ifrs conceptual framework

TRANSCRIPT

IFRS CONCEPTUALFRAMEWORK

Financial Reporting

MARCH 12, 2015PROF.WAQAR HASSAN RANDHAWA Hailey college of Commerce

Hailey College Of Commerce Financial Reporting Notes G1, G2 (Morning & After noon)

B.com (Hons) 8th Semester, M.com (3.5 years) 4thSemester

This section relates to what I call the ‘pillars of accounting’,a very important area, without which the ‘top floor’ of yourknowledge cannot be built. The foundations of this ‘building’were built in prior years of accounting study. If you feel thatthere may be cracks in your foundation, right now is the time tofix them by revising your work from prior years.

The Framework

The Framework is technically not a standard but the foundation forall standards and interpretations. It therefore does not overrideany of the IFRSs but should be referred to as the basic logicwhen interpreting and applying a difficult IFRS (the term IFRSincludes the standards and the interpretations).

ScopeThe Conceptual Framework deals with:

(a) The objective of financial statements

(b) The qualitative characteristics that determine the usefulnessof information in financial statements

(c) The definition, recognition and measurement of the elementsfrom which financial statements are constructed

(d) Concepts of capital and capital maintenance

Course Instructor Waqar Hassan Randhawa ACA (ICAEW) FCCA (UK) [email protected]

Hailey College Of Commerce Financial Reporting Notes G1, G2 (Morning & After noon)

B.com (Hons) 8th Semester, M.com (3.5 years) 4thSemester

The objective of general purpose financialreportingThe Conceptual Framework states that:

'The objective of general purpose financial reporting is toprovide information about the reporting Entity that is useful toexisting and potential investors, lenders and other creditors inmaking Decisions about providing resources to the entity.'

These users need information about:

The economic resources of the entity

The claims against the entity

Changes in the entity's economic resources and claims

Information about the entity's economic resources and the claimsagainst it helps users to assess the entity's liquidity andsolvency and its likely needs for additional financing.

Information about a reporting entity's financial performance (thechanges in its economic resources and claims) helps users tounderstand the return that the entity has produced on itseconomic resources. This is an indicator of how efficiently andeffectively management has used the resources of the entity andis helpful in predicting future returns.

The objective of financial statements is to provide informationthat is useful to a wide range of users regarding the entities:

• Financial position: found mainly in the statement of financialposition;

Course Instructor Waqar Hassan Randhawa ACA (ICAEW) FCCA (UK) [email protected]

Hailey College Of Commerce Financial Reporting Notes G1, G2 (Morning & After noon)

B.com (Hons) 8th Semester, M.com (3.5 years) 4thSemester

• Financial performance: found mainly in the statement ofcomprehensive income;

• Changes in financial position: found mainly in the statement ofchanges in equity; and

Management’s stewardship of the resources entrusted to it.

It is important to note that users are not limited toshareholders and governments, but include, amongst others,employees, lenders, suppliers, competitors, customers and thegeneral public.

Underlying assumptionAccruals basisThe Conceptual Framework makes it clear that this information shouldbe prepared on an accruals basis

Accruals basis. The effects of transactions and other events arerecognized when they occur (and not as cash or its equivalent isreceived or paid) and they are recorded in the accounting recordsand reported in the financial statements of the periods to whichthey relate.

Financial statements prepared under the accruals basis show userspast transactions involving cash and also obligations to pay cashin the future and resources which represent cash to be receivedin the future.

Going concernGoing concern. The entity is normally viewed as a going concern,that is, as continuing in operation for the foreseeable future.

Course Instructor Waqar Hassan Randhawa ACA (ICAEW) FCCA (UK) [email protected]

Hailey College Of Commerce Financial Reporting Notes G1, G2 (Morning & After noon)

B.com (Hons) 8th Semester, M.com (3.5 years) 4thSemester

It is assumed that the entity has neither the intention nor thenecessity of liquidation or of curtailing materially the scale ofits operations.

It is assumed that the entity has no intention to liquidate or curtail major operations. If it did, then the financial statements would be prepared on a different (disclosed) basis.FAST FORWARD

Qualitative characteristics of useful financialinformation

Chapter 3 of the Conceptual Framework distinguishes betweenfundamental and enhancing qualitative characteristics, foranalysis purposes. Fundamental qualitative characteristicsdistinguish useful financial reporting information frominformation that is not useful or misleading. Enhancingqualitative characteristics distinguish more useful informationfrom less useful information.

The two fundamental qualitative characteristics arerelevance and faithful representation

Relevance

Relevant information is capable of making a difference in the decisions made by users. It is capable of making a difference in decisions if it has predictive value, confirmatory value or both.

