fiscal management in adjustment lending

TRANSCRIPT

________ -m" Ai'~~4 -,4

~~~ -~~~~~~-7

4:

A WorldBank Oera"IT

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Fiscal Managementin Adjustment Lending

Other Titles in the SeriesPREPARED BY THE WORLD BANK OPERATIONS EVALUATION DEPARTMENT

Reforming Agriculture: The World Bank Goes to Market(1997)*

Paddy Irrigation and Water Management in Southeast Asia(1997)*

1995 Evaluation Results(1997)*

Zambia Country Assistance Review: Turning an Economy Around(1997)*

Aga Khan Rural Support Program: A Third Evaluation(1996)*

Lending for Electric Power in Sub-Saharan Africa(1996)*

Industrial Restructuring: World Bank Experience, Future Challenges(1996)*

Social Dimensions of Adjustment: World Bank Experience, 1980-93(1996)*

1994 Evaluation Results(1996)*

Ghana Country Assistance Review: A Study in DevelopmentEffectiveness(1995)*

Evaluation and Development: Proceedings of the 1994 WorldBank Conference(1995)

Developing Industrial Technology: Lessons for Policy and Practice(1995)*

The World Bank and Irrigation(1995)*

1993 Evaluation Results(1995)*

Structural and Sectoral Adjustment: World Bank Experience, 1980-92(1995)*

Gender Issues in World Bank Lending(1995)*

The World Bank's Role in Human Resource Development in Sub-Saharan Africa: Education, Training, and Technical Assistance(1994)*

1992 Evaluation Results(1994)*

New Lessons from Old Projects: The Workings of Rural Developmentin Northeast Brazil(1993; contains summaries in French, Portuguese, and Spanish)

World Bank Approaches to the Environment in Brazil(1993; contains summaries in French, Portuguese, and Spanish)

Trade Policy Reforms under Adjustment Programs(1992)*

World Bank Support for Industrialization in Korea, India,and Indonesia(1992)*

Population and the World Bank: Implications from Eight Case Studies(1992)*

The Aga Khan Rural Support Program in Pakistan:Second Interim Evaluation(1990)*

*Contains summaries in French and Spanish.

Fiscal Managementin Adjustment Lending

Jayati Datta-Mitra

THE WORLD BANK

WASHINGTON, D.C.

Copyright C 1997The Intemational Bank for Reconstructionand Development/THE WORLD BANK1818 H Street, N.W.Washington, D.C. 20433, U.S.A.

All rights reservedManufactured in the United States of AmericaFirst printing June 1997

The opinions expressed in this report do not necessarily represent the views of the World Bank orits member governments. The World Bank does not guarantee the accuracy of the data included inthis publication and accepts no responsibility whatsoever for any consequence of their use. Theboundaries, colors, denominations, and other information shown on any map in this volume donot imply on the part of the World Bank Group any judgment on the legal status of any territory orthe endorsement or acceptance of such boundaries.

The material in this publication is copyrighted. Requests for permission to reproduce portions of itshould be sent to the Office of the Publisher at the address shown in the copyright notice above.The World Bank encourages dissemination of its work and will normally give permission prompt-ly and, when the reproduction is for noncommercial purposes, without asking a fee. Permission tocopy portions for classroom use is granted through the Copyright Clearance Center, Inc., Suite 910,222 Rosewood Drive, Danvers, Massachusetts 01923, U.S.A.

Cover photo by Angie Gentile-Blackwell.

Library of Congress Cataloging-in-Publication Data

Datta-Mitra, Jayati.Fiscal management in adjustment lending / Jayati Datta-Mitra.

p. cm. - (A World Bank operations evaluation study, ISSN1011-0984)

Includes bibliographical references.ISBN 0-8213-3965-61. Fiscal policy-Developing countries. 2. Loans, Foreign-

Developing countries. 3. World Bank. 4. Budget deficits-Developing countries. 5. Structural adjustment (Economic policy)-Developing countries. I. World Bank. II. Title. III. Series.HJ1620.D377 1997332.1'532-dc2l 97-19151

CIP

Contents

Foreword xiPr6logo xiiiAvant-propos xvAcknowledgments xviiAbbreviations and acronyms xviii

Summary 1Resumen 8Resume 16

1. Setting the stage 25

The typical crisis profile 25The centrality of fiscal reform 27Coverage of the report 27

2. Fiscal management in SALs/SECALs: a close-up view 30

What was the quality of fiscal diagnosis? 31Was the quality of conditionality adequate? 39Was implementation adequate? 43Conclusions 45Lessons 47

3. Tax reform 51

What the study found 51Principles of tax reform 52Precision and content of tax conditionality 54How successfully were tax conditionalities implemented? 61How effective was tax reform? 61Lessons and directions for the future 66

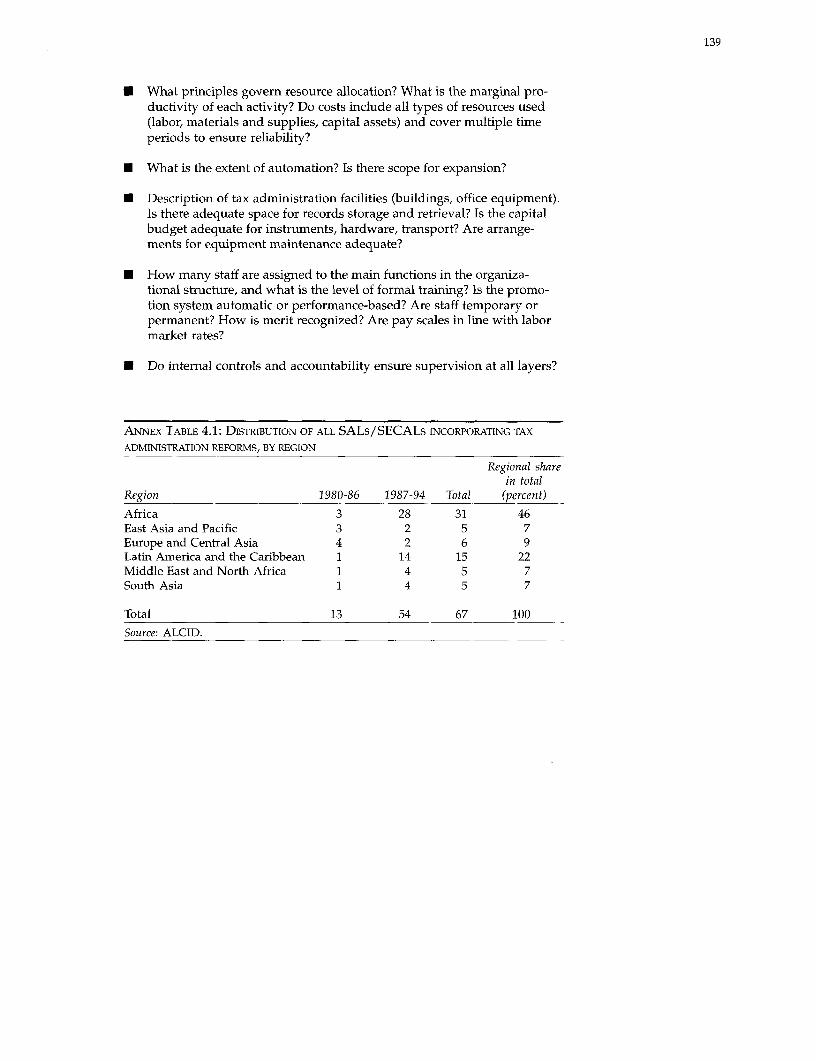

4. Tax administration reform 71

