france exporting

TRANSCRIPT

Leonard SahlingGlobal ResearchProLogis Research GroupDenver CO, USA+1 (303) 567 [email protected]

France is caught up in a sweeping pan-European logistics revolution, and so are the French logistics property markets.

Inrecentyears,capitalhasstreamedintoFrance’sdistributionpropertymarkets,bolsteringpricesandcompressingyields.Theyieldsdeclinedanadditional125-to-150basispointsduring2005-06andcurrentlyrangebetween5.9-to-6.5%.

Tenyearsago,Francehadvirtuallynomoderndistributionfacilities,andthosethatdidexistwereoperatedmostlybyowneroccupants.

Frenchwarehousesbuiltbefore1995wereconstructedmostlyona build-to-suit basis specific to the requirements of owner-users. Today,manyofthoseolderwarehousesareborderingonfunctionalobsolescence.

3PLshaveemergedasakeyplayerthroughoutEurope,helpingcompanies design and operate efficient, pan-European distribution networks. The 3PLs also constitute a key lessee of modern, efficient distributionfacilities.

France’scentrallocationwithinEuropemakesitanessentiallocationforretailers,wholesalers,andotheruserstoincludeinanypan-Europeanlogisticsstrategy.

Today, tens of millions of square metres of large, modern distribution spaceareinoperationinFrance.Manyarebuild-to-suits,butthemajorityweretargetedforlessee-usersanddesignedtosuitawiderangeofend-users.

ThesenewmoderndistributionfacilitiesarelocatedinFrance’smajorlogisticshubs,includingParis/Ile-de-France,Lyon,Lille,andMarseille.

AlthoughFrancehasanamplesupplyofrawland,localmunicipalitiestightlycontrolbothitspricinganditsreleaseforsaleanddevelopment.Consequently, land prices tend not to fluctuate in terms of regular marketcycles.

Inside this Issue…

Global Property Market ReviewEuropean Distribution and Warehouse Markets

France’s Logistics Property Markets — Distribution Gateway to Southern Europe

Overview and Summary .....................................2

Investment Climate ............................................3

Economic Structure ............................................4

Location, Location, Location ...............................6

Europe’s Logistics Revolution .............................7

New Breed of Warehouses ..................................8

Current Market Conditions .................................9

Market Rents ................................................... 11

Contractual Rent Indexation ............................. 12

Developable Land ............................................ 13

Local Planning Rules and Permitting ................ 13

Conclusion ....................................................... 14

From the Editor ................................................ 15

Lisa GrahamEuropean ResearchProLogis Research GroupParis, France+33 (0)6 72 01 53 [email protected]

Fall 2007

� • Global Property Market Review — France

Overview and SummaryFranceiscaughtupinapan-Europeanlogisticsrevolution.Thisup-heavalisrootedintwosweepingeconomictrends—theexpansionandintegrationoftheEconomicUnion(EU)andtheglobalizationofsupplychains.

AstheEUhasgrown,companiesthroughoutEuropehavestrivedtobroadentheirdistributionnetworksfromanationaltoacross-borderperspective.WithFrance’scentrallocationandextensivehighwaysystem,mostcompaniesincorporateoneormoreFrenchhubsintotheirpan-Europeandistributionnetworks.Bythemid-1990s, the first wave of property investors had recognized this nascent opportunity, and the influx of capital was used to build a new“breed”ofmodern,largedistributionfacilities.

When the dot-com bubble burst in 2001, financial markets trembled worldwide,andinvestorsreactedbyincreasingtheirexposuretodirectandindirectinvestmentsinrealestate.DespiteFrance’spersistent,post-2000macroeconomicmalaise,itslogisticspropertymarketshavethrived.Investmentcapitalhascontinuedtostreamintothismarket,adding to its liquidity and further fueling its growth.

Francetodaypossessesthebiggestinventoryoflarge,moderndistributionfacilitiesontheContinent.Itslogisticspropertymarkethas attained a size sufficient to provide ample-enough liquidity and stabilitytoattractglobalinvestors.Since1999,investmentsinthelogisticspropertymarkethaveyieldedthesecond-highestincomereturnsofallthecommercialpropertytypesinFrance.

As the EU has grown, companies

throughout Europe have strived to

broaden their distribution networks

from a national to a cross-border

perspective.

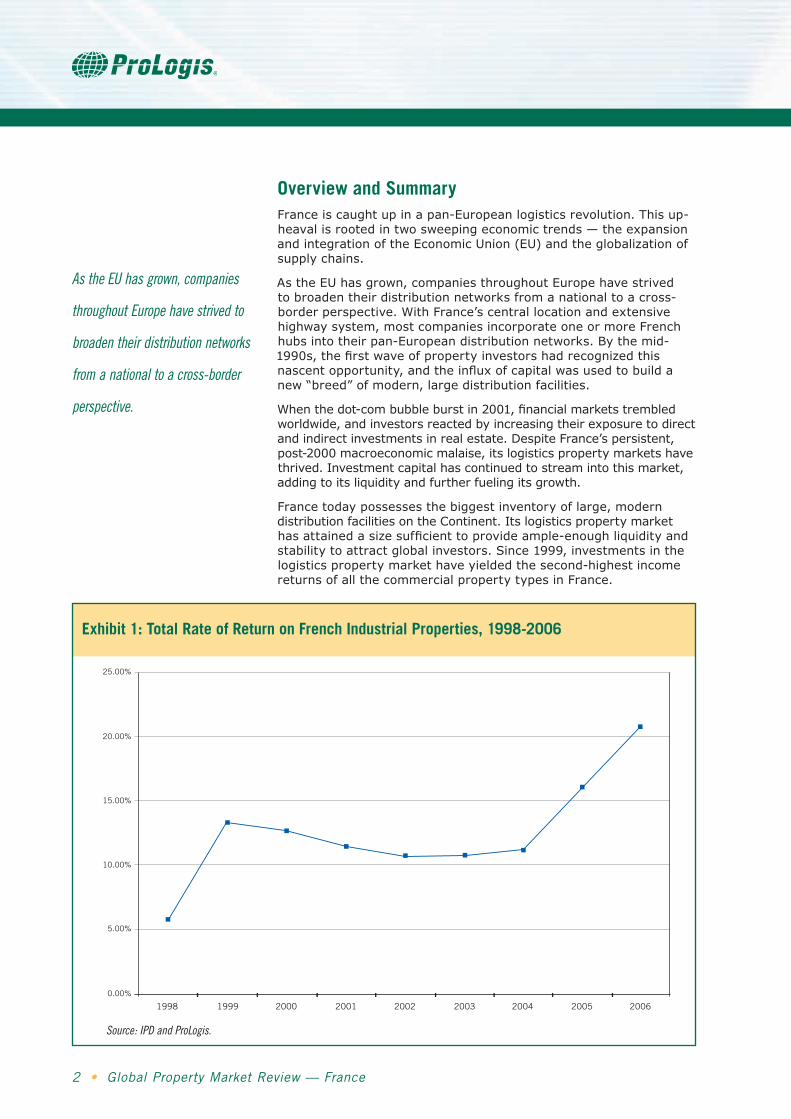

Exhibit 1: Total Rate of Return on French Industrial Properties, 1998-2006

1998 1999 2000 2001 2002 2003 2004 2005 2006

25.00%

20.00%

15.00%

10.00%

5.00%

0.00%

Source: IPD and ProLogis.

