csr magisterij turker me

TRANSCRIPT

Influence of CSR Aspects on

Organizational Commitment What influence do the different CSR aspects have on the organizational commitment of Douwe

Egberts employees?

Name: T.A.M. Wijnants

ANR: 435337

Supervisor: Drs. Ir. K.M. Thomas

Second Reader: Dr. A.J.A.M. Naus

Number of words: 13.830

Faculty: Tilburg School of Economics and Management, Tilburg University

Thesis: Master thesis of the department of Organization & Strategy

Educational program: Master Strategic Management

Date of defence: 24th of August 2011

Master Thesis T.A.M. Wijnants

Influence of CSR Aspects on Organizational Commitment

1

Management summary

The main theoretical contribution of this research is to show that every Corporate Social

Responsibility (CSR) aspect influences organizational commitment. Finding out which aspects

influence organizational commitment of employees positively can contribute to making

communication of CSR more efficient and effective. To this CSR and organizational commitment are

defined and the influence of this relationship is reviewed in past literature. After assessing CSR

models of past research a new well based model is built to research the influence of CSR aspects on

organizational commitment. Using the organizational commitment questionnaire (OCQ) the

organizational commitment per aspect is measured and the variances of the results are analysed.

Resulting in the conclusion that the CSR aspects and the CSR dimensions they belong to have a

positive influence on organizational commitment. However there is found now statistically

significant difference between the means of organizational commitment of these aspects.

Foreword

After an extensive search for a topic during a graduation internship at Douwe Egberts/Sara Lee (DE)

this research idea was born out of a brainstorm with the Corporate Social Responsibility (CSR) team.

The CSR team had already done quite some research on what the company exactly did on CSR and

how they could communicate this in a clear way. After evaluating the whole introduction, one of the

main conclusions was they did not know what the employees thought of CSR and their role in it.

What do the employees find interesting and how could they be involved in the CSR projects in order

to feel proud and committed to the company. So this research will be done to answer these

questions but even more to demonstrate that creating awareness of CSR among employees can be

done more efficiently and effectively by researching the needs of the employees.

Firstly I would like to take this opportunity to thank the following persons that helped me during my

thesis. Starting with Marketing Manager Corporate Social Responsibility Paul Schoon of Douwe

Egberts for his cooperation in my research among the employees of Douwe Egberts. Thanks to him,

the entire research is made possible and the response rate of the questionnaire would never have

been this large without his cooperation. Moreover, I would like to thank Drs. Ir. KM Thomas for the

quality advice and active support during the writing process of my thesis. Thanks to her motivation

and confidence in my work, I was constantly encouraged to successfully conclude my thesis. I would

also like to thank Dr. A.J.A.M. Naus for his advice on the statistical part of my research. The

enthusiasm about my dataset and the suggestions of the possibilities of my data had a contagious

effect to get the most out of my results. Finally, I would like to thank my parents who supported me

during my entire study, in good and bad times the kept faith in my abilities.

Master Thesis T.A.M. Wijnants

Influence of CSR Aspects on Organizational Commitment

2

Table of contents

Management summary ....................................................................................................................... 1

Foreword ............................................................................................................................................. 1

1: Introduction ......................................................................................................................................... 4

1.1: Background .................................................................................................................................. 4

1.2: Problem indication ....................................................................................................................... 5

1.3: Problem statement ...................................................................................................................... 6

1.4: Research strategy ......................................................................................................................... 6

1.5: Structure of the thesis ................................................................................................................. 6

2: Theoretical framework ........................................................................................................................ 7

2.1 CSR defined in literature ............................................................................................................... 7

2.2 Aspects of CSR ............................................................................................................................... 8

2.3 Organizational commitment of employees ................................................................................ 10

2.4 Effect of CSR on organizational commitment of employees ...................................................... 12

2.5 CSR Aspects and the DE employees’ organizational commitment ............................................. 14

2.5.1 People .................................................................................................................................. 14

2.5.2 Planet ................................................................................................................................... 15

2.5.3 Profit .................................................................................................................................... 16

2.6 Overview ..................................................................................................................................... 17

3: Research methodology ...................................................................................................................... 18

3.1 Research method ........................................................................................................................ 19

3.2 Research approach ...................................................................................................................... 19

3.3 Sample choice and sampling ....................................................................................................... 20

3.4 Collecting data using questionnaire ............................................................................................ 20

3.4.1 Dependent variable ............................................................................................................. 20

3.4.2 Independent variables ......................................................................................................... 21

3.4.3 Control variables .................................................................................................................. 22

3.4.4 Conditions of questionnaire ................................................................................................ 23

3.5 Data analysis ............................................................................................................................... 23

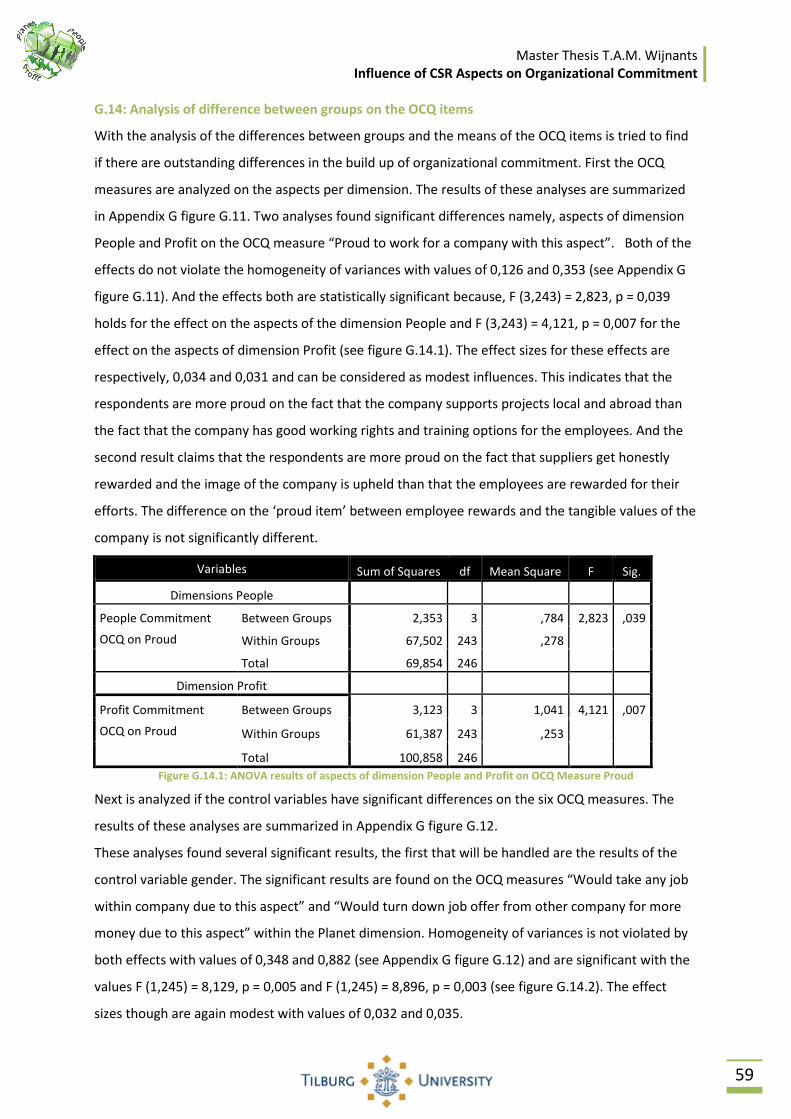

4: Results and Analysis .......................................................................................................................... 24

4.1 Results on Control Variables ....................................................................................................... 25

4.2 Ranking Aspects .......................................................................................................................... 26

4.3 Reliability OCQ Measures ............................................................................................................ 27

4.4 One-way between groups ANOVA for aspects on organizational commitment ........................ 27

4.5 Information questions ................................................................................................................. 29

4.6 Influence of control variables on differences between groups .................................................. 30

5: Conclusions, Limitations and Recommendations ............................................................................. 35

5.1 Conclusions ................................................................................................................................. 35

5.2 Limitations ................................................................................................................................... 37

Master Thesis T.A.M. Wijnants

Influence of CSR Aspects on Organizational Commitment

3

5.3 Recommendations ...................................................................................................................... 37

References ............................................................................................................................................. 39

Master Thesis T.A.M. Wijnants

Influence of CSR Aspects on Organizational Commitment

4

1: Introduction

In this chapter the motivation for the research and the structure of this paper are introduced. First

the background of the problem that is dealt with in this research is outlined. In paragraph 1.2 the

problem itself is defined in the problem indication. This indication leads to the formulation of the

problem statement and the resulting research questions in paragraph 1.3. Paragraph 1.4 briefly

discusses the research strategy and finally in paragraph 1.5 the structure of the rest of the research is

clarified.

1.1: Background

There is a lot of discussion about the definition of Corporate Social Responsibility (CSR) and how it is

implemented by companies. The CSR definition of Brundtland (1987): “Paths of progress which meet

the needs and aspirations of the present generation without compromising the ability of future

generations to meet their needs.” is used by a lot of companies including Douwe Egberts (DE) where

this research takes place. DE actively uses the definition within their CSR program as a benchmark for

all CSR projects that are undertaken. Since DE realizes that CSR can play a very important role in

business they actively invest in CSR. Past research has shown that solid CSR initiatives and projects

seen from the resource based view can be a rare resource of a company and difficult to imitate.

Therefore it can create a real competitive advantage for a company in the long run (Graafland, 2002).

Porter and Kramer (2006) state that environmental consciousness can improve business performance

because environment friendly companies can create competitive advantage with cost reduction,

differentiation, positive image and strategic vision. So in order to perform well, a company needs to

invest in the future and show to their stakeholders that the company works in a profitable but

sustainable way.

DE is already involved in several CSR initiatives and projects for many years. These projects and

initiatives are communicated separately to the outside world as well as the employees, but they are

never combined in a simple and clear overview. So in order to get a good overview for the company

itself and all its stakeholders, a communication plan for these CSR initiatives and projects is

developed. With this communication material DE is able to show to its stakeholders in which

projects the company is involved and what the company does for the environment and society. Last

December this communication plan called “More Sustainable from Cultivation to Cup” has been

launched for the employees. With the brochures and flyers of this plan it is easy to show employees,

customers and prospects what DE has to offer on the area of CSR (see Appendix A figure A.1).

Master Thesis T.A.M. Wijnants

Influence of CSR Aspects on Organizational Commitment

5

1.2: Problem indication

To make the communication plan that DE launches a success in their communication to the

stakeholders, the plan needs to be adopted in the best way possible by the employees. The

communication plan is evaluated by 100 employees and results show that there are multiple subjects

of the communication plan that can be improved. The top three recommendations are:

• Workers want more specific information about certain projects (18%)

• The employees want to stay up to date on the status of the projects (10%)

• The employees would like to participate and contribute to the projects (9%)

Recent scientific research confirms that information and participation are important to employees.

Even the smallest initiatives that employees can be informed of and participate in have large

influence on their commitment towards their company (Nord and Fuller, 2009). Kim, Lee, Kim and

Lee (2010) claim that participation to CSR has a more direct influence on the commitment of

employees towards a company then the single associated feeling with CSR projects.

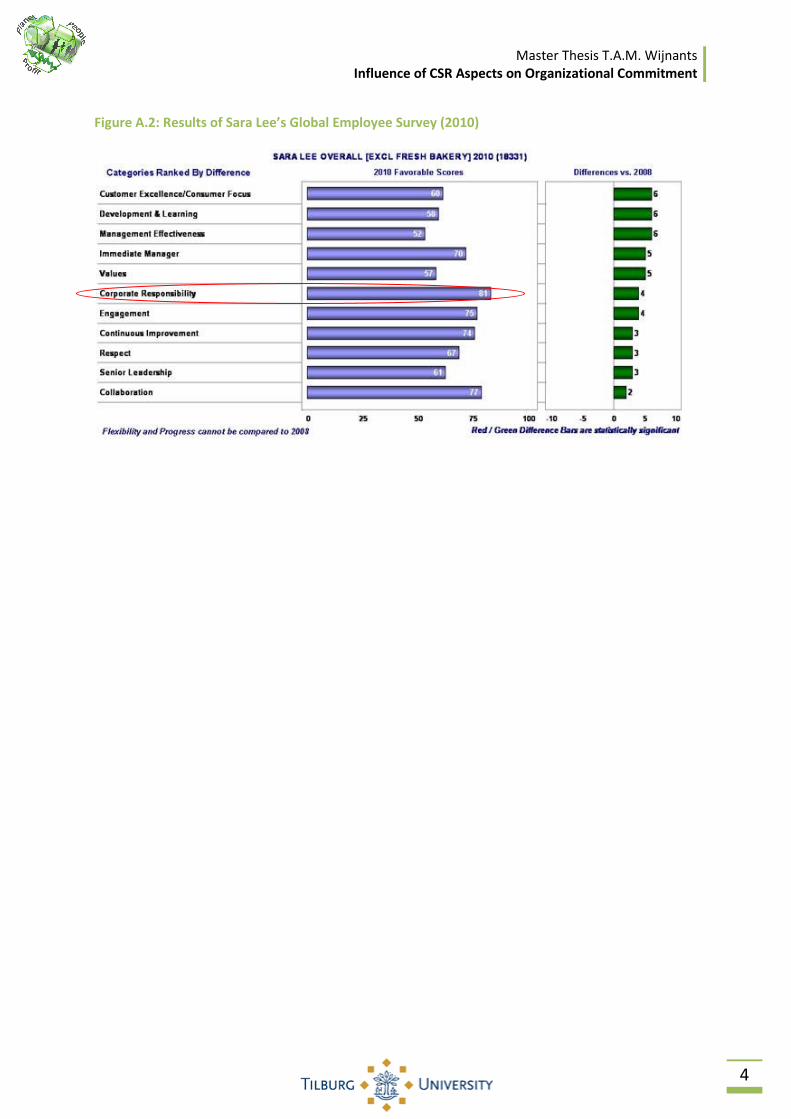

The importance of CSR to the employees of DE is also proven by a global survey among the staff of

the parent company Sara Lee. In these standings Corporate Responsibility was put as the number

one priority of employees scoring 81 points out of 100 on importance (see Appendix A figure A.2). In

order to make CSR a success at DE, the employees need to believe and feel that they can identify

themselves with the projects. So DE has to meet their employees in their needs in order to keep

them committed to the company. Thus the needs of the employees should be researched. With this

knowledge the company is able to focus their information flow on the most influential aspects,

therefore informing their employees more efficiently. With these updates employees can be better

informed about CSR and as implied in prior research, become more committed towards DE.

The main theoretical contribution of this research is to show that every CSR aspect influences

organizational commitment. Finding out which aspects influence organizational commitment of

employees positively can contribute to making communication of CSR more efficient and effective.

Subsequently, employees are more committed to their company and become ‘ambassadors’ of the

CSR aspects. With the support of the employees the CSR aspects can be built into a sustainable

strategic competitive advantage.

Master Thesis T.A.M. Wijnants

Influence of CSR Aspects on Organizational Commitment

6

1.3: Problem statement

Following this problem indication the next problem statement is formulated:

What influence do the different CSR aspects have on the organizational commitment of Douwe

Egberts employees?

Derived from this problem statement the next research questions are formulated:

1. How is CSR defined?

2. How can CSR be divided in aspects of People, Planet and Profit?

3. What determines organizational commitment of employees?

4. What effect does CSR have on the organizational commitment of (DE) employees?

1.4: Research strategy

To define the variables that are used in this research, past literature on these subjects will be

consulted. To complete the framework and to make sure the composed model for this research is

applicable for practice, CSR reports of companies in the Fast Mover Consumer Goods (FMCG)

industry are reviewed. Finally the variables and the relationship of these variables in the model are

tested with an online questionnaire among the employees of DE. The results are analyzed to find if

and what kind of relationship there is between the variables of CSR aspects and organizational

commitment.

1.5: Structure of the thesis

In chapter two the research questions are answered. The first four paragraphs in chapter two deal

with one research question each and lastly paragraph 2.5 explains the formulated model. These

answers provide the theoretical framework for this research. The subsequent methodology chapter

explains how this research is composed and conducted. The results and analysis of this research are

presented in the fourth chapter. In chapter five the research questions and therefore the problem

statement is answered , resulting in derived conclusions in paragraph 5.1. Lastly, limitations and

resulting recommendations for future research are presented in respectively paragraph 5.2 and 5.3.

Master Thesis T.A.M. Wijnants

Influence of CSR Aspects on Organizational Commitment

7

2: Theoretical framework

This chapter starts with defining CSR in paragraph 2.1. In paragraph 2.2 the models that are built to

measure CSR are reviewed. Paragraph 2.3 discusses what determines organizational commitment of

employees. In paragraph 2.4 the role that CSR plays on employees and their organizational

commitment is explained. Subsequently paragraph 2.5 elucidates the model of CSR aspects as

defined for this research. In the last paragraph the model that is used to measure the organizational

commitment towards the CSR aspects is shown and the findings of this complete chapter are

summarized.

2.1 CSR defined in literature

In prior research the definition of CSR has been used in various ways by many authors. In the 1980’s

the Brundtland report establishes the connection between environmental degradation and social-

economic development. The environmental sustainability can only be accomplished if subjects as

poverty and lack of education, for example, are addressed. Brundtland (1987) summarizes the ideas

of research until this point in time in the definition: “Paths of progress which meet the needs and

aspirations of the present generation without compromising the ability of future generations to meet

their needs.” In the 1990’s, Elkington shed his light on the consequences of sustainable development

for companies. He states that companies have environmental, social and economic impacts on

society and should contribute to sustainable development. A company that takes its responsibility

and has a positive impact on these elements gains the trust of society and ensures the continuity of

the company itself. Corporate sustainability requires companies to perform responsibly in the

economic, environmental, and social dimensions. Elkington (1997) refers to this as “the triple bottom

line” of people, planet and profit of which companies need to satisfy the needs of their stakeholders.

In the past years CSR has increasingly been in the news, with bans of products by consumers and

campaigns against brands. The previously mentioned bans and campaigns are both consequences of

companies that violate their social responsibility. Examples of these consequences can be found in

Appendix B.1.

As already stated before the concept of CSR seems difficult to pin down in previous literature and it is

difficult to judge what is part of CSR and what is not. In 1999 the Social Economic Council (SER) was

asked by the Dutch government to prepare a report about CSR. The SER report examines the

evolution of CSR and the role of companies in society and was published in 2001. The SER came up

with the next definition of Corporate Social Responsibility, which incorporates two elements. The SER

builds on the triple P bottom line of Elkington, because companies can not only create economic

value but can also create value on the environmental and social dimension. The second element in

the SER rapport is the relationship of the company with its stakeholders and the society as a whole. A

Master Thesis T.A.M. Wijnants

Influence of CSR Aspects on Organizational Commitment

8

company is described as a form of a cooperation of different stakeholders; the company has to

balance partially between conflicting interests of these stakeholders. If a company wants to maintain

good stakeholder relations it has to be transparent and open up their way of doing business to all

stakeholders. Therefore they have to stay in a continuous interactive dialogue with all the interested

parties of the company. The SER distinguishes between primary and other stakeholders. Primary

stakeholders are employees and shareholders, because they have structural contact with the

managers of the company. Other stakeholders are consumers, suppliers, competitors, the

government and the society as a whole. They are all in contact with the company and have a certain

interest in the companies’ activities. This last definition by the SER will be used in this research.

Hereafter CSR is defined for this research, by covering the different aspects that of CSR.

2.2 Aspects of CSR

This paragraph reviews in which aspects of people, planet and profit CSR can be divided according to

literature. In literature models are built to measure the level of CSR that is applied by a company.

