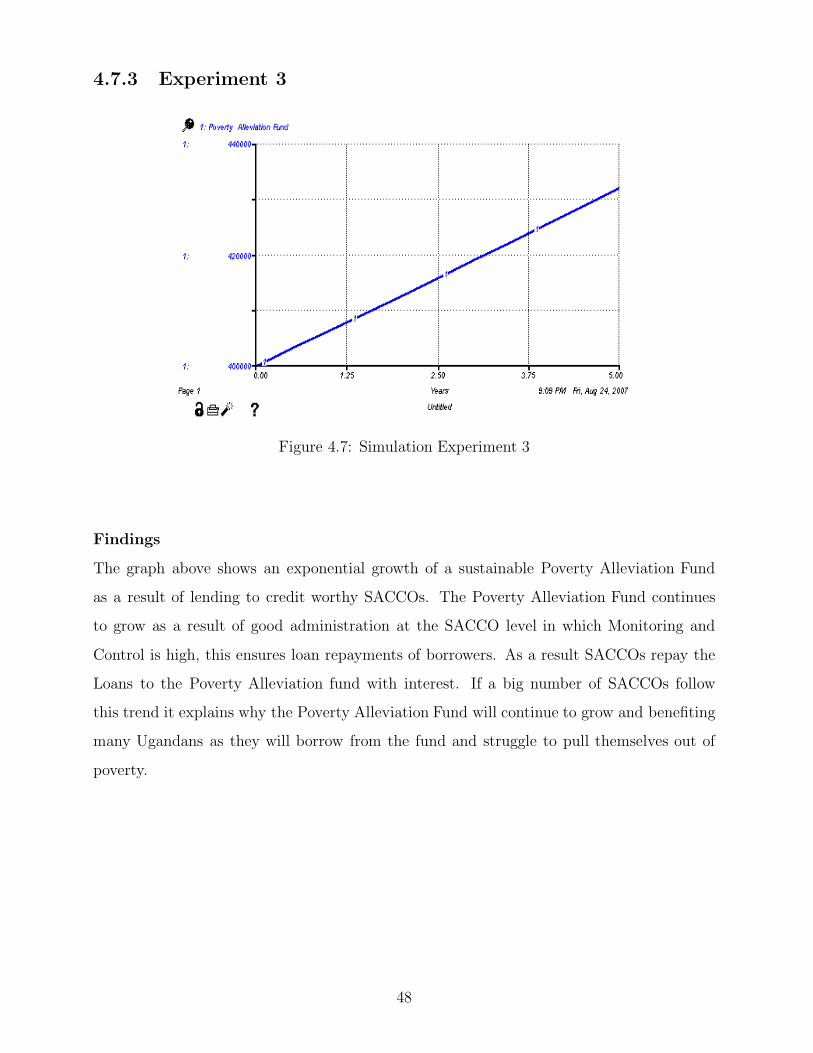

loan servicing

TRANSCRIPT

A Simulation Model of Loan Servicing forSavings and Credit Cooperative

Organizations (SACCOs) under the PovertyAlleviation Program

by

SSEWANKAMBO DAMIAN

2005/HD18/4053UBIFA(Mak), PGDCS(Mak)

[email protected], +256 752 436 317

A Project Report Submitted to School of Graduate Studies in

Partial Fulfillment for the Award of Master of Science inComputer Science Degree of Makerere University

Option: Computer Information Systems

October, 2007

Declaration

I Ssewankambo Damian do hereby declare that this Project Report is original and has notbeen published or submitted for any other degree award to any other University before.

Signed: .......................................................... Date: ...........................................Ssewankambo DamianBIFA(Mak), PGDCS(Mak)Department of Information SystemsFaculty of Computing and Information Technology, Makerere University

Approval

This Project Report has been submitted for Examination with the approval of the followingsupervisors.

Signed: .......................................................... Date: ...........................................Prof. V. Baryamureeba, PhDSupervisorDepartment of Computer ScienceFaculty of Computing and Information Technology, Makerere University

Signed: .......................................................... Date: ...........................................Ms. Agnes RwashanaBAC (Mak), Msc (Mak)Assistant SupervisorDepartment of Information SystemsFaculty of Computing and Information Technology, Makerere University

ii

Dedication

This work is dedicated to my beloved parents Mr. Sekiziyivu Damian and Ms. TeddyKyebonere.

iii

Acknowledgments

I would like to thank my Father and Mother for the moral and financial support they havegiven me throughout this course.

Special thanks to my supervisor Professor Venansius Baryamureeba for the intellectual guid-ance and advice given to me, without which this work would not have been a success.

My thanks go to Dr. Ddembe Williams, Dr. Tom Wanyama, Ms. Agnes Rwashana and Mr.Paul Ssemaluulu who were always there for me.

My thanks also go to my colleagues Sarah Nsibirwa Nsubuga, Kabuye Patrick and BulegaWilson with whom we formed a Simulation and Modeling discussion group.

Iam grateful to my sisters Vivian Nakabugo, Frances Namuli ,Cissy Nakanjako and JoselineNassali who have always been supportive.

Lastly I thank all those who contributed to this work in one way or another, I will alwaysappreciate your contributions.

MAY THE ALMIGHTY GOD BLESS YOU ALL.

iv

Contents

Declaration . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . iApproval . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . iiDedication . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . iiiAcknowledgements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . iv. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . viList of Figures . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . viiList of Tables . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . viiiAcronyms . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ixAbstract . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . xi

1 INTRODUCTION 11.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

1.1.1 Background to the Study . . . . . . . . . . . . . . . . . . . . . . . . . 21.2 Statement of the problem . . . . . . . . . . . . . . . . . . . . . . . . . . . . 51.3 Objectives . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

1.3.1 Scope . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 71.3.2 Significance of the study . . . . . . . . . . . . . . . . . . . . . . . . . 81.3.3 Conceptual Framework . . . . . . . . . . . . . . . . . . . . . . . . . . 91.3.4 Research Contributions . . . . . . . . . . . . . . . . . . . . . . . . . . 11

2 LITERATURE REVIEW 122.1 Review of Loan Servicing Case Studies . . . . . . . . . . . . . . . . . . . . . 122.2 System Dynamics/Simulation Models in Credit Evaluation . . . . . . . . . . 14

2.2.1 Stock and Flow Diagram of a Credit Evaluation System . . . . . . . . 142.2.2 Running of a Simulation . . . . . . . . . . . . . . . . . . . . . . . . . 15

2.3 Modeling and Simulation Systems . . . . . . . . . . . . . . . . . . . . . . . 162.4 Strengths and weaknesses of simulation . . . . . . . . . . . . . . . . . . . . 17

2.4.1 Strengths of simulation . . . . . . . . . . . . . . . . . . . . . . . . . 172.4.2 Weaknesses of Simulation . . . . . . . . . . . . . . . . . . . . . . . . 19

2.5 State of the art and practice in loan servicing . . . . . . . . . . . . . . . . . 202.5.1 Loan Products . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 202.5.2 Loan servicing tips . . . . . . . . . . . . . . . . . . . . . . . . . . . . 202.5.3 Characteristics of loans . . . . . . . . . . . . . . . . . . . . . . . . . 21

2.6 Poverty Alleviation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 212.6.1 How income poverty is measured. . . . . . . . . . . . . . . . . . . . . 212.6.2 Trends in income poverty and inequality . . . . . . . . . . . . . . . . 222.6.3 Role of Empowerment in Poverty Alleviation . . . . . . . . . . . . . . 23

v

2.6.4 Divestiture of Micro Credit Schemes as a Tool in Fighting Poverty . . 242.6.5 Role of Decentralization in Fighting Poverty . . . . . . . . . . . . . . 252.6.6 Impact of credit in Poverty Alleviation . . . . . . . . . . . . . . . . . 26

2.7 Loan Recovery . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 262.8 Targets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 262.9 Critique on the Literature . . . . . . . . . . . . . . . . . . . . . . . . . . . . 272.10 Conclusion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27

3 METHODOLOGY 283.1 Review of methodologies . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28

3.1.1 Case Study. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 283.1.2 Viable Systems . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 293.1.3 Dynamic Synthesis Methodology . . . . . . . . . . . . . . . . . . . . 29

3.2 How the specific objectives were achieved . . . . . . . . . . . . . . . . . . . . 323.2.1 Identify shortcomings with the current approaches . . . . . . . . . . . 323.2.2 Identify Variables . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 333.2.3 Simulation Model Development . . . . . . . . . . . . . . . . . . . . . 333.2.4 Validation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 34

4 PRESENTATION OF RESULTS 354.1 Shortcomings with the current approaches . . . . . . . . . . . . . . . . . . . 354.2 Identified Variables . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38

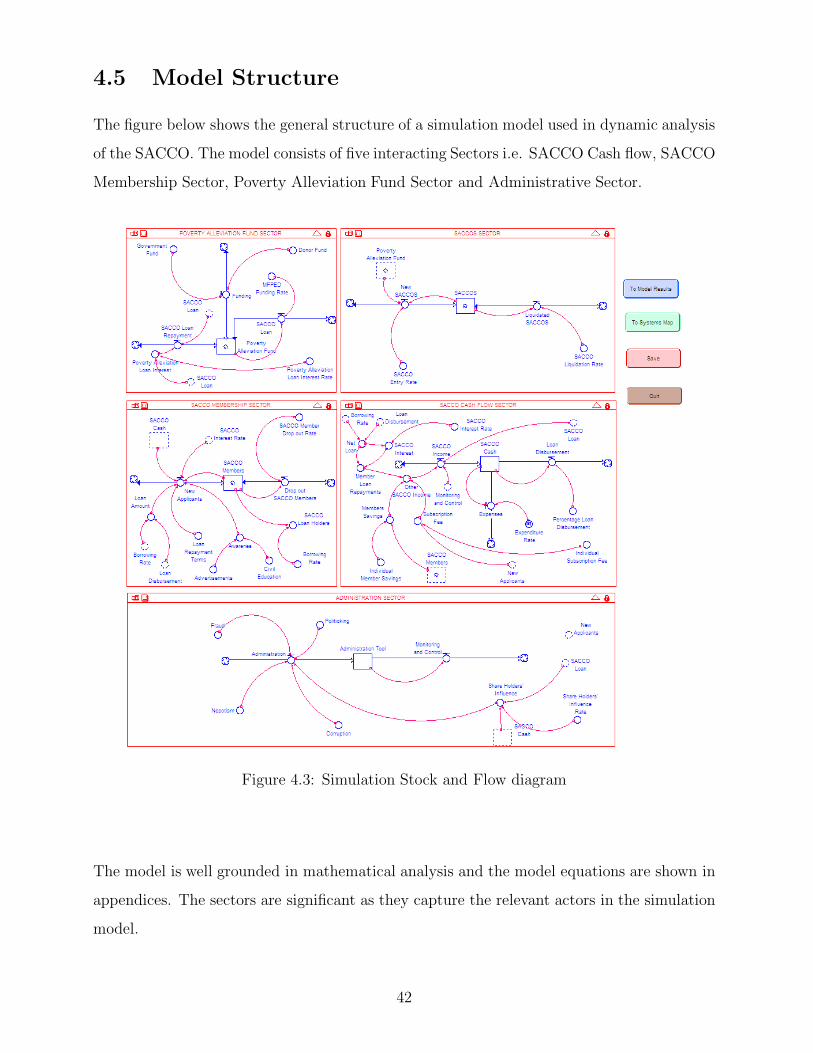

4.2.1 Definition of variables . . . . . . . . . . . . . . . . . . . . . . . . . . 384.3 Causal loop Diagram . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 414.4 Modeling Decisions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 414.5 Model Structure . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42

