hong kong exchanges and clearing limited

TRANSCRIPT

This document is downloaded from CityU Institutional Repository,

Run Run Shaw Library, City University of Hong Kong.

Title Hong Kong Exchanges and Clearing Limited

Author(s) Li, Fei (李飛)

Citation Li, F. (2011). Hong Kong Exchanges and Clearing Limited (Outstanding Academic Papers by Students (OAPS)). Retrieved from City University of Hong Kong, CityU Institutional Repository.

Issue Date 2011

URL http://hdl.handle.net/2031/6444

Rights This work is protected by copyright. Reproduction or distribution of the work in any format is prohibited without written permission of the copyright owner. Access is unrestricted.

1

IS6912 Information Systems Project

Hong Kong Exchanges and Clearing Limited

LI Fei

2

Table of Content

Abstract ......................................................................................................................... 4

Hong Kong Exchanges and Clearing Limited (A) .................................................... 5

Company Overview ............................................................................................................ 5

Business Performance ........................................................................................................ 6

Growth Fuelled by Mainland Listing ................................................................................. 6

Competitive Landscape in Mainland China ....................................................................... 7

History ....................................................................................................................... 7

International Board .................................................................................................... 7

Moves by HKEx ................................................................................................................. 8

Consultation on Acceptance of Mainland Accounting and Auditing Stands ............ 9

Consultation on Proposed Listing Rules for Mineral and Exploration Companies . 11

Change in Chief Executive ...................................................................................... 12

RMB Internationalization ................................................................................................. 13

Conclusion ........................................................................................................................ 14

Exhibit 1: Products & Services of HKEx ................................................................. 15

Exhibit 2: Number of IPO Transactions ................................................................... 16

Exhibit 3: Number of Listed Companies inHKEx ................................................... 16

Exhibit 4:Market Capitalization ............................................................................... 17

Exhibit 5: Number of Listed Companies by Industry Classification........................ 18

Exhibit 6: Primary Market Driven by Mainland Listings in HKEx ......................... 18

Exhibit 7: Performance of Mainland Enterprises in 2009 ........................................ 19

Exhibit 8: Biographical Information of Charles LI .................................................. 20

Exhibit 9: Financial Highlights ................................................................................ 21

Exhibit 10: Organizational Chart ............................................................................. 22

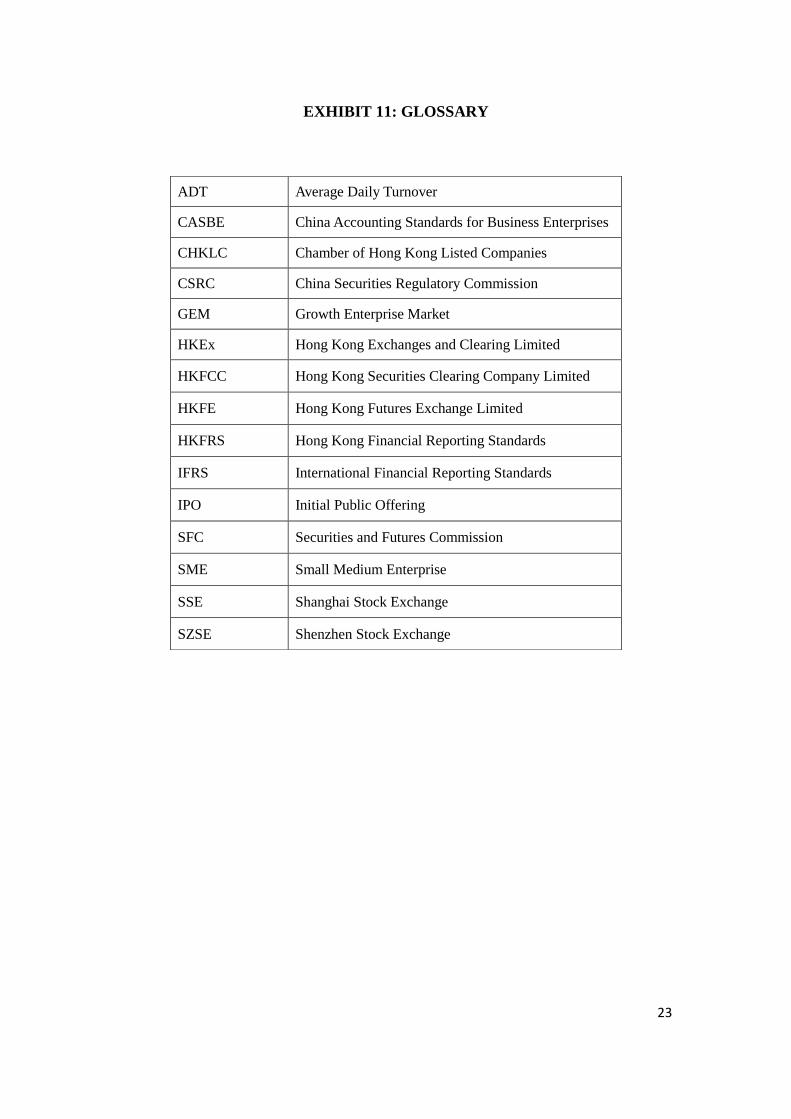

Exhibit 11: Glossary ................................................................................................. 23

Hong Kong Exchanges and Clearing Limited (B) .................................................. 24

Business Performance ...................................................................................................... 24

Strategic Plan 2010-2012 ................................................................................................. 24

New Competitive Landscape............................................................................................ 25

HKEX’s Preparation for RMB Products .......................................................................... 26

Exhibit 1: Recors Set in 2010 ................................................................................... 28

Exhibit 2: IPO Equity Funds Raised ........................................................................ 29

Exhibit 3: Organizational Chart ............................................................................... 30

Exhibit 4: HKEx’s Preparations for Trading and Clearing of RMB Products ......... 31

3

Exhibit 5: RMB Deports in HONG KONG ............................................................. 32

Exhibit 6: Total Equity Funds Raised ...................................................................... 33

Exhibit 7: Market Value of Shares of Domestic-listed Compaines.......................... 34

Exhibit 8: Ten Largest IPO Funds Raised by Newly Listed Companies in 2010 .... 35

Case Analysis .............................................................................................................. 36

Executive Summary ........................................................................................................ .36

Situation Analysis ............................................................................................................ 36

Market Environment Analysis - Five Forces Model ............................................... 36

Nonmarket Environment Analysis .......................................................................... 38

SWOT Analysis ....................................................................................................... 39

Analysis of the personnel change ............................................................................ 40

Strategic Alternatives ....................................................................................................... 40

Recommendation .............................................................................................................. 41

Do not accept mainland accounting and auditing stands ......................................... 42

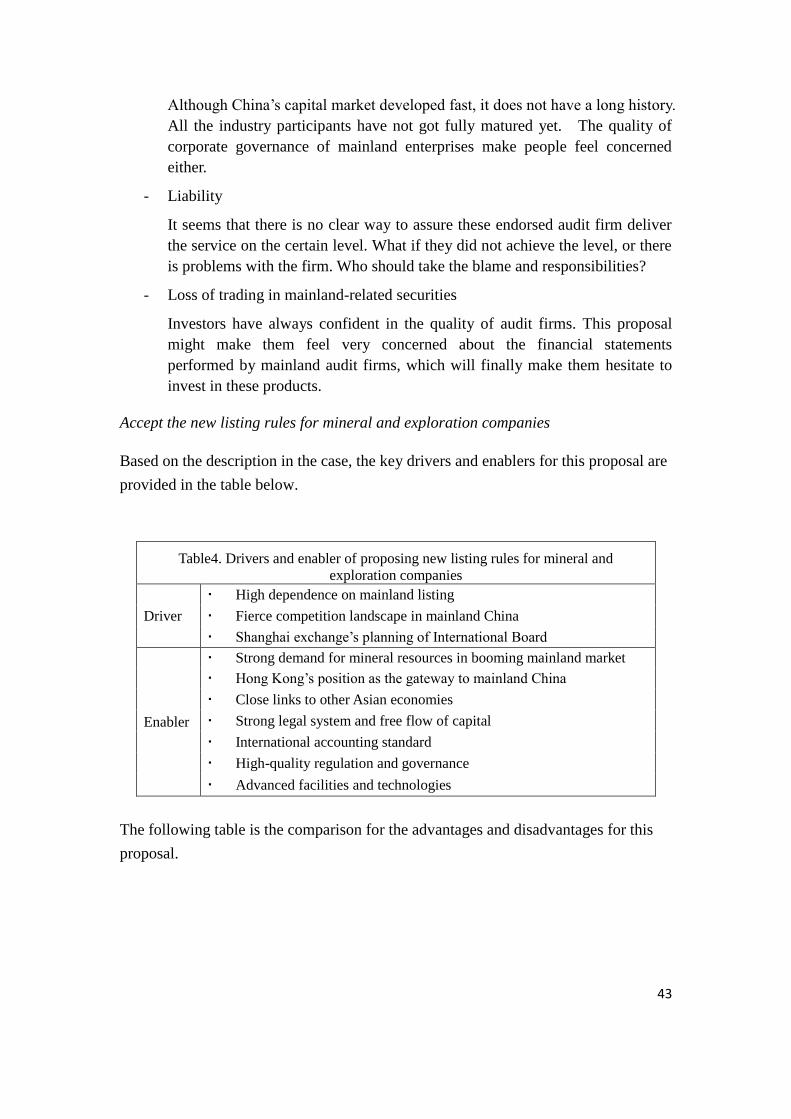

Accept the new listing rules for mineral and exploration companies ...................... 43

Develop RMB Products ........................................................................................... 44

4

Abstract

Hong Kong Exchanges and Clearing Limited (“HKEx”) is a listed company,

regulating all the core stocks and derivative marketplace in Hong Kong. This project

focused on HKEx’s strategic alternatives towards Shanghai Stock Exchange’s (“SSE”)

rise in recent years. HKEx and SSE are the core parts in respective finance industries.

Debates over the sibling rivalry between them have increased year after year.

Therefore, the target of this project is to analyze the competitive landscape HKEx

faced, describe the strategic alternatives HKEx may have, and provide solution that

can address this situation and support HKEx’s further development.

The project is divided into 2 parts, case study and case analysis. The first part

included A Case and B Case. A Case described the background of HKEx, SSE as well

as China’s capital market. Then it introduced HKEx’s planning about accepting

mainland accounting standards, make new listing rules to mineral and exploration

companies, and developing RMB products. B Case presented the new competitive

landscape and HKEx’s strategic plan 2010-2012, followed by HKEx’s preparations

for RMB products. For the second part, first I described its external and internal

environment with five-force model and SWOT analysis. Then strategic alternatives

were introduced. I made recommendations to HKEx with judgments at last.

5

Hong Kong Exchanges and Clearing Limited (A)

The Hong Kong Stock Exchange (“HKEx”) had long played a key role in reinforcing

Hong Kong's position as an international financial centre. It had made a significant

contribution to transforming the local financial services industry into a regional

market place that was home to many global financial firms.1 It had also significantly

benefited from the growing economic power of mainland China. However, in 2009,

China’s State Council issued a guideline to make Shanghai an international financial

centre and shipping hub by 2020.2 The Shanghai Stock Exchange (“SSE”), which

played a central role in promoting Shanghai’s development, clearly stood to gain from

this announcement. The future of the HKEx, as the premier stock exchange and

clearing house in the region, was placed into doubt. HKEx was faced with a number

of challenges in this situation, to assure its survival and continued growth into the

future.