When deciding what is relevant, one must consider the users’ needsin decision-making:

Course Instructor Waqar Hassan Randhawa ACA (ICAEW) FCCA (UK) [email protected]

Hailey College Of Commerce Financial Reporting Notes G1, G2 (Morning & After noon)

B.com (Hons) 8th Semester, M.com (3.5 years) 4thSemester

A user will use financial statements to predict, for example, thefuture asset structure, profitability and liquidity of thebusiness and to confirm his previous predictions. The predictiveand confirmatory role of the financial statements is thereforevery important to Consider when presenting financial statements. By way of example,unusual items should be displayed separately because these, bynature, are not expected to recur frequently.

A user will use financial statements to predict, for example, thefuture asset structure, profitability and liquidity of thebusiness and to confirm his previous predictions. The predictiveand confirmatory role of the financial statements is thereforevery important to

The relevance of information is affected by its nature and itsmateriality

Materiality. Information is material if omitting it or misstatingit could influence decisions that users make on the basis offinancial information about a specific reporting entity. Consider the materiality of the size of the item or the potentialerror in user-judgment if it were omitted or misstated

Materiality is a term that you will encounter very often in yourstudies and is thus important for you to understand. TheFramework explains that you should consider something (an amountor some other information) to be material: If the economic decisions of the users could be influenced if it were misstated oromitted. Materiality is considered to be a ‘threshold’ or ‘cut-off point’to help in determining what would be useful to users and is

Course Instructor Waqar Hassan Randhawa ACA (ICAEW) FCCA (UK) [email protected]

Hailey College Of Commerce Financial Reporting Notes G1, G2 (Morning & After noon)

B.com (Hons) 8th Semester, M.com (3.5 years) 4thSemester

therefore not a primary qualitative characteristic. For example,all revenue types above a certain amount may be considered to bematerial to an entity and thus the entity would disclose eachrevenue type separately.

Faithful representationFinancial reports represent economic phenomena in words and numbers. To be useful, financial information must not only represent relevant phenomena but must faithfully represent the phenomena that it purports to represent.

To be a faithful representation information must be complete, neutral and free from error

A complete depiction includes all information necessary for auser to understand the phenomenon being depicted, including allnecessary descriptions and explanations

A neutral depiction is without bias in the selection orpresentation of financial information. This means thatinformation must not be manipulated in any way in order toinfluence the decisions of users.

Free from error means there are no errors or omissions in thedescription of the phenomenon and no Errors made in the processby which the financial information was produced. It does not meanthat no Inaccuracies can arise, particularly where estimates haveto be made.

Most financial statements have some level of risk that not alltransactions and events have been properly identified and thatthe measurement basis used for some of the more complex

Course Instructor Waqar Hassan Randhawa ACA (ICAEW) FCCA (UK) [email protected]

Hailey College Of Commerce Financial Reporting Notes G1, G2 (Morning & After noon)

B.com (Hons) 8th Semester, M.com (3.5 years) 4thSemester

transactions might not be the most appropriate. Sometimes eventsor transactions can be so difficult to measure that the entitychooses not to include them in the financial statements. The mostcommon example of this is the internal goodwill that the entityis probably creating but which it cannot recognise due to theinability to clearly identify it and the inability to measure itreliably.

Substance over form This is not a separate qualitative characteristic under theConceptual Framework. The IASB says that to do so would beredundant because it is implied in faithful representation.Faithful representation of a Transaction is only possible if itis accounted for according to its substance and economic reality.

This requires that the legal form of a transaction be ignored ifthe substance or economic reality thereof differs. A typicalexample here is a lease agreement (the legal document). The term‘lease’ that is used in the legal document suggests that you areborrowing an asset in exchange for payments (rental) over aperiod of time. Many of these so-called lease agreements resultin the lessee (the person ‘borrowing’ the asset) keeping theasset at the end of the ‘rental’ period. This means that thelease agreement is actually, in substance, not a lease but anagreement to purchase (the ‘lessee’ was actually purchasing theasset and not renting the asset). This lease is referred to as afinance lease, but as accountants, we will recognize thetransaction as a purchase (and not as a pure lease).

Enhancing qualitative characteristics

Course Instructor Waqar Hassan Randhawa ACA (ICAEW) FCCA (UK) [email protected]

Hailey College Of Commerce Financial Reporting Notes G1, G2 (Morning & After noon)

B.com (Hons) 8th Semester, M.com (3.5 years) 4thSemester

Comparability

Comparability is the qualitative characteristic that enablesusers to identify and understandSimilarities in, and differences among, items. Information abouta reporting entity is more useful if it can be compared withsimilar information about other entities and with similarinformation about the same Entity for another period or date.

