global entertainment & media outlook 2020-2024 - iab hong

TRANSCRIPT

Global E&M Outlook 2020-2024: Hong Kong summary

Global Entertainment & Media Outlook 2020-2024: Hong Kong summary

October 2020

Global E&M Outlook 2020-2024: Hong Kong summary

Contents

Overview: Entertainment & Media

Outlook - Global and Hong Kong

New trend

Segment deep dive

01

02

03

03

15

32

2

Global E&M Outlook 2020-2024: Hong Kong summary

Overview:

Entertainment &

Media Outlook –

Global and

Hong Kong

3Global E&M Outlook 2020-2024: Hong Kong summary

Global E&M Outlook 2020-2024: Hong Kong summary

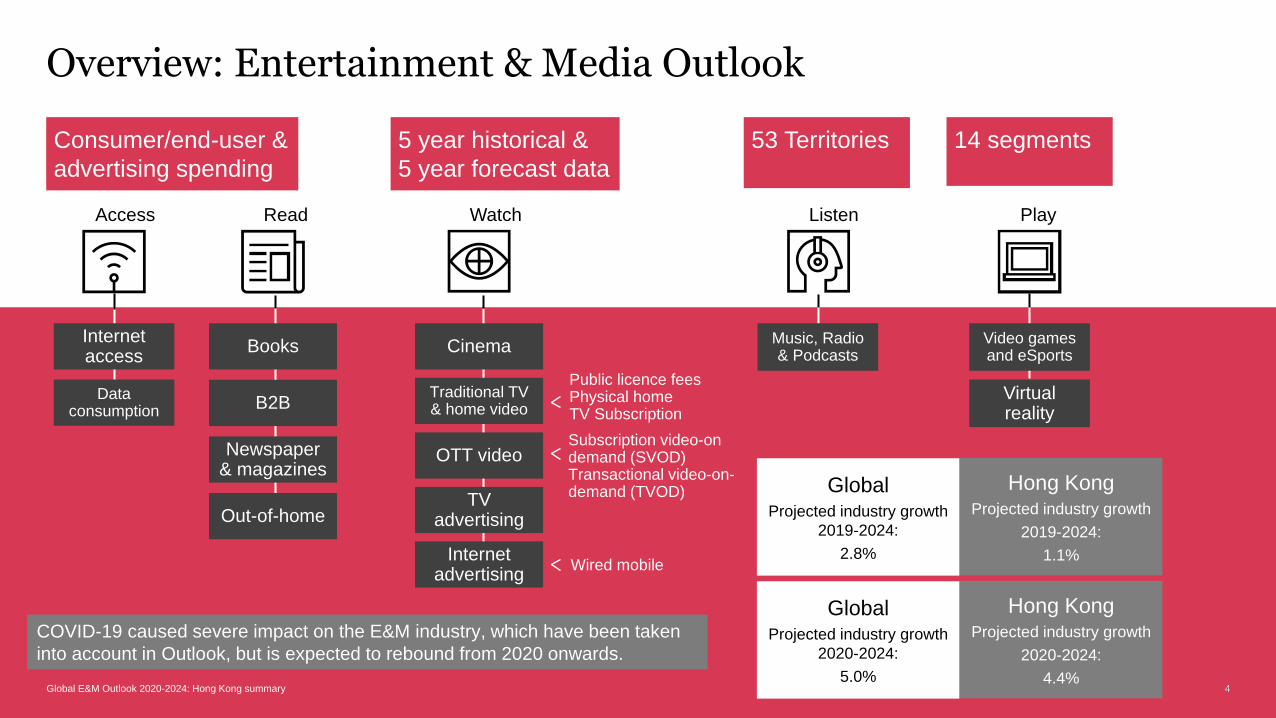

Overview: Entertainment & Media Outlook

4

Hong Kong Projected industry growth

2019-2024:

1.1%

GlobalProjected industry growth

2019-2024:

2.8%

PlayListenWatchReadAccess

Internet access

Books CinemaMusic, Radio& Podcasts

Video games and eSports

B2B

Newspaper & magazines

Out-of-home

Traditional TV & home video

OTT video

TV advertising

Internet advertising

Virtual reality

Consumer/end-user &

advertising spending

5 year historical &

5 year forecast data

53 Territories 14 segments

Wired mobile

Subscription video-on demand (SVOD) Transactional video-on-demand (TVOD)

Public licence feesPhysical homeTV Subscription

Data consumption

4Global E&M Outlook 2020-2024: Hong Kong summary

Hong Kong Projected industry growth

2020-2024:

4.4%

GlobalProjected industry growth

2020-2024:

5.0%

COVID-19 caused severe impact on the E&M industry, which have been taken

into account in Outlook, but is expected to rebound from 2020 onwards.

Global E&M Outlook 2020-2024: Hong Kong summary

Pulling the future forward: The entertainment and media industry reconfigures amid recovery

5

• Consumer habits can take a lifetime to learn—but just a lockdown to

lose. In only a few short months, COVID-19 accelerated ongoing changes in

consumers’ behaviour, pulling forward a series of digital disruptions that would

have occurred in future years

• New opportunities for new business models present themselves to meet

consumers who are predominantly at home and online – businesses are

creating new arrangements and combinations aimed at opening up new

revenue opportunities

• Consumer spending trumps advertising – E&M companies are increasingly

in the business of delivering experiences and content directly to consumers,

not delivering audiences and eyeballs to advertisers

• Reconfiguration is underway as consumers and businesses adapt. Although

there will still be challenges for E&M companies as we move beyond the

pandemic, the digital migration that it has pulled forward will also generate

opportunities in all segments

Global Entertainment & Media Outlook perspectives

Overview: Entertainment & Media Outlook – Global and Hong Kong

Global E&M Outlook 2020-2024: Hong Kong summary

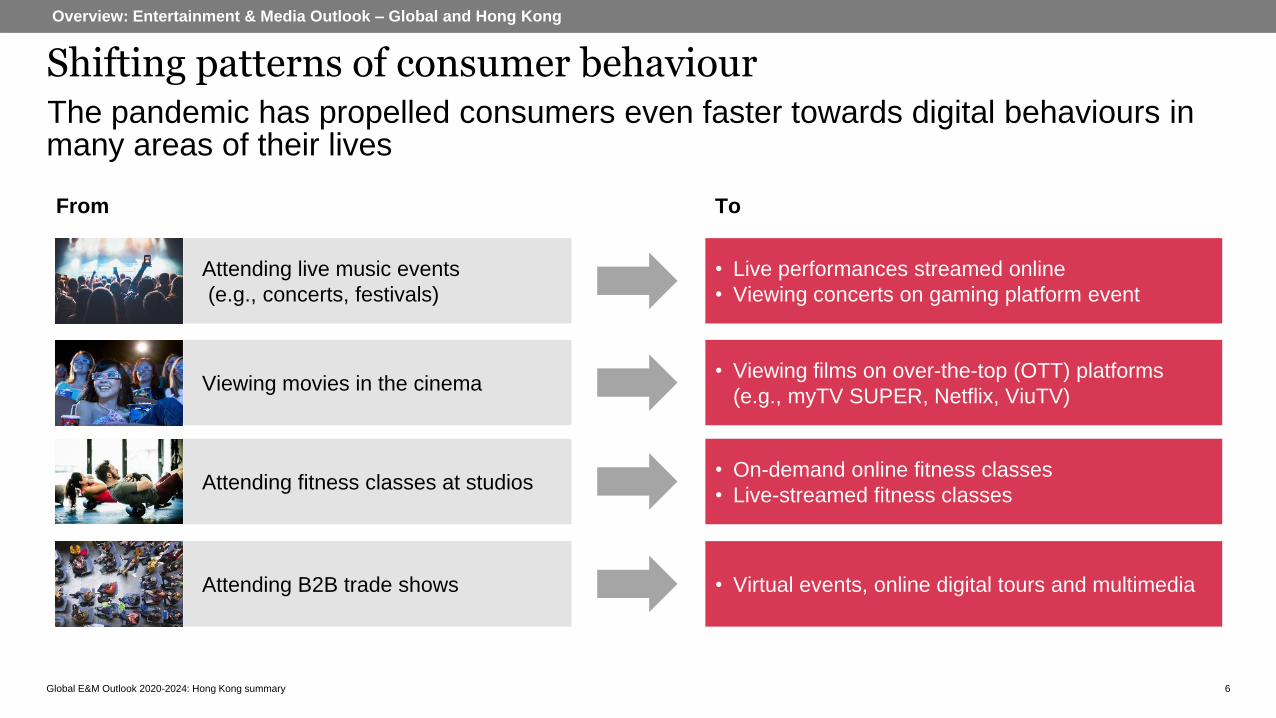

Shifting patterns of consumer behaviour

6

The pandemic has propelled consumers even faster towards digital behaviours in many areas of their lives

Overview: Entertainment & Media Outlook – Global and Hong Kong

From To

Attending live music events

(e.g., concerts, festivals)

Viewing movies in the cinema

Attending fitness classes at studios

• Live performances streamed online

• Viewing concerts on gaming platform event

• Viewing films on over-the-top (OTT) platforms

(e.g., myTV SUPER, Netflix, ViuTV)

• On-demand online fitness classes

• Live-streamed fitness classes

Attending B2B trade shows • Virtual events, online digital tours and multimedia

Global E&M Outlook 2020-2024: Hong Kong summary

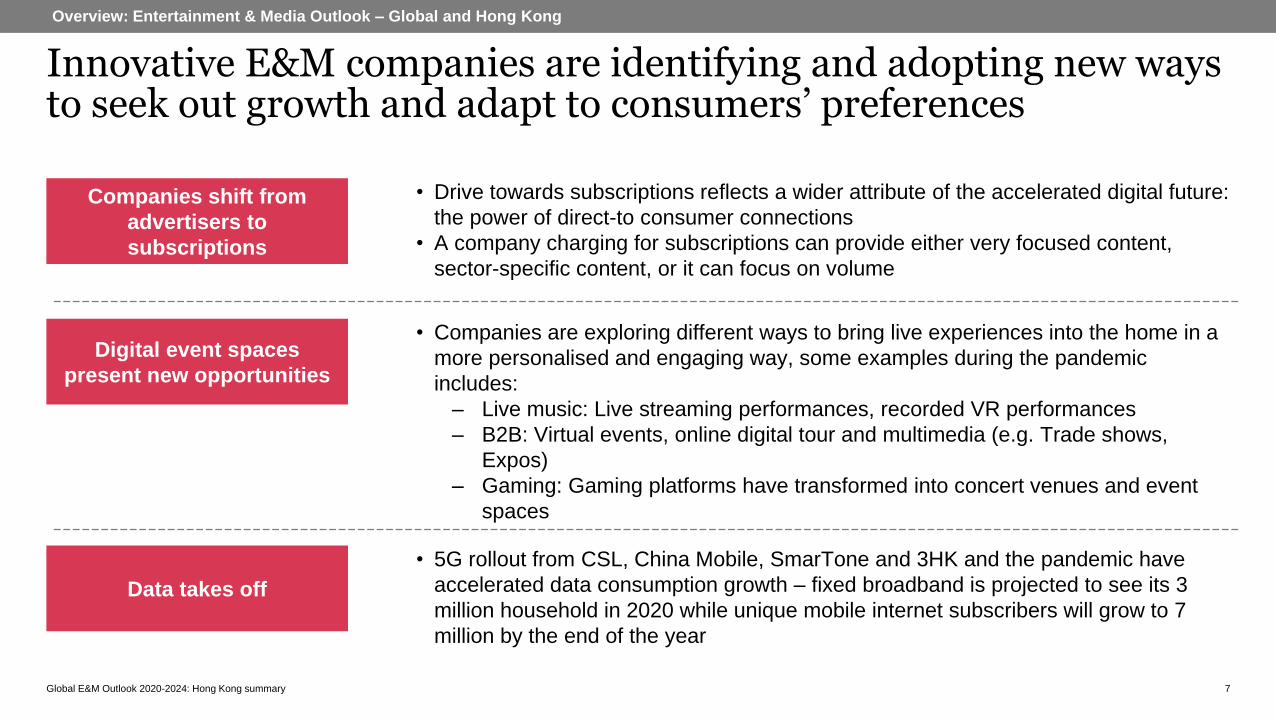

Innovative E&M companies are identifying and adopting new ways to seek out growth and adapt to consumers’ preferences

7

Overview: Entertainment & Media Outlook – Global and Hong Kong

Companies shift from

advertisers to

subscriptions

• Drive towards subscriptions reflects a wider attribute of the accelerated digital future:

the power of direct-to consumer connections

• A company charging for subscriptions can provide either very focused content,

sector-specific content, or it can focus on volume

Digital event spaces

present new opportunities

• Companies are exploring different ways to bring live experiences into the home in a

more personalised and engaging way, some examples during the pandemic

includes:

– Live music: Live streaming performances, recorded VR performances

– B2B: Virtual events, online digital tour and multimedia (e.g. Trade shows,

Expos)

