city of fort bragg

TRANSCRIPT

City Council

City of Fort Bragg

Meeting Agenda

416 N Franklin Street

Fort Bragg, CA 95437

Phone: (707) 961-2823

Fax: (707) 961-2802

THE FORT BRAGG CITY COUNCIL MEETS CONCURRENTLY AS

THE FORT BRAGG MUNICIPAL IMPROVEMENT DISTRICT NO. 1

AND THE FORT BRAGG REDEVELOPMENT SUCCESSOR

AGENCY

Town Hall, 363 N. Main Street6:00 PMMonday, December 9, 2019

CALL TO ORDER

PLEDGE OF ALLEGIANCE

ROLL CALL

AGENDA REVIEW

1. MAYOR’S RECOGNITIONS AND ANNOUNCEMENTS

1A. 19-533 Presentation of Proclamation to Ricardo Garcia for Providing Life-Saving

Actions

18-2019 Ricardo Garcia Commendation

18-2019 Ricardo Garcia Commendation Spanish

Attachments:

1B. 19-532 Receive Presentation from Mendocino Coast Humane Society Executive

Director Chuck Tourtillott

MCHS Presentation Summary 120919

MCHS_City Council Presentation 12-09-19

Attachments:

1C. 19-528 Presentation by Mendocino County Fifth District Supervisor Ted Williams

on the County's Proposed Transient Occupancy Tax (TOT) on

Campground and Recreational Vehicle Parks

2. PUBLIC COMMENTS ON: (1) NON-AGENDA, (2) CONSENT CALENDAR & (3)

CLOSED SESSION ITEMS

MANNER OF ADDRESSING THE CITY COUNCIL: Any member of the public desiring to address the City

Council may submit a Speaker Card to the City Clerk and proceed to the podium after being recognized by the

Presiding Officer. Speakers will be called up in the order the Speaker Cards are received. Those who have not

filled out a Speaker Card will be given an opportunity to speak after all those who have filled out Speaker Cards

have spoken. All remarks and questions shall be addressed to the City Council; no discussion or action will be

taken pursuant to the Brown Act. No person shall speak without being recognized by the Mayor or acting

Mayor. Written comments may be submitted to the City Clerk, 416 N. Franklin Street, Fort Bragg, CA 95437,

or emailed to [email protected].

Page 1 City of Fort Bragg Printed on 12/4/2019

December 9, 2019City Council Meeting Agenda

TIME ALLOTMENT FOR PUBLIC COMMENT ON NON-AGENDA ITEMS: Thirty (30) minutes shall be allotted

to receiving public comments. If necessary, the Mayor or acting Mayor may allot an additional 30 minutes to

public comments after Conduct of Business to allow those who have not yet spoken to do so. Any citizen, after

being recognized by the Mayor or acting Mayor, may speak on any topic that may be a proper subject for

discussion before the City Council for such period of time as the Mayor or acting Mayor may determine is

appropriate under the circumstances of the particular meeting, including number of persons wishing to speak or

the complexity of a particular topic. Time limitations shall be set without regard to a speaker’s point of view or

the content of the speech, as long as the speaker’s comments are not disruptive of the meeting.

BROWN ACT REQUIREMENTS: The Brown Act does not allow action or discussion on items not on the

agenda (subject to narrow exceptions). This will limit the Council's response to questions and requests made

during this comment period.

3. STAFF COMMENTS

4. MATTERS FROM COUNCILMEMBERS

5. CONSENT CALENDAR

All items under the Consent Calendar will be acted upon in one motion unless a Councilmember requests that

an individual item be taken up under Conduct of Business.

5A. 19-525 Adopt Resolution of the Fort Bragg City Council Amending the FY 2019-20

Budget (Amendment No. 2020-06) Approving the Use of $91,000.00 of

General Fund Fund Balance to Make a Prepayment to CalPERS Against

the City’s Unfunded Pension Liability ( Account 110-0000-0220)

RESO Unfunded Pension Liability PrepaymentAttachments:

5B. 19-529 Adopt by Title Only and Waive the Second Reading of Ordinance

955-2019 Repealing and Replacing Chapter 6.10 (Weed Abatement

Procedures) and Adding Chapter 6.11 (Integrated Pest Management) to

Title 6 (Health and Sanitation) of the Fort Bragg Municipal Code

ORD 955-2019Attachments:

5C. 19-487 Approve Maddy Act Notice Providing List of Appointed Terms Expiring in

