macq-ro insights

TRANSCRIPT

Please refer to page 41 for important disclosures and analyst certification, or on our website www.macquarie.com/research/disclosures.

GLOBAL

Why this issue matters to investors

1) President Trump is attempting to bring

factories back to the US. To succeed,

economic incentives have to be altered

2) This is possible through a radical

reduction in US corporate tax rates and

import tariffs

3) A 45% tariff on Chinese imports into the

US would result in an estimated 14%

volume decline in Chinese imports

4) A 20% tariff on all US imports would result

in an estimated 4% volume decline in total

US imports

5) Profits are highly vulnerable. Rather than

Asian exporters, it is safer for investors to

seek MNCs that are regionally self-

sufficient

Other related reports:

14 February 2017 The Global Macro outlook: Policy shifts in the US

19 January 2017 Fortress America: Buy America! Trade policy is great again

31 January 2017 An activist US trade policy a.k.a. protectionism

25 January 2017 Global slump scenarios, and the EM economies that concern us the most

11 January 2017 Following the new smart money

Analyst(s) Macquarie Capital Securities (Japan) Limited Peter Eadon-Clarke +81 3 3512 7850 [email protected] Nara Song +81 3 3512 7878 [email protected] Macquarie Capital Markets Canada Ltd. David Doyle, CFA +1 416 848 3663 [email protected]

1 March 2017

Macq-ro insights Factory Asia at risk: the numbers President Trump is attempting to roll back the ICT revolution’s 30-year impact on

multinationals (MNCs) sliced and diced supply chains, and to bring factories

back to the US. To succeed, economic incentives have to be altered.

Dramatic developments on US trade policy, the Budget and tax reform are

expected. Whilst attention is focussed currently on the potential for import tariffs,

the upcoming legislation for a radical reduction in US corporate tax rates (from

35% to say 20%) would also contribute to a revival in US-based manufacturing.

Whilst it is not clear yet how President Trump will proceed on trade, candidate

Trump provided a detailed roadmap in a speech on 28 June 2016, pages 2-3.

We believe Factory Asia is facing its most serious challenge in decades.

A 45% tariff on Chinese imports into the US would result in an estimated 14%

volume decline in Chinese imports. US domestic production would replace half;

other countries would supply the balance. The impact on US GDP would be

marginal, possibly positive. The real damage arrives with retaliation, pages 4-6.

Estimated decline in Chinese imports on a 45% tariff scenario

Pass-through rate (%) Price elasticity of US consumer demand to Chinese Imports 0.4 0.6 0.8 1.0

20 3.6 5.4 7.2 9.0 40 7.2 10.8 14.4 18.0

60 10.8 16.2 21.6 27.0 80 14.4 21.6 28.8 36.0

Source: Macquarie Research, March 2017

A 20% tariff on all US imports, tax reform’s possible border tax adjustment,

would result in an estimated 4% volume decline in total US imports.

Whilst the 45% tariff scenario results in only a 1.3% volume decline in total US

imports, there is a high risk of immediate retaliation, in our opinion. The second

scenario is likely to face a WTO challenge first.

Profits are highly vulnerable, reflecting the need to absorb part of the tariff

imposition, as well as the negative volume effect. An analysis of the textiles and

footwear sector by Terence Chang et al, Quantifying the US border tax impact,

estimated base case profit declines of 39% for HK/China footwear companies

and -18% for apparel companies. Given their extensive engagement in Factory

Asia, we judge many Japanese MNCs to be at risk. Rather than Asian exporters,

it is safer for investors to seek MNCs that are regionally self-sufficient.

East Asian growth: The integrated export supply-chain of Factory Asia means

that any fall in US imports from China has negative spill-over consequences

across East Asia. The resulting negative impact on real GDP growth is estimated

to be broadly similar across East Asian countries, though North East Asia

appears to be hit proportionally a little harder than ASEAN, page 28.

Lower trend growth in East Asia appears likely as the contribution from capital

deepening becomes less. We use trend growth rates as the anchor around

which our forecasts oscillate. We reduce our East Asia trend growth forecast by

0.2 ppt to 4.5% pa, from page 24.

Macquarie Research Macq-ro insights

1 March 2017 2

Candidate Trump on trade Whilst it is not clear yet how President Trump will proceed, candidate Trump provided a detailed roadmap in a speech on 28 June 2016.

The source of the potential 45% tariff on Chinese imports is explained on page 6.

28 June 2016, Pennsylvania, Trump’s speech on trade, selected quotes:

Hillary Clinton unleashed a trade war against the American worker when she supported one

terrible trade deal after another – from NAFTA to China to South Korea. A Trump

administration will end that war by getting a fair deal for the American people. The era of

economic surrender will finally be over.

Our politicians have aggressively pursued a policy of globalization, moving our jobs, our

wealth and our factories to Mexico and overseas. Globalization has made the financial elite,

who donate to politicians, very, very wealthy. I used to be one of them. I hate to say it, but I

used to be one. But it has left millions of our workers with nothing but poverty and heartache.

When subsidized foreign steel is dumped into our markets, threatening our factories, the

politicians have proven, folks, have proven they do nothing.

We allowed foreign countries to subsidize their goods, devalue their currencies, violate their

agreements and cheat in every way imaginable, and our politicians did nothing about it.

Trillions of our dollars and millions of our jobs flowed overseas as a result.

Today, we import nearly US$800bn more in goods than we export. We can’t continue to do

that. This is not some natural disaster, it’s a political disaster and politician-made disaster.

Very simple. And it can be corrected and we can correct it fast when we have people with the

right thinking.

And listen to this. The first Republican president, Abraham Lincoln, warned that, quote “the

abandonment of the protective policy by the American government will produce want and ruin

among our people.” He understood it much better than our current politicians, that’s why he

was Abraham Lincoln, I guess.

Ladies and gentlemen, it is time to declare our economic independence once again. I’ll do it.

No doubt about it. Not even a little doubt. It also means reversing two of the worst legacies of

the Clinton years. At the center of the catastrophe are two trade deals…

First, the North American Free Trade Agreement, or the disaster called NAFTA.

Second, China’s entry into the World Trade Organization.

China’s entrance into the WTO has enabled the greatest job theft in the history of our country

I have been talking about for many years. And you know what? Nobody listened. But they are

listening now. Almost half of our entire manufacturing trade deficit in goods with the world is

the result of trade with China.

Trade reform and the negotiation of great trade deals is the quickest way to bring our jobs

back to our country.

A Trump administration will change our failed trade policies, and I mean quickly. Here are

seven steps I would pursue right away to bring back our jobs.

Number one, I am going to withdraw the United States from the Trans-Pacific Partnership,

which has not yet been ratified.

I am going to appoint the toughest and smartest, and I know them all, trade negotiators to

fight on behalf of American workers.

I am going to direct the secretary of commerce to identify every violation of trade agreements

a foreign country is currently using to harm you, the American worker. I will then direct all

appropriate agencies to use every tool under American and international law to end these

abuses. And abuse is the right word.

Here are seven

steps I would

pursue right away to

bring back our jobs

We allowed foreign

countries to

subsidize their

goods, devalue their

currencies, violate

their agreements

and cheat in every

way imaginable, and

our politicians did

nothing about it

Macquarie Research Macq-ro insights

1 March 2017 3

Number four. I'm going to tell our NAFTA partners that I intend to immediately renegotiate the

terms of that agreement to get a better deal by a lot. Not just a little, by a lot for our workers.

And if they don't agree to a renegotiation, which they might not because they are so used to

having their own way -- not with Trump they won't have their own way. Then, I will submit

under Article 2205 of the NAFTA Agreement that America intends to withdraw from the deal.

Number five. I'm going to instruct my treasury secretary to label China a currency

manipulator, which should have been done years ago. Any country that devalues their

currency in order to take unfair advantage of the United States, which is many countries, will

be met with sharply. And that includes tariffs and taxes.

Number six, I'm going to instruct the U.S. trade representative to bring trade cases against

China, both in this country and at the WTO. China's unfair subsidy behavior is prohibited by

the terms of its entrance to the WTO and I intend to enforce those rules and regulations. And

basically, I intend to enforce the agreements from all countries, including China.

Seven, if China does not stop its illegal activities, including its theft of American trade secrets,

I will use every lawful -- this is very easy. This is so easy. I love saying this. I will use every

lawful presidential power to remedy trade disputes, including the application of tariffs

consistent with Section 201 and 301 of the Trade Act of 1974, and Section 232 of the Trade

Expansion Act of 1962.

And when they say trade expansion, they're talking about other countries, they're not talking

about us because there is no expansion. They get the expansion, we get the joblessness.

That's the way it works. It's not going to happen anymore. President Reagan deployed similar

trade measures when motorcycle and semiconductor imports threatened U.S. industry. I

remember. His tariff on Japanese motorcycles was 45 percent and his tariff to shield

America's semiconductor industry was 100 percent, and that had a big impact, folks. A big

impact.

A new era of prosperity will finally begin. America will be independent once more.

Independent once more. Doesn't that sound great? Under a Trump presidency, the American

worker will finally have a president who will protect them and fight for them. We will stand up

to trade cheating. Cheating. Cheaters, that's what they are. Cheaters. We will stand up to

trade cheating anywhere and everywhere it threatens the American job.

Will President Trump implement Candidate Trump’s policies?

Following the US election on 8 November 2016, financial markets embraced the “Reflation

trade” and as shown in Fig 1 and Fig 2, both the real yield, the growth proxy, and the inflation

compensation element continued rising until late December.

However since late December, growth expectations have fallen, whilst inflationary

expectations have continued to rise: a combination consistent with the bond market

discounting a higher probability of protectionist policies being implemented.

Fig 1 The real yield component, the growth proxy Fig 2 The US inflation compensation element

Note: The above is the 10-year US TIPS yield

Source: St. Louis, Macquarie Research, March 2017

Note: The 10-year US bond yield minus the 10-year US TIPS yield:

Source: Datastream ,Macquarie Research, March 2017

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

10/2016 11/2016 12/2016 01/2017 02/2017

10 year TIPS yield

1.6

1.7

1.8

1.9

2

2.1

2.2

10/2016 11/2016 12/2016 01/2017 02/2017

Inflation compensation

If China does not

stop its illegal

activities, including

its theft of American

trade secrets, I will

use every lawful --

this is very easy.

