financial fragility and financial crisis in mexico

TRANSCRIPT

FINANCIAL FRAGILITY AND FINANCIAL CRISIS IN MEXICO

Julio López Gallardo, Juan Carlos Moreno-Brid and Martín Puchet Anyul*Universidad Nacional Autonoma de México and Economic Commission

for Latin America and the Caribbean(February 2004; revised January 2005)

ABSTRACT

The objective of this paper is to show how Mexico’s strategy of financial deregulation and liberaliza-tion set the stage for the crisis that the country suffered in December 1994. The theoretical underpin-ning is Post-Keynesian, and more precisely, a Minsky-inspired analytical perspective extended to theopen economy. In the first section the authors carry out a theoretical discussion dealing with somePost-Keynesian theories of the business cycle. A second section is devoted to examining and identify-ing the stylized facts in the evolution of the Mexican economy, with special emphasis on the interac-tion between the financial and real variables. In the last section the authors propose a simplified modelwhich shows how and why a strategy of financial deregulation and liberalization may lead to finan-cial fragility and to a crisis.

1. INTRODUCTION

After the traumatic experience of the early 1980s, which saw an ill-managedoil boom turn into a major financial crisis,1 Mexico completely overhauledits economic strategy. The economic role of the state was forsaken, thedomestic market was opened-up to imports, international financial transac-tions were fully liberalized and the domestic financial sector was re-privatizedand deregulated.

Metroeconomica 57:3 (2006) 365–388

© 2006 The AuthorsJournal compilation © 2006 Blackwell Publishing Ltd, 9600 Garsington Road, Oxford, OX42DQ, UK and 350 Main St, Malden, MA 02148, USA

* The authors would like to thank Josep González Calvet and two anonymous referees of thisjournal for their very useful comments, to Elvio Accinelli for his technical support and to Alejandro Cruz for his extremely efficient and enthusiastic research assistance. The opinions hereexpressed are the responsibility of the authors and do not necessarily coincide with those of theinstitutions with which they are affiliated.1 In 1955–56 there was a balance-of-payments crisis that was rapidly corrected through a depre-ciation of the exchange rate and a selective—rather expansionary—fiscal policy. This adjust-ment strategy succeeded, besides avoiding a full fledged financial crisis, in placing the Mexicaneconomy in a long-term path of high and sustained growth with relatively low inflation thatwould last practically until the 1970s. This period is known as the ‘Desarrollo Estabilizador’ inMexico’s economic history.

366 Julio López Gallardo et al.

© 2006 The AuthorsJournal compilation © 2006 Blackwell Publishing Ltd

The objective of this paper is to show how the strategy of financial dereg-ulation and liberalization set the stage for the crisis that Mexico suffered inDecember 1994; a crisis that caused real GDP to fall in 1995 by about 6 percent with respect to the level it had achieved one year earlier. Our theoreti-cal underpinning is Post-Keynesian, and more precisely, a Minsky-inspiredanalytical perspective extended to the open economy. Thus, this paper canbe read from two different perspectives. It can be read as an analysis ofMexico’s 1994–95 crisis, seen with the perspective of the Post-Keynesianbusiness cycle theory. It can also be read as a present-day reflection on andextension to an open economy of Post-Keynesian business cycle theory, illus-trated with the particular case of the Mexican experience.

The structure of the paper is as follows. In the second section we carry outa theoretical discussion dealing with some Post-Keynesian theories of thebusiness cycle. A third section is devoted to examining and identifying thestylized facts in the evolution of the Mexican economy, with special empha-sis on the interaction between the financial and real variables. In section 4we propose a simplified model that shows how and why a strategy of finan-cial deregulation and liberalization may lead to financial fragility and to acrisis. Final remarks are in section 5.

2. THEORETICAL DISCUSSION

Growth in capitalist economies is subject to cycles that, under certain cir-cumstances, may turn into crises. The original Post-Keynesian theoretical literature on the subject, on which our approach relies, was formulatedassuming a closed economy and in this context we can distinguish two per-spectives. The first one was put forward by Kalecki, who developed a busi-ness cycle theory whereby investment decisions are a function of the changesin the factors determining the rate of profit and of the current entrepreneurialsavings. In his theory Kalecki integrated in a novel way financial considera-tions, which enter via an argument related to firms’ own financial resourcesand the principle of increasing risk. Nevertheless, he implicitly assumed thatmonetary conditions remained unchanged, and that the reaction of firms tofinancial conditions does not vary during the course of the cycle.2

The second approach was formulated by Minsky (1975, 1982), who identi-fied the varying target rate of indebtedness of firms and of lending of banks

2 Note, however, that in Kalecki (1942), where he presented a second version of his model headmitted, en passant, the elasticity of investment decisions to firm’s internal savings may in factchange.

Financial Fragility and Financial Crisis in México 367

© 2006 The AuthorsJournal compilation © 2006 Blackwell Publishing Ltd

as one of the underlying causes of the cycle.3 Of course, the recognition of theinfluence of firms’ indebtedness in their investment decisions was not new;and in fact it played a significant role in the analytical framework and in theempirical reflection of the man to whom we pay homage today. Thus, inSteindl’s (1952) original stagnation theory, unwanted changes (i.e. an unfore-seen rise) in the gearing ratio make it difficult for capitalist economies to spon-taneously overcome the tendency towards stagnation brought about when therate of growth of investment tends to decline. But the idea of a cycle of finan-cial origin is mostly associated with Minsky, while the seminal contribution ofSteindl in this area has largely gone unnoticed (but see Lavoie, 1995).

It may be recalled that in the Minsky closed-economy story the cyclicalupswing is brought about because, after a period of tranquility, firms andbanks become more optimistic, so that investment and demand for externalfinance—i.e. liquidity provided by the financial system—rises at a faster paceand supply of finance accommodates this thanks to financial innovationsimplemented by banks. Now, the boom looses momentum because externalfinance to firms is increasingly restricted, becoming more expensive and moredifficult to get. More precisely, the hike of the indebtedness coefficients givesrise to a situation of ‘financial fragility’, in the sense that the ratio of privatedebt to capital or to profits increases progressively reaching critical levels and,accordingly, financial factors have an ever greater bearing on the develop-ment of the economy. If domestic credit supply is not forthcoming, eitherbecause banks become more cautious or because monetary authorities imple-ment restraining measures, the boom would get busted as firms would beforced to downgrade their investment projects and ultimately their businessperspectives. Investment growth is thus reduced and, if accompanied with aslowdown in the rate of expansion of the other determinants of profits, thiswill feed back into slower growth of effective demand and of profits. Hencethe rate of profits will decline and the economy will enter a downward spiral.Without adequate policies—fiscal and monetary—the subsequent slowdownor recession may turn into a full-blown debt crisis.

If we extend his analysis to an open economy,4 we must take into accountthat the upswing gives rise to an important imbalance, of external nature, asimports rise faster than exports and thus increasingly put pressure on the

3 Although Minsky made extensive use of, and acknowledged the importance of Kalecki’stheory of profits, to the best of our knowledge he never recognized how much his theory ofinvestment owed to Kalecki’s principle of increasing risk. See Nasica (2000) for an excellent pres-entation and development of the literature concerning Minsky’s model, and for a most usefullist of references.4 See Arestis and Glickman (2002) for an interesting extension of Minsky’s ideas to the openeconomy.

368 Julio López Gallardo et al.

© 2006 The AuthorsJournal compilation © 2006 Blackwell Publishing Ltd

availability of foreign exchange. To be more precise on the nature of thisimbalance, as exports fail to grow in tandem with the domestic upswing, debtrequirements and financial external fragility increase.

External financial fragility has a microeconomic and a macroeconomicdimension. The former takes place when the mismatch between earnings andpayments in foreign currency in the balance sheets of economic agentsreaches a critical level. The latter can be identified as a situation in which acountry is at high risk of holding insufficient foreign reserves to satisfy thedemand to convert a large proportion of the cumulative saving done innational currency, into foreign currency.