What the study found 71The ends and means of tax administration reform 71Bank involvement in tax administration reform 75Tracking implementation of reforms 79Measuring outcomes 80Lessons 81

5. Public expenditure reform 83

What the study found 83A framework for evaluating public sector reforms 85Expenditure patterns before adjustment lending 87

vii

viii

Bank conditionalities 88Implementation of conditionalities 94How effective were expenditure reform conditions? 96Lessons 104

6. Fiscal adjustment under SALs and SECALs: an aggregateview and conclusions 106

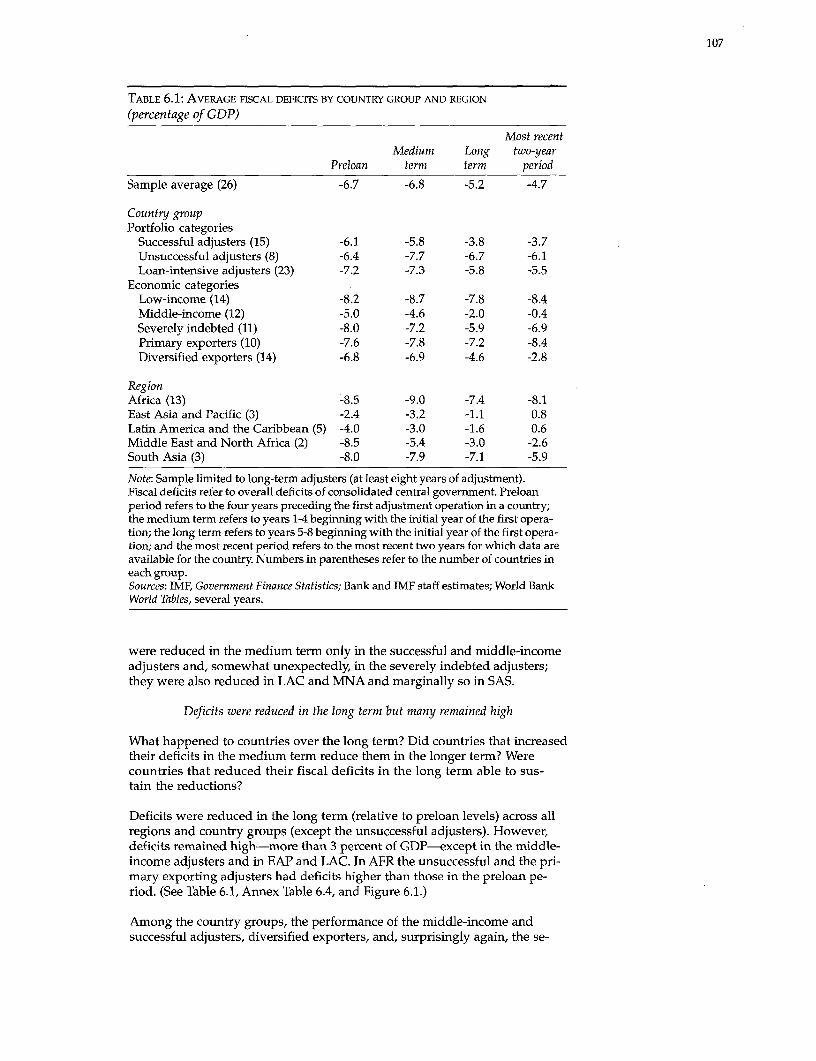

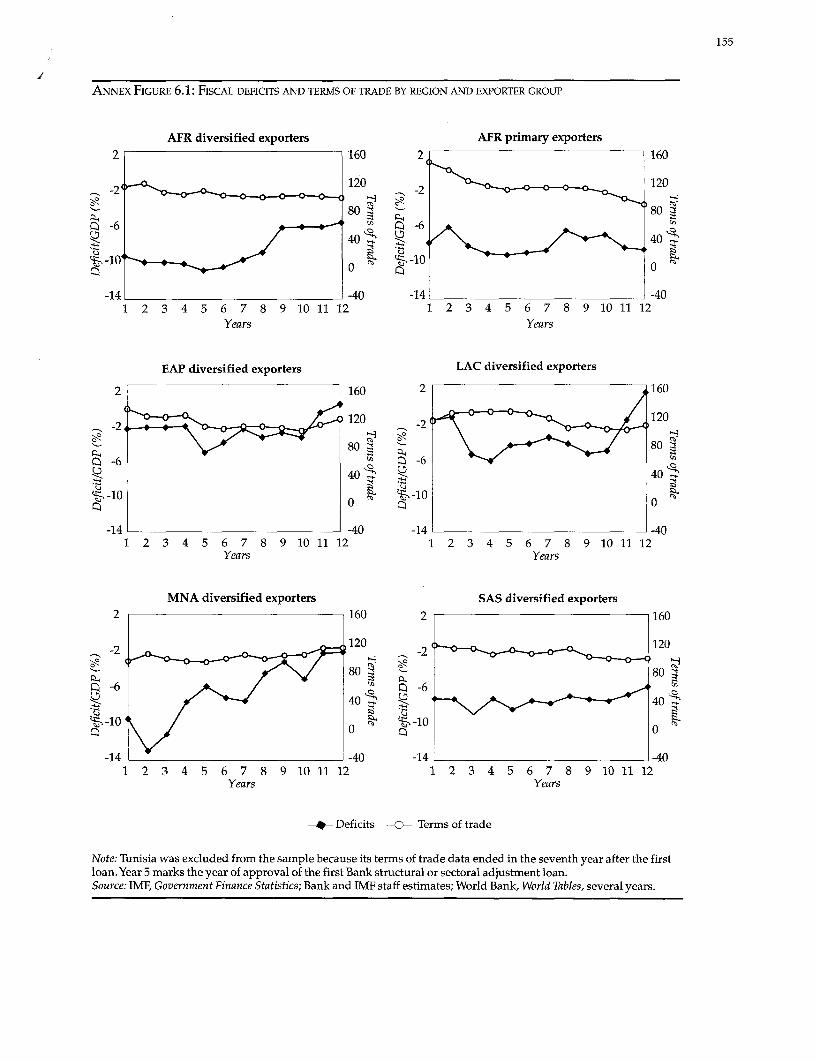

Were fiscal deficits reduced? 106How did external factors affect fiscal outcomes? 109How was fiscal adjustment achieved? 111Recommendations 113

Annexes 121

Bibliography 167

Supplement 173

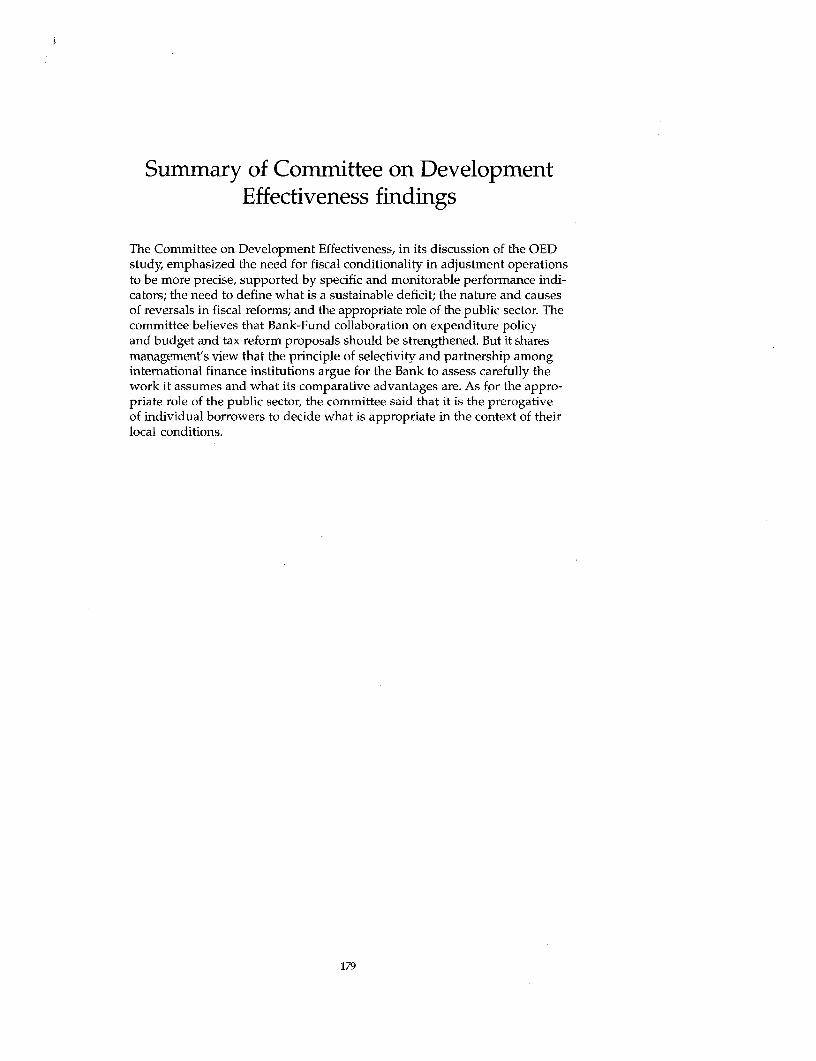

Introductory note 174Management response 175Summary of Committee on Development Effectiveness findings 179

Boxes

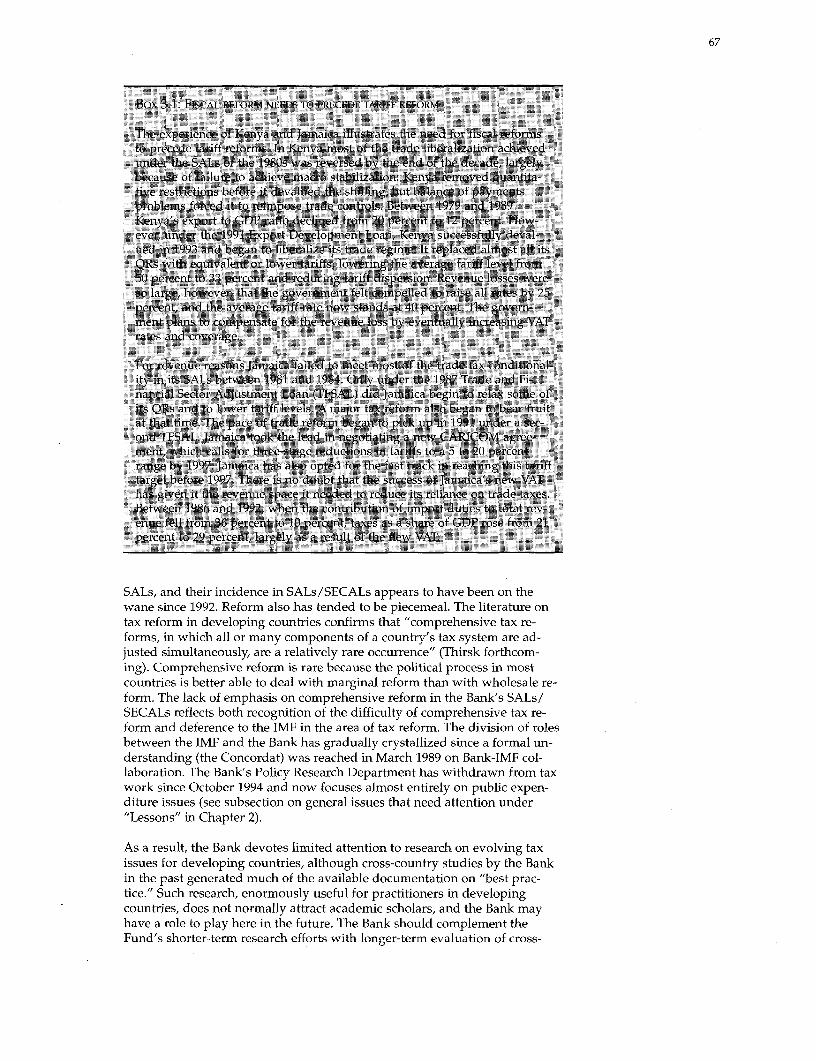

2.1 Basic elements of diagnosis 312.2 Examples of quasi-fiscal activities of financial systems 342.3 Evaluating conditionality 403.1 Fiscal reform needs to precede tariff reform 676.1 Determining the solvency of the public sector 113

Figures

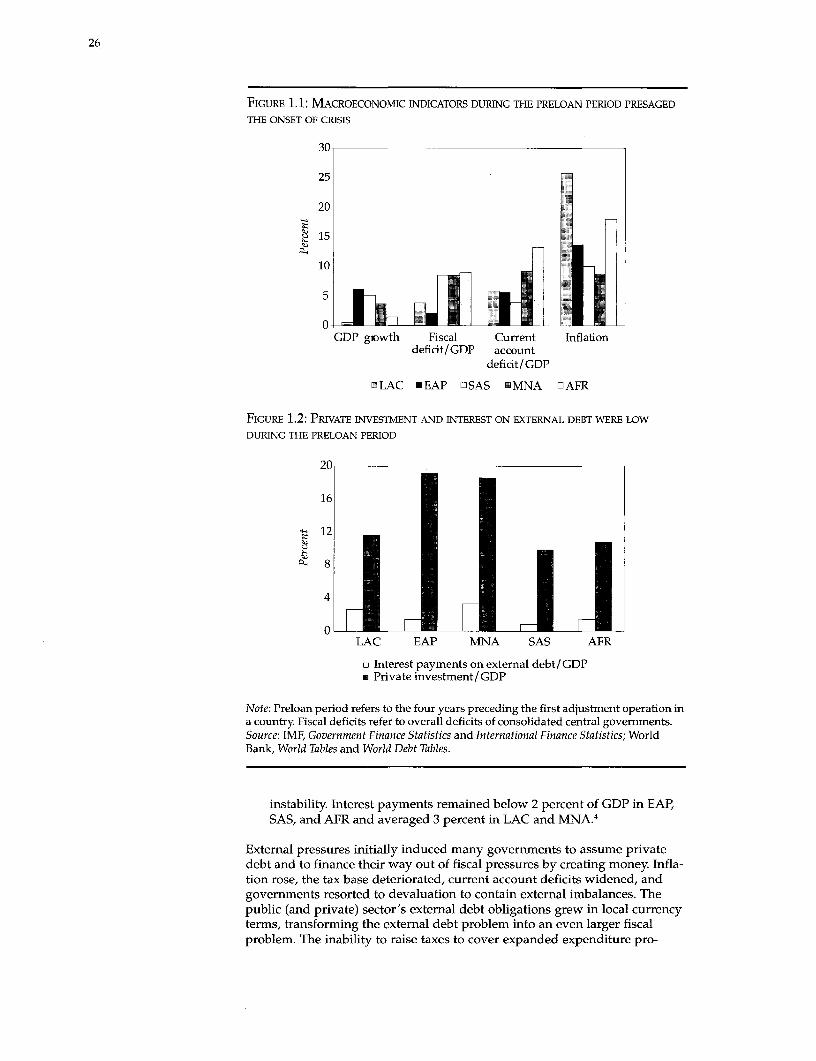

1.1 Macroeconomic indicators during the preloan periodpresaged the onset of crisis 26

1.2 Private investment and interest on external debt werelow during the preloan period 26

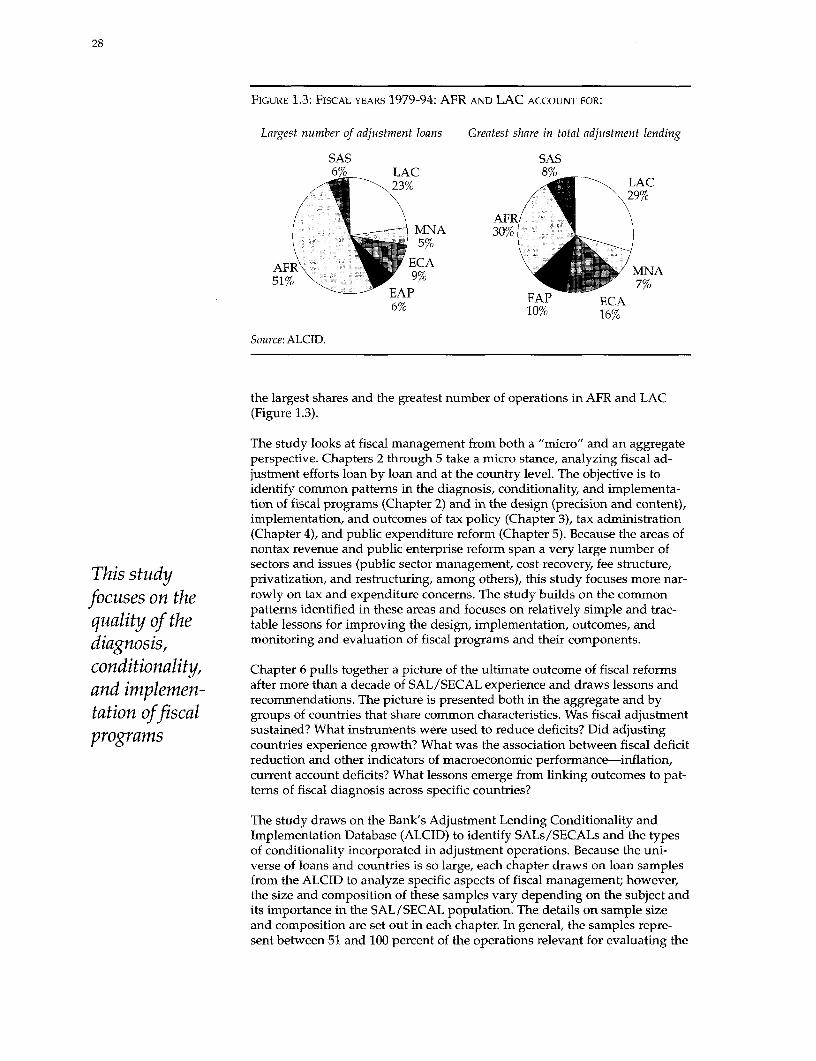

1.3 Fiscal years 1979-94: AFR and LAC account for largest number ofadjustment loans and greatest share in total adjustment lending 28

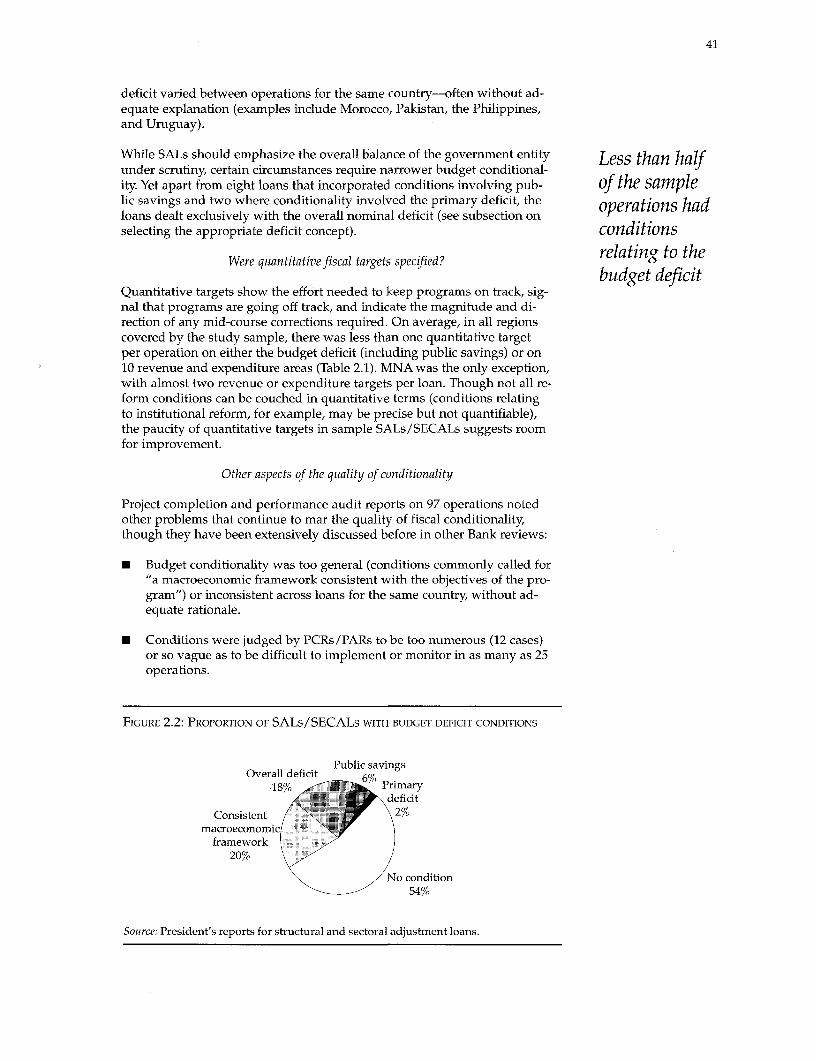

2.1 Coverage of fiscal accounts was specified in only halfof the 129 SALs/SECALs 32

2.2 Proportion of SALs/SECALs with budget deficit conditions 416.1 Change in fiscal deficits by region and country group 108

Tables

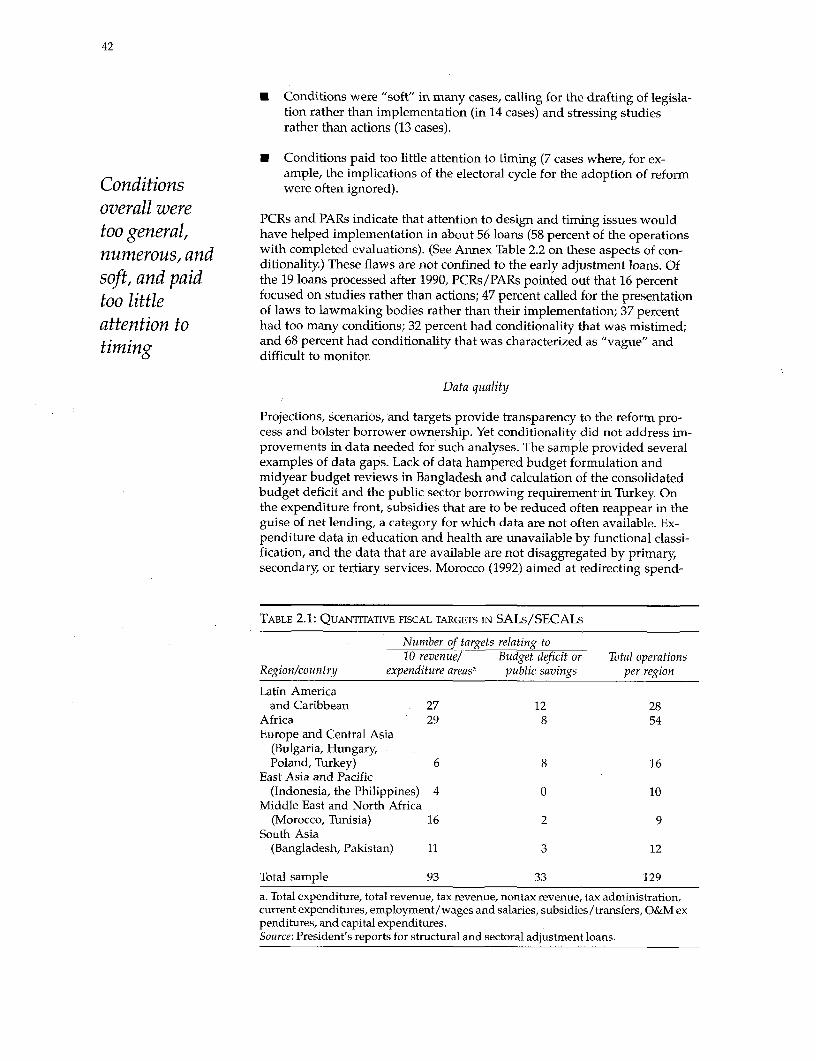

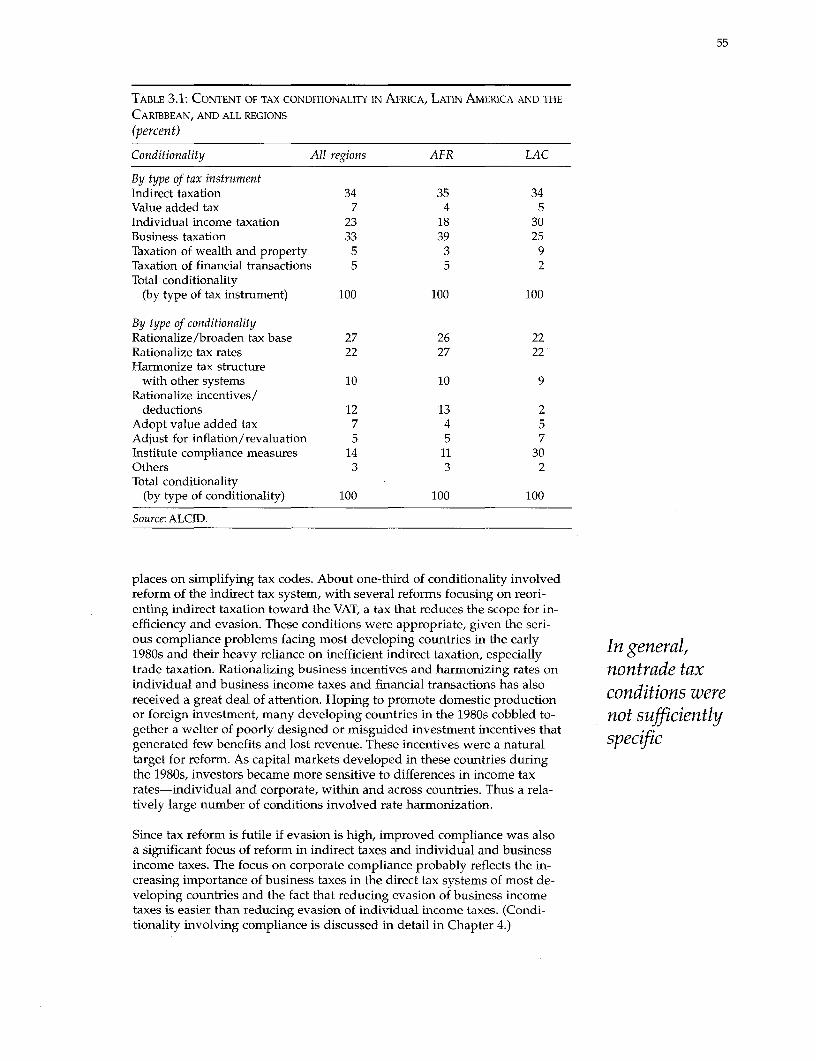

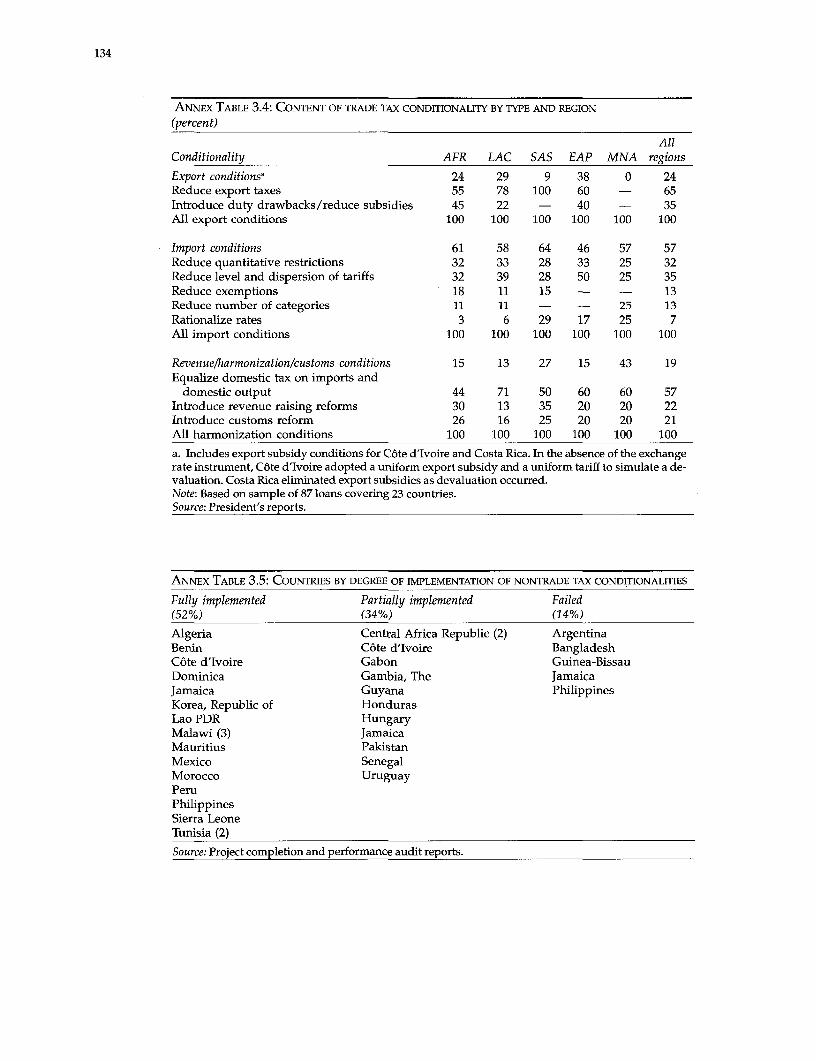

2.1 Quantitative fiscal targets in SALs/SECALs 423.1 Content of tax conditionality in Africa, Latin America and

the Caribbean, and all regions 553.2 Trade tax conditionality by type and region 593.3 Types of trade tax conditionality by region and country 603.4 Tax structure before and after adjustment 623.5 Diagnosis of need for revenue reform and performance 653.6 Successful and less successful trade adjusters 664.1 Sample SALs/SECALs incorporating tax administration

reforms by region and period 754.2 Specificity of tax administration reform conditionalities by region 77

ix

4.3 Sample conditionalities by level of precision 774.4 Specific tax administration reform conditionalities by region 775.1 Composition of central government expenditures, regional

averages, 1970-79 875.2 Public current expenditures per pupil by level of education 885.3 Loan conditions by expenditure reform objective, 1980-94 895.4 Countries facing civil service conditions 905.5 Loan conditions by equity objective, 1980-94 935.6 Implementation of Bank conditions on public expenditures 955.7 Diagnosis of need for total expenditure reform and performance 955.8 Diagnosis of need for capital expenditure reform and performance 975.9 Diagnosis of need for current expenditure reform and performance 985.10 Changes in wage expenditure shares, before and after adjustment 995.11 Changes in central government expenditures on education,

before and after adjustment 1015.12 Changes in central government expenditures on health 1015.13 Expenditure inflexibility 1025.14 Primary enrollment ratios in countries with education conditions 1035.15 Enrollment ratios and the gender gap in primary education 1036.1 Average fiscal deficits by country group and region 107

Foreword

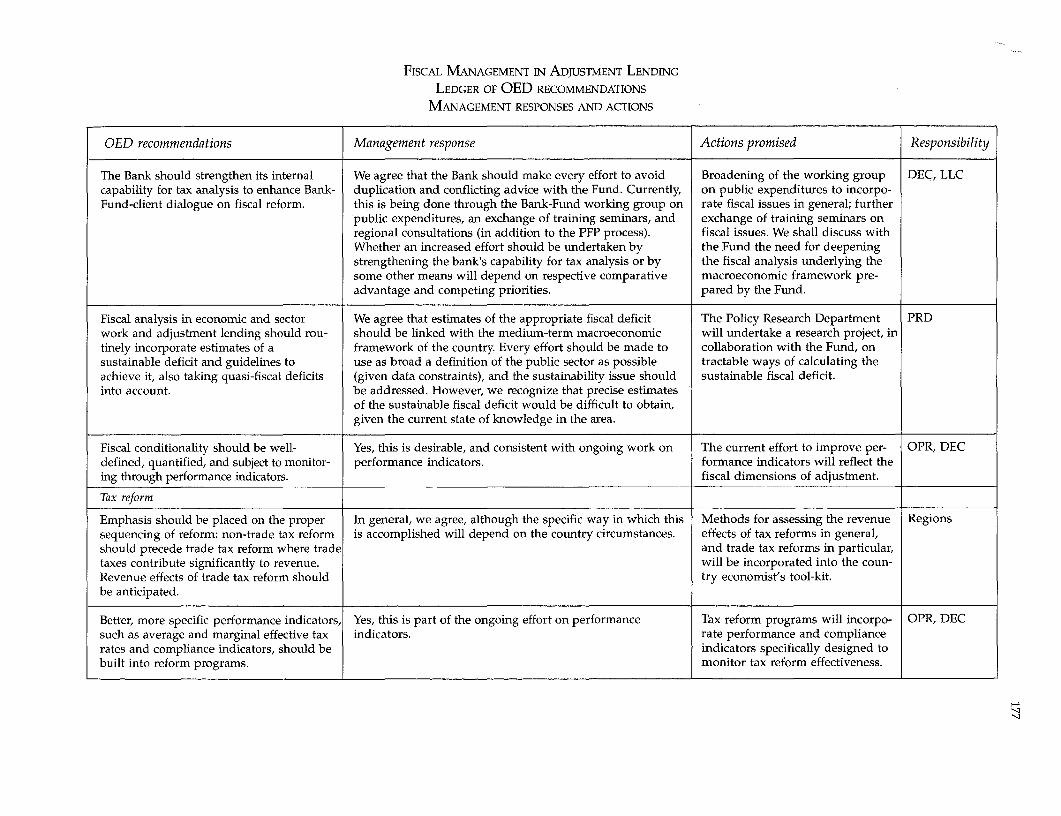

Fiscal balance is central to the success of adjustment. This study, preparedby the World Bank's Operations Evaluation Department, analyzes theBank's experience with fiscal management in 250 adjustment operationsin 86 countries. It examines the fiscal record in a sample of 26 countries(134 operations) grouped by region, portfolio characteristics, and economictraits. The study confirms that fiscal deficit reduction is associated with im-proved external balances and economic growth and that it takes sustained,long-term effort, and continual vigilance against reversals. Contrary to theview prevailing in the early years of adjustment operations, the study sug-gests that fiscal mismanagement, not exogenous shocks, was the principalcause of persistent budget deficits.

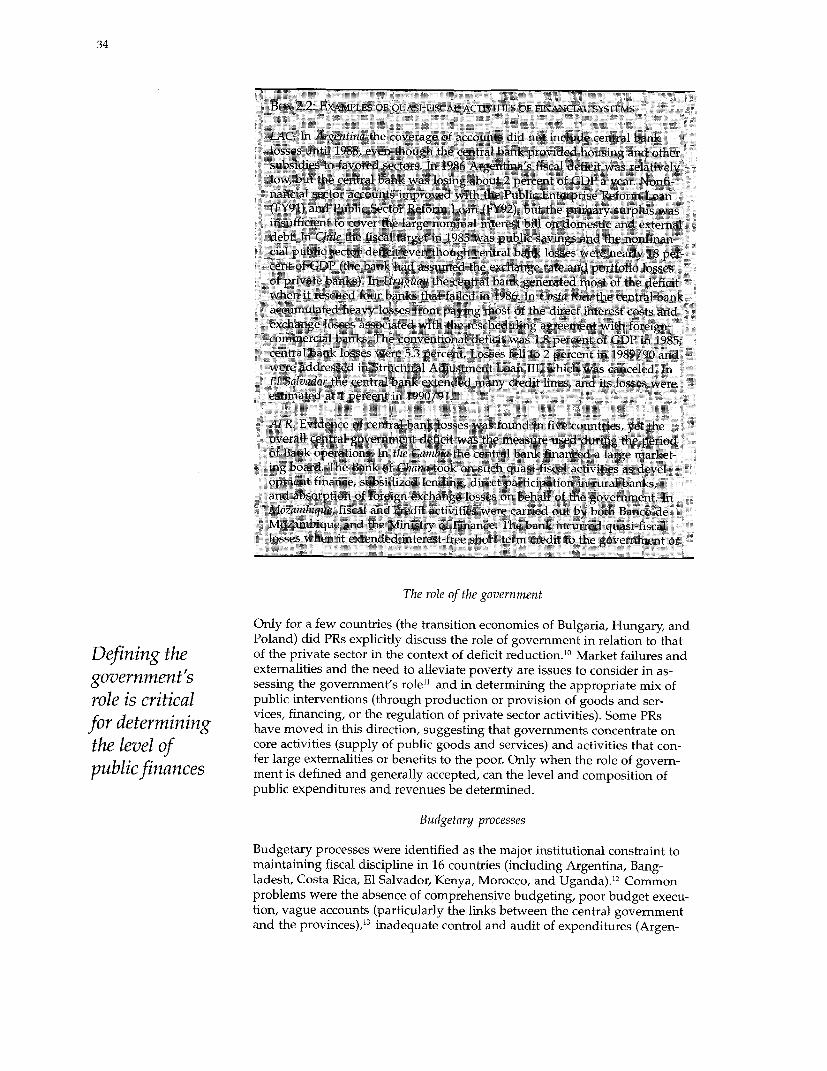

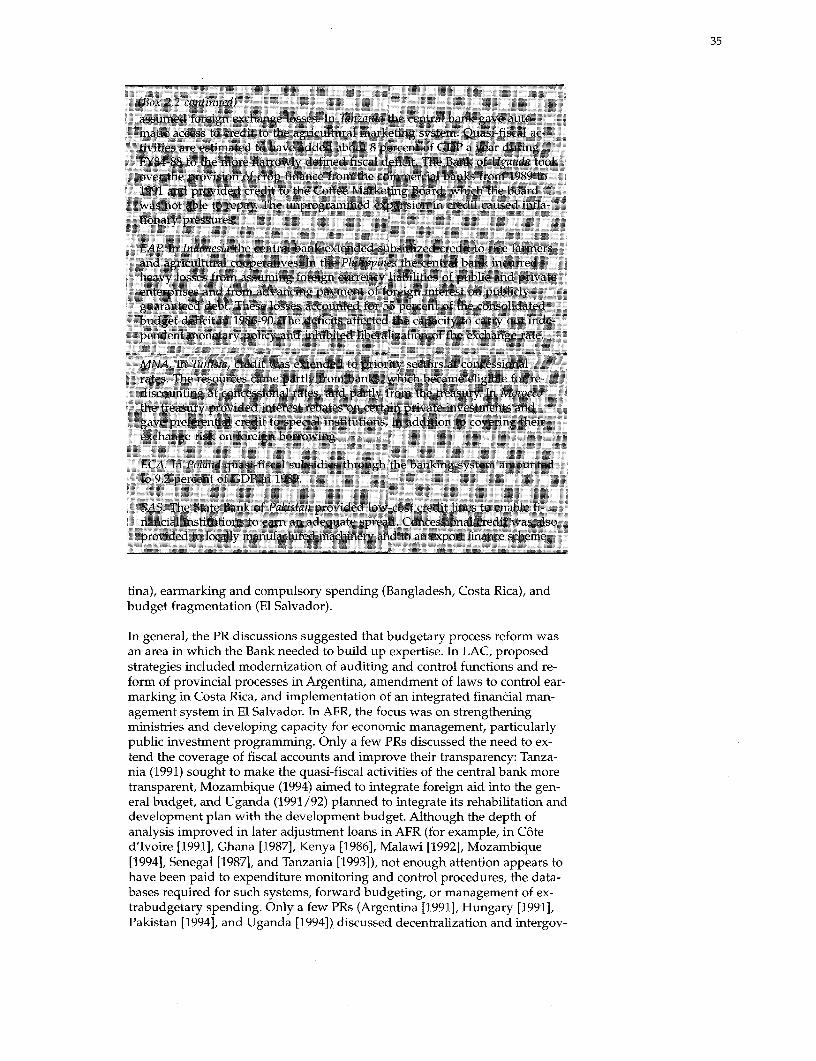

