micro finance report

TRANSCRIPT

1. IntroductionMany people, particularly those living on low incomes,

cannot access mainstream financial products such as bank

accounts and low cost loans. This financial exclusion

imposes real costs on individuals, their families and the

communities in which they live.

Households that operate without mainstream banking services:

are unable to make savings via direct debits on utility

bills, are more vulnerable to loss or theft and may face

additional barriers to employment. In addition, they are far

more likely to use the alternative credit market - and pay

interest many times that of a standard personal loan, often

contributing to spiraling debt. In addition, for those who

do get into debt or who struggle to make payments, the

supply of free face-to-face money advice falls far short of

demand. Unrestrained access to public goods and services is

the sine qua non of an open and efficient society. As banking

services are in the nature of public good, it is essential

that availability of banking and payment services to the

entire population without discrimination is the prime

objective of the public policy.

1.1 What is Financial Inclusion?Financial inclusion is providing financial services at an

affordable cost to the disadvantaged and low income groups.

1

Some of the financial services include giving loans,

credits, providing banking facilities etc.

1.2 What is Micro-Finance?‘Micro-finance’ is often used interchangeably with

‘Financial inclusion’. But, it mostly consists of giving

micro-credit, micro-savings, micro-insurance etc.

1.3 Micro-finance Definition According to International Labor Organization (ILO),“Microfinance is an economic development approach thatinvolves providing financial services through institutionsto low income clients”.

In India, Microfinance has been defined by “The NationalMicrofinance Taskforce, 1999” as “ provision of thrift,credit and other financial services and products of verysmall amounts to the poor in rural, semi-urban or urbanareas for enabling them to raise their income levels andimprove living standards”.

"The poor stay poor, not because they are lazy but becausethey have no access to capital."The dictionary meaning of‘finance’ is management of money. The management of moneydenotes acquiring & using money. Micro Finance is buzzingword, used when financing for micro entrepreneurs. Conceptof micro finance is emerged in need of meeting special goalto empower under-privileged class of society, women, andpoor, downtrodden by natural reasons or men made; caste,creed, religion or otherwise. The principles of MicroFinance are founded on the philosophy of cooperation and itscentral values of equality, equity and mutual self-help. Atthe heart of these principles are the concept of humandevelopment and the brotherhood of man expressed through

2

people working together to achieve a better life forthemselves and their children.

Traditionally micro finance was focused on providing a verystandardized credit product. The poor, just like anyoneelse, (in fact need like thirst) need a diverse range offinancial instruments to be able to build assets, stabilizeconsumption and protect themselves against risks. Thus, wesee a broadening of the concept of micro finance--- ourcurrent challenge is to find efficient and reliable ways ofproviding a richer menu of micro finance products. MicroFinance is not merely extending credit, but extending creditto those who require most for their and family’s survival.It cannot be measured in term of quantity, but due weightage to quality measurement. How credit availed is used tosurvive and grow with limited means.

1.4 Difference between Financial Inclusion and

Micro-FinanceMicro-Finance is a subset of Financial Inclusion. Apart from

providing micro-credit, micro-savings, micro-insurance,

Financial Inclusion also consists of other ways of bringing

deprived society in to financial service system by educating

them about financial system, offering the policies of their

interest etc.

2. Objective of studyTo understand what financial inclusion means, to study about

the organizations involved in it, the situation in Andhra

Pradesh and give suggestions for financial inclusion.

3

3. MethodologyStep 1 – Collection of information related to Financial

Inclusion.

Step 2 – Collection of information about organization

involved in Financial Inclusion.

Step 3 – Associating with an organization for studying

Financial Inclusion.

Step 4 – Conducting a survey to collect information.

Step 5 – Giving suggestions.

4. The scope of financial inclusionThe scope of financial inclusion can be expanded in two

ways.

Through state-driven intervention by way of statutory

enactments ( for instance the US example, the Community

Reinvestment Act and making it a statutory right to have

bank account in France).

Through voluntary effort by the banking community itself for

evolving various strategies to bring within the ambit of the

banking sector the large strata of society.

4

When bankers do not give the desired attention to certain

areas, the regulators have to step in to remedy the

situation. This is the reason why the Reserve Bank of India

is placing a lot of emphasis on financial inclusion.

In India the focus of the financial inclusion at present is

confined to ensuring a bare minimum access to a savings bank

account without frills, to all. Internationally, the

financial exclusion has been viewed in a much wider

perspective. Having a current account / savings account on

its own, is not regarded as an accurate indicator of

financial inclusion. There could be multiple levels of

financial inclusion and exclusion. At one extreme, it is

possible to identify the ‘super-included’, i.e., those

customers who are actively and persistently courted by the

financial services industry, and who have at their disposal

a wide range of financial services and products. At the

other extreme, we may have the financially excluded, who are

denied access to even the most basic of financial products.

In between are those who use the banking services only for

deposits and withdrawals of money. But these persons may

have only restricted access to the financial system, and may

not enjoy the flexibility of access offered to more affluent

customers.

4.1 Consequences of financial exclusion

5

Consequences of financial exclusion will vary depending on

the nature and extent of services denied. It may lead to

higher incidence of crime, general decline in investment,

difficulties in gaining access to credit or getting credit

from informal sources at exorbitant rates, and increased

unemployment, etc. The small business may suffer due to

loss of access to middle class and higher-income consumers,

higher cash handling costs, delays in remittances of money.

According to certain researches, financial exclusion can

lead to social exclusion.

5. Micro-finance and Poverty AlleviationMost poor people manage to mobilize resources to develop

their enterprises and their dwellings slowly over time.

Financial services could enable the poor to leverage their

initiative, accelarating the process of building incomes,

assets and economic security. However, conventional finance

institutions seldom lend down-market to serve the needs of

low-income families and women-headed households. They are

very often denied access to credit for any purpose, making

the discussion of the level of interest rate and other terms

of finance irrelevant. Therefore the fundamental problem is

not so much of unaffordable terms of loan as the lack of

access to credit itself (Kim 1995).

The lack of access to credit for the poor is attributable to

practical difficulties arising from the discrepancy between

6

the mode of operation followed by financial institutions and

the economic characteristics and financing needs of low-

income households. For example, commercial lending

institutions require that borrowers have a stable source of

income out of which principal and interest can be paid back

according to the agreed terms. However, the income of many

self employed households is not stable, regardless of its

size. A large number of small loans are needed to serve the

poor, but lenders prefer dealing with large loans in small

numbers to minimize administration costs. They also look for

collateral with a clear title - which many low-income

households do not have. In addition bankers tend to consider

low income households a bad risk imposing exceedingly high

information monitoring costs on operation.

Over the last ten years, however, successful experiences in

providing finance to small entrepreneur and producers

demonstrate that poor people, when given access to

responsive and timely financial services at market rates,

repay their loans and use the proceeds to increase their

income and assets. This is not surprising since the only

realistic alternative for them is to borrow from informal

market at an interest much higher than market rates.

Community banks, NGOs and grassroots savings and credit

groups around the world have shown that these

microenterprise loans can be profitable for borrowers and

7

for the lenders, making microfinance one of the most

effective poverty reducing strategies.

6. History of Micro-finance The first instance of Micro-Finance dates back to as far as

19th century. Friedrich Wilhelm Raiffeisen conceived the

idea of cooperative self-help during his tenure as the mayor

of Flammersfeld. Raiffeisen was moved to action by the

poverty of the recently freed serfs, and by the degree of

exploitation they faced from local moneylenders. He was

inspired by observing the suffering of the farmers in the

hands of loansharks. He founded the first cooperative

lending bank, in 1864.

In 1959, Dr. Akhtar Hameed Khan a social activist pioneered

microfinance activities

in Bangladesh and Pakistan. He developed Comilla model,

which provided a methodology of implementation in the areas

of agricultural and rural development on the principle of

grassroots level cooperative participation by the people.

Some salient features of the Comilla Model are:

Involvement of both public and private sectors in the

process of rural development and refining them to suit the

needs.

Development of a institutional leaderships in every

village to manage and sustain the development efforts.

8

Decentralized of various government departments and the

representatives of public organizations.

Education the people and improving the technology

Focus on community development, target group approach,

and intensive area development.

Muhammad Yunus, the founder of Grameen Bank in Bangledesh,

was inspired by Mr Akthar Hameed Khan and

the terrible Bangladesh famine of 1974 to make a small loan

of $27 to a group of 42 families so that they could create

small items for sale. This led to development of Grameen

Bank.

6.1 Role of Microfinance:

Ø Microfinance helps poor households meet basic needs andprotects them against risks.

Ø The use of financial services by low-income householdsleads to improvements in household economic welfare andenterprise stability and growth.

Ø By supporting women’s economic participation, microfinanceempowers women, thereby promoting gender-equity andimproving household well being.

Ø The level of impact relates to the length of time clientshave had access to financial services.

Microfinance Today

In the 1970s a paradigm shift started to take place. Thefailure of subsidized government or donor driveninstitutions to meet the demand for financial services in

9

developing countries let to several new approaches. Some ofthe most prominent ones are presented below. Bank Dagan Bali(BDB) was established in September 1970 to serve low incomepeople in Indonesia without any subsidies and is now “well-known as the earliest bank to institute commercialmicrofinance”. While this is not true with regard to theachievements made in Europe during the 19th century, itstill can be seen as a turning point with an ever increasingimpact on the view of politicians and development aidpractitioners throughout the world. In 1973 ACCIONInternational, a United States of America (USA) based nongovernmental organization (NGO) disbursed its first loan inBrazil and in 1974 Professor Muhammad Yunus started whatlater became known as the Grameen Bank by lending a total of$27 to 42 people in Bangladesh. One year later the Self-Employed Women’s Association started to provide loans ofabout $1.5 to poor women in India. Although the latterexamples still were subsidized projects, they used a morebusiness oriented approach and showed the world that poorpeople can be good credit risks with repayment ratesexceeding 95%, even if the interest rate charged is higherthan that of traditional banks. Another milestone was thetransformation of BRI starting in 1984. Once a loss makinginstitution channeling government subsidized credits toinhabitants of rural Indonesia it is now the largest MFI inthe world, being profitable even during the Asian financialcrisis of 1997 – 1998.