This is particularly important to be able to make a company accountable for its responsibilities and to

be able to assess its performance in this regard. Therefore it is necessary to develop methods to be

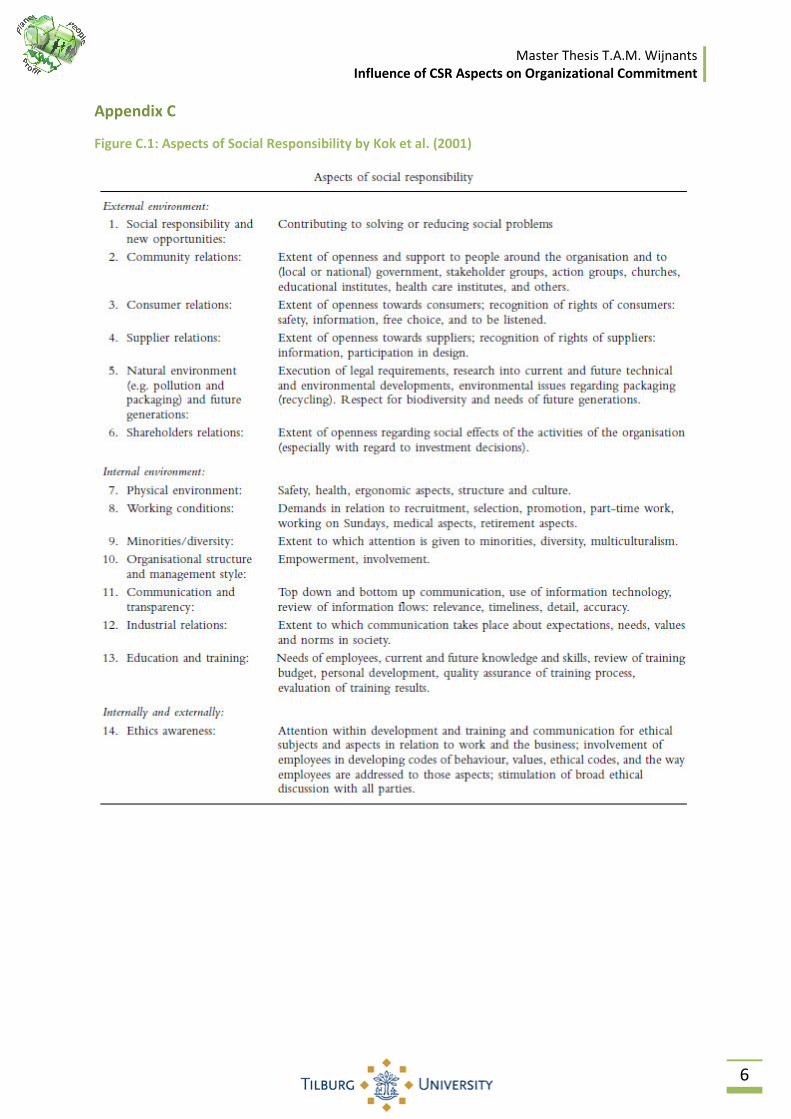

able to assess the CSR performance of a company. In 2001 Kok, van der Wiele, McKenna and Brown

tried to create a CSR audit to let CSR play a larger part in Quality Awards like the European Quality

Award. This distinction is awarded annually by the European Foundation for Quality Management to

the organization that is the best proponent in Europe of Total Quality Management. This was the

beginning of measurement of CSR, when it was only a part of the total quality of management by a

company. The aspects used in this audit are divided in external and internal environment. See Figure

C.1 in appendix C to view all the aspects Kok et al. (2001) used. What started as just a part of a total

quality framework later became a benchmark on its own. Graafland, Eijffinger, Stoffele, Smid, and

Coldeweijer (2004) created a CSR benchmark after research among Dutch companies that makes it

possible to compare the scores of companies and creates more transparency. With a mark for CSR

stakeholders are able to judge how responsible the company really is and is not judged on some eye-

catching incidents. By benchmarking a company knows where it stands in comparison to their

contenders and is able to evaluate and improve the process. These CSR benchmarks divide CSR into

different aspects in order to rate the total CSR activity of a company. The rating of Graafland et al.

(2004) is partly based on opinions of different stakeholders about the activity of the company in the

different aspects. Company reports on CSR and other public sources are also consulted to rate the

performance on CSR. This is to ensure non-biased answers of the stakeholders. Nowadays, these

company CSR reports are more reliable due to guidelines like the Global Reporting Initiative (GRI)

Sustainability Reporting Guidelines (2011). The GRI is an organization that standardized the

sustainability reporting, after thorough research and cooperation with progressive companies and

Master Thesis T.A.M. Wijnants

Influence of CSR Aspects on Organizational Commitment

9

research specialists, and wrote a guideline for companies to make the reporting of companies less

biased and more comparable. Benchmarks like Graafland et al. (2004) also use this GRI reporting

guideline (2011) to select their indicators for CSR. The aspects used in the benchmark of Graafland et

al. (2004) are related to economic, ecological and social sustainability for the different stakeholders.

This is completely in line with the CSR definition of the SER (2001). The measure is built on only Dutch

companies, and since the Netherlands is a rather small player globally, the results should be tested in

a larger economy. The aspects of CSR used by this research are shown in Figure C.2 of appendix C.

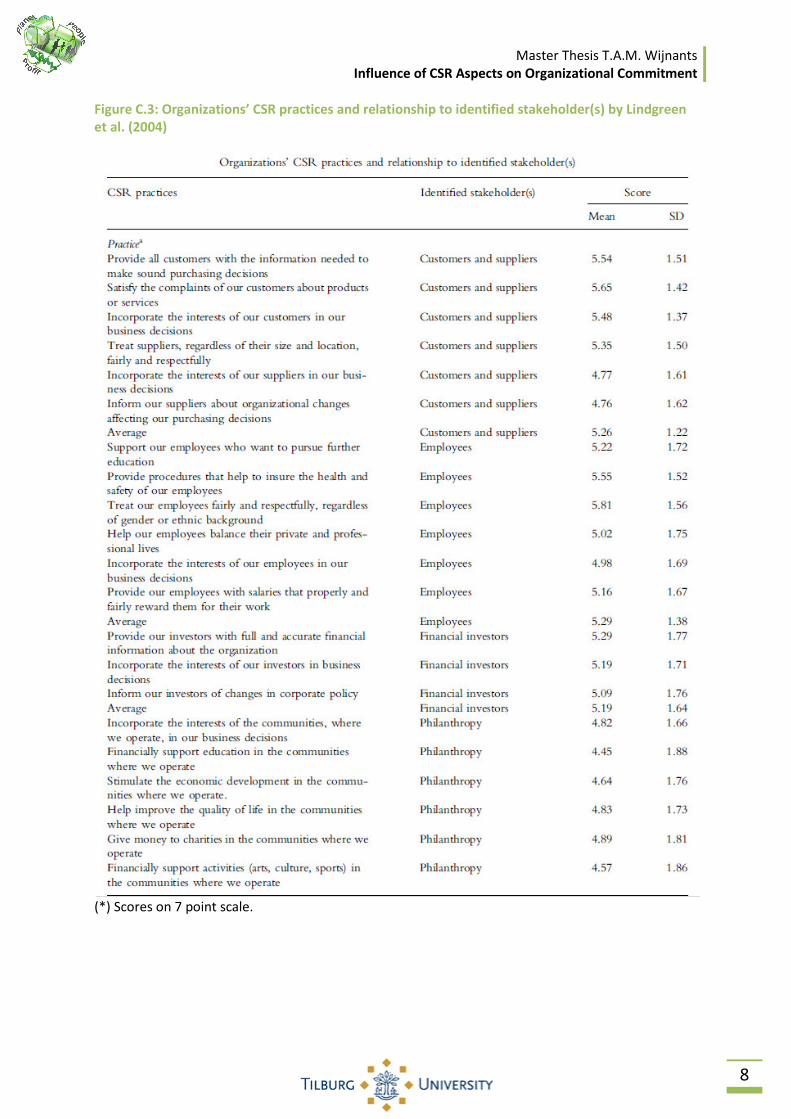

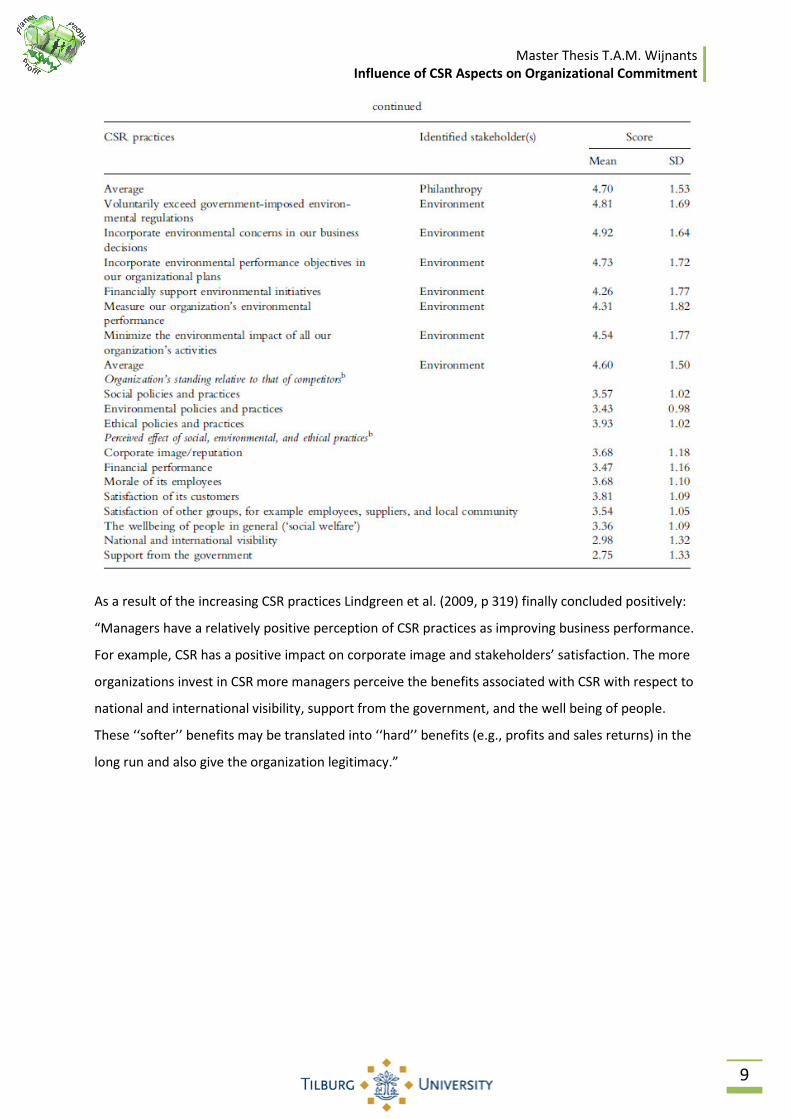

Lindgreen, Swaen and Johnston (2009) investigate 401 U.S. organizations at their actual CSR practices

related to their different stakeholder groups. The general conclusion in this research is that every

company has different priorities in CSR. The choice for particular CSR practices depends on the type

of stakeholders the organization considers important. In general the employees are seen as the most

important stakeholders following this research. On a seven-point scale the employees indicate that

their organizations have adopted the most specific CSR practices relating to employees with a mean

of 5,29 (see Figure C.3 of appendix C). On a seven-point scale with a seven for well adopted and a

one for badly adopted, this is a very positive score and above the highest average score of all

stakeholders. The CSR practices Lindgreen et al. used in their research along with their main

conclusion can be viewed in Figure C.3 of appendix C. To measure CSR more accurately the aspect list

becomes longer and longer. This makes it difficult to do research due to the extensive

questionnaires. With long surveys, leading to a declined response rate and affected reliability. So

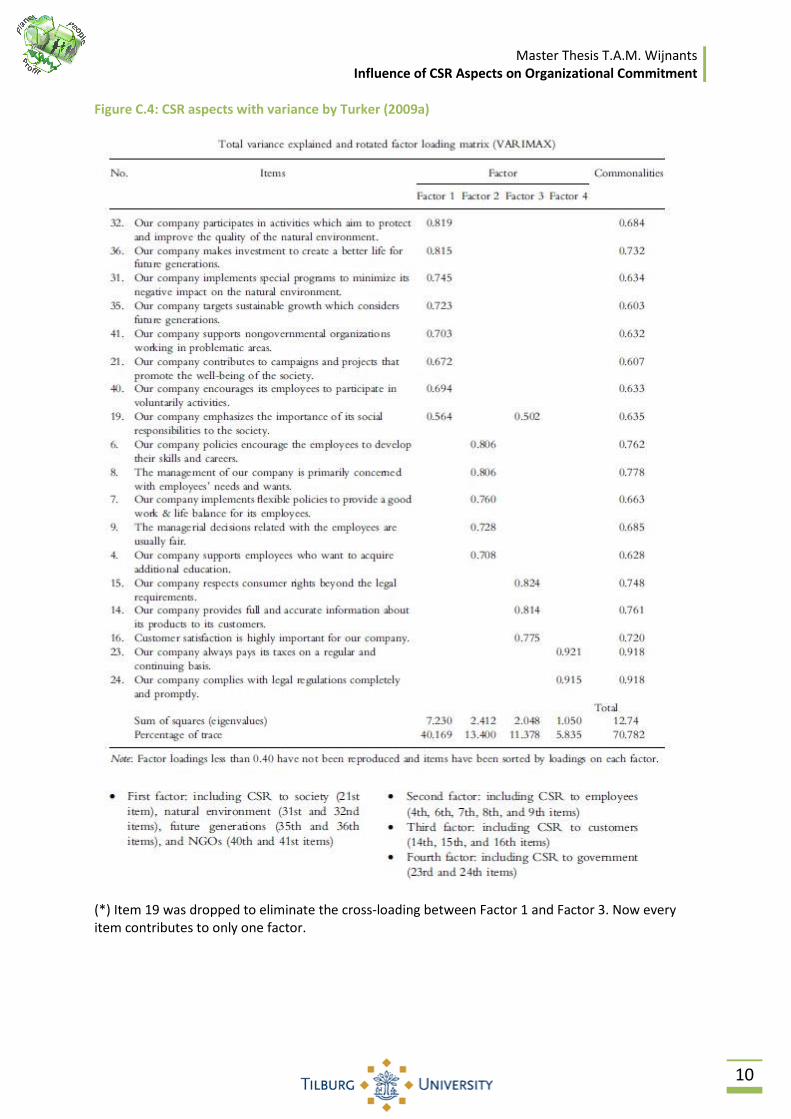

Turker (2009a) tried to shrink the list of aspects to a level where the model is still reliable. This

research starts with aspects derived from multiple scales in previous literature. After several pilots

the list shrunk to eighteen aspects that were used in the final survey. After analysis one aspect was

dropped and the remaining aspects explained 71% of the model. The CSR aspects that were used in

the final survey are displayed in Figure C.4 of appendix C. When a benchmark is built on a research in

just one single country it tends to be biased and cannot be generalized over more countries. This is a

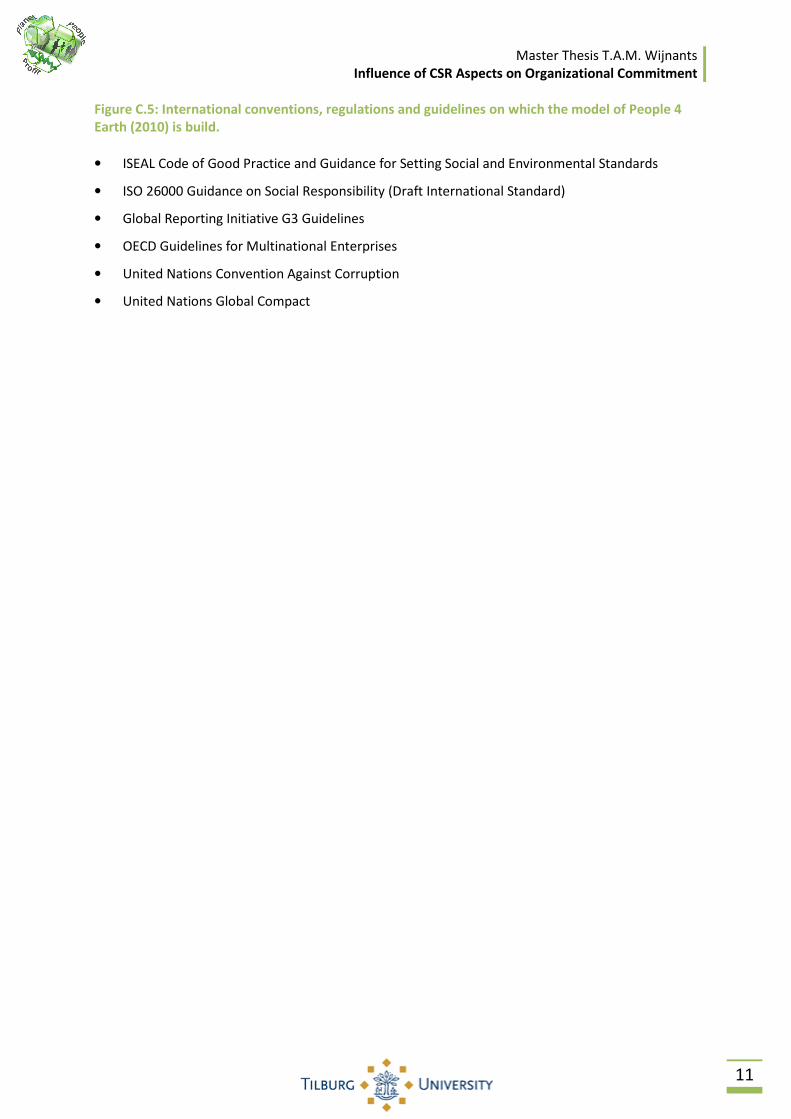

fact for all previously mentioned studies. In 2010 the independent global non-profit organization

People 4 Planet launched their benchmark of Global Sustainability Standards for Products. They fill

the gap of a lacking global standard for sustainability on multiple dimensions. The transparency of

CSR efforts improves even more when the benchmarking of companies is done by independent

institutes (Graafland et al., 2004). Such a generally accepted, global sustainable product standard

that is developed and supported by a multi-stakeholder process provides an easy understandable

framework for a complex project. It is a foothold for companies to enhance product sustainability

and a structure to apply specific standards for a product. And finally the standard makes it possible to

provide uniform information for the stakeholders.

Master Thesis T.A.M. Wijnants

Influence of CSR Aspects on Organizational Commitment

10

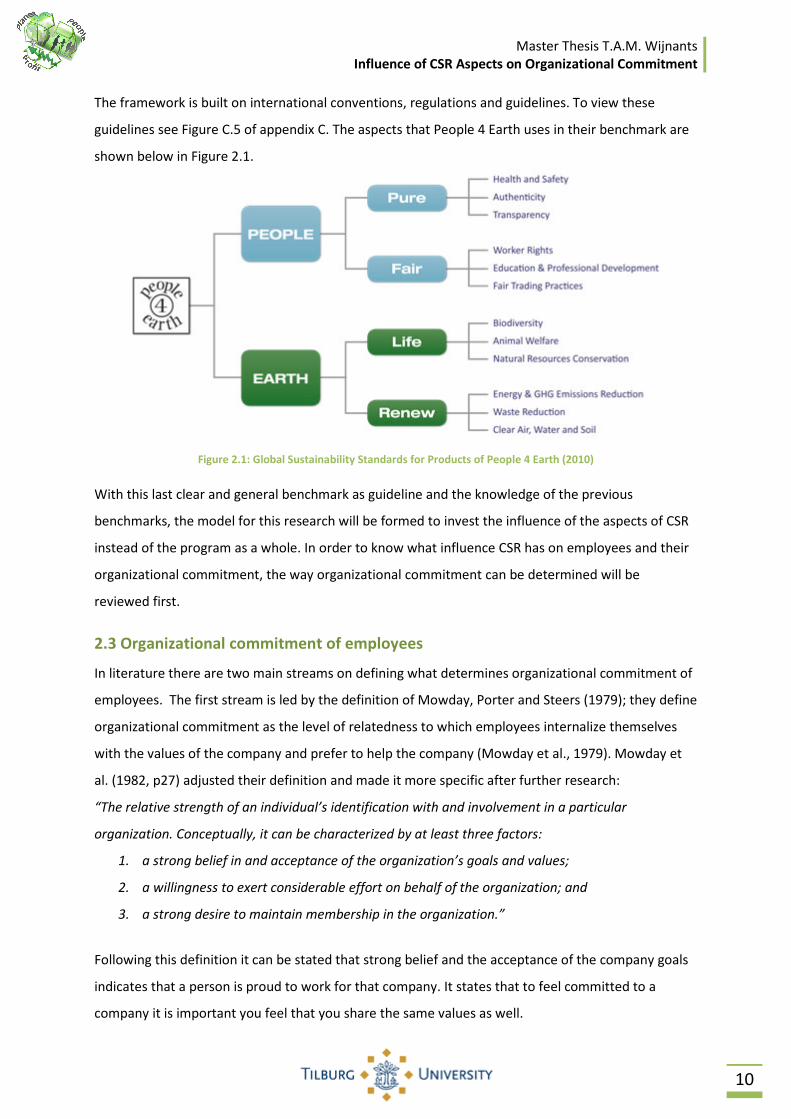

The framework is built on international conventions, regulations and guidelines. To view these

guidelines see Figure C.5 of appendix C. The aspects that People 4 Earth uses in their benchmark are

shown below in Figure 2.1.

Figure 2.1: Global Sustainability Standards for Products of People 4 Earth (2010)

With this last clear and general benchmark as guideline and the knowledge of the previous

benchmarks, the model for this research will be formed to invest the influence of the aspects of CSR

instead of the program as a whole. In order to know what influence CSR has on employees and their

organizational commitment, the way organizational commitment can be determined will be

reviewed first.

2.3 Organizational commitment of employees

In literature there are two main streams on defining what determines organizational commitment of

employees. The first stream is led by the definition of Mowday, Porter and Steers (1979); they define

organizational commitment as the level of relatedness to which employees internalize themselves

with the values of the company and prefer to help the company (Mowday et al., 1979). Mowday et

al. (1982, p27) adjusted their definition and made it more specific after further research:

“The relative strength of an individual’s identification with and involvement in a particular

organization. Conceptually, it can be characterized by at least three factors:

1. a strong belief in and acceptance of the organization’s goals and values;

2. a willingness to exert considerable effort on behalf of the organization; and

3. a strong desire to maintain membership in the organization.”

Following this definition it can be stated that strong belief and the acceptance of the company goals

indicates that a person is proud to work for that company. It states that to feel committed to a

company it is important you feel that you share the same values as well.

Master Thesis T.A.M. Wijnants

Influence of CSR Aspects on Organizational Commitment

11

These two determinants can be retrieved from the first part of the definition. That putting effort in

and working hard for the company contributes to the involvement of an employee with the

company, can be derived from the second part of the definition. And in the last part loyalty seems to

determine a large part of organizational commitment (Mowday, 1998).

