comparative study of the effects of aflatoxin b1 metabolites and α-amanitin on rat liver rna...

TRANSCRIPT

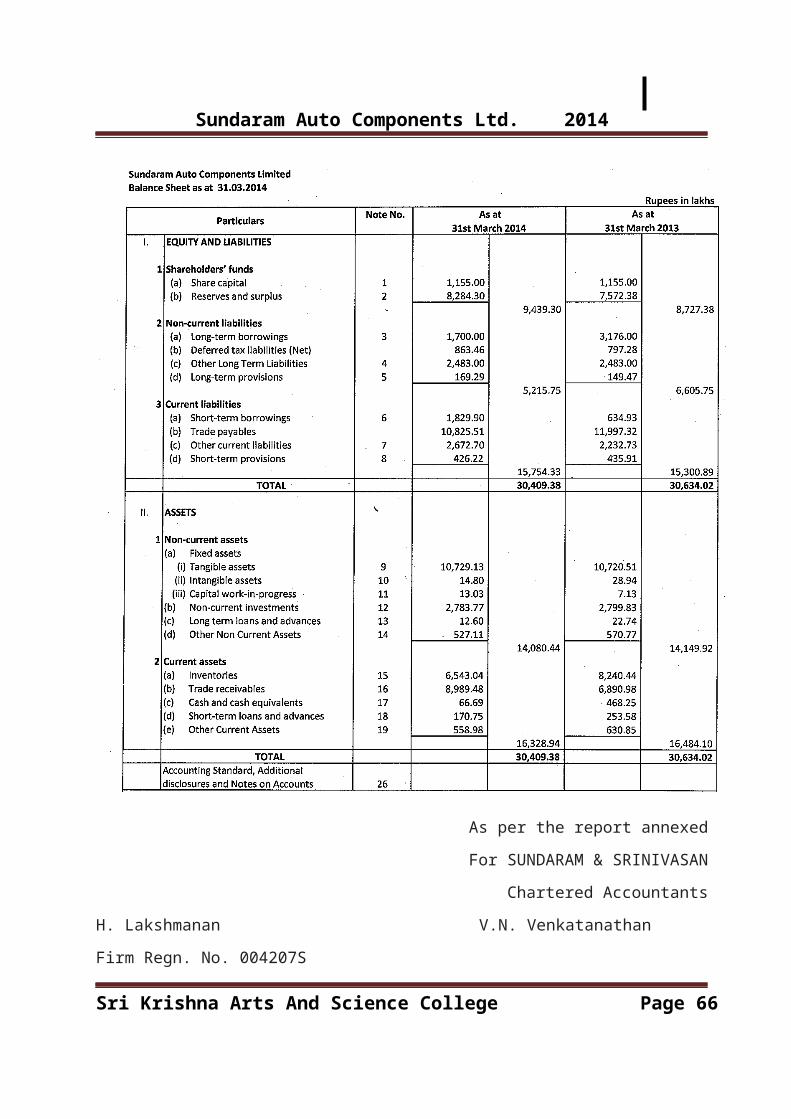

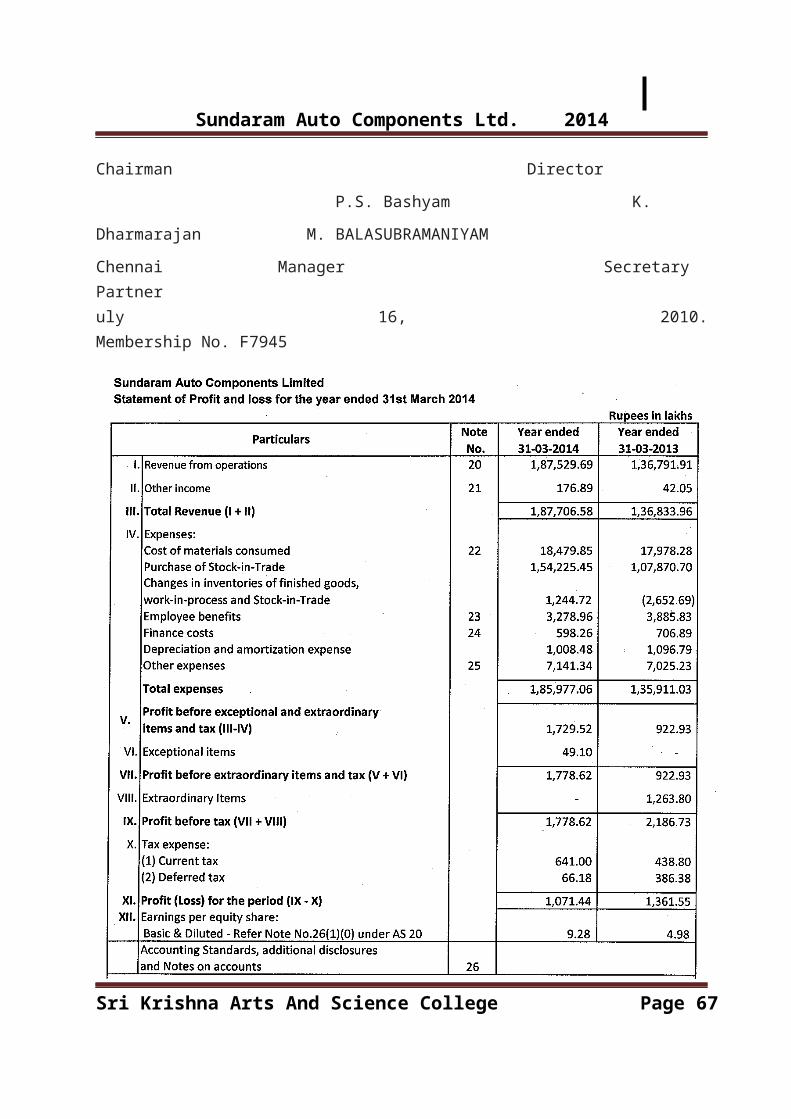

Sundaram Auto Components Ltd. 2014

INDUSTRY PROFILEINTRODUCTION:

The Indian auto component industry is one of the

country's rising industries with tremendous growth prospects.

From a low-key supplier providing components exclusively to

the domestic market, the industry has emerged as one of the

key auto components centres in Asia and is today seen as a

significant player in the global automotive supply chain.

India is now a supplier of a range of high-value and critical

automobile components to global auto makers such as General

Motors, Toyota, Ford and Volkswagen, amongst others.

The industry currently accounts for almost seven per cent

of India's gross domestic product (GDP) and employs about 19

million people, both directly and indirectly. The ever-

increasing development in infrastructure, big domestic market,

increasing purchasing power and stable government framework

have made India a favourable destination for investment, as

per the vision of Automotive Mission Plan (AMP)2006-2016.

COMPANY PROFILE:

“SUNDARAM AUTO COMPONENTS LIMITED”

HISTORY:

Sri Krishna Arts And Science College Page 1

Sundaram Auto Components Ltd. 2014

Sundaram Auto Components Ltd Plastics Division was

established is 1988. Over the years, it has diversified into

automotive, electrical and appliances industry along the way

proving itself as a total solution provider in plastics. Three

state-of-the-art manufacturing facilities at strategic

locations with in-house mold manufacturing & painting and

driven by highly qualified team ensures meeting varied

customer requirements.

The company has grown length and breadth and caters to

wide customer base and has proved its credentials as a total

solution provider for injection moulded plastic components.

HIGHLIGHTS:

SACL plastic division have its roots in one of the

India’s most reputed business houses “TVS group”. TVS groups

were started in 1911 by Shri T.V.Sundaram Iyengar, the TVS

group played a pioneering role in the intergeneration of

India’s automobile industry; and is today by far the largest

manufacturer and distributor of auto components in the

country, a multimillion, multi business conglomerate

consisting of over 40 blue-chip companies.

Sri Krishna Arts And Science College Page 2

Sundaram Auto Components Ltd. 2014

To bring the vision of their founder to reality, they

practice Total Quality Management (TQM) at all levels

supported by the five pillars of TQM. Total employee

involvement and cross functional problem solving approach

contribute to a steady stream of continuous improvements. As a

part of TVS group they nurture the talents of the employees

and bring the best out of them by providing excellent work

environment& career development.

Care for the environment gains new momentum through

recycling of resources and extensive tree planting and land

reclamation projects. Customer satisfaction, Quality,

continuous improvements as the goal, plastics are poised to

take on the opportunities and challenges of the future.

SACL – Plastics Division serves customers from different

segments of industry like Automobile (four wheeler, two

wheeler),Electrical and Electronics, Home appliances and

Sports goods.

SACL – Plastics Division continuously focuses on

implementing new and innovative technologies in its

manufacturing processes to meet ever-increasing customer

expectations.

The manufacturing facility is a modern state-of-the-art unit

equipped with electronically controlled injection moulding

machines supported by auxiliary equipments, CAD/CAM/CAE

Sri Krishna Arts And Science College Page 3

Sundaram Auto Components Ltd. 2014

facilities capable of developing and delivering products with

high consistency and accuracy.

BOARD OF DIRECTORS:

H. LAKSHMANAN, Chairman

C.N. PRASAD

V. N. VENKATANATHAN

K. N. RADHAKRISHNAN

S. G. MURALI

VISION OF SACL:

To be environmental friendly and socially responsible

manufacturer of automotive components, for engineering

applications using processes capable of providing high quality

products to customers in global markets and to provide

fulfillment and prosperity to employees and suppliers.

MISSION OF SACL:

Satisfy customers through a proactive approach by producing

high quality products using cost effective manufacturing

processes and on time delivery.

Sri Krishna Arts And Science College Page 4

Sundaram Auto Components Ltd. 2014

Achieve objectives through total Employee involvement.

Constantly strive to reduce costs and maintain

competitive advantage.

Support suppliers and enable them to continually upgrade

themselves.

Conduct business with uncompromising integrity.

QUALITY POLICY:

Sundaram Auto Components Ltd is committed to achieve

total customer satisfaction by providing products and services

of the right quality, on time delivery and at the agreed

price. This will be achieved through continuous improvements

of their process and total employee involvement activities.

SACL FOCUS ON THE FOLLWING FIELDS:

Two wheelers

Auto components

Distribution & Logistics

Financial Services

Electronics & IT.

MOTIVATIONAL FACTORS:

SACL – Plastics Division, as an organization, is

committed towards improving the environmental performance, and

Sri Krishna Arts And Science College Page 5

Sundaram Auto Components Ltd. 2014

creating awareness and educating its employees, suppliers, and

interested parties on the benefits of the EMS.

SACL – Plastics Division, as an organization, is

committed towards controlling the impacts arising out of its

activities on the environment by implementing EMS and adhering

to the legal obligations.

SACL – Plastics Division, as a committed citizen, look

forward to an improved environment and achieving

Benefits to the organization, employees, public and other

interested parties.

Better living conditions for the present and future

generations.

Better work environment.

Financial benefits by better utilization of resources and

waste reduction.

Improved organizational image and access to international

market.

Some of the eco friendly measures taken by the SACL – Plastics

Division are:

Using recycling trolleys and bins for transporting the

products to customers,

Considerable reduction in the usage of wooden cases for

packing, by replacing them with hard cardboard boxes.

Sri Krishna Arts And Science College Page 6

Sundaram Auto Components Ltd. 2014

Usage of canteen waste as manure

Storing and disposal of scrap after segregation,

Re-cycling of plastic raw material.

Re-using of mould inserts.

Re-using of water used for mould cooling.