Budget deficits-accompanied by rising external debt and a growing ratioof debt to GDP-remain high, and there have been some reversals, particu-larly in Africa and among low-income and severely indebted adjusters andprimary exporters. Fiscal success was limited in part because reform pro-grams (1) failed to address the role of the state, a critical factor determiningthe level of public finances; (2) treated fiscal issues separately from othermacroeconomic reforms and ignored fiscal sustainability and solvency;(3) paid scant attention to fiscal deficit coverage, measurement, and data;and (4) were couched in conditionality that was too soft, ambiguous, orinconsistent.

Countries reduced deficits by increasing revenue and to a lesser extent bylowering capital spending; targeted cuts in current expenditures provedmore elusive. Revenues increased, not by imposing higher tax rates, butby broadening and simplifying the tax base. Tax conditionality (affectingpolicy as well as administration) was imprecise and did not build in perfor-mance monitoring indicators. And expenditure conditions focused on shiftsin expenditure, not outcomes.

The study offers a number of recommendations for the Bank and its borrowers:

* Estimate the level of the sustainable deficit and provide guidelinesfor achieving it in Bank economic and sector work and adjustmentlending.

* Improve sequencing of tax reform, for example, by ensuring that non-tax trade reform precedes trade tax reform and that tax administrationreform precedes or accompanies tax policy reform.

* Consider explicitly the role of the state and the appropriate mix ofpublic/private provision of services in recommending public expendi-ture reform.

* Include poverty alleviation and equity objectives in public expendi-ture reform.

xi

xii

* Build adequate monitoring and performance indicators for both tax andexpenditure reforms.

* Enhance Bank-Fund coordination, in support of the Fund's lead role ingiving fiscal advice, by strengthening the Bank's ability to analyze taxesand expenditures.

Robert PicciottoDirector GeneralOperations Evaluation

Prologo

El equilibrio fiscal es esencial para la eficacia del ajuste. En este estudio,preparado por el Departamento de Evaluaci6n de Operaciones del BancoMundial, se analiza la experiencia del Banco en materia de gesti6n fiscal en250 operaciones de ajuste realizadas en 86 paises. Se examina el historial fis-cal de una muestra de 26 paises (134 operaciones) agrupados por regiones,caracteristicas econ6micas y de la cartera. El estudio confirma que la reduc-ci6n del deficit fiscal se vincula con la mejora de la balanza de pagos y elaumento del crecimiento econ6mico, y que para lograrla se necesita unesfuerzo sostenido a largo plazo y la vigilancia constante para que no seproduzcan retrocesos. A diferencia de la opini6n predominante en los pri-meros anios de las operaciones de ajuste, el estudio revela que la principalcausa de la persistencia de los deficit presupuestarios era la mala gesti6nfiscal y no las conmociones externas.

El nivel de los deficit presupuestarios -unidos a una deuda externa yuna relaci6n deuda-PIB crecientes- sigue siendo alto, y se han observadoalgunos retrocesos, sobre todo en los paises de Africa y las naciones deingreso bajo y gravemente endeudadas en proceso de ajuste y exportadorasde productos primarios. El exito fiscal se vio en parte limitado porque losprogramas de reforma: (1) no abordaron el papel que cabe al estado, unfactor crucial para determinar el nivel de las finanzas publicas; (2) trataronlos problemas fiscales en forma independiente de otras reformas macro-econ6micas e ignoraron la sostenibilidad fiscal y la solvencia; (3) presta-ron escasa atenci6n a la cobertura del d6ficit fiscal, su medici6n y datosconexos, y (4) contenfan condicionalidades demasiado blandas, ambiguaso incongruentes.

Los pafses redujeron los deficit aumentando los ingresos y, en menor medi-da, reduciendo el gasto de capital; result6 mas dificil aplicar reduccionesespecificas de los gastos corrientes. Los ingresos aumentaron gracias a laampliaci6n y simplificaci6n de la base imponible, y no mediante la aplica-ci6n de tasas impositivas mas altas. La condicionalidad de orden tributario(que afectaba a las politicas y la administraci6n) era imprecisa y no incor-poraba indicadores de seguimiento de los resultados. Ademas, las condicionesdel gasto se centraron en el desplazamiento de estos y no en los resultados.

El estudio contiene varias recomendaciones para el Banco y sus prestata-rios, a saber:

* Estimar el nivel de deficit sostenible y establecer directrices paraalcanzarlo en los estudios econ6micos y sectoriales del Banco y en elfinanciamiento para fines de ajuste.

