pre-listing statement - sharedata online

TRANSCRIPT

PRE-LISTING STATEMENTFriday, 28 March 2014

PRE-LISTING STATEMENT

The definitions and interpretations commencing on pages 13 to 18 of this pre-listing statement have, where applicable, been used in these cover pages.

This pre-listing statement is prepared and issued in terms of the Listings Requirements, for the purpose of providing information with regard to the company and is issued in respect of:

• aprivateplacementtoraiseuptoapproximatelyR400millionbywayofaprivateplacingbywayofanofferforsubscriptiontoinvitedqualifyinginvestorsforuptoamaximumof53200000privateplacementsharesinthecompanyatanissuepricetobedeterminedbydemandandforwhichanindicativeissuepriceofR7,52perprivateplacementsharehasbeenused in this pre-listing statement; and

• thesubsequentlistingofallthesharesofthecompanyinthe“RealEstate–RetailREIT”sectoroftheJSE.

2014

Opening date of the private placement (09:00) Monday, 31 March

Closing date of the private placement (12:00)* Wednesday, 2 April

ResultsoftheprivateplacementreleasedonSENS Wednesday,2April

Results of the private placement published in the press on Thursday, 3 April

Proposed date of listing (09:00) Monday, 7 April

* Invited investors must advise their CSDP or broker of their acceptance of the private placement shares in the manner and cut-off time stipulated by their CSDP or broker.

IMPORTANT POINTS TO NOTE

Theoffer,intheformoftheprivateplacement,isbeingmadetoinvitedinvestorsonlyandwillcompriseuptoamaximumof53200000privateplacementsharesatanindicativeissuepriceofR7,52perprivateplacementshare.

Applicants will only be permitted to apply for shares with a minimum total acquisition cost, per single addressee acting as principal, of greater than or equal to R1 million unless the applicant is a person, acting as principal, whose ordinary business, or part of whose ordinary business, is to deal in securities, whether as principal or agent (in reliance on section 96(1)(a)(i) and 96(1)(b) of the Companies Act) or such applicant falls within one of the other specified categories of persons listed in section 96(1) of the Companies Act.

Prospective investors should not treat the contents of this pre-listing statement as advice relating to legal, taxation, investment or any other matters and should consult their own professional advisors concerning the consequences of their acquiring, holding or disposing of offer shares. Prospective investors should inform themselves as to:

• thelegalrequirementswithintheirowncountriesforthepurchase,holding,transferordisposalofoffershares;

• anyforeignexchangerestrictionsapplicabletothepurchase,holding,transferordisposalofoffershareswhichtheymightencounter;and

• theincomeandothertaxconsequenceswhichmayapplytothemasaresultofthepurchase,holding,transferordisposal of offer shares. Prospective investors must rely upon their own representatives, including their own legal advisors and accountants, and not those of the company, as to legal, tax, investment or any other related matters concerning Safari and an investment therein.

SAFARI INVESTMENTS RSA LIMITED(IncorporatedintheRepublicofSouthAfrica)

(Registrationnumber2000/015002/06)Sharecode:SAR|ISIN:ZAE000188280

(“Safari”or“thecompany”)

The information contained in this document constitutes factual information as contemplated in section 1(3)(a) of the South African Financial Advisory and Intermediary Services Act 2002 and should not be construed as an express or implied recommendation, guidance or proposal that any particular transaction in respect of the offer shares is appropriate to the particular investment objectives, financial situations or needs of a prospective investor.

Immediatelypriortotheprivateplacementandthelisting:

• theauthorisedsharecapitalofthecompanycomprised500000000ordinarysharesofnoparvalue;

• theissuedsharecapitalofthecompanycomprised120864827ordinarysharesofnoparvalue;and

• thecompanyhadnotreasurysharesinissue.

AssumingthattheprivateplacementisfullysubscribedattheindicativeissuepricepershareofR7,52,immediatelyaftertheprivate placement and listing:

• theauthorisedsharecapitalofthecompanywillcomprise500000000ordinarysharesofnoparvalue;

• theissuedsharecapitalofthecompanywillcompriseamaximumof174064827ordinarysharesofnoparvalue;and

• thecompanywillhavenotreasurysharesinissue.

On listingon the JSE, assuming that theprivateplacement is fully subscribedat the indicative issuepriceofR7,52, theanticipatedmarketcapitalisationofthecompanyshouldbeapproximatelyR1,276billion.

On listing and thereafter, all shares of the company will rank pari passu in all respects. There are no convertibility or redemption rights relating to any of the private placement shares offered in terms of the private placement. The private placement shares willonlybe issued indematerialised form.Nocertificatedprivateplacementshareswillbe issued.There isno intentiontoextendapreferenceonallotmentof theprivateplacementshares toanyparticularcompanyorgroup, in theeventofanoversubscription of the private placement shares pursuant to the private placement. There will be no fractions of private placement shares offered or issued in terms of the private placement. The private placement will not be underwritten.

The listing is not conditional on raising a minimum amount in terms of the private placement. The net proceeds of the private placementwillbeusedbySafaritosettleinterest-bearingdebtandstrengthenthebalancesheetforongoingactivities.

TheJSEhasgrantedSafarialistingofuptoamaximumof174064827sharesinthe“RealEstate–RetailREIT”sectorofthemainboardoftheJSE,intermsoftheFTSEclassification,undertheabbreviatedname“Safari”,JSEsharecode“SAR”andISINZAE000188280witheffectfromthecommencementoftradeonMonday,7April2014,subjecttoobtainingaspreadofshareholdersacceptabletotheJSEincompliancewiththeListingsRequirements.

The directors, whose names appear on page 1 of this pre-listing statement, collectively and individually accept full responsibility for the accuracy of the information given herein and certify that to the best of their knowledge and belief there are no facts that have been omitted which would make any statement false or misleading, that all reasonable enquiries to ascertain such facts have been made and that this pre-listing statement contains all information required by common law and the Listings Requirements.

The corporate advisors, bookrunners, sponsor, independent reporting accountants and auditors, attorneys, communication advisor, transfersecretariesand independentpropertyvaluer,whosenamesaresetout in the“Corporate informationandadvisors”sectiononpage1ofthispre-listingstatement,haveconsentedinwritingandhavenot,priortothepublicationofthispre-listing statement, withdrawn their consent to the inclusion of their names in the capacities stated and, where applicable, to their reports being included in this pre-listing statement.

As the offer is not an offer to the public as contemplated under the Companies Act, a copy of this pre-listing statement is not requiredtoberegisteredwithCIPCpursuanttotheCompaniesAct.

OFFERS IN SOUTH AFRICA ONLY

This pre-listing statement is not an invitation to the public to subscribe for securities, but is issued in compliance with the Listings Requirements of the JSE Limited, for providing information to the public with regard to the company. This pre-listing statement is not an invitation to the public to subscribe for securities, but is issued in compliance with the Listings RequirementsoftheJSELimited,forprovidinginformationtothepublicwithregardtothecompany.Thispre-listingstatementhasbeenissuedinconnectionwiththeprivateplacementofferinSouthAfricaonlyandisaddressedonlytopersonstowhomthe private placement offer may lawfully be made. The distribution of this pre-listing statement and the making of an offer through this private placement may be restricted by law. Persons into whose possession this pre-listing statement comes must inform themselves about and observe any such restrictions. This pre-listing statement does not constitute an offer of, or invitationtosubscribefor,anyofthesharesinanyjurisdictioninwhichsuchoffer,subscriptionorsalewouldbeunlawful.NoonehastakenanyactionthatwouldpermitanofferingofsharestooccuroutsideofSouthAfrica.

FORWARD LOOKING STATEMENTS

This pre-listing statement includes forward looking statements. Forward looking statements are statements including, but notlimitedto,anystatementsregardingthefuturefinancialpositionofSafarianditsfutureprospects.Theseforwardlookingstatements have been based on current expectations and projections about future results,which, although the directorsbelieve them to be reasonable, are not a guarantee of future performance.

Anabridgedversionofthispre-listingstatementwillbereleasedonSENSonFriday,28March2014andpublishedinthepresson Monday, 31 March 2014.

Date of issue: Friday, 28 March 2014

Thispre-listingstatementisavailableonlyinEnglish.CopiesmaybeobtainedfromtheregisteredofficesofSafariinPretoria,thetransfersecretaries,thesponsorandattorneys’officesinJohannesburg,detailsofwhicharesetout inthe“Corporateinformation”sectionofthispre-listingstatement.

Lead bookrunner and corporate advisor

Sponsor andjoint bookrunner

Joint corporate advisor and joint bookrunner

Attorneys Independent reporting accountants and auditors

Communications advisor

Transfer secretaries

Independent valuer

1

CORPORATE INFORMATION

DIRECTORS OF SAFARI MH Tsolo (independent non-executive chairman)FJJMarais(chief executive officer)K Pashiou (executive director)PA Pienaar (executive director)DEvanStraten(executive financial director)AEWentzel(independent non-executive director)JPSnyman (independent non-executive director)SJKruger(non-executive director)M Minnaar (non-executive director)JCVerwayen(non-executive director)

REGISTERED OFFICE OF SAFARI

c/o Company Secretarial ServicesBlock A, Brooklyn Office Park105NicolsonStreet,Brooklyn0181

Place of incorporation:SouthAfricaDate of incorporation:7July2000

COMPANY SECRETARY

Safari Retail Proprietary Limited(Registrationnumber2008/011620/07)

420 Friesland Lane, Lynnwood, Pretoria 0081

Postal 420 Friesland Lane, Lynnwood, Pretoria 0081

Represented by:DirkEngelbrechtBComm LLB

TRANSFER SECRETARIES

Computershare Investor Services Proprietary Limited(Registrationnumber2004/003647)

70MarshallStreet,Johannesburg2001

POBox61051,Marshalltown2107

ATTORNEYS

Edward Nathan Sonnenbergs Inc(Registrationnumber2006/018200/21)

150WestStreet,Sandton2196

POBox783347,Sandton2146

AUDITORS

Mazars Inc5StDavidsPlace,Parktown2193

POBox6697,Johannesburg2000

INDEPENDENT REPORTING ACCOUNTANTS

Mazars Inc5StDavidsPlace,Parktown2193

POBox6697,Johannesburg2000

INDEPENDENT VALUER

Mills Fitchet (Tvl) cc(RegistrationnumberCK89/40464/23)

No17TudorPark,61HillcrestAvenueOerderPark,Randburg2115

POBox35345,Northcliff2115

SPONSOR AND JOINT BOOKRUNNER

PSG Capital Proprietary Limited(Registrationnumber1951/002280/06)

1st Floor, Ou Kollege Building35KerkStreet,Stellenbosch7599

POBox7403,Stellenbosch7599

LEAD BOOKRUNNER AND CORPORATE ADVISOR

DEA-RU Proprietary Limited(Registrationnumber2004/018276/07)

7SunPlace,Sharonlea,Olivedale2158

JOINT CORPORATE ADVISOR

Fanus Kruger Consulting cc(Registrationnumber2006/173299/23)

PropateezOfficePark98BeyersNaudeDrive,Rustenburg0300

COMMUNICATIONS ADVISOR

Instinctif Proprietary Limited (Registration number 97/02334/07)

FountainGrove,5SecondRoad,Hydepark Sandton2196

POBox413187,Craighall2024

2

TABLE OF CONTENTS

The definitions and interpretations commencing on pages 13 to 18 of this pre-listing statement have been used in the following table of contents.