In February 1997 more than 2,900 policymakers, microfinancepractitioners and representatives of various educationalinstitutions and donor agencies from 137 different countriesgathered in Washington D.C. for the first Micro CreditSummit. This was the start of a nine year long campaign toreach 100 million of the world poorest households withcredit for self employment by 2005. According to theMicrocredit Summit Campaign Report 67,606,080 clients havebeen reached through 2527 MFIs by the end of 2002, with41,594,778 of them being amongst the poorest before theytook their first loan. Since the campaign started the

10

average annual growth rate in reaching clients has beenalmost 40 percent. If it has continued at that speed morethan 100 million people will have access to microcredit bynow and by the end of 2005 the goal of the microcreditsummit campaign would be reached. As the president of theWorld Bank James Wolfensohn has pointed out, providingfinancial services to 100 million of the poorest householdsmeans helping as many as 500 – 600 million poor people.

1. Strategic Policy Initiatives

Some of the most recent strategic policy initiatives in thearea of Microfinance taken by the government and regulatorybodies in India are:Working group on credit to the poor through SHGs, NGOs, NABARD, 1995The National Microfinance Taskforce, 1999Working Group on Financial Flows to the Informal Sector (set up by PMO), 2002Microfinance Development and Equity Fund, NABARD, 2005Working group on Financing NBFCs by Banks- RBI

2. Activities in Microfinance

Microcredit: It is a small amount of money loaned to aclient by a bank or other institution. Microcredit can beoffered, often without collateral, to an individual orthrough group lending.

Micro savings: These are deposit services that allow one tosave small amounts of money for future use. Often withoutminimum balance requirements, these savings accounts allowhouseholds to save in order to meet unexpected expenses andplan for future expenses

Micro insurance: It is a system by which people, businessesand other organizations make a payment to share risk. Accessto insurance enables entrepreneurs to concentrate more on

11

developing their businesses while mitigating other risksaffecting property, health or the ability to work.

Remittances: These are transfer of funds from people in oneplace to people in another, usually across borders to familyand friends. Compared with other sources of capital that canfluctuate depending on the political or economic climate,remittances are a relatively steady source of funds.

3. Legal Regulations

Banks in India are regulated and supervised by the ReserveBank of India (RBI) under the RBI Act of 1934, BankingRegulation Act, Regional Rural Banks Act, and theCooperative Societies Acts of the respective stategovernments for cooperative banks.NBFCs are registered underthe Companies Act, 1956 and are governed under the RBI Act.There is no specific law catering to NGOs although they canbe registered under the Societies Registration Act, 1860,the Indian Trust Act, 1882, or the relevant state acts.There has been a strong reliance on self-regulation for NGOMFIs and as this applies to NGO MFIs mobilizing depositsfrom clients who also borrow. This tendency is a concern dueto enforcement problems that tend to arise with self-regulatory organizations. In January 2000, the RBIessentially created a new legal form for providingmicrofinance services for NBFCs registered under theCompanies Act so that they are not subject to any capital orliquidity requirements if they do not go into the deposittaking business. Absence of liquidity requirements isconcern to the safety of the sector.

12

7. Grameen Bank – A Pioneer of Micro-FinanceThe Grameen Bank (literally, "Bank of the Villages", in

Bangla) is the outgrowth of Muhammad Yunus' ideas. The bank

13

began as a research project by Yunus and the Rural Economics

Project at Bangladesh's University of Chittagong to test his

method for providing credit and banking services to the

rural poor. In 1976, the village of Jobra and other villages

surrounding the University of Chittagong became the first

areas eligible for service from Grameen Bank. The Bank was

immensely successful and the project, with government

support, was introduced in 1979 to the Tangail District (to

the north of the capital, Dhaka). The bank's success

continued and it soon spread to various other districts of

Bangladesh and in 1983 it was transformed into an

independent bank by the legislature of Bangladesh. Bankers

from ShoreBank, a community development bank in Chicago,

helped Yunus with the official incorporation of the bank

under a grant from the Ford Foundation. The bank's repayment

rate was hit following the 1998 flood of Bangladesh before

recovering again in recent years.

The Grameen Bank lending system is simple but effective. To

obtain loans, potential borrowers must form a group of five,

gather once a week for loan repayment meetings, and to start

with, learn the bond rules and "16 Decisions" which they

chant at the start of their weekly session. These decisions

incorporate a code of conduct that members are encouraged to

follow in their daily life e.g. production of fruits and

vegetables in kitchen gardens, investment for improvement of

housing and education for children, use of latrines and safe

14

drinking water for better health, rejection of dowry in

marriages etc. Physical training and parades are held at

weekly meetings for both men and women and the "16

Decisions" are chanted as slogans. Though according to the

Grameen Bank management, observance of these decisions is

not mandatory , in actual practice it has become a

requirement for receiving a loan.

Number of groups in the same village are federated into a

Centre. The organisation of members in groups and centres

serves a number of purposes. It gives individuals a measure

of personal security and confidence to take risks and launch

new initiatives.

The formation of the groups - the key unit in the credit

programme - is the first necessary step to receive credit.

Loans are initially made to two individuals in the group,

who are then under pressure from the rest of the members to

repay in good time. If the borrowers default, the other

members of the group may forfeit their chance of a loan. The

loan repayment is in weekly installments spread over a year

and simple interest of 20% is charged once at the year end.

The groups perform as an institution to ensure mutual

accountability. The individual borrowing member is kept in

line by considerable pressure from other group members.

Credibility of the entire group and future benefits in terms

of new loans are in jeopardy if any one of the group members

defaults on repayment.

15

There have been occasions when the group has decided to fine

or expel a member who has failed to attend weekly meetings

or willfully defaulted on repayment of a loan. The members

are free to leave the group before the loan is fully repaid;

however, the responsibility to pay the balance falls on the

remaining group members. In the event of default by the

entire group, the responsibility for repayment falls on the

centre.

The Grameen Bank has provided an inbuilt incentive for

prompt and timely repayment by the borrower i.e. gradual

increase in the borrowing eligibility of subsequent loans.

A survey has shown that about 42% of the members had no

income earning occupation (though some may have been unpaid

family workers in household enterprises) at the time of

application of the first loan. Thus, the Grameen Bank has

helped to generate new jobs for a large proportion of the

members. Only insignificant portion of the loans (6 per

cent) was diverted for consumption and other household

needs.

About 50 per cent of the loans taken by male members were

for the purpose of trading and shop keeping. 75 per cent of

loans given to female members were utilised for livestock,

poultry raising, processing and manufacturing activity.

16

7.1 Financial needs and financial services

In developing economies and particularly in the rural areas,many activities that would be classified in the developedworld as financial are not monetized: that is, money is notused to carry them out. Almost by definition, poor peoplehave very little money. But circumstances often arise intheir lives in which they need money or the things money canbuy.In Stuart Rutherford’s recent book .The Poor and TheirMoney, he cites several types of needs:•Lifecycle Needs: such as weddings, funerals, childbirth,education, homebuilding, widowhood, old age.

•Personal Emergencies: such as sickness, injury,unemployment, theft, harassment or death.

•Disasters: such as fires, floods, cyclones and man-madeevents like war or bulldozing of dwellings.

17

•Investment Opportunities: expanding a business, buying landor equipment, improving housing, securing a job (which oftenrequires paying a large bribe), etc.Poor people find creative and often collaborative ways tomeet these needs, primarily through creating and exchangingdifferent forms of non-cash value. Common substitutes forcash vary from country to country but typically includelivestock, grains, jewellery and precious metals.

As Marguerite Robinson describes in The MicrofinanceRevolution, the 1980s demonstrated that “microfinance couldprovide large-scale outreach profitably,” and in the 1990s,“microfinance began to develop as an industry”. In the2000s, the microfinance industry’s objective is to satisfythe unmet demand on a much larger scale, and to play a rolein reducing poverty. While much progress has been made indeveloping a viable, commercial microfinance sector in thelast few decades, several issues remain that need to beaddressed before the industry will be able to satisfymassive worldwide demand.

The obstacles or challenges to building a sound commercialmicrofinance industry include:

•Inappropriate donor subsidies•Poor regulation and supervision of deposit-taking MFIs•Few MFIs that mobilize savings•Limited management capacity in MFIs•Institutional inefficiencies•Need for more dissemination and adoption of rural,agricultural microfinance methodologies

7.2 Criticism- Gina Neff of the Left Business Observer

has described the microcredit movement as a privatization of

public safety-net programs. Enthusiasm for microcredit among

18

government officials as an anti-poverty program can motivate

cuts in public health, welfare, and education spending. Neff

maintains that the success of the microcredit model has been

judged disproportionately from a lender's perspective

(repayment rates, financial viability) and not from that of

the borrowers. For example, the Grameen Bank's high

repayment rate does not reflect the number of women who are

repeat borrowers, and have become dependent on loans for

household expenditures rather than capital investments.

Studies of microcredit programs have found that women often

act merely as collection agents for their husbands and sons,

such that the men spend the money themselves while women are

saddled with the credit risk.As a result, borrowers are kept

out of waged work and pushed into the informal economy.

Bangladesh's Finance and Planning Minister M. Saifur Rahman

charges that some microfinance institutions use excessive

interest rates

8. Financial Inclusion in other countriesA Financial Inclusion Task Force has been set up in UK. The

Financial Inclusion Task Force in UK has identified three

priority areas for the purpose of financial inclusion,

viz., access to banking, access to affordable credit and

access to free face-to-face money advice. UK has established

a Financial Inclusion Fund to promote financial inclusion

and assigned responsibility to banks and credit unions in

19

removing financial exclusion. Basic bank no frills accounts

have been introduced. An enhanced legislative environment

for credit unions has been established, accompanied by

tighter regulations to ensure greater protection for

investors.