The second stream on research of organizational commitment is led by Meyer and Allen (1991). They

propose a new organizational commitment definition with three components. They state that

organizational commitment is a psychological state that shows the employee’s relationship with a

company and has an impact on the decision to stay at a company. The three components in this

definition of organizational commitment are:

1. Affective Commitment: An employees’ psychological attachment to the company.

2. Continuance Commitment: Costs for the employee associated with leaving the company.

3. Normative Commitment: Perceived obligation to remain at the company.

As they explain themselves: “Affective commitment refers to the employee’s emotional attachment

to, identification with and involvement in the organization. Employees with a strong affective

commitment continue employment with the organization because they want to do so. Continuance

commitment refers to an awareness of the costs associated with leaving the organization. Employees

whose primary link to the organization is based on continuance commitment remain because they

need to do so. Finally normative commitment reflects a feeling of obligation to continue

employment. Employees with a high level of normative commitment feel that they ought to remain

with the organization.” (Meyer and Allen, 1991, p 67)

Both streams developed Organizational Commitment Questionnaires (OCQ) to measure how these

determinants of organizational commitment together can be measured and determine the level of

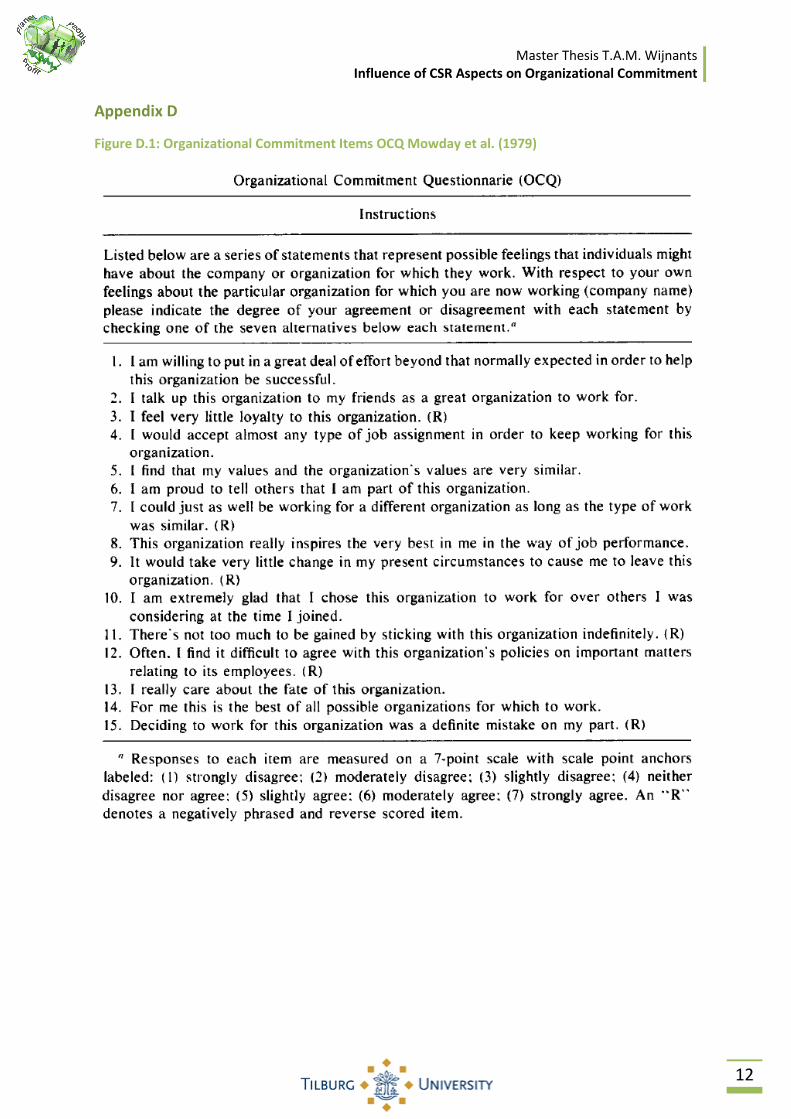

organizational commitment of an employee. The Organizational Commitment Questionnaire (OCQ)

developed by Mowday et al. (1979) was the first designed instrument to measure the organizational

commitment. The OCQ instrument contained initially fifteen items to measure the determinants of

organizational commitment and therefore the value of organizational commitment in total (see

appendix D Figure D.1 for the items). The research was held among 2563 employees working in a

wide variety of jobs in different public and private companies, so the OCQ is considered to be

generalizable. The representative research proved to be a good predictive and reliable instrument

after multiple tests on validity and reliability. In later research Mowday et al. (1982) conclude that

after reviewing the results and performing additional tests, very similar results were obtained with a

questionnaire of nine items, as compared to the initial fifteen entries in the first study. So the

questionnaire can be reduced but the reliability of the results stays nearly the same.

Master Thesis T.A.M. Wijnants

Influence of CSR Aspects on Organizational Commitment

12

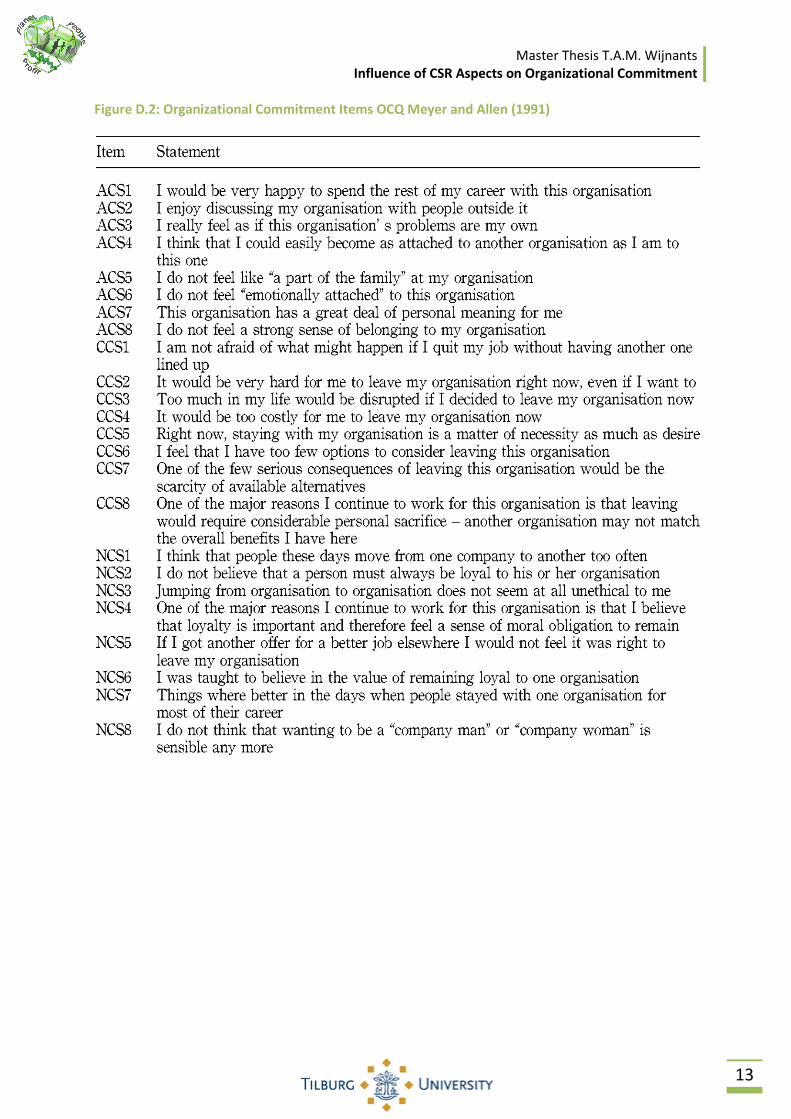

The initial OCQ model by Myer and Allen (1991) contains twenty-four items to determine the three

commitment components (see Figure D.2 of appendix D to view the items). After a review on their

results and more research on other respondents, Meyer and Allen (1993) concluded that eighteen

items were also sufficient enough to reliably measure organizational commitment.

Both OCQ measurements are still in use; the OCQ by Mowday et al. (1982) however is regarded to be

predominantly assessing the affective form of commitment (Mowday, 1998). Previous analytic

studies have shown that each form of commitment is associated with labour turnover and intentions

to leave the organization but suggest that a stronger relationship exists between affective

commitment and a couple of other desirable employee outcomes such as: attendance, job

performance, stress health, work-nonwork conflict (Meyer, Stanley, Herscovitch and Topolnytsky,

2002). Moreover affective commitment above others is fairly strongly related to positive attitudes in

the workplace. This implies that affective commitment is considered to be the most important

component of commitment for the positive approach of commitment. Studies investigating the

relationship between CSR performance and commitment have typically focused on affective

commitment (Brammer, Millington & Rayton, 2007) because of this. Another reason for the choice of

affective commitment in relation to CSR research is that being a member of a favourably reputable

organization can enhance an employee’s social identity and influence the affective component rather

than continuance and normative components (Turker, 2009b). For these reasons the choice is made

to research the relationship between the affective component of organizational commitment and the

aspects of CSR in this paper. And since the scale of OCQ by Mowday et al. (1982) is the most

frequently used and reliable measure of affective commitment (Turker, 2009b), this measurement

will be the guideline in the measurement of organizational commitment in this research. The next

paragraph reviews the effect that the already reviewed CSR has on organizational commitment.

2.4 Effect of CSR on organizational commitment of employees

Branco and Rodgriues (2006) use the resource based perspectives to research why firms engage in

CSR activities. The result reveals that companies engage in CSR because they believe it helps them to

gather a competitive advantage. The results of this research shows that the external benefits of CSR

can directly be related to the effect on corporate reputation. Therefore, Branco and Rodgriues (2006)

state that firms with a good social responsibility reputation can improve relations with internal and

external factors. Accordingly they can even attract better employees or increase current employees

motivations, morale, commitment and loyalty to the company.

Most studies have focused on the external part of CSR by looking at the influence of CSR on

prospective employees. These studies show how a socially responsible reputation of a company

influences corporate attractiveness for prospective employees such as students, or MBA students

(Albinger and Freeman, 2000; Blackhaus, Stone and Heiner, 2002).

Master Thesis T.A.M. Wijnants

Influence of CSR Aspects on Organizational Commitment

13

The effect of CSR on organizational attractiveness is stronger for people who are looking for a job and

have plenty of job choices (Albinger and Freeman, 2000). When these jobseekers already have more

knowledge of CSR or are directly involved with issues that a CSR project of a company deals with,

they are even more sensitive to CSR (Blackhaus et al., 2002). This shows that people would take a job

only to be able to work for a certain company, implying that CSR has an influence on this loyalty

point of organizational commitment. Montgomery and Ramus (2003) even found that MBAs are

willing to partly ignore the financial benefits in order to work for a company with a good reputation

of CSR. This implies that employees would turn down offers with higher salaries to be able to work

for a certain company. This shows that CSR influences organizational commitment on this loyalty

item. The image of a company can be formed by CSR even if the applicant has had no previous

interaction with a company, because a company’s social performance sends signals to prospective

job applicants about what it would be like to work for this company (Greening and Turban, 2000).

CSR can, therefore, be seen as useful for attracting the most qualified employees and is an important

component of corporate attractiveness, corporate image and reputation.

CSR directed towards employees can be perceived positively by both prospective employees and

current employees. According to social identity theory corporate social performance can be

expected to contribute positively to the attraction, retention and motivation of employees because

they are likely to identify strongly with positive organizational values (Peterson, 2004). Identification

with organizational values is also a determinant of organizational commitment as mentioned in

paragraph 2.3. So it can be stated that CSR has in influence on the organizational values.

Commitment of employees towards these values of CSR is very important, for example

environmental policy demonstrates that employees’ support is necessary to secure that the CSR

programs and policies are executed effectively (Ramus and Steger, 2000). This research also shows

that employees are the most important link to implement CSR strategies.

The last decades, people have become more aware of the extent and consequences of environment

degradation. Therefore employees prefer to work in socially responsible companies and their

organizational commitment level is positively affected by CSR to society, natural environment, next

generations, nongovernmental organizations employees and customers (Turker, 2009b). CSR gives a

good example of what the company stands for and gives an employee a weapon to defend

themselves and the company to external stakeholders. Good deeds of companies motivate

employees to discuss with others outside the company and feel a strong sense of commitment to the

company (Stawiski, Deal and Gentry, 2010). Generally stated, if an employee starts to be proud of

being a member of socially responsible organization, his or her work attitudes can be influenced

positively (Brammer et al., 2007; Peterson, 2004). Being proud and loyal to a company are also

important determinants of organizational commitment as mentioned earlier in paragraph 2.3.

Master Thesis T.A.M. Wijnants

Influence of CSR Aspects on Organizational Commitment

14

So past literature shows that CSR clearly has an influence on these determinants. The research of

Bhattacharya et al. (2008) found the following positive outcomes of CSR on employees organizational

commitment:

• Internal (mind of an employee): high level of commitment to their own work, greater morale,

dedication to excellence in work tasks. This all leads to satisfaction in their job, a sense of pride

towards the company and a feeling of well being in general.

• External (behaviour of an employee):

Reduction in absenteeism and employee retention, these aspects inspires the employees to work

harder, be more productive and focus more on quality.

Working harder is indicated in paragraph 2.3 as one of the determinants of organizational

commitment as well and this research shows CSR has an influence on this determinant. Now the

determinants of organizational commitment and the influence of CSR on them is reviewed, the

model that is composed and used in this research is explained in the next paragraph.

2.5 CSR Aspects and the DE employees’ organizational commitment

With the knowledge of past literature a simple but well substantiated model is built. The model

contains twelve aspects equally divided over the three dimensions of CSR that are mentioned by

Elkington (1997) and the definition of SER (2001). The guideline for the people and planet dimension

is the model of People 4 Earth (2010) supported by the other models discussed in paragraph 2.2. The

profit dimension is mainly formed by the other models discussed in 2.2 since People 4 Earth (2010)

does not include this dimension. All dimensions are also checked on their role in actual CSR reports.

The dimension people will be handled first in 2.5.1, followed by planet in 2.5.2 and profit in 2.5.3.

