fixed income 2 level ii 2020 - dbf finance

TRANSCRIPT

CFA®Preparationwww.dbf-finance.com

LuisM.deAlfonso

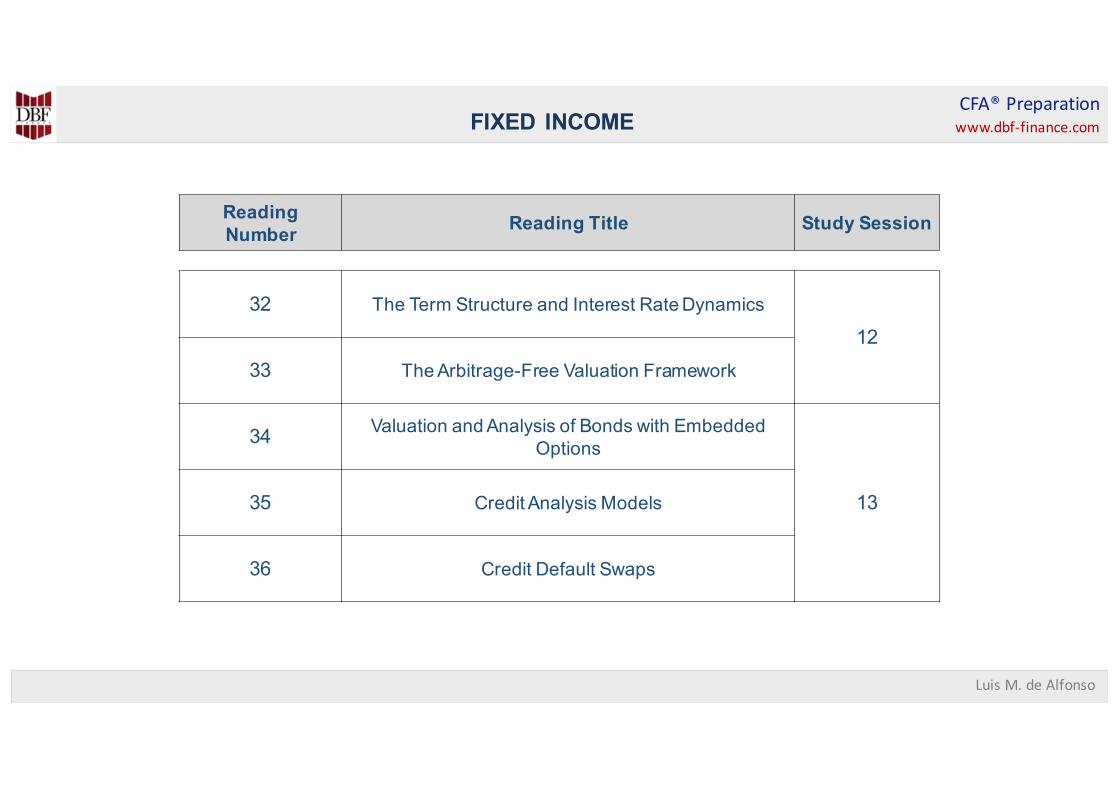

FIXED INCOME

Reading Number Reading Title Study Session

32 The Term Structure and Interest Rate Dynamics

1233 The Arbitrage-Free Valuation Framework

34 Valuation and Analysis of Bonds with EmbeddedOptions

1335 Credit Analysis Models

36 Credit Default Swaps

CFA®Preparationwww.dbf-finance.com

LuisM.deAlfonso

FIXED INCOME

The Arbitrage-Free ValuationFramework

Study Session 12

Reading Number 33

CFA®Preparationwww.dbf-finance.com

LuisM.deAlfonso

FI – The Arbitrage-Free Valuation Framework

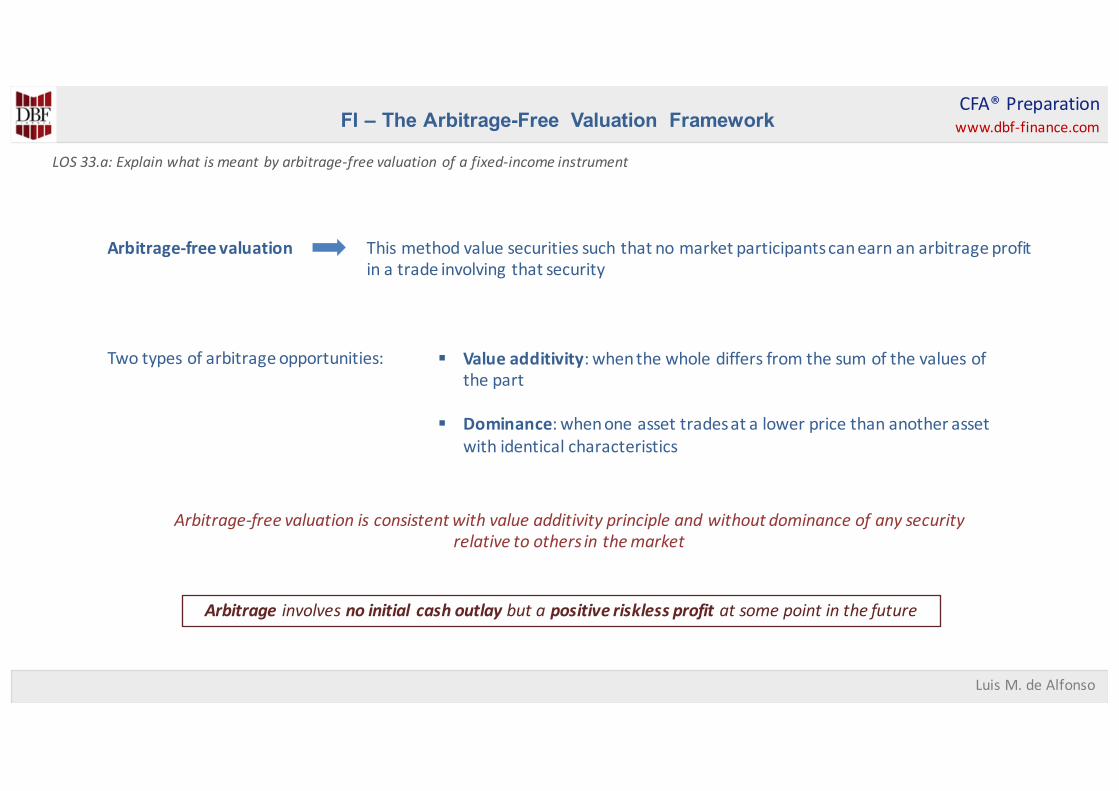

LOS33.a:Explain what is meant by arbitrage-freevaluation ofafixed-income instrument

Arbitrage-freevaluation This method value securities such that nomarket participantscanearn an arbitrageprofitinatrade involving that security

Two types ofarbitrageopportunities: § Value additivity:whenthe whole differs from the sumofthe values ofthe part

