elena zins_thesis.pdf - sistema de bibliotecas fgv

TRANSCRIPT

1

FUNDAÇÃO GETULIO VARGAS

ESCOLA DE ADMINISTRAÇÃO DE EMPRESAS DE SÃO PAULO

HOUSING MICROFINANCE IN BRAZIL

An exploratory study

ELENA ZINS

SÃO PAULO

2021

2

ELENA ZINS

HOUSING MICROFINANCE IN BRAZIL

An exploratory study

Dissertation presented to Escola de

Administração de Empresas de São Paulo of

Fundação Getulio Vargas, as a requirement to

obtain the title of Master in International

Management (MPGI).

Knowledge Field: International Economic and

Finance

Adviser: Prof. Dr. Lauro Emilio Gonzalez

Farias

SÃO PAULO

2021

3

Zins, Elena.

Housing microfinance in Brazil : an exploratory study / Elena Zins. - 2021.

142 f.

Orientador: Lauro Gonzalez.

Dissertação (mestrado profissional MPGI) – Fundação Getulio Vargas, Escola de Administração de Empresas de São Paulo.

1. Finanças - Aspectos sociais. 2. Microfinanças. 3. Habitação - Brasil - Aspectos sociais. I. Gonzalez, Lauro. II. Dissertação (mestrado profissional MPGI) – Escola de Administração de Empresas de São Paulo. III. Fundação Getulio Vargas. IV. Título.

CDU 336(81)

Ficha Catalográfica elaborada por: Isabele Oliveira dos Santos Garcia CRB SP-

010191/O

Biblioteca Karl A. Boedecker da Fundação Getulio Vargas - SP

4

ELENA ZINS

HOUSING MICROFINANCE IN BRAZIL

An exploratory study

Thesis presented to Escola de Administração de

Empresas de São Paulo of Fundação Getulio

Vargas, as a requirement to obtain the title of

Professional Master in International

Management (MPGI).

Knowledge Field: International Economics

and Finance

Approval Date: 19/01/2021

Committee members:

_____________________________________

Prof. Dr. Lauro Emilio Gonzalez Farias

_____________________________________

Prof. Dr. Edgard Elie Roger Barky

_____________________________________

Prof. Dr. Tânia Pereira Christopoulos

5

Acknowledgements

I would like to thank my supervisor, Prof. Lauro Emilio Gonzalez, for helping me to achieve

another important milestone in my academic journey.

I would like to express my extreme gratitude to the professionals who accepted to dedicate

some of their time to share their experience, knowledge and opinions with me, as well as

providing me some guidance for my research for some of them. The interviews conducted gave

me invaluable material for this research.

My sincere thanks also go to my friends and my housemates for their patience when hearing

my countless concerns, complains and doubts related to my thesis the nine last months.

Lastly, I would like to express my gratitude to my family, especially my mother, which has

been unconditionally supporting me in every aspect of my academic journey at FGV-EAESP,

despite the long distance between my home country and Brazil.

6

Abstract

The housing deficit and lack of access to credit, notably for the low-income populations, are

striking problems in emerging countries, especially in Brazil. The fiscal pressure on public

housing programs is increasing, what suggests new solutions must be implemented to alleviate

this problem.

Housing microfinance is an embryonic but promising market-based practice that could at least

partly meet the vast demand for housing finance among low-income populations in Brazil.

In this context, this thesis aims at exploring the challenges of housing microfinance expansion

in the specific context of Brazil. The methodological approach of this study was to collect both

qualitative data. The interviews combined with the secondary data enabled us to provide an

overview of the current housing microfinance initiatives in the country, of the market gap that

could be filled, of challenges impacting its development as well as expected future development

in the market.

The results indicate that despite the existence of a market gap that could be filled by housing

microfinance and some small-scale success examples of the practice in the country, there is a

conjunction of politic, socio-economic and regulatory factors hindering the development of

housing microfinance. Overall, experts do not believe there will be an expansion of housing

microfinance in Brazil, at least in the near future. The paper ends by outlining key avenues for

future research.

Keywords: financial inclusion, housing microfinance, housing deficit, low-income populations

7

Resumo

O déficit habitacional e a falta de acesso ao crédito, em particular para as populações de baixa

renda, são problemas alarmantes nos países emergentes, especialmente no Brasil. A pressão

fiscal sobre os programas habitacionais públicos está aumentando, o que sugere que novas

soluções devem ser implementadas para aliviar este problema.

O microfinanciamento habitacional é uma prática baseada no mercado embrionária, mas

promissora que poderia, pelo menos em parte, atender à vasta demanda por financiamento

habitacional entre as populações de baixa renda no Brasil.

Neste contexto, esta tese visa explorar os desafios da expansão das microfinanças habitacionais

no contexto específico do Brasil. A abordagem metodológica deste estudo foi a de coletar dados

qualitativos. As entrevistas combinadas com os dados secundários nos permitiram fornecer uma

visão ampla da atual oferta e demanda de microfinanças habitacionais no Brasil, de vários

aspectos que impactam seu desenvolvimento, assim como o desenvolvimento futuro esperado

no mercado.

Os resultados indicam que apesar da existência de uma lacuna no mercado que poderia ser

preenchida pelas microfinanças habitacionais e alguns exemplos de sucesso em pequena escala

da prática no país, existe uma conjunção de fatores políticos, sócio-econômicos e regulatórios

que dificultam o desenvolvimento das microfinanças habitacionais. Em geral, os especialistas

não acreditam que haverá uma expansão das microfinanças habitacionais no Brasil, pelo menos

no futuro próximo. A pesquisa termina delineando as principais vias para pesquisas futuras.

Palavras-chave: inclusão financeira, microfinanças habitacionais, déficit habitacional,

populações de baixa renda

8

Table of contents

1. Introduction ....................................................................................................................... 12

2. Literature review on Housing Microfinance ..................................................................... 13

a. Definition ...................................................................................................................... 14

b. Function and impacts .................................................................................................... 17

c. Constraints and challenges ............................................................................................ 22

d. Factors for housing microfinance expansion ................................................................ 24

e. Summary ....................................................................................................................... 26

3. Housing Microfinance in the Brazilian context ................................................................ 27

a. Microfinance ................................................................................................................. 27

b. Housing deficit .............................................................................................................. 33

c. Housing financing options for low-income households ................................................ 36

d. Summary ....................................................................................................................... 42

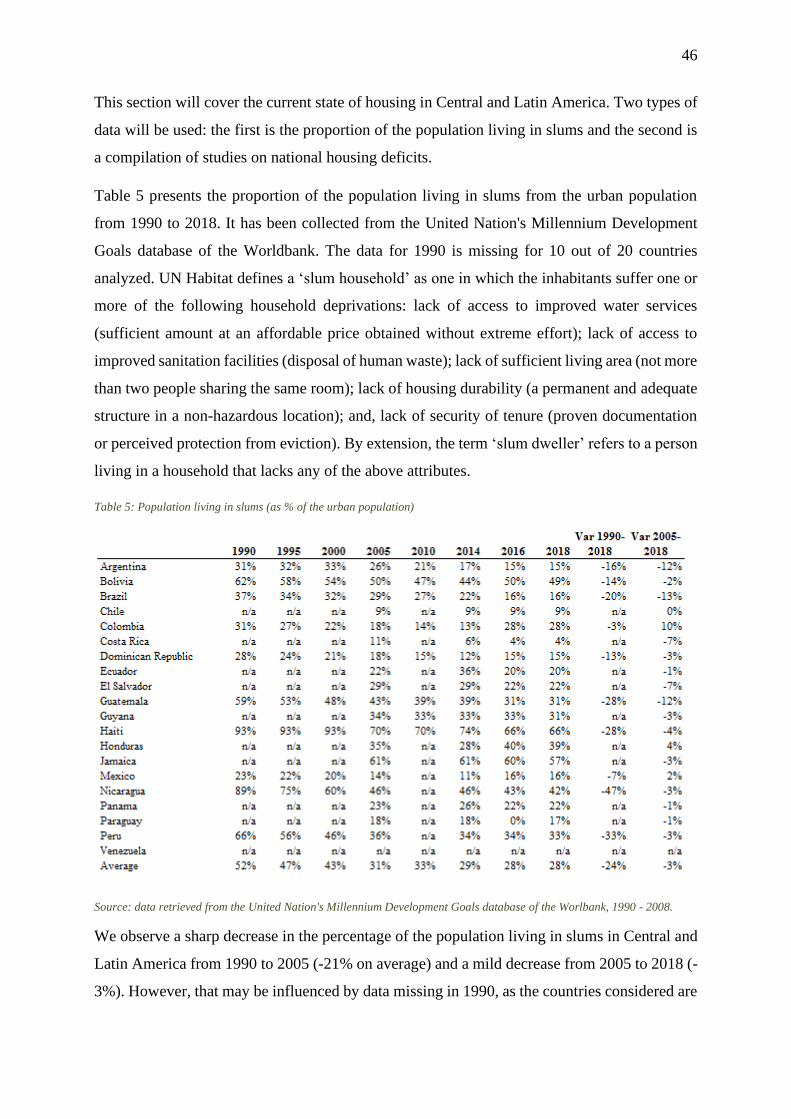

4. Overall view of housing and HMF Experiences in Latin America................................... 43

a. Housing deficit .............................................................................................................. 44

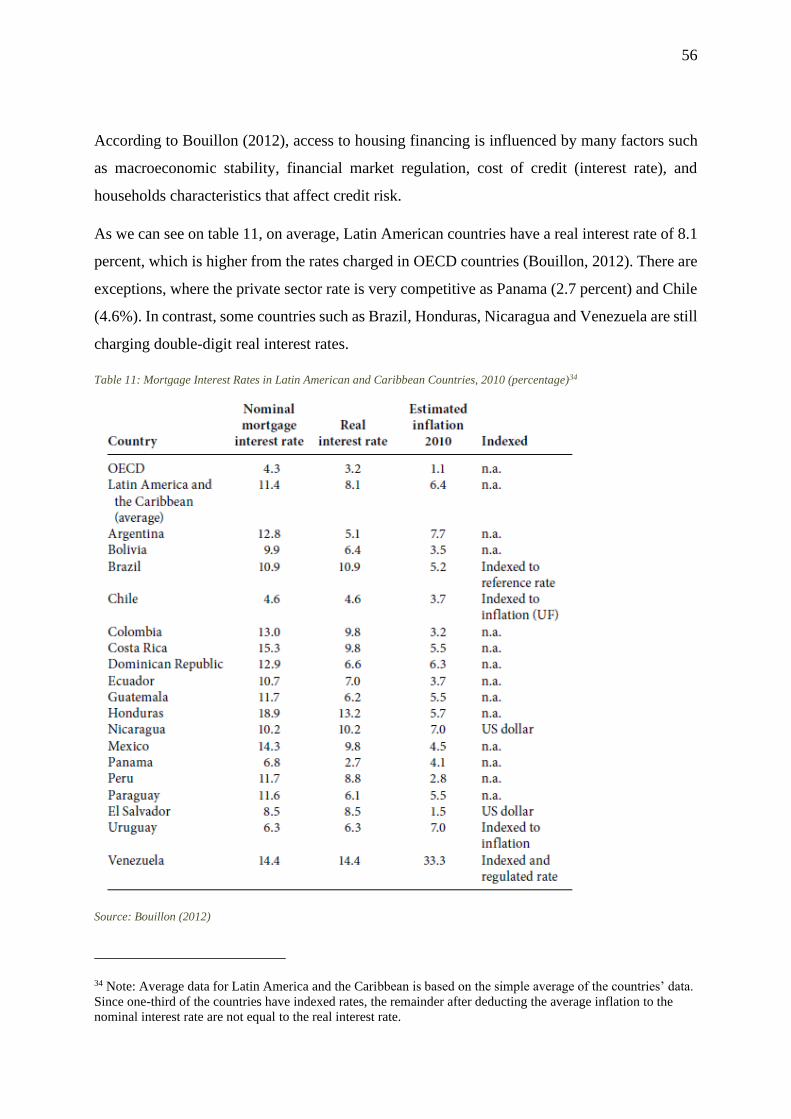

b. Loan and mortgage context ........................................................................................... 53

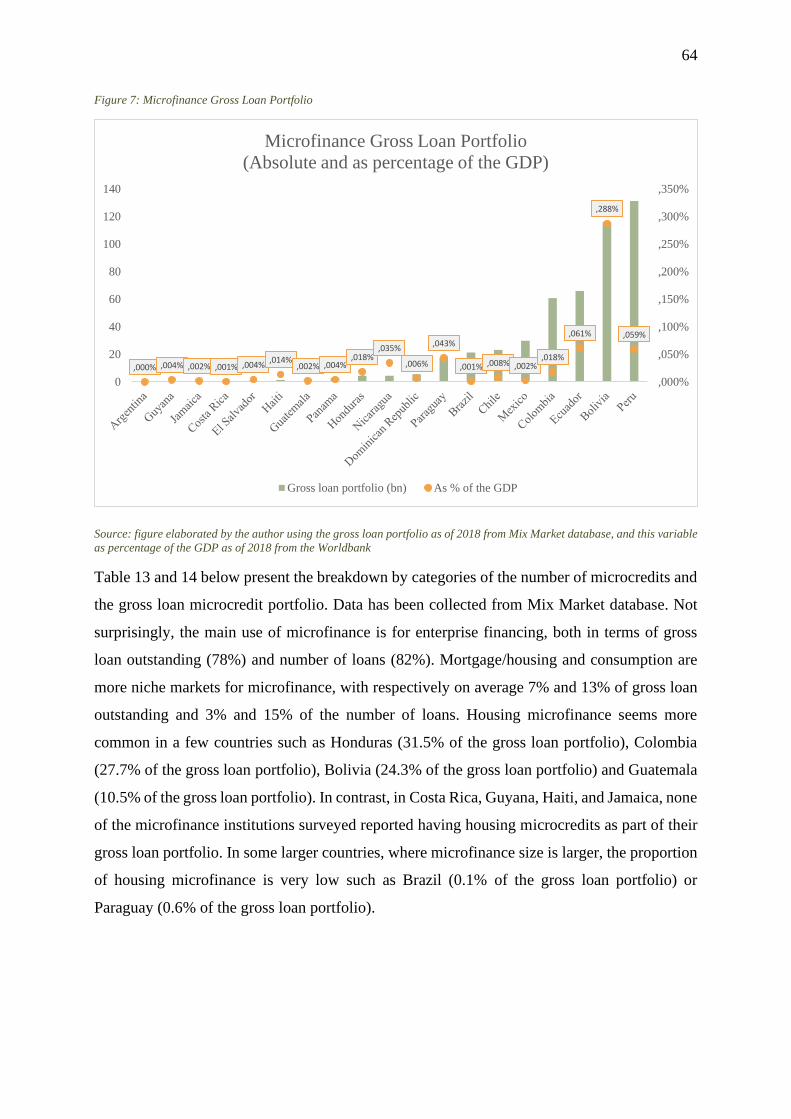

c. Assessment of housing policies ..................................................................................... 57

