leviathan's wells. a political economy of oil nationalization

TRANSCRIPT

Leviathan’s Wells A Political Economy of Oil Nationalization Sjoerd ten Wolde Pre-master’s student, Faculty of Economics and Business Administration, Vrije Universiteit Amsterdam Email: [email protected] Abstract: Foreign investment in oil production is characterized by high levels of risk, due to a government’s sovereign powers to nationalize these investments. This paper investigates the political and economic factors underlying governments’ decisions regarding the expropriation of oil investments. Moreover, it explores the strategic reaction of the investing transnational oil firm to this inherent sovereign risk. This is done through the analysis of a formal game-theoretic model of the production phase of oil extraction. It is found that governments are more likely to nationalize when public and elite support for the political leaders is low. Also, strong institutional constraints and a firm rule of law may withhold governments from expropriating through imposing high transaction costs. Firms primarily base their investment decisions on the government’s expected strategy, taxes and rents, interest rates, and the costs and benefits of additional investment. From these findings, the paper concludes that the political nature of oil investment warrants more knowledge and caution regarding the domestic political situation of oil-producing countries. Keywords: Nationalization; Expropriation; Political institutions; Rule of law; Oil production; Oil investment; Public support; Elite support Final version: June 30, 2010

“For by Art is created that great Leviathan called a Commonwealth or State, which is but

an Artificial Man; though of greater stature and strength than the Natural, for whose protection and defense it was intended; and in which, the Sovereignty is an Artificial Soul, as giving life

and motion to the whole body.” - Thomas Hobbes1

I INTRODUCTION Petroleum is not only the fuel of today’s global economy, but also of a great many of the international conflicts of our age. Growing ever scarcer, a myriad of contenders are figuratively and literally fighting over the control of the sources of this black gold. The protagonists of this standoff are two types of actors: states and transnational oil companies (TOCs). While fruitful cooperation between the two is commonplace, their often opposing interests ensure that conflicts still abound. One of the most important manifestations of this clash of interests is the phenomenon of nationalization: the complete seizure of the assets of a TOC by a foreign government. This risk of expropriation2 may have severe consequences for investment decisions made by both TOCs and national oil companies (NOCs). Moreover, the actual execution of such an expropriation may reverberate throughout the global economy for years. A substantive body of economic work has been published regarding the reasons and incentives underlying expropriatory decisions. Most of the models employed, however, fail to take account of the political dimension. Expropriation and nationalization not only take place

1 Leviathan (1651), Introduction 2 Please note that ‘nationalization’ and ‘expropriation’ are used interchangeably in this paper.

2 Sjoerd ten Wolde

because of their direct economic benefits to a government, but also due to the limited time horizon of political leaders, their popularity, their elite support, or the institutions constraining them. This paper shall set out to model this aspect of oil investment decisions, together with the ‘orthodox’ economic aspects. The present analysis aims to provide the reader with both an intuitive understanding of the political economy of oil nationalization, and a formal model and testable hypotheses. Chapter 2 presents the paper’s research objectives, methods and central concepts. Following this, Chapter 3 will give a concise introduction into the global oil market, its actors, market structure and central problems. Subsequently, in Chapter 4 the formal, game-theoretic model shall be introduced. In Chapter 5, this basic model shall be expanded upon through some formal extensions. Finally, the conclusion shall discuss our findings and their implications for real-life economic situations. 2 RESEARCH OBJECTIVES AND METHODOLOGY The prime objective of this study is to examine the influence of political variables on the decisions of governments to nationalize and of transnational oil companies to invest in oil-producing countries. Specifically, we are interested in the influence that popular support for the government, elite support, and institutional constraints bear upon petroleum-investment decisions, and how these decisions affect the efficiency and overall profits in oil production. As a subsidiary objective, we are interested in the effect that other relevant variables – prices, taxes, oil-field yields, or the efficiency of NOCs – have upon actors’ strategies and overall welfare. Therefore, the central problem could be framed as follows:

“In what way are the strategic decisions made by governments and transnational oil companies in oil investment affected by popular support, elite support, and institutional constraints?”

We shall examine this through analyzing what gains are to be had through cooperation of the government and TOC, what motivates the actors in their decisions and how individual and overall welfare is affected.

The paper departs from a rational-actor perspective, analyzing the conditions and incentives underlying oil investment and production through game-theoretical principles. Although the assumption of rationality may not be fully adequate, since topics such as a ‘people’s right’ to oil reserves oftentimes arouse strong passions, the analysis of rational incentives may serve to explain general tendencies, trends and the context within which nationalization takes place.

This paper investigates the problem through a formal model, analyzing the interaction of several variables. Several hypotheses are generated; the present paper does not, however, attempt to refute these hypotheses itself. Of course, the conjectured hypotheses would be well-served by empirical testing and in-depth qualitative analysis. 3 INTERNATIONAL OIL INVESTMENT This chapter serves as a brief introduction into the topic at hand: oil production. It will describe the structure and idiosyncrasies of the oil industry as an economic market. Moreover, it will address the political context underlying (international) oil investments. Finally, four central problems in international oil investment are discussed.

Leviathan’s Wells. A Political Economy of Oil Nationalization 3

3.1 Oil production Activities in the oil industry are generally divided into two phases: upstream production and downstream production. Whereas downstream production refers to the refining, packaging and selling of petroleum products, upstream activities are constituted primarily by the exploration, extraction and production of crude oil, natural gas and other by-products. As the present paper is focused on the upstream part of oil production, some of the main features of crude oil production shall here be presented. The key characteristics of production are: (i) the primacy of economic and technological constraints over geological constraints, (ii) the sophistication of oil technology, and (iii) different degrees of economic risk in different phases of production. An important feature of oil production is the fact that the amount of crude oil effectively extracted from a reservoir (the so-called ‘recovery factor’) is often merely a small part of the total amount of oil present (Hyne 2001: p.432). These recovery factors – usually ranging from 5% to 75% of the total oil in place – not only depend on the geological idiosyncrasies of the site, but more importantly on the investments being made by the extracting party. If these investments are not made timely, subsequent recovery of the reserves is generally harder and more costly (Hyne 2001; Mitchell, Morita, Selley & Stern 2001: p.46). This is especially important because insufficient investment by oil companies may lead to a loss in long-term profits for both the company and the country owning the oil field (cf. Pindyck 1978). Hence, economic and technological constraints usually prevail over geological factors in petroleum extraction. A second attribute of oil production is constituted by the technical nature of its extraction. Although there has been a strong proliferation of technical knowledge in the past decades, lack of technological knowledge and experience may prove a strong barrier to efficient production. This applies specifically to national oil companies: apart from managerial suboptimality, a lack of technical know-how often impedes efficient production by these companies. This partly explains why, across the board, national oil companies often function less efficiently (Eller, Hartly & Meddock III 2010). Thirdly, different phases in the extraction process entail different economic risks. One can broadly distinguish between the following stages: the exploration phase, the development phase, and the production phase. Even before any oil has been produced, petroleum exploration already demands for significant investments. For this reason governments often relegate exploration and its associated economic risks to private companies (Manzano & Monaldi 2008: p.76). Likewise, when in the development phase, short-run profitability may be low before learning-by-doing effects and increased knowledge about the oil field result in full-fledged production. Hence, oil extraction usually requires extensive sunk costs (Manzano & Monaldi 2008: p.61; Favero, Pesaran & Sharma 1994). Apart from this, risks and profitability differ hugely between different oil fields. For these reasons, one could characterize the oil industry as a capital-intensive industry in which investment decisions strongly influence long-run possibilities and profitability. Because of high technological and capital-related barriers, entry conditions are harsh, even for already existing companies wanting to invest in new oil fields. This applies especially for national oil companies, specifically those who do not possess great capital reserves and those who are inefficient or lack specific technical knowledge. Lastly, it is a high-risk industry, in which governments are often unwilling or unable to bear the risks and costs of exploration and development.

4 Sjoerd ten Wolde

3.2 Actors and market structure In the upstream market, three types of actors define the state of affairs: governments, national oil companies, and transnational oil companies. These will be discussed here. Governments of sovereign states have the ultimate say over oil resources, as virtually all exploitable global oil reserves are located in sovereign territory3. The legal doctrine of sovereignty gives states full ownership rights over all their resources – even after granting concessions. The risk emanating from this structure of governance is usually referred to as ‘sovereign risk’. The final authority to make agreements and execute policies rests with the internationally recognized government of a state. Some so-called rentier states are severely dependent on their income from oil rents and taxes: Saudi Arabia, Venezuela and Mexico are striking examples of this. This often puts heavy pressure on governments to increase their income from oil production and rents4. National oil companies are companies instituted by a state. Although they may have significant autonomy in some cases, it is the government of the state that exercises control over them (Eller, Hart & Medlock III 2010). As Eller, Hart and Medlock remark, these companies’ goals are not necessarily restricted to making profit: NOCs may have subsidiary tasks such as social development, creating employment or maintaining clientelistic relations, as Venezuela’s PDVSA illustrates (ibid: p.2). A prime characteristic of many of these companies is their relative lack of efficiency and technological know-how when producing autonomously (ibid.). Although there are strong differences between the myriad of NOCs, this inefficiency has prompted many governments to engage in production-sharing agreements between their NOC and transnational oil companies. Also, a number of countries allow TOCs to operate independently. Lastly, transnational oil companies are significant players in the market. Contrary to popular belief, however, TOCs are only involved in approximately half of the world’s oil production (Mitchell, Morita, Selley & Stern 2001: p.137). Access to substantial sources of oil is increasingly hard for TOCs, as many oil reserves are located either in politically unstable countries or countries barring TOCs from domestic oil production (Eller, Hartley & Medlock III 2010: p.2). Nonetheless, these companies have a strong bargaining asset in their technological prowess. As such, they are often indispensable partners for NOCs which have not managed to make the technological and organizational leap required for contemporary efficient oil production (Mommer 2000: p.1).

The global oil market is often characterized as an oligopoly, with relatively few companies controlling the market and many consumers buying their products. Although this qualification certainly applies for the downstream market – as the actions of the OPEC cartel in the 1970s have demonstrated –, the upstream market is far more monopolistic in its nature. With the virtual absence of major discoveries in recent decades, and most important oil fields being in the hands of Middle Eastern states and their national oil companies, the granting of oil concessions is most definitely a seller’s market (cf. Manzano & Monaldi 2008: p.66; Mommer 2000: p.38). Especially salient in this context is the bargaining power that the doctrine of state sovereignty gives to governments. This gives states the possibility to unilaterally change agreements and to exercise eminent domain, thereby expropriating investments. As demonstrated by the Sakhalin affair in which the Russian Federation bereft Shell from its control over the Sakhalin II project, this very fact may give states a leverage that by far exceeds that of oil companies.

