measuring business excellence

TRANSCRIPT

Measuring Business ExcellenceBalanced scorecard: a rising trend in strategic performance measurementKhim Ling SimHian Chye Koh

Article information:To cite this document:Khim Ling SimHian Chye Koh, (2001),"Balanced scorecard: a rising trend in strategic performance measurement", Measuring BusinessExcellence, Vol. 5 Iss 2 pp. 18 - 27Permanent link to this document:http://dx.doi.org/10.1108/13683040110397248

Downloaded on: 17 March 2015, At: 22:44 (PT)References: this document contains references to 19 other documents.To copy this document: [email protected] fulltext of this document has been downloaded 6045 times since 2006*

Users who downloaded this article also downloaded:Helen Atkinson, (2006),"Strategy implementation: a role for the balanced scorecard?", Management Decision, Vol. 44 Iss 10 pp.1441-1460 http://dx.doi.org/10.1108/00251740610715740Meena Chavan, (2009),"The balanced scorecard: a new challenge", Journal of Management Development, Vol. 28 Iss 5 pp. 393-406http://dx.doi.org/10.1108/02621710910955930Ulf Johanson, Matti Skoog, Andreas Backlund, Roland Almqvist, (2006),"Balancing dilemmas of the balanced scorecard", Accounting,Auditing & Accountability Journal, Vol. 19 Iss 6 pp. 842-857 http://dx.doi.org/10.1108/09513570610709890

Access to this document was granted through an Emerald subscription provided by 516270 []

For AuthorsIf you would like to write for this, or any other Emerald publication, then please use our Emerald for Authors serviceinformation about how to choose which publication to write for and submission guidelines are available for all. Please visitwww.emeraldinsight.com/authors for more information.

About Emerald www.emeraldinsight.comEmerald is a global publisher linking research and practice to the benefit of society. The company manages a portfolio of more than290 journals and over 2,350 books and book series volumes, as well as providing an extensive range of online products and additionalcustomer resources and services.

Emerald is both COUNTER 4 and TRANSFER compliant. The organization is a partner of the Committee on Publication Ethics (COPE)and also works with Portico and the LOCKSS initiative for digital archive preservation.

*Related content and download information correct at time of download.

Dow

nloa

ded

by U

nive

rsiti

Keb

angs

aan

Mal

aysi

a A

t 22:

44 1

7 M

arch

201

5 (P

T)

BALANCED SCORECARD: A RISING TRENDIN STRATEGIC PERFORMANCE

MEASUREMENT

Khim Ling Sim and Hian Chye KohKhim L. Sim, PhD, is an Assistant Professor of Accountancy at Western New England College. Her research interests

include management control systems, organizational learning, organizational reengineering in new manufacturingpractices, performance measures and performance evaluations. She has published in journals such as Journal of

Management Accounting Research, International Review of Accounting, International Journal of Operationsand Production Management, among others. She is currently a member of Institute of Management Accounting,

American Accounting Association, and Institute of Decision Sciences. Dr Sim can be contacted at [email protected] ortel: (413) 782 1506. Hian Chye Koh, PhD, a Certified Public Accountant, is an Associate Professor and Vice-Dean

(Business) of the Nanyang Business School (Singapore). He has published widely in international journals andconferences and serves as a consultant to several statutory boards and organizations. His current interest is in strategic

data analysis. Dr Koh can be contacted at [email protected] or tel: (65) 790 5646.

Abstract The long-term survival of a business is dependent upon

meeting market needs through a long-term value creation process.

Traditional performance measurement systems have been criticized

as being too narrowly focused on financial figures and functional

level performance such that they often fail to capture organizational

long-term business success. In contrast, the balanced scorecard calls

on managers to first make a commitment to introduce an array of

measures or scorecards that will guide their decisions away from the

narrowly focused financial measures. These scorecards, in turn, serve

as dials on a dashboard and guide businesses into greater

profitability as managers position themselves to better serve their

employees, customers, and shareholders at large. Using information

collected from 83 electronics companies located within the USA,

results from the study provide support for the balanced scorecard.

Specifically, findings show that manufacturing plants that have

strategically linked their corporate goals or objectives to their

performance measurement systems, via the scorecard, performed

better than those that do not.

Keywords Balanced scorecard, Performance measurement,

Just-in-time, TQM, Electronics industry,

Performance improvement

Do your performance measurement systems

measure up?

The pressure of reporting corporate performance based

on non-financial as well as financial measures has

intensified over the last few years. For example, the

Conference Board of the Canadian Institute of

Chartered Accountants (CICA) reported that traditional

accounting-based performance measures are excessively

historical; they lack predictive power and reward the

wrong behavior and do not capture key business changes

until it is too late. The Conference Board also concludes

that these measures give inadequate consideration to

such resources as intellectual capital (Waterhouse,

1999). Accordingly, the Board suggests that strategically

oriented performance measurement systems should

measure non-financial as well as financial outcomes.

Likewise, a report by the American Institute of Certified

Public Accountants (AICPA) recommends that

companies should disclose leading, non-financial

measures on key business processes such as product

quality, cycle time, innovation, and employee

satisfaction (AICPA Report, 1994, p. 143).

Coincidentally, a survey conducted by the Institute of

Management Accounting in the USA, lends some

support for the recommendations made by the CICA

and AICPA (IMA, 1996). For example, the survey

shows that only 15 percent of the respondents indicated

that their measurement systems supported top

management's business objectives well, while 43 percent

of the respondents rated their measurement systems as

less than adequate or poor. On the other hand, 60

percent of these respondents reported that they were

undertaking a major overhaul or were planning to

replace their current performance measurement systems.

