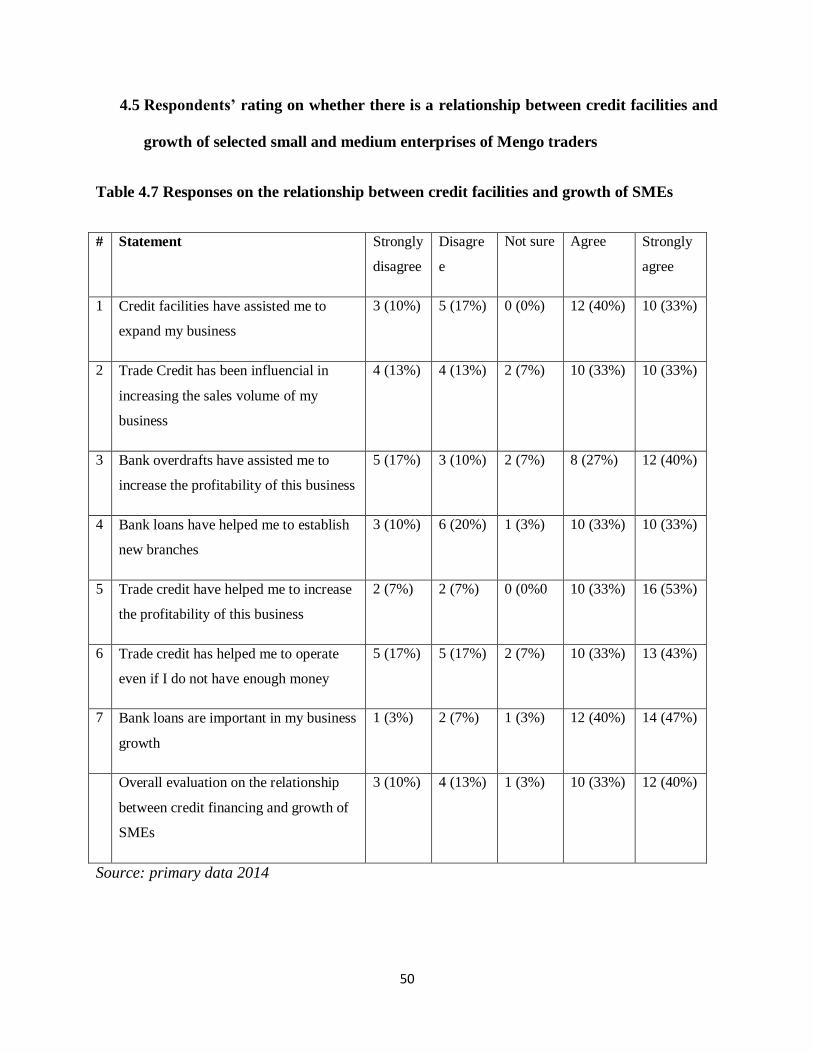

credit financing and growth of smes

TRANSCRIPT

i

CREDIT FINANCING AND THE GROWTH OF SMALL AND

MEDIUM ENTERPRISES

A case of selected Small and Medium Enterprises in Mengo trading center

BY

SIMON PETER KYOMUHENDO

Reg No. 11/2/330/E/1366

A RESEARCH REPORT SUBMITTED TO THE FACULTY OF BUSINESS ADMINISTRATION

IN PARTIAL FULFILLMENT OF THE REQUIREMENTS FOR THE AWARD OF A

BACHELOR OF SCIENCE IN ACCOUNTING AND FINANCE DEGREE OF NDEJJE

UNIVERSITY

APRIL 2014

ii

DECLARATION

I SIMON PETER KYOMUHENDO Registration Number 11/2/330/E/1366,

declare that this is my original work and has never been presented to any university

or higher institution of learning

Signature; ………………….

Simon Peter Kyomuhendo

Date; ……………………

iii

APPROVAL

I confirm that the work reported in this research was carried out by the candidate

Mr. Simon Peter Kyomuhendo under my supervision

Signature………………………. Date………………………………

Dr. Henry Buwule Musoke

Senior Lecturer, Ndejje University

iv

DEDICATION

I would like to dedicate this research report to my dear mother Nakibuka Mary

Gorretti Mwesigwa, my beautiful sisters Rachael Sebowa Tumusiime, Asiimwe

Lydia, Katushabe Oliver, Kyakuhaire Hellen, Mirembe Jacinta, as well as my

brothers Mwesigwa Steven Junior and Muhumuza David. Who tirelessly

encouraged and supported me financially, spiritually and materially throughout the

entire course of study.

v

ACKNOWLEDGEMENT

I would like to extend my sincere gratitude to my research supervisor, Dr Henry

Buwule Musoke, for the tireless support, assistance and encouragement that has

helped me to come up with this study.

Special thanks goes to my fellow students especially members of family 28,

lecturers, Staffs and the entire management of Ndejje University, for the positive

critiquing and driving motivation.

Furthermore, I thank my family most especially my mother Mary Gorretti

Nakibuka, my sisters Rachael Sebowa Tumusiime and Asiimwe Sarah Lydia as

well as my Brother Mwesigwa Steven Junior, all of who has supported me

financially, emotionally and materially through this study

Finally, I thank the Almighty God for His grace, love, peace and guidance, because

without Him, I would not have done anything.

vi

ABSTRACT

This study was conducted to find out the relationship between credit financing and the growth of

Small and Medium Enterprises in Mengo trading center.

The study was set to address the following specific objectives: to examine the nature of credit

financing facilities offered to the small and medium enterprises at Mengo treading centre, to

determine the level of growth of small and medium enterprises at Mengo trading centre, to

determine the relationship between credit financing facilities and growth of small and medium

enterprises.

The researcher used a descriptive and analytical research design to establish a relationship

between the two variables and to exhaust all areas in the research.

A sample size of 30 Small and Medium Enterprises from Mengo Trading center was used and

sampled. Questionnaires and interviews were used to collect data which were processed by

tabulation, and also narrations inform of description were accounted for easy understanding of

the findings.

The findings indicated that 70% respondents were in agreement that credit financing is very

important for the growth of their businesses.

The overall evaluation of the study found out a positive relationship between credit financing and

growth of Small and Medium Enterprises in Mengo trading center.

The study concludes that credit financing facilities are very paramount for the growth of Small

and Medium Enterprises.

The study recommended that among other things, there is need to revise the lending policies,

terms and conditions for loans, so that they favor the Small and Medium Enterprises. In addition,

the interest rates on loans need to be reduced.

vii

LIST OF TABLES

Table 4.1; Respondents’ gender ………………………………………………………………28

Table 4.2; Respondents’ age ………………………………………………………………….33

Table 4.3; Respondents’ education levels ……………………………………………………34

Table 4.4 Respondents’ years of working with the SME ……………………………………31

Table 4.5 credit financing ……………………………………………………………………32

Table 4.6; Response on growth of SMEs ……………………………………………………37

Table 4.7 Response on the relationship between credit financing and growth of SMEs ……40

Table 4.8; Correlation ………………………………………………………………………..43

viii

LIST OF FIGURES

Figure 1; Conceptual framework …………………………………………………………….7

Figure 4.1; Respondent’s gender …………………………………………………………..28

Figure 4.2; Respondent’s age ………………………………………………………………29

Figure 4.3; Respondents’ education level ………………………………………………….34

i

TABLE OF CONTENTS

DECLARATION ................................................................................................................................... ii

APPROVAL ......................................................................................................................................... iii

DEDICATION ...................................................................................................................................... iv

ACKNOWLEDGEMENT ..................................................................................................................... v

ABSTRACT .......................................................................................................................................... vi

LIST OF TABLES ................................................................................................................................ vii

LIST OF FIGURES ...............................................................................................................................viii

CHAPTER ONE .................................................................................................................................... 1

INTRODUCTION. ................................................................................................................................ 1

Back ground to the study ......................................................................................................................... 1

Statement of the problem ....................................................................................................................... 3

Objectives of the study ........................................................................................................................... 4

General objective..................................................................................................................................... 4

Specific objectives .................................................................................................................................. 4

Research questions ................................................................................................................................. 5

Scope of the study ................................................................................................................................... 5

Time scope ............................................................................................................................................. 5

Geographical scope ................................................................................................................................. 5

Subject scope ......................................................................................................................................... 6

Significance of the study ......................................................................................................................... 6

Conceptual frame work ........................................................................................................................... 7

Operational definition of key terms .......................................................................................................... 8

CHAPTER TWO................................................................................................................................. 10

LITERATURE REVIEW ...................................................................................................................... 10

2.1Introduction ...................................................................................................................................... 10

Small and medium enterprises in Uganda .............................................................................................. 10

The concept of credit financing. ............................................................................................................. 11

Sources of credit .................................................................................................................................... 13

Bank loans............................................................................................................................................ 14

Types of bank loans ............................................................................................................................... 14

Secured loans ....................................................................................................................................... 14

Unsecured loans ................................................................................................................................... 15

ii

Transaction loans.................................................................................................................................. 15

Trade credit ........................................................................................................................................... 16

Bank Overdraft facility ......................................................................................................................... 16

Business growth .................................................................................................................................... 17

Indicators of growth in SME’s ............................................................................................................... 17

Business expansion............................................................................................................................... 18

Sales volume increase ............................................................................................................................ 18

Increased profitability ........................................................................................................................... 19

Increase in the market share ................................................................................................................... 20

Relationships between Credit Financing and Growth of SMEs. .............................................................. 20

Credit financing and growth of SMEs ................................................................................................... 20

Bank loans and growth of SMEs ............................................................................................................ 20

Trade credit and growth of SMEs .......................................................................................................... 23

Bank overdrafts and growth of SMES ................................................................................................... 24

Summary of Literature. .......................................................................................................................... 24

CHAPTER THREE............................................................................................................................. 26

METHODOLOGY ................................................................................................................................ 26

Introduction ........................................................................................................................................... 26

Research design ..................................................................................................................................... 26

Survey population ................................................................................................................................. 26

Sample size, sampling procedures and Sampling design ......................................................................... 27

Sample size ........................................................................................................................................... 27

Sampling design .................................................................................................................................... 27

Data collection procedures ..................................................................................................................... 28

Data Methods collection, Methods, sources, and Instruments ............................................................... 28

Data sources .......................................................................................................................................... 28

Primary data ......................................................................................................................................... 28

Secondary data ..................................................................................................................................... 28

Data collection method ......................................................................................................................... 29

Administering Questionnaires ............................................................................................................... 29

Data collection instruments ................................................................................................................... 29

Self-administered questionnaires ........................................................................................................... 29

iii

Interview guides .................................................................................................................................... 29

Limitations of the study ......................................................................................................................... 31

CHAPTER FOUR ............................................................................................................................... 32

PRESENTATION AND DISCUSSION OF THE FINDINGS ........................................................... 32

Introduction .......................................................................................................................................... 32

Demographic Characteristics of Respondents ........................................................................................ 32

Age group (gender) ............................................................................................................................... 33

Respondents’ age group ........................................................................................................................ 34

Level of Education ................................................................................................................................. 36

Ownership of the SME ........................................................................................................................... 37

Line category of business ....................................................................................................................... 38

Duration the employees have been in the firm ...................................................................................... 39

Credit financing ..................................................................................................................................... 40

The relationship between credit financing and growth of SMEs. ............................................................ 53

CHAPTER FIVE ................................................................................................................................. 54

SUMMARY OF FINDINGS, CONCLUSION AND RECOMMENDATION .................................. 54

5.0 Introduction ................................................................................................................................... 54

Summary of key findings ....................................................................................................................... 54

Credit financing facilities. ...................................................................................................................... 54

Growth of SMEs in Mengo trading center .............................................................................................. 55

Relationship between micro finance activities and performance of small scale businesses ...................... 55

Recommendations ................................................................................................................................. 56

Areas for further research ...................................................................................................................... 57

REFERENCES .................................................................................................................................... 58

APPENDIX A; INTRODUCTORY LETTER .................................................................................... 60

APPENDIX B; QUESTIONNAIRE .................................................................................................... 61

1

CHAPTER ONE

1.0INTRODUCTION.

