lending relationships in the interbank market

TRANSCRIPT

Lending Relationships in the Interbank Market∗

João F. Cocco†

Francisco J Gomes‡

Nuno C. Martins§

July 2005

∗We would like to thank Viral Acharya, Andrea Buraschi, Jennifer Conrad, Francesca Cornelli, Denis

Gromb, Michel Habib, Philipp Hartmann, Narayan Naik, Jose Peydro-Alcayde, Mitchell Petersen, Maximiano

Pinheiro, Raghuram Rajan, Rafael Repullo, Henri Servaes and seminar participants at the Bank of England,

Banco de Portugal, Cass Business School, European Central Bank, London Business School, London School

of Economics, the 2002 European Winter Meetings of the Econometric Society, the 2004 American Finance

Association meetings, and the 2005 Conference on Competition, Stability, and Integration in European Bank-

ing for helpful comments and suggestions. We are especially grateful to an anonymous referee for detailed and

constructive comments. The analysis, opinions and findings of this paper represent the views of the authors,

they are not necessarily those of the Banco de Portugal.†London Business School, Regent’s Park, London NW1 4SA, UK, and CEPR. Email [email protected].‡London Business School, Regent’s Park, London NW1 4SA, UK, and CEPR. Email [email protected]§Universidade Nova de Lisboa and Banco de Portugal, Av. Almirante Reis, 71, 1150-012 Lisboa, Portugal.

E-mail [email protected]

1

Abstract

We use a unique dataset to study lending relationships in the interbank market. We explic-

itly control for the endogeneity of lending relationships, and find that borrowers pay a lower

interest rate on loans from banks with whom they have a stronger relationship. Moreoever,

we find that smaller banks, banks with lower return on assets, banks with a higher propor-

tion of non-performing loans, and banks subject to more volatile liquidity shocks rely more

on lending relationships. Finally, we find evidence that smaller banks with limited access to

international markets tend to rely on lending relationships when borrowing in the domestic

interbank market. This provides evidence that banks rely on lending relationships to overcome

monitoring and default risk problems, and for insurance purposes.

1 Introduction

Many interactions between economic agents are of a frequent and repeated nature. In such

a setting agents may establish relationships, and equilibrium outcomes may be very different

from those that arise in a spot market. One important setting in which there are frequent

and repeated interactions between agents is the interbank market. Our paper studies the role

of lending relationships in this market.

Understanding lending behavior and price formation in the interbank market is important

for banks who use it to engage in unsecured borrowing and lending of funds. It is also

important for monetary authorities, since the interbank market lies at the heart of monetary

policy. Moreover, it is in this market that the overnight rate is determined, which is the

shortest-term market interest rate, and as such it has a crucial role in term structure models.

The interbank market is fragmented in nature. For direct loans, which account for most

of the lending volume, the loan’s amount and interest rate are agreed on a one-to-one basis

between borrower and lender. Other banks do not have access to the same terms, and do

not even know that the loan took place. When quotes are posted on screens, they are merely

indicative. This market structure allows banks to establish lending relationships.1

But which economic purpose do lending relationships in interbank markets serve? The

literature has focused on the function of these markets has distributors of liquidity. In the

model of Ho and Saunders (1985), the reserve position of each bank is affected by stochastic

deposits and withdrawals by customers. As a result banks trade in order to meet their reserve

requirements. Similarly, in the model of Bhattacharya and Gale (1987) banks borrow and

lend funds in order to insure against intertemporal liquidity shocks. In the model of Allen and

Gale (2000) liquidity shocks arise from uncertainty in the timing of depositors’ consumption.

Banks hold deposits with banks in other regions to insure against liquidity shocks in their

own region. Finally, in the model of Freixas, Parigi and Rochet (2000) the uncertainty and

1The issue of price formation and the properties of prices in centralized versus fragmented markets has

been the subject of much research (see for example Wolinsky, 1990, Biais, 1993, and O’Hara, 1995).

1

interbank lending arise from consumers’ uncertainty about where to consume. A common

feature to these (and other) models of the interbank market are liquidity shocks, that give

rise to borrowing and lending. Lending relationships may provide insurance against liquidity

shocks.

Another important strand of the literature focuses on the role of peer monitoring in inter-

bank markets (see the models of Rochet and Tirole, 1996, Freixas and Holthausen, 2005, and

the empirical analysis in Furfine, 2001). Peer monitoring is important because of the large

and unsecured nature of the loans. Thus, lending relationships may help overcome agency

problems.

In addition to focusing on lending relationships in the interbank market, the main novelty

of our analysis is that we recognize that the decision of whether to rely on lending relationships

is an endogenous choice, and our econometric approach treats it as such. For this reason we

are able to provide new insights into the determinants of lending relationships.

We use a unique dataset that contains information on all direct loans that took place in

the Portuguese interbank market between January 1997 and August 2001. The Portuguese

interbank market is in many respects typical and, although smaller, it is organized similarly

to the US Fed Funds market. Our dataset identifies the date, interest rate, amount, maturity,

lender and borrower of each loan. Thus, we can track loans between each and every pair

of banks, and with other banks over time. Using this information, we construct dynamic

measures of relationships based on the intensity of pair-wise lending activity. Our dataset

also includes daily information on each bank’s reserve deposits, and quarterly information

on banks’ balance sheet variables including total assets, return on assets and proportion of

non-performing loans.

We first investigate the link between the loan interest rate and relationship measures. To

address the endogeneity issue we estimate instrumental variables regressions, in which we

explore the time-series dimension of our dataset by using lagged relationship measures as

instruments. Obviously such instruments are not available in cross-sectional data, which is

typically used in the existing literature on lending relationships. Importantly, we find that

2

borrowers pay a lower interest rate on loans from banks with whom they have a stronger

lending relationship. We also find that once we control for the endogeneity of lending rela-

tionships, several other explanatory variables are no longer important for explaining the loan

interest rate.

The instrumental variables regressions allow us to identify the causal link between rela-

tionship measures and the loan interest rate, but they do not explain the determinants of

lending relationships. To do so we estimate a seemingly unrelated regressions system of equa-

tions, with the amount lent, the interest rate, and the relationship measures for lender and

borrower as dependent variables. This allows us to simultaneously study the determinants of

loan pricing, loan amount, and of lending relationships.

Our main findings are as follows. First, we find that borrowers with lower return on

assets and with a higher proportion of non-performing loans are more likely to rely on lending

relationships. These results provide empirical support for an explanation of these relationships

based on default risk and monitoring.

We use the information on each bank’s reserve deposits to construct a measure of liquidity

shocks which is equal to the daily change in these deposits. We find that borrowers with

more volatile liquidity shocks are more likely to rely on lending relationships. They tend to

do so with lenders who have less volatile liquidity shocks, and also with whom they have

less correlated shocks. In addition, borrowers are more likely to rely on lending relationships

when they experience a larger imbalance in their reserve deposits. This provides evidence that

banks rely on lending relationships for insurance.

We find that small borrowers are more likely to establish relationships and that they tend

to choose larger banks as their preferred lenders. Furthermore, large banks tend to be net

borrowers, while small banks tend to be net lenders in the market. Interestingly, this pattern

of trade is also a distinctive feature of the US Fed Funds market (Furfine, 1999, Ho and

Saunders, 1985).

Finally, we investigate how banks’ ability to access international markets affect the nature

of lending relationships in the domestic interbank market. We find that small banks and banks

3

with a higher proportion of non-performing loans tend to have limited access to international

markets, and that they tend concentrate their borrowing when borrowing funds in the domestic

interbank market. This result may be due to peer monitoring across borders being less efficient

than at the domestic level, as in the model of Freixas and Holthausen (2005).

Our results for the pricing or interbank loans are consistent with those of Furfine (2001)

for the Fed Funds market. We find that, controlling for the degree of lending relationship and

holding the size of the counterparty fixed, larger banks borrow and lend at more favorable

terms. Banks with higher return on assets lend at higher interest rates. This is consistent

with these banks having a higher opportunity cost of lending funds in the interbank market,

and requiring a higher interest rate to do so. Borrowers with a higher proportion of non-

performing loans tend to pay higher interest rates. Again controlling for the degree of lending

relationship, we find that more profitable banks lend less, and banks with a higher proportion

of non-performing loans lend more and borrow less. Thus banks that have better investment

opportunities tend to be net borrowers.

There is a large literature on lending relationships that focuses on bank-firm relationships.

It has found evidence that lending relationships help overcome constraints that arise from

monitoring and default risk between borrower and lender of funds,2 and allow banks to provide

insurance to firms in the form of interest-rate smoothing.3 Thus this literature focuses on long-

term relationships between banks and firms, by which banks acquire inside knowledge about

firm characteristics or the project that is being financed. Although somewhat related, it is

important to note that these relationships are of a different nature than the ones that we

study in our paper, which are transaction based.

The paper proceeds as follows. Section 2 describes the data, our relationship metrics and

reports some summary statistics. Section 3 studies the pricing of interbank loans. Section 4

2See Berger and Udell (1995), Lummer and McConnell (1989), Petersen and Rajan (1994), Slovin, Sushka,

and Poloncheck (1993).3See Berger and Udell (1992), Berlin and Mester (1999), Petersen and Rajan (1995), or Ongena and Smith

(2000) for a survey of the literature on bank lending relationships.

4

investigates the determinants of lending relationships. Section 5 presents additional evidence

on the determinants of lending relationships, that allows us to be more precise with respect

to their nature. Section 6 reports some robustness checks. Section 7 concludes.

2 The Data

2.1 Description

We combine information from three different datasets, which we have obtained from the Por-

tuguese Central Bank. The first dataset has information on all direct loans in the Portuguese

interbank market from January 1997 to August 2001. The Portuguese interbank market is a

typical interbank market, and although of a smaller size, it functions in a similar way to the

Fed Funds market. Each loan may be either borrower or lender initiated. When a bank wishes

to borrow or lend funds, it approaches another bank, identifies itself, and asks for prices, i.e.

interest rates, for borrowing and lending funds at a given maturity. It is very rare that banks

asking for quotes are turned down, or simply refused funds. But banks do provide different

quotes for different banks that approach them, and it is common practice for banks to shop

around for the best rates.

Our dataset is unique in that it comprises all direct loans, and contains information on

the loan’s date, amount, interest rate, and maturity, as well as the identity of the lender and

the borrower. Being able to identify the lender and borrower for each loan and to observe all

loans over a long period of time is crucial for our study of lending relationships. Even though

interbank loans are privately negotiated, they must be reported to the central bank, who is

responsible for their settlement, by debiting and crediting the reserve accounts of borrowers

and lenders.

We restrict our analysis to overnight loans, i.e. loans maturing on the next business day.

We do so because the interbank market is mainly a market for short-term borrowing and

lending of funds: during our sample period there were 44, 768 overnight loans accounting for

5

over 75 percent of the total amount lent (casual evidence suggests that this is a common

feature in most interbank markets). Even though credit risk for loans of overnight maturity

may be small, it is important to note that these are large and uncollaterized loans, with an

average loan amount of roughly twelve million euros. Therefore we expect that even small

differences across banks in credit risk are reflected on the loan interest rate.

The second dataset provides daily information on the balance in banks’ reserve accounts. It

allows us to study how banks’ reserve position affects their behavior in the interbank market.

The third dataset contains quarterly information on bank characteristics, including total

assets, financial and profitability ratios and credit risk variables. This dataset also allows us

to determine whether the bank belongs to a banking group, defined in terms of control of the

institution. We exclude loans between banks belonging to the same group, which leaves us

with a total of 37, 701 overnight loans.

2.2 Measuring Lending Relationships

We measure lending relationships by the intensity of lending activity between banks. We use

two alternative measures. Our first measure is based on how concentrated the banks’ lending

and borrowing activity is. More precisely, for every given lender (L) and every borrower (B),

we compute a lender preference index (LPI), equal to the ratio of total funds that L has

lent to B during a given year/quarter, over the total amount of funds that L has lent in the

interbank market during that same year/quarter.4 Let F j−→ki denote the amount lent by bank

j to bank k on loan i then:

LPI%L,B,q =Xi∈q

FL−→Bi /

Xi∈q

FL−→alli (1)

where q denotes year/quarter. This ratio is more likely to be high if L relies on B more than

on other banks to lend funds in the market.4We discuss our choice of time period in detail below.

