planning, scheduling and budgeting value-added chains

TRANSCRIPT

Computers and Chemical Engineering 28 (2004) 45�/61

www.elsevier.com/locate/compchemeng

Planning, scheduling and budgeting value-added chains

M. Badell, J. Romero, R. Huertas, L. Puigjaner *

Chemical Engineering Department, Universitat Politecnica de Catalunya, ETSEIB-DEQ, Av. Diagonal 647 Pab. G-2, 08028 Barcelona, Spain

Abstract

This paper addresses the implementation of financial cross functional links with the enterprise value-added chain including

retrofitting activities at plant level when scheduling, planning and budgeting in short term planning in batch process industries. The

main idea is achieving financial-supply chain integration into advanced planning and schedule (APS) enterprise systems (Badell &

Puigjaner (2001a). Discover a powerful tool for scheduling in ERM systems. Hydrocarbon Processing, 80 (3), 160; Badell & Puigjaner

(2001b). Advanced enterprise resource management systems. Computers & Chemical Engineering, 25 , 517). The platform built

combines a deterministic cash flow management model with an advanced schedule algorithm using a MILP formulation. The

modelling framework created can support the budgeting activity of the entire enterprise functionality, being now the budget the core

document for enterprise management. The benefits of this work are shown through a case study that illustrates the modelling

framework, the information flows and procedures necessary to implement a financial/supply chain scheduling methodology for the

use of financial managers during planning and budgeting activities in process industries.

# 2003 Elsevier Ltd. All rights reserved.

Keywords: Financial integration; Planning; Scheduling; Budgeting; Value-added chain; Batch process industry

1. Introduction

The importance of financial and cash management

was recognised 50 years ago. Howard and Upton (1953)

affirmed: ‘‘The effective control of cash is one of the

most important requirements of financial management.

Cash is the lifeblood of business enterprise, and its

steady and healthy circulation throughout the entire

business operation has been shown repeatedly to be the

basis of business solvency’’. The importance of an

effective and steady cash control acknowledged by

Howard and Upton long ago at the present is bigger

due to the increased mobility of capital. Further, since

that time the working capital of companies drop

soundly. The dynamical economy continuously in-

creases production alternatives and hence makes in-

tractable the empiric management of the enterprise

financial resources. Up till now the cash control to

achieve a steady liquidity circulation is not achieved.

Besides the complexity of the new economy and its

pitfalls, a topical review of historical guidelines and

* Corresponding author. Tel.: �/34-93-401-6678; fax: �/34-93-401-

7150.

E-mail address: [email protected] (L. Puigjaner).

0098-1354/03/$ - see front matter # 2003 Elsevier Ltd. All rights reserved.

doi:10.1016/S0098-1354(03)00163-7

approaches in integration and cash management model-

ling would help in the orientation. Budgeting models for

financial control emerged earlier than operation sche-

dules. Their initial sequential approach focused (for

example, on individual financing/investment asset eva-

luation and its earnings/repayments timing) was later

developed toward the simultaneous consideration of

financial decisions. These included cash flow synchro-

nisation, resources and financing distribution and the

investment of the excess cash in marketable securities

(Charnes, Cooper, & Ijiri, 1963; Robichek, 1967; Orgler,

1969, 1970; Srinivasan, 1986).

Particularly Charnes went beyond about the success

of optimisation advances in production sheduling mod-

els. In his opinion, for a number of reasons the

applications were concentrated in the production area,

but there was no motive for not applying the same

techniques in financial planning, including purchases

and product sales, or even more, in joint operating and

financial planning. About the same approach Robichek

recognised that in order to reach the overall optimum in

short and long term capital budgeting the solution must

be determined simultaneously and not by sequencial

actions, but he also emphasised that the new develop-

ments in linear programming and financial management

Nomenclature

The notation, in alphabetical order, firstly the indicators that provide flexibility to the budget in the

deterministic cash flow linear programming model.

g ; h ; I ; j ; purchase or financing incidence; type of payment; maturity period; time periodA average required cash balance over T periods

Ar accounts receivable at the end of period r

ah ,g ,j technical coefficient of payment xh ,g ,j

Bo cash balance at the beginning of the first periodBx upper limit on accounts payable at the horizonBj cash balance in period j

Ch ,g ,j net return from payment xh ,g ,j

Di ,j net return from investment in marketable securities yi ,j

di ,j technical coefficient of security purchases yi ,j

Ei ,j net cost of security sales zi ,j

ei ,j technical coefficient of security sales zi ,j

Fh ,j net cost of short-term financingkh number of intervals in which a payment k (type h ) can be made

Lh ,g total amount of obligation type h incurred in period g

Mj minimum cash balance in period j

Nj fixed net cash flow in period j

Pr other current liabilities at end of period r

q number of payment types involving accounts payableQ quick ratioRh total amount available for short-term financing from source h

s number of regular payment types (accounts payable and notes payable)Si total maturity value of securities in existing portfolio maturing in period i

T number of periods in the modeltj length in days of period j

u total number of payment types (h�/1. . . q , q�/1 . . . s , s�/1. . . u)

v indicator of the last type of financing (h�/s�/1. . . u , u�/1. . . v)

wh ,g amount borrowed from source h in period g

xh ,g ,j amount of payment type h which is scheduled to be paid in j for an obligation incurred in g

yi ,j amount invested in period j in a security maturing in period i

zi ,j amount sold in period j from a security maturing in period I

M. Badell et al. / Computers and Chemical Engineering 28 (2004) 45�/6146

were still not mature to let them capture the whole

financial problem within a single straightforward treat-

ment. In his opinion the reason for considering isolated

subproblems in financial management was that the

overall financing problem was too complex to be

analysed all at once. At the same period Lerner

(Robichek, 1967) at a Conference in Stanford University

in 1966 remarked that financial officers must support

decision making considering all of them simultaneously.

In his opinion the stronger companies would work in 6

months with integrated financial modelling. Unfortu-

nately, his forecast was excessively optimistic.

On the operative side, a huge number of models,

specially in the last 25 years, have been developed to

perform short term scheduling and longer term planning

of batch plant production to optimise quality or cost-

related performance measures (Shah, 1998). Since the

beginning the feasibility of scheduling and planning

models’ output was supported by another model, the

material resource planning (MRP) system, which

emerged earlier than production scheduling.

Until now both models*/schedule and MRP*/re-

main as independent subsystems when discarding un-feasible plans during the hierarchical planning based on

the material logic. Certainly, these old planning struc-

tures are not enough to sustain the ongoing age of

discontinuity of products and processes. Having the

hierarchical planning a rustic trial and error loop

between MRP and the scheduling model to evaluate

the viability of the proposed plan, cannot offer the

necessary uphold to an economy that must respond to afinancial logic dynamically.

However, very limited works were reported on the

joint financial and operative modelling. If in practice the

financial matters are not still integrated on their own to

M. Badell et al. / Computers and Chemical Engineering 28 (2004) 45�/61 47

support financial decision making, one of the main

reasons is because until today scheduling/planning and

budgeting modelling have been treated as separate

problems and were implemented in independent envir-onments. Financial integration must have degrees of

freedom to change the production decisions in order to

flatten cash flows profiles and leverage earnings. On the

financial side, an effective cash plan and control is still

not operative as production schedules do, and one of the

first reasons could be that the current accounting

systems are not forward looking. Accounting systems

must play a similar role for cash flow as MRP plays tomaterials. By analogy cash flow management needs a

forward-looking ‘bill of finances explosion’, with in-

dividual models to simulate the financing rate of return

in the same manner as materials within MRP systems

have a precise inventory status with all information

about inflows and outflows and inventory models for

each item.

