challenges faced by micro finance institutions in credit

TRANSCRIPT

[jiC

C H A L L E N G E S F A C E D BY M I C R O F INANCE

INSTITUTIONS IN C R E D I T MANAGEMENT ^

B Y

I R E N E M U K I T I

United States Internaucriai ...,v Africa - Library

A Project Report Submitted to the Chandaria School of Business in

Partial Fulfilment of the Requirements for the Degree of Masters in

Business Administration (MBA)

USIU-A

400000005080

UNITED STATES INTERNATIONAL U N I V E R S I T Y

F A L L 2013

STUDENT'S DECLARATION

I , the undersigned, declare that this is my original work and has not been submitted to any

other college, institution or university other than the United States International

University in Nairobi for academic credit.

Signed Date: 3 ^ 1 ̂ ' 1 ^ H

Irene Mukiti ID No: 623287

This project report has been presented for examination with my approval as the appointed

supervisor.

Signed: ( j g ^ ^ ^ Date: H

Dr. Amos Njuguna

Signed: (f^f^ Date:

Dean, Chandaria School of Business

ii

COPYRIGHT

All rights reservd.No part of this project may be reproduced, stored in a retrieval system,

or transmitted in any form or by any means, electronic, mechanical, photocopying,

recording or otherwise without prior written permission from the author.

Irene Ngali Mukiti. Copyright © 2013

iii

ABSTRACT

The main purpose of this research was to determine and identify the challenges faced by

micro finance institutions (MFIs) in credit management in Kenya. The study was guided

by the following research quesfions: What are the exposing factors to credit risk among

microfinance institutions? What is the relationship between credit management policy and

, customer retention? What are the guiding principles and practices that can be used to

manage credit risk in microfinance institutions?

In order to achieve the above, the study adopted a descriptive research design in order to

obtain the data that is necessary, which in essence facilitated the collection of the private

data as a way of getting into the research objectives. The population under study was 54

micro finance institutions. The collection of the private data was done using structured

questiormaires that were pilot tested in order to ensure that there was reliability as well as

validity. The coding of the data was done with the use of Microsoft Excel as weH as

Statistical Package for Social Sciences (SPSS) in order to generate the descriptive

statistics for instance frequencies and percentages.

Data analysis was done through descriptive and inferential statistics which included

percentages, frequencies, and regression tables. Data was presented in pictorial

representation in the form of tables and figures.

The study findings reveled that there are various exposing factors to credit risk among

microfinance institutions in Kenya. Specifically the majority of the respondents were of

the opinion that loans to individuals, highly contributed to credit risk, followed by

involvement in foreign exchange trade, operational risk, prevailing inflation rates,

prevailing interest rates group loans and finally, investment in bonds and equities. This

implies that indeed issuance of loans to individuals is highly risk as compared to groups.

It also implies that investment bonds and equities are less risky.

Additionally it was revealed that there is a positive relationship between credit

management policy measures and customer retention. Similarly the majority of the

respondents agree on the various credit management policy measures by the MFIs.

Specifically it was revealed that majority of the respondents agree that repeat customers

are asked for collateral security each time they get a loan. Similarly majority of the

respondents agree that customers are frequently trained on the different products offered

iv

by the MFI. In the same regard, majority of the respondents agree that credit officers

verify information provided by the loan applicant each time. Additionally majority of the

respondents agree that managers establish long-term business relationship with customers

through continued communication, as well interest rates are competitively set compared

to other MFIs. Finally respondents agree that credit time and duration issued are

dependent on the loan type. These findings imply that indeed, MFIs do not discriminate

among different customers when it comes to credit policy measures. However, MFIs seek

continued customer relations in order to enhance customer retention

The study also revealed that the credit control policy implemented determines the risk

exposure. It was also revealed that the Management Information System adopted by an

MFI helps in risk reduction. Fureth maintaining an appropriate credit administration and

monitoring of customers helps reduce on risk. Finally, it was revealed that efficient

internal controls, supervision and audit are adequate to mitigate credit risk.

The study concludes that that there is a positive relationship between credit management

policy measures and customer retention. The study also concludes that the credit control

policy implemented determines the risk exposure. Finally, the study concludes that

efficient internal controls, supervision and audit are adequate to mitigate credit risk.

In light of the findings on this objective, the study recommends that MFI officials should

be able to identify the inadequacy of collateral security/equitable mortgage against loan.

The institutions should review the unrealistic terms and schedule of repayment. The

institution should also impose proper follow up measures to ensure that clients use loans

for purpose approved for. The study also recommends that since poor customers generally

have no credit history and little collateral, MFIs must use innovative lending practices to

reduce risks associated with asymmetric information between lender and borrower. The

best way to retain these customers is upon the manager's initiative in developing

voluntary savings products where customers save money which can be helpful for MFIs

in mobilizing savings to lend out at low cost compared to the market. Further the study

recommends that entrepreneurs should address labor problems in the market.

V

ACKNOWLEDGEMENT

I would like to thank God almighty for His guidance and providence all through my

studies, I also appreciate and thank Dr. Amos Njuguna my supervisor for his support ,

guidance, timely and wise counsel during the preparation of this project report.To the

different staff of all the Micro fmance institutions visited during the research period thank

you for your cooperation. Finally special thanks to my family for their continued support

and encouragement all through my studies and to all friends made a great contribution to

this project .God bless you all.