6

Similarly, we compute a borrower preference index (BPI) as the ratio of total funds that

B has borrowed from L in a given year/quarter, as a fraction of the total amount of funds

that B has borrowed in the market in that same year/quarter:

BPI%L,B,q =Xi∈q

FL−→Bi /

Xi∈q

F any−→Bi . (2)

Our second measure of lending relationships is simply the (absolute) number of different

banks to which bank L lent funds during year/quarter q, and similarly the number of different

banks from which bank B borrowed funds during year/quarter q:

LPI#L,q = Number of banks to which bank L lent funds in year/quarter q (3)

BPI#B,q = Number of banks from which bank B borrowed funds in year/quarter q (4)

Thus our first measure of lending relationships is a relative measure, while our second

measure is an absolute one. Elsas, Heinemann, and Tyrell (2004) solve a model in which for

some borrowers it is optimal to rely on multiple but asymmetric financing, i.e. borrowing a

large amount from a single bank, and the remaining amount from several other banks. This

asymmetry in financing can not be captured by the absolute number of different lenders.

For this reason we have decided to use both an absolute and a relative measure of lending

relationships. As one might expect, the correlation between these measures is negative. The

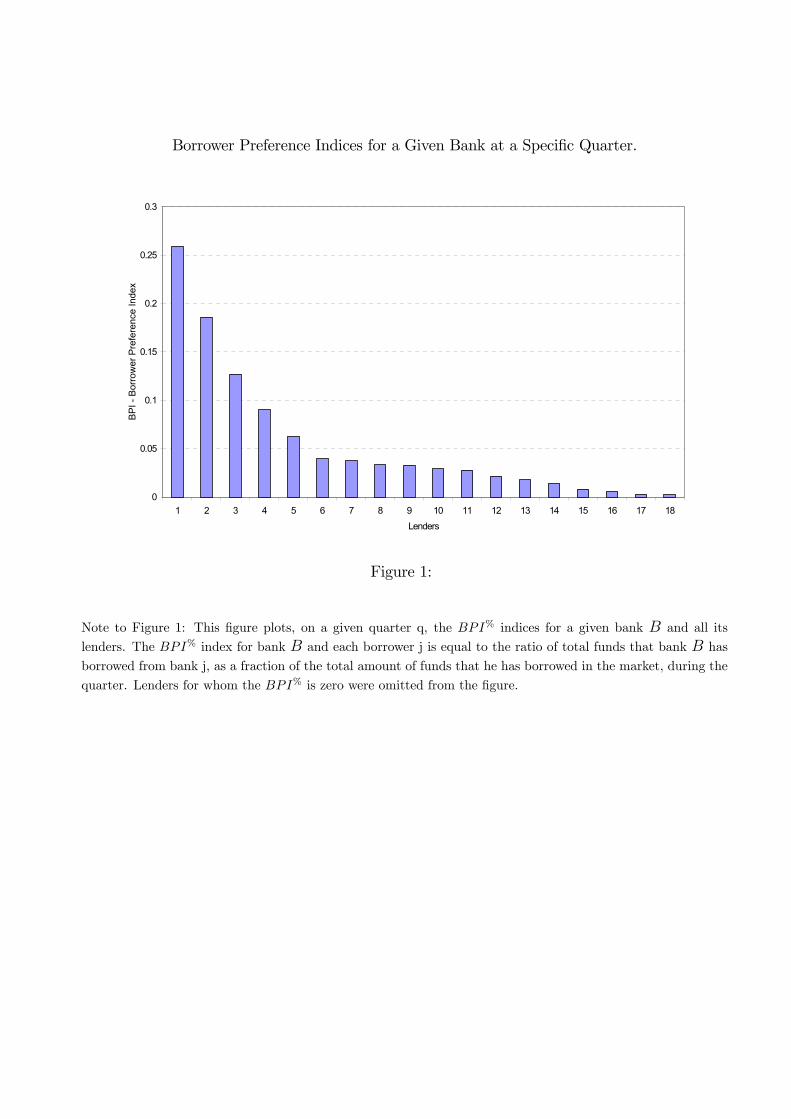

correlation between the BPI% and BPI# indices is equal to −0.46, while the correlationbetween the LPI% and LPI# indices is equal to −0.42Figure 1 plots, for a given quarter and for a given borrower, its BPI% indices with different

lenders. The most important lender for this borrower during this quarter is the bank labeled

as lender one, from which it borrowed roughly a quarter of the total funds that it borrowed

during the quarter. This figure illustrates that in our data there are asymmetries in financing,

with some lenders being much more important than others.

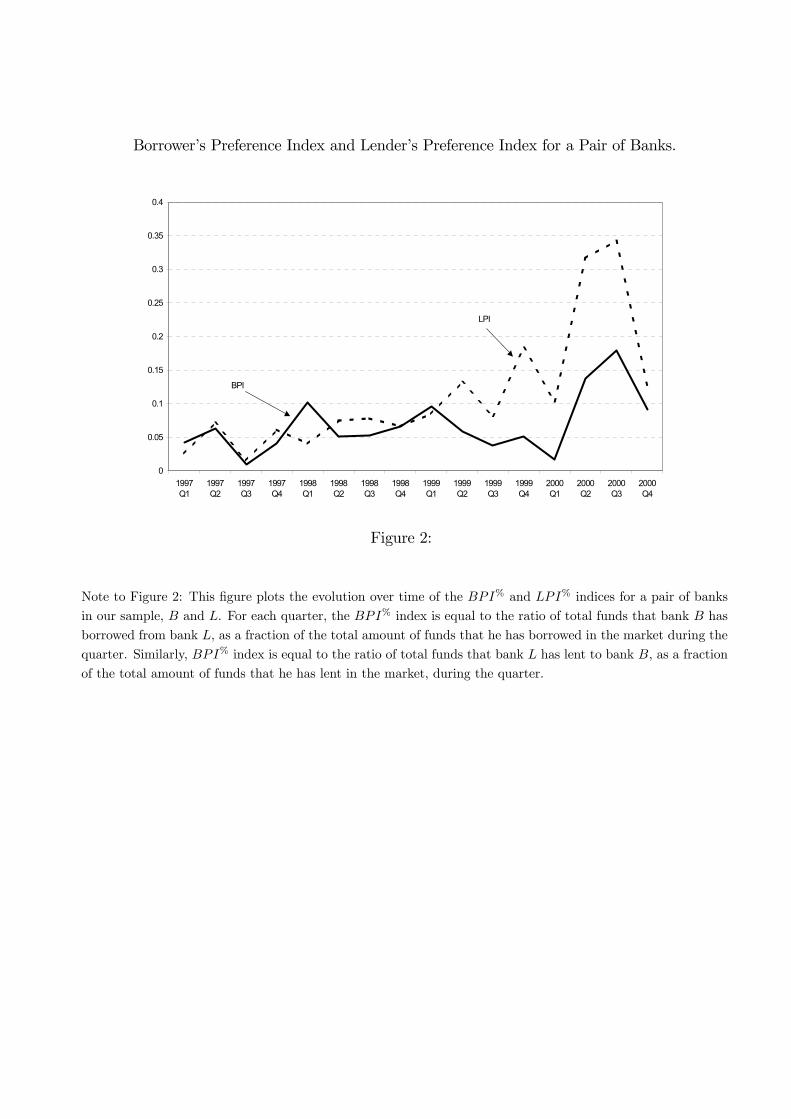

As an illustrative example of the time-series dimension of our relationship measures, Figure

2 plots the evolution of the LPI% and BPI% indices for a pair of banks in our sample, L and

7

B. This time-series dimension of our data is important because it will allow us to deal with

the issue of the endogeneity of lending relationships. More precisely, since there is a time-

series dimension in our data we will be able to use lagged relationship measures as (exogenous)

instruments. Figure 2 also illustrates that there is time variation in our relationship measures.

In our regressions the explanatory power comes both from cross-sectional differences across

banks, as well as changes over time in bank characteristics.

We have chosen the calendar quarter to measure lending relationships. To some extent this

choice is arbitrary. A lending relationship should be fairly stable over time, but not immutable

through time. In addition, there is a practical reason to choose the calendar quarter as unit of

analysis, since some of our bank data is quarterly, namely information about the banks’ assets,

profitability and credit risk. In section 6 we show that the results are robust to alternative

ways of measuring relationships.

2.3 Profitability and Credit Risk Variables

One possible motive for lending relationships is that they may help overcome agency problems

that arise from asymmetric information between borrowers and lenders of funds. Rochet and

Tirole (1996) solve a model of the interbank market in which monitoring plays an important

role.5 For this reason we include as explanatory variables total assets, the quarterly return

on assets (ROA), and the proportion of non-performing loans (NPL). The latter is defined as

loans that are past-due for a period exceeding 90 days, over total outstanding credit granted

by the bank. Obviously, the latter includes loans granted to individuals and firms, and not

only to other banks.

5Broecker (1990), Flannery (1996), and Freixas and Holthausen (2005) also solve models of the interbank

market with asymmetric information and credit risk. Freixas and Holthausen (2005) solve such a model in an

international setting, when cross-country information is noisy.

8

2.4 Insurance variables

A second possible reason for banks to establish lending relationships is to obtain insurance

against idiosyncratic liquidity shocks, arising from withdrawals by retail depositors. A bank

may borrow the funds needed to meet unexpectedly large withdrawals from other banks in the

interbank market (see the models of Ho and Saunders, 1985, Bhattacharya and Gale, 1987,

and Freixas, Parigi and Rochet, 2000).

If lending relationships are important for insurance purposes, we might expect banks sub-

ject to more volatile liquidity shocks to rely more on them. To investigate this hypothesis we

construct a measure of volatility of liquidity shocks, equal to the standard deviation of the

daily change in the bank’s reserve deposits that is not due to loans in the interbank market.

We compute this measure for each bank and quarter, and normalize it by the bank’s average

quarterly reserves.

One may expect that lending relationships are more valuable for both borrowing and

lending banks when their liquidity shocks are less correlated. That is, when borrowing banks

need funds lending banks are more likely to have a surplus of funds. For each quarter, we

measure the correlation between each two banks’ daily change in reserve deposits that is not

due to loans in the interbank market.6

Banks may borrow funds to satisfy reserve requirements. Over a given reserve maintenance

period (or settlement period) a given bank’s average reserves must not fall below a given

proportion of its short-term liabilities (mostly customer deposits).7 It is therefore natural to

expect that banks’ reserve position, when they borrow or lend funds in the interbank market,

affect the interest rate on the loans, and with whom they interact. To investigate these effects

we construct a proxy for each bank’s reserve requirements, equal to the average of the daily

6Note that the argument that lending relationships are more valuable when banks have less correlated

shocks does not require that the correlation be negative.7Campbell (1987), Hamilton (1996), Hartmann et al. (2001), and Spindt and Hoffmeister (1988) have

noticed how shortages of liquidity at the end of the maintenance period often lead to special behavior of

overnight rates during those days.

9

deposits in the bank’s reserve account over the reserve maintenance period. We then measure

surplus deposits for bank i on day t (SDit) as the ratio between the current average level of

deposits in the reserve account (since the start of the current reserve requirement period) and

our proxy for reserve requirements:

SDit =

Xs∈{m(t):s6t}

Depositis

/nt Xs∈m(t)

Depositis

/n

(5)

where m(t) refers to the days in the same reserve maintenance period as day t, and nt and

n are the up to t and the total number of days in the maintenance period, respectively. In

words, this variable measures the average deposits in the bank’s reserve account up to day t of

the current reserve maintenance period, relative to the average deposits in the account during

the same reserve maintenance period. It captures the extent to which a bank’s requirements

imply a need for or an excess of funds. As before we compute the average value of this variable

over each quarter, for those days in which the bank intervened in the interbank market.

