financial statements, creative accounting, and roles of auditors

TRANSCRIPT

1

Financial Statements, Creative Accounting, and Roles of Auditors: The

Case of Bangladesh

ABSTRACT

Based mainly on archival sources and interviews of accounting academics and

professionals, this paper examines financial statements, creative accounting, and roles

and responsibilities of auditors in Bangladesh. Like other countries, financial statements

in Bangladesh are intended to provide divergent users a true and fair view of the

business result of a company during a stipulated period of time and the state of affairs

at a particular date. The professional auditors' functions in connection with these

statements include examination of the books of accounts on the basis of which these

are prepared; verification that financial statements conform to legal requirements and

conventional accounting practices; certification that these statements exhibit accurate,

authentic, and undistorted business results and financial positions, and attestation that

such statements do not conceal any irregularities in connection with their preparation,

presentation, and certification. The users rely on such audited reports and use them to

achieve their respective objectives. If those reports misrepresent or conceal companies'

performance and positions, and the users suffer any loss from actions based on such

reports, they can sue the auditors in the court of justice and bring complaints to the

professional accounting institution. Financial and audit integrity is also essential in order

to promote a strong and reliable capital market and attract foreign investment. This

paper critically examines the existing provisions of the Companies Act, legal,

professional and ethical codes of conduct, and the role of the court in resolving audit

related cases in Bangladesh. It is suggested that a strong coordinated role of the

government and professional bodies is required to ensure proper user protection.

Keywords: Audit function, Auditor responsibility, Bangladesh, codes of ethical conduct,

creative accounting, financial statements.

2

INTRODUCTION: RESEARCH OBJECTIVE AND METHOD

Professional auditors and accountants in Bangladesh are surrounded, guided, and

conditioned by a wide array of national and social, conventional, legal, ethical, and

professional rules and norms, and these frame the horizon of their professional and

occupational duties and responsibilities. Regional and international professional forums

and bodies, international developmental agencies, and multinational investors'

requirements also influence activities, organisation, and management of their

professional bodies. The two most important functions that need to be performed are

auditing of financial statements and issuing reports. This paper gives an account of

auditors` responsibilities and liabilities in connection with financial statements that they

audit, but fail to report on window‐dressing and cooking of books and other mollified

and fraudulent practices, and thus cause damages to the users.

Methods used to conduct this research include survey of literature, examination of

web sites of different national and international professional bodies and related

organisations, examination of audited financial reports and statements as found in

annual reports of several state‐owned enterprises in Bangladesh, telephonic interview

of several prominent accounting scholars and professionals, and informal contacts with

some professional accountants and their client companies.

FINANCIAL STATEMENTS: OBJECTIVES AND PRINCIPLES

For joint stock companies in Bangladesh, legislations are the primary and most

important sources and guidelines to keep books of accounts, make accounting

statements, conduct audits, and making report to the users. In accordance with Section

181 of the Companies Act, 1994, a joint stock company shall keep accounting

statements of all receipts and payments, all sales and purchases of goods, and all assets

and liabilities. In order to determine profit or loss of business activities during a

particular period, which is normally a year, a profit and loss account and to show the

state of financial position at a specific date which is usually the last day of that period, a

balance sheet is prepared (GOB/MOL, 1994). To be more specific and realistic, financial

3

statements in Bangladesh include three sets of statements, namely a profit and loss

account divided into manufacturing account, trading account, profit and loss account,

and profit and loss appropriation account as per necessity and custom; a balance sheet;

and needful supplementary statements (Khan, 2000). The supplementary statements

are prepared to support and explain information included in the above financial

statements. Some of such statements and explanatory notes are cash flow and fund

flow statements that are now treated as integral part of financial statements and should

be read and refereed to together in order to get a clear picture of the business results

and financial position of the company (Rahman, 1982). However, sole trader companies,

partnership firms, government organisations and institutions, private business

enterprises, non‐governmental organisations and societies, and non‐profit organisations

are also required to keep records of transactions and make periodical financial

statements to show their performance and positions.

In addition to legal requirements, the financial statements serve many purposes of

divergent interest groups and parties. A manufacturing account shows the performance

of an enterprise that is engaged in manufacturing of goods and services as reflected in

the cost of products or services manufactured, and it is prepared after taking into

account all direct costs and expenses incurred in connection therewith (Khan, 200;

Banerjee, 2005). The trading account shows the gross business result which is either

gross profit or loss and occurs due to buying and selling of goods, which can be both

manufactured inside the company or purchased from other companies. The profit and

loss account shows net business results, i.e., the net profit or loss after deducting all

indirect and administrative expenses. The profit and loss appropriation account is

mostly prepared by a public joint stock company, and shows how the final profit or loss

of an accounting year is disposed of among various portfolios and stakeholders. These

can be called accounting of produces, sales, expenses, net profit or loss, and

disbursement of profit and loss for a given period of time, which is most commonly a

year.

The second most important financial statement is the balance sheet, which shows a

summarized financial position as reflected in assets, liabilities, working capital, net

4

worth, and bank loans, stock, and debentures on a specific point of time. In a true sense,

it shows the position of the fundamental accounting equation (Assets = Liabilities +

Proprietorship) at a particular point of time (Khan, 2006; Ahmed 2007). The

supplementary statements show detailed transactions done in a particular account, or

position of affairs and performance in a specific area, or an account of importance.

These accounts and statements look very simple in literature and practice, but from the

very start of the history of company accounting in this country and in other parts of the

globe, these are essentially needed for any commercial enterprise. Laws make them

binding, parties other than management and owners use these for their respective

interests, and the government requires these to see the aggregate result of business

activities. These seem deceptively simple, but practically very difficult in that they need

to show the business results and positions accurately. Accountants all over the globe are

dying hard to keep such accounts in conformity with laws, concepts, and conventions;

accounting scholars teaches their arts and science of keeping such accounts; and

employers give on‐the‐job training to develop skills of their accounting staff to keep

accounts and make statements and reports in readily usable forms and formats.

The sacred creed underlying all the above financial statements is that of a “true and

fair view” in that these exhibit and disclose the true and fair view of the performance‐

either profit or loss‐of the company's business activities for the period for which these

are prepared; and show the true and fair view of the state of financial position at a

particular date as shown by assets, liabilities, and equities, which may change in value

and quality due to use, lapse of time, and changes that circumscribe business function,

operation, and management of a concerned company (Tandon, Sudharsanam &

Sundharabahu, 2001; Ullah, 2001; Gupta, 2007; Saeed, 2008; Gill, 2009). All material

changes of positions must be supported by supplementary statements‐notes, other

statements, and explanatory materials‐prepared also on the similar principle of “true

and fair view”.

One statutory requirement is that all such accounts and statements be prepared

and audited by professional accountants who are chartered and/or certified public

accountants as per the law of the country. The Security and Stock Exchange Commission

5

requires all listed companies on the Dhaka and Chittagong Stock Exchanges to follow

International Accounting Standards (IAS). Other parties interested in accounting

statements in Bangladesh are investors, management, lenders, creditors, the

government and its agencies, share brokers, and foreign business partners. Unlike

developed nations, customers, employees, suppliers and trade partners, the general

public, and academia possess inertia toward to companies’ reports and statements.

Stock markets nowadays, however, drew attention of private and institutional investors,

as a result of which companies are increasingly careful to improve the qualitative

aspects of their accounts and audit statements.

As induced from IAS and international accounting and auditing bodies, financial

statements should pass the test of four qualitative characters, such as,

understandability, relevance, reliability, and comparability. Relevance involves

materiality and reliability includes faithful representation, substance over form,

neutrality, prudence, and completeness (Alexander & Simon, 2000). Although not

directly refereed to the IAS, the Company Act 1994 stipulates that accounting

statements must adhere to principle and spirit to achieve such qualities to fulfill all

implicit and explicit objectives of such financial statements (MOL/GOB, 1994).

Companies and firms follow and adopt various formats in producing accounting and

other financial statements as stipulated in the Company Act. Although accountants

adhere to the principles of this Act, many follow the so called British format where items

are shown in horizontal orders with debits in the left hand column and credits in the

right hand column and the American format of expenditures shown at first in landscape

format followed by the income items in the similar format. In the balance sheet

especially assets and liabilities are grouped to facilitate ratio and other analyses for

decision‐making by interested parties and users. In practice, all company accounts in

Bangladesh are required to be kept in accordance with double entry book keeping

principles, although proprietary and partnership firms and many non‐governmental

organisations and other organisations keep account on the single entry system.

However, this happens mostly due to ignorance on the double entry system.

6

Vide Sections 181‐184 of the Companies Act 1994 in Bangladesh, books of accounts

and accounting statements are needed to keep records of all amounts of money

received and expended, all sales and purchases, assets and liabilities, and particulars

relating to utilization of material, labor, and overhead items in connection with

production, processing, manufacturing, marketing and distribution of goods and

services. These are intended to give a true and fair view of the business affairs and

explain transactions carried out. The books of accounts and related documents are

open to inspection by the Registrar of Joint Stock Companies and any authorized

government agency and office. It is a mandatory requirement on the part of the Board

to present a balance sheet together with a profit and loss account or an income and

expenditure account of a financial year in the annual general meeting of that year

(MOL/GOB, 1994). All these must be audited and certified by a professional accountant.

