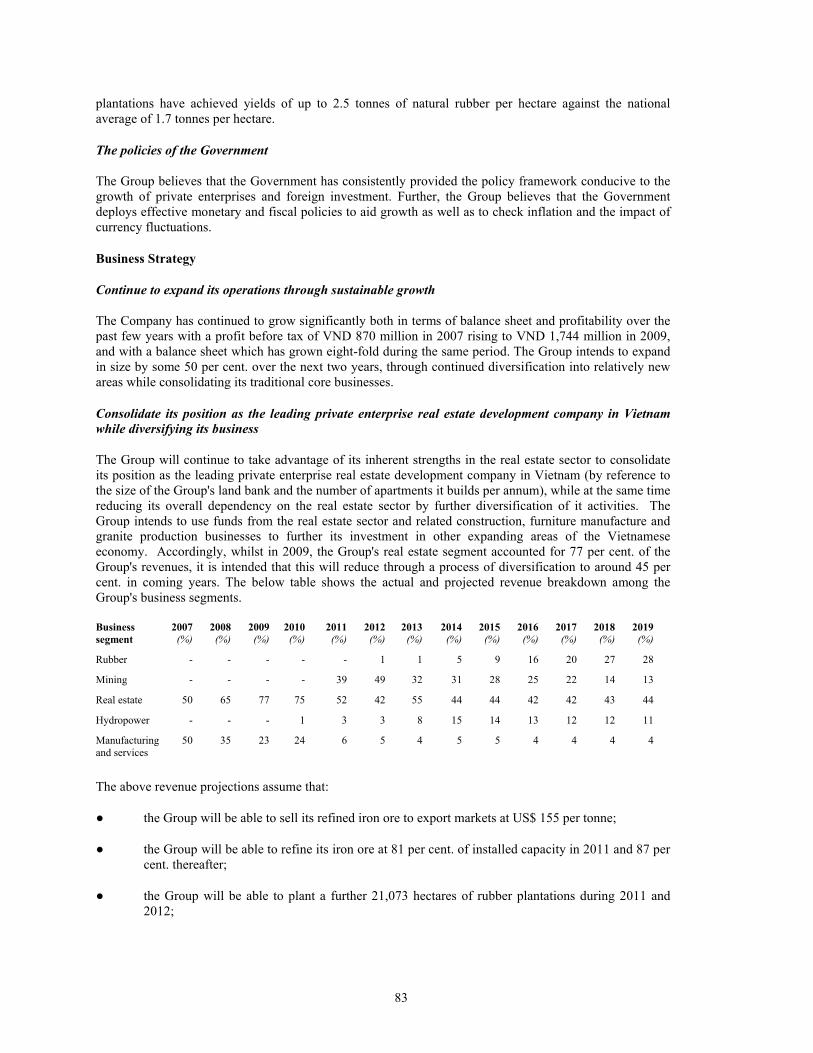

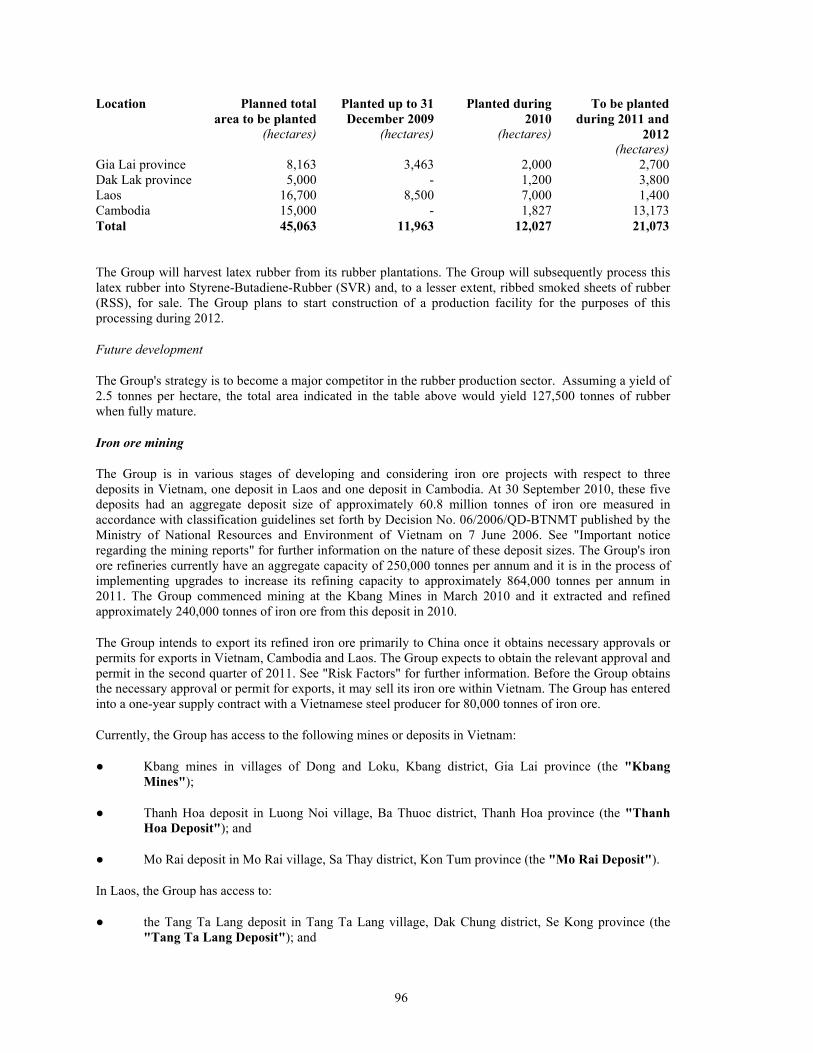

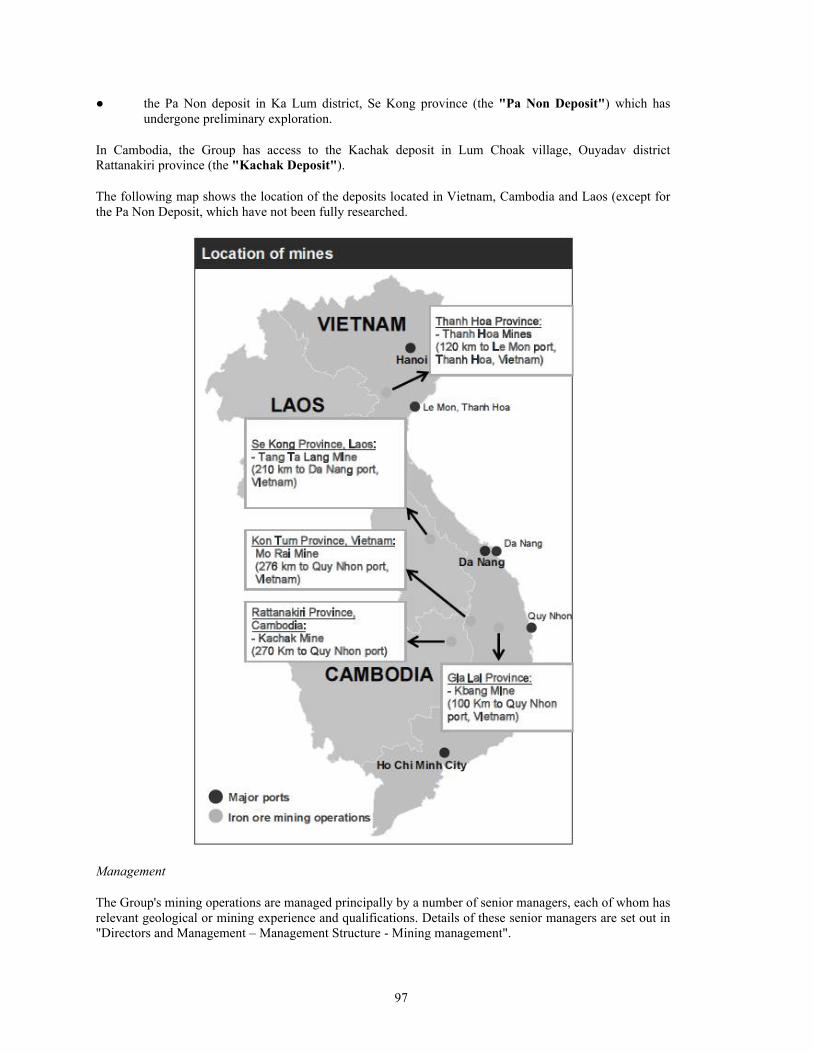

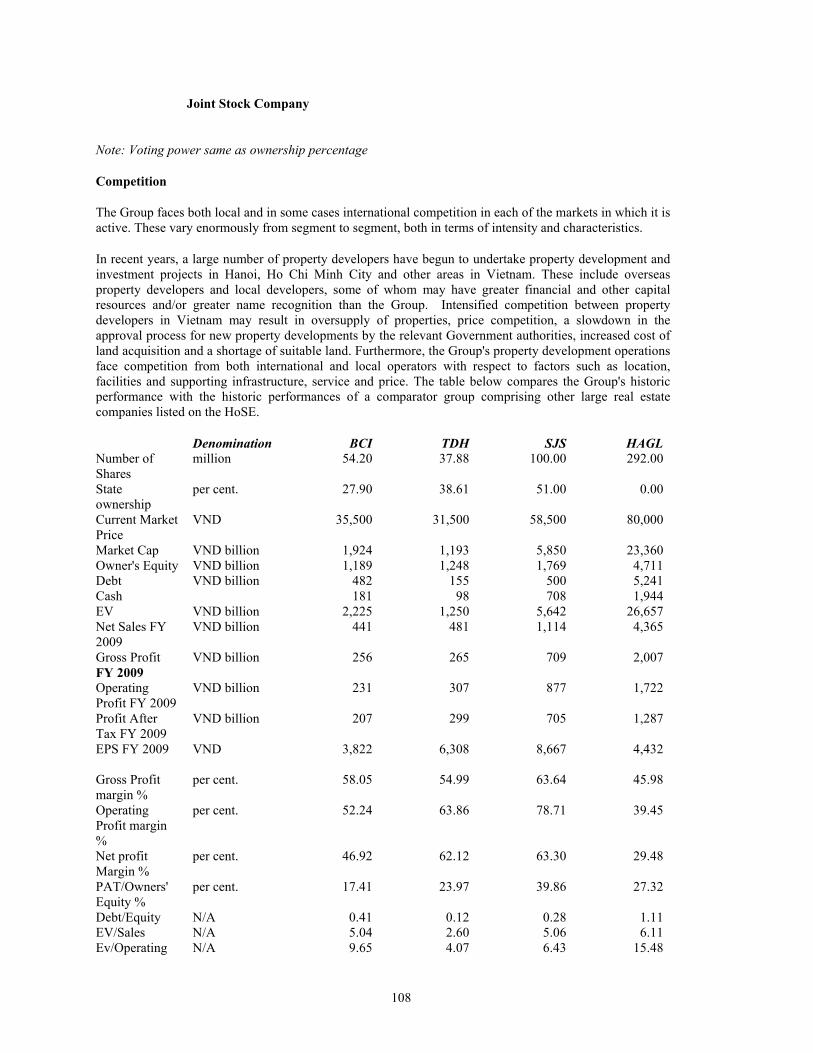

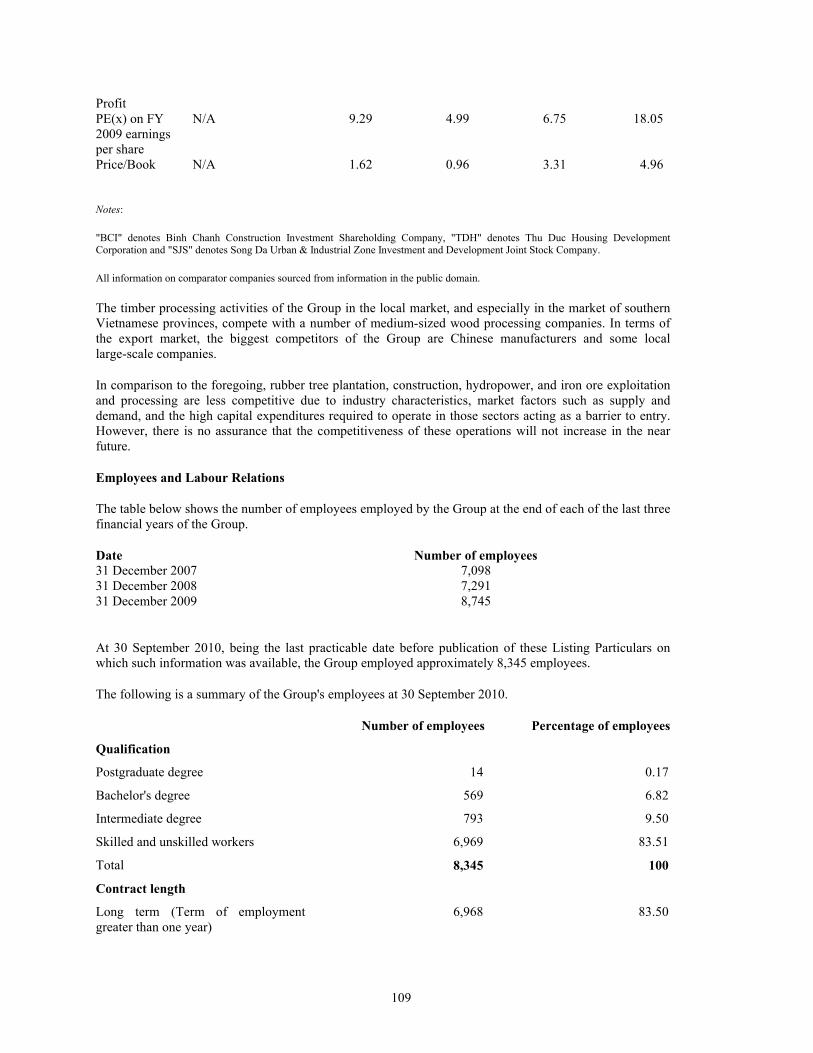

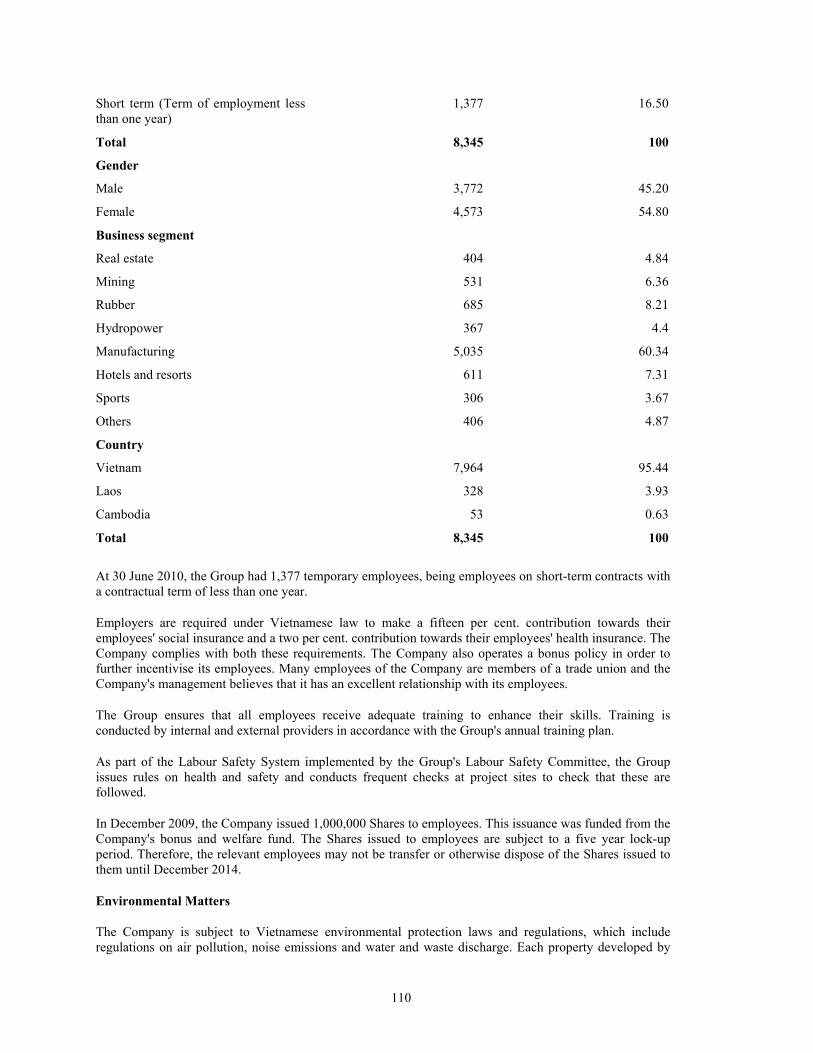

hoang anh gia lai joint stock company - rns submit

TRANSCRIPT

This is a document comprising Listing Particulars in respect of up to 200,000,000 Global Depositary Receipts representing up to 200,000,000 Shares of par value VND 10,000 each in the Company. 16,216,250 unlisted GDRs were issued pursuant to a Deposit Agreement on 6 December 2010. Upon issuance of the GDRs, the Company issued a Preferential Allotment Letter constituting an undertaking to issue the New Shares on a date specified in the Preferential Allotment Letter. At such time, the Preferential Allotment Letter represented the Deposited Property. The New Shares were issued by the Company on 20 December 2010 and deposited as Deposited Shares in accordance with the Deposit Agreement. Upon such deposit, each GDR represented one underlying New Share. The GDRs are denominated in US Dollars.

Application has been made to the UK Listing Authority for the GDRs to be admitted to the Official List and application has been made to the London Stock Exchange to admit the GDRs to trading under the symbol "HAG" on the Professional Securities Market through its International Order Book. The Professional Securities Market is not a regulated market for the purposes of Directive 2004/39/EC (the Markets in Financial Instruments Directive). It is expected that admission to the Official List and to trading on the Professional Securities Market will become effective and that unconditional dealings in the GDRs through the International Order Book will commence on or about 23 March 2011. Application has been made for the admission of 200,000,000 GDRs to the Official List, comprising 24,324,375 GDRs that have been issued at the date of these Listing Particulars and up to 175,675,625 GDRs which may be issued from time to time in accordance with the terms of the Deposit Agreement. All of the Existing Shares were admitted to trading on the HoSE before the issuance of the New Shares. The New Shares were admitted to trading on the HoSE on 12 January 2011. The 8,108,125 Shares deposited in accordance with the terms of the Deposit Agreement pursuant to a bonus share issue on 26 January and which are represented by GDRs were admitted to trading on the HoSE on 28 February 2011. The Company applied for approval from the SSC for the issue of the New Shares which are represented by the GDRs and this approval was granted on 19 November 2010.

These Listing Particulars do not constitute, nor do they contain, and should not be construed as, an offer or invitation to subscribe for or purchase any securities in the Company.

The GDRs are of a specialist nature and should normally only be bought and traded by investors who are particularly knowledgeable in investment matters. Investing in the GDRs involves risks. See "Risk Factors" beginning on page 21 to read about factors that investors should consider before buying the GDRs.

The GDRs and the Shares represented by such GDRs have not been and will not be registered under the Securities Act or any state securities laws in the United States, but were issued and will be issued outside the United States in reliance on the exception from registration under the Securities Act provided by Regulation S. The GDRs may not be offered, sold, pledged or otherwise transferred to any person located in Vietnam, residents of Vietnam, or to, or for the account or benefit of such persons, except as permitted by applicable Vietnamese laws and regulations. The GDRs are not transferable except in accordance with the restrictions described under "Transfer Restrictions".

HOANG ANH GIA LAI JOINT STOCK COMPANY(established in the Socialist Republic of Vietnam as a joint stock company under the Law on Enterprises

No.60/2005/QH11 with Business Registration Certificate number 5900377720)

Listing of up to 200,000,000 Global Depositary ReceiptsRepresenting up to 200,000,000 Shares, par value VND 10,000 each

Elara Capital PLCSole Lead Manager and Bookrunner

Sacombank Securities Joint Stock CompanyFinancial Adviser

The date of these Listing Particulars is 18 March 2011

2

The GDRs have initially been issued in global form. The GDRs issued in global form are and will be evidenced by a Master GDR in registered form. On 6 December 2010, the Master GDR was deposited with a common depositary for and registered in the name of BT Globenet Nominees Ltd. as nominee for Deutsche Bank AG, London Branch as common depositary for Euroclear and Clearstream, Luxembourg for onward delivery. Interests in the Master GDR will be exchangeable for, and GDRs may be issued in the form of, GDRs in definitive form, as set out in "Summary of Provisions relating to the GDRs while in Master Form" and "Transfer Restrictions". The GDRs have and will be issued pursuant to the Deposit Agreement, by and among the Company and the Depositary. A GDR represented by an individual definitive certificate will not be eligible for clearing and settlement through Euroclear or Clearstream, Luxembourg or for trading on the Professional Securities Market.

The Company accepts full responsibility for the information contained in these Listing Particulars and, having taken all reasonable care to ensure that such is the case, declares that the information contained in these Listing Particulars is, to the best of its knowledge, in accordance with the facts and contains no omission likely to affect its import.

This document comprises Listing Particulars for the purposes of the Listing Rules made by the Financial Services Authority. These Listing Particulars are being furnished by the Company in connection with the Listing. The information contained herein has been provided by the Group and other sources identified herein.

The distribution of these Listing Particulars in certain jurisdictions may be restricted by law. Persons into whose possession these Listing Particulars come are required by the Company to inform themselves about and to observe any such restrictions. For a description of restrictions on offers and sales of the GDRs and distribution of these Listing Particulars, see "Terms and Conditions of the Global Depositary Receipts" and "Transfer Restrictions". No person is authorised to give any information or to make any representation not contained in these Listing Particulars and any information or representation not so contained must not be relied upon as having been authorised on behalf of the Company. The delivery of these Listing Particulars at any time does not imply that the information contained in it is correct as at any time subsequent to its date.

The Depositary and the Sole Lead Manager and Bookrunner have not separately verified the information contained in these Listing Particulars. Accordingly, no representation, warranty or undertaking, express or implied, is made and no responsibility is accepted by the Depositary or the Sole Lead Manager and Bookrunner as to the accuracy or completeness of the information contained in these Listing Particulars or any other information supplied in connection with the GDRs or the Shares and nothing contained herein is, or shall be relied upon as, a promise or representation by the Depositary or the Sole Lead Manager and Bookrunner as to the past or the future. Each person receiving these Listing Particulars acknowledges that such person has not relied on the Depositary or the Sole Lead Manager and Bookrunner in connection with its investigation of the accuracy of such information or any investment decision and each such person must rely on their own examination of the Company and the merits and risks involved in investing in the GDRs.

The Company applied for approval from the SSC for the issue of the New Shares and such approval was granted by the SSC on 19 November 2010. A copy of these Listing Particulars will be delivered to the SSC for record purposes only.

Shares evidenced by the GDRs may not be withdrawn by Holders of GDRs during the Lock-up Period (as defined elsewhere in this document). The GDRs will be fully transferable during the Lock-up Period but may not be withdrawn from the depositary facility. For risks in relation to the Lock-up Period, see "Risk Factors – Risks Associated with the GDRs and the Shares". After the expiry of the Lock-up Period, a Holder may request the Depositary to withdraw from the depositary facility the Shares represented thereby and transfer the funds raised from the sale of such Shares on the secondary market to the Holder. The Shares represented by the GDRs have been and will be registered in the name of the Depositary and the Depositary has issued and will issue the GDRs pursuant to the terms of the Deposit Agreement. Beneficial interests in the Master GDR are and will be shown on, and transfers thereof will be effected through, records maintained by Euroclear and Clearstream, Luxembourg and their direct and indirect participants. Beneficial interests in the GDRs represented by an individual definitive certificate will be entered into the register maintained by the Depositary and transfers or cancellations thereof shall be effected through the register via the Depositary or its agent in accordance with the terms of the Deposit Agreement.

NOTICE IN CONNECTION WITH THE UNITED STATES OF AMERICA

This document is not for publication or distribution directly or indirectly in or into any jurisdiction in which the same would be unlawful. This document is for information purposes only and does not constitute an offer or invitation to acquire or dispose of GDRs or Shares in the United States or any other jurisdiction.

The GDRs have not been and will not be registered under the Securities Act or any state securities laws in the United States and may not be offered, sold, resold or otherwise transferred within the United States except pursuant to an exemption from, or in a transaction not subject to, the registration requirements of the Securities Act and applicable state securities laws. Accordingly, the GDRs have been issued outside the United States in reliance on the exemptions from registration provided by Regulation S.