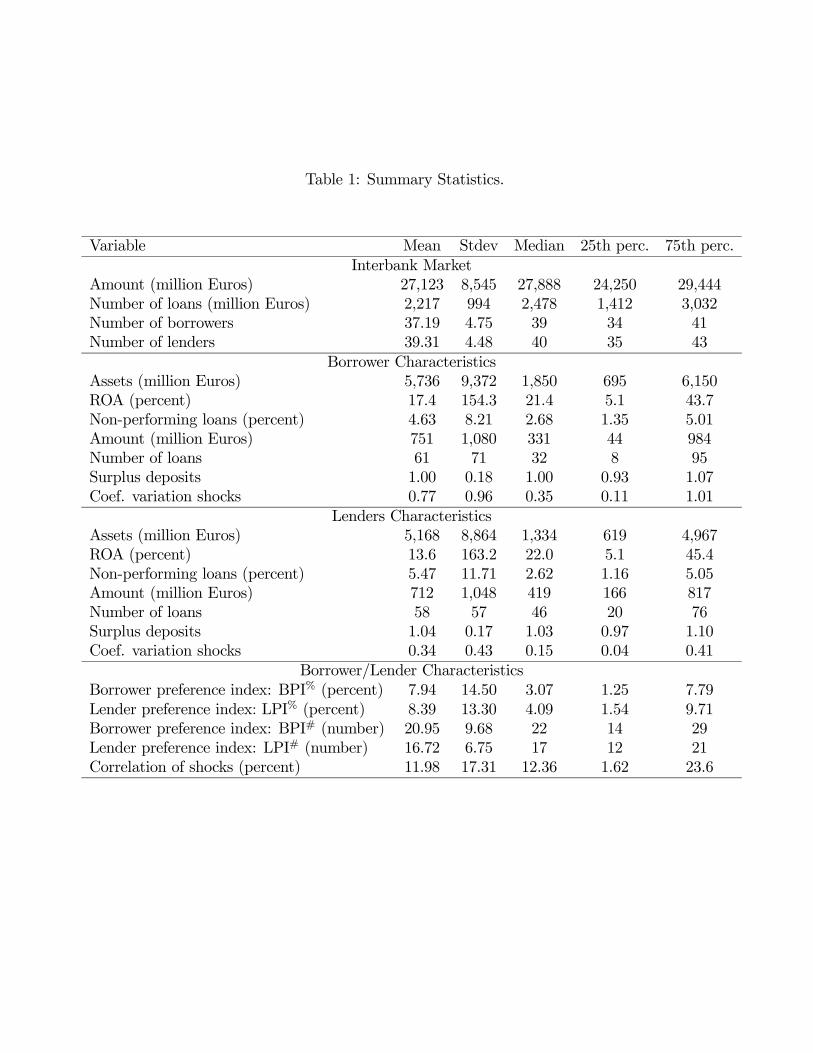

2.5 Summary statistics

Table 1 reports summary statistics. The first panel shows information on the Portuguese

interbank market. The average total amount lent in each quarter is 27,123 million euros, with

an average 2,217 loans. Thus, the average loan amount is roughly twelve million euros. The

average number of different borrowers (lenders) in each quarter is 37 (39).

The next two panels of Table 1 report summary statistics for borrowing and lending banks,

respectively, on total assets (Assets), quarterly return on assets (ROA), and proportion of

non-performing loans (NPL). Table 1 reports that on average borrowing banks are larger (as

measured by total assets), have a higher ROA and a smaller proportion of NPL than lending

banks. This is consistent with borrowing banks having better investment opportunities than

lending banks, which explains why they show up as borrowers in the market.

10

Table 1 also reports information on total amount and number of loans made and received

by each bank in the interbank market during the quarter. On average each borrower receives

751 million Euros in 61 loans, while each lender loans out 712 million Euros in 58 loans.8

Table 1’s last panel shows summary statistics for the relationship metrics, and for the

correlation of shocks. The average BPI% is 7.94 percent, and the average LPI% is 8.39

percent. These averages are significantly higher than the median values (3 and 4 percent

respectively), a sign of a skewed distribution. That is banks borrow/lend relatively little from

most banks, but large amounts from a few of them. This is why it is important to consider

these measures of relationships, in addition to simply the number of different borrowers and

lenders, whose summary statistics are shown in the next two rows of Table 1.

Table 1’s last row reports summary statistics for the correlation of shocks (as defined in

section 2.4). As one would expect, these correlations tend to be positive, with an average

value of 12 percent. There is also significant cross-section dispersion, with the 25th percentile

equal to 1.6 percent and the 75th percentile equal to 23.6 percent.

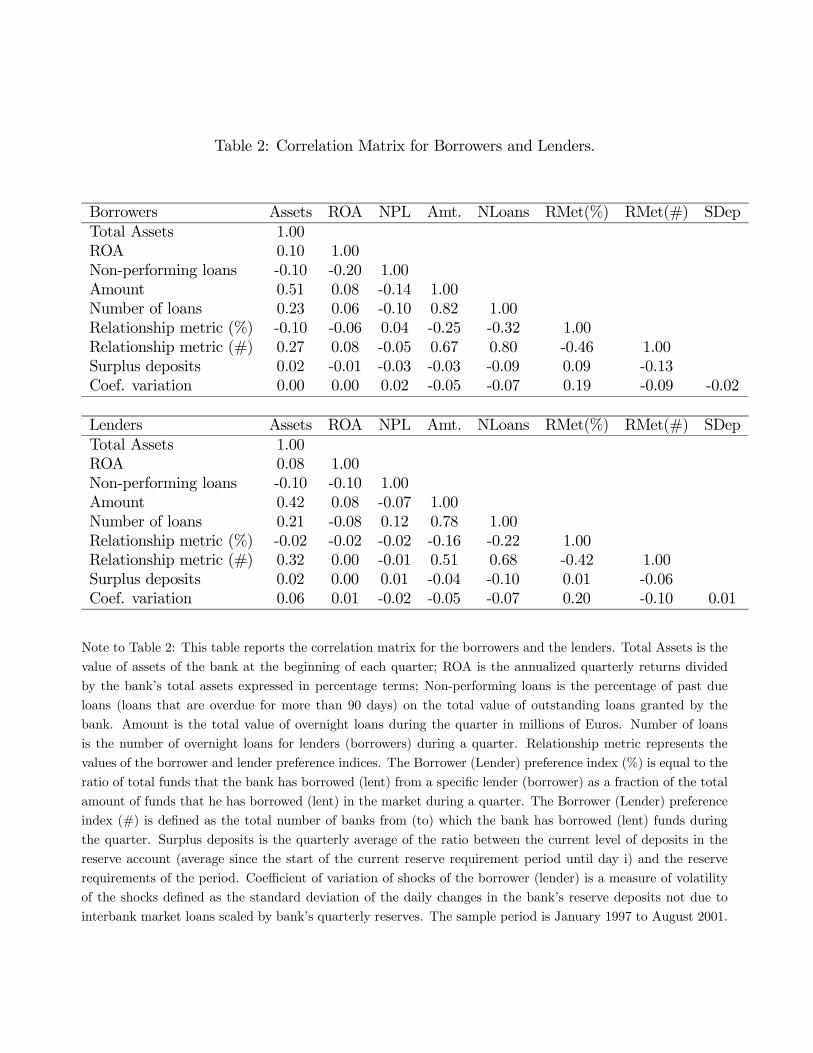

Table 2 shows the correlation matrix between several variables for borrowers and lenders.

The largest correlations are between total assets, total amount lent/borrowed in the interbank

market, and number of loans. Banks with more assets tend to be more active in the interbank

market both in terms of total amount borrowed/lent and number of loans. For both borrowers

and lenders of funds the LPI% andBPI% indices are negatively correlated with size, measured

by total assets, amount and number of loans. As expected, larger banks also lend and borrow

funds from a larger number of different banks: the correlations between the LPI# and BPI#

indices and total assets, amount, and number of loans are large and positive.

8The average amount and number of loans for borrowing and lending banks are not exactly equal because

there is a different number of borrowing and lending banks in the market.

11

3 Pricing of Interbank Loans

This section investigates the determinants of the interest rate on interbank market loans.

In most interbank markets the central bank sets a target rate. For this reason we focus on

explaining the difference between the interest rate on a given loan and the average interest

rate on overnight loans. Some numbers are helpful for understanding the daily variability in

interest rates in our sample. The standard deviation of interest rates on a given day is on

average 8 basis points. Moreover, this is naturally a strongly skewed distribution. While the

median standard deviation is 6 basis points, in ten percent of the days the standard deviation

of interest rates is higher than 18 basis points.

We proceed as follows. First for a loan from bank L to bank B on day t, we calculate the

difference between the interest rate (iL,B,t) and the average (market-wide) overnight interest

rate on the same day (it), divided by the standard deviation of overnight interest rates for

that day (σit). This is to account for the well-documented GARCH effects in interbank market

interest rates (Hamilton, 1996). Since our unit of observation is year/quarter, we then obtain

the average interest rate difference for all loans from bank L to bank B during year/quarter

q, with q = 1, ..., 19, as:

iqL,B =1

Tq

Xt∈q(iL,B,t − it)/σ

it (6)

where Tq denotes the number of trading days in period q.9

We first study how interest rates so defined depend on size, profitability and relationship

measures in a univariate framework. We then turn our attention to multivariate analysis that

9The exact formula is slightly more complicated, since we must account for the possibility of more than

one loan between the same pair of banks on a given day. If we let index j denote different loans between the

same pair of banks on a given day, the exact formula is:

iqB,L =1

Tq

Xt∈q

1

JL,B,t

Xj

(iL,B,t,j − it)/σit

where JL,B,t denotes the number of loans from L to B on day t.

12

include these and other explanatory variables. Finally, in section 3.3, we recognize that our

relationship measures are endogenous, and estimate instrumental variables (IV) regressions to

address the endogeneity issue. These IV regressions also allow us to identify the causal link

between relationship measures and the loan interest rate.

3.1 Univariate analysis

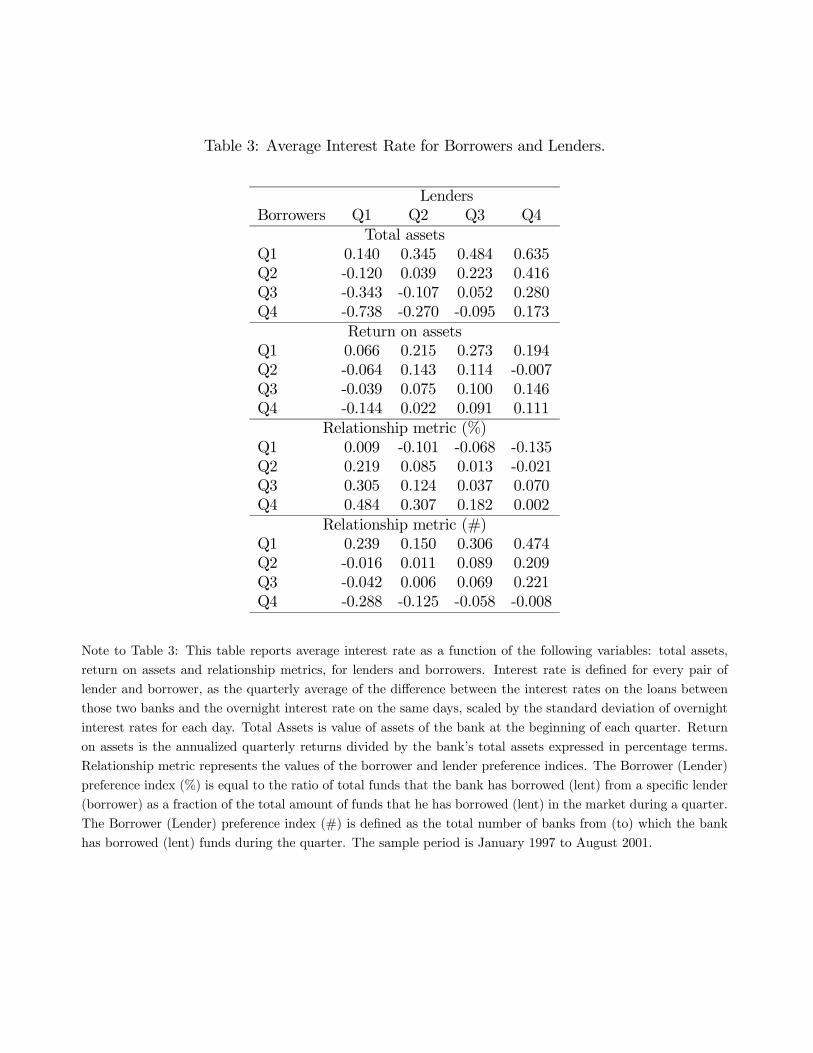

Table 3 reports the average interest rate (iqL,B) as a function of different characteristics of both

borrowing and lending banks. In the first panel we focus on Total Assets. There is evidence

that in the Fed Funds market larger banks tend to obtain more favorable interest rates when

borrowing or lending (Allen and Saunders, 1986, Stigum, 1990, Furfine, 2001). Table 3’s first

panel reports the interest rate differential on loans between banks in the different quartiles of

the total assets distribution (quartile 1 regroups the smallest banks). Each column regroups

lenders, while each row regroups borrowers.

