pension funds - some varied perspectives

TRANSCRIPT

Pension Funds – Some Varied Perspectives

Submitted By:-

Harish K. Raman

Symbiosis Law School, Pune

(Constituent of Symbiosis International

University)

BBA.LL.B(C)

P.R.N. No.-13010124268

E-Mail Address - [email protected];

Pension Funds - Some Varied Perspectives

Abstract :-

“Will I have enough to live on when I retire?” This question of old age financial security is

being asked across the world with growing apprehension. India is no exception. Three reports

have examined old age financial security for Indians and are now being studied for

implementation by the government. Keeping this in mind a brief introduction into the

functioning and need of pension funds has been given. PFRDA has been focused on.

Background of PFRDA and NPS has been explained as also their applicability. National

Pension Scheme has also been discussed. Implementation and Impact of NPS has been

explained in detail. Employees' Provident Fund Organisation is another organ set up by the

Government whose role has been looked into. Changes around the world and the change in

global finance markets has been discussed. Wealth and Investments which form an important

part of any financial system have also been explained. Operating Expenses which herald a

change in markets have been focused on. Answer to an ongoing debate in today’s world

Public or Private Management and which to choose has been provided. Several practical

recommendations which can improve the financial standing and gain have also been

discussed.

Key Words: Pension Fund, Pension Fund Regulatory Development Authority (PFRDA),

National Pension Scheme (NPS), Employees' Provident Fund Organisation (EPFO), Public

Pension Fund Management

Pension Funds - Some Varied Perspectives

Introduction

Nearly one eighth of world’s elderly population lives in India. The vast majority of this

population is not covered by any formal pension scheme. Instead, they are dependent on their

own earning and transfer from their children. These informal systems of old age income

security are imperfect and are becoming increasingly strained. People above the age of 60

years have grown at an annual rate of growth of 3.8 percent (75.9 million in 2001 and 55.3

million in 1991) during the period 1991-2001, as against the annual growth of 1.8% for the

general population.

A Pension Fund is basically a fund established by an employer to facilitate and organize the

investment of employees' retirement funds contributed by the employer and employees. The

pension fund is a common asset pool meant to generate stable growth over the long term, and

provide pensions for employees when they reach the end of their working years and

commence retirement.

Pension funds are commonly run by some sort of financial intermediary for the company and

its employees, although some larger corporations operate their pension funds in-house.

Pension funds control relatively large amounts of capital and represent the largest

institutional investors in many nations.

Pension Policy in India has traditionally been based on financing through employer and

employee participation. As a result, the coverage has been restricted to the organized sector

and a vast majority of the workforce in the unorganized sector has been denied access to

formal channels of old age financial support. Only about 12 per cent of the working

population in India is covered by some form of retirement benefit scheme. Besides the

problem of limited coverage, the existing mandatory and voluntary private pension system is

characterized by limitations like fragmented regulatory framework, lack of individual choice

and portability and lack of uniform standards. High incidence of administrative cost and low

real rate of returns characterize the existing system, which has become unsustainable.

Pension Fund Regulatory Development Authority and National Pension

Scheme

By a notification issued by the Ministry of Law and Justice dated September 18, 2013, the

Pension Fund Regulatory and Development Authority Act, 2013 ("Act") was brought into

effect. Before this, the Pension Fund Regulatory and Development Authority ("PFRDA") was

an interim regulator. The Act intends to promote old age income security by establishing,

developing and regulating pension funds and to protect the interests of subscribers to its

schemes. The Act covers National Pension Scheme ("NPS") and any other pension scheme

not regulated by other enactment like Employees' Pension Scheme, 1995, Employees'

Provident Funds and Miscellaneous Provisions Act, 1952 etc.

In light of the above development, the present bulletin highlights the applicability of the Act

and NPS which is a voluntary retirement savings scheme and has been designed to enable the

subscriber to make optimum decisions regarding his future and provide for his old age

through systemic savings. The bulletin discusses the proposed structure and any implication

on private companies.