Global Property Market Review — France • �

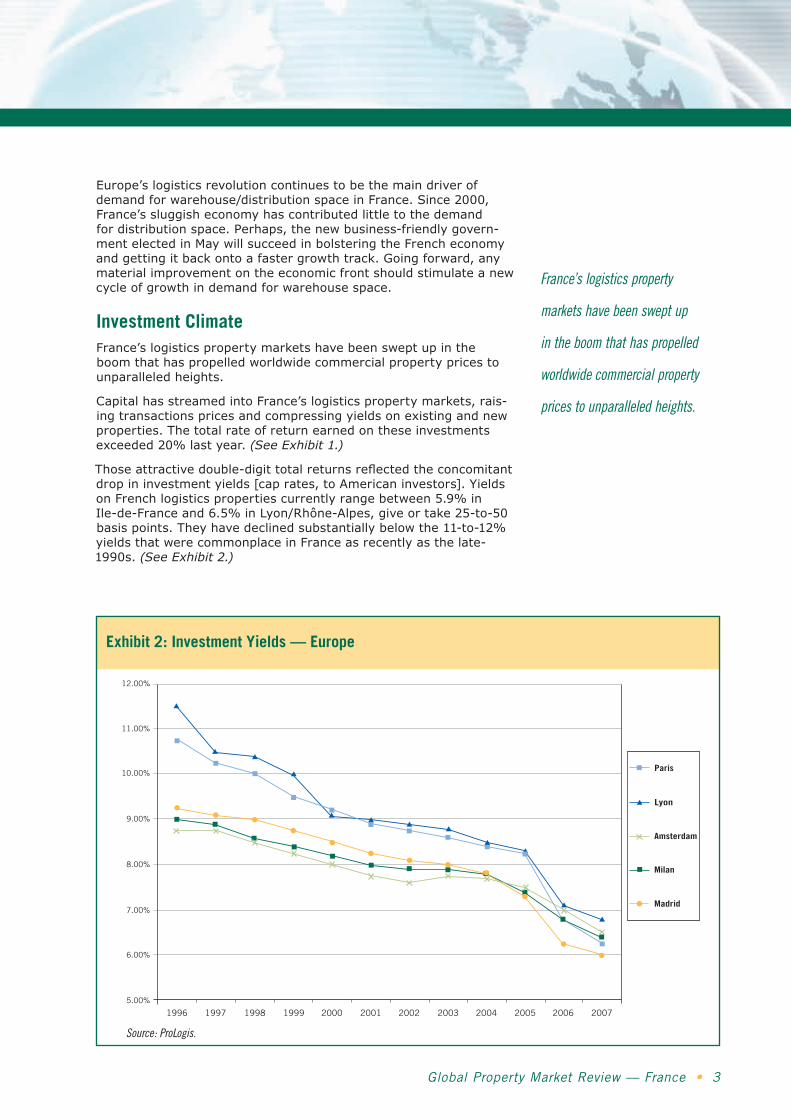

Exhibit 2: Investment Yields — Europe

Europe’slogisticsrevolutioncontinuestobethemaindriverofdemandforwarehouse/distributionspaceinFrance.Since2000,France’ssluggisheconomyhascontributedlittletothedemandfordistributionspace.Perhaps,thenewbusiness-friendlygovern-mentelectedinMaywillsucceedinbolsteringtheFrencheconomyandgettingitbackontoafastergrowthtrack.Goingforward,anymaterialimprovementontheeconomicfrontshouldstimulateanewcycleofgrowthindemandforwarehousespace.

Investment Climate France’slogisticspropertymarketshavebeensweptupintheboomthathaspropelledworldwidecommercialpropertypricestounparalleledheights.

CapitalhasstreamedintoFrance’slogisticspropertymarkets,rais-ingtransactionspricesandcompressingyieldsonexistingandnewproperties.Thetotalrateofreturnearnedontheseinvestmentsexceeded20%lastyear.(See Exhibit 1.)

Those attractive double-digit total returns reflected the concomitant dropininvestmentyields[caprates,toAmericaninvestors].YieldsonFrenchlogisticspropertiescurrentlyrangebetween5.9%inIle-de-Franceand6.5%inLyon/Rhône-Alpes,giveortake25-to-50basispoints.Theyhavedeclinedsubstantiallybelowthe11-to-12%yieldsthatwerecommonplaceinFranceasrecentlyasthelate-1990s.(See Exhibit 2.)

France’s logistics property

markets have been swept up

in the boom that has propelled

worldwide commercial property

prices to unparalleled heights.

12.00%

11.00%

10.00%

9.00%

8.00%

7.00%

6.00%

5.00%

Milan

Madrid

Amsterdam

Paris

Lyon

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Source: ProLogis.

� • Global Property Market Review — France

Attheirpresentlowlevels,theyieldsonFrenchlogisticspropertiesaligncloselywiththoseforcomparableinvestmentsinothermain-streamEuropeanmarkets,indicativeofFrance’selevatedstatusintheeyesofglobalinvestors.Thoughlessglamorousthanothercom-mercialpropertymarkets,France’slogisticspropertymarketshaveprovidedconsistentlyhighperformance.Since1998,thetotalreturnforthesectoraveraged12.4%ayear,thesecond-highestreturnafterthe17.4%returnearnedbyretailpropertiesandslightlyabovetheall-propertytotalreturnof11.8%.

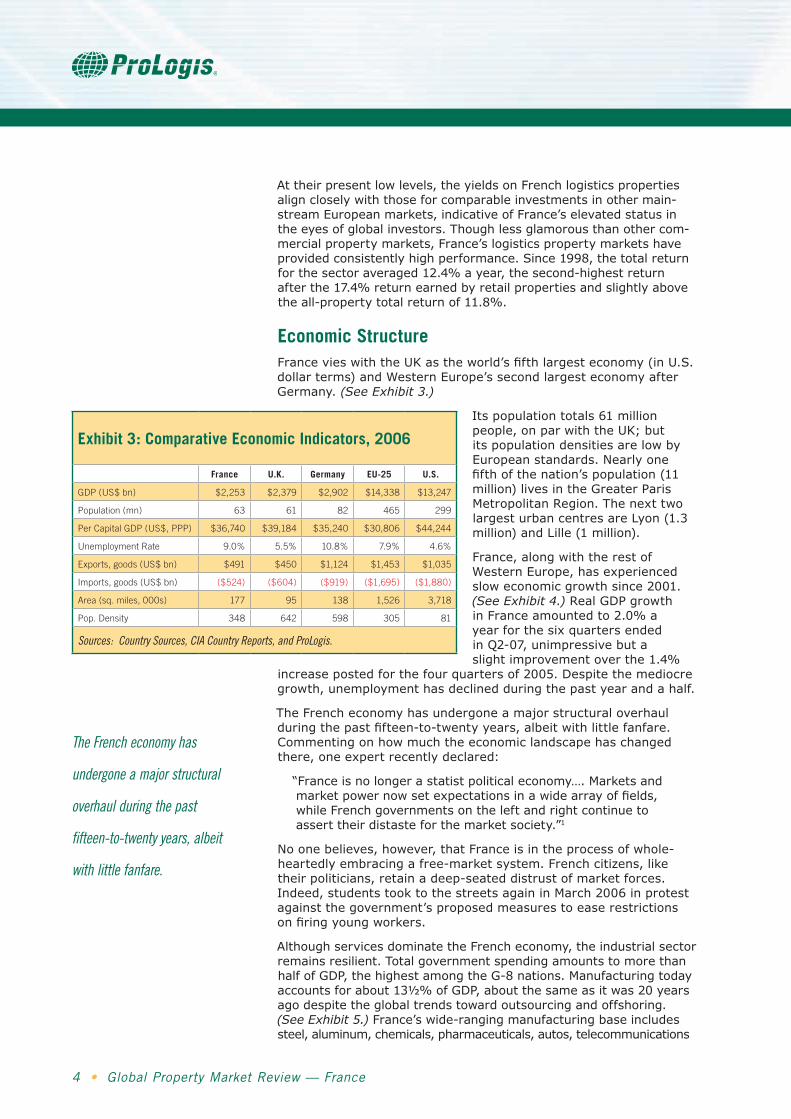

Economic Structure France vies with the UK as the world’s fifth largest economy (in U.S. dollarterms)andWesternEurope’ssecondlargesteconomyafterGermany.(See Exhibit 3.)