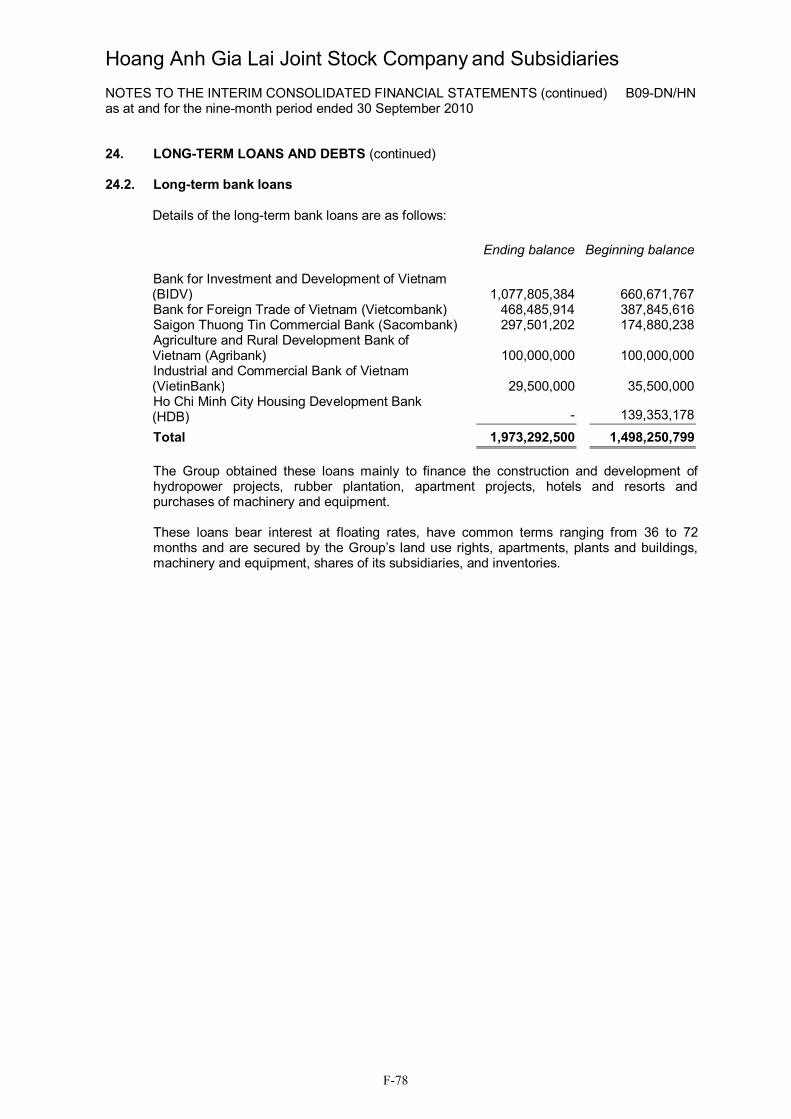

The GDRs have not been approved or disapproved by the SEC, any state securities commission in the United States or any other regulatory authority in the United States, nor have any of the foregoing authorities passed on or endorsed the merits of the GDRs or the accuracy or adequacy of the information contained in this document. Any representation to the contrary is a criminal offence in the United States.

NOTICE TO PERSONS IN THE UNITED KINGDOM

These Listing Particulars are only being distributed to and are only directed at (i) persons who are outside the United Kingdom or (ii) investment professionals falling within Article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (the "Order") or (iii) high net worth entities, and other persons to whom it may lawfully be communicated, falling within Article 49(2)(a) to (d) of the Order (all such persons together being referred to as "relevant persons"). The GDRs are only available to, and any invitation, offer or agreement to

3

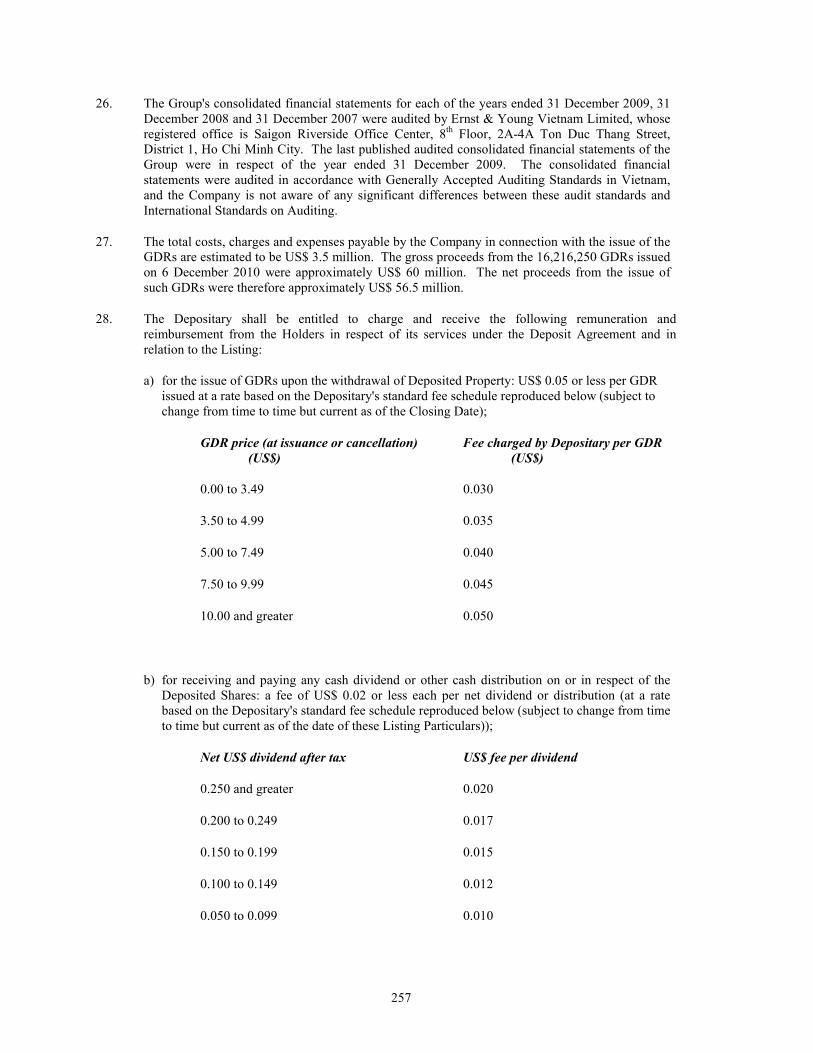

subscribe, purchase or otherwise acquire such GDRs will be engaged in only with, relevant persons. Any persons who are not a relevant person should not act or rely on this document or any of its contents.

NOTICE TO PERSONS IN THE EUROPEAN ECONOMIC AREA

In any European Economic Area Member State that has implemented the Prospectus Directive, this communication is only addressed to and is only directed at qualified investors in that Member State within the meaning of the Prospectus Directive.

These Listing Particulars have been prepared on the basis that any offer of GDRs in a Relevant Member State will be made pursuant to an exemption under the Prospectus Directive, as implemented in that Relevant Member State, from the requirement to publish a prospectus for offers of GDRs. Accordingly, any person making or intending to make any offer with the European Economic Area of GDRs which are the subject of the Listing may only do so in circumstances in which no obligation arises for the Company to publish a prospectus pursuant to Article 3 of the Prospectus Directive or supplement a prospectus pursuant to Article 16 of the Prospectus Directive, in each case, in relation to such offer. TheCompany has not authorised, nor does it authorise, the making of any offer of GDRs in circumstances in which an obligation arises for the Company to publish or supplement a prospectus for such offer.

Each person in a Relevant Member State who receives any communication in respect of, or who acquires any GDRs in connection with, the Listing will be deemed to have represented, warranted and agreed to the Company that:

(a) it is a qualified investor within the meaning of the law in that Relevant Member State implementing Article 2(1)(e) of the Prospectus Directive; and

(b) in the case of any GDRs acquired by it as a financial intermediary, as that term is used in Article 3(2) of the Prospectus Directive, (i) the GDRs acquired by it in the offer have not been acquired on behalf of, nor have they been acquired with a view to their offer or resale to, persons in any Relevant Member State other than qualified investors, as that term is defined in the Prospectus Directive or (ii) where GDRs have been acquired by it on behalf of persons in any Relevant Member State other than qualified investors, the offer of those GDRs to it is not treated under the Prospectus Directive as having been made to such persons.

For the purposes of this representation, the expression an "offer" in relation to any GDRs in any Relevant Member State means the communication in any form and by any means of sufficient information on the terms of the offer and any GDRs to be offered so as to enable an investor to decide to purchase or subscribe for the GDRs, as the same may be varied in that Relevant Member State by any measure implementing the Prospectus Directive in that Relevant Member State.

NOTICE TO PERSONS IN SINGAPORE

These Listing Particulars have not been registered as a prospectus with the Monetary Authority of Singapore. Accordingly, these Listing Particulars and any other document or material in connection with the offer or sale, or invitation for subscription or purchase, of the GDRs may not be circulated or distributed, nor may the GDRs be offered or sold, or be made the subject of an invitation for subscription or purchase, whether directly or indirectly, to the public or any member of the public in Singapore other than (a) to an institutional investor specified in Section 274 of the Securities and Futures Act of Singapore (the "Securities and Futures Act"); (b) to a sophisticated investor, and in accordance with the conditions, specified in Section 275 of the Securities and Futures Act; or (c) otherwise pursuant to, and in accordance with the conditions of, any other applicable provision of the Securities and Futures Act.

SUMMARY .................................................................................................................................................................9

SUMMARY OF THE GDRS.....................................................................................................................................16

RISK FACTORS........................................................................................................................................................21

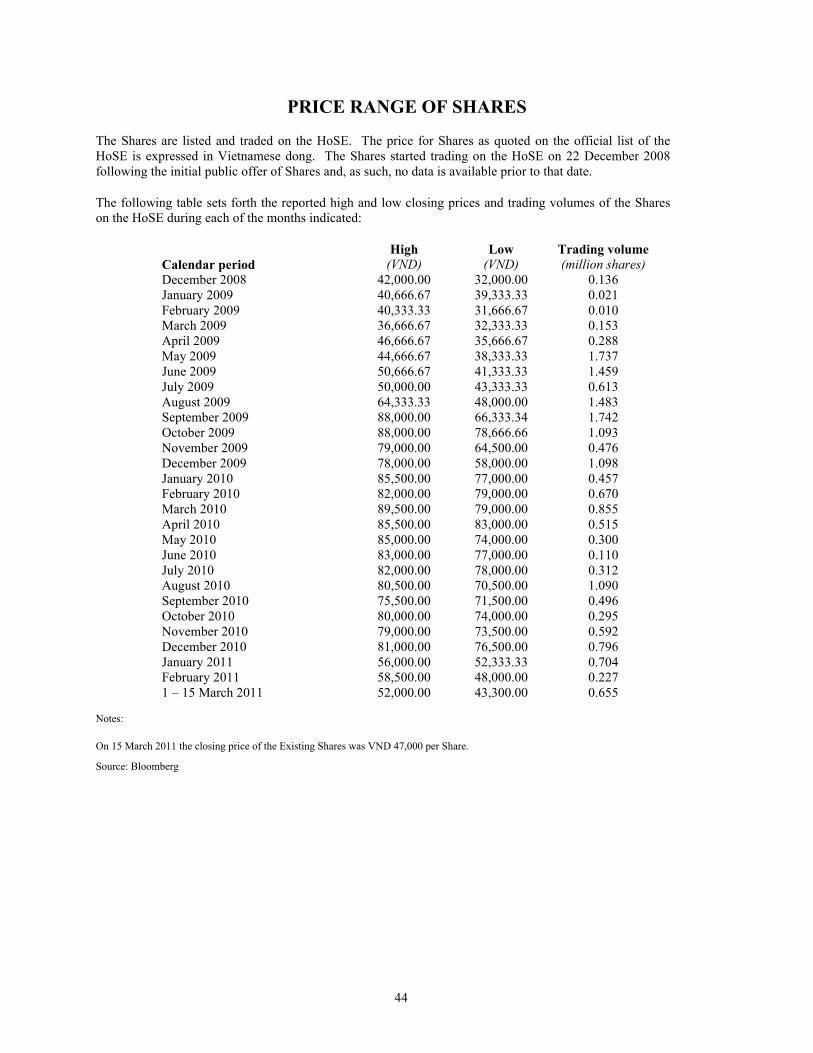

PRICE RANGE OF SHARES ...................................................................................................................................44

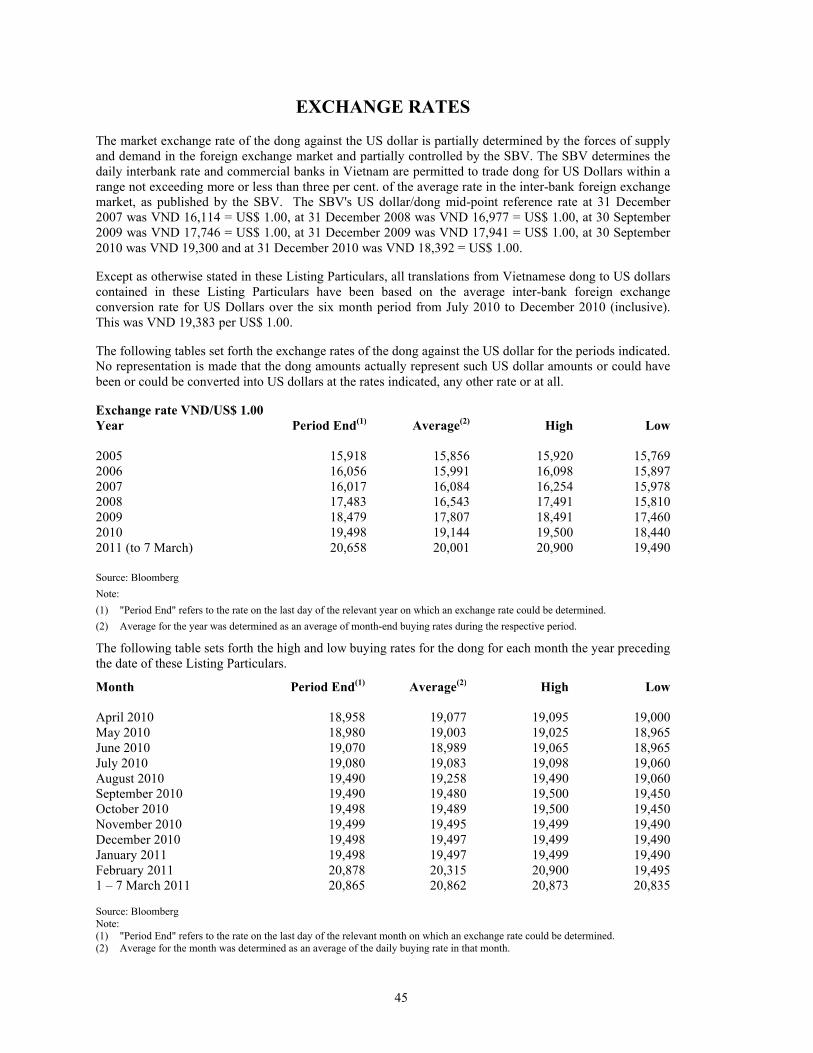

EXCHANGE RATES ................................................................................................................................................45

USE OF PROCEEDS AND DIVIDEND POLICY....................................................................................................46

MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS.....................................................................................................................................................48

MARKET AND INDUSTRY OVERVIEW ..............................................................................................................74

BUSINESS.................................................................................................................................................................80

VIETNAMESE REGULATORY LAW OVERVIEW ............................................................................................114

SUMMARIES OF THE MINING EXPLORATION SURVEYS............................................................................140

DIRECTORS AND MANAGEMENT ....................................................................................................................183

MAJOR SHAREHOLDERS....................................................................................................................................192

VIETNAMESE SECURITIES MARKET ...............................................................................................................194

DESCRIPTION OF THE SHARES.........................................................................................................................200

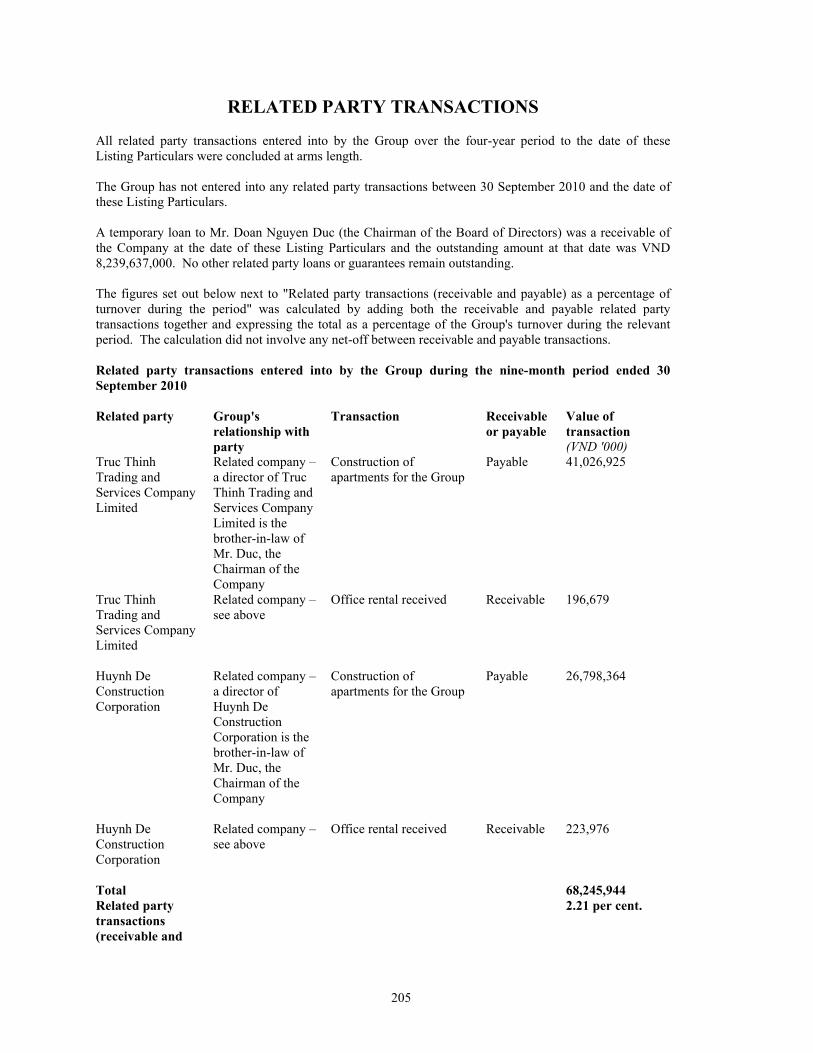

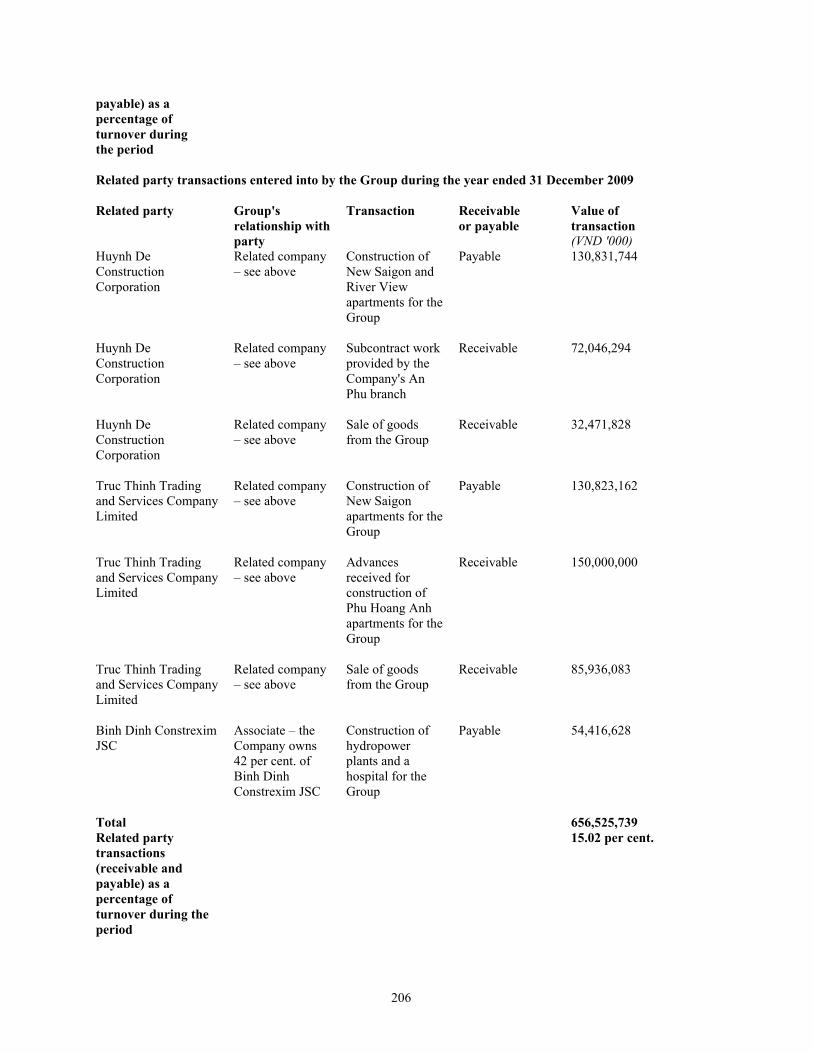

RELATED PARTY TRANSACTIONS ..................................................................................................................205

TERMS AND CONDITIONS OF THE GLOBAL DEPOSITARY RECEIPTS.....................................................210

SUMMARY OF PROVISIONS RELATING TO THE GDRS WHILE IN MASTER FORM ...............................229

INFORMATION RELATING TO THE DEPOSITARY ........................................................................................231

TRANSFER RESTRICTIONS ................................................................................................................................232

FOREIGN INVESTMENT AND EXCHANGE CONTROLS................................................................................234

VIETNAMESE REGULATORY APPROVALS AND FILINGS ..........................................................................238

TAXATION .............................................................................................................................................................239

ENFORCEABILITY OF CIVIL LIABILITIES ......................................................................................................245

GENERAL INFORMATION ..................................................................................................................................246

SUMMARY OF SIGNIFICANT DIFFERENCES BETWEEN VIETNAMESE VAS AND IFRS........................261

DEFINITIONS........................................................................................................................................................ 271

INDEX TO FINANCIAL STATEMENTS............................................................................................................. 274

FINANCIAL STATEMENTS .................................................................................................................................F-1