Because a fast-growing economy breeds enthusiastic expectations andbanks (both domestic and international) are in the business of profiteeringafter all—with ‘herd’-like behavior (Steindl, 1990, pp. 371–5)—during theearly phase of the upswing it may be easy to finance the external imbalancewith resources provided by international creditors. However, with debt per-sistently rising, eventually at a faster pace than exports, or income, or both,international banks would have to reassess the solvency of the thriving debtorsand of the country as a whole, and decide to accept or not a systematic increasein their exposure. Thus, an excessive external exposure, or worsening interna-tional financial or trading conditions, may also put an end to the upswing andbring about the downturn. Most importantly, considering the volatility andinterdependence of private agents’ expectations in modern global capitalism,a credit restriction—by increasing interest rates or contracting the availablefunds for lending—in the international capital markets may lead eventually toa financial crisis. Also, a foreign recession may be imported by provoking a fallof exports’ earnings, either because they cut down the volumes exported orbecause they cause unit prices to decline. The possibility of any compensa-tional policies aiming to put a stop to the downward spiral, which requireforeign defensive indebtedness, is more difficult than in the closed economy, asit depends on the international financial system’s flexibility. If foreign creditswere to be rationed this could force one after another round of cuts in domes-tic expenditure and profits, and further abase investment.

The influence of institutional changes can easily be incorporated into theprevious analytical framework. Steindl provided two very interesting exam-ples, related with the changing financial environment in a closed economy.Thus, in Steindl (1952), he showed that the institutional innovation associ-ated with the development of the capital stock market in the US economystimulated the rate of capital accumulation—and, accordingly, prevented thetendency towards stagnation to emerge earlier than it actually did—thanksto the decline it brought about in the cost of external financial resources tofirms. He remarked that, surprisingly, this very important development had

Financial Fragility and Financial Crisis in México 369

© 2006 The AuthorsJournal compilation © 2006 Blackwell Publishing Ltd

not been given much consideration either in the theoretical or in the empir-ical literature of his time.

His second example was related to the emergence of a steady stream ofnew durable and relatively expensive consumer goods, and the parallel gen-eralization of consumer credit at advanced stages of capitalist development(Steindl, 1964).5 He argued that the first phenomenon might have imparteda downward bias to the long-run development of the economy if the pur-chase of durable goods had required a rise in the saving coefficient. He addedthat such a situation was prevented by the massive expansion of consumercredit, which ultimately brought about a decline in the medium time-lagbetween personal income and personal expenditure, thus contributing to anupward drift in the long-run rate of growth of capitalist economies.

Minsky envisioned institutional changes as ‘thwarting mechanisms’ thatwould somehow put limits, or floors, to the spontaneous development of thesystem (Minsky and Ferri, 1992). But, following the two examples providedby Steindl, we can also consider some institutional changes as ‘triggeringmechanisms’, which may disrupt a dynamic process that would otherwise besmooth and tranquil, and turn it into a trajectory leading to cycles or evento a chaotic development. For example, such a change, or a bifurcation, maycome about if a ‘positive financial shock’ happens to take place—e.g. if finan-cial reforms are implemented that allow banks to expand lending beyond the‘paying capacity’ of the economy. Also, the ‘triggering mechanism’ may berelated to too relaxed conditions in the world financial system. As we arguebelow, in Mexico’s experience the 1988–94 mini-boom that led to the 1995crisis, was the consequence of a combination of an ill-conceived and drasticfinancial deregulation that led to an excessive opening-up to financial inflows,mainly short-term capital.

We shall later put forward a very simplified analytical model where weattempt to identify the main interactions between the real and the financialsectors of a semi-industrialized economy, on the basis of which we can studyfinancial crises. But before that, we shall give an account of Mexico’s expe-rience and of the road to the crisis.

3. MEXICO’S EXPERIENCE

Let us first consider the basic institutional facts. Until the beginning of the1980s Mexico’s central bank set the deposit interest rates that financial insti-tutions were allowed to pay to depositors and credit was regulated through

5 It is unfortunate that our author did not include this very important essay in Steindl (1990).

370 Julio López Gallardo et al.

© 2006 The AuthorsJournal compilation © 2006 Blackwell Publishing Ltd

a complex system of reserve coefficients and preferential lending rates forspecific sectors or activities. In the mid- and late 1980s institutional reformsbegan to be executed that led to deregulation, re-privatization6 and liberal-ization of Mexico’s financial system, went along the following lines (Mantey,1996; Tello, 2004). The first step was the implementation of a system of auc-tions, whereby the interest rates were established for commercial bankdeposits at the central bank and lending from the central to commercialbanks. Later on, in the second half of the 1980s, the mandatory reserve ratioof banks was drastically reduced (from 50 per cent to 10 per cent) and theinterest rates for some specific banking instruments were liberalized. In turn,commercial banks were given complete freedom to allocate according to theirown preferences the resources obtained from these instruments. This reformwas followed by the full and complete liberalization of domestic interest ratesin 1988. The banking system was re-privatized in 1990, and a year later themandatory reserve ratio was eliminated for all banking liabilities denomi-nated in domestic currency. In 1993 commercial banking portfolio investmentwas completely deregulated.

On the other hand, by the end of the 1980s, banks were permitted toborrow abroad—although with some minor restrictions—and non-residentswere allowed to invest in domestic financial assets with practically no limitation.

Finally, it may be worth mentioning that the functioning of Mexico’s stockmarket was not modified to any important degree in the course of thereforms, and remained extremely shallow. Very few firms, about 200 in all,trade their shares in the Bolsa Mexicana de Valores (Mexican StockExchange). These are all gigantic firms whose aggregate sales represent about30 per cent of Mexico’s GDP. On the other hand, shares do not figure promi-nently within the assets of the private sector. In 1998 they represented lessthan 1 per cent of the total assets of pension funds, and a bit over 1 per centof the total assets of commercial funds.

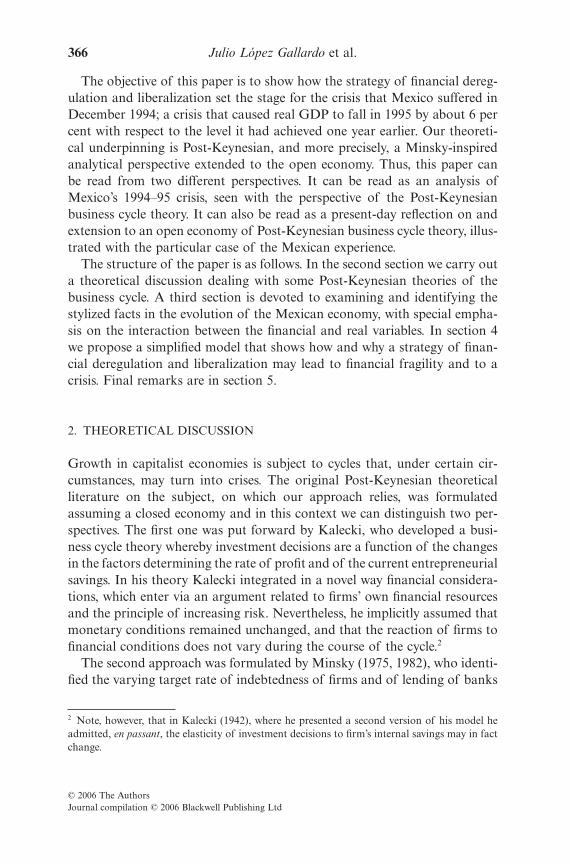

We now describe the main features of Mexico’s macroeconomic evolutionafter the reforms. To motivate our story, we make use of figures that shedlight on peculiar but important aspects of this country’s development.7

The first point worth mentioning is that after a protracted period of stag-nation following the 1982–83 crisis, economic growth resumed from aboutthe mid-1987 onwards, and continued up until December 1994, when thecrisis erupted (see figure 1). However, the economy’s growth rate was modest,especially when compared with Mexico’s historical growth record.