Company Overview

The HKEx controlled the Stock Exchange of Hong Kong Limited (“SEHK”), Hong

Kong Futures Exchange Limited (“HKFE”), and Hong Kong Securities Clearing

Company Limited (“HKFCC”). It was set up under Hong Kong’s comprehensive

market reform of the stock and futures markets in 1999.3 Before that, the main

securities trading market in Hong Kong was the Stock Exchange of Hong Kong

Limited, which was created after the unification of four exchanges (Hong Kong Stock

Exchange, Far East Exchange, Kam Ngan Stock Exchange, and Kowloon Stock

Exchange) in 1980.4

The HKEx was listed in 2000 as a “market-driven organization”, responsible to its

shareholders. About half of its directors in the board were directly appointed by the

Hong Kong’s government. The government was also HKEx’s top shareholder, which

increased its equity holding to 5.88 per cent of HKEx’s total shares with its huge

foreign-exchange reserves in September 2007.5 HKEx also operated and regulated

the securities and derivatives marketplace in Hong Kong, responsible for the

regulation of listed companies, administration of rules, and the services to customers.6

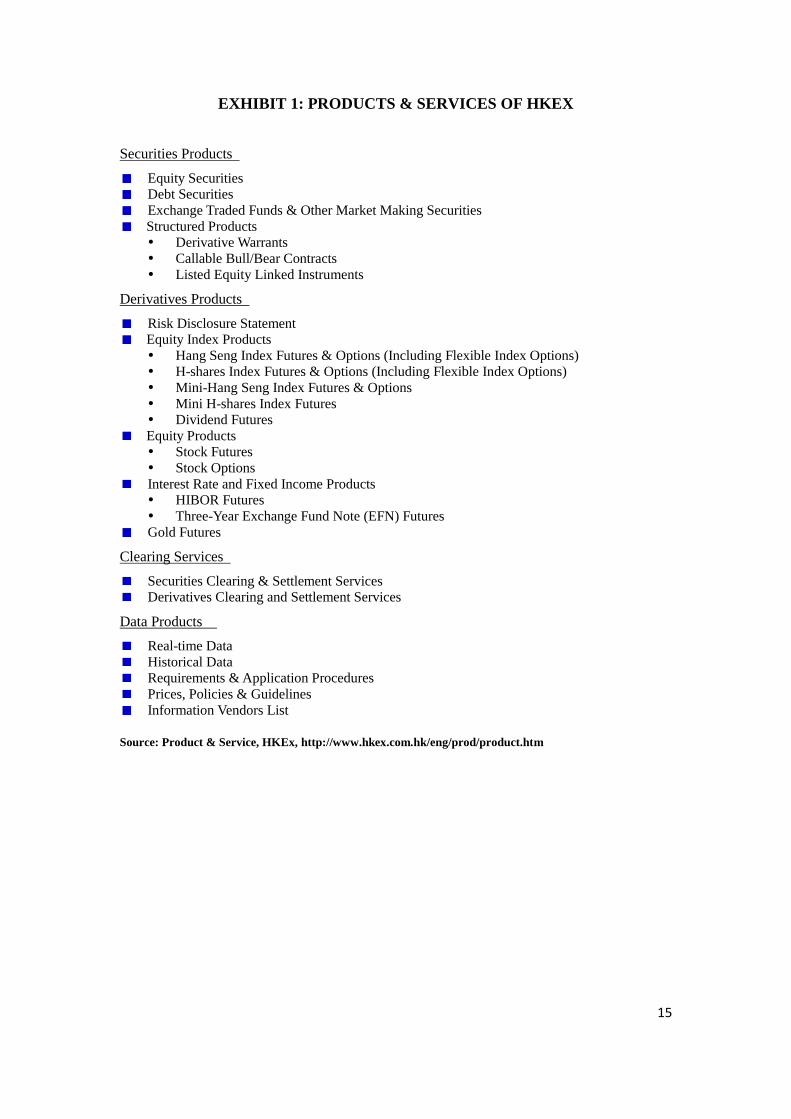

A variety of securities and derivatives [see Exhibit 1] could be traded on HKEx’s

markets. Clearing services and comprehensive pre-trade and post-trade services were

also available.7 Under Hong Kong’s existing laws, any organization that wanted to

hold more than 5 per cent of HKEx’s total shares must receive the approval from the

Hong Kong’s government first.

1 Company Profile, http://www.hkex.com.hk/eng/exchange/corpinfo/profile.htm 2 http://news.sina.com.cn/c/2009-03-26/031017482257.shtml 3 Company Profile, http://www.hkex.com.hk/eng/exchange/corpinfo/profile.htm 4 History of HKEx and its Markets, 24 July 2009,

http://www.hkex.com.hk/eng/exchange/corpinfo/history/history.htm 5 http://www.zaobao.com/finance/pages/comment070912.html 6 Company Profile, http://www.hkex.com.hk/eng/exchange/corpinfo/profile.htm 7 Product & Service, http://www.hkex.com.hk/eng/prod/product.htm

6

Business Performance

In respect of listing, HKEx vetted 150 listing applications in 2009 and the numbers of

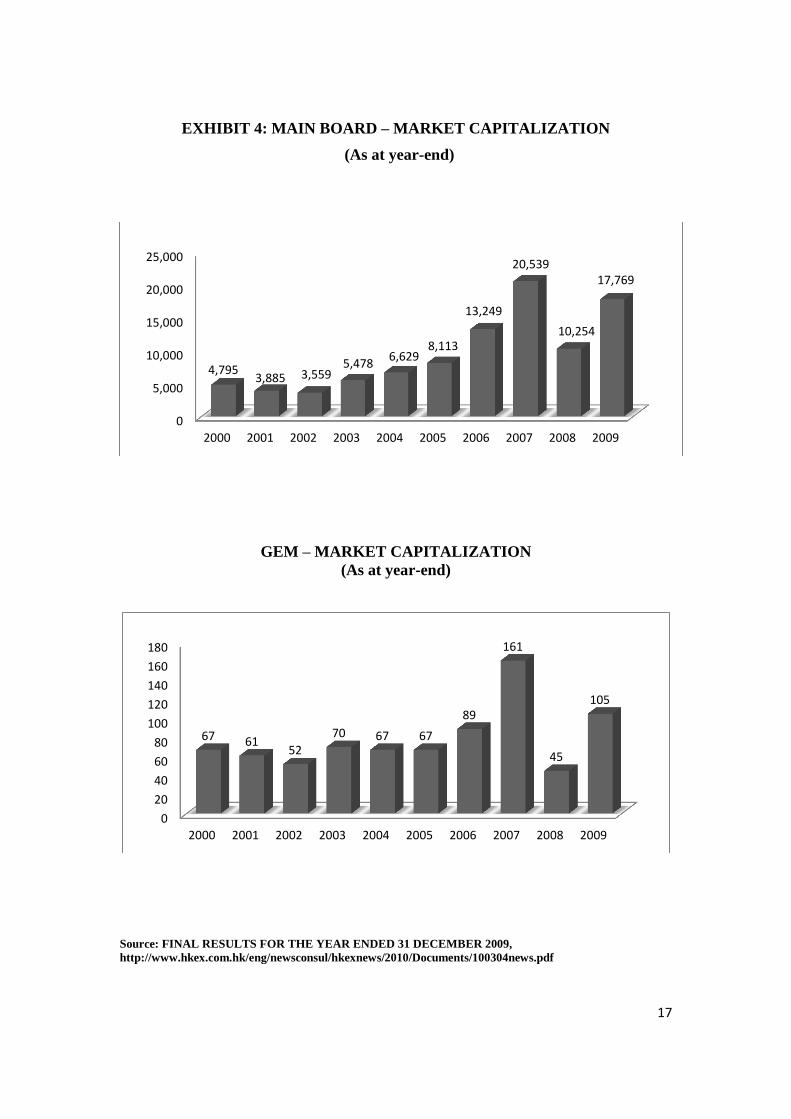

newly listed companies on the Main Board and the Growth Enterprise Market (GEM)

– a new ventures exchange - were 68 and 5 respectively [See Exhibit 2].8 By the

end of 2009, there were 1,145 companies listed on the Main Board and 174 on the

GEM, with a market capitalisation of HK$17,769 billion and HK$105 billion

respectively [See Exhibit 3 & 4].9 Total equity funds raised from the Main Board and

the GEM were HK$ 638 billion and 4.384 billion respectively.10

The listed

companies on the HKEx were largely centred around consumer goods, services,

properties and construction, IT, industrial goods, financials and materials [See Exhibit

5].11

In 2009, HKEx’s annual revenue and other income was HK$7.035 billion and the

profit before taxation was HK$5.542 billion, each decreased 7 per cent over 2008.

The average daily turnover value on the stock exchange was HK$62.3 billion in 2009.

The profit attribute to shareholders was HK$4.704 billion and the basic earnings per

share were HK$4.38, dropped about 8 per cent from previous year. The dividend

payout ratio remained almost fixed in 90 per cent.12

Growth Fuelled by Mainland Listing

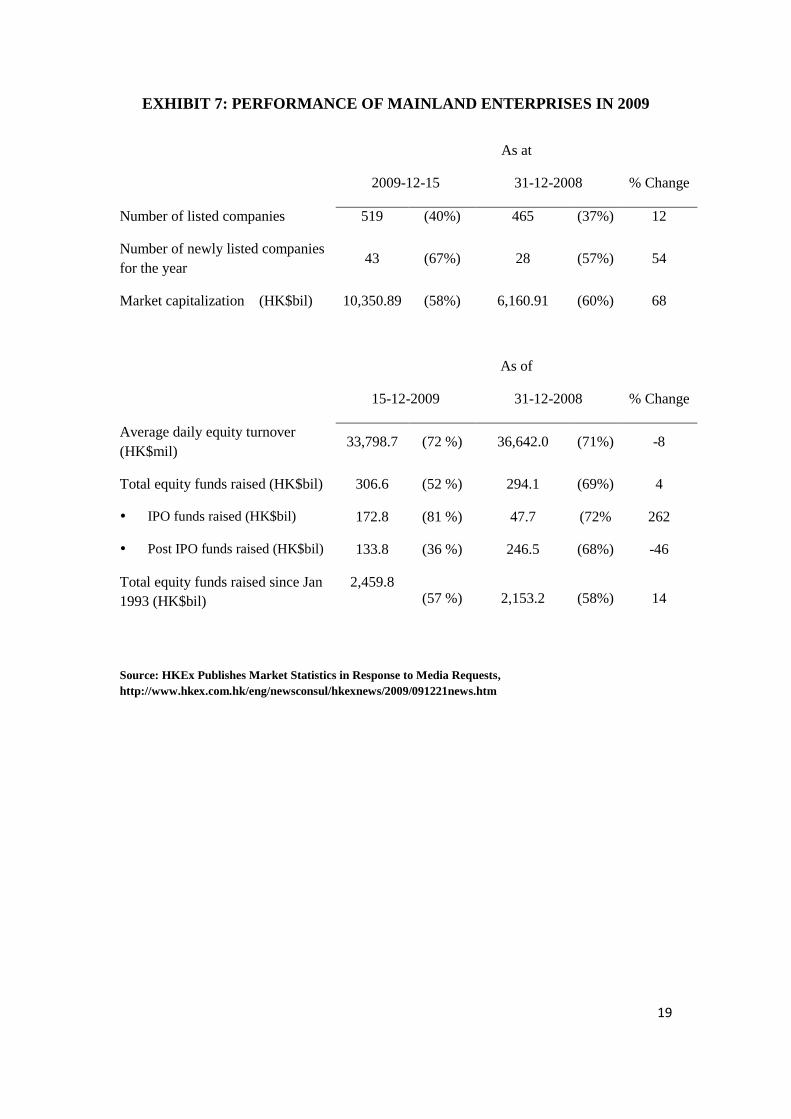

In recent years, the HKEx had seen a big jump in activity from mainland-based

enterprises [See Exhibit 6 & 7]. In 2009, 40 per cent of the total 1,319 listed

companies were mainland-related enterprises, with a market capitalization of

HK$ 10.44 trillion, making up 58 per cent of the total.13

In particular,

mainland-related enterprises accounted for 83 per cent of total IPO funds raised by

HKEx in 2009. In fact, fuelled by this growth, the HKEx ranked first in all IPO equity

funds raised worldwide in 2009. Mainland-related enterprises also represented 72 per

cent of the average daily equity turnover at HKEx.