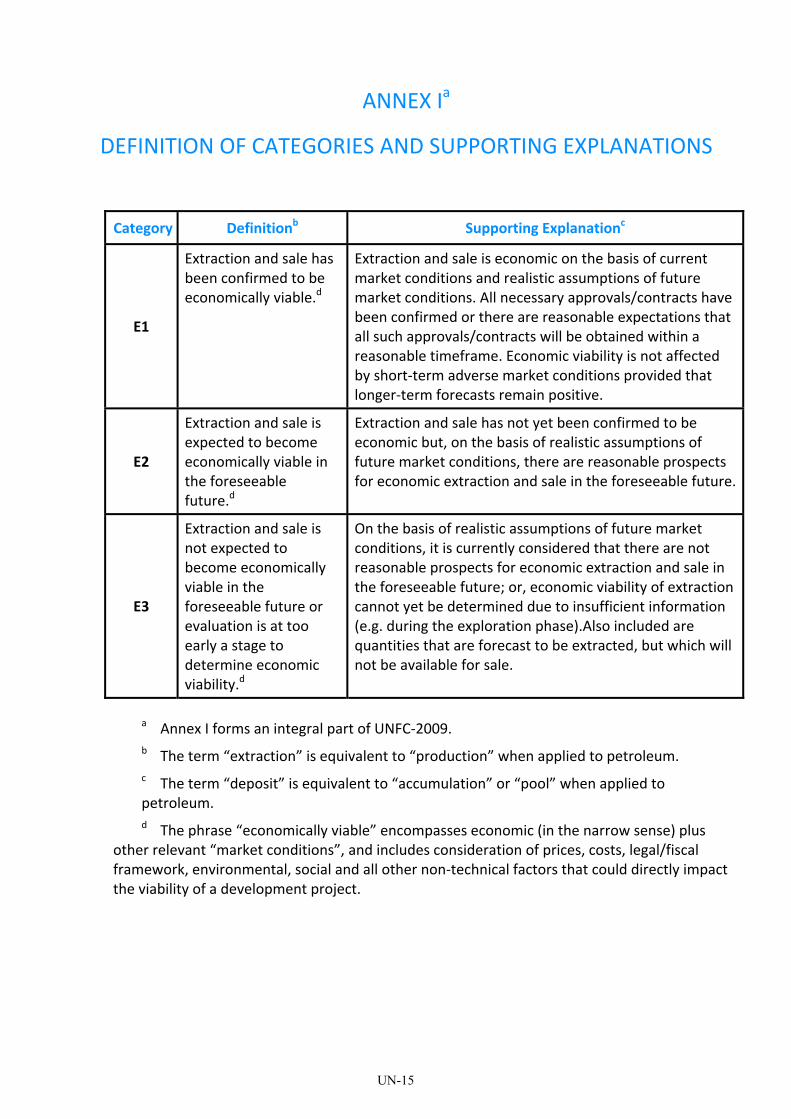

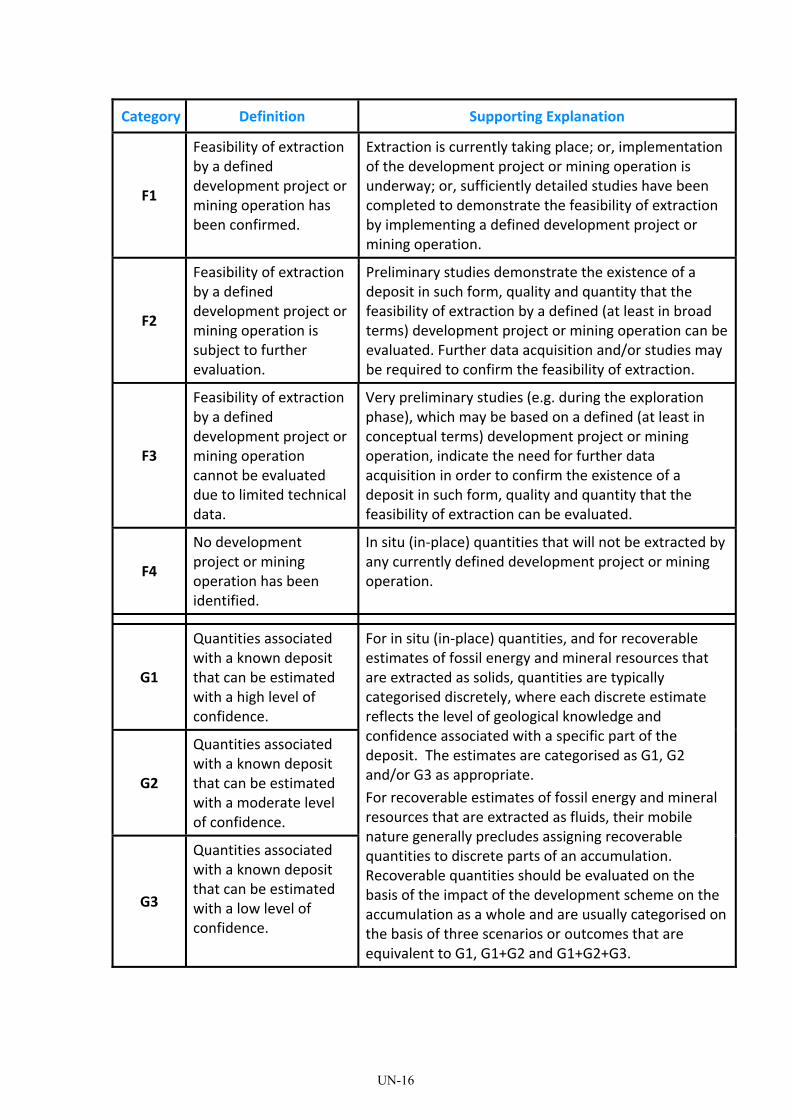

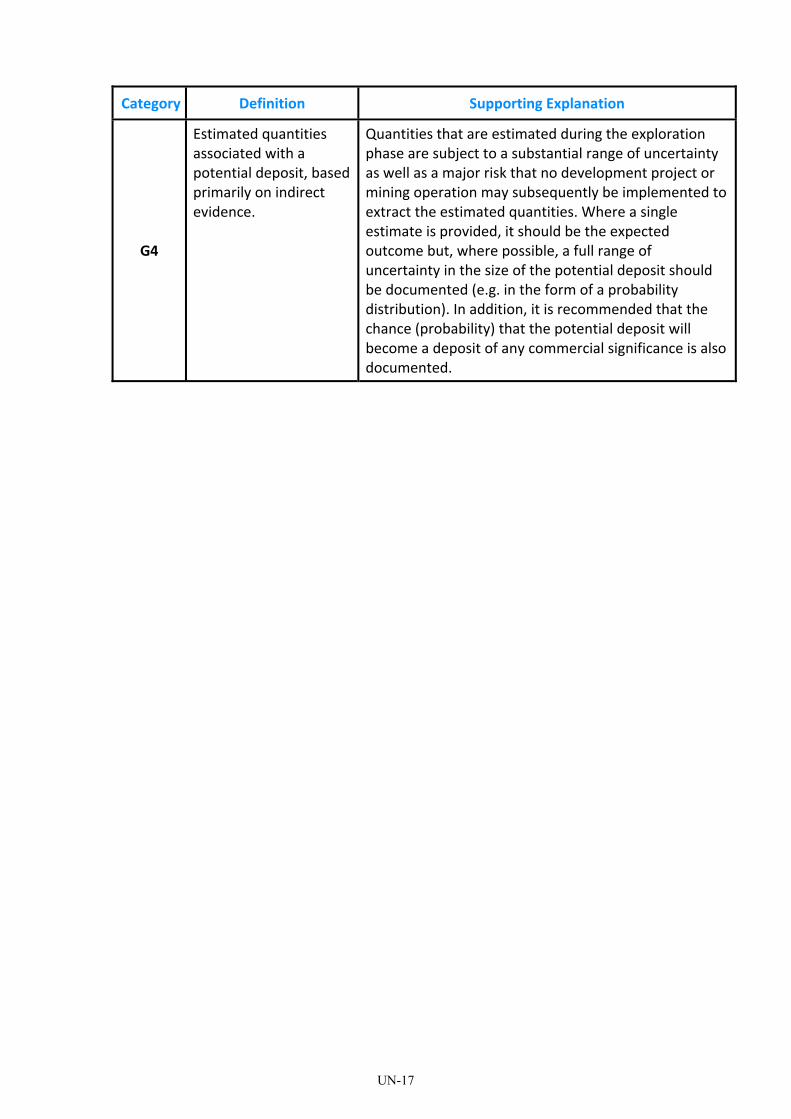

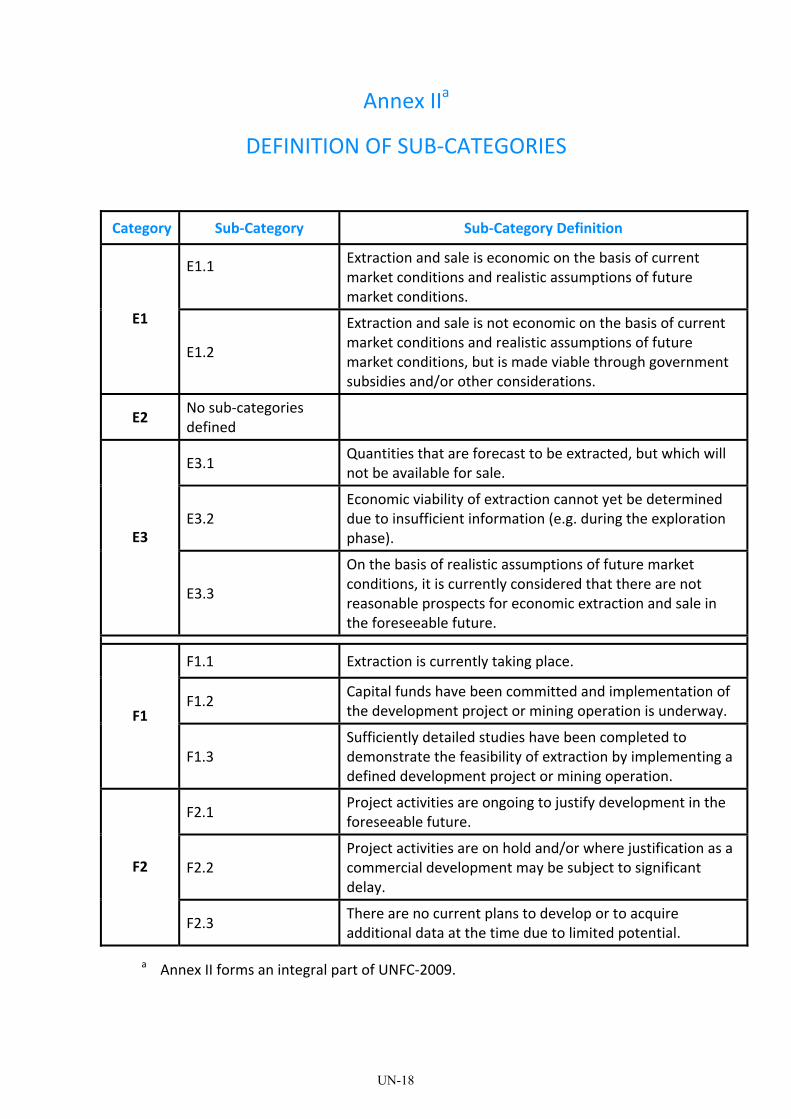

UNITED NATIONS FRAMEWORK CLASSIFICATION FOR FOSSIL ENERGY AND MINERALS...........UN-1

5

AVAILABLE INFORMATION

The Company will furnish the Depositary with copies of its annual audited financial statements in English prepared in conformity with VAS. In accordance with the terms of the Deposit Agreement, the Company will also furnish the Depositary with unaudited quarterly and (if produced) semi-annual interim financial information in English prepared in accordance with Vietnamese Securities Laws. The Company will also arrange for the prompt transmittal to the Depositary of sufficient copies in English of any notices, reports or communications that are made generally available by the Company to the holders of Shares or other deposit property, and upon receipt of any such notices, the Depositary has agreed to furnish such notices to Holders in accordance with the Terms and Conditions of the GDRs, including making copies of such notices available upon request at its specified office and the specified office of any of the Depositary's agents.

INVESTMENT IN VIETNAM

The GDRs may not be offered or sold directly or indirectly in Vietnam or to, or for the benefit of, any resident in Vietnam (which term as used in these Listing Particulars shall have the same meaning as that defined in the 2005 Ordinance on Foreign Exchange, which include (a) any corporation or other entity incorporated under the laws of Vietnam and operating in Vietnam (a "Vietnamese entity"), and (b) any Vietnamese citizen residing abroad for a period of less than 12 months or any Vietnamese entity's representative office established in any other country). Unless permitted under Vietnamese Securities Laws, no advertisement, invitation or document relating to the GDRs has or will be issued in Vietnam.

ENFORCEMENT OF FOREIGN JUDGMENTS IN VIETNAM AND SERVICE OF PROCESS

The Company is a joint stock company incorporated under the laws of Vietnam. All of the Company's directors and executive officers are residents of Vietnam. Further, a substantial portion of the assets of such persons and the Company are located in Vietnam. As a result, it may not be possible for investors to effect service of process upon the Company or such persons in jurisdictions outside Vietnam or to enforce judgments obtained against the Company or such persons outside Vietnam. Any judgment of a foreign court (such as a United States court) in respect of a commercial or civil matter may be recognised and enforced in Vietnam provided that (i) such judgment is not considered by a Vietnamese court as being ineffective or as being "contradictory to primary principles of the Vietnam law" pursuant to Article 356 of the 2004 Code on Civil Proceedings, and (ii) the question of whether such judgment is qualified to be recognised by a Vietnamese court for enforcement on a reciprocal basis will be decided by such Vietnamese court at its sole discretion. Further information on the enforceability of civil liabilities in Vietnam can be found at "Enforceability of Civil Liabilities".

PRESENTATION OF FINANCIAL AND OTHER INFORMATION

References in these Listing Particulars to "Vietnam" are to the "Socialist Republic of Vietnam"; references to the "Government" are to the Government of Vietnam. Unless the context otherwise requires, references to the "Company" are to Hoang Anh Gia Lai Joint Stock Company, and references to the "Group" are to the Company and its subsidiaries and subsidiary undertakings. Certain other terms used in these Listing Particulars, including certain capitalised terms and other terms, are defined in "Definitions".

The Company prepares its consolidated financial statements in accordance with VAS, which differ in certain respects from generally accepted accounting principles in other countries. VAS differs in certain significant respects from IFRS. For a comparison of accounting principles in Vietnam and accounting principles under IFRS, see "Summary of Significant Differences between VAS and IFRS". The Company publishes its consolidated financial statements in Vietnamese dong.

6

In these Listing Particulars, all references to "Vietnamese dong", "dong" and "VND" are to the legal currency of Vietnam and all references to "dollars", "USD", "US dollars", and "US$" are to the legal currency of the United States. Solely for the convenience of the reader, these Listing Particulars present translations of certain dong amounts into US dollars at specified rates. This should not be construed as a representation that those Vietnamese dong or US dollar amounts could have been, or could be, converted into US dollars or Vietnamese dong, as the case may be, at any particular rate, or at all. Except as otherwise stated in these Listing Particulars, all translations from Vietnamese dong to US dollars contained in these Listing Particulars have been based on the average inter-bank foreign exchange conversion rate for US Dollars over the six month period from July 2010 to December 2010 (inclusive). This was VND 19,383 per US$ 1.00.

In these Listing Particulars, where information has been presented in thousands or millions of units, amounts may have been rounded up or down. Accordingly, totals of columns or rows of numbers in tables may not be equal to the apparent total of the individual items and actual numbers may differ from those contained in these Listing Particulars due to rounding. The English names of the Vietnamese nationals, entities, departments, facilities, laws, regulations, certificates, titles and the like are translations of their Vietnamese names and are included for identification purposes only. In the event of any inconsistency, the Vietnamese name prevails.

Any information sourced from a third party has been accurately reproduced and, as far as the Company is aware and has been able to ascertain from information published by such third party, no facts have been omitted which render the reproduced information inaccurate or misleading. Where third party information has been used, the source of this information has been identified.

INDUSTRY AND MARKET DATA

Information regarding market position, growth rates and other industry data pertaining to the Company's business contained in these Listing Particulars consists of estimates based on data reports compiled by professional organisations and analysts, on data from other external sources and on the Company's knowledge of its markets. This data is subject to change and cannot be verified with complete certainty due to limits on the availability and reliability of the raw data and other limitations and uncertainties inherent in any statistical survey. In many cases, there is no readily available external information (whether from trade associations, government bodies or other organisations) to validate market-related analyses and estimates, so the Company relies on internally developed estimates. While the Company has compiled, extracted and reproduced market or other industry data from external sources, including third parties or industry or general publications, the Company accepts responsibility for accurately reproducing such data. However, the Company has not independently verified that data and does not make any representation regarding the accuracy of such data. Similarly, while the Company believes its internal estimates to be reasonable, such estimates have not been verified by any independent sources and the Company cannot assure potential investors as to their accuracy.

FORWARD-LOOKING STATEMENTS

These Listing Particulars contain forward-looking statements that involve risks and uncertainties. These statements relate to future estimates or events or the Group's future financial performance and include, but are not limited to, statements concerning:

● the Group's ability to implement its strategy, including anticipated benefits and risks;

● the Group's ability to develop and expand its business;

● the Group's capital expenditure plans, including estimates of future acquisition, and the Group's ability to satisfy its capital needs;

● the Group's future results;

7

● the anticipated size or trends of the market segments in which the Group competes and the anticipated competition in those markets; and

● government regulation.

Furthermore, in some cases, investors can identify forward-looking statements by terminology such as "may", "will", "could", "should", "expect", "plan", "intend", "anticipate", "believe", "estimate", "predict", "potential" or "continue" and the negative of such terms or other comparable terminology. These statements are only predictions. Actual events or results may differ materially. In evaluating these statements, investors should specifically consider various factors, including the risks outlined in the "Risk Factors" section. These factors may cause the Group's actual results to differ materially from any forward-looking statement. Except as required by law, the Group undertakes no obligation to update any forward-looking statements after the date of these Listing Particulars or to conform these statements to actual results or to changes in the Group's expectations.

The forward-looking statements contained in these Listing Particulars are based on the beliefs of management, as well as the assumptions made by and information currently available to management. Although the Group believes that the expectations reflected in such forward-looking statements are reasonable at this time, the Group cannot make any assurances that such expectations will prove to be correct. Given these uncertainties, investors are cautioned not to place undue reliance on such forward-looking statements. Important factors that could cause actual results to differ materially from the Group's expectations are contained in cautionary statements in these Listing Particulars, including, without limitation, in conjunction with the forward-looking statements included in these Listing Particulars and specifically under "Risk Factors". If any of these risks and uncertainties materialise, or if any of the Group's underlying assumptions prove to be incorrect, the Group's actual results of operations or financial condition could differ materially from that described herein as anticipated, believed, estimated or expected. All subsequent written and oral forward-looking statements attributable to the Group are expressly qualified in their entirety by reference to these cautionary statements.

8

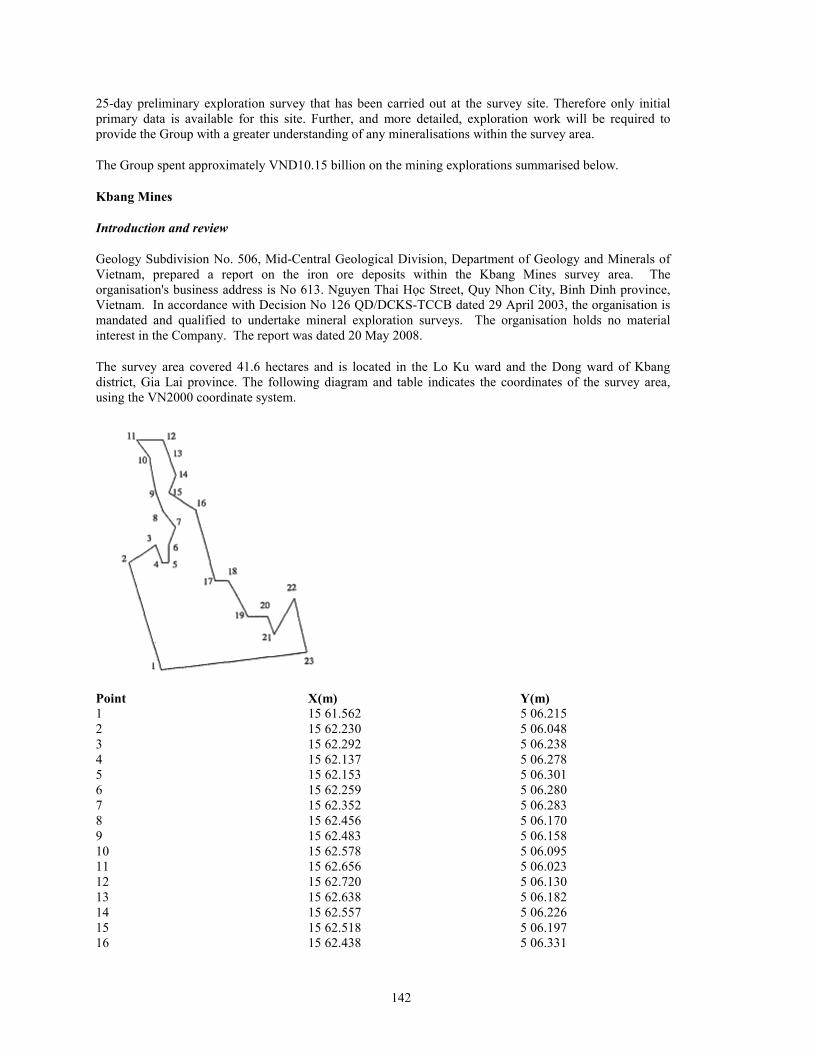

THE COMPANY

Hoang Anh Gia Lai Joint Stock CompanyNo 15 Truong Chinh Street

Phu Dong CommunePleiku City

Gia Lai Province

DEPOSITARY

Deutsche Bank Trust Company Americas60 Wall Street

New York, NY 10005

CUSTODIAN

Deutsche Bank AG, Ho Chi Minh City Branch

Saigon Centre, 65 Le Loi Boulevard

District 1, Ho Chi Minh City

SOLE LEAD MANAGER AND BOOKRUNNER

FINANCIAL ADVISER

Elara Capital PLC29 Marylebone Road

London NW1 5JX

Sacombank Securities Joint Stock Company

278 Nam Ky Khoi Nghia Street District 3, Ho Chi Minh City

LEGAL ADVISERS TO THE SOLE LEAD MANAGER AND BOOKRUNNER

As to US and English lawMayer Brown International LLP

201 BishopsgateLondon EC2M 3AF

As to Vietnamese lawMayer Brown JSM

12th FloorPacific Place Building83B Ly Thuong KietHoan Kiem District

Hanoi

LEGAL ADVISERS TO THE DEPOSITARY

Linklaters LLPOne Silk Street

London EC2Y 8HQ

INDEPENDENT STATUTORY AUDITORS TO THE COMPANY

Ernst & Young Vietnam LimitedSaigon Riverside Office Center

8th Floor2A-4A Ton Duc Thong Street

District 1Ho Chi Minh City

9

SUMMARY

Information on the Group – Overview

Hoang Anh Gia Lai Joint Stock Company is currently the largest private sector company, by market capitalisation, listed on the HoSE. At 15 March 2011, its market capitalisation was approximately VND 21,962 billion.

The Group primarily operates in the following business sectors: real estate, rubber plantations, iron ore mining, hydropower and manufacturing. Although originally focused in the Gia Lai province of Vietnam, the Group has expanded its activities throughout Vietnam and into the neighbouring states of Laos and Cambodia. The Group exports its furniture products throughout Asia, Europe and the Americas.

Competitive Strengths

The Company believes that its success and future prospects and the success and future prospects of the Group of which it is the ultimate parent company are linked to the following competitive strengths:

● The Group is a large diversified group with strong financial performance.

● The Group leverages the intrinsic natural advantages of Vietnam and its key geo-political location.

● The Group has built a balanced portfolio of complementary businesses.

● The Group's activities have allowed it to build a strong brand within the Vietnamese market.

● The Company has sought to reward its shareholders through dividends and bonus share issues.

● The Group is efficiently run and has a competitive advantage over state-owned enterprises.

● The Group believes that the Government has consistently provided the policy framework conducive to the growth of private enterprises and foreign investment.

Business Strategy

The Group's current business strategy is to:

● Continue to expand its operations through sustainable growth.

● Consolidate its position as the leading private enterprise real estate development company in Vietnam while diversifying its business.

● Become one of the largest producers of natural rubber in Vietnam.

● Establish itself as a major mining presence in Southeast Asia.

● Make itself one of the leading private suppliers of hydropower in Vietnam.

● Consolidate its position and increase profitability in the manufacturing and granite production sectors.

Summary of Risk Factors

The Group's business, financial condition, the industries and markets in which it operates and the GDRs are subject to certain risks including, but not limited to the following risks.

Risks relating to the Group's business and the industries in which it operates

General risks relating to the Group's business

10

● The Group's diversification strategy may not be successful.

● The Group's expansion and diversification is dependent upon its ability to obtain funding.

● Government regulations impose significant costs on the Group's operations, and future regulations could increase those costs or limit the Group's ability to produce and sell its products.

● The Group's business will be affected if the Group is not able to compete effectively.

● The Group may not purchase sufficient insurance to cover risks in its business operations.

● The Group may be unable to attract and retain a highly-skilled and experienced workforce and management.

● Relocation of incumbent residents and businesses on the Group's sites may cause delays and increase its costs.

● The Company's results of operations depend on those of its subsidiaries and affiliates.

● There may be conflicts between the interests of the real estate, rubber plantation, iron ore mining, hydropower and manufacturing divisions.

● Opposition from local communities and other parties.

● Shortages or increased costs of materials and skilled labour could increase costs and delay projects.

● The Group relies upon third party suppliers.

● The current global economic slowdown may negatively impact the Group.

● The Company's controlling Shareholder may be able to take actions that do not reflect the will or best interests of other Shareholders.

● Certain of the Group's existing projects are being developed without necessary government approvals, permits or licences and development and operation of certain projects are not fully in compliance with applicable laws and regulations.

● The Group has limited customers for its new business.

Real estate risks

● The Group's business is dependent on the Vietnamese real estate market.

● Demand for properties developed by the Group may fluctuate.

● Delay or failure by the Group in acquiring, developing and constructing its projects could have a material adverse effect on its real estate business.

● Property transfers and registration of land title in Vietnam is complex and subject to delays.

● Market values in an illiquid market may be difficult to ascertain.

● Uncertain property values may fluctuate.

● Purchasers of pre-sold properties may be entitled to remedies against the Group in certain circumstances.

● The Group may not be able to acquire land use rights at acceptable prices.

11

Rubber risks

● Any significant downturn in the Chinese economy may decrease rubber exports.

● The Group's business may vary with fluctuations in the production costs and the prices for natural rubber.

● The Group's rubber plantation sites may not yield sufficient volume of rubber and are subject to natural disasters.

● Elimination of tax incentives could have a material adverse effect on the rubber plantation business.

● Due to a change in the Group's revenue recognition policy for pre-completion sale of its apartments, the Group's historical financial condition and results of operations may not be fully comparable to its future financial condition and results of operations.

Iron ore mining risks

● The Group operates in a competitive industry.

● The Group's mining operations are subject to operating risks that could result in decreased iron ore production which could, in turn, reduce its revenues.

● Disruptions to or increased costs of transport services may affect the Group's ability to deliver iron ore to customers.