Consistency, although related to comparability, is not the same.It refers to the use of the same methods for the same items (i.e.consistency of treatment) either from period to period within areporting entity or in a single period across entities.

The disclosure of accounting policies is particularly importanthere. Users must be able to distinguish between differentaccounting policies in order to be able to make a validcomparison of similar items in the accounts of differententities.

When an entity changes an accounting policy, the change isapplied retrospectively so that the results from one period tothe next can still be usefully compared.

Comparability is not the same as uniformity. Entities shouldchange accounting policies if those policies becomeinappropriate. Corresponding information for preceding periodsshould be shown to enable comparison over time.

Financial statements should be comparable from one year to thenext: therefore, accounting policies must be consistentlyapplied, meaning that transactions of a similar nature should betreated in the same way that they were treated in the priorCourse Instructor Waqar Hassan Randhawa ACA (ICAEW) FCCA (UK) [email protected]

Hailey College Of Commerce Financial Reporting Notes G1, G2 (Morning & After noon)

B.com (Hons) 8th Semester, M.com (3.5 years) 4thSemester

years; and from one entity to the next: therefore entities mustall comply with the same standards, so that when comparing twoentities a measure of comparability is guaranteed.

As a result of requiring comparability, users need to be providedwith information for the comparative year and should be providedwith the accounting policies used by the entity (and any changesthat may have been made to the accounting policies used in aprevious year).

Verifiability

Verifiability helps assure users that information faithfullyrepresents the economic phenomena it purports to represent. Itmeans that different knowledgeable and independent observerscould reach consensus that a particular depiction is a faithfulrepresentation.

Information that can be independently verified is generally moredecision-useful than information that cannot.

Timeliness

Timeliness means having information available to decision-makersin time to be capable of influencing their decisions. Generally,the older information is the less useful it is.

Information may become less useful if there is a delay inreporting it. There is a balance between timeliness and theCourse Instructor Waqar Hassan Randhawa ACA (ICAEW) FCCA (UK) [email protected]

Hailey College Of Commerce Financial Reporting Notes G1, G2 (Morning & After noon)

B.com (Hons) 8th Semester, M.com (3.5 years) 4thSemester

provision of reliable information. If information is reported ona timely basis when not all aspects of the transaction are known,it may not be complete or free from error.

Conversely, if every detail of a transaction is known, it may betoo late to publish the information because it has becomeirrelevant. The overriding consideration is how best to satisfythe economic decision-making needs of the users.

Understandability

Classifying, characterising and presenting information clearlyand concisely makes it understandable.

Financial reports are prepared for users who have a reasonableknowledge of business and economic activities and who review andanalyse the information diligently. Some phenomena are inherentlycomplex and cannot be made easy to understand. Excludinginformation on those phenomena might make the information easierto understand, but without it those reports would be incompleteand therefore misleading. Therefore matters should not be leftout of financial statements simply due to their difficulty aseven well-informed and diligent users may sometimes need the aidof an advisor to understand information about complex economicphenomena.

Course Instructor Waqar Hassan Randhawa ACA (ICAEW) FCCA (UK) [email protected]

Hailey College Of Commerce Financial Reporting Notes G1, G2 (Morning & After noon)

B.com (Hons) 8th Semester, M.com (3.5 years) 4thSemester

The cost constraint on useful financial reporting

This is a pervasive constraint, not a qualitative characteristic.When information is provided, its benefits must exceed the costsof obtaining and presenting it. This is a subjective area andthere are other difficulties: others, not the intended users, maygain a benefit; also the cost may be paid by someone other thanthe users. It is therefore difficult to apply a cost-benefitanalysis, but preparers and users should be aware of theconstraint.