It is generally believed that the best performance

measures are those linked to a business' strategy. In

addition, performance measures should be focused, and

should reward behavior that contributes to business

M e a s u r i n g B u s i n e s s E x c e l l e n c e 5 , 2 2 0 0 1 , p p . 1 8 - 2 6 , # M C B U n i v e r s i t y P r e s s , 1 3 6 8 - 3 0 4 7

The current issue and full text archive of this journal is available athttp://www.emerald-library.com/ft

1 8

Dow

nloa

ded

by U

nive

rsiti

Keb

angs

aan

Mal

aysi

a A

t 22:

44 1

7 M

arch

201

5 (P

T)

success (see Kaplan and Norton, 1992; 1996a; 1996b;

Atkinson and Epstein, 2000). Given recent development

in the performance measurement literature (see above),

more executives around the world have begun to

question whether their performance measurement

systems measure up. There is also a growing interest in

whether non-financial measures such as customer

satisfaction, employee satisfaction, or innovation, are

useful indicators of a firm's future performance.

Likewise, practitioners have begun to look into the

implementation of balanced scorecards as a means to

overcome the limitations of the traditional performance

measurement system. Accordingly, the purpose of this

study is to investigate whether

there are any linkages between

business success and the use of

strategically linked performance

measures, which include both

non-financial and financial

performance measures.

What Is a balanced scorecard?

Proponents of the balanced

scorecard (see Kaplan and

Norton 1992; 1996a; 1996b)

have long suggested the use of

non-financial performance

measures via three additional

perspectives (i.e. customer,

internal business process, and

learning and innovation) to

supplement traditional financial

measures. According to Kaplan

and Norton (1996b, p. 75),

`̀ Used this way, the scorecard

addresses a serious deficiency in

traditional management

systems: their inability to link a

company's long-term strategy

with its short-term actions''. According to a recent

balanced scorecard report, various surveys estimate that

40-50 percent of large organizations have begun

implementing this concept (Balanced Scorecard Report,

1999a). So, what is a balanced scorecard?

Robert Kaplan, of the Harvard Business School, and

David Norton, the president of a Massachusetts

consulting firm, developed the balanced scorecard

(BSC) in the early 1990s. It was built around the

premise that companies can no longer gain sustainable

competitive advantage solely by developing tangible

assets. To phrase it differently, the ability of a company

to build its `̀ intangible assets'' or `̀ intellectual capital''

has become a critical success factor in creating and

sustaining competitive advantage (see also MobilizingInvisible Assets by Hiroyuki Itami, 1987). According to

Kaplan and Norton (1996a; 1996b), the four

perspectives of the BSC, as presented in Figure 1, will

enable companies to track financial results and

simultaneously monitor progress in building the

capabilities that are necessary for acquiring the

`̀ intellectual capital'' or `̀ intangible assets'' needed for

future business growth and for providing keener

competition (Kaplan and Norton (1992; 1996a; 1996b)

provide further discussion on the balanced scorecard).

Many big corporations in the USA have implemented

the BSC. Although the satisfaction rate varies across

companies, many have achieved some phenomenal

results. These companies include the Mobil US

Marketing and Refining (Mobil USM&R) Division,

Chadwick Inc., the City of

Charlotte (see Harvard Business

School Publishing, cases

number 9-197-025, 9-196-124,

and 9-199-036, respectively),

and Sears Roebuck and

Company, among others. For

example, within two years after

the implementation of the BSC,

Mobil's growth and productivity

strategy has dramatically

improved Mobil USM&R

division's position from the last

place (in 1992 and 1993) to first

place in the industry with profits

of 56 percent above the industry

average. The productivity

strategy also created a

20 percent reduction in the cost

to refine, market, and deliver a

gallon of gasoline. With better

utilization of the existing

resources, Mobil showed an

annual improvement in cash

flow of almost $1.2 billion in

1996. According to Brian Baker (the president of the

North America Marketing and Refining Division), six

years later, the company remains on course towards its

strategic vision (Balanced Scorecard Report, 1999b).

The experience of Sears Roebuck and Company was

equally encouraging. During the early 1990s, Sears

Roebuck and Company had some of the worst

performance in its history. For example, the company

net loss was $3.9 billion in 1992. Within two years after

the implementation of the BSC, Sears reported a 4

percent increase in employee satisfaction and customer

satisfaction. The increase in customer satisfaction led to

an estimated $200 million increase in revenue. The extra

revenues also increase Sears' market capitalization by

almost $250 million (Rucci et al., 1998).

Despite an increased interest from practitioners in the

implementation of the BSC, large scale empirical

findings on BSC implementation remains scarce. In a

M e a s u r i n g B u s i n e s s E x c e l l e n c e 5 , 2 2 0 0 1

``Accordingly, the

purpose of this study is

to investigate whether

there are any linkages

between business

success and the use of

strategically linked

performance measures,

which include both

non-financial and

financial performance

measures.''

1 9

Dow

nloa

ded

by U

nive

rsiti

Keb

angs

aan

Mal

aysi

a A

t 22:

44 1

7 M

arch

201

5 (P

T)

1996 survey conducted by Tower Perrin Consulting

firm, 64 percent of the respondents rated `̀ satisfaction or

value received'' from BSC implementation higher than

that from performance measurement approaches used in

the past. In contrast, only 37 percent of the respondents

reported `̀ employee understanding of performance

measures and goals'' from BSC implementation higher

than that from performance measurement systems used

in the past (Ittner and Larcker, 1998). However, a

survey of vice presidents of quality for major US firms

conducted by professors from the Wharton School fails

to relate customer and quality measures to accounting

and stock returns (Ittner and Larcker, 1998).