● Reserve and resource estimates are uncertain.

● The Group's profitability depends upon its ability to successfully exploit existing reserves.

● The marketability and prices of iron ore may fluctuate.

● The Group is in the process of obtaining exploitation permits and other permits, licences and approvals in connection with several of its iron ore projects.

● The Group's operations may substantially impact the environment.

● The Group may not be able to export iron ore to overseas markets.

Hydropower risks

● Delay or failure by the Group in developing and completing its development projects may adversely affect the Group's power production levels.

● The Group's hydropower operations may be materially adversely affected by climate change.

● Increased demand for water in other sectors may affect the Group's operations.

● Plant and machinery supplies and failures may disrupt hydropower operations.

● The financial performance of the Group's hydropower operations may be adversely affected by changes to its off-take agreements with EVN.

● The Group's hydro projects may not be eligible for CERs under the CDM.

Manufacturing risks

12

● The Group's furniture manufacturing business may be adversely affected by price and availability of raw materials.

● Demand for the Group's furniture products may fluctuate.

● Tariff changes on wood and furniture may have a material effect on the competition faced by the Group.

Risks relating to Vietnam

● The Group may not be able to enforce its rights effectively through legal proceedings in Vietnam.

● The Group's operations may be subject to environmental regulations.

● The Group's operations may be subject to economic, political and economic risks.

● The Vietnamese economy is subject to periods of high inflation.

● The Group is exposed to currency risks.

● Corporate disclosure, accounting and governance standards in Vietnam do not require the level of disclosure applicable in other non-emerging market jurisdictions.

● Any downgrade of Vietnam's sovereign debt rating by an international rating agency could have a negative impact on the Group's results of operations and financial condition.

● The tax status of the Group may change.

● The Group's ability to raise foreign capital may be constrained by Vietnamese law.

● The Group may not be able to grant mortgages over land.

Risks associated with the GDRs and the Shares

● The GDRs may not be a suitable investment for all investors.

● Future issuances and sales of GDRs and equity securities by the Company may affect the market price of the GDRs and the Shares.

● An active market for the GDRs may not develop.

● The trading price of emerging market securities are subject to substantial volatility.

● The market price of GDRs may decrease after they are admitted to trading and Holders will bear the risk of fluctuations in the price of the underlying Shares.

● Legal protections available to Holders may be limited.

● Fluctuations in the exchange rate between the Vietnamese dong and the US dollar could have a material adverse effect on the value of the GDRs and the Shares represented by such GDRs, independent of the Group's operating results.

● The Depositary's announcement obligations on purchase or disposal of Shares may result in substantial volatility in the trading price of the GDRs and/or the price of the Shares.

● Holders will not be able to withdraw any Deposited Property for a period of at least 12 months from the date of the deposit of Shares by the Company.

13

● Shares purchased by the Depositary on behalf of depositors will also be subject to lock-up until expiry of the Lock-up Period.

● Holders may only withdraw Deposited Property by instructing the Depositary to sell Deposited Property in the local market.

● Holders will have no voting rights.

● Holders may be subject to taxation in Vietnam.

● Vietnamese laws contain provisions that limit the foreign ownership rights of non-Vietnamese persons, which could materially impact the price of the Shares and GDRs.

● Holders or Shareholders may not receive cash dividends on such Shares or GDRs.

● The Depositary may withhold acceptance of funds for deposit, refuse to purchase Shares, withhold delivery or registration of issuance or transfer of all or part of the Shares and/or GDRs or withhold adjustment of the Master GDR to reflect increases in Shares represented thereby.

● The Depositary may refuse to accept funds for the purchase of Shares on behalf of depositors and/or may refuse to purchase Shares on behalf of depositors.

● The Depositary may not be able to purchase Shares or a sufficient number of Shares.

● The Depositary may not be able to sell Deposited Property and/or any sale of Deposited Property may be at a price lower than that expected by Holders.

● The Depositary may refuse to sell Deposited Property or deliver the proceeds from any such sale.

● Fees, taxes, duties, charges, costs and expenses under the Deposit Agreement in connection with the purchase and/or sale of Shares by the Depositary will be borne by the Holder.

