india daily, july 28, 2010

TRANSCRIPT

For Private Circulation Only. FOR IMPORTANT INFORMATION ABOUT KOTAK SECURITIES’ RATING SYSTEM AND OTHER DISCLOSURES. REFER TO THE END OF THIS MATERIAL.

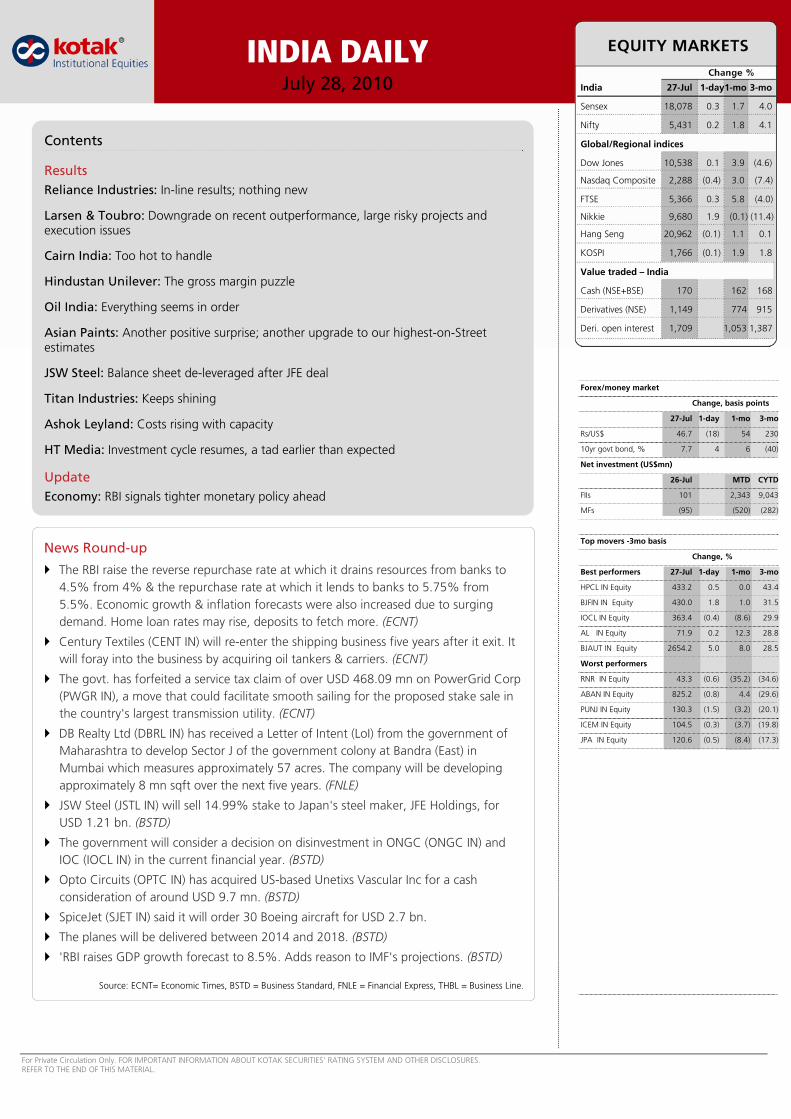

INDIA DAILYJuly 28, 2010 India 27-Jul 1-day1-mo 3-mo

Sensex 18,078 0.3 1.7 4.0

Nifty 5,431 0.2 1.8 4.1

Global/Regional indices

Dow Jones 10,538 0.1 3.9 (4.6)

Nasdaq Composite 2,288 (0.4) 3.0 (7.4)

FTSE 5,366 0.3 5.8 (4.0)

Nikkie 9,680 1.9 (0.1) (11.4)

Hang Seng 20,962 (0.1) 1.1 0.1

KOSPI 1,766 (0.1) 1.9 1.8

Value traded – India

Cash (NSE+BSE) 170 162 168

Derivatives (NSE) 1,149 774 915

Deri. open interest 1,709 1,053 1,387

Forex/money market

Change, basis points

27-Jul 1-day 1-mo 3-mo

Rs/US$ 46.7 (18) 54 230

10yr govt bond, % 7.7 4 6 (40)

Net investment (US$mn)

26-Jul MTD CYTD

FIIs 101 2,343 9,043

MFs (95) (520) (282)

Top movers -3mo basis

Change, %

Best performers 27-Jul 1-day 1-mo 3-mo

HPCL IN Equity 433.2 0.5 0.0 43.4

BJFIN IN Equity 430.0 1.8 1.0 31.5

IOCL IN Equity 363.4 (0.4) (8.6) 29.9

AL IN Equity 71.9 0.2 12.3 28.8

BJAUT IN Equity 2654.2 5.0 8.0 28.5

Worst performers

RNR IN Equity 43.3 (0.6) (35.2) (34.6)

ABAN IN Equity 825.2 (0.8) 4.4 (29.6)

PUNJ IN Equity 130.3 (1.5) (3.2) (20.1)

ICEM IN Equity 104.5 (0.3) (3.7) (19.8)

JPA IN Equity 120.6 (0.5) (8.4) (17.3)

Contents

Results Reliance Industries: In-line results; nothing new

Larsen & Toubro: Downgrade on recent outperformance, large risky projects and execution issues

Cairn India: Too hot to handle

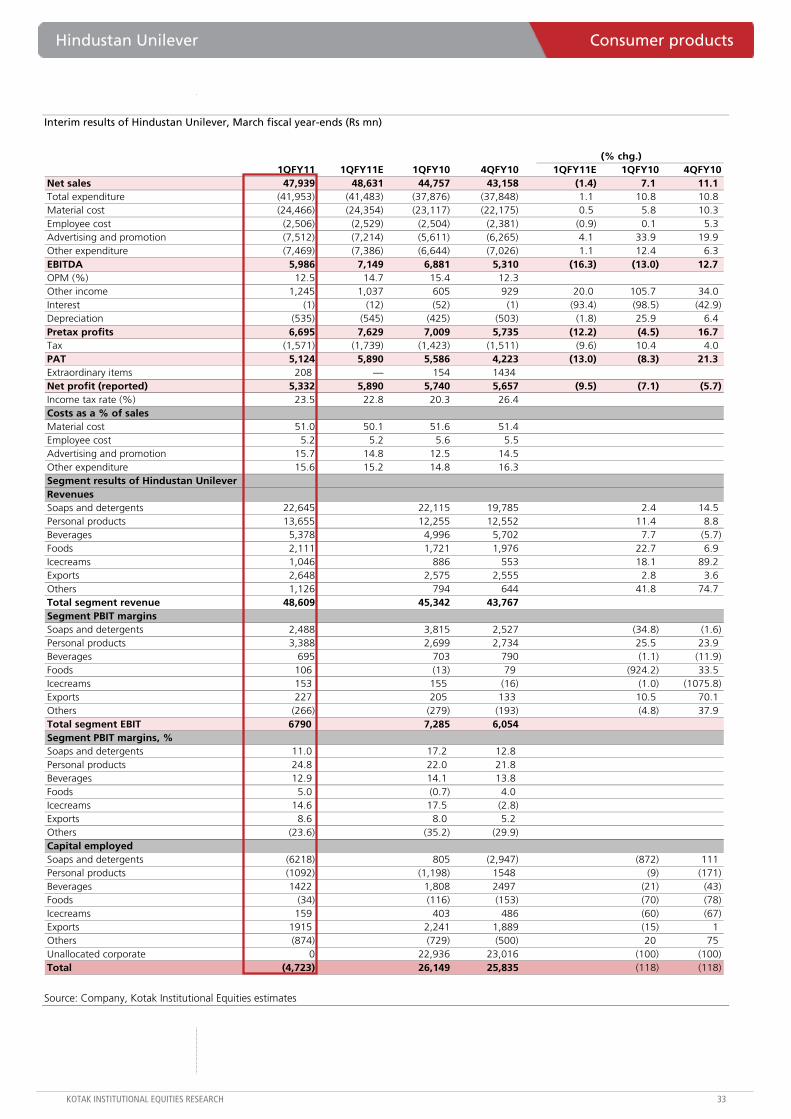

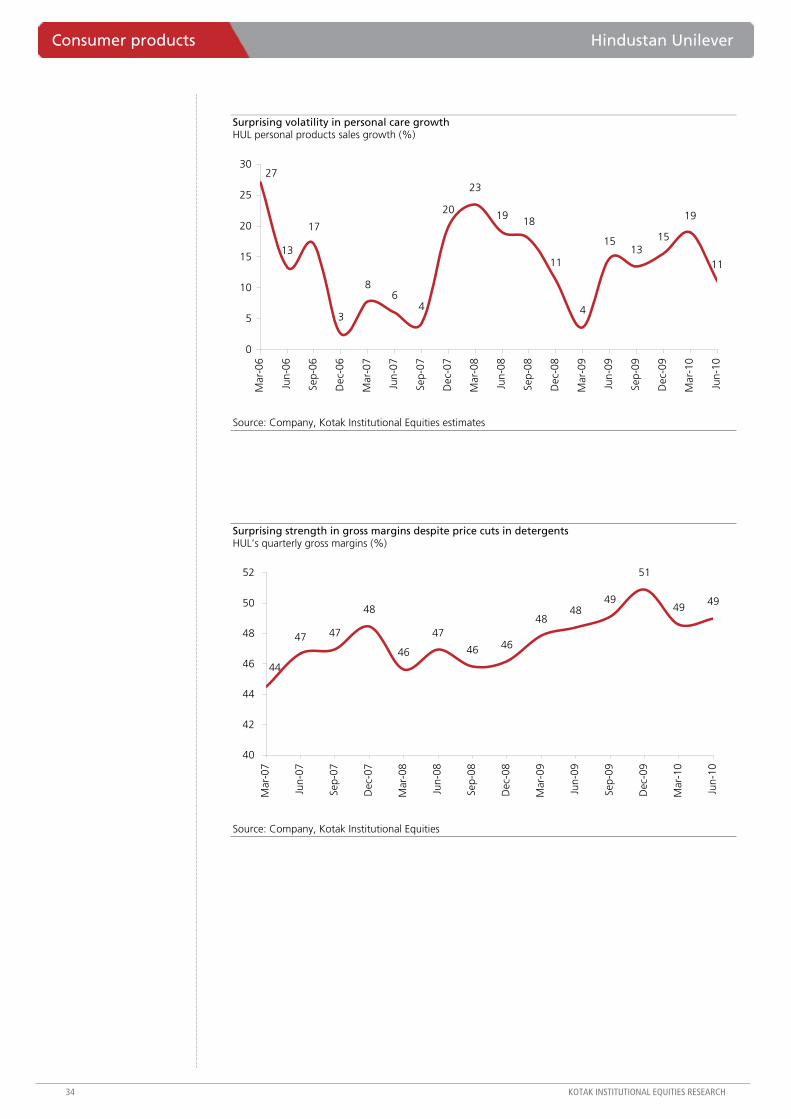

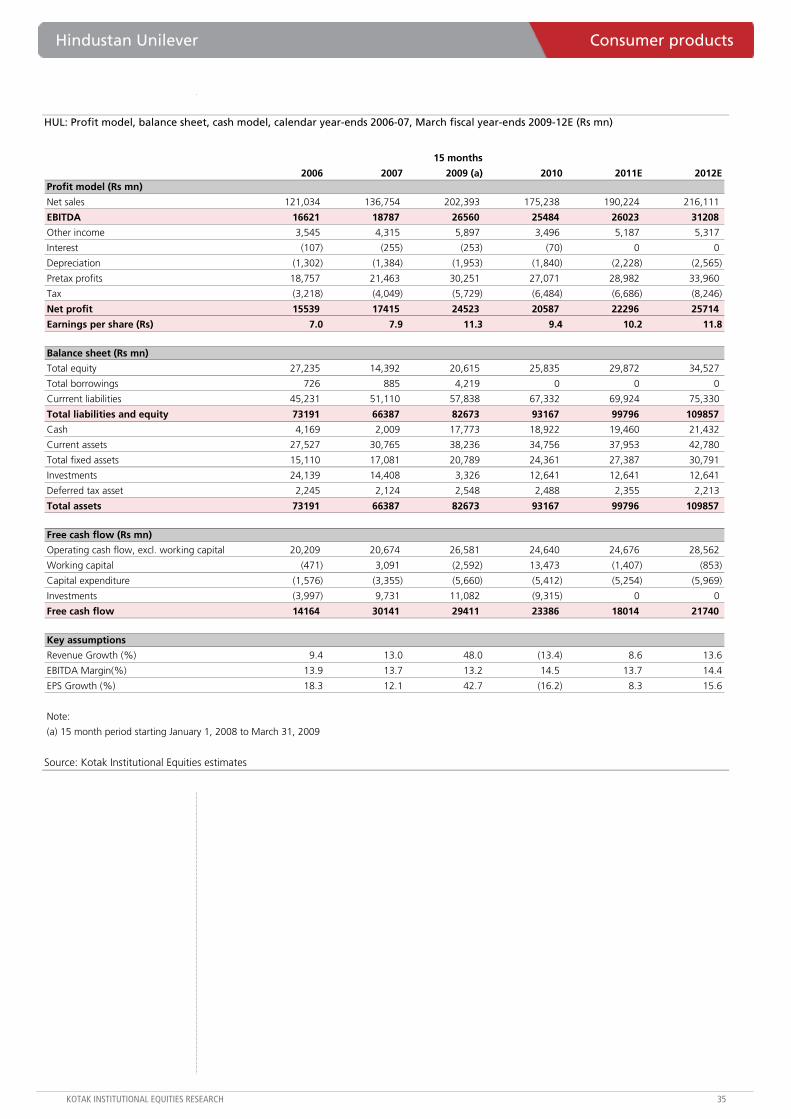

Hindustan Unilever: The gross margin puzzle

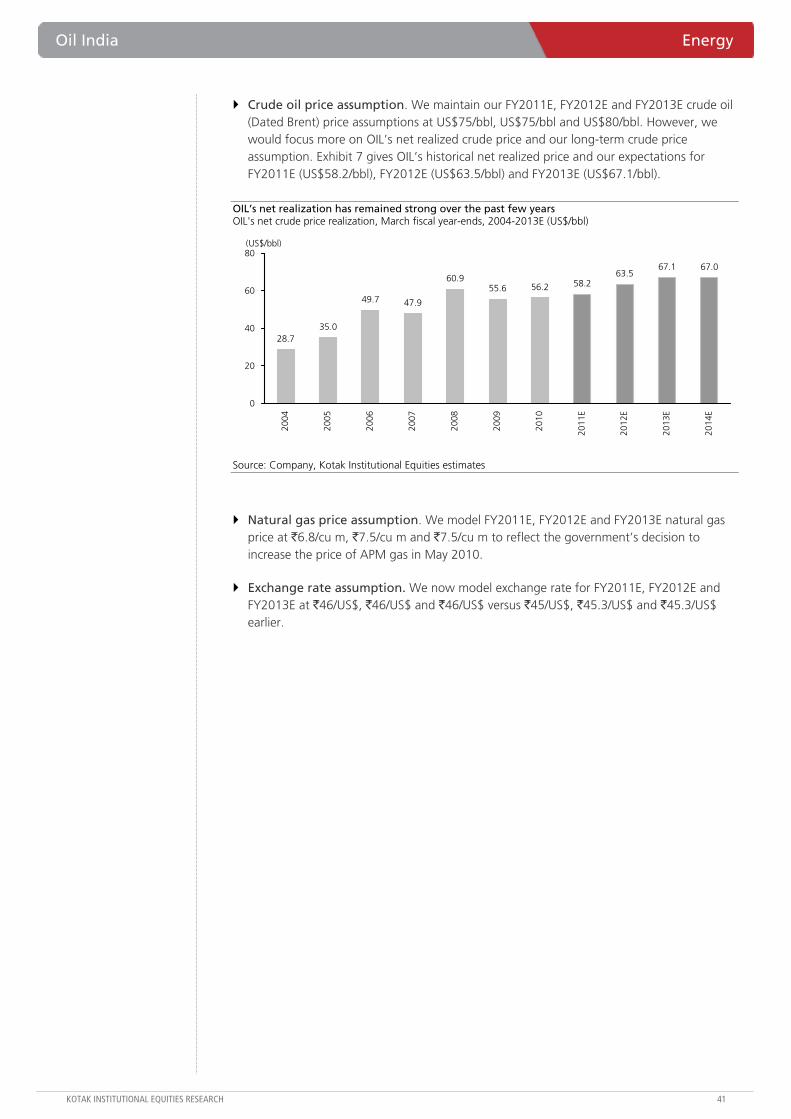

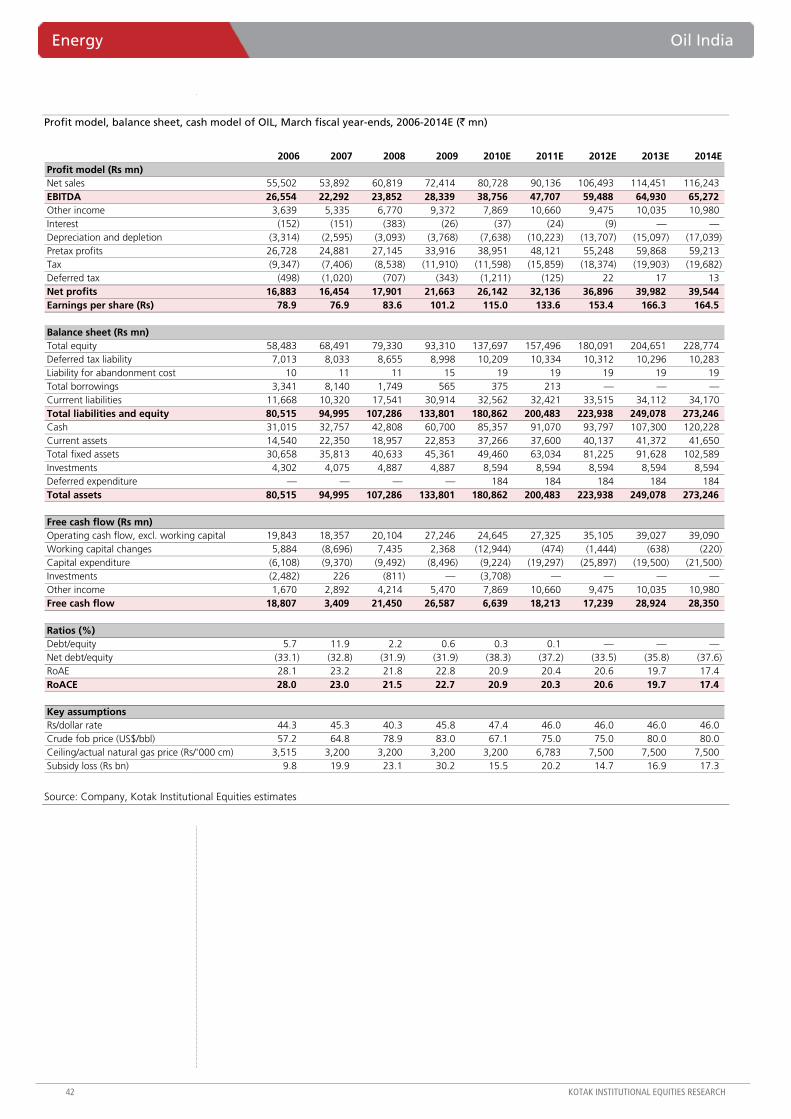

Oil India: Everything seems in order

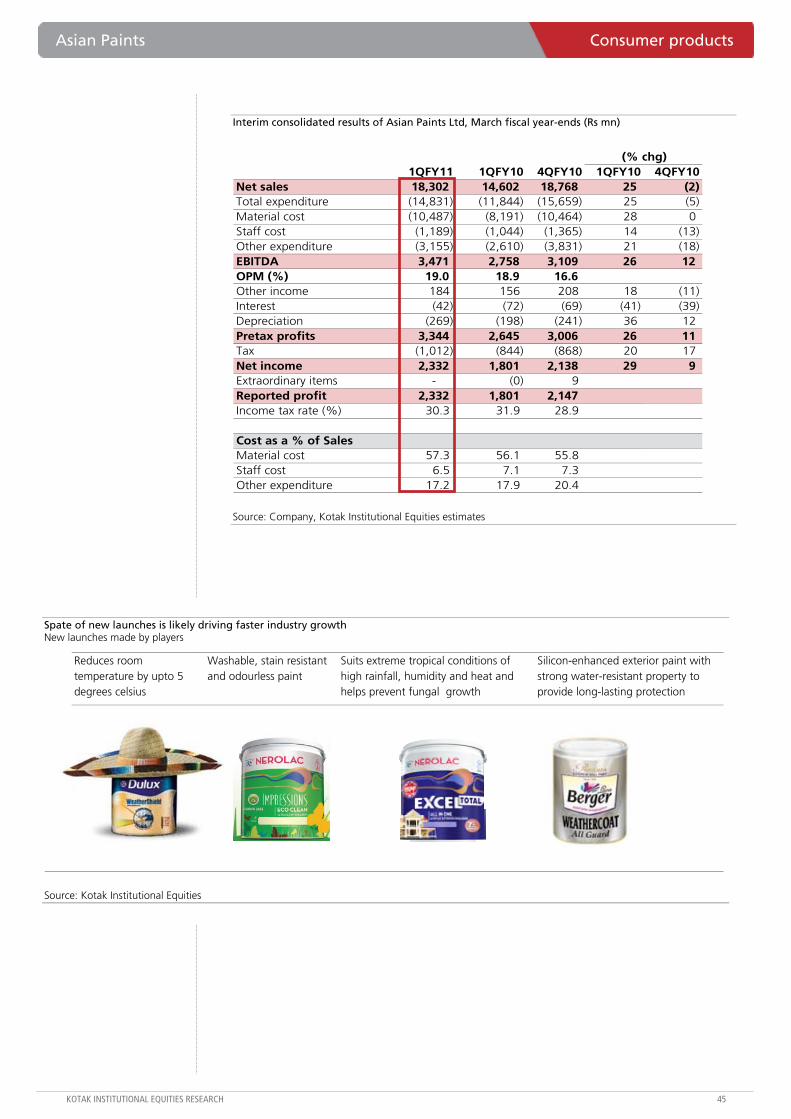

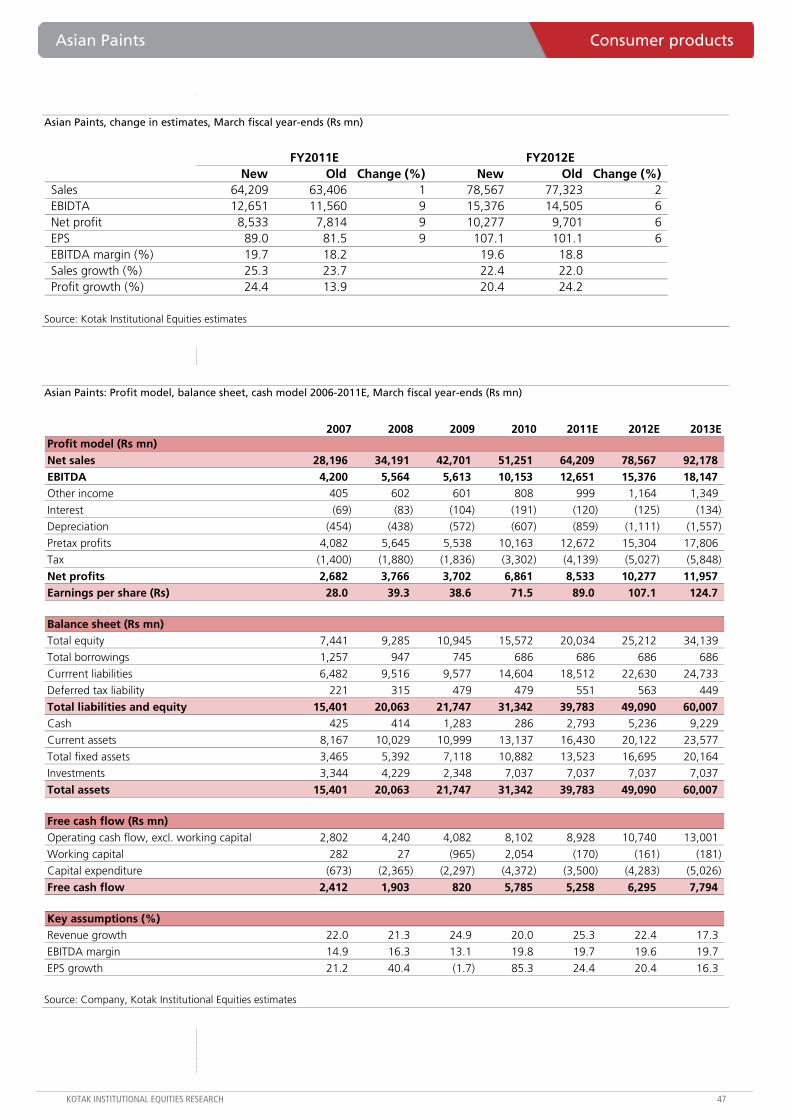

Asian Paints: Another positive surprise; another upgrade to our highest-on-Street estimates