From the perspective of mainland enterprises, there were a variety of advantages of

listing in Hong Kong. Hong Kong was the ‘window to the world’ for many Chinese

firms – it was widely respected as a leading international financial centre, it already

hosted many of the region’s leading firms, it had a well-established legal system, and

it provided a strong and attractive foundation for issuers to raise funds. Furthermore,

Hong Kong has zero capital flow restrictions, currency convertibility and free

8 FINAL RESULTS FOR THE YEAR ENDED 31 DECEMBER 2009,

http://www.hkex.com.hk/eng/newsconsul/hkexnews/2010/Documents/100304news.pdf 9 FINAL RESULTS FOR THE YEAR ENDED 31 DECEMBER 2009,

http://www.hkex.com.hk/eng/newsconsul/hkexnews/2010/Documents/100304news.pdf 10 FINAL RESULTS FOR THE YEAR ENDED 31 DECEMBER 2009,

http://www.hkex.com.hk/eng/newsconsul/hkexnews/2010/Documents/100304news.pdf 11 FINAL RESULTS FOR THE YEAR ENDED 31 DECEMBER 2009,

http://www.hkex.com.hk/eng/newsconsul/hkexnews/2010/Documents/100304news.pdf 12

FINAL RESULTS FOR THE YEAR ENDED 31 DECEMBER 2009,

http://www.hkex.com.hk/eng/newsconsul/hkexnews/2010/Documents/100304news.pdf 13 FINAL RESULTS FOR THE YEAR ENDED 31 DECEMBER 2009,

http://www.hkex.com.hk/eng/newsconsul/hkexnews/2010/Documents/100304news.pdf

7

transferability of securities.14

However, there were still a few barriers to overcome.

For example, the HKEx did not accept mainland accounting standards.

Competitive Landscape in Mainland China

History

In 1990, the establishment of the Shanghai Stock Exchange marked the starting point

of China’s capital market ambitions. At the beginning, the market capitalization of

SSE was RMB1, 234 billion, with only 30,000 investors and 25 registered members.15

The inception of the Shenzhen Stock Exchange (“SZSE”) could be traced back to

1986, the beginning of the joint-stock system reform of state-owned corporations in

Shenzhen. Unlike other exchanges organized as corporations, both of SSE and SZSE

were membership institutions, directly governed by the China Securities Regulatory

Commission (“CSRC”).16

Within 20 years, both stock exchanges made great advances. A series of new products

were introduced on both exchanges, demonstrating the growth and diversification of

trading varieties in the Chinese capital market.17

In particular, the launch of the

Growth Enterprises Market (“GEM”) and the Small and Medium Enterprises (“SME”)

Board in SZSE provided a vehicle for small- and medium-sized enterprises in

mainland China to raise funds.

During this process of development, the equity division reform - the biggest

institutional reform in China’s capital market - played a vital role in the great

development of China’s stock market. This reform was designed to eliminate the

discrepancy in the circulation systems of tradable share and non-tradable share, which

had an important influence on improving the quality of listed companies.18

After its

completion, China’s stock market changed from an equity-divided market to an

all-floating one.19

Other changes were also being instituted. For example, the

comprehensive management of securities companies was overhauled. These changes

have effectively reduced the level of systemic risk in China’s capital market.

Starting with the equity division reform, the SSE stepped into the ranks of the main

stock exchanges worldwide. Remarkably, the market capitalization of SSE jumped

from RMB2.3 trillion in 2005 to RMB18.5 trillion in 2009. Its average daily volume

soared from 8.6 billion in 2005 to 142 billion in 2009, an increase of 1,700 per cent.20

International Board

In March 2009, China’s State Council issued a guideline to make Shanghai an

international financial centre and shipping hub by 2020.21

On 8 April 2009, together

14 Advantages of Listing in Hong Kong, http://www.hkex.com.hk/eng/listing/listhk/advantages_of_listing.htm 15 http://www.cnstock.com/index/gdbb/201012/1054853.htm 16 About SSE, http://www.sse.com.cn/sseportal/en/c01/p996/c1501_p996.shtml 17 http://www.cnstock.com/index/gdbb/201012/1054853.htm 18 Notice of the State Council on Approving and Forwarding CSRC’s Opinions on Improving Quality of Listed

Companies, http://www.csrc.gov.cn/pub/csrc_en/laws/rfdm/AdministrativeLaws/200907/t20090728_119362.htm 19 Q&A by CSRC Spokesman on Hot Issues, CSRC, 15 August 2008,

http://www.csrc.gov.cn/pub/csrc_en/newsfacts/release/200809/t20080903_69038.htm 20 http://news.sohu.com/20101219/n278389185.shtml 21 http://news.sina.com.cn/c/2009-03-26/031017482257.shtml

8

with a few other cities, Shanghai was approved as a pilot RMB settlement centre for

international trade.22

Hand in hand with these changes were plans to add international listings to the SSE,

accommodating itself with Shanghai’s upcoming role of international financial

centre.23

Originally, all foreign companies who wanted to tap China’s market could

only choose to list on the HKEx, while the introduction of an International Board on

the SSE would allow them to list on the domestic stock market directly.

The International Board would provide a platform for the world's most famous

companies to list, which would boost the attractiveness and competitiveness of the

SSE. The Shanghai government also hoped that the change would mark the return of

red-chip companies24

to mainland China. In this case, Hong Kong listed firms would

be encouraged to list on the domestic stock markets. In fact, it appeared likely that the

first companies to be listed on the International Board would be red-chip companies,

local blue-chip companies in Hong Kong, and some international giants, like HSBC,

that were now listed in Hong Kong. Meanwhile foreign enterprises were expressing

their strong willingness to list on SSE, including HSBC, Standard Chartered, NYSE

Euronext, Bank of East Asia and the Development Bank of Singapore. Duncan

Niederauer, chief executive of NYSE Euronext said:

“NYSE Euronext is gunning to be the first company to list on the international board

of the Shanghai Stock Exchange whenever it is thrown open for foreign firms. On

some technical aspects, we are working with the CSRC to discuss which is the right

shape or structure for the listing.”25

The benefits for foreign companies listing in mainland China were substantial. They

would be able to enhance their visibility and increase brand awareness within the

Chinese markets. Plus, they would have direct access to RMB funding to further

expand their business in China without the concerns of foreign exchange risks.

Although there was no specific timetable for this launch, a document issued by the

State Council in 2009 made it clear that eligible foreign enterprises wishing to issue

RMB denominated shares would be authorized to do so in due time.26

Moves by HKEx

Faced with the strong ambition and government backing of the SSE, people in Hong

Kong worried that the HKEx would become marginalized. HKEx Chairman Ronald

Arculli argued that the competition between them was not a zero-sum game. He said,

“Even with the Mainland continuing to gradually open up and come the day when

capital controls are lifted, Shanghai and Hong Kong will still be distinct markets with

their own areas of strengths, and appeal to different types of investors. The Chinese

22 http://news.xinhuanet.com/fortune/2009-04/09/content_11152584.htm 23 The International Board can allow enterprises that are registered outside of China to apply to be listed on the

Shanghai Stock Exchange 24 Red chip companies are enterprises that are incorporated outside of the mainland China and are controlled by

Mainland Government entities. 25 NYSE looks at Shanghai float, http://www.chinadaily.com.cn/bizchina/2009-05/14/content_7775756.htm 26 http://finance.sina.com.cn/stock/y/20100307/21127516612.shtml

9

market continues to grow bigger every year and is large enough to support more than

one successful financial center. There is certainly room for Shanghai and Hong Kong,

as well as other Chinese cities, to thrive.” Ronald Arculli said.

27

However, the legislative councillor (accountancy) of HKSAR, Paul Chan Mo Po

noted that Shanghai’s ambitions to be an international financial centre was a warning

for Hong Kong. He argued that although many people believed China had a massive

potential market to support the development of more than one financial centre, there

were few international examples of countries being able to support more than one

financial centre. He also said although there were several famous exchanges in Japan,

people would only have room in their memories for Tokyo Stock Exchange.28

Consultation on Acceptance of Mainland Accounting and Auditing Stands

It was clear that, in the absence of credible local alternatives, the HKEx benefited

great deal from growth and development within China. However, faced with huge

opportunities for development, SSE would be more capable of maintaining and

attracting local listing resources. Therefore it became extremely challenging for

HKEx to develop business in mainland China.

In August 2009, HKEx published consultation paper on “acceptance of mainland

accounting and auditing standards and mainland audit firms for mainland incorporated

companies listed in Hong Kong”.29

Mark Dickens, HKEx's Head of Listing, said

“Our proposed framework recognizes that Mainland accounting and auditing

standards have converged with international standards.”30

At present, the exchange only accepted the use of Hong Kong Financial Reporting

Standards (“HKFRS”) and International Financial Reporting Standards (“IFRS”), and

generally accepted accounting principles in US or other accounting standards under

certain circumstances.31

It did not, however, accept mainland accounting standards.

This restriction proved to be a big impediment for mainland firms wishing to list on

the exchange. The differences in accounting standards were significant, and many

mainland firms were hesitant to change their practices and conform to international

standards. However, this proposal could allow mainland issuers to make their

financial statements using mainland accounting standards and have them audited with

endorsed mainland audit firms, which could reduce their compliance cost, increase

market efficiency, and promote timely disclosure of information to investors.32

When responded to this consultation paper, president of The Hong Kong Society of

Financial Analysis Mr Karl Lung said,

“An effective way of financial reporting could be anticipated by preparing financial

statements under one standard. Investors are going to be well protected with one

single standard consistently applied. Capital markets from both sides will have an

27 HKEx Chairman Ronald Arculli’s Speech at Macquarie’s China/Hong Kong Conference,

http://www.hkex.com.hk/eng/newsconsul/speech/2009/sp090518.htm 28 http://www.takungpao.com.hk/news/09/08/31/ZJ-1134804.htm 29 HKEx News Release, http://www.hkex.com.hk/eng/newsconsul/hkexnews/2009/090828news.htm 30 HKEx News Release, http://www.hkex.com.hk/eng/newsconsul/hkexnews/2009/090828news.htm 31 Advantages of Listing in Hong Kong, http://www.hkex.com.hk/eng/listing/listhk/advantages_of_listing.htm 32

HKEx News Release, http://www.hkex.com.hk/eng/newsconsul/hkexnews/2009/090828news.htm

10

equal starting point in valuing a listed company; resulting in a more efficient market

and efficient resources allocation.”33

However, industry participants in Hong Kong, on average, questioned the reliability

of financial reports under mainland accounting stands, as well as the credibility of

regulation in China. They also generally took a sceptical attitude about to regulate

mainland audit firms involved in this process.

Jamie Allen, secretary-general of the Asian Corporate Governance Association, said he

was concerned that “Hong Kong’s Securities and Futures Commission (“SFC”) would

not have oversight over the mainland auditing companies providing these financial

statements because they would be supervised by Beijing’s Ministry of Finance.”34

He

also asked,

“If there is a problem with mainland auditing firms, the SFC is working with one hand

tied behind its back. How do we know the Ministry of Finance is going to discipline

these firms?”35

The Chamber of Hong Kong Listed Companies (“CHKLC”) raised a number of other

issues. For example, mainland audit industry had not reached the international level

and the audit firms might be inexperienced in the Hong Kong listing rules.36

Besides,

mainland regulatory authorities might not know very well about the Hong Kong

accounting and auditing practices.37

The Professional Commons of Hong Kong did not agree with the proposed

framework. They stated the reasons in regard of international standard, quality control,

convergence of CASBE with HKFRS, mainland audit firms and sponsors.

“We don’t agree such an important issue, being affecting the future listing qualities of

Hong Kong’s IPOs and listed issuers, to be effected by amending the Listing Rules

and granting waivers by the SFC… Moreover, whose responsibility to assure to the

market that the level of quality assurance equivalence has been achieved, and how

this will be conveyed to the market. Without a clear understanding about the

regulatory regime of Mainland auditors/reporting accountants and what appropriate

sanctions can be applied against them, sufficient comfort will not be given to the

public or investors as the quality, standard and reliability of Mainland auditors. It

would be difficult and too high a risk for Hong Kong sponsors to give the required

declaration. It also not clear whether and how investors/sponsors can take legal

action against Mainland audit firms.”38

One retail investor, who opposed the proposal either, responded the consultation

paper anonymously.

