euro zone crisis

TRANSCRIPT

Executive summary

This study is about the Euro Zone crisis and how the Italian

Economy deals with it. In the first part, the analysis and

description of the Euro zone crisis is done briefly and while in

the second part, the description of the Italian economy is

explained briefly. The study also shows how the Euro zone crisis

has affected the Italian economy.

Introduction to Euro zone Crisis

The euro zone crisis was triggered in 2010 by doubts about

the Greek government's ability to service its debt. Investor

reluctance to buy its bonds spread to affect the bond issues

of several other euro zone members, including Ireland and

Portugal; and by late 2011, it was having some effect upon

the bonds of many of its members, even including Germany.

Euro zone loans to Greece, Ireland, and Portugal had failed

to restore investor confidence, and the austerity conditions

attached to those loans were hampering their recovery from

the Great Recession.

Some other member governments were finding it difficult to

roll-over maturing debt, and it came to be realized that the

resources that would be needed to rescue larger members such

as Spain or Italy could be greater than their euro zone

partners could raise. What had been uncertainty about the

fiscal sustainability of a few peripheral members had grown

into uncertainty about the sustainability of the euro zone

system itself.

To make matters worse, the euro zone fell back into

recession in the third quarter of 2012 as the crisis started

to bite more deeply into the core northern economies.

Confidence was partially restored in the course of 2012,

despite the partial default of the Greek government, by the

European Central Bank's willingness to buy bonds that had

been issued by distressed member governments, but there was

awareness of the need for further measures.

As a long-term measure, 25 European Union governments agreed

to a set of balanced-budget undertakings termed the "Fiscal

Compact", and there was agreement in principle to a "Compact

for Growth and Jobs" but the only early action under

consideration was the creation of a banking union to relieve

the pressure on member governments to recapitalize their

banks. Proposals for debt mutualisation, for example by the

creation of "Eurobonds", were firmly rejected.

Background to the crisis

Euro zone

- The euro zone was launched in 1991 as an economic and

monetary union that was intended to increase economic

efficiency while preserving financial stability.

- Financial vulnerability to asymmetric shocks as a result of

disparities among member economies was intended to be

countered in the medium term by limits on public debt and

budget deficits, and in the long term, by progressive

economic convergence.

- By the early years of the 21st century, however, it had

became apparent that the fiscal limits could not be

enforced, and that membership had enabled the governments of

some countries - notably Greece - to borrow on more

favorable terms than had previously been available.

- It had also become evident that membership had reduced the

international competitiveness of low-productivity countries

- such as Greece -, and that it had raised the

competitiveness of high-productivity countries - such as

Germany.

- For those and other reasons, it now appears that there had

been divergence rather than convergence among the economies

of the euro zone, and that their vulnerability to external

shocks had been increased rather diminished.

Members

The original members of the euro zone are: Belgium, Germany,

Ireland, Spain, France, Italy, Luxembourg, the Netherlands,

Austria, Portugal and Finland;

Greece joined in 2001;

Slovenia joined in 2007;

Cyprus and Malta joined in 2008;

Slovakia joined in 2009;

Estonia joined in 2011.

Membership

- In 1991, leaders of the 15 countries that then made up the

European Union, set up a monetary union with a single

currency.

- There were strict criteria for joining (including targets

for inflation, interest rates and budget deficits), and

other rules that were intended to preserve its members'

fiscal sustainability were added later.

- No provision was made for the expulsion of countries that

did not comply with its rules, neither for the voluntary

departure of those who no longer wished to remain, but it

was intended to impose financial penalties for breaches.

- The non-members of the euro zone among members of the

European Union are Denmark, Estonia, Latvia, Lithuania,

Hungary, Poland, Romania, Sweden and the United Kingdom.

Monetary policy

- The monetary policy of the euro zone during its first decade

was conducted in accordance with accepted international

practice.

- The remit given to the European Central Bank assigned

overriding importance to price stability, but also required

it "without prejudice to the objective of price stability"

to "support the general economic policies in the Community"

including a "high level of employment" and "sustainable and

non-inflationary growth.

- In its initial response to the recession of 2009 the Bank

lagged behind other central banks in the adoption of

expansionary monetary policies.

- It eventually made a series of reductions to its discount

rate bringing it down to 1 per cent by the second quarter of

2009.

- When it became clear that those moves had not achieved the

intended easing of the credit crunch it was decided in May

to adopt the controversial and largely untried policy of

quantitative easing.

Fiscal policies

- The Euro zone does not intervene in member governments'

fiscal policies except to monitor, and attempt to enforce,

compliance with the Stability and growth pact. Early

breaches of the pact were followed by a renegotiation that

relaxed its provisions, but there were some further breaches

of the relaxed rules.

- In 2008, the European Commission warned that the euro zone’s

average public debt could reach 84 per cent of GDP by 2010,

and that there were high levels of public debt in Ireland,

Spain and France and Greece.

- In February 2010, euro zone ministers gave assurances that

the euro was not in danger and instructed Greece to reduce

public expenditure and increase taxation in order to reduce

its debt.

Developing crisis

- During 2010, prospective investors became increasingly

reluctant to buy the bonds issued by five euro zone

governments (Portugal, Ireland, Italy, Greece and Spain) at

the offered interest rates, and the governments concerned

had to make a succession of increases in those rates.

- Two of those governments - Greece and Ireland - eventually

decided that, without help, they would not be able to

continue to finance their budget deficits, and they sought -

and received - loans from other European governments.

- Those loans failed to reassure potential investors, and in

November they demanded further increases in the interest

rates on the government bonds of all five governments

(including those of Portugal, Spain and Italy, because of

fears of contagion from Greece and Ireland).

Prospect

- The euro zone crisis has drawn attention to a moral hazard

that is inherent in the design of the euro zone.

- The governments of countries such as Greece are enabled in

effect to pledge the resources of the union's more

creditworthy members such as Germany against their own

borrowings.

- A no bail-out clause in the Maastricht Treaty was intended

to deter abuse, but the time inconsistency of that deterrent

was revealed when it was realized that the contagion costs

of not bailing out the Greek government would exceed the

costs of a bailout.

- By December 2010, there was widespread uncertainty about

future prospects for the euro zone and beyond.

- There were doubts about the willingness of European

governments to provide further financial support to the five

"PIIGS" governments, and speculation that financing

difficulties might spread to affect other governments.

- Some commentators considered it inevitable that one or other

of the PIIGS governments would default on, or restructure,

its loans, and other commentators forecast departures from

the euro zone by governments wishing to escape its

restraints.

- There were even those who envisaged wholesale departures,

leading to a collapse of the common currency - an outcome

that would impose substantial losses upon countries with

investments in euro-denominated securities, and could

threaten the stability of the international financial

system.

The European Central Bank

- The European Central Bank is the core of the "Euro system"

that consists also of all the national central banks of the

member countries of the Union (whether or not they are

members of the euro zone).