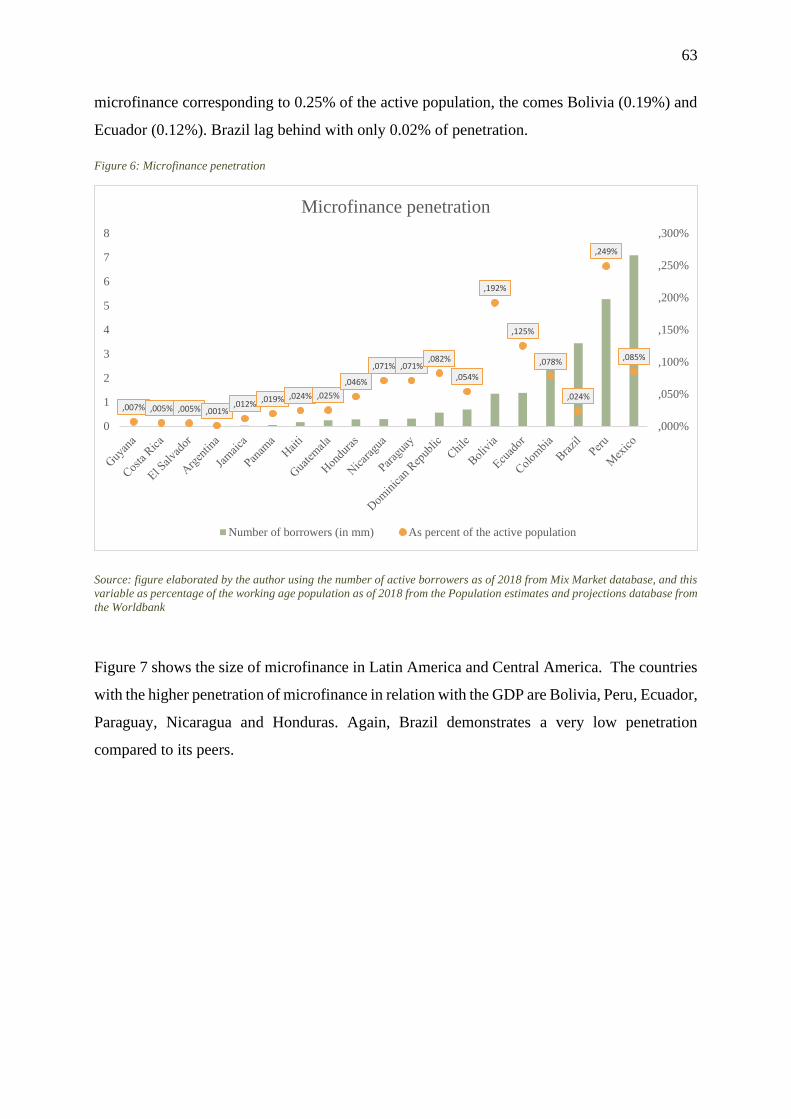

d. Microfinance ................................................................................................................. 62

e. Summary ....................................................................................................................... 66

5. Methodology ..................................................................................................................... 66

6. Empirical results ............................................................................................................... 71

a. The current state of the practice .................................................................................... 71

b. Legal Framework .......................................................................................................... 76

c. Market gap ..................................................................................................................... 77

d. Challenges ..................................................................................................................... 80

e. Best practices ................................................................................................................. 88

f. Future perspectives ........................................................................................................ 89

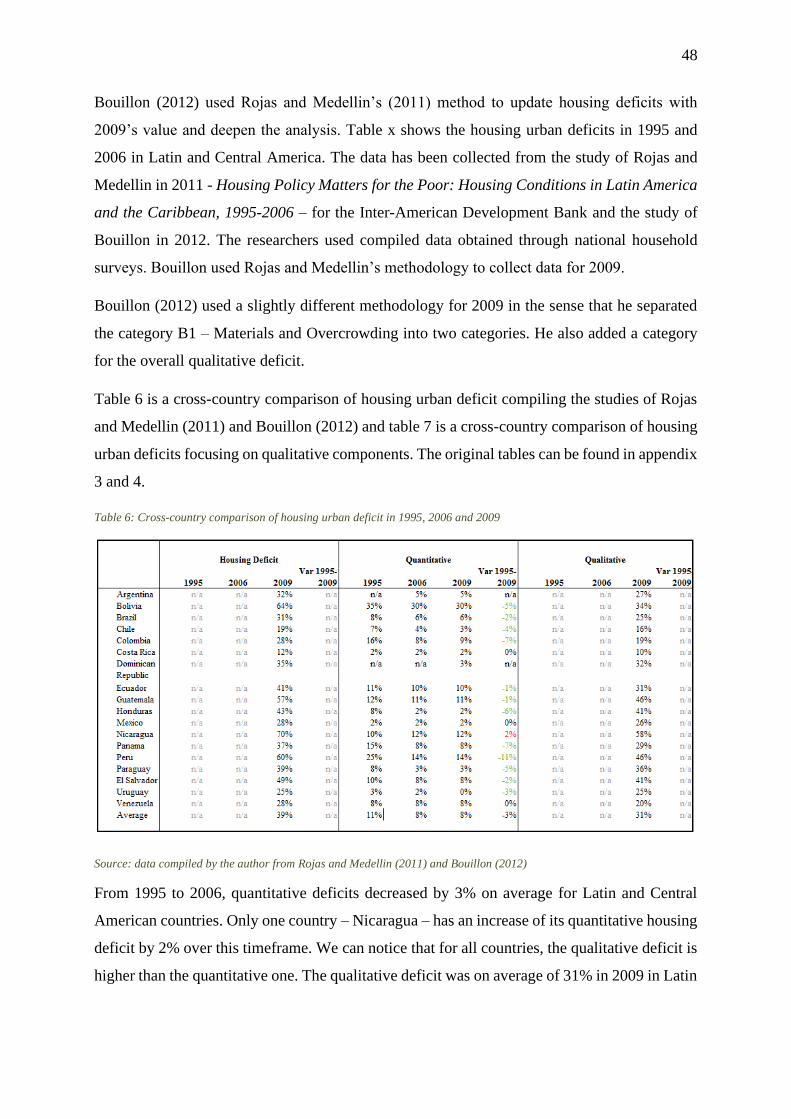

g. Policy recommendations ............................................................................................... 90

h. Summary ....................................................................................................................... 91

7. Concluding remarks .......................................................................................................... 92

8. References ......................................................................................................................... 95

9. Appendices ...................................................................................................................... 104

9

List of tables

Table 1: Housing microfinance products profiles .................................................................... 15

Table 2: Summary of the best practices of housing microfinance using the framework of

Escobar and Merrill, crossed with other researches ................................................................. 16

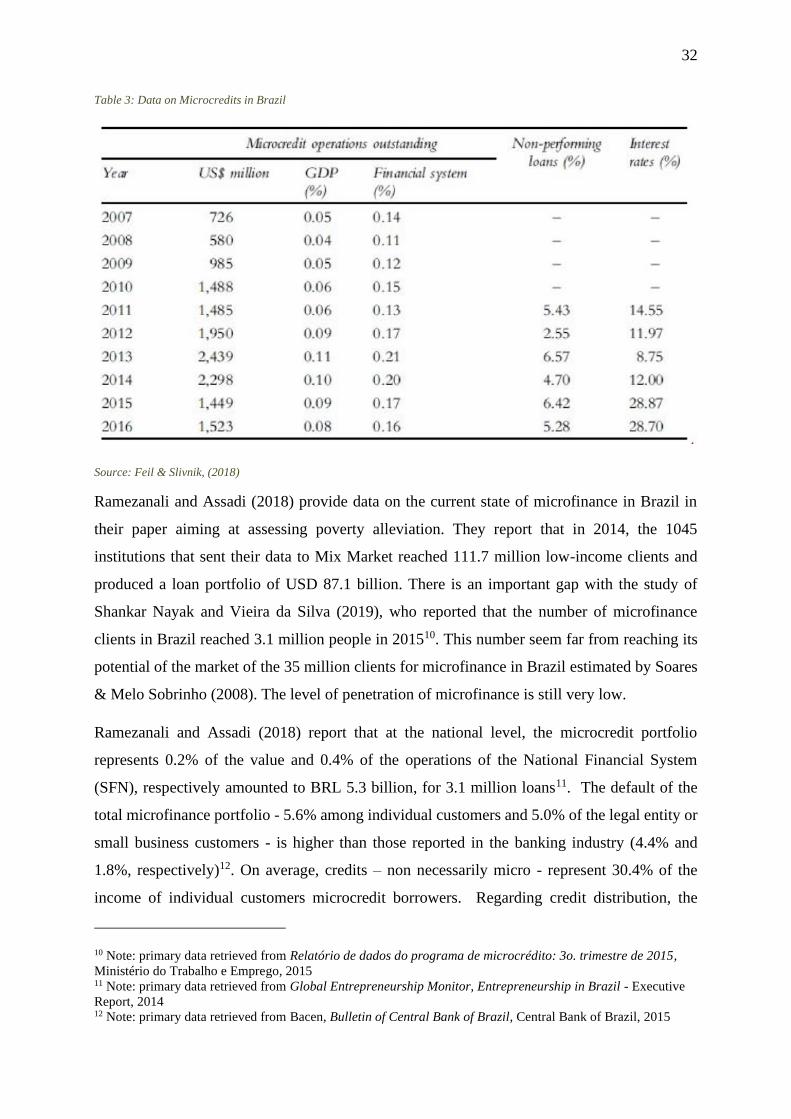

Table 3: Data on Microcredits in Brazil ................................................................................... 32

Table 4: Rules of the program My House My Life .................................................................. 37

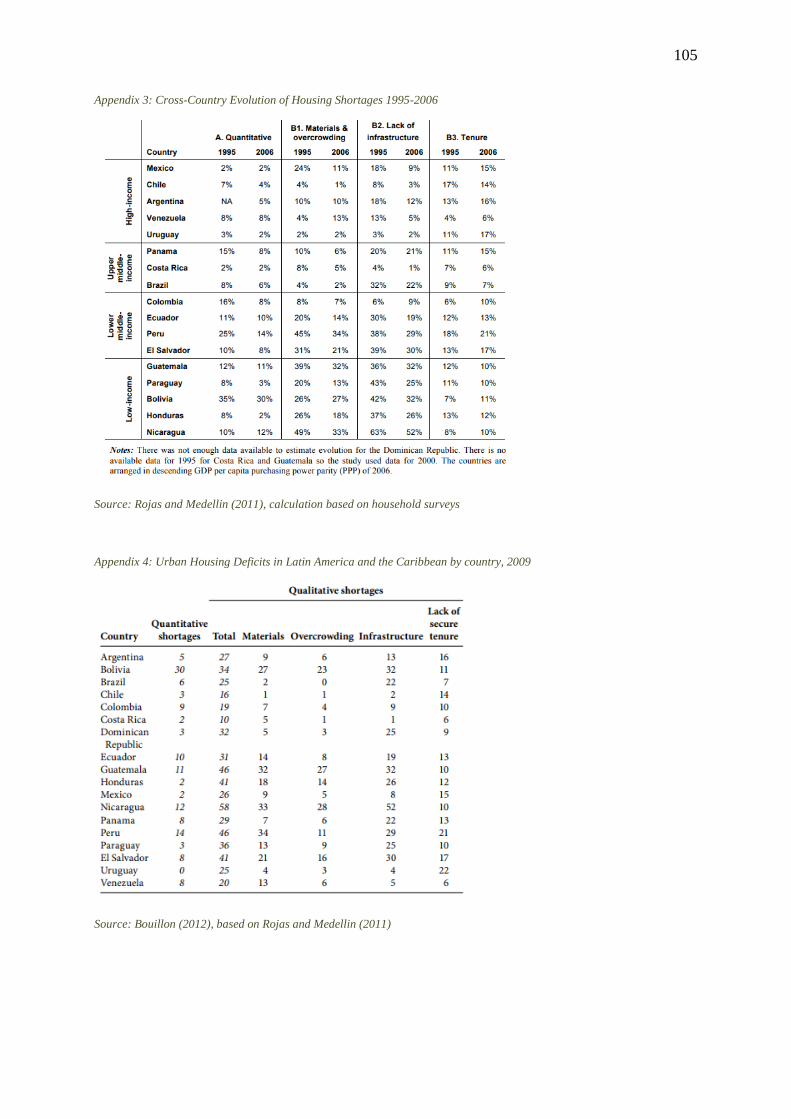

Table 5: Population living in slums (as % of the urban population) ........................................ 46

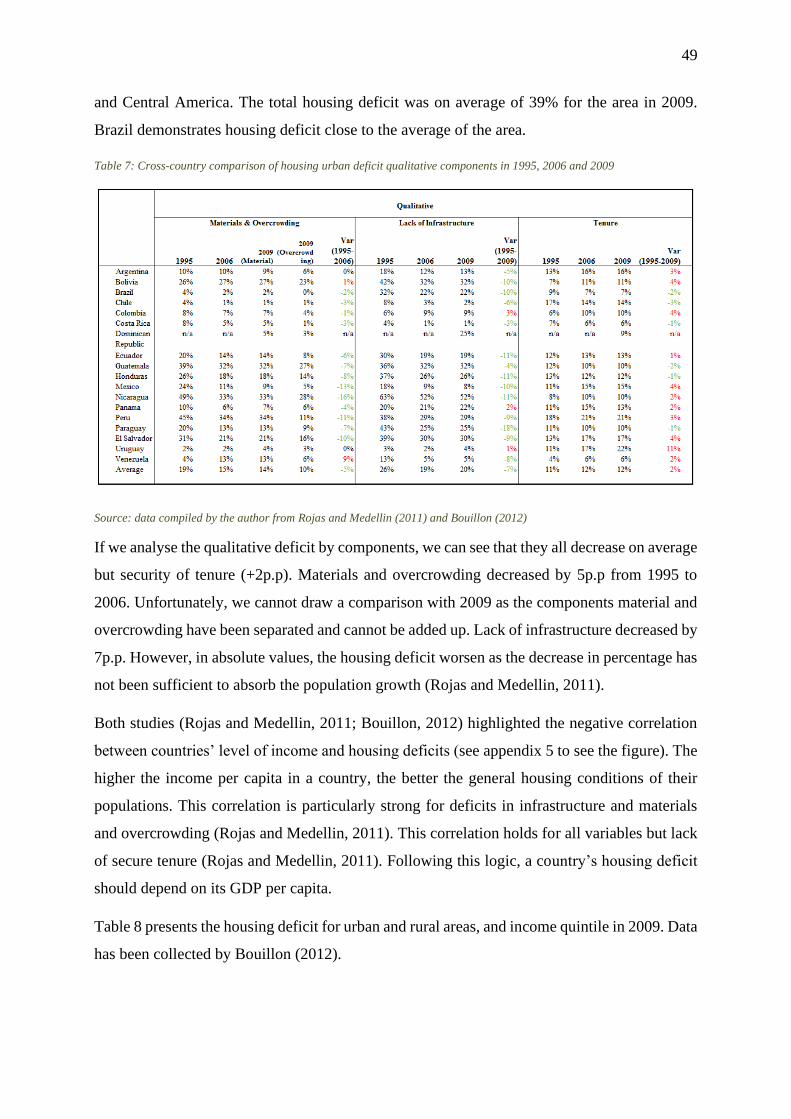

Table 6: Cross-country comparison of housing urban deficit in 1995, 2006 and 2009 ........... 48

Table 7: Cross-country comparison of housing urban deficit qualitative components in 1995,

2006 and 2009 .......................................................................................................................... 49