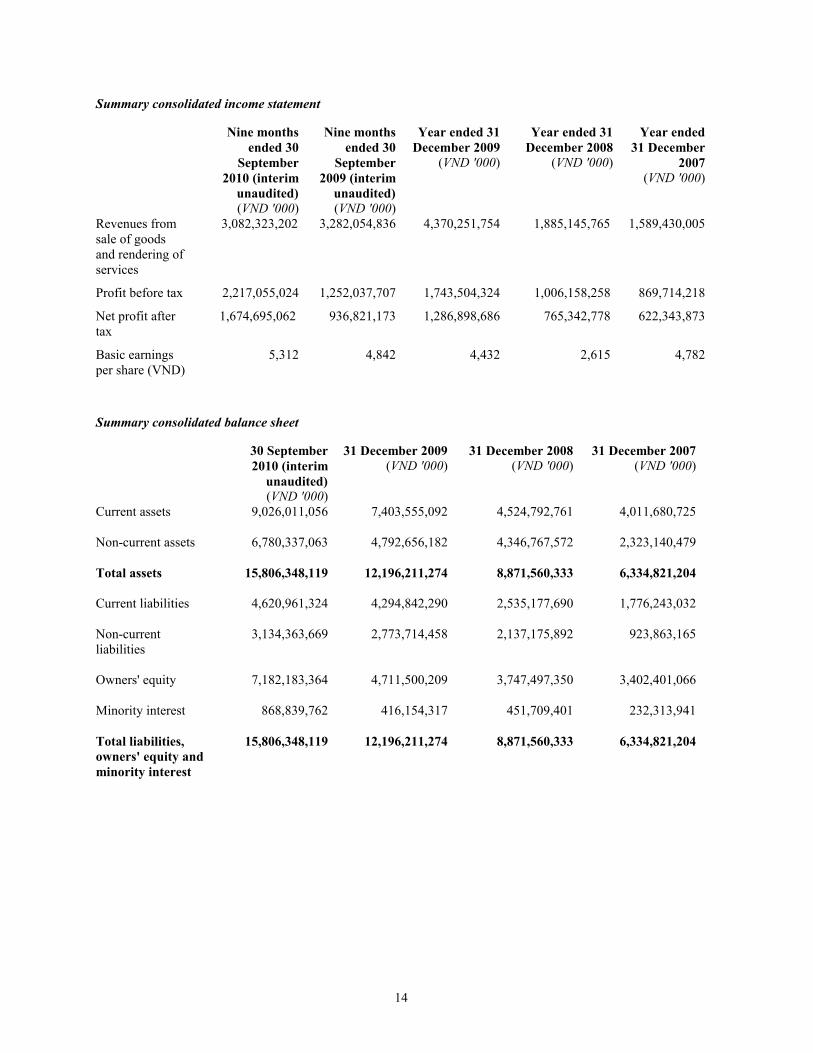

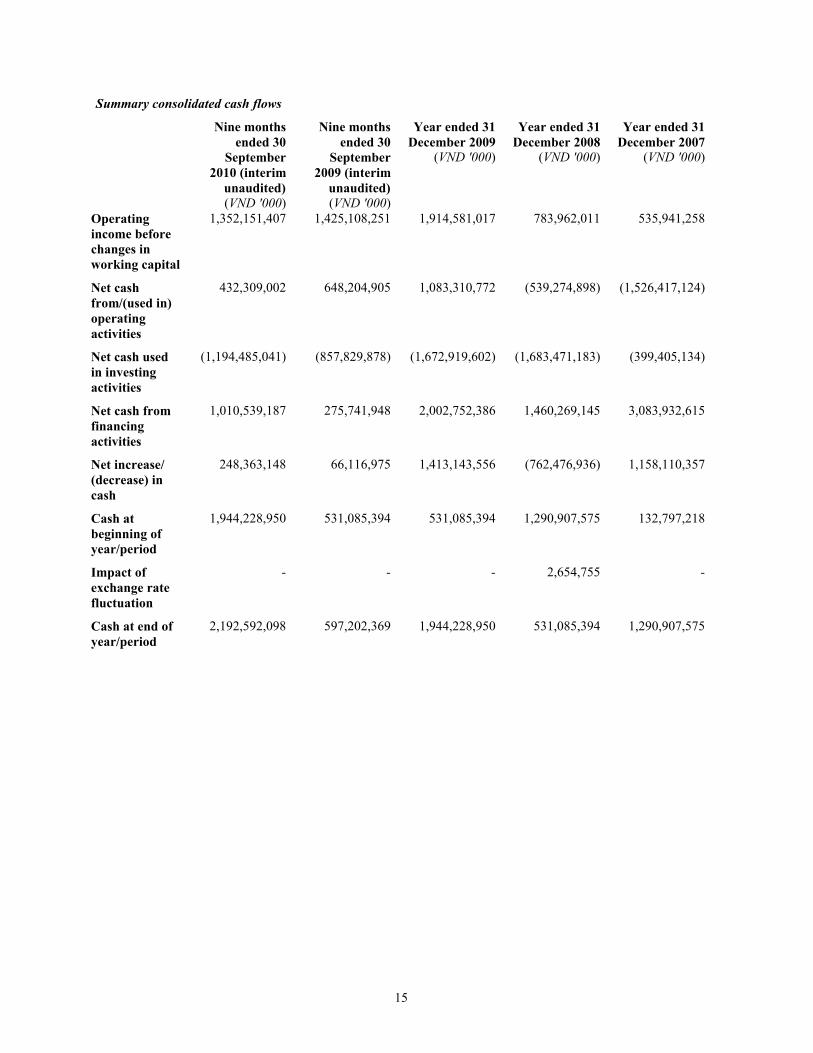

Summary of Financial Information

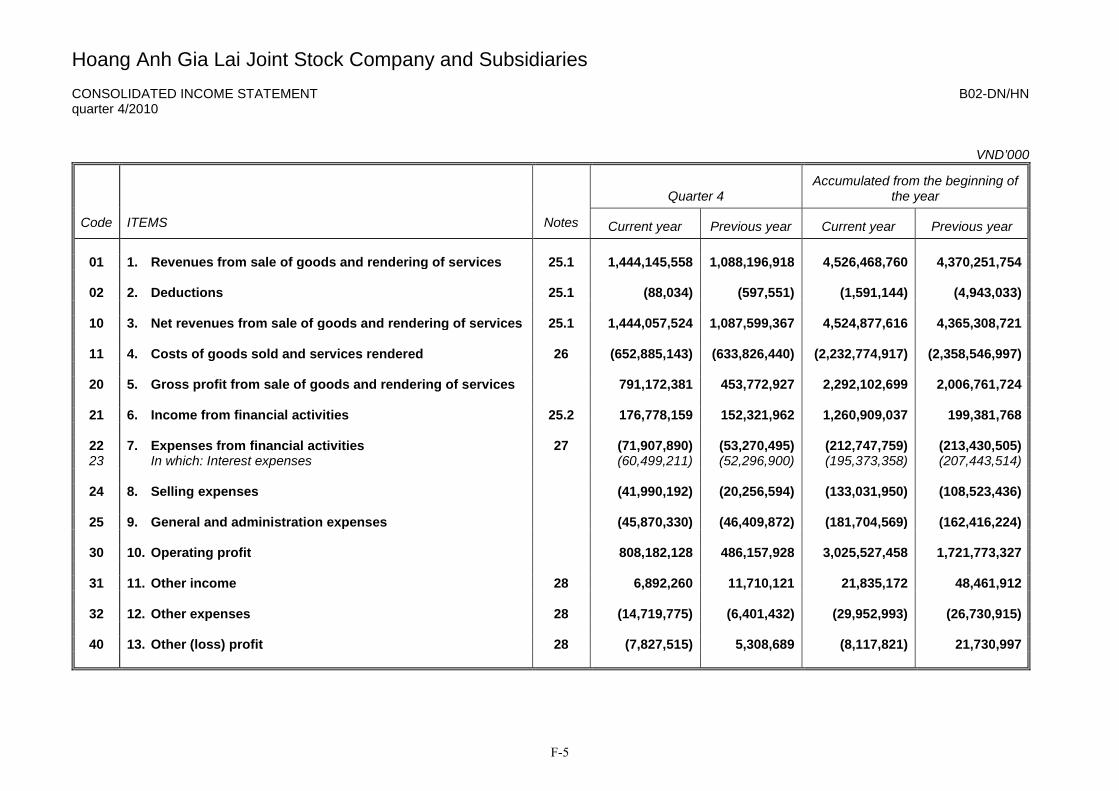

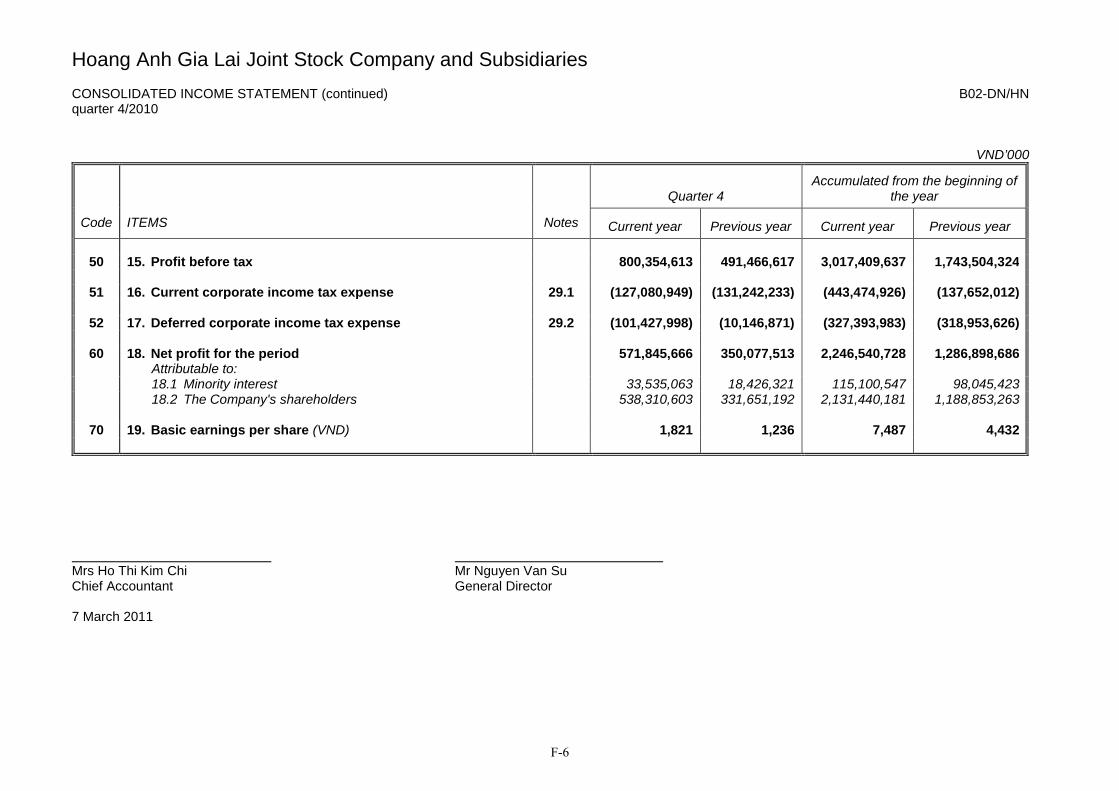

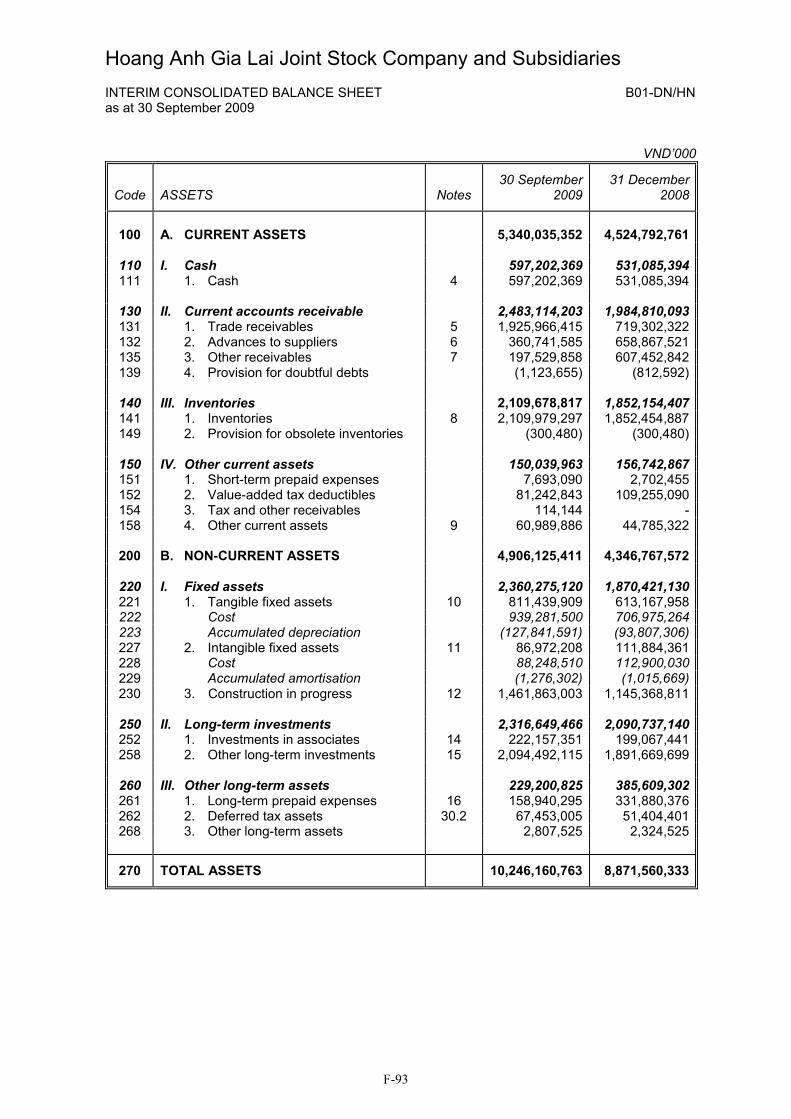

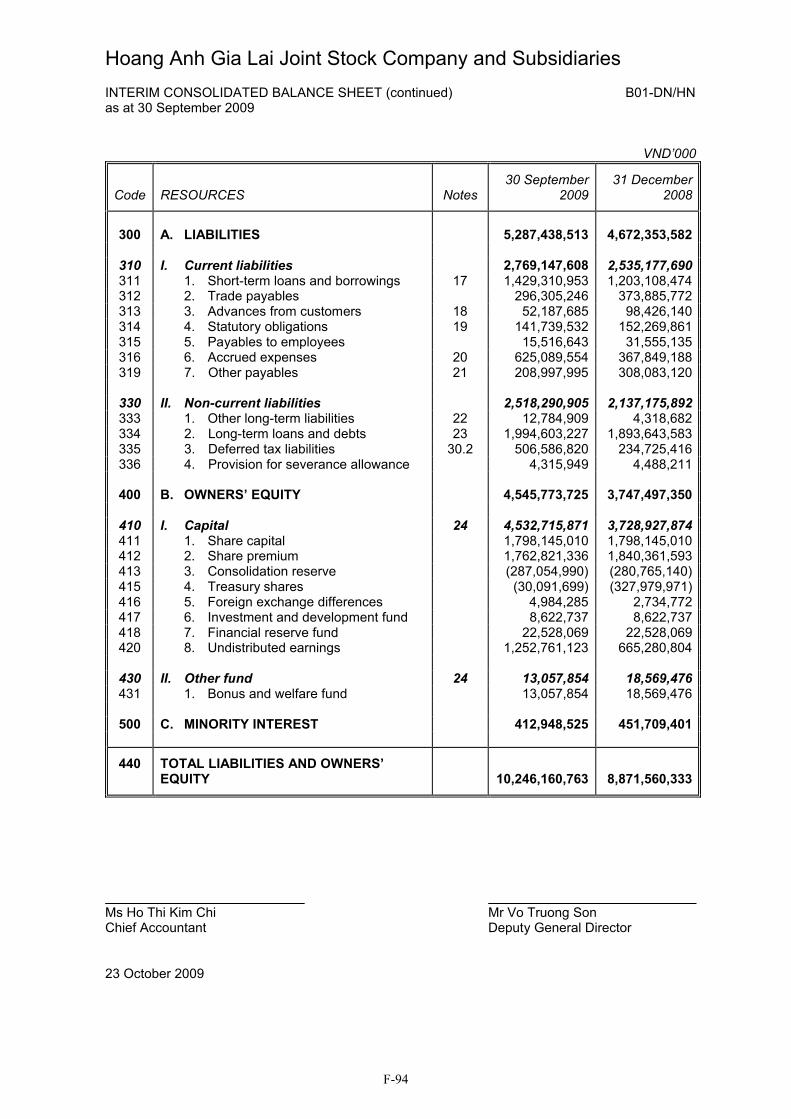

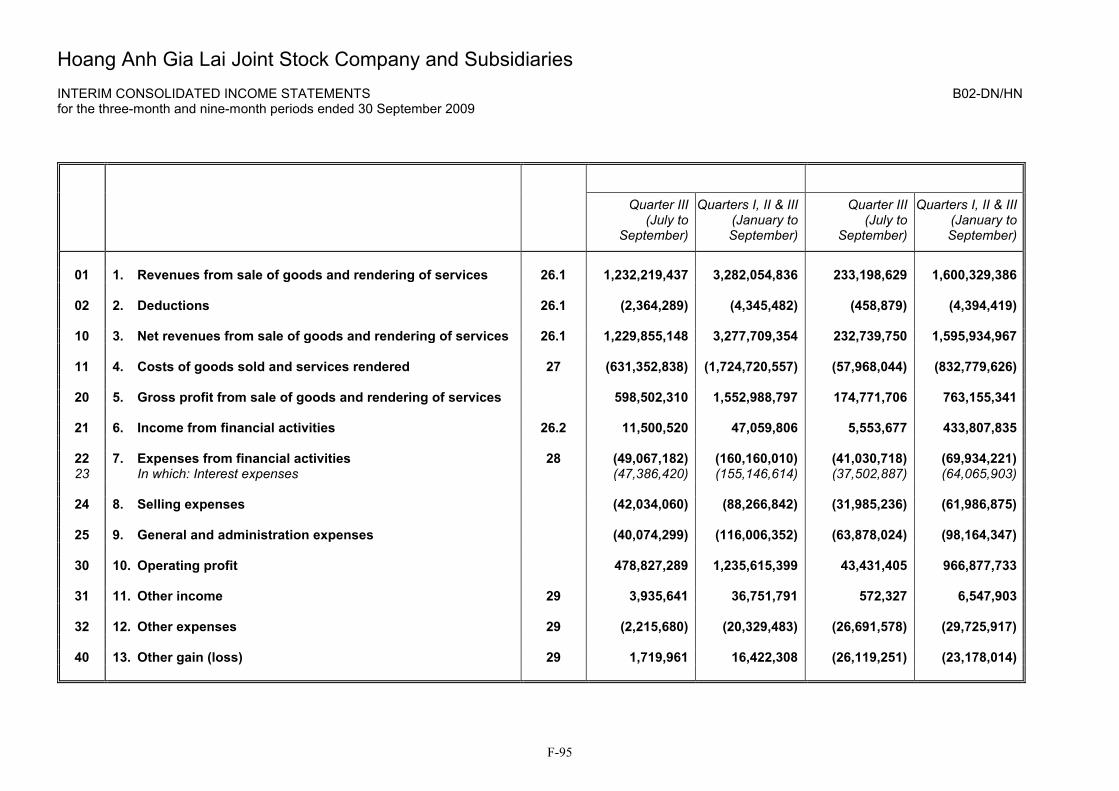

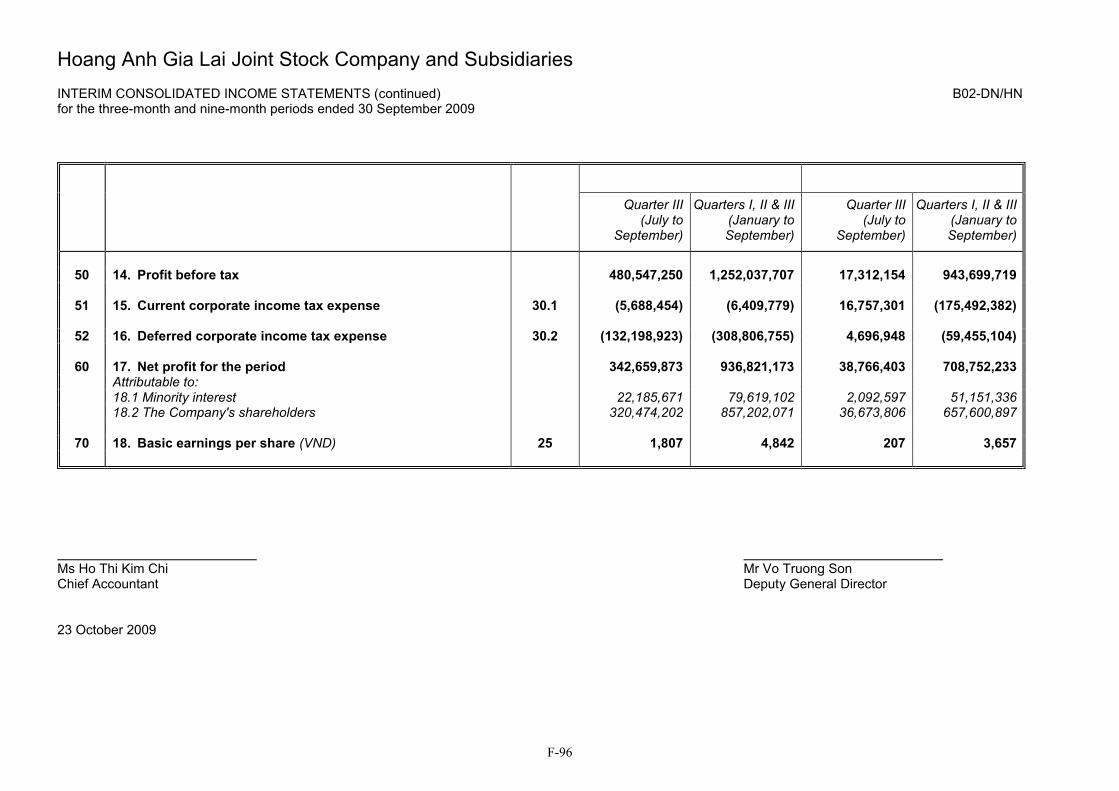

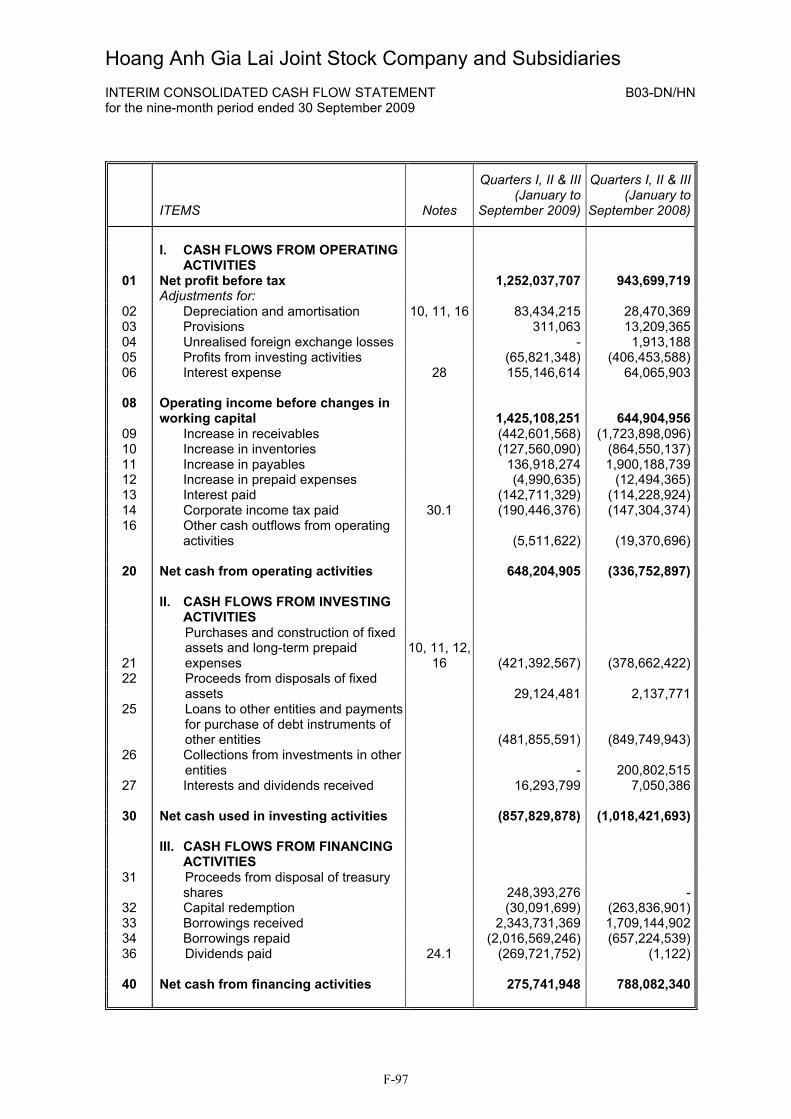

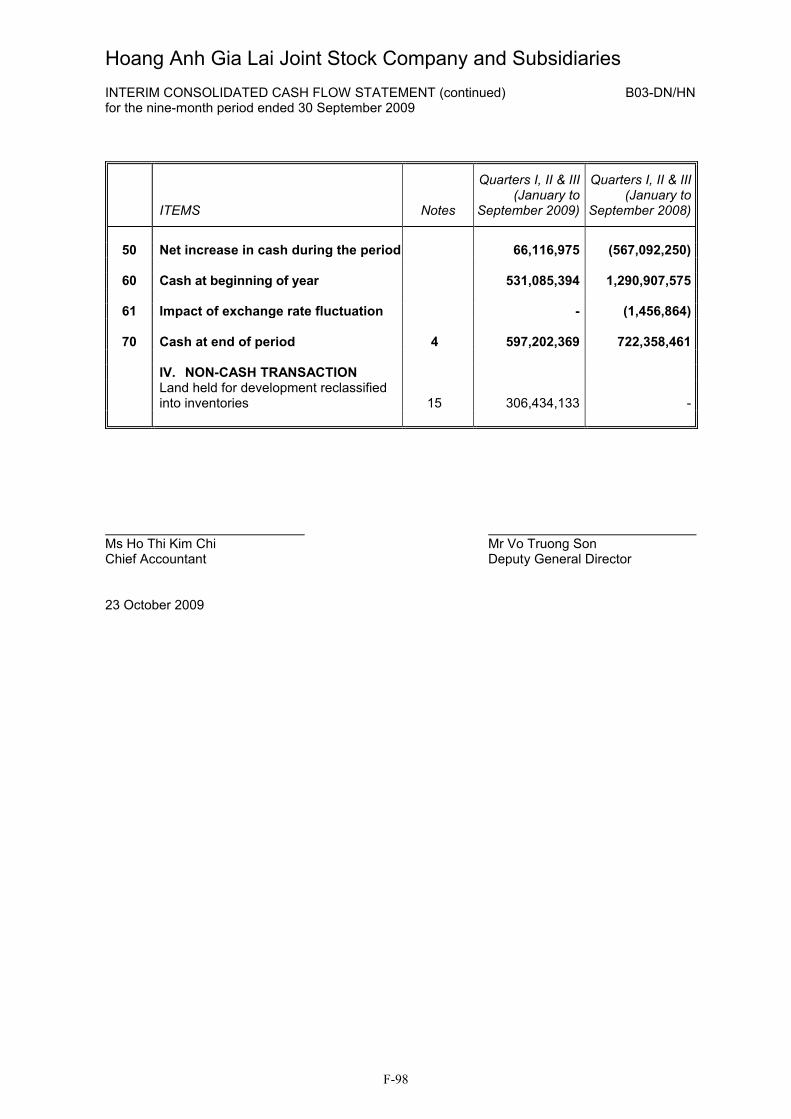

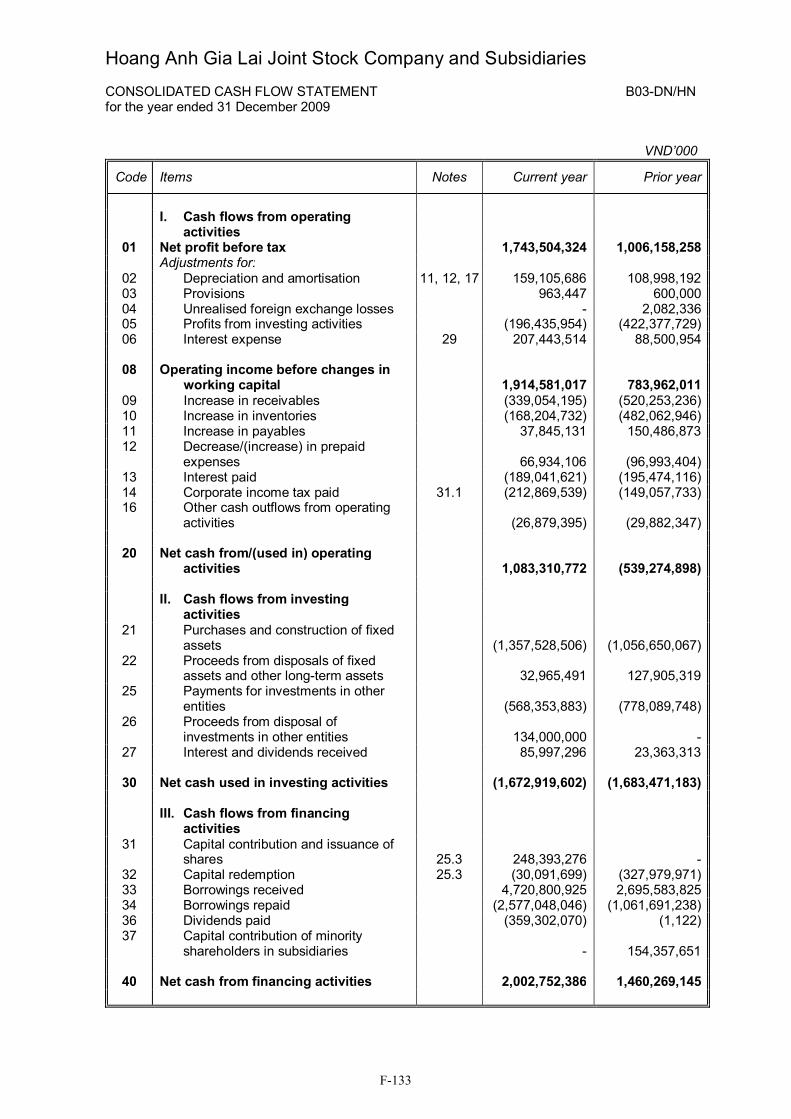

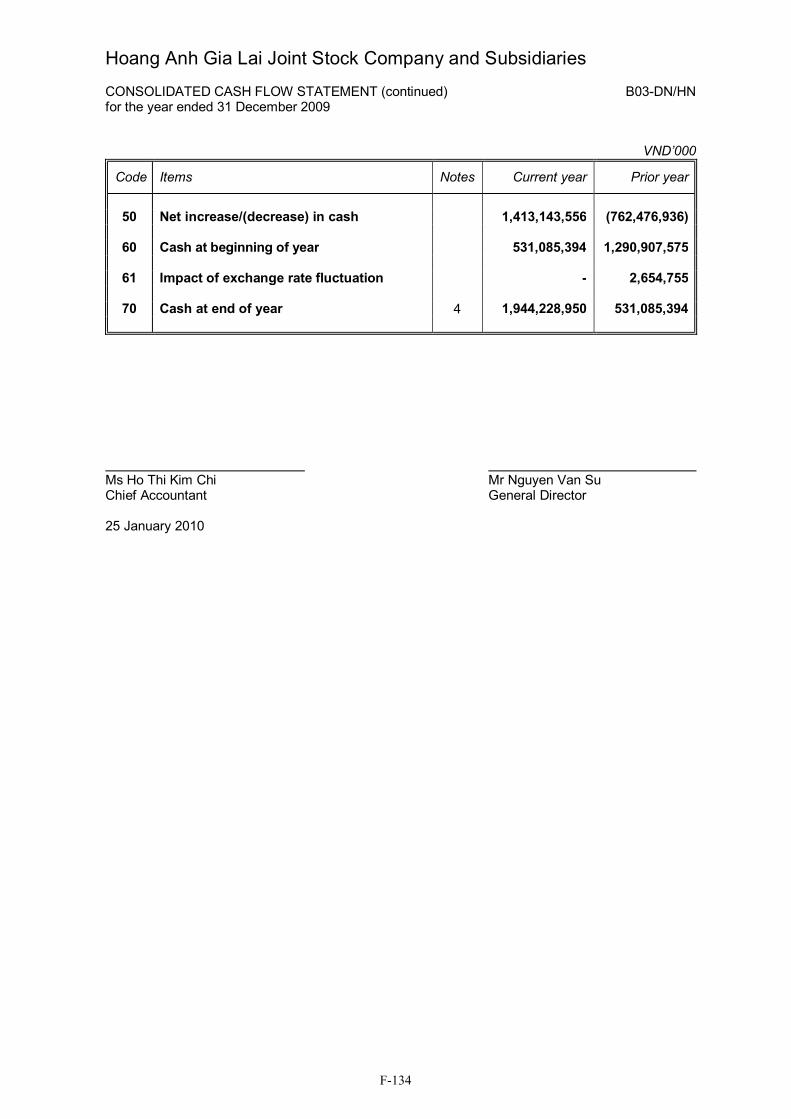

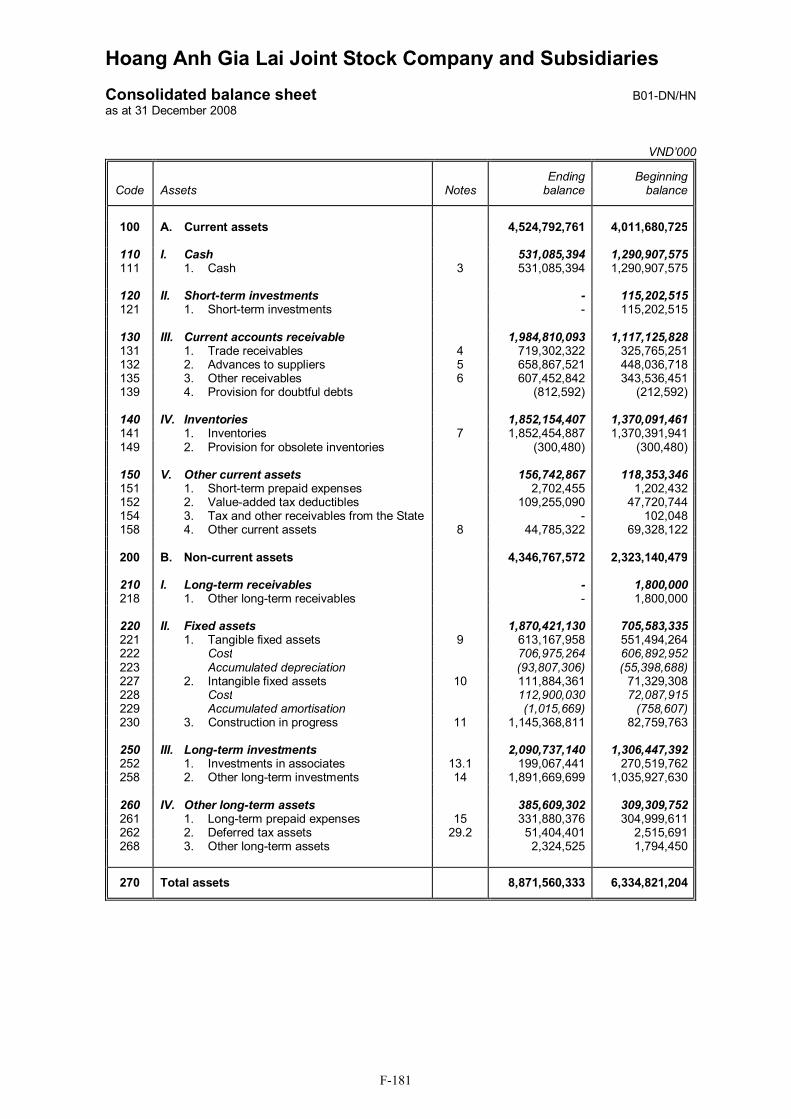

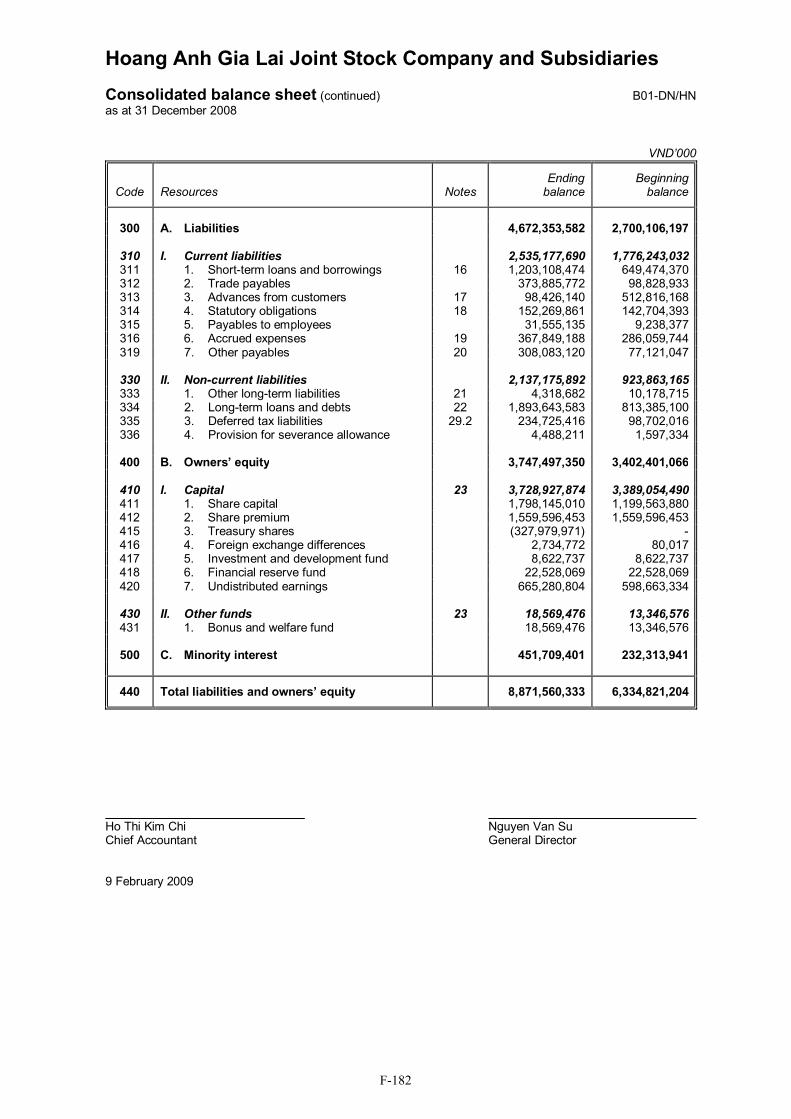

The following tables set forth selected consolidated financial information on the Group for each of the three years ended 31 December 2009, 2008 and 2007, and the nine month periods ended 30 September 2010 and 30 September 2009. This information is qualified in its entirety by reference to the Group's audited financial statements and the related notes thereto prepared in accordance with VAS and included elsewhere in these Listing Particulars. The Group's financial statements as of each of the years ended 31 December 2009, 2008 and 2007 were audited by Ernst & Young Vietnam Limited. The Company's financial statements for the nine month periods ended 30 September 2010 and 30 September 2009 are unaudited.

THE FINANCIAL INFORMATION OF THE GROUP INCLUDED IN THESE LISTING PARTICULARS HAS NOT BEEN PREPARED IN ACCORDANCE WITH IFRS AND THERE MAY BE MATERIAL DIFFERENCES IN THE FINANCIAL INFORMATION HAD IFRS BEEN APPLIED TO THE FINANCIAL INFORMATION. A DESCRIPTION OF THE SIGNIFICANT DIFFERENCES BETWEEN VAS AND IFRS IS INCLUDED IN THESE LISTING PARTICULARS UNDER "SUMMARY OF SIGNIFICANT DIFFERENCES BETWEEN VAS AND IFRS".

THE CONSOLIDATED FINANCIAL STATEMENTS AS OF AND FOR THE PERIODS ENDED 31 DECEMBER 2007, 31 DECEMBER 2008 AND 31 DECEMBER 2009 WERE EACH AUDITED IN ACCORDANCE WITH GENERALLY ACCEPTED AUDITING STANDARDS IN VIETNAM.

14

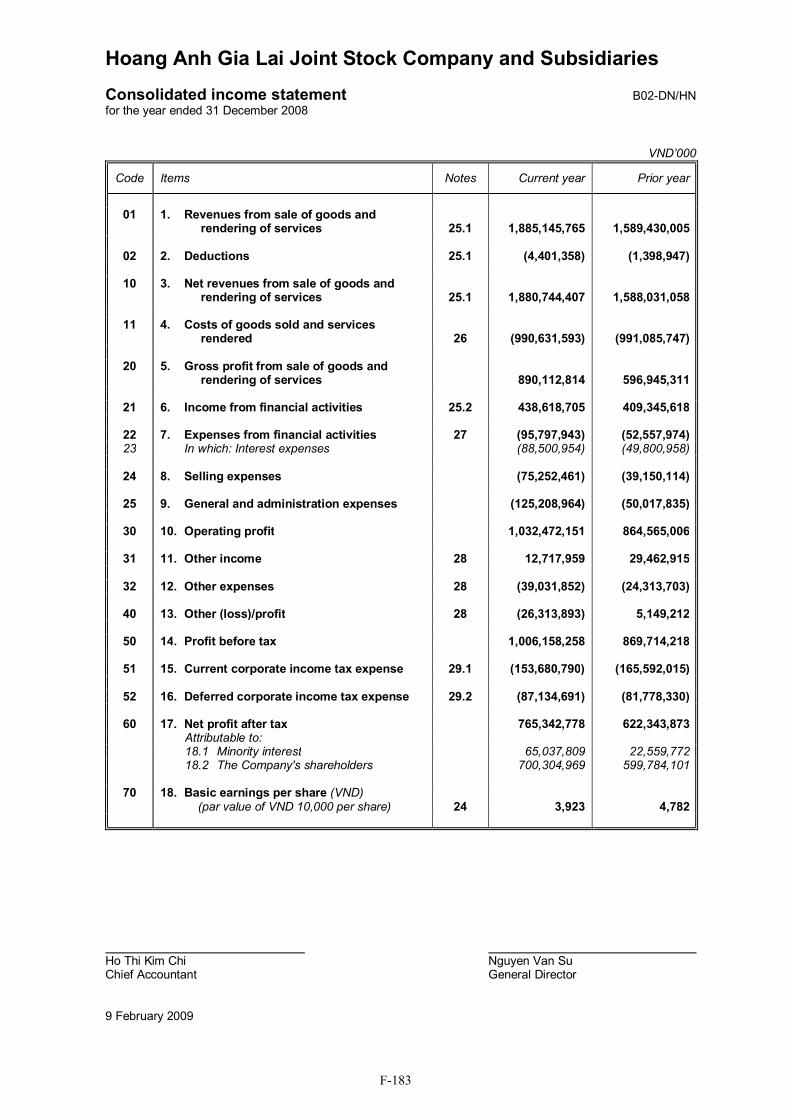

Summary consolidated income statement

Nine months ended 30

September 2010 (interim

unaudited)(VND '000)

Nine months ended 30

September 2009 (interim

unaudited)(VND '000)

Year ended 31 December 2009

(VND '000)

Year ended 31 December 2008

(VND '000)

Year ended 31 December

2007(VND '000)

