financial advice: an improvement for worse?

TRANSCRIPT

Financial Advice: An Improvement for Worse?∗

Yigitcan Karabulut†

Goethe University Frankfurt

This draft: June 17, 2013

Abstract

In this paper, I analyze the role of �nancial advisors in individual investment decisions

and ask whether �nancial advice is a reliable substitute for individuals' �nancial literacy.

I report two main �ndings. First, I �nd that individuals who tend to be �nancially less

sophisticated are more likely to consult professional advisors, which supports the notion

that �nancial advice serves as a substitute for �nancial literacy. Second, when I analyze

the impact of �nancial advice on portfolio choice, I show that, if anything, use of �nancial

advice does not improve the quality of individuals' investment decisions. For example,

I document that advised investors earn lower raw and risk-adjusted returns than self-

directed investors, even before deducting advisory fees and transaction costs. Overall, the

evidence presented in this study casts doubts on the ability of �nancial advice to serve as

an e�ective substitute for �nancial literacy.

Keywords: Financial advice, individual investors, household �nance.

JEL Codes: D12, D14, D8, D18.

∗I would like to thank Ben Craig, Andreas Hackethal, Michael Haliassos, Orcun Kaya, Isabel Schnabeland seminar participants at the 2011 European Retail Investment Conference, the 2010 Annual Meeting of theEuropean Finance Association, the 2010 Annual Meeting of the German Finance Association, 8th. Workshop onMoney, Banking and Financial Markets, the 2010 PhD Workshop of the French Finance Association, Universityof Mainz and University of Frankfurt for helpful comments and discussions.†Please address all correspondence to Yigitcan Karabulut, Goethe University Frankfurt, Department of

Money and Macroeconomics, House of Finance, Grueneburgplatz 1, 60323, Frankfurt, Germany, E-mail:[email protected], Phone: +49-69-798-33859. The usual disclaimer applies.

1 Introduction

In recent years individuals have become increasingly active in �nancial markets. Accordingly,

both the stock market participation rates and portfolio shares of households in risky assets have

risen signi�cantly over the last two decades (Bilias, Georgarakos, and Haliassos, 2008).1 Amajor

reason for the spread of the `equity culture' is the growing responsibility of individuals to save

for retirement (Campbell, 2006; Lusardi and Mitchell, 2007; van Rooij, Lusardi, and Alessie,

2011). In particular, demographic transitions have caused policymakers in many countries to

reform traditional bene�t pension plans and to adapt de�ned contribution schemes, which shift

the responsibility and risks of retirement �nancing to individuals (Lusardi and Mitchell, 2007,

2011). For example, Ryan, Trumbull, and Tufano (2011) report that American households held

approximately 420 billion USD in de�ned contribution plans in 1985, which had risen to 3.3

trillion USD by 2009.

Meanwhile, �nancial markets become more complex in the wake of recent �nancial market

innovations. On the one hand, the advent of more sophisticated �nancial instruments creates

the possibility of more-customized �nancial products and services, which can better suit the

needs of individuals (Lusardi and Mitchell, 2011). On the other hand, the increase in the

number of investment options makes it di�cult for individuals to invest wisely (Hortascu and

Syverson, 2004).

The increasing responsibility of individuals to make important economic decisions, coupled

with the higher sophistication of �nancial markets, raises the question of whether households

are well-equipped to cope with these decisions, including how much to save and invest, how

to allocate investments over di�erent asset classes and so on. Recent research documents that

many households do not possess a su�cient level of �nancial literacy (Lusardi and Mitchell,

2007), lack information (Guiso and Jappelli, 2006) and exhibit behavioral biases (Kahneman,

Knetsch, and Thaler, 1991), which often lead to suboptimal �nancial decisions (e.g., Barber

and Odean, 2000, 2001; Polkovnichenko, 2005; Campbell, 2006; Goetzmann and Kumar, 2008).

Indeed, individuals' limited ability to make informed decisions can incur substantial welfare

costs, not only for individuals themselves but for society at large. For example, Boeri and

Guiso (2007) and Akerlof and Shiller (2009) argue that the low �nancial literacy of the U.S.

households is one of the driving forces of the recent subprime crisis.2 Thus, an important issue is

1For a more detailed discussion about the composition of household portfolios, see, for example, the contri-butions in Guiso, Haliassos, and Japelli (2001).

2In a recent paper, Gerardi, Goette, and Meier (2010) address this issue and show that there is indeed a

1

determining how to improve the quality individuals' �nancial decisions. The literature suggests

three potential remedies to overcome the obstacles faced by individuals toward making sound

�nancial decisions: �nancial advice, �nancial literacy education and default options. In this

paper, I focus on the role of professional advice in individuals' investment decisions and ask

whether �nancial advice is a reliable substitute for individuals' �nancial literacy.3

To answer this question, I focus on three key issues. First, I analyze how the decision

to have a �nancial advisor correlates with the demographics and �nancial characteristics of

individuals. The purpose of this analysis is to gauge whether �nancial advice serves as a

substitute for �nancial literacy. Second, I investigate the relationship between �nancial advice

and portfolio performance to quantify the potential welfare e�ects of �nancial advice. Third,

to examine the channels through which �nancial advisors can a�ect portfolio performance, I

compare the portfolio choices of advised and self-directed investors along several dimensions,

including their trading behavior, diversi�cation choices and asset allocation decisions. I attempt

to address these issues using a unique database from a large German commercial bank that

includes personal characteristics, end-of-month portfolio positions, trades and information on

use of �nancial advice for each sampled individual.

I obtain the following results in this study. First, individuals who tend to be �nancially less

sophisticated are more likely to consult professional advisors, which supports the notion that

�nancial advice serves as a substitute for �nancial literacy. This �nding is intuitive because

investors with low levels of �nancial literacy are shown to be particularly in need of investment

guidance (Lusardi and Mitchell, 2007). Thus, there is considerable scope for �nancial advice

to help these individuals. At the same time, however, the fact that �nancial advice resembles

a `credence good', i.e., individuals are generally neither ex-ante nor ex-post able to assess its

quality, coupled with the multitasking of an advisor, i.e., selling and advising, can create in-

centives for �nancial advisors to exploit individuals' lack of �nancial literacy.4 The analysis of

the welfare e�ects of �nancial advice provides to some extent an indication of which of these

opposing e�ects is dominant. I observe that advised investors earn lower raw and risk-adjusted

negative association between individuals' �nancial literacy and mortgage delinquencies and defaults.3Use of �nancial advice is widespread. For example, a recent survey in the EU indicates that 80 percent of

respondents seek professional advice before purchasing any investment products (Chater, Huck, and Inderst,2010). In another survey in the U.S., Hung et al. (2008) document that 73 percent of all investors make use of�nancial advice when making investment decisions.

4See, for example, the models of Inderst and Ottaviani (2009, 2012) who formally demonstrate that thepossibility of abuse and costly incentive problems is especially severe when sales agents have to perform thedual task of promoting new customers and providing advice to them.

2

returns than self-directed investors, even before deducting advisory fees and transaction costs.

This �nding is consistent with the results of previous studies, such as Hackethal, Haliassos,

and Jappelli (2012), who show that independent �nancial advisors negatively a�ect portfolio

performance. Interestingly, I �nd that the negative e�ect of �nancial advisors is more pro-

nounced among investors with lower investment-income ratios who presumably do not correct

for the underlying con�ict of interest and take advisors' recommendations at face value. These

�ndings demonstrate the possible agency con�ict between professional advisors and individuals

with limited �nancial literacy.

Of course, individuals actively choose whether to make use of �nancial advice, which suggests

that consulting a professional advisor may re�ect an endogenous choice. For example, an

investor who realizes poor portfolio performance can make use of �nancial advice in the hope

that professionals will help him or her to improve his or her performance results. To address

this potential bias, I also use instrumental variable (IV) techniques when testing the e�ects of

�nancial advice on portfolio performance. Even after controlling for the endogeneity of �nancial

advice, I still �nd a negative e�ect of �nancial advisors on portfolio performance, although the

IV coe�cients are larger in magnitude. Overall, the bene�ts of �nancial advice, if present at

all, seem to fall along dimensions other than portfolio performance.