This paper addresses a financial and operatingscheduling/planning modelling framework, simulating

the output of MRP models and cash flows, the latter to

substitute delayed information of accounting systems.

The cash flow and budgeting model will be coupled with

an advanced planning and scheduling procedure using a

MILP formulation. In this paper the model develop-

ment will be exposed through a case study to suggest

that a new conceptual approach in enterprise manage-ment systems, consisting of the joint integration of

enterprise finance with the company operations model,

is a must to improve overall earnings and reach stock-

holder-oriented objectives. This case study includes a

complex decision scenario with retrofitting activities at

plant level, which results will be described subsequently.

2. Objectives

The aim of this work is to propose the use of

advanced planning and schedule (APS) tools backed

up with the appropriate models to make joint financial

and operative integrations in order to support and

change the current position of chief financial officers

(CFO) during complex decision-making when planning

in chemical process industries. This approach changesnot only the sequential analysis of financial actions to a

simultaneous one in order to improve financial manage-

ment quality, but gives the possibility of considering

operative production tasks as variable decisions. There-

fore the scope is enhanced by coupling financial short-

term projection with the value-added chain and other

enterprise planning activities.

While inventory control methods have long beendeveloped for increasing the efficiency of inventory

management, a similar need for updated cash inventory

is not achieved owing to the backward-looking ap-

proach of accountancy. An updated cash inventory

control is absolutely necessary to execute joint financial

and operative scheduling models.

The best manner of having early warning of financialproblems ahead is to manage with a proactive approach

to prevent illiquidity. This provides to the CFO the same

possibilities*/but regarding cash management*/that

since several decades ago had been covered for the

inventory manager to lower inventory-carrying costs

and identify material shortages before their production

lines shutdown. The substitution of intuitive sequential

decision making by a time-phased simultaneous optimi-sation of the enterprise activities to evaluate plans and

budgets offsetting the constrained net cash requirements

could increment value to shareholders while satisfying

customers. The methodology heightens the decision-

making capacity of the CFO levering its possibilities to

the new breakthroughs necessary today. This approach

is not available in the literature neither in software

market.

3. The enterprise financial organisation

The CFO has a key leadership role on the top

management team and is heavily involved in strategy

and decision making about planning, budgeting and

evaluation tasks. With a global enterprise and opera-

tional oversight the CFO can distribute resourcesoptimally through the entity functionality. Cash man-

agement and related financial instruments on a short-

term basis are part of financial officer’s tasks. However,

long range decisions, such as capital budgeting, funds,

dividend policy, merges or fusions are usually of higher

priority than cash management. But the outcome of

long range decisions is usually an input of cash manage-

ment tasks and this low prioritised work is the most timeconsuming management task in decision making and

could be the first step on the way to firm insolvency.

Because of the long time horizon of capital budgets,

they are usually divided into annual periods. Hence, the

first period of the capital budget is the horizon for the

cash management model, e.g. for the short-term plan

and budget. A joint time period means that the two

types of financial decisions are interrelated, so theyshould be considered jointly. If they are considered

independently sub-optimal decisions are obtained. Thus

a vision of both underlying functions is therefore very

convenient.

In the annual plan, when elapsed first periods, say a

month, the whole annual model is re-computed while

planning the next second month. So constantly only the

decisions of the first month of the plan are applied.However, their longer-run effects for the resting months

of the year are always visualised. With this move the

model updates with fresh data the ‘past’ future of the

M. Badell et al. / Computers and Chemical Engineering 28 (2004) 45�/6148

latter annual computation when each new computation

is performed. This ensures the optimal fulfilment of long

term capital budgets year by year and hence marks the

difference with the historic accountancy approach bylooking forward to the near future.

Regrettably CFOs are now forced to make short-term

decisions without including simultaneously the effect on

the underlying capital budget in course and for their job

use out of date, estimated or anecdotal information. A

cash inventory in real time, as all material resources

have in MRP systems, is not yet available. Notice that

MRP systems, which support the feasibility of operativeplans and schedules, is forward-looking during the

BOM explosion.

Due to the fact that the feasibility of financial

projections is achieved through the support of accoun-

tancy information, at the present financial management

is like driving a truck by looking through the rear-view

mirror. In that position it is not possible to see where the

entity is going, only where it has already been, notknowing if damage was provoked. Sometime later,

issues show up in the financial results what really

happened and maybe how easy it would have been to

avoid the damage. At this point it is usually too late,

comings and goings have already become problems.

This delayed analysis is typically done on an ad-hoc

basis when the fireman syndrome appears, rather than

as an integrated and comprehensive approach to proac-tive managerial performance. Worse yet is that there is

no consciousness of these shortcomings.

As a consequence of these pitfalls many subjective

rules are used to address financial issues. When the

minimum net cash balance is not achieved the main

solution is to borrow the amount required. But other

management decisions for short-run financing exist, as

speeding up collections or delaying payments. Manytimes these decisions to avoid cash shortage are made

independently from other financing-investment deci-

sions or bank services. On the other hand many times

the payment schedules are determined automatically,

and are no longer subject to joint consideration with the

investment-financing decisions makers.

Also automatically investing the surplus cash is not a

good rule, it must be found the best possible way ofreproduction. When a cash surplus can be used to retire

debt, other decisions less profitable, as purchasing short

term marketable securities, must be rejected. Only if all

alternatives are not profitable, net cash flow should be

higher or lower than minimal.

But sequential actions not only are regarding time,

sometimes are segmented by departments or by teams.

While each division forecasts its own needs or surplus,financing and investment decisions are made by the

head office. Also many firms tend to separate the

management of marketable securities from other cash

management decisions. New analytical models must be

developed for solving these problems since traditional

methods are today inadequate. In most cases the

analytical approach represents a significant improve-

ment over simple rules of thumb and subjective decisionmaking. The complexity of cash management problems

stems from the large number of relevant decision

variables, their interrelationship within each time peri-

ods and among time periods and the high frequency

with which these decisions have to be made.

Unlike capital budgeting, the management of working

capital concentrates on short term financial decisions

and, therefore, is closely related to cash management. Itis the management of liquid assets, which can be divided

into four major categories: cash, marketable securities,

accounts receivable and inventories. In Fig. 1 the control

of the cash flow of the working capital is achieved by

placing the finances in the prevalent position in the

integrated multi-functional approach. The commercial

supply chain operations are represented within the

operative schedule to make out the real time inventoryof cash represented in the net cash flow profile. This

constitutes a new approach not considered in enterprise

systems standards.

4. Enterprise-control system integration standard in

batch industry

With the aim of providing solutions with an approx-imation to the standard terminology and approaches a

brief review of the postulates on which standards are

based on is necessary. The material logic of the pioneer

MRP systems still remains as the kernel of most of the

current commercial enterprise systems that consider

operation planning while financial logic is absent being

crucial to integration. Therefore, there is a gap between

shop floor and business level related to e-business due tothe absence of a financial cross-functional factory-to-

business link. The standards developed are not yet able

to standardise the financial logic because it never was

used, creating, for this reason, the mentioned gap. The

ANSI/ISA’s S88.01 standard Batch Control was devel-

oped by the International Society for Measurement &

Control (ISA) and published in 1995 by ISA and

American National Standards Institute (ANSI). TheS88.02 Batch Control Part 2: Data structures and

Language Guidelines, has been published and covers

in detail the areas of storing and exchanging batch

control data and also provides detail about what a batch

recipe actually looks like. The ISA-SP95 Enterprise-

Control System Integration Part 1: Models and Termi-

nology (draft) is based and complaint with S88.