Background of PFRDA and NPS

In the 2003-04 budget, a new pension system was introduced by the government based on

defined contribution, to be shared equally between the government and its employees. Under

such scheme there was no contribution from the government in respect of individuals who are

not government employees. The Ministry of Finance was empowered to oversee and

supervise the pension funds. The government approved the proposal to implement the new

restructured defined contribution pension system on October 10, 2003. PFRDA Bill also

known as Pension Bill was first time introduced in the Parliament in 2005 to replace the

ordinance that came in 2004 to set up PFRDA but could not be passed. An interim PFRDA

was constituted on November 14, 2008. The PFRDA Bill, 2011 was reintroduced on March

24, 2011 and was referred to the standing committee on finance on March 29, 2011 for

examination. Based on their recommendations of the standing committee, some amendments

were incorporated in the Bill, which was also approved by the cabinet. Both the houses of

Parliament on September 4, 2013 and September 6, 2013 respectively passed the PFRDA

Bill, 2013. The said Bill has also received the assent of the President on September 18, 2013.

Applicability of PFRDA and NPS

The Act applies to NPS but not to other specific pension schemes or funds or to the insurance

contracts under which payment of money is assured on death, any pension scheme exempted

by central government, persons appointed before January 1, 2004 to public services or All

India services. NPS is available to all citizens of India on voluntary basis and is mandatory

for employees of central government (except armed forces) appointed on or after January 1,

2004. All Indian citizens between the age of 18 and 55 can join the NPS.

The NPS will work on defined contribution basis and will have two tiers, Tier-I and Tier-II.

Both Tier-I (Pension Account) and Tier-II (Savings Account) will be pure retirement savings

products, the only distinction being Tier-I is a non-withdrawable account while Tier- II is a

withdrawable account to meet financial contingencies. Contribution to Tier-I is mandatory for

all government employees joining government service on or after January 1, 2004 whereas

Tier-II will be optional and at the discretion of government employees.

All assets, liabilities, debts, obligations, sums of money due, suits and legal proceedings

related to the "Interim PFRDA" has been transferred to PFRDA on and from the date of

establishment of the PFRDA.

National Pension Scheme

The NPS reflects government's effort to find sustainable solutions to the problem of

providing adequate retirement income. In NPS, every subscriber will have an individual

pension account (Tier-I). Withdrawals up to 25% of contribution are allowed by subscribers.

Recordkeeping, accounting and switching of options by the subscriber are the responsibilities

of Central Recordkeeping Agency ("CRA"). There is a facility of portability of pension

accounts in case of change of employment but the collection and transmission of

contributions shall be carried out through CRA only. There is no assurance of benefits except

market based guarantee mechanism. The subscriber will have to purchase an annuity from

any life insurance company while taking exit from NPS. A subscriber may also have an

additional account under NPS with an additional feature that the subscriber may withdraw

part or all of his money at any time from the additional account (Tier-II).

Implementation of NPS

In Tier-I, every subscriber shall have an individual pension account. A non-government

employee needs to contribute at least four times in a year and each contribution should not be

less than INR 500. Therefore, the minimum contribution3 to the scheme should not be less

than INR 6000 every year. Government employees will have to make a contribution of 10%

of their basic pay plus Dearness Allowance ("DA"), which will be deducted from his salary

every month. An equal contribution will be made by the government. Tier-I contributions

will be kept in Tier-I Account.

A government employee can exit at or after the age of 60 years from the Tier-I of the scheme.

At exit, it would be mandatory for him to invest 40% of pension wealth to purchase an

annuity from an Insurance Regulatory and Development Authority regulated life insurance

company, which will provide pension for the lifetime of the employee and his dependent

parents/spouse. In the case of government employees who leave NPS before attaining the age

of 60, the mandatory annuitization would be 80% of the pension wealth.

The Tier-II enables the existing Tier - I account holders to build savings through investments

over and above those in the Tier I pension account. Tier-II contributions will be kept in a

separate account that will be withdrawable at the option of the Government servant.

