effects of loan portfolio diversification on performance of savings and credit on co-operative...

TRANSCRIPT

EFFECTS OF LOAN PORTFOLIO DIVERSIFICATION ON PERFORMANCE OFSAVINGS AND CREDIT ON CO-OPERATIVE SOCIETIES; A CASE STUDY OF

MARAKWET TEACHER’S SACCO LTD.

PRESENTER:

COURSE CODE:

PAPER CODE:

INDEX NO:

SUPERVISOR:

PRESENTED TO:

i

DECLARATIONI declare that this is my original work and has not been

presented to any other institution or examination body and it

should not be reproduced without my concern and that of Eldoret

Polytecnic.

NAME :

SIGN: …………………………

DATE: …………………………

SUPERVISOR

This project has been submitted for examination with my approval

as the project supervisor.

NAME:

SIGN: …………………

ii

DATE:……………........

DEDICATION

I dedicate this work to all those who gave me all support in the

coming up of this project, first of ……………..

iii

ACKNOWLEDGEMENT

I would like to acknowledge the efforts of my parents for the

provision of financial support. I also acknowledge the guidance

and encouragement given to me by my siblings and my colleagues in

school. I also acknowledge the staff of Marakwet Teachers Sacco

for the contribution they gave during my study at their

organization.

iv

ABSTRACTThe aim of this study is to determine the effects of loans

portfolio diversification on the performance of Marakwet

Teacher’s Sacco Ltd. The main objective of the study is to find

out how loan portfolio affects the performance, how does the

diversification influence loan sales, how it affects the

financial position and the customer base. Members of Sacco’s have

been affected by different loans offered by SACCOs this makes the

management to be on the run introducing different loans to their

v

customers. For a Sacco to be able to effectively compete with

other upcoming banking institutions it must among other things

introduce a variety of services so as to improve its objective

achievement for both members and management. This may not work

well until an optimal level of loans portfolio diversification is

reached.

The study employed a case study research design which is believed

to be an intensive descriptive and holistic analysis of the

single entity. The study targeted a population of 49 which

consisted of Junior Employees 39 and Management level employees

10. From the targeted population stratified sampling was used to

pick the sample size for the study. I used questionnaires and

interviews as data collection instruments. Microsoft Excel was

used to capture the data then analyzed by tables and graphs.

The study established that the loan portfolio diversification has

an effect on the SACCO performance and there are some challenges

faced in the management of the portfolio like inadequate sales

promotion strategies, customer preferences and choice, customer

inadequate information on various loans and iintense competition

from other SACCOs. The study recommends the following as

necessary to make loan portfolio diversification successful.

Undertake effective sales promotion to help customers understand

various loans offered and the SACCO should try to educate its

customers on the benefits of other loans as per the circumstance

so that to have good balance on all the loans offered. I

vi

recommend also further research into the sector to ensure that

the strategies work effectively and a research be done to

identify the effects of management skills of the employees on the

performance and the same should be done on the banks.

Table of ContentsDECLARATION..................................................ii

DEDICATION...................................................iiiABSTRACT......................................................vTable of Contents............................................vi

LIST OF ABBREVIATIONS AND ACRONYMS..........................viii1.0 INTRODUCTION...............................................11.1 Background of the study....................................11.1.1 Concept of SACCOs in Kenya...............................11.1.2 Concept of Loan Diversification..........................21.1.2.1 Types of Loans Offered.................................31.1.3 Marakwet Teachers Sacco..................................41.1.3.1 Society catchment area.................................41.2 The Problem Statement......................................51.3 Research Questions.........................................61.4 Significance of the study..................................61.5 Scope and Delimitations of the study.......................71.6 Conceptual Framework.......................................8CHAPTER TWO....................................................92.0 INTRODUCTION...............................................92.1 Review of Theories.........................................92.1.1 Trade Theory and Structural Diversification..............92.1.2 Classical Portfolio Theory..............................112.2 Criticisms of the Theories................................132.3 Empirical Review..........................................142.4 Knowledge Gap.............................................15CHAPTER THREE.................................................173.0 INTRODUCTION..............................................173.1 Research Design...........................................173.2 Target Population.........................................17

vii

3.3 Sampling Procedures.......................................183.4 Data Collection Procedures................................183.4.1 Simple Random Sampling..................................183.4.2 Stratified Sampling.....................................193.4.3 Data Collection Instruments.............................193. 4.3.1 Questionnaires.......................................193. 4.3.2 Interviews...........................................193.5 Validity and Reliability..................................203.6 Data Analysis Procedures..................................20CHAPTER FOUR..................................................214.0 DATA ANALYSIS, PRESENTATION AND INTERPRETATION............214.1 Background Information....................................214.1.1 Gender of the Respondents...............................214.1.2 Respondent’s Educational Level..........................224.1.3 Respondents’ Position in the Company....................234.1.4 Working Years of Service................................24Article I...................................4.2 Specific Objectives

244.2.1 What are the types of loans offered by the Marakwet Teacher’s SACCO...............................................244.2.2 Main reason(s) for offering Variety of loans............254.2.3 Types of loans Preferred by the Customers...............264.2.4 Reasons why Customers prefer any given loan service.....274.2.5 Effects of loan Portfolio diversification on financial performance...................................................284.2.6 Main Indicators of Performance in the Organization......294.2.7 Challenges the SACCO is facing in Managing loan Portfolio..............................................................29CHAPTER FIVE..................................................315.0 SUMMARY OF FINDINGS, CONCLUSION AND RECOMMENDATIONS.......315.1 Introduction..............................................315.2 Summary of the Findings...................................315.2.1 Demographic Information.................................315.2.2 Types of loans offered by the Marakwet Teacher’s SACCO. .325.2.3 Reasons for offering Variety of loans...................325.2.4 Types of loans Preferred by the Customers...............335.2.5 Reasons why Customers prefer any given loan service.....335.2.6 Effects of loan Portfolio diversification on financial performance...................................................33

viii

5.2.7 Main Indicators of Performance in the Organization......335.2.8 Challenges the SACCO is facing in Managing loan Portfolio..............................................................345.3 Conclusions...............................................345.4 Recommendations...........................................355.5 Suggestions for Further Research..........................35REFERENCES....................................................35

LIST OF ABBREVIATIONS AND ACRONYMS

SACCOS- Savings and Credit Cooperative Society

ATM- Automated Teller Machine

KNUT- Kenya National Union of Teachers

TSC- Teachers Service Commission

NPL-Non-performing loan

ix

LLP-Loan Loss Provision

SNC-Syndicated National Credits

CHAPTER ONE

x

1.0 INTRODUCTION

1.1 Background of the study

Co-operative is an autonomous association of persons united

voluntarily cooperate or their mutual economic, social, cultural

needs and aspirations through a jointly owned and democratically

controlled enterprise. A cooperative society is a business entity

geared towards the promotion of the Welfare and economic

interacts of their members and this is in turn will contribute

towards the attainment of the overall national development goals

of poverty alleviation and wealth creation. Cooperative Values

has it’s based on: self-help, self responsibility, decorative

control, equity, equality and solidarity. In the tradition of

their founders, cooperatives members believe in the ethical

values, honesty, openness, social responsibility and caring for

other.

Cooperative principles are the guidelines by which cooperative

put their values into practice and also determine the attitude

that provides the movement with its procedures and distinctive

characteristics. These include; voluntary and open membership,

democratic member control, member economic participation,

autonomy and independence, education, training and information,

cooperation among cooperatives and concern for the community

xi

1.1.1 Concept of SACCOs in Kenya

The cooperative movement in Kenya was started by the European

farmers at Lumbwa. Kipkelion in Kericho district in 1908. It was

aimed at promoting production and marketing. Those formed by

Africans were not recognized until 1930’s when the colonial

government had a change of heart. In 1940s the British government

agreed to introduce cooperative in Africa colonies. Consequently,

Kenya enacted the cooperative ordinance in 1945 followed by the

creation of a department under the registrar of cooperatives in

1946, whose objectives were to form and promote form produce then

market the idea of marketing cooperative in Africa land units.

After independence, the cooperative movement assisted in

mobilizing and raising the necessary capital for the acquisition

of business and forms, formerly owned by European settlers. A

need for a ministry responsible for development and guidance of

expanding cooperative movement arose. Hence the formation of the

Ministry of Cooperatives Development and Marketing in 1963.

Much recognition was given to the cooperatives as a tool of

development in 1965 with the government’s policy paper: seasonal

paper number 10 of 1965. The governments realized that the

cooperatives could be used as a tool of attainment of African

socialism by Africans. This led to the enactment of cooperative

xii

society Act of 1963 CAP 490 (Revised in 1967) which made the

provision for appointment of commissioner for cooperatives.

In 1997, the government introduced a new cooperative societies

Act number 6 to govern the operation of cooperatives under a

liberalized economy. As a result the government reduced its power

of influence and left the cooperatives to exercises some self-

regulation without much interference.

An amendment of the cooperative societies Act of 1997 was made in

2004. Its aim was to improve the economy through cooperatives.

Thus the government continued, from then onwards, to emphasize on

the benefits of movement in Kenya since it uplifts the country’s

economy. (Gamba and Kono, 2003)

1.1.2 Concept of Loan Diversification

Portfolio diversification is the means by which investors

minimize or eliminate their exposure to company-specific risk,

minimize or reduce systematic risk and moderate the short-term

effects of individual asset class performance on portfolio value.

In a well-conceived portfolio, this can be accomplished at a

minimal cost in terms of expected return. Such a portfolio would

be considered to be a well-diversified.

Although the concepts relevant to portfolio diversification are

customarily explained with respect to the stock markets, the same

underlying principals apply to the loans investments. For

instance, loans have specific risk that can be diversified away

xiii

in the same manner as that of stocks.

1.1.2.1 Types of Loans Offered

Development Loans; It’s a loan whose maximum repayment period is

48 months. Interest rate is 1% per month on reducing balance. The

amount of loan awarded depends on deposits. Sometimes the SACCO

gives this loan three times the customer’s deposit. This deposit

may be in form of their shares in the SACCO or real deposit.

School Fees Loan; It’s a loan whose maximum repayment period is

12 months; this means that the loan only covers one year.

Interest rate is 1% per month on reducing balance, as the balance

goes down the amount of interest paid declines. Amount of loan

awarded depends on deposits, the higher the deposit the more the

amount loaned.

College Fees Loan; This resembles school fees loan but differs on

the loan period. It’s a loan whose maximum repayment period is 24

months. Interest rate is 1% per month on reducing balance. Amount

of loan awarded depends on deposits. It is convenient when it is

two years unlike one year in the above loan.

Emergency Loan; It’s a loan whose maximum amount issued without

documentation is Kshs. 20,000. Any amount exceeding this should

have supportive documentation. Maximum emergency loan amount is

Kshs 150,000.Interest rate is 3% per month on reducing balance.

Amount of loan awarded depends on deposits. This loan has less

xiv

processing time and paper work. The loan is not limited to any

period of repayment; however the loan is expensive when it is

held for a long time.

Development Loan; This loan is being offered for development

purposes. The amount of loan offered to members depends on the

number of shares being held by the member. Members are qualified

to have this loan upto three (*3) times the shares held by the

member. This loan is repayable within 36 months.

Salary in advance; It’s a loan whose interest will be charged at

the rate of 5 % flat rate and recoverable within one month and

this product only applies to those members whose salaries is

channeled through FOSA. This service is payable within 5 months

for members. The documentation that is required is the salary

slip. The loan is normally based on the salary expected. The

lender also faces some sort of risk and the urgency of the loan

making it expensive.