6 By the end of 1982 the banking system had been nationalized.7 Please note, in the figures the arrows indicate the reference axis for the respective variables.

Financial Fragility and Financial Crisis in México 371

© 2006 The AuthorsJournal compilation © 2006 Blackwell Publishing Ltd

In spite of the mildness of the recovery, the import elasticity of demanddramatically rose and the current account balance significantly deteriorated.This latter feature can be explained, on the one hand, by the steady appreci-ation of the domestic currency shown also in figure 1 (on which more later),8

and on the other hand, by the dismantling of the previous system of pro-tection of the domestic market (Moreno-Brid, 2001). Anyway, full liberal-ization of capital movements and privatization of public enterprises, coupledwith high domestic interest rates and with a relatively low price of Mexico’sfinancial and real wealth instruments, attracted large inflows of foreignresources that financed the current account deficit.

The inflow of foreign capital contributed to the expansion of the mone-tary base and the resources of the banking system. Simultaneously, the dereg-ulation of the financial domestic sector enlarged banks’ freedom to manageassets and liabilities, to reduce their reserve requirements and to innovatewith new financial instruments.

13.8

13.9

14.0

14.1

14.2

14.3

0.00

0.01

0.01

0.01

0.01

1980 1985 1990 1995 2000

<-----------------GDP

Realexchangerate--------------->

Figure 1. GDP and the real exchange rate.

8 The real exchange rate r shown in figure 1 is defined as: r = (p/Ep*), where E is the nominalexchange rate (say pesos per dollar), p* is the price index of international prices and p is the price index of domestic prices. Hence, a rise in r denotes a currency appreciation. We thus depart from the Latin American tradition where the real exchange rate is usually definedas q = E(p*/p).

372 Julio López Gallardo et al.

© 2006 The AuthorsJournal compilation © 2006 Blackwell Publishing Ltd

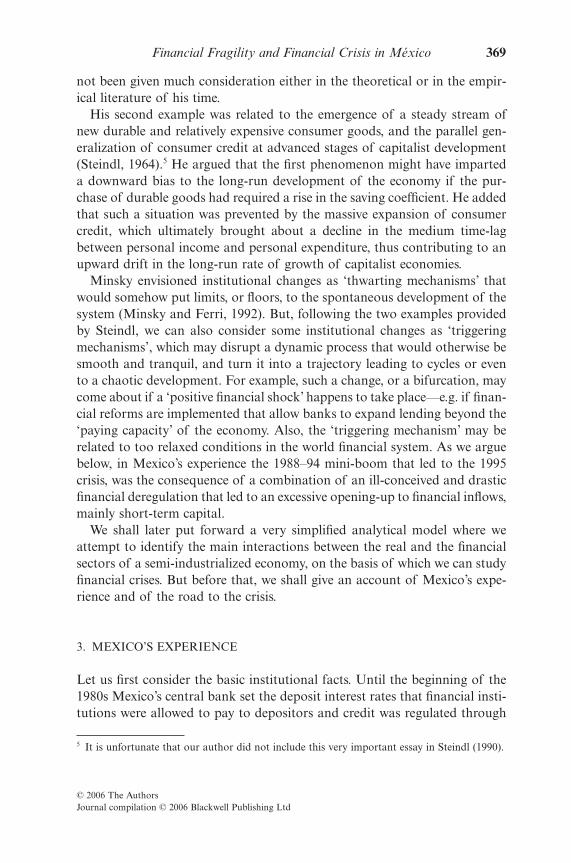

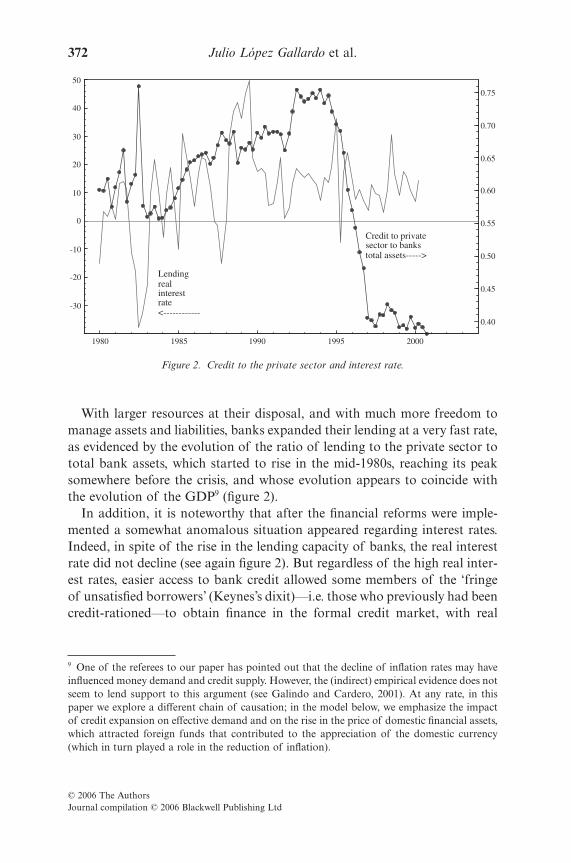

With larger resources at their disposal, and with much more freedom tomanage assets and liabilities, banks expanded their lending at a very fast rate,as evidenced by the evolution of the ratio of lending to the private sector tototal bank assets, which started to rise in the mid-1980s, reaching its peaksomewhere before the crisis, and whose evolution appears to coincide withthe evolution of the GDP9 (figure 2).

In addition, it is noteworthy that after the financial reforms were imple-mented a somewhat anomalous situation appeared regarding interest rates.Indeed, in spite of the rise in the lending capacity of banks, the real interestrate did not decline (see again figure 2). But regardless of the high real inter-est rates, easier access to bank credit allowed some members of the ‘fringeof unsatisfied borrowers’ (Keynes’s dixit)—i.e. those who previously had beencredit-rationed—to obtain finance in the formal credit market, with real

-30

-20

-10

0

10

20

30

40

50

0.40

0.45

0.50

0.55

0.60

0.65

0.70

0.75

1980 1985 1990 1995 2000

Lendingrealinterestrate<------------

Credit to privatesector to banks total assets----->

Figure 2. Credit to the private sector and interest rate.

9 One of the referees to our paper has pointed out that the decline of inflation rates may haveinfluenced money demand and credit supply. However, the (indirect) empirical evidence does notseem to lend support to this argument (see Galindo and Cardero, 2001). At any rate, in thispaper we explore a different chain of causation; in the model below, we emphasize the impactof credit expansion on effective demand and on the rise in the price of domestic financial assets,which attracted foreign funds that contributed to the appreciation of the domestic currency(which in turn played a role in the reduction of inflation).

Financial Fragility and Financial Crisis in México 373

© 2006 The AuthorsJournal compilation © 2006 Blackwell Publishing Ltd

interest rates that were probably below what they were in the informalmarket. In other words, a larger part of latent demand for credit could nowmanifest itself as actual demand.