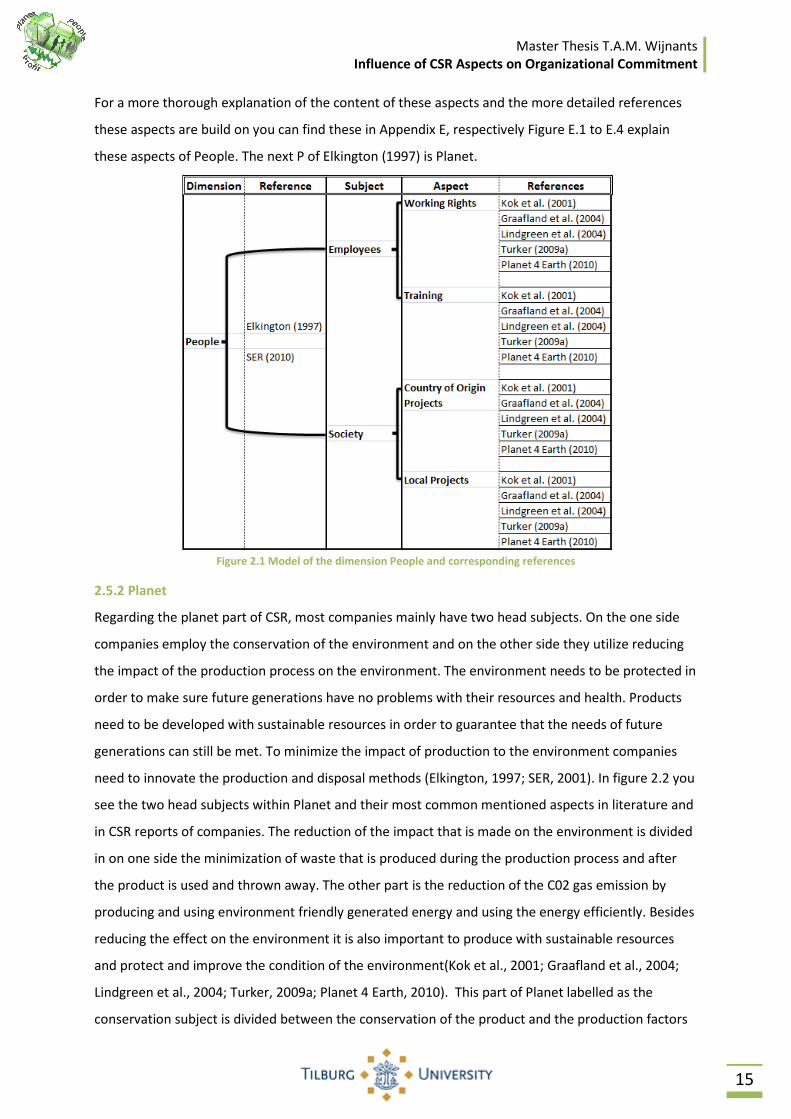

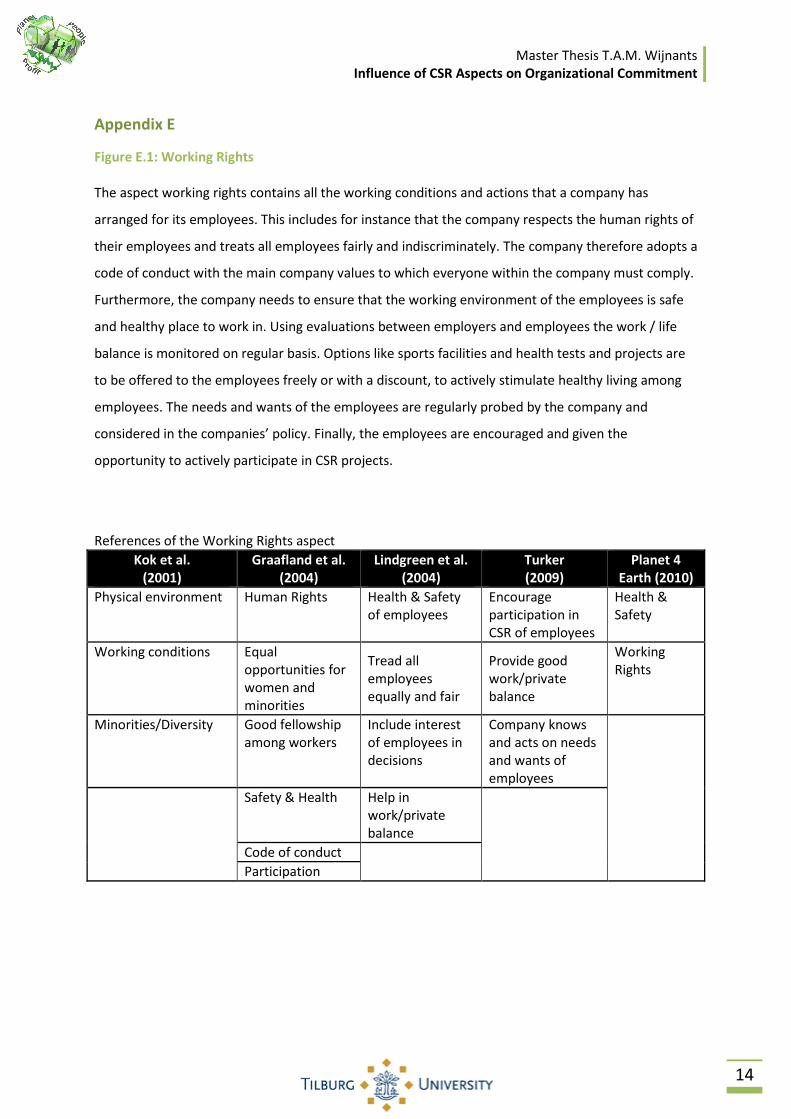

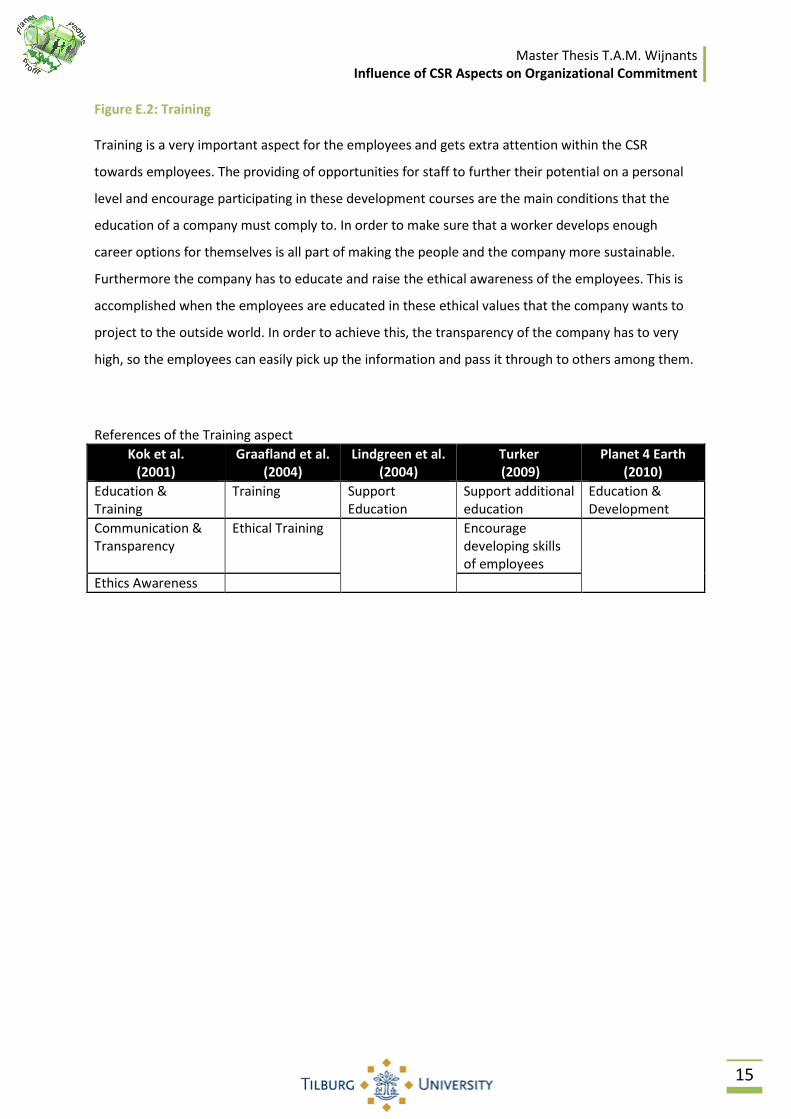

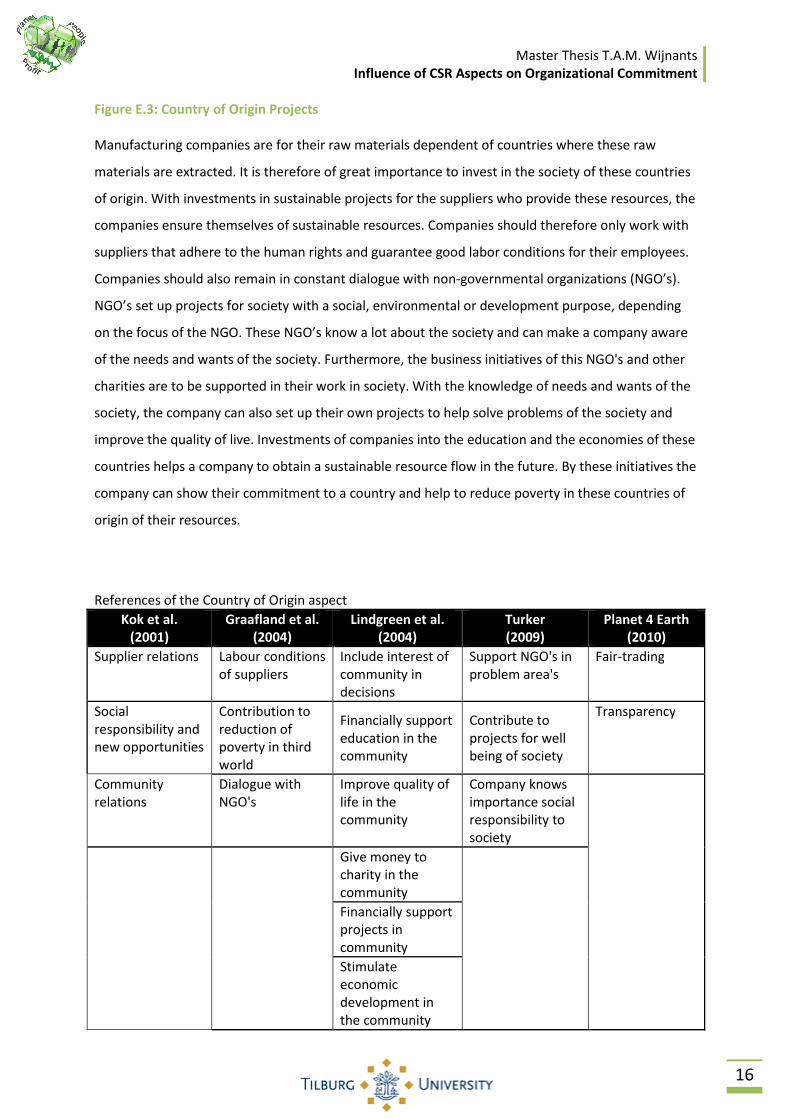

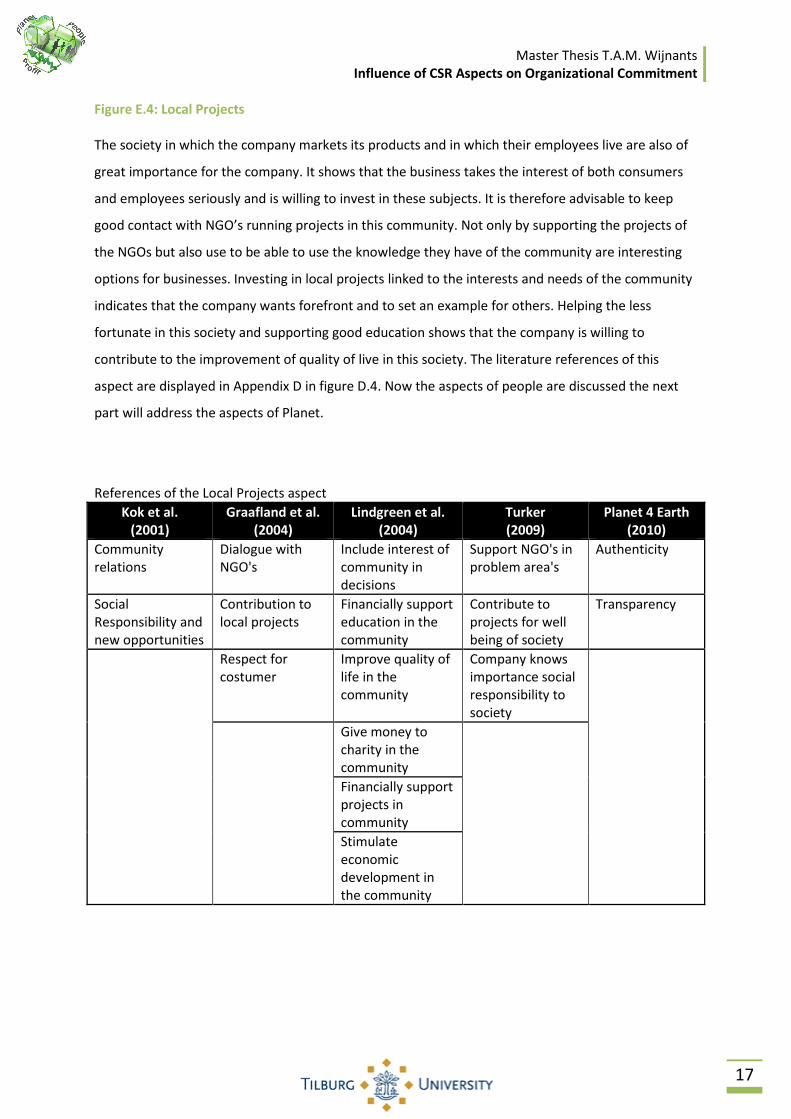

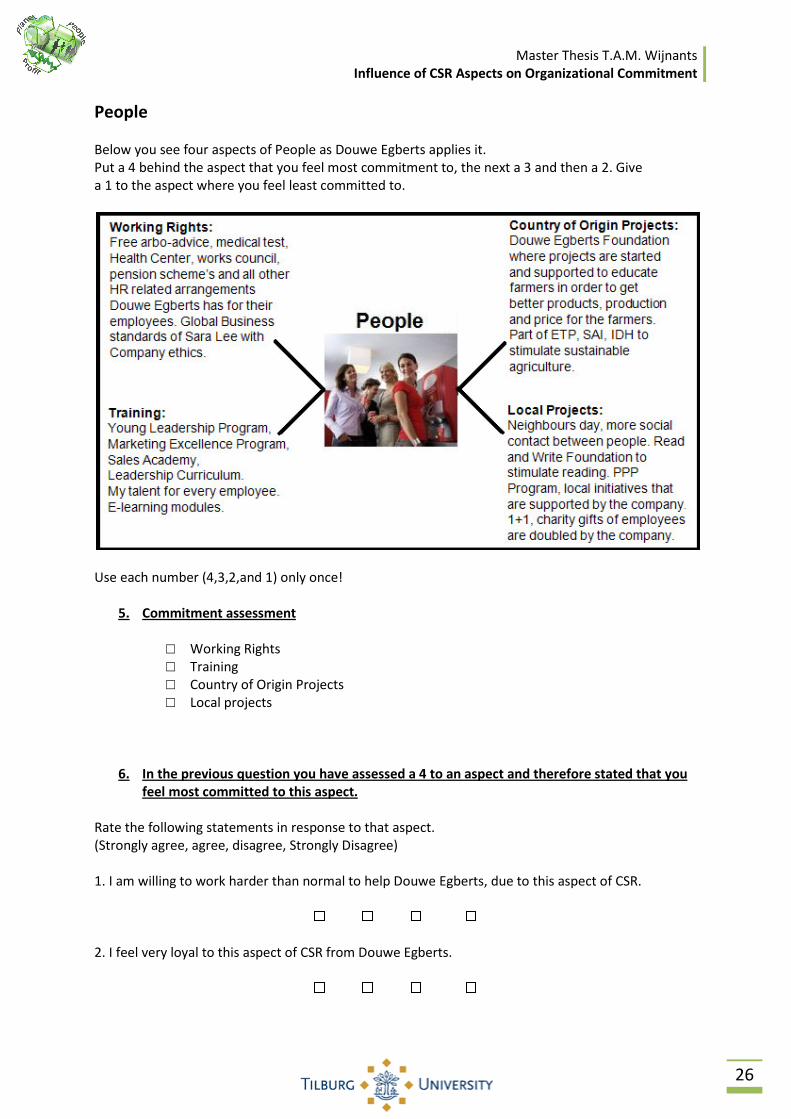

2.5.1 People

The dimension People contains two large focus groups that a producing company works with. The

employees are an important focus group because they produce, transport and sell the products of

the company. The society is the other large focus group of people that a company does their

business with; the company buys products from and sells products to the society (Elkington, 1997;

SER, 2001). In figure 2.1 these two focus groups are placed as subjects within People and their most

common mentioned aspects in literature and CSR reports of companies. The aspects of the subject

employees are divided in the working rights that a company handles and the training opportunities

the employees are offered (Kok et al., 2001; Graafland et al., 2004; Lindgreen et al., 2004; Turker,

2009a; Planet 4 Earth, 2010). The subject society is divided in the projects that are supported in the

country of origin of the main raw materials production and the projects that are established in the

local market where the product is produced and sold (Kok et al., 2001; Graafland et al., 2004;

Lindgreen et al., 2004; Turker, 2009a; Planet 4 Earth, 2010).

Master Thesis T.A.M. Wijnants

Influence of CSR Aspects on Organizational Commitment

15

For a more thorough explanation of the content of these aspects and the more detailed references

these aspects are build on you can find these in Appendix E, respectively Figure E.1 to E.4 explain

these aspects of People. The next P of Elkington (1997) is Planet.