* Mejorar la secuencia de la reforma tributaria, por ejemplo, asegurandoque esta se vea precedida por la reforma comercial no tributaria, y quela reforma de la administraci6n tributaria se introduzca antes que lareforma de la politica impositiva o en forma simultanea.

xiii

xiv

* Al recomendarse la reforma del gasto piublico, considerar expresamenteel papel que cabe al estado y la combinaci6n adecuada de prestaci6n deservicios por los sectores piiblico y privado.

* Incluir objetivos de equidad y reducci6n de la pobreza en la reforma delgasto publico.

* Formular indicadores adecuados de seguimiento y los resultados de lareforma impositiva y del gasto.

* Mejorar la coordinaci6n entre el Banco y el Fondo, respaldando lafunci6n rectora que cabe al Fondo en materia de asesoramiento fiscalmediante el fortalecimiento de la capacidad del Banco para el analisisde los impuestos y el gasto.

Robert PicciottoDirector GeneralEvaluaci6n de Operaciones

Avant-propos

L'equilibre budgetaire est a la base de la reussite de l'ajustement. La pre-sente etude, preparee par le Departement de l'evaluation des operationsde la Banque mondiale, analyse l'experience de la Banque en matiere degestion budgetaire dans le cadre de 250 operations d'ajustement meneesdans 86 pays. Elle examine les resultats budgetaires d'un echantillon de 26pays (134 operations) regroupes par region, caracteristiques du portefeuilleet particularites 6conomiques. L'etude confirme que la reduction du deficitbudgetaire est liMe a l'amelioration des comptes exterieurs et a la croissanceeconomique, et qu'il faut consentir un effort soutenu et de longue haleine etfaire preuve d'une vigilance de tous les instants si l'on veut eviter un retouren arriere. Contrairement aux theses qui avaient cours durant les premieresann6es des operations d'ajustement, l'etude laisse entendre que c'est lamauvaise gestion budgetaire, et non les chocs exogenes, qui sont la causeprincipale de d6ficits budgetaires persistants.

Les deficits budg6taires - qui vont de pair avec l'alourdissement de la detteext6rieure et l'augmentation du ratio d'endettement par rapport au PIB -restent eleves et l'on a assist6 a un certain nombre de revirements, en par-ticulier en Afrique et parmi les pays a faible revenu et lourdement endettes,engag6s dans la voie de l'ajustement et exportateurs de produits primaires.Le caractere limite de la r6ussite budgetaire tient en partie au fait que lesprogrammes de reforme: (1) n'ont pas su apprehender la question du r6lede l1'tat, determinant fondamental du niveau des finances publiques; (2) onttraite separement les problemes budgetaires d'une part et les autres reformesmacro6conomiques d'autre part, sans tenir compte des aspects de soutena-bilite ou de solvabilite budgetaires; (3) n'ont guere prete attention aux mo-yens a mettre en oeuvre pour prendre veritablement en compte le d6ficitbudgetaire, le mesurer et rassembler des donnees statistiques; et (4) etaientfondes sur des conditions trop laxistes, ambigues ou incoherentes.

Les pays ont reduit leur deficit en augmentant leurs recettes et, dans unemoindre mesure, en diminuant leurs depenses d'6quipement, mais les objec-tifs de compression des depenses courantes se sont r6veles plus difficiles aatteindre. Les recettes ont augmente non pas par suite d'un relevement destaux d'imposition, mais du fait de l'6largissement et de la simplification del'assiette fiscale. Les conditions d'ordre fiscal (influant sur les politiquesautres que commerciale ainsi que sur l'administration fiscale) etaient im-precises et n'incorporaient pas d'indicateurs de suivi des performances.De plus, les conditions relatives aux d6penses ne portaient plus sur lesresultats, mais sur les r6orientations des d6penses.

L'6tude offre un certain nombre de recommandations a la Banque et ases emprunteurs:

* Estimer le niveau de deficit soutenable et fournir, dans les etudes eco-nomiques et sectorielles et les prets d'ajustement de la Banque, deslignes directrices pour y parvenir.

xv

xvi

* Am6liorer 1'echelonnement des mesures de reforme fiscale, par exempleen veillant a ce que les mesures de reforme commerciale non fiscales pre-cedent les mesures fiscales et que la reforme de l'administration fiscaleprec&de ou accompagne la reforme de la politique fiscale.

* Examiner explicitement, lors -de la formulation de recommandationsconcernant la r6forme des depenses publiques, le role de l'etat et larepartition appropri&e des services a assurer respectivement par lessecteurs public et prive.

* Prendre en compte, dans la reforme des d6penses publiques, les objec-tifs de reduction de la pauvrete et d'equite.

* Ptablir des indicateurs adequats de suivi et de performance pour lareforme de la fiscalite comme pour celle des depenses.

* Renforcer la coordination entre la Banque et le Fonds pour aider le Fondsa jouer le r6le pilote qui est le sien en matiere de conseils fiscaux en ren-dant la Banque mieux a meme d'analyser les impots et les depenses.

Robert PicciottoDirecteur g6neralEvaluation des operations

Acknowledgments

The report was prepared by Jayati Datta-Mitra (Principal Evaluation Officer).Members of the team included Amaresh Bagchi ("Tax administration re-form"); Vandana Chandra and Salman Anees ("Fiscal management underSALs/SECALs: an aggregate view and conclusions"); Poonam Gupta ("Fis-cal management in SALs/SECALs: a close-up view"); Anwar Shah (PrincipalEvaluation Officer), Jeff Huther, Sandra Roberts, and Ylbin Xiang ("Public ex-penditure reform"); Wayne Thirsk and Harry Watson ("Tax reform"). JohnDiamond, Mohammad Emran, and Monica Rubio provided initial researchsupport. Meta de Coquereaumont, Barbara Kami, and Alison Strong editedthe grey cover version of this report. Angie Gentile-Blackwell copyeditedand produced the published version. Jasmine Mason-Anderson, NormaNamisato, and Geri Wise provided administrative assistance. The reportwas issued by the Country Policy, Industry, and Finance Division (ManuelPefialver, Division Chief) of the Operations Evaluation Department (Fran-cisco Aguirre-Sacasa, Director) under the Director-General, OperationsEvaluation, Robert Picciotto.

xvii

Abbreviations and acronyms

AFR Africa Regional OfficeALCID Adjustment Lending Conditionality and

Implementation DatabaseEAP East Asia and Pacific Regional OfficeECA Europe and Central Asia Regional OfficeESW Economic and sector workGDP Gross domestic productGNP Gross national productICR Implementation completion reportIBRD International Bank for Reconstruction and DevelopmentIDA International Development AssociationIMF International Monetary FundLAC Latin America and Caribbean Regional OfficeMNA Middle East and North Africa Regional OfficeOED Operations Evaluation DepartmentO&M Operations and maintenancePAR Performance audit reportPCR Project completion reportPR President's reportQR Quantitative restrictionRMSM Revised Minimum Standard ModelSAL Structural adjustment loanSAS South Asia Regional OfficeSECAL Sectoral adjustment loanTAR Tax administration reformTFSAL Trade and financial sector adjustment loanTIN Tax identification numberVAT Value added tax

xviii

FISCAL MANAGEMENT INADJUSTMENT LENDING

Summary

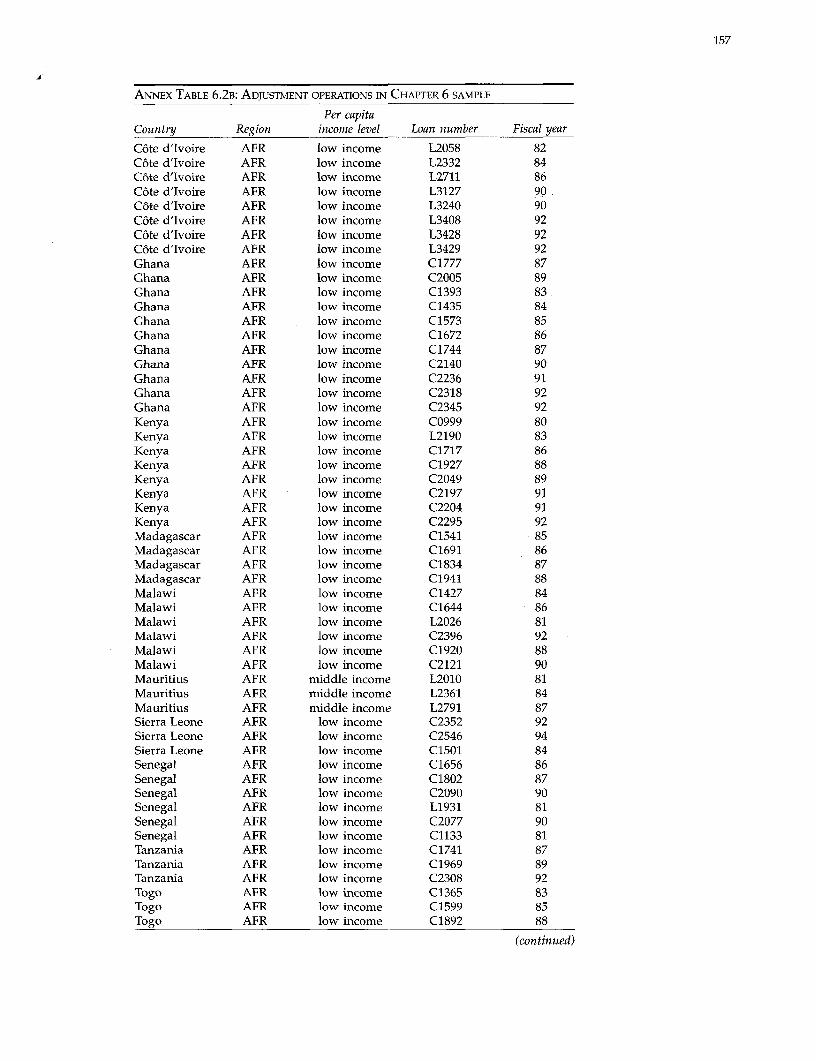

The World Bank initiated structural adjustment lending in the early 1980sto help developing countries out of the economic crises into which externalshocks and macroeconomic mismanagement had plunged them. By the early1990s about two-thirds of the Bank's clients had initiated policy reforms sup-ported by structural or sectoral adjustment loans (SALs/SECALs). A largenumber of these loans-about 250 SALs/SECALs to 86 countries between fis-cal years 1979 and 1994-had fiscal reform components. This study assesseshow well Bank-supported fiscal adjustment worked and reflects on how loanperformance can be improved in future operations.

What the study found

The principal findings of the study are that (a) successful fiscal management Fi scalrequires sustained, long-term effort, (b) lower fiscal deficits are associatedwith faster economic growth, (c) sustained deficit reductions were achieved adjustment isprimarily through revenue enhancement, while expenditure reduction tar- a long-termgets were more elusive, and (d) the fiscal reform component of Bank-sup-ported adjustment lending had only limited success because of the frag- processmented treatment of fiscal issues and the vague conditionality of loans.

General findings

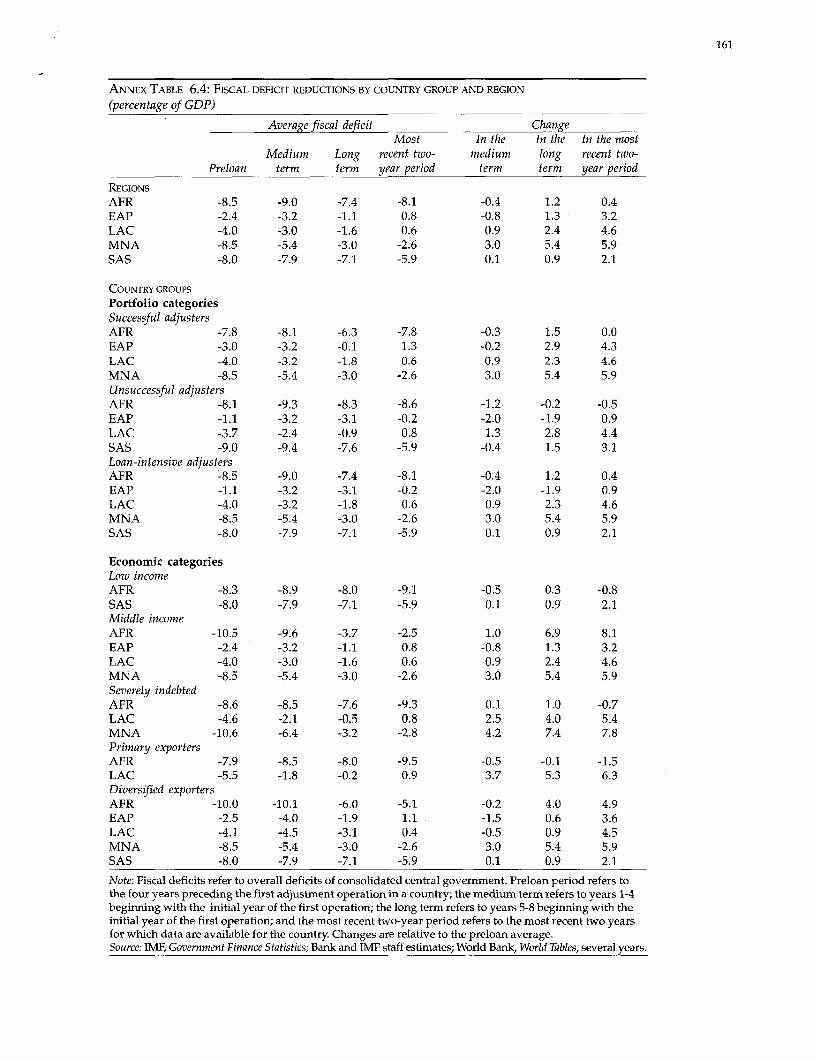

Management of fiscal deficits requires sustained, long-term adjustment effort. Defi-cits of SAL/SECAL countries rose in the medium term; only in the long term(five to eight years following the first loan) were there substantive signs ofbudgetary improvements. Though deficits were lower in the most recenttwo years (relative to the four-year preloan period) in SAL/SECAL coun-tries as a whole, deficits continued at well above 3 percent of GDP, and therewere significant reversals in deficit reduction in Africa among low-income andseverely indebted adjusters and primary exporters. The low-income and pri-mary exporter groups showed no improvement relative to the preloan period.

The principal source of large fiscal deficits was fiscal mismanagement, notexogenous shocks. Though the foreign interest burden did not constrain ad-justment in several SAL/SECAL countries, the growing ratio of external debtto gross domestic product (GDP) across most regions indicates that the im-provements in fiscal management were not strong enough to sustain sol-vency in many of the client countries.

Deficit reduction leads to improved external balances and stimulates growth. Be-cause fiscal deficits can contribute to many economic ills (inflation, creditshortages, distorted interest and exchange rates, current account imbalances),they can crowd out private investment and hurt economic growth. Although

1

2

growth performance was uneven across regions, the data confirm that whileother conditions are also necessary for growth, good fiscal managementhelps. The data also indicate a strong association between improvements infiscal deficits and in current account deficits.

Sustained deficit reductions were achieved primarily through revenue enhancementsand to a lesser extent through reductions in capital spending. Targeted reductions incurrent expenditures proved to be more elusive. Fiscal adjustments were not sus-

Sustained def cit tained in countries that reduced their deficits through short-term shifts in rev-enue or expenditure. Most countries that made fiscal improvements over the

reduction is longer term did so by increasing revenue (not by increasing tax rates but by

achieved broadening tax bases and simplifying tax systems). Countries with worseningfiscal deficits generally increased current expenditures without increasing

primarily revenues. Current and capital expenditure strategies were consistent acrossthrough revenue country groups and regions and over time: all regions and country groups

except the Middle East and North Africa (MNA) and the middle-income ad-enhancements justers increased current expenditures, and all groups except East Asia and

Pacific (EAP) pruned capital expenditures relative to the preloan period. Re-ductions in current expenditures, while considered necessary in many cases,were only achieved in a small number of countries.

The record of borrower compliance with Bank conditions was excellent, yetBank-supported adjustment lending had only limited fiscal success becausefiscal issues were treated in a fragmented manner and conditionality wasvague. The poor quality of fiscal data undoubtedly contributed to the diffi-culties of identifying the components of fiscal accounts and the budgetaryimplications of changes in fiscal and other macroeconomic policies. Mostoperations paid little attention to coverage, measurement, or sustainability ofthe deficit or to the role of the public sector (a critical factor determining thelevel of the public finances). Though fiscal policy is only one aspect of a largeradjustment program of interdependent policy reforms, few operations dis-cussed the relationship between fiscal deficits (and the instruments for reduc-ing them) and the other macroeconomic variables and structural reform mea-sures underway or planned. The complex issues connected with budgetaryreform (budgetary discipline, identification of strategic priorities, technicalefficacy, accountability, information systems). Conditionality on the budgetdeficit or public savings was too general, inconsistent between loans for thesame country, or subject to different interpretations. The vagueness of fiscalconditions made implementation and monitoring difficult or impossible (in68 percent of operations covered by project completion and performance au-dit reports-PCRs and PARs). Conditions were "soft," calling for legislationto be drafted rather than implemented (47 percent) and stressing studiesrather than implementation (16 percent). Conditionality was occasionallypoorly timed (32 percent).