To promote environmental consciousness in the employees,

the Organization has embarked on an extensive environmental

awareness-building programme, through Total Employee

Involvement. The various interactions between employees are

being highlighted through Safety competitions; quiz programmes

and periodic visit of employees to organization having well

established EMS.

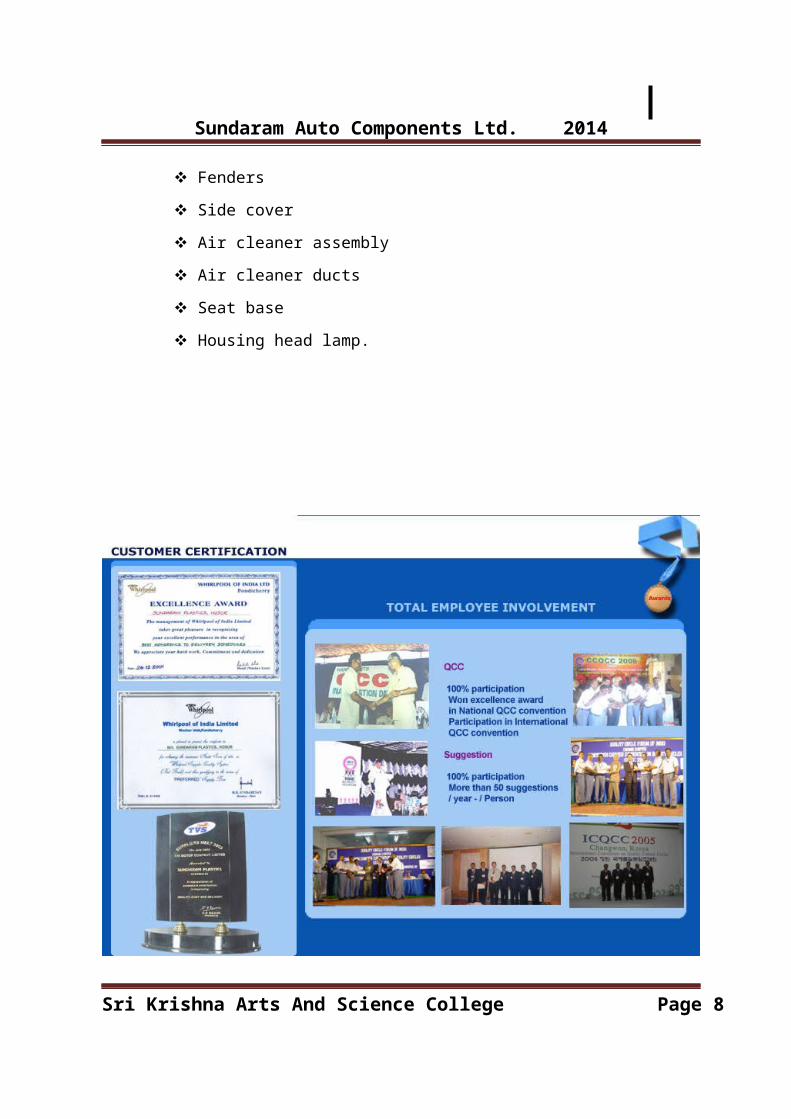

PRODUCTS OF SACL:

FOUR WHEELER PARTS:

Cylinder head cover

Radiator fan

Timing belt cover

Glove box

Oil separator

Water connector

Transmission components.

TWO WHEELER PARTS:

Tail cover

Sri Krishna Arts And Science College Page 7

Sundaram Auto Components Ltd. 2014

Fenders

Side cover

Air cleaner assembly

Air cleaner ducts

Seat base

Housing head lamp.

Sri Krishna Arts And Science College Page 8

Sundaram Auto Components Ltd. 2014

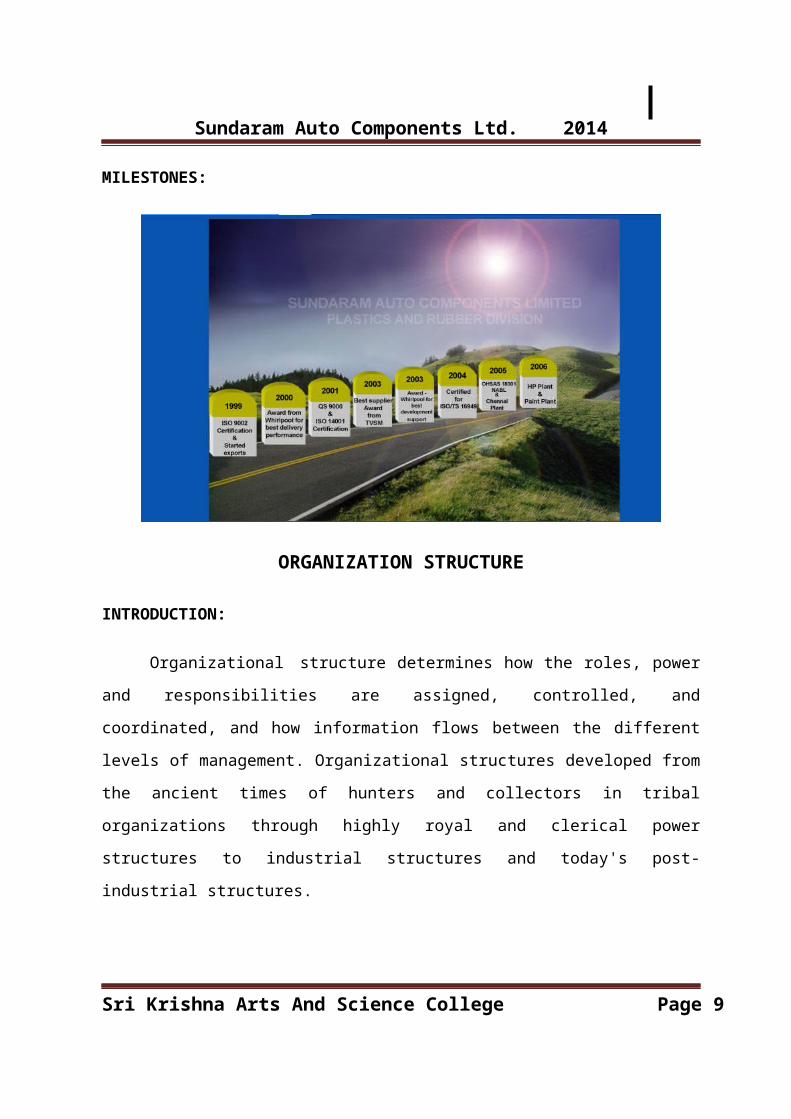

MILESTONES:

ORGANIZATION STRUCTURE

INTRODUCTION:

Organizational structure determines how the roles, power

and responsibilities are assigned, controlled, and

coordinated, and how information flows between the different

levels of management. Organizational structures developed from

the ancient times of hunters and collectors in tribal

organizations through highly royal and clerical power

structures to industrial structures and today's post-

industrial structures.

Sri Krishna Arts And Science College Page 9

Sundaram Auto Components Ltd. 2014

1. It provides the foundation on which standard operating

procedures and routines rest.

2. It determines which individuals get to participate in

which decision-making processes, and thus to what

extent their views shape the organization’s actions.

3. Organizational structure allows the expressed

allocation of responsibilities for different functions

and processes to different entities such as the branch,

department, workgroup and individual.

4. An organizational structure defines how activities such

as task allocation, coordination and supervision are

directed towards the achievement of organizational

aims.

5. An organization can be structured in many different

ways, depending on their objectives. The structure of

an organization will determine the modes in which it

operates and performs.