A last defining characteristic of the oil market is the strong fluctuation of market prices. Not only is the market dependent on changing market fundamentals, it is also 3 There are exceptions to this, such as the hotly contested Arctic, and the high seas. 4 Dependence on income from natural-resource industries may lead to economic and political problems. For a discussion on this so-called ‘resource curse’, see for instance Mehlum, Moene and Thorvik (2006).

Leviathan’s Wells. A Political Economy of Oil Nationalization 5

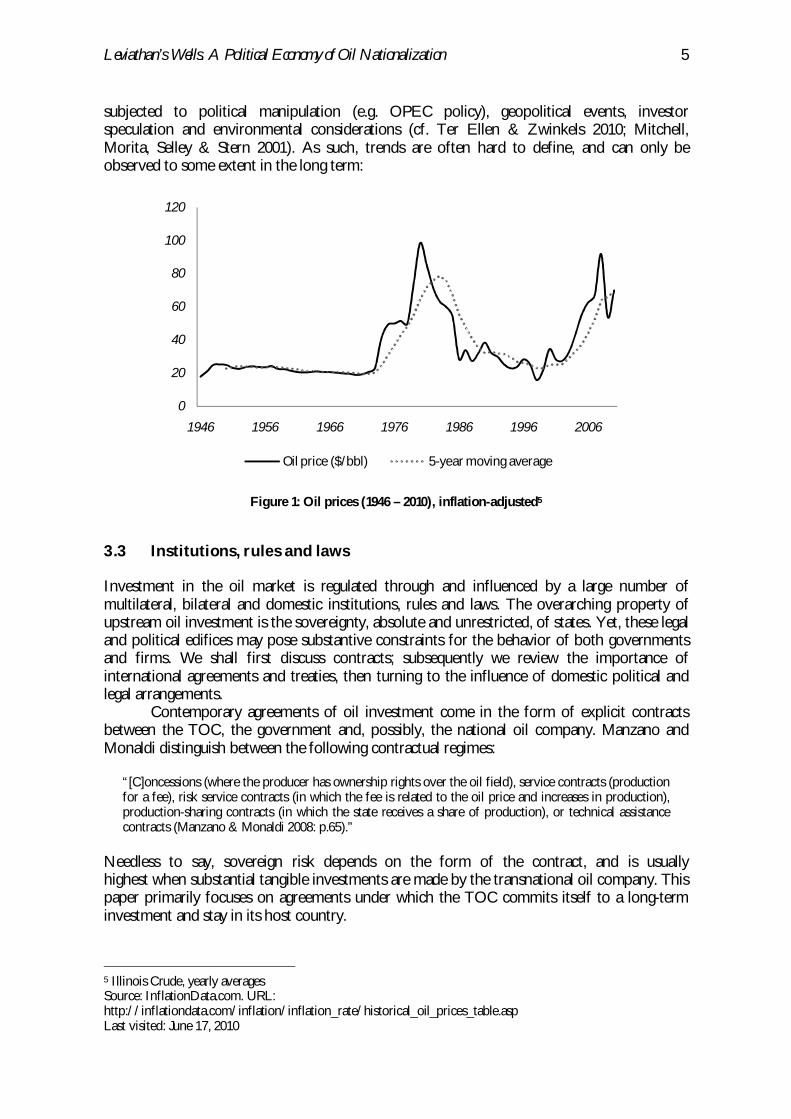

subjected to political manipulation (e.g. OPEC policy), geopolitical events, investor speculation and environmental considerations (cf. Ter Ellen & Zwinkels 2010; Mitchell, Morita, Selley & Stern 2001). As such, trends are often hard to define, and can only be observed to some extent in the long term:

Figure 1: Oil prices (1946 – 2010), inflation-adjusted5

3.3 Institutions, rules and laws Investment in the oil market is regulated through and influenced by a large number of multilateral, bilateral and domestic institutions, rules and laws. The overarching property of upstream oil investment is the sovereignty, absolute and unrestricted, of states. Yet, these legal and political edifices may pose substantive constraints for the behavior of both governments and firms. We shall first discuss contracts; subsequently we review the importance of international agreements and treaties, then turning to the influence of domestic political and legal arrangements. Contemporary agreements of oil investment come in the form of explicit contracts between the TOC, the government and, possibly, the national oil company. Manzano and Monaldi distinguish between the following contractual regimes:

“[C]oncessions (where the producer has ownership rights over the oil field), service contracts (production for a fee), risk service contracts (in which the fee is related to the oil price and increases in production), production-sharing contracts (in which the state receives a share of production), or technical assistance contracts (Manzano & Monaldi 2008: p.65).”

Needless to say, sovereign risk depends on the form of the contract, and is usually highest when substantial tangible investments are made by the transnational oil company. This paper primarily focuses on agreements under which the TOC commits itself to a long-term investment and stay in its host country.

5 Illinois Crude, yearly averages Source: InflationData.com. URL: http://inflationdata.com/inflation/inflation_rate/historical_oil_prices_table.asp Last visited: June 17, 2010

0

20

40

60

80

100

120

1946 1956 1966 1976 1986 1996 2006

Oil price ($/bbl) 5-year moving average

6 Sjoerd ten Wolde

When a TOC invests in the host country, it subjects itself to the present national laws and the will of the ruling executive. A great number of countries, nonetheless, have concluded either bilateral or multilateral investment treaties (specifically the recent Energy Charter Treaty6) with other countries. If both the host country and the TOC’s country of origin is party to such a treaty, both can relegate disputes to a body of international arbitration – for this purpose, the International Centre for Settlement of Investment Disputes (ICSID) is currently the most utilized forum (Joffé et al. 2009: p.7,11). Although matters of sovereignty constrain the power of such bodies, these investment treaties may pose formidable obstacles to both governments and TOC in weaseling out, primarily in the form of transaction costs. Perhaps more important, however, are the constraints and possibilities that national institutions bring about for the executive. A strong rule of law and a system of constraints on the executive branch of government may lead to higher political transaction costs of nationalization. Well-defined property rights may lead to a lower likelihood of expropriation; likewise, local laws regulating or forbidding nationalization make it more costly for a government to expropriate. Conversely, institutionally underdeveloped countries are often prone to bouts of nationalization (cf. Knack & Keefer 1995). 3.4 Central problems in oil production Because of the specific nature of the oil industry, there are some common difficulties in international oil production and investment. Federico Sturzenegger has identified four central problems in oil production contracts (Sturzenegger, in Manzano & Manaldi 2008: p.99-100). These problems are the following:

1. Time inconsistency. Perhaps the paramount problem in oil production and investment is that a government has strong incentives to lure international oil companies into investing in the country’s oil production through offering attractive business opportunities, tax holidays, and the like. Once the investment has been done, however, the state has an incentive to renege on its promises and increase its taxation or nationalize the investments (Manzano & Monaldi 2008: p.75).

2. The tension between rent extraction and keeping incentives intact. While a government will want to appropriate as large a part of the rents as possible, it also wants to keep in place the incentives for an international oil company to keep on producing and investing. Theoretically, (high) taxation could lead to suboptimal production levels (cf. Perloff 2009: p.192-193).

3. Asymmetric information. A common problem in oil production is constituted by a lack of information on the government’s part about both the (technical) requirements of oil operations and about the actual production and profits realized by the international oil company. This may result in more bargaining power for the oil company, as well as in suboptimal rent extraction (Manzano & Monaldi 2008: p.73). One way for a government to resolve this problem is through employing a national oil company, possibly operating in conjunction with the international oil company. This may partly resolve both the lack of technological know-how and the knowledge about output and profits.

Alternatively, there may be a lack of information on the part of the international oil company regarding political decisions. While the company, through repeated interaction and observed actions, may have essential information about the current government’s intentions, it is unknowledgeable about the actions of subsequent governments. Although such events as coups d’état and revolutions may pose

6 See http://www.encharter.org/ for more information on the ENC.

Leviathan’s Wells. A Political Economy of Oil Nationalization 7

significant problems of risk for the company, even democratic rotations of power can lead to significant policy shifts.

4. Agency problems with state production. In an ideal situation, the state would be indifferent between having a state oil company produce all oil or outsourcing this production to private oil companies and capturing all surplus. In reality, however, state production may run into problems of agency and efficiency. The form and shape of this problem largely depends on the autonomy awarded to the state oil company and the regulating institutions (Manzano & Monaldi 2008). If state companies are under political control, there is often a problem of too much rent extraction, leaving the companies little room for the necessary investments. Also, political rent seeking may pose a problem to the efficacy of the oil operations. When state companies are strongly autonomous, on the other hand, the state may not be able to adequately capture all rents.

The interaction between governments and international petroleum companies is heavily influenced by the way both parties have been able to resolve these problems. For instance, Brazil’s national oil company Petrobras is widely deemed to be effective, independent and trustworthy, thus increasing Brazil’s bargaining power and reducing its information asymmetry. On the other hand, the firing of a substantial part of Venezuela’s PDVSA cadre in December 2002 by Hugo Chávez’s government has substantially reduced Venezuela’s access to information (Eller, Hartley & Medlock III 2010; Manzano & Monaldi 2008). Thus, the institutional, political and economic quirks of a country have a profound effect on oil investment.

4 A MODEL OF OIL INVESTMENT This chapter will define the game-theoretical model underlying the present analysis. First, the basic intuitions that form the foundation of the model are discussed. Subsequently, a one-shot game is presented. After that, this game is expanded into a repeated game, with a government discount function based on domestic political circumstances. This game will consequently be analyzed, laying bare the mechanics of the model. 4.1 Some basic intuitions Our abstraction of the process of oil investment into a game follows some basic intuitions about investments in the oil industry. These involve the importance of sovereignty, the assumption that national oil firms produce less efficiently, the existence of an explicit or implicit contract, and the long-term importance of political factors. Firstly, the quintessential matter in any investment deal struck between a government and a private company is the notion of sovereignty: the state always has the unilateral capacity to change a contract or nationalize the whole enterprise (see Section 3.2). Although states may have compelling reasons to refrain from it, the mere possibility of nationalization is always a background factor in petroleum investment.