This is so easy. I

love saying this. I

will use every lawful

presidential power

to remedy trade

disputes, including

the application of

tariffs consistent

with Section 201

and 301 of the Trade

Act of 1974, and

Section 232 of the

Trade Expansion

Act of 1962

Macquarie Research Macq-ro insights

1 March 2017 4

Tariffs: concepts and numbers The following uses the methodology laid in out the paper Trump’s Tariffs: A dissent of 5 April

2016 by J.W. Mason.

A 45% tariff on Chinese imports

Assumption #1 Chinese exported/US importer pass-through rate: 40%

So a 45% tariff leads to a US consumer price rise of 18% (45 times 0.4). This is the split

between how much of the tariff is absorbed by the producers, importers in squeezed profit

margins, and how much is paid by consumers.

As an offset to squeezed RMB profit margins, another effect could be a fall in the value of the

RMB versus the US$, which reduces the Chinese cost of production in US$ terms. Please

see assumption #4 below.

Assumption #2 Price elasticity of US consumer demand to Chinese goods is 0.8

So an 18% increase in price leads to a 14% decrease in Chinese imports. This assumption

and the next one are about how the consumer reacts: do they pay the higher price which

leads to a fall in spending on other goods and services (real incomes fall), do they switch to

alternative imports at the old price (GDP neutral), or do they switch to domestically produced

goods boosting US growth (on a variety of assumptions)?

The import price elasticity tends to be lower the greater the complexity of the product e.g.

capital goods and/or intangible aspects such as brand. We assume China’s exports to the US

are mainly simple consumer goods.

Fig 3 Estimated decline in Chinese imports on a 45% tariff scenario

Pass-through rate (%) Price elasticity of US consumer demand to Chinese Imports 0.4 0.6 0.8 1.0

20 3.6 5.4 7.2 9.0 40 7.2 10.8 14.4 18.0

60 10.8 16.2 21.6 27.0 80 14.4 21.6 28.8 36.0

Source: Macquarie Research, March 2017

Assumption #3 Substitution 50% domestic, 50% foreign non-China

For simplicity, let’s assume these are supplied at the same price, but are of a lower quality.

This assumption gives the US total import price elasticity (0.5).

The following table gives an indication of the variation of estimates around this assumption.

Fig 4 US trade (import, export) price elasticities, survey of estimates (to one decimal point)

Study Years Imports Exports Measure

Income Price Income Price (see note)

Herve et al. (2010) n/a 1.2 0.3 1.0 0.6 C

Wu (2008) 1960-1998 2.2 0.2 1.6 1.4 E

Kwack et al. (2007) 1984-2003 1.9 0.9 P

Crane, Crowley and Quayyum (2007) 1955-2006 2.0 0.6 2.3 0.6 P, E

Bahmani-Oskooee and Ardalani (2006) 1991-2002 1.8 0.1 2.5 0.8 E

Mann and Plck (2005) 1980-2003 2.2 0.3 1.4 0.2 P

Chinn (2005) 1975-2004 2.4 0.2 1.9 0.8 E

Hooper, Johnson and Marquez (1998) 1960-1994 2.1 0.5 1.3 1.0 P

Senhadji (1998), Senhadji and Montenegro (1999) 1960-1993 2.5 0.5 1.0 0.7 P

Wren-Lewis and Driver (1998) 1980-1995 2.4 0.2 1.2 0.7 E

Marquez (1999) 1973-1985 1.9 0.8 1.4 0.8 P

Housthakker and Magee (1969) 1951-1966 1.7 1.0 1.0 1.5 P

Note: The far right column indicates if “price’ was measured with an import price index (P), the exchange rate (E), or competiveness, i.e. relative wages (C). The “P” estimates are the most relevant for a tariff

Source: Trump’s Tariffs: A Dissent by J.W. Mason (April 2016), Macquarie Research, March 2017

The import volume

decline equals:

Tariff rate times

Pass-through rate

times

Price elasticity of

US consumer

demand

A 14% decrease in

Chinese imports

Macquarie Research Macq-ro insights

1 March 2017 5

Assumption #4 The RMB remains broadly flat with the US$ in year one

As noted in assumption #3 other non-US countries are taking market share from China. This

would be expected to put downward pressure on the RMB exchange rate. We assume the

PBoC intervenes to offset this. We believe Chinese policymakers are keen to manage

exchange rate expectations, and to avoid depreciation expectations becoming entrenched.

Some additional implications

1) The 45% tariff on Chinese imports: the impact on US household income, as

measured by the increase in the US import bill, Fig 5.

Fig 5 US household income impact: the increased US import bill (as a % of GDP)

As a percentage of GDP Before After Change % change

Total US imports 15.50 15.31 -0.19 -1.2

Import substitution (US production) 0.19 0.19 na

US Imports from China (volume) 2.70 2.32 -0.38 -14.0

China import price 1.00 1.18 +0.18 +18.0

US imports from non-China (volume) 12.80 12.99 +0.19 +1.5

Non-China import prices 1.00 1.00 0.00 0.0

Weighted overall import prices 1.00 1.03 0.03 3.2%

US import bill 15.50 15.73 +0.23 +1.5

Note: the import substitution, US production does not include multiplier effects in this table, i.e. the need to build new factories equipped with machinery

Source: Macquarie Research, March 2017

2) The China tariff impact on the US CPI

0.19 (China’s current share of US imports) times

0.15 (gross imports to US GDP) times

0.86 (remaining Chinese imports) times

18% (pass-through of tariff to CPI)

= 0.44% (Strictly, this measures the price impact on GDP, and thus we are assuming that this

flows through one-to-one to the 70% of GDP which is consumption)

Assumption #5: the multiplier effect of a fall in real incomes, perhaps compounded by

an asset market effect: a US income multiplier of 1.5 over two years

3) The impact on US GDP

Fig 6 The 45% China tariff impact on US GDP: Marginal, possibly positive

Negative US incomes are reduced by 0.23% of GDP (the increase in the import bill, Fig 5, grey highlights) multiplied by the 1.5 income multiplier = a loss of 0.35% of GDP

Positive Import substitution - imports from China are about 2.8% of US GDP times 7% (0.5 times 14%, the amount of reduced Chinese imports substituted by domestic production) = 0.20% of GDP. There is an income multiplier on this too, 1.5 times = a gain of 0.30% of GDP (*)

Positive In addition, US tax revenues go up as the 45% tariff is levied on the remaining Chinese imports: 0.19 times 0.15 times 0.86 times 45% = 1.1% of GDP. This could be used by the US government to increase US public sector expenditures or cut other taxes, stimulating the economy

Note: (*) Please note that import substitution, domestic production takes into account the current resource constraints of the US economy through the assumption of a US income multiplier of 1.5 over two years. This incorporates the capex expenditures, the resultant inflation consequences and any growth dampening policy response by the US Fed. Source: Macquarie Research, March 2017

Real damage arrives with retaliation (at the same 45% tariff rate)

US exports to China are 0.7% of US GDP, and the pass-through rate is likely to be higher on

more complex goods, say 60%. The price elasticity is also probably higher, as for a relatively

poor China, US products are likely more discretionary (Chinese consumers are more price-

sensitive). Let’s say that there is a 1.5 price elasticity of Chinese demand to US exports. 45%

times 0.6 times 1.5 times (equals a 40.5% decline in US exports to China) times 0.7 times the

1.5 US income multiplier = a loss of 0.43% of US GDP.

The impact on US

household income,

as measured by the

increase in the US

import bill

The impact on the

US CPI

The impact on US GDP

A loss of 0.4% of

US GDP

Macquarie Research Macq-ro insights

1 March 2017 6

The source of the 45% tariff number

Peter Navarro is the director of the National Trade Council. The National Trade Council will

be a newly formed body under the Trump Administration to “advise the President on

innovative strategies in trade negotiations, coordinate with other agencies to assess US

manufacturing capabilities and the defence industrial base, and help match unemployed

American workers with new opportunities in the skilled manufacturing sector.”

On 21 July 2016, the LA Times published an Op-ed by Peter Navarro: “Trump's 45% tariff on

Chinese goods is perfectly calculated”. To quote:

Trump’s suggestion of a 45% tariff on Chinese imports would, by my calculations, be an

appropriate level. More than 10 years ago, I began analyzing exactly how China’s state-run

industries significantly undercut foreign manufacturers and found that lower labor costs

accounted for only 39% of China’s price advantage. Five other unfair trade practices — the

aforementioned illegal export subsidies and currency manipulation along with intellectual

property theft and lax worker safety and environmental regulations — are the bigger story.

Fig 7 comes from Peter Navarro’s referred to 2006 paper: The Economics of the “China

Price”

Fig 7 Relative contributions of the eight China Price drivers, %, total 100%

1 Wages 39.41 2 Subsidies 16.71 3 Network clustering 16.02 4 Undervalued currency 11.44 5 Counterfeiting & Piracy 8.63 6 FDI 3.09 7 Health & Safety 2.44 8 Environmental 2.26

Source: The Economics of the “China Price” by Peter Navarro (2006), Macquarie Research, March 2017

Wages, network clustering and (possibly) FDI are acknowledged as largely “fair” advantages,

and ignoring the undervalued currency, the remaining four items highlighted in grey add to

30%. It appears that the overall estimates are still believed to be broadly valid. To quote Peter

Navarro’s 21 July 2016 Op-ed again:

When I added up the effects of such practices in China in 2006, they accounted for 43.7% of

the artificially low price of Chinese manufactured goods — almost exactly the amount of

Trump’s proposed tariffs. In the decade since my study was conducted, China’s cheating has

only worsened and become more institutionalized. For example, the bipartisan Commission

on the Theft of American Intellectual Property in 2013 estimated that the U.S. loses more than

$300 billion a year to intellectual property theft and blames China for 50% to 80% of the

problem.

A 20% across the board tariff (the possible border tax adjustment)

For a fuller discussion of this, please see David Doyle’s 19 January 2017 Fortress America: Buy America! Trade policy is great again.

Whilst the same methodology is used, and the same 40% pass-through to US prices is assumed, the price elasticity of US consumer demand to all imports is lower, say 0.5 (versus 0.8 for Chinese imports), and domestic substitution in this scenario is 100%.

A 20% tariff times a 0.40 pass-through (so an 8% increase in import prices) times a 0.5 price

elasticity of US consumer demand implies a 4% drop in import volumes. Imports are 15.5% of

US GDP, so this is equivalent to a 0.6% of US GDP.