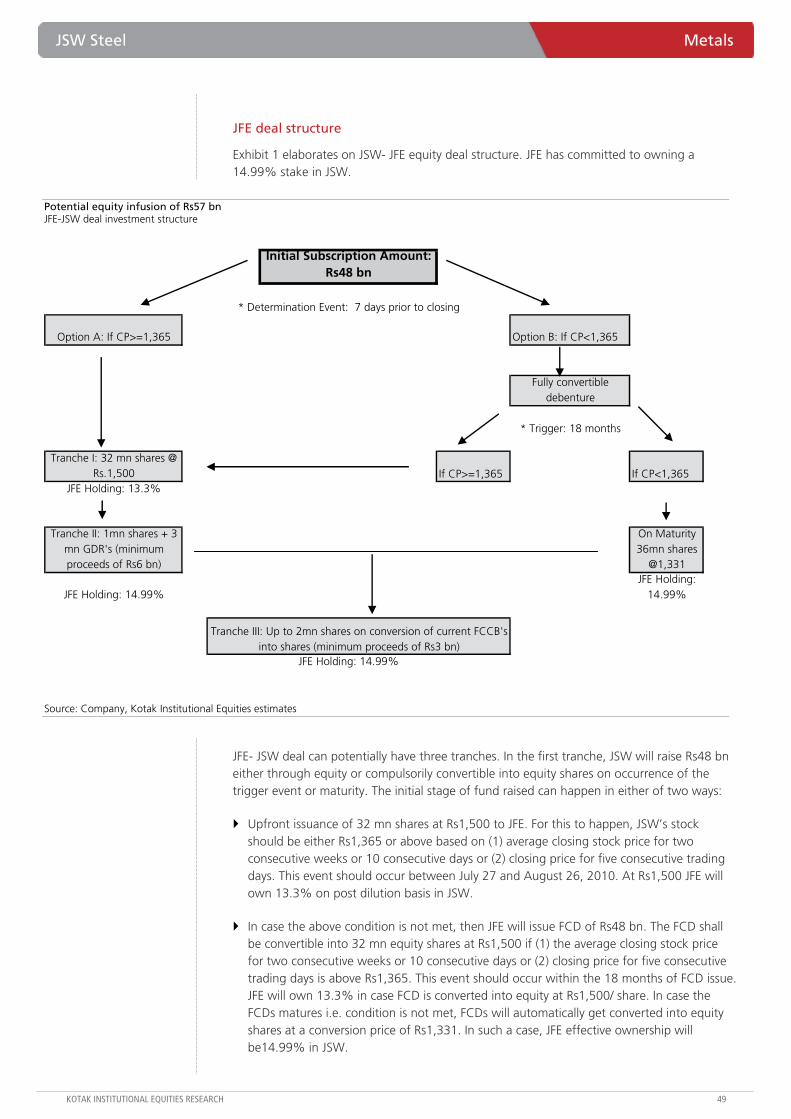

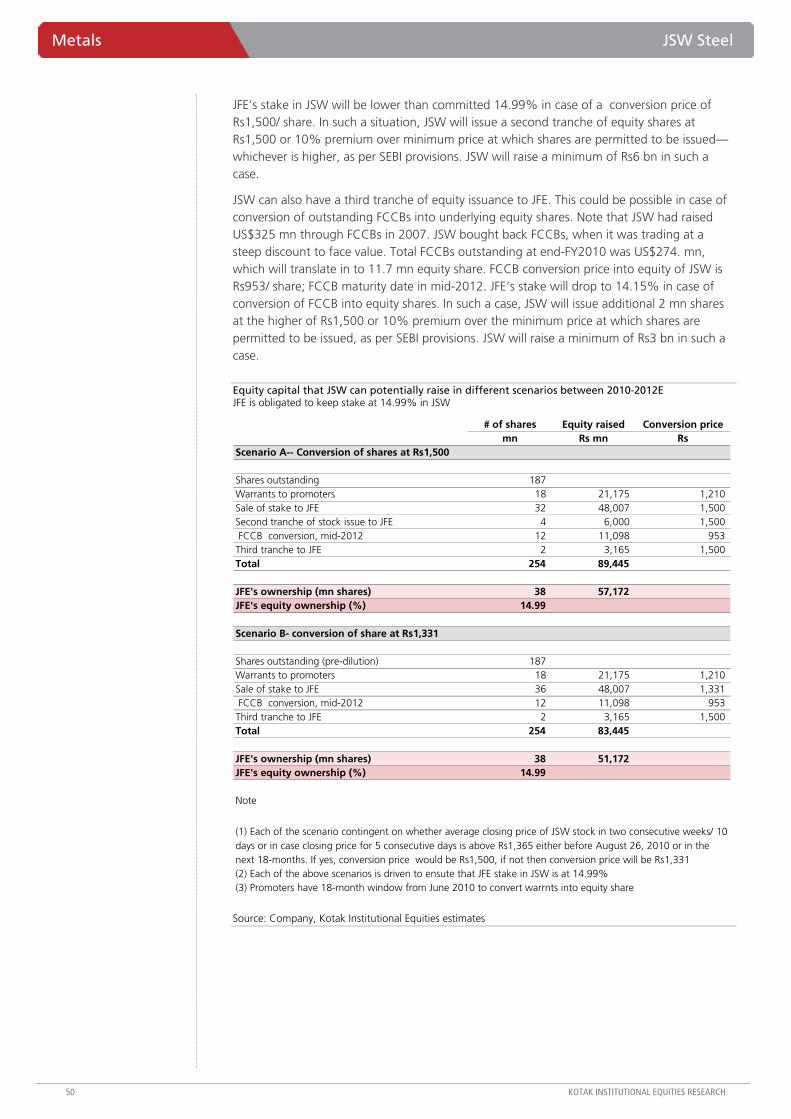

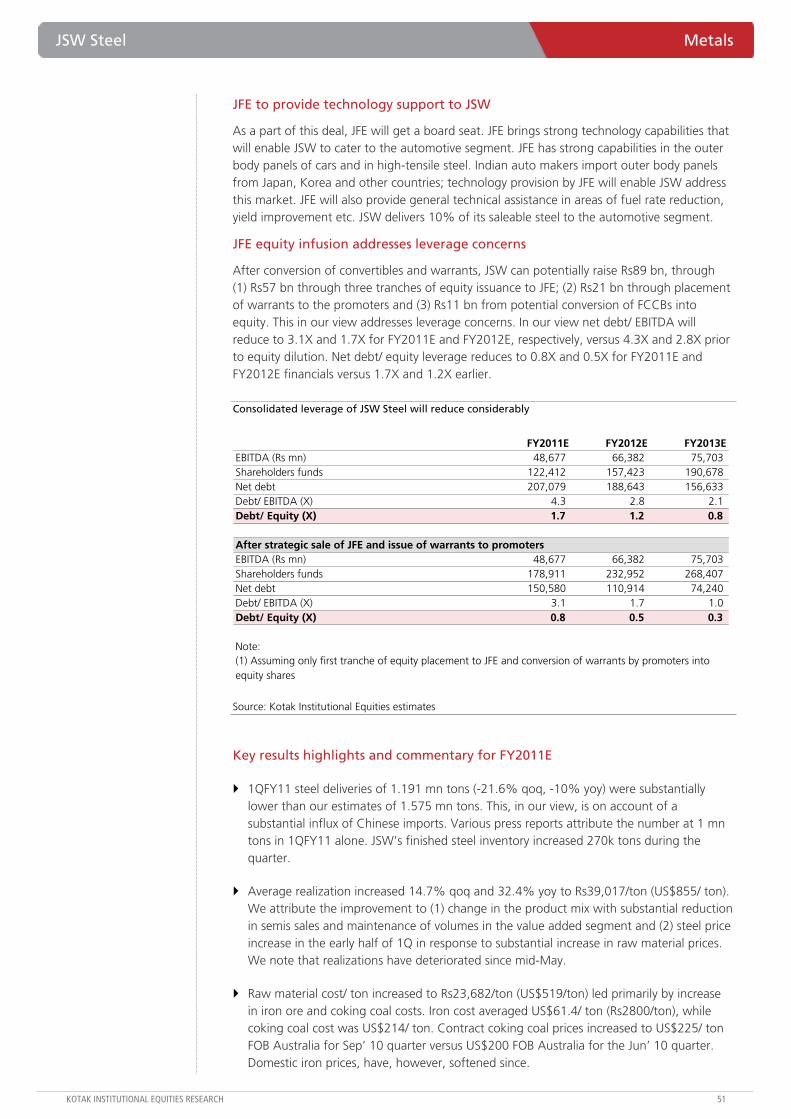

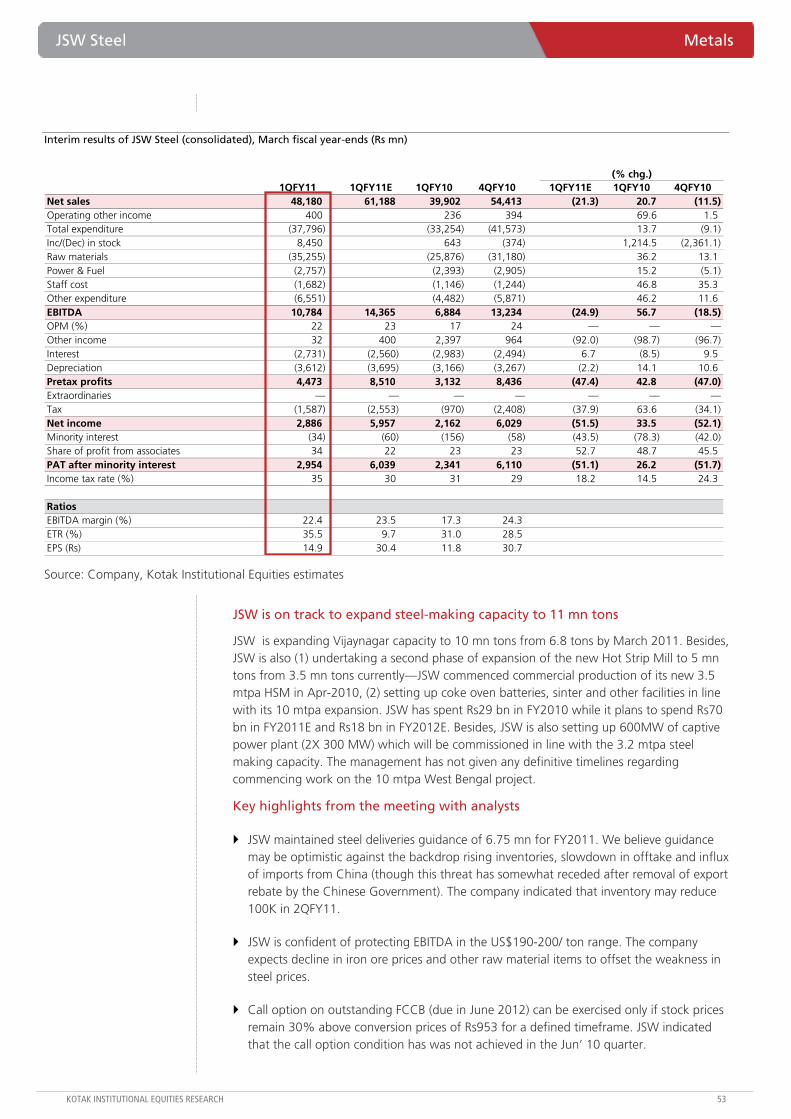

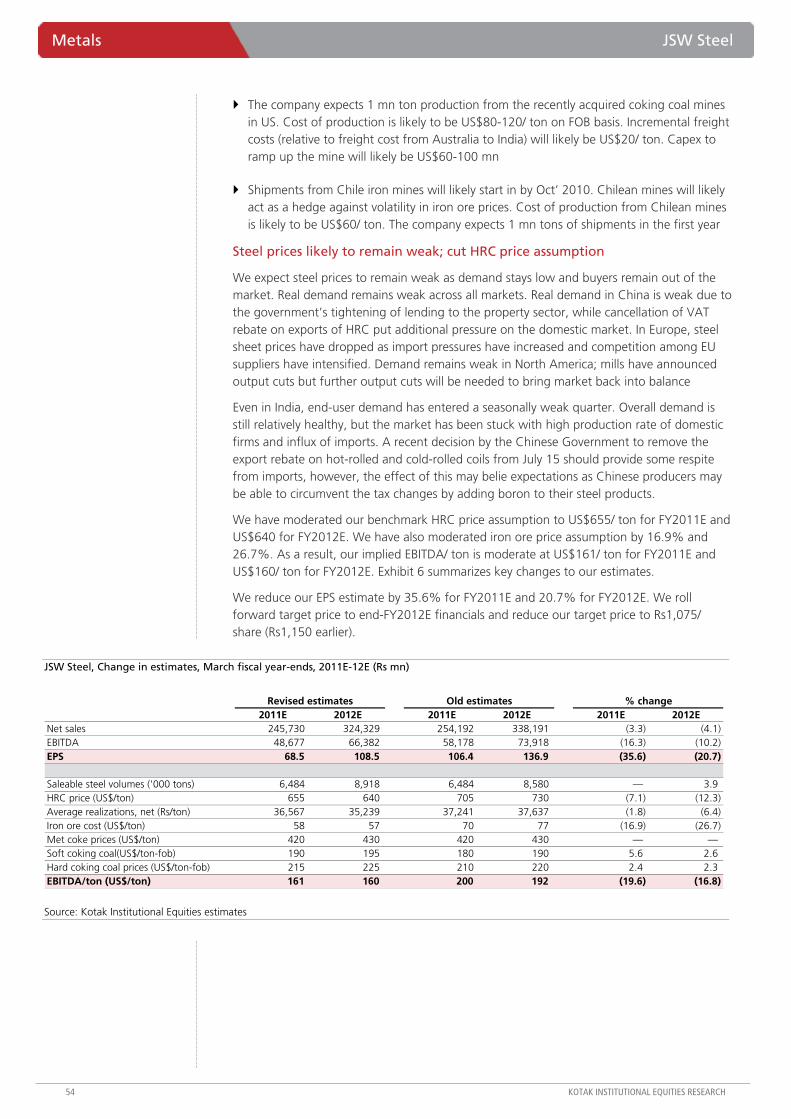

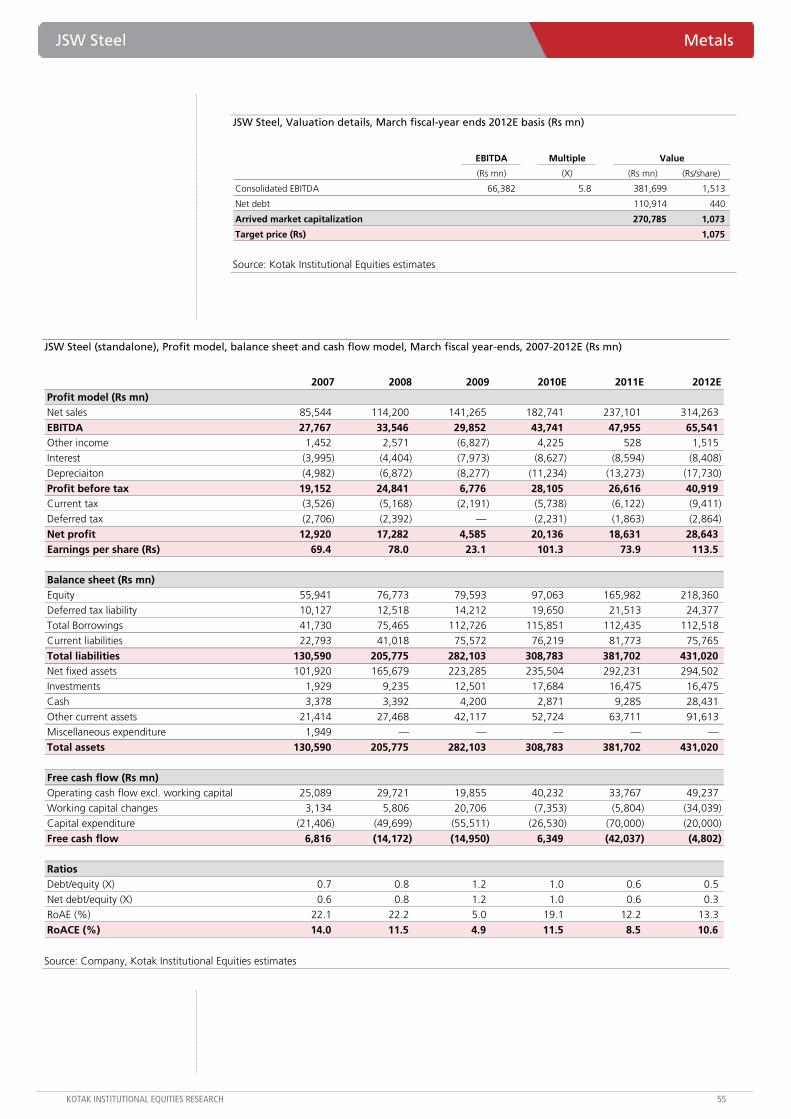

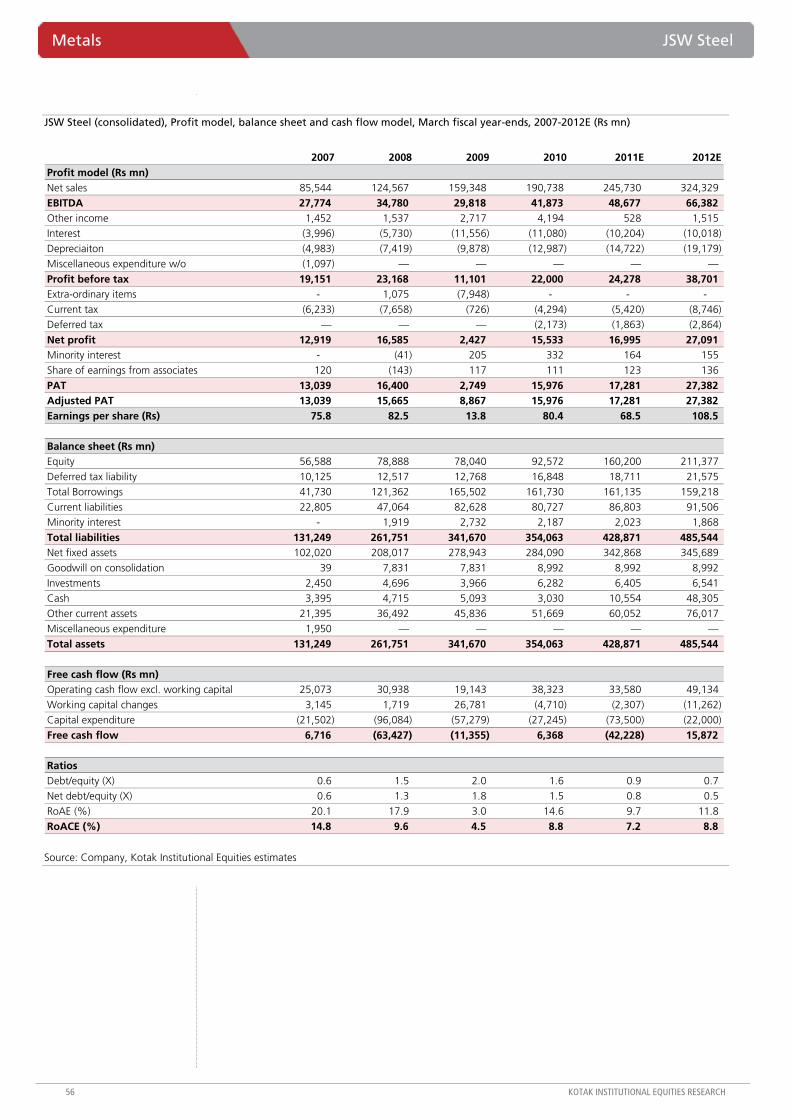

JSW Steel: Balance sheet de-leveraged after JFE deal

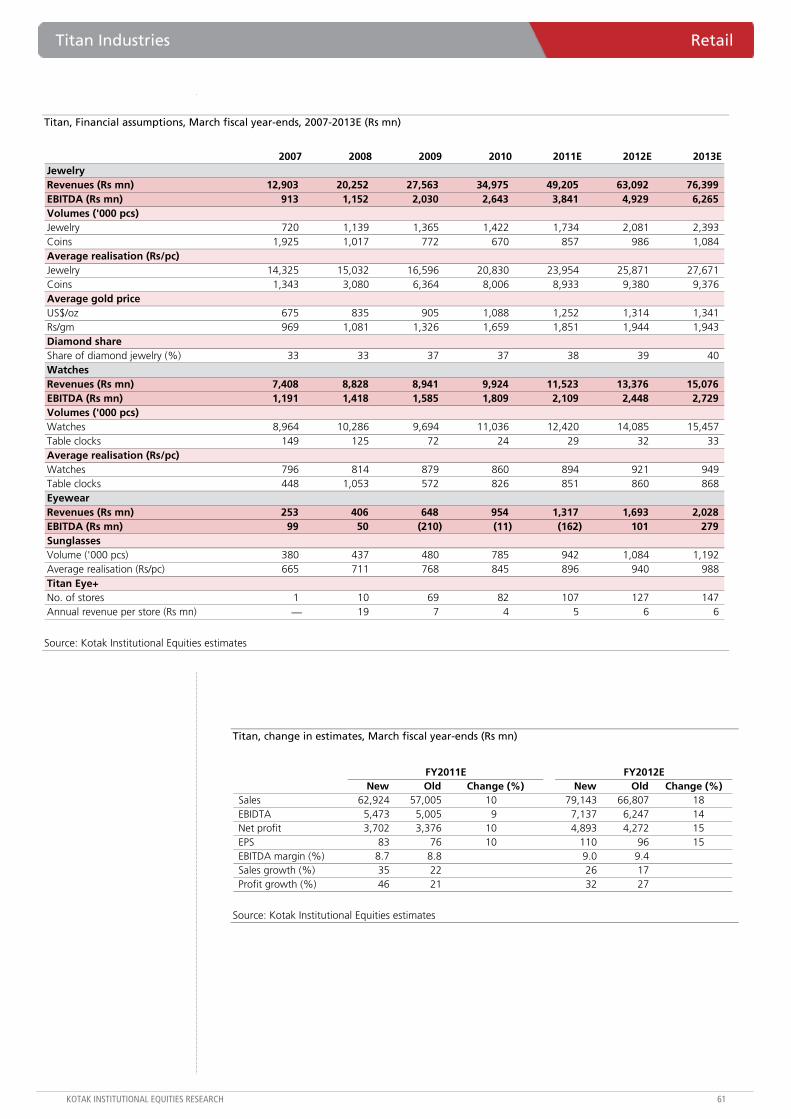

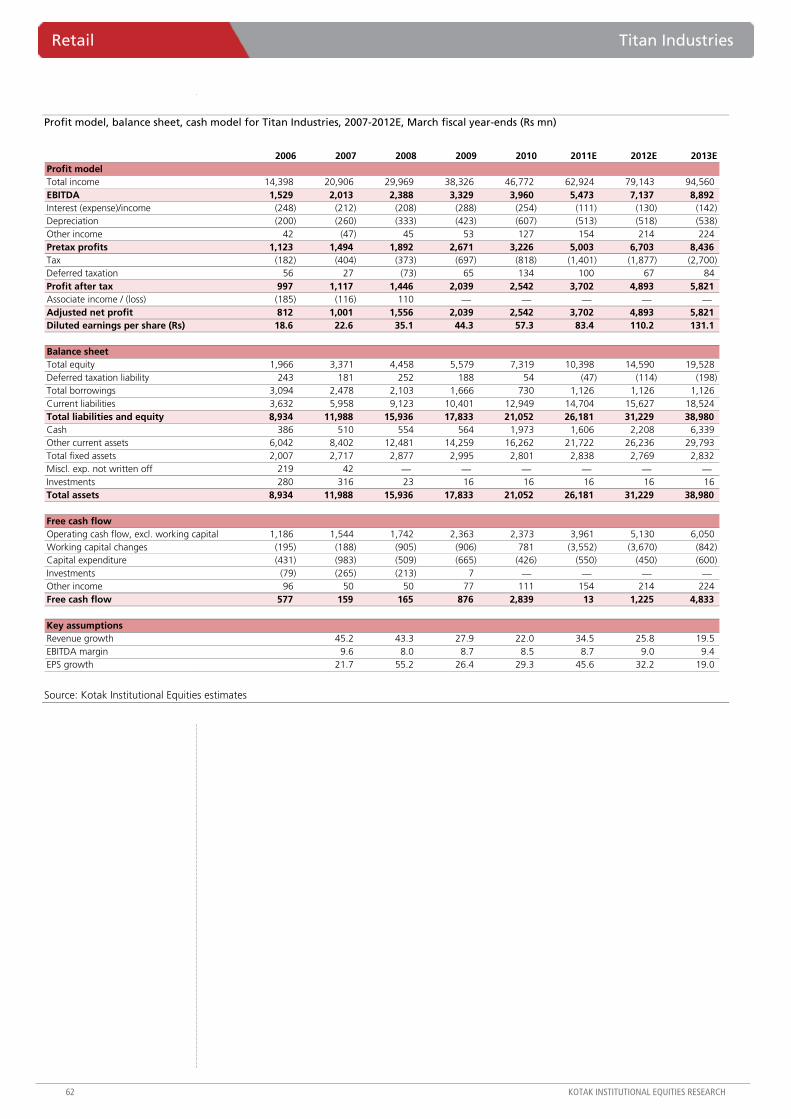

Titan Industries: Keeps shining

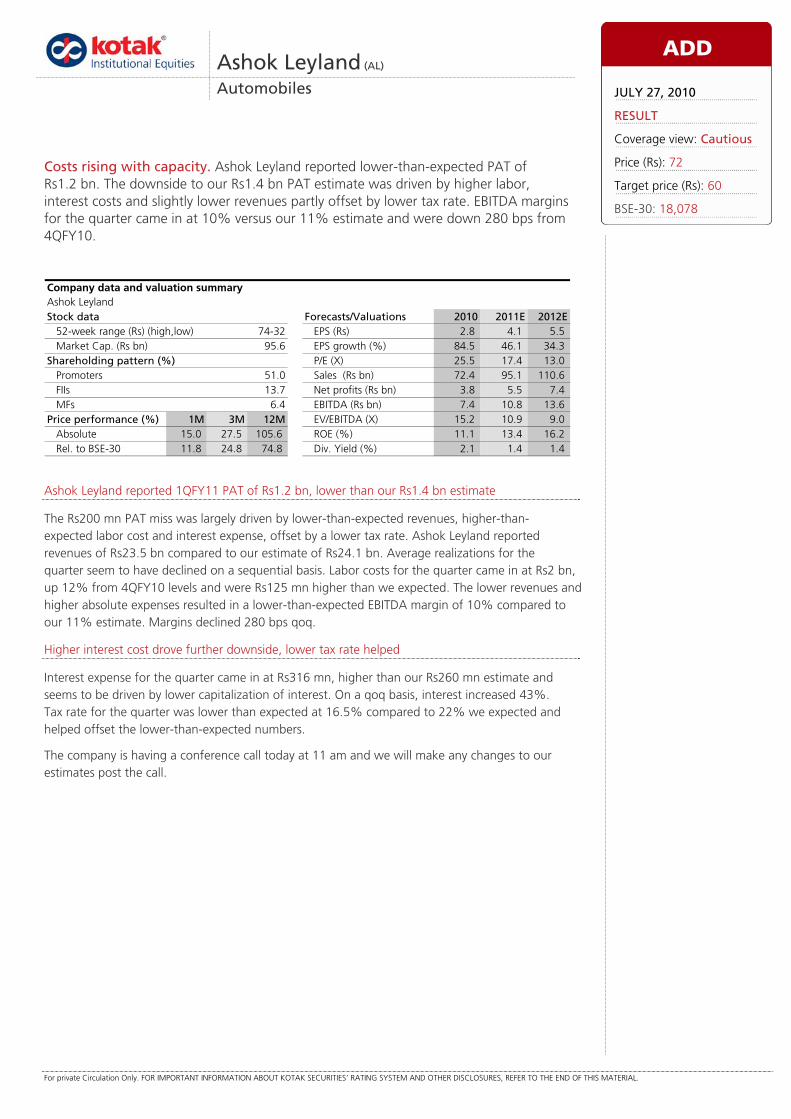

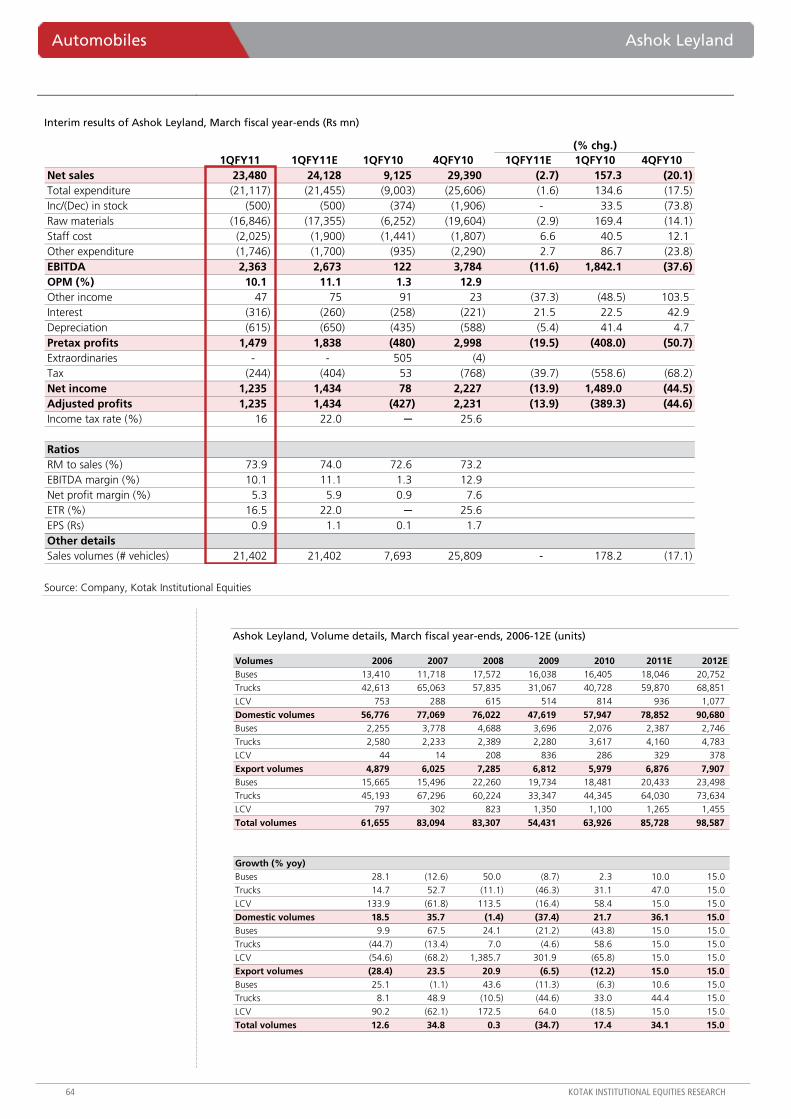

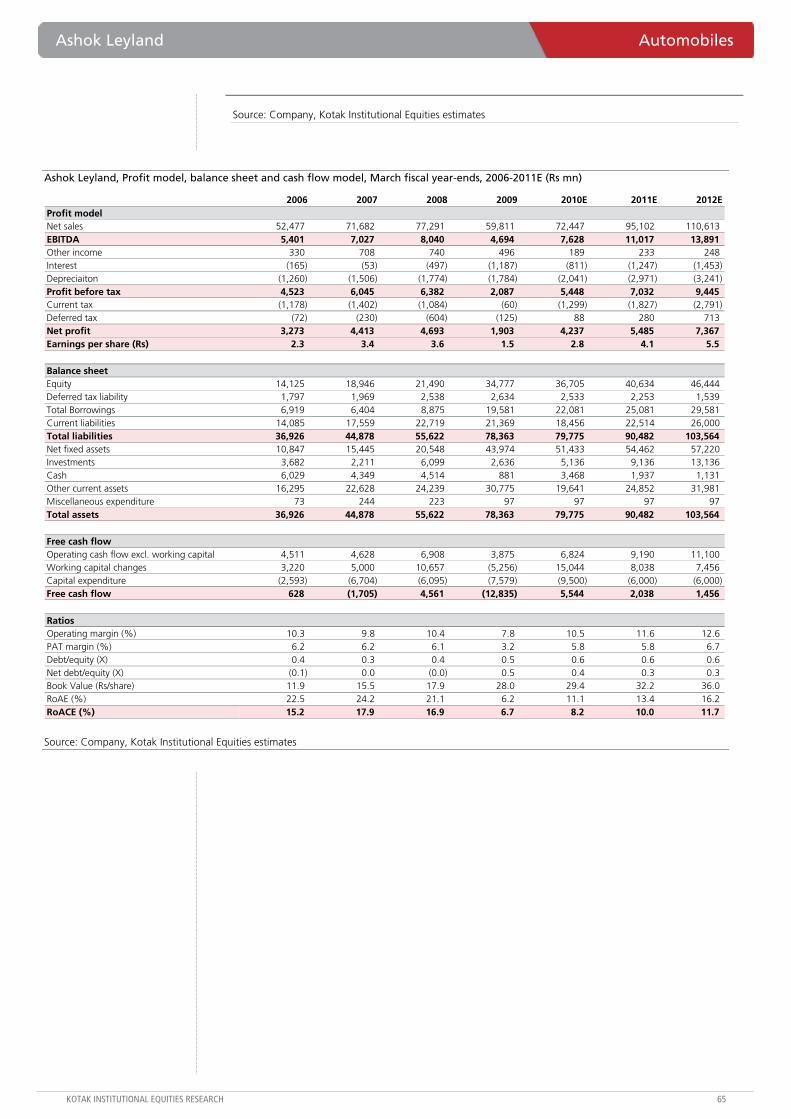

Ashok Leyland: Costs rising with capacity

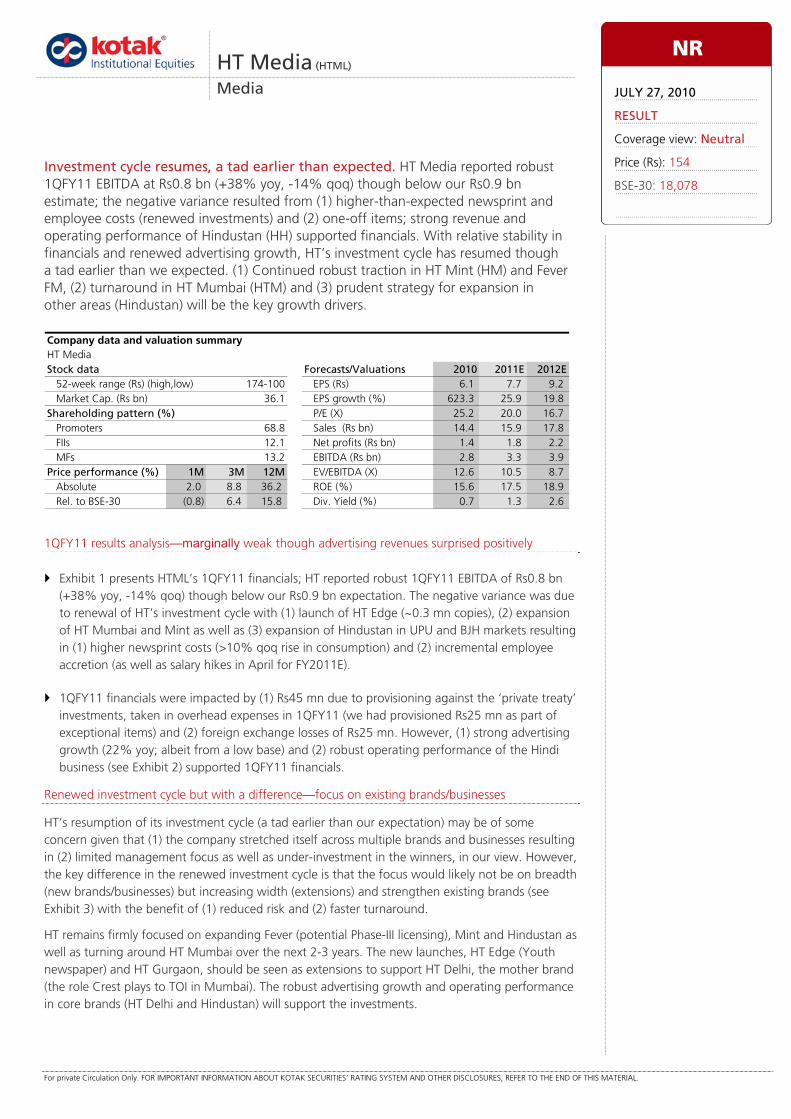

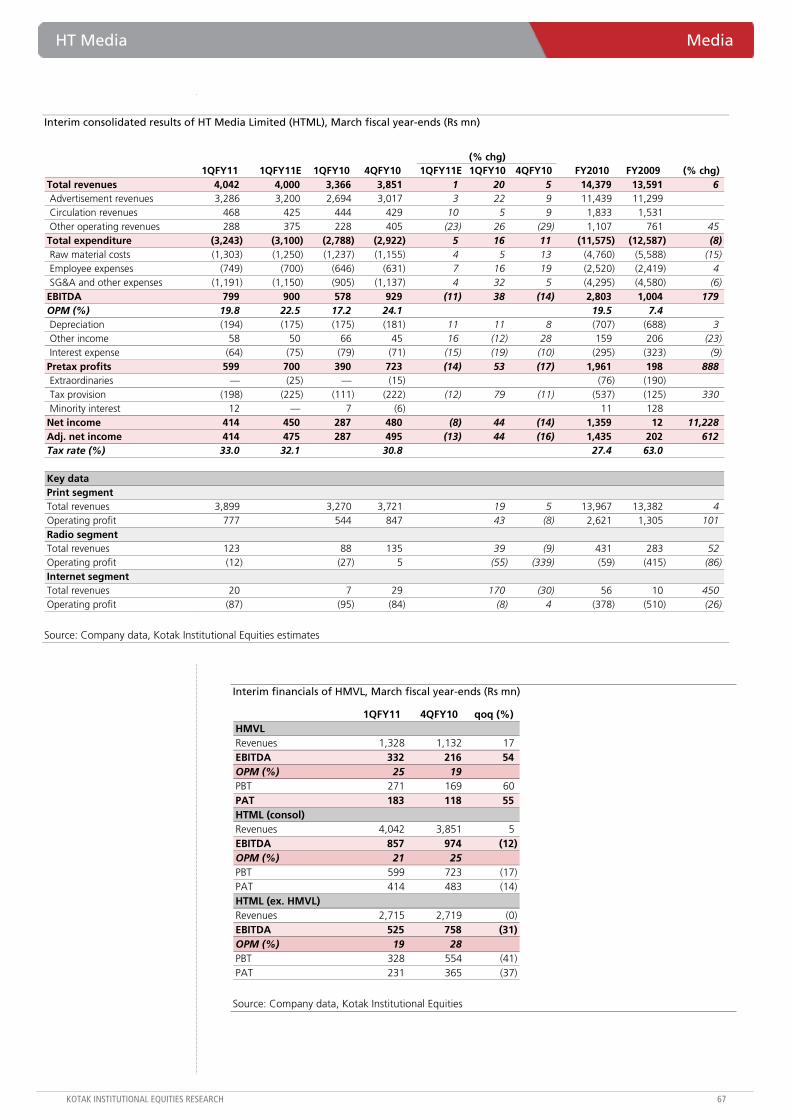

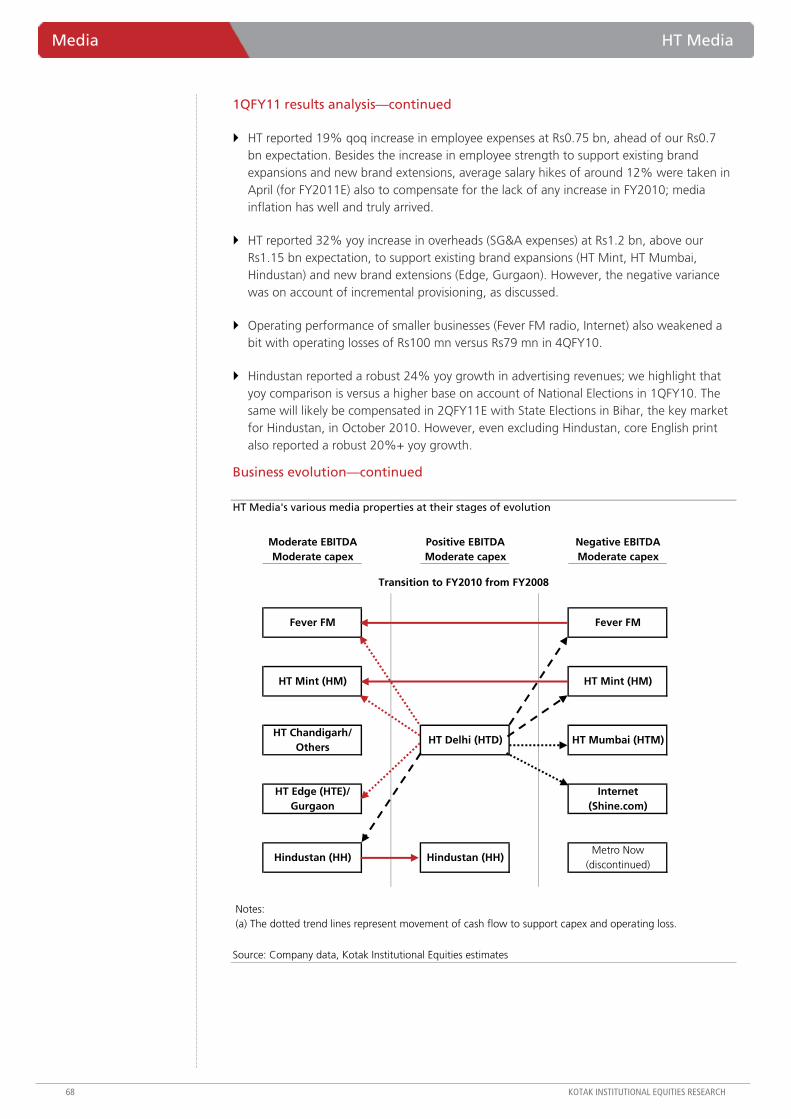

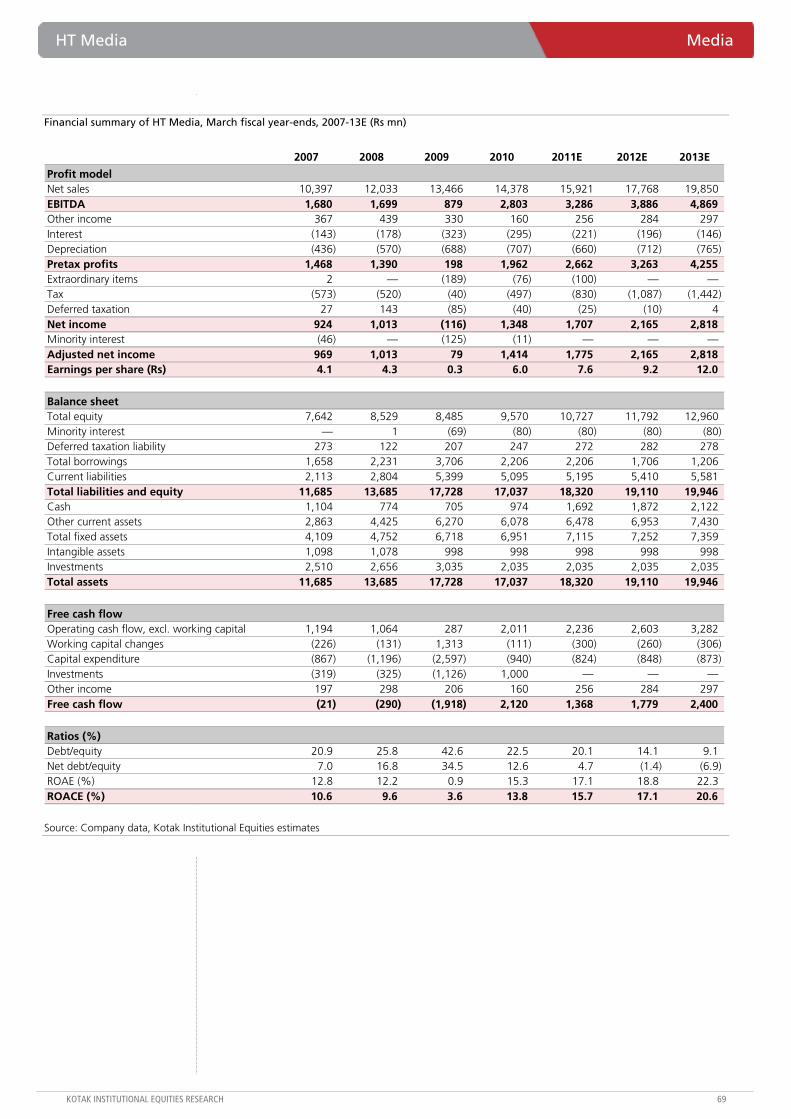

HT Media: Investment cycle resumes, a tad earlier than expected

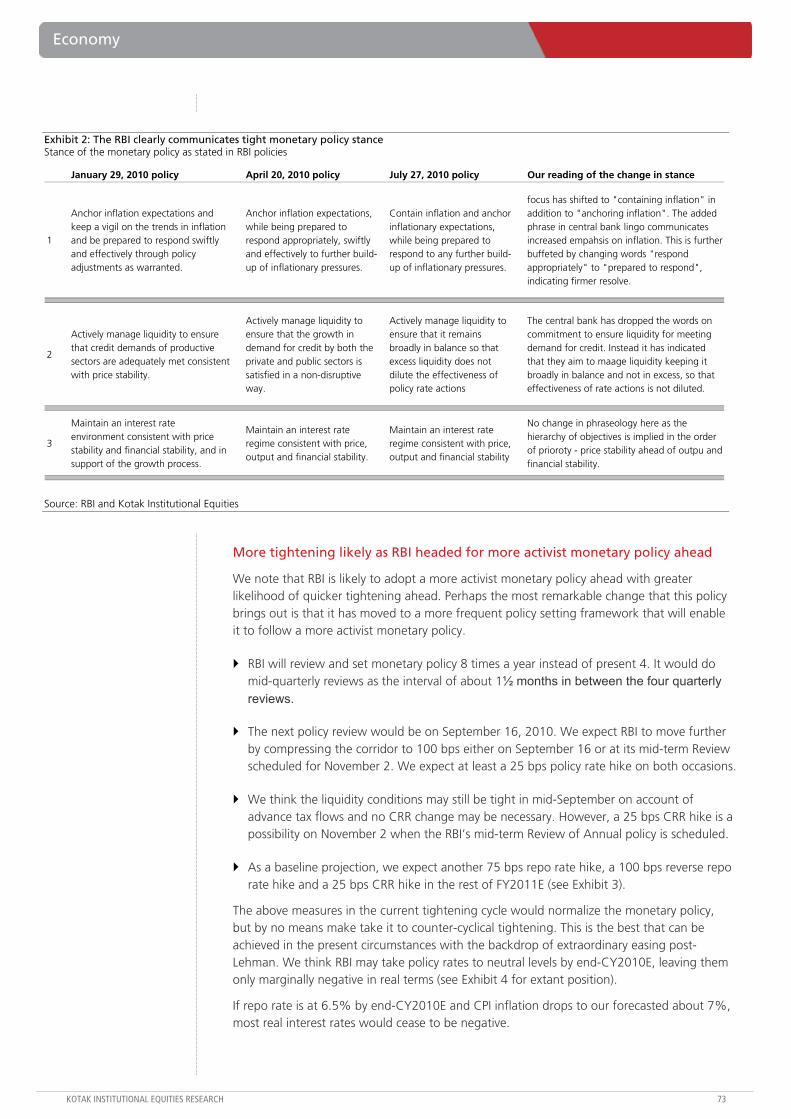

Update Economy: RBI signals tighter monetary policy ahead

News Round-up

The RBI raise the reverse repurchase rate at which it drains resources from banks to 4.5% from 4% & the repurchase rate at which it lends to banks to 5.75% from 5.5%. Economic growth & inflation forecasts were also increased due to surging demand. Home loan rates may rise, deposits to fetch more. (ECNT)

Century Textiles (CENT IN) will re-enter the shipping business five years after it exit. It will foray into the business by acquiring oil tankers & carriers. (ECNT)

The govt. has forfeited a service tax claim of over USD 468.09 mn on PowerGrid Corp (PWGR IN), a move that could facilitate smooth sailing for the proposed stake sale in the country's largest transmission utility. (ECNT)

DB Realty Ltd (DBRL IN) has received a Letter of Intent (LoI) from the government of Maharashtra to develop Sector J of the government colony at Bandra (East) in Mumbai which measures approximately 57 acres. The company will be developing approximately 8 mn sqft over the next five years. (FNLE)

JSW Steel (JSTL IN) will sell 14.99% stake to Japan's steel maker, JFE Holdings, for USD 1.21 bn. (BSTD)

The government will consider a decision on disinvestment in ONGC (ONGC IN) and IOC (IOCL IN) in the current financial year. (BSTD)

Opto Circuits (OPTC IN) has acquired US-based Unetixs Vascular Inc for a cash consideration of around USD 9.7 mn. (BSTD)

SpiceJet (SJET IN) said it will order 30 Boeing aircraft for USD 2.7 bn.

The planes will be delivered between 2014 and 2018. (BSTD)

'RBI raises GDP growth forecast to 8.5%. Adds reason to IMF's projections. (BSTD)

Source: ECNT= Economic Times, BSTD = Business Standard, FNLE = Financial Express, THBL = Business Line.

For private Circulation Only. FOR IMPORTANT INFORMATION ABOUT KOTAK SECURITIES’ RATING SYSTEM AND OTHER DISCLOSURES, REFER TO THE END OF THIS MATERIAL.

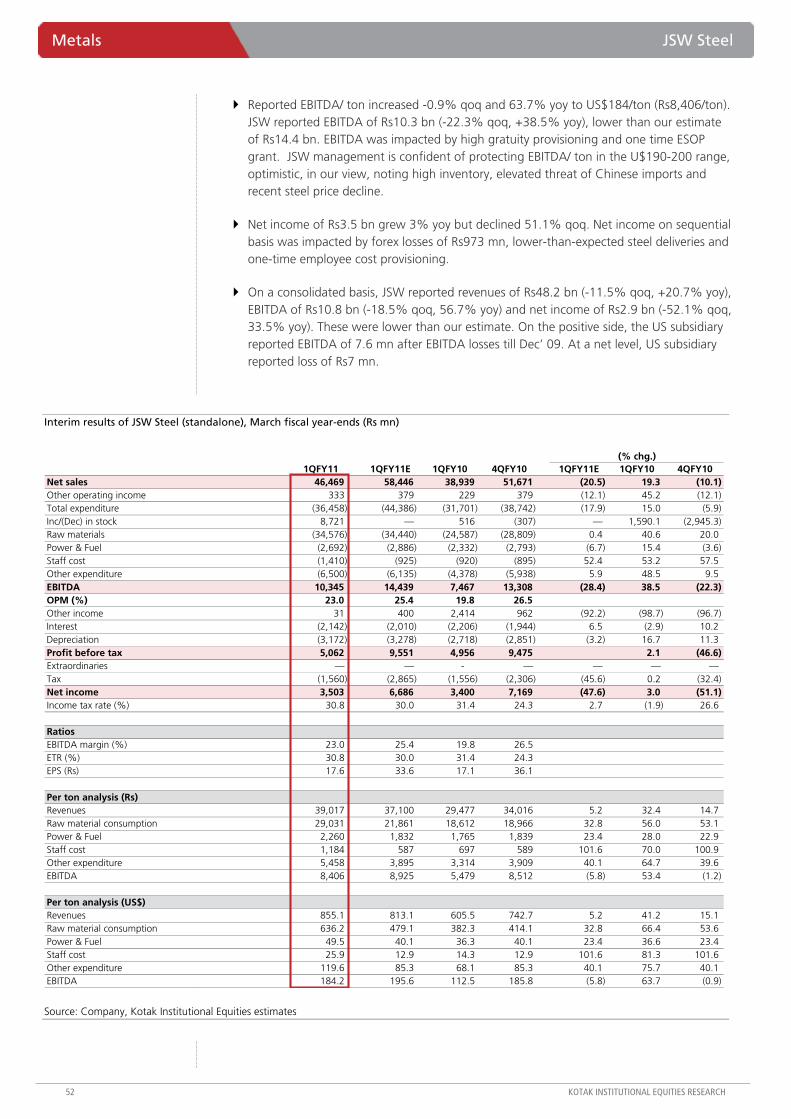

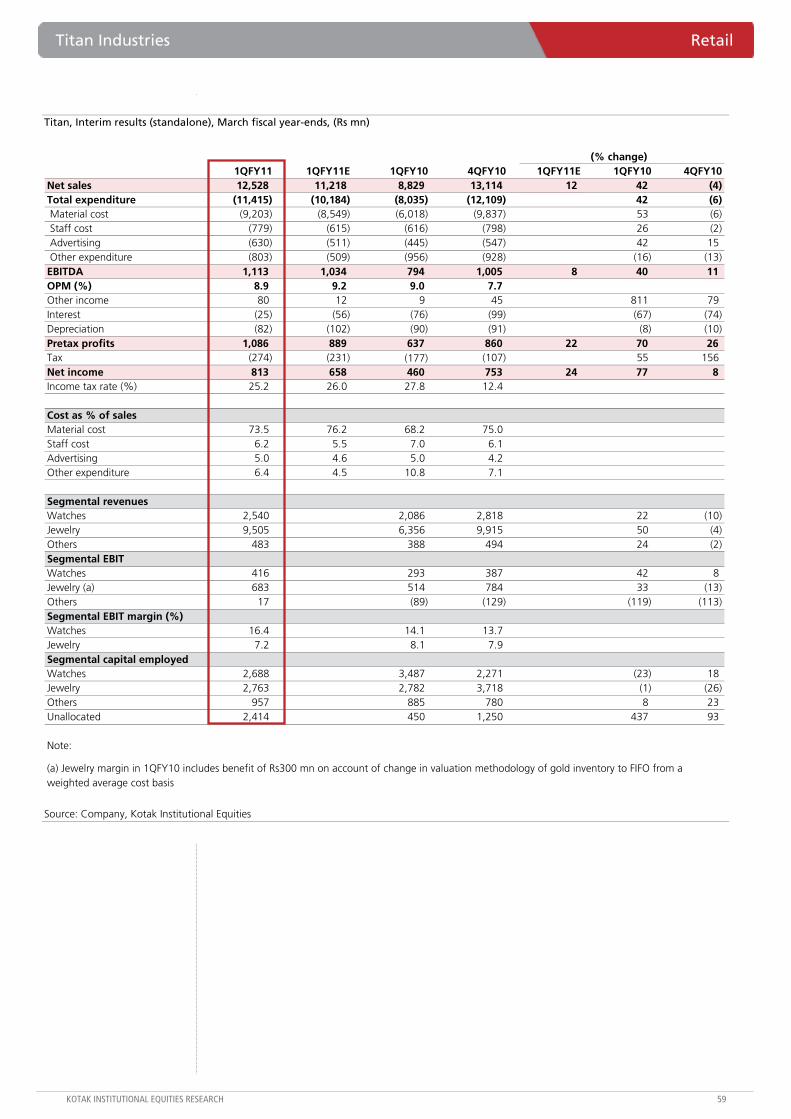

Strong growth in EBITDA yoy but up modest 2.3% qoq and 2.1% below our expectation

RIL’s 1QFY11 EBITDA increased 46% yoy and 2.3% qoq to `93.4 bn but was marginally below our `95.4 bn estimate. Higher refining and E&P volumes and higher refining margins drove yoy and qoq performance. 1QFY11 refining margin was US$7.3/bbl (+US$0.5/bbl yoy and -US$0.2/bbl qoq), chemical segment performed strongly but KG D-6 gas volumes stagnated at 60 mcm/d.