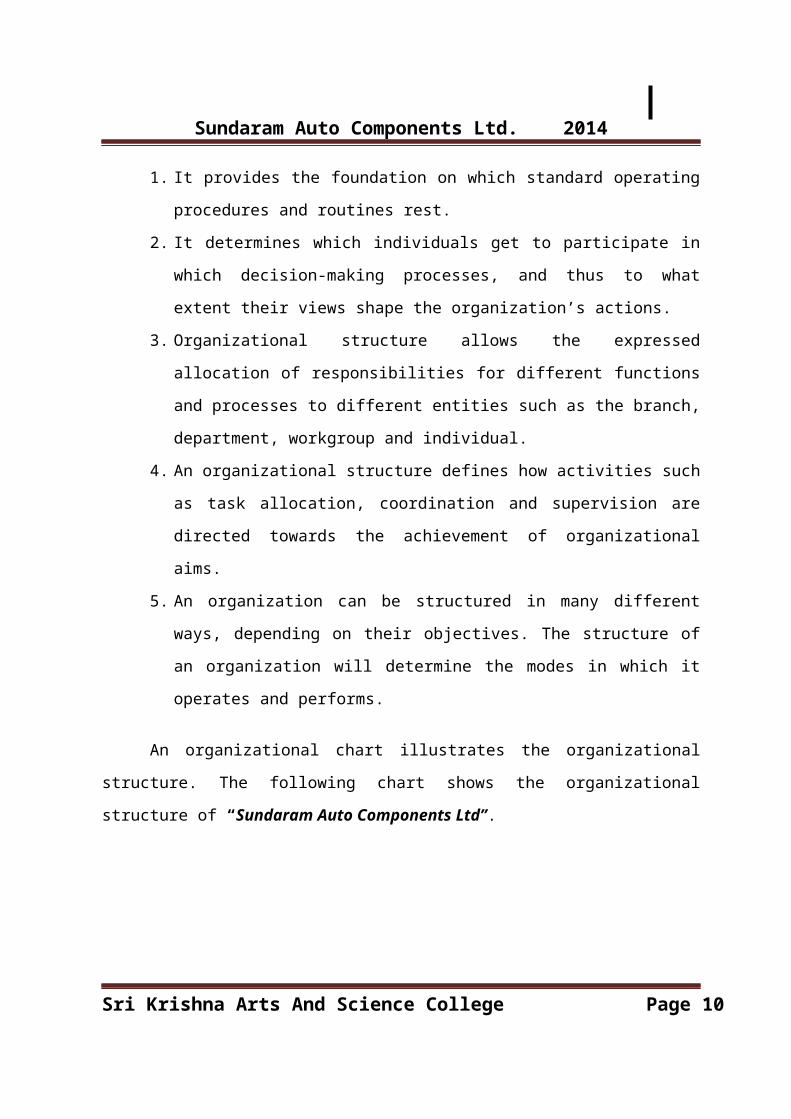

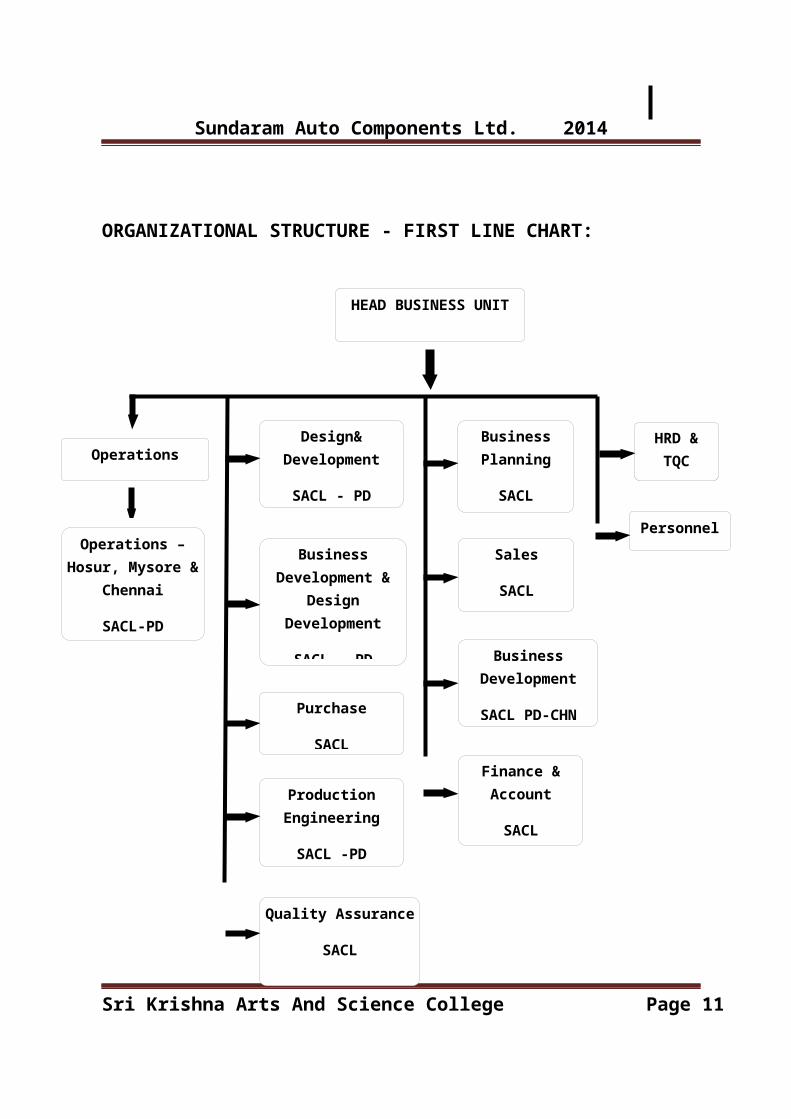

An organizational chart illustrates the organizational

structure. The following chart shows the organizational

structure of “Sundaram Auto Components Ltd”.

Sri Krishna Arts And Science College Page 10

Sundaram Auto Components Ltd. 2014

ORGANIZATIONAL STRUCTURE - FIRST LINE CHART:

Sri Krishna Arts And Science College Page 11

ProductionEngineering

SACL -PD

Purchase

SACL

Design&Development

SACL - PD

BusinessDevelopment &

DesignDevelopment

SACL - PD

Operations –Hosur, Mysore &

Chennai

SACL-PD

HEAD BUSINESS UNIT

Quality Assurance

SACL

OperationsBusinessPlanning

SACL

Personnel

HRD &TQC

Finance &Account

SACL

BusinessDevelopment

SACL PD-CHN

Sales

SACL

Sundaram Auto Components Ltd. 2014

AREA OF INTREST (FINANCE DEPARTMENT):MISSION:

Ensure complete and accurate accounting of all

transactions and to report all financial information in

accordance with state and local laws. Develop and implement

systems to clearly chart the financial health of organization.

PURPOSE:

Manage overall F&A activity of the plant & provide

financial advice and support to management to enable them to

make sound business decisions. Manager’s purpose is to manage

overall activity of the plant.

ROLE DESCRIPTION:

Responsible for the entire financial strategy of the

organization.

Responsible for managing funds, internal control systems

and audits, external compliances and general accounting.

Analyzing and interpretation of financial data .

Providing information on cost allocation & controls.

Control and analyze stock variance.

Sri Krishna Arts And Science College Page 12

Sundaram Auto Components Ltd. 2014

Comparison of results against budgeted income and

expenditure analysis etc.,

Cost reduction and PIP (Profit Improvement Plan)

Validation.

Financial forecasting and advising senior management on

financial implications.

Liaison with Auditors for Internal, External and

Statutory audits.

Improve profitability by controlling fixed cost and

reviewing cost reduction projects.

Exercise Costing & Budgetary Controls.

Plan and conduct feasibility study of capital

investments.

Train, retain, motivate and manage performance of the

team members.

Sri Krishna Arts And Science College Page 13

Sundaram Auto Components Ltd. 2014

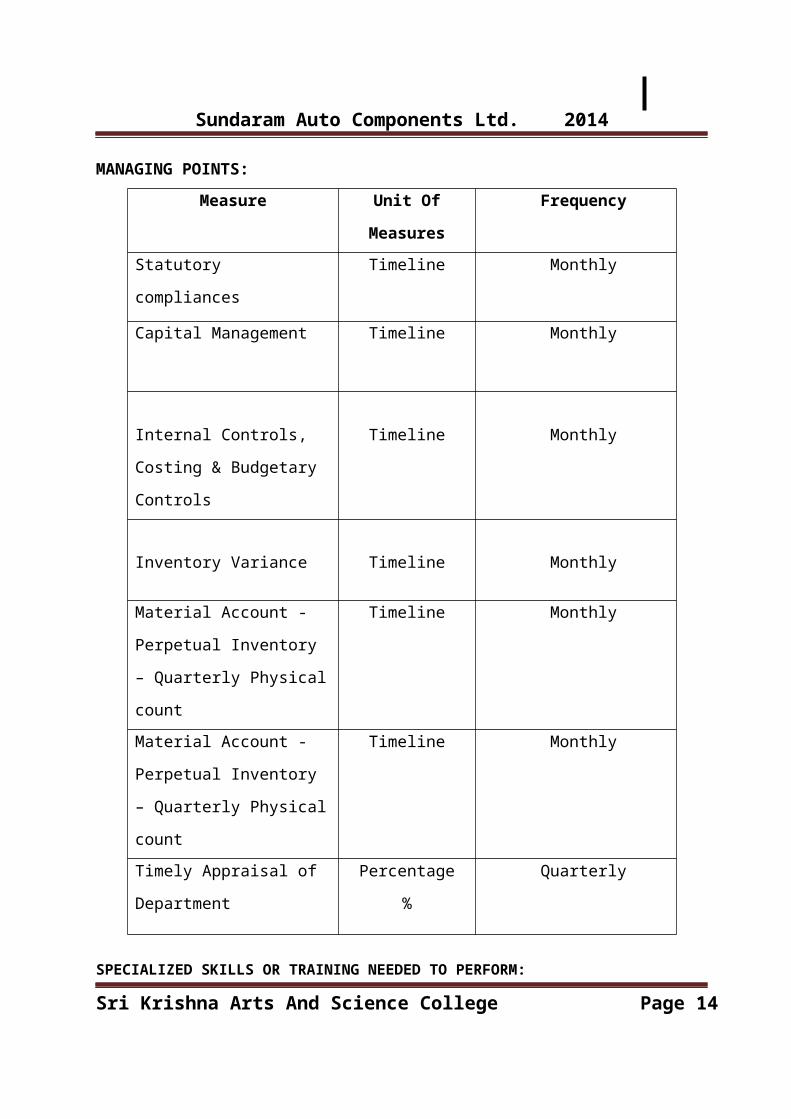

MANAGING POINTS:

SPECIALIZED SKILLS OR TRAINING NEEDED TO PERFORM:

Sri Krishna Arts And Science College Page 14

Measure Unit Of

Measures

Frequency

Statutory

compliances

Timeline Monthly

Capital Management Timeline Monthly

Internal Controls,

Costing & Budgetary

Controls

Timeline Monthly

Inventory Variance Timeline Monthly

Material Account -

Perpetual Inventory

– Quarterly Physical

count

Timeline Monthly

Material Account -

Perpetual Inventory

– Quarterly Physical

count

Timeline Monthly

Timely Appraisal of

Department

Percentage

%

Quarterly

Sundaram Auto Components Ltd. 2014

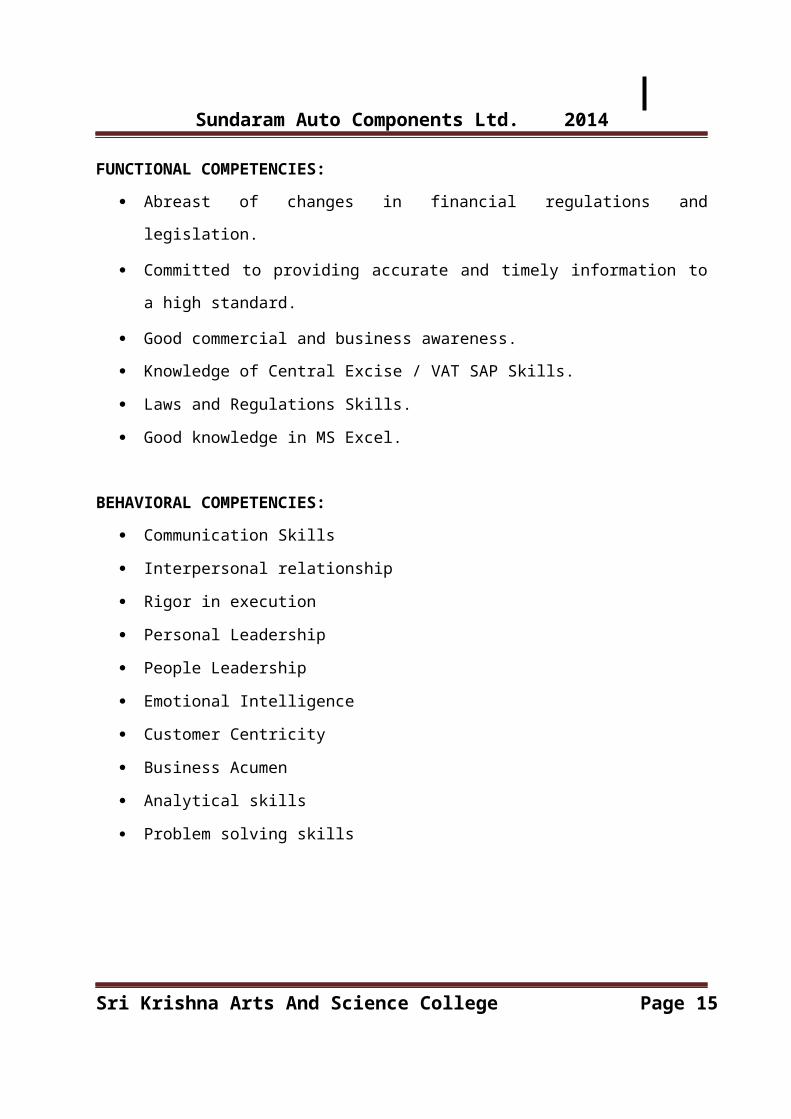

FUNCTIONAL COMPETENCIES:

Abreast of changes in financial regulations and

legislation.

Committed to providing accurate and timely information to

a high standard.

Good commercial and business awareness.

Knowledge of Central Excise / VAT SAP Skills.

Laws and Regulations Skills.

Good knowledge in MS Excel.

BEHAVIORAL COMPETENCIES:

Communication Skills

Interpersonal relationship

Rigor in execution

Personal Leadership

People Leadership

Emotional Intelligence

Customer Centricity

Business Acumen

Analytical skills

Problem solving skills

Sri Krishna Arts And Science College Page 15

Sundaram Auto Components Ltd. 2014

UNIQUE SELLING PROPOSITION (USP)

INTRODUCTION:

The factor or consideration presented by a seller as the

reason that one product or service is different from any better

than that of the competition.

The USP of a company determines what place a brand

(tangible good or service) should occupy in the consumer's mind

compared to the competition. The model directs managers to

determine the cognitive gap, locating "which functional benefit

in a given category is most valued by consumers and least

dominated by other brands." It is also commonly known as

mindshare marketing, the aim is to stake a claim to the

cognitive association in consumers' minds, connecting the brand

trademark with the benefit claim as "simply and consistently

and frequently” as possible.