Figure 2.1 Model of the dimension People and corresponding references

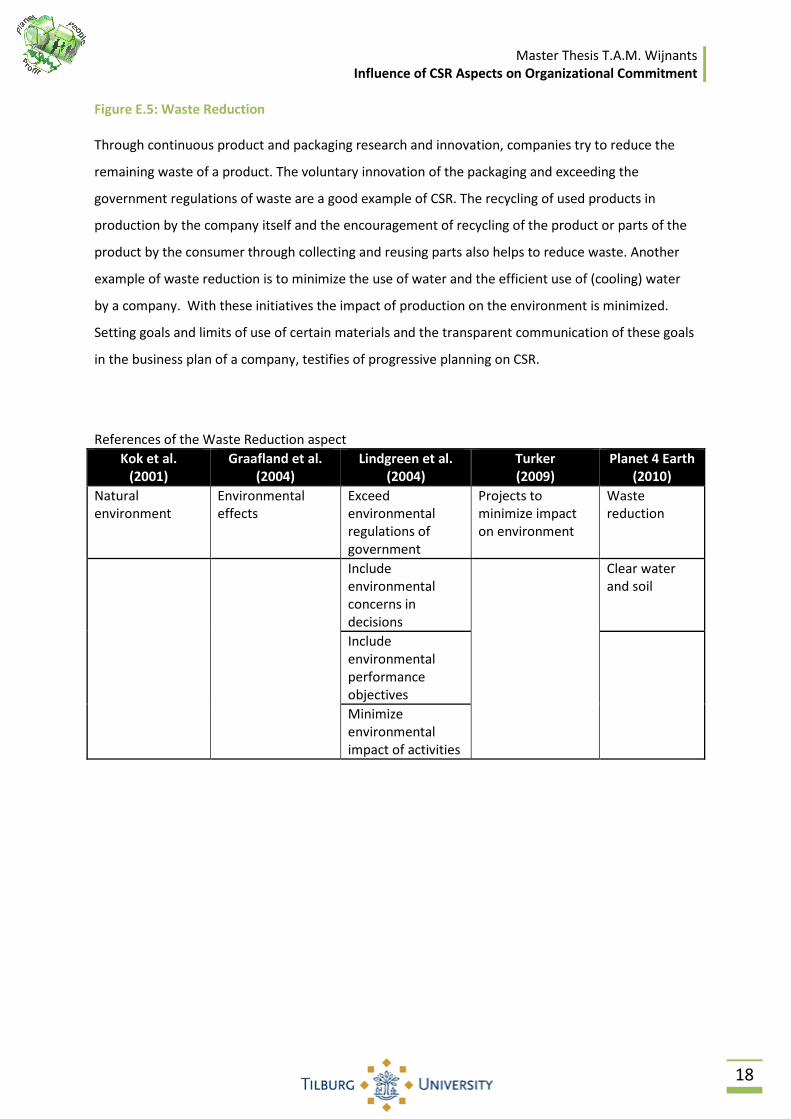

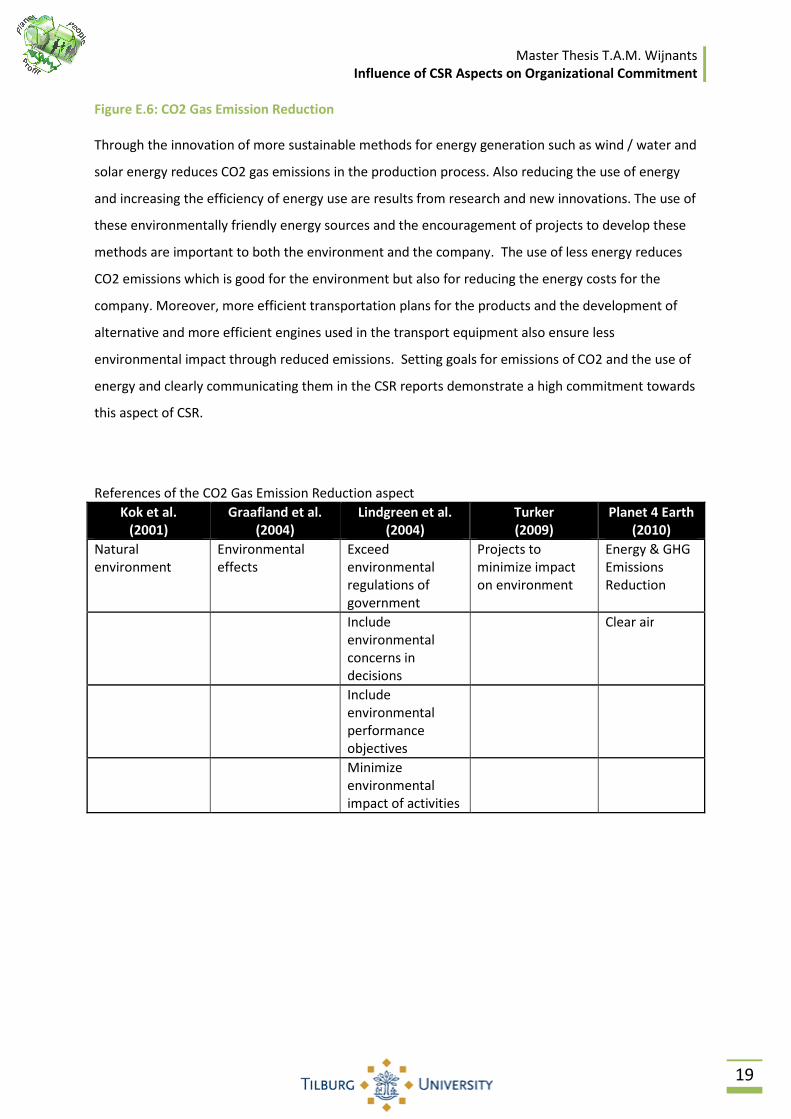

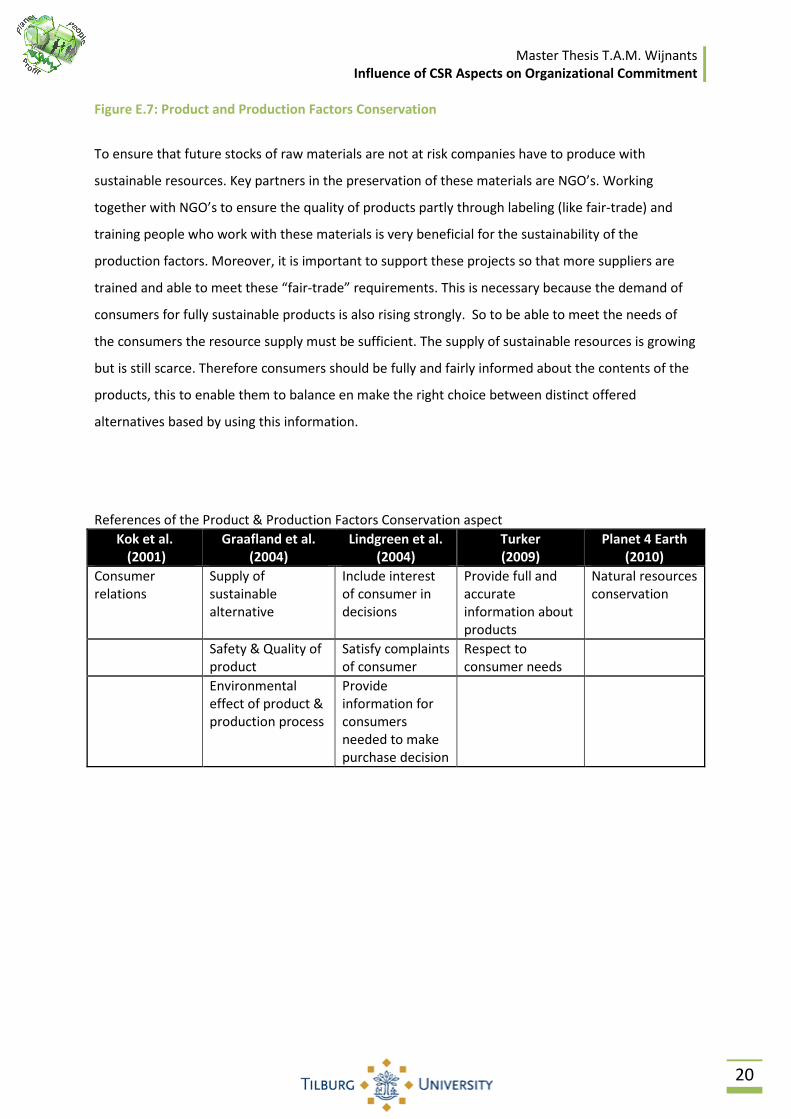

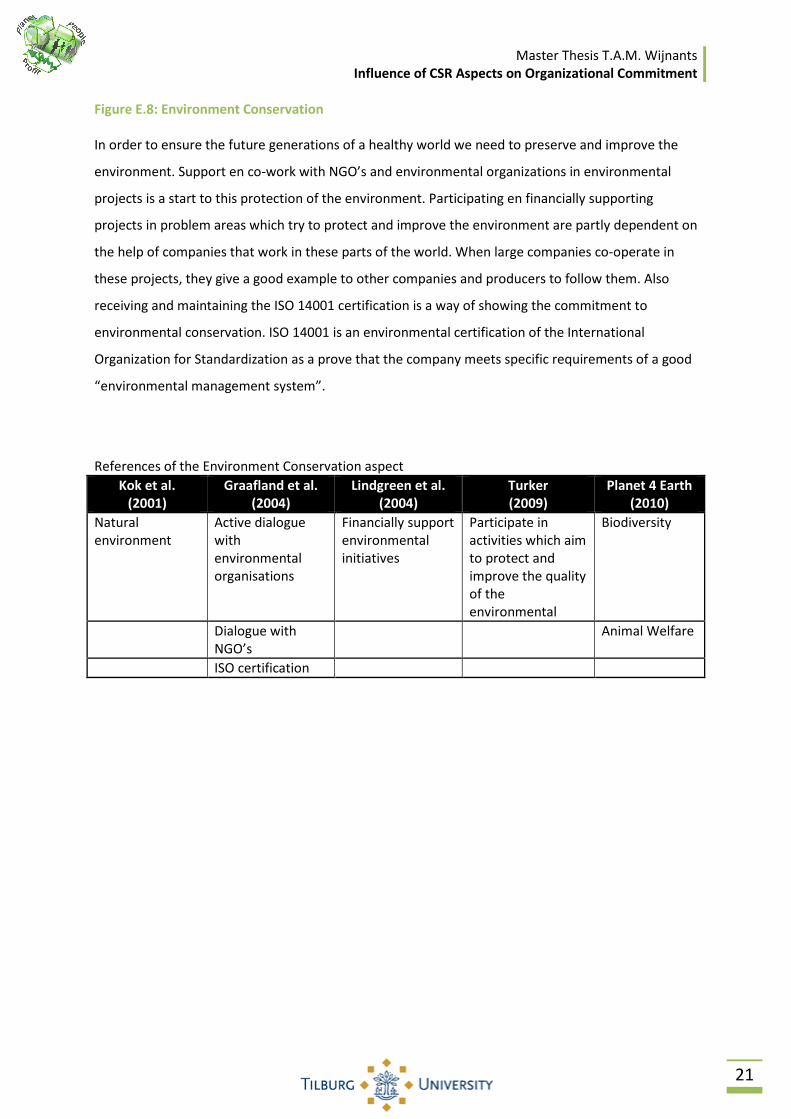

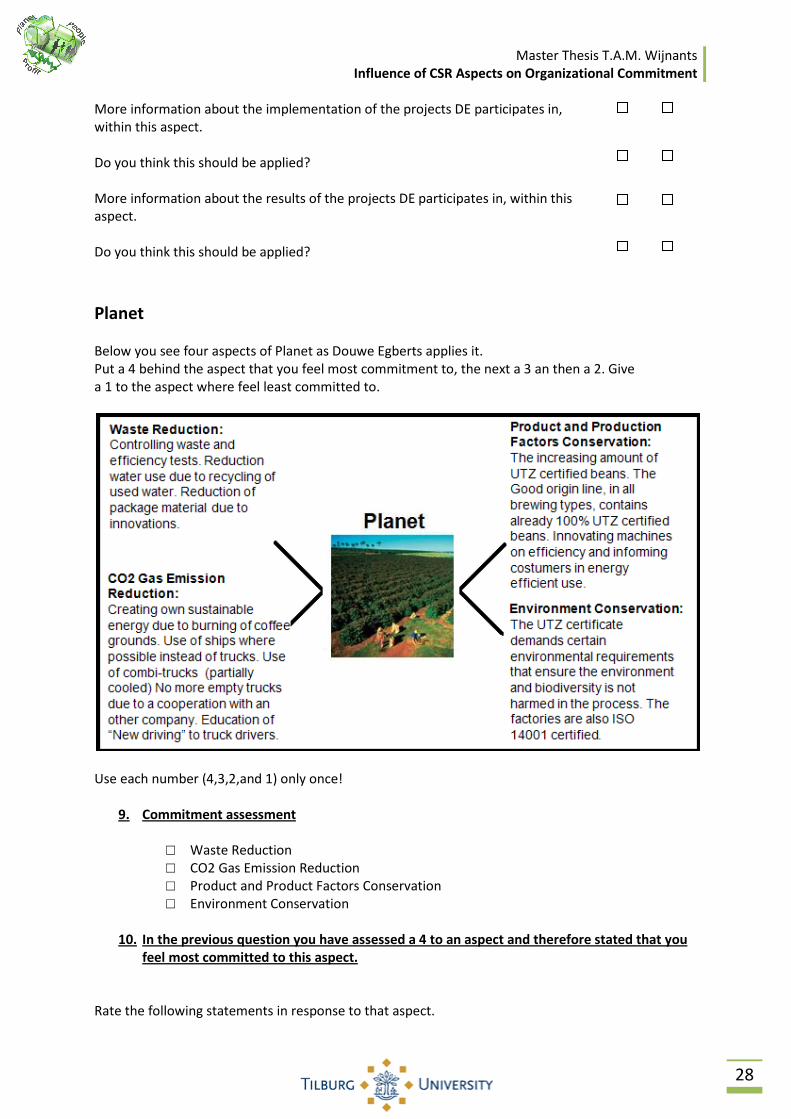

2.5.2 Planet

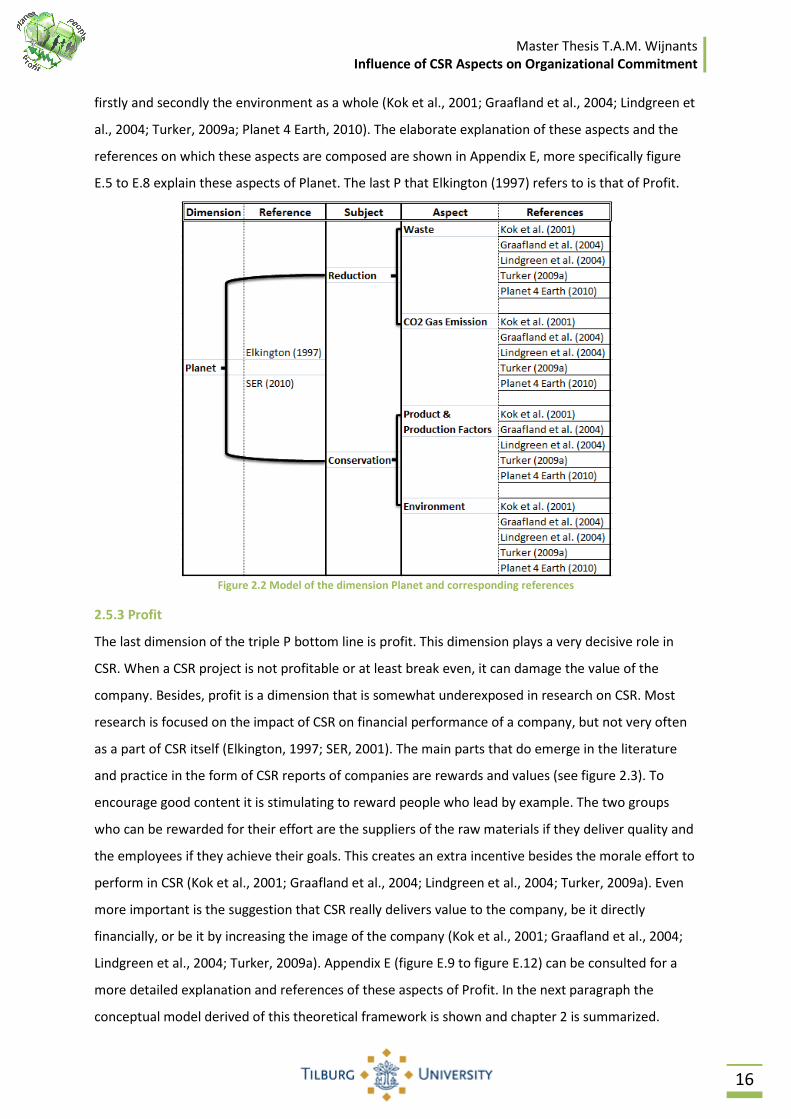

Regarding the planet part of CSR, most companies mainly have two head subjects. On the one side

companies employ the conservation of the environment and on the other side they utilize reducing

the impact of the production process on the environment. The environment needs to be protected in

order to make sure future generations have no problems with their resources and health. Products

need to be developed with sustainable resources in order to guarantee that the needs of future

generations can still be met. To minimize the impact of production to the environment companies

need to innovate the production and disposal methods (Elkington, 1997; SER, 2001). In figure 2.2 you

see the two head subjects within Planet and their most common mentioned aspects in literature and

in CSR reports of companies. The reduction of the impact that is made on the environment is divided

in on one side the minimization of waste that is produced during the production process and after

the product is used and thrown away. The other part is the reduction of the C02 gas emission by

producing and using environment friendly generated energy and using the energy efficiently. Besides

reducing the effect on the environment it is also important to produce with sustainable resources

and protect and improve the condition of the environment(Kok et al., 2001; Graafland et al., 2004;

Lindgreen et al., 2004; Turker, 2009a; Planet 4 Earth, 2010). This part of Planet labelled as the

conservation subject is divided between the conservation of the product and the production factors

Master Thesis T.A.M. Wijnants

Influence of CSR Aspects on Organizational Commitment

16

firstly and secondly the environment as a whole (Kok et al., 2001; Graafland et al., 2004; Lindgreen et

al., 2004; Turker, 2009a; Planet 4 Earth, 2010). The elaborate explanation of these aspects and the

references on which these aspects are composed are shown in Appendix E, more specifically figure

E.5 to E.8 explain these aspects of Planet. The last P that Elkington (1997) refers to is that of Profit.

Figure 2.2 Model of the dimension Planet and corresponding references

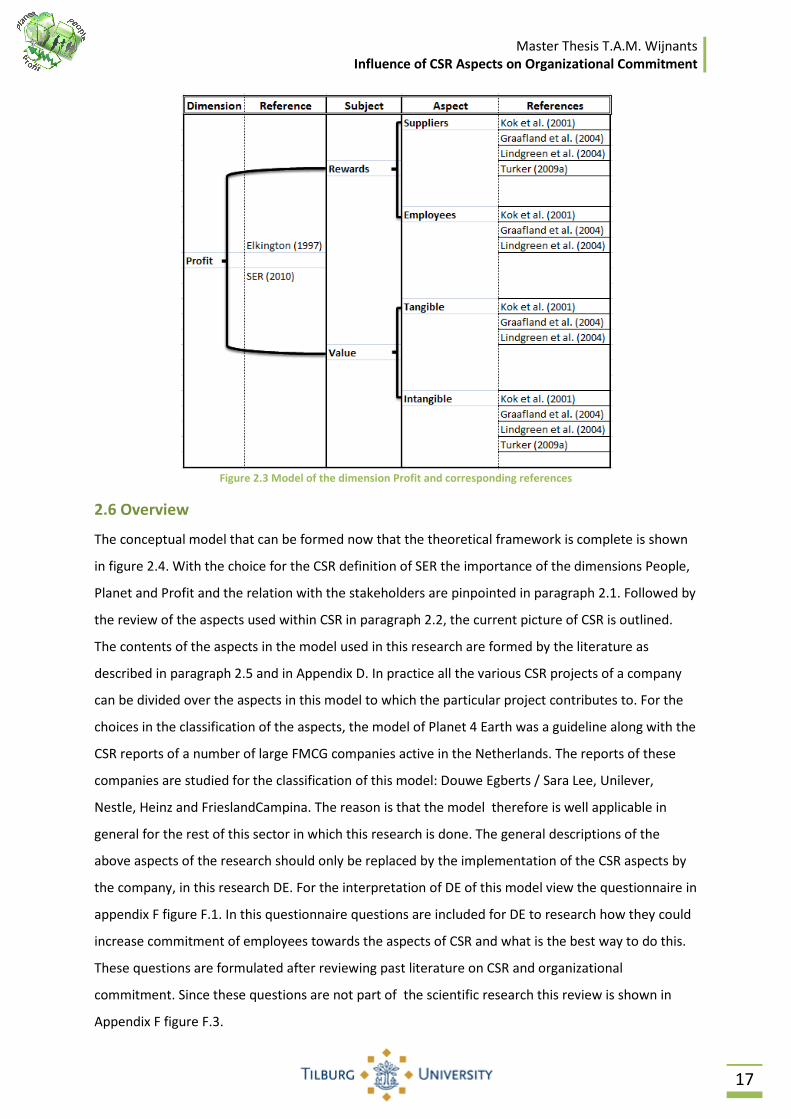

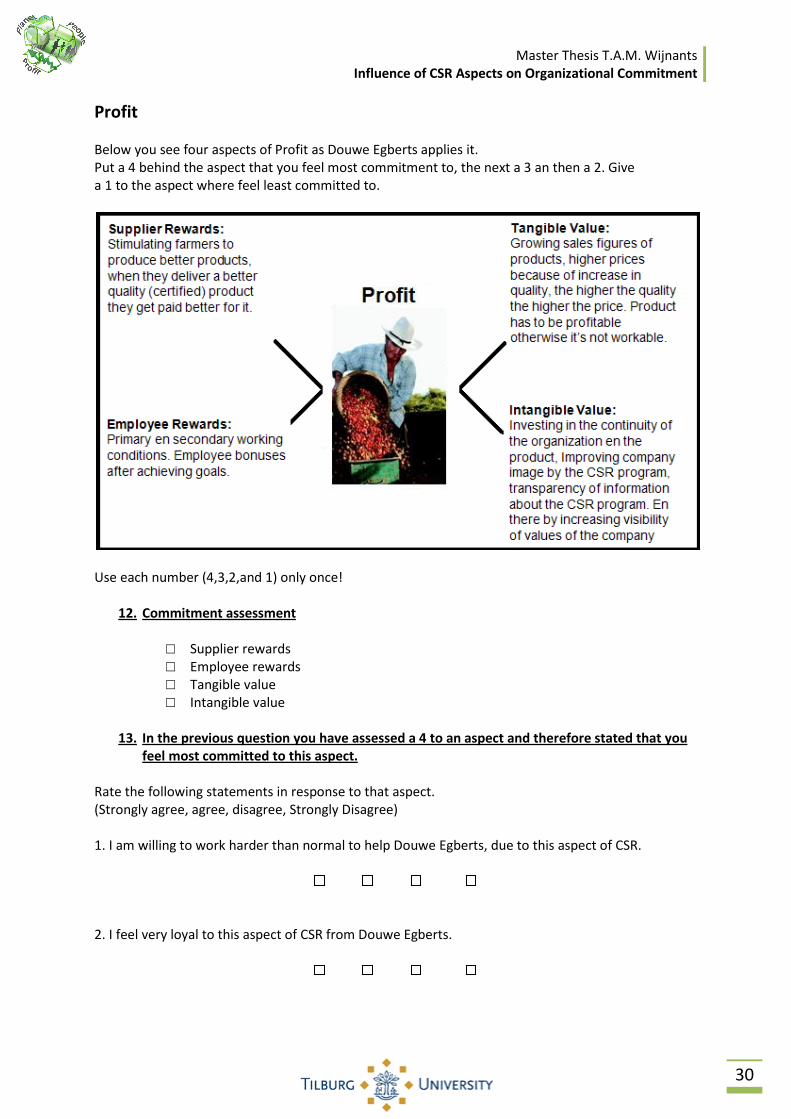

2.5.3 Profit

The last dimension of the triple P bottom line is profit. This dimension plays a very decisive role in

CSR. When a CSR project is not profitable or at least break even, it can damage the value of the

company. Besides, profit is a dimension that is somewhat underexposed in research on CSR. Most

research is focused on the impact of CSR on financial performance of a company, but not very often

as a part of CSR itself (Elkington, 1997; SER, 2001). The main parts that do emerge in the literature

and practice in the form of CSR reports of companies are rewards and values (see figure 2.3). To

encourage good content it is stimulating to reward people who lead by example. The two groups

who can be rewarded for their effort are the suppliers of the raw materials if they deliver quality and

the employees if they achieve their goals. This creates an extra incentive besides the morale effort to

perform in CSR (Kok et al., 2001; Graafland et al., 2004; Lindgreen et al., 2004; Turker, 2009a). Even

more important is the suggestion that CSR really delivers value to the company, be it directly

financially, or be it by increasing the image of the company (Kok et al., 2001; Graafland et al., 2004;

Lindgreen et al., 2004; Turker, 2009a). Appendix E (figure E.9 to figure E.12) can be consulted for a

more detailed explanation and references of these aspects of Profit. In the next paragraph the

conceptual model derived of this theoretical framework is shown and chapter 2 is summarized.

Master Thesis T.A.M. Wijnants

Influence of CSR Aspects on Organizational Commitment

17

Figure 2.3 Model of the dimension Profit and corresponding references

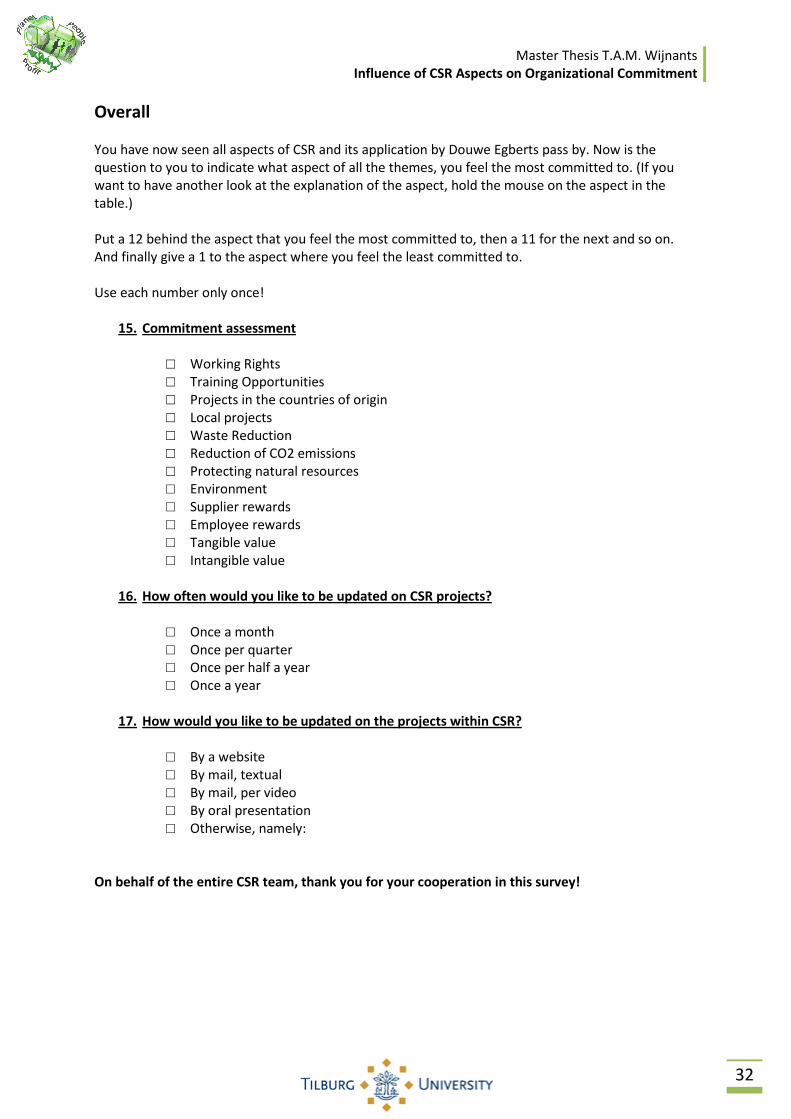

2.6 Overview

The conceptual model that can be formed now that the theoretical framework is complete is shown

in figure 2.4. With the choice for the CSR definition of SER the importance of the dimensions People,

Planet and Profit and the relation with the stakeholders are pinpointed in paragraph 2.1. Followed by

the review of the aspects used within CSR in paragraph 2.2, the current picture of CSR is outlined.

The contents of the aspects in the model used in this research are formed by the literature as

described in paragraph 2.5 and in Appendix D. In practice all the various CSR projects of a company

can be divided over the aspects in this model to which the particular project contributes to. For the

choices in the classification of the aspects, the model of Planet 4 Earth was a guideline along with the

CSR reports of a number of large FMCG companies active in the Netherlands. The reports of these

companies are studied for the classification of this model: Douwe Egberts / Sara Lee, Unilever,

Nestle, Heinz and FrieslandCampina. The reason is that the model therefore is well applicable in

general for the rest of this sector in which this research is done. The general descriptions of the

above aspects of the research should only be replaced by the implementation of the CSR aspects by

the company, in this research DE. For the interpretation of DE of this model view the questionnaire in

appendix F figure F.1. In this questionnaire questions are included for DE to research how they could

increase commitment of employees towards the aspects of CSR and what is the best way to do this.

These questions are formulated after reviewing past literature on CSR and organizational

commitment. Since these questions are not part of the scientific research this review is shown in

Appendix F figure F.3.

Master Thesis T.A.M. Wijnants

Influence of CSR Aspects on Organizational Commitment

18

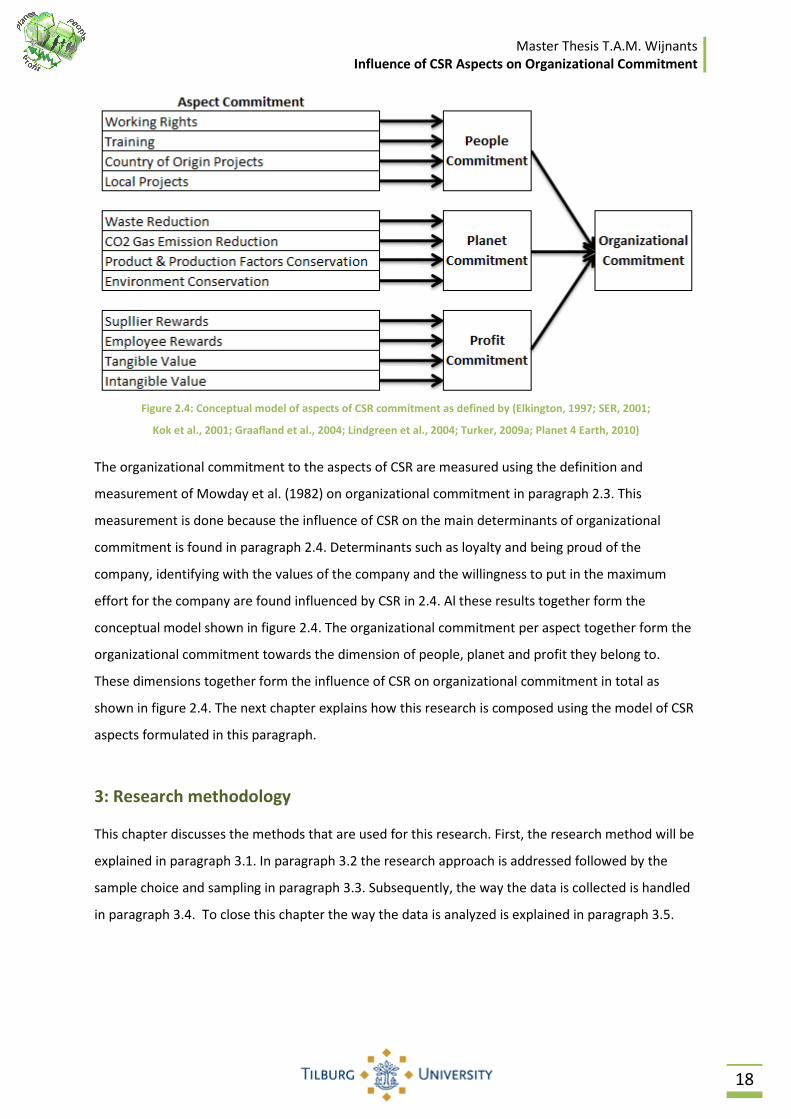

Figure 2.4: Conceptual model of aspects of CSR commitment as defined by (Elkington, 1997; SER, 2001;

Kok et al., 2001; Graafland et al., 2004; Lindgreen et al., 2004; Turker, 2009a; Planet 4 Earth, 2010)

The organizational commitment to the aspects of CSR are measured using the definition and

measurement of Mowday et al. (1982) on organizational commitment in paragraph 2.3. This

measurement is done because the influence of CSR on the main determinants of organizational

commitment is found in paragraph 2.4. Determinants such as loyalty and being proud of the

company, identifying with the values of the company and the willingness to put in the maximum

effort for the company are found influenced by CSR in 2.4. Al these results together form the

conceptual model shown in figure 2.4. The organizational commitment per aspect together form the

organizational commitment towards the dimension of people, planet and profit they belong to.