DD&A increased sharply yoy but grew modestly qoq

DD&A jumped 86% yoy to `34.9 bn reflecting full commissioning of new SEZ refinery and higher KG D-6 production volumes. However, flat volumes in KG D-6 gas production and moderate growth in oil volumes resulted in a more modest growth on a qoq basis (+2.7% qoq). Interest expense climbed 18% yoy to `5.4 bn reflecting lower interest capitalized (`1 bn versus `4.4 bn in 1QFY10). RIL’s effective tax rate increased to 19.7% against 19.3% in 4QFY10.

Cut EPS estimates for FY2011E and FY2012E

We have cut FY2011E and FY2012E EPS to `59 and `74 from `63 and `80 previously. The changes reflect (1) lower gas production at RIL’s KG D-6 gas production, (2) lower chemical and refining margins, (3) weaker Indian Rupee-US Dollar assumptions and (4) minor other changes. We see downside risks to earnings from (1) higher-than-expected taxation, (2) lower-than-expected gas production and (3) weaker-than-expected chemical and refining margins; both continue to be very weak.

SOTP-based valuation of `1,060 on FY2012E basis; retain SELL

Our revised SOTP-based 12-month fair valuation for RIL stock is `1,060 based on FY2012E estimates versus `985 previously based on average of FY2011E and FY2012E estimates. We use 7X and 7.5X EBITDA multiple to value the chemicals and refining businesses and factor in `73 of fair valuation of potential upside from gas discoveries in KG D-3, KG D-9 and MN D-4 blocks.

.dot

Reliance Industries (RIL)

Energy

In-line results; nothing new. RIL reported 1QFY11 net income at `48.5 bn, modestly lower than our `49.8 bn estimate. The negative variance was due to lower-than-expected refining margin, which offset higher other income. We have cut chemical and refining margins resulting in FY2011E EPS at `59 (-6.2%) and FY2012E EPS at `74.4 (-7.2%). We retain our SELL rating on the stock as it offers modest upside to our 12-month SOTP-based fair valuation of `1,060.

Reliance IndustriesStock data Forecasts/Valuations 2010 2011E 2012E

52-week range (Rs) (high,low) EPS (Rs) 49.6 59.0 74.4Market Cap. (Rs bn) 3,135.2 EPS growth (%) (1.8) 18.8 26.2

Shareholding pattern (%) P/E (X) 21.2 17.9 14.2Promoters 41.1 Sales (Rs bn) 1,924.6 2,585.3 2,693.2FIIs 21.3 Net profits (Rs bn) 162.4 193.0 243.5MFs 2.6 EBITDA (Rs bn) 309.4 378.1 418.5

Price performance (%) 1M 3M 12M EV/EBITDA (X) 11.4 8.8 7.3Absolute (0.9) (0.7) 8.6 ROE (%) 11.4 12.3 13.9Rel. to BSE-30 (3.6) (2.9) (7.7) Div. Yield (%) 0.6 0.7 0.9

Company data and valuation summary

1,185-841

SELL

JULY 28, 2010

RESULT

Coverage view: Cautious

Price (Rs): 1,054

Target price (Rs): 1,060

BSE-30: 18,078

QUICK NUMBERS

• 1QFY11 EBITDA increased 2% qoq, 2% below estimate

• Refining margin declined US$0.2/bbl qoq

• KG D-6 gas production stagnant at 60 mcm/d

Reliance Industries Energy

KOTAK INSTITUTIONAL EQUITIES RESEARCH 3

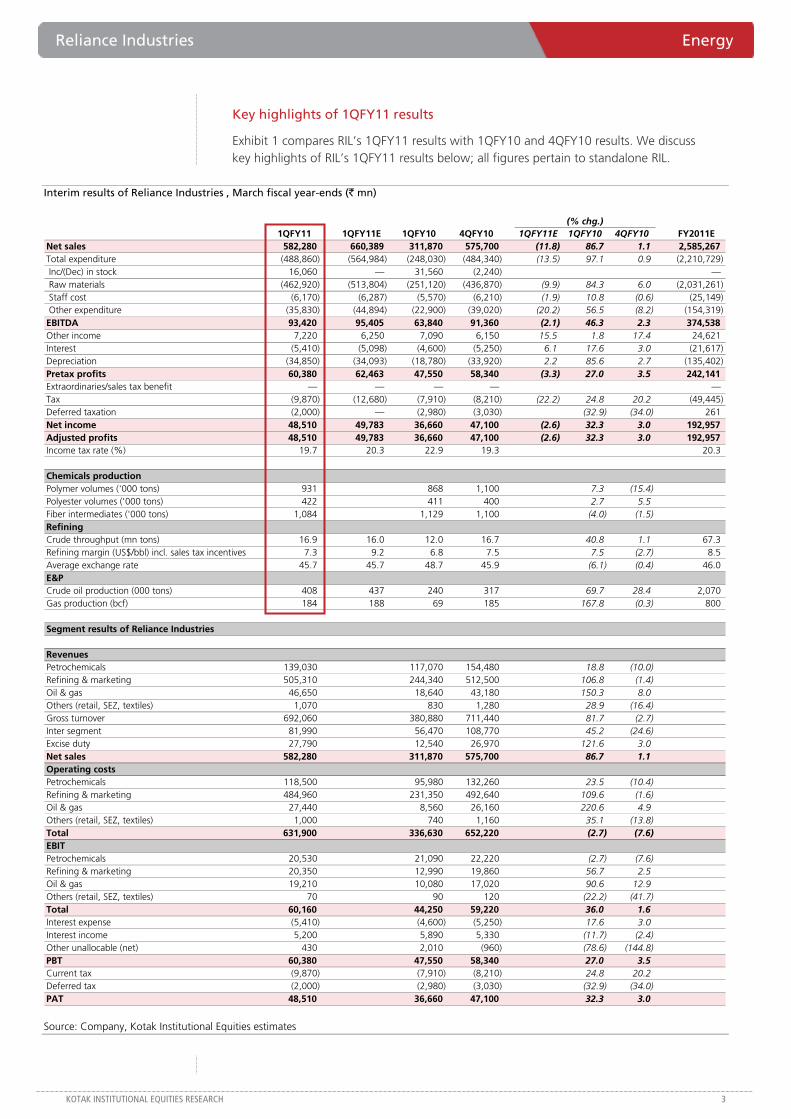

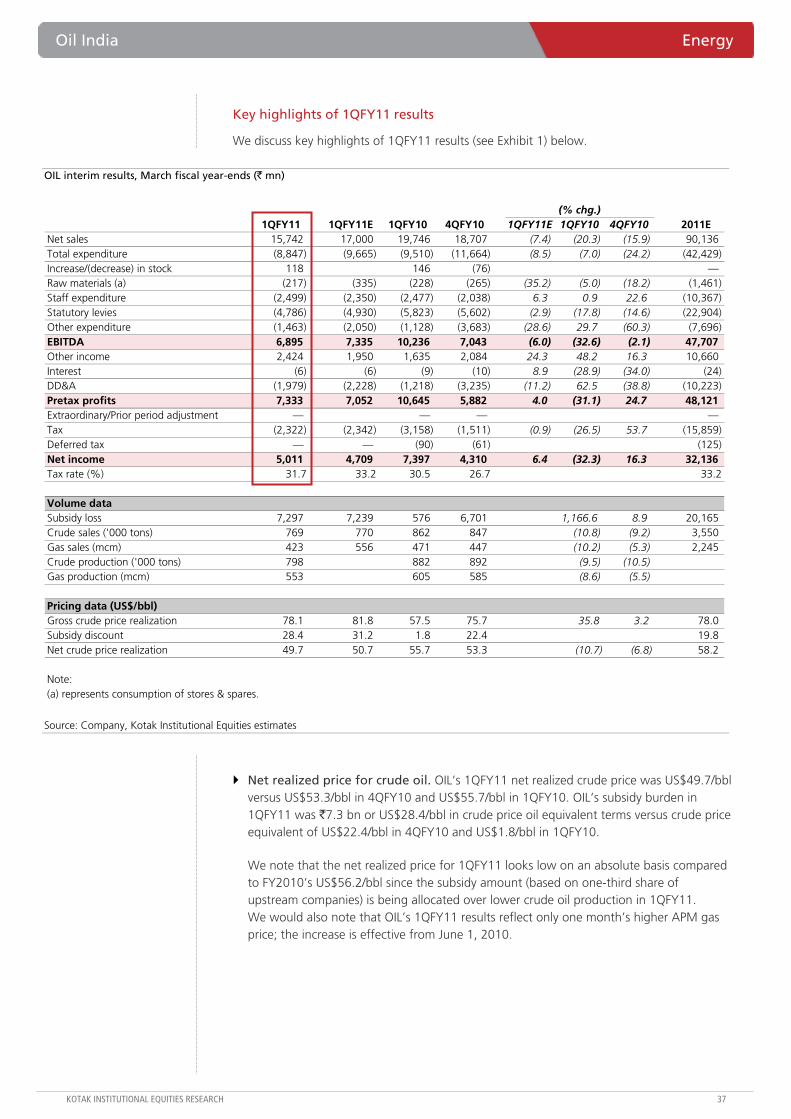

Key highlights of 1QFY11 results

Exhibit 1 compares RIL’s 1QFY11 results with 1QFY10 and 4QFY10 results. We discuss key highlights of RIL’s 1QFY11 results below; all figures pertain to standalone RIL.