Itspopulationtotals61millionpeople,onparwiththeUK;butitspopulationdensitiesarelowbyEuropeanstandards.Nearlyonefifth of the nation’s population (11 million)livesintheGreaterParisMetropolitanRegion.ThenexttwolargesturbancentresareLyon(1.3million)andLille(1million).

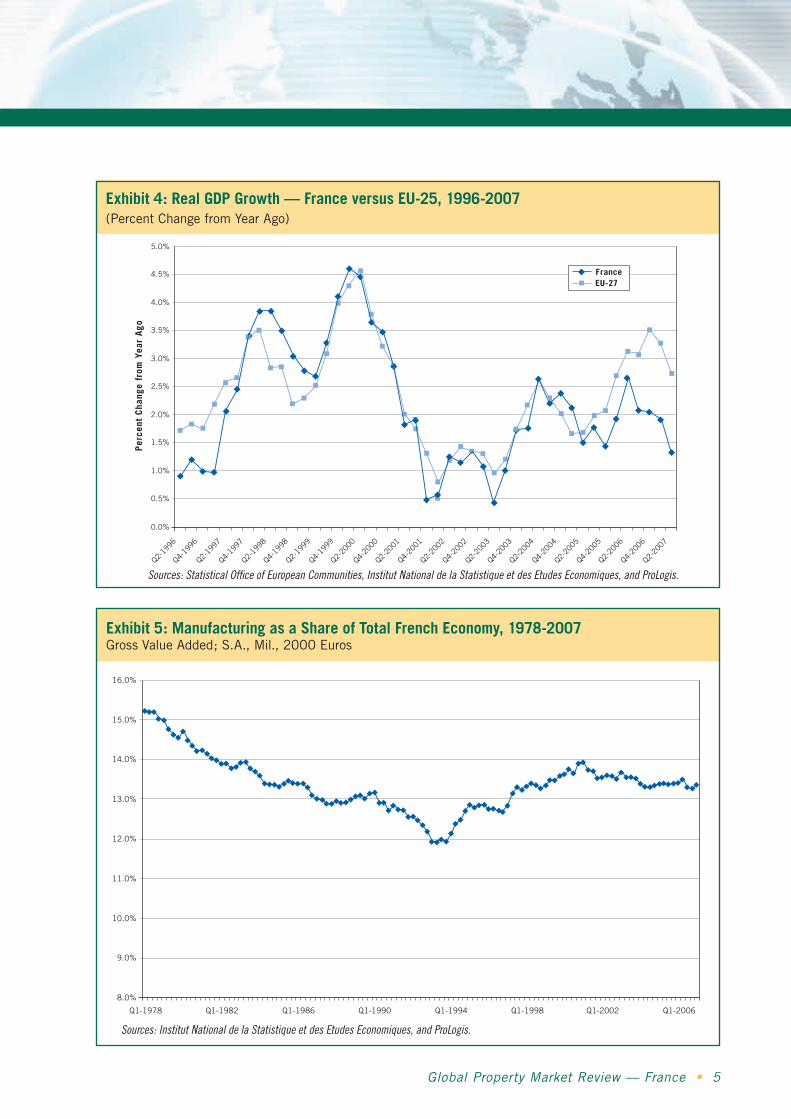

France,alongwiththerestofWesternEurope,hasexperiencedsloweconomicgrowthsince2001.(See Exhibit 4.)RealGDPgrowthinFranceamountedto2.0%ayear for the six quarters ended inQ2-07,unimpressivebutaslightimprovementoverthe1.4%

increase posted for the four quarters of 2005. Despite the mediocre growth,unemploymenthasdeclinedduringthepastyearandahalf.

TheFrencheconomyhasundergoneamajorstructuraloverhaulduring the past fifteen-to-twenty years, albeit with little fanfare. Commentingonhowmuchtheeconomiclandscapehaschangedthere,oneexpertrecentlydeclared:

“Franceisnolongerastatistpoliticaleconomy….Marketsandmarket power now set expectations in a wide array of fields, whileFrenchgovernmentsontheleftandrightcontinuetoasserttheirdistasteforthemarketsociety.”1

Noonebelieves,however,thatFranceisintheprocessofwhole-heartedlyembracingafree-marketsystem.Frenchcitizens,liketheirpoliticians,retainadeep-seateddistrustofmarketforces.Indeed,studentstooktothestreetsagaininMarch2006inprotestagainstthegovernment’sproposedmeasurestoeaserestrictionson firing young workers.

AlthoughservicesdominatetheFrencheconomy,theindustrialsectorremainsresilient.TotalgovernmentspendingamountstomorethanhalfofGDP,thehighestamongtheG-8nations.Manufacturingtodayaccountsforabout13½%ofGDP,aboutthesameasitwas20yearsagodespitetheglobaltrendstowardoutsourcingandoffshoring.(See Exhibit 5.)France’swide-rangingmanufacturingbaseincludessteel,aluminum,chemicals,pharmaceuticals,autos,telecommunications

Exhibit 3: Comparative Economic Indicators, 2006

France U.K. Germany EU-25 U.S.

GDP (US$ bn) $2,253 $2,379 $2,902 $14,338 $13,247

Population (mn) 63 61 82 465 299

Per Capital GDP (US$, PPP) $36,740 $39,184 $35,240 $30,806 $44,244

Unemployment Rate 9.0% 5.5% 10.8% 7.9% 4.6%

Exports, goods (US$ bn) $491 $450 $1,124 $1,453 $1,035

Imports, goods (US$ bn) ($524) ($604) ($919) ($1,695) ($1,880)

Area (sq. miles, 000s) 177 95 138 1,526 3,718

Pop. Density 348 642 598 305 81

Sources: Country Sources, CIA Country Reports, and ProLogis.

The French economy has

undergone a major structural

overhaul during the past

fifteen-to-twenty years, albeit

with little fanfare.

Global Property Market Review — France • �

Exhibit 4: Real GDP Growth — France versus EU-25, 1996-2007(Percent Change from Year Ago)

Exhibit 5: Manufacturing as a Share of Total French Economy, 1978-2007Gross Value Added; S.A., Mil., 2000 Euros

0.0%

0.5%

1.0%

1.5%

2.0%

3.0%

4.0%

5.0%

2.5%

3.5%

4.5%

Per

cent

Cha

nge

from

Yea

r A

go

EU-27France

Q2-19

96Q4-

1996

Q2-19

97Q4-

1997

Q2-19

98Q4-

1998

Q2-19

99Q4-

1999

Q2-20

00Q4-

2000

Q2-20

01Q4-

2001

Q2-20

02Q4-

2002

Q2-20

03Q4-

2003

Q2-20

04Q4-

2004

Q2-20

05Q4-

2005

Q2-20

06Q4-

2006

Q2-20

07

Sources: Statistical Office of European Communities, Institut National de la Statistique et des Etudes Economiques, and ProLogis.

8.0%

9.0%

10.0%

11.0%

12.0%

13.0%

14.0%

15.0%

16.0%

Q1-1978 Q1-1982 Q1-1986 Q1-1990 Q1-1994 Q1-1998 Q1-2002 Q1-2006

Sources: Institut National de la Statistique et des Etudes Economiques, and ProLogis.

� • Global Property Market Review — France

equipment, fashion and luxury goods, military arms, rail transport equip-ment,andaerospace.

