capital budgeting lecture

TRANSCRIPT

Topic 4 Capital Budgeting - Part 1

What is capital budgeting?

Analysis of potential additions to fixed assets.

Long-term decisions; involve large expenditures.

Very important to firm’s future.

Methods of Project Evaluation

1. Non-discounted cash flow methods - payback period - accounting rate of return

2. Discounted cash flow methods - internal rate of return - net present value

Payback Period

The amount of time required for an investment to generate cash flows to recover its initial cost.

An investment is acceptable if its calculated payback is less than some prescribed number of years.

Payback Period IllustratedInitial outlay -$1 000

Year Cash flow 1 $200 2 400 3 600

Accumulated Year Cash flow 1 $200 2 600 3 1 200

Payback period = 2.67 years

Example

Year 0 1 2 3 PaybackProject A -50 1 49 0 2 yearsProject B -50 49 0 1 3 yearsProject C -50 0 0 500 3 years

Decision:Choose project A

But clearly wrong!

Advantages of Payback Period

No need for detailed analysis. Simple to calculate and understand. Adjusts for uncertainty of later cash flows. Biased towards liquidity.

Disadvantages of Payback Period

Time value of money and risk ignored. Ad hoc determination of acceptable payback period.

Ignores cash flows beyond the cut-off date. Biased against long-term projects.

Accounting Rate of Return (ARR) Measure of an investment’s profitability.

A project is accepted if ARR > target average return.

book value averageprofitnet average ARR

ARR Example Year

1 2 3Sales $440 $240 $160Expenses 220 120 80Gross profit 220 120 80Depreciation 80 80 80

Earnings before taxes 140 40 0Taxes (25%) 35 10 0Net profit $105 $30 $0

Assume initial investment = $240

ARR Example (continued)

$120 2

$0 $240 2

valueSalvage investment Initial book value Average

$45 3

$0 $30 $105 profit net Average

37.5% $120$45

book value Averageprofitnet Average ARR

Disadvantages of ARR The measure is not a ‘true’ reflection of return.

Time value of money is ignored.

Ad hoc determination of target average return.

Uses profit and book value instead of cash flow and market value.

Advantages of ARR Easy to calculate and understand.

Considers all profits of the project.

Net Present Value (NPV)

Net present value is the difference between an investment’s market value (in today’s dollars) and its cost (also in today’s dollars).

Net present value is a measure of how much value (in dollars) is created by undertaking this investment.

Steps

1. Estimate CFs (inflows & outflows).2. Assess riskiness of CFs.3. Determine r = discount rate for the

project.4. Find NPV 5. Accept if NPV > 0

NPV Illustrated

0 1 2

Initial outlay($1 100)

Revenues $1 000Expenses 500Cash flow $ 500

Revenues $2 000Expenses 1 000Cash flow$1 000

– $1 100.00

+454.55

+826.45+$181.00

$500 1.10

$1 000 (1.10)

2

NPV

NPV

An investment should be accepted if the NPV is positive and rejected if it is negative.

Estimation of the future cash flows and the discount rate are important in the calculation of the NPV.

Internal Rate of Return (IRR)

The discount rate which makes the Present value of the Project’s Future Cash flows equal to the cost of the Project.

A project is accepted if its IRR is > the required rate of return.

Generally found by trial and error.

Internal Rate of Return: IRR

0 1 2 3

CF0 CF1 CF2 CF3Cost Inflows

IRR is the discount rate that forcesPV inflows = cost. This is the sameas forcing NPV = 0.

IRR ExampleInitial outlay = -$200

Year Cash flow 1 $ 50 2 100 3 150

Find the IRR such that NPV = 0 50 100 150 0 = -200 + + + (1+IRR)1 (1+IRR)2 (1+IRR)3

50 100 150 200 = + + (1+IRR)1 (1+IRR)2 (1+IRR)3

IRR Example (continued)Trial and Error Discount ratesNPV 0% $100 5% 68 10% 41 15% 18 20% -2

IRR is just under 20% -- about 19.44%

Rationale for the IRR Method

If IRR > r, then the project’s rate of return is greater than its cost-- some return is left over to boost shareholders’ returns.

Example: r = 10%, IRR = 15%.Profitable.

IRR Acceptance Criteria

If IRR > r, accept project.If IRR < r, reject project.