In order to successfully market itself, every business

owner needs to focus on what's special and different about the

Sri Krishna Arts And Science College Page 16

Sundaram Auto Components Ltd. 2014

business. The best way to do this is to try to express this

uniqueness in a single statement. The key to effective selling

in this situation is what advertising and marketing

professionals call a "unique selling proposition" (USP).

USP of Finance Department:

To ensure complete and accurate accounting of all

transactions and to report all financial information in

accordance with state and local laws. Develop and implement

systems to clearly chart the financial health of organization.

Manage overall F&A activity of the plant & provide financial

advice and support to management to enable them to make sound

business decisions.

Elements of USP:

It is truly unique, which is tough to do in a world of

copycats & benchmarking.

The USP includes an implied action.

A guarantee or assurance is offered in the statement.

It is short.

It is easily understood.

Uniqueness can be sought in a number of ways:

By offering the lowest price.

By offering the highest quality.

Sri Krishna Arts And Science College Page 17

Sundaram Auto Components Ltd. 2014

By being exclusive. In the information age, this is an

increasingly common type of USP. More and more firms offer

a unique packaging of information or knowledge.

By offering the best customer service.

By offering the widest choice.

By giving the best guarantee.

Some ways to use USP:

Sound-bites or elevator speeches

Marketing messages

Brochures

Value Propositions

Advertising

Press Releases

Proposals

Benefits of a USP:

A strong USP will drive sales and make communications with

potential customers more effective.

A good USP will help employees and friends of the company

understand the value of the products or services.

If the USP is truly unique, it will differentiate from the

competitors. Competing on differentiation instead of price

is a stronger competitive position.

Sri Krishna Arts And Science College Page 18

Sundaram Auto Components Ltd. 2014

The USP can speed up sales and open doors because it is

easy to understand.

INSTITUTIONAL REQUIREMENTS

ACCOUNTS PAYABLE PROCESS:

The accounts payable process or function is immensely

important since it involves nearly all of a company's payments

outside of payroll. The accounts payable process might be

carried out by an accounts payable department in a large

corporation, by a small staff in a medium-sized company, or by

a bookkeeper or perhaps the owner in a small business.

Regardless of the company's size, the mission of accounts

payable is to pay only the company's bills and invoices that

are legitimate and accurate. This means that before a vendor's

invoice is entered into the accounting records and scheduled

for payment, the invoice must reflect:

what the company had ordered

what the company has received

the proper unit costs, calculations, totals, terms, etc.

Sri Krishna Arts And Science College Page 19

Sundaram Auto Components Ltd. 2014

To safeguard a company's cash and other assets, the accounts

payable process should have internal controls. A few reasons for

internal controls are to:

Prevent paying a fraudulent invoice

Prevent paying an inaccurate invoice

Prevent paying a vendor invoice twice

Be certain that all vendor invoices are accounted for

Periodically companies should seek professional assistance to

improve its internal controls.

The accounts payable process must also be efficient and

accurate in order for the company's financial statements to be

accurate and complete. Because of double-entry accounting an

omission of a vendor invoice will actually cause two accounts

to report incorrect amounts.

For example, if a repair expense is not recorded in a timely

manner:

1. The liability will be omitted from the balance sheet, and

2. The repair expense will be omitted from the income

statement.

If the vendor invoice for a repair is recorded twice, there

will be two problems as well:

1. The liabilities will be overstated, and

2. Repairs expense will be overstated.

Sri Krishna Arts And Science College Page 20

Sundaram Auto Components Ltd. 2014

In other words, without the accounts payable process being

up-to-date and well run, the company's management and other

users of the financial statements will be receiving inaccurate

feedback on the company's performance and financial position.

A poorly run accounts payable process can also mean

missing a discount for paying some bills early. If vendor

invoices are not paid when they become due, supplier

relationships could be strained. This may lead to some vendors

demanding cash on delivery. If that were to occur it could have

extreme consequences for a cash-strapped company.

Just as delays in paying bills can cause problems, so

could paying bills too soon. If vendor invoices are paid

earlier than necessary, there may not be cash available to pay

some other bills by their due dates.

PURCHASE ORDER:

A purchase order or PO is prepared by a company to

communicate and document precisely what the company is ordering

from a vendor. The paper version of a purchase order is a

multi-copy form with copies distributed to several people.

The people or departments receiving a copy of the PO include:

the person requesting that a PO be issued for the goods or

services

the accounts payable department

Sri Krishna Arts And Science College Page 21

Sundaram Auto Components Ltd. 2014

the receiving department

the vendor

the person preparing the purchase order

The purchase order will indicate a PO number, date of

order, company name, vendor name, name and phone number of a

contact person, a description of the items being purchased, the

quantity, unit prices, shipping method, date needed, and other

pertinent information. One copy of the purchase order will be

used in the three-way match.

RECEIVING REPORT:

A receiving report is a company's documentation of the

goods it has received. The receiving report may be a paper form

or it may be a computer entry. The quantity and description of

the goods shown on the receiving report should be compared to

the information on the company's purchase order.

After the receiving report and purchase order information

are reconciled, they need to be compared to the vendor invoice.

Hence, the receiving report is the second of the three

documents in the three-way match.

VENDOR INVOICE:

Sri Krishna Arts And Science College Page 22

Sundaram Auto Components Ltd. 2014

The supplier or vendor will send an invoice to the company

that had received the goods and/or services on credit. When the

invoice or bill is received, the customer will refer to it as a

vendor invoice. Each vendor invoice is routed to accounts

payable for processing. After the invoice is verified and

approved, the amount will be credited to the company's Accounts

Payable account and will also be debited to another account

(often as an expense or asset).

A common technique for verifying a vendor invoice is the

three-way match.

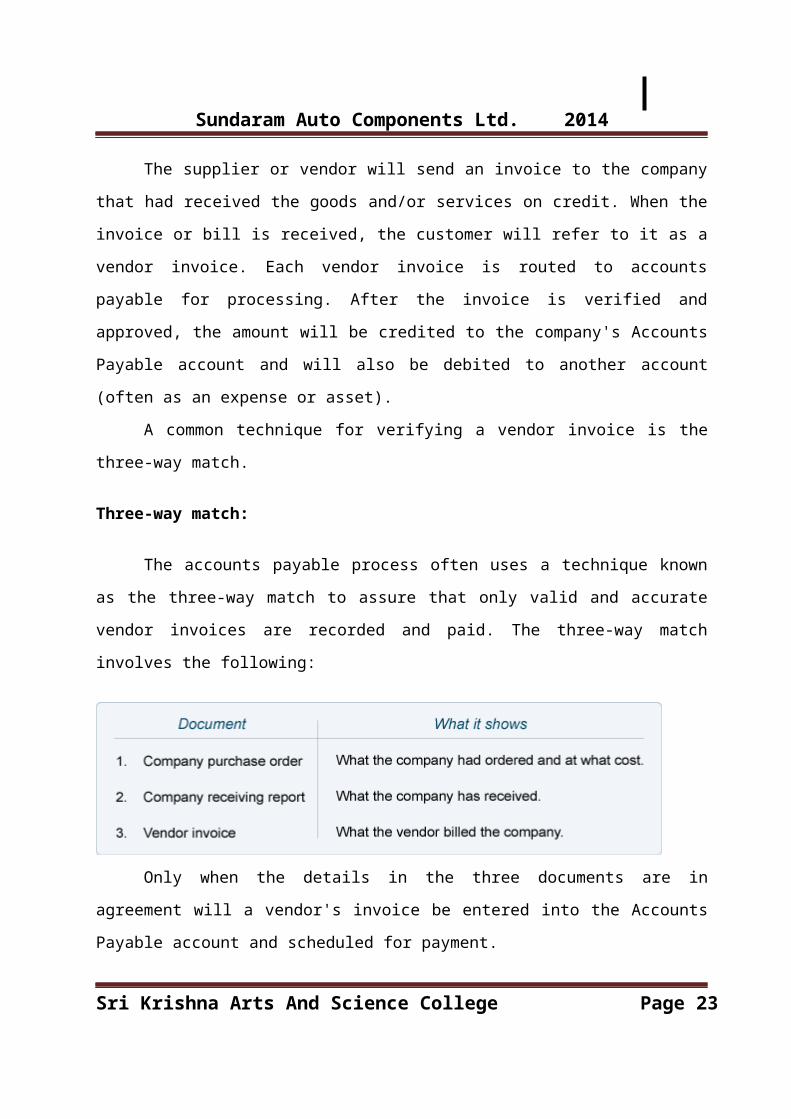

Three-way match:

The accounts payable process often uses a technique known

as the three-way match to assure that only valid and accurate

vendor invoices are recorded and paid. The three-way match

involves the following:

Only when the details in the three documents are in

agreement will a vendor's invoice be entered into the Accounts

Payable account and scheduled for payment.

Sri Krishna Arts And Science College Page 23

Sundaram Auto Components Ltd. 2014

Good internal control of a company's resources is enhanced

when the company assigns a separate employee with a specific,

limited responsibility. The following chart illustrates the

concept of the separation (or segregation) of duties involving

accounts payable:

When the duties are separated, it will require more than

one dishonest person to steal from the company. Hence, small

companies without sufficient staff to separate employees'

responsibilities will have a greater risk of theft.

The three-way match involves comparing the following

information:

1. The description, quantity, cost and terms on the company's

purchase order.

2. The description and quantity of goods shown on the receiving

report.

3. The description, quantity, cost, terms, and math on the

vendor invoice.

Sri Krishna Arts And Science College Page 24

Sundaram Auto Components Ltd. 2014

After determining that the information reconciles, the

vendor invoice can be entered into the liability account

Accounts Payable. The information entered into the accounting

software will include invoice reference information (vendor

name or code, invoice number and date, etc.), the amount to be

credited to Accounts Payable, the amount(s) and account(s) to

be debited and the date that the payment is to be made. The

payment date is based on the terms shown on the invoice and the

company's policy for making payments.

Lastly, the documents should be stamped or perforated to

indicate they have been entered into the accounting system thus

avoiding a duplicate payment.

VOUCHERS:

Some companies use a voucher in order to document or

"vouch for" the completeness of the approval process. A voucher

can be visualized as a cover sheet for attaching the supporting

documents (purchase order, receiving report, vendor's invoice,

etc.) and for noting the approvals, account numbers, and other

information for each vendor invoice or bill.

Sri Krishna Arts And Science College Page 25

Sundaram Auto Components Ltd. 2014

When the vendor invoice is paid, the voucher and its

attachments (including a copy of the check that was issued)

will be stored in a paid voucher/invoice file. If paper

documents are involved, an office machine could perforate the

word "PAID" through the voucher and its attachments. This is

done to assure that a duplicate payment will not occur.

The unpaid invoices and vouchers will be held in an open

file.

Vendor invoices without purchase orders or receiving reports:

Not all vendor invoices will have purchase orders or

receiving reports. Hence, the three-way match is not always

possible. For example, a company does not issue a purchase

order to its electric utility for a pre-established amount of

electricity for the following month. The same is true for the

telephone, natural gas, sewer and water, freight-in, and so on.

There are also payments that are required every month in

order to fulfill lease agreements or other contracts. Examples

include the monthly rent for a storage facility, office rent,

automobile payments, equipment leases, maintenance agreements,

etc. Even though these obligations will not have purchase

orders, the responsibility is unchanged: pay only the amounts

that are legitimate and accurate.