The exchange rate assumption needs to be made explicit. Unlike the managed RMB

exchange rate, the other major trading partners of the US have floating exchange rates.

For simplification, we’ve embedded the exchange rate move into the pass-through rate. So a

40% pass-through rate implies that 60% is absorbed by profit margins and exchange rate

movements combined. By way of reference, 93% of all US imports are priced in the US$.

In the decade since

my study was

conducted, China’s

cheating has only

worsened and

become more

institutionalized

Trump’s suggestion

of a 45% tariff on

Chinese imports

would, by my

calculations, be an

appropriate level

A 4% decrease in

total import

Macquarie Research Macq-ro insights

1 March 2017 7

Trade related numbers

Fig 8 has basic trade data for East Asian countries; whilst the two following pages (page 8

and page 9) provide detailed data on the US trade balance.

A 14% decrease in Chinese imports to the US would reduce overall Chinese exports by 2.5%

(14 times 0.18, Fig 8 highlighted in grey), as a first round effect.

Fig 8 2015 export data, East Asian countries

Exports to: (in US$bn) Exports to: (% of total exports)

Exports GDP Exports/GDP a) US b) China c) Japan a) US b) China c) Japan (US$bn) (US$bn) (%)

Japan 625 4,384.5 14.3 126 109 NA 20.2 17.5 NA China 2,281 10,959.9 20.8 411 NA 136 18.0 NA 6.0 South Korea 527 1,378.9 38.2 70 137 26 13.3 26.0 4.9 Taiwan 280 525.2 53.4 34 74 20 12.0 26.4 7.0 Hong Kong 465 309.2 150.5 44 250 16 9.5 53.7 3.4

Vietnam 164 191.4 85.8 35 22 14 21.0 13.2 8.4 Thailand 211 395.6 53.3 24 23 20 11.2 11.1 9.4 Malaysia 200 297.1 67.3 19 26 19 9.4 13.0 9.5 Singapore 352 292.8 120.1 24 48 15 6.9 13.7 4.3 Philippines 59 292.2 20.1 9 6 12 15.0 10.9 21.1 Indonesia 150 861.0 17.5 16 15 18 10.8 10.0 12.0 ASEAN-6 1,136 2,330.0 48.8 127 140 98 11.2 12.3 8.6

Note: GDP is Oxford Economics, Exports data are from Datastream and IMF

Source: Oxford Economics, Datastream, IMF, Macquarie Research, March 2017

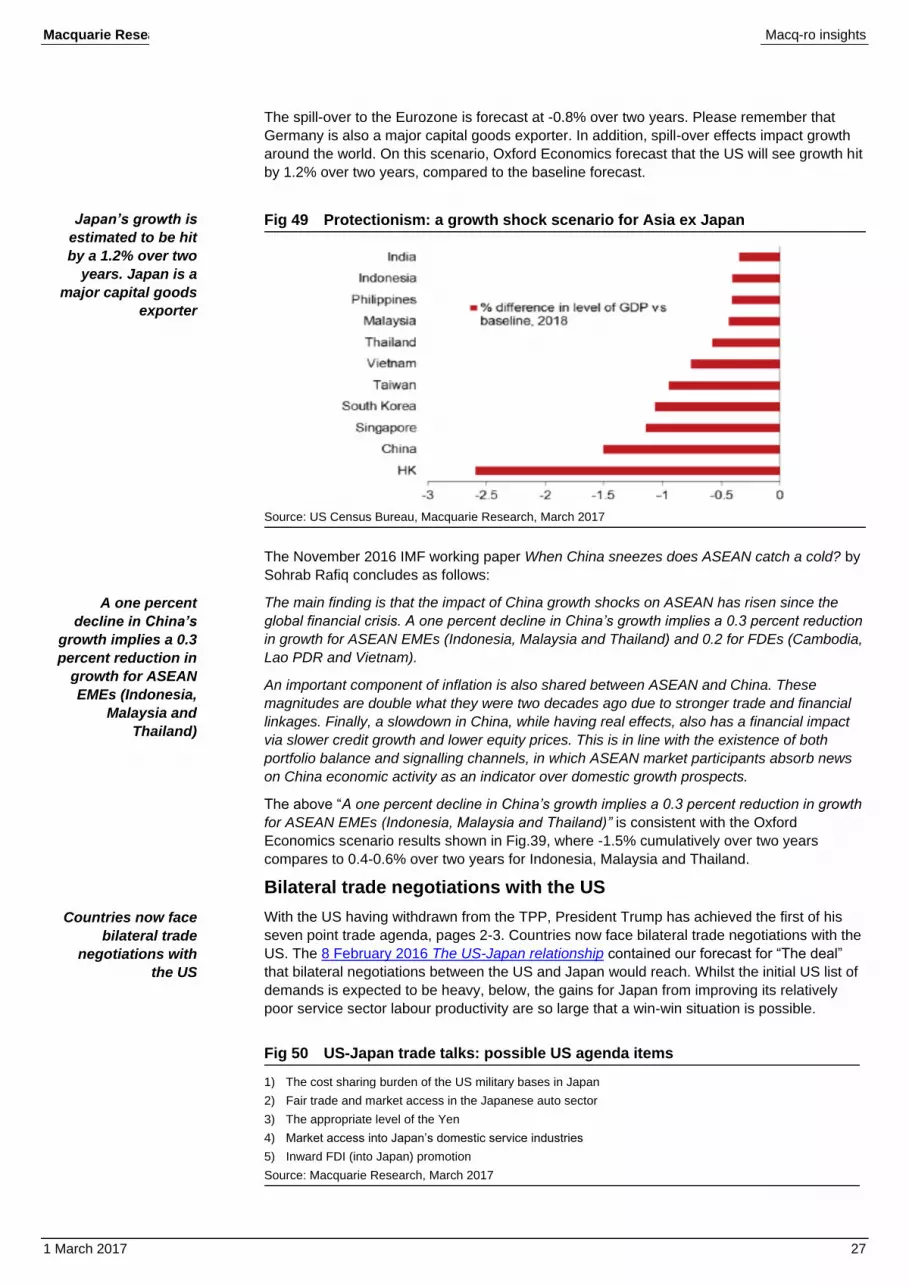

In our opinion, President Trump, wearied by the implications of the US being the ‘consumer of

last resort’, wants to rebalance the US economy, and bring factories back to the US.

This implies that President Trump probably focusses more on the trade balance (goods only)

than the current account which includes the services balance. Fig.9 contrasts the trade

balance positions of Factory Asia and the US. In line with other advanced economies, the US

has a growing surplus on its services balance.

The trade surplus of Factory Asia is now materially bigger than in the years leading to the

Global Financial Crisis (GFC). We believe that this ‘savings surplus’ was one of the main

drivers of the decline in global real interest rates, a contributor to the debt build-up in

advanced economies’ private sectors prior to the GFC.

Ten years later this global ‘fault line’ still exists.

Fig 9 Trade account balances: Factory Asia in surplus, the US in deficit

Note: Factory Asia is the aggregate of Japan, China, Korea, Taiwan, HK, and the ASEAN-5

Source: IMF, Datastream , Macquarie Research, March 2017

Please see page 29 for a chart of the current account balances of Factory Asia and the US.

-1200

-800

-400

0

400

800

1200 (USbn$)

Factory Asia

United States

The trade surplus of

Factory Asia is now

materially bigger

than in the years

leading to the

Global Financial

Crisis

Ma

cq

ua

rie R

esea

rch

M

acq-ro

insig

hts

1 M

arc

h 2

01

7

8

Fig 10 US Exports and Imports – snapshot by major trade partner and major product

Source: Bureau of Economic Analysis, Macquarie Research, March 2017

Trade Partner

Exports of

goods and

services

(millions of

USD) Goods total

Foods, feeds,

and beverages

Industrial

supplies and

materials

Capital goods

except

automotive

Automotive

vehicles, parts,

and engines

Consumer

goods except

food and

automotive

Other general

merchandise Services total

Maintenance

and repair

services Transport

Travel (for all

purposes

including

education)

Insurance

services

Financial

services

Charges for

the use of

intellectual

property

Telecom,

computer, and

information

services

Other business

services

Government

goods and

services

Euro Area 346,859 201,149 9,267 50,053 75,280 13,258 47,084 5,936 145,710 5,046 14,312 23,257 1,693 14,342 38,483 5,958 41,796 822

China 164,435 111,970 17,755 31,209 43,907 11,070 7,079 748 52,466 1,518 4,704 31,581 700 3,067 5,869 710 3,816 502

Canada 324,102 269,704 23,418 70,122 70,307 59,015 35,172 10,127 54,397 2,152 8,007 14,914 1,941 6,172 8,186 3,312 9,303 409

Mexico 261,868 230,622 16,234 76,561 82,312 33,524 14,653 7,205 31,245 723 3,981 16,985 396 1,444 3,326 1,128 2,793 468

Japan 106,141 61,959 11,124 14,913 22,709 2,034 8,974 2,173 44,184 1,163 9,219 11,435 2,025 3,843 6,973 1,494 7,403 627

United Kingdom 122,491 56,655 1,876 10,312 22,624 3,712 12,061 2,436 65,837 2,799 7,443 12,836 2,728 13,815 9,227 4,440 12,352 196

OPEC 107,885 71,451 6,149 12,366 30,700 9,119 5,837 6,666 36,434 3,227 3,178 12,994 322 2,566 1,743 2,272 5,813 4,320

South Korea 60,999 41,509 5,526 11,632 16,640 2,564 2,873 2,263 19,490 656 2,359 8,535 213 968 4,462 326 1,628 347

India 40,202 20,370 977 6,388 5,114 304 5,547 681 19,833 351 1,868 11,304 96 839 2,388 1,299 1,294 391

Brazil 54,309 28,828 659 12,040 12,408 1,032 2,198 490 25,482 607 4,330 9,217 396 1,620 3,333 4,197 1,632 150

Taiw an 37,938 26,293 2,897 5,443 14,564 279 1,217 1,846 11,645 938 2,128 2,244 42 650 4,270 149 602 624

Singapore 43,079 26,452 637 6,639 15,745 253 2,060 953 16,627 1,243 638 973 394 1,107 2,737 1,073 8,228 233

Australia 45,122 22,639 1,369 3,370 8,587 2,686 3,673 2,694 22,483 970 1,275 8,372 1,387 3,385 2,673 1,387 2,598 436