Irene N. Mukiti

USIU, Fall 2013

vi

T A B L E OF CONTENTS

STUDENT'S DECLARATION ii

COPYRIGHT iii

ABSTRACT iv

ACKNOWLEDGEMENT vi

TABLE OF CONTENTS vii

LIST OF TABLES x

LIST OF FIGURES xi

ABBREVIATIONS xii

CHAPTER ONE 1

1.0 INTRODUCTION 1

1.1 Background of the Study 1

1.2 Statement of the Problem 4

1.3 Purpose of the Study 4

1.4 Research Questions 4

1.5 Significance of the Study 5

1.6 Scope of the study 5

1.7 Definition of Terms 5

1.8 Chapter summary 6

CHAPTER TWO 7

2.0 L ITERATURE R E V I E W 7

2.1 Introduction 7

2.2 Espousing Factors to Credit Risk among Microfinance Institutions 7

vii

2.3 Credit Management policies and Customer Retention 10

2.4 Guiding Principles and Practices to Manage Credit Risk in Microfinance Insfitutions 15

2.5 Chapter Summary 21

CHAPTER T H R E E 22

3.0 METHODOLOGY 22

3.1 Introduction 22

3.2 Research Design 22

3.3 Population and Sampling 22

3.4 Data Collection Methods 24

3.5 Research Procedures 24

3.6 Data Analysis Methods 24

3.7 Chapter Summary 25

CHAPTER FOUR 26

4.0 DATA ANALYSIS AND PRESENTATION 26

4.1 Introduction 26

4.2 Background Information 26

4.3 Exposing Factors to Credit Risk among Microfinance Institufions 28

4.4 Relafionship between Credit Management Policy and Customer Retention 33

4.5 Guiding Principles and Practices to Manage Credit Risk 34

4.6 Chapter Summary 38

vii i

CHAPTER F I V E 39

5.0 DISCUSSION, CONCLUSIONS AND RECOMMENDATIONS 39

5.1 Introduction 39

5.2 Summary 39

5.3 Discussion 41

5.4 Conclusions 46

5.5 Recommendations 47

REFERENCES 49

APPENDICES 52

APPENDIX I : L E T T E R OF INTRODUCTION 52

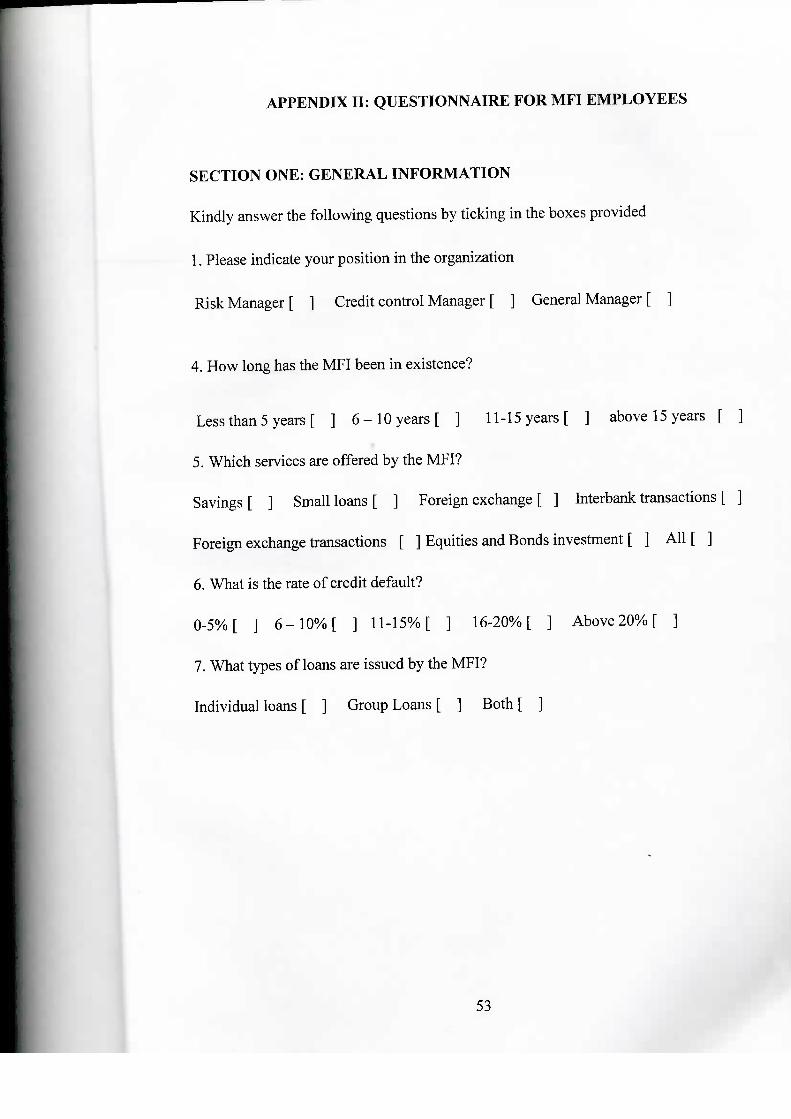

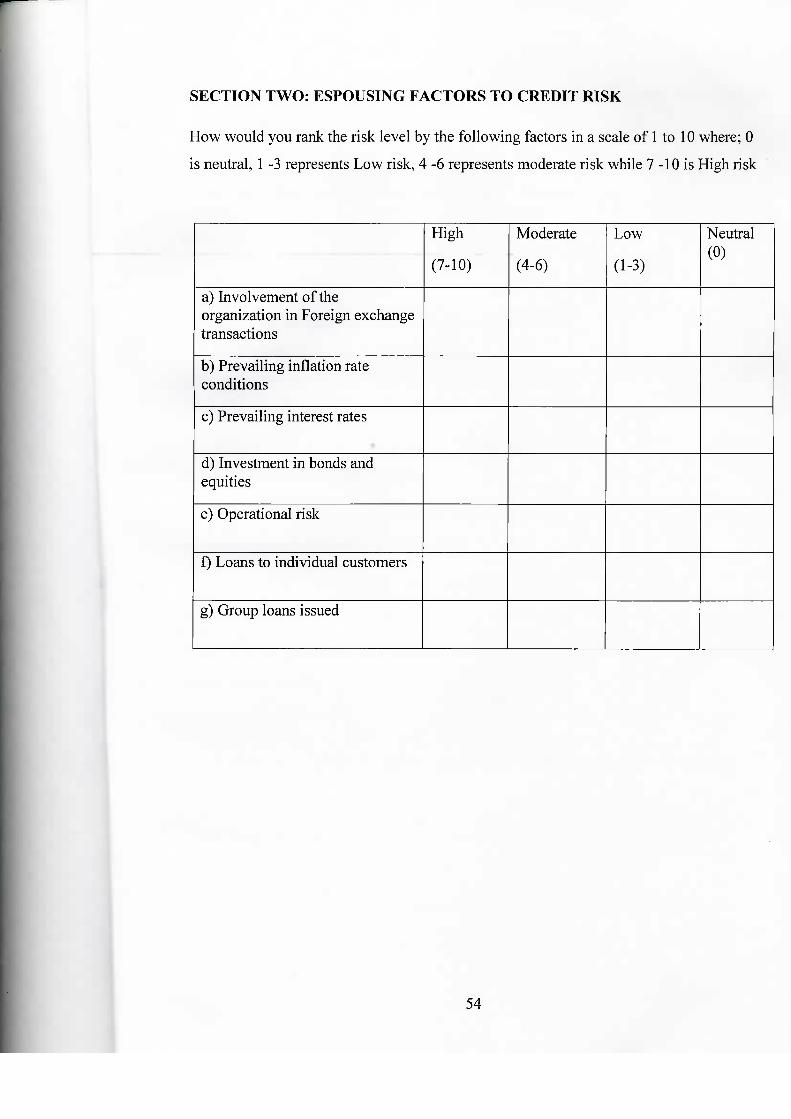

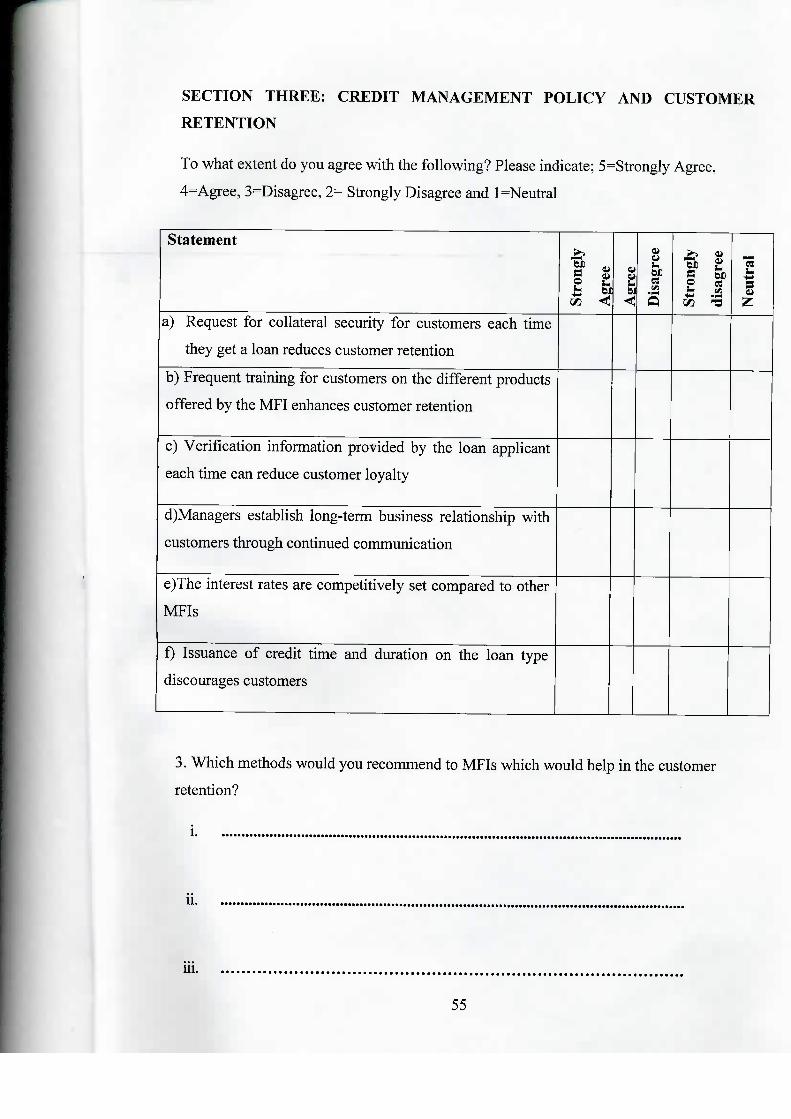

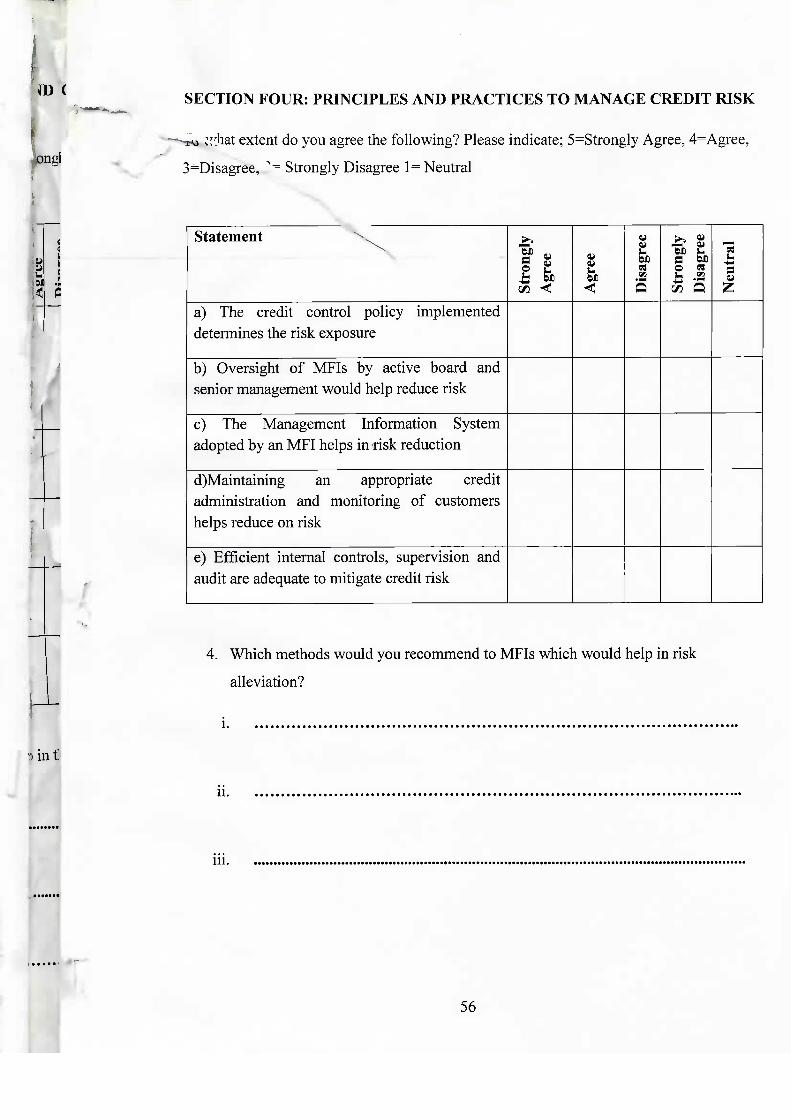

APPENDIX I I : QUESTIONNAIRE FOR MFI E M P L O Y E E S 53

APPENDIX I I I : BUDGET 57

ix

L IST OF T A B L E S

Table 4.1 Position in the Company 26

Table 4.2: Years in Existence 27

Table 4.3: Relationship between Credit Management Policy and Customer Retention....34

X

LIST OF FIGURES

Figure 4.1: Type of Loans 28

Figure 4.2: Exposing Factors to Credit Risk among Microfinance Insfitutions 28

Figure 4.3: Loans to Groups 29

Figure 4.4: Loans to Individuals 30

Figure 4.5: Operafion Risk 30

Figure 4.6: Investment in Bonds 31

Figure 4.7: Prevailing Interest Rates 31

Figure 4.8: Prevailing Inflation Rates 32

Figure 4.9: Prevailing Inflation Rates 32

Figure 4.10: Relationship between Credit Management Policy and Customer Retention 33

Figure 4.11: Credit Control Policy Implemented Determines Risk Exposure 35

Figure 4.12: Oversight of MFIs by senior management would help Reduce Risk 36

Figure 4.13: Management Informafion System adopted by an MFI helps in Risk

Reduction 36

Figure 4.14: Maintaining an Appropriate Credit Administration 37

Figure 4.15: Efficient Internal Controls, Supervision and Audit 38

xi

ABBREVIATIONS

CR Credit Risk

CRM Credit Risk Management

FI Financial Institutions

MFIs Micro fmance institutions

MSEs Micro and Small Enterprises

SME Small and medium enterprise

KWFT Kenya Women Finance Trust

xi i

CHAPTER ONE

1.0 INTRODUCTION

l.lBackground of the Study

Financial institutions (FIs) are very important in any economy. Their role is similar to that

of blood arteries in the human body, because FIs pump financial resources for economic

growth from the depositories to where they are required. Microfinance institutions are FIs

and are key providers of financial information to the economy. They play even a most

critical role to emergent economies where borrowers have no access to capital markets.

There is evidence that well-functioning Microfinance institutions accelerate economic

growth (Richard et al., 2008).

Microfinance has been defined as the provision of financial services such as deposits,

loans, payment services, money transfers and insurance to low-income, poor and

excluded people enabling them to raise their income and living standards (Aghion and

Morduch, 2005). It consists of lending and recycling very small amounts of money for

short periods of time. Microfinance or microcredit has therefore been associated with

helping empower the poor to account properly and independently for their small

businesses and thus manage their livelihoods better (Richard et al., 2008). On the other

hand, poverty alleviation has been a long term goal of governments and key international

institutions such as the World Bank and United Nations seeking more effective ways of

reaching the poor. The importance of microfinance as a targeted strategy for poverty

alleviation lies in its ability to reach the grassroots with financial services based more on

a "bottom-up" as opposed to "top-down" approach (Dixon et al., 2006).

When Muhammad Yunus, an economics professor at a Bangladesh university, started

making small loans to local villagers in the 1970s, it was unclear where the idea would

go. Around the world, scores of state-run banks had already tried to provide loans to poor

households, and they left a legacy of inefficiency, corruption, and millions of dollars of

squandered subsidies. Today, Muhammad Yunus is recognized as a visionary in a

movement that has spread globally, claiming over 65 million customers at the end of

2002 (Richard et al., 2008). They are served by microfinance institutions that are

providing small loans without collateral, collecting deposits, and, increasingly, selling

1

insurance, all to customers who had been written off by commercial banks as being

unprofitable (Aghion and Morduch, 2005).

Indonesia was the first developing country to establish large scale commercial

microfinance systems (Richard et a l , 2008). Banks in developing countries typically

serve no more than 20% of the population leaving the rest with little, i f any, access to

financial services. The unserved majority which employs as much as 60% of the

economically active population depends on informal and semi-formal sources of finance

(Aghion and Morduch, 2005). Most of the entities providing microfinance services are

non-formal and semi-formal institutions not subject to prudential regulations which apply

to banks and other formal-sector institutions. The ability of most micro finance

institutions (MFIs) to leverage capital and mobilize external resources is generally

limited. To support outreach to low-income clients, donated resources are generally

leveraged and augmented by borrowing from formal financial institutions or large

institutional and individual investors, or accepting limited deposits from the public

(Greuning, Gallardo and Randhawa, 1998).

Credit risk arises fi-om uncertainty in a given counterparty's ability to meet its obligations.

The increasing variety in the types of counterparties and the ever-expanding variety in the

forms of obligations have meant that credit risk management has jumped to the forefront

of risk management activities carried out by firms in the financial services industry

(Fatemi and Fooladi, 2006).

Risk taking is an inherent element and integral part of financial services in general and of

microfinance in particular and, indeed, profits are in part the reward for successful risk

taking in business (Aghion and Morduch, 2005). On the other hand, excessive and poorly

managed credit can lead to losses and thus endanger the safety and soundness of

microfinance institutions and safety of microfinance institution's depositors.