– Gaming: Gaming platforms have transformed into concert venues and event

spaces

Data takes off

• 5G rollout from CSL, China Mobile, SmarTone and 3HK and the pandemic have

accelerated data consumption growth – fixed broadband is projected to see its 3

million household in 2020 while unique mobile internet subscribers will grow to 7

million by the end of the year

Global E&M Outlook 2020-2024: Hong Kong summary

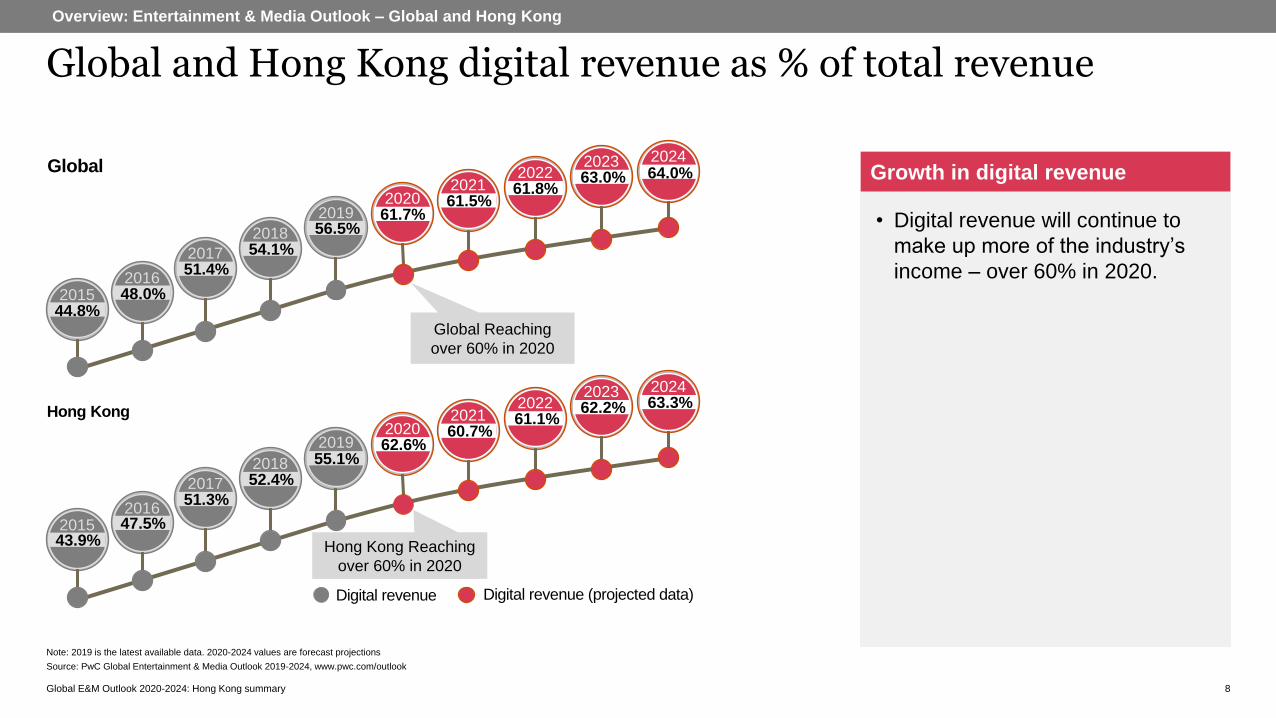

Global and Hong Kong digital revenue as % of total revenue

8

Overview: Entertainment & Media Outlook – Global and Hong Kong

• Digital revenue will continue to

make up more of the industry’s

income – over 60% in 2020.

Growth in digital revenue

在过去21年历史中,从未出现过如此糟糕的年份

Digital revenue Digital revenue (projected data)

44.8%2015 48.0%

201651.4%2017 54.1%

2018 56.5%2019 61.7%

2020 61.5%2021 61.8%

2022 63.0%2023

64.0%2024

Global Reaching

over 60% in 2020

43.9%2015 47.5%

201651.3%2017 52.4%

2018 55.1%2019 62.6%

2020 60.7%2021 61.1%

2022 62.2%2023

63.3%2024

Hong Kong Reaching

over 60% in 2020

Global

Hong Kong

Note: 2019 is the latest available data. 2020-2024 values are forecast projections

Source: PwC Global Entertainment & Media Outlook 2019-2024, www.pwc.com/outlook

Global E&M Outlook 2020-2024: Hong Kong summary

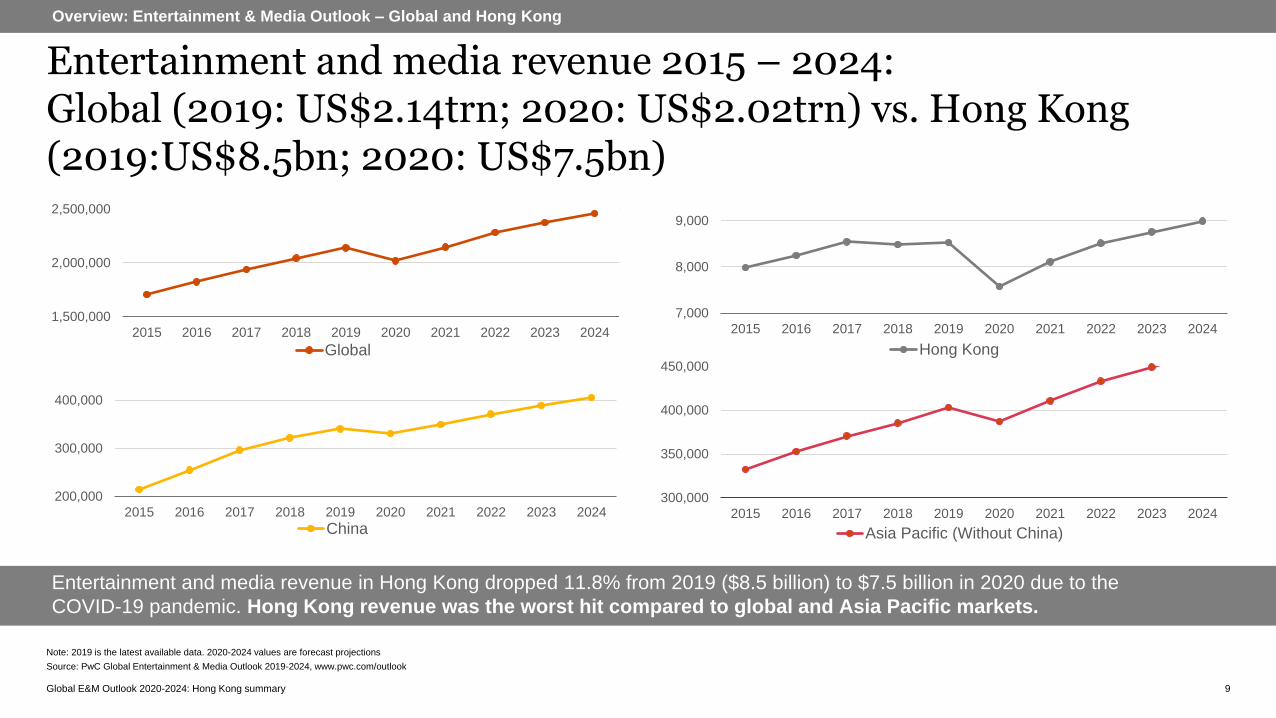

Entertainment and media revenue 2015 – 2024:Global (2019: US$2.14trn; 2020: US$2.02trn) vs. Hong Kong (2019:US$8.5bn; 2020: US$7.5bn)

9

Overview: Entertainment & Media Outlook – Global and Hong Kong

Entertainment and media revenue in Hong Kong dropped 11.8% from 2019 ($8.5 billion) to $7.5 billion in 2020 due to the

COVID-19 pandemic. Hong Kong revenue was the worst hit compared to global and Asia Pacific markets.

2019至2024年复合年均增长率(有/无互联网接入)

1,500,000

2,000,000

2,500,000

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024

Global

7,000

8,000

9,000

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024

Hong Kong

Note: 2019 is the latest available data. 2020-2024 values are forecast projections

Source: PwC Global Entertainment & Media Outlook 2019-2024, www.pwc.com/outlook

200,000

300,000

400,000

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024

China

300,000

350,000

400,000

450,000

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024

Asia Pacific (Without China)

Global E&M Outlook 2020-2024: Hong Kong summary

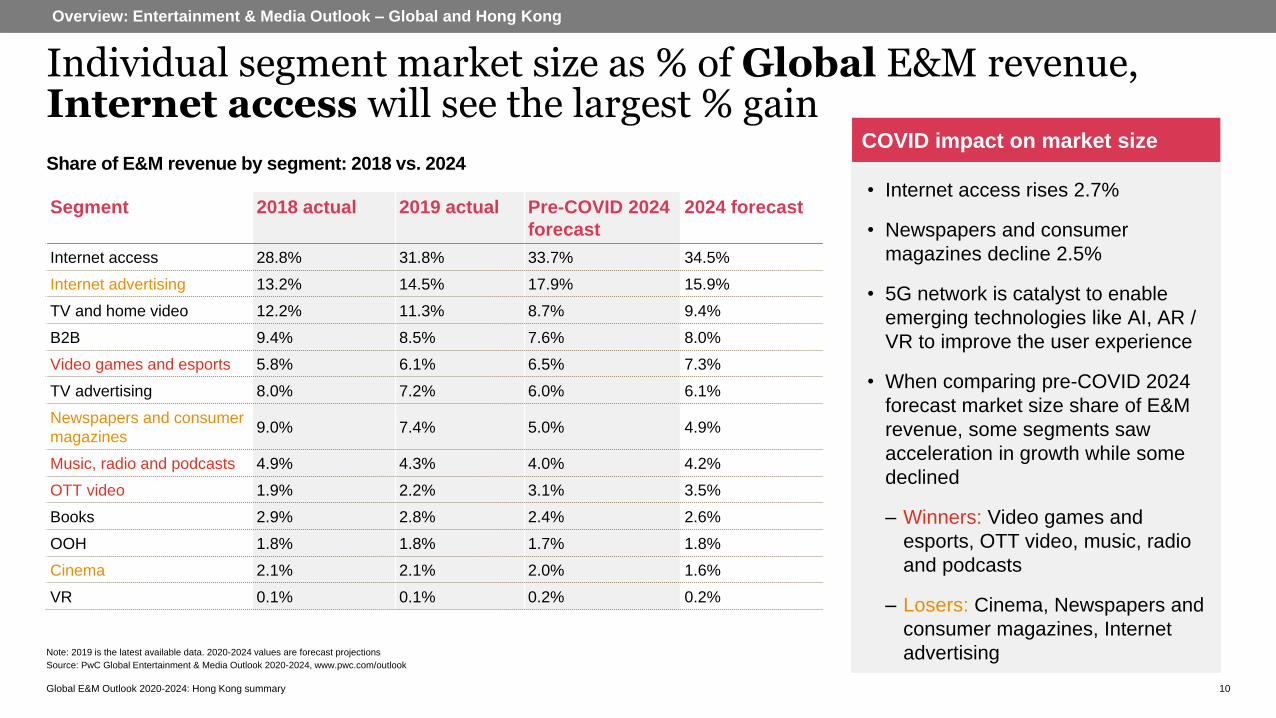

Individual segment market size as % of Global E&M revenue, Internet access will see the largest % gain

10

Overview: Entertainment & Media Outlook – Global and Hong Kong

Source: PwC Global Entertainment & Media Outlook 2020-2024, www.pwc.com/outlook

Note: 2019 is the latest available data. 2020-2024 values are forecast projections