Course Instructor Waqar Hassan Randhawa ACA (ICAEW) FCCA (UK) [email protected]

Hailey College Of Commerce Financial Reporting Notes G1, G2 (Morning & After noon)

B.com (Hons) 8th Semester, M.com (3.5 years) 4thSemester

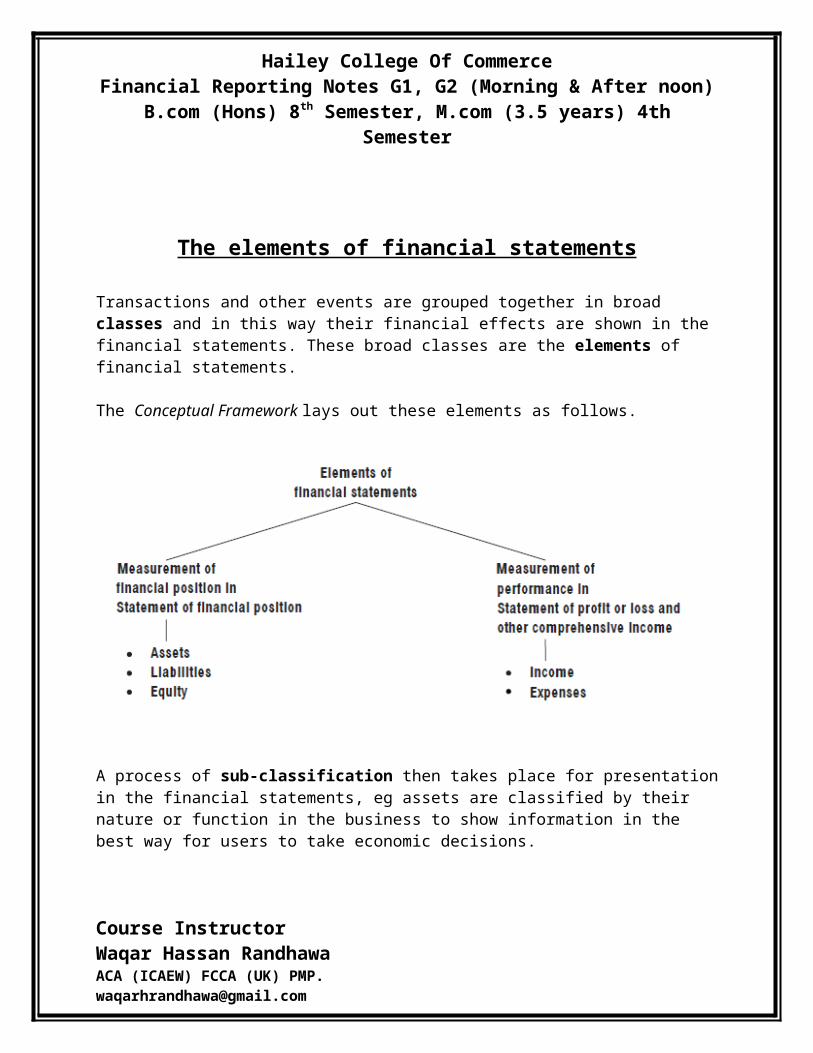

The elements of financial statements

Transactions and other events are grouped together in broad classes and in this way their financial effects are shown in the financial statements. These broad classes are the elements of financial statements.

The Conceptual Framework lays out these elements as follows.

A process of sub-classification then takes place for presentationin the financial statements, eg assets are classified by their nature or function in the business to show information in the best way for users to take economic decisions.

Course Instructor Waqar Hassan Randhawa ACA (ICAEW) FCCA (UK) [email protected]

Hailey College Of Commerce Financial Reporting Notes G1, G2 (Morning & After noon)

B.com (Hons) 8th Semester, M.com (3.5 years) 4thSemester

Financial position

We need to define the three terms listed under this headingabove.

Asset. A resource controlled by an entity as a result of pastevents and from which future economic benefits are expected toflow to the entity.

Liability. A present obligation of the entity arising from pastevents, the settlement of which isexpected to result in an outflow from the entity of resourcesembodying economic benefits.

Equity. The residual interest in the assets of the entity afterdeducting all its liabilities.

These definitions are important, but they do not cover thecriteria for recognition of any of these items, his means thatthe definitions may include items which would not actually berecognised in the statement of financial position because they

Course Instructor Waqar Hassan Randhawa ACA (ICAEW) FCCA (UK) [email protected]

Hailey College Of Commerce Financial Reporting Notes G1, G2 (Morning & After noon)

B.com (Hons) 8th Semester, M.com (3.5 years) 4thSemester

fail to satisfy recognition criteria particularly the probableflow of any economic benefit to or from the business.

Assets:

Future economic benefit. The potential to contribute,directly or indirectly, to the flow of cash and cash equivalentsto the entity. The potential may be a productive one that is partof the operating activities of the entity. It may also take theform of convertibility into cash or cash equivalents or acapability to reduce cash outflows, such as when an alternativemanufacturing process lowers the cost of production.

Assets are usually employed to produce goods or services forcustomers; customers will then pay for these. Cash itself rendersa service to the entity due to its command over other resources.

The existence of an asset, particularly in terms of control, isnot reliant on:(a) Physical form (hence patents and copyrights); nor(b) Legal rights (hence leases).