4.5.1 POVERTY ALLEVIATION FUND SECTOR . . . . . . . . . . . . . 434.5.2 SACCOS SECTOR . . . . . . . . . . . . . . . . . . . . . . . . . . . . 434.5.3 SACCO CASH FLOW SECTOR . . . . . . . . . . . . . . . . . . . . 434.5.4 SACCO MEMBERSHIP SECTOR . . . . . . . . . . . . . . . . . . . 444.5.5 ADMINISTRATION SECTOR . . . . . . . . . . . . . . . . . . . . . 45

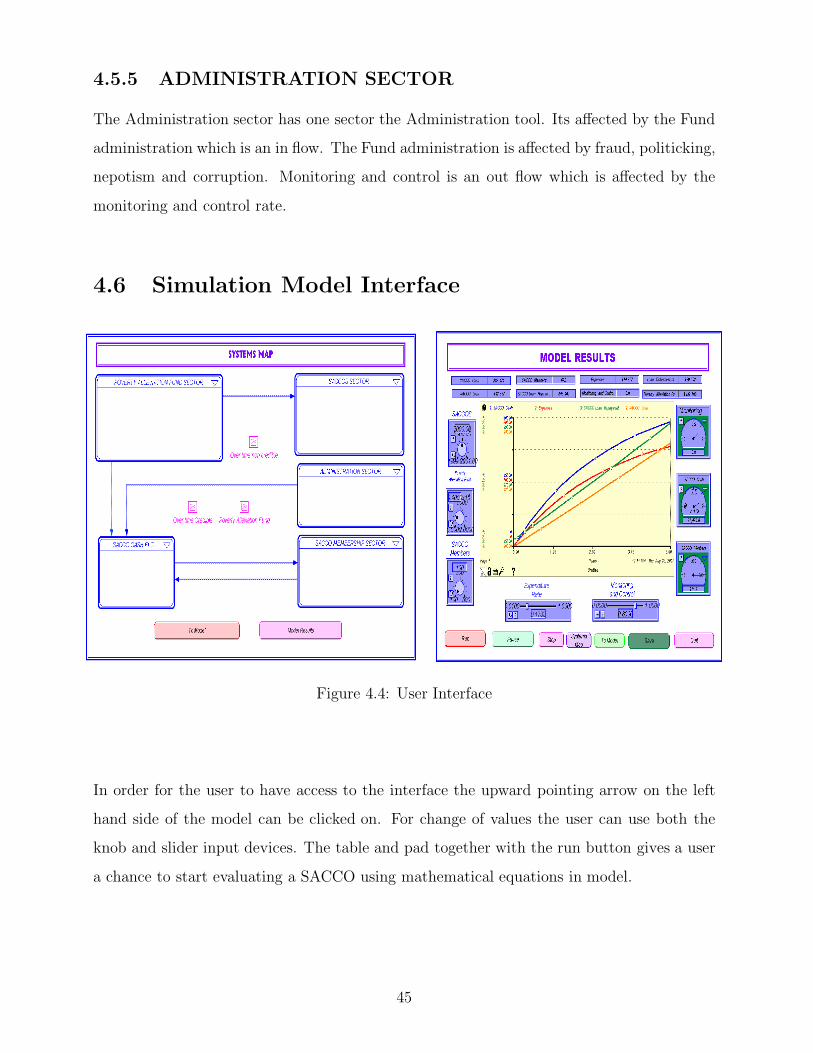

4.6 Simulation Model Interface . . . . . . . . . . . . . . . . . . . . . . . . . 454.7 Initial Conditions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 46

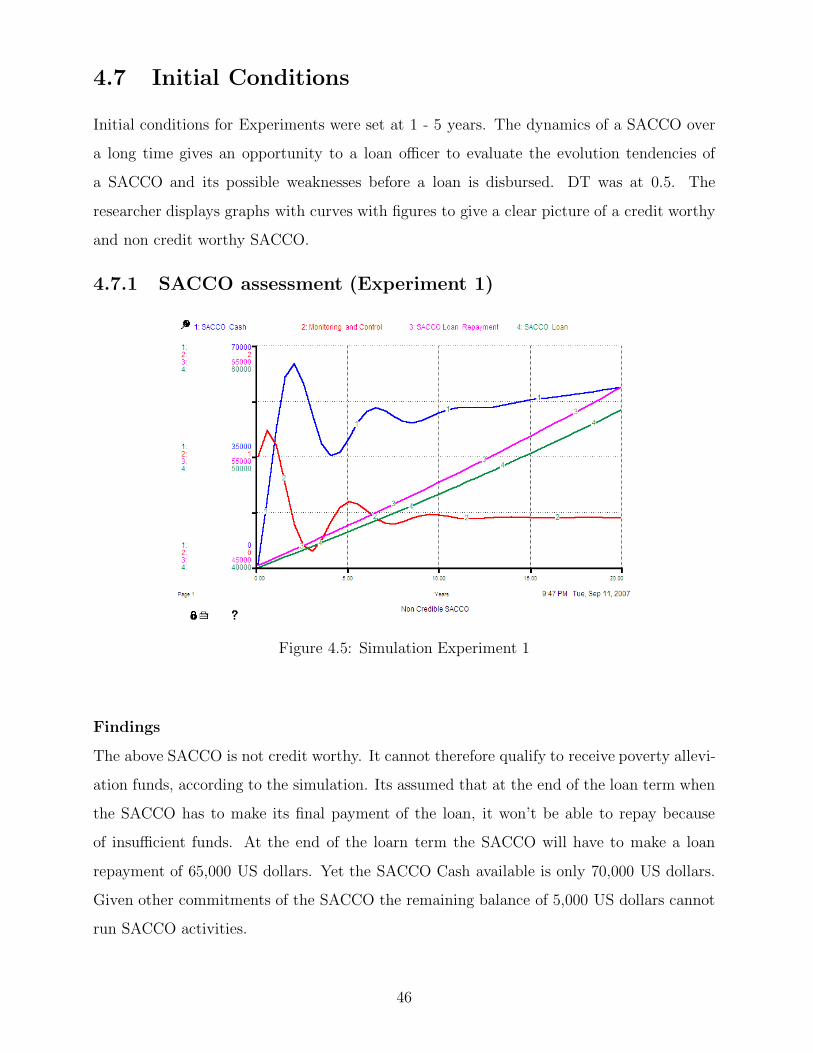

4.7.1 SACCO assessment (Experiment 1) . . . . . . . . . . . . . . . . . . . 464.7.2 SACCO assessment (Experiment 2) . . . . . . . . . . . . . . . . . . . 474.7.3 Experiment 3 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 48

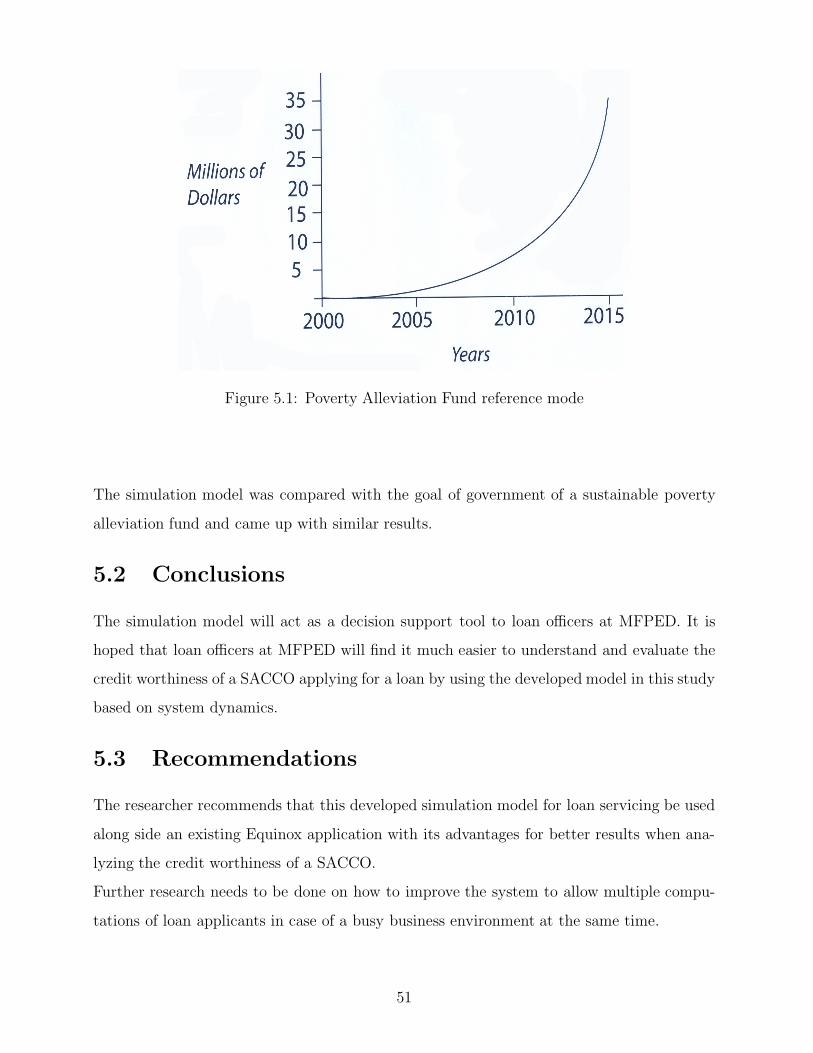

5 DISCUSSION, CONCLUSIONS AND RECOMMENDATIONS 495.1 Discussion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 495.2 Conclusions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 515.3 Recommendations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 51REFERENCES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 52APPENDIX A: INTERVIEW GUIDE . . . . . . . . . . . . . . . . . . . . . . . . 56APPENDIX B: MODEL EQUATIONS . . . . . . . . . . . . . . . . . . . . . . . . 58

vi

List of Figures

1.1 Shows the trend of fighting poverty in Uganda. . . . . . . . . . . . . . . . . . 51.2 Behavior over time graph representing the standards of living and inequality

in relation to the introduction of new poverty alleviation schemes and theirefficiency (MFPED, 2005[27]). . . . . . . . . . . . . . . . . . . . . . . . . . . 6