Sri Krishna Arts And Science College Page 26

Sundaram Auto Components Ltd. 2014

“AUTOMATION OF VENDOR PAYMENT PROCESS TO AVOID HIGH LEAD

TIME”

INTRODUCTION:

Automation of vendor payment is a term used to describe

the ongoing effort of many companies to streamline the business

process of their accounts payable departments. The accounts

payable department's main responsibility is to process and

review transactions between the company and its suppliers. In

other words, it is the accounts payable department's job to

make sure all outstanding invoices from their suppliers are

approved, processed, and paid. Processing an invoice includes

recording important data from the invoice and inputting it into

the company’s financial, or bookkeeping, system. After it is

accomplished, the invoices must go through the company’s

respective business process in order to be paid.

Today’s competitive business environment requires that

companies continually seek to cut costs and improve the bottom

line. As a result, corporate executives are sharpening their

focus on operational, back-office efficiencies as a source of

Sri Krishna Arts And Science College Page 27

Sundaram Auto Components Ltd. 2014

savings and liquidity. One area that has been a major focus of

this effort is the Accounts Payable process.

IMPORTANCE OF THE PROBLEM:

More time required for cheque payment processing.

High lead time to realize the cheques by suppliers after

payment made on due date.

Less control over cash flow.

Misplacement of cheques during correspondence.

Issues in Cheque management- Cheque return due to

signature mismatch, damage of instrument, wrong vendor

name etc.,

Transaction cost on account of postage and cheque leafs.

EFFECTS OF THE PROBLEM:

Time lag in payment to important suppliers.

Late payment interest to suppliers.

Delay in instant advance payment.

Unentitled to vendor discounts.

Loss of reputation.

CAUSES AND EFFECTS DIAGRAM:

Sri Krishna Arts And Science College Page 28

Sundaram Auto Components Ltd. 2014

OBSERVATION (CHECK SHEET) :

Existing payment process needs to be automated to meet the

business needs.

Current payment process demands more human interventions.

Dependent on paper based instruments.

Opportunity for payment process streamlining.

Sri Krishna Arts And Science College Page 29

Sundaram Auto Components Ltd. 2014

Scope for complete automation of payment mechanism in

phased manner.

STRATEGY USED - WHY WHY ANALYSIS:

WHY WHY ANALYSIS is a method of questioning that leads to

the identification of the root cause(s) of a problem. A why-why

is conducted to identify solutions to a problem that address

it’s root cause(s). Rather than taking actions that are

merely band-aids, a why-why helps to identify how to really

prevent the issue from happening again. A why-why is most

Sri Krishna Arts And Science College Page 30

Lead time 7 days

Sundaram Auto Components Ltd. 2014

effective in a team setting or with more than one person

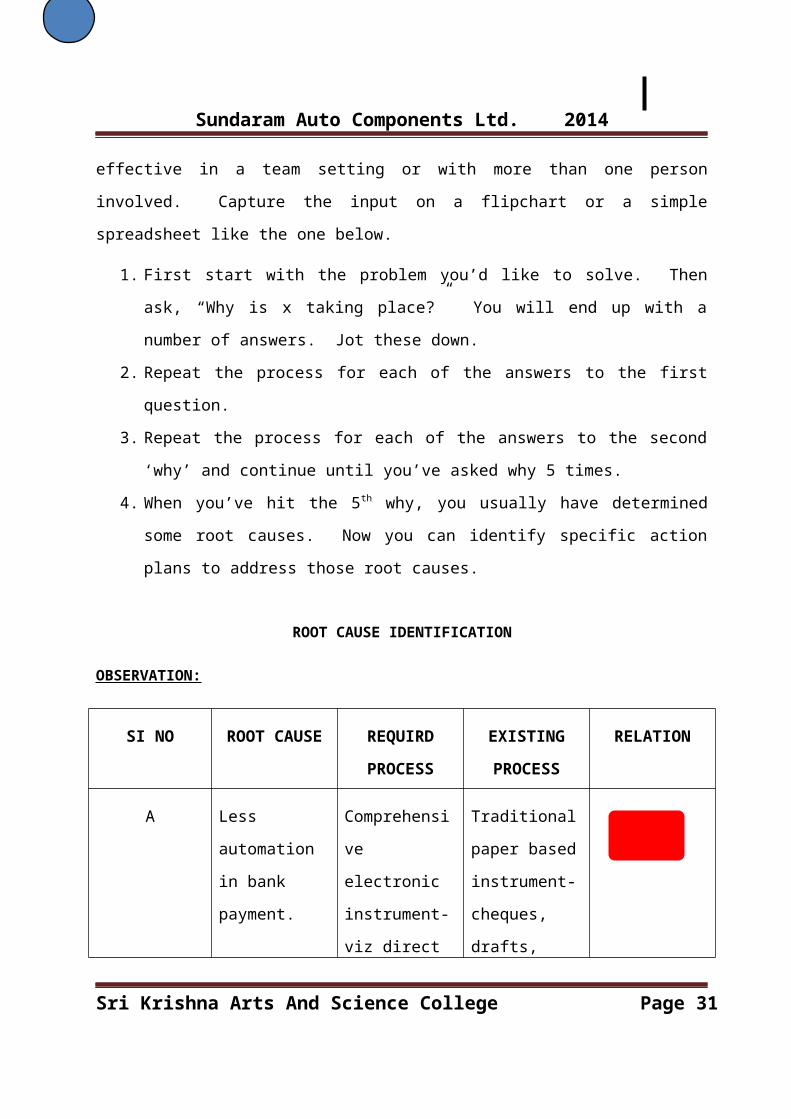

involved. Capture the input on a flipchart or a simple

spreadsheet like the one below.

1. First start with the problem you’d like to solve. Then

ask, “Why is x taking place?” You will end up with a

number of answers. Jot these down.

2. Repeat the process for each of the answers to the first

question.

3. Repeat the process for each of the answers to the second

‘why’ and continue until you’ve asked why 5 times.

4. When you’ve hit the 5th why, you usually have determined

some root causes. Now you can identify specific action

plans to address those root causes.

ROOT CAUSE IDENTIFICATION

OBSERVATION:

SI NO ROOT CAUSE REQUIRD

PROCESS

EXISTING

PROCESS

RELATION

A Less

automation

in bank

payment.

Comprehensi

ve

electronic

instrument-

viz direct

Traditional

paper based

instrument-

cheques,

drafts,

Sri Krishna Arts And Science College Page 31

Lead time 7 days

Sundaram Auto Components Ltd. 2014

debit,

RTGS, NEFT,

ECS.

payorder.

B Less

control

over

liquidity

management

Payment to

be made in

a single

day

Payment

happening

anywhere

between 3

to 7 days.

C Delay in

clearance

in

instrument

of banks

No

clearance

Lead time

in bank

clearance-

2to3 days.

Sri Krishna Arts And Science College Page 32

CLOSE RELATIONSHIPMEDIUM RELATIONSHIP

Sundaram Auto Components Ltd. 2014

KEY BENEFITS:

Every business is familiar with the arduous process of

paying bills for goods and services, not to mention the sea of

paper and the information management challenges it creates.

Regardless of a company’s size, nearly every enterprise must

respond to invoices for utilities, rent, and goods or services

in order to perform without interruption. Failure to pay

promptly can result in severe penalties or worse – no lights.

The approval of invoices and resolving of billing

discrepancies can require many man hours. Inefficiencies may

Sri Krishna Arts And Science College Page 33

Automated payment process through Corporate banking

Sundaram Auto Components Ltd. 2014

prevent organizations from taking advantage of invoice

discounts and may result in late payment fees, or even damage

to a company’s reputation. Invoice digital capture and

automated workflow address these challenges.

Together, they provide a seamless flow of accurate and

timely information, expediting processing and saving precious

human capital for more important projects.

• Reduced payment processing time

• Mass approval of payment to vendors

• Transactions can be traced through unique transaction

reference numbers.

• Transaction cost can be passed on to vendors

• Faster reconciliation of bank transactions

• Improvement in productivity

• No change in quality

• Transaction Cost -Saving of Rs 2 Lakhs per annum

• Timely payment to suppliers.

STANDARDISATION:

Sri Krishna Arts And Science College Page 34

Sundaram Auto Components Ltd. 2014

Proposed to make payment through electronic

mode for all the vendors in phased manner.

Periodic review of payment automation to

utilize the payment solution offered by the

banking system from time-to-time.

APPLICATION OF TECHNOLOGY

INJECTION MOULDING:

Injection moulding is a manufacturing process for

producing parts by injecting material into a mould. Injection

moulding can be performed with a host of materials, including

metals, glasses, elastomers, confections, and most commonly

thermoplastic and thermosetting polymers. Material for the part

is fed into a heated barrel, mixed, and forced into a mold

cavity where it cools and hardens to the configuration of the

cavity.[1]:240 After a product is designed, usually by an

Sri Krishna Arts And Science College Page 35

Sundaram Auto Components Ltd. 2014

industrial designer or an engineer, moulds are made by a mould

maker (or toolmaker) from metal, usually either steel or

aluminium, and precision-machined to form the features of the

desired part. Advances in technology now also allow for 3D

printing of injection moulds for certain applications, using

photopolymer plastics which do not melt during the injection

process. Injection moulding is widely used for manufacturing a

variety of parts, from the smallest components to entire body

panels of cars.

Parts to be injection moulded must be very carefully designed

to facilitate the moulding process; the material used for the

part, the desired shape and features of the part, the material

of the mould, and the properties of the moulding machine must

all be taken into account. The versatility of injection

moulding is facilitated by this breadth of design

considerations and possibilities.

Today with the growing competition, customers are

demanding quick response with minimum cost. Lead-time reduction

has long been recognized as an important metric to improve the

responsiveness. Lead-time as it is defined, is, “The total time

required to complete one unit of a product or service”.

Management of time specifically lead-time, is a competitive

advantage, and delivery lead-time reduction within the logistic

network is the mechanism for time-based competition.

Sri Krishna Arts And Science College Page 36

Sundaram Auto Components Ltd. 2014

In the current project work, Inventory Optimization is

done to a Distribution Center to reduce its lead time and

improve its responsiveness towards the customers. Pre-

positioning of inventory to optimize it is one way of reducing

the lead time.

The aim of the project is, to reduce the lead time of the

customer orders for a distribution center. The current system

which is being followed consists of a long waiting time for the

customers. With the present inventory arrangement, the lead

time for the orders being processed is high which is making the

process slow. The distribution center consists of levels into

which the inventory is arranged .There is no specific criteria

following currently for this process. So when a customer places

an order and after the order receipt is received, the customer

is made to wait for a long time until the order is being

processed.

After the receipt for an order is received, the employees

have to manually fill the order by picking the products from

the stock, which is randomly placed in the entire distribution

center. Even for a single product the employee has to travel in

the entire levels for filling it, which is creating a lot of

unwanted motion. This is contributing a high lead time which is

resulting in customer unsatisfaction.

Sri Krishna Arts And Science College Page 37

Sundaram Auto Components Ltd. 2014

Major emphasis is done on the inventory arrangement so as to

reduce the time taken to fill the orders, through which the

lead time can be reduced considerably. The flaws in the current

system are studied and data is collected relevantly to apply

the required tools.

The customer orders data is collected. Data mining

techniques are applied to analyze the data. The frequently

repeated items together were found out from the customer

orders. With the frequent item sets the inventory is rearranged

as clusters. Sku Clustering is done in the inventory

arrangement in the entire stocks. Now with the clustering of

the sku’s there is more chance that, more likely ordered

products are nearby. So this reduced the time taken to fill the

orders. So as the products are near by the orders are filled

faster than earlier. Through which the customer waiting time is

reduced. The lead time is reduced considerably which resulted

in increased customer satisfaction.