Transactions or events in the past give rise to assets; thoseexpected to occur in the future do not in themselves give rise toassets. For example, an intention to purchase a non-current assetdoes not, in itself, meet the definition of an asset.

Course Instructor Waqar Hassan Randhawa ACA (ICAEW) FCCA (UK) [email protected]

Hailey College Of Commerce Financial Reporting Notes G1, G2 (Morning & After noon)

B.com (Hons) 8th Semester, M.com (3.5 years) 4thSemester

Liabilities:

An essential characteristic of a liability is that the entity has a present obligation.

Obligation. A duty or responsibility to act or perform in acertain way. Obligations may be legally enforceable as aconsequence of a binding contract or statutory requirement.Obligations also arise, however, from normal business practice,custom and a desire to maintain good business relations or act inan equitable manner

It is important to distinguish between a present obligation and afuture commitment. A management decision to purchase assets inthe future does not, in itself, give rise to a presentobligation.

Settlement of a present obligation will involve the entity givingup resources embodying economic benefits in order to satisfy theclaim of the other party. This may be done in various ways, notjust by payment of cash.

Liabilities must arise from past transactions or events. In thecase of, say, recognition of future rebates to customers based onannual purchases, the sale of goods in the past is thetransaction that gives rise to the liability.

Equity

Equity is defined above as a residual, but it may be sub-classified in the statement of financial position. This willindicate legal or other restrictions on the ability of the entity

Course Instructor Waqar Hassan Randhawa ACA (ICAEW) FCCA (UK) [email protected]

Hailey College Of Commerce Financial Reporting Notes G1, G2 (Morning & After noon)

B.com (Hons) 8th Semester, M.com (3.5 years) 4thSemester

to distribute or otherwise apply its equity. Some reserves arerequired by statute or other law, eg for the future protection ofcreditors. The amount shown for equity depends on the measurementof assets and liabilities. It has nothing to do with the marketvalue of the entity's shares.

Performance

Profit is used as a measure of performance, or as a basis forother measures (eg Earnings per share). It depends directly onthe measurement of income and expenses, which in turn depend (inpart) on the concepts of capital and capital maintenance adopted.

The elements of income and expense are therefore defined.

Income. Increases in economic benefits during the accountingperiod in the form of inflows orEnhancements of assets or decreases of liabilities that result inincreases in equity, other than those relating to contributionsfrom equity participants.

Expenses. Decreases in economic benefits during the accountingperiod in the form of outflows or depletions of assets orincurrences of liabilities that result in decreases in equity,other than those relating to distributions to equityparticipants.

Income and expenses can be presented in different ways in thestatement of profit or loss and other comprehensive income, toprovide information relevant for economic decision-making. Forexample, income and expenses which relate to continuing

Course Instructor Waqar Hassan Randhawa ACA (ICAEW) FCCA (UK) [email protected]

Hailey College Of Commerce Financial Reporting Notes G1, G2 (Morning & After noon)

B.com (Hons) 8th Semester, M.com (3.5 years) 4thSemester

operations are distinguished from the results of discontinuedoperations.

Income

Both revenue and gains are included in the definition of income.Revenue arises in the course of ordinary activities of an entity.

Gains. Increases in economic benefits. As such they are nodifferent in nature from revenue.

Gains include those arising on the disposal of non-currentassets. The definition of income also includes unrealized gains,eg on revaluation of marketable securities.

Expenses

As with income, the definition of expenses includes losses aswell as those expenses that arise in the course of ordinaryactivities of an entity.

Losses. Decreases in economic benefits. As such they are nodifferent in nature from other expenses.

Losses will include those arising on the disposal of non-currentassets. The definition of expenses will also include unrealizedlosses, eg the fall in value of an investment.

Course Instructor Waqar Hassan Randhawa ACA (ICAEW) FCCA (UK) [email protected]

Hailey College Of Commerce Financial Reporting Notes G1, G2 (Morning & After noon)

B.com (Hons) 8th Semester, M.com (3.5 years) 4thSemester

Recognition of the elements of financialstatements

Items which meet the definition of assets or liabilities maystill not be recognised in financial statements because they mustalso meet certain recognition criteria.