This chapter gives the background of the study, statement of the problem, purpose of the study,

objectives, research questions, scope of the study, significance of the study and the conceptual

framework. In the recent years, many authors have emphasized on the role of credit facilities on

the growth and the general performance of Small and Medium Enterprises (SMEs).

Many Non-Government organizations and other government organizations have struggled to

make sure that small and Medium Enterprises (SMEs) flourish. Despite their efforts and the

different political campaigns to end the poverty endemic, these efforts have realized both

positive and negative impacts. This study therefore will explore the relationship between credit

financing and the growth of small and Medium Enterprises (SMEs).

1.1Back ground to the study

Credit financing is a strategy that involves borrowing money from a lender with the

understanding that the full amount will be paid in future usually with an interest (Stearns, 1997).

He further says that credit financing involves any money or financial instrument extended to the

borrower by the lender from which the later expects a refund of both principal and interest. The

interest rate charged on the borrowed funds reflects the level of the risk that the lender

undertakes when securing the loan. Kakuru (2000) argues that credit financing includes both

secured and unsecured loans. He further says that security for the loans involves a form of

collateral as an assurance for the loan. Therefore if the debtor defaults on the loan, that collateral

is forfeited to satisfy payment of the debt.

2

Growth of small and medium enterprises SMEs involves increased level of output, increased

number of employee performance, increased level of creativity and innovation, industrial

restructuring and wealth generation in both developing and developed economies Uganda

Investment Report (UIA, 2008). According to Matly and Westhead (2005), healthy and growing

SMEs are perceived to be crucial for sustainable competitive and economic development at local,

regional and national levels.

In Uganda, SME’s are enterprises employing more than 5 but mot exceeding a maximum of

50employees, with the value of assets, including land, building and working capital of less than

Ug.shs 50 million (US$ 30,000) and annual income turnover of between Ug.shs10-50 million

(US$ 6,000-30,000) (Kasekende and Opondo, 2003).

Small and medium enterprises are businesses which are independently owned and operated by a

few individuals. They can be defined in terms of sales volume and number of employees in the

business indicated by structural development, profitability and employment levels. They mainly

engage in buying produce, market vending, catering and confectionery, shop keeping, second

hand clothing, health/herbal services, secretarial services, telephone services, handicraft,

transport and many others Uganda Bureau of Statistics report (UBOS, 2004).

Mengo traders finance their businesses with commercial banks loans, overdrafts, leasing

facilities, trade financing and loans from money lenders. These loans are taken in different loan

sizes and their repayment period differs depending on the lending authority. Although traders are

exposed to all these credit financing options, most of them have failed to grow and expand and

profitability has remained low meaning credit financing has not made a positive impact on the

businesses in that area. It has been attributed that poor credit financing caused by lack of

3

collateral security, low rate of repayment, high deficiency rates, and poor business plans might

be discouraging the financial institutions to offer them credit services (UIA report, 2008).

1.2Statement of the problem

Credit financing directly affects the growth of small and medium enterprises (Padey, 2000).

Proper management of debts lead to growth and smooth operation of businesses and poor

management of debts will not only cripple the ability of commercial banks and other lending

institutions to offer credit facilities to small and medium enterprises but threatens their

profitability and survival (UIA Report, 2008).

Traders in Mengo trading center finance their businesses with loans from commercial banks,

overdrafts, leasing facilities, trade financing and money lenders. These loans are taken in

different loan sizes and their repayment period differs depending on the lending authority.

Traders either take group or individual loans depending on the size of the loans and the purpose

to which these loans are to be put and the progress of each group or individual in the lending

cycle. The loan sizes also depend on the collateral security and the capacity of the group or

individual to pay (UIA report, 2008).

Despite the fact that a lot of efforts have been put in providing Mengo traders with bank loans

and trade credit as a form of credit financing to promote their growth, this has not been the case

as majority lack collateral security, many are offered small loan sizes with high interest rates,

short loan periods, the rapidly growing inflation rate and high deficiency. This discourages the

financial institutions to offer them credit services thus threatening their profitability survival and

ability to grow. As a failure to perform their operations, many traders have lost their businesses

since they cannot be sustained with their own equity.

4

It is likely that the cause of low growth of small and medium enterprises could be due to

inadequate funding, planning, limited credit financing (UIA Report, 2008).

The study therefore sought to investigate the effect of credit financing on the growth of small and

medium enterprises.

1.3 Objectives of the study

1.3.1 General objective

The general objective of the study was to investigate the relationship between credit financing

and the growth of selected small and medium enterprises in Mengo, Lubaga division, Kampala

district.

1.3.2 Specific objectives

The study was guided by the following specific objectives:

1. To examine the nature of credit financing facilities offered to the small and medium

enterprises at Mengo treading centre

2. To determine the level of growth of small and medium enterprises at Mengo trading

centre

3. To determine the relationship between credit financing facilities and growth of small

and medium enterprises.

5

1.4 Research questions

What is the nature of credit financing facilities offered to the small and medium enterprises at

Mengo treading centre?

What is the effect of credit financing on growth of small and medium enterprises at Mengo treading

centre?

What is the relationship between credit financing facilities and growth of small and medium

enterprises?

1.5 Scope of the study

1.5.1 Time scope

The study covered a period of two years starting from 2012 - 2014. This period was chosen

because it was long enough to enable the researcher to analyse the relationship between credit

financing and growth of Small and Medium Enterprises.

1.5.2 Geographical scope

The study was carried out from Mengo trading centre, Rubaga Division Kampala District of

Uganda. This area was considered because it was within the researchers’ area of location, that is

between the location of the university and the area of residence of the researcher thus being

convenient in terms of data collection.

6

1.5.3 Subject scope

The study covered the concept of credit facilities as the independent variable and the dependent

variable was growth of Small and Medium Enterprises (SME’s). It examined credit financing

components which were conceptualized as; bank loans, trade credits and bank overdrafts. The

dependent variable which was the growth of small and medium enterprises was conceptualized

through indicators like profitability, sales volume increase, increased product range and

expansion of small and medium enterprises

1.6 Significance of the study

1. The study was to help provide an up-to-date literature on the relationship between access

to credit facilities and the growth of small and medium enterprises to future researchers.

2. The result of the study could assist policy makers to determine whether provision of

micro credit by credit institutions can foster the growth of SMEs.

3. The research findings if published would provide necessary guide lines to government

and financial institutions hence leading to the improvement in service delivery

4. The study could also help small and medium enterprises to learn how to improve their

conditions in order to overcome the challenges in the credit market so as to achieve

sustainable development.

7

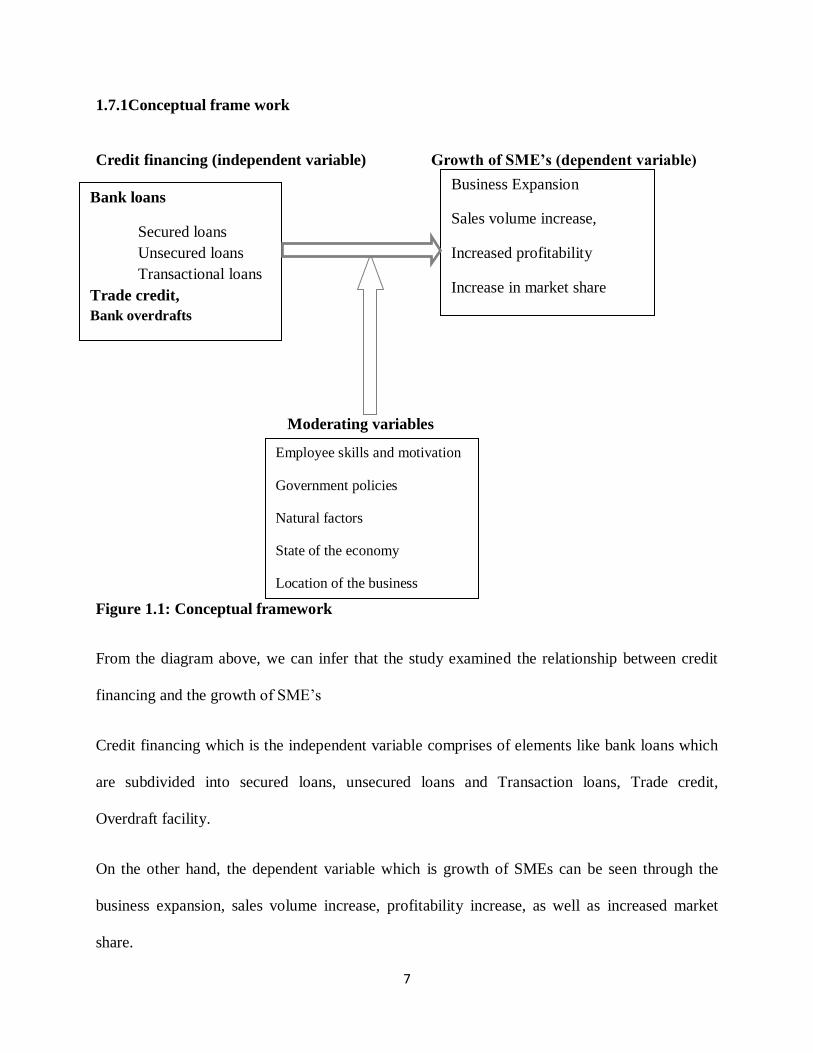

1.7.1Conceptual frame work

Credit financing (independent variable) Growth of SME’s (dependent variable)

Moderating variables

Figure 1.1: Conceptual framework

From the diagram above, we can infer that the study examined the relationship between credit

financing and the growth of SME’s

Credit financing which is the independent variable comprises of elements like bank loans which

are subdivided into secured loans, unsecured loans and Transaction loans, Trade credit,

Overdraft facility.

On the other hand, the dependent variable which is growth of SMEs can be seen through the

business expansion, sales volume increase, profitability increase, as well as increased market

share.

Bank loans

Secured loans

Unsecured loans

Transactional loans

Trade credit,

Bank overdrafts

Business Expansion

Sales volume increase,

Increased profitability

Increase in market share

Employee skills and motivation

Government policies

Natural factors

State of the economy

Location of the business

8

Furthermore, the intervening variables in the relationship between independent variable and

dependent variable included, employee motivation and skills, government policies, natural

factors, state of the economy, location of the business, among others

1.7.2 Operational definition of key terms

Credit financing: For the purpose of this study, credit financing refers to type of loan or any

financial assistance made to a business or corporate finance context. Specific types of credit

facilities are: revolving credit, term loans, committed facilities, letters of credit and most retail

credit accounts.

