depositary receipts: concept, evolution and recent trends

TRANSCRIPT

Depositary Receipts: Concept, Evolution and Recent Trends

Manoj Kumar1

1 Manoj Kumar is a faculty member at Kirloskar Institute of Advanced Management Studies, Harihar. He holds a doctorate from the Shailesh J Mehta School of Management, Indian Institute of Technology, Powai, Bombay. He can be contacted at: [email protected]

Abstract

The trend towards the internationalisation of financial markets has gained impetus during the last two decades, driven mainly by the sophistication in IT and capital market participants (borrowers, investors and financial intermediaries), greater co-operation between financial regulators, the lowering of capital barriers across national boundaries and the liberalisation of capital markets in emerging economies. Many companies are looking beyond their domestic financial markets to develop an investor base and to raise international capital. By the end of December 2001, there were 2465 foreign companies listed on the major stock exchanges of the world. A vast majority of foreign firms choose to cross-list their stock through the use of depositary receipts (DRs), which have become the popular mode of financing. The 1990s saw an increased flow of DR programmes, especially from the emerging markets. In April 1992, the government permitted Indian companies to raise equity capital by issuing DR programmes in the international financial markets and of all the emerging markets, India has the maximum number of DR programmes. This paper aims at understanding the conceptual framework of DR programmes and studying the evolution of DR markets, including the introduction and development of DR programmes issued by Indian firms.

Introduction

The trend towards the internationalisation of financial markets has gained impetus during the last two

decades, driven mainly by the sophistication in IT and capital market participants (borrowers, investors

and financial intermediaries), greater co-operation between financial regulators, the lowering of capital

barriers across national boundaries and the liberalisation of capital markets in emerging economies2.

Many companies are looking beyond their domestic financial markets to develop an investor base and to

raise international capital3. By the end of December 2001, there were 2465 foreign companies listed on

the major stock exchanges of the world. A vast majority of foreign firms choose to cross-list their stock

through the use of depositary receipts (DRs), which have become the popular mode of financing. The

1990s saw an increased flow of DR programmes, especially from the emerging markets. In April 1992,

the government permitted Indian companies to raise equity capital by issuing DR programmes in the

international financial markets and of all the emerging markets, India has the maximum number of DR

programmes.

This paper aims at understanding the conceptual framework of DR programmes and studying the

evolution of DR markets, including the introduction and development of DR programmes issued by

Indian firms. The remaining paper is organized as follows: Section I provides a conceptual framework

for the DR programs. Section II traces the historical evolution and growth of DR markets, including the

developments pertaining to the Indian DR programs. Finally, summary and conclusions of this chapter

are presented in the Section III.

I. Conceptual Framework

We initiate our discussion by explaining the structure, issuing process and trading mechanism for a

typical DR program. Next, the various types of DR programs are explained.

1.1 Structure, Issuing Process and Trading Mechanism

A depositary receipt is a negotiable instrument denominated in US dollars or Euro (or in a currency other

than the domestic currency of the issuer company), which is issued to the investors in one or more

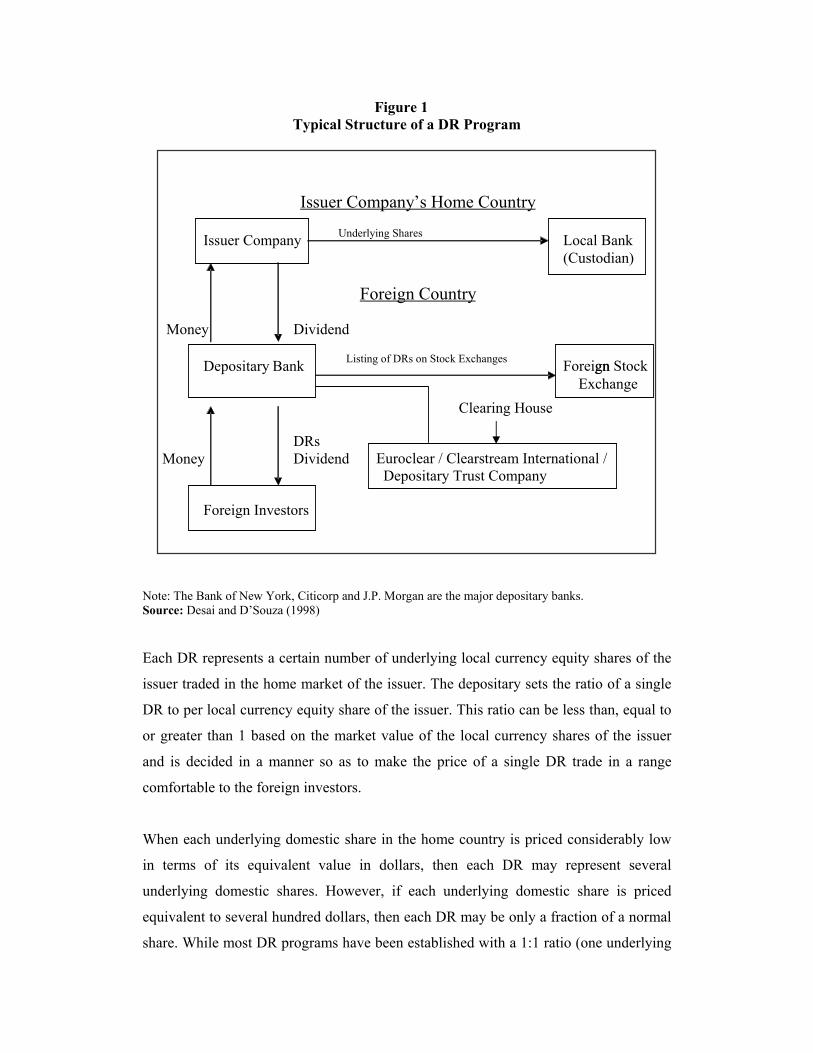

foreign countries. Figure 2.1 depicts the mechanism for floatation of a DR program. DRs are issued by

the overseas depositary bank (henceforth also referred to as depositary) to the international investors

either against the issuer’s local currency shares registered in depositary’s name in the shareholder books

of the company or against the physical delivery of local currency shares of the issuer company to the

depositary or, more commonly, to a domestic custodian bank appointed by the depositary. The

depositary in respect of a DR program is located in a foreign country, where as the custodian is located

in a home country of the issuer company (henceforth also referred to as issuer).

2 ‘Emerging economies’ or ‘Emerging markets’ or ‘Emerging countries’ or ‘Developing markets’ mainly cover countries that the World Bank, the International Finance Corporation (IFC)and the United Nations have determined to have a low or middle-income economy (with per capita income less than $9,361 in1998). Stock markets in these countries have not yet developed to the same levels of sophistication and market capitalisation as in a number of developed countries. By the end of 1999, the IFC identified 81 countries to be emerging economies. (Source: IFC, 2000)

Figure 1

Typical Structure of a DR Program

Note: The Bank of New York, Citicorp and J.P. Morgan are the major depositary banks. Source: Desai and D’Souza (1998)

Each DR represents a certain number of underlying local currency equity shares of the

issuer traded in the home market of the issuer. The depositary sets the ratio of a single

DR to per local currency equity share of the issuer. This ratio can be less than, equal to

or greater than 1 based on the market value of the local currency shares of the issuer

and is decided in a manner so as to make the price of a single DR trade in a range

comfortable to the foreign investors.

When each underlying domestic share in the home country is priced considerably low

in terms of its equivalent value in dollars, then each DR may represent several

underlying domestic shares. However, if each underlying domestic share is priced

equivalent to several hundred dollars, then each DR may be only a fraction of a normal

share. While most DR programs have been established with a 1:1 ratio (one underlying

Issuer Company’s Home Country Issuer Company Underlying Shares Local Bank

(Custodian)

Foreign Country Money Dividend Depositary Bank Listing of DRs on Stock Exchanges Foreign gn Stock Exchange

DRs Money Dividend Euroclear / Clearstream International / Depositary Trust Company

Clearing House

Foreign Investors

share equals one depositary share), some of DR programs have ratios ranging from

100,000:1 to 1:100.

Appropriate ratio is decided by the depositary bank at the inception of the DR program

with counseling from the issuer, investors, brokers, investment bankers and

underwriters. The ratio can be adjusted at a future date to address changes in market

conditions. Alternately, the issuer may undertake a stock split of the underlying

domestic shares so as to keep the market price of a single DR within a comfortable

price range for the foreign investors. In setting the ratio, three factors are decisive. First,

the issuer decides the ratio in a manner so that DR prices conform to the price range at

which most securities of companies in the issuer's industry generally trade. Second,

issuer wants to conform to the average price range at which most shares listed on the

stock exchange trade. Finally, ratio is decided to give a sense of ‘just pricing’ to the

prospective investors.

In order to establish a DR program, issuer selects a depositary, a custodian bank and an

advisory team constituted of lawyers, accountants, and investment bankers. While the

advisory team plays a crucial role during the initial floatation and listing process of the

DR program, the role of the depositary and the custodian bank is crucial even after the

initial floatation and listing process gets over. They are responsible for managing the

issue on an on-going basis. The issuer appoints custodian bank in consultation with the

depositary bank. The issuer and the depositary bank enter into a depositary agreement

that sets forth the terms of the DR program. The agreement stipulates the rights and

responsibilities of the issuer, depositary and the investors investing in the DR program.

The issuer, on an on-going basis, deals only with the depositary bank in regards to

payments, notices or rights/bonus issues related to the DR issues. The depositary

agreement, as a general rule, sets forth an obligation of the depository to provide notice

of shareholder meetings and other information about the issuer company to the

investors so as to enable them to exercise their shareholders rights. While for GDR

investors voting rights rests with the depository bank, ADR investor are allowed to

exercise their voting rights in individual capacity. Depositary bank is also responsible

for secondary market transfers / cancellations of DRs. The depositary agreement also

set out the amount payable as administration fee from the issuer for the services offered

by the depositary.

The issuer represented by its directors, officers, US agents, underwriters, experts, legal

advisors, auditors and accountants involved in preparation of the registration statement

has liabilities under the US securities laws for false or misleading statements in or

omissions from its filings to SEC. Besides, individuals are also held personally liable

for false or misleading statements in or omissions from the filings for which they are

responsible. Preparation of the filing includes (a) ‘due diligence’ investigation, usually

conducted by the outside legal advisor; (b) audit of the financial information provided

by the accounting firm; and (c) outside experts’ conclusions.

The roles of different market intermediaries involved in issuing and listing of a DR

program are as follows:

(a) Issuer Company is responsible for (i) preparing the issue proposal, (ii) determining

the financial objectives, (iii) obtaining the required approvals from Board of

Directors, shareholders and regulators as may be needed, (iv)deciding the type of

DR program to be issued, (v) providing financial information to accountants, and

(vi) developing investor relations plan.

(b) Lead Manager (Investment Banker) is responsible for (i) marketing the issue to the

investors; (ii) conducting the road show; (iii) advising the issuing company on the

type of DR program, pricing of the security; (iv) obtaining CUSIP or ISIN4

number; (v) obtaining DTC, Euroclear, Clearstream International, and PORTAL

eligibility as may be needed; and (vi) appointing the legal advisers so as to ensure

the accuracy of the information in the prospectus.

(c) Co-Managers / Underwriters assist the lead manager in fulfilling its obligations to

the issuer company. Underwriters subscribe to the unsubscribed portion of the

issue or else buy the portion of DRs to further sell it to the investors.

(d) Depositary is the bank authorized by the issuer company to issue DRs against the

equity shares of the issuer company deposited with domestic custodian. It is the

4 CUSIP stands for Committee on Uniform Securities Identification Procedure, set up by the American Bankers Association to create identifying numbers for all securities trading in the U.S. The assignment of CUSIP numbers is by a subsidiary of Standard & Poor, the rating agency. Every security, mutual fund, option, warrants, bond, common share has its own 9-digit CUSIP number that appears on the certificate of ownership. Recently, because of the volume of issues, some numbers now are letters. The last digit is a "check digit" which can be used to verify the others. The CUSIP for IBM is 59200102. ISIN (International Securities Identification Numbers) is international system that corresponds to CUSIP. It uses a 12- digit number, not letters, and is used by the European settlement systems, CLEARSTREAM INTERNATIONAL (Luxembourg) and EUROCLEAR (a Brussels-based subsidiary of Morgan Guaranty).

overseas agent of the issuer company who issues the DRs to the investors in lieu of

shares allotted to him/her. The physical possession of the shares rests with the

domestic custodian although the ownership of the shares vests with the DR

investors. Banks such as the Bank of New York, Citibank and J.P. Morgan have

been acting as the depositaries in many DR programs. The legal relationship

between the DR investor and the depository bank is that of trust. The depository is

the registered owner of the shares and its name appears in the ‘Register of

Members’ of the issuer company. The most important role of a depositary bank is

that of stock transfer agent and registrar. Therefore all major depositary banks

maintain the sophisticated stock transfer systems. Depositary bank is responsible

for (i) advising the structure of DR program; (ii) appointing the custodian; (iii)

assisting in complying to the regulatory requirements for floating DR program; (iv)

coordinating with lawyers, accountants and investment bankers to ensure that all

program implementation steps are completed; (v) preparing and issuing the DR

certificates; (vi) enlisting the market makers (vii) faxing the announcement of

program establishment to brokers and traders; and (viii) acting as the liaison

between the issuer, the securities markets participants, and the DR holders once a

depositary receipt facility is established.

(e) Brokers are responsible for (i) submitting the required forms to become a market

maker in a DR program; (ii) making securities available to the investors; and (iii)

executing and settling the trades.

(f) Custodian is the banking company situated in the issuer’s home country appointed

as a custodian of the underlying shares of the issuer company. Custodian is

responsible for (i) holding the underlying shares in the account of depositary; (ii)

communicating with depositary on corporate actions and related issues; and (iii)

transmitting dividend payments to the investors through depositary.