Because of the mixed findings, this study aims to

provide additional information related to the use of non-

financial performance measures. The findings are based

on the experiences of 83 electronic companies that were

located in the USA, with an annual sales ranging from

$10 million to $2 billion. A survey instrument was used

and a majority of the respondents in this study are top-

level executives or directors of manufacturing. The

results of this study provide further evidence that

manufacturing plants that have strategically linked their

corporate goals or objectives to their performance

measurement systems, via the scorecard in the four

perspectives, performed better than those that do not.

Descriptive statistics of sample companies

Table I (Panel A) provides information on the job title of

the respondents in this study. As noted, a majority of the

respondents belong to middle and upper management,

who tend to be closely involved in strategic planning and

decision making. Table I (Panel B) provides descriptive

statistics of workplace practices of the sample

companies. It is noted that 70 percent of the 83 sample

companies have some kind of total quality management

(TQM) program, 64 percent have implemented a just-

in-time (JIT) program, while about 75 percent are

heavily involved in work team practices. Finally, more

than half of the companies are using some kind of

workers' incentive plans. Using this database, Sim et al.(1999) reported that companies that made use of

incentive plans while focusing on the implementation of

TQM, JIT, and work teams, were associated with better

customer, delivery, and quality performance. Given this

finding, the database is expected to be a good source to

validate the BSC framework.

The theoretical framework

Consistent with the latest developments in the

performance measurement literature such as those

advocated by proponents of the BSC, it is expected that

companies that continuously improve their capabilities

(e.g. by implementing advanced workplace practices,

which are to be monitored via the innovation and

learning perspective) should achieve better performance

in their internal business process perspective which will,

in turn, lead to better performance in their customer

perspective. All such efforts should lead to improved

financial performance. Accordingly, Figure 2 provides a

BSC framework relevant to this study, keeping in mind

that the focus of the scorecard is on business unit

performance (i.e. performance of the manufacturing

division)[1]. Finally, Table II provides detailed

information or the scorecard (i.e. goals and measures)

used in this study.

M e a s u r i n g B u s i n e s s E x c e l l e n c e 5 , 2 2 0 0 1

Figure 1 Ð The balanced scorecard

2 0

Dow

nloa

ded

by U

nive

rsiti

Keb

angs

aan

Mal

aysi

a A

t 22:

44 1

7 M

arch

201

5 (P

T)

M e a s u r i n g B u s i n e s s E x c e l l e n c e 5 , 2 2 0 0 1

Table I Ð Summary statistics of the 83 electronics companies

A. Job title of respondents

Job title used by respondents Number of respondents Percentage

Plant manager, manufacturing manager, or operations manager 23 28

VP of operations, VP of engineering, VP of manufacturing, or VP of quality 24 29

Director of operations, director of manufacturing, or director of manufacturing and engineering 14 17

CEO, president and CEO, executive VP, or president 5 6

Miscellaneous titles used, e.g. material manager, test manager, sourcing and fabricationmanager, or product integrity manager 11 13

No information on job title 6 7

Total respondents 83 100

B. Advanced workplace practices (n = 83)

Variable No formal program 1-2 years 3-4 years > 4 years

Years of TQM experience 25 (30%) 19 (23%) 22 (27%) 17 (20%)

Years of JIT experience 30 (36%) 22 (27%) 15 (18%) 16 (19%)

Variable Fixed payFixed + noncash reward

Fixed + individual-basedcash reward

Fixed + group-basedcash reward

Worker compensation 37 (45%) 7 (8%) 13 (16%) 26 (31%)

Scale ranging from 1-7 (strongly disagree = 1, 4 = neither disagree or agree, 7 = strongly agree)

Variable 1-3 3.1-4.9 5-7

Work team practices 3 (3%) 18 (22%) 62 (75%)

Figure 2 Ð The balanced scorecard for a manufacturing division ± a theoretical model

2 1

Dow

nloa

ded

by U

nive

rsiti

Keb

angs

aan

Mal

aysi

a A

t 22:

44 1

7 M

arch

201

5 (P

T)