These dimensions together form the influence of CSR on organizational commitment in total as

shown in figure 2.4. The next chapter explains how this research is composed using the model of CSR

aspects formulated in this paragraph.

3: Research methodology

This chapter discusses the methods that are used for this research. First, the research method will be

explained in paragraph 3.1. In paragraph 3.2 the research approach is addressed followed by the

sample choice and sampling in paragraph 3.3. Subsequently, the way the data is collected is handled

in paragraph 3.4. To close this chapter the way the data is analyzed is explained in paragraph 3.5.

Master Thesis T.A.M. Wijnants

Influence of CSR Aspects on Organizational Commitment

19

3.1 Research method

For this study primary, secondary and tertiary literature sources are used. For the research of CSR a

number of primary sources such as CSR reports from companies are used, but also publications and

reports from governments and independent organizations about CSR. For the definitions and

relationships between CSR and commitment secondary literature such as journals and books are the

main literature sources. These journals and books were found through tertiary literature sources

such as indexes of the search portal of the University of Tilburg and the online academic citation

index of Web of Science (Saunders, Lewis and Thornhill , 2009). Search terms such as CSR,

sustainability, employees, commitment and derivatives thereof are used to collect literature for this

research. The sources used for this study are of course selected by relevance of the information for

this research. Only the weight and reliability of the research is checked by the impact factor of the

journal in which the research is published and/or the number of times the research is cited since the

publication. Consulted sources are for instance highly respected journals as Academy of

Management Journal. However sources also include journals related to the main topics of CSR such

as the Journal of Business Ethics. For organizational commitment is the Human Resource

Management Review a good example. Ultimately, the snowball technique is applied to the already

found literature through search results to make sure that the widest and fullest possible picture of

the issues can be outlined(Saunders et al, 2009).

3.2 Research approach

The approach of this research can be termed as deductive since the relationship between two

variables is researched and the decisive factors that influence this relationship are determined.

Thereafter this relationship is measured with the use of a newly formed model. Firstly both variables,

CSR and organizational commitment, are defined using academic literature. Also, the literature is

used to examine past research on the relationship between these variables. After this framework is

clear, this research tries to find out how this relationship between these variables is established.

After the results of this research are shown, these results are used to draw conclusions about the

additional effects of these outcomes for practice and future research. Therefore the purpose of this

study is therefore ‘descripto-explanatory’ (Saunders et al, 2009).

The research is based on primary quantitative data that tries to indicate a relationship between

variables. Since this data is collected only once among a large population of people, the easiest way

to obtain and process this data is by using the survey strategy. To be more precise the questionnaire

data collection technique is employed (Saunders et al, 2009). Since the questionnaire was only sent

out once to one sample group, this research can be called cross-sectional (Saunders et al, 2009).

Master Thesis T.A.M. Wijnants

Influence of CSR Aspects on Organizational Commitment

20

3.3 Sample choice and sampling

This research uses a questionnaire to obtain the data needed to study the relationship between CSR

and organizational commitment of employees. Since the chance of a case to be selected for this

research is equal to all cases the sampling technique is considered as a probability type (Saunders et

al, 2009). The sampling frame of this research is clear and is formed by the employees of DE. The

total amount of employees of DE in the Netherlands is 2229 and 1000 of them are in possession of a

corporate email address. After ten days 299 employees had responded to the questionnaire. The

survey software allowed students to do free research until a maximum of 300 respondents. Since the

company did not want to invest in the possibility to enter more respondents, the questionnaire

closed and the sample size was complete at a total amount of response of 30% of the approached

sample. So the first 299 respondents that reacted to the questionnaire form the sample used in this

research. A sample size of 243 respondents would make the sample reliable for a 90% confidence

level to generalize over the whole population (Pallant, 2010).

3.4 Collecting data using questionnaire

The primary data is collected by a protected online questionnaire among all the employees that are

in possession of a corporate email address. All questions used in this questionnaire are closed

questions because of the large sample and the convenience for data analysis (Saunders et al., 2009).

For the composition of the questionnaire it is important to have a clear view on the dependent,

independent and the control variables that are going to be measured. First the dependent variable

will be handled in paragraph 3.4.1 followed by the independent variable in paragraph 3.4.2 and the

control variables in paragraph 3.4.3. This paragraph is concluded by subparagraph 3.4.4 that shows

the conditions under which the questionnaires are completed.

3.4.1 Dependent variable

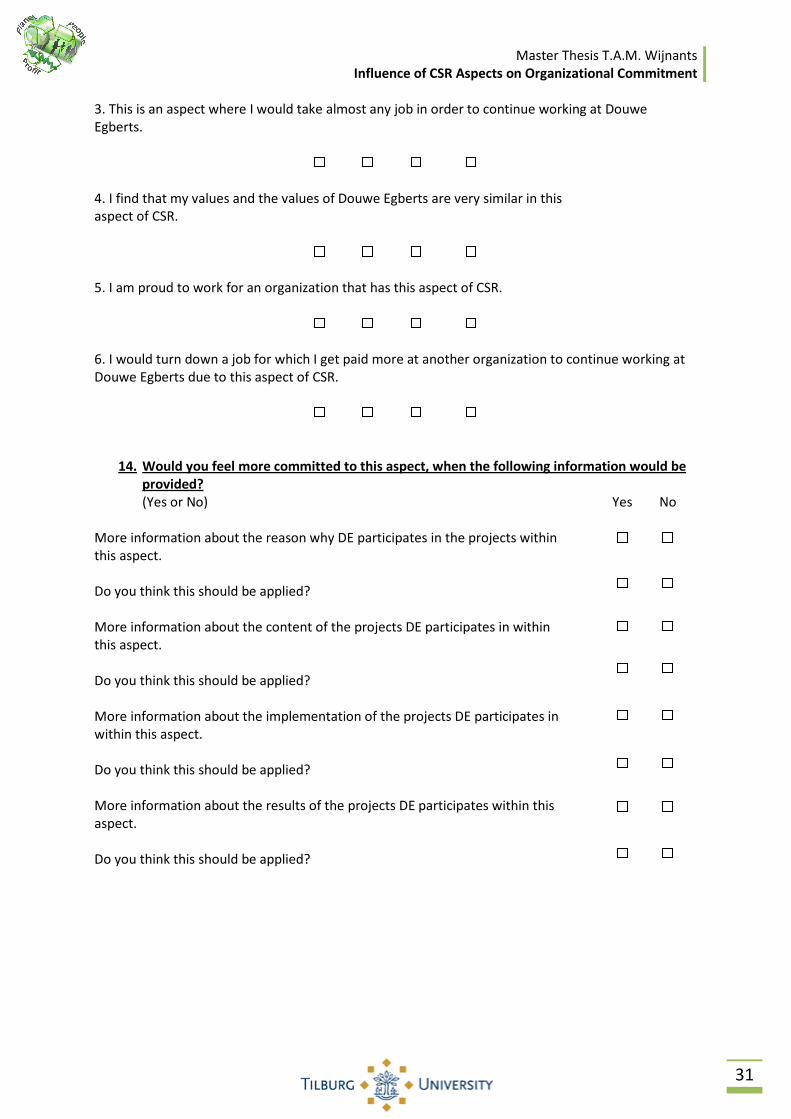

The dependent variable in this research is organizational commitment and the opinion of the

employees is asked in the different dimensions of CSR. The measurement of this variable will be on a

scale based on six questions as used by Marsden, Kalleberg and Cook (1993). The questions used in

this research constructing the scale that is analyzed are shown in figure 3.1.

Master Thesis T.A.M. Wijnants

Influence of CSR Aspects on Organizational Commitment

21

Figure 3.1: Adjusted six questions commitment measure

The wordings of these questions correspond to that used by Marsden et al. (1993) and are only

rephrased to make them applicable to this research (Saunders et al., 2009). This measure was chosen

because the organizational commitment is being measured three times, for every CSR dimension. To

keep the survey feasible for the respondents, but still reliable for research the six questions based

scale of Marsden was used. The main determinants of organizational commitment that are measured

in this six items OCQ are derived from the definition of Mowday et al. (1982) as stated earlier.

Question one to five bear a close resemblance to items one, three, four, five and six of the fifteen

item Organizational Commitment Questionnaire (OCQ) of Mowday et al (1982, p221) which are the

same questions as in the earlier published OCQ of 1979 (see Appendix D.1). The six questions that

are used in this research capture the major aspects of organizational (affective) commitment

definition measured by the OCQ (see Mowday et al. 1982 p 27).

Question one reflects the component of willingness to exert effort on behalf of the organization,

which covers the second part of definition (see page 10 for the definition). Question four and five

concern the belief in and acceptance of the organization’s goals and values of the employees; which

refers to the first part of the definition. Question number two, three and six measure the desire to

maintain membership in the organization, representing the third part of the definition. All questions

are answered on a four point scale, so this kind of question is called a rating question put together in

a matrix for a clear overview (Saunders et al., 2009). In a four point scale the respondent is forced to

make a choice between positive and a negative answer to the question. The coding for these

questions is a one for ‘totally disagree’ and a four for ‘totally agree’. Respondents will be assigned

the mean of their scores on the six items as their score on the commitment scale of an aspect. In the

research of Marsden (1993) the internal consistency reliability of the sample was an acceptable

reliability of .74. This means that this measure explains 74% of the model. In the next paragraph the

independent variables will be clarified.

3.4.2 Independent variables

The independent variables of this research are formed by the CSR aspects within the CSR dimensions.

The model that is built and explained in paragraph 2.5 summarizes these aspects. This framework is

filled in with the context of the CSR program of the company that is researched, DE in this case. The

questions that answer to the independent value are ranking questions. The respondent is asked per

dimension to rank the aspects; with this technique the relative importance between the aspects of

Master Thesis T.A.M. Wijnants

Influence of CSR Aspects on Organizational Commitment

22

the same dimension is discovered (Saunders et al., 2010).

A one is given to the aspect the respondent feel least committed to, a two and a three are given to

the following aspects and finally a four to the aspect they feel most committed to. When the most

important aspect of a dimension is found it can be researched separately on the level of

organizational commitment. The reason to only measure the commitment for this aspect is when the

commitment was measured for all aspects, the questionnaire would become too long and

monotonous. This would result in a drastic drop of the response rate to the questionnaire. Now that

the independent value is clear the final subparagraph defines the control variables that are

researched.

3.4.3 Control variables

Besides the main variables this research controls for a range of variables that have been identified as

significant control variables of affective commitment and CSR. These control variables have been

used in earlier research on organizational commitment. Meyer et al. (2002) researched several

determinants of commitment and found positive correlations for age and the length of employment

in the company (organizational tenure) with affective commitment. Age has an influence on the

effect of CSR on organizational commitment because people in different stages of their life, find

different things important. This view on life changes due to the experiences they have gained

(Turker, 2009b). Organizational tenure also has an effect worth mentioning on organizational

commitment. When employees gain experience with a company they tend to get more attached to

it. Also long serving employees retrospectively develop affective commitment with a company,

otherwise they would have already left the company (Meyer et al., 1997). For gender, education and

marital status Meyer et al. (2002) found no significant correlation in their research. However, there

are several researches that claim the influence of gender on CSR and commitment. Since man and

women have different work characteristics they judge commitment differently (Marsden et al. 1993).

Decisions concerning attitudes and values, which holds for CSR, can be subject to significant gender

differences (Greening and Turban, 2000). While men attach more value to instrumental or economic

concerns woman are more likely to be concerned with discretionary behaviour within a company.

This is supported by Peterson (2004) who suggests that the relationship between organizational

commitment and discretionary measures of corporate social responsibility is stronger for women

than for men. Also corporate charitable behaviour, which is usually considered to be discretionary, is

viewed more favourably by women than men. Age, gender and tenure are considered relevant and

important determinants in multiple researches (Brammer , 2007; Peterson, 2004; Turker, 2009b). The

control variable of function of an employee within the company has been added in recent research.

Strong evidence has been found a positive relationship between leadership and organizational

commitment (Walumbwa and Lawler, 2002). So differences in the function layers of a company

Master Thesis T.A.M. Wijnants

Influence of CSR Aspects on Organizational Commitment

23

regarding CSR and commitment are to be expected (Brammer, 2007).

These control variables are added to this questionnaire for DE to be able to directly inform groups of

employees on CSR aspects that these groups find important and feel most committed to. These

control variables are defined as attribute questions (Saunders et al., 2009). They are handled with

the category questions collection because with categories it is easy to compare groups of people and

also the anonymity of the respondents is guaranteed in this way.

3.4.4 Conditions of questionnaire

Before the final questionnaire was sent out, a control group of ten employees of DE participates in a

pilot questionnaire. This pilot tests if the questionnaire is clear, measures the right variables in a

correct way and to estimate the time it takes to complete the questionnaire. These respondents also

critically review whether the questionnaire is translated in a clear and correct way. With the

feedback of this control group the final survey is composed and published online. The link of the

questionnaire is protected and only accessible to the receivers of the mail. It is also possible to fill in

the questionnaire only once per mail receivers, this to prevent a possible sabotage of the

questionnaire and the out coming data. From the moment the employees receive the mail with the

link to the questionnaire they have four weeks to respond, receiving a reminder one week before the

deadline. The questionnaire is sent out by the Marketing Manager Corporate Social Responsibility of

the company; this is done to show that the company attaches great importance to the research and

to try to increase the response rate of the questionnaire. In the accompanying letter the importance

to the employees themselves is explained and it is used to inform the respondents that the data will

also be used for a graduation research. The final questionnaire that is used in this research can be

found in appendix F figure F.1. Questions seven, eight, eleven and fourteen to seventeen are used by

DE to make the information sources about CSR for employees more efficient.

As mentioned in previous literature CSR has an impact on organizational commitment. Added to this

knowledge we know that CSR consists of several components. Combining all this knowledge, this

study wants to explore how every aspect of CSR contributes to organizational commitment. In the

next paragraph the way the data is analyzed is explained.

3.5 Data analysis

Firstly the data is checked for errors. After checking the control variables no deviations to what is

expected are found. At the check up of the dimension variables twenty-five cases are excluded

because they did not fill in the ranking questions correctly. The respondents did not use every

number between one and four only once. In the final check of the ranking to the complete model of

aspects another amount of thirteen cases are excluded because they did not use every number

between one and twelve only once. These cases are deleted ‘case listwise’ (Pallant, 2010), which

Master Thesis T.A.M. Wijnants

Influence of CSR Aspects on Organizational Commitment

24

means they are completely deleted from the data set, not only for the missing value.

The reason to do is to prevent that respondents are only partly influencing the data. After a review

for normality of the measures, fourteen outliers were also deleted from the data set. With these

deviations deleted the error free sample contained 247 respondents. That is more than the 243

respondents needed to make the research for 90% reliable with a 5% confidence interval to the

complete population of 2229.

To check the reliability of the scales used to measure organizational commitment the Cronbach’s

Alpha is checked for every measure of the aspects separately and the dimensions separately. When

the measures are checked on reliability the data variances of the data are compared using a one-way

between-groups analysis of variance (ANOVA) to compare groups. One-way means the comparison

of one independent value which has a number of different levels on the dependent variable. These

levels correspond in this case to the different aspects of a dimension on organizational commitment.

Between-groups means that every group contains different respondents. The assumptions needed to

perform ANOVAs are tested for these measures. The ANOVAs are used to research whether there are

significant differences between the variances of organizational commitment between the aspects of

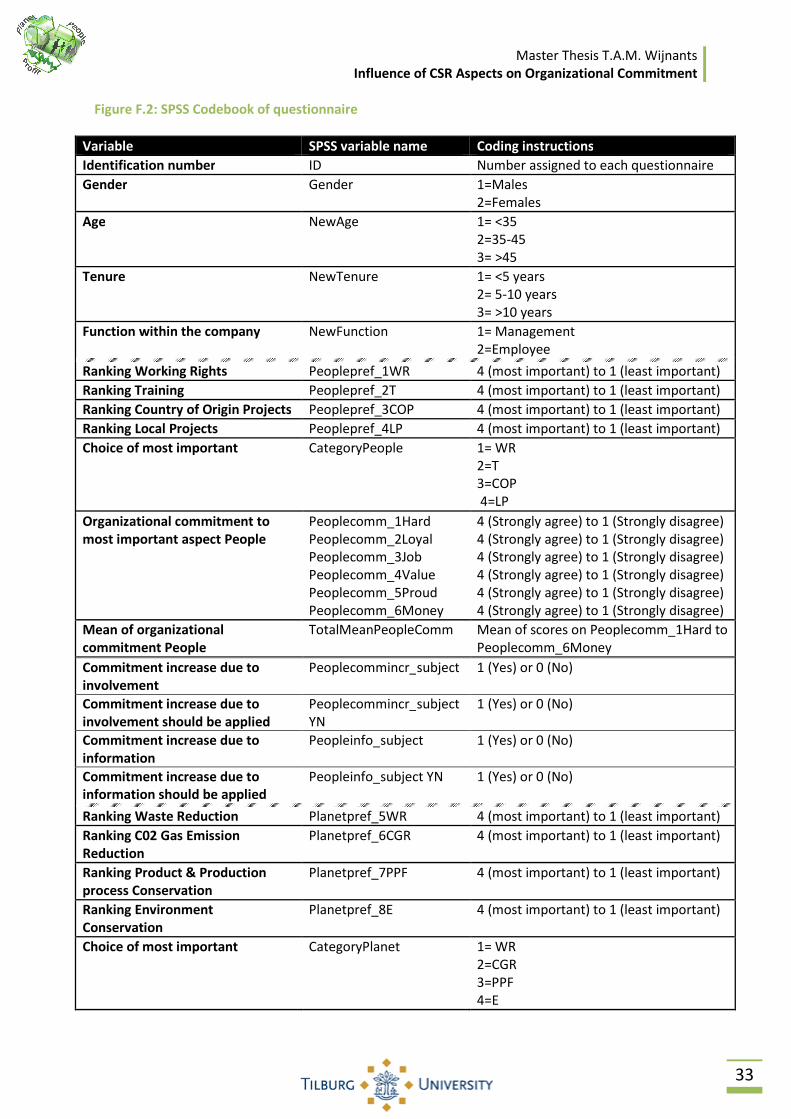

CSR. The data is analyzed using SPSS and the codebook of the data set is shown in Appendix F figure

F.2. Now it is clear how the research is composed and conducted the results and analysis are handled

in the next chapter.

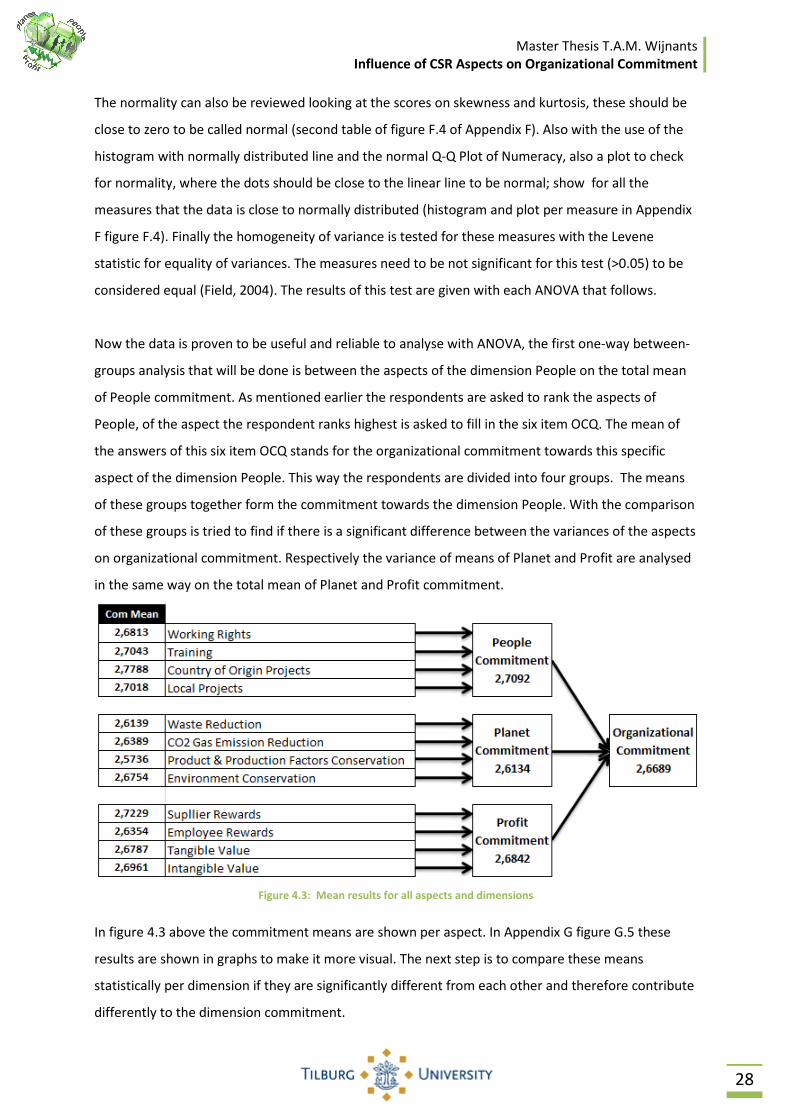

4: Results and Analysis

In this chapter the direct result of the questionnaires will be given and the analysis of the obtained

data will be illustrated. First the results for the descriptive statistics of the control variables will be

given and analysed in paragraph 4.1. Secondly the results of the ranking questions will be given in

paragraph 4.2, followed by the analysis of the OCQ measure and the differences between the aspects

per dimension in paragraph 4.3 and 4.4. Then the results of the information questions of the

questionnaire will be handled in paragraph 4.5 to close the chapter with further interesting analysis

on differences between groups of the data in paragraph 4.6.