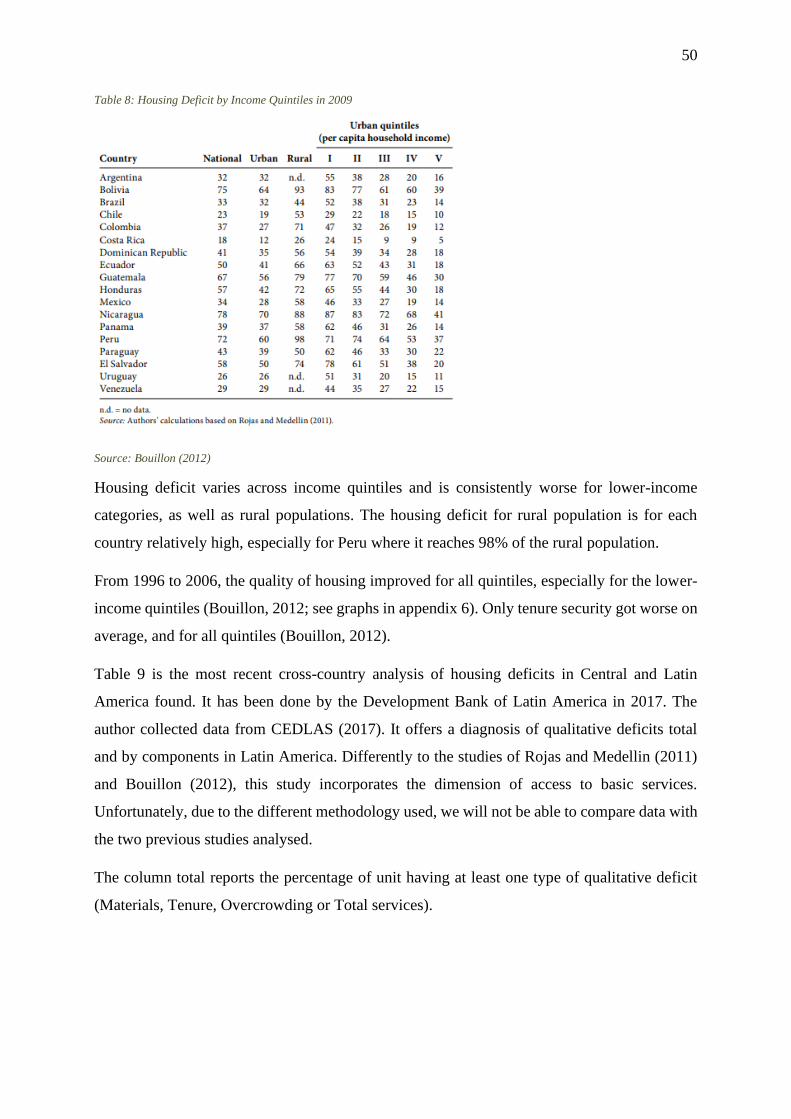

Table 8: Housing Deficit by Income Quintiles in 2009 ........................................................... 50

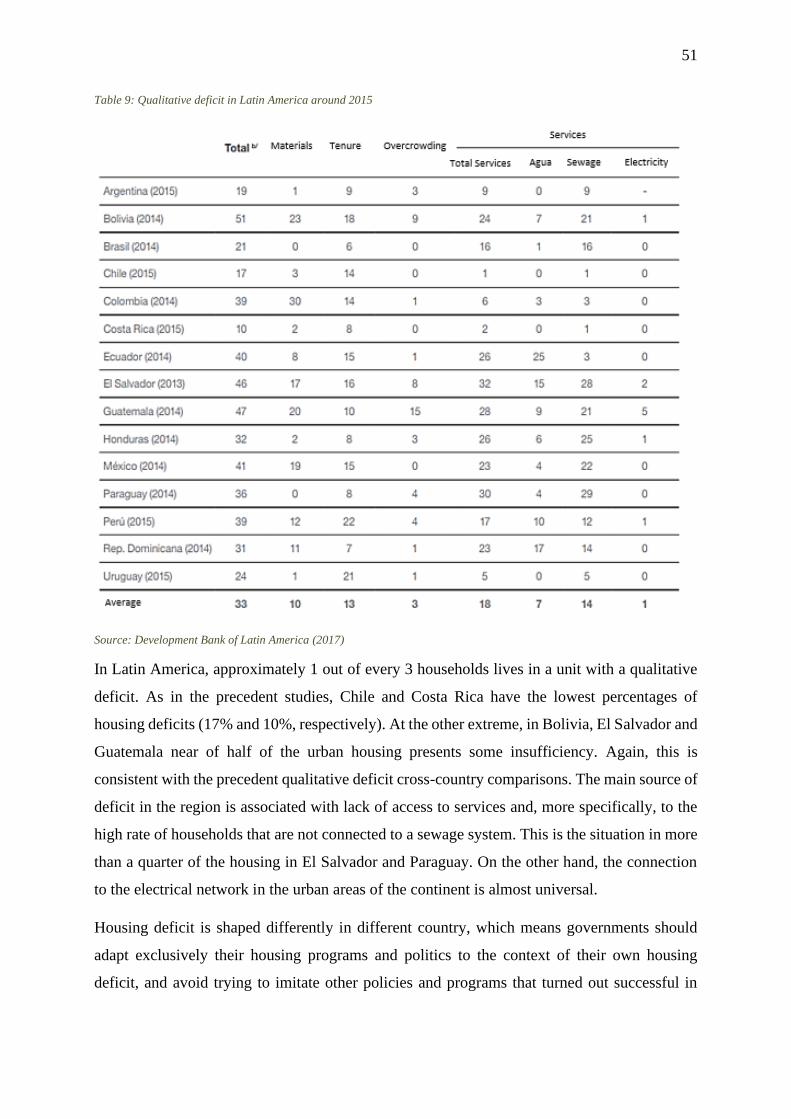

Table 9: Qualitative deficit in Latin America around 2015 ..................................................... 51

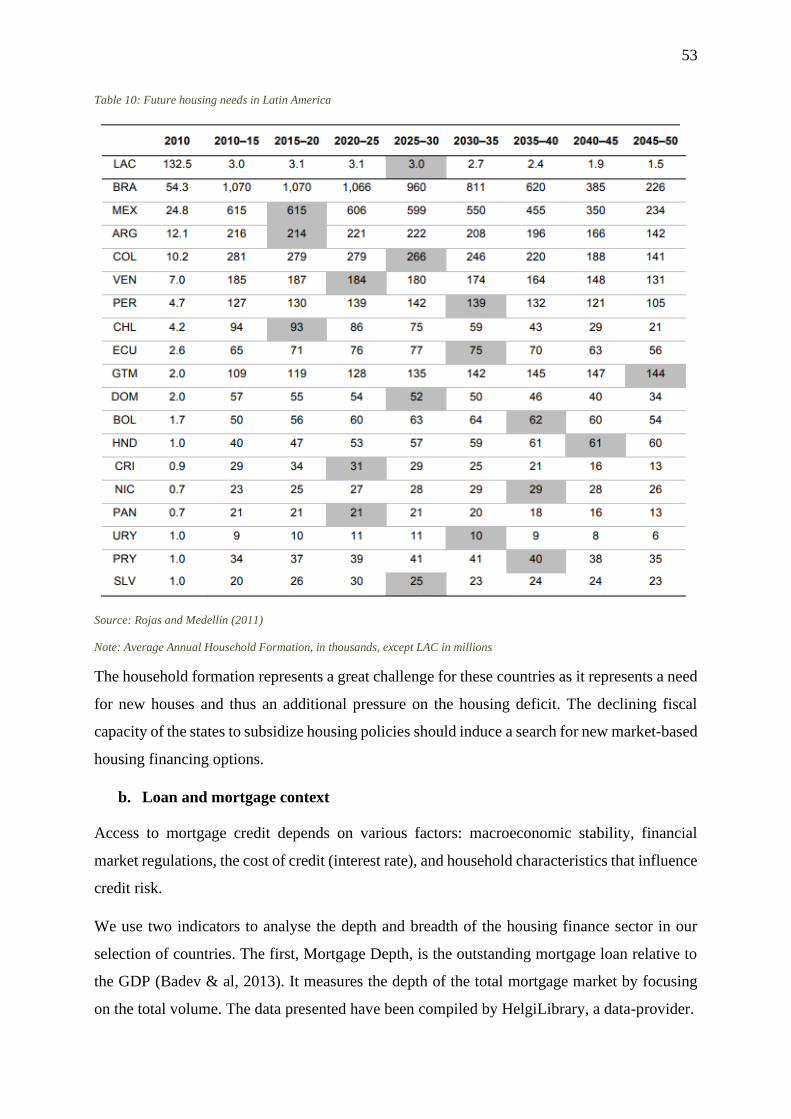

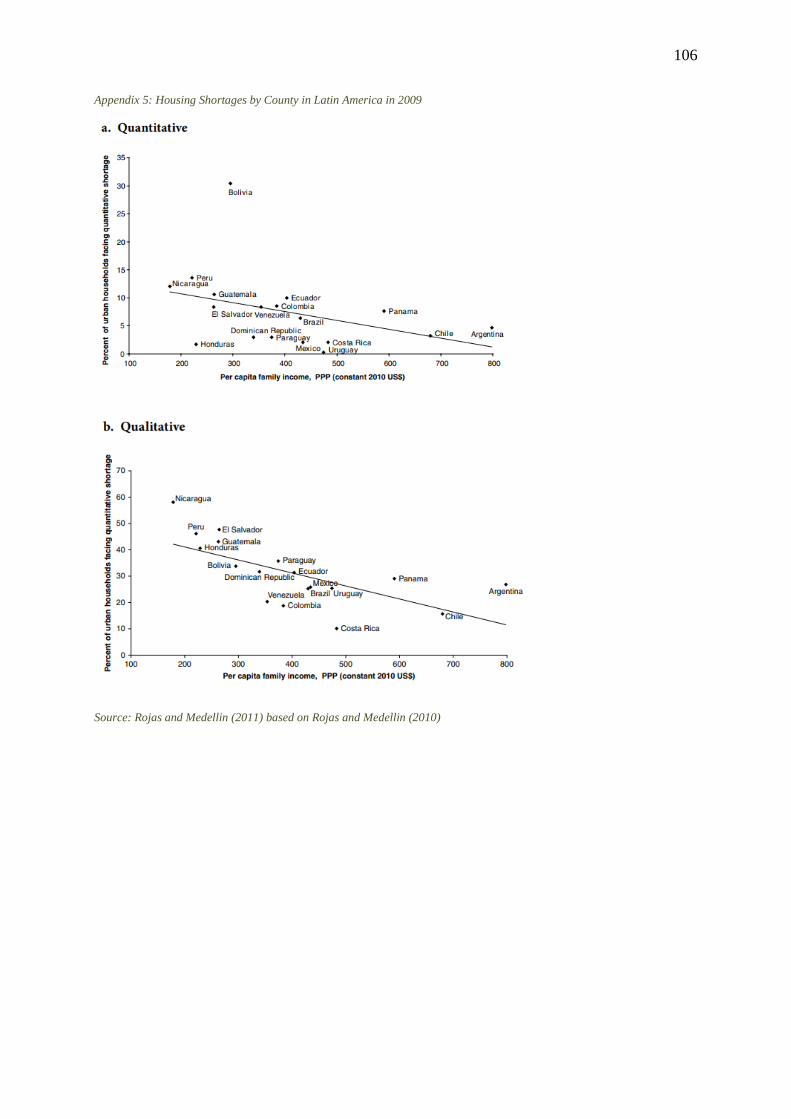

Table 10: Future housing needs in Latin America ................................................................... 53

Table 11: Mortgage Interest Rates in Latin American and Caribbean Countries, 2010

(percentage) .............................................................................................................................. 56

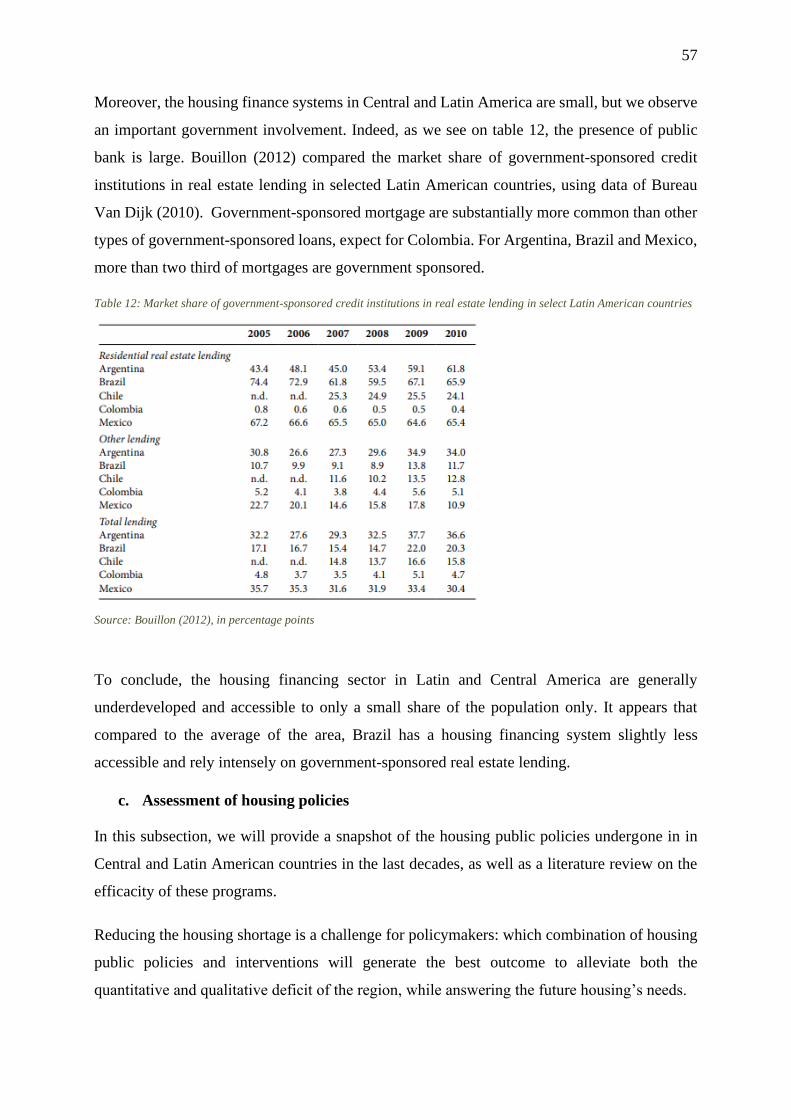

Table 12: Market share of government-sponsored credit institutions in real estate lending in

select Latin American countries ............................................................................................... 57