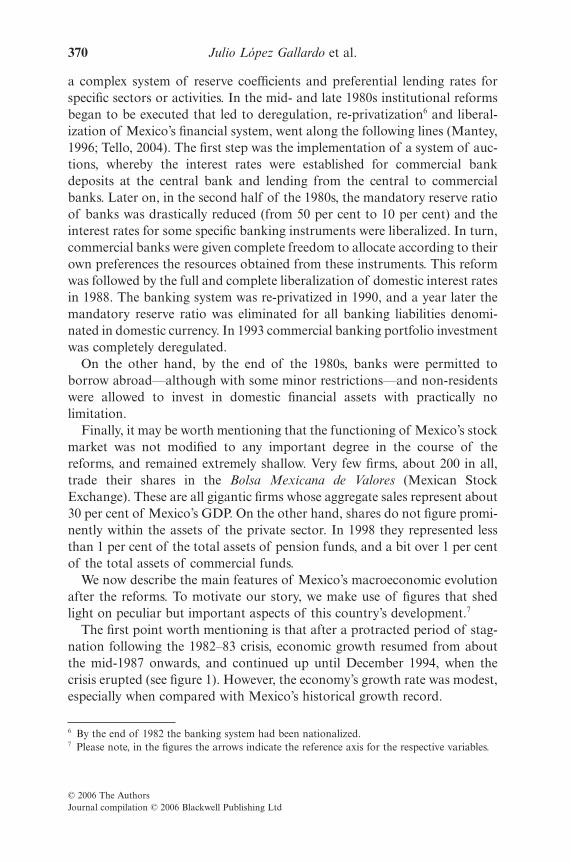

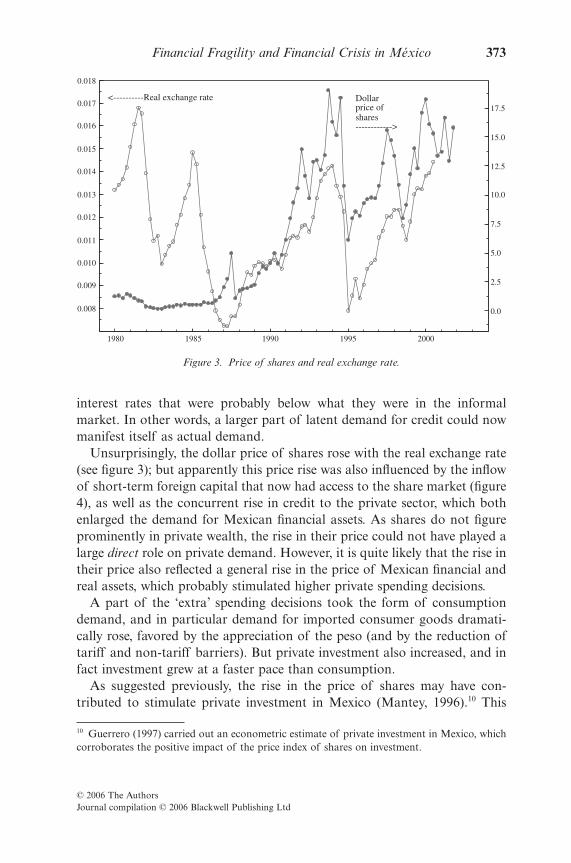

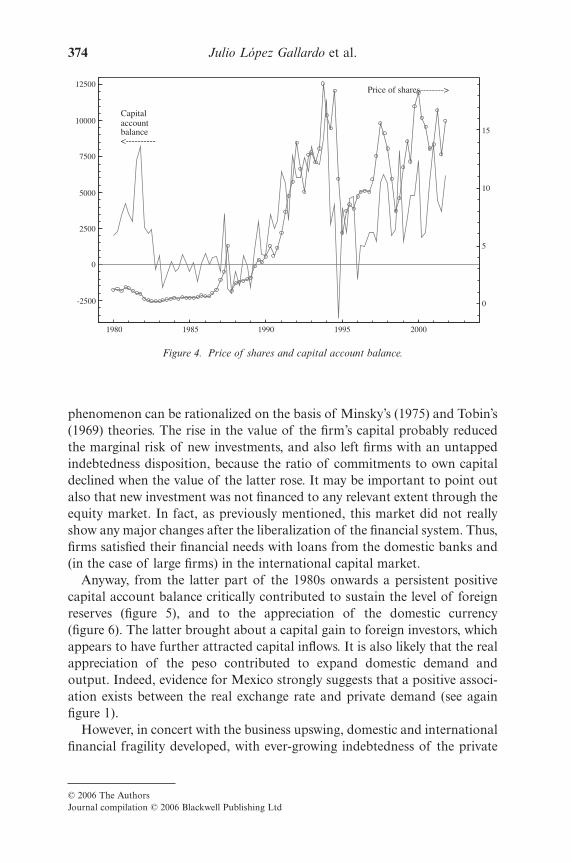

Unsurprisingly, the dollar price of shares rose with the real exchange rate(see figure 3); but apparently this price rise was also influenced by the inflowof short-term foreign capital that now had access to the share market (figure4), as well as the concurrent rise in credit to the private sector, which bothenlarged the demand for Mexican financial assets. As shares do not figureprominently in private wealth, the rise in their price could not have played alarge direct role on private demand. However, it is quite likely that the rise intheir price also reflected a general rise in the price of Mexican financial andreal assets, which probably stimulated higher private spending decisions.

A part of the ‘extra’ spending decisions took the form of consumptiondemand, and in particular demand for imported consumer goods dramati-cally rose, favored by the appreciation of the peso (and by the reduction oftariff and non-tariff barriers). But private investment also increased, and infact investment grew at a faster pace than consumption.

As suggested previously, the rise in the price of shares may have con-tributed to stimulate private investment in Mexico (Mantey, 1996).10 This

0.008

0.009

0.010

0.011

0.012

0.013

0.014

0.015

0.016

0.017

0.018

0.0

2.5

5.0

7.5

10.0

12.5

15.0

17.5

1980 1985 1990 1995 2000

<----------Real exchange rate Dollar price ofshares------------>

Figure 3. Price of shares and real exchange rate.

10 Guerrero (1997) carried out an econometric estimate of private investment in Mexico, whichcorroborates the positive impact of the price index of shares on investment.

374 Julio López Gallardo et al.

© 2006 The AuthorsJournal compilation © 2006 Blackwell Publishing Ltd

phenomenon can be rationalized on the basis of Minsky’s (1975) and Tobin’s(1969) theories. The rise in the value of the firm’s capital probably reducedthe marginal risk of new investments, and also left firms with an untappedindebtedness disposition, because the ratio of commitments to own capitaldeclined when the value of the latter rose. It may be important to point outalso that new investment was not financed to any relevant extent through theequity market. In fact, as previously mentioned, this market did not reallyshow any major changes after the liberalization of the financial system. Thus,firms satisfied their financial needs with loans from the domestic banks and(in the case of large firms) in the international capital market.

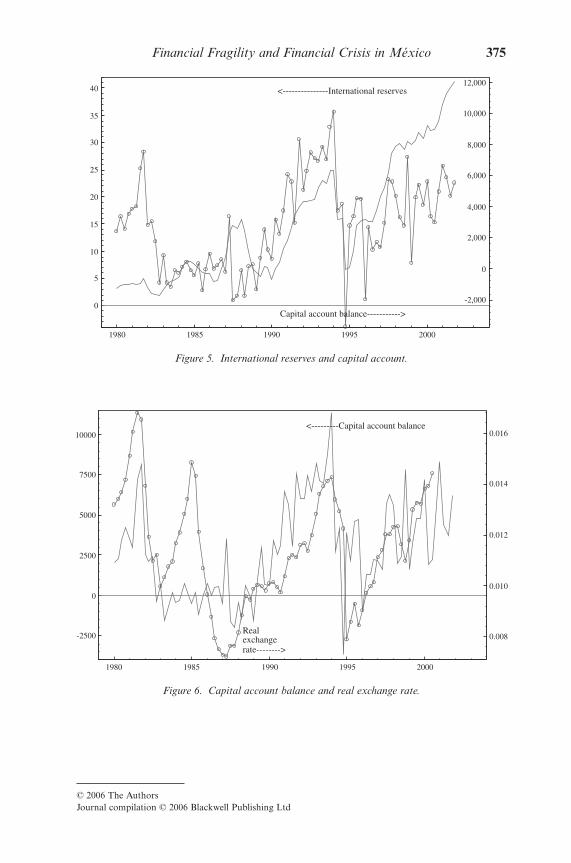

Anyway, from the latter part of the 1980s onwards a persistent positivecapital account balance critically contributed to sustain the level of foreignreserves (figure 5), and to the appreciation of the domestic currency (figure 6). The latter brought about a capital gain to foreign investors, whichappears to have further attracted capital inflows. It is also likely that the realappreciation of the peso contributed to expand domestic demand andoutput. Indeed, evidence for Mexico strongly suggests that a positive associ-ation exists between the real exchange rate and private demand (see againfigure 1).