France’smembershipintheexpandingEUhasbeeninstrumentalinunleashingkeencompetitiveforceswithintheFrencheconomy.ManyFrenchcompanieshaveinturntakenadvantageoftheopportunitiesofferedbyanexpandingworldmarketandthrived.DozensofthemappearedonForbes’2003listoftheworld’sbestbigcompanies,includingPeugeot,Renault,BNPParibas,Publicis,Rallye, Michelin, L’Oreal, Lagardere, Christian Dior, Thomson, Sanofi-Synthelabo,PernodRicard,andAirbus.2

LabormarketrigiditiesremaintheAchilles’heeloftheFrencheconomy.Nationalworkrules,forexample,makeitcumbersomeandcostlyforemployerstodismissemployeesandmanagetheirworkforces.Hence,employersarereluctanttohirenewfull-timeemployees,labor-marketturnoverhasslowedtoacrawl,overalljoblessnessremainshigh,andsomesocio-demographicgroupsarenotwellintegratedintotheworkforce.

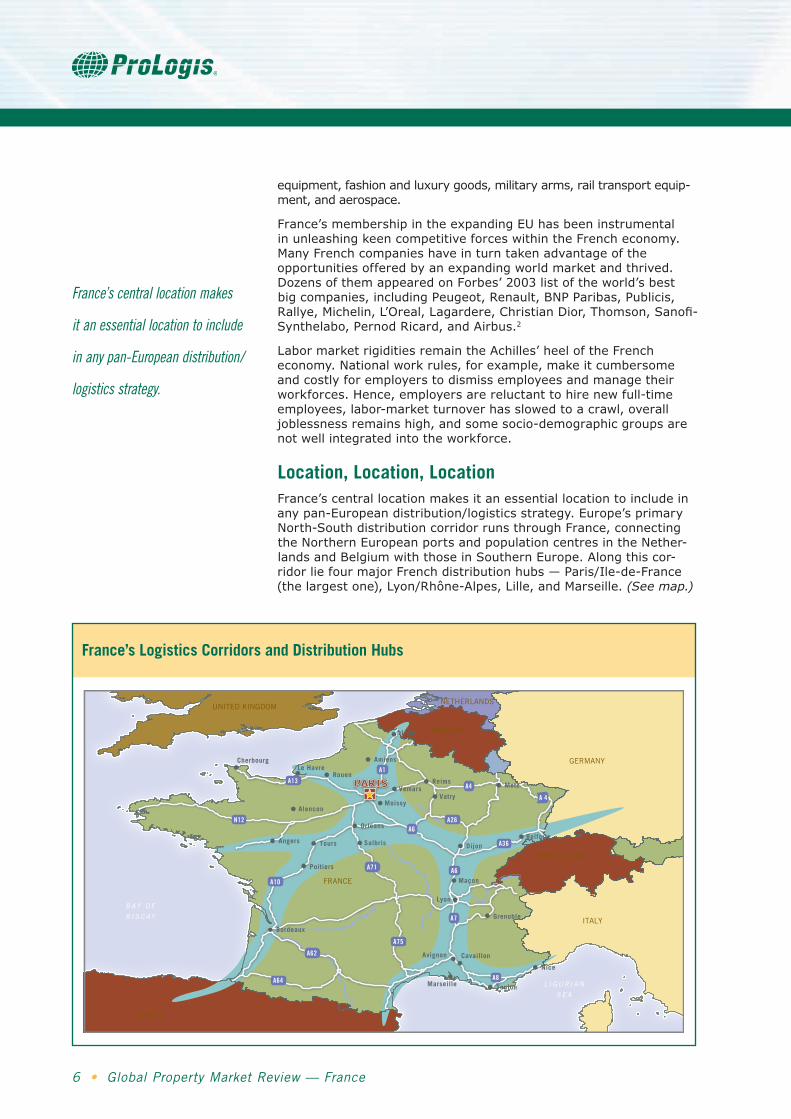

Location, Location, Location France’scentrallocationmakesitanessentiallocationtoincludeinanypan-Europeandistribution/logisticsstrategy.Europe’sprimaryNorth-SouthdistributioncorridorrunsthroughFrance,connectingtheNorthernEuropeanportsandpopulationcentresintheNether-landsandBelgiumwiththoseinSouthernEurope.Alongthiscor-ridorliefourmajorFrenchdistributionhubs—Paris/Ile-de-France(thelargestone),Lyon/Rhône-Alpes,Lille,andMarseille.(See map.)

France’s Logistics Corridors and Distribution Hubs

France’s central location makes

it an essential location to include

in any pan-European distribution/

logistics strategy.

L I G U R I A N

S E A

B AY O F

B I S C AY

RouenLe Havre

Reims

Amiens

Alencon

Salbris

Moissy

VemarsVatry

Grenoble

Avignon

Marseille

Poitiers

Cherbourg

Cavaillon

Angers

Orleans

Tours Dijon

Bordeaux

Nice

Toulon

Metz

Maçon

Lyon

Belforte

Lille

PARIS

FRANCE

BELGIUM

SWITZERLAND

ITALY

UNITED KINGDOMNETHERLANDS

GERMANY

SPAIN

A26A6

A8

A13

A36

A7

A6

A4

N12

A71

A1

A10

A75

A 4

A62

A64

Global Property Market Review — France • �

France’slandtransportinfra-structureisarguablyoneofthebestinEuropeandcontinuestoimprove.Duringthepastdecade,theFrenchgovern-menthasfundedasubstan-tialexpansionofitsnationalnetworkofmotorways.Trucksaccountforabout75%oftotalfreightshipments.Railfreightplaysalesserbutstillsig-nificant role — which at 17% is oneofthehighestratesintheEU.France’sfreightrailwaysre-portedlyhandlemostlybever-agesandhouseholdappliancesinadditiontobulkgoodssuchascoalandaggregates.

ImprovementshavealsobeenmadetoFrance’sports.LeHavreisFrance’slargestcon-tainerport(andEurope’stenthlargestport),havinghandled2.13million TEUs [twenty-foot equivalent units] in 2006. (Container-izedfreightiswhatmattersmostformoderndistributionfacilities.)MarseilleisFrance’ssecondlargestportwith0.94millionTEUs,andDunkirkisthethirdlargestwith0.20millionTEUs.

Europe’s Logistics Revolution In 1992, twelve European countries ratified an agreement to band togetherandlaunchedtheEuropeanUnion(EU).Intheensuingyears,FranceandherEUpartnershavepursuedeconomicintegra-tionandopenbordersinaccordwiththeMaastrichtcriteria.TheireffortsspearheadedtheEuropeanlogisticsrevolution.

AsbordersdisappearedwithintheEU,companiesinFranceandtherestofEuropefoundthemselvesoperatingona“leveler”playingfield — albeit against more competitors. Impelled by the heightened competition, companies redoubled their efforts to find ways to re-duce their operating costs or increase their efficiency.

Threemajortrendshaveemerged:

• Companieshaveturnedtoglobalsourcingforintermediatemate-rials and components to incorporate into their finished products.

• Companieshaveattemptedtoidentifytheircorecompetenciesandoutsourceeverythingelsetothird-partyproviders.

• Companieshavestrivedtoremovecapital-intensiveassetsfromtheir books and redeploy the capital into alternative, more profit-ableuses.

In their intensifying quest for a competitive edge, European companies haverecognizedtheimportancebutintrinsiccomplexityofsupplychains — and the difficulty of getting them to operate properly. They alsohaverealizedthatlogisticsandsupplychainoperationsarenottheircorecompetencyandhaveturnedtothird-partylogisticsproviders (3PLs) for expertise and help — either to figure out how toimprovetheirlogisticsandsupplychainoperationsortotakecommand of those operations and run them more efficiently.

France’s land transport infrastructure is arguably one of the best in Europe, and France continues to fund new improvements to its infrastructure.

As borders disappeared within the

EU, companies in France and the

rest of Europe found themselves

operating on a “leveler” playing

field — albeit against more

competitors.