1.3 Conceptual Framework . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

2.1 The figure shows the structure of the cash, bank credit and account receivables. 15

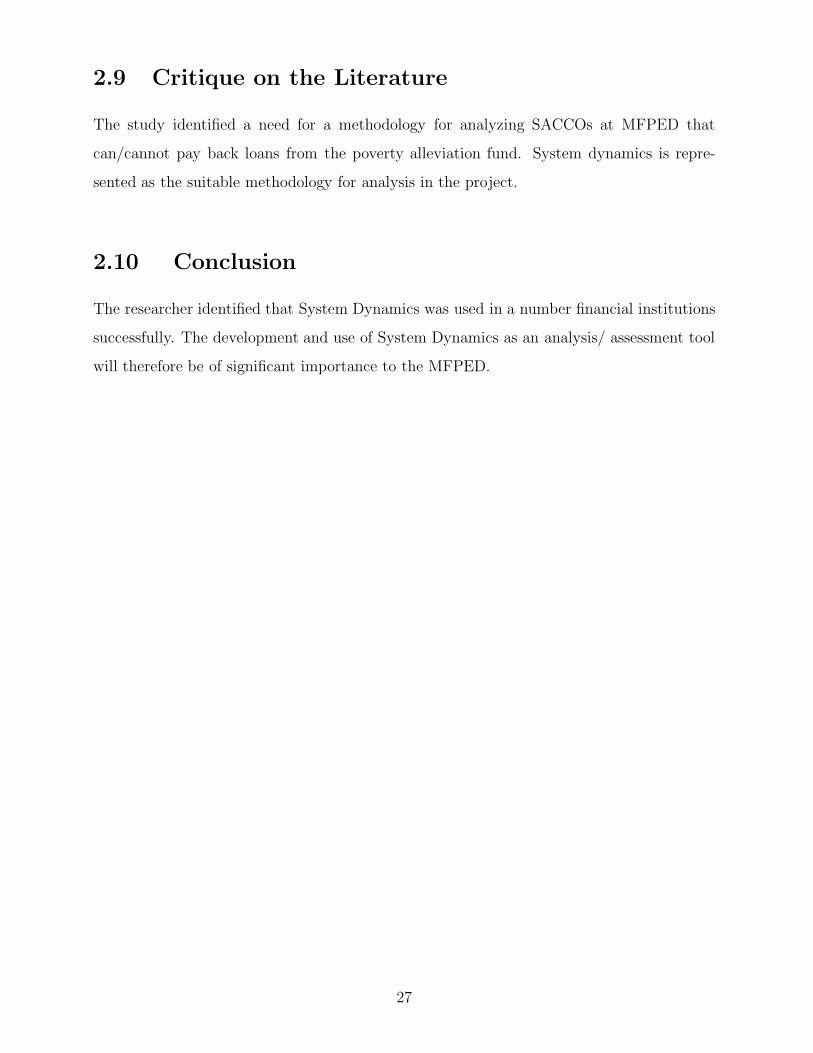

3.1 The Dynamic Synthesis Methodology. Adapted from (Williams, 2004) [46] . 303.2 System Dynamics Modeling. Adapted from (Richard and Pugh,1981)[38]. . . 31

4.1 Micro finance Institutions Model. Adapted from (Gary,2000)[13]. . . . . . . . 384.2 Causal Loop Diagram for the proposed Simulation Model . . . . . . . . . . . 414.3 Simulation Stock and Flow diagram . . . . . . . . . . . . . . . . . . . . . . . 424.4 User Interface . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 454.5 Simulation Experiment 1 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 464.6 Simulation Experiment 2 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 474.7 Simulation Experiment 3 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 48

5.1 Poverty Alleviation Fund reference mode . . . . . . . . . . . . . . . . . . . . 51

vii

List of Tables

2.1 Levels of Poverty . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 222.2 Poverty by occupational group . . . . . . . . . . . . . . . . . . . . . . . . . . 24

3.1 Methodologies explored . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28

viii

LIST OF ABBREVIATIONS

ACORD: Agency for Cooperation and Research in Development.AFCAP: African Pilot Capacity Building ProgrammeAMFIU: Association of Micro enterprise Finance Institutions of Uganda.BOU: Bank of UgandaCBOs: Community Based OrganizationsCDW: Community Development WorkerCGAP: Consultative Group to Assist the Poorest.CMF: Center for Micro Enterprise Finance.DANIDA: Danish International Development Agency.DFD: Development Finance Department, Bank of UgandaDFID: Department for International Development.ECS: Entandikwa Credit SchemeFEW: Financial Extension WorkerGOU: Government of Uganda.GTZ: German Technical Cooperation. (Deutsche Cresellschaft fur Technische Zusammenar-beit)IMF: International Monitory FundIFAD: International Fund for Agriculture DevelopmentLTV: Loan to Value ratiosMCC: Micro Finance Competence CenterMDIs: Micro Deposit-taking InstitutionsMFF: Micro Finance Forum.MFIs: Micro Finance Institutions.MFPED: Ministry of Finance, Planning and Economic DevelopmentMGLSD: Ministry of Gender, Labour and Social DevelopmentMTCS: Medium Term Competitiveness Strategy for the Private SectorNAADS: National Agricultural Advisory Services ProgrammeNGOs: Non Government OrganizationsNPART: Non-Performing Assets Recovery TrustNURP I : Northern Uganda Rehabilitation ProjectOSS: Operational Self SufficiencyPAP: Poverty Alleviation ProjectPAPSCA: Programme for Poverty Alleviation and Social Costs of Structural AdjustmentPEAP: Poverty Eradication Action PlanPMA: Plan for the Modernization of AgriculturePMA: Plan for Modernization of AgriculturePRESTO: Private Enterprise Support, Training and Development Programme.PRSPs: Poverty Reduction Strategy PapersPSDP: Private Sector Development Programme.RMSP: Rural Micro Finance Support ProjectSACCOS: Savings and Credit Cooperative OrganizationsSME: Small and Medium Sized EnterpriseSPEED: Support for Private Enterprise Expansion and Development.STELLA: Systems Thinking Educational Learning Laboratory with Animation

ix

SUFFICE: Support to Feasible Financial Institutions and Capacity Building Efforts.UBOS: Uganda Bureau of StatisticsUCA: Uganda Cooperative Alliance.UCAP: Uganda Micro Finance Capacity-Building FrameworkUNDP: United Nations Development Programme.UNHCR: United Nations High Commissioner for RefugeesUSAID: United States Agency for International Development.YES: Youth Entrepreneurs Scheme

x

Abstract

Evaluating credit worthy SACCOs that receive Poverty Alleviation Funds has been consid-

ered as one of the main dilemmas that loan officers at the Ministry of Finance Planning and

Economic Development (MFPED) in Uganda have to face in order to reduce the probability

of default. The lending process involves application for loans from MFPED to the successful

or unsuccessful repayment of the loan.

The objective of the Project report was to develop a simulation model that can be used

to analyze SACCOs that can / cannot pay back borrowed poverty alleviation funds to the

MFPED. This objective was achieved through the use of Systems Thinking Educational

Learning Laboratory with Animation (STELLA) software. In developing the simulation

model the concepts of System Dynamics were used. The Dynamic Synthesis Methodology

was used in the development process of the model because its a proven methodology used

by experienced modelers.

The experiments carried out indicate that SACCOs that apply for poverty alleviation funds

can be easily evaluated based on the risk assessment of the credit worthiness a SACCO

under different (What - if) scenarios. As a diagnostic tool this Simulation Model provides

an insight into the underlying structures of a SACCO from which behavior over time and

discreet events emerge. Loan officers can therefore use this Model to give advice to non

credit worthy SACCOs on how to improve on the performance of their organizations so as

to be worthy of receiving funding from the MFPED and rid themselves of poverty.

The researcher recommends that further research be made on how the system can accommo-

date multiple users simultaneously evaluating credit worthy applicants in a busy networked

environment.

xi

Chapter 1

INTRODUCTION

1.1 Introduction

The Poverty Eradication Action Plan (PEAP) is Uganda’s comprehensive Development

Framework. The PEAP has guided the formulation of government policy since its inception

in 1997. It is hoped that under this plan, Uganda will be transformed into a modern economy

in which agents in all sectors can participate in economic growth (MFPED, 2005) [27].

This implies that a number of conditions must be met:-

(i) The economy requires structural transformation, including the modernization of agri-

culture and the development of industries which build on demand and supply linkages

from agriculture.

(ii) The poor must be able to participate in this growth, both by expanding smallholder

agriculture and by expanding employment in industry and services, as well as in rural

non farm enterprises.

(iii) The economic growth must be sustainable

However in order for all the above conditions to be met, there must be cooperation in form

of loan repayment from the general public that receives loans under the project. This will

therefore benefit the wider community by expanding beneficiary base.

1

1.1.1 Background to the Study

Over the last 19 years, the Government of Uganda(GOU) implemented policies geared to-

wards eradicating poverty. These policies involved lending money to individuals through

state credit programs which included

(i) The Entandikwa Credit Scheme (ECS);

”Entandikwa” means ”start up capital”. The credit scheme was a start up capital

fund targeting poor people, with the aim of helping them to improve their economic

status. Under the scheme, 30 percent of the credit was allocated to women and youth

(International Labour Organization, 2003) [19]. Entandikwa was a government admin-

istered programme that disbursed start up loans under the Ministry of Finance. ECS

was apparently proposed by Parliament in 1993 as a way to cover the credit needs of

war-ravaged areas (originally slated for 14 districts). Probably due to political pressure

it was extended to all districts (in fact to all 214 constituencies) in the country with a

fixed (and equal) amount of loan capital being provided per constituency, thereby con-

firming the political nature of the change. It began lending in 1995 and by June 1996

had disbursed US Dollars 7.42 million in GOU money (there was no donor support

to this programme). However the exercise collapsed because the borrowers failed to

pay back (Dichter and Kamuntu, 1997) [9]. According to Moses Byaruhanga the Pres-

idential Advisor on Political Affairs, the government of Uganda suffered a shs.9b loss

through the Entandikwa Schemme. It failed due to poor management and inadequate

loan repayment.” (AGOA News, 2005) [2].

(ii) The Youth Entrepreneurship Scheme (YES).

This scheme was an intervention to mope up unemployment by enabling the affected

majority - youth to be self sustaining (Parliament, 2003) [33]. It was a credit scheme

funded directly through the treasury (Okrut et al., 2004)[32].

(iii) Poverty Alleviation Project (PAP).

The Poverty Alleviation Project was introduced to check the growing poverty levels

with in the rural population. In this project poor landless people would get government

2

loans to buy land, cultivate on it and earn a living as a way of pulling themselves out

of poverty.

(iv) Rural Farmers Scheme (RFS).

This scheme targeted rural farmers. Through this scheme farmers would be given seeds

or animals to rare, machinery such as tractors and technical advice about modern

farming methods. After a given period of time or after harvesting the beneficiaries

were expected to repay the loan depending on the assistance given so as to benefit

other farmers.

(v) Cooperative Credit Scheme (CCS).

Cooperative societies were the beneficiaries of the Cooperative Credit Scheme. Under

this project cooperative societies would borrow from the scheme and pay back a loan

after a specified period of time.

It should be noted that the performance of the schemes was adversely affected by very poor

loan recovery, inefficiency and high management costs which consequently led to under per-

formance or collapse. The view that prevailed for many years was that micro borrowers were

too poor to pay back their loans.

Poverty had increased from 33.8 percent in 1999/00 to 37.7 percent in 2002/03. However

government’s target is to have 28 percent of poor in overall population by 2014/2015 (MF-

PED, 2005) [24]).

More needs to be done to ensure that all Ugandans move and stay out of poverty. The cur-

rent Poverty Eradication Action Plan (2004/5 - 2007/8), has one of its major strategic points

as; instituting a micro-finance delivery system relying on Savings and Cooperative Credit

Organizations (SACCOs) which are made up of individuals. Here government lends money

to a SACCO through the MFPED at low interest rates. The organization/SACCO then

divides funds among members. However there should be a mechanism for analyzing whether

SACCOs can be able to pay back the money to the poverty alleviation fund/MFPED.

3

Existing case studies of loan servicing in state credit programs/SACCOs include:- Manual

system, Loan performer application, and Equinox application. These systems are robust in

the scheduling of payment times of borrowers, data storage and are easy to use. However they

do not evaluate the credit worthiness and ability of the SACCOs to pay back loans over time.

The Simulation Model developed by the researcher evaluates the credit worthiness and the

ability of a SACCO to pay back a loan over time. This simulation model caters for ”WHAT

IF” incidences and help the Loan Officer take decisions from an informed point of view

about credible borrowers. Its logical to argue that this simulation model for loan servicing

can be used along side an existing Equinox application with its advantages for better results

when analyzing the credit worthiness of a SACCO. Therefore there was a need to develop a

simulation model that could be used to identify unsound SACCOs.

4

1.2 Statement of the problem

The Government of Uganda has implemented policies geared towards eradicating poverty.