Consequently, microfinance institutions may fail to meet its social and financial

objectives. This implies that proactive risk management is essential to the long term

sustainability of microfinance institutions (MFIS). Therefore, it is believed that effective

risk management allows MFIs to capitalize on new opportunities and to minimize threats

to their financial viability (NBE, 2010).

2

According to Ahamed (2010), credit policy is a management philosophy for spelling out

the decision variables of credit standards, credit terms and collection efforts by which

managers in MFIs have an influence on their operations. The credit policy impacts on the

impact of MFIs depending on the lending approaches used to screen clients for credit

facilities which are either liberal or stringent in nature. These approaches are effective and

efficient provided managers are competent with the relevant skills, knowledge and

experience of leading teams to achieve the set targets.

However, lack of collateral and high interest rates as an impediment to access to loans

from Micro finance institutions (MFIs) by micro entrepreneurs (Ahamed, 2010). Micro

entrepreneurs who secure fiinds from such institutions spend the bulk of their returns on

investment in paying the cost of capital, thus leaving them with none or little savings for

reinvestment. As a result, the majority of micro enterprises fail to grow into Small and

eventually Medium enterprises. Therefore, to bring the youth on board, the Kenyan

government with the support of development partners in 2006 established a youth

enterprise development ftmd that is channelled to Micro finance Institutions and other

financial intermediaries for onward lending to the youth without collateral (Ahamed,

2010). Such a fund attracts a greatly reduced cost of capital which stands at 8% per

annum as a strategy to make the fund affordable to the youth who in many cases do not

have collateral and therefore ideal for start-ups. Given that the vision of micro finance is

to promote the growth of micro enterprises, MFIs and other financial intermediaries have

experienced rapid growth to support the micro enterprises. One such institution is the

Kenya Rural Enterprise Program (K-REP) , a non-governmental organization that was

started in 1984 under the funding of the US AID (Simeyo et al, 2011).

To date, a number of MFIs and financial intermediaries including K-REP, Equity bank,

Kenya women finance trust (KWFT) and Faulu Kenya provide micro finance services to

the low income groups for purposes of starting or developing income generating

activities. Financial services deepening (FSD), (2009) indicates that MSEs access to

credit has increased greatly from 7.5% in 2006 to 17.9% in 2009 (Simeyo et al, 2011).

3

1.2 Statement of the Problem

Microfinance institutions face various risks that can be categorized into three groups,

financial risk with credit risk being a component, operational risk and strategic risk

(Teferri, 2000). These risks have different impact on the performance of MFIs. The

magnitude and the level of loss caused by customer risk compared to others is severe to

cause bank or MFI failures. Over the years, there have been an increased number of

significant bank problems in both matured and emerging economies. Various researchers

have studied reasons behind bank and MFIs problems and identified several factors.

Credit problems, especially weakness in credit risk management, have been identified to

be a part of the major reasons behind banking difficulties (Simeyo et al, 2011). Loans

constitute a large proportion of CR as they normally account for 10-15 times the equity of

an MFI. Thus, banking business is likely to face difficulties when there is a slight

deterioration in the quality of loans. Poor loan quality has its roots in the information

processing mechanism (Teferri, 2000). These problems are at their acute stage in

developing countries. The problem often begins right at the loan application stage and

increases ftorther at the loan approval, monitoring and controlling stages, especially when

credit risk management guidelines in terms of policy strategies and procedures for credit

processing do not exist or weak or incomplete (Richard et al., 2008).

Studies conducted so far on Micro enterprises (Teferri, 2000) and on manufacturing firms'

case located in Kenya do not specifically touch the case of micro finance institutions.

This study therefore tried to narrow the research gap paying attention to this sector of the

economy. Studies done on micro enterprises are meant to evaluate the institutional

sustainability of the credit scheme. This study therefore sought to examine broadly

challenges faced by micro finance institutions in credit management.

1.3 Purpose of the Study

The purpose of the study was to determine and identify the challenges faced by micro

finance institutions in credit management in Kenya.

1.4 Research Questions

1.4.1 What are the exposing factors to credit risk among microfinance institutions?

1.4.2 What is the relationship between credit management policy and customer retention?

4

1.4.3 What are the guiding principles and practices that can be used to manage credit risk

in microfinance institutions?

1.5 Significance of the Study

The following subsection presents a detailed summary of the importance of the study to

the various institutions and individuals.

1.5.1 Microfinance institutions

It will help micro finance institutions know the impact they have on their clients and how

to ensure efficient running between the two parties when it comes to credit issuing and

repayment.

1.5.2 Government

The study will be of help to the government and policy makers to put in place laws and

regulations that support credit management systems by banks and MFIs. The study wil l

recommend areas of improvement in debt collection for the sake of sound collection of

loans in microfinance institutions sector, boost the confidence of savers and borrowers

who transact with these microfinance institutions.

1.5.3 Scholars and researchers

The study will contribute to the existing body of knowledge on microfinance institutions

to academicians and make recommendations arising from its findings for further research

on this or other related areas of study.

1.6 Scope of the study

To cover all the regions in the entire country was impossible because of the limited time

frame and amount of funds for this research. For this reason, the study was limited to

Nairobi and targeted microfinance institutions.

1.7 Definition of Terms

1.7.1 Entrepreneur

An entrepreneur is a person who organizes and manages a business undertaking and

assumes a risk of a business enterprise for the sake of profits (Dessler, 2000).

5

1.7.2 Micro finance institutions (MFI)

Microfinance is the provision of financial services in small increments, typically to very

poor people (Robinson, 2001).

1.7.3 Portfolio Management

Portfolio management can be defined as the monitoring the performance of a firms total

loan fund (SEEP, 2009).

1.7.4 Loan Portfolio

This can be defined as the outstanding principal balance of all of the MFI 's outstanding

loans including current, delinquent and restructured loans due within 2months, but not

loans that have been written off (SEEP, 2009).

1.7.5 Portfolio at Risk .

Portfolio at risk is the value of all loans outstanding that have one or more installments of

principal past due more than a certain number of days (SEEP, 2009).

1.8 Chapter summary

The chapter has given a background of the study which indicates the origin of micro

finance institutions and shows their importance in the current world especially to small

and medium entrepreneurs and most important the credit management faced by MFIs. It

has also highlighted the purpose of the study which was to determine and identify the

challenges faced by micro finance institutions in credit management in Kenya. The

chapter also presented the research questions, justification of the study, scope of the study

and definition of terms. The next chapter gives a review of literature relating to

challenges faced by microfinance institutions in credit management. The third chapter

covers the research methodology while the fourth chapter provides the research findings

lastly final chapter gives a summary of the findings, conclusion and recommendations.

CHAPTER TWO

2.0 LITERATURE R E V I E W

2.1 Introduction

The purpose of this chapter was to determine and identify the challenges faced by micro

fmance institutions in credit management in Kenya This chapter addresses the espousing

factors to credit risk among microfinance institutions, the relationship between credit

management policy and customer retention and the guiding principles and practices can

be used to manage credit risk in microfinance institutions.

2.2 Espousing Factors to Credit Risk among Microfinance Institutions

According to Ogilo (2012), Financial institutions have faced difficulties over the years for

a multitude of reasons, the major cause of serious banking problems continues to be

directly related to lax credit standards for borrowers and counterparties, poor portfolio

risk management or a lack of attention to changes in economic or other circumstances that

can lead to a deterioration in the credit standing of a bank's counterparties. For most

banks and MFIs, loans are the largest and most obvious source of credit risk however,

other sources of credit risk exist throughout the activities of a bank, including in the

banking book and in the trading book, and both on and off the balance sheet. Banks and

FMIs are increasingly facing credit risk (or counterparty risk) in various financial

instruments other than loans, including acceptances, interbank transactions, trade

financing, foreign exchange transactions, financial futures, swaps, bonds, equities,

options, and in the extension of commitments and guarantees, and the settlement of

transactions.

Watkins and Hicks (2009), indicate that microfinance institutions have become an

integral part in the financial market by making microloans to low-income borrowers

mostly in the developing and transition economies. Microfinance has been argued to

charge high interest rates to ensure that their organizations are financially sustainable.

The two place arguments that by doing so, microfinance institutions ensure permanence

and expansion of the services they provide.

7

Yehuala (2008), concurring that microfinance charges higher interest rates, notes that

loan size rather than interest charged is what is relevant in making loan acquisition

decision. Loan provided by formal financial institutions is usually small, due to the risk

averseness, and a gap is created which is filled by accessing money from private lenders

at a higher interest rate. However, Peace (2011) contradicts that position by stating that

interest rate is a relevant factor in loan acquisition decision as it is set by institutions to

sort potential borrowers.

Applying stringent lending criteria to low-income borrowers may in effect lead to their

exclusion from the financial system which is not socially acceptable or legitimate. At the

same time, failure to accommodate for credit risk increases the likelihood of loan default

which in the short term increases financial institutions costs and in the long term is passed

on to other borrowers in the form of more expensive and or less accessible retail credit.

Failure to differentiate lending policies to reflect credit risk may lead all borrowers to

suffer through reduced availability of low cost credit. The likelihood of this is increased

by the moral hazard problem that households when applying for funding, overstate their

ability to meet the repayment schedule of the lender (Ralston, D and Wright, A , 2003).

2.2.1 Credit Risk Types

Operational risk is the risk of direct or indirect loss resulting from inadequate or failed

intemal processes, people and systems or from external events or unforeseen

catastrophes. It includes the exposure to loss resulting from the failure of a manual or

automated system to process, produce or analyse transactions in an accurate, timely and

secure manner. Operational risk therefore is imbedded in all of the microfinance

institution's operations including those supporting the management of other risks (NBE,

2010).

Managing operational risk is an important feature of sound risk management practice in

any microfinance institution (NBE, 2010). The exact approach chosen by an individual

microfinance institution will depend on a range of factors, including its size and

sophistication and the nature and complexity of its activities. Common operational risks

in MFIs include the following: The system does not correctly reflect loan tracking, e.g.

information on amount disbursed, payment received, current status of outstanding

8

balance, aging of loan by portfolio outstanding (Steinwand, 2000). Lack of effectiveness

and insecurity of management information system in general and the portfolio

management system in particular e.g. software does not have intemal safety features,

inaccurate MIS and untimely reports; Inconsistencies between the loan management

system data and the accounting system data; Treating rescheduled loan as on-site loans;

Lack of portfolio related fraud controls; Loan tracking information is not adequate. The

most important types of operational risk could also involve breakdowns in intemal

systems and controls and corporate govemance. Such breakdowns can often lead to

financial losses through error, fraud or inefficiency. Other aspects of operational risk

include major failure of information technology systems or events such as natural and

other disasters. As microfinance institutions become more reliant on technology to

support various aspects of their operations, the potential failure of a technology based

system is of growing concem in the context of the management of operational risk (NBE,

2010).

Foreign exchange risk is the potential for loss of eamings or capital resulting from

fluctuations in currency values (Tamil, 2010). Microfinance institutions most often

experience foreign exchange risk when they borrow or mobilize savings in one currency

and lend in another (Robinson, 2001). For example, MFIs that offer dollar savings

accounts and lend in the local currency risk financial loss i f the value of the local

currency weakens against the dollar. Altematively, i f the local currency strengthens

against the dollar, the MFI experiences a financial gain. Due to the potential severity of

the downside risk, an MFI should avoid funding the loan portfolio with foreign currency

unless it can match its foreign liabilities with foreign assets of equivalent duration and

maturity. In Ghana, the appreciation of the dollar actually caused many MFIs that were

dependent on dollar-denominated loans to begin mobilizing local savings in 1999 to

reduce the currency mismatch of assets and liabilities. To reduce investment portfolio

risk, treasury managers stagger investment maturities to ensure that the MFI has the long-

term funds needed for growth and expansion. In addition, they consider the credit,

inflation, and currency risks that might threaten the value of the principal investment.

Short-term investments, for example, carry less risk of losing value due to inflation

(Steinwand, 2000).