Page

Corporate information 1

Salient features 4

1. Introduction 4

2. Natureofbusinessandbusinessstrategy 4

3. Prospects 6

4. REITlegislation,REITtaxationstatusandcorporategovernance 7

5. Detailsofprivateplacement 8

6. StatementastolistingontheJSE 8

7. Action required 8

8. Salientfinancialinformation 8

9. Further copies of the pre-listing statement 11

Important dates and times 12

Definitions and interpretations 13

Section one – details of the private placement 19

1. Purpose of the private placement and the listing 19

2. Salientdatesandtimes 19

3. Particulars of the private placement 19

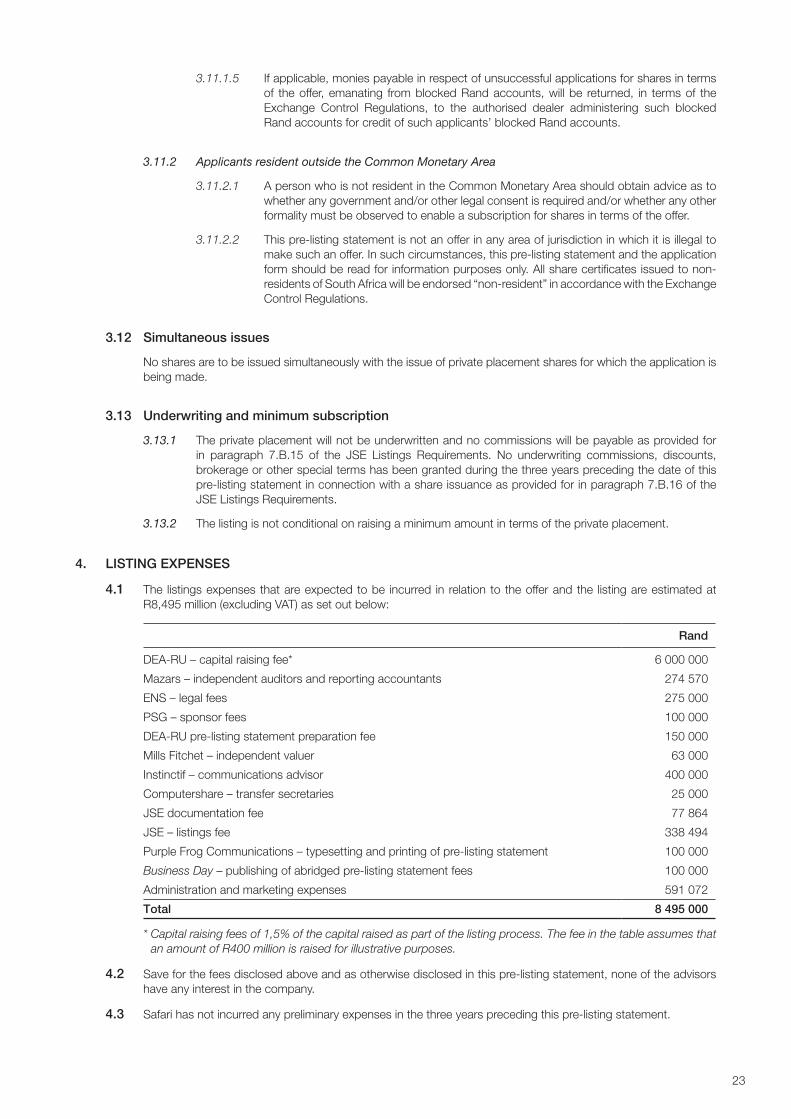

4. Listingsexpense 23

The business 24

5. Incorporation,historyandnatureofthebusiness 24

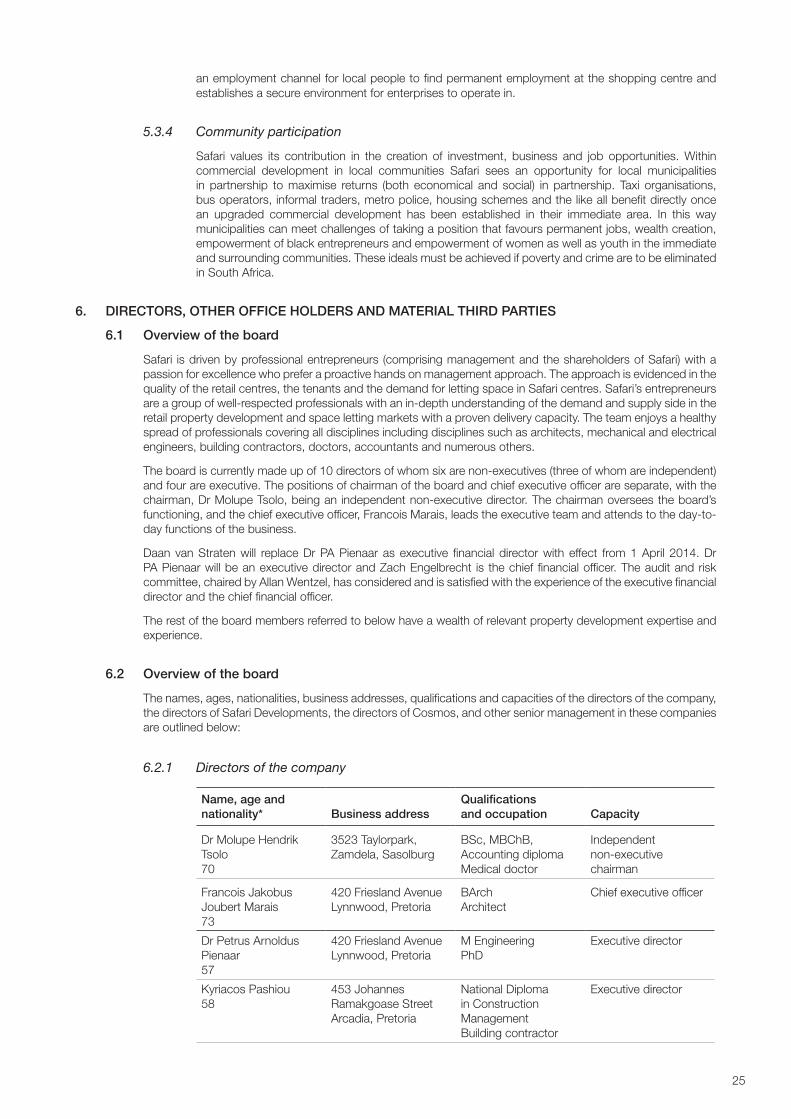

6. Directors,otherofficeholdersandmaterialthirdparties 25

7. History,stateofaffairsandprospectsofthegroup 35

8. Analysis of the property portfolio 43

9. Development and management of the property portfolio 47

Financial information 54

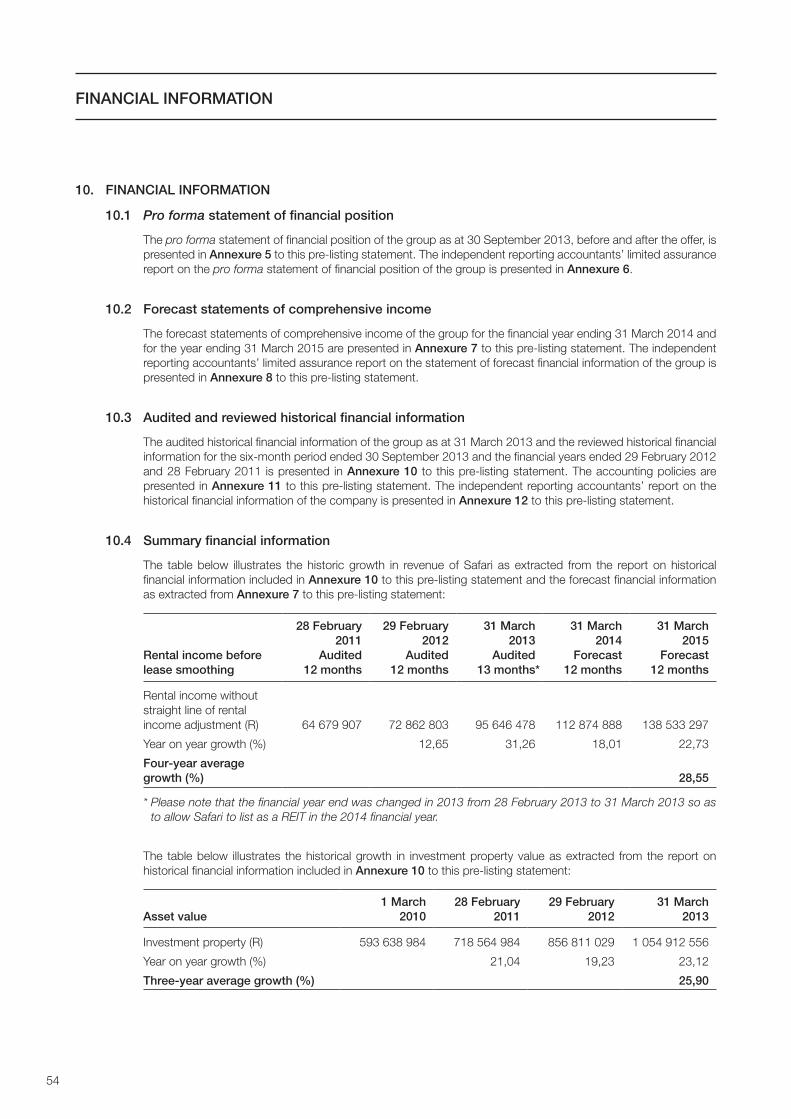

10. Financialinformation 54

11. Dividendsanddistributionpolicy 55

12. Materialchanges 55

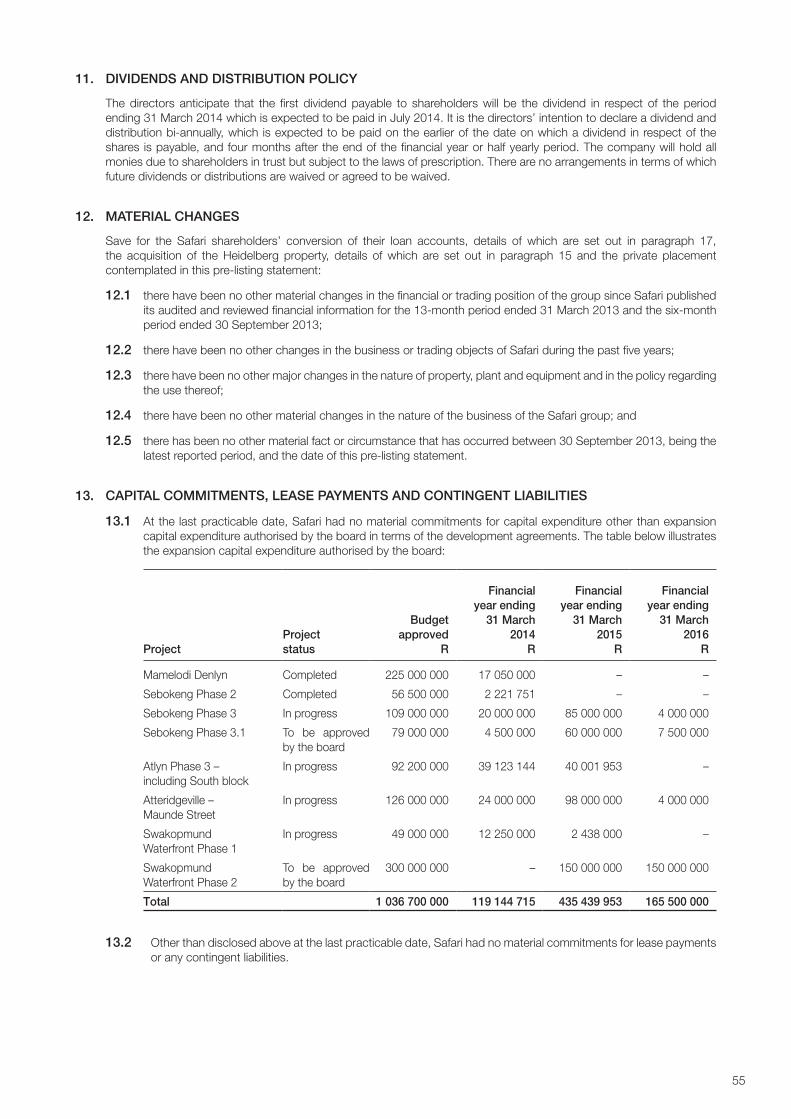

13. Capitalcommitments,leasepaymentsandcontingentliabilities 55

14. Loans 56

3

Page

15. TheHeidelbergacquisitionandpropertyacquiredortobeacquired 56

16. Propertydisposedofortobedisposedof 57

Share capital 58

17. Authorisedandissuedsharecapital 58

18. Adequacyofworkingcapital 59

19. Unissuedshares 59

20. Optionsandpreferentialrightsinrespectofshares 59

21. Generalauthoritytoissuesharesforcashandtorepurchaseshares 59

22. Otherlistings 60

23. Majorandcontrollingshareholders 60

General information 61

24. Promoters’andotherinterests 61

25. Materialcontracts 61

26. Experts’consents 61

27. Governmentprotectionandinvestmentencouragementlaw 62

28. Litigationstatement 62

29. Documentsavailableforinspection 62

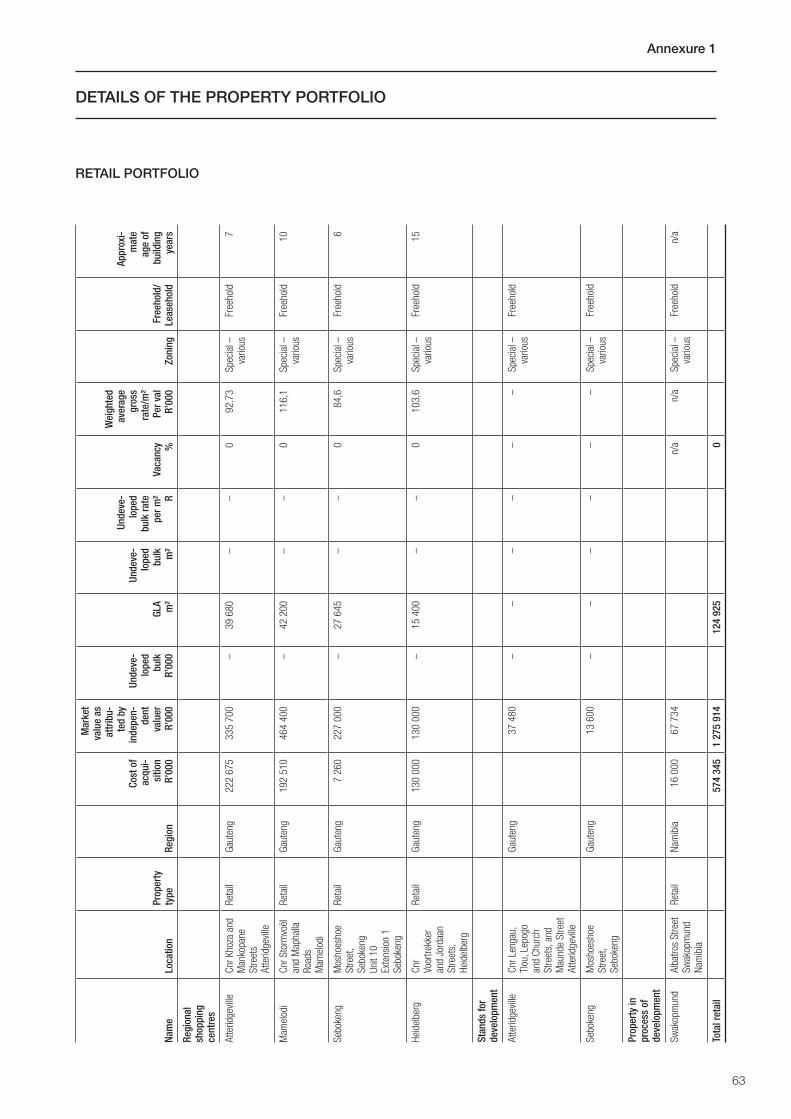

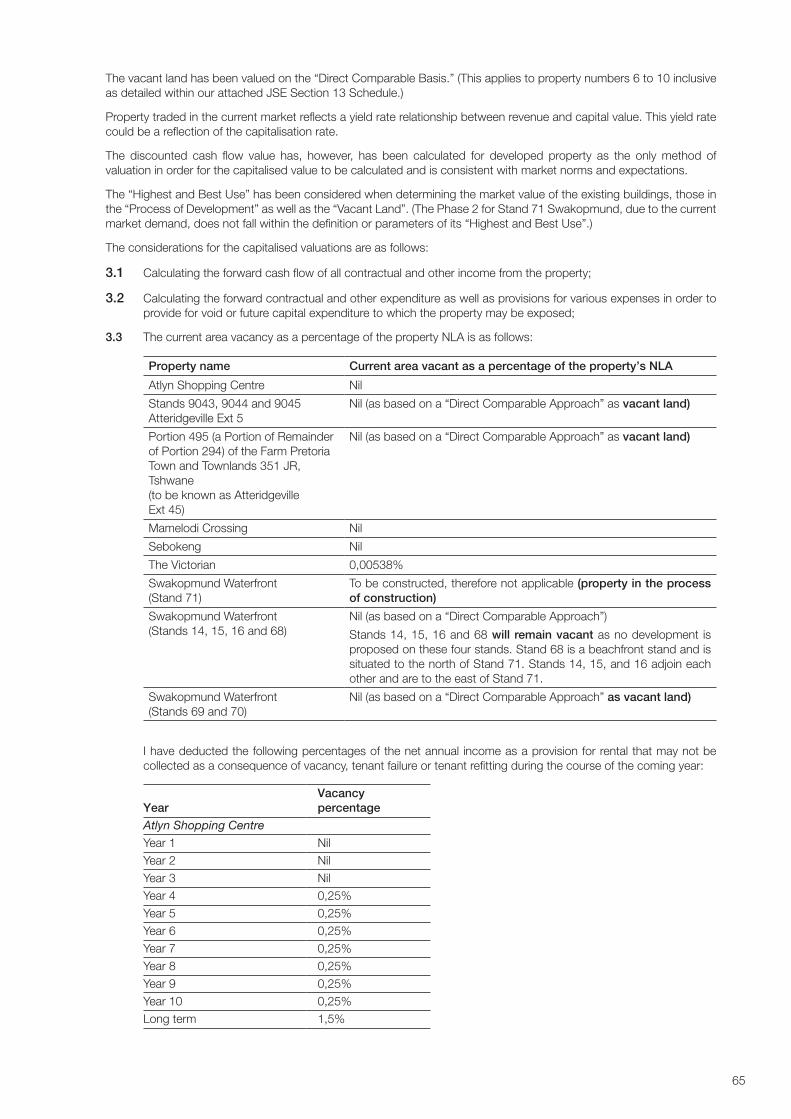

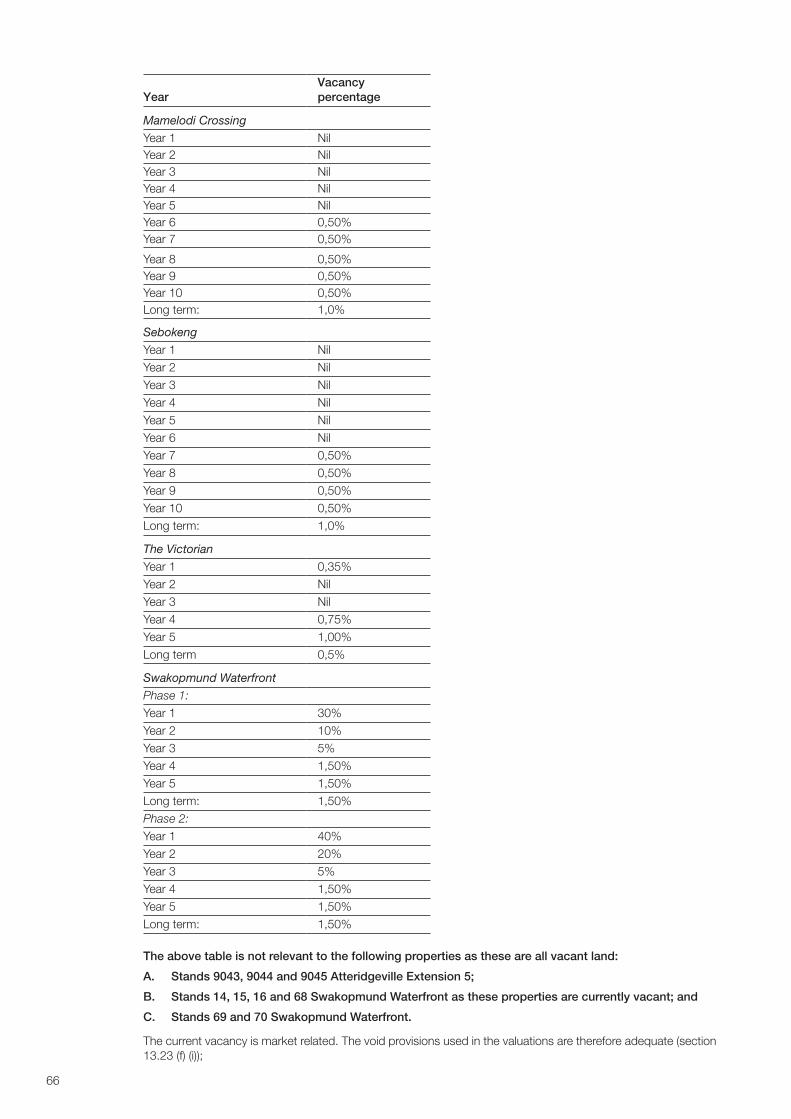

Annexure 1 Detailsofthepropertyportfolio 63

Annexure 2 MillsFitchetindependentvaluer’spropertyvaluationreport 64

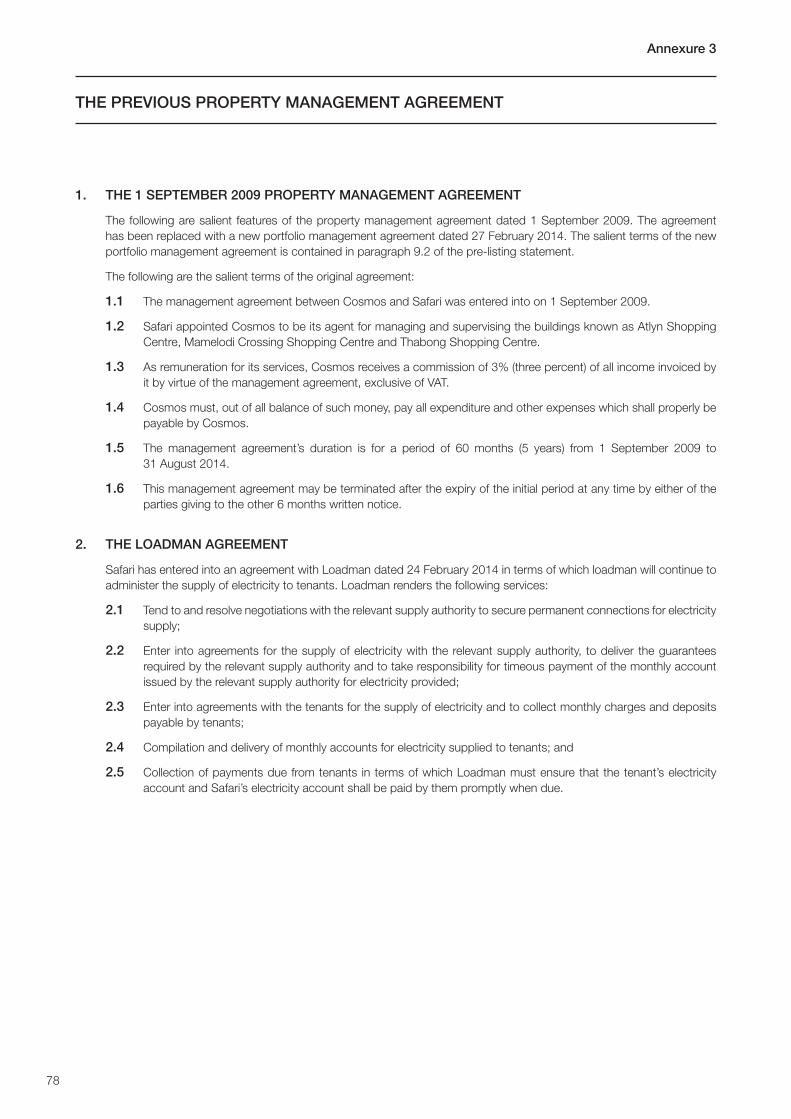

Annexure 3 The previous property management agreement 78

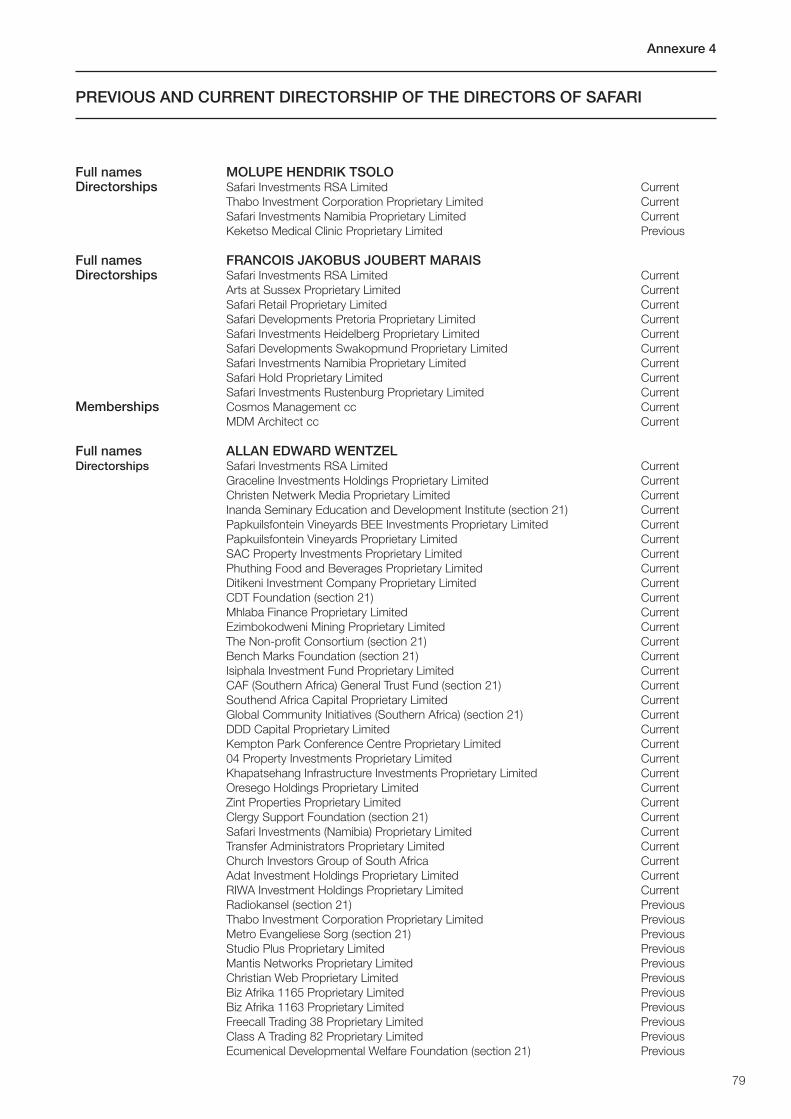