FOSA Loan; The minimum amount granted is Kshs 10,000 and maximum

amount is Kshs.500, 000. The maximum repayment period is 12

months. The interest rate is 1.5 % per month flat rate. This is

regarded to be the cheapest loan that can be advanced to a

member, based on the rate and the amount loanable. It requires

all necessary documentation for one to qualify for this type of

loan.

xv

1.1.3 Marakwet Teachers Sacco

MARAKWET TEACHERS SACCO SOCIETY LTD was born through the

splitting from Keiyo/Marakwet Teachers Sacco Society.MTSS was

registered by the commissioner or for co-operatives development

on 3rd July 1996.The societies proponents visualized on the

future hence they sought to harness their individual resources

together to form a common pool from which they could raise their

fund to realize theire development goals. The society started off

with only 873 members but currently it stands at 5094 members.

1.1.3.1 Society catchment area.

The Sacco draws its membership mainly from employees of TSC and

those related institutions such as Education officers and members

of KNUT local branch. The Sacco has also opened the common bond

to include members of the civil service e.g. chiefs, clerks etc.

The proponents of this society visualized the future hence sought

to harness their individual resources together to form a pool

from which they could raise to realize their development goals.

The members are drawn from all over the region of Marakwet

districts (east and west) and other interested persons outside

the region who meet the terms and conditions of the Sacco. Some

delegates are elected to represent the SACCO in mattersxvi

pertaining the society and interests of members.

FOSA services are offered by the SACCO- these are banking

services such as FOSA loans, sms alerts, fixed deposits

facilities, cheque advance, M-banking, salary advance, ATM

facilities, and salary processing. Other FOSA products include: -

savings account, children’s account, medical account, Christmas

account, group account, cheque advance repayable at maturity of

the cheque,

1.2 The Problem Statement

Loan advancement is an integral part of Sacco’s income. The price

that customers pay for the loans makes the largest portion of

reported profits. Whether diversified Loan advancement has an

effect on the success of a SACCO is the most critical question in

SACCO’s operation. A diversified loan service means wider

coverage of the customers. Loan diversification results to

variety of loans on offer; this will impact on the demand. The

well-being ranking exercise seen in SACCOSs show that both poor

and well-off people are members of SACCOSs.

However, the membership size by well-being status differs due to

the products that the SACCOs offer. They are providing services

for a larger proportion of poor people than the self-promoted

ones. SACCOs are focused on providing their services, both social

and financial, for as many poor people as possible, whereas on

xvii

the other hand SACCOs mainly focused on providing financial

services, rather than social services for their members.

There are other problems that need to be to be addressed like,

loan delay due to loan procedures that negatively impact the

society’s loan policy. This is because of inadequate funds, some

incompetent staff who process loans according to whom they know

regardless of the members ability and erroneous loan application

by members due to misunderstanding especially by the members.

Variety loans or single loans the SACCOs management needs to

balance between different loans. This study endeavors to find out

which is the optimal loan diversification for the SACCO to

maximize on its performance.

1.3 Research Questions

In order to solve the research problem the following questions

need to be taken into account.

i. Does loan diversification influence loan sales?

ii. What are the types of loans offered by SACCOs?

iii. Does loan diversification directly affect SACCOs’

financial performance?

iv. Do the customers have any significant influence on

types of loans to be offered?

v. Does loan portfolio diversification influence the SACCOs

membership?

xviii

1.4 Significance of the study

Research findings of this study will be useful to the following

groups

Academics; Credit and portfolio diversification is an area of

study in colleges, universities and other private studies. This

group will use the research findings to broaden their

understanding on issues relating to portfolio diversification and

credit risks therein. Also the study will open up areas, which

need further research.

The financial analyst; this study will help since they will get

additional information for their clients. It will also help them

in preparation of their annual bulletins or professional

magazines. Stockbrokers need it to advice investors.

The public or shareholders; by undertaking this study, members

and shareholders will understand the need for diversification,

the type of portfolio diversification that is optimal. It also

helps potential customers in their decision-making.

SACCOs; SACCOs can compare their loan diversification and

performance using findings of this study whether the policy is in

the view to maximize the wealth of their shareholders.

The government agencies; this enables the government agencies to

know the tax payable by the SACCO in view of interests charged on

loans.

To the management; this study will enable to guide the management

xix

in designing an effective diversification policy. Effective

diversification policy assists in realization of the objective of

the firm that is maximization of profits. This study will help

management not only exercise the management on the degree of

judgment to establish a sound policy and also in timing of

investment opportunities.

1.5 Scope and Delimitations of the study

The data being used is taken from primary source originating from

the Marakwet Teacher’s Sacco staff therefore the data is only

relevant and can only be used fully by Marakwet Teacher’s Sacco,

the result and the interpretation are completely rigid and from

the viewpoint of the researcher. Among the different aspect of

SACCO disbursement only loan diversification is taken for

consideration, the data being taken into account only relates to

the financial information of Marakwet Teacher’s SACCO Limited

before and after loan portfolio diversification.

xx

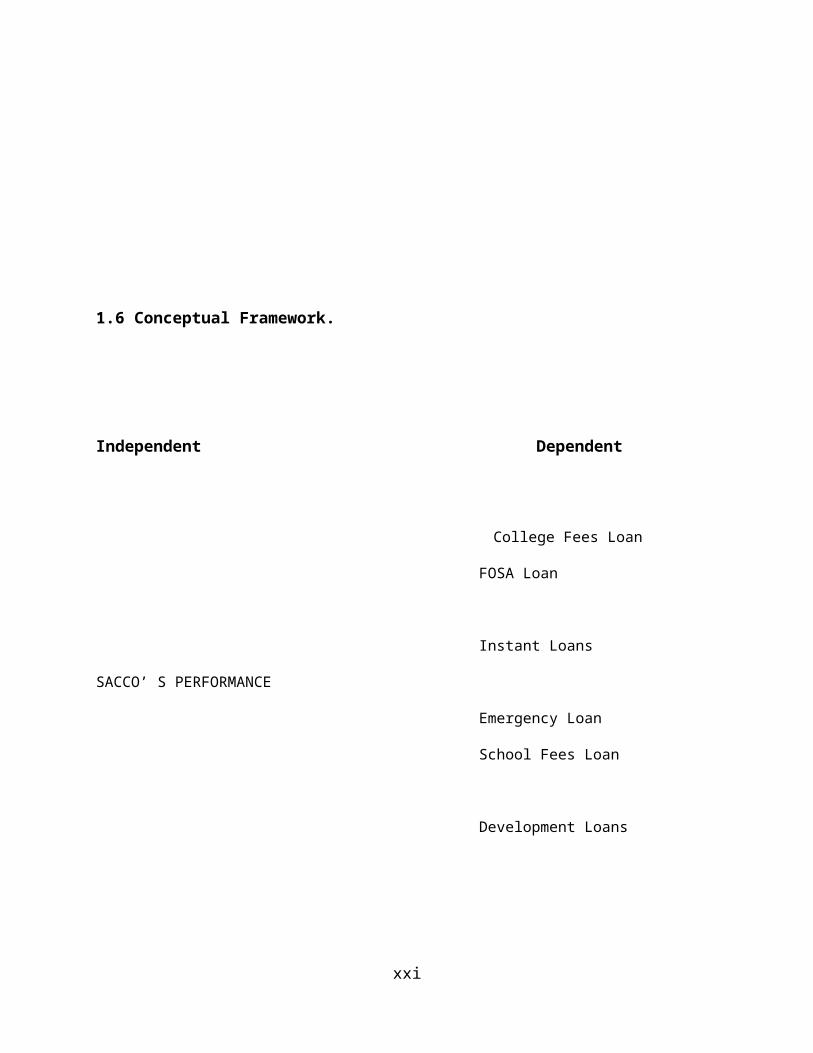

1.6 Conceptual Framework.

Independent Dependent

College Fees Loan

FOSA Loan

Instant Loans

SACCO’ S PERFORMANCE

Emergency Loan

School Fees Loan

Development Loans

xxi

Fig; 1 conceptual framework

CHAPTER TWO

2.0 INTRODUCTION

2.1 Review of Theories

2.1.1 Trade Theory and Structural Diversification

Economic sectors generate positive externalities and that these

externalities may not spread rapidly around the globe and can act

as a constraint to structural diversification since they cause

technological disparities to persist. The traditional

interpretation of comparative advantage is based on the

assumption of constant returns to scale, that’s when inputs to

production are doubled output doubles as well. In the presence of

economies of scale, the larger the scale on which production

takes place, the more efficient is productions meaning doubling

the inputs to production will more than double its output.

Economies of scale at the firm level, internal economies of

scale, must be distinguished from those occurring at the sectoral

level, external economies of scale or external economies, in

xxii

order to analyze their impact on market structure and structural

diversification. "External economies of scale occur when the cost

per unit depends on the size of the sector but not necessarily on

the size of any one firm. Internal economies of scale occur when

the cost per unit depends on the size of an individual firm but

not necessarily on that of the sector, (Krugman and Obstfeld,

1994).

Internal economies of scale allow large firms to obtain a cost

advantage over small ones and are therefore likely to give rise

to an imperfectly competitive market structure. By contrast,

external economies of scale need not lead to imperfect

competition because individual firms may remain small, even

though important advantages for the large scale arise at the

sectoral level.

The limited size of a market constrains both the variety and

quantity of services that a country can produce efficiently when

there are internal economies of scale. Firms operating on a

relatively large domestic market will tend to have more sales and

hence lower average unit costs than those operating on a small

domestic market. Given their cost advantages, these firms will be

more competitive on international markets and therefore find it

easier to establish export activities. This suggests that

countries with a relatively large domestic market will find it

easier to diversify into activities were internal economies of

scale are large. Economies of scale arise at the sectoral rather

than at the firm level, for example when production is

xxiii

concentrated in one or a few locations, thereby reducing the

sector's cost without necessarily affecting the size of

individual firms in this sector. The geographical concentration

of production sites may give rise to a local market for a greater

variety of support services for a larger supply of specialized

skilled labour, (Kamp, A., 2006)

The presence of strong external economies of scale tends to lead

to a situation where a country that has established a large

production of a good will produce it at a low cost, since its

producers are able to take advantage, for example, of the easy

and cheap availability of both support services and skilled

labour. This cost advantage constitutes a barrier to entry for

other countries to this sector even though the sector may have a

perfectly competitive market structure; this is because the

country that is trying to enter production in this sector will

not have the gradual accumulation of networks of firms that gives

rise to external economies, like the country with long

established activities in this sector.

The accumulation of knowledge is probably the main source of

dynamic scale economies. Dynamic internal economies of scale

arise when the costs of a firm depend on production experience,

that’s its cumulative output to date, rather than on the scale of

its current output. The inverse relationship between unit cost

and cumulative output can be expressed through a downward sloping

learning curve. Dynamic external economies arise when the

xxiv

improvement which an individual firm achieved in its products or

its production technique is imitated by its competitors; as a

result, knowledge spills over from the firm that initially

invested in knowledge accumulation to other firms that have not

made any specific investment in such knowledge.

Whether or not externalities in this learning process spill over

internationally has important implications for trade patterns.

With a full international spillover of learning externalities,

producers in all countries have access to the same body of

technical information; as a result, the accumulation of knowledge

through learning does not affect their relative abilities to

produce any specific good. A country's trade pattern must then be

determined by other factors, such as its initial conditions in

terms of factor endowment. By contrast, if the extent of

knowledge spillovers is limited to national borders, sector-

specific knowledge stocks accumulate in proportion to local

activity in this sector alone. Both domestic and foreign

producers learn and become more productive in sectors in which

they always have been active; as a result, initial patterns of

trade get locked in - history matters for the determination of a

country's opportunities for structural diversification. The

dismal conclusion would be that countries which, for whatever

historic reasons, are late-comers in the process of structural

diversification risk being trapped in a low-development

equilibrium Kamp et al ,2005

xxv

The initial advantage in structural diversification will

perpetuate itself and serve as a barrier to competitive entrants

is based on two assumptions: first, the learning-by-doing

benefits of skill-intensive activities are assumed to accrue

entirely to producers within a country, that’s knowledge

spillovers across national boundaries are assumed to be zero.