When I turn to other portfolio decisions, I �nd that the extent of portfolio under-diversi�cation

is greater among self-directed investors, indicating that �nancial advisors appear to moderate

both home bias and equity under-diversi�cation. The latter �nding is consistent with the view

that �nancial advisors respond to monetary incentives and promote mutual funds, which in

turn improves equity diversi�cation. Similarly, use of �nancial advice lowers the number of

trades, whereas it shows no signi�cant e�ect on account turnover. At the same, however,

I document that advised investors rebalance their portfolios less frequently, and thus, their

portfolios display a higher degree of inertia. I note that these �ndings remain the same even

after controlling for the possible endogeneity of �nancial advice. Finally, the examination of

asset allocation in advised and self-managed portfolios suggests that �nancial advisors do not

improve the asset allocation decisions of individuals. In fact, self-directed customers exhibit

better asset allocation and timing abilities than advised customers, which could partly explain

the underperformance of advised portfolios. In summary, it appears that the use of �nancial

advice does not improve the quality of individuals' investment decisions.

This paper contributes to the growing empirical literature on the role of �nancial advice in

3

individual investment decisions (Bergstresser, Chalmers, and Tufano, 2009; Hackethal, Halias-

sos, and Jappelli, 2012; Mullainathan, Noth, and Schoar, 2012; Kramer, 2012). For example,

Bergstresser, Chalmers, and Tufano (2009) indirectly investigate the impact of �nancial advice

by comparing the performance and other dimensions of mutual funds sold directly to investors

with those sold through brokers. The researchers �nd little evidence that �nancial advice adds

value. In an audit study, Mullainathan, Noth, and Schoar (2012) use mystery shopping in the

U.S. to test whether �nancial advice helps biased investors to correct their �nancial decisions.

The authors conclude that �nancial advice fails to improve the investment decisions of indi-

viduals. In another paper, using administrative data, Chalmers and Reuter (2012) �nd that

use of �nancial advice contributes to lower portfolio returns and higher market risk. Overall,

consistent with these papers, the evidence in my paper casts doubt on the ability of �nancial

advice to serve as an e�ective substitute for �nancial literacy.

The remainder of the paper is organized as follows. Section 2 describes the data and

variables I use in the empirical analysis. In Section 3, I outline the identi�cation strategy.

Section 4 analyzes the question of who has a �nancial advisor, whereas Section 5 investigates

the welfare e�ects of �nancial advice by comparing advised and self-directed portfolios. In

Section 6, I analyze the possible channels through which �nancial advice a�ects individual

portfolios. Section 7 concludes the paper.

2 Data, Variable De�nitions and Descriptive Statistics

The primary database is a record of the trades and monthly portfolio positions of 3,032 indi-

vidual investors with accounts at one of the largest German commercial banks from January

2003 to October 2005. In total, there are 100,056 investor-month observations, or an average

of 33 observation months per individual, resulting in a strongly balanced panel.5

The database indicates the end-of-month portfolios of the sampled individuals and records

all of their trades at a monthly frequency. Moreover, the data also provide detailed demographic

and investor-type information of sampled individuals such as age, gender, profession, self-

reported risk preference (ranges from very safe to very risky), self-reported monthly labor

income, self-reported �nancial competence and place of residence, detailed at the parish level.6

5Although I have 34 observation months per individual in the original data, I exclude the �rst month (i.e.,January 2003) from the sample because the portfolio returns cannot be de�ned for this month.

6The original data set provides information for 5,051 individuals. Nonetheless, I had to exclude 2,019individuals (a total of 68,646 observations) from the sample due to incomplete information on labor income

4

In the Data Appendix, I provide a detailed description of all variables employed in the analysis.

The bank collects the demographic and investor-type information when an individual opens an

account at the bank and updates this information in case the bank receives any new information

from the customer in the interim.

The sample bank also keeps records of whether its customers make use of �nancial advice

that is o�ered by professional advisors at the bank's local branches. More speci�cally, when

opening an investment account, every bank customer is randomly assigned to a �nancial advisor

at the local branch, regardless of whether they make use of the �nancial advice provided. When

an individual investor places an order via internet, phone or fax in the bank's trading system,

the bank's information system directly shows that order to the corresponding �nancial advisor,

who makes an entry to record whether the customer's order is based on a recommendation

provided by the advisor. It is important to note that the sample bank does not use these

entries to assess the quality of advice or the performance of its advisors. Therefore, bank

advisors face no direct or indirect incentives to provide misleading information to the system.

Based on the entries of the bank employees, I calculate a �nancial advice variable for each

sampled individual that measures the degree of use of �nancial advice. This variable is cal-

culated as the ratio of advised trades relative to all trades executed by the customer over the

sample period:

Financial Advice Intensityi =

∑Tt Advised Tradesit∑T

t All Tradesit(1)

Here, i indexes the sampled individual and t refers to the monthly time period. By de�nition,

Financial Advice Intensityi is a continuous variable and can take a value between zero and one,

where zero implies self-managed accounts and one suggests full delegation of portfolio decisions

to the professional advisors.7

In addition, I create several control variables to account for the e�ects of investor biases.

First, I construct a variable to control for investor overcon�dence, which has been extensively

documented among individual investors (Odean, 1998a; Barber and Odean, 2000, 2001; Guiso

(1,500 individuals), place of residence (201 individuals) and regional variables employed as instruments in themultivariate analysis (318 individuals), respectively.

7By de�nition, the �nancial advice variable can only be computed if an investor makes a trade, i.e., thedenominator in Equation 1 is greater than zero. Otherwise, it would be missing. In approximately 81 percent of100,056 investor-month observations, I observe no trade. Therefore, to have a meaningful measure of �nancialadvice, I aggregate both the advised and non-advised trades over the entire sample period for each sampledindividual and construct the �nancial advice variable.

5

and Jappelli, 2006). Investors with this biased perception tend to overestimate their own valu-

ations of the stock market and concern themselves less about the beliefs of others. Accordingly,

greater overcon�dence leads to increased trading (Barber and Odean, 2000), greater risk taking

(Odean, 1998a) and deterring individuals from seeking professional advice (Guiso and Jappelli,

2006). Following Goetzmann and Kumar (2008) and Bailey, Kumar, and Ng (2008), investor

overcon�dence is measured with a dummy variable set to one for investors who fall in the high-

est portfolio turnover quartile and the lowest risk-adjusted performance quartile as measured by

the Sharpe ratio, that is, those investors who trade the most but attain the worst performance.

In addition, I also include a male gender dummy variable in the regressions, given that male

investors are more likely to be overcon�dent (Barber and Odean, 2001).

Another psychological bias that is shown to a�ect investor behavior is the competence

e�ect (Heath and Tversky, 1991; Graham, Harvey, and Huang, 2009). The competence e�ect

posits that individuals are more willing to bet on their own judgments when their subjective

competence in an area is higher (Heath and Tversky, 1991). Thus, this investor bias is relevant

to investor behavior, particularly, to the decision to make use of �nancial advice. To account

for this e�ect, I use information on the self-perceived �nancial knowledge and skills of the bank

customers. Speci�cally, the bank asks the individuals to rate their �nancial knowledge on a

scale from 1 (very poor) to 6 (very good) when opening an account. Based on this information,

I measure investor competence with a dummy variable set to one for investors who rate their

�nancial knowledge as `very good' and zero otherwise. Finally, I de�ne a derivative dummy

that is set to one if an investor held any derivative products (e.g., options, futures, etc.) in his

portfolio during the sample period. As noted by Bailey, Kumar, and Ng (2008), this variable

serves as a good proxy for (relatively) more sophisticated individual investors who may also

have a preference for speculation.

In Panel A of Table 1, I �rst present descriptive statistics regarding the characteristics of

the investors in the �nal sample. Unless noted otherwise, the mean and the standard deviation

are always calculated on the full pooled sample. The investors are, on average, 56 years old

and have an average portfolio value of 50,901 Euro. The majority of the bank customers,

approximately 39.5 percent, are occupied as employees, whereas the share of blue-collar workers

and retirees account for 4.0 and 21.5 percent, respectively. Approximately 21 percent of the

individuals in the sample report to take above-average �nancial risk (i.e., Risky and Very risky),

whereas 18 percent of them are willing to take below-average risk (i.e., Very safe and Safe).

6

Furthermore, the mean (median) value of the �nancial advice intensity is 47.1 (50) percent,

indicating that approximately one in every two trades made by the sampled investors is based

on the recommendations of �nancial advisors.

When I turn to investor biases, I observe that 5.6 percent of the sampled individuals tend

to display overcon�dent behavior. Interestingly, the share of investors who rate their �nancial

knowledge as `very good' is also equal to 5.6 percent. Although the shares of `overcon�dent'

and `competent' investors are identical in the �nal sample, only 3 percent of the overcon�dent

investors report to a have higher subjective competence, which implies that investor overcon-

�dence does not seem to subsume the competence e�ect although both concepts are closely

related.