However, in concert with the business upswing, domestic and internationalfinancial fragility developed, with ever-growing indebtedness of the private

-2500

0

2500

5000

7500

10000

12500

0

5

10

15

1980 1985 1990 1995 2000

Capitalaccountbalance<----------

Price of shares-------->

Figure 4. Price of shares and capital account balance.

Financial Fragility and Financial Crisis in México 375

© 2006 The AuthorsJournal compilation © 2006 Blackwell Publishing Ltd

0

5

10

15

20

25

30

35

40

-2,000

0

2,000

4,000

6,000

8,000

10,000

12,000

1980 1985 1990 1995 2000

<---------------International reserves

Capital account balance----------->

Figure 5. International reserves and capital account.

-2500

0

2500

5000

7500

10000

0.008

0.010

0.012

0.014

0.016

1980 1985 1990 1995 2000

<---------Capital account balance

Realexchangerate-------->

Figure 6. Capital account balance and real exchange rate.

376 Julio López Gallardo et al.

© 2006 The AuthorsJournal compilation © 2006 Blackwell Publishing Ltd

sector vis-à-vis the banking sector, and of the national economy vis-à-visforeign lenders.

Indeed, between 1988 and 1994 the share of outstanding credit of firmswith the banking system rose from being equivalent to 8.9 per cent of GDPin 1988 to 35.5 per cent in 1994. The figures for households show an evengreater increase; i.e. their share rose from 14.2 per cent to 55.3 per cent(OECD, 1995). On the other hand, the share of government loans in totalloans from the banking system declined from being a little above 60 per centin 1988 to less than 10 per cent in 1994. These two phenomena, the rise inprivate indebtedness and the decline in the share of lending to the govern-ment from banks, we take as prima facie evidence of a rise in domestic finan-cial fragility. In fact, it appears that the reduction in the share of the safe(government) loans in the total loans of the banks contributed to the rise ofnon-performing loans, whose share in the total assets of the banking systemgrew from less than 1 per cent in 1988 to over 5 per cent in 1994.11

As regards external financial fragility, at the microeconomic level the inflowof foreign funds resulted in heavy external indebtedness of the private sector,including the banks; the exposure of the latter in foreign currency rose fromabout 19,000 (million of dollars) in December 1992, to about 24,000 inDecember 1993, and to 25,000 in December 1994. Also, during the course ofthe business upswing important signs of macroeconomic internationalfragility appeared. Perhaps the most salient sign was the rise in the ratio ofthe accumulated current account deficit to GDP, which steadily and persist-ently grew, and the ratio of M2 to international reserves, which started togrow prior to the crisis.

As the crisis itself showed, Mexico’s booming current account deficit hadgone too far, bringing about a critical level of external financial fragility. Butwhat is also striking is that the critical indicators, and particularly the ratioof M2 to international reserves, whose rise is considered in the empirical lit-erature as one of the most clear signs that can anticipate a crisis, was ratherstable (and below what it had been in the recent past) for quite some timeafter the current account balance had been showing a high deficit.

In fact, notwithstanding the deterioration of the current account, Mexico’snew strategy received not only abundant foreign funds, but also praise frominternational financial institutions. In the domestic front, and in spite of themildness of the upswing, and of the mounting evidence of financial stress offirms and banks, expectations also improved. According to the survey of

11 González (1997) estimated an econometric model for non-performing loans for the 1980–95period, where the importance of the deregulation of credit and of the share of government loansin total loans is confirmed.

Financial Fragility and Financial Crisis in México 377

© 2006 The AuthorsJournal compilation © 2006 Blackwell Publishing Ltd

entrepreneurial opinion that Mexico’s central bank conducts twice a year, inthe second semester of 1986 the proportion of respondents that consideredthe economic climate as good was the same as the proportion that consid-ered the economic climate as bad (at about 20 per cent each). A year laterthe proportion of the former rose (to 30 per cent) while that of the latter fell(to 14 per cent), and in the second semester of 1989 the respective propor-tions were 67 per cent and 3 per cent. Finally, in the second semester of 1994(i.e. just before the crisis), the proportions were 64 per cent and 2 per cent,respectively (Cruz, 2004).

There was certainly an ideological preconception, which helps one under-stand why in spite of the ever-growing current account deficit in a context ofa quite modest business upswing, the international financial institutions, thepress and domestic opinion maintained their support for Mexico’s economicstrategy, and why in spite of the rise in the dollar price of Mexico’s financialassets the inflow of foreign funds could continue.12 In fact, one is remindedof the beauty contest analogy so convincingly put forward by Keynes—herethe ideal type of beauty had taken the shape of the strategy advocated bythe Washington consensus.

Another reason comes from the difficulty to evaluate the soundness orotherwise of foreign indebtedness, since Mexico’s fundamentals appeared atfirst sight satisfactory and the signs coming from the market were in any casefar from clear. As previously mentioned, investment had grown and capaci-ties had expanded. On the other hand, exports were growing at a relativelyfast rate, in spite of the appreciation of the currency. Also, the curse of infla-tion appeared to have been defeated. Finally, it was not easy for the economicauthorities, for both economic and political reasons, to depreciate the domes-tic currency in order to redress the foreign balance.

The benevolence of international financial institutions and foreigninvestors lasted approximately until the first quarter of 1994 (although expec-tations of domestic entrepreneurs remained optimistic until the crisiserupted). The capital account balance and the reserve position deterioratedin the course of 1994 (see figure 5). Even though the former remained posi-tive, and reserves were at a relatively high level until the crisis erupted inDecember 1994, in the course of that year the government had to offer evermore favorable conditions to foreign investors in order to attract foreignfunds, and the composition of the latter dramatically changed. Thus, theshare accounted for by short-term capital inflows over total capital inflowsrose about 50 per cent with respect to the previous year.

12 The rise in the dollar price of shares coincided with the rise in the price of shares in the USA,so that their relative price did not grow.

378 Julio López Gallardo et al.

© 2006 The AuthorsJournal compilation © 2006 Blackwell Publishing Ltd

However, what is also remarkable is that when a shift of opinion of foreignagents appears to have taken place, this was due to events to a large extentexogenous to the evolution of the Mexican economy. These events had to dowith the rise in international interest rates, and with domestic political eventsthat appeared as capable of destabilizing the ruling regime. Recall, the Zap-atista uprising had taken place in January of 1994, later came the assassina-tions first of the presidential candidate of the ruling party, and later of thesecretary general of that same party, which all provoked a change in this gen-erous attitude.

Of course, with the above we do not want to imply that the crisis was theconsequence of exogenous factors. In fact, the ultimate cause of the crisiswas the ever-growing external financial fragility Mexico’s economy was accu-mulating. But the precise date when the crisis erupted was certainly deter-mined by factors that were not only economic sensu strictu.

We shall now take stock of the previous theoretical and historical discus-sion in order to specify a model capable of explaining a balance-of-paymentscrisis, and the collapse of the domestic currency under conditions of imper-fect information and a confidence breakdown.

4. MODELING THE DEVELOPMENT OF FINANCIAL FRAGILITY ANDA FINANCIAL CRISIS

The main features of the model we shall develop are the following.13 First,we assume that output is governed by aggregate demand, and we posit thatdemand is affected by the trade balance and by domestic autonomous expen-diture; the latter is assumed to depend on the availability of credit and onthe distribution of income. Second, the economy is assumed to be open toforeign capital inflows, but domestic and international financial assets areimperfect substitutes. Third, we assume ‘credit rationing’. More specifically,we suppose that the volume of credit, and thus the quantity of money, issupply determined, by the supply from banks, and not by demand. This is arather extreme assumption, but we adopt it here as a simple device in orderto stress a peculiarity of Mexico and possibly other semi-industrializedeconomies, where small- and medium-sized firms are indeed credit rationed,and large firms tend to have recourse to foreign credit. Thus, although we

13 Our model owes a lot to Bhaduri (2003), Erturk (2004), and most especially to Frenkel (1983).The latter is particularly important in the Latin American context because, to our knowledge,it was the first to put forward the interrelationship between high domestic interest rates, foreigncapital inflows, domestic credit expansion and external financial fragility.