These policies involve lending money to individuals through state credit programs (En-

tandikwa Credit Scheme, Youth Entrepreneurship Scheme, Poverty Alleviation Project, Ru-

ral Farmers Scheme and Cooperative Credit Scheme) which have continuously collapsed due

to inadequate loan repayment to the poverty alleviation fund. Currently a new credit scheme

in which loans are disbursed to Savings Credit and Cooperative Organizations (SACCOs)

has been launched under the Ministry of Finance Planning and Economic Development.

However, there is no system used in assessing the performance of SACCOs that receive loans

from the scheme and their ability to payback these loans. This is an inadequate way of

planning for the poverty alleviation funds. The ministry in its planning and management

approach to these funds has shown a great loophole in this sector hence the need to use

Systems Dynamics as a tool that can analyze borrowers that can / cannot pay back loans

so as to ensure the sustain ability of the poverty alleviation fund.

Poverty Alleviation Dynamic Theory

Figure 1.1: Shows the trend of fighting poverty in Uganda.

The government’s experiences in fighting poverty are represented by Shifting the burden

archetype. Over the years the low standards of living faced by the population have prompted

5

government to introduce new poverty alleviation schemes as a quick solution to alleviating

poverty. The quick solution portrays the government as an entity trying to solve the poverty

problem.

The side effect of introducing new poverty alleviation schemes is that the causes of fail-

ure in administration of previous schemes are not investigated exorbitantly to eliminate the

reoccurance of past mistakes as aresult it leads to the lack of an adequate administration

tool. Despite the fact that government and the development partners through the MFPED

have continually allocated resources to alleviate poverty through poverty alleviation schemes,

poverty still looms among Ugandans. Lack of an adequate administration tool reduces the

chance of getting a fundamental solution, which is an effective poverty alleviation scheme.

However if an adequate administration tool is got an efficient poverty alleviation scheme

will be got. Though it will take some time (delay) before tangible results are seen the low

standards of living will be reduced hence reducing poverty. At the same time there will be

more support for an efficient poverty alleviation scheme. With the cause of failure of previous

schemes the current scheme (SACCOs) can be a success if the past deficiencies are addressed.

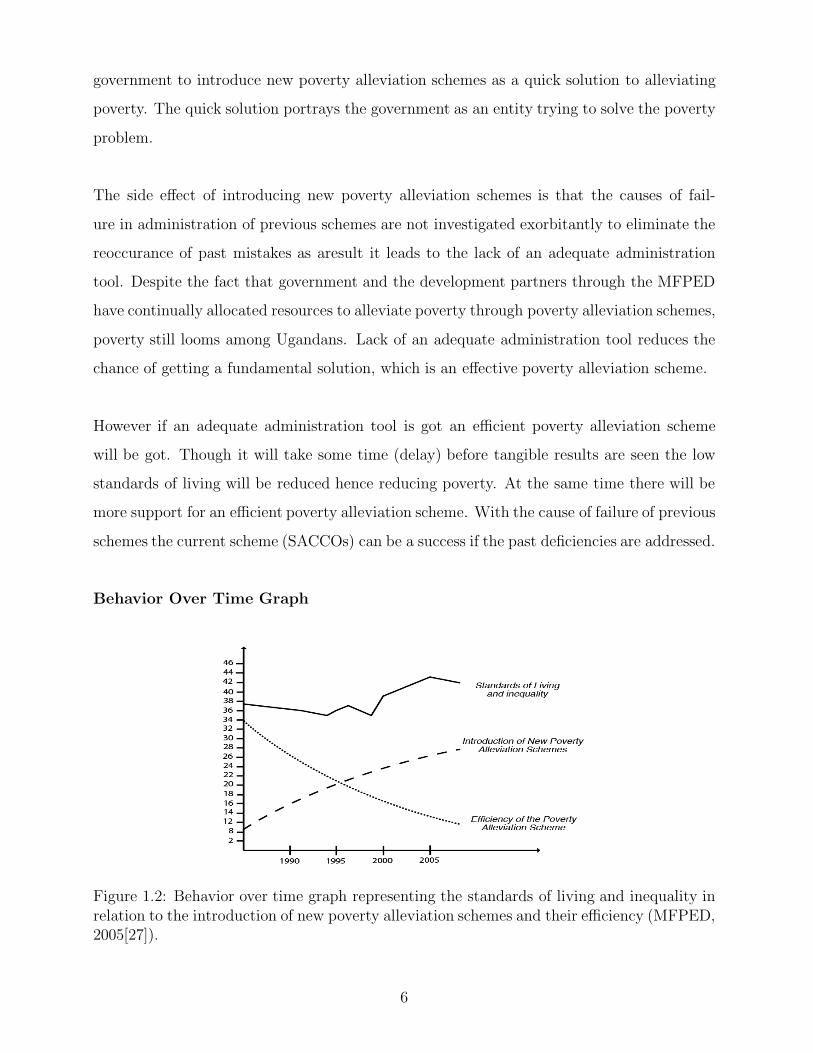

Behavior Over Time Graph

Figure 1.2: Behavior over time graph representing the standards of living and inequality inrelation to the introduction of new poverty alleviation schemes and their efficiency (MFPED,2005[27]).

6

Each time an intervention is made by introducing a new poverty alleviation scheme to re-

duce on the low standards of living a temporary improvement is registered but short lived.

Poverty remains as well as becoming worse.

1.3 Objectives

Main Objective:

The main objective of the study was to develop a Simulation model that can be used to

analyze SACCOs that can / cannot pay back poverty alleviation funds.

Specific Objectives:

(i) To identify shortcomings with the current approaches used in determining SACCOs

that receive loans from the poverty alleviation fund.

(ii) To identify variables for inclusion in the Simulation Model.

(iii) To develop a simulation model as a decision support tool for identifying credible SAC-

COs.

(iv) To validate the simulation model with existing case studies.

1.3.1 Scope

The research focused on analysis of SACCOs and their ability to pay back loans offered by

the Poverty Alleviation Scheme. It also examined the factors, which influenced positively

and negatively the performance of SACCOs. All these were put together to form a simulation

model, from which various simulations were made. The period of study considered is 2000

to 2006.

Area and population study

The study was conducted in Uganda in Kampala district at the MFPED, Post Bank head-

quarters and in Wakiso district at Wakiso Self Help Savings and Credit Cooperative or-

ganization . The office of the SACCOs coordinator at the MFPED and Wakiso Self Help

7

Savings and Credit Cooperative organization officials were visited to gather the necessary

information needed for the research. People from within the SACCO and from outside, were

interviewed so as to gather their experience in the poverty alleviation.

1.3.2 Significance of the study

(i) The simulation model will help loan officers responsible for issuing poverty alleviation

funds make meaningful decisions quickly and from an informed position. Simulation

can improve the education, effectiveness and help to develop the art of decision -

making. Simulation can be used as a facilitator of communicating ideas up and down

with in the organization(Greasley, 2004) [15].

(ii) Sustainability of the poverty alleviation fund will be achieved. The system will be

able to analyze and eliminate unsound SACCOs. In this arrangement credit worthy

SACCOs will be able to receive loans and through effective loan repayment the poverty

alleviation fund will grow because of interest, benefiting a bigger fraction of the pop-

ulation hence poverty alleviation.

(iii) The Simulation Model will lead to better management since the system will be eliminat-

ing unsound SACCOs from receiving loans. Therefore the borrowers will be expected

to meet their repayment commitments without the MFPED alocating much resources

for SACCOs to be closely monitored.

(iv) With the development of a Simulation Model as an analysis and assessment tool, loan

officers will be able to advise SACCOs on how to improve on performance depending

on analysis given by the system. System Dynamics models help to understand the

relationship between behavior patterns and system structure. Problems related to

system behavior can then be solved by changing the system structure (Marquez and

Blanchar, 2004) [26].

(v) To the government of Uganda through the MFPED this study will be applicable in

its planning procedures. Through simulations the MFPED will be able evaluate its

progess on the fight against poverty.

8

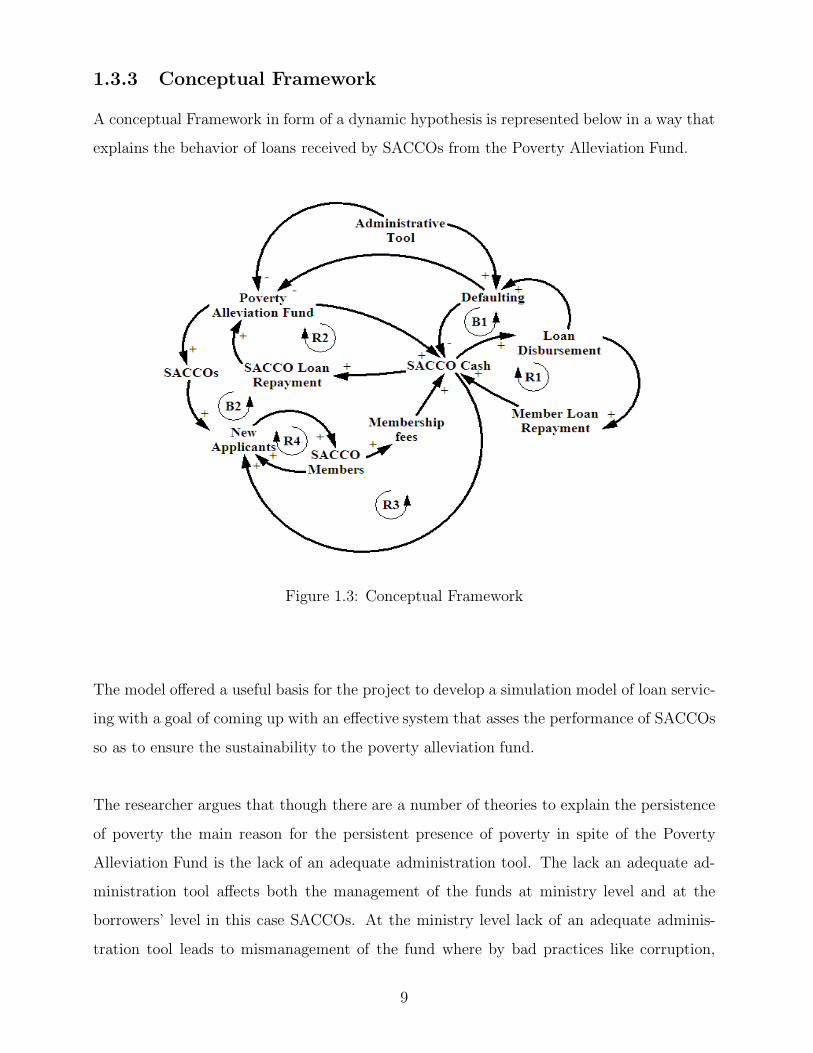

1.3.3 Conceptual Framework

A conceptual Framework in form of a dynamic hypothesis is represented below in a way that

explains the behavior of loans received by SACCOs from the Poverty Alleviation Fund.

Figure 1.3: Conceptual Framework

The model offered a useful basis for the project to develop a simulation model of loan servic-

ing with a goal of coming up with an effective system that asses the performance of SACCOs

so as to ensure the sustainability to the poverty alleviation fund.

The researcher argues that though there are a number of theories to explain the persistence

of poverty the main reason for the persistent presence of poverty in spite of the Poverty

Alleviation Fund is the lack of an adequate administration tool. The lack an adequate ad-

ministration tool affects both the management of the funds at ministry level and at the

borrowers’ level in this case SACCOs. At the ministry level lack of an adequate adminis-

tration tool leads to mismanagement of the fund where by bad practices like corruption,

9

politicking and nepotism are not checked. At the borrowers level the lack of an adequate

administration tool makes monitoring and control of funds impossible, this leads to default-

ing of loans by borrowers. With massive defaulting of members in a SACCO, loans from

the Poverty Alleviation Fund cannot be paid back by a SACCO hence making the Poverty

Alleviation Scheme ineffective. If all SACCOs fail to return the borrowed funds the scheme

collapses.