Secondly, nationally owned oil companies are, in general, not able to produce as efficiently as private oil companies (Eller, Hartley & Medlock III 2010). This may be due, for example, to agent-principal problems, politicization of the company’s business, or lack of technological know-how. Indeed, if governments were able to produce as efficiently as privately owned companies, they would not have an incentive to invite private firms, for they would be able to maximize their income without any outside help. Although empirically some NOCs, such as Saudi Arabia’s SaudiAramco or China’s CNOOC, are quite efficient, most are well below TOCs’ levels of efficiency (ibid.). Hence, a government could theoretically appropriate more oil income through the employment of international oil companies, as long

8 Sjoerd ten Wolde

as it sets its taxes and rents correctly. In the game portrayed here, we therefore assume that there is an efficiency-related incentive for a government to invite a TOC. A third intuition is that the cooperation between a government and an oil firm involves an implicit or (more likely) an explicit contract. The most fundamental requirement of this contract is that the government not abuse its sovereign powers to expropriate the investments of the firm. The contract sets out the applying tax rates and oil rents to be paid. It may also stipulate that the oil firm must invest in the exploration and exploitation of the oil fields, that it must provide for local employment opportunities, that its conduct be ethical and appropriate, and similar clauses. The breaking up of such contracts more often than not results in a severe drop in trust. Fourthly, the model reflects the intuition that political factors are paramount in the long run. While a one-shot game in reality (e.g. a short project) may primarily be dependent on the economic profits, long-term cooperation strongly depends on the reputation, reliability and incentives of a government and its institutional system. Especially investment decisions are heavily influenced by the ‘discount factor’ of both the government and the oil firm. This intuition clearly favors stable political institutions and broad public and elite support of the government when it comes to the likelihood of an optimal outcome.

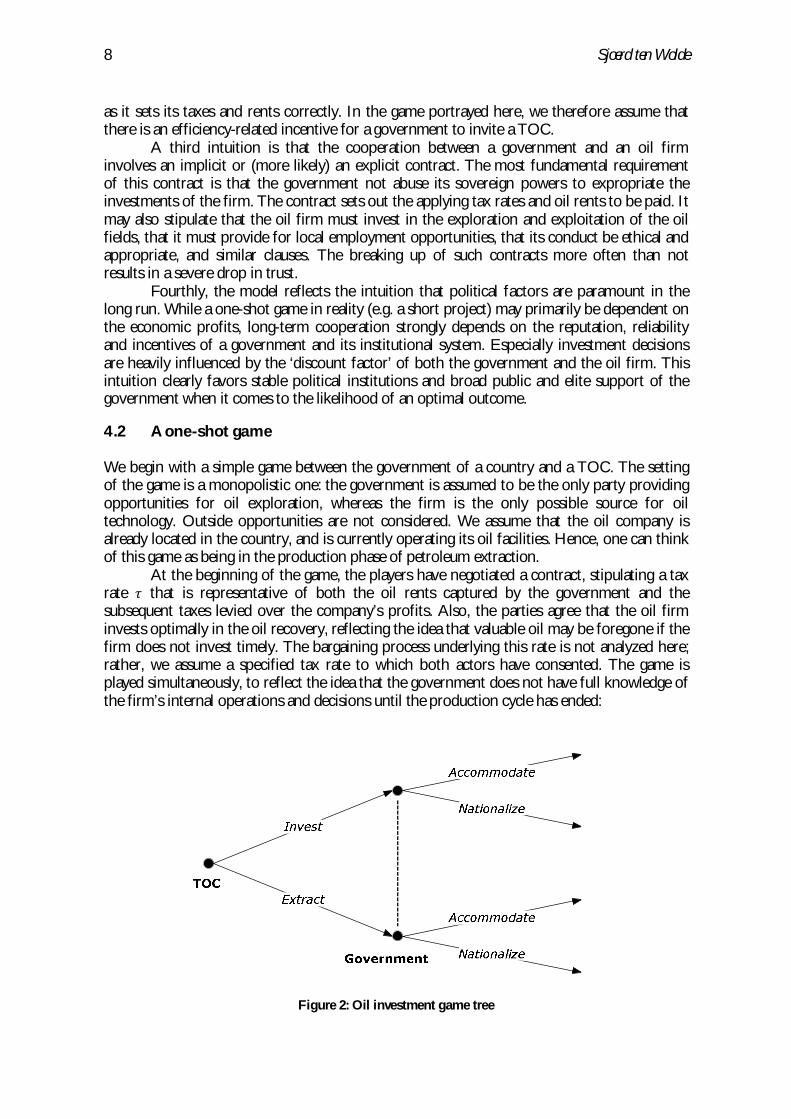

4.2 A one-shot game We begin with a simple game between the government of a country and a TOC. The setting of the game is a monopolistic one: the government is assumed to be the only party providing opportunities for oil exploration, whereas the firm is the only possible source for oil technology. Outside opportunities are not considered. We assume that the oil company is already located in the country, and is currently operating its oil facilities. Hence, one can think of this game as being in the production phase of petroleum extraction. At the beginning of the game, the players have negotiated a contract, stipulating a tax rate 휏 that is representative of both the oil rents captured by the government and the subsequent taxes levied over the company’s profits. Also, the parties agree that the oil firm invests optimally in the oil recovery, reflecting the idea that valuable oil may be foregone if the firm does not invest timely. The bargaining process underlying this rate is not analyzed here; rather, we assume a specified tax rate to which both actors have consented. The game is played simultaneously, to reflect the idea that the government does not have full knowledge of the firm’s internal operations and decisions until the production cycle has ended:

Figure 2: Oil investment game tree

Leviathan’s Wells. A Political Economy of Oil Nationalization 9

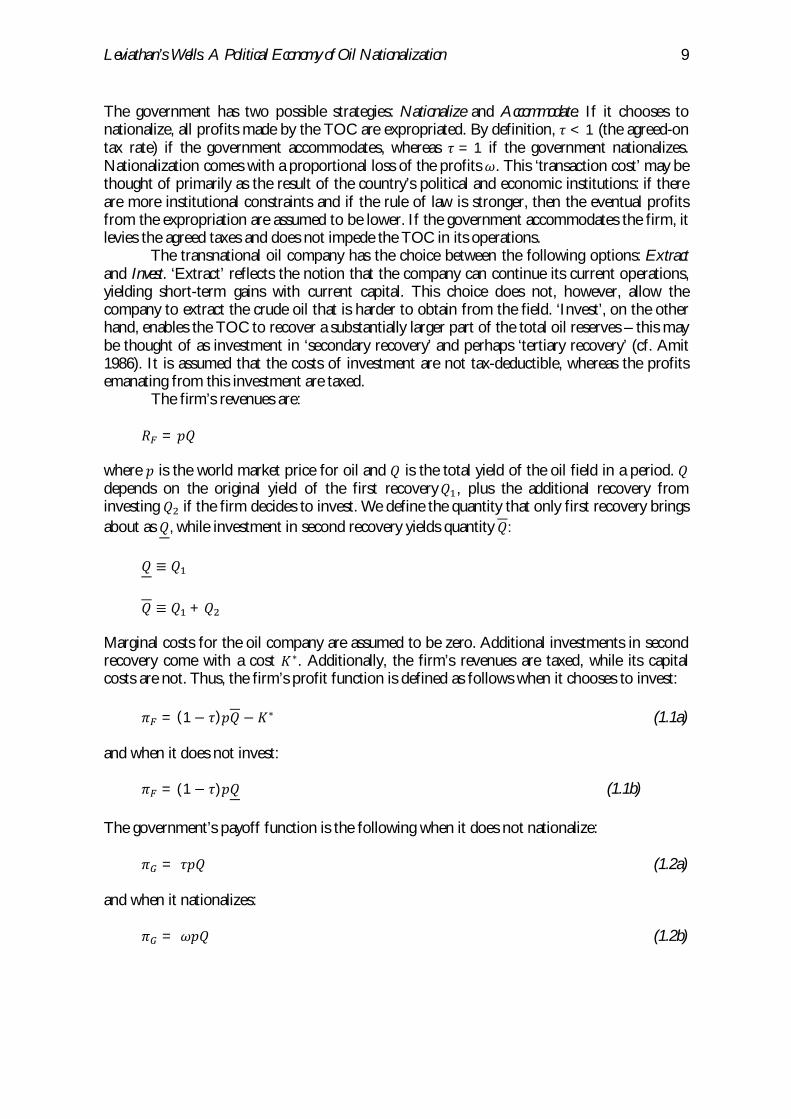

The government has two possible strategies: Nationalize and Accommodate. If it chooses to nationalize, all profits made by the TOC are expropriated. By definition, 휏 < 1 (the agreed-on tax rate) if the government accommodates, whereas 휏 = 1 if the government nationalizes. Nationalization comes with a proportional loss of the profits 휔. This ‘transaction cost’ may be thought of primarily as the result of the country’s political and economic institutions: if there are more institutional constraints and if the rule of law is stronger, then the eventual profits from the expropriation are assumed to be lower. If the government accommodates the firm, it levies the agreed taxes and does not impede the TOC in its operations. The transnational oil company has the choice between the following options: Extract and Invest. ‘Extract’ reflects the notion that the company can continue its current operations, yielding short-term gains with current capital. This choice does not, however, allow the company to extract the crude oil that is harder to obtain from the field. ‘Invest’, on the other hand, enables the TOC to recover a substantially larger part of the total oil reserves – this may be thought of as investment in ‘secondary recovery’ and perhaps ‘tertiary recovery’ (cf. Amit 1986). It is assumed that the costs of investment are not tax-deductible, whereas the profits emanating from this investment are taxed.