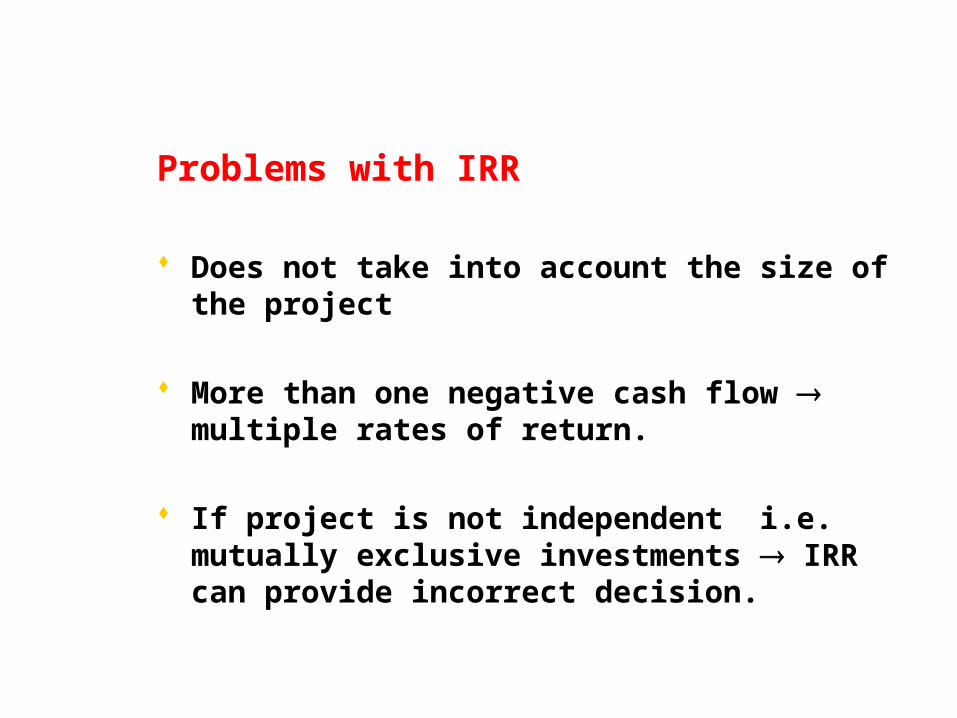

Problems with IRR

Does not take into account the size of the project

More than one negative cash flow multiple rates of return.

If project is not independent i.e. mutually exclusive investments IRR can provide incorrect decision.

Multiple Rates of ReturnAssume you are considering a project for which the cash flows are as follows:

Year Cash flows

0 -$252 1 1 431 2 -3 035 3 2 850 4 -1 000

Multiple Rates of ReturnWhat’s the IRR? Find the rate at which

the computed NPV = 0:

at 25.00%:NPV = 0 at 33.33%:NPV = 0 at 42.86%:NPV = 0 at 66.67%:NPV = 0

Two questions:1.What’s going on here?2.How many IRRs can there be?

Multiple Rates of Return$0.06

$0.04

$0.02

$0.00

($0.02)

NPV

($0.04)

($0.06)

($0.08)

0.2 0.28 0.36 0.44 0.52 0.6 0.68

IRR = 25%

IRR = 33.33%

IRR = 42.86%

IRR = 66.67%

Discount rate

90 1,09090

0 1 2 10YTM = ?

How is a project’s IRR related to a bond’s YTM?

If a 9% Coupon 10 year $1000 bond sells for $1,134.20 what is the YTM (cost of debt, interest rate in the market place)

-1,134.2

YTM = 7.08%

...

90 1,09090

0 1 2 10IRR = ?

If an investment project costs $1,134.20 and generates cash inflows of $90 for the next 9 years and $1090 at end of year 10, what is the IRR?

Answer: 7.08%

IRR and YTM are the same thing. A bond’s YTM is the IRR if you invest in the bond.

-1,134.2

IRR = 7.08%

...

What is the difference between independent and mutually exclusive projects?Projects are:

Independent, if the cash flows of one are unaffected by the acceptance of the other.

Mutually Exclusive, if the acceptance of one project results in the rejection of another project.

NPV and IRR always lead to the same accept/reject decision for independent projects:

r > IRRand NPV < 0.

Reject.