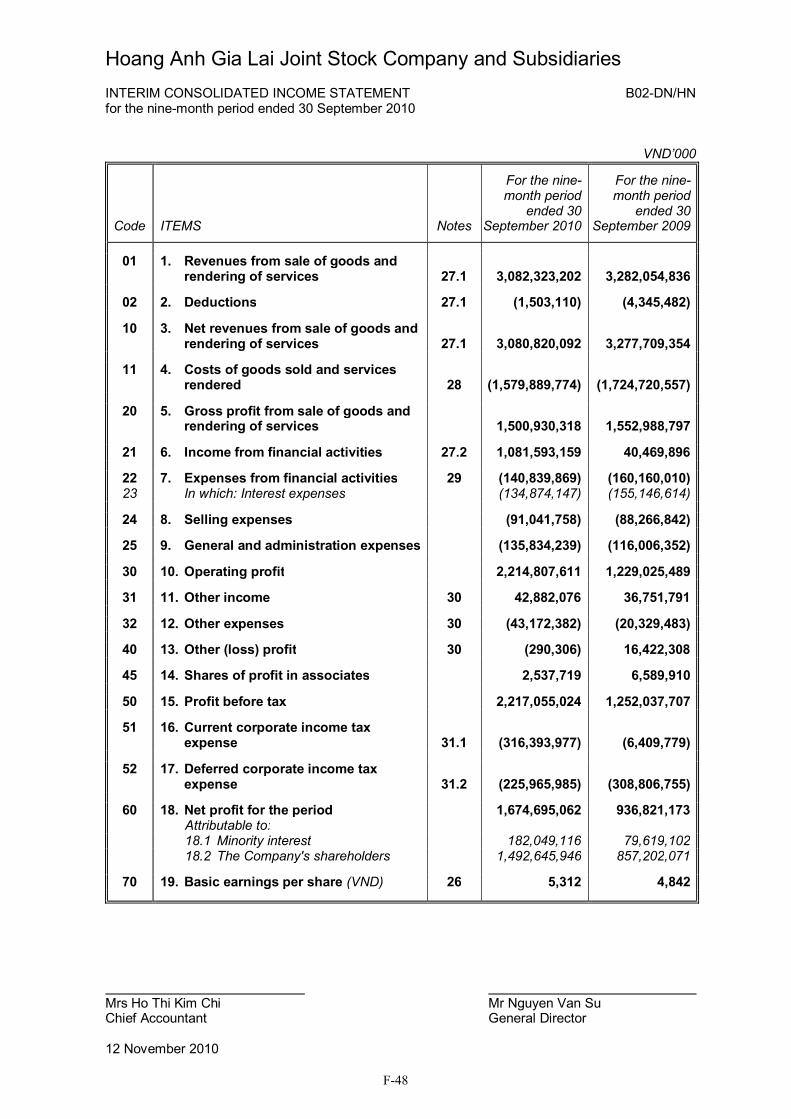

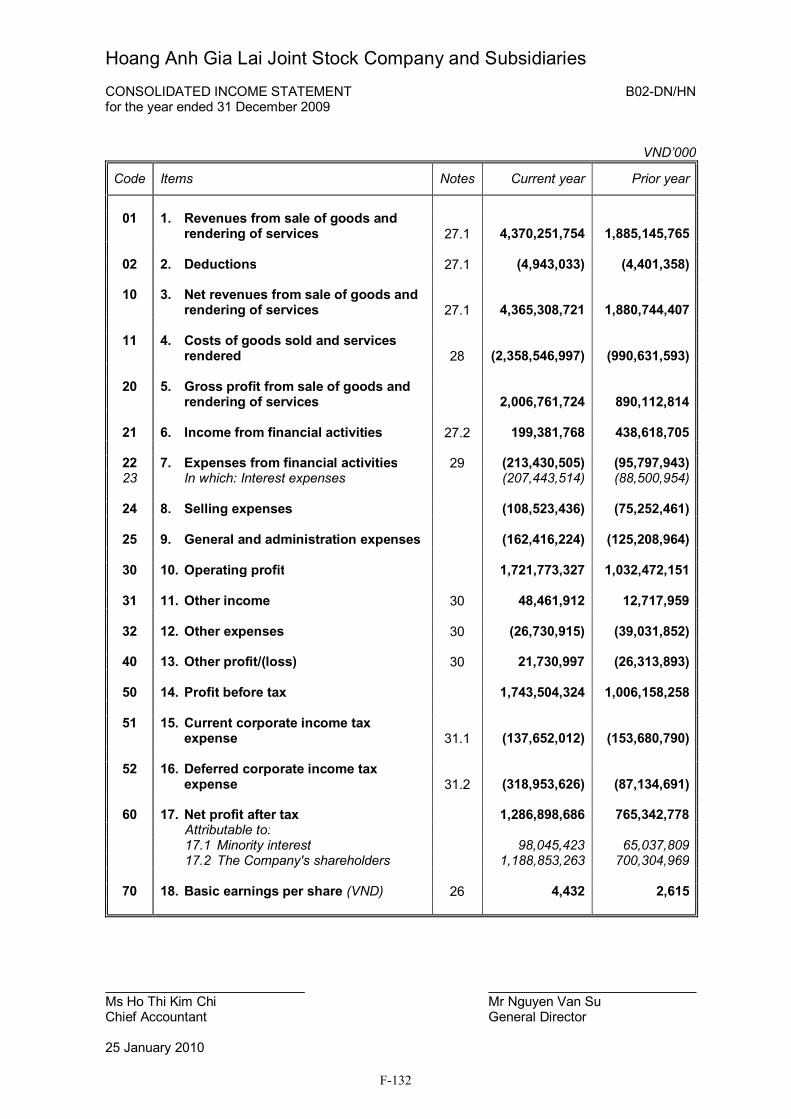

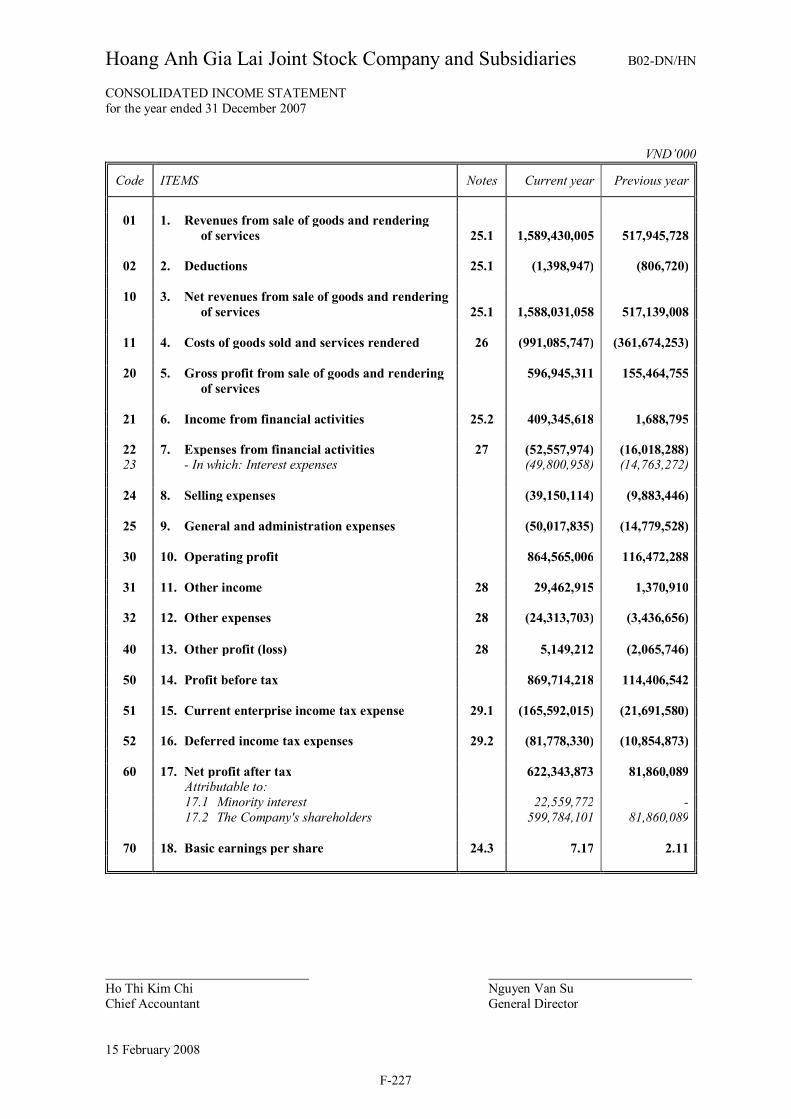

Revenues from sale of goods and rendering of services

3,082,323,202 3,282,054,836 4,370,251,754 1,885,145,765 1,589,430,005

Profit before tax 2,217,055,024 1,252,037,707 1,743,504,324 1,006,158,258 869,714,218

Net profit after tax

1,674,695,062 936,821,173 1,286,898,686 765,342,778 622,343,873

Basic earnings per share (VND)

5,312 4,842 4,432 2,615 4,782

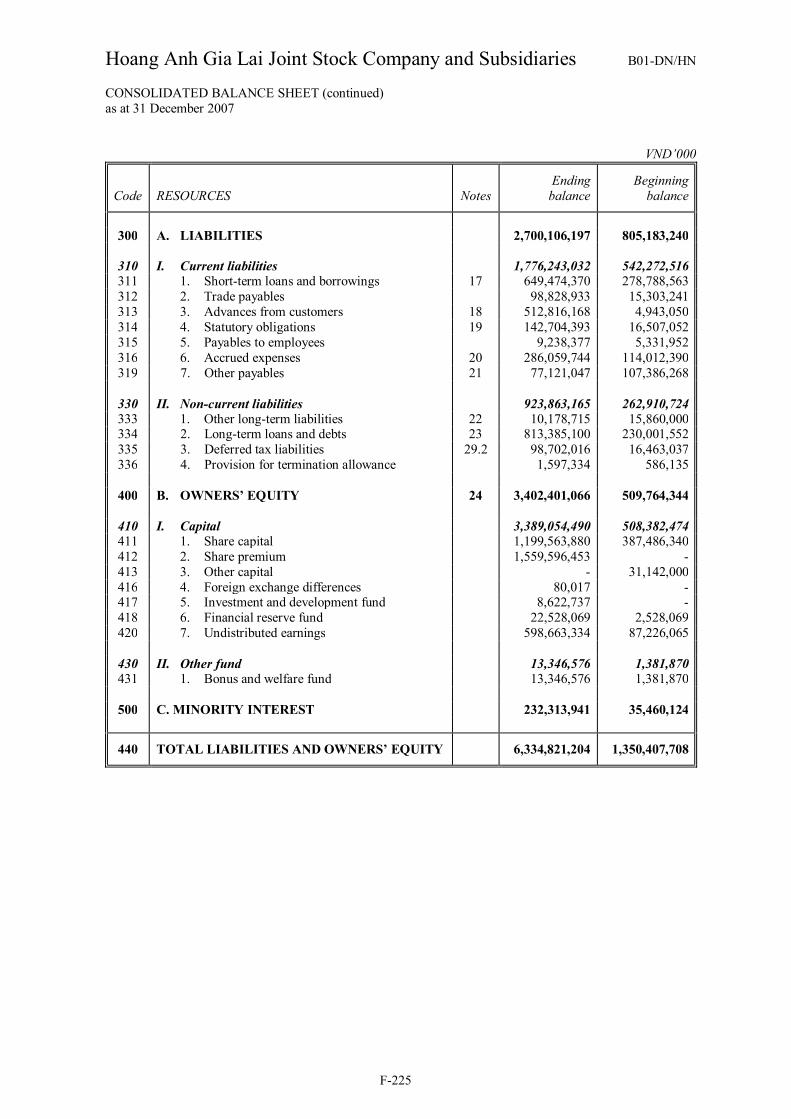

Summary consolidated balance sheet

30 September 2010 (interim

unaudited)(VND '000)