So the Inventory principles are applied to reduce the lead

time. Eventhough this may not be the entire solution to the

problem, but to some extent this is a solution which improves

the efficiency considerably.

Sri Krishna Arts And Science College Page 38

Sundaram Auto Components Ltd. 2014

WORK FLOW CHART

CASH:

In this site the person has the responsibility to control

cash flow of the firm. He will control all the cash in and out

from the firm. Before make or received a payment from clients,

he will get the approval from the authorized person for

verification and sign if agreed. Usually the firm use computer

system to update and control cash in and out from client and

firm. The system that they use is Microsoft word and Microsoft

excel. All the clients can make a payment either by cash or

cheque. This firm paid their staff salary through bank such as

ICICI Bank, SBI Bank, and others. It was an easy way to pay

salary to the permanent staffs. Besides that they were also pay

to the staff if they have taken overtime.

Sri Krishna Arts And Science College Page 39

FINANCECASHPAYABLESRECEIVABLESGENERAL LEDGERTAXATIONMANAGEMENT INFORMATION SYSTEM

Sundaram Auto Components Ltd. 2014

Cash management is an extremely important area for a

firm’s success. Cash management is a main area of working

capital management. At the organizational level the

responsibilities of a chief financial officer can be presented

as follows:

Capital management.

Risk management.

Strategic planning.

Investor relations.

Financial reporting.

Risk management.

Hedging and insurance management.

Accounts receivable management.

Accounts payable management.

Bank relations.

Insurance risk.

Undertake short-term investments.

Inter-group borrowing and lending.

Bank relations, credit facilities operations.

International taxation.

BILLS PAYABLE:

Bills payable is a concept used in the areas of finance

and accounting. The term can be defined in three ways:

Sri Krishna Arts And Science College Page 40

Sundaram Auto Components Ltd. 2014

Bills payable can be the funds that a bank borrows from

other banks. These are typically due in the very short

term and are used to provide liquidity to the receiving

bank.

Bills payable can be short-term notes issued by a business

that are due on demand or by a specific date. The duration

of these forms of indebtedness tend to be quite short.

Bills payable can be the same as accounts payable, which

are usually comprised of invoices from suppliers that are

received and recorded by a business within the current

liabilities section of the balance sheet. These

liabilities may be recorded as accrued liabilities, if a

liability is present as of the end of a reporting period,

but no invoice from a supplier has yet been received.

Bills payable is an older term, and is more commonly found

in the English system of accounting than the American system.

PAYMENT PROCESS:

- Automated payment process through corporate banking.

Finance Dept. Decides to initiate payments by RTGS/NEFT.

Bank entry will be posted in SAP and a separate RTGS/NEFT

request file will be generated.

File authorized through SBI Portal.

Sri Krishna Arts And Science College Page 41

Sundaram Auto Components Ltd. 2014

Cross verifies transmission authenticity for security

purpose.

Fund transferred to beneficiary bank account through

RTGS/NEFT/DC.

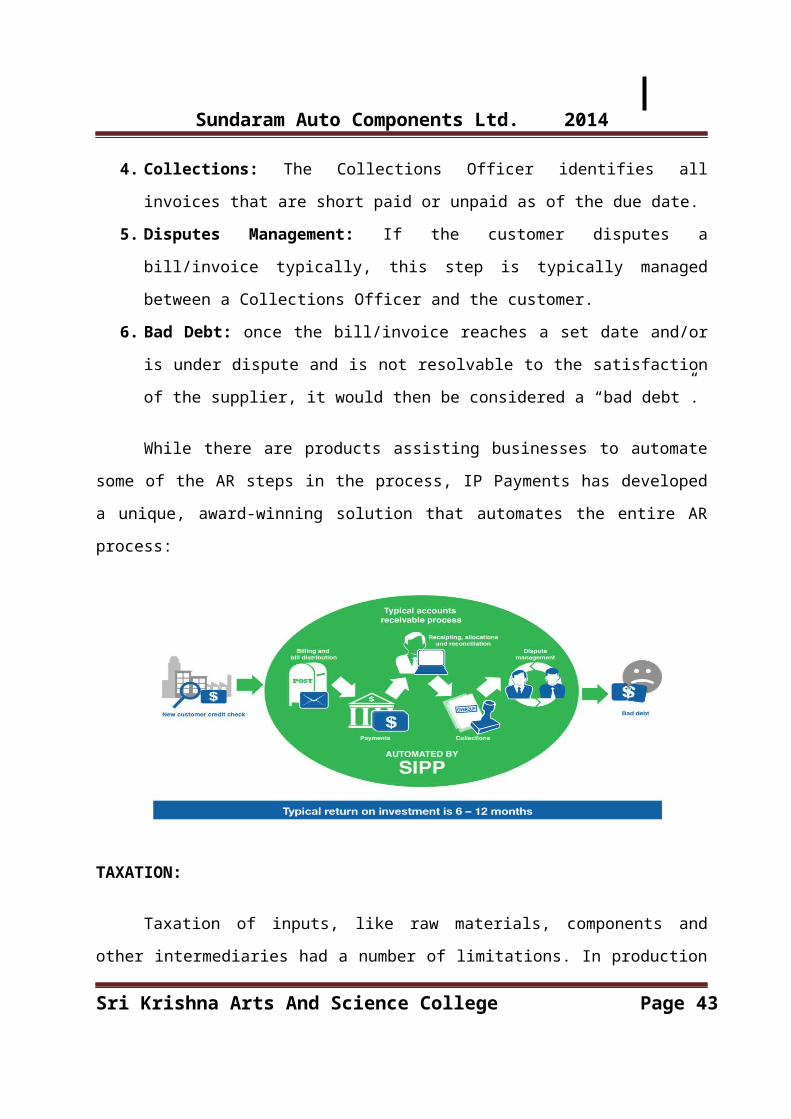

ACCOUNTS RECEIVABLES PROCESS:

The Accounts Receivable process is the process by which

businesses receive payments from customers for goods or

services sold.

The process has several steps:

1. Credit Decisions: The supplier of goods and services

checks if the prospective customer is of sufficient credit

worthiness to warrant the supply of the products or

services under an account arrangement.

2. Billing and Bill Distribution: Happens once the

good/services have been supplied. Payments are completed

by the customer once they are ready to pay.

3. Receipting, Allocations and Reconciliation: This step is

undertaken by an Accounts Receivables Officer. The AR

Officer identifies a payment deposited into the supplier

bank account, receipts it into the AR system, allocates

it to an invoice and reconciles to ensure that the payment

is correct.

Sri Krishna Arts And Science College Page 42

Sundaram Auto Components Ltd. 2014

4. Collections: The Collections Officer identifies all

invoices that are short paid or unpaid as of the due date.

5. Disputes Management: If the customer disputes a

bill/invoice typically, this step is typically managed

between a Collections Officer and the customer.

6. Bad Debt: once the bill/invoice reaches a set date and/or

is under dispute and is not resolvable to the satisfaction

of the supplier, it would then be considered a “bad debt”.

While there are products assisting businesses to automate

some of the AR steps in the process, IP Payments has developed

a unique, award-winning solution that automates the entire AR

process:

TAXATION:

Taxation of inputs, like raw materials, components and

other intermediaries had a number of limitations. In production

Sri Krishna Arts And Science College Page 43

Sundaram Auto Components Ltd. 2014

process, raw material passes through various processes stages

till a final product emerges. Thus, output of the first

manufacturer becomes input for second manufacturer and so on.

When the inputs are used in the manufacture of product `A', the

cost of the final product increases not only on account of the

cost of the inputs, but also on account of the duty paid on

such inputs. As the duty on the final product is on ad valorem

basis and the final cost of product `A' includes the cost of

inputs, inclusive of the duty paid, duty charged on product `A'

meant doubly taxing raw materials. In other words, the tax

burden goes on increasing as raw material and final product

passes from one stage to other because, each subsequent

purchaser has to pay tax again and again on the material which

has already suffered tax. This is called cascading effect or

double taxation.

This very often distorted the production structure and did

not allow the correct assessment of the tax incidence.

Therefore, the Government tried to remove these defects of the

Central Excise System by progressively relieving inputs from

excise and countervailing duties. An ideal system to realize

this objective would have been to adopt value added taxation

(VAT). However, on account of some practical difficulties it

was not possible to fully adopt the value added taxation.

Sri Krishna Arts And Science College Page 44

Sundaram Auto Components Ltd. 2014

Hence, Government evolved a new scheme, `MODVAT' (Modified

Value Added Tax). MODVAT Scheme which essentially follows VAT

Scheme of taxation. i.e. if a manufacturer a purchases certain

components (raw materials) from another manufacturer B for use

in its product. B would have paid excise duty on components

manufactured by it and would have recovered that excise duty in

its sales price from A. Now, A has to pay excise duty on

product manufactured by it as well as bear the excise duty paid

by the supplier of raw material B. Under the MODVAT scheme, a

manufacturer can take credit of excise duty paid on raw

materials and components used by him in his manufacture. It

amounts to excise duty only on additions in value by each

manufacturer at each stage.

The MODVAT scheme is regulated by Rules 57A to 57U of the

Central Excise Rules and the notifications issued there under

(The Central Excise Rules, 2002 (Section 143 of the Finance

Act, 2002).

MODVAT Scheme ensures the revenue of the same order and at

same time the price of the final product could be lower. Apart

from reducing the costs through elimination of cascade effect,

and bringing in greater rationalization in tax structure and

also bringing in certainty in the amount of tax leviable on the

final product, this scheme will help the consumer to understand

precisely the impact of taxation on the cost of any product and

Sri Krishna Arts And Science College Page 45

Sundaram Auto Components Ltd. 2014

will, therefore, enable consumer resistance to unethical

attempts on the part of manufacturers to raise prices of final

products, attributing the same to higher taxes.

Subsequently, MODVAT scheme was restructured into CENVAT

(Central Value Added Tax) scheme. A new set of rules 57AA to

57AK , under The CENVAT Credit Rules, 2004, were framed and

whatever restrictions were there in MODVAT Scheme were put to

an end and comparatively, a free hand was given to the

assesses. Under the CENVAT Scheme, a manufacturer of final

product or provider of taxable service shall be allowed to take

credit of duty of excise as well as of service tax paid on any

input received in the factory or any input service received by

manufacturer of final product.

The term "Input" means: -

1. All goods, except light diesel oil, high speed diesel oil

and motor spirit, commonly known as petrol, used in or in

relation to the manufacture of final products whether

directly or indirectly and whether contained in the final

product or not and includes lubricating oils, greases,

cutting oils, coolants, accessories of the final products

cleared along with the final product, goods used as

paint, or as packing material, or as fuel, or for

generation of electricity or steam used in or in relation

to manufacture of final products or for any other

Sri Krishna Arts And Science College Page 46

Sundaram Auto Components Ltd. 2014

purpose, within the factory of production.

2. All goods, except light diesel oil, high speed diesel oil,

motor spirit, commonly known as petrol and motor

vehicles, used for providing any output service;

Explanation 1 :

The light diesel oil, high-speed diesel oil or motor

spirit, commonly known as petrol, shall not be treated as an

input for any purpose whatsoever.