Small and Medium Enterprises (SME’s)In Uganda, SME’s are enterprises employing not

more than maximum of 50employees, with the value of assets, including land, building and

working capital of less than Ug.shs 50 million (US$ 30,000) and annual income turnover of

between Ug.shs10-50 million (US$ 6,000-30,000) (Kasekende and Opondo, 2003). Small

enterprises outnumber large companies by a wide margin and also employ many more people.

SMEs are also said to be responsible for driving innovation and competition in many economic

sectors.

Uganda Investment Authority (UIA). The Uganda Investment Authority (UIA) is a semi-

autonomous government agency operating in partnership with the private sector and Government

of Uganda to drive national economic growth and development.

Business growth- For the purpose of this study, growth as the ability of an organization to meet

required standards in its operations, increase its market share, improve its facilities, increase its

9

profitability and ensure return on investments to its shareholders, and also witness total waste

reduction through optimal capacity utilization and operational efficiency.

Micro finance institutions (MFIs) Bank of Uganda defines MFIs as non-government

institutions, saving and credit corporations that provide savings and micro loans not exceeding us

$1000 to poor individuals, enterprises or groups for purpose of engaging in viable economic

activities where there are difficulties in accessing financial services from the formal banking

sector.

10

CHAPTER TWO

LITERATURE REVIEW

2.1Introduction

In this chapter a theoretical and practical relationship between credit financing and growth of

small and medium enterprises was looked at as studied by different authors. In so doing the

subject of inquiry was extracted in light with the previous conducted research and scholarly

work.

2.2 Small and medium enterprises in Uganda

SMEs are widely defined in terms of their characteristics, which include the size of the capital

investment, the number of employees, the turnover, the management style, the location and the

market share (Okello et al, 2007). There is no generally agreed definition of SMEs globally.

Different researchers and policy makers (Kasekende, 2001; Mwenda and Muuka, 2004; MOF,

2001) have used different definitions for SMEs. The number of persons employed, investment in

plant and machinery and sales turnover are all used to define SMEs (Najjemba, 2000)

However, international organizations such as the World Bank and the International Finance

Corporations (2002), define SMEs as enterprises that require small amounts of capita to

establish, small number of employees or in most cases personally handled by the owner, and

referred to as micro-businesses hence to them, they are “mini businesses” or “Bop businesses”

Country context plays a major role in determining the nature of these characteristics, especially,

the size of investment in capital accumulation and the number of employees. For developing

countries, SMEs would generally mean enterprises with less than 50 workers.

11

In Uganda, SME’s are enterprises employing not more than maximum of 50employees, with the

value of assets, including land, building and working capital of less than Ug.shs 50 million (US$

30,000) and annual income turnover of between Ug.shs10-50 million (US$ 6,000-30,000)

(Kasekende and Opondo, 2003). These SMEs are in farming, buying produce, market vending,

catering and confectionary, shop keeping, second hand clothes and shoes, health services,

stationary among others. Majority of these businesses operate in shared premises and start

operations before acquiring licenses (Byaruhanga, 2012)

2.3The concept of credit financing.

A credit is borrowing money from an outside source with a promise to return the principal in

addition to an agreed upon level of interest. The most popular source of credit financing is the

bank, but can also be issued by a private company or even a friend or a family member (Richard,

2009).

Ledger wood, 1999 and Wright, 1999: Micro finance is the provision of financial services to low

income clients or solidarity lending groups including consumers and the self-employed who

traditionally lack access to banking and related services from most formal financial institutions

because of their business savings level and credit needs are small. These financial services

commonly take the form of loans (microcredit) and micro-savings, though some microfinance

institutions will offer other services such as micro-insurance and payment services, deposit

taking, retail financing services, consultancy and training in business management to catch up

with competition. Others are money transfer, safe custody of valuable items, health care schemes

and salary based loan products. They lend to the poor who have few assets that cannot be secured

by a bank as collateral (Hernando de Soto polar, 1989). MFIs in Uganda include money lenders,

micro finance agencies, NGOs, rural farmers schemes and savings societies.

12

Credit financing is a strategy that involves borrowing money from a lender with an

understanding that full amount will be paid in future with an interest (Stearns, 1997). He

emphasizes that credit financing is basically money that you borrow to run your business being

divided into two categories based on the type of loan you are seeking either long term or short

term credit financing. Long term credit financing usually applies to assets your business is

purchasing such as equipment, buildings, land, or machinery. With long term credit financing,

the scheduled repayment of the loan and the estimated useful life of the assets extends over more

than one year. Short term credit financing usually applies to money needed for the day-to-day

operations of the business such as purchasing inventory, supplies or paying the wages of

employees. Short term credit financing is referred to as an operating loan or short term loan

because the scheduled repayment takes place in less than one year.

Hansen, 2000 said that MFIs could act as an efficient vehicle for the intermediation of finance

institutions and the small scale enterprises. Micro finance provides the needed opportunity for

entrepreneurs to start or improve business in order to make profit and improve their lives (Allan

et al., 2008; Brana, 2008; Lans et al., 2008; Majumdar, 2008; Roslan and Mohd, 2009; Salman,

2009; Shane 2003; Tata and Prasad 2008)

According to Enterprise Uganda report, 2003, credit financing is a useful strategy particularly for

small and medium enterprises with good credit history. However, the report further states that

small businesses should think carefully before committing their businesses to credit financing

options to avoid cash problems and reduced flexibility.

Women entrepreneurs mostly in developing countries have no easy access to credit for their

entrepreneurial activity and are the most vulnerable to poverty (Ibru, 2009; Iganiga, 2008;

13

Iheduru, 2002; Kuzilwa, 2005; Lakwo, 2007; May, 2007; Okpukpara, 2009). Majority of

Uganda’s MFIs clients are women; loans to female clients constitute around 75% of the loan

portfolio and 80% of the savings portfolio, MFPED 2000. This is because Women are thought to

benefit the whole family and strengthen role of women in society and women are proven to be

better loan payers (Wright et al 1999; Mutesasira et al 1999; Barnes et al., 1998). They are the

most beneficiaries from products offered by MFIs. They enhance their status financially socially

and even politically. Equip them with skills through training. Despite of this, micro finance

activities have shown little potential to thoroughly change existing inequalities in power relations

or the role of women in society (Buckley 1996; Goetz and Gupta 1996; Hulme and Mosley

1996).

MFIs advice small scale entrepreneurs on the viable business venture to undertake and on how

best to go about the operation of the business, this helps boost efficiency and their performance

thus enabling growth (Ledger wood, 1999).

2.4 Sources of credit

Any business regardless of its size may at one time or the other develops the need for credit

services in order for it to have sufficient capital in order to finance its operations. Such credit

may be short-term and long-term capital. Long term capital is normally required by businesses

for making long term investments such as buildings, machinery. Short term capital on the other

hand, is required essentially for financing the daily operations of the business (Kakuru, 2001).

14

2.4.1 Bank loans

In finance, a bank loan is a debt evidenced by a note which specifies, among other things, the

principal amount, interest rate, and date of repayment. A loan entails the reallocation of the

subject asset(s) for a period of time, between the lender and the borrower.

In a loan, the borrower initially receives or borrows an amount of money, called the principal,

from the lender, and is obligated to pay back or repay an equal amount of money to the lender at

a later time. Typically, the money is paid back in regular installments, or partial repayments; in

an annuity, each installment is the same amount.

The loan is generally provided at a cost, referred to as interest on the debt, which provides an

incentive for the lender to engage in the loan. In a legal loan, each of these obligations and

restrictions is enforced by contract, which can also place the borrower under additional

restrictions known as loan covenants. Although this article focuses on monetary loans, in

practice any material object might be lent (Vincent J. 1991).

2.4.2 Types of bank loans

2.4.2.1 Secured loans

A secured loan is a loan in which the borrower pledges some asset (e.g. a car or property) as

collateral. A mortgage loan is a very common type of debt instrument, used by many individuals

to purchase housing. In this arrangement, the money is used to purchase the property. The

financial institution, however, is given security, a lien on the title to the house, until the mortgage

is paid off in full. If the borrower defaults on the loan, the bank would have the legal right to

repossess the house and sell it, to recover sums owing to it.

15

2.4.2.2 Unsecured loans

Unsecured loans are monetary loans that are not secured against the borrower's assets. These

may be available from financial institutions under many different guises or marketing packages

which include but not limited to: credit card debt, personal loans, bank overdrafts, credit

facilities or lines of credit, corporate bonds (may be secured or unsecured)

The interest rates applicable to these different forms may vary depending on the lender and the

borrower. These may or may not be regulated by law. Interest rates on unsecured loans are nearly

always higher than for secured loans, because an unsecured lender's options for recourse against

the borrower in the event of default are severely limited. An unsecured lender must sue the

borrower, obtain a money judgment for breach of contract, and then pursue execution of the

judgment against the borrower's unencumbered assets (that is, the ones not already pledged to

secured lenders). In insolvency proceedings, secured lenders traditionally have priority over

unsecured lenders when a court divides up the borrower's assets. Thus, a higher interest rate

reflects the additional risk that in the event of insolvency, the debt may be uncollectible.

2.4.2.3 Transaction loans

According to Kakuru (2001), a transaction loan refers to a business dealing that is closed for a

particular period of time. There are some loans that can be obtained by the businessman for

general purpose and these can be referred to as general loans. Some of the costs that are

associated with these types of loans include interest, commitment fee, and compensatory

balance.

16

2.4.3 Trade credit

Trade credit arises in situations where the supplier do not require immediate payments for

whatever batches of goods and services that have been supplied to a business until the given

credit period. In other words, this is a short term source of credit and in most cases it is less than

one year and because it gives the firm the time to invest in the money it would have otherwise

use to pay the supplier and possibly pay more pressing expenses (Kakuru, 2001).

Trade credit contract terms as well as the volume of trade credit are important parts of trade

credit since they determine the implicit interest rate on trade credit, in other words the price of

trade credit. Contract terms include discounts for early payment, size of the discount, length of

the discount period, final payment due date, and late payment penalty fee. When the delivery and

payment do not occur at the same time, payment arrangements define credit terms (Ng. et al.

1999). The seller may require the payment before the delivery (CBD-cash before delivery) or

cash on delivery (COD), where the buyer bears most of the risk.

2.4.4 Bank Overdraft facility

This is a situation where owners of business ventures are allowed to overdraw their accounts. For

instance if a firm has something like 60 million shillings on its account, a financial institution to

which that businessman is a client may allow him or her to overdraw a maximum of 20m such

that at any one time, the firm can be able to tap a total of 40m from its account (Kakuru, 2001).

An overdraft can also be defined as an agreement where a customer can purchase goods on

account (without paying cash), paying the supplier at a later date. Usually when the goods are

delivered, a trade credit is given for a specific amount of days for example 30, 60 or 90 days.

17

Jewelry businesses sometimes extend credit to 180 days or longer. Basically, this is a credit a

company gives to another for the purchase of goods and services

The amount of days for which a credit is given is determined by the company allowing the credit,

and is agreed upon by both the company allowing the credit and the company receiving it. With

the extension of the payment date, the company receiving the credit essentially could sell the

goods and use the net proceeds to pay back the debt. This type of credit is sometimes given to

encourage sales. At times, a supplier may give a discount, if the customer pays within a certain

period of time.

2.5 Business growth

Ronstadt (2000) defined business growth as a company’s increase in its product sales, market

share, brand recognition, customer loyalty, opening of new branches through expansions and

acquisitions, an optimal capital structure and increased profitability and return on investments.