Total of above 1,715,430 1,169,601 97,888 311,048 420,897 138,850 148,428 44,218 545,833 21,393 63,442 164,647 12,333 53,818 93,670 27,745 99,258 9,525

US Total 2,201,653 1,455,593 131,758 383,174 520,175 150,787 193,608 56,776 746,062 26,147 84,807 206,326 17,743 95,023 121,300 37,288 138,055 19,370

Trade Partner

Imports of

goods and

services

(millions of

USD) Goods total

Foods, feeds,

and beverages

Industrial

supplies and

materials

Capital goods

except

automotive

Automotive

vehicles, parts,

and engines

Consumer

goods except

food and

automotive

Other general

merchandise Services total

Maintenance

and repair

services Transport

Travel (for all

purposes

including

education)

Insurance

services

Financial

services

Charges for

the use of

intellectual

property

Telecom,

computer, and

information

services

Other business

services

Government

goods and

services

Euro Area 442,586 331,073 20,497 51,638 92,276 48,120 99,166 19,249 111,514 1,235 21,658 25,371 6,530 2,901 12,888 5,778 28,510 6,643

China 477,769 461,942 5,752 42,135 168,068 18,948 221,652 5,353 15,827 520 4,346 4,521 55 583 426 923 4,341 112

Canada 311,773 282,365 23,798 119,066 34,076 65,711 18,016 17,833 29,406 1,559 5,853 6,605 467 1,827 1,362 4,170 7,306 258

Mexico 323,357 300,315 24,637 28,994 89,818 106,428 39,096 8,160 23,041 232 3,030 14,731 28 329 653 962 2,953 126

Japan 162,814 132,214 875 15,087 49,482 52,235 10,868 3,433 30,601 122 8,250 2,935 358 1,489 10,773 438 3,172 3,062

United Kingdom 105,526 53,802 2,586 9,900 13,527 9,140 12,146 6,423 51,724 2,533 7,969 8,247 4,275 8,536 3,685 2,320 13,413 746

OPEC 82,806 72,042 4,362 55,194 1,341 948 8,009 1,863 10,764 50 3,375 2,990 39 440 342 240 1,438 1,851

South Korea 81,637 70,910 661 11,928 17,443 25,970 13,409 1,500 10,726 16 5,657 1,200 98 249 216 60 1,055 2,176

India 70,839 44,737 2,771 8,167 4,278 1,243 27,611 666 26,101 20 547 3,203 49 522 371 14,808 6,536 43

Brazil 31,024 24,396 2,697 11,503 5,163 1,051 1,473 1,951 6,629 510 779 945 31 449 1,449 449 1,974 45

Taiw an 46,632 39,048 432 6,954 19,426 3,213 7,452 1,572 7,583 37 5,016 1,311 12 137 34 50 928 58

Singapore 25,601 18,583 65 3,992 8,342 46 3,712 2,290 7,019 620 1,202 536 205 821 115 387 3,005 126

Australia 17,347 9,932 3,263 2,304 1,547 317 1,407 954 7,415 33 1,019 1,797 505 796 577 301 2,177 211

Total of above 2,179,711 1,841,359 92,396 366,862 504,787 333,370 464,017 71,247 338,350 7,487 68,701 74,392 12,652 19,079 32,891 30,886 76,808 15,457

US Total 2,692,256 2,194,719 129,332 432,747 592,752 350,727 585,227 86,558 497,538 8,530 96,415 119,645 47,644 24,612 42,010 37,053 100,882 20,747

US Exports 4Q15 through 3Q16

US Imports 4Q15 through 3Q16

Goods Services

Goods Services

Ma

cq

ua

rie R

esea

rch

M

acq-ro

insig

hts

1 M

arc

h 2

01

7

9

Fig 11 US net exports and total trade – snapshot by major trade partner and major product

Source: Bureau of Economic Analysis, Macquarie Research, March 2017

Trade Partner

Net exports of

goods and

services

(millions of

USD) Goods total

Foods, feeds,

and beverages

Industrial

supplies and

materials

Capital goods

except

automotive

Automotive

vehicles, parts,

and engines

Consumer

goods except

food and

automotive

Other general

merchandise Services total

Maintenance

and repair

services Transport

Travel (for all

purposes

including

education)

Insurance

services

Financial

services

Charges for

the use of

intellectual

property

Telecom,

computer, and

information

services

Other business

services

Government

goods and

services

Euro Area (95,727) (129,924) (11,230) (1,585) (16,996) (34,862) (52,082) (13,313) 34,196 3,811 (7,346) (2,114) (4,837) 11,441 25,595 180 13,286 (5,821)

China (313,334) (349,972) 12,003 (10,926) (124,161) (7,878) (214,573) (4,605) 36,639 998 358 27,060 645 2,484 5,443 (213) (525) 390

Canada 12,329 (12,661) (380) (48,944) 36,231 (6,696) 17,156 (7,706) 24,991 593 2,154 8,309 1,474 4,345 6,824 (858) 1,997 151

Mexico (61,489) (69,693) (8,403) 47,567 (7,506) (72,904) (24,443) (955) 8,204 491 951 2,254 368 1,115 2,673 166 (160) 342

Japan (56,673) (70,255) 10,249 (174) (26,773) (50,201) (1,894) (1,260) 13,583 1,041 969 8,500 1,667 2,354 (3,800) 1,056 4,231 (2,435)

United Kingdom 16,965 2,853 (710) 412 9,097 (5,428) (85) (3,987) 14,113 266 (526) 4,589 (1,547) 5,279 5,542 2,120 (1,061) (550)

OPEC 25,079 (591) 1,787 (42,828) 29,359 8,171 (2,172) 4,803 25,670 3,177 (197) 10,004 283 2,126 1,401 2,032 4,375 2,469

South Korea (20,638) (29,401) 4,865 (296) (803) (23,406) (10,536) 763 8,764 640 (3,298) 7,335 115 719 4,246 266 573 (1,829)

India (30,637) (24,367) (1,794) (1,779) 836 (939) (22,064) 15 (6,268) 331 1,321 8,101 47 317 2,017 (13,509) (5,242) 348

Brazil 23,285 4,432 (2,038) 537 7,245 (19) 725 (1,461) 18,853 97 3,551 8,272 365 1,171 1,884 3,748 (342) 105

Taiw an (8,694) (12,755) 2,465 (1,511) (4,862) (2,934) (6,235) 274 4,062 901 (2,888) 933 30 513 4,236 99 (326) 566

Singapore 17,478 7,869 572 2,647 7,403 207 (1,652) (1,337) 9,608 623 (564) 437 189 286 2,622 686 5,223 107

Australia 27,775 12,707 (1,894) 1,066 7,040 2,369 2,266 1,740 15,068 937 256 6,575 882 2,589 2,096 1,086 421 225

Total of above (464,281) (671,758) 5,492 (55,814) (83,890) (194,520) (315,589) (27,029) 207,483 13,906 (5,259) 90,255 (319) 34,739 60,779 (3,141) 22,450 (5,932)

US Total (490,603) (739,126) 2,426 (49,573) (72,577) (199,940) (391,619) (29,782) 248,524 17,617 (11,608) 86,681 (29,901) 70,411 79,290 235 37,173 (1,377)

Trade partner

Total trade of

goods and

services

(millions of

USD) Goods total

Foods, feeds,

and beverages

Industrial

supplies and

materials

Capital goods

except

automotive

Automotive

vehicles, parts,

and engines

Consumer

goods except

food and

automotive

Other general

merchandise Services total

Maintenance

and repair

services Transport

Travel (for all

purposes

including

education)

Insurance

services

Financial

services

Charges for

the use of

intellectual

property

Telecom,

computer, and

information

services

Other business

services

Government

goods and

services

Euro Area 789,445 532,222 29,764 101,691 167,556 61,378 146,250 25,185 257,224 6,281 35,970 48,628 8,223 17,243 51,371 11,736 70,306 7,465

China 642,204 573,912 23,507 73,344 211,975 30,018 228,731 6,101 68,293 2,038 9,050 36,102 755 3,650 6,295 1,633 8,157 614

Canada 635,875 552,069 47,216 189,188 104,383 124,726 53,188 27,960 83,803 3,711 13,860 21,519 2,408 7,999 9,548 7,482 16,609 667

Mexico 585,225 530,937 40,871 105,555 172,130 139,952 53,749 15,365 54,286 955 7,011 31,716 424 1,773 3,979 2,090 5,746 594

Japan 268,955 194,173 11,999 30,000 72,191 54,269 19,842 5,606 74,785 1,285 17,469 14,370 2,383 5,332 17,746 1,932 10,575 3,689

United Kingdom 228,017 110,457 4,462 20,212 36,151 12,852 24,207 8,859 117,561 5,332 15,412 21,083 7,003 22,351 12,912 6,760 25,765 942

OPEC 190,691 143,493 10,511 67,560 32,041 10,067 13,846 8,529 47,198 3,277 6,553 15,984 361 3,006 2,085 2,512 7,251 6,171

South Korea 142,636 112,419 6,187 23,560 34,083 28,534 16,282 3,763 30,216 672 8,016 9,735 311 1,217 4,678 386 2,683 2,523

India 111,041 65,107 3,748 14,555 9,392 1,547 33,158 1,347 45,934 371 2,415 14,507 145 1,361 2,759 16,107 7,830 434

Brazil 85,333 53,224 3,356 23,543 17,571 2,083 3,671 2,441 32,111 1,117 5,109 10,162 427 2,069 4,782 4,646 3,606 195

Taiw an 84,570 65,341 3,329 12,397 33,990 3,492 8,669 3,418 19,228 975 7,144 3,555 54 787 4,304 199 1,530 682

Singapore 68,680 45,035 702 10,631 24,087 299 5,772 3,243 23,646 1,863 1,840 1,509 599 1,928 2,852 1,460 11,233 359

Australia 62,469 32,571 4,632 5,674 10,134 3,003 5,080 3,648 29,898 1,003 2,294 10,169 1,892 4,181 3,250 1,688 4,775 647

Total of above 3,895,141 3,010,960 190,284 677,910 925,684 472,220 612,445 115,465 884,183 28,880 132,143 239,039 24,985 72,897 126,561 58,631 176,066 24,982

US Total 4,893,909 3,650,312 261,090 815,921 1,112,927 501,514 778,835 143,334 1,243,600 34,677 181,222 325,971 65,387 119,635 163,310 74,341 238,937 40,117

Goods Services

US Net Exports 4Q15 through 3Q16

US Total trade 4Q15 through 3Q16

Goods Services

Macquarie Research Macq-ro insights

1 March 2017 10

Factory Asia The discussion that follows focusses on a possible 45% tariff on Chinese exports. As the

above has illustrated this is a serious situation for Factory Asia. We need to go further than

the 14% fall in China’s export volumes to the US to include:

1) The country sources of the value-added in China’s exports. There is an East Asian

integrated supply chain, that often culminates in the final assembly in China before

shipment to the US

2) An allowance for the countries that might supply the substitute imports to the US.