2020

12092019 MADDY ACT NOTICEAttachments:

5D. 19-512 Receive and File Minutes of October 2, 2019 Finance and Administration

Committee Meeting

FACM20191002Attachments:

5E. 19-514 Receive and File Minutes of August 21, 2019 Public Safety Committee

Meeting

PSCM2019-08-21Attachments:

5F. 19-531 Receive and File Minutes of October 9, 2019 Public Works and Facilities

Committee Meeting

Page 2 City of Fort Bragg Printed on 12/4/2019

December 9, 2019City Council Meeting Agenda

PWM 10092019Attachments:

5G. 19-536 Approve Minutes of November 25, 2019

CCM2019-11-25Attachments:

6. DISCLOSURE OF EX PARTE COMMUNICATIONS ON AGENDA ITEMS

7. PUBLIC HEARING

When a Public Hearing has been underway for a period of 60 minutes, the Council must vote on whether to

continue with the hearing or to continue the hearing to another meeting.

8. CONDUCT OF BUSINESS

8A. 19-530 Receive Report and Consider Adoption of City Council Resolution

Approving Professional Services Agreement with R.E.Y. Engineers, Inc. to

Provide Design and Engineering Services for the 2020 Maple Street

Storm Drain and Alleys Rehab Project, City Project No. PWP-00116, and

Authorizing City Manager to Execute Contract (Amount Not to Exceed

$144,342.00; Account No.405-4870-0731)

12092019 2020 Maple Street Project Design

Att 1 - RESO 2020 Maple St Project Design

Attachments:

8B. 19-520 Receive Report and Recommendation from the Election Systems Review

Ad Hoc Committee

12092019 ERC Report

Public report - elections review - FINAL

Attachments:

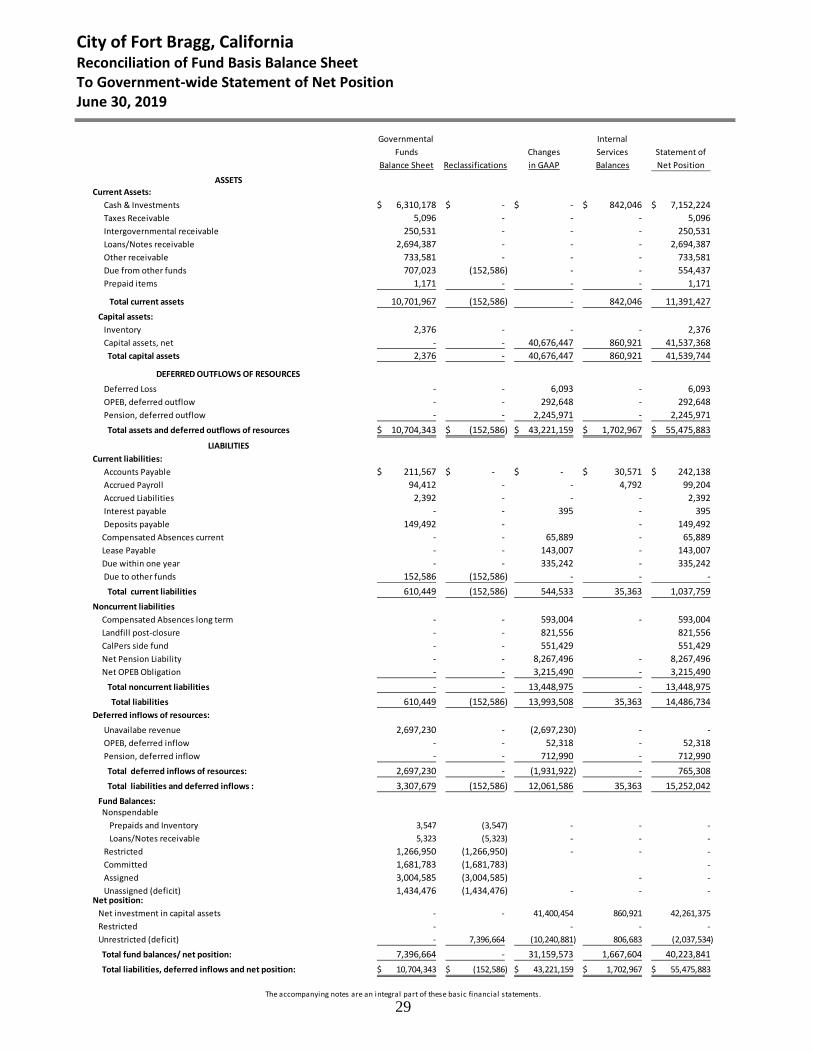

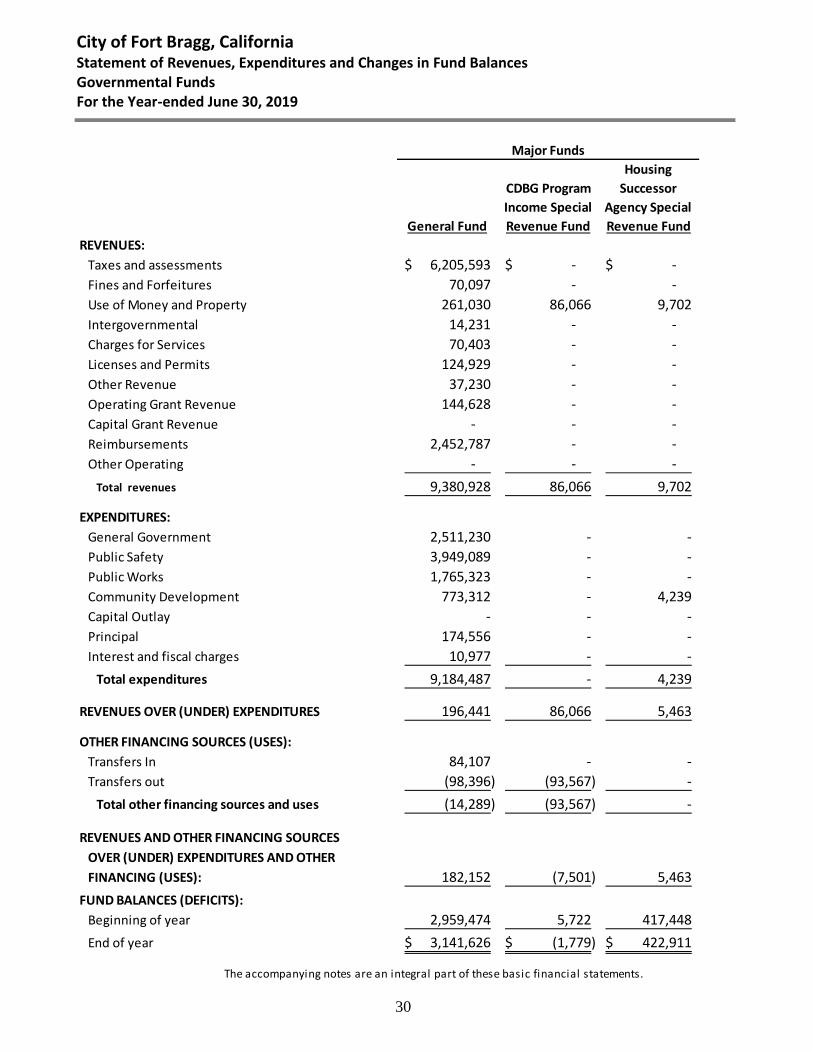

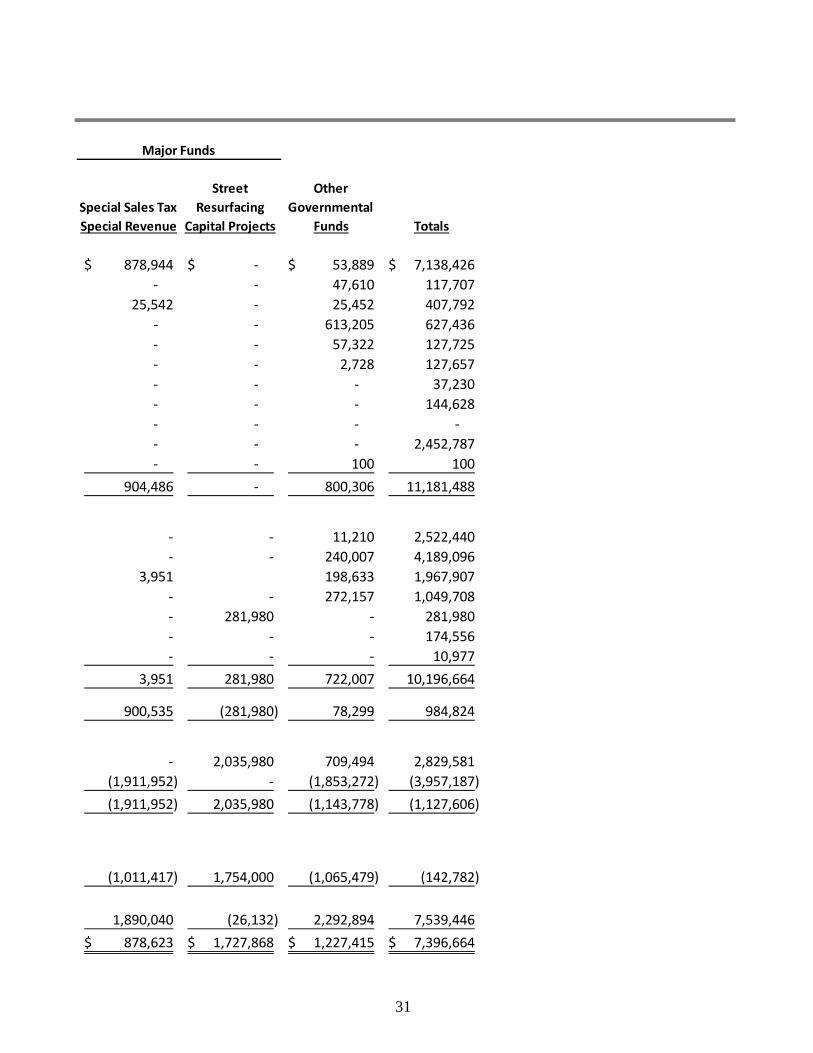