Financial Fragility and Financial Crisis in México 379

© 2006 The AuthorsJournal compilation © 2006 Blackwell Publishing Ltd

share the usual assumption of the Post-Keynesian school that credit andmoney are endogenous for the private sector as a whole, we distance our-selves from the so-called ‘horizontalist approach’. Finally, in order to sim-plify matters the model will be specified in linear terms.

The model is composed of the following set of equations:14

(1)

(2)

(3)

(4)

(5)

(6)

(7)

(8)

Equation (1) specifies the current account deficit B, which depends on the real exchange rate r, and the level of output Y. We assume that the Marshall–Lerner conditions holds, and that a higher level of output is associated with a higher level of imports, and hence with a larger currentaccount deficit. Please note that for the sake of simplicity we disregard factorpayments.

Equation (2) states that net capital inflows F (net of profit remittancesabroad, of amortization payments etc.) responds to the level of the domestic interest rate on government bonds i, and to the dollar value ofdomestic financial assets , where = Qr according to equation (5), Q beingthe price in pesos of domestic assets. Thus, we assume, on the basis ofMexico’s experience, that a capital gain brought about by higher demand fordomestic assets, and by appreciation of the currency, further stimulate capitalinflows.15

˙ ;r R R= −( ) >q q 0

R F B= +

Q qC=

Q Qr=

C c R c i c cR i R i= − >; , 0

Y y r y C y yr C r C= + >; , 0

F f i f Q f fi Q i Q= + >; , 0

B b r b Y b br Y r Y= − >; , 0

14 br is the partial derivative of B with respect to r, etc.15 In a more realistic version of the model, it could be assumed that the relationship between and F is non-linear; however, we do not explore this issue, which is left for future research.

Q

380 Julio López Gallardo et al.

© 2006 The AuthorsJournal compilation © 2006 Blackwell Publishing Ltd

Equation (3) states that gross output Y depends on the real exchange rate andon credit availability C.16 We assume that credit availability raises outputthrough its impact on effective demand, and that currency depreciation dimin-ishes effective demand. Our reasons for the latter assumption are as follows.First, currency depreciation will probably bring about inflationary pressures,which may be followed by a deflationary monetary and policy stance. Second,if depreciation does not bring about wage inflation, it will entail a reduction inreal wages, or at least a reduction of the share of wages in value added. The con-sequent shift from profits to wages will induce a rise of the share of saving thatwill diminish the value of the multiplier. Finally, currency depreciation will raisethe indebtedness ratio of firms indebted in foreign currency that may discour-age new investment. Thus, unless net exports rise very strongly (which willdepend on the price elasticity of exports and imports), output is likely to fall.17

Equation (4) specifies the factors affecting domestic credit C, namely, thechange in foreign reserves R, and the domestic interest rate i. It is assumedthat foreign reserves are the only source of the monetary base, and that banklending rises when foreign reserves rise. On the other hand, a higher rate ofinterest on government bonds, which are the only safe financial assets, dis-courages bank lending because banks can earn profits without taking anyrisk. We assume that the domestic interest rate is always above the interna-tional interest rate. In equation (6) we posit that the peso price of domesticassets depends on the availability of credit.

Finally, the dynamics of the model is made explicit in equations (7) and(8), where we take R and r as our state variables. The change in reserves bydefinition depends on (net) capital inflows F, and on the current accountbalance B. Furthermore, the currency tends to appreciate whenever the levelof reserves exceeds a given value .18R

16 The variable C denotes the stock of credit outstanding, and not the flow of new credit.Anyway, our conclusions would not change if we assumed that output depends on the flow ofnew credit.17 It is usually taken for granted that the depreciation of the currency will be expansionary pro-vided the ‘Marshall–Lerner condition’ is fulfilled. However, this is not necessarily the case. Seethe classic paper by Krugman and Taylor (1978). By the way, since a currency depreciation withconstant money wages is analogous to a reduction of real wages, we are implicitly assuming a‘wage-led’ regime, using the terminology coined by Bhaduri and Marglin (1990).18 The theory underpinning equation (8) views the dynamics of the exchange rate as dependent,in the first place, on the change in the country’s net assets of foreign exchange (since foreignreserves are by definition equal to the foreign asset position but less than the foreign liabilityposition). In the second place, the dynamics depends on conventions. More specifically, is tobe taken as that the level of reserves that foreign exchange operators consider sufficient (or safe)for a given country. Thus, is not a target level of reserves fixed by the authorities, but a con-vention determined by the market. As Keynes pointed out long ago, conventions need not beclosely related to economic fundamentals, and they can abruptly change.

R

R

Financial Fragility and Financial Crisis in México 381

© 2006 The AuthorsJournal compilation © 2006 Blackwell Publishing Ltd

Upon substitutions we specify (7) and (8) as functions of r and R.19 Thenwe have

(9)

(10)

where the positive parameters are

We find now the equilibrium points (R*, r*) such that (9) and (10) are both

equal to zero. From (10) we get R* = . And from (9) we get .

Since the system is non-linear, we take the best linear approximation usingthe standard procedure. The Jacobian evaluated at the equilibrium pointturns out to be

(11)

The dynamical behavior of the model in its linearized form is given by thesigns of the trace and determinant of (11):20

Jdr c dR b

R r* ** *

,( ) =− −

q 0

rcR adR b

***

= −−

R

d f qcQ R=

c b y cY C R=

b b b y f qc ir Y r Q i= + +

a f i b y c ii Y C i= +

r R R= −( )q

R a br cR drR= − − +

19 The steps are as follows:

20 Recall that when det(J) < 0 we have a saddle point; and when det(J) > 0 we have a sink iftr(J) < 0, and a source when tr(J) > 0.

R F B f i f Q b r b Y

f i f qC b r b y r y C

f i b r b y r f qr b y C

f i b r b y r f qr b y

i Q r Y

i Q r r Y r C

i r Y r Q Y C

i r Y r Q Y C

= + = + − − ( ) ( )= + − − +( ) ( ) ( ) ( )= − − + −( )= − − + −

from 1 and 2

from 5 , 6 and 3

(( ) −[ ] ( )= +( ) − + +( )

− ( ) + ( )

c R c i

f i b y c i b r b y f qc i r

b y c R f qc r

R i

i Y C i r Y r Q i

Y C R Q RR

from 4

382 Julio López Gallardo et al.

© 2006 The AuthorsJournal compilation © 2006 Blackwell Publishing Ltd

(12)

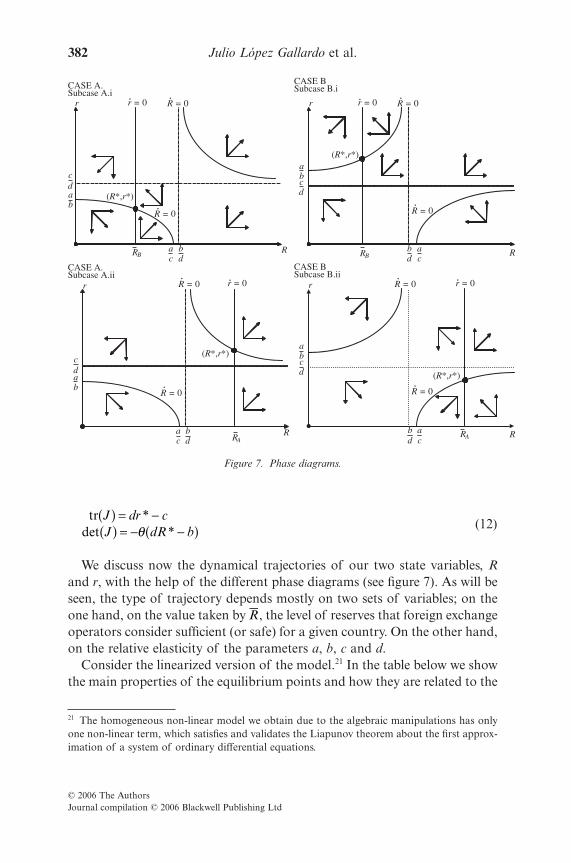

We discuss now the dynamical trajectories of our two state variables, Rand r, with the help of the different phase diagrams (see figure 7). As will beseen, the type of trajectory depends mostly on two sets of variables; on theone hand, on the value taken by , the level of reserves that foreign exchangeoperators consider sufficient (or safe) for a given country. On the other hand,on the relative elasticity of the parameters a, b, c and d.