A civil rights law, namely Community Reinvestment Act (CRA)

in the United States prohibits discrimination by banks

against low and moderate income neighborhoods. The CRA

imposes affirmative and continuing obligations on banks to

serve the needs for credit and banking services of all the

communities in which they are chartered. In fact, numerous

studies conducted by Federal Reserve and Harvard University

demonstrated that CRA lending is a win-win proposition and

profitable to banks. In this context, it is also interesting

to know the other initiative taken by a state in the United

States. Apart from the CRA experiment, armed with the

sanction of Banking Law, the State of New York Banking

Department, with the objective of making available the low

cost banking services to consumers, made mandatory that each

banking institution shall offer basic banking account and in

case of credit unions the basic share draft account, which

is in the nature of low cost account with minimum

facilities.

9. Financial Inclusion in India

20

In India, banks made an entry in rural areas initially to

provide an alternative to the rural money lenders who

provided credit support, but not without exploiting the

rural poor. After the nationalization in 1969, commercial

banks in the country took upon themselves a massive task of

improving access of the poor to formal credit and accelerate

the flow of credit to the rural economy. Their role in

poverty alleviation was more appreciated when the

Government, as a major paradigm shift, decided to launch a

direct attack on poverty, through its special employment

generation strategies and productive asset creation programs

like Integrated Rural Development Program (IRDP)

A World Bank study assessing access to financial

institutions found that amongst rural households in Andhra

Pradesh and Uttar Pradesh, 59% lack access to deposit

account and 78% lack access to credit. Considering that the

majority of the 360 million poor households (urban and

rural) lack access to formal financial services, the numbers

of customers to be reached, and the variety and quantum of

services to be provided are really large.

9.1 Microfinance in India

At present lending to the economically active poor bothrural and urban is pegged at around Rs 7000 crores in theIndian banks’ credit outstanding. As against this, accordingto even the most conservative estimates, the total demandfor credit requirements for this part of Indian society issomewhere around Rs 2,00,000 crores.

21

Microfinance changing the face of poor India

Micro-Finance is emerging as a powerful instrument forpoverty alleviation in the new economy. In India, micro-Finance scene is dominated by Self Help Groups (SHGs) -Banks linkage Programme, aimed at providing a cost effectivemechanism for providing financial services to the 'unreachedpoor'. In the Indian context terms like "small and marginalfarmers", " rural artisans" and "economically weakersections" have been used to broadly define micro-financecustomers. Research across the globe has shown that, overtime, microfinance clients increase their income and assets,increase the number of years of schooling their childrenreceive, and improve the health and nutrition of theirfamilies.

A more refined model of micro-credit delivery has evolvedlately, which emphasizes the combined delivery of financialservices along with technical assistance, and agriculturalbusiness development services. When compared to the widerSHG bank linkage movement in India, private MFIs have hadlimited outreach. However, we have seen a recent trend oflarger microfinance institutions transforming into Non-BankFinancial Institutions (NBFCs). This changing face ofmicrofinance in India appears to be positive in terms of theability of microfinance to attract more funds and thereforeincrease outreach.

In terms of demand for micro-credit or micro-finance, thereare three segments, which demand funds. They are:

•At the very bottom in terms of income and assets, are thosewho are landless and engaged in agricultural work on aseasonal basis, and manual laborers in forestry, d foremost,consumption credit during those months when they do not getlabour work, and for contingencies such as illness. Theyalso need credit for acquiring small productive assets, suchas livestock, using which they can generate additionalincome.

22

• The next market segment is small and marginal farmers andrural artisans, weavers and those self-employed in the urbaninformal sector as hawkers, vendors, and workers inhousehold micro-enterprises.This segment mainly needs credit for working capital, asmall part of which also serves consumption needs. Thissegment also needs term credit for acquiring additionalproductive assets, such as irrigation pump sets, bore wellsand livestock in case of farmers, and equipment (looms,machinery) and work sheds in case of non-farm workers.

• The third market segment is of small and medium farmerswho have gone in for commercial crops

Such as surplus paddy and wheat, cotton, groundnut, andothers engaged in dairying, poultry, fishery, etc. Amongnon-farm activities, this segment includes those in villagesand slums, engaged in processing or manufacturing activity,running provision stores, repair workshops, tea shops, andvarious service enterprises. These persons are not alwayspoor, though they live barely above the poverty line andalso suffer from inadequate access to formal credit.

Well these are the people who require money and withMicrofinance it is possible. Right now the problem is that,it is SHGs' which are doing this and efforts should be madeso that the big financial institutions also turn up andstart supplying funds to these people. This will lead to abetter India and will definitely fulfill the dream of ourlate Prime Minister, Mrs. Indira Gandhi, i.e. Poverty.

One of the statements is really appropriate here, which isas: “Money, says the proverb makes money. When you have gota little, it is often easy to get more. The great difficultyis to get that little.” Adams Smith.

Today India is facing major problem in reducing poverty.About 25 million people in India are under below poverty

23

line. With low per capita income, heavy population pressure,prevalence of massive unemployment and underemployment , lowrate of capital formation , misdistribution of wealth andassets , prevalence of low technology and poor economicsorganization and instability of output of agricultureproduction and related sectors have made India one of thepoor countries of the world.

Present Scenario of India:

India falls under low income class according to World Bank.It is second populated country in the world and around 70 %of its population lives in rural area. 60% of people dependon agriculture, as a result there is chronic underemploymentand per capita income is only $ 3262. This is not enough toprovide food to more than one individual . The obviousresult is abject poverty , low rate of education, low sexratio, exploitation. The major factor account for highincidence of rural poverty is the low asset base. Accordingto Reserve Bank of India, about 51 % of people house possessonly 10% of the total asset of India .This has resulted lowproduction capacity both in agriculture (which contributearound 22-25% of GDP ) and Manufacturing sector. Ruralpeople have very low access to institutionalizedcredit( from commercial bank).

The micro-finance scene in India is dominated by Self Help

Groups (SHGs) - Banks linkage program for over a decade now.

As the formal banking system already has a vast branch

network in rural areas, it was perhaps wise to find ways and

means to improve the access of rural poor to the existing

banking network. This was tried by routing financial

services through Self-Help Groups [4], formed as grass

24

roots level institutions developed for social/economic and

financial intermediation for focusing on the poor.

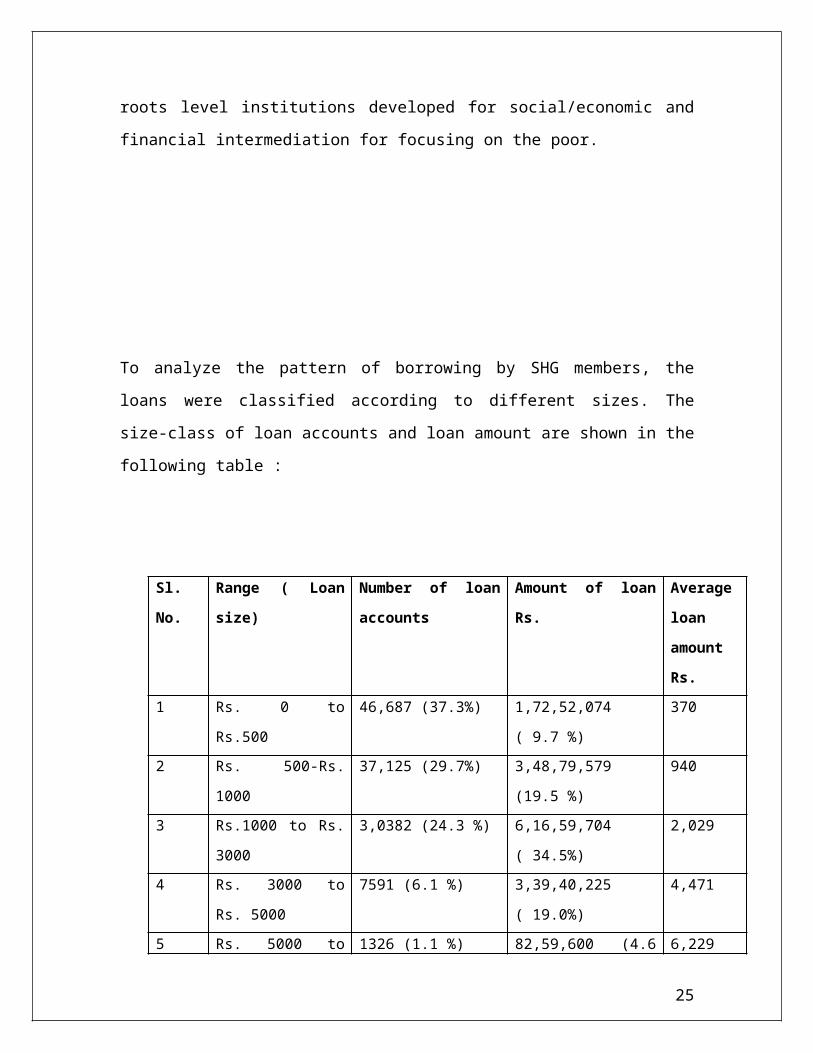

To analyze the pattern of borrowing by SHG members, the

loans were classified according to different sizes. The

size-class of loan accounts and loan amount are shown in the

following table :

Sl.

No.

Range ( Loan

size)

Number of loan

accounts

Amount of loan

Rs.

Average

loan

amount

Rs. 1 Rs. 0 to

Rs.500

46,687 (37.3%) 1,72,52,074

( 9.7 %)

370

2 Rs. 500-Rs.

1000

37,125 (29.7%) 3,48,79,579

(19.5 %)

940

3 Rs.1000 to Rs.

3000

3,0382 (24.3 %) 6,16,59,704

( 34.5%)

2,029

4 Rs. 3000 to

Rs. 5000

7591 (6.1 %) 3,39,40,225

( 19.0%)

4,471

5 Rs. 5000 to 1326 (1.1 %) 82,59,600 (4.6 6,229

25

Rs. 7000 %)6 Rs. 7000 to

Rs. 10000

1329 (1.1 5) 1,23,93,264 (6.9

%)

9,325

7 Rs. 10,000 to

Rs. 15,000

366 (0.3%) 48,61,456 (2.7

%)

13,283

8 Rs. 15,000 and

above

229 (0.2 %) 54,74,722 (3.1

%)

23,907

Total 1,25,035 (100%) 17,87,20,624

(100%)

1,429

It can be seen that the size of loan accounts was very small

as nearly about 91 % loan accounts were in the size class

below Rs. 3000.