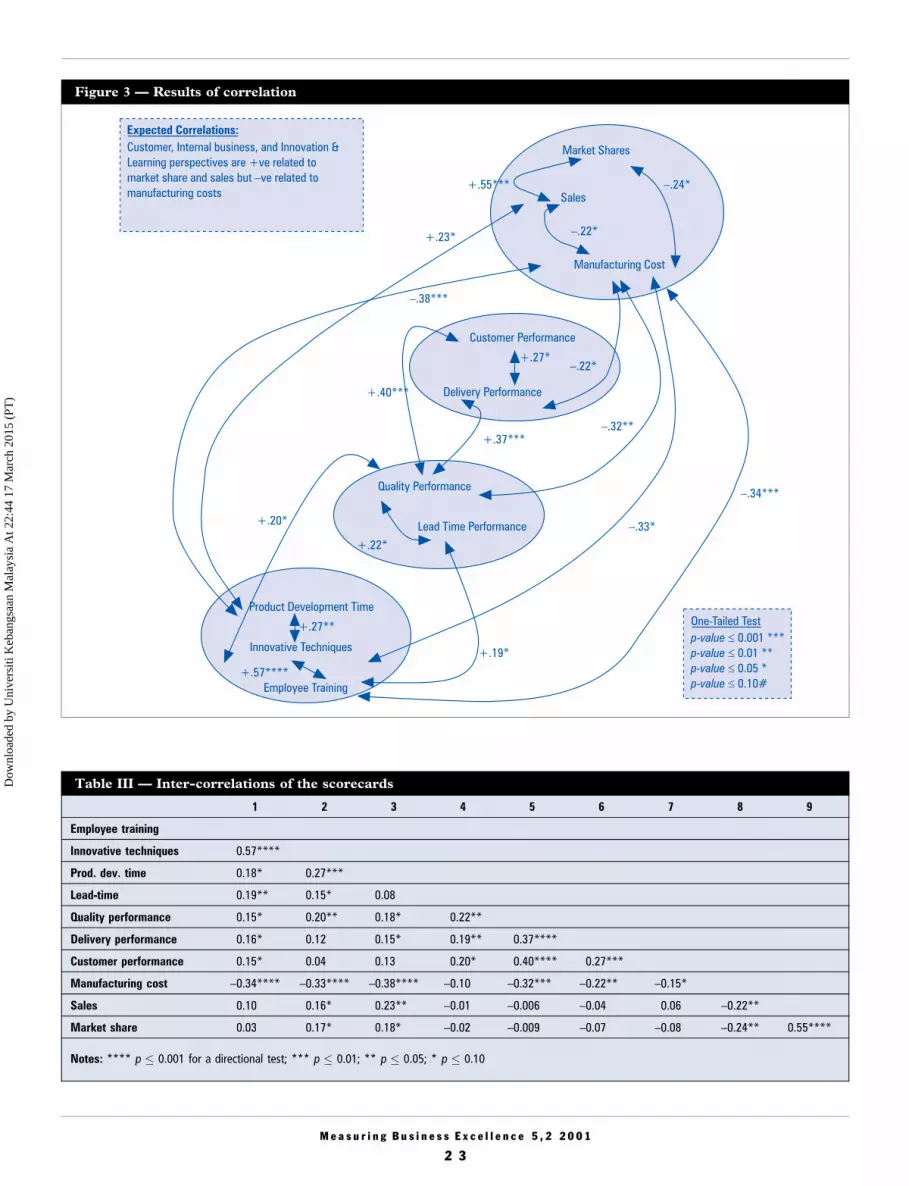

Are the analyses holding up?

Kaplan and Norton (1996b) suggest the use of

correlation analysis to test the expected relationships in

the scorecards. Accordingly, results of correlation are

presented in Figure 3 as well as Table III. Figure 3

shows how the four perspectives are interrelated, while

Table III presents results of inter-correlations among the

scorecards (i.e. goals and measures). For example,

innovative techniques and employee training are

positively correlated to shorter product development

time. In many instances, innovative techniques and

shorter product development time are positively related

to internal business process perspective (i.e. quality

performance and lead time performance), while quality

performance is positively related to the customer

perspective (customer and delivery performance).

Finally, customer performance is negatively related to

manufacturing costs (i.e. lower manufacturing costs are

associated with higher customer satisfaction), while

manufacturing costs are negatively related to sales

(i.e. lower manufacturing costs are associated with

higher sales) and market share (i.e. lower manufacturing

costs are associated with higher market share).

Accordingly, the results are consistent with many of the

expectations outlined in Figure 2, the theoretical model.

Nevertheless, what appear to be equally if not more

interesting are the correlations of the innovation and

learning perspective with the other perspectives. Given

the importance of the innovation and learning

perspective, the next section discusses these

relationships.

Core competencies ± innovation and continuous

employee training

Long-term survival of a business is dependent upon

meeting market needs through long-term value creation

process. Historically, the operations process, or

operational excellence, has been the focus of this value

creation process. In contrast, recent developments in the

literature have called for a shift in emphasis to the

`̀ innovation process'' (see Kaplan and Norton, 1996a;

Simons, 2000). In the innovation process, managers

identify new customers, new markets, and the emerging

needs of the existing and future customers. With intense

competition, current technology and employee skills

often quickly become obsolete or inadequate to keep

pace with the changing needs of the customers.

Accordingly, businesses continue to invest in employee

training while searching for breakthrough technology in

order to excel. Proponents for BSC have suggested that

the innovation and learning perspective could be used to

monitor this long-term value creation process.

Surprisingly, few organizations have maintained a good

scorecard that is relevant to this important process. For

example, Frigo and Krumwiede (1999) reported that the

majority of BSC users in their study rate the

effectiveness of their organization's performance

measures in the innovation perspective as `̀ less than

adequate to poor''.