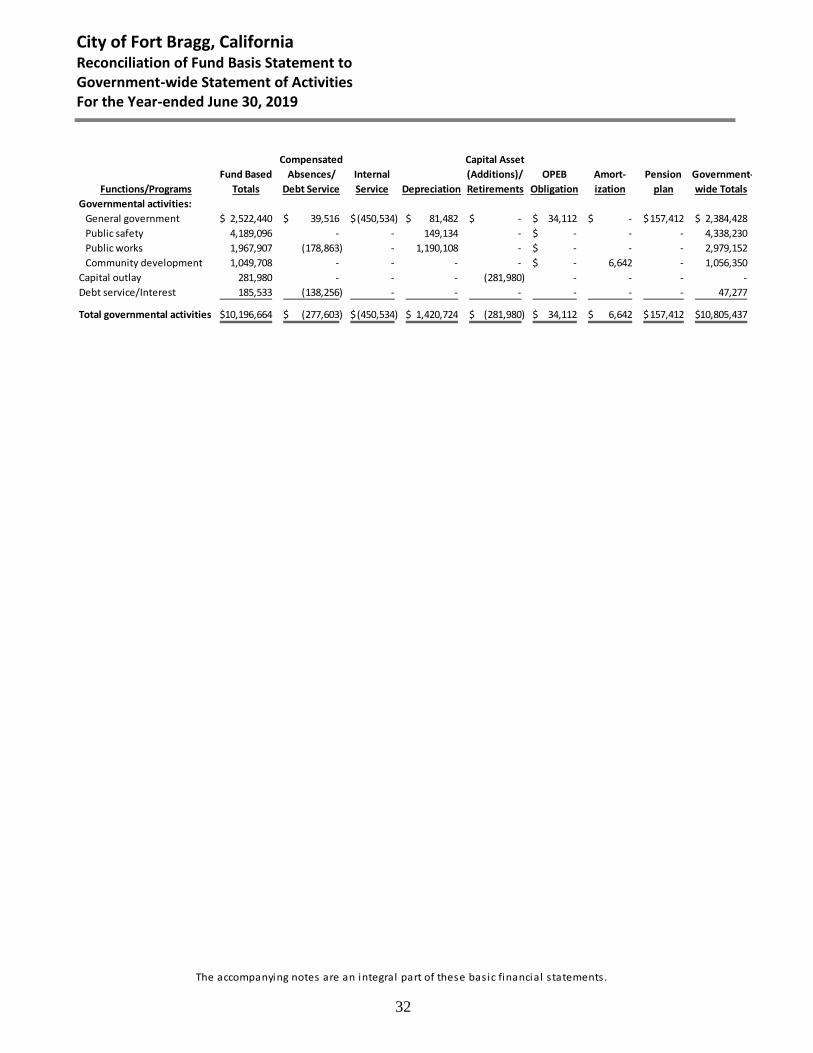

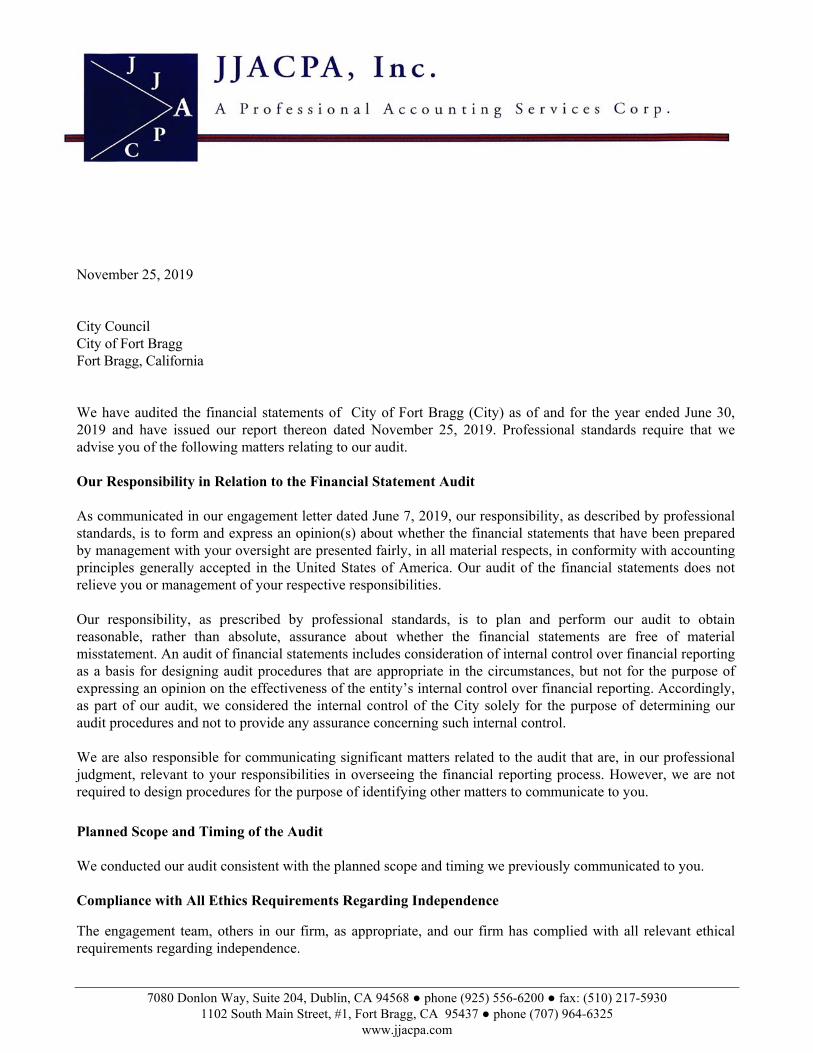