33 http://www.hkex.com.hk/chi/newsconsul/mktconsul/responses/Documents/cp200908r_IN16.pdf 34 HK opens door to Chinese accounting standards,

http://www.ft.com/cms/s/0/e33293a4-044e-11e0-8a3c-00144feabdc0.html#axzz1LlbGUKYd 35 HK opens door to Chinese accounting standards,

http://www.ft.com/cms/s/0/e33293a4-044e-11e0-8a3c-00144feabdc0.html#axzz1LlbGUKYd 36 http://www.hkex.com.hk/chi/newsconsul/mktconsul/responses/Documents/cp200908r_IN14.pdf 37 http://www.hkex.com.hk/chi/newsconsul/mktconsul/responses/Documents/cp200908r_IN14.pdf 38 http://sc.hkex.com.hk/TuniS/www.hkex.com.hk/chi/newsconsul/mktconsul/marketconsultation_c.htm

11

“It makes the financial statement non-comparable with those presented in HKFRS.

Investors invested in those companies through IPO because of the high integrity of

HK auditors. Allowing such changes does not make sense and unfair to those

investors already invested in those companies. The proposal would adversely affect

the accounting/audit employment sector. The new proposal has make Hong Kong

losing its control on maintaining integrity of capital market.”39

Hong Kong’s capital market had a long history and the local enterprises had always

performed exceedingly well in corporate governance. In this regard, mainland firms

lagged far behind local firms. According to the Transparency International, in 2010,

Hong Kong ranked 13th on the Corruption Perceptions Index, while China only

ranked number 78, same ranking with Columbia, Lesotho and Serbia.40

As result,

perhaps one big potential impact was the influences on international investors, which

had always been confident in local audit firms. With the boom of Chinese market,

these investors had attached high importance to mainland-related securities on HKEx.

This proposal might make them feel very concerned, because it disenabled them to

rely on the local regulatory authorities to regulate related mainland audit firms.41

Consultation on Proposed Listing Rules for Mineral and Exploration Companies

Faced with the intense competition in mainland China and SSE’s planning of

international board, HKEx kicked off its efforts for market diversification, trying to

reduce its heavy dependence on mainland China. The HKEx aimed at attracting more

international enterprises, especially for mineral and exploration companies. For these

companies, HKEx integrated all profound benefits from both eastern and western

markets. On the one hand, the booming mainland China leaded to a strong demand for

mineral resources on the market, while Hong Kong had close links to many Asian

economies and was the key gateway to mainland China. In this regard, the HKEx had

been seen as an ideal access point to the rapidly booming and growing mainland

market. On the other hand, HKEx had strong legal system, regulatory framework,

accounting standards and advanced infrastructures with international standards.42

Therefore, in September 2009, HKEx consulted the public about the proposed listing

rules for mineral and exploration companies, to strengthen its role as an important

listing centre for mineral and exploration companies.43

The proposal included

revising eligibility requirements, specific continuing disclosure obligations, specific

disclosure requirements of entering into major transactions, and the requirements to

update previously published statements on reserves and resources.44

For example, a

mineral and exploration company wanted to list had to “provide a report on its

reserves and resources under internationally recognized mineral reporting codes”.45

Exploration companies must have identified resources to protect investors as “they

39 http://www.hkex.com.hk/chi/newsconsul/mktconsul/responses/Documents/cp200908r_AN01.pdf 40 http://www.transparency.org/policy_research/surveys_indices/cpi/2010/results 41 http://chinese.wsj.com/big5/20101220/hkv100229.asp 42 Advantages of Listing in Hong Kong, http://www.hkex.com.hk/eng/listing/listhk/advantages_of_listing.htm 43 HKEx News Release, http://www.hkex.com.hk/eng/newsconsul/hkexnews/2009/090911news.htm 44 HKEx News Release, http://www.hkex.com.hk/eng/newsconsul/hkexnews/2009/090911news.htm 45

CONSULTATION PAPER ON NEW LISTING RULES FOR MINERAL AND EXPLORATION

COMPANIES, http://www.hkex.com.hk/eng/newsconsul/mktconsul/documents/cp200909m_e.pdf

12

will not be exposed to the high risks of failure of early stage.”46

Mark Dickens,

HKEx’s Head of Listing, said,

“Our proposals are aimed at updating Hong Kong’s regulatory framework for listed

mineral and exploration companies, bringing the framework into line with

international best practice and ensuring investors will be provided with information

that is both material and reliable.”

Under this new listing rule, the time for companies to get ready for listing could be

extended two to three times above, and the listing cost would also rise on a big scale.

But it could “improve disclosure standard s for circulars and listing documents” and

“facilitate timely dispatch of circulars for investors to make informed decisions”.

American Appraisal China Limited agreed with this proposal. They said,

“In view of the risks involved in exploration it would make sense to only allow listing

of exploration companies with controlling interests in such businesses. It could also

make sense to adopt terminology that clearly separates exploration and production

activities due to the different risk profile.”47

However, CanAlaska Uranium Limited did not agree on it. They argued that,

“Such a restriction would preclude the listing of mineral/resource investment funds

and royalty companies under the Mineral and Exploration Companies categorization.

These entities represent a vital, active and complementary component of the capital

market for resource companies elsewhere in global markets and are sought-out by

investor for their professional capabilities in serving to diversify investment risk.”48

Change in Chief Executive

During SSE’s planning for further development, HKEx was undergoing the

transferring of power for chief executive. Charles Li was the only candidate in the

selection of a new Chief Executive for the HKEx.49

He was chosen due to his

extensive knowledge of both mainland and western financial markets. As the first

Mainland-born Chief Executive, Charles Li would join the firm from October 2009

and officially succeeded the outgoing CEO on 16 January 2010.50

About the competition between Hong Kong and Shanghai, Li viewed it as a process

of using core competencies to gain deserved market share.

“While competition drives Hong Kong, rivalries should not be seen as a "zero-sum

game" or a "life-or-death struggle." Hong Kong markets also have much room to

grow due to the vast potential of the mainland. Both Hong Kong and HKEx should

seek to maintain their international character and not rely solely on being China's

46 CONSULTATION PAPER ON NEW LISTING RULES FOR MINERAL AND EXPLORATION

COMPANIES, http://www.hkex.com.hk/eng/newsconsul/mktconsul/documents/cp200909m_e.pdf 47 http://www.hkex.com.hk/eng/newsconsul/mktconsul/responses/documents/cp200909mr_in1.pdf 48 http://www.hkex.com.hk/eng/newsconsul/mktconsul/responses/documents/cp200909mr_in5.pdf 49 http://orientaldaily.on.cc/cnt/finance/20090605/00273_001.html 50 Appointment of Charles Li as the Next Chief Executive of HKEx and Renewal of Senior Executives’ Contracts,

http://www.hkex.com.hk/eng/newsconsul/hkexnews/2009/090603news.htm

13

window to the world or depend too heavily on favourable policies from Beijing.”

Charles Li said. 51

RMB Internationalization

Amid the global financial turmoil of 2008 and 2009, many traditional financial hubs

faced the prospect of recession. China’s huge foreign-exchange reserves were also

under great pressure. These events strengthened China’s determination to strengthen

and internationalize the RMB. It was felt that a powerful international financial centre

in China would dramatically facilitate the internationalization of the RMB. Therefore

the guideline to make Shanghai an international financial centre was also a critical

step toward RMB Internationalization. The planned international listings on the

Shanghai Exchange could also enhance the movement of capital between internal and

external markets, and then accelerate the continuous two-way interchange of RMB

within and outside China.

The development of RMB-denominated financial products in overseas markets could

highly boost RMB Internationalization. Undoubtedly, the easiest way for overseas

shareholders to invest in RMB-denominated financial products was in overseas capital

markets. At this point, Hong Kong was the natural choice for this role.

Internationalized currency should be capable of acting as pricing currency, settlement

currency and reserve currency. Considering that the wider the range of

RMB-denominated products, the faster the boot-up process of RMB’s role as

settlement currency would be, HKEx’s role of providing RMB-denominated products

would be significant in promoting RMB internationalization. More important, this

would create great opportunities for HKEx’s further development in this process.

In July 2009, China announced a pilot initiative that expanded the settlement

agreement of cross-border trade transactions in RMB between Hong Kong and five

mainland cities.52

However, trading in RMB didn’t flourish indeed in Hong Kong

after the launch of this project. Li indicated this was mainly caused several factors,

including poor channel for RMB to flow into Hong Kong, limited cash amount of

RMB in Hong Kong, and the lack of the investment offerings in RMB.53

By the end of 2009, there was only a total of 63 billion of RMB deposit in Hong Kong,

which was far from enough to support the transaction. Moreover, mainland regulators

had not ease the restriction for RMB to flow back into China and the cross-border

trade transactions in RMB yet. So there was currently no effective way for RMB to

flow into Hong Kong and flow back in mainland China. Besides, investors didn’t

have enough RMB to invest and it also took time to get through the red tape about the

change between RMB and HK dollar. As a result, HKEx was faced with great

difficulties and obstacles for the planning of RMB products. Even worse, most of

these issues were out of its control.

51 Charles Li: HKEx to Retain International Character, http://english.caijing.com.cn/2009-06-05/110178498.html 52 Beijing’s dollar trap,

http://www.ft.com/cms/s/0/ed6fd068-7d20-11de-b8ee-00144feabdc0.html#axzz1KBw23xSF 53 http://the-sun.on.cc/cnt/finance/20100126/00434_013.html

14

Conclusion

Normally, HKEx released its strategic plan on January. However, Li decided to

postpone the announcement until March 2010, in order to give himself enough time to

consider all the options.54

He wanted to make sure that he addressed the main

challenges facing the exchange, including the rising status of the SSE and

international board. He also had to decide whether or not to move beyond mainland

market, such as focus on mineral and exploration companies worldwide, or further

expand mainland market and offer more opportunities to mainland firms wishing to

list on the exchange, such as RMB securities and mainland accounting standards.

54 http://hk.news.yahoo.com/article/100125/9/gabx.html

15

EXHIBIT 1: PRODUCTS & SERVICES OF HKEX

Securities Products

Equity Securities

Debt Securities

Exchange Traded Funds & Other Market Making Securities

Structured Products

Derivative Warrants

Callable Bull/Bear Contracts

Listed Equity Linked Instruments

Derivatives Products

Risk Disclosure Statement

Equity Index Products

Hang Seng Index Futures & Options (Including Flexible Index Options)

H-shares Index Futures & Options (Including Flexible Index Options)

Mini-Hang Seng Index Futures & Options

Mini H-shares Index Futures

Dividend Futures

Equity Products

Stock Futures

Stock Options

Interest Rate and Fixed Income Products

HIBOR Futures

Three-Year Exchange Fund Note (EFN) Futures

Gold Futures

Clearing Services

Securities Clearing & Settlement Services

Derivatives Clearing and Settlement Services

Data Products

Real-time Data

Historical Data

Requirements & Application Procedures

Prices, Policies & Guidelines

Information Vendors List

Source: Product & Service, HKEx, http://www.hkex.com.hk/eng/prod/product.htm

16

EXHIBIT 2: NUMBER OF IPO TRANSACTIONS

2009 2008 2007 2006 2005

New listing applications accepted 123 137 125 88 111

Applications listed 93 57 96 65 76

Companies listed on Main Board pursuant to Chapter 64 29 78 54 55

Investment vehicles listed on Main Board 19 7 11 3 6

Transfer of listing from GEM to Main Board 4 18 4 2 2

Companies listed on GEM 5 2 2 6 10

Deemed new listings 1 1 1 0 3

New listing applications rejected 0 1 0 7 5

New listing applications withdrawn 3 8 3 4 5

Applications in process as at year-end 31 27 42 29 32

Active applications with approval granted but not

yet listed at year-end 12 24 9 6 6

Source: FINAL RESULTS FOR THE YEAR ENDED 31 DECEMBER 2009,

http://www.hkex.com.hk/eng/newsconsul/hkexnews/2010/Documents/100304news.pdf

EXHIBIT 3: NUMBER OF LISTED COMPANIES IN HKEX

2009 2008 2007 2006 2005

Main Board 1,145 1,087 1,048 975 934

GEM 174 174 193 198 201

Total 1,319 1,261 1,241 1,173 1,135

Source: FINAL RESULTS FOR THE YEAR ENDED 31 DECEMBER 2009,

http://www.hkex.com.hk/eng/newsconsul/hkexnews/2010/Documents/100304news.pdf

17

EXHIBIT 4: MAIN BOARD – MARKET CAPITALIZATION

(As at year-end)

GEM – MARKET CAPITALIZATION

(As at year-end)