Thus the problem concerning implementation offinancial recipes is not considered in these standards.

In the production environment the recipe is defined as:

‘‘Associated with each product is a directed network of

Fig. 1. Scheme of the enterprise system proposed to control working capital by cash management.

M. Badell et al. / Computers and Chemical Engineering 28 (2004) 45�/61 49

tasks, where the directed arcs in the network indicate the

precedence order among tasks and at the same time

represent the direction of material flow between tasks.

Each product has a distinct recipe.’’ Although recipe is

only associated with production, by analogy the term

can be enlarged for financial operations and financial

assets. Indeed, from a financial viewpoint, plants act as

money factories where the cash can be seen as a raw

material or a resource that flows continuously in and

out through pipelines from sources to destinations (see

Fig. 2). So we used for commercial operations the same

model and nomenclature as the production recipes but

by means of virtual processing units related to financial

tasks as unit operations do to operation.Fig. 3 shows details of the output when the proposed

financial recipes are used to represent the commercial

supply chain operations as a real functional factory-to-

business link.

As can be seen in Fig. 4, with this modelling

framework*/and as already happens with multiplant

operating schedules*/finances of multisite enterprises

would easily be managed by an overall partnership

interoperable platform shared by the high level business

management. The enterprise cash management inter-

operating sites are freely regulated between certain

bounds, based on the analysis of the optimal overall

alternative. The data retrieved and the integrated models

support the linkage of the firm’s strategic focus and

other organisational constraints in a computer-aided

decision tool to support the optimal enterprise-wide

financial decision-making.

5. Previous work in cash management models

The cash balances normally fluctuate due to the lack

of synchronisation between cash inflows (receipts fromaccounts receivable and cash sales) and outflows (pay-

ments on accounts and notes payable). The schedule of

flows must be simultaneously determined to make trade-

off solutions. The cash management problem consists of

optimally financing net outflows through a line of

credit, pledging accounts receivable, selling marketable

securities or investing the net inflows in marketable

securities considering yield and transaction costs.A review of the previous theoretical works in the

literature reveals that while in the area of deterministic

models of cash management most of them were devel-

oped focusing more in the individual financial decision

types, at the stochastic side of cash management models

two basic approaches were developed. Baumol’s model

(1952) had an inventory approach assuming certainty.

Cash was treated similarly as holding inventory andpayments were assumed at a constant rate. On the

contrary Miller and Orr (1966) (see Fig. 5) used their

predictions about economies of scale in corporate cash

Fig. 2. Flows of money in the enterprise scenario.

M. Badell et al. / Computers and Chemical Engineering 28 (2004) 45�/6150

demand assuming uncertainty and interest rate effects.

The transactions motive for holding cash was based on

the fact that perfect forecasts of cash were virtually

impossible to achieve because the timing of inflows

depend on payments of customers.Since the 1960s linear programming was introduced

to the area of finance to consider the intertemporal

aspects in the financial environment. On the determi-

nistic side the model proposed by Orgler (1969) was

based on keeping a minimum cash while all excess is

invested in marketable securities as shown in the right

side of Fig. 5.

The positive peaks of cash are due to the span

between cash inflows and buys of marketable securities

and the cash income from sale of securities and pay of

liabilities. The outflows of cash are controllable and

hence not stochastic in the deterministic model. A large

portion of the inflows are predictable while others

consist of controlled inputs (e.g. selling marketable

securities from the initial portfolio prior to maturity).

The intertemporal features of cash management were

treated using unequal periods in a linear programming

model to capture the day-to-day aspect of the cash

management problem. Cash deposits in excess as a

‘minimum’ cash balance requirement improve the firm’s

credit conditions. Consequently, determining the ‘mini-

Fig. 3. A money-time-based schedule. Right:

mum’ cash balance is also a part of the cash manage-

ment problem (Srinivasan, 1986).

The research in cash management modelling was

more based in decomposition techniques paying less

attention to broader enterprise objectives. The whole

sequence of interrelated problems in an enterprise was

not considered, likely due to the lack of adequate

software and computers. The target was to minimize

the cost from the cash budget over the planning horizon

subject to the constraints involving decision variables.

The unequal periods reduced the effect of uncertainty by

increasing the number of periods at the beginning, for

which the cash needs were determined with precision,

and lumping the remaining periods with forecasts less

accurate. In order to synchronise in the most profitable

form the cash inflows/outflows of financial operations,

were kept fixed the resting segments of the enterprise

planning decisions. Enterprises today do not have

appropriate and well tested integrated commercial soft-

ware tools, neither completely defined the theory to

develop them to provide reliable answers for internal/

external decision making focused on treasury and over-

all integration.

Nowadays the majority of finance software applica-

tions are commercial off-the-shelf packages with indivi-

dual analysis of financial items in toolboxes. Model-

based software on financial matters only offers service

to aid financial operations in the different types of

decisions and value market, timing the individual

functions to calculate the basic analytical tasks of

financial operations. There are no tools to simulate the

enterprise scenario as a whole.

The approach of this paper modifies the traditional

way of working when uses the simultaneous analysis of

actions to better assess the current role. The scope is

enhanced by coupling the financial short-term projec-

tion with supply chain planning and asset investments

considering them as variable decisions to be properly

a brewery financial-production schedule.

Fig. 4. Multisite enterprise cash management by overall control of the safety stock of cash.

M. Badell et al. / Computers and Chemical Engineering 28 (2004) 45�/61 51

interconnected in the set of decisions necessary for

optimal overall financial-operation management.

To shift the finance function from a paper driven

clerical role to a more active role as value producer,advisor and strategist, complex objective functions have

to be developed and permanently enhanced. The goal

must be not to let that the financial viability become

threatened by poor cash flow decisions in the firm.

6. The modelling framework

In this work financial objectives are placed in

dominant position during simultaneous financial-supply

chain synchronisation while testing different alterna-tives. The supply chain manages a demand, whose

accomplishment will depend on the plant capacity and

hence will be determined by a production scheduler tool

(the APS tool). On the other hand, a budgeting tool

determines the financial performance where cash flow is

managed. Hence, through this synchronisation between

supply-chain demand (as a function of plant capacity

through the APS tool) and the financial performance (asa function of the cash availability through the budgeting

tool) is possible the visibility of the cumbersome

Fig. 5. Securities investments at A�/A?, sales at B?B in Miller and Orr model;

sales and buys.

interactions between the plant floor and the supply

chain decision-making. The blind position of the CFO

can disappear being able to improve enterprise competi-

tiveness by knowing where the money is and where it

will be by the on line cash inventory profile, in part as a

result of the supply chain commercial scheduled deci-

sions.

The data necessary for managing the cash account of

a business firm include purchases, sales, collections on

accounts receivable, sources of short-term financing and

yields on short-term marketable securities. When the

solution method is segmented with the firm’s operation,

the production information requires the use of offline

forecasts, which always introduce an element of un-

certainty relative to the cash management problem.