Balunywa (1998) looks at business growth as the ability of an organization to meet required

standards in its operations, increase its market share, improve its facilities, increase its

profitability and ensure return on investments to its shareholders, and also witness total waste

reduction through optimal capacity utilization and operational efficiency.

2.5.1 Indicators of growth in SME’s

The indictors of business growth include the following; increased sales and revenues. Increasing

sales and revenues should be experienced by the enterprise in the goods or services such a

company offers. For example, a company should be able to see a difference in production output

of one month from another and also increased output should be corresponding with increasing

18

demand for such products which results into increasing sales and revenues, month by month,

translating into year by year increases in production and sales (Ronstadt, 2000).

2.5.2 Business expansion

This is where a company expands its activities and not only occupies a large position of the

physical existing markets but also the biggest part of the consumers’ minds with what is being

offered by that company. Increasing market share may take the form of increasing sales by being

able to sell at lower prices than the competitors, increasing the range of products and product

lines, increasing distribution channels and sales outlets, boosting various marketing drives such

as vigorous advertising in all media available to essentially place an organization’s products in

the minds of the consumers among other significant activities (Balunywa, 1998).

2.5.3 Sales volume increase

Sales volume refers to the amount or number of units that are sold of a particular product or

service. Profits depend on growing sales and managing costs, which include variable and fixed

costs. Variable costs depend on sales volumes because they involve direct raw materials and

labor costs. Small and large businesses incur fixed costs, even if they have no sales. Fixed costs

are constant at certain levels of production and sales. Outside of these levels, fixed costs may

vary with sales volumes. Sales are the lifeblood of any successful business. An increase in sales,

all other things equal, usually translates into higher profitability (Byaruhanga, 2012). Sales

volume refers to the number or quantity of products sold and can be expressed in either shillings

or percentage terms.

19

2.5.4 Increased profitability

A financially stable enterprise applies optimal use of both debt and owner’s equity and a

company which is no longer struggling with financial problems as most companies do is seen to

be setting off from its starting feet to greater business horizons thus looked at as a growing

company. Such a company will never lack funding since financial Institutions will start looking

at it as a potential client and they are ready to lend it money as need may be. On the other hand,

if the company does not want to employ so much debt in its business, it is easy to sale off its

shares and gets the required capital or funds and potential shareholders will come panting for the

offer (Sekajja, 1997). Growth in profitability is also one of the indicators of economic activity.

Such growth should be reflected in profitable enterprises, and conversion into medium or large

enterprises. In addition, SMEs growth can be measured in terms of profits. Profit making

organisations look at the rate of return on the resources of the firm (Pandey, 1996)

If the level of profits of the firm is high, then the company can retain some of the profits for

reinvestment (Yaron, Benjamin and Piprek, 1996). These are referred to as retained earnings

which are undistributed portions of the company that are regarded as a source of owned capital.

These profits are converted into reserves and used for the financing requirements of the

company. This process of re-investing a portion of the profits of the company is called pouching

back of profits or internal financing (Kakuru, 2001). Sandee (1999), Rural people do not make

enough profits that can be ploughed back for re/investment thus creating a barrier in financing

their business.

20

2.5.5 Increase in the market share

Growth of an SME can also be measured basing on the increase in the market share. According

to Kotler (2000), the company’s growth will be determined by the increase in rate of growth of

its market share. The increase in the market share will be reflected in the increased sales volume

and establishment of distributional channels for the goods and services to the target segment

2.6 Relationships between Credit Financing and Growth of SMEs.

2.6.1 Credit financing and growth of SMEs

Lack of access to credit financing may in one way or the other deter the growth and development

of small and medium enterprises simply because these proprietors may lack the ability to acquire

sufficient funds in order to finance their activities. Such phenomenon is most prevalent in areas

where there are no or sufficient bank outlets as compared to other businessmen in urban centers.

Even the few financial institutions that are available impose high interest rates on their loans

hence affecting the proper functioning of these SMEs.

2.6.2 Bank loans and growth of SMEs

The financing of small and medium enterprises (SMEs) has been a topic of keen interest in

recent years because of the key role that SMEs play in economic development and their

potentially important contribution to economic diversification and employment (Ayyagari et

al.,2007; Beck et al., 2005a). In developing economies including Sub-Saharan Africa, SMEs are

typically more credit-constrained than large firms, severely affecting their possibilities to grow

(Beck et al, 2005b; Beck and Demirguc-Kunt, 2006; Beck et al, 2006; Ayyagari et al, 2008; Beck

et al, 2008a; Ayyagari et al, 2012). As regards extending financing to SMEs, banks have an

important role to play in Sub-Saharan Africa due to their dominance in the financial systems and

21

the limitations of informal finance, especially as regards serving the higher end of the SME

market (Ayyagari et al, 2012). The evidence suggests that competition, especially as introduced

by innovators, is important to encourage banks to venture into the SME space and to move them

out of their comfort zone in countries like Uganda where high interest rates on Government

securities area disincentive to intensify lending to SMEs. Providing a conducive lending

environment and encouraging competition through allowing banks to innovate, for instance

through agency or mobile banking, seems to be an important role to play for Government.

Equally important is to ensure that an effective credit bureau is in operation, and that the

securitization and realization of (movable) collateral is efficient. Nevertheless, while a conducive

legal and regulatory framework is necessary to support SME lending over time, it is not

sufficient and growth can happen even if the enabling environment is still developing, as is the

case in Kenya. The extent to which commercial banks lend to SMEs depends on a range of

country- and bank-specific factors. Among the main factors impacting bank financing for SMEs

are inter alia the macroeconomic environment, the legal and regulatory framework, the state of

the financial sector infrastructure, bank-internal limitations in terms of capacity and technology,

and SME specific factors, particularly the SME landscape in terms of number, size, and focus of

operation, as well as the opaqueness of information (Berger and Udell, 1998; Beck et al, 2008b;

De la Torre et al, 2010; Beck et al, 2011). Due to the opaqueness of SMEs, i.e. the challenges

associated with ascertaining the reliability of information provided, it has conventionally been

assumed that small and domestic banks applying relationship lending are better equipped to lend

to SMEs (Berger and Udell, 1995; Berger et al, 2001; Mian 2006; among others). Recently,

however, this view has been challenged with the argument that large and foreign banks are also

22

able to lend to SMEs effectively by using arms-length technology and centralized organizational

structures (Berger and Udell, 2006; Berger et al, 2007; de la Torre et al, 2010; Beck et al, 2011).

Professor Dean Karlan of Yale University stated that many of the benefits from micro credit are

in fact loaned to people with existing businesses and not to those seeking to establish new

businesses, and to those who want to supplement the family income. Thus concludes that micro

finance was not necessarily bad and can generate some positive benefits, despite some lenders

charge a high interest (40- 60%). To further the point stated by Professor Karlan, micro financing

begets the general tendency of a small business initially supported on credit to gain profits with

time and generate micro savings. In his latest study, the famous two time Pulitzer Prize winner,

Nicholas Dona bet Kristof states that there is no evidence of any negative influence of micro

financing but countless examples of people now looking at the bigger picture and saving for

better things have surfaced.

Micro finance activities have capacity to reduce poverty, contribution to food security, change

social relations for the better and reduce vulnerability. Ishengoma, 2004 and Kimuyu, 2004

confirm the importance of SSB‟s access to productive resources (micro finance). They help poor

diversify their income sources, build up physical , human and social assets, focus on good money

management, rebuild household’s base of income and assets after economic shocks have

occurred and to smooth consumption (Sebstad and Chen, 1996; Hulme ,1998; Ito,1998; Cohen

,1997; Cohen, 1999). However most criticism of micro finance have actually been criticism of

micro credit, being delivered in the absence of other micro finance services such as savings,

remittances, payments and insurance. They charge high interest rates. For instance Mohammed

Yunus, 2008 argue that MFIs that charge more than 15% above their long-term operating costs

should face penalties and poor should be the beneficiaries of micro finance. Milford Bateman,

23

the author of Why doesn’t micro finance work? , argues that micro credit offers only an illusion

of poverty reduction and concludes that it is a development policy blunder of quite historic

proportions.

Micro credit can be used to acquire financial assets to expand business capital and generate more

profits, working capital, attain productive assets. Savings as a micro finance factor enable people

with few assets to save, since they could make weekly savings as well as contribute to group

savings, and such savings are mobilized by the MFIs for further lending to other clients and

finance small emergencies through holding small amounts held in highly liquid form (Mkpado

and Arene, 2007).

2.6.3 Trade credit and growth of SMEs

In a model without bank loans, Bougheas et al. (2009) show that, for a given liquidity, an

increase in production will require an increase in trade credit. A higher production is associated

with a higher production cost which, for a given (insufficient) amount of liquidity, implies that

these SMEs will need to take more trade credit. So trade credit works as an alternative mean to

finance production. Also Cu~nat (2007) argues that fast growing SMEs may finance themselves

with trade credit when other types of finance are not sufficiently available. Fisman and Love

(2003) extend the analysis to link trade credit substitutability for institutional financing and the

overall development of the financial sector. They find evidence that industries that use more

trade credit grow relatively faster in countries with poorly developed financial markets. More

empirical support of a link between trade credit and SME performance comes from Boissay and

Gropp (2007), who show that SMEs that are confronted with a liquidity shortage (shock) try to

overcome this distressed situation by passing on one fourth of the shock to their suppliers by

taking more trade credit.

24

2.6.4 Bank overdrafts and growth of SMES

Overdrafts have traditionally been a basic building block for small businesses, allowing them

some breathing space in their cash flow. Banks are being forced to hold more capital against the

loans they write, and that capital has to come from somewhere. Small business overdrafts are an

easy target for banks, as they can be withdrawn with little or no notice. In addition to reducing

the value of overdrafts being used by small businesses, banks have also been decreasing SMEs'

agreed overdraft facilities - the short-term credit lines available to businesses if needed. Says

Philip W (2002), "We have frequently heard from our customers in recent months that their

banks are lowering agreed overdraft limits, and creating situations where costs like VAT bills

can create an unnecessary cash flow crisis." This show how crucial it can be for businesses to

explore alternative forms of funding that can provide the flexibility they need. If businesses find

that their overdrafts disappear just when they need them most, it can unnecessarily threaten the

viability of otherwise healthy businesses. Philip White explains: "An overdraft can be withdrawn

by a bank at any time, meaning that any capital investment programme that relies upon one

doesn't have a solid foundation." "Asset finance, on the other hand, remains in place so long as

the business is able to keep up repayments on it. As the economy begins to recover and more

businesses look to invest in growth, it's important that they look beyond banks for the lending

they need."

2.5 Summary of Literature.

In final analysis, the role played by financial institutions in providing credit facilities has greatly

fostered the growth of small and medium enterprises and it cannot be under estimated as the

literature above reveals. However given the high level of inaccessibility of these business

25

enterprises mostly in developing countries, MFIs have made it difficult for the owners of small

and medium enterprises to access credit facilities and therefore this study is aimed at making a

clear analysis of the roles and contribution of these credit financing facilities towards the growth

of SMEs. Therefore, the two variables have a relationship.

26

CHAPTER THREE

METHODOLOGY

3.1 Introduction

This chapter contains the different methods that were used in data collection and it outlines the

research design, the survey population, the sampling design, sample size, data collection sources,

methods and instruments, data collection procedures that were used in selecting the sample, and

the methods of analyzing and disseminating the data.