Annexure 4 PreviousandcurrentdirectorshipofthedirectorsofSafari 79

Annexure 5 Pro formastatementoffinancialpositionofSafari 83

Annexure 6 IndependentReportingAccountants’assurancereportonthecompilationof pro formastatementoffinancialpositionofSafari 88

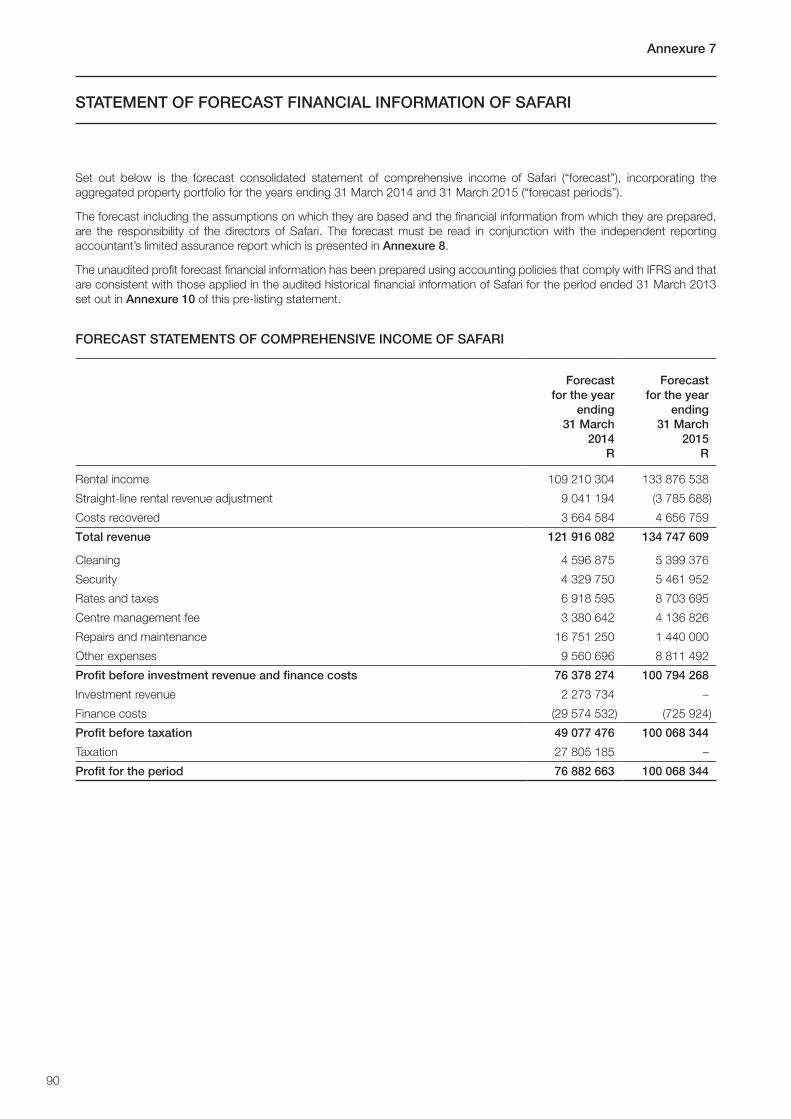

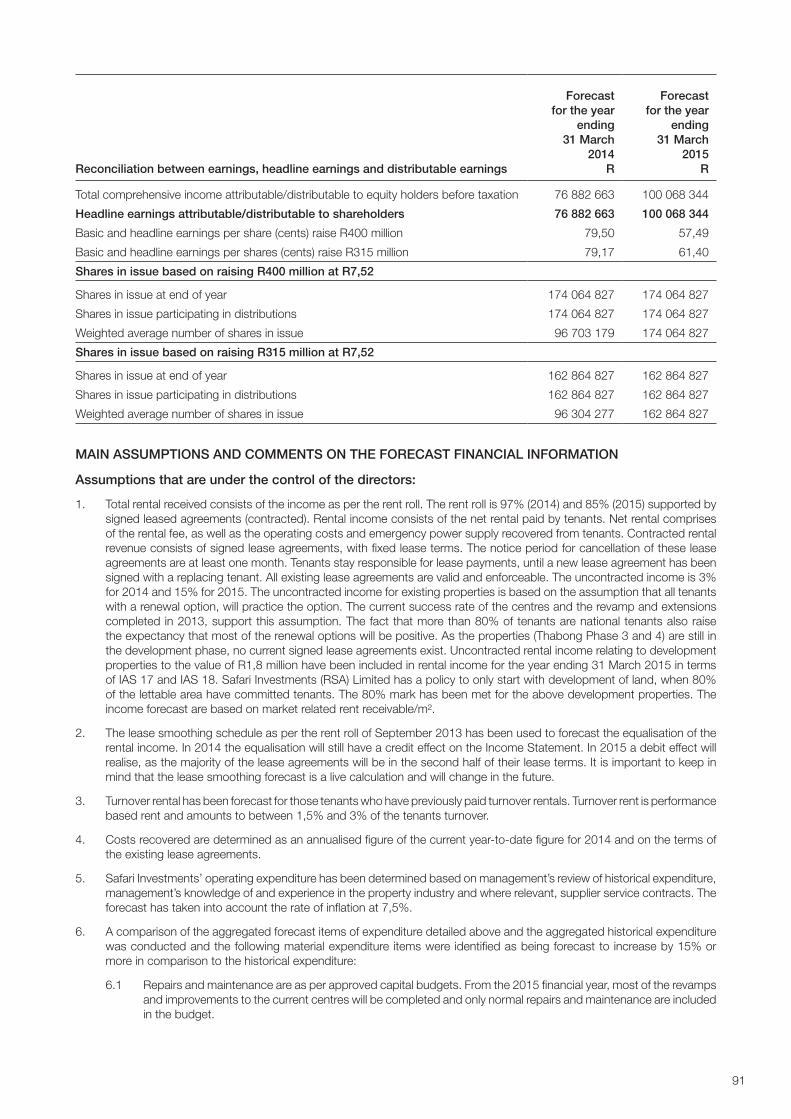

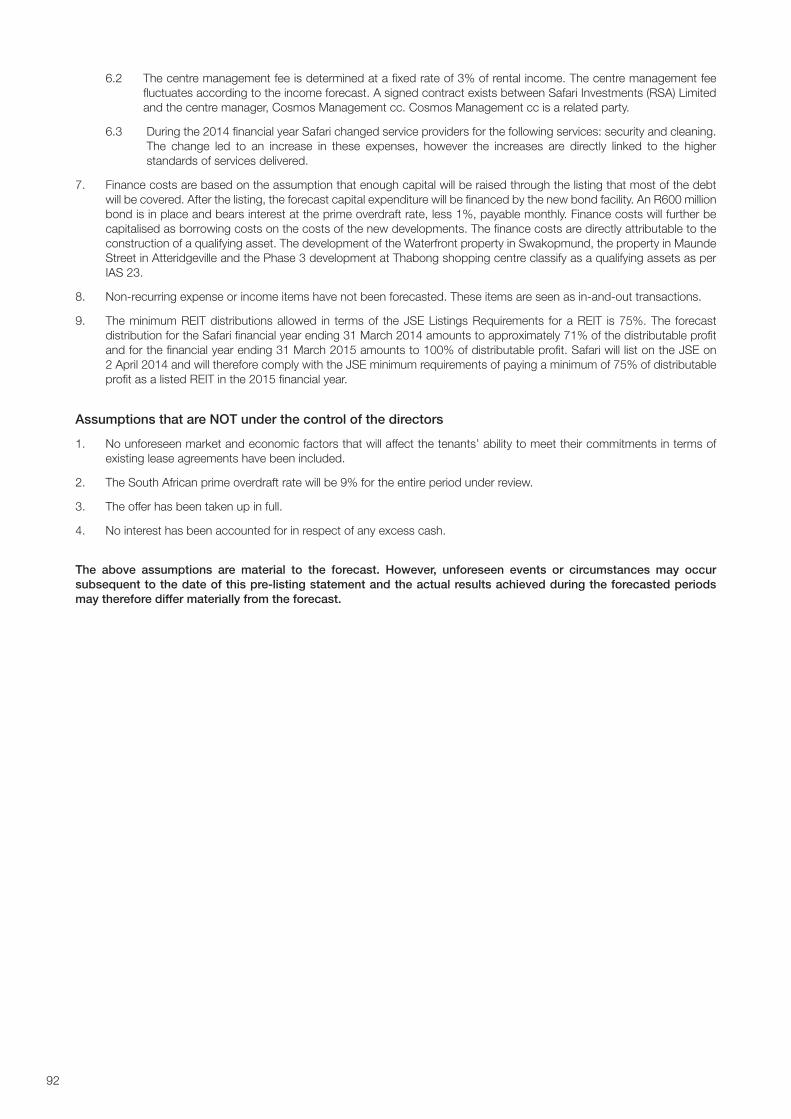

Annexure 7 StatementofforecastfinancialinformationofSafari 90

Annexure 8 IndependentReportingAccountants’limitedassurancereportonthe forecastinformationofSafari 93

Annexure 9 IndependentReportingAccountants’limitedassurancereporton theexistenceandrecognitionandmeasurementoftheHeidelbergproperty 97

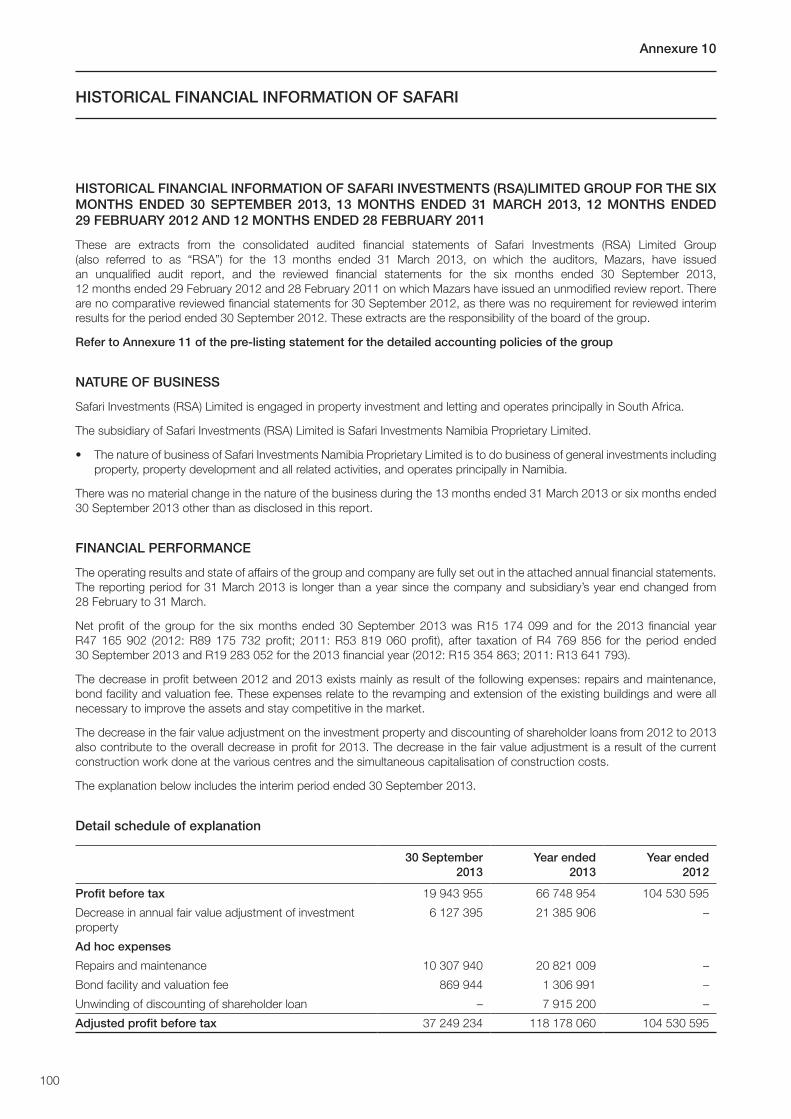

Annexure 10 HistoricalfinancialinformationofSafari 100

Annexure 11 AccountingpoliciesofSafari 136

Annexure 12 IndependentReportingAccountants’reportonthehistoricalfinancialinformationofSafari 144

Annexure 13 Summaryofthedevelopmentagreements 146

Annexure 14 SalientfeaturesoftheMemorandumofIncorporation 152

Annexure 15 Corporategovernancestatement 157

Application form (blue) Attached

4

SALIENT FEATURES

The information set out in this salient features section of the pre-listing statement is only an overview and is not intended to be comprehensive.Itshouldbereadinconjunctionwiththeinformationcontainedinothersectionsofthispre-listingstatementtogainacomprehensiveoverviewoftheSafarigroupandtheprivateplacement.Thedefinitionsandinterpretationsgivenonpages 13 to 18 of this pre-listing statement apply, mutatis mutandis, to the salient features as set out below.

1. INTRODUCTION

SafariInvestmentsisbuiltonawellestablishedbusinessmodelwithasuccessfulhistoryandtrackrecord.Safariwasincorporatedasapubliccompanyon7July2000byitsfoundingshareholders.Thecompanyhasinthepast10yearsmanaged to establish a sought-after retail portfolio, focused on high growth township areas.

InJuly2013,theexistingshareholdersofSafariconvertedpersonalloanaccountstothevalueofR186millionintoSafarishares and as such remain committed to the future of the company. The main focus of the company is to invest into quality income-generating properties including vacant land with development potential, as well as new property ventures underdevelopmentinbothSouthAfricaandinternationally.