Although our model is also affected by uncertainty, it

makes the difference due to the fact that it is connected

to the supply chain through the purchases of raw

materials to suppliers and through the sales of final

products to the customers as decision variables in the

form shown in Fig. 6. If uncertainty is relatively

unimportant owing to the short-term nature of the

problem, it is very important the fact of considering

fixed the production decisions, e.g. the purchases and

the deterministic model without bounds, where peaks are provoked by

M. Badell et al. / Computers and Chemical Engineering 28 (2004) 45�/6152

sales, which remove almost all the problem degrees of

freedom to obtain best solutions.

The selection of an APS tool as the overall framework

to support the joint modelling approach proposed was

not fortuity. A brief review of enterprise software

systems is necessary. Enterprise software refers to a

well organised system, where software and information

are efficiently integrated giving access to all the organi-

sation with a high level of accuracy and minimal manual

intervention, eliminating duplications and functional

‘islands’.APS approach relies on models that permit to

schedule resources assuming finite capacity. APS is

based on complex algorithms, simulation engines and

other technologies that have no linkage with enterprise

resource planning (ERP) transaction systems. This tool

has evolved with a continuous improvement coupled

with the incorporation of new technologies, as schedul-

ing logic (Layden, 1998) and Gantt charts, which permit

people to view resource profiles and schedules and

interactively update them. The evolution of APS also

became linked to the evolution of the computer,

mathematical models and optimisation techniques. La-

ter on logic was developed for specific scheduling issues

like sequencing activities or calculating lot sizes. As

computers were able to take a more complete view of

planning problems, they considered an entire manufac-

turing site and identified the sequence of operations that

minimised makespan or maximised profit. Afterwards

industry connected the management of product recipes

to the production equipment to execute plans. Thus

much of the analysis that executes APS tools is above

the transactional scope. APS takes data from an ERP

system and incorporates advanced calculation techni-

ques to develop directly precise business plans. APS

eliminates the trial end error process linked to material

resource planning in transactional systems as ERP

because APS is designed to simultaneously coordinate

their material and capacity resources with their business

Fig. 6. Financial links with the supply chain affected by uncertainty.

rules (objectives and priorities) and constraints. Because

of APS’ ability to give companies realistic plans,

companies are able to provide their customers with

capable-to-promise accurate information and meetproactively their JIT (just in time) shipment. In the

mid 1980s many major chemical companies realised that

they were becoming limited in their ability to offset

manufacturing process and started examining their

supply chain activities, the today basic trend in these

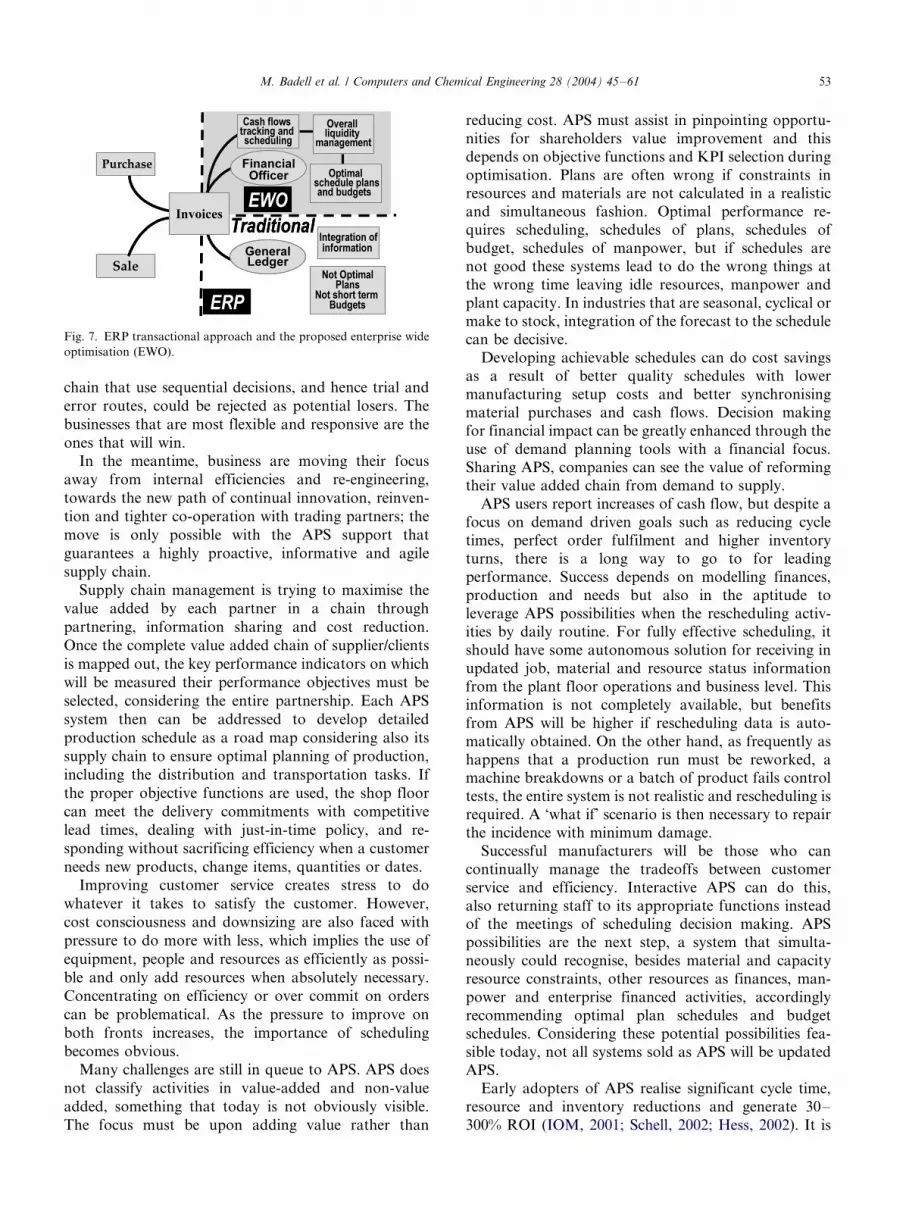

research branch (Fig. 7).

On the contrary the transactional systems architecture

that ERP systems have, limited the planning andscheduling capabilities to MRP, CRP, etc. until rela-

tively recently. ERP systems are linked with MRP

systems through a trial and error loop to let production

plans test its material feasibility. ERP or SCM solutions

must be very reactive on trying to deadlines.

However, in 2000 APS market had an inflection point

(McCall, 2001). An inflection point is provoked when

the fundamental technology on which applications arecreated shifts to such a degree that the applications must

be developed over again. Besides coming out with new

applications, APS vendors had to invest in research and

development (R&D) or collaboration. Now ERP ven-

dors are introducing APS tools within its system. While

the ERP framework moves to a metamorphosis from its

transactional approach to the advanced planning and

scheduling framework, an APS implant in ERP canovercome the limitations and bridge the gap between the

two approaches. ERP vendors may say that a good ERP

system can provide the same functionality of APS, but

this is only real when it has embedded a true APS that

adds business value increasing its usability for ‘what-if’

scenarios (Shobry, 1998; Fraser, 1999; IOM, 2001;

http://www.autofieldguide.com/).

From the viewpoint of human factors, APS equippedwith integrated enterprise modelling systems, will influ-

ence towards favourable changes. While production

planners are more concerned with the efficiency side of

production, others claim due date fulfilment or inform

in response to illiquidity situations. Management’s time

is consumed in production meetings where jobs, custo-

mers and receivables unpaid are reviewed and priori-

tised. Then manufacturing efficiency is disrupted, setupsare shutdown, outside processes are employed or over-

time is expended. The staff occupation in meetings of

today displaces other jobs that could make crisis

tomorrow.