The firm’s revenues are:

푅 = 푝푄

where 푝 is the world market price for oil and 푄 is the total yield of the oil field in a period. 푄 depends on the original yield of the first recovery 푄 , plus the additional recovery from investing 푄 if the firm decides to invest. We define the quantity that only first recovery brings about as 푄, while investment in second recovery yields quantity 푄:

푄 ≡ 푄

푄 ≡ 푄 + 푄 Marginal costs for the oil company are assumed to be zero. Additional investments in second recovery come with a cost 퐾∗. Additionally, the firm’s revenues are taxed, while its capital costs are not. Thus, the firm’s profit function is defined as follows when it chooses to invest:

휋 = (1− 휏)푝푄 − 퐾∗ (1.1a) and when it does not invest:

휋 = (1− 휏)푝푄 (1.1b) The government’s payoff function is the following when it does not nationalize:

휋 = 휏푝푄 (1.2a)

and when it nationalizes:

휋 = 휔푝푄 (1.2b)

10 Sjoerd ten Wolde

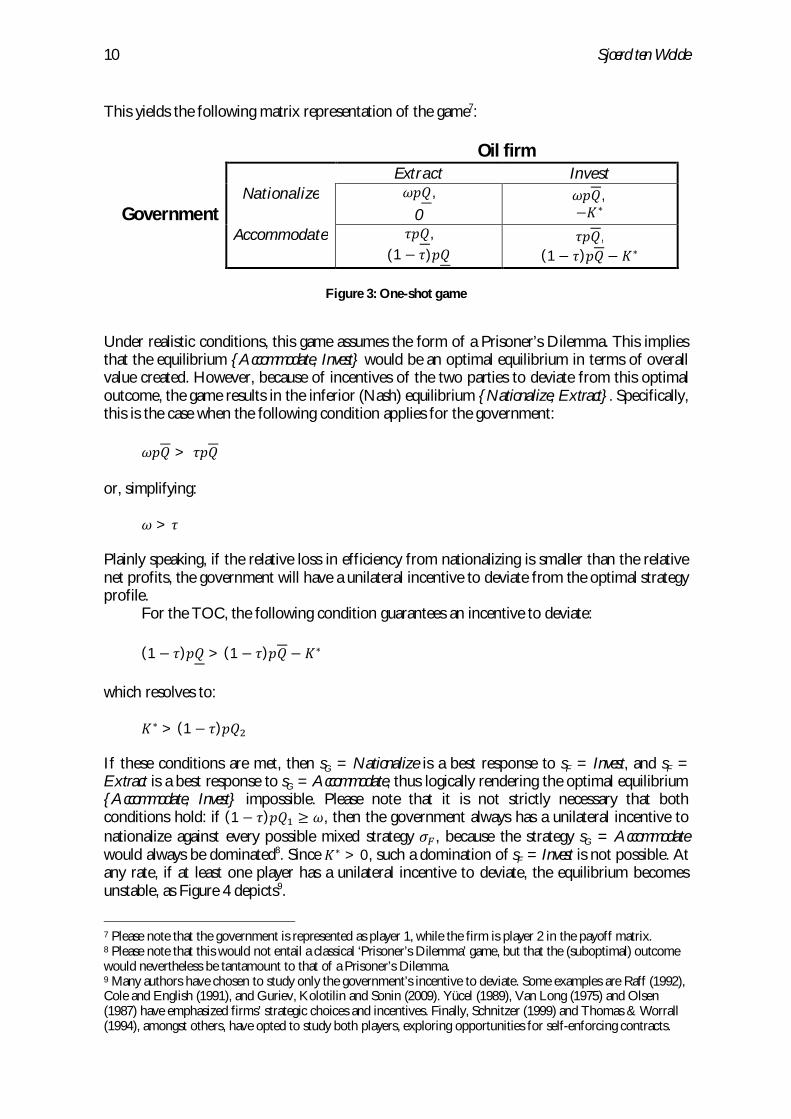

This yields the following matrix representation of the game7:

Oil firm

Government

Extract Invest Nationalize

휔푝푄,

0 휔푝푄, −퐾∗

Accommodate

휏푝푄, (1 − 휏)푝푄

휏푝푄, (1− 휏)푝푄 − 퐾∗

Figure 3: One-shot game

Under realistic conditions, this game assumes the form of a Prisoner’s Dilemma. This implies that the equilibrium {Accommodate, Invest} would be an optimal equilibrium in terms of overall value created. However, because of incentives of the two parties to deviate from this optimal outcome, the game results in the inferior (Nash) equilibrium {Nationalize, Extract}. Specifically, this is the case when the following condition applies for the government:

휔푝푄 > 휏푝푄

or, simplifying:

휔 > 휏

Plainly speaking, if the relative loss in efficiency from nationalizing is smaller than the relative net profits, the government will have a unilateral incentive to deviate from the optimal strategy profile.

For the TOC, the following condition guarantees an incentive to deviate:

(1 − 휏)푝푄 > (1 − 휏)푝푄 − 퐾∗ which resolves to:

퐾∗ > (1 − 휏)푝푄 If these conditions are met, then sG = Nationalize is a best response to sF = Invest, and sF = Extract is a best response to sG = Accommodate, thus logically rendering the optimal equilibrium {Accommodate, Invest} impossible. Please note that it is not strictly necessary that both conditions hold: if (1 − 휏)푝푄 ≥ 휔, then the government always has a unilateral incentive to nationalize against every possible mixed strategy 휎 , because the strategy sG = Accommodate would always be dominated8. Since 퐾∗ > 0, such a domination of sF = Invest is not possible. At any rate, if at least one player has a unilateral incentive to deviate, the equilibrium becomes unstable, as Figure 4 depicts9.

7 Please note that the government is represented as player 1, while the firm is player 2 in the payoff matrix. 8 Please note that this would not entail a classical ‘Prisoner’s Dilemma’ game, but that the (suboptimal) outcome would nevertheless be tantamount to that of a Prisoner’s Dilemma. 9 Many authors have chosen to study only the government’s incentive to deviate. Some examples are Raff (1992), Cole and English (1991), and Guriev, Kolotilin and Sonin (2009). Yücel (1989), Van Long (1975) and Olsen (1987) have emphasized firms’ strategic choices and incentives. Finally, Schnitzer (1999) and Thomas & Worrall (1994), amongst others, have opted to study both players, exploring opportunities for self-enforcing contracts.

Leviathan’s Wells. A Political Economy of Oil Nationalization 11

Oil firm

Government

Extract Invest

Nationalize

Suboptimal

Accommodate

Optimal

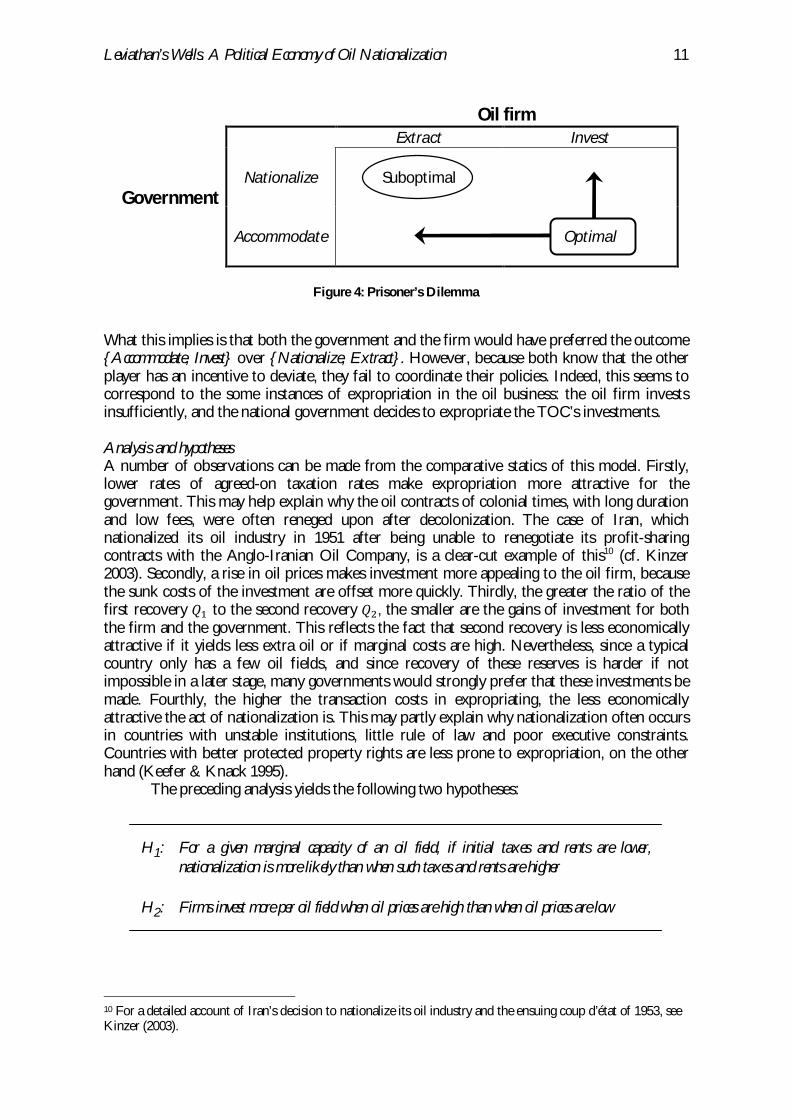

Figure 4: Prisoner’s Dilemma

What this implies is that both the government and the firm would have preferred the outcome {Accommodate, Invest} over {Nationalize, Extract}. However, because both know that the other player has an incentive to deviate, they fail to coordinate their policies. Indeed, this seems to correspond to the some instances of expropriation in the oil business: the oil firm invests insufficiently, and the national government decides to expropriate the TOC’s investments. Analysis and hypotheses A number of observations can be made from the comparative statics of this model. Firstly, lower rates of agreed-on taxation rates make expropriation more attractive for the government. This may help explain why the oil contracts of colonial times, with long duration and low fees, were often reneged upon after decolonization. The case of Iran, which nationalized its oil industry in 1951 after being unable to renegotiate its profit-sharing contracts with the Anglo-Iranian Oil Company, is a clear-cut example of this10 (cf. Kinzer 2003). Secondly, a rise in oil prices makes investment more appealing to the oil firm, because the sunk costs of the investment are offset more quickly. Thirdly, the greater the ratio of the first recovery 푄 to the second recovery 푄 , the smaller are the gains of investment for both the firm and the government. This reflects the fact that second recovery is less economically attractive if it yields less extra oil or if marginal costs are high. Nevertheless, since a typical country only has a few oil fields, and since recovery of these reserves is harder if not impossible in a later stage, many governments would strongly prefer that these investments be made. Fourthly, the higher the transaction costs in expropriating, the less economically attractive the act of nationalization is. This may partly explain why nationalization often occurs in countries with unstable institutions, little rule of law and poor executive constraints. Countries with better protected property rights are less prone to expropriation, on the other hand (Keefer & Knack 1995). The preceding analysis yields the following two hypotheses:

H1: For a given marginal capacity of an oil field, if initial taxes and rents are lower,

nationalization is more likely than when such taxes and rents are higher H2: Firms invest more per oil field when oil prices are high than when oil prices are low

10 For a detailed account of Iran’s decision to nationalize its oil industry and the ensuing coup d’état of 1953, see Kinzer (2003).

12 Sjoerd ten Wolde

4.4 A repeated game with political discount function The preceding analysis made it abundantly clear that, in situations of limited interaction and a lack of institutional constraints, optimal oil investment is unlikely to occur. Indeed, this scenario could well take place in countries where the prospects for further interaction are minute – for instance, if there are few oil reserves, or if the national oil company is not likely to cooperate on other projects. In most real-life situations, however, there is repeated interaction. Therefore, this section explores the implications of repeating the above game.