Consider the linearized version of the model.21 In the table below we showthe main properties of the equilibrium points and how they are related to the

R

det *J dR b( ) = − −( )qtr J dr c( ) = −*

CASE A.Subcase A.i

CASE A.Subcase A.ii

RBR

ca

db

dc

ba

r

(R*,r*)

(R*,r*)

(R*,r*)

(R*,r*)

r

dc

ba

ca

db

AR R

CASE B Subcase B.i

CASE B Subcase B.ii

r r = 0

r = 0

R = 0r = 0 R = 0

R = 0r = 0R = 0

ba

dc

BRdb

ca R

R = 0R = 0

R = 0 R = 0

db

ca R

r

AR

ba

dc

Figure 7. Phase diagrams.

21 The homogeneous non-linear model we obtain due to the algebraic manipulations has onlyone non-linear term, which satisfies and validates the Liapunov theorem about the first approx-imation of a system of ordinary differential equations.

Financial Fragility and Financial Crisis in México 383

© 2006 The AuthorsJournal compilation © 2006 Blackwell Publishing Ltd

level of and the structural parameters of the model. Note that the equi-librium point is unique in each one of the cases and subcases describedbelow:

ParametersLow (a/c) < (b/d) (a/c) > (b/d)High (a/c) < (b/d) (a/c) > (b/d)

To start with, it may be pointed out that when (a/c) > (b/d), then we have

(13)

Now, an interesting feature of the model is that the left-hand side param-eters of (13) are related with the financial side of the economy, while theright-hand side parameters are related to the real side of the economy. Itappears, therefore, that the stability properties of our model are closelyrelated with the relative strength of the financial vis-à-vis the real side of theeconomy. On the other hand, it must be mentioned that our assumptionregarding the value taken by yr, the partial derivative of demand to the realexchange rate, also plays a role in connection with the stability conditions.The latter are more easy to be met when demand reacts positively to a risein the real exchange rate than when the opposite is the case.

Let us now dwell further on the mathematical properties of the model.Take first the case when the strength of the ‘financial’ parameters is low

vis-à-vis the strength of the ‘real’ parameters, which we label Case A; thenwe have two subcases:

(i) When is low, the equilibrium point is a sink. Thus, the system is stable.(ii) When is high, then the equilibrium point is a saddle point. There is

only one convergent path. The saddle point is above the (a/b) ratio.

On the contrary, in what we label Case B, namely when the strength of the‘financial’ parameters is high vis-à-vis the strength of the ‘real’ parameters,then we have again two subcases:

(i) When is low, the equilibrium point is a source. Thus, the system isunstable.

(ii) When is high, then the equilibrium point is again a saddle point.There is only one convergent path. The saddle point is below the (a/b)ratio.

R

R

RR

ac

bd

f f q b y b b yi Q r c r y r< ⇔ < +( )

R

R

384 Julio López Gallardo et al.

© 2006 The AuthorsJournal compilation © 2006 Blackwell Publishing Ltd

The model in its non-linearized form gives rise to the following dynamicalconfiguration.

(a) low, and whatever (a/c) < (b/d) or (a/c) > (b/d), then the paths followedby the state variables are spirals. In the first case, the system convergestowards the equilibrium point, while in the second one it diverges fromit. In this sense, the stability properties are the same as in the linearizedversion of the system.

(b) high, and whatever (a/c) < (b/d) or (a/c) > (b/d), then the paths followedby the state variables are saddle points.

As was mentioned, when is low, both in Case A and in Case B the equi-librium point is a spiral. However, no limit cycle can be said to exist. In orderfor a limit cycle to appear, it is necessary that non-linearities occur in any oneof the original behavioral equations. In our model, the non-linearities arisedue to the algebraic transformations of the original equations.

Finally, it should be noticed that it is possible that in:

Case A: (a/c) < < (b/d), then no equilibrium point exists; or inCase B: (b/d) < < (a/c), no equilibrium point exists.

Notice also that instability of the exchange rate r and of the level ofreserves R implies that the current account balance will also be unstable, butin the opposite direction. Indeed, the dynamics of the current accountbalance can be easily shown to be

(14)

We reconsider now the most important results from an economic per-spective. In the first place, the value taken by , the level of reserves thatforeign exchange operators consider sufficient (or safe), plays a fundamentalrole regarding the trajectory of the state variables and of the system. Stabil-ity only can arise when is low. The question arises, why is this so? In ouropinion, this occurs because, when is low, then even a small accelerationof output will tend to bring about a negative value for in (8). Accordingly,the exchange rate will depreciate. Now, depreciation of the exchange rate willhave a negative impact on demand and output, as well as on the dollar priceof domestic assets, which will tend to dampen capital inflows; which in turnwill tend to dampen growth in R.

On the other hand, a low is merely a necessary, not a sufficient condi-tion. Stability requires also that condition (13), (a/c) < (b/d), be fulfilled. Itwould appear, therefore, that when financial variables speedily react tostimuli, then any shock that takes the economy away from its equilibrium willmove it further and further away from equilibrium.

R

rR

R

R

˙ ˙ ˙ ˙B b r b y c R y rr y C r r= − − +( )

RR

R

R

R

Financial Fragility and Financial Crisis in México 385

© 2006 The AuthorsJournal compilation © 2006 Blackwell Publishing Ltd

Nevertheless, we should also mention that policies can play a role in orderto ensure that the conditions for stability are met; namely, the economicauthorities could implement measures to establish Case A. Recall first thatwe have distinguished three regions depending on the value taken by vis-à-vis the parameters of the model. In Case A, when < (a/c), we are in thelow zone sensu strictu. Then for (a/c) < < (b/d) we are in a zone where noequilibrium can exist. Finally, when > (b/d), this is the high zone. Now,stable equilibrium can occur only in the low zone. However, the value of thelow zone is not a given constant. Even when conventions are such that thevalue of is high, what matters is not its absolute value, but rather its valuevis-à-vis the parameters of our model, namely fi, fQ, q, br, yc, by and yr. Buteven though these appear as parameters, the monetary authorities could exertan influence upon them.

5. FINAL REMARKS

On the basis of our analysis of Mexico’s recent experience with financialderegulation and liberalization, we have set up a model that appears to val-idate, in an open economy context, the conjectures about the volatility ofcapitalist economies put forward by two authors that have been frequentlycited in this paper, Steindl and Minsky. In one of his last contributions, theformer remarked that ‘Contrary to some opinions . . . diversity of expecta-tions is a condition for the attainment and maintenance of equilibrium in[speculative] markets’ (Steindl, 1990, p. 371). And expectations need in factdiverge among operators in the financial markets, especially in order forcapital inflows to be not too sensitive to changes in the interest rate and inthe dollar price of domestic assets (low value for fi and fQ); which are impor-tant conditions on which stability depends. Minsky, on the other side,asserted in several places his belief that capitalist economies with developedand complicated financial structures are liable to fluctuate, and may even behighly unstable; thus requiring thwarting mechanisms to set limits and floorsto these fluctuations (see especially Minsky and Ferri, 1992).