The company is managed by a professional and committed management team with more than 200 years of property developmentandmanagementexperience.Theteamhasbeensuccessfulinpropertydevelopment,redevelopmentanddeal-making.Theyhavetheabilitytosuccessfullymanageastrong,profitableandgrowingportfolio;andanexcellentreputationforachievingthemostoutofpropertyassetsthroughkeystrategicrelationships.SafariDevelopmentsalsoprovidesaccesstoapipelineofoff-marketpropertiesandexclusivedevelopmentopportunities.

2. NATURE OF BUSINESS AND BUSINESS STRATEGY

Safarioffersanexceptional long-termsustainableportfolio,aswellasanoutstandingopportunity toenter thehighlydesirable retail property market in high growth areas, including townships. The company serves as a platform for smaller investorstomakeaninvestmentinqualityretailpropertyassetsandformspartofthepensionplanofitsapproximately150currentshareholders.

Safari’sprimaryinvestmentfocusisonqualityincomeproducingpropertiesthroughretailinvestmentsanddevelopmentsin retail centres held directly or indirectly. The company’s development arm covers greenfields developments of land intoretailcentresandbrownfieldsdevelopmentthroughrefurbishment,upgradeorotherimprovementtoexistingretailbuildings.AllpropertiesintheSafariportfolioweredevelopedbySafariDevelopments.

Safarihasastrongfocusonpreviouslydisadvantagedcommunitiesandunder-resourcedareaswhere itestablishes,developments and promotes quality assets that uplift and benefit communities by providing a desirable and high-end shoppingexperienceclosertowheretheylivetherebysignificantlyreducingcommutingtimeandcostassociatedwithtravelling to regional centres. This approach also targets the problem of limited tradability of retail properties in these areas resulting in significantly improved opportunities for the communities in which its property assets are located. Safari’sportfolioprovidesstableincomeandbalancesheetstrengthtosecureandfundhigh-growthopportunitieswithinitsdevelopments.TheSafarimanagementhasastrongtrackrecordinsuccessfullybringingnewprojectsintofruitionandfollowsaconservativephasedapproachtogreenfieldsdevelopmentsSafari’sinvestmentstrategyhasbeentoutiliseits broad internal skills to undertake retail developments. These have primarily targeted high growth, and high growth township areas in Gauteng. Whilst undertaking developments from the outset does entail significant risks, it is also where greatershareholdervaluecanbecreated.Tominimisefinancialrisk,Safarifollowsastaggereddevelopmentapproach.

Ineachofthekeyproperties,theinitialphaseoftheretailcentrehasbeenrelativelysmall,withthepotentialforexpansion.Once the centre has gained traction amongst customers and the demand for retail space increased, further phases have been rolled out. This approach has been replicated across the initial three centres in the portfolio which are now entering their thirdor fourthdevelopmentphases. Inaddition, eachphasehasgenerally seenan improvement in the tenantquality,withtheextensionsprimarilydrivenbythelargenationalretailers.Thus,between80%and90%ofSafari’sGLAisnowtenantedbynationalretailers.Inspiteofthis,Safarialsobelievesthatretainingandsupportinglocalisedshopsservicingthecommunity’sspecificneedsisjustasimportantasattractingnationalbrands.

Anotherkeyobjectivehasbeentodevelopcentreswithinkeycatchmentareas.Additionallythestrategicpositioningof the retail centres, and planned developments, ensures that properties are optimally placed to take full advantage of both current and future growth patterns amongst retailers. This is achieved through the development of centres in strong regional nodes, a strategy that both attracts top quality national retailers as well as reduces the risk of potential competitors entering the market.

5

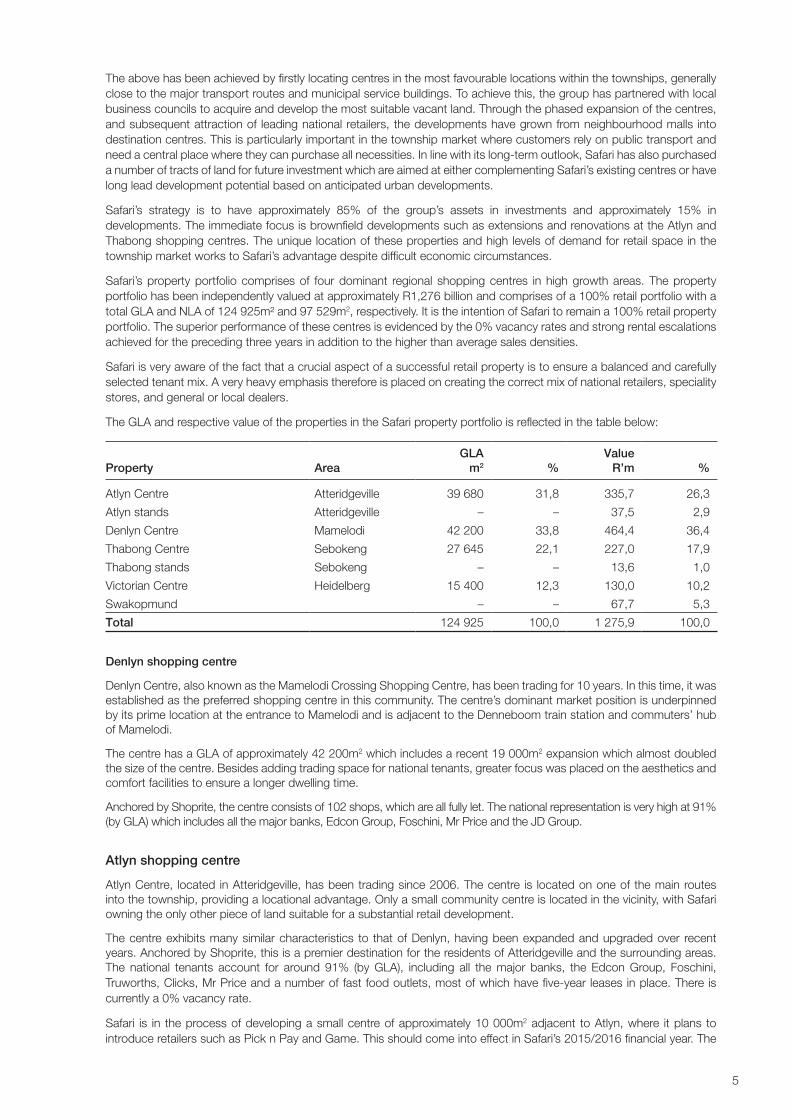

The above has been achieved by firstly locating centres in the most favourable locations within the townships, generally closetothemajortransportroutesandmunicipalservicebuildings.Toachievethis,thegrouphaspartneredwithlocalbusinesscouncilstoacquireanddevelopthemostsuitablevacantland.Throughthephasedexpansionofthecentres,and subsequent attraction of leading national retailers, the developments have grown from neighbourhood malls into destination centres. This is particularly important in the township market where customers rely on public transport and needacentralplacewheretheycanpurchaseallnecessities.Inlinewithitslong-termoutlook,SafarihasalsopurchasedanumberoftractsoflandforfutureinvestmentwhichareaimedateithercomplementingSafari’sexistingcentresorhavelong lead development potential based on anticipated urban developments.

Safari’s strategy is to have approximately 85% of the group’s assets in investments and approximately 15% indevelopments.TheimmediatefocusisbrownfielddevelopmentssuchasextensionsandrenovationsattheAtlynandThabong shopping centres. The unique location of these properties and high levels of demand for retail space in the townshipmarketworkstoSafari’sadvantagedespitedifficulteconomiccircumstances.

Safari’spropertyportfoliocomprisesof fourdominant regional shoppingcentres inhighgrowthareas.ThepropertyportfoliohasbeenindependentlyvaluedatapproximatelyR1,276billionandcomprisesofa100%retailportfoliowithatotalGLAandNLAof124925m²and97529m2,respectively.ItistheintentionofSafaritoremaina100%retailpropertyportfolio.Thesuperiorperformanceofthesecentresisevidencedbythe0%vacancyratesandstrongrentalescalationsachieved for the preceding three years in addition to the higher than average sales densities.

Safariisveryawareofthefactthatacrucialaspectofasuccessfulretailpropertyistoensureabalancedandcarefullyselectedtenantmix.Averyheavyemphasisthereforeisplacedoncreatingthecorrectmixofnationalretailers,specialitystores, and general or local dealers.

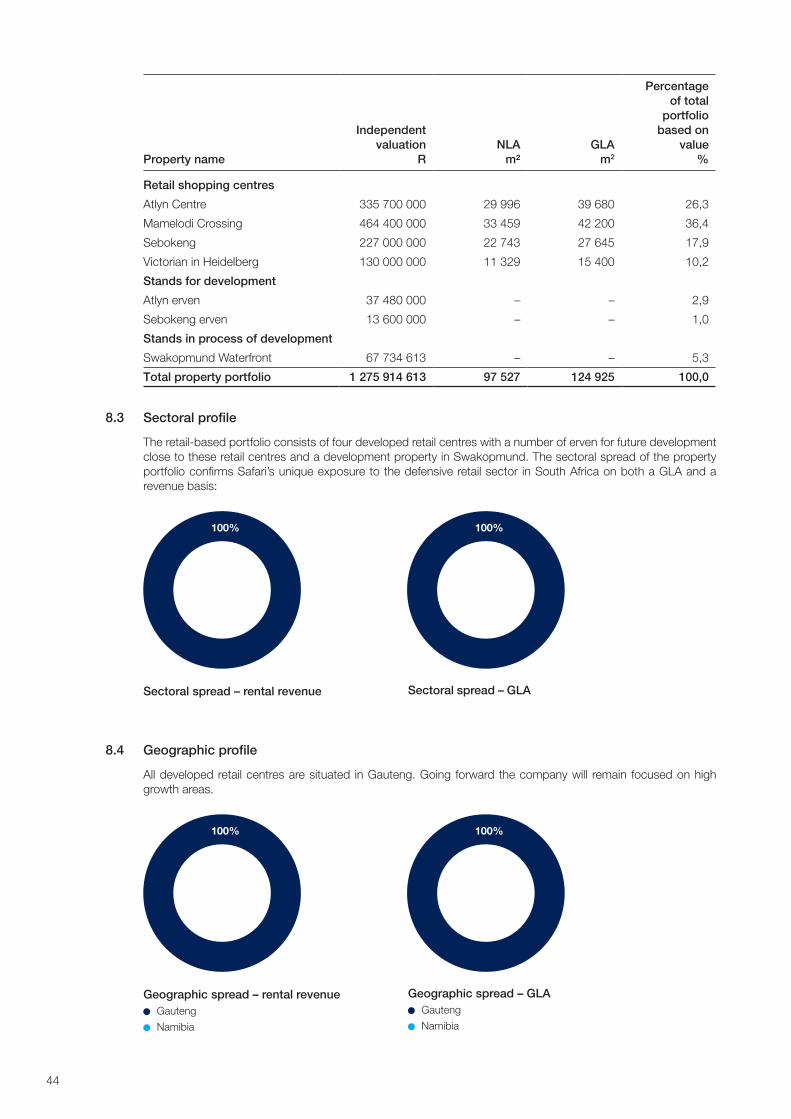

TheGLAandrespectivevalueofthepropertiesintheSafaripropertyportfolioisreflectedinthetablebelow:

Property AreaGLA

m2 % Value

R’m %

Atlyn Centre Atteridgeville 39680 31,8 335,7 26,3

Atlyn stands Atteridgeville – – 37,5 2,9

Denlyn Centre Mamelodi 42 200 33,8 464,4 36,4

Thabong Centre Sebokeng 27645 22,1 227,0 17,9

Thabong stands Sebokeng – – 13,6 1,0

VictorianCentre Heidelberg 15400 12,3 130,0 10,2

Swakopmund – – 67,7 5,3

Total 124925 100,0 1275,9 100,0

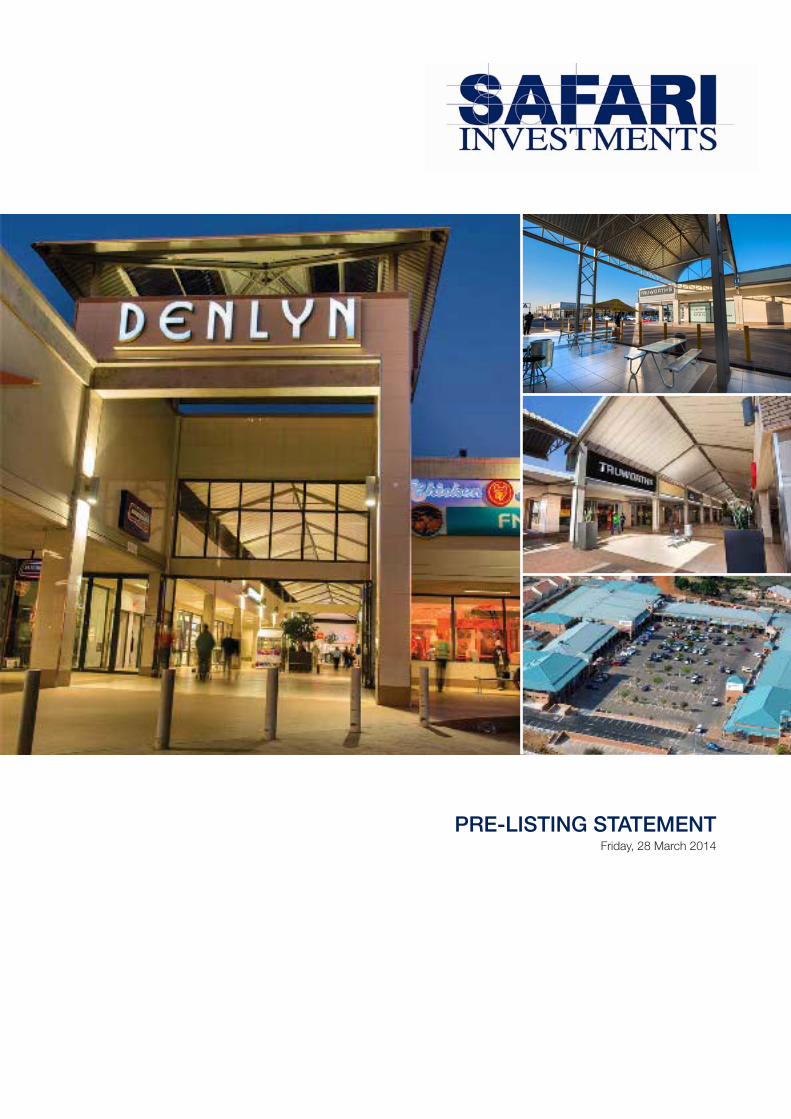

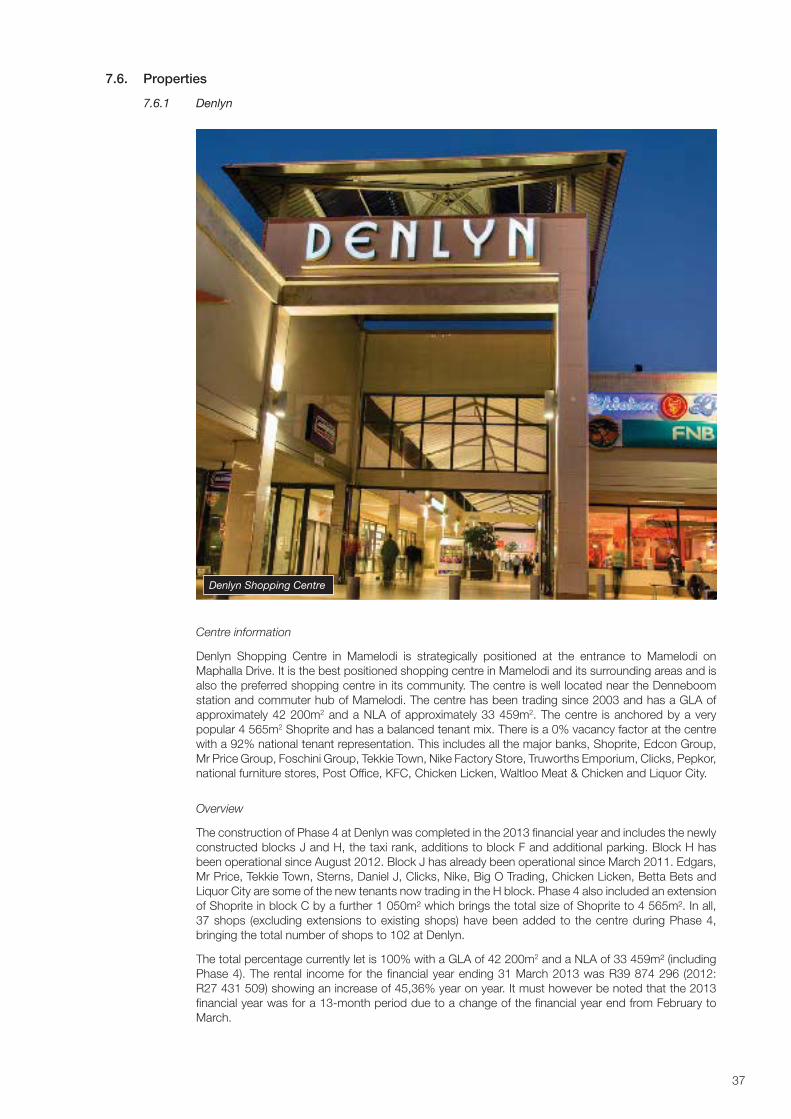

Denlyn shopping centre

DenlynCentre,alsoknownastheMamelodiCrossingShoppingCentre,hasbeentradingfor10years.Inthistime,itwasestablished as the preferred shopping centre in this community. The centre’s dominant market position is underpinned byitsprimelocationattheentrancetoMamelodiandisadjacenttotheDenneboomtrainstationandcommuters’hubof Mamelodi.