§ Dominance:whenone asset tradesatalower price than another assetwith identical characteristics

Arbitrage-freevaluation is consistentwith value additivity principle andwithout dominance ofany securityrelative toothers inthemarket

Arbitrage involves noinitial cashoutlay but apositiveriskless profit atsome point inthe future

CFA®Preparationwww.dbf-finance.com

LuisM.deAlfonso

FI – The Arbitrage-Free Valuation Framework

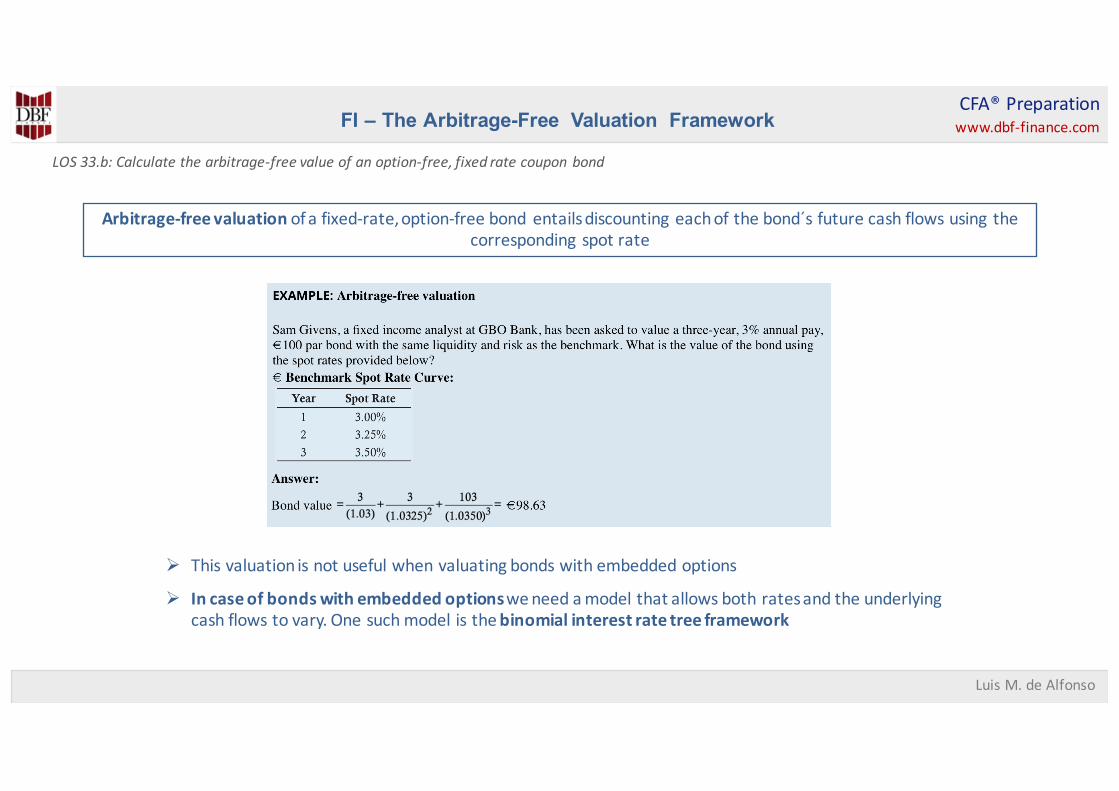

LOS33.b:Calculate the arbitrage-freevalue ofan option-free,fixed rate coupon bond

Arbitrage-freevaluation ofafixed-rate,option-freebond entailsdiscounting eachofthe bond´sfuture cashflows using thecorresponding spotrate

Ø This valuation is not useful when valuating bonds with embedded options

Ø Incaseofbondswith embedded optionsweneed amodel that allows both ratesandthe underlyingcashflows tovary.One suchmodel is thebinomialinterest rate tree framework