Segment 2018 actual 2019 actual Pre-COVID 2024

forecast

2024 forecast

Internet access 28.8% 31.8% 33.7% 34.5%

Internet advertising 13.2% 14.5% 17.9% 15.9%

TV and home video 12.2% 11.3% 8.7% 9.4%

B2B 9.4% 8.5% 7.6% 8.0%

Video games and esports 5.8% 6.1% 6.5% 7.3%

TV advertising 8.0% 7.2% 6.0% 6.1%

Newspapers and consumer

magazines9.0% 7.4% 5.0% 4.9%

Music, radio and podcasts 4.9% 4.3% 4.0% 4.2%

OTT video 1.9% 2.2% 3.1% 3.5%

Books 2.9% 2.8% 2.4% 2.6%

OOH 1.8% 1.8% 1.7% 1.8%

Cinema 2.1% 2.1% 2.0% 1.6%

VR 0.1% 0.1% 0.2% 0.2%

Share of E&M revenue by segment: 2018 vs. 2024

• Internet access rises 2.7%

• Newspapers and consumer

magazines decline 2.5%

• 5G network is catalyst to enable

emerging technologies like AI, AR /

VR to improve the user experience

• When comparing pre-COVID 2024

forecast market size share of E&M

revenue, some segments saw

acceleration in growth while some

declined

– Winners: Video games and

esports, OTT video, music, radio

and podcasts

– Losers: Cinema, Newspapers and

consumer magazines, Internet

advertising

COVID impact on market size

Global E&M Outlook 2020-2024: Hong Kong summary

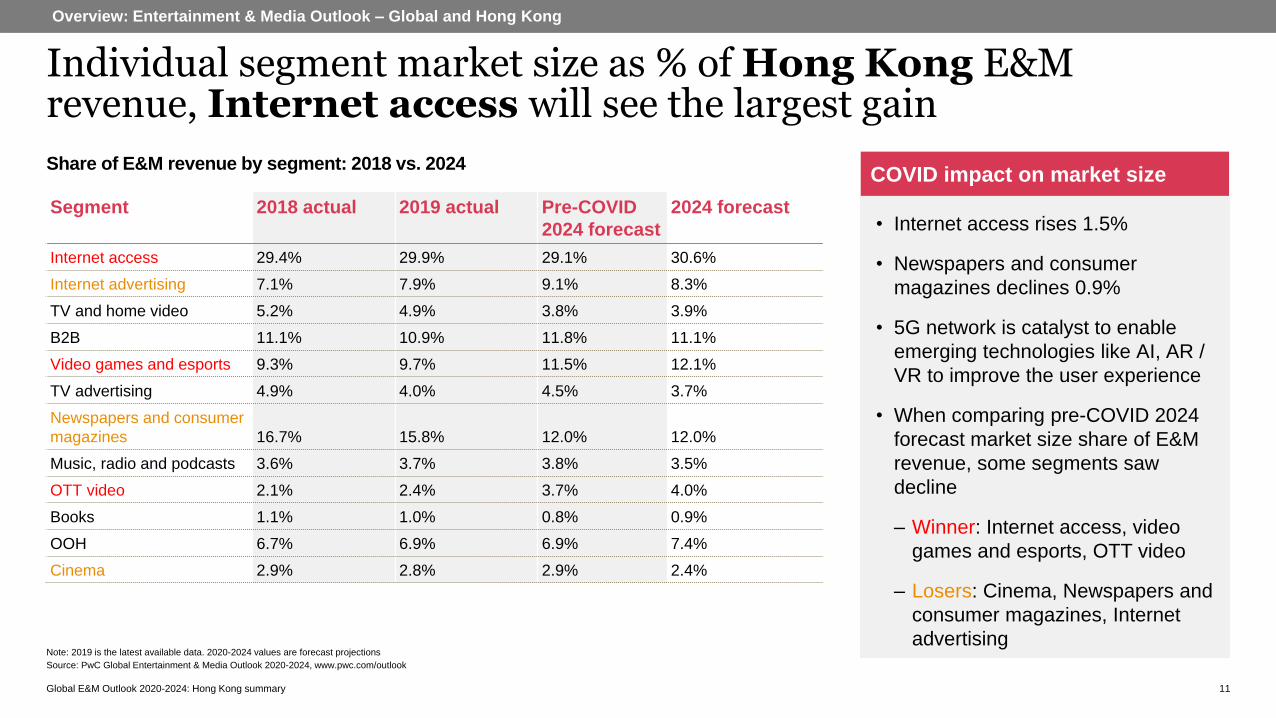

Individual segment market size as % of Hong Kong E&M revenue, Internet access will see the largest gain

11

Overview: Entertainment & Media Outlook – Global and Hong Kong

Source: PwC Global Entertainment & Media Outlook 2020-2024, www.pwc.com/outlook

Note: 2019 is the latest available data. 2020-2024 values are forecast projections

Segment 2018 actual 2019 actual Pre-COVID

2024 forecast

2024 forecast

Internet access 29.4% 29.9% 29.1% 30.6%

Internet advertising 7.1% 7.9% 9.1% 8.3%

TV and home video 5.2% 4.9% 3.8% 3.9%

B2B 11.1% 10.9% 11.8% 11.1%

Video games and esports 9.3% 9.7% 11.5% 12.1%

TV advertising 4.9% 4.0% 4.5% 3.7%

Newspapers and consumer

magazines 16.7% 15.8% 12.0% 12.0%

Music, radio and podcasts 3.6% 3.7% 3.8% 3.5%

OTT video 2.1% 2.4% 3.7% 4.0%

Books 1.1% 1.0% 0.8% 0.9%

OOH 6.7% 6.9% 6.9% 7.4%

Cinema 2.9% 2.8% 2.9% 2.4%

Share of E&M revenue by segment: 2018 vs. 2024

• Internet access rises 1.5%

• Newspapers and consumer

magazines declines 0.9%

• 5G network is catalyst to enable

emerging technologies like AI, AR /

VR to improve the user experience

• When comparing pre-COVID 2024

forecast market size share of E&M

revenue, some segments saw

decline

– Winner: Internet access, video

games and esports, OTT video

– Losers: Cinema, Newspapers and

consumer magazines, Internet

advertising

COVID impact on market size

Global E&M Outlook 2020-2024: Hong Kong summary

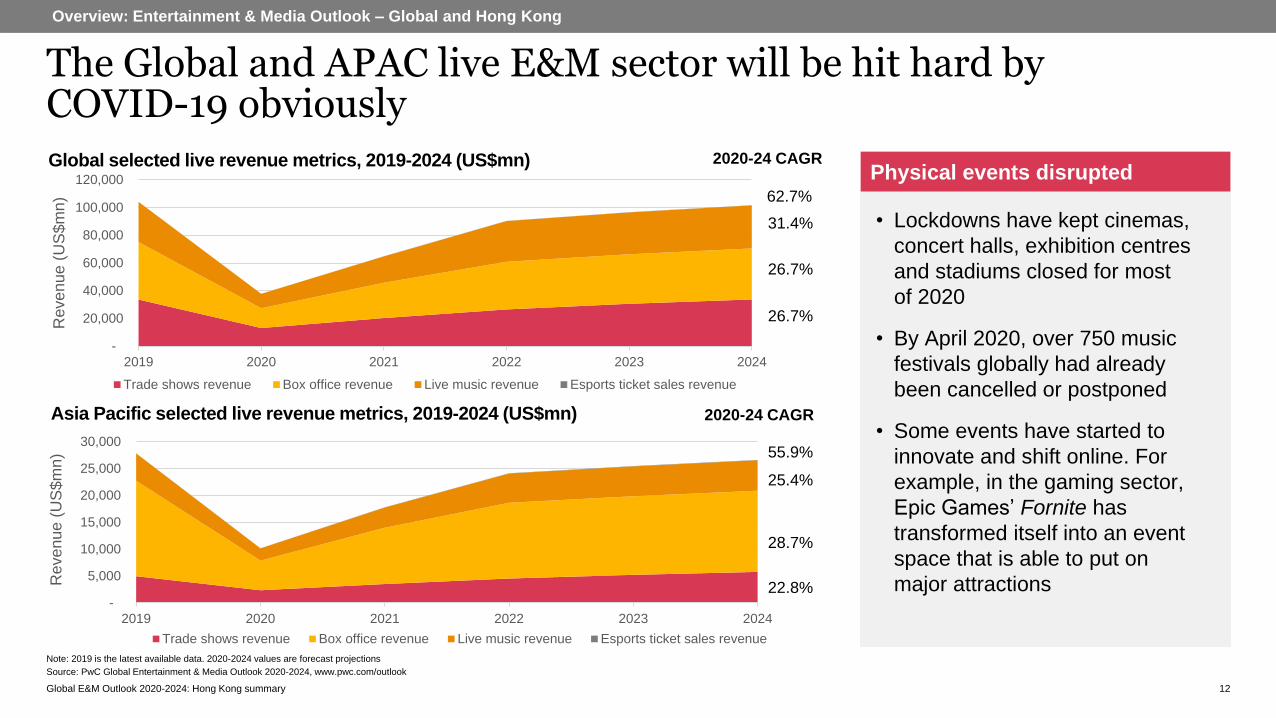

The Global and APAC live E&M sector will be hit hard by COVID-19 obviously

12

Overview: Entertainment & Media Outlook – Global and Hong Kong

Source: PwC Global Entertainment & Media Outlook 2020-2024, www.pwc.com/outlook

Note: 2019 is the latest available data. 2020-2024 values are forecast projections

Global selected live revenue metrics, 2019-2024 (US$mn)

• Lockdowns have kept cinemas,

concert halls, exhibition centres

and stadiums closed for most

of 2020

• By April 2020, over 750 music

festivals globally had already

been cancelled or postponed

• Some events have started to

innovate and shift online. For

example, in the gaming sector,

Epic Games’ Fornite has

transformed itself into an event

space that is able to put on

major attractions

Physical events disrupted

-

20,000

40,000

60,000

80,000

100,000

120,000

2019 2020 2021 2022 2023 2024

Revenue (

US

$m

n)

Trade shows revenue Box office revenue Live music revenue Esports ticket sales revenue

Asia Pacific selected live revenue metrics, 2019-2024 (US$mn)

-

5,000

10,000

15,000

20,000

25,000

30,000

2019 2020 2021 2022 2023 2024

Revenue (

US

$m

n)

Trade shows revenue Box office revenue Live music revenue Esports ticket sales revenue

55.9%

2020-24 CAGR

25.4%

28.7%

22.8%

62.7%

2020-24 CAGR

31.4%

26.7%

26.7%

Global E&M Outlook 2020-2024: Hong Kong summary

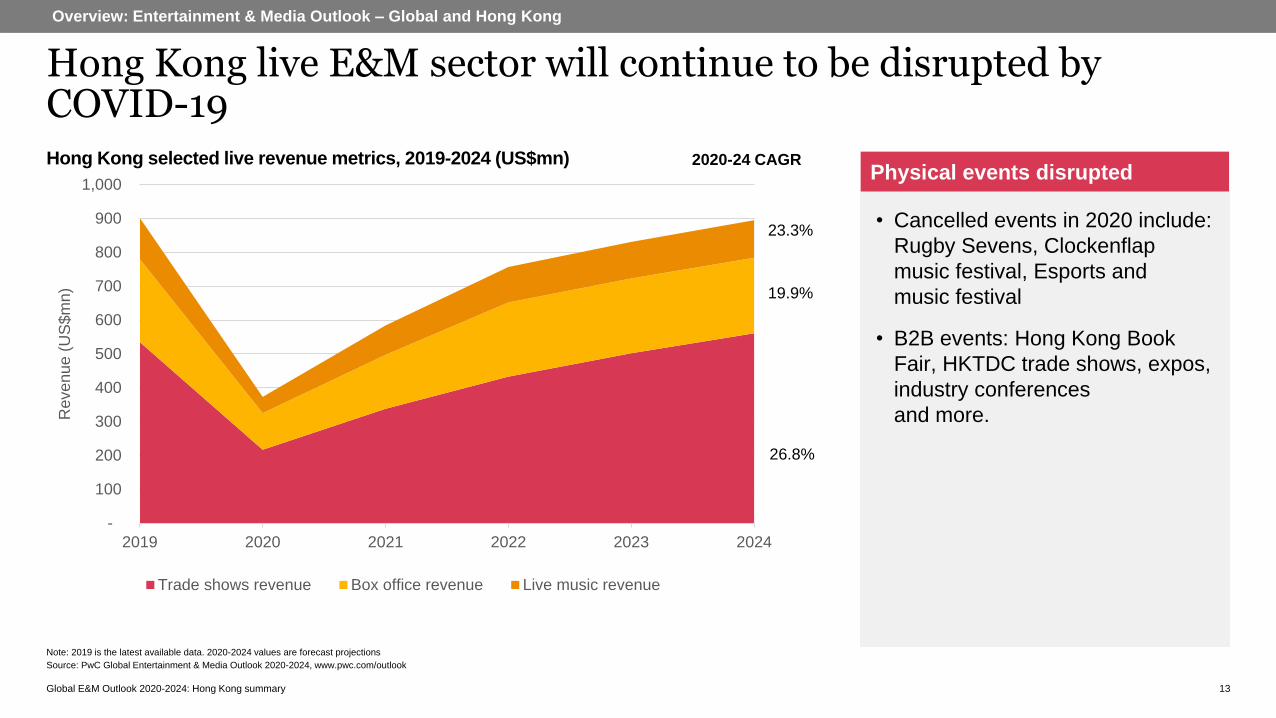

Hong Kong live E&M sector will continue to be disrupted by COVID-19

13

Overview: Entertainment & Media Outlook – Global and Hong Kong

Source: PwC Global Entertainment & Media Outlook 2020-2024, www.pwc.com/outlook

Note: 2019 is the latest available data. 2020-2024 values are forecast projections

Hong Kong selected live revenue metrics, 2019-2024 (US$mn)

-

100

200

300

400

500

600

700

800

900

1,000

2019 2020 2021 2022 2023 2024

Reven

ue (

US

$m

n)

Trade shows revenue Box office revenue Live music revenue

23.3%

2020-24 CAGR

19.9%

26.8%

• Cancelled events in 2020 include:

Rugby Sevens, Clockenflap

music festival, Esports and

music festival

• B2B events: Hong Kong Book

Fair, HKTDC trade shows, expos,

industry conferences

and more.