But the problem not only concerns the single en-

terprise. The natural way to achieve more, once

individual organisations had achieved efficiency, is to

extend the organisation management to its supply chain.From supplier’s supplier to customer’s customer, each

link gives an impact in the responsiveness and agility of

the whole chain. One malfunction and the entire system

is no longer responding accurately. The slow links of the

Fig. 7. ERP transactional approach and the proposed enterprise wide

optimisation (EWO).

M. Badell et al. / Computers and Chemical Engineering 28 (2004) 45�/61 53

chain that use sequential decisions, and hence trial and

error routes, could be rejected as potential losers. The

businesses that are most flexible and responsive are the

ones that will win.

In the meantime, business are moving their focus

away from internal efficiencies and re-engineering,

towards the new path of continual innovation, reinven-

tion and tighter co-operation with trading partners; the

move is only possible with the APS support that

guarantees a highly proactive, informative and agile

supply chain.

Supply chain management is trying to maximise the

value added by each partner in a chain through

partnering, information sharing and cost reduction.

Once the complete value added chain of supplier/clients

is mapped out, the key performance indicators on which

will be measured their performance objectives must be

selected, considering the entire partnership. Each APS

system then can be addressed to develop detailed

production schedule as a road map considering also its

supply chain to ensure optimal planning of production,

including the distribution and transportation tasks. If

the proper objective functions are used, the shop floor

can meet the delivery commitments with competitive

lead times, dealing with just-in-time policy, and re-

sponding without sacrificing efficiency when a customer

needs new products, change items, quantities or dates.

Improving customer service creates stress to do

whatever it takes to satisfy the customer. However,

cost consciousness and downsizing are also faced with

pressure to do more with less, which implies the use of

equipment, people and resources as efficiently as possi-

ble and only add resources when absolutely necessary.

Concentrating on efficiency or over commit on orders

can be problematical. As the pressure to improve on

both fronts increases, the importance of scheduling

becomes obvious.

Many challenges are still in queue to APS. APS does

not classify activities in value-added and non-value

added, something that today is not obviously visible.

The focus must be upon adding value rather than

reducing cost. APS must assist in pinpointing opportu-

nities for shareholders value improvement and this

depends on objective functions and KPI selection during

optimisation. Plans are often wrong if constraints inresources and materials are not calculated in a realistic

and simultaneous fashion. Optimal performance re-

quires scheduling, schedules of plans, schedules of

budget, schedules of manpower, but if schedules are

not good these systems lead to do the wrong things at

the wrong time leaving idle resources, manpower and

plant capacity. In industries that are seasonal, cyclical or

make to stock, integration of the forecast to the schedulecan be decisive.

Developing achievable schedules can do cost savings

as a result of better quality schedules with lower

manufacturing setup costs and better synchronising

material purchases and cash flows. Decision making

for financial impact can be greatly enhanced through the

use of demand planning tools with a financial focus.

Sharing APS, companies can see the value of reformingtheir value added chain from demand to supply.

APS users report increases of cash flow, but despite a

focus on demand driven goals such as reducing cycle

times, perfect order fulfilment and higher inventory

turns, there is a long way to go to for leading

performance. Success depends on modelling finances,

production and needs but also in the aptitude to

leverage APS possibilities when the rescheduling activ-ities by daily routine. For fully effective scheduling, it

should have some autonomous solution for receiving in

updated job, material and resource status information

from the plant floor operations and business level. This

information is not completely available, but benefits

from APS will be higher if rescheduling data is auto-

matically obtained. On the other hand, as frequently as

happens that a production run must be reworked, amachine breakdowns or a batch of product fails control

tests, the entire system is not realistic and rescheduling is

required. A ‘what if’ scenario is then necessary to repair

the incidence with minimum damage.

Successful manufacturers will be those who can

continually manage the tradeoffs between customer

service and efficiency. Interactive APS can do this,

also returning staff to its appropriate functions insteadof the meetings of scheduling decision making. APS

possibilities are the next step, a system that simulta-

neously could recognise, besides material and capacity

resource constraints, other resources as finances, man-

power and enterprise financed activities, accordingly

recommending optimal plan schedules and budget

schedules. Considering these potential possibilities fea-

sible today, not all systems sold as APS will be updatedAPS.

Early adopters of APS realise significant cycle time,

resource and inventory reductions and generate 30�/

300% ROI (IOM, 2001; Schell, 2002; Hess, 2002). It is

M. Badell et al. / Computers and Chemical Engineering 28 (2004) 45�/6154

impossible to forecast a real ROI for ERP systems when

less than 20% (Funk, 2001) are successes, more than

80% are failures, which means not achieving 70% of

projected gain. This is likely motivated because APSsystems add more ‘brains’ behind. However, nowadays

they need the sensors and organisation created by ERP

and plant systems to manage the data needed to

simulate business. Whatever the reasons and challenges

of other technologies and even the past implementation

integration failures, the APS system passed the real test

with ROIs not obtained by others. A lot of advantages

were the reasons for its preference as framework tointeractively integrate enterprise functionality. APS

systems are a step forward.

7. Formulation of the problem

In our formulation we create in the APS systems the

computer models that enable the simultaneous planning

of all resources/constraints (materials, labour, machines,tools, etc.) on a global basis. Consequently our ap-

proach enhances the APS achievements when creates a

software package (stand alone or coupled with ERP

systems) that meets a new enterprise-wide optimisation

in the financial management. It consists in using all the

possibilities to reproduce money and to change the

actual enterprise post calculated operative-economic

picture by outdated accountancy drivers updatingthem in real time with a future viewpoint using financial

drivers and optimal budgetary policy. As a result the

focus will not be on the past but on the future and it is

expressed not with the accountancy measures but with

the financial cash flows. This is feasible due to the

robust cash flow information captured directly from the

production and value-added chain actors. This makes

possible the connection of all company functionalitythrough their expenses and yields measured in a

common performance measure.

The suggested approach is based on a unequal multi-

ple-period linear programming model which includes as

decision variables payments, short-term financing, cash

balance and securities transactions, for which both the

amount and maturity are explicitly defined and conse-

quently derived by the model. The model’s objectivefunction represents the horizon value of net revenues

obtained from cash transactions over the entire planning

period and is maximised subject to a set of subjective

and institutional constraints. When subjective con-

straints are incorporated managerial risk preferences

are implemented. The model may start with daily

intervals and end with monthly periods that cover the

main portion of the horizon or vice versa. At the end offirst period the model is re-computed so that only first

period decisions are implemented while their effects over

the entire horizon are taken into account. As a result the

model used is able to ‘remember’ the future instead of

remembering the past, as current accountancy practices

does.

The size of inventories or the credits to customers are

decision variables within the model. The payments to

providers are scheduled within the time span and subject

to the credit terms specified by the firm’s creditors.

Daily disbursements, which are controlled by a financial

officer with respect to their size and timing, are

associated with accounts payable. Because of discounts

on accounts payable and interest savings on other types

of controllable payments, total payments may be less

than the amount payable. This aspect of the payment

schedule is taken into consideration by multiplying the

payment with an adjusting coefficient which is based on

the discount rate or interest savings. For instance, a

payment on a 2%-10 days, net-30 days account payable

is divided by a technical coefficient during the first 10

days after the purchase period. Other payments, as the

payroll, whose size and timing are predetermined, are

still considered as fixed cash outflows but should be

modelled to flatten overtime peaks by flexible manage-

ment. It is assumed a lower bound on cash holdings. If a

production schedule violates the cash flow, it is con-

sidered unfeasible and a hard constraint demands for

another plan solution avoiding trial and error proce-

dures involving human intervention. If the violation of

due date far outweigh the benefits of working without

minimum cash rupture, due date is fulfilled or vice versa.