CFA®Preparationwww.dbf-finance.com

LuisM.deAlfonso

FI – The Arbitrage-Free Valuation Framework

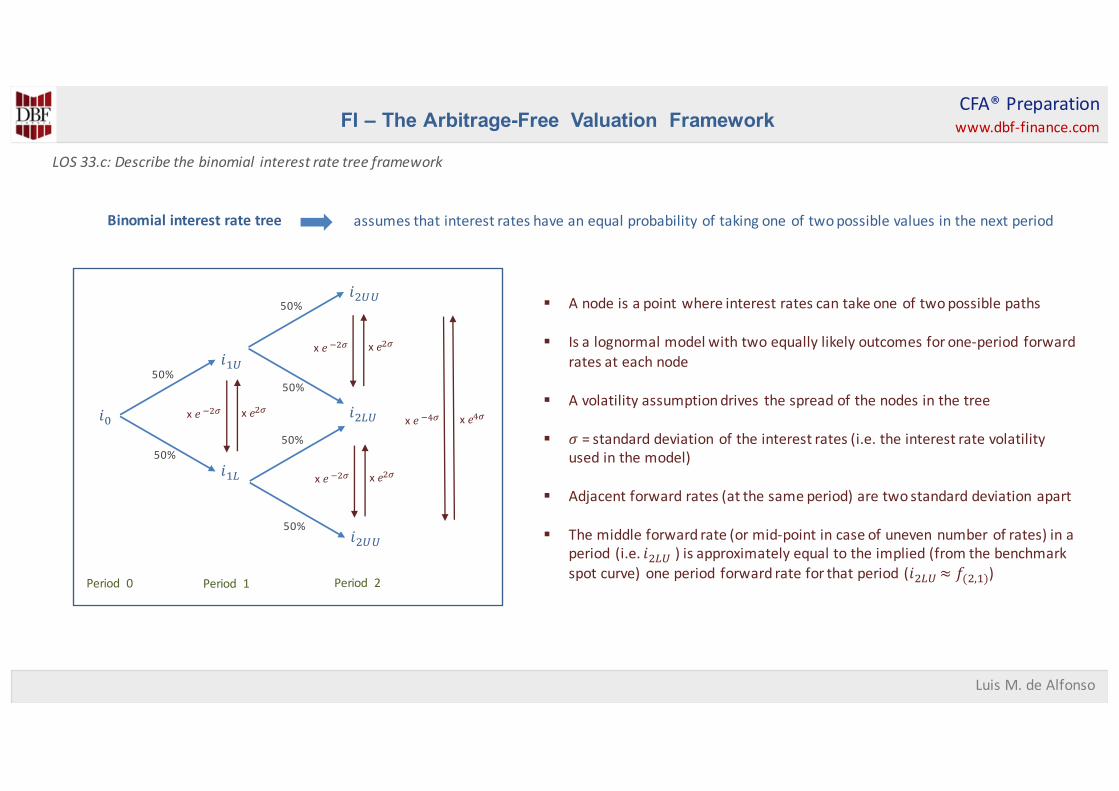

LOS33.c:Describethe binomial interest rate tree framework

Binomialinterest rate tree assumes that interest rates have an equal probability oftaking one oftwopossible values inthe next period

𝑖"

𝑖#$

𝑖#%50%

50%

𝑖&$%

𝑖&%%50%

50%

𝑖&%%

50%

50%

x𝑒&(x𝑒 )&(

x𝑒&(x𝑒 )&(

x𝑒&(x𝑒 )&(

x𝑒*(x𝑒 )*(

Period 0 Period 1 Period 2

§ Anode is apoint where interest rates cantake one oftwopossible paths

§ Is alognormal model with two equally likely outcomes for one-period forwardrates ateach node

§ Avolatility assumptiondrives the spreadofthe nodes inthe tree

§ 𝜎 =standarddeviation ofthe interest rates (i.e.the interest rate volatilityused inthe model)

§ Adjacent forwardrates (atthe same period)aretwo standarddeviation apart

§ The middle forwardrate (or mid-point incaseofuneven number ofrates)inaperiod (i.e.𝑖&$% )is approximately equal tothe implied (from the benchmarkspotcurve)one period forwardrate for that period (𝑖&$% ≈ 𝑓(&,#))