Physical events disrupted

Global E&M Outlook 2020-2024: Hong Kong summary

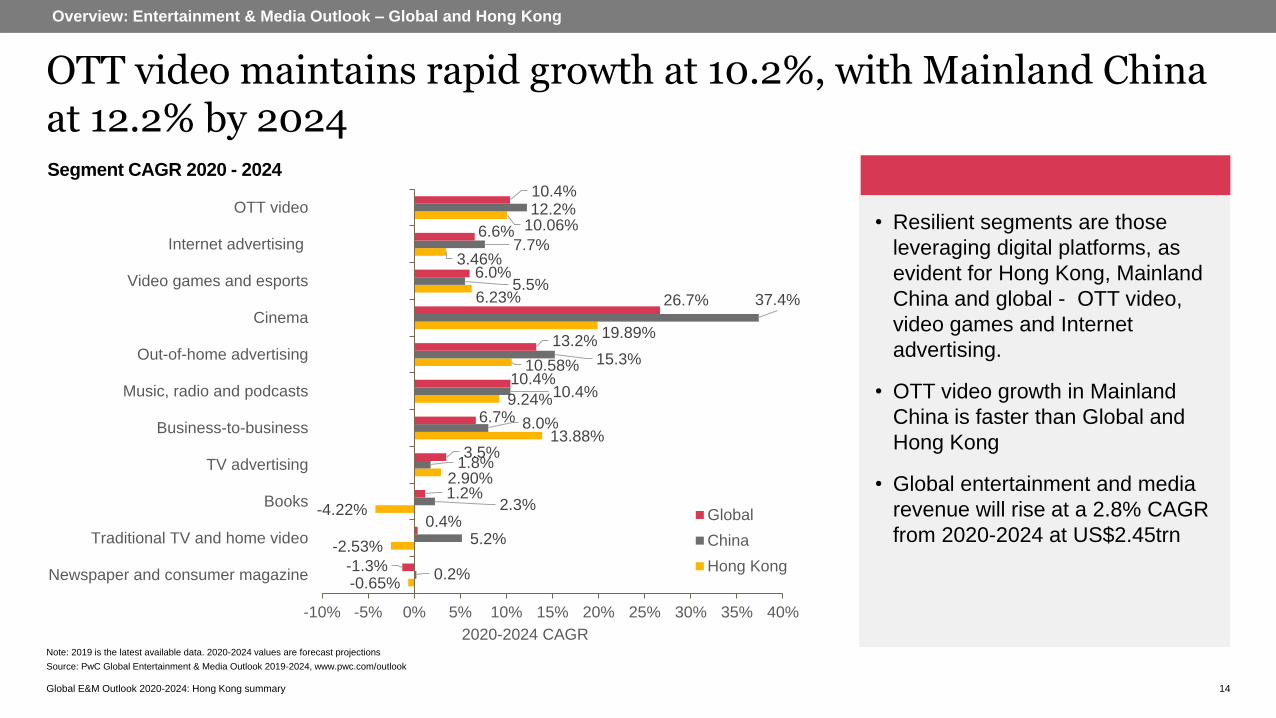

Segment CAGR 2020 - 2024

Note: 2019 is the latest available data. 2020-2024 values are forecast projections

Source: PwC Global Entertainment & Media Outlook 2019-2024, www.pwc.com/outlook

14

Overview: Entertainment & Media Outlook – Global and Hong Kong

• Resilient segments are those

leveraging digital platforms, as

evident for Hong Kong, Mainland

China and global - OTT video,

video games and Internet

advertising.

• OTT video growth in Mainland

China is faster than Global and

Hong Kong

• Global entertainment and media

revenue will rise at a 2.8% CAGR

from 2020-2024 at US$2.45trn

OTT video maintains rapid growth at 10.2%, with Mainland China at 12.2% by 2024

-0.65%

-2.53%

-4.22%

2.90%

13.88%

9.24%

10.58%

19.89%

6.23%

3.46%

10.06%

0.2%

5.2%

2.3%

1.8%

8.0%

10.4%

15.3%

37.4%5.5%

7.7%

12.2%

-1.3%

0.4%

1.2%

3.5%

6.7%

10.4%

13.2%

26.7%

6.0%

6.6%

10.4%

-10% -5% 0% 5% 10% 15% 20% 25% 30% 35% 40%

Newspaper and consumer magazine

Traditional TV and home video

Books

TV advertising

Business-to-business

Music, radio and podcasts

Out-of-home advertising

Cinema

Video games and esports

Internet advertising

OTT video

2020-2024 CAGR

Global

China

Hong Kong

Global E&M Outlook 2020-2024: Hong Kong summary

Segment

deep dives

15Global E&M Outlook 2020-2024: Hong Kong summary

Global E&M Outlook 2020-2024: Hong Kong summary

Segment

deep diveInternet advertising

16Global E&M Outlook 2020-2024: Hong Kong summary

Global E&M Outlook 2020-2024: Hong Kong summary

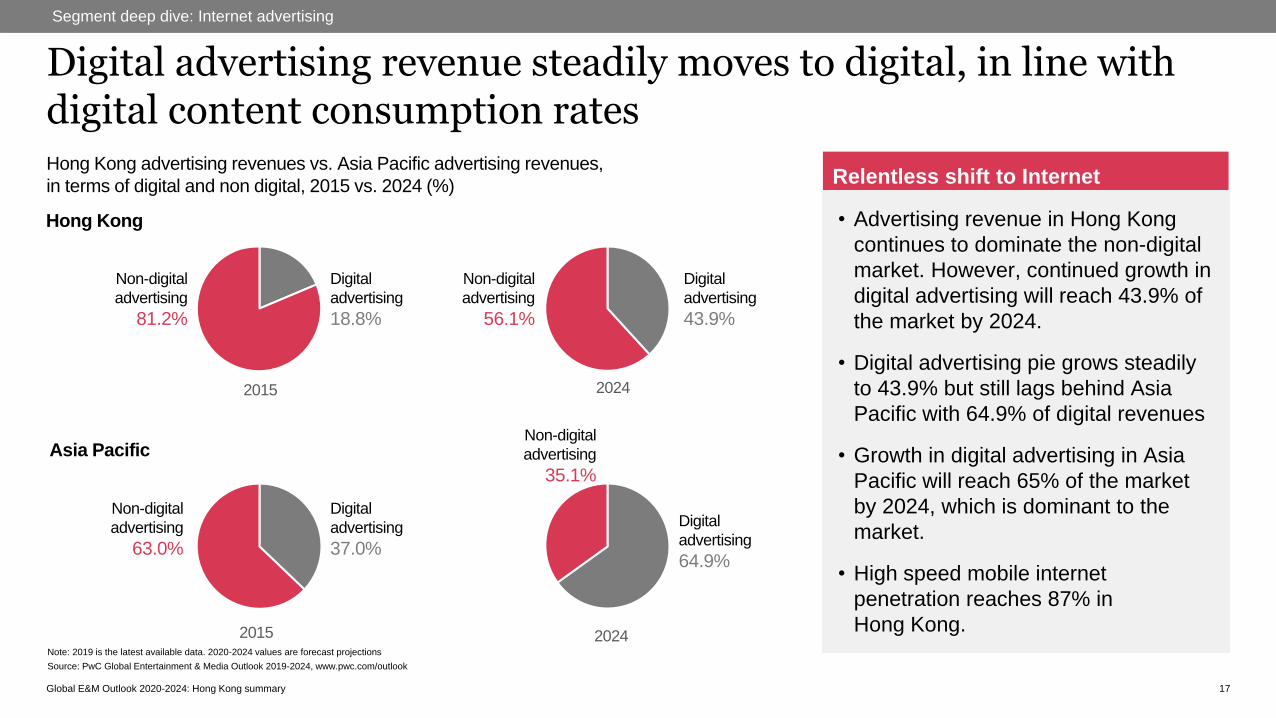

Relentless shift to Internet

17

Hong Kong advertising revenues vs. Asia Pacific advertising revenues,

in terms of digital and non digital, 2015 vs. 2024 (%)

Segment deep dive: Internet advertising

• Advertising revenue in Hong Kong

continues to dominate the non-digital

market. However, continued growth in

digital advertising will reach 43.9% of

the market by 2024.

• Digital advertising pie grows steadily

to 43.9% but still lags behind Asia

Pacific with 64.9% of digital revenues

• Growth in digital advertising in Asia

Pacific will reach 65% of the market

by 2024, which is dominant to the

market.

• High speed mobile internet

penetration reaches 87% in

Hong Kong.

Digital advertising revenue steadily moves to digital, in line with digital content consumption rates

17

2015 2024

Digital

advertising

18.8%

Non-digital

advertising

81.2%

Digital

advertising

43.9%

Non-digital

advertising

56.1%

Note: 2019 is the latest available data. 2020-2024 values are forecast projections

Source: PwC Global Entertainment & Media Outlook 2019-2024, www.pwc.com/outlook

Digital

advertising

37.0%

Non-digital

advertising

63.0%

2015 2024

Digital

advertising

64.9%

Non-digital

advertising

35.1%

Hong Kong

Asia Pacific

Global E&M Outlook 2020-2024: Hong Kong summary

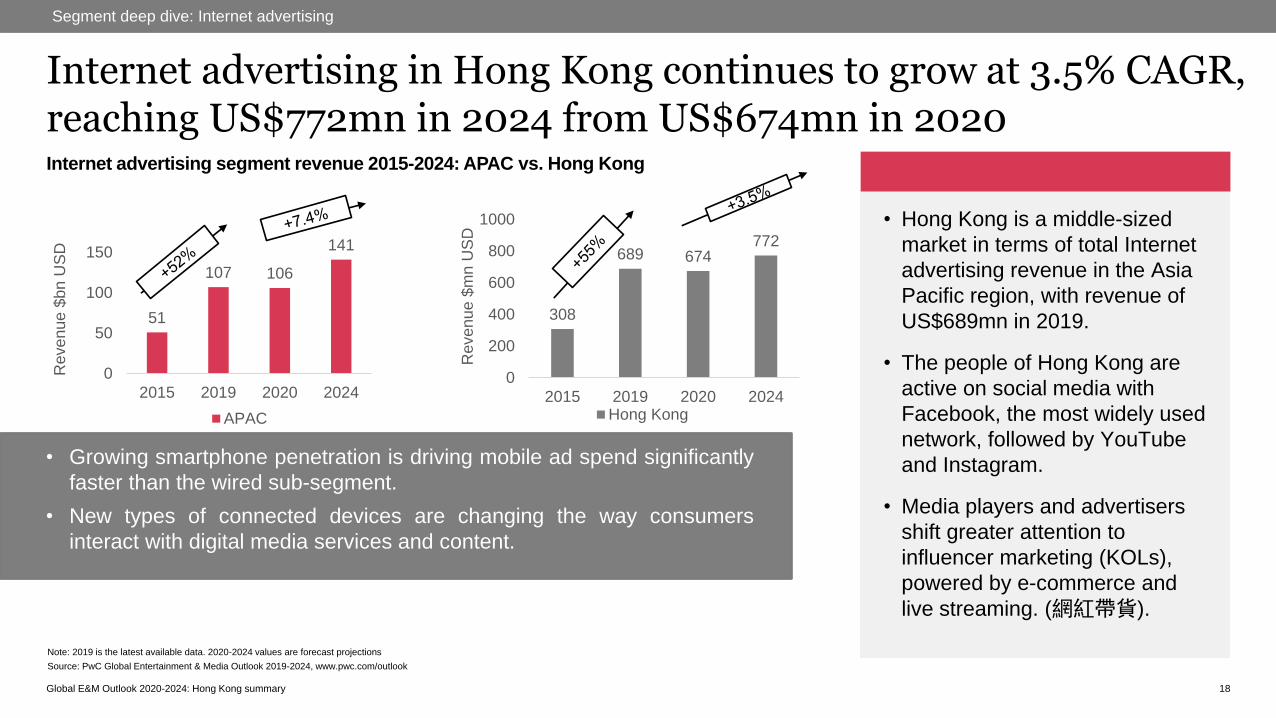

• Growing smartphone penetration is driving mobile ad spend significantly

faster than the wired sub-segment.

• New types of connected devices are changing the way consumers

interact with digital media services and content.

Internet advertising segment revenue 2015-2024: APAC vs. Hong Kong

308

689 674772

0

200

400

600

800

1000

2015 2019 2020 2024

Revenue $

mn U

SD

Hong Kong

51

107 106

141

0

50

100

150

2015 2019 2020 2024

Revenue $

bn U

SD

APAC

Segment deep dive: Internet advertising

18

• Hong Kong is a middle-sized

market in terms of total Internet

advertising revenue in the Asia

Pacific region, with revenue of

US$689mn in 2019.

• The people of Hong Kong are

active on social media with

Facebook, the most widely used

network, followed by YouTube

and Instagram.

• Media players and advertisers

shift greater attention to

influencer marketing (KOLs),

powered by e-commerce and

live streaming. (網紅帶貨).

Internet advertising in Hong Kong continues to grow at 3.5% CAGR, reaching US$772mn in 2024 from US$674mn in 2020

Note: 2019 is the latest available data. 2020-2024 values are forecast projections

Source: PwC Global Entertainment & Media Outlook 2019-2024, www.pwc.com/outlook

Global E&M Outlook 2020-2024: Hong Kong summary

至 2024年来自中国 OTT 视频市场的收入

Segment deep dive: Internet advertising

19

• Hong Kong wired internet

advertising remains stagnant.

• Mobile internet advertising is

growing at 7.62% CAGR and

gaining market share.

• In line with 5G uptake and rising

consumption of OTT video, this

will spur growth in mobile internet

advertising.

Mobile Internet advertising growth at 7.62% CAGR to reach US$377mn in 2024, bypassing wired paid search

0

50

100

150

200

250

300

350

400

HK Mobile Internet advertising

HK Wired paid search Internet advertising

0

50

100

150

200

250

300

350

400

450

HK Mobile Internet advertisingHK Wired Internet advertising

Hong Kong mobile vs. wired Internet

advertising revenue (US$ mn)

Hong Kong mobile Internet advertising

vs. wired paid search Internet

advertising revenue(US$ mn)

7.62%

2020--24

CAGR

0.13%

2020--24

CAGR

7.62%

2020--24

CAGR

-0.92%

2020--24

CAGR

Note: 2019 is the latest available data. 2020-2024 values are forecast projections

Source: PwC Global Entertainment & Media Outlook 2019-2024, www.pwc.com/outlook

Revenue $

mn U

SD

Revenue $

mn U

SD

Global E&M Outlook 2020-2024: Hong Kong summary 20

Segment deep dive: Internet advertising

Hong Kong mobile video Internet advertising vs total wired display Internet

advertising 2015-2024 (US$ mn)

Video will become an increasingly

important part of the mobile display

mix due to:

• Continued focus on video by

mobile social platforms;

• Shifts towards out-stream video

inventory on publishers’ mobile

sites and apps;

• Increased mobile video

consumption driven by faster and

more reliable mobile connectivity.