The new integrated financial approach guides the

organisation through optimal schedule budgets with

electronic Gantt charts and reschedules updates. Once

the scenario is erected, a set of cross-functional links via

performance measures, predictors and drivers must be

established to begin the simulations of alternatives (Fig.

8). From the APS block it is obtained the information

regarding the constraints of the functions taken into

account in a given case. The subjective constraints of the

institution and CFO are added to specify the simulation

model. With these elements the budget model is

specified where different simulations of alternatives

can be tested. When the initial model is obtained, then

it is optimised with a linear programming formulation.

Finally the optimal budget accepted is applied and

monitored. If incidences occur violating the budget

schedule, a reschedule is done.

Having financial managers a tailor-made scheduling

tool to simulate and test different budget schedule

alternatives with information and transparency of the

limitations and interactions occurring at plant and

business level within each alternatives, best operations

such as discounting, levering, investment in marketable

securities, acquiring credit and loans, pledging, advan-

cing and many others can heighten the corporate value

status.

M. Badell et al. / Computers and Chemical Engineering 28 (2004) 45�/61 55

The modelling framework of the system capable of

making the simultaneous optimisation of the supply-

chain, retrofitting decisions and financial operations

consists of a linear programming model with rollinghorizon possibilities that uses an optimal operative

production schedule solution with customer satisfaction

in order to determine the optimal budget and cash flow

plan of the company.

8. Budgeting modelling framework for optimalretrofitting

A 4 month time horizon is chosen, divided unequally

into four periods of 10, 20, 30 and 60 days, respectively;

i.e. period 1 has 10 days, period 2 has 20 days, etc. (see

Fig. 9).

This case study is based on a batch specialty chemical

plant. A number of products are produced in differentequipment units, where switch-over times and cost

between products is of special concern. An advanced

planning and scheduling algorithm is available. In this

case study it is studied the plant retrofit to improve the

switch-over between products, reducing the cleaning

time required, in order to be able to assume a higher

product demand. Hence, first, modifying and expanding

budget model is analysed the maximum retrofit invest-ment having a financial capacity limited by the liquidity

requirements of the CFO. Second, interacting the

budgeting with the designed APS tool, a retrofit

investment is proposed considering the expected future

plant financial behaviour after the retrofit (Fig. 10).

The objective function, to maximise in time horizon

T , is the sum of payments taking or not the prompt

payment discounts, Xg ,j , and marketable securitiesrevenues, (yi ,j �/zi ,j), deducting costs of the short term

Fig. 8. Management functional links in financial/supply chain integra-

tion.

credit line, wh ,g and of the retrofit loan, Rg . Technical

coefficients C , D , E , and F adjust quantities depending

on the timing of periods when actions incur; of maturity,

i , payment, g , sales, j , credit, h , etc.

REVENUE

�XT

j

Cg;jXg;j�XT�1

j�2

XT

j�1

(Di;jyi;j�Ei;jzi;j)

�XT

g�1

Fh;gwh;g�XT

g�1

Rg (1)

Production expenses during the week will consider

initial zero stock and raw material needs. The economicsituation of the case study is based on the information

given. The initial working capital considered is 100

monetary units (mu). The minimum net cash flow

allowed (Mj ), beneath which a short-term financing

source must be found, is determined by the CFO taking

into account the variability of cash outflow. The

following hard constraint is then introduced.

bj �Mj j� 1; . . . ; T (2)

The portfolio of marketable securities held by the firm

at the beginning of the first period includes several sets

of securities with known face values in mu and maturity

periods, only one maturing beyond the horizon (S1�/

250, S2�/190, S3�/1900, S4�/1500, S5�/2250). Allmarketable securities can be sold prior to maturity at

a discount or loss for the firm. Revenues and costs

associated with the transactions in marketable securities

are given by technical coefficients Dij and Eij .

Xt�1

j�1

dt;jyt;j i�2; . . . ; T where Dij �1�dij (3)

Fig. 9. Budget time horizon of 120 days in four unequal periods.

Fig. 10. Enterprise capacity for retrofitting investment (Y retrofit, X

years, Z budget revenue).

M. Badell et al. / Computers and Chemical Engineering 28 (2004) 45�/6156

Xi�1

j�1

et;jzt;j 5Si i�2; . . . ;T�1 where Eij

�1�eij (4)

A short term financing source is represented by a

constrained (850 mu) open line of credit. Under an

agreement with the bank loans can be obtained at the

beginning of any period and are due after 1 year at a

monthly interest rate of 0.5%. Early repayments are not

permitted. The costs of taking a loan relevant for

measuring the performance of the cash managementdecisions are given by technical coefficients Fh,g .

XT

g�1Fh;gwh;g5Kh h�1; . . . ; v (5)

The payment decisions to be considered correspond toaccounts payable with 2% 10 days, net 30 days terms of

credit (2-10/N-30). All payments of raw materials must

be fulfilled within the horizon (L1�/803, L2�/2409,

L3�/3212, L4�/7227). In consequence, all obligations

for raw materials prior to period 1 have been met.

Purchases of raw materials of periods 1, 2, 3 and 4 are

the variable decisions that connect the production with

the finances for the material resource planning (MRP)supply. It is assumed that all bills are received in the first

half of the respective periods and that payments,

including sales of final products, are made at the

beginning of the periods. Any part of the bills can be

paid either at the first 10 days with a 2% discount or at

face value after 30 days. It remains to be decided upon

what part of the bills to pay in which period. The

payments are constrained by the following equation:

XT

j�gah;g;jxh;g;j 5Lh;g

g�T�h�1; . . . ; T

h�1; . . . ; s

�(6)

The net cash flows expected in periods 1, 2, 3 and 4

are variable decisions decided depending on the schedul-

ing solution. The minimum cash balance requirement

for all four periods was assumed 100. Other receipts and

disbursements as payroll, loan repayment or sales (6863mu/month) are entered as time fixed net cash flows. A

requirement that the average daily cash balance be at

least a known figure is incorporated.

The monthly retrofit credit cost is calculated as

�in(1 � i)n

(1 � i)n � 1�1

�loan

12n;

where i is the medium term loan interest technical

coefficient and n the years of loan repayment.

Several possibilities to ‘balance’ the cash budget in

periods in terms of their respective cost can be obtained.

The enterprise has the following management guide-lines: fulfil customer due dates evaluating its cost

expressed as plant capacity drops; take all discounts if

possible; use fully the line of credit; delay selling

marketable securities as long as possible, but sell them

if it is necessary to get a discount. With this input is

determined an output, the cash budget, with the best

timing of payments, investments, sales of marketable

securities and financing decisions.

9. The scheduling modelling framework: a case study

The case study consists of a batch specialty chemical

plant with two different batch reactors (R1 and R2).

Each production recipe basically consists of the reaction

phase. Hence, raw materials are transferred from stock

to the reactor, where several substances react, and, at

the end of the reaction phase, products are directly

transferred to lorries to be transported to differentcustomers. Plant product portfolio is around 60 differ-

ent products using up to 15 different substances.

Production times range from 3 to 34 h. Product

switch-over basically depends on the nature of both

substances involved in the precedent and following

batch. Cleaning time ranges from 0 up to 6 h.