The following are the relationships that can be drawn from the conceptual framework.

(i) SACCO Cash increases Loan disbursement to members. Loan disbursement in turn

increases the number of members making repayments (Member Loan Repayments) to

the pool (SACCO Cash). This increases the SACCO Cash since members pay back

loans with interest.

(ii) SACCO Cash increases Loan disbursement. Loan disbursement increases the risk of

defaulting cases (Defaulting). Defaulting reduces SACCO Cash.

(iii) When the Poverty Alleviation Fund lends money to a SACCO inform of loans the

SACCO Cash increases. SACCO Cash in turn increases SACCO loan repayment.

SACCO loan repayment with interest increases the poverty Alleviation Fund.

(iv) The ability of a SACCO to mobilize a lot of funds (SACCO Cash) attracts new appli-

cants to the SACCO. New applicants increase the number of SACCO members. An

increase in SACCO members leads to an increase in Membership fees collected. An

increase in membership fees collected increases the SACCO cash.

(v) The availability of the poverty alleviation funds attracts new SACCOs to be formed

so as to benefit from the loans. SACCOs formed and have received loans attract new

applicants to the SACCO. New applicants lead to an increase in SACCO members.

An increase in SACCO members leads to an increase in membership fees collected. An

increase in membership fees collected lead to an increase to SACCO cash. SACCO cash

increases SACCO loan repayment. SACCO loan repayment with interest increases the

Poverty Alleviation Fund.

10

(vi) An inadequate administration tool of the management and oversight of the Poverty

Alleviation Fund leads to the loss of funds or collapse of the fund making it ineffective

in alleviating poverty. An inadequate administration tool at the same time reduces

the ability of SACCOs to monitor their activities effectively leading to defaulting of

members hence making a SACCO unable to pay back poverty alleviation funds.

1.3.4 Research Contributions

This Project Report made a contribution to the literature in terms of analyzing SACCOs

that can / cannot pay back poverty alleviation loans to the Ministry of Finance Planning and

Economic Development. The resulting tool will help SACCO Loan Managers at the MFPED

cut down debates on decisions regarding applicant SACCOs to receive poverty alleviation

funding, reduce loan losses and help researchers analyse related problems.

11

Chapter 2

LITERATURE REVIEW

Introduction

In this Chapter the researcher reviewed literature on loans, loan systems, system dynamics /

simulation and poverty in Uganda and abroad in the quest of developing a simulation model

based on standards and facts. This was of essence in developing a system that evaluates

credit worthy SACCOs putting the conditions / complexities of Uganda into perspective.

2.1 Review of Loan Servicing Case Studies

The researcher in this part presents loan servicing case studies that have been used in state

credit programs by lending authorities in Uganda. They include the following:-

(i) Manual System

At the time of launching the Entandikwa Credit Scheme and the Youth Entrepreneur-

ship scheme in the 1990s, loan accounting systems were not available to Lenders situ-

ated at county level. Lenders were relying on the ordinary manual system evaluating

the credit worthiness of potential borrowers. Given the lack of proper documentation

of financial records of potential borrowers (small entrepreneurs) and the high demand

of State loan (Entandikwa) the lenders were undergoing tremendous pressure of a slow

complex system which they couldn’t manage efficiently hence severe loan losses.

(ii) Loan Performer Application

With the introduction of the Poverty Alleviation Project (PAP) lenders were to use

the Loan Performer Application. Some of the major weakness with this application

included the following:- The application was slow and continuously broke down. When

12

repayments of loans in arrears were made twice in a day Loan Performer got confused

regarding the balances. If the user imported a pre-payment for a loan on declining

balance with interest recalculated, this resulted in negative principal balances (Loan-

performer, 1993)[25]. The system could not help the lender make analysis on ”WHAT

IF” incidences and credit worthiness of borrowers. In fact this system did not perform.

(iii) Equinox

Equinox is the application used to schedule payment times and identify SACCOs in

arrears. However it should be noted it doesnot evaluate the credit worthiness of a

SACCO. Its robust with the ability of handling complex and huge number of accounting

tasks (Equinoxco, 2004)[10]. It can be centralized through the use of the network.

However just like Loan Performer it can not carry out analysis under ”WHAT IF”

incidences.

System Dynamics Simulation Modeling has alternatively been identified as the available so-

lution of credible SACCO evaluation. Given the uncertainities(”WHAT IF”) factors that

occur in everyday business dealings a simulation Model is best positioned to handle any

changes in the business environment and its impact on a SACCO over time. System Dy-

namics mimics the dynamic world we leave in.

Most simulation models are computer-based models that perform a series of calculations

under a range of scenarios and assumptions. Simulation models project future cash flows,

income, and expenses. These assumptions include different loan growth and funding plan

scenarios and other assumptions about how a banks assets and liabilities will be replaced.

They can be used to measure risk from either an earnings or economic perspective. The

models simulate or project a banks risk exposure under a variety of assumptions and scenarios

and, thus, can be used to isolate sources of a banks risk exposure or quantify certain types

of risk. To do so, a bank performs a series of simulations and applies different assumptions

and scenarios to each simulation (Piget and Oslo, 1998) [35].

In a previous study (Welch et al., 1990 [43] examined how computer simulation can generate

quality. This can be a good methodology for eliminating unreliable SACCOs and businesses

from acquiring poverty alleviation fund loans.

13

(Bruce and Simon, 1992)[6] demonstrated how computer simulation, instead of algebraic

calculations, can replace some simple binomial calculations.

Successfully introducing a product / State loan scheme based on a new technology can give

company/MFPED significant advantages and ability to drive down the cost (Kim and Coyle,

1993)[22]. IT-enabled transactions (loan servicing predictions) help organizations / MFPED

create value by enhancing interaction with suppliers and customers (Glazer, 1993)[14].

2.2 System Dynamics/Simulation Models in Credit Eval-

uation

The Use of System Dynamics Models to evaluate the Credit Worthiness of Firms (Alfredo

and Raed, 2004) [3] was developed to evaluate credit worthy firms in Jordan that would ben-

efit from bank loans. More and more, small firms could have credit without serious check

of their credit status due to the weakness in the risk assessment approaches that existed.

This expansion policy increased the default rate and number of bankruptcy cases. These

problems required different ways to help the credit officers in banks to understand the credit

worthiness of firms.

The researcher has realized a close link in the quest of identifying credit worthy firms in

Jordan and credit worthy SACCOs in Uganda all in an effort of identifying bad creditors

since there are no strong risk assessment approaches that exit.

2.2.1 Stock and Flow Diagram of a Credit Evaluation System

Assets modeled (Figure 2.1) are cash, account receivable, inventory (finished product), while

the liabilities are accounts payable, long term debt and bank credit.

With the model, the credit officer can be able to test the effect of a new loan on the firm.

Some variables represent the parameters that the credit officers can change through the

simulation to test their different scenarios. At the same time switching of pages to the cal-

culation of financial ratios to evaluate the firm’s performance is done.

14

Figure 2.1: The figure shows the structure of the cash, bank credit and account receivables.

However the researcher discovered this model developed in Jordan is shallow since it does

not critically represent entities outside an organization that affect a firm and its credit wor-

thiness in the long run.

2.2.2 Running of a Simulation

It is based on System Dynamics model which allows the analyst to:

(i) Use the firms finances as inputs to calculate the financial ratios for the current financial

situation and before obtaining the new loan.

(ii) Allow the analyst or the user to measure the firms performance under different what - if

scenarios through the changes in its financial ratios when implementing these scenarios.

(iii) Allow the credit officer to analyze the firm’s loan application through simulating the

impact of the requested loan on the firm’s future performances.

A Simulation Model of Loan Servicing for Savings and Credit Cooperative organizations

developed in this project registers the successes of running the simulation of the Jordanian

model as well as other benefits such as aspects of business life like delays and many others

15

are reflected.

Its on the basis of this simulation (Jordanian model) as an insight that a Simulation of

Model of loan servicing for SACCOs was developed though with different parameters that

represent the state of SACCOs in Uganda.

2.3 Modeling and Simulation Systems

System Dynamics Simulation Modeling is based on understanding the formulations, devel-

oping the causal loop diagrams, developing the stocks and flows diagrams, validation, and

testing. Causal loop diagrams are the basis on which the SD model is built. They depict,

graphically, the interactions and cause-and-effect relationships among the different system

parameters (Hines, 2000)[17].

Computer simulation, has become a useful part of modeling many systems in economics to

gain insight into the operation of those systems. Computer simulations are often considered

to be human out of the loop simulations (Richardson, 1995)[36].

The three essences for all computer simulation models are theory, data and program. To

develop a computer model to simulate the behavior of a system, detailed knowledge (theory

and data) about that system are fundamental. A given computer program is thus the main

tool to express the logic of theory in computer codes (Chi, 2000)[8]. Simulation in the study

having occured, theory about loan servicing was analyzed, the data about the methodology

followed to disburse funds was evaluated so as to come out with a model that aids decision

makers to determine borrowers that can/cannot service loans.

Further more (Aghie and Popplewell, 1997)[1] notes that, computer simulation has been clas-

sified as one of the best problem-solving tools, permitting experimentation with a model. It

has been pointed out also that simulation is an excellent tool for forecasting outcomes, an-

alyzing entire problems and finding total solutions, economically. These capabilities should

help managers to implement correct decisions first time.

16

Simulation is one of the most powerful analysis tools available to those responsible for the

design and operation of complex systems. (Welgama and Mills, 1995)[44] State that, it

is a method that ”mimics” the operating behaviour of the system. Some of the benefits

of simulation are the possibility of exploring new policies, operating procedures and so on,

without disrupting ongoing operations, and the ability to gain insights into system variables.

Simulation involves the process of abstraction, construction of the model and conducting

experiments.

2.4 Strengths and weaknesses of simulation

2.4.1 Strengths of simulation

Computer simulation techniques, developed over 30 years, are recognized as a powerful

tool used to understand and resolve even very complex problems (Aghaie and Popplewell,

1997)[1].This underscores the need to use Simulation for determining SACCOs that can pay

back poverty alleviation funds.

(Greasley, 2004)[15] suggests that simulation can improve the education, effectiveness and

help to develop the art of decision-making. Furthermore, he proposes its use as a facilitator

of communicating ideas up and down within an organization. This is a clear indication that

Simulation will help loan officers at MFPED make quick decisions.

Simulation has been successfully used in statistical process control (SPC) (Aghaie and Pop-

plewell, 1997)[1].

Simulation is an important decision making and problem-solving tool that according to

(Holst and Bolmsj, 2001)[18] finds its typical application in three main areas such as:

(i) Explorative studies of existing systems to improve them;

(ii) Studies of existing systems with some changes made to them, similar to the first purpose

but used to validate a specific alternative, e.g. proposed investment; and

(iii) Design and validation of new systems

17

A good simulation model can reliably predict the performance of the existing system under

different conditions. In the practical cases described by (OKane, 2004)[31], simulation models

were then developed to simulate alternative ”what-if” scenarios. (Greasley, 2004)[15] used

simulation, in a practical case, to predict improvements in the system performance.

By analysing the beahviour of the system and considering the goals and objectives of the sys-

tem, it is possible to enhance system design. Simulation can virtually guarantee the design

of better performing manufacturing facilities Greasley (2004)[15]. Designing manufacturing

systems before implementing them in practice is a task that simulation modeling is ideally

suited to (Baldwin et al., 2000)[4].