ThecentrehasaGLAofapproximately42200m2 which includes a recent 19 000m2expansionwhichalmostdoubledthesizeofthecentre.Besidesaddingtradingspacefornationaltenants,greaterfocuswasplacedontheaestheticsandcomfort facilities to ensure a longer dwelling time.

AnchoredbyShoprite,thecentreconsistsof102shops,whichareallfullylet.Thenationalrepresentationisveryhighat91%(byGLA)whichincludesallthemajorbanks,EdconGroup,Foschini,MrPriceandtheJDGroup.

Atlyn shopping centre

AtlynCentre, located inAtteridgeville,hasbeentradingsince2006.Thecentre is locatedononeofthemainroutesintothetownship,providingalocationaladvantage.Onlyasmallcommunitycentreislocatedinthevicinity,withSafariowning the only other piece of land suitable for a substantial retail development.

Thecentreexhibitsmanysimilarcharacteristics to thatofDenlyn,havingbeenexpandedandupgradedover recentyears.AnchoredbyShoprite,thisisapremierdestinationfortheresidentsofAtteridgevilleandthesurroundingareas.The national tenants account for around 91% (byGLA), including all themajor banks, the EdconGroup, Foschini,Truworths, Clicks, Mr Price and a number of fast food outlets, most of which have five-year leases in place. There is currentlya0%vacancyrate.

Safari is in theprocessofdevelopingasmallcentreofapproximately10000m2adjacent toAtlyn,where itplans tointroduceretailerssuchasPicknPayandGame.ThisshouldcomeintoeffectinSafari’s2015/2016financialyear.The

6

centrewillbejoinedtothelargerAtlyncentreviaagreenspaceandwalkingpath.ThiswillenhancetheenvironmentalappealofthenodeandfurtherentrenchSafari’sdominantpositioninthearea.

Thabong shopping centre

Thabong shopping centre used to be a smaller community centre in Sebokengwhich started trading in 2007 andcurrentlyservesasaregionalcentre.ThecentreislocatedwithinthemajorbusinessdistrictofSebokengandadjacentto the main hospital. While the centre does face some competition from nearby shopping centres, management has focusedonattractingthecorrecttenantmixtomakethecentrethepreferredshoppingdestinationinthearea.

Thabong’skeyadvantageisitsexpansionpotentialbeingsituatedona10hapieceofland,mostofwhichisundeveloped.Anapproximate10000m2GLAextensionisinprogressandisplannedforcompletionandoccupationbynewadditionalanchortenantstowardsthefirstquarterof2015,bringingthecentreGLAto41000m2. Currently Thabong is anchored bySpar,withotherkeynationaltenantsbeingFoschiniGroupbrands,JDGroup,LewisGroupandPepStores.Asacommunitycentre, theproportionofnational retailersofaround80% isslightly less than theSafari’s largercentres.However,astheextensionisbeingdesignedspecificallytoaccommodatenewnationalretailers(PicknPay,Edgars,Woolworths),theproportionshouldincreasetothe90%level.

Victorian shopping centre

TheVictorianCentreinHeidelbergisawellestablishedcommunitycentre,havingtradedfor16years.Whilethecentrehas provided a popular shopping destination in the town, a regional mall is currently being built a few kilometres away. Nevertheless,keynationaltenantshaveindicatedthattheywillremaininTheVictorianCentreandanumberofextensionsand refurbishments to stores were completed over the past year. The centre is anchored by Pick n Pay, with key tenants beingMrPrice,TotalsportsandCNA.Nationalretailerscompriseapproximately95%ofthetenants.

Swakopmund

Internationally, Safari is in the process of developing a new regional destination centre in the Namibian town ofSwakopmund.ThepropertyisonaprimebeachfrontpieceoflandapproximatelyfourkilometresfromtheSwakopmundcentralbusinessdistrict.Thefirstphaseofthedevelopmentwillbetheconstructionofapproximately16000m2 to 20 000m2 of retail space,overlooking thewaterfront.While relatively small incomparison toSouthAfricancentres, theSwakopmundretaildevelopmentwillprovidetheonly“one-stop”shoppingdestinationinthearea.Landpreparationiswell underway, with the bulk earthworks having been installed. The planned completion date for the centre is anticipated to be 24 months away depending on the construction commencement date.

3. PROSPECTS

WhiletheboardofSafarirecognisestheconstraintsandchallengesfacedbytheSouthAfricaneconomyatpresentandgoing forward, it is confident that the group will continue to show positive revenue and capital growth, given the quality of its investmentpropertiesanddevelopmentpipeline.The long-termobjectiveofSafari istogrowitsassetbasebyredevelopingitsexistingpropertyportfolioandbyinvestinginwell-pricedincomeproducingpropertiestooptimisecapitaland income returns over time for shareholders. The company will redevelop properties to enhance value and support longer-termincomeandcapitalgrowthwhilstalsoexpandingitsdevelopmentpipelinetosustainlong-termprospectsthrough opportunities and strategic relationships.

Safariplanstocontinuewithitscurrentprojects,beingextensionstosomecentresandtheSwakopmundwaterfrontproject.Centreextensionsareconsideredtobelowrisk,astenantshavebeensecuredandtheretailpatternsarewellunderstood.Beingagreenfieldsdevelopment,however,theSwakopmundprojectdoesentailgreaterrisk,althoughthiswillbemitigatedbythephaseddevelopmentoftheproject,forwhichanchorretailtenantshavealreadybeensecured.WhileSafariwouldconsideracquisitions,bulkingupscaleisnotconsideredakeyobjectiveandthefocuswillratherbeonpotentialacquisitionsthatofferappealingdevelopmentopportunitieswhereSafaricandeployitsin-houseskills.ThecurrentvaluepipelineofpotentialprojectsunderconsiderationisinexcessofR1billion.

TheprimaryobjectivesofSafariareto:

• provideanincomestreamthroughrentalincomefromtheinvestmentproperties;

• growitsassetbasebydevelopingandinvestinginfairlyvaluedincomeproducingproperties;

• manageandredevelopaqualityretailpropertyportfoliothatprovidesgoodgrowthopportunities;

• optimisecapitalgrowth;and

• allowshareholderstoparticipateinthenetincome(afterprovidingforrelatedexpenditure)bydistributingsurplusnetcash income to shareholders.

7

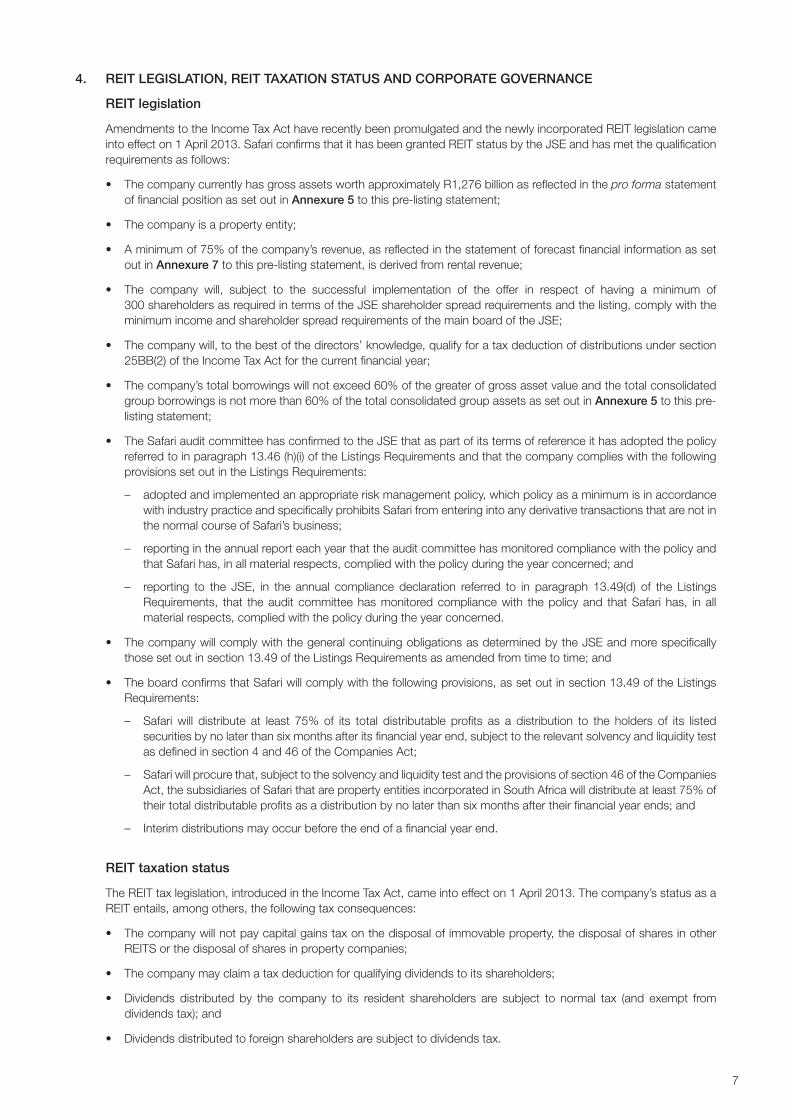

4. REIT LEGISLATION, REIT TAXATION STATUS AND CORPORATE GOVERNANCE

REIT legislation

AmendmentstotheIncomeTaxActhaverecentlybeenpromulgatedandthenewlyincorporatedREITlegislationcameintoeffecton1April2013.SafariconfirmsthatithasbeengrantedREITstatusbytheJSEandhasmetthequalificationrequirements as follows:

• ThecompanycurrentlyhasgrossassetsworthapproximatelyR1,276billionasreflectedinthepro forma statement of financial position as set out in Annexure 5 to this pre-listing statement;

• Thecompanyisapropertyentity;

• Aminimumof75%ofthecompany’srevenue,asreflectedinthestatementofforecastfinancialinformationassetout in Annexure 7 to this pre-listing statement, is derived from rental revenue;

• The company will, subject to the successful implementation of the offer in respect of having a minimum of 300shareholdersasrequiredintermsoftheJSEshareholderspreadrequirementsandthelisting,complywiththeminimumincomeandshareholderspreadrequirementsofthemainboardoftheJSE;

• Thecompanywill,tothebestofthedirectors’knowledge,qualifyforataxdeductionofdistributionsundersection25BB(2)oftheIncomeTaxActforthecurrentfinancialyear;

• Thecompany’stotalborrowingswillnotexceed60%ofthegreaterofgrossassetvalueandthetotalconsolidatedgroupborrowingsisnotmorethan60%ofthetotalconsolidatedgroupassetsassetoutinAnnexure 5 to this pre-listing statement;

• TheSafariauditcommitteehasconfirmedtotheJSEthataspartofitstermsofreferenceithasadoptedthepolicyreferredtoinparagraph13.46(h)(i)oftheListingsRequirementsandthatthecompanycomplieswiththefollowingprovisions set out in the Listings Requirements:

– adoptedandimplementedanappropriateriskmanagementpolicy,whichpolicyasaminimumisinaccordancewithindustrypracticeandspecificallyprohibitsSafarifromenteringintoanyderivativetransactionsthatarenotinthenormalcourseofSafari’sbusiness;

– reportingintheannualreporteachyearthattheauditcommitteehasmonitoredcompliancewiththepolicyandthatSafarihas,inallmaterialrespects,compliedwiththepolicyduringtheyearconcerned;and

– reporting to the JSE, in the annual compliance declaration referred to in paragraph 13.49(d) of the ListingsRequirements, that theauditcommitteehasmonitoredcompliancewith thepolicyand thatSafarihas, inallmaterial respects, complied with the policy during the year concerned.

• ThecompanywillcomplywiththegeneralcontinuingobligationsasdeterminedbytheJSEandmorespecificallythose set out in section 13.49 of the Listings Requirements as amended from time to time; and

• TheboardconfirmsthatSafariwillcomplywiththefollowingprovisions,assetoutinsection13.49oftheListingsRequirements:

– Safari will distribute at least 75%of its total distributable profits as a distribution to the holders of its listedsecuritiesbynolaterthansixmonthsafteritsfinancialyearend,subjecttotherelevantsolvencyandliquiditytestasdefinedinsection4and46oftheCompaniesAct;

– Safariwillprocurethat,subjecttothesolvencyandliquiditytestandtheprovisionsofsection46oftheCompaniesAct,thesubsidiariesofSafarithatarepropertyentitiesincorporatedinSouthAfricawilldistributeatleast75%oftheirtotaldistributableprofitsasadistributionbynolaterthansixmonthsaftertheirfinancialyearends;and

– Interimdistributionsmayoccurbeforetheendofafinancialyearend.

REIT taxation status

TheREITtaxlegislation,introducedintheIncomeTaxAct,cameintoeffecton1April2013.Thecompany’sstatusasaREITentails,amongothers,thefollowingtaxconsequences:

• Thecompanywillnotpaycapitalgainstaxonthedisposalofimmovableproperty,thedisposalofsharesinotherREITSorthedisposalofsharesinpropertycompanies;

• Thecompanymayclaimataxdeductionforqualifyingdividendstoitsshareholders;

• Dividends distributed by the company to its resident shareholders are subject to normal tax (and exempt fromdividendstax);and

• Dividendsdistributedtoforeignshareholdersaresubjecttodividendstax.

8

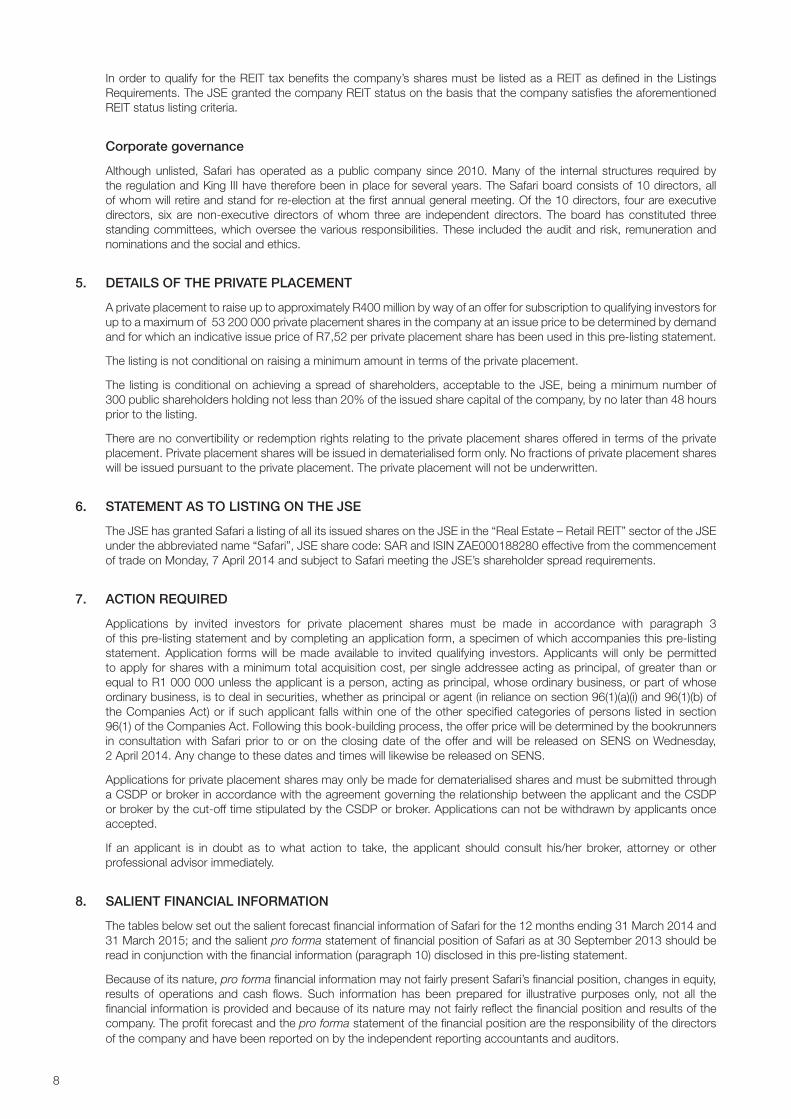

InordertoqualifyfortheREITtaxbenefitsthecompany’ssharesmustbelistedasaREITasdefinedintheListingsRequirements.TheJSEgrantedthecompanyREITstatusonthebasisthatthecompanysatisfiestheaforementionedREITstatuslistingcriteria.

Corporate governance

Althoughunlisted,Safari hasoperatedasapublic companysince2010.Manyof the internal structures requiredbytheregulationandKingIIIhavethereforebeeninplaceforseveralyears.TheSafariboardconsistsof10directors,allofwhomwillretireandstandforre-electionatthefirstannualgeneralmeeting.Ofthe10directors,fourareexecutivedirectors, six are non-executivedirectors ofwhom three are independentdirectors. Theboardhas constituted threestanding committees, which oversee the various responsibilities. These included the audit and risk, remuneration and nominations and the social and ethics.