CFA®Preparationwww.dbf-finance.com

LuisM.deAlfonso

FI – The Arbitrage-Free Valuation Framework

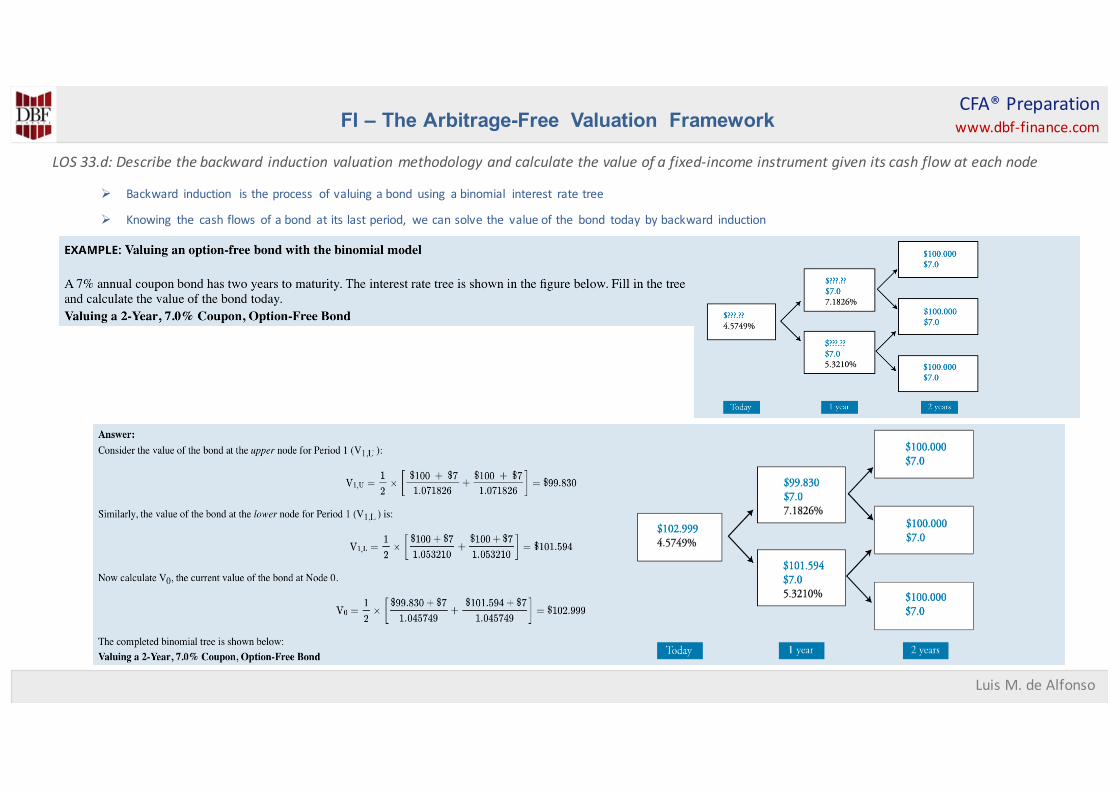

LOS33.d:Describethe backward induction valuation methodology andcalculate the value ofafixed-income instrument given its cashflow ateach node

Ø Backward induction is the process ofvaluing abond using abinomial interest rate tree

Ø Knowing the cashflows ofabond atits last period, we cansolve the value ofthe bond today by backward induction