Interim results of Reliance Industries , March fiscal year-ends (` mn)

(% chg.)1QFY11 1QFY11E 1QFY10 4QFY10 1QFY11E 1QFY10 4QFY10 FY2011E

Net sales 582,280 660,389 311,870 575,700 (11.8) 86.7 1.1 2,585,267 Total expenditure (488,860) (564,984) (248,030) (484,340) (13.5) 97.1 0.9 (2,210,729) Inc/(Dec) in stock 16,060 — 31,560 (2,240) — Raw materials (462,920) (513,804) (251,120) (436,870) (9.9) 84.3 6.0 (2,031,261) Staff cost (6,170) (6,287) (5,570) (6,210) (1.9) 10.8 (0.6) (25,149) Other expenditure (35,830) (44,894) (22,900) (39,020) (20.2) 56.5 (8.2) (154,319) EBITDA 93,420 95,405 63,840 91,360 (2.1) 46.3 2.3 374,538 Other income 7,220 6,250 7,090 6,150 15.5 1.8 17.4 24,621 Interest (5,410) (5,098) (4,600) (5,250) 6.1 17.6 3.0 (21,617) Depreciation (34,850) (34,093) (18,780) (33,920) 2.2 85.6 2.7 (135,402) Pretax profits 60,380 62,463 47,550 58,340 (3.3) 27.0 3.5 242,141 Extraordinaries/sales tax benefit — — — — —Tax (9,870) (12,680) (7,910) (8,210) (22.2) 24.8 20.2 (49,445) Deferred taxation (2,000) — (2,980) (3,030) (32.9) (34.0) 261 Net income 48,510 49,783 36,660 47,100 (2.6) 32.3 3.0 192,957 Adjusted profits 48,510 49,783 36,660 47,100 (2.6) 32.3 3.0 192,957 Income tax rate (%) 19.7 20.3 22.9 19.3 20.3

Chemicals productionPolymer volumes ('000 tons) 931 868 1,100 7.3 (15.4) Polyester volumes ('000 tons) 422 411 400 2.7 5.5 Fiber intermediates ('000 tons) 1,084 1,129 1,100 (4.0) (1.5) RefiningCrude throughput (mn tons) 16.9 16.0 12.0 16.7 40.8 1.1 67.3 Refining margin (US$/bbl) incl. sales tax incentives 7.3 9.2 6.8 7.5 7.5 (2.7) 8.5 Average exchange rate 45.7 45.7 48.7 45.9 (6.1) (0.4) 46.0 E&PCrude oil production (000 tons) 408 437 240 317 69.7 28.4 2,070 Gas production (bcf) 184 188 69 185 167.8 (0.3) 800

Segment results of Reliance Industries

RevenuesPetrochemicals 139,030 117,070 154,480 18.8 (10.0) Refining & marketing 505,310 244,340 512,500 106.8 (1.4) Oil & gas 46,650 18,640 43,180 150.3 8.0 Others (retail, SEZ, textiles) 1,070 830 1,280 28.9 (16.4) Gross turnover 692,060 380,880 711,440 81.7 (2.7) Inter segment 81,990 56,470 108,770 45.2 (24.6) Excise duty 27,790 12,540 26,970 121.6 3.0 Net sales 582,280 311,870 575,700 86.7 1.1 Operating costsPetrochemicals 118,500 95,980 132,260 23.5 (10.4) Refining & marketing 484,960 231,350 492,640 109.6 (1.6) Oil & gas 27,440 8,560 26,160 220.6 4.9 Others (retail, SEZ, textiles) 1,000 740 1,160 35.1 (13.8) Total 631,900 336,630 652,220 (2.7) (7.6) EBITPetrochemicals 20,530 21,090 22,220 (2.7) (7.6) Refining & marketing 20,350 12,990 19,860 56.7 2.5 Oil & gas 19,210 10,080 17,020 90.6 12.9 Others (retail, SEZ, textiles) 70 90 120 (22.2) (41.7) Total 60,160 44,250 59,220 36.0 1.6 Interest expense (5,410) (4,600) (5,250) 17.6 3.0 Interest income 5,200 5,890 5,330 (11.7) (2.4) Other unallocable (net) 430 2,010 (960) (78.6) (144.8) PBT 60,380 47,550 58,340 27.0 3.5 Current tax (9,870) (7,910) (8,210) 24.8 20.2 Deferred tax (2,000) (2,980) (3,030) (32.9) (34.0) PAT 48,510 36,660 47,100 32.3 3.0

Source: Company, Kotak Institutional Equities estimates

Energy Reliance Industries

4 KOTAK INSTITUTIONAL EQUITIES RESEARCH

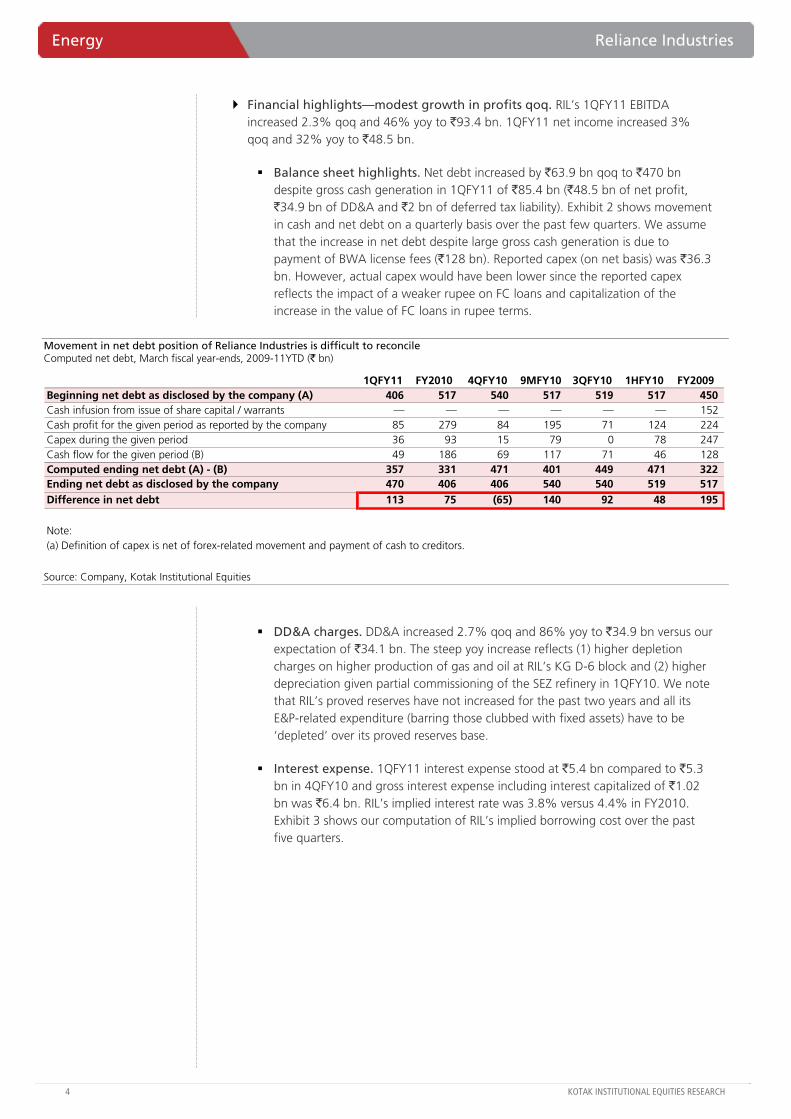

Financial highlights—modest growth in profits qoq. RIL’s 1QFY11 EBITDA increased 2.3% qoq and 46% yoy to `93.4 bn. 1QFY11 net income increased 3% qoq and 32% yoy to `48.5 bn.

Balance sheet highlights. Net debt increased by `63.9 bn qoq to `470 bn despite gross cash generation in 1QFY11 of `85.4 bn (`48.5 bn of net profit, `34.9 bn of DD&A and `2 bn of deferred tax liability). Exhibit 2 shows movement in cash and net debt on a quarterly basis over the past few quarters. We assume that the increase in net debt despite large gross cash generation is due to payment of BWA license fees (`128 bn). Reported capex (on net basis) was `36.3 bn. However, actual capex would have been lower since the reported capex reflects the impact of a weaker rupee on FC loans and capitalization of the increase in the value of FC loans in rupee terms.

Movement in net debt position of Reliance Industries is difficult to reconcile Computed net debt, March fiscal year-ends, 2009-11YTD (` bn)

1QFY11 FY2010 4QFY10 9MFY10 3QFY10 1HFY10 FY2009Beginning net debt as disclosed by the company (A) 406 517 540 517 519 517 450 Cash infusion from issue of share capital / warrants — — — — — — 152 Cash profit for the given period as reported by the company 85 279 84 195 71 124 224 Capex during the given period 36 93 15 79 0 78 247 Cash flow for the given period (B) 49 186 69 117 71 46 128 Computed ending net debt (A) - (B) 357 331 471 401 449 471 322 Ending net debt as disclosed by the company 470 406 406 540 540 519 517 Difference in net debt 113 75 (65) 140 92 48 195

Note:(a) Definition of capex is net of forex-related movement and payment of cash to creditors.

Source: Company, Kotak Institutional Equities

DD&A charges. DD&A increased 2.7% qoq and 86% yoy to `34.9 bn versus our expectation of `34.1 bn. The steep yoy increase reflects (1) higher depletion charges on higher production of gas and oil at RIL’s KG D-6 block and (2) higher depreciation given partial commissioning of the SEZ refinery in 1QFY10. We note that RIL’s proved reserves have not increased for the past two years and all its E&P-related expenditure (barring those clubbed with fixed assets) have to be ‘depleted’ over its proved reserves base.

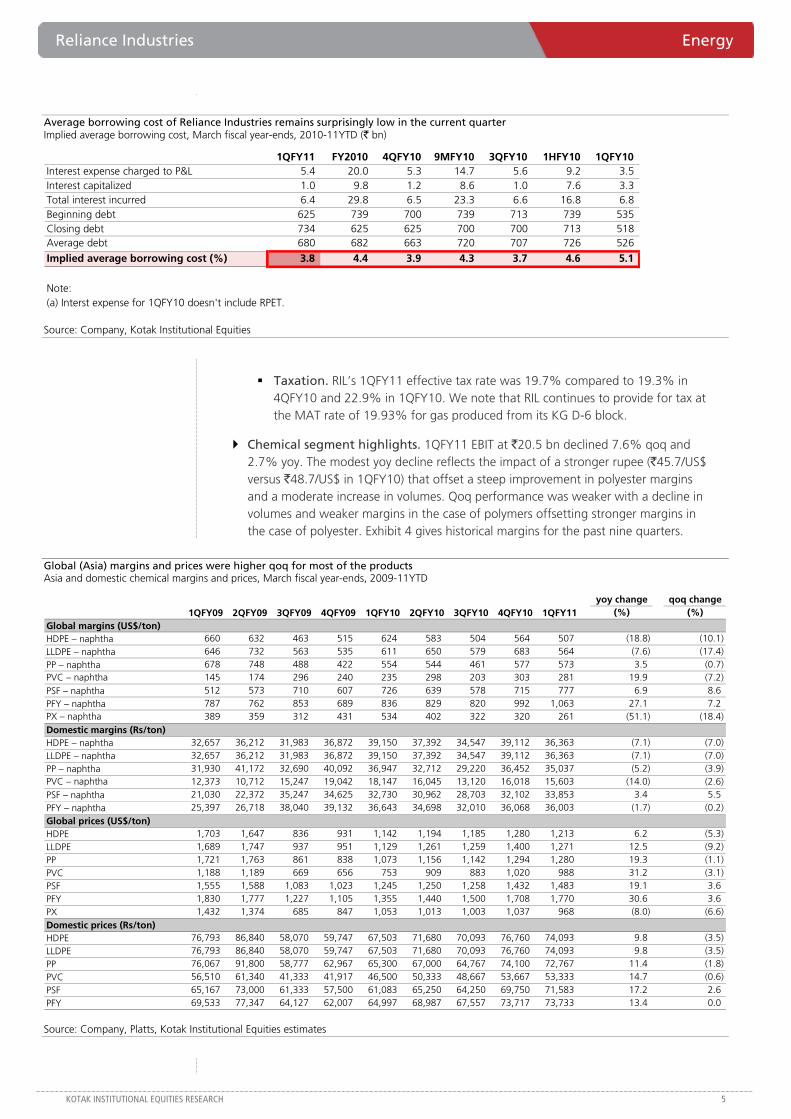

Interest expense. 1QFY11 interest expense stood at `5.4 bn compared to `5.3 bn in 4QFY10 and gross interest expense including interest capitalized of `1.02 bn was `6.4 bn. RIL’s implied interest rate was 3.8% versus 4.4% in FY2010. Exhibit 3 shows our computation of RIL’s implied borrowing cost over the past five quarters.

Reliance Industries Energy

KOTAK INSTITUTIONAL EQUITIES RESEARCH 5

Average borrowing cost of Reliance Industries remains surprisingly low in the current quarter Implied average borrowing cost, March fiscal year-ends, 2010-11YTD (` bn)

1QFY11 FY2010 4QFY10 9MFY10 3QFY10 1HFY10 1QFY10Interest expense charged to P&L 5.4 20.0 5.3 14.7 5.6 9.2 3.5 Interest capitalized 1.0 9.8 1.2 8.6 1.0 7.6 3.3 Total interest incurred 6.4 29.8 6.5 23.3 6.6 16.8 6.8 Beginning debt 625 739 700 739 713 739 535 Closing debt 734 625 625 700 700 713 518 Average debt 680 682 663 720 707 726 526

Implied average borrowing cost (%) 3.8 4.4 3.9 4.3 3.7 4.6 5.1

Note:(a) Interst expense for 1QFY10 doesn't include RPET.

Source: Company, Kotak Institutional Equities

Taxation. RIL’s 1QFY11 effective tax rate was 19.7% compared to 19.3% in 4QFY10 and 22.9% in 1QFY10. We note that RIL continues to provide for tax at the MAT rate of 19.93% for gas produced from its KG D-6 block.

Chemical segment highlights. 1QFY11 EBIT at `20.5 bn declined 7.6% qoq and 2.7% yoy. The modest yoy decline reflects the impact of a stronger rupee (`45.7/US$ versus `48.7/US$ in 1QFY10) that offset a steep improvement in polyester margins and a moderate increase in volumes. Qoq performance was weaker with a decline in volumes and weaker margins in the case of polymers offsetting stronger margins in the case of polyester. Exhibit 4 gives historical margins for the past nine quarters.

Global (Asia) margins and prices were higher qoq for most of the products Asia and domestic chemical margins and prices, March fiscal year-ends, 2009-11YTD

yoy change qoq change1QFY09 2QFY09 3QFY09 4QFY09 1QFY10 2QFY10 3QFY10 4QFY10 1QFY11 (%) (%)

Global margins (US$/ton)HDPE – naphtha 660 632 463 515 624 583 504 564 507 (18.8) (10.1) LLDPE – naphtha 646 732 563 535 611 650 579 683 564 (7.6) (17.4) PP – naphtha 678 748 488 422 554 544 461 577 573 3.5 (0.7) PVC – naphtha 145 174 296 240 235 298 203 303 281 19.9 (7.2) PSF – naphtha 512 573 710 607 726 639 578 715 777 6.9 8.6 PFY – naphtha 787 762 853 689 836 829 820 992 1,063 27.1 7.2 PX – naphtha 389 359 312 431 534 402 322 320 261 (51.1) (18.4) Domestic margins (Rs/ton)HDPE – naphtha 32,657 36,212 31,983 36,872 39,150 37,392 34,547 39,112 36,363 (7.1) (7.0) LLDPE – naphtha 32,657 36,212 31,983 36,872 39,150 37,392 34,547 39,112 36,363 (7.1) (7.0) PP – naphtha 31,930 41,172 32,690 40,092 36,947 32,712 29,220 36,452 35,037 (5.2) (3.9) PVC – naphtha 12,373 10,712 15,247 19,042 18,147 16,045 13,120 16,018 15,603 (14.0) (2.6) PSF – naphtha 21,030 22,372 35,247 34,625 32,730 30,962 28,703 32,102 33,853 3.4 5.5 PFY – naphtha 25,397 26,718 38,040 39,132 36,643 34,698 32,010 36,068 36,003 (1.7) (0.2) Global prices (US$/ton)HDPE 1,703 1,647 836 931 1,142 1,194 1,185 1,280 1,213 6.2 (5.3) LLDPE 1,689 1,747 937 951 1,129 1,261 1,259 1,400 1,271 12.5 (9.2) PP 1,721 1,763 861 838 1,073 1,156 1,142 1,294 1,280 19.3 (1.1) PVC 1,188 1,189 669 656 753 909 883 1,020 988 31.2 (3.1) PSF 1,555 1,588 1,083 1,023 1,245 1,250 1,258 1,432 1,483 19.1 3.6 PFY 1,830 1,777 1,227 1,105 1,355 1,440 1,500 1,708 1,770 30.6 3.6 PX 1,432 1,374 685 847 1,053 1,013 1,003 1,037 968 (8.0) (6.6) Domestic prices (Rs/ton)HDPE 76,793 86,840 58,070 59,747 67,503 71,680 70,093 76,760 74,093 9.8 (3.5) LLDPE 76,793 86,840 58,070 59,747 67,503 71,680 70,093 76,760 74,093 9.8 (3.5) PP 76,067 91,800 58,777 62,967 65,300 67,000 64,767 74,100 72,767 11.4 (1.8) PVC 56,510 61,340 41,333 41,917 46,500 50,333 48,667 53,667 53,333 14.7 (0.6) PSF 65,167 73,000 61,333 57,500 61,083 65,250 64,250 69,750 71,583 17.2 2.6 PFY 69,533 77,347 64,127 62,007 64,997 68,987 67,557 73,717 73,733 13.4 0.0

Source: Company, Platts, Kotak Institutional Equities estimates

Energy Reliance Industries

6 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Polymer production volumes increased 7.3% yoy to 0.93 mn tons but declined 15.4% qoq reflecting shutdown at its Hazira and Nagothane cracker complexes. Polyester volumes increased 2.7% yoy and 5.5% qoq to 0.42 mn tons. As per the company, domestic polymer demand was largely flat yoy while domestic fiber and yarn demand increased 10% yoy in 1QFY11.

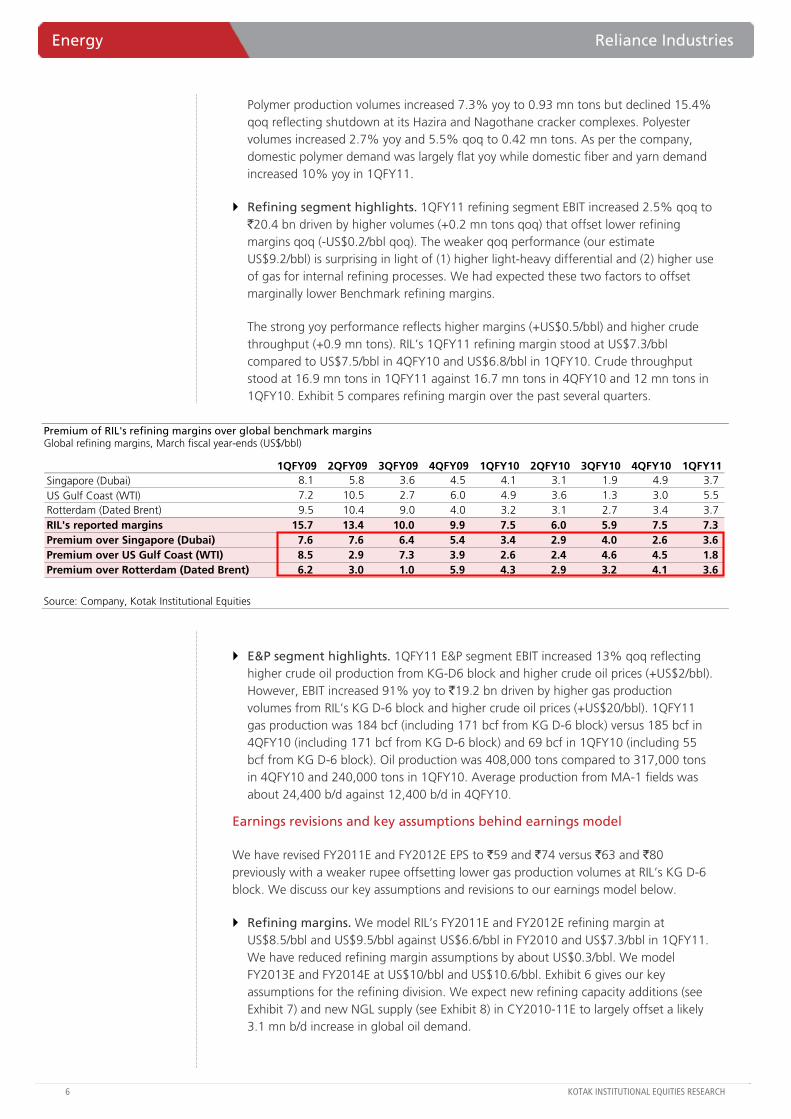

Refining segment highlights. 1QFY11 refining segment EBIT increased 2.5% qoq to `20.4 bn driven by higher volumes (+0.2 mn tons qoq) that offset lower refining margins qoq (-US$0.2/bbl qoq). The weaker qoq performance (our estimate US$9.2/bbl) is surprising in light of (1) higher light-heavy differential and (2) higher use of gas for internal refining processes. We had expected these two factors to offset marginally lower Benchmark refining margins.

The strong yoy performance reflects higher margins (+US$0.5/bbl) and higher crude throughput (+0.9 mn tons). RIL’s 1QFY11 refining margin stood at US$7.3/bbl compared to US$7.5/bbl in 4QFY10 and US$6.8/bbl in 1QFY10. Crude throughput stood at 16.9 mn tons in 1QFY11 against 16.7 mn tons in 4QFY10 and 12 mn tons in 1QFY10. Exhibit 5 compares refining margin over the past several quarters.

Premium of RIL's refining margins over global benchmark margins Global refining margins, March fiscal year-ends (US$/bbl)

1QFY09 2QFY09 3QFY09 4QFY09 1QFY10 2QFY10 3QFY10 4QFY10 1QFY11Singapore (Dubai) 8.1 5.8 3.6 4.5 4.1 3.1 1.9 4.9 3.7 US Gulf Coast (WTI) 7.2 10.5 2.7 6.0 4.9 3.6 1.3 3.0 5.5 Rotterdam (Dated Brent) 9.5 10.4 9.0 4.0 3.2 3.1 2.7 3.4 3.7 RIL's reported margins 15.7 13.4 10.0 9.9 7.5 6.0 5.9 7.5 7.3 Premium over Singapore (Dubai) 7.6 7.6 6.4 5.4 3.4 2.9 4.0 2.6 3.6 Premium over US Gulf Coast (WTI) 8.5 2.9 7.3 3.9 2.6 2.4 4.6 4.5 1.8 Premium over Rotterdam (Dated Brent) 6.2 3.0 1.0 5.9 4.3 2.9 3.2 4.1 3.6

Source: Company, Kotak Institutional Equities

E&P segment highlights. 1QFY11 E&P segment EBIT increased 13% qoq reflecting higher crude oil production from KG-D6 block and higher crude oil prices (+US$2/bbl). However, EBIT increased 91% yoy to `19.2 bn driven by higher gas production volumes from RIL’s KG D-6 block and higher crude oil prices (+US$20/bbl). 1QFY11 gas production was 184 bcf (including 171 bcf from KG D-6 block) versus 185 bcf in 4QFY10 (including 171 bcf from KG D-6 block) and 69 bcf in 1QFY10 (including 55 bcf from KG D-6 block). Oil production was 408,000 tons compared to 317,000 tons in 4QFY10 and 240,000 tons in 1QFY10. Average production from MA-1 fields was about 24,400 b/d against 12,400 b/d in 4QFY10.

Earnings revisions and key assumptions behind earnings model

We have revised FY2011E and FY2012E EPS to `59 and `74 versus `63 and `80 previously with a weaker rupee offsetting lower gas production volumes at RIL’s KG D-6 block. We discuss our key assumptions and revisions to our earnings model below.

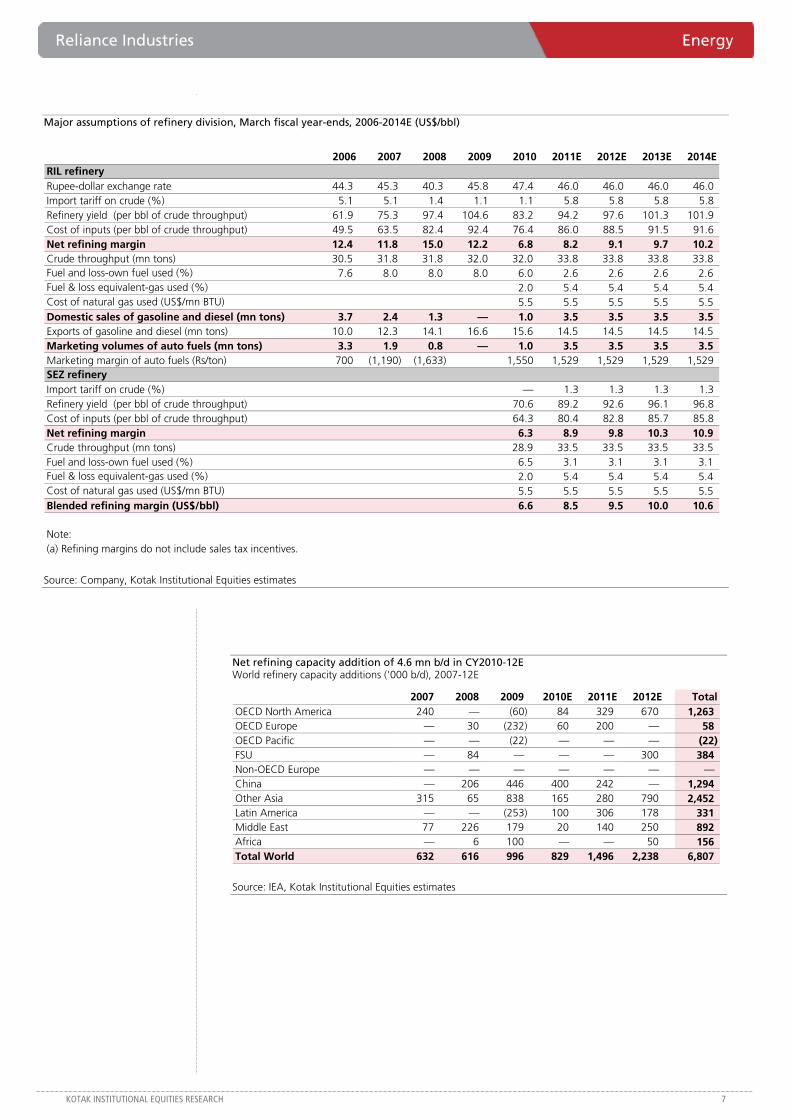

Refining margins. We model RIL’s FY2011E and FY2012E refining margin at US$8.5/bbl and US$9.5/bbl against US$6.6/bbl in FY2010 and US$7.3/bbl in 1QFY11. We have reduced refining margin assumptions by about US$0.3/bbl. We model FY2013E and FY2014E at US$10/bbl and US$10.6/bbl. Exhibit 6 gives our key assumptions for the refining division. We expect new refining capacity additions (see Exhibit 7) and new NGL supply (see Exhibit 8) in CY2010-11E to largely offset a likely 3.1 mn b/d increase in global oil demand.

Reliance Industries Energy

KOTAK INSTITUTIONAL EQUITIES RESEARCH 7

Major assumptions of refinery division, March fiscal year-ends, 2006-2014E (US$/bbl)

2006 2007 2008 2009 2010 2011E 2012E 2013E 2014ERIL refineryRupee-dollar exchange rate 44.3 45.3 40.3 45.8 47.4 46.0 46.0 46.0 46.0 Import tariff on crude (%) 5.1 5.1 1.4 1.1 1.1 5.8 5.8 5.8 5.8 Refinery yield (per bbl of crude throughput) 61.9 75.3 97.4 104.6 83.2 94.2 97.6 101.3 101.9 Cost of inputs (per bbl of crude throughput) 49.5 63.5 82.4 92.4 76.4 86.0 88.5 91.5 91.6 Net refining margin 12.4 11.8 15.0 12.2 6.8 8.2 9.1 9.7 10.2 Crude throughput (mn tons) 30.5 31.8 31.8 32.0 32.0 33.8 33.8 33.8 33.8 Fuel and loss-own fuel used (%) 7.6 8.0 8.0 8.0 6.0 2.6 2.6 2.6 2.6 Fuel & loss equivalent-gas used (%) 2.0 5.4 5.4 5.4 5.4 Cost of natural gas used (US$/mn BTU) 5.5 5.5 5.5 5.5 5.5 Domestic sales of gasoline and diesel (mn tons) 3.7 2.4 1.3 — 1.0 3.5 3.5 3.5 3.5 Exports of gasoline and diesel (mn tons) 10.0 12.3 14.1 16.6 15.6 14.5 14.5 14.5 14.5 Marketing volumes of auto fuels (mn tons) 3.3 1.9 0.8 — 1.0 3.5 3.5 3.5 3.5 Marketing margin of auto fuels (Rs/ton) 700 (1,190) (1,633) 1,550 1,529 1,529 1,529 1,529SEZ refineryImport tariff on crude (%) — 1.3 1.3 1.3 1.3 Refinery yield (per bbl of crude throughput) 70.6 89.2 92.6 96.1 96.8 Cost of inputs (per bbl of crude throughput) 64.3 80.4 82.8 85.7 85.8 Net refining margin 6.3 8.9 9.8 10.3 10.9 Crude throughput (mn tons) 28.9 33.5 33.5 33.5 33.5 Fuel and loss-own fuel used (%) 6.5 3.1 3.1 3.1 3.1 Fuel & loss equivalent-gas used (%) 2.0 5.4 5.4 5.4 5.4 Cost of natural gas used (US$/mn BTU) 5.5 5.5 5.5 5.5 5.5 Blended refining margin (US$/bbl) 6.6 8.5 9.5 10.0 10.6

Note:(a) Refining margins do not include sales tax incentives.