9

According to Rosenberg (1999), Micro Finance Institutions (MFIs) are increasingly a

central source of credit for the poor in many countries. Weekly collection of repayment

instalments by bank personnel is one of the key features of microfinance that is believed

to reduce default risk in the absence of collateral and make lending to the poor viable.

Some of the factors that lead to loan default include; inadequate or non-monitoring of

micro and small enterprises by banks, leading to defaults, delays by banks in processing

and disbursement of loans, diversion of funds, over concentration of decision making,

where all loans are required by some banks to be sanctioned by Area/Head Offices.

Weekly collection of repayment instalments by bank personnel is one of the key features

of microfinance that is believed to reduce default risk in the absence of collateral and

make lending to the poor viable (Vogelgesang, 2003). In addition, frequent meetings with

a loan officer may improve client trust in loan officers and their willingness to stay on

track with repayments.

2.3 Credit Management policies and Customer Retention

According to Ralston and Wright (2003), attracting and retaining profitable customers,

and increasing reviews from those customers are a priority of managers of all firms in

today's globalised marketplace. It is particularly important in the highly competitive retail

financial services market where the core business of banking continues to be the

profitable management of risk. For banks and other financial services firms, risk

management is consistent with their profit maximizing objectives which is evidenced by

provision of tailor made products and personal loan packages to profitable low income

customers (Kenny, 2010).

For MFIs managers need to reduce the risk of loan default because the institutions'

financial viability is weakened by the loss of principal and interest the cost of carry and

the opportunity cost of management time taken to recover capital at risk (Harris, 2001).

Yet on the other hand, MFIs operate under the objective of maximizing benefits to

members, which includes the social role of providing loans to help customers achieve

their standards of living goals. This social role can conflict with financial viability i f it

means managers become less stringent in the application of sound lending practices to

access and monitor the credit risk of borrowers (Ralston, D and Wright, A , 2003).

10

The purpose of customer retention is to ensure that an institution maintains relationships

with value adding customers. Such an objective is attained when retained customers are

offered quality goods and services which fulfil their needs (Kenny, 2010). According to

Harris (2001), customers who willingly renew their loan contracts are more satisfied with

the services than those who do not. The satisfied customers therefore utter positive word

of mouth which influences the beliefs, feelings and behaviours of other customers which

facilitates the efforts of micro finances in extending outreach to customers (Harris, 2001).

Similarly loan applications are shorter for retained customers because loan officers take

little fime to conduct on site business evaluation for each loan (Kenny, 2010). This is also

true for clients with good repayment records whose costs of serving lowers the

transaction costs leading to efficiency, increased number of client reached and at the

same time enabling loan officers to have time of marketing and educating more customers

about financial products hence lowering the acquisition costs for customers (Craig, 2010).

Customer retention facilitates outreach by improving efficiency and enhancing

productivity as repeat borrowers with good repayment records require less time to

manage than new clients (Harris, 2001). This effect of improved efficiency is helpful to

MFIs serving the lower market segment because of compensation for the small loan

balances given out. Likewise retained customers reduce the lending risks due to the fact

that sufficient information is built on their cash flows and business performance which

facilitates MFIs to make optimal credit decisions while modifying the lending terms as

per the identified risks (Micro save, 2010). Dawkins (2010) shows that retained customers

who are loyal and satisfied by the services generate increasing profits over time for MFIs

due to the lower acquisition costs, higher loan balances which are used to subsidize the

cost structure inform of interest rates and processing fees to new customers. However, not

all customers are interested in borrowing all the time (Clark, 2010).The best way to retain

these customers is upon the manager's initiative in developing voluntary savings products

where customers save money which can be helpful for MFIs in mobilizing savings to lend

out at low cost compared to the market (Craig, 2010). The next subsection looks at the

collateral requirements.

11

2.3.1 The collateral Requirements

One reason for the development of the microfinance industry is that traditional banks do

not serve persons who cannot offer traditional collateral. Many micro lending

methodologies use peer groups, restrictive product terms and compulsory savings as

collateral substitutes. Subsequent lending innovations provide microloans with non-

traditional collateral, such as household assets and consigners' (Harris, 2001). Pawn

lending and asset leasing are other methods of overcoming collateral constraints. Perhaps

more important than the type of collateral is how it is used. In microfinance, collateral is

primarily employed as an indication of the applicant's commitment. It is rarely used as a

secondary repayment source because the outstanding balance is so small that it is not

cost-effective to liquidate the collateral, much less legally register it i f such a service is

available (Peace, 2011). Only when clients are not acting in good faith do micro lenders

take a hard line stance and seize collateral. Consequently, MFIs tend to be less concerned

about the ratio of the loan size to the value of collateral than how the clients would feel i f

the collateral was taken from them. As the loan size increases, however, this soft

approach to collateral needs to change so those larger loans are indeed backed by

appropriate security (Churchill and Coster, 2001).

Since poor customers generally have no credit history and little collateral, MFIs must use

innovative lending practices to reduce risks associated with asymmetric information

between lender and borrower. In fact, several studies have focused on understanding the

mechanisms of lending practices such as group loans, a type of joint-liability loan,

whereby the MFI delegates screening, monitoring, and contract enforcement costs to a

group, and individual uncollateralized loans, whereby repayment is secured with a

promise of access to larger loans in the futiu-e conditional on current loan repayment

(Hartarska, Cropper and Caudill, 2012).

According to Christl and Pribil (2004), that evaluation of the collateral provided by the

credit applicant is an essential element in the credit approval process and thus has an

impact on the overall assessment of the credit risk involved in a possible exposure. The

main feature of a collateralized credit is not only the borrowers personal credit standing,

which basically determines the probability of default, but the collateral which the lender

can realize in case the customer defaults and which thus deter-mines the MFIs loss. Via

12

the risk component of loss given default and any other requirements concerning credit

risk mitigation techniques, the value of the collateral is included in calculating the capital

requirement under Basel I I . In order to calculate the risk parameters under Basel I I

correctly, it is important for the valuation of the collateral to be effected completely

independently of the calculation of the borrowers probability default in the credit rating

process.

2.3.2 Education and Training To Customers

MFI staff and the customers need sufficient training so that they can understand the

numerous regulations, policies, and procedures governing loan funds. Audit reports have

found that deficiencies in loan and grant oversight are not due to a lack of policies, but

rather that existing policies are not being followed (Harris, 2001). Federal, State, and

local government offices are responsible for ensuring that staffs are properly trained to

fulfil grant requirements (Peace, 2011). It is essential that grantees also receive training,

particularly small entities not familiar with all of the regulations and policies. Improving

skills of staff can be a long-term process that needs a strategic approach. When the

Environmental Protection Agency. Providing training of staff helps to ensure that eligible

recipients understand how to apply for loans and properly use the funds (Bangladesh

Bank, 2005).

A critical step towards service excellence is investing in the skills and knowledge

development of servers, giving them the preparation to serve and, in so doing, stoking

their desire to serve. The training should focus on the understanding of why service

excellence is important both to the organization and the individual employees, not just

how and what needs to be done. The combination of developing skills, on-the-job

knowledge, and internalizing organizational goals should be the key purpose of the

employee training. It can stimulate their enthusiasm about their work and about new

challenges to satisfy customer expectations. Employee development starts from recruited

personnel who have the ability, desire and personality to be excellent service providers

(Kim and Kleiner, 1996). The next subsection looks at the accountability to staff

13

2.3.3 Accountability of Staff

According to Symonds, Wright and Ott (2007), customer-led MFIs lay the foundation for

a deeper relationship from the outset. Through a carefully crafted after-sale process, they

capitalize on the enthusiasm new customers bring to their selection of product and

provider by arranging an initial welcoming call in the first week and initiating a month-

by-month follow-up program to help customers better understand account features. They

monitor this "overinvestment" in new customers to determine how customers are using

the bank's services and systematically track any potential problems that could cause a

new customer to defect. When they spot mishaps successive months of late fees, for

instance they act pre-emptively to correct the problem and rescue the relationship. Senior

managers, troubled by the periodic peaks in attrition among new customers, should see a

big opportunity to get more value out of their customer-acquisition investments by

helping new members discover service features that best suited their needs.

Tracking how well staffs deliver on promises is integral to the leaders' approach to

managing the customer relationship. What customers experience day by day in contacts

they have with each branch office or call centre determines the quality of the on-going

relationship. For clear account statements, an orderly branch appearance and easy to

understand product information which can be thought of as "hygiene factors" customers

expect execution to be error-free (or that, in its breach, the bank will make promptly

acknowledge its mistake and work to regain the customer's good wil l (Harris, 2001).

Thus, many banks need to invest in improving basic processes first before they can begin

exceeding customer expectations (Symonds, Wright and Ott, 2007).

Converting customers into loyalists and, even better, making them recruiters of still more

customers requires a disciplined, muhiyear initiative (Peace, 2011). The process of

becoming a customer-led bank begins with a commitment to eliminate self-defeating

behaviours that blind the organization to customers' needs. Putting customer loyalty at

the heart of growth requires banks to master new disciplines (Tamil, 2010). They must

learn to nurture the loyal core of their customer base and hone skills for spotting and

attracting the right new customers. Retail bank executives across the world are awakening

to the realization that long-term growth and profitability hinge on their ability to attract

14

and retain loyal customers. That recognition has been a long time in coming. It's being

spurred by a potent combination of increasing competition, regulatory scrutiny and

customers' easier access to a broad range of new products and services and thus MFIs

should adapt these practices. The literature has established various policy measures on

credit management, and indeed it is evident that the various measures put in place, are

sufficient enough to deal with the riskiness of MFIs, however the literature has not

comprehensively articulated how such policy measures can enhance customer retention.

In this regard therefore the study sought to fill in these gaps, by seeking to establish how

such measures enhance customer retention.

2.4 Guiding Principles and Practices to Manage Credit Risk in Microfinance

Institutions

According to Ralston and Wright (2003), sound lending procedures in retail financial

institutions involve identifying high-risk applicants, modifying loan conditions such as

security requirements and monitoring repayments post-loan approval. For managers of

MFIs this procedure is complicated by the need to balance between the institutions' social

objective of improving loan accessibility to the poor and the possibility of reducing the

institutions viability through loan default. Customers experiencing some bankruptcy-

related default on personal loans indicate that managers do not impose more stringent

lending conditions on high-risk borrowers. However, social and viability objectives could

be better balanced through careful loan monitoring and timely arrears practices. The next

subsection looks at the adequate control over credit risk.

2.4.1 Adequate Control over Credit Risk

A number of techniques are available to microfinance institutions to assist in the

mitigation of credit risk. Group collateral and guarantees are the most commonly used.

Various forms of other collateral and guarantees (Including physical collateral, personal

guarantees etc.) could also be used. Notwithstanding the use of various mitigation

techniques individual credit transactions should be entered into primarily on the strength

of the borrower's repayment capacity (Harris, 2001). Microfinance institutions should

also be mindful that the value of collateral might well be impaired by the same factors

that have led to the diminished recoverability of the credit. Microfinance institutions

15

should have policies covering the acceptability of various forms of collateral, procedures

for the ingoing valuation of such collateral, and a process to ensure that collateral is, and

continues to be enforceable and realizable (Harris, 2001). With regard to guarantees,

microfinance institutions should evaluate the level of coverage being provided in relation

to the credit-quality and legal capacity of the guarantor and should be careful when

making assumptions about implied support from third parties including government

entities (NBE,2010).

Similar to capital market investors, which rely on external credit ratings provided by

rating agencies, banks and MFIs can assign intemal credit ratings to evaluate the credit

worthiness of borrowers (Peace, 2011). These ratings provide a screening tactic to

alleviate asymmetric information problems between borrowers and lenders. Such

transaction-based lending technologies have become even more important with the

introduction of Basel I I , which has pushed banks to adopt new credit risk management

techniques, including credit-scoring models, to analyse credit worthiness (NBE, 2010).