CFA®Preparationwww.dbf-finance.com

LuisM.deAlfonso

FI – The Arbitrage-Free Valuation Framework

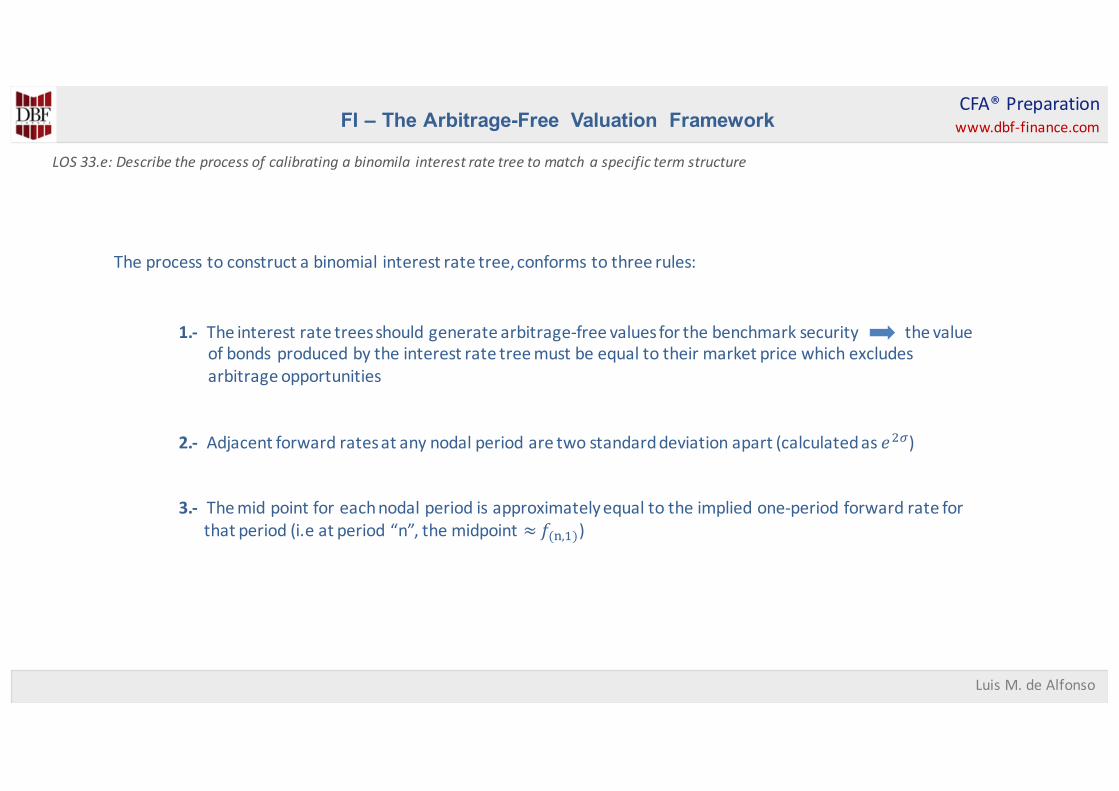

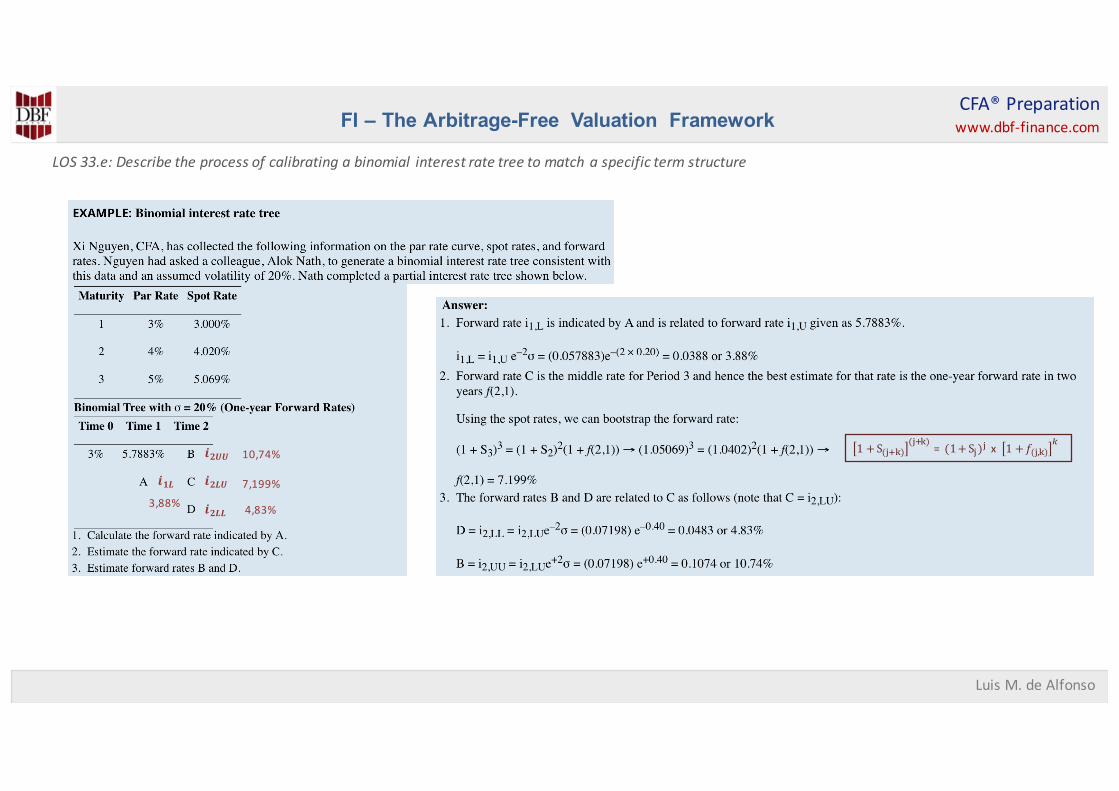

LOS33.e:Describethe process ofcalibrating abinomila interest rate tree tomatchaspecific term structure

The process toconstruct abinomialinterest rate tree,conforms tothree rules:

1.- The interest rate treesshould generate arbitrage-freevalues for the benchmark security the valueofbonds produced by the interest rate treemust beequal totheir market price which excludesarbitrageopportunities

2.- Adjacent forwardratesatany nodalperiod aretwo standarddeviation apart (calculatedas𝑒&()

3.- Themid point for eachnodalperiod is approximatelyequal tothe implied one-period forwardrate forthat period (i.e atperiod “n”,the midpoint ≈𝑓(1,#))

CFA®Preparationwww.dbf-finance.com

LuisM.deAlfonso

FI – The Arbitrage-Free Valuation Framework

LOS33.e:Describethe process ofcalibrating abinomial interest rate tree tomatchaspecific term structure

𝒊𝟐𝑼𝑼

𝒊𝟐𝑳𝑼

𝒊𝟐𝑳𝑳

𝒊𝟏𝑳

1 +S(:;<)(:;<)