The rationale of making profit and loss appropriation account is that all profits after the

payment of mandatory tax belongs to the shareholder or owners and accrues to them as

dividend. Carrying a part of that to any reserve account indeed implies forsaking current

gain by them. Any allocation to reserve and sinking funds implies it should be made for

such purposes as strengthening the financial position of the company, and, therefore,

should be agreed upon, disclosed, and explained by management to the stakeholders.

Regarding the form and contents of balance sheet and profit and loss account, the

law stipulates that “the balance sheet of a company shall contain a summary of the

assets and of the capital and liabilities of the company, giving a true and fair view of

affairs as at the end of the financial year, and it shall, subject to the provisions of this

section be in the forms set out in Part‐I of Schedule I, or in such form as may be

approved by the government; and in preparing the balance sheet due regard shall be

paid to the general instructions for preparation of balance sheet under the heading

“Notes” at the end of Part I” mentioned above. On the other hand, the “profit and loss

account of a company shall give a true and fair view of the profit and or loss of the

company for the financial year and shall, and (the author adds the italicized words)

comply with the requirements of Part II of Schedule XI” of this law (MOL/GOB, 1994).

The spirit and rationale of law everywhere is the same, but this regulations in the

7

Companies Law of Bangladesh was highly influenced by laws in neighboring India and in

the United Kingdom which, in fact, formulated and enacted this and most other laws for

its colonies in South Asia.

This law also stipulates that the balance sheet and the profit and loss account shall

be authenticated by a board member; certified copies of such documents shall be filed

to the Registrar of the Joint Stock Companies; and these shall be sent to shareholders

and stockholders before the annual general meeting (Companies Act, 1994,sections,

189, 190, 191& 193). This are, in fact, intended to establish disclosure, stakeholders’

governance, and government control, and prevent malicious practices. These also help

keep accounts and books by accounting staff and conduct audit by both internal and

external auditors.

CREATIVE ACCOUNTING FOR WINDOW‐DRESSING OF FINANCIAL STATEMENTS

According to the prevailing laws and customs in Bangladesh, financial statements

must show the true and fair view of performance and state of affairs of the company in

the most accurate form and understandable way. Window‐dressing is a process of

manipulation in those statements, and intends to give users a more favorable

impression of performance and the position of the company, which can otherwise be

disclosed had there not been any such manipulations (Shukla, Grewal & Gupta, 1997;

Khan, 2000; Ahmed, 2007). The practice is not necessarily fraudulent, but it is willful and

a sheer maneuver to show a better performance and state of affairs. In reality, the state

of affairs shown thus is not typical of what prevailed throughout the year (Khan, 2000).

It is done in meticulous way, and is also called creative accounting. Companies take

resort to it to show stronger business position than competitors, influence prices in the

stock market, sale new stock or bond issue, bluff tax authority, conceal liquidity crisis,

defend hostile takeover bid, avoid statutory M&A, evade managerial inefficiency, pay or

receive shoddy bonus, and deceive individual investors who mostly do not possess

knowledge of accounting, or stock market.

8

According to the Dictionary of Accounting Terms, window dressing makes a

company looking better financially than what it really is. The Dictionary of Finance and

Investment Terms puts it in a little different way that trading activity at the end of the

accounting period is designed to dress up a portfolio to be presented to clients or

shareholders. This includes all accounting gimmickry, e.g., omitting certain expenses,

concealing certain liabilities, delaying write‐offs, anticipating sales, and other such

actions, which may or may not be fraudulent, but are designed to make a financial

statement show a more favorable condition than what actually exists. The Dictionary of

Banking Terms defines it as special adjustments in the financial position done often to

give the appearance of adequate liquidity in order to comply with reporting

requirements (All Business, 2009). Such other definitions are innumerable in textbooks,

online materials, and research papers and monograms. Thus definitions, styles, and

motives of creative accounting and window dressing differ among industries,

organizations, companies, firms, and even countries. Allen (2003) finds that the US

banks make systematic upward window dressing adjustment in assets and liabilities

especially federal funds, repurchase agreements, certificates of deposit, and Eurodollar

deposits on the last day of the quarter. Griffiths (1989) humorously calls window

dressing creative accounting whereby, “every company in the country is fiddling its

profits. Every set of published accounts is based on books which have been gently

cooked or completely roasted. The figures which are fed twice a year to the investing

public have been changed to protect the guilty. It is the biggest con trick since the

Trojan Horse”. He further argues that although the accounting standard regimes have

undergone drastic changes in the 1990s, there still exits a plethora of devices which a

company can adopt to show their performance and position in a better way (Griffiths,

1995).

Although practiced world‐wide, creative accounting to window‐dress financial

statements is under no circumstances a good accounting practice if considered from the

point of view of accuracy, fair practice of management, and ethics and good behavior of

the accounting and auditing professions. The Enron Sandal of window‐dressing, which

erupted in 2001 and disrupted the accounting and auditing professions and their

9

regulatory bodies and forums all over the globe, is the biggest of such practices ever

known to the government administrations and business communities. Ranked six

consecutive years as the most innovative company of the USA, Enron’s published

financial appearance was galvanized by “institutionalized, systematic, and creatively

planned accounting fraud”, and the hand that charted and certified its bright picture

was the Arthur Andersen accounting firm (MacLean & Elkind, 2003; Hodak, 2007).

Account books were cooked by using accounting loopholes to disguise bank loans

amounting to US$3.9 billion taken between 1992 to 2001, and those were shown as

swaps transactions to hedge commodities trades, and thus the increase in debts was

misrepresented to show reduced risks (Steil, 2002). The Enron case shows how a

company can capitalize on assets of others for minting rich profits and returns from risky

business and can embark on deceptive rhetoric on intellectual ability of top executives

and maneuver market, industry, credit raters, and government (BusinessWeek, 2001).

Innumerable accounting scandals can be found in every country throughout the

globe. Most of the notorious accounting scandals of the 1980s and the 1990s took place

in the developed countries, and involve both world‐class companies and

audit/accounting firms, who possess superb accounting regimes, accounting and

auditing standards, and many surveillance authorities. Window dressing goes unnoticed

and undetected in the developing countries where regulatory regimes and protections

are not adequately developed and lax, and accounting and auditing professions are

controlled and commanded by the powerful social elites. The so‐called India’s Enron is

that of the Satyam Scandal of 2009, where the founder chairman of the company

inflated cash and bank balances by over 50 billion rupees (about 1 billion US dollars),

and questions the credibility of corporate governance and risks of investment emerging

markets where internal authorities push for lower standards (Bangladesh News, 2009).

Enron’s auditor was Arthur Anderson, and Satyam’s was PricewaterhouseCoopers, both

from the USA. Accounting G3‐the USA, the UK, and Australia possesses all scandalous

incidences of the corporate world.

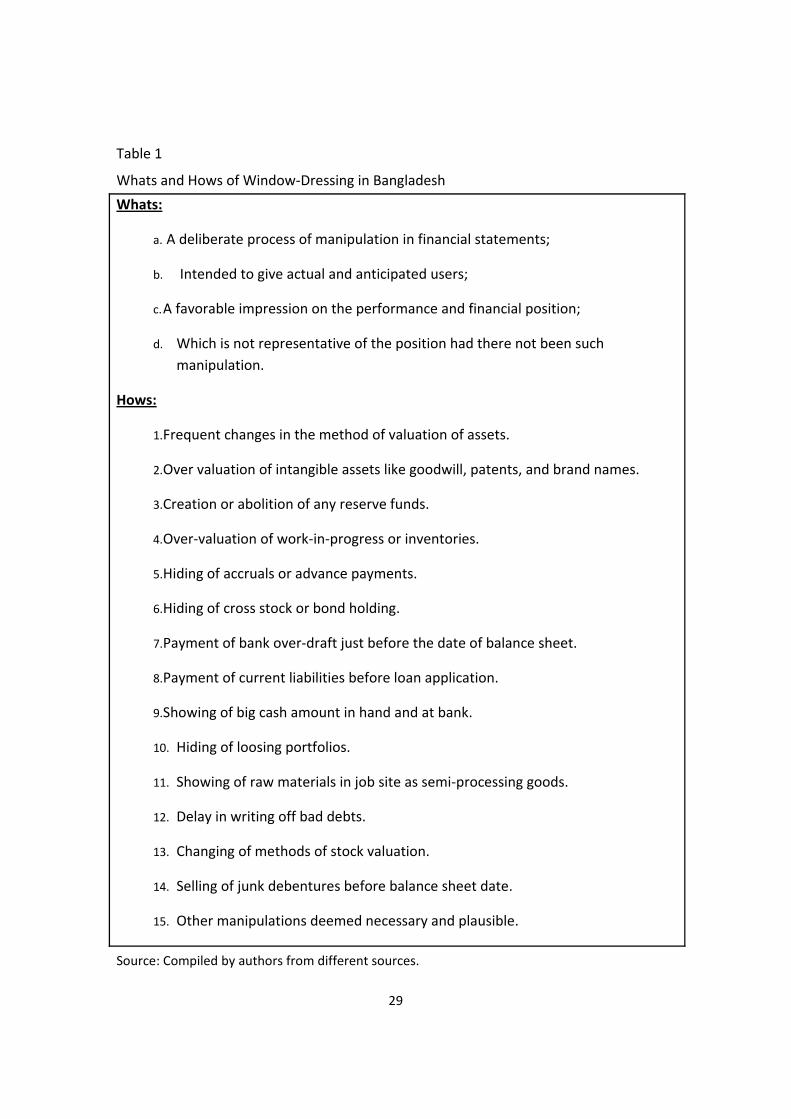

The way in which a window‐dressing is done differs from case to case. But the

common practices are frequent changes in the method of valuation of assets, creation

10

of different reserve funds, under‐or‐over valuation of goodwill, showing of fictitious

transactions, and so forth (see Table 1).