NPV ($)

r (%)IRR

IRR > rand NPV > 0Accept.

0

IRR, NPV and Mutually Exclusive Projects

Discount rate2% 6% 10% 14% 18%

6040200

– 20– 40

Net present value

– 60– 80

– 10022%

IRR A IRR

B

0

14012010080

160 Year

0 1 2 3 4Project A: – $350 50 100 150 200Project B: – $250 125 100 75 50

26%

Crossover Point

IRR vs NPV

IRR NPV selects project selects project

if r = 4% B A

if r = 6% B A

if r = 12% B B

if r = 15% B B

Reinvestment Rate Assumptions

NPV assumes reinvest at r (opportunity cost of capital).

IRR assumes reinvest at IRR.

Reinvest at opportunity cost, r, is more realistic, so NPV method is best. NPV should be used to choose between mutually exclusive projects.

Which methods do companies use? USA study by Ryan

Australian study by Freeman & Hobbes

Always or often used (>=75% )

Net Present Value (NPV) 85%Internal rate of return (IRR) 77%Payback 53%Discounted Payback 38%Profitability Index 21%Accounting rate of return 15%M odified internal rate of return (M IRR) 9%

Econom ic Value Added (EVA) 31%

NPV 75%IRR 72%DCF Profitability Index 23%Payback 44%Accounting return on Investm ent (ARO I) 33%O ther 49%

When calculating NPV’s consider: Include all incremental cash flows.

In undertaking a Project Evaluation need to consider what difference it makes to the total cash flows of the firm whether the firm does or does not undertake the project under consideration.

What to do about ?• sunk costs• opportunity costs• side effects

Ignore Sunk Costs Sunk costs are unavoidable (incurred in the past) cash outflows, no longer relevant to influencing whether a project should be undertaken

Example $10,000 payment to be made to a marketing company for assessing the market for a project which costs $125,000, and yields net cash flows of $75,000 for 2 years when the discount rate is 10%. Should the project be taken on?

Project NPV if:(incorrectly) include marketing costs:-135+75/(1.1)1+75/(1.1)2

= -4.8 => reject

(correctly) exclude marketing costs:-125+75/(1.1)1+75/(1.1)2

= 5.2 => accept

Include Opportunity Costs If project uses resources which could be put to some other use (ie. has an opportunity cost), then $ value of alternative use must be included as cash outflow

Example A company owns machinery which has been leased out generating income of $3m per year. The machinery will now be used in a project which yields $20m for 2 years and costs $30m (opportunity cost of capital is 10%). Should the project be taken on?

Project NPV if:

(incorrectly) ignore foregone lease income as a cash outflow:-30+20/(1.1)1+20/(1.1)2

= 4.7m => accept

(correctly) include foregone lease income as cash outflow:

