mid-term evaluation of regional venture capital funds

TRANSCRIPT

Date

September 2011

MID-TERM EVALUATION OF REGIONAL VENTURE CAPITAL FUNDS IMPLEMENTATION AND LESSONS LEARNT

Regional Venture Capital Funds Mid-term evaluation

2

Contents Abstract 4 1. Introduction 7 1.1 Background – on publicly-financed venture capital funds 7 1.2 Ongoing evaluation 10 1.3 This year’s evaluation 11 1.4 Data sources 13 1.5 Explanation of concepts 15 1.6 Conclusions from first year of ongoing evaluation 17 1.7 Report structure 18 2. InternationAL AND SWEDISH EXPERIENCES 18 2.1 International experiences 19 2.2 Swedish pilot projects 24 3. venture capital fund operationS in the pAst year 29 4. The venture capital funds’ INVESTMENTS 32 4.1 The venture capital funds’ investment activity 33 4.2 The venture capital funds’ investment activity and portfolio compositions 37 4.3 Expected investment activity during 2012-2014 61 5. DEVELOPMENT AND ADDITIONALITY OF THE COMPANY 66 5.1 Description of the companies 66 5.2 Achievement of objectives 69 5.3 Additionality in companies 74 5.4 Summary and discussion 74 6. PrivatE CO-INVESTORS 76 6.1 Description of private co-investors 76 6.2 The private co-investors and the investment’s achievement of objectives 78 6.3 Additionality – does the investment contribute to an increase in access to capital and

willingness to invest/investment activity? 81 6.4 Summary and discussion 82 7. REGIONAL COOPERATION 84 7.1 Forms and degrees of cooperation 85 7.2 Factors affecting the degree of cooperation 86 7.3 Summary and recommendations 88 8. DisCussion AND CONCLUSIONS 90 8.1 Results and recommendations 90 8.2 Ongoing evaluation work in 2012-2014 96 9. APPENDICES 98 9.1 Appendix 1: The investment’s programme logic 98 9.2 Appendix 2: EVCA:s industry sector classification 100 9.3 Appendix 3: Delayed, changed and additional investment decisions101 9.4 Appendix 4: Venture capital funds’ investment processes 102 10. ReferenCES 107

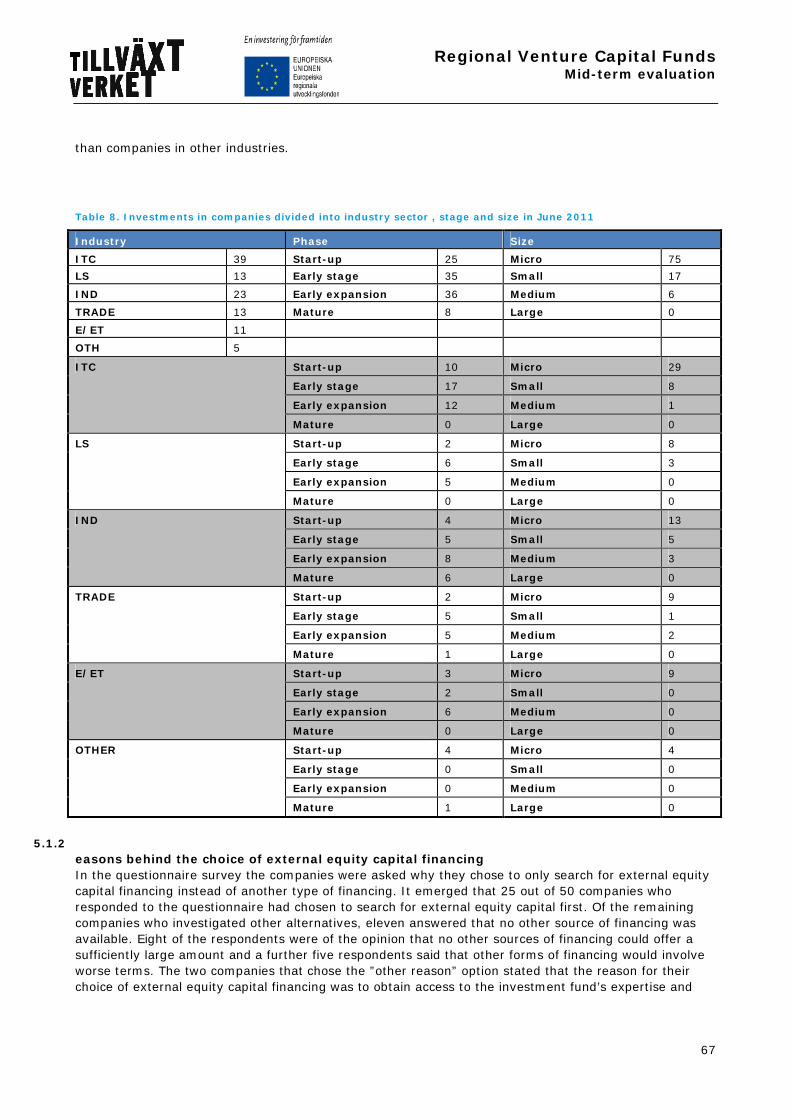

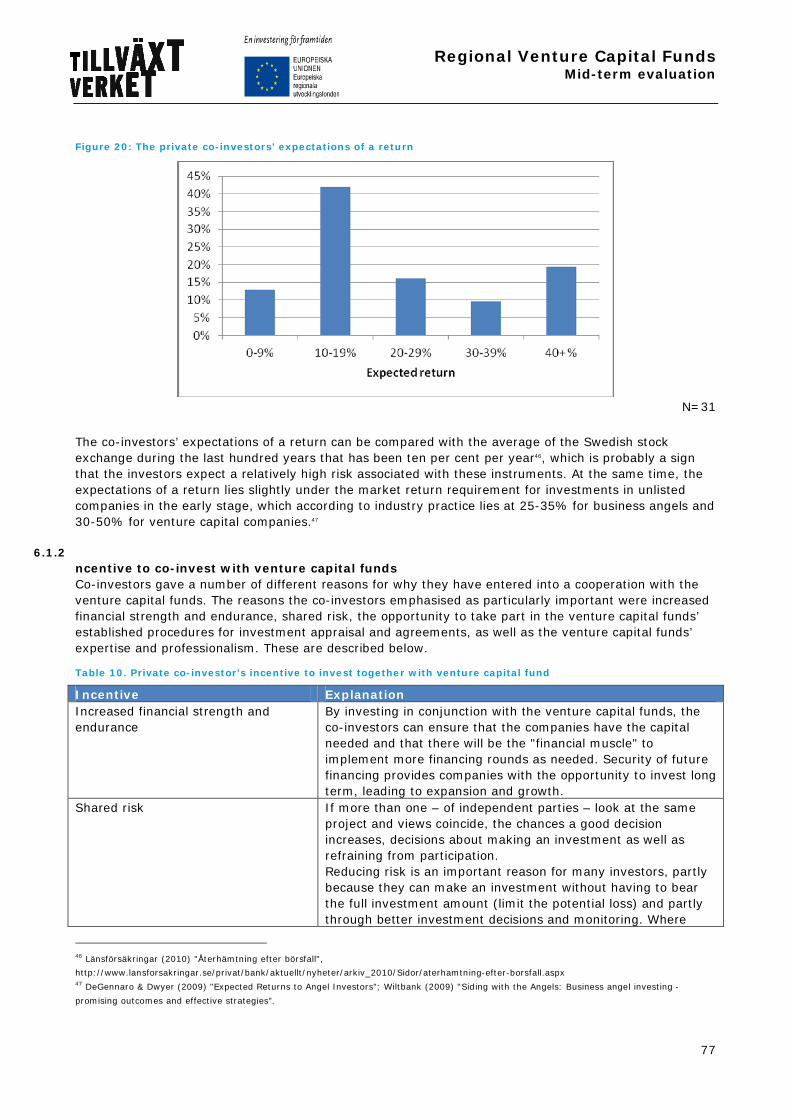

List of tables and figures Table 1. Mid-term evaluation’s topics, questions and data collection methods ................................... 12 Table 2. Non-response analysis of companies.............................................................................. 13 Table 3. The venture capital funds’ accumulated rate of investment up to and including June 2011 ...... 34 Table 4. Horizontal criteria....................................................................................................... 37 Table 5: Forecast of disbursed EU funds..................................................................................... 62