Insert Table 1 here

In Bangladesh, creative accounting to window dress accounts exists in many forms,

levels, and colors. Sen and Inanga (2005) reports a number cases of creative accounting,

and concludes that window‐dressing of financial statements has seriously violated all

known ethical standards. Alam (1988) observes creative accounting as a threat which

may even crash in the fledgling stock market of this country.

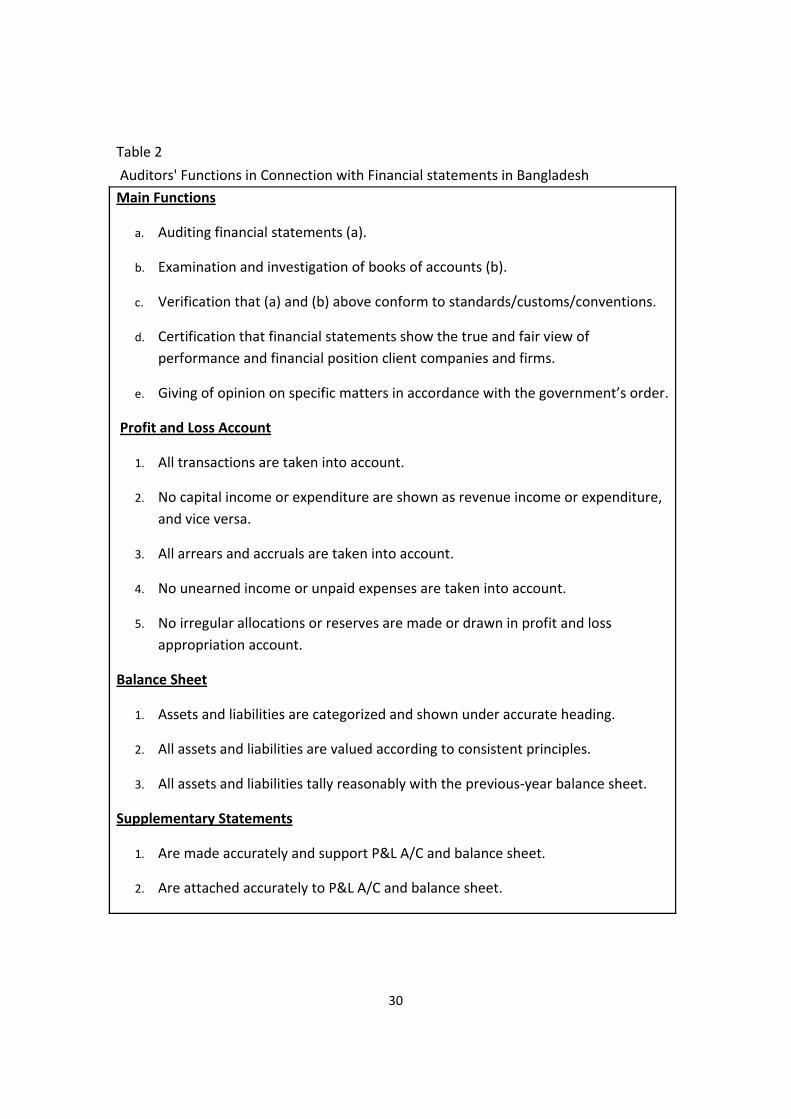

FINANCIAL STATEMENTS AND FUNCTIONS OF AUDITORS

The first and foremost function of the accounting profession in Bangladesh is to

audit the financial statements of clients and certify their accuracy and authenticity. In

connection with the profit and loss account, the auditor must ascertain that every

business transaction of the accounting year has been properly taken into account; no

capital income or expenditure has been shown as revenue income or expenditure or

vice versa; all arrears and accruals have been taken into account; and no unearned

incomes or expenses have been included. In connection with the profit and loss

appropriation account, he or she must be careful to pinpoint that no irregular

allocations or reserves have been made to bluff tax or dividend payment, nor has any

formerly earmarked allocation or reserve been drawn to inflate dividend payment,

which show favorable business performance ultimately influence the market price of

the company’s share (Khan, 2000).

In connection with the balance sheet, the auditor must examine that all assets and

liabilities are properly categorized and exhibited under accurate heading, have been

valued accurately, and are authentic in existence; the supporting supplementary

statements of accounts are correct; and must verify that all items shown in the current

balance sheet are similar to those in the previous year’s balance sheet. He or she must

also confirm that all supplementary statements have been made accurately and support

11

P&L A/C and balance sheet and attached to them accurately and understandably.

Finally, an auditor is required to certify that the profit and loss account and balance

sheet exhibit the true and fair view of the business performance and financial position

of the company (Ullah, 2001).

Insert Table 2 here

In true sense, this certification is a testimonial to the stewardship function of

accountant, internal auditor, and finally management of a company, which according to

some scholars is reporting on stewardship. Under all circumstances, however, it is

expected that auditors give due attention to accounting customs and conventions

prevailing in the country and laws and regulations of the government and professional

bodies and exercise fair practices in view of professional ethics and code of conducts,

either implicit or explicit.

IMPORTANT FACTORS THAT GOVERN FUNCTIONS OF AUDITORS

Accounting Conventions

While doing audit, the auditors are obliged to see that the account books and

records have been kept in compliance with the universally accepted accounting

concepts, standards, and customary conventions, and those that prevail in the country.

They are to examine whether all assets and liabilities have been valued on a consistent

basis; whether accounts of various branches, projects, and ventures have been kept

uniformly; whether all material transactions have been taken into account accurately;

whether all tangible and intangible assets and liabilities have been disclosed fully;

whether any change of accounting principles has been reported objectively, and so on

(Khan, 2000; Anthony, Kaplan & Young, 2005). In other words, there are required to

conduct their jobs in close conformity with the nine universally accepted accounting

concepts and four conventions, which equally hold truth in the case of Bangladesh

Laws and Rules and National and International Regulatory Organisations

12

In Bangladesh, financial reporting is a mandatory requirement for all companies

incorporated under the Companies Act of 1913. The Companies Act of 1994 has been

enacted to replace this old law, but it also possesses similar requirements on reporting.

The detailed rules and methods relating to the preparation and presentation of

accounting books and statements have been set out in Sections 181 to 191 and those

relating to auditing and investigation in Sections 195 to 221. The Schedule II to this Act

has specified formats for P&L A/C and balance sheet; the methods according to which

these are to be prepared; the items to be incorporated therein; and the order to be

followed in listing them (MOL/GOB, 1994).

The two principal national institutions that regulate accounting professions in the

country are the Institute of Chartered Accountants of Bangladesh (ICAB) and the

Institute of Cost and Management Accountants of Bangladesh (ICMAB). Although

professional and functional asymmetry does exist between these organisations, they

organize the profession, develop the modus operandi of awarding membership, and

regulate examinations, and offer courses and curriculum that must be fulfilled by every

individual willing to pursue a career of professional accountant and thereby professional

auditors. Unlike educational institutions which come under the administrative

jurisdiction of the Ministry of Education, these two are administered by the Ministry of

Commerce of the government.

Established in 1973 under the Bangladesh Chartered Accountants Order 1973

(Presidential Order No. 2of 1973), the ICAB is the national professional accounting body

and offers rigorous top‐quality education and training for the would‐be accounting

professionals and inculcates high values and professionalism among its students and

members. The ICAB’s stated mission is to provide leadership in the development,

enhancement, and coordination of the accountancy profession in order to enable it to

provide services of consistently high quality in the public interest (ICAB, 2009). To

achieve this mission it has set forth objectives to regulate accountancy profession,

administer its members and student, implement professional ethics and code of

conduct for its members, offer specialized training in accounting, auditing, taxation,

corporate law, management consultancy, IT, and related disciplines, foster acceptance

13

of IAS and International Standards Auditing (ISA), and adapt and incorporate those into

Bangladesh Accounting Standards (BAS) and Bangladesh Standards on Auditing (BSA),

keep abreast of all developments, diffuse knowledge on accounting, auditing, IT, and

related fields, and liaise with regional and international forums of accountants (ICAB,

2009).

The ICAB has developed professional code of conducts, ethics guidelines,

practicing rules, and punitive measures for any breach of such rules, code, and ethics.