Specific findings on aspects offiscal reform

Revenue reform. The Bank's advice on tax reform has generally been consistentwith best practice as set out in the Bank's Lessons of Tax Reform (1991). Taxadministration reforms have generally been consistent with state-of-the-artrecommendations for improving taxpayer compliance and operation of taxdepartments. But some problems remain. Revenues rose in only 17 of the 26countries where tax measures (base broadening, simplification, or rationaliza-tion) had been identified as necessary and as likely to boost revenue. Weak-nesses in tax administration appear to at least partly explain why revenue fellshort of expectations in several countries (Bulgaria, C6te d'Lvoire, Hungary,Senegal, Venezuela) and why revenue increases, where they occurred, failed

3

to have the desired fiscal impact (Bangladesh, Pakistan, Uganda). Tax admin-istration was also neglected in some early SALs (Bangladesh, C6te d'Ivoire,Hungary, Pakistan, Uganda).

In general, conditions on nontrade tax reforms have constituted only a smallcomponent of SALs/SECALs and have been selective rather than comprehen-sive. In 92 SALs/SECALs covering 53 countries with nontrade tax conditions,conditionality sought largely to broaden direct and indirect tax bases and tolower marginal income tax rates in order to make tax systems simpler, moreefficient, and easier to administer. Typically, conditionality supported govern-ment reform initiatives or piggybacked on other institutional initiatives. TheBank generally deferred to the International Monetary Fund's (IMF or Fund)lead in nontrade tax reform in countries where the Fund was involved in thetax area.

About 40 percent of conditionality was quantitative and easily monitorable:meeting certain quantitative criteria or making specific changes in tax basesor rate structures. However, about 48 percent of conditions stipulated specificstatutory changes but did not provide quantitative measures of performance;these conditions generally specified the direction of change in the tax codewithout mentioning the magnitude of change expected. About 12 percent of Nontrade taxconditions lacked both quantitative and qualitative criteria. Thus about 60 riform supportedpercent of conditions left open the possibility of poor outcomes: some could ' t Bbe satisfied de jure by minor alterations in the tax code; others simply could by the Banknot be adequately monitored or evaluated. was generally

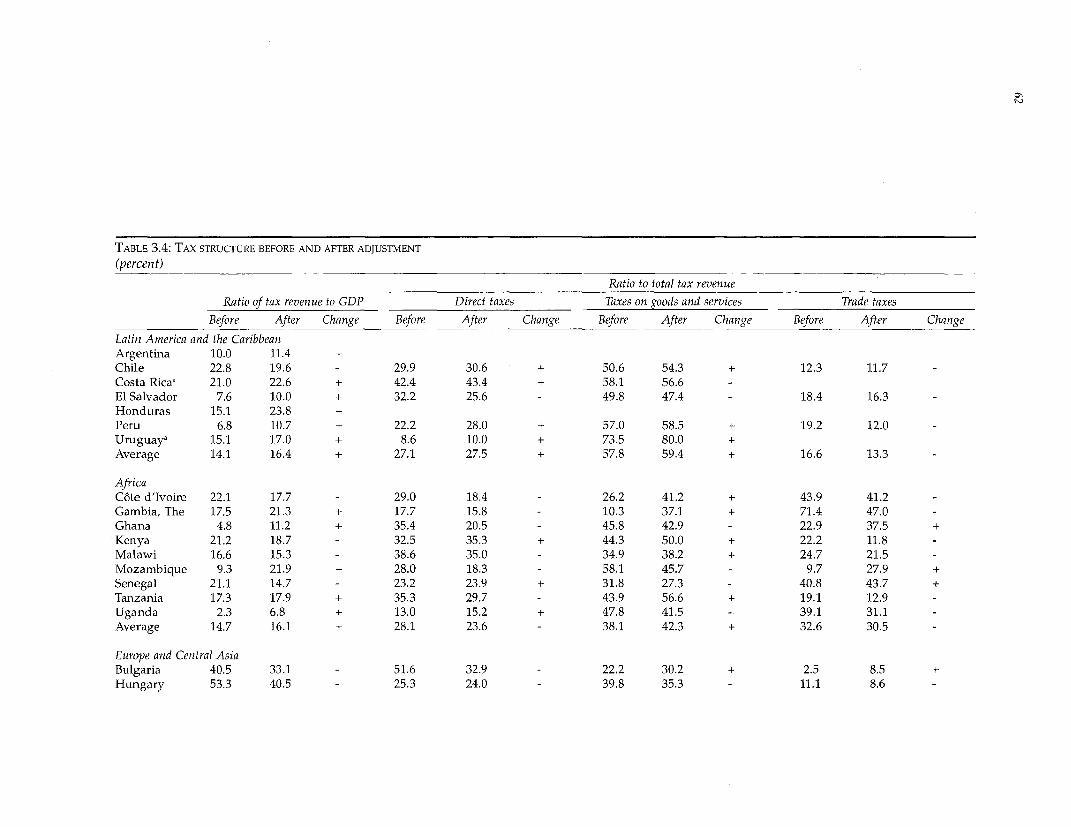

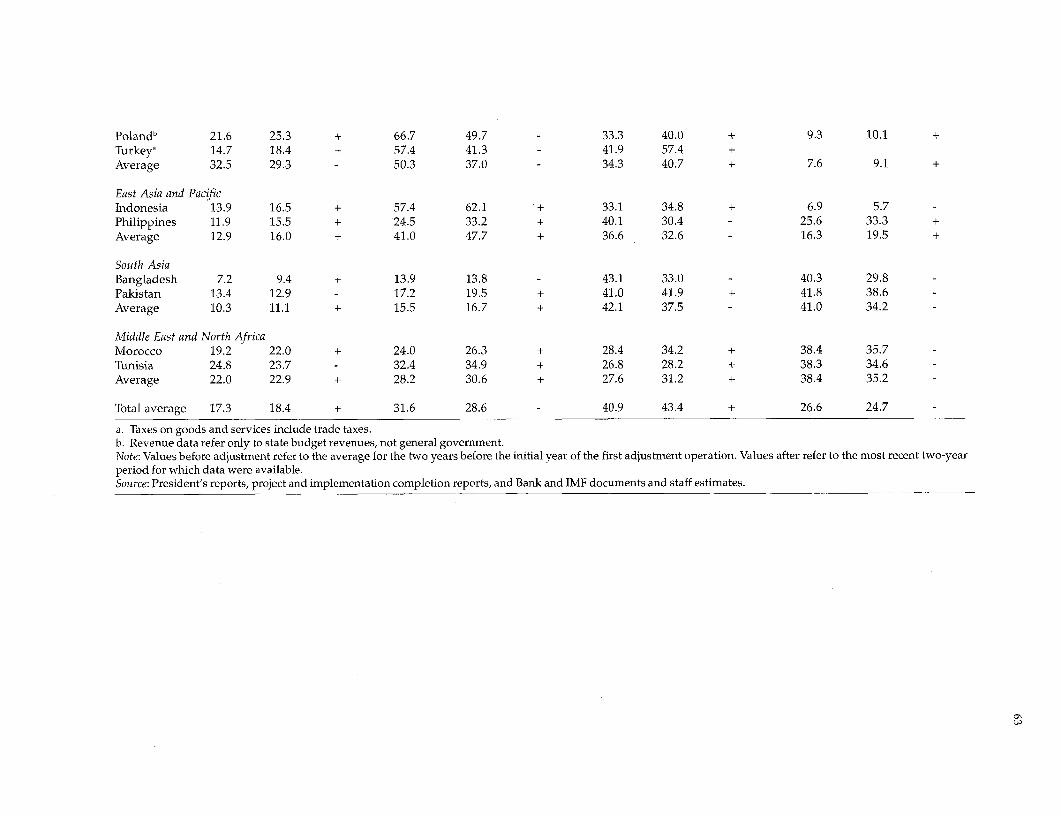

None of the SALs/SECALs specified pre-reform benchmarks such as mar- selective andginal effective tax rates. Partly as a result, none of the PCRs/PARs could difficult toevaluate implementation and outcomes in terms of changes in these rates,and very few verified compliance by comparing the record before and after monitor andreform. Thus the effectiveness of tax conditionality was generally evaluated evaluate; thein terms of statutory compliance (fulfillment of conditions stipulating chan-ges in tax statutes) or increases in tax ratios even though such ratios are af- record on tradefected by many other factors. Although few conditions called specifically for tax reforms wasincreases in tax rates, tax ratios did increase (through increases in tax bases)in a large number of countries. The shifts in tax structure that followed tax betterreform were generally consistent with Lessons of Tax Reform (World Bank1991a)-in the direction of less reliance on trade taxes and greater relianceon domestic indirect taxes.

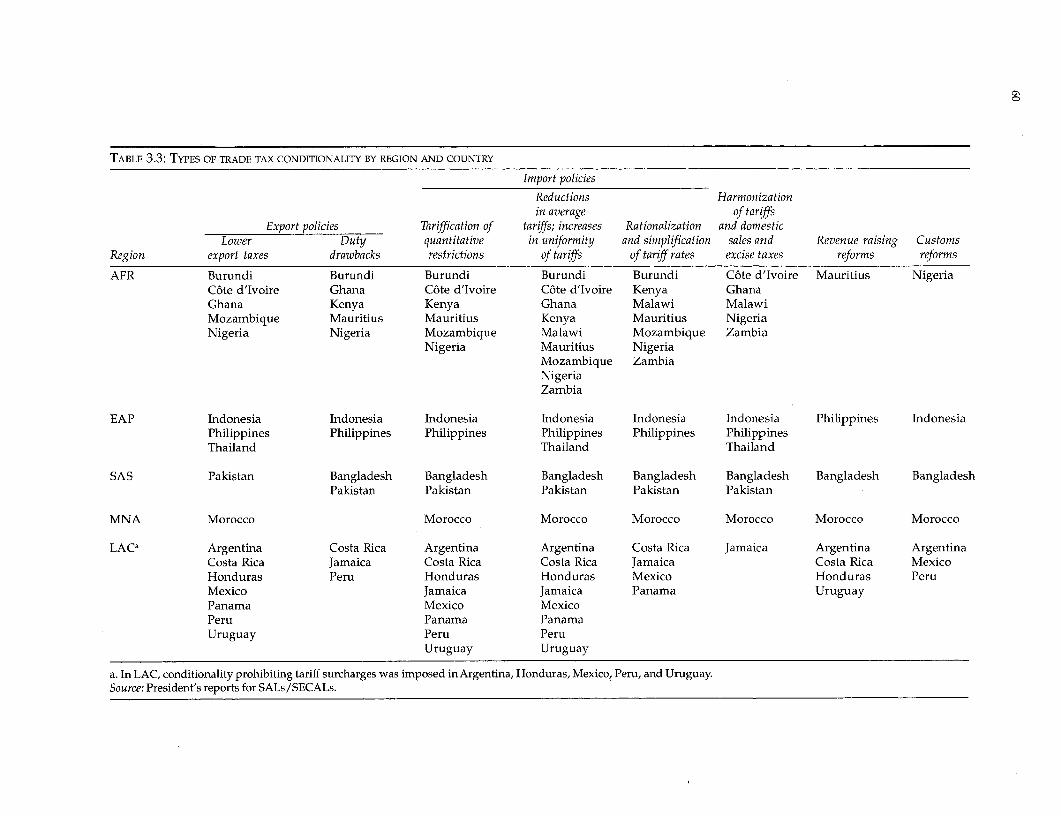

The record for trade taxes was much better. In a sample of 83 operationscovering 23 countries with trade tax conditions (out of a total of 171 opera-tions in 75 countries), conditionality was specific, and reform objectives werespelled out as clear-cut, quantified policy targets to be reached before a speci-fied deadline. Such precision makes compliance relatively easy to monitor.Though compliance was good, the pace of reform varied, often depending onhow well trade reform was synchronized with other reforms. Revenue pres-sures often held up trade reform. So did insufficient progress on stabilization.Little effort was made to quantify the revenue effects of trade reforms; inad-equate attention went to harmonizing sales and excise taxes for imports anddomestic goods.

Though the Bank's involvement in tax administration reform has increasedsignificantly since 1987, the record suggests piecemeal reform rather thana comprehensive reform strategy. Only 40 percent of conditionality wascouched in precise terms. PCRs/PARs that tracked implementation of con-ditionality pronounced compliance to be high, but without monitorable per-

4

formance indicators such findings are not very persuasive. The most com-mon yardstick was the ratio of taxes to GDP, even though tax collections areaffected by many factors other than administration. As with nontrade tax re-form, imprecision and a paucity of monitorable indicators impaired the qual-ity of tax administration conditionality.

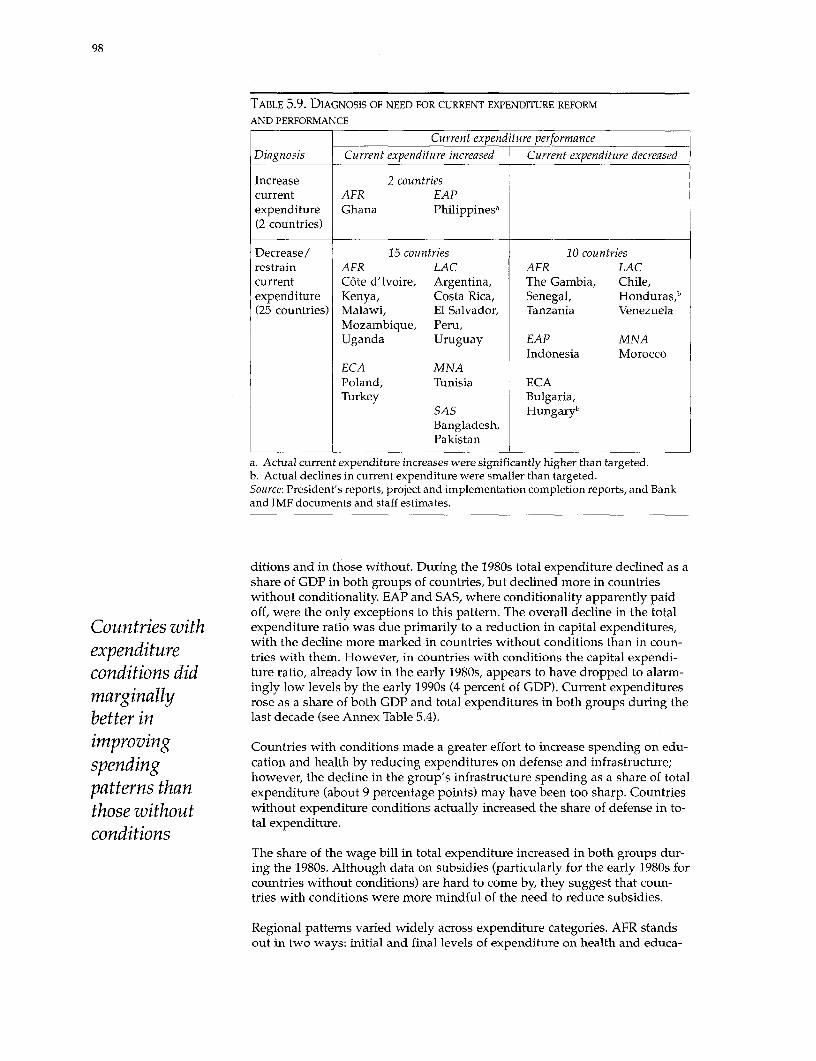

Expenditure reform. The Bank has frequently helped countries define expendi-ture reform; expenditure conditions were incorporated in 219 operations in83 countries during FY79-94. In general, expenditure reform efforts havebeen broadly consistent with the directions discussed in Bank reports on ad-justment lending (World Bank 1988a, 1990a, 1992a, b; Jayarajah and Branson1995). Conditions have focused on reducing and restructuring capital expen-ditures, reducing subsidies, reforming public employment and cutting thepublic wage bill, emphasizing operations and maintenance (O&M) of exist-ing facilities, and increasing social sector spending (though attention to pov-erty reduction has been weak).