=(1+S:): x 1 +𝑓(:,<)=

3,88%7,199%

10,74%

4,83%

CFA®Preparationwww.dbf-finance.com

LuisM.deAlfonso

FI – The Arbitrage-Free Valuation Framework

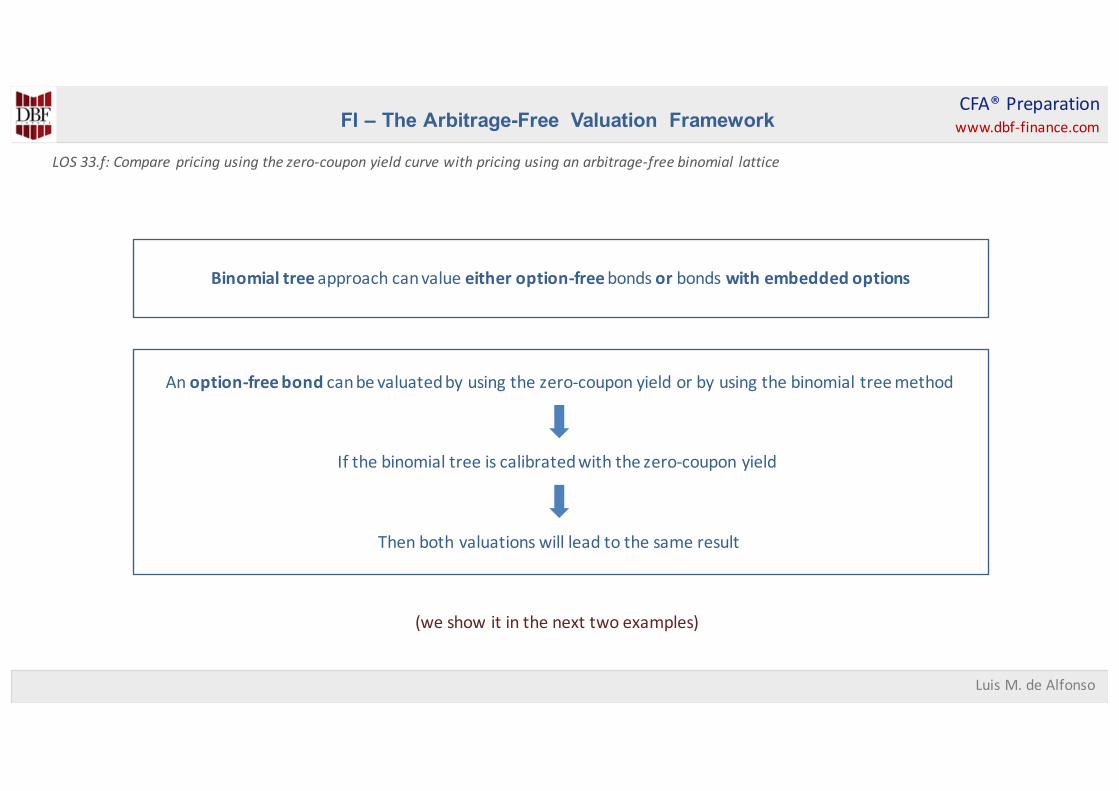

LOS33.f:Comparepricing using the zero-coupon yield curvewith pricing using an arbitrage-freebinomial lattice

An option-freebondcanbevaluatedby using the zero-coupon yield or by using the binomialtreemethod

If the binomialtree is calibratedwith the zero-coupon yield

Then both valuations will leadtothe same result

Binomialtreeapproach canvalue either option-freebonds or bonds with embedded options

(we showit inthe next two examples)

CFA®Preparationwww.dbf-finance.com

LuisM.deAlfonso

FI – The Arbitrage-Free Valuation Framework

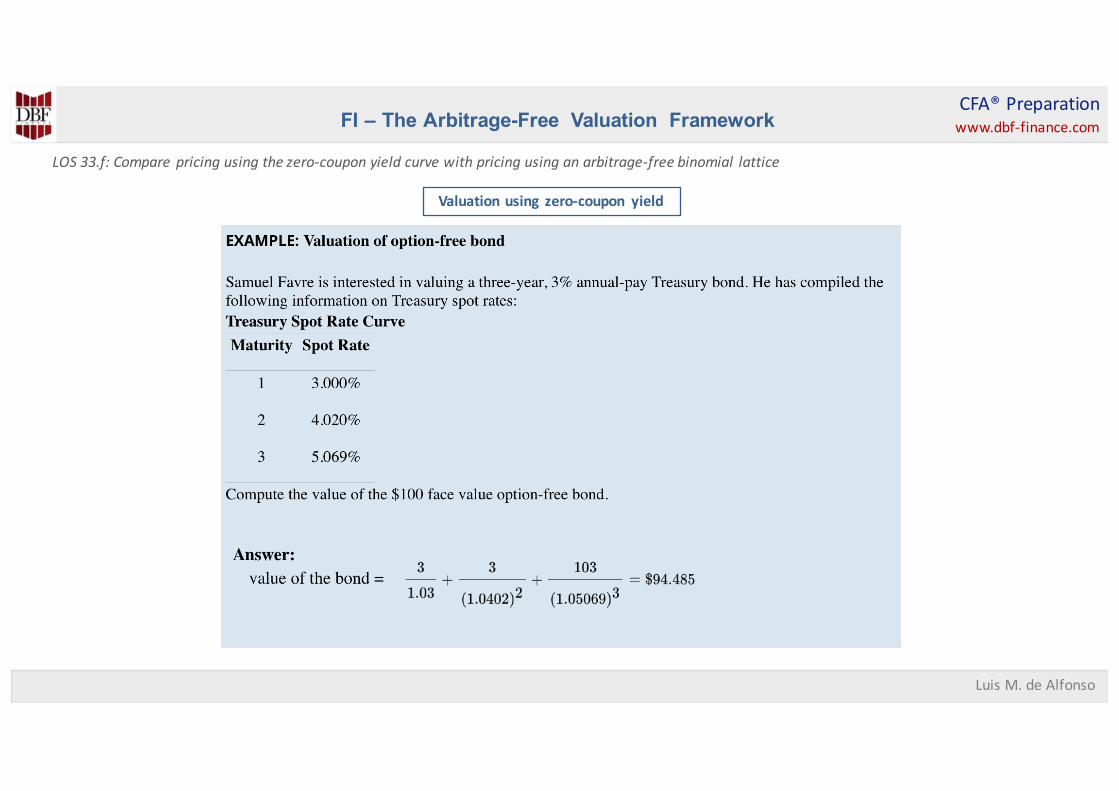

LOS33.f:Comparepricing using the zero-coupon yield curvewith pricing using an arbitrage-freebinomial lattice