In the analysis of the impact of �nancial advice on portfolio choice, I �rst focus on the per-

formance aspect. More speci�cally, I analyze how �nancial-advisor-assisted accounts perform in

comparison to self-managed portfolios. To do so, I compute the monthly portfolio returns using

the modi�ed version of the Dietz (1968) measure, assuming that all dividends and interests are

paid in the middle of a given month and reinvested:

Returngrossit =

(Portfolioit − Portfolioit−1)− (Purchasesit − Salesit)Portfolioit−1 + (Purchasesit − Salesit + Cashit) · 0.5

(2)

Here, i indexes the sampled investor and t refers to the monthly time period. Returngrossit

represents the portfolio returns before deducting any transaction costs; Portfolioit is the market

value of the portfolio of investor i at the end of month t; Purchasesit and Salesit denote the

cumulative purchases and sales in month t, respectively. Finally, Cashit represents the cash

proceeds from dividends or coupons.8

Next, I calculate the portfolio returns net of transaction costs (i.e., advisory fees, trading

costs, etc.) in a manner analogous to that used to formulate Equation 2:

Returnnetit =

(Portfolioit − Portfolioit−1)− (Purchasesit − Salesit)− CostsitPortfolioit−1 + (Purchasesit − Salesit + Cashit) · 0.5

(3)

Using the net monthly returns as computed in Equation 3, I then calculate the abnormal

returns for each individual portfolio with respect to the CAPM and the four-factor model that

includes Fama and French (1993) factors and the Carhart (1997) momentum factor, respec-

8Note that the results of the portfolio performance tests presented in the next section are robust to adoptingdi�erent assumptions about the timing of transactions, i.e., at the beginning or end of a given month.

7

tively:

Returnnet1it = ai + bi ·RMRFt + ei,t (4)

Returnnet1it = αi + β1i ·RMRFt + β2i · SMBt + β3i ·HMLt + β4i · UMDt + εi,t (5)

Here, ai and αi denote the one-factor alpha and four-factor alpha, respectively. Returnnet1it

is the net monthly return on the portfolio of investor i in excess of the risk-free rate, which is

captured by monthly returns on the JP Morgan 3 Month Euro Cash Index. RMRFt denotes

the excess return on the market portfolio that is approximated by the comprehensive German

CDAX Performance Index. SMBt, HMLt and UMDt correspond to monthly returns on size,

value premium and momentum portfolios, respectively. The size portfolio return (SMB) is

approximated by the di�erence in monthly returns on the small cap SDAX index and the large

cap DAX 30 index. The book-to-market portfolio return (HML) is approximated by the return

di�erence between the MSCI Germany Value Index and the MSCI Germany Growth Index.

Finally, the momentum portfolio return (UMD) is the di�erence in monthly returns between

a group of stocks with recent above-average returns and another set of stocks that displayed

below-average returns.9

To ensure that the results of the performance tests are not driven by any outliers, I winsorize

the performance measures at the �rst and ninety-ninth percentile; i.e., I set all observations

that fall beyond these tolerances to the �rst and ninety-ninth percentile values, respectively.

Panel B of Table 1 presents summary statistics for these variables.

3 Endogeneity of Financial Advice: Identi�cation Strategy

One important feature of my analysis is that I treat the decision to consult a �nancial advisor

as an endogenous choice and tackle the arising endogeneity issue in the econometric analysis. I

argue that there are two possible mechanisms through which the decision to consult a �nancial

advisor can be endogenous.

The �rst possible mechanism is the omitted variable bias. Although having a rich data

set at the individual level allows me to account for a large set of investor controls, still, some

9The group with above-average returns is de�ned as the top 30 percent of stocks from the CDAX index overthe past 11 months, and the below-average group contains the lowest 30 percent of stocks from the same indexover the same period.

8

unobserved individual characteristics such as level of social capital or trading experience can

simultaneously a�ect both the decision to seek �nancial advice and the portfolio choices of

individuals. Statistically, unobserved in�uences could induce a correlation between the �nancial

advice variable and the error term even after controlling for observable characteristics, which

would render ordinary least squares (OLS) estimates inconsistent.

Clearly, the natural way to solve this problem is to exploit the panel dimension of the data

and use panel regression techniques such as �xed e�ects or random e�ects, which would enable

me to control for omitted individual e�ects in the regressions. In my case, however, the �xed

e�ects estimator is not feasible because almost all investor controls do not vary over time, and

thus, the individual �xed e�ects would be perfectly correlated with them. Therefore, I use the

random e�ects approach, which does not have this problem.

Second, any relationship between portfolio choice and having a �nancial advisor could re�ect

`reverse' causality; that is, the decision to make use of �nancial advice can be endogenously

determined by the portfolio choices of individuals. For example, investors who exhibit poor

portfolio performance can consult �nancial advisors in the hope that professional advisors would

help them to improve their performance results (Hackethal, Haliassos, and Jappelli, 2012). This

situation would generate a spurious correlation between the left-hand side variables and the

�nancial advice variable, which would not allow me to render a causal interpretation of the

estimated coe�cient with respect to �nancial advice.

To overcome the identi�cation problem, I use an instrumental variables (IV) technique,

which is conducted in the two stage least squares (2SLS) fashion. Conceptually, there are two

conditions that a variable must satisfy to be considered a valid instrument. First, it must be

correlated with the endogenous �rst-stage variable, which is, in my case, use of �nancial advice.

This condition ensures that variations in the IV induce variations in the endogenous variable.

Second, the IV must be uncorrelated with the error term in the equation of interest, which

ensures that the latent characteristics do not contaminate the induced variations.

Keeping these caveats in mind, I instrument the �nancial advice variable with two regional

variables that are constructed from primary information regarding the 5-digit zip code of res-

idence. In particular, I use the number of psychotherapists and number of all bank branches

in a parish where the sampled individual is located.10 As I will show shortly, both of these

10The data on the number of psychotherapists in a given parish is hand-collected from the web site ofthe German Psychotherapists Association (Deutsche Psychotherapeuten Vereinigung). The information on thenumber of bank branches is provided by an independent commercial data provider. Furthermore, it is importantto note that the variable for the number of bank branches includes not only the branches of the sampled bank

9

instruments meet the two criteria that I outlined above, i.e., they are highly correlated with

the �nancial advice variable and do not have any direct e�ect on the variables of interest.

The motivation for the use of the number of psychotherapists and number of bank branches

as instruments is as follows. With respect to the former, individuals living in neighborhoods

with a higher number of therapists are more likely to seek professional help or advice when

they are confronted with di�culties or challenges in their daily lives. Thus, I assume that

these people also have a higher tendency to consult professionals when they are confronted

with essential economic decisions, such as where to invest or how to allocate their savings

among alternative investment options. Therefore, my prior is that this variable is positively

associated with use of �nancial advice. With respect to the latter, investors living in parishes

with a greater concentration of banks can potentially obtain investment-relevant information

from local sources or advice from other third parties in a more convenient way, which together

could lower the tendency to seek professional �nancial advice. Therefore, I expect the number

of bank branches to be negatively associated with the decision to make use of �nancial advice.

Although both of these factors are likely to be exogenous with respect to portfolio per-

formance and the investment choices of individuals, a careful reader could be skeptical of the

validity of these instruments. More speci�cally, these factors may have served as a proxy for

another regional variable that has a direct e�ect on the variables of interest. For example, some

unobserved regional characteristics correlated with the instruments, such as the level of social

capital (e.g., trust levels) in the parish, can potentially a�ect both the portfolio choices of the

individuals and their tendency to seek �nancial advice. This situation is problematic, however,

because the instruments may thus not be orthogonal to the error process. To overcome, or

at least to minimize, the severity of this problem, I include regional dummy variables that

account for possible latent regional characteristics and capture the direct e�ects of the location

of individuals.

The excluded instruments, i.e., number of psychotherapists and bank branches in a given

parish, are assumed to be correlated with the �nancial advice variable but uncorrelated with

the error term in the equation of interest. To further ensure the quality of these instruments,

I perform two speci�cation tests from the �rst-stage regressions, in which the �nancial advice

variable is regressed on the full set of instruments. First, as I over-identify each speci�cation to

achieve stronger identi�cation, I am able to use over-identi�cation tests such as the Hansen-J

but also the branches of all banks in a given parish.

10

statistic, which allow me to test for the statistical exogeneity of the instruments. Indeed, I

observe that the Hansen-J test statistics for over-identi�cation fail to reject the null of valid

instruments, suggesting that the instruments satisfy the orthogonality condition (χ2-test=0.868;

p-value=0.351).