(g) Investor Relations Firm is responsible for (i) developing a long-term investor

relationship program with specific and measurable goals and objectives; and (ii)

placing tombstone advertisement for announcing establishment of the program.

(h) Legal Advisors assist the issuing company, lead manager, co-managers and the

underwriters in the preparation of the prospectus, depository agreement, indemnity

agreement and subscription agreement. They are also responsible for filing the

appropriate statements for registration and/or establishing exemptions from certain

procedures.

(i) Auditors must be appointed by the issuing company. Typically, it is one amongst

the big international accounting firms. They prepare the auditor’s report for

inclusion in the prospectus, provide requisite consent and comfort letters and

reconcile the issuing company’s accounts with International Accounting Standards

(IAS) or US Generally Accepted Accounting Principles (GAAP). They also

participate in the due diligence meetings for enabling the issuing company to

comply with proper disclosures relating to the issue.

(j) Listing Agent is often an investment or merchant bank, stockbroker, accountancy

or law firm, or other financial adviser. Normally the lead manager will also act as

the listing agent, but it is not uncommon to appoint a separate listing agent. All

companies seeking the listing of DRs in Europe have to appoint a listing agent,

which must be authorised by the listing authority to participate in securities issues.

The listing agent, who must meet certain qualifications, provides the link between

the company, depositary and the listing authority. The listing agent should be

appointed at an early stage in the process of listing, as his responsibilities include:

assessing the company’s suitability for a listing in LSE or LxSE; advising on all

aspects of the listing rules; reviewing the prospectus; appointing legal advisers to

ensure the information in the prospectus is accurate and that investors have all the

information they require to make an informed decision; confirming to the listing

authority that all the requirements of its listing rules have been met; and

communicating with the listing authority and seeking approval of the prospectus.

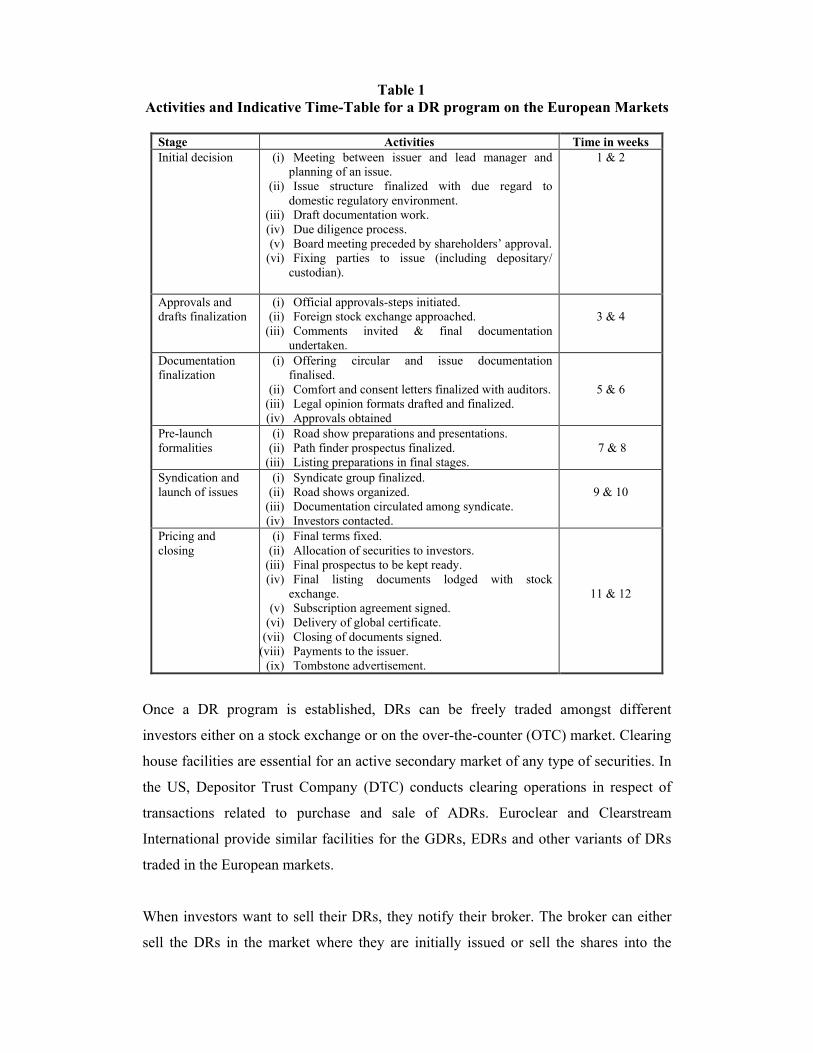

Launching a DR program is a time consuming process, more so, if the issue is a level–

III ADR program. Establishing a level-II or a level-III DR program requires a period of

18-30 weeks as against a period of 11-13 weeks for a level–I or the GDR issue. Table

1 depicts the activities and an indicative timeframe for launching a typical GDR

program.

Table 1 Activities and Indicative Time-Table for a DR program on the European Markets

Stage Activities Time in weeks Initial decision (i) Meeting between issuer and lead manager and

planning of an issue. (ii) Issue structure finalized with due regard to

domestic regulatory environment. (iii) Draft documentation work. (iv) Due diligence process. (v) Board meeting preceded by shareholders’ approval.

(vi) Fixing parties to issue (including depositary/ custodian).

1 & 2

Approvals and drafts finalization

(i) Official approvals-steps initiated. (ii) Foreign stock exchange approached.

(iii) Comments invited & final documentation undertaken.

3 & 4

Documentation finalization

(i) Offering circular and issue documentation finalised.

(ii) Comfort and consent letters finalized with auditors. (iii) Legal opinion formats drafted and finalized. (iv) Approvals obtained

5 & 6

Pre-launch formalities

(i) Road show preparations and presentations. (ii) Path finder prospectus finalized.

(iii) Listing preparations in final stages.

7 & 8

Syndication and launch of issues

(i) Syndicate group finalized. (ii) Road shows organized.

(iii) Documentation circulated among syndicate. (iv) Investors contacted.

9 & 10

Pricing and closing

(i) Final terms fixed. (ii) Allocation of securities to investors.

(iii) Final prospectus to be kept ready. (iv) Final listing documents lodged with stock

exchange. (v) Subscription agreement signed.

(vi) Delivery of global certificate. (vii) Closing of documents signed.

(viii) Payments to the issuer. (ix) Tombstone advertisement.

11 & 12

Once a DR program is established, DRs can be freely traded amongst different

investors either on a stock exchange or on the over-the-counter (OTC) market. Clearing

house facilities are essential for an active secondary market of any type of securities. In

the US, Depositor Trust Company (DTC) conducts clearing operations in respect of

transactions related to purchase and sale of ADRs. Euroclear and Clearstream

International provide similar facilities for the GDRs, EDRs and other variants of DRs

traded in the European markets.

When investors want to sell their DRs, they notify their broker. The broker can either

sell the DRs in the market where they are initially issued or sell the shares into the

issuer company’s home market. Secondary market trading in DRs is constituted of two

types of market transactions, viz., the intra-market transaction and the cross-border

transaction.

The intra-market transactions follow the settlement procedures setout for the trading in

domestic securities of the country where DRs are issued. In a typical intra-market

transaction, DR certificates are transferred from the seller’s account to the buyer’s

account. A high liquidity level is necessary for intra-market transaction to get executed.

Most secondary market transactions in ADRs are settled via intra-market trading due to

the high liquidity levels in the ADR markets.

In a cross-border transaction, brokers, either through their own international offices or

through a local broker in the issuer company’s home market, will sell the shares back

into the home market. In order to settle the trade, the broker will surrender the DRs to

the depository bank with instructions to deliver the shares to the buyer in the home

market. The depository bank will cancel the DRs and instruct the custodian to release

the underlying shares and deliver them to the local broker who purchased the shares.

The broker will arrange for the foreign currency to be converted into the appropriate

currency (US dollars or Euro) for payment to the DR holder.

The cross-border transactions in DRs are, typically, executed to take advantage of the

price differentials between the DR prices and the prices of equivalent underlying

domestic shares. Besides, lack of liquidity in DR markets also prompts the cross-border

transactions. Most transactions in the Indian GDRs are executed as cross-border

transactions.

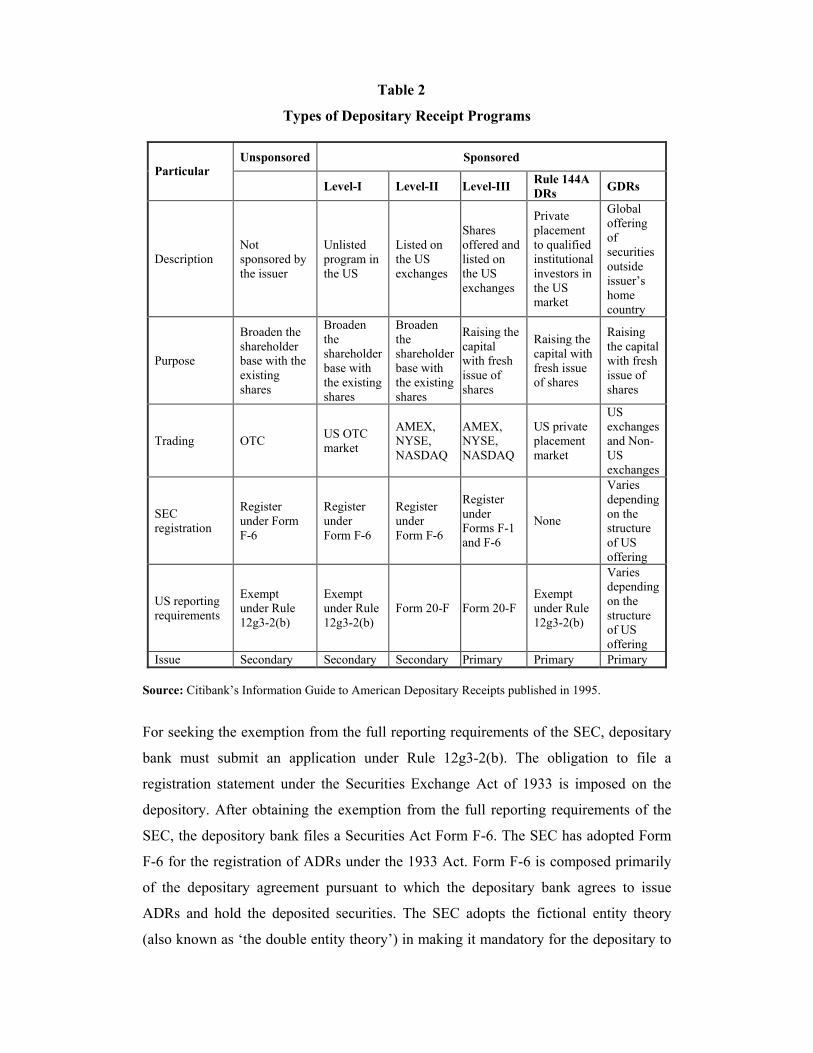

1.2 Types of Depositary Receipt Programs

Issuer Company has the option of issuing one or more types of the available choices of

DR programs. A broader classification of DR programs is on the basis of the countries

where DR programs are issued and or listed. While American Depositary Receipts

(ADRs) are issued and or listed only in the US markets, Global Depositary Receipts

(GDRs) are simultaneously issued and or listed in the more than one market, typically

in the European and US markets. DR programs can also be classified into the following

four categories based on the regulatory complexity of the issuance process, purpose and

the post issuance reporting requirements of the program (Table 2).

(a) Unsponsored American Depositary Receipts.

(b) Sponsored American Depositary Receipts.

(c) Privately Placed Depositary Receipts.

(d) Global Depositary Receipts and Its Variants.

(a) Unsponsored American Depositary Receipts: These are issued by one or more

depositaries in response to market demand but without a formal agreement with the

issuer company. Unsponsored DRs are created in order to satisfy the investors’ demand

for the securities of a particular foreign company. When investors show their buying

interest in the shares of a particular foreign company, broker(s) purchase those shares

listed on the company's home market and request the delivery of the shares to the

depositary bank’s custodian operating in that country. The broker then converts the US

dollars or Euro received from the investor into the corresponding foreign currency in

order to make payment for the purchased shares from the company’s home market. On

the same day custodian notifies the depositary bank that the delivery of the shares has

been received. Upon such notification, DRs are issued and delivered to the initiating

broker(s), who then delivers the DRs to the investor. If the DR facility is established

without the active participation of the issuer company, then the fee payable to the

depositary bank is borne by the holders of unsponsored DRs.

Table 2

Types of Depositary Receipt Programs

Unsponsored Sponsored Particular

Level-I Level-II Level-III Rule 144A DRs GDRs

Description Not sponsored by the issuer

Unlisted program in the US

Listed on the US exchanges

Shares offered and listed on the US exchanges

Private placement to qualified institutional investors in the US market

Global offering of securities outside issuer’s home country

Purpose

Broaden the shareholder base with the existing shares

Broaden the shareholder base with the existing shares

Broaden the shareholder base with the existing shares

Raising the capital with fresh issue of shares

Raising the capital with fresh issue of shares

Raising the capital with fresh issue of shares

Trading OTC US OTC market

AMEX, NYSE, NASDAQ

AMEX, NYSE, NASDAQ

US private placement market

US exchanges and Non-US exchanges

SEC registration

Register under Form F-6

Register under Form F-6

Register under Form F-6

Register under Forms F-1 and F-6

None

Varies depending on the structure of US offering

US reporting requirements

Exempt under Rule 12g3-2(b)

Exempt under Rule 12g3-2(b)

Form 20-F Form 20-F Exempt under Rule 12g3-2(b)

Varies depending on the structure of US offering

Issue Secondary Secondary Secondary Primary Primary Primary Source: Citibank’s Information Guide to American Depositary Receipts published in 1995.