Members are required to submit at least one a year two annual audit compliance

reports ‐cold file review report and whole firm review report ‐ stating how effectively

they are complying with the ICAB rules of practice and standards. The former report is

designed to objectively examine an audit assignment after its completion, and addresses

audit accuracy in terms of procedures, standards, and practicing rules as articulated by

the ICAB (ICAB, 2009a). The latter one reports on the firm’s procedures in respect of all

matters in connection with all audit assignments, and also confirms the matter of the

cold file review (ICAB, 2009b). It also requires member firms to submit an annual audit

quality control report called the Bangladesh Standard on Quality Control I (BSQC I),

which aims to establish standards and guidelines regarding a member’s responsibility

for quality control of audits, reviews of historical financial information, and other

services of engagement with clients (ICMAB, 2009c). An annual audit return is also

designed for submission furnishing all information regarding partners, number of

clients, number of audits performed, use of audit manual, submission of audit

compliance review (ACR), and specialized clients, if any (ICMAB, 2009d).

In order to achieve its stated objectives, the ICAB holds offices in Dhaka and

Chittagong and chapters in the UK (London) and North America (Ontario, Canada), and

its affiliates simultaneously possess membership in CPA bodies in the UK, Australia, the

USA, and Canada. Bangladesh, represented by the ICAB, is a member of the

International Federation of Accountants (IFAC), and is thereby automatically a member

of the International Accounting Standards Committee (IASC). The ICAB has ratified

and/or adapted a number of IAS and has developed its own standards to customize and

incorporate the needs of the country. It is also a member of the South Asian Federation

14

of Accountants (SAFA) and the Confederation of Asian and Pacific Accountants (CAPA).

SAFA and CAPA are regional forums of professional accountants and conduct research,

seminar, workshop, and lecture to standardize accounting and auditing practices,

exchange and diffuse information among professions, and achieve uniformity of

practices among the member nations in this region.

The second professional accounting institution, the Institute of Cost and

Management Accountants of Bangladesh (ICMAB), was established in 1977 vide the Cost

and Management Accountants Ordinance, 1977(Ordinance No. LIII of 1977) and is

regulated vide the Cost and Management Accountants Regulations, 1980 (as amended

up to date) to impart training and education in the field of cost and management

accounting. It possesses four domestic branch offices in the divisional headquarters of

Chittagong, Rajshahi, Khulna, and Comilla, and a Chapter in Canada. It aims to augment

economic and industrial development of the country by promoting and regulating cost

and management accounting education, research, and profession. Especially, in order to

develop a cost and management accountant (CMA) profession in the country, it plans

and offers education and training to its students, members, and corporate managers,

helps develop, adopt, and implement international financial reporting standards (IFRS),

and formulates, adopts, and implements cost accounting and auditing standards (CAAS),

and its members conduct cost audit of the companies stipulated in the Companies Act,

1994 (ICMAB, 2009). Interestingly, almost all ICAB members and many academics

possess qualification and certification of this institute, as a result of which a good

network prevails across the accounting profession in this country. Though it is not

mandatory, as per Proviso 1 (d) of Section 181 and Section 220 of the Companies Act

1994, the government may order companies engaged in production, distribution,

marketing, transportation, processing, manufacturing, milling extraction, and mining

activity to audit cost accounts by a CMA (MOL/GOB, 1994).

Thirdly, all companies listed on the Dhaka Stock Exchange and Chittagong Stock

Exchange is required to follow all ratified and adapted IASs and ISAs in their accounting

and auditing functions. The Ministries of Commerce, Finance, and Law exercise direct

and indirect control on accounting institutions. The public sector enterprises that fall

15

under jurisdiction of the Presidential Order 27 on the nationalization of industrial

enterprises also need to keep accounts and statements and audit those (MOL/GOB,

1972). Public enterprises need to produce a variety of monthly financial statements to

the corporation head offices (Hoque & Hopper, 1994), and are compelled follow a triple

audit system: periodic audit by internal auditors from a corporation head office,

statutory audit by professional auditors, and commercial audit by the government

auditors (Khondaker, 1997).

Fourthly, established in 1973, the Comptroller and Auditor‐General (CAG) is

constitutionally the supreme audit authority in the country, and is empowered to audit

accounts of all public enterprises where the government holds 50 percent or more

shares, and accounts and statements of all statutory public and local government

organizations. It conducts independent audit and evaluation through its own staff and

makes report, which ultimately goes to the parliament for debate, discussion, and

approval (Khondaker, 1989; Shamsuzzaman & Rahman, 2003).

ICAB wants all its members to comply with its guidelines on the quality of their

services to clients, which include among others reporting on the availability of

documents relating of accounts audited, their adherence to generally accepted

accounting principles and practices, disclosures, and supplementary statements (ICAB,

2009). Similarly, ICMAB and CAG require their members and staff to comply with audit

requirement, investigate into the matters of suspicion, and report of all material

defaults in accounting procedures and accounting statements.

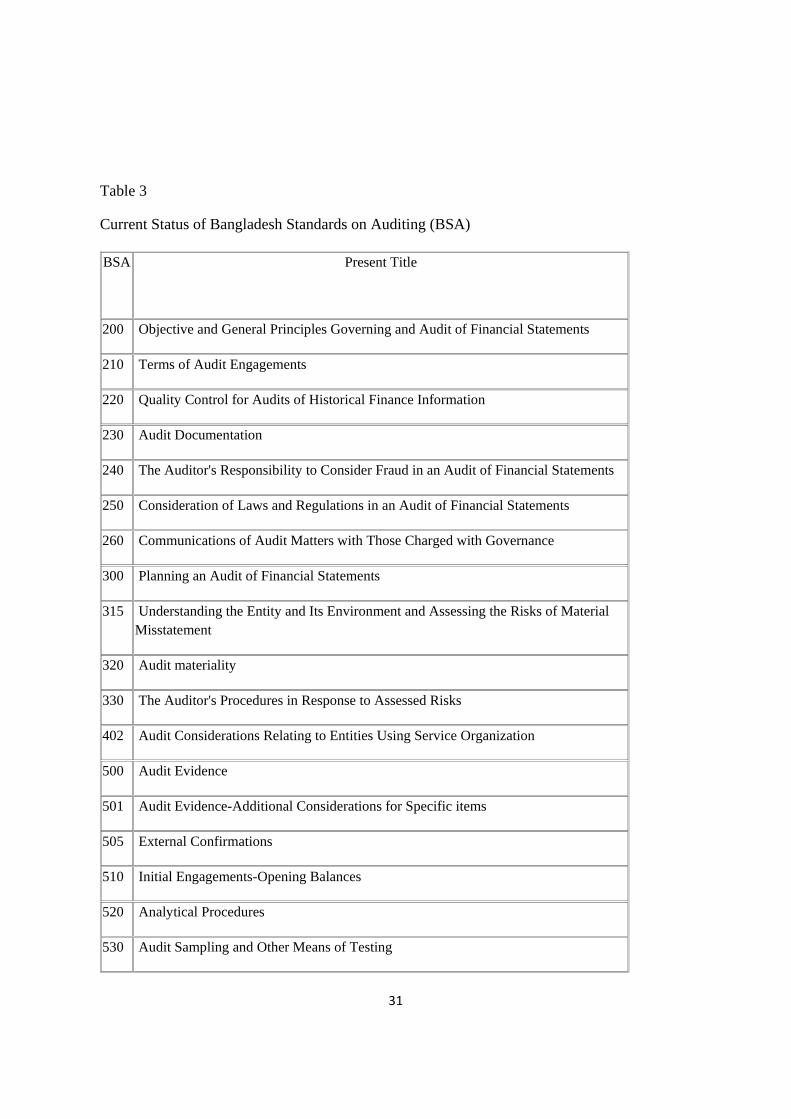

Professional Practices: Bangladesh Standards of Auditing (BSA) and International

Standards of Auditing (ISA)

In Bangladesh auditors derive their powers and authorities from laws and regulation

of which the Companies Act is the most important one, and the others being rules,

regulations, and procedures of the ICAB, ICMAB, and CAG. Especially, the Companies Act

has articulated principles and regulations, according to which even a qualified and

registered member of the ICAB or ICMAB can be disqualified from becoming an auditor

and powers and rights as an auditor can be relinquished. Sections 210‐221 of this Act

16

relate to the appointment, remuneration, removal, qualification and disqualification,

power and duties, obligation to attend AGM, certification and authentication of audit

reports, and penalty for non‐compliance with laws and provisions (MOL/GOB, 1994).

These standards and rules together with the customized and adapted international

standards and conventions have established the framework, principle, and guideline for

auditors’ functions in this country. Any violation of these is regarded as professional

offence of negligence and misconduct, and makes members accountable to the

Institutes as well as to the court of justice in the country. The Bangladesh Chartered

Accountants Ordinance, 1973, as for example, requires its affiliated members to bring all

actions that deem to be subversive to the provision of this Ordinance to its notice, and

urges them to include such actions in their reports.