According to the NBE report (2010), small business loans and retail credit are less

sensitive to systematic risk and their maturities are shorter under Basel I I , retail credit and

loans to low income earners are treated differently than corporate loans, such that they

require less regulatory capital for given probabilities of defaults. However, Basel I I also

assumes that a smaller borrower suffers a greater probability of default. Basel I I

encourages banks to update their intemal systems and procedures to manage their

customer loans. Banks can create their own credit-scoring models, so SMEs seeking bank

financing must overcome the doubts created by the banks' intemal rating models and

analyses of their probability of default I f a firm knows its own creditworthiness, it might

have a better chance of gaining fair treatment from lenders, reducing the loan interest rate,

and mitigating the average cost of capital. Moreover, this knowledge would increase

transparency in the credit process, which itself would be beneficial (Gama and Geraldes,

2012). The next subsection looks at how an active board and senior management

oversight helps to enhance customer retention.

16

2.4.2 Active Board and Senior Management Oversight

The board of directors is responsible for approving and reviewing the liquidity risk

management strategy and policies of the microfinance institution (Peace, 2011). Each

microfinance institution should develop a strategy that sets the objectives of ensuring that

the microfinance institution at all times, has adequate levels of liquidity to meet its

operational needs and should adopt the necessary policies and procedures to achieve this

objective. At a minimum, the board should: Understand the nature and level of

institution's liquidity risk; At all-time be informed of the institution's liquidity risk;

approve broad business strategies, policies, guidelines and intemal control and limits for

managing and monitoring liquidity; establish tolerance levels in respect of liquidity risk;

establish clear levels of delegation within the liquidity management function; ensure that

the microfinance institution's management adopts procedures to enable the achievement

of the objectives set out in the strategy and poHcies; ensure that the management

measures, monitors and controls liquidity risk; effectively communicate the strategies and

policies to all relevant microfinance institution personnel; ensure that the liquidity

management framework is regularly reviewed; ensure that the management information

systems are in place which can adequately measure, monitor, control and report liquidity

risk (NBE,2010).

The board of directors should have responsibility for approving and periodically (at least

annually) reviewing the credit risk strategy and significant credit risk policies of the bank

(NBE, 2010). The strategy should reflect the bank's tolerance for risk and the level of

profitability the bank expects to achieve for incurring various credit risks. Senior

management should have responsibility for implementing the credit risk strategy

approved by the board of directors and for developing policies and procedures for

identifying, measuring, monitoring and controlling credit risk (Peace, 2011). Such

policies and procedures should address credit risk in all of the bank's activities and at

both the individual credit and portfolio levels. MFIs should identify and manage credit

risk inherent in all products and activities and should ensure that the risks of products and

activities new to them are subject to adequate risk management procedures and controls

before being introduced or undertaken, and approved in advance by the board of directors

17

or its appropriate committee. The following subsection looks at how management

information system enhances customer retention.

2.4.3 Management Information System

To properly control risks, an MFI needs a strong information system. Being that risk

management is a dynamic three-step cycle in which MFIs identify their risks, design and

implement controls to mitigate these risks, and establish systems to monitor them. These

monitoring systems are then used to help identify additional risks, setting in motion a

dynamic process (Christen, 2000). Management information systems (MIS) lie at the

heart of this dynamic, serving as the primary link between these three elements. Whether

computerized or manual, an effective MIS provides critical information for risk

identification, acts as a mechanism for systematizing business processes and controls, and

offers a tool for monitoring organizational performance and pinpointing future risk areas.

As such, MIS is the foundation for effective risk management. MIS includes all the

systems used for generating the information that guides management in its decisions and

action. Good information is essential for an MFI to perform efficiently and effectively.

MIS must be accurate and easy to use. By transforming data, or unprocessed facts, into

information through a systematic process, management information systems provide tools

for identifying, controlling and monitoring key risks within an organization. The better

the information, the better the MFI can manage its risks (Waterfield and Ramsing, 1998).

Good MIS assists MFI 's maximize their outreach to the poor so that economies of scale

can be enjoyed fully. Appropriate MIS goes a long way to assist programs with an easy

was to analyse data for improving their program design and to assist in the development

of products that are geared to meeting the needs of the people (Christen, 2000).

According to Gibbons (2000), there is a need to improve the capacity of programs to

handle greater responsibilities and be able to control greater amounts of funds. It is

important for programs to update and improve other essential systems as well, like

computerized MIS and plarming with the micro finance so as to give management the

tools they need. The next subsection reviews literature on efficient intemal controls,

supervision and audit can be used to mitigate risk.

18

2.4.4 Efficient Internal Controls, Supervision and Audit To Mitigate Credit Risk

According to Tinsley (2005), organizations that award loans need good intemal control

systems to ensure that funds are properly used and achieve intended results. These

systems, which must be in place prior to grant or loan award, can serve as the basis for

ensuring funds are awarded to eligible entities for intended purposes, and are managed

appropriately. Intemal control systems that are not adequately designed or followed make

it difficult for managers to determine whether funds are properly used (Christen, 2000).

There are four areas where intemal controls are important; Preparing policies and

procedures before issuing loans, consolidating information systems to assist in managing

grants, providing loan management training to staff and grantees and coordinating

programs with similar goals and purposes.

Having regulations and intemal operating procedures in place prior to awarding loans

enables agencies to set clear expectations. Policies serve as guidelines for ensuring that

new loan programs include provisions for holding awarding organizations and grantees

accountable for properly using funds and achieving agreed-upon results (Tinsley, 2005).

Although different programs may need different procedures, general policies should be

established that all programs must follow (Tinsley, 2005).

MFIs should have a segregated intemal audit and control department charged with

conducting audits of all departments the intemal audit should verify the continuing

adequacy and applicability of credit risk management policies and procedures provide an

independent assessment of the credit portfolios' existence, quality and value, the integrity

of the credit process, and promotes detection of problems relating thereto (Tinsley, 2005).

Every year, intemal audit should prepare an auditing plan to be approved by the board

according to which the audits are carried out. This auditing plan should be carried out in a

risk-oriented maimer, taking into account size and nature of the credit institution, as well

as type, volume, complexity, and risk level of the MFI's activities (Kim and Kleiner,

2006).

The frequency of auditing the individual audit areas should be stipulated in the MFI 's

intemal guidelines for intemal auditing. A comprehensive written audit report has to be

19

prepared following each audit. It will usually be expedient to first report to the head of the

audited organizational unit on the audit's findings in the course of a final meeting and to

offer the opportunity to comment on the findings, with these comments to be taken into

account in the audit report. Subsequently, all top executives and department heads are

informed accordingly. It is the task of intemal auditing to monitor the swift correction of

any problems detected in the audit as well as the implementation of its recommendations

in a suitable form, and i f necessary to schedule a follow-up audit (Kim and Kleiner,

2006).

According to Kim and Kleiner (2006), assessments of intemal audit should, at a

minimum, randomly test all aspects of credit risk management in order to determine that;

Credit activities are in compliance with the MFI's credit and accounting policies and

procedures, and with the laws and regulations to which these credit activities are

subjected to, existing credit facilities are duly authorized, and are accurately recorded and

appropriately valued on the books of the MFI , credit exposures are appropriately rated,

credit files are complete, potential problem accounts are being identified on a timely basis

and determine whether the FI 's provision for credit losses is adequate, credit risk

management information reports are adequate and accurate, improvement in the quality of

credit portfolio and appraise top management (Bangladesh Bank, 2005). The following

subsection presents policies and strategies and allocation credit facilities.

2.4.5 Policies and Strategies and Allocation of Credit Facilities

Every MFI should have a credit risk policy document that should include risk

identification, risk measurement, risk grading techniques, reporting and risk control or

mitigation techniques, documentation, legal issues and management of problem facilities

(NBE, 2010). The senior management of the MFI should develop and establish credit

policies and credit administration procedures as a part of overall credit risk management

framework and get those approved from Board. Such policies and procedures shall

provide guidance to the staff on various types of lending including Corporate, SME,

Consumer, Housing etc. Credit risk policies should; Provide detailed and formalized

credit evaluation and appraisal process, provide risk identification, measurement,

monitoring and control, define target markets, risk acceptance criteria, credit approval

20

authority, credit maintenance procedures and guidelines for portfolio management, be

communicated to branch offices. Al l dealing officials should clearly, understand the

MFFs approach for credit sanction and should be held accountable for complying with

established policies and procedures. Clearly spell out roles and responsibilities of units

and staff involved in management of credit in order to be effective, these policies must be

clear and communicated down the line. Further any significant deviation from these

policies must be communicated to the top management and corrective measures should be

taken. It is the responsibility of senior management to ensure effective implementation of

these policies duly approved by the Board (Bangladesh Bank, 2005).

A thorough credit and risk assessment should be conducted prior to the granting of a

facility, and at least annually thereafter for all facilities. The results of this assessment

should be presented in a Credit Application that originates from the relationship manager

or account officer and is reviewed by Credit Risk Management for identification and

probable mitigation of risks. The relationship manager should be the owner of the

customer relationship, and must be held responsible to ensure the accuracy of the entire

credit application submitted for approval. He or she must be familiar with the MFI's

Lending Guidelines and should conduct due diligence on new borrowers, principals, and

guarantors. It is essential that they know their customers and conduct due diligence on

new borrowers, principals, and guarantors to ensure such parties are in fact who they

represent themselves to be. A l l MFI 's should have established Know Your Customer and

Money Laundering guidelines which should be adhered to at all times (Bangladesh Bank,

2005).

2.5 Chapter Summary

The purpose of this chapter was to determine and identify the challenges faced by micro

finance institutions in credit management in Kenya This chapter addressed the espousing

factors to credit risk among microfinance institutions, the relationship between credit

management policy and customer retention and the guiding principles and practices can

be used to manage credit risk in microfinance institutions. The following chapter presents

the research methodology to be used in the study.

21

CHAPTER T H R E E

3.0 METHODOLOGY

3.1 Introduction

The objective of this research was to determine the challenges microfinance institutions

face in credit management. This chapter addresses the research design that was employed

in the study. It discusses the research design, population and sample, data collection,

research procedure and data analysis methods. A summary of the chapter wil l be provided

at the end.

3.2 Research Design

Bums and Groove (2001) state that designing a study helps researches to plan and

implement the study in a way that will help them obtain the intended results. This

increased the chances of obtaining information that could be associated with the real

situation. The research design employed in the study was descriptive survey which

enabled the researcher to present variables under investigation. The study was conducted

in natural settings and sought to retrieve the information from the respondent. It involved

a small sample of total population. Using the research methods mentioned above, the

researcher was able to obtain information on the challenges that MFIs face in credit

management in Kenya.

3.3 Population and Sampling

3.3.1 Population

Population refers to the entire group of people, events or things of interest that the

researcher wishes to investigate (Saunders, Lewis and Thomhill, 2009). Fifty four MFIs

in Kenya were identified for data collection. Cooper and Schindler (2008) define a

population as the total of the elements (an element is the subject on which measurement is

being taken) upon which inferences can be made. The study focused on the population

that is located in Nairobi comprising of all licensed MFIs offering products and services

to their customers. The study population consisted of all MFIs currently operating in

Kenya, there are fifty four MFIs currently operating in Kenya and registered as members

of the Association of Microfinance Institutions in Kenya (AMFI-K) . The MFIs were

specific to those that are located in Nairobi and had operations in rural areas of Central

22

Kenya. The Microfinance Institutions had to be issuing credit to either groups or

individuals in Kenya. The MFIs were either receiving deposits or were pure credit.

3.3.2 Sampling Design

According to Ross Kenneth (2005), sampling design is generally conducted in order to

permit the detailed study of part rather than the whole population. The information

derived from the resulting sample is customarily employed to develop useful

generalizations about the population. These generalizations may be in the form of

estimates of one or more characteristics associated with the population, or they may be

concerned with estimates of the strength of relationships between characteristics within

the population. The researcher wil l only focus on MFIs in Nairobi.