M e a s u r i n g B u s i n e s s E x c e l l e n c e 5 , 2 2 0 0 1

Table II Ð A framework of the balanced scorecard for a manufacturing division

Perspective Goals Performance measures

Innovation and learning Be innovative and continually improveour manufacturing skills

Employee training (average across three indicators)(1) management devotion to quality improvement(2) quality related training provided to employees(3) Percent of employees who have quality as a major responsibility

Innovative techniques (average across three indicators):(1) quality function deployment technique(2) Taguchi methods(3) continuous process improvement technique

New product development time

Internal business process To improve manufacturing efficiency Quality performance (average across five indicators)(1) cost of scrap(2) units reworked(3) units of defect(4) warranty cost(5) sales returned

Performance in manufacturing lead time

Customer Delight the customers Customer performance (average across three indicators)(1) customer perceived product durability and reliability(2) customer perceived overall product performance(3) customer complaints

Delivery performance(1) Percent delivered to schedule

Financial Reward shareholders by cutting costsand improving sales

Manufacturing costsSalesMarket share

2 2

Dow

nloa

ded

by U

nive

rsiti

Keb

angs

aan

Mal

aysi

a A

t 22:

44 1

7 M

arch

201

5 (P

T)

M e a s u r i n g B u s i n e s s E x c e l l e n c e 5 , 2 2 0 0 1

Figure 3 Ð Results of correlation

Table III Ð Inter-correlations of the scorecards

1 2 3 4 5 6 7 8 9

Employee training

Innovative techniques 0.57****

Prod. dev. time 0.18* 0.27***

Lead-time 0.19** 0.15* 0.08

Quality performance 0.15* 0.20** 0.18* 0.22**

Delivery performance 0.16* 0.12 0.15* 0.19** 0.37****

Customer performance 0.15* 0.04 0.13 0.20* 0.40**** 0.27***

Manufacturing cost ±0.34**** ±0.33**** ±0.38**** ±0.10 ±0.32*** ±0.22** ±0.15*

Sales 0.10 0.16* 0.23** ±0.01 ±0.006 ±0.04 0.06 ±0.22**

Market share 0.03 0.17* 0.18* ±0.02 ±0.009 ±0.07 ±0.08 ±0.24** 0.55****

Notes: **** p � 0.001 for a directional test; *** p � 0.01; ** p � 0.05; * p � 0.10

2 3

Dow

nloa

ded

by U

nive

rsiti

Keb

angs

aan

Mal

aysi

a A

t 22:

44 1

7 M

arch

201

5 (P

T)

Contributions

One major contribution of this study lies in the

identification of the performance measures for the

innovation and learning perspective. Consistent with the

BSC literature (e.g. Kaplan and Norton, 1992; 1996a;

1996b; Atkinson and Epstein, 2000), employee training

is included as one of the performance measures.

However, it must also be borne in mind that a good

scorecard should not lead to `̀ information overload''.

Thus, this study includes only techniques that are truly

innovative (see Table II for the three techniques selected

for this study). Finally, product development time is

included as the third measure for the innovation and

learning perspective, because

both empirical and anecdotal

evidence have increasingly

viewed `̀ time to market'' as a key

to success and profitability

(Cooper and Kleinschmidt,

1994; Choperana, 1996; DroÈge

et al., 2000)[2].

Our results as presented in

Figure 3 show that employee

training is positively related to

delivery and customer

performance; it is also related to

lower manufacturing costs.

Similarly, innovative techniques

are related to lower

manufacturing costs, higher

sales, and greater market share,

while shorter product

development time[3] is related

to lower manufacturing costs,

higher sales, and greater market

share. These results are further

illustrated in Table IV. For

example, companies that

reported that their

manufacturing costs `̀ decreased

tremendously'' also scored

higher in the scale of 1-7 in employee training and

innovative techniques; they also reported better

improvement in product development time as compared

to companies that reported that their manufacturing

costs only `̀ increased slightly''. These results were

statistically significant. Likewise, companies that

reported `̀ tremendous increase'' in their market share

and sales also reported a higher score in innovative

techniques as well as a better improvement in product

development time as compared to companies that

reported only `̀ slightly decrease'' in market share and

sales. Again, except for one result which is marginally

supported, the remaining results are statistically

significant.

Although many of the results are consistent with

theories in the performance literature, a correlation test

does not allow us to make statements about cause and

effect. Accordingly, additional analysis that allows us to

make better inferences was conducted. When collecting

the above data, we were also interested in whether

advanced workplace practices add value to businesses.

Thus, we asked questions related to these issues. Results

of regression analysis are presented in Table V.

In the above analysis, we predicted that the

implementation of advanced workplace practices

(i.e. years of implementing TQM and JIT, the use of

incentive plans, work team, TQM and JIT) are positively

related to business performance,

such as higher market share,

higher sales and lower

manufacturing costs. Results of

regression analysis provide

support for our expectations.

For example, findings show that

`̀ years of implementing TQM''

and `̀ years of implementing

JIT'' are positively related to

greater market share. In

addition, the implementation of

work team is also positively

related to greater marker share.

Similarly, results indicate that

work team and TQM are

positively related to lower

manufacturing costs. On the

other hand, it appears that

companies in their early stage of

JIT implementation show

greater reduction in

manufacturing costs than

companies that had

implemented JIT for a longer

period. It is plausible that these

results are due to `̀ diminishing

returns'' after implementing JIT

for a longer period of time.

Although not directly related to the primary objective of

this study, results of regression analysis enhance the

current study by providing important insights into

business strategy (i.e. the implementation of advanced

workplace practices), performance measures, and

business success.

Conclusion

Using information collected from 83 companies,

correlation and regression results provide support for the

BSC. Specifically, findings suggest that the BSC can be

used as a tool for monitoring the long-term value

creation process. Undoubtedly, providing training to

employees or implementing innovative techniques

M e a s u r i n g B u s i n e s s E x c e l l e n c e 5 , 2 2 0 0 1

``Although not directly

related to the primary

objective of this study,

results of regression

analysis enhance the

current study by

providing important

insights into business

strategy (i.e. the

implementation of

advanced workplace

practices),performance

measures, and business

success.''