Regional Venture Capital Funds Mid-term evaluation

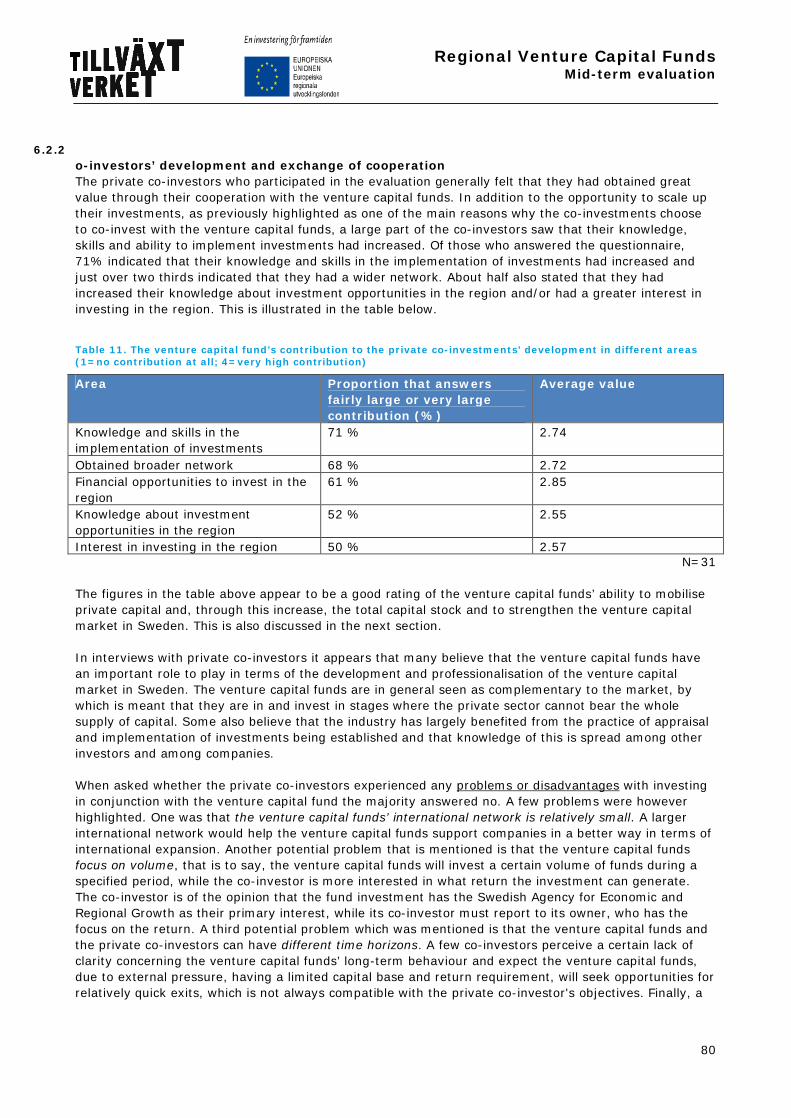

3

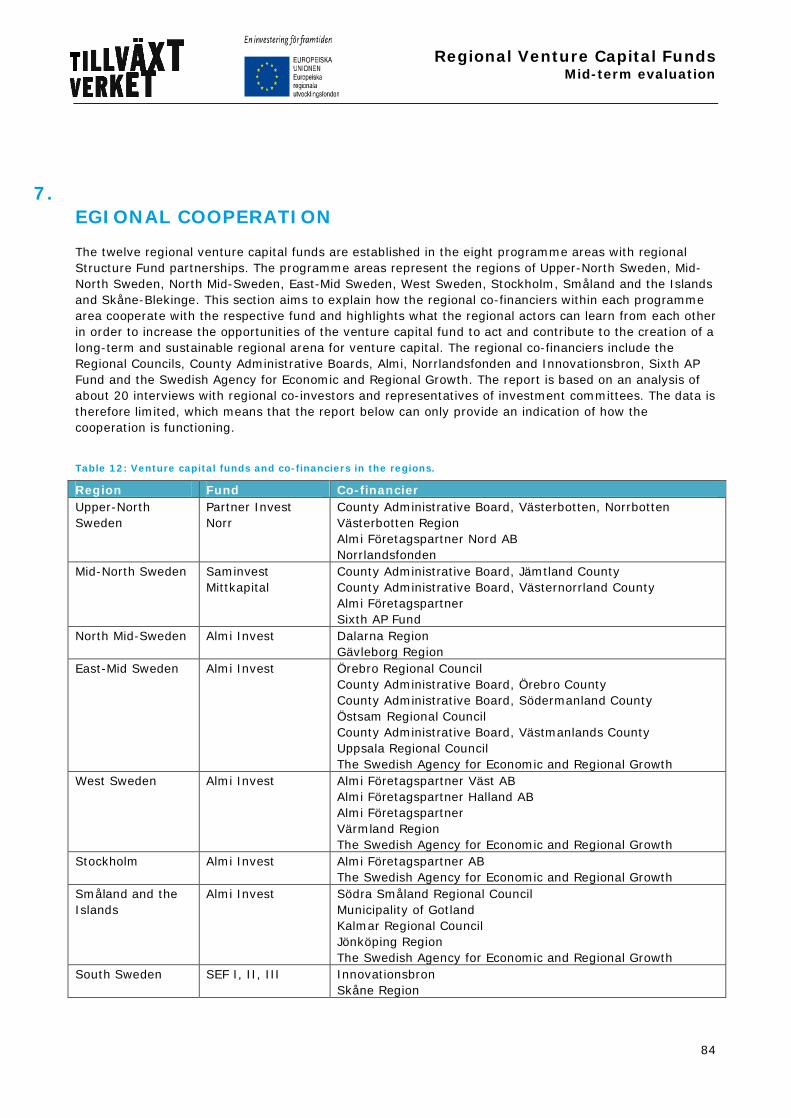

Table 6: Required future investment rate for four venture capital funds........................................... 64 Table 7: Forecast of decided EU funds........................................................................................ 65 Table 8. Investments in companies divided into industry sector, stage and size in June 2011 .............. 67 Table 9: Has the company brought in further external capital since financing from the investment fund has been received?................................................................................................................. 73 Table 10. Private co-investor’s incentive to invest together with venture capital fund ......................... 77 Table 11. The venture capital fund’s contribution to the private co-investments’ development in different areas (1=no contribution at all; 4=very high contribution) ............................................................ 80 Table 12: Venture capital funds and co-financiers in the regions..................................................... 84 Figure 1. Map of fund portfolios for regional funds.......................................................................... 9 Figure 2. Invested EU-funds as a percentage of target for the whole project period ........................... 36 Figure 3: Rate of investment and portfolio composition (Almi Invest Östra Mellansverige)................... 39 Figure 4: Rate of investment and portfolio composition (Almi Invest Stockholm) ............................... 41 Figure 5: Rate of investment and portfolio composition (Almi Invest Småland och Öarna)................... 43 Figure 6: Rate of investment and portfolio composition (Almi Invest Västsverige).............................. 45 Figure 7: Rate of investment and portfolio composition (Almi Invest Västsverige - Värmland).............. 47 Figure 8: Rate of investment and portfolio composition (Almi Invest Norra Mellansverige) .................. 49 Figure 9: Rate of investment and portfolio composition (Almi Invest Partnerinvest i Norr)................... 51 Figure 10: Rate of investment and portfolio composition (Partnerskapsfonden Mittsverige - Saminvest) 54 Figure 11: Rate of investment and portfolio composition (Mittkapital Jämtland/Västernorrland) ........... 55 Figure 12: Rate of investment and portfolio composition (SEF I)..................................................... 58 Figure 13: Rate of investment and portfolio composition (SEF II-III)............................................... 59 Figure 14: Reasons behind choice of external equity capital financing.............................................. 68 Figure 15: Risks associated with investment ................................................................................. 1 Figure 16: Overall risk of investment........................................................................................... 1 Figure 17: Areas of application of capital investment .................................................................... 71 Figure 18: To what extent will the company use the capital investment for different purposes (average divided per fund).................................................................................................................... 72 Figure 19: Additional impact of the additional capital.................................................................... 73 Figure 20: The private co-investors’ expections of a return............................................................ 77 Figure 21. Co-investors’ expected contribution to company’s development and company’s expectations (1=no contribution at all; 4=very high contribution)..................................................................... 79 Figure 23: Degree and form of cooperation................................................................................. 85 Figure 24: Regional structures and processes.............................................................................. 87

Regional Venture Capital Funds Mid-term evaluation

4

ABSTRACT

This is a mid-term evaluation of the initiative comprising twelve nationwide regional venture capital funds, which are operated in the form of ERDF-funded projects with regional co-financing. The background to the initiative is the interest expressed by the European Commission and national and regional players in working with revolving financial instruments in the form of equity capital, in order to address the identified lack of capital for financing small and medium-sized enterprises (SMEs) with growth ambitions. The aim of the venture capital funds, which were founded in 2009, is to increase access to equity capital for small and medium-sized enterprises in Sweden. Because the venture capital funds are run as projects, they are referred to as fund projects. The project period is from 01/01/2009 to 31/12/2014. The project owner must submit a final report on the use of ERDF funds in the project by 31/03/2015. ERDF funds that have not been invested in portfolio companies at least once prior to 31/12/2014 must be paid back to the EU Commission. Available funds that are not liable for repayment are retained after the final accounting for the region. During the project period, funds can be reallocated from fund projects to other structural fund projects. The initiative is subject to ongoing evaluation, which means that its progress will be regularly monitored and evaluated. This will contribute to learning about the initiative's implementation and results. Ramböll Management has been commissioned to conduct the ongoing evaluation of the twelve fund projects between autumn 2009 and spring 2015. The ongoing evaluation is summarised in a yearly report, and this present report constitutes the ongoing evaluation for 2011 and the mid-term evaluation of the, initiative. 1 The mid-term evaluation was conducted and the report written by Sofia Avdeitchikova PhD (external project manager, CIRCLE, Lund University), Ulrika Ekström (internal project manager, Ramböll Management) and Martin Fröberg and Marcus Holmström (both at Ramböll Management). The Swedish Agency for Economic and Regional Growth Report and the CEOs of the venture capital funds were consulted during the mid-term evaluation process. The CEOs also received a written version of the report on which they were able to submit comments. The purpose of the mid-term evaluation is to provide the Swedish Agency for Economic and Regional Growth, the venture capital funds and other stakeholders with early indications of how the initiative stands in relation to defined goals and to highlight any difficulties in the implementation process. The mid-term evaluation is about how the involved players (project owners, funded companies, regional and private co-financiers) are working within the framework of the fund projects and their perception of the value of the initiative in areas such as investment activity, development of companies and the initiative's capacity to increase access to capital in the regions. The mid-term evaluation also highlights cooperation in the regions and identifies challenges and success factors in the continuing work with the funds, in order to provide knowledge about the initiative's long-term effects on capitalisation in the region. Consequently, the mid-term evaluation has been designed to answer the following overarching questions:

• Where do the venture capital funds stand in relation to the defined rate of investment goals? • What is the status of the venture capital funds' portfolios with regard to the initiative's mission,

the size of the companies, the stage of development, industry diversification etc.? • What do the companies get out of the investors' involvement? Can a positive development in the

companies be observed? • Are there signs that the venture capital funds are helping to improve the capital position of

companies; in other words, is the initiative creating additionality? • How is the cooperation with the regional co-financiers working?

1 The first ongoing evaluation report, Start av regionala riskkapitalfonder (Start of regional venture capital funds), was issued in 2010 (Swedish

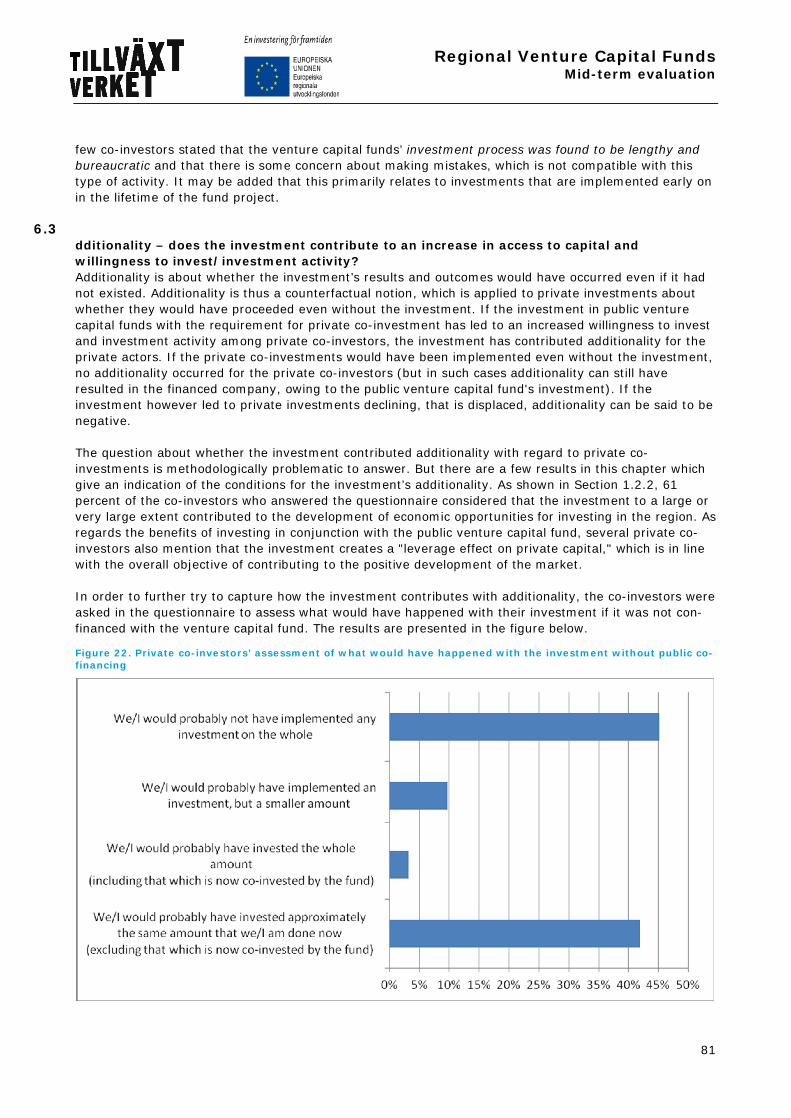

Agency for Economic and Regional Growth Report 0072).