Insert Table 3 here

Professional Ethics and Code of Conducts

People engaged in the accounting/auditing professions all over the world are

required to oblige with many professional principles and regulations. Following the

Enron scandal, the US Congress has enacted the Sarbanese‐Oxley Act, 2002 and made it

mandatory for all practicing accounting firms in that country to register with the Public

Accounting Oversight Board (PCAOB) that monitors compliance of such firms with laws,

standards, and ethics. Similar legalizations are being adopted in the UK and other EU

nations, Japan, and Australia. Except the Satyam scandal of 2009, no big accounting

scandal has yet been reported in the South Asian Association for Regional Cooperation

(SAARC) countries. The SAFA, the regional forum of professional accountants, has

developed a code of ethics, where the ICAB played the prime role, and it endorsed it

with a very strong urge on the members to comply with those in their practices (SAFA,

2004; ICAB, 2009). In addition to these, it has adopted IFAC Code of Ethics and IFAC

Standards of Ethics, and has formulated its own Code of Ethics as derived from the

Bangladesh Chartered Accountants Ordinance, Schedule C, Part I (ICAB, 1973). These

professional codes of ethics in principle vary among accountants in practice, members in

17

service as management consultants, and members engaged in mechanized accounting

and computer services (ICAB, 2009).

Breach of the code of behavior as charted out in the ICAB Ordinance is regarded as

professional misconduct. Thus, a professional accountant shall be guilty of professional

misconduct if he or she involves in any of the following actions, namely and most

importantly, professional service partnership with an unqualified non‐accountant

person; payment of a part of professional remuneration to a person otherwise

unrelated to ICAB; assuming responsibility of auditing a company without consulting the

previous auditor; accepting appointment as auditor without confirming the

requirements of appointment as stipulated in the Companies Act; accepting terms and

conditions of work that amounts to be non‐competitive for a professional auditor; sub‐

letting work to a non‐certified professional; soliciting clients through direct or indirect

promotional activities and social contacts; receiving fees for professional services

depending on business profit or loss of the client; failing to draw attention to any breach

of the generally accepted accounting principles by the client in the audit report; failing

to report any known material misstatement in a financial statement; showing gross

negligent in conducting professional duties; failing to obtain sufficient information from

clients to qualify audit report; failing to submit any report required by the ICAB council;

and divulging information received during professional engagement with a client to a

third party without its prior consent (ICAB, 1973).

As mentioned before, the SAFA has developed its code of ethics keeping in view the

region’s unique professional environment, and advocates six fundamental principles of

integrity, objectivity, professional competence, due diligence, confidentiality, and

professional behavior to be followed by professional accountants (SAFA, 2004). These

in fact follow from the global effort under auspices of the IASB and IFAC to establish and

restore public confidence in accountants and accountancy professions that was lost

during the high profile accounting frauds in the USA in 2001‐2 and other developed

countries.

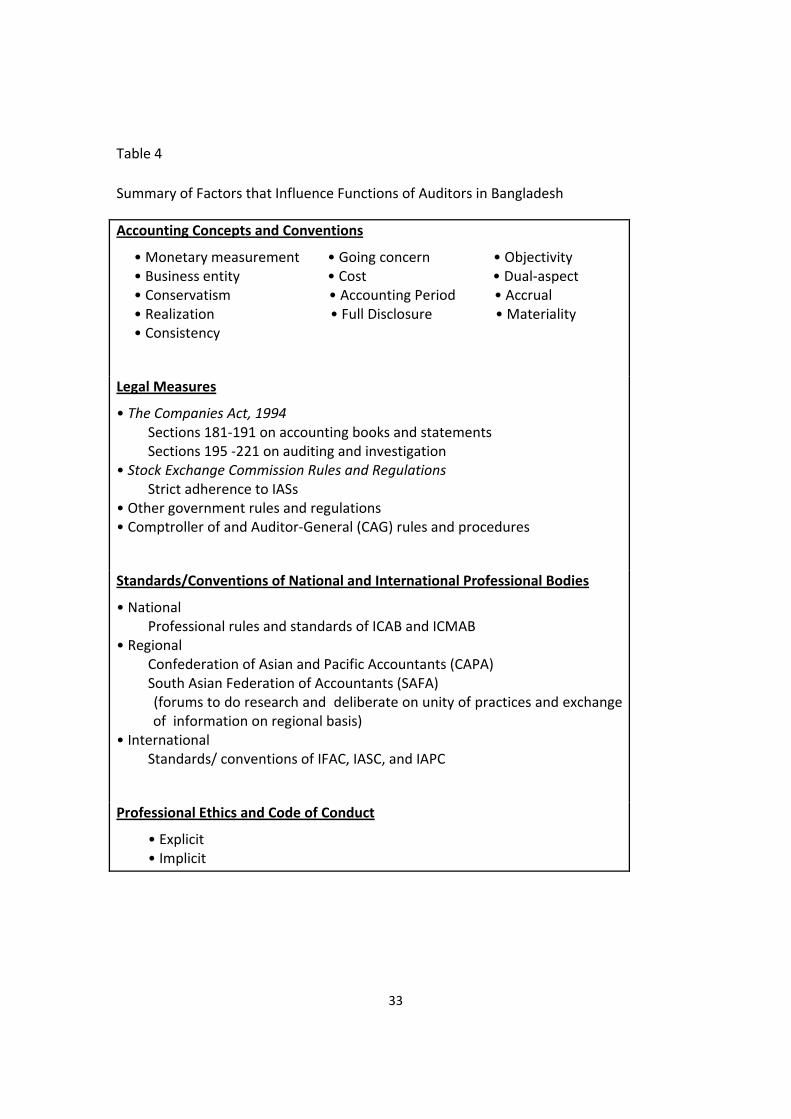

Thus, it is evident from this section that multiple government agencies, professional

institutes, and laws and regulations condition, determine, and govern functions of

18

auditors in Bangladesh. These national factors receive further impetus and force from

the regional and international accounting and auditing professional bodies and

institutions. All such factors are summarized in Table 4. Although the degree of

influence of the individual category of factors on auditor’s functions varies, together

these define the boundary and framework of auditors functions in this country. The

Companies Act, 1994 constitutes the foundation for all accounting and auditing

requirements in connection with joint stock companies, and is referred to for all other

types of business organizations. However, this law is stubbornly silent about the BAS,

BSA, IAS, and IFRS (IAS Plus, 2007), which gives rise to camouflaged views and

confusions among internal and external accountants and auditors. The Securities and

Exchange Commission (SEC) of Bangladesh regulates financial reporting of the listed

companies and urges on those to follow the provisions of the Securities Exchange Rules,

1987 and to comply with the IASs (MOF/GOB, 1987), which are adapted in the BAS. The

ICAB Technical and Research Committee develop national standards called BASs based

on the IAS, but reportedly the BAS are neither mandatory nor enforceable through the

ICAB bye‐laws (IAS Plus, 2007). Here lies the crux of international compatibility of

accounting and auditing professions and practices in Bangladesh. Also, the non‐listed

companies and SMEs are not required to comply with both national and international

standards – a practice that gives rise to double standard among accountants.

Insert Table 4 here

Furthermore, the rules and regulations that apply to banks, insurance companies,

and some other designated institutions differ significantly. The Banking Company Act of

1991, for example, stipulates that reporting formats and disclosures must conform with

the BAS 30, which is very similar to the IAS 30. However, as found in Siddiqui and Podder

(2002) banks did not fully comply with the requirements of the BAS and the auditors

even did not issue any qualified audit reports. This thrusts questions on the

independence, objectivity, and competence of the auditors. The same is also true with

the insurance companies, which are regulated under the Insurance Act of 1938 (IAS Plus,

2007). All old laws and regulations, including even the relatively new Companies Act of

1994, need revisions to incorporate provisions to make BAS and BSA mandatory.

19

AUDITORS' LIABILITY IN CONNECTION WITH CREATIVE ACCOUNTING

Theoretically, auditors’ offenses in connection with creative accounting practices to

window‐dress financial statements can be labeled as professional negligence,

misfeasance (breach of trust or duty imposed by law), and professional misconduct for

which they can be prosecuted under civil and criminal laws of the country (Tandon et

al., 2001; Ullah, 2001; Gupta, 2007). Most of these happen due to non‐compliance with

professional codes of conduct and ethics, failure to follow accounting and auditing

standards, and malicious accomplices with the clients.

Also, auditors’ responsibility is one of the most debated and controversial topics

among auditors, politicians, media, regulating authorities, and the public (Gay, Schelluch

& Reid, 1997). The debate has more exacerbated by the collapse of big corporations

such as Enron and WorldCom (Lee, Ali & Gloeck, 2008). Debacles of Enron, AIG,

WorldCom, Subeam, and Madoff in the USA, Paramalt in Italy, Satyam in India, OneTel in

Australia, and several other big frauds in Germany and South Korea prove that

accounting scandals are blind to geography (Financial Week, 2009), goodwill, and

national status of companies and audit firms. Financial report users perceive auditors

duties to be detecting and reporting on frauds more than looking into compliance with

statutes and audit standards (Lee et al., 2008). Auditors assume both professional and

legal duties while scrutinizing their clients’ financial statements (Ang & Lim, 2008).