With a view to enhancing the financial inclusion, as a

proactive measure, the RBI in its Annual Policy Statement

for the year 2005-06, while recognizing the concerns in

regard to the banking practices that tend to exclude rather

than attract vast sections of population, urged banks to

review their existing practices to align them with the

objective of financial inclusion. In the Mid Term Review of

the Policy (2005-06), RBI exhorted the banks, with a view

to achieving greater financial inclusion, to make available

a basic banking ‘no frills’ account either with nil or very

minimum balances as well as charges that would make such

accounts accessible to vast sections of the population. The

nature and number of transactions in such accounts would be

restricted and made known to customers in advance in a

26

transparent manner. All banks are urged to give wide

publicity to the facility of such no frills account so as to

ensure greater financial inclusion.

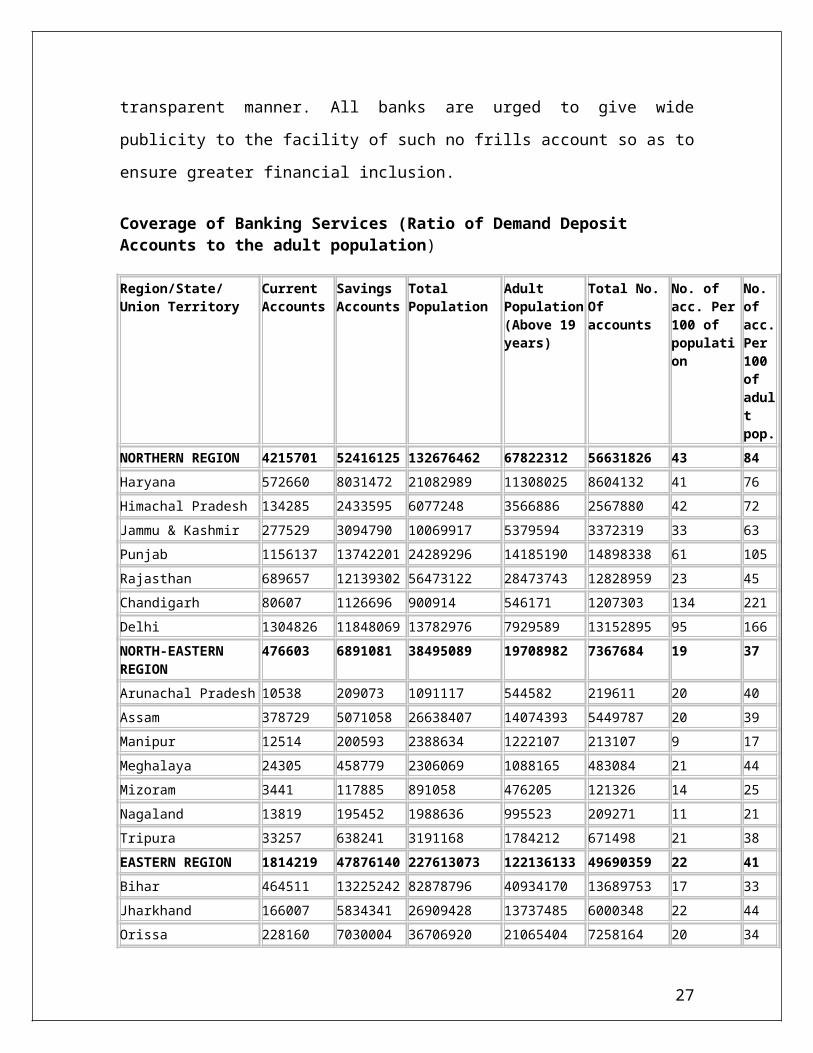

Coverage of Banking Services (Ratio of Demand Deposit Accounts to the adult population)

Region/State/Union Territory

Current Accounts

Savings Accounts

Total Population

Adult Population(Above 19 years)

Total No. Of accounts

No. of acc. Per100 of population

No. of acc.Per 100 of adult pop.

NORTHERN REGION 4215701 52416125 132676462 67822312 56631826 43 84Haryana 572660 8031472 21082989 11308025 8604132 41 76Himachal Pradesh 134285 2433595 6077248 3566886 2567880 42 72Jammu & Kashmir 277529 3094790 10069917 5379594 3372319 33 63Punjab 1156137 13742201 24289296 14185190 14898338 61 105Rajasthan 689657 12139302 56473122 28473743 12828959 23 45Chandigarh 80607 1126696 900914 546171 1207303 134 221Delhi 1304826 11848069 13782976 7929589 13152895 95 166NORTH-EASTERN REGION

476603 6891081 38495089 19708982 7367684 19 37

Arunachal Pradesh 10538 209073 1091117 544582 219611 20 40Assam 378729 5071058 26638407 14074393 5449787 20 39Manipur 12514 200593 2388634 1222107 213107 9 17Meghalaya 24305 458779 2306069 1088165 483084 21 44Mizoram 3441 117885 891058 476205 121326 14 25Nagaland 13819 195452 1988636 995523 209271 11 21Tripura 33257 638241 3191168 1784212 671498 21 38EASTERN REGION 1814219 47876140 227613073 122136133 49690359 22 41Bihar 464511 13225242 82878796 40934170 13689753 17 33Jharkhand 166007 5834341 26909428 13737485 6000348 22 44Orissa 228160 7030004 36706920 21065404 7258164 20 34

27

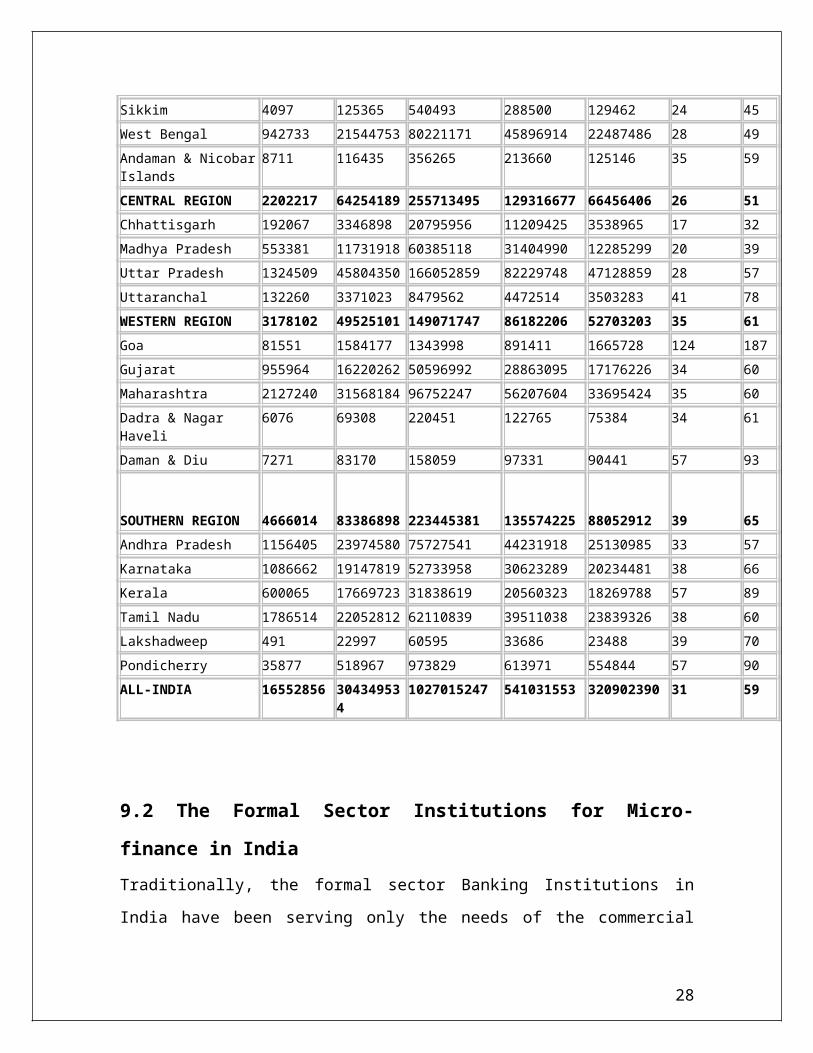

Sikkim 4097 125365 540493 288500 129462 24 45West Bengal 942733 21544753 80221171 45896914 22487486 28 49Andaman & NicobarIslands

8711 116435 356265 213660 125146 35 59

CENTRAL REGION 2202217 64254189 255713495 129316677 66456406 26 51Chhattisgarh 192067 3346898 20795956 11209425 3538965 17 32Madhya Pradesh 553381 11731918 60385118 31404990 12285299 20 39Uttar Pradesh 1324509 45804350 166052859 82229748 47128859 28 57Uttaranchal 132260 3371023 8479562 4472514 3503283 41 78WESTERN REGION 3178102 49525101 149071747 86182206 52703203 35 61Goa 81551 1584177 1343998 891411 1665728 124 187Gujarat 955964 16220262 50596992 28863095 17176226 34 60Maharashtra 2127240 31568184 96752247 56207604 33695424 35 60Dadra & Nagar Haveli

6076 69308 220451 122765 75384 34 61

Daman & Diu 7271 83170 158059 97331 90441 57 93

SOUTHERN REGION 4666014 83386898 223445381 135574225 88052912 39 65Andhra Pradesh 1156405 23974580 75727541 44231918 25130985 33 57Karnataka 1086662 19147819 52733958 30623289 20234481 38 66Kerala 600065 17669723 31838619 20560323 18269788 57 89Tamil Nadu 1786514 22052812 62110839 39511038 23839326 38 60Lakshadweep 491 22997 60595 33686 23488 39 70Pondicherry 35877 518967 973829 613971 554844 57 90ALL-INDIA 16552856 30434953

41027015247 541031553 320902390 31 59

9.2 The Formal Sector Institutions for Micro-

finance in India Traditionally, the formal sector Banking Institutions in

India have been serving only the needs of the commercial

28

sector and providing loans for middle and upper income

groups. Similarly, for housing the HFIs have generally not

evolved a lending product to serve the needs of the Very LIG

primarily because of the perceived risks of lending to this

sector. Following risks are generally perceived by the

formal sector financial institutions:

Credit Risk

High transaction and service cost

Absence of land tenure for financing housing

Irregular flow of income due to seasonality

Lack of tangible proof for assessment of income

Unacceptable collaterals such as crops, utensils and

jewellery

As far as the formal financial institutions are concerned,

there are Commercial Banks, Housing Finance Institutions

(HFIs), NABARD, Rural Development Banks (RDBs), Land

Development Banks Land Development Banks and Co-operative

Banks (CBs).