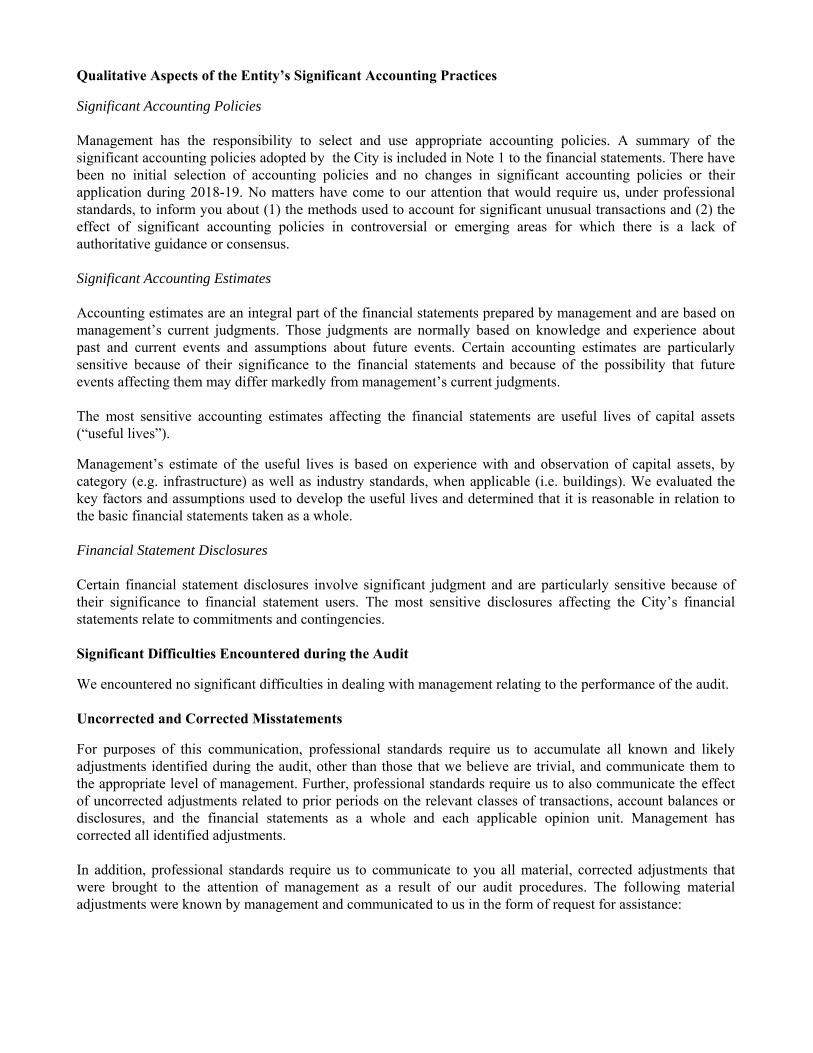

8C. 19-523 Receive Presentation From JJACPA, Inc. and Finance Director Victor