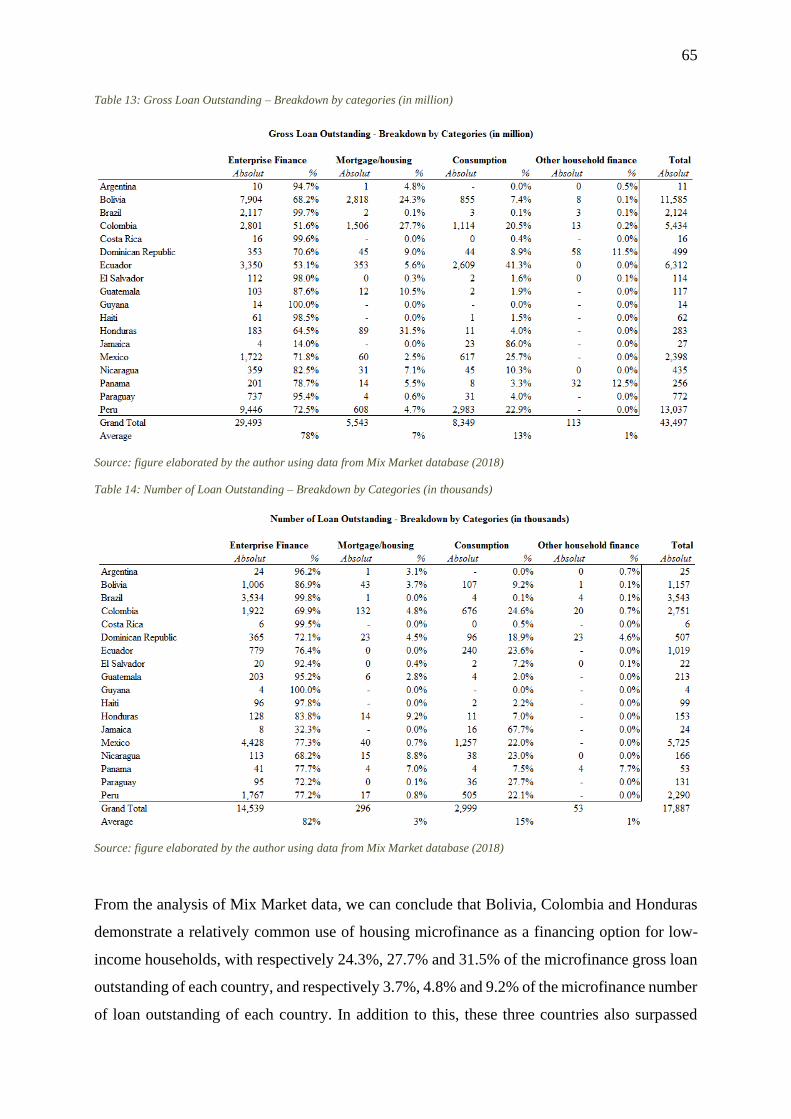

Table 13: Gross Loan Outstanding – Breakdown by categories (in million) ........................... 65

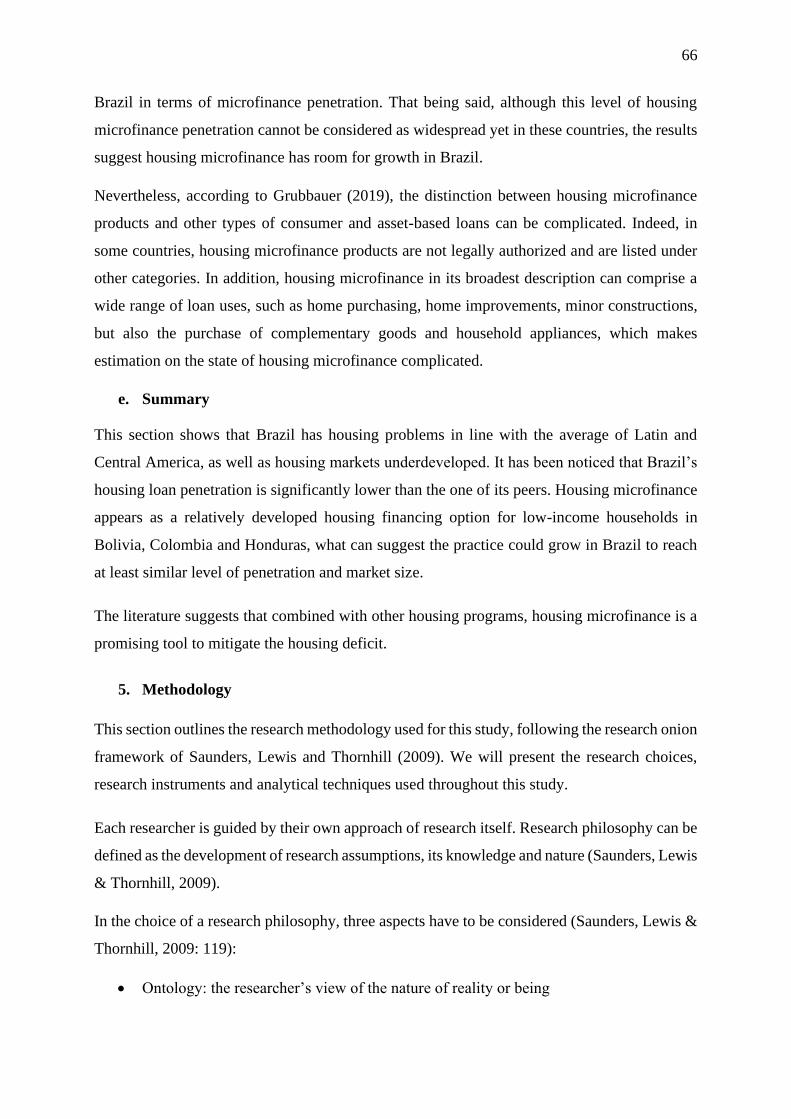

Table 14: Number of Loan Outstanding – Breakdown by Categories (in thousands) ............. 65

Table 15: List of Experts interviewed ...................................................................................... 71

Table 16: Mapping of the existing offer ................................................................................... 72

10

List of figures

Figure 1: Framework for understanding the business case for housing microfinance ............. 26

Figure 2: Units delivered, through the program My House My Life ....................................... 38

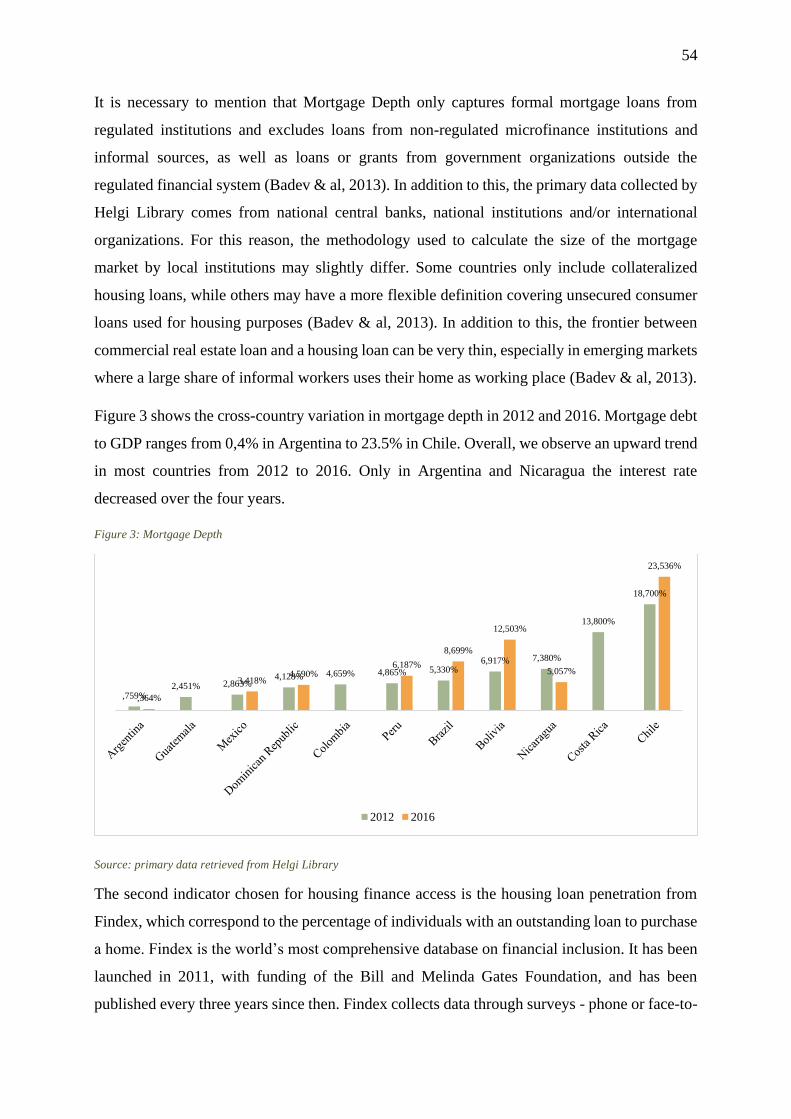

Figure 3: Mortgage Depth ........................................................................................................ 54

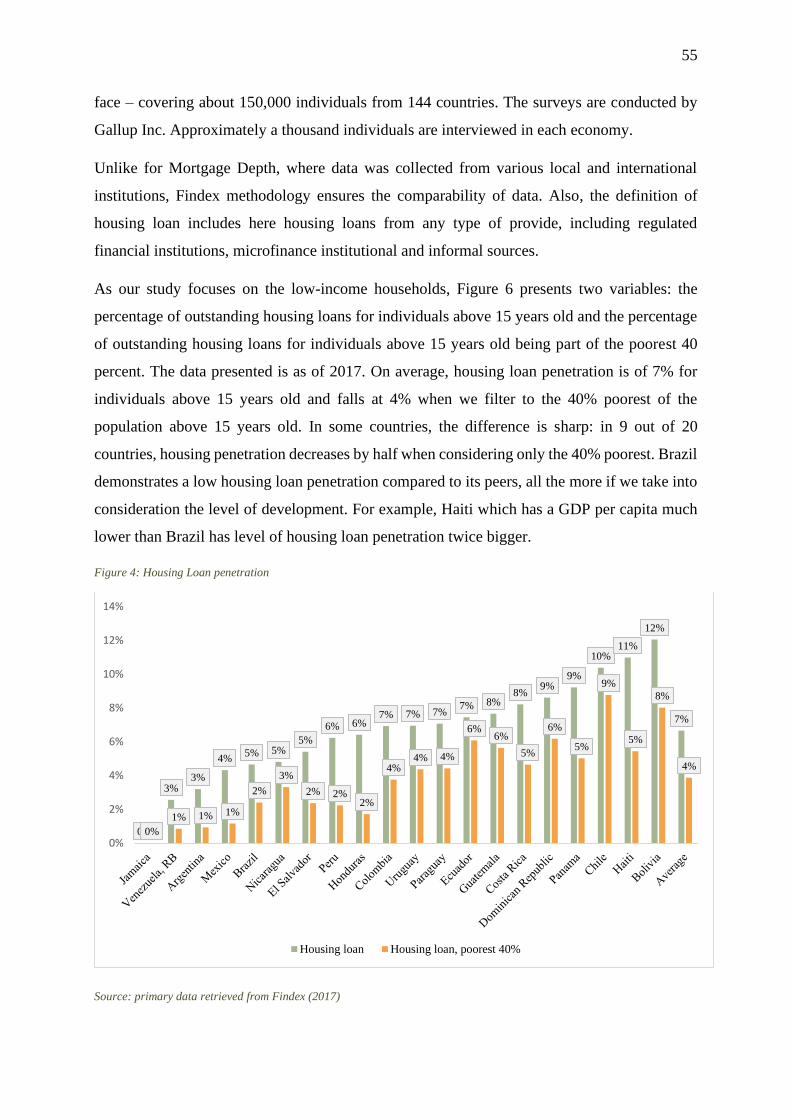

Figure 4: Housing Loan penetration ......................................................................................... 55

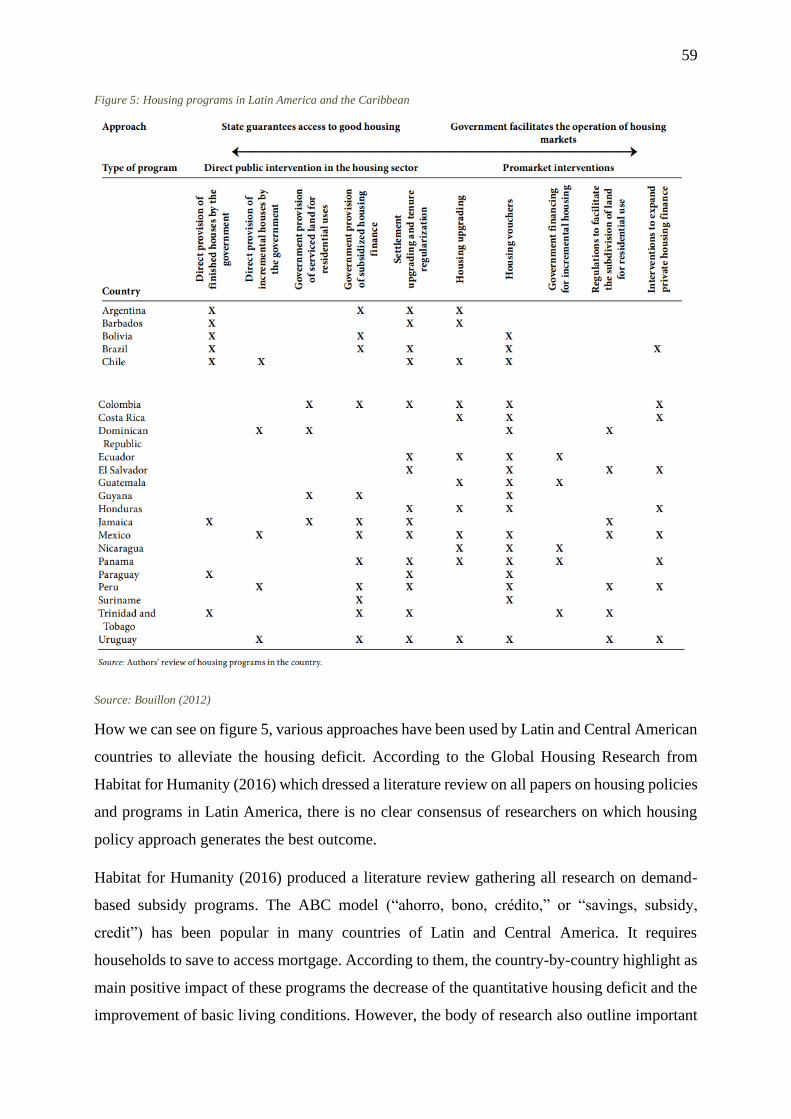

Figure 5: Housing programs in Latin America and the Caribbean .......................................... 59

Figure 6: Microfinance penetration .......................................................................................... 63

Figure 7: Microfinance Gross Loan Portfolio .......................................................................... 64

11

List of Acronyms and Terms

ABRAINC Brazilian Association of Real Estate Developers

BNDES National Bank for Economic and Social Development

ETGF Employment Time Guarantee Fund

HMF Housing Microfinance

MFI Microfinance Institution

MCMV My House My Life

NGO Nongovernmental Organization

PNMPO National Program of Oriented Productive Microcredit

HMFI Housing Microfinance Institution

LIH Low-income Households

12

1. Introduction

In the 1990s and early 2000s, housing policies in South America shifted from state-based to

market-based solutions (Datta & Jones, 1999 in Grubbauer, 2018). Structural adjustment

policies imposed by the World Bank and the International Monetary Fund contributed to

develop housing finance systems and promote homeownership. Latin America can be

considered as a pioneer in housing microfinance and inspired the world with the success stories

of MiBanco in Peru and BancoSol in Bolivia (Ferguson, 2008).