As regards the Co-operative Structures, the Urban Co.op

Banks (UCB) or Urban Credit Co.op Societies (UCCS) are the

two primary co-operative financial institutions operating in

the urban areas. There are about 1400 UCBs with over 3400

branches in India having 14 million members, Their total

lending outstanding in 1990-91 has been reported at over Rs

80 billion with deposits worth Rs 101 billion.

29

Similarly there exist about 32000 credit co.op societies

with over 15 million members with their total outstanding

lending in 1990-91 being Rs 20 billion with deposits of Rs

12 billion.

Few of the UCCS also have external borrowings from the

District Central Co.Op Banks (DCCBs) at 18-19%. The loans

given by the UCBs or the UCCS are for short term and

unsecured except for few which are secured by personal

guarantees. The most effective security being the group or

the peer pressure.

The Government has taken several initiatives to strengthen

the institutional rural credit system. The rural branch

network of commercial banks have been expanded and certain

policy prescriptions imposed in order to ensure greater flow

of credit to agriculture and other preferred sectors. The

commercial banks are required to ensure that 40% of total

credit is provided to the priority sectors out of which 18%

in the form of direct finance to agriculture and 25% to

priority sector in favour of weaker sections besides

maintaining a credit deposit ratio of 60% in rural and semi-

urban branches. Further the IRDP introduced in 1979 ensures

supply of credit and subsidies to weaker section

beneficiaries. Although these measures have helped in

widening the access of rural households to institutional

credit, vast majority of the rural poor have still not been

covered. Also, such lending done under the poverty

30

alleviation schemes suffered high repayment defaults and

left little sustainable impact on the economic condition of

the beneficiaries.

9.3 The Existing Informal financial sourcesThe informal financial sources generally include funds

available from family sources or local money lenders. The

local money lenders charge exorbitant rates, generally

ranging from 36% to 60% interest due to their monopoly in

the absence of any other source of credit for non-

conventional needs. Chit Funds and Bishis are other forms of

credit system operated by groups of people for their mutual

benefit which however their own limitations have.

Lately, few of the NGOs engaged in activities related to

community mobilization for their socio-economic development

have initiated savings and credit programmes for their

target groups. These Community based financial systems

(CBFS) can broadly be categorized into two models: Group

Based Financial Intermediary and the NGO Linked Financial

Intermediary.

Most of the NGOs like SHARAN in Delhi, FEDERATION OF THRIFT

AND CREDIT ASSOCIATION (FTCA) in Hyderabad or SPARC in

Bombay have adopted the first model where they initiate the

groups and provide the necessary management support. Others

31

like SEWA in Ahmedabad or BARODA CITIZEN's COUNCIL in Baroda

pertain to the second model.

The experience of these informal intermediaries shows that

although the savings of group members, small in nature do

not attract high returns, it is still practised due to

security reasons and for getting loans at lower rates

compared to that available from money lenders. These are

short term loans meant for crisis, consumption and income

generation needs of the members. The interest rates on such

credit are not subsidised and generally range between 12 to

36%. Most of the loans are unsecured. In few cases personal

or group guarantees or other collaterals like jewellery is

offered as security.

While a census of NGOs in micro-finance is yet to be carried

out, there are perhaps 250-300 NGOs, each with 50-100 Self

Help Groups (SHG). Few of them, not more than 20-30 NGOs

have started forming SHG Federations. There are also

agencies which provide bulk funds to the system through

NGOs. Thus organizations engaged in micro finance activities

in India may be categorized as Wholesalers, NGOs supporting

SHG Federations and NGOs directly retailing credit borrowers

or groups of borrower.

The Wholesalers will include agencies like NABARD, Rashtriya

Mahila Kosh-New Delhi and the Friends of Women's World

Banking in Ahmedabad. Few of the NGOs supporting SHG

Federations include MYRADA in Bangalore, SEWA in Ahmedabad,

32

PRADAN in Tamilnadu and Bihar, ADITHI in Patna, SPARC in

Mumbai, ASSEFA in Madras etc. While few of the NGOs directly

retailing credit to Borrowers are SHARE in Hyderabad, ASA in

Trichy, RDO Loyalam Bank in Manipur.

9.4 Strengths of Informal Sector A synthesis that can be evolved out of the success of

NGOs/CBOs engaged in microfinance is based on certain

preconditions, institutional and facilitating factors.

Preconditions to Success: Those NGOs/ CBOs have been successful that have instilled

financial value/ discipline through savings and have

demonstrated a matching value themselves before lending. A

recovery system based on social intermediation and various

options including non-financial mechanisms has proved to be

effective. Another important feature has been the community

governance. The communities in which households are direct

stake holders have successfully demonstrated the success of

programs. A precondition for success is to involve community

directly in the program. Experience indicates that savings

and credit are both critical for success and savings should

33

precede credit. Chances of success more with women: Programs

designed with women are more successful.

Operating Indicators : The operating indicators show that programs which are

designed taking into account the localized and geographical

differences have been successful. Effective and responsive

accounting and monitoring mechanisms have been an important

and critical ingradient for the success of programs. The

operational success has been more when interest rates are at

or near market rates: The experience of NGOs/CBOs indicates

that low income households are willing to pay market rates.

The crucial problem is not the interest rates but access to

finance. Eventually in absence of such programs households

end up paying much higher rates when borrowing from informal

markets. Some NGOs have experimented where members of

community decide on interest rates. This is slightly

different from Thailand experience where community decides

on repayment terms and loan amount. A combination of the

three i.e. interest rates, amount and repayment period if

decided by community, the program is most likely to succeed.

A program which is able to leverage maximum funds from

formal market has been successful. Experience indicates that

it is possible to leverage higher funds against deposits.

The spreads should be available to meet operational costs of

NGOs. Most of the directed credit program in India like Kfw

34

have a ceiling on the maximum interest rate and the spread

available to NGOs. A flexible rate of interest scheme would

indicate a wider spread for NGOs. Selected non-financial

services, viz. business, marketing support services enhance

success. Appropriate incentives for borrowing and proper

graduation of credit has been essential component of

success. A successful program can not be generalized for all

needs and geographical spread. The programs which are simple

and replicable in similar contexts have contributed to

success.

Betterment in quality of life through better housing or

better economic opportunities is a tangible indicator of

success. The programs which have been able to demonstrate on

some measurable scale that the quality of life has improved

have been successful. To be successful the program

productivity with outreach should match. The credit

mechanism should be flexible meeting multiple credit needs:

The programs which have taken care of other needs such as

consumption, marriage etc. besides the main shelter,

infrastructure or economic needs are successful.

Facilitating Factor Another factor that has contribiuted to the success is the

broad environment. A facilitative environment and enabling

regulatory regime contributes to the success. The NGOs/CBOs

which have been able to leverage funds from formal programs

35

have been successful. An essential factor for success is

that all development programs should converge across

sectors.

9.5 Credit Mechanisms Adopted by HDFC (India) for

Funding the Low Income Group Beneficiaries HDFC has been making continuous and sustained efforts to

reach the lower income groups of society, especially the

economically weaker sections, thus enabling them to realize

their dreams of possessing a house of their own.

HDFCs' response to the need for better housing and living

environment for the poor, both, in the urban and rural

sectors materialized in its collaboration with Kreditanstalt

fur Wiederaufbau (KfW), a German Development bank. KFW

sanctioned DM 55 million to HDFC for low cost housing

projects in India. HDFCs' approach to low-income lending has

been extremely professional and developmental in nature.

Negating the concept of dependence, HDFCs' low cost housing

schemes are marked by the emphasis on peoples participation

and usage of self-help approach wherein the beneficiaries

contribute both in terms of cash and labour for construction

of their houses. HDFC also ensures that the newly

constructed houses are within the affordability of the

beneficiaries, and thus promotes the usage of innovative low

cost technologies and locally available materials for

construction of the houses.

36

For the purpose of actual implementation of the low cost

housing projects, HDFC collaborates with organisations,

both, Governmental and Non-Governmental. Such organisations

act as co-ordinating agencies for the projects involving a

collective of individuals belonging to the Economically

Weaker Sections. The projects could be either in urban or

rural areas.

The security for the loan is generally the mortgage of the

property being financed. The construction work is regularly

monitored by the co-coordinating agencies and HDFC. The

loans from HDFC are disbursed depending upon the stages of

construction. To date, HDFC has experienced 100% recovery

for the loans disbursed to various projects.

10. Self Help Groups (SHGs)

Self- Help Groups (SHGs) Play today a major role in Povertyalleviation in rural India. A growing number of poor people(Mostly women) in various part of India are members of SHGsand actively engage in savings credit (S/C), as well s inother activities ( income generation, natural resourcesmanagement, literacy, child care and nutrition, etc.). TheS/C focus in the SHG is the prominent element and offers achance to create some control over capital, albeit in verysmall amounts. The SHG sys tem has proven to be veryrelevant and effectively in offering women the possibilityto break gradually away from exploitation and isolation.

10.1 How self help groups work

NABARD (1997) defines SHGs as “small, economicallyhomogenous affinity groups of rural poor, voluntarily formed

37

to save and mutually contribute to a common fund to be lentto its members as per the group members’ decision”Most SHGs in India have 10 to 25 members, who can be eitheronly men, or only women, or only youth, or mix of these. Aswomen’s SHG or sangha have been promoted by a wide range ofgovernment and non-governmental agencies, they can now makeup 90% of all SHGs.