Master Thesis T.A.M. Wijnants

Influence of CSR Aspects on Organizational Commitment

25

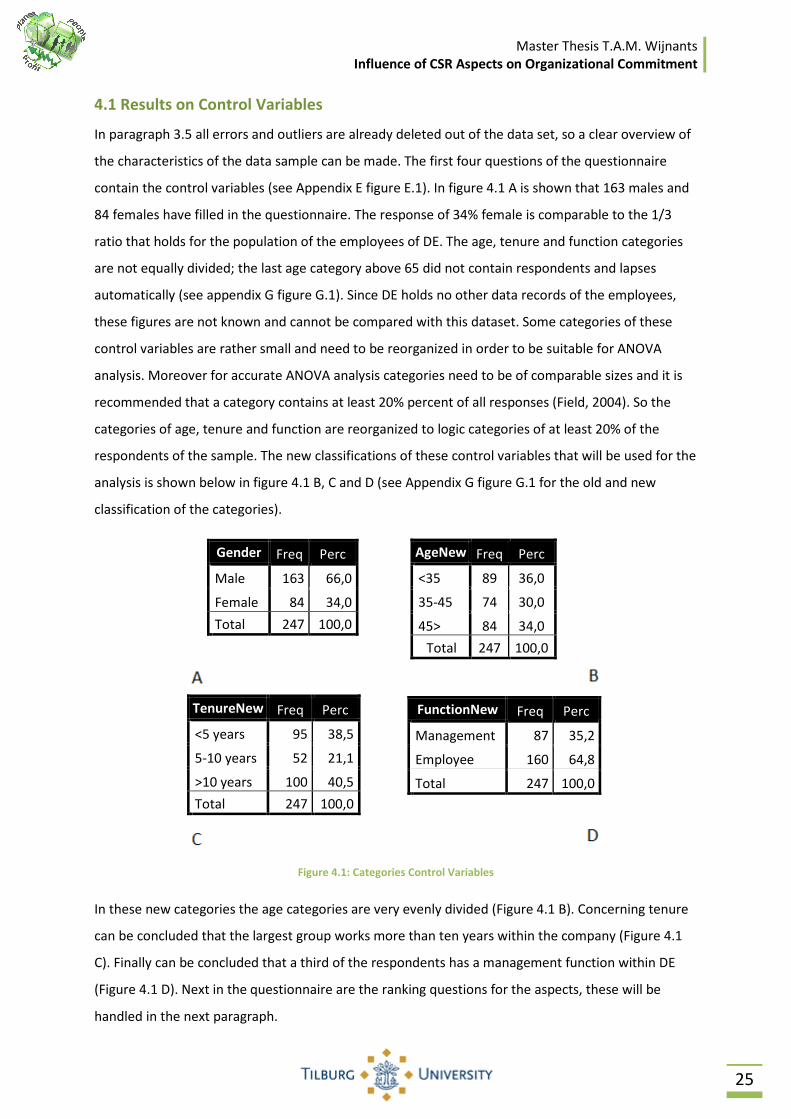

4.1 Results on Control Variables

In paragraph 3.5 all errors and outliers are already deleted out of the data set, so a clear overview of

the characteristics of the data sample can be made. The first four questions of the questionnaire

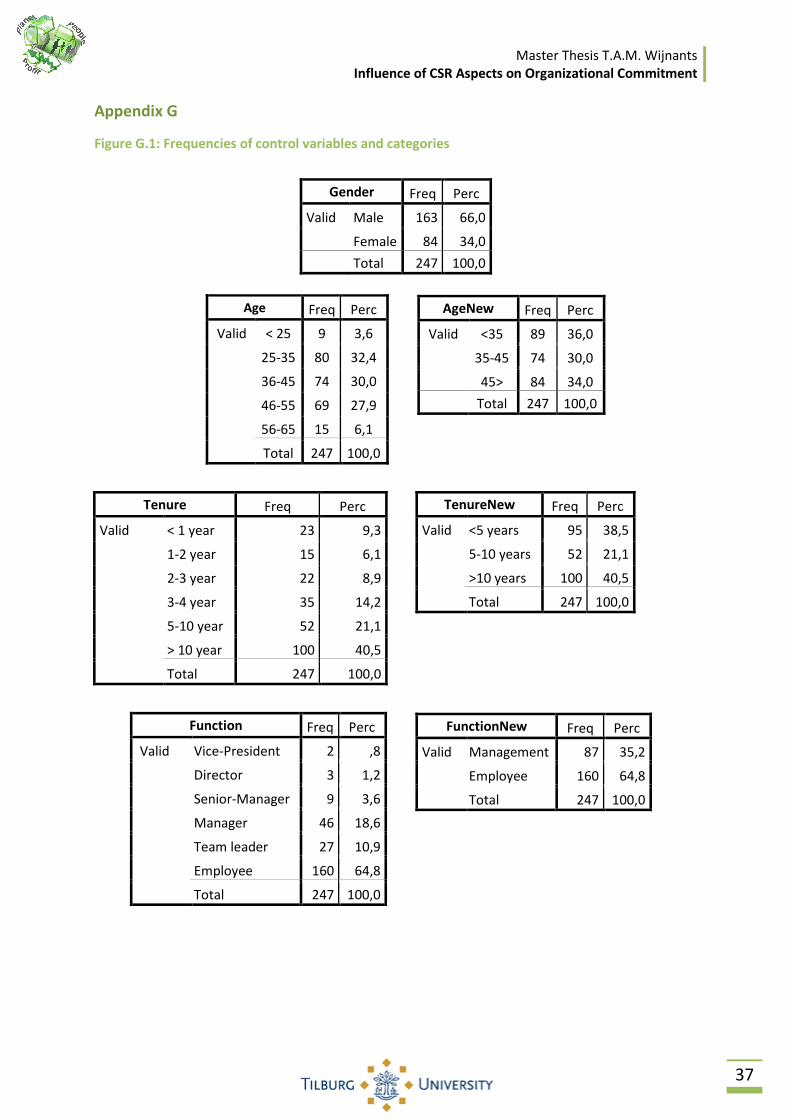

contain the control variables (see Appendix E figure E.1). In figure 4.1 A is shown that 163 males and

84 females have filled in the questionnaire. The response of 34% female is comparable to the 1/3

ratio that holds for the population of the employees of DE. The age, tenure and function categories

are not equally divided; the last age category above 65 did not contain respondents and lapses

automatically (see appendix G figure G.1). Since DE holds no other data records of the employees,

these figures are not known and cannot be compared with this dataset. Some categories of these

control variables are rather small and need to be reorganized in order to be suitable for ANOVA

analysis. Moreover for accurate ANOVA analysis categories need to be of comparable sizes and it is

recommended that a category contains at least 20% percent of all responses (Field, 2004). So the

categories of age, tenure and function are reorganized to logic categories of at least 20% of the

respondents of the sample. The new classifications of these control variables that will be used for the

analysis is shown below in figure 4.1 B, C and D (see Appendix G figure G.1 for the old and new

classification of the categories).

Figure 4.1: Categories Control Variables

In these new categories the age categories are very evenly divided (Figure 4.1 B). Concerning tenure

can be concluded that the largest group works more than ten years within the company (Figure 4.1

C). Finally can be concluded that a third of the respondents has a management function within DE

(Figure 4.1 D). Next in the questionnaire are the ranking questions for the aspects, these will be

handled in the next paragraph.

AgeNew Freq Perc

<35 89 36,0

35-45 74 30,0

45> 84 34,0

Total 247 100,0

Gender Freq Perc

Male 163 66,0

Female 84 34,0

Total 247 100,0

TenureNew Freq Perc

<5 years 95 38,5

5-10 years 52 21,1

>10 years 100 40,5

Total 247 100,0

FunctionNew Freq Perc

Management 87 35,2

Employee 160 64,8

Total 247 100,0

Master Thesis T.A.M. Wijnants

Influence of CSR Aspects on Organizational Commitment

26

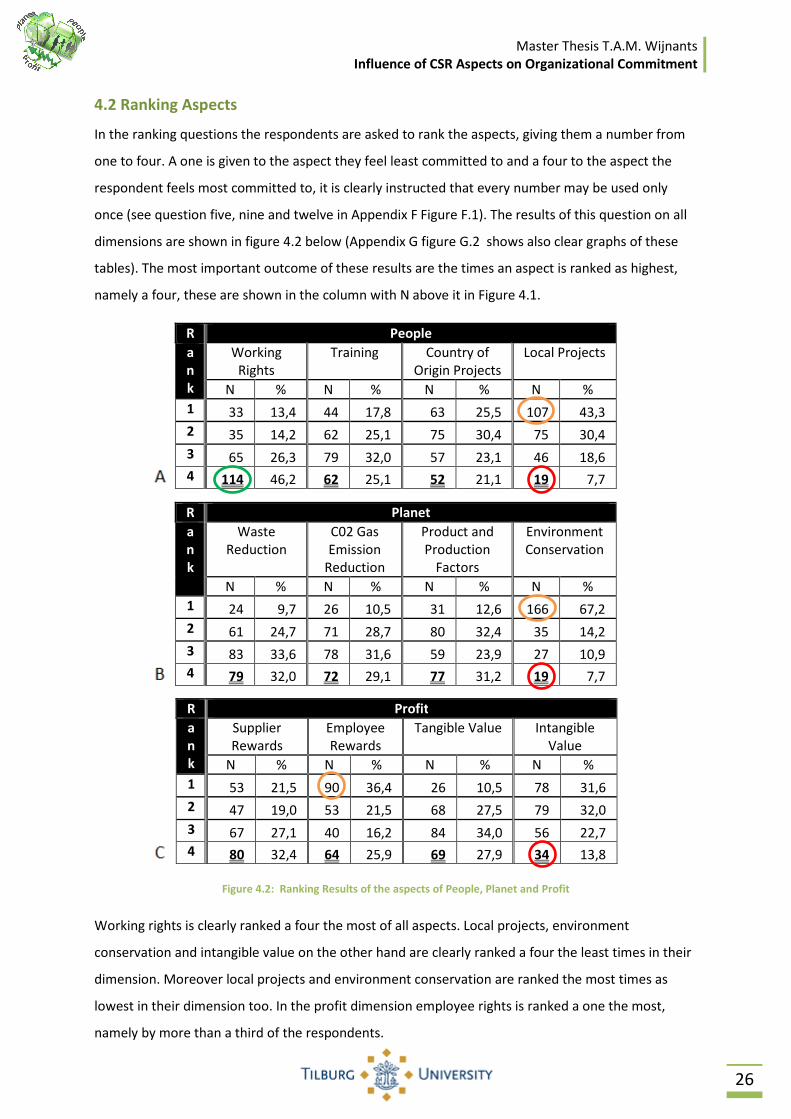

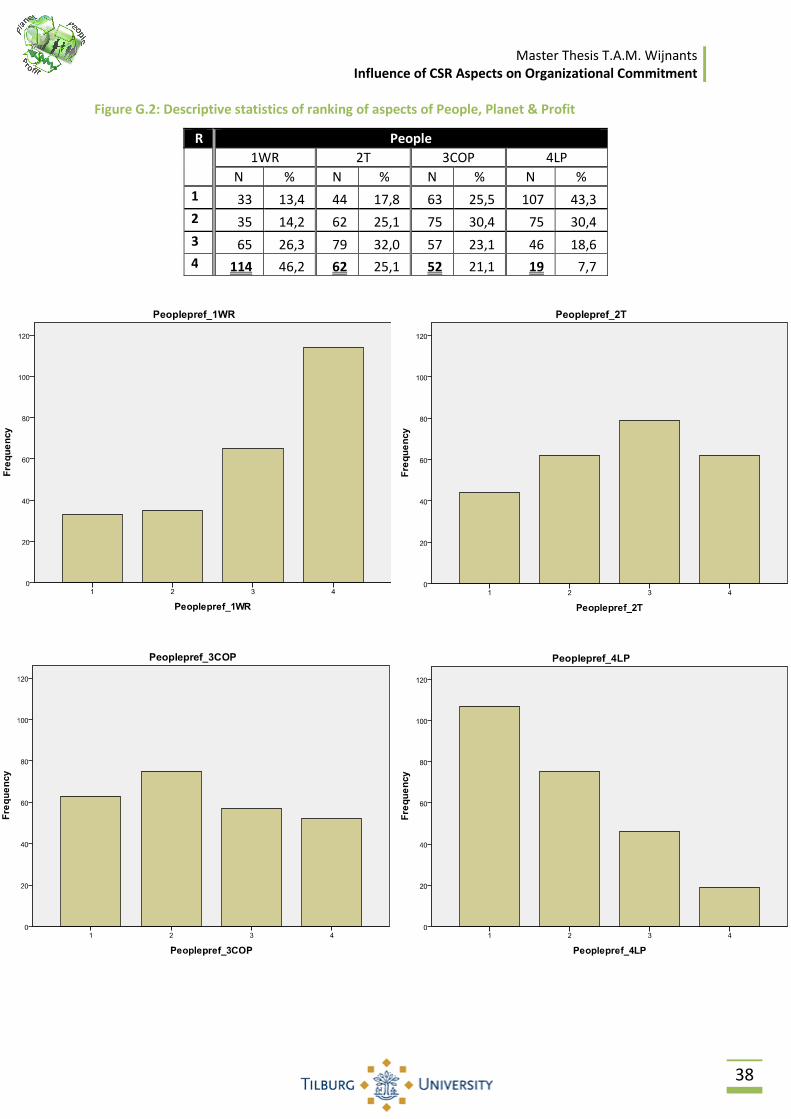

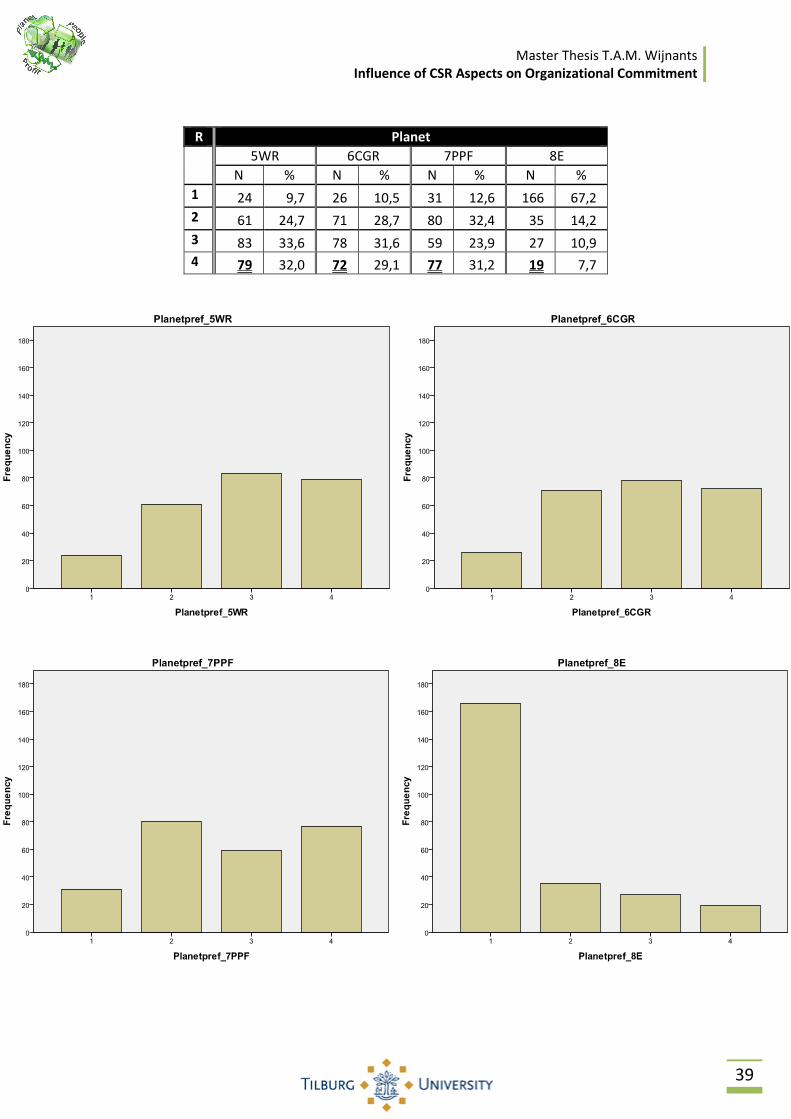

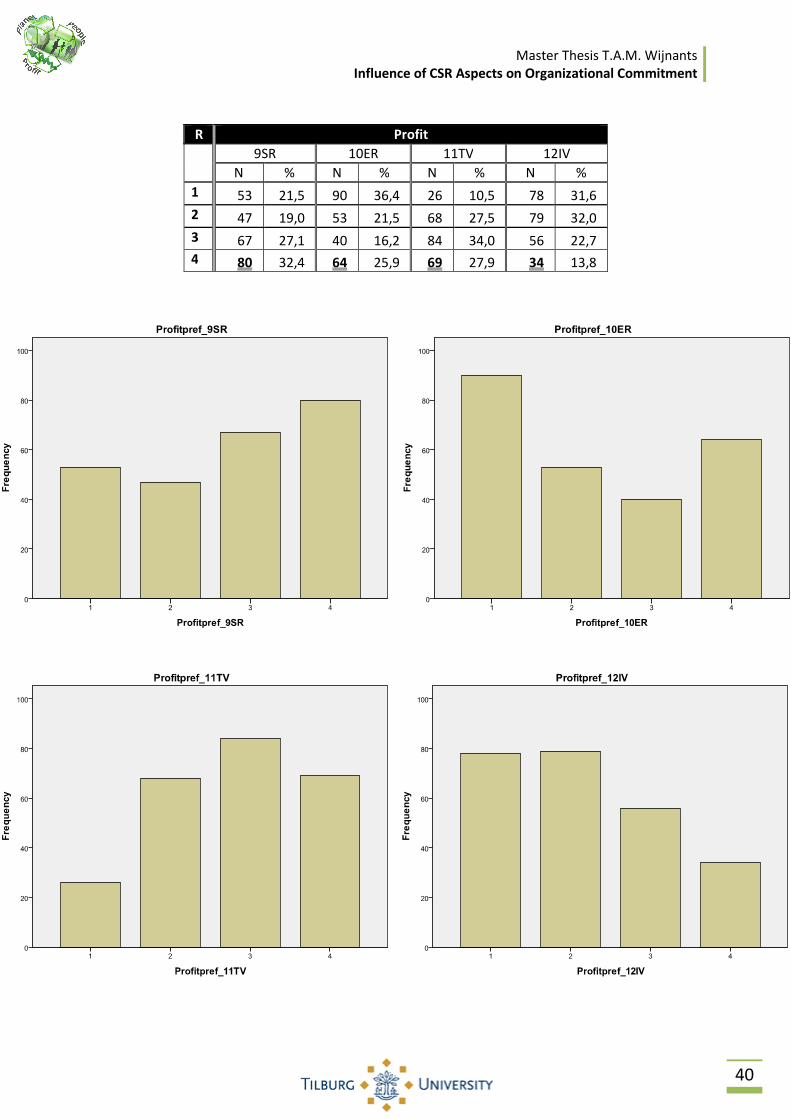

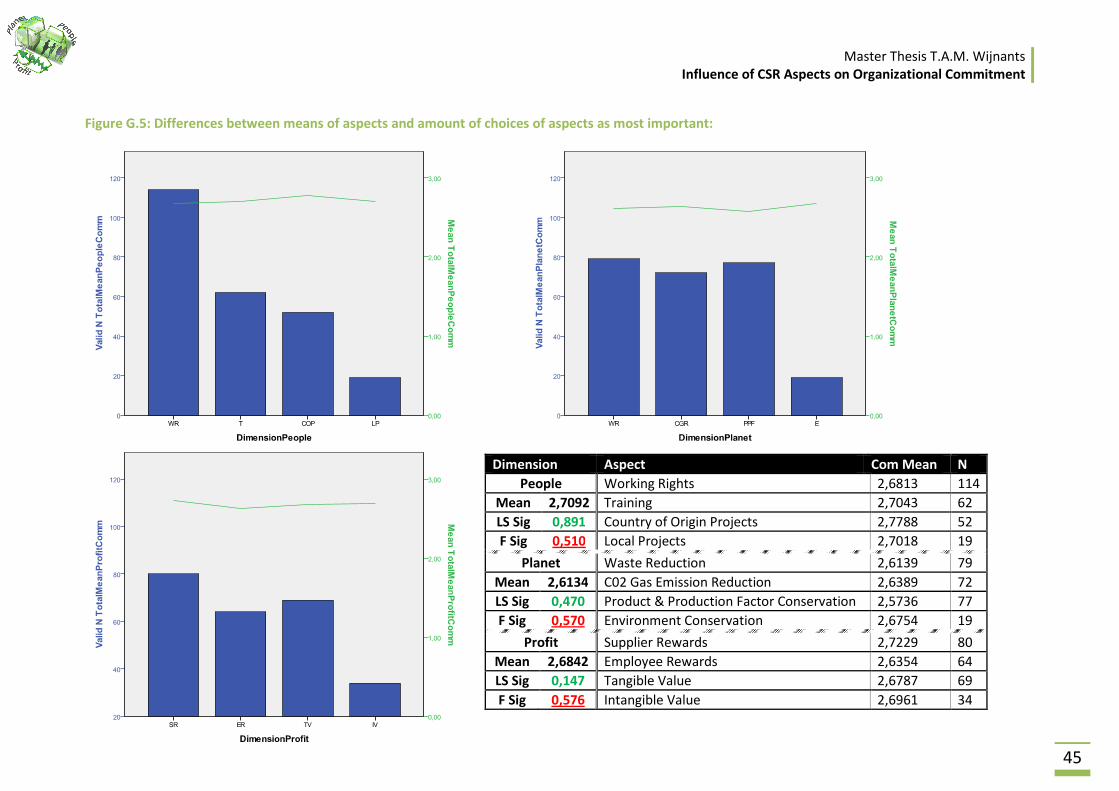

4.2 Ranking Aspects

In the ranking questions the respondents are asked to rank the aspects, giving them a number from

one to four. A one is given to the aspect they feel least committed to and a four to the aspect the

respondent feels most committed to, it is clearly instructed that every number may be used only

once (see question five, nine and twelve in Appendix F Figure F.1). The results of this question on all

dimensions are shown in figure 4.2 below (Appendix G figure G.2 shows also clear graphs of these

tables). The most important outcome of these results are the times an aspect is ranked as highest,

namely a four, these are shown in the column with N above it in Figure 4.1.