The first panel of Table 3 shows that in our data larger banks tend to obtain more favorable

rates. The patterns are remarkably clear. Holding the quartile of the borrowing bank fixed,

the interest rate increases with the size of the lender. Similarly, holding the size of the lending

bank fixed, the interest rate decreases with an increase in the size of the borrower.10

Table 3’s second panel reports interest rate differentials as a function of the quartiles of the

ROA distribution (Quartile 1 includes the banks with the lowest ROA). Although the interest

rate patterns are not as clear as for total assets, more profitable borrowing banks seem to pay

a lower interest rate than less profitable ones. Similarly, more profitable lending banks tend

to receive a higher interest rate, at least when we compare quartiles 1 and 4.

Table 3’s last two panels report interest rate differentials, but now as a function of the

relationship measures. The third panel reports the interest rate differentials as a function

of BPI% and LPI%.11 The results appear to suggest that borrowers (lenders) tend to pay

10The results are similar when we use other measures of size, such as total amount lent/borrowed in the

interbank market or number of loans.11Note that in the previous two panels all loans for a given lender in a given quarter would appear in the

13

(receive) higher (lower) interest rates on loans with banks with whom they have a more

intense lending relationship. As the next section shows, the reason for this result is that the

decision of whether to rely on lending relationships is endogenous, and correlated with bank

characteristics that also affect the interest rate on the loan. The last panel of Table 4 reports

interest rate differentials as a function of BPI# and LPI#. The patterns, although not always

monotonic across quartiles, are symmetric to those in the previous panel, as one might have

expected from the negative correlation between the two measures.

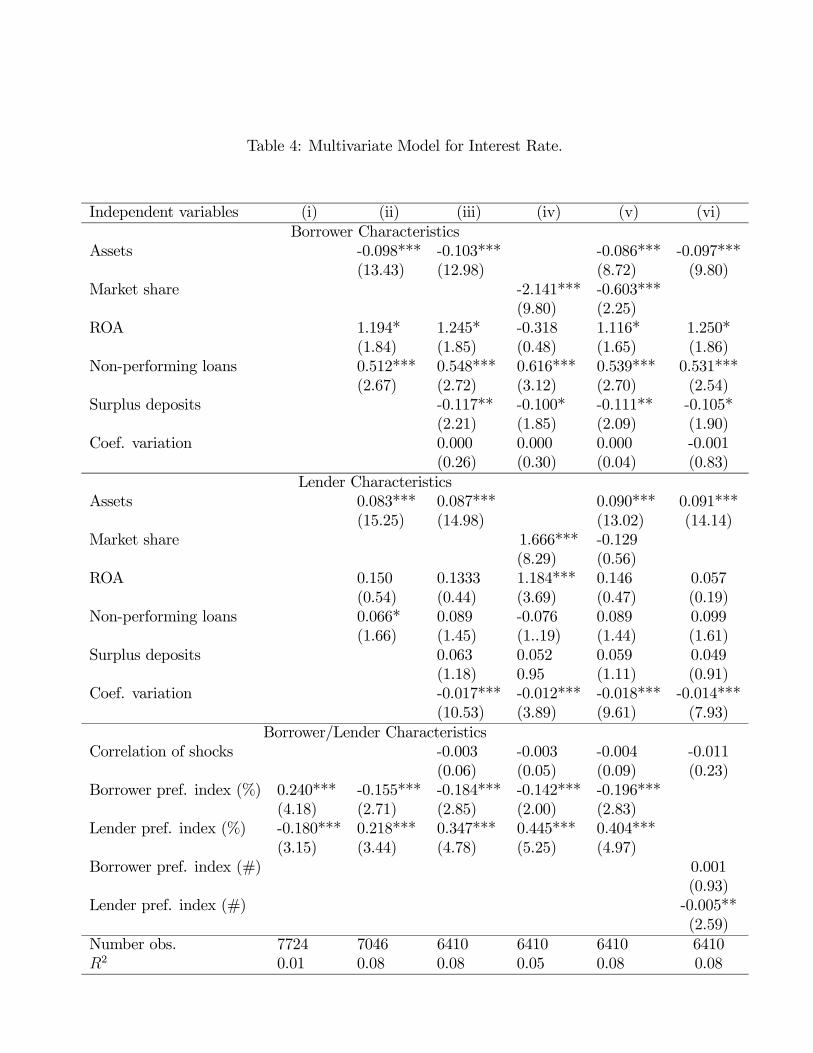

3.2 Multivariate Analysis

We first estimate the unconditional correlation between the relationship metrics and the loan

interest rate:

iqL,B = α+ γBPI%,qL,B + κLPI%,qL,B + βqDq + uqL,B (7)

where q indexes year/quarter, Dq are time (year/quarter) dummies, the subscripts L and B

refer to lending and borrowing bank, respectively, and uqL,B is the residual. Column (i) of

Table 4 shows the estimation results. The results confirm the ones previously obtained in the

univariate analysis (third panel of Table 3) and the coefficients are statistically significant in

both cases.

Next we include size, ROA and NPL as additional independent variables. The regression

that we estimate is:

iqL,B = α+Xj=L,B

£β1j Si ze

qj + β2jROA

qj + β3jNPLq

j

¤+γBPI%,qL,B+κLPI%,qL,B+βqDq+uqL,B (8)

As a size measure we use the logarithm of total assets. Finally, we include as independent

variables those related to insurance motives. These include the net reserve position of borrow-

ers and lenders when they borrow or lend funds in the interbank market (surplus deposits, or

same column, depending on its total assets or ROA. In the third panel, a given lender may have a LPI with

a borrower that is in top quartile of the distribution of LPI indices, and a LPI with another borrower that

is in the bottom quartile. The interest rate differential for loans with the former shows up in Table 3 under

column Q4, whereas for the loans with the latter shows up under column Q1.

14

SD), the coefficient of variation of their liquidity shocks (CVB and CVL), and the correlation

of liquidity shocks between lender and borrower (θL,B):

iqL,B = α+Xj=L,B

£β1j Si ze

qj + β2jROA

qj + β3jNPLq

j + β4jSDqj + β5jCV

qj

¤+β6θL,B + γBPI%,qL,B + κLPI%,qL,B + βqDq + uqL,B (9)

Including the relationship metrics as exogenous variables may seem surprising, given our

previous discussion on the endogeneity of lending relationships. However, these equations are

typically estimated in the lending relationships literature. Later on we will explicitly recognize

the endogeneity problem, both with IV regressions and with SUR estimation. Comparing

these results with those obtained when controlling for endogeneity allows us to investigate

the potential biases introduced by treating the lending relationship measures as independent

variables in the interest rate equation.

Columns (ii) and (iii) of Table 4 show the estimation results. Interestingly, once we include

the logarithm of total assets, ROA, and NPL as independent variables the estimated coeffi-

cients on the relationship variables revert sign (column (ii)). Thus lenders receive a higher

interest rates on loans to borrowers with whom they have a lending relationship, and borrow-

ers pay a lower interest rate on loans from banks with whom they have a lending relationship.

This result is the opposite of the unconditional results, and shows how crucial it is to control

for bank characteristics in the pricing of interbank loans.

The signs of the estimated coefficients of the size variables, positive for lenders and negative

for borrowers, confirm that in the market larger banks receive better interest rates, whichever

side of the market they are in. The estimated positive coefficient on the ROA of borrowers is

intuitive. Borrowers with a higher ROA have a more profitable application for the funds, and

are willing to pay a higher interest rate for the funds they borrow. Similarly, the estimated

coefficient on the ROA of lenders is positive, although not statistically significant. A higher

ROA means that lenders have a higher opportunity cost of lending in the interbank market,

and require a higher interest rate to do so.

15

The effects of credit risk are captured by the proportion of non-performing loans (NPL)

variable. We find that borrowers with a higher proportion of NPL tend to pay higher interest

rates on loans in the interbank market, a result which is statistically significant at the one per-

cent level. We also estimate a positive coefficient on NPL of lenders, but it is not statistically

significant when we include the insurance variables (column (iii)).

The results in column (iii) of Table 4 show that borrowers with a lower surplus deposit

pay on average a higher interest rate on their loans. The magnitude of the coefficient is also

economically significant: a 1% shortage of funds leads to an interest rate premium of 0.12

standard deviations. The coefficient on SDqL is not statistically significant. What seems to

matter for lenders is the volatility of liquidity shocks: the more volatile they are the lower

is the interest rate that lenders receive on interbank market loans. Finally, the estimated

coefficient on θL,B is not significantly different from zero.

In columns (iv) and (v) we investigate why larger banks receive better rates. The fact that

borrowers’ size matters is intuitive and could be due to better information being available

for larger banks, or to larger banks being too-big-to-fail. However, the reason why larger

lenders receive better rates is less clear. A possible reason may be the bilateral nature of

the market. In a market with pairwise meetings such as the interbank market, the relative

bargaining power of borrower and lender of funds will affect the interest rate on the loan. If

size is correlated with bargaining power, then larger lenders (and larger borrowers) will receive

better interest rates on their loans.12

In order to investigate this, and for each lender (and borrower) in our sample, we have

calculated their respective market shares. That is: the total amount that the lender has lent

(the borrower has borrowed) in the interbank market, over the total amount lent/borrowed

by all banks in the market. Market shares thus calculated are positively correlated with bank

size, as measured by the logarithm of total assets, with coefficients of correlation equal to 0.59

(0.74) for lenders (borrowers). In columns (iv) and (v) of Table 4 we report the estimation

12See Osborne and Rubinstein (1990) for a textbook treatment of models of bilateral markets that predict

this result.

16

results when we include market shares as explanatory variables for the interest rate on the

loans. We find that lenders/borrowers with larger market shares receive better rates (column

(iv)). When in column (v) we include both market shares and the logarithm of total assets

as independent variables we find that the explanatory power of both variables is diminished,

reflecting the fact that they are co-linear.

The last column of Table 4 reports the estimation results when we use BPI# and LPI# as

relationship measures. The effects of the size, profitability, credit risk, and insurance variables

on the interest rate are similar to those reported in column (iii) and therefore we refrain from

commenting on them. Interestingly, the estimated coefficient on BPI# is not statistically

significant, while the estimated coefficients on BPI% was significant. Thus it seems that for

borrowers of funds it is important to use as a measure of the strength of the relationship a

variable that reflects the (possible) asymmetric nature of the financing, such as borrowing

a large amount from a single bank, and the remaining amount from several other banks.

Obviously this asymmetry in financing can not captured by the number of different lenders

(the BPI# variable).