5. DETAILS OF THE PRIVATE PLACEMENT

AprivateplacementtoraiseuptoapproximatelyR400millionbywayofanofferforsubscriptiontoqualifyinginvestorsforuptoamaximumof53200000privateplacementsharesinthecompanyatanissuepricetobedeterminedbydemandandforwhichanindicativeissuepriceofR7,52perprivateplacementsharehasbeenusedinthispre-listingstatement.

The listing is not conditional on raising a minimum amount in terms of the private placement.

Thelisting isconditionalonachievingaspreadofshareholders,acceptabletotheJSE,beingaminimumnumberof 300publicshareholdersholdingnotlessthan20%oftheissuedsharecapitalofthecompany,bynolaterthan48hoursprior to the listing.

There are no convertibility or redemption rights relating to the private placement shares offered in terms of the private placement.Privateplacementshareswillbeissuedindematerialisedformonly.Nofractionsofprivateplacementshareswill be issued pursuant to the private placement. The private placement will not be underwritten.

6. STATEMENT AS TO LISTING ON THE JSE

TheJSEhasgrantedSafarialistingofallitsissuedsharesontheJSEinthe“RealEstate–RetailREIT”sectoroftheJSEundertheabbreviatedname“Safari”,JSEsharecode:SARandISINZAE000188280effectivefromthecommencementoftradeonMonday,7April2014andsubjecttoSafarimeetingtheJSE’sshareholderspreadrequirements.

7. ACTION REQUIRED

Applications by invited investors for private placement shares must be made in accordance with paragraph 3 of this pre-listing statement and by completing an application form, a specimen of which accompanies this pre-listing statement. Application forms will be made available to invited qualifying investors. Applicants will only be permitted to apply for shares with a minimum total acquisition cost, per single addressee acting as principal, of greater than or equal to R1 000 000 unless the applicant is a person, acting as principal, whose ordinary business, or part of whose ordinarybusiness,istodealinsecurities,whetherasprincipaloragent(inrelianceonsection96(1)(a)(i)and96(1)(b)ofthe Companies Act) or if such applicant falls within one of the other specified categories of persons listed in section 96(1)oftheCompaniesAct.Followingthisbook-buildingprocess,theofferpricewillbedeterminedbythebookrunnersinconsultationwithSafariprior tooron theclosingdateof theofferandwillbe releasedonSENSonWednesday, 2April2014.AnychangetothesedatesandtimeswilllikewisebereleasedonSENS.

Applications for private placement shares may only be made for dematerialised shares and must be submitted through aCSDPorbrokerinaccordancewiththeagreementgoverningtherelationshipbetweentheapplicantandtheCSDPorbrokerbythecut-offtimestipulatedbytheCSDPorbroker.Applicationscannotbewithdrawnbyapplicantsonceaccepted.

If an applicant is in doubt as towhat action to take, the applicant should consult his/her broker, attorney or otherprofessional advisor immediately.

8. SALIENT FINANCIAL INFORMATION

ThetablesbelowsetoutthesalientforecastfinancialinformationofSafariforthe12monthsending31March2014and31March2015;andthesalientpro formastatementoffinancialpositionofSafariasat30September2013shouldbereadinconjunctionwiththefinancialinformation(paragraph10)disclosedinthispre-listingstatement.

Because of its nature, pro formafinancialinformationmaynotfairlypresentSafari’sfinancialposition,changesinequity,results of operations and cash flows. Such information has been prepared for illustrative purposes only, not all thefinancialinformationisprovidedandbecauseofitsnaturemaynotfairlyreflectthefinancialpositionandresultsofthecompany. The profit forecast and the pro forma statement of the financial position are the responsibility of the directors of the company and have been reported on by the independent reporting accountants and auditors.

9

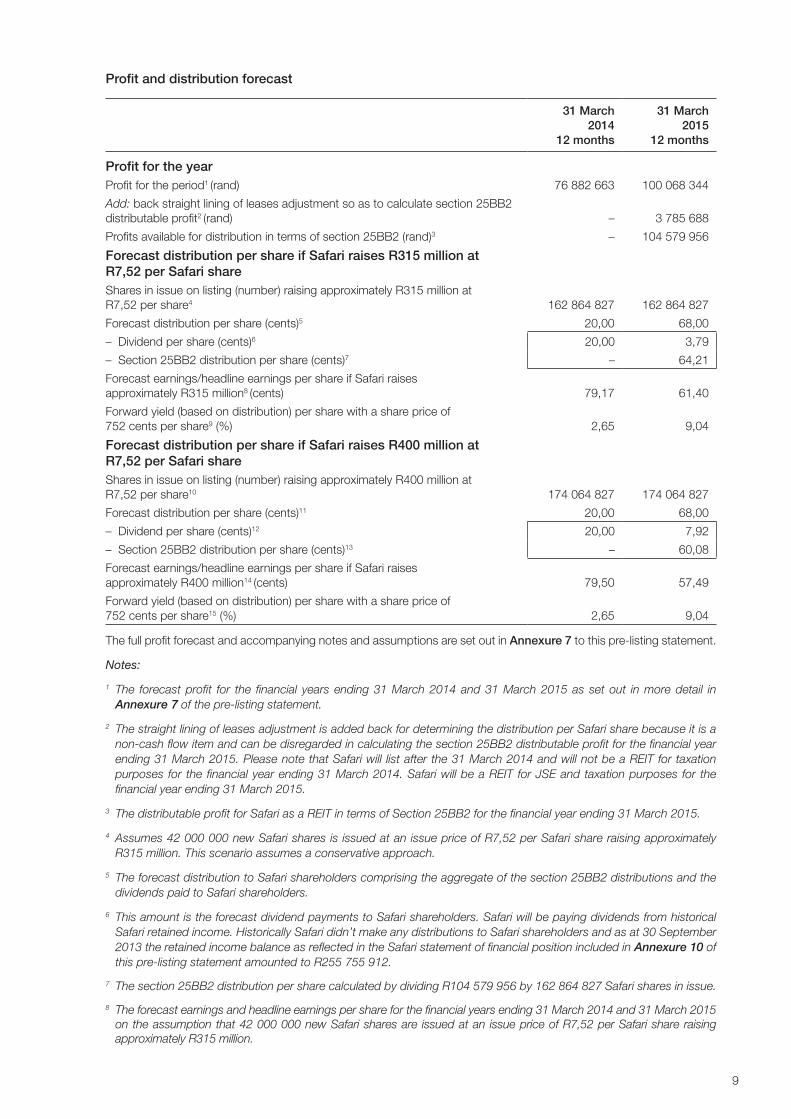

Profit and distribution forecast

31 March 2014

12 months

31 March 2015

12 months

Profit for the yearProfit for the period1 (rand) 76 882 663 100 068 344

Add: back straight lining of leases adjustment so as to calculate section 25BB2 distributable profit2 (rand) – 3 785 688

Profits available for distribution in terms of section 25BB2 (rand)3 – 104 579 956

Forecast distribution per share if Safari raises R315 million at R7,52 per Safari shareShares in issue on listing (number) raising approximately R315 million at R7,52 per share4 162 864 827 162 864 827

Forecast distribution per share (cents)5 20,00 68,00

– Dividend per share (cents)6 20,00 3,79

– Section 25BB2 distribution per share (cents)7 – 64,21

Forecast earnings/headline earnings per share if Safari raises approximately R315 million8 (cents) 79,17 61,40

Forward yield (based on distribution) per share with a share price of 752 cents per share9 (%) 2,65 9,04

Forecast distribution per share if Safari raises R400 million at R7,52 per Safari shareShares in issue on listing (number) raising approximately R400 million at R7,52 per share10 174 064 827 174 064 827

Forecast distribution per share (cents)11 20,00 68,00

– Dividend per share (cents)12 20,00 7,92

– Section 25BB2 distribution per share (cents)13 – 60,08

Forecast earnings/headline earnings per share if Safari raises approximately R400 million14 (cents) 79,50 57,49

Forward yield (based on distribution) per share with a share price of 752 cents per share15 (%) 2,65 9,04

The full profit forecast and accompanying notes and assumptions are set out in Annexure 7 to this pre-listing statement.

Notes:

1 The forecast profit for the financial years ending 31 March 2014 and 31 March 2015 as set out in more detail in Annexure 7 of the pre-listing statement.

2 The straight lining of leases adjustment is added back for determining the distribution per Safari share because it is a non-cash flow item and can be disregarded in calculating the section 25BB2 distributable profit for the financial year ending 31 March 2015. Please note that Safari will list after the 31 March 2014 and will not be a REIT for taxation purposes for the financial year ending 31 March 2014. Safari will be a REIT for JSE and taxation purposes for the financial year ending 31 March 2015.

3 The distributable profit for Safari as a REIT in terms of Section 25BB2 for the financial year ending 31 March 2015.

4 Assumes 42 000 000 new Safari shares is issued at an issue price of R7,52 per Safari share raising approximately R315 million. This scenario assumes a conservative approach.

5 The forecast distribution to Safari shareholders comprising the aggregate of the section 25BB2 distributions and the dividends paid to Safari shareholders.

6 This amount is the forecast dividend payments to Safari shareholders. Safari will be paying dividends from historical Safari retained income. Historically Safari didn’t make any distributions to Safari shareholders and as at 30 September 2013 the retained income balance as reflected in the Safari statement of financial position included in Annexure 10 of this pre-listing statement amounted to R255 755 912.

7 The section 25BB2 distribution per share calculated by dividing R104 579 956 by 162 864 827 Safari shares in issue.

8 The forecast earnings and headline earnings per share for the financial years ending 31 March 2014 and 31 March 2015 on the assumption that 42 000 000 new Safari shares are issued at an issue price of R7,52 per Safari share raising approximately R315 million.

10

9 The forward yield per Safari share in issue expressed as a % calculated by dividing the forecast distribution per Safari share by the issue price per Safari share.

10 Assumes 53 200 000 new Safari shares are issued at an issue price of R7,52 per Safari share raising approximately R400 million.

11 The forecast distribution to Safari shareholders comprising the aggregate of the section 25BB2 distributions and the dividends paid to Safari shareholders.

12 The forecast dividend payment by Safari to Safari shareholders from historical Safari retained income. As at 30 September 2013 the retained income balance as reflected in the Safari statement of financial position included in Annexure 10 of this pre-listing statement amounted to R255 755 912.

13 The section 25BB2 distribution per share calculated by dividing R104 579 956 by 174 064 827 Safari shares in issue.

14 The forecast earnings and headline earnings per share for the financial years ending 31 March 2014 and 31 March 2015 on the assumption that 53 200 000 new Safari shares are issued at an issue price of R7,52 per Safari share raising approximately R400 million.

15 The forward yield per Safari share in issue expressed as a % calculated by dividing the forecast distribution per Safari share by the issue price per Safari share.

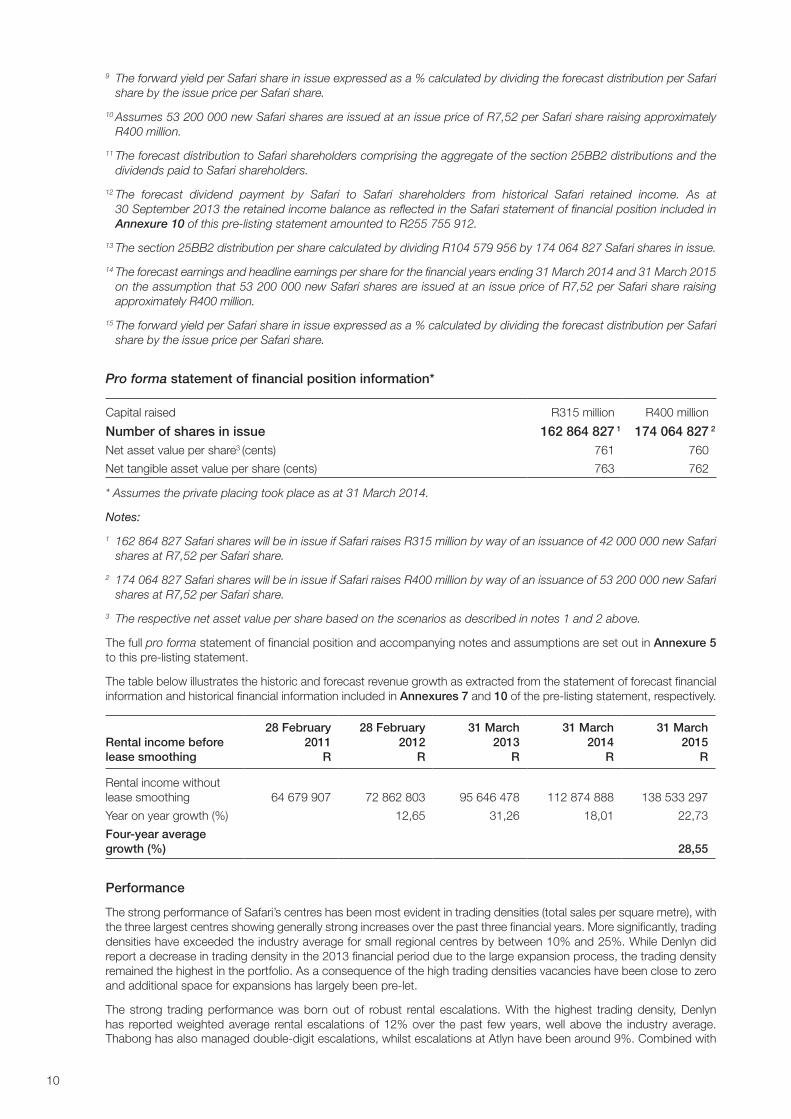

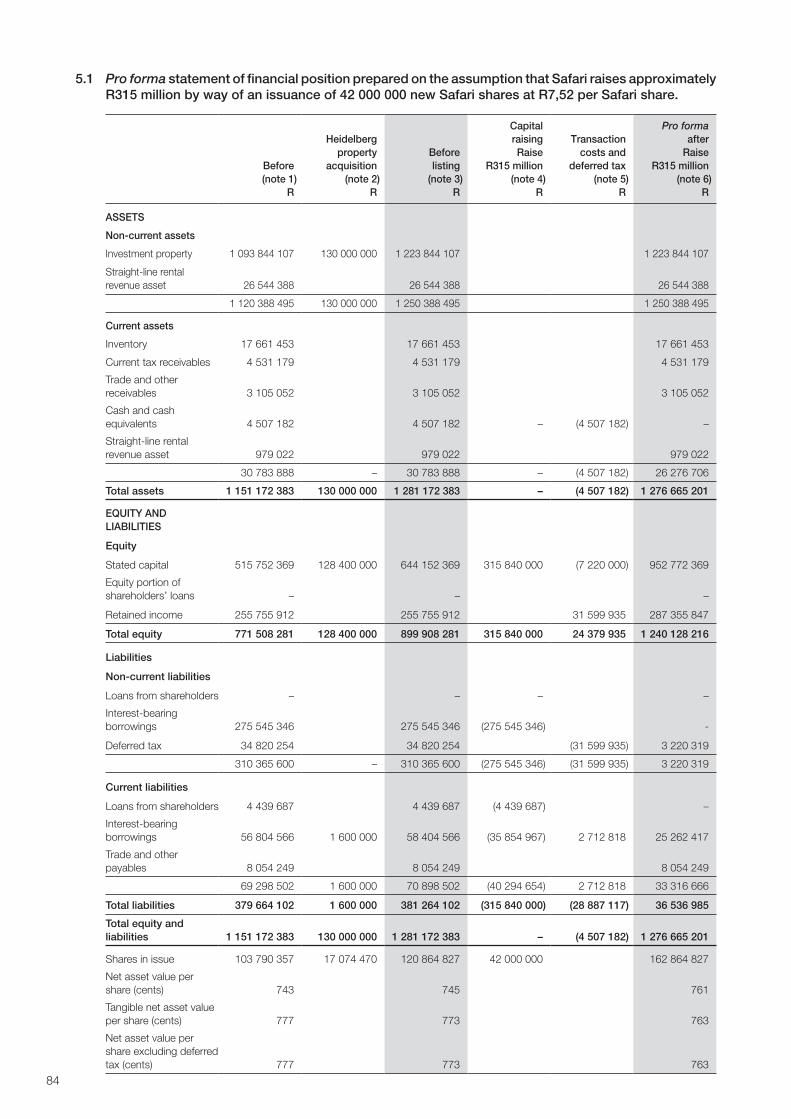

Pro forma statement of financial position information*

Capital raised R315 million R400 million

Number of shares in issue 162 864 827)1 174 064 827)2

Net asset value per share3 (cents) 761 760

Net tangible asset value per share (cents) 763 762

* Assumes the private placing took place as at 31 March 2014.

Notes:

1 162 864 827 Safari shares will be in issue if Safari raises R315 million by way of an issuance of 42 000 000 new Safari shares at R7,52 per Safari share.

2 174 064 827 Safari shares will be in issue if Safari raises R400 million by way of an issuance of 53 200 000 new Safari shares at R7,52 per Safari share.

3 The respective net asset value per share based on the scenarios as described in notes 1 and 2 above.

The full pro forma statement of financial position and accompanying notes and assumptions are set out in Annexure 5 to this pre-listing statement.

The table below illustrates the historic and forecast revenue growth as extracted from the statement of forecast financial information and historical financial information included in Annexures 7 and 10 of the pre-listing statement, respectively.