Source: FINAL RESULTS FOR THE YEAR ENDED 31 DECEMBER 2009,

http://www.hkex.com.hk/eng/newsconsul/hkexnews/2010/Documents/100304news.pdf

0

5,000

10,000

15,000

20,000

25,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

4,795 3,885 3,559

5,478 6,629

8,113

13,249

20,539

10,254

17,769

0

20

40

60

80

100

120

140

160

180

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

67 61 52

70 67 67

89

161

45

105

18

EXHIBIT 5: NUMBER OF LISTED COMPANIES BY INDUSTRY

CLASSIFICATION

– Main Board and GEM (as at year-end)

2009 2008 2007 2006 2005

Energy 44 34 28 21 20

Materials 105 93 81 69 62

Industrial Goods 111 113 114 103 92

Consumer Goods 330 327 336 327 317

Services 209 198 188 168 165

Telecommunications 18 17 18 16 17

Utilities 32 24 20 22 22

Financials 102 100 103 103 100

Properties & Construction 191 174 166 158 151

Information Technology 154 158 161 161 162

Conglomerates 23 23 26 25 26

Total 1,319 1,216 1,241 1,173 1,134

Source: FINAL RESULTS FOR THE YEAR ENDED 31 DECEMBER 2009,

http://www.hkex.com.hk/eng/newsconsul/hkexnews/2010/Documents/100304news.pdf

EXHIBIT 6: PRIMARY MARKET DRIVEN BY MAINLAND LISTINGS IN

HKEX

Source; HKEx’s Strategies in Capturing Mainland Opportunities and Becoming Globally Competitive

http://www.hkex.com.hk/eng/newsconsul/speech/2010/Documents/sp100426.pdf

19

EXHIBIT 7: PERFORMANCE OF MAINLAND ENTERPRISES IN 2009

As at

2009-12-15 31-12-2008 % Change

Number of listed companies 519 (40%) 465 (37%) 12

Number of newly listed companies

for the year 43 (67%) 28 (57%) 54

Market capitalization (HK$bil) 10,350.89 (58%) 6,160.91 (60%) 68

As of

15-12-2009 31-12-2008 % Change

Average daily equity turnover

(HK$mil) 33,798.7 (72 %) 36,642.0 (71%) -8

Total equity funds raised (HK$bil) 306.6 (52 %) 294.1 (69%) 4

IPO funds raised (HK$bil) 172.8 (81 %) 47.7 (72% 262

Post IPO funds raised (HK$bil) 133.8 (36 %) 246.5 (68%) -46

Total equity funds raised since Jan

1993 (HK$bil)

2,459.8

(57 %) 2,153.2 (58%) 14

Source: HKEx Publishes Market Statistics in Response to Media Requests,

http://www.hkex.com.hk/eng/newsconsul/hkexnews/2009/091221news.htm

20

EXHIBIT 8: BIOGRAPHICAL INFORMATION OF CHARLES LI

Mr Li Xiaojia, Charles

Other major offices:

Shanghai Pudong Development Bank Co Ltd (“SPDB”) (listed on the Shanghai Stock

Exchange)– non-executive director (2008~)

China Vanke Co Ltd (“China Vanke”) (listed on the Shenzhen Stock Exchange)–

non-executive director (2008~)

China Entrepreneurs Forum – director (2005~)

Past offices:

JP Morgan China – chairman (2003-2009)

Merrill Lynch China (1994-2003: president (1999-2003))

Brown & Wood, New York – associate (1993-1994)

Davis Polk & Wardwell, New York – associate (1991-1993)

Qualifications:

Bachelor of Arts in English Literature (Xiamen University, China)

Master of Arts in Journalism (University of Alabama, USA)

Juris Doctor (Columbia University, USA)

Source: Change in Chief Executive and Directorate,

http://www.hkex.com.hk/eng/newsconsul/hkexnews/2010/Documents/100115news.pdf

21

EXHIBIT 9: FINANCIAL HIGHLIGHTS

Source: FINAL RESULTS FOR THE YEAR ENDED 31 DECEMBER 2009,

http://www.hkex.com.hk/eng/newsconsul/hkexnews/2010/Documents/100304news.pdf

2009 2008 Change

KEY MARKET STATISTICS Average daily turnover value on the

Stock Exchange $62.3 billion $72.1 billion (14%)

Average daily number of derivatives contracts

traded on the Futures Exchange 206,458 207,052 (0%)

Average daily number of stock options contracts

traded on the Stock Exchange 191,676 225,074 (15%)

2009

$’000

2008

$’000 Change

RESULTS

Revenue and other income 7,035,040

1,492,949

7,549,090

1,620,953

(7%)

(8%) Operating expenses

Profit before taxation 5,542,091

(838,047)

5,928,137

(799,506)

(7%)

5% Taxation

Profit attributable to shareholders 4,704,044 5,128,631 (8%)

Basic earnings per share $4.38

$4.36

$4.78

$4.75

(8%)

(8%) Diluted earnings per share

Interim dividend per share $1.84

$2.09

$2.49

$1.80

(26%)

16% Final dividend per share

$3.93 $4.29 (8%)

Dividend payout ratio 90% 90% N/A

2009 2008 Change

KEY ITEMS IN CONSOLIDATED

STATEMENT OF FINANCIAL POSITION

Shareholders’ funds ($’000) 8,027,326 7,293,614 10%

Total assets 2 ($’000) 45,332,002 62,822,112 (28%)

Net assets per share $7.46 $6.79 10%

22

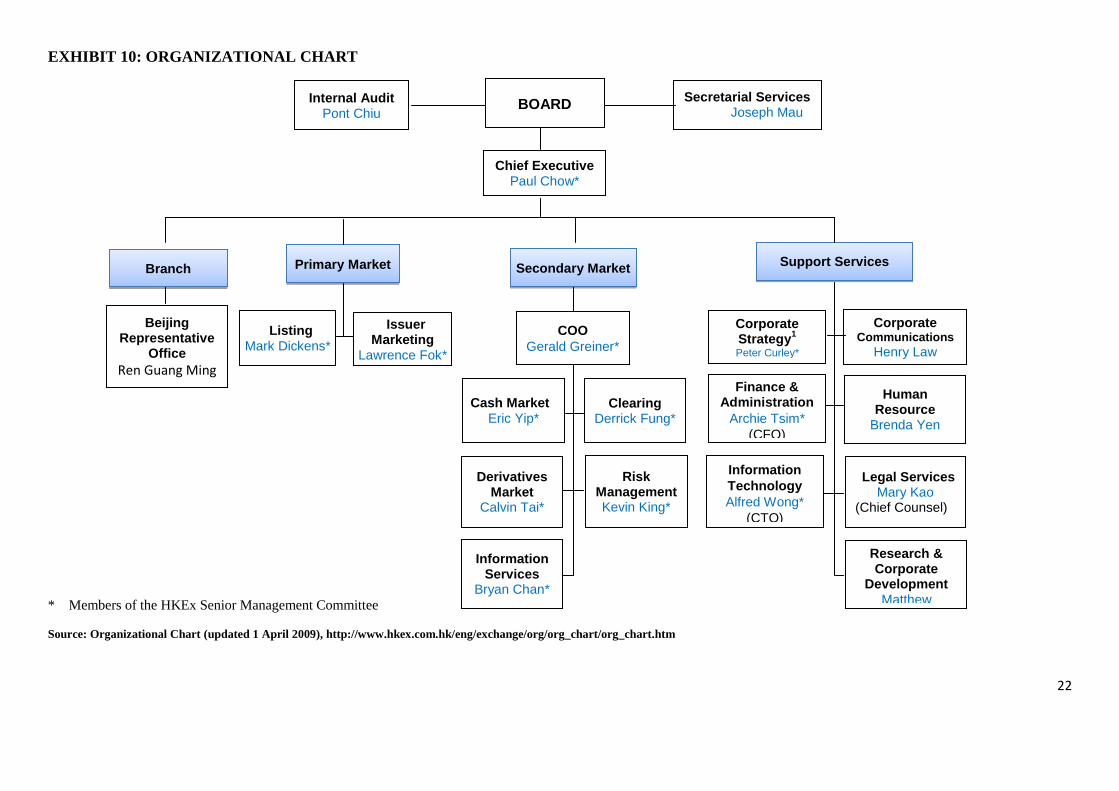

EXHIBIT 10: ORGANIZATIONAL CHART

* Members of the HKEx Senior Management Committee

Source: Organizational Chart (updated 1 April 2009), http://www.hkex.com.hk/eng/exchange/org/org_chart/org_chart.htm

Secretarial Services Joseph Mau

Internal Audit Pont Chiu

Chief Executive Paul Chow*

Primary Market Secondary Market Support Services

Listing Mark Dickens*

Finance & Administration

Archie Tsim*

(CFO)

COO

Gerald Greiner*

Information Services

Bryan Chan*

Risk Management Kevin King*

Clearing Derrick Fung*

Cash Market Eric Yip*

Derivatives Market

Calvin Tai*

Research & Corporate

Development Matthew Harrison

Legal Services Mary Kao

(Chief Counsel)

Human Resource

Brenda Yen

Information

Technology

Alfred Wong*

(CTO)

Corporate Communications

Henry Law

BOARD

Corporate Strategy

1

Peter Curley*

Beijing Representative

Office

Ren Guang Ming

Issuer Marketing

Lawrence Fok*

Branch

23

EXHIBIT 11: GLOSSARY

ADT Average Daily Turnover

CASBE China Accounting Standards for Business Enterprises

CHKLC Chamber of Hong Kong Listed Companies

CSRC China Securities Regulatory Commission

GEM Growth Enterprise Market

HKEx Hong Kong Exchanges and Clearing Limited

HKFCC Hong Kong Securities Clearing Company Limited

HKFE Hong Kong Futures Exchange Limited

HKFRS Hong Kong Financial Reporting Standards

IFRS International Financial Reporting Standards

IPO Initial Public Offering

SFC Securities and Futures Commission

SME Small Medium Enterprise

SSE Shanghai Stock Exchange

SZSE Shenzhen Stock Exchange

24

Hong Kong Exchanges and Clearing Limited (B)

Facing the emerging opportunities of the further opening up of China’s capital market

and the intense competition from exchanges, HKEx announced its Strategic Plan

2010–2012 on 4 March, 2010, two months after the appointment of Charles Li went

into effect.55

Apart from further emphasizing the importance of mainland business,

there were also new additions to its focus, such as developing new RMB products to

leverage China.