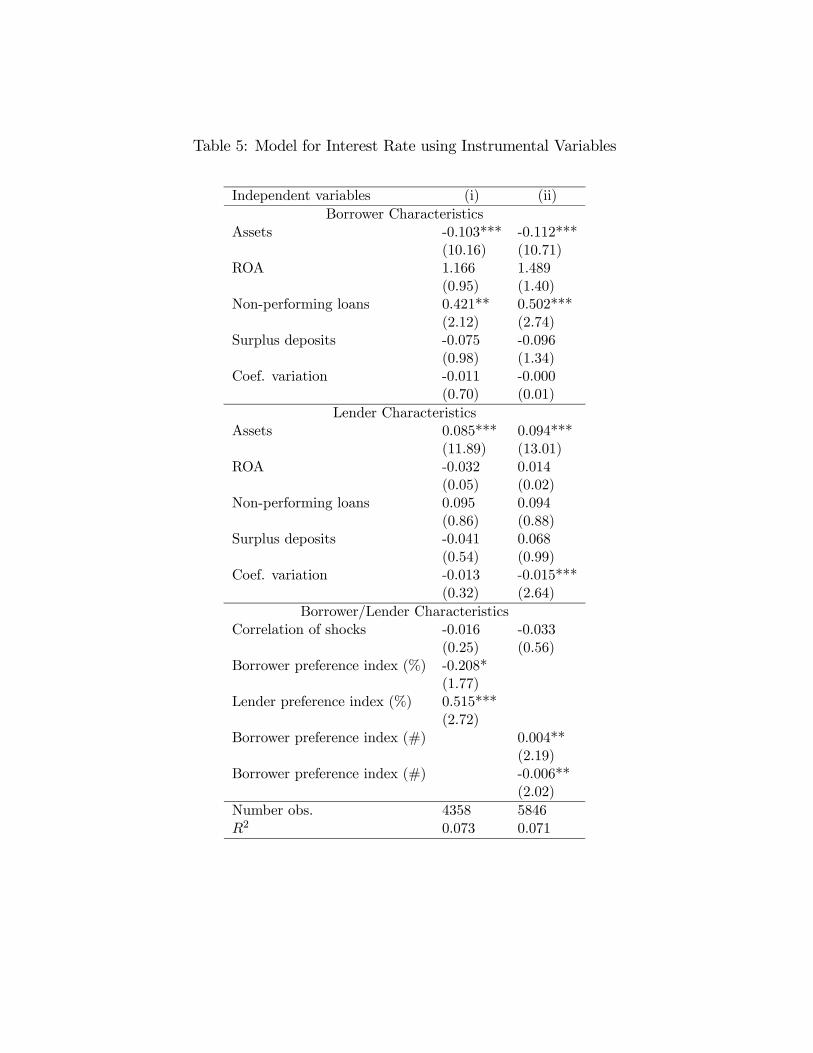

3.3 Instrumental Variables Regressions

In order to address the issue of the endogeneity of the relationship measures we estimate

instrumental variables (IV) regressions. These regressions allow us to identify the causal link

between the relationship measures and the loan interest rate. This is a departure from most

of the existing literature on lending relationships, which does not address the endogeneity of

the relationship measures.

The validity of the IV approach depends crucially on the quality of the instruments used

in the first stage regression. Good instruments include those which are simultaneously pre-

determined and highly correlated with the relationship metrics. Therefore, we explore the

time-series dimension of our data set, and use the lagged relationship measures as instruments.

Obviously, such instruments are not available in cross sectional data, which is typically used

17

in the existing literature on lending relationships. The quality of these instruments can be

measured by the R-squared of the first-stage regressions: for the BPI% (LPI%) measure it is

equal to 67% (78%), and for the BPI# (LPI#) measure it is equal to 49% (52%).13

The estimation results for the second stage regressions are shown in Table 5. The t-

statistics (reported below the estimated coefficients) have been adjusted for first-stage esti-

mation error. When we compare the results in Table 5 to those in Table 4 we can draw the

following conclusions. First, the coefficients on total assets and non-performing loans remain

essentially unchanged. Larger banks tend to receive higher interest rates when they lend, and

pay lower interest rates when they borrow. Borrowers with more default risk pay on average a

higher interest rates on their loans, while the lender’s default risk is now clearly non-significant

in both regressions.

Second, the estimated coefficient on the surplus deposit of borrowers is no longer significant,

and the estimated coefficient on the coefficient of variation of lenders is only significant in (ii).

Thus the level of significance of the insurance variables is reduced once we control for the

endogeneity of lending relationships. This suggests that relationships are important because

they allow banks to obtain insurance in the interbank market. In the next section we will

study the determinants of lending relationships.

Third, the estimated coefficients on the relationship variables are significant throughout,

and have the same signs as in Table 4. Moreover, the magnitude of the estimated coefficients

is either unchanged or even slightly increased (in absolute value). This result implies that,

at least in our dataset, the endogeneity problem does not affect the inference regarding the

causal link between lending relationships and interest rates. Of course, one should be careful

about generalizing this result to other applications, since we have only shown that it holds in

our data. Furthermore, and even though the estimated coefficients on the relationship metrics

are robust to an IV approach, the inference on the coefficients of some of the insurance

13We have also estimated the IV regressions using the first lag of all the explanatory variables in equation

(9) as instruments in the first-state regression. The first stage R2 was almost unaffected and the second stage

results were the same and are therefore not reported.

18

variables changes. If these are only control variables, then this is not an issue. However,

if one is interested in the economic interpretation of those coefficients, then controlling for

endogeneity is important.

4 The Determinants of Lending Relationships

The instrumental variables regressions that we have estimated in the previous section allow us

to estimate the effects of lending relationships on the interest rate on the loan, but they do not

explain the determinants of lending relationships. In this section we investigate which bank

characteristics explain the decision of whether or not to rely on lending relationships. We do

so in a setting in which we allow the loan amount and interest rate to be correlated with the

identity of the borrowing and lending banks or on whether they have a lending relationship.

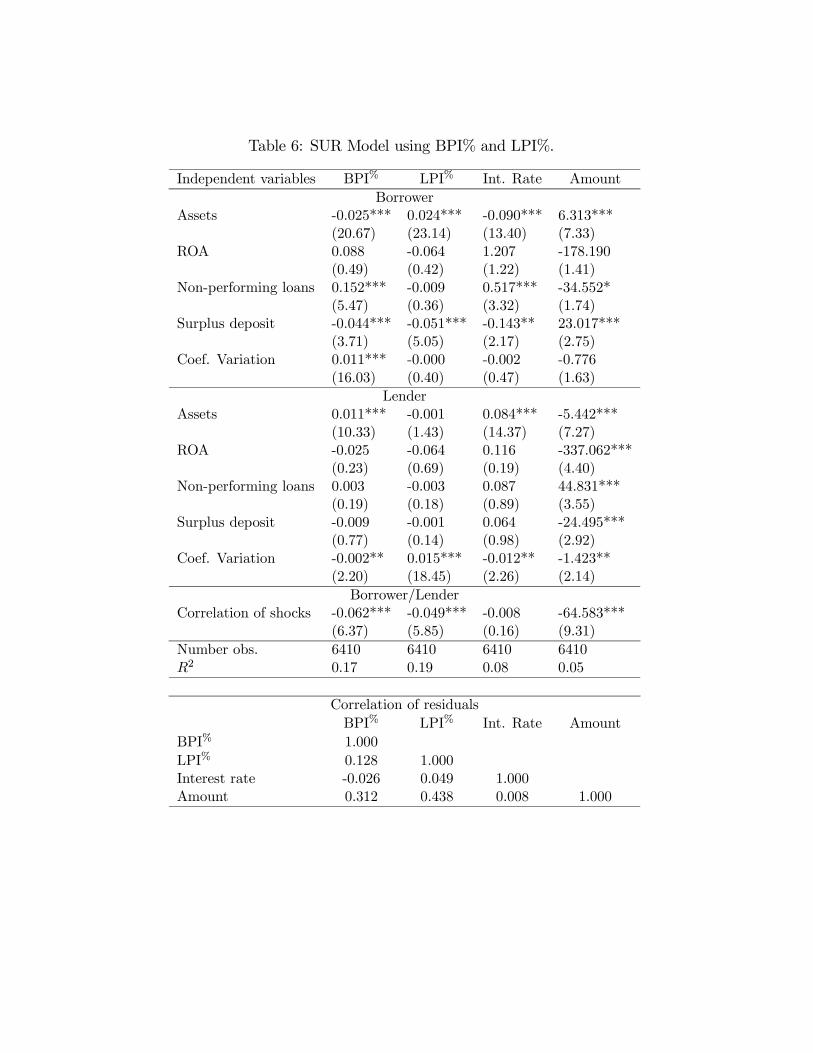

More precisely, we now estimate a seemingly unrelated regressions (SUR) system of equa-

tions, with the amount lent, interest rate, and the relationship measures between lender and

borrower (LPI and BPI) as endogenous dependent variables. Thus, we estimate simultane-

ously the following system of equations:

iqL,B = α1+Xj=L,B

£β11jSize

qj + β12jROA

qj + β13jNPLq

j + β14jSDqj + β15jCV

qj

¤+β16θB,L+β

q1Dq1+uqL,B

(10)

BPI%,qL,B = α2+Xj=L,B

£β21jSize

qj + β22jROA

qj + β23jNPLq

j + β24jSDqj + β25jCV

qj

¤+β26θB,L+β

q2Dq2+εqL,B

(11)

LPI%,qL,B = α3+Xj=L,B

£β31jSize

qj + β32jROA

qj + β33jNPLq

j + β34jSDqj + β35jCV

qj

¤+β36θB,L+β

q3Dq3+ξqL,B

(12)

Ln(V qL,B) = α4+

Xj=L,B

£β41jSize

qj + β42jROA

qj + β43jNPLq

j + β44jSDqj + β45jCV

qj

¤+β46θB,L+β

q4Dq4+vqL,B

(13)

where V qL,B is the total amount of funds lent by bank L to bank B during quarter q, and Ln

denotes logarithm. In this section we focus our attention on the LPI% and BPI% indices.

19

The results for the LPI# and BPI# are similar and reported in section 6. We estimate a

reduced form system, and therefore allow for contemporaneous correlation across the different

innovations (u, ε, ξ and v). As before, we include time dummies in all equations.

4.1 BPI and LPI equations

Table 6 shows the estimation results for BPI% and LPI% indices. The results for the BPI%

equation are shown in the second column. In this equation we try to determine which borrower

and lender characteristics explain the variation in BPI% indices. In other words, who are the

borrowers’ who have higher relationship indices, and who are the lenders with whom they

have higher indices.

The negative coefficient on the logarithm of total assets of borrowers means that small

borrowers rely more on lending relationships. The estimated coefficient on the total assets of

lender in the BPI% equation is positive and statistically significant, meaning that small bor-

rowers tend to have large banks as their preferred lenders. These results suggest a dichothomy

between large and small banks in the market, an issue that we explore further in section 5.1.

Interestingly, we find that borrowers with higher default risk are more likely to rely on

lending relationships: the estimated coefficient on NPL of borrowers is positive and significant.

In addition, borrowers with a large proportion of NPL pay higher interest rates on their loans

(the estimated coefficient on NPL in the interest rate equation is positive). From these two

results one may reasonably expect that banks which borrow funds from banks with whom

they have a lending relationship pay higher rates. This may seem inconsistent with the result

in Table 4 that loan rates tend to be lower for banks borrowing from lenders with whom they

have large relationship indices.

The key to understanding this apparent inconsistency is to note that we do not find that

unconditionally borrowers with a high default risk and large BPI indices pay lower interest

rates. In fact the reverse is true: large values for BPI indices tend to be associated with higher

interest rates (Table 3, and column (i) in Table 4). It is only when controlling for default risk

20

that the estimated coefficient on the BPI index is negative (Table 4 column (ii)), but even so

it is an order of magnitude smaller than the coefficient on the default risk variable. That is:

borrowers with a high proportion of NPL pay on average higher interest rates. However, the

interest rate premium is smaller if they borrow funds from a lender with whom they have a

high BPI.