Damiani on the Comprehensive Annual Financial Report (CAFR) for the

Year Ended June 30, 2019 for the City of Fort Bragg and Consider

Accepting the CAFR as Presented

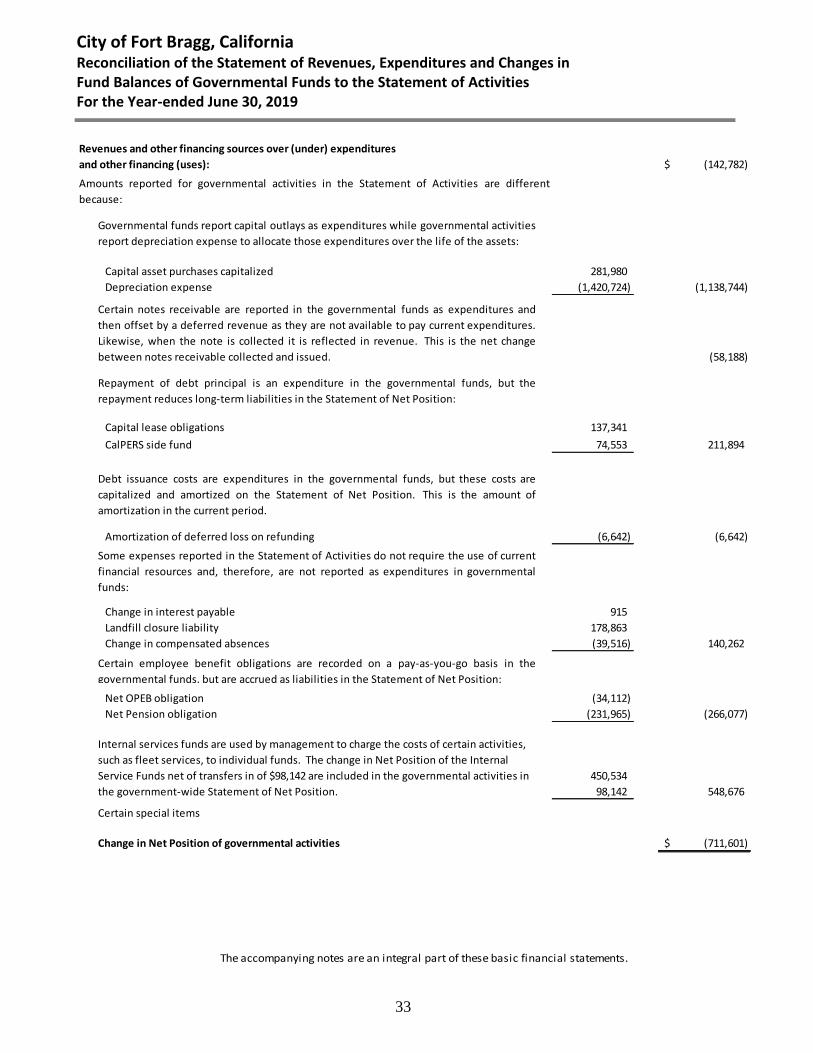