Where knowledge spillovers are concentrated within national

borders, countries' learning experience differ and the historical

coincidence of inheriting even a small lead in knowledge puts a

country in a position of self-perpetuating structural

diversification and development, thereby increasing the gap in

other countries. By contrast, where knowledge spillovers are

international in scope, other countries can share in the benefits

of knowledge accumulation and thereby improve their structural

diversification and development opportunities, provided their

social capability in knowledge absorption allows them to master

this knowledge. Second, the argument of the perpetuation of an

initial advantage in structural diversification is further based

on the assumption that learning-by doing is unbounded and that

therefore producing different goods is associated with

permanently differing learning potentials. The following chapter

will show that this latter assumption may be unrealistic.

xxvi

2.1.2 Classical Portfolio Theory

Classical portfolio theory in the sense of Markowitz (1952)

states that a portfolio is well diversified if there is no

portfolio which has, at the same time, lower risk and at least as

much expected return. However, this concept cannot be transferred

easily to loan portfolios for the many reasons. Fist, the

classical portfolio theory is based on mean-variance-efficiency.

However, the return distribution of loan portfolios is highly

skewed so that the variance is an inappropriate risk measure and

the mean variance-concept is no longer justified on the basis of

the expected utility theory. Secondly, even if the mean-variance

framework were appropriate for loan portfolios, the problem to

estimate the necessary input parameters would remain. In order to

determine the composition of mean-variance efficient portfolios

one needs, among others, the correlations of the portfolio’s

assets; but the correlations among loans cannot be estimated

precisely, at least with the limited data which we usually have.

Accepting the inappropriateness of the Markowitz-concept in this

context, we resort to more heuristic concepts and we use the loan

portfolio concentration and the loan portfolio’s distance to a

benchmark as diversification measures. In the context of

portfolio theory, an investor invests his money into different

assets, for the SACCO loaning to different industries, that’s

loans granted to firms of one industry are seen as one asset.

In the sense of Markowitz diversification is a means to change

xxvii

the risk of a portfolio. Keeping monitoring abilities and

monitoring costs constant, the default risk of a SACCO is likely

to decrease when a SACCO’s loan portfolio gets better

diversified. This view seems to be predominant in the German

financial institutions investment plans stipulating that a

SACCO’s sum of large loans is limited to eight times the SACCO’s

liable capital.

Winton (1999) shows that diversification does not need to lower

the SACCO s’ default risk. This model result is based on the idea

that specialized SACCOs can benefit from their screening and

monitoring advantages. However, it must be taken into

consideration that the results of the model rely to some degree

on the assumption that there are only two sectors in the model

economy. Thus, within the Winton model diversification is an” all

or nothing” decision. To explain the relationship of

diversification and return there seems to be a tradeoff between

the benefits from risk diversification and specialization.

Thus, the theory investigated the relationship of risk and loan

portfolio diversification. While return figures can easily be

derived from balance sheet data it is by far less clear how the

risk of a SACCO’s loan portfolio should be estimated. A common

approach to measure the SACCO’s risk is to use the loan loss

provision ratio (LLP) or the non-performing loan ratio (NPL).

Acharya et al. (2004) refer to these ratios as a measure for the

bank’s risk in the loan portfolio. They admit that this

xxviii

interpretation is questionable: The risk of a loan portfolio is

its unexpected loss, not the losses that are expected. However,

the denominators of the loan loss provision ratio and of the non-

performing loan ratio are also determined by losses that were

expected when originating the loans. Theses expected losses

should be reflected in a risk-adjusted pricing and therefore not

be considered as risk. Consequently, doesn’t only measure the

risk in the bank’s loan portfolio by the loan loss provision

ratio and the non-performing loan ratio but also by the

fluctuation of these variables in the course of time. The theory

defines the variables LLP and NPL as the standard deviations of a

bank’s loan loss provision ratio and non-performing loan ratio,

respectively.

nplb,t = _ + _ · smb,t−1 + 0 · zb,t−1 + μb + _t + "b (9)

In the regressions above, llpb,t and nplb,t denote the loan loss

provision ratios and the non-performing loan ratios of SACCO b at

time t, sm is one of our specialization measures, and z is a

vector of control variables. Again, μb and _t represent SACCO

individual and time individual fixed effects.

The specialization measures ‘sm’ are defined such that high

degrees of specialization are associated with high values while

low values stand for diversification. Therefore a positive sign

for the coefficient if diversification tends to reduce the risk

of a SACCO expected. On the other hand, if focused SACCO s tend

to identify effectively the low-risk borrowers and thereby reduce

xxix

their risk, we will find a negative relation between the SACCO s’

risk and their specialization measure.

2.2 Criticisms of the Theories

Should a bank diversify its loan portfolio or should a bank hand

out loans only to those groups whose income generation is very

familiar with? If a loan were a liquid asset with exogenous

payoff, the question would clearly be answered in favor of risk

diversification. However, loans cannot be traded in a liquid

market and the bank can at least in part determine the payoff of

the loan: Depending on its screening and monitoring abilities, a

bank can prevent or at least mitigate the information asymmetry

problems associated with the loan contract and can thereby reduce

the riskiness of the payoff.

The initial advantage in structural diversification will

perpetuate itself and serve as a barrier to competitive entrants

is based on two assumptions: first, the learning-by-doing

benefits of skill-intensive activities are assumed to accrue

entirely to producers within a country, that’s knowledge

spillovers across national boundaries are assumed to be zero.

Where knowledge spillovers are concentrated within national

borders, countries' learning experience differ and the historical

coincidence of inheriting even a small lead in knowledge puts a

country in a position of self-perpetuating structural

diversification and development, thereby increasing the gap in

other countries.xxx

2.3 Empirical Review

The theoretical literature on the question whether or not to

diversify does not offer an unanimous recommendation. Whereas

Diamond (1984) comes to the conclusion that a bank maximizes the

gains from delegated monitoring by perfect diversification,

Hellwig (1998) extends the Diamond (1984) model and shows that

banks may be well advised to concentrate at least on some large

projects to reduce the monitoring costs. Stomper (2004) shows in

an equilibrium model that both types of banks exist in

equilibrium: those that are perfectly diversified and those that

are specialized.

Winton (1999) explicitly models the tradeoff between

diversification and specialization. In his model the gains from

diversification and those from focusing depend on the riskiness

of the bank. According to his model the gains from

diversification are most dominant when the bank has a medium risk

level; for low risk and for high risk banks it pays to run a

specialization strategy. Whereas Lang and Stulz (1994) and Berger

and Ofek (1995) find a discount for diversified firms, Campa and

Kedia (2002) argue that this diversification-discount is rather

due to the underlying characteristics of the diversified firms

than to the decision for diversification. Stiroh (2004) and

xxxi

Laderman (2000) empirically analyze the benefits from strategic

diversification in the case of banks.

According to their studies the gains from diversification in

terms of reduced risk are only weak. Heitfield et al. (2005)

analyze portfolios of Syndicated National Credits (SNC). They

show that the portfolio risk goes up when the name and industry

concentration is increased. However, their results are barely

surprising because in their study the loan parameters are

exogenous and therefore the banks’ screening and monitoring

abilities remain unconsidered.

The empirical study of Acharya et al. (2004) is based on the

theoretical results of Winton (1999). They analyze the portfolio

diversification as well as risk and return figures of Italian

banks and conclude that “diversification, per se, is no guarantee

of superior performance or greater bank safety and soundness”.

Elyasiani and Deng (2004) carry out a corresponding study for the

banks in the United States. They find that diversified banks have

lower returns, but at the same time these banks are less risky,

hinting at a typical tradeoff of risk and return. Hayden et al.

(2005) perform a study close to Acharya et al. (2004) with data

for German banks. They find that diversified banks tend to show

weaker results than specialized banks. Their study is the one

most closely related to my own work.

xxxii

2.4 Knowledge Gap

The portfolio composition in my study is calculated from the

borrowers’ statistics, whereas Hayden et al. (2005) use

individual loan data which is taken from the German credit

register. The problem with the credit register is that it only

covers loans of more than 1.5 million Euros, whereas the

borrowers’ statistics comprises all national lending.

Winton (1999) explicitly models the tradeoff between

diversification and specialization. In his model the gains from

diversification and those from focusing depend on the riskiness

of the bank. According to his model the gains from

diversification are most dominant when the bank has a medium risk

level; for low risk and for high risk banks it pays to run a

specialization strategy.

Lang and Stulz (1994) and Berger and Ofek (1995) find a discount

for diversified firms, Campa and Kedia (2002) argue that this

diversification-discount is rather due to the underlying

characteristics of the diversified firms than to the decision for

diversification. Little has been understood about the

diversification and its effects on profitability. This is the

reason for the study of diversification of loan portfolio by the

researcher to bring out the actual impact on profitability. Lack

xxxiii

of a clear explanation on the relationship of diversification and

profitability has left many loan managers guessing.

xxxiv

CHAPTER THREE

3.0 INTRODUCTION

3.1 Research Design

Kothari (2003) define the research design as what, when, how

much, by what means concerning an enquiry or a study. A research

design is the arrangement of conditions for collection and

analysis of data in a manner that aims to combine relevance to

the research purpose, a research design is the conceptual

structure within which research is conducted; it constitutes the

blueprint for collection, measurement and analysis of data.

The study applied a case study research design; as such it was an

intensive descriptive and holistic analysis of Marakwet Teachers

SACCO as a single entity. It is an investigation of single entity

in order to gain insight into the larger cases. According to Oso

(2005) in a case where the number of organizations that can be

investigated are few, a small sample is available and an in-depth

analysis is necessary, a case study is the most appropriate.

3.2 Target Population

The target population is the loan department employees of

Marakwet Teacher’s Savings and Credit Co-Operative Society. The

target population was divided into two strata that are senior

xxxv

management level employees and junior employees. These include

the Customer care, credit officers, accountants, branch marketing

managers and branch manager. The reason for selection of the

target population was dueto the convenience, time allowed and

financial resources available to me.