Source: Company, Kotak Institutional Equities estimates

Net refining capacity addition of 4.6 mn b/d in CY2010-12E World refinery capacity additions ('000 b/d), 2007-12E

2007 2008 2009 2010E 2011E 2012E TotalOECD North America 240 — (60) 84 329 670 1,263 OECD Europe — 30 (232) 60 200 — 58 OECD Pacific — — (22) — — — (22)FSU — 84 — — — 300 384 Non-OECD Europe — — — — — — —China — 206 446 400 242 — 1,294 Other Asia 315 65 838 165 280 790 2,452 Latin America — — (253) 100 306 178 331 Middle East 77 226 179 20 140 250 892 Africa — 6 100 — — 50 156 Total World 632 616 996 829 1,496 2,238 6,807

Source: IEA, Kotak Institutional Equities estimates

Energy Reliance Industries

8 KOTAK INSTITUTIONAL EQUITIES RESEARCH

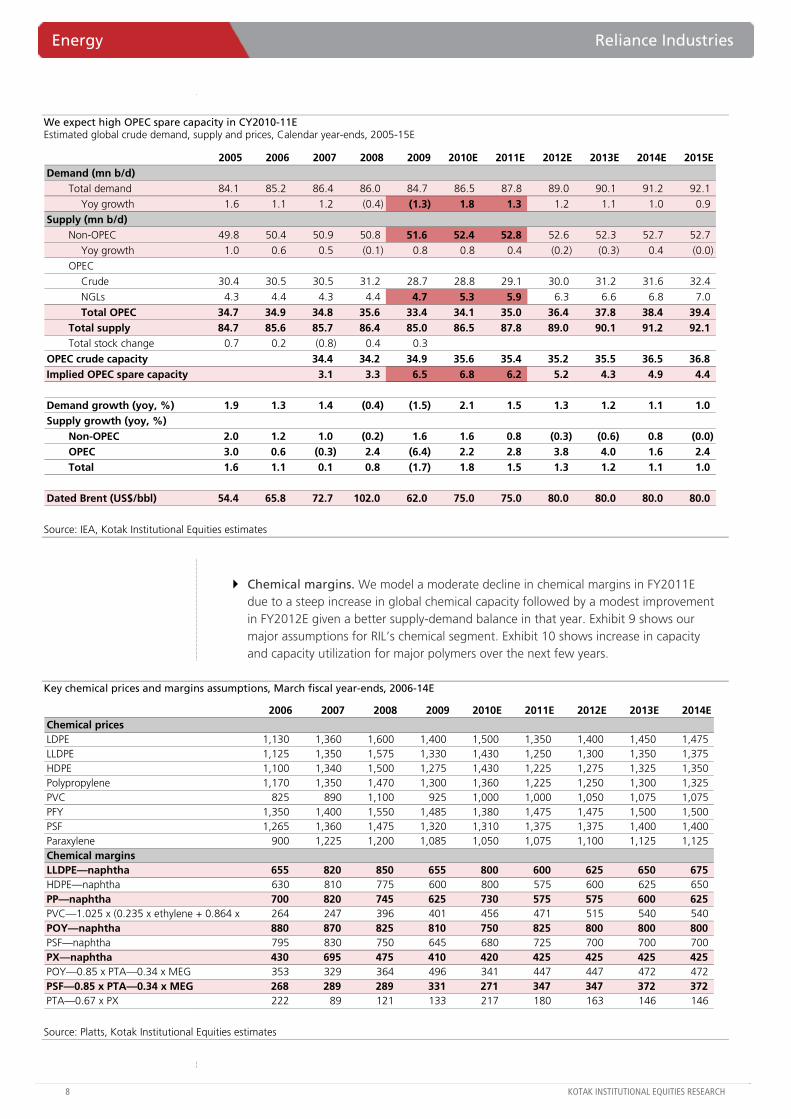

We expect high OPEC spare capacity in CY2010-11E Estimated global crude demand, supply and prices, Calendar year-ends, 2005-15E

2005 2006 2007 2008 2009 2010E 2011E 2012E 2013E 2014E 2015EDemand (mn b/d)

Total demand 84.1 85.2 86.4 86.0 84.7 86.5 87.8 89.0 90.1 91.2 92.1Yoy growth 1.6 1.1 1.2 (0.4) (1.3) 1.8 1.3 1.2 1.1 1.0 0.9

Supply (mn b/d)Non-OPEC 49.8 50.4 50.9 50.8 51.6 52.4 52.8 52.6 52.3 52.7 52.7

Yoy growth 1.0 0.6 0.5 (0.1) 0.8 0.8 0.4 (0.2) (0.3) 0.4 (0.0)OPEC

Crude 30.4 30.5 30.5 31.2 28.7 28.8 29.1 30.0 31.2 31.6 32.4NGLs 4.3 4.4 4.3 4.4 4.7 5.3 5.9 6.3 6.6 6.8 7.0

Total OPEC 34.7 34.9 34.8 35.6 33.4 34.1 35.0 36.4 37.8 38.4 39.4Total supply 84.7 85.6 85.7 86.4 85.0 86.5 87.8 89.0 90.1 91.2 92.1Total stock change 0.7 0.2 (0.8) 0.4 0.3

OPEC crude capacity 34.4 34.2 34.9 35.6 35.4 35.2 35.5 36.5 36.8Implied OPEC spare capacity 3.1 3.3 6.5 6.8 6.2 5.2 4.3 4.9 4.4

Demand growth (yoy, %) 1.9 1.3 1.4 (0.4) (1.5) 2.1 1.5 1.3 1.2 1.1 1.0Supply growth (yoy, %)

Non-OPEC 2.0 1.2 1.0 (0.2) 1.6 1.6 0.8 (0.3) (0.6) 0.8 (0.0)OPEC 3.0 0.6 (0.3) 2.4 (6.4) 2.2 2.8 3.8 4.0 1.6 2.4Total 1.6 1.1 0.1 0.8 (1.7) 1.8 1.5 1.3 1.2 1.1 1.0

Dated Brent (US$/bbl) 54.4 65.8 72.7 102.0 62.0 75.0 75.0 80.0 80.0 80.0 80.0

Source: IEA, Kotak Institutional Equities estimates

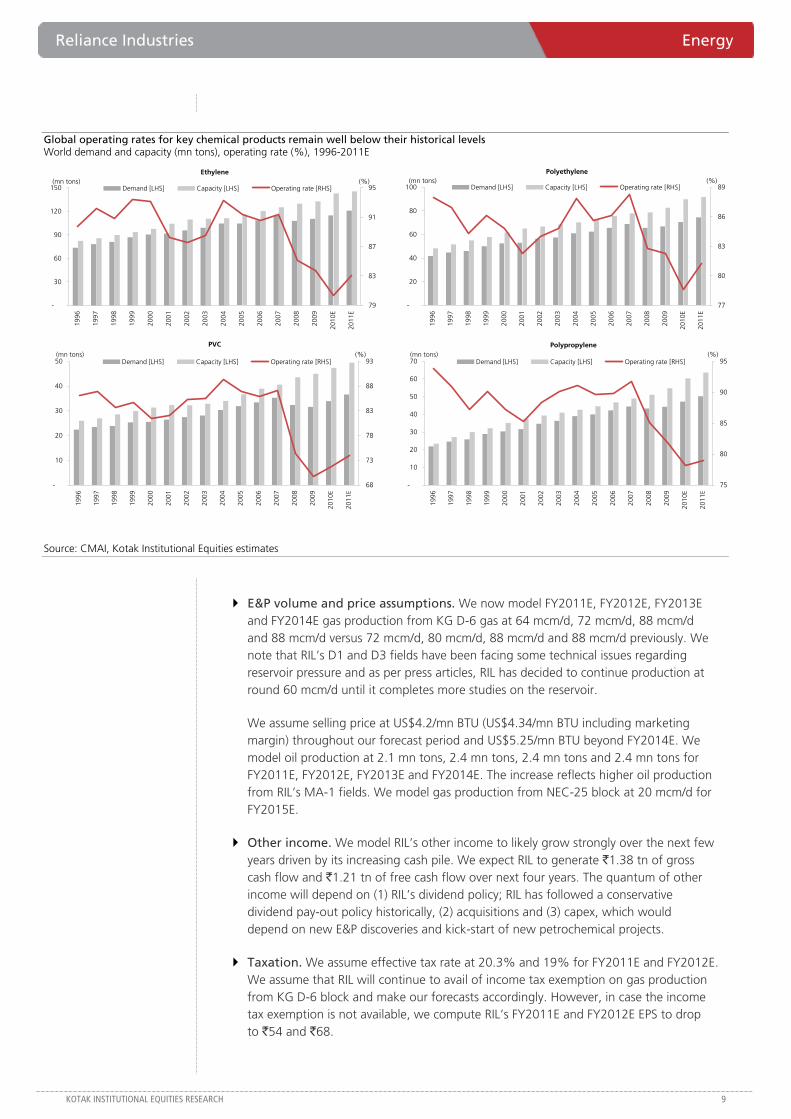

Chemical margins. We model a moderate decline in chemical margins in FY2011E due to a steep increase in global chemical capacity followed by a modest improvement in FY2012E given a better supply-demand balance in that year. Exhibit 9 shows our major assumptions for RIL’s chemical segment. Exhibit 10 shows increase in capacity and capacity utilization for major polymers over the next few years.

Key chemical prices and margins assumptions, March fiscal year-ends, 2006-14E

2006 2007 2008 2009 2010E 2011E 2012E 2013E 2014EChemical pricesLDPE 1,130 1,360 1,600 1,400 1,500 1,350 1,400 1,450 1,475LLDPE 1,125 1,350 1,575 1,330 1,430 1,250 1,300 1,350 1,375HDPE 1,100 1,340 1,500 1,275 1,430 1,225 1,275 1,325 1,350Polypropylene 1,170 1,350 1,470 1,300 1,360 1,225 1,250 1,300 1,325PVC 825 890 1,100 925 1,000 1,000 1,050 1,075 1,075PFY 1,350 1,400 1,550 1,485 1,380 1,475 1,475 1,500 1,500PSF 1,265 1,360 1,475 1,320 1,310 1,375 1,375 1,400 1,400Paraxylene 900 1,225 1,200 1,085 1,050 1,075 1,100 1,125 1,125Chemical marginsLLDPE—naphtha 655 820 850 655 800 600 625 650 675 HDPE—naphtha 630 810 775 600 800 575 600 625 650 PP—naphtha 700 820 745 625 730 575 575 600 625 PVC—1.025 x (0.235 x ethylene + 0.864 x 264 247 396 401 456 471 515 540 540 POY—naphtha 880 870 825 810 750 825 800 800 800 PSF—naphtha 795 830 750 645 680 725 700 700 700 PX—naphtha 430 695 475 410 420 425 425 425 425 POY—0.85 x PTA—0.34 x MEG 353 329 364 496 341 447 447 472 472 PSF—0.85 x PTA—0.34 x MEG 268 289 289 331 271 347 347 372 372 PTA—0.67 x PX 222 89 121 133 217 180 163 146 146

Source: Platts, Kotak Institutional Equities estimates

Reliance Industries Energy

KOTAK INSTITUTIONAL EQUITIES RESEARCH 9

Global operating rates for key chemical products remain well below their historical levels World demand and capacity (mn tons), operating rate (%), 1996-2011E

-

30

60

90

120

150

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

E

2011

E

(mn tons)

79

83

87

91

95(%)

Demand [LHS] Capacity [LHS] Operating rate [RHS]

-

20

40

60

80

100

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

E

2011

E

(mn tons)

77

80

83

86

89(%)

Demand [LHS] Capacity [LHS] Operating rate [RHS]

-

10

20

30

40

50

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

E

2011

E(mn tons)

68

73

78

83

88

93(%)

Demand [LHS] Capacity [LHS] Operating rate [RHS]

-

10

20

30

40

50

60

70

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

E

2011

E

(mn tons)

75

80

85

90

95(%)

Demand [LHS] Capacity [LHS] Operating rate [RHS]

Ethylene Polyethylene

PVC Polypropylene

Source: CMAI, Kotak Institutional Equities estimates

E&P volume and price assumptions. We now model FY2011E, FY2012E, FY2013E and FY2014E gas production from KG D-6 gas at 64 mcm/d, 72 mcm/d, 88 mcm/d and 88 mcm/d versus 72 mcm/d, 80 mcm/d, 88 mcm/d and 88 mcm/d previously. We note that RIL’s D1 and D3 fields have been facing some technical issues regarding reservoir pressure and as per press articles, RIL has decided to continue production at round 60 mcm/d until it completes more studies on the reservoir.

We assume selling price at US$4.2/mn BTU (US$4.34/mn BTU including marketing margin) throughout our forecast period and US$5.25/mn BTU beyond FY2014E. We model oil production at 2.1 mn tons, 2.4 mn tons, 2.4 mn tons and 2.4 mn tons for FY2011E, FY2012E, FY2013E and FY2014E. The increase reflects higher oil production from RIL’s MA-1 fields. We model gas production from NEC-25 block at 20 mcm/d for FY2015E.

Other income. We model RIL’s other income to likely grow strongly over the next few years driven by its increasing cash pile. We expect RIL to generate `1.38 tn of gross cash flow and `1.21 tn of free cash flow over next four years. The quantum of other income will depend on (1) RIL’s dividend policy; RIL has followed a conservative dividend pay-out policy historically, (2) acquisitions and (3) capex, which would depend on new E&P discoveries and kick-start of new petrochemical projects.

Taxation. We assume effective tax rate at 20.3% and 19% for FY2011E and FY2012E. We assume that RIL will continue to avail of income tax exemption on gas production from KG D-6 block and make our forecasts accordingly. However, in case the income tax exemption is not available, we compute RIL’s FY2011E and FY2012E EPS to drop to `54 and `68.

Energy Reliance Industries

10 KOTAK INSTITUTIONAL EQUITIES RESEARCH

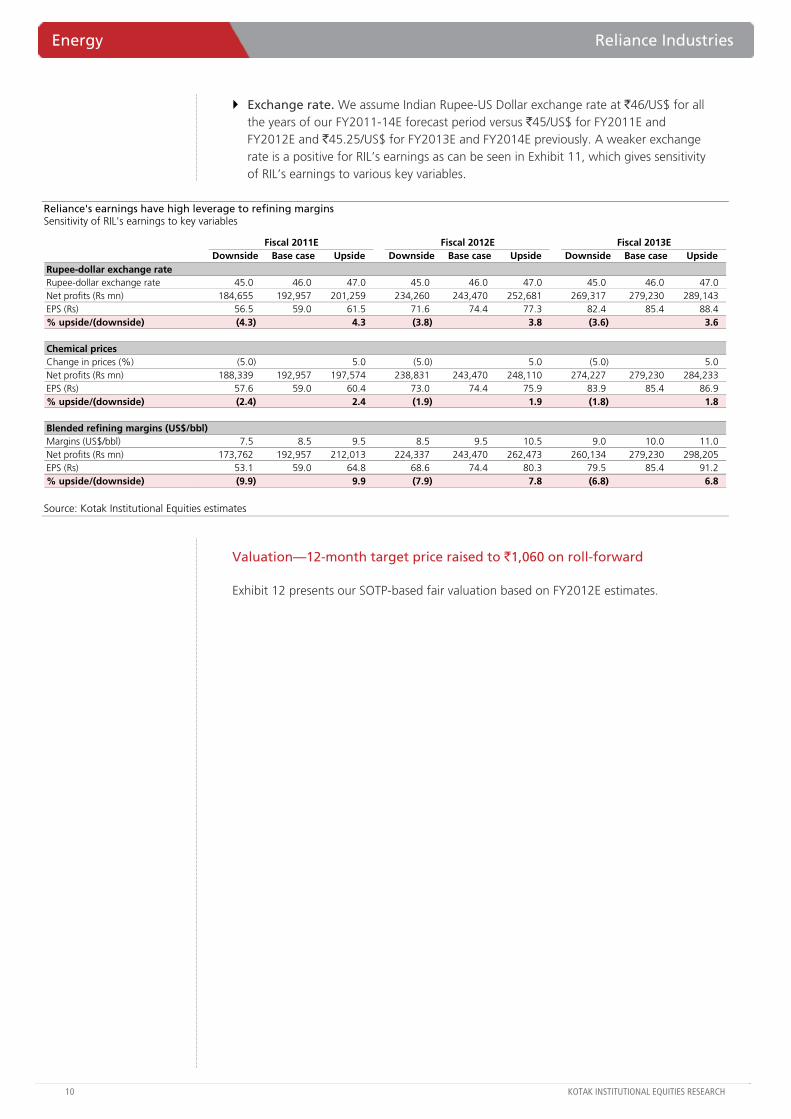

Exchange rate. We assume Indian Rupee-US Dollar exchange rate at `46/US$ for all the years of our FY2011-14E forecast period versus `45/US$ for FY2011E and FY2012E and `45.25/US$ for FY2013E and FY2014E previously. A weaker exchange rate is a positive for RIL’s earnings as can be seen in Exhibit 11, which gives sensitivity of RIL’s earnings to various key variables.

Reliance's earnings have high leverage to refining margins Sensitivity of RIL's earnings to key variables

Fiscal 2011E Fiscal 2012E Fiscal 2013EDownside Base case Upside Downside Base case Upside Downside Base case Upside

Rupee-dollar exchange rateRupee-dollar exchange rate 45.0 46.0 47.0 45.0 46.0 47.0 45.0 46.0 47.0 Net profits (Rs mn) 184,655 192,957 201,259 234,260 243,470 252,681 269,317 279,230 289,143 EPS (Rs) 56.5 59.0 61.5 71.6 74.4 77.3 82.4 85.4 88.4 % upside/(downside) (4.3) 4.3 (3.8) 3.8 (3.6) 3.6

Chemical pricesChange in prices (%) (5.0) 5.0 (5.0) 5.0 (5.0) 5.0 Net profits (Rs mn) 188,339 192,957 197,574 238,831 243,470 248,110 274,227 279,230 284,233 EPS (Rs) 57.6 59.0 60.4 73.0 74.4 75.9 83.9 85.4 86.9 % upside/(downside) (2.4) 2.4 (1.9) 1.9 (1.8) 1.8

Blended refining margins (US$/bbl)Margins (US$/bbl) 7.5 8.5 9.5 8.5 9.5 10.5 9.0 10.0 11.0 Net profits (Rs mn) 173,762 192,957 212,013 224,337 243,470 262,473 260,134 279,230 298,205 EPS (Rs) 53.1 59.0 64.8 68.6 74.4 80.3 79.5 85.4 91.2 % upside/(downside) (9.9) 9.9 (7.9) 7.8 (6.8) 6.8

Source: Kotak Institutional Equities estimates

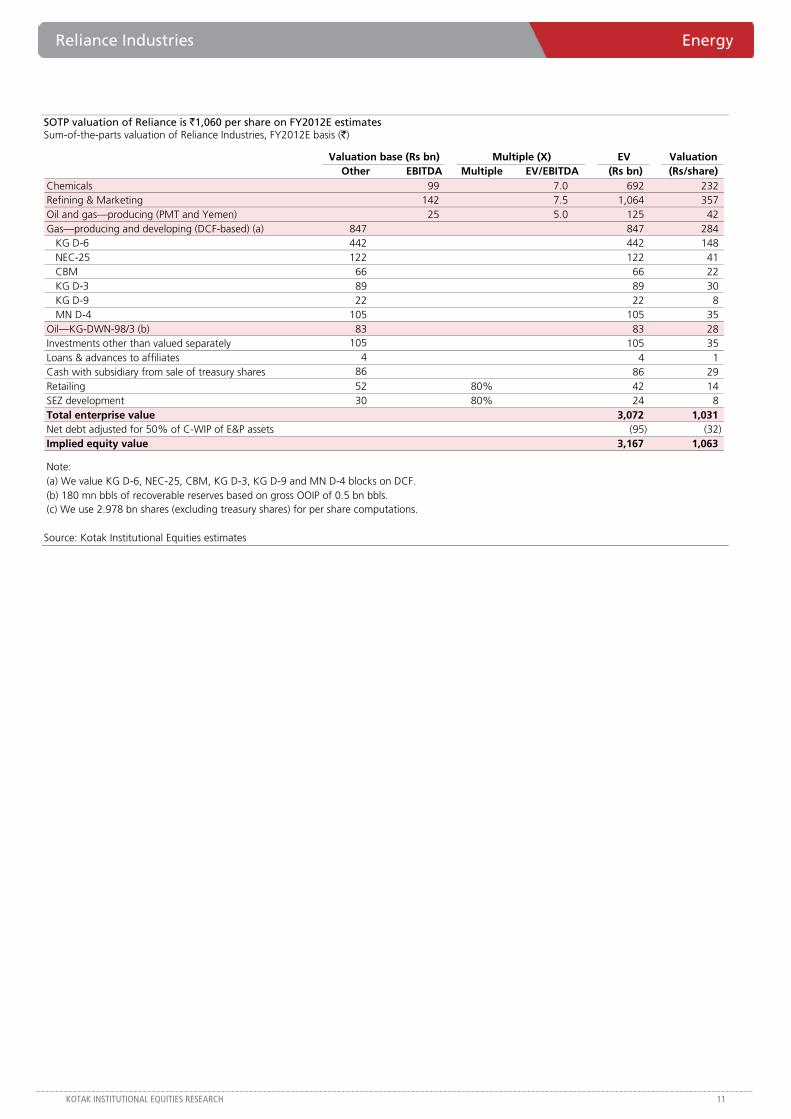

Valuation—12-month target price raised to `1,060 on roll-forward

Exhibit 12 presents our SOTP-based fair valuation based on FY2012E estimates.

Reliance Industries Energy

KOTAK INSTITUTIONAL EQUITIES RESEARCH 11

SOTP valuation of Reliance is `1,060 per share on FY2012E estimates Sum-of-the-parts valuation of Reliance Industries, FY2012E basis (`)

Valuation base (Rs bn) Multiple (X) EV ValuationOther EBITDA Multiple EV/EBITDA (Rs bn) (Rs/share)

Chemicals 99 7.0 692 232Refining & Marketing 142 7.5 1,064 357Oil and gas—producing (PMT and Yemen) 25 5.0 125 42Gas—producing and developing (DCF-based) (a) 847 847 284 KG D-6 442 442 148 NEC-25 122 122 41 CBM 66 66 22 KG D-3 89 89 30 KG D-9 22 22 8 MN D-4 105 105 35Oil—KG-DWN-98/3 (b) 83 83 28Investments other than valued separately 105 105 35Loans & advances to affiliates 4 4 1Cash with subsidiary from sale of treasury shares 86 86 29Retailing 52 80% 42 14SEZ development 30 80% 24 8Total enterprise value 3,072 1,031Net debt adjusted for 50% of C-WIP of E&P assets (95) (32)Implied equity value 3,167 1,063

Note:(a) We value KG D-6, NEC-25, CBM, KG D-3, KG D-9 and MN D-4 blocks on DCF.(b) 180 mn bbls of recoverable reserves based on gross OOIP of 0.5 bn bbls.(c) We use 2.978 bn shares (excluding treasury shares) for per share computations.

Source: Kotak Institutional Equities estimates

Energy Reliance Industries

12 KOTAK INSTITUTIONAL EQUITIES RESEARCH

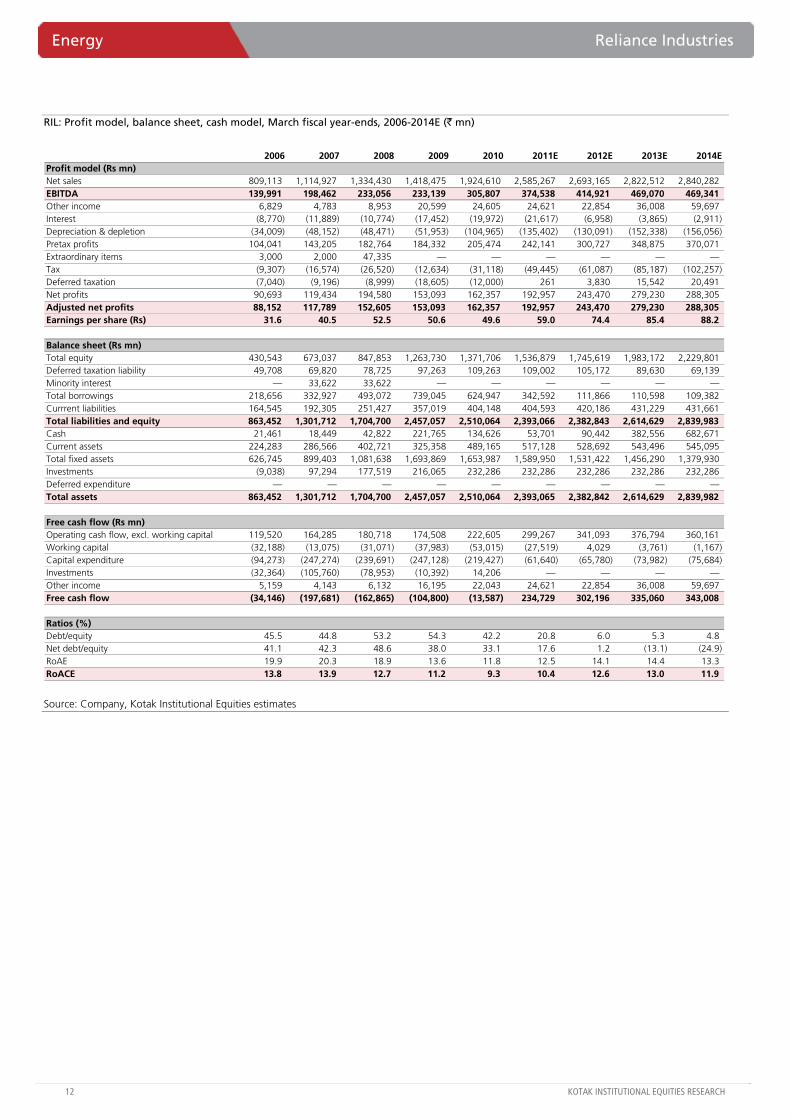

RIL: Profit model, balance sheet, cash model, March fiscal year-ends, 2006-2014E (` mn)

2006 2007 2008 2009 2010 2011E 2012E 2013E 2014EProfit model (Rs mn)Net sales 809,113 1,114,927 1,334,430 1,418,475 1,924,610 2,585,267 2,693,165 2,822,512 2,840,282EBITDA 139,991 198,462 233,056 233,139 305,807 374,538 414,921 469,070 469,341Other income 6,829 4,783 8,953 20,599 24,605 24,621 22,854 36,008 59,697Interest (8,770) (11,889) (10,774) (17,452) (19,972) (21,617) (6,958) (3,865) (2,911)Depreciation & depletion (34,009) (48,152) (48,471) (51,953) (104,965) (135,402) (130,091) (152,338) (156,056)Pretax profits 104,041 143,205 182,764 184,332 205,474 242,141 300,727 348,875 370,071Extraordinary items 3,000 2,000 47,335 — — — — — —Tax (9,307) (16,574) (26,520) (12,634) (31,118) (49,445) (61,087) (85,187) (102,257)Deferred taxation (7,040) (9,196) (8,999) (18,605) (12,000) 261 3,830 15,542 20,491Net profits 90,693 119,434 194,580 153,093 162,357 192,957 243,470 279,230 288,305Adjusted net profits 88,152 117,789 152,605 153,093 162,357 192,957 243,470 279,230 288,305Earnings per share (Rs) 31.6 40.5 52.5 50.6 49.6 59.0 74.4 85.4 88.2

Balance sheet (Rs mn)Total equity 430,543 673,037 847,853 1,263,730 1,371,706 1,536,879 1,745,619 1,983,172 2,229,801Deferred taxation liability 49,708 69,820 78,725 97,263 109,263 109,002 105,172 89,630 69,139Minority interest — 33,622 33,622 — — — — — —Total borrowings 218,656 332,927 493,072 739,045 624,947 342,592 111,866 110,598 109,382Currrent liabilities 164,545 192,305 251,427 357,019 404,148 404,593 420,186 431,229 431,661Total liabilities and equity 863,452 1,301,712 1,704,700 2,457,057 2,510,064 2,393,066 2,382,843 2,614,629 2,839,983Cash 21,461 18,449 42,822 221,765 134,626 53,701 90,442 382,556 682,671Current assets 224,283 286,566 402,721 325,358 489,165 517,128 528,692 543,496 545,095Total fixed assets 626,745 899,403 1,081,638 1,693,869 1,653,987 1,589,950 1,531,422 1,456,290 1,379,930Investments (9,038) 97,294 177,519 216,065 232,286 232,286 232,286 232,286 232,286Deferred expenditure — — — — — — — — —Total assets 863,452 1,301,712 1,704,700 2,457,057 2,510,064 2,393,065 2,382,842 2,614,629 2,839,982

Free cash flow (Rs mn)Operating cash flow, excl. working capital 119,520 164,285 180,718 174,508 222,605 299,267 341,093 376,794 360,161Working capital (32,188) (13,075) (31,071) (37,983) (53,015) (27,519) 4,029 (3,761) (1,167)Capital expenditure (94,273) (247,274) (239,691) (247,128) (219,427) (61,640) (65,780) (73,982) (75,684)Investments (32,364) (105,760) (78,953) (10,392) 14,206 — — — —Other income 5,159 4,143 6,132 16,195 22,043 24,621 22,854 36,008 59,697Free cash flow (34,146) (197,681) (162,865) (104,800) (13,587) 234,729 302,196 335,060 343,008

Ratios (%)Debt/equity 45.5 44.8 53.2 54.3 42.2 20.8 6.0 5.3 4.8 Net debt/equity 41.1 42.3 48.6 38.0 33.1 17.6 1.2 (13.1) (24.9) RoAE 19.9 20.3 18.9 13.6 11.8 12.5 14.1 14.4 13.3 RoACE 13.8 13.9 12.7 11.2 9.3 10.4 12.6 13.0 11.9

Source: Company, Kotak Institutional Equities estimates

For private Circulation Only. FOR IMPORTANT INFORMATION ABOUT KOTAK SECURITIES’ RATING SYSTEM AND OTHER DISCLOSURES, REFER TO THE END OF THIS MATERIAL.