Government will not make any contribution to Tier-II account. No additional CRA charges

will be levied for account opening and annual maintenance in respect of Tier-II. However,

CRA will charge separately for each transaction in Tier II, the charges being identical to the

transaction charge structure in Tier-I. There is no limit on number of withdrawals. Separate

nomination can be made for Tier-II account. The subscriber would have the same choice of

Pension Fund Managers ("PFM") and schemes as in the case of Tier-I account. Facility of

only one-way transfer of savings from Tier-II to Tier-I is available. An active Tier I account

will be a pre-requisite for opening of a Tier-II account.

In cases of discharge/death of the employee, the amount of accumulated funds in the NPS

account will be paid to the employee/family of the employee. The amount of monthly-

annuitized pension from the date of discharge/death will be worked out in accordance with

the regulations notified by PFRDA.

Impact of NPS

NPS has been notified for tax benefit purposes. Under this, both employee and employer's

contributions are eligible for income tax deduction up to 10% of basic plus DA under section

80CCD5 of the Income Tax Act, 1961 within INR 1 lakh limit as specified under Section

80CCE6. The employer can claim tax benefit for its contribution by showing it as business

expense in the profit and loss account.

The NPS contribution will be in addition to Employee Provident Fund investments. Employer

can simply deduct the contribution from employee's salary. It saves a big part of the salary

and helps in availing tax exemptions too. Other than central and state government employees,

mandated to make contribution to NPS, those working in entities registered under the

Companies Act, Cooperative Acts, registered partnership firms, proprietorship concerns,

trusts and societies can avail additional tax exemption under this model. Corporate houses

willing to join NPS can do so by tying up with one of the PFRDA-approved points of

presence ("POP"), which facilitate account opening and act as an intermediary between the

subscriber and NPS intermediaries such as CRA. It is also beneficial for professionals as they

can become the part of CRA and can also act as PFM. Due to the above mentioned benefits,

many private limited companies are switching to NPS.

The limitation under this scheme is that the total amount of the contribution should not be

more than 10% otherwise the additional amount will not qualify for the tax benefit.