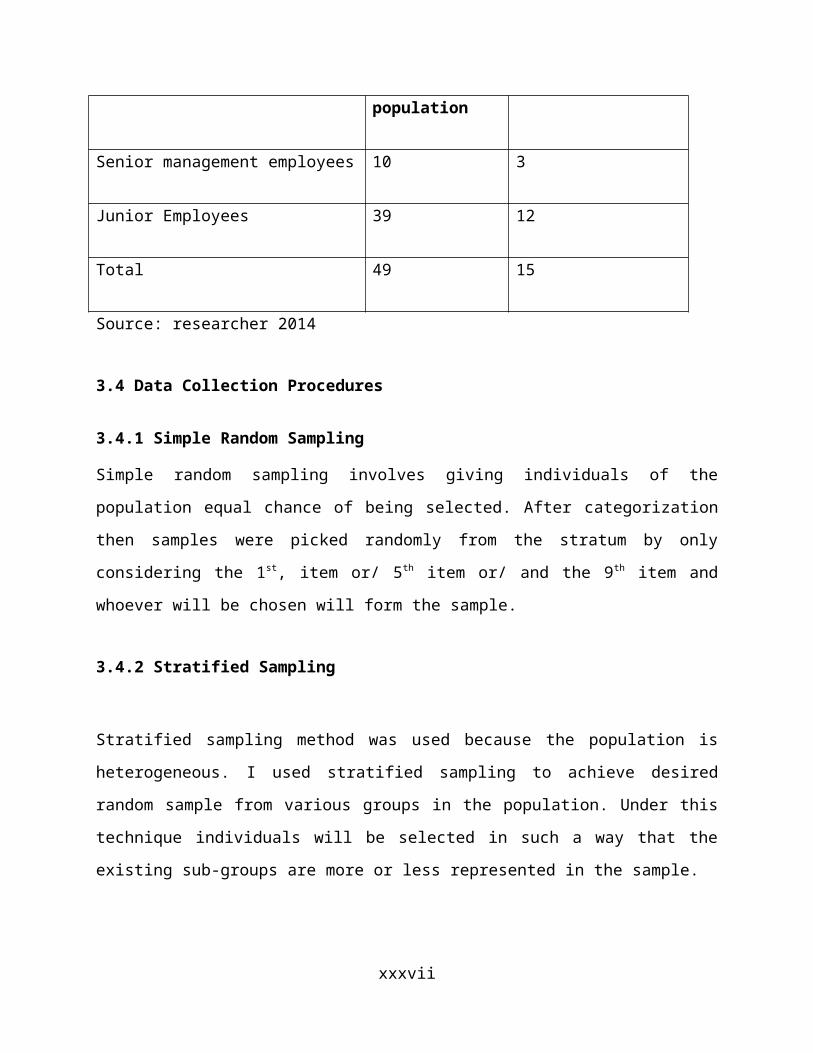

3.3 Sampling Procedures

The target population of the study will be 49 respondents and a

sample size of 15 respondents. Sampling is a procedure of

selecting a part of the population on which research is to be

conducted. It ensures that conclusions from the study can be

generalized to the entire population.I employed stratified random

sampling procedure. Stratified sampling was preferred as it is

suitable to include the elements from each of the categories and

it enabled to divide the population into two strata then get 30%

as representatives from the strata randomly. The strata are made

up of management level employees and junior employees. A 30% is

assumed to be representative of the general population (Mugenda

and Mugenda 2003). It further ensures that the whole population

is represented.

Table 1: Target population and sample size

Category Target Sample (30%)

xxxvi

population

Senior management employees 10 3

Junior Employees 39 12

Total 49 15

Source: researcher 2014

3.4 Data Collection Procedures

3.4.1 Simple Random Sampling

Simple random sampling involves giving individuals of the

population equal chance of being selected. After categorization

then samples were picked randomly from the stratum by only

considering the 1st, item or/ 5th item or/ and the 9th item and

whoever will be chosen will form the sample.

3.4.2 Stratified Sampling

Stratified sampling method was used because the population is

heterogeneous. I used stratified sampling to achieve desired

random sample from various groups in the population. Under this

technique individuals will be selected in such a way that the

existing sub-groups are more or less represented in the sample.

xxxvii

3.4.3 Data Collection Instruments

For the purpose of collecting the data, questionnaires and

interviews were used.

3. 4.3.1 Questionnaires

Questionnaires assisted in collecting opinions from respondents.

They are useful since the numbers of people from whom the facts

will be collected will be many and the questionnaires will create

uniformity of responses. They are inexpensive, quick and reliable

way of gathering information. This is due to the fact that

individuals can maintain anonymity and therefore, provide real

facts. The questionnaires will be open and closed ended

questions.

3. 4.3.2 Interviews

This involves face to face interaction and discussion. Responses

will be recorded for analysis. The questions that will be asked

are designed to cover issues to do with product diversification

and its effects on performance of SACCOs.

The interview will be guided by the use of structured question.

The questions will be both open and closed ended.

xxxviii

3.5 Validity and Reliability

Validity is the extent to which differences found with a

measuring tool reflect true differences among the sources. The

purpose of validity in the study is to seek relevant evidence

that confirms the answers found with the measurement device which

is the nature of the problem. The validity of the instrument was

ensured through constructive criticism from friends and research

assistant. The items were revised and improved accordingly. On

the other hand reliability is the accuracy and precision of a

measurement procedure. The reliability of the instrument was

improved through pre-testing. Pre-testing involves relying on

colleagues and friends to refine measuring instrument. Validity

and reliability of the instruments was done in order to limit the

distorting effects of random efforts on the findings.

3.6 Data Analysis Procedures

The data collected from several sources for the purpose of the

study will be adopted and reorganized. Data capturing will be

done using Excel sheets. The data from the completed sheets will

be recorded and analyzed using tables and graphs in a summarized

pattern in the response to the study problem.

xxxix

CHAPTER FOUR

4.0 DATA ANALYSIS, PRESENTATION AND INTERPRETATION

4.1 Background Information

The researcher sought this information to find out the kind of

persons he was dealing with. This information includes gender of

the respondents, educational level and working experience of the

respondents

4.1.1 Gender of the Respondents

The study sought to establish gender of the respondents so as to

establish on the criteria used by the management in its

employment. In most organizations, private, public, profit making

or non-profit making, there has been call to enhance equity and

gender balance in all appointments. The researcher was thus

motivated to determine whether the organization employs or

observes gender balance in its employment. Table 4.1 shows gender

distribution in the organization.

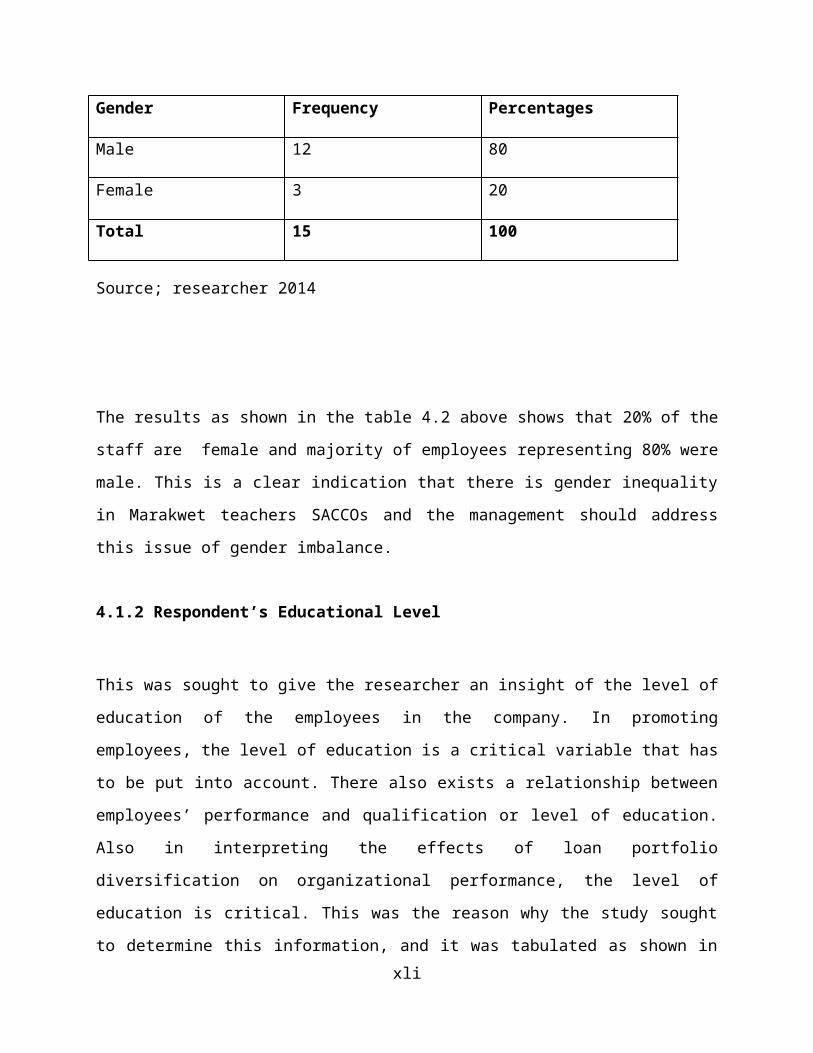

Table 4.2 Gender of the respondents

xl

Gender Frequency Percentages

Male 12 80

Female 3 20

Total 15 100

Source; researcher 2014

The results as shown in the table 4.2 above shows that 20% of the

staff are female and majority of employees representing 80% were

male. This is a clear indication that there is gender inequality

in Marakwet teachers SACCOs and the management should address

this issue of gender imbalance.

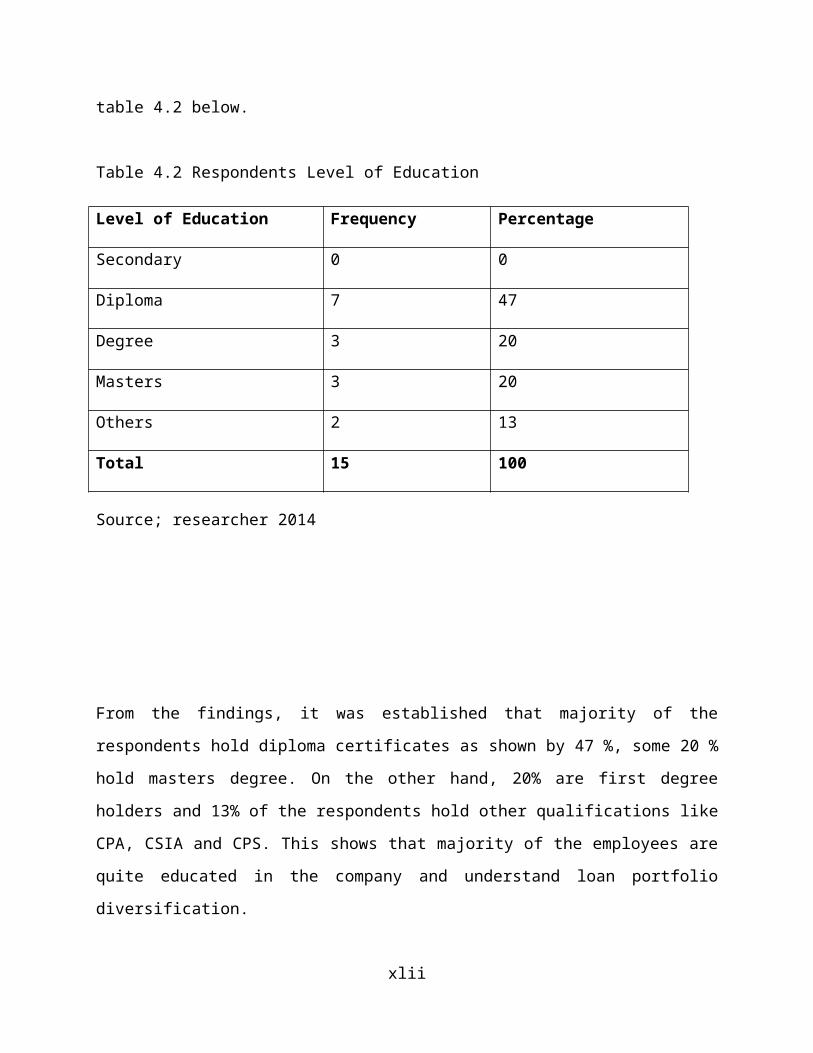

4.1.2 Respondent’s Educational Level

This was sought to give the researcher an insight of the level of

education of the employees in the company. In promoting

employees, the level of education is a critical variable that has

to be put into account. There also exists a relationship between

employees’ performance and qualification or level of education.

Also in interpreting the effects of loan portfolio

diversification on organizational performance, the level of

education is critical. This was the reason why the study sought

to determine this information, and it was tabulated as shown inxli

table 4.2 below.