31 December 2009(VND '000)

31 December 2008(VND '000)

31 December 2007(VND '000)

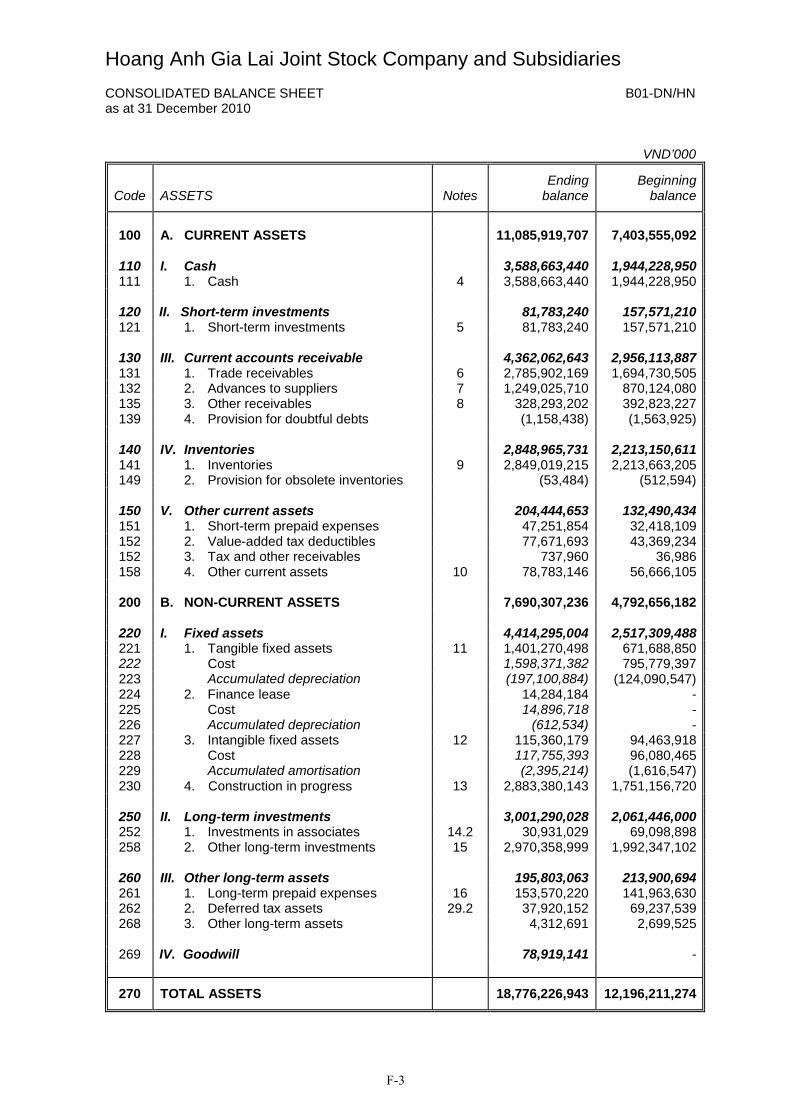

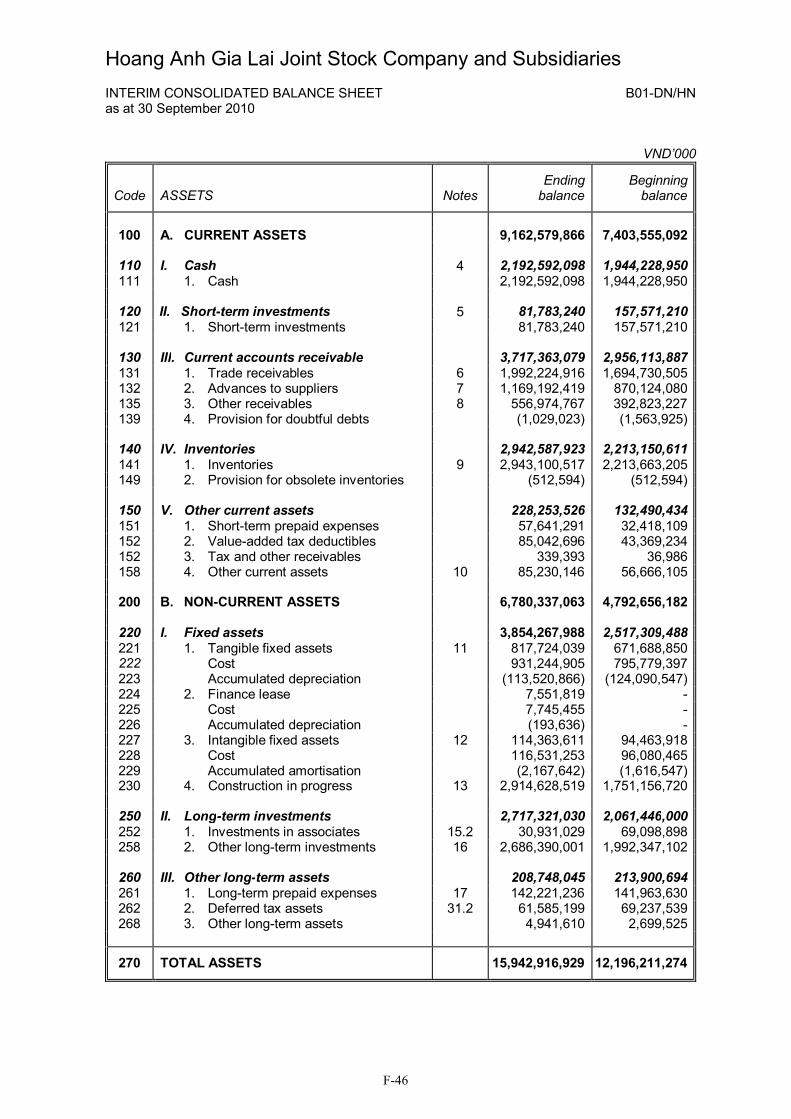

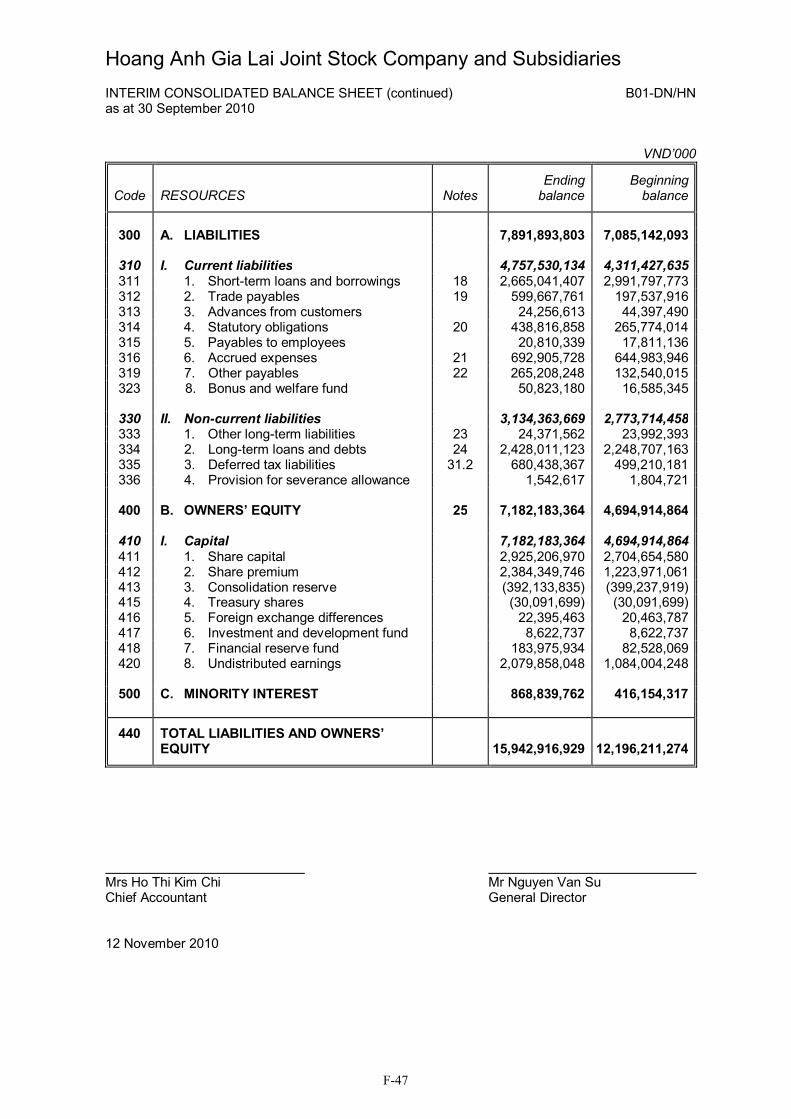

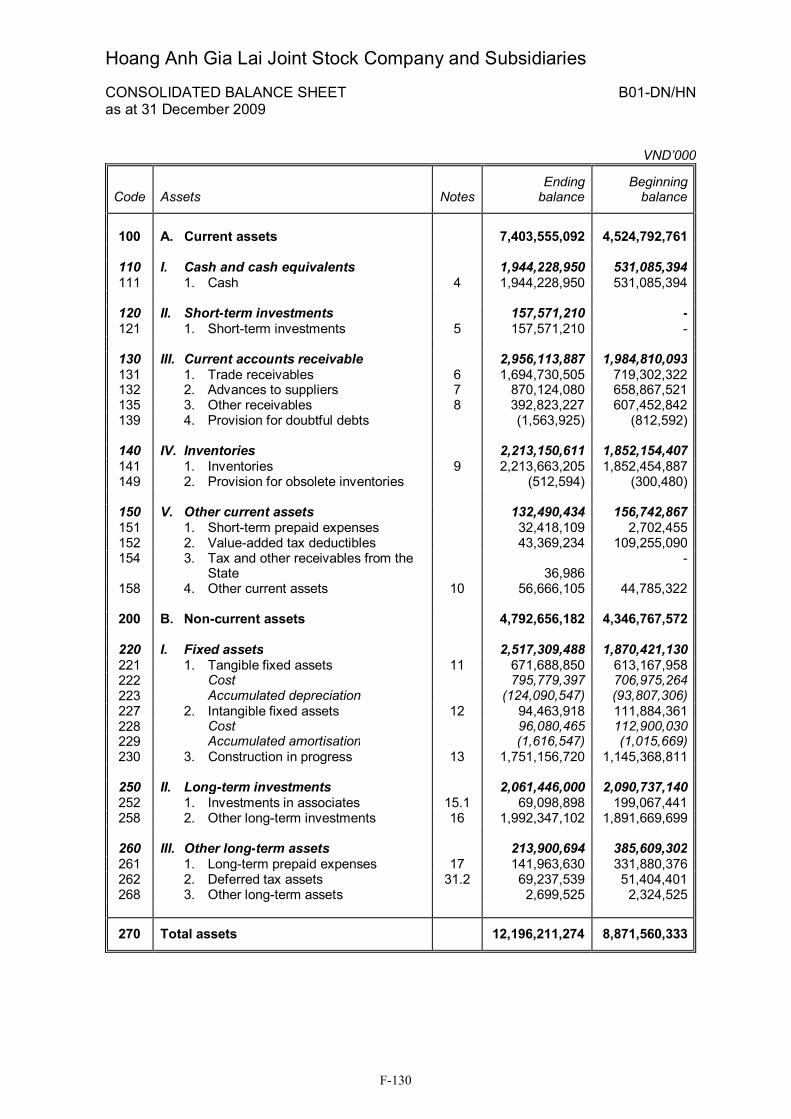

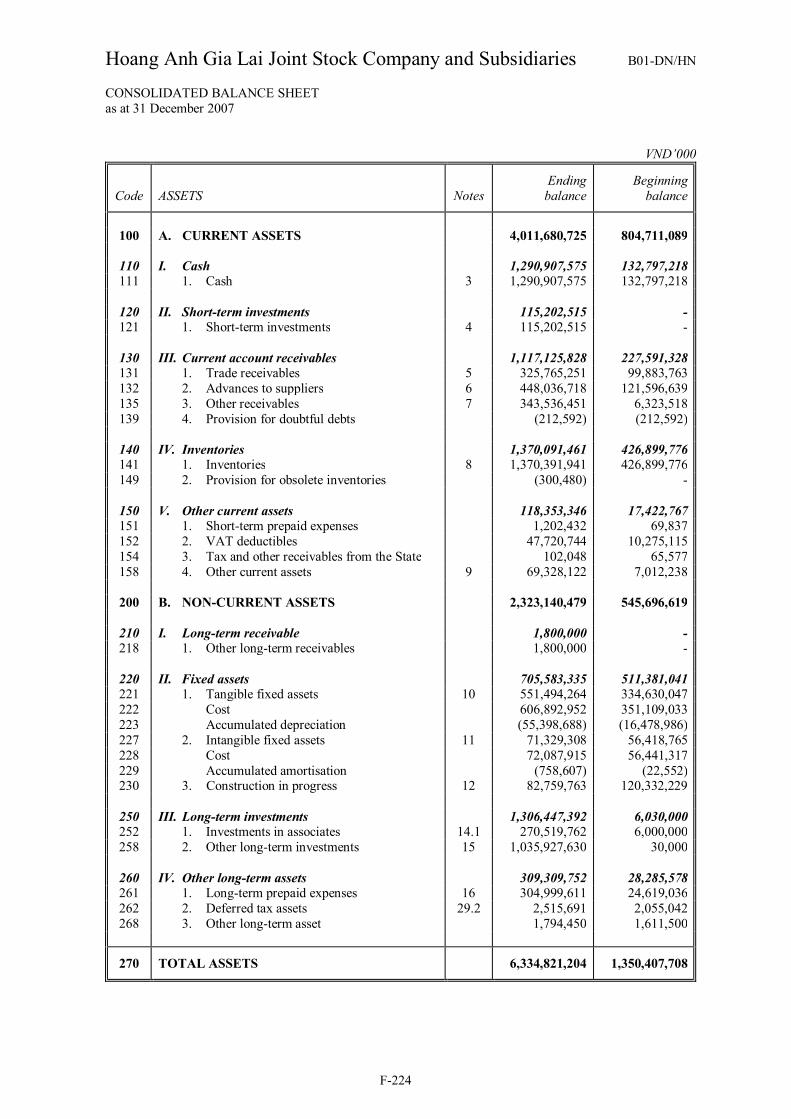

Current assets 9,026,011,056 7,403,555,092 4,524,792,761 4,011,680,725

Non-current assets 6,780,337,063 4,792,656,182 4,346,767,572 2,323,140,479

Total assets 15,806,348,119 12,196,211,274 8,871,560,333 6,334,821,204

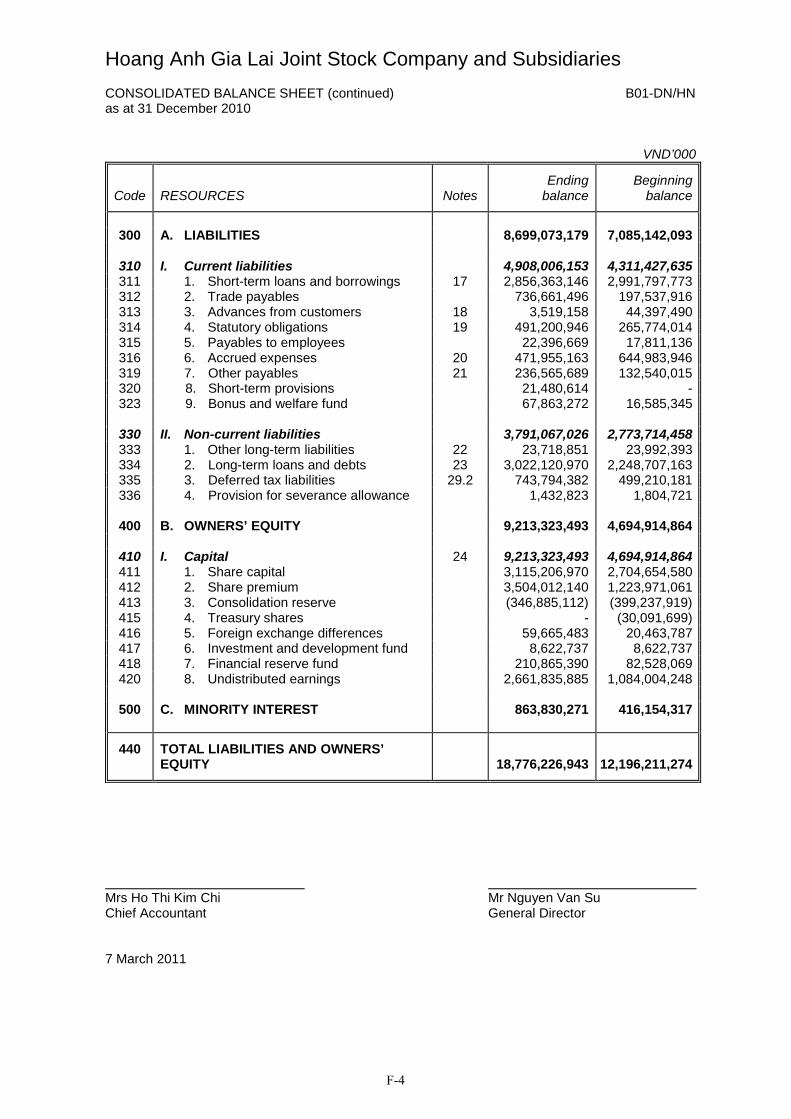

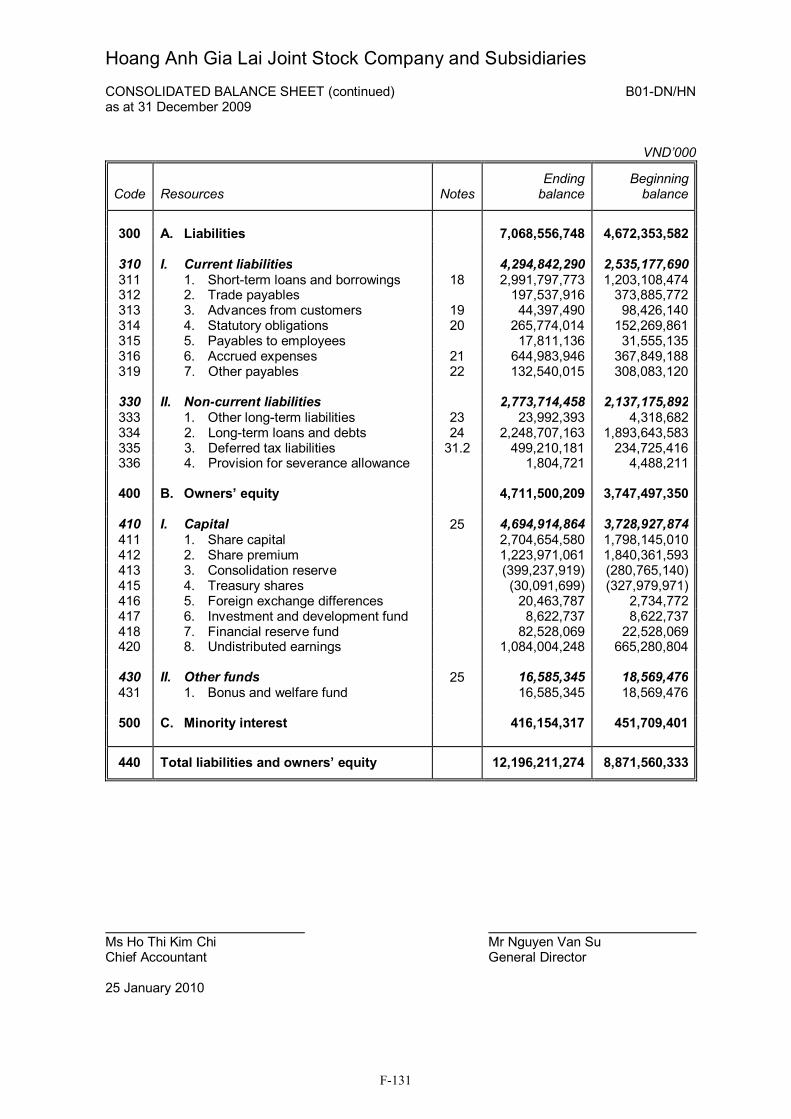

Current liabilities 4,620,961,324 4,294,842,290 2,535,177,690 1,776,243,032

Non-current liabilities

3,134,363,669 2,773,714,458 2,137,175,892 923,863,165

Owners' equity 7,182,183,364 4,711,500,209 3,747,497,350 3,402,401,066

Minority interest 868,839,762 416,154,317 451,709,401 232,313,941

Total liabilities, owners' equity and minority interest

15,806,348,119 12,196,211,274 8,871,560,333 6,334,821,204

15

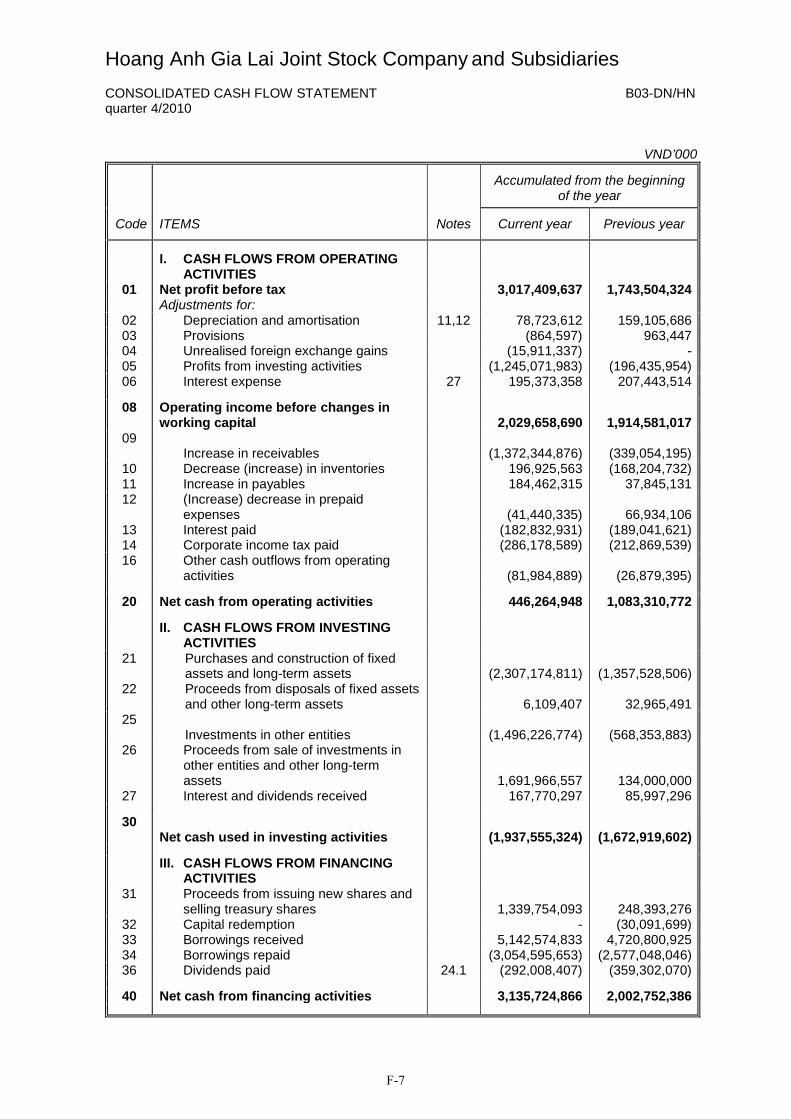

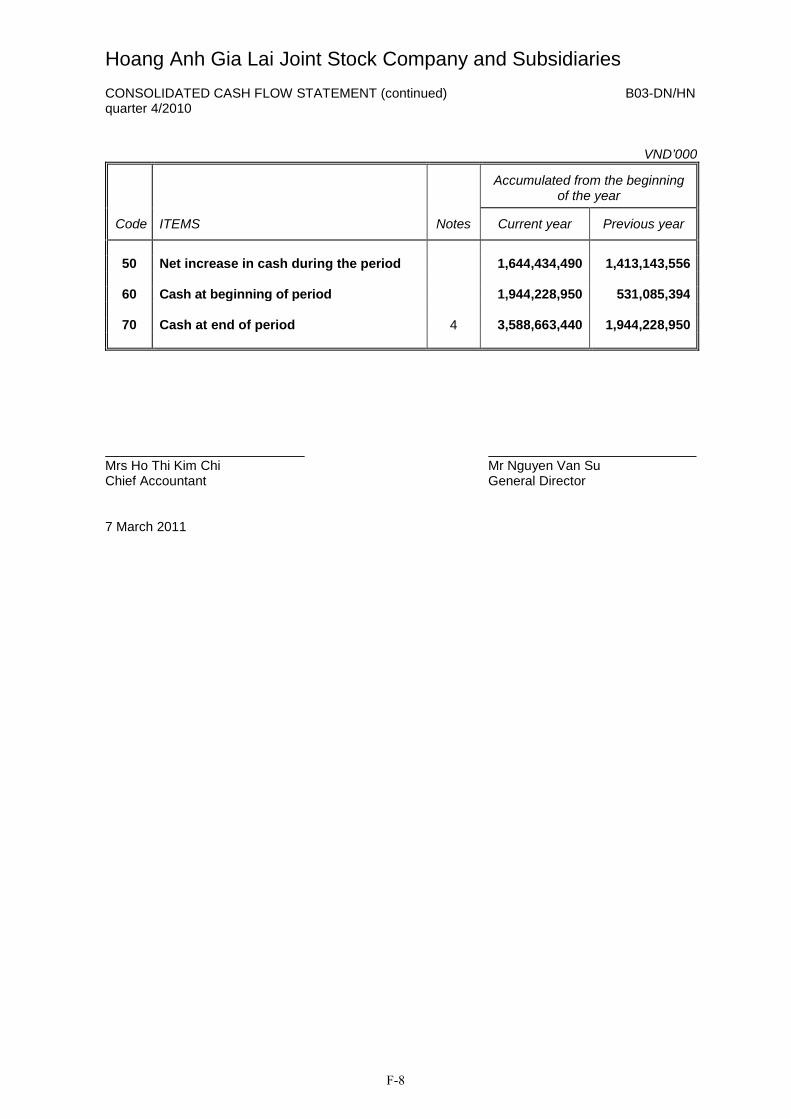

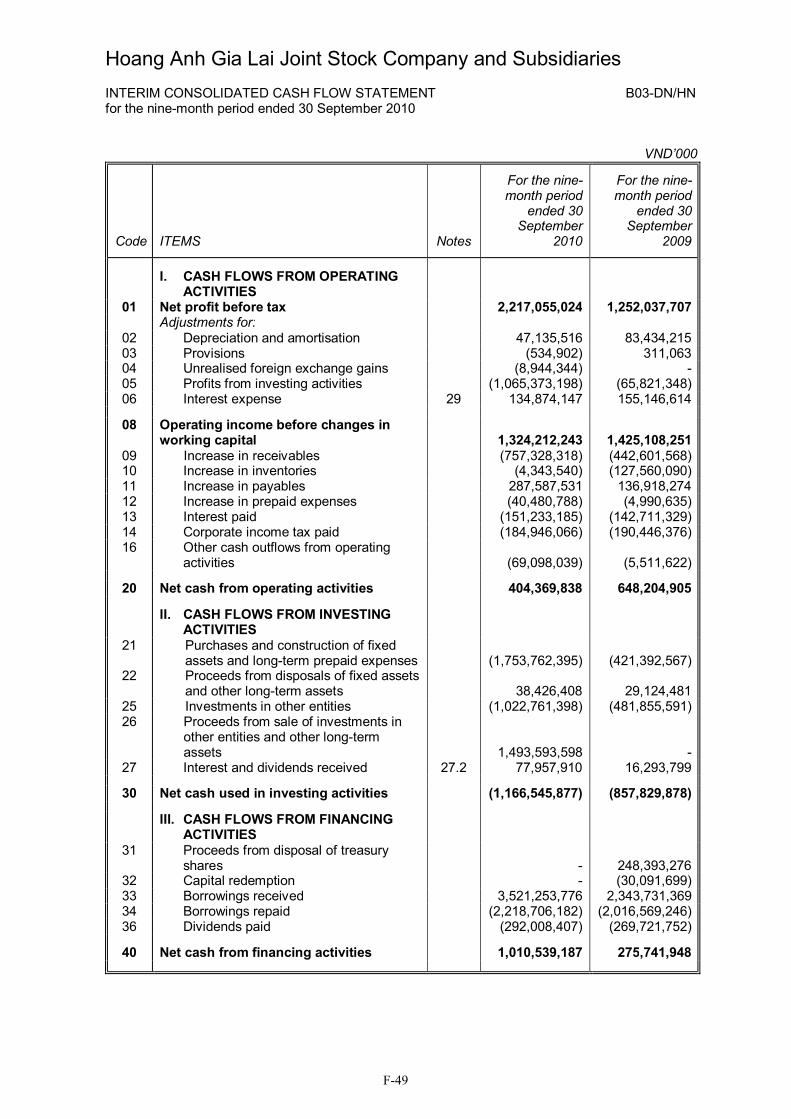

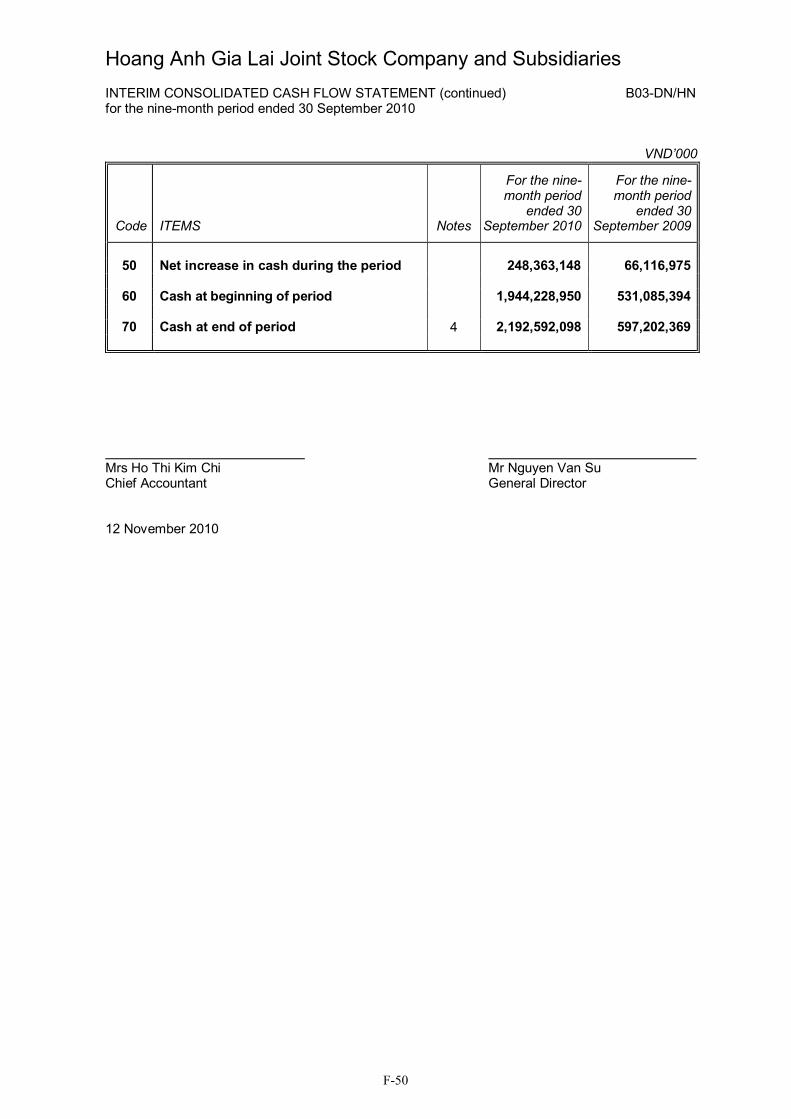

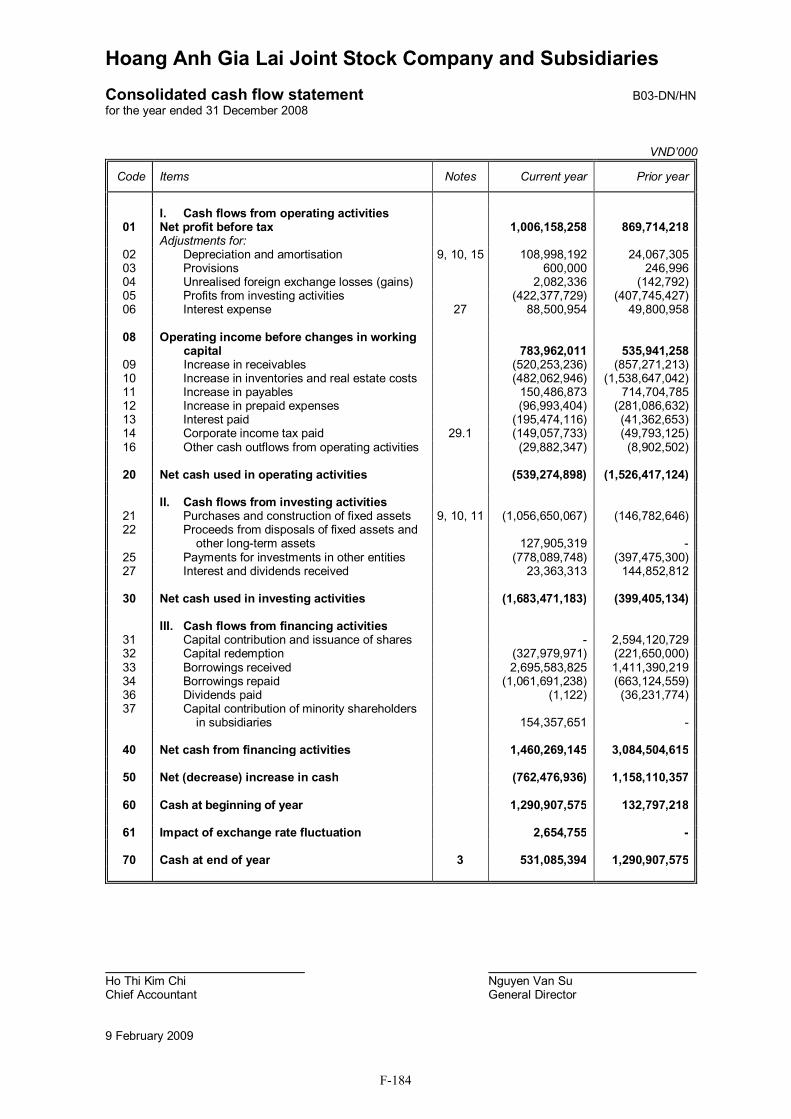

Summary consolidated cash flows

Nine months ended 30

September 2010 (interim

unaudited)(VND '000)

Nine months ended 30

September 2009 (interim

unaudited)(VND '000)

Year ended 31 December 2009

(VND '000)

Year ended 31 December 2008

(VND '000)

Year ended 31 December 2007

(VND '000)

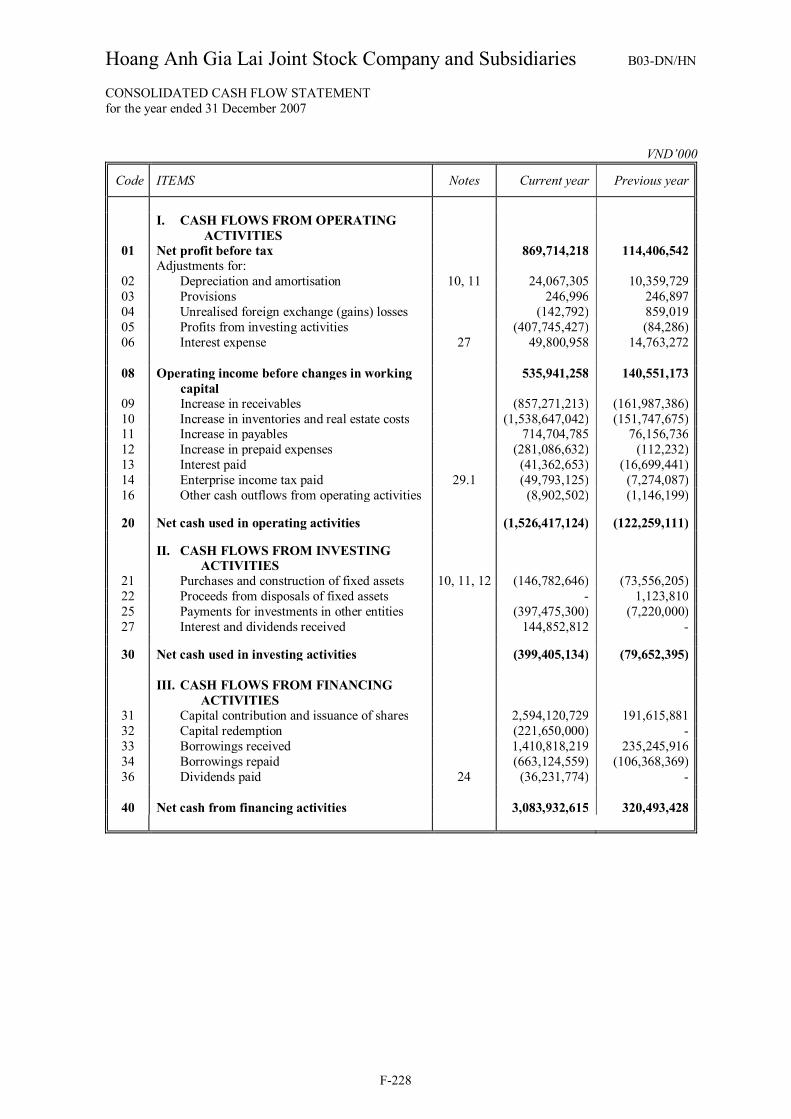

Operating income before changes in working capital

1,352,151,407 1,425,108,251 1,914,581,017 783,962,011 535,941,258

Net cash from/(used in) operating activities

432,309,002 648,204,905 1,083,310,772 (539,274,898) (1,526,417,124)

Net cash used in investing activities

(1,194,485,041) (857,829,878) (1,672,919,602) (1,683,471,183) (399,405,134)

Net cash from financing activities

1,010,539,187 275,741,948 2,002,752,386 1,460,269,145 3,083,932,615

Net increase/(decrease) in cash

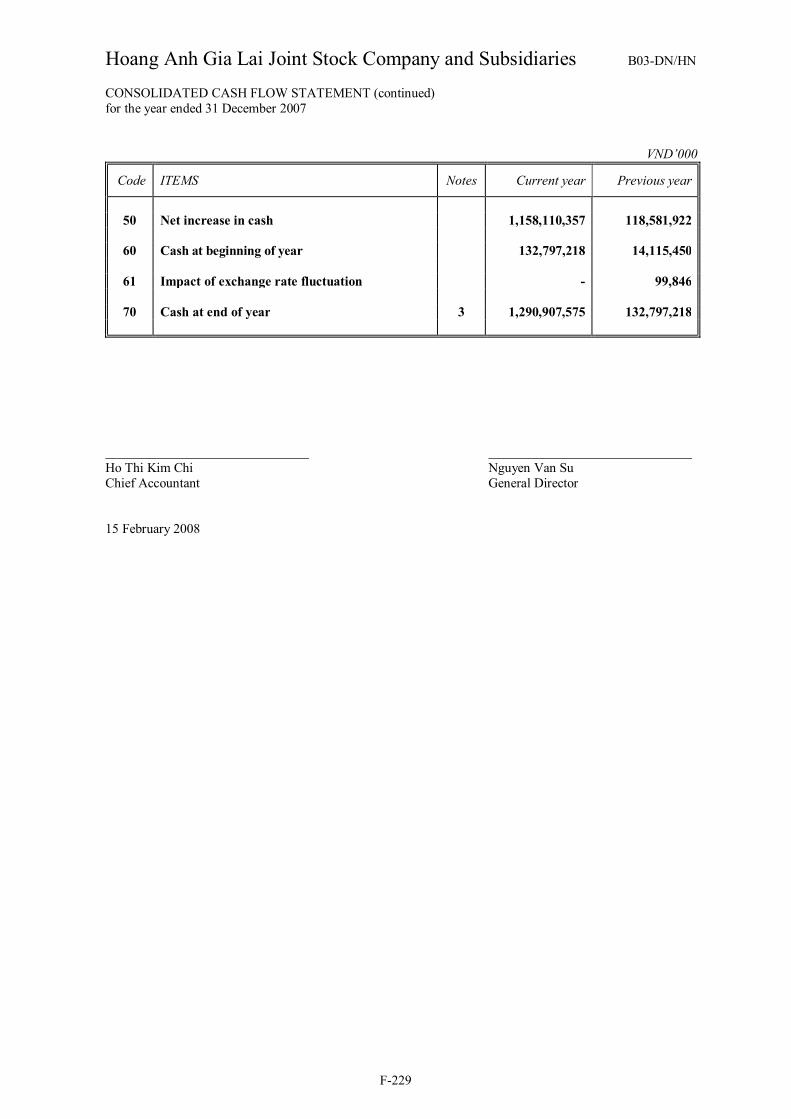

248,363,148 66,116,975 1,413,143,556 (762,476,936) 1,158,110,357

Cash at beginning of year/period

1,944,228,950 531,085,394 531,085,394 1,290,907,575 132,797,218

Impact of exchange rate fluctuation

- - - 2,654,755 -

Cash at end of year/period

2,192,592,098 597,202,369 1,944,228,950 531,085,394 1,290,907,575

16

SUMMARY OF THE GDRS

The following is a general summary of the terms of the GDRs. This summary is derived from and should be read in conjunction with the Terms and Conditions of the Global Depositary Receipts that are set out in full elsewhere in these Listing Particulars, which shall prevail to the extent of any inconsistency with the terms set out in this section. Capitalised terms used herein and not otherwise defined have the respective meanings given to such terms in the Terms and Conditions of the Global Depositary Receipts or the Definitions section.