The folk theorem applies to the game: for sufficiently high discount rates, the game may end up in the Pareto-efficient equilibrium. This paper postulates, however, that the government’s discount rate is not exogenously given. Rather, political leaders’ time horizon is determined primarily by considerations of political survival. Except for extreme cases of graft, one can assume that governments try to gain as much from their control over oil fields as possible in order to garner political support and to be able to execute their political plans11. As Bueno de Mesquita et al. remark, ‘[t]he incumbent wants to maximize her discretionary resources’ (2003: p.96). Thus, politicians will be especially preoccupied with factors such as popular and elite support for their governance. Although the salience of these factors may vary between democracies and authoritarian systems, both are very much defining for every political leader’s perspective on the politics of oil. We shall here employ a two-pronged approach to governments’ discount rates. Our model incorporates (i) public support for the government, and (ii) the (political) elite’s support for the government. The thought behind this is that, in any given country, the political leadership’s survival is dependent on at least one of these groups’ backing. Bueno de Mesquita et al. (2003) point out that the size of the supporting classes (the so-called ‘selectorate’) differs strongly between nations, and is of paramount importance to a country’s economic policies. The degree in which each group’s endorsement matters is a function of the country’s political system: while autocracies tend to favor elite support over public support, in more democratic countries public opinion usually holds sway over the government’s survival12. The government’s discount factor, then, assays the degree in which the government thinks it is able to postpone current gains in order to achieve greater gains later on. This leads to the following formula for the discount factor:

훿 (푎,휑, 휇) = 푎휑 + (1− 푎)휇 (2.1) in which 휑 stands for a measure of public support between 0 and 1, and 휇 is a measure of elite support between 0 and 1. 푎 is a coefficient between 0 and 1 reflecting the relative importance of each variable. This coefficient is assumed to depend on the level of democracy, with 0 standing for full-fledged authoritarianism and 1 being ‘perfect democracy’.

With regard to the discount factor of the transnational oil company, it is assumed that the firm discounts the future in terms of the real world interest rate 푟. Thus, we end up with the following discount rate:

훿 (푟) = (2.2)

This model assumes a grim trigger strategy: if either the government or the oil company decides to defect, the other player will play the defecting strategy for the remainder of the game. In the

11 It should be noted that this notion is compatible with both ‘benevolent’ rule – in which case the oil funds get used for ‘common’ purposes – and with clientelistic forms of government, which need funds to keep 12 Democracy is here regarded as a continuous variable, not a categorical one.

Leviathan’s Wells. A Political Economy of Oil Nationalization 13

case of the government this is the choice to nationalize the oil investments. The oil firm, on the other hand, withdraws from the country for the remainder of the game.

A new feature we introduce here is the notion that, once it nationalizes, the government will produce the oil itself (e.g. through its own national oil company) for all remaining periods. Reflecting the idea that national oil companies are, in general, less efficient in their production, the government cannot invest in second recovery, and produces:

푄 = 휃푄

in which 휃 is an efficiency coefficient, and 0 ≤ 휃 ≤ 1. Thus, the income for the government after nationalizing will be the following in every period:

휋 = 푝휃푄

In an infinitely repeated game, this yields the following payoff function if the government decides to cooperate and does not nationalize:

훿 휋 =휏푝푄

1 − 훿

Which simplifies to:

휋 (휏,푄,푎,휑, 휇) =( )

(2.3a) If the government does decide to nationalize, it will earn the following income:

훿 휋 = 휔푝푄 + 훿 푝휃푄 + 훿 푝휃푄 + 훿 푝휃푄 +⋯ = 휔푝푄 +훿 푝휃푄1 − 훿

Which could be written down as:

휋 (휏,푄,푎,휑, 휇) = 휔푝푄 +[ ( ) ]

( ) (2.3b)

Then, the oil firm’s payoffs when it cooperates are:

훿 휋 = [(1− 휏)푝푄 − 퐾][1 + 훿 + 훿 + 훿 +⋯ ] =(1− 휏)푝푄 − 퐾

1 − 훿

Inserting 훿 = 1/(1 + 푟), we obtain:

휋 (휏,푄,퐾, 푟) = (1− 휏)푝푄 − 퐾∗ + ( ) ∗ (2.4a)

14 Sjoerd ten Wolde

If the oil company decides to deviate, it will obtain the following profits13:

훿 휋 = (1− 휏)푝푄

Thus:

휋 (휏,푄) = (1 − 휏)푝푄 (2.4b) For clarity, we here summarize the government’s and TOC’s set of payoffs:

휋 (휏) =

⎩⎪⎨

⎪⎧ 휏푝푄

1 − 푎휑 − (1 − 푎)휇, 푖푓 푎푙푙 휏 < 1

휔푝푄 +[푎휑 + (1 − 푎)휇]푝휃푄1 − 푎휑 − (1− 푎)휇

, 푖푓 휏 = 1

휋 (퐾) = (1− 휏)푝푄 − 퐾∗ +(1− 휏)푝푄 − 퐾∗

푟 , 푖푓 푎푙푙 퐾 = 퐾∗

(1 − 휏)푝푄 , 푖푓 퐾 < 퐾∗

Self-enforcing contracts For a production contract to be self-enforcing, the parties must agree on a tax rate that is both acceptable to the oil firm and which does not induce the government to break its promises and nationalize (Watson 2002: p.116). Thus, there are two restrictions: an upper bound emanating from the oil firm’s profit maximization, and a lower bound resulting from the government’s inability to commit credibly to low tax regimes.

The following condition must hold for the government:

휏푝푄1 − 푎휑 − (1 − 푎)휇

≥ 휔푝푄 +[푎휑 + (1− 푎)휇]푝휃푄1 − 푎휑 − (1 − 푎)휇

This could be reformulated in terms of the negotiated tax rate:

휏 ≥ 휔 + [푎휑 − (1 − 푎)휇][(휃푄 푄)⁄ − 휔] In words, this means that the negotiators must take account of the transaction costs of

nationalization, the efficiency of autonomous oil production, and the geological and market conditions underlying the project. Perhaps most importantly, moreover, they must take heed of the government´s popular and elite support. In a way, surprisingly enough, a more instable political environment could give governments greater political clout in negotiations over taxation and oil rents – this would strongly resemble a ‘tied hands’ strategy (Schelling 1960); (see Figure 5). 13 It is assumed here that the oil company still pays its taxes when it deviates, even if it knows that it will get booted out of the country. While this need not necessarily occur in reality, the host country could of course always resort to arrests, violence, etc. to force an outgoing company to pay its taxes.

Leviathan’s Wells. A Political Economy of Oil Nationalization 15

For the firm, the upper boundary is:

(1 − 휏)푝푄 − 퐾∗ +(1 − 휏)푝푄 − 퐾∗

푟≥ (1− 휏)푝푄

Which, expressed in the tax rate, boils down to:

휏 ≤ 1−퐾∗(1 + 1 푟)⁄

푝푄(1 + 1 푟)⁄ − 푝푄

or, equivalently:

(1 − 휏) ≥퐾∗(1 + 1 푟)⁄

푝푄(1 + 1 푟)⁄ − 푝푄

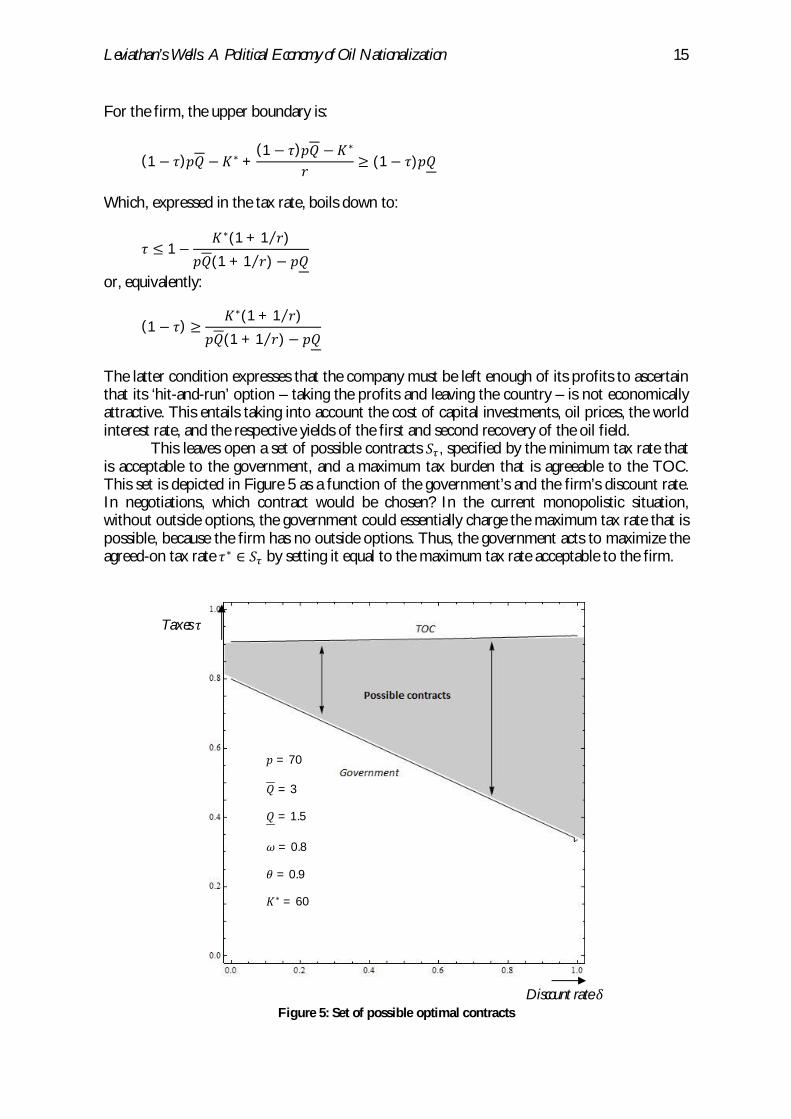

The latter condition expresses that the company must be left enough of its profits to ascertain that its ‘hit-and-run’ option – taking the profits and leaving the country – is not economically attractive. This entails taking into account the cost of capital investments, oil prices, the world interest rate, and the respective yields of the first and second recovery of the oil field. This leaves open a set of possible contracts 푆 , specified by the minimum tax rate that is acceptable to the government, and a maximum tax burden that is agreeable to the TOC. This set is depicted in Figure 5 as a function of the government’s and the firm’s discount rate. In negotiations, which contract would be chosen? In the current monopolistic situation, without outside options, the government could essentially charge the maximum tax rate that is possible, because the firm has no outside options. Thus, the government acts to maximize the agreed-on tax rate 휏∗ ∈ 푆 by setting it equal to the maximum tax rate acceptable to the firm.