Table 4.2 Respondents Level of Education

Level of Education Frequency Percentage

Secondary 0 0

Diploma 7 47

Degree 3 20

Masters 3 20

Others 2 13

Total 15 100

Source; researcher 2014

From the findings, it was established that majority of the

respondents hold diploma certificates as shown by 47 %, some 20 %

hold masters degree. On the other hand, 20% are first degree

holders and 13% of the respondents hold other qualifications like

CPA, CSIA and CPS. This shows that majority of the employees are

quite educated in the company and understand loan portfolio

diversification.

xlii

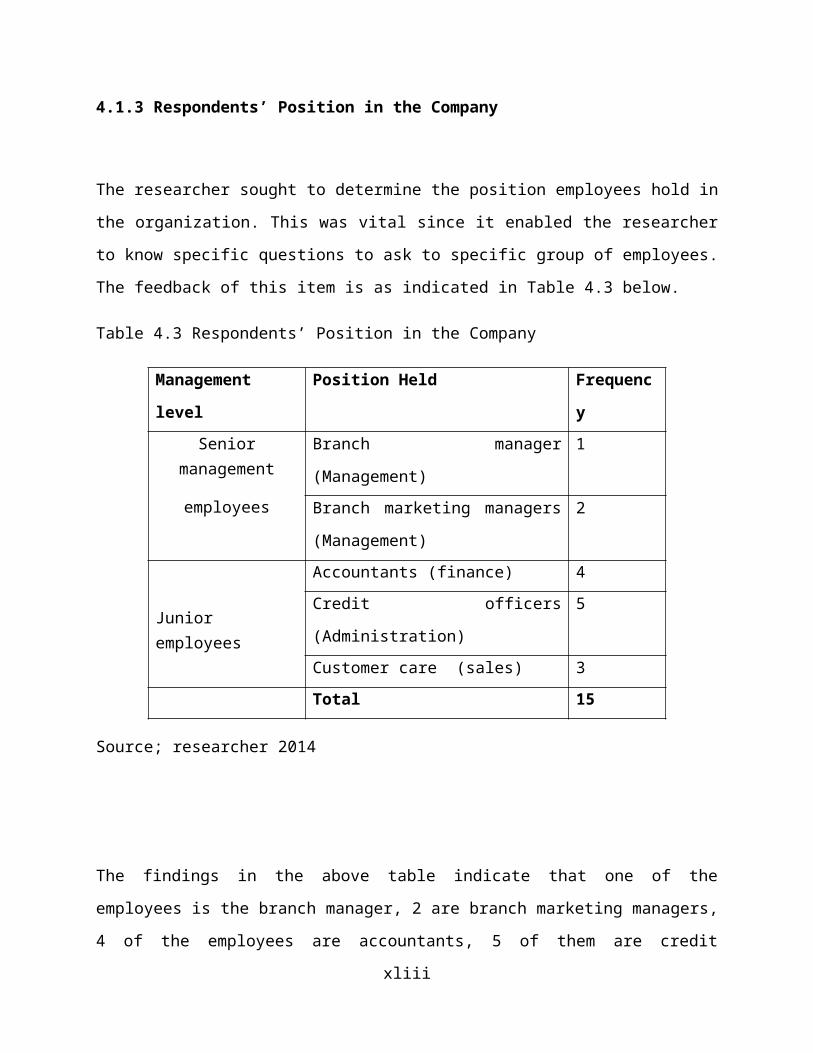

4.1.3 Respondents’ Position in the Company

The researcher sought to determine the position employees hold in

the organization. This was vital since it enabled the researcher

to know specific questions to ask to specific group of employees.

The feedback of this item is as indicated in Table 4.3 below.

Table 4.3 Respondents’ Position in the Company

Management

level

Position Held Frequenc

ySenior

management

employees

Branch manager

(Management)

1

Branch marketing managers

(Management)

2

Junior employees

Accountants (finance) 4Credit officers

(Administration)

5

Customer care (sales) 3Total 15

Source; researcher 2014

The findings in the above table indicate that one of the

employees is the branch manager, 2 are branch marketing managers,

4 of the employees are accountants, 5 of them are credit

xliii

officers, and other 3 are Customer care staff. These findings

show that the company is fairly balanced in terms of employees in

various departments of positions.

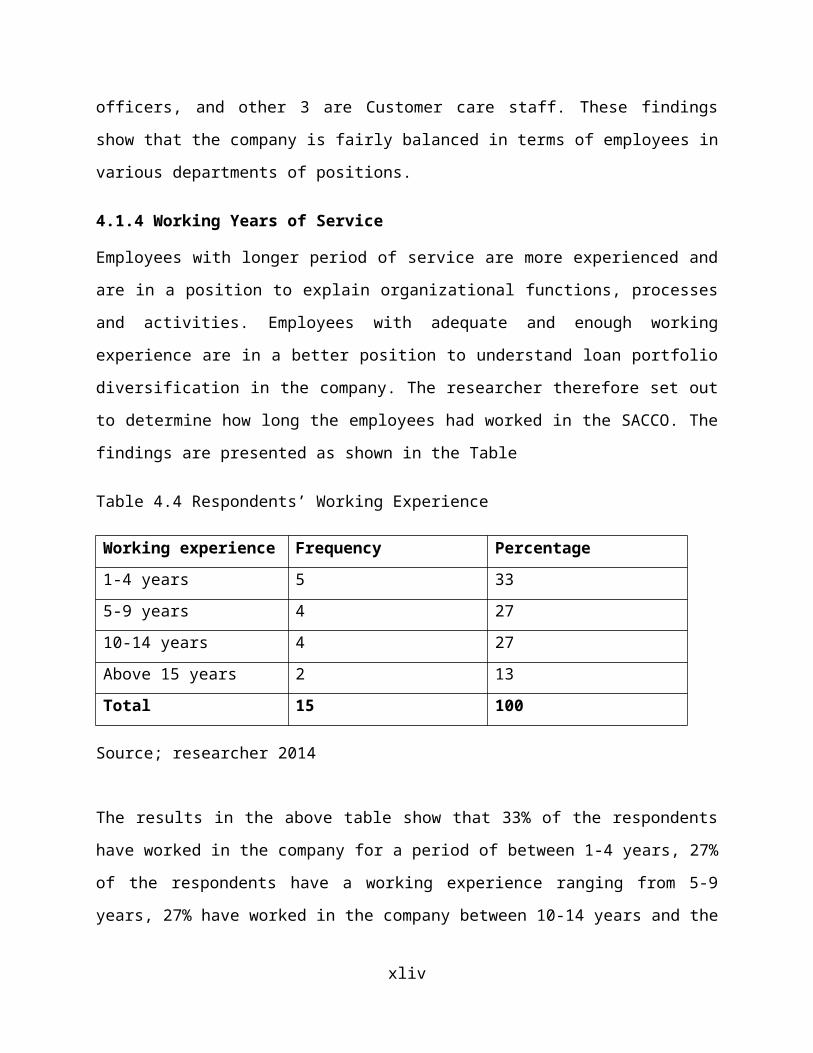

4.1.4 Working Years of Service

Employees with longer period of service are more experienced and

are in a position to explain organizational functions, processes

and activities. Employees with adequate and enough working

experience are in a better position to understand loan portfolio

diversification in the company. The researcher therefore set out

to determine how long the employees had worked in the SACCO. The

findings are presented as shown in the Table

Table 4.4 Respondents’ Working Experience

Working experience Frequency Percentage1-4 years 5 335-9 years 4 2710-14 years 4 27Above 15 years 2 13Total 15 100

Source; researcher 2014

The results in the above table show that 33% of the respondents

have worked in the company for a period of between 1-4 years, 27%

of the respondents have a working experience ranging from 5-9

years, 27% have worked in the company between 10-14 years and the

xliv

remaining 13% have a working experience of over 15 years. These

findings show that majority of the respondents have worked for

relatively long periond in the company and thus are in a better

position to understand loan portfolio diversfication in the

company.

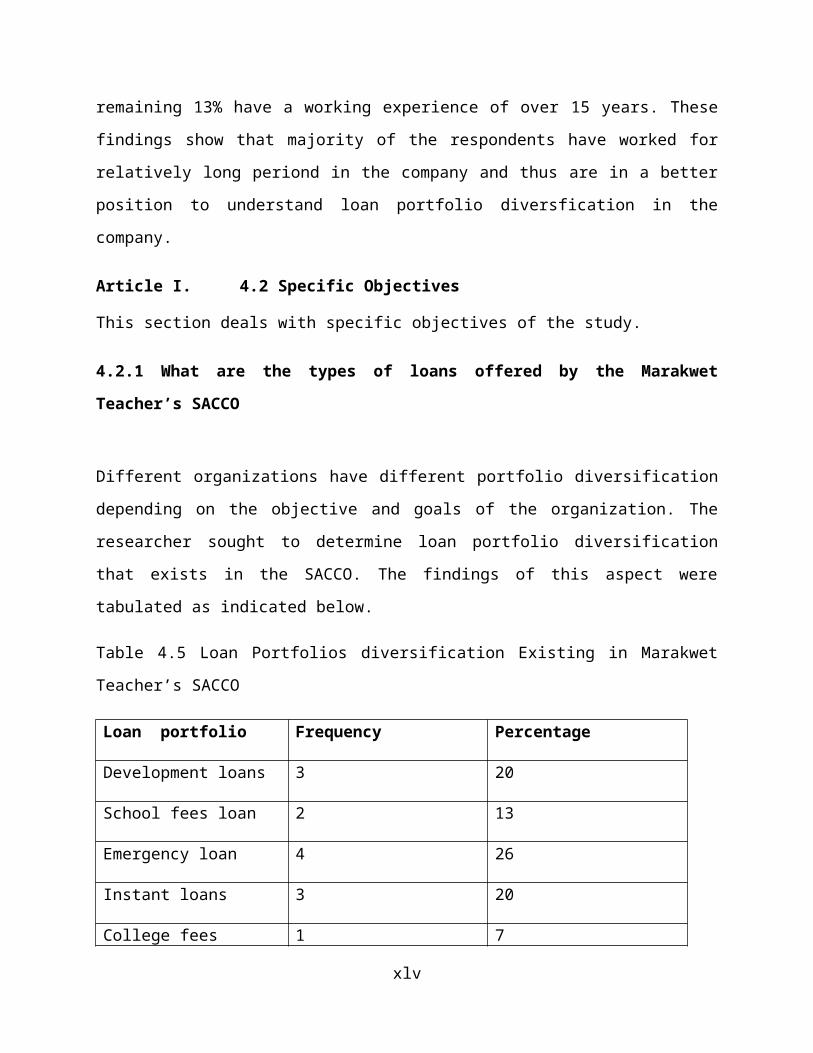

Article I. 4.2 Specific Objectives

This section deals with specific objectives of the study.

4.2.1 What are the types of loans offered by the Marakwet

Teacher’s SACCO

Different organizations have different portfolio diversification

depending on the objective and goals of the organization. The

researcher sought to determine loan portfolio diversification

that exists in the SACCO. The findings of this aspect were

tabulated as indicated below.

Table 4.5 Loan Portfolios diversification Existing in Marakwet

Teacher’s SACCO

Loan portfolio Frequency Percentage

Development loans 3 20

School fees loan 2 13

Emergency loan 4 26

Instant loans 3 20

College fees 1 7

xlv

Salary advance 1 7

FOSA loan 1 7

Total 15 100

Source; researcher 2014

The table above indicates that 20% of the respondents indicated

that development loans and instant loans is one of loan

diversification used by the SACCO, majority of the respondents as

shown by 26% cited emergency loan , 13% felt school fees loan and

FOSA loan, Salary advance and college fees loans 7% each. This

indicates that the company offers wide variety of loan portfolio

diversification to its customers.