Importance of mobile video

advertising rises

0

20

40

60

80

100

120

140

160

180

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024

Mobile other display Internet advertising

Mobile video Internet advertising

Mobile paid search Internet advertising

5.33%

2020--24

CAGR

11.47%

2020--24

CAGR

8.23%

2020--24

CAGR

Hong Kong mobile video Internet advertising grows at 11.47% to US$57mn in 2020, similar to Asia Pacific growth of 19.24%

Note: 2019 is the latest available data. 2020-2024 values are forecast projections

Source: PwC Global Entertainment & Media Outlook 2019-2024, www.pwc.com/outlook

Global E&M Outlook 2020-2024: Hong Kong summary

Segment deep diveOTT video

21Global E&M Outlook 2020-2024: Hong Kong summary

Global E&M Outlook 2020-2024: Hong Kong summary

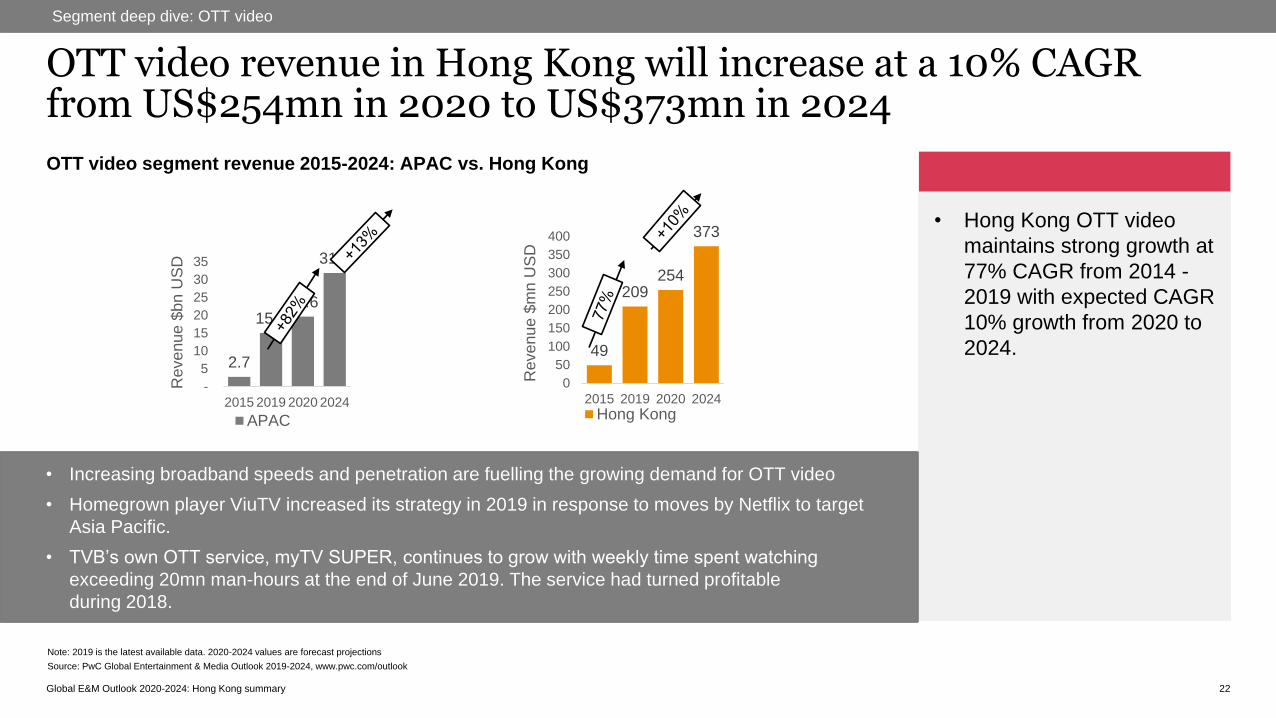

OTT video segment revenue 2015-2024: APAC vs. Hong Kong

Segment deep dive: OTT video

22

OTT video revenue in Hong Kong will increase at a 10% CAGR from US$254mn in 2020 to US$373mn in 2024

• Hong Kong OTT video

maintains strong growth at

77% CAGR from 2014 -

2019 with expected CAGR

10% growth from 2020 to

2024.

• Increasing broadband speeds and penetration are fuelling the growing demand for OTT video

• Homegrown player ViuTV increased its strategy in 2019 in response to moves by Netflix to target

Asia Pacific.

• TVB’s own OTT service, myTV SUPER, continues to grow with weekly time spent watching

exceeding 20mn man-hours at the end of June 2019. The service had turned profitable

during 2018.

Note: 2019 is the latest available data. 2020-2024 values are forecast projections

Source: PwC Global Entertainment & Media Outlook 2019-2024, www.pwc.com/outlook

2.7

15.019.6

31.9

-

5

10

15

20

25

30

35

2015 2019 2020 2024

Revenue $

bn U

SD

APAC

49

209254

373

0

50

100

150

200

250

300

350

400

2015 2019 2020 2024

Revenue $

mn U

SD

Hong Kong

Global E&M Outlook 2020-2024: Hong Kong summary

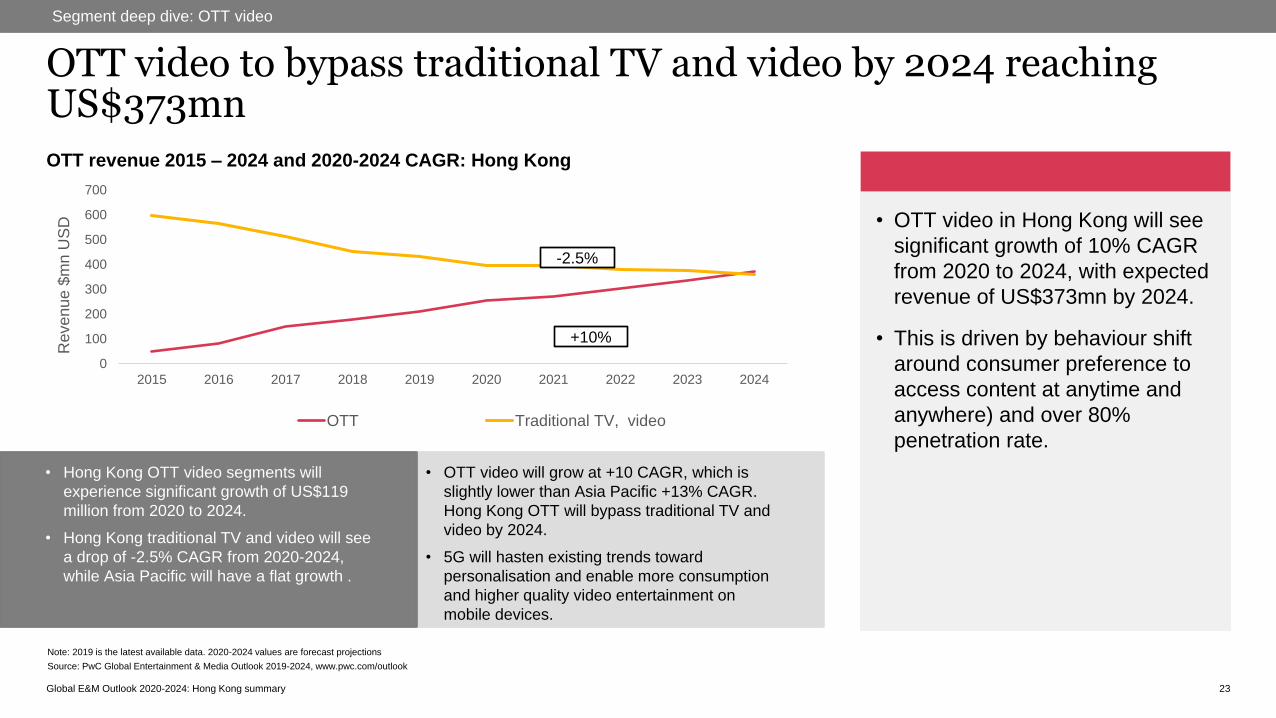

OTT revenue 2015 – 2024 and 2020-2024 CAGR: Hong Kong

Segment deep dive: OTT video

23

OTT video to bypass traditional TV and video by 2024 reaching US$373mn

• OTT video in Hong Kong will see

significant growth of 10% CAGR

from 2020 to 2024, with expected

revenue of US$373mn by 2024.

• This is driven by behaviour shift

around consumer preference to

access content at anytime and

anywhere) and over 80%

penetration rate.

• OTT video will grow at +10 CAGR, which is

slightly lower than Asia Pacific +13% CAGR.

Hong Kong OTT will bypass traditional TV and

video by 2024.

• 5G will hasten existing trends toward

personalisation and enable more consumption

and higher quality video entertainment on

mobile devices.

• Hong Kong OTT video segments will

experience significant growth of US$119

million from 2020 to 2024.

• Hong Kong traditional TV and video will see

a drop of -2.5% CAGR from 2020-2024,

while Asia Pacific will have a flat growth .

Note: 2019 is the latest available data. 2020-2024 values are forecast projections

Source: PwC Global Entertainment & Media Outlook 2019-2024, www.pwc.com/outlook

0

100

200

300

400

500

600

700

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024

Revenue $

mn U

SD

OTT Traditional TV, video

-2.5%

+10%

Global E&M Outlook 2020-2024: Hong Kong summary

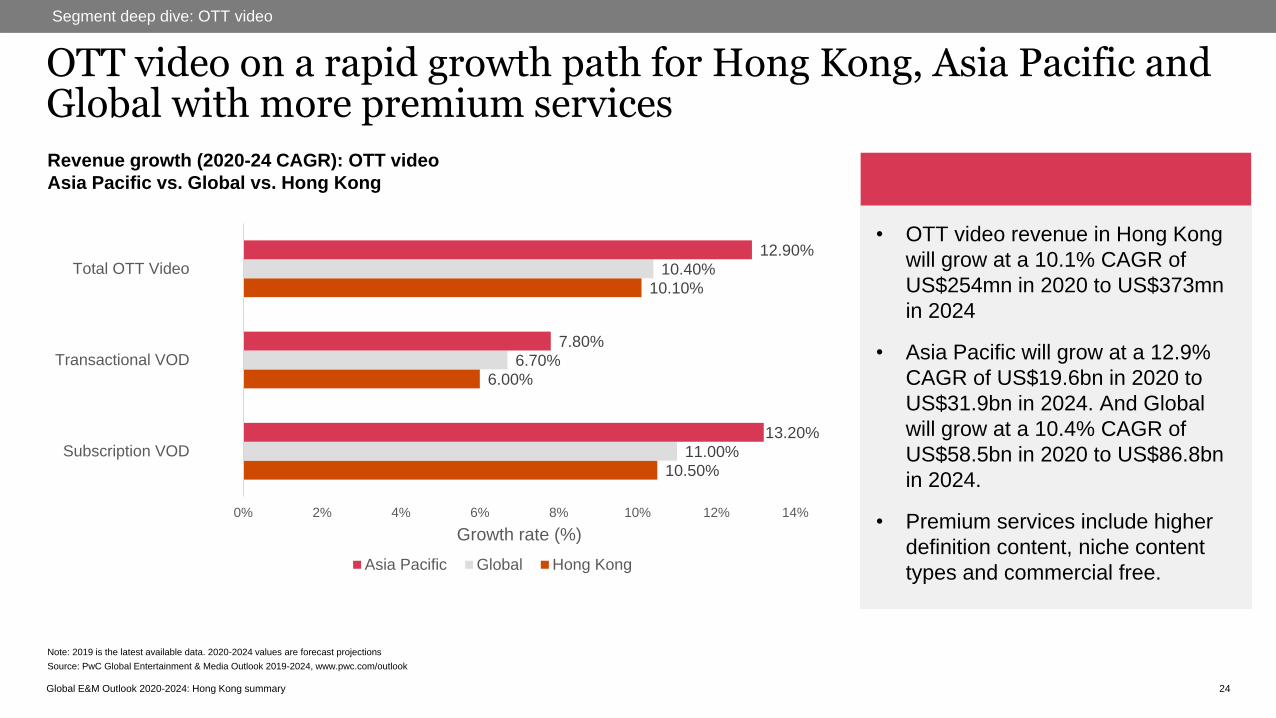

Revenue growth (2020-24 CAGR): OTT video

Asia Pacific vs. Global vs. Hong Kong

Segment deep dive: OTT video

24

OTT video on a rapid growth path for Hong Kong, Asia Pacific and Global with more premium services

Note: 2019 is the latest available data. 2020-2024 values are forecast projections

Source: PwC Global Entertainment & Media Outlook 2019-2024, www.pwc.com/outlook

• OTT video revenue in Hong Kong

will grow at a 10.1% CAGR of

US$254mn in 2020 to US$373mn

in 2024

• Asia Pacific will grow at a 12.9%

CAGR of US$19.6bn in 2020 to

US$31.9bn in 2024. And Global

will grow at a 10.4% CAGR of

US$58.5bn in 2020 to US$86.8bn

in 2024.