Business Performance

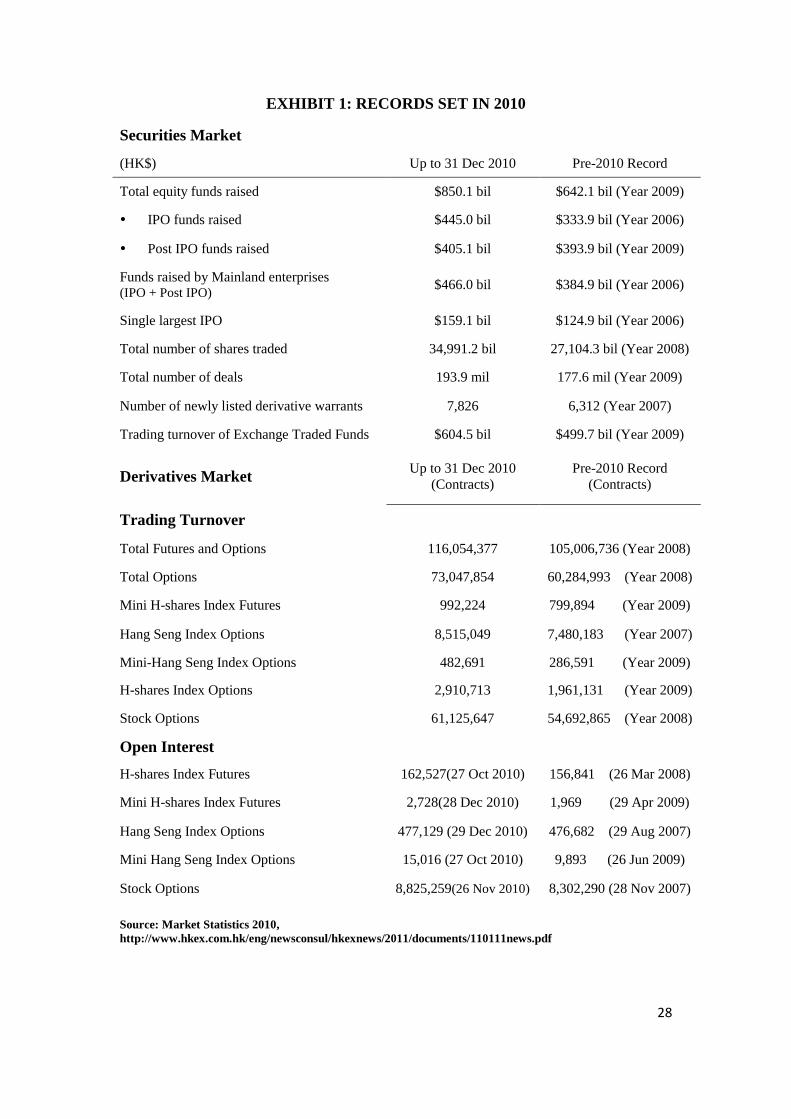

2010 was an extraordinary year for HKEx, in which it had set a series of new records

[see Exhibit 1]. According to HKEx, it set high record for both IPOs and Total Funds

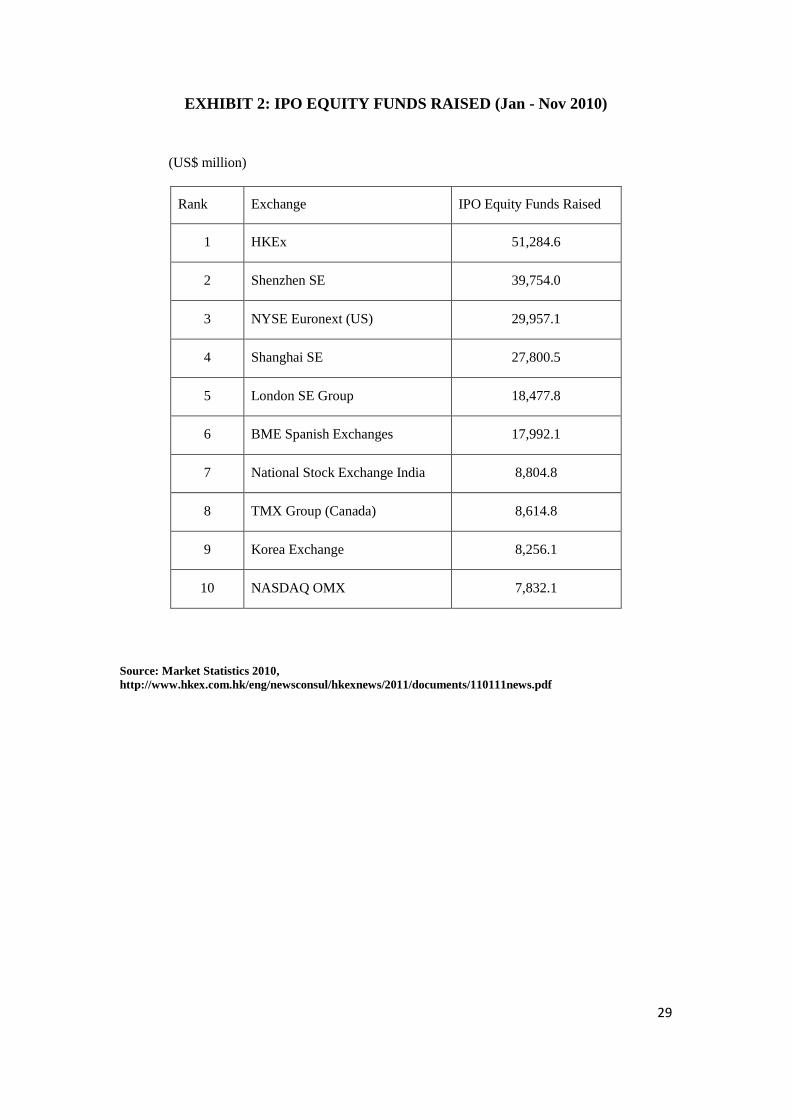

Raised in 2010 and its IPOs ranked first in the world for the second year in a row [see

Exhibit 2].56

Mainland enterprises also had good performances in this year. As at the

end of 2010, a total of 66 new mainland companies were listed on HKEx, growing 38

per cent compared with the same period in 2009.57

HKEx’s effort in attracting global

listing companies was also worth noting. In 2010 multiple large-scale international

companies, including Prudential Plc, AIA, and United Company RUSAL Plc, had

chosen to list in Hong Kong. The IPO funds raised in HKEx was HK$ 445billion in

2010, 45 per cent of which was brought by international listings. By contrast, this

figure was only 5 per cent in 2007.58

Strategic Plan 2010-2012

Against the backdrop of opportunities and competitions ahead, HKEx developed its

new vision in this strategic plan, to making itself the leading exchange by combining

the best characteristics of Chinese and international markets.59

In particular, HKEx

had positioned itself as “the China exchange of choice for global investors and issuers,

and the international exchange of choice for issuers and investors from Greater

China”.60

With this vision, Mr Li explained the direction of the new strategic plan:

The plan involves enlarging our product offering, investor base and geographic

coverage. More specifically, we will work to introduce renminbi products and enable

participation of more Mainland investors in our markets. We want to be on hand to

forge new ground in support of Mainland policy evolution and make our platform an

effective one for the trading of renminbi products.61

55 HKEx Chief Executive Charles Li’s Elaboration on HKEx’s Strategic Plan 2010-2012

http://www.hkex.com.hk/eng/newsconsul/hkexnews/2010/Documents/1003047news.pdf 56 2011 HKEx Annual Media Luncheon,

http://www.hkex.com.hk/eng/newsconsul/hkexnews/2011/documents/1101113news.pdf 57 Market Statistics 2010, http://www.hkex.com.hk/eng/newsconsul/hkexnews/2011/documents/110111news.pdf 58 2011 HKEx Annual Media Luncheon,

http://www.hkex.com.hk/eng/newsconsul/hkexnews/2011/documents/1101113news.pdf 59 FINAL RESULTS FOR THE YEAR ENDED 31 DECEMBER 2009,

http://www.hkex.com.hk/eng/newsconsul/hkexnews/2010/Documents/100304news.pdf 60 FINAL RESULTS FOR THE YEAR ENDED 31 DECEMBER 2009,

http://www.hkex.com.hk/eng/newsconsul/hkexnews/2010/Documents/100304news.pdf 61

HKEx Chief Executive Charles Li’s Elaboration on HKEx’s Strategic Plan 2010-2012

http://www.hkex.com.hk/eng/newsconsul/hkexnews/2010/Documents/1003047news.pdf

25

The Strategic Plan 2010–2012 comprised three integrated parts: core strategy,

extension strategy and expansion strategy.62

Typically, it covered five key focus areas,

namely primary market, RMB, clearing structure, trading structure and IT.63

In the

following three-year period, the strategic plan would be implemented through a series

of initiatives, which would be confirmed by HKEx’s annual budget and operating

plan.64

At this stage, HKEx identified 19 initiatives to achieve its objectives.65

In this strategic plan, HKEx’s planning of introducing RMB Products included the

creation of a platform to support multi-currency products, and making effort to

become the destination of RMB-based products outside mainland China.66 At this

stage, HKEx would focus on identifying new RMB products, coordinating with

authorities for cross-border RMB-related business, and developing related clearing, IT

platforms and infrastructures etc.67

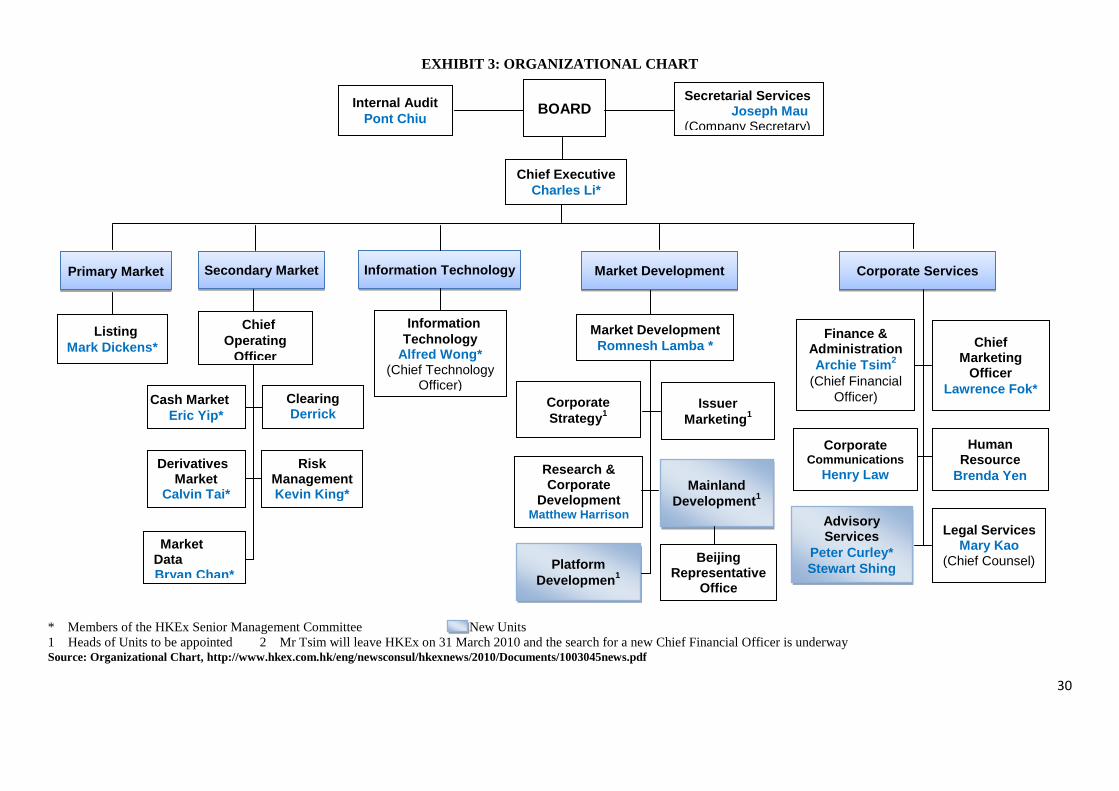

In order to align with its strategic direction, HKEx revised its organization structure

[see Exhibit 3] at the same time. The most noticeable change was the establishment of

a new market development group. A mainland Development department was also

established under this division.68

Leading by Romnesh Lamba, who joined HKEx in

February 2010 as Executive Vice President, this new division would focus on

capturing mainland-related opportunities, broadening HKEx's issuer base, assessing

product development and enhancing HKEx’s competitiveness.69

New Competitive Landscape

On 5 March, 2010, the Premier of the State Council Wen Jiabao delivered the Report

on the Work of the Government.70

It is said in this report that China would

“vigorously develop the financial market and encourage financial innovation” and

“promote pilot projects for the use of the renminbi in cross-border trade, and

gradually develop overseas financial activities using the renminbi”.71

This had made

it clear that China would develop overseas financial activities using RMB, which also

further confirmed the future establishment of International Board and the approval of

foreign companies to issue RMB-dominated shares in China.