Complaints and litigations by the client or any other interested party give rise to

liability, which can be categorized as liabilities to the clients and liabilities to the third

parties. The first category arises due to professional negligence in carrying out assigned

responsibilities and for committing misfeasance. When sued, the court in Bangladesh

takes necessary investigation under the Penal Code or Code of Criminal Procedure 1898

(Act V of 1889) depending on the nature of the offense. The court may refer to all

principles and rules that regulate the affairs of the accounting and auditing profession in

the country. The final verdict of the court, whether it is financial penalty or professional

penalty, is given with due references to precedence and verdict earlier cases, if any

exists (Tandon et al., 2001).Under Section 219 of the Companies Act, the court can

impose a fine of TK. 1,000 in any case of negligence or misfeasance, and if that arises

20

due to non‐compliance with the requirements under Sections 213 (i.e., failure to access

to the books, accounts, and vouchers of the client, failure to make report on profit or

loss and clients affairs and conformity of those with books, accounts and information

received, etc.) and Section 215 (i.e., failure to sign audit report and any other

documents as required of the client by law) of the Companies Act. Similarly, for any

fraudulent statement in connection can with the balance sheet, profit and loss account,

or any supplementary statements under Section 397 of the above Act, the court can give

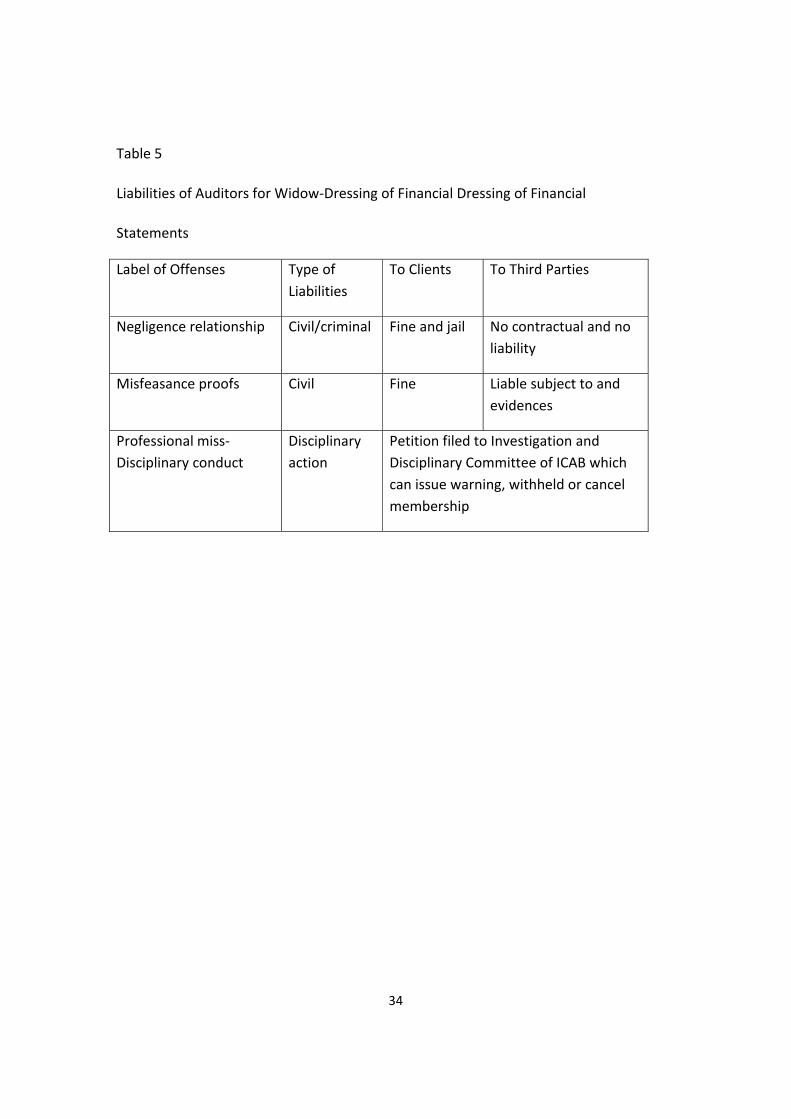

verdict of imprisonment extending up to five years (MOL/GOB, 1994). Table 5 shows a

summary of the various offenses and liabilities for those.

Insert Table 5 here

An aggrieved party can also lodge complaints with the ICAB or ICMAB, where the

accountants are registered and affiliated. It is mandatory on the part of professional

auditors in Bangladesh to strictly observe and adhere to guidelines mentioned in the

first part of the Schedule C of the ICAB Ordinance of 1973. If they fail to follow any of

the rules in the Ordinance, charges for professional misconduct can be filed with the

Disciplinary Committee of the Institute. In such cases, with due investigation in to the

content of this complaints, the Committee may either issue a tough note of warning, or

may cancel, or even withheld membership of the offender, which precludes such a

member from undertaking any professional activity (ICAB, 2009).

Auditors' liabilities to third parties such as banker, creditor, income tax authority,

financial institution, and prospective investors in shares and debentures are normally

categorized as liability for professional negligence and liability for fraudulent practices.

For professional negligence, according to the prevailing court verdicts still referred to as

precedence, auditors have almost no liability since they are not under any contractual

relationships with such third parties. However, for fraudulent practices, they are held

liable if the aggrieved party can prove that the auditors' reports were materially falsified

or distorted; the auditors knowingly gave such falsified report; it acted candidly upon

the report of the auditors and incurred losses; and the auditors have given consent to

include their reports along with financial statements (Tandon et al., 2001; Ullah, 2001;

Gupta, 2007).

21

SUMMARY AND CONCLUSION

In Bangladesh, auditor’s responsibility is a highly confused concept among layman

users and even professional Chartered Accountants (CA). One famous CA who holds a

PhD in addition to Bachelor and Master Degrees in Accounting and once held the

position of Vice President and President of ICAB observes the situation as: “the common

confusion, particularly in the eye of layman, is to see the auditors as responsible for the

accounts. The users of accounts sometimes confuse this view. The directors of the

company are statutorily responsible for the accounts, which is also not clear to the users

of accounting reports in Bangladesh. The auditor’s responsibility begins and ends with

his expression of an opinion on the audit report. The audit report is the formal

communication about the accounts between the auditors of the enterprise and the

persons to whom they report to, either shareholders, or the government, whosoever is

appropriate” (Ahmed, 2006). It is thus seen that the professional auditors absolve their

responsibilities with audit report to third parties.

As Hall and Renner (1991) observed, auditors may fail to detect and report a material

error or misstatement in accounts due to three reasons, namely, they are either

negligent or incompetent, or they lack integrity, or they are deliberately deceived by

directors. Management may create undue and servile pressure on auditors and

sometime intimidates to abandon audit engagement (Fearnly, Beattie & Brandt, 2005).

In Bangladesh despite the claim of excellence of professional education curriculum,

toughness of article‐ship, low rate of passing in the CA examination, and robust

professional practicing regulations, the level of educational achievement and

professional understanding and thereby professional efficiency is not uniform

throughout the accounting profession. It is serious a question whether all members

equally understand ICAB rules and guides, manuals and forms, government laws and

gazettes, and especial the audit manual in English which alone is 223 pages. The code of

conduct of the SAFA has taken over the website of the ICAB, which raises question on

the availability of distinctive ethics code in Bangladesh. Another issue is, how far the

code of ethics for the CAG auditors differ or coincide with that of the ICAB and whether

some of those can be adapted for the ICAB, needs debate and deliberation. From

22

informal connections with some CA, it seems they speak much about their elitist status,

how Board members and internal auditors scare auditors and audit clerks‐cum‐articled

CA students, and how their remunerations and audit fees can be increased, and they

deliberately avoid questions on why the number of CA in the country is still less than

one thousand.

From the legal point of view, auditors in Bangladesh have definite liabilities for

cooking of financial statements. Given that the provisions of laws are implemented

properly, however, it cannot be said that the amount of liability is sufficient to redress

losses that may occur to any party. Enough legal measures still do exists to stop

window‐dressing. The amount of fine that can be imposed on an auditor is less than

US$15, which is rather ridiculous if considered how colossal the loss to a part can be.

There exist very few evidences where the court fined and imprisoned an auditor or the

ICAB canceled the registration of its members for not reporting on creative practices in

financial statements.

Bangladesh is now at the threshold of business, industrial, and economic

developments, and the role of auditors in connection with financial statements and

audit reports is of paramount importance since the parties interested in such

statements have no other alternative ways but to rely on them. From interviews, it

seems that window‐dressing is notoriously endemic, but not much care is taken by the

ICAB and its members, clients, and government agencies. Holding a ratio of less than

seven CAs per one million population, CA are highly educated and as a profession

extremely remunerating. They are very influential among economic and power

polarizing classes, develop and maintain many formal and informal networks with

industry owners, corporate management, bureaucrats, and political power elites

through blood and matrimonial relationships, alma mater connections, ministerial and

advisory appointments in the government, and even act as lobbying agents. Such

relations dilute professional ethics and code of conducts, governance and fiduciary

relationships, and professional obligations of care and trust.