To aid in judgements, there is a more detailed history of the evolution of Factory Asia from

page 14. First, we capture the essence of the situation on this and the next page.

A visual history of the emergence of Factory Asia

As the joint WTO & Ide-Jetro paper Trade patterns and global value chains in East Asia

notes, supplying demand in the US from East Asia began in the 1960s with mass

consumption and mass marketing. In 1970 Japan led the way, with Hong Kong the leading

Asian Tiger at that time, Fig 12. By 1990, Fig 13, South Korea and China had begun to

emerge, but Japan remained the dominant exporter to the US market.

Fig 12 Total US trade with selected Asian partners (US$bn), 1970

Fig 13 Total US trade with selected Asian partners (US$bn), 1990

Source: WTO, Macquarie Research, March 2017 Source: WTO, Macquarie Research, March 2017

Fig 14 Total US trade with selected Asian partners (US$bn), 2000

Fig 15 Total US trade with selected Asian partners (US$bn), 2009

Source: WTO, Macquarie Research, March 2017 Source: WTO, Macquarie Research, March 2017

0

1

2

3

4

5

6

7

0 1 2 3 4 5 6

Japan Singapore India Thailand China Republic of Korea Hong Kong Chinese Taipei Malaysia

(US imports)

(US exports)0

20

40

60

80

100

120

0 10 20 30 40 50 60

Japan Singapore India Thailand China Republic of Korea Hong Kong Chinese Taipei Malaysia

(US imports)

(US exports)

0

20

40

60

80

100

120

140

160

180

0 20 40 60 80

Japan Singapore India Thailand China Republic of Korea Hong Kong Chinese Taipei Malaysia

(US imports)

(US exports) 0

50

100

150

200

250

300

350

400

0 20 40 60 80 100

Japan Singapore India Thailand China Republic of Korea Hong Kong Chinese Taipei Malaysia

(US imports)

(US exports)

Macquarie Research Macq-ro insights

1 March 2017 11

Whilst from 1990 the narrative remains in country terms, it becomes increasingly misleading.

Whilst previously Japanese companies were predominantly producing and exporting from

Japan, now begins an aggressive slicing and dicing of their supply chains via FDI throughout

East Asia.

Fig 14 shows the situation on the eve of China’s December 2001 WTO entry. China had

already grown in importance relative to Japan, but as pages 14-23 explain, this reflected the

relocation of Japanese final assembly plants to China at an accelerating pace since 1992. In

terms of the source of East Asian exports to the US, in 2009, at the time of the Global

Financial Crisis (GFC), China had become dominant, Fig 15.

Fig 16 has the most recent data.

Fig 16 Total US trade with selected Asian partners, 2015

Source: BEA, Macquarie Research, March 2017

Identifying the country of origin of the value added in goods imported into the US (rather than

attributing everything to the final exporting country) is possible through using Input-Output

tables, the topic of the next section.

Fig 17 is one proxy for the importance of Japanese and other multinationals (MNCs). Please

note that number of Japanese affiliates in China that import and export at 2,260 compares to

the total of the US, Germany, Taiwan, South Korea and France of 2,207. As financial centres,

we chose to exclude HK and Singapore in this comparison. Please also note that Japan’s

affiliates are extensively represented across other East Asia nations (grey highlights).

Fig 17 Global value chain (GVC)-FDI, the most common bilateral pairs

Destination Origin Number of affiliates that import and export % of total affiliates

PRC Japan 2,260 81 PRC Hong Kong 1,314 76 PRC US 646 74 PRC Germany 625 76 PRC Taipei, China 401 79 PRC South Korea 358 86 PRC Singapore 337 71 Vietnam Japan 306 72 Thailand Japan 258 64 Indonesia Japan 214 53 Taipei, China Japan 212 74 PRC France 177 77 Malaysia Japan 175 78 Philippines Japan 171 69 Singapore Japan 164 54

Note: Asian economic integration report 2016 by the ADB. GVC-FDI refers to foreign affiliates engaged in both exports and imports. ADB calculations from data sourced from the Dun & Bradsheet D&B Worldbase

Source: ADB, Macquarie Research, March 2017

0

50

100

150

200

250

300

350

400

0 10 20 30 40 50 60 70 80 90 100

Japan Singapore India ThailandChina Republic of Korea Hong Kong Chinese Taipei Malaysia

(US imports)

(US exports)

Whilst from 1990 the

narrative remains in

country terms, it

becomes

increasingly

misleading

Whilst previously

Japanese

companies were

predominantly

producing and

exporting from

Japan, now begins

an aggressive

slicing and dicing of

their supply chains

via FDI throughout

East Asia

One proxy for the

importance of

Japanese and other

multinationals

Macquarie Research Macq-ro insights

1 March 2017 12

Sources of Value Added in Gross exports Conventional trade statistics measure the value of commerce between two countries, rather

than attributing the value-added in the goods. This has become increasingly important as

supply chains have sliced and diced activities. The following draws on the IMF 2013 working

paper Export performance in Europe: What do we know from supply links? By Jesmin

Rahman & Tianli Zhao. The vibrancy of Factory Europe is perhaps underappreciated.

The value-added of gross exports is subdivided by the location of value-added (domestic,

foreign) and for domestic value-added by the stage of production, Fig 18. Components 1 and

2 are stand-alone exports whilst components 3, 4 and 5 are parts of supply chains.

Domestic value-added intermediate exports, components 3 and 4, processed further in to

exports are “upstream”.

Component 5, the foreign-value-added going into final exports is “downstream”. The higher

the percentage the more likely the country is the downstream final assembler.

Fig 18 Decomposition of gross exports into five value-added components

Note: From the IMF working paper Export performance in Europe: What do we know from supply links? By Jesmin Rahman & Tianli Zhao (2013) which draws on Koopman, Powers, Wang & Wei (2011): Give credit where credit is due, Tracing value-added in global production chains

Source: IMF, Macquarie Research, March 2017

Fig.19 has the available data, comparing 2008 versus 1995. Please note that for Asia-Pacific

countries the slicing and dicing of MNC supply chains has led to:

1) A lower share of domestic value-added in gross exports, and a higher share of

foreign value-added (shaded in light brown). Japan has gone from 6.7% to 19.8%,

China from 17.5% to 31.4%, South Korea from 26.9% to 43.9% and Taiwan from

35.9% to 48.6%.

2) A relative increase in component 3, the export of intermediates which are processed

and then re-exported to third countries, shaded in pale red. Japan has gone from

14.3% to 21.1%, China from a modest 8.9% to a still modest 11.8%, South Korea

from 13.5% to 16.2%, and Taiwan from 10.4% to an impressive 20.8%.

3) The US and Germany are highlighted in pale green for comparison. Please note the

relatively high component 4 scores (exported intermediates that return home) in both

cases, but especially the US. This shows the importance of NAFTA trade.

4) Summing all three supply-chain components (3, 4 and 5), and comparing 1995 with

2008, the US has gone from 33.0% to 41.7%, Germany from 35.3% to 48.4% and

Japan from 22.6% to 42.2%, for increases of 8.7%, 13.1% and 19.6% respectively.

Whilst Japan has evolved the most rapidly since 1995, Germany remains the most

advanced.

Whilst Japan has

evolved the most

rapidly since 1995,

Germany remains

the most advanced

Conventional trade

statistics measure

the value of

commerce between

two countries,

rather than

attributing the

value-added in the

goods

Ma

cq

ua

rie R

esea

rch

M

acq-ro

insig

hts

1 M

arc

h 2

01

7

13

Fig 19 Value-Added Decomposition of Exports in Manufacturing: DVA is Domestic value added, FVA is Foreign value added, all numbers % unless otherwise stated

Country of Region

Decomposition in export of manufacturing good 1995 Decomposition in export of manufacturing good 2008

Gross manufacturing export (US$m)

DVA in direct

exports of final goods

DVA in intermediates

absorbed by direct importer

Indirect DVA exports to

third countries

Returned DVA FVA Total

Gross manufacturing export (US$m)

DVA in direct

exports of final goods

DVA in intermediates

absorbed by direct importer

Indirect DVA exports to

third countries

Returned DVA FVA Total

(1) (2) (3) (4) (5) (1) (2) (3) (4) (5)

CHN 136,325 50.6 22.6 8.9 0.4 17.5 100 1,803,921 35.4 19.8 11.8 1.5 31.4 100 JPN 399,313 39.3 38.0 14.3 1.6 6.7 100 723,610 29.2 28.7 21.1 1.3 19.8 100 KOR 119,391 29.5 29.6 13.5 0.4 26.9 100 424,822 18.8 20.7 16.2 0.4 43.9 100 TWN 108,406 28.7 24.8 10.4 0.2 35.9 100 254,976 10.6 19.8 20.8 0.2 48.6 100 INDIA 32,005 40.8 36.1 10.8 0.1 12.2 100 176,800 32.9 24.3 14.1 0.4 28.3 100 IDN 36,721 30.4 38.6 11.7 0.2 19.1 100 97,085 19.3 38.9 20.3 0.3 21.2 100 AUS 30,659 30.7 39.4 13.9 0.2 15.8 100 94,421 21.6 33.9 20.8 0.5 23.1 100

USA 479,211 35.6 31.4 11.0 8.9 13.1 100 1,001,641 30.9 27.5 14.8 6.8 20.1 100 CAN 158,479 27.6 34.4 7.1 0.8 30.2 100 300,671 26.3 30.9 9.9 1.0 32.0 100 MEX 54,824 31.5 25.4 7.6 0.3 35.2 100 199,372 28.3 23.4 9.4 0.5 38.5 100 BRA 41,011 24.4 50.0 16.3 0.3 9.0 100 145,530 32.8 32.6 18.6 0.4 15.6 100