Explanation 2:

Inputs include goods used in the manufacture of capital

goods which are further used in the factory of the

manufacturer;"

The term "Input service" means any service: -

1. Used by a provider of taxable service for providing an

output service; or

2. Used by the manufacturer, whether directly or indirectly,

in or in relation to the manufacture of final products and

clearance of final products from the place of removal,

And includes services used in relation to setting up,

modernization, renovation or repairs of a factory, premises of

Sri Krishna Arts And Science College Page 47

Sundaram Auto Components Ltd. 2014

provider of output service or an office relating to such

factory or premises, advertisement or sales promotion, market

research, storage upto the place of removal, procurement of

inputs, activities relating to business, such as accounting,

auditing, financing, recruitment and quality control, coaching

and training, computer networking, credit rating, share

registry and security, inward transportation of inputs or

capital goods and outward transportation upto the place of

removal;"

Manufacturer and service providers can avail CENVAT credit

of capital goods used by them. The plant and machinery and

allied items are purchased by a manufacturer. Such goods known

as capital goods may be duty paid. The capital goods shall be

used in manufacture of final products or for providing output

service. The CENVAT credit in respect of duty paid on capital

goods shall be taken only for an amount not exceeding fifty

percent of the duty paid in the same financial year and the

credit of balance amount can be take in any financial year

subsequent to the financial year in which the capital goods

were received.

Duty Paying Documents against which CENVAT credit can be

availed are:-

Sri Krishna Arts And Science College Page 48

Sundaram Auto Components Ltd. 2014

Invoice issued by,

A manufacture of inputs or capital goods,

An importer,

An importer from his depot or premises of consignment

agent,

Provided the depot/ premises is registered with

central excise,

A first/second stage dealer.

A supplementary invoice.

A bill of entry.

A certificate issued by appraiser of customs.

An invoice/bill/challan issued by providers of input

service.

A challan evidencing payment of service tax.

Credit of duty is allowed only if all the conditions given

below are met:-

The basic criteria for availment of credit of duty paid on

inputs or capital goods is that the goods shall be used in

manufacture of final products.

The goods shall be accompanied with proper prescribed

documents.

The final products shall not be exempt from whole of duty

or chargeable to nil rate of duty.

Sri Krishna Arts And Science College Page 49

Sundaram Auto Components Ltd. 2014

ROLE DESCRIPTION:

Candidate should be well versed with both direct and

indirect taxes; filing of returns, assessments and audits.

- Preparation of Income Tax Return, Working for filling

of TDS Return on quarterly basis

- Working with Consultant to provide the required data

for assessment and appeal proceeding.

- working with Chartered Accountants to collect the

certificate and filed forms

- Preparation of computation of wealth tax and filling

of return

- Working with Transfer pricing consultant to provide

the required data for assessments

- Working for payment of Service Tax, Maintaining

records of payment of Service Tax & Excise

- Working with consultants / Sales Tax Commissioner for

providing data and any other requirement

- Downloading of C-Forms and sending to Vendor after

signature

- Reconciliation of vendor accounts and follow up for

confirmation/statements

- Working for filling of VAT Return with the Department

Sri Krishna Arts And Science College Page 50

Sundaram Auto Components Ltd. 2014

- Providing data for Annual Vat Audit and finalize the

same

- Dealing with Internal Custom Department for exchange

of information as and when required.

- Associate with Tax Auditor for providing the related

working for Tax Audit and filling of Returns.

- Providing data to parent company at the time of

consolidation of accounts.

- Providing related documents for Cost Audit.

SWOT ANALYSIS

INTRODUCTION:

SWOT analysis looks at the strengths and weaknesses, and

the opportunities and threats of the business faces. By

focusing on the key factors affecting the business, now and in

the future, a SWOT analysis provides a clear basis for

examining the business performance and prospects. This briefing

outlines:

• Typical strengths, weaknesses, opportunities and threats,

and how to identify them.

Sri Krishna Arts And Science College Page 51

Sundaram Auto Components Ltd. 2014

• How to use SWOT analysis to drive the business forward.

STRENGTHS:

Strengths are usually easy to identify, through the

continuing dialogue with customers and suppliers. The records

(eg. sales) will also help to indicate areas which are

particularly strong (eg. rising sales for a particular

product).

For most businesses, strengths will fall into four distinct

categories.

1. Sound finances may give you advantages over the competitors.

Important factors might include:

• Positive cash flow.

• Growing turnover and profitability.

• Skilled financial management, good credit control and few

bad debts.

• A strong balance sheet.

• Access to extensive credit, a strong credit rating, and a

good relationship with the bank and other sources of finance.

2. Marketing may be the key to the success.

The business may enjoy:

• Market leadership in a profitable niche.

• A good reputation and a strong brand name.

• An established customer base.

Sri Krishna Arts And Science College Page 52

Sundaram Auto Components Ltd. 2014

• A strong product range.

• Effective research and development, use of design

and innovation.

• A skilled sales force.

• Thorough after-sales service.

• Protected intellectual property (eg registered

designs, patented products).

3. Management and personnel skills and systems may provide

equally

Important underpinnings for success.

These may include factors such as:

• Management strength in depth.

• The ability to make quick decisions.

Skilled employees, successful recruitment, and effective

training and development.

• Good motivation and morale.

• Efficient administration.

4. Strengths in production may include the right premises and

plant, and good sources of materials or sub-assemblies.

The business may benefit from:

• Modern, low-cost production facilities.

• Spare production capacity.

• A good location.

Sri Krishna Arts And Science College Page 53

Sundaram Auto Components Ltd. 2014

• Effective purchasing and good relationships with

suppliers.

Be aware that strengths are not always what they seem.

Strengths may imply weaknesses (for example, market leaders are

often complacent and bureaucratic) and often imply threats (for

example, the star salesman may be a strength — until he

resigns).

WEAKNESSES:

The weaknesses are often known but ignored. A SWOT

analysis should be the starting point for tackling

underperformance in the business.

1. Poor financial management may result in situations where:

• Insufficient funds are available for investment in new

plant or product development.

• All available security, including personal assets and

guarantees, is already pledged for existing

borrowings.

• Poor credit control leads to unpredictable cash flow.

2. Lack of marketing focus may lead to:

• Unresponsive attitudes to customer requirements.

• A limited or outdated product range.

Sri Krishna Arts And Science College Page 54

Sundaram Auto Components Ltd. 2014

• Complacency and a failure to innovate.

• Over-reliance on a few customers.

3. Management and personnel weaknesses are often hard to

recognize, except with hindsight. Familiar examples are:

• Failure to delegate and train successors.

• Expertise and control locked up in a few key

personnel.

• Inability to take outside advice.

• High staff turnover.

4. Inefficient production, premises and plant can undermine

any business, however hard people work.

Typical problems include:

• Poor location and shabby premises.

• Outdated equipment, high cost production and low

productivity.

• Long leases tying the business to unsuitable premises

or equipment.

• Inefficient processes.

OPPORTUNITIES:

Sri Krishna Arts And Science College Page 55

Sundaram Auto Components Ltd. 2014

External changes provide opportunities that well managed

businesses can turn to their advantage.

1) Changes involving organizations and individuals which

directly affect the business may open up completely new

possibilities. For example:

• Deterioration in a competitor’s performance, or the

insolvency of a competitor.

• Improved access to potential new customers and markets

(eg overseas).

• Increased sales to existing customers, or new leads

gained through them.

• The development of new distribution channels (eg the

Internet).

• Improved supply arrangements, such as just-in-time

supply or outsourcing non-core activities.

• The opportunity to recruit a key employee from a

competitor.

• The introduction of financial backers who are keen to

fund expansion.

2) The broader business environment may shift in the

favour. This may be caused by:

• Political, legislative or regulatory change.

For example, a change in legislation that requires customers to

purchase a product.

• Economic trends.

Sri Krishna Arts And Science College Page 56

Sundaram Auto Components Ltd. 2014

For example, falling interest rates reducing the cost of

capital.

• Social developments.

For example, demographic changes or changing consumer

requirements leading to an increase in demand for the products.

• New technology.

For example, new materials, processes and information

technology.

THREATS:

Threats can be minor or can have the potential to destroy

the business.

I. Changes involving organizations and individuals that

directly affect the business can have far-reaching

effects. For example:

• Improved competitive products or the emergence of new

competitors.

• Loss of a significant customer.

Sri Krishna Arts And Science College Page 57

Sundaram Auto Components Ltd. 2014

• Creeping over-reliance on one distributor or group of

distributors.

• Failure of suppliers to meet quality requirements.

• Key personnel leaving, perhaps with trade secrets.

• Lenders reducing credit lines or increasing charges.

• A rent review threatening to increase costs, or the

expiry of a lease.

• Legal action (eg being sued by a customer).

II. The broader business environment may alter to the

disadvantage. This may be the result of:

• Political, legislative or regulatory change.

For example, new regulation increasing the costs or requiring

product redesign.

• Economic trends.

For example, lower exchange rates reducing the income from

overseas.

• Social developments.

For example, consumer demands for ‘environmentally-friendly’

products.

• New technology.

For example, technology that makes the products obsolete or

gives competitors an advantage.

Sri Krishna Arts And Science College Page 58

Sundaram Auto Components Ltd. 2014

CONCLUSION:

During my training, I found lead – time payment process to

be a drawback. It involves steps which are very complicated,

thereby resulting in delayed payment. So, the suppliers of the

company hesitate to supply materials for further production and

flourishment of the company, so annual production will be

decreased and the annual turnover will be affected on the

whole. So I would suggest a new method called as “AUTOMATIC

PAYMENT PROCESS” which reduces complications in payment,

thereby improving the production process.

The study is to determine the factors related to financial

activities engaged by the employees. And to evaluate the

effectiveness of the Financial Engagement SACL. This study is

to find out the satisfaction levels of the Employees with the

current system.

Monitor quality and standards of performance.

Ensure effective control of resources.

Provide information on key areas for management decision-

making.

Indicate profitable financial returns.

Sri Krishna Arts And Science College Page 59

Sundaram Auto Components Ltd. 2014

Contains an investors / lenders exit strategy.

Ensure fast financing results.

Contains a financial risk sensitivity analysis.

The main objective of the industrial training is to

provide an opportunity to undergraduates to identify, observe

and practice how accounting is applicable in the real industry.

It is not only to get experience on technical practices but

also to observe management practices and to interact with

fellow workers.

Auditors’ Report to the Shareholders of Sundaram Auto

Components Limited, Chennai for the year ended 31st March 2010:

1) We have audited the attached balance sheet of M/s.

Sundaram Auto Components Limited, Chennai 600 006 as at 31st

March 2010 and the profit and loss account for the year ended

on that date annexed thereto and the cash flow statement for

the year ended on that date. These financial statements are the

Sri Krishna Arts And Science College Page 60

Sundaram Auto Components Ltd. 2014

responsibility of the Company’s management. Our responsibility

is to express an opinion on these financial statements based on

our audit.

2) We have conducted our audit in accordance with

auditing standards generally accepted in India. These standards

require that we plan and perform the audit to obtain reasonable

assurance about whether the financial statements are free of

material misstatement. An audit includes examining, on a test

basis, evidence supporting the amounts and disclosures in the

financial statements. An audit also includes assessing the

accounting principles used and significant estimates made by

management, as well as evaluating the overall presentation of

the financial statements. We believe that our audit provides a

reasonable basis for our opinion.