Valuation using zero-coupon yield

CFA®Preparationwww.dbf-finance.com

LuisM.deAlfonso

FI – The Arbitrage-Free Valuation Framework

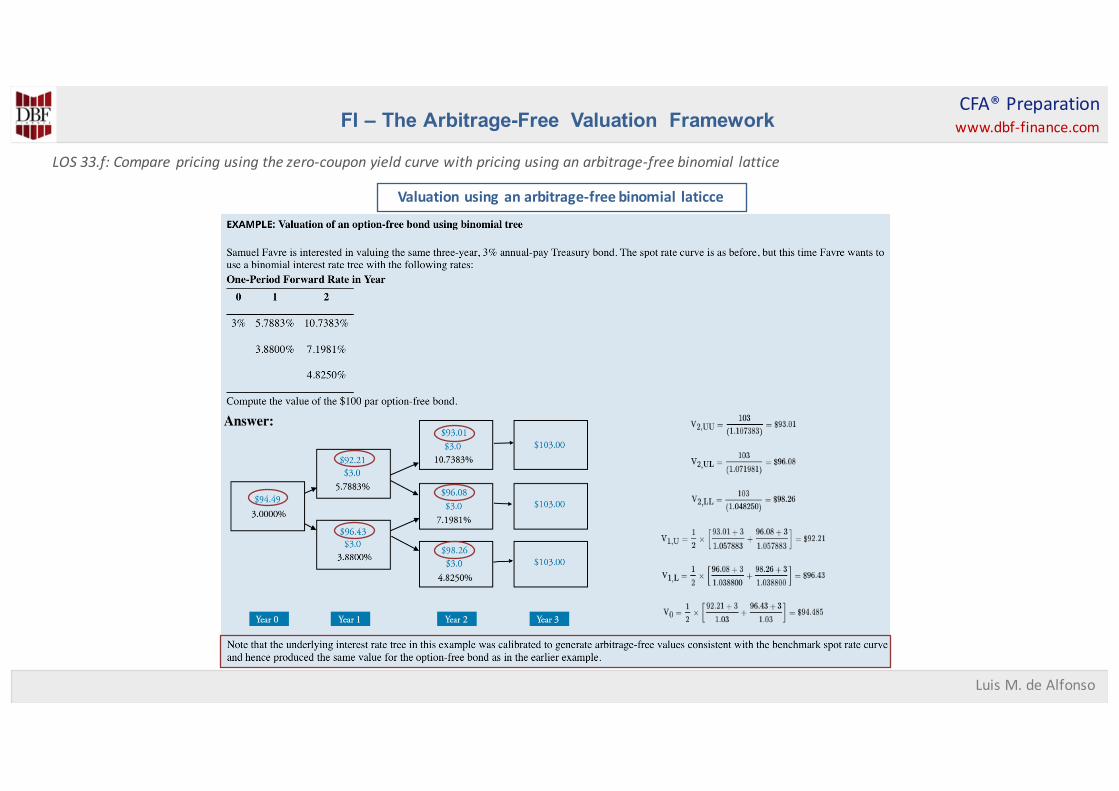

LOS33.f:Comparepricing using the zero-coupon yield curvewith pricing using an arbitrage-freebinomial lattice

Valuation using an arbitrage-freebinomial laticce

CFA®Preparationwww.dbf-finance.com

LuisM.deAlfonso

FI – The Arbitrage-Free Valuation Framework

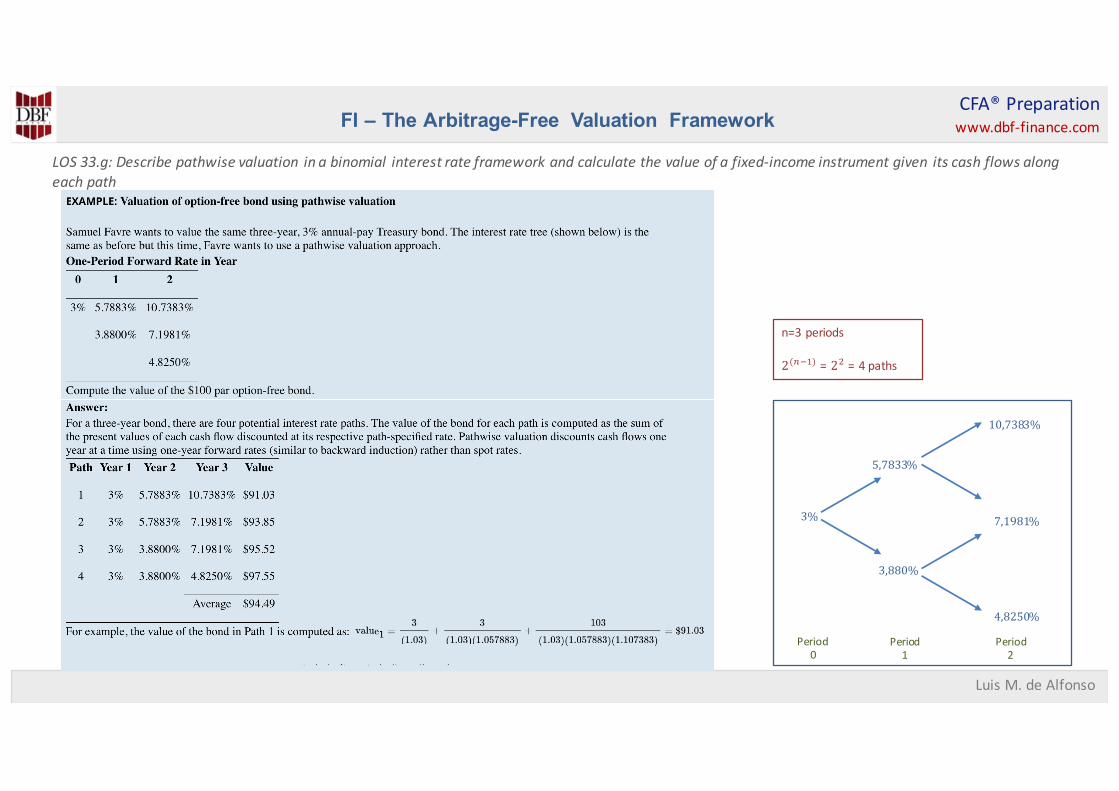

LOS33.g:Describepathwise valuation inabinomial interest rate framework andcalculate the value ofafixed-income instrument given its cashflows alongeach path