Recognition. The process of incorporating in the statement offinancial position or statement of profit or loss and othercomprehensive income an item that meets the definition of anelement and satisfies the following criteria for recognition:

(a) It is probable that any future economic benefitassociated with the item will flow to or from the entity

(b) The item has a cost or value that can be measured withreliability

Probability of future economic benefits

Probability here means the degree of uncertainty that the futureeconomic benefits associated with an item will flow to or from

Course Instructor Waqar Hassan Randhawa ACA (ICAEW) FCCA (UK) [email protected]

Hailey College Of Commerce Financial Reporting Notes G1, G2 (Morning & After noon)

B.com (Hons) 8th Semester, M.com (3.5 years) 4thSemester

the entity. This must be judged on the basis of thecharacteristics of the entity's environment and the evidenceavailable when the financial statements are prepared.

Reliability of measurementThe cost or value of an item, in many cases, must be estimated.The Conceptual Framework states, however, that the use of reasonableestimates is an essential part of the preparation of financialstatements and does not undermine their reliability. Where noreasonable estimate can be made, the item should not berecognised, although its existence should be disclosed in thenotes, or other explanatory material. Items may still qualify forrecognition at a later date due to changes in circumstances orsubsequent events.

Assets which cannot be recognisedThe recognition criteria do not cover items which many businessesmay regard as assets. A skilled workforce is an undoubted assetbut workers can leave at any time so there can be no certaintyabout the probability of future economic benefits. A company mayhave come up with a new name for its product which is greatlyincreasing sales but, as it did not buy the name, the name doesnot have a cost or value that can be reliably measured, so it isnot recognised.

Recognition of items

Course Instructor Waqar Hassan Randhawa ACA (ICAEW) FCCA (UK) [email protected]

Hailey College Of Commerce Financial Reporting Notes G1, G2 (Morning & After noon)

B.com (Hons) 8th Semester, M.com (3.5 years) 4thSemester

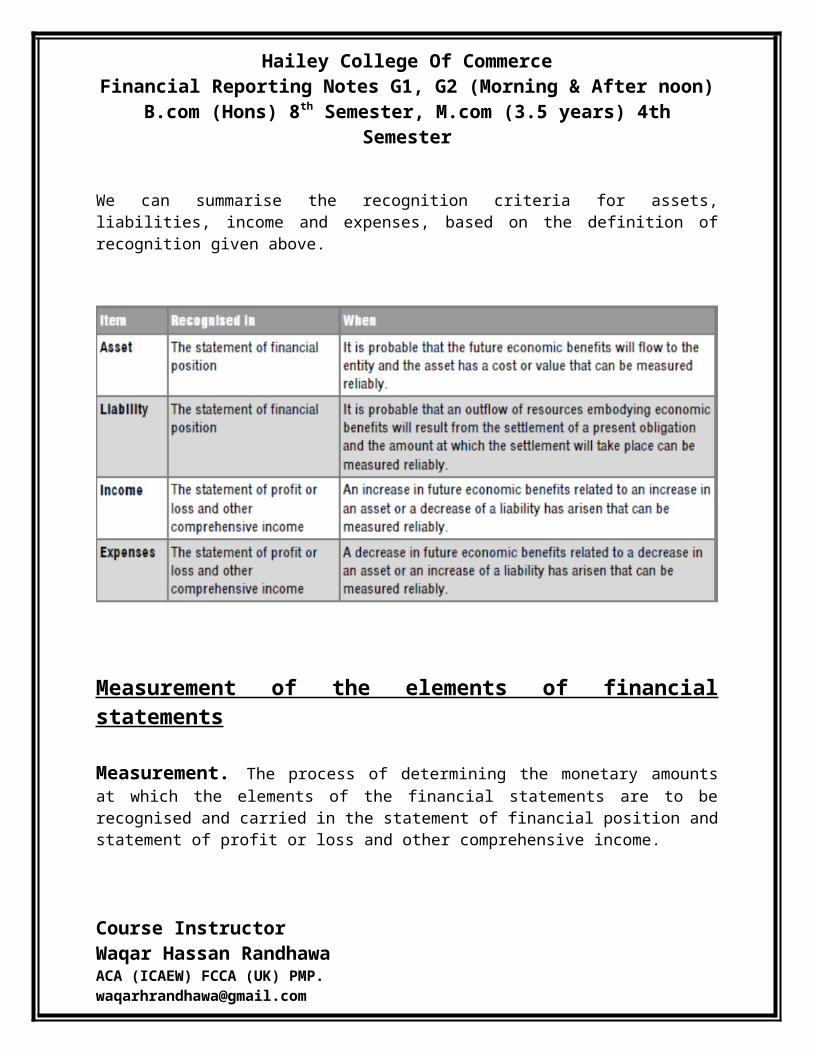

We can summarise the recognition criteria for assets,liabilities, income and expenses, based on the definition ofrecognition given above.