-30+17/(1.1)1+17/(1.1)2

= -0.5m => reject

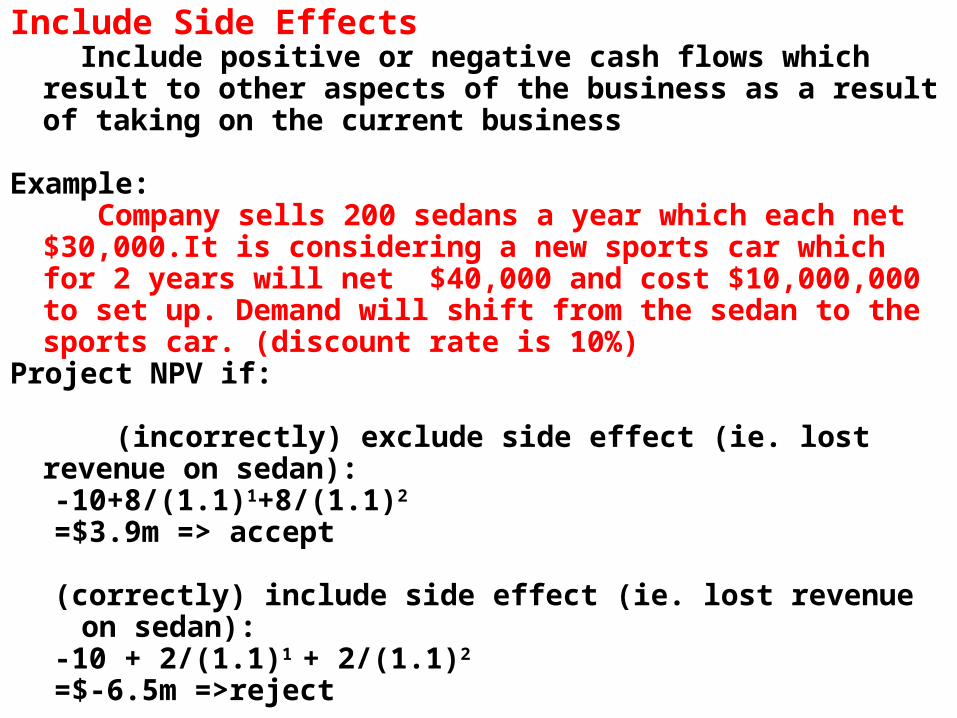

Include Side Effects Include positive or negative cash flows which result to other aspects of the business as a result of taking on the current business

Example: Company sells 200 sedans a year which each net $30,000.It is considering a new sports car which for 2 years will net $40,000 and cost $10,000,000 to set up. Demand will shift from the sedan to the sports car. (discount rate is 10%)

Project NPV if:

(incorrectly) exclude side effect (ie. lost revenue on sedan):-10+8/(1.1)1+8/(1.1)2

=$3.9m => accept

(correctly) include side effect (ie. lost revenue on sedan):

-10 + 2/(1.1)1 + 2/(1.1)2

=$-6.5m =>reject

Consistency

Inflation•If cash flows are nominal cash flows, ie the effect of inflation has not been removed, then the discount rate has to be a nominal discount rate.•If the cash flows are real, ie the effect of inflation has been removed the discount rate has to be a real discount rate.•If the analysis is done correctly it should not matter whether it is done in real or nominal termsTax•If the cash flows are after tax cash flows the discount rate has to be an after tax discount rate.•If the cash flows are before tax cash flows the discount rate has to be a before tax discount rate.•If the analysis is done properly it should not matter whether it is done in pre tax or after tax cash flows

Working capital requirements::

investment in long term assets generally requires support of current assets

initial outflow in current assets necessary to support investment represents cash outflow . This is assumed to be returned as a cash inflow at the end of the project's life

current assets are financed in part by current liabilities, thus net working capital is the cash flow considered

What about Financing Costs?

The costs of financing can be taken account of in either the cash flows or the discount rate.

In our analysis we will be taking account of the financing costs in the discount rate /required rate of return so therefore it is important it is not also taken into account in the cash flows or else there would be double counting.

The required rate of return is the return that the firm has to earn on the project in order to satisfy the providers of financial capital to the project

Net Cash Flows Vs Accounting Entries

Net Cash Flows and Accounting Profit Are Not Equivalent

Accounting entries:: allow for subjectivity and manipulation due to accounting system's inherent problems

Net cash flowsNet cash flows:: timing and magnitude of cash flows are of importance

cash pays expenses; cash can be invested

Taxation 3 major impacts:

• represents a cash outlay• depreciation tax deduction provides a ‘tax shield’

• Capital gains( losses) increases ( decreases) amount of tax paid

Disposal of assets – gain/loss on disposal of assets

If the salvage value > book value, a profit/gain is made on disposal. This profit/gain is subject to tax.

If the salvage value < book value, the ensuing loss on disposal is a tax deduction.

Capital gains

don’t confuse these with gain/loss on disposal of assets

Capital gains made on the sale of assets such as rental property are subject to taxation.

Capital losses are not a tax deduction but can be offset against future capital gains.

Investment Allowance Incentive to encourage investment - cash inflow

ExampleExample:: investment allowance of 18% i.e. 18% of the cost of an investment is an allowable deduction when assessing income tax payable, initial outlay $1000, tax rate 40%

$$ $$ RevenueRevenue 500500 500500

less investment allowanceless investment allowance (180)(180) Taxable incomeTaxable income 320320 500500

less tax (0.4)less tax (0.4) (128)(128) (200)(200) The tax bill is reduced by $200 - $128 = $72.00

or or

Tax Benefit or Tax saving = 0.18 * 1000 * Tax Benefit or Tax saving = 0.18 * 1000 * 0.40 0.40

= $ = $ 72.0072.00