Brazil did not take this path and housing microfinance is still virtually non-existent, although

the housing deficit for low-income population is important. First through the Government

Severance Indemnity Fund for Employees (FGTS), and since its creation in 2009, through the

housing program My House My Life, the government has provided to low-income households

loans, which cannot properly be labelled as microcredits due to a number of factors as the very

high level of subsidizes (Ferguson, 2008). However, these state programs, offering very

advantageous loan conditions, almost completely undermined commercially-viable

microfinance institutions in Brazil (Ferguson, 2008). As stated Ramezanali and Assadi (2018,

p60), “after more than a decade of state-based policies supported by a buoyant commodity

market that turned out finally to be a kind of Dutch Disease and the worst economic

crisis since the 1930s, Brazil seems to consider more private and market-based initiatives

for eradicating poverty.” This crisis embodied the opportunity for microfinance to flourish and

catch up with some of its neighbouring countries, which had developed significantly more

proportionally. Since 2015, as Brazil weathered a political crisis, and is now going through a

recession, the government disposes less liquidities for social assistance, anti-poverty and credit

programs. In that context, housing microfinance could reveal as an effective solution to alleviate

housing problems, solve a market failure and relieve the burden of the state of its housing

programs.

Housing microfinance has the potential to help solving a critical problem in developing

countries: the lack or poor state of housing for low- and moderate-income population. This

practice can be described as “small, non-mortgage-backed loans offered in succession to

support the existing incremental building practices of low-income population” (Habitat for

Humanity, 2019). The borrowed funds are typically allocated for self-help home improvements

and expansion, but also for new constructions of basic core units (Ferguson, 2000). This

practice meets more adequately the needs of this population strata.

13

The objective of this thesis is to understand the challenges relative to housing microfinance

expansion in Brazil. As it happened in other Latin American countries, housing microfinance

could take over state-housing programs, which would create a financially sustainable housing

financing option for low-income population, as well as generate economic growth, from the

perspective of the state and the borrowers. However, the practice has developed less than in

other countries of the area, such as Peru with MiBanco and Bolivia with BancoSol. It seems

relevant to attempt to assess the challenges of HMF specific to the Brazilian context.

The proposed study seeks at filling a research gap on the challenges to the development of HMF

initiatives in Brazil, by providing an overview on the current supply and demand, the factors

influencing the development of the practice in Brazil as well as future perspectives. No study

tackled this issue in the Brazilian context so far. The closest study in this context which can be

cited is the study of Cities Alliance and the City of São Paulo in 2007, assessing the potential

of housing microfinance in São Paulo state. Since then, many factors changed such as the

creation of My House My Life, the regulation and the economic context.

In order to impact how the expansion of housing microfinance would impact the country, the

research question will be the follow:

What are the challenges relative to the expansion of housing microfinance in Brazil?

In exploring the research question, we will aim at understanding:

• The current state of the practice in Brazil

• The challenges related to the development of housing microfinance

• Its perspective of development

Although the literature concerning housing microfinance is rich, the importance and originality

of the study is that it crosses the practice of housing microfinance with the Brazilian context.

2. Literature review on Housing Microfinance

In this first subsection, we will attempt at providing to the reader an exhaustive overview of the

theoretical framework of HMF and some more practical elements on its successes, failures, and

challenges.

In the last two decades, there has been an increasing interest in for this topic. Nevertheless,

major research in the topic was published about twenty years ago and the relevance of the

findings in the current context, which has evolved considerably since, is questionable. Lastly,

14

some significant research gaps have been identified in the topic, such as the immediate impact

of HMF (Grubbauer, 2018).

a. Definition

In Housing Microfinance: Toward a Definition, Daphnis (2004) defines housing microfinance

as “a discrete area of practice that intersects housing finance and microfinance”1. This approach

emerged to fill the gap created by the limitations of housing finance and the revolution of

microfinance. Mortgage lending never offered financially viable options for low-income

populations: impoverished people could not afford to borrow enough to finance a complete

home unless the repayments were stretched over a long period of time. The terms of the lending

not fitting the repayment abilities of base of the pyramid households, the default risk was too

high for financial institutions. To fill this void, governments of developing countries attempted

at creating non-commercial schemes for the financing of complete homes for poor people.

Although these programs can be effective in a specific national context, they tend to be

excessively bureaucratic and have never reached enough efficiency to lead to worldwide

replication (Daphnis, 2004). The revolution in microfinance provided empirical evidences that

economically active poor people can repay their loan. Housing microfinance has emerged based

on the potential that microfinance could go beyond income-generating uses – microenterprises

- to personal asset building.

In this context, housing microfinance can be more practically described as “small, non-

mortgage-backed loans offered in succession to support the existing incremental building

practices of low-income population” (Habitat for Humanity, 2017). Incremental building

accounts for up to 90% of residential development in developing countries and follows the

following pattern: acquisition of a lot, building a small core unit, and expanding and improving

the core unit (Habitat for Humanity, 2014).

According to Ferguson (2004), this practice appears as an intermediate step in interest rate,

term, form of collateral/guarantee, and other respects between housing finance and

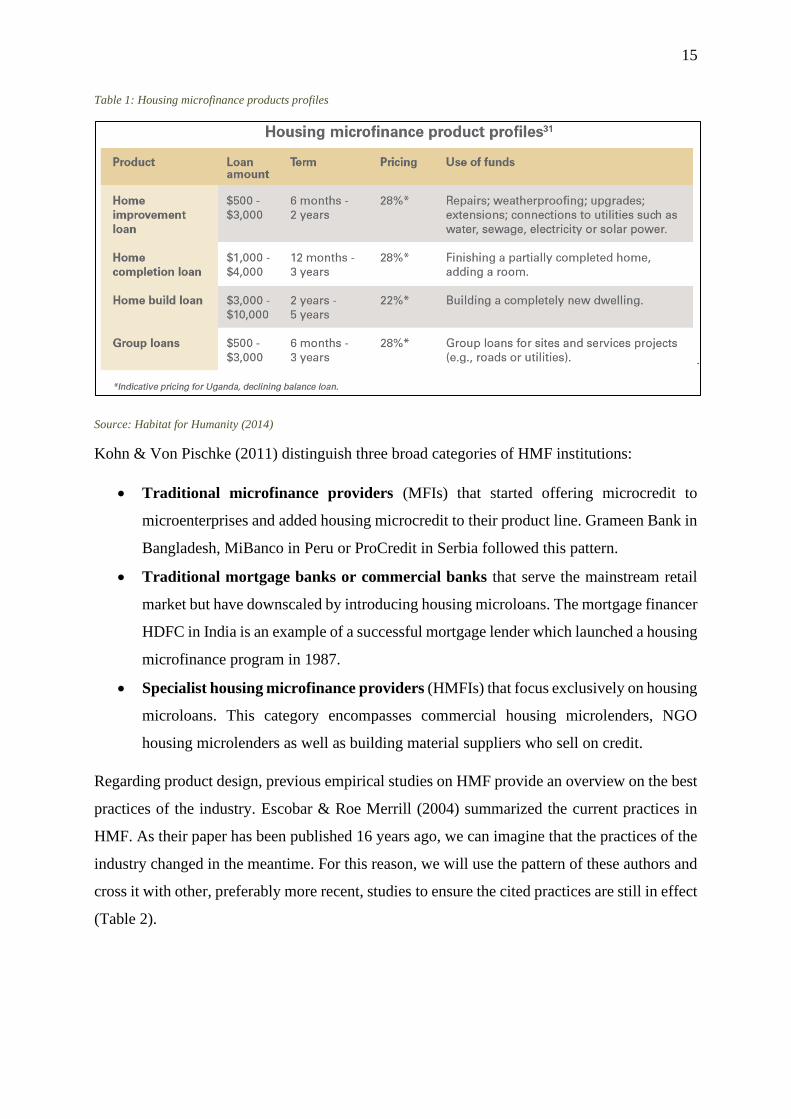

microfinance. The table below is presenting the product profiles of HMF products.

1 Daphnis, F., Housing Microfinance: Toward a Definition In Daphnis, F., Ferguson, 2004, Housing

Microfinance: A guide to practice, 2004, Kumarian Press Inc

15

Table 1: Housing microfinance products profiles

Source: Habitat for Humanity (2014)

Kohn & Von Pischke (2011) distinguish three broad categories of HMF institutions:

• Traditional microfinance providers (MFIs) that started offering microcredit to

microenterprises and added housing microcredit to their product line. Grameen Bank in

Bangladesh, MiBanco in Peru or ProCredit in Serbia followed this pattern.

• Traditional mortgage banks or commercial banks that serve the mainstream retail

market but have downscaled by introducing housing microloans. The mortgage financer

HDFC in India is an example of a successful mortgage lender which launched a housing

microfinance program in 1987.

• Specialist housing microfinance providers (HMFIs) that focus exclusively on housing

microloans. This category encompasses commercial housing microlenders, NGO

housing microlenders as well as building material suppliers who sell on credit.

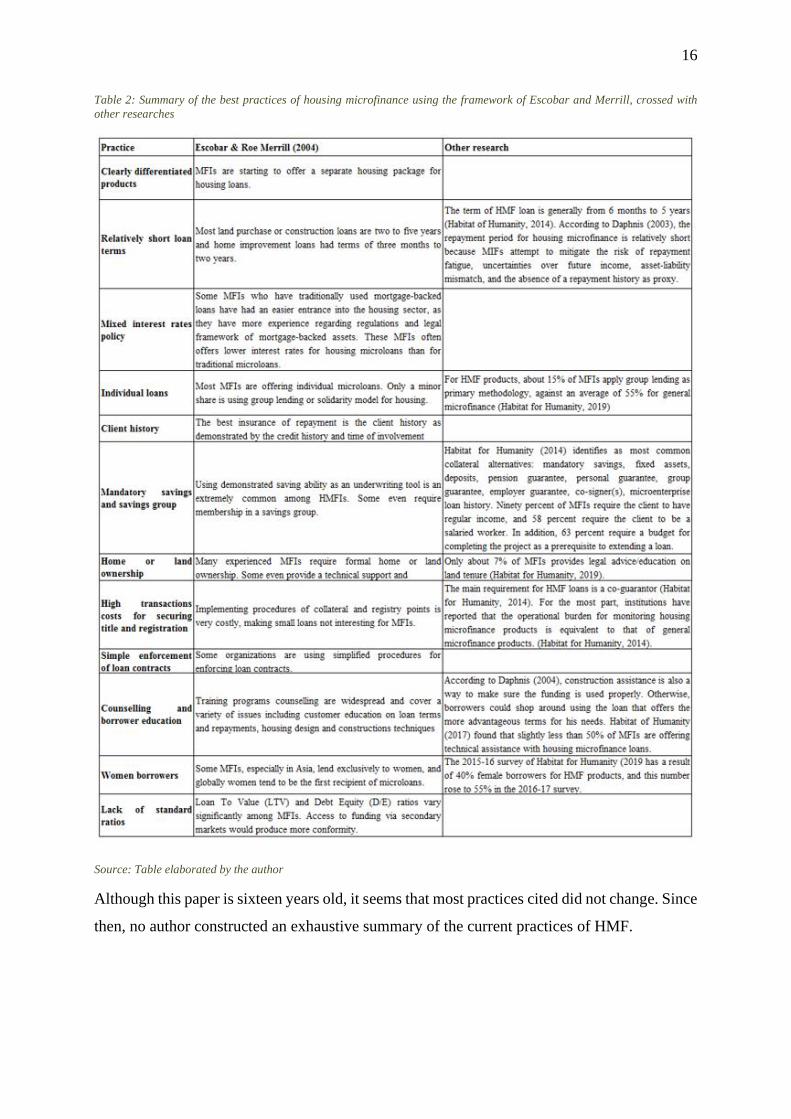

Regarding product design, previous empirical studies on HMF provide an overview on the best

practices of the industry. Escobar & Roe Merrill (2004) summarized the current practices in

HMF. As their paper has been published 16 years ago, we can imagine that the practices of the

industry changed in the meantime. For this reason, we will use the pattern of these authors and

cross it with other, preferably more recent, studies to ensure the cited practices are still in effect

(Table 2).

16

Table 2: Summary of the best practices of housing microfinance using the framework of Escobar and Merrill, crossed with

other researches

Source: Table elaborated by the author

Although this paper is sixteen years old, it seems that most practices cited did not change. Since

then, no author constructed an exhaustive summary of the current practices of HMF.

17

b. Function and impacts

Housing microfinance holds importance on two perspectives: (1) to meet the demand for

housing financing of the impoverished people in emerging countries who are excluded from the

conventional lending practices and (2) to contribute to the development of financial institutions

who have low-income people as a significant share of their client base, especially microfinance

institutions (Ferguson, 2004).

To begin with, we can claim that housing microfinance is important, as it fills a market void

created by the failure of traditional mortgage finance to meet the need of the low-income

consumers. At most, in middle-income countries, a third of households has access to mortgages

(Porteous, 2011). In low-income countries, this proportion is much lower. Ferguson (2004)

explained this market void by the following factors:

• Real interest rates are generally high (more than 10%) and lead to high debt

service

• Long-term funding on domestic markets in emerging countries are generally

unavailable, which creates interest-rate risk for mortgage lending and greatly

limits the supply of mortgage money

• Formal-sector systems are expensive, including those for registry of property

rights, land-use development, and property transfer taxes, what push most low-

moderate-income families into the informal sector

• The poor functioning of rental markets makes home rental an undesirable or

unavailable option for low-income households in developing countries, while it

is the norm in developed countries

• Long-term debt is conflicting survival strategies of low-income households –

especially working in the informal sector – which face revenues instability

• The fiscal capacity of most governments to fund the subsidies necessary for

affordable housing projects is declining

Facing the lack of financing options, low income households generally spread the costs of

housing over long timespan rather than trying to pay for a complete unit upfront as it generally

occurs for middle-class families in developed countries. They typically afford home ownership

through self-home building over a time span of 5 to 20 years (Ferguson, 2003). Research also

highlighted that low-income families tend to prefer incrementally improving their home than

buying a new property elsewhere, as they would lose the social capital of their relationships

18

with families and friends in the neighbourhood (Ferguson, 2004). However, traditional

commercial banks generally only provide loans for new commercially built units.

Furthermore, in developing countries, homeownership is particularly important. For a large

share of low-income people in the developing world, it is the most important asset they will

ever own. Owning their home serves as a shelter against life uncertainties such as illness,

unemployment, and highly fluctuating income (Ferguson, 2004), as well as family inheritance

(Bonduniba, 2016). In addition, as exposed Daphnis (2004), home can constitute a productive

asset for the home-based microentrepreneurs. For these reasons, the homeownership rate is

generally high in developing countries, although mortgage finance is much less advanced than

it is in developed countries.

In the view of MFIs, there is a preference for homeownership among the lowest socioeconomic

groups which can trigger their willingness to access affordable finance.

In addition, research has showed that 20% of microentrepreneurs microcredits are already

directed to home improvement (Habitat for Humanity, 2019). When housing microfinance is

not an option, poor borrowers make the rational choice of recurring to productive microcredits

to finance their home improvements as it offers better repayment terms than do informal sources

of money lending, such as loan sharks (Daphnis, 2004). The effective interest rate on small

loans in the informal credit market is about 100% per year and can be even higher for very

small loans (Schmidt, 2010). Furthermore, microenterprise microfinance represents a way for

families to invest in their productive activity thanks to these supplementary funds, while

keeping their savings for home improvements. The expansion of HMF would properly answer

a need that already exists.