Figure 5: Set of possible optimal contracts Discount rate 훿

푝 = 70

푄 = 3

푄 = 1.5

휔 = 0.8

휃 = 0.9

퐾∗ = 60

Taxes 휏

16 Sjoerd ten Wolde

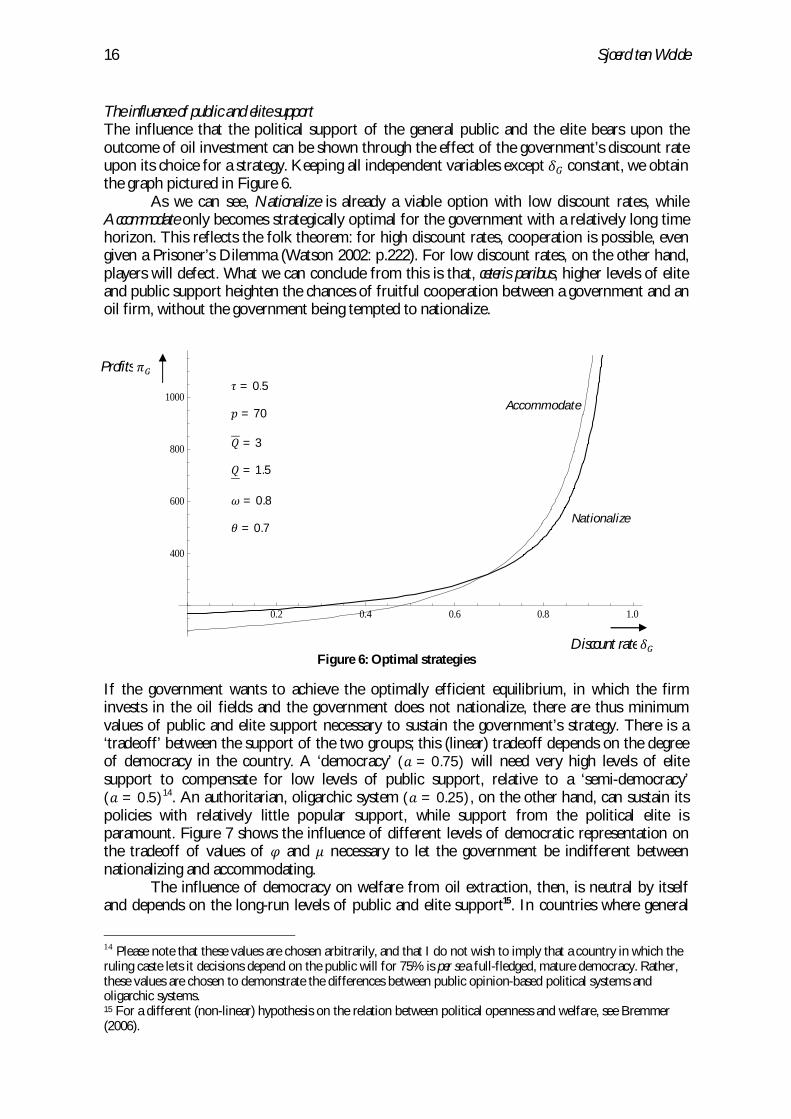

The influence of public and elite support The influence that the political support of the general public and the elite bears upon the outcome of oil investment can be shown through the effect of the government’s discount rate upon its choice for a strategy. Keeping all independent variables except 훿 constant, we obtain the graph pictured in Figure 6.

As we can see, Nationalize is already a viable option with low discount rates, while Accommodate only becomes strategically optimal for the government with a relatively long time horizon. This reflects the folk theorem: for high discount rates, cooperation is possible, even given a Prisoner’s Dilemma (Watson 2002: p.222). For low discount rates, on the other hand, players will defect. What we can conclude from this is that, ceteris paribus, higher levels of elite and public support heighten the chances of fruitful cooperation between a government and an oil firm, without the government being tempted to nationalize.

Figure 6: Optimal strategies

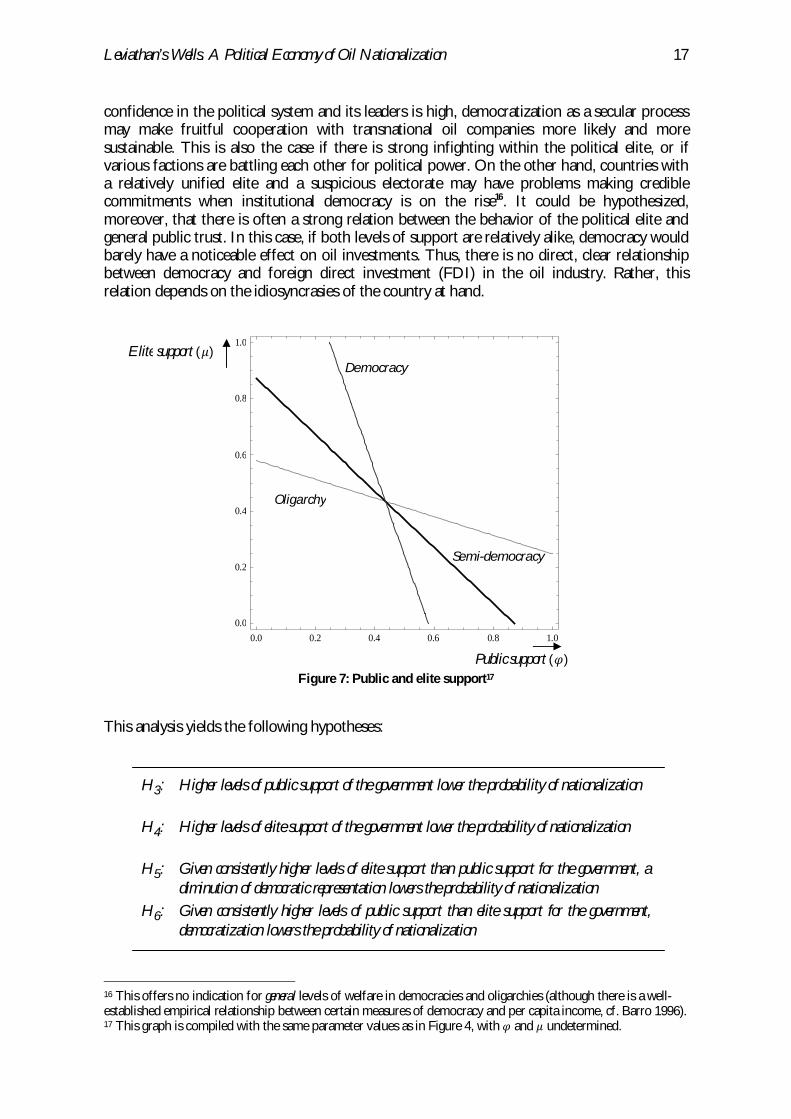

If the government wants to achieve the optimally efficient equilibrium, in which the firm invests in the oil fields and the government does not nationalize, there are thus minimum values of public and elite support necessary to sustain the government’s strategy. There is a ‘tradeoff’ between the support of the two groups; this (linear) tradeoff depends on the degree of democracy in the country. A ‘democracy’ (푎 = 0.75) will need very high levels of elite support to compensate for low levels of public support, relative to a ‘semi-democracy’ (푎 = 0.5)14. An authoritarian, oligarchic system (푎 = 0.25), on the other hand, can sustain its policies with relatively little popular support, while support from the political elite is paramount. Figure 7 shows the influence of different levels of democratic representation on the tradeoff of values of 휑 and 휇 necessary to let the government be indifferent between nationalizing and accommodating.

The influence of democracy on welfare from oil extraction, then, is neutral by itself and depends on the long-run levels of public and elite support15. In countries where general

14 Please note that these values are chosen arbitrarily, and that I do not wish to imply that a country in which the ruling caste lets it decisions depend on the public will for 75% is per se a full-fledged, mature democracy. Rather, these values are chosen to demonstrate the differences between public opinion-based political systems and oligarchic systems. 15 For a different (non-linear) hypothesis on the relation between political openness and welfare, see Bremmer (2006).

Accommodate

Nationalize

0.2 0.4 0.6 0.8 1.0

400

600

800

1000

Discount rate 훿

Profits 휋 휏 = 0.5

푝 = 70

푄 = 3

푄 = 1.5

휔 = 0.8

휃 = 0.7

Leviathan’s Wells. A Political Economy of Oil Nationalization 17

confidence in the political system and its leaders is high, democratization as a secular process may make fruitful cooperation with transnational oil companies more likely and more sustainable. This is also the case if there is strong infighting within the political elite, or if various factions are battling each other for political power. On the other hand, countries with a relatively unified elite and a suspicious electorate may have problems making credible commitments when institutional democracy is on the rise16. It could be hypothesized, moreover, that there is often a strong relation between the behavior of the political elite and general public trust. In this case, if both levels of support are relatively alike, democracy would barely have a noticeable effect on oil investments. Thus, there is no direct, clear relationship between democracy and foreign direct investment (FDI) in the oil industry. Rather, this relation depends on the idiosyncrasies of the country at hand.

Figure 7: Public and elite support17

This analysis yields the following hypotheses:

H3: Higher levels of public support of the government lower the probability of nationalization H4: Higher levels of elite support of the government lower the probability of nationalization H5: Given consistently higher levels of elite support than public support for the government, a

diminution of democratic representation lowers the probability of nationalization H6: Given consistently higher levels of public support than elite support for the government,

democratization lowers the probability of nationalization

16 This offers no indication for general levels of welfare in democracies and oligarchies (although there is a well-established empirical relationship between certain measures of democracy and per capita income, cf. Barro 1996). 17 This graph is compiled with the same parameter values as in Figure 4, with 휑 and 휇 undetermined.