� • Global Property Market Review — France

Inturn,the3PLshaveeagerlysteppedforwardtohelpcompaniescreateworld-classsupplychainsandnavigatethecomplexitiesofborderlesstrade.OutsourcingtrendsinFrancerevealthattheemergenceandexpansionof3PLshavebeenanimportantsourceofdemandfornewwarehouseanddistributionspaceaccountingforanaverageof45%ofoveralltakeupduring2000-05and60%oftakeupduring2006.[Note:eightofProLogis’toptenleasingcustomersinFranceare3PLs,includingDeutschePostAG,IDLogisticsFrance,andGeodis.]

While3PLsweregainingmarketshare,retailerswereconcentratingon supply chain efficiencies to reduce their costs. As retailers merged and expanded across the continent, distribution was quickly becomingpan-European.Thesolutionwasalargerwarehousethatcouldserveasanationalorregionaldistributionbase.

RetailershavebecomeanotherimportantsourceofdemandformodernwarehousespaceinFrance.Theyaccountedforroughlyonethirdoftotaltakeupbetween2001and2006.Forexample,CarrefourandAuchan,France’stwoleadinghypermarketchains,relyonlargewarehousesincentrallocationstodistributegoodswithinFranceaswellasacrossbordersintoItalyandSpain.

New Breed of Warehouses Tenyearsago,therewerefewmoderndistributionfacilitiesinFrance,andthosethatdidexistthenwereoperatedalmostexclusivelybyowner-occupants.

Thepre-1995warehouseshadbeenbuiltmostlybyindependentgeneralcontractorshiredbytheowner-occupants.Fewoftheseolderwarehouseshadbeenbuiltforlessee-users.Instead,owner-occupantshadcontractedtohavewarehousesbuilt-to-suittheirspecific needs. Most of these “build-to-suits” were financed with a credit bail — a French version of a financial lease that permitted the lessor(usuallyabank)todepreciatethevalueofthelandandbuild-ingoverthetermoftheleaseandthenawarded100%ownershiptotheuser-occupantattheendofthelease.(See box.)

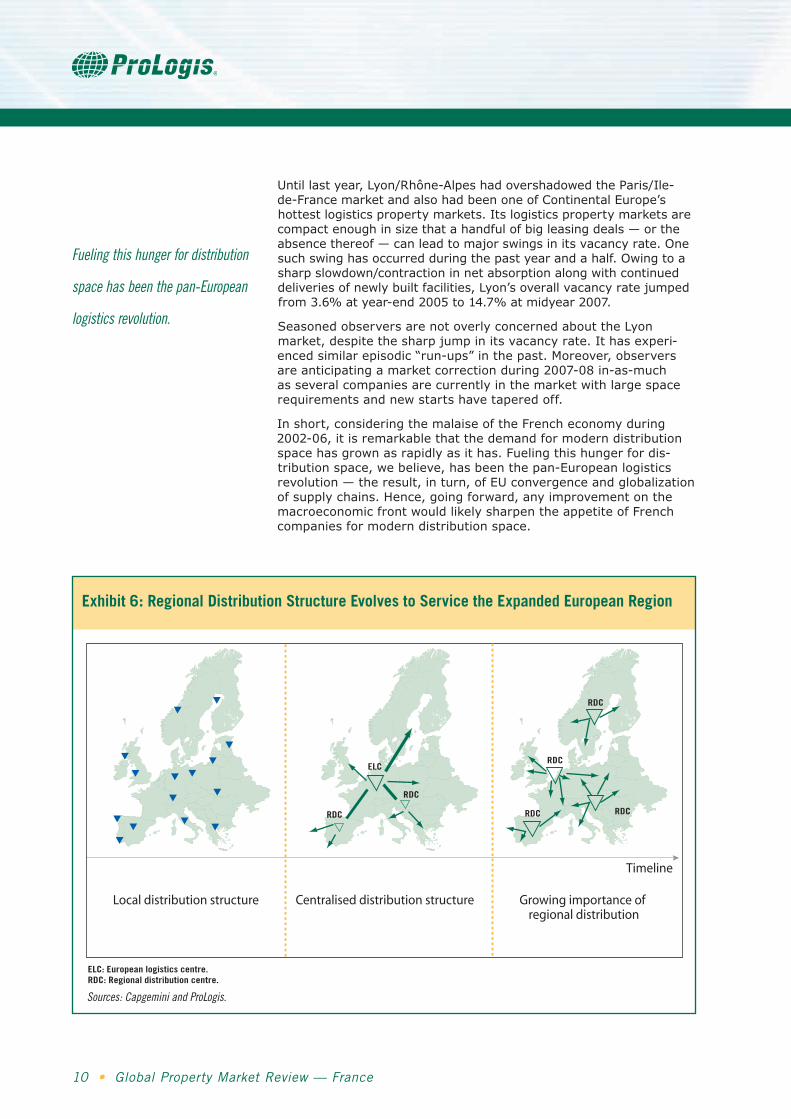

Thoseolderfacilities,however,wereill-suitedtothenewcompeti-tiveenvironmentthatmaterializedaftertheEUwascreatedin1992.Withthedisappearanceofcountryborders,companiesoperatinginEuropehavesoughttore-designtheirdistributionnetworks.For-merly,thosecompaniescustomarilyoperatedoneormorefacilitiesineverycountrywheretheymarketedtheirgoods.Today,theyrelyonfewerbutbiggerso-calledregionaldistributioncenters,eachoneservicingalargegeographicregionthatmaycutacrosscountryboundaries.(See Exhibit 6.)

Moderndistributionfacilitiesaredesignedtofacilitatetherapidthroughput of goods from suppliers to final users. Hence, the new facilitiestendtobebiggerwithhigherceilings,moredockdoors,andmoreoutsideparkingspacefortrailerswaitingtobeunloadedorpickedup.France’sprototypicalmoderndistributionfacilityspans at least 10,000 square metres [m2] of floorspace, with ceiling heights of at least 9 metres, load-bearing floors to support at least 5tonsperm2,oneloadingdockforevery1,000m2,andtruck-turn-ingareasofatleast35metres.

This new breed of distribution facility first appeared in France during themid-to-late1990s.Ascapitalinvestmentandexpertisestreamed

The 3PLs have eagerly stepped

forward to help companies create

world-class supply chains and

navigate the complexities of

borderless trade.

Those older facilities were ill-

suited to the new competitive

environment that materialized

after the EU was created in 1992.

Global Property Market Review — France • �

intothecountry,France’smoderndistributionpropertymarketbe-gan to take form. For the first time, distribution facilities were built expresslyforthefor-leasemarket,developedonaspeculativebasis,anddesignedtobeadaptabletoamultitudeofend-users.

Current Market Conditions Bymidyear2007,France’stotalstockoflarge,moderndistribu-tionfacilitieshadgrowntoabout15-to-20millionm2or160-to-215million square feet (MSF). (“Large” facilities are those with gross floor area exceeding 10,000 m2.)Nooneknowsforsure,butthetotalstockofwarehouse/distributionspaceinFranceisthoughttobeintherangeof85-to-90millionm2(or900-to-1,000MSF)—thevastmajorityofwhichisborderingonfunctionalobsolescence.

WehaveusedDTZ’sdatabasetotrackmarketconditionsinthetwolargestFrenchdistributionhubs—Paris/Ile-de-FranceandLyon/Rhône-Alpes.Thecurrentstockoflarge,modernfacilitiesinthosetwomarketstotaled13millionm2(or140MSF)atmidyear2007

—10millionm2inParis/Ile-de-Franceand3millionm2inLyon.