Furthermore, housing microfinance can contribute to the development of financial institutions

that have low/moderate households as part of their clients such as microfinance institutions

(Ferguson, 2004). The larger amount, longer terms and lower delinquency rates of housing

microfinance in comparison to microfinance for entrepreneurs can help microfinance

institutions to increase their profitability and diversify their risk, if costs can be kept under

control (Schuman, 2004). Besides, the addition of housing microfinance products can

“differentiate an institution, improve branding, and lead to crossselling of other products”

(SEEP, 2014, p20). It represents an opportunity for existing MIFs to scale up through the

increase of loan volume in a market where microenterprise microfinance is saturated (Ferguson,

2003).

19

In addition, housing microfinance can have an impact on the macro-level. If we consider

housing microfinance is a housing financing option for some low-income households that

would otherwise have no access to housing financing, it can lead to renovation, expansion and

construction projects that would otherwise not see the light of the day, and thereby boost the

housing industry. In the 70s, we observed a shift of opinion towards the housing industry:

initially perceived as a social expenditure and drag on growth, it has increasingly been seen as

a growth contributor (Harris & Arku, 2006). Indeed, the housing industry affects economic

development through many aspects, being a major employer with large multiplier effects. This

industry, encompassing building materials, construction, real estate and financial industries,

generally represents 9% of jobs in the economy worldwide (Ferguson, 2003). As we observed

in the United States in 2001 and 2002, it also contributes to help economies find their way out

of recession (Ferguson, 2003). However, in many developing economies, the mortgage market

is small and the housing microfinance market underdeveloped, making the housing industry

minor. The democratization of housing microfinance could change this paradigm and unlock

this as-yet-untapped potential.

According to Prior and Argandoña (2008), there is a close relationship between the level of

economic development of a country and the level of development of its financial system.

Indeed, many empirical studies suggest that the development of the financial system promote

economic growth, particularly in emerging countries (King & Levine 1993, Demirguc ̧-Kunt

& Maksimovic 1996, Rajan & Zingales 1998, Beck & al. 2000).

Overall, housing microfinance is believed to be a growth contributor, but there is a research gap

on the impact of housing microfinance on poverty alleviation.

Initially perceived as ethically progressist, microfinance came under heavy criticisms the past

years. An evident example of the conflict between commercial and developmental aspirations

is the successful IPO of the Mexican-based microfinance institution Compartamos (Hudon &

Sandberg, 2013). This success resulted from the strategy of the MFI to charge excessive interest

rate to the borrowers, which thereby made Compartamos highly profitable. Other MFIs have

been accused of using exploitative lending techniques which were pushing borrowers into “debt

traps”. The effectiveness of microfinance towards poverty alleviation started to be called into

question. In some cases, these criticisms led to a severe political reaction. For example, in

Ecuador, India and Nicaragua, the authorities closed branches of large MFIs. Also, in more than

forty developing countries, we observed the introduction of mandatory interest rates ceilings to

prevent MFIS of using abusing pricing practices. These scandals highlight the difficulty of

20

reconcile conflicting interest for for-profit MIFs, namely being profitable while offering fair

microcredit terms.

In developing countries, most of the poor, especially women, lack access to basic financial

services which are necessary for them to manage their life and break the vicious circle of

poverty which is characterised by low incomes, low savings and low investments. Muhammad

Yunus, the founder of Grameen Bank, claimed that access to credit should be considered a

human right as it will help to put “poverty in museums”2. A growing body of literature has

investigated the socio-economic impact of microfinance: the results are mixed.

Pitt & Khander (1998) found a significant positive effect on the overall level of wellbeing of

poor households, measured by some indicators such as schooling of children, especially when

the woman is the participant of the program. Some studies suggest that microfinance

contributed importantly to the income generation activity (Samer & al, 2015) but had modest

impact on other indicators such as education, health or female empowerment (Kondo & al,

2008; Setboonsarng,& Parpiev, 2008). Some other studies contradict these results and find a

positive relationship between microfinance and children education (Holvoet, 2003; Noreen &

al, 2011). Many other studies show, however, that the effects of microfinance on alleviating

poverty are relatively small, or even non-existent (Duvendack & Palmer-Jones, 2012; Hermes,

2014; Ali & Mughal, 2019). According to Remazanali & Assadi (2018), microfinance is an

effective tool for poverty alleviation for the less severe poverty cases, but with limited impact

on core poverty. Another analysis, from Morduch (1998), is that microfinance does not reduce

poverty, but vulnerability, by increasing resilience of poor households.

Remazanali & Assadi (2018) intended to answer to this question using Brazil as case study.

They conclude their paper on the fact that microfinance contributed to mitigate socioeconomic

disparities, through the generation of jobs and income, but fail to significantly alleviate poverty

due to low coverage. The authors outline that the outcome of microfinance is highly dependent

to the economic and political context. Their study focused on productive microcredits, which

is the most common type of microfinance in Brazil.

All the studies mentioned in the two last paragraphs are generally focusing on productive

microcredits, the most common type of microfinance. Some can argue that the results of these

research are not relevant for housing microfinance, however we believe they are interesting

2 Yunus, M., (2006) Nobel Lecture, URL: https://www.nobelprize.org/prizes/peace/2006/yunus/26090-

muhammad-yunus-nobel-lecture-2006-2/

21

insights on the topic. Indeed, as mentioned earlier, it has been proven that 20% of productive

microcredits are actually directed to home improvement (Habitat for Humanity, 2019). Besides,

productive microcredits also allow families to save more funds for home improvement, which

means the impact of general microfinance can be relevant as it is closely related to housing

microfinance. Only one study aiming at assessing the impact of HMF towards poverty has been

identified so far. The findings suggest that HMF has a positive impact on home improvements

and the delivery of affordable houses to the LIHs, as well as on household empowerment

encompassing the dimensions of financial inclusion, social inclusion and economic security

(Odongo, 2016). Nevertheless, Odongo’s findings must be considered carefully as the diversity

of MFIs practices require additional empirical evidences to properly assess the link between

HMF and poverty alleviation.

Bondinuba & al (2020) argues that the application of microenterprise finance concepts in HMF

can be very detrimental to the lowest socioeconomic groups. In conventional microenterprise,

microloans are granted to acquire more capital, expand the business, and ultimately lead to a

business income increase. However, in the case of HMF, the funds are directed to the

improvement of a house which does not generate any income to reimburse the loan, pushing

the borrower into the debt trap. The pressure of the debt repayment can lead borrowers to recur

to alternative sources of funding only to reimburse the initial microloan. Besides, the cost and

prices of building material may be very unstable in developing economies, resulting from

external macro-factors. Also, countries with unpredictable and regularly escalating inflation

induce concerns to both MIFs and the poorest of the poor borrowers. Lastly, regulations

concerning urban development may also evolve due to the fast urbanisation, which can lead the

low-income borrowers to lose their land for new developments.

As said Bertrand Renaud, former senior housing finance advisor for the World Bank, housing

microfinance is continually facing the challenge of reconciling “three particularly conflicting

objectives: affordability for the households, viability for the financial institutions, and resources

mobilization for the expansion of the sector”3

Grubbauer (2019) outlines the lack of academic research on the impact of housing

microfinance, from both the perspectives of the housing market and the households of the

3 Renaud, B. cited in Reckford, J., Step by step: supporting incremental building through housing microfinance,

Habitat for Humanity, Shelter Report, 2014, URL:

https://reliefweb.int/sites/reliefweb.int/files/resources/2014_shelter_rpt_final.pdf

22

borrower. The author claimed that there is no sufficient evidence ensuring the social impacts of

housing microfinance envisioned by the industry, namely “largely improving quality of life and

happiness, sanitation and health, and security of tenure” (Habitat for Humanity, 2015, p. 27).

c. Constraints and challenges

In this section, we will discuss some inherent constraints and challenges that MFIs, investors,

and clients face that are prohibitive to the full realisation of the market opportunities of HMF

portfolios in the low-income housing market.

Prior & Argandoña (2009) identified four factors hampering the development of microfinance

in developing countries. They defend the position that the lack of access to financial services in

developing countries is mainly due to a supply problem. According to them, “the business

models used by the financial institutions operating in these countries are inadequate and

inefficient, as they are unable to profitably serve the low-income segments.” (p.354). Although

these factors are referring to general microfinance, they are applicable to HMF and provide

valuable insights on current issues for the expansion of HMF. The first of these factors is the

high cost and price of financial services. Indeed, the weak financial penetration is closely related

to the low overall level of efficiency, due to high operating costs and to the scarce presence of

active financial institutions. These institutions are stimulated to serve only high-income client

due to the low level of competition. Secondly, they reported a geographical issue. The density

of bank branches is low in developing countries as the potential customers in these areas are

low-income and do not generate sufficient income to cover the costs of traditional bank

branches. Thirdly, Prior & Argandoña (2009) reported that there is a lack of appropriate

methodologies for analysing credit risks. The low level of bancarization and the vast informal

economy makes difficult in collecting credit history and repayment, and thus estimate the credit

risks. Fourthly, they identified the lack of an appropriate regulatory framework for microfinance

is an obstacle to its spread, as it generates high regulation costs, complex bureaucratic

requirements and variation from country to country. These issues are maximized by the diverse

nature of MFIs (NGOs, social enterprises, financial institutions). Nonbanks MFIs are not

subjected to the financial regulation followed by central banks and are not eligible financial

intermediaries, which prevent them from diversifying their products, such as offering saving

accounts (Arun, 2005). An appropriate regulatory framework creates the conditions for a MFIs

to expand and reach financial sustainability through subsidizes.

23

Several authors support the hypothesis that market saturation can negatively impact MFIs

portfolios, which is apparent because of expanding credit in the saturated market to the pool of

borrowers, thereby deteriorating portfolio quality, and with that raising exposure to risky loans

(Gonzalez, 2010; Lutzenkirchen & Weistroffer, 2012; Mia & al (2017). Gonzalez (2010) argues

that when market penetration rates exceed 10% of the total population, portfolio quality

diminishes. Lutzenkirchen & Weistroffer (2012) explain this trend by the fact that when the

potential pool of new clients falls, MFIs in fast growing markets have trouble acquiring new

low-risk borrowers among the poor and end up granting credits to subprime borrowers.

Secondly, MFIs facing high growth do not hire and train cannot keep up with hiring and training

new staff, so that the case-load of loan officers increases, while quality of monitoring decreases.

Specifically, Habitat for Humanity (2019) listed the three main related risks to housing

microfinance for MFIs as follows: (1) client repayment consideration, (2) nonfinancial

constraints and (3) tenure security. The most major risk concerns the ability of the client to

repay the instalments, which is a common concern when dealing with clients with inconsistent

or even unpredictable income is a common concern throughout the microfinance sector. Then

comes the nonfinancial constraints, that is the insufficient ability of housing microfinance

clients to budget or plan for the project. A way to solve this issue is by providing technical

assistance or housing support services. These services may include construction guidance,

assistance in budgeting for the project, legal assistance in securing formal recognition of land

tenure, and even home maintenance skills. Lastly, tenure security is a big concern as in regions

that lack sufficient regulation, homeowners might not be able to prove their ownership. In that

case, the financial providers would have extremely limited recourse on the property if the client

defaulted. Also, an external party could lay claim to the property and ask the residents to leave.

To face this issue, MFIs have to assess the land tenure risks in the region it operates and

adequately price this risk into the product terms.

There is one last constraint faced by MIFs when offering housing microfinance products:

offering stand-alone products with no records on the borrower (Ferguson, 2004). Indeed, the

strongest pressure to repay a loan comes from the ability of the lender to cut future access to

credit to the borrower. In the situation of microlending for microenterprises, they depend on

microfinance institutions for a continuous stream of small working capital requirements,

equipment, or other types of loans, creating a strong business relationship. In the context of

housing microfinance, the borrower may need only one larger credit rather than a sequence of

small loans, which would constitute a stand-alone product. If housing microfinance institutions

24

do not share their information about risky clients, the repayment incentives for the whole

industry weakens.

d. Factors for housing microfinance expansion

Housing microfinance is a relatively new financial product. According to the survey of Habitat

for Humanity (2017)4, this new financial practice expanded significantly around 2005, with the

number of financial institutions offering housing microfinance products nearly doubling

between 2006 and 2011. About 16 percent of total reporting institutions launched housing

microfinance products within the first year of the organization’s founding and 41 percent

introduced housing finance products within 5 years of company’s existence. Globally, housing

microfinance is growing as 64% of MIFs reported that housing microfinance products are

growing as a percentage of their portfolio.

On a global scale, housing microfinance still account only for a minor proportion of

microfinance. A 2011 report found that housing microcredits accounted for less than 2% of the

overall microfinance sector (Habitat for Humanity, 2015).

Some factors in developing economies are fundamental to create an attractive and sound

environment for MIFs expansion. According to Ferguson (2003), the potential for expansion of

housing microfinance institutions is greatest in countries where: (1) macro-financial conditions

create high real interest rate (10% and above) that make traditional mortgage finance affordable

for only a small share of the population, (2) land tenure problems are widespread, and the legal

structure makes taking and/or executing mortgage liens difficult, costly and rare, (3) the great

bulk of the population is low- to moderate income, (4) urbanization is fast, and hence housing

problems are great, (5) a high share of the population has rights to land shorts of full legal title

via purchase or invasion, (6) a strong microfinance industry exists.

A more recent study conducted in Ghana ranked the motivations of MIFs to enter the housing

market in a developing country (Bondinuba & al, 2020). The interest in profit have been listed

as the top motivation for MIFs to offer housing microfinance products. Then, the second strong

determinant of MIFs motivation to enter the market the easy of entry into the market, which

depends on a set of factors such as the prevailing regulatory environment, the availability of

funding, affordable land, among others. The third factor is the interest in growth which mainly

4 Note: the survey of Habitat for Humanity is based on the answers of 101 financial institutions offering housing

microfinance products of a fairly even regional distribution. Results might be biased due to the limited sample.

25

rest on the estimated size of the low-income housing market. Lastly, the desire of

homeownership which is shaped by cultural specificities is an important factor to consider.

The survey of Habitat for Humanity (2017) obtain different results regarding the top reasons

for MIFs to offer housing microfinance products, which can be explain by the different angle

chosen in the survey to tackle the issue. In this report, the main drivers turned out to be social

impact (90%), demand from loyal clients (56%) and portfolio diversification (40%) and attempt

to tap into a new market or grow clientele bases (39%). Institutions are validating missional

alignment (social impact) and considering how the product contributes to the business strategy

of the institution (retain clients or expand market). If we segment by institutional types, we

observe subtle variations in the results. “Social impact” was the most frequently listed motivator

across all institutional types5. For cooperatives and foundations, NGOs and microfinance banks,

“growth in response to demand from loyal clients” was the second most frequently cited

motivator. As we could expect, no NGOs cited profitability, while 53 percent of microfinance

banks, 25 percent of nonbanking financial institutions and 11 percent of cooperatives and

foundations cited profitability as a top three motivator. For microfinance banks, profitability

ranks third. This variation reminds us that the institutional type of the MIFs has a strong

influence on its mission and way of working.

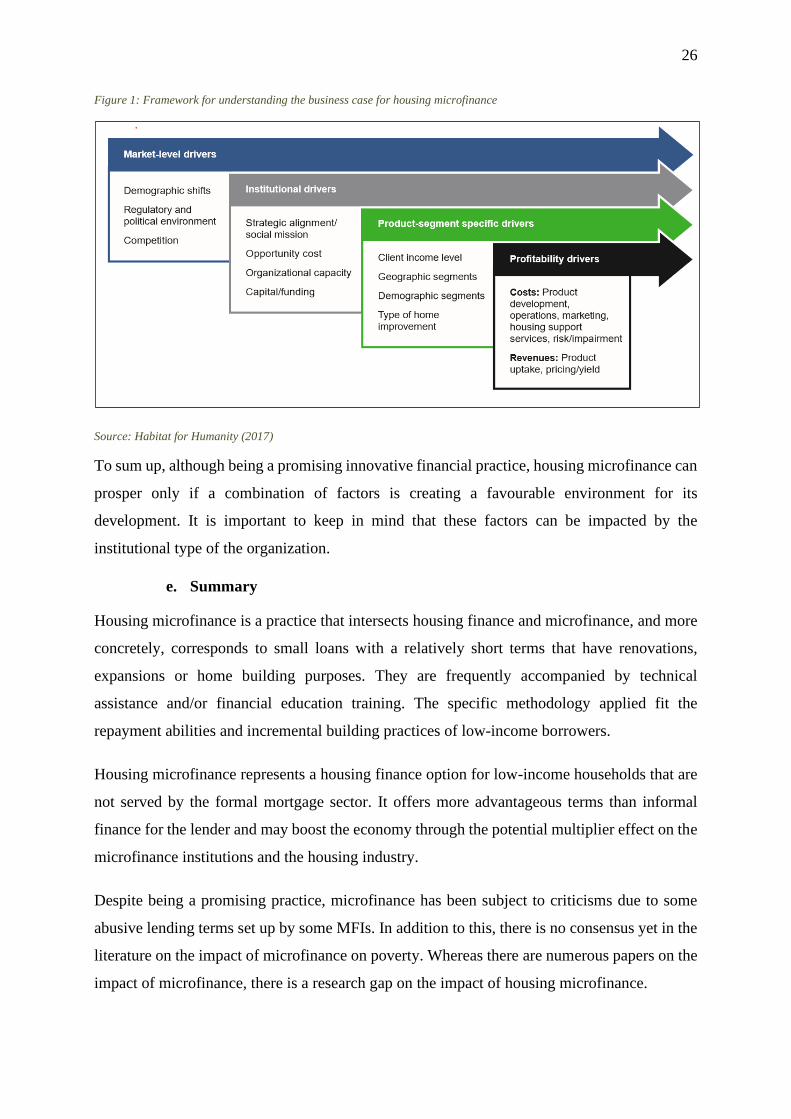

Habitat for Humanity (2017) created a framework, that you can see below, providing valuable

insights to financial institutions in the launch and expansion of housing microfinance products

(Figure 1). The framework aims at covering all drivers related to housing microfinance, namely

market-level drivers, institutional drivers, product-segment specific drivers and profitability

drivers.

5 Note: institutional types are divided among four categories in the study: (1) Cooperatives and foundations, (2)

Nongovernmental organizations, (3) Nonbanking financial institutions, (4) Microfinance banks

26

Figure 1: Framework for understanding the business case for housing microfinance

Source: Habitat for Humanity (2017)

To sum up, although being a promising innovative financial practice, housing microfinance can

prosper only if a combination of factors is creating a favourable environment for its

development. It is important to keep in mind that these factors can be impacted by the

institutional type of the organization.

e. Summary

Housing microfinance is a practice that intersects housing finance and microfinance, and more

concretely, corresponds to small loans with a relatively short terms that have renovations,

expansions or home building purposes. They are frequently accompanied by technical

assistance and/or financial education training. The specific methodology applied fit the

repayment abilities and incremental building practices of low-income borrowers.

Housing microfinance represents a housing finance option for low-income households that are

not served by the formal mortgage sector. It offers more advantageous terms than informal

finance for the lender and may boost the economy through the potential multiplier effect on the

microfinance institutions and the housing industry.

Despite being a promising practice, microfinance has been subject to criticisms due to some

abusive lending terms set up by some MFIs. In addition to this, there is no consensus yet in the

literature on the impact of microfinance on poverty. Whereas there are numerous papers on the

impact of microfinance, there is a research gap on the impact of housing microfinance.

27

On a global scale, housing microfinance is still minor, what can be related to the risks previously

highlighted that are supported by microfinance institutions.

3. Housing Microfinance in the Brazilian context

This chapter will focus on the Brazilian context. It seems relevant in this topic to provide to the

reader some knowledge concerning general microfinance evolution, as HMF is a subpart of this

practice. This subsection will cover the history of microfinance in Brazil, the regulatory

framework of the practice in the country, its current state as well as some insights on the housing

deficit and housing financing options for low-income households. The housing deficit and

housing problem for the poorest ones in Brazil has been subject to important research but

generally under the prism of public policies, and not market-based solutions. Also, in order to

assess the potential contribution of HMF, this topic reveal necessary for the reader to understand

the pool of options the base of the pyramid population has in housing financing. Except for the

state-program My House My Life, researchers have not treated this subject in much details. In

this part, focusing exclusively on the Brazilian context seemed crucial as these alternative

housing financing options are shaped by the political, economic and cultural Brazilian history

and practices.

a. Microfinance

According to Oikawa Cordeiro (2020), Brazil “has a trajectory that stand out the microfinance

world” (p7). Brazil was a pioneer in the creation of what is considered the “new wave” of

microcredit, having started its first microcredit program even before Bangladesh, which is

generally cited as a success example of microfinance. Also, it regulated the sector much earlier

than most countries of the global south. Despite this pioneering role, the microcredit sector in

Brazil did not develop much and is still very limited today. After the election of the Worker’s

Party (PT) in 2003, the state started to play a major role, either through subsidy policies, or

through the control of interest rates, and more generally, by strategically leading the sector

(Oikawa Cordeiro, 2019).

Several authors outline the change in the general characteristics of these projects (Lima, 2009;

Marques, 2009; Feil & Slivnik, 2019). Initially, there was a greater presence of international

organizations and NGOs, such as the World Bank, the Inter-American Development Bank and

Acción International, acting either through funding or technical support. However, their

28

presence declined drastically over the years, concomitantly with the growth of the state’s

presence in the sector which started mainly with Lula administration in 2003.

The following paragraphs will describe chronologically and in more details the trends evoked

above.

The history of microcredit in Brazil started in 1973 in Recife with the Projeto Uno organized

by Banco Economico. The program’s main purpose was to offer a small line of credit to

informal workers with no collateral, an innovative idea at the time. Despite its innovative

business model and eighteen years of existence, the program got shut down due to its lack of

financial sustainability (Santos & Gois, 2011). Following UNO’s creation, several NGO

oriented towards microcredit have been created in the country, with a significant share of these

receiving financial support from US-based development organizations (Feil & Slivnik, 2019).

However, all these early attempts revealed difficult to operate and gradually shut down. Most

of them were unable to reach sufficient scale and financial sustainability and were strongly

affected by the monetary instability that ravaged the country during the 1980s and beginning of

the 1990s (Feil & Slivnik, 2019).

Several authors report that it is in the second half of the 1990s, after monetary stability had been

achieved by the Real Plan (1994), that microfinance institutions, known as Banco do Povo,

started to mushroom in the country as a result of organized civil society and a number of

municipal and state initiatives (Carvalho de Franca Filho & al, 2012, Feil & Slivnik, 2019). The

federal government had decided to boost the microcredit sector and for that purpose, operated

legal and regulatory changes and implemented several new policies and programs to create

supportive conditions for microcredit expansion. In 1996, the first major public intervention

aiming at supporting microcredit activity was conducted by the National Bank for Economic

and Social Development6 (BNDES) which created the Popular Productive Credit Program and

the Institutional Development Program. These two organizations had as purpose to create the

basis for the expansion of microfinance in Brazil.

According to Feil & Slivnik, (2019), the most successful program began on year later, in 1997,

with the creation of CrediAmigo by Banco do Nordeste. Its success can be attributed to its

6 Note: BNDES is a federal-owned development bank and is the main financing agent for development in the

country.

29

methodology with the focus on loan officers, social collateral and low bureaucratie. Currently,

the program has two million customers and is self-sustainable.

Several authors consider that the election of the left-oriented Workers Party and Lula in 2003

represents a turning point in the democratization of access to credits and others financial

services in Brazil (Barone & Sader, 2008; Carvalho de Franca Filho & al, 2012; Oikawa

Cordeiro 2019; Feil & Slivnik, 2019). Despite being one of the largest economies in the world,

wealth distribution was – and still is – highly unequal, and regional disparities extremely

important. To address these issues, Lula’s administration worked at facilitating mass financial

inclusion by the poor, to increase consumption. For this purpose, the famous cash-transfer

program Bolsa Familia has been created and there was a major expansion of microcredits for

consumption needs. Bringing an end to the neoliberal trends of the 1980 and 1990s reducing

the interventionism of the state, Lula’s government began to restore the role of the government

as the promoter of economic growth and long-term planning (Feil & Slivnik, 2019).

According to Feil & Slivnik (2019), a more comprehension policy toward financial inclusion

started to be delineated after 2003, with numerous measures to expand the supply of financial

services to low-income populations. The main measures were the facilitation to simplification

of the process of opening bank accounts, the stimulus to the formation of credit cooperatives

and the introduction of a two percent reserve requirement on demand deposits by the Central

Bank to microcredit lines. This third measure was an attempt of the BCB to bring the private

financial sector into the microfinance industry. According to Feil & Slivnik (2019), this

regulatory initiative constituted an important tool to stimulate financial institutions to supply

microcredit at relatively low interest rates.

In 2005, the federal government conceived a more comprehensive microcredit policy: created

the National Program of Oriented Productive Microcredit (PNMPO)7. PNMPO aimed at

fostering job creation and income for micro-entrepreneurs, providing resources for microcredit

operations, offering technical support to microcredit providers (Feil & Slivnik, 2019).

According to Feil & Slivnik (2019), PNMPO evolved following the introduction of the

CRESCER program, which pushed the microfinance sector to put more emphasis for business

investment rather than consumption needs. The CRESCER program sets interest rates for

microcredit in a maximum of 8% per year, which is low for Brazilian standards (Feil & Slivnik;

7 Note: the National Program of Oriented Productive Microcredit (PNMPO) have been created through the

enactment of Law 11,110 the 25th of April 2005

30

2019). Barone and Sander (2008) argue that in practice, PNMPO acts as an articulating

institution between productive oriented microcredit institutions, banks and other operators of

public resources, by providing support, promotion and structuring of the microfinance sector.

Thus, it performs other functions that overlap the functions already exercised by BNDES,

duplicating institutional structures and dividing efforts.

Regarding the legal framework, in the two last decades, the Brazilian government has fostered

the development of productive-oriented microcredits through legal instruments but restrained

consumer microcredits.

According to Shankar Nayak & Vieira da Silva (2019), two legal milestones shape the sector

in Brazil until today. First, the Law 10.735/ 2003, according to which all financial institutions

are required to allocate 2% of their direct deposits to microcredit. These are called the Inter-

finance Deposits of Microcredit (DIM). Its objective is to stimulate the performance of the

private financial sector in the microfinance sector. Second is the creation of the National

Program of Productive Oriented Microcredit (PNMPO), by the federal government,

institutionalized by the Law 11.110/2005, which expands the resources directed to the

microcredit sector and formats its operations, limiting, for example, the interest rate at 2% per

month.

Since the resolution 4000/2011 of 2011, the Central Bank of Brazil requires that 80% of the

compulsory applications should go to operations with low-income individuals to stimulate

entrepreneurship, with an emphasis on the development of local communities (Shankar Nayak

& Vieira da Silva, 2019).

Nevertheless, the high operational costs, the lack of expertise in the market combined with these

normative restrictions such as the cap on interest rates, have been reported to be significant

obstacles for private banking institutions to develop their microfinance activities (Chaves,

2011).

More recently, the regulatory framework of microcredit experienced some changes, aiming at

restraining consumer microcredits8 and expanding productive microcredits (Shankar Nayak &

Vieira da Silva, 2019). In 2018, the Brazilian Congress has approved a new law for microcredit

8 Valente, G. Governo acaba com microcrédito para consumo e expande operações para empreendedores , 2019,

URL: https://oglobo.globo.com/economia/governo-acaba-com-microcredito-para-consumo-expande-operacoes-

para-empreendedores-23558271

31

operations (Law 13636/2018). Access has been increased to microentrepreneurs with annual

gross income of up to 200 thousand reais and the maximum limit for the total balance of the

operations contracted by the client increased from 40,000 reais to 80,000 reais. The law also

extends the sources of microcredit financing. Since then, the monitoring of the use of money

by entrepreneurs can be done electronically. This should lower the cost of this type of operation

and encourage more banks to operate in this market and fintechs to expand. Under the current

microcredit rule, banks cannot charge interest higher than 3% per month on these contracts. The

Contract Opening Fee (TAC) is limited to 4% of the total financing amount. As the allocation

of 2% of their direct deposits to microcredit operation did not change, the volume of money

available should not increase at first. This new set of regulations also restrained consumer

microcredit to only one item of consumption: the assisted technologies which encompasses

wheelchairs, hearing aids, equipment for the blind, for example9.

For now, the Brazilian microcredit regulation does not allow financial institutions to offer

microcredits for housing financing and we observe a trend to foster income-generating

microcredits but limit other types of microcredits.

The next paragraphs will aim at evaluating the current state of microfinance in Brazil.

Despite the recent developments and improvements, the size of microfinance in Brazil remains

low compared to the national financial system (Table 3; Feil & Slivnik, 2018). Although its

volume has more than doubled from 2007 to 2016, its proportion only slightly increased in

percentage of the GDP and percentage of the financial system. Both in volume and proportion,

the microfinance industry peaked in 2013, when the interest rates reached its lowest level. In

2016, microcredit operations amounted USD 1,523 million, accounted for 0,08% of the GDP

and 0,16% of the financial system, and had an average interest rate of 28,70%.

9 Ibid

32

Table 3: Data on Microcredits in Brazil

Source: Feil & Slivnik, (2018)

Ramezanali and Assadi (2018) provide data on the current state of microfinance in Brazil in

their paper aiming at assessing poverty alleviation. They report that in 2014, the 1045

institutions that sent their data to Mix Market reached 111.7 million low-income clients and

produced a loan portfolio of USD 87.1 billion. There is an important gap with the study of

Shankar Nayak and Vieira da Silva (2019), who reported that the number of microfinance

clients in Brazil reached 3.1 million people in 201510. This number seem far from reaching its

potential of the market of the 35 million clients for microfinance in Brazil estimated by Soares

& Melo Sobrinho (2008). The level of penetration of microfinance is still very low.

Ramezanali and Assadi (2018) report that at the national level, the microcredit portfolio

represents 0.2% of the value and 0.4% of the operations of the National Financial System

(SFN), respectively amounted to BRL 5.3 billion, for 3.1 million loans11. The default of the

total microfinance portfolio - 5.6% among individual customers and 5.0% of the legal entity or

small business customers - is higher than those reported in the banking industry (4.4% and

1.8%, respectively)12. On average, credits – non necessarily micro - represent 30.4% of the

income of individual customers microcredit borrowers. Regarding credit distribution, the

10 Note: primary data retrieved from Relatório de dados do programa de microcrédito: 3o. trimestre de 2015,

Ministério do Trabalho e Emprego, 2015 11 Note: primary data retrieved from Global Entrepreneurship Monitor, Entrepreneurship in Brazil - Executive

Report, 2014 12 Note: primary data retrieved from Bacen, Bulletin of Central Bank of Brazil, Central Bank of Brazil, 2015

33

authors note geographical variations. The Northeast region accounts for 52.1% of the national

portfolio in value and 35% of the number of transactions. The average value per transaction is

50% higher than the national average. The Southeast is the second largest microcredit portfolio,

accounting for 22.6% of the national value. These disparities can be explained by the wide

disparities in poverty in Brazil, the Northeast being the poorest state of the country.

Pedroza (2011) highlighted the low penetration rate of microfinance in Brazil (8,1%) compared

to other Latin American countries, such as Bolivia (43,5%) and Peru (33,9%), where

microfinance is an important component of their financial markets (Shankar Nayak & Vieira

da Silva, 2019). Soares and Melo Sobrinho (2008) estimated a potential market of 16 million

micro-entrepreneurs in Brazil, and an effective demand of 12 billion reals (U.S.$3.2 billion) in

microcredit operations, which as we saw in the previous paragraph, is yet far to be met.

Housing microfinance is virtually non-existent in Brazil. So far, there is only one study

launched by City Alliance in 2007 assessing the viability of housing microfinance in the state

of São Paulo. However, with the creation of My House My Life, the development of

microfinance in Brazil and the regulatory evolution, the results are partly outdated. As

mentioned previously, the central bank does not allow financial institutions to offer housing

microcredits, which can explain the little amount of research on housing microfinance in the

Brazilian context. We can conclude that there is a research gap in that topic, as literature

exploring low-income housing is focusing on state-based alternatives.

b. Housing deficit

This subsection will cover diverse aspects of the question, such as the general pattern of LIHs

housing construction or improvement pattern, the estimated demand, the current housing

deficit, and the factors causing these issues. Then, we will move on to the state-program My

House My Life and alternative options offered for housing financing for LIHs.

The lack or poor quality of housing is a major issue for LIHs in Brazil. Gonzalez & Deak (2018)

performed a study on the evolution of housing access in Brazil from 1995 to 2015. They report

in 2015, a housing deficit of 6 million of families, which corresponds to 9.3% of families in

Brazil.13 Considering the timeframe 2007 to 2015, they observe an improving of housing access

till 2013, when the housing deficit started to worsen, both in absolute and relative values. In

13 Note: primary data retrieved from Fundação João Pinheiro

34

2014, about half (48%) of the housing deficit was fuelled by the excessive burden of the housing

related costs (rent, charges, ect…)14. The other half of the housing deficit is made up by family

cohabitation (31%), precarious housing (14%) and house crowding (6%). Family cohabitation

and precarious housing are the categories that decreased significantly both in absolute and

relative percentage. Precarious housing fell from 23% (1.4 million units) in 2007 to 14% (0.9

million units) in 2014. Family cohabitation decreased by 8% over this timeframe (from 39% -

2.5 million units - in 2007 to 31% - 1.9 million units - in 2014). House crowding remained

stable over time (6% - 0.3 million units). The excessive burden of the housing related costs is

the parameter that increased the most. It rose from 32% to 48% (2.0 to 2.9 million units). This

last parameter increased greatly, driven by the valorisation of real estate prices over this

timeframe, which has not been accompanied by a valorisation of wages of the same magnitude.

According to a technical report from FGV to Abrainc (Brazilian Association of Real Estate

Developers), the most vulnerable families, those which earn less than three minimum wages15

, represent 91.7% of the total housing deficit and 100% among those who spend too much on

housing-related costs16.

Nevertheless, despite the housing shortage, Brazil does have a significant number of vacant

units despite the housing shortage (Business Call to Action and Aspen Network of Development

Entrepreneurs, 2014). There are estimated to be at least 7 million empty homes, of which 70%

are in urban areas. Most vacant units are situated in the south-eastern region, with 1,33 million

units in São Paulo. The number of vacant buildings almost equals the units needed to eradicate

the shortage of housing. At least 6.3 million of the 7 million units are in suitable condition to

be occupied and would provide housing for about 19 million people. However, the murky legal

status of the buildings is one of the problems in coping with empty property and recent housing

policies have not dealt with this issue, although these empty units could be used to reduce the

housing crisis with sufficient public policy and private intervention.

Previous research has highlighted the demand for home improvements or expansion.

In 2007, a study conducted by Ashoka explored consumer credits on building material

confirmed the demand for home improvements or expansion. Out of the 237 households

14 Note: housing costs are said excessive when they exceed 30% of income 15 Note: three minimum wages equated BRL 2,994 in 2019 16 Study cited in Antunes, L., Minha Casa perto do fim?, UOL Economia, URL:

https://economia.uol.com.br/reportagens-especiais/minha-casa-minha-vida-dez-anos/#tematico-1

35

studied, 91% declared to intend to pursue home improvement or home expansion (Ferguson &

Smets, 2010).

A more recent study conducted by Plano CDE and the Center for Microfinance and Financial

Inclusion Studies from FGV (2016) on the social classes C, D & E found that home

improvement (22%) is the third most chosen answer to the question “What would you do if you

had extra money?”, after saving (48%) and pay debt (26%). Therefore, we believe that as

international research outlined, LIHs improve their home gradually and that a large share of

this population wishes to expand or improve their home.

Also, as mentioned earlier, research has showed that 20% of microentrepreneurs microcredits

are already directed to home improvement (Habitat for Humanity, 2019). The study of

Ramezanali and Assadi (2018) on microfinance in Brazil corroborates these results: 35% of

microloans have for main purpose housing17. The reported proportion in Brazil is higher than

the worldwide average; that can be related to the fact that HMF is not legally authorized for

financial institutions in Brazil, only productive microcredits are. Thus, microentrepreneurs

would more redirect the purpose of their microloans to housing as they lack other options.

The pattern of housing building for LIHs in Brazil is consistent with the research discussed in

the previous section: slum-dwellers build their home incrementally.

A study conducted by Cities Alliance with the Municipality of Sao Paulo in 2007 highlighted

that incremental self-constructions (often carried out over several years) represent 77% of

housing units built annually in Brazil. In classes C, D and E they represent 99% of the buildings.

Regarding financing, 62% are self-financed, a percentage that rises to 92% for classes D, E. All

the households surveyed declared having built their house themselves and extended it over time.

In the case of the group with residents of buildings, almost all residents still need to renovate

their apartments, as these are delivered by the government without internal and external

finishing. The external renovation is the first thing to be done by the new residents.18 Only part

of the participants (40%) managed to carry out the internal renovation of the apartment, in a

period that varied from 1 to 3 years of living in the building.19 The payment of utility bills,

which many residents coming from slums did not previously pay, put a financial pressure on

the slum-dwellers and leads them to postpone investments in internal renovations of the

17 Note: primary source of the chart is Cidadania Financiera of 2015 18 Note: refers to renovation of the floor, the gate, the stairwell window 19 Note: refers to renovation of the flooring, painting, plaster or putty

36

apartments. In the case of collective housing, 58% of participants stated that they had renovated

their apartment. Most of them discounted the investment made in the improvement out of the

rent. Therefore, in the case of both favelas and apartments, there is an extended period of time

until the improvement or expansion of the unit is carried out.

A report published by Business Call to Action and Aspen Network of Development

Entrepreneurs (2014) on housing of LIHs states that most self-construction is performed by the

residents themselves, representing over 70% of building material transactions in the

construction sector.

c. Housing financing options for low-income households

In this subsection, we will present financing options in Brazil that are accessible to LIHs. We

will begin with the most popular – My House My Life and consumer credits – and move on to

housing cooperatives and housing consortium, and finish with informal housing finance.

Created in 2009, My House My Life is the largest housing policy operating in Brazil. 2007 and

2008 were years of intense growth in Brazil (6.1% and 5.1%) but it was benefiting mainly to

families with middle- and high-income, according to Ana Maria Castelo, coordinator of Civil

Construction Studies at IBRE/FGV (Brazilian Institute of Economics at Fundação Getulio

Vargas).20 The subprime crises outbreaking in the US in 2008 generated concerns on the credit

offer in Brazil. The government of Lula first strengthened the real estate credits offer in public

banks and announced in March the creation of the program My House My Life. Its aim was to

decrease the housing deficit for low-income people, as well as stimulate the economy which

was facing the effect of the subprime crises at that time.21 The program was aiming at building

one million of accommodations for the low-income population at the cost of BRL$34bn through

loans and subsidizes (BRL$60.8bn corrected from inflation - 2019)22. Since 2019, the

subsidizes are fully financed by the Employment Time Guarantee Fund Fundo (ETGF).

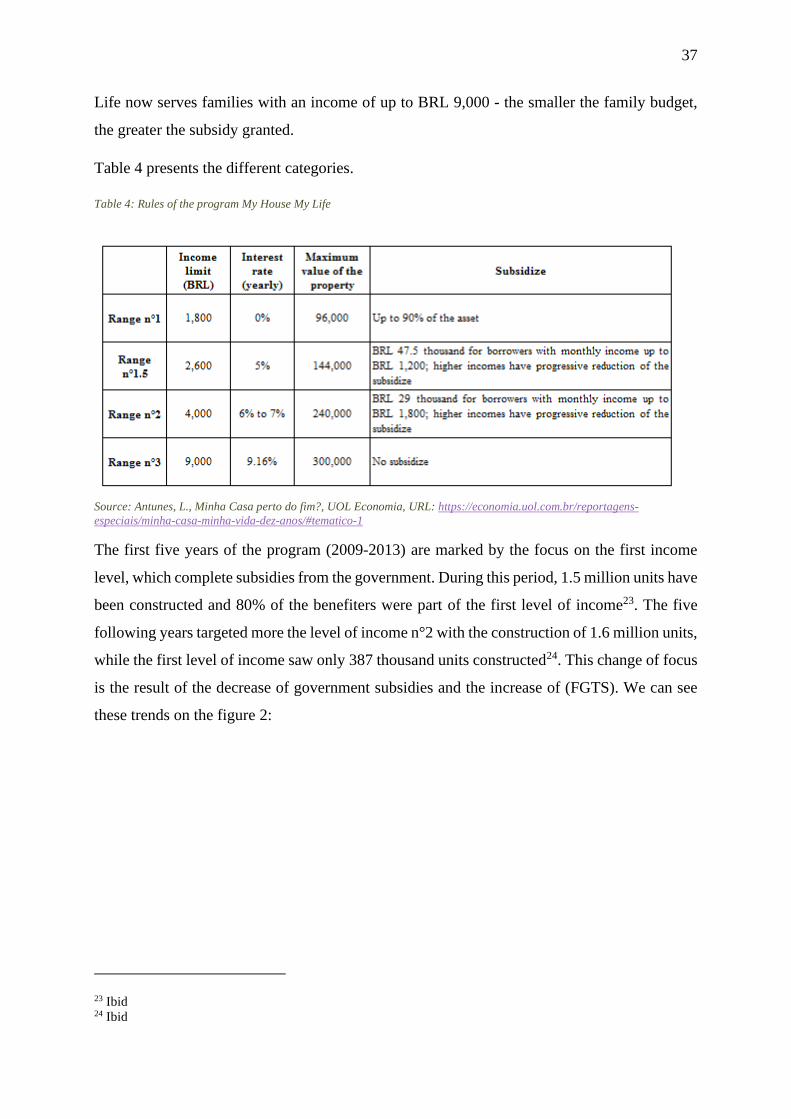

The program was organized by levels of revenue and corresponding rate, maximum value of

the unit and level of subsidize. The income range have been modified in 2016. My House My

20 Antunes, L., Minha Casa perto do fim?, UOL Economia, URL: https://economia.uol.com.br/reportagens-

especiais/minha-casa-minha-vida-dez-anos/#tematico-1 21 Ibid 22 Ibid

37

Life now serves families with an income of up to BRL 9,000 - the smaller the family budget,

the greater the subsidy granted.

Table 4 presents the different categories.

Table 4: Rules of the program My House My Life

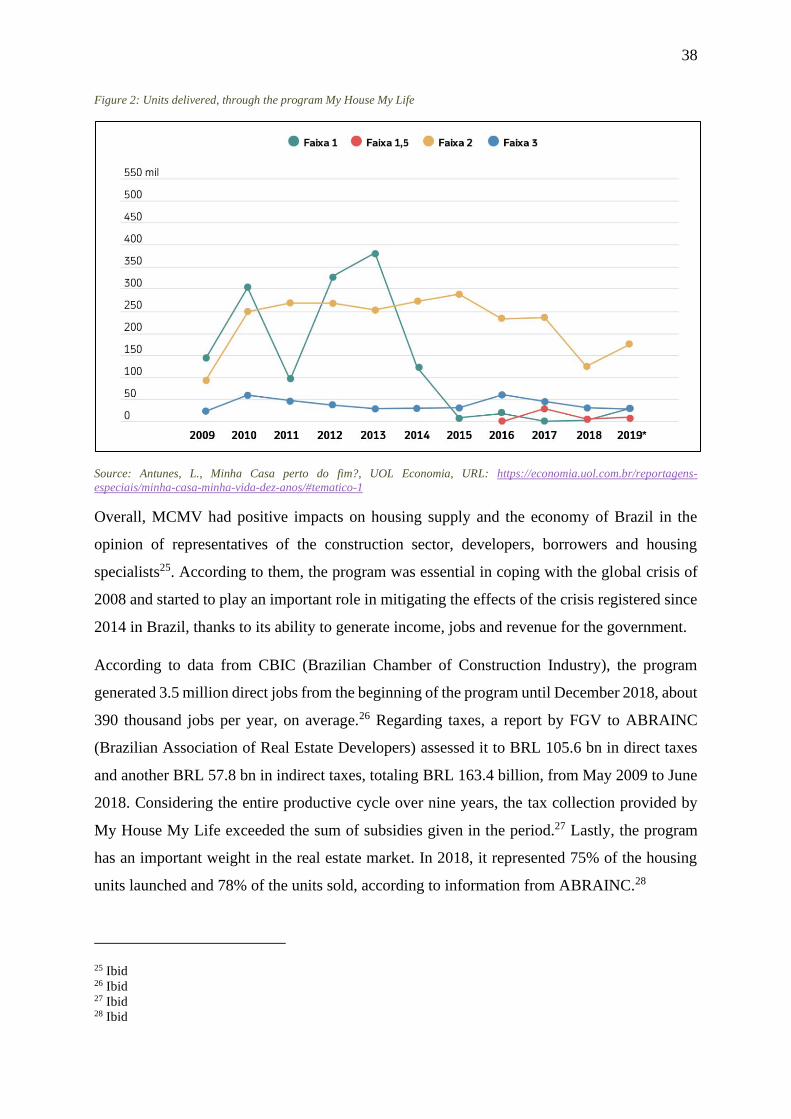

The first five years of the program (2009-2013) are marked by the focus on the first income

level, which complete subsidies from the government. During this period, 1.5 million units have

been constructed and 80% of the benefiters were part of the first level of income23. The five

following years targeted more the level of income n°2 with the construction of 1.6 million units,

while the first level of income saw only 387 thousand units constructed24. This change of focus

is the result of the decrease of government subsidies and the increase of (FGTS). We can see

these trends on the figure 2:

23 Ibid 24 Ibid

Source: Antunes, L., Minha Casa perto do fim?, UOL Economia, URL: https://economia.uol.com.br/reportagens-

especiais/minha-casa-minha-vida-dez-anos/#tematico-1

38

Figure 2: Units delivered, through the program My House My Life

Source: Antunes, L., Minha Casa perto do fim?, UOL Economia, URL: https://economia.uol.com.br/reportagens-