- Its governing body consists of the six members of its

Executive Board, and the governors of the national central

banks of the 17 euro zone countries.

- It is responsible for the execution of the Union's monetary

policy. Its statutory remit requires that, "without

prejudice to the objective of price stability", it is to

"support the general economic policies in the Community"

including a "high level of employment" and "sustainable and

non-inflationary growth".

- The bank's governing board sets the euro zone’s discount

rates and has been responsible for the introduction and

management of refinancing operations.

- Article 101 of the European Treaty expressly forbids the ECB

from lending to governments and Article 103 prohibits the

euro zone from becoming liable for the debts of member

states.

The Stability and Growth Pact

- The Stability and Growth Pact that was introduced as part of

the Maastricht Treaty in 1992 set arbitrary limits upon

member countries' budget deficits and levels of public debt

at 3 per cent and 60 per cent of GDP respectively.

- Following multiple breaches of those limits by France and

Germany, the pact has since been renegotiated to introduce

the flexibility announced as necessary to take account of

changing economic conditions.

- Revisions introduced in 2005 relaxed the pact's enforcement

procedures by introducing "medium-term budgetary objectives"

that are differentiated across countries and can be revised

when a major structural reform is implemented; and by

providing for abrogation of the procedures during periods of

low or negative economic growth.

- A clarification of the concepts and methods of calculation

involved was issued by the European Union's The Economic and

Financial Affairs Council in November 2009 which includes an

explanation of its excessive deficit procedure.

- According to the Commission services 2011 spring forecasts,

the government deficit exceeded 3% of GDP in 22 of the 27

European Union countries in 2010.

The European Financial Stability Facility

- In May 2010, the Council of Ministers established a

Financial Stability Facility (EFSF) to assist euro zone

governments in difficulties "caused by exceptional

circumstances beyond their control".

- It was empowered to rise up €440 billion by issuing bonds

guaranteed by member states.

- It was to supplement an existing provision for loans of up

to €60 billion by the European Financial Stability Mechanism

(EFSM), and loans by the International Monetary Fund.

- Proposals to leverage the €440 billion by loans from the

European Central Bank were not authorized until October

2011.

- Loans are subject to conditions negotiated with European

Commission and the IMF, and accepted by the euro zone

Finance Ministers.

- The EFSF and the EFSM were replaced in 2013 by a permanent

crisis resolution regime, called the European Stability

Mechanism (ESM), which is to be a supranational institution,

established by international treaty, with an independent

decision-making power. (A comprehensive explanation of the

EFSF and the ESM is available in question-and-answer form.)

Pre-crisis performance

- Neither a 1999-2008 growth rate comparison, nor a 2008-2011

growth rate comparison shows a significant difference

between the performance of the euro zone as a whole and of

the European Union as a whole, However, there is clear

evidence that the Great Recession had imposed an asymmetric

shock on the euro zone, causing downturns of above average

severity in the economies of the PIIGS countries (Portugal,

Italy, Ireland, Greece and Spain), that are attributable to

departures from currency area criteria, including large

differences in member country trade balances, limited labour

mobility and price flexibility.

The PIIGS

- The economies of the PIIGS countries differed in several

respects from those of the others.

- Unlike most of the others, they had developed deficits on

their balance of payments current accounts (largely

attributable to the effect of the euro's exchange rate upon

the competitiveness of their exports).

- Deleveraging of corporate and household debt had amplified

the effects of the recession to a greater extent -

especially in those with larger-than-average financial

sectors, and those that had experienced debt-financed

housing booms.

- In common with the others, they had developed cyclical

deficits under the action of their economies' automatic

stabilizers and of their governments' discretionary fiscal

stimuli, and increases in existing structural deficits as a

result of losses of revenue-generating productive capacity.

- In some cases, their budget deficits had been further

increased by subventions and guarantees to distressed banks

Causes of the Euro Crisis

Rising household and government debt levels

- In 1992, members of the European Union signed the Maastricht

Treaty, under which they pledged to limit their deficit

spending and debt levels. However, a number of EU member

states, including Greece and Italy, were able to circumvent

these rules, failing to abide by their own internal

guidelines, sidestepping best practice and ignoring

internationally agreed standards.

- This allowed the sovereigns to mask their deficit and debt

levels through a combination of techniques, including

inconsistent accounting, off-balance-sheet transactions as

well as the use of complex currency and credit derivatives

structures. The complex structures were designed by

prominent U.S.investment banks, who received substantial

fees in return for their services.

- The adoption of the euro led to many Euro zone countries of

different credit worthiness receiving similar and very low

interest rates for their bonds and private credits during

years preceding the crisis. As a result, creditors in

countries with originally weak currencies (and higher

interest rates) suddenly enjoyed much more favorable credit

terms, which spurred private and government spending and led

to an economic boom. In some countries such as Ireland and

Spain low interest rates also led to a housing bubble, which

burst at the height of the financial crisis.

- A number of economists have dismissed the popular belief

that the debt crisis was caused by excessive social welfare

spending. According to their analysis, increased debt levels

were mostly due to the large bailout packages provided to

the financial sector during the late-2000s financial crisis,

and the global economic slowdown thereafter.

- The average fiscal deficit in the euro area in 2007 was only

0.6% before it grew to 7% during the financial crisis. In

the same period, the average government debt rose from 66%

to 84% of GDP.

- Excessive lending by banks and not deficit spending created

this crisis. Government's mounting debts are a response to

the economic downturn as spending rises and tax revenues

fall, not its cause.

Trade imbalances

- Commentator and Financial Times journalist Martin Wolf has

asserted that the root of the crisis was growing trade

imbalances. He notes in the run-up to the crisis, from 1999

to 2007, Germany had a considerably better public debt and

fiscal deficit relative to GDP than the most affected euro

zone members.

- In the same period, these countries (Portugal, Ireland,

Italy and Spain) had far worse balance of payments

positions. Whereas German trade surpluses increased as a

percentage of GDP after 1999, the deficits of Italy, France

and Spain all worsened.

- A trade deficit by definition requires a corresponding

inflow of capital to fund it, which can drive down interest

rates and stimulate the creation of bubbles: "For a while,

the inrush of capital created the illusion of wealth in

these countries, just as it did for American homeowners:

asset prices were rising, currencies were strong, and

everything looked fine.

- But a bubble always burst sooner or later, and yesterday’s

miracle economies have become today’s basket cases, nations

whose assets have evaporated but whose debts remain all too

real."

- A trade deficit can also be affected by changes in relative

labour costs, which made southern nations less competitive

and increased trade imbalances.

- Since 2001, Italy's unit labor costs rose 32% relative to

Germany's Greek unit labour costs rose much faster than

Germany's during the last decade.

- However, most EU nations had increases in labour costs

greater than Germany's. Those nations that allowed "wages to

grow faster than productivity" lost competitiveness.

Germany's restrained labour costs, while a debatable factor

in trade imbalances, are an important factor for its low

unemployment rate.