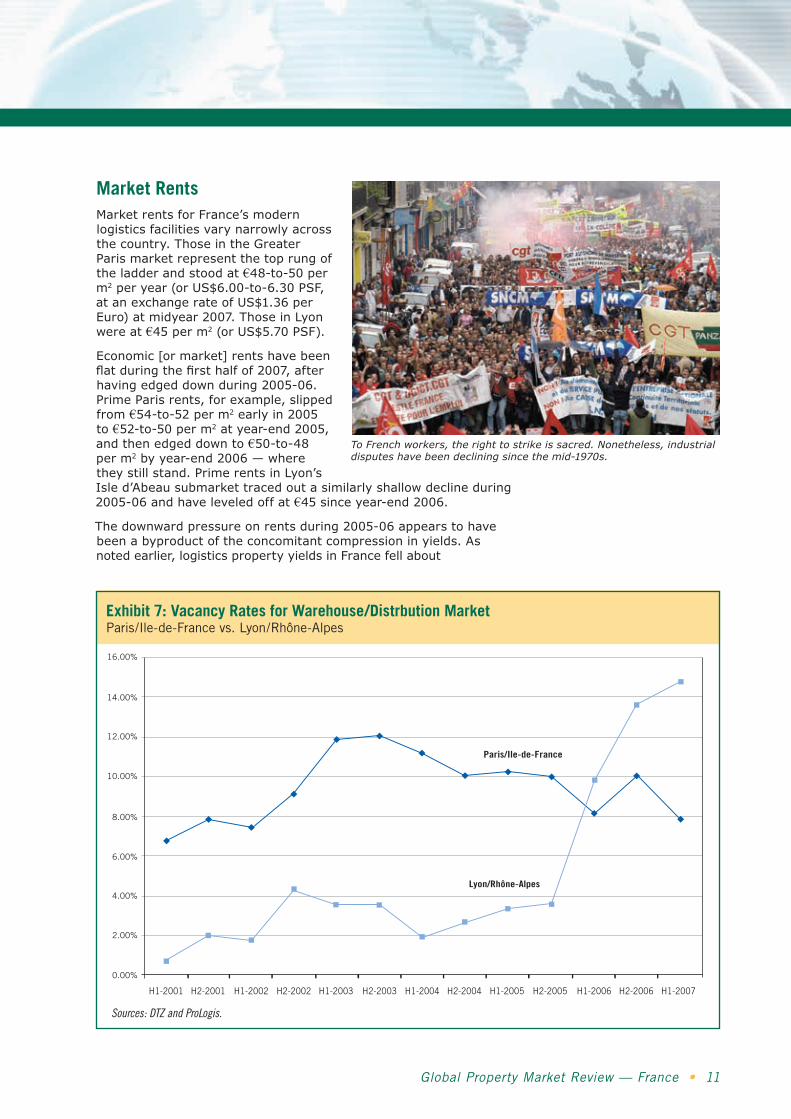

Paris/Ile-de-Franceistodaythehealthierofthetwomarkets.Grant-ed,thegrowthinitsoccupiedspace(realizeddemand)dideaseto4.7%lastyearfromthe6.8%ayearrateaveragedduringtheprevi-ous four years. But realized demand gunned ahead during the first halfof2007,growingata4.3%rate(notannualized).From2003through the first half of 2007, the demand for distribution space in theParis/Ile-de-Franceregionhasoutpacednewdeliveries,anditsoverallvacancyratehasrecededfromthepeakof12.0%reachedatyear-end2003to7.9%atmidyear2007.(See Exhibit 7.)

For the first time, distribution

facilities were built expressly for

the for-lease market, developed on

a speculative basis, and designed

to be adaptable to a multitude of

end-users.

Garonor and Sogaris — Exceptions to the RulePriortothemid-1990s,weknowofonlytwoFrenchdevelopmentcompanies—GaronorS.A.andSogaris—thatdeviatedfromalong-standingtraditionofbuildingwarehousesforowner-occupiers.

Asmentionedinthetext,thepre-1995warehouseswerebuiltmostlybyindependentcontractorshiredbytheowner-occupants.These facilities were financed using a credit-bail — i.e., tax efficient commercialmortgagethatwasoff-balancesheetandpermittedaccelerateddepreciationoflandandbuildings.

Despitethetaxincentivesthatfavouredownership,somecompaniesoperatinginFrancestillpreferredtoleasewarehousespace,ratherthan own it. Recognizing a potentially profitable niche, Garonor S.A. andSogariseachbegantodevelopwarehousespaceforlease,creatinglogisticsparksnearmajorairportsandmotorways.GaronorS.A.wasa private developer acquired by ProLogis in December 1998; Sogaris isownedbyvariousparapublicentitiesandcontinuestodevelopwarehouses.

Today,theblocksofleasedwarehousespacebuiltbythesetwomaverickdevelopersconstitutethemainexceptionstotherulethatpre-1995warehouseswerebuiltby,andfor,owner-occupants.However,whencombined,theseblocksofspaceamounttolessthanone million square metres of older warehouse space — a drop in the bucket,sotospeak,whencomparedtoatotalinventorythoughttobe85-to-90millionm2.

10 • Global Property Market Review — France

Untillastyear,Lyon/Rhône-AlpeshadovershadowedtheParis/Ile-de-FrancemarketandalsohadbeenoneofContinentalEurope’shottestlogisticspropertymarkets.Itslogisticspropertymarketsarecompactenoughinsizethatahandfulofbigleasingdeals—ortheabsencethereof—canleadtomajorswingsinitsvacancyrate.Onesuchswinghasoccurredduringthepastyearandahalf.Owingtoasharpslowdown/contractioninnetabsorptionalongwithcontinueddeliveriesofnewlybuiltfacilities,Lyon’soverallvacancyratejumpedfrom3.6%atyear-end2005to14.7%atmidyear2007.

SeasonedobserversarenotoverlyconcernedabouttheLyonmarket,despitethesharpjumpinitsvacancyrate.Ithasexperi-encedsimilarepisodic“run-ups”inthepast.Moreover,observersareanticipatingamarketcorrectionduring2007-08in-as-muchasseveralcompaniesarecurrentlyinthemarketwithlargespacerequirements and new starts have tapered off.

Inshort,consideringthemalaiseoftheFrencheconomyduring2002-06,itisremarkablethatthedemandformoderndistributionspacehasgrownasrapidlyasithas.Fuelingthishungerfordis-tributionspace,webelieve,hasbeenthepan-Europeanlogisticsrevolution—theresult,inturn,ofEUconvergenceandglobalizationofsupplychains.Hence,goingforward,anyimprovementonthemacroeconomicfrontwouldlikelysharpentheappetiteofFrenchcompaniesformoderndistributionspace.

Fueling this hunger for distribution

space has been the pan-European

logistics revolution.

ELC: European logistics centre.RDC: Regional distribution centre.

Local distribution structure Centralised distribution structure Growing importance of regional distribution

Timeline

ELC

RDC

RDC

RDC

RDC RDC

RDC

Exhibit 6: Regional Distribution Structure Evolves to Service the Expanded European Region

Sources: Capgemini and ProLogis.

Global Property Market Review — France • 11

Market Rents MarketrentsforFrance’smodernlogisticsfacilitiesvarynarrowlyacrossthecountry.ThoseintheGreaterParismarketrepresentthetoprungoftheladderandstoodat€48-to-50perm2peryear(orUS$6.00-to-6.30PSF,atanexchangerateofUS$1.36perEuro)atmidyear2007.ThoseinLyonwereat€45perm2(orUS$5.70PSF).

Economic[ormarket]rentshavebeenflat during the first half of 2007, after havingedgeddownduring2005-06.PrimeParisrents,forexample,slippedfrom€54-to-52perm2earlyin2005to€52-to-50perm2atyear-end2005,andthenedgeddownto€50-to-48perm2byyear-end2006—wheretheystillstand.PrimerentsinLyon’sIsled’Abeausubmarkettracedoutasimilarlyshallowdeclineduring2005-06andhaveleveledoffat€45sinceyear-end2006.

Thedownwardpressureonrentsduring2005-06appearstohavebeenabyproductoftheconcomitantcompressioninyields.Asnotedearlier,logisticspropertyyieldsinFrancefellabout

Exhibit 7: Vacancy Rates for Warehouse/Distrbution MarketParis/Ile-de-France vs. Lyon/Rhône-Alpes

To French workers, the right to strike is sacred. Nonetheless, industrial disputes have been declining since the mid-1970s.