3.3.2.1 Sampling Frame

Sampling frame can be defined as the list of elements from which the sample was actually

drawn from (Cooper & Schindler, 2000). It is also knovra as the working population. The

sampling frame was the list of members of the Association of Microfinance Institutions in

Kenya (AMFI-K) which can be sourced from their website.

3.3.2.2 Sampling Technique

The study employed a census survey approach and as such, all the fifty three MFIs in the

population were studied. This means that all the MFIs were approached to participate in

the study. The choice for census is based on the fact that the entire population is

sufficiently small with only 54 MFIs. The census method has an advantage in that it

helped obtain data from each of the companies which then provided greater accuracy and

reliability.

3.3.2.3 Sampling Size

According to Cheston (2002), sample size depends on projects, project purpose, project

complexity, amount of errors willing to be tolerated, time constraints, financial

constraints and previous research in the areas. The choice for census is based on the fact

that the entire population is sufficiently small with only 53 MFIs. The census method has

an advantage in that it helped obtain data from each of the companies which then

provided greater accuracy and reliability.

23

3.4 Data Collection Methods

Data collection is an important aspect of any study type of research study. Inaccurate data

collection can impact negatively on the study and leads to invalid results. This study used

both primary data and secondary data. The research instrument used in collection of

primary data was questionnaires. The questionnaires were administered to ensure that

detailed and in depth information was generated through probing the respondent. The

questionnaires were then pre-set in order to remove any error and omissions. The

secondary data was obtained from various library books, referenced journals, research

papers and various websites regarding MFIs and credit management.

3.5 Research Procedures

Before the actually administering the questiormaire, a pilot study was done to ensure that

all questions were clear and understandable. The pilot study was administered to the

senior officers of two MFIs and revision of the questionnaire done accordingly. After

revisions on the questionnaires, they were administered via email as well as through drop

and pick to the respondents. In order to ensure a favourable response rate, the

questionnaire was issued with a cover letter that explained how the respondents were

chosen, anonymity of the identity of the respondents and a surety of sharing the results of

the research. This process took two weeks.

3.6 Data Analysis Methods

After data was collected it was prepared before being analyzed. The data was edited to do

away with omissions, improve legibility and consistency and coding was appropriately

done so as to assist in interpreting, classifying and recording of data. Tabulation was the

form in which data was recorded and categorized in order for it to be analyzed.

Data analysis was done through descriptive and regression statistics. This included

percentages, frequencies, and regression tables. Data was presented in pictorial

representation in the form of tables and figures. The tool that was used for analysis of

data collected was Statistical Package for Social Sciences (SPSS).

24

3.7 Chapter Summary

The chapter explains the research methodology used the population and the sample size,

so as to the give accurate information. The research design employed in the study was

descriptive survey which enabled the researcher to present variables under investigation.

It explains the data collection methods and tools. Data analysis was done through

descriptive and regression statistics. This included percentages, frequencies, and

regression tables. Data was presented in pictorial representation in the form of tables and

figures. The next chapter will help evaluate the findings, conclusions and give the

appropriate recommendations which will be based on this chapter.

25

CHAPTER FOUR

4.0 DATA ANALYSIS AND PRESENTATION

4.1 Introduction

This chapter presents the results and findings of the study on the research questions with

regards to the data collected from the MFIs in Kenya. The initial section covers the

background information with respect to the respondent as well as the company

background that relates to MFIs. This was to enable the researcher to know the nature and

type of the MFI , while the second was on the exposing factors to credit risk among

microfinance institutions. The third section was on the relationship between credit

management policy and customer retention and the fourth section was on the guiding

principles and practices that can be used to manage credit risk in microfinance

institutions. ^

4.2 Background Information

This section offers the backgroimd information with regards to the respondents' gender,

level of education as well as the experience in the industry. This was put into

consideration because of the meaningful contribution it offers to the study as the variables

help to provide the logic behind the responses issued by the respective respondents. Fifty

four questiormaires were issued to the respondents out of this, fifty three were returned.

This indicated a 97% response rate.

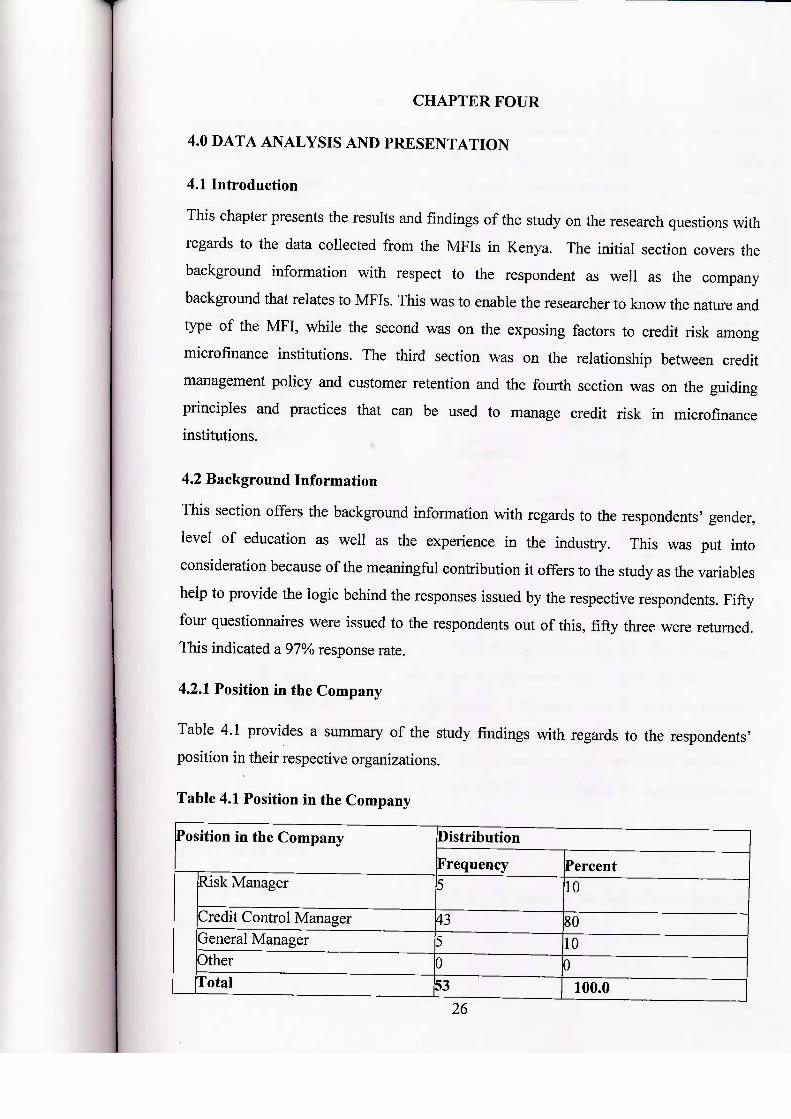

4.2.1 Position in the Company

Table 4.1 provides a summary of the study findings with regards to the respondents'

position in their respective organizations.

Table 4.1 Position in the Company

Position in the Company Distribution

Frequency Percent Risk Manager 5 10

Credit Control Manager 43 80 General Manager 5 10 Other 0 0

Total 53 100.0

26

Whereas 80 % of the respondents were in the credit control management only 10 % of the

respondents were either risk managers or general managers. None of the respondents

were from the other categories. The study findings show that indeed, the respondents

were directly involved in the strategic decision making by these organizations and

therefore likely to provide first-hand information on the variables of the study.

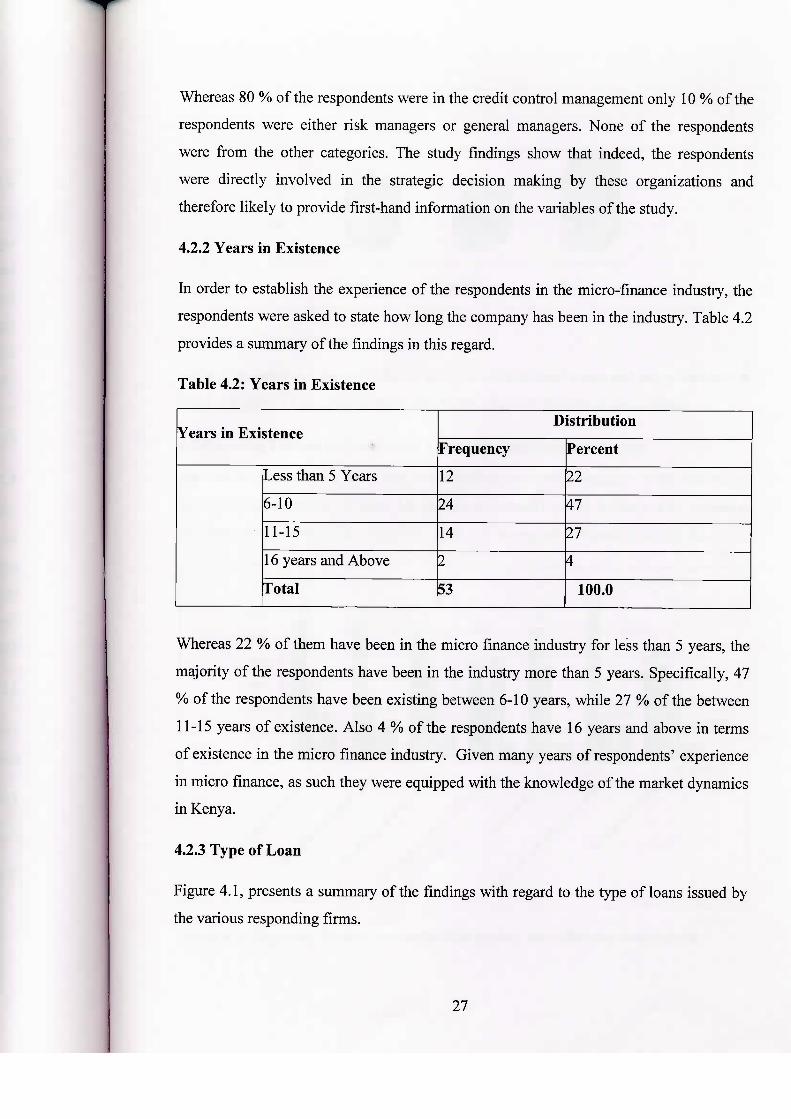

4.2.2 Years in Existence

In order to establish the experience of the respondents in the micro-finance industry, the

respondents were asked to state how long the company has been in the industry. Table 4.2

provides a summary of the findings in this regard.

Table 4.2: Years in Existence

Years in Existence Distribution

Frequency Percent

Less than 5 Years 12 22

6-10 24 47

11-15 14 27

16 years and Above 2 4

Total 53 100.0

Whereas 22 % of them have been in the micro fmance industry for less than 5 years, the

majority of the respondents have been in the industry more than 5 years. Specifically, 47

% of the respondents have been existing between 6-10 years, while 27 % of the between

11-15 years of existence. Also 4 % of the respondents have 16 years and above in terms

of existence in the micro fmance industry. Given many years of respondents' experience

in micro finance, as such they were equipped with the knowledge of the market dynamics

in Kenya.