Some calculations help to clarify this important point. Consider an increase in the pro-

portion of NPL from the 25th to the 75th percentile, while everything else remains the same.

Using the estimated coefficients in the third column of table 4 we see that the interest rate

on the loan increases by 2 basis points.14 However, if the increase in the proportion of NPL is

accompanied by an increase in the BPI index from the 25th to the 75th percentile, the increase

in interest rate is only 0.6 basis points. If instead we consider an increase in the proportion of

NPL from the 10th to the 90th percentile the increase in interest rate is 20 basis points when

the BPI index is unchanged, and 5 basis points when the BPI index also increases from the

10th to the 90th percentile.15

Several of the insurance variables are also significant. The estimated negative coefficient

on the surplus deposit of borrowers implies that they are more likely to borrow funds from

lenders with whom they have large relationship indices when they have a larger shortage of

funds. Borrowers with more volatile liquidity shocks tend to rely more on lending relationships

(the coefficient on CV qB is positive), and they tend to do so with lenders that have less volatile

liquidity shocks (the estimated coefficient on CV qL in the BPI% equation is negative and

statistically significant). This supports the idea that lending relationships are important for

insurance purposes. Finally, the correlation variable is also significant and it has a negative

coefficient, which is consistent with the mutual insurance hypothesis. Borrowers are more likely

to have lending relationships with lenders when their liquidity shocks are less correlated. In

14Due to our scaling of the dependent variable we need to multiply the increase by the standard deviation

of the interest rate.15The effect of NPL on the interest rate may be larger because default risk is likely to be correlated with

bank size, for which we are also controlling in Table 4.

21

such case the insurance benefits of the relationship are likely to be larger.

The third column of Table 6 reports the results for the LPI% equation. Similarly to the

borrowers, we find that small lenders are more likely to have higher relationships indices, and

that they tend to do so higher indices with large borrowers (the estimated coefficient on total

assets of lenders is negative and on the total assets of borrowers is positive). The estimated

coefficient on the credit risk of lenders is not statistical significant. This is consistent with the

results for the interest rate regression reported in Table 4. It is natural to expect that what

matters in a loan is the credit risk of the borrower, and not that of the lender.

In the LPI% equation, the estimated coefficient on the reserve imbalance of borrowers is

negative and statistically significant. This means that banks that borrow funds at times when

their reserve imbalance is larger tend to borrow funds from lenders which have high relationship

indices with them (recall that the reserve imbalance variable for borrowers is defined in such a

way that a lower value means a higher imbalance). Thus loans that take place when reserves

imbalances are larger tend to be associated with higher relationship indices. This result comes

from the time-series dimension of our panel.

In addition, lenders with more volatile liquidity shocks tend to have higher relationship

indices with borrowers that face less volatile liquidity shocks, although the estimated coefficient

for borrowers is not significantly different from zero. As in the BPI% equation, the estimated

coefficient on the correlation variable is negative, consistent with the mutual insurance motive

for establishing relationships.

As a whole, columns two and three of Table 6 show that it is mostly borrower characteristics

that explain variation in the BPI% and LPI% indices. Among the lender characteristics the

only two that seem to be important are the logarithm of total assets and liquidity risk. One

might have an a priori expectation that for non-secure loans such as interbank market loans,

borrowers’ characteristics are more important for explaining the terms of the loan than lenders’

characteristics. Table 6 suggests that this reasoning carries through when explaining lending

relationships.

22

4.2 Interest rate and loan volume equations

The fourth column of Table 6 shows the results for the interest rate equation. This equation

is similar to that estimated in specification (iii) of Table 4, except that now we do not include

the LPI and BPI indices as independent variables, but instead treat them as endogenous when

estimating the system of equations. The main noticeable difference relative to the results in

Table 4 is that the estimated coefficient for the borrower’s ROA is now non-significant. Given

that several papers on lending relationships rely on regressions of the price of the loan on

relationship measures and other control variables, it is re-assuring to find out that in our data

the results for this regression are robust to an approach that treats the relationship measures

as endogenous variables.

In the last column of Table 6 we report the results for loan volume (the fourth equation

in the SUR system). We find that larger banks borrow larger amounts. Interestingly, we

find that more profitable banks lend less (the estimated coefficients on ROAqL is negative).

In addition, we find that banks with a higher proportion of non-performing loans lend more

and borrow less (the estimated coefficients on NPLqL and NPLq

B are positive and negative,

respectively). The estimated coefficients for ROA and NPL are consistent with banks that

have better investment opportunities borrowing more and lending less. Finally, the estimated

coefficients on surplus deposit show that banks which have smaller imbalances tend to rely on

larger loans with any particular bank.

4.3 Correlation of residuals

At the bottom of Table 6 we show the estimated correlation matrix of residuals in the SUR

system of equations. This allows us to study the correlation between the different endoge-

nous variables. However, we should point out that since our SUR system is a reduced form

estimation, these correlations are not partial derivatives, i.e. when we look at the correlation

between the residuals in two different equations we are not holding the other endogenous

variables constant.

23

Larger residuals for the BPI equation are associated with lower interest rates, and larger

residuals for the LPI equation are associated with higher interest rates. Thus, borrowers

pay lower interest rates when they borrow funds from banks with whom they have a lending

relationship, and lenders receive a higher interest rate when they lend funds to banks with

whom they have a lending relationship. Although the signs of the correlations between the

LPI and BPI and interest rate are intuitive, the magnitude of the correlation is fairly small.

From Table 6 we see that the largest correlations are of amount lent with LPI and BPI, which

are equal to 0.44 and 0.31, respectively. This finding supports the idea that relationships have

the greatest effect on the provision of credit, and not on the price at which banks are able to

borrow or lend.

5 Further Evidence on the Determinants of Lending

Relationships

In this section we provide further evidence on the determinants of lending relationships, that

allows us to be more precise as to their exact nature.16

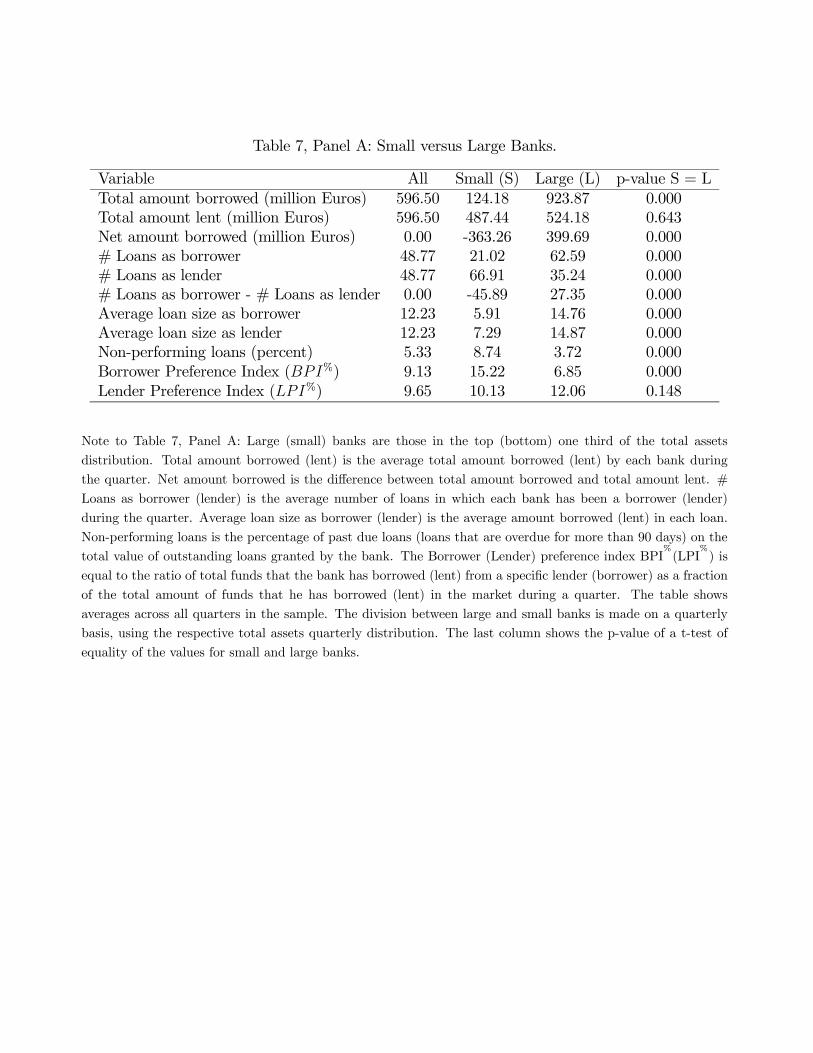

5.1 Small versus Large Banks

The estimation results in the previous sections show that bank size is an important determi-

nant of interbank market interest rates, and of lending relationships. In this section we explore

further the role of bank size in the market structure. In order to do so, and for each quarter

in our sample, we classify banks into large and small, based on the quarterly distribution of

bank assets. Large (small) banks are those whose assets are larger (smaller) than percentile

66 (33) of this distribution. We then compare several variables for small and large banks.

The first two rows of Table 7, Panel A report the average amount borrowed/lent per bank

16We would like to thank an anonymous referee for suggestions that have led us to investigate the questions

in this section.

24

and quarter over the whole sample period. The third row reports the net amount borrowed,

which is simply the difference between the first two. The second column shows the results for

all banks, i.e. not conditional on bank size, while columns three and four show the results for

small and large banks, respectively. On average, and per quarter, each bank in our sample

has lent/borrowed 596.5 million euros. There are significant differences between small and

large banks: large banks tend to be net borrowers, with an average net amount borrowed

roughly equal to 400 million euros, while small banks tend to be net lenders, with an average

net amount lent equal to 363 million euros.

Interestingly, this pattern of trade, in which large banks tend to be net buyers of liquidity

and small banks tend to be net sellers, is also a distinctive feature of the US Fed Funds market

(see for example Furfine, 1999, or Ho and Saunders, 1985).17 It can be rationalized by the

model of Ho and Saunders (1985). If large banks are better able to diversify their risk exposure

than small banks, then larger banks will be more rate sensitive than small banks, and the

slopes of the demand functions for interbank funds of large banks will be more price-elastic

than those of small banks. An important policy implication is that open market operations by

the central bank will be more effective when targeted at large rather than small institutions.

Table 7, Panel A also reports information on the number of loans and average loan amount.

Large (small) banks tend to transact mostly as borrowers (lenders), reflecting the fact that

they tend to be net borrowers (lenders) in the market. Unsurprisingly, average loan amount

for small banks is significantly lower than average loan amount for large banks.

The last three rows of Table 7, Panel A report the proportion of non-performing loans,

and relationship indices. Small banks tend to have a significantly higher proportion of non-

preforming loans than large banks. Furthermore, they tend to have significantly higher BPI

indices than large banks when borrowing funds. This suggests that small banks when bor-

rowing funds find it optimal to concentrate their borrowing. Interestingly, the same is not

17See also Stigum’s (1990) description of the Fed Funds market: “To cultivate correspondents that will sell

funds to them, large banks stand ready to buy whatever sums these banks offer, whether they need all these

funds or not."

25

true when lending funds, since there are no statistically significant differences in LPI indices

between small and large banks.

We have also investigate the likelihood that banks appear on both sides of the market, i.e.

as lenders and borrowers over a given time period. Panel B of Table 7 reports that 66.1%

(50.2%) of all banks have been on average active market participants on both sides of the

market at least once a month (week).

Panel B of Table 7 also reports summary statistics for bank assets and proportion of non-

performing loans as a function of how often banks appear on both sides of the market. It

shows that large banks are more likely to appear on both sides of the market, and in this way

act as intermediaries. In addition, banks that reverse their positions more frequently tend to

have a significantly lower proportion of non-performing loans. Naturally, banks with lower

credit risk are better-suited to act as intermediaries. Finally, we have investigated whether

the volatility of liquidity shocks differs depending on the frequency with which banks appear

on both sides of the market, but found no statistically significant differences.