The rules and regulations of SHGs vary according to thepreferences of the members and those facilitating theirformation. A common characteristics of the groups is thatthey meet regularly (typically once per week or once perfortnight) to collect the savings from members, decide towhich member to give a loan, discuss joint activities (suchas training, running of a communal business, etc.), and tomitigate any conflicts that might arise. Most SHGs have anelected chairperson, a deputy, a treasurer, and sometimesother office holders.

Most SHGs start without any external financial capital bysaving regular contribution by the members. Thesecontributions can be very small(e.g. 10 Rs per week).After aperiod of consistent savings(e.g. 6 months to one year) theSHGs start to give loans from savings in the form of smallinternal loans for micro enterprise activities andconsumption. Only those SHGs that have ultilized their ownfunds well are assisted with external funds through linkageswith banks and other financial intermediaries.

However, it is generally accepted that SHGs often do notinclude the poorest of poor, for reasons such as:

(a) Social Factors (the poorest are often those whoare socially marginalized because of caste affiliationand those who are most skeptical o the potentialbenefits of collective action).

(b) Economic factors (the poorest often do not havefinancial resources to contribute to the savings and

38

pay membership fees; they are often the ones whomigrate during lean seasons thus making groupmembership difficult).

(c) Intrinsic biases of the implementingorganizations( as the poorest of the poor are the mostdifficult to reach and motivate, implementing agenciestend to leave them out, preferring to focus on the nextwealth category).

10.2 Sources of capital and links between SHGs and Banks

SHGs can only fulfill a role in the rural economy if groupmembers have access to financial capital and markets fortheir products and services. While the groups initiallygenerate their own savings through thrift(whereby thriftimplies savings created by postponing almost necessaryconsumption, while savings imply the existence of surpluswealth),their aim is often to link up with financialinstitutions in order to obtain further loans forinvestments in rural enterprises. NGOs and banks are givingloans to SHGs either as “matching loans” (whereas the loanamount is proportionate to the group’s savings) or as fixedamounts, depending on the group’s record of repayment,recommendations by group facilitators, collateralprovided ,etc.

10.3 How SHGs save

Self-help groups mobilize savings from their members, andmay then on-lend these funds to one another, usually atapparently high rates of interest which reflect the members’understanding of the high returns they can earn on the smallsums invested in their micro enterprises, and the evenhigher cost of funds from money lenders. If they do not wishto use the money, they may deposit it in a bank. If themembers’ need for funds exceeds the group’s accumulatedsavings, they may borrow from a bank or other organization,

39

such as micro-finance non-government organization, toaugment their own fund.

The system is very flexible. The group aggregates the smallindividual saving and borrowing requirements of its members,and the bank needs only to maintain one account for thegroup as a single entity. The banker must assess thecompetence and integrity of the group as a micro-bank, butonce he has done this he need not concern himself with theindividual loans made by the group to its members, or theuses to which these loans are put. He can treat the group asa single customer, whose total business and transactions areprobably similar in amount to the average for his normalcustomers, because they represent the combined bankingbusiness of some twenty ‘micro-customers’. Any bank branchcan have a small or a large number of such accounts withouthaving to change its methods of operation.

Unlike many customers, demand from SHGs is not price-sensitive. Illiterate village women are sometimes betterbanker than some with more professional qualifications.They know that rapid access to funds is more important thantheir cost, and they also know, even though they might notbe able to calculate figures, that the typical micro-enterprise earns well over 500% return on the small suminvested in it (Harper,M,1997,p.15). The groups thus chargethemselves high rates of interest; they are happy to takeadvantage of the generous spread that the NABARD subsidizedbank lending rate of 12% allows them, but they also willingto borrow from NGO/MFIs which on-lend funds from SIDBI at15%, or from ‘new generation’ institutions such as BasixFinance at 18.5% or 21%.

10.4 SHGs-Bank Linkage Model

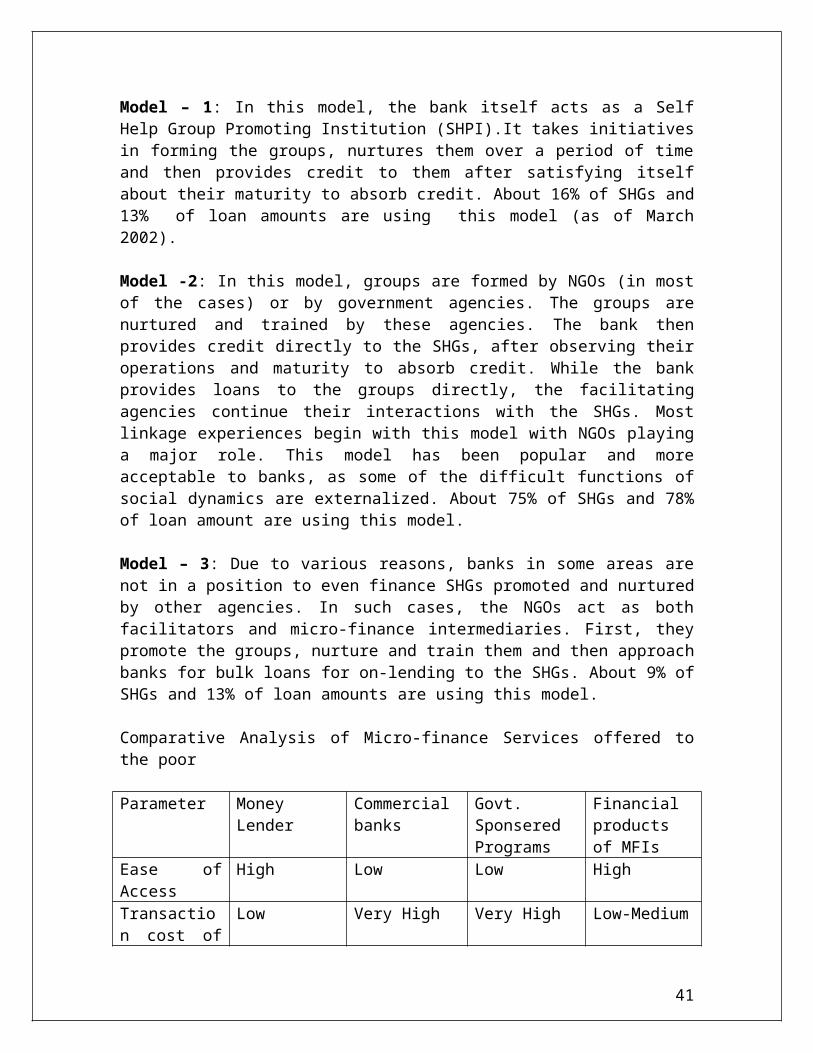

NABARD is presently operating three models of linkages ofbanks with SHGs and NGOs:

40

Model – 1: In this model, the bank itself acts as a SelfHelp Group Promoting Institution (SHPI).It takes initiativesin forming the groups, nurtures them over a period of timeand then provides credit to them after satisfying itselfabout their maturity to absorb credit. About 16% of SHGs and13% of loan amounts are using this model (as of March2002).

Model -2: In this model, groups are formed by NGOs (in mostof the cases) or by government agencies. The groups arenurtured and trained by these agencies. The bank thenprovides credit directly to the SHGs, after observing theiroperations and maturity to absorb credit. While the bankprovides loans to the groups directly, the facilitatingagencies continue their interactions with the SHGs. Mostlinkage experiences begin with this model with NGOs playinga major role. This model has been popular and moreacceptable to banks, as some of the difficult functions ofsocial dynamics are externalized. About 75% of SHGs and 78%of loan amount are using this model.

Model – 3: Due to various reasons, banks in some areas arenot in a position to even finance SHGs promoted and nurturedby other agencies. In such cases, the NGOs act as bothfacilitators and micro-finance intermediaries. First, theypromote the groups, nurture and train them and then approachbanks for bulk loans for on-lending to the SHGs. About 9% ofSHGs and 13% of loan amounts are using this model.

