increasing transparency and financial accountability in the health sector: why performance-based...

TRANSCRIPT

Increasing transparency and financial accountability in the health sector:

Why performance-based budgeting is not the answer

141st Annual Meeting of the APHA, Boston MATaryn Vian, SM, PhD

Boston University School of Public [email protected]

Presenter Disclosures

The following personal financial relationships with commercial interests relevant to this presentation existed during the past 12 months:

Taryn Vian

No relationships to disclose

Rationale Research questions Methods Findings Conclusions

Outline

Performance based budgeting (PBB) to align spending decisions with expected performance

Meant to increase government accountability and effectiveness

International experience so far is mixed Does this reform work? If so, how?

Rationale

Lesotho is implementing PBB as part of larger public finance reforms, but hospitals are experiencing problems

Analysis of reform implementation in the health sector, using a theoretical model, could suggest ways to improve progress

Rationale for Lesotho

“The concept is simple—objectives, results, and resources should all be linked...The application is

difficult.”Auditor General of Canada

Transformational Change Model

Source: VanDeusen Lukas, C., S. K. Holmes, et al. (2007). "Transformational change in health care systems: An organizational model." Health Care Management Review 32(4): 309-320

To improve our understanding of PBB in the health sector To help improve public policy in Lesotho To inform research on organizational change and public

finance reform

Purpose

Progress: What progress has been made in implementing reforms?

Perceptions: What attitudes do people have about the reforms?

Factors: What are the factors related to progress in implementation? Can Transformational Change (TC) model help explain progress? How might the model be improved?

Research Questions

Multiple case study research approach Unit of analysis: hospital Triangulation through multiple data sources

◦ plans◦ budgets◦ performance reports◦ 52 interviews

Analysis: ◦ Sequential individual cases, cross-case analysis ◦ Modified grounded theory approach

Methods

Source: Lesotho DHS 2004

Cases in StudyHospital/

Characteristic Hospital A Hospital B Hospital C Hospital D

Level of Facility

District

District

Regional

Regional

Beds

107

108

207

117

Patient

Satisfaction

73%

82%

9%

42%

Accreditation (passing is

>80%; 11 total areas)

2 areas >80% 4 areas >50%

0 areas >80% 2 areas >50%

0 areas >80% 2 areas >50%

1 areas >80% 4 areas >50%

Annual admissions

3,254 4,394 5,446 2,613

General Outpatient visits

36,409 28,153 20,014 17,741

Doctors/nurses 3/29 4/35 7/36 4/27

Findings

Dimension/ Measure

Hospital Average A B C D

Dimension 1: Evidence that Performance Plans Exist Availability of plan ●● ●● ●● ●● Modest Organization of plan ● ●● ●● ●● Modest Accountability structure ●●● ●● ●● ●● Modest Defined activities/outputs ● ●● ●● ● Modest to little Participation ●● ● ●● ● Modest to little Baseline data ○ ○ ○ ○ None Institutionalization ○ ○ ○ ○ None Acceptance ● ○ ● ○ Little to none Dimension 2: Evidence that Performance-based Budgets Exist Availability of budget ●● ● ●● ●● Modest Organization of budget ● ●● ●● ●● Modest Output/activity costing ○ ● ● ○ Little to none Institutionalization ○ ○ ○ ○ None Acceptance ○ ○ ○ ○ None Dimension 3: Evidence of Performance Monitoring & Reporting Data systems oriented to PBB

● ● ○ ● Little

Performance reporting ●● ○ ○ ● Little Financial reporting ○ ○ ○ ○ None Dimension 4: Evidence that Performance Information is Used …To make or change work plans

● ○ ○ ● Little to none

…To develop budgets ● ○ ○ ○ Little to none …To monitor efficiency and effectiveness

○ ○ ○ ○ None

…To communicate within hierarchy (internal accountability)

○ ○ ○ ○ None

…To communicate to the public (external accountability)

○ ○ ○ ○ None

Dimension/ Measure

Hospital Average A B C D

Dimension 1: Evidence that Performance Plans Exist Availability of plan ●● ●● ●● ●● Modest Organization of plan ● ●● ●● ●● Modest Accountability structure ●●● ●● ●● ●● Modest Defined activities/outputs ● ●● ●● ● Modest to little Participation ●● ● ●● ● Modest to little Baseline data ○ ○ ○ ○ None Institutionalization ○ ○ ○ ○ None Acceptance ● ○ ● ○ Little to none Dimension 2: Evidence that Performance-based Budgets Exist Availability of budget ●● ● ●● ●● Modest Organization of budget ● ●● ●● ●● Modest Output/activity costing ○ ● ● ○ Little to none Institutionalization ○ ○ ○ ○ None Acceptance ○ ○ ○ ○ None Dimension 3: Evidence of Performance Monitoring & Reporting Data systems oriented to PBB

● ● ○ ● Little

Performance reporting ●● ○ ○ ● Little Financial reporting ○ ○ ○ ○ None Dimension 4: Evidence that Performance Information is Used …To make or change work plans

● ○ ○ ● Little to none

…To develop budgets ● ○ ○ ○ Little to none …To monitor efficiency and effectiveness

○ ○ ○ ○ None

…To communicate within hierarchy (internal accountability)

○ ○ ○ ○ None

…To communicate to the public (external accountability)

○ ○ ○ ○ None

Little progress in implementing PBB at any of the hospitals

More progress on performance-based planning than on other measures

Some efforts to develop performance budgets, but lack of systems, poor understanding of “outputs”

Little or no monitoring or use of data

Q 1: Measuring Progress

Misalignment of StructureHospital Functional Structure MTEF Program StructureDMO Office General Admin & ManagementAdministration (incl. maintenance, minor Administration works, drivers & admin staff, manage Infrastructure Development & Maint. service contracts, e.g. food for patients) Maintenance of EquipmentAccounts Financial ManagementHuman Resources Short-term TrainingNursing Curative Outpatient Department Inpatient Services MCH Outpatient Services Wards Pharmaceuitical Services Operating Theatre Laboratory Services Mental Health Observation Unit Radiology ServicesPharmacy DisabilityRadiology PhysiotherapyLaboratoryART Clinic

What is an “Output”?