• Premium services include higher

definition content, niche content

types and commercial free.

10.50%

6.00%

10.10%

11.00%

6.70%

10.40%

13.20%

7.80%

12.90%

0% 2% 4% 6% 8% 10% 12% 14%

Subscription VOD

Transactional VOD

Total OTT Video

Growth rate (%)

Asia Pacific Global Hong Kong

Global E&M Outlook 2020-2024: Hong Kong summary

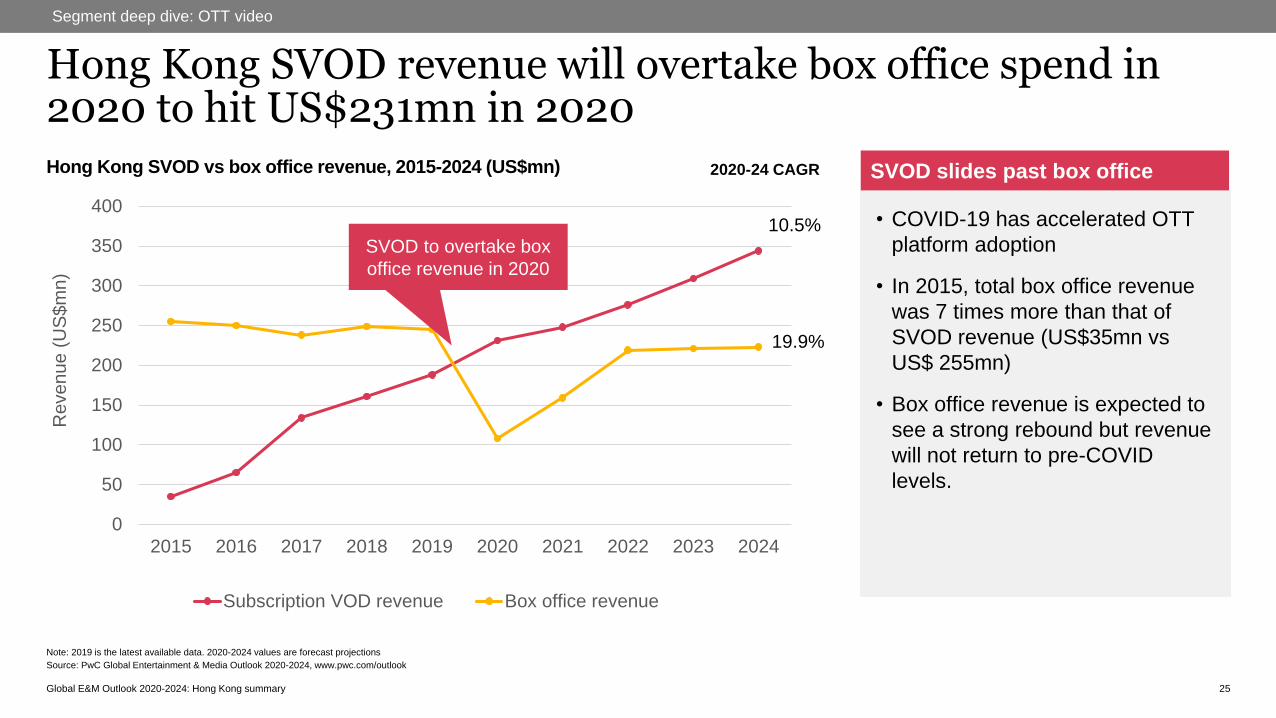

Hong Kong SVOD revenue will overtake box office spend in 2020 to hit US$231mn in 2020

25

Segment deep dive: OTT video

Source: PwC Global Entertainment & Media Outlook 2020-2024, www.pwc.com/outlook

Note: 2019 is the latest available data. 2020-2024 values are forecast projections

0

50

100

150

200

250

300

350

400

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024

Reven

ue

(U

S$m

n)

Subscription VOD revenue Box office revenue

Hong Kong SVOD vs box office revenue, 2015-2024 (US$mn)

• COVID-19 has accelerated OTT

platform adoption

• In 2015, total box office revenue

was 7 times more than that of

SVOD revenue (US$35mn vs

US$ 255mn)

• Box office revenue is expected to

see a strong rebound but revenue

will not return to pre-COVID

levels.

SVOD slides past box office

SVOD to overtake box

office revenue in 2020

10.5%

19.9%

2020-24 CAGR

Global E&M Outlook 2020-2024: Hong Kong summary

Segment deep diveVideo games

26Global E&M Outlook 2020-2024: Hong Kong summary

Global E&M Outlook 2020-2024: Hong Kong summary 27

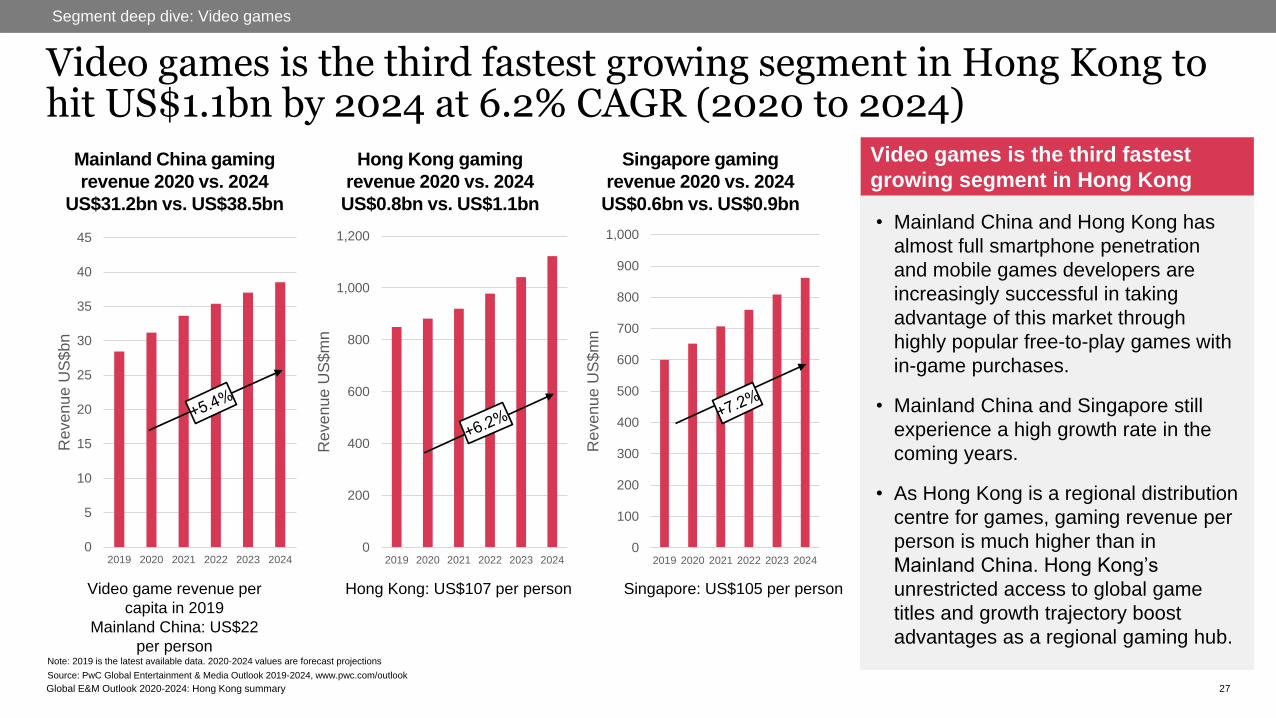

Segment deep dive: Video games

Video games is the third fastest growing segment in Hong Kong to hit US$1.1bn by 2024 at 6.2% CAGR (2020 to 2024)

• Mainland China and Hong Kong has

almost full smartphone penetration

and mobile games developers are

increasingly successful in taking

advantage of this market through

highly popular free-to-play games with

in-game purchases.

• Mainland China and Singapore still

experience a high growth rate in the

coming years.

• As Hong Kong is a regional distribution

centre for games, gaming revenue per

person is much higher than in

Mainland China. Hong Kong’s

unrestricted access to global game

titles and growth trajectory boost

advantages as a regional gaming hub.

Video games is the third fastest

growing segment in Hong KongMainland China gaming

revenue 2020 vs. 2024

US$31.2bn vs. US$38.5bn

0

5

10

15

20

25

30

35

40

45

2019 2020 2021 2022 2023 2024

Revenue U

S$bn

Note: 2019 is the latest available data. 2020-2024 values are forecast projections

Source: PwC Global Entertainment & Media Outlook 2019-2024, www.pwc.com/outlook

Hong Kong gaming

revenue 2020 vs. 2024

US$0.8bn vs. US$1.1bn

0

200

400

600

800

1,000

1,200

2019 2020 2021 2022 2023 2024

Revenue U

S$m

n

Singapore gaming

revenue 2020 vs. 2024

US$0.6bn vs. US$0.9bn

0

100

200

300

400

500

600

700

800

900

1,000

2019 2020 2021 2022 2023 2024

Revenue U

S$m

nVideo game revenue per

capita in 2019

Mainland China: US$22

per person

Hong Kong: US$107 per person Singapore: US$105 per person

Global E&M Outlook 2020-2024: Hong Kong summary 28

Segment deep dive: Video games

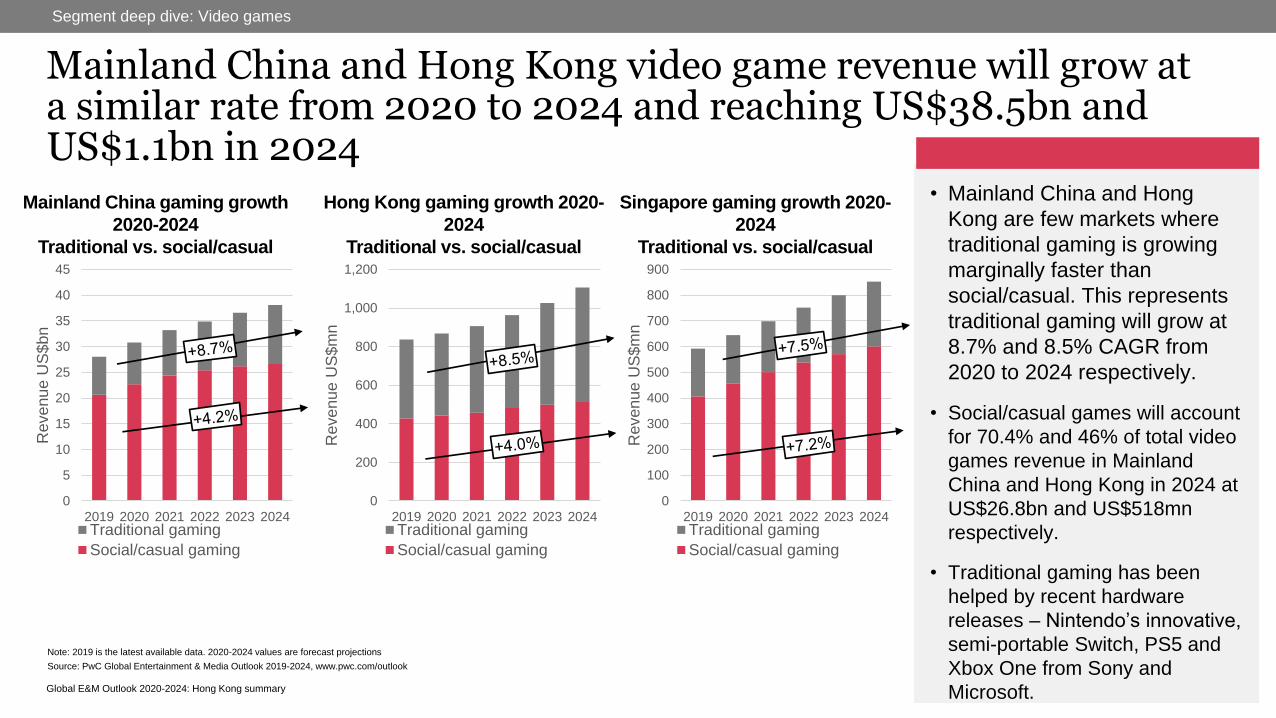

Mainland China and Hong Kong video game revenue will grow at a similar rate from 2020 to 2024 and reaching US$38.5bn and US$1.1bn in 2024

• Mainland China and Hong

Kong are few markets where

traditional gaming is growing

marginally faster than

social/casual. This represents

traditional gaming will grow at

8.7% and 8.5% CAGR from

2020 to 2024 respectively.

• Social/casual games will account

for 70.4% and 46% of total video

games revenue in Mainland

China and Hong Kong in 2024 at

US$26.8bn and US$518mn

respectively.

• Traditional gaming has been

helped by recent hardware

releases – Nintendo’s innovative,

semi-portable Switch, PS5 and

Xbox One from Sony and

Microsoft.