Smaller banks are less likely to act as intermediaries, and are more likely to act as lenders.

But is it the case that when they need to borrow funds they do so from banks to whom they

usually lend funds? In order to investigate this we have estimated the probability that small

banks borrow funds from a bank to whom they usually lend funds, where the latter means a

bank in top fifty percent (one third) of the distribution of LPI indices for that small bank.

This probability is as high as 66.88% (54.58% for the one-third cutoff). The corresponding

probabilities for all banks, i.e. not conditional on bank size, are smaller and equal to 59.28%

(48.43%). Thus small banks, when reversing roles, tend to rely more on banks with whom

they usually interact on the other side of the market than the average bank in our sample.

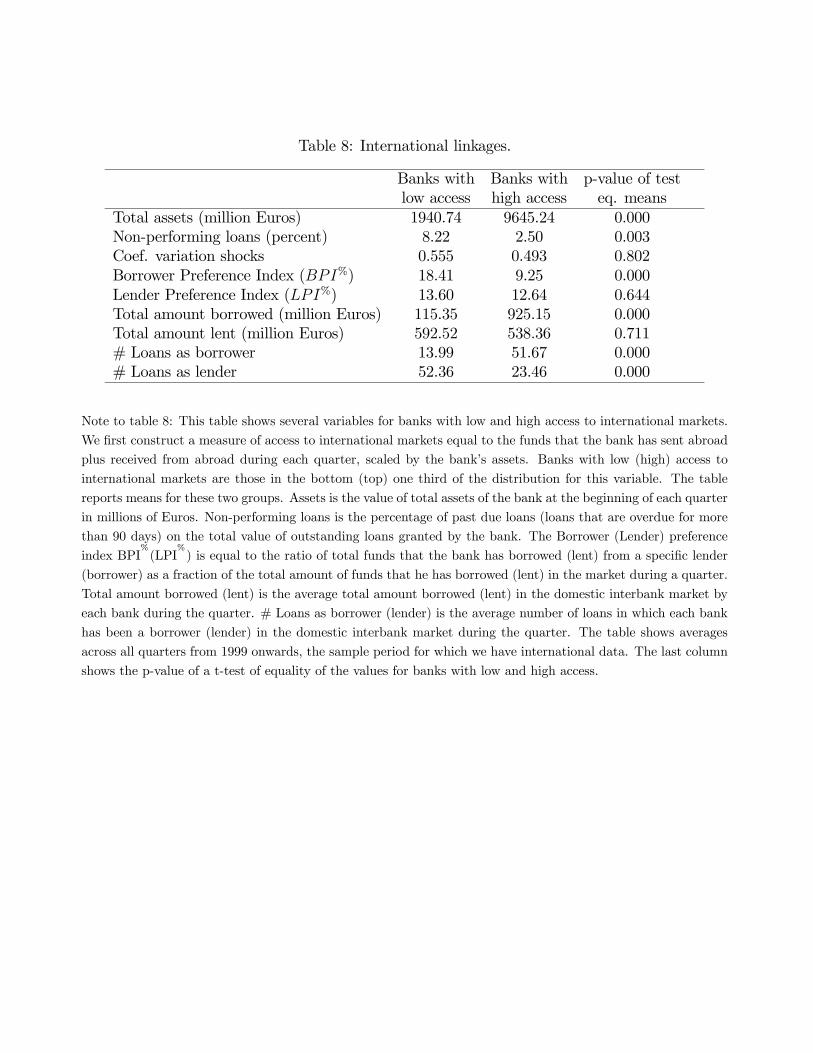

5.2 International Linkages

Unfortunately our main dataset only includes information on loans in the domestic interbank

market. However, and in order to explore international linkages between domestic and foreign

26

banks, we have obtained data from a different dataset, namely from the Trans-European

Automated Real-time Gross settlement Express Transfer system (TARGET). This is the real-

time gross settlement system for the euro offered by the Eurosystem. It is mainly used for

the settlement of large-value euro interbank transfers. This dataset contains information on

the identity of both the sender and receiver of funds, and on the amount transferred. It has

some shortcomings. First, transfers of funds between a pair of banks may be due to a variety

of reasons, other than interbank loans. For example, if a large individual client of a foreign

bank decides to transfer funds to a domestic bank, this transfer of funds will show up in the

dataset, and cannot be distinguished from an interbank loan. Second, this dataset is only

available from 1999 onwards, or roughly the second half of the sample period.

We use this dataset to investigate how international linkages relate to the nature of lend-

ing relationships in the domestic interbank market. This is particularly interesting because

the Euro area seems to be characterized by a two-tier structure, in which only large banks

are usually able to access foreign interbank markets for liquidity, and in which small banks

tend to do their interbank business through large domestic banks (European Central Bank,

2000). With this in mind, we first construct a measure of access to international markets, by

calculating the total amount of funds that each domestic bank has received from plus sent

abroad during each quarter. We then scale this variable by bank size, as measured by total

bank assets.18

We think that this variable is a better measure of access to international markets, than

simply the difference between funds received from abroad and funds sent abroad scaled by

bank assets. This is because a domestic bank may find it easy to access international interbank

markets, but during a given time period it may neither be net borrower nor net lender in these

18We have calculated alternative measures of access to international markets equal to the total amount of

funds that each domestic bank has received from abroad during the quarter scaled by bank assets, and equal

to the total amount of funds that each domestic bank has sent abroad during the quarter scaled by bank

assets. The correlation coefficient between these two variables is 0.97, and the correlation coefficients between

them and the total amount of funds sent plus received from abroad scaled by bank assets are over 0.99.

27

markets. In this case the latter variable would be zero. We classify banks into low and high

access to international markets, according to this measure. Banks with high (low) access are

those in the top (bottom) one third of the distribution of this variable. Table 8 shows the

results for the mean of several variables for each of these two groups. The last column shows

the p-value for a t-test of equality of means.

The first row confirms the result that banks with better access to international markets

tend to be larger: the difference in total bank assets between the two groups is almost five-

fold. Interestingly, we find that banks with low access to international markets tend to have a

much higher proportion of non-performing loans. Furthermore, these banks, when borrowing

funds in the domestic interbank market, find it optimal to concentrate their loans: their BPI

indices are much higher than those with high access to international market. This result is

consistent with peer monitoring across borders being less efficient than at the domestic level,

as in the model of Freixas and Holthausen (2005). It suggests that in international unsecured

credit markets such as interbank markets, peer monitoring plays an important role in that

it allows liquidity to flow across borders. However, an alternative explanation is that large

banks are perceived by international markets as being too-big-too-fail, and for this reason

they can borrow internationally at low rates. In either case, our results suggest that domestic

regulators should direct their policies towards an improvement of the cross-border information

available, particularly so on small banks, so as to enhance cross-border market integration.

Finally, we find that banks with high access to international markets tend to have a lower

coefficient of variation of liquidity shocks, but the difference relative to banks with low access

to international markets is not statistically significant.

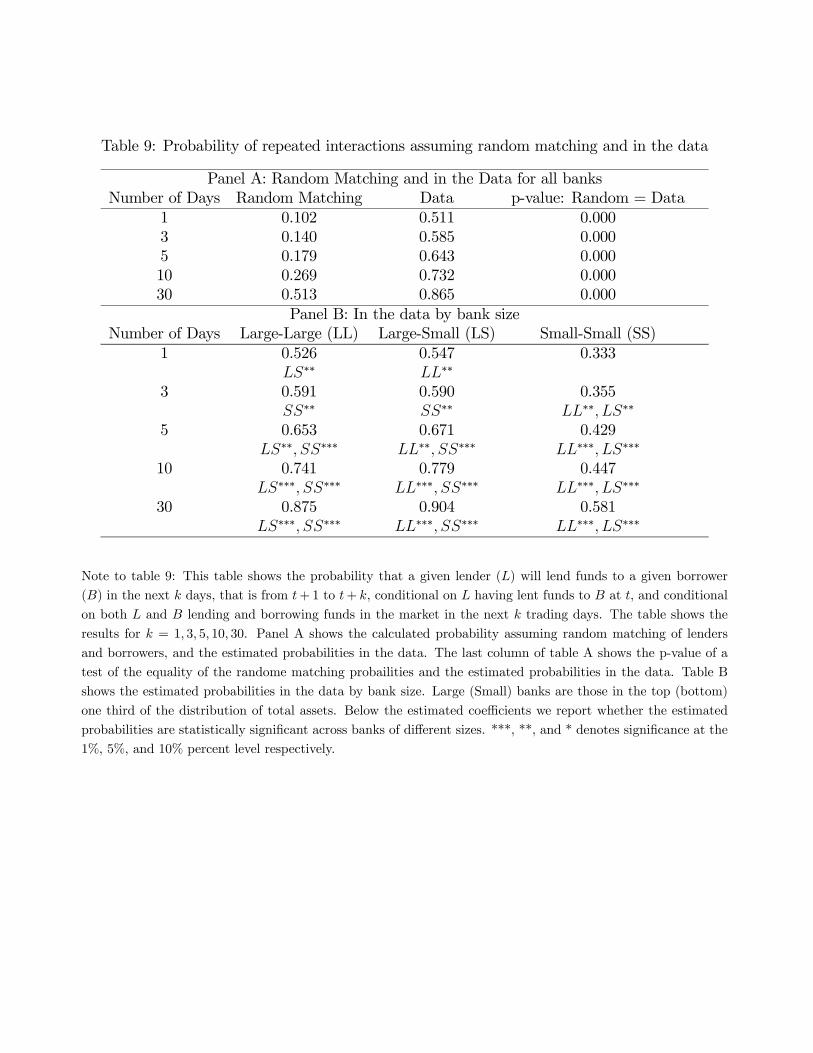

5.3 Time-series probabilities of repeated interactions

In order to better understand the time-series dimension of the relationship between borrowers

and lenders we estimate the probability of repeated interactions. More precisely, we estimate

the probability that a given lender (L) will lend funds to a given borrower (B) in the next k

28

days, that is from t+1 to t+ k, conditional on L having lent funds to B at t, and conditional

on both L and B lending and borrowing funds in the market in the next k days. Thus, we are

trying to answer the following question: given that B has borrowed from L at t, and given

that B needs funds again sometime within the next k trading days, how likely is it that it will

borrow from L again?

Before we turn to the estimation results let us first calculate what we should expect to

observe if the matching mechanism was completely random. The average number of loans on

a given day is 43.31, and the average daily number of active lenders in the market is 23.1.

This corresponds to an average of 1.87 loans per lender each day. Since the average daily

number of active borrowers is 17.95, if the matching was completely random the probability

of a lender lending to the same borrower at t+ 1, conditional on having done so at t and on

both lender and borrower being active in the market at t+ 1, is 10.2%.19 This probability is

roughly one fifth of the value that we have estimated in the data, and equal to 51% (Table

9, Panel A). This probability increases to 64% if we consider k equal to five, and if we take

a 30-day window the probability is as high as 87%. These probabilities are much larger than

those we would obtain with a random matching mechanism, which are 18% and 51% for a five

and a thirty-day window, respectively. The differences are statistically significant at the 1%

significance level. Thus, in the interbank market, lenders frequently use previous borrowers

and vice-versa, and much more frequently than one would obtain if the matching mechanism

was random.

With our previous analysis of bank size in mind, in Panel B of Table 9 we take this

analysis in that direction. In particular we estimate and find that the probability of repeated

interaction is higher if one of the banks is small (asset size below percentile 33) and the other

one is large (asset size above percentile 66). When both the borrower and the lender are

large the probability of repeated interaction is lower, and it is lowest when both lender and

19With probability 1/17.95 the bank lends to the same borrower in its first loan, plus with probability

(1−1/17.95) it does not lend to the same borrower in the first loan, but it does so with probability 0.87/17.95in the 0.87 remaining loan, so that the probability is 1/17.95 + (1− 1/17.95)× 0.87/17.95.

29

borrower are small. These estimated probabilities suggest that lending relationship are most

important when between small and large banks in the domestic market. In panel B of Table

9, below the estimated probabilities, we report whether these probabilities are statistically

different from one another. It is important to note that for k equal to one we do not find

that the probability of SS is significantly different than LL or LS because there are very few

observations for SS and k = 1.