What is more, we hope to have shown that instability due to financialfactors is not a problem affecting only developed economies but also, andperhaps with vengeance, less developed ones as well. We think that condi-tions for instability can be expected to arise rather easily, following financialliberalization and deregulation in economies of this type. As seen in Mexico’sexperience, in particular capital inflows turned out to be very responsive torises in both the price of assets and the interest rate; the price of assetsstrongly responded to expansion of credit, and bank lending also swiftly

R

RR

RR

386 Julio López Gallardo et al.

© 2006 The AuthorsJournal compilation © 2006 Blackwell Publishing Ltd

responded to a greater availability of resources. We can then easily under-stand why in Mexico the exchange rate appreciated and foreign reserves wereincreasing, in spite of the deterioration in the current account situation.

Of course, the persistent deterioration of the current account that accom-panied the appreciation of the currency and the growth of reserves could notlast forever. But the precise date when the situation would explode cannot bemade precise with this, or with any other model. Rather, the only thing thatthe model can tell us is that an unstable situation was developing, and thatthe economy, under the prevailing rules, did not endogenously give birth toforces that would contribute to offsetting the tendency towards instability.

In Mexico’s case, we may posit that during a first stage, the accumulation ofan increasing current account deficit did not pose grave problems. The gov-ernment acquired increased legitimacy and the country had a very good press,and further the renegotiation of the servicing of the external debt reducedforeign payments. But at a later stage, together with the accumulation of anever-increasing current account deficit, its sustainable value was also reduceddue to adverse economic and political events, national and international.Thus, the crisis was the consequence of the simple unfolding of the economicexpansion, in the context of an ever-increasing external financial fragility. Inother words, even a moderate growth rate and an unchanged governmentpolicy stance became extremely risky, and actually were not sustainable anylonger under the existing institutional framework—i.e. in a financially veryopen economy—because the danger existed that investors might easily switchfrom peso-denominated to dollar-denominated financial assets.

The question finally arises, why there is no evidence that a new crisisappears on the horizon, in spite of Mexico’s economy operating under essen-tially the same institutional setting? Answering this question in full wouldprobably require another document. However, we could suggest very brieflythat some of the reasons may have to do with changes in the speed of reac-tion of the financial parameters of the model, and especially in fi, fQ and q.That is, the reactions of capital inflows to changes in the interest rates andin the value of domestic assets, and of the price of financial assets to creditexpansion, may be now less strong than they were before the crisis, preciselybecause a deep crisis took place.22

22 Of course, factors left outside of the model may be also playing a role. Thus, in a recent workBlecker (2004) discusses some of these factors. On the one hand, when the peso became over-valued in 2001–2, the government was able to devalue it without inviting a speculative attack.In addition, rise of the share of FDI (foreign direct investment) over ‘hot money’ helped to sta-bilize Mexico’s balance of payments. Finally, Mexico’s growth slowdown since 2001 has had theeffect of reducing import demand and thereby preventing an excessive trade deficit.

Financial Fragility and Financial Crisis in México 387

© 2006 The AuthorsJournal compilation © 2006 Blackwell Publishing Ltd

REFERENCES

Arestis, P., Glickman, M. (2002): ‘Financial crisis in Southeast Asia: dispelling illusion the Minskyan way’, Cambridge Journal of Economics, 26, pp. 237–60.

Bhaduri, A. (2003): ‘Capital flows, the balance of payments and the exchange rate’, in Dutt, A.,Ros, J. (eds): Development Economics and Structuralist Macroeconomics: Essays in Honorof Lance Taylor, Edward Elgar, Cheltenham.

Bhaduri, A., Marglin, S. (1990): ‘Unemployment and the real wage: the economic basis for con-testing political ideologies’, Cambridge Journal of Economics, 14, pp. 375–93.

Blecker, R. (2004): ‘The North American economies after NAFTA: a critical appraisal’, Inter-national Journal of Political Economy, 33 (1) (Fall 2003 issue, published 2005), pp. 5–27.

Cruz, M. (2004): ‘The 1994–95 Mexican financial crisis: a further analysis using a Post-Keynesian approach’, PhD thesis, University of Manchester.

Erturk, K. (2004): ‘Reflections on currency crises’, Investigación Económica, 53 (248), pp. 15–40.Frenkel, R. (1983): ‘Mercado financiero, expectativas cambiales, y movimientos de capital’, El

Trimestre Económico, 50, pp. 2041–76.Galindo, L. M., Cardero, M. E. (2001): ‘El proceso de monetización en México: la experiencia

reciente’, Aportes, 6 (17), pp. 37–56.González, C. (1997): ‘Determinantes de la cartera vencida en México: un análisis de cointe-

gración y modelo de corrección de errores’, Unpublished MA thesis, Maestría en CienciasEconómicas, Universidad Nacional Autónoma de México.

Guerrero, C. (1997): ‘Los determinantes de la inversión privada en México’, Unpublished MAthesis, Maestría en Ciencias Económicas, Universidad Nacional Autónoma de México.

Kalecki, M. (1942): ‘Studies in economic dynamics’, included in Osiatynsky, J. (ed.) (1991): Col-lected Works of Michal Kalecki, vol. II, Oxford University Press, Oxford.

Krugman, P., Taylor, L. (1978): ‘Contractionary effects of devaluation’, Journal of InternationalEconomics, 8, pp. 445–56.

Lavoie, M. (1995): ‘Interest rates in Post-Keynesians models of growth and distribution’,Metroeconomica, 46 (2), pp. 146–77.

Mantey, G. (1996): ‘La liberalizaciòn financiera en Mèxico y su efecto en el ciclo econòmico’,Economìa Aplicada Nr. 26, Maestria en Ciencias económicas, UNAM, Mexico.

Minsky, H. (1975): John Maynard Keynes, Columbia University Press, New York.Minsky, H. (1982): Can ‘It’ Happen Again? Essays on Instability and Finance, M. E. Sharpe, New

York.Minsky, H., Ferri, P. (1992): ‘Market processes and thwarting systems’, Structural Change and

Economic Dynamics, I, pp. 79–91.Moreno-Brid, J. C. (2001): ‘Liberalización Comercial y la Demanda de Importaciones en

México’, Investigación Económica, 62 (240), pp. 13–51.Nasica, E. (2000): Finance, Investment and Economic Fluctuations: An Analysis in the Tradition

of Hyman P. Minsky, Edward Elgar, Cheltenham.OECD (1995): ‘Mexico’, in Economic Surveys, OECD, Paris.Steindl, J. (1952): Maturity and Stagnation in American Capitalism, Basil Blackwell, Oxford.Steindl, J. (1964): ‘On maturity in capitalist economies’, in Problems of Economic Dynamics and

Planning, Polish Scientific Publishers, PWN, Warsaw.Steindl, J. (1990): Economic Papers 1941–88, St. Martin, New York.Tello, C. (2004): ‘Transición financiera en México’, Nexos, 320, pp. 19–30.Tobin, J. (1969): ‘A general equilibrium approach to monetary theory’, Journal of Money, Credit

and Banking, 1, pp. 15–29.

388 Julio López Gallardo et al.

© 2006 The AuthorsJournal compilation © 2006 Blackwell Publishing Ltd

Julio Gallardo Juan Carlos Moreno-BridUniversidad Nacional Autonoma de Mexico Economic Commission for Latin Facultad de Economía America and the Caribbean (CEPAL)Ciudad Universitaria Organisation of the United NationsMéxico D.F. 56-22-21-10 y 56-22-21-86 Presidente Masaryk 29, piso 13E-mail: [email protected] Mexico D.F

Mexico 11570Martin Puchet E-mail: [email protected] Nacional Autonoma de MexicoFacultad de EconomíaCiudad UniversitariaMéxico D.F. 56-22-21-10 y 56-22-21-86E-mail: [email protected]