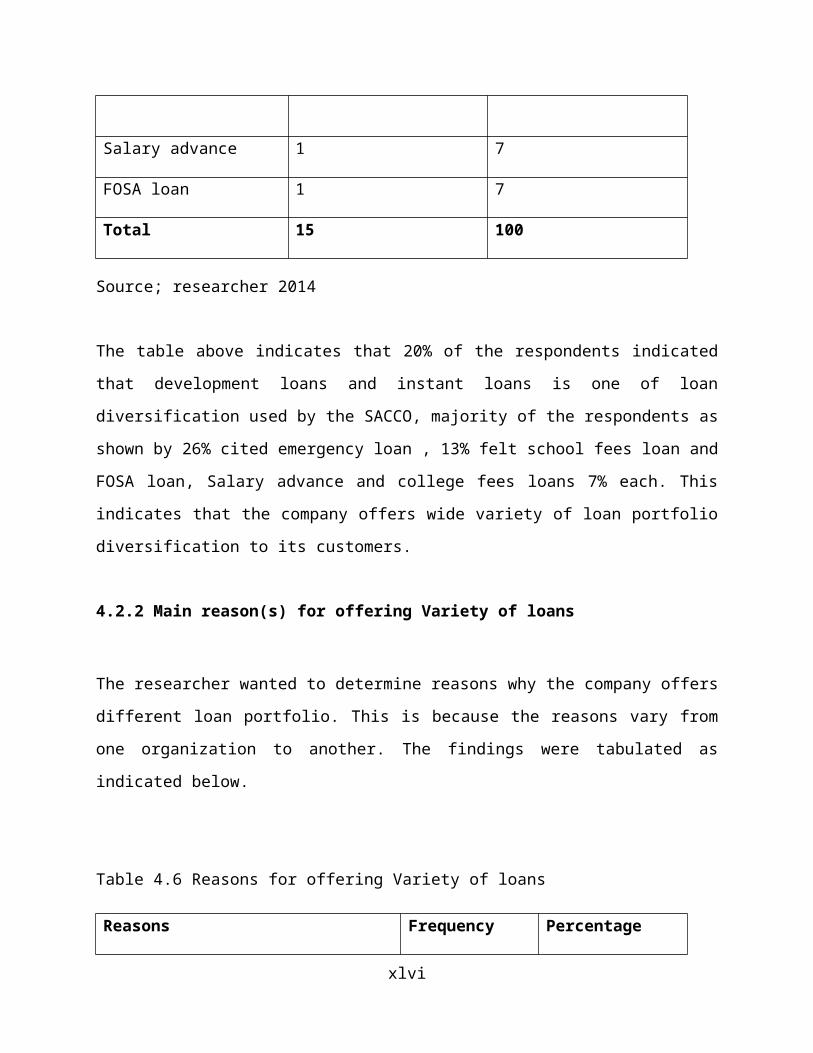

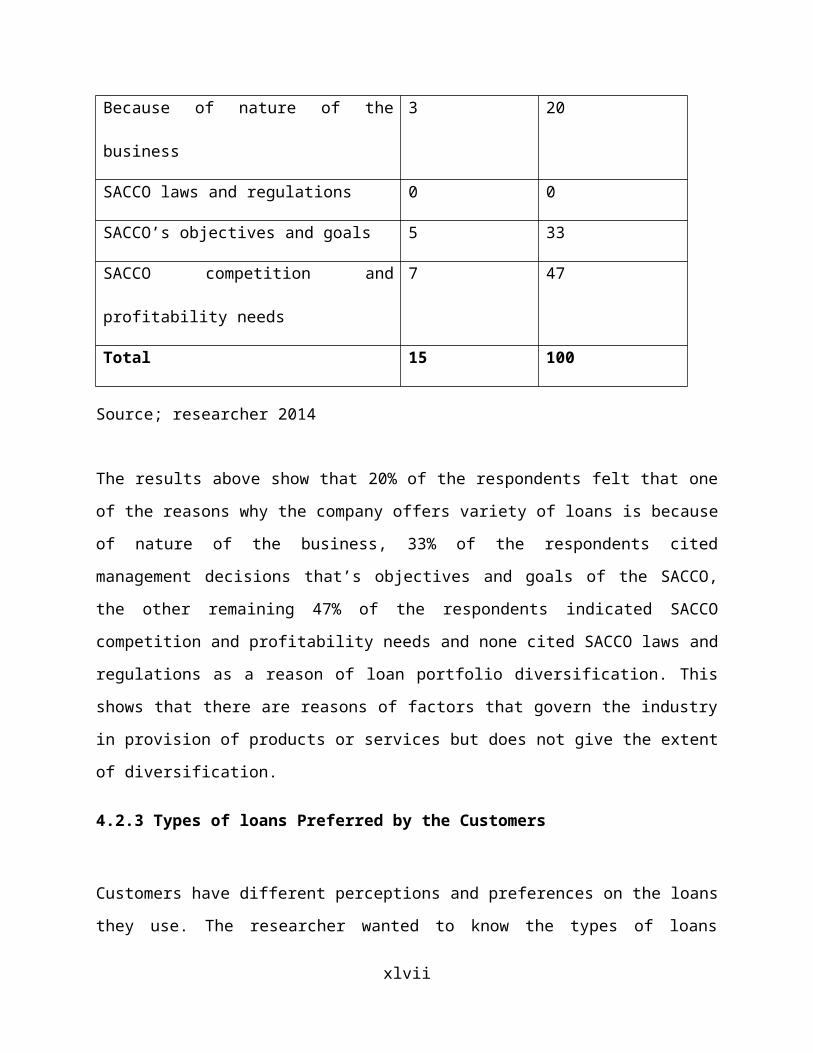

4.2.2 Main reason(s) for offering Variety of loans

The researcher wanted to determine reasons why the company offers

different loan portfolio. This is because the reasons vary from

one organization to another. The findings were tabulated as

indicated below.

Table 4.6 Reasons for offering Variety of loans

Reasons Frequency Percentage

xlvi

Because of nature of the

business

3 20

SACCO laws and regulations 0 0

SACCO’s objectives and goals 5 33

SACCO competition and

profitability needs

7 47

Total 15 100

Source; researcher 2014

The results above show that 20% of the respondents felt that one

of the reasons why the company offers variety of loans is because

of nature of the business, 33% of the respondents cited

management decisions that’s objectives and goals of the SACCO,

the other remaining 47% of the respondents indicated SACCO

competition and profitability needs and none cited SACCO laws and

regulations as a reason of loan portfolio diversification. This

shows that there are reasons of factors that govern the industry

in provision of products or services but does not give the extent

of diversification.

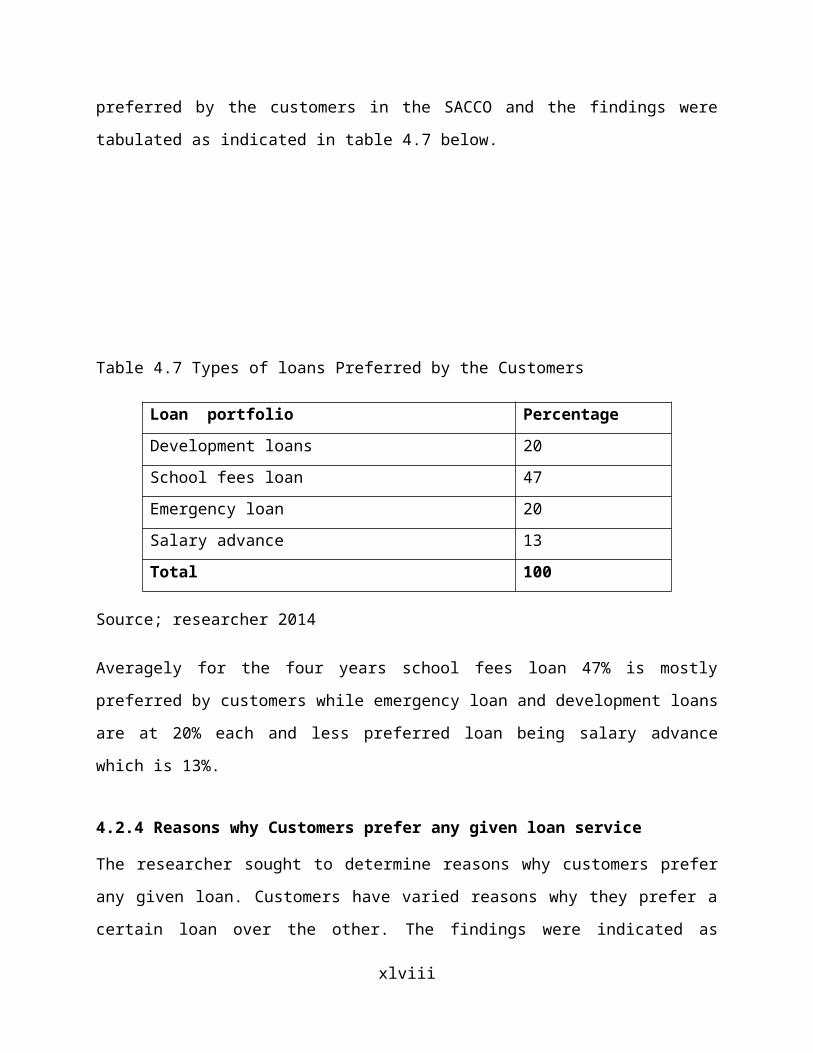

4.2.3 Types of loans Preferred by the Customers

Customers have different perceptions and preferences on the loans

they use. The researcher wanted to know the types of loans

xlvii

preferred by the customers in the SACCO and the findings were

tabulated as indicated in table 4.7 below.

Table 4.7 Types of loans Preferred by the Customers

Loan portfolio PercentageDevelopment loans 20School fees loan 47Emergency loan 20Salary advance 13Total 100

Source; researcher 2014

Averagely for the four years school fees loan 47% is mostly

preferred by customers while emergency loan and development loans

are at 20% each and less preferred loan being salary advance

which is 13%.