- The euro locks countries into an exchange rate amounting to

“very big bet that their economies would converge in

productivity.” If not, workers would move to countries with

greater productivity. Instead the opposite happened: the gap

between German and Greek productivity increased resulting in

a large current account surplus financed by capital flows.

The capital flows could have been invested to increase

productivity in the peripheral nations. Instead capital

flows were squandered in consumption and consumptive

investments.

Loss of confidence

- Prior to development of the crisis it was assumed by both

regulators and banks that sovereign debt from the euro zone

was safe.

- Banks had substantial holdings of bonds from weaker

economies such as Greece which offered a small premium and

seemingly were equally sound.

- As the crisis developed it became obvious that Greek, and

possibly other countries', bonds offered substantially more

risk. Contributing to lack of information about the risk of

European sovereign debt was conflict of interest by banks

that were earning substantial sums underwriting the bonds.

- The loss of confidence is marked by rising sovereign CDS

prices, indicating market expectations about countries'

creditworthiness.

- Investors have doubts about the possibilities of policy

makers to quickly contain the crisis. Since countries that

use the euro as their currency have fewer monetary policy

choices (e.g., they cannot print money in their own

currencies to pay debt holders), certain solutions require

multi-national cooperation. Further, the European Central

Bank has an inflation control mandate but not an employment

mandate, as opposed to the U.S. Federal Reserve, which has a

dual mandate.

- Heavy bank withdrawals have occurred in weaker Euro zone

states such as Greece and Spain. Bank deposits in the Euro

zone are insured, but by agencies of each member government.

- If banks fail, it is unlikely the government will be able to

fully and promptly honor their commitment, at least not in

euros, and there is the possibility that they might abandon

the euro and revert to a national currency; thus, euro

deposits are safer in Dutch, German, or Austrian banks than

they are in Greece or Spain.

- As of June, 2012, many European banking systems were under

significant stress, particularly Spain. A series of "capital

calls" or notices that banks required capital contributed to

a freeze in funding markets and interbank lending, as

investors worried that banks might be hiding losses or were

losing trust in one another.

- In June 2012, as the euro hit new lows, there were reports

that the wealthy were moving assets out of the Euro zone and

within the Euro zone from the South to the North. Between

June 2011 and June 2012 Spain and Italy alone have lost 286

bn and 235 bn euros.

- Altogether Mediterranean countries have lost assets worth

ten per cent of GDP since capital flight started in end of

2010.Mario Draghi, president of the European Central Bank,

has called for an integrated European system of deposit

insurance which would require European political

institutions craft effective solutions for problems beyond

the limits of the power of the European Central Bank. As of

June 6, 2012, closer integration of European banking

appeared to be under consideration by political leaders

Monetary policy inflexibility

- Membership in the Euro zone established a single monetary

policy, preventing individual member states from acting

independently. In particular they cannot create Euros in

order to pay creditors and eliminate their risk of default.

Since they share the same currency as their (euro zone)

trading partners, they cannot devalue their currency to make

their exports cheaper, which in principle would lead to an

improved balance of trade, increased GDP and higher tax

revenues in nominal terms.

- In the reverse direction moreover, assets held in a currency

which has devalued suffer losses on the part of those

holding them. For example, by the end of 2011, following a

25 % fall in the rate of exchange and 5 % rise in inflation,

euro zone investors in Pound Sterling, locked into euro

exchange rates, had suffered an approximate 30 % cut in the

repayment value of this debt.

The PIIGS crisis (March 2010 to October 2011)

Overview

- The Great Recession brought about large increases in the

indebtedness of the euro zone governments and by 2009,

twelve member states had public debt/GDP ratios of over 60%

of GDP.

- Concern developed in early 2010 concerning the fiscal

sustainability of the economies of the "PIIGS" countries

(Portugal, Ireland, Italy, Greece and Spain) and a euro zone

fund was set up to assist members in difficulty.

- Bond markets were eventually reassured by the conditional

loans provided to Ireland, but despite a euro zone loan to

Greece, they demanded increasing risk premiums for lending

to its government.

- In late 2010 there were signs of contagion of market fears

by the governments of other euro zone countries, and it

appeared that the integrity of the euro zone was being put

in question.

The Greek problem

- In April 2010, the Greek government faced the prospect of

being unable to fund its maturing debts.

- Its problems arose from large increases in its sovereign

spreads reflecting the bond market's fears that it might

default - fears that were based upon both its large budget

deficits, and its limited economic prospects.

- In May 2010, the Greek government was granted a €110 billion

rescue package, financed jointly by the euro zone

governments and the IMF.

- Further increases in spreads showed that those rescue

packages had failed to reassure the markets.

The Irish problem

- Between 2009 and 2010 Ireland's budget deficit increased

from 14.2 per cent to 32.4 per cent of GDP, as a result

mainly of one-off measures in support of the banking sector.

November 2010 the government applied for financial

assistance from the EU and the IMF.

- By the autumn of 2011 the government's programmes of tax

increases had brought about a major improvement in fiscal

sustainability, bringing down its budget deficit from 32.4

percent to an expected 10.6 percent of GDP and enabling the

government to return to the bond market.

Contagion among the PIIGS

- Signs began to appear of the contagion of the bond market

fears from Greece to other PIIGS countries, particularly

Portugal and Spain.

- Portugal received an EU/IMF rescue package in May 2011, and

Greece was assigned a second package in July, neither of

which restored the bond market's confidence in euro zone

sovereign debt.

- There was a dramatic increase in measures of the market

assessment of default risk, implying a 98 per cent

probability of a Greek government default.

- Also in 2011, there was a major decline in confidence in

euro zone banks, following rumors that losses on Greek bonds

had left them undercapitalized.

- What had started as a Greek crisis was developing into a

euro zone crisis because the rescue packages that could be

needed for the much bigger economies of Spain or Italy were

expected to be larger than the euro zone could afford. Bond

market concern about the sustainability of Italy's public

debt was reflected in a progressive rise in the yield on its

10-year government bonds during 2011, and by October it had

risen to over 5 percent.

Policy responses

Overview

- On the 26th of October, a meeting of euro zone leaders was

held, the declared purpose of which was to restore

confidence by adopting a "comprehensive set of additional

measures reflecting our strong determination to do whatever

is required to overcome the present difficulties".

- One set of measures that was adopted for that purpose,

acknowledged the Greek government's inability to repay its

debt in full, and provided for the restructuring of that

debt, and for the financial support necessary for the

government's survival.

- A second set was intended to provide an insurance against

the contagion by other euro zone countries of the Greek

government's difficulties and to assure the markets that

sufficient euro zone funds would be available to cope with

contagion should it occur.

- Thirdly, and in view of the market's awareness that a rescue

of the Italian government would impose a major drain on

those funds, the leaders sought to strengthen that

government's defenses against default

Restructuring the Greek debt

- The rescue package for Greece included a 50 percent write-

off of the Greek government's debt (as had been agreed with

the Institute of International Finance representing the

world's banks), and a €130 billion conditional loan.