Measurement of the elements of financialstatements

Measurement. The process of determining the monetary amountsat which the elements of the financial statements are to berecognised and carried in the statement of financial position andstatement of profit or loss and other comprehensive income.

Course Instructor Waqar Hassan Randhawa ACA (ICAEW) FCCA (UK) [email protected]

Hailey College Of Commerce Financial Reporting Notes G1, G2 (Morning & After noon)

B.com (Hons) 8th Semester, M.com (3.5 years) 4thSemester

This involves the selection of a particular basis of measurement.A number of these are used to different degrees and in varyingcombinations in financial statements. They include the following.

– Historical cost– Current cost– Realisable (settlement) value– Present value of future cash flows

Historical cost. Assets are recorded at the amount of cash orcash equivalents paid or the fair value of the considerationgiven to acquire them at the time of their acquisition.Liabilities are recorded at the amount of proceeds received inexchange for the obligation, or in some circumstances (forexample, income taxes), at the amounts of cash or cashequivalents expected to be paid to satisfy the liability in thenormal course of business.

Current cost. Assets are carried at the amount of cash or cashequivalents that would have to be paid if the same or anequivalent asset was acquired currently.

Liabilities are carried at the undiscounted amount of cash orcash equivalents that would be required to settle the obligationcurrently.

Realizable (settlement) value.

Realizable value. The amount of cash or cash equivalents thatcould currently be obtained by selling an asset in an orderlydisposal.

Course Instructor Waqar Hassan Randhawa ACA (ICAEW) FCCA (UK) [email protected]

Hailey College Of Commerce Financial Reporting Notes G1, G2 (Morning & After noon)

B.com (Hons) 8th Semester, M.com (3.5 years) 4thSemester

Settlement value. The undiscounted amounts of cash or cashequivalents expected to be paid to satisfy the liabilities in thenormal course of business.

Present value. A current estimate of the present discounted valueof the future net cash flows in the normal course of business.

Historical cost is the most commonly adopted measurement basis,but this is usually combined with other bases, eg inventory iscarried at the lower of cost and net realisable value.

Recent standards use the concept of fair value, which is definedby IFRS 13 as 'the price that would be received to sell an assetor paid to transfer a liability in an orderly transaction betweenmarket participants at the measurement date'.

ILLUSTRATION OF MEAAUREMENT

A machine was purchased on 1 January 2015 for PKR.3m. That wasits original cost. It has a useful like of 10 years and under thehistorical cost convention it will be carried at original costless accumulated depreciation. So in the financial statements at31 December 2016 it will be carried at:

3m – (0.3 X 2) = PKR 2.4m

The current cost of the machine, which will probably also be itsfair value, will be fairly easy to ascertain if it is not toospecialised. For instance, two year old machines like this onemay currently be changing hands for PKR 2.5m, so that will be anappropriate fair value.

Course Instructor Waqar Hassan Randhawa ACA (ICAEW) FCCA (UK) [email protected]

Hailey College Of Commerce Financial Reporting Notes G1, G2 (Morning & After noon)

B.com (Hons) 8th Semester, M.com (3.5 years) 4thSemester

The net realizable value of the machine will be the amount thatcould be obtained from selling it, less any costs involved inmaking the sale. If the machine had to be dismantled andtransported to the buyer's premises at a cost of PKR 200,000, theNRV would be $2.3m.

The replacement cost of the machine will be the cost of a newmodel less two year's depreciation. The cost of a new machine maynow be PKR3.5m. Assuming a ten-year life, the replacement costwill therefore be PKR 2.8m.

The present value of the machine will be the discounted value ofthe future cash flows that it is expected to generate. If themachine is expected to generate $500,000 per annum for theremaining eight years of its life and if the company's cost ofcapital is 10%, present value will be calculated as:

500,000 X 5.335* = PKR 2667,500* Cumulative present of PKR 1 per annum for eight yearsdiscounted at 10%

Course Instructor Waqar Hassan Randhawa ACA (ICAEW) FCCA (UK) [email protected]

Hailey College Of Commerce Financial Reporting Notes G1, G2 (Morning & After noon)

B.com (Hons) 8th Semester, M.com (3.5 years) 4thSemester

The IASB and current accounting standards

The IASB's predecessor body, the IASC, had issued 41International Accounting Standards (IASs) and on 1 April 2001 theIASB adopted all of these standards and now issues its ownInternational Financial Reporting Standards (IFRSs). So farfourteen new IFRSs have been issued.

Due process

The overall agenda of the IASB will initially be set bydiscussion with the IFRS Advisory Council. The process fordeveloping an individual standard would involve the followingsteps.