39%

13%

26%

22%

Procurement

Staff Training

Patient Care

Other

Liter of fuel

Staff trained

MeetingProcurement

Staff Training

Patient Care

Other

Patient visit

“We look at what we have achieved, in terms of what we got last time...like how many computers. We do the subtraction—we asked for 5 computers last year and only got 3, so we still need 2.”

Accountant

Input-oriented Budgeting Approach

KnowledgeResultsSuccess

factors

Q 2: Perceptions

“These things...we hear about them [but] it is mainly something that concerns people in Accounts...it is not really a health initiative.”

Most unit heads did not know there was a budget reform…

“We work the wards, …… they go to meetings.” (Hospital Matron)

-

Professional Boundaries

The Accountant did not let you get anything. We always wondered—what is really happening? I planned and made the budget, so I know it is really there, and then you have to ask, what happened to the money?

Hospital Matron

Result: Lack of Transparency

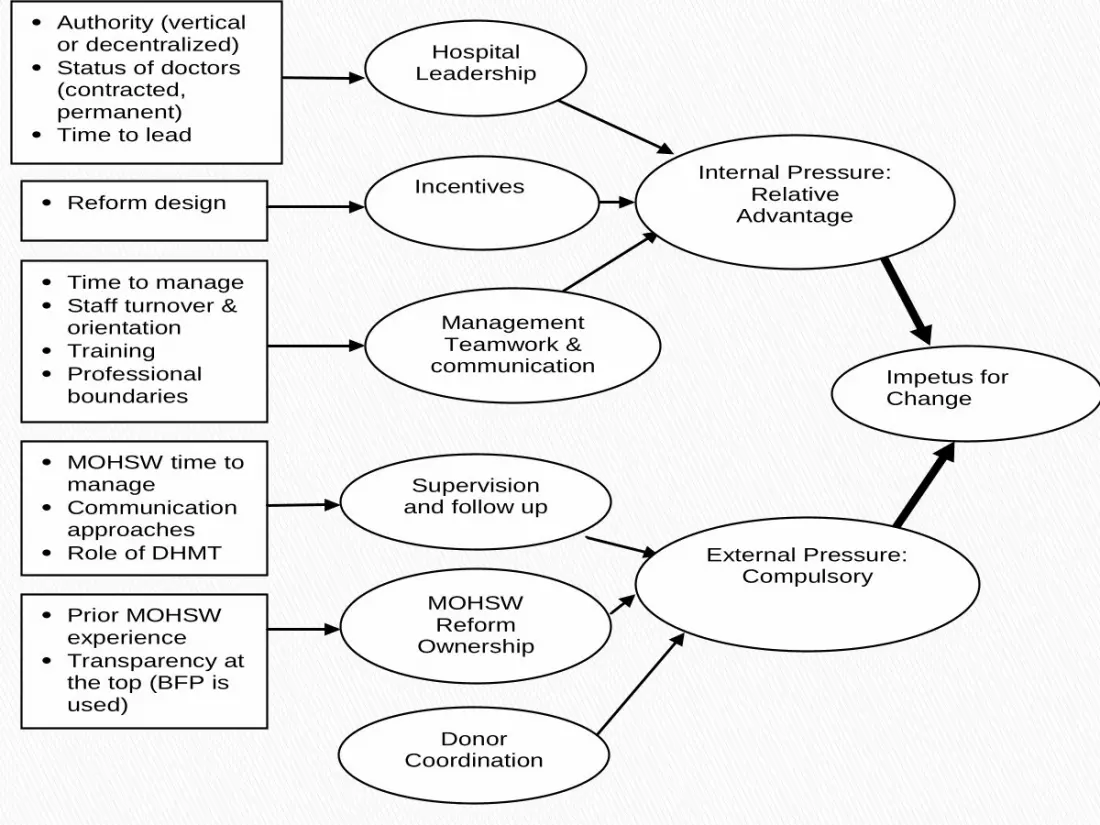

Q 3: Implementation Factors

Impetus for Change

Internal Pressure: Relative

Advantage

Hospital Leadership

Incentives

Management Teamwork &

communication

Time to manage Staff turnover &

orientation Training Professional

boundaries MOHSW time to

manage Communication

approaches Role of DHMT Prior MOHSW

experience Transparency at

the top (BFP is used)

Reform design

Supervision and follow up

External Pressure: Compulsory

MOHSW Reform

Ownership

Donor Coordination

Authority (vertical or decentralized)

Status of doctors (contracted, permanent)

Time to lead

1. Develop leadership2. Redesign reform (SII)

• simplify• incentives• integrate components

3. Strengthen capacity4. Breakdown professional silos

Levers to Influence Reform Progress

1. PBB reform may help improve accountability, but must be adapted for LDCs.

2. Organizational change theory may explain reform progress once prerequisites are in place. Focus on building impetus for change.

3. Explore other strategies and stay committed to the goal of greater accountability in government.

Conclusion

The Lesotho-Boston Health Alliance and Carrie CafaroStudy participants from Lesotho

Many thanks to…

Photo: Libby Cunningham