Hong Kong gaming growth 2020-

2024

Traditional vs. social/casual

0

200

400

600

800

1,000

1,200

2019 2020 2021 2022 2023 2024

Revenue U

S$m

n

Traditional gaming

Social/casual gaming

Note: 2019 is the latest available data. 2020-2024 values are forecast projections

Source: PwC Global Entertainment & Media Outlook 2019-2024, www.pwc.com/outlook

Mainland China gaming growth

2020-2024

Traditional vs. social/casual

0

5

10

15

20

25

30

35

40

45

2019 2020 2021 2022 2023 2024

Revenue U

S$bn

Traditional gaming

Social/casual gaming

Singapore gaming growth 2020-

2024

Traditional vs. social/casual

0

100

200

300

400

500

600

700

800

900

2019 2020 2021 2022 2023 2024

Re

ven

ue

US

$m

n

Traditional gaming

Social/casual gaming

Global E&M Outlook 2020-2024: Hong Kong summary 29

Segment deep dive: Video games

Video games top countries by 2024 revenue and growth 2020-2024

US, Mainland China, Japan and South Korea dominates the video game market. They will represent 61% market share by 2024 t 61

Top 10 video game countries

by revenue 2024

1. Mainland China

2. US

3. Japan

4. South Korea

5. UK

6. Germany

7. France

8. Italy

9. India

10.Canada

Country on both lists

India

Top 10 countries with highest

CAGR 2020-2024

1. Pakistan

2. Nigeria

3. India

4. Peru

5. Egypt

6. Norway

7. Philippines

8. Indonesia

9. Kenya

10.Brazil

Note: 2019 is the latest available data. 2020-2024 values are forecast projections

Source: PwC Global Entertainment & Media Outlook 2019-2024, www.pwc.com/outlook

Global E&M Outlook 2020-2024: Hong Kong summary 30

Segment deep dive: Video games

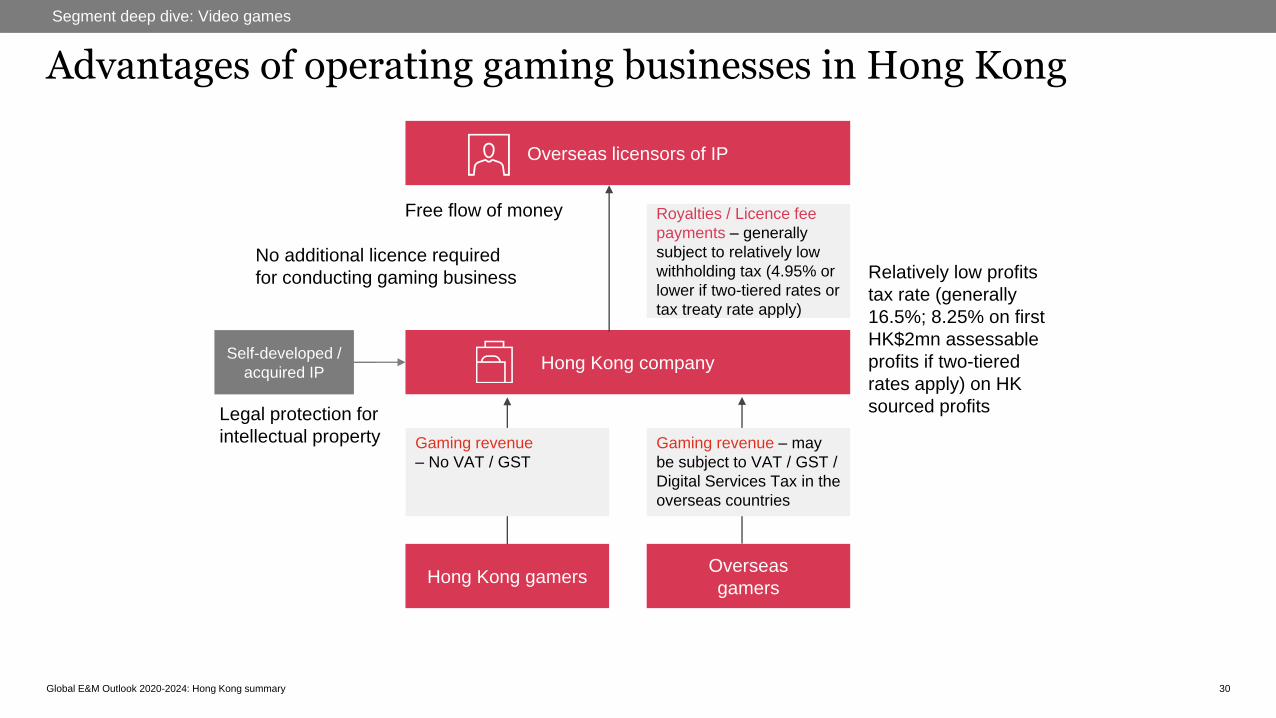

Advantages of operating gaming businesses in Hong Kong

Overseas licensors of IP

Hong Kong company

Relatively low profits

tax rate (generally

16.5%; 8.25% on first

HK$2mn assessable

profits if two-tiered

rates apply) on HK

sourced profitsLegal protection for

intellectual property

Free flow of money

No additional licence required

for conducting gaming business

Self-developed /

acquired IP

Hong Kong gamersOverseas

gamers

Gaming revenue – may

be subject to VAT / GST /

Digital Services Tax in the

overseas countries

Gaming revenue

– No VAT / GST

Royalties / Licence fee

payments – generally

subject to relatively low

withholding tax (4.95% or

lower if two-tiered rates or

tax treaty rate apply)

Global E&M Outlook 2020-2024: Hong Kong summary 31

Segment deep dive: Video games

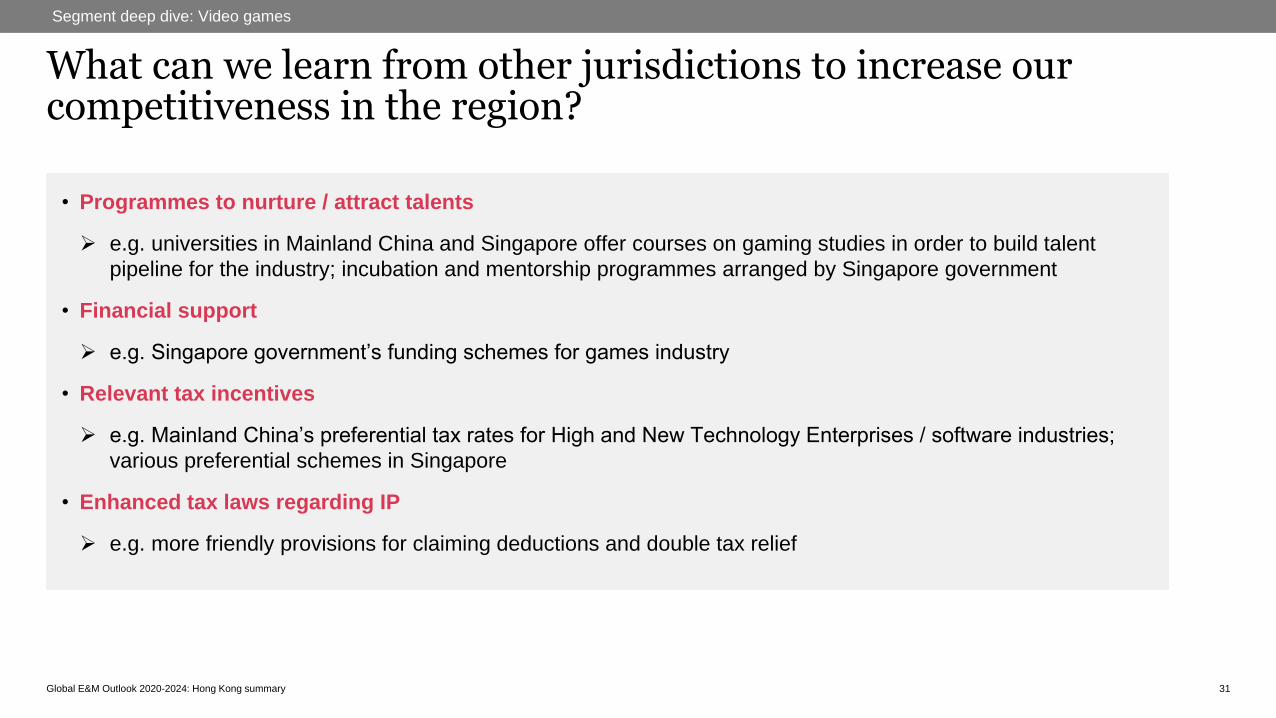

What can we learn from other jurisdictions to increase our competitiveness in the region?

• Programmes to nurture / attract talents

➢ e.g. universities in Mainland China and Singapore offer courses on gaming studies in order to build talent

pipeline for the industry; incubation and mentorship programmes arranged by Singapore government

• Financial support

➢ e.g. Singapore government’s funding schemes for games industry

• Relevant tax incentives

➢ e.g. Mainland China’s preferential tax rates for High and New Technology Enterprises / software industries;

various preferential schemes in Singapore

• Enhanced tax laws regarding IP

➢ e.g. more friendly provisions for claiming deductions and double tax relief

Global E&M Outlook 2020-2024: Hong Kong summary

New trendSmart speakers,

podcasts

32Global E&M Outlook 2020-2024: Hong Kong summary

Global E&M Outlook 2020-2024: Hong Kong summary

New trend

33

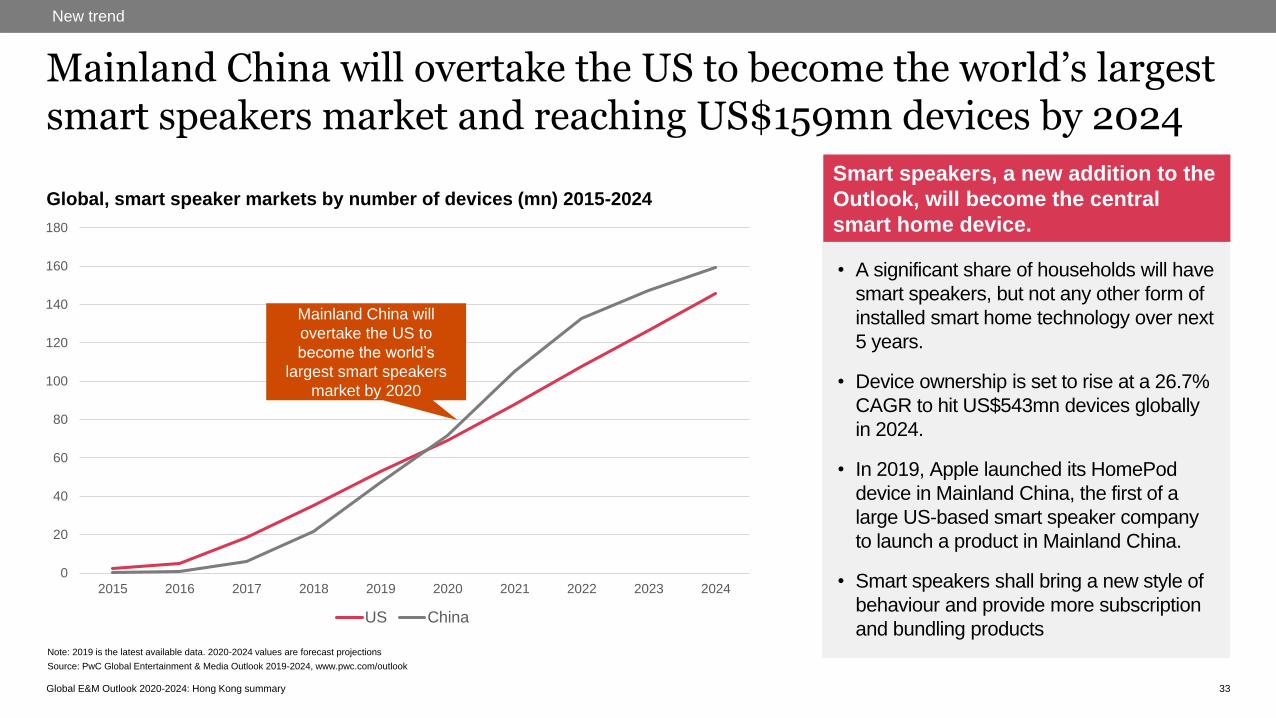

• A significant share of households will have

smart speakers, but not any other form of

installed smart home technology over next

5 years.

• Device ownership is set to rise at a 26.7%

CAGR to hit US$543mn devices globally

in 2024.

• In 2019, Apple launched its HomePod

device in Mainland China, the first of a

large US-based smart speaker company

to launch a product in Mainland China.

• Smart speakers shall bring a new style of

behaviour and provide more subscription

and bundling products

Smart speakers, a new addition to the

Outlook, will become the central

smart home device.