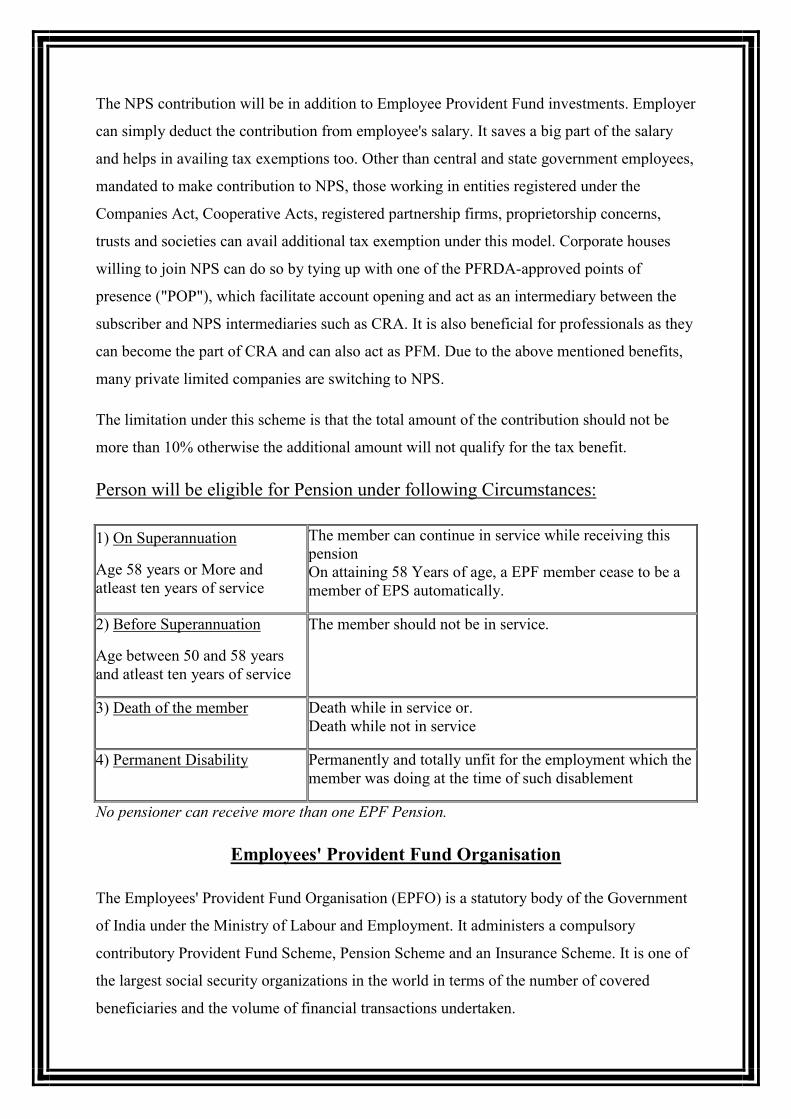

Person will be eligible for Pension under following Circumstances:

1) On Superannuation

Age 58 years or More and atleast ten years of service

The member can continue in service while receiving this pension On attaining 58 Years of age, a EPF member cease to be a member of EPS automatically.

2) Before Superannuation

Age between 50 and 58 years and atleast ten years of service

The member should not be in service.

3) Death of the member Death while in service or. Death while not in service

4) Permanent Disability Permanently and totally unfit for the employment which the member was doing at the time of such disablement

No pensioner can receive more than one EPF Pension.

Employees' Provident Fund Organisation

The Employees' Provident Fund Organisation (EPFO) is a statutory body of the Government

of India under the Ministry of Labour and Employment. It administers a compulsory

contributory Provident Fund Scheme, Pension Scheme and an Insurance Scheme. It is one of

the largest social security organizations in the world in terms of the number of covered

beneficiaries and the volume of financial transactions undertaken.

The EPFO has the dual role of being the enforcement agency to oversee the implementation

of the EPF& MP Act and as a service provider for the covered beneficiaries throughout the

country. To this end, the Our Commissioners of the Regional and Sub Regional Offices of

Organisation are vested with vast powers under the statute conferring quasi- judicial authority

for search and seizure of records, assessment of financial liability on the employer, levy of

damages, attachment and auction of a defaulter's property, prosecution and arrest and

detention in civil prison.

Changes Around the World

Recent years have witnessed intense pension reform efforts in countries around the globe,

which have often involved an increased use of funded pension programmes managed by the

private sector. There is a growing need among policy makers and the regulatory community,

as well as among private sector participants, to compare programme developments and

experiences to those of other countries. Because funded arrangements are likely to play an

increasingly important role in delivering retirement income security in many countries, and

because the investment of pension assets will increasingly affect securities markets in future

years, the availability of an accurate, comprehensive, comparable and up-to-date body of

international statistics is a necessary tool for policy-makers, regulators and market

participants.

The Working Party on Private Pensions and its Task Force on Pension Statistics launched the

Global Pension Statistics' project (GPS) in 2002. The GPS provides a valuable means for

measuring and monitoring the pension industry, and permit inter-country comparisons of

current statistics and indicators on key aspects of retirement systems across OECD and non-

OECD countries. Data are collected on an ongoing basis so that trends can be readily

identified and analysed. The statistics cover an extensive range of indicators and relate to a

wide definition of private pension plans, themselves subdivided into detailed categories using

coherent statistical concepts, definitions and methodologies.

Structure of Pension Systems Private pension plans can be financed through pension funds,

pension insurance contracts, book reserves or other vehicles (bank or investment companies

managed funds). They could be linked to an employment relationship, making them

occupational pension plans, or they may be based on contracts between individuals and

private pension providers, making them personal pension plans.