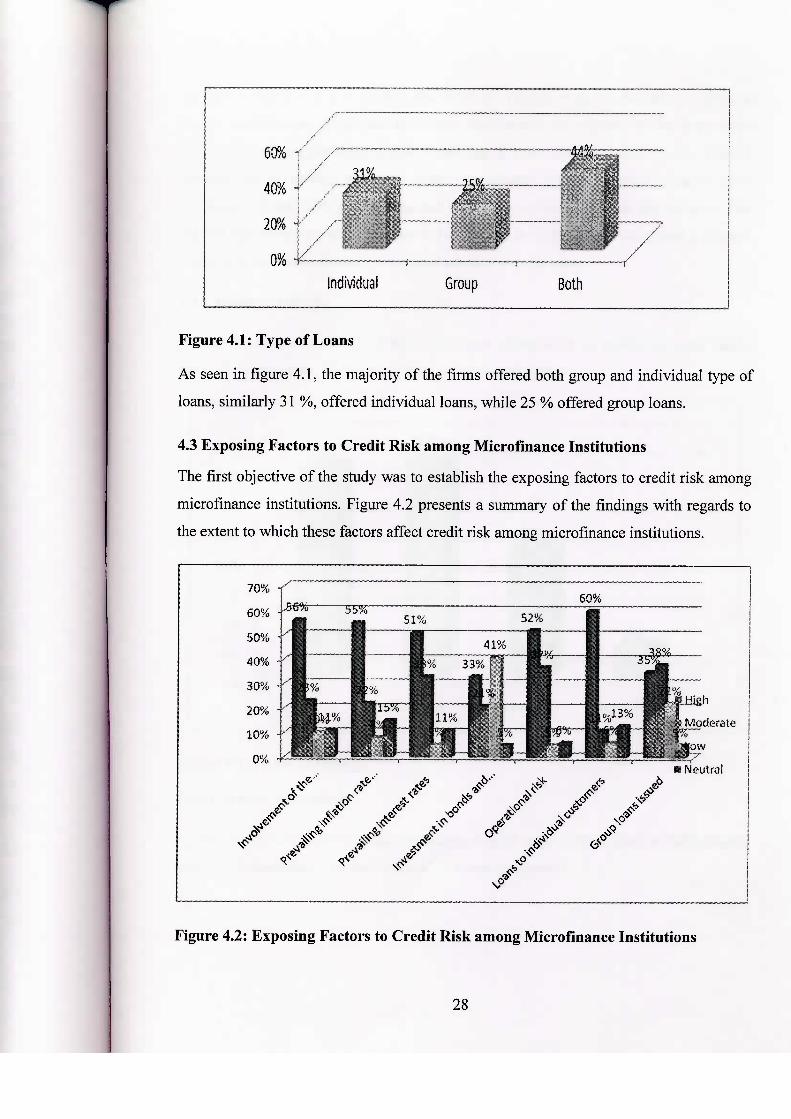

4.2.3 Type of Loan

Figiu-e 4.1, presents a summary of the findings with regard to the type of loans issued by

the various responding firms.

27

0% — f

Individual Group Both

Figure 4.1: Type of Loans

As seen in figure 4.1, the majority of the firms offered both group and individual type of

loans, similarly 31 %, offered individual loans, while 25 % offered group loans.

4.3 Exposing Factors to Credit Risli among Microfinance Institutions

The first objective of the study was to establish the exposing factors to credit risk among

microfinance institutions. Figure 4.2 presents a summary of the findings with regards to

the extent to which these factors affect credit risk among microfinance institutions.

70% •

60% -

50%

40%

30% j

20%

10%

0%

60% 5S%

51% 52%

High

Moderate

NO" J -

\

|OW

Neutral

Figure 4.2: Exposing Factors to Credit Risk among Microfinance Institutions

28

As seen in figure 4.2, it is evident that there are various exposing factors to credit risk

among microfinance institutions in Kenya. Specifically, the majority of the respondents

were of the opinion that loans to individuals, highly contributed to credit risk, followed by

involvement in foreign exchange trade, operational risk, prevailing inflation rates,

prevailing interest rates group loans and finally, investment in bonds and equities. This

implies that indeed issuance of loans to individuals is highly risk as compared to groups.

It also implies that investment bonds and equities are less risky.

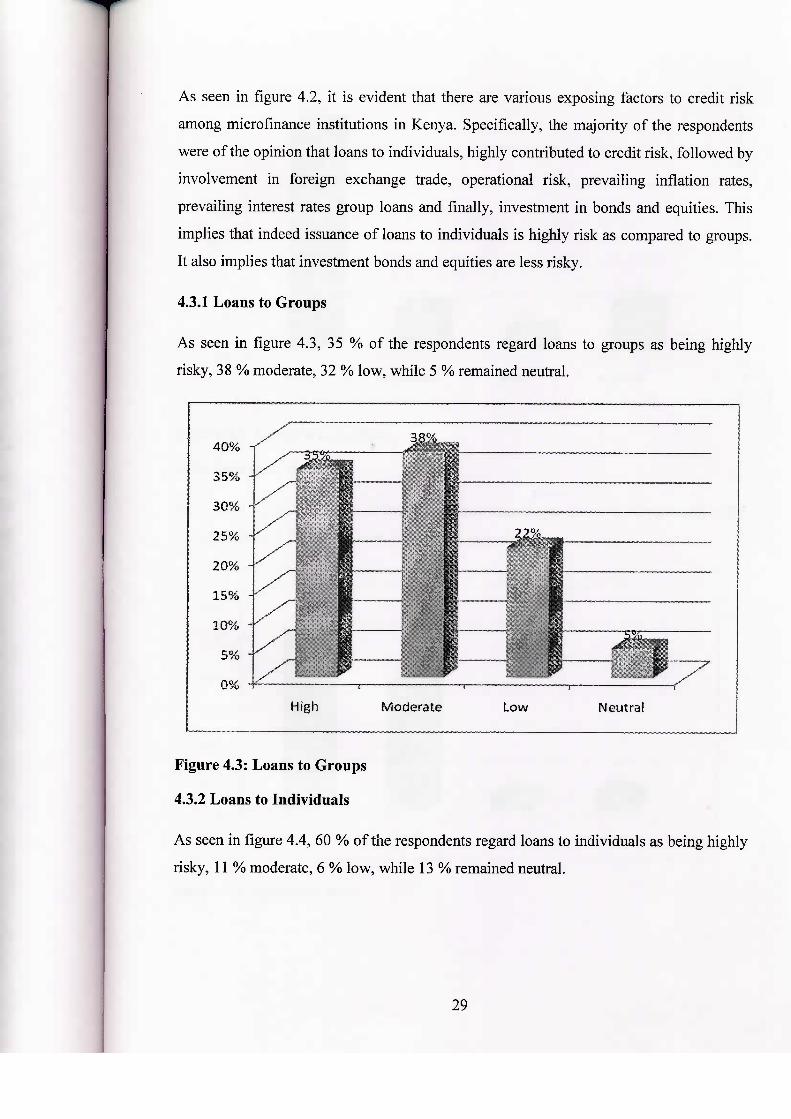

4.3.1 Loans to Groups

As seen in figure 4.3, 35 % of the respondents regard loans to groups as being highly

risky, 38 % moderate, 32 % low, while 5 % remained neutral.

High Moderate Low Neutral

Figure 4.3: Loans to Groups

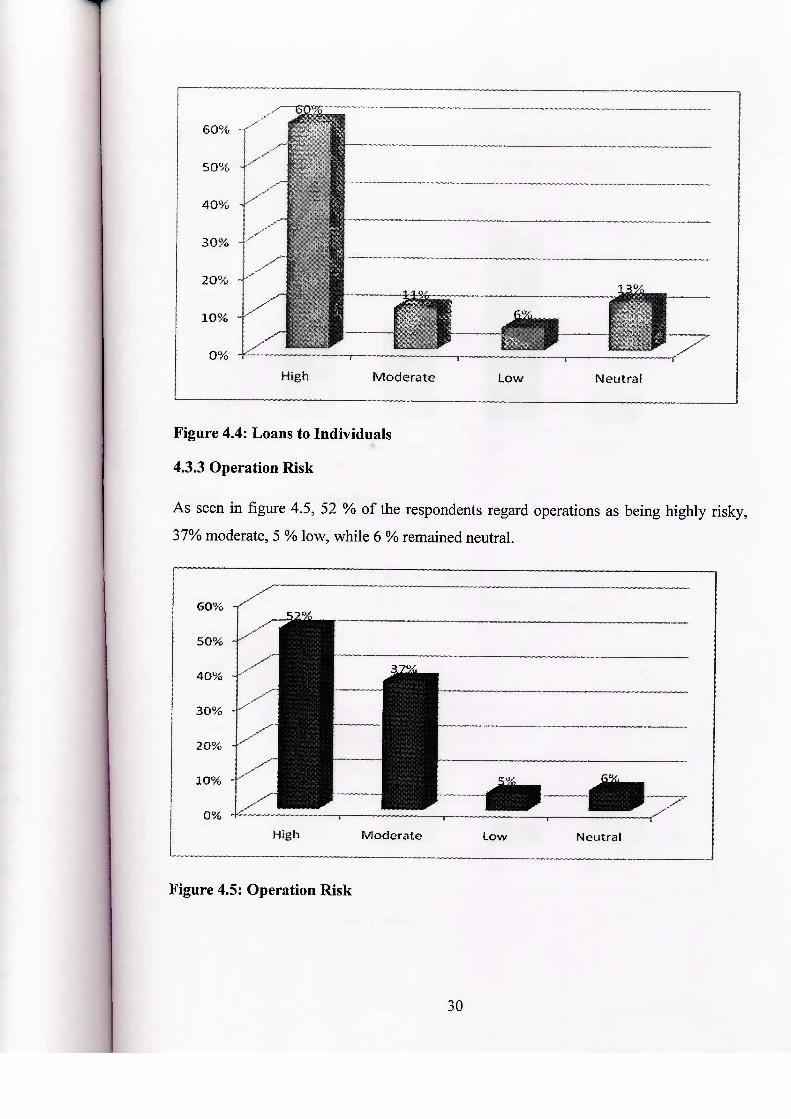

4.3.2 Loans to Individuals

As seen in figure 4.4, 60 % of the respondents regard loans to individuals as being highly

risky, 11 % moderate, 6 % low, while 13 % remained neutral.

29

10%

0% . ^ - O ^

High Moderate Low Neutral

Figure 4.4: Loans to Individuals

4.3.3 Operation Risk

As seen in figure 4.5, 52 % of the respondents regard operations as being highly risky,

37% moderate, 5 % low, while 6 % remained neutral.

High Moderate Low Neutral

Figure 4.5: Operation Risk

30

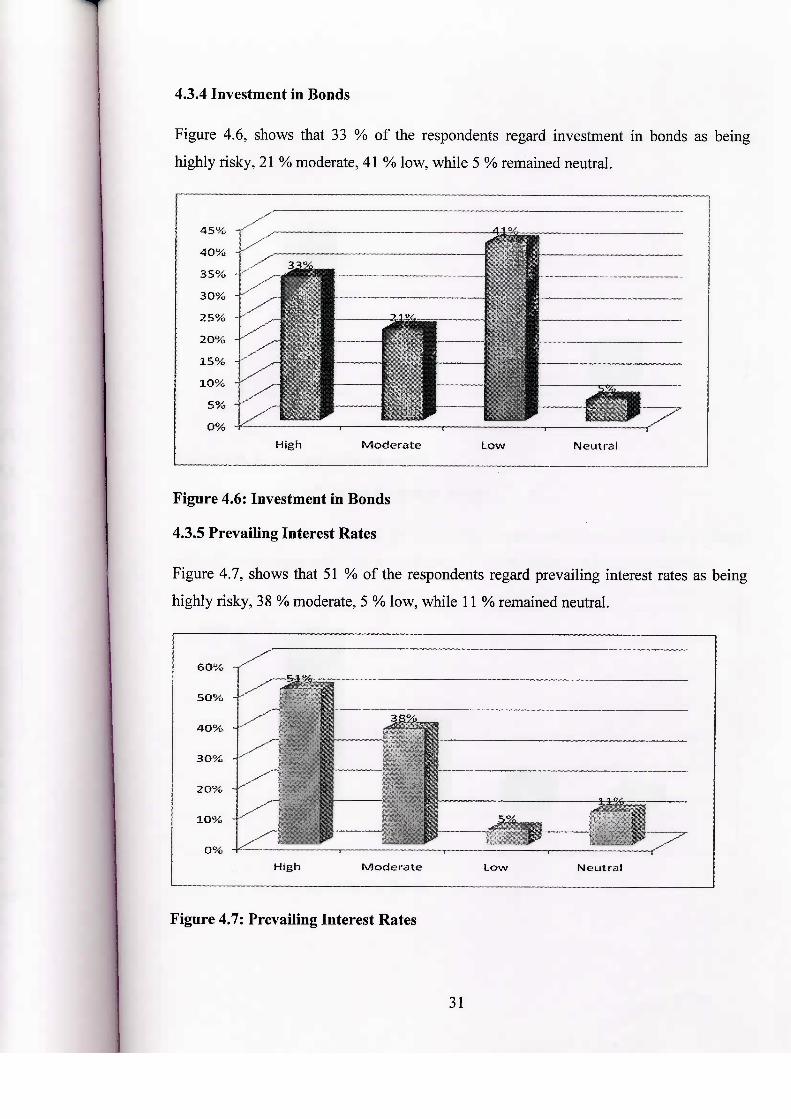

4.3.4 Investment in Bonds

Figure 4.6, shows that 33 % of the respondents regard investment in bonds as being

highly risky, 21 % moderate, 41 % low, while 5 % remained neutral.