H1-2001 H2-2001 H1-2002 H2-2002 H1-2003 H2-2003 H1-2004 H2-2004 H1-2005 H2-2005 H1-2006 H2-2006 H1-2007

16.00%

14.00%

12.00%

10.00%

4.00%

6.00%

8.00%

0.00%

2.00%

Paris/Ile-de-France

Lyon/Rhône-Alpes

Sources: DTZ and ProLogis.

1� • Global Property Market Review — France

125-to-150basispointsduringthepasttwoyears,parallelingasimilardeclineinmanyothercountries.Inthefaceoftherapidrun-upinpropertyprices,developersandinvestorshavebeenwillingtoac-cept lower required or asking rents inanefforttoacceleratelease-upwhile still enjoying healthy profit margins.

Lookingahead,analystsgener-allyforeseemodestrentgrowthincomingyears.Yieldcompressionisthoughttohavelargelyrunitscourse.Moreover,withconstruc-tioncostshavingrisensharplyinrecentyearsandwiththeEUeconomyhavingshiftedintohighergear,thestageissetformodestrentgrowth.

Contractual Rent IndexationFrance’sstandardcommercialleaseisthebail commercial.Itsterms and conditions were codified into French commercial law un-der a decree that first took effect on September 30, 1953, and, as such,arestandardizednationwide.

AllcommercialleasesinFrancehaveastandardnine-yeartermwith“breaks”atthethirdandsixthyears—theso-called“3-6-9”structure.However,boththetenantandthelandlordareabletowaiveanyofthebreakoptionsinordertohavealongercontractualcommitment—andusuallyalowerrentaswell.“Plain-vanilla”build-to-suitfacilitiesareoftenleasedforasix-yearterm.

Atthethirdandsixthyearbreakpoints,tenantshavetherighttoterminatetheirleasesprematurely,withoutpenalty.Butaslongastheleaseremainsineffect,thecontractualrentswillbeadjustedannually to reflect movements in an index of construction costs. Attheendoftheninthyear,thetenanthastheautomaticrighttorenewhislease,whilethelandlordhastherighttoadjustthecon-tractualrenttotheprevailingmarketlevel.

Withmarketrentshavingedgeddowninrecentyears,agaphasopenedupbetweencontractualrentsandmarketrents.From2002-05,thecostofconstructionindexcompiledbyINSEEincreased3.9%ayear,onaverage;anditjumped7.5%lastyear.Hence,foraleasesignedthreeyearsago,thegapcurrentlyexceeds15%.Asthisgapwidens,tenantsareunderincreasingpressureeithertobreaktheirleasesorrenegotiatetheircontractualrents.

Andthat’spreciselywhattenantshavedone.Leasetake-upshitarecord-highlevelof1.2millionm2inGreaterParislastyear.[“Take-up,” sometimes referred to as gross absorption, is equal to the square footageencompassedinnewlysignedleases.]Atthesametime,netabsorptioninGreaterPariseasedslightlyfromitspreviouspace.

Incontrast,theLyonmarkethasexperiencedanevenmoredramaticdisparitybetweentake-upandnetabsorption.Lastyear,take-upthereamountedto359,000m2, its best showing in five

As the gap between contractual

and market rents widens, tenants

are under increasing pressure

either to break their leases or

renegotiate their contractual rents.

Many of France’s older warehouse facilities built before 1995 are ill-suited to the new competitive environment that materialized after the EU was created in 1992.

Global Property Market Review — France • 1�

years(thoughnotarecordhigh).Atthesametime,netabsorptionamountedtominus108,000m2inLyon.

Developable Land UnliketheUK,Francehasanamplesupplyofdevelopableland.However,thelocalmunici-palitieslandbankalldevelopablelandzonedforcommercialuses,includingdistribution,andtightlycontrolitsreleaseforsaleanddevelopment. Consequently, land pricesinFrancearelesspronetocyclicalswingsthanthoseinothercountries.

With modern distribution facilities requiring bigger tracts of land, thelocalmunicipalitieshavecreatednewindustriallogisticszonesalong major distribution corridors where the first logistics parks were constructed.TheSenartandMarne-la-ValleesubmarketsinIle-de-France(Paris)andtheIsled’AbeausubmarketoutsideLyonarethreeexamplesofthenewzoneswherestrategiclocationscombinedwithamplelandhavemadeitpossibletocreateprimedistributionhubs.

TheParis/Ile-de-FrancemarketservesasbothFrance’slargestcon-sumermarketanditsprincipaltransport/distributionhub.ThebulkofFrance’saircargoisroutedthroughParis-CharlesdeGaulleandParis-OrlyAirports.ParisisalsothejunctionpointforFrance’smajormotorways.Asaresult,landpricesinParis/Ile-de-France,whichrangebetween€50-to-80perm2(orUS$275,000-to-450,000peracre),correspondmorecloselytoEurope’sothermajorcapitalcitiesratherthantotherestofFrance.

LandpricesconvergeintherestofFrancewithsmallvariationsdueprimarilytotheavailabilityofdevelopablelandzonedforlogistics.Landisgenerallymoreexpensiveinareaswherelogisticsware-housedevelopmentsareincompetitionwithalternativeuses.Landpricescurrentlyrangebetween€38-to-42perm2inLyon/Rhône-Alpesandbetween€35-to-38perm2inMarseille.

Local Planning Rules and PermittingTheeaseofobtaininglocalplanningpermissiontobuilddistributionfacilitiesvariesbymunicipality.Whilesomeauthoritiesareada-mantlyopposedtologisticsuses(e.g.Oise,northofParis)owingtoconcerns about environmental pollution or traffic congestion, others (e.g.ToulouseandLeHavre)arefavorablydisposedtowarehousingdevelopmentowingtojobcreationandbroadertaxbases.

Thenormalpermitprocedureincludesapublicinvestigationfocusingonanypotentiallynegativeimpactsontheenvironmentandsur-roundingcommunityinadditiontothesecurityofemployees.Thepermitting process can be quite lengthy compared to other EU coun-tries—takingaslongas12months.However,sincethelocalpermitproceduresareveryexplicit,adeveloperwillusuallyhaveagoodindicationofthelikelihoodthathisprojectwillbeapprovedwhenhefirst applies.