DEU 511,451 36.3 28.3 14.3 2.7 18.3 100 1,434,387 29.5 22.2 16.5 2.1 29.8 100 FRA 261,160 37.1 25.6 13.8 1.4 22.1 100 576,334 32.8 19.7 15.5 1.2 30.9 100 ITA 219,179 41.7 25.0 11.9 0.8 20.6 100 515,486 34.3 21.1 15.6 0.9 28.1 100 GBR 225,865 36.3 25.6 13.8 1.3 23.0 100 403,728 32.3 21.5 16.4 1.1 28.6 100 NLD 148,442 28.9 21.2 12.9 0.7 36.4 100 329,863 24.0 15.5 13.8 0.5 46.2 100 ESP 86,279 37.8 24.9 12.9 0.6 23.7 100 269,583 30.3 19.7 14.5 0.9 34.7 100 BEL 134,844 24.0 19.2 12.3 0.5 44.0 100 267,975 18.0 14.7 13.4 0.3 53.7 100 SWE 77,872 29.1 27.7 15.3 0.4 27.5 100 176,392 23.7 20.7 16.1 0.3 39.2 100 POL 23,293 36.4 27.7 16.4 0.2 19.3 100 168,624 28.6 17.7 16.9 0.4 36.4 100 AUT 47,262 27.1 27.9 16.1 0.5 28.4 100 156,202 23.1 19.0 17.7 0.4 39.8 100 TUR 24,664 50.2 23.4 11.2 0.1 15.1 100 136,191 31.7 22.1 13.9 0.2 32.1 100 CZE 16,880 23.5 25.5 15.4 0.7 34.9 100 135,925 19.8 14.5 15.0 0.2 50.5 100 IRL 40,338 33.2 16.6 8.5 0.1 41.6 100 117,948 26.1 14.3 9.2 0.1 50.3 100 RUS 27,595 14.7 47.9 24.8 0.6 12.0 100 111,251 13.2 43.5 32.1 1.0 10.3 100 FIN 39,298 23.6 34.4 17.1 0.3 24.7 100 102,544 18.5 25.9 18.4 0.2 37.0 100 DNK 48,727 44.8 19.1 9.9 0.2 26.1 100 94,058 35.6 17.0 13.3 0.2 33.8 100 HUN 8,703 29.4 22.0 13.2 0.1 35.4 100 86,360 18.7 12.1 12.9 0.2 56.1 100 SVK 7,467 18.1 27.5 17.7 0.5 36.1 100 60,929 18.7 13.7 15.8 0.2 51.6 100 PRT 21,379 40.0 19.3 9.3 0.2 31.2 100 51,345 28.7 19.1 13.0 0.3 38.9 100 ROM 6,475 30.1 28.5 14.4 0.1 26.9 100 38,436 25.7 20.9 18.4 0.3 34.7 100 SVN 7,850 30.8 21.3 11.1 0.0 36.7 100 26,238 24.2 15.9 15.0 0.1 44.9 100 GRC 4,282 42.1 22.4 10.9 0.2 24.4 100 17,847 26.7 18.6 12.3 0.3 42.2 100 BGR 3,444 28.7 22.8 9.7 0.0 38.8 100 17,499 17.5 16.0 13.2 0.1 53.2 100 LTU 1,660 24.9 23.3 10.9 0.0 40.9 100 14,435 20.3 15.6 11.3 0.2 52.7 100 LUX 6,635 11.2 21.5 16.5 0.1 50.8 100 13,346 11.6 15.3 17.5 0.1 55.5 100 EST 1,380 28.7 20.3 10.7 0.1 40.2 100 8,650 20.9 21.1 16.2 0.1 41.7 100 LVA 871 29.5 28.4 13.5 0.0 28.6 100 5,598 24.4 21.6 14.9 0.3 38.8 100 MLT 1,363 15.9 11.7 7.3 0.0 65.1 100 2,763 17.5 13.5 12.7 0.0 56.4 100 CYP 848 42.9 13.9 3.9 0.0 39.2 100 1,457 29.7 18.3 10.7 0.1 41.2 100

Rest of the world 418,354 30.3 25.9 9.7 2.4 31.8 100 1,647,992 19.9 21.2 11.1 3.6 44.2 100

Total 58% 14% 28% 56% 16% 38%

Note: From the IMF working paper Export performance in Europe: What do we know from supply links? By Jesmin Rahman & Tianli Zhao (2013). Source: IMF, Macquarie Research, March 2017

Macquarie Research Macq-ro insights

1 March 2017 14

Japan & Factory Asia Multinationals (MNCs) deployed the ICT revolution over the 20 years up until 2008, and the

Global Financial Crisis, into what many call “Globalisation’s second unbundling”, the slicing

up of supply chains around the world. MNCs have been the primary transmission mechanism,

and have been rewarded by the increased global share of income going to capital. For more

analysis, please see the 20 May 2016 Macq-ro insights: from labour to capital.

Fig 20 comes from the February 2007 ADB working paper: Managing the Noodle Bowl: The

fragility of East Asian regionalism by Richard Baldwin. Richard Baldwin’s new book The Great

Convergence: Information technology and the new globalization (2016) is recommended.

Fig 20 Japanese plants in emerging East Asia

Fig 21 BITs, worldwide

Note: The figure shows the sum of plants in the auto and electrical machinery industries. From the February 2007 ADB working paper: Managing the Noodle Bowl: The fragility of East Asian regionalism by Richard Baldwin, which cites Fujita and Hamaguchi (2006): The coming age of China-plus-one

Source: ADB above, Macquarie Research, March 2017

Source: UNCTAD, Macquarie Research, March 2017

As noted by Richard Baldwin and Javier Lopez-Gonzales in their 2012 Supply-chain trade: A

portrait of global patterns and several testable hypotheses there was a demand pull element

into EM economies as well as a MNC supply-push seeking lower labour costs:

Developing nations that had eschewed trade liberalisation for decades, suddenly embraced

openness that facilitated international production sharing. They slashed tariffs unilaterally

(especially on intermediates), signing Bilateral Investment Treaties (BITs, which are mostly

unilateral concessions to rich-nation firms seeking to invest), signing Regional Trade

Agreements (RTAs) with ‘deep’ provisions that are pro-supply-chain (e.g. assurances for

intellectual property, capital movements, inward investments, competition policy, business

visas, etc.).

Please see Fig 21.

The result has been regional supply chains built around Factory Asia, Factory North America

and Factory Europe.

Headquarter economies (Japan, US, Germany), those with advanced technology and high

wages, have outsourced slices of their supply chains to factory economies, those with low

wages.

Exceptions to this image include China, which has progressed to exporting low-tech industrial

intermediates, and Japan, whose high tech industrial intermediates are also exported to

Factory North America and Factory Europe.

This has important consequences for estimating the economic impact of protectionism.

The following pages focus on the evolution of Factory Asia, drawing on the reports below.

0

500

1000

1500

2000

2500

3000

3500

0

50

100

150

200

250

1959

1962

1965

1968

1971

1974

1977

1980

1983

1986

1989

1992

1995

1998

2001

2004

2007

2010

2013

2016

Number of new BITs signed per year [LHS]

Accumulated newly created BITs [RHS]

Globalisation’s 2nd

unbundling

Factory Asia,

Factory North

America and

Factory Europe

Macquarie Research Macq-ro insights

1 March 2017 15

Fig 22 The US-Japan relationship, recommended articles

Author Title

Fukunari Kimura International production and distribution networks in East Asia: 18 facts, mechanics, and policy implications (2006) Shujiro Urata Free trade agreements: A catalyst for Japan’s economic revitalisation (2005) Shujiro Urata Changing competitiveness of the Japanese manufacturing sector and firms in regional production networks in

Asia, chapter 5 of the ADB-KERI Future of Factory Asia (2014)

Shujiro Urata Japan’s trade policy with Asia, from the Japan MOF Public Policy Review Vol.10, No.1 (2014) Richard Baldwin, Tadashi Ito, Hitoshi Sato

Portrait of factory Asia: Production network in Asia and its implication for growth – the ‘smile curve’ (2014)

ADB Asian economic integration report 2016: What drives FDI in Asia and the Pacific? (2016)

Source: Macquarie Research, March 2017

Japan and the development of Factory Asia

Fig 23 and Fig 24 show how Japanese direct exports to the US and the EU have been

broadly stagnant since 1989 in yen value terms, and have fallen as a percentage of total

Japanese exports from 51% to 35%.

Exports to East Asia have grown strongly over the period.

Fig 23 Japanese exports to the US and by region, 1988 to 2016, ¥tr

Source: RIETI, Macquarie Research, March 2017

Fig 24 Japanese exports by region (shares), 1988-2016, %

Source: RIETI, Macquarie Research, March 2017

0

10

20

30

40

50

60

70

80

90

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

(trJPY)

US EU Korea TaiwanSingapore Hong Kong ASEAN IndiaChina Others Exports

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

(trJPY)

US EU Korea Taiwan Singapore Hong Kong ASEAN India China Others

Japanese direct

exports to the US

and the EU have

been broadly

stagnant since 1989

in yen value terms…

…and have fallen as

a percentage of total

Japanese exports

from 51% to 35%

Macquarie Research Macq-ro insights

1 March 2017 16

Fig.25 and Fig 26 show a similar pattern for Japanese imports.

Fig 25 Japanese imports by region, 1988-2016, ¥tr

Source: RIETI, Macquarie Research, March 2017

Fig 26 Japanese imports by region (shares), 1988-2016, %

Source: RIETI, MOF, Macquarie Research, March 2017

In terms of the share of Japanese trade, it is only China that has shifted materially from 1988

to now. As a share of Japanese exports China’s share has grown from 3% to 23%, whilst

China’s share of Japanese imports has grown from 5% to 21%.

Developing in tandem, Fig 27 shows the waves of Japanese FDI into China from 1980 to

2011, and the related market opening policies (Fig 28). For example, the middle 1990’s was a

period of major realised investment, following the 1994 reforms.

Fig 27 also has data on the number of FDI cases into China each year, and with cases

consistently measured in thousands, it reflects that even Japan’s SME sector embraced the

lower wage cost opportunity in China.

Japan’s companies began to internationalise from the late 1980s. Fig 29, and this provides a

context for the China FDI waves of Fig 27.

The US and EU have dominated M&A activity (Fig 29, lower panel) which is included in total

FDI flows (Fig 29, upper panel) when at least a 10% stake is acquired. FDI flows to China

have been overwhelmingly greenfield investment until 2015.