Wealth and Investments

These indicators refer to the trend in pension fund assets and asset allocation. The default

queries are proposed for pension funds, therefore excluding data pertaining to book reserve

systems (as they exist in Austria and Germany for example), pension insurance contracts

(available in most OECD countries) and funds managed as part of financial institutions.

However, the default options can be modified to comply with users' needs.

Operating Expenses

Pension fund operating expenses comprise all costs arising from the general administration of

the plan/fund that are treated as plan/fund expenses (i.e. administrative costs and investment

management costs). The efficiency of private pension systems can be assessed by looking at

the costs in relation to assets under management.

Equity allocations by Japan pension funds have risen from 22% in 2003 to 40% in 2013,

while equity allocations by U.K. pension funds have fallen from 65% to 50% in the same

period. The Netherlands’ equity allocations fell from 40% to 35%, and Canada’s allocation to

equities fell from 55% to 48%. U.S. and Australia pension funds have maintained the highest

allocation to equities over time, reaching 57% and 54% in 2013, respectively.

Japan pension funds still have the highest allocation to bonds (51%), but this represents a

significant reduction since 2003, when 71% of its assets were in bonds. Netherlands pension

funds have increased their allocation to bonds during this period (from 45% to 50%), as have

U.K. funds (31% to 33%) — the only two countries in the study to have done so.

Allocations to alternative assets, especially real estate (and to a lesser extent, hedge funds,

private equity and commodities), for the P7 markets have grown from 5% to 18% since 1995.

In the past decade, most countries have increased their exposure to alternative assets, with

Australia increasing the most (from 8% to 25%), followed by Canada (from 8% to 21%) and

the U.K. (from 3% to 14%). Allocations to alternatives in the Netherlands and Switzerland

have remained constant during the same period.

There is a clear sign of reduced home bias in equities, with the average weight of domestic

equities in pension fund portfolios falling from around 65% in 1998 to just over 44% in 2013.

Perhaps surprisingly, during the past 10 years, U.S. pension funds remained the market with

the highest bias to domestic equities, while Canadian funds have had the lowest allocation to

domestic equities. Regarding home bias in fixed-income investments, the average allocation

to domestic bonds as a percentage of total bonds has remained high since the inception of this

research, when it was over 88%. Last year, it was around 80%.

During the 10-year period from 2003 to 2013, the CAGR of DC assets was 9%, compared to

5% for DB assets. DC pension assets have grown from 38% in 2003 to 47% in 2013.

Australia has the highest proportion of DC to DB pension assets: 84% to 16%, compared to

83% to 17% in 2012. Only Australia and the U.S. have a larger proportion of DC assets to

DB assets.

Japan, Canada and the Netherlands are markets dominated by DB pensions, with 97%, 96%

and 95% of assets, respectively, invested in these types of pensions. Historically only DB,

these markets are now showing small signs of a shift toward DC.

In the U.K. and Australia, the private sector holds the biggest portion of pension assets,

accounting for 88% and 84%, respectively, of total assets in 2012. Japan and Canada are the

only two markets where the public sector holds more pension assets than the private sector,

holding 71% and 55% of total assets, respectively.

Public or Private Management

Indians do not have the first pillar funded and supported by government and, therefore, the

second pillar becomes the basic pillar – a core retirement plan. In this plan people are looking

for secured income when they retire, and, therefore, as recommended by the World Bank the

plan should be publicly managed. Problems with privatization include the following:

1. Current retirement benefits are barely adequate and a retiree wants a reliable source of

income. Privatization contains no social insurance components like disability and survivors’

benefits. Retirees would have to buy them separately. Benefits may be reduced by as much as

30 per cent in some cases.

2. Having individual retirement accounts in private pension funds would be prohibitively

expensive to administer. In some cases where contributions are small (say Rs. 100 a month),

administrative costs may be as high as 25 per cent of contributions.