3) As required by the Companies (Auditor’s Report)

Order, 2003 and amended by the Companies (Auditor’s Report)

(Amendment) Order, 2004 issued by the Central Government in

terms of sub-section (4A) of Section 227 of the Companies Act,

1956, we enclose in the Annexure, a statement on the matters

specified in paragraphs 4 and 5 of the said Order.

4) Further to our comments in the Annexure, referred to

above, we state that –

Sri Krishna Arts And Science College Page 61

Sundaram Auto Components Ltd. 2014

i. We have obtained all the information and

explanations, which to the best of our knowledge and belief

were necessary for the purposes of our audit;

ii. In our opinion, proper books of accounts, as

required by law have been kept by the Company so far as appears

from our examination of such books;

iii. The balance sheet, profit and loss account and

cash flow statement dealt with by this report are in agreement

with the books of accounts;

iv. In our opinion, the Balance Sheet, Profit and

Loss account and the Cash Flow Statement dealt with by this

report comply with the accounting standards referred to in sub-

section (3C) of Section 211 of the Companies Act, 1956;

v. On the basis of written representations received

from the directors of the Company as on 31st March 2010 and

taken on record by the Board of Directors, we report that none

of the directors are disqualified from being appointed as a

director in terms of clause (g) of sub-section (1) of Section

274 of the Companies Act, 1956 on the said date;

vi. In our opinion and to the best of our

information and according to the explanations given to us, the

said accounts read together with the notes thereon give the

information required by the Companies Act, 1956, in the manner

so required and give a true and fair view in conformity with

the accounting principles generally accepted in India;

Sri Krishna Arts And Science College Page 62

Sundaram Auto Components Ltd. 2014

In so far as it relates to the Balance

Sheet, of the state of affairs of the Company as at 31st March

2010;

In so far as it relates to the Profit and

Loss account, of the profit of the Company for the year ended

on that date; and

In so far as it relates to the Cash Flow

Statement, of the cash flows for the year ended on that date.

For SUNDARAM & SRINIVASAN

Chartered Accountants

Firm Regn. No. 004207S

Place: Chennai

Date: July 16, 2010

M.BALASUBRAMANIYAM

Partner

Membership No. F7945

Sri Krishna Arts And Science College Page 63

Sundaram Auto Components Ltd. 2014

Annexure referred to in the report of even date on the accounts

for the year ended 31.03.2014.

The company has maintained proper records showing full

particulars including quantitative details and situation

of fixed assets.

The inventory has been physically verified at reasonable

interval during the by the management.

The company has neither taken nor granted any loan to /

from companies, firms and other parties covered in the

register maintained under section 301 of the companies

act 1956.

The company has an internal audit system, which in

auditor’s opinion is commensurate with its size and

nature of its business.

The company has not accepted any deposit from the

public.

The company does not cover under the Employees’ State

Insurance Act.

The company has not used fund raised on short term basis

for long term investments.

The company has not allotted any shares on preferential

basis to parties and companies covered in the register

maintained under section 301 of the Companies Act, 1956.

According to the information, the company has not

granted loans and advance on the basis of security by

Sri Krishna Arts And Science College Page 64

Sundaram Auto Components Ltd. 2014

way of pledge of shares, debentures and other

securities.

The company has not availed any fresh loan during the

year.

During the year, the company has not issued any secured

debentures.

Based on the audit procedures adopted information and

explanations given to us by the management no funds or

on by the company has been noticed or reported during

the course of audit.

For SUNDARAM & SRINIVASAN Chartered Accountants Firm Regn. No. 004207S

Place: Chennai M.BALASUBRAMANIYA PartnerDate: 31.03.2014 Membership No. F7945

Sri Krishna Arts And Science College Page 65

Sundaram Auto Components Ltd. 2014

As per the report annexed

For SUNDARAM & SRINIVASAN

Chartered Accountants

H. Lakshmanan V.N. Venkatanathan

Firm Regn. No. 004207S

Sri Krishna Arts And Science College Page 66

Sundaram Auto Components Ltd. 2014

Chairman Director

P.S. Bashyam K.

Dharmarajan M. BALASUBRAMANIYAM

Chennai Manager Secretary Partneruly 16, 2010.Membership No. F7945

Sri Krishna Arts And Science College Page 67

Sundaram Auto Components Ltd. 2014

As per the report annexed

For SUNDARAM & SRINIVASAN

Chartered Accountants

H. Lakshmanan V.N. Venkatanathan

Firm Regn. No. 004207S

Chairman Director

P.S. Bashyam K. Dharmarajan M.

BALASUBRAMANIYAM

Chennai Manager Secretary

Partner

July 16, 2010

Membership No. F7945

Sri Krishna Arts And Science College Page 68

Sundaram Auto Components Ltd. 2014

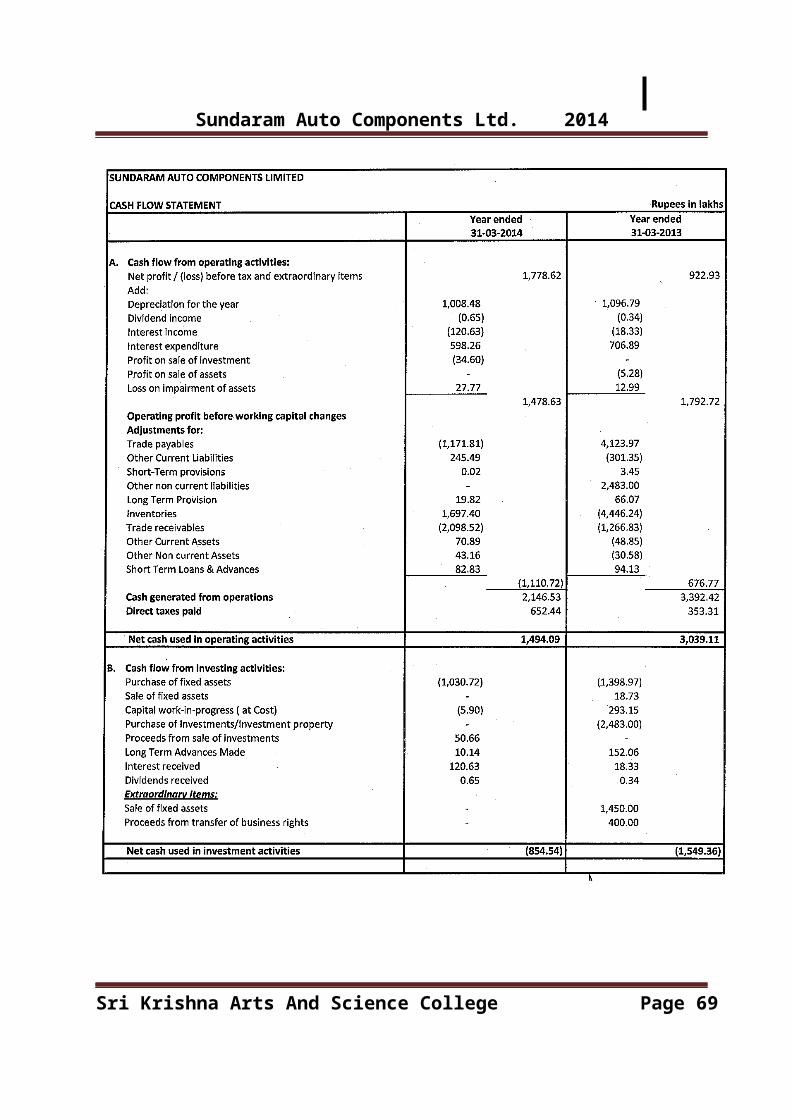

Sri Krishna Arts And Science College Page 69

Sundaram Auto Components Ltd. 2014

As per the report annexed

For SUNDARAM & SRINIVASAN

Chartered Accountants

H. Lakshmanan V.N. Venkatanathan

Firm Regn. No. 004207S

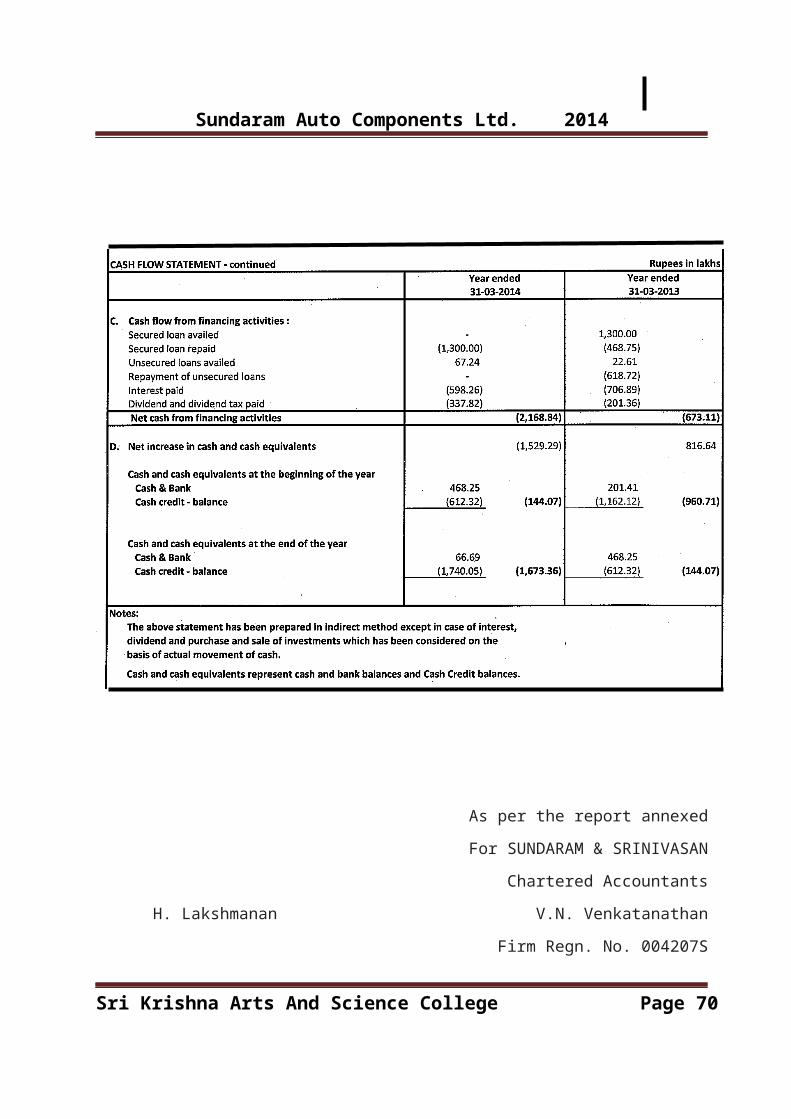

Sri Krishna Arts And Science College Page 70

Sundaram Auto Components Ltd. 2014

Chairman Director

P.S. Bashyam K. Dharmarajan M.

BALASUBRAMANIYAM

Chennai Manager Secretary

Partner

July 16, 2010

Membership No. F7945

TWO WHEELER PARTS

Sri Krishna Arts And Science College Page 71

Sundaram Auto Components Ltd. 2014

FOUR WHEELER PARTS

Sri Krishna Arts And Science College Page 72

Sundaram Auto Components Ltd. 2014

Sri Krishna Arts And Science College Page 73

Sundaram Auto Components Ltd. 2014

DIAPHRAGMS AND HOSES

INJUCTION MOULDING AREA

Sri Krishna Arts And Science College Page 74

Sundaram Auto Components Ltd. 2014

MANUFACTURING FACILITIES

Sri Krishna Arts And Science College Page 75

Sundaram Auto Components Ltd. 2014

Sri Krishna Arts And Science College Page 76