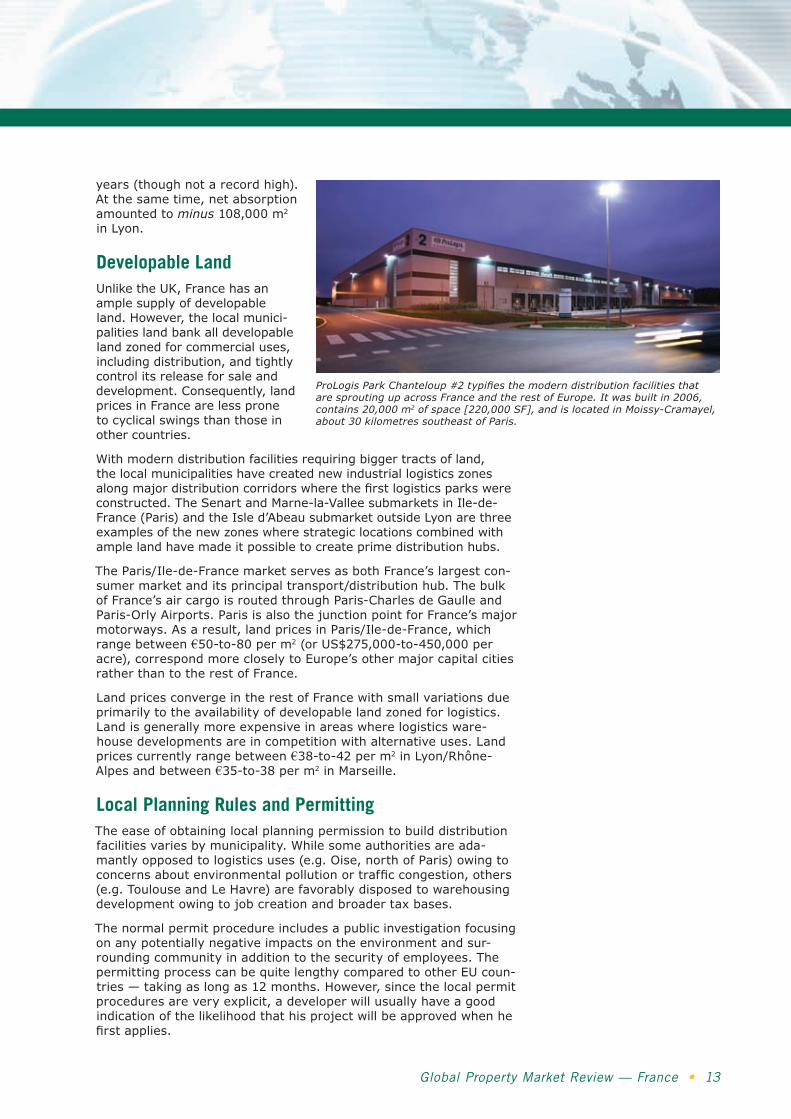

ProLogis Park Chanteloup #2 typifies the modern distribution facilities that are sprouting up across France and the rest of Europe. It was built in 2006, contains 20,000 m2 of space [220,000 SF], and is located in Moissy-Cramayel, about 30 kilometres southeast of Paris.

1� • Global Property Market Review — France

ConclusionFranceiscaughtupinasweepingpan-Europeanlogisticsrevolution,andsoaretheFrenchlogisticspropertymarkets.

Tenyearsago,Francehadvirtuallynomoderndistributionfacilitiesavailable,andthefacilitiesthatdidexistthenwereoperatedmostlybyowneroccupants.Whereastheold-stylefacilitiesweredesignedstrictlyforstorage,thenewonesaredesignedtofacilitatetherapidthroughputofgoods—theHolyGrailforsupplychainexecutives.Today,France’stotalstockofsuchfacilitieshasgrowntoabout15-to-20 million square metres, and the vast majority of these modern facilitieswerebuiltforlease.

To date, property investors have profited handsomely from this transformation,andtheycanlookforwardtocontinuedhealthyreturns.Indeed,consideringthatFrance’seconomyappearstobeescaping finally from the doldrums that have dogged it for the past eightyearsorso,anyimprovementontheeconomicfrontislikelytobolsterthedemandformoderndistributionfacilities.

Endnotes1PepperD.Culpepper,“Capitalism,Coordination,andEconomicChange:theFrenchPoliticalEconomysince1985,”inChanging France: the Politics that Markets Make,editedbyPepperD.Culpepper,etal,Palgrave-Macmillan,2006,p.29.

2SophieMeunier,“FranceandGlobalizationin2003,”U.S.-FranceAnalysisSeries,May2003,TheBrookingsInstitution,pp.1-2.

Global Property Market Review — France • 1�

ThisreportonFranceisthesecondinaseriesinvestigatinghowthe

European logistics property markets operate. (The first one dealt

withtheUKmarkets.)Eachcountry’slogisticspropertymarkets

havetheirownidiosyncrasies,andourgoalistounderstandtheir

differencesaswellastheircommonalities.

We’vealreadyhighlightedthemaintakeawaysfromthisreporton

pageone;there’snoneedtorepeatthemhere.Whatsurprised

me most is the finding that France really did not have any logistics

propertymarketsuntiltheearlytomid-1990s—atleast,notinthe

senseoforganized,well-utilizedexchangesforleaseddistribution

spaceandforthesaleandpurchaseoflogisticsproperties.Such

exchangeswereunneededbecause,priortotheearly’90s,virtually

allFrenchwarehouseswereownedbytheiruser-occupants.

Today,well-functioningmarketsforleasingdistributionspaceandforbuyingorsellingdistributionproperties

notonlyexistinFrance,buthavegrownlargeenoughtoprovidelessees,owners,andinvestorswithhigh

degrees of liquidity. Indeed, as indicated in the text, France today possesses the largest inventory of large,

moderndistributionfacilitiesontheContinent.TheFrenchmaydislikecompetitivemarkets,buttheyare

pragmaticenoughtorealizethattheymusthavemoderndistributionfacilitiestocompeteeffectivelywithin

theEU“sweepstakes.”

From the Editor…

About ProLogis

Leonard Sahling

First Vice President

ProLogis Research Group

+1 (303) 576 2766

Lisa Graham

Director of European Research

ProLogis Research Group

Paris, France

+33 (0)6 72 01 53 08

ProLogisistheworld’slargestowner,manager,anddeveloperofdistributionfacilities,withoperationsin105marketsacrossNorthAmerica,Europe,andAsia.Thecompanyhas$29.9billionofassetsowned,managed,and under development, comprising 447 million square feet (42 million square meters) in 2,523 properties asofJune30,2007.ProLogis’customersincludemanufacturers,retailers,transportationcompanies,third-party logistics providers and other enterprises with large-scale distribution needs. Headquartered in Denver,Colorado,ProLogisemploysmorethan1,300peopleworldwide.

©Copyright2007ProLogis.Allrightsreserved.

ThisinformationshouldnotbeconstruedasanoffertosellorthesolicitationofanoffertobuyanysecurityofProLogis.Wearenotsolicitinganyactionbasedonthismaterial.ItisforthegeneralinformationofProLogis’customersandinvestors.

Thisreportisbased,inpart,onpublicinformationthatweconsiderreliable,butwedonotrepresentthatitisaccurateorcomplete,anditshouldnotbereliedonassuch.Norepresentationisgivenwithrespecttotheaccuracyorcompletenessoftheinformationherein.Opinionsexpressedareourcurrentopinionsasofthedateappearingonthisreportonly.ProLogisdisclaimsanyandallliabilityrelatingtothisreport,including,withoutlimitation,anyexpressorimpliedrepresentationsorwarrantiesforstatementsorerrorscontainedin,oromissionsfrom,thisreport.

Anyestimates,projectionsorpredictionsgiveninthisreportareintendedtobeforward-lookingstatements.Althoughwebelievethattheexpectationsinsuchforward-lookingstatementsarereasonable,wecangivenoassurancethatanyforward-lookingstatementswillprovetobecorrect.Suchestimatesaresubjecttoactualknownandunknownrisks,uncertainties,andotherfactorsthatcouldcauseactualresultstodiffermateriallyfromthoseprojected.Theseforward-lookingstatementsspeakonlyasofthedateofthisreport.Weexpresslydisclaimanyobligationorundertakingtoupdateorreviseanyforward-lookingstatementcontained herein to reflect any change in our expectations or any changeincircumstancesuponwhichsuchstatementisbased.

Nopartofthismaterialmaybe(i)copied,photocopied,orduplicatedinanyformbyanymeansor(ii)redistributedwithoutthepriorwrittenconsentofProLogis.

1007-3000 P20303

1� • Global Property Market Review — France

ProLogis-Europe

Customer Service Headquarters

Schiphol Blvd., Tower F, 6th Floor

World Trade Center

Schiphol Airport 1118BG

Amsterdam, Netherlands

+31 (0)20 655 66 66

www.prologis.com

ProLogis Corporate Headquarters

4545 Airport Way

Denver, CO 80239

303.567.5000

800.566.2706

www.prologis.com

ProLogis Supply Chain Research ReportsAdditionalsupplychainresearchreportsareavailable.TodownloadPDFs

oftheseadditionalreports,pleasegotowww.prologisresearch.com.