December 2010 marked the 20th Anniversary of the China’s capital market. By the

end of 2010, a total of 2063 companies listed on the mainland exchanges, with the

62 A Quick Guide to HKEx Strategic Plan 2010-2012

http://www.hkex.com.hk/eng/newsconsul/hkexnews/2010/Documents/1003046news.pdf 63

The HKEx Strategic Plan 2010–2012,

http://www.hkex.com.hk/eng/exchange/invest/finance/2009/documents/f108_09.pdf 64 FINAL RESULTS FOR THE YEAR ENDED 31 DECEMBER 2009,

http://www.hkex.com.hk/eng/newsconsul/hkexnews/2010/Documents/100304news.pdf 65 FINAL RESULTS FOR THE YEAR ENDED 31 DECEMBER 2009,

http://www.hkex.com.hk/eng/newsconsul/hkexnews/2010/Documents/100304news.pdf 66 FINAL RESULTS FOR THE YEAR ENDED 31 DECEMBER 2009,

http://www.hkex.com.hk/eng/newsconsul/hkexnews/2010/Documents/100304news.pdf 67 FINAL RESULTS FOR THE YEAR ENDED 31 DECEMBER 2009,

http://www.hkex.com.hk/eng/newsconsul/hkexnews/2010/Documents/100304news.pdf 68 HKEx announces revised corporate structure,

http://www.hkex.com.hk/eng/newsconsul/hkexnews/2010/1003045news.htm 69 HKEx announces revised corporate structure,

http://www.hkex.com.hk/eng/newsconsul/hkexnews/2010/1003045news.htm 70 Report on the Work of the Government (2010),

http://www.gov.cn/english/official/2010-03/15/content_1556124.htm 71 Report on the work of the government, Wen Jiabao, 5 March 2010

26

market capitalization of RMB26.54 trillion.72

China's A-share market took third place

with a stock market value of US$3.83 trillion, only after US (US$ 15.26 trillion) and

Japan (US$ 3.87 trillion).73

Furthermore, by means of merger, acquisition,

restructuring, and overall listing, an array of listed companies had been further

developed and optimized.74

On this basis, the blue-chip structure at SSE had basically

taken shape. The construction of blue-chip market was an important part of SSE’s

efforts to become a global and highly developed stock exchange. Moreover, SSE had

also basically concluded its preparatory work concerning listing and trading on the

International Board.75

In the international market, competitions between exchanges were getting more and

more intensified, especially for the surge of merger and acquisition in exchange

industry. On 22 October 2010, Singapore Exchange (SGX) and the Australian

Securities Exchange (ASX) announced their preparation for their historic US$14

billion alliance.76

If the deal was successful, it would create a new centre for trading

in Asia to attract major investors and issuers.77

Also, it would provide Australians

with future opportunities to invest in Asian market. Besides, SGX had already been

far more aggressive than HKEx in adopting advanced technologies, such as dark

pools.78

Moving into 2011, the storm became even fiercer. In February 2011,

Deutsche Boerse submitted a tender for NYSE Euronext, London Stock Exchange

announced to take over Toronto Stock Exchange parent TMX Group Inc., and BATS

Global Markets said it would buy Chi-X Europe.79

All these events happened within

three weeks.

In this regard, HKEx Chairman Ronald Arculli said,

We would keep our ears and eyes open, we would look at developments that are going

on in other markets - we do not rule out doing joint ventures or strategic alliances,

but we don't see that equity is necessary a component of any possible co-operation.

HKEX’s Preparation for RMB Products

After the release of HKEx Strategic Plan 2010-2012, HKEx had also done a series of

work to prepare for the trading and clearing of the RMB products [see Exhibit 4]. On

22 October 2010, the first RMB-dominated exchange traded product, RMB bonds

issued by Asian Development Bank, was listed in HKEx. In order to further expand

the RMB business, a revised Settlement Agreement on the Clearing of RMB

Businesses was signed on 19 July 2010,80

which could greatly ease the restrictions to

72 http://www.bosidata.com/jinrongshuju1103/L216189GT2.html 73 http://www.cnstock.com/index/gdbb/201012/1056340.htm 74 Geng: Promote Innovation for Blue-chip Market Construction,

http://www.sse.com.cn/sseportal/en/jsp/news.html

75 SSE Completes Preparatory Work for Int'l Board, http://www.sse.com.cn/sseportal/en/jsp/news.html

76 Asian bid for $14bn merger with ASX

http://www.temasekreview.com/2010/10/23/asian-bid-for-14bn-merger-with-asx/ 77 Merger could threaten Hong Kong Exchange, Bernard Cheng, 25 October 2010,

http://bernardcheng.wordpress.com/2010/10/25/65/ 78 For HKEx, A Threat From South, http://cn.wsj.com/gb/20101025/hkv134350_ENversion.shtml 79

SGX CEO says no more concessions on $7.7 billion ASX bid,

http://www.reuters.com/article/2011/03/01/us-finance-summit-exchanges-idUKTRE72026B20110301 80 Mainland, HK revise agreement for RMB clearing biz in HK,

http://www.chinadaily.com.cn/china/2010-07/19/content_11021000.htm

27

use RMB in Hong Kong. After the signing of this agreement, a series of

RMB-dominated products were introduced in session by financial institutions in Hong

Kong.

In 2010, the amount of RMB deposits and RMB trade settlement both experienced a

tremendous growth in Hong Kong [see Exhibit 5], but RMB deposits still represented

less than 5 per cent of total deposit in Hong Kong.81

81 2011 HKEx Annual Media Luncheon,

http://www.hkex.com.hk/eng/newsconsul/hkexnews/2011/documents/1101113news.pdf

28

EXHIBIT 1: RECORDS SET IN 2010

Securities Market

(HK$) Up to 31 Dec 2010 Pre-2010 Record

Total equity funds raised $850.1 bil $642.1 bil (Year 2009)

IPO funds raised $445.0 bil $333.9 bil (Year 2006)

Post IPO funds raised $405.1 bil $393.9 bil (Year 2009)

Funds raised by Mainland enterprises

(IPO + Post IPO) $466.0 bil $384.9 bil (Year 2006)

Single largest IPO $159.1 bil $124.9 bil (Year 2006)

Total number of shares traded 34,991.2 bil 27,104.3 bil (Year 2008)

Total number of deals 193.9 mil 177.6 mil (Year 2009)

Number of newly listed derivative warrants 7,826 6,312 (Year 2007)

Trading turnover of Exchange Traded Funds $604.5 bil $499.7 bil (Year 2009)

Derivatives Market Up to 31 Dec 2010

(Contracts)

Pre-2010 Record

(Contracts)

Trading Turnover

Total Futures and Options 116,054,377 105,006,736 (Year 2008)

Total Options 73,047,854 60,284,993 (Year 2008)

Mini H-shares Index Futures 992,224 799,894 (Year 2009)

Hang Seng Index Options 8,515,049 7,480,183 (Year 2007)

Mini-Hang Seng Index Options 482,691 286,591 (Year 2009)

H-shares Index Options 2,910,713 1,961,131 (Year 2009)

Stock Options 61,125,647 54,692,865 (Year 2008)

Open Interest

H-shares Index Futures 162,527(27 Oct 2010) 156,841 (26 Mar 2008)

Mini H-shares Index Futures 2,728(28 Dec 2010) 1,969 (29 Apr 2009)

Hang Seng Index Options 477,129 (29 Dec 2010) 476,682 (29 Aug 2007)

Mini Hang Seng Index Options 15,016 (27 Oct 2010) 9,893 (26 Jun 2009)

Stock Options 8,825,259(26 Nov 2010) 8,302,290 (28 Nov 2007)

Source: Market Statistics 2010,

http://www.hkex.com.hk/eng/newsconsul/hkexnews/2011/documents/110111news.pdf

29

EXHIBIT 2: IPO EQUITY FUNDS RAISED (Jan - Nov 2010)

(US$ million)

Rank Exchange IPO Equity Funds Raised

1 HKEx 51,284.6

2 Shenzhen SE 39,754.0

3 NYSE Euronext (US) 29,957.1

4 Shanghai SE 27,800.5

5 London SE Group 18,477.8

6 BME Spanish Exchanges 17,992.1

7 National Stock Exchange India 8,804.8

8 TMX Group (Canada) 8,614.8

9 Korea Exchange 8,256.1

10 NASDAQ OMX 7,832.1

Source: Market Statistics 2010,

http://www.hkex.com.hk/eng/newsconsul/hkexnews/2011/documents/110111news.pdf

30

EXHIBIT 3: ORGANIZATIONAL CHART

* Members of the HKEx Senior Management Committee New Units

1 Heads of Units to be appointed 2 Mr Tsim will leave HKEx on 31 March 2010 and the search for a new Chief Financial Officer is underway

Source: Organizational Chart, http://www.hkex.com.hk/eng/newsconsul/hkexnews/2010/Documents/1003045news.pdf

Chief Executive

Charles Li*

Secretarial Services Joseph Mau (Company Secretary)

Internal Audit

Pont Chiu

Market Development Primary Market Secondary Market Corporate Services Information Technology

Listing

Mark Dickens*

Market Development

Romnesh Lamba * Chief Marketing

Officer

Lawrence Fok*

Finance & Administration

Archie Tsim2

(Chief Financial

Officer)

Information

Technology

Alfred Wong* (Chief Technology

Officer)

Chief

Operating

Officer

Gerald Greiner*

Market Data Bryan Chan*

Risk Management Kevin King*

Clearing Derrick Fung*

Cash Market

Eric Yip*

Derivatives Market

Calvin Tai*

Platform

Developmen1

Mainland

Development1

Research & Corporate

Development Matthew Harrison

Issuer

Marketing1

Legal Services Mary Kao

(Chief Counsel)

Human Resource

Brenda Yen

Advisory Services

Peter Curley*

Stewart Shing

Corporate Communications

Henry Law

BOARD

Corporate

Strategy1

Beijing Representative

Office

31

EXHIBIT 4: HKEX’S PREPARATION FOR TRADING AND CLEARING OF

RMB PRODUCTS

SEHK Circulars

Additional RMB Readiness Test from 24 to 27 March

Simulation Test for Trading of Renminbi (RMB) Products on 19 March

Test for Simulating Electronic Initial Public Offer (EIPO) Subscription, Trading, Clearing

and Money Settlement of Listed Renminbi (RMB) Products

Revised Calculation of Market Turnover Disseminated on AMS/3 Information Pages

P.788 and 8788 and Line 23 of Stock Pages

Calculation of Stamp Duty and Trading Related Fees for Transactions in Non-Hong Kong

Dollar Currencies

Listing of the First Renminbi (RMB) Denominated Exchange Traded Product on 22

October 2010

Exchange Participants' Preparation for Trading and Clearing of Renminbi (RMB)

Denominated Products

Testing Sessions for Simulating Trading in Renminbi (RMB) Products

Operational Readiness for Trading of Renminbi (RMB) Products

HKSCC Circulars

For CCASS Participants

Additional Renminbi (RMB) Readiness Test from 24 to 27 March 2011

Renminbi (RMB) Payment Pilot Run on Thursday 17 March 2011 and Clearing

Simulation Test for RMB Securities on Sunday 20 March 2011 (For Direct Clearing

Participants Only)

Renminbi (RMB) Payment Pilot Run on Thursday 17 March 2011 and Clearing

Simulation Test for RMB Securities on Sunday 20 March 2011 (For Custodian, General

Clearing and Stock Pledgee Participants Only)

Test for Simulating Electronic Initial Public Offer (EIPO) Subscription, Trading, Clearing

and Money Settlement of Listed Renminbi (RMB) Products

Calculation of CCASS Fees for Transactions in Non-Hong Kong Dollar Currencies

Questionnaire on Preparation for Settlement of Renminbi (RMB) Denominated Products

Operational Readiness for CCASS Money Settlement in Renminbi (RMB)

For CCASS Designated Banks

Setup of Renminbi (RMB) Designated Bank Account in CCASS and Payment Pilot Run

HKCC / SEOCH Circulars

Acceptance of RMB as Cash Collateral for Margin Requirements

Source: Preparation for Trading and Clearing of Renminbi (RMB) Products,

http://www.hkex.com.hk/eng/market/sec_tradinfra/prepareRMB/prepareRMB.htm

32

EXHIBIT 5: RMB DEPOSITS IN HONG KONG

CUMULATIVE RMB TRADE SETTLEMENT

Source: 2011 HKEx Annual Media Luncheon,

http://www.hkex.com.hk/eng/newsconsul/hkexnews/2011/documents/1101113news.pdf

33

EXHIBIT 6: TOTAL EQUITY FUNDS RAISED (Jan - Nov 2010)

(US$ million)

Rank Exchange Total Equity Funds Raised

1 NYSE Euronext (US) 180,652.0

2 BM&F BOVESPA (Brazil) 97,494.9

3 HKEx 87,144.7

4 Shanghai SE 76,051.1

5 London SE Group 56,639.2

6 NYSE Euronext (Europe) 54,834.3

7 Shenzhen SE 51,237.0

8 Tokyo SE 49,133.2

9 TMX Group (Canada) 42,835.8

10 National Stock Exchange India 33,998.1

Source: Market Statistics 2010,

http://www.hkex.com.hk/eng/newsconsul/hkexnews/2011/documents/110111news.pdf

34

EXHIBIT 7: MARKET VALUE OF SHARES OF DOMESTIC-LISTED

COMPANIES

(Main and Parallel Markets)