- The Greek government responded to the conditions for the

loan by calling a referendum to enable the Greek people to

decide whether to accept the package.

- At an emergency summit on 2nd November, however, Greek Prime

Minister Papandreou was persuaded by French President

Sarkozy and German Chancellor Merkel that the subject of the

referendum should be whether Greece should remain within the

euro zone, rather than the acceptability of the rescue

package.

- He was also told that the €8 billion tranche of the EU/IMF

loan that (needed to avoid a default in December) would be

withheld until after the referendum.

- Acknowledging the prospect that the referendum could result

in the departure of Greece from the euro zone, Jean-Claude

Juncker, the Chairman of the Euro group of euro zone Finance

Ministers announced that preparations for that outcome were

in hand.

- The next day Prime Minister Papandreou announced his

willingness to cancel the referendum, and that he had

obtained agreement of opposition leaders to do so.

- On the 6th of November party leaders agreed to form a

coalition government under a new Prime Minister.

- A new government was formed with Lucas Papa demos as Prime

Minister of Greece, and the terms of the EU rescue were

agreed.

Strengthening the firewall

- The "firewall measures" that were proposed in order to limit

contagion by European governments and their banks included a

4- to 5-fold increase in the size of the European Financial

Stability Facility and the recapitalization of selected euro

zone banks.

The larger PIIGS

- There was concern about the short-term fiscal stability of

Italy and Spain in view of the large sums that would be

required to roll-over debts that are due to mature in 2012 -

amounts that are much larger than those needed to rescue

Greece (approximately €300 billion for Italy and €150

billion for Spain).

- Market concern arose from doubts about the willingness of

the euro zone leaders to commit themselves to the continuing

support of Italy and Spain, and about their ability to raise

the necessary funds.

- In December 2011, with sovereign bond yields at around 7 per

cent for Italy and 6 per cent for Spain, it appeared

questionable whether those countries would be able to raise

the funds required by further bond issues.

- On 12th January, however, Spain and Italy sold about €22bn

of government debt at sharply lower costs than at previous

auctions.

- In June 2012 the Spanish government requested, and was

granted, a €100bn loan from the European Union to re

capitalize its banks

The euro zone crisis (November 2011 to present)

Overview

- Bond market investors were not immediately reassured by the

decisions of October 2011 and there was a loss of confidence

that extended briefly beyond the PIIGS group.

- Despite the new Italian government's acceptance of the

measures had been agreed, the yields on its bonds rose to

over 7 per cent.

- However, the December offer by the European Central Banks to

lend unlimited amounts to euro zone banks at an interest

rate of 1 per cent, was followed by a marked reduction in

the yields on Italian and Spanish government bonds and,

following the Bank's subsequent bond purchases, there was a

general recovery of investor confidence.

- In other respects the crisis deepened, with falling growth

and deteriorating economic in Portugal, Italy, Greece and

Spain, and in the euro zone as a whole.

- Also, there is continuing uncertainty concerning the fiscal

sustainability of Greece and Spain.

The larger PIIGS

- There was concern about the short-term fiscal stability of

Italy and Spain in view of the large sums that would be

required to roll-over debts that are due to mature in 2012 -

amounts that are much larger than those needed to rescue

Greece (approximately €300 billion for Italy and €150

billion for Spain).

- Market concern arose from doubts about the willingness of

the euro zone leaders to commit themselves to the continuing

support of Italy and Spain, and about their ability to raise

the necessary funds.

- In December 2011, with sovereign bond yields at around 7 per

cent for Italy and 6 per cent for Spain, it appeared

questionable whether those countries would be able to raise

the funds required by further bond issues.

- On 12th January, however, Spain and Italy sold about €22bn

of government debt at sharply lower costs than at previous

auctions.

- In June 2012 the Spanish government requested, and was

granted, a €100bn loan from the European Union to re

capitalize its banks

Proposals

A number of different long-term proposals have been put forward

by various parties to deal with the Euro zone crises, these

include;

European fiscal union

- Increased European integration giving a central body

increased control over the budgets of member states was

proposed on June 14, 2012 by Jens Weidmann President of the

Deutsche Bundesbank, expanding on ideas first proposed by

Jean-Claude Trichet, former president of the European

Central Bank. Control, including requirements that taxes be

raised or budgets cut, would be exercised only when fiscal

imbalances developed.

- This proposal is similar to contemporary calls by Angela

Merkel for increased political and fiscal union which would

"allow Europe oversight possibilities.

European bank recovery and resolution authority

- European banks are estimated to have incurred losses

approaching €1 trillion between the outbreak of the

financial crisis in 2007 and 2010.

- The European Commission approved some €4.5 trillion in state

aid for banks between October 2008 and October 2011, a sum

which includes the value of taxpayer-funded

recapitalizations and public guarantees on banking debts.

- On 6 June 2012, the European Commission adopted a

legislative proposal for a harmonized bank recovery and

resolution mechanism.

- The proposed framework sets out the necessary steps and

powers to ensure that bank failures across the EU are

managed in a way which avoids financial instability.

- The new legislation would give member states the power to

impose losses, resulting from a bank failure, on the

bondholders to minimize costs for taxpayers. The proposal is

part of a new scheme in which banks will be compelled to

“bail-in” their creditors whenever they fail, the basic aim

being to prevent taxpayer-funded bailouts in the future.

- The public authorities would also be given powers to replace

the management teams in banks even before the lender fails.

Each institution would also be obliged to set aside at least

one per cent of the deposits covered by their national

guarantees for a special fund to finance the resolution of

banking crisis starting in 2018.

Eurobonds

- A growing number of investors and economists say Eurobonds

would be the best way of solving a debt crisis, though their

introduction matched by tight financial and budgetary

coordination may well require changes in EU treaties.

- On 21 November 2011, the European Commission suggested that

euro bonds issued jointly by the 17 euro nations would be an

effective way to tackle the financial crisis.

- Using the term "stability bonds", Jose Manuel Barroso

insisted that any such plan would have to be matched by

tight fiscal surveillance and economic policy coordination

as an essential counterpart so as to avoid moral hazard and

ensure sustainable public finances.

European Monetary Fund

- On 20 October 2011, the Austrian Institute of Economic

Research published an article that suggests transforming the

EFSF into a European Monetary Fund (EMF), which could

provide governments with fixed interest rate Eurobonds at a

rate slightly below medium-term economic growth (in nominal

terms).

- These bonds would not be tradable but could be held by

investors with the EMF and liquidated at any time. Given the

backing of all euro zone countries and the ECB "the EMU

would achieve a similarly strong position vis-a-vis

financial investors as the US where the Fed backs government

bonds to an unlimited extent."