For seeking the exemption from the full reporting requirements of the SEC, depositary

bank must submit an application under Rule 12g3-2(b). The obligation to file a

registration statement under the Securities Exchange Act of 1933 is imposed on the

depository. After obtaining the exemption from the full reporting requirements of the

SEC, the depository bank files a Securities Act Form F-6. The SEC has adopted Form

F-6 for the registration of ADRs under the 1933 Act. Form F-6 is composed primarily

of the depositary agreement pursuant to which the depositary bank agrees to issue

ADRs and hold the deposited securities. The SEC adopts the fictional entity theory

(also known as ‘the double entity theory’) in making it mandatory for the depositary to

file Form F-6. Under this theory the depositary bank assumes the issuers responsibility

to file a registration documents with the SEC and is required to sign Form F-6 on behalf

of issuer. However, the depositary and its officers remain shielded from any liability

arising from the content of the registration document. The filing of Form F-6 is

obligatory even in case of the sponsored DR programs. However, the issuer is a party to

the depositary agreement of the sponsored programs, and hence is liable for any

liability arising from the content of the registration document.

Unsponsored ADR programs are exempted from the SEC’s reporting requirements and

can only be traded on the over-the-counter market5 and listed in the pink sheets.

Unsponsored ADR programs have several advantages over the sponsored ADR

programs. First, they are relatively inexpensive and easier way for expanding the

investor base in the US. Second all costs associated with establishment of an

unsponsored ADR program are borne by the investor. Third, SEC registration and

reporting requirements are minimal. Fourth, the issuer is not a party to the depository

agreement, or a registration applicant and therefore is not subject to any US liability

arising in connection with the ADR program.

Some examples of the unsponsored DR programs, which have their origination in the

recent past are – the Telefonos de Mexico’s DR program listed on NASDAQ, and the

Wal-Mart de Mexico’s DR program traded on OTC market of U.S.A. However,

unsponsored DR programs have become a rarity in the recent years (only three new

unsponsored DR programs were established from 1983 to 1994). Foreign companies,

which are popular amongst the investors, most willingly sponsor their DR program(s).

The main reasons for the gradual obsolescence of unsponsored DR programs in the

recent years are: (i) the issuer being not a party to the depository agreement has little

control over the unsponsored DR program; (ii) the unsponsored programs can easily be

duplicated by other depository banks as there is no need of any consent from the issuer

company; (iii) conversion of a unsponsored DR program into a sponsored DR program

5 In OTC market, transactions are conducted through telephones and computer networks connecting the dealers of the traded securities. OTC trading in US is done in either of the following two ways: (a) National Quotation Bureau for brokers and dealers (the market maker community) daily publishes and distributes the pink sheets (named for their color) to the brokers and dealers. These sheets provide the detailed information about the prices and the market makers for the OTC stocks. The pink sheets are not available to the general public. (b) OTC Bulletin Board (OTCBB) is a regulated transaction and dealer-driven quotation service. Data available through this service may include real-time quotes and last sale prices in domestic securities and indicative prices in foreign securities and DRs. It also lists the market makers for OTC issues and allows them to enter quotes and indications of share volume twice a day.

is very expensive for the issuer as it requires a payment of the cancellation fees for the

outstanding unsponsored DRs; and (iv) unsponsored DRs have low liquidity, as they

are restricted from trading on the regular stock exchanges.

(b) Sponsored American Depositary Receipts: Issuer takes the initiative of launching a

sponsored DR program by appointing the depositary and other intermediaries involved

in a DR program. Sponsored DR programs offer several advantages to the issuer. First,

issuer has complete control over the sponsored DR facility. Second, issuer can choose

from the several types of sponsored DR programs, some of which can be used for

raising the fresh capital and for listing on the foreign stock exchange(s).

Sponsored DRs to be issued in the US markets must be registered with SEC using the

Form F-6. The filing in the Form-6 is made pursuant to provisions of the Securities Act

1933. It incorporates by reference various provisions of the depositary agreement.

Typically, the Form F-6 for a sponsored DR program is executed by the depository

bank, but must also be signed by a majority of the issuer’s board of directors, who

undertake, if necessary, to make the required future disclosures.

Security Exchange Commission (SEC) of US recognises following types of the

sponsored ADRs:

(I.) Level-I American Depositary Receipts; and

(II.) Level-II and Level-III American Depositary Receipts.

(I.) Level-I American Depositary Receipts: Level-I ADR programs are not allowed to

list on the regular US stock exchanges. However, they are allowed to be traded on the

US OTC market6 and or on some stock exchanges outside the US. In US their prices

are published daily in the pink sheets. A few brokers may act as market makers and

provide their two-way quotes in the pink sheets for level-I ADRs. The brokers, who

want to transact in level-I ADRs deal with the brokers listed as market makers for a

particular ADR program on the pink sheets. A broker may elect to list as a market

maker for a level-I ADR program because of the following reasons: (i) the program is

6 As per a new rule, effective since April 1st 1998, level-I ADRs were made ineligible from inclusion on the OTC Bulletin Board (OTCBB). To be eligible for the OTCBB after April 1st 1998, an ADR program must be registered with the SEC pursuant to Section 12 of the 1934 Securities Exchange Act. Therefore, an ADR program has to be level-II or level-III program in order to remain eligible for quotation on OTCBB.

known or perceived to be an attractive to the DR investors (institutional or retail); (ii)

the brokerage firm follows the company from research perspective; (iii) the investment

banking side of the brokerage firm has client interest in the issuer; (iv) the brokerage

firm serves the retail investor base for which listing on the pink sheets are viewed as

business-generating; (v) high liquidity in the issuer’s underlying stocks listed on the

issuer’s home market; (vi) issuer’s high earnings and sales growth potential; and (vii)

possibility of the arbitrage opportunities. A broker may also be formally solicited by the

issuer to become the market maker for its DR program. A market maker is not

necessarily required for ADRs to be bought or sold in the OTC market.

Level-I ADR programs are exempted from the reporting requirements of the SEC under

the Rule 12g3-2(b). It is not necessary for the level-I issuers to recast or reconcile their

financial statements as per the US Generally Accepted Accounting Principles (GAAP).

Moreover, level-I issuers do not have to file a Form 20-F7 with the SEC. However,

Rule 12g3-2(b) requires that the issuers of level-I ADR programs must provide the SEC

on Form 6-K with English translations or summaries of information that is: sent to

shareholders, made public in the home market, or provided to a local exchange(s).

Due to relatively easy regulatory framework for the level-I issuers, SEC does not allow

the level-I ADR programs to list on the US stock exchanges. Similarly, level-I ADR

programs can not be used as a means of raising fresh capital from the US capital

markets. However, a level-I ADR program offer an easy and relatively inexpensive way

for the issuers to gauge the interest of US investors in their securities and to familiarize

their name to the US investors.

Many well known multinational companies have established level-I programs viz.

Roche Holding, ANZ Bank, South African Brewery, Guinness, Cemex, Jardine

Matheson Holding, Dresdner Bank, Mannesmann, RWE, CS Holding, Shiseido, Nestle,

Rolls Royce, Volkswagen etc. In addition, numerous companies such as RTZ, Elf

7 Securities of non-US private issuers must be registered with SEC on Form F-6 under the Securities Act 1933, before they can be listed on a US national securities exchange or quoted on NASDAQ. Under the Securities Exchange Act 1934, once a non-US private issuer has listed its securities or registered a securities offering under the Securities Act 1933, it must thereafter file annual reports on Form 20-F that serves as both a registration statement under the Securities Exchange Act 1934, and an annual report for non-US private issuers. An annual report on Form 20-F must be filed within six months after the end of the fiscal year covered by that report. Form 20-F calls for financial statements and other specific disclosures about the firm's business. The issuer may use non-US GAAP if a reconciliation statement to US GAAP is presented for material differences in earnings, earnings per share and balance sheet items.

Aquitaine, Glaxo Wellcome, Western Mining, Hanson, Medeva, Bank of Ireland,

Astra, Telebrás and Ashanti Gold Fields Company Ltd. started with a level-I program

and have upgraded to a level-II or level-III program.

(II.) Level-II and Level-III Depositary Receipts: Level-II and Level-III ADR programs

are listed on the US stock exchange(s). Listed ADRs are more widely covered by the

US financial press and analysts, and hence substantially improves the visibility for

issuer in the US financial press. This in turn promotes more active trading and a greater

liquidity in the level-II and level-III ADR programs. Level-II and level- III ADRs may

also be simultaneously listed on exchanges outside the US.

In level-I and level-II ADR programs, brokers buy the already issued equity shares of

the issuer in the issuer’s home market and deposit them with the custodian bank. The

companies are not permitted to raise the fresh capital from the US markets through the

issue of level-I and level-II ADR programs. However, companies that wish to raise

fresh capital can do so by issuing the level III ADR programs. In a level-III program,

the issuer raises fresh capital by offering the new shares to US investors.

The regulatory requirements of the exchange listed ADR programs (level-II and level-

III) are more stringent than the level-I DR programs. For issuing level-II and level-III

ADR programs, the issuer must fulfill with the registration procedures as set out in the

Securities Exchange Act of 1934 and the listing requirements of the stock exchange(s).

For all intents and purposes, the issuers of level-II and level-III DR programs are

regulated in exactly the same way as any other publicly listed US company. The

Securities Exchange Act of 1934 prescribes similar registration and reporting

requirements for establishing the level-II and level-III ADR programs with some

additional requirements for level-III ADR programs. For issuing the level-II or level-III

ADR programs, the issuer must register and report to SEC by filing the initial

registration statement and their annual reports on Form 20-F8. The issuers of level-II

ADR programs are required to partially reconcile their financial statements to US

8 Form 20-F has two sets of (mutually exclusive) financial statement requirements, referred to as Item 17 (''low disclosure'') and Item 18 (''high disclosure''). Item 17 contains the minimum disclosure requirements and generally does not require US GAAP disclosures if those disclosures are not required under the home exchange listing. Item 17 does not require footnote disclosures about income taxes, leases, pensions, non-consolidated affiliated, related parties, and/or complete industry and geographic segment information. Item 18, which must be completed in a level-III DR program, mandates these disclosures. It is not mandatory for the level-II DR issuers to fill item 18 in the form.

GAAP. However, there is no need for individual business segments of the issuer to

reconcile their financial statements to the US GAAP.

The additional requirements for the level-III ADR program are as follows. First, the

issuer must submit Form F-1 to the SEC to register the underlying securities to be

offered under level-III ADR program. Second, the issuer has to fully reconcile its

financial statements to US GAAP so as to fulfill the requirements of filing of Form 20-

F (or include US GAAP financials).

(c) Privately Placed - Rule 144A Depositary Receipts (RADRs): Private placement of

ADRs is a comparatively cheaper and faster mode of raising the capital than the level-

III ADR offerings. Issuers, therefore, often raise the capital through the private

placement of sponsored DRs in the foreign markets. A non-US issuer can privately

place its ADRs with the US investors pursuant to the Regulation D and Rule 144A.

Regulation D, adopted by SEC in 1982, establishes certain conditions under which a

securities offering made in US territory is considered a private offering, and is therefore

not subject to the requirements of advance filing with the SEC and provision of a

prospectus. Under Rule 144A, adopted by SEC in April 1990, non-US firms are

allowed to privately place their ADRs for trading among the qualified institutional

buyers (QIBs) in US. As per Rule 144A, a QIB is (i) any institution that owns and

invests on a discretionary basis not less than US $100 million in securities of issuers

that are not affiliated to it or (ii) an entity entirely owned by the QIBs. Rule 144A

greatly increased the liquidity of privately placed securities by allowing QIBs to resell

the RADRs privately to the other QIBs without any holding period requirement.

RADRs offerings are exempted from certain disclosure and reporting requirements

designed to protect individual investors, such as prospectus delivery and periodic

financial reporting. Securities offered in the Rule 144A market do not have to be

registered under the Securities Act and issuers do not have to comply with the periodic

reporting requirements of the Exchange Act.

To float ADRs under Rule 144A it is necessary that the same class of securities have

not been listed on a US securities exchange or quoted on NASDAQ, at the time of

issuance of securities under Rule 144A. This condition is applied to prevent the

development of dual markets for the same security. The prohibition of resale of shares

to non-QIBs expires after three years, and the shares can then be traded on the broader

level-I OTC market. The seller of the RADRs must take reasonable steps to ensure that

purchaser is aware of seller’s reliance on the exemption from the registration

requirements of the Securities Act. Rule 144A also requires that the security holder and

holder’s prospective purchaser must have the right to obtain from foreign private issuer,

at the request of the holder, a reasonably current brief statement of the issuer’s

business, products and services; and the issuer’s most recent balance sheet, profit and

loss statements, retained earnings statements, and similar financial statements for the

prior two years. This information need not be prepared in accordance with US GAAP.

The process of doing private a placement involves the drafting of an offering circular

that in general has the same content as a prospectus. It is to provide information about

the company and the issuing securities. As the offering circular is not subject to the

SEC registration, the disclosure of the financial information provided therein must

comply only with accounting principles of the issuer’s home country and is primarily

product of negotiations of the issuer and the investment banker. Typically, the issuer

includes in the offering circular a set of financial statements which, although are

prepared in accordance with the accounting principles of the issuer’s home country, are

“Americanized” in terms of style and presentation. In addition, the issuer may provide

reconciliation to the US GAAP of the most significant financial data.

RADRs are traded by US market makers on a private screen-based listing service

system known as PORTAL9 administered by the National Association of Securities

Dealers (NASD). Secondary trading of the Rule 144A securities involves substantial

paperwork, associated with the necessity of proving eligibility of securities for the Rule

144A exemption and eligibility of the buyers to participate in the transactions. Rule

144A allows the issuer to raise only a relatively small amount of money (US $30-$50

millions). However, issuing of RADRs allows foreign issuers to assess investor appetite

for their securities before listing or publicly offering their DRs to the full spectrum of

US investors.