0

10

20

30

40

50

60

70

80

90

100

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

(trJPY)

US EU Korea TaiwanSingapore Hong Kong ASEAN IndiaChina Others Exports

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

(trJPY)

US EU Korea Taiwan Singapore Hong Kong ASEAN India China Others

Japanese direct

imports from the US

and the EU have

grown modestly

since 1989 in yen

value terms…

…and have fallen as

a percentage of total

Japanese imports

from 35% to 25%

Even Japan’s SME

sector embraced the

lower wage cost

opportunity in China

Ma

cq

ua

rie R

esea

rch

M

acq-ro

insig

hts

1 M

arc

h 2

01

7

17

Fig 27 Japan FDI into China, 1996-2010

Note: The FDI value for 2011 is the sum of January to November 2011. Source: Invest In China, Macquarie Research, March 2017

Fig 28 Procession of Japan's FDI into China

1980s 1H 1980s 2H 1990s 1H 1990s 2H 2000 onwards

Reasons for investment

Cheap and good labour pool The previous + infrastructure, marketisation

The previous + parts procurement (Pearl River Delta)

The previous + domestic market (Yangtze Delta), entry into WTO, R&D

Main regions Dalian Dalian, Pearl River Delta Pearl River Delta, Yangtze Delta Pearl River Delta, Yangtze Delta, Beijing Main industries Textiles, sundry goods, food Textiles, sundry goods, food, electric

appliances, machinery, motorbikes, automobiles

Textiles, sundry goods, food, electric appliances, electric devices, machinery, chemistry, electric device components, machinery parts

Textiles, sundry goods, food, electric appliances, electric devices, machinery, chemistry, electric device components, machinery parts, software development, R&D centre, automobile

Major policies July 1979: Foreign investment granted

legal status in China 1980: 4 Special Economic Zones (SEZs) (Shenzhen, Zhuhai, Shantou, Xiamen) established 1983: Regulations for the Implementation of the Law of the People's Republic of China on Joint Ventures using China and Foreign Investment promulgated, further liberalising domestic market and clarifying business environment 1984: 14 SEZs established in coastal cities

1985: 12 of the 14 SEZs designated as Technology Promotion Zones to expedite transfer of technology. Development Triangles including the Yangtze River delta, Pearl River delta, and Min Nan region in Fujian were opened to foreign investors. 1986: Favourable regulations and provisions established to promote export-oriented JVs and JVS using advanced technologies. Wholly foreign-owned enterprises allowed. '22 Article Provisions' gave foreign enterprises preferential treatment, with freedom to import inputs, right to retain/swap foreign exchange, privileged access to utilities, etc.

1994: New proposals to attract FDI into specific sectors to match domestic industrial objectives: agriculture, hydropower, communications, energy and raw material sectors. Tightened procedures for contract approvals and foreign enterprise registrations. Increased penalties if agreements unfulfilled.

1995: Provisional Guidelines for Foreign Investment Projects took effect. Priority given to FDI in agriculture, energy, transportation, telecommunications, basic raw materials, and high-technology industries. Those advancing into the central and central west region strongly encouraged. Guiding Catalogue of Foreign Investment Projects categorised investments into four categories: Encouraged, Restricted, Prohibited and Permitted.

Dec 2001: China joins the WTO. 2007: Third update to the Catalogue of Industries for Guiding Foreign Investment. Encouraged sectors include high-tech, equipment manufacturing, and new material production industries. Areas such as recycling industry, clean production, renewable energy, ecological environment protection, and comprehensive utilisation of resource encouraged.

Source: MOF, Macquarie Research, March 2017

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

Japan's Realised FDI Value in China (LHS) # of cases (RHS) # of cases(US$mn)

Ma

cq

ua

rie R

esea

rch

M

acq-ro

insig

hts

1 M

arc

h 2

01

7

18

Fig 29 Japanese FDI outflow (top panel) and M&A outflow (lower panel)

M&A outflow

Note: Western Europe includes Germany, UK, France, Netherlands, Italy, Belgium, Luxembourg, Switzerland, Sweden, and Spain. M&A outflow data for 1983-1995 are from FactSet, 1996-2011 are from RECOF. Transaction values are converted from JPY to USD using the annual average exchange rate from Federal Reserve. Please also note the data availability between 1983-1995: North America (1990-) and Western Europe (1993-). RECOF: the source of the M&A outflow chart was modified in 2014 and the data categories have slightly changed.

Source: MOF, JETRO, RECOF , Macquarie Research, March 2017

-10

10

30

50

70

90

110

130

150

170

190

198

3

198

4

198

5

198

6

198

7

198

8

198

9

199

0

199

1

199

2

199

3

199

4

199

5

199

6

199

7

199

8

199

9

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

201

5

201

6

(US$bn) North America Western Europe China South Korea Other Asia Others

0

20

40

60

80

100

120

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

(US$bn)

North America Western Europe China South Korea Other Asia Others

Macquarie Research Macq-ro insights

1 March 2017 19

Fig 30 provides a summary of the FDI flows, presented in cumulative stock terms, whilst Fig

31 does the same for company overseas affiliate sales. Asia has been an important

contributor in both cases.

Fig 30 Japan’s Outward FDI Stock by Region

Note: data from https://www.jetro.go.jp/en/reports/statistics/

Source: Jetro, Macquarie Research, March 2017

Fig 31 Sales of Overseas Affiliates of Japanese Companies by Regions

Source: METI, Macquarie Research, March 2017

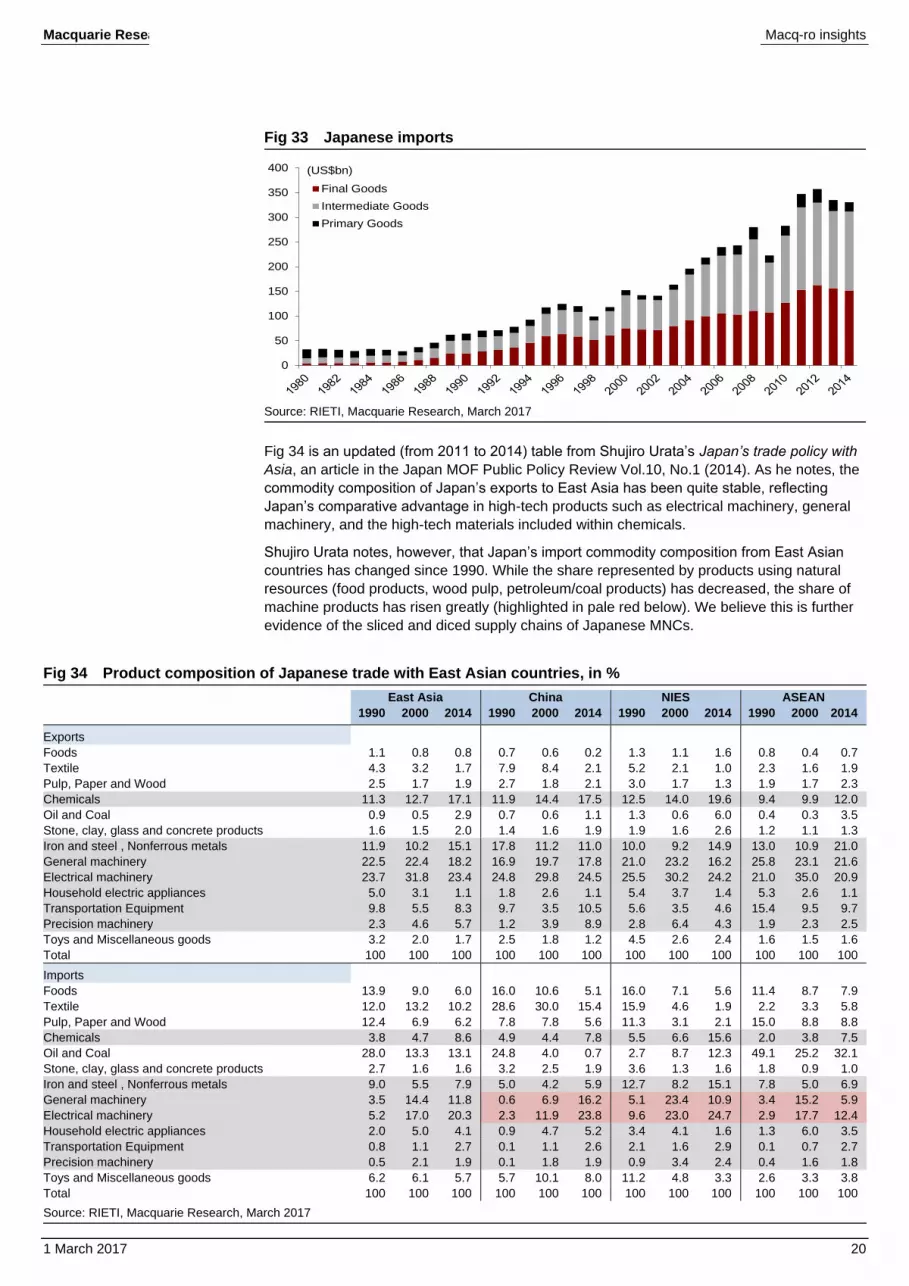

Next we present charts of Japanese exports and imports classified into primary, intermediate

and final goods. As expected, the growth in intermediate goods has been very strong,

especially in the case of Japanese exports.

Fig 32 Japanese exports

Source: RIETI, Macquarie Research, March 2017

0

200

400

600

800

1,000

1,200

1,400 (US$bn)

Asia North America

Latin America Oceania

Europe Middle East

Africa

0

50

100

150

200

250

300

350

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

(10trJPY)

Africa Oceania

Europe Middle East

South America North America

Asia

0

50

100

150

200

250

300

350

400

450

500 (US$bn)

Final Goods

Intermediate Goods

Primary Goods

The growth in

intermediate goods

has been very

strong

Macquarie Research Macq-ro insights

1 March 2017 20

Fig 33 Japanese imports

Source: RIETI, Macquarie Research, March 2017

Fig 34 is an updated (from 2011 to 2014) table from Shujiro Urata’s Japan’s trade policy with

Asia, an article in the Japan MOF Public Policy Review Vol.10, No.1 (2014). As he notes, the

commodity composition of Japan’s exports to East Asia has been quite stable, reflecting

Japan’s comparative advantage in high-tech products such as electrical machinery, general

machinery, and the high-tech materials included within chemicals.