3. Privatization gets the employer off the hook. Risk shifts from corporations to employees.

Most employees prefer the stability of pension plans to higher volatile monetary value of the

fund. For less wealthy, assured income has always been economically better than higher but

volatile and uncertain financial wealth.

4. There would be the added problem of agency risk, which has not been taken note of.

Government would have to add a so-called ‘0 pillar’ that will guarantee a minimum pension

to employees whose own defined pension falls below a specified minimum. Along with tax

subsidy, policy makers should factor into the cost of government providing guarantees for

policyholders.

The priority should, therefore, be putting in place a policy vision and road map with specific

goals in relation to pre-determined milestones. These include the tax financed and means-

tested system for lower income groups. If government cannot afford it, then it has no moral or

political justification to even consider providing further tax benefits to privileged income

groups. If there are no government funds for the first pillar, the third pillar should remain out

of policy discussions. Emphasis should be on strengthening the second pillar.

Conclusion And Recommendations

Pension reforms would not occur overnight. Thus, the focus should be on improving existing

systems rather than replace them with new ones. Efforts should be made to find ways of

supporting new systems that may supplement existing systems. Since the tax-paying

population is small, an exclusive focus on tax incentives as a vehicle to encourage savings is

misplaced. Proper estimate of the “tax expenditure” (that is, forgone revenues) that results

from current tax preferences for retirement savings and explicit decisions about the

appropriate size and progressivity of these preferences need to be made. Government’s

contingent liabilities on account of minimum pension guarantee also need to be taken into

account before any change in policy is made. Participants’ interests and associated

government costs in the form of government grants, administrative costs by its agencies

(EPFO, post office, bank branches, etc.), and funds required to guarantee minimum pension

should all be taken into account in recommending any institutional arrangement.

In the government sector, reforms should focus on strengthening the existing PAYG system

through adjusting the system parameters. Pension outlays can be lowered by reducing the

replacement rates, that is, the ratio of pensions to wages, or by moving toward less generous

pension indexation formulas that give less weight to wages and more weight to inflation,

raising the retirement age in line with life expectancy, and rationalizing disability, survivors’

benefit, etc.

Private firms, particularly insurers and fund management companies, may be lobbying hard

to acquire new business or being hired by EPFO to manage its Rs. 500 billion corpus without

guaranteeing anything in return except lofty promises. However, government must be

cautious about these moves. In privatizing the basic pension system for its citizens,

intermediation costs and agency risk cannot be ignored. Since politicians cannot stop being

playing Santa Clauses and causing havoc with government finances, one should not imagine

that fund managers would discipline them and solve the problem. Given so many scams in

the past, it is more likely that they will join the bandwagon in sharing the spoils at

participants’ and/or government expense. All this serves to spotlight the role that the

government must play in creating a pension system with appropriate safeguards for inherent

risks and ensure that appropriate parties bear them. If private fund managers are willing to

guarantee performance, it may be worth trying. EPFO finances need closer scrutiny to

examine its viability and to provide efficient services it must have trained manpower and

technology savvy administration.

The priority should, therefore, be putting in place a policy vision and road map with specific

goals in relation to pre-determined milestones. These should include a tax financed and

means-tested system for lower income groups. If government cannot afford it, then it has no

moral or political justification to even consider providing further tax benefits to privileged

income groups. If there are no government funds for the first pillar in the World Bank

recommended multi-pillar system, the third pillar should remain out of policy discussions.

Emphasis should be on strengthening the second pillar. Suggested reforms neither enhance

efficiency nor make the social security system more equitable. It would only privatize the

gains while costs and risk for the government would increase considerably. It would only

help well-off segment of society in availing more tax concessions. Present problem in the

government pension system is due to successive governments behaving like Santa Clauses

ignoring the cost to exchequer. Fund managers would not be able to solve these problems.