Countries with Countries with expenditure conditions did only marginally better than coun-tries without them in improving expenditure patterns. Countries with condi-

expenditure tions had greater success in increasing social spending and cutting subsidies

conditions did and defense spending, and they ended the period with lower wage expendi-tures than countries without conditions. Although both groups started out

only marginally with roughly equal ratios of total expenditure to GDP, countries with condi-

better than tions had less success in cutting total expenditure. Success has been limitedin restructuring current expenditures away from wages and subsidies and to-

countries without ward nonwage O&M, and attempts to cut public employment have generally

in improving been short-lived or modest. Countries with capital expenditure conditionsended the period with very low levels of capital expenditures, reflecting re-

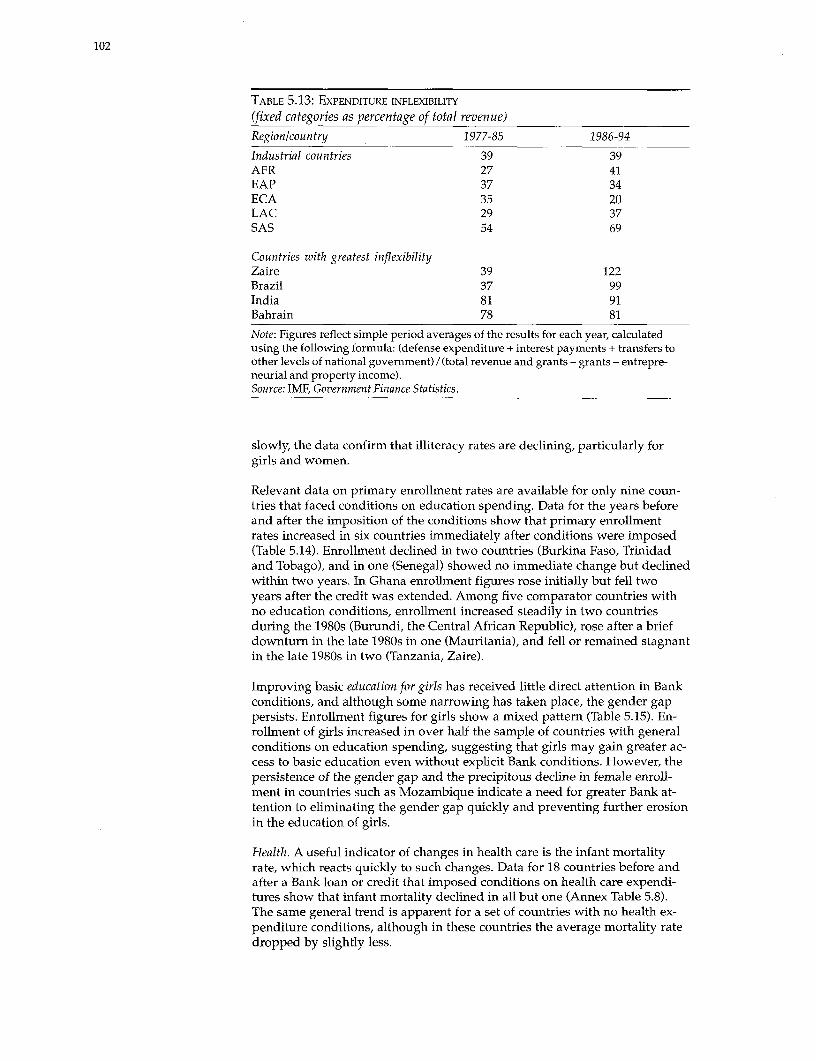

expenditure latively large cuts in infrastructure spending. One reason for the relativelypnatterns modest performance on the expenditure front may be the inflexibility that af-

flicts budgets in many countries; Bank adjustment lending made little head-way in this area.

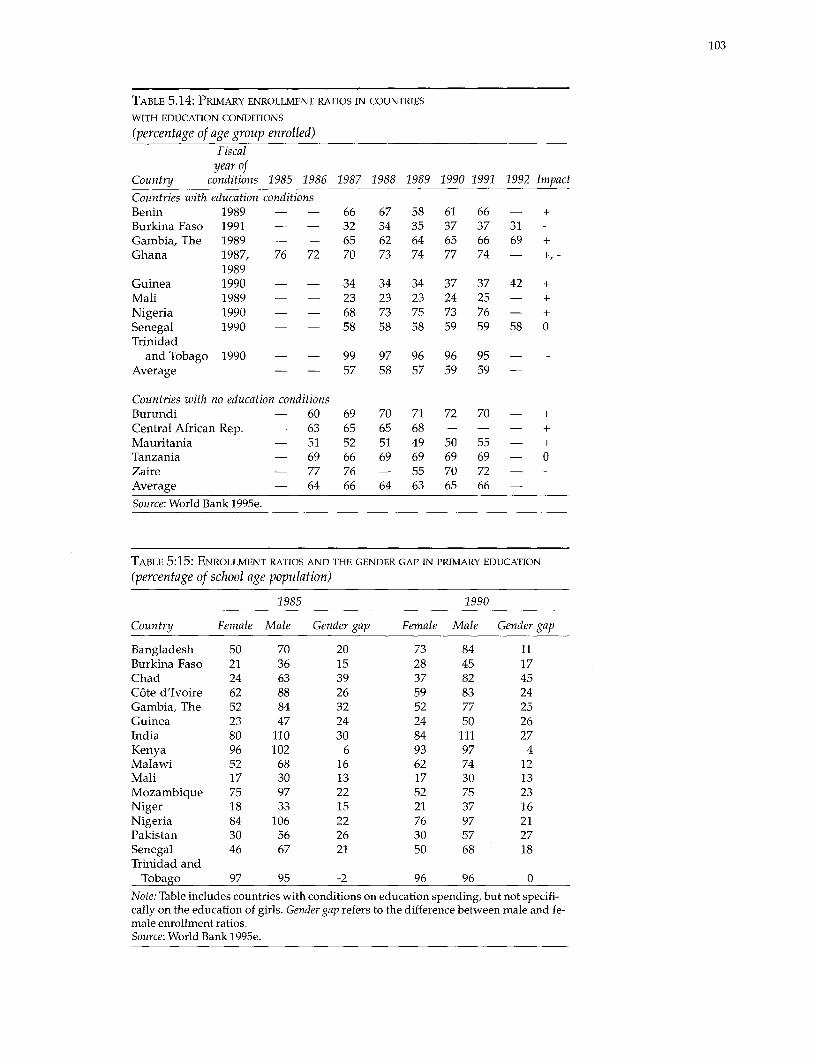

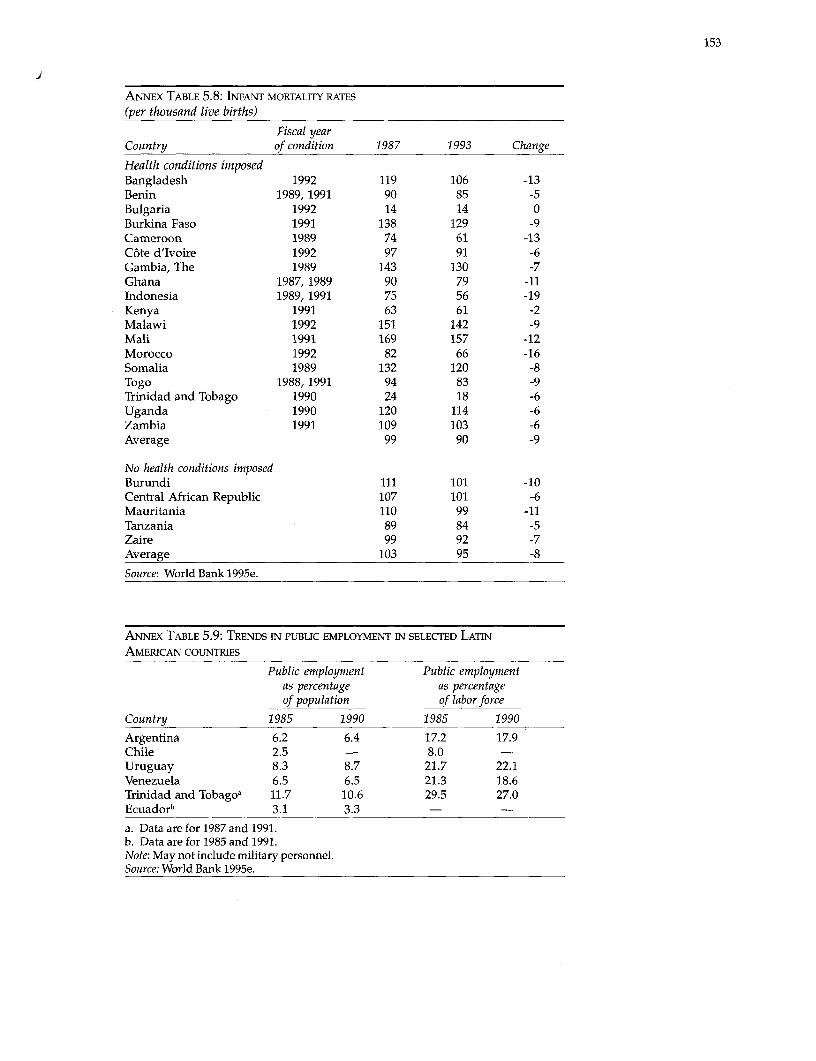

In countries with education and health conditions, both sectors increasedtheir shares in total spending. Yet education and health expenditure ratioswere only marginally better in countries with such conditions than in coun-tries without. For both groups of countries illiteracy rates declined, particu-larly for girls and women, as did infant mortality rates. Cost-recovery effortsin the social sectors were limited. One reason that Bank conditions may havehad little additional impact on social sectors is that the Bank emphasized themeans rather than the ends of expenditure reform. Conditions focused onchanging expenditures in specific functional categories or sectors rather thanon the relation between inputs (such as level of expenditures), outputs (en-rollment rates, graduation rates), and final outcomes (rates of literacy; mor-tality; access to basic services, particularly by the poor and needy).

What can be done?

Suggested priorities for Bank work

On Bank-Fund coordination. The centrality of fiscal reform to macroeconomicstability and growth has been well recognized by the Bank and the Fund, andthe two institutions have worked out a division of labor in recent years. TheFund takes a lead in issues relating to taxes and the aggregate level of spend-ing, whereas the Bank leads on sectoral spending issues. Although this divi-sion of labor works well for the most part, it cannot be viewed inflexibly.

5

Thus while respecting the Fund's lead role in giving fiscal advice, the Bankneeds to take a more hands-on approach to the design of fiscal reforms inadjustment lending, particularly where the Fund may not be directly in-volved. For example, the Bank needs to consider the relationships betweentax policy reforms undertaken in adjustment programs and other structuralreforms (as in private sector development, financial and capital market re-forms); between the size and role of the government and the level of thepublic finances; between the financing of the budget and the level and com-position of public expenditures; and between tax and expenditure decisionsand poverty programs. The Bank needs to build up analytical capacity toadvise staff on fiscal and adjustment issues, to identify best practice, and toanalyze new fiscal policy issues that are likely to assume importance in thefuture (financial sector taxation, environmental taxes). In this respect, theBank's Policy Research Department, which withdrew from tax analysis in Oc-tober 1994 to concentrate on expenditure issues, needs to correct the balance.Such a capability will enhance Bank-Fund coordination and strengthen dia-logue on fiscal issues. The Bank and Fund are exploring new and existing chan-nels for improving coordination in the preparation of country macroeconomicframeworks (policy framework papers, public expenditure reviews, Bank coun-try assistance strategy papers, Fund country assistance briefs). The Bank andFund also need to collaborate in improving their own fiscal databases and clientfiscal data systems. A lot can be

On loan conditions. Fiscal conditionality in adjustment operations needs to done to improvebe more specific and precise, supported by specific and monitorable per- the qualityformance indicators, and focused on fiscal (and related macroeconomic)outcomes in addition to the means of reform. Conditionality should stress of fiscalimplementation of new laws as much as enactment and implementation of di Istudy recommendations more than the preparation of studies. condionalty

Onfiscal deficits. The Bank needs to ensure greater precision on several fronts:

* The coverage of fiscal accounts needs to be expanded and the transpar-ency of accounts improved. This implies a need to incorporate state, lo-cal, and municipal accounts into the fiscal accounts, track quasi-fiscaldeficits, and work out the implications of implicit taxes, subsidies, andgovernment guarantees.

* The appropriate measure of the deficit for tackling the problem at handneeds to be identified. In most countries, the overall deficit may be ap-propriate; in some, it may be the operational or the structural deficit; inothers, public savings may need to be the focus; in yet others, primarydeficits may need monitoring.

* Fiscal accounts must be better integrated into the macroeconomicframework of analysis to enable more dynamic analysis of fiscal andother macroeconomic adjustments. This is essential for estimating thesustainable deficit; identifying tradeoffs among acceptable levels of bor-rowing, inflation, interest rates, and other macroeconomic variables;and setting quantitative targets for achieving a sustainable deficit andmonitoring macroeconomic outcomes.

On tax reform. The main areas of Bank attention should be:

* Simplification and base broadening. Bank work in tax reform should con-tinue to stress broadening and simplifying tax bases for easier adminis-tration and better compliance.

6

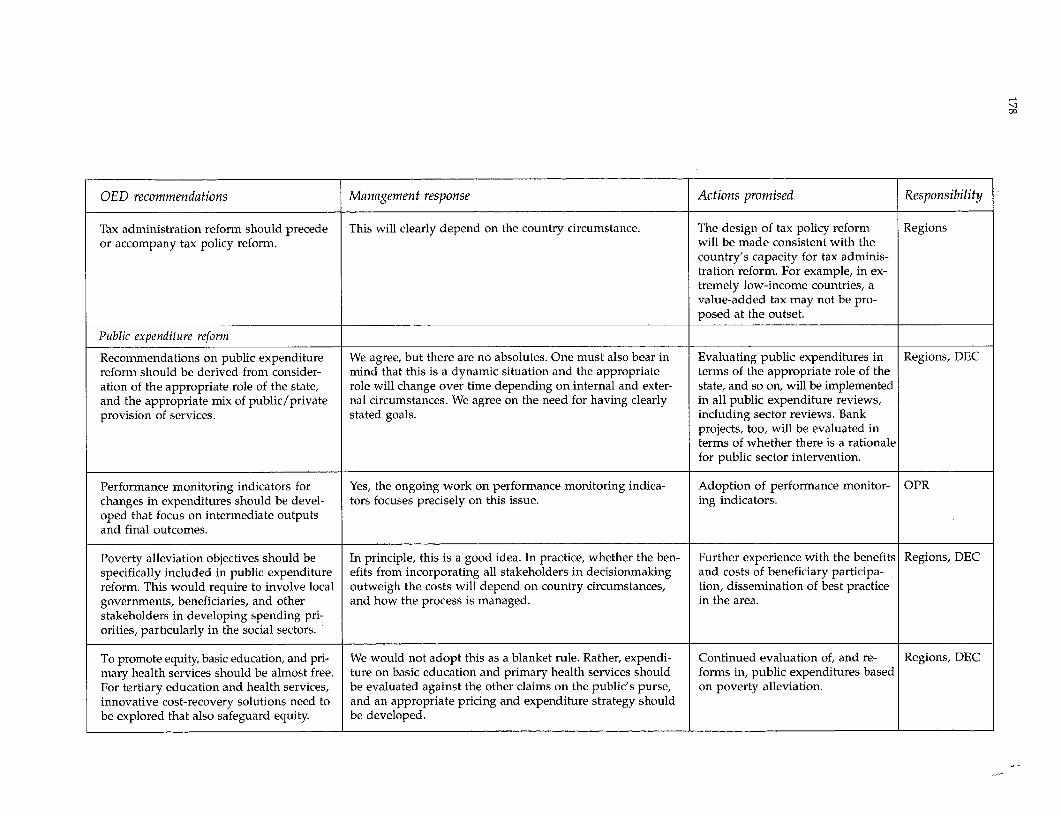

* Sequencing of tax reform. The Bank needs to emphasize the proper se-quencing of tax reform. If trade taxes contribute significantly to revenue,nontrade tax reforms to enhance revenue may need to precede trade taxreform. Reforms in tax administration should precede or accompany taxstructure reform.

* Environment, equity, and private sector development concerns. Bank work ontax reform should involve considerations of environmental concerns; thetax system should also not adversely affect equity/poverty reduction orthe intemational competitiveness of the economy

* Tax administration. Tax administration reform should focus on a condu-cive legal environment, taxpayer education, information systems (usedby tax departments), audits, withholding and presumptive taxation, andimprovements in value-added tax (VAT) administration.

* Monitoring progress. Building better performance indicators into tax andtax administration reform programs would benefit design, implementa-tion, and evaluation and focus attention on the goals of reform. Perfor-mance indicators should cover effective tax rates and, for tax administra-tion, cost and output measures.

On public expenditure reform. The Bank should focus on:

* Establishing the basisfor the recommendations. Recommendations on publicexpenditure reform should be derived from considerations of the appro-priate role of government. Govemments need to be persuaded to moveaway from a command and control culture toward a service deliveryoutlook. They also need to be encouraged to invite local governments,potential beneficiaries, and other stakeholders to participate in discus-sions on development and spending priorities, particularly in social sec-tors. This would entail reform of budgetary processes and institutions.

* Clarifying the goals of reform. Focusing on the ultimate goals of expendi-ture reform right from the start is important both for the proper selectionof expenditure (or other) instruments and for better implementation. TheBank needs to promote the development of appropriate performancemonitoring indicators that include intermediate (short-run) outputs andfinal (long-run) outcomes as well as measures of the level and composi-tion of expenditure.

* Increasing attention to expenditure composition. When deficit reduction is amajor objective, both current and capital expenditures need to be exam-ined, with special attention to inflexible and unproductive expenditures(such as defense and subsidies not oriented to the poor). Although theBank's emphasis on capital spending cuts was warranted in countrieswhere large capital projects did not meet the basic needs of the popula-tion, in some countries capital spending shares (of total spending orGDP) have fallen to levels that may be retarding growth. In these coun-tries and in others where much of the population lacks access to basicservices, basic investments may need a boost.

* Emphasizing poverty alleviation. Expenditure programs have greater po-tential than revenue reforms as instruments for reducing poverty. Thusthe Bank needs to pursue expenditure solutions for better targeting ofsubsidy programs and better access by the poor to basic services. TheBank might also seek innovative solutions to the problems of poverty,

7

such as using education programs to teach poor households about safewater and sanitation practices. The Bank also needs to encourage clientsto direct resources to rural areas, where most of the poor live.

* Promoting equity. Basic education and health services should be almostfree to ensure universal coverage, while innovative cost-recovery solu-tions that also promote equity are needed for tertiary education andhealth services.