3.2 Research design

A correlational, cross-sectional survey design which was analytical and descriptive in nature was

used. The study utilized a cross-sectional survey design because it is flexible in both quantitative

and qualitative data collection. This design enabled the study to be carried out at a particular time

and the notion of combining quantitative and qualitative data in a case study research offered the

promise of getting closer to the whole of a case in a way that a single method study cannot be

achieved. Quantitative data analysis was used to describe the statistics of the scores using indices

that describe the current situation and investigate the associations between the study variables

using information gained from the questionnaires. The researcher used both qualitative and

quantitative methods in order to enable all stakeholders and involved parties to understand the

study findings and recommendations.

3.3 Survey population

The study examined Small and Medium Enterprises in Mengo trading center. Then the survey

design consisted of manufacturing SMEs, restaurants, retail shops and boutiques. Different

respondents constituting business proprietors, employees of small and medium enterprises and

27

officials of the financial institutions that are operating in Mengo trading centre in Rubaga

division, Kampala district will constitute the study population.

3.4 Sample size, sampling procedures and Sampling design

3.4.1Sample size

Collecting the data from the entire population may not be possible because of the cost and time

that will be involved in collecting and analyzing it. The researcher therefore purposefully selected

respondents who own, manage, or run small and medium enterprises. The researcher employed a

sample size of 28 respondents from Mengo Sub County, which was the area of study. This

sample size was determined scientifically using the Krejcie and Morgan’s 1970 table because of

its simplicity in determining the sample size not forgetting the time factor.

3.4.2 Sampling procedure:

The study included only small scale businesses. These were numerous in number and found in

the informal sector that is everywhere in the country. For study purposes, Mengo trading center

was chosen. However the study was unable to reach the entire population in the named center.

The researcher stratified the population into five strata that is retail shops, manufacturing SMEs,

restaurant business, tailoring and boutiques. Random sampling was used to select the sampling

frame, they were allocated numbers that were written on papers shuffled and respondents where

got by picking a paper randomly until the required respondents were got.

3.4.3 Sampling design

The researcher purposely selected business owners due to the vital information they possess. He

further stratified the population into two strata, that is to say, managerial and non-managerial

staff to avoid any bias. Simple random sampling was used to select the respondents in each

28

stratum because of its simplicity. A list of managers with their subordinates was used to select

the sampling frame; they were allocated numbers written on small pieces of paper, mixed up and

respondents were selected by picking on a paper randomly until all the required number of

respondents are obtained.

3.5 Data collection procedures

The researcher will obtain an introductory letter from the Ndejje University which will be

presented to the Rubaga Division headquarters for permission to conduct this study. This will

assist in the pre-test. The Questionnaires will be administered to the respondents and they will

fill at their time of convenience and then collected after three weeks. During data collection, the

rights of individuals will be respected. . The pilot test will be carried out to ensure the validity

and reliability of the research instruments.

3.6 Data Methods collection, Methods, sources, and Instruments

3.6.1 Data sources

3.6.1.1 Primary data

This is data which is original that is it has not been worked on that is processed and analyzed,

still so fresh from the field. This was collected from owners of small and medium enterprises in

Mengo Sub County.

3.6.1.2 Secondary data

This is data which is already collected by other researchers. It is data which is not fresh from the

field; that is it has already been analyzed and processed and in most cases it is just referred to.

This data was got from textbooks, journals, internet and dissertations of Ndejje University.

29

3.6.2 Data collection method

The researcher used collected data through administering questionnaires, and interviews to

obtain up-to-date information.

3.6.2.2 Administering Questionnaires

The researcher collected data by administering questionnaires were the respondents filled them

and the researcher used responses to make conclusion.

3.6.2.2 Interviews

These involved face-to-face interactions with the respondents where the interviewer asked

questions that respondents answered.

3.6.3 Data collection instruments

Data will be collected using different instruments which include;

Self-administered questionnaires

Questionnaires were prepared and sent to selected respondents. The researcher comprehensively

explained to the respondents the purpose of the study within the questionnaire. The

questionnaires comprised of both structured and unstructured questions. Information was

gathered through the use of self- administered questionnaires using a 5 linkert scale of strongly

agree (5)-strongly disagree (1). Respondents were given questionnaires and guided on how to fill

the questions independently. The forms were returned after completion.

Interview guides

The researcher also used interview guides to collect data from the field. The respondents who

were interviewed included managers and non-managerial staff of small and medium enterprises

30

so as to get a general picture on the role of credit finance to the growth of small and medium

enterprises.

3.7.1 Data analysis

After collection of data, the researcher studied the responses from the questionnaires so as to

make sure that the information obtained is complete, consistent, accurate and reliable. Analysis

of the data was done using both qualitative and quantitative methods in order to make the

findings easy to understand and make conclusion to the stakeholders. Descriptive analysis was

done using MS- Excel. This is because Ms Excel could easily generated charts and graphs.

Quantitative data processed by coding and sorting it to ensure that they matched with study

objectives. After this, it was analyzed using SPSS and later interpretation derived using mean

scores which were later used to interpret the findings. SPSS was used because of its accuracy in

statistical data analysis and presentation A higher mean score for a positive statement meant that

majority of the respondents tended to agree with such a statement and vice versa. For negative

statements a lower mean score meant that majority of the respondents agreed to the statement

and vice versa. The researcher used Statistical Package for Social Scientists (SPSS) to establish

the relationship between the study variables. The data was tabulated and collected into

percentages, deriving frequency tables afterwards.

3.8 Ethical issues and considerations

Respondents who required for anonymity were granted it but were requested to sign a consent

form that was to be distributed with the questionnaires because the study was carried out in their

work place and sources to earn a living at times assistants were used to limit suspicious and

beliefs that the research was to cover up for competitors strategy. The introduction letter from the

31

university was used to reduce suspicions from MFIs officers and the traders and ease access to

information. The researcher was subject to the ethics approval of Ndejje University

3.9.1 Limitations of the study

The researcher was faced with a number of problems and challenges that included;

Time; Since the researcher was not on a full time programme, time was a limiting factor. Much

time was spent while carrying out interviews and many respondents were too busy while others

had limited time for the study.

Funds; Since the project was privately sponsored, funds to support activities like transport,

typing, printing, photocopy, binding, stationary, surfing on the internet and other activities were

not readily available. As a solution to this problem, the researcher mobilized some of his savings

and sought for some funds from friends and relatives so as to finish this study.

Limited literature; The researcher was faced with a problem of limited literature specific to the

subject under study. The researcher had to use Internet to access more data. Some of the

available data was old and outdated. Current data was obtained from traders, business owners

(entrepreneurs) and workers. Access to new material on Internet was not easy since some files

require one to had to have password and username in order to access them and they were at times

not easy to understand

32

CHAPTER FOUR

PRESENTATION AND DISCUSSION OF THE FINDINGS

4.1 Introduction

This Chapter is about presentation and discussion of the findings.

This presentation and discussion of the findings were done in relation to the study objectives.

The general objective was to identify the relationship between credit financing and the growth of

SMEs. The specific objectives included; to establish the nature of credit financing facilities

offered to the small and medium enterprises at Mengo trading centre, to determine the level of

growth of small and medium enterprises at Mengo trading centre and to determine the

relationship between credit financing facilities and growth of small and medium enterprises.

4.2 Demographic Characteristics of Respondents

The respondent’s basic information was looked at in terms of gender, group (age), number of

years working with the SME and level of education.

33

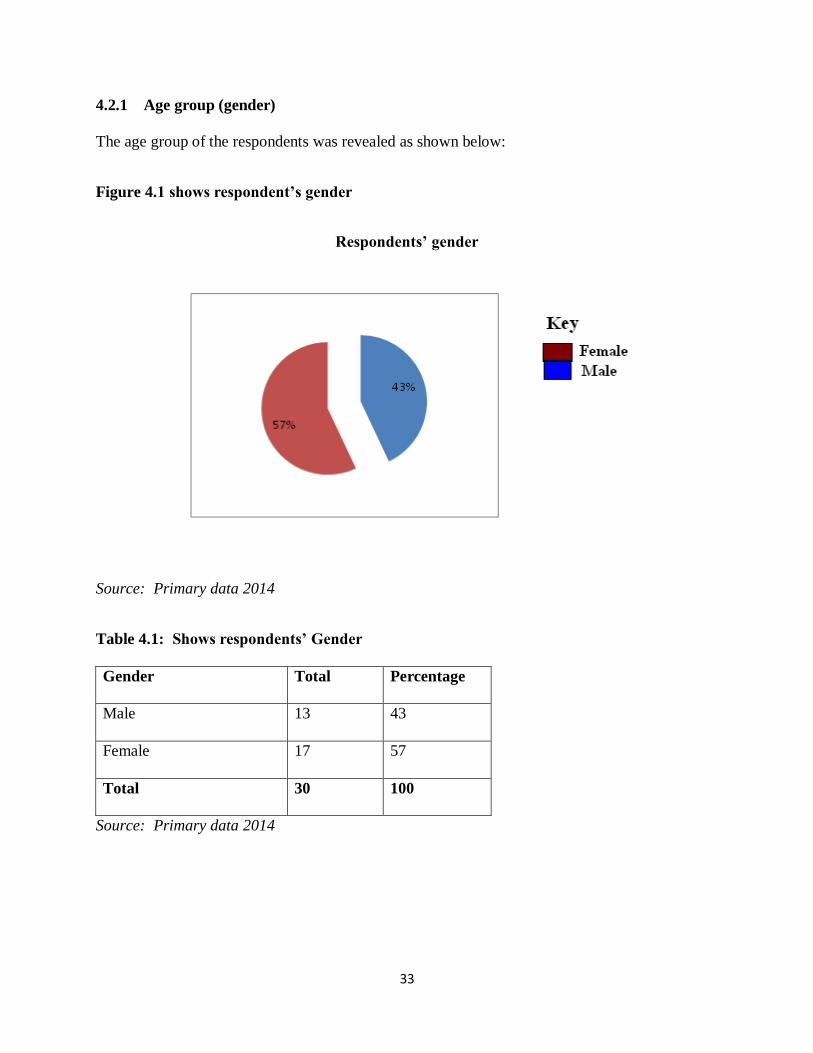

4.2.1 Age group (gender)

The age group of the respondents was revealed as shown below:

Figure 4.1 shows respondent’s gender

Respondents’ gender

Source: Primary data 2014

Table 4.1: Shows respondents’ Gender

Gender Total Percentage

Male 13 43

Female 17 57

Total 30 100

Source: Primary data 2014

34

From table 4.1, 43% of the respondents were males while 57% of them were females. This

implies that the data obtained was gender unbiased because the employees of small and medium

enterprises are more of females than males.