Questions also remain on the quality of auditing, which seems extremely gorgeous

as per ICAB rules and regulations. Dubious accuracy of accounting reports, untoward

23

transactions affecting minority shareholders, creditors, and tax collecting institutions,

and inadequately transparent external reports are found in the privatized enterprises

(Uddin & Hopper, 2003). An audit expectation gap between the CAG and the users of

audit reports exists in the public sector contrary to the fact that such reports are strictly

examined by the Public Accounts Committee, the parliament, and international funding

agencies (Chowdhury, Innes & Kouhy, 2005). This induces to deduce that such gap also

prevails in the private sector enterprises.

Under the US Common Law, auditors were originally liable to clients and primary

beneficiaries, which the Restatement of (Second) of Torts has limited only to losses

suffered by users whose reliance is specifically for foreseen by auditors (Huss, 1991).

Here, public accountants have also ethical duty toward the public and stockholders and

are obliged to give correct audit reports and avoid audit negligence (Brecht, 1992).

Enron’s auditor Arthur Andersen was found guilty in the court of public opinion, and it

had to pay heavy penalty in terms of deserting of clients, fleeing of employees,

allegation of perjury, and eroding corporate values and legacy (Thomas, 2002).

Punishment was also given to its accountants for non compliance with legal

requirements and professional negligence. The Sarbanes‐Oxley Act of 2002, mentioned

before also, was an eventual outcome of Enron to defense audit malpractices in publicly

traded companies, to establish new auditor independence rules, to create a Public

Company Accounting Oversight Board, to tighten corporate governance and certification

requirements and statuses of limitations, and to impose penalties for negligence

(Grubbs & Ethridge, 2007).

In Australia, damage suits can be brought under Tort, and auditors can be made

liable to the shareholders, the auditee company, and to the third parties, provided that

the plaintiff can sufficiently prove its reliance on auditor’s report, proven breach of

negligence by auditor, a causal relationship between the negligence and the loss it

suffered, and the existence of a duty of due care (Leung, Coram & Cooper, 2007). As the

Australian High Court held in Esanda Finance v Peat Marwick Hungerfords case in 1997,

auditors do not owe a duty of care to a third party, but liability does exist provided the

audit firm knew in advance that a third party were to rely on its work in relation to a

24

specific transaction (O’Leary, 1998). In New Zealand, however, auditors are entitled to

append a disclaimer in their audit reports to avoid tortuous risk of professional

negligence litigation by third parties (Keenan, 2008).

In Bangladesh public surveillance authority on accounting profession is non‐existent

and litigation under the Penal Code or Tort are very rare. Disclaimer is not yet thought in

Bangladesh and other SAARC countries. A lack of basic knowledge and expertise in

accounting and auditing debars third parties to understand accounting statements and

challenge auditors’ reports even if they suffer economic losses. Such users do not have

enough courage to employ lawyers, go to the legal bodies, and to bring legal charges

against management and auditors for distorted audit statements and reports. And this

situation is further aggravated due to the absence of government mechanisms to

safeguard general users of audit reports. However, much research, debate, and

deliberation is needed among government agencies, users of audit reports, ICAB and

ICMAB, and academics to see how window‐dressing takes place through creative

accounting practices, what the accounting profession thinks on creative accounting and

window‐dressing, how window‐dressing can be kept within a tolerable limit and

boundaries of business and management ethics, and what should constitute an

adequate liability of auditors if losses incur to the users of their reports.

REFERENCES

Ahmed, J. (2006). Roadmap for accountancy profession in Bangladesh. The Financial

Express, February 19, Sunday.

Ahmed, N. (2007). Financial accounting – A Simplified Approach, New Delhi: Atlanta

Publishers.

Alam, A. S. (1988). Creative Accounting – Is It Leading Us Towards a Stock Market

Crash?. The Cost and Management Accountant, ICMAB, Dhaka, 16(5).

Alexander, D., Archer, S. (2000). (2001). Miller International Accounting Standards

Guide. San Diego, Harcourt Professional Publishing, 208‐209 and 33.04.

25

All Business. (2009). Business Glossary‐Window Dressing Definition. Accessed on

December 12, 2009, [available at:

http://www.allbusiness.com/glossaries/window‐dressing/4941928‐1.html].

Allen, L. (2003). Bank window dressing: Theory and Evidence. Science Direct Journal of

Banking and Finance, Elsevier B.V. Accessed on December 10, 2009, [available at:

http://www.sciencedirect.com/].

Ang, C.H., Lim, K. (2008). Who Left the Gates Unlocked? Reconciling the Duties of

Auditors and Company Directors. Singapore Academy of Law Journal, 20 (SAcLJ).

Anthony, A. A., Kaplan, R., Young, M.S. (2005). Management Accounting, Boston:

Pearson.

Bangladesh News (2009). Satyam scandal highlights emerging market risks. Accessed on

December 16, 2009, [available at: http://www.independent–bangladesh.com/ ].

Benarjee, B. (2006). Cost Accounting: Theory and Practice, New Delhi: Prentice‐Hall of

India Pvt. Ltd.

BusinessWeek (2001). The Fall of Enron. Accessed on December 12, 2009, [at

http://www.businessweek.com/magazine/content/01_51/b3762001.htm].

Brecht, D.H. (1991). Accountants’ duty to the public for audit negligence: self‐regulation

and legal liability. Business & Professional Ethics Journal, 10.

Chowdhury, R., Innes, J., Kouhy, R. (2005). The public sector audit expectations gap in

Bangladesh. Managerial Auditing Journal, 20(8/9).

Fearnly, S., Beattie, V.A., Brandt, R. (2005). Auditor Independence and Audit Risk: A

Reconceptualization. Journal of International Accounting Research, 4(1): 39‐72.

Financial Week (2009). Getting away with it: Accounting scandals blind to geography,

research shows. Financial Week. Accessed on December 24, 2009, [available at

http://www.financialweek.com/article/2009109/REG].

Gay, G, Schelluch, P., Reid, I. (1997). Users’ Perceptions of the Auditing Responsibilities

for the Prevention, Detection and Reporting of Fraud, Other Illegal Acts and

Error. Australian Accounting Review, 7(1): 51‐61.

Gill, G.S. (2007). Modern Auditing and Assurance Services, London: John Willey & Sons.

Government of the Peoples' Republic of Bangladesh (GOB), Ministry of Law or MOL

(1994). The Companies Act, 1994 (As Amended up‐to‐date), Dhaka: MOL.

Griffiths, I. (1986). Creative Accounting‐How to Make your Profits What You Want Them

to Be, London: Sidgwick & Jakson Ltd.

Griffiths, I. (1995). New Creative Accounting‐How to Make your Profits What You Want

Them to Be, London: Plagrave McMillan.

26

Grubbs, J.K., Ethridge, Jr., Jack, R. (2007). Auditor negligence liability to third parties

revisited. Journal of Legal, Ethical and Regulatory Issues, 6(1).

Gupta, K. (2002). Contemporary Auditing, New Delhi: Tata McGraw‐Hill.

Hall, W.D., Renner, A.J. (1991). Lessons auditors ignore at their own: Part two. Journal of

Accountancy, June, 63‐71.

Hodak, M. (2007). The Enron Scandal, New York: New York University/ Hodak Value

Advisors.

Hus, F.H. (1991). Legal liability: Exploring instrumental reasoning and the evolution of

the auditor’s duty. Critical Perspectives on Accounting, 2(2): 171‐83.

IAS Plus (2007). Accounting Standards Updates by Jurisdiction. Accessed on December

16, 2009, [Available at: http://www.iasplus.com/country/banglade.htm] .

ICAB (2009). Bangladesh Standards on Auditing (BSA)‐Current Status of Adoption of ISA.

Assessed on December 17, 2009, [available at http://www.icab/org/bd/bas.php].

ICAB (2009). The Institute of Chartered Accountant of Bangladesh – A Brief Outline.

Accessed on December 17, 2009, [available at http://www.icab/org/bd/bas.php].

ICAB (2009a). Cold File Audit Compliance Report. Dhaka: ICAB.

ICAB (2009b). Whole Firm Audit Compliance Report. Dhaka: ICAB.

ICAB (2009c). Bangladesh Standard on Quality Control I. Dhaka: ICAB.

ICAB (2009d). Annual Return. Dhaka: ICAB.

ICAB (2009). Professional Misconduct. Accessed on December 8, 2009, [available at

http://www.icab.org.bd/code_conduct.php].

ICMAB, Auditing, http://www.ismab.org.bd/New ‐Syllabus/Auditing.html (retrieved on

December 12).

ICAB (2009). Annual Return – A Return that needs to be Furnished Annually by all

Practicing Firms to the Quality Assurance Department of the Institute of

Chartered Accountants of Bangladesh. Dhaka: ICAB.

Keenan, M. (200?). The Auditors’ Dilemma: To Disclaim or Not Disclaim. University of

Auckland Business Review, 10(1).

Khan, A. R. (2000). Business Ethics. Dhaka: Ruby Publications, 96‐107.

Khan, M. M. (2000). Advanced Accounting, I (reprinted edition), Dhaka: Ideal Library,

873‐897.