In �nite samples, however, having valid instruments is not su�cient to ensure the consistency

of the IV approach (Staiger and Stock, 1997). In addition, the excluded instruments have to

correlate strongly with the endogenous �rst-stage variable. Accordingly, I �nd that the joint-

test of signi�cance for the excluded instruments exceeds Stock and Yogo (2002)'s critical values

for 10 percent maximal size distortion (F -statistics=24.54; p-value<0.01), which indicates that

the excluded instruments are strongly correlated with the �nancial advice variable and thus do

not su�er from a weak instrument problem.11 Overall, the speci�cation tests imply that the

instruments appear to meet the two necessary conditions.

4 Who seeks Financial Advice?

I begin the analysis by investigating the determinants of seeking �nancial advice. To do so,

I construct an indicator variable for having a �nancial advisor. In particular, I de�ne an

individual investor as advised if more than half of his trades are based on the recommendations

of the bank advisors and zero otherwise.12 Using probit regressions, I then model having a

�nancial advisor as a function of various investor characteristics such as age, profession, investor

biases, risk preference and monthly salary.

My proposed model is reported in Table 2. I report the marginal e�ects rather than the

original probit coe�cients, along with heteroscedasticity-consistent standard errors. As shown

in column (i), male and high-income investors are less likely to consult �nancial advisors when

making investment decisions. These �ndings are consistent with the existing literature that

shows that the levels of �nancial literacy is particularly lower among females and low-income

individuals (Campbell, 2006; Lusardi and Mitchell, 2007). In other words, the lower demand

of high-income and male investors for �nancial advice supports the notion that �nancial advice

serves as a substitute for the �nancial literacy of individuals. Next, I observe that the demand

11For a comprehensive discussion on the weak instrument problem, see, for example, Stock and Yogo (2002)and Stock, Wright, and Yogo (2002).

12The choice of the threshold value (i.e., 0.50) is motivated by the fact that 0.50 is equal to the sample medianof the �nancial advice intensity variable (see Equation 1). This enables me to have two equal-sized groups. Inote that I have tried various speci�cations with di�erent threshold values and I obtain qualitatively similarresults.

11

for �nancial advice increases with the willingness to take �nancial risk and age. Each of these

e�ects is economically highly signi�cant. Regarding the latter, ceteris paribus, individuals

who are older than 60 are 23.2 percentage points more likely to seek �nancial advice than

younger investors in the under-30 age group. With respect to profession, all of the estimated

coe�cients are positive (relative to the omitted group of `Retiree'), except the dummy variable

for being an employee. One possible interpretation that is consistent with this �nding is the

opportunity costs argument. For example, the possible time and opportunity costs associated

with managing a portfolio may be higher for individuals who are occupied as executive employee.

Therefore, these individuals may delegate portfolio decisions to professionals to minimize the

arising opportunity costs.

In this respect, I document that male, younger and high-income individuals more likely to

bet on their own judgments and manage their portfolios on their own. When I turn my attention

to the e�ects of investor biases, I �nd that the demand for �nancial advice is signi�cantly

lower among biased investors - those scoring high on overcon�dence and the competence e�ect.

The adverse e�ect of overcon�dence is in line with existing evidence indicating that these

investors concern themselves less about the opinions of others and thus are less willing to rely

on information or recommendations provided by professionals (Barber and Odean, 2001; Guiso

and Jappelli, 2006). Similarly, the negative association between the competence e�ect and

having a �nancial advisor is also intuitive. As noted previously, the competence e�ect posits

that people with this biased perception are more willing to bet on their own judgments (Heath

and Tversky, 1991; Graham, Harvey, and Huang, 2009). The results shown in Table 2 support

this conjecture. I observe a signi�cant negative e�ect of competence on the decision to have a

�nancial advisor. In particular, investors with higher perceived competence are 10.1 percentage

points less likely to be matched with a �nancial advisor. Finally, I �nd that those investors

who invest in particularly risky products (i.e., derivatives) are also less willing to demand for

�nancial advice.

In speci�cation (ii) in Table 2, I regress the �nancial advice dummy on the full set of in-

struments, including the two regional variables; number of psychotherapists and bank branches

in the parish. I �nd that both instruments exhibit the predicted signs, and the coe�cient

estimates are both statistically and economically signi�cant. The demand for �nancial advice

is greater for individuals who live in neighborhoods with a higher number of therapists and a

lower number of bank branches. In other words, investors who are likely to seek professional

12

help from psychotherapists and those who are less likely to have access to investment-relevant

information from local sources or advice from other third parties tend to make use of �nancial

advice.

In summary, the evidence described in this section reveals two interesting facts about the

determinants of �nancial advice. First, �nancial advisors tend to be matched with those in-

vestors who are likely to be less �nancially sophisticated, suggesting that �nancial advice serves

as a substitute for �nancial literacy. Second, investor biases such as overcon�dence and the

competence e�ect appear to be important factors that deter individuals from seeking profes-

sional advice, even though �nancial advisors can potentially insulate those individuals from

these behavioral biases. In the following, I turn to the e�ects of �nancial advice on individual

portfolios to test whether �nancial advice is an e�ective substitute for �nancial literacy.

5 Portfolio Performance and Financial Advice

In this section, the portfolio performance of advised investors is compared to that of self-

directed investors, with the goal of identifying whether use of �nancial advice contributes to

improvements in portfolio performance.

First, I focus on the e�ects of �nancial advisors on net monthly portfolio returns as de�ned

in Equation 3. Table 3 reports the estimation results, along with standard errors clustered

at the zip-code level. Estimates of four di�erent speci�cations are reported in the table. Re-

gression (i) shows the pooled OLS results without time and region �xed e�ects; (ii) shows the

pooled OLS results with time and region �xed e�ect; (iii) shows the results of a random e�ects

estimator that accounts for unobserved investor heterogeneity; and (iv) shows the results of

the instrumental variable regressions. These regressions, and all those that follow, also include

suppressed dummies for monthly time and regions.

Clearly, the main variable of interest in my model is the degree of �nancial advice that is

calculated as the ratio of advised trades to all trades made by the investor. Interestingly, I �nd

an adverse e�ect of professional �nancial advice on the net monthly portfolio returns, regardless

of whether controlling for time and region �xed e�ects; unobserved individual heterogeneity or

the possible endogeneity of �nancial advice. The moderating e�ect of �nancial advisors is both

statistically and economically signi�cant at the one-percent level in all four speci�cations. For

example, based on the OLS coe�cient, a one unit increase in the degree of �nancial advice is

13

associated with a decrease of 11 basis points in the monthly returns, which corresponds to a

reduction of 1.32 percent in the annual rate of return. However, these results need to be inter-

preted with caution, given that use of �nancial advice can re�ect an endogenous choice. When

I correct for endogeneity, I also �nd qualitatively similar results, although the IV coe�cient is

larger in magnitude.

It is also worth brie�y discussing some of the other controls in the regressions and their

importance. First, and not surprisingly, I �nd that investor overcon�dence is negatively as-

sociated with monthly returns. The negative e�ect of overcon�dence on portfolio returns is

consistent with the �ndings reported in the literature that such investors trade securities too

frequently and thus exhibit poor performance (Barber and Odean, 2000, 2001). I also �nd that

income-rich individuals tend to realize higher portfolio returns, perhaps due to their higher lev-

els of �nancial literacy (Campbell, 2006; Lusardi and Mitchell, 2007). With respect to the risk

tolerance of investors, all of the estimated coe�cients are positive and statistically signi�cant

(relative to the omitted group of `Very Safe'), implying that portfolio returns increase with the

risk tolerance of investors. Finally, I observe a signi�cant negative e�ect of age on portfolio

returns. For example, individual investors who are older than 60 earn on average 3.12% lower

returns annually than the investors in the under-30 age group. This �nding is interesting. On

the one hand, older individuals are likely to have more investment experience that they have

accumulated over time (Korniotis and Kumar, 2011). On the other hand, aging is likely to have

an adverse e�ect on the cognitive abilities of people (Agarwal, Driscoll, Gabaix, and Laibson,

2009; Christelis, Japelli, and Padula, 2010). Because I am not able to control for those e�ects

separately, the age variable is likely to capture these confounding e�ects. Hence, the negative

coe�cient on age suggests that age-driven increases in investment experience seem to be o�set

by the age-driven decline in the ability of investors to make e�ective investment decisions.

One natural explanation why collaboration with professional advisors negatively a�ects port-

folio returns is the fees paid to bank for �nancial advice. For example, Bergstresser, Chalmers,

and Tufano (2009) note that brokered-channel mutual fund customers pay more than twice as

much loads and fees as direct-channel customers. In other words, the possible bene�ts of �nan-

cial advice can be partially or entirely o�set by its direct costs. Consistent with this conjecture,

in an unreported analysis, I �nd that advised customers incur signi�cantly higher transaction

costs than self-directed investors (59.24 Euro versus 43.74 Euro; t-statistics=7.741).13 To ad-

13The transaction costs are computed on a monthly frequency and contain fees paid to banks for �nancialadvice, trading costs and portfolio management fees.

14

dress this possibility, I next investigate the e�ect of �nancial advice on gross portfolio returns

as de�ned in Equation 2. The right-hand-side variables are exactly the same as in Table 3, and

the dependent variable is now gross monthly returns before deducting any transaction costs.

As reported in Table 4, both the OLS and the IV regressions yield negative and statistically

signi�cant estimates for the use of �nancial on gross portfolio returns; however, as before the

IV estimate is greater in magnitude. In other words, the transaction costs explanation is not

supported by the data: the advised investors earn lower returns even before deducting any

transaction costs.

The evidence described so far suggests that advisor-assisted portfolios underperform self-

managed portfolios. However, the �rst moment of portfolio returns has yet to be explored. Put

di�erently, �nancial advice could still create value by reducing investors' exposure to portfolio

risk, thus increasing the risk-adjusted returns.

In Table 5, I investigate the e�ects of �nancial advice on risk-adjusted returns. Speci�cations

(i) and (ii) use a one-factor alpha as the performance measure, whereas I use a four-factor alpha

as the dependent variable in regressions (iii) and (iv).14 Consistent with prior evidence, I �nd

that use of �nancial advice also reduces risk-adjusted returns. Both the OLS and the IV

coe�cients are negative and statistically signi�cant at the one-percent level. This remains true

for both risk-adjusted performance measures. It is not unexpected that the recommendations

of the �nancial advisors in my sample do not produce persistent positive alphas for their

clients. In fact, most existing studies show that professional money managers do not consistently

outperform passive benchmarks (Jensen, 1968; Malkiel, 1995; Desai and Jain, 1995). However, it

is still somewhat surprising that �nancial advisors do not even contribute to better performance

relative to self-directed customers.15

Finally, I investigate whether the e�ect of �nancial advice varies across individuals with po-

tentially di�erent incentives. To address this issue, I split the sample into two subsamples based

on the investment-income ratio of individuals. Following Graham, Harvey, and Huang (2009), I

14Over the sample period, I calculate a one-factor alpha and a four-factor alpha for each customer portfo-lio separately based on a single-factor and a four-factor model as described in Equation 4 and Equation 5,respectively. This reduces my sample size to 3,032, i.e., to the number of individual investors in the �nalsample. Therefore, I use cross-sectional OLS and IV regressions in analyzing the e�ects of �nancial advice onrisk-adjusted returns.

15I acknowledge that these results need to be interpreted with caution. For instance, I ignore the possibletime and opportunity costs associated with managing a portfolio due to the di�culty of estimating these costs.Consider, for example, the time and opportunity costs of managing a portfolio exceeding both direct andindirect costs of �nancial advice. In this case, collaboration with advisors could still be better than the casewhen investors have to incur high costs in managing their own portfolios.

15

�rst calculate the investment-income ratio by dividing the time-series average of portfolio value

by labor income and then de�ne the investors who fall above (below) the cross-sectional median

value as high- (low-) incentive investors. Table 6 shows the e�ect of bank advisors on portfolio

performance for each subgroup separately. Both the OLS and IV regressions yield strong and

negative estimates for use of �nancial advice among low-incentive investors, whereas I �nd no

signi�cant e�ect of �nancial advice for high-incentive investors, i.e., higher investment-income

ratio. One possible interpretation that is consistent with this �nding is that high-incentive

investors may expend more e�ort, for example, in information search and acquisition processes

when making investment decisions. Accordingly, these investors can �lter out possible `poor'

recommendations of banks advisors. By contrast, low-incentive investors may conduct only a

very limited search and take advisors' recommendations at face value (also not correcting for

the underlying con�ict of interest), which can possibly lead to poor portfolio performance.

In summary, I �nd no evidence that use of �nancial advice contributes to better account

performance. On the contrary, investors who manage their accounts on their own realize better

performance results. However, it is not clear through which channel �nancial advisors in�uence

portfolio performance negatively. To address this issue, I next analyze the e�ects of �nancial

advice on investment mistakes and the dynamic asset allocation decisions of individual investors.

6 Investment Mistakes, Asset Allocation and Financial Ad-

vice

In this section, I analyze the possible channels through which �nancial advisors can a�ect the

portfolio performance of individuals. First, I analyze the impact of �nancial advice on investors'

diversi�cation choices. Then, I turn to the e�ect of professional advisors on the trading behavior

of individuals. Finally, I examine the asset allocation recommendations of �nancial advisors

and assess their market timing abilities.

6.1 Portfolio Diversi�cation and Financial Advice

Standard models of portfolio choice suggest that investors should hold diversi�ed portfolios

to eliminate non-compensated idiosyncratic risk. In reality, however, individual investors are

typically underdiversi�ed (Barber and Odean, 2000; Polkovnichenko, 2005; Goetzmann and

Kumar, 2008) and do not diversify internationally (French and Poterba, 1991; Kang and Stulz,

16

1997; Coval and Moskowitz, 1999; Bailey, Kumar, and Ng, 2008). There is thus considerable

scope for �nancial advisors to improve portfolio diversi�cation.

To assess the impact of �nancial advisors on the diversi�cation choices of individual in-

vestors, I focus on two diversi�cation measures. The �rst measure is the share of mutual funds

in the stock portfolio, which captures the extent of equity portfolio diversi�cation. The second

diversi�cation measure is the percentage of domestic securities in the equity portfolio, which

measures the extent to which investors exhibit a home bias.

Because I de�ne the measures of diversi�cation only for stockholders, the regression esti-

mates can be a�ected by selection bias. Therefore, I use the procedure proposed by Heckman

(1979) to counter the potential bias due to sample selection. Speci�cally, I begin by estimating

a probit model, where the decision to invest in stocks is modeled as a function of observable

investor characteristics, monthly time e�ects and regional controls. To develop this model,

following Vissing-Jorgensen (2002), I use the one-lagged Euro amount invested in stocks as the

excluded variable. The use of this exclusion restriction is motivated by stock market entry

costs.16 Then, I compute the inverse Mills ratio (IMR) from the selection equation and add

this ratio to the corresponding estimation model of portfolio diversi�cation.

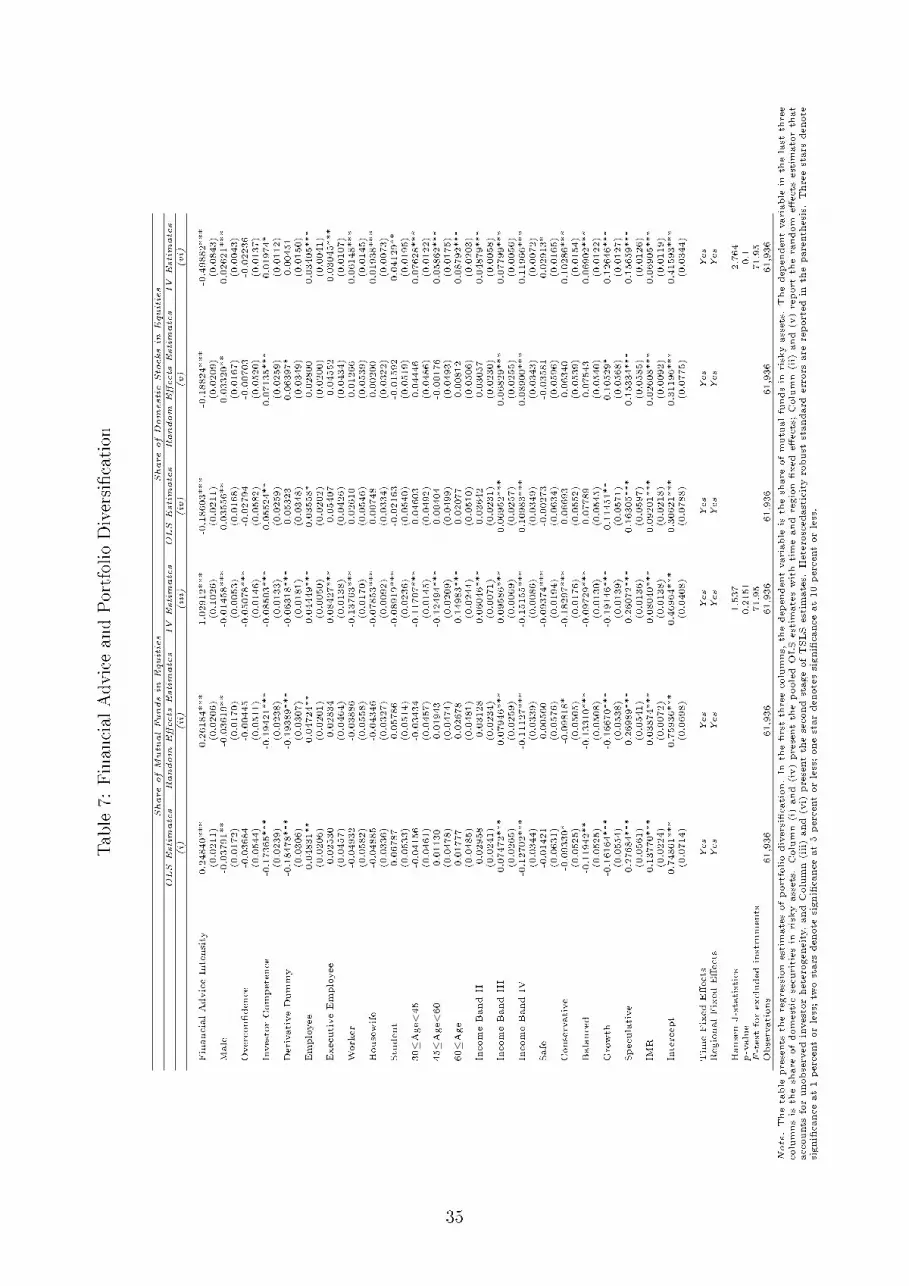

I begin, in columns (i) to (iii) of Table 7, by testing the e�ects of �nancial advice on equity

portfolio diversi�cation. In all three speci�cations, I �nd that the coe�cient estimates of

the �nancial advice variable is positive and statistically signi�cant, which suggests that advised

investors hold better diversi�ed portfolios. In fact, the positive contribution of �nancial advisors

to equity diversi�cation is not surprising, given the monetary incentives of advisors to promote

mutual funds. Speci�cally, �nancial advisors may be rationally responding to their incentives

and directing their clients to mutual funds to receive higher commissions, which in turn improves

equity diversi�cation.

A similar perspective on the role of �nancial advice applies to improving international

diversi�cation. Both the OLS and the IV coe�cients are statistically signi�cant at the one-

percent level, and the IV coe�cient is larger in magnitude, -0.498 versus -0.186. In other words,

�nancial advisors seem to encourage cross-border investments, and thus, equity home bias is

less pronounced for advised investors.17

16For a detailed discussion about the e�ects of entry costs on stock market participation, see, for example,Vissing-Jorgensen (2002) and Haliassos and Michaelides (2003).

17One can argue that bank advisors promote foreign investments presumably because international ordersare associated with higher commissions. However, the sampled bank charges a �xed commission rate for bothdomestic and international stocks, which does not support this explanation. In particular, the sampled bank

17

Controlling for other variables, income-rich individuals are more likely to own international

equity securities. The positive association between international diversi�cation and income is

consistent with the information-costs-based explanation that the �xed costs of learning about

foreign securities may deter individuals from investing in international securities (Kang and

Stulz, 1997). I also �nd that the coe�cients for investor competence are positive and highly

statistically signi�cant, indicating that investors who perceive themselves to be more competent

tend to avoid foreign stocks. In fact, the adverse e�ect of investor competence is somewhat

puzzling and does not support the view that investors with higher perceived knowledge and

skills are more willing to invest in foreign assets (Graham, Harvey, and Huang, 2009). Finally,

I observe that home bias increases with the risk tolerance of individuals, which is consistent

with the predictions of Goetzmann and Kumar (2008).

6.2 Trading Behavior and Financial Advice

Financial theory provides two competing perspectives on trading activity. The �rst hypothesis

suggests that rational agents either should not trade for speculative reasons (Milgrom and

Stokey, 1982) or they should only trade when the marginal bene�t of the trade equals or

exceeds its marginal costs, increasing their expected utility (Grossman and Stiglitz, 1980). An

alternative perspective is found in the overcon�dence models of Odean (1998b) and Gervais and

Odean (2001). According to these models, investors will trade to their detriment. Using data

from a large U.S. discount broker, Barber and Odean (2000, 2001) test these distinct theories

and show that individual investors overtrade to their detriment because of high transaction

costs.

Hence, a priori, �nancial advisors can have two opposing e�ects on the trading behavior

of individuals. On the one hand, use of professional advice can limit excessive trading and

associated transaction costs because professionals are shown to be less subject to investor

biases (List, 2003; Haigh and List, 2005). On the other hand, the fact that �nancial advisors

generate higher trading commissions through the purchases of their clients can create incentives

for advisors to increase their trading frequency (Shapira and Venezia, 2001). In Table 8, I

investigate which of these e�ects is stronger.

I begin by testing the e�ects of professional advice on the trading frequency. In columns

charges a commission rate of 100 basis points for purchases or sales of all stocks, regardless of whether they aredomestic or foreign.

18

(i) to (iii), the dependent variable is the natural logarithm of monthly number of trades. The

regression results in the �rst three columns suggest that the e�ect of �nancial advice on trading

frequency is negative and statistically signi�cant, indicating that trading frequency decreases

with use of �nancial advice. This result supports the notion that �nancial advisors seem to

limit overtrading. However, given that sales commissions depend on trading volume rather

than number of trades, �nancial advisors can face incentives to increase account turnover.

To address this possibility, in columns (iv)-(vi), I investigate the relation between �nancial

advice and portfolio turnover. Following Barber and Odean (2001), I calculate the monthly

portfolio turnover as the sum of one half of the monthly purchase turnover and one half of the

monthly sales turnover. When I turn my attention to portfolio turnover, I observe that �nancial

advice displays no signi�cant e�ect on account turnover. This remains true when I control for

unobserved individual heterogeneity and the possible endogeneity of the use of �nancial advice.

In summary, the possible positive and negative e�ects of �nancial advice on individual trading

behavior tend to cancel out each other.

With respect to behavioral biases, I �nd strong evidence that portfolio turnover increases

with both overcon�dence and investor competence. Each of these e�ects is economically signif-

icant. Based on the IV coe�cient, the monthly turnover in overcon�dent investors' accounts

is 344 basis points more than that in unbiased investors' accounts. Similarly, investors who

feel more competent trade 240 basis points more than those who do not exhibit a competence

e�ect, which con�rms the �ndings of (Graham, Harvey, and Huang, 2009). Of the other control

variables, I observe that younger, income-rich and less risk-averse investors also turn over their

portfolios more frequently.

The results presented so far suggest that �nancial advisors lower the number of trades,

whereas they show no signi�cant e�ect on portfolio turnover. In fact, investors with a target

risk level should periodically rebalance their portfolios to maintain the desired risk pro�le,

for example, in response to passive changes in their portfolios or to changes in demographic

characteristics (e.g., aging).18 Based on the evidence presented in Table 8, a natural question

to ask is whether advised portfolios are characterized by inertia. To answer this question, I

next investigate the relation between �nancial advice and the portfolio rebalancing decisions of

individuals.

18As I noted earlier, the empirical literature based on administrative data �nds evidence of overtrading (e.g.,Odean (1998a); Barber and Odean (2000)), whereas another strand of research that focuses on survey data andretirement accounts documents substantial inertia in household portfolios (Agnew, Balduzzi, and Sunden, 2003;Bilias, Georgarakos, and Haliassos, 2010).

19

First, I need to establish an appropriate de�nition of portfolio rebalancing. Following Al-

varez, Guiso, and Lippi (2012), I use a broad notion of portfolio rebalancing. In particular, I

assume that a portfolio rebalancing occurs when there is a net sale in one asset class and a

net purchase in another. Likewise, in their model, Bonaparte, Cooper, and Zhu (2012) also

attribute the simultaneous purchases and sales of two di�erent asset classes to the rebalancing

purposes of households. Furthermore, to keep the analysis simple, I restrict my attention to two

broad asset classes, (i) risky assets (including stocks, retail derivatives and real estate funds)

and (ii) risk-free assets (including direct and indirect bonds, cash and money market funds).

Because I am interested in the e�ects of �nancial advice on the simultaneous portfolio

decisions of individuals, I require an empirical model that allows me to estimate the joint

probability of trading risky and risk-free assets in opposite directions. For this purpose, I

employ a bivariate probit model. Table 9 reports the marginal e�ects for the joint probability

of trading risky and risk-free assets. Columns (i) and (iii) report the joint probability of

selling risky assets and buying risk-free assets, whereas Columns (ii) and (iv) present the joint

probability of buying risky assets and selling risk-free assets. Note that, in speci�cations (iii)

and (iv), I control for the possible endogeneity of �nancial advice by replacing the �nancial

advice variable with its �tted value from the instrumental variable regression.19

Table 9 presents the estimation results. I report the marginal e�ects rather than original

probit coe�cients, along with standard errors clustered at the zip-code level. Both the OLS

and IV estimates yield a negative and signi�cant e�ect of �nancial advice on the rebalancing

decisions of individuals. Based on the IV estimates, ceteris paribus, a unit increase in the �nan-

cial advice intensity decreases the probability of portfolio rebalancing by 4.1 to 7.4 percentage

points, indicating that advised portfolios display a higher degree of inertia.

One possible explanation for the adverse e�ect of advisors on portfolio rebalancing is the

trail commissions attached to mutual funds. Speci�cally, investment �rms pay brokers (�nan-

cial advisors) trail commissions for every subsequent year the customer holds their products.

Accordingly, these commissions could create incentives for advisors not to encourage portfolio

rebalancing that may lead to portfolio inertia.

Controlling for other investor characteristics, I observe that high-income investors tend to

rebalance their portfolios more frequently. This result is consistent with the adjustment costs

19In the portfolio rebalancing regressions, I restrict my attention to those individuals who hold risky assetsin their portfolios. Risky assets include stocks (both direct and indirect), retail derivatives (i.e., certi�cates),derivatives and mixed mutual funds. Therefore, I have a total of 68,251 observations in these regressions.

20

explanation of Bonaparte, Cooper, and Zhu (2012), who argue that higher transaction costs

associated with stock trading contribute to infrequent portfolio adjustments. With respect

to behavioral biases, I �nd that both overcon�dence and investor competence increase the

probability of rebalancing portfolios. This �nding is also consistent with the positive e�ect of

these biases on trading frequency and account turnover. Put di�erently, it seems that investors

with these biased perceptions do not only randomly buy and sell securities (i.e., churning) but

they also tend to deliberately rebalance their portfolios (Calvet, Campbell, and Sodini, 2009).

6.3 Asset Allocation, Market Timing and Financial Advice

Finally, I compare the asset allocation decisions of advised and self-directed investors. As

noted by Bergstresser, Chalmers, and Tufano (2009), professionals can create value by providing

superior asset allocation recommendations. In other words, �nancial advisors could raise (lower)

the portfolio weights among di�erent asset classes prior to a rise (fall) in the market, which

would help individuals to market-time (Bollen, 2001).

To analyze this possibility, following the procedure described in Bergstresser, Chalmers, and

Tufano (2009), I investigate the asset allocation recommendations of �nancial advisors at the

aggregate level. Speci�cally, I restrict my attention to the stock, bond and cash holdings of in-

dividuals, which are assumed to represent their entire portfolios. Then, I calculate the portfolio

weight of each asset class in the aggregated advised and self-managed portfolios correspond-

ingly. The choice of these asset classes is dictated by the availability of relevant benchmark

indices that are used in the computation of monthly portfolio returns, which allows me to isolate

the possible e�ects of individual security selection. In particular, I use the MSCI World Index,

Barclays European Aggregate Bond Index and monthly Euribor rates as benchmark indices for

stock, bond and cash holdings, respectively. To evaluate the market timing abilities of �nancial

advisors, I compare, at the aggregate level, the cumulative value of 1 Euro over 34 months

invested at the beginning of the observation period and rebalanced periodically in each month

according to the corresponding portfolio weights in the advised and self-managed portfolios.

Figure 1 depicts the cumulative value of 1 Euro invested using the advised and self-managed

asset allocation weights. The results show that the asset allocation weights of self-directed in-

vestors leads to a signi�cantly higher cumulative wealth than those of advised investors (1.14

Euro versus 0.964 Euro). When the mean monthly returns of aggregated portfolios are con-

trasted, I observe that self-managed portfolios realize 43.92 basis points, whereas advised in-

21

vestors achieve -9.424 basis points returns per month. The di�erence is also statistically highly

signi�cant (t-statistics=4.078; p-value<0.001). Similarly, when the volatility of returns is con-

sidered and risk adjustment has been carried out, I �nd that self-managed portfolios produce

a signi�cantly higher Sharpe ratio than the advised portfolios (0.28 versus -0.06 per month).

As a whole, this simple exercise implies that the involvement of �nancial advisors does

not lead to superior asset allocation, which could potentially explain the underperformance of

advised portfolios relative to self-directed portfolios.

7 Conclusion

In this paper, I analyze the role of �nancial advice in individual investment decisions and ask

whether �nancial advice is a reliable substitute for individuals' �nancial literacy.

I begin the analysis by showing that individuals who tend to be �nancially less sophisti-

cated seem to be matched with �nancial advisors, which supports the view that professional

�nancial advice serves as a substitute for �nancial literacy. In fact, this �nding suggests that

there is a large scope for �nancial advisors to improve individual �nancial decisions because

these individuals are particularly in need of investment guidance. Nevertheless, the credence

good characteristic of �nancial advice, coupled with the multitasking of an advisor, can create

incentives for �nancial advisors to exploit individuals' lack of �nancial literacy.

To investigate which of these e�ects is dominant, I next turn to the welfare e�ects of �nancial

advice by contrasting advised and self-managed portfolios. I document that advised investors

earn lower raw and risk-adjusted returns than self-directed investors even before I deduct the

advisory fees and transactions costs. This �nding reveals the possible agency con�ict between

�nancial advisors and individuals with limited �nancial literacy.

To analyze the possible channels through which �nancial advisors a�ect portfolio perfor-

mance, I �nally compare the portfolio choices of advised and self-directed investors along sev-

eral dimensions, including their trading behavior, diversi�cation choices and asset allocation

decisions. I �rst show that �nancial advisors improve portfolio diversi�cation by encouraging

cross-border investments and investments in mutual funds. The latter �nding supports the

idea that �nancial advisors respond to monetary incentives and promote mutual funds. Fur-

thermore, the use of �nancial advice does not show any signi�cant e�ect on portfolio turnover,

whereas it lowers the likelihood of portfolio rebalancing. Finally, I show that use of �nancial ad-

22

vice does not improve the asset allocation decisions of investors. On the contrary, self-managed

portfolios exhibit better asset allocation and market timing than advised portfolios, which can

partly explain the underperformance of advised portfolios.

Overall, the presented evidence in this paper casts doubts on the ability of professional

advice to serve as a reliable substitute for �nancial literacy.

23

References

Agarwal, S., J. C. Driscoll, X. Gabaix, and D. Laibson (2009). The age of reason: Financial

decisions over the life-cycle and implications for regulation. Brookings Papers on Economic

Activity 2, 51�118.

Agnew, J., P. Balduzzi, and A. Sunden (2003). Portfolio choice and returns in a large 401(k)

plan. American Economic Review 93 (2000-06), 193�205.

Akerlof, G. and R. Shiller (2009). Animal Spirits: How human psychology drives the economy,

and why it matters for global capitalism. Princeton University Press.

Alvarez, F. E., L. Guiso, and F. Lippi (2012). Durable consumption and asset management

with transaction and observation costs. American Economic Review 102, 2272�2300.

Bailey, W., A. Kumar, and D. Ng (2008). Foreign investments of u.s. individual investors:

Causes and consequences. Management Science 54, 443�459.

Barber, B. M. and T. Odean (2000). Trading is hazardous to your wealth: The common stock

investment performance of individual investors. Journal of Finance 55 (2), 773�806.

Barber, B. M. and T. Odean (2001). Boys will be boys: Gender, overcon�dence, and common

stock investment. The Quarterly Journal of Economics 116 (1), 261�292.

Bergstresser, D., J. M. R. Chalmers, and P. Tufano (2009). Assessing the costs and bene�ts of

brokers in the mutual fund industry. Review of Financial Studies 22 (10), 4129�4156.

Bilias, Y., D. Georgarakos, and M. Haliassos (2008). Equity culture and the distribution of

wealth. Center for Financial Studies Working Paper 2005/20, Goethe University Frankfurt.

Bilias, Y., D. Georgarakos, and M. Haliassos (2010). Portfolio inertia and stock market �uctu-

ations. Journal of Money, Credit and Banking 42, 715�742.

Boeri, T. and L. Guiso (2007). Subprime crisis: Greenspan's legacy. Technical report, Voxeu.org.

Bollen, N. P. B. (2001). On the timing ability of mutual fund managers. Journal of Fi-

nance 56 (3), 1075�1094.

Bonaparte, Y., R. Cooper, and G. Zhu (2012). Consumption smoothing and portfolio rebal-

ancing: The e�ects of adjustment costs. Journal of Monetary Economics 59, 751�768.

24

Calvet, L. E., J. Y. Campbell, and P. Sodini (2009). Fight or �ight? portfolio rebalancing by

individual investors. Quarterly Journal of Economics 124 (14177), 301�348.

Campbell, J. Y. (2006). Household �nance. Journal of Finance 61 (12149), 1553�1604.

Carhart, M. M. (1997). On persistence in mutual fund performance. Journal of Finance 52,

57�82.

Chalmers, J. and J. Reuter (2012). What is the impact of �nancia advisors on retirement

portfolio choices and outcomes? Working Paper 18158, NBER.

Chater, N., S. Huck, and R. Inderst (2010). Consumer decision-making in retail investment

services. Report to the european commission.

Christelis, D., T. Japelli, and M. Padula (2010). Cognitive abilities and portfolio choice. Eu-

ropean Economic Review 54, 18�38.

Coval, J. D. and T. J. Moskowitz (1999). Home bias at home: Local equity preference in

domestic portfolios. Journal of Finance 54 (501), 2045�2073.

Desai, H. and P. C. Jain (1995). An analysis of the recommendations of the "superstar" money

managers at barron's annual roundtable. Journal of Finance 50 (4), 1257�73.

Dietz, P. O. (1968). Components of a measurement model: Rate of return, risk and timing.

Journal of Finance 23, 267 � 275.

Fama, E. F. and K. R. French (1993). Common risk factors in the returns on stock and bonds.

Journal of Financial Economics 33, 3�56.

French, K. R. and J. M. Poterba (1991). Investor diversi�cation and international equity

markets. American Economic Review 81 (2), 222�26.

Gerardi, K., L. Goette, and S. Meier (2010). Financial literacy and subprime mortgage del-

iquency: Evidence from a survey matched to administrative data. Working paper, Federal

Reserve Bank of Atlanta.

Gervais, S. and T. Odean (2001). Learning to be overcon�dent. Review of Financial Studies 14,

1�27.

25

Goetzmann, W. N. and A. Kumar (2008). Equity portfolio diversi�cation. Review of Fi-

nance 12 (3), 433�463.

Graham, J. R., C. R. Harvey, and H. Huang (2009). Investor competence, trading frequency,

and home bias. Management Science 55 (11426).

Grossman, S. and J. Stiglitz (1980). On the impossibility of informationally e�cient markets.

American Economic Review 70 (4), 393�408.

Guiso, L., M. Haliassos, and T. Japelli (Eds.) (2001). Household Portfolios. MIT Press.

Guiso, L. and T. Jappelli (2006). Information acquisition and portfolio performance. CEPR

Discussion Papers 5901.

Hackethal, A., M. Haliassos, and T. Jappelli (2012). Financial advisors: A case of babysitters?

Journal of Banking & Finance 36, 509�524.

Haigh, M. S. and J. A. List (2005). Do professional traders exhibit myopic loss aversion? an

experimental analysis. Journal of Finance 60, 523�534.

Haliassos, M. and A. Michaelides (2003). Portfolio choice and liquidity constraints. Interna-

tional Economic Review 44 (1), 143�177.

Heath, C. and A. Tversky (1991). Preference and belief: Ambiguity and competence in choice

under uncertainty. Journal of Risk and Uncertainty 4 (1), 5�28.

Heckman, J. J. (1979). Sample bias as a speci�cation error. Econometrica 47(1), 153�162.

Hortascu, A. and C. Syverson (2004). Product di�erentiation, search costs, and competition

in the mutual fund industry: A case study of s&p 500 index funds. Quarterly Journal of

Economics 119, 403�456.

Hung, A. A., N. Clancy, J. Dominitz, E. Talley, C. Berrebi, and F. Suvankulov (2008). In-

vestor and industry perspectives on investment advisers and broker-dealers. Technical report,

RAND Center for Corporate Ethics and Governance.

Inderst, R. and M. Ottaviani (2009). Misselling through agents. American Economic Review 99,

883�908.

26

Inderst, R. and M. Ottaviani (2012). Financial advice. Journal of Economic Literature 50,

494�512.

Jensen, M. C. (1968). The performance of mutual funds in the period 1945-1964. Journal of

Finance 23, 389�416.

Kahneman, D., J. L. Knetsch, and R. H. Thaler (1991). The endowment e�ect, loss aversion,

and status quo bias: Anomalies. Journal of Economic Perspectives 5 (1), 193�206.

Kang, J. K. and R. M. Stulz (1997). Why is there a home bias? an analysis of foreign portfolio

equity ownership in japan. Journal of Financial Economics 46 (5166), 3�28.

Korniotis, G. M. and A. Kumar (2011). Do older investors make better investment decisions?

Review of Economics and Statistics 93, 244�265.

Kramer, M. M. (2012). Financial advice and individual investor portfolio performance. Finan-

cial Management 41, 395�428.

List, J. A. (2003). Does market experience eliminate market anomalies? The Quarterly Journal

of Economics 118 (1), 41�71.

Lusardi, A. and O. S. Mitchell (2007). Baby boomer retirement security: The roles of planning,

�nancialliteracy, and housing wealth. Journal of Monetary Economics 54, 205�224.

Lusardi, A. and O. S. Mitchell (2011). The outlook for �nancial literacy. Working Paper 17077,

NBER.

Malkiel, B. G. (1995). Returns from investing in equity mutual funds 1971-1991. Journal of

Finance 50, 549�572.

Milgrom, P. and N. Stokey (1982). Information, trade and common knowledge. Journal of

Economic Theory 26, 17�27.

Mullainathan, S., M. Noth, and A. Schoar (2012). The market for �nancial advice: An audit

study. Working Paper 17929, NBER.

Odean, T. (1998a). Are investors reluctant to realize their losses? Journal of Finance 53 (5),

1775�1798.

27

Odean, T. (1998b). Volue, volatility, price, and pro�t when all traders are above average.

Journal of Finance 53, 1887�1934.

Polkovnichenko, V. (2005). Household portfolio diversi�cation: A case for rank-dependent

preferences. Review of Financial Studies 18 (4), 1467�1502.

Ryan, A., G. Trumbull, and P. Tufano (2011). A brief postwar history of u.s. consumer �nance.

Business History Review 85, 461�498.

Shapira, Z. and I. Venezia (2001). Patterns of behavior of professionally managed and inde-

pendent investors. Journal of Banking and Finance 25 (8), 1573�1587.

Stock, J. H., J. H. Wright, and M. Yogo (2002). A survey of weak instruments and weak iden-

ti�cation in generalized method of moments. Journal of Business & Economic Statistics 20,

518�529.

Stock, J. H. and M. Yogo (2002). Testing for weak instruments in linear iv regression. NBER

Working Paper 284.

van Rooij, M., A. Lusardi, and R. Alessie (2011). Financial literacy and stock market partici-

pation. Journal of Financial Economics 101, 449�472.

Vissing-Jorgensen, A. (2002). Towards an explanation of household portfolio choice heterogene-

ity: Non�nancial income and participation cost structures. Working Paper 8884, NBER.

28

Table 1: Summary Statistics

Mean Median Standard deviation No of Obs

A. Explanatory variables

Financial advice intensity 0.471 0.500 0.416 100,056Investor biases:Investor overcon�dence 0.056 0.000 0.231 100,056Derivative dummy 0.026 0.000 0.160 100,056Investor competence 0.056 0.000 0.230 100,056Demographics:Male 0.474 0.000 0.499 100,056Retiree 0.215 0.000 0.411 100,056Housewife 0.093 0.000 0.290 100,056Student 0.060 0.000 0.237 100,056Employee 0.394 0.000 0.489 100,056Executive employee 0.028 0.000 0.166 100,056Blue-collar worker 0.041 0.000 0.197 100,056Age<30 0.065 0.000 0.246 100,05630≤Age<45 0.201 0.000 0.401 100,05645≤Age<60 0.252 0.000 0.434 100,05660≤Age 0.482 0.000 0.500 100,056Income band I 0.230 0.000 0.421 100,056Income band II 0.417 0.000 0.493 100,056Income band III 0.254 0.000 0.435 100,056Income band IV 0.099 0.000 0.298 100,056Individual risk preference:Very safe 0.068 0.000 0.252 100,056Safe 0.122 0.000 0.327 100,056Conservative 0.289 0.000 0.453 100,056Balanced 0.311 0.000 0.463 100,056Risky 0.120 0.000 0.325 100,056Highly risky 0.091 0.000 0.287 100,056Instruments:No of bank branches in the parish (in ln) 3.885 3.818 1.432 100,056No of psychotherapists in the parish (in ln) 1.153 1.099 0.889 100,056

B. Explained variables