Regional Venture Capital Funds Mid-term evaluation

5

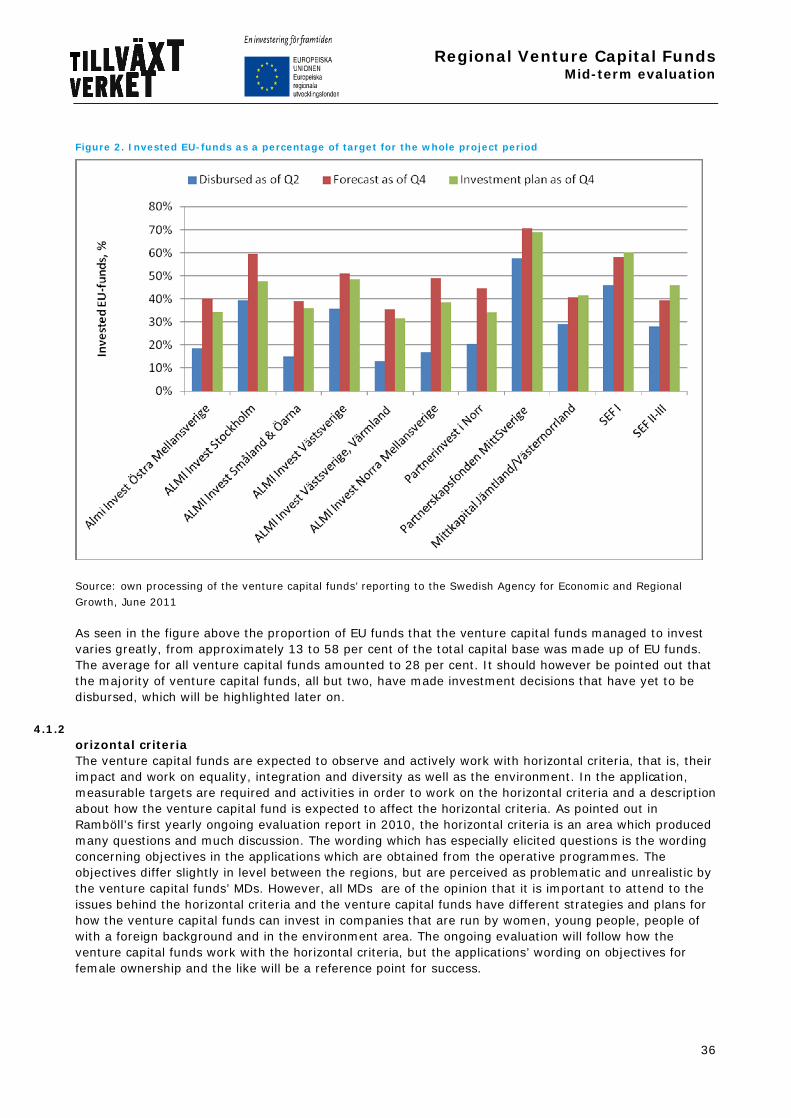

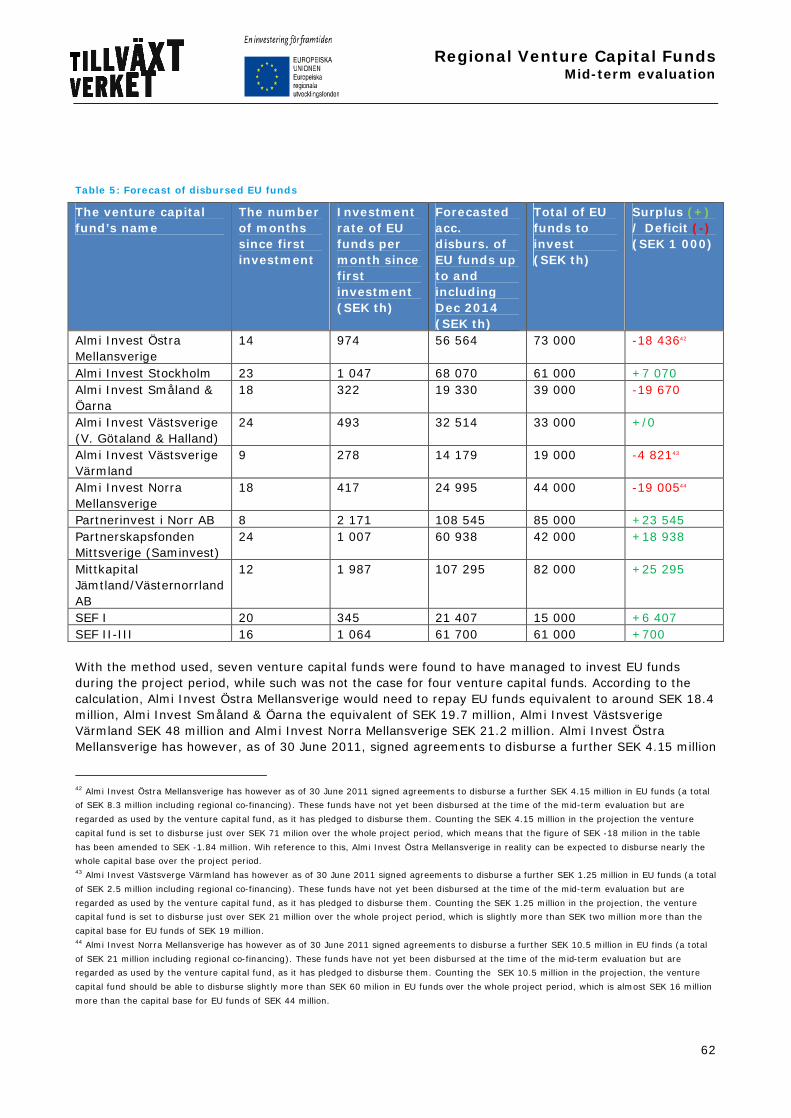

When the first evaluation of the regional venture capital fund initiative was made halfway through 2010 as part of this ongoing evaluation assignment, most of the venture capital funds were still in a start-up phase. Several venture capital funds had a slow start, which was largely due to delays in disbursement of the regional co-financing, the need to develop procedures for the assessment and implementation of investments and long-drawn-out recruitment processes. The economic situation in Sweden and the world was relatively uncertain which meant that many companies were cautious about investing in expansion and there appeared to be relatively little capital in the market available for new investments. Generally speaking, many venture capital funds saw it would be a challenge to ensure a sufficient flow of good potential deals and suitable investment partners, particularly in regions dominated by large companies and industrial environments which have not historically had a culture of venture capital financing. In addition, regulations governing the activities of the ERUF-financed venture capital funds were perceived as creating ambiguities, which took up a great deal of time and led to frustration and unnecessarily long investment processes. The venture capital funds appear to have made a good start to their activities during the last year, and most of them are in line with or close to the planned investment rate. The composition of the venture capital funds' portfolio is generally good, which means the investments have largely focused on small enterprises in early development stages. This is in line with the overall objective of the initiative, which is to address the gap in the supply of capital to small and medium-sized enterprises and to do so in a market-complementary way, i.e., not competing with the private market. The mid-term evaluation includes an assessment of whether the venture capital funds' rate of investment by the end of 2011 will be in line with the accumulated investment plan which runs until the end of December 2011 (short-term) and also an assessment of whether it is likely that the venture capital funds will manage to invest the entire capital base made up of EU funds during the full project period (long-term). In the short term, it is Ramböll's view that there is a risk that the rate of investment, particularly for Almi Invest Småland & Öarna, Almi Invest Västsverige Värmland, Partnerinvest i Norr, Mittkapital Jämtland/Västernorrland and SEF II-III, may be below the projected rate of investment at the end of 2011. This assessment is based on the EU funds paid out by the venture capital funds up until the end of Q2 2011 and the size of any additional investment decisions. Other factors considered in the assessment include the dealflow, and qualitative aspects such as the investment climate in a particular region, perceived access to private capital and the intensity of the funds' marketing and networking efforts. On the basis of the venture capital funds' average monthly EU funds disbursement since the initiative started in 2009, it is Ramböll's assessment that there may be a long-term risk that Almi Invest Östra Mellansverige, Almi Invest Småland & Öarna, Almi Invest Västsverige Värmland and Almi Invest Norra Mellansverige will not manage to invest the entire capital base made up of EU funds before the end of the project period. However, if the assessment takes into account whether the above-named venture capital funds have entered into legal agreement to pay out additional EU funds, this risk is eliminated or at least significantly reduced. On the basis of the venture capital funds' total investment decisions, the funds are all expected to be able to use the entire capital base made up of EU funds before the end of the project period. However, the decision as to whether the venture capital funds will be liable for repayments to the European Commission is not based on their investment decisions, but on their actual disbursement of funds to portfolio companies. However, given that the venture capital funds also pay out the funds for which decisions have been made, the results indicate that they should all be able to invest their EU funds during the project period.

Several venture capital funds report that interest from the companies has exceeded expectations. Because the majority of the venture capital funds have existing and established local networks in their regions, only a relatively low level of resources has needed to be channelled on marketing, and the funds have experienced a positive attitude and confidence from companies and private co-investors alike. A number of the venture capital funds' CEOs say they have been pleasantly surprised at the relatively high

Regional Venture Capital Funds Mid-term evaluation

6

quality of the investment objects and the good industry diversification, even outside the large urban areas. The companies which have received funding under the initiative are generally highly satisfied with their relationship with both the venture capital fund and the private co-investors. The companies have used the capital primarily for market development, product development and skills acquisition, and the majority of companies that have received funding from the venture capital funds are experiencing a high investment value. Companies are tending to find that the investment has contributed to faster expansion, more opportunities to obtain other external financing, a higher ambition level, increased production capacity and professionalisation of board work. Many of the companies also believe that the investment will ultimately lead to increased expertise and better profitability. One-third of the companies that participated in the evaluation process have received additional equity capital from new external shareholders after the initial investment has been made, suggesting that the companies have become more attractive to investors. Consequently, there is evidence that the initiative is making a positive contribution to the companies' growth and to increasing knowledge about venture capital, thereby contributing to the achievement of the initiative's objectives.

The private co-investors are experiencing a number of values and benefits in investing with a public venture capital fund. For example, the portfolio companies benefit from their venture capital fund's investment procedures, expertise and professionalism, and the risk associated with private capital is shared. In addition, the private co-investors report that the cooperation has increased their knowledge and skills in the area of implementation of investments and that they have developed wider networks. This must be seen as a good testimonial for the initiative and is in line with its overall objective, namely to contribute to the development of private co-investment partners.

Cooperation between the venture capital funds and regional co-financiers differs from region to region and even within regions. The degree of contact and cooperation also differs among regional co-financiers. Structural conditions such as the region's industry structure, market maturity and equity financing experience, and other factors such as support-building efforts when the venture capital fund was established, common goals and personal abilities affect cooperation between a private equity fund and its co-financiers. This in turn affects the possibilities for establishing a sustainable venture capital arena.

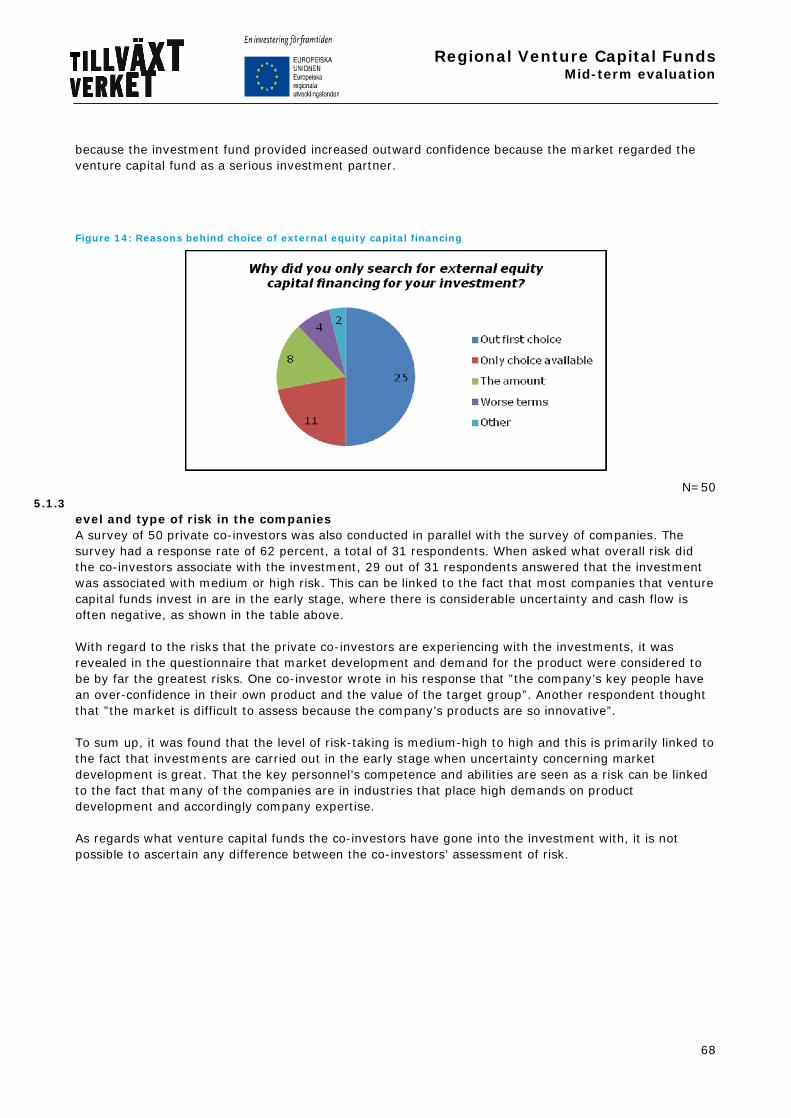

The overall question of whether the capital supply situation for businesses and the capital market has improved as a result of the initiative is difficult to answer, although there are indications that the initiative has helped to address the equity gap identified in the companies that have received funding and has also attracted private capital. Just over one-fifth of the companies that participated in the Ramböll evaluation decided to go ahead with the venture capital fund investment as no other source of investment was considered possible. A further quarter of the companies said that other investment sources were available but that they did not offer equivalent conditions. These figures together provide a certain indication that the initiative has filled a market need. Almost half of the private co-investors who participated in the evaluation said they would probably not have made the investment at all without the venture capital fund's co-investment. Almost ten percent said they probably would have made an investment, but the amount would have been lower. This indicates that the initiative has resulted in an increased volume of private capital investment. Consequently, there is at present no evidence that the investment has crowded out the private capital.