Here, plant retrofit to improve product switch-over is

envisaged. In order to estimate the weekly raw materialliabilities and sales, a Montecarlo simulation of weekly

product demand has been scheduled minimising switch-

over and production cost. As stated, product demand is

generally higher than plant capacity, being this unsa-

tisfied demand the reason of the besought retrofit.

Therefore, the scheduling algorithm not only sequences

batches but also chooses which products out of the

demand portfolio will be produced in a weekly horizon.Being i�/1. . . n the different demand products, Yi is a

binary variable that equals to 1 if product i is included

into plant schedule and, equals to 0 otherwise. As a first

M. Badell et al. / Computers and Chemical Engineering 28 (2004) 45�/61 57

approach, the selection of products is considered out of

the budget optimisation.

The objective of the scheduling algorithm is to

maximise in a week horizon (168 h) the benefit obtainedfrom producing a number of products of the demand

portfolio considering each product hourly contribution

to profit1 (Bi ) minus the required cleaning cost (CCi,i ?),

Eq. (7).

Objective_Function

max

�Xi

BiYi�X

e

Xk

Xi

Xi0

CCi;i0xi;k;exi;k�1;e

�

Production_horizon

TFk;e5168 h (7)

where xi ,k ,e is the assignment binary variable of batch i

at position k in the sequence at equipment unit e . This

objective function is maximised subject to constraints of

timing and batch sequence as follows,

Schedule_Timing

TFk;e�TIk;e�X

i

TOPixi;k;e�X

i

�X

i0

CTi;i0xi;k;exi;k�1;e k

]1

TFk;e�TIk;e�X

i

TOPixi;k;e k�1

TIk]TFk�1;e k]1

TIk;e�0 k�1

Batch_sequencing

Xe

Xk

xi;k;e�Yi

Xi

xi;k;e51

Xi

xi;k;e5X

i

xi;k�1;e k]1 (8)

where TOPi is the processing time of batch i , CTi,i’ the

cleaning time when switching-over from product i to i ?,TFk,e and TIk,e the ending and initial times of job k inthe sequence at equipment unit e . This formulation,

introducing aggregated variables for xi ,k ,e xi ,k�1, e ,

gives a MILP formulation that is solved using GAMS-

CONOPT.

1 A rough-cut sales contribution to profit expressed as difference

between price and cost of raw materials.

For instance, consider the weekly product demand,

the cleaning time and the product benefit of equipment

unit R1 shown at Table 1.

In order to solve the problem in an efficient way,firstly the six products with more hourly contribution to

profit are scheduled and then the rest. This strategy,

though might loose some optimality, improves revenues,

profit and permits to solve in less than 20 CPU seconds

at a 1 GHz machine the combinatorial explosion

problem. The procedure concludes that the optimal

number of products to be contemplated in the plant

schedule is ten out of the 13 to be produced in thefollowing order:

prod 20, prod 18, prod 3, prod 22, prod 19, prod 10,prod 6, prod 4, prod 23, prod 15, prod 13, prod 2 and

prod 16

with an overall cleaning cost of 2 mu. Hence, raw

material weekly liabilities and weekly sales for period

and for this reactor are of 350 and 600, mu respectively.

Applying this strategy to the other plant reactor unit

and for several product demand profiles, the estimated

weekly raw materials liabilities and sales are of 709 and

1480, respectively. With this data, the budget withoutconsidering retrofit is shown in Table 2.

10. Retrofitting case

In order to increase plant capacity it is decided to

improve the product switch-over. Investing on a new

cleaning device switch-over times can be reduced in a

60%. We can install this device in one reactor unit or in

both as a function of what investment the enterprisefinancial capacity can afford. Other decision variable is

the loan repayment span; if the loan is paid very quickly

the company will run out of cash and if very slowly the

enterprise will be paying more interests. Finally, it

should also be decided how much the enterprise needs

to invest.

In order to analyse the investment capability of the

batch specialty chemical enterprise under study it is usedthe budgeting model (Eqs. (1)�/(6)) for different repay-

ment spans and required revenues. The result is shown

in Fig. 11. It can be observed how increasing revenues

decrease the available funds. The optimum repayment

span is found where the enterprise net cash flow

balances the interest expenses.

Lets consider that 10 000 mu is the required invest-

ment to install the two cleaning devices in both reactorunits. It is decided a tighten-belt policy during the

retrofitting period reducing the cash inflows in a 2%. A

medium-term loan is negotiated at an 8% annual

interest.

Tab

le1

Typ

ica

lw

eek

lyp

rod

uct

dem

an

do

fre

act

or

un

itR

1

Pro

du

ctP

roce

ssin

gti

me

(h)

Co

ntr

ibu

tio

nto

pro

fit

(mu

)

Cle

an

ing

ma

trix

La

stp

rod

uct

/nex

t

pro

du

ct

Pro

d

20

Pro

d

18

Pro

d

8

Pro

d

12

Pro

d

3

Pro

d

22

Pro

d

19

Pro

d

10

Pro

d

8

Pro

d

4

Pro

d

23

Pro

d

15

Pro

d

13

Pro

d

2

Pro

d

16

Pro

d2

09

3P

rod

20

33

33

03

33

36

33

33

Pro

d1

84

2P

rod

18

60

03

60

00

36

00

30

Pro

d8

17

.52

.5P

rod

86

30

36

00

03

63

02

53

Pro

d1

21

23

Pro

d1

26

30

36

00

03

63

03

3

Pro

d3

9.5

3P

rod

36

33

36

33

33

63

30

3

Pro

d2

23

49

Pro

d2

20

33

33

33

33

63

33

3

Pro

d1

91

44

Pro

d1

96

00

03

60

03

63

03

0

Pro

d1

01

03

Pro

d1

06

30

03

60

03

63

03

3

Pro

d6

73

Pro

d6

63

00

36

00

36

30

25

3

Pro

d4

55

3P

rod

46

30

03

63

00

63

03

3

Pro

d2

33

49

Pro

d2

36

33

33

63

33

33

33

3

Pro

d1

55

2P

rod

15

25

02

52

52

52

50

25

25

25

25

25

25

0

Pro

d1

31

34

Pro

d1

36

30

03

60

00

36

33

3

Pro

d2

17

7P

rod

26

32

53

06

33

25

36

33

3

Pro

d1

66

3P

rod

16

60

00

36

00

03

60

00

3

M. Badell et al. / Computers and Chemical Engineering 28 (2004) 45�/6158

According to Fig. 11, the optimal repayment span of

the loan is of 4 years, so the repayments of 273 mu/

month will total 13 130 mu including interests. Table 3,

and Fig. 11 in schedule format, show the budget of thisretrofitting period. A cash outflow of 18 759 mu is

obtained, less than the 19 126 mu obtained prior retro-

fitting, due to the four loan repayments included in the

horizon (1092 mu).

It can be observed how critical is a good budget

management during a retrofitting period where enter-

prise company revenues could be very sharp. In the

optimal budgets the level of cash is maintained as nearas possible to the minimum level by ad hoc analysis

when a cash surplus appear, only disrupting when any

feasible profitable action can be applied (Fig. 12).

While budgets let CFO to focus the future in the short

and long term planning horizon, from a supervision

point of view the analysis of unexpected cash flow

demands can be definitively accomplished via monitor-

ing budgeting performance in ‘real time’. A cash deficitcould be solved delaying liability payments, selling

marketable securities, negotiating a loan or receivable

by commercial papers. Similarly the use of idle cash can

be systematically evaluated and could be used to buy

marketable securities, necessary assets in plant or to

advance credit/loan repayments saving money to the

firm.