Inflow skew can’t explain nil growth in E&C; lengthening execution cycle and client side issues can

Revenues disappoint—attributed to several large orders in initial stage of execution. Sedate revenue growth of 6.4% yoy—attributed to orders being in the initial phase of execution led by back-ended nature of inflows in FY2010. We highlight that there is only a marginal increase in skew versus long-term trends and that cannot explain almost nil growth in E&C. Lengthening execution cycle and client side issues can explain revenue growth issues.

Higher-than-expected margins help meet PAT-level estimates. The stronger-than-expected EBITDA margin of 12.8% (versus estimate of 10.5%, up 150 bps yoy) led to a net profit of Rs6.7 bn, broadly in line with our estimate and about 15% up on a yoy basis.

E&C segment leads margin expansion, but revenue growth purely from product segments. E&C segment recorded flat yoy revenues; growth of 25-30% was driven by product segments. However, margin expansion was primarily led by E&C segment (up 190 bps).

Order inflows of Rs156 bn in 1QFY11, up 63% yoy, were driven by L&T’s own 2X660 MW order worth Rs52 bn. Order backlog of Rs1,078 bn (up 50% yoy) provides visibility of 2.3 years.

Management maintains guidance; subsidiaries record very strong performance

Management has maintained its full-year order inflow growth guidance of 25% and revenue growth guidance of 20% for FY2011E. Despite sedate revenue growth in 1QFY11, the management expects to meet its full-year revenue growth guidance based on execution pick-up in 2H11E of orders won in 2H10. L&T Infotech reported a strong revival in revenues (up 19.5%) and the financial services subs continued to record strong performance (revenues up 45% and 72%).

Outperformance, execution issues and risky development business prompts downgrade

Revise standalone estimates to Rs63.9 and Rs78.2 (from Rs64.2 and Rs80.9) and consolidated estimates to Rs71.7 and Rs89 (from Rs71.4 and Rs90.7) for FY11E-12E. Downgrade to ADD on (1) recent outperformance, (2) likely aggravation of near-term returns dilution and execution risks with increasing dependence on large development projects such as Metro and thermal power, (3) continued execution issues and (4) limited upside to FY2012E-based target price (Rs2,075).

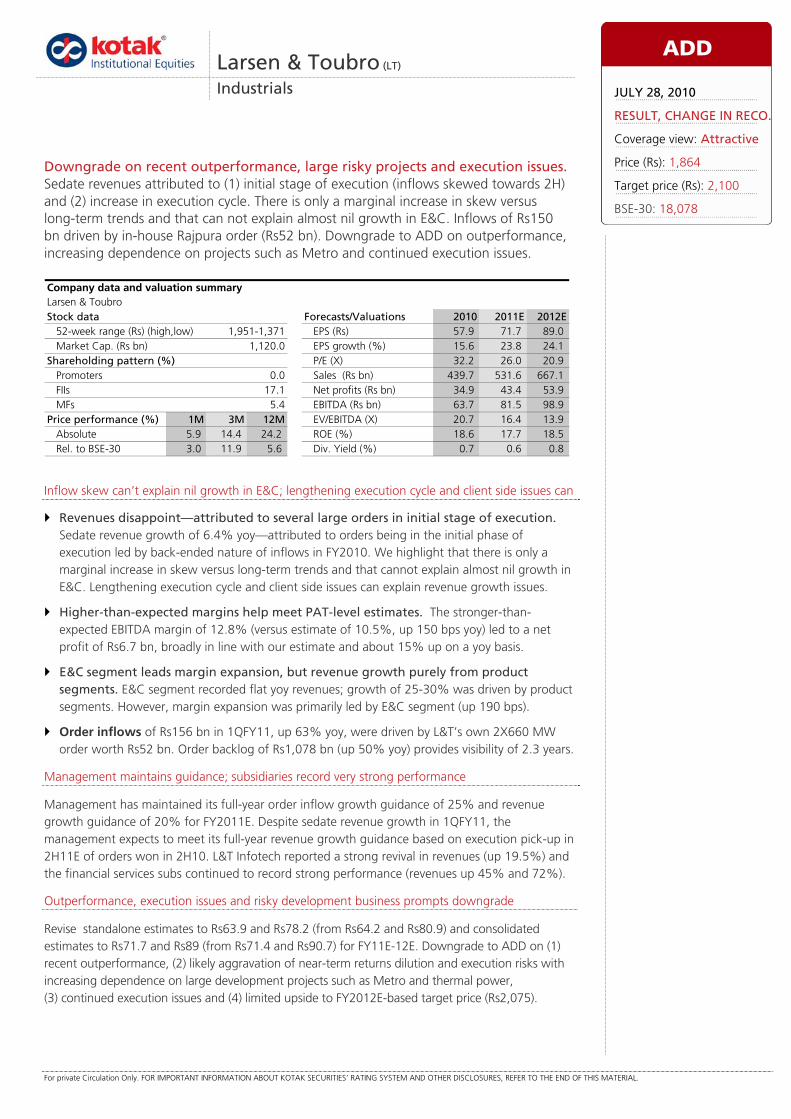

Larsen & Toubro (LT)

Industrials

Downgrade on recent outperformance, large risky projects and execution issues. Sedate revenues attributed to (1) initial stage of execution (inflows skewed towards 2H) and (2) increase in execution cycle. There is only a marginal increase in skew versus long-term trends and that can not explain almost nil growth in E&C. Inflows of Rs150 bn driven by in-house Rajpura order (Rs52 bn). Downgrade to ADD on outperformance, increasing dependence on projects such as Metro and continued execution issues.

Larsen & ToubroStock data Forecasts/Valuations 2010 2011E 2012E

52-week range (Rs) (high,low) EPS (Rs) 57.9 71.7 89.0Market Cap. (Rs bn) 1,120.0 EPS growth (%) 15.6 23.8 24.1

Shareholding pattern (%) P/E (X) 32.2 26.0 20.9Promoters 0.0 Sales (Rs bn) 439.7 531.6 667.1FIIs 17.1 Net profits (Rs bn) 34.9 43.4 53.9MFs 5.4 EBITDA (Rs bn) 63.7 81.5 98.9

Price performance (%) 1M 3M 12M EV/EBITDA (X) 20.7 16.4 13.9Absolute 5.9 14.4 24.2 ROE (%) 18.6 17.7 18.5Rel. to BSE-30 3.0 11.9 5.6 Div. Yield (%) 0.7 0.6 0.8

Company data and valuation summary

1,951-1,371

ADD

JULY 28, 2010

RESULT, CHANGE IN RECO.

Coverage view: Attractive

Price (Rs): 1,864

Target price (Rs): 2,100

BSE-30: 18,078

Industrials Larsen & Toubro

14 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Revenues disappoint—slow as several large projects in initial stage of execution

L&T reported disappointing revenues of Rs79 bn, about 15% below our estimates of Rs93 bn, recording modest 6.4% growth yoy. Our strong revenue growth estimate of 25% yoy was based on execution of the order backlog and a pick-up in execution of the orders that had slowed down in the first nine months of FY2010. The sedate revenue growth was attributed to (1) several large projects being in the initial stages of execution (due to the back-ended nature of order inflows in FY2010)—the management expects execution of these orders to pick up in 2HFY10, (2) increase in average execution-cycle of the backlog; about a third of the current order book comprise of orders with an execution cycle of 3-5 years and (3) higher international order inflows which is yet to translate into revenues.

Higher-than-expected EBITDA margin helps meet PAT-level estimates; margins likely to remain flat for full-year FY2011E

L&T reported a stronger-than-expected EBITDA margin of 12.8%, up 150 bps yoy and about 230 bps higher than our estimate of 10.5%. The gross margin of L&T (net of variable expenses—raw material, subcontracting and other manufacturing expenses) expanded by 190 bps yoy to 24.6% in 1QFY11 from 22.8% in 1QFY10. We had expected a slight contraction in margins as we believed that the uptick in commodity prices in 4QFY10 would adversely impact the raw material costs. L&T did report a 120 bps increase in raw material expenses as a percentage of sales; however, this was completely offset by decrease in subcontracting expenses as a percentage of sales leading to the gross margin expansion. The lower subcontracting expense in the quarter was attributed to completion of a large order in the previous quarter (Delhi airport order). The higher-than-expected EBITDA margin led to a net profit of Rs6.7 bn, broadly inline with our estimate and about 15% up on a yoy basis.

The management suggested that the full-year FY2011E margin is likely to remain broadly at FY2010 levels of about 13%. The margin expansion witnessed in 1QFY11 is unlikely to sustain for the remaining of FY2011.

Larsen & Toubro Industrials

KOTAK INSTITUTIONAL EQUITIES RESEARCH 15

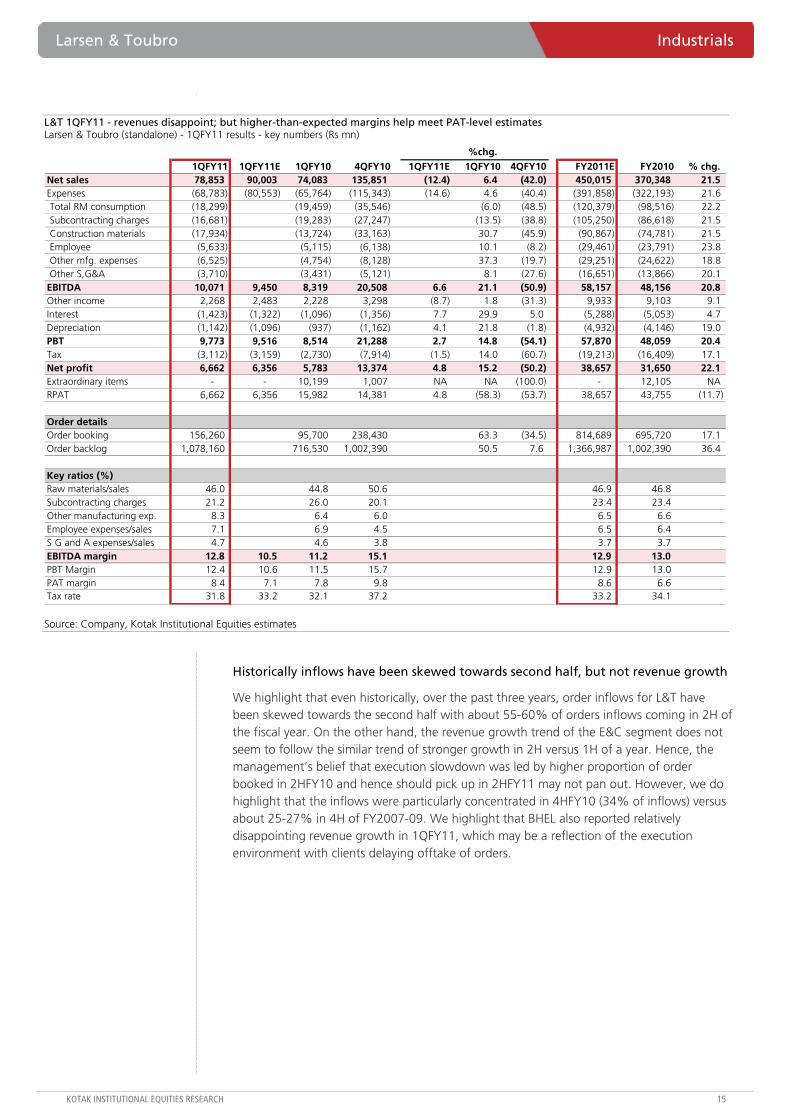

L&T 1QFY11 - revenues disappoint; but higher-than-expected margins help meet PAT-level estimates Larsen & Toubro (standalone) - 1QFY11 results - key numbers (Rs mn)

%chg.1QFY11 1QFY11E 1QFY10 4QFY10 1QFY11E 1QFY10 4QFY10 FY2011E FY2010 % chg.

Net sales 78,853 90,003 74,083 135,851 (12.4) 6.4 (42.0) 450,015 370,348 21.5 Expenses (68,783) (80,553) (65,764) (115,343) (14.6) 4.6 (40.4) (391,858) (322,193) 21.6 Total RM consumption (18,299) (19,459) (35,546) (6.0) (48.5) (120,379) (98,516) 22.2 Subcontracting charges (16,681) (19,283) (27,247) (13.5) (38.8) (105,250) (86,618) 21.5 Construction materials (17,934) (13,724) (33,163) 30.7 (45.9) (90,867) (74,781) 21.5 Employee (5,633) (5,115) (6,138) 10.1 (8.2) (29,461) (23,791) 23.8 Other mfg. expenses (6,525) (4,754) (8,128) 37.3 (19.7) (29,251) (24,622) 18.8 Other S,G&A (3,710) (3,431) (5,121) 8.1 (27.6) (16,651) (13,866) 20.1 EBITDA 10,071 9,450 8,319 20,508 6.6 21.1 (50.9) 58,157 48,156 20.8 Other income 2,268 2,483 2,228 3,298 (8.7) 1.8 (31.3) 9,933 9,103 9.1 Interest (1,423) (1,322) (1,096) (1,356) 7.7 29.9 5.0 (5,288) (5,053) 4.7 Depreciation (1,142) (1,096) (937) (1,162) 4.1 21.8 (1.8) (4,932) (4,146) 19.0 PBT 9,773 9,516 8,514 21,288 2.7 14.8 (54.1) 57,870 48,059 20.4 Tax (3,112) (3,159) (2,730) (7,914) (1.5) 14.0 (60.7) (19,213) (16,409) 17.1 Net profit 6,662 6,356 5,783 13,374 4.8 15.2 (50.2) 38,657 31,650 22.1 Extraordinary items - - 10,199 1,007 NA NA (100.0) - 12,105 NARPAT 6,662 6,356 15,982 14,381 4.8 (58.3) (53.7) 38,657 43,755 (11.7)

Order detailsOrder booking 156,260 95,700 238,430 63.3 (34.5) 814,689 695,720 17.1 Order backlog 1,078,160 716,530 1,002,390 50.5 7.6 1,366,987 1,002,390 36.4

Key ratios (%)Raw materials/sales 46.0 44.8 50.6 46.9 46.8 Subcontracting charges 21.2 26.0 20.1 23.4 23.4 Other manufacturing exp. 8.3 6.4 6.0 6.5 6.6 Employee expenses/sales 7.1 6.9 4.5 6.5 6.4 S G and A expenses/sales 4.7 4.6 3.8 3.7 3.7 EBITDA margin 12.8 10.5 11.2 15.1 12.9 13.0 PBT Margin 12.4 10.6 11.5 15.7 12.9 13.0 PAT margin 8.4 7.1 7.8 9.8 8.6 6.6 Tax rate 31.8 33.2 32.1 37.2 33.2 34.1

Source: Company, Kotak Institutional Equities estimates

Historically inflows have been skewed towards second half, but not revenue growth

We highlight that even historically, over the past three years, order inflows for L&T have been skewed towards the second half with about 55-60% of orders inflows coming in 2H of the fiscal year. On the other hand, the revenue growth trend of the E&C segment does not seem to follow the similar trend of stronger growth in 2H versus 1H of a year. Hence, the management’s belief that execution slowdown was led by higher proportion of order booked in 2HFY10 and hence should pick up in 2HFY11 may not pan out. However, we do highlight that the inflows were particularly concentrated in 4HFY10 (34% of inflows) versus about 25-27% in 4H of FY2007-09. We highlight that BHEL also reported relatively disappointing revenue growth in 1QFY11, which may be a reflection of the execution environment with clients delaying offtake of orders.

Industrials Larsen & Toubro

16 KOTAK INSTITUTIONAL EQUITIES RESEARCH

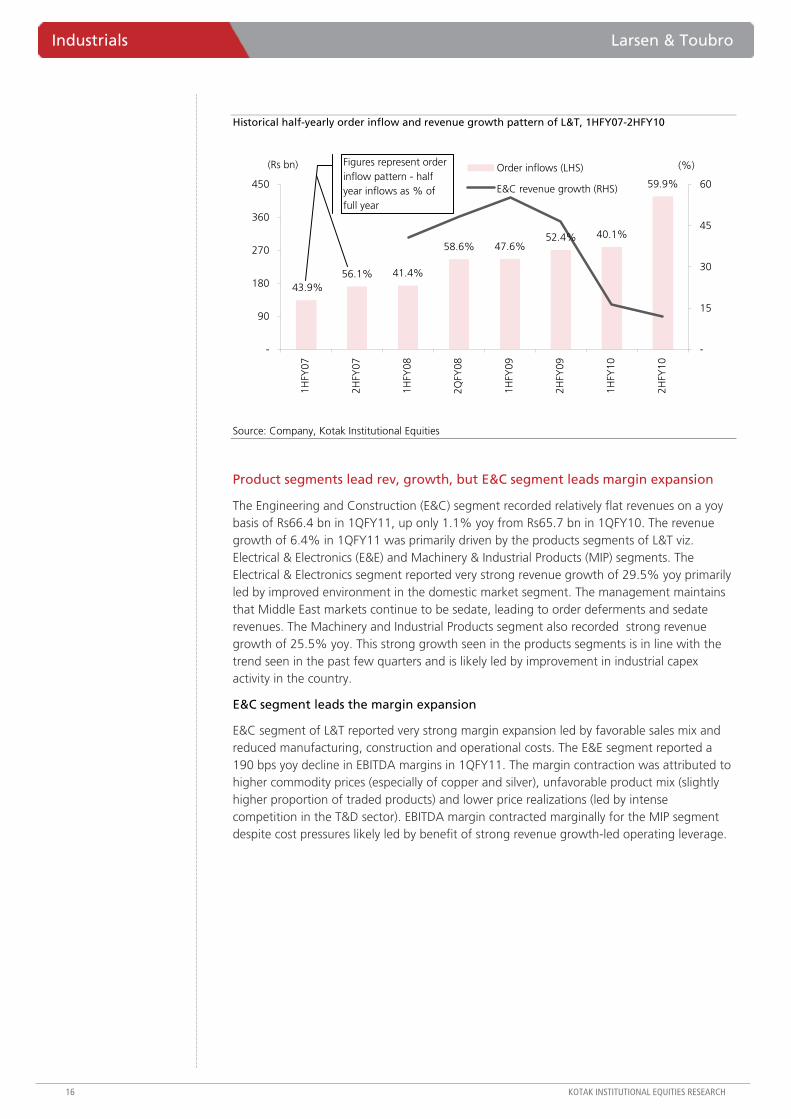

Historical half-yearly order inflow and revenue growth pattern of L&T, 1HFY07-2HFY10

56.1% 41.4%

58.6% 47.6%52.4% 40.1%

59.9%

43.9%

-

90

180

270

360

450

1HFY

07

2HFY

07

1HFY

08

2QFY

08

1HFY

09

2HFY

09

1HFY

10

2HFY

10

(Rs bn)

-

15

30

45

60

(%)Order inflows (LHS)

E&C revenue growth (RHS)

Figures represent order inflow pattern - half year inflows as % of full year

Source: Company, Kotak Institutional Equities

Product segments lead rev, growth, but E&C segment leads margin expansion

The Engineering and Construction (E&C) segment recorded relatively flat revenues on a yoy basis of Rs66.4 bn in 1QFY11, up only 1.1% yoy from Rs65.7 bn in 1QFY10. The revenue growth of 6.4% in 1QFY11 was primarily driven by the products segments of L&T viz. Electrical & Electronics (E&E) and Machinery & Industrial Products (MIP) segments. The Electrical & Electronics segment reported very strong revenue growth of 29.5% yoy primarily led by improved environment in the domestic market segment. The management maintains that Middle East markets continue to be sedate, leading to order deferments and sedate revenues. The Machinery and Industrial Products segment also recorded strong revenue growth of 25.5% yoy. This strong growth seen in the products segments is in line with the trend seen in the past few quarters and is likely led by improvement in industrial capex activity in the country.

E&C segment leads the margin expansion

E&C segment of L&T reported very strong margin expansion led by favorable sales mix and reduced manufacturing, construction and operational costs. The E&E segment reported a 190 bps yoy decline in EBITDA margins in 1QFY11. The margin contraction was attributed to higher commodity prices (especially of copper and silver), unfavorable product mix (slightly higher proportion of traded products) and lower price realizations (led by intense competition in the T&D sector). EBITDA margin contracted marginally for the MIP segment despite cost pressures likely led by benefit of strong revenue growth-led operating leverage.

Larsen & Toubro Industrials

KOTAK INSTITUTIONAL EQUITIES RESEARCH 17

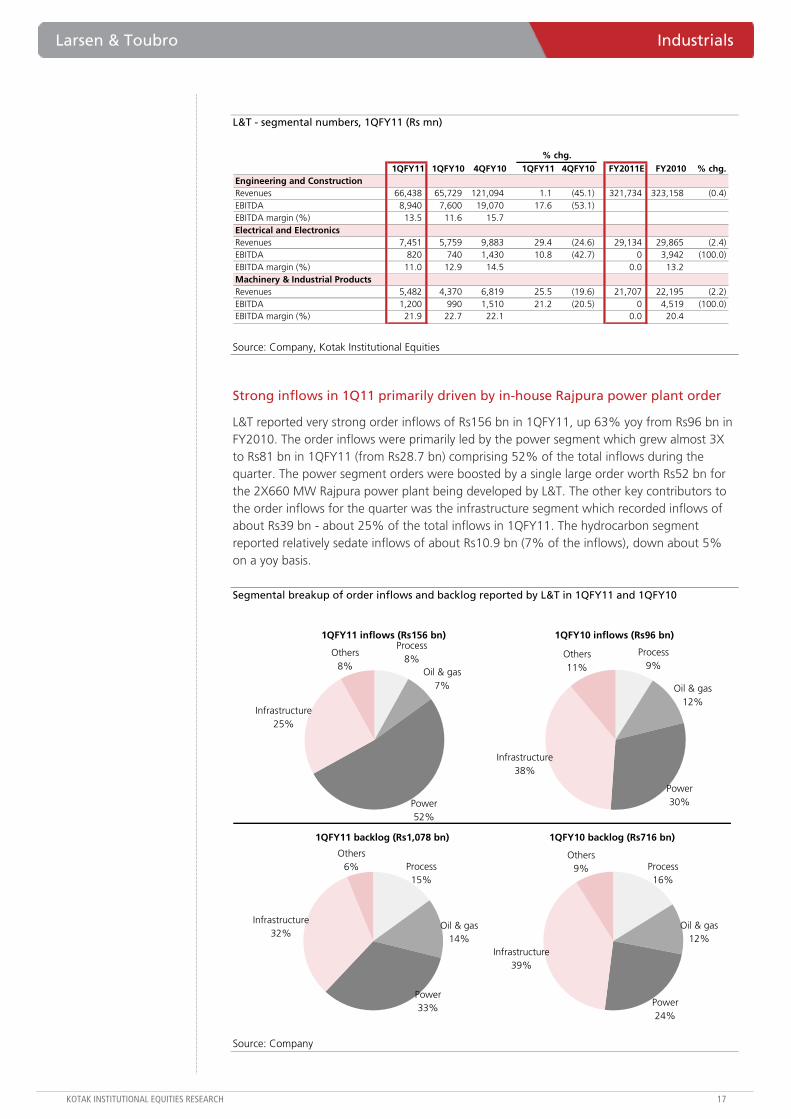

L&T - segmental numbers, 1QFY11 (Rs mn)

1QFY11 1QFY10 4QFY10 1QFY11 4QFY10 FY2011E FY2010 % chg.Engineering and ConstructionRevenues 66,438 65,729 121,094 1.1 (45.1) 321,734 323,158 (0.4)EBITDA 8,940 7,600 19,070 17.6 (53.1)EBITDA margin (%) 13.5 11.6 15.7Electrical and ElectronicsRevenues 7,451 5,759 9,883 29.4 (24.6) 29,134 29,865 (2.4)EBITDA 820 740 1,430 10.8 (42.7) 0 3,942 (100.0)EBITDA margin (%) 11.0 12.9 14.5 0.0 13.2Machinery & Industrial ProductsRevenues 5,482 4,370 6,819 25.5 (19.6) 21,707 22,195 (2.2)EBITDA 1,200 990 1,510 21.2 (20.5) 0 4,519 (100.0)EBITDA margin (%) 21.9 22.7 22.1 0.0 20.4

% chg.

Source: Company, Kotak Institutional Equities

Strong inflows in 1Q11 primarily driven by in-house Rajpura power plant order

L&T reported very strong order inflows of Rs156 bn in 1QFY11, up 63% yoy from Rs96 bn in FY2010. The order inflows were primarily led by the power segment which grew almost 3X to Rs81 bn in 1QFY11 (from Rs28.7 bn) comprising 52% of the total inflows during the quarter. The power segment orders were boosted by a single large order worth Rs52 bn for the 2X660 MW Rajpura power plant being developed by L&T. The other key contributors to the order inflows for the quarter was the infrastructure segment which recorded inflows of about Rs39 bn - about 25% of the total inflows in 1QFY11. The hydrocarbon segment reported relatively sedate inflows of about Rs10.9 bn (7% of the inflows), down about 5% on a yoy basis.

Segmental breakup of order inflows and backlog reported by L&T in 1QFY11 and 1QFY10

1QFY11 inflows (Rs156 bn)

Infrastructure25%

Oil & gas7%

Process8%

Others8%

Power52%

1QFY10 inflows (Rs96 bn)

Power30%

Others11%

Process9%

Oil & gas12%

Infrastructure38%

1QFY11 backlog (Rs1,078 bn)

Power33%

Others6% Process

15%

Oil & gas14%

Infrastructure32%

1QFY10 backlog (Rs716 bn)

Infrastructure39%

Oil & gas12%

Process16%

Others9%

Power24%

Source: Company

Industrials Larsen & Toubro

18 KOTAK INSTITUTIONAL EQUITIES RESEARCH

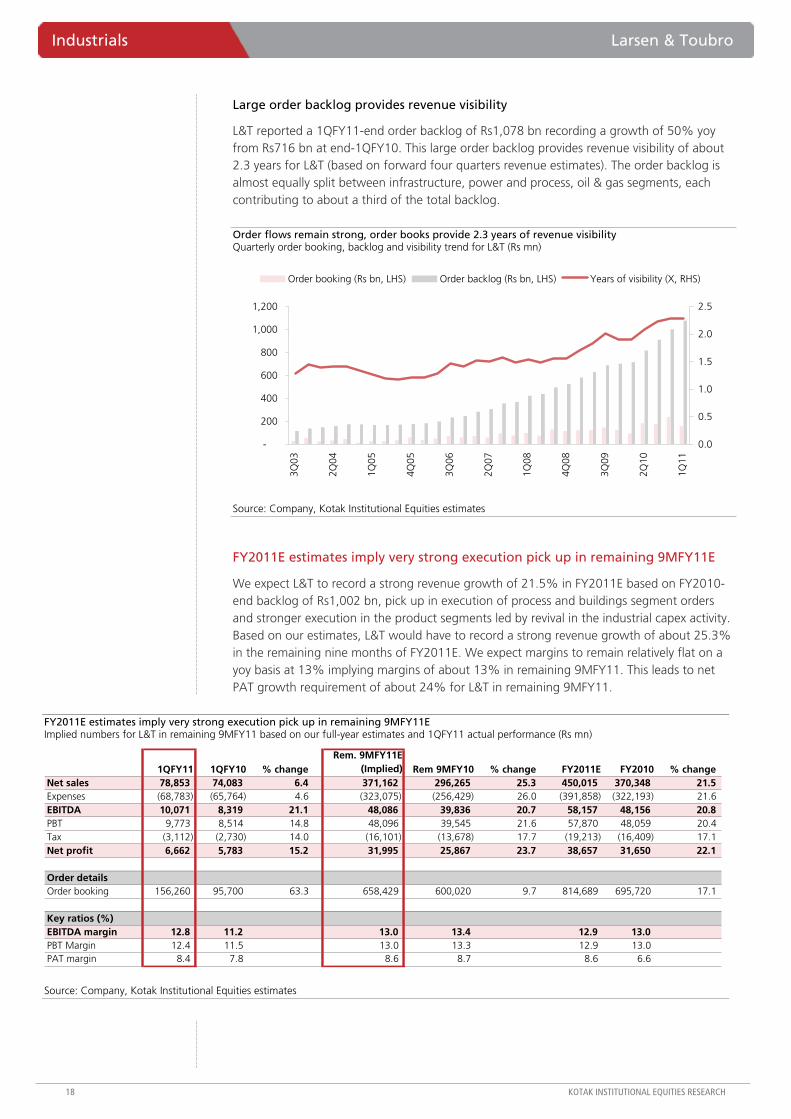

Large order backlog provides revenue visibility

L&T reported a 1QFY11-end order backlog of Rs1,078 bn recording a growth of 50% yoy from Rs716 bn at end-1QFY10. This large order backlog provides revenue visibility of about 2.3 years for L&T (based on forward four quarters revenue estimates). The order backlog is almost equally split between infrastructure, power and process, oil & gas segments, each contributing to about a third of the total backlog.

Order flows remain strong, order books provide 2.3 years of revenue visibility Quarterly order booking, backlog and visibility trend for L&T (Rs mn)

-

200

400

600

800

1,000

1,2003Q

03

2Q04

1Q05

4Q05

3Q06

2Q07

1Q08

4Q08

3Q09

2Q10

1Q11

0.0

0.5

1.0

1.5

2.0

2.5

Order booking (Rs bn, LHS) Order backlog (Rs bn, LHS) Years of visibility (X, RHS)

Source: Company, Kotak Institutional Equities estimates

FY2011E estimates imply very strong execution pick up in remaining 9MFY11E

We expect L&T to record a strong revenue growth of 21.5% in FY2011E based on FY2010-end backlog of Rs1,002 bn, pick up in execution of process and buildings segment orders and stronger execution in the product segments led by revival in the industrial capex activity. Based on our estimates, L&T would have to record a strong revenue growth of about 25.3% in the remaining nine months of FY2011E. We expect margins to remain relatively flat on a yoy basis at 13% implying margins of about 13% in remaining 9MFY11. This leads to net PAT growth requirement of about 24% for L&T in remaining 9MFY11.