Regional Venture Capital Funds Mid-term evaluation

7

1. NTRODUCTION

In 2009, twelve regional public venture capital funds were set up in Sweden. The venture capital funds are run as projects within the framework of the eight regional Structural Fund programmes and financed by the European Regional Development Fund (ERDF) and a number of regional financiers. Several actors have been commissioned to be project owners and operate one or more of these projects: Innovationsbron, Almi Invest, Saminvest, the Norrland Fund (Norrlandfonden) and the Sixth AP Fund (Sjätte AP-fonden). The regional investments are therefore called “fund projects” whose overall aim is to “offer market complementary instruments within the framework of the Structural Fund programme” and to examine how different forms of public investments can contribute to an increase in the availability of equity capital for small and medium-sized enterprises (SMEs) in Sweden. Ramböll has been commissioned to carry out an ongoing, learning review and evaluation (ongoing evaluation) of the twelve fund projects between autumn 2009 and spring 2015. The ongoing evaluation is summarised in one report per year and this report is the ongoing evaluation report for 20112. This year’s report is also the mid-term evaluation of the initiatives prescribed by the guidelines of the Swedish Agency for Economic and Regional Growth. The mid-term evaluation is an integrated part of the ongoing evaluation report and is in practice an analysis of the first two years of operation of the fund projects. The mid-term evaluation aims to provide the Swedish Agency for Economic and Regional Growth, the venture capital funds and other relevant actors with early indications of how the investments stand in relation to the objectives set and highlight weaknesses in the implementation process. The mid-term evaluation looks at how the actors involved (project owners, portfolio companies who received funding and private co-financiers) are operating within the framework of the fund projects and their perceived value of the investment with regard to for example investment activity, company development and the investment’s ability to increase the availability of capital in the regions. The mid-term evaluation will also highlight cooperation in the regions and identify challenges and success factors in the continued work with the funds. This is done in order to provide knowledge about the long-term effects of the investment on the supply of capital in the regions.

1.1 ackground – on publicly-financed venture capital funds The European Regional Development Fund (ERDF) aims to strengthen the economic and social cohesion in the EU by correcting imbalances between its regions. Through the fund a number of different types of aid were distributed during the year: various types of financing instruments, direct financing aid for companies, aid for infrastructure investments and more. During the 1994-1999 programming period, the number of Structural Funds that were used for venture capital funds in Europe grew from being almost non-existence. The background to this was the assessment that there was a shortage of venture capital available for small and medium-sized enterprises with growth ambitions. Before the 2000-2006 programming period, investments of ERDF-financed venture capital funds increased. The Commission also encouraged member countries to re-orientate company-focussed financing investments away from traditional grants to other forms of financing, like venture capital. Part of the argument for this re-orientation was the lack of venture capital; a structure of revolving venture capital funds can provide less reduction of competition whilst opening the way for a reflux of capital (venture capital funds can provide returns that in turn can be reinvested). Moreover, there were positive experiences of ERDF-financed venture capital funds. In the present 2007-2013 programming period more venture capital funds than ever were invested in SMEs. 2 The ongoing evaluation’s first report in Swedish was published 2010, Start av regionala riskkapitalfonder, Swedish Agency for Economic and

Regional Growth 0072

Regional Venture Capital Funds Mid-term evaluation

8

In Sweden, the first ERDF-financed venture capital funds were set up in 2005 when a decision by the government and parliament made these types of investments possible. The initiative was taken after the European Commission in a report from 2002 identified Sweden as one of four countries that still only applied direct grants in its various Structural Fund programmes. Three pilots involving regional partnership funds were launched within the then Objective 2 in West Sweden, Gotland and Mid-North Sweden3, where regional Almi companies set up subsidiaries that managed the partnership funds. The pilots were structured so as to promote a change from being a passive partner to an active private co-investor and were based on a model for public venture capital funds that was developed in Scotland. The pilots were concluded in June 2008, with the exception of follow-up investments in existing portfolio companies.4 In 2006, the European Investment Fund (EIF) carried out an analysis of the need and opportunities to enhance SMEs’ access to capital with Structural Funds in Sweden with the JEREMIE initiative (Joint European Resources for Micro to Medium Enterprises)5. The initiative aims to stimulate development of SMEs by improving access to microcredits, venture capital and loan guarantees. The basis for the financing from the ERDF comes with the requirement of both national public co-financing and private co-financing.6 The ERDF also opens up other ways of working with the supply of capital for SMEs. As an alternative to JEREMIE, the Structural Fund partnerships of the eight programme areas and Nutek/the Swedish Agency for Economic and Regional Growth (in its capacity as the managing authority for ERDF) provided financing actors with the opportunity to apply for ERDF funds for part-financing of guarantees or venture capital funds. Like JEREMIE, this approach aims to create revolving financing tools for equity that goes into SMEs with growth ambitions. The announcement resulted in twelve regional venture capital funds being established.

3Almi Företagspartner Örebro Ab started the wholly-owned subsidiary Vestra Partnerinvest, Almi Företagspartner Mitt AB the wholly-owned

subsidiary Saminvest and Almi Företagspartner Gotland AB started Region Invest AB. 4 See Chapter 2.2 for a summary of the results from the pilot initiative in 2005-2008. 5 JEREMIE is a joint initiative from the European Commission and the European Investment Fund which was introduced in October 2005. 6 EIF identified shortages in the supply of capital and recommended that Sweden invests in a national JEREMIE fund. There was also found to be

great interest in venture capital investment, but also major problems in obtaining national co-financing in certain regions. In addition, the

applicable legislation (including the Public Procurement Act) made it technically very complicated to establish a JEREMIE fund in Sweden.

Regional Venture Capital Funds Mid-term evaluation

9

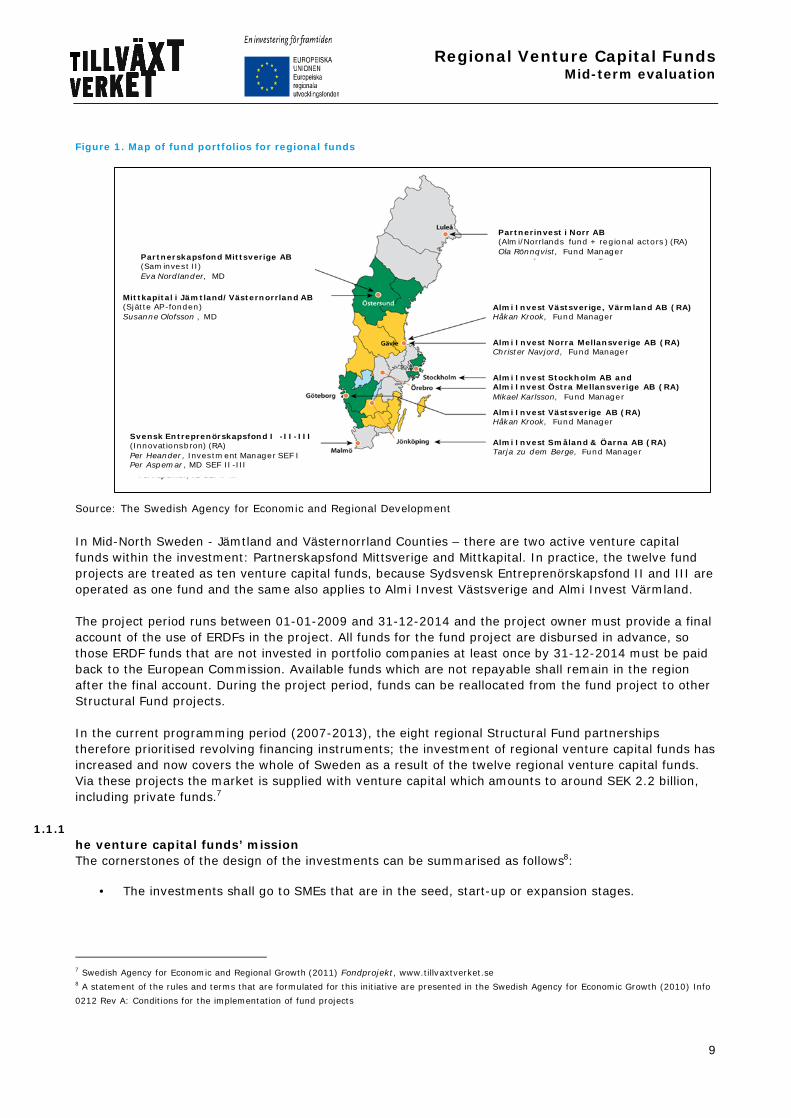

Figure 1. Map of fund portfolios for regional funds

Source: The Swedish Agency for Economic and Regional Development

In Mid-North Sweden - Jämtland and Västernorrland Counties – there are two active venture capital funds within the investment: Partnerskapsfond Mittsverige and Mittkapital. In practice, the twelve fund projects are treated as ten venture capital funds, because Sydsvensk Entreprenörskapsfond II and III are operated as one fund and the same also applies to Almi Invest Västsverige and Almi Invest Värmland. The project period runs between 01-01-2009 and 31-12-2014 and the project owner must provide a final account of the use of ERDFs in the project. All funds for the fund project are disbursed in advance, so those ERDF funds that are not invested in portfolio companies at least once by 31-12-2014 must be paid back to the European Commission. Available funds which are not repayable shall remain in the region after the final account. During the project period, funds can be reallocated from the fund project to other Structural Fund projects. In the current programming period (2007-2013), the eight regional Structural Fund partnerships therefore prioritised revolving financing instruments; the investment of regional venture capital funds has increased and now covers the whole of Sweden as a result of the twelve regional venture capital funds. Via these projects the market is supplied with venture capital which amounts to around SEK 2.2 billion, including private funds.7

1.1.1 he venture capital funds’ mission The cornerstones of the design of the investments can be summarised as follows8:

• The investments shall go to SMEs that are in the seed, start-up or expansion stages.