An issuer may have non-US tranche of its RADR program privately placed in the US

markets. While the US portion is structured as a private offering in accordance with 9 PORTAL is an acronym for Private Offerings, Re-sales and Trading through Automated Linkages

Rule 144A, the non–US tranche may be sold to non-US investors in reliance with

Regulation S of the Securities Act.

Regulation S, adopted by SEC in 1990, specifically allows an issuer to make a private

offering in the US concurrently with an offering not registered under the Securities Act

outside US. Regulation S clarifies the conditions under which an issue is considered to

be made outside the US, and hence not subjected to SEC regulations.

An issue is considered to be made outside the US when the following three conditions

are met: (i) the buyer is outside US territory; (ii) the securities are not offered or

advertised in the US; and (iii) during a specific period (up to one year depending on

how much interest there is in the securities in the US) the securities are not offered,

advertised or sold to US investors directly or indirectly, with the exception of QIBs.

The GDR structures described later have been developed to enable the non-US issuer to

make a global offering in reliance on Regulation S.

In early 1990s SEC created a regulation that allows a non-US issuer to establish a

registered and non-restricted level-I ADR program along with the RADRs for the same

class of underlying stock. This facility is termed as "side-by-side".

(d) Global Depositary Receipts and Its Variants: During 1990s, the surge in capital

raised through DR programs prompted the emerging markets issuers to create several

innovative DR programs. Emerging markets issuers realized that there are numerous

advantages of floating DR programs on the less stringent European markets or

elsewhere. Floating a GDR program on the European market is easier and faster than

floating an ADR program on the US market. Issuer does not have to fulfill the onerous

regulatory requirements of SEC. This prompted the development of GDR programs and

their several variants, for example, Euro Depositary Receipt (EDR), Retail Depositary

Receipt (RDR) and Singapore Depositary Receipt (SDR) programs (Kulikov, 2000).

Citibank introduced the first GDR program in December 1990 for the Samsung

International, a Korean company.

GDRs allow an issuer to raise capital simultaneously in multiple markets through a

global offering. GDR issues have a wider geographical coverage vis-à-vis an ADR or

an EDR or SDR issue. A GDR offering allows the issuer to broaden shareholder base

by simultaneously accessing the several capital markets outside their home market. In

past GDR issues have concurrently been done in Europe and America. A number of

GDR programs are listed at LSE and LxSE. While individual and institutional investors

invest in ADRs, only the latter buy GDRs. Some GDR programs have a parallel 144A

facility. If there is no 144A facility, the 40-day rule applies that enables US investors to

invest in any DR issue done outside US. The 40-day rule provides that if a foreign issue

is "seasoned", then US investors can purchase it on the foreign market. The big hurdle

is whether the foreign market allows foreigners to invest.

GDRs are traded over-the-counter, by telephone or by screen, although many GDR

programs are also listed in London or Luxembourg exchanges. Most GDR offerings

consist of a US tranche that may be a level-III ADR program or privately placed RADR

program. The non-US tranche is sold outside the US (typically in the European

markets) in accordance with Regulation S.

There are many variations for structuring GDR issues. For example, global offerings

have used GDRs that are listed on the NYSE and there have been several GDR

offerings with no US component. The flexibility of the GDR structure has made it a

popular and rapidly growing capital-raising tool. GDRs can be issued in either the

public or private markets in the US or other countries. The links that exist between

Euroclear and Clearstream International in Europe and DTC in the US allow for

efficient and trouble-free settlement of securities between these two major markets.

Several region-specific DR programs have also evolved during the 1990s. An issuer

can establish a DR program that taps only Singapore, European, Asian and/or Latin

American investors and does not offer shares in the US. Such DRs allow the issuers to

choose the investor base they wish to access. SDRs are traded on the Singapore Stock

Exchange. They enable the issuers to establish their presence in the Singapore capital

market. SDRs also position an issuer to benefit from future growth in the Asia/Pacific

region. Daimler-Benz AG was the first company to establish a SDR program in May

1994.

Similarly, EDRs are designed to attract new capital and investors from within the Euro

community. EDRs are priced in euros and all distributions (dividends, stock splits, and

rights issues) are made in euros. The potential market for EDRs includes: institutional

investors diversifying holdings from EU issuers into favorable global sectors; and

individual investors adopting an equity culture, and seeking global renowned issuers.

EDRs can be listed or traded on exchanges such as London, Luxembourg, Paris,

Frankfurt, Brussels, Amsterdam and Vienna.

Lately many new stock exchanges have started listing DR programs viz., Berlin,

Frankfurt, Munich, Toronto, Budapest, Brussels, Johannesburg and Amsterdam. There

are other stock exchanges that are giving a serious consideration for allowing the

foreign companies to list their DRs on these exchanges viz., Hong Kong, Shanghai,

ShenZen and Bombay Stock Exchange.

II. Evolution and Growth of DR Markets

In this section, we first present a historical perspective of growth and evolution of DR

markets in the international arena. Next, we discuss the Indian DR programs and

provide the regulatory framework for Indian firms to issue and list their DR programs

on the foreign markets. Important statistics and major trends for the Indian DR

programs are also covered.

2.1 International Scenario Initial DR programs were originally developed to address the concerns of US investors,

interested in investing internationally. Prior to the introduction of ADRs, US investors

were reluctant to invest directly in offshore securities because of the cumbersome

buying and settlement procedures. In 1927, Morgan Guarantee Trust of New York

(predecessor of current bank J.P. Morgan) created the first ever ADR program for a UK

retailer ‘Selfridge Provincial Stores Limited’. Another 17 ADR programs were opened

around that time and three of them still survive viz., BAT Industries, Cortlaulds plc,

and The General Electric Company. Introduction of ADRs eased the process of

investing in the UK stocks for the US investors.

The early growth, wherein 18 ADR programs were established, came to an abrupt halt

at the time when stock markets crashed in 1929. Following the recovery from market

crash, the Great Depression of 1933 adversely affected the demand for fresh capital. By

the time the demand for fresh capital again started to pick up, the outbreak of World

War II led to the institution of extensive capital controls, in 1939. These controls made

it illegal to sell domestic securities to foreigners, as well as to buy foreign securities.

Therefore, until early 1950s no fresh ADR programs were established.

In its present form ADRs came into existence in 1955, when the SEC introduced its

Form S-12 for registering all ADR programs. Australian and South African mining

companies were the first to introduce DRs in a form as they exist today. Subsequently

several Japanese firm also issued ADRs during 1960s. In 1970s and 1980s several more

firms from other countries also adopted the DR route for raising capital and/or listing in

major capital markets. During 1970s and 1980s a few countries also allowed the

domestic companies to directly sell and list their equity stocks on the foreign markets.

During 1990s there was a spurt in number of DR programs (also an increase in number

of cross-listed equity issues) due to the following reasons. First, the regulatory changes

introduced by SEC during 1990s attracted fresh foreign issuers to the US markets.

Under Rule 144A, institutional buyers were exempted from a requirement to hold

privately placed securities for two years before trading them. This increased the

liquidity and marketability of privately-placed ADRs (Mullin, 1993). Second, London

Stock Exchange (LSE) in 1994 introduced regulations which enable foreign-issuers to

list sterling denominated DR programs on the exchange. Subsequently, the mandatory

requirement for all foreign-issuers to list their DR programs on LSE was also removed.

Third, the massive wave of privatizations of public enterprises during

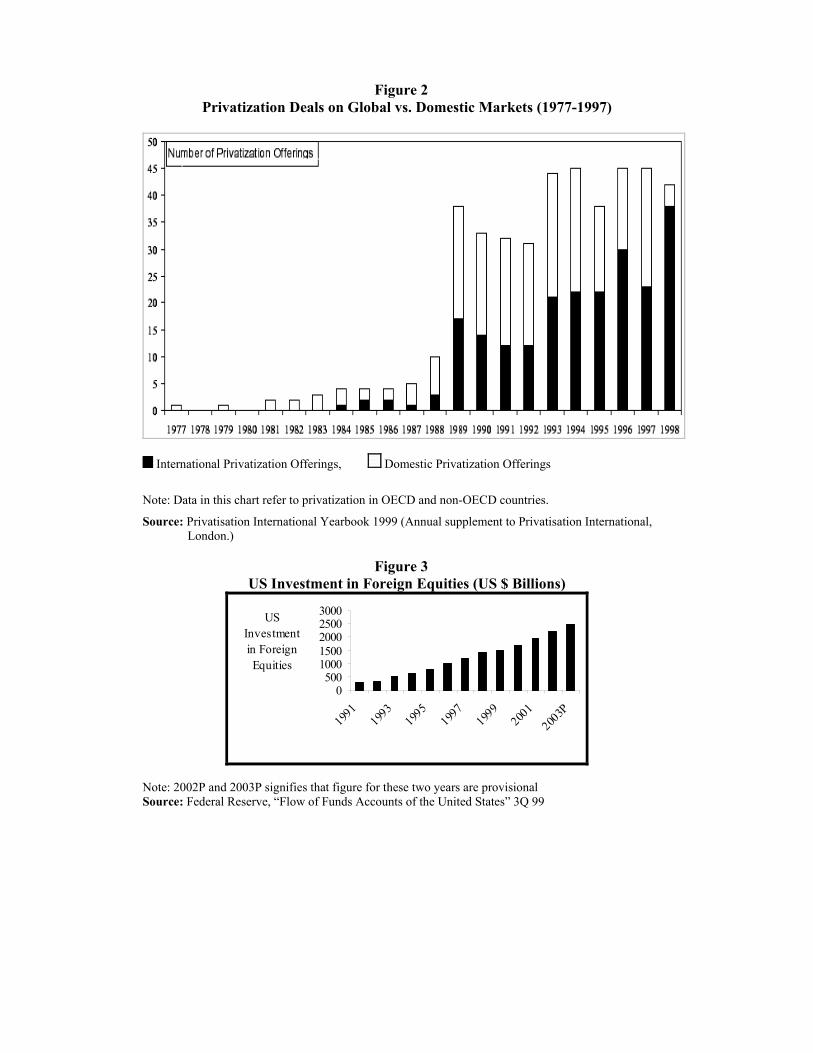

1990s also contributed to growth in number of international offerings (Figure 2).

Among the 650 major privatizations during 1990s, about 150 involved an equity issue

on non-domestic markets, yielding an approximately $52 billions Government revenue

(Source: Privatisation International).

The following facts are indicative of the growth experienced by DR market during

1990s (BONY, 2000, 2001, and 2002):

(a) US investment in the foreign equity has increased from US $279 billions during

1991 to US $1943 billion during 2001 (Figure 3).

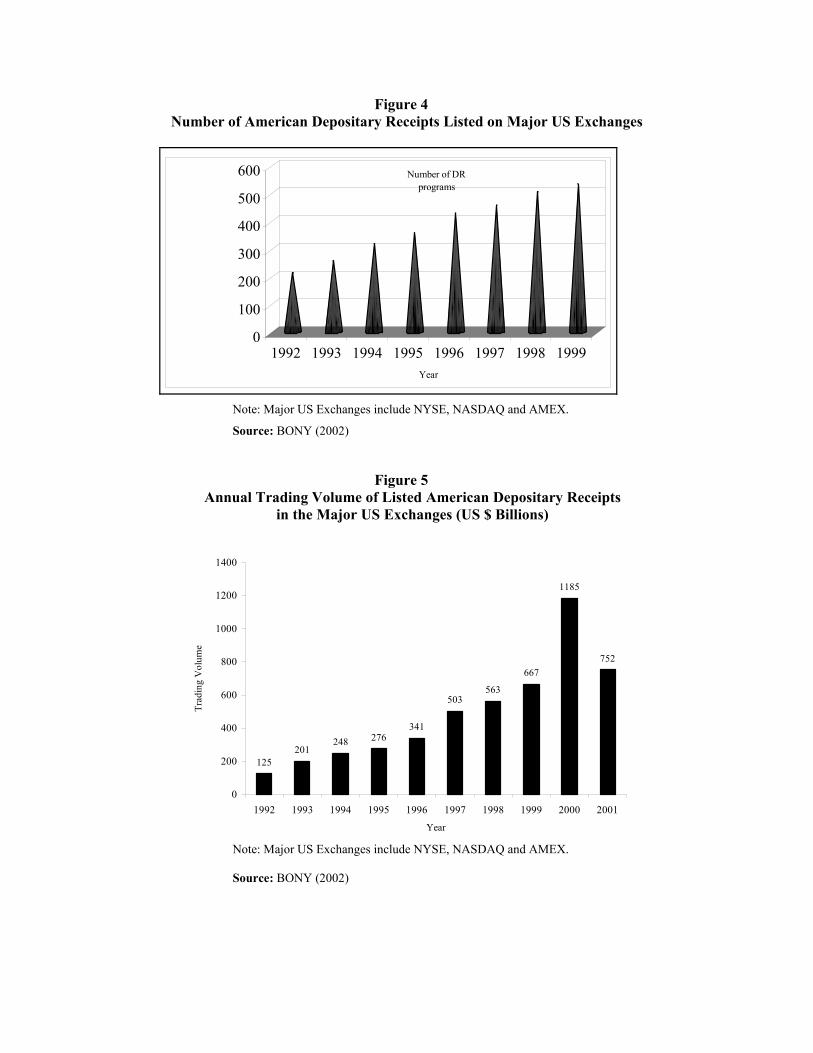

(b) The number of ADR programs listed on three major stock exchanges of US,

viz., NYSE, NASDAQ and AMEX has increased from 215 in 1992 to 623 in

2001 (Figure 4). Similarly, the total number of DR programs has grown from

924 in 1992 to over 1558 programs in December 2001. The number of countries

that have issued their DR programs has gone up from 24 in 1990 to 78 in 2001.