(As at the end of November 2010)

(US$ million)

November 2010 December 2009

Exchange Rank Market value Rank Market value % Change

NYSE Euronext (US) 1 13,040,691.5 1 11,837,793.3 10.2

NASDAQ OMX 2 3,649,044.0 4 3,239,492.4 12.6

Tokyo SE 3 3,541,793.5 3 3,306,082.0 7.1

London SE Group 4 3,353,840.2 2 3,453,622.1 -2.9

HKEx 5 2,695,931.6 7 2,305,142.8 17.0

NYSE Euronext (Europe) 6 2,695,282.5 5 2,869,393.1 -6.1

Shanghai SE 7 2,680,723.4 6 2,704,778.5 -0.9

TMX Group 8 2,002,393.9 8 1,676,814.2 19.4

Bombay SE 9 1,540,338.9 11 1,306,520.3 17.9

BM&F BOVESPA (Brazil) 10 1,447,045.2 10 1,337,247.7 8.2

Source: Market Statistics 2010,

http://www.hkex.com.hk/eng/newsconsul/hkexnews/2011/documents/110111news.pdf

35

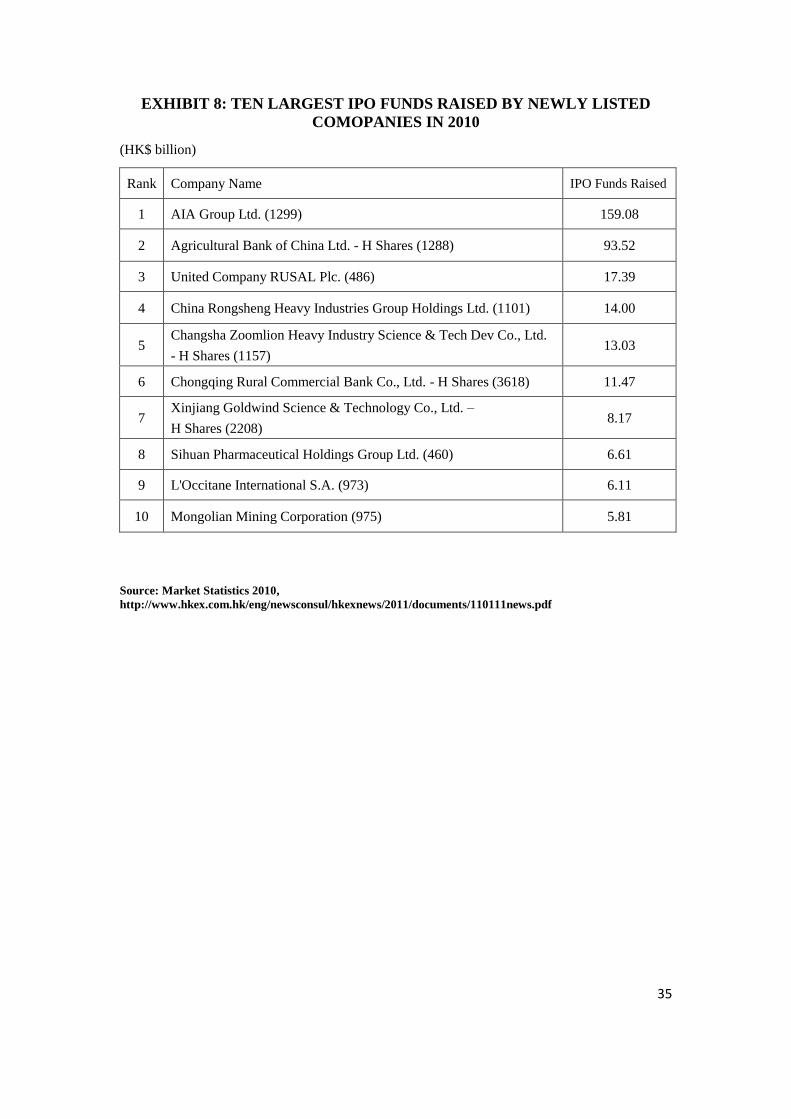

EXHIBIT 8: TEN LARGEST IPO FUNDS RAISED BY NEWLY LISTED

COMOPANIES IN 2010

(HK$ billion)

Rank Company Name IPO Funds Raised

1 AIA Group Ltd. (1299) 159.08

2 Agricultural Bank of China Ltd. - H Shares (1288) 93.52

3 United Company RUSAL Plc. (486) 17.39

4 China Rongsheng Heavy Industries Group Holdings Ltd. (1101) 14.00

5 Changsha Zoomlion Heavy Industry Science & Tech Dev Co., Ltd.

- H Shares (1157) 13.03

6 Chongqing Rural Commercial Bank Co., Ltd. - H Shares (3618) 11.47

7 Xinjiang Goldwind Science & Technology Co., Ltd. –

H Shares (2208) 8.17

8 Sihuan Pharmaceutical Holdings Group Ltd. (460) 6.61

9 L'Occitane International S.A. (973) 6.11

10 Mongolian Mining Corporation (975) 5.81

Source: Market Statistics 2010,

http://www.hkex.com.hk/eng/newsconsul/hkexnews/2011/documents/110111news.pdf

36

Case Analysis

_

Executive Summary

Focused on Shanghai Stock Exchange’s rise in recent years, the case provides

HKEx’s alternative options towards the competitive landscape. Located in the

booming Chinese market with most potential, the sibling rivalry between Hong Kong

and Shanghai has arisen for a long time. HKEx and Shanghai Stock Exchange (SSE),

the core part in respective finance industries, would certainly compete for the leading

exchange in China.

Preferential policies, along with China’s fast-growing capital market, make SSE a

promising challenger. No doubt the stock exchange of Hong Kong, which has relied

on mainland listing resources for many years exclusively, became palpably nervous.

Faced with the challenges from rivals, issuers, investors as well as government, HKEx

took steps, appointed the first mainland-born chief executive, and even forecasted the

new opportunity for further development. Which alternatives should HKEx took, and

whether or not HKEx can capture new opportunity as well as fend off competitors

with its new chief executive and strategies are the key.

Situation Analysis

Market Environment Analysis - Five Forces Model

Power of buyers and suppliers

In the perfectly or imperfectly competitive markets, prices of goods and

services are almost determined by the markets. While in the exchange

industry, exchanges are highly regulated and protected by the governments

because of their roles in finance area. Therefore issuers and investors are put

at the passive positions in receiving the prices and fees without bargaining

power.

New market entrants

Perhaps we can say that stock exchanges are in an oligopoly situation in the

domestic market while they are in a competitive situation in the global

markets. In order to maintain financial stability, it’s impossible for

individuals and institutions to break into this field. So existed participants in

this field face few threats from new entrants.

Substitute products

In highly developed countries, there are more than one exchanges existing at

the same time, such as NYSE Euronext and NASDAQ, which differ a lot in

visions, positions, target customers and so on. So each exchange in the world

37

plays as a monopolist in respective regions. As a result, substitute products

and services for one exchange are existed in the global market, and these

products or services are imperfect substitutes. Because with the transfer of

territory, both market and nonmarket environment, including policies, laws,

culture and investors have changed correspondingly.

Besides there is a key issue that issuers cannot ignore. Exchanges didn’t

make an agreement on the acceptation of accounting standards worldwide,

which means issuers faced with various barrier to entry when make decisions.

In recent years, with the rapid development of the trade liberalization all over

the world, various barriers presented weak step by step. Exchanges tend to

lower the barrier to entry by accepting accounting standards in a broader

sense, to attract more potential listing recourse. For example, HKEx

published the consultation paper on accepting of mainland accounting and

auditing standards and mainland audit firms for mainland incorporated

companies listed in Hong Kong in 2009. This new rule can greatly reduce the

compliance cost and can eventually raise mainland issuers’ motivations to list

in Hong Kong.

Another key issue about substitute is the domestic demand in each market.

The market with plenty of investors can lead to high market turnover. Also

issuers can achieve more exposure to this market with more issuers.

Therefore the marketplace that each exchange existed in is also a critical

consideration to issuers. HKEx’s decade-long boom owed a lot to its position

as the gateway of mainland China. We can find from a series of key statistics,

including market capitalization, average daily equity turnover and IPO funds

raised, mainland-related enterprises make great contributions to HKEx.

Existing competitive rivalry

Exchange’ revenue comes from trading fees, listing fees, income from sale of

information, and so on. Based on the local market with fixed number of local

investors, the best way to generate income for exchange is attracting more

companies to list, which is also an important indicator of its competitive

competencies. For this reason, we can notice the growing tendencies in

competition for listing resource in this industry.

In a certain sense, competition between various exchanges is also the

competition between financial industries of different countries. So this

competition also exists in the attractions and competitiveness of different

financial markets.

With the raise of emerging markets in China, especially after the equity

division reform, Shanghai Exchange has gradually evolved into a major

exchange, with the market capitalization soaring from RMB2.3 trillion in

2005 to RMB18.5 trillion in 2010. In the international scale, competitions

38

have become much stiffer.

Nonmarket Environment Analysis

As mentioned above, exchanges are highly regulated and protected by the

governments. So except for market environment, exchanges are also operated in

nonmarket environment. Although HKEx was listed in 2000 and directly supervised

and controlled by the management and the board. Its top shareholder is the Hong

Kong government and about half of the directors in the board are directly appointed

by the government. As a result, its business practices, rules and strategic planning can

be influenced by the authorities and government. In the meantime, HKEx is also a

member of regulator of the securities and derivatives marketplace in Hong Kong. So

the nonmarket environment and issues are especially important for it.

According to the description in the following table, HKEx’s nonmarket environment

kept changing and progressing in the form of legislation and regulation. Therefore, if

HKEx wants to continue its longstanding success and leave its mainland rivals far

behind, it has to be successful in the market as well as in the nonmarket environment.

Table1. HKEx’s non-market environment

Issues

In 1999, Hong Kong’s government make a comprehensive market

reform of the stock and futures markets, and HKEx was set up during

this reform.

P#

1

It showed in the law any organization that wanted to hold more than 5

per cent of HKEx’s total shares must receive the approval from the

Hong Kong’s government first.

1

In 2007, Hong Kong’s government increased its equity holding to 5.88

per cent of HKEx’s total shares with its huge foreign-exchange

reserves.

1

March 2009, China’s State Council issued a guideline to make

Shanghai an international financial centre and shipping hub by 2020. 3

April 2009, Shanghai was approved as the pilot RMB settlement centre

for international trade. 4

China’s State Council made it clear eligible abroad enterprises which

wanted issue RMB denominated shares would be authorized in due

time.

4

In July 2009, China announced a pilot initiative that expanded the

settlement agreement of cross-border trade transactions in RMB

between Hong Kong and five mainland cities

9

39

Interests

• Organized Interests Finance Industry, Exchanges, Shareholders, Issuers

• Unorganized Interests Investors

Institutions

• Legislative

China’s State Council

Hong Kong Government

• Administrative and Regulatory Agencies

Hong Kong Monetary Authority (HKMA)

Hong Kong Securities and Futures Commission

China Securities Regulatory Commission

• Nongovernment

Public sentiment

News media

SWOT Analysis

Table2. SWOT Analysis to HKEX

Strength Weakness

Market

- Hong Kong is widely respected as a leading

international financial centre.

- Hong Kong has close links to many Asian

economies and is the key gateway to mainland

China.

- Hong Kong has already hosted many of the region’s

leading firms.

- Limited local marketplace and fixed

number of local investors

- Have great dependence on mainland

China and listing of mainland

enterprises.

- Fall behind of SSE in terms of

average daily trading volume (ADT).

Non-market

- Hong Kong has a well-established legal system, and

it provided a strong and attractive foundation for

issuers to raise funds.

- Hong Kong has zero capital flow restrictions,

currency convertibility and free transferability of

securities.

Opportunity Threat

Market - Opening up of China’s capital market - Rise of rivals

Non-market - RMB internationalization

40