The Company ......................................... Hoang Anh Gia Lai Joint Stock Company incorporated in the Socialist Republic of Vietnam with limited liability.

The GDRs............................................... Each GDR represents one Share. The GDRs are currently evidenced by a single Master GDR in registered form. There are limitations on redeposits of Shares that have been withdrawn from the GDR deposit facilities and restrictions on deposits of Shares acquired in the open market. The GDRs and the Shares represented thereby are subject to restrictions on transfer. See "Terms and Conditions of the Global Depositary Receipts" and "Transfer Restrictions".

Closing Date........................................... On 6 December 2010

Book-Entry and Definitive Certificate Delivery ................................ On 6 December 2010, the Company delivered an undertaking

by way of a Preferential Allotment Letter to the Depositary to issue the New Shares on 20 December 2010. Upon receipt andconfirmation of the Preferential Allotment Letter by the Custodian, the Preferential Allotment Letter was deposited as Deposited Property and the Depositary executed and delivered the Master GDR evidencing the GDRs on the Closing Date and delivered such Master GDR to a common depositary for Euroclear and Clearstream, Luxembourg. On 20 December 2010, the Company issued the New Shares, which were deposited with the Custodian in accordance with the terms of the Deposit Agreement. Except as described in "Summary of Provisions relating to the GDRs while in Master Form", beneficial interests in the Master GDRs are and will be shown on, and transfers thereof will be effected only through, book-entry records maintained by Euroclear and Clearstream, Luxembourg and their direct and indirect participants and accountholders. Subject to certain conditions, definitive certificated GDRs will be delivered to any Holder having instructed, or deemed to have instructed, the Depositary to issue and deliver the same. See "Summary of Provisions Relating to the GDRs while in Global Form".

Issue of additional GDRs ....................... Under the terms of the Deposit Agreement, additional GDRs may be issued only in respect of (i) Shares issued as a dividend or free distribution in respect of the Deposited Shares pursuant to Condition 5, (ii) Shares subscribed or acquired by Holders from the Company through the exercise of rights distributed by the Company to such persons in respect of the Deposited Shares pursuant to Condition 7, (iii) securities issued by the Company to the Holders in respect of Deposited

17

Shares as a result of any change in par value, subdivision, consolidation or other reclassification of Deposited Shares pursuant to Condition 10, and (iv) any other Shares in issue or purchased by the Depositary pursuant to Condition 1(B).

Deposit of funds for purchase of Shares to be represented by GDRs..... Subject to applicable laws and regulations, the Terms and

Conditions of the Global Depositary Receipts and receipt of such documents and information as the Depositary or the Custodian may deem necessary or appropriate, the Depositary will accept the deposit of funds from depositors to be applied towards the purchase of Shares in respect of which further GDRs are to be issued, with such additional Shares being deposited with the Depositary and forming Deposited Property.

Purchase of Shares by the Depositary on behalf of depositors......... Upon each occasion when funds for the purchase of Shares are

deposited with the Depositary pursuant to the Conditions, the Depositary will use reasonable endeavours, subject to all applicable laws and regulations, and providing it has been pre-funded, indemnified and/or secured to its satisfaction, to apply such funds for the purchase of such number of Shares specified by the depositor in the notice delivered pursuant to the Deposit Agreement at the then-prevailing market price. Following any such purchase of Shares, the Depositary will issue the corresponding number of GDRs and will make the appropriate entries in the Register to show such issue and either (i) make the appropriate entries on the Master GDR to reflect the increase in the number of GDRs evidenced by the Master GDR or (ii) issue a further Master GDR in respect of the new issue of GDRs (which further Master GDR may or may not have a temporary ISIN as appropriate in the circumstances) and shall notify the Clearing Systems (and/or the common depositary on their behalf) and the Company of such increase. The Depositary shall, if after accepting funds for the purchase of Shares it is unable using reasonable endeavours to purchase such number of Shares specified by the depositor in its notice, contact the depositor (or its broker-dealer acting as agent on its behalf) for further instructions.

Lock-up Period....................................... The Deposited Property may not be withdrawn at any time during the period of 12 months from 20 December 2010, being the date on which the Deposited Shares were deposited with the Custodian in accordance with the terms of the Deposit Agreement, or such other statutory period as may apply to the holding of the Shares by the Custodian pursuant to Vietnamese law and regulations relating to private placements in effect from time to time. In addition, any purchase of Shares by the Depositary on behalf of depositors in the secondary market at any time during the Lock-up Period will also be subject to lock-up until expiry of the Lock-up Period and Holders will not be able to withdraw such Deposited Property until expiry of the Lock-up Period.

18

Withdrawal of Deposited Property......... Subject to expiry of the Lock-up Period, upon request by any Holder in accordance with the Conditions for withdrawal of Deposited Property (and upon compliance therewith, including the delivery of certifications and/or evidence satisfactory to the Depositary) the Depositary shall, subject to the requirements of law or of any government or governmental authority, body or commission, or any other reason, sell or procure the sale of (either by public or private sale and otherwise at its discretion, subject to Vietnamese law and regulations) the Deposited Property (other than the Deposited Property held in cash), and shall distribute the proceeds of such sale, less all fees, taxes, duties, charges, costs and expenses incurred or that may be incurred by or on behalf of the Depositary with respect to such sale, as a cash distribution to the person or persons specified in the order for withdrawal, save in certain circumstances as specified in the Terms and Conditions of the Global Depositary Receipts.

Fees in connection with purchase of Shares and/or sale of Deposited Property by the Depositary..................... The payment of any fees, taxes, duties, charges, costs and

expenses (including, without limitation, any taxes in connection with the purchase of Shares, any registration fees and any fees imposed by the London Stock Exchange or the HoSE (or such other stock exchange(s) in Vietnam where the Shares may be listed from time to time)) incurred or that may be incurred by or on behalf of the Depositary with respect to the acceptance of a deposit, the purchase of Shares or the issue of GDRs, as necessary, may be deducted by the Depositary in advance of any purchase of Shares from the funds deposited by such depositor with the Depositary. All fees, taxes, duties, charges, costs and expenses incurred or that may be incurred by or on behalf of the Depositary with respect to any sale of Shares by the Depositary in connection with a withdrawal of Deposited Property shall be deducted from the proceeds of such sale. In addition, in accordance with Vietnamese regulations the Depositary will appoint a Vietnamese broker to carry out any purchase of Shares and/or sale of Deposited Property. Any fees and commissions of such broker in connection with the purchase of Shares and/or the sale of Deposited Property will be borne by the relevant depositor of funds or the Holder, as the case may be. Pursuant to current restrictions imposed by Vietnamese law and regulations, the Depositary may only appoint one broker at any one time.

New Shares............................................. The New Shares were issued by the Company on 20 December 2010 and deposited as Deposited Shares in accordance with the Deposit Agreement. Upon such deposit, each GDR represented one underlying New Share. The Existing Shares were not initially deposited with the Depositary and represented by GDRs but such Shares may be deposited with the Depositary by Shareholders at a later date in accordance with the Conditions.

Dividends ............................................... Holders will be entitled to receive dividends, subject to the terms of the Deposit Agreement, to the same extent as the

19

holders of Shares, less the fees, taxes, duties, charges, costs and expenses payable under such Deposit Agreement, including any Vietnamese tax applicable to such dividends. Cash dividends on the Shares, if any, will be paid in dong and, subject to any restrictions imposed by Vietnamese law, regulations or applicable permits, will be converted into US dollars by the Depositary in the manner provided in the Deposit Agreement and distributed to Holders. See "Taxation — Vietnamese Tax Considerations". The Company has not paid any dividends since 26 August 2010.

Taxation.................................................. For a discussion of certain tax considerations relevant to an investment in the GDRs, see "Taxation".

Voting Rights of Holders ....................... Holders will have no voting rights with respect to the Deposited Shares deposited with the Custodian pursuant to the terms of the Deposit Agreement. The Depositary will not exercise any voting rights in respect of the Deposited Shares unless it is required to do so by law. If so required, the Depositary will, at the direction of the Board of Directors (subject to the advice of legal counsel taken by the Depositary and the Company, at the expense of the Company) either vote as directed by the Board of Directors or give a proxy or power of attorney to vote the Deposited Shares in favour of a director of the Company or other person or vote in the same manner as those Shareholders designated by the Board of Directors. A valid corporate decision of the Company will bind the Depositary and the Holders notwithstanding these restrictions on voting rights. The Depositary shall in no circumstances exercise any discretion with respect to the voting of the Deposited Shares.

Restriction on Disposition ofSecurities ................................................ The GDRs, and the Shares represented by such GDRs, have

not been, and will not be, registered under the Securities Act. Offers and sales of the GDRs will be subject to certain restrictions described in "Transfer Restrictions".

Depositary for the GDRs........................ Deutsche Bank Trust Company Americas.

Governing Law....................................... The Deposit Agreement is governed by English law.

Listing and Trading Markets for the GDRs................................................ Application has been made for the GDRs to be listed on the

Official List and, with respect to GDRs in global form, admitted to trading on the Professional Securities Market.

A GDR represented by an individual definitive certificate will not be eligible for clearing and settlement through Euroclear or Clearstream, Luxembourg or for trading on the Professional Securities Market.

Listing and Trading Market forShares .................................................... The Existing Shares and the New Shares have been admitted

to listing on the HoSE. The approval from the SSC for the issuance of the New Shares was granted on 19 November

20

2010 and the New Shares were admitted to trading on the HoSE on 12 January 2011. The 8,108,125 Shares deposited in accordance with the terms of the Deposit Agreement pursuant to a bonus share issue on 26 January and which are represented by GDRs were admitted to trading on the HoSE on 28 February 2011.

Dilution................................................... The issue of the New Shares which are represented by GDRs resulted in a 6.1 per cent. dilution in Shareholders' shareholdings.

Government Approvals .......................... Vietnamese regulations are silent as to what approval or permission a company issuing GDRs needs to obtain from any of the regulatory authorities in Vietnam. In the absence of specific provisions of the Vietnamese Securities Laws legislating for GDRs representing listed shares of companies incorporated in Vietnam, the Company has consulted with the SSC on a no-names basis and the SSC advised that no such approval was required. See "Vietnamese Regulatory Approvals and Filings — Approvals".

GDR Security Codes .............................. Master GDR ISIN: US4337181030

Master GDR Common Code: 056263730

Master GDR CUSIP: 433718103

21

RISK FACTORS

Investing in the GDRs involves a high degree of risk. Any potential investor should pay particular attention to the fact that the Group operates in Vietnam, under a legal and regulatory environment, which, in some respects, may differ from that which prevails in other countries. Prospective investors should carefully consider the risks described below, in addition to the other information contained in these Listing Particulars, before making any investment decision relating to the GDRs or the Shares represented by the GDRs. The occurrence of any of the following events could have a material adverse effect on the Group's business, results of operations, financial condition and future prospects and cause the market price of the GDRs and the underlying Shares to fall significantly and/or its ability to pay dividends could be impaired. This section describes the material and principal risks specific to the Group and the markets it operates in. Additional risks not currently known to the Group or that the Group currently deems immaterial may also adversely affect the market price of the GDRs and the underlying Shares.

1. Risks Relating to the Group's business and the industries in which it operates

General risks relating to the Group's business

The Group's diversification strategy may not be successful

Historically, the Group's principal business has been within the real estate sector. In 2009, approximately 77 per cent. of the Group's revenues were generated by its real estate business. The Group aims to increase its turnover and profitability through further diversification into the rubber, iron ore, and hydropower industry sectors. In addition, it is expected that the Group's growth strategy will deliver a more balanced segmental revenue profile, enhanced margins, tax benefits and higher earnings per share growth. There can be no assurance that the Group will be able to achieve all or any of its objectives, and even if achieved, within the anticipated time frame and budget.

Although the Group has gained considerable project management experience from its real estate activities and has recruited managers with experience in the industries within which its new businesses operate, there can be no assurance that the Group's management will be able to successfully execute its strategy of expanding and diversifying into new areas of business which are substantially unrelated to its current principal business. As the Group continues to grow, it must continue to improve its technical and operational knowledge, optimise allocation of resources and implement an effective internal management system. The Group needs to continue to recruit and provide training for qualified personnel in order to support its expanding operations. Furthermore, the Group needs to manage relationships with a greater number of customers, suppliers, contractors, service providers, lenders, other third parties and relevant governmental authorities. The Group will also need to further strengthen its internal control and compliance functions to ensure that its is able to comply with its future legal and contractual obligations. There can be no assurance that the Group will not experience issues such as construction delays or operational difficulties at new locations or difficulties in expanding its existing businesses and operations. Similarly, there can be no assurance that the Group will be able to attract and hire competent personnel and implement its training programs to support its expanding businesses.

Until recently, substantially all of the Group's business operations were in Vietnam. While the Group intends to continue to concentrate its resources in Vietnam, it has expanded to Cambodia, Laos and Thailand. These countries may differ from Vietnam in terms of, among other factors, economic development, regulatory environment, business practices, quality of suppliers and contractors, pricing, availability of bank financing, mortgage financing and customer tastes and preferences. Accordingly, the Group's experience in Vietnam may not be applicable to other countries and it may be at a competitive disadvantage compared to other businesses with a more established presence in those countries. An unsuccessful expansion into these new countries may increase the Group's operating costs and impair its overall profitability and in turn materially and adversely affect its business, prospects, financial condition and results of operations.

22

The Group's ability to diversify its operations could be limited by many factors beyond its control, including the Group's ability to raise sufficient financing, restrictions under the Group's existing or future debt agreements, competition from other companies, external contractors and engineers, and granting ofconsents and permits from relevant government departments. These risks are described in greater detail in this section. The Group's inability to complete its projects as planned may have a material adverse effect on the growth prospects of the Group or the results of the operations or financial condition of the Group.

The Group may not be able to refinance its indebtedness as it matures

The Group maintains significant indebtedness to finance its project development activities. At 30 September 2010, the Group's total consolidated indebtedness, representing its current and non-current bank and other loans, was VND5,093,053 million, of which VND2,665,041 million was due within one year or on demand. The Group's short term capital needs are to finance its working capital requirements and are generally met using short-term loans secured by land use rights, plant, machinery and equipment and inventories. Other sources of short term liquidity include cash balances and receipts from operations. The Group's long-term capital needs include the financing of its current and future real estate projects, the development of its hydropower, iron ore and rubber plantations businesses and purchases of machinery and equipment. The Group believes that, because of its anticipated strong cash flows in the future, it will be able to repay its debts as they fall due. However, any material deterioration in the Group's cash position in the future, as a result of unforeseen events or matters beyond its control, will require it to use cash generated from operating activities or some other sources to repay its debt when it becomes due. There can be no assurance that the Group's business will generate sufficient cash flow from operations to repay its borrowings as they mature. Repaying borrowings with cash generated by operating activities will divert the Group's financial resources away from the development of its businesses.

The Group's operations may be restricted by the terms of the notes to be issued by the Company, which could limit the Group's ability to plan for or to react to market conditions

At the date of these Listing Particulars, the Company was in the process of offering senior notes to potential investors (the "Notes"). The Company is expecting to raise approximately US$ 200m from this offering. The Notes will be secured on a pledge of the shares held by the Company (and other Group companies) in its subsidiary guarantors (Hoang Anh Gia Lai Wooden Furniture Joint Stock Company, Hoang Anh Gia Lai Hydropower Joint Stock Company, Hoang Anh Construction and Development House Joint Stock Company, HAGL Mineral Joint Stock Company and HAGL Rubber Joint Stock Company.) and will be senior in right of payment to certain future subordinated indebtedness of the Company or the guarantors, but will be subordinated to certain existing indebtedness. The indenture governing the Notes will, among other things (and subject to certain important exceptions and qualifications), limit the Company's and the subsidiary guarantors' ability to:

● incur or guarantee additional indebtedness and issue disqualified or preferred stock;

● declare dividends on capital stock or purchase or redeem capital stock;

● make investments or other specified restricted payments;

● sell assets;

● create charges;

● enter into sale and leaseback transactions;

● engage in any business other than permitted business (broadly, any business that is the same as, or reasonably related, ancillary or complementary to, any of the businesses in which the Group is engaged on at the date of the indenture);

23

● enter into agreements that restrict the subsidiaries' ability to pay dividends, transfer assets or make intercompany loans;

● enter into transactions with shareholders or affiliates; and

● effect a consolidation or merger.

Some of the Group's existing indebtedness contain negative covenants that restrict the operations of its businesses, its ability to incur additional loans and declare dividends and most of its indebtedness is secured by charges on its assets. See "Management's Discussion and Analysis of Financial Condition and Results of Operations – Capital resources and expenditures" for details of the covenants which apply to this indebtedness.

The Group expects that future indebtedness will contain similar restrictive covenants and may create similar charges on its assets. The Group may lose part or all of the charged assets if the Group cannot repay or refinance such borrowings as they mature, which could materially and adversely affect its business, prospects, financial condition and results of operations. However, the Group believes that the current risk of losing part or all of such assets is remote as the Group anticipates receiving strong cashflows in the future, which will allow it to meet its payment obligations under the Notes. However, these covenants could limit the Group's ability to plan for or react to market conditions or to meet its capital needs. The Group's ability to comply with these covenants may be affected by events beyond its control, and it may have to curtail some of its operations and growth plans to maintain compliance. However, the Group does not currently anticipate having to take any such action to maintain compliance.

The Group's expansion and diversification is dependent upon its ability to obtain funding

The Group requires capital for, among other purposes, expanding its operations, making acquisitions, managing acquired assets, acquiring new equipment, maintaining the condition of its existing equipment and maintaining compliance with laws and regulations. For the years ending 31 December 2011, 2012 and 2013, the Group plans to incur capital expenditures of US$ 195.8m, US$ 215.3m and US$ 67.8m, respectively. These amounts are significantly greater than the Group's historical capital expenditures. To the extent that cash generated internally and cash available under the Group's existing credit facilities are not sufficient to fund its capital requirements, the Group will require additional debt or equity financing, which may not be available on favourable terms, or at all. Future debt financing, if available, may result in increased finance charges, increased financial leverage, decreased income available to fund further expansion and the imposition of restrictive covenants on the Group's businesses and operations. In addition, future debt financing may limit the Group's ability to withstand competitive pressures and render the Group's business more vulnerable to economic downturns. If the Group fails to generate or obtain sufficient additional capital in the future, it could be forced to reduce or delay capital expenditures, sell assets or restructure or refinance indebtedness.

Accordingly, the Group's planned and any proposed future expansions and projects may be materially and adversely affected if the Group is unable to obtain funding for such capital expenditures on satisfactory terms, on a timely basis or at all, including as a result of any of the Group's existing facilities becoming repayable before their due dates. In addition, there can be no assurance that the Group's planned or any proposed future expansions and projects will be completed on time or within budget, which may adversely affect the Group's cash flow.

The Group has not obtained certain approvals, permits and licences for the development and operation of several of its existing projects

The Group has not obtained certain approvals, permits and licences for the development and operation of several of its existing projects. These are set out below:

24

● Planting activities have commenced at the Group's rubber plantation project at Chu Prong district, Gia Lai province, although the Group has not been issued with an investment certificate. However, the land area had already been allocated to the Group by the People's Committee of Gia Lai Province. The Group is currently seeking an investment certificate.

● The Group has commenced construction of its hydropower projects at Ba Thuoc 2 and Dakpsi 2B without construction permits. The Group believes that it does not need construction permits for these projects and has received verbal confirmation from the relevant governmental organisations that this is the case. However, it is seeking a formal waiver of the construction permit requirement. It has received such waivers in respect of its other hydropower plants in relation to which construction activities have commenced.

Pursuant to applicable laws and regulations, the Group may be subject to certain potential administrative liabilities and sanctions due to the lack of necessary approvals, such as fines (ranging from VND 10,000,000 to VND 15,000,000 for failure to obtain an investment certificate for a project), temporary or permanent suspension of construction or operations or compulsory termination of investment activities. The Group believes that the risk of such sanctions is remote.

In addition, the development and operation of some of the Group's projects are not in compliance with the applicable laws and regulations, which may cause a material adverse impact on its businesses. The Company's subsidiaries in Cambodia and Laos have historically not been in full compliance with the applicable labour laws and regulations due to their operations without necessary labour registration, social security registration and excessive non-Laotian employees. The Group has already initiated necessary actions to remedy such non-compliance and has not been fined, penalised or received any notice of suspension from the relevant authorities. However, the relevant governmental authorities may still have the power to impose administrative sanctions upon the Group based on certain of its prior non-compliances during the relevant statutory limitation period, within the specified timeframe even though such non-compliances are remedied in the future. In these circumstances, the Group may incur additional financial burdens to pay fines (which cannot be estimated) and it may not be able to maintain its project development schedule due to suspension of operations. However, the Group does not believe that the imposition of such sanctions is likely.

Government regulations impose significant costs on the Group's operations and future regulations could increase those costs or limit the Group's ability to produce and sell its products

The industries which the Group operates are subject to regulation by Vietnamese law with respect to matters such as limitations on land use, employee health and safety, land permits and licensing requirements, water pollution, protection of human health, plant life and wildlife, the discharge of materials into the environment, surface subsidence from underground mining, and reclamation and restoration of properties. In particular, certain statutory and regulatory permits and approvals may be required in order for the Group to carry out its activities and operations. In particular, most of the Group's hydropower, iron ore mining and rubber plantations projects are at an early stage of development. The Group is in varying stages of applying for and obtaining the necessary licences, approvals and permits with respect to each of these projects and in many instances are in direct discussions with the relevant governmental agencies, authorities and ministries to apply for and obtain these licences, approvals and permits. There can be no assurance that the relevant authorities will issue any such permits and approvals in the time frame anticipated, or at all.

Even if the Group obtains the required licences, permits and approvals, its operations may be subject to continued review and the governing regulations are subject to change. Further, the Group's contractors and other counterparties may also be required to obtain approvals, licences, registrations and permits with respect to the services they provide to the Group. There can be no assurance that such contractors or counterparties will have obtained and maintain the validity of such approvals, licences, registrations and permits.

25

The possibility also exists that new legislation and/or regulations and orders may be adopted that may materially adversely affect the Group's operations and cost structure. New legislation or administrative regulations, including proposals related to the protection of environment that would further regulate and tax the industries the Group operates in, may also require the Group or its customers to change operations significantly or incur increased costs. These regulations, if enacted in the future, could have a material adverse effect on the Group's financial condition and results of operations.

The Group's business will be affected if the Group is not able to compete effectively