- To ensure fiscal discipline despite lack of market pressure,

the EMF would operate according to strict rules, providing

funds only to countries that meet fiscal and macroeconomic

criteria. Governments lacking sound financial policies would

be forced to rely on traditional (national) governmental

bonds with less favorable market rates.

- Furthermore, banks would no longer be able to unduly benefit

from intermediary profits by borrowing from the ECB at low

rates and investing in government bonds at high rates

Impact on the Italian Economy

The Quiet Collapse of the Italian Economy

- While attention on the Euro crisis has been focusing

primarily on Greece and Cyprus, it is no mystery that Italy,

alongside with Spain, constitutes the real challenge for the

future of the common currency, in any direction events will

be unfolding.

- In the relative silence of the international press, Italy’s

macroeconomic situation has been showing no sign of

improvement, and indeed numerous indicators portray a

national economy which finds itself in a depression, rather

than in a however severe recession. It is no overstatement

that the Italian economy is currently collapsing.

- Italy is the third largest economy of the Euro zone (after

Germany and France), holds the largest public debt (over €2

trillion), which has been growing at an astonishing pace,

even in more recent times and particularly as a ratio to GDP

(130%), since the latter is contracting fast. How is this

sustainable?

- Well, it is not. But for the moment, thanks to the ECB

direct interventions (€102.8 billion of Italian bond

purchases in 2011-12) and especially to the LTRO mechanisms,

the finances of the Italian state can still be kept afloat.

- Italian banks have been absorbing €268 billion of liquidity

issued by the ECB by means of the LTRO programme. In its

essence, the mechanism is the following: because the ECB

cannot lend liquidity directly to the states, except in

times of absolute emergency and for the stabilization of

financial markets in the short term (as happened in 2011),

it lends money to the banks, which in turn purchase

government-issued bonds.

- Interestingly, the LTRO scheme has also become an instrument

for the relatively orderly withdrawal of international

investors from Italy, especially French and German, whose

share of public debt has fallen from 51% to 35%, mirroring

the rise of Italian banks purchasing public debt.

- This is an important signal, which goes in the opposite

direction of an increased interdependency as would be

expected from a monetary union in preparation for a

political union.

- It is arguable that many investors are actually

systematically reducing their exposure in South Europe,

possibly hoping that a future breakup of the common currency

will have less harmful consequences if their involvement in

the financial and economy destiny of those countries is

curtailed to the minimum. For Eurosceptics, it is a signal

that, once all foreign investors withdraw, Italy will be

left to its fate.

- The truth is that the Italian state went bankrupt in summer

2011, when interest rates on the national debt went out of

control, and as a result Italy lost access to the financial

markets.

- Of course, because of the sheer dimensions of Italy as an

economy and as a debtor, the ECB and political authorities

in Europe have agreed to create around the country’s

finances the appearance of a market, which is in fact, as

the numbers above show, largely artificial. Ideally, Italy

should stay on this artificial support until the economic

conditions improve and confidence is restored to such a

level that the country will have again access to a “normal”

credit market.

- However, this is not happening and there is no sign it is

going to happen in the years to come.

- The situation of the Italian economy is simply dramatic.

Recently, a study has appeared which reveals how the current

crisis (2007-2013) is in many ways much worse than the 1929-

1934 contraction.

- In the present crisis, investments have collapsed by 27.6%

in the five year period, against 12.8% in the interwar

depression.

- GDP has declined by 6.9% against 5.1%. Italy, with the

second largest manufacturing sector in Europe after

Germany, has lost about 24% of its industrial production,

going back to the 1980s level.

- No data is currently showing any sign of recovery. From the

beginning of this year, the country has lost over 31,000

companies. Every day 167 retail units are lost, signaling an

authentic disintegration of the retail sector.

- The automotive sector, a crucially important one for the

Italian economy, has been constantly contracting: from about

2.5 million cars sold in 2007, sales in 2012 reached only

the 1.4 million mark (the 1979 level) and they are still

contracting this year. Construction, the other pillar of the

national economy, is in rout: the 14% slump in 2012 is only

the last in a series of difficult years.

- Home sales have dropped by 29% in 2012 against the already

miserable 2011, to the 1985 level of 444,000 units, about

half the number of 2006.

- Of course, the consequences of this economic disaster in

terms of loss of employment are dire: unemployment is now at

almost 12% and growing fast.

- The Italian state has so far managed to defend its financial

position by means of increased taxation, limited spending

cuts and more borrowing. The borrowing scheme has been

engineered with the help of the ECB and the banking sector.

- Under pressure from the European Union, Italy has committed

to a rigorous budget and it has even introduced a balanced-

budget amendment in its constitution. Absurdly, the Italian

state runs a surplus when public debt interest payments are

excluded, but this only appears to be because, purely and

simply, the state often “forgets” to pay its suppliers (the

outstanding debt to private companies is in the €90-€130

billion range, depending on the criteria for calculation).

- Now, it is not difficult to imagine that, in a few months,

despite the new taxes, the sheer collapse of entire sectors

of the economy will cause a rapid contraction of tax

revenues.

- The Italian state cannot possibly accumulate even more debt

at a faster pace (at least for Italy, the austerity debate

makes little sense). Italy will simply run out of options,

and it will require additional measures from the EU. But

because of the sheer size of the economy and the public

debt, this is simply impossible.

- In the absence of any political consensus around a radically

different monetary policy of the ECB, i.e. unlimited QE,

which will probably never materialize, and which will

clearly not solve any of the country’s structural problems,

the only realistic scenario will be that of a debt

restructuring or renegotiation, as suggested by Nouriel

Roubini in a precise analysis published more than 18 months

ago.

- The collapse of the Italian state finances is rapidly

approaching. It will have an enormous impact on the Euro

zone and the European Union.

The Demise of Italy and the Rise of Chaos

- Future historians will probably regard Italy as the perfect

showcase of a country which has managed to sink from the

position of a prosperous, leading industrial nation just two

decades ago to a condition of unchallenged

economic desertification, total demographic mismanagement,

rampant “third worldisation”, plummeting cultural production

and a complete political-constitutional chaos.

- The government knows perfectly well that the situation is

unsustainable, but for the moment it is only capable to

resorting to an extremely short-sighted VAT rate increase

(to a staggering 22%), which will depress consumption even

more, and to vague proclaims about the necessity of shifting

the tax burden way from wages and companies to financial

rents, although the chances of this to be implemented are

essentially negligible

- Indeed, it is not impossible for an economy which has lost

about 8% of its GDP to have one or more quarters in positive

territory. However, it is a profound distortion of

elementary semantics to call a (perhaps) +0.3% annual

rebound as “recovery”, considering the economic disaster

unfolding in the last five years. More correct would be to

talk about a transition from a severe recession to some sort

of stagnation.But unfortunately, like characters of a Greek

tragedy; Italian leaders were deprived by the gods even of

this illusionary and pitiful dream of stagnation. Economic

data of the summer months indicate that the economic

downturn is far from being over.