Simulation models can be more realistic. A simulation model can accommodate various

business forecasts and allow flexibility in running sensitivity analyzes. For instance, basis

risk can be evaluated by varying the spreads between the indices the bank uses to price its

products.

Perhaps the strongest advantage of simulation models is that they can present risk in terms

that are meaningful and clear to senior management and boards of directors.

Simulation models can vary greatly in their complexity and accuracy. As the cost of com-

puting technology has declined, simulation models have improved. Some simulation models

can:

(i) Handle the intermediate principal amortizations of products such as installment loans.

(ii) Handle caps and floors on adjustable rate loans and prepayment of mortgages or

mortgage-backed securities under various interest rate scenarios (embedded options).

(iii) Handle nonstandard swaps and futures contracts.

(iv) Change spread relationships to capture basis risk.

(v) Model a variety of interest rate movements and yield curve shapes.

(vi) Test for internal consistency among assumptions.

(vii) Analyze market or economic risk as well as risk to interest income.

18

2.4.2 Weaknesses of Simulation

System dynamics are more accessible to a wider range of people and practically are often

used to clarify conceptual relationships before the formal models are introduced. However,

casual loop diagrams have some problems in addressing system dynamics issues. Firstly,

casual loop diagrams cannot effectively address delays an important notion in the field of

system dynamics. A simple cross over the link can qualitatively indicate the existence of

a delay, but it cannot show the magnitude of the delay. Its limitation in terms of quan-

tities representation also applies to other building blocks of causal loop diagrams, such as

positive and negative signs. This is also an essential and natural part of SD research. In

addition, a crux problem with causal loop diagrams is that they make no distinction between

information links and rate-to-level links (Richardson, 1986)[37]. In the future work, formal

quantitative models will be applied to address quantitative relationships.

Although offering greater versatility than the alternatives, simulation is not always objec-

tive. A simulation can misrepresent the banks current risk position because it relies on

managements assumptions about the banks future business.

The myriad of assumptions that underlie most simulation models can make it difficult to

determine how much a variable contributes to changes in the value of the target account.

For this reason, many banks supplement their earnings simulation measures by isolating

the risk inherent in the existing balance sheet using gap reports or measurements of risk

to the economic value of equity. In measuring their earnings at risk, many bankers limit

the evaluation of their risk exposures to the following two years because interest rate and

business assumptions that project further are considered unreliable. As a result, banks that

use simulation models with horizons of only one or two years do not fully capture their long-

term exposure. A bank that uses a simulation model to measure the risk solely to near-term

earnings should supplement its model with gap reports or economic value of equity models

that measure the amount of long-term repricing exposures (Piget and Oslo, 1998)[35].

19

2.5 State of the art and practice in loan servicing

Loan servicing

Is a term referring to the steps taken to maintain a loan from the time it is closed until the

last payment is received and the obligation is paid. Steps may include billing the borrower,

collecting payments, escrowing tax and insurance payments, and making contract changes

(Heartland, 2006) [16]. On the other hand Loan servicing is refered to as the act of collecting

loan payments, handling property tax and insurance escrows, fore closing on defaulted loans

and remitting payments to the investors (Fairvalley, 2006) [11].

2.5.1 Loan Products

Some of the loan products provided include the following:-

(i) Working capital loans. These loans are targeted to individuals who have an enterprise

that is not the primary means of generating income for the individual. Working capital

loans are designed for investing in activities that support the enterprise’s business cycle.

(ii) Welfare loans. These loans are designed to respond to life cycle crises that members

have to deal with. These loans take care of needs such as education, medical expenses,

legal fees etc. Members have to stipulate the reason for which they are taking the loan

in order to quality for consideration.

(iii) Development loan. These are loan capital investment that are made presumably to

increase the holding of productive land, building houses, purchasing inputs. It’s a

financing instrument with a term of a minimum of five years.

2.5.2 Loan servicing tips

(i) Posting protocol: Adopt a standard payment application protocol (e.g. late fee, inter-

est, then principle) common in most servicing systems.

(ii) Ticklers: Ensure post - closing follow-up items are addressed, e.g. annual financial

statements, tax payments and filling.

(iii) Data quality and data integrity: Set - up loans timely and accurately pre/post closing

and compare terms to loan documentation. Any loan modifications should be immedi-

20

ately updated In system to avoid future payment posting discrepancies that can affect

repayment history records.

(iv) Immediate application of funds received: Post payments received as soon as practical

to limit number of returned payments (insufficient funds) and loan delinquencies. Post

using effective date of payment (i.e. date payment received). Encourage Automated

clearing House or electronic funds transfer payment whenever possible to ensure timely

payment receipt from borrower.

(vi) Variable rate loans: Use common index that investors are accustomed to purchasing.

Ensure index rate is updated when rates change and that proper rate is utilized to

avoid future principal and interest payment allocation issues (Wallstreet, 2006)[42].

2.5.3 Characteristics of loans

From the supply side, loans are provided with the following being the standard requirements

that borrowers are supposed to meet.

(i) Loan size. Maximum loan size is based on one’s ability to repay.

(ii) Collateral for the loans. These may include shares, guarantors or other assets.

(iii) Loan term. This depends on the agreed time frame.

(iv) Loan fees. These may include loan appraisal fees.

(vi) Equity requirements

(vii) Loan repayment dates/times.

2.6 Poverty Alleviation

2.6.1 How income poverty is measured.

Using a national survey on household expenditure (which has been conducted in most years

since 1992), statisticians calculate the real household expenditure per adult equivalent. This

measure includes home-produced food as well as goods purchased from the market, and ad-

justs household size for the number of people of different ages, to give an accurate reflection

21

of the relation between the household’s total expenditure and its members’ consumption

needs. It also corrects for inflation. Households whose real expenditure per adult equivalent

falls below a given level (the poverty line) are considered poor. The poverty line used in

Uganda is an absolute, not a relative one; it measures the level of expenditure needed to

secure basic food consumption needs (taking into account regional variations in food prices)

and a corresponding level of non-food consumption. Poverty can be measured by the head-

count -the proportion of people below the poverty line -or by the poverty gap and depth of

poverty, which also takes into account the distance below the poverty line (MFPED, 2005)

[27].

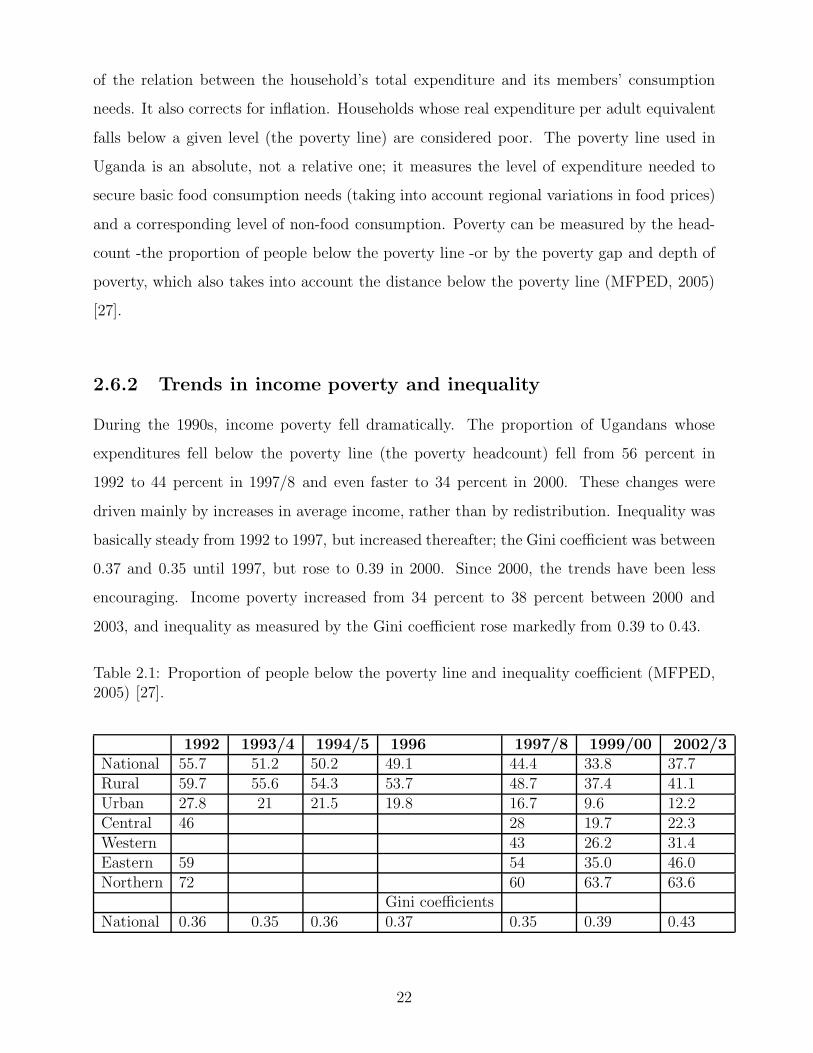

2.6.2 Trends in income poverty and inequality

During the 1990s, income poverty fell dramatically. The proportion of Ugandans whose

expenditures fell below the poverty line (the poverty headcount) fell from 56 percent in

1992 to 44 percent in 1997/8 and even faster to 34 percent in 2000. These changes were

driven mainly by increases in average income, rather than by redistribution. Inequality was

basically steady from 1992 to 1997, but increased thereafter; the Gini coefficient was between

0.37 and 0.35 until 1997, but rose to 0.39 in 2000. Since 2000, the trends have been less

encouraging. Income poverty increased from 34 percent to 38 percent between 2000 and

2003, and inequality as measured by the Gini coefficient rose markedly from 0.39 to 0.43.

Table 2.1: Proportion of people below the poverty line and inequality coefficient (MFPED,2005) [27].

1992 1993/4 1994/5 1996 1997/8 1999/00 2002/3National 55.7 51.2 50.2 49.1 44.4 33.8 37.7Rural 59.7 55.6 54.3 53.7 48.7 37.4 41.1Urban 27.8 21 21.5 19.8 16.7 9.6 12.2Central 46 28 19.7 22.3Western 43 26.2 31.4Eastern 59 54 35.0 46.0Northern 72 60 63.7 63.6

Gini coefficientsNational 0.36 0.35 0.36 0.37 0.35 0.39 0.43

22

There has been extensive discussion of the relation of these findings to participatory evidence.

While the participatory data show less perceived improvement, this arises partly because

the period of comparison was different. While most Ugandan households in 2000 were

economically better off than they had been in 1992, they were not necessarily better off than

they or their parents had been in the 1960s or early1970s, because of the decline in incomes

during the 1970s and early 1980s. The Gini coefficient results have a number of implications

for poverty in the period 2000-2003:

(i) Poverty rose in almost all regions of the country, with a particularly sharp rise in the

East. However, the North (in which poverty fell slightly, although it must be noted

that the sample excludes the insecure areas of Pader, Kitgum and Gulu) remains the

poorest region in the country.

(ii) The regional shares of population changed markedly, with an increase in the share of

the East and a reduction in the share of the North. This partly reflects the movement

of some displaced persons to the East because of insecurity.

(iii) Inequality increased markedly, with the Gini coefficient rising from 0.39 to 0.43.

(iv) The sectoral shares of household heads changed dramatically, with a major shift out of

crop agriculture. This may be partly due to a change in the sample, although the share

of households owning land is constant across the two surveys. This is accompanied by

a large drop in consumption of home-produced food, while consumption of purchased

food increased.