Till 1981 there were only five countries, viz., Hong Kong, South Africa, Japan,

Australia and the United Kingdom that had any DR program.

(c) The total annual trading volumes in listed DRs increased from $125 billions in

1992 to $1185 billions in 2000 at compound annual growth rate of 32.5 percent

(Figure 5). Though annual trading during 2001 has fallen to $752 dollars due

to the recessionary phase in the world economy.

(d) Number of public DR programs has increased from an annual average of 47

programs during the 1992-1995 to 63 programs during 1996-2001. Similarly the

average annual dollar amount raised through public DR programs has increased

from $8572 millions during 1992-1995 to $13995 millions during 1996-2001.

(e) Total global market capitalization of companies that have DR programs exceeds

$6 trillion at the close of 1999.

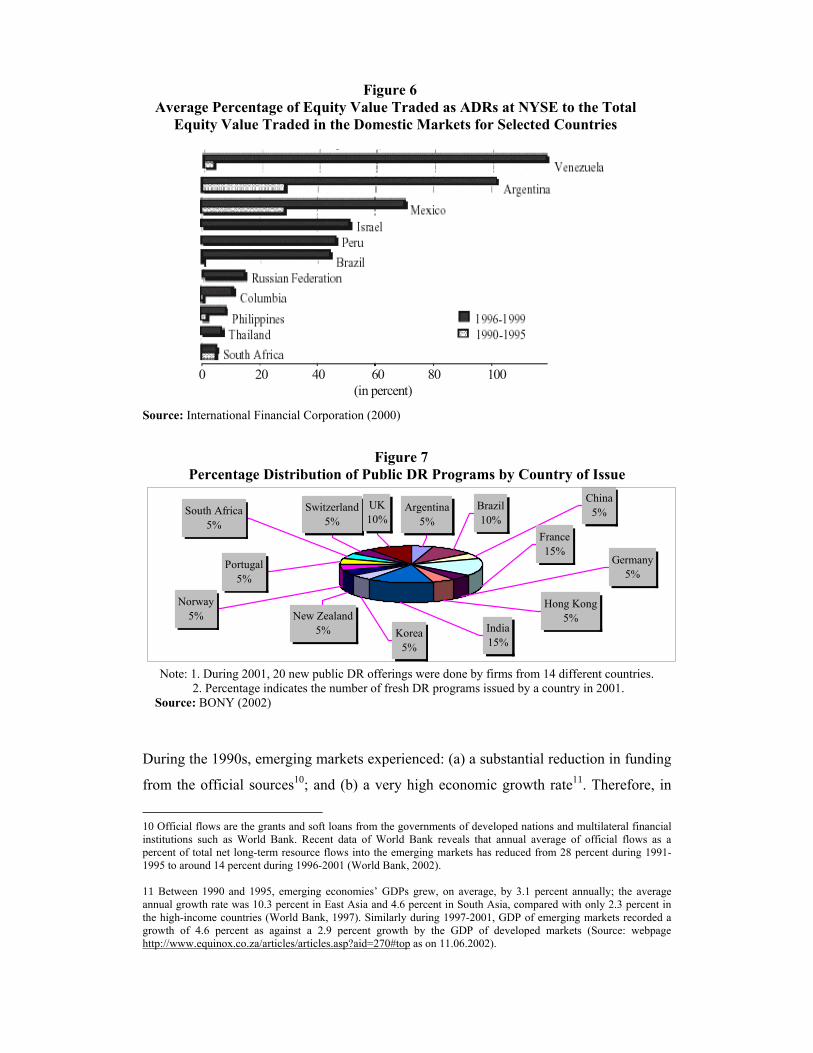

(f) There is an upward trend in the percentage of equity value traded in form of DR

programs in the foreign markets (Figure 6).

Figure 2 Privatization Deals on Global vs. Domestic Markets (1977-1997)

International Privatization Offerings, Domestic Privatization Offerings

Note: Data in this chart refer to privatization in OECD and non-OECD countries. Source: Privatisation International Yearbook 1999 (Annual supplement to Privatisation International,

London.)

Figure 3 US Investment in Foreign Equities (US $ Billions)

0500

10001500200025003000

1991

1993

1995

1997

1999

2001

2003P

US Investment in Foreign Equities

Note: 2002P and 2003P signifies that figure for these two years are provisional Source: Federal Reserve, “Flow of Funds Accounts of the United States” 3Q 99

Figure 4

Number of American Depositary Receipts Listed on Major US Exchanges

0

100

200

300

400

500

600 Number of DR programs

1992 1993 1994 1995 1996 1997 1998 1999Year

Note: Major US Exchanges include NYSE, NASDAQ and AMEX.

Source: BONY (2002)

Figure 5 Annual Trading Volume of Listed American Depositary Receipts

in the Major US Exchanges (US $ Billions)

201248 276

341

503563

667

1185

752

125

0

200

400

600

800

1000

1200

1400

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

Year

Trad

ing

Vol

ume

Note: Major US Exchanges include NYSE, NASDAQ and AMEX.

Source: BONY (2002)

Figure 6 Average Percentage of Equity Value Traded as ADRs at NYSE to the Total

Equity Value Traded in the Domestic Markets for Selected Countries

0 20 40 60 80 100 (in percent) Source: International Financial Corporation (2000)

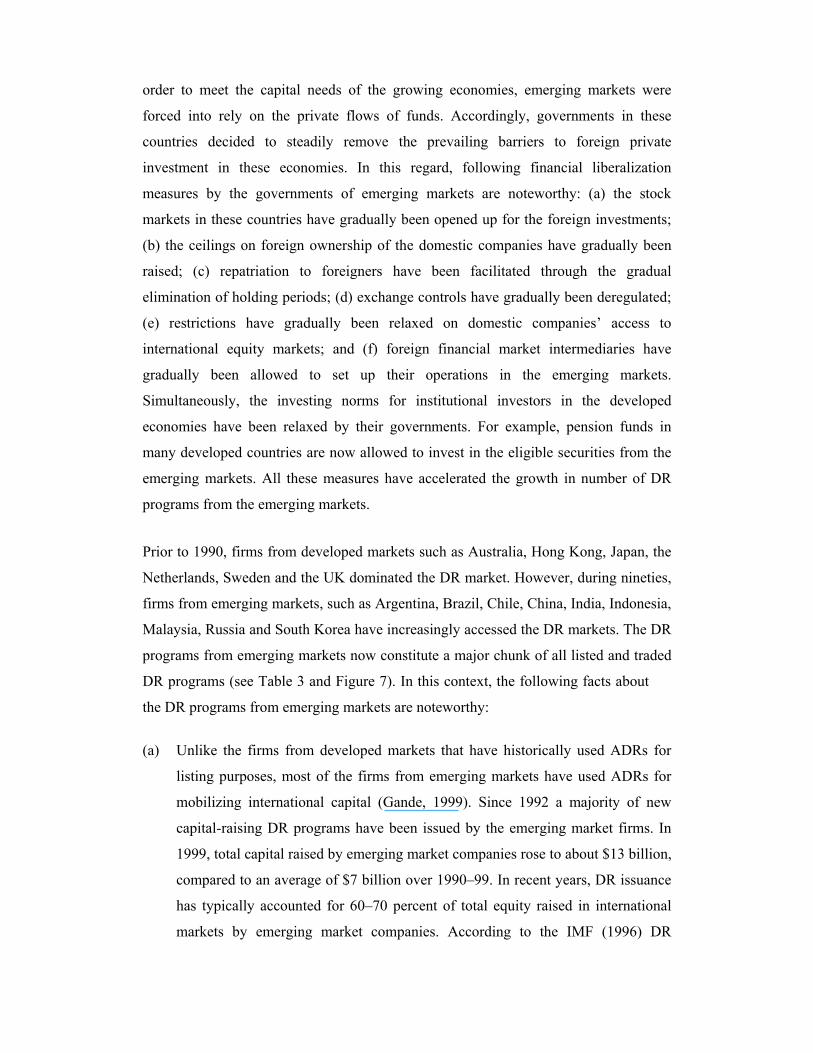

Figure 7 Percentage Distribution of Public DR Programs by Country of Issue

Germany5%

Hong Kong5%

India15%

Korea5%

New Zealand5%

Norway5%

Portugal5%

South Africa5%

Switzerland5%

UK10%

Argentina5%

Brazil10%

China5%

France15%

Note: 1. During 2001, 20 new public DR offerings were done by firms from 14 different countries. 2. Percentage indicates the number of fresh DR programs issued by a country in 2001.

Source: BONY (2002)

During the 1990s, emerging markets experienced: (a) a substantial reduction in funding

from the official sources10; and (b) a very high economic growth rate11. Therefore, in

10 Official flows are the grants and soft loans from the governments of developed nations and multilateral financial institutions such as World Bank. Recent data of World Bank reveals that annual average of official flows as a percent of total net long-term resource flows into the emerging markets has reduced from 28 percent during 1991-1995 to around 14 percent during 1996-2001 (World Bank, 2002). 11 Between 1990 and 1995, emerging economies’ GDPs grew, on average, by 3.1 percent annually; the average annual growth rate was 10.3 percent in East Asia and 4.6 percent in South Asia, compared with only 2.3 percent in the high-income countries (World Bank, 1997). Similarly during 1997-2001, GDP of emerging markets recorded a growth of 4.6 percent as against a 2.9 percent growth by the GDP of developed markets (Source: webpage http://www.equinox.co.za/articles/articles.asp?aid=270#top as on 11.06.2002).

order to meet the capital needs of the growing economies, emerging markets were

forced into rely on the private flows of funds. Accordingly, governments in these

countries decided to steadily remove the prevailing barriers to foreign private

investment in these economies. In this regard, following financial liberalization

measures by the governments of emerging markets are noteworthy: (a) the stock

markets in these countries have gradually been opened up for the foreign investments;

(b) the ceilings on foreign ownership of the domestic companies have gradually been

raised; (c) repatriation to foreigners have been facilitated through the gradual

elimination of holding periods; (d) exchange controls have gradually been deregulated;

(e) restrictions have gradually been relaxed on domestic companies’ access to

international equity markets; and (f) foreign financial market intermediaries have

gradually been allowed to set up their operations in the emerging markets.

Simultaneously, the investing norms for institutional investors in the developed

economies have been relaxed by their governments. For example, pension funds in

many developed countries are now allowed to invest in the eligible securities from the

emerging markets. All these measures have accelerated the growth in number of DR

programs from the emerging markets.

Prior to 1990, firms from developed markets such as Australia, Hong Kong, Japan, the

Netherlands, Sweden and the UK dominated the DR market. However, during nineties,

firms from emerging markets, such as Argentina, Brazil, Chile, China, India, Indonesia,

Malaysia, Russia and South Korea have increasingly accessed the DR markets. The DR

programs from emerging markets now constitute a major chunk of all listed and traded

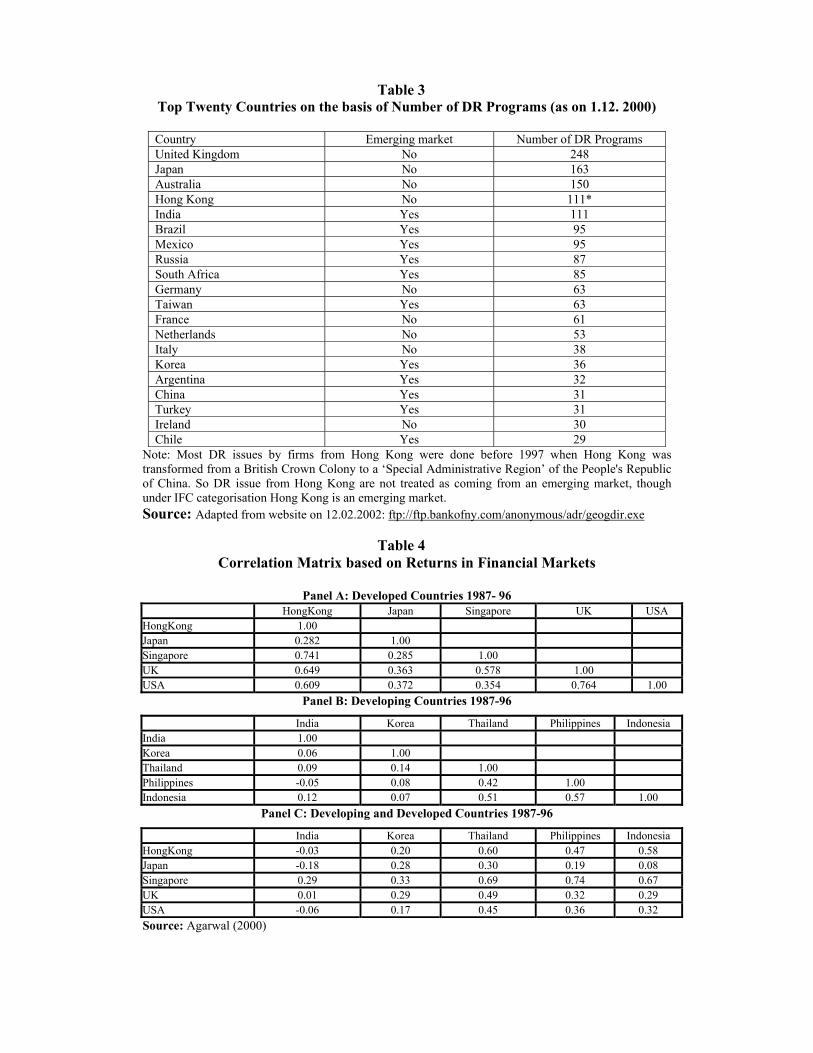

DR programs (see Table 3 and Figure 7). In this context, the following facts about

the DR programs from emerging markets are noteworthy:

(a) Unlike the firms from developed markets that have historically used ADRs for

listing purposes, most of the firms from emerging markets have used ADRs for

mobilizing international capital (Gande, 1999). Since 1992 a majority of new

capital-raising DR programs have been issued by the emerging market firms. In

1999, total capital raised by emerging market companies rose to about $13 billion,

compared to an average of $7 billion over 1990–99. In recent years, DR issuance

has typically accounted for 60–70 percent of total equity raised in international

markets by emerging market companies. According to the IMF (1996) DR

programs by emerging markets accounted for 77 per cent of their total equity

issuance in 1994, but this ratio dropped sharply to 48.8 per cent in 1995.