It can be concluded that in order to effectively invest and manage huge funds belonging to a

large number of subscribers and to ensure the integrity of NPS, establishment of a statutory

PFRDA with well defined powers, duties and responsibilities would benefit all the

subscribers of the NPS. The new law could help in bringing new pension products in the

market, thereby giving choice to customers. Competition could also improve quality of

service and returns. If these measures are successful, these could help in mobilising

substantial long-term funds, which can be used to build infrastructure. It is mandatory to use

40% of pension wealth to purchase the annuity at the time of the exit (i.e. after the age of 60

years). This provision has been made in the New Pension Scheme with an intention that the

retired government servants should get regular monthly income during their retired life.

References :-

1. International Monetary Fund. (2004). Risk Management and the Pension Fund Industry,

International Monetary Fund.

2. Government Accountability Office. (2013). Defined Benefit Pension Plans: Recent

Developments Highlight Challenges of Hedge Fund and Private Equity Investing.

Createspace.

3. van Nunen, A. (2013). Fiduciary Management. Wiley.

4. Bedi, Rahul. (2009). Corporate Governance Triangle in the Post Sarbanes-Oxley Period:

Attitudes of Three Anchors - Executive Management, Independent Directors, and Long

Term Pension Fund Shareholders. LAP Lambert Academic Publishing.

5. United States Congress Committee & Mourlon, Michel Felix. (2010). Targeted Pension

Fund Investment for Economic Growth and Development; Hearing Before the Joint

Economic Committee, Congress of the United. Cambridge Scholars Publishing.

6. Woolfe, Jeremy. (2014, June 5). Pension funds await decision on derivative-trade

exemption ruling. Investments & Pensions Europe.

7. EMPLOYEE'S PENSION SCHEME, 1995, (Updated as on 01.10.2008). Retreived From

http://www.epfindia.com/Circulars/EPS95_update102008.pdf

8. THE PENSION FUND REGULATORY AND DEVELOPMENT AUTHORITY ACT,

2013, NO. 23 OF 2013, [18th September, 2013.]. Retreived From

http://indiacode.nic.in/acts-in-pdf/232013.pdf

9. INCOME-TAX ACT, 1961, [43 OF 1961], [AS AMENDED BY FINANCE ACT, 2008].

Retreived From http://tkbsen.in/wp-content/uploads/2013/06/Income-Tax-Act-1961.pdf

Corporates should run their own Pension Funds for their non-EPFO category employees

and invest funds in the equity market. (2014, June 5). Business Standard

10. Pension funds key to creation of robust domestic institutional network: Sinha. (2014, May

15). Business Line

11. Sebi, exchanges pitch for pension money in capital markets. (2014, Jun 1). The Economic

Times.

12. Lukewarm response to Indian diaspora pension scheme. (2014, 13 May). Jagran Post.

13. Bank Track. What is a pension fund?.

14. Zaidi, Babar. National Pension Scheme funds hit by downturn. (2013, September 9). The

Economic Times.

15. Beware of tax implications on pension funds. (2008, January 18). The Economic Times.

16. Reuters. ING's Polish unit to sell remaining stake in pension fund for $80 million. (2014,

May 7). The Economic Times.

17. FDI in pension fund management can wait. (2007, May 15). The Economic Times.

18. Goswami, Ranadev. INDIAN PENSION SYSTEM: PROBLEMS AND PROGNOSIS.

Fellow, Indian Institute of Management Bangalore. Retreived From

http://www.actuaries.org/EVENTS/Seminars/Brighton/presentations/goswami.pdf

19. Srinivas, P. S. & Thomas, Susan. Institutional Mechanisms in Pension Fund

Management: Lessons from Three Indian Case Studies. Economic and Political Weekly,

Vol. 38, No. 8, Money, Banking and Finance (Feb. 22-28, 2003), pp. 706-711+713-

714+716-717.

20. IMAM, ASHRAF. PENSION FUND MANAGEMENT IN INDIA: GOVERNMENT

ROLE AND REGULATORY ISSUES. ZENITH, International Journal of

Multidisciplinary Research, Vol.1 Issue 7, November 2011, ISSN 2231 5780.