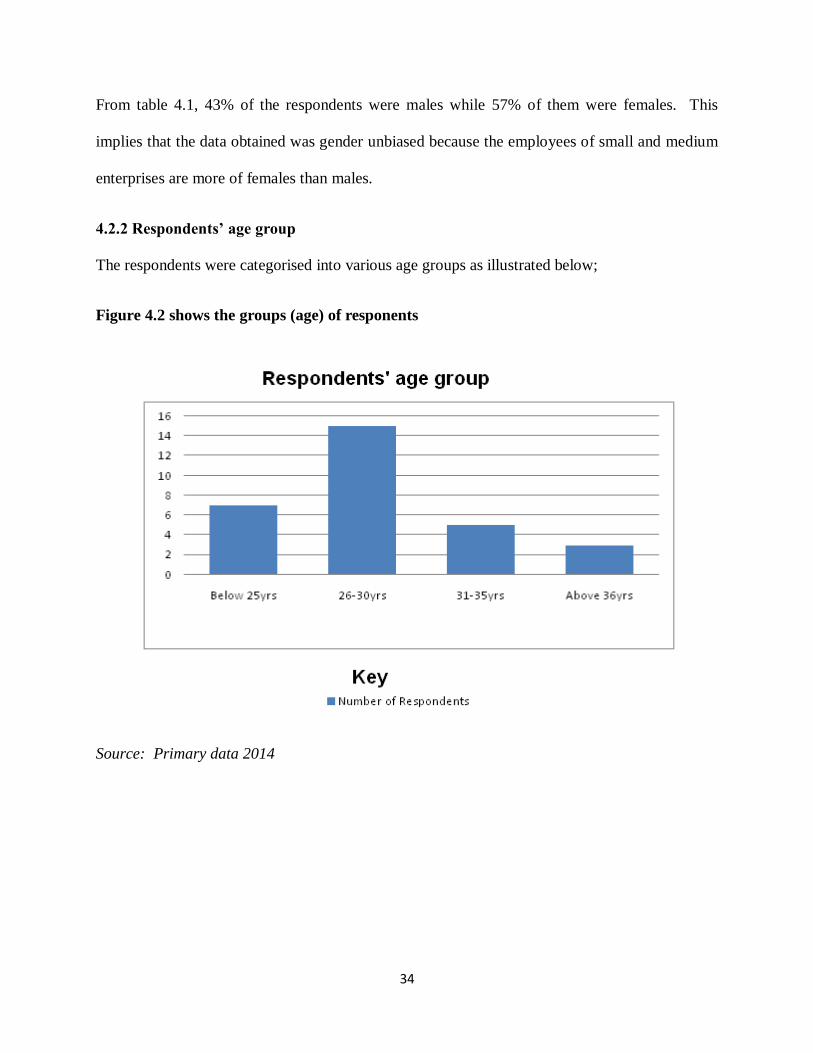

4.2.2 Respondents’ age group

The respondents were categorised into various age groups as illustrated below;

Figure 4.2 shows the groups (age) of responents

Source: Primary data 2014

35

Table 4.2 show the number of respondents

Group Number of Respondents Percentage of respondents

Below 25yrs 7 23%

26-30yrs 15 50%

31-35yrs 5 17%

Above 36yrs 3 10%

Total 30 100%

Source: Primary data 2014

From table4.2, 7 respondents (23%) were below 25 years of age, 15 respondents were between

26-30 years, 5 respondents (17%) were between 31-35 years and 3 respondents (10%) were

above 36 years of age. Majority of the respondents were therefore aged between 26-30 years

which is a very active and productive age bracket.

36

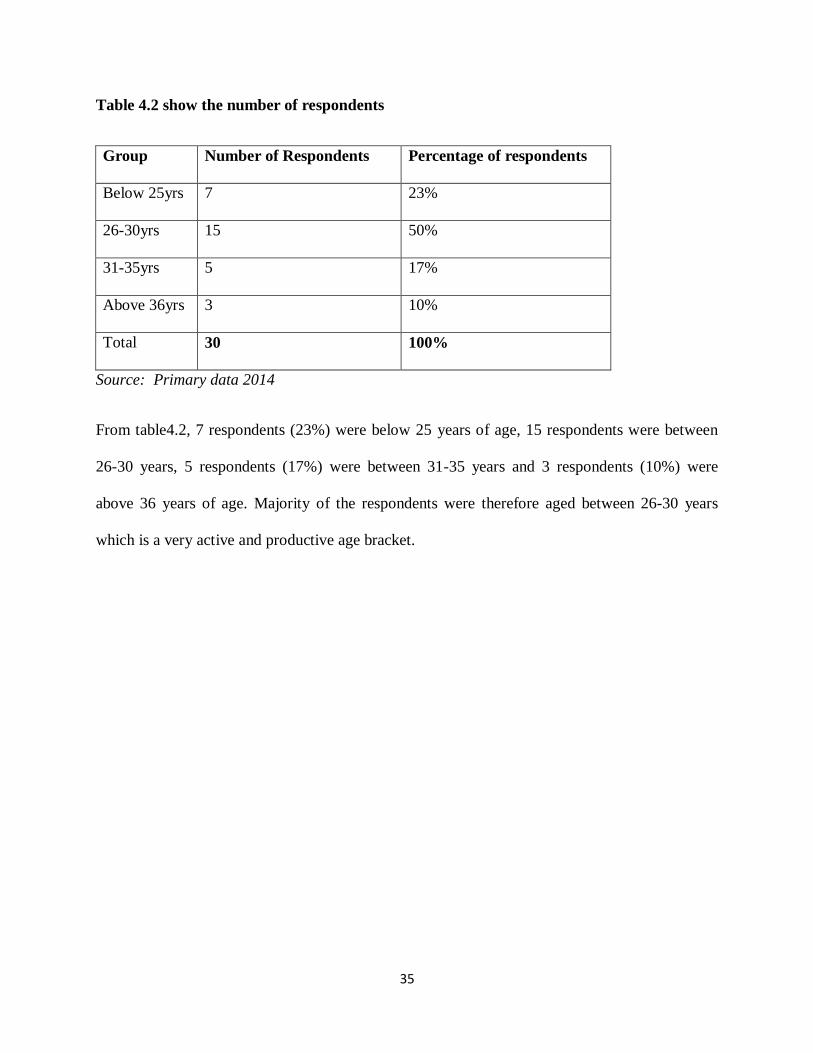

4.2.3 Level of Education

The response about the education level of the respondents was presented below:

Figure 4.3; Respondents’ level of education

Source: Primary data 2014

37

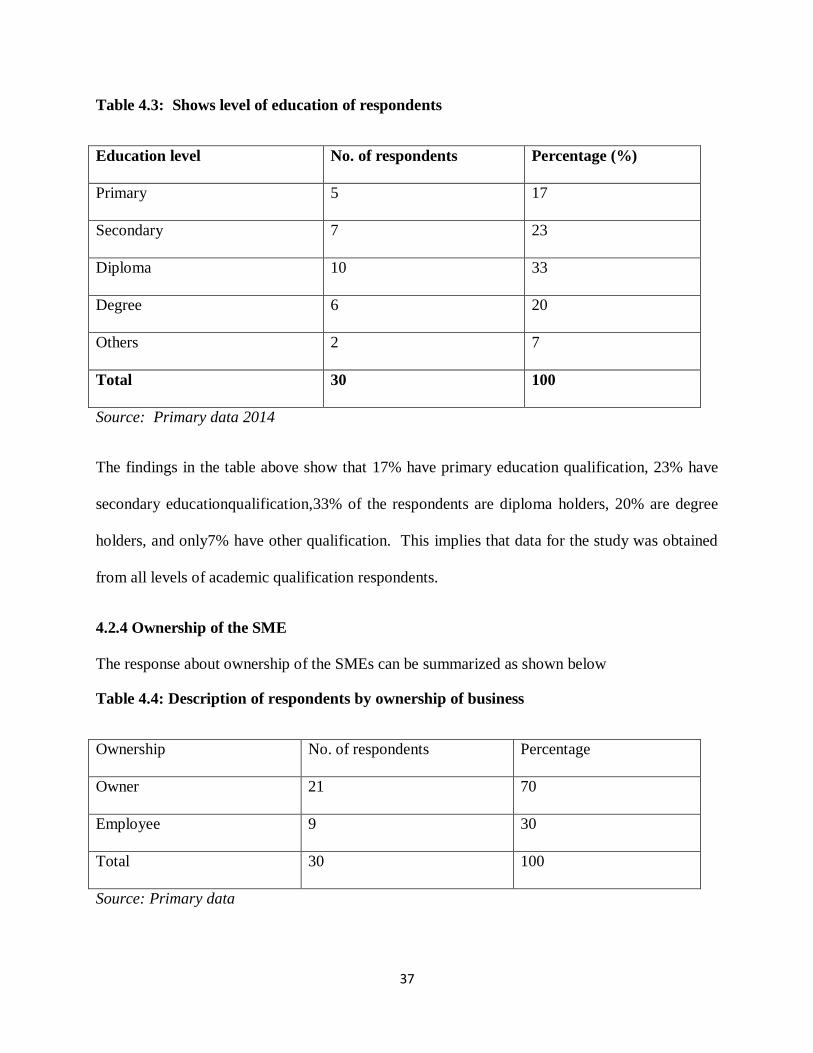

Table 4.3: Shows level of education of respondents

Education level No. of respondents Percentage (%)

Primary 5 17

Secondary 7 23

Diploma 10 33

Degree 6 20

Others 2 7

Total 30 100

Source: Primary data 2014

The findings in the table above show that 17% have primary education qualification, 23% have

secondary educationqualification,33% of the respondents are diploma holders, 20% are degree

holders, and only7% have other qualification. This implies that data for the study was obtained

from all levels of academic qualification respondents.

4.2.4 Ownership of the SME

The response about ownership of the SMEs can be summarized as shown below

Table 4.4: Description of respondents by ownership of business

Ownership No. of respondents Percentage

Owner 21 70

Employee 9 30

Total 30 100

Source: Primary data

38

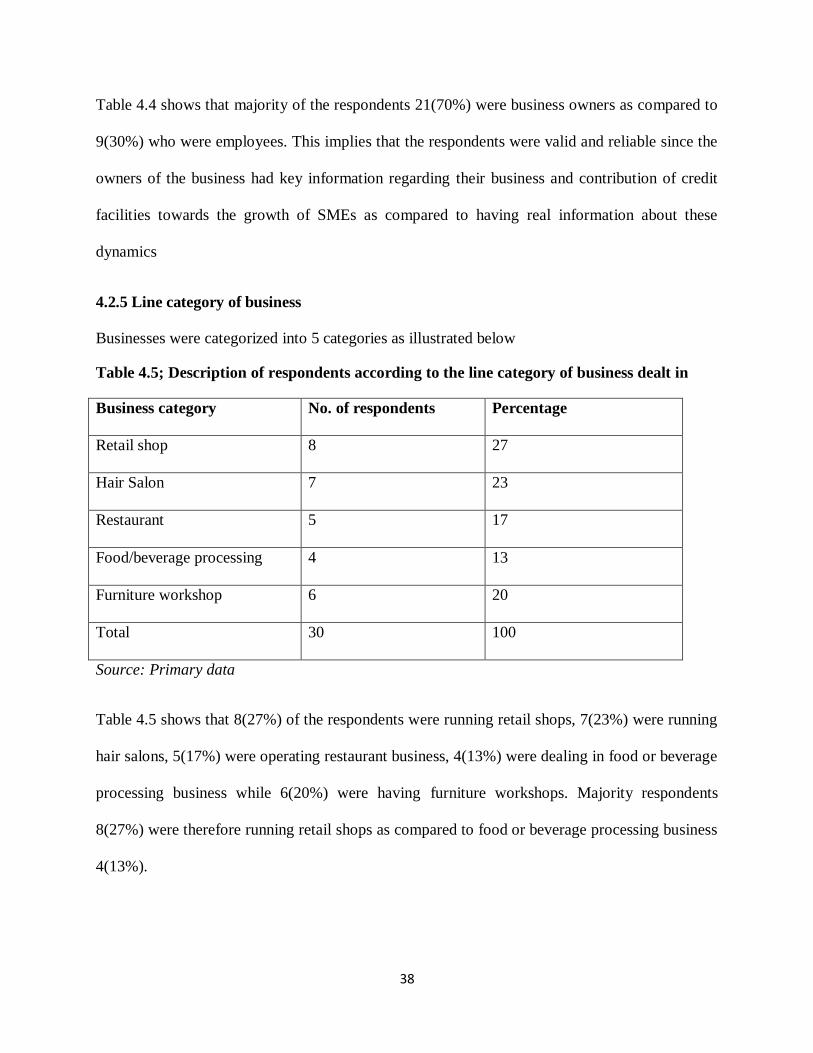

Table 4.4 shows that majority of the respondents 21(70%) were business owners as compared to