The increase in poverty is particularly marked for households in crop agriculture, although

other sectors such as trade and hotels also show large increases. By contrast, workers in

government services experienced reductions in poverty (MFPED, 2005) [27].

2.6.3 Role of Empowerment in Poverty Alleviation

The steps taken by Government through various social policies and programmes for disad-

vantaged groups like, women, widows, the youth, the elderly, neglected children and orphans,

23

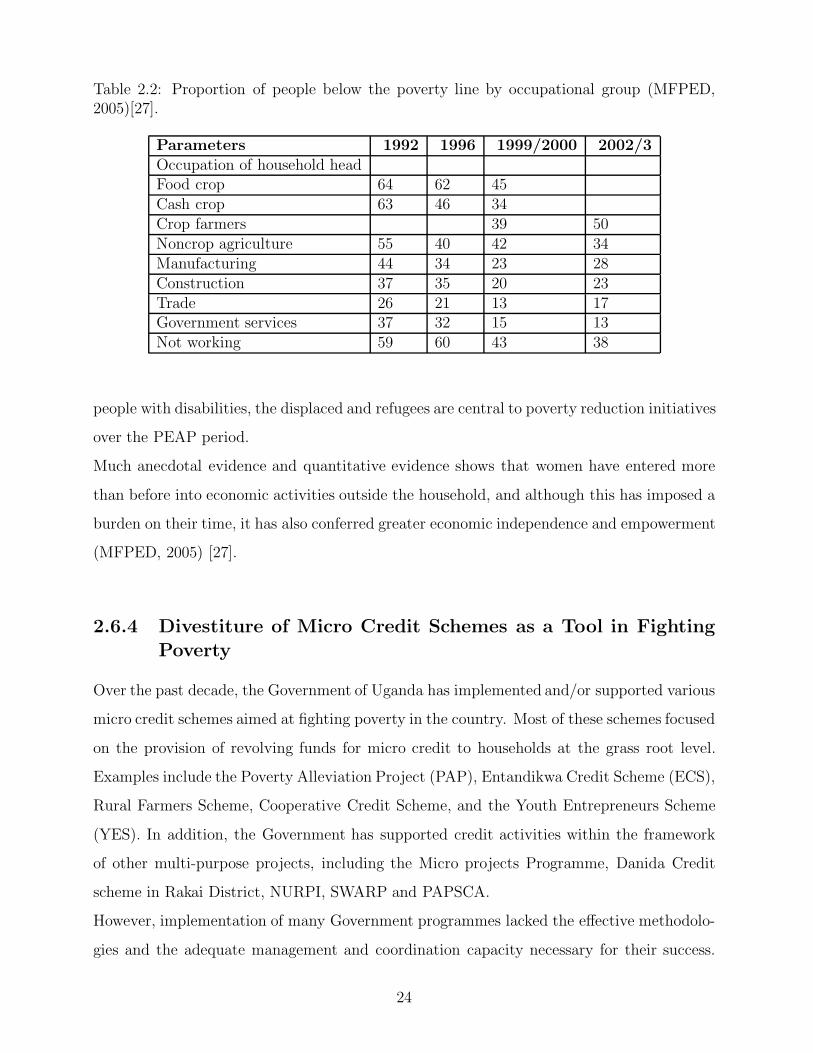

Table 2.2: Proportion of people below the poverty line by occupational group (MFPED,2005)[27].

Parameters 1992 1996 1999/2000 2002/3Occupation of household headFood crop 64 62 45Cash crop 63 46 34Crop farmers 39 50Noncrop agriculture 55 40 42 34Manufacturing 44 34 23 28Construction 37 35 20 23Trade 26 21 13 17Government services 37 32 15 13Not working 59 60 43 38

people with disabilities, the displaced and refugees are central to poverty reduction initiatives

over the PEAP period.

Much anecdotal evidence and quantitative evidence shows that women have entered more

than before into economic activities outside the household, and although this has imposed a

burden on their time, it has also conferred greater economic independence and empowerment

(MFPED, 2005) [27].

2.6.4 Divestiture of Micro Credit Schemes as a Tool in Fighting

Poverty

Over the past decade, the Government of Uganda has implemented and/or supported various

micro credit schemes aimed at fighting poverty in the country. Most of these schemes focused

on the provision of revolving funds for micro credit to households at the grass root level.

Examples include the Poverty Alleviation Project (PAP), Entandikwa Credit Scheme (ECS),

Rural Farmers Scheme, Cooperative Credit Scheme, and the Youth Entrepreneurs Scheme

(YES). In addition, the Government has supported credit activities within the framework

of other multi-purpose projects, including the Micro projects Programme, Danida Credit

scheme in Rakai District, NURPI, SWARP and PAPSCA.

However, implementation of many Government programmes lacked the effective methodolo-

gies and the adequate management and coordination capacity necessary for their success.

24

As a result, the performance of the schemes was adversely affected by very poor loan recov-

ery, inefficiency and high management costs which consequently led to under-performance

and/or collapse (Nannyonjo and Nsubuga, 2004)[28].

The government’s own credit programmes (Entandikwa and PAP) suffer badly from being

government run. Both are viewed as unsuccessful and as having contributed further to a

dependency culture. While there is evidence that PAP has learned some lessons and has

begun to achieve a minimum of financial success, there remain bureaucratic and political in-

terference, operational inefficiencies, lack of logistical support, poor motivation among front

line workers, and undue complexity of goals and missions (Ditcher and Kamuntu, 1997) [9].

2.6.5 Role of Decentralization in Fighting Poverty

Decentralized government structures are central to Uganda’s mode of governance as spelt

out in the 1995 Constitution and the 1997 Local Government Act. Moreover, the decentral-

ization process is at the heart of the Poverty Eradication Action Plan, which sets out the

strategy through which the GOU aims to eradicate poverty. The GOU has over the years

strengthened the decentralized structures through increasing their autonomy, and widening

their participation in decision making in order to enhance the efficiency and effectiveness in

allocation of resources towards the achievement of the PEAP objectives in line with local

priorities. The government also recognizes that effective monitoring and evaluation is essen-

tial for ensuring that budgetary allocations are fully translated into outputs and outcomes.

To this effect, the GOU has put in place a monitoring network comprising representatives

from the central government, line ministries, donors and the civil society. In addition, efforts

have been made to improve transparency and accountability by stepping up public informa-

tion through the media and use of notice boards in public places such as schools and places

of worship. Strong decentralized structures will facilitate the work of CDWs and FEWs

through better coordination and wider participation (Nannyonjo and Nsubuga, 2004) [28].

25

2.6.6 Impact of credit in Poverty Alleviation

Credit is considered to be an essential input to increase agricultural productivity, mainly

land and labour. It is believed that credit boosts income levels, increases employment at the

household level and thereby alleviates poverty. Credit enables poor people to overcome their

liquidity constraints and undertake some investments, especially in improved farm technol-

ogy and inputs, thereby leading to increased agricultural production. Furthermore credit

helps poor people to smooth out their consumption patterns during the lean periods of the

year. By so doing, credit maintains the productive capacity of poor rural households. The

World Bank in also observed that improved consumption is an investment in the productiv-

ity of the labour force (Okrut et al., 2004) [32].

2.7 Loan Recovery

With regard to the unsuccessful GOU Entandikwa scheme, there is need for efforts to recover

the outstanding loans as writing them off will not only have negative effects on the entire

private sector micro finance industry, but will also result in increased and willful default-

ing. One option for the GOU is to hand over the portfolio to court bailiffs, lawyers and/or

the Non Performing Assets Recovery Trust (NPART), which will continue recovery of the

loans. Another option is to sale the loan portfolio to financial institutions, which will pro-

vide additional financial services to the clients subsequent to full recovery of the outstanding

Entandikwa loans (Nannyonjo and Nsubuga, 2004)[28].

2.8 Targets

The income-based interpretation of the poverty reduction goal is the PEAP target of reduc-

ing the incidence of household poverty to 10 percent by 2017. In comparison, the Millennium

Development Goal for poverty eradication translates into a target of 28 percent poverty by

2015. This target is considerably less ambitious than the PEAP target (Uganda Debt Net-

work, 2003) [41].

26

2.9 Critique on the Literature

The study identified a need for a methodology for analyzing SACCOs at MFPED that

can/cannot pay back loans from the poverty alleviation fund. System dynamics is repre-

sented as the suitable methodology for analysis in the project.

2.10 Conclusion

The researcher identified that System Dynamics was used in a number financial institutions

successfully. The development and use of System Dynamics as an analysis/ assessment tool

will therefore be of significant importance to the MFPED.

27

Chapter 3

METHODOLOGY

3.1 Review of methodologies

The researcher explored three methodologies of research which included Case Study, Viable

Systems and Dynamic Synthesis. A comprehensive study was done about the three method-

ologies to select the best to be used in the development of the research. Dynamic synthesis

was selected as the most appropriate methodology to be used in the research as others had

serious shortcomings.

Table 3.1: Rankings of the three explored methodologies.

No. Functionality Case Study Viable Systems Dynamic Synthesis1 Accuracy YES YES YES2 Focus YES YES YES3 Non Biased NO NO YES4 Ease to use YES NO YES5 Inclusive NO NO YES6 Ranking 2 3 1

3.1.1 Case Study.

Case Study is an exploratory (single in-depth study) or explanatory (cross-case analysis) re-

search strategy, which involves an empirical investigation of a particular contemporary phe-

nomenon within its real life context using multiple sources of evidence (Williams,2000)[48].

A frequent criticism of case study methodology is that its dependence on a single case ren-

ders it incapable of providing a generalizing conclusion. It is also stated that they can also

lead to bias (Williams, 2004) [46].There are no really good methodological frameworks for

28

conduct of case studies or use of case study research.

3.1.2 Viable Systems

Viable Systems Methodology (VSM) posists an organizational structure which must exist in

order for an entity to be viable i.e. able to survive.

3.1.3 Dynamic Synthesis Methodology

Dynamic Synthesis Methodology refers to the integration of theoretical concepts and struc-

turing of parts and elements of a process over time in such a manner to form a formal

functional entity, underpinned by synthesis as philosophy of science. (Williams, 2004)[46]

The researcher used Dynamic Synthesis Methodology which is the tested methodology used

by advanced modelers. Williams(2004)[46 ] States that the Dynamic Synthesis Methodol-

ogy is grounded on well tested and developed theoretical anchors and builds on an existing

epistemological philosophy of science in the acquisition of knowledge, as a basis for theory

building and extension in the field of System dynamics.

Combining case study and System dynamics modeling makes Dynamic Synthesis Method-

ology a powerful empirical research method that potentially makes useful contribution to

body of System Dynamics (Williams, 2004)[46].

The Dynamic Synthesis Methodology (DSM) includes six iterative research process phases,

namely: Problem Statement, Field Studies, System Dynamics Model Building, Case Studies,

Simulation Experiments and Model Use and Theory Extension. The process diagram that

outlines this iterative research process, which was used to conduct the research study, is

illustrated below.

29

Figure 3.1: The Dynamic Synthesis Methodology. Adapted from (Williams, 2004) [46]

The Problem Statement

The problem statement was the basis of the research on SACCOs credit worthiness, Williams

(2004)[46] states that the statement of the problem is an important early phase in modeling

and analysis. The word ”problem statement” is used in preference to research question(s)

because modeling and analysis being part of System dynamics requires solving problems

rather than answering questions

Field Study

Field studies and supporting data collection methods provide invaluable insights and discov-

eries during the System dynamics research. Field study is a term that applies to variety of

research methods, raging from low to high constraints (Williams, 2000)[46].

The researcher carried out a field study at The Ministry of Finance Planning and Economic

Development. The Office of the SACCOs coordinator was visited to gather the necessary

30

information.