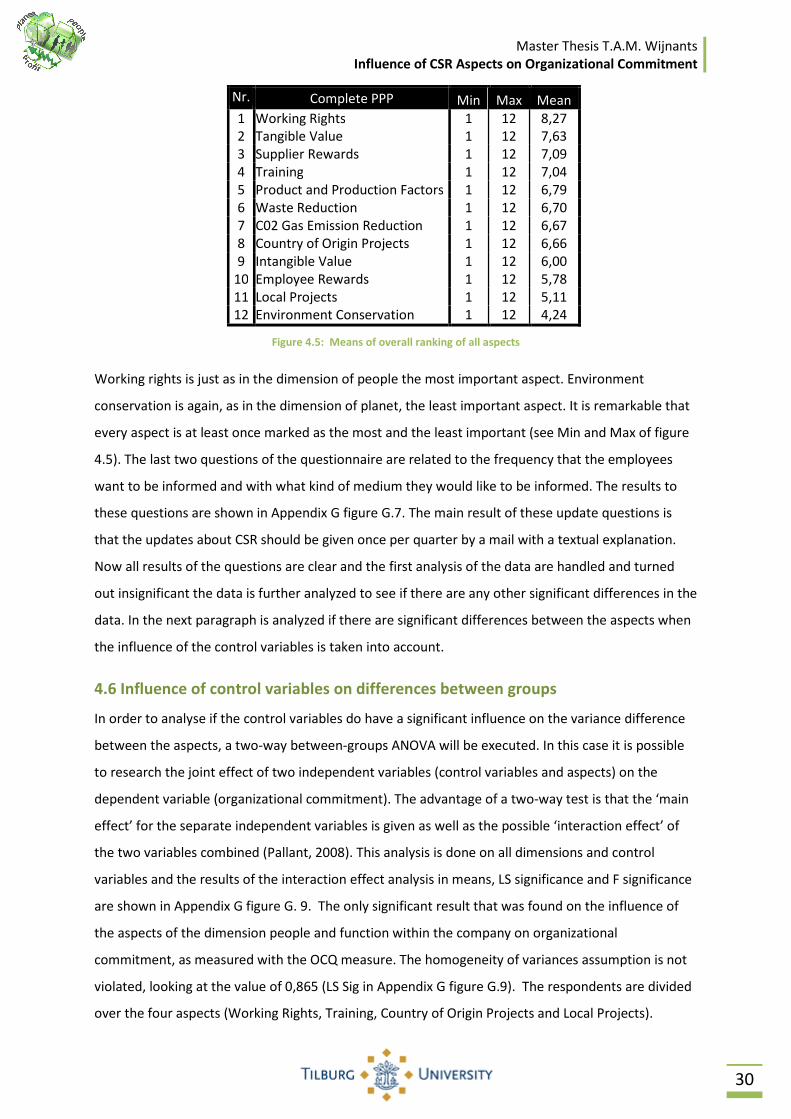

Figure 4.2: Ranking Results of the aspects of People, Planet and Profit

Working rights is clearly ranked a four the most of all aspects. Local projects, environment

conservation and intangible value on the other hand are clearly ranked a four the least times in their

dimension. Moreover local projects and environment conservation are ranked the most times as

lowest in their dimension too. In the profit dimension employee rights is ranked a one the most,

namely by more than a third of the respondents.

R People

a

n

k

Working

Rights

Training Country of

Origin Projects

Local Projects

N % N % N % N %

1 33 13,4 44 17,8 63 25,5 107 43,3

2 35 14,2 62 25,1 75 30,4 75 30,4

3 65 26,3 79 32,0 57 23,1 46 18,6

4 114 46,2 62 25,1 52 21,1 19 7,7

R Planet

a

n

k

Waste

Reduction

C02 Gas

Emission

Reduction

Product and

Production

Factors

Environment

Conservation

N % N % N % N %

1 24 9,7 26 10,5 31 12,6 166 67,2

2 61 24,7 71 28,7 80 32,4 35 14,2

3 83 33,6 78 31,6 59 23,9 27 10,9

4 79 32,0 72 29,1 77 31,2 19 7,7

R Profit

a

n

k

Supplier

Rewards

Employee

Rewards

Tangible Value Intangible

Value

N % N % N % N %

1 53 21,5 90 36,4 26 10,5 78 31,6

2 47 19,0 53 21,5 68 27,5 79 32,0

3 67 27,1 40 16,2 84 34,0 56 22,7

4 80 32,4 64 25,9 69 27,9 34 13,8

Master Thesis T.A.M. Wijnants

Influence of CSR Aspects on Organizational Commitment

27

In the next question the respondent is asked to fill in the six item OCQ measure for the aspect he

ranked with a four. In the next paragraph the results of these OCQ are checked for their reliability.

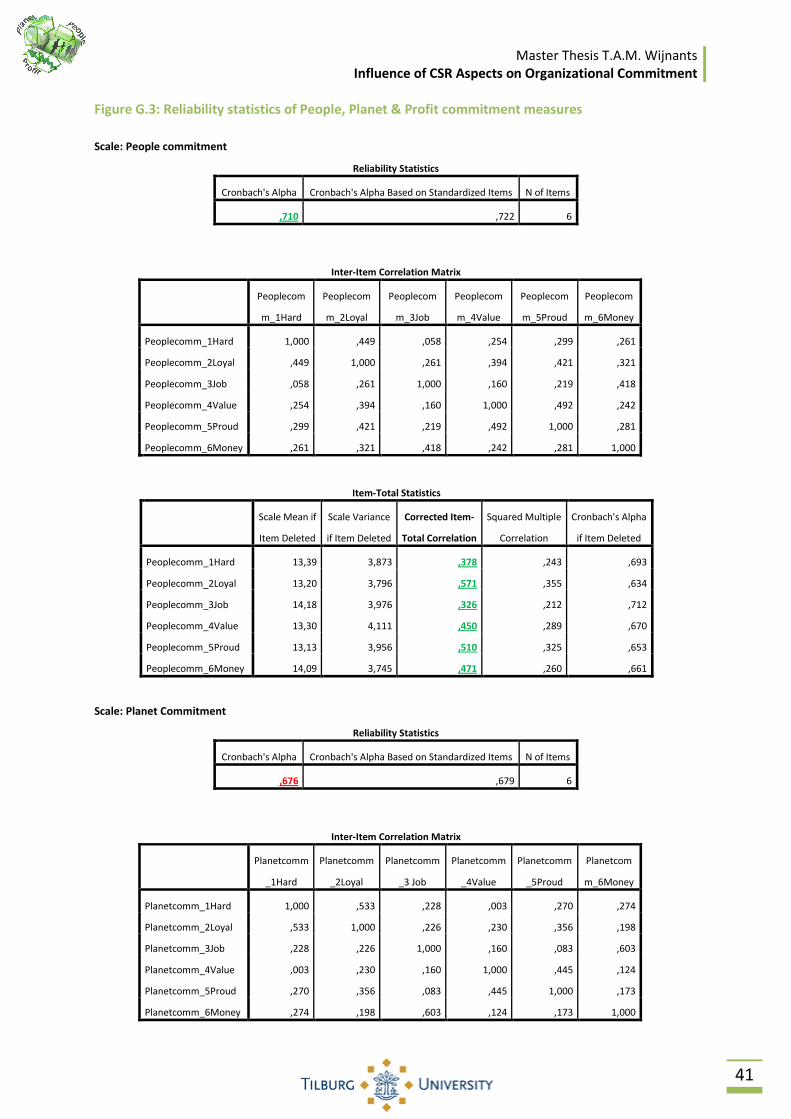

4.3 Reliability OCQ Measures

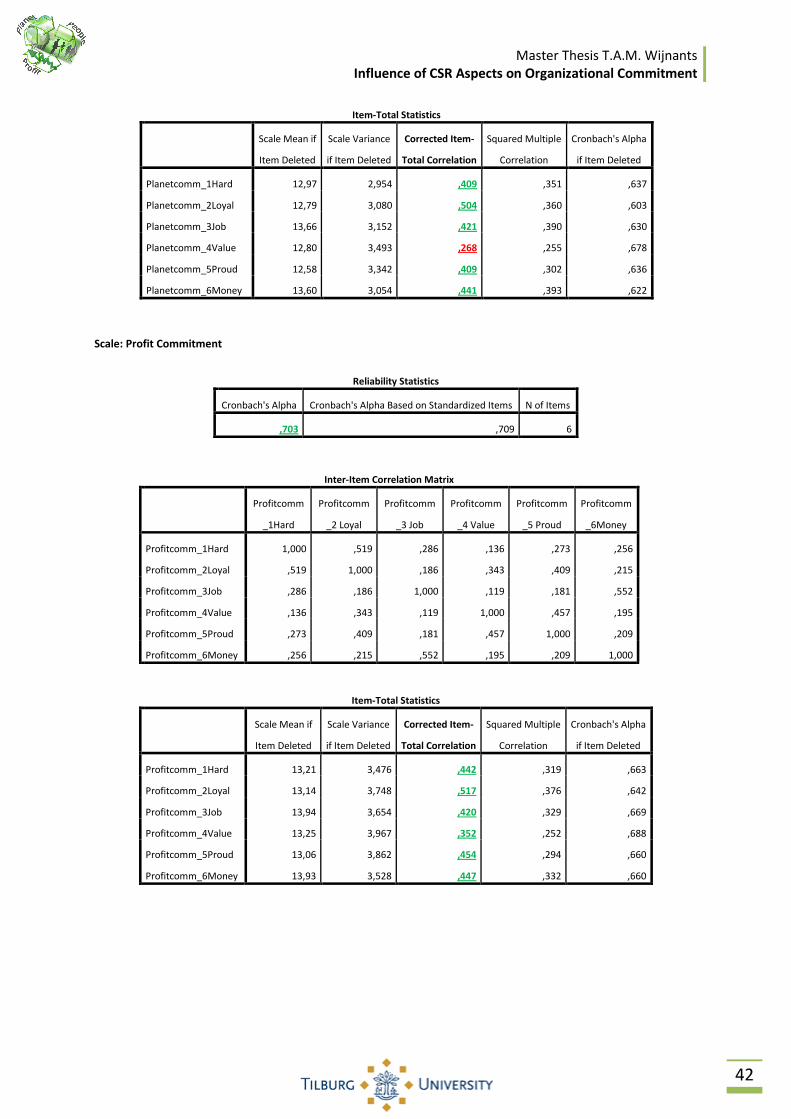

The OCQ measures for People, Planet and Profit commitment are tested for their reliability (see

Appendix G figure G.3 for the tables). The Cronbach’s Alpha for People commitment is 0,710 for

Planet commitment 0,676 and for Profit commitment 0,703. A Cronbach’s Alpha value shows the

internal consistency of a measurement tool, in other words it indicates to which extent a number of

items in a test measure the same concept. Scores higher than 0,7 are considered as acceptable (Field,

2004). Since no scores in the correlation matrix are negative, suggesting the items measure

something different, all these items measure the same characteristic. Also practical every item scores

more than 0,3 on the corrected Item-Total Correlation which also points to the fact that all items

measure the same subject (Pallant, 2010). Despite the lower score on Planet commitment and the

below 0,3 score of the ‘value item’ in this specific measurement the construct will be considered as

generally reliable because the influence when this item is deleted is minimal to the construct. And

since this construct is used before in prior research and scored an acceptable Cronbach’s Alpha of

0,74 the construct is considered as a reliable measure for organizational commitment. Since the

OCQ measures are considered reliable the organizational commitment scores on the different

aspects are going to be compared using ANOVA in the next paragraph.

4.4 One-way between groups ANOVA for aspects on organizational commitment

ANOVA is short for Analysis of Variances and compares the variances of different groups if the differ

from one another and therefore perfectly suitable for this research. In order to be able to perform an

ANOVA some assumptions must be applicable to the data. The data has to be measured at an

interval or ratio level. The sampling of a measurement needs to be random and the observations

need to be independent to perform ANOVA. Finally the distribution of the data needs to be normal

and the variability of the scores for each group needs to be similar, also called ‘Homogeneity of

variance’ (Pallant et al., 2010; Field, 2004). The commitment measure in this research is measured

with a four-point Likert scale which is a scale on an interval level. Since this research is mailed to the

respondents and filled in separately by the first 299 respondents, the assumptions of the data being

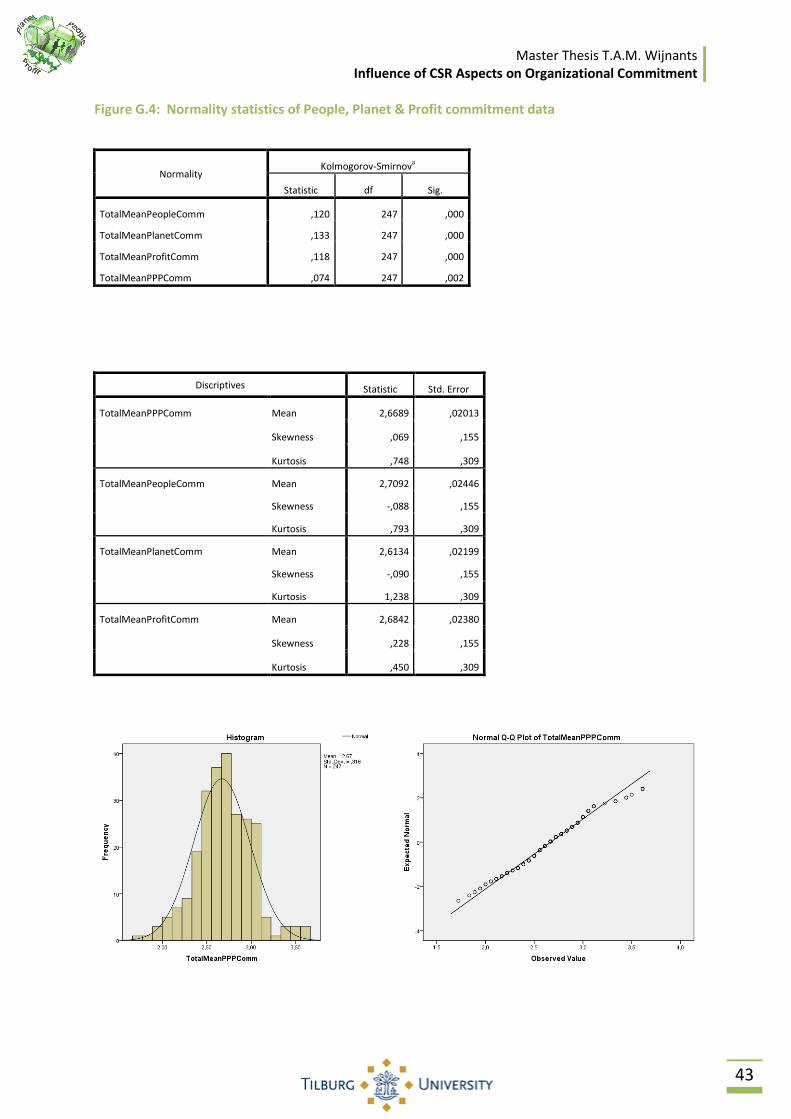

independent and random holds for this research. For normality the measures are tested using the

Kolmogorov-Smirnov test. This test controls if a distribution is normal around the expected value. As

you can see in the first table of figure G.3 of appendix G, the measures violate this assumption since

the significance is below 0.05. The violation of normality should not cause problems with large

samples (>30) at least if there close to normally distributed (Pallant 2010).

Master Thesis T.A.M. Wijnants

Influence of CSR Aspects on Organizational Commitment

28

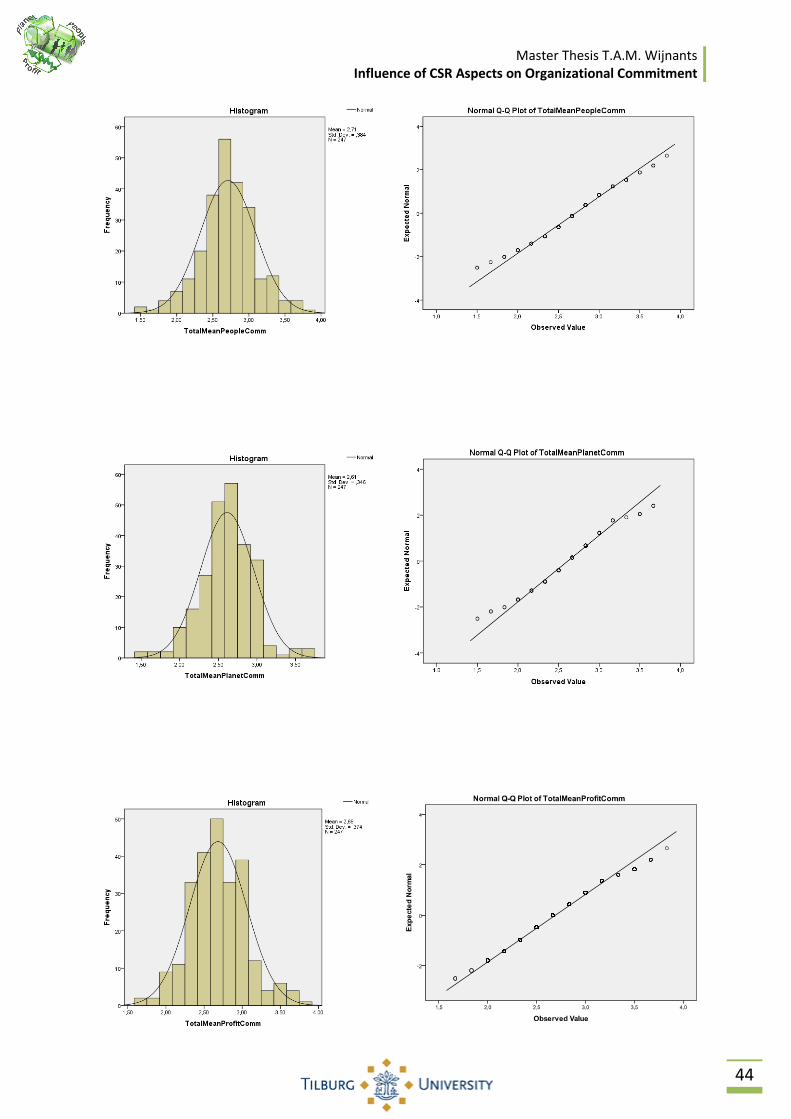

The normality can also be reviewed looking at the scores on skewness and kurtosis, these should be

close to zero to be called normal (second table of figure F.4 of Appendix F). Also with the use of the

histogram with normally distributed line and the normal Q-Q Plot of Numeracy, also a plot to check

for normality, where the dots should be close to the linear line to be normal; show for all the

measures that the data is close to normally distributed (histogram and plot per measure in Appendix

F figure F.4). Finally the homogeneity of variance is tested for these measures with the Levene