(b) Some companies from emerging countries have changed their domicile country

and have listed on the exchange of their new domicile country. This is done to

reduce the risk premium which investor associate with companies from emerging

markets. Two South African companies changed their domicile country to UK.

(c) Many newly listed companies from emerging markets have had their initial public

offerings in mature markets, bypassing local markets completely. For example,

Internet companies from Israel and Latin America have recently chosen to list

directly on the NASDAQ.

(d) While DR programs from Latin American firms dominated the market for new

DR issues during the first part of 1990s, DR programs from Asian firms

dominated the market for new DR issues during 1999 and 2000.

(e) There has been a significant increase in the capital raised in technology, media,

and telecommunications sectors, which accounted for almost half of the capital

raised by emerging markets in 1999.

DR Programs from emerging markets were an instant hit amongst international

investing community. According to Porter (1993) this is so because emerging markets

(a) represent a fast growing part of the world economy; (b) have delivered superior

returns (c) are attractively valued; (d) represent huge marketplaces; and (e) are

underweighted in global portfolios. Agarwal (2000) showed that during 1987-96 the

correlation between financial markets return of US and UK was about 0.76 as against a

low correlation of developed markets with emerging markets (Table 4). Though the

correlation between the nations has changed over the years, but the correlation between

the developed and emerging countries continues to be lower (Shashikanth et al., 1998).

Therefore interest in the DR programs from emerging countries is also due to the

greater diversification potential of these programs from the perspective of an

international investor.

Table 3 Top Twenty Countries on the basis of Number of DR Programs (as on 1.12. 2000)

Country Emerging market Number of DR Programs United Kingdom No 248 Japan No 163 Australia No 150 Hong Kong No 111* India Yes 111 Brazil Yes 95 Mexico Yes 95 Russia Yes 87 South Africa Yes 85 Germany No 63 Taiwan Yes 63 France No 61 Netherlands No 53 Italy No 38 Korea Yes 36 Argentina Yes 32 China Yes 31 Turkey Yes 31 Ireland No 30 Chile Yes 29

Note: Most DR issues by firms from Hong Kong were done before 1997 when Hong Kong was transformed from a British Crown Colony to a ‘Special Administrative Region’ of the People's Republic of China. So DR issue from Hong Kong are not treated as coming from an emerging market, though under IFC categorisation Hong Kong is an emerging market. Source: Adapted from website on 12.02.2002: ftp://ftp.bankofny.com/anonymous/adr/geogdir.exe

Table 4 Correlation Matrix based on Returns in Financial Markets

Panel A: Developed Countries 1987- 96

HongKong Japan Singapore UK USA HongKong 1.00 Japan 0.282 1.00 Singapore 0.741 0.285 1.00 UK 0.649 0.363 0.578 1.00 USA 0.609 0.372 0.354 0.764 1.00

Panel B: Developing Countries 1987-96

India Korea Thailand Philippines Indonesia India 1.00 Korea 0.06 1.00 Thailand 0.09 0.14 1.00 Philippines -0.05 0.08 0.42 1.00 Indonesia 0.12 0.07 0.51 0.57 1.00

Panel C: Developing and Developed Countries 1987-96

India Korea Thailand Philippines Indonesia HongKong -0.03 0.20 0.60 0.47 0.58 Japan -0.18 0.28 0.30 0.19 0.08 Singapore 0.29 0.33 0.69 0.74 0.67 UK 0.01 0.29 0.49 0.32 0.29 USA -0.06 0.17 0.45 0.36 0.32 Source: Agarwal (2000)

2.2 Indian Depositary Receipts - Regulatory Framework and Trends In July 1991, the Indian government announced the New Industrial Policy (NIP) to

liberalize its economy. The Securities and Exchange Board of India (SEBI) was created

with statutory authority to oversee India’s capital markets in 1992. SEBI initiated its

reform process and introduced changes in several areas of Indian capital market.

However, we focus here on reforms related to investments in Indian firms by foreign

investors and to Indian firms’ ability to raise capital abroad.

In the Indian context, the precarious foreign exchange situation in 1991 prompted the

Indian government to liberalize the flow of capital into the country. Therefore, in

September 1992, government permitted Foreign Institutional Investors (FIIs)12 to invest

in Indian securities under specific guidelines issued by the Reserve Bank of India (RBI)

and the SEBI. Other sources of foreign investment include Non-Resident Indians

(NRIs), Overseas Corporate Bodies13 (OCBs), DRs and Euro-Convertible Bonds. FIIs

are required to register themselves with SEBI before they invest in the Indian capital

market. Application for registration should be made by FIIs to SEBI in the prescribed

form in duplicate. One copy of the application will be forwarded by SEBI to the RBI

which in turn will grant permission under FERA 1973 to the bank branch designated by

the applicant FII to buy/sell securities. Initial permission will be valid for five years and

will be operative only after obtaining registration from SEBI. This permission will be

renewed for a further period of five years on request. The RBI’s permission would

enable the FIIs to buy/sell the securities and remit the income/dividend/sale proceeds

after payment of applicable taxes through the designated bank branch. FIIs must also

register with the SEC or comparable regulatory body in their respective countries of

domicile or incorporation to assure the credibility of FIIs.

Indian regulations allow FIIs to buy and sell Indian securities with their total holding of

an individual firm being restricted to 30 per cent of issued capital (the limit can be

raised to 49% with the approval of the board of directors of the company concerned),

12 Foreign Institutional Investors (FIIs) include pension funds, mutual funds, investment trusts, investment trusts, asset management companies, nominee companies & incorporated portfolio managers. 13 Overseas Corporate Bodies (OCBs) include overseas companies, partnership firms, trusts, societies, and other corporate bodies which are owned directly or indirectly to the extent of at least 60 per cent, by individuals of Indian nationality or origin resident outside India.

and holdings by a single FII are limited to 10 per cent of issued capital. The ceiling of

30 per cent or 49 per cent, as the case may be, applicable for investment by FIIs will

not include investments made by NRIs/OCBs under the Portfolio Investment Scheme.

It will also not include direct foreign investment by an FII as a foreign collaborator and

investment by FIIs through offshore funds, DRs, and Euro-Convertible Bonds. Indian

Government permitted Indian firms to raise funds from the international market by their

DRs in April 1992.

The Indian DRs can be denominated in any freely convertible currency and may be

listed on any international stock exchange. Initially, only one-way fungibility of DRs

was allowed, i.e., investors owning DRs were allowed to convert them into underlying

Indian shares after a delay of 45 days from the closing date of the issue. However, once

converted, these Indian shares could not be converted back into DRs. In February 2001,

Indian government allowed two-way fungibilty in Indian DRs. A two-way fungibility

means foreign investors owning Indian DRs and Indian companies can convert their

ADRs/GDRs into shares tradable at Indian stock exchanges and vice-versa. There are

no end-use restrictions on GDR/ADR issue proceeds, except restrictions on investment

in stock markets and real estate.

Subsequent transactions in Indian DRs in the foreign markets by non-residents are not

subject to Indian capital gains taxes, but the dividends are taxed at a rate of 9.75

percent. If non-residents hold DRs for more than a year before converting them to

underlying shares, resulting capital gains are treated as long-term capital gains and are

taxed accordingly. However, if DRs are converted into underlying shares prior to one

year, resulting gains are treated as short-term gains. No wealth or gift is payable by

holders of Indian DRs.

A foreign investor, interested in investing in Indian equities, has primarily two avenues

of doing so. One is to register officially as a FII and buy and sell equities in the Indian

stock market; the other avenue is to buy GDRs of Indian firms in overseas markets.

Both these investments carry their own tax and transactional implications. In the case of

FIIs, legal and institutional restrictions make it difficult for small and medium foreign

investors to invest directly in the Indian stock market. For such individual investors,

GDRs offer an attractive alternate avenue for investing in Indian equities. Indian

citizens, who are residents of India, are restricted from buying or selling shares in

foreign countries. Mutual funds are permitted to invest in ADRs/GDRs up to 10 per

cent of the net assets managed by them as on the date of the last audited balance sheet,

subject to a maximum of $50 million per mutual fund. The Indian rupee is not fully

convertible and Indian residents are not allowed to hold foreign currency accounts.

Earlier, the approval of Ministry of Finance was necessary for issuing DRs. Now

companies can raise money through DRs under an automatic route without the prior

approval of the Ministry of Finance. However, the companies will have to fulfill the

mandatory approval requirements under FDI policy and the provisions of FERA/FEMA

prior to the overseas issue. The issue-related expenses (covering both fixed expenses

like underwriting, commissions, lead managers, charges, legal expenses and other

reimbursable expenses) are subject to a ceiling of 4 per cent in the case of GDRs and 7

percent in the case of listing on US exchange. Issue expenses beyond the ceiling require

the prior approval of RBI. The issuing companies will have to furnish full particulars of

the issue, including the underlying equity shares representing the ADRs, to the Ministry

of Finance and the Reserve Bank of India within 30 days of the completion of this

offering. There is no restriction on the number of ADRs/GDRs to be floated by a

company or a group of companies in a financial year.