7 Swedish Agency for Economic and Regional Growth (2011) Fondprojekt, www.tillvaxtverket.se 8 A statement of the rules and terms that are formulated for this initiative are presented in the Swedish Agency for Economic Growth (2010) Info

0212 Rev A: Conditions for the implementation of fund projects

Partnerskapsfond Mittsverige AB(Saminvest II)Eva Nordlander, MD

Mittkapital i Jämtland/Västernorrland AB(Sjätte AP-fonden)Susanne Olofsson , MD

Svensk Entreprenörskapsfond I -II-III(Innovationsbron) (RA)Per Heander, Investment Manager SEF IPer Aspemar , MD SEF II -III

Partnerinvest i Norr AB(Almi/Norrlands fund + regional actors ) (RA)Ola Rönnqvist, Fund Manager

Almi Invest Västsverige, Värmland AB (RA)Håkan Krook, Fund Manager

Almi Invest Norra Mellansverige AB (RA)Christer Navjord, Fund Manager

Almi Invest Stockholm AB andAlmi Invest Östra Mellansverige AB (RA)Mikael Karlsson, Fund Manager

Almi Invest Västsverige AB (RA)Håkan Krook, Fund Manager

Almi Invest Småland & Öarna AB (RA)Tarja zu dem Berge, Fund Manager

Regional Venture Capital Funds Mid-term evaluation

10

• The venture capital funds shall be complementary to the market. This means, inter alia, that the venture capital funds shall address a gap in the supply of capital among SMEs with high growth potential and not compete with the private market.

• The venture capital funds shall invest in conjunction with a private commercial independent actor and the investment must be made on equal terms.

• The venture capital funds shall revolve i.e. that when the funds’ holding is realised the funds must be reinvested in the region. This also means that the funds shall strive to maintain their capital base. There shall however be no formal requirement that the venture capital funds must generate a return.

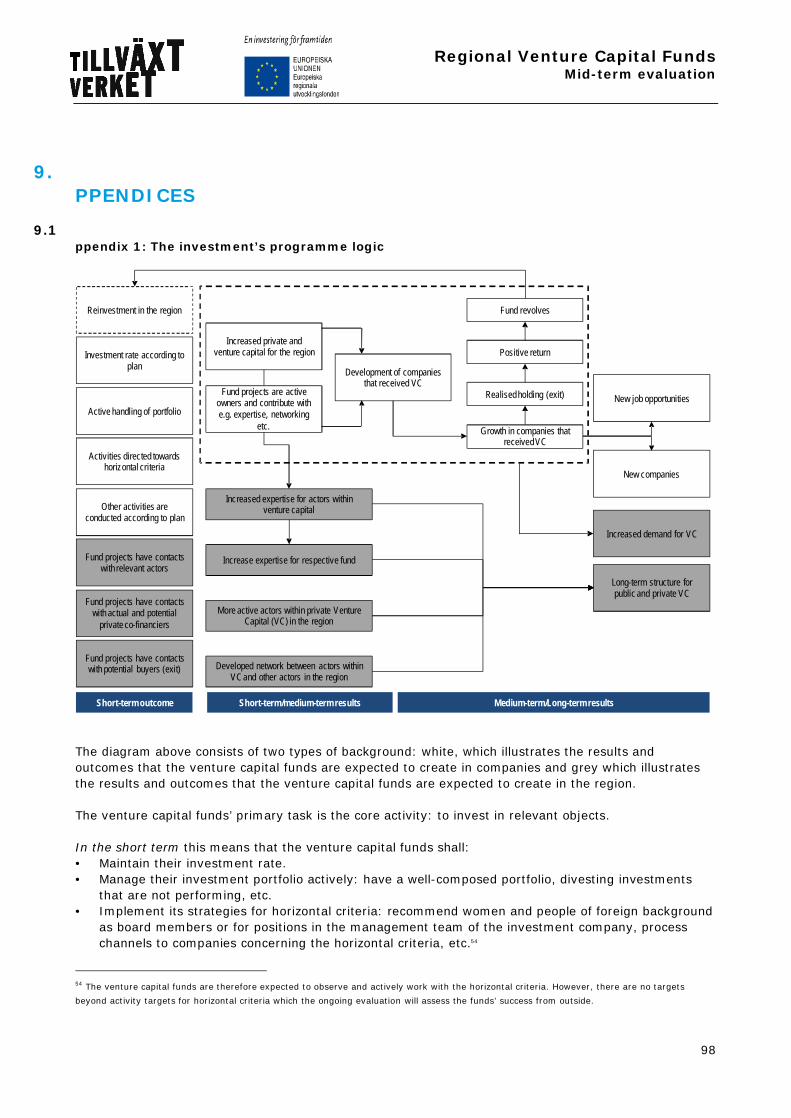

According to the text of the announcement, the goal of the project is that “more companies shall start and grow in the regional programme areas through an improved supply of capital to small and medium-sized enterprises in the early stage.”9. The venture capital funds are also expected to contribute to the development and professionalisation of the venture capital market in Sweden. The formal structure of objectives relating to the results and outcomes that the initiative is expected to produce are presented in Appendix 1.

1.2 ngoing evaluation In principle, all Structural Fund-financed projects with financing from the EU of SEK 10 million or more and projects of “special interest” must implement an ongoing evaluation of itself. The Swedish Agency for Economic and Regional Growth, which is the managing authority for the eight regional Structural Fund programmes in Sweden, has chosen to invest additional funds to commission joint ongoing evaluation of the twelve fund projects in conjunction with the project owners. The aim is to be able to make comparisons between the venture capital funds’ structure, conditions and results, and not least to allow the ongoing evaluation to be an arena for an exchange of experiences between the venture capital funds. The overall approach also provides the Swedish Agency for Economic and Regional Growth with good conditions for learning about how different structures and administrative frameworks impact the venture capital funds’ way of working and what results are generated. Ramböll has been commissioned to carry out the ongoing evaluation of the twelve fund projects between autumn 2009 and spring 2015. The contract was awarded by the Swedish Agency for Economic and Regional Growth’s Evaluation Group for the regional Structural Fund programme, which is also responsible for the ongoing evaluation. The ongoing evaluation will monitor the fund projects on an ongoing basis and will be based on a learning approach where feedback takes place through seminars, workshops and yearly written reports. The yearly reports describe, account for and analyse the implementation and results of the project and discuss current questions in the venture capital funds’ life cycle. The point of evaluating on an ongoing basis is that it provides greater opportunities for learning and development of an investment during its implementation. One problem that the European Commission, the Swedish Agency for Economic and Regional Growth and other actors have noted is that evaluations are often made too late for recommendations to be used for developing and improving investments. In the guideline for evaluation of the Structural Funds for the 2007-2013 period, the Swedish Agency for Economic and Regional Growth states that the overall objective of ongoing evaluation is to create the conditions for continuous learning in the project and that the ongoing evaluation should have a forward-looking and development-supporting approach. The insights and experiences that the evaluation provides will not only be conveyed back to the evaluation object: the venture capital funds’ management, board, employees and financiers. The ongoing 9 http://www.tillvaxtverket.se/download/18.74f57d0f1283a4f88ff800020468/M%C3%A5lindikatorerna+i+fondprojekten.pdf

Regional Venture Capital Funds Mid-term evaluation

11

evaluation will also actively contribute to a wider public debate concerning financing issues by addressing itself to actors like entrepreneurs, private investors, the Ministry of Enterprise, Energy and Communications, the authority for the Swedish Agency for Economic and Regional Growth, regional stakeholders, researchers in business financing and more. Aside from the ongoing evaluation, the authority also carries out work for Growth Analysis commissioned by the Ministry of Enterprise, Energy and Communications and which involves a further evaluation that includes research overviews, international experiences of venture capital investments, outcome evaluation, etc. Ramböll and the Swedish Agency for Economic and Regional Growth cooperate and work towards maintaining a continuous dialogue that supports both the ongoing evaluation and the future outcome evaluation. During the first year (autumn 2009-spring 2010) the ongoing evaluation fulfilled an ex ante evaluation, which must be implemented before a venture is started in order to analyse the relevance, design and objectives structure of the investment. In the case of this analysis, this was done after the investment had been designed, at the same time that the venture capital funds had begun their operative work. Central questions during the first year of the ongoing evaluation revolved around what the venture funds were to achieve in order to be seen as successful, how the business got started and whether the funds were designed so that they can be expected to achieve success. This mid-term evaluation will provide the Swedish Agency for Economic and Regional Growth, venture capital funds and other relevant actors with early indications of how the investment stands in relation to the objectives set and how the implementation is progressing.

1.3 his year’s evaluation The evaluation work began in autumn 2009 and will be carried out on an ongoing basis until the spring of 2015. During this period the project will continuously be developed and undergo different phases, which means that different evaluation questions will arise at different stages in the development of the venture capital funds. Therefore it is important that the evaluation is designed in such a way that it allows the results to be delivered during the time of the venture capital funds’ life cycle when they can be put to practical use in the project. This means that the ongoing evaluation work has not been planned in detail from the start in terms of precisely stipulating what questions will be answered and how this will be done. Ramböll has therefore created a structure where the ongoing evaluation, in conjunction with the project owners and the Swedish Agency for Economic and Regional Growth, makes decisions about what questions are relevant to ask at different times in order to evaluate the implementation of the fund project’s achievement of its objectives and what methods are appropriate in order to answer these questions in a reliable manner. This year’s evaluation – mid-term evaluation – has been designed to answer the following overall questions: • How do the venture capital funds stand in relation to the targets set with regard to the rate of

investment? • How do the venture capital funds’ portfolios look with regard to the investment’s mission10, the size of

the company, stage of development, industry diversification, etc.? • What did the business gain from the investors’ involvement? Can a positive development of the

company be observed? • Are there signs that the venture capital funds are contributing towards the improvement in the

supply of capital situation for companies, i.e. does the investment create additionality? • How is the cooperation with the regional co-financiers functioning? In order to answer the questions above, the mid-term evaluation is divided according to the different actors that are covered by the investment: venture capital funds, private investors and the companies. In

10 See above in Section 1.1.1 Venture capital funds’ mission

Regional Venture Capital Funds Mid-term evaluation

12

the table below the topics of the evaluation, questions and data collection methods are presented which are used to answer the respective question. The methodological approaches and the data sources are briefly presented in the next section.

Table 1. Mid-term evaluation’s topics, questions and data collection methods

Area Questions Method/data collection Venture capital funds’ operation during the past year

How did the venture capital funds’ operation proceed? What has happened since the follow-up a year ago? Weaknesses and successes? Lessons from last year?

• Interviews with the venture capital funds’ MDs

• Written communication with venture capital funds’ MDs

How does the venture capital funds’ investment activity stand in relation to the investment targets set? How does the expected investment activity look for the rest of the project period (forecast)?

Venture capital funds’ investments

How are the venture capital funds’ investment portfolios composed? Are the portfolio compositions reasonable in relation to the mission of the investment and overall objectives?

• Interviews with the venture capital funds’ MDs

• The Swedish Agency for Economic and Regional Growth’s summaries of the venture capital funds’ reporting

• Reporting from the venture capital funds to the Swedish Agency for Economic and Regional Growth

Who are the private investors and what characterises their investment behaviour? To what extent can private co-investors contribute to the financed company’s development and how they develop themselves as a result of the investment?

Private co-investors

Has the investment elicited any more new investors in the market and contributed additionality i.e. led to increased investment interest and investment activity among existing investors?

• Questionnaire to private co-investors

• Interviews with private co-investors

Ramböll has carried out the evaluation in four main phases. In Phase 1, the questionnaires sent to private co-investors and companies were designed. In Phase 2, interviews were conducted with venture capital funds, companies and private co-investors. In Phase 3, the venture capital funds’ yearly reports of indicators and investments made were studied and compiled. In the fourth and final phase, the collected material was analysed and the present report was compiled. Work in the different phases has been done in continuous dialogue with the Swedish Agency for Economic and Regional Growth.

Regional Venture Capital Funds Mid-term evaluation

13

The ongoing evaluation work during 2011 has been carried out by Ulrika Ekström (internal project manager at Ramböll Management Consulting), Sofia Avdeitchikova (external project manager), formerly at Ramböll Management Consulting and now researcher at Lund University, Martin Fröberg and Marcus Holmström at Ramböll Management Consulting. Ingrid Rydell at Ramböll Management Consulting, responsible for method during the first year of the ongoing evaluation rejoined the team during autumn 2011 after parental leave.