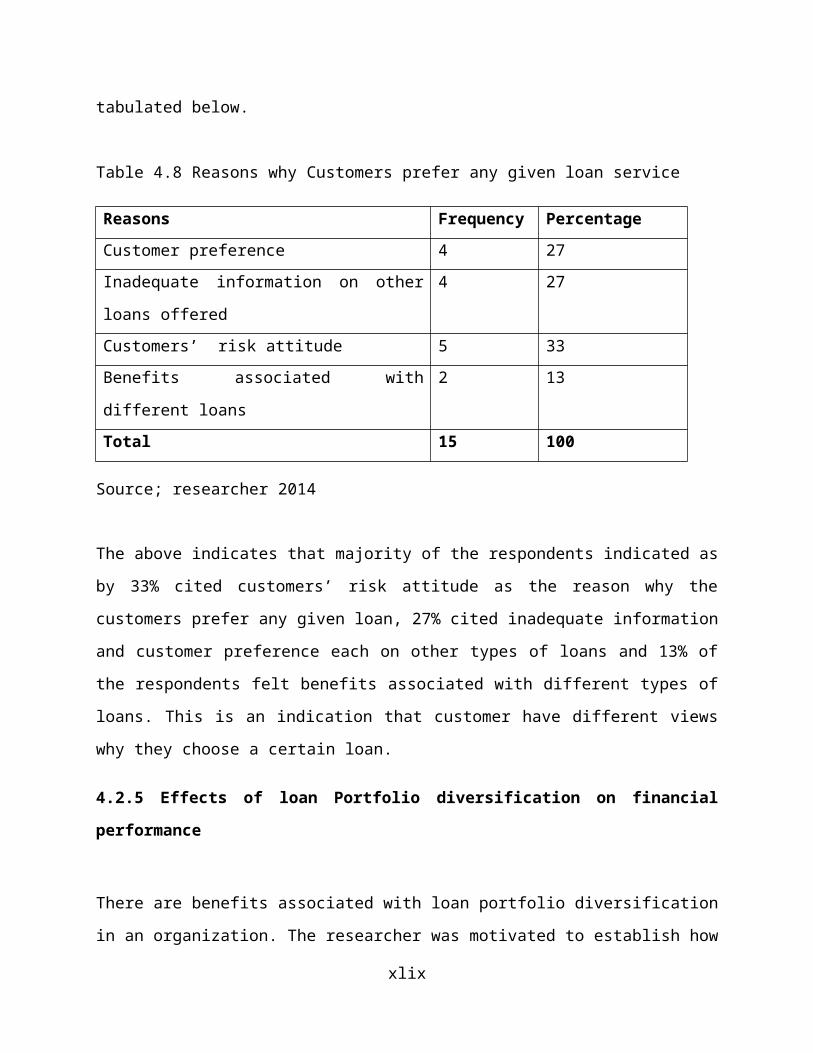

4.2.4 Reasons why Customers prefer any given loan service

The researcher sought to determine reasons why customers prefer

any given loan. Customers have varied reasons why they prefer a

certain loan over the other. The findings were indicated as

xlviii

tabulated below.

Table 4.8 Reasons why Customers prefer any given loan service

Reasons Frequency PercentageCustomer preference 4 27Inadequate information on other

loans offered

4 27

Customers’ risk attitude 5 33Benefits associated with

different loans

2 13

Total 15 100

Source; researcher 2014

The above indicates that majority of the respondents indicated as

by 33% cited customers’ risk attitude as the reason why the

customers prefer any given loan, 27% cited inadequate information

and customer preference each on other types of loans and 13% of

the respondents felt benefits associated with different types of

loans. This is an indication that customer have different views

why they choose a certain loan.

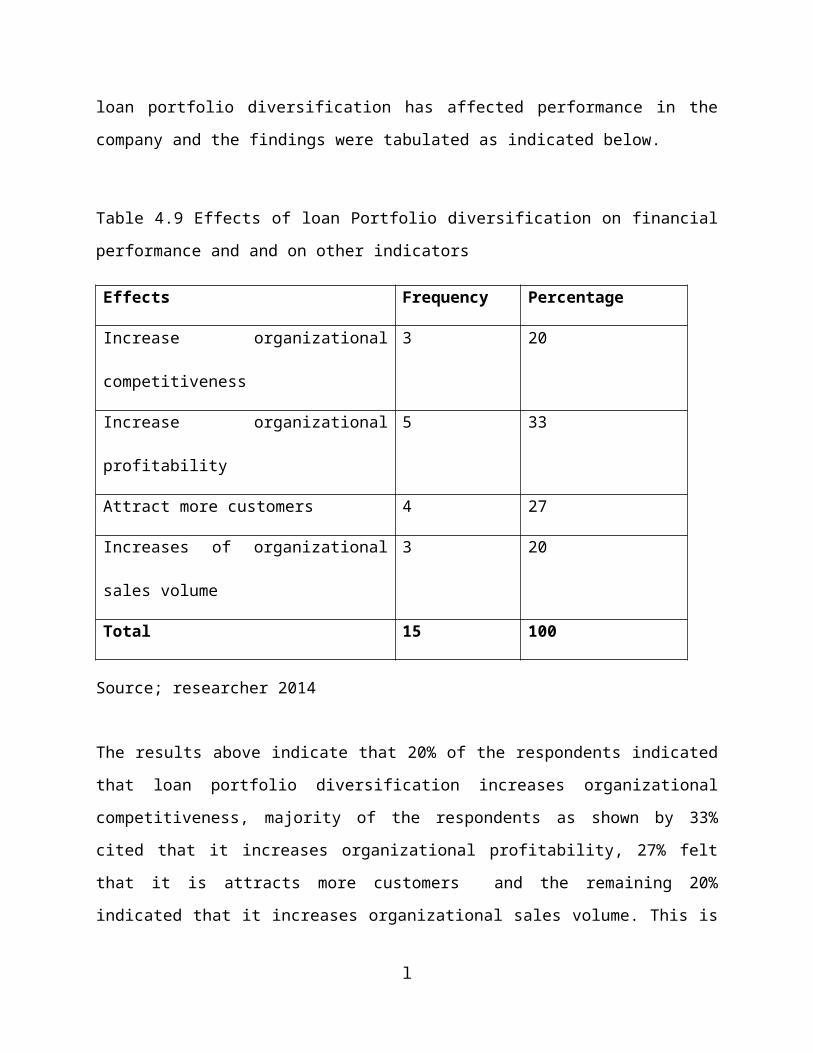

4.2.5 Effects of loan Portfolio diversification on financial

performance

There are benefits associated with loan portfolio diversification

in an organization. The researcher was motivated to establish how

xlix

loan portfolio diversification has affected performance in the

company and the findings were tabulated as indicated below.

Table 4.9 Effects of loan Portfolio diversification on financial

performance and and on other indicators

Effects Frequency Percentage

Increase organizational

competitiveness

3 20

Increase organizational

profitability

5 33

Attract more customers 4 27

Increases of organizational

sales volume

3 20

Total 15 100

Source; researcher 2014

The results above indicate that 20% of the respondents indicated

that loan portfolio diversification increases organizational

competitiveness, majority of the respondents as shown by 33%

cited that it increases organizational profitability, 27% felt

that it is attracts more customers and the remaining 20%

indicated that it increases organizational sales volume. This is

l

a clear indication that loan portfolio diversification is

beneficial to a company.

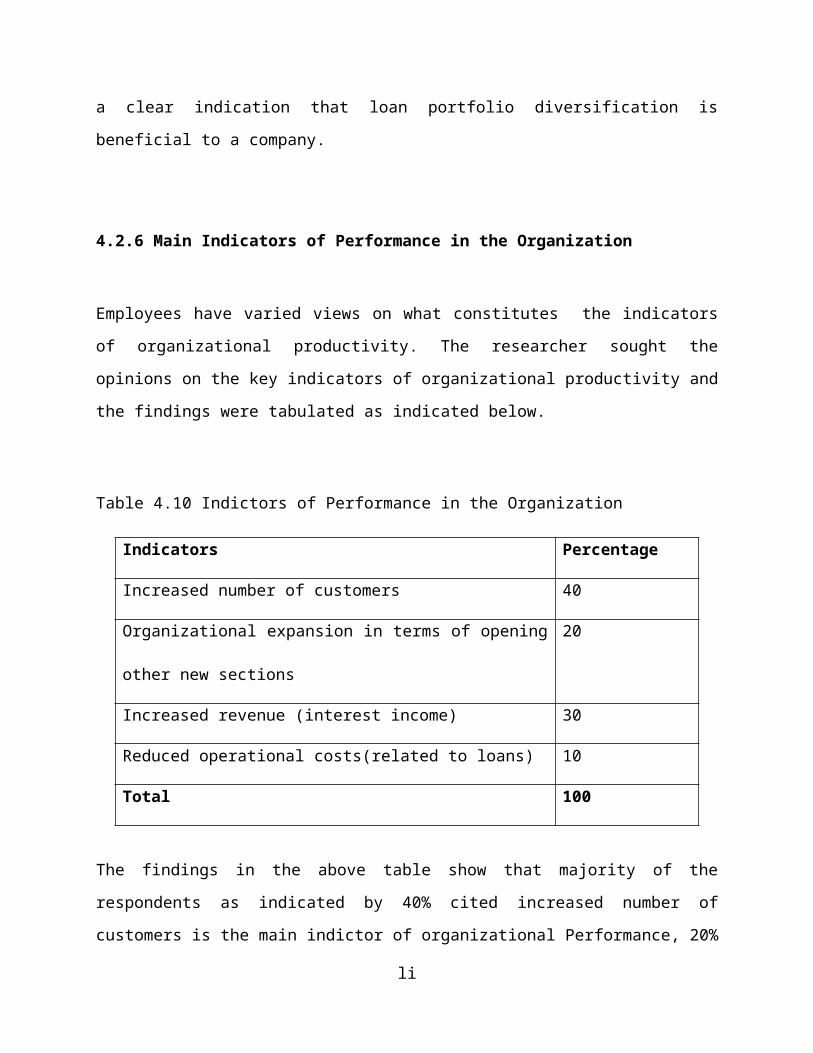

4.2.6 Main Indicators of Performance in the Organization

Employees have varied views on what constitutes the indicators

of organizational productivity. The researcher sought the

opinions on the key indicators of organizational productivity and

the findings were tabulated as indicated below.

Table 4.10 Indictors of Performance in the Organization

Indicators Percentage

Increased number of customers 40

Organizational expansion in terms of opening

other new sections

20

Increased revenue (interest income) 30

Reduced operational costs(related to loans) 10

Total 100

The findings in the above table show that majority of the

respondents as indicated by 40% cited increased number of

customers is the main indictor of organizational Performance, 20%

li

cited organizational expansion in terms of opening other new

sections, 30% indicated increased organizational revenue based on

the interest income and some 10% of the respondents felt reduced

operational costs such as bad debts written off. These findings

show that there are various indicators of Performance.

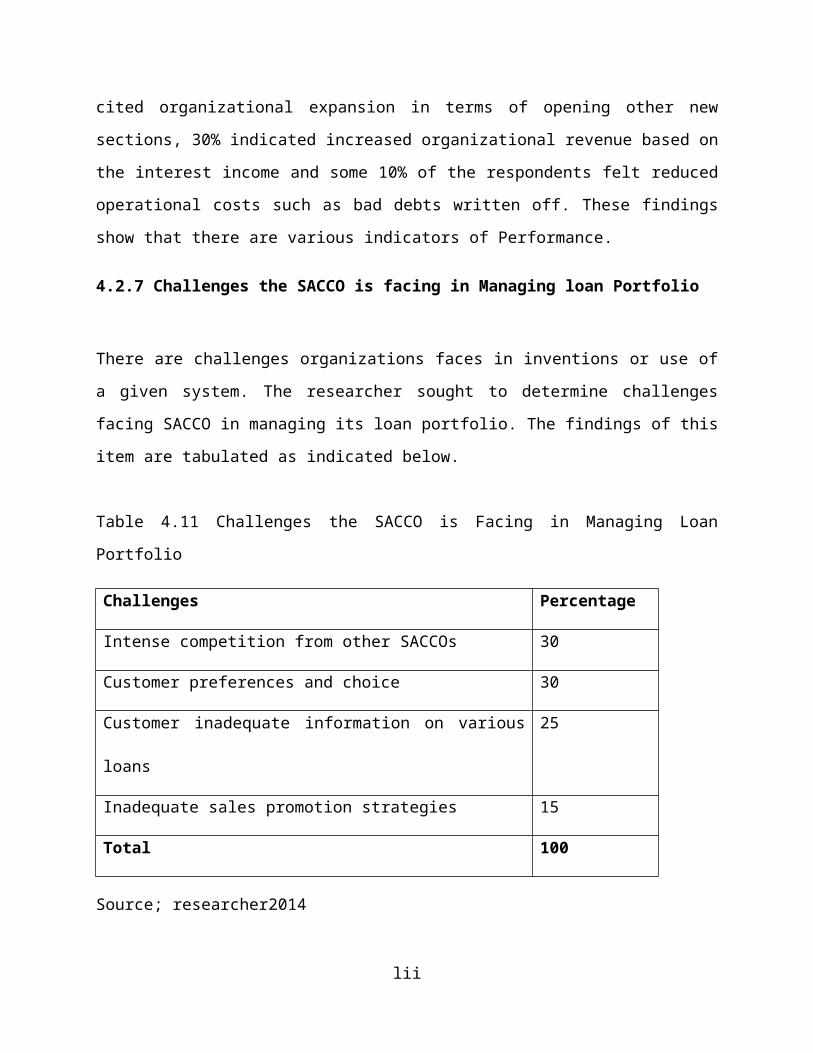

4.2.7 Challenges the SACCO is facing in Managing loan Portfolio

There are challenges organizations faces in inventions or use of

a given system. The researcher sought to determine challenges

facing SACCO in managing its loan portfolio. The findings of this

item are tabulated as indicated below.