2 4

Dow

nloa

ded

by U

nive

rsiti

Keb

angs

aan

Mal

aysi

a A

t 22:

44 1

7 M

arch

201

5 (P

T)

M e a s u r i n g B u s i n e s s E x c e l l e n c e 5 , 2 2 0 0 1

Table V Ð Further evidence ± advanced workplace practicesa are value-added to businesses

Change in market share Change in salesChange in manufacturing

costs

Expected signsa Coefficient (t-value) Coefficient (t-value) Coefficient (t-value)

Intercept 3.61 (44.4)*** 4.06 (43.9)*** 1.99 (23.3)***TQM-time + 0.12 (1.98)* 0.11(1.60) ±0.06 (±0.87)JIT-time + 0.11 (2.07)* ±0.07 (±1.12) 0.11 (1.94)*Incentive plans + 0.10 (0.55) 0.23 (1.13) ±0.07 (±0.40)Work team + 0.21 (2.29)** 0.21 (2.07)* ±0.18 (±1.94)*TQM + ±0.6 (±0.53) ±0.001 (±0.01) ±0.24 (±1.90)*JIT + ±0.27 (±1.66) ±0.24 (±1.25) 0.06 (0.35)

Adj R2 0.128 0.095 0.17Overall F 2.96** 2.37* 3.67**n 81 80 79

Notes:TQM-time and JIT-time were measured in years of implementing the TQM or JIT program. Incentive plans is a dichotomous variable, with `̀ 1'' representing theuse of incentive pay while `̀ 0'' representing the use of fixed-pay for the employees. Finally, work team, TQM, and JIT were measured using a scale of 1-7a The expected signs are for sales and market share. These signs will be negative for manufacturing costsAll t-tests were one-tailed tests: *** p � 0.001; ** p � 0.01; * p � 0.05

Table IV Ð Interrelationship of the innovation and learning perspective with the financial perspective

Performance measures from innovation andlearning perspective

Manufacturing costsincrease slightly

(= 4)

Manufacturing costdecreased tremendously

(=1) t-value Results supported?

Mean score for employee training 3.96 (n = 6) 5.49 (n = 21) 3.02**** SupportedMean score for innovative techniques 2.71 (n = 7) 4.08 (n = 21) 3.08**** SupportedMean score for percent change in product

development timea 9% (n = 6) 39% (n = 19) 3.16**** Supported

Performance measures from innovation andlearning perspective

Sales decreased slightly(=2)

Sales increasedtremendously (=5) t-value Results supported?

Mean score for innovative techniques 2.78 (n = 6) 3.81 (n = 26) 2.09** SupportedMean score for percent change in product

development time 18% (n = 4) 38% (n = 25) 1.61* Marginally supported

Performance measures from innovation andlearning perspective

Market share decreasedslightly (=2)

Market share increasedtremendously (=5) t-value Results supported?

Mean score for innovative techniques 3.38 (n = 7) 4.48 (n = 7) 1.89** SupportedMean score for percent change in product

development time 12% (n = 5) 37% (n = 8) 2.31** Supported

Notes:Respondents were asked to identify changes in manufacturing costs, sales, and market share in the last 3 years using the scale of 1-5 (decreased tremendously =1, no change = 3, increased tremendously = 5). Similar questions were asked with respect to the use of innovative techniques and employee training using thescale of 1-7 (strongly disagree/little or none = 1, neither disagree or agree = 4, strongly agree/consistent use = 7). It is interesting to note that no respondentmarked increased tremendously in manufacturing cost in the survey; similarly, no respondent marked decreased tremendously in sales or market share. Consistentwith the theories from BSC, it is hypothesized that manufacturing plants that reported tremendous decrease in manufacturing costs should score higher in theinnovation and learning perspectives than those plants that reported slightly increase in manufacturing costs. Likewise, it is hypothesized that manufacturingplants that reported tremendous increase in sales or market share should score higher in the innovation and learning perspectives than those plants that reportedslightly decrease in sales and market share. Results from t-statistics supported the expectationsAll t-tests were one-tailed tests: **** p � 0.001; *** p � 0.01; ** p � 0.05; * p � 0.10a Respondents were asked to report the average time to market a new product for the most recent year (t) and two years ago (t-2). Percent change in

product development time was calculated using the following formula: [(time to market in yeart±2 ± time to market in yeart)/time to market in yeart±2 * 100percent]

2 5

Dow

nloa

ded

by U

nive

rsiti

Keb

angs

aan

Mal

aysi

a A

t 22:

44 1

7 M

arch

201

5 (P

T)

consumes a significant amount of resources. Top

management often wonders about the payback of this

type of investment. The findings of this study provide

useful information in this regard. Finally, the significant

correlations of product development time with the three

financial indicators are consistent with the current body

of literature. For example, prior research studies have

shown that first-to-market products often command

higher initial prices and then garner dominant market

share and greater customer loyalty. Significant cost

benefits are also associated with compressing the new

product development process (DroÈge et al., 2000).

Accordingly, managers may want to closely monitor

their time to market new products. A slack in this

indicator often signals retarding sales or a sluggish

market share ahead.

One limitation of our study is the small sample size.

Nevertheless, results in this study have shown that

manufacturing plants that have strategically linked their

corporate goals or objectives to their performance

measurement systems, via the scorecard in the four

perspectives, performed better than those that do not.