1.4 ata sources The primary data sources used for this report are telephone interviews with the venture capital funds’ MDs, private co-investors and companies as well as questionnaires to co-investors and companies that received financing. Quantitative data from the Swedish Agency for Economic and Regional Growth and the venture capital funds related to the reporting of indicators and implemented investments has also been analysed. The different data sources are briefly presented below.

1.4.1 uestionnaires Questionnaire to the company The purpose of the questionnaire to the company has been to obtain information about the companies that received financing from the venture capital funds concerning, among other things, their financing history and perceived ”capital gap”, ambitions for growth and vision of the company’s future development, preferences for venture capital as a source of financing and expectations and perceived impact of the investment upon the company’s business. Contact information for the companies that received financing was made available by the regional capital funds. Ramböll received contact details of 87 companies, of which 54 wholly or partially answered the questionnaire, representing a response rate of 62 per cent. The respondents were given three weeks to answer the questionnaire and two reminders were sent out during this time. A good response rate depends on which target group the questionnaire is aimed at, what relationship the sender has to the respondents and how the questionnaire is designed. In the case of online questionnaires response frequencies above 55 per cent are usually considered to be good. All venture capital funds are represented in the company questionnaire11, but in cases where the number of respondents from companies that received financing by a given fund are very few, Ramböll has for privacy reasons chosen not to disclose which fund the company has cooperated with. A non-response analysis was also conducted in order to examine whether there are differences between companies that have answered the questionnaire and non-respondents i.e. how representative the companies that answered the questionnaire are of all companies that the report aims to study. The non-response analysis was done with respect to the variables that were available for all companies: the company’s stage of development, industry sector and size (number of employees). The results are reported in Table 2. Non-response analysis of companies The stage and industry sector distributions used in the table are reported in Appendix 2.

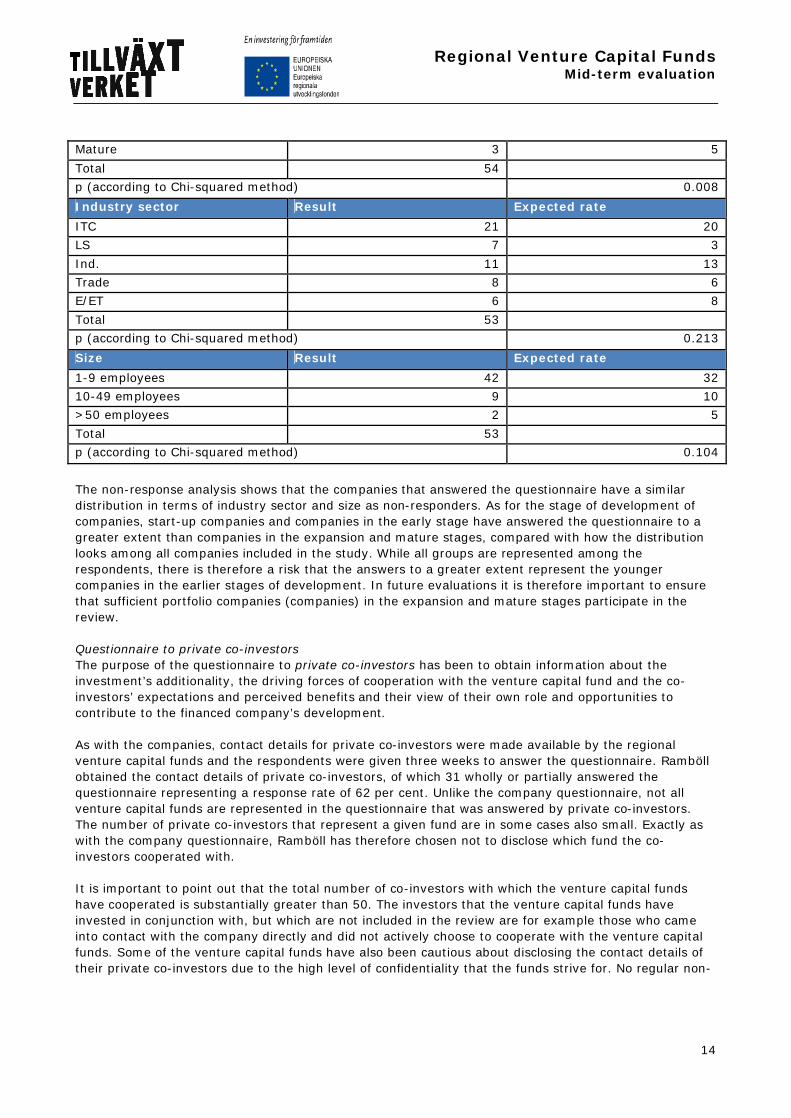

Table 2. Non-response analysis of companies12

Stage Result Expected rate Start-up 14 10 Early stage 22 13 Expansion 15 23

11 The venture capital funds run by Almi Invest are in this respect regarded as one fund as is also the case with Sydsvensk Entreprenörsfond I, II

and III. 12 The analysis was carried out using the Chi-Square function, which compares the distribution of the studied group and the expected distribution

if the two studied groups (respondents and non-respondents) had been identical. The function also calculates the probability (p) that differences

between actual and expected values are by chance. If the probability is less than 5% (p<0.05) differences are usually considered to be significant.

Regional Venture Capital Funds Mid-term evaluation

14

Mature 3 5 Total 54 p (according to Chi-squared method) 0.008

Industry sector Result Expected rate ITC 21 20 LS 7 3 Ind. 11 13 Trade 8 6 E/ET 6 8 Total 53 p (according to Chi-squared method) 0.213

Size Result Expected rate 1-9 employees 42 32 10-49 employees 9 10 >50 employees 2 5 Total 53 p (according to Chi-squared method) 0.104

The non-response analysis shows that the companies that answered the questionnaire have a similar distribution in terms of industry sector and size as non-responders. As for the stage of development of companies, start-up companies and companies in the early stage have answered the questionnaire to a greater extent than companies in the expansion and mature stages, compared with how the distribution looks among all companies included in the study. While all groups are represented among the respondents, there is therefore a risk that the answers to a greater extent represent the younger companies in the earlier stages of development. In future evaluations it is therefore important to ensure that sufficient portfolio companies (companies) in the expansion and mature stages participate in the review. Questionnaire to private co-investors The purpose of the questionnaire to private co-investors has been to obtain information about the investment’s additionality, the driving forces of cooperation with the venture capital fund and the co-investors’ expectations and perceived benefits and their view of their own role and opportunities to contribute to the financed company’s development. As with the companies, contact details for private co-investors were made available by the regional venture capital funds and the respondents were given three weeks to answer the questionnaire. Ramböll obtained the contact details of private co-investors, of which 31 wholly or partially answered the questionnaire representing a response rate of 62 per cent. Unlike the company questionnaire, not all venture capital funds are represented in the questionnaire that was answered by private co-investors. The number of private co-investors that represent a given fund are in some cases also small. Exactly as with the company questionnaire, Ramböll has therefore chosen not to disclose which fund the co-investors cooperated with. It is important to point out that the total number of co-investors with which the venture capital funds have cooperated is substantially greater than 50. The investors that the venture capital funds have invested in conjunction with, but which are not included in the review are for example those who came into contact with the company directly and did not actively choose to cooperate with the venture capital funds. Some of the venture capital funds have also been cautious about disclosing the contact details of their private co-investors due to the high level of confidentiality that the funds strive for. No regular non-

Regional Venture Capital Funds Mid-term evaluation

15

response analysis could be done because some background information about the co-investments who did not answer the questionnaire was not available.

1.4.2 elephone interviews Within the framework of the mid-term evaluation, Ramböll has conducted interviews with four groups of respondents:

• Telephone interviews with all fund MDs

• 20 interviews with companies that received financing

• Ten interviews with private co-investors

• 20 interviews with the funds’ regional co-financiers

The companies and private investors who participated in the surveys were asked to state whether they took part in a telephone interview. The selection of interviews with the companies was then done to ensure variation in the companies’ industry sector affiliation and size. All venture capital funds are represented in the interviews with companies, while ten of twelve venture capital funds are represented in the interviews with co-investors. Ramböll has used semi-structured interviews, which means that an interview guide has been used to ensure that the same issues are addressed by all respondents, at the same time as there is room for follow-up questions and further discussion.

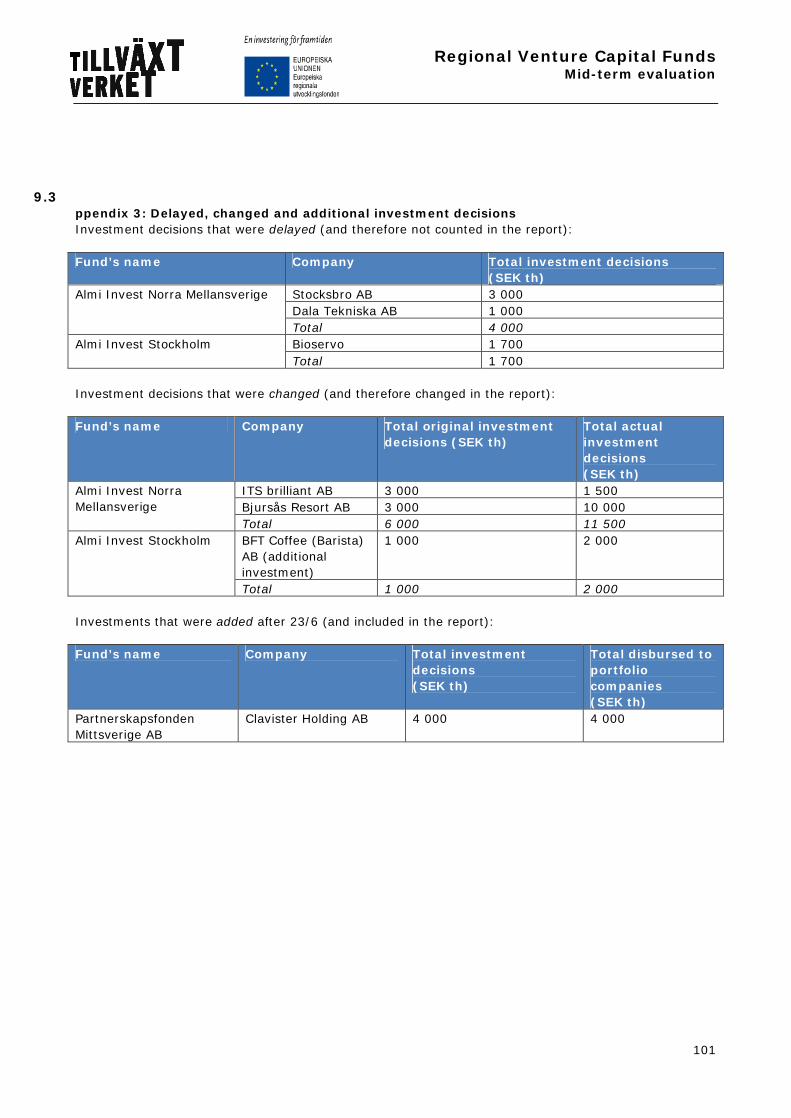

1.4.3 he venture capital funds’ reporting In addition to the questionnaires, the venture capital funds reporting to the Swedish Agency for Economic and Regional Growth regarding the implemented investments and other indicators consists of the quantitative data sources in this report. The reporting consists of an account of the investments the venture capital funds have made with information about the companies that received financing. The information includes the venture capital funds’ investment decisions, disbursed investments, number of employees in the company that the venture capital funds decided to invest funds in and certain information concerning horizontal criteria, for example the participating company’s ownership structure according to gender. The reporting for this report was submitted on 23 June 2011 and the funds were given the opportunity to make adjustments relating to activities up to 30 June 2011. These adjustments are presented in Appendix 3.