Mainland China will overtake the US to become the world’s largest smart speakers market and reaching US$159mn devices by 2024

Note: 2019 is the latest available data. 2020-2024 values are forecast projections

Source: PwC Global Entertainment & Media Outlook 2019-2024, www.pwc.com/outlook

Global, smart speaker markets by number of devices (mn) 2015-2024

0

20

40

60

80

100

120

140

160

180

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024

US China

Mainland China will

overtake the US to

become the world’s

largest smart speakers

market by 2020

Global E&M Outlook 2020-2024: Hong Kong summary

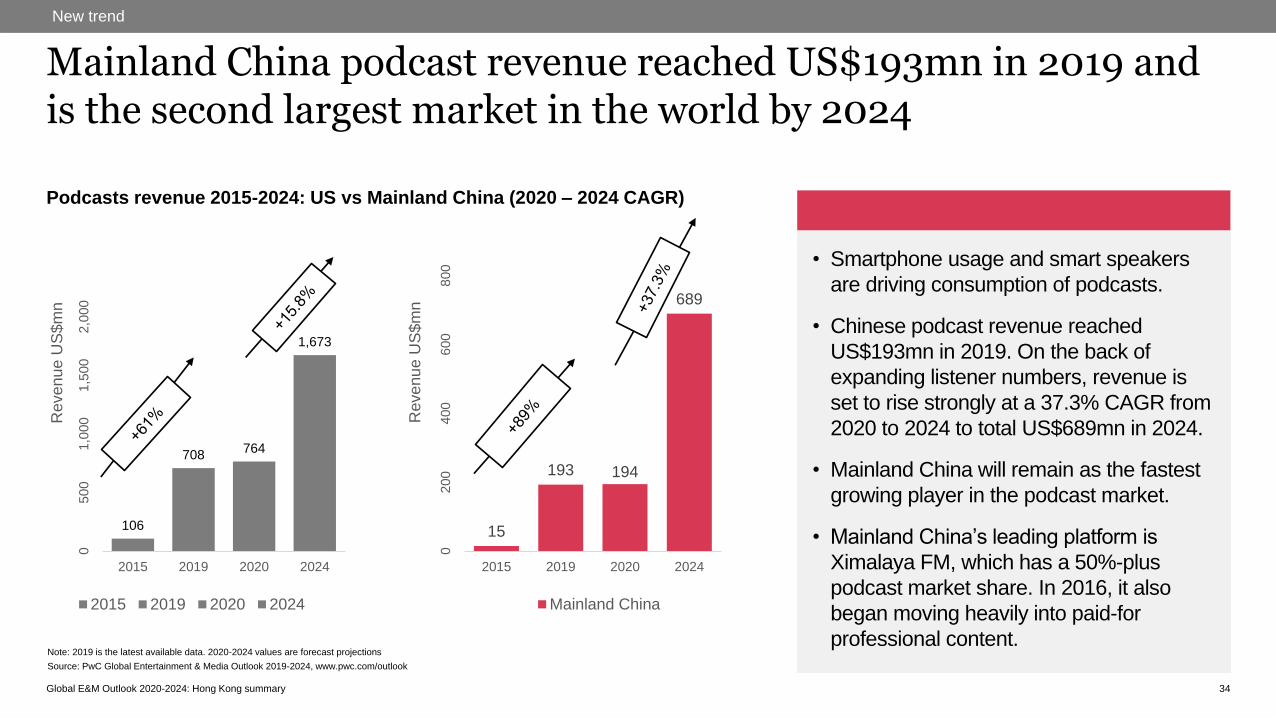

New trend

34

• Smartphone usage and smart speakers

are driving consumption of podcasts.

• Chinese podcast revenue reached

US$193mn in 2019. On the back of

expanding listener numbers, revenue is

set to rise strongly at a 37.3% CAGR from

2020 to 2024 to total US$689mn in 2024.

• Mainland China will remain as the fastest

growing player in the podcast market.

• Mainland China’s leading platform is

Ximalaya FM, which has a 50%-plus

podcast market share. In 2016, it also

began moving heavily into paid-for

professional content.

Mainland China podcast revenue reached US$193mn in 2019 and is the second largest market in the world by 2024

Note: 2019 is the latest available data. 2020-2024 values are forecast projections

Source: PwC Global Entertainment & Media Outlook 2019-2024, www.pwc.com/outlook

Podcasts revenue 2015-2024: US vs Mainland China (2020 – 2024 CAGR)

106

708764

1,673

05

00

1,0

00

1,5

00

2,0

00

2015 2019 2020 2024

Revenue U

S$m

n

2015 2019 2020 2024

15

193 194

689

02

00

400

600

800

2015 2019 2020 2024

Revenue U

S$m

n

Mainland China

Global E&M Outlook 2020-2024: Hong Kong summary

New trend

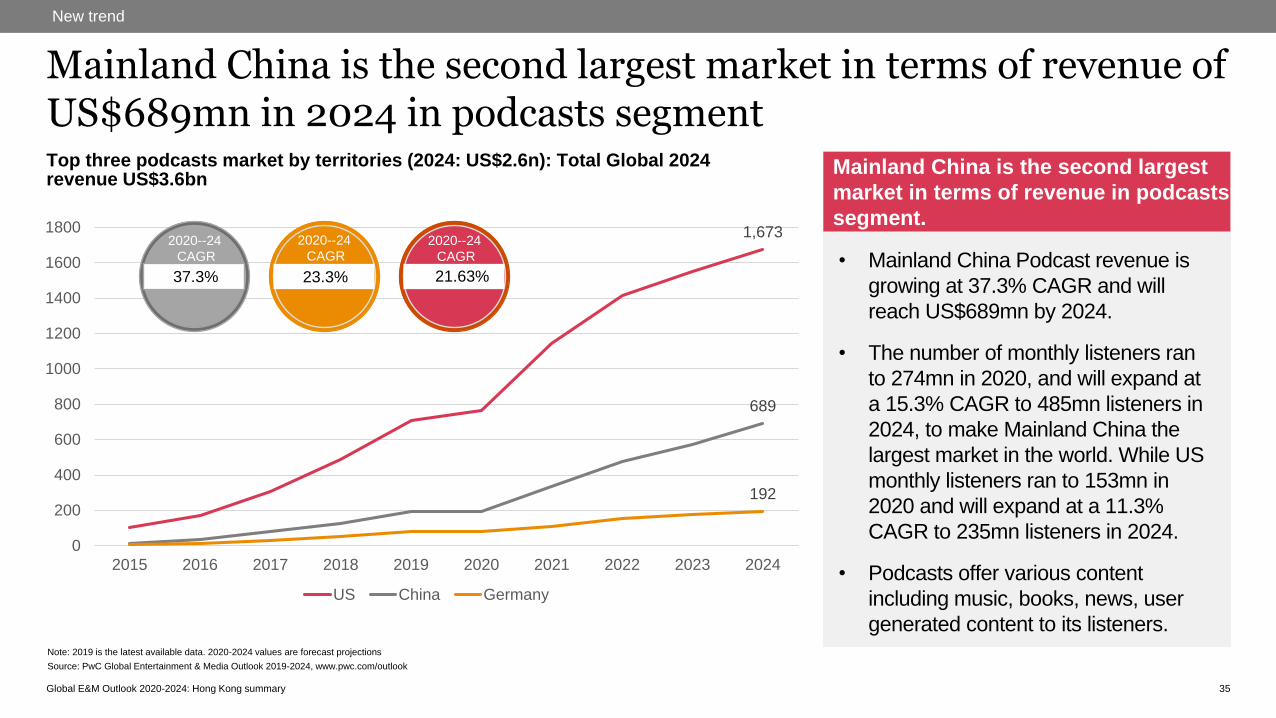

35

• Mainland China Podcast revenue is

growing at 37.3% CAGR and will

reach US$689mn by 2024.

• The number of monthly listeners ran

to 274mn in 2020, and will expand at

a 15.3% CAGR to 485mn listeners in

2024, to make Mainland China the

largest market in the world. While US

monthly listeners ran to 153mn in

2020 and will expand at a 11.3%

CAGR to 235mn listeners in 2024.

• Podcasts offer various content

including music, books, news, user

generated content to its listeners.

Mainland China is the second largest market in terms of revenue of US$689mn in 2024 in podcasts segment

Note: 2019 is the latest available data. 2020-2024 values are forecast projections

Source: PwC Global Entertainment & Media Outlook 2019-2024, www.pwc.com/outlook

Top three podcasts market by territories (2024: US$2.6n): Total Global 2024 revenue US$3.6bn

1,673

689

192

0

200

400

600

800

1000

1200

1400

1600

1800

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024

US China Germany

37.3%

2020--24

CAGR

23.3%

2020--24

CAGR

21.63%

2020--24

CAGR

Mainland China is the second largest

market in terms of revenue in podcasts

segment.

Global E&M Outlook 2020-2024: Hong Kong summary

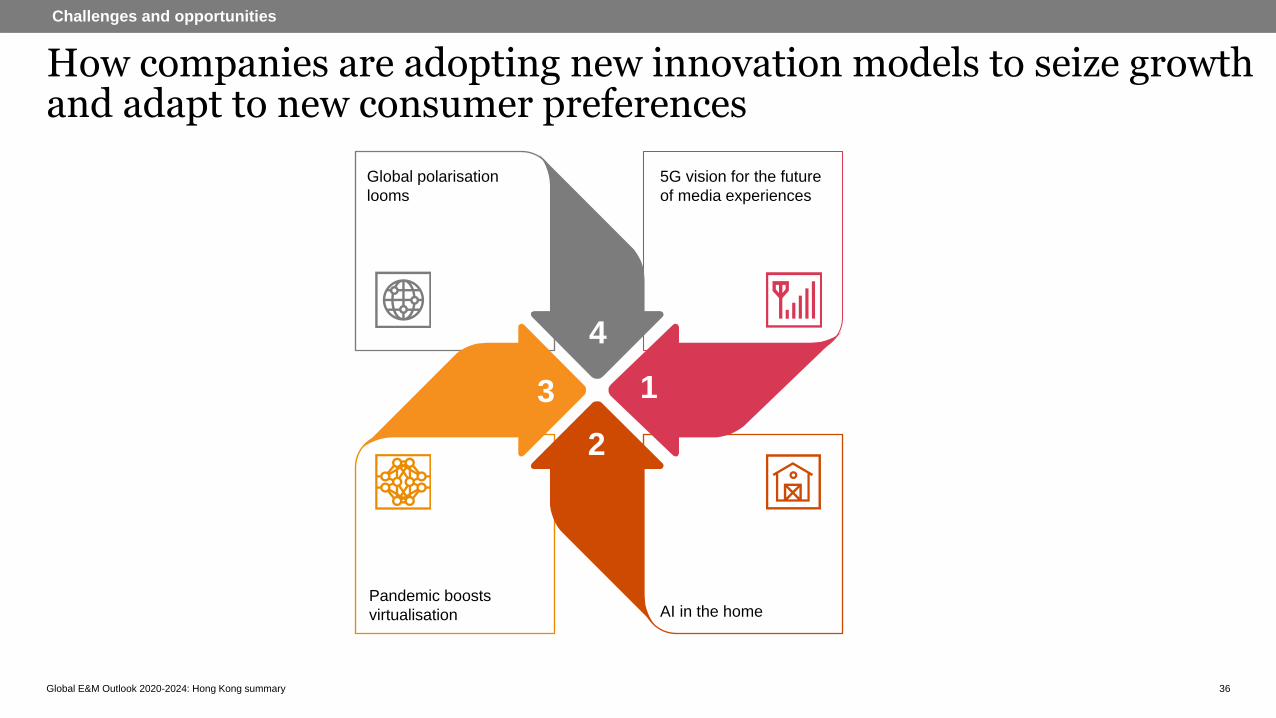

How companies are adopting new innovation models to seize growth and adapt to new consumer preferences

36

Challenges and opportunities

4

1

2

3

Global polarisation

looms

5G vision for the future

of media experiences

Pandemic boosts

virtualisation AI in the home

Global E&M Outlook 2020-2024: Hong Kong summary 37

About the Global Entertainment & Media Outlook and glossary

• PwC’s 21st annual edition of the Global Entertainment &

Media Outlook is a comprehensive online source of

global analysis for consumer and advertising spending.

With like-for-like, five-year historical and five-year

forecast data and commentary for 14 defined industry

segments in 53 territories, the Outlook makes it easy to

compare and contrast consumer and advertising

spending across segments and territories. Find out

more at www.pwc.com/outlook.

• A total of 53 countries are represented within the

Outlook spread across North America, Western

Europe, Central Europe, Middle East & Africa, Latin

America and Asia Pacific.

Global Entertainment & Media Outlook

• Revenue includes: Advertising and consumer

revenue streams

• Digital revenue - Digital is revenue delivered through

the Internet. Internet access revenue is obviously

included in, and the majority part of, “digital.” In

advertising, this is effectively Internet advertising and

digital OOH advertising. In consumer it's areas like OTT

video revenue, digital forms of

books/newspaper/magazine purchases, video game

downloads and online/microtransaction revenue, VR

revenue, and digital music revenue (downloads,

streaming, ringtones).

Glossary

Global E&M Outlook 2020-2024: Hong Kong summary

Key contacts

38

Cecilia Yau

PwC Mainland China and

Hong Kong Media Leader

Wilson Chow

PwC Global TMT Industry Leader

pwc.com/outlook

Thank you.

The information contained in this presentation is of a general nature only. It is not meant to be comprehensive and does not constitute the rendering of legal, tax or other

professional advice or service by PricewaterhouseCoopers Ltd ("PwC"). PwC has no obligation to update the information as law and practices change. The application

and impact of laws can vary widely based on the specific facts involved. Before taking any action, please ensure that you obtain advice specific to your circumstances

from your usual PwC client service team or your other advisers.

The materials contained in this presentation were assembled in Oct 2020 and were based on the law enforceable and information available at that time.

© 2020 PricewaterhouseCoopers Limited. All rights reserved. PwC refers to the Hong Kong member firm, and may sometimes refer to the PwC network. Each member

firm is a separate legal entity. Please see www.pwc.com/structure for further details.