Another mathematically identicalapproach tovaluationusing thebackward induction method inabinomialtree is thepathwisevaluation approach

Foran n-period binomialtree,there are2 ?)# possible paths

CFA®Preparationwww.dbf-finance.com

LuisM.deAlfonso

FI – The Arbitrage-Free Valuation Framework

LOS33.g:Describepathwise valuation inabinomial interest rate framework andcalculate the value ofafixed-income instrument given its cashflows alongeach path

3%

3,880%

5,7833%

7,1981%

10,7383%

4,8250%

Period0

Period1

Period2

n=3periods

2 ?)# =2& =4paths

CFA®Preparationwww.dbf-finance.com

LuisM.deAlfonso

FI – The Arbitrage-Free Valuation Framework

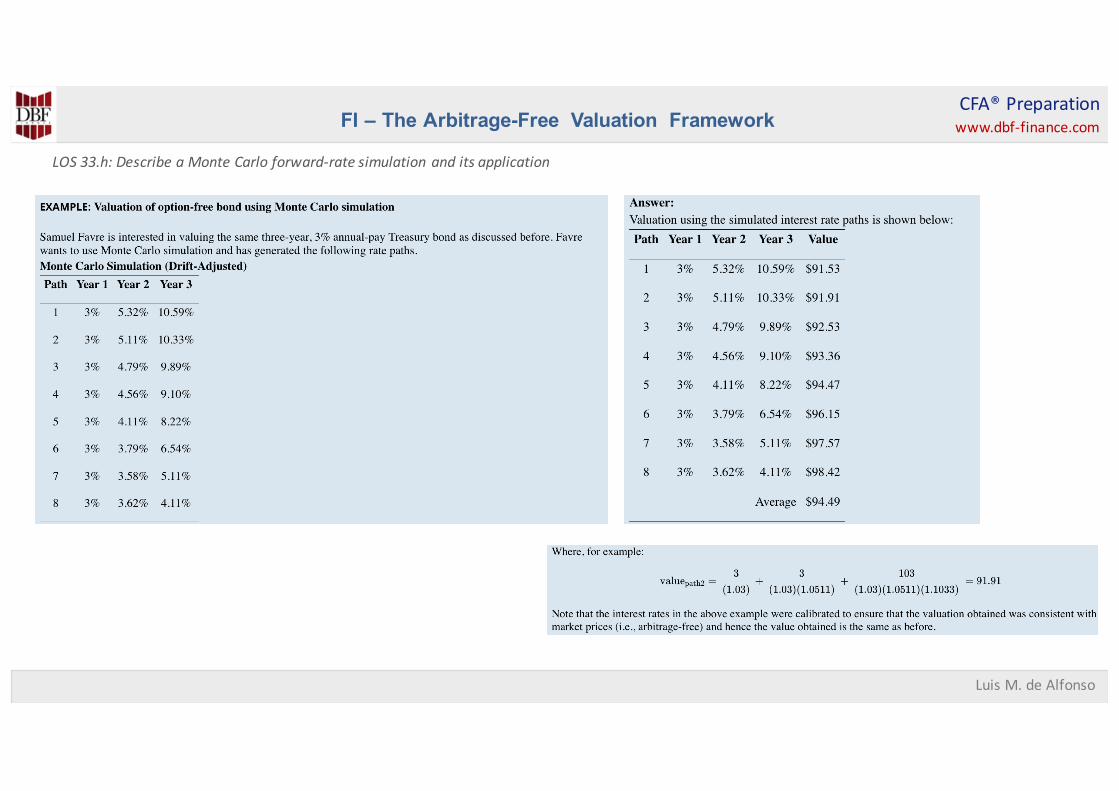

LOS33.h:DescribeaMonteCarloforward-rate simulation andits application

Ø Mortgage-backedsecuritieshavepath dependent cashflows on account ofthe embedded prepayment option

Ø An important assumption ofthe binomialvaluation process is that the value ofthe cashflows atagiven pointintimeis independent ofthe path that interest rates followed uptothat point (i.e.thebinomialvaluationprocess cannot beusedwhen cashflows arepath dependent)

Ø Becauseofpath dependency ofcashflows ofmortgage-backedsecurities,the binomialtreebackwardinduction process cannot beused tovalue such securities

Ø MonteCarlosimulationmethod should beused for valuing MBS,asthis method canbeusedwhen cashflowsarepath dependent

Ø MonteCarlosimulation method usespathwise valuationandalargenumber ofrandomly generatedsimulatedpaths,using amodel that incorporates avolatility assumption andan assumed probability distribution

CFA®Preparationwww.dbf-finance.com

LuisM.deAlfonso

FI – The Arbitrage-Free Valuation Framework

LOS33.h:DescribeaMonteCarloforward-rate simulation andits application