9(30%) who were employees. This implies that the respondents were valid and reliable since the

owners of the business had key information regarding their business and contribution of credit

facilities towards the growth of SMEs as compared to having real information about these

dynamics

4.2.5 Line category of business

Businesses were categorized into 5 categories as illustrated below

Table 4.5; Description of respondents according to the line category of business dealt in

Business category No. of respondents Percentage

Retail shop 8 27

Hair Salon 7 23

Restaurant 5 17

Food/beverage processing 4 13

Furniture workshop 6 20

Total 30 100

Source: Primary data

Table 4.5 shows that 8(27%) of the respondents were running retail shops, 7(23%) were running

hair salons, 5(17%) were operating restaurant business, 4(13%) were dealing in food or beverage

processing business while 6(20%) were having furniture workshops. Majority respondents

8(27%) were therefore running retail shops as compared to food or beverage processing business

4(13%).

39

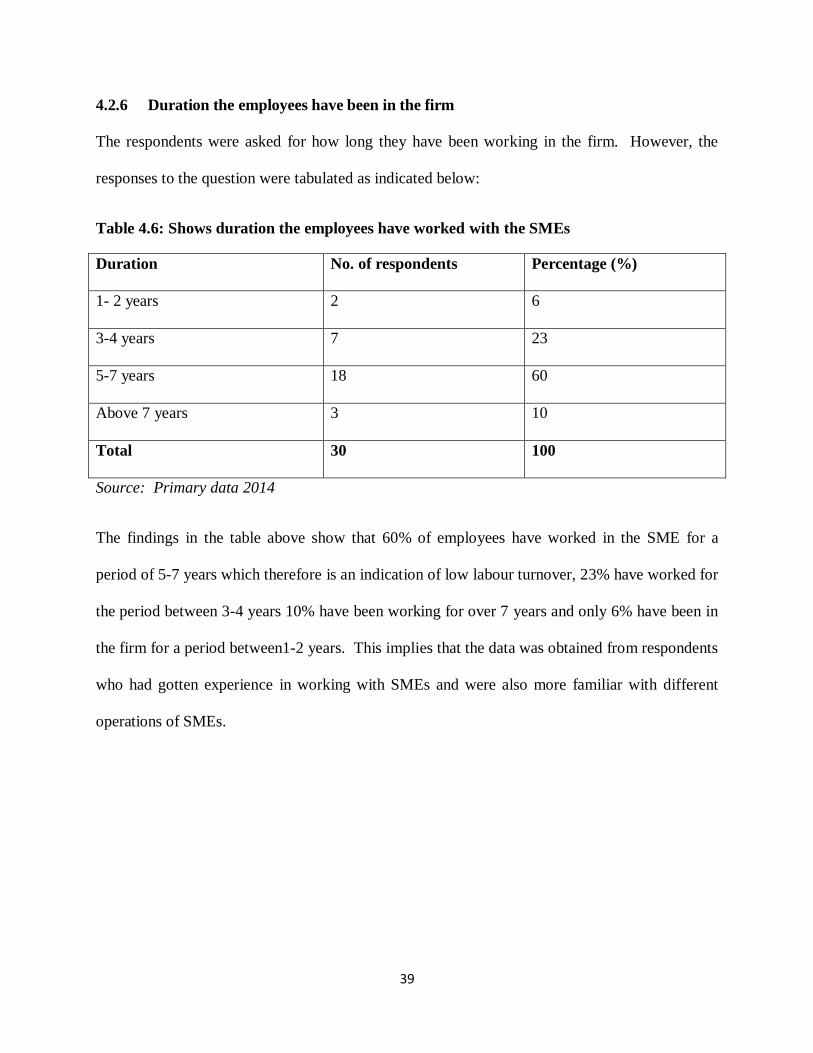

4.2.6 Duration the employees have been in the firm

The respondents were asked for how long they have been working in the firm. However, the

responses to the question were tabulated as indicated below:

Table 4.6: Shows duration the employees have worked with the SMEs

Duration No. of respondents Percentage (%)

1- 2 years 2 6

3-4 years 7 23

5-7 years 18 60

Above 7 years 3 10

Total 30 100

Source: Primary data 2014

The findings in the table above show that 60% of employees have worked in the SME for a

period of 5-7 years which therefore is an indication of low labour turnover, 23% have worked for

the period between 3-4 years 10% have been working for over 7 years and only 6% have been in

the firm for a period between1-2 years. This implies that the data was obtained from respondents

who had gotten experience in working with SMEs and were also more familiar with different

operations of SMEs.

40

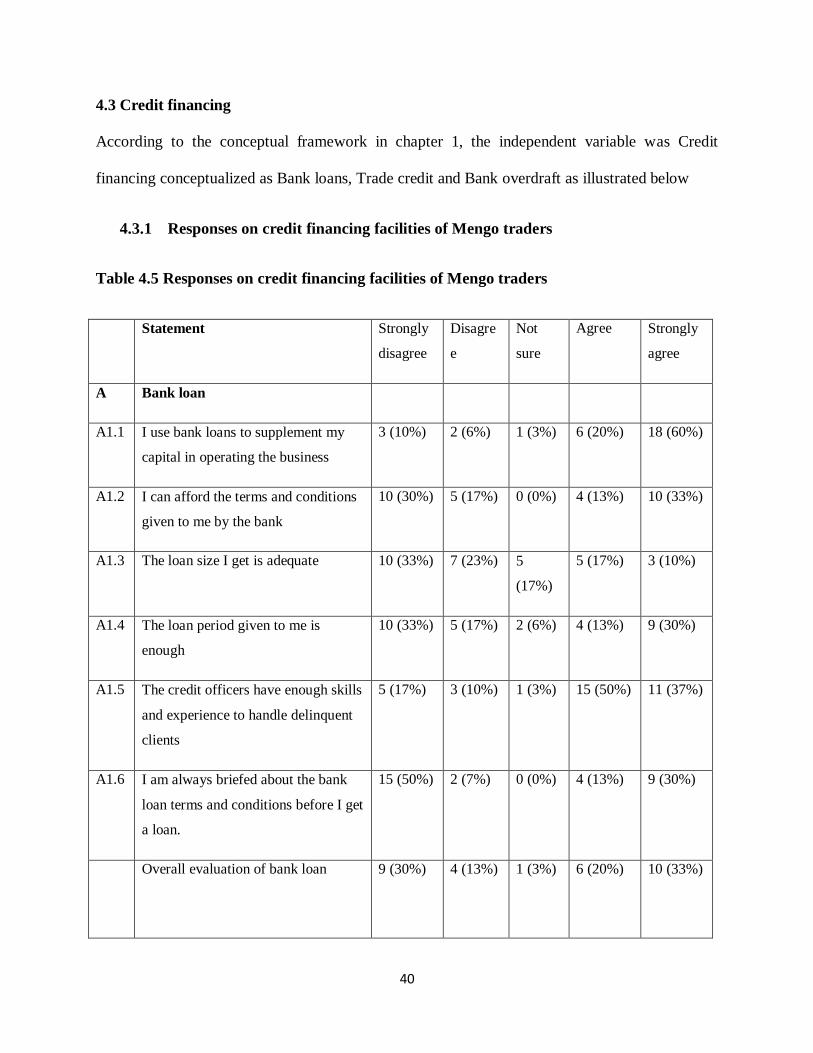

4.3 Credit financing

According to the conceptual framework in chapter 1, the independent variable was Credit

financing conceptualized as Bank loans, Trade credit and Bank overdraft as illustrated below