- A recent study indicates that 15% of Italy’s manufacturing

industry, which before the crisis was the largest in Europe

after Germany’s, has been destroyed, and about 32,000

companies have disappeared.

- This data alone shows the immense amount of essentially

irreparable damage which the country is undergoing. In the

author’s view, this situation has its roots in the immensely

degraded political culture of the country’s elite, which, in

the last few decades, has negotiated and signed countless

international agreements and treaties without ever

considering the real economic interest of the country and

without any meaningful planning of the nation’s future.

- Italy could not have entered the last wave of globalization

under worse conditions. The country’s leadership never

recognized that indiscriminate opening to Asia’s light

industrial products would destroy Italy’s once leading

industries in the same sectors.

- They signed the euro treaties promising to the European

partner’s reforms which have never been implemented, but

fully committing themselves to austerity policies. They

signed the Dublin Regulation on EU borders knowing perfectly

well that Italy is not even remotely able (as shown by the

continuous influx of illegal migrants in Lampedusa and the

inevitable deadly incidents) to patrol and protect its

borders. Consequently, Italy has found itself locked up in a

web of legal structures which are making the complete demise

of the nation practically certain.

- Italy has currently the highest taxation levels on companies

in the EU and one of the highest in the world. This factor,

together with a fatal mix of awful financial management,

inadequate infrastructure, ubiquitous corruption and an

inefficient bureaucracy, which includes the slowest and most

unreliable justice system in Europe, is pushing all

remaining entrepreneurs out of the country.

- This time not only towards cheap labour destinations, such

as East or South Asia, but a large flux of Italian companies

is pouring in neighboring Switzerland and Austria, where,

despite the relatively high labour costs, companies will

find a real state cooperating with them, instead of

sabotaging them.

- The demise of Italy as an industrial nation is also

reflected by the unprecedented level of brain drain, with

tens of thousands young researchers, scientists, technicians

emigrating to Germany, France, Britain, Scandinavia, as well

as to North America and East Asia.

- Thus, everybody in the country producing anything of value,

together with most of the educated people is leaving,

planning to leave, or would like to leave. Indeed, Italy has

become a place for some sort of demographic pillaging from

the perspective of other, more organized countries, which

have long seen the opportunity to easily attract highly

qualified workers, often trained at the expenses of the

Italian state, simply by offering them reasonable economic

prospects which they will never see if they remain in Italy.

- All this seems not to preoccupy the Italian political

leadership. On the one hand, the country is the prisoner of

a cultural duopoly: it is either the Catholic culture, or

the socialist culture. Both are preoccupied with universal

ambitions (somehow eschatological and increasingly anti-

modernist) which make the national perspective unviable to

them. Indeed, the Italian state was created by liberal-

conservative and monarchist modernists, sometimes animated

by virulent forms of anticlericalism, essentially the

opposite of the current political elite.

- It is not surprising that what the former accomplished gets

dismantled by the latter. The problem is not so much,

however, the dismantling of the nation state, but that the

nation state is not going to be replaced by any meaningful

political project, leaving its space, essentially, to chaos.

- Italy has entered a period of constitutional anomaly.

Because party politicians have brought the country to a

near-collapse in 2011, an event which would have had severe

consequences globally, the country has been essentially

taken over by a small number of technocrats coming from the

President of the Republic’s office, the bureaucrats of

several key ministries and the Bank of Italy. Their task is

to guarantee stability to Italy vis-à-vis the EU and the

financial markets at any cost. This has been so far achieved

by sidelining both the political parties and the parliament

to unprecedented levels, and with a ubiquitous and

constitutionally questionable interventionism from the

President of the Republic, who has extended his powers well

beyond the boundaries of the still officially parliamentary

republican order.

- The President’s interventionism is particularly evident in

the creation of the Monti government and in the current

Letta government, which are both direct expression of the

Quirinale.

- The point here is that, where politicians have failed,

bureaucrats and technocrats hope to succeed. The illusion,

which many Italians are cultivating by believing that the

President, the Bank of Italy and the bureaucracy know better

how to save the country, is now widespread. They will be

bitterly disappointed. The current leadership, both

technocratic and political, has no ability, and perhaps even

no intention, to save the country from ruin. On the

contrary, it would be easy to argue that Monti’s policies

have exacerbated the already severe recession. Letta is

following exactly the same path. But everything has to

be sacrificed in the name of stability. The technocrats

share the same cultural backgrounds of the political

parties, and in symbiosis with them have managed to rise to

their current positions: it is therefore hopeless to think

that they will obtain better results, since they are also

unable to have any sort of long term vision for the country.

They are actually the guarantors of Italy’s demise.

- In conclusion, the rapidity of the decline is truly

breathtaking. This is certainly not exclusive to Italy, as

arguably most if not all Western countries are undergoing

rampant third worldisation.

- Italy has simply less economic and social “capital” to burn

in comparison to Germany and other Nordic countries. But it

must be clear that, continuing on this way, there will be

nothing left of Italy as a modern industrial nation in less

than a generation. But just in another decade or so entire

regions of the country, such as Sardinia or Liguria, will be

so much demographically compromised that they may never

recover.

- The founders of the Italian state one hundred and fifty-two

years ago had fought and even died hoping to bring

Italy back to a central position as a cultural and economic

powerhouse within the Western world, as the one it occupied

in the late middle Ages and Renaissance.

- That project has now completely failed, with the abandonment

the very cultural idea of having any meaningful political

ambition going beyond the sheer day-to-day management on the

one hand, and the messianic (but effectively pointless)

universalism of saving the world on the other even at the

expenses of one’s own political community.

- Unless some sort of miracle occurs, it may take centuries to

reconstruct Italy. At the moment, it seems to be a

completely lost cause.