1.5 xplanation of concepts A number of specialist terms are used in this initiative. We briefly discuss the concepts that are central to this report below. Additionality Additionality is one of the fundamental principles of the European Union’s aid policy, which says that Community aid shall complement the Member States’s own contributions and not reduce them.13 The establishment of public venture capital funds may lead to the private venture capital market developing more slowly or a reduction in the amount of private venture capital.14 Displacement effects like these mean that private venture capital is reduced and replaced with public capital.15 There may also be a risk

13 The Swedish Agency for Economic and Regional Growth (2010) "Staten och riskkapitalet" 2010:01, s. 73 14 Leleux, B., Surlemont, B. och Wacquier, H. (1998) i Reynolds, P.D., Bygrave, W.D., Carter, N.M., Manigart, S., Mason, C.M., Meyer, D.G., Shaver, K.G. (eds.), Frontiers of entrepreneurship research, Babson College, State versus private capital: cross-spawning or crowding-out? A Pan-

European Analysis. 15 Jyoti, K. and Sandler, T. (2000) Partners in giving: the crowding-in effects of UK government grants, European Economic Review, 44.

Regional Venture Capital Funds Mid-term evaluation

16

that public venture capital funds succeed in financing good projects by not requiring as high a return as private venture capital funds and thereby out-compete private investors who have to settle for inferior objects.16 Business angel A business angel is a private person who directly or through a company invests in companies. The business angel invests equity capital and provides business knowledge, skills and contacts to unlisted companies. This may for example be a person who sold his or her company and now wants to invest some of the capital of the company. Business angels act as a complement to formal venture capital in that they usually go in at the early stage of the company’s growth phases than risk capital investors. "Private investor" is a broader concept than business angel. 17 Pari passu The venture capital funds’ investments must be made together with and on equal terms (pari passu) as one or more private independent co-investors. The private co-investors must stand for at least 50 per cent of the investment, but can stand for more. On equal terms means that the fund project and private investors invest with the same requirements and rights. A private independent commercial co-investor is in normal circumstances expected to be a venture capital company or a business angel i.e. a private person who invests his or her own funds for a share in the ownership of the company or a company that wants to invest in another company.18 In Paragraph 5 of the fund project’s special conditions it states: "To ensure that the project owner's individual investments are made on a commercial basis, at least one private commercial operator must invest at the same time in the portfolio company with at least the same amount and on equal terms." Investments in the fund project must therefore be co-financed on equal terms between the public and the private commercial venture capital.19 Mittkapital Jämtland/Västernorrland, which are owned by the Sixth AP Fund (Sjätte AP-fonden) and Sydsvensk Entreprenörsfond (SEF) I are however exceptions to this rule. Venture capital Venture capital is investment in companies not listed on a public list (i.e. stock exchange or another marketplace). The main part of a venture capital investment in general is made up of so called "equity", but it is also common for some intermediate forms between equity and loan capital to exist, such as convertible loans. A venture capital investment therefore means that the investor is, or has the potential to become, a part-owner of the company. Venture capital is not only a capital investment, but also assumes that the investor gets actively involved in the ownership, for example, through representation on the company’s board. Venture capital investment is also often limited in time so that the venture capital company has a goal to dispose of their investment in the foreseeable future (usually 5-7 years). Venture capital investments are typically minority investments in unlisted companies, often young companies in the early stage but also companies in their expansion phase. Venture capital is often

16 Manigart, S., De Waele, K., Wright, M., Robbie, K., Desbrières, P, Sapienza, H. and Beekman, A. (2001) Determinants of required returns in

venture capital investments: A five country study, Journal of Business Venturing, 17(4). 17 Expowera (2008) http://www.expowera.se/mentor/ekonomi/finansiering_affarsanglar.htm, obtained on 17-05-2011, The Swedish Agency for

Economic and Regional Growth (2011)

http://www.tillvaxtverket.se/huvudmeny/insatserfortillvaxt/kapitalforsorjning/affarsanglar.4.21099e4211fdba8c87b800017075.html, obtained on

17-05-2011, Företagande.se (2011) http://www.foretagande.se/Om-affarsanglar.html, obtained on 17-05-2011 18 Mittkapital Jämtland/Västernorrland is however an exception to this rule. 19 The Swedish Agency for Economic and Regional Growth (2010) Diskussionsunderlag för fondprojektens genomförande: Regionalfonderna i

Sverige 2009-2014, Info 0212, s. 15

Regional Venture Capital Funds Mid-term evaluation

17

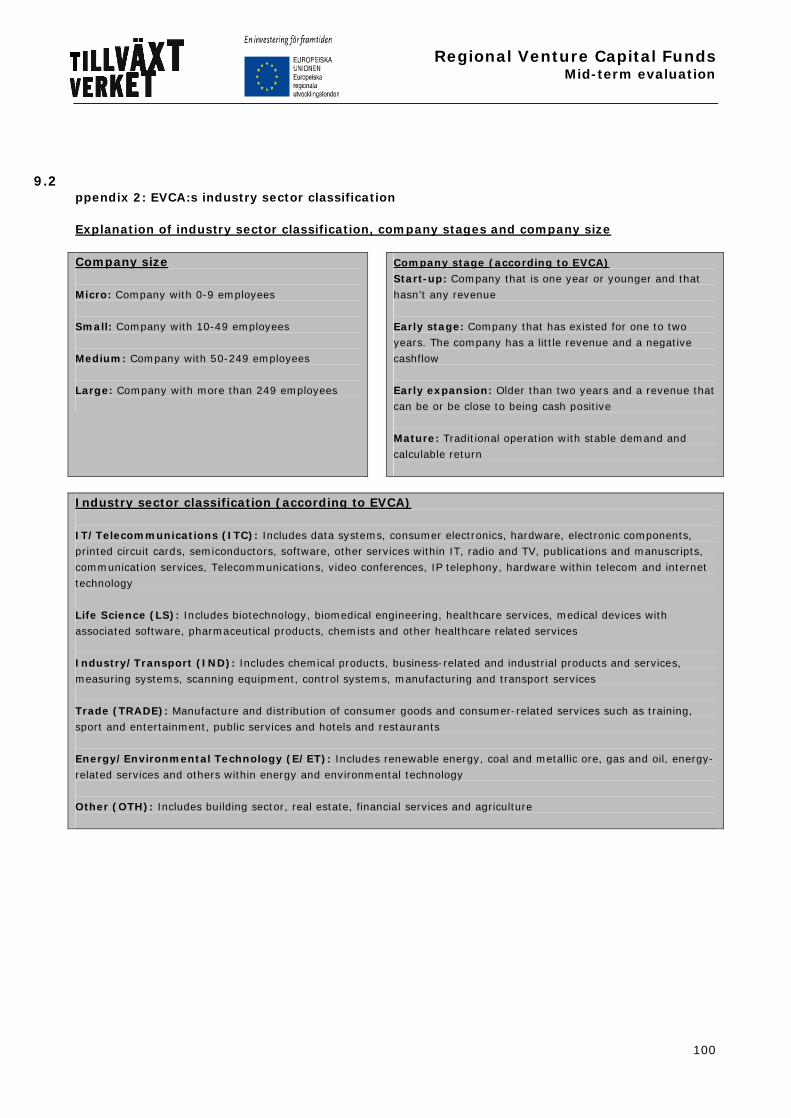

invested by a specialised manager who hopes to maximize the return on investment (ROI). Because the risk the investor takes on is relatively large, they generally go into a company only if they believe they can obtain a quick and large return20. Risk capital The term "risk capital" refers to the financing of a company’s equity capital during the early growth stages (seed, start-up and expansion stages), such as informal investment by business angels, venture capital and alternative stock markets that specialise in small and medium-sized enterprises, including growth companies21. The companies’ stages of development The European Union uses the following definitions for the different stages at which the investor may enter: seed capital, start-up capital, expansion capital and replacement capital22, of which the latter is not covered by venture capital definitions (see above). The different terms are defined in order below. Seed capital Financing of analysis, assessment and development of a new concept prior to start-up. Start-up capital Financing of product development and initial marketing for companies that have not sold their product or service commercially and are not yet generating a profit. Expansion capital Financing of growth and expansion in a company that may break even or go into profit – the financing is used to increase production capacity, for market or product development or as additional working capital. Replacement capital Purchase of existing shares in a company from another private equity investment company or from another or other shareholder(s) - Replacement capital is also called "secondary purchase." The European Private Equity and Venture Capital Association (EVCA) uses similar subdivisions, but chooses instead to separate the stages as start-up, early-stage, early expansion and mature companies. The exact definitions are presented in Appendix 2, in which EVCA’s industry sector classification is also shown. In this report, EVCA’s definitions are used because the venture capital funds have chosen to document their investments based on these, which is also industry practice.

1.6 onclusions from first year of ongoing evaluation The aim of the ongoing evaluation during 2009 and 2010 was to analyse the venture capital funds’ mission, design and objectives structure, to illustrate how the venture capital funds started their activities and to define the key success factors of the venture capital funds’ work and the challenges ahead. The dialogue with the venture capital funds’ MDs and with the Swedish Agency for Economic and Regional Growth revealed that the investment tussled with a number of problems which delayed the start of the venture capital funds and took the focus away from core activities. The biggest problem was a delay in disbursement of regional co-financing, problems in recruiting MDs for all of the venture capital funds, lack of clarity and disagreement about the chief objectives and mission of the venture capital funds and uncertainty regarding how the rules should be interpreted. The latter was perceived as a big problem because interpretation of the rules was done afterwards i.e. when the venture capital funds had already started and were then applied retrospectively.

20 Isaksson, A. (2000) Venture capital – begrepp och definitioner. Published in The Swedish Private Equity & Venture Capital Association’s (SVCA) Register of Members 2000/2001. 21 The Swedish Agency for Economic and Regional Growth (2010) Info 0212 Rev A: Förutsättningar för fondprojektens genomförande. 22 The Swedish Agency for Economic and Regional Growth (2010) Info 0212 Rev A: Förutsättningar för fondprojektens genomförande.

Regional Venture Capital Funds Mid-term evaluation

18

Other challenges that have affected and continue to be expected to be central to the venture capital funds' operations are primarily the difficulty in finding good investment objects and financially strong and competent private co-investors and finding ways to "invest right" - in line with the guidelines for the venture capital funds’ work and with the potential of a good return. While the first two challenges have been experienced more in regions with a less developed private equity market and whose business structure is based on companies that have traditionally not been the subject of venture capital financing, it seems that the final challenge has applied to all regions. Despite the challenges the funds experienced a lot of interest and a positive reception from companies, private investors and regional actors and had a good belief in the future. There seemed to be a confidence in the initiative and in the organisations that are implementers of fund projects. During the first year of operation (the majority of venture capital funds have been running for less than that), 759 investment proposals were received and 59 investments were implemented, amounting to a value of SEK 277 million, including private co-investment. All venture capital funds intended to make up for the delay which occurred during the first year and over time invest in line with their planned investment rate. Based on the conclusions of the ongoing evaluation in 2009 and 2010, it is of major importance, within the framework of this mid-term evaluation, to answer how the problems and challenges outlined above have been handled by both venture capital funds and the Swedish Agency for Economic and Regional Growth.

1.7 eport structure This report consists of eight chapters. The next chapter presents international and previous Swedish experiences of similar public investments in capital and the supply of expertise to small and medium- sized enterprises in the early stages. After that, in Chapter Three, an overall picture is given of the venture capital funds' activities during the past year. Chapter Four deals with the venture capital funds, investment activity and forecasts for the remaining project period are presented. The portfolio compositions of the venture capital funds are presented and discussed, with respect to the financed company’s stage of development, size and industry sector affiliation. Chapter Five deals with the consequences of the investment in terms of development and additionality of the financed companies, while Chapter Six deals with the private co-investors’ perceived value of the investment and contributions to the development of the financed companies. Chapter Seven discusses regional cooperation and, finally, in Chapter Eight, the report's final discussion and conclusions are presented, in which the long-term impact of the initiative on access to capital for companies and investment activity of private investors is discussed.