FISCAL MANAGEMENT INADJUSTMENT LENDING

Resumen

El Banco Mundial comenz6 a efectuar prestamos para fines de ajuste estruc-tural a principios de los afios ochenta con objeto de ayudar a los paises endesarrollo a superar la crisis econ6mica que sufrian como consecuencia delas conmociones externas y la mala gesti6n macroecon6mica. Al inicio deldecenio de 1990 unos dos tercios de los clientes del Banco habian empren-dido el proceso de reforma de sus politicas con el apoyo de prestamos paraajuste estructural o para ajuste sectorial. Muchos de estos pr6stamos -

alrededor de 250 otorgados a 86 paises entre los ejercicios de 1979 y 1994-tenian componentes de reforma fiscal. En este estudio se analiza la eficaciadel apoyo brindado por el Banco para el ajuste fiscal y se consideran mediosde mejorar el desempefno de los prestamos futuros para ese fin.

Resultados del estudio

Las principales conclusiones del estudio son las siguientes: (a) una gesti6nfiscal eficaz requiere esfuerzos sostenidos a largo plazo; (b) un nivel mas ba-jo de d6ficit fiscales esta relacionado con un crecimiento econ6mico mas ra-pido; (c) las reducciones sostenidas de los deficit se lograron principalmentea traves del incremento de los ingresos, pero los resultados fueron menossatisfactorios en lo que respecta a la rebaja de los gastos, y (d) el exito delcomponente de reforma fiscal de los prestamos para fines de ajuste del Bancos6lo ha sido limitado debido al enfoque fragmentario de las cuestiones fis-cales y a la imprecisi6n de la condicionalidad de esas operaciones.

Conclusiones generales

La gesti6n de los deficitfiscales exige esfuerzos sostenidos de ajuste a largo plazo.Los deficit de los paises receptores de prestamos para ajuste estructural ypara ajuste sectorial aumentaron a plazo mediano; s6lo a largo plazo (entrecinco y ocho afios despues del primer prestamo) hubo indicios importantesde mejoras presupuestarias. Si bien en los dos afios mas recientes los deficithan sido menores en el conjunto de paises receptores de esos prestamos (enrelaci6n con el cuatrienio anterior a su aprobaci6n), en Africa y en los paisesde ingreso bajo y gravemente endeudados en proceso de ajuste y en los ex-portadores de productos primarios se registraron fuertes reveses. En estosdos ultimos grupos no hubo mejoras en relaci6n con el periodo anterior alos prestamos.

La causa principal de los cuantiosos deficit fiscales fue la mala administra-ci6n fiscal, y no las conmociones ex6genas. Si bien la carga de los interesesexternos no limit6 el ajuste en varios de los paises receptores de prestamospara ajuste estructural y para ajuste sectorial, la creciente relaci6n deudaexterna-producto intemo bruto (PIB) en la mayoria de las regiones indica

8

9

que las mejoras en la gesti6n fiscal no fueron suficientemente profundas paramantener la solvencia en muchos de los paises clientes.

La rebaja de los deficit resulta en saldos externos mas satisfactorios y estimula elcrecimiento. Puesto que los d6ficit fiscales pueden contribuir a muchos malesecon6micos (inflaci6n, escasez de credito, distorsi6n de las tasas de interesy los tipos de cambio, desequilibrios en la cuenta corriente), es posible quedesplacen a la inversi6n privada y perjudiquen el proceso de crecimientoecon6mico. El desempeno en materia de crecimiento vari6 de una regi6n aotra, pero los datos confirman que, a pesar de que otras condiciones tambienson necesarias en ese sentido, una buena gesti6n fiscal contribuye al creci-miento. Los datos apuntan tambi6n a la existencia de un s6lido nexo entrelas mejoras de los deficit fiscales y de los deficit en cuenta corriente.

Las reducciones sostenidas de los deficit fiscales se alcanzaron principalmentegracias a incrementos de los ingresos y, en menor medida, a la disminuci6n de losgastos de capital. Los resultadosfueron menos satisfactorios en lo referente a lasmetas relacionadas con el recorte de los gastos corrientes. La mayoria de los pai-ses que mejoraron su situaci6n fiscal lograron ese objetivo mediante incre-mentos de los ingresos. Los pafses cuyos deficit fiscales se agravaron en gen-eral incrementaron sus gastos corrientes sin al mismo tiempo elevar sus in-gresos. Las estrategias en materia de gastos corrientes y de capital fueronsemejantes en los diversos grupos de paises y regiones y a traves del tiem-po: todas las regiones y grupos de paises, con excepci6n de Oriente Medioy Norte de Africa y los paises de ingreso mediano abocados al proceso deajuste, elevaron sus gastos corrientes, y todos los grupos, salvo Asia orientaly el Pacifico, recortaron sus gastos de capital en comparaci6n con el periodoanterior a los prestamos. La reducci6n de los gastos corrientes, aunque enmuchos casos se consideraba necesaria, iinicamente se alcanz6 en un peque-iio numero de paises.

El historial de cumplimiento por los prestatarios de las condiciones esta-blecidas por el Banco fue excelente, pero en el plano fiscal el exito de losprestamos para fines de ajuste respaldados por la instituci6n s6lo fue limi-tado debido al enfoque fragmentario de las cuestiones fiscales y a la impre-cisi6n de la condicionalidad. La calidad deficiente de los datos fiscales indu-dablemente increment6 la dificultad de identificar los componentes de lascuentas fiscales y las repercusiones presupuestarias de los cambios en lapolitica fiscal y otras politicas macroecon6micas. En la mayor parte de lasoperaciones se prest6 poca atenci6n a la cobertura, medici6n o sostenibilidadde los deficit y a la funci6n del sector publico (factor de importancia criticapara determinar el nivel de las finanzas piiblicas). Aunque la politica fiscal ess6lo uno de los aspectos de un programa mas amplio de ajuste que involucrela reforma de politicas relacionadas entre si, en pocas operaciones se abord6la relaci6n entre los d6ficit fiscales y los instrumentos para reducirlos y otrasvariables macroecon6micas y medidas de reforma estructural. Tampoco seadopt6 un enfoque integral de las complejas cuestiones que entrafia la refor-ma presupuestaria (disciplina presupuestaria, participaci6n de los beneficia-rios locales en las decisiones en materia de gastos, eficacia tecnica, responsa-bilidad, sistemas de informaci6n). En lo que respecta al deficit presupues-tario o al ahorro piublico, la condicionalidad fue demasiado general, no fuecoherente en los diversos prestamos a un mismo pais o estuvo abierta ainterpretaciones diferentes. La imprecisi6n de las condiciones fiscales hizoque su aplicaci6n y seguimiento resultaran dificiles o imposibles (el 68 porciento de las operaciones sobre las que se han preparado informes de termi-naci6n y de evaluaci6n ex post). Las condiciones fueron "blandas", puesrequerian la formulaci6n de legislaci6n mas bien que su aplicaci6n (47 por

10

ciento), y hacian hincapie en la elaboraci6n de estudios y no en la ejecuci6n(16 por ciento). La condicionalidad en ocasiones tambi6n adoleci6 de defi-ciencias en lo que respecta a su oportunidad (32 por ciento).

Resultados especfficos en determinados aspectos de la reforma fiscal

Reforma en el drea de los ingresos. La asesoria brindada por el Banco acerca dela reforma tributaria en general se ha ajustado a las practicas 6ptimas deli-neadas en su publicaci6n Lessons of Tax Reform (Lecciones de la reforma tri-butaria) (1991a). En la esfera de la administraci6n tributaria, las reformas engeneral han estado en consonancia con las recomendaciones mas avanzadaspara mejorar el cumplimiento por los contribuyentes y el funcionamientode los departamentos de impuestos. Pero persisten algunos problemas. Losingresos s6lo se elevaron en 17 de los 26 paises en los que se habia deter-minado que era necesario adoptar medidas impositivas (ampliaci6n de labase, simplificaci6n o racionalizaci6n) y que estas medidas probablementeincrementarian los ingresos. Las deficiencias de la administraci6n tributariaparecen explicar, por lo menos parcialnente, por qu6 en varios paises (Bul-garia, C6te d'Ivoire, Hungria, Senegal, Venezuela) los ingresos no estuvierona la altura de las expectativas y por qu6 en los casos en que si se registraronaumentos estos no tuvieron el efecto fiscal deseado (Bangladesh, PakistAn,Uganda). En algunos de los primeros prestamos para ajuste estructural(Bangladesh, C6te d'Ivoire, Hungria, Pakistan, Uganda), tampoco se prest6la atenci6n debida a la administraci6n tributaria.

En general, las condiciones vinculadas con las reformas tributarias no rela-cionadas con el comercio s6lo han constituido un pequeino componente delos prestamos para ajuste estructural y para ajuste sectorial, y han sido decaracter selectivo mas bien que integral. En 92 de estos prestamos que in-cluian condiciones tributarias no relacionadas con el comercio, correspon-dientes a 53 paises, en gran medida la condicionalidad se orientaba a am-pliar las bases de los impuestos directos e indirectos y rebajar las tasasmarginales del impuesto sobre la renta con objeto de lograr que el sistemaimpositivo fuera mas sencillo, mas eficiente y mas facil de administrar.Tipicamente, la condicionalidad respaldaba iniciativas de reforma guber-namentales o acompafiaba a otras iniciativas institucionales. En generalel Banco sigui6 la orientaci6n del Fondo Monetario Internacional (FMI oFondo) en lo relativo a las reformas tributarias no relacionadas con el co-mercio en los paises en que el Fondo actuaba en la esfera de los impuestos.

Alrededor del 40 por ciento de la condicionalidad era de indole cuantitativay susceptible de facil seguimiento: consistia en el cumplimiento de deter-minados criterios cuantitativos o la implantaci6n de cambios especificos enla base tributaria o en la estructura de las tasas. Sin embargo, alrededor del48 por ciento de las condiciones requerian la introducci6n de cambios legis-lativos especificos, pero no comprendian indices cuantitativos del desem-pefno; estas condiciones en general especificaban la orientaci6n de la modi-ficaci6n del c6digo tributario sin mencionar la magnitud prevista de esamodificaci6n. Aproximadamente el 12 por ciento de las condiciones careciande criterios tanto cuantitativos como cualitativos. De modo que alrededordel 60 por ciento de las condiciones dejaban abierta la posibilidad de que losresultados fueran deficientes: algunas podian cumplirse de jure implantandopequefios cambios en el c6digo tributario; en el caso de otras sencillamenteno era posible un seguimiento o evaluaci6n retrospectiva adecuados.

En ninguno de los prestamos para ajuste estructural o para ajuste sectorial sesefnalaban puntos de referencia especificos anteriores a la reforma, como las

11

tasas impositivas marginales efectivas. En parte como consecuencia de ello,ninguno de los informes de terminaci6n y evaluaci6n ex post pudo analizarla ejecuci6n y los resultados desde la perspectiva de los cambios en esastasas, y muy pocos verificaron el cumplimiento comparando la situaci6n an-tes y despues de la reforma. En consecuencia, la efectividad de la condicio-nalidad en el plano tributario en general se evalu6 en funci6n del cumpli-miento en el terreno legislativo (cumplimiento de las condiciones que reque-rian la implantaci6n de cambios en las leyes tributarias) o de aumentos delos coeficientes tributarios, a pesar de que estos ultimos se ven afectados pormuchos otros factores. Si bien pocas condiciones exigian especificamente elincremento de las tasas impositivas, los coeficientes tributarios si se elevaronen un gran numero de paises (como resultado de aumentos de la base tribu-taria). Los cambios en la estructura impositiva a raiz de la reforma tributariaen general estaban en consonancia con lo establecido en la publicaci6n Les-sons of Tax Reform (Banco Mundial 1991a), o sea, menor dependencia de losimpuestos al comercio y mayor apoyo en los impuestos internos indirectos.

El historial es mucho mas satisfactorio en lo que respecta a los impuestos alcomercio. En una muestra de 83 operaciones correspondientes a 23 paises enlas que habia condiciones relativas a los impuestos al comercio (de un totalde 171 operaciones en 75 paises), la condicionalidad era especifica, y losobjetivos de la reforma estaban formulados en forma de metas de politicacuantitativas concretas que debian alcanzarse dentro del plazo especificadoa ese efecto. Con ese grado de precisi6n el seguimiento del cumplimientoresulta relativamente facil. Aunque el historial de cumplimiento fue bueno,el ritmo de la reforma vari6 de un caso a otro, y en muchas ocasiones depen-di6 del grado de sincronizaci6n de la reforma comercial con la reforma enotras areas. En muchos casos las presiones en materia de ingresos retrasaronla reforma comercial. Lo mismo puede decirse del progreso insuficiente enlo que respecta a la estabilizaci6n. Se hicieron pocos esfuerzos por cuanti-ficar los efectos de la reforma comercial en los ingresos, y no se prest6 ladebida atenci6n a la armonizaci6n de los impuestos a las ventas y los im-puestos al consumo en lo que atafie a las importaciones y a los bienes deproducci6n nacional.

La reforma de la administraci6n tributaria en general ha adolecido de impre-cisi6n y no ha sido susceptible de seguimiento. A pesar de que la participa-ci6n del Banco en la reforma de la administraci6n tributaria se ha intensifi-cado considerablemente desde 1987, todo sugiere que el proceso de reformaha sido fragmentario y que no se ha seguido una estrategia integral. S61o enun 40 por ciento de los casos la condicionalidad estaba formulada en termi-nos concretos. Los informes de terminaci6n y de evaluaci6n ex post que anali-zaron esa cuesti6n encontraron que el cumplimiento de la condicionalidadfue alto, pero dada la inexistencia de indicadores del desempenlo suscepti-bles de seguimiento esa conclusi6n no es muy significativa. El indice usadomas frecuentemente fue la relaci6n impuestos-producto interno bruto, apesar de que la recaudaci6n de impuestos se ve afectada por muchos otrosfactores ademas de la administraci6n. Al igual que en el caso de la reformatributaria no relacionada con el comercio, la imprecisi6n y la escasez de indi-cadores susceptibles de seguimiento repercutieron negativamente en la cali-dad de la condicionalidad en el area de la administraci6n tributaria.

Reforma en el drea de los gastos. Con frecuencia el Banco ha ayudado a lospaises a definir los parametros de la reforma en esta esfera: en los ejerciciosde 1979-94 se incluyeron condiciones relativas a los gastos en 219 operacio-nes correspondientes a 83 paises. En general, los esfuerzos de reforma de losgastos han estado en consonancia con los lineamientos formulados en los

12

informes del Banco sobre los prestamos para fines de ajuste (Banco Mundial1988a, 1990a, 1992a, b; Jayarajah y Branson 1995). Las condiciones se hancentrado en la disminuci6n y reestructuraci6n de los gastos de capital, la rebajade los subsidios, la reforma del empleo en el sector puiblico y la reducci6n de losgastos salariales en ese sector, el enfasis en el funcionamiento y manteninijentode las instalaciones existentes y el incremento de los gastos en el sector social(aunque no se prest6 la debida atenci6n a la meta de aliviar la pobreza).

El desempefio de los paises para los que se establecieron condiciones relati-vas a los gastos fue s6lo marginalmente mas satisfactorio que el de los de-mas paises en cuanto al mejoramiento de las pautas del gasto. Esos paisestuvieron mas exito en lo que respecta al aumento de los gastos para finessociales y la reducci6n de los subsidios y los gastos de defensa, y terminaronel periodo con un nivel mas bajo de gastos salariales que los paises a los queno se aplicaron tales condiciones. Aunque inicialmente ambos grupos de pai-ses tenian relaciones gastos totales-PIB aproximadamente iguales, los paisescon condiciones tuvieron menos exito en la reducci6n de los gastos totales.Su exito fue limitado en lo que atafie a la reestructuraci6n de los gastos co-rrientes, en el sentido de reducir los correspondientes a salarios y subsidios eincrementar los orientados a actividades de funcionamiento y mantenimien-to no salariales; las tentativas de reducir el empleo en el sector publico engeneral han sido de corta duraci6n o de poca envergadura. Los paises concondiciones relativas a los gastos de capital terminaron el periodo con nive-les muy bajos de gastos de ese tipo, lo que indica la existencia de reduccionesrelativamente grandes de los gastos por concepto de infraestructura. Unaraz6n de este desempefio mas bien modesto en el area de los gastos puederadicar en la falta de flexibilidad de que adolecen los presupuestos de mu-chos paises; los prestamos para fines de ajuste del Banco hicieron pocasaportaciones en esta esfera.

En los paises para los que se establecieron condiciones relacionadas con lossectores de educaci6n y salud, aument6 la participaci6n de ambos sectoresen el gasto total. Sin embargo, los coeficientes de gastos en educaci6n y saluds6Lo fueron marginalmente mas satisfactorios en los paises con tales condi-ciones que en los demas. Las tasas de analfabetismo, particularmente deninias y mujeres, y las tasas de mortalidad infantil bajaron en ambos gruposde paises. Los esfuerzos de recuperaci6n de costos en los sectores socialesfueron limitados. Una raz6n que explica por que es posible que las condicio-nes establecidas por el Banco hayan tenido poco efecto adicional en los sec-tores sociales es que la instituci6n hizo hincapie en los medios mas bien queen la finalidad de la reforma de los gastos. Las condiciones se centraron en lamodificaci6n de los gastos en determinadas categorfas funcionales o sectoresmAs bien que en la relaci6n entre insumos (como el nivel de los gastos), pro-ductos (tasas de matricula y de graduaci6n) y resultados finales (tasas dealfabetizaci6n; mortalidad; acceso a los servicios basicos, particularmentepor parte de los pobres y necesitados).