Shujiro Urata notes, however, that Japan’s import commodity composition from East Asian

countries has changed since 1990. While the share represented by products using natural

resources (food products, wood pulp, petroleum/coal products) has decreased, the share of

machine products has risen greatly (highlighted in pale red below). We believe this is further

evidence of the sliced and diced supply chains of Japanese MNCs.

Fig 34 Product composition of Japanese trade with East Asian countries, in %

East Asia China NIES ASEAN

1990 2000 2014 1990 2000 2014 1990 2000 2014 1990 2000 2014

Exports

Foods 1.1 0.8 0.8 0.7 0.6 0.2 1.3 1.1 1.6 0.8 0.4 0.7

Textile 4.3 3.2 1.7 7.9 8.4 2.1 5.2 2.1 1.0 2.3 1.6 1.9

Pulp, Paper and Wood 2.5 1.7 1.9 2.7 1.8 2.1 3.0 1.7 1.3 1.9 1.7 2.3

Chemicals 11.3 12.7 17.1 11.9 14.4 17.5 12.5 14.0 19.6 9.4 9.9 12.0

Oil and Coal 0.9 0.5 2.9 0.7 0.6 1.1 1.3 0.6 6.0 0.4 0.3 3.5

Stone, clay, glass and concrete products 1.6 1.5 2.0 1.4 1.6 1.9 1.9 1.6 2.6 1.2 1.1 1.3

Iron and steel , Nonferrous metals 11.9 10.2 15.1 17.8 11.2 11.0 10.0 9.2 14.9 13.0 10.9 21.0

General machinery 22.5 22.4 18.2 16.9 19.7 17.8 21.0 23.2 16.2 25.8 23.1 21.6

Electrical machinery 23.7 31.8 23.4 24.8 29.8 24.5 25.5 30.2 24.2 21.0 35.0 20.9

Household electric appliances 5.0 3.1 1.1 1.8 2.6 1.1 5.4 3.7 1.4 5.3 2.6 1.1

Transportation Equipment 9.8 5.5 8.3 9.7 3.5 10.5 5.6 3.5 4.6 15.4 9.5 9.7

Precision machinery 2.3 4.6 5.7 1.2 3.9 8.9 2.8 6.4 4.3 1.9 2.3 2.5

Toys and Miscellaneous goods 3.2 2.0 1.7 2.5 1.8 1.2 4.5 2.6 2.4 1.6 1.5 1.6

Total 100 100 100 100 100 100 100 100 100 100 100 100

Imports

Foods 13.9 9.0 6.0 16.0 10.6 5.1 16.0 7.1 5.6 11.4 8.7 7.9

Textile 12.0 13.2 10.2 28.6 30.0 15.4 15.9 4.6 1.9 2.2 3.3 5.8

Pulp, Paper and Wood 12.4 6.9 6.2 7.8 7.8 5.6 11.3 3.1 2.1 15.0 8.8 8.8

Chemicals 3.8 4.7 8.6 4.9 4.4 7.8 5.5 6.6 15.6 2.0 3.8 7.5

Oil and Coal 28.0 13.3 13.1 24.8 4.0 0.7 2.7 8.7 12.3 49.1 25.2 32.1

Stone, clay, glass and concrete products 2.7 1.6 1.6 3.2 2.5 1.9 3.6 1.3 1.6 1.8 0.9 1.0

Iron and steel , Nonferrous metals 9.0 5.5 7.9 5.0 4.2 5.9 12.7 8.2 15.1 7.8 5.0 6.9

General machinery 3.5 14.4 11.8 0.6 6.9 16.2 5.1 23.4 10.9 3.4 15.2 5.9

Electrical machinery 5.2 17.0 20.3 2.3 11.9 23.8 9.6 23.0 24.7 2.9 17.7 12.4

Household electric appliances 2.0 5.0 4.1 0.9 4.7 5.2 3.4 4.1 1.6 1.3 6.0 3.5

Transportation Equipment 0.8 1.1 2.7 0.1 1.1 2.6 2.1 1.6 2.9 0.1 0.7 2.7

Precision machinery 0.5 2.1 1.9 0.1 1.8 1.9 0.9 3.4 2.4 0.4 1.6 1.8

Toys and Miscellaneous goods 6.2 6.1 5.7 5.7 10.1 8.0 11.2 4.8 3.3 2.6 3.3 3.8

Total 100 100 100 100 100 100 100 100 100 100 100 100

Source: RIETI, Macquarie Research, March 2017

0

50

100

150

200

250

300

350

400 (US$bn)

Final Goods

Intermediate Goods

Primary Goods

Macquarie Research Macq-ro insights

1 March 2017 21

Extended supply chains require low friction costs as well as robust ICT systems. Fig 35

shows Japan’s Free Trade Agreements, which are predominately with other Asian countries.

Fig 36 gives an indication of customs and logistic ease across Asia, with Mexico included for

comparison purposes.

Fig 35 Japan’s completed FTAs

FTA Partners Start of negotiation Signing of FTA Enactment of FTA

In effect Singapore Jan-01 Jan-02 Nov-02

Mexico Nov-02 Sep-04 Mar-05

Malaysia Jan-04 Dec-05 Jul-06

Chile Feb-06 Mar-07 Sep-07

Thailand Feb-04 Apr-07 Nov-07

Indonesia Jul-05 Aug-07 Jul-08

Brunei Jun-06 Jun-07 Jul-08

ASEAN Apr-05 Apr-08 Dec-08

Philippines Feb-04 Sep-06 Dec-08

Switzerland May-07 Feb-09 Sep-09

Vietnam Jan-07 Dec-08 Oct-09

India Jan-07 Feb-11 Aug-11

Peru May-09 May-11 Mar-12

Australia Apr-07 Jul-14 Jan-15

Mongolia Jun-12 Feb-15 Jun-16

Source: Ministry of Foreign Affairs, Macquarie Research, March 2017

Fig 36 Efficiency of international logistics: 2016

Country Ranking (out of 160

countries) Score (1-5) Customs Infrastructure International

shipments Logistics

competence Tracking &

tracing Timeliness

Singapore 5 4.1 4.2 4.2 4.0 4.1 4.1 4.4 Hong Kong, China 9 4.1 3.9 4.1 4.1 4.0 4.0 4.3 Japan 12 4.0 3.9 4.1 3.7 4.0 4.0 4.2 Korea, Rep. 24 3.7 3.5 3.8 3.6 3.7 3.8 4.0 Taiwan 25 3.7 3.2 3.6 3.6 4.0 3.6 4.3 China 27 3.7 3.3 3.8 3.7 3.6 3.7 3.9 Malaysia 32 3.4 3.2 3.5 3.5 3.3 3.5 3.7 India 35 3.4 3.2 3.3 3.4 3.4 3.5 3.7 Thailand 45 3.3 3.1 3.1 3.4 3.1 3.2 3.6 Mexico 54 3.1 2.9 2.9 3.0 3.1 3.4 3.4 Indonesia 63 3.0 2.7 2.7 2.9 3.0 3.2 3.5 Vietnam 64 3.0 2.8 2.7 3.1 2.9 2.8 3.5 Brunei 70 2.9 2.8 2.8 3.0 2.6 2.9 3.2 Philippines 71 2.9 2.6 2.6 3.0 2.7 2.9 3.4 Cambodia 73 2.8 2.6 2.4 3.1 2.6 2.7 3.3 Myanmar 113 2.5 2.4 2.3 2.2 2.4 2.6 2.9 Lao PDR 152 2.1 1.9 1.8 2.2 2.1 1.8 2.7

Note: Myanmar and Lao PDR score poorly below, implying that despite low wage levels, both need to make considerable progress in their infrastructure facilities before they will be able to join the East Asian export supply chain in any scale

Source: World Bank, Logistics Performance Index, Macquarie Research, March 2017

For two Japanese MNCs, Fig 38 shows their East Asia ex Japan factory network: Canon

(7751 JP, ¥3,305, Neutral, TP: ¥3,350, Damian Thong) and Panasonic (recommendation

details below).

Fig 37 has the recommendation details for some of, we believe, Japan’s major exporters.

However, Japanese companies rarely release export data. The website “World’s Top

Exporters” is recommended for readers who wish to explore further.

Fig 37 Some of Japan’s major exporters, recommendation details

Stock Ticker Rec C/P T/P To TP

(%) Stock Ticker Rec C/P T/P To TP

(%)

Toyota Motor 7203 OP 6,448 7,900 22.5 Panasonic 6752 OP 1,259 1,450 15.2 Honda Motor 7267 OP 3,553 4,300 21.0 Sony 6758 OP 3,486 4,250 21.9 Nissan Motor 7201 OP 1,112 1,530 37.6 Toshiba 6502 OP 224 315 40.7 Hitachi 6501 OP 633 755 19.3 Nippon Steel SM 5401 OP 2,808 3,000 6.9 JX Holdings 5020 OP 532 630 18.4 MHI 7011 N 444 470 5.9

Note: Share prices as of 24 February. Source: Macquarie Research, March 2017

Japan’s Free Trade

Agreements are

predominately with

other Asian

countries

Canon and

Panasonic

Japanese

companies rarely

release export data

Ma

cq

ua

rie R

esea

rch

M

acq-ro

insig

hts

1 M

arc

h 2

01

7

22

Fig 38 Examples of Japanese MNC factory networks in East Asia ex-Japan: Canon and Panasonic

Panasonic

1. Panasonic Industrial Devices Singapore, 2. Panasonic Industrial Devices Malaysia Sdn. Bhd. 3. PT. Panasonic Industrial Devices Batam, 4. Panasonic Manufacturing (Thailand) Co., Ltd, 5. Panasonic Industrial Devices Vietnam Co.,Ltd, 6. P.T SANYO Jaya Components Indonesia, 7. Panasonic Precision Devices Philippines Corporation, 8. Panasonic Industrial Devices (Tianjin) Co.,Ltd, 9. Panasonic Industrial Devices (Beijing) Co., Ltd, 10. Panasonic Industrial Devices (Qingdao) Co.,Ltd, 11. Panasonic Industrial Devices Taiko (Shenzhen) Co, 12. Panasonic Electronic Devices (Jingmen) Co.,Ltd, 13. Panasonic Industrial Devices (Hong Kong) Co.,Ltd

Canon