As each decision influence the magnitude of eachother’s decision the simultaneous solution is obliged to

achieve the overall best balance. Besides, the simulation

enables testing different alternatives during planning

introducing constraints and modifying the formulations.

With all the operation and financial information online

with absolute transparency of the limitations and

interactions occurring at plant and business level within

each alternative still the intuitive proper selection is theheart of cash management.

11. Conclusions

The concept behind improved ERP systems is the

overall integration of the whole enterprise functionality

into the management systems through financial links.

Converting current ERP software systems in realmanagement decision tools requires crucial changes in

approach.

The models presented here search the most efficient

cash source providing the exact quantity that strictly

satisfies the punctual necessity without obeying fixed

bound constraints. The cash profile crawls on its

optimal level bound when working out other preferen-

tial action is impossible. The overall KPI is the max-imisation of shareholder value-added within a budgetary

modelling framework with output in schedule format

consisting in an electronic Gantt chart with profile views

Table 2

Optimal budget prior retrofitting period

F.O. max revenue 400 mu PERIOD 1 (10 days) PERIOD 2 (20 days) PERIOD 3 (30 days) PERIOD 4 (60 days)

Cash balance BoP 100 100 100 100

Receipts

Sale of MS 0 2339(S3�S4) 0 0

MS maturity 250(S1) 440(S2�S2*) 0(S3) 1049(S4)

Sale of product 0 0 11 840 13 320

Cash available 350 2879 11 940 14 469

Disbursements

Payments of RM 0 2779(98%L1�L2) 2779(98%L3) 6253(98%L4)

Payroll 0 0 100 300

Retrofitting Without retrofit Without retrofit Without retrofit Without retrofit

Total liabilities 0 0 2879 6553

Excess (shortage) 250 100 100 100

Invest 250 0 8960 7816

Borrow 0 0 0 0

Cash balance EoP 100 100 100 100

Total output (Cash EoP�/100�/S5�/2250�/New Portfolio MS�/16 776)�/19 126 mu

* Investment maturing in horizon.

M. Badell et al. / Computers and Chemical Engineering 28 (2004) 45�/61 59

of shareholder value. The securities portfolio acts as a

diversified buffer of liquid funds that can make a

worthwhile contribution to firm’s wealth avoiding the

perishable spoil of finances. A case study was presented

to use the integrated approach to analyse the investment

in facilities the enterprise can afford in function of its

finances. The work done prototypes a stand alone/

complementary tool for enterprises when transactional

systems type ERP are in use.

Today’s short lifecycle of products and processes

require sharp and finely tuned management actions

Fig. 11. Optimal budget post retro

that must be guided by scheduling tools. Additionally,

such actions must be able to keep track of money

movements concerning supply chain events, synchronise

cash inflows with outflows and ensure a safety cash

stock solving peaks by making full use of the scheduling

possibilities with finite resources.

The new times don’t go leaving space to lose

opportunities. The possibilities of the company to

produce benefits should entirely be taken. In the same

manner as MRP systems did with inventory control,

now would be obligatory to help the enterprise liquidity

fitting in Gantt chart format.

Table 3

Optimal budget post retrofitting period

F.O. max revenue 201 mu PERIOD 1 (10 days) PERIOD 2 (20 days) PERIOD 3 (30 days) PERIOD 4 (60 days)

Cash balance BOP 100 100 100 100

Receipts

Sale of MS 0 2708(S3�S4) 0 0

MS maturity 250(S1) 440(S2�S2*) 0(S3) 676(S4)

Sale of products 0 0 12 920 14 535

Cash available 350 3247 13 020 15 311

Disbursements

Payments of RM 0 3148(98%L1�L2) 3148(98%L3) 7082(98%L4)

Payroll 0 0 100 300

Retrofitting 0 0 273 819

Total liabilities 0 3147 3521 8201

Excess (shortage) 350 100 9499 100

Invest 250 0 9399 7010

Borrow 0 0 0 0

Cash balance EoP 100 100 100 100

Total output (Cash EoP�/100�/S5�/2250�/New Portfolio MS�/16 409)�/18 759

Fig. 12. The control of the model (right) leaves inoperable any cash

upper bound.

M. Badell et al. / Computers and Chemical Engineering 28 (2004) 45�/6160

management with computer-aided planners of its finan-

cial resources. With these tools CFO could locate in time

the proper figure to put in the right place knowing

exactly its effect and the cash inventory status, some-

thing impossible to do now.

Thus CFO could effectively lead a ‘proactive’ for-

ward-looking management with computer-aided bud-

geting systems. Budgets let to focus the future in the

short and long term planning horizon. Armed with up to

the minute information on the overall budget status,

costs and schedules, allocation of resources, reschedules

and cost of capital, the CFO is prepared and available to

respond quickly to events as they arise. With the

proposed simulation framework can be obtained in

time automatic optimal budgets.

A new financial paradigm is acting and it is necessary

to catch its compass. This work constitutes an advance

in the challenge to link finance with the enterprise

functionality based on a forward-looking approach thatproactively synchronises cash inflows and outflows. The

methodology here prescribed leads to a competent,

rigorous and consistent financial system prototype well

suited to the coming competitive business environment

in an era of higher capital mobility.

Acknowledgements

Financial support from European Community by

VIPNET (G1RD-CT-2000-003181) and GCO (BRPR-

CT98-9005) projects is gratefully acknowledged.

References

Baumol, W. J. (1952). The transactions demand for cash: an inventory

theoretic approach. Quarterly Journal of Economics 66 (4), 545.

Charnes, A., Cooper, W. W., & Ijiri, Y. (1963). Breakeven budgeting &

programming to goals. Journal of Accounting Research 1 (1), 16.

Fraser, J. (1999) APS to ERP: how tight a link? APS , May.

Funk, G. (2001). Enterprise integration: join the successful 20%.

Hydrocarbon Processing 80 , 4.

Hess, E. (2002) Make advanced planning & scheduling work for your

company, APS , May.

Howard, B. B., & Upton, M. (1953). Introduction to business finance

(p. 188). New York: McGraw Hill.

IOM Control (2001), ERP survey, Institute Operation Management 27,

8.

Layden, J. (1998) The evolution of scheduling logic, APS , 8.

McCall, J. (2001) APS technology obsolete?, Integrated Solutions ,

April.

M. Badell et al. / Computers and Chemical Engineering 28 (2004) 45�/61 61

Miller, M. H., & Orr, R. (1966). A model of the demand for money by

firms. The Quarterly Journal of Economics 80 (3), 413.

Orgler, Y. E. (1969). An unequal-period model for cash management

decisions. Management Science 20 (10), 1350.

Orgler, Y. E. (1970). Cash management . Wadsworth.

Schell, D. (2002) Overcoming intricacies of ERP system implementa-

tion. Integrated Solutions , 2.

Robichek, A. (1967). Financial research and management decisions .

New York: Wiley.

Shah, N. (1998). Single and multisite planning and scheduling: current

status and future challenges. FOCAPO American Institute of

Chemical Engineering Journal Symposium Series 94 (320),

91.

Shobry, D. E. (1998). The history of APS, APS , Sept.

Srinivasan, V. (1986). Deterministic cash flow management. Omega ,

14(2), 145.

http://www.autofieldguide.com/ (2001). Integrating APS and ERP is

getting easier, Industry Directions.