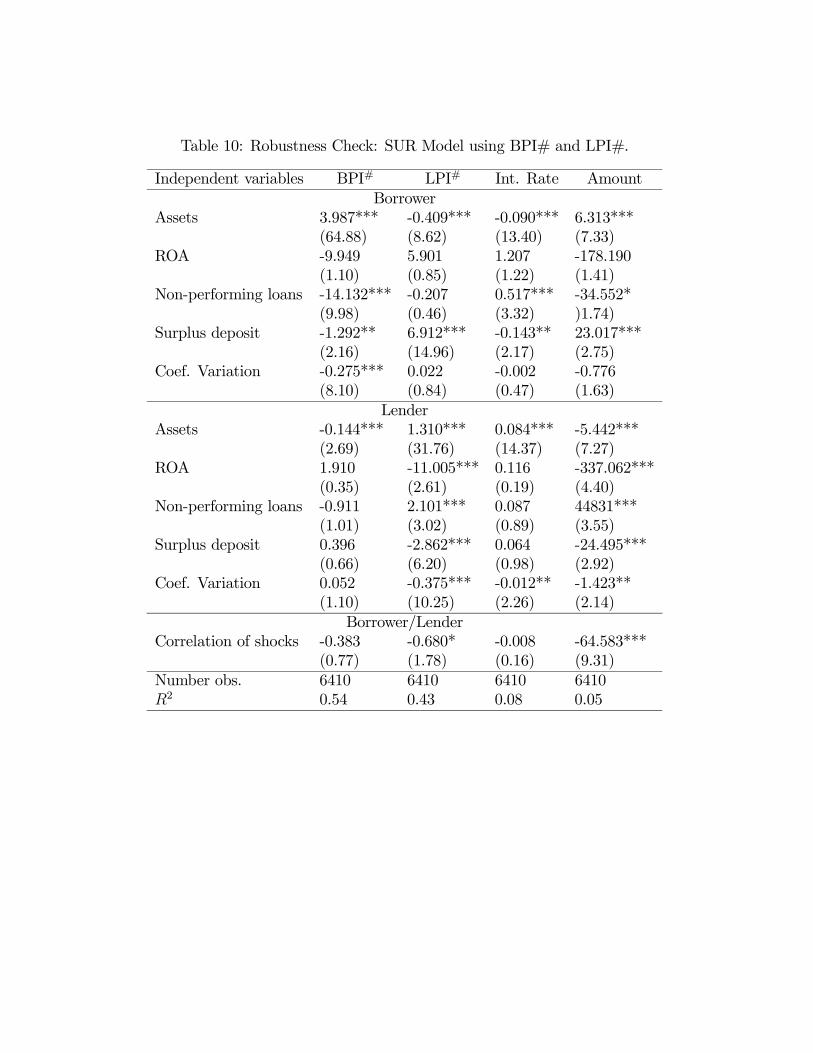

6 Robustness checks

In Tables 10 through 11 we present several different robustness checks, in which we estimate

the SUR system using alternative measures of lending relationships. Table 10 reports the

estimation results for the previously constructed BPI# and LPI# indices. In interpreting

the results in this table one should recall that a higher index means that banks rely less on

lending relationships. That is the interpretation is symmetric to that of the BPI% and LPI%

indices. The results in Table 10 are similar to those in Table 6, except for the fact that in the

third column the NPL of lenders is positive and statistically significant. Thus lenders with

a higher NPL tend to rely more on lending relationships. This is the opposite of what one

might have a priori expected. However, this result is not robust to other relationship measures

(Tables 6 and 11).

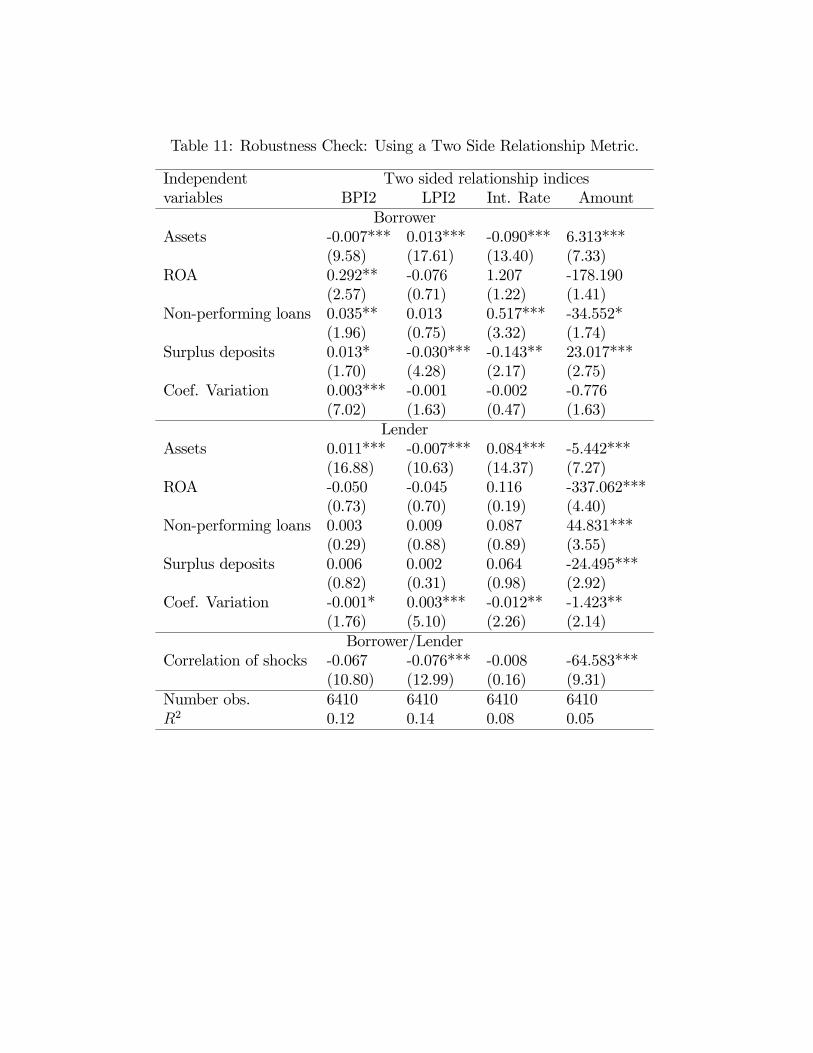

We have constructed the LPI% as being equal to the total amount that bank L has lent to

bank B as a fraction of the total amount that bank L has lent in the interbank market during

the quarter. However, during the same quarter bank L may borrow funds from bank B. We

now investigate the robustness of the results to measures that take into account a two-sided

relationship factor. More precisely, the relationship measures are:

BPI2L,B,q =Xi∈q

¡FL−→Bi + FB−→L

i

¢/Xi∈q

¡F all−→Bi + FB−→all

i

¢(14)

LPI2L,B,q =Xi∈q

¡FL−→Bi + FB−→L

i

¢/Xi∈q

¡FL−→alli + F all−→L

i

¢(15)

30

Thus the borrower preference index is now defined as the total amount bank B borrowed from

plus lent to bank L divided by the total amount of funds that B has borrowed plus lent in the

market during quarter q. The estimation results for these alternative relationship measures

are reported in Table 11. Although there are some differences in magnitude and statistical

significance of some of the estimated coefficients, the results are similar to those we obtained

before.

Finally, we have constructed lender and borrower preference indices similar to LPI% and

BPI% but using number of loans instead of loan amounts. That is the lender preference index

was constructed as the number of times that L has lent funds to B during quarter q, as a

fraction of the total number of times that bank L has lent funds in the interbank market

during the same quarter. The results were similar and are not reported.

7 Conclusion and Policy Implications

Interbank markets play an important role in distributing liquidity across the financial system.

It is in this market that banks borrow and lend funds among themselves, allowing for the

transfer of liquidity from banks that have excess funds to those that are short. However, since

interbank market loans are unsecured, they also increase the exposure of lenders to borrowers.

In this paper we have studied lending relationships in a typical interbank market.

There are at least two sets of reasons why banks may benefit from lending relationships.

First, in the models of Ho and Saunders (1985), Bhattacharya and Gale (1987), and Freixas,

Parigi and Rochet (2000) banks borrow and lend funds in the interbank market to insure

against idiosyncratic liquidity shocks that arise from the behavior of retail depositors. Thus,

banks may form lending relationships for insurance purposes. Second, Rochet and Tirole

(1996) present a model of the interbank market in which asymmetric information and mon-

itoring play an important role. Thus, banks may rely on lending relationships to overcome

problems that arise from asymmetric information on credit worthiness.

We have provided evidence that supports both of these motives for the existence of lending

31

relationships. Importantly, we have done so by explicitly recognizing that these relationships

are endogenous, and addressing the issue by estimating instrumental variables regressions and

a system of seemingly unrelated regressions. We have found that smaller banks, with lower

return on assets, banks with a higher proportion of non-performing loans and banks that are

subject to more volatile liquidity shocks rely more on lending relationships, and that they tend

to form relationships with large banks, and banks that are subject to less volatile liquidity

shocks.

In order to be more precise as to the exact nature of lending relationships, we have inves-

tigated the role of bank size in the market structure. Interestingly, we have found that large

banks tend to be net buyers of liquidity and small banks tend to be net sellers. This pattern of

trade is also a distinctive feature of the US Fed Funds market (see for example Furfine, 1999,

or Ho and Saunders, 1985). It can be rationalized by the model of Ho and Saunders (1985).

If large banks are better able to diversify their risk exposure than small banks, then large

banks will be more rate sensitive than small banks, and the slopes of the demand functions

for interbank funds of large banks will be more price-elastic than those of small banks. One

important policy implication is that open market operations by the central bank will be more

effective when targeted at large rather than small institutions.

We have also investigated how access to international markets affects the nature of lending

relationships in the domestic market. We have found that large domestic banks tend to

have better access to international markets. Interestingly, we have found that banks with low

access to international markets tend to have a much higher proportion of non-performing loans.

Furthermore, these banks, when borrowing in the domestic interbank market, find it optimal

to concentrate their loans. This result is consistent with peer monitoring across borders being

less efficient than at the domestic level, as in the model of Freixas and Holthausen (2005).

It suggests that in international unsecured credit markets such as interbank markets, peer

monitoring plays an important role in that it allows liquidity to flow across borders. However,

an alternative explanation is that large banks are perceived by international markets as being

too-big-too-fail, and for this reason they can borrow internationally. In either case, our results

32

suggest that domestic regulators should direct their policies towards an improvement of the

cross-border information available, particularly so on small banks, so as to enhance cross-

border market integration.

33

8 References

Allen, Franklin and Douglas Gale, 2000, “Financial Contagion,” Journal of Political Econ-

omy, 108, pp. 1-33.

Allen, Linda, and Anthony Saunders, 1986, “The Large-small Bank Dichotomy in The Federal

Funds Market,” Journal of Banking and Finance, 10, pp. 219-230.

Berger Allen N. and Gregory F. Udell, 1992, “Some Evidence on the Empirical Significance

of Credit Rationing,” Journal of Political Economy, 100, pp. 1047-1077.

Berger Allen N. and Gregory F. Udell, 1995, “Relationship Lending and Lines of Credit in

Small Firm Finance,” Journal of Business, 68, pp. 351-381.

Berlin, Mitchell, and Loretta Mester, 1999, “Deposits and Relationship Lending,” Review of

Financial Studies, 12, pp. 579-607.

Bhattacharya, Sudipto and Douglas Gale, 1987, Preference Shocks, Liquidity, and Central

Bank Policy, in W. Barnett and K. Singelton (eds.), New Approaches to Monetary

Economics, Cambridge University Press.

Biais, Bruno, 1993, “Price Formation and Equilibrium Liquidity in Fragmented and Central-

ized Markets,” Journal of Finance, 48, pp. 157-185.