iQue puede hacerse?

Prioridades sugeridas para las actividades del Banco

En el area de la coordinaci6n Banco-Fondo. Tanto el Banco como el Fondo reco-nocen debidamente la importancia fundamental de la reforma fiscal parala estabilidad macroecon6mica y el crecimiento, y en los iiltimos afios hanconvenido en una divisi6n de sus actividades en esa esfera. El Fondo toma lainiciativa en las cuestiones relacionadas con los impuestos y el nivel global

13

del gasto, mientras que el Banco lo hace en las cuestiones relacionadas con losgastos sectoriales. Aunque en general esta divisi6n de las actividades funcionaen forma satisfactoria, no puede considerarse como una norma inflexible. Demodo que el Banco, al mismo tiempo que respeta el papel principal del Fondoen el suministro de asesoria fiscal, necesita participar mas activamente en laformulaci6n de las reformas fiscales en el marco de los prestamos para finesde ajuste, sobre todo en los casos en que es posible que el Fondo no tenga unaparticipaci6n directa. Por ejemplo, el Banco tiene que tomar en cuenta la rela-ci6n entre las reformas de la politica tributaria emprendidas en virtud de pro-gramas de ajuste y otras reformas estructurales (como las reformas relaciona-das con la promoci6n del sector privado y los mercados financieros y de capi-tal); entre las dimensiones y el papel del gobierno y el nivel de las finanzaspiIblicas; entre la financiaci6n del presupuesto y el nivel y composici6n de losgastos publicos, y entre las decisiones en materia de impuestos y gastos y losprogramas de lucha contra la pobreza. Es necesario que el Banco establezcala capacidad analitica requerida para asesorar a los funcionarios acerca delas cuestiones fiscales y de ajuste, para identificar las practicas 6ptimas ypara analizar los problemas emergentes de poliftica fiscal que probablementerevestiran importancia en el futuro (tributaci6n del sector financiero, impues-tos ambientales). En este sentido, es preciso que el Departamento de Investi-gaciones sobre Politicas de Desarrollo del Banco, que en octubre de 1994 dej6de realizar analisis impositivos para concentrarse en las cuestiones relacio-nadas con los gastos, tome medidas para modificar esa situaci6n. Su capaci-dad en esta esfera estrecharia la coordinaci6n Banco-Fondo y fortaleceria eldidalogo sobre cuestiones fiscales. El Banco y el Fondo estan explorando caucesnuevos y ya existentes para mejorar la coordinaci6n respecto de la preparaci6nde documentos generales de politica macroecon6mica (documentos sobre para-metros de politica econ6mica, analisis de los gastos publicos, documentos delBanco sobre estrategias de asistencia a los paises, documentos del Fondo deorientaci6n sobre la estrategia para los pafses). El Banco y el Fondo tambientienen que colaborar en la tarea de mejorar sus propias bases de datos fiscalesy los sistemas de datos fiscales de los clientes.

En el drea de las condiciones de los prestamos. En las operaciones de ajuste lacondicionalidad fiscal necesita ser mas especifica y precisa, estar respaldadapor indicadores del desempefio concretos y susceptibles de seguimiento yprestar especial atenci6n, ademas de a los medios de alcanzar la reforma, alos resultados fiscales (y otros macroecon6micos conexos). La condiciona-lidad deberia otorgar tanta importancia a la aplicaci6n de nuevas leyes comoa su promulgaci6n, y deberia hacer mas hincapie en la puesta en practica delas recomendaciones de los estudios que en su preparaci6n.

En el drea de los deficit fiscales. El Banco necesita asegurar la existencia de mayorprecisi6n en varios frentes:

* Es preciso ampliar la cobertura de las cuentas fiscales y mejorar sutransparencia. Esto entrafia la incorporaci6n de las cuentas provinciales,locales y municipales en las cuentas fiscales; el seguimiento de los d6ficitcuasifiscales, y la determinaci6n de las repercusiones de los impuestosimplicitos, los subsidios y las garantias gubernamentales.

* Tiene que identificarse el indice apropiado del deficit para abordar elproblema en cuesti6n. El deficit global puede ser el indice apropiado enla mayoria de los paises, pero en algunos puede serlo el deficit operacio-nal o estructural; en ciertos paises la atenci6n quizas deba centrarse en elahorro publico, y en otro grupo puede requerirse el seguimiento de losdeficit primarios.

14

* Las cuentas fiscales deben integrarse mejor en el marco macroecon6micode analisis para poder estudiar en forma mas dinamica los ajustes fisca-les y otros ajustes macroecon6micos. Esto es esencial para estimar el de-ficit sostenible; para identificar las ventajas y desventajas de diversosniveles aceptables de endeudamiento, inflaci6n, tasas de interes y otrasvariables macroecon6micas, y para establecer metas cuantitativas parael logro de niveles sostenibles de d6ficit y el seguimiento de los resul-tados macroecon6micos.

En el area de la reforma tributaria. Las cuestiones principales en las que elBanco deberia centrarse son las siguientes:

* Simplificacion y ampliaci6n de la base tributaria. Las actividades del Bancoen materia de reforma tributaria deberian seguir haciendo hincapie enla ampliaci6n y simplificaci6n de la base tributaria a fin de facilitar laadministraci6n e incrementar el cumplimiento.

* Secuencia apropiada de las medidas de reforma tributaria. El Banco tiene queprestar especial atenci6n a la secuencia apropiada de las medidas dereforma tributaria. En los casos en que los impuestos al comercio contri-buyen en forma significativa a los ingresos, las reformas tributarias norelacionadas con el comercio cuyo objetivo es elevar los ingresos tal veztengan que preceder a las relacionadas con el comercio, que por lo gen-eral resultan en niveles de ingreso mas bajos. Las reformas de la admi-nistraci6n tributaria deben preceder o acompafiar a la reforma de laestructura impositiva.

* Consideraciones relacionadas con el medio ambiente, la equidad y la promo-ci6n del sector privado. Las actividades del Banco en la esfera de la refor-ma tributaria deben tener en cuenta las consideraciones pertinentes decaracter ambiental; ademas, el sistema tributario no debe repercutirnegativamente en la equidad y la lucha contra la pobreza ni en lacompetitividad intemacional de la economia.

* Administraci6n tributaria. La reforma de la administraci6n tributariadeberia centrarse en el establecimiento de un marco legal propicio, laformaci6n de los contribuyentes, los sistemas de informaci6n (emplea-dos por los departamentos de impuestos), las auditorias, los impuestosretenidos en la fuente y los impuestos sobre la renta presuntiva, y elperfeccionamiento de la administraci6n de los impuestos al valoragregado (IVA).

* Seguimiento de los progresos. La incorporaci6n de indicadores mas efica-ces del desempefio en los programas de reforma de los impuestos y suadministraci6n redundaria en mejoras en el disenlo, ejecuci6n y evalua-ci6n retrospectiva, y atraeria la atenci6n a las metas de la reforma. Estosindicadores deberian abarcar las tasas impositivas efectivas y, en el casode la administraci6n tributaria, los indices de los costos y resultados.

En el area de la reforma de los gastos. El Banco deberia centrarse en:

* El establecimiento de la base para las recomendaciones. Las recomendacionespara la reforma del gasto publico deben fundamentarse en considera-ciones relativas a la funci6n gubemamental apropiada. Es necesariopersuadir a los gobiemos de que pasen de una cultura de direcci6n ycontrol a una de suministro de servicios. Asimismo es preciso alentar-los a que inviten a las administraciones locales, los posibles beneficia-

15

rios y otros interesados a participar en conversaciones sobre prioridadesen materia de desarrollo y gasto, particularmente en los sectores so-ciales. Esto entrafiaria la reforma de los procesos presupuestarios ylas instituciones.

* La aclaraci6n de las metas de la reforma. A fin de seleccionar los instrumen-tos adecuados en materia de gastos (o de otros rubros) y de propiciaruna mayor eficiencia en la ejecuci6n, es importante centrar la atenci6ndesde el principio en las metas finales de la reforma de los gastos. ElBanco necesita fomentar el desarrollo de indicadores apropiados deldesempefno que comprendan resultados intermedios (a corto plazo) yresultados finales (a largo plazo) y tambien indices del nivel y compo-sici6n de los gastos.

* Una mayor atenci6n a la composici6n de los gastos. En los casos en que lareducci6n de los deficit es un objetivo importante, es necesario analizarlos gastos tanto corrientes como de capital, y prestar especial atenci6n alos gastos inflexibles e improductivos (como los de defensa y los subsi-dios no orientados a la poblaci6n pobre). Si bien el enfasis del Banco enla rebaja de los gastos de capital ha estado justificado en los paises enque los proyectos grandes de capital no se orientaban a la atenci6n de lasnecesidades basicas de la poblaci6n, en algunos paises esos gastos (comoproporci6n de los gastos totales o del PIB) han caido a niveles que pue-den estar retrasando el crecimiento. En estos paises y en otros en quegran parte de la poblaci6n carece de acceso a los servicios fundamen-tales, puede ser necesario incrementar las inversiones basicas.

* El enfasis en el alivio de la pobreza. El potencial de los programas de gastoses mayor que el de las reformas de los ingresos en lo que se refiere a lareducci6n de la pobreza. Es preciso, por lo tanto, que el Banco busque enel ambito de los gastos los medios de lograr una mejor focalizaci6n delos programas de subsidios y un mayor acceso de la poblaci6n pobre alos servicios basicos. El Banco tambien podria tratar de encontrar solu-ciones innovadoras a los problemas de la pobreza, como programas paraimpartir informaci6n sobre la potabilidad del agua a los hogares pobresy enseniarles buenas practicas sanitarias. Asimismo, el Banco necesitaalentar a los clientes a que encaucen recursos hacia las zonas rurales,pues es en ellas que vive la mayoria de la poblaci6n pobre.

* La promoci6n de la equidad. Los servicios bAsicos de educaci6n y saluddeben ser casi gratuitos para asegurar una cobertura universal, mientrasque en el caso del nivel terciario de esos servicios deben aplicarse solu-ciones innovadoras de recuperaci6n de costos que tambien fomentenla equidad.

FISCAL MANAGEMENT INADJUSTMENT LENDING

Resume

La Banque mondiale a lance son programme de pret a l'ajustement structu-rel au debut des ann6es 80 pour aider les pays en developpement a sortirde la crise economique dans laquelle les chocs exterieurs et leur mauvaisegestion macroeconomique les avaient plonges. Au debut des annees 90, presde deux tiers des clients de la Banque avaient entrepris des reformes appu-yees par des prets a l'ajustement structurel ou sectoriel (PAS/PASEC). Ungrand nombre de ces prets (environ 250 PAS/PASEC ont et6 consentis a 86pays entre les exercices 79 et 94) comprenaient une composante << reformedes finances publiques »>. Les auteurs de la presente etude evaluent lesprogres realises grace aux ajustements que la Banque a appuy6s dans cedomaine et cherchent a voir comment les prets pourraient devenir plusperformants a l'avenir.

Conclusions de l1'tude

L'etude a abouti aux quatre grandes conclusions suivantes: (a) une sainegestion des finances publiques passe par une action soutenue sur une longueduree; (b) la reduction du d6ficit budgetaire et l'acc6leration de la croissanceeconomique vont de pair; (c) les reductions durables du d6ficit sont davan-tage le resultat d'une augmentation des recettes que d'une compression desd6penses; et (d) le succes limite des composantes "< reforme des financespubliques >> appuyees par la Banque tient au fait que les questions budg&-taires n'ont pas ete traitees de facon suffisamment globale et que les clausesde conditionnalite des prets etaient peu explicites.

Constatations d'ordre general

La gestion du deficit budgetaire passe par une action soutenue sur une longue du-ree. Le deficit des pays beneficiaires de PAS et de PASEC a augmente a mo-yen terme; l'amelioration de la situation budgetaire ne s'est vraiment faitsentir qu'a long terme (de cinq a huit ans apres l'octroi du premier pret).Bien que le deficit ait baisse au cours des deux dernieres annees (par rap-port a la periode de quatre ans ayant precede l'octroi des prets) dans lespays ben6ficiaires de PAS/PASEC, pris dans leur ensemble, on a constated'importants retoumements de situation dans les pays d'Afrique, ainsi quechez les exportateurs de produits primaires et parmi les pays a faible reve-nu et gravement endettes qui avaient pris des mesures d'ajustement. Legroupe des pays a faible revenu et celui des exportateurs de produits pri-maires n'ont enregistre aucun progres sur ce plan par rapport a la periodeavant l'octroi des prets.

Les deficits budgetaires importants ont avant tout ete dus a une mauvaisegestion des finances publiques, et non a des chocs exogenes. Bien que la

16

17

charge des int6rets en devises etrangeres n'ait pas entrave I'ajustement deplusieurs pays beneficiaires de PAS/PASEC, I'accroissement du ratio detteexterieure-produit int6rieur brut (PIB) dans la plupart des regions du mondemontre que l'assainissement des finances publiques n'a pas et suffisantpour assurer la solvabilite de nombreux pays clients.

La reduction du deficit conduit a une amelioration de la balance exterieure et sti-mule la croissance. Le deficit budgetaire pouvant etre l'une des causes denombreux maux economiques (inflation, rarete du credit, distorsion destaux d'int&r&t et de change), il peut faire fuir l'investissement prive et pena-liser la croissance economique. Bien que celle-ci ait ete inegale d'une regiona l'autre, les donnees montrent qu'une saine gestion des finances publiquesaide a obtenir de bons resultats, meme si d'autres conditions doivent aussietre reunies. Les chiffres montrent aussi que la reduction du deficit budge-taire et l'amelioration du deficit des comptes courants sont etroitement liees.

La reduction durable du deficit a surtout et lefait d'un accroissement des recetteset, dans une moindre mesure, d'une compression des depenses d'equipement. Lareduction ciblee de certaines depenses defonctionnement ne s'est pas traduite pardes resultats aussi nets. La plupart des pays ayant ameliore leur situationbudgetaire y sont parvenus en augmentant les recettes. En regle g6nerale,les pays dont le deficit budgetaire s'est creuse avaient accru leurs depensesde fonctionnement sans augmenter leurs recettes. En matiere de depensesde fonctionnement et d'equipement, les strategies ont ete appliquees defacon uniforme dans le temps, d'un groupe de pays a l'autre et d'une regiona l'autre. En effet, a l'exception du Moyen-Orient et de l'Afrique du Nord(MNA) et des pays a revenu intermediaire ayant applique un programmed'ajustement, l'ensemble des r6gions et des groupes de pays ont accru leursdepenses de fonctionnement et, a l'exception de l'Asie de l'Est et du Pacifi-que (EAP), tous les groupes ont tailk dans leurs depenses d'equipement parrapport a la periode avant l'octroi des prets. Bien que jugee necessaire dansde nombreux cas, une compression des d6penses de fonctionnement n'estintervenue que dans un petit nombre de pays.

On peut dresser un bilan tres positif du respect des conditions de la Banquepar les emprunteurs, meme si les operations de pret a l'ajustement n'ont euqu'un succes limite sur le plan budgetaire. En effet, les aspects budg6tairesn'ont pas et6 traites de facon suffisamment globale et les clauses de condi-tionnalite etaient trop vagues. La mauvaise qualite des donnees sur les fi-nances publiques a incontestablement contribue aux problemes rencontrespour faire ressortir les differentes composantes des comptes publics et mettreen evidence les incidences sur le budget de la reorientation de la politiquebudgetaire et des autres mesures macroeconomiques. La couverture du defi-cit, sa mesure et son caractere soutenable, ou encore le r6le du secteur public(un facteur qui determine tres largement le niveau des finances publiques),sont des questions auxquelles on n'a guere prete attention dans la plupartdes op6rations. Bien que la politique budgetaire ne soit que l'un des aspectsd'un programme plus large d'ajustement comportant des reformes inter-dependantes, peu d'operations ont et l'occasion d'examiner la relation en-tre le deficit budgetaire et les instruments pour le faire reculer, ou entre lesautres variables economiques et les mesures de reforme structurelle. Lesquestions complexes li6es a la reforme budgetaire (discipline budgetaire,participation des beneficiaires locaux aux choix de depenses a engager, effi-cacite sur le plan technique, gestion responsable, systemes informatiques,etc.) n'ont pas non plus ete abordces de facon globale. Les clauses de con-ditionnalite applicables au d6ficit budgetaire ou a l'epargne publique etaienttrop generales, variaient d'un pret a l'autre dans le meme pays ou faisaient

18

l'objet d'interpr6tations diff6rentes. Le manque de pr6cision des conditionsli6es aux aspects budg6taires a fait que l'ex6cution et le suivi ont 6t6 diffi-ciles ou impossibles a realiser (dans 68 pour cent des operations couvertespar des rapports de fin d'ex6cution et d'evaluation r6trospective - RFE etRER). Les conditions etaient peu contraignantes, portant davantage sur lar6daction que sur l'application de textes l6gislatifs et reglementaires (47pour cent) et mettant plus l'accent sur la r6alisation d'6tudes que sur leurexecution (16 pour cent). Dans certains cas, les conditions pr6vues devaient&re appliqu6es a un moment peu opportun (32 pour cent).

Constatations sur des aspects precis de la reforme des finances publiques