FY2011E estimates imply very strong execution pick up in remaining 9MFY11E Implied numbers for L&T in remaining 9MFY11 based on our full-year estimates and 1QFY11 actual performance (Rs mn)

1QFY11 1QFY10 % changeRem. 9MFY11E

(Implied) Rem 9MFY10 % change FY2011E FY2010 % changeNet sales 78,853 74,083 6.4 371,162 296,265 25.3 450,015 370,348 21.5 Expenses (68,783) (65,764) 4.6 (323,075) (256,429) 26.0 (391,858) (322,193) 21.6 EBITDA 10,071 8,319 21.1 48,086 39,836 20.7 58,157 48,156 20.8 PBT 9,773 8,514 14.8 48,096 39,545 21.6 57,870 48,059 20.4 Tax (3,112) (2,730) 14.0 (16,101) (13,678) 17.7 (19,213) (16,409) 17.1 Net profit 6,662 5,783 15.2 31,995 25,867 23.7 38,657 31,650 22.1

Order detailsOrder booking 156,260 95,700 63.3 658,429 600,020 9.7 814,689 695,720 17.1

Key ratios (%)EBITDA margin 12.8 11.2 13.0 13.4 12.9 13.0 PBT Margin 12.4 11.5 13.0 13.3 12.9 13.0 PAT margin 8.4 7.8 8.6 8.7 8.6 6.6

Source: Company, Kotak Institutional Equities estimates

Larsen & Toubro Industrials

KOTAK INSTITUTIONAL EQUITIES RESEARCH 19

Management maintains FY2011E guidance of 25% order inflow growth and 20% execution growth

L&T management has retained its full-year FY2011E guidance of 25% growth in order inflows and 20% growth in 20%. The 25% order inflow growth target includes the Rs121 bn potential orders for the Hyderabad Metro project as well as certain road development projects where L&T has been awarded the project but is awaiting financial closure. Despite sedate revenue growth in 1QFY11 the management has retained its full-year revenue growth guidance of 20%. The management cited that as majority of order inflows in FY2010 (about 60%) was booked in 2HFY10 the revenues in this fiscal is also likely to be skewed towards the second half. On an average, a large order takes about six months for the initial monetization and engineering activities. The revenues from the order would start kicking in only six months post winning the order. Hence, L&T management expects execution to record a sharp pick up in 2HFY11.

Seemed more confident on inflow guidance versus revenues—a bit surprising

L&T management seemed much more confident of achieving its full-year inflow growth guidance of 25% (likely led by large infrastructure and power projects) than its revenue growth guidance of 20%. We find this a bit surprising as we believe revenues are likely to be relatively more in control/ in the hands of the company versus order inflows.

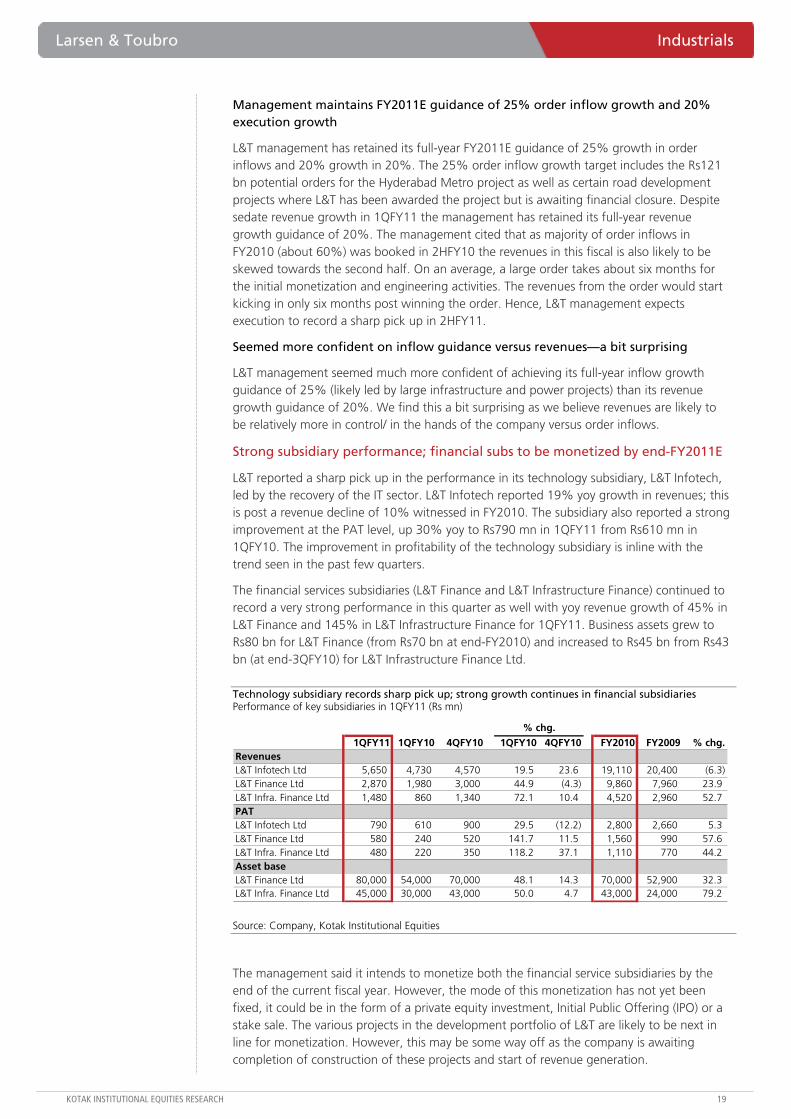

Strong subsidiary performance; financial subs to be monetized by end-FY2011E

L&T reported a sharp pick up in the performance in its technology subsidiary, L&T Infotech, led by the recovery of the IT sector. L&T Infotech reported 19% yoy growth in revenues; this is post a revenue decline of 10% witnessed in FY2010. The subsidiary also reported a strong improvement at the PAT level, up 30% yoy to Rs790 mn in 1QFY11 from Rs610 mn in 1QFY10. The improvement in profitability of the technology subsidiary is inline with the trend seen in the past few quarters.

The financial services subsidiaries (L&T Finance and L&T Infrastructure Finance) continued to record a very strong performance in this quarter as well with yoy revenue growth of 45% in L&T Finance and 145% in L&T Infrastructure Finance for 1QFY11. Business assets grew to Rs80 bn for L&T Finance (from Rs70 bn at end-FY2010) and increased to Rs45 bn from Rs43 bn (at end-3QFY10) for L&T Infrastructure Finance Ltd.

Technology subsidiary records sharp pick up; strong growth continues in financial subsidiaries Performance of key subsidiaries in 1QFY11 (Rs mn)

1QFY11 1QFY10 4QFY10 1QFY10 4QFY10 FY2010 FY2009 % chg.RevenuesL&T Infotech Ltd 5,650 4,730 4,570 19.5 23.6 19,110 20,400 (6.3) L&T Finance Ltd 2,870 1,980 3,000 44.9 (4.3) 9,860 7,960 23.9 L&T Infra. Finance Ltd 1,480 860 1,340 72.1 10.4 4,520 2,960 52.7 PATL&T Infotech Ltd 790 610 900 29.5 (12.2) 2,800 2,660 5.3 L&T Finance Ltd 580 240 520 141.7 11.5 1,560 990 57.6 L&T Infra. Finance Ltd 480 220 350 118.2 37.1 1,110 770 44.2 Asset baseL&T Finance Ltd 80,000 54,000 70,000 48.1 14.3 70,000 52,900 32.3 L&T Infra. Finance Ltd 45,000 30,000 43,000 50.0 4.7 43,000 24,000 79.2

% chg.

Source: Company, Kotak Institutional Equities

The management said it intends to monetize both the financial service subsidiaries by the end of the current fiscal year. However, the mode of this monetization has not yet been fixed, it could be in the form of a private equity investment, Initial Public Offering (IPO) or a stake sale. The various projects in the development portfolio of L&T are likely to be next in line for monetization. However, this may be some way off as the company is awaiting completion of construction of these projects and start of revenue generation.

Industrials Larsen & Toubro

20 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Annual report highlights working capital improvement, returns dilution and moderate capex

Key highlights from L&T’s annual report include:

Net adjusted working capital surprisingly low at 12 days on better credit and advances; strong operating cash: L&T reported surprisingly low working capital of just 12 days of sales (adj. for loans & advances to subsidiaries) from 29 days in FY2009. The reduction in working capital, led by better credit terms and customer advances, led to strong operating cash generation of Rs41 bn. The operating cash, funds from QIP/FCCB (Rs29 bn) and divestiture (Rs12 bn) were applied towards capex (Rs14 bn), increase in investments in subsidiaries (Rs28 bn) and increase in current investments (Rs31 bn).

Large investments in new businesses and infrastructure projects lead to near-term returns dilution. Reported RoCE and RoE has diluted to 16% (from 21.5%) and 20.6 (from 28.4%) over the last two years. L&T has, over the last year, made several large investments into new business areas such as power equipment and development and several infrastructure SPVs. However, L&T’s RoCE adjusted for investment in subsidiaries and non-business related loans & advances to subsidiaries has remained very high at 30% for the past three years. Projects such as Hyd. metro would exacerbate the problem.

Buys 4.6% in IDPL implying Rs53 bn value; Seawoods stuck others (Tamco, FZE, Associates) do well. L&T has bought back 4.6% in IDPL from IDF for Rs2.45 bn, implying valuation of Rs53 bn, (our estimate of Rs82 bn). External investors were inducted to bring arms length relationship between development and construction however intention to pursue growth across verticals, large projects (Hyd. metro) and asymmetric benefits for partners must have led to buy back. Seawoods remains stuck (Rs8.5 bn equity and likely Rs11 bn debt); however, other subs do well (Tamco - Rs0.75 bn PAT, Associate PAT of Rs1.9 bn versus Rs1.4 bn, FZE PAT positive versus Rs3 bn loss).

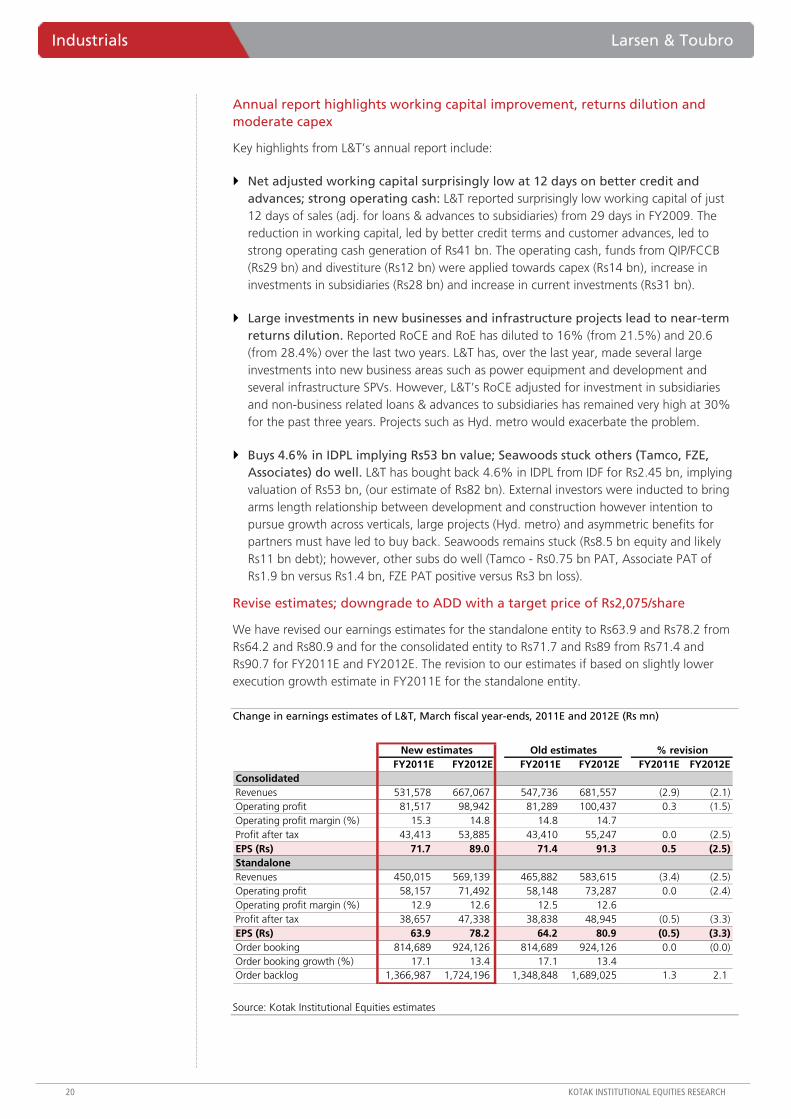

Revise estimates; downgrade to ADD with a target price of Rs2,075/share

We have revised our earnings estimates for the standalone entity to Rs63.9 and Rs78.2 from Rs64.2 and Rs80.9 and for the consolidated entity to Rs71.7 and Rs89 from Rs71.4 and Rs90.7 for FY2011E and FY2012E. The revision to our estimates if based on slightly lower execution growth estimate in FY2011E for the standalone entity.

Change in earnings estimates of L&T, March fiscal year-ends, 2011E and 2012E (Rs mn)

FY2011E FY2012E FY2011E FY2012E FY2011E FY2012EConsolidatedRevenues 531,578 667,067 547,736 681,557 (2.9) (2.1)Operating profit 81,517 98,942 81,289 100,437 0.3 (1.5)Operating profit margin (%) 15.3 14.8 14.8 14.7Profit after tax 43,413 53,885 43,410 55,247 0.0 (2.5)EPS (Rs) 71.7 89.0 71.4 91.3 0.5 (2.5)StandaloneRevenues 450,015 569,139 465,882 583,615 (3.4) (2.5)Operating profit 58,157 71,492 58,148 73,287 0.0 (2.4)Operating profit margin (%) 12.9 12.6 12.5 12.6Profit after tax 38,657 47,338 38,838 48,945 (0.5) (3.3)EPS (Rs) 63.9 78.2 64.2 80.9 (0.5) (3.3)Order booking 814,689 924,126 814,689 924,126 0.0 (0.0)Order booking growth (%) 17.1 13.4 17.1 13.4Order backlog 1,366,987 1,724,196 1,348,848 1,689,025 1.3 2.1

New estimates Old estimates % revision

Source: Kotak Institutional Equities estimates

Larsen & Toubro Industrials

KOTAK INSTITUTIONAL EQUITIES RESEARCH 21

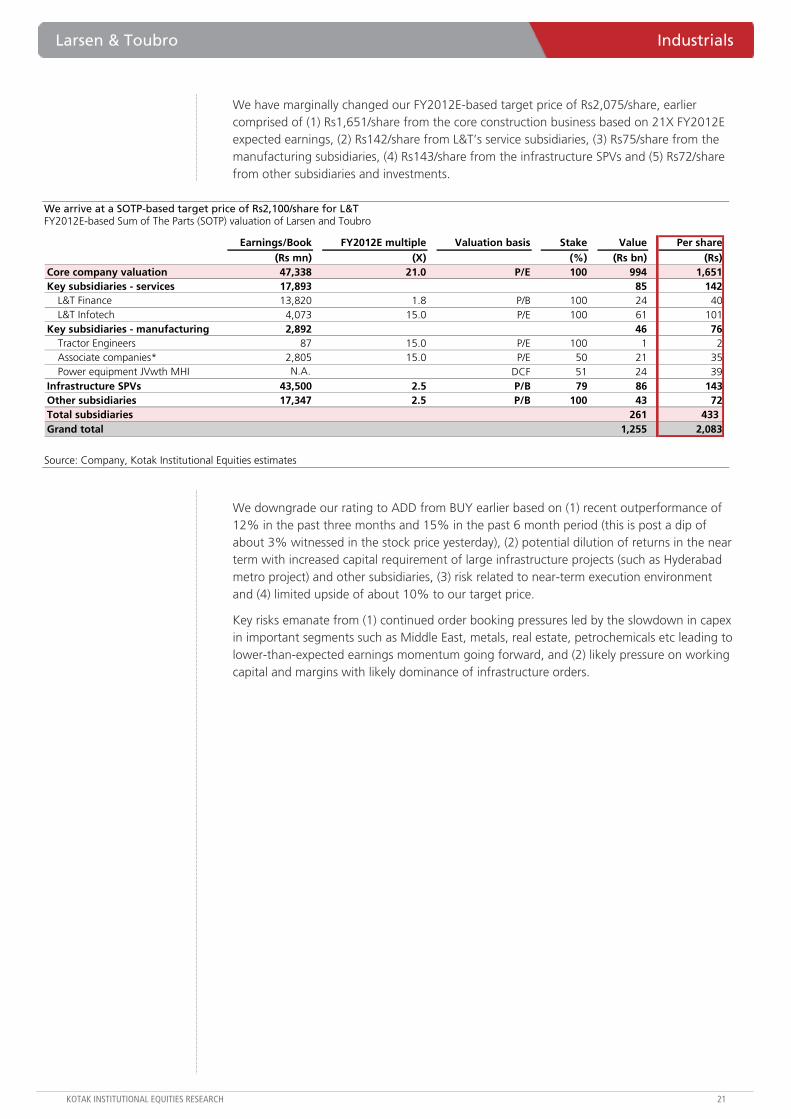

We have marginally changed our FY2012E-based target price of Rs2,075/share, earlier comprised of (1) Rs1,651/share from the core construction business based on 21X FY2012E expected earnings, (2) Rs142/share from L&T’s service subsidiaries, (3) Rs75/share from the manufacturing subsidiaries, (4) Rs143/share from the infrastructure SPVs and (5) Rs72/share from other subsidiaries and investments.

We arrive at a SOTP-based target price of Rs2,100/share for L&T FY2012E-based Sum of The Parts (SOTP) valuation of Larsen and Toubro

Earnings/Book FY2012E multiple Valuation basis Stake Value Per share (Rs mn) (X) (%) (Rs bn) (Rs)

Core company valuation 47,338 21.0 P/E 100 994 1,651 Key subsidiaries - services 17,893 85 142

L&T Finance 13,820 1.8 P/B 100 24 40 L&T Infotech 4,073 15.0 P/E 100 61 101

Key subsidiaries - manufacturing 2,892 46 76 Tractor Engineers 87 15.0 P/E 100 1 2 Associate companies* 2,805 15.0 P/E 50 21 35 Power equipment JVwth MHI N.A. DCF 51 24 39

Infrastructure SPVs 43,500 2.5 P/B 79 86 143 Other subsidiaries 17,347 2.5 P/B 100 43 72 Total subsidiaries 261 433 Grand total 1,255 2,083

Source: Company, Kotak Institutional Equities estimates

We downgrade our rating to ADD from BUY earlier based on (1) recent outperformance of 12% in the past three months and 15% in the past 6 month period (this is post a dip of about 3% witnessed in the stock price yesterday), (2) potential dilution of returns in the near term with increased capital requirement of large infrastructure projects (such as Hyderabad metro project) and other subsidiaries, (3) risk related to near-term execution environment and (4) limited upside of about 10% to our target price.

Key risks emanate from (1) continued order booking pressures led by the slowdown in capex in important segments such as Middle East, metals, real estate, petrochemicals etc leading to lower-than-expected earnings momentum going forward, and (2) likely pressure on working capital and margins with likely dominance of infrastructure orders.

Industrials Larsen & Toubro

22 KOTAK INSTITUTIONAL EQUITIES RESEARCH

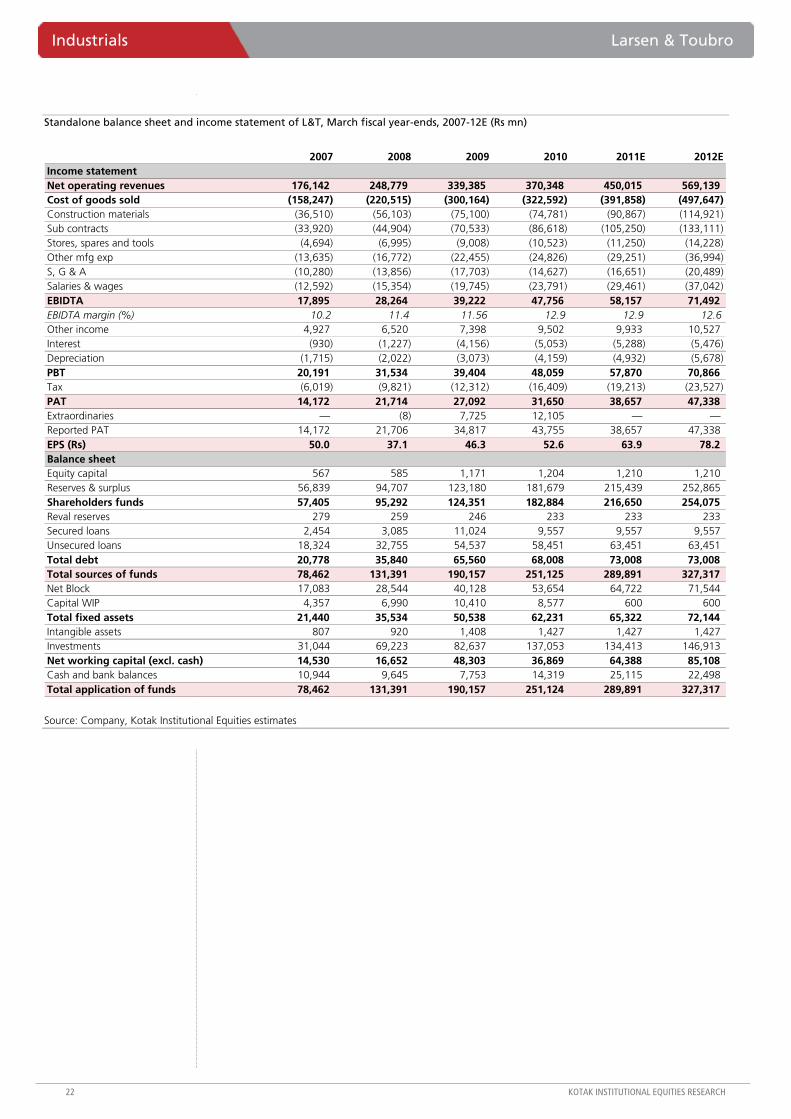

Standalone balance sheet and income statement of L&T, March fiscal year-ends, 2007-12E (Rs mn)

2007 2008 2009 2010 2011E 2012EIncome statementNet operating revenues 176,142 248,779 339,385 370,348 450,015 569,139Cost of goods sold (158,247) (220,515) (300,164) (322,592) (391,858) (497,647)Construction materials (36,510) (56,103) (75,100) (74,781) (90,867) (114,921)Sub contracts (33,920) (44,904) (70,533) (86,618) (105,250) (133,111)Stores, spares and tools (4,694) (6,995) (9,008) (10,523) (11,250) (14,228)Other mfg exp (13,635) (16,772) (22,455) (24,826) (29,251) (36,994)S, G & A (10,280) (13,856) (17,703) (14,627) (16,651) (20,489)Salaries & wages (12,592) (15,354) (19,745) (23,791) (29,461) (37,042)EBIDTA 17,895 28,264 39,222 47,756 58,157 71,492EBIDTA margin (%) 10.2 11.4 11.56 12.9 12.9 12.6Other income 4,927 6,520 7,398 9,502 9,933 10,527Interest (930) (1,227) (4,156) (5,053) (5,288) (5,476)Depreciation (1,715) (2,022) (3,073) (4,159) (4,932) (5,678)PBT 20,191 31,534 39,404 48,059 57,870 70,866Tax (6,019) (9,821) (12,312) (16,409) (19,213) (23,527)PAT 14,172 21,714 27,092 31,650 38,657 47,338Extraordinaries — (8) 7,725 12,105 — —Reported PAT 14,172 21,706 34,817 43,755 38,657 47,338EPS (Rs) 50.0 37.1 46.3 52.6 63.9 78.2Balance sheetEquity capital 567 585 1,171 1,204 1,210 1,210 Reserves & surplus 56,839 94,707 123,180 181,679 215,439 252,865 Shareholders funds 57,405 95,292 124,351 182,884 216,650 254,075 Reval reserves 279 259 246 233 233 233 Secured loans 2,454 3,085 11,024 9,557 9,557 9,557 Unsecured loans 18,324 32,755 54,537 58,451 63,451 63,451 Total debt 20,778 35,840 65,560 68,008 73,008 73,008 Total sources of funds 78,462 131,391 190,157 251,125 289,891 327,317 Net Block 17,083 28,544 40,128 53,654 64,722 71,544 Capital WIP 4,357 6,990 10,410 8,577 600 600 Total fixed assets 21,440 35,534 50,538 62,231 65,322 72,144 Intangible assets 807 920 1,408 1,427 1,427 1,427 Investments 31,044 69,223 82,637 137,053 134,413 146,913 Net working capital (excl. cash) 14,530 16,652 48,303 36,869 64,388 85,108 Cash and bank balances 10,944 9,645 7,753 14,319 25,115 22,498 Total application of funds 78,462 131,391 190,157 251,124 289,891 327,317

Source: Company, Kotak Institutional Equities estimates

For private Circulation Only. FOR IMPORTANT INFORMATION ABOUT KOTAK SECURITIES’ RATING SYSTEM AND OTHER DISCLOSURES, REFER TO THE END OF THIS MATERIAL.

Lower-than-expected oil production from Rajasthan mars 1QFY11 results

Cairn reported 1QFY11 net revenues at `8.4 bn (+21.3% qoq and +310% yoy) and EBITDA at `6.1 bn (+64.7% qoq and +359% yoy) sharply lower than our estimate of `10.2 bn and `8.2 bn. The negative variance is due to (1) lower-than expected oil production at 44,381 b/d from its key Rajasthan block versus our estimate of 47,454 b/d and (2) higher DD&A charge at `1.7 bn versus our estimated `725 mn. 1QFY11 crude price realization was US$72/bbl versus US$71/bbl in 4QFY10 and US$60.2/bbl in 1QFY10. 1QFY11 gas realization was US$4.6/mcf versus US$4.4/mcf in 4QFY10 and US$4/mcf in 1QFY10.

Stock price movement suggests correlation with crude prices seems to have fizzled out

We are surprised by the increase in Cairn’s stock price in the past three months despite a sharp correction in crude oil prices over the same period. We note that crude oil prices (Dated Brent) have correctly sharply by 11.4% in the past three months; however, Cairn’s stock price is up by 9.5% over the same period. Cairn stock price seems to be moving up more in line with its parent’s stock price while correlation with crude price and Indian stock market is quite low of late.

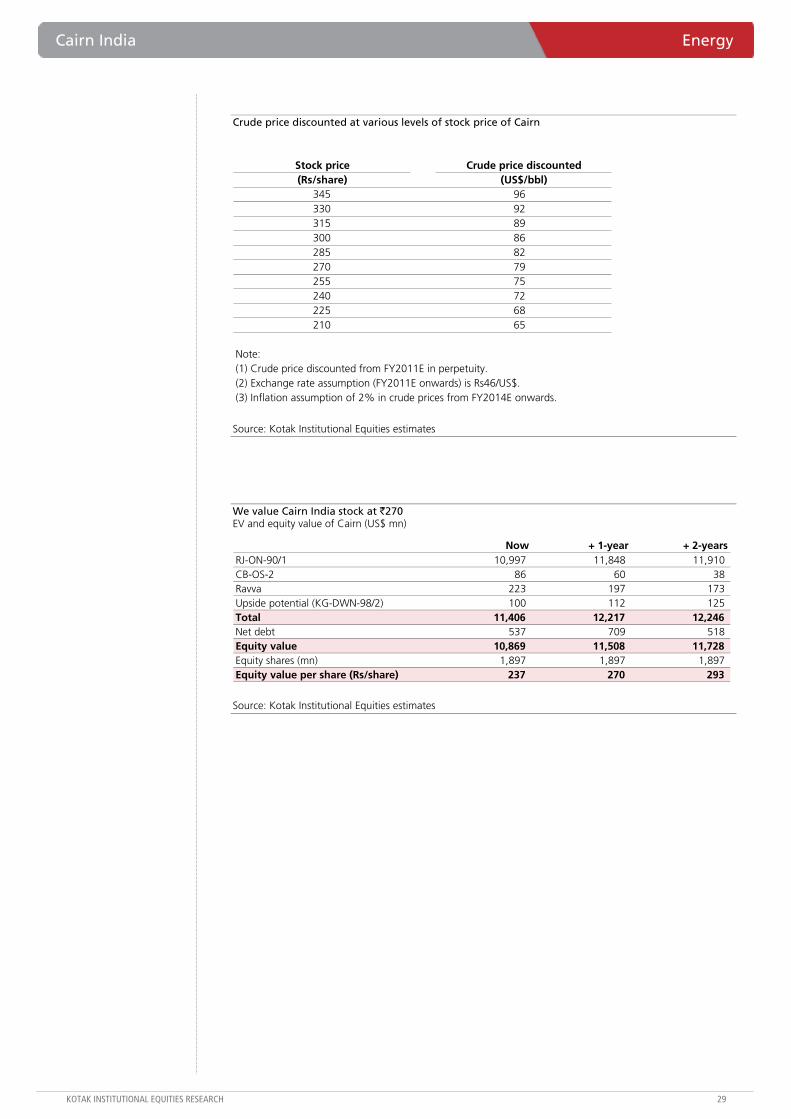

Valuations hard to justify; maintain SELL with revised 12-month DCF-based target price of `270

We maintain our SELL rating on the stock noting 19% potential downside to our 12-month DCF-based target price of `270. The upward revision to target price reflects higher inflation-adjusted long-term crude prices in perpetuity. We rule out a multiple-based approach as earnings over the next 2-3 years would reflect (1) peak level of production, (2) low level of government share and (3) payment of tax at MAT rate. We believe DCF is the appropriate methodology as it best captures the specifics of a production sharing contract as Cairn’s share of profits/cash flow from its Rajasthan block will change over time.