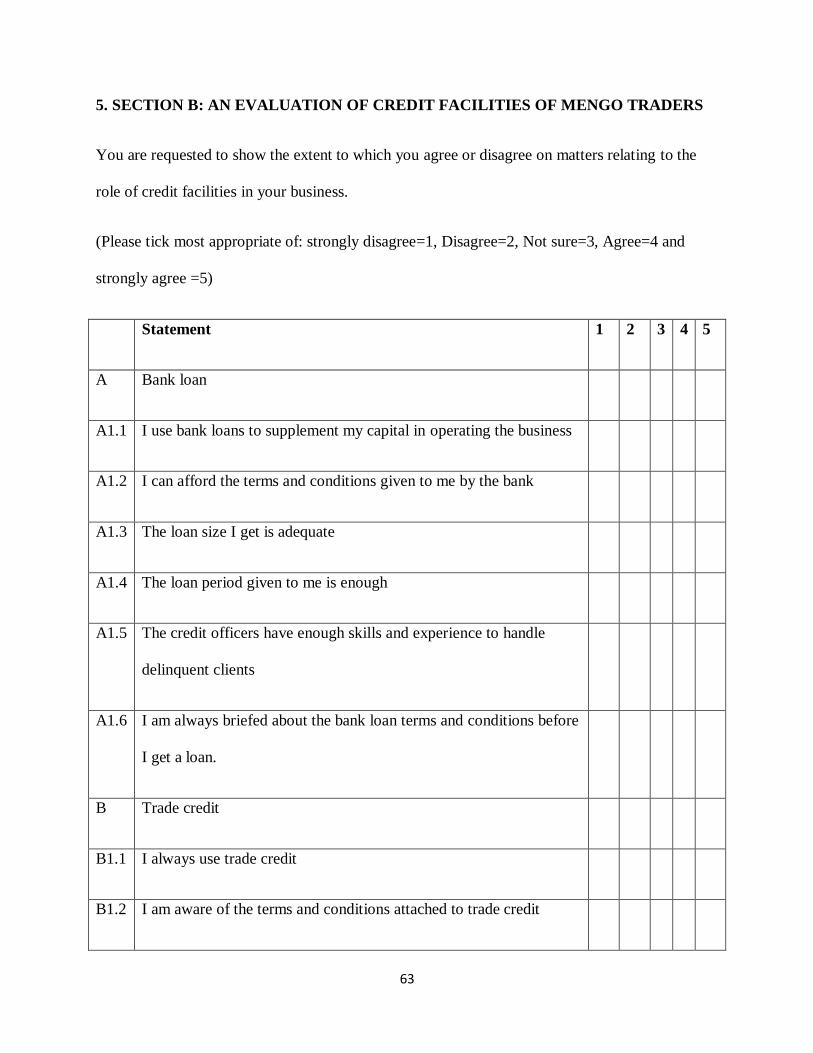

4.3.1 Responses on credit financing facilities of Mengo traders

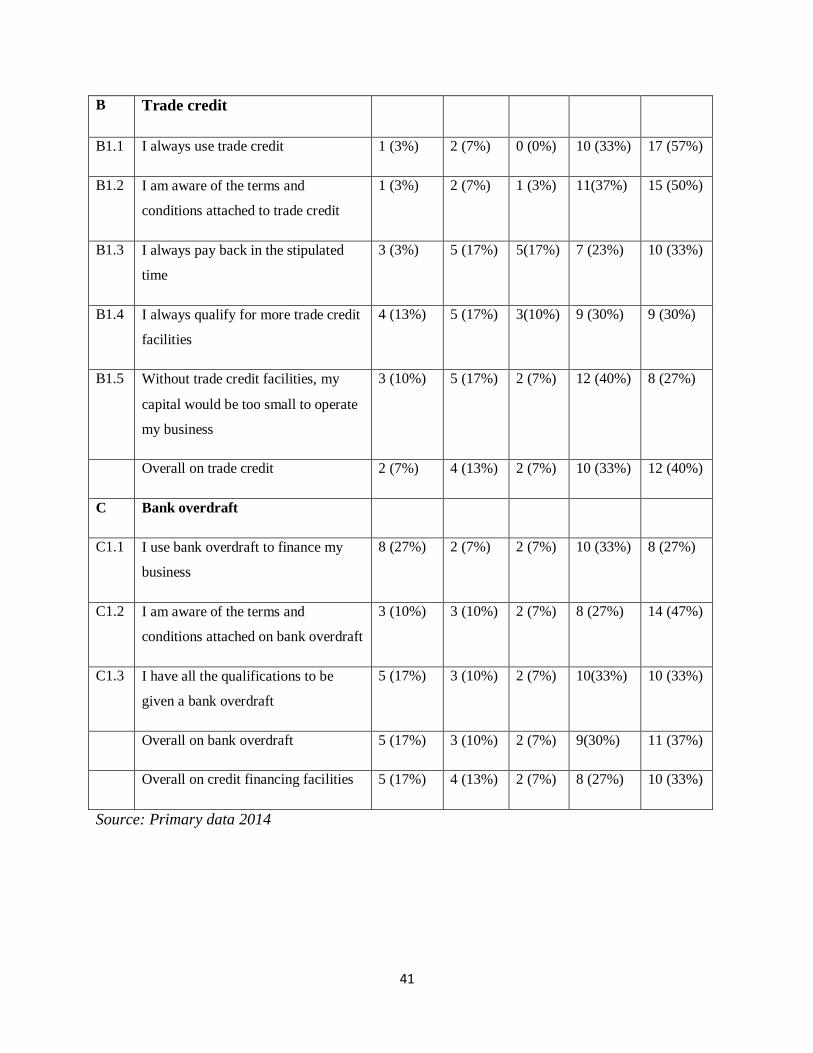

Table 4.5 Responses on credit financing facilities of Mengo traders

Statement Strongly

disagree

Disagre

e

Not

sure

Agree Strongly

agree

A Bank loan

A1.1 I use bank loans to supplement my

capital in operating the business

3 (10%) 2 (6%) 1 (3%) 6 (20%) 18 (60%)

A1.2 I can afford the terms and conditions

given to me by the bank

10 (30%) 5 (17%) 0 (0%) 4 (13%) 10 (33%)

A1.3 The loan size I get is adequate 10 (33%) 7 (23%) 5

(17%)

5 (17%) 3 (10%)

A1.4 The loan period given to me is

enough

10 (33%) 5 (17%) 2 (6%) 4 (13%) 9 (30%)

A1.5 The credit officers have enough skills

and experience to handle delinquent

clients

5 (17%) 3 (10%) 1 (3%) 15 (50%) 11 (37%)

A1.6 I am always briefed about the bank

loan terms and conditions before I get

a loan.

15 (50%) 2 (7%) 0 (0%) 4 (13%) 9 (30%)

Overall evaluation of bank loan 9 (30%) 4 (13%) 1 (3%) 6 (20%) 10 (33%)

41

B Trade credit

B1.1 I always use trade credit 1 (3%) 2 (7%) 0 (0%) 10 (33%) 17 (57%)

B1.2 I am aware of the terms and

conditions attached to trade credit

1 (3%) 2 (7%) 1 (3%) 11(37%) 15 (50%)

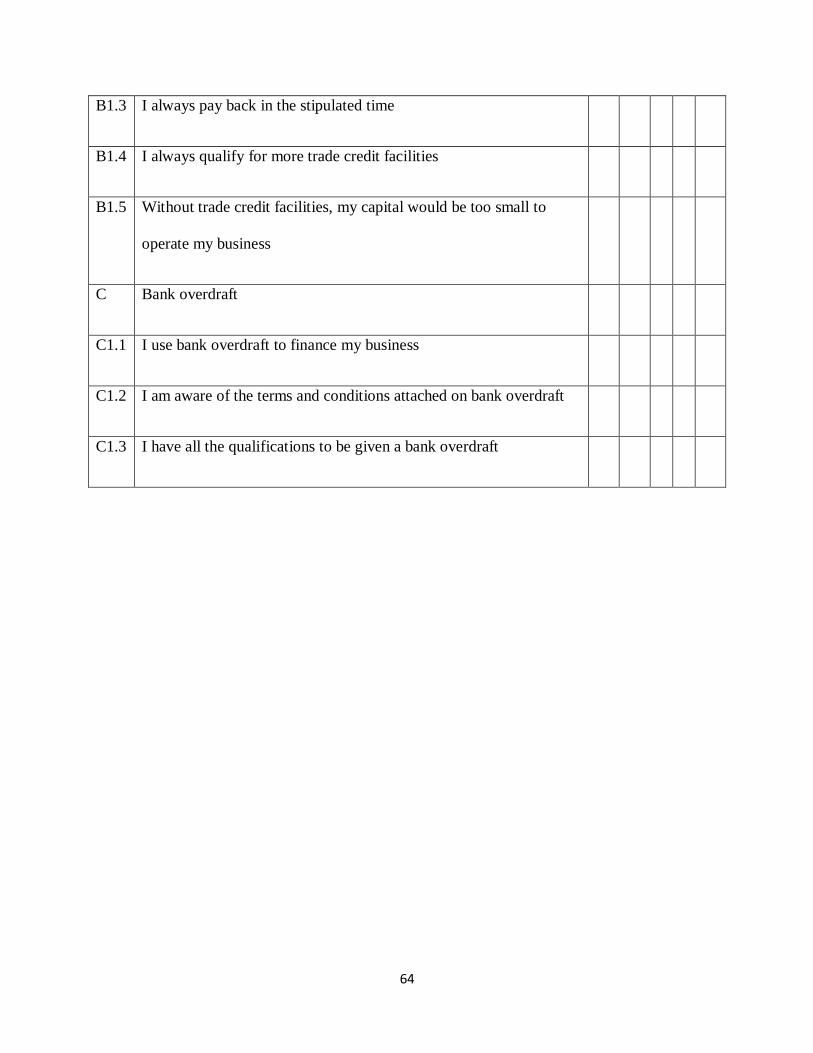

B1.3 I always pay back in the stipulated

time

3 (3%) 5 (17%) 5(17%) 7 (23%) 10 (33%)

B1.4 I always qualify for more trade credit

facilities

4 (13%) 5 (17%) 3(10%) 9 (30%) 9 (30%)

B1.5 Without trade credit facilities, my

capital would be too small to operate

my business

3 (10%) 5 (17%) 2 (7%) 12 (40%) 8 (27%)

Overall on trade credit 2 (7%) 4 (13%) 2 (7%) 10 (33%) 12 (40%)

C Bank overdraft

C1.1 I use bank overdraft to finance my

business

8 (27%) 2 (7%) 2 (7%) 10 (33%) 8 (27%)

C1.2 I am aware of the terms and

conditions attached on bank overdraft

3 (10%) 3 (10%) 2 (7%) 8 (27%) 14 (47%)

C1.3 I have all the qualifications to be

given a bank overdraft

5 (17%) 3 (10%) 2 (7%) 10(33%) 10 (33%)

Overall on bank overdraft 5 (17%) 3 (10%) 2 (7%) 9(30%) 11 (37%)

Overall on credit financing facilities 5 (17%) 4 (13%) 2 (7%) 8 (27%) 10 (33%)

Source: Primary data 2014

42

Evaluation of bank loans

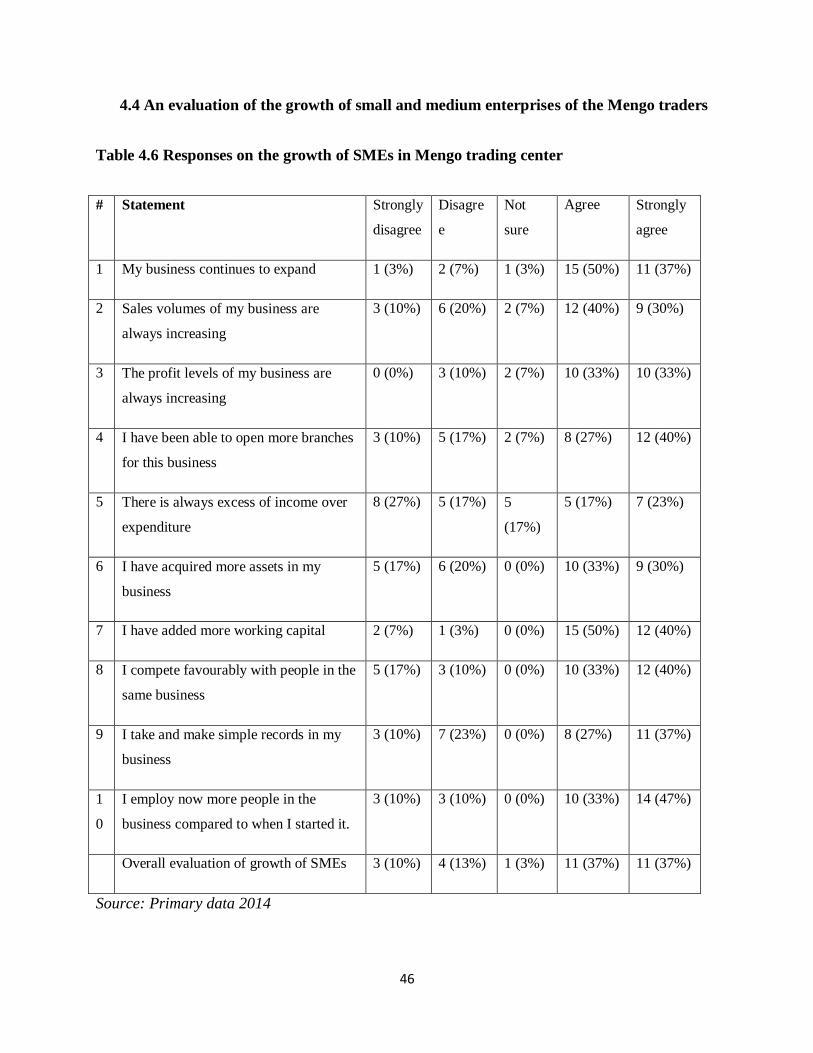

Table4.5 shows that, 10% of the respondents strongly disagreed that they do not use bank loans

to supplement their capital in operating the business, 6% disagreed, 3% were not sure, 20%