Semi-democracy

Democracy

Oligarchy

0.0 0.2 0.4 0.6 0.8 1.00.0

0.2

0.4

0.6

0.8

1.0Elite support (휇)

Public support (휑)

Oligarchy

18 Sjoerd ten Wolde

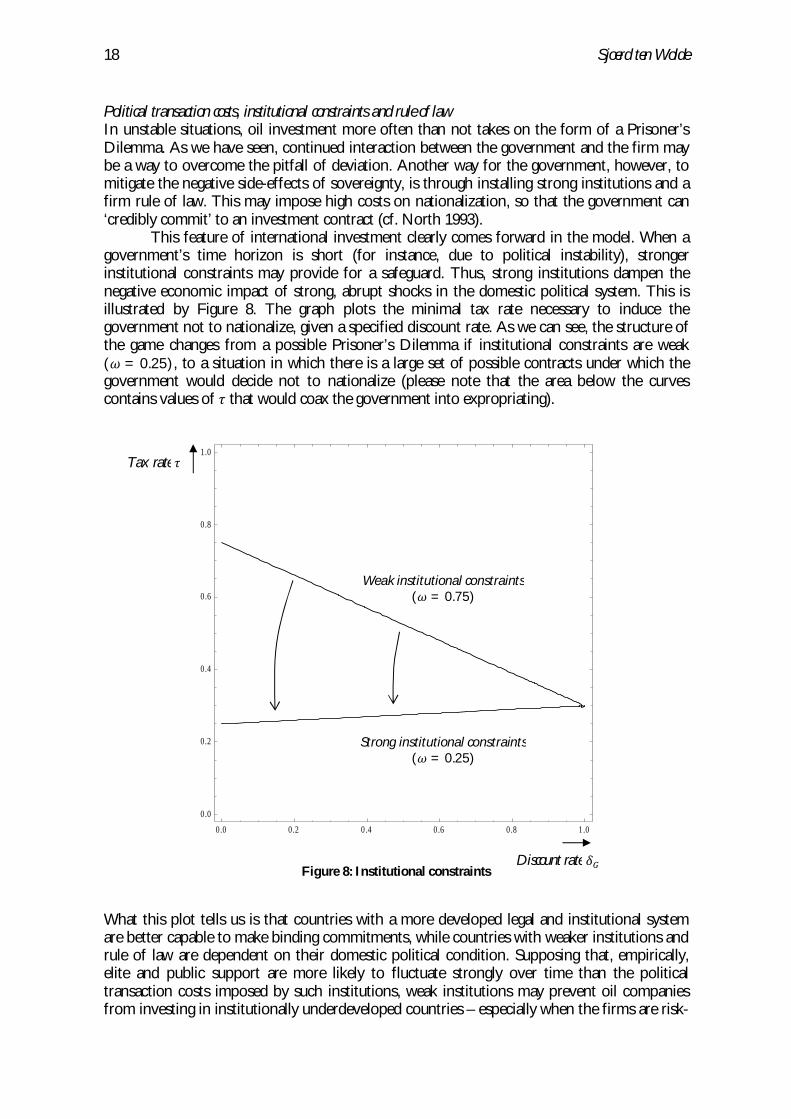

Political transaction costs, institutional constraints and rule of law In unstable situations, oil investment more often than not takes on the form of a Prisoner’s Dilemma. As we have seen, continued interaction between the government and the firm may be a way to overcome the pitfall of deviation. Another way for the government, however, to mitigate the negative side-effects of sovereignty, is through installing strong institutions and a firm rule of law. This may impose high costs on nationalization, so that the government can ‘credibly commit’ to an investment contract (cf. North 1993). This feature of international investment clearly comes forward in the model. When a government’s time horizon is short (for instance, due to political instability), stronger institutional constraints may provide for a safeguard. Thus, strong institutions dampen the negative economic impact of strong, abrupt shocks in the domestic political system. This is illustrated by Figure 8. The graph plots the minimal tax rate necessary to induce the government not to nationalize, given a specified discount rate. As we can see, the structure of the game changes from a possible Prisoner’s Dilemma if institutional constraints are weak (휔 = 0.25), to a situation in which there is a large set of possible contracts under which the government would decide not to nationalize (please note that the area below the curves contains values of 휏 that would coax the government into expropriating).

Figure 8: Institutional constraints

What this plot tells us is that countries with a more developed legal and institutional system are better capable to make binding commitments, while countries with weaker institutions and rule of law are dependent on their domestic political condition. Supposing that, empirically, elite and public support are more likely to fluctuate strongly over time than the political transaction costs imposed by such institutions, weak institutions may prevent oil companies from investing in institutionally underdeveloped countries – especially when the firms are risk-

Weak institutional constraints

( = 0.75)

Strong institutional constraints

( = 0.25)

0.0 0.2 0.4 0.6 0.8 1.00.0

0.2

0.4

0.6

0.8

1.0

Discount rate 훿

Tax rate 휏

Weak institutional constraints (휔 = 0.75)

Strong institutional constraints (휔 = 0.25)

Leviathan’s Wells. A Political Economy of Oil Nationalization 19

averse. Thus, strong constraints on the executive branch may serve as a protective cushion in politically volatile times. We could distill the following hypotheses from the preceding analysis:

H7: More robust institutions, a stronger rule of law, and/or more constitutional constraints lower the probability of nationalization

H8: More robust institutions, a stronger rule of law, and/or more constitutional constraints

lead to higher rates of petroleum-related investment World interest rate As we have seen, the influence of the domestic political environment is of quintessential importance to the government’s decision to nationalize or not. While the firm’s discount rate, determined by the costs of raising capital, is also an essential variable, its effect on the outcome of the investment game is arguably less important. Theoretically, the model attributes less influence to the firm’s discount rate. Empirically, real interest rates often vary less than domestic political variables. Nevertheless, we shall here briefly examine the effect of interest rates on the firm’s behavior:

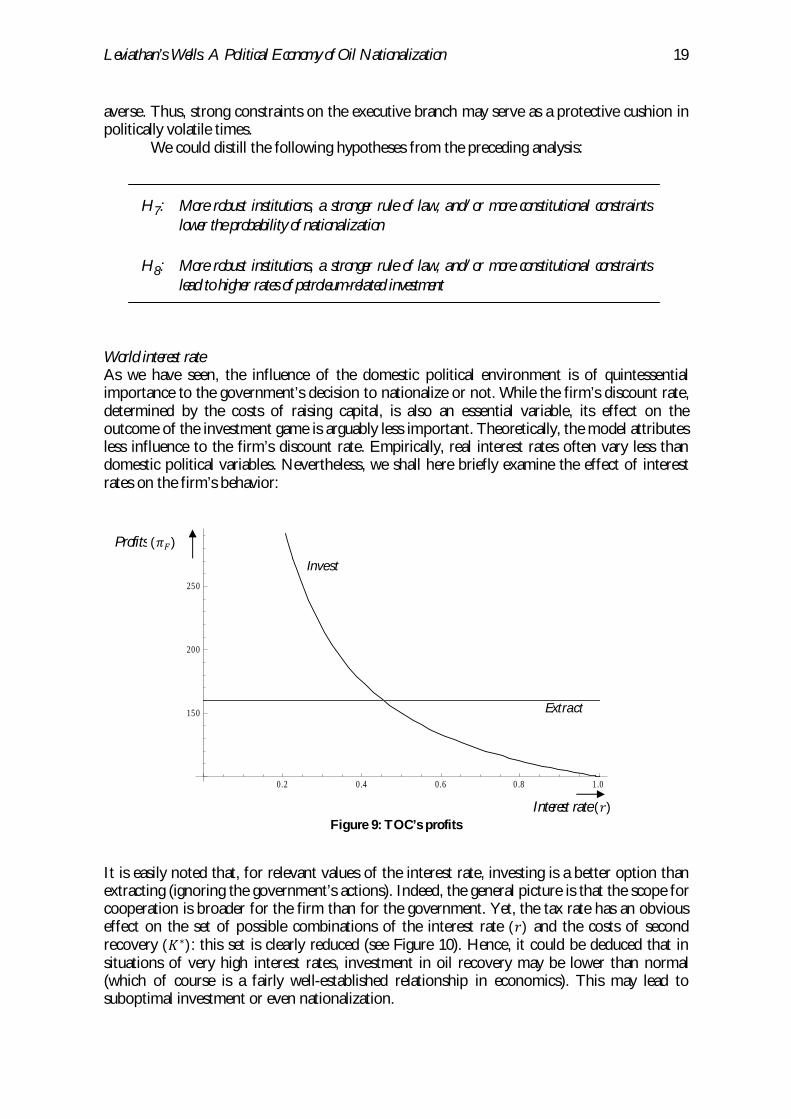

Figure 9: TOC’s profits

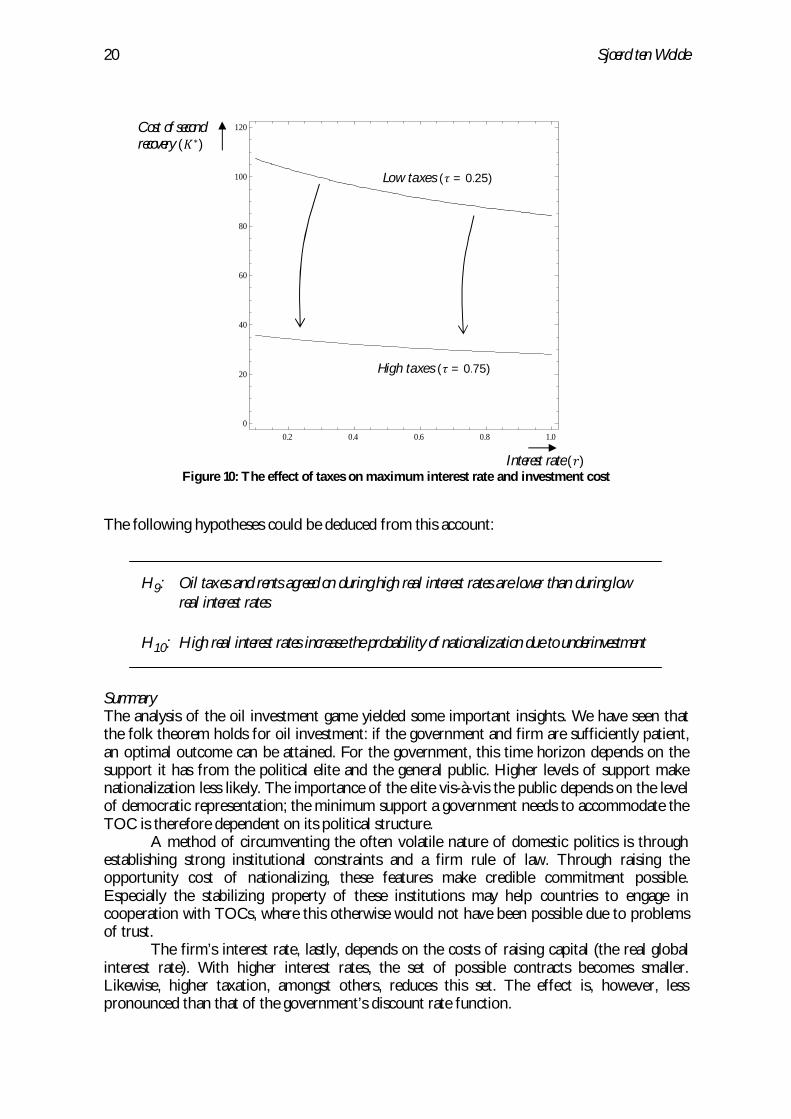

It is easily noted that, for relevant values of the interest rate, investing is a better option than extracting (ignoring the government’s actions). Indeed, the general picture is that the scope for cooperation is broader for the firm than for the government. Yet, the tax rate has an obvious effect on the set of possible combinations of the interest rate (푟) and the costs of second recovery (퐾∗): this set is clearly reduced (see Figure 10). Hence, it could be deduced that in situations of very high interest rates, investment in oil recovery may be lower than normal (which of course is a fairly well-established relationship in economics). This may lead to suboptimal investment or even nationalization.