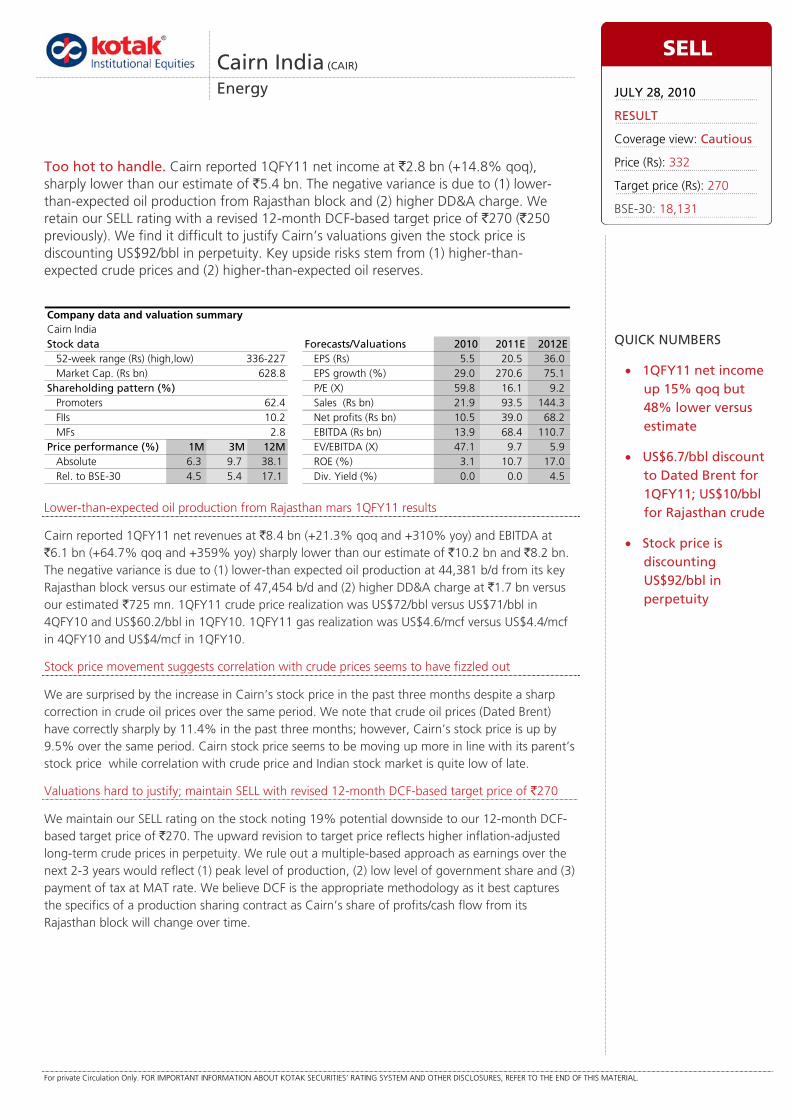

Cairn India (CAIR)

Energy

Too hot to handle. Cairn reported 1QFY11 net income at `2.8 bn (+14.8% qoq), sharply lower than our estimate of `5.4 bn. The negative variance is due to (1) lower-than-expected oil production from Rajasthan block and (2) higher DD&A charge. We retain our SELL rating with a revised 12-month DCF-based target price of `270 (`250 previously). We find it difficult to justify Cairn’s valuations given the stock price is discounting US$92/bbl in perpetuity. Key upside risks stem from (1) higher-than-expected crude prices and (2) higher-than-expected oil reserves.

Cairn IndiaStock data Forecasts/Valuations 2010 2011E 2012E

52-week range (Rs) (high,low) EPS (Rs) 5.5 20.5 36.0Market Cap. (Rs bn) 628.8 EPS growth (%) 29.0 270.6 75.1

Shareholding pattern (%) P/E (X) 59.8 16.1 9.2Promoters 62.4 Sales (Rs bn) 21.9 93.5 144.3FIIs 10.2 Net profits (Rs bn) 10.5 39.0 68.2MFs 2.8 EBITDA (Rs bn) 13.9 68.4 110.7

Price performance (%) 1M 3M 12M EV/EBITDA (X) 47.1 9.7 5.9Absolute 6.3 9.7 38.1 ROE (%) 3.1 10.7 17.0Rel. to BSE-30 4.5 5.4 17.1 Div. Yield (%) 0.0 0.0 4.5

Company data and valuation summary

336-227

SELL

JULY 28, 2010

RESULT

Coverage view: Cautious

Price (Rs): 332

Target price (Rs): 270

BSE-30: 18,131

QUICK NUMBERS

• 1QFY11 net income up 15% qoq but 48% lower versus estimate

• US$6.7/bbl discount to Dated Brent for 1QFY11; US$10/bbl for Rajasthan crude

• Stock price is discounting US$92/bbl in perpetuity

Energy Cairn India

24 KOTAK INSTITUTIONAL EQUITIES RESEARCH

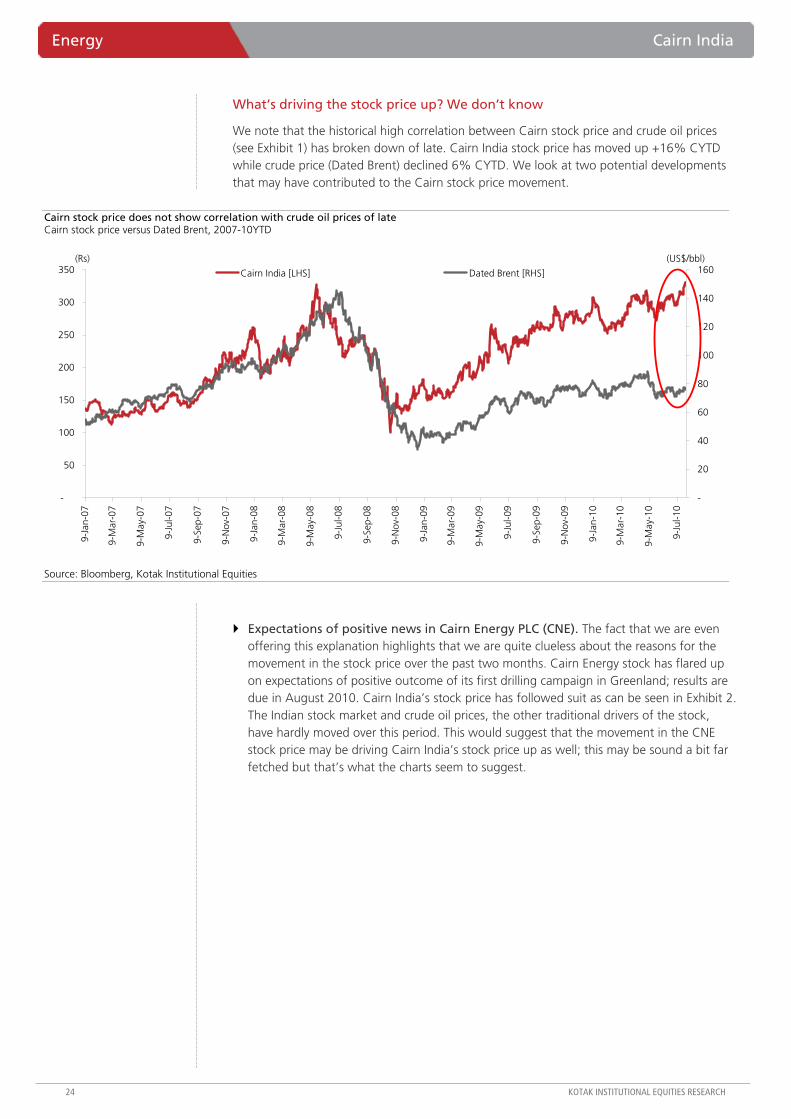

What’s driving the stock price up? We don’t know

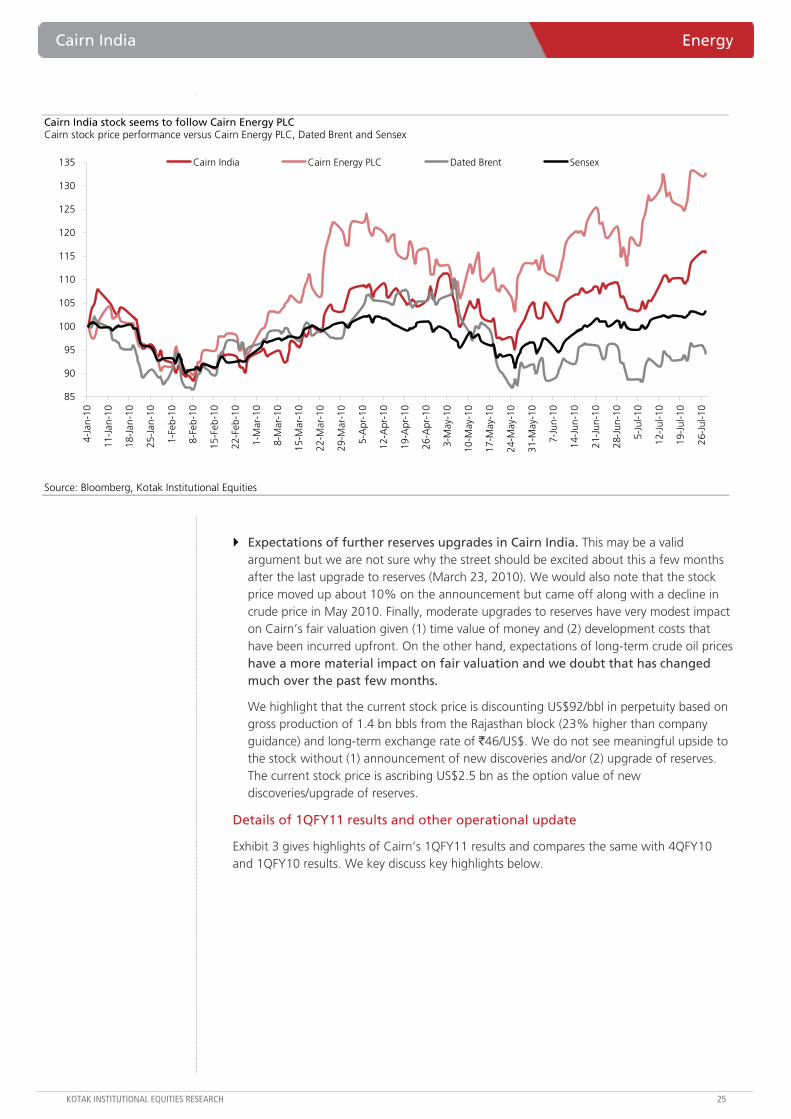

We note that the historical high correlation between Cairn stock price and crude oil prices (see Exhibit 1) has broken down of late. Cairn India stock price has moved up +16% CYTD while crude price (Dated Brent) declined 6% CYTD. We look at two potential developments that may have contributed to the Cairn stock price movement.

Cairn stock price does not show correlation with crude oil prices of late Cairn stock price versus Dated Brent, 2007-10YTD

-

50

100

150

200

250

300

350

9-Ja

n-07

9-M

ar-0

7

9-M

ay-0

7

9-Ju

l-07

9-Se

p-07

9-N

ov-0

7

9-Ja

n-08

9-M

ar-0

8

9-M

ay-0

8

9-Ju

l-08

9-Se

p-08

9-N

ov-0

8

9-Ja

n-09

9-M

ar-0

9

9-M

ay-0

9

9-Ju

l-09

9-Se

p-09

9-N

ov-0

9

9-Ja

n-10

9-M

ar-1

0

9-M

ay-1

0

9-Ju

l-10

-

20

40

60

80

100

120

140

160Cairn India [LHS] Dated Brent [RHS]

(Rs) (US$/bbl)

Source: Bloomberg, Kotak Institutional Equities

Expectations of positive news in Cairn Energy PLC (CNE). The fact that we are even offering this explanation highlights that we are quite clueless about the reasons for the movement in the stock price over the past two months. Cairn Energy stock has flared up on expectations of positive outcome of its first drilling campaign in Greenland; results are due in August 2010. Cairn India’s stock price has followed suit as can be seen in Exhibit 2. The Indian stock market and crude oil prices, the other traditional drivers of the stock, have hardly moved over this period. This would suggest that the movement in the CNE stock price may be driving Cairn India’s stock price up as well; this may be sound a bit far fetched but that’s what the charts seem to suggest.

Cairn India Energy

KOTAK INSTITUTIONAL EQUITIES RESEARCH 25

Cairn India stock seems to follow Cairn Energy PLC Cairn stock price performance versus Cairn Energy PLC, Dated Brent and Sensex

85

90

95

100

105

110

115

120

125

130

135

4-Ja

n-10

11-J

an-1

0

18-J

an-1

0

25-J

an-1

0

1-Fe

b-10

8-Fe

b-10

15-F

eb-1

0

22-F

eb-1

0

1-M

ar-1

0

8-M

ar-1

0

15-M

ar-1

0

22-M

ar-1

0

29-M

ar-1

0

5-A

pr-1

0

12-A

pr-1

0

19-A

pr-1

0

26-A

pr-1

0

3-M

ay-1

0

10-M

ay-1

0

17-M

ay-1

0

24-M

ay-1

0

31-M

ay-1

0

7-Ju

n-10

14-J

un-1

0

21-J

un-1

0

28-J

un-1

0

5-Ju

l-10

12-J

ul-1

0

19-J

ul-1

0

26-J

ul-1

0

Cairn India Cairn Energy PLC Dated Brent Sensex

Source: Bloomberg, Kotak Institutional Equities

Expectations of further reserves upgrades in Cairn India. This may be a valid argument but we are not sure why the street should be excited about this a few months after the last upgrade to reserves (March 23, 2010). We would also note that the stock price moved up about 10% on the announcement but came off along with a decline in crude price in May 2010. Finally, moderate upgrades to reserves have very modest impact on Cairn’s fair valuation given (1) time value of money and (2) development costs that have been incurred upfront. On the other hand, expectations of long-term crude oil prices have a more material impact on fair valuation and we doubt that has changed much over the past few months.

We highlight that the current stock price is discounting US$92/bbl in perpetuity based on gross production of 1.4 bn bbls from the Rajasthan block (23% higher than company guidance) and long-term exchange rate of `46/US$. We do not see meaningful upside to the stock without (1) announcement of new discoveries and/or (2) upgrade of reserves. The current stock price is ascribing US$2.5 bn as the option value of new discoveries/upgrade of reserves.

Details of 1QFY11 results and other operational update

Exhibit 3 gives highlights of Cairn’s 1QFY11 results and compares the same with 4QFY10 and 1QFY10 results. We key discuss key highlights below.

Energy Cairn India

26 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Interim results of Cairn India (` mn)

(% chg.)1QFY11 1QFY11E 1QFY10 4QFY10 1QFY11E 1QFY10 4QFY10 2011E

Income from operations 8,406 10,241 2,050 6,928 (17.9) 310.1 21.3 93,507 Total expenditure (2,347) (2,080) (728) (3,250) 12.8 222.2 (27.8) (26,299) Inc/(Dec) in stock 670 155 (700) Operating expenses (2,188) (1,400) (440) (1,843) 56.3 397.2 18.7 (5,886) Staff cost (189) (280) (215) (268) (32.5) (12.1) (29.5) (1,179) Government taxes/share of profit — — — — (17,634) Other expenditure (640) (400) (228) (439) 59.9 180.5 45.8 (1,600)EBITDA 6,059 8,161 1,321 3,678 (25.8) 358.6 64.7 67,208 Other income 281 1,025 1,290 879 (72.6) (78.2) (68.1) 1,158Interest (493) (950) (7) (19) (48.1) 6,647.9 2,520.2 (2,446)Exploration costs written off (322) (650) (309) (1,219) (50.5) 4.1 (73.6) (1,800)DD&A (1,660) (725) (413) (382) 128.9 301.5 334.9 (9,203)Pretax profits 3,866 6,861 1,882 2,938 (43.6) 105.5 31.6 54,917 Extraordinaries/sales tax benefit — — (1,637) — —Tax (296) (1,451) (208) (208) (79.6) 42.1 42.1 (14,005)Deferred taxation (756) — 418 (278) (1,960)Net income 2,814 5,396 454 2,452 (47.8) 519.3 14.8 38,952 Minority interest — — — — —Net income after minority interest 2,814 5,396 454 2,452 (47.8) 519.3 14.8 38,952 Income tax rate (%) 27.2 21.4 (85.9) 16.5 29.1

Production, selling price dataProduction volume, gross ('000 boepd) 95.0 99.3 59.5 69.0 59.7 37.7 151.6 Production volume, net ('000 boepd) 44.8 47.5 15.9 26.3 181.5 70.2 84.1 Rajasthan 31.1 33.5 — 12.3 70.5 CB-OS-2 5.4 5.5 5.8 5.7 (6.7) (4.9) 4.9 Oil 3.3 3.1 4.0 3.3 (17.3) (0.8) 3.1 Gas (mn cf/d) 12.8 13.0 10.9 13.4 16.9 (4.2) 9.9 Ravva 8.3 8.5 10.1 8.4 (17.6) (0.5) 8.7 Oil 6.5 6.3 8.2 6.7 (21.0) (2.4) 6.8 Gas (mn cf/d) 11.0 11.8 11.3 10.7 (2.7) 3.1 10.3 Selling price, oil (US$/bbl) 72.0 72.6 60.2 71.0 19.6 1.4 68.1 Selling price, gas (US$/mcf) 4.6 4.9 4.0 4.4 15.0 4.1 4.9 Exchange rate (Rs/US$) 45.7 45.7 48.7 45.9 (6.2) (0.4) 46.0

Source: Company, Kotak Institutional Equities estimates

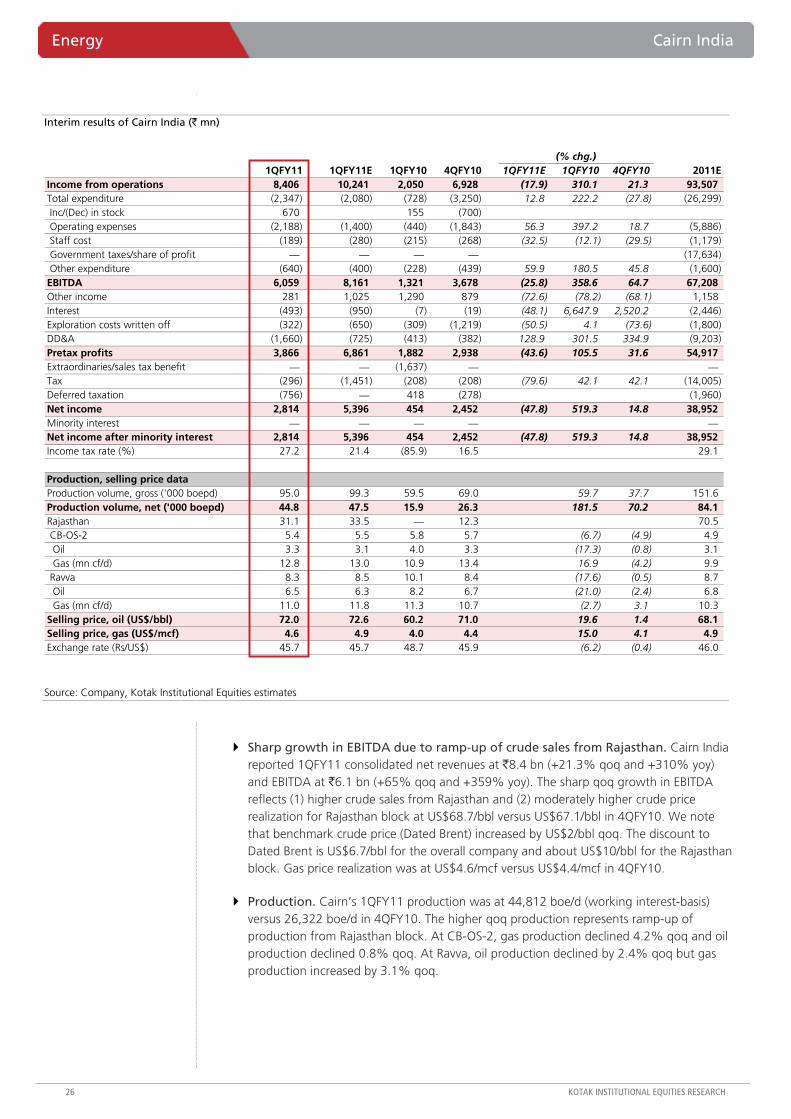

Sharp growth in EBITDA due to ramp-up of crude sales from Rajasthan. Cairn India reported 1QFY11 consolidated net revenues at `8.4 bn (+21.3% qoq and +310% yoy) and EBITDA at `6.1 bn (+65% qoq and +359% yoy). The sharp qoq growth in EBITDA reflects (1) higher crude sales from Rajasthan and (2) moderately higher crude price realization for Rajasthan block at US$68.7/bbl versus US$67.1/bbl in 4QFY10. We note that benchmark crude price (Dated Brent) increased by US$2/bbl qoq. The discount to Dated Brent is US$6.7/bbl for the overall company and about US$10/bbl for the Rajasthan block. Gas price realization was at US$4.6/mcf versus US$4.4/mcf in 4QFY10.

Production. Cairn’s 1QFY11 production was at 44,812 boe/d (working interest-basis) versus 26,322 boe/d in 4QFY10. The higher qoq production represents ramp-up of production from Rajasthan block. At CB-OS-2, gas production declined 4.2% qoq and oil production declined 0.8% qoq. At Ravva, oil production declined by 2.4% qoq but gas production increased by 3.1% qoq.

Cairn India Energy

KOTAK INSTITUTIONAL EQUITIES RESEARCH 27

Cairn’s entitlement was 74% in Rajasthan output. We note that Cairn’s entitlement in its Rajasthan block was 74% versus its participating interest of 70% in the block. This is on account of cairn’s entitlement to recover the initial exploration expenses that were incurred by cairn solely. The management has guided that Cairn’s entitlement will be at 74% for FY2011E.

DD&A charges up 335% qoq. Cairn reported DD&A expenses at `1.7 bn (+335%qoq and +302% yoy). The sharp increase in DD&A expenses reflects (1) higher depreciation charge due to commissioning of the pipeline in 1QFY11 and (2) higher depletion charge due to higher production.

Other income was 68% lower qoq. Cairn’s other income was lower at `281 mn (-68% qoq) as 4QFY10 other income included forex gains. We note that 1QFY11 other expenditure includes `413 mn as foreign exchange fluctuation loss.

Execution on track with commissioning of Train 3 at its Rajasthan block. Cairn commissioned the second train with a capacity of 50,000 b/d in May 2010 and the third train with a capacity of 50,000 b/d in June 2010. Cairn is currently producing over 100,000 b/d.

Earnings revision and key assumptions

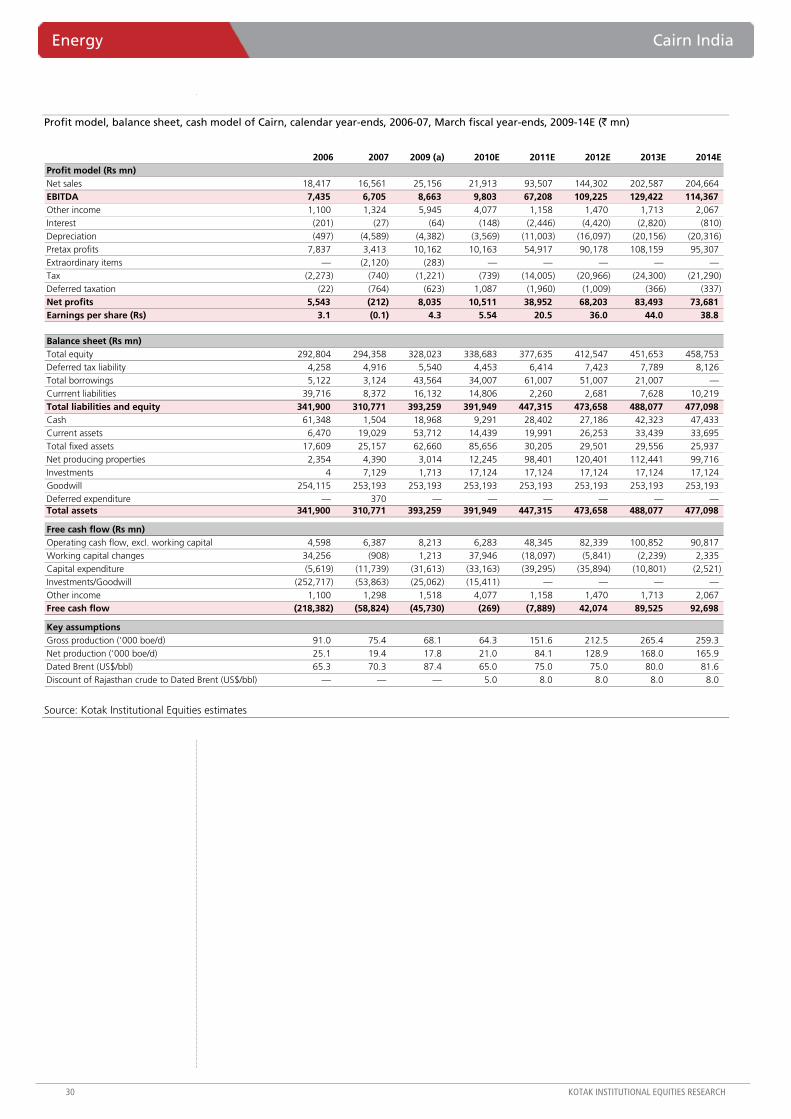

We have fine-tuned our FY2011E, FY2012E and FY2013E EPS to `21, `36 and `44 from `28, `40 and `48 to reflect (1) moderately higher production and (2) weaker rupee. We discuss our key assumptions behind earnings estimates below.

Production. We model gross production from Rajasthan block at 5 mn tons (101,000 b/d) for FY2011E, 8.3 mn tons (167,000 b/d) for FY2012E and 11.3 mn tons (225,000 b/d) for FY2013E. We assume gross production of 1.4 bn bbls (1.13 bn bbls net to Cairn) over the life of the field.

Crude price assumption. We maintain our crude price (Dated Brent) assumptions at US$75/bbl for FY2011E, US$75/bbl for FY2012E and US$80/bbl for FY2013E. However, we increase crude prices by 2% in perpetuity beyond FY2013E to reflect the impact of inflation. We model discount for Rajasthan crude to Dated Brent at US$8/bbl (US$6/bbl previously).

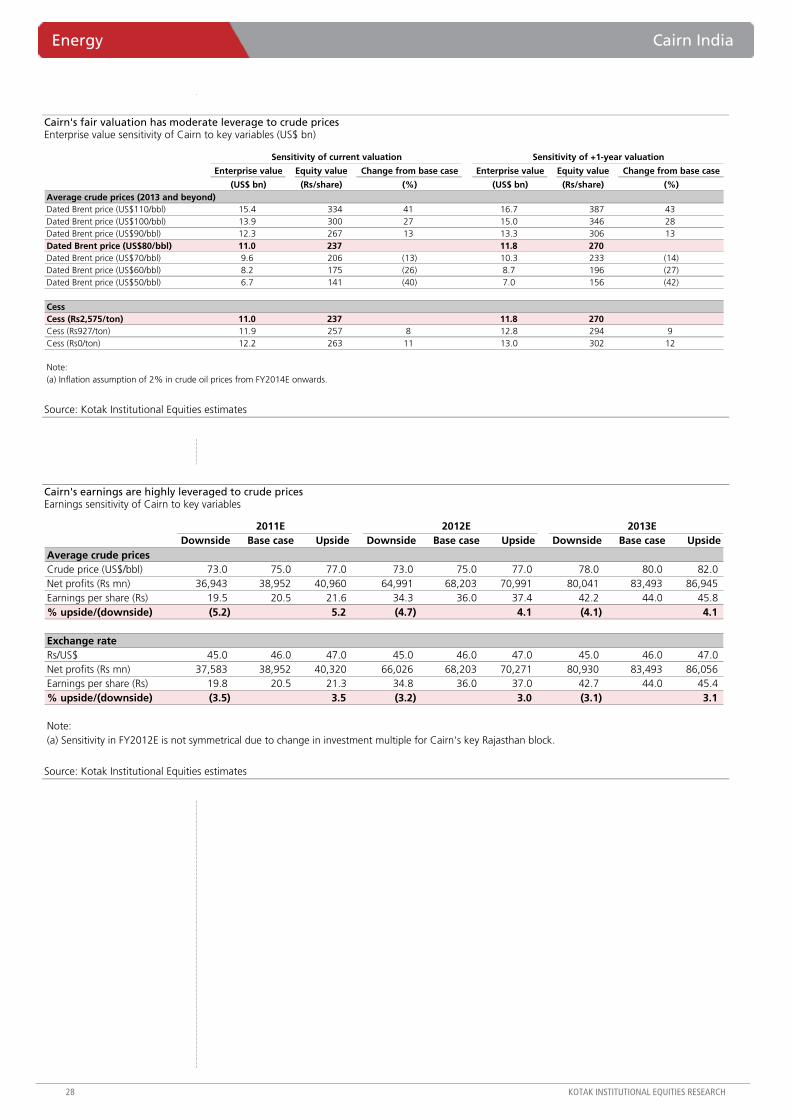

Cess. Our earnings estimates and valuation for Cairn India reflect payment of cess on crude oil from its Rajasthan block. Cairn is paying cess under protest and we believe it is best to factor in the payment for making financial estimates. Our fair valuation of `271 assumes cess payment at `2,575/ton. Our fair valuation of the stock would increase by `294 if we assume that Cairn will have to bear cess at `927/ton and it would increase by `302 if we assume Cairn will not have to bear any cess (see Exhibit 4).

Energy Cairn India

28 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Cairn's fair valuation has moderate leverage to crude prices Enterprise value sensitivity of Cairn to key variables (US$ bn)

Sensitivity of current valuation Sensitivity of +1-year valuation

Enterprise value Equity value Change from base case Enterprise value Equity value Change from base case

(US$ bn) (Rs/share) (%) (US$ bn) (Rs/share) (%)Average crude prices (2013 and beyond)Dated Brent price (US$110/bbl) 15.4 334 41 16.7 387 43Dated Brent price (US$100/bbl) 13.9 300 27 15.0 346 28Dated Brent price (US$90/bbl) 12.3 267 13 13.3 306 13Dated Brent price (US$80/bbl) 11.0 237 11.8 270 Dated Brent price (US$70/bbl) 9.6 206 (13) 10.3 233 (14)Dated Brent price (US$60/bbl) 8.2 175 (26) 8.7 196 (27)Dated Brent price (US$50/bbl) 6.7 141 (40) 7.0 156 (42)

CessCess (Rs2,575/ton) 11.0 237 11.8 270 Cess (Rs927/ton) 11.9 257 8 12.8 294 9Cess (Rs0/ton) 12.2 263 11 13.0 302 12

Note:(a) Inflation assumption of 2% in crude oil prices from FY2014E onwards.

Source: Kotak Institutional Equities estimates

Cairn's earnings are highly leveraged to crude prices Earnings sensitivity of Cairn to key variables