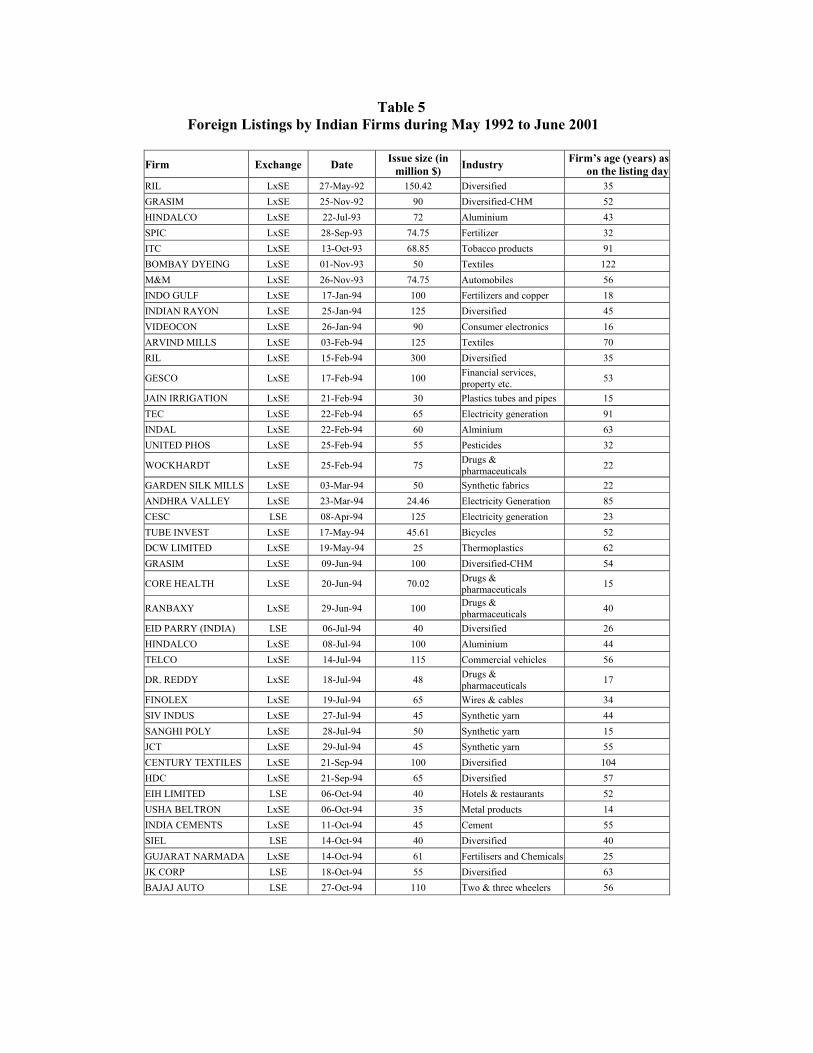

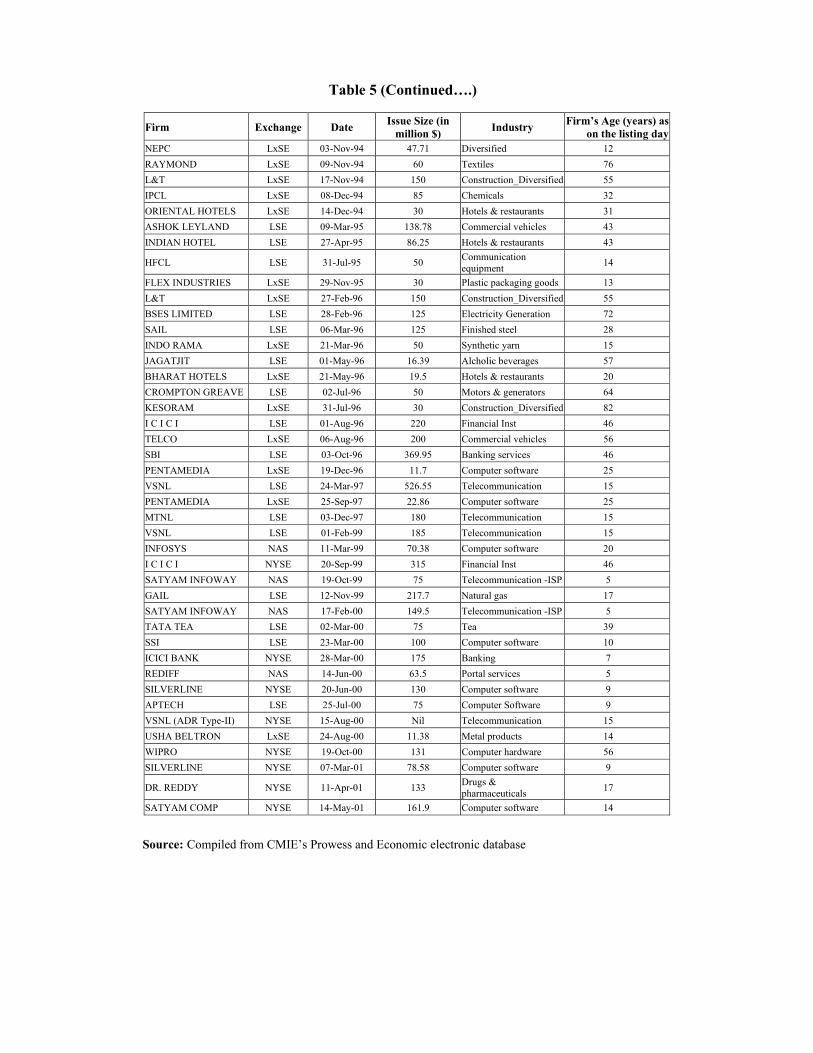

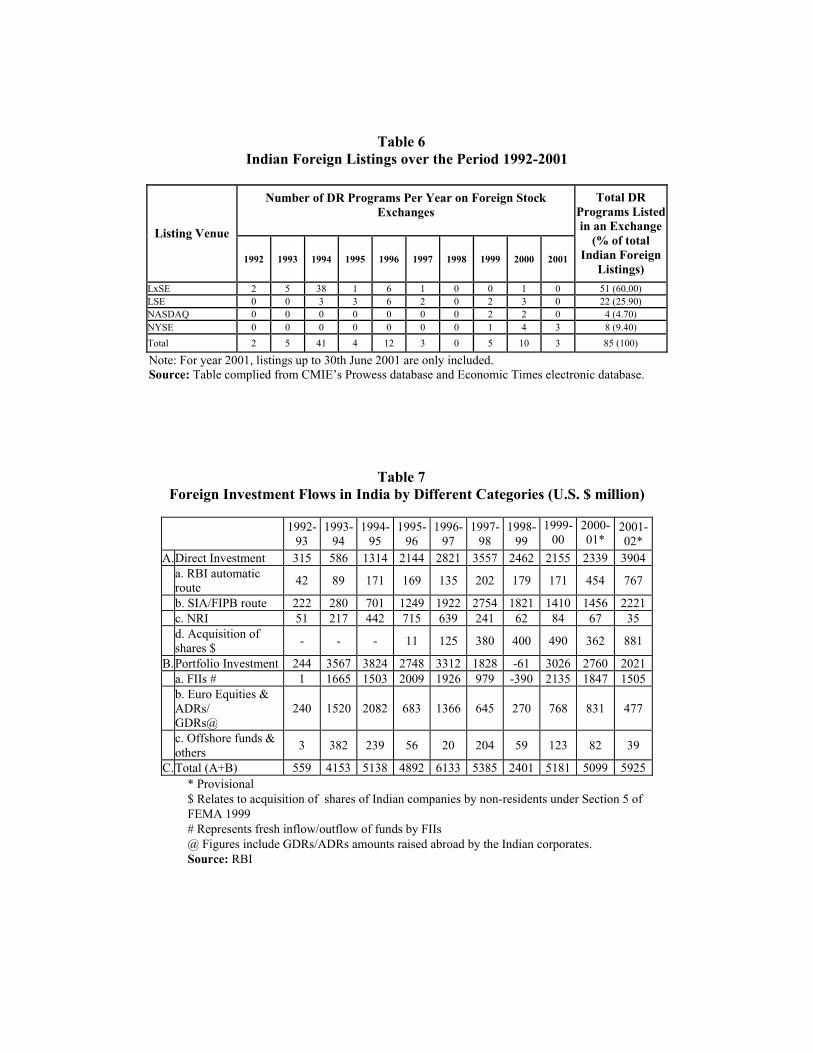

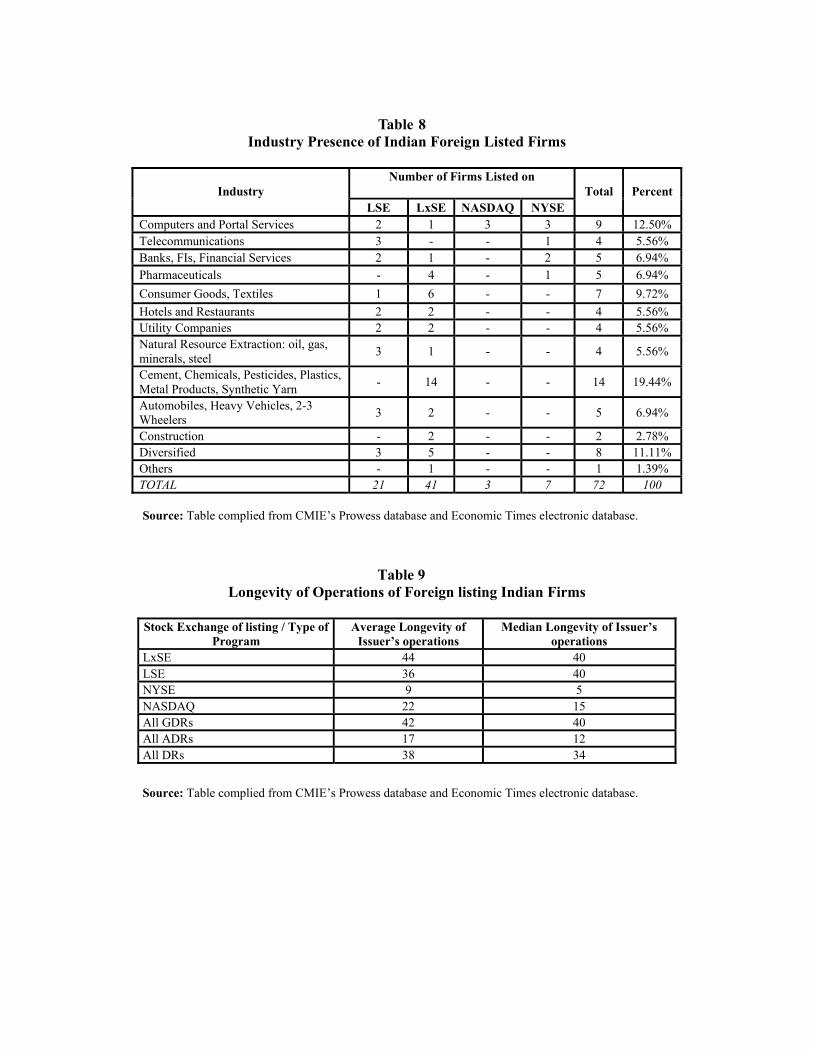

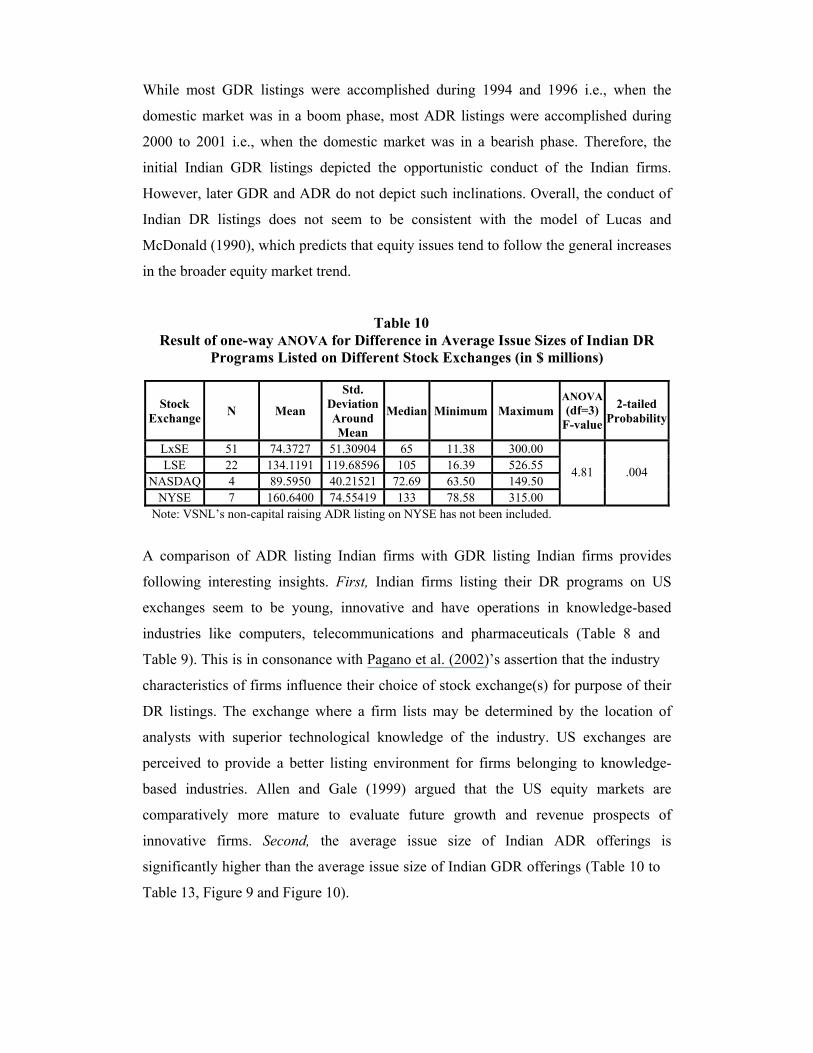

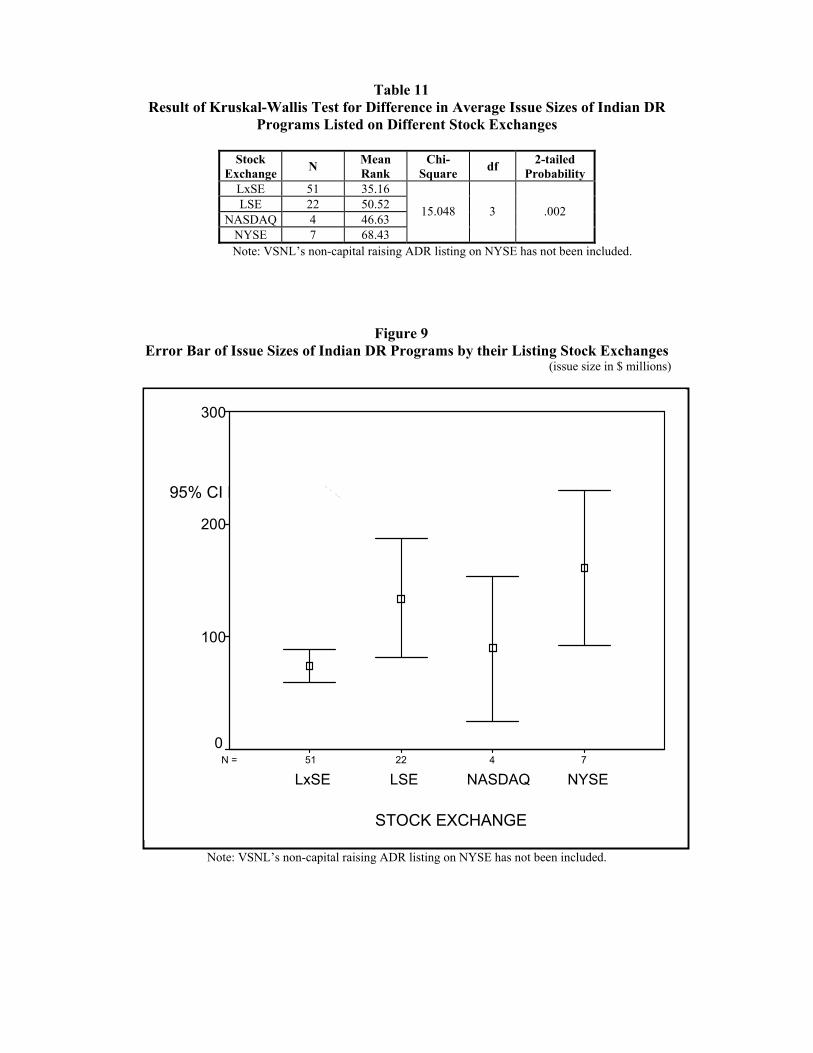

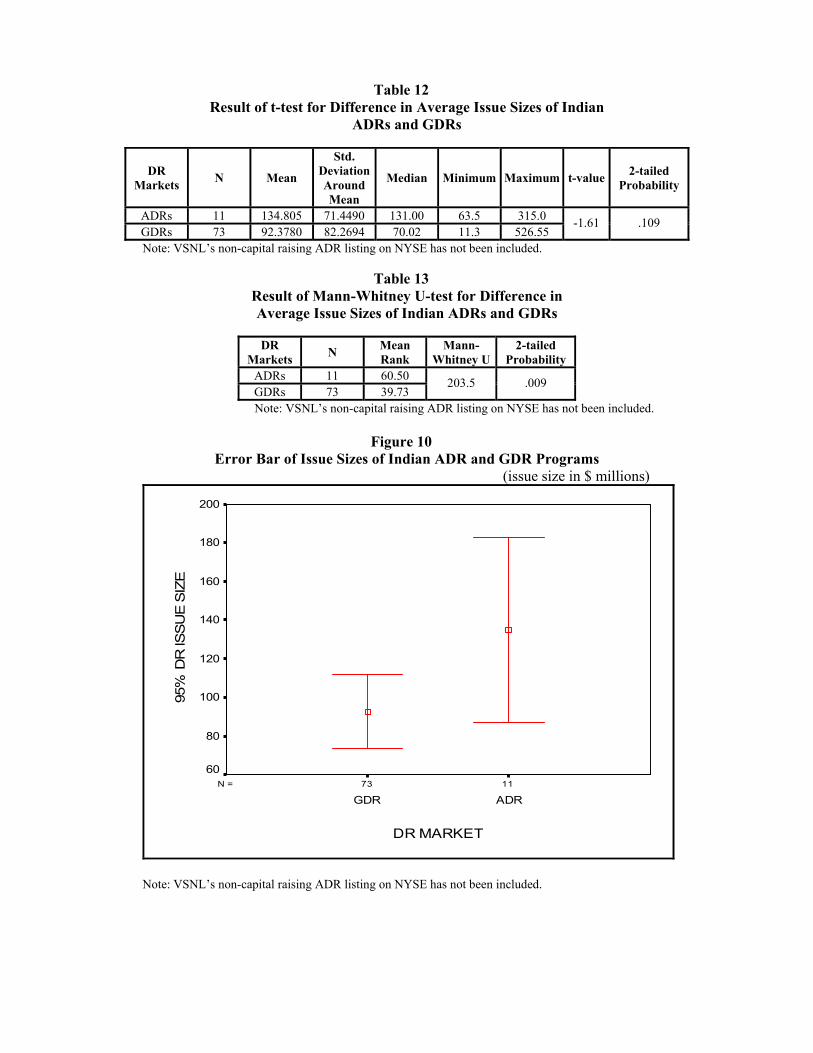

From April 1992 to June 2001 seventy-two Indian firms took advantage of this

opportunity and raised foreign equity capital by issuing eighty-five DR programs listed