Present Condition

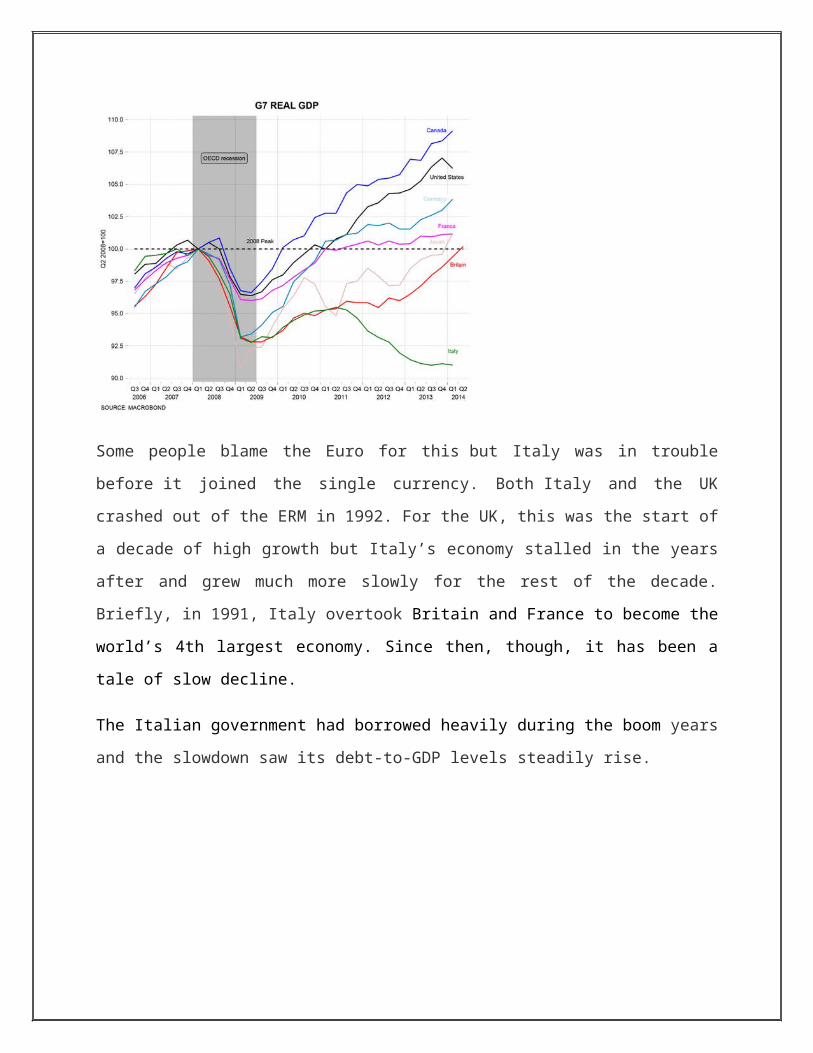

The country slid into recession again this year, wiping out not

only its post-recession growth but much of its growth since it

joined the Euro.

The pattern of Italy’s GDP growth has become detached from that

of the rest of the G7. Since the crash, all the other major

economies have grown, albeit at different rates. Italy, though,

is on a severe downward slide.

Some people blame the Euro for this but Italy was in trouble

before it joined the single currency. Both Italy and the UK

crashed out of the ERM in 1992. For the UK, this was the start of

a decade of high growth but Italy’s economy stalled in the years

after and grew much more slowly for the rest of the decade.

Briefly, in 1991, Italy overtook Britain and France to become the

world’s 4th largest economy. Since then, though, it has been a

tale of slow decline.

The Italian government had borrowed heavily during the boom years

and the slowdown saw its debt-to-GDP levels steadily rise.

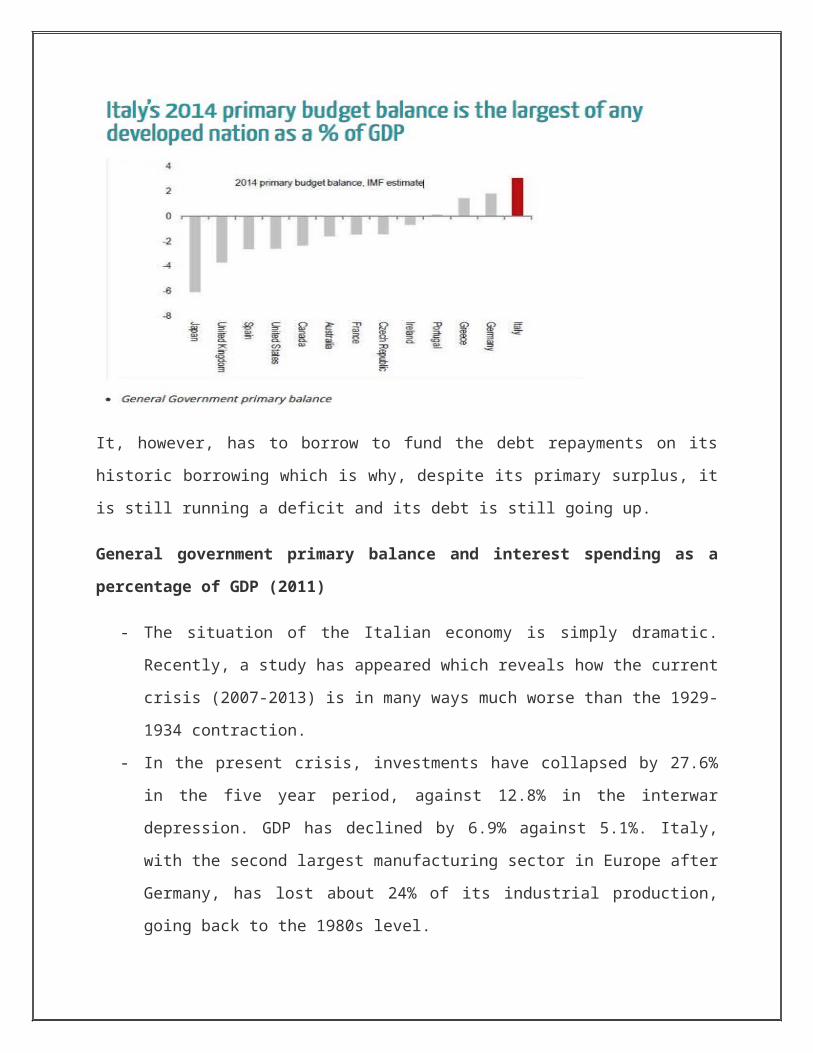

Italy reduced its deficits drastically in the 1990s. For many

years now, it has run a primary surplus. This means that, before

debt interest, its government revenue is higher than its public

spending. Unlike many other countries, including Britain and the

USA, it is not borrowing to fund public services and social

security.

It, however, has to borrow to fund the debt repayments on its

historic borrowing which is why, despite its primary surplus, it

is still running a deficit and its debt is still going up.

General government primary balance and interest spending as a

percentage of GDP (2011)

- The situation of the Italian economy is simply dramatic.

Recently, a study has appeared which reveals how the current

crisis (2007-2013) is in many ways much worse than the 1929-

1934 contraction.

- In the present crisis, investments have collapsed by 27.6%

in the five year period, against 12.8% in the interwar

depression. GDP has declined by 6.9% against 5.1%. Italy,

with the second largest manufacturing sector in Europe after

Germany, has lost about 24% of its industrial production,

going back to the 1980s level.

- No data is currently showing any sign of recovery. From the

beginning of this year, the country has lost over 31,000

companies. Every day 167 retail units are lost, signalling

an authentic disintegration of the retail sector.

- The automotive sector, a crucially important one for the

Italian economy, has been constantly contracting: from about

2.5 million cars sold in 2007, sales in 2012 reached only

the 1.4 million mark (the 1979 level) and they are still

contracting this year.

- Construction, the other pillar of the national economy, is

in rout: the 14% slump in 2012 is only the last in a series

of difficult years.