2. NTERNATIONAL AND SWEDISH EXPERIENCES

This chapter summarises the initial experiences of public investments of capital and the supply of expertise to companies in the early stage in Finland, Scotland and Norway. Secondly, it presents a summary of the contents of Ramboll Management's evaluation of the Swedish pilot investments in three regional venture capital funds from April 201123, focusing on the conclusions drawn about the pilot fund's achievement of its objectives, models and lessons learnt prior to today's twelve fund projects.

23 Ramböll (2011) Utvärdering: Pilotsatsning på regionala investeringsfonder

Regional Venture Capital Funds Mid-term evaluation

19

2.1 nternational experiences This section is a brief summary of a draft report written in Norwegian that the Swedish Agency for Growth Policy Analysis (Growth Analysis) compiled.24 The section in its entirety is therefore Ramböll’s rendering of the draft that Growth Analysis provided.25 Growth Analysis will deliver its final version of the report that is reproduced here. Finland – The VIGO programme In Finland, public and private actors have desired a stronger coordination of existing financing instruments for companies in the early stage, at the same time as they saw that potential growth companies, in addition to capital, have a need for the supply of expertise. Inspired by the Israeli Yozma "business incubator" model, the Finnish Ministry of Employment and the Economy launched the VIGO programme in 2009. The programme The goal of VIGO is to stimulate the growth of new technology-based growth companies and establish a "fast track" to financing, at the same time companies are provided with expertise. After a bidding competition involving 43 participating networks, the programme selected six networks, consisting of serial entrepreneurs, investors and business developers with international experience. The main idea is that when a certified VIGO incubator chooses to engage in a project with its own time and money, this triggers support from Tekes’ YIE programmes and investment from the Seed Fund Vera26. The experienced business developers contribute to a more rapid and better development of companies and help them in their internationalisation process. In their investments the individual VIGO actors focus on specific industries. There are no geographic restrictions, but the idea is that industry diversification will contribute to geographic distribution. A steering committee composed of representatives from venture capital environments, the Ministry, Tekes and Vera Venture is responsible for the programme’s development. The programme has therefore been developed in collaboration between the private and public actors. The VIGO programme is thus operating outside the traditional structures in Finland. Since VIGO does not contribute any financing, the input of public resources to run the programme was relatively small. The individual VIGO networks have slightly different models, but usually partners in an individual VIGO network invest their own time and money in the portfolio company and usually have a stake of around 20 per cent. The incentive for the partners in a VIGO network is primarily a return on investments, but they can also get parts of their salaries covered by the contribution that companies get through a management fee. VIGO however receives no public funding. Experiences so far The first two years of the programme have been far from trouble-free. The idea was that each VIGO network would create a "fast track" to public financing, but from the incubator’s point of view the decision-making processes were found to be slow and not at all predictable. The VIGO network first does its own evaluation of the project and after that Tekes and Seed Vera Venture do their own evaluations of each individual project. The result is a turnaround time of at least two to three months and less predictability. The private actors believe that decisions should essentially lie with them but entrusting decisions to private actors radically goes against how both Seed Veraventure and Tekes usually work. But the decision process as it is done now appears to be inefficient in that the three actors are doing their 24 The Swedish Agency for Economic and Regional Growth (2011) Staten och riskkapitalet, delrapport 2 25 Ramböll Management has therefore not made any of its own analyses of the content. 26 Tekes, The Finnish Funding Agency for Technology and Innovation, supports R & D and develops instruments to support the commercialisation

of high technology companies. This has largely taken place through different types of financial contributions to potential growth companies.

Through the initiative of Young Innovative Entrepreneurs (YIE) from 2008, young businesses can receive up to one million Euros in financial contributions and loans (contributions makes up about 75 per cent). Seed Fund Vera was founded in 2005 by Finnvera, a state-owned

organisation that since 2003 gradually took over the role of Finland’s financing actor in the seed stage. Seed Fund Vera has 96 million Euros in

management capital and in 2011 expanded with capital from the ERDF.

Regional Venture Capital Funds Mid-term evaluation

20

evaluations independently of each other. The private actors are sceptical about giving Tekes a more central role in the programme for fear that the programme will become bureaucratic, as this is one of "many" programmes that Tekes manages. The public actors for their part emphasise that this is taxpayers' money and that the types of decisions that are made must be quality controlled. Tekes also points out that they have a role in protecting the entrepreneur's interests as otherwise there is a risk of them being steamrollered by the private VIGO network. The VIGO programme has only been in operation for a short time but there are some indications that the programme has had some success. One is international financing, where several companies have attracted international venture capital financing. This indicates that the international network is very useful when it comes to strengthening the legitimacy of the potential growth company in the international market. The way forward The VIGO programme was initially set up for a period of three plus a further three years, which means that it will be evaluated after three years. In addition, it experimented with the setting up of a "micro-seeding fund" linked to the individual VIGO networks in 2011. The funds will be set up in cooperation with Seed Veraventure and have a budget of 5 million Euros. In 2011, a number of VIGO networks wanted to expand, but in this context a larger diversification of industry sectors is preferred (of the six existing VIGO networks three focus on ICT). All the parties involved expressed strong interest in developing the concept further and look at this first period as a pilot initiative, in which actors test things out and try to adapt the system to the Finnish context. Scotland – Scottish Co-Investment Fund The Scottish Co-Investment Fund (SCF) was launched in 2003 with a capital of 48 million pounds, including financing from the ERDF. The fund provided equity capital to companies with good growth potential and often with their own technology. SCF acted as a fund on commercial grounds and thereby expected to generate a financial return (through share dividends, partial exits, etc). What was special about SCF was that it was a co-investment fund, which means that its own equity was invested on equal terms (pari passu) with investors from the private sector and followed the private actor’s investment decisions. SCF was a passive investor and owner (so-called sleeping partner). Due diligence and the investment decisions were carried out by the co-investors themselves, given that the investment fulfilled the SCF’s basic investment criteria. The fund participated in investments of up to two million pounds and co-invested amounts between 100 000 and one million pounds. The SCF started with 15 partners and twelve investors in 2003 and has since developed to a level of around 55-60 investments a year and 28 partners. Most partners are syndicates of business angels. Two key conditions for the establishment, design and later success of the SCF was that there were substantial tax incentives and an infrastructure that attracted private co-investors. Through the Enterprise Investment Scheme (EIS) investors receive tax reductions when they went in with new equity into small companies. Under certain conditions the investor can get back 20 per cent of the invested sum, a level which was raised to 30 per cent in 2011. It is also possible to avoid taxation of profits or write off the loss in order to get reduced income tax when the equity stake is sold. Evaluation of the Scottish Co-Investment Fund The Centre for Strategy and Evaluation Services carried an evaluation of the SCF in 2007, based on analyses of the venture capital funds’ data and results, questionnaires to the funds and companies and interviews. The evaluation showed that the venture capital funds in the SCF had addressed areas that are characterised by market failure. The funds have involved additionality because companies that did not have access to financing alternatives or needed additional funds received financing. The first Growth

Regional Venture Capital Funds Mid-term evaluation

21

Analysis Interim Report27 however established that no connection had been made between the received aid and the company’s development in terms of size, growth and profitability. The funds were also assessed to have contributed to the strengthening of the regional finance markets. By making public funds available, regional willingness to invest increased. Because the SCF is a co-investment fund, the private investors obtained both financial leverage on the invested funds and a spreading of risk. In the evaluation, the conclusion was drawn that the projects the SCF co-financed would not have been carried out by investors without aid. The form of co-investment also means that the SCF is primarily attractive to informal venture capitalists, such as business angels and networks. In 2006 and 2007, Scottish Government Social Research also carried out an evaluation which, among other things, pointed out that, since the SCF follows the private actors’ investment decisions, the geographical distribution of the investments is largely influenced by where the private actors are located. This is considered to have resulted in a large proportion of the investments initially being made in eastern Scotland around Edinburgh, where there were already active investment environments. The Centre for Strategy and Evaluation Services also found in its assessment that an overall displacement of private investors was not likely because the SCF only co-invests in companies in conjunction with other investors. SCF has however had an ambitious returns target and, to achieve this, the SCF makes investments and exits that give the greatest possible return i.e. at a stage when private financiers can take over. This is considered to have involved a substantial risk of direct displacement of private investors - but there is no evidence that displacement occurred. The evaluation also showed difficulties in steering equity investment from the growth regions to regions with little or no growth. Similar difficulties have been noted in Sweden, where there is an in-built conflict of interest where investment companies on the one hand must handle tasks that they consider the market does not manage and, on the other hand, operate under market conditions. The combined effects of the SCF initiative for the Scottish market were, at the time of evaluation, relatively small both in terms of loan and equity capital. The role of the funds in the early stages of owner-financing, however, was significant. The evaluation also established that it was too early to draw any far-reaching conclusions about the sustainability of the investment, that is, whether the funds would be self-sufficient. Probably a long-term public commitment is required since it takes time before the funds generate enough income to become self-sufficient. Growth Analysis points out in Interim Report 2 that, even if the SCF has largely succeeded in building a more well-functioning market for investments in the early stage, the situation is relatively vulnerable since there may be confusion about whether the SCF will exist in future. The question of the fund's long-term existence is a challenge given that the political leadership is something that changes over time. It was further pointed out that, even if the SCF has a good track record in terms of investment, there is greater uncertainty associated with realizing value from their investment portfolio. SCF aims to be "evergreen" (revolving) since revenues from sales cover the need for new investments. The financial crises of recent years has led to the investment cycle taking longer than planned and there are currently only a few examples of investments that have been sold at a profit. Norway – the Norwegian seed capital scheme The first pure private venture fund in Norway was established in the early 1980s. During the following years, a number of funds were established but after ”the crash” in 1987 many of these had problems. When portfolio companies developed poorly, it was difficult to start new funds. But the industry later had a solid growth and before the IT bubble burst in 2001 a robust environment had emerged. This resulted in stronger competition for both capital and projects and contributed to professionalisation and later internationalisation of the industry. In recent years, there has been a very strong growth in the industry. in 2004, the Norwegian funds had NOK 18 billion in assets under management and in 2010 the amount

27 Growth Analysis (2010) ”Staten och riskkapitalet” 2010:01

Regional Venture Capital Funds Mid-term evaluation

22

had risen to around NOK 60 billion. However, the overwhelming majority of this growth came within ”the buy-out segment” and not within classic venture or in the early stage/seed stage. The growth within seed financing has primarily come through the state-initiated seed stage funds that were established in 1998 and 2006. The public actor, Innovation Norway, has monitoring and management responsibility for the investments. The organisation has a number of instruments to assist both new and established businesses. The first seed fund was established in 1997 as a cooperative project between the Ministry of Trade and industry, The Norwegian Industrial and Regional Development Fund, now Innovation Norway and Norsk Investorforum. Seed Capital 1 – 1997/98 In the first seed capital scheme, the state took part in the financing of a seed fund though the supply of loan capital, while equity capital was to be disbursed by private investors. The seed capital would in this way trigger private capital and supply expertise to companies in the early stages. The first fund to be set up was the nationwide START Fund with a total management capital of NOK 320 million. The state went in with so-called liability loans equivalent to NOK 160 million. In addition to this, five smaller regional funds were established. A traditional model of management (General Partners) and private actors (Limited Partners) were chosen. As a risk-relief element a reserve fund was established. Financial results and lessons learnt The fund’s financial results were considered to be very poor. Some of the reasons for the first scheme’s poor results are assessed to be the following:

• The risk relief was too small • Too little focus on management (lacking expertise) • Very little expertise about exits in management environment • The funds were too small • The model of liability loans has not been successful