Course Instructor Waqar Hassan Randhawa ACA (ICAEW) FCCA (UK) [email protected]

Hailey College Of Commerce Financial Reporting Notes G1, G2 (Morning & After noon)

B.com (Hons) 8th Semester, M.com (3.5 years) 4thSemester

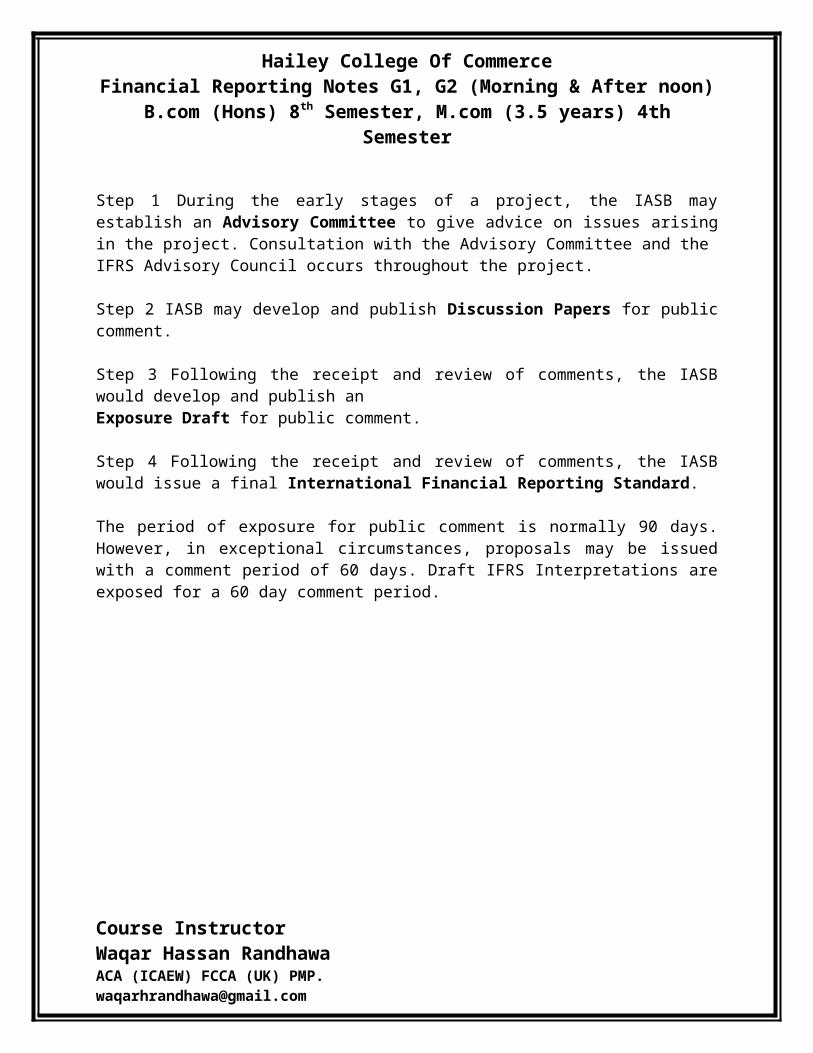

Step 1 During the early stages of a project, the IASB mayestablish an Advisory Committee to give advice on issues arisingin the project. Consultation with the Advisory Committee and theIFRS Advisory Council occurs throughout the project.

Step 2 IASB may develop and publish Discussion Papers for publiccomment.

Step 3 Following the receipt and review of comments, the IASBwould develop and publish anExposure Draft for public comment.

Step 4 Following the receipt and review of comments, the IASBwould issue a final International Financial Reporting Standard.

The period of exposure for public comment is normally 90 days.However, in exceptional circumstances, proposals may be issuedwith a comment period of 60 days. Draft IFRS Interpretations areexposed for a 60 day comment period.

Course Instructor Waqar Hassan Randhawa ACA (ICAEW) FCCA (UK) [email protected]

Hailey College Of Commerce Financial Reporting Notes G1, G2 (Morning & After noon)

B.com (Hons) 8th Semester, M.com (3.5 years) 4thSemester

Course Instructor Waqar Hassan Randhawa ACA (ICAEW) FCCA (UK) [email protected]

Hailey College Of Commerce Financial Reporting Notes G1, G2 (Morning & After noon)

B.com (Hons) 8th Semester, M.com (3.5 years) 4thSemester

Course Instructor Waqar Hassan Randhawa ACA (ICAEW) FCCA (UK) [email protected]