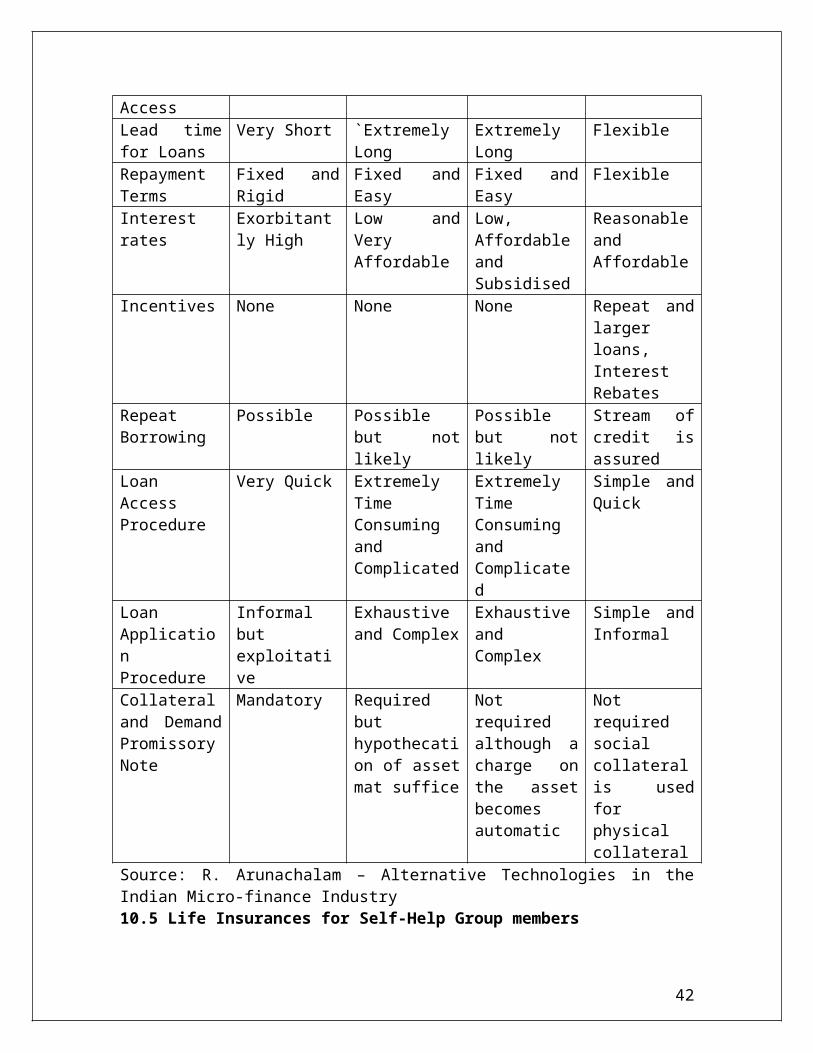

Comparative Analysis of Micro-finance Services offered tothe poor

Parameter MoneyLender

Commercialbanks

Govt.SponseredPrograms

Financialproductsof MFIs

Ease ofAccess

High Low Low High

Transaction cost of

Low Very High Very High Low-Medium

41

Access Lead timefor Loans

Very Short `ExtremelyLong

ExtremelyLong

Flexible

RepaymentTerms

Fixed andRigid

Fixed andEasy

Fixed andEasy

Flexible

Interestrates

Exorbitantly High

Low andVeryAffordable

Low,AffordableandSubsidised

ReasonableandAffordable

Incentives None None None Repeat andlargerloans,InterestRebates

RepeatBorrowing

Possible Possiblebut notlikely

Possiblebut notlikely

Stream ofcredit isassured

LoanAccessProcedure

Very Quick ExtremelyTimeConsumingandComplicated

ExtremelyTimeConsumingandComplicated

Simple andQuick

LoanApplicationProcedure

Informalbutexploitative

Exhaustiveand Complex

ExhaustiveandComplex

Simple andInformal

Collateraland DemandPromissoryNote

Mandatory Requiredbuthypothecation of assetmat suffice

Notrequiredalthough acharge onthe assetbecomesautomatic

Notrequiredsocialcollateralis usedforphysicalcollateral

Source: R. Arunachalam – Alternative Technologies in theIndian Micro-finance Industry10.5 Life Insurances for Self-Help Group members

42

The United India Insurance Company has designed two PLLIs(Personal Line Life Insurance) for women in rural areas. Thecompany will be targeting self-help groups, of which thereare around 200,000 in the country, with 15-20 women in agroup. The two policies are

(1) The Mother Teresa Women & Children Policy, withthe aim of giving to the woman in the event ofaccidental death of her husband and to support herminor children in the event of her death , and

(2) The Unimicro Health Scheme, giving personalaccident and hospitalization covers besides cover fordamage of dwelling due to fire and allied perils.

11. Weaknesses of Existing Microfinance Models One of the most successful models discussed around the world

is the Grameen type. The bank has successfully served the

rural poor in Bangladesh with no physical collateral relying

on group responsibility to replace the collateral

requirements. This model, however, has some weaknessed. It

involves too much of external subsidy which is not

replicable Grameen bank has not oriented itself towards

mobilising peoples' resources. The repayment system of 50

weekly equal instalments is not practical because poor do

not have a stable job and have to migrate to other places

for jobs. If the communities are agrarian during lean

seasons it becomes impossible for them to repay the loan.

Pressure for high repayment drives members to money lenders.

Credit alone cannot alleviate poverty and the Grameen model

43

is based only on credit. Micro-finance is time taking

process. Haste can lead to wrong selection of activities and

beneficiaries.

Another model is Kerala model (Shreyas). The rules make it

difficult to give adequate credit {only 40-50 percent of

amount available for lending). In Nari Nidhi/Pradan system

perhaps not reaching the very poor.

Most of the existing microfinance institutions are facing

problems regarding skilled labour which is not available for

local level accounting. Drop out of trained staff is very

high. One alternative is automation which is not looked at

as yet. Most of the models do not lend for agriculture.

Agriculture lending has not been experimented.

Risk Management : yield risk and price risk

Insurance & Commodity Future Exchange could be explored

All the models lack in appropriate legal and financial

structure. There is a need to have a sub-group to brainstorm

on statutory structure/ ownership control/ management/

taxation aspects/ financial sector prudential norms. A

forum/ network of micro-financier (self regulating

organization) is desired.

A New Paradigm A new paradigm that emerges is that it is very critical to

link poor to formal financial system, whatever the mechanism

may be, if the goal of poverty allieviation has to be

44

achieved. NGOs and CBOs have been involved in community

development for long and the experience shows that they have

been able to improve the quality of life of poor, if this is

an indicator of development. The strengths and weaknesses of

existing NGOs/CBOs and microfinance institutions in India

indicate that despite their best of efforts they have not

been able to link themselves with formal systems. It is

desired that an intermediary institution is required between

formal financial markets and grassroot. The intermediary

should encompass the strengths of both formal financial

systems and NGOs and CBOs and should be flexible to the

needs of end users. There are, however, certain unresolved

dilemmas regarding the nature of the intermediary

institutions. There are arguments both for and against each

structure. These dilemmas are very contextual and only

strengthen the argument that no unique model is applicable

for all situations. They have to be context specific.

11.1 Dilemmas in Micro-Finance

Community Based Investor Owned

Community Managed

Community (self)

financed

Integrated (social &

finance)

Professionally managed

Accepting outside funds for

on-lending

Minimalist (finance only)

For profit

45

Non profit / mutual

benefit

Only for poor

'Self regulated'

For all under served

clients

Externally regulated

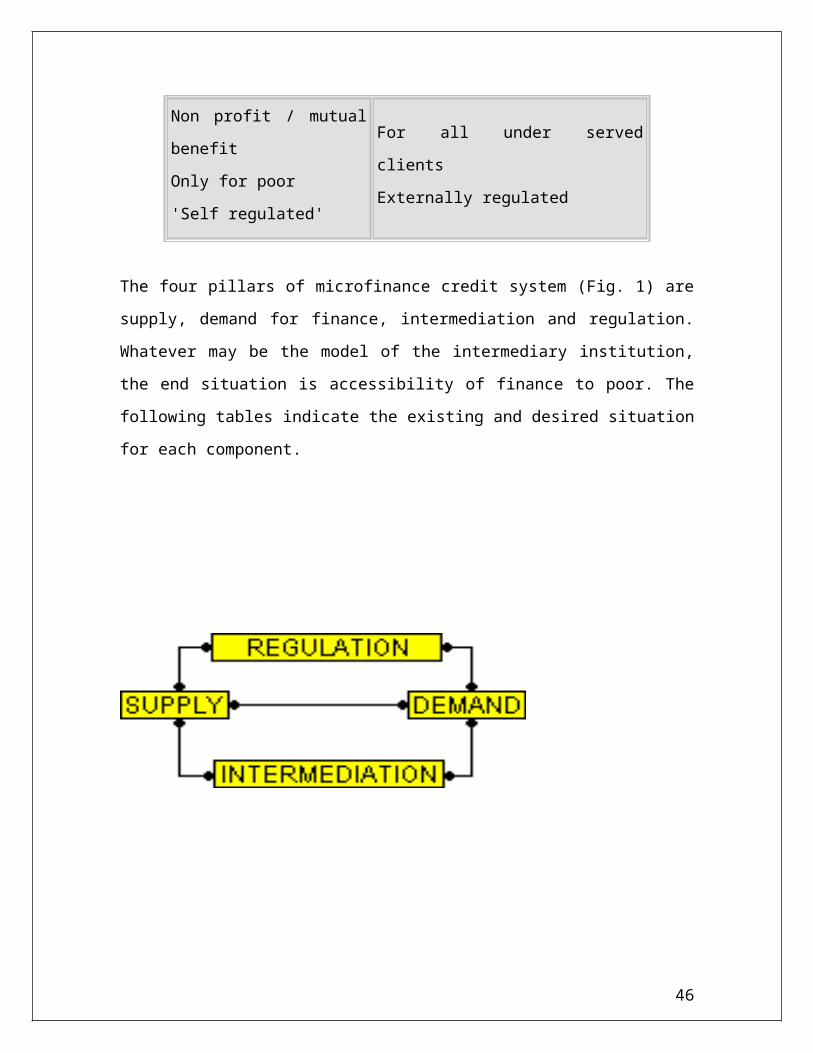

The four pillars of microfinance credit system (Fig. 1) are

supply, demand for finance, intermediation and regulation.

Whatever may be the model of the intermediary institution,

the end situation is accessibility of finance to poor. The

following tables indicate the existing and desired situation

for each component.

46

DEMAND

Existing Situation Desired Situation

fragmented

Undifferentiated

Addicted, corrupted by

capital & subsidies

Communities not aware of

rights and

responsibilities

Organized

Differentiated (for

consumption, housing)

De-addicted from

capital & subsidies

Aware of rights and

responsibilities

SUPPLY

Existing Situation Desired Situation

Grant based

(Foreign/GOI)

Directed Credit -

unwilling and corrupt

Not linked with

mainstream

Mainly focussed for

credit

Regular fund sources

(borrowings/deposits)

Demand responsive

Part of mainstream

(banks/FIs)