High Moderate Low Neutral

Figure 4.6: Investment in Bonds

4.3.5 Prevailing Interest Rates

Figure 4.7, shows that 51 % of the respondents regard prevailing interest rates as being

highly risky, 38 % moderate, 5 % low, while 11 % remained neutral.

6 0 %

'— l̂ilttiiii 5 0 % -

4 0 % -

3 0 % -

2 0 % -

i o % -. . ^

o% High Moderate Low Neutral

Figure 4.7: Prevailing Interest Rates

31

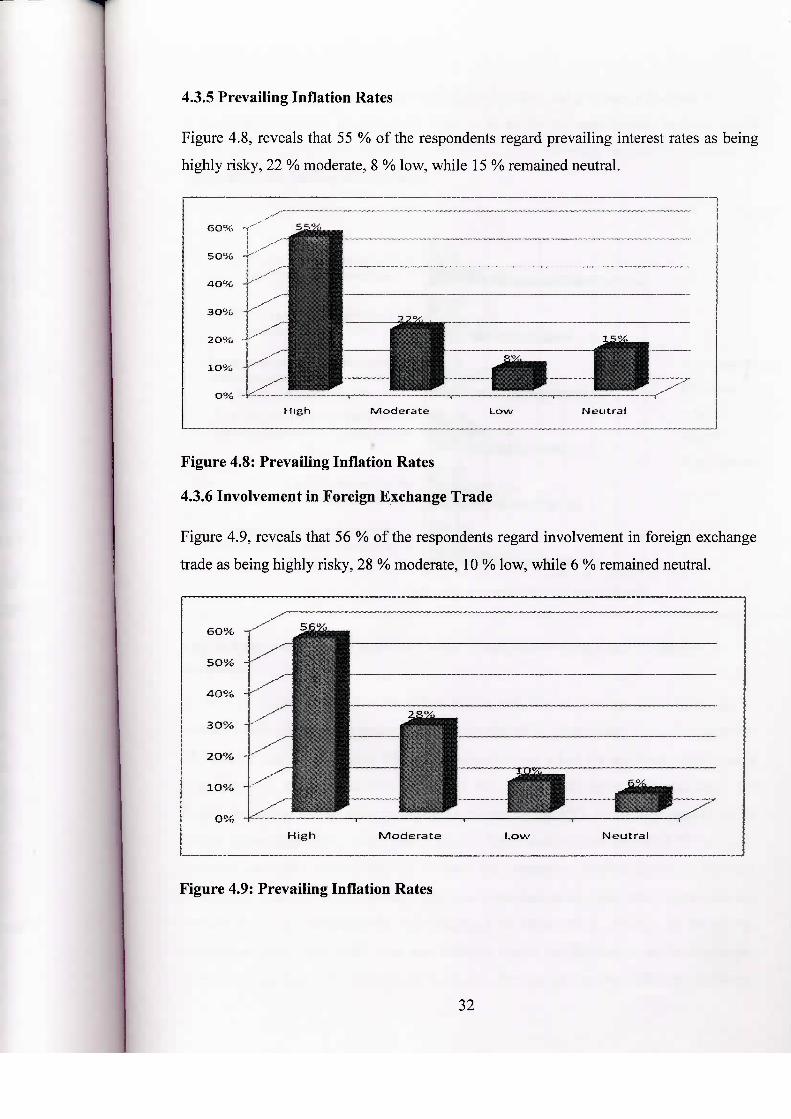

4.3.5 Prevailing Inflation Rates

Figure 4.8, reveals that 55 % of the respondents regard prevailing interest rates as being

highly risky, 22 % moderate, 8 % low, while 15 % remained neutral.

60'X> -

5 0 % - " "

4 0 % - "" '

High Moderate Low Neutral

Figure 4.8: Prevailing Inflation Rates

4.3.6 Involvement in Foreign Exchange Trade

Figure 4.9, reveals that 56 % of the respondents regard involvement in foreign exchange

trade as being highly risky, 28 % moderate, 10 % low, while 6 % remained neutral.

High M o d e r a t e L o w Neutral

Figure 4.9: Prevailing Inflation Rates

32

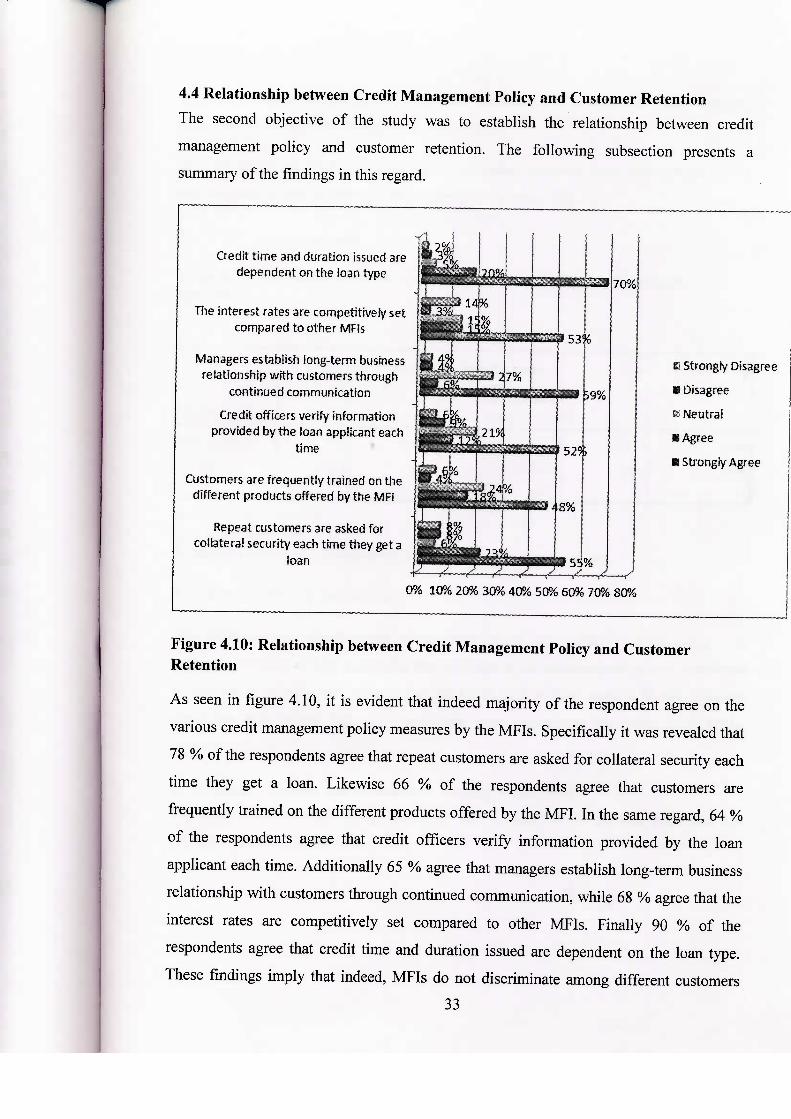

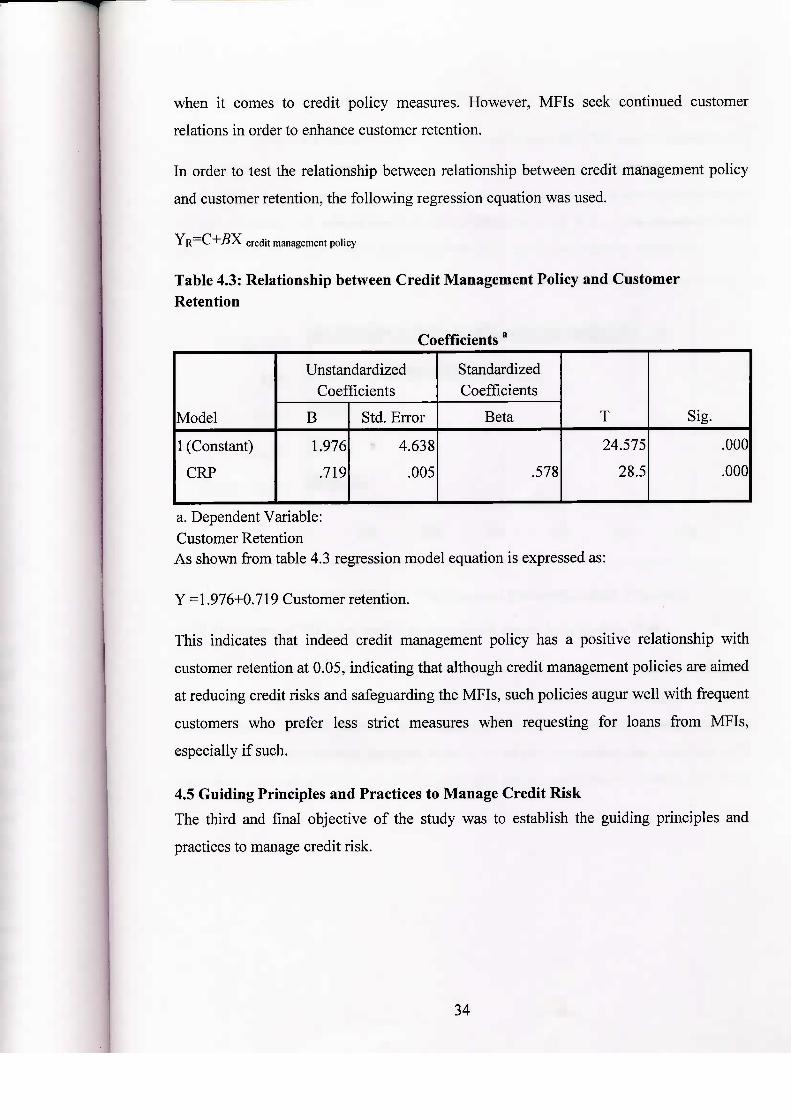

4.4 Relationship between Credit Management Policy and Customer Retention

The second objective of the study was to establish the relationship between credit

management policy and customer retention. The following subsection presents a

summary of the findings in this regard.

Credit time and duration issued are

dependent on the loan type

The interest rates are competitively set

compared to other MFIs

Managers establish long-term business

relationship with customers through

continued communication

Credit officers verify information

provided by the loan applicant each

time

Customers are frequently trained on the

different products offered by the MFI

Repeat customers are asked for

collateral security each time they get a

loan

• Strongly Disagree

• Disagree

it Neutral

• Agree

• Strongly Agree

0% 10% 20% 30% 40% 50% 60% 70% 80%

Figure 4.10: Relationship between Credit Management Policy and Customer Retention

As seen in figure 4.10, it is evident that indeed majority of the respondent agree on the

various credit management policy measures by the MFIs. Specifically it was revealed that

78 % of the respondents agree that repeat customers are asked for collateral security each

time they get a loan. Likewise 66 % of the respondents agree that customers are

frequently trained on the different products offered by the MFI . In the same regard, 64 %

of the respondents agree that credit officers verify information provided by the loan

applicant each time. Additionally 65 % agree that managers establish long-term business

relationship with customers through continued communication, while 68 % agree that the

interest rates are competitively set compared to other MFIs. Finally 90 % of the