Consistent with the current body of literature, this study

has also demonstrated that non-financial measures are

often useful indicators of financial performance for

manufacturing companies. Most important, it is hoped

that the study will encourage more managers to

strategically link their long-term value creation process

to the performance measurement system. Last but not

least, it should be added that the model presented in this

study should be considered as a template and not a

`̀ cure-all'' solution. MBE

Notes

1. Although return on investment is an important performance

measure for a business unit, it is not captured in our study due to

perceived difficulties in getting this information from the

respondents, a majority of whom are plant managers or directors

of operations.

2. Employee satisfaction is a good measure for the innovation and

learning perspective. Its exclusion from this study is mainly due

to the perceived difficulties in collecting this information, since

the questionnaire was sent to the director of manufacturing.

3. Shorter product development time is often the end results of

increased employee training and the use of innovative

techniques.

References

American Institute of Certified Public Accountants (1994), Improving

Business Reporting ± A Customer Focus, AICPA, New York, NY.

Atkinson, A. and Epstein, M. (2000), `̀ Measure for measure'', CMA

Magazine, Vol. 74 No. 7, pp. 22-8.

Balanced Scorecard Report (1999a), Insight, Experience and Ideas for

Strategy-focused Organizations, Article Reprint No. B9911F,

Harvard Business School Publishing, Boston, MA.

Balanced Scorecard Report (1999b), Insight, Experience and Ideas for

Strategy-focused Organizations, Article Reprint No. B9911B,

Harvard Business School Publishing, Boston, MA.

Choperana, A.M. (1996), `̀ Fast cycle time ± driver of innovation and

cycle time'', Research Technology Management, May-June,

pp. 36-49.

Cooper, R.G. and Kleinschmidt, E.J. (1994), `̀ Determinants of

timeliness in product development'', Journal of Product Innovation

Management, Vol. 11, pp. 381-96.

DroÈge, C., Jayaram, J. and Vickery, S. (2000), `̀ The ability to minimize

the timing of new product development and introduction: an

examination of antecedent factors in the North American

automobile supplier industry'', Journal of Production Innovation

Management, Vol. 17, pp. 24-40.

Frigo, M.L. and Krumwiede, K.R. (1999), `̀ Balanced scorecards: a

rising trend in strategic performance measurement'', Journal of

Strategic Performance Measurement, Vol. 3, February-March,

pp. 42-8.

Institute of Management Accountants (IMA) (1996), Are Corporate

America's Financial Measurements Outdated?, IMA, Montvale, NJ.

Itami, H. (1987), Mobilizing Invisible Assets, Harvard University Press,

Cambridge, MA.

Ittner, C.D. and Larcker, D.F. (1998), `̀ Innovations in performance

measurement: trends and research implications'', Journal of

Management Accounting Research, Vol. 10, pp. 205-38.

Ittner, C.D., Larcker, D.F. and Meyer, M. (1997), `̀ Performance,

compensation, and the balanced scorecard'', working paper,

University of Pennsylvania.

Kaplan, R.S. and Norton, D.P. (1992), `̀ The balanced scorecard ±

measures that drive performance'', Harvard Business Review,

January-February, pp. 71-9.

Kaplan, R.S. and Norton, D.P. (1996a), Translating Strategy into

Actions: The Balanced Scorecard, Harvard Business School Press,

Boston, MA.

Kaplan, R.S. and Norton, D.P. (1996b), `̀ Using the balanced

scorecard as a strategic management systems'', Harvard Business

Review, January-February, pp. 75-85.

Rucci, A.J., Kirn, S.P. and Quinn, R.T. (1998), `̀ The employee-

customer-profit chain at Sears'', Harvard Business Review,

Vol. 76, January-February, pp. 82-97.

Sim, K.L., Killough, L.N. and Curatola, A.P. (1999), `̀ An

examination of organizational design and performance

improvement in the manufacturing industry'', International

Review of Accounting, Vol. 4, pp. 1-21.

Simons, R. (2000), Performance Measurement and Control Systems for

Implementing Strategy, Prentice-Hall, Englewood Cliffs, NJ.

Waterhouse, J.M. (1999), `̀ Reporting practices: measuring up'',

CA Magazine, March, pp. 41-8.

M e a s u r i n g B u s i n e s s E x c e l l e n c e 5 , 2 2 0 0 1

2 6

Dow

nloa

ded

by U

nive

rsiti

Keb

angs

aan

Mal

aysi

a A

t 22:

44 1

7 M

arch

201

5 (P

T)

This article has been cited by:

1. Mohamed El-Mekawy, Lazar Rusu, Erik Perjons. 2015. An evaluation framework for comparing business-IT alignmentmodels: A tool for supporting collaborative learning in organizations. Computers in Human Behavior . [CrossRef]

2. Bruce Gurd, Panayiotis Ifandoudas. 2014. Moving towards agility: the contribution of a modified balanced scorecard system.Measuring Business Excellence 18:2, 1-13. [Abstract] [Full Text] [PDF]

3. Adrian Payne, Pennie Frow. 2014. Developing superior value propositions: a strategic marketing imperative. Journal of ServiceManagement 25:2, 213-227. [Abstract] [Full Text] [PDF]

4. Adrian Payne, Pennie Frow. 2014. Deconstructing the value proposition of an innovation exemplar. European Journal ofMarketing 48:1/2, 237-270. [Abstract] [Full Text] [PDF]

5. Sangjae Lee, Sung Bum Park, Gyoo Gun Lim. 2013. Using balanced scorecards for the evaluation of “Software-as-a-service”.Information & Management 50, 553-561. [CrossRef]

6. André de Waal, Karima Kourtit. 2013. Performance measurement and management in practice. International Journal ofProductivity and Performance Management 62:5, 446-473. [Abstract] [Full Text] [PDF]