- Home sales have dropped by 29% in 2012 against the already

miserable 2011, to the 1985 level of 444,000 units, about

half the number of 2006. Of course, the consequences of this

economic disaster in terms of loss of employment are dire:

unemployment is now at almost 12% and growing fast.

- The speed of Italy’s decline is astonishing. Italians once

celebrated displacing Britain and France as the world’s 4th

largest economy. Now, a mere twenty or so years later, a

knackered state, with hardening arteries and on ECB

medication, is trying to outrun a rising tide of debt, and

losing. It is a depressing and rather frightening story

Italy In trouble

- Italy has massive debts totaling €1.9 trillion, but for many

years its life in the red has not been considered a problem

worth more than the odd grumble as it has always been able

to keep up with repayments.

- That has changed dramatically. The reason why Italy has come

under such heavy fire from investors is that it is seen as

weak link in the Euro zone thanks to both the size of the

debt pile and most importantly its debt to GDP ratio, which

is the second highest in the EU at 120 per cent of GDP.

- The wave of fear washing over the Euro zone economies has

seen the cost of servicing that debt rise dramatically and

that is bad news for Italy, which also suffers from very

slow growth and so cannot boost its power to repay the debt.

- Over the next year the country needs to borrow about €360bn,

mostly to repay its debts, and the markets fear that it will

not be able to afford to do this as investors demand higher

and higher rates of return for buying debt that they see as

increasingly risky prospect.

- The benchmark measure for the cost of servicing the debt is

the yield on ten-year Italian Government bonds, which is

essentially the return that investors require in exchange

for buying them.

- This yield has rocketed up to almost 7.5% today compared to

4.1% a year ago and an average of about 5% over the past 12

months.

- Borrowing costs above 7% triggered bailouts worth around

€250bn in Greece, Ireland and Portugal, but the fear is that

Italy has too much debt to be rescued – hence the desperate

rush to boost the Euro zone bailout fund.

Is this a big problem

- The big problem now is that the Euro zone crisis has

deepened and banks and institutional investors have begun to

shun what they see as risky assets - Italian bonds now fall

firmly into that pile.

- As investors dump Italian bonds into a market where demand

is falling they have to be offered cheaper to find a buyer.

- When the price of these second-hand existing bonds falls but

their interest rate stays the same, the yield rises.

- The knock-on effect of this is that Italy will have to offer

higher rates when it comes to issuing new debt to match the

return investors could get from buying second-hand Italian

bonds instead.

- The last ten-year auction saw Italy sell debt at 6.06% at

the end of October.

- The Bank of Italy maintains that it can afford to pay up to

8 per cent on new ten-year bond issues and still balance the

books, but the big risk is that banks and institutional

investors continue to shun the nation’s debt and the cost of

servicing that spirals even higher

- Italy is already borrowing money to keep up repayments on

its debts. If it gets to the point where it cannot auction

enough debt to keep this up at an affordable rate, it would

be faced with the prospect of defaulting on its debts.

- This scenario, which is spooking investors, is similar to

what happened to Greece, Portugal and Ireland and triggered

bailouts for them.

- The fear is that as Italy’s debts are so big, the Euro zone

cannot afford to bail it out, especially as the domino

effect means that the markets may then start shunning the

bonds of next weakest link in the euro area.

Solutions

Strengthening Italy's policies

- A programme of reform proposed by the Italian Government was

itemized in the summit communiqué, and Prime Minister

Berlusconi was called upon to submit "an ambitious

timetable" for its implementation.

- The reforms that were promised in response in his "letter of

intent" are reported to include also a reduction in the size

of the civil service, a €15 billion privatization of state

assets and the promotion of private sector investment in the

infrastructure.

- It was approved on the 12th of November by the Italian

parliament as the Financial Stability Law, and Berlusconi

was replaced as Prime Minister by the eminent economist,

Mario Monti.

Bail out fund

- After being criticised for months of dithering, the Euro

zone nations have been trying to hammer out a decisive plan

to deal with the debt crisis that is picking off countries

one by one.

- The solution they have come up with is boosting the EU

bailout fund, the European Financial Stability Fund, EFSF,

to €1 trillion, a level that leaders see as being big enough

to stand behind any of the troubled Euro zone countries debt

repayments.

- Unfortunately, this plan has not come to fruition swiftly

enough to head off the crisis before it managed to engulf

Italy.

- One of the reasons behind this is that while the Euro zone

leaders announced at the end of October that they agreed in

principle to boost the fund’s firepower from €440bn to €1

trillion, they didn’t actually have a concrete plan of how

to do this.

- The hope appeared to be that the Euro zone could tap up

strong emerging market economies, such as China and Russia,

and sovereign wealth funds for support through a ‘special

purpose investment vehicle’, on the basis that a stronger

fund would benefit the global economy and put the banking

system less at risk.

- However, the subsequent G20 summit in Cannes last week was

overshadowed by Greece’s political instability and ended

with no such pledge of support.

- One other solution put forward is a massive dose of

quantitative easing, with the European Central Bank printing

funds to buy troubled governments’ debt and drive down

yields.

- The Euro zone has so far avoided QE, fearing its potentially

inflationary after-effects, and politically it remains

hugely unpopular with Germany, which holds the power among

the euro nations.

- If QE were to arrive for the Euro zone it would require a

dramatic change in the ECB’s stance and it could come with

major concessions from member countries to the ECB on how

their economies are controlled.

Present condition of Italian Economy

Italy and France sought to present a united front yesterday as

grim economic news threatened to push Europe back into recession

and exacerbate a spiralling debt crisis.

European leaders are scrambling again to stem the march of the

crisis, which pushed the euro to a 16-month low against the US

dollar yesterday, drove Italy's borrowing rates to unsustainable

levels, and is threatening France's prized AAA credit rating.

With the debt jitters affecting core economies, economic

indicators show that even powerhouse Germany hasn't been spared.

Economic sentiment and retail sales are falling across the

region, according to new data released yesterday, while

unemployment in the 17-nation eurozone is stuck at 10.3pc.

Conclusion

Euro zone crisis was an outcome of an unstable economic

structure. In order to boost consumption, people and the

government were encouraged to spend on credit. And this credit

comes as a loan from future and when it reaches its tipping

point, we find ourselves in recession.

Thus I say that for a sustainable development we should always

take the middle path, i.e. the “mean way”. Savings may be a new

term for west but it is built in value in the eastern culture.

Collectiveness is always better than individualism.

It is time that the Italian economy act fast , it should try to

come out of the rat race of GDP growth, and instead focus on

sustainable development. One of the main reasons Italy economy

collapsed was they didn’t take the mean way for economic

liberation.

The crisis has impacted on a system that had deteriorated

following twenty years of political instability and economic

decline. Thus , it has only worsened the conditions of a country

which is already in crisis. The circumstances responsible for

Italy’s decline and the avoidance of the structural reforms have

resulted in the inability to rescue the country and reforming

system.

In conclusion, the global Euro zone crisis has had a great impact

on the Italian economy.