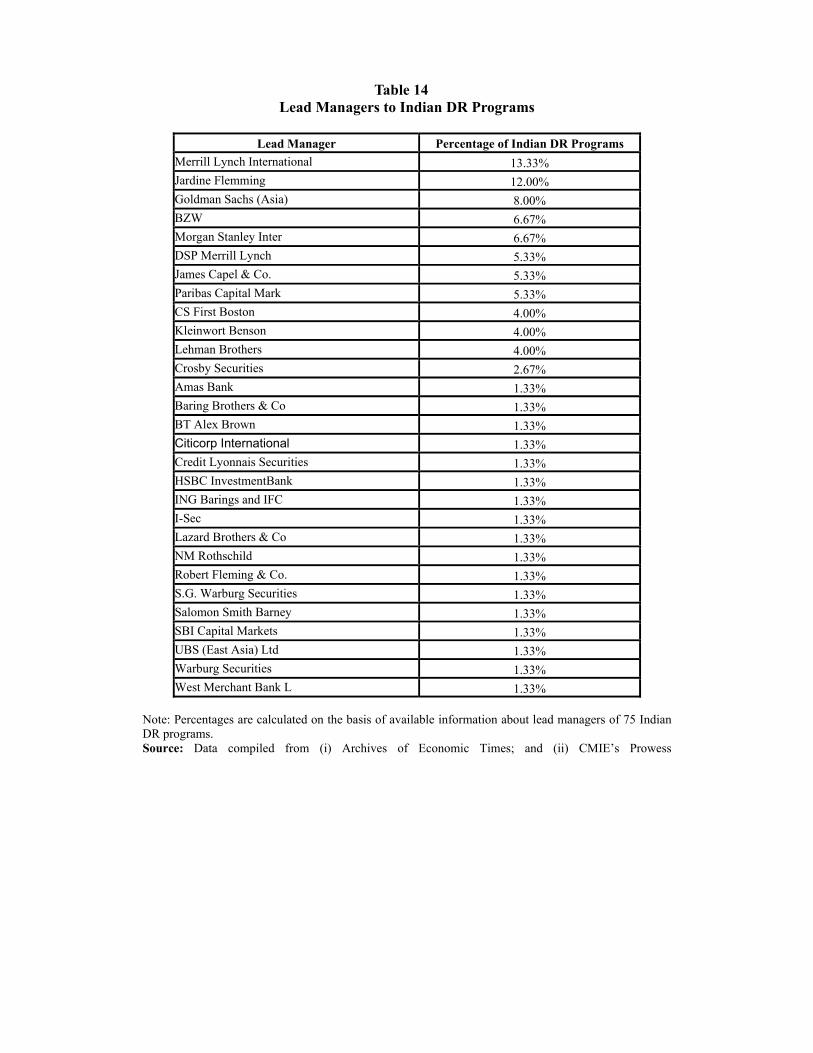

on the foreign markets (Table 5 and Table 6). These programs have contributed

positively towards the aggregate foreign investment coming into India (Table 7).

Indian DR programs are listed at Luxembourg Stock Exchange (LxSE), London Stock

Exchange (LSE), NASDAQ and New York Stock Exchange (NYSE). Of all the

emerging markets, India has maximum number of DR programs (Table 3).

Table 6 depicts the time-pattern and geography of Indian foreign listings from May

1992 to June 2001. Initial DR programs by the Indian firms were listed at the LxSE due

to the mild securities’ regulations and the easy listing norms of the Luxembourg

market. The choice of LxSE for initial foreign listings by Indian firms were in

consonance Foerster and Karolyi (1993)’s assertion that initial foreign listings by firms

of any country are accomplished on markets which are easier to enter. In second phase

many Indian firms listed their DR programs at the LSE. Since 1999, most fresh Indian

DR programs are being accomplished at the stringent US stock exchanges. While the

listings on US market require stringent disclosures and recasting of firms’ financial

statements as per US GAAP, listings on LxSE and LSE comes much easier without any

additional disclosures and recasting of the financial accounts.

The temporal shift in choice of foreign listing venues by the Indian firms could be

attributed to prescription of higher mandatory levels of financial disclosures and

transparency for the Indian firms by the SEBI. During the early nineties, most Indian

firms did not have level of financial transparency as desired by the US GAAP and SEC.

Therefore, initially Indian firms refrained from listing on the US exchanges. However,

during the course of 1990s, Indian financial market regulators introduced several

reforms to improve the level of financial transparency of the Indian firms. These

financial sector reforms positively influenced the capability of Indian firms to tap the

US markets. Therefore, of late, many Indian firms have listed their DR programs on the

US exchanges also. Amongst the US exchanges, it is the NYSE which is most stringent

in its listing norms. Listing on NASDAQ is easier compared to the listing on the

NYSE. So initial Indian firms tapping the US markets listed on NASDAQ. However,

subsequently a few Indian firms have also listed on the NYSE. Lately, some of the

Indian firms have also delisted their GDR programs from the LSE and LxSE due to the

poor liquidity on these exchanges and have instead, listed their fresh DR programs on

the US exchanges14. Overall, it seems that gradually US exchanges are becoming more

favourable destination for fresh DR listings by the Indian firms. This observation is in

consonance with the Pagano et al. (2002)’s finding that European exchanges have been

losing out to US exchanges in attracting the fresh foreign listings.

14 Dr Reddy’s Laboratories, MTNL, VSNL have delisted their GDR programs.

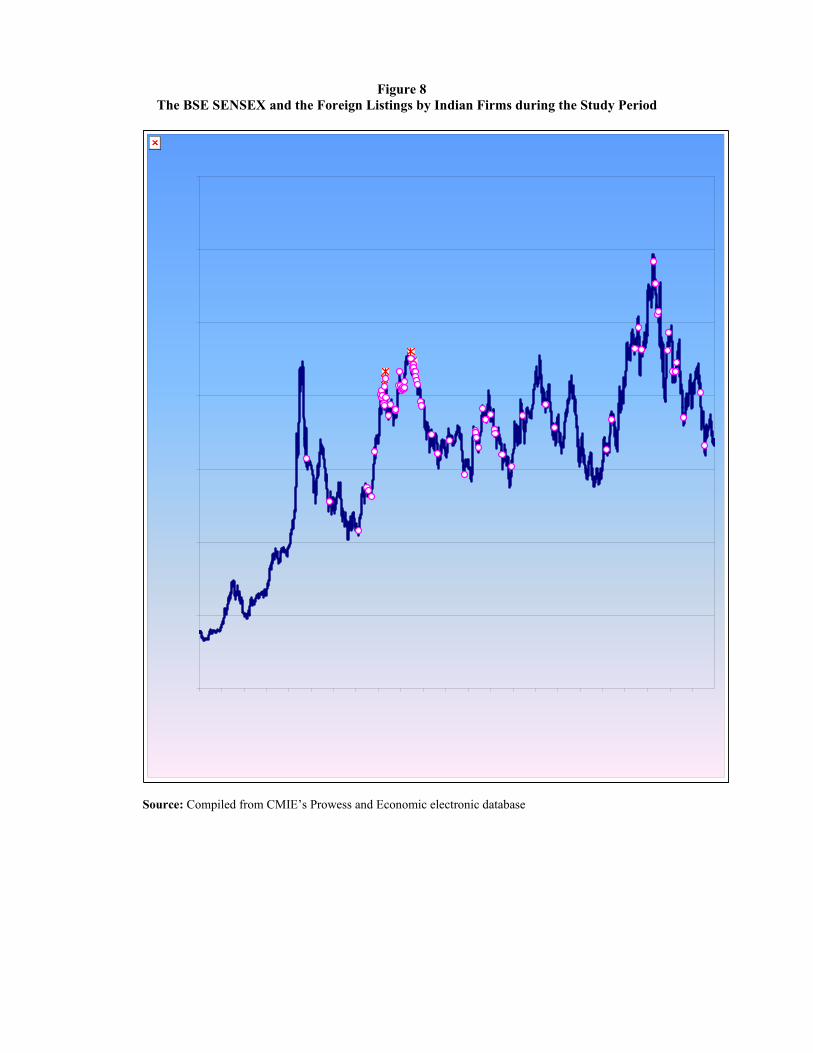

Table 6 and Figure 8 depicts that there have been three periods characterised by

high foreign listing activity by the Indian firms. In 1994 alone, forty-one DR listings

were accomplished. Similarly, year 1996 and 2000 are marked with a large number of

DR listings by the Indian firms. Figure 2.8 simultaneously depicts the closing value of

the BSE SENSEX on a particular day and the number of Indian DR programs listed on

that day. India entered the international arena in May 1992, with the first GDR issue by

Reliance Industries Limited on LxSE. In November 1992, Grasim Industries also issued

their GDR program on the LxSE. Then, the GDR markets witnessed a lull till 1993-end

in the wake of the securities scam and the consequent fall in the domestic markets.

The lull period during 1993 was followed by a surge in number of Indian GDR

programs during 1994 and again during 1996. Patil (1994) associated the bunching of

Indian GDR issues during the above periods to the pent up overseas demand for Indian

papers and the existing costly procedure of flotation in the domestic market. A high

degree of foreign listing activity by the Indian firms during 1994 and 1996 was also

attributable to the (a) increased allocation of investible funds by the international

investors to the emerging markets like India; and (c) desire of many Indian firms to

raise the funds during the boom phase of the domestic markets so as to get a better

pricing for their DR programs.

There were infrequent fresh DR listings by the Indian firms during 1995, mainly due to

the uncertain domestic political environment. Similarly, there was a two-year lull

period in foreign listings activity during 1997 and 1998 owing to the economic crises in

the South-east Asian markets.

Foreign listing activity by Indian firms regained momentum during 1999 with the

successful ADR issue by Infosys Technologies Limited. During 2000, there was a spurt

in number of Indian foreign listings because of the fresh policy initiatives by Indian

government, which simplified approval mechanisms for software, information

technology, telecommunication, biotechnology and pharmaceutical firms for issuing

DR programs in the foreign markets. These firms used the foreign listings to (a) attain a

better valuation for their firms; and (b) meet their requirements of large amount of

funds, not easily available from the Indian markets.

Table 5

Foreign Listings by Indian Firms during May 1992 to June 2001

Firm Exchange Date Issue size (in million $) Industry Firm’s age (years) as

on the listing dayRIL LxSE 27-May-92 150.42 Diversified 35 GRASIM LxSE 25-Nov-92 90 Diversified-CHM 52 HINDALCO LxSE 22-Jul-93 72 Aluminium 43 SPIC LxSE 28-Sep-93 74.75 Fertilizer 32 ITC LxSE 13-Oct-93 68.85 Tobacco products 91 BOMBAY DYEING LxSE 01-Nov-93 50 Textiles 122 M&M LxSE 26-Nov-93 74.75 Automobiles 56 INDO GULF LxSE 17-Jan-94 100 Fertilizers and copper 18 INDIAN RAYON LxSE 25-Jan-94 125 Diversified 45 VIDEOCON LxSE 26-Jan-94 90 Consumer electronics 16 ARVIND MILLS LxSE 03-Feb-94 125 Textiles 70 RIL LxSE 15-Feb-94 300 Diversified 35

GESCO LxSE 17-Feb-94 100 Financial services, property etc. 53

JAIN IRRIGATION LxSE 21-Feb-94 30 Plastics tubes and pipes 15 TEC LxSE 22-Feb-94 65 Electricity generation 91 INDAL LxSE 22-Feb-94 60 Alminium 63 UNITED PHOS LxSE 25-Feb-94 55 Pesticides 32

WOCKHARDT LxSE 25-Feb-94 75 Drugs & pharmaceuticals 22

GARDEN SILK MILLS LxSE 03-Mar-94 50 Synthetic fabrics 22 ANDHRA VALLEY LxSE 23-Mar-94 24.46 Electricity Generation 85 CESC LSE 08-Apr-94 125 Electricity generation 23 TUBE INVEST LxSE 17-May-94 45.61 Bicycles 52 DCW LIMITED LxSE 19-May-94 25 Thermoplastics 62 GRASIM LxSE 09-Jun-94 100 Diversified-CHM 54

CORE HEALTH LxSE 20-Jun-94 70.02 Drugs & pharmaceuticals 15

RANBAXY LxSE 29-Jun-94 100 Drugs & pharmaceuticals 40