7. Naqi Sayed. 2013. Ratify, reject or revise: balanced scorecard and universities. International Journal of Educational Management27:3, 203-220. [Abstract] [Full Text] [PDF]

8. Sany Sanuri Mohd Mokhtar. 2013. The effects of customer focus on new product performance. Business Strategy Series 14:2/3,67-71. [Abstract] [Full Text] [PDF]

9. Bunjongjit Rompho, Sununta Siengthai. 2012. Integrated performance measurement system for firm's human capital building.Journal of Intellectual Capital 13:4, 482-514. [Abstract] [Full Text] [PDF]

10. Fu-Hsiang Chen, Tsung-Shin Hsu, Gwo-Hshiung Tzeng. 2011. A balanced scorecard approach to establish a performanceevaluation and relationship model for hot spring hotels based on a hybrid MCDM model combining DEMATEL and ANP.International Journal of Hospitality Management 30, 908-932. [CrossRef]

11. Samuel Azasu. 2011. Ownership and size as predictors of incentive plans within Swedish real estate firms. Property Management29:5, 454-467. [Abstract] [Full Text] [PDF]

12. Md Habib‐Uz‐Zaman Khan, Abdel K. Halabi, Kurt Sartorius. 2011. The use of multiple performance measures and thebalanced scorecard (BSC) in Bangladeshi firms. Journal of Accounting in Emerging Economies 1:2, 160-190. [Abstract] [FullText] [PDF]

13. Milind T. Phadtare. 2010. Developing Balanced Scorecard: Case of Three Construction Firms of Small Size. Journal of Asia-Pacific Business 11, 135-157. [CrossRef]

14. Mar Vila, Gerard Costa, Xari Rovira. 2010. The creation and use of scorecards in tourism planning: A Spanish example.Tourism Management 31, 232-239. [CrossRef]

15. 강강강, 강강강. 2010. Analysis of the Casual Relationships between Service Business Performance using Performance Measures.Jounal of Korea Service Management Society 11, 87-110. [CrossRef]

16. André de Waal, Karima Kourtit, Peter Nijkamp. 2009. The relationship between the level of completeness of a strategicperformance management system and perceived advantages and disadvantages. International Journal of Operations & ProductionManagement 29:12, 1242-1265. [Abstract] [Full Text] [PDF]

17. Meena Chavan. 2009. The balanced scorecard: a new challenge. Journal of Management Development 28:5, 393-406. [Abstract][Full Text] [PDF]

18. Karima Kourtit, Peter Nijkamp, Andre A. de Waal. 2009. Strategic Performance Management and creative industry.International Journal of Foresight and Innovation Policy 5, 65. [CrossRef]

19. Scott B. Jackson, Thomas J. Lopez, Austin L. Reitenga. 2008. Accounting fundamentals and CEO bonus compensation.Journal of Accounting and Public Policy 27, 374-393. [CrossRef]

20. Ruzita Jusoh, Daing Nasir Ibrahim, Yuserrie Zainuddin. 2008. The performance consequence of multiple performancemeasures usage. International Journal of Productivity and Performance Management 57:2, 119+-136. [Abstract] [Full Text][PDF]

21. Monica Franco‐Santos, Mike Kennerley, Pietro Micheli, Veronica Martinez, Steve Mason, Bernard Marr, Dina Gray, AndrewNeely. 2007. Towards a definition of a business performance measurement system. International Journal of Operations &Production Management 27:8, 784-801. [Abstract] [Full Text] [PDF]

Dow

nloa

ded

by U

nive

rsiti

Keb

angs

aan

Mal

aysi

a A

t 22:

44 1

7 M

arch

201

5 (P

T)

22. Tariq H. Ismail. 2007. Performance evaluation measures in the private sector: Egyptian practice. Managerial Auditing Journal22:5, 503-513. [Abstract] [Full Text] [PDF]

23. Nagarajah Lee. 2006. Measuring the performance of public sector organisations: a case study on public schools in Malaysia.Measuring Business Excellence 10:4, 50-64. [Abstract] [Full Text] [PDF]

24. Mohd Zulkifli Mokhtar, Yusuf Karbhari, Kamal Naser. 2005. Company Financial Performance and ISO 9000 Registration:Evidence from Malaysia. Asia Pacific Business Review 11, 349-367. [CrossRef]

25. Ramakrishnan Ramanathan. 2004. Business excellence of industrial groups in Oman. Measuring Business Excellence 8:4, 34-44.[Abstract] [Full Text] [PDF]

26. Silvia Ondategui-Parra, Jui G. Bhagwat, Kelly H. Zou, Adheet Gogate, Lisa A. Intriere, Pauline Kelly, Steven E. Seltzer,Pablo R. Ros. 2004. Practice Management Performance Indicators in Academic Radiology Departments1. Radiology 233,716-722. [CrossRef]

27. Rodney A Stewart, Sherif Mohamed. 2004. Evaluating web-based project information management in construction: capturingthe long-term value creation process. Automation in Construction 13, 469-479. [CrossRef]

28. Kamal Naser, Yusuf Karbhari, Mohammad Zulkifli Mokhtar. 2004. Impact of ISO 9000 registration on company performance.Managerial Auditing Journal 19:4, 509-516. [Abstract] [Full Text] [PDF]

Dow

nloa

ded

by U

nive

rsiti

Keb

angs

aan

Mal

aysi

a A

t 22:

44 1

7 M

arch

201

5 (P

T)