Rental income before lease smoothing

28 February 2011

R

28 February 2012

R

31 March 2013

R

31 March 2014

R

31 March 2015

R

Rental income without lease smoothing 64 679 907 72 862 803 95 646 478 112 874 888 138 533 297

Year on year growth (%) 12,65 31,26 18,01 22,73

Four-year average growth (%) 28,55

Performance

The strong performance of Safari’s centres has been most evident in trading densities (total sales per square metre), with the three largest centres showing generally strong increases over the past three financial years. More significantly, trading densities have exceeded the industry average for small regional centres by between 10% and 25%. While Denlyn did report a decrease in trading density in the 2013 financial period due to the large expansion process, the trading density remained the highest in the portfolio. As a consequence of the high trading densities vacancies have been close to zero and additional space for expansions has largely been pre-let.

The strong trading performance was born out of robust rental escalations. With the highest trading density, Denlyn has reported weighted average rental escalations of 12% over the past few years, well above the industry average. Thabong has also managed double-digit escalations, whilst escalations at Atlyn have been around 9%. Combined with

11

theexpansionsof the tradingarea,Denlynreported22%growth in rental income in the2013financialperiod,whileThabongandAtlynreported20%and17%growthrespectively.Victoriandeliveredescalationsinlinewiththemarket.

Despite the strong escalations achieved, average rental rates remain well below the sector average. Based on industry datatheaveragerentalforsmallregionalcentresisaroundR250/m2 and R170/m2 for community centres. This compares to average rentals between R92/m2 and R109/m2forSafari’sproperties.Thisisaclearsuggestionthatsubstantialroomforrentalincomegrowthexistsimmediately,evenifindustryrentalsbegintostagnatesomewhat.

Rentalincomeisforecasttoincreaseduringthe2014financialyear,largelyduetotheextensionsatDenlyncomingonstreamforthefullyear.Double-digitgrowthratesarealsoexpectedfromAtlynandThabong.AsTheVictorianhasbeenacquiredclosetotheyearend,itscontributiontothe2014yearislow.PleasenotethatSafari’s2013financialperiodwasa13-monthperiodduetothechangeinyearendfromFebruarytoMarchsoastoallowSafaritolistasaREIT.

Tenant quality and lease expiry

Safari’stenantmixisunderpinnedbynationalretailers,banks,restaurantsandfastfoodchains.Inthisregard,amongstthe fourproperties,A-grade tenantsaccount foraround69%of theGLAand58%of rental income,whileB-gradetenantscomprise18%ofGLAand21%ofrentalsrespectively.C-gradetenantsaregenerallystandalonebusinesses,providing specific services to the community. Focusing on tenant concentrations, the top-10 tenant groups across the portfolioaccountfor41,5%.Ofthis,fourtenantscontributebetween6%and7%each(Shoprite,Edcon,FoschiniGroup,Pepkor)andthreebetween4%and5%(Truworths,MrPriceGroupandSpar).Safarievidencesafavourableoverallleaseprofile.ExpiriesbyGLAarelongdated,withalmost60%onlymaturingfrom2018onwards.Thisequatestoaround44%leasesbyrentalincome.ThedifferentialbetweenGLAandrentalincomeexpiriescanbeattributedtothehighportionanchortenantswithleaseperiodsof10yearsormore,withmultipleoptionalextensions.Assuchtenantstendtopayalowerrentalratepersquaremetre,theirproportionalcontributiontoleasesbyincomeislowerthanbyGLA.Incontrast,private tenants tend to pay higher per metre rentals and sign shorter dated leases.

With regard tomaturitiesby rental income,a relativelyevendispersion isapparent,withbetween15%and20%ofleasesexpiringinanygivenyear,Safari’sleasematurityprofileisexpectedtolengthenevenfurtherasnewtenantsareintroducedintothecentresthroughthevariousextensionsunderway.Whilelongerdatedleasesdooffergreaterincomestability and reduce portfolio risk, theymay limit Safari’s ability to pass through higher rental escalations.However,includedinalllong-termleaseagreementsareturnoverclausesthatenableSafaritobenefitfromincreasedfoottraffic,compensating somewhat for potential lower escalations.

The table below illustrates the historical growth in investment property value as extracted from the report on historical financial information included in Annexure 10 to this pre-listing statement:

Asset value1 March

2010 28 February

2011 29 February

2012 31 March

2013

Investmentproperty(R) 593638984 718564984 856811029 1054912556

Yearonyeargrowth(%) 21,04 19,23 23,12

Three-year average growth (%) 25,90

Gearing and future extensions

Thelistingsproceedswillbeutilisedtosettlealloutstandingdebt,withapproximatelyR58millionretainedincash.ThiswillfreeuptheentireR600millionAbsadebtfacilitytobeutilisedfornewcapex.WhilethecurrentR600millionAbsafacilityissufficienttosupporttheprojectpipeline,Safariplanstodiversifyfundingthroughadomesticmedium-termnoteissuance.

9. FURTHER COPIES OF THE PRE-LISTING STATEMENT

Further copies of this pre-listing statement may be obtained during normal business hours from Monday, 31 March 2014 from:

• SafariInvestments(RSA)Limited,420FrieslandLane,Lynnwood,Pretoria0081;

• ComputershareInvestorServicesProprietaryLimited,GroundFloor,70MarshallStreet,Johannesburg2001;

• EdwardNathanSonnenbergsInc,150WestStreet,Sandton2196;and

• PSGCapitalProprietaryLimited,1stFloor,OuKollegeBuilding,35KerkStreet,Stellenbosch7599.

12

IMPORTANT DATES AND TIMES1

The definitions and interpretations commencing on pages 13 to 18 of this pre-listing statement apply to these important dates and times:

2014

Abridgedpre-listingstatementreleasedonSENSon Friday,28March

Abridged pre-listing statement published in the press on Monday, 31 March

Opening date of the private placement (9:00) Monday, 31 March

Closing date of the private placement (12:00)2 Wednesday, 2 April

ResultsoftheprivateplacementreleasedonSENSon Wednesday,2April

Notificationofallotmentstosuccessfulinvitedinvestorsby Wednesday,2April

Results of the private placement published in the press on Thursday, 3 April

ListingofsharesandthecommencementoftradingontheJSEon(9:00) Monday,7April

AccountsatCSDPorbrokerupdatedandcreditedinrespectofdematerialised shareholders3 Monday, 7 April

Notes:

1 All references to dates and time are to local dates and times in South Africa. These dates and times are subject to amendment. Any such amendment will be released on SENS and published in the press.

2 Invited investors must advise their CSDP or broker of their acceptance of the private placement in the manner and cut-off time stipulated by their CSDP or broker.

3 CSDPs effect payment on a delivery-versus-payment basis.

13

DEFINITIONS AND INTERPRETATIONS

In thispre-listingstatementand theannexureshereto,unlessotherwise indicated, thewords in thefirstcolumnhave themeanings stated opposite them in the second column, words in the singular include the plural and vice versa, words importing one gender include the other genders and references to a person include references to an entity and vice versa.

“Absa” Absa Bank Limited, (registration number 1986/004794/06), a public company dulyincorporatedandregisteredinaccordancewiththelawsofSouthAfrica;

“acquisition” or theacquisitionbySafarioftheHeidelbergpropertyandcertainassumedliabilities“Heidelberg acquisition” ofHeidelberginexchangeforafreshissuanceofsharesbySafari;

“ALSI” theFTSE/JSEAllShareIndex;

“anchor tenant” the leading tenant in a shopping centre whose prestige and brand recognition is anticipated to attract other tenants and shoppers and who usually occupies the largest percentage of gross lettable area in the shopping centre;

“annual budget” the budget including revenues, operating and capital investment expenditures, otherexpenditureandcashflowforafinancialyearofeachlettingenterprise;

“application form” the blue application form, attached to and forming part of this pre-listing statement, which qualifying investors are required to complete and return in accordance with the instructions contained therein in order to be considered for participation in the offer;

“Attorneys Act” AttorneysAct,No53of1979,asamended;

“Bloomberg” a real-time, online, subscription provider of up-to-date business news and financial information which delivers international breaking news, live stock market data and an online database providing current and historical financial quotes, financial statement data for listed companies, business newswires, statistics on financial markets and global economies, as well as a portal to company, industry and economic research;

“board” theboardofdirectorsofSafari,thedetailsofwhicharesetoutinparagraph6andAnnexure 4 of this pre-listing statement;

“bookrunner(s)” DEA-RUasleadbookrunnerandPSGasjointbookrunner;

“business day” anydayotherthanaSaturday,SundayorofficialpublicholidayinSouthAfrica;

“CAGR” Compound Annual Growth Rate;

“certificated shareholders” Safarishareholderswhoholdcertificatedshares;

“certificated shares” Safarishareswhichhavenotbeendematerialised intotheStratesystem,title towhich isrepresented by share certificates or other physical documents of title;

“CGT” CapitalGainsTaxasleviedintermsoftheIncomeTaxAct;

“CIPC” theCompaniesandIntellectualPropertyCommission,establishedintermsofsection185ofthe Companies Act;

“common monetary area” collectively, South Africa, the Republic of Namibia and the Kingdoms of Lesotho andSwaziland;

“Companies Act” theCompaniesAct,No2008(ActNo71of2008),asamended;

“Companies Regulations” theCompaniesRegulations,2011promulgatedinGovernmentGazetteNo34239intermsof section 223 of the Companies Act;

“corporate advisor(s)” DEA-RU and FKC, full details of which are set out in the “Corporate information andadvisors”sectionofthispre-listingstatement;

“Cosmos” Cosmos Management Close Corporation (registration number 1989/037137/23), a close corporationincorporatedandregisteredinSouthAfrica.Themember’sinterestinCosmosisheld55%byFJJMarais(SafariCEO),15%byEleGrange,20%byWVenterand10%byML de Klerk;

14

“CPI” consumerpriceindex,showingtheaveragepricelevelofabasketofgoodsandservicesbought by a typical consumer or household and which changes over time, as determined andpublishedbyStatisticsSouthAfricafromtimetotime;

“CSDP” a CentralSecuritiesDepositoryParticipantinSouthAfricaappointedbyashareholderforthepurposes of, and in regard to, dematerialisation and to hold and administer securities or an interest in securities on behalf of a shareholder;

“Deeds Office” therelevantofficeoftheRegistrarofDeedshavingjurisdictionoverthelandinquestion;

“dematerialise” or the process whereby ownership of shares as evidenced by share certificates and/or “dematerialisation” some other documents of title are converted to an electronic form as dematerialised shares

underStrate and recorded in the sub-register of shareholdersmaintainedbyaCSDPorbroker;

“dematerialised shareholders” Safarishareholderswhoholddematerialisedshares;

“dematerialised shares” SafarishareswhichhavebeenincorporatedintotheStratesystem,titletowhichisnolongerrepresented by share certificates or physical documents of title;

“development agreement(s)” thewrittendevelopmentagreementsenteredintobetweenSafariDevelopmentsandSafari,as more fully describe in Annexure 13;

“development manager” SafariDevelopments;

“developments” projectsentailingthedevelopmentofimmovableproperty;

“direct property portfolio” thosepropertiesheldbySafarianditssubsidiaries,assetoutinAnnexure 1;or “property portfolio”

“director” adirectorofSafariasdefinedintheCompaniesAct;

“distributable income” or gross income,asdefined in the IncomeTaxAct lessdeductionsandallowancesthatare“distributable profit” permittedtobedeductedbyaREITintermsoftheIncomeTaxAct,otherthanthequalifying

distribution,asdefined in termsof section25BBof the IncomeTaxAct,beingqualifyingdistributions that form part of distributable profit;

“documents of title” share certificates, certified transfer deeds, balance receipts and any other documents of title to shares acceptable to the board;

“Exchange Control the Exchange Control Regulations of South Africa issued under the CurrencyRegulations” andExchangesAct(ActNo9of1933),asamended;

“Financial Markets Act” FinancialMarketsAct,No19of2012,asamendedfromtime-to-time;

“Financial Year” thefinancialyearofSafariwhichcommenceson1Aprilofeachyearandendson31Marchof the following year;

“GLA” the total area of a building that can be let to a tenant plus supplementary areas which include forexamplestorerooms,balconies,terraces,patiosandsignage/advertisingareas;

“government” thegovernmentofSouthAfrica;

“GR” GrossRental,beingbasicrentalplusoperationalcosts,excludingratesandtaxes,measuredin Rands;

“group” in relation to a company (wherever incorporated), any company that is a subsidiary (being its holding company) and any other subsidiaries of any such holding company and each companyinagroupthatisamemberofthegroup.Unlessthecontextotherwiserequires,theapplication of the definition of group to any company at any time will apply to the company as it is at that time;

“Heidelberg property” portion 3 of erf 3523 Heidelberg Township, registration J.R. Gauteng measuring 3,4hectaresandheldbySafariHeidelbergbydeedoftransferT164635/2004;

“Heidelberg property theagreementbetweenSafariandSafariHeidelbergintermsofwhichSafariacquiredtheacquisition agreement” HeidelbergpropertyfromSafariHeidelbergdated24January2014;

“Income Tax Act” theIncomeTaxAct,No58of1962,asamended;

“independent reporting Mazars, a partnership formed in terms of the laws of South Africa, full details ofaccountants and auditors” whicharesetoutinthe“Corporateinformation”section;or “independent reporting accountants” or “Mazars”

15

“independent property valuer” theindependentpropertyvaluerofSafaribeingMillsFitchet;

“intangible assets” anintangibleassetasdefinedandrecognisedintermsofIFRS;

“investment committee” a committee to be established by Safari and appointed by the board to consider andmotivate investment opportunities, details of which are set out in paragraph 9.3 of this pre-listing statement;

“invited investors” those specifically identified persons including individuals, financial institutions and selected retail investors to whom the offer under the private placement will be addressed and made;

“IFRS” InternationalFinancialReportingStandards;

“JIBAR” JohannesburgInter-BankAgreedRate;

“JSAPY” theFTSE/JSESouthAfricaListedPropertyIndex;

“JSE” JSE Limited (registration number 2005/022939/06), licensed as an exchange under theFinancialMarketsAct(ActNo19of2012)asamended,andapubliccompanyregisteredandincorporatedintermsofthelawsofSouthAfrica;

“JSE Guaranteed Fund” a fund consisting of assets acquired and liabilities incurred by the trustees of the JSEGuaranteeFundTrust(master’sreferencenumberIT9150/2005);whichvestinthetrustees;

“King III” theCodeofCorporatePracticesandConduct inSouthAfrica, representingprinciplesofgood corporate governance as laid out in the King Report, as amended from time to time;

“land” immovable property;

“last practicable date” the last day before the finalisation of this pre-listing statement being Friday, 14 March 2014;

“lease agreements” theleaseagreementsenteredintobetweentheSafarigroupandthetenantsofthelettingenterprises;

“letting enterprise” the business of letting a building or part thereof;

“listing” thelistingofalltheissuedsharesofthecompanyinthe“RealEstate–RetailREIT”sectorofthemainboardoftheJSE,expectedtobeonMonday,7April2014;

“Listings Requirements” theListingsRequirements,asamendedbytheJSEfromtimetotime;

“Loadman” AfricanElectrical TechnologiesProprietaryLimited (registrationnumber1994/000780/07),trading as Loadman, a private company incorporated on 10 February 1994. The shares inLoadmanareheld25%bythePETrust,25%bytheTJTrust,25%bytheIJTrustand 25%by theSchuldFamilyTrust.ThedirectorsofLoadmanarePPVEOlivier,JBTheron,SJFStapelbergandHLSchuldwhoarealsobeneficiariesofthevarioustrustslistedabove.NoneofthedirectorsortheirrespectivetrustsarerelatedpartiestoSafariasdefinedintheJSEListingsRequirementsandnodirectorofSafariortheirassociateshaveanyinterestorbenefit in the Loadman electrification agreement;

“Loadman electrification theagreemententeredintobetweenSafariandLoadmandated24February2014.Abriefagreement” summary of this agreement is included in Annexure 3 of the pre-listing statement;

“loan agreement between the loan agreement entered into between Safari and Absa Mortgage Fund ManagersSafari and Absa” dated1July2013;

“m2” or “sqm” square metres;

“Mills Fitchet” the independent and professional property valuer of the group, full details of which are set outinthe“Corporateinformation”section;

“MOI” the Memorandum of Incorporation of the company, extracts of which are set out in Annexure 14;

“NAV” NetAssetValue,beingthevalueofallthegroup’sassetsaftersubtractingthevalueofallitsliabilitiesasdeterminedinaccordancewiththeconsolidatedfinancialstatementsofSafaripreparedinaccordancewithIFRS;

“Nedbank” NedbankLimited(registrationnumber1951/000009/06),apubliccompanydulyincorporatedandregisteredinaccordancewiththelawsofSouthAfrica;

“net income” grossincome,asdefinedintheIncomeTaxAct;lessdirectpropertyexpenses,administrationexpensesandfinancecosts;

16

“NLA” NetLettableArea,beingthetotalareaofabuildingthatcanbelettoatenant.NLAisthusGLA minus supplementary areas;

“node” a narrowly particularised and localised position or place; a spot; or area;

“offer” or “private placing” aprivateplacingbywayofanoffer forsubscriptionofup toamaximumof53200000shares in the share capital ofSafari toqualifying Investors at an indicative issuepriceofapproximatelyR7,52;

“own-name dematerialised dematerialisedSafarishareholderswho/whichhaveelectedown-nameregistration;shareholders”

“portfolio development and the agreement entered into between Safari and Safari Developments datedprocurement agreement” 27 February 2014;

“property portfolio theagreemententeredintobetweenSafariandCosmosdated27February2014;management agreement”