Khondaker, M.R. (1982). Business Organization and the Development of Accounting.

Unpublished Masters Thesis, Department of Accounting, Faculty of Commerce,

University of Dhaka, Bangladesh.

Khondaker. M.R. (1989). Solving the Problems of Government Control and Management

Autonomy in the Public Sector of Bangladesh: Some Lessons from Japan and the

27

U.K. The Annual Bulletin of the Institute of Business Research, Chuo University,

Number 16.

Khondaker, M.R. (1997). Japanese Style Management for Bangladesh Public Sector‐the

case of jute industry, Dhaka: NSU‐NFU.

Lee, T., Ali, A., Gloeck, J.D. (2008). A Study of auditors’ responsibility for fraud detection

in Malaysia, South African Journal of Accountability and Auditing Research, 8, 27‐

34.

Leung, P., Coram, P., Cooper, B. (2007). Modern Auditing & Assurance Services,

Australia, Milton: John Wiley & Sons.

Mclean, B., Elkind, P. (2003). Smartest Guys in the Room: The Amazing Rise and

Scandalous Fall of Enron, New York: Portfolio Hardcover.

Ministry of Finance (MOF)/GOB (1987). The Securities and Exchange Rules, 1987, Dhaka:

MOL/GOB.

MOL/GOB (1972). The Bangladesh Industrial Enterprise (Nationalization) Order, 1972,

Dhaka: MOL/GOB. Ministry of Law (MOL), Government of Bangladesh (GOB)

1994. The Companies Act (Bangladesh), 1994, Dhaka: MOL/GOB.

O’Leary, Conor (1998). Auditors’ liability to third parties ‐ the door remains open.

Managerial Auditing Journal, 13(9), 521‐24.

Saeed, K.A. (2008). Auditing, Lahore: Accounting and Taxation Services Institutes.

Sen, D.K., Inanga, E.L. (2009). Creative Accounting in Bangladesh and Global

Perspectives. Accessed on December 31, 2009, [available at

http://www.web2.msm.nl/news/articles/050707papers/0206_Sen_Inanga.PDF].

Shamsuzzaman, M.. Rahman, N. (2003). Audit Profile: Office of the Comptroller and

Auditor‐General of Bangladesh. International Journal of Government Auditing,

30(2).

Shukla, M.C., Grewal, T.S., Gupta, S.P. (1997). Advanced Accounts, New Delhi: S. Chand

& Co Ltd.

Siddiqui, J., Podder, J. (2002). Effectiveness of Bank Audit in Bangladesh. Managerial

Auditing Journal, 17(8), 502‐510.

South Asian Federation of Accountants (SAFA) (2004). Code of Ethics for Professional

Accountants in SAFA Countries. Dhaka: SAFA Ethics & Independence Committee.

Steil, B. (2002). Enron and Italy: Parallels between Rome’s Efforts to qualify for euro

entry and financial chicanery in Texas. Financial Times, accessed on December

10, 2009, [available at: http://www.cfr.org/publication/4455/enron_and‐

italy.html.

28

Thomas, C.B. (2002). Called to Account. Financial Times, accessed on December 10,

2009, [available at

http://www.time.com/time/printout/0,8816,236006,00.html/]

Tandon, B. N., Sudharsanam, S., Sundharabahu, S. (2001). A Handbook of Practical

Auditing, New Delhi: S. Chand & Co. (revised edition), 594‐630.

Uddin, S., Hopper, T. (2003). Accounting for Privatisation in Bangladesh: Testing World

Bank Claims. Critical Perspectives on Accounting, 14(7), 734‐74.

Ullah, W. (2001). Auditing (sixth reprinted edition), Dhaka: Abadi Publications, Chs. 9,

10, 11, 12 & 14.

29

Table 1

Whats and Hows of Window‐Dressing in Bangladesh

Whats:

a. A deliberate process of manipulation in financial statements;

b. Intended to give actual and anticipated users;

c. A favorable impression on the performance and financial position;

d. Which is not representative of the position had there not been such

manipulation.

Hows:

1.Frequent changes in the method of valuation of assets.

2.Over valuation of intangible assets like goodwill, patents, and brand names.

3.Creation or abolition of any reserve funds.

4.Over‐valuation of work‐in‐progress or inventories.

5.Hiding of accruals or advance payments.

6.Hiding of cross stock or bond holding.

7.Payment of bank over‐draft just before the date of balance sheet.

8.Payment of current liabilities before loan application.

9.Showing of big cash amount in hand and at bank.

10. Hiding of loosing portfolios.

11. Showing of raw materials in job site as semi‐processing goods.

12. Delay in writing off bad debts.

13. Changing of methods of stock valuation.

14. Selling of junk debentures before balance sheet date.

15. Other manipulations deemed necessary and plausible.

Source: Compiled by authors from different sources.

30

Table 2

Auditors' Functions in Connection with Financial statements in Bangladesh

Main Functions

a. Auditing financial statements (a).

b. Examination and investigation of books of accounts (b).

c. Verification that (a) and (b) above conform to standards/customs/conventions.

d. Certification that financial statements show the true and fair view of

performance and financial position client companies and firms.

e. Giving of opinion on specific matters in accordance with the government’s order.

Profit and Loss Account

1. All transactions are taken into account.

2. No capital income or expenditure are shown as revenue income or expenditure,

and vice versa.

3. All arrears and accruals are taken into account.

4. No unearned income or unpaid expenses are taken into account.

5. No irregular allocations or reserves are made or drawn in profit and loss

appropriation account.

Balance Sheet

1. Assets and liabilities are categorized and shown under accurate heading.

2. All assets and liabilities are valued according to consistent principles.

3. All assets and liabilities tally reasonably with the previous‐year balance sheet.

Supplementary Statements

1. Are made accurately and support P&L A/C and balance sheet.

2. Are attached accurately to P&L A/C and balance sheet.

31

Table 3

Current Status of Bangladesh Standards on Auditing (BSA)

BSA

Present Title

200 Objective and General Principles Governing and Audit of Financial Statements

210 Terms of Audit Engagements

220 Quality Control for Audits of Historical Finance Information

230 Audit Documentation

240 The Auditor's Responsibility to Consider Fraud in an Audit of Financial Statements

250 Consideration of Laws and Regulations in an Audit of Financial Statements

260 Communications of Audit Matters with Those Charged with Governance

300 Planning an Audit of Financial Statements

315 Understanding the Entity and Its Environment and Assessing the Risks of Material Misstatement

320 Audit materiality

330 The Auditor's Procedures in Response to Assessed Risks

402 Audit Considerations Relating to Entities Using Service Organization

500 Audit Evidence

501 Audit Evidence-Additional Considerations for Specific items

505 External Confirmations

510 Initial Engagements-Opening Balances

520 Analytical Procedures

530 Audit Sampling and Other Means of Testing

32

540 Audit of Accounting Estimates

545 Auditing Fair Value Measurements and Disclosures

550 Related Parties

560 Subsequent Events

570 Going Concern

580 Management Representations

600 Using the Work of Another Auditor

610 Considering the Work of Internal Auditing

620 Using the Work of an Expert

700 The Independent Auditor's Report on Complete Set of General Purpose Financial Statements

710 Comparatives

720 Other Information in Documents Containing Audited Financial Statements

800 The Auditor's Report on Special Purpose Audit Engagements

1000 Inter-Bank Confirmation Procedures

1004 The Relationship Between Bank Supervisions and Banks' External Auditors

1005 The Special Considerations in the Audit of Small Entities

1014 Reporting by Auditors on Compliance with International Financial Reporting Standards

Source: ICAB (2009).

33

Table 4

Summary of Factors that Influence Functions of Auditors in Bangladesh

Accounting Concepts and Conventions

• Monetary measurement • Going concern • Objectivity • Business entity • Cost • Dual‐aspect • Conservatism • Accounting Period • Accrual • Realization • Full Disclosure • Materiality • Consistency

Legal Measures

• The Companies Act, 1994 Sections 181‐191 on accounting books and statements Sections 195 ‐221 on auditing and investigation • Stock Exchange Commission Rules and Regulations Strict adherence to IASs • Other government rules and regulations • Comptroller of and Auditor‐General (CAG) rules and procedures

Standards/Conventions of National and International Professional Bodies

• National Professional rules and standards of ICAB and ICMAB • Regional Confederation of Asian and Pacific Accountants (CAPA) South Asian Federation of Accountants (SAFA) (forums to do research and deliberate on unity of practices and exchange

of information on regional basis) • International Standards/ conventions of IFAC, IASC, and IAPC

Professional Ethics and Code of Conduct

• Explicit • Implicit

34

Table 5

Liabilities of Auditors for Widow‐Dressing of Financial Dressing of Financial

Statements

Label of Offenses Type of

Liabilities

To Clients To Third Parties

Negligence relationship Civil/criminal Fine and jail No contractual and no

liability

Misfeasance proofs Civil Fine Liable subject to and

evidences

Professional miss‐

Disciplinary conduct

Disciplinary

action

Petition filed to Investigation and

Disciplinary Committee of ICAB which

can issue warning, withheld or cancel

membership