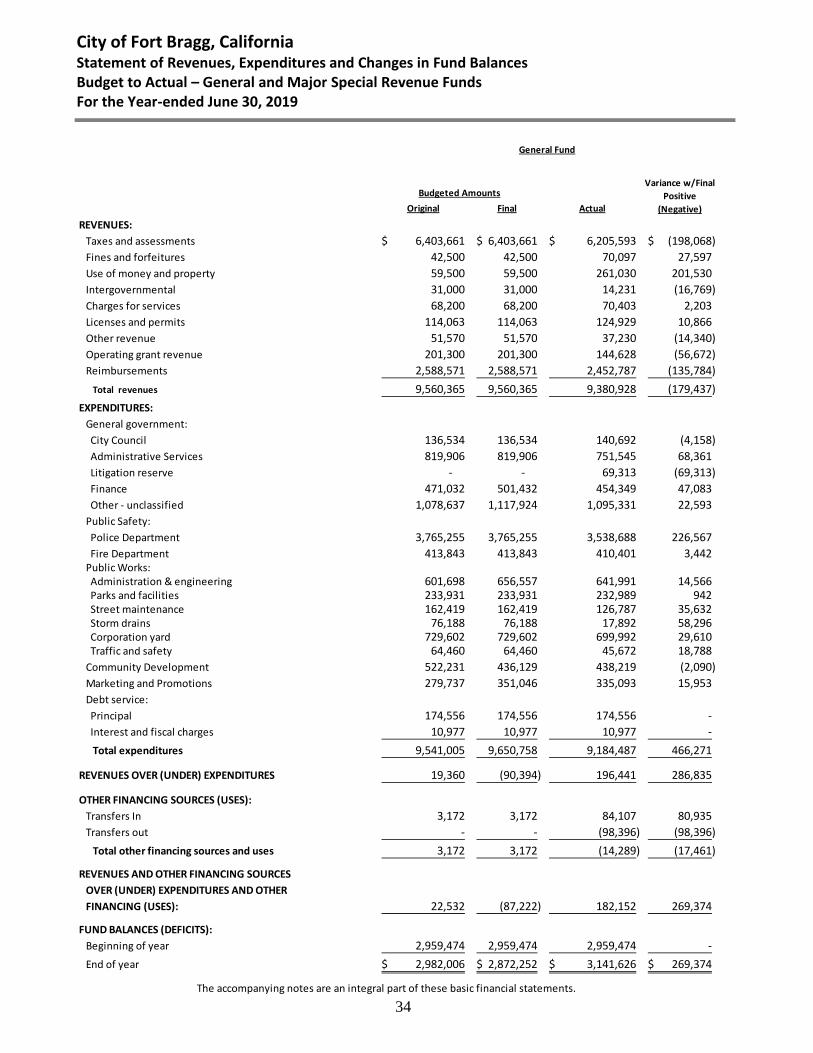

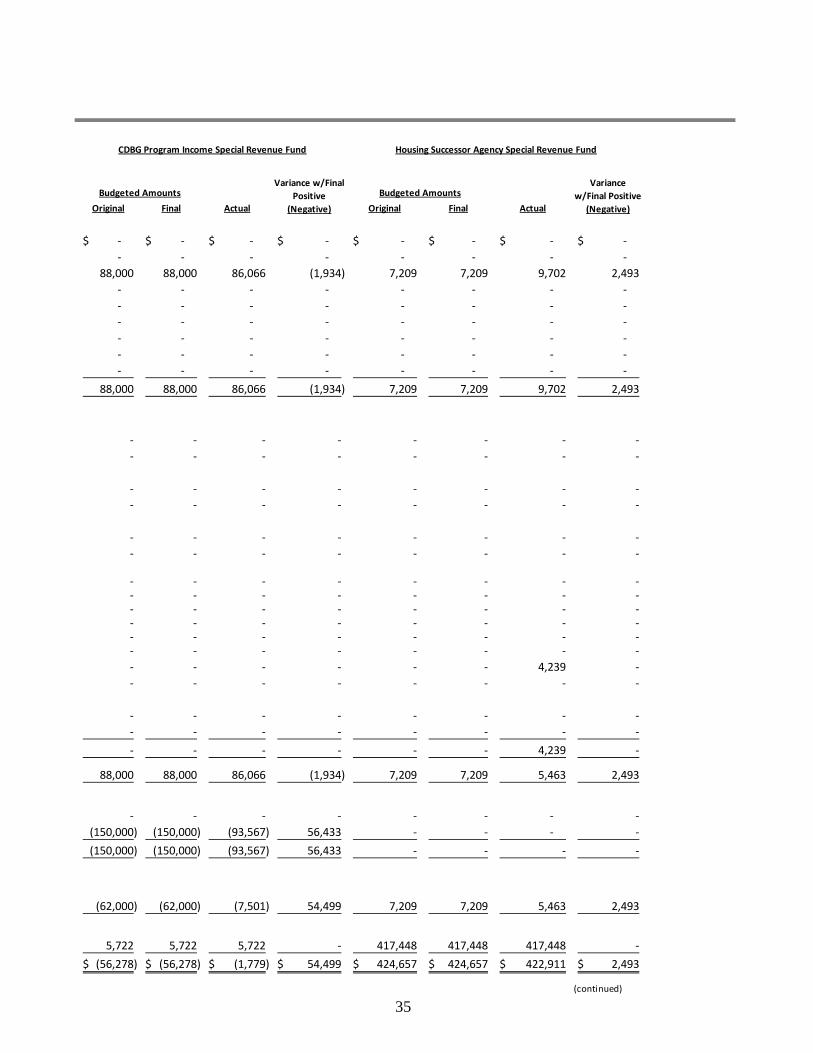

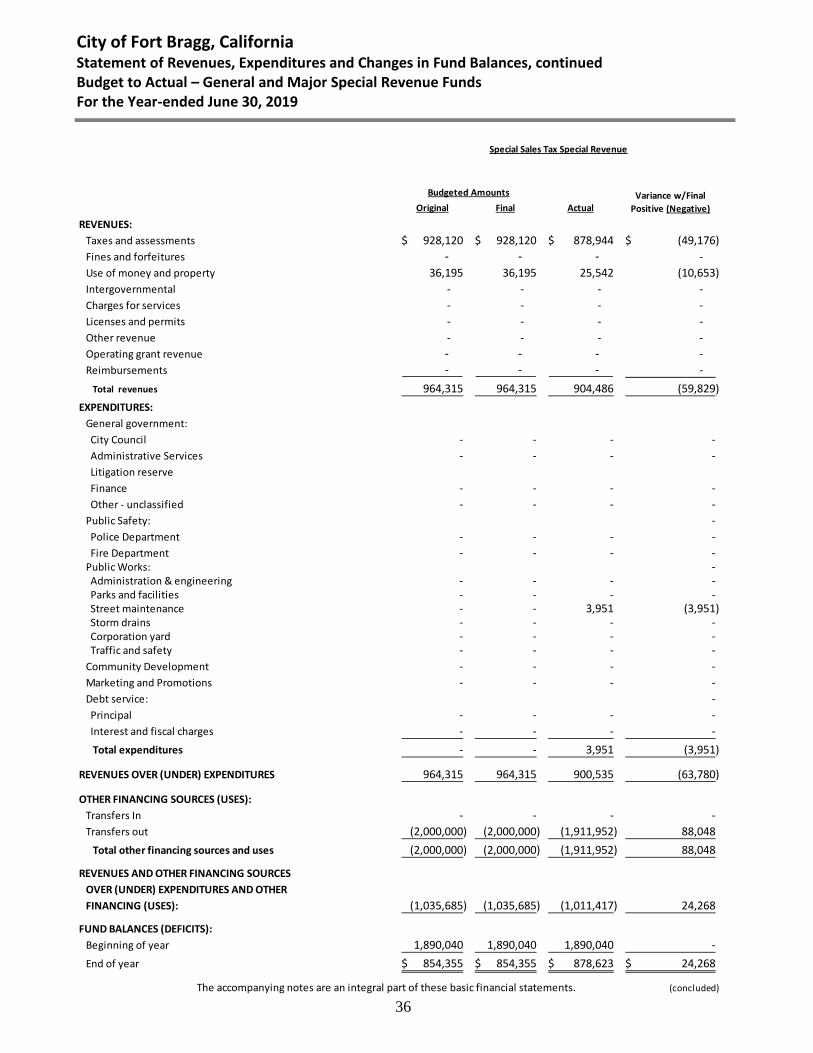