Add savings and insurance

Reduce dominance of informal,

unregulated suppliers

47

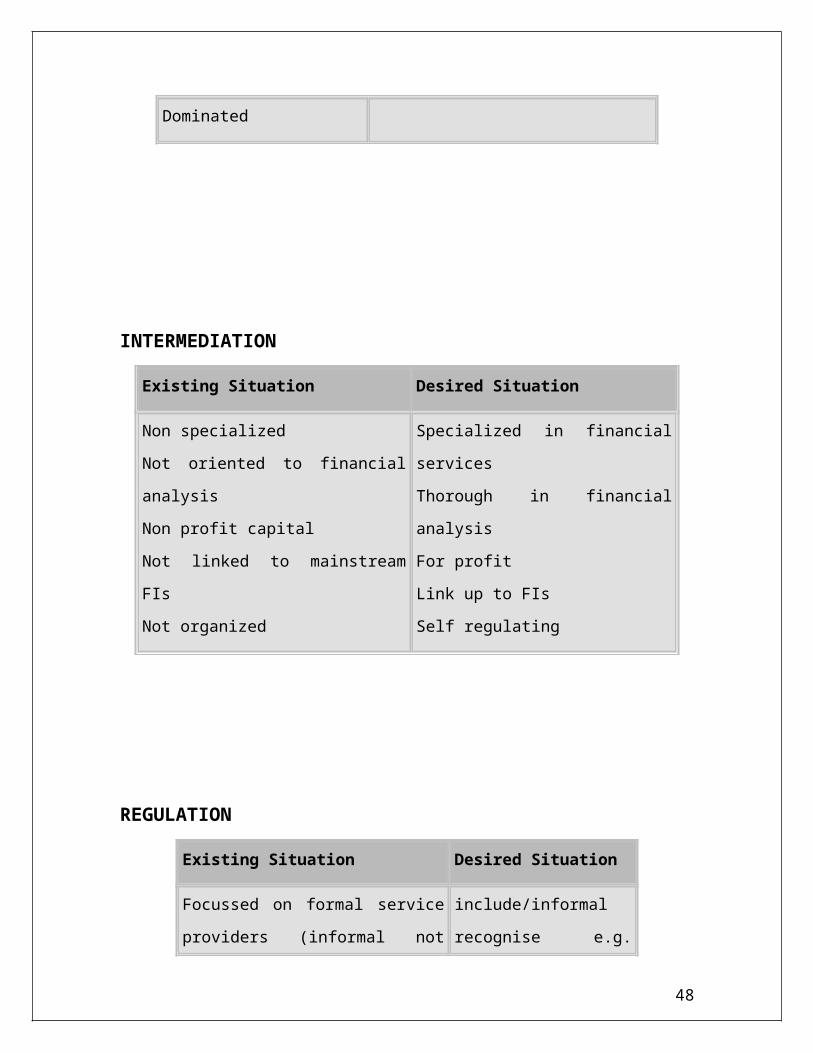

Dominated

INTERMEDIATION

Existing Situation Desired Situation

Non specialized

Not oriented to financial

analysis

Non profit capital

Not linked to mainstream

FIs

Not organized

Specialized in financial

services

Thorough in financial

analysis

For profit

Link up to FIs

Self regulating

REGULATION

Existing Situation Desired Situation

Focussed on formal service

providers (informal not

include/informal

recognise e.g.

48

regulated)

regulating the wrong things

e.g. interest rates

Multiple and conflicting

(FCRA, RBI, IT, ROC,

MOF/FIPB, ROS/Commerce)

Negatively oriented

SHGs

Regulate rules of

game

Coherence and

coordination

across regulators

Enabling

environment

11.2 Demand side barriers Reasons for remaining outside mainstream financial services

are complex and interrelated. This study was tasked with

confirming and building upon existing knowledge of the

demand side barriers preventing financially excluded people

from accessing banking and affordable credit. Below is a

summary of the key demand side barriers identified in the

research.

Lack of awareness: Financially excluded people are not all

aware of the existence and

features of basic bank accounts, or the fact that these are

easier to obtain than current

accounts. Awareness of sources of affordable credit, such as

credit unions and

49

Community Development Initiative Funds (CDIFs), is extremely

low.

Lack of perceived advantage: Many financially excluded

people without bank accounts

do not see a compelling reason for opening one. Those who do

not priorities having a bank account are satisfied with

their existing approaches to managing their finances, and

some are also distrustful of banks. In addition, some feel

that their incomes are too low to

Warrant having or using a bank account.

Socio-cultural factors: Socio-cultural factors act as a

strong barrier for financially excluded people to change

their financial situation. Many have been operating outside

mainstream banking for some time, and this is what people

close to them also do. There is a perception that banks are

‘not for poor people’, along with a preference for dealing

in Cash.

Attraction of alternatives: People without any account are

managing in cash and by using other people’s accounts where

necessary. The development of benefits (and wages for some)

being paid electronically has compelled some people to take

up a bank account.

However, for many, a more straightforward alternative for

benefits payments is a Post Office Card Account (POCA). In

terms of credit, many borrow from family and friends, and

50

catalogues and doorstep lenders are also frequently

mentioned.

Control: There are significant fears around being less able

to keep track of spending and to resist temptation by moving

from cash to an account. People have particular worries

around managing timings of incomings and outgoings with

Standing Orders and Direct Debits. Some have also had

previous experiences with debt from bank loans and

overdrafts, and there is great reluctance to take the ‘risk’

of getting into the situation again.

Confusion and complexity: This is a theme that covers a

multitude of factors when opening an account, including

onerous ID requirements (a particularly strongly voiced

theme in this research), complex paperwork, lack of

understanding of terms and conditions, and difficulty

comparing features from bank to bank. Most are therefore not

confident about opening a bank account and even fewer are

confident about the prospect of borrowing money from a bank.

Fear and mistrust of banks and banking: Financially excluded

people often refer to feeling intimidated when entering a

bank. The daunting physical environment, described by one

person as like ‘going to court’, contributes to this

feeling. It also relates to the perception that people with

less money are treated poorly by bank staff. There is also

fear and uncertainty about bank charges and penalties, as

well as about fraud and the security of accounts. Mistrust

51

of banks is particularly evident amongst the financially

excluded.

Banks are perceived to be out for themselves and not to act

in their customers’ best interests. There is even some

perception that banks will try to ‘trick’ the less well off

and financially illiterate into getting into debt.

Perceived (and experienced) supply side barriers: Another

important barrier which directly impacts on demand is the

concern amongst the financially excluded about whether or

not they will ‘qualify’ for a bank account or loan. If they

have poor credit histories, they worry about these issues

coming to light and about being humiliated by being turned

down as a result. They believe that banks will be reluctant

to offer services to them and that there will be lengthy and

onerous processes to go through.

Perceived benefits Benefits of banking are not top of mind which is another

factor in why many financially excluded people have not

attempted to open an account. On prompting, however, some

benefits of bank accounts can be identified. These include:

Better security: operating in cash makes people more

vulnerable to loss or theft;

Protection from spending: not having cash ‘burning a hole in

your pocket’;

52

More convenient: access to cash points 24/7, paying by debit

card etc;

Direct payments of wages and benefits: POCAs are an

alternative for benefits, but

this is not the case for wages;

Access to direct debits: perceived to be easier for bill

paying and there is also some

recognition that there are discounts available for direct

debit users in some cases

(however, direct debits are also a feature that causes

concern);

Access to specific products and services: e.g. those only

available to people with

Debit/credit cards or the ability to pay by direct debit;

and access to other bank services: e.g. mortgages.

Financially excluded people find it much more difficult to

identify the benefits of mainstream borrowing. While some

expect the rates to be better, bank loans and credit are

regarded by the financially excluded to be so out of reach

to them as to be irrelevant.

As such, the perceived barriers of mainstream banking and

credit currently substantially

Outweigh the benefits. There are also some indications that

financial excluded people currently accept paying over the

odds and being excluded from information and services. This

53

level of acceptance also needs to be addressed to motivate

greater take-up of mainstream financial products.

11.3 Overcoming barriers Overcoming the demand side barriers to financial inclusion

requires a programme of initiatives focused on every stage

of the banking process:

Making people aware of the banking products they are

eligible for;

Actively promoting the benefits of basic bank accounts;

Making it easier and assisting people to open the

account;

Helping people to use them fully;

Ensuring product features meet their needs; and

Assisting them if they get into difficulty.

As the financially excluded will not normally proactively

seek out solutions for themselves, a sustained campaign,

with significant outreach activity, will be required to

encourage greater take-up and use of mainstream financial

products and services. Local intermediaries (both statutory

and non-statutory) potentially have a significant role here.

Crucially the style as well as the substance of banks and

banking needs to be addressed in order to become more

approachable to the financially excluded.

54

Encouragingly, however, the majority would want to open a

bank account and access affordable credit if the barriers

were addressed.

11.4 Methods and types of services The key to facilitating greater access to banking and

affordable credit for the financially excluded is ensuring

services are as local and community based as possible. There

is a strong preference for face-to-face contact but

telephone potentially can complement this, particularly for

information and advice.

There are a number of things that banks can do to become

less practically and emotionally intimidating to financially

excluded people.

Other service models also provide some valuable learnings:

Credit Unions: common bond; friendly staff; local and

convenient; whole family eligible to join; and

Provident Financial: notwithstanding the cost of credit,

people appreciate being visited

at home, by someone local, who understands their situation.

Features Once explained, the basic bank account appeals to this

audience. In

55

particular, they value the presence of a buffer zone and

debit card, and the absence of a tempting and risky

overdraft facility.

Additional features that people would find useful

for bank accounts

include: Consistent minimum standards across all basic bank accounts

and providers;

Reducing the ID requirements;

Ensuring that the account can be opened with a minimal

amount;

Extending the buffer zone facility from cash withdrawals

to Direct

Debits;

A method whereby the Direct Debit date can be made more

flexible to coincide with an incoming credit;

Providing regular statements without extra charge to help

customers

keep track of payments; and

Providing warnings if the customer is about to go into

the red. Much can be learnt from the Credit Union model for

its features as well as its style of service with respect to

borrowing.

Key aspects of its appeal are:

Relatively low interest for borrowing;

56

Built-in control – customers can only borrow what they

can afford to pay back;

Flexibility of repayments and the ability to agree

payment terms that suit customers; and

Encouraging saving, as customers need to save before they

are eligible to borrow.

Even Provident Financial, with its comparatively much higher

rates of interest, provides some learning’s on what features

of loans are valued by financially excluded people. These

include

Being relatively easy to qualify;

Ability to borrow small amounts; and

Flexibility of repayments – particularly payment holidays

and the ability to pay back more or less depending on

circumstances.

11.5 Supply side barriersAnother important barrier which directly impacts on demand

is concern amongst financially excluded people about whether

or not they will ‘qualify’ for a bank account or loan. Those

with poor credit histories are concerned that these issues

may come to light and cause them humiliation, and they are

reluctant to put themselves through this experience. There

is a general belief that banks will be reluctant to offer

services to ‘people like them’ because of their financial

situation. This is particularly the case with loans. These

57

views are often based on previous experiences of trying and