0.2 0.4 0.6 0 .8 1 .0

150

200

250

Invest

Extract

Interest rate (푟)

Profits (휋 )

20 Sjoerd ten Wolde

Figure 10: The effect of taxes on maximum interest rate and investment cost

The following hypotheses could be deduced from this account:

H9: Oil taxes and rents agreed on during high real interest rates are lower than during low

real interest rates H10: High real interest rates increase the probability of nationalization due to underinvestment

Summary The analysis of the oil investment game yielded some important insights. We have seen that the folk theorem holds for oil investment: if the government and firm are sufficiently patient, an optimal outcome can be attained. For the government, this time horizon depends on the support it has from the political elite and the general public. Higher levels of support make nationalization less likely. The importance of the elite vis-à-vis the public depends on the level of democratic representation; the minimum support a government needs to accommodate the TOC is therefore dependent on its political structure. A method of circumventing the often volatile nature of domestic politics is through establishing strong institutional constraints and a firm rule of law. Through raising the opportunity cost of nationalizing, these features make credible commitment possible. Especially the stabilizing property of these institutions may help countries to engage in cooperation with TOCs, where this otherwise would not have been possible due to problems of trust. The firm’s interest rate, lastly, depends on the costs of raising capital (the real global interest rate). With higher interest rates, the set of possible contracts becomes smaller. Likewise, higher taxation, amongst others, reduces this set. The effect is, however, less pronounced than that of the government’s discount rate function.

0.2 0.4 0.6 0.8 1.00

20

40

60

80

100

120Cost of second recovery (퐾∗)

Interest rate (푟)

High taxes (휏 = 0.75)

Low taxes (휏 = 0.25)

Leviathan’s Wells. A Political Economy of Oil Nationalization 21

5 CONCLUSION “Oil is like a wild animal. Whoever captures it has it.”, oil entrepreneur Jean Paul Getty once remarked. In this age of increasing demand and scarcity, national states have managed to capture the vast majority of oil sources. These states are often more concerned with their own well-being or that of their citizens than with the profits of foreign oil companies. These foreign oil firms, on the other hand, are increasingly obliged to bow to the will of their host countries. In many instances, nonetheless, the relationship between states and transnational oil companies is symbiotic, rather than adversarial. The general inefficiency of national oil companies forces governments to seek help from foreign companies. Notwithstanding this symbiosis, however, there is often strong mutual distrust. This paper has investigated the political and economic factors underlying investment and nationalization decisions. Using a formal game-theoretic model, we have explored the notion of petroleum investment as a Prisoner’s Dilemma, in which optimal outcomes are only possible under certain conditions. A one-shot game yielded the conclusion that, in circumstances where repeated interaction is absent, the outcome of an investment game will tend to be suboptimal for both players. Subsequently, we analyzed the behavior of the players in an infinitely repeated game, in which the government had the option to nationalize and to (inefficiently) produce its own oil. This analysis yielded a number of insights. (i) First, governments are more likely to nationalize oil investments when public and elite support are low. The relative importance of the general public and the political elite depends on the degree of democratic representation of the country; hence, oil investment is influenced in different ways by democratization, depending on the long-run support of these two groups. (ii) Second, strong institutional constraints and a consolidated rule of law heighten the political transaction costs of nationalization, thereby rendering expropriation less likely. Developed institutions may therefore act as a safeguard against the negative impact on investment of bouts of political instability, dissatisfaction with a government, and the like. (iii) Third, firms are more prone to underinvestment when interest rates are high. This may lead to nationalization if the low levels of production make expropriation and subsequent national production more attractive. However, the effect of the interest rate on the probability of nationalization seems to be weaker than that of the aforementioned factors. Oil investment is a deeply political business. As we have seen, governmental decisions get made not only on the basis of potential profits, but also on their political merits. The government’s time horizon therefore depends strongly on the institutional structure of the country, and the support of the government from elite groups and the general population. This observation warrants more research with respect to the exact nature of decision-making in oil; especially empirical studies would contribute to the profession’s body of knowledge. Moreover, more sensitivity of those ‘in the business’ to political factors could prevent disastrous investments – and perhaps even unethical decisions and behavior. In the near future, it is likely that we will see more international conflicts revolving around oil, as states will feel the temptation of their inner Leviathan. A deeper understanding of the motives driving the actors involved would therefore contribute to better outcomes and wiser decisions before investments are made. It is a scarce world after all, but scarcity need not lead to misery.

22 Sjoerd ten Wolde

BIBLIOGRAPHY AGUIAR, M., M. AMADOR & G. GOPINATH (2009). ‘Expropriation Dynamics’. American

Economic Review, vol. 99, no. 2, pp. 473-479 BARRO, R.J. (1996). ‘Democracy and Growth’. Journal of Economic Growth, vol. 1, no. 1, pp. 1-27 BOHN, H. & R.T. DEACON (2000). ‘Ownership Risk, Investment, and the Use of Natural

Resources’. The American Economic Review, vol. 90, no. 3, pp. 526-549 BOYARCHENKO, N. (2007). ‘Turning Off the Tap: Determinants of Expropriation in the

Energy Sector’. Working Paper BREMMER, I. (2006). The J Curve: A New Way to Understand Why Nations Rise and Fall. New York:

Simon & Schuster BUENO DE MESQUITA, B., A. SMITH, R.M. SIVERSON & J.D. MORROW (2003). The Logic of

Political Survival. Cambridge, MA: The MIT Press COLE, H.L. & W.B. ENGLISH (1991). ‘Expropriation and Direct Investment’. Journal of

International Economics, vol. 30, no. 3-4, pp. 201-227 DUNCAN, R. (2005). ‘Price or Politics? An Investigation of the Causes of Expropriation’.

Working Paper ELLER, S.L., P.R. HARTLEY & K.B. MEDLOCK III (2010). ‘Empirical Evidence on the

Operational Efficiency of National Oil Companies’. Empirical Economics, forthcoming GIBBONS, R. (1992). A Primer in Game Theory. Harlow: Prentice Hall GURIEV, S., A. KOLOTILIN & K. SONIN (2010). ‘Determinants of Nationalization in the Oil

Sector: A Theory and Evidence from Panel Data’. Journal of Law, Economics and Organization, forthcoming

HYNE, N.J. (2001). Nontechnical Guide to Petroleum Geology, Exploration, Drilling and Production. 2nd Edition. Tulsa: Penn Well Corporation.

JOFFÉ, G., P. STEVENS, T. GEORGE, J. LUX & C. SEARLE (2009). ‘Expropriation of Oil and Gas Investments: Historical, Legal and Economic Perspectives in a New Age of Resource Nationalism’. Journal of World Energy Law & Business, vol. 2, no. 1, pp. 3-23

KNACK, S. & P. KEEFER (1995). ‘Institutions and Economic Performance: Cross Country Tests Using Alternative Institutional Measures’. Economics and Politics, vol. 7, no. 3, pp. 207-227

LE CALVEZ, M. (2009). ‘El Impacto de las Políticas Nacionales en los Rediseños de Gobernanza Petrolera en Ecuador y Venezuela’. América Latina Hoy, vol. 53, pp. 67-83

LONG, N.V. (1975). ‘Resource Extraction under the Uncertainty about Possible Nationalization’. Journal of Economic Theory, vol. 10, pp. 42-53

LI, Q. (2009). ‘Democracy, Autocracy, and Expropriation of Foreign Direct Investment’. Comparative Political Studies, vol. 42, no. 8, pp. 1098-1127

MANZANO, O. & F. MONALDI (2008). ‘The Political Economy of Oil Production in Latin America’. Economía, vol. 9, no. 1, pp. 59-103

MEHLUM, H., K. MOENE & R. TORVIK (2006). ‘Institutions and the Resource Curse’. The Economic Journal, vol. 116, pp. 1-20

MITCHELL, J., K. MORITA, N. SELLEY & J. STERN (2001). The New Economy of Oil. Impacts on Business, Geopolitics and Society. London: Royal Institute of International Affairs

MOMMER, B. (2000). ‘The Governance of International Oil: The Changing Rules of the Game’. OIES Paper WPM 26, Oxford Institute for Energy Studies

NORTH, D.C. (1993). ‘Institutions and Credible Commitment’. Journal of Institutional and Theoretical Economics, vol. 149, pp. 11-23

PERLOFF, J.M. (2009). Microeconomics. Fifth Edition. Pearson/Addison-Wesley RAFF, H. (1992). ‘A Model of Expropriation with Asymmetric Information’. Journal of

International Economics, vol. 33, no. 3-4, pp. 245-265

Leviathan’s Wells. A Political Economy of Oil Nationalization 23

SCHNITZER, M. (1999). ‘Expropriation and Control Rights: A Dynamic Model of Foreign Direct Investment’. International Journal of Industrial Organization, vol. 17, no. 8, pp. 1113-1137

TER ELLEN, S. & R.C.J. ZWINKELS (2010). ‘Oil Price Dynamics: A Behavioral Finance Approach with Heterogeneous Agents’. Energy Economics, forthcoming

THOMAS, J. & T. WORRALL (1994). ‘Foreign Direct Investment and the Risk of Expropriation’. The Review of Economic Studies, vol. 61, no. 1, pp. 81-108

WAELDE, T.W. (1996). ‘International Energy Investment’. Energy Law Journal, vol. 17, pp. 191-215

WATSON, J. (2002). Strategy. An Introduction to Game Theory. New York/London: W.W. Norton WYDICK, B. (2008). Games in Economic Development. Cambridge: Cambridge University Press