System Dynamics Model Building

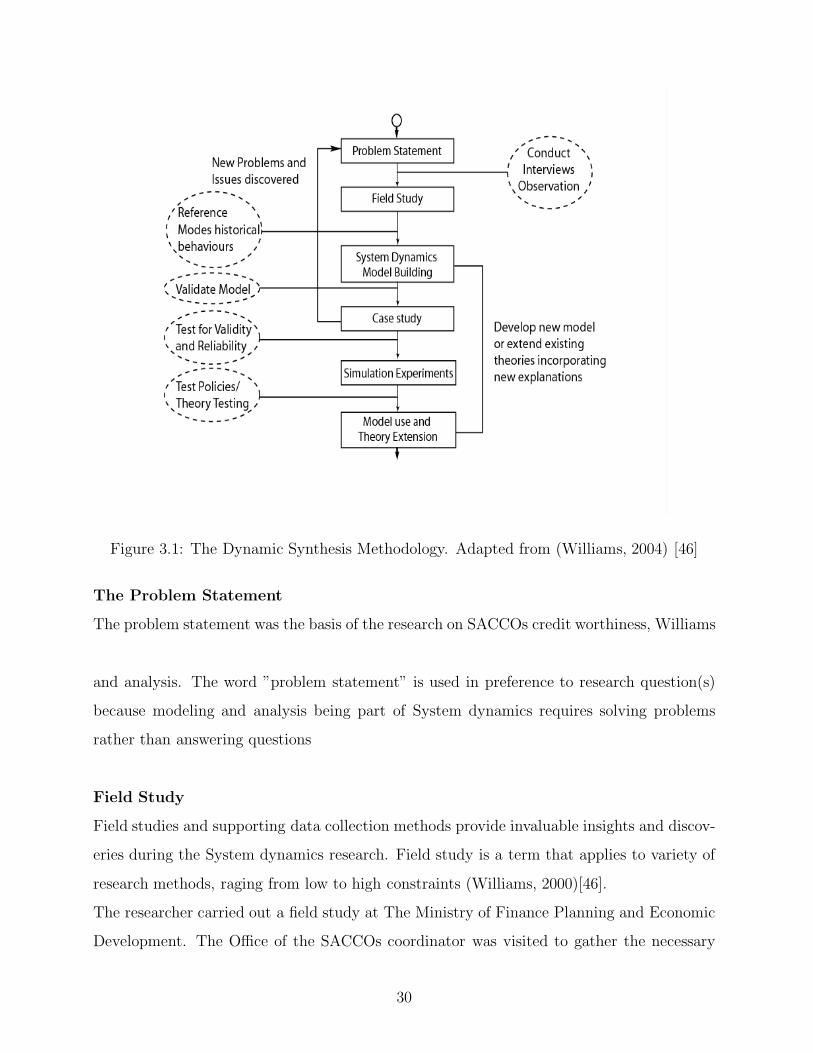

Richardson and Purgh (1981) [38] suggest that a system dynamics modeling effort begins

and ends with understanding as shown below:-

Figure 3.2: System Dynamics Modeling. Adapted from (Richard and Pugh,1981)[38].

Case Studies

Case Study is an exploratory (single in-depth study) or explanatory (cross-case analysis) re-

search strategy, which involves an empirical investigation of a particular contemporary phe-

nomenon within its real life context using multiple sources of evidence (Williams,2000)[48].

The researcher carried out a case study at Wakiso Self Help Savings and Credit Cooperative

Organization in Wakiso District Uganda.

Simulation Experiments

Simulation models are abstracts of the real world view of a system or problem being solved.

During the course of simulation, the model mimics important elements of what is being

simulated. The model is used as a vehicle for experimentation in a ”trial and error” way

to demonstrate the likely effects of various policies. Those policies, which produce the best

result in the model, will be implemented in real life (Williams,2004)[46].

31

Model Use and Theory Extension

The System dynamics modeling approach takes a philosophical position that feedback struc-

tures are responsible for the changing patterns of behaviour we experience in complex prob-

lems. System Thinking /System Dynamics notation can be used to model and test different

hypotheses propounded about RE process modeling and analysis. A dynamic hypothesis,

can be tested verbally, or as a causal loop diagram or as a stock and flow diagram. In view of

SD’s capacity to deal with the dynamic complexity created by interdependencies, feedback,

time delays and non-linearity (Williams,2000)[46].

3.2 How the specific objectives were achieved

The specific objectives are listed below and the techniques that were used to achieve them

are laid out as follows:-

3.2.1 Identify shortcomings with the current approaches

Data Collection Methods

The researcher used interviews and reviewing existing literature on the shortcomings with

current approaches used in loan disbursement to SACCOs.

The researcher conducted interviews with two MFPED officials that took decisions and

oversaw loan disbursement to SACCOs. An interview guide was used and questions were

designed to enable interviewees air out deficiencies with the current approaches of loan dis-

bursement. This helped to gain an insight into major problems as well as offering solutions.

Interviews also allowed the researcher access first hand information and also established a

relationship with the interviewees.

Existing documentation were reviewed which included Reports, Papers and Journals etc. at

the MFPED and World Bank libraries regarding approaches that were used in determing

SACCOs that received Poverty Alleviation Funds were incorporated in the report.

Observation enabled the researcher crosscheck the validity and accuracy of information gath-

ered through interviews and reviewed literature.

32

3.2.2 Identify Variables

The variables used in the simulation model were got through reviewing of literature and

interviews with the use of an interview guide.

3.2.3 Simulation Model Development

Simulation Model Development involved both Design and Implementation. The Design or

blue print of a simulation is the Causal loop diagram. It was drawn showing the cause and

effect tendencies of SACCO activities, this then lead to Implementation.

The methodology that was used in the implementation of the project, is Systems Dynamics

its based on the use of simulation models. Systems Thinking Educational Learning Labora-

tory with animation (STELLA) is a computer simulation program which was used to develop

models. STELLA provides a framework and an easy-to-understand graphical interface for

observing the quantitative interaction of variables within a system. The graphical interface

was used to describe and analyze very complex mathematical systems.

In Implementation A systems dynamics model was built based on the field study results

which provided a descriptive model. The Causal Loop Diagrams, was later converted to

stock and flow diagrams which is a formal quantitative model of the problem in question.

Mathematical relationships between and among variables which enable the simulation of the

model are defined after which simulations of the key variables are run. The simulation was

an imitation (on a computer) of a system as it progressed through time. The Purpose is to

obtain a better understanding of the system as well as the identification of the area which

needs improvement, on which future decision of the organization are based.

As a consequence, the model will be used as a supportive tool for decision making rather

than making decisions on behalf of the user. It’s on the results of the simulation model that

the MFPED will base its decision as regards giving loans to credible SACCOS made of small

scale entrepreneurs. System dynamics is the best suitable methodology through which this

can be determined because of the following reasons;

33

(i) It expresses all variables into cause and effect relationship. This is essential because

many people would think of another problem being the cause of poor loan repayment

out, yet the problem is somewhere else.

(ii) Many times systems fail and management has to look outside the organization for the

cause of the problem, yet the problem is within. So systems dynamics comes in to give

a solution to the problems by analyzing each sector, and identifying the origin of the

problem, and how it relates with the other entities.

(iii) System dynamics enables the user to have results of a long period of time. Having this

type of problem requires adequate planning for a long or short period of time. System

Dynamics provides this solution by enabling the simulator have results for the period

of time for proper planning.

(iv) ) System dynamics does not provide solutions to problems, but the problem is high-

lighted and this prompts management to dig deep into the highlighted problem to see

how to solve the problem.

3.2.4 Validation

Law and Kelton(1991)[23] suggests that if a model is ”valid”, then the decisions made with

the model should be similar to those that would be made by physically experimenting with

the system. A model is said to be credible when a simulation model and its results are

accepted by managers/customers as being valid, and used as an aid (tool) in making many

decisions.

Williams (2004)[46], states that building valid and credible process models is an important

aspect of a researcher’s representation of the actual system being studied.

Values were tested by the researcher on the model with available case studies and ministry

data to ensure that values are acceptable and that credible and reliable figures are produced

by the model after its run. This aimed at removing exaggerations and possible causes of

error.

34

Chapter 4

PRESENTATION OF RESULTS

4.1 Shortcomings with the current approaches

In the new poverty alleviation scheme of disbursing loans to SACCOs the researcher identi-

fied and investigated shortcomings of current approaches used in determining SACCOs that

receive poverty alleviation funds.

Current approaches used in the evaluation of SACCOs that receive loans.

The researcher discovered that loan officers use Traditional judgmental approaches for eval-

uation of SACCOs that receive loans. Assessing the credibility of a SACCO is a major

aspect that is looked at by loan officers when selecting SACCOs that qualify for a loan.

For a SACCO to be declared credible the following factors have to be considered to the

satisfaction of loan officers:-

(i) The SACCO had to produce a Registration Certificate certified by the Ministry of

Tourism Trade and Industry which registers SACCOs under the Cooperatives statute

an omnibus law for all types of cooperatives.

(ii) Management is evaluated. The managers must be known in areas they come from.

These leaders must produce introduction letters from the Local Council 1 (one) chair-

person.

(iii) Objectives of the SACCO should be convincing to loan officers and aimed to uplift

SACCO members from poverty.

(iv) Evidence of SACCO activity inform of financial documents i.e. balance sheet must be

35

submitted to loan officers.

The researcher found out that though the Traditional judgmental methods may select good

and bad creditors its not entirely accurate because of the following reasons:-

(i) Loan officers make decisions based on the past data of the SACCO which have no

bearing on the future events.

(ii) They give a static picture where as we live in a dynamic world. They also provide a

shallow view whereas it would be much more useful if a holistic picture of the SACCO’s

ability to survive the period of the loan and make repayment.

(iii) Often Balance Sheets of SACCOs can be ”adjusted” to portray a rosier picture of the

financial health of the SACCO than actually exists so the financial ratios based on to

give loans are rendered inappropriate.

(iv) The Traditional judgmental approach is not entirely correct because its based on prob-

ability.

(v) Does not consider ”what if” possibilities which may occur in the business environment

and affect the performance of SACCOs and their ability to pay back the loans under

different pressures.

(vi) These methods do not include the effect of delays in the business environment. In all

aspects of business life, there are delays - Some serious and some not. These delays can

have non - linear effects which are a breeding ground for chaotic behavior where small

changes in some parameters can result in massive changes in the financial position of

the SACCO.

The researcher would encourage the use of Traditional Judgmental approach of assessing

credible SACCOs alongside the proposed approach of using Simulation modeling. The ad-

vantages of the proposed approach are further explained below.

Proposed approach

The researcher proposed system dynamics with the use of Simulation and modeling as the

new approach because of the following reasons:-

36

(i) Complexity. Operations of the inner workings of a SACCO are complex for loan officers

to come up with a correct decision using the traditional judgmental approach. However

Simulation and modeling allows one to measure soft relationships using graphs. Such a

technique for representing non - measurable features coupled with advanced modeling

software such as STELLA interface eases significantly the modeling task.

(ii) Simulation and modeling is flexible enough to permit dynamic runs which give signifi-

cant advantage over Traditional judgmental approach in understanding the pattern of

behavior of a candidate SACCO.

(iii) Interconnectedness. Variables of the SACCO do not work in isolation but affect one

another. It is difficult to predict the effect of the interconnections through the use

of traditional judgmental approach. However Simulation and modeling easily predicts

event by running simulations based on cause and effect of variables.

(iv) Simulation and modeling allows easy insertion of delays and non - linearity, which is

always important in the case on credit analysis, this allows system dynamics models