“pre-listing statement” alldocumentscontainedinthisbounddocument, includingtheannexuresheretoandtheapplication form, dated Friday, 28 March 2014;

“press” the Business Day newspaper;

“prime rate” the publicly quoted basic rate of interest from time to time published by Absa as being the prime overdraft rate;

“promoter” the party(ies) responsible for the formation of a company to be listed, or acquired by an existingissuer,andwhoearn(s)afeetherefrom,incashorotherwise;

“property portfolio manager” Cosmos, as the property portfolio manager of the property portfolio;or “portfolio manager”

“property portfolio theagreemententeredintobetweenSafariandCosmosdated27February2014;management agreement”

“property portfolio” or the portfolio of properties and the details of which are set out in Annexure 1 to this“properties” pre-listing statement;

“purchase consideration” thetotalamountofR128400000paidbySafaritotheHeidelbergshareholdersbywayofor “Heidelberg purchase a fresh issuance of 17 074 470 Safari shares at R7,52 per Safari share to Heidelbergconsideration” shareholdersonregistrationoftheHeidelbergpropertyintothenameofSafari;

“qualifying investors” invited investors applying as principals for a minimum subscription of R1 million in shares unless such applicant is a person, acting as principal, whose ordinary business, or part of whose ordinary business, is to deal in securities, whether as principal or agent (in reliance on section96(1)(a)(i)and96(1)(b)oftheCompaniesAct)orsuchapplicantfallswithinoneoftheotherspecifiedcategoriesofpersonslistedinsection96(1)oftheCompaniesAct;

“R” or “Rand” or “ZAR” SouthAfricanRand,thelawfulcurrencyofSouthAfrica;

“registered owners” the owners of the Land registered as such in the Deeds Office;

“REIT” RealEstateInvestmentTrust,acompanylistedontheJSEwhichhasreceivedREITstatusin termsof theListingsRequirementsandwhichqualifies for taxdeduction in respectofdistributionsundertheprovisionsofsection25BBoftheIncomeTaxAct;

“SA” or “South Africa” theRepublicofSouthAfrica;

“Safari” or “the company” Safari InvestmentsRSALimited(registrationnumber2000/015002/06),apubliccompanyincorporatedon7July2000inaccordancewiththelawsofSouthAfrica(previouslyknownasSafariInvestmentsSebokengProprietaryLimited),tobelistedontheJSEandclassifiedasaREIT;

“Safari Atteridgeville” SafariInvestmentsAtteridgevilleProprietaryLimited(registrationnumber2004/029742/07), a private company incorporated in South Africa. On 1 March 2009 Safari Atteridgevilleenteredintoanamalgamationtransactionascontemplatedinsection44oftheIncomeTaxAct,No58of1962(asamended)throughthesaleof therespectivebusinessesofSafariPretoriaandSafariAtteridgevilleasgoingconcernstoSafariinoneindivisibleamalgamationtransaction.All theSafariAtteridgevilleshareholderswereabsorbed intoSafariandSafariAtteridgeville was liquidated;

17

“Safari Developments” SafariDevelopments (Pretoria)ProprietaryLimited (registrationnumber2000/024887/07), a private company incorporated in South Africa. The shares in Safari Developments are held25%byPaceProjectsProprietaryLimitedwhosesharesareheld100%byKPashiou, adirectorofSafari;25%bySJKruger,adirectorofSafari;25%byJCVerwayen,adirectorofSafari;and25%bySafariholdofwhich100%isheldbyFJJMarais,theSafariCEO;

“Safari group” SafarianditssubsidiarySafariNamibia;

“Safari Heidelberg” Safari Investments(Heidelberg)ProprietaryLimited(registrationnumber1996/015306/07),aprivatecompany incorporated in1996 inSouthAfrica.Theshares inSafariHeidelbergareheldbytheAJSWTrust(2,2%),CELamprecht(1,2%),ChrisandNelsiaVisserFamilieTrust(1,8%),DATrust(0,5%),DeVilliers&SchoemanTrust(3,1%),DeVilliersCilliersTrust(1,0%), FAPashiouTrust (4,9%), FrancoisMaraisTrust (5,6%),GAPashiouTrust (4,9%),GroveEiendomsTrust(2,5%),IJTrust(2,7%),Jannie&AdriVerwayenTrust(3,3%),JanniedeBeerFamilyTrust(7,1%),JCHavinga(0,9%),JCMCInvestmentConsultantsProprietaryLimited(0,8%),JHLamprecht(2,3%),JPvanderMerwe(0,6%),KAPashiouTrust(4,9%),KD Brandt (4,2%),MRC Trust (5,6%), Paula Prinsloo (1,5%), PE Trust (3%), PlentytradeProprietaryLimited (15,8%),RASkinnerKonstruksieCC(2,3%),RikaVenterFamilieTrust(3,8%),SSesTrust(2%),SchuldFamilyTrust(2,7%),SSLTrust(0,8%),TheAMPInvestmentTrust(2,3%),TheFloodInvestmentTrust(3,2%)andtheTJTrust(2,7%);

“Safari Namibia” Safari Investments Namibia Proprietary Limited, registration number 2002/246, a privateunlistedcompany incorporated inNamibia (previouslyknownasSwakopmundWaterfrontPropertyCompany),awhollyownedsubsidiaryofSafariwithregisteredaddress14StarfishRoad,SealaVieNo2,Mile4,Swakopmund;

“Safari Pretoria” Safari Investments Pretoria Proprietary Limited, registration number 2000/030872/07, aprivatecompanyincorporatedinSouthAfrica.On1March2009SafariPretoriaenteredintoanamalgamationtransactionascontemplatedinsection44oftheIncomeTaxAct,No58of1962(asamended)throughthesaleoftherespectivebusinessesofSafariPretoriaandSafariAtteridgevilleasgoingconcernstoSafariinoneindivisibleamalgamationtransaction.AlltheSafariAtteridgevilleshareholderswereabsorbedintoSafariandSafariPretoriawasliquidated;

“Safari Retail” SafariRetailProprietaryLimited,registrationnumber2008/011620/07,aprivatecompanyincorporatedinSouthAfrica.ThesharesinSafariRetailisheld60%byFJJMaraistheSafarichiefexecutiveofficer,20%byHPienaarand20%byZEngelbrechttheSafarichieffinancialofficer;

“Safarihold” Safarihold Proprietary Limited (registration number 1983/012478/07), a private companyincorporated in South Africa owned 50% by theMRC Trust (Master’s reference numberIT 4930/02) a family trust ofwhichMCMarais, FJJMarais and JA Janse vanRensburgaretrusteesandCKruger,HHKlerck,JHRKlerkandTRoodearebeneficiariesand50%bytheFrancoisMaraisTrust(Master’sreferencenumberIT177/85)afamilytrustofwhich FJJMarais,WEJohnsonandJHBoshoffaretrusteesandMCMarais,RSLMarais,WMaraisand FH Marais are beneficiaries;

“SA” or “South Africa” theRepublicofSouthAfrica;

“SAPOA” SouthAfricanPropertyOwnersAssociation;

“SARB” SouthAfricanReserveBank;

“SARS” theCommissioneroftheSouthAfricanRevenueService;

“SENS” theStockExchangeNewsServiceoftheJSE;

“share” or “shares” anoparvalueordinaryshareintheissuedsharecapitalofSafari;

“shareholder(s)” or “Safari theholderorholdersofsharesinSafari;shareholder(s)”

“Sponsor” PSGCapitalProprietaryLimited,fulldetailsofwhicharesetoutinthe“Corporateinformationandadvisors”sectionofthispre-listingstatement;

“Strate” Strate Limited (registration number 1998/022242/06), a public company registered andincorporatedintermsofthelawsofSouthAfrica,whichislicensedtooperate,intermsoftheFinancialMarketsAct(ActNo19of2012),asamended,andwhichisresponsiblefortheelectronicsettlementsystemusedbytheJSE;

“STT” SecuritiesTransferTax,asdeterminedintheSouthAfricanSecuritiesTransferTaxAct,No25of 2007;

18

“subsidiary” asubsidiarytoSafariasdefinedintheCompaniesAct;

“tangible NAV” NetAssetValuelessintangibleassets;

“transfer” theregistrationoftransferoftherelevantimmovablepropertyintothenameofSafariorthegroup in the relevant deeds registry office;

“transfer secretaries” or Computershare Investor Services Proprietary Limited (registration number“Computershare” 2004/003647/07)aprivatecompany registeredand incorporated in termsof the lawsof

SouthAfrica,fulldetailsofwhicharesetoutinthe“Corporateinformation”section;

“VAT” ValueaddedtaxasdefinedintheValueAddedTaxAct(ActNo89of1991),asamended;

“VWAP” VolumeWeightedAveragePrice;and

“yield” the distribution available to a holder of a share in any 12-month period or any financial year, as the case may be, divided by the relevant market price of that security.

19

SECTION ONE – DETAILS OF THE PRIVATE PLACEMENT

1. PURPOSES OF THE PRIVATE PLACEMENT AND THE LISTING

1.1 The principal rationale for the Listing of the company is to:

1.1.1 provide qualifying investors with an opportunity to participate over the long term in the income streams andfuturecapitalgrowthofSafari;

1.1.2 obtain an increased spread of shareholders to enhance the liquidity and tradeability of the shares;

1.1.3 provideSafariwithaccesstoacentre’stradingfacilitytherebyprovidingliquiditytoshareholders;

1.1.4 provideSafariwithaccesstocapitalmarketsandaplatformtoraisefundingtopursuegrowthandinvestment opportunities in the future; and

1.1.5 enhancethepublicprofileandgeneralawarenessofSafari.

1.2 The main purpose of this pre-listing statement is to:

1.2.1 provide investors with relevant information relating to the company, property portfolio, directors and property managers;

1.2.2 communicate the strategy and vision of the company;

1.2.3 undertaketheprivateplacingofuptoamaximumof53200000shareswithinvestors;and

1.2.4 set out the salient details of the offer and the procedure for participating therein.

1.3 ThenetproceedsoftheprivateplacementwillbeusedbySafaritosettleinterest-bearingdebtandstrengthenthe balance sheet for ongoing activities.

2. SALIENT DATES AND TIMES

2014

Opening date of the private placement (9:00) Monday, 31 March

Closing date of the private placement (12:00) Wednesday, 2 April

Notificationofallotmentstosuccessfulinvitedinvestorsby Wednesday,2April

ResultsoftheprivateplacementreleasedonSENSon Wednesday,2April

Results of the private placement published in the press on Thursday, 3 April

AccountsatCSDPorbrokerupdatedanddebitedinrespectofdematerialised shareholders Monday, 7 April

ListingofsharesandthecommencementoftradingontheJSEon(9:00) Monday,7April

Thedatesandtimesinthispre-listingstatementaresubjecttochangeandanychangeswillbereleasedonSENSandpublished in the press.

3. PARTICULARS OF THE PRIVATE PLACEMENT

3.1 Details of the private placement

3.1.1 A private placement to raise up to R400 million by way of an offer for subscription to invited investors foruptoamaximumof53200000privateplacementsharesinthecompanyatanissuepricetobedeterminedbydemandandforwhichanindicativeissuepriceofR7,52perprivateplacementsharehas been used in this pre-listing statement.

3.1.2 Theprivateplacementshares issuedintermsofthispre-listingstatementwillbeallottedsubjecttotheprovisionsoftheMOIandwillrankpari passuinallrespectsincludingdistributions,withallexistingissued shares in the company.

3.1.3 There are no convertibility or redemption provisions relating to any shares.

20

3.1.4 OnlynoparvalueshareswillbeissuedasprovidedforintheMOI.

3.1.5 The private placement shares will only be issued in dematerialised form. No certificated privateplacement shares will be issued.

3.1.6 Nofractionsofprivateplacementshareswillbeofferedintermsoftheprivateplacement.Anyexcessfunds received from applicants resulting from fractional entitlements will be refunded.

3.1.7 The directors will not increase the number of shares offered in terms of the private placement.

3.1.8 Nosharehasanyspecialrightstodividends,capitalorprofitsofthecompany.

3.1.9 TherewillbenootherclassesofsharesauthorisedorinissuebySafariatthedateoflisting.

3.1.10 There are no shares held in treasury.

3.2 Conditions to the listing

3.2.1 The listing issubject to theachievementofaspreadofshareholdersacceptable to theJSE,beingaminimumof300publicshareholdersholdingnot lessthan20%oftheissuedsharecapitalofthecompany.Safariexpectstomeettheserequirementsaftertheprivateplacement.

3.2.2 The offer and listing are conditional on obtaining the minimum spread of shareholders required under the Listings Requirements failing which, the private placing and any acceptance thereof shall not be of any force or effect and no person shall have a claim whatsoever against the company or any other person as a result of the failure of such condition.

3.3. Procedures for acceptance

3.3.1 The private placement is open to invited investors only.

3.3.2 The private placement shares will only be issued in dematerialised form. No certificated privateplacement shares will be issued.

3.3.3 Qualifying investors wishing to participate in the offer should contact the bookrunner prior to the cut-off timeanddateforprovidingapplicationsreferredtoinparagraph2headed“salientdatesandtimes”above.

3.3.4 The following parties may not participate in the private placement:

3.3.5.1 any person who may not lawfully participate in the private placement; and/or

3.3.5.2 any investor who has not been invited to participate; and/or

3.3.5.3 any person acting on behalf of a minor or deceased estate.

3.3.5 Noapplicationswillbeacceptedafter12:00onWednesday,2April2014.

3.3.6 Applications submitted by qualifying investors are irrevocable until the date of listing and may not be withdrawnoncereceivedbythetransfersecretaries,CSDPorbrokers.

3.3.7 Nopersonacquiringsharesbyvirtueofsection96(1)(b)oftheCompaniesActshallbepermittedtouse an agent.

3.3.8 Application forms must be completed in accordance with the provisions of this pre-listing statement and the instructions contained in the application form.

3.3.9 Copies or reproductions of the application form will be accepted at the discretion of the board.

3.3.10 Any alterations on the application form must be authenticated by full signature.

3.3.11 Receipts will not be issued for applications, application monies or supporting documents received.

3.3.12 Eachapplicationwillberegardedasasingleapplication.

3.3.13 Applications must be for a minimum of R1 000 000 per person acting as principal. Thereafter applications should be in multiples of no less than 1 000 shares.

3.3.14 Sharesmaynotbeappliedforinthenameofaminororadeceasedestate.

3.3.15 Nodocumentaryevidenceofcapacityneedaccompanytheapplicationform,butSafarireservestheright to call upon any selected qualifying investor to submit such evidence for noting, which evidence will be returned at the risk of the qualifying investor.

3.3.16 The board reserve the right to accept or refuse any applications, either in whole or in part, or to abate any or all applications (whether or not received timeously) in such manner as they may determine, in the event of an oversubscription.

21

3.4 Representation

AnyqualifyinginvestorapplyingfororacceptingsharesintheoffershallbedeemedtohaverepresentedtoSafarithat such investor was in possession of a copy of this pre-listing statement at that time. Any party applying for oracceptingsharesonbehalfofaqualifying investorshallbedeemedtohaverepresentedtoSafari that it isduly authorised to do so and warrants that it and the qualifying investor for whom it is acting as agent is duly authorised to do so in accordance with all relevant laws and such investor guarantees the payment of the issue price and that a copy of this pre-listing statement was in the possession of such investor for whom it is acting as agent.

3.5 Allocation and oversubscription

3.5.1 The basis of allocation of the issued shares will be determined by the bookrunner in consultation with Safari.ItisintendedthatnoticeofallocationwillbegivenonWednesday,2April2014.Dependingonthe level of demand, applicants may receive no shares or fewer than the number of shares applied for.Anydealing insharesprior todeliveryofsuchshares isentirelyat theapplicant’sownrisk.Nopreference of allotment will be given to any particular company or group.

3.5.2 In theeventofanoversubscription, theboardshall, in itssolediscretion,determineanappropriateallocation mechanism, such that the private placement shares will be allocated on an equitable basis, calculated in such a way that a person will not, in respect of his application receive an allocation of a lesser number of shares than any other invited investor applying for the same number or a lesser number of shares. Theboardwill also take into account the spread requirements of the JSE, theliquidity of the shares and consider the potential shareholder base that the board wishes to achieve.

3.6 Dematerialisation of the issued shares

ShareswillbeissuedbySafaritosuccessfulapplicantsindematerialisedformonly.Accordingly,allsuccessfulapplicantsmustappointaCSDP,directlyorthroughabroker,toreceiveandholdthedematerialisedsharesontheirbehalf.Shouldashareholder requireaphysicalcertificate forhis/hershares,suchshareholderwillhaveto materialise their shares following the listing, for which a fee will be charged, and should therefore contact its CSDPtodoso.Itisnotedthattherearerisksassociatedwithholdingsharesincertificatedform,includingtheriskoflossortaintedscript,whicharenolongercoveredbytheJSEGuaranteeFund.Allshareholderswhoelectto convert their dematerialised shares into certificated shares will have to dematerialise their shares should they wishtotradethemunderthetermsofStrate(seeparagraph3.8headed“Strate”below).

Eachapplicant’sdulyappointedCSDPorbrokerwillreceivethedematerialisedsharesontheirbehalfwhichisexpectedtooccuronMonday,7April2014duringtheStratesettlementruns.

3.7 Payment and delivery of shares

3.7.1 Eachsuccessfulapplicantmust,assoonaspossibleafterbeingnotifiedofanallocationofshares,forward to: