final report quantitative research report: ‘attitudes towards online shopping and knowledge about...

TRANSCRIPT

FINAL REPORT

QUANTITATIVE RESEARCH REPORT: ‘Attitudes towards online shopping and knowledge about shopping

online securely’

PREPARED FOR: NSW Fair Trading

30 October 2012

PREPARED BY: Stancombe Research + Planning P/L

18 Glenmore Road Paddington, NSW 2021

ABN: 70 056 731 670

ACN: 056 731 670

QUANTITATIVE RESEARCH REPORT: ‘Attitudes towards online shopping and knowledge about shopping online securely’. Prepared by Stancombe Research & Planning for NSW Fair Trading, 2012.

2

Table of contents 1 Executive summary ....................................................................................3

1.1 Background ..........................................................................................3 1.2 Research objectives .............................................................................3

1.2.1 Consumer specific objectives.........................................................3 1.2.2 Business specific objectives...........................................................4

1.3 Methodology.........................................................................................4 1.3.1 Research design ............................................................................4 1.3.2 Sample structure............................................................................5 1.3.3 Analysis and reporting of results ....................................................5

1.4 Key findings and implications ...............................................................6 2 Background ................................................................................................8

2.1 Research background ..........................................................................8 2.2 Research objectives .............................................................................9

2.2.1 Consumer specific objectives.........................................................9 2.2.2 Business specific objectives.........................................................10

3 Methodology.............................................................................................12 3.1.1 Research design ..........................................................................12 3.1.2 Sample structure..........................................................................14 3.1.3 About this report...........................................................................15

4 Key Themes .............................................................................................17 4.1 The PayPal disparity ..........................................................................17 4.2 The disconnect over drivers of online shopping .................................17 4.3 Australian consumer law ....................................................................18 4.4 Online security concerns ....................................................................18

5 Online Shopping and Selling Behaviours .................................................19 5.1 Frequency of shopping, goods and services purchased ....................19 5.2 Seller origin, payment and delivery methods......................................20

6 Drivers and Barriers to Shopping and Selling Online................................22 6.1 Consumer and business drivers.........................................................22 6.2 Consumer and Business Barriers.......................................................23 6.3 Negative experiences.........................................................................24

7 Awareness and Behaviours to Online Security.........................................26 7.1 Awareness of security indicators ........................................................26 7.2 Australian consumer law ....................................................................27

8 Summary and Conclusions.......................................................................28 9 Appendices...............................................................................................31

9.1 Appendix 1: Consumer Questionnaire................................................31 9.2 Appendix 2: Business Questionnaire..................................................46

Index of tables Table 1 Survey structure 14 Table 2 Consumer sample 15 Table 3 SMS sample 15 © State of New South Wales through NSW Fair Trading, 2012

QUANTITATIVE RESEARCH REPORT: ‘Attitudes towards online shopping and knowledge about shopping online securely’. Prepared by Stancombe Research & Planning for NSW Fair Trading, 2012.

3

1 Executive summary

1.1 Background

NSW Fair Trading has identified the fact that, while much research has been

conducted about Australians’ online shopping behaviours, there has been little

research into attitudes towards it or into safety and security measures taken.

With the growth in Australian consumers shopping online and Australian

businesses selling online, and in the context of a growing number of

complaints about online shopping received by NSW Fair Trading, this topic is

worthy of deeper understanding and exploration.

1.2 Research objectives This research aims to provide understanding and quantification of consumer

and business attitudes towards online shopping and knowledge about

shopping online securely and provides recommendations to improving the

experience for both consumers and small-medium businesses.

Two consumer groups and two business groups were surveyed.

Consumers:

• NSW People who have shopped online in the last year

• NSW People who have not-shopped online in the last year

Businesses:

• Small to Medium Businesses (SMBs) with an existing online business

payment option

• SMBs who do not sell online, but have an online presence

1.2.1 Consumer specific objectives

The objectives specific to NSW consumers were as follows:

• Measure how often Australians are shopping online

• Determine which types of goods are bought online

• Determine which payment methods are used when shopping online

• Confirm the drivers and barriers to shopping online, in particular,

the security concerns about online shopping

QUANTITATIVE RESEARCH REPORT: ‘Attitudes towards online shopping and knowledge about shopping online securely’. Prepared by Stancombe Research & Planning for NSW Fair Trading, 2012.

4

• Ascertain the source of concerns related to shopping online (e.g.

personal experience, friends’ experiences, media reports etc.)

• Measure awareness of indicators or signs that an online shopping

site is safe and secure

• Measure the incidence of negative experiences with online

shopping, with detail around the types of problems

• Establish whether there are any differences in attitudes towards

domestic online retail and international

1.2.2 Business specific objectives

The objectives specific to NSW Small to Medium Businesses were as

follows:

• Ascertain the proportion of sales made online

• Determine which types of goods are sold online

• Determine which payment methods are offered for online shopping

• Confirm the drivers and barriers to selling online

• Determine the measures taken by online retailers to indicate their

site is safe and secure

• Measure SMB perceptions of the impact of consumer concerns

about online shopping on their business

• Measure the incidence of negative customer feedback or issues

with online sales

1.3 Methodology

1.3.1 Research design

Two bespoke and complementary 15-minute online surveys were used

to target consumer and business audiences respectively. The

complementary nature of the surveys allowed for comparison between

consumer and business points of view in developing the online shopping

insights. The 15-minute duration of the surveys permitted the gathering

of detailed information to develop comprehensive insights, and the

online survey instrument was highly suited to the context of the study.

QUANTITATIVE RESEARCH REPORT: ‘Attitudes towards online shopping and knowledge about shopping online securely’. Prepared by Stancombe Research & Planning for NSW Fair Trading, 2012.

5

The sample was drawn from an online panel and appropriate

respondents identified using existing profile information, before being

invited to complete the survey via email. In determining appropriate

respondents, consumers were screened based on gender, age, and

location; businesses were screened based on business

owner/manager/decision maker, number of employees, and location.

1.3.2 Sample structure

Two separate samples were used, one consumer (n=1000) and one

business (n=201). The consumer and business surveys aimed to

represent the New South Wales (NSW) consumer population who use

the Internet, and NSW Small to Medium Business population with an

online presence respectively. Demographic breakdowns of the

consumer and SMB samples are detailed in tables 2 and 3.

1.3.3 Analysis and reporting of results

This study produced results from both the consumer and business

viewpoints. Results from the consumer viewpoint are considered in total,

and compared between different subgroups (e.g. Website or online,

Online auction, Group buying voucher). One-tailed statistical significance

tests were conducted to test for differences between the responses of

subgroups, as well as against the total. Where significant differences are

reported, a confidence interval of 95% has been used. Similarly, results

from the business viewpoint are considered in total, and by Business

website as a subgroup. One-tailed statistical significant tests were also

applied to test for differences, and a 95% confidence interval was also

used. Where possible, consumer and business viewpoints are compared

to provide a contrast and build a more meaningful representation of the

online shopping picture. Consequently, results from both the consumer

and business viewpoints are reported, and the validity of results is

determined through statistical significance.

QUANTITATIVE RESEARCH REPORT: ‘Attitudes towards online shopping and knowledge about shopping online securely’. Prepared by Stancombe Research & Planning for NSW Fair Trading, 2012.

6

1.4 Key findings and implications

Combining the consumer and SMB perspectives revealed a number of key

themes from the research. Firstly, there is a disparity in the importance of

using PayPal as a payment method. From the consumer perspective, PayPal

is the first choice payment method. 59% of consumers use PayPal when

shopping from websites. Additionally, 13% of consumers can cite, without

prompting, that PayPal is a security feature when shopping online.

Conversely, less than half of SMBs offer a PayPal payment option. Even

though 11% of SMBs recognise PayPal as a security feature, the primary

payment methods from the business perspective are credit card and bank

transfer. PayPal could be promoted among SMBs as a way of offering

customers what they want and subsequently alleviating some potential

security concerns.

Second, there is a fundamental disconnect between consumers and

businesses over the drivers of online shopping. Overall, 58% of consumers

spontaneously mentioned access to lower prices as a reason for shopping

online. Similarly, 61% mentioned lower prices when prompted. Conversely,

when prompted, only 35% of SMBs cited the ability to offer discounts to

customers as a reason for selling online. Further, the main motive (71%)

reported by SMBs for selling online was to reach a broader customer base.

Interestingly, approximately 60% of both consumers and businesses cited

convenience as a reason for shopping online; this represents a mutual middle

ground. Nevertheless, consumers are driven to shop online primarily by the

access to lower prices, whereas businesses are far less concerned with

providing this value proposition to consumers. SMBs need to be aware that

consumers expect lower prices when shopping online.

Third, consumers and businesses are confused as to whether or how

Australian Consumer Law applies to online shopping. Around half (51%) of

consumers make online purchases from auction websites, however both

consumers (54%) and SMBs (54%) are largely unsure how Australian

Consumer Law may or may not apply to private sellers. Similarly, 6% of

QUANTITATIVE RESEARCH REPORT: ‘Attitudes towards online shopping and knowledge about shopping online securely’. Prepared by Stancombe Research & Planning for NSW Fair Trading, 2012.

7

consumers have reported receiving damaged goods, and another 6% have

reported ordering goods they never received. Also, 13% of SMBs claim to

have received reports of missing goods, and 9% damaged goods. Despite

these rates of incidence, large proportions of both consumers (46%) and

SMBs (42%) are unsure who is responsible for replacing damaged or missing

goods. These examples suggest consumers are making purchasing decisions

irrespective of the added risks of not understanding the legal context.

Consequently, there is scope to educate consumers and SMBs about the

application of Australian Consumer Law.

Fourth, security is a concern when shopping online. The majority (88%) of

those who do not shop online cite security concerns as a barrier. Of those

who do shop online, 2% claim to have been victim of fraud when shopping

online. When thinking of features that may identify a secure website, just

under half (47%) of consumers are aware of ‘Https’ indicating a secure site,

and 11% are aware of ‘the padlock symbol’. Importantly, while 68% of SMBs

are aware of ‘https’ as a security feature, only around half (52%) offer this

security when selling online. Consumers are largely unsure of what indicates

a secure site for online shopping, and the majority of businesses are aware

but far fewer provide the security as part of their value proposition to

customers. As a result, there is a need to raise awareness among consumers

of ‘https’ sites and perhaps some room to promote their use among SMBs. It

may be beneficial to raise ‘padlock symbol’ awareness alongside an ‘https’

promotion.

QUANTITATIVE RESEARCH REPORT: ‘Attitudes towards online shopping and knowledge about shopping online securely’. Prepared by Stancombe Research & Planning for NSW Fair Trading, 2012.

8

2 Background

2.1 Research background

Online shopping is a rapidly growing phenomenon. The topic attracts regular

mainstream media attention and is common conversation across social media

and face-to-face. The latest NAB Online Retail Sales Index 1 found that

Australians spent more than $11 billion in online retail sales in the 12 months

to April 2012. This represents around five percent (5%) of all retail spending in

Australia. The Australian Productivity Commission2 estimates that online retail

shopping will increase by between ten precent (10%) and fifteen percent

(15%) per annum over the next three years, while some commentators predict

even stronger growth.

Three main factors have been previously found to drive retail online shopping

frequency among Australian consumers. These include: 1) lower prices, 2)

convenience, and 3) a wider range of goods to choose from. Additionally,

online access is becoming easier and more frequent. New mobile electronic

devices such as smart phones and tablets are stimulating further growth in

online sales together with online price comparison sites and apps.

Some research into only shopping behaviours has previously been

conducted. Contrary to popular belief, the majority of online sales are made

with domestic retailers. According to the 2012 NAB Online Retail Sales Index3

almost three quarters of online sales were made with domestic retailers. Fair

Trading received more than 7,000 complaints about online shopping issues in

the last financial year. 1 NAB (2012) “NAB Online Retail Sales Index Monthly update – August 2012”. Retrieved from: http://business.nab.com.au/nab-online-retail-sales-index-monthly-update-august-2012-1433/. 26 Oct 2012 2 APC (2011) “Trends and issues related to online retailing – December 2011”. Retrieved from: http://www.pc.gov.au/projects/inquiry/retail-industry/report. 26 Oct 2012 3 NAB (2012) “NAB Online Retail Sales Index Monthly update – August 2012”. Retrieved from: http://business.nab.com.au/nab-online-retail-sales-index-monthly-update-august-2012-1433/. 26 Oct 2012

QUANTITATIVE RESEARCH REPORT: ‘Attitudes towards online shopping and knowledge about shopping online securely’. Prepared by Stancombe Research & Planning for NSW Fair Trading, 2012.

9

Australians spent more than $11bn on online retail sales in the 12 months to

April 2012, and 5% of all retail spending in Australia is online. In the U.K,

approximately three-quarters of Internet users are worried about identity theft,

viruses, or ‘being conned’. 14 per cent of online shoppers said they had ‘lost

out’ or ‘been scammed’ while shopping online. Generally, a lack of trust was a

key feature of the British public’s attitude towards shopping over the Internet.

While much is known about online shopping behaviours, little (if any) research

had been done into Australians’ attitudes towards online shopping, nor into

their knowledge about shopping securely online or which warning signs to

look for. This research aimed to fill these information gaps.

2.2 Research objectives This research aims to provide understanding and quantification of consumer

and business attitudes towards online shopping and knowledge about

shopping online securely and provides recommendations to improving the

experience for both consumers and small-medium businesses.

Two consumer groups and two business groups were surveyed.

Consumers:

• NSW People who have shopped online in the last year

• NSW People who have not-shopped online in the last year

Businesses:

• Small to Medium Businesses (SMBs) with an existing online business

payment option

• SMBs who do not sell online, but have an online presence

2.2.1 Consumer specific objectives

The objectives specific to NSW consumers were as follows:

• Measure how often Australians are shopping online

• Determine which types of goods are bought online

• Determine which payment methods are used when shopping online

QUANTITATIVE RESEARCH REPORT: ‘Attitudes towards online shopping and knowledge about shopping online securely’. Prepared by Stancombe Research & Planning for NSW Fair Trading, 2012.

10

• Confirm the drivers and barriers to shopping online, in particular,

the security concerns about online shopping

• Ascertain the source of concerns related to shopping online (e.g.

personal experience, friends’ experiences, media reports etc.)

• Measure awareness of indicators or signs that an online shopping

site is safe and secure

• Measure the incidence of negative experiences with online

shopping, with detail around the types of problems

• Measure awareness of rights and responsibilities when shopping

online

• Establish whether there are any differences in attitudes towards

domestic online retail and international.

2.2.2 Business specific objectives

The objectives specific to NSW Small to Medium Businesses were as

follows:

• Ascertain the proportion of sales made online

• Determine which types of goods are sold online

• Determine which payment methods are offered for online shopping

• Confirm the drivers and barriers to selling online

• Determine the measures taken by online retailers to indicate their

site is safe and secure

• Measure SMB perceptions of the impact of consumer concerns

about online shopping on their business

• Measure the incidence of negative customer feedback or issues

with online sales

• Measure awareness of rights and responsibilities when shopping

online.

QUANTITATIVE RESEARCH REPORT: ‘Attitudes towards online shopping and knowledge about shopping online securely’. Prepared by Stancombe Research & Planning for NSW Fair Trading, 2012.

11

QUANTITATIVE RESEARCH REPORT: ‘Attitudes towards online shopping and knowledge about shopping online securely’. Prepared by Stancombe Research & Planning for NSW Fair Trading, 2012.

12

3 Methodology

3.1.1 Research design

Two bespoke and complementary 15-minute online surveys were used

to target consumer and Small to Medium Businesses (SMB) audiences

respectively. The complementary nature of the surveys allowed for

comparison between consumer and SMB points of view in developing

the online shopping insights. The 15-minute duration of the surveys

permitted the gathering of detailed information to develop

comprehensive insights, and the online survey instrument was highly

suited to the context of the study. Specifically, the questionnaire targeted

online behaviours and online retail offerings, drivers and barriers to

shopping and selling online, online shopping and selling experiences,

and online shopping and selling security issues. Both surveys are

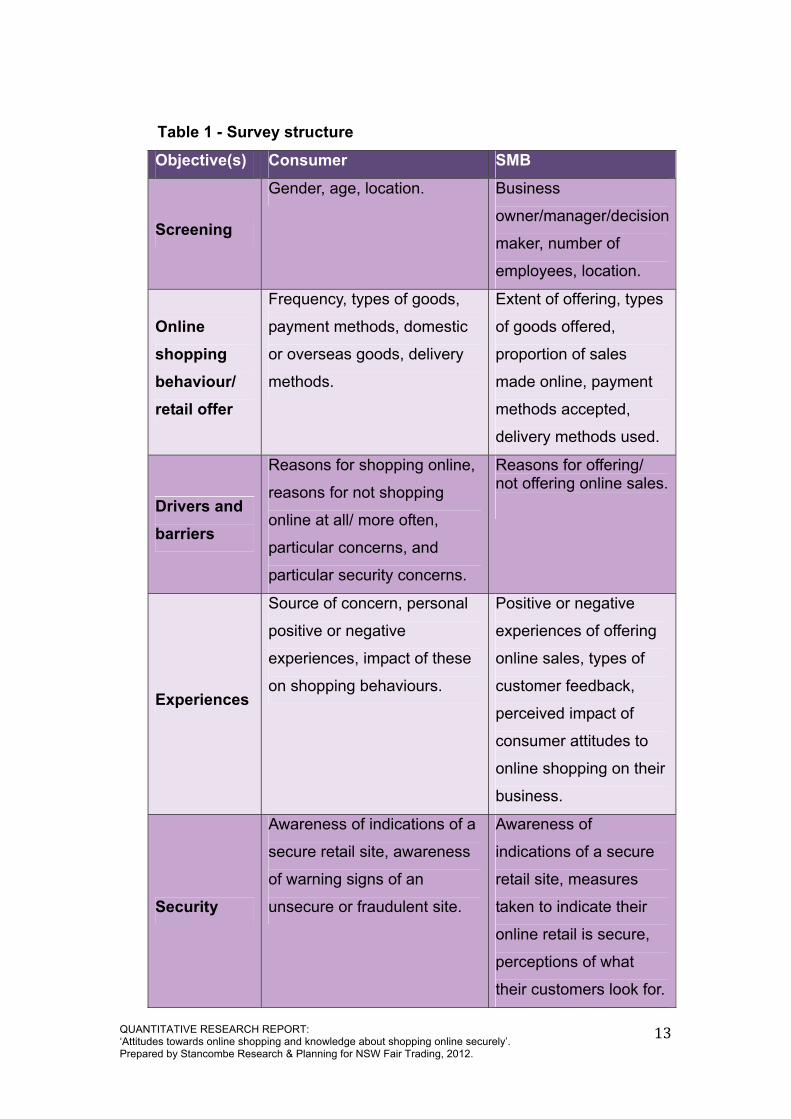

appended as Appendix 1 and Appendix 2. Table 1 provides details of the

survey structure.

The sample was drawn from an online panel and appropriate

respondents were identified using existing profile information before

being invited to complete the survey via email. In determining

appropriate respondents, existing panel information was used to screen

respondents based on gender, age, and location; businesses were

screened based on business owner/manager/decision maker, number of

employees, and location. Table 2 details the consumer sample, and

Table 3 the SMB sample.

QUANTITATIVE RESEARCH REPORT: ‘Attitudes towards online shopping and knowledge about shopping online securely’. Prepared by Stancombe Research & Planning for NSW Fair Trading, 2012.

13

Table 1 - Survey structure

Objective(s) Consumer SMB

Screening

Gender, age, location. Business

owner/manager/decision

maker, number of

employees, location.

Online shopping behaviour/ retail offer

Frequency, types of goods,

payment methods, domestic

or overseas goods, delivery

methods.

Extent of offering, types

of goods offered,

proportion of sales

made online, payment

methods accepted,

delivery methods used.

Drivers and barriers

Reasons for shopping online,

reasons for not shopping

online at all/ more often,

particular concerns, and

particular security concerns.

Reasons for offering/ not offering online sales.

Experiences

Source of concern, personal

positive or negative

experiences, impact of these

on shopping behaviours.

Positive or negative

experiences of offering

online sales, types of

customer feedback,

perceived impact of

consumer attitudes to

online shopping on their

business.

Security

Awareness of indications of a

secure retail site, awareness

of warning signs of an

unsecure or fraudulent site.

Awareness of

indications of a secure

retail site, measures

taken to indicate their

online retail is secure,

perceptions of what

their customers look for.

QUANTITATIVE RESEARCH REPORT: ‘Attitudes towards online shopping and knowledge about shopping online securely’. Prepared by Stancombe Research & Planning for NSW Fair Trading, 2012.

14

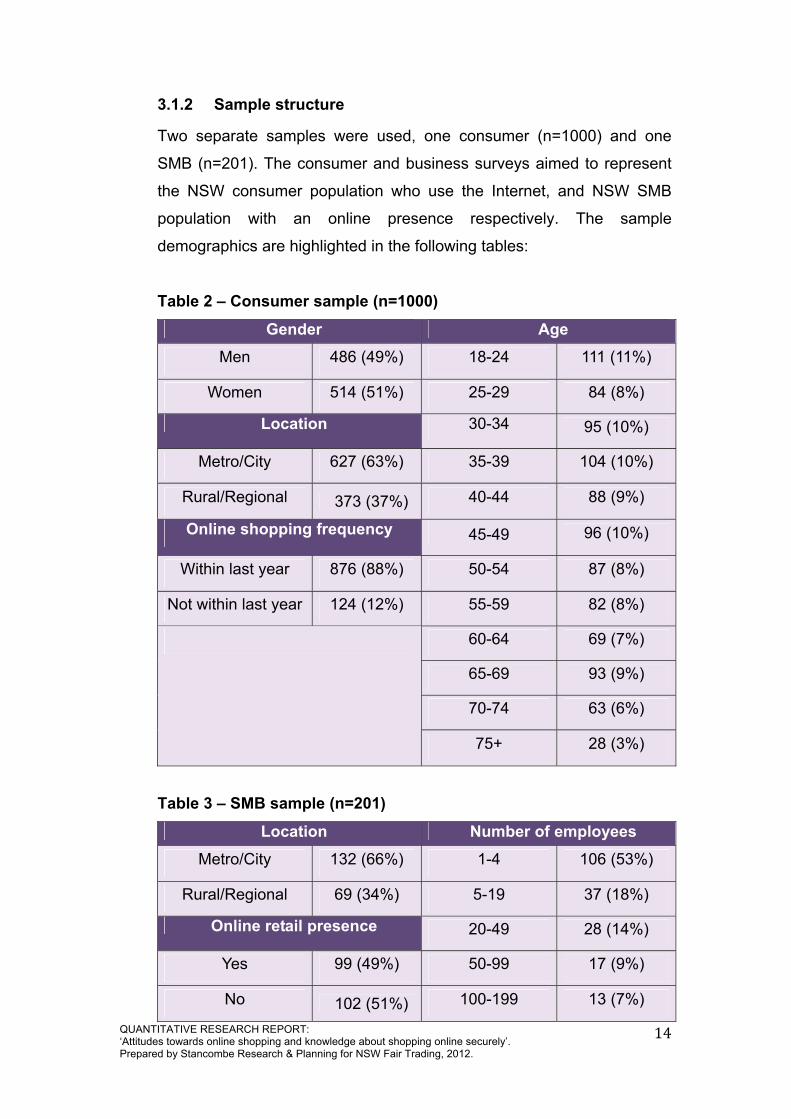

3.1.2 Sample structure

Two separate samples were used, one consumer (n=1000) and one

SMB (n=201). The consumer and business surveys aimed to represent

the NSW consumer population who use the Internet, and NSW SMB

population with an online presence respectively. The sample

demographics are highlighted in the following tables:

Table 2 – Consumer sample (n=1000)

Gender Age Men 486 (49%) 18-24 111 (11%)

Women 514 (51%) 25-29 84 (8%)

Location 30-34 95 (10%)

Metro/City 627 (63%) 35-39 104 (10%)

Rural/Regional 373 (37%) 40-44 88 (9%)

Online shopping frequency 45-49 96 (10%)

Within last year 876 (88%) 50-54 87 (8%)

Not within last year 124 (12%) 55-59 82 (8%)

60-64 69 (7%)

65-69 93 (9%)

70-74 63 (6%)

75+ 28 (3%)

Table 3 – SMB sample (n=201)

Location Number of employees Metro/City 132 (66%) 1-4 106 (53%)

Rural/Regional 69 (34%) 5-19 37 (18%)

Online retail presence 20-49 28 (14%)

Yes 99 (49%) 50-99 17 (9%)

No 102 (51%) 100-199 13 (7%)

QUANTITATIVE RESEARCH REPORT: ‘Attitudes towards online shopping and knowledge about shopping online securely’. Prepared by Stancombe Research & Planning for NSW Fair Trading, 2012.

15

3.1.3 About this report

This report represents key findings from the NSW Fair Trading

commissioned research into online retail shopping in NSW.

Samples in this study are drawn from NSW consumers and businesses

(SMBs). Responses from consumers and businesses are examined from

both total and subgroup perspectives. Specifically, subgroups were

based on the channels by which consumers made online purchases and

business made sales. More specifically, consumer purchasing

subgroups included website or online, online auction, and group buying

voucher. Comparatively, business website was the single subgroup for

SMBs. However, responses were not always mutually exclusive. In other

words, respondents may belong to multiple purchasing subgroups. For

example, fifteen hundred and forty six (1546) responses were derived

from one thousand (1000) consumer respondents. Specifically, of the

consumer respondents, seven hundred and forty one (741) used website

or online, fife hundred and fourteen (514) used online auction, and two

hundred and nineteen (219) used group buying vouchers.

Statistical tests (one-tailed) were undertaken to establish whether

differences between the responses of subgroups within each sample, as

well as between subgroups and total, were statistically significant at the

95% confidence level. This infers that the differences are not due to the

random statistical variation inherent in all data, as they do not overlap

within the ‘margins of error’ associated with the results. To understand

this, margins of error depend on the base size of the sub-group in

question but also the extremeness of response. For example, the margin

of error for a sample size of 1000, such as the NSW consumer sample,

is approximately 3% for a response of 50% and this gets smaller with

responses closer to the extremes e.g. 1.9% error for a response of 90%.

In other words, assuming a 95% confidence level, if a result based on

the consumer sample is reported as 50%, we can be 95% certain that

the true result is between 47% and 53%.

QUANTITATIVE RESEARCH REPORT: ‘Attitudes towards online shopping and knowledge about shopping online securely’. Prepared by Stancombe Research & Planning for NSW Fair Trading, 2012.

16

The margins of error will be larger for any analysis using sub-samples of

the total population e.g. those who purchase via a website or online

store, etc. Consequently, it may not be viable to compare results

between sub groups with small base sizes, e.g. why SMBs are not split

into three subgroups. This also explains why differences between sub

groups may be large but may not be statistically significant.

QUANTITATIVE RESEARCH REPORT: ‘Attitudes towards online shopping and knowledge about shopping online securely’. Prepared by Stancombe Research & Planning for NSW Fair Trading, 2012.

17

4 Key Themes

4.1 The PayPal disparity

The importance of PayPal differs from consumer and business

viewpoints. From the consumer perspective, PayPal is the first choice

payment method. Specifically, 59% of consumers use PayPal when

shopping from websites. Additionally, 13% of consumers can cite,

without prompting, that PayPal is a security feature when shopping

online. Despite the strong consumer preference for using PayPal when

shopping online, less than half of SMBs offer a PayPal payment option;

the primary payment methods from the business perspective are credit

card and bank transfer. Considering online security, 11% of SMBs

recognise PayPal as a security feature. Despite common ground

between consumers and SMBs regarding PayPal security benefits, a

key disparity in the use of PayPal is evident between consumers and

SMBs.

4.2 The disconnect over drivers of online shopping There is a large disconnect between why consumers shop online and

why SMBs sell online. 58% of consumers spontaneously mentioned

access to lower prices as a reason for shopping online. Similarly, 61%

mentioned lower prices when prompted. Conversely, zero percent (0%)

of SMBs spontaneously suggested offering lower prices. However, when

prompted, 35% of SMBs cited the ability to offer discounts to customers

as a reason for selling online. Further, the main motive (71%) reported

by SMBs for selling online was to reach a broader customer base.

Interestingly, approximately 60% of both consumers and businesses

cited convenience as a reason for shopping online; this represents a

shared middle ground. Nevertheless, consumers are driven to shop

online primarily by the access to lower prices, whereas businesses are

far less concerned with providing this value proposition to consumers.

QUANTITATIVE RESEARCH REPORT: ‘Attitudes towards online shopping and knowledge about shopping online securely’. Prepared by Stancombe Research & Planning for NSW Fair Trading, 2012.

18

4.3 Australian consumer law Consumers and SMBs were asked to state whether example

applications of Australia Consumer Law in the online shopping context

were true or false. Generally, consumers and SMBs are confused as to

whether or how Australian Consumer Law applied. About half (51%) of

consumers make online purchases from auction websites, however both

consumers (54%) and SMBs (54%) are largely unsure how Australian

Consumer Law may or may not apply to private sellers. Similarly, 6% of

consumers reported receiving damaged goods, and another 6% have

reported they ordered goods they never received. Also, 13% of SMBs

claim to have received reports of missing goods, and 9% damaged

goods. Despite these rates of incidence, large proportions of both

consumers (46%) and SMBs (42%) are unsure who is responsible for

replacing damaged or missing goods. These examples suggest

consumers are making purchasing decisions irrespective of the added

risks of not understanding the legal context.

4.4 Online security concerns Security is a concern when considering shopping online. The vast

majority (88%) of those who do not shop online cite security concerns as

a barrier. Of those who do shop online, 2% claim to have been victim of

fraud when shopping online. When thinking of features that may identify

a secure website, just under half (47%) of consumers are aware of

‘https’ indicating a secure site, and 11% are aware of ‘the padlock

symbol’. Importantly, while 68% of SMBs are aware of ‘https’ as a

security feature, only 52% offer this security when selling online. 41% of

consumers are largely unsure of what indicates a secure site for online

shopping. The same percentage (41%) of businesses are also unaware,

yet 76% take some steps to indicate to customers that the site is safe

and secure to buy from.

QUANTITATIVE RESEARCH REPORT: ‘Attitudes towards online shopping and knowledge about shopping online securely’. Prepared by Stancombe Research & Planning for NSW Fair Trading, 2012.

19

5 Online Shopping and Selling Behaviours

5.1 Frequency of shopping, goods and services purchased

The majority (88%) of the NSW population who use the internet shop

online, although only half of SMBs in the state sell online. 88% of the

NSW online population has shopped online via some method in the last

year, whereas 49% of SMBs with an online presence had sold goods or

services online during the same period. More specifically, of those

consumers who did shop online in the last year (n=741), 45% shop online

once a month, and 70% at least every few months. Conversely, of the

cumulative SMBs online business channels (n=126), 55% sell less than

30% of their products or services online. When consumers shop online,

90% have done so from home, and around 20% from work. A computer or

laptop has been used by around 90% of consumers, 15% have purchase

via a smartphone, and 10% via tablet. Most online shopping is done via a

computer or laptop from home, and there is a disparity between the

percentage and frequency of consumers shopping online and SMBs

selling online.

To purchase products or services online, consumers most frequently use

common websites or online stores. In fact, approximately 75% of

consumers buy from these channels. Online auctions also play a

substantial role with 50% of consumers reporting the use of this channel.

Additionally, group-buying vouchers are used by approximately 30% of

consumers. Generally, discretionary spending dominates the online

consumer market. For example, roughly 35% of people bought

books/CD’s/DVDs, whereas around 10% bought groceries online.

However, certain products and services are more commonly purchased

through specific channels. Online auctions play a significant role for

physical goods, and group-buying vouchers occupy a niche space for

leisure and services. For example, 49% of those consumers who have

used a group-buying voucher did so to purchase meals at restaurants.

QUANTITATIVE RESEARCH REPORT: ‘Attitudes towards online shopping and knowledge about shopping online securely’. Prepared by Stancombe Research & Planning for NSW Fair Trading, 2012.

20

Comparatively, 7% of those who used a website or online store, and only

2% of those who used an online auction, did so to buy meals at

restaurants. While online purchasing may be common, the channel used

to buy a particular product or service may differ greatly.

5.2 Seller origin, payment and delivery methods

The majority of goods and services consumers purchase online come

from within Australia. Just under half of all online purchases are from

sellers based only in Australia, a further one-third (30%) are mostly from

Australian sellers, and around 15% are half from Australian businesses

and half from overseas businesses. The remainder of online purchases,

roughly 10%, are mostly or all from sellers based overseas. Similarly,

from the SMB perspective, just over half of sales are to NSW customers

and a further one-third is mostly to Australians. However, this could be

partly a function of a high Australia dollar impacting exports. Importantly,

there is some variance in consumer purchases by channel used.

Consumers using websites or online stores, and online auctions, are more

likely to purchase from overseas sellers compared to using group buying

vouchers. Moreover, due to the nature of the channel, group-buying

vouchers are almost exclusively purchased from domestic sellers.

Nevertheless, the majority of online purchases being from local sellers is

true across all online purchasing channels.

PayPal is the most common online payment method used by consumers.

Considering all types of online purchases, approximately three in every

five consumers have used PayPal in the last year. This compares to

roughly two in every five using credit card, and one in five for debit card,

while bank transfers are around one in ten. Conversely, just less than one

half (47%) of SMBs have accepted payment via PayPal in the last year,

yet approximately two-thirds (64%) have accepted credit card payments.

Amazingly, 65% of SMBs reported accepting payment via bank transfer,

compared to 10% of consumers making payment. Similarly, one-third of

SMBs have accepted cash on delivery although only one in ten

consumers have reported using this method. These staggering

QUANTITATIVE RESEARCH REPORT: ‘Attitudes towards online shopping and knowledge about shopping online securely’. Prepared by Stancombe Research & Planning for NSW Fair Trading, 2012.

21

differences highlight the disparity between payment methods of NSW

consumers and NSW SMBs, and suggest local SMBs could be missing

out on sales.

Standard mail is used to deliver the majority of goods purchased online.

Almost three-fifths (57%) of consumers received goods purchased online

by standard mail, and just more than one-third (35%) via courier. This

trend increases with purchases via website or online store, compared to

other methods. SMBs align with consumers in reporting that standard mail

and courier are the most common delivery methods used. Additionally,

the majority of online sales are received within 2-3 business days, and

over four in five purchases are received within 4-5 working days. The

standard mail and courier delivery methods represent a safe and secure

way to deliver and receive goods.

QUANTITATIVE RESEARCH REPORT: ‘Attitudes towards online shopping and knowledge about shopping online securely’. Prepared by Stancombe Research & Planning for NSW Fair Trading, 2012.

22

6 Drivers and Barriers to Shopping and Selling Online

6.1 Consumer and business drivers

The drivers for consumer online shopping and SMB online selling differ

greatly. From the consumer perspective, the top-of-mind reasons for

shopping online are access to cheaper products and discounts.

Approximately three in five (58%) online consumers reported this

spontaneously. Roughly one-third (30%) of online shoppers suggested

convenience was a benefit to shopping online, whereas less than one-fifth

(16%) shopped online because they could not find the product locally.

This suggests just more than four in five (84%) online purchases are

substitutes for locally available physical store based products or services.

However, when prompted, convenience becomes an equally important

driver of online consumer purchasing as price, around three in five (60%)

consumers report this. While price (61%) and convenience (60%)

standout as the two key drivers, choice (38%) and availability (37%) are

acknowledged as important secondary considerations. Convenience

seems most applicable to shopping via websites, while group-buying

vouchers are attractive for online-only discounts, and are the most likely

to be purchase spontaneously. Ultimately, the role of online shopping

form the consumer perspective is not to offer enjoyment or relief from

physical shopping, rather its role is largely functional.

The picture is vastly different from the SMB perspective. The standout

top-of-mind reason for selling online for SMBs is to reach a wider

customer base. Approximately two in five (39%) businesses

spontaneously reported this as a benefit to selling online; efficiency (18%)

and cost-effectiveness (16%) also feature. However, when prompted,

most SMBs identified reaching more or niche customers, and

convenience for both themselves and customers, as reasons for online

selling. While consumers (60%) and SMBs (61%) are in consensus over

the convenience of online shopping, the low prices that are a priority for

QUANTITATIVE RESEARCH REPORT: ‘Attitudes towards online shopping and knowledge about shopping online securely’. Prepared by Stancombe Research & Planning for NSW Fair Trading, 2012.

23

consumers (61%) are very low (35%) from the SMB perspective. Due to

the disparity between consumer and business drivers for participating in

the online marketplace, the clear takeout message is that SMBs are not

taking a customer-centric approach to online sales.

6.2 Consumer and Business Barriers

Safety concerns and a need to seeing a product before buying are the two

barriers to online shopping prevalent from the consumer viewpoint. Of the

responses (372) by those consumers who had not shopped online in the

last year, just over one-third (36%) spontaneously cited safety concerns

as a reasons preventing them from shopping online. This was closely

followed by the need to see a product before purchasing it, at around one-

quarter (27%) of offline customers. Specifically, when prompted, payment

security (38%) and not knowing exactly what you are getting (31%) were

the two key barriers. However, tied in with this are concerns about quality

(27%), delivery (26%), and returns (27%). When exploring these concerns

by online purchasing channel, strong lack of understanding for the way

online auctions (17%) and group buying vouchers (22%) operate was

discovered. This compares to a 9% lack of understanding for website and

online stores. Consequently, the key barriers for consumers to shopping

online are themes of security, knowing what is being purchased, and

understanding.

The barriers to selling online from the SMBs perspective are much

clearer. The top-of-mind barrier for SMBs was that the product or service

offering is not conducive to online sales (25%). This suggests that most

SMBs offering products or services suitable for online sale will attempt to

sell online. Beyond the perceived plausibility issues of online sale as a

barrier for business to sell online, some SMBs reported control over

pre/post sale service (9%) and safety concerns (4%). Specifically, around

10% of SMBs not currently online value their service to customers to the

point that it becomes a barrier to transacting online. In other words, some

SMBs (10%) believe their service based value proposition would be at risk

QUANTITATIVE RESEARCH REPORT: ‘Attitudes towards online shopping and knowledge about shopping online securely’. Prepared by Stancombe Research & Planning for NSW Fair Trading, 2012.

24

by moving online. Nevertheless, suitability of the online marketplace for

the products or services is the key barrier to online sales for SMBs.

6.3 Negative experiences

Online consumers are impacted by negative experiences in multiple ways.

one in five (21%) shoppers have had some kind of negative experience

with goods taking longer than expected to arrive. This represents the most

common negative experience online. Generally though, the problems

experienced vary little (<3%) between the online purchasing channels.

Otherwise, the most prevalent problems are with goods not meeting

expectations (10%) or problems with delivery (10%), perhaps justifying

consumer concerns over these issues. Incidences of fraud or incorrect

charges when shopping online are very low (2%) – it seems consumer

concern outweighs the actual risk. However, one-quarter (26%) of online

shoppers who have had a negative experience say it made them more

reluctant to shop online. Nevertheless, negative experiences with online

shopping do not tend to deter customers generally. Rather, they may be

cautious of a particular seller in the future (26%), and/or read the fine print

more thoroughly (21%). Further, about one-fifth (18%) of consumers who

have had a negative online experience (435) claim the problem was

resolved easily which led to them being more confident to shop online.

Overall, the impact of negative experiences on online customers is varied.

Comparatively, awareness of other people’s negative online experiences

is more detrimental to those offline shoppers. Of those who have not

shopped online in the last year, the quality of goods or services not

meeting the expected standards was the most commonly known negative

experience of online shopping (13%). This suggests bad experiences

relating to quality are a more ‘voiced’ complaint than duration of delivery

(10%). Beyond this, minimal differentiation was made between other

types of negative online experience. Most of these experiences are

associated with websites and online stores, since, as aforementioned,

online auctions and group buying vouchers are poorly understood offline

consumers. Ultimately, awareness of other people’s negative online

QUANTITATIVE RESEARCH REPORT: ‘Attitudes towards online shopping and knowledge about shopping online securely’. Prepared by Stancombe Research & Planning for NSW Fair Trading, 2012.

25

experiences magnifies the general reluctance of offline consumers to

shop online (32%).

Reports received by businesses relating to online sales supports the

consumer findings. With the exception of goods not arriving within

expected timeframes, businesses are generally aware of negative online

experiences just as much as consumers. Although fewer SMBs than

consumers reported ‘goods taking longer than expected to arrive’, it is

likely that businesses would not get to hear about this if the goods

eventually arrived. It may be that not meeting timeframe expectations

could be silently turning customers away. Nevertheless, customer

feedback has had positive impacts on businesses. Approximately three-

quarters (72%) of SMBs have made changes to their sales operations as

a result. More specifically, around one-third (33%) of SMBs responded by

making terms and conditions clearer, and one-quarter (26%) included

more detailed product descriptions. Similarly, two-thirds (66%) of those

businesses not online and who have witnessed negative online

experiences also improved their business operations.

QUANTITATIVE RESEARCH REPORT: ‘Attitudes towards online shopping and knowledge about shopping online securely’. Prepared by Stancombe Research & Planning for NSW Fair Trading, 2012.

26

7 Awareness and Behaviours to Online Security

7.1 Awareness of security indicators

Most consumers can identify indicators of online shopping security. To

identify safety when shopping online, consumers chiefly look for familiar

brands (16%), secure payment certifications (15%), and PayPal (13%).

The key warning signs for consumers are bad feedback or ratings (16%),

or unfamiliarity with a website (12%). Interestingly, most of those who

have not shopped online in the last year find it difficult to recognise any

sort of online safety indicators (64%). Also, almost two-thirds (65%)

concede they cannot recognise any safety indicators of online shopping,

or simply do not know. However, about one in ten (9%) could mention a

padlock security symbol, and about one in twenty (6%) ‘https’.

Nevertheless, there is a very apparent lack of understanding of online

shopping from the offline cohort.

Strangely, offline SMBs are better at recognising security indicators of

online shopping than those online SMBs. Among those online, PayPal

(11%) and secure sites (18%) are the most commonly identified security

indications. Disturbingly, 41% of online SMBs are not aware of anything

that might make customers suspect a site may not be safe and secure to

buy from. Consequently, these SMBs are less able to ensure safe selling

practices for their customers. This figure reduces to around 25% when

among offline SMBs. Many more offline SMBs can name PayPal (6%

more), https (11% more), or general website quality (7% more), as

indicators of security or warning signs for consumers shopping online.

When prompted, both consumers and SMBs are far more aware of online

shopping security measures. Generally, consumers have quite high

awareness (>65%) of most online security measures, though there is

room for education around https (47%), and verifying addresses (39%).

Interestingly, ‘check a seller’s reputation’ was markedly lower for those

QUANTITATIVE RESEARCH REPORT: ‘Attitudes towards online shopping and knowledge about shopping online securely’. Prepared by Stancombe Research & Planning for NSW Fair Trading, 2012.

27

using group buying vouchers (18% lower). Consumers could be so

tempted by the price discounts of group buying vouchers that they forego

this security step. Comparatively, among both online and offline

businesses, SMBs have better knowledge than consumers about https

(18% more), and businesses providing a physical address (25% more).

7.2 Australian consumer law

Both consumers and businesses are largely confused as to the

application of Australian Consumer Law to online shopping scenarios.

More than half of consumers (54%) and the same amount of SMBs (54%)

are unsure how Australian Consumer Law may or may not apply to

private sellers versus businesses. Very similar findings point to both

consumers (46%) and SMBs (42%) misunderstandings of whether or not

Australian Consumer Law applies to who is responsible for goods

damaged in transit. Despite the confusion surrounding the application of

Australian Consumer Law, SMBs go some way towards ensuring

customers are aware of their rights and responsibilities. In particular,

publishing terms and conditions on their websites (59%), returns policy

(52%), and expected delivery timings (45%). Clearly though, much could

be done to improve both consumer and SMB understandings of the

application of Australia Consumer Law.

QUANTITATIVE RESEARCH REPORT: ‘Attitudes towards online shopping and knowledge about shopping online securely’. Prepared by Stancombe Research & Planning for NSW Fair Trading, 2012.

28

8 Summary and Conclusions

8.1 Key themes Five key themes were discovered from this research. These include: the

PayPal disparity, the disconnect over drivers of online shopping, Australian

consumer law, and Online security concerns.

Since PayPal is the first choice payment method from the consumer

perspective (59%), yet less than half of SMBs offer this payment method

(47%), can the use of PayPal be promoted among SMBs as a way of offering

customers what they want and alleviating potential security concerns?

Consumers (61%) cite lower prices as a reason for shopping online, whereas

only 35% SMBs mentioned this value proposition. Moreover, the main reason

(71%) SMBs are driven to sell online is to reach a broader customer base.

Therefore, there is a disconnect between consumers and SMBs as to the

primary reasons they shop/sell online. SMBs need to be aware that

consumers expect lower prices when shopping online.

Consumers (54%) and SMBs (54%) are largely unsure how Australian

Consumer Law may or may not apply to private sellers. Similarly, large

proportions of both consumers (46%) and SMBs (42%) are unsure who is

responsible for replacing damaged or missing goods. There is scope to

educate consumers and SMBs about the application of Australian Consumer

Law and, in particular, who is responsible for goods lost or damaged in transit.

47% of consumers are aware of ‘https’ indicating a secure site, and 11% are

aware of ‘the padlock symbol’. While 68% of SMBs are aware of ‘https’ as a

security feature, only 52% offer this security when selling online. There is a

need to raise awareness among consumers of https sites and perhaps some

room to promote their use among SMBs. With the padlock symbol having

higher awareness than ‘https’ it may be beneficial to promote the two

alongside each other.

QUANTITATIVE RESEARCH REPORT: ‘Attitudes towards online shopping and knowledge about shopping online securely’. Prepared by Stancombe Research & Planning for NSW Fair Trading, 2012.

29

8.2 Online shopping and selling behaviours The majority (88%) of NSW’s online population shop online, particularly for

discretionary spending, though only half (49%) of SMBs in the state sell

online. When online, websites are the most commonly used (74%) but online

auctions also play a significant role (51%), particularly for physical goods.

Group buying vouchers occupy a niche space for leisure and services (26%).

Consumers use PayPal most of all to shop online (63%) but SMBs may be

missing out here by not offering this method – just under half of them do

(47%). After PayPal, credit cards are the most commonly used (42%), and

debit cards (23%) when shopping through websites or online stores. The

majority (74%) of online shopping is for goods from within Australia, though a

quarter (26%) of consumers make half or more of their purchases overseas.

Most goods arrive to consumers by standard mail (57%) although SMBs are

just as likely to use couriers as standard mail (48%), a sensible way to ensure

goods arrive safely. Further, SMBs report that most goods (72%) arrive within

2-3 business days and it’s likely that this has set consumer expectations for

delivery times – leaving potential for delays.

8.3 Drivers and barriers to shopping and selling online The key reason for consumers to shop online is to access lower prices (61%),

though this is at odds with SMBs’ reasons for selling online: to reach a wider

range of customers (71%). Consumers and SMBs do align on the

convenience online shopping offers (both 60%) and this is a key benefit to

both parties. However, that convenience may be marred slightly when goods

take longer to arrive – the most common complaint by consumers that may

not be getting fed back to SMBs. The key barrier for consumers to shopping

online is concerns over the security of their financial details (38%), though not

knowing exactly what’s being purchased is a close second (31%). The latter is

borne out of goods being unsuitable (10%), of lower quality than expected

(10%), or not matching the description online (7%) are the next most common

problems consumers experience. Negative experiences have made some

consumers check policies more carefully and avoid problem sellers (28%),

while SMBs have taken positive steps to displaying policies more clearly and

QUANTITATIVE RESEARCH REPORT: ‘Attitudes towards online shopping and knowledge about shopping online securely’. Prepared by Stancombe Research & Planning for NSW Fair Trading, 2012.

30

ensuring descriptions of goods are detailed and accurate (33%). For SMBs,

the key barrier to selling online is that it is not a suitable channel for their

offering (25%).

8.4 Awareness and behaviours relating to online security Consumers are most comfortable shopping via familiar sites (16%

spontaneous) and are well versed in the basic security measures: keeping

records (68%), not giving out details and passwords (71), checking bank

statements (72%). They claim to look for ‘secure payment’ options (15%

spontaneous) but awareness of https sites as a security feature is relatively

low (47%). PayPal is known to be a secure method of payment and is sought

out by consumers (13% spontaneous). Among SMBs, there is room for

improvement – while most have some security measures in place for online

customers (68%), they are certainly not covering them all. There is some

room for education among both consumers (43%) and SMBs (40%) as to

when Australian consumer law applies given that there is confusion over its

application to private sellers. There is also some room for education among

consumers (37%) and SMBs (38%) as to who is responsible for goods that

are lost in transit or arrive damaged.

QUANTITATIVE RESEARCH REPORT: ‘Attitudes towards online shopping and knowledge about shopping online securely’. Prepared by Stancombe Research & Planning for NSW Fair Trading, 2012.

31

9 Appendices

9.1 Appendix 1: Consumer Questionnaire Project Click

Consumer Questionnaire V3 Intro Thank you for agreeing to take part in this survey, which should take you around 15 minutes to complete. We value your opinion so please be honest and open in your responses. This survey is being conducted by Stancombe Research & Planning, an independent market research organisation. All of your responses will be kept strictly confidential, and will only be analysed as part of a wider group. Similarly you will not be identified, and no-one will contact you as a result of any information you provide. Screening and Demographics ASK ALL S0. Do you or any members of your household work in any of the following industries? MR Marketing or market research 1 PR or journalism 2 Advertising 3 CLOSE Telecommunications 4 Healthcare 5 Government 6 Financial services 7 None of these 97 CONTINUE ASK ALL S1. Are you male or female? SR Male 1 Female 2 CHECK

QUOTAS

QUANTITATIVE RESEARCH REPORT: ‘Attitudes towards online shopping and knowledge about shopping online securely’. Prepared by Stancombe Research & Planning for NSW Fair Trading, 2012.

32

ASK ALL S2. What is your age in years? PROGRAMMER PLEASE CAPTURE AGE BRACKET 18-24 1 25-29 2 30-34 3 35-39 4 40-44 5 45-49 6 50-54 7 55-59 8 60-64 9 65-69 10 70-74 11 75+ 12

CHECK QUOTAS

ASK ALL S3. Where do you currently live? SR Sydney 1 Newcastle 2 Central Coast 3 Wollongong 4 Albury 5 Maitland 6 Wagga Wagga 7 Port Macquarie 8 Tamworth 9 Orange 10 Dubbo 11 Bathurst 12 Lismore 13 Coffs Harbour 14 Richmond 15 Nowra 16 Elsewhere in NSW 17

CHECK QUOTAS

Outside of NSW 18 CLOSE Thank you, you have qualified to complete the remainder of the survey.

QUANTITATIVE RESEARCH REPORT: ‘Attitudes towards online shopping and knowledge about shopping online securely’. Prepared by Stancombe Research & Planning for NSW Fair Trading, 2012.

33

ASK IF S3=17 S4. Which of the following best describes the area you live in? SR Regional city (80,000 or more inhabitants) 1 Large town (40,000 – 79,999 inhabitants) 2 Small town (2,000 – 39,999 inhabitants) 3 Village or remote location (Less than 2000 inhabitants) 4 Don’t know 99 ASK ALL S5. Which of the following best describes your household status? SR Single, living with parents 1 Single, living alone 2 Single or couple, sharing with other adults 3 Single, living with children in the household 4 Married/ de facto, no children in the household 5 Married/ de facto, with children in the household 6 Divorced, separated or widowed, no children in the household 7 Divorced, separated or widowed, with children in the household 8 Other 98 Prefer not to say 96 ASK ALL S6. What is your current employment status? SR Employed full-time (35+ hours a week) 1 Employed part-time 2 Home duties 3 Student 4 Retired/ superannuated 5 Looking for work 6 Pensioner 7 Other 98 Prefer not to say 96

QUANTITATIVE RESEARCH REPORT: ‘Attitudes towards online shopping and knowledge about shopping online securely’. Prepared by Stancombe Research & Planning for NSW Fair Trading, 2012.

34

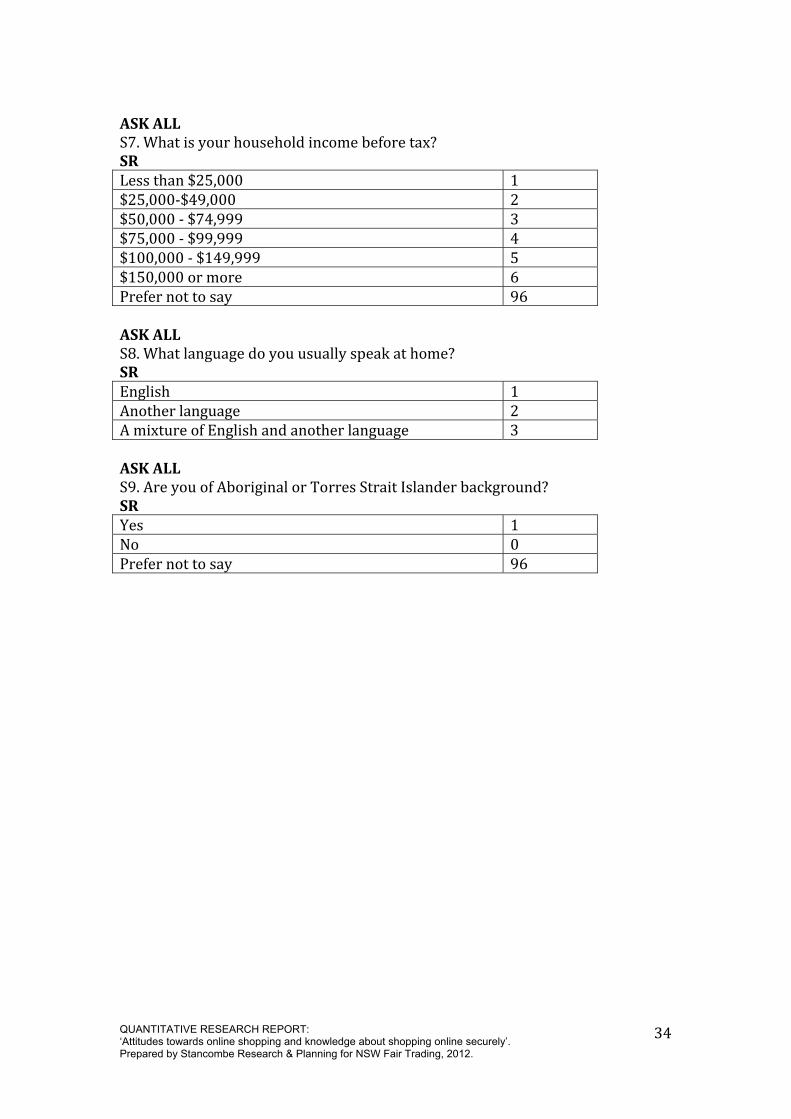

ASK ALL S7. What is your household income before tax? SR Less than $25,000 1 $25,000-$49,000 2 $50,000 - $74,999 3 $75,000 - $99,999 4 $100,000 - $149,999 5 $150,000 or more 6 Prefer not to say 96 ASK ALL S8. What language do you usually speak at home? SR English 1 Another language 2 A mixture of English and another language 3 ASK ALL S9. Are you of Aboriginal or Torres Strait Islander background? SR Yes 1 No 0 Prefer not to say 96

QUANTITATIVE RESEARCH REPORT: ‘Attitudes towards online shopping and knowledge about shopping online securely’. Prepared by Stancombe Research & Planning for NSW Fair Trading, 2012.

35

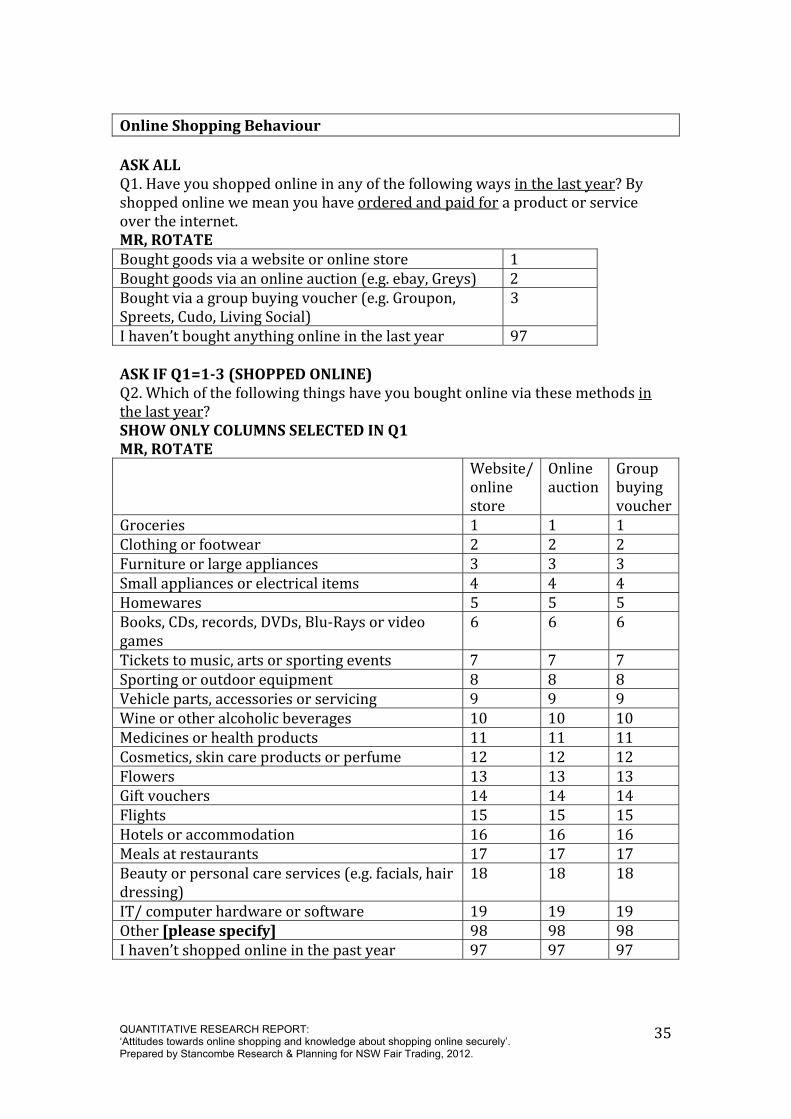

Online Shopping Behaviour ASK ALL Q1. Have you shopped online in any of the following ways in the last year? By shopped online we mean you have ordered and paid for a product or service over the internet. MR, ROTATE Bought goods via a website or online store 1 Bought goods via an online auction (e.g. ebay, Greys) 2 Bought via a group buying voucher (e.g. Groupon, Spreets, Cudo, Living Social) 3 I haven’t bought anything online in the last year 97 ASK IF Q1=1-3 (SHOPPED ONLINE) Q2. Which of the following things have you bought online via these methods in the last year? SHOW ONLY COLUMNS SELECTED IN Q1 MR, ROTATE Website/ online store Online auction Group buying voucherGroceries 1 1 1 Clothing or footwear 2 2 2 Furniture or large appliances 3 3 3 Small appliances or electrical items 4 4 4 Homewares 5 5 5 Books, CDs, records, DVDs, Blu-Rays or video games 6 6 6 Tickets to music, arts or sporting events 7 7 7 Sporting or outdoor equipment 8 8 8 Vehicle parts, accessories or servicing 9 9 9 Wine or other alcoholic beverages 10 10 10 Medicines or health products 11 11 11 Cosmetics, skin care products or perfume 12 12 12 Flowers 13 13 13 Gift vouchers 14 14 14 Flights 15 15 15 Hotels or accommodation 16 16 16 Meals at restaurants 17 17 17 Beauty or personal care services (e.g. facials, hair dressing) 18 18 18 IT/ computer hardware or software 19 19 19 Other [please specify] 98 98 98 I haven’t shopped online in the past year 97 97 97

QUANTITATIVE RESEARCH REPORT: ‘Attitudes towards online shopping and knowledge about shopping online securely’. Prepared by Stancombe Research & Planning for NSW Fair Trading, 2012.

36

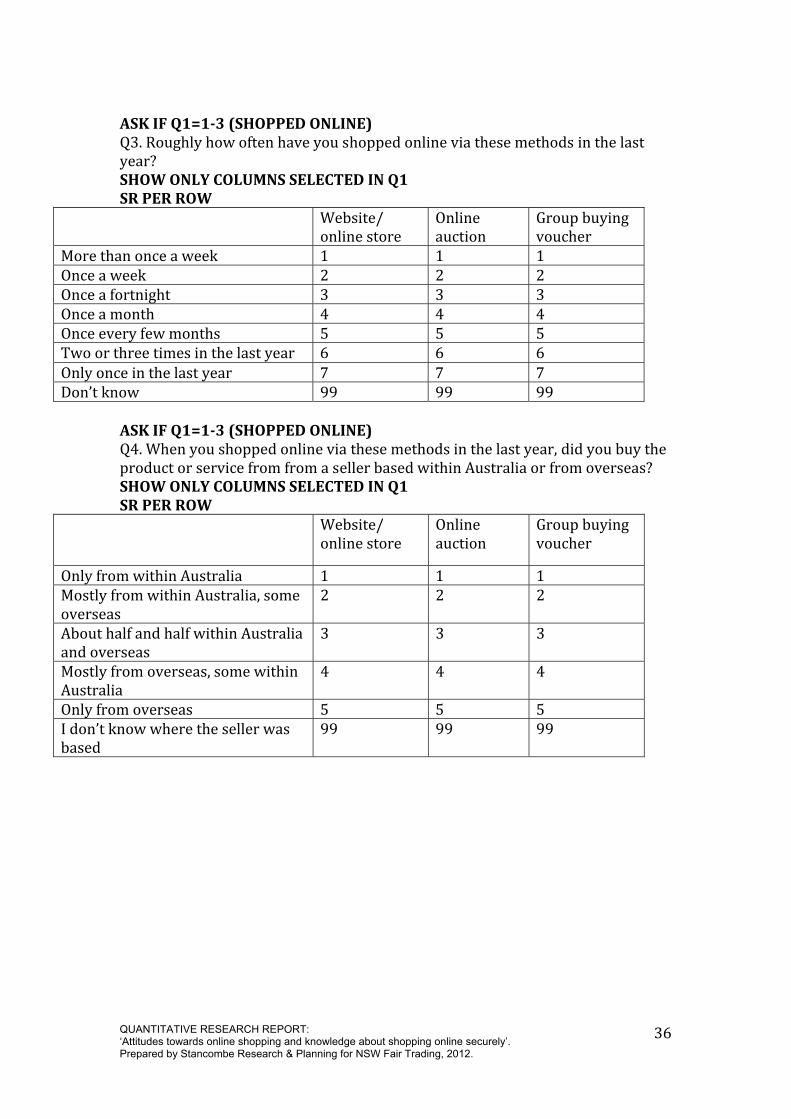

ASK IF Q1=1-3 (SHOPPED ONLINE) Q3. Roughly how often have you shopped online via these methods in the last year? SHOW ONLY COLUMNS SELECTED IN Q1 SR PER ROW Website/ online store Online auction Group buying voucher More than once a week 1 1 1 Once a week 2 2 2 Once a fortnight 3 3 3 Once a month 4 4 4 Once every few months 5 5 5 Two or three times in the last year 6 6 6 Only once in the last year 7 7 7 Don’t know 99 99 99 ASK IF Q1=1-3 (SHOPPED ONLINE) Q4. When you shopped online via these methods in the last year, did you buy the product or service from from a seller based within Australia or from overseas? SHOW ONLY COLUMNS SELECTED IN Q1 SR PER ROW Website/ online store Online auction Group buying voucher Only from within Australia 1 1 1 Mostly from within Australia, some overseas 2 2 2 About half and half within Australia and overseas 3 3 3 Mostly from overseas, some within Australia 4 4 4 Only from overseas 5 5 5 I don’t know where the seller was based 99 99 99

QUANTITATIVE RESEARCH REPORT: ‘Attitudes towards online shopping and knowledge about shopping online securely’. Prepared by Stancombe Research & Planning for NSW Fair Trading, 2012.

37

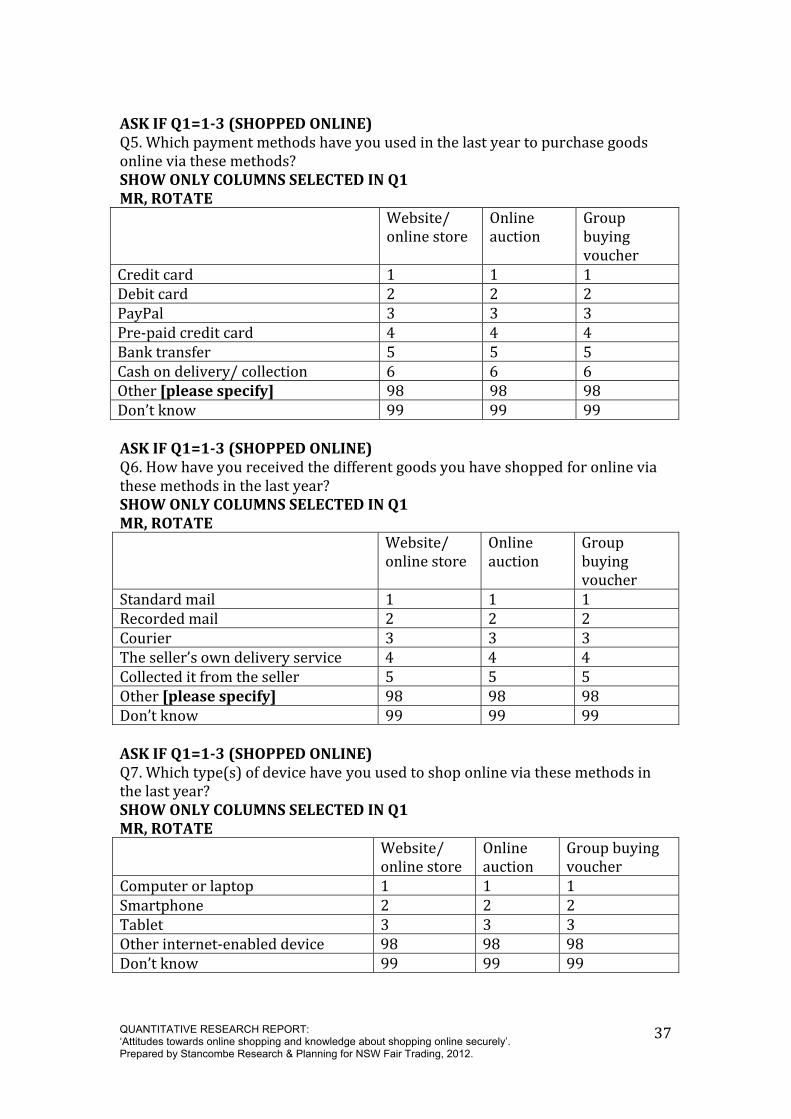

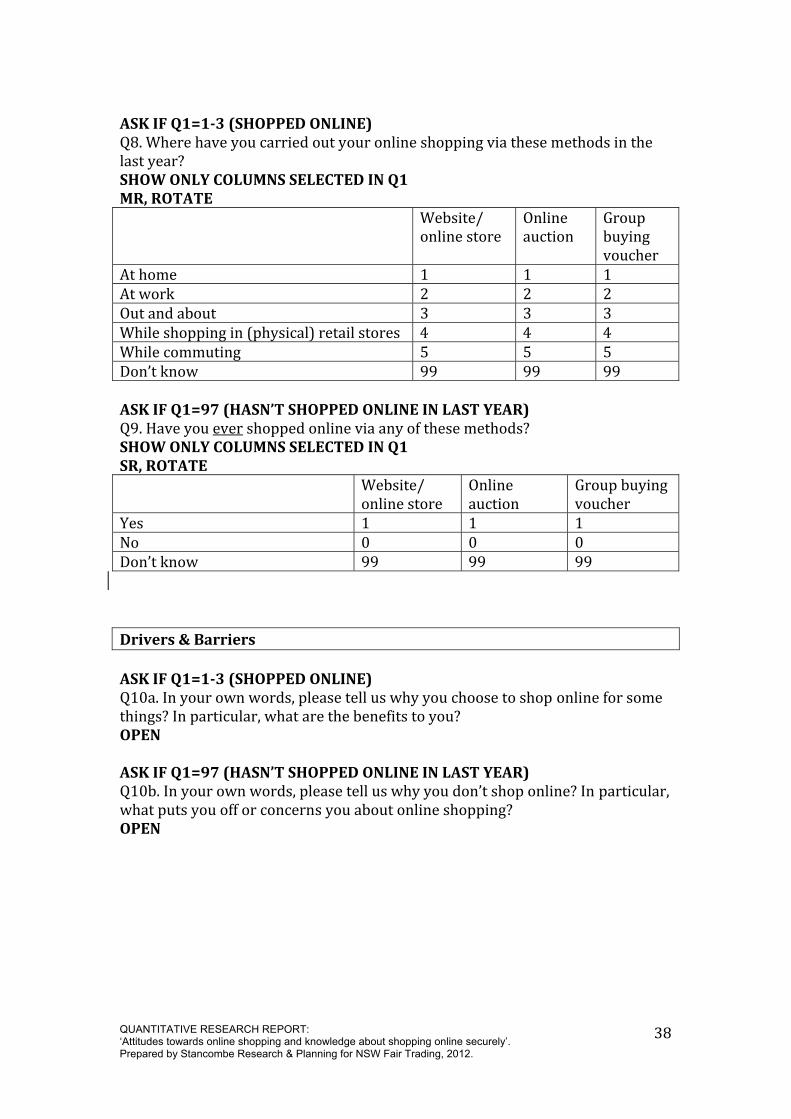

ASK IF Q1=1-3 (SHOPPED ONLINE) Q5. Which payment methods have you used in the last year to purchase goods online via these methods? SHOW ONLY COLUMNS SELECTED IN Q1 MR, ROTATE Website/ online store Online auction Group buying voucher Credit card 1 1 1 Debit card 2 2 2 PayPal 3 3 3 Pre-paid credit card 4 4 4 Bank transfer 5 5 5 Cash on delivery/ collection 6 6 6 Other [please specify] 98 98 98 Don’t know 99 99 99 ASK IF Q1=1-3 (SHOPPED ONLINE) Q6. How have you received the different goods you have shopped for online via these methods in the last year? SHOW ONLY COLUMNS SELECTED IN Q1 MR, ROTATE Website/ online store Online auction Group buying voucher Standard mail 1 1 1 Recorded mail 2 2 2 Courier 3 3 3 The seller’s own delivery service 4 4 4 Collected it from the seller 5 5 5 Other [please specify] 98 98 98 Don’t know 99 99 99 ASK IF Q1=1-3 (SHOPPED ONLINE) Q7. Which type(s) of device have you used to shop online via these methods in the last year? SHOW ONLY COLUMNS SELECTED IN Q1 MR, ROTATE Website/ online store Online auction Group buying voucher Computer or laptop 1 1 1 Smartphone 2 2 2 Tablet 3 3 3 Other internet-enabled device 98 98 98 Don’t know 99 99 99

QUANTITATIVE RESEARCH REPORT: ‘Attitudes towards online shopping and knowledge about shopping online securely’. Prepared by Stancombe Research & Planning for NSW Fair Trading, 2012.

38

ASK IF Q1=1-3 (SHOPPED ONLINE) Q8. Where have you carried out your online shopping via these methods in the last year? SHOW ONLY COLUMNS SELECTED IN Q1 MR, ROTATE Website/ online store Online auction Group buying voucher At home 1 1 1 At work 2 2 2 Out and about 3 3 3 While shopping in (physical) retail stores 4 4 4 While commuting 5 5 5 Don’t know 99 99 99 ASK IF Q1=97 (HASN’T SHOPPED ONLINE IN LAST YEAR) Q9. Have you ever shopped online via any of these methods? SHOW ONLY COLUMNS SELECTED IN Q1 SR, ROTATE Website/ online store Online auction Group buying voucher Yes 1 1 1 No 0 0 0 Don’t know 99 99 99 Drivers & Barriers ASK IF Q1=1-3 (SHOPPED ONLINE) Q10a. In your own words, please tell us why you choose to shop online for some things? In particular, what are the benefits to you? OPEN ASK IF Q1=97 (HASN’T SHOPPED ONLINE IN LAST YEAR) Q10b. In your own words, please tell us why you don’t shop online? In particular, what puts you off or concerns you about online shopping? OPEN

QUANTITATIVE RESEARCH REPORT: ‘Attitudes towards online shopping and knowledge about shopping online securely’. Prepared by Stancombe Research & Planning for NSW Fair Trading, 2012.

39

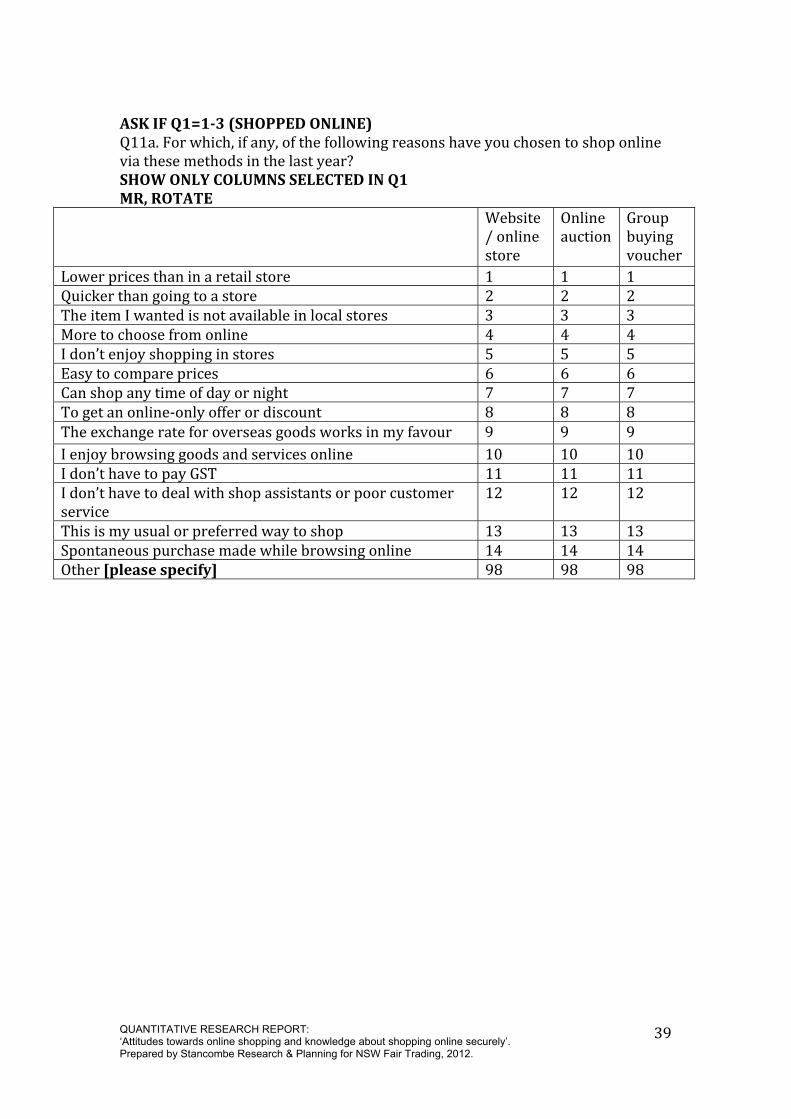

ASK IF Q1=1-3 (SHOPPED ONLINE) Q11a. For which, if any, of the following reasons have you chosen to shop online via these methods in the last year? SHOW ONLY COLUMNS SELECTED IN Q1 MR, ROTATE Website/ online store Online auction Group buying voucher Lower prices than in a retail store 1 1 1 Quicker than going to a store 2 2 2 The item I wanted is not available in local stores 3 3 3 More to choose from online 4 4 4 I don’t enjoy shopping in stores 5 5 5 Easy to compare prices 6 6 6 Can shop any time of day or night 7 7 7 To get an online-only offer or discount 8 8 8 The exchange rate for overseas goods works in my favour 9 9 9 I enjoy browsing goods and services online 10 10 10 I don’t have to pay GST 11 11 11 I don’t have to deal with shop assistants or poor customer service 12 12 12 This is my usual or preferred way to shop 13 13 13 Spontaneous purchase made while browsing online 14 14 14 Other [please specify] 98 98 98

QUANTITATIVE RESEARCH REPORT: ‘Attitudes towards online shopping and knowledge about shopping online securely’. Prepared by Stancombe Research & Planning for NSW Fair Trading, 2012.

40

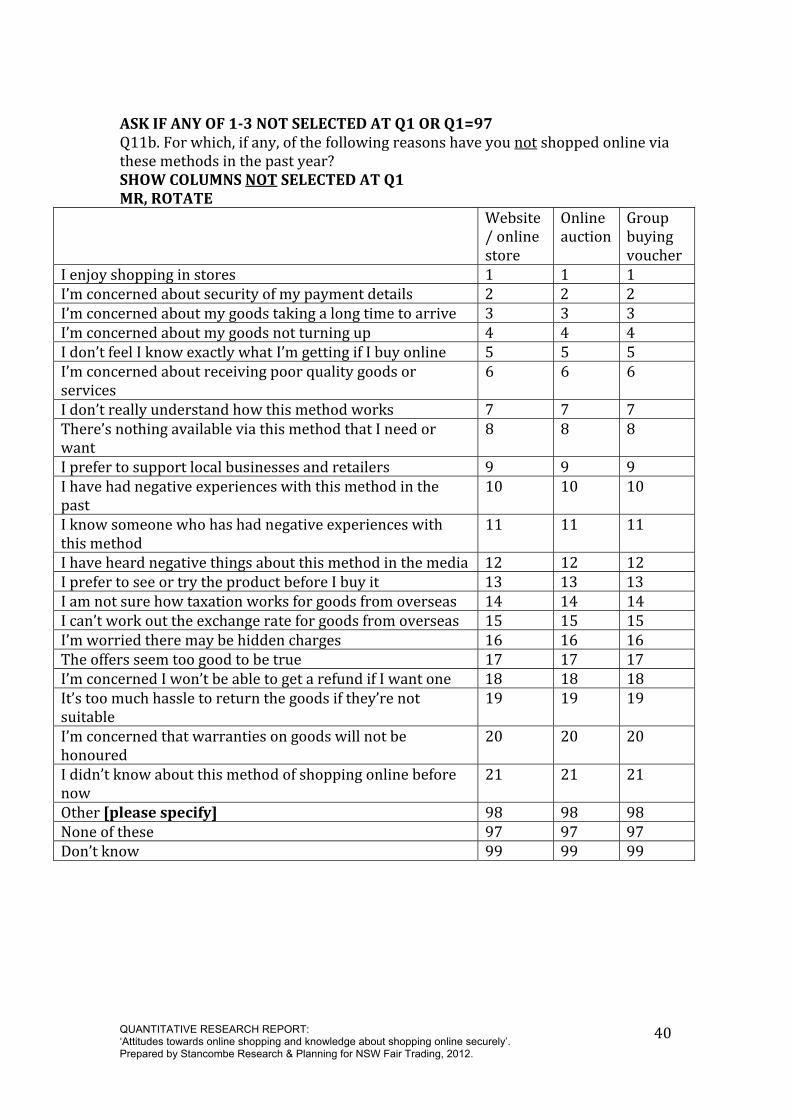

ASK IF ANY OF 1-3 NOT SELECTED AT Q1 OR Q1=97 Q11b. For which, if any, of the following reasons have you not shopped online via these methods in the past year? SHOW COLUMNS NOT SELECTED AT Q1 MR, ROTATE Website/ online store Online auction Group buying voucher I enjoy shopping in stores 1 1 1 I’m concerned about security of my payment details 2 2 2 I’m concerned about my goods taking a long time to arrive 3 3 3 I’m concerned about my goods not turning up 4 4 4 I don’t feel I know exactly what I’m getting if I buy online 5 5 5 I’m concerned about receiving poor quality goods or services 6 6 6 I don’t really understand how this method works 7 7 7 There’s nothing available via this method that I need or want 8 8 8 I prefer to support local businesses and retailers 9 9 9 I have had negative experiences with this method in the past 10 10 10 I know someone who has had negative experiences with this method 11 11 11 I have heard negative things about this method in the media 12 12 12 I prefer to see or try the product before I buy it 13 13 13 I am not sure how taxation works for goods from overseas 14 14 14 I can’t work out the exchange rate for goods from overseas 15 15 15 I’m worried there may be hidden charges 16 16 16 The offers seem too good to be true 17 17 17 I’m concerned I won’t be able to get a refund if I want one 18 18 18 It’s too much hassle to return the goods if they’re not suitable 19 19 19 I’m concerned that warranties on goods will not be honoured 20 20 20 I didn’t know about this method of shopping online before now 21 21 21 Other [please specify] 98 98 98 None of these 97 97 97 Don’t know 99 99 99

QUANTITATIVE RESEARCH REPORT: ‘Attitudes towards online shopping and knowledge about shopping online securely’. Prepared by Stancombe Research & Planning for NSW Fair Trading, 2012.

41

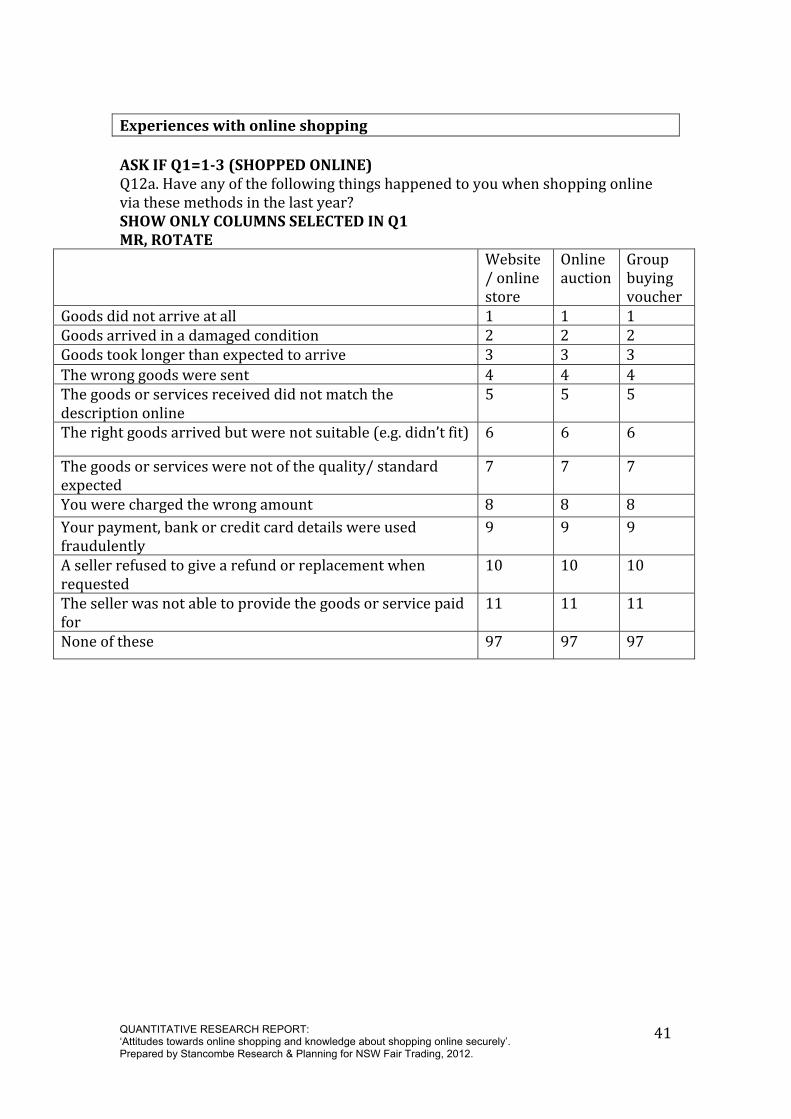

Experiences with online shopping ASK IF Q1=1-3 (SHOPPED ONLINE) Q12a. Have any of the following things happened to you when shopping online via these methods in the last year? SHOW ONLY COLUMNS SELECTED IN Q1 MR, ROTATE Website/ online store Online auction Group buying voucher Goods did not arrive at all 1 1 1 Goods arrived in a damaged condition 2 2 2 Goods took longer than expected to arrive 3 3 3 The wrong goods were sent 4 4 4 The goods or services received did not match the description online 5 5 5 The right goods arrived but were not suitable (e.g. didn’t fit) 6 6 6 The goods or services were not of the quality/ standard expected 7 7 7 You were charged the wrong amount 8 8 8 Your payment, bank or credit card details were used fraudulently 9 9 9 A seller refused to give a refund or replacement when requested 10 10 10 The seller was not able to provide the goods or service paid for 11 11 11 None of these 97 97 97

QUANTITATIVE RESEARCH REPORT: ‘Attitudes towards online shopping and knowledge about shopping online securely’. Prepared by Stancombe Research & Planning for NSW Fair Trading, 2012.

42

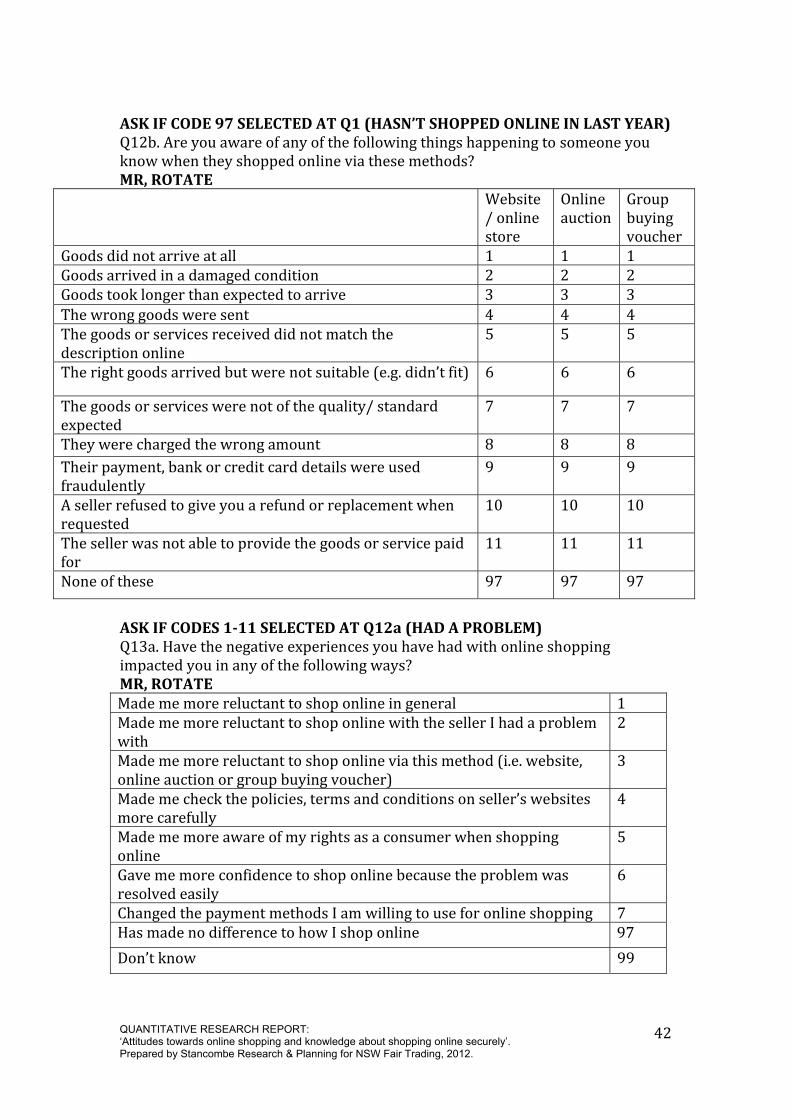

ASK IF CODE 97 SELECTED AT Q1 (HASN’T SHOPPED ONLINE IN LAST YEAR) Q12b. Are you aware of any of the following things happening to someone you know when they shopped online via these methods? MR, ROTATE Website/ online store Online auction Group buying voucher Goods did not arrive at all 1 1 1 Goods arrived in a damaged condition 2 2 2 Goods took longer than expected to arrive 3 3 3 The wrong goods were sent 4 4 4 The goods or services received did not match the description online 5 5 5 The right goods arrived but were not suitable (e.g. didn’t fit) 6 6 6 The goods or services were not of the quality/ standard expected 7 7 7 They were charged the wrong amount 8 8 8 Their payment, bank or credit card details were used fraudulently 9 9 9 A seller refused to give you a refund or replacement when requested 10 10 10 The seller was not able to provide the goods or service paid for 11 11 11 None of these 97 97 97 ASK IF CODES 1-11 SELECTED AT Q12a (HAD A PROBLEM) Q13a. Have the negative experiences you have had with online shopping impacted you in any of the following ways? MR, ROTATE Made me more reluctant to shop online in general 1 Made me more reluctant to shop online with the seller I had a problem with 2 Made me more reluctant to shop online via this method (i.e. website, online auction or group buying voucher) 3 Made me check the policies, terms and conditions on seller’s websites more carefully 4 Made me more aware of my rights as a consumer when shopping online 5 Gave me more confidence to shop online because the problem was resolved easily 6 Changed the payment methods I am willing to use for online shopping 7 Has made no difference to how I shop online 97 Don’t know 99

QUANTITATIVE RESEARCH REPORT: ‘Attitudes towards online shopping and knowledge about shopping online securely’. Prepared by Stancombe Research & Planning for NSW Fair Trading, 2012.

43

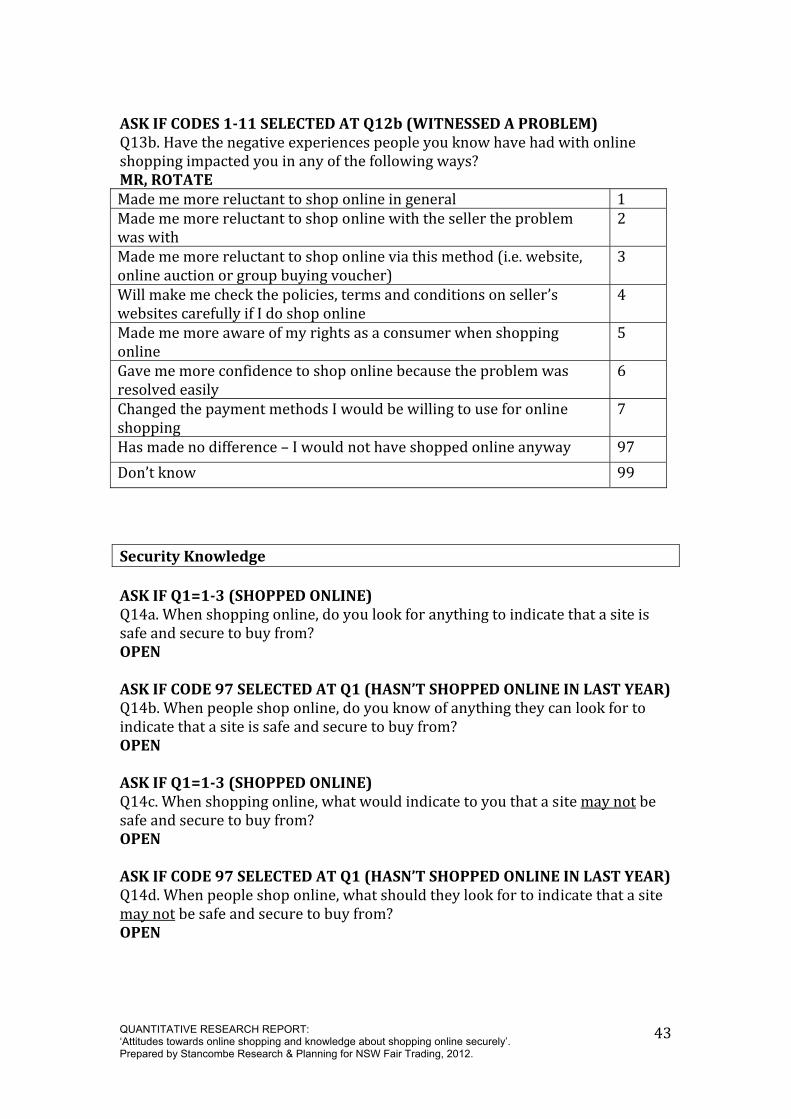

ASK IF CODES 1-11 SELECTED AT Q12b (WITNESSED A PROBLEM) Q13b. Have the negative experiences people you know have had with online shopping impacted you in any of the following ways? MR, ROTATE Made me more reluctant to shop online in general 1 Made me more reluctant to shop online with the seller the problem was with 2 Made me more reluctant to shop online via this method (i.e. website, online auction or group buying voucher) 3 Will make me check the policies, terms and conditions on seller’s websites carefully if I do shop online 4 Made me more aware of my rights as a consumer when shopping online 5 Gave me more confidence to shop online because the problem was resolved easily 6 Changed the payment methods I would be willing to use for online shopping 7 Has made no difference – I would not have shopped online anyway 97 Don’t know 99 Security Knowledge ASK IF Q1=1-3 (SHOPPED ONLINE) Q14a. When shopping online, do you look for anything to indicate that a site is safe and secure to buy from? OPEN ASK IF CODE 97 SELECTED AT Q1 (HASN’T SHOPPED ONLINE IN LAST YEAR) Q14b. When people shop online, do you know of anything they can look for to indicate that a site is safe and secure to buy from? OPEN ASK IF Q1=1-3 (SHOPPED ONLINE) Q14c. When shopping online, what would indicate to you that a site may not be safe and secure to buy from? OPEN ASK IF CODE 97 SELECTED AT Q1 (HASN’T SHOPPED ONLINE IN LAST YEAR) Q14d. When people shop online, what should they look for to indicate that a site may not be safe and secure to buy from? OPEN

QUANTITATIVE RESEARCH REPORT: ‘Attitudes towards online shopping and knowledge about shopping online securely’. Prepared by Stancombe Research & Planning for NSW Fair Trading, 2012.

44

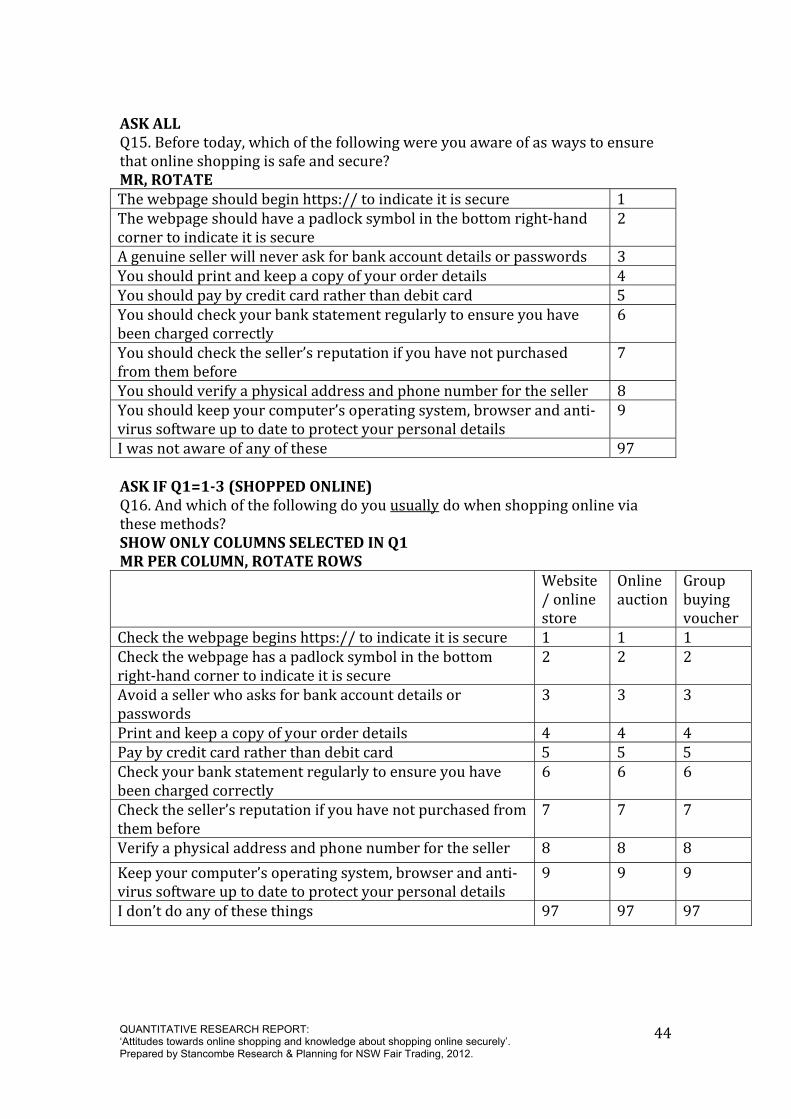

ASK ALL Q15. Before today, which of the following were you aware of as ways to ensure that online shopping is safe and secure? MR, ROTATE The webpage should begin https:// to indicate it is secure 1 The webpage should have a padlock symbol in the bottom right-hand corner to indicate it is secure 2 A genuine seller will never ask for bank account details or passwords 3 You should print and keep a copy of your order details 4 You should pay by credit card rather than debit card 5 You should check your bank statement regularly to ensure you have been charged correctly 6 You should check the seller’s reputation if you have not purchased from them before 7 You should verify a physical address and phone number for the seller 8 You should keep your computer’s operating system, browser and anti-virus software up to date to protect your personal details 9 I was not aware of any of these 97 ASK IF Q1=1-3 (SHOPPED ONLINE) Q16. And which of the following do you usually do when shopping online via these methods? SHOW ONLY COLUMNS SELECTED IN Q1 MR PER COLUMN, ROTATE ROWS Website/ online store Online auction Group buying voucher Check the webpage begins https:// to indicate it is secure 1 1 1 Check the webpage has a padlock symbol in the bottom right-hand corner to indicate it is secure 2 2 2 Avoid a seller who asks for bank account details or passwords 3 3 3 Print and keep a copy of your order details 4 4 4 Pay by credit card rather than debit card 5 5 5 Check your bank statement regularly to ensure you have been charged correctly 6 6 6 Check the seller’s reputation if you have not purchased from them before 7 7 7 Verify a physical address and phone number for the seller 8 8 8 Keep your computer’s operating system, browser and anti-virus software up to date to protect your personal details 9 9 9 I don’t do any of these things 97 97 97

QUANTITATIVE RESEARCH REPORT: ‘Attitudes towards online shopping and knowledge about shopping online securely’. Prepared by Stancombe Research & Planning for NSW Fair Trading, 2012.

45

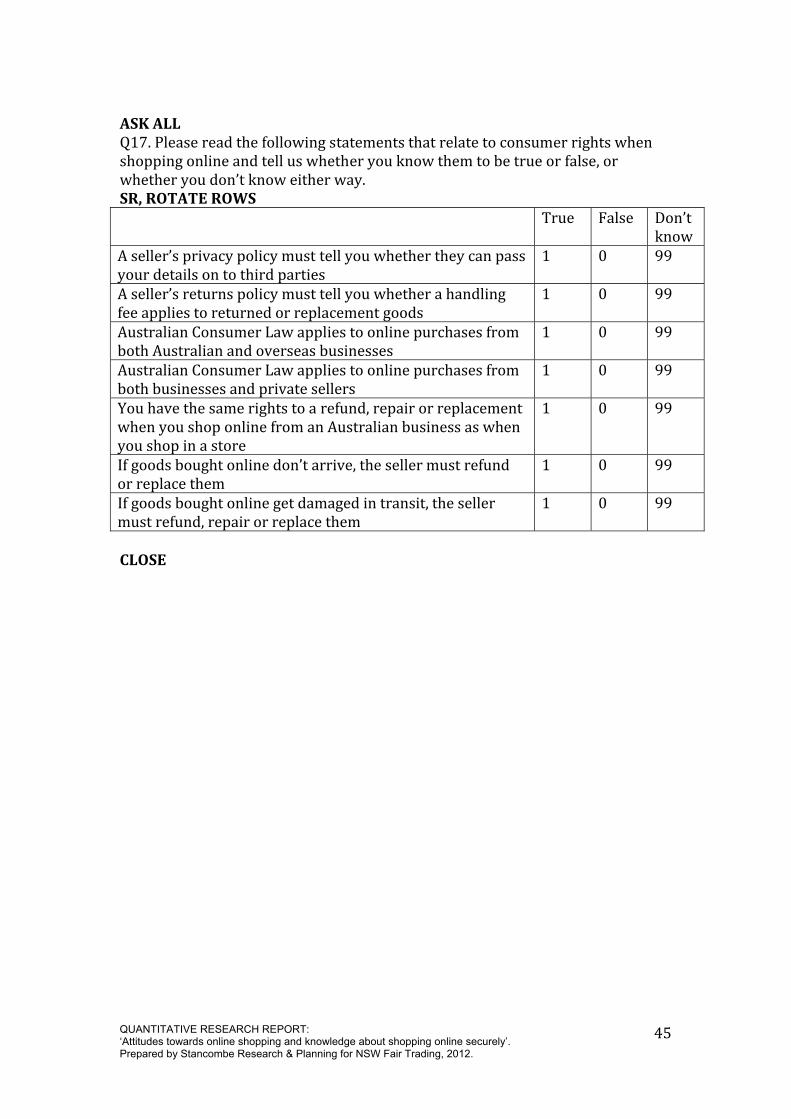

ASK ALL Q17. Please read the following statements that relate to consumer rights when shopping online and tell us whether you know them to be true or false, or whether you don’t know either way. SR, ROTATE ROWS True False Don’t know A seller’s privacy policy must tell you whether they can pass your details on to third parties 1 0 99 A seller’s returns policy must tell you whether a handling fee applies to returned or replacement goods 1 0 99 Australian Consumer Law applies to online purchases from both Australian and overseas businesses 1 0 99 Australian Consumer Law applies to online purchases from both businesses and private sellers 1 0 99 You have the same rights to a refund, repair or replacement when you shop online from an Australian business as when you shop in a store 1 0 99 If goods bought online don’t arrive, the seller must refund or replace them 1 0 99 If goods bought online get damaged in transit, the seller must refund, repair or replace them 1 0 99 CLOSE

QUANTITATIVE RESEARCH REPORT: ‘Attitudes towards online shopping and knowledge about shopping online securely’. Prepared by Stancombe Research & Planning for NSW Fair Trading, 2012.

46

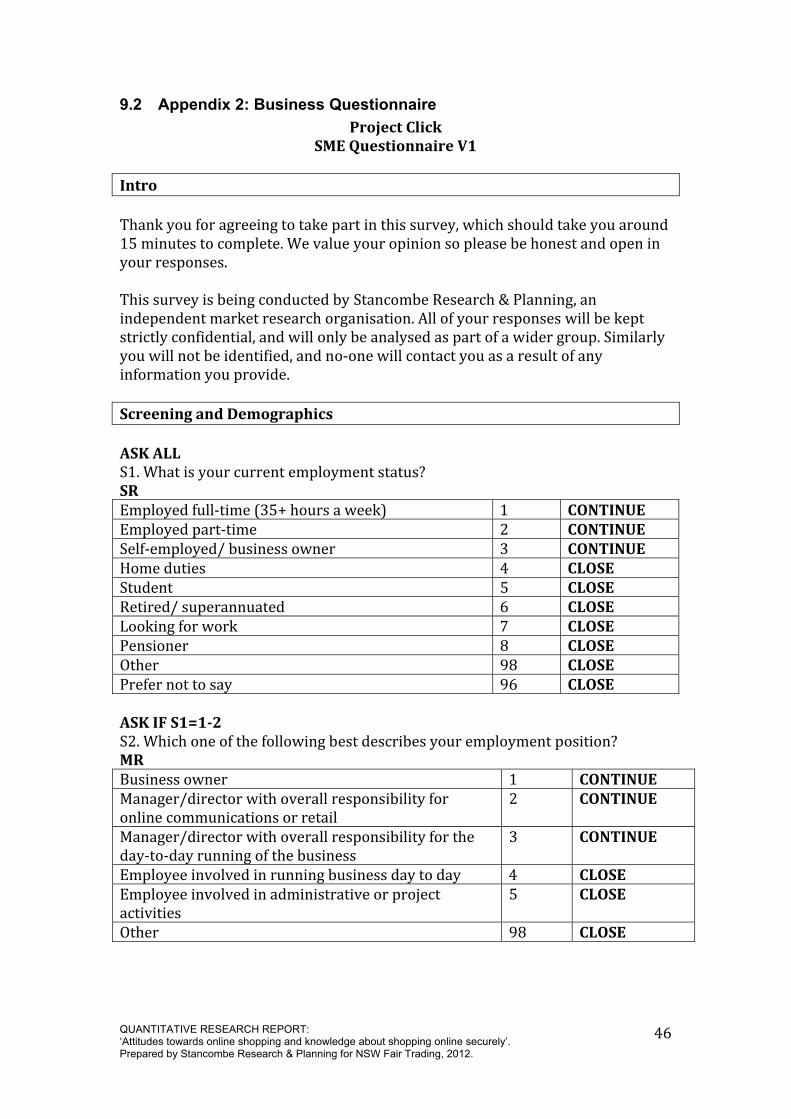

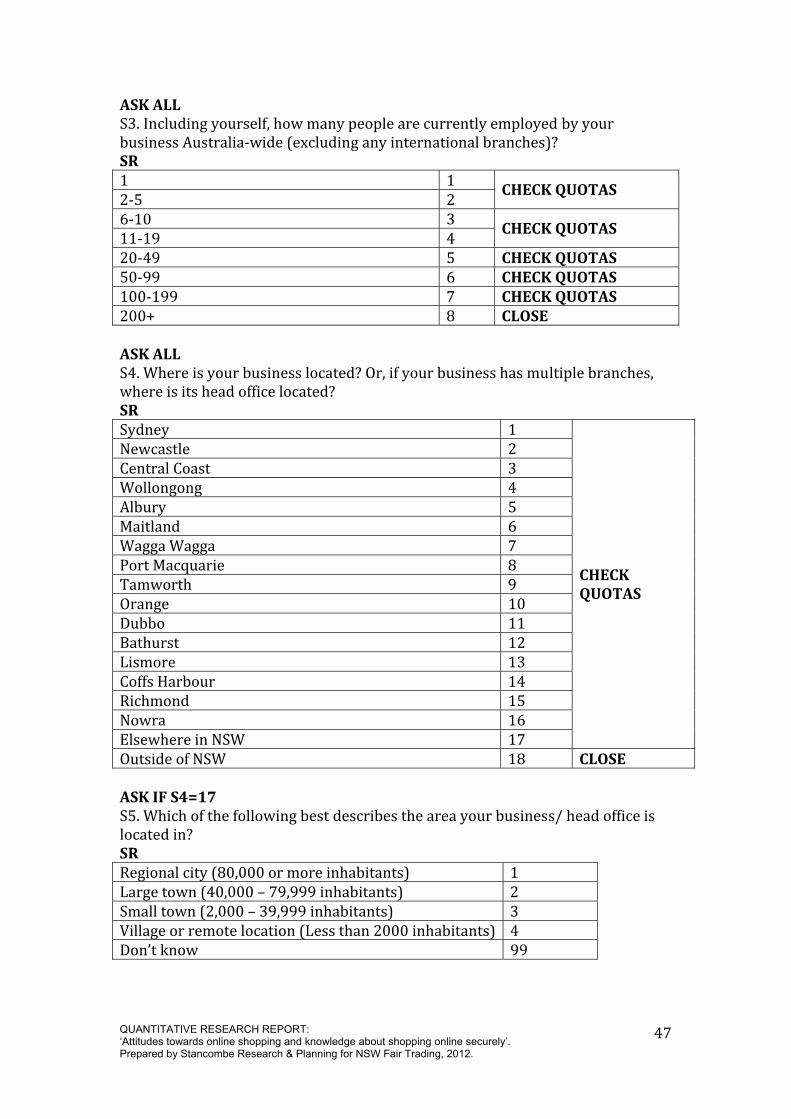

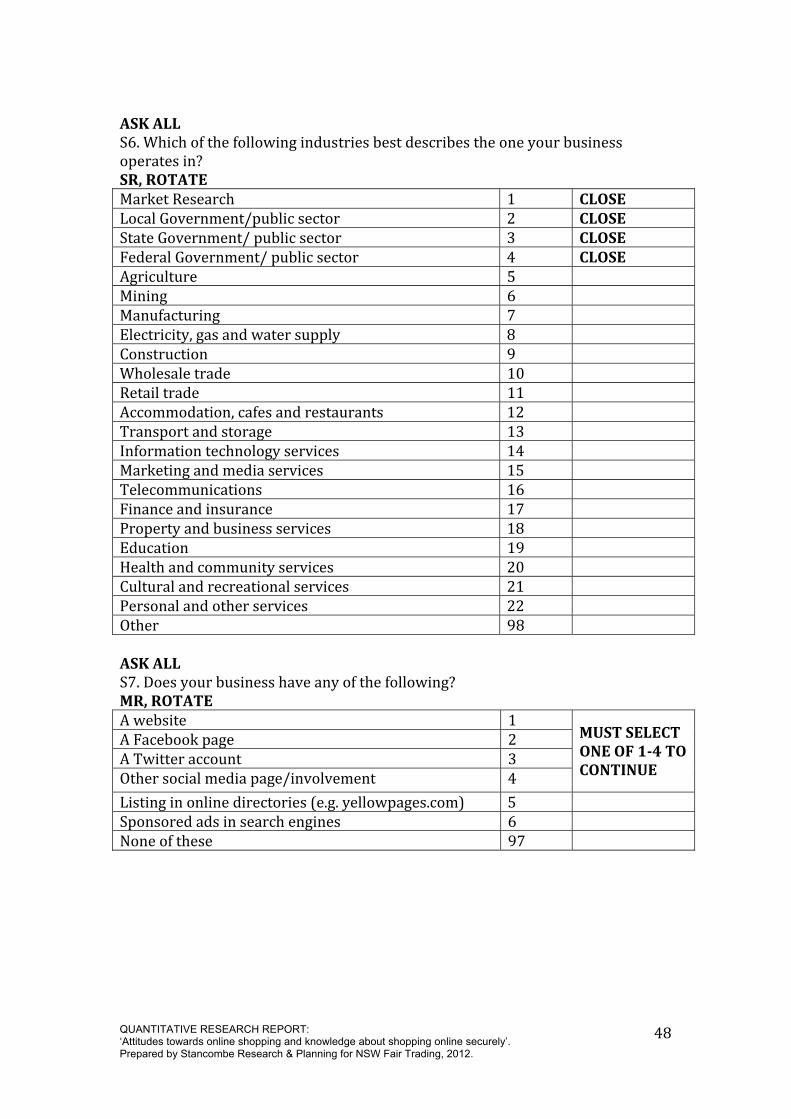

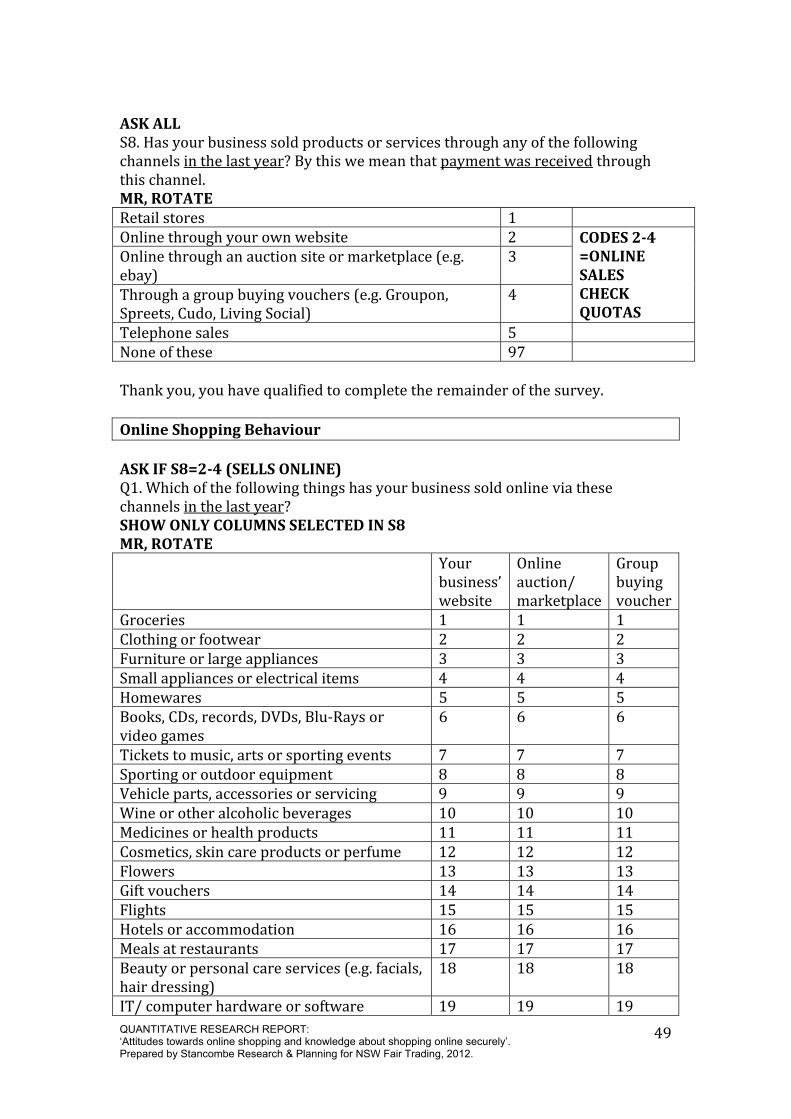

9.2 Appendix 2: Business Questionnaire Project Click