Table 4.11 Challenges the SACCO is Facing in Managing Loan

Portfolio

Challenges Percentage

Intense competition from other SACCOs 30

Customer preferences and choice 30

Customer inadequate information on various

loans

25

Inadequate sales promotion strategies 15

Total 100

Source; researcher2014

lii

The results above show that 30% of the respondents indicated that

one of the challenges faced in loan portfolio diversification is

intense competition from other companies that is difficult to

merge, another 30% indicated customer preferences and choice that

cannot be easily be predicted, 25% cited customer inadequate

information on various classes of loans and the remaining 15%

felt inadequate sales promotion strategies as another challenge.

This shows that there are a number of challenges faced in loan

portfolio diversification.

CHAPTER FIVE

5.0 SUMMARY OF FINDINGS, CONCLUSION AND RECOMMENDATIONS

5.1 Introduction

This chapter presents the discussion of the findings,

conclusions, recommendations and suggestions for further

research. This study was carried out with the main purpose of

finding out the effects of loan portfolio diversification on

liii

organizational performance.

5.2 Summary of the Findings

5.2.1 Demographic Information

a) Gender of the Respondents

Gender of the respondents was studied. From the results 20% of

the staff were female and 80% were male. There is gender

inequality in the company

b) Respondent’s Educational Level

Educational level of the respondents indicated that majority of

the respondents hold diploma certificates as shown by 47 %, some

20 % hold maters degree. On the other hand, 20% are first degree

holders and 13% of the respondents hold other qualifications like

CPA and CPS.

c) Respondents’ Position in the Company

The findings in the above table indicate that one of the

employees is the branch manager, 2 are branch marketing managers,

4 of the employees are accountants, 5 of them are credit

officers, and other 3 are Customer care staff. These findings

show that the company is fairly balanced in terms of employees in

various departments of positions.

liv

d) Working Years of Service

The results established that that 33% of the respondents have

worked in the company for a period of between 1-4 years, 27% of

the respondents have a working experience ranging from 5-9 years,

27% have worked in the company between 10-14 years and the

remaining 13% have a working experience of over 15 years. These

findings show that majority of the respondents have worked for

relatively long periond in the company and thus are in a better

position to understand loan portfolio diversfication in the

company.

5.2.2 Types of loans offered by the Marakwet Teacher’s SACCO

The field findings established that 20% of the respondents

indicated that development loans and instant loans is one of loan

diversification used by the SACCO, majority of the respondents as

shown by 26% cited emergency loan, 13% felt school fees loan and

FOSA loan, Salary advance and college fees loans 7% each. This

indicates that the company offers wide variety of loan portfolio

diversification to its customers.

5.2.3 Reasons for offering Variety of loans

It was found out that 20% of the respondents felt that one of the

reasons why the company offers variety of loans is because of

lv

nature of the business, 33% of the respondents cited management

decisions that’s objectives and goals of the SACCO, the other

remaining 47% of the respondents indicated SACCO competition and

profitability needs and none cited SACCO laws and regulations as

a reason of loan portfolio diversification. This shows that there

are reasons of factors that govern the industry in provision of

products or services but does not give the extent of

diversification.

5.2.4 Types of loans Preferred by the Customers

Averagely for the four years school fees loan 47% is mostly

preferred by customers while emergency loan and development loans

are at 20% each and less preferred loan being salary advance

which is 13%.

5.2.5 Reasons why Customers prefer any given loan service

The field findings indicated that majority of the respondents

indicated by 33% cited customers’ risk attitude as the reason why

the customers prefer any given loan, 27% cited inadequate

information and customer preference each on other types of loanslvi

and 13% of the respondents felt benefits associated with

different types of loans. This is an indication that customers

have different views why they choose a certain loan

5.2.6 Effects of loan Portfolio diversification on financial

performance

The results indicated that 20% of the respondents indicated that

loan portfolio diversification increases organizational

competitiveness, majority of the respondents as shown by 33%

cited that it increases organizational profitability, 27% felt

that it is attracts more customer and the remaining 20% indicated

that it increases organizational sales volume. This is a clear

indication that loan portfolio diversification is beneficial to a

company.

5.2.7 Main Indicators of Performance in the Organization

The findings established that majority of the respondents as

indicated by 40% cited increased number of customers is the main

indictor of organizational Performance, 20% cited organizational

expansion in terms of opening other new sections, 30% indicated

increased organizational revenue based on the interest income and

some 10% of the respondents felt reduced operational costs such

as bad debts written off. These findings show that there are

various indicators of Performance.lvii

5.2.8 Challenges the SACCO is facing in Managing loan Portfolio

The results established that 30% of the respondents indicated

that one of the challenges faced in product mix portfolio is

intense competition from other companies that is difficult to

merge, another 30% indicated customer preferences and choice that

cannot be easily changed, 25% cited customer inadequate

information on various classes of insurance and the remaining 15%

felt inadequate sales promotion strategies as another challenge.

This shows that there are a number of challenges faced in product

mix portfolio.

5.3 Conclusions

Based on the findings of this study of determining the effects of

loan portfolio diversification on the performance of the SACCO,

the researcher made the following conclusions.

Loan portfolios diversification existing in Marakwet Teacher’s

SACCO and it includes FOSA loan, salary advance, college fees,

instant loans, development loans, school fees loan and emergency

loan

The major effects of this loan portfolio diversification on

lviii

performance, increased organizational competitiveness, increased

organizational profitability in terms of interest income,

attraction of more customers and increased organizational sales

volume.

Major Challenges Marakwet Teacher’s SACCO is facing in managing

its loan portfolio diversification include Inadequate sales

promotion strategies ,Intense competition from other companies,

Customer preferences and choice and Customer inadequate

information on various loans.

5.4 Recommendations

Based on finding and conclusions of the study the researcher felt

that the following recommendations are necessary to make loan

portfolio diversification successful.

There is need to carry out effective sales promotion to help

customers understand various loans offered by the SACCO.

The company should try to educate its customers on the benefits

of other loans as per the circumstance so that to have good

balance on all the loans offered.

5.5 Suggestions for Further Research

For SACCO, financial sub-sector to grow there is need for the

sector to ensure that it adequately strengthen itself and come up

lix

with solid solutions that can be implemented. Despite the fact

that there are certain self-advanced strategies that can be

adopted by the sub-sector itself, there are also external efforts

that can still be made. This requires further research into the

sector to ensure that the strategies work effectively.There is

also need for further research to identify the effects of

management skills of the SACCO employees on the performance and

the same should be done on the banks.

REFERENCES

Acharya, V., Hasan, I., Saunders, A., 2004. Should Banks Be

Diversified? Evidence from Individual Bank Loan Portfolios.

Working Paper, London Business School, London, forthcoming in:

Journal of Business (July 2006).

Berger, P. G., Ofek, E., 1995. Diversification’s Effect on Firm

Value. Journal of Financial Economics 37, 39–65.

Boyd, J. H., Runkle, D. E., 1993. Size and Performance of Banking

Firms. Journal of Monetary Economics 31, 47–67.

Campa, J. M., Kedia, S., 2002. Explaining the Diversification

Discount. The Journal of Finance 57 (4), 1731–1762.

De Nicol´o, G., 2001. Size, Charter Value and Risk in Banking: An

International Perspective. Working Paper 689, Board of Governors

of the Federal Reserve System.

Diamond, D., 1984. Financial Intermediation and Delegated lx

Monitoring. Review of Economic Studies 51, 393–414.

Elyasiani, E., Deng, S., 2004. Diversification Effects on the

Performance of Financial Services Firms. Working Paper, Temple

University, Philadelphia.

Gamba B and Kombo G., 2003. Cooperative Management in Developing

Countries

Hayden, E., Porath, D., von Westernhagen, N., 2005. Does

Diversification Improve the Performance of German Banks? Evidence

from Individual Bank Loan Portfolios.

Heitfield, E., Burton, S., Chomsisengphet, S., 2005. The Effects

of Name and Sector Concentrations on the Distribution of Losses

for Portfolios of Large Wholesale Credit Exposures. Working

Paper, Board of Governors of the Federal Reserve System.

Kamp, A., 2006. Diversifikation versus Spezialisierung von

Kreditportfolios – Eine Empirische Analyse. Ph.D. thesis,

University of M¨unster.

Kamp, A., Pfingsten, A., Porath, D., 2005. Do Banks Diversify

Loan Portfolios? A Tentative Answer Based on Individual Bank Loan

Portfolios. Working Paper 03/2005, Deutsche Bundesbank, Frankfurt

am Main.

Kothari C.R (2003) Research Methodology. (4th Edition) Continuum,

lxi

London

Krugman, S., Obstfeld, A. P., 1994. A Theory of Optimal Bank

Size. Oxford Economic Papers 44, 725–749.

Laderman, E. S., 2000. The Potential Diversification and Failure

Reduction Benefits of Bank Expansion into Nonbanking Activities.

Working Paper 2000-01, Federal Reserve Bank of San Francisco.

Lang, G., Welzel, P., 1997. Gr¨oße und Kosteneffizienz im

deutschen Bankensektor. Zeitschrift f¨ur Betriebswirtschaft 67

(3), 269–283.

Lang, L., Stulz, R., 1994. Tobin’s q, Corporate Diversification,

and Firm Performance. Journal of Political Economy 102, 1248–

1280.

Markowitz, H. M., 1952. Portfolio Selection. Journal of Finance

7, 77–91.

McFadden, R. L., 2005. Optimal Bank Size From the Perspective of

Systemic Risk. Working Paper, Universit´e de Paris 1 - Sorbonne -

Panth´eon.

Mwingi Mwalimu SACCO Research by KUSCO March 2003.

Mugenda and Mugenda AG (2003) Research Methods Qualitative and

quantitative approaches, Act press, Nairobi

Oso, Y. and Onen, D. (2005), A general Guide to Writing Research

Proposal and Report. lxii

Pfingsten, A., Rudolph, K., 2002. German Banks’ Loan Portfolio

Composition: Market-Orientation vs. Specialisation. Working Paper

02-02, Institut f¨ur Kreditwesen, M¨unster.

Roll, R., 1992. Industrial Structure and the Comparative Behavior

of International Stock Market Indices. Journal of Finance 42, 3–

41.

Stiroh, K. J., 2004. Diversification in Banking: Is Noninterest

Income the Answer? Journal of Money, Credit, and Banking 36 (5),

853–882.

Stomper, A., 2004. A Theory of Banks’ Industry Expertise, Market

Power, and Credit Risk. Working Paper, University of Vienna.

Winton, A., 1999. Don’t Put All Your Eggs in One Basket?

Diversification and Specialization in Lending. Working Paper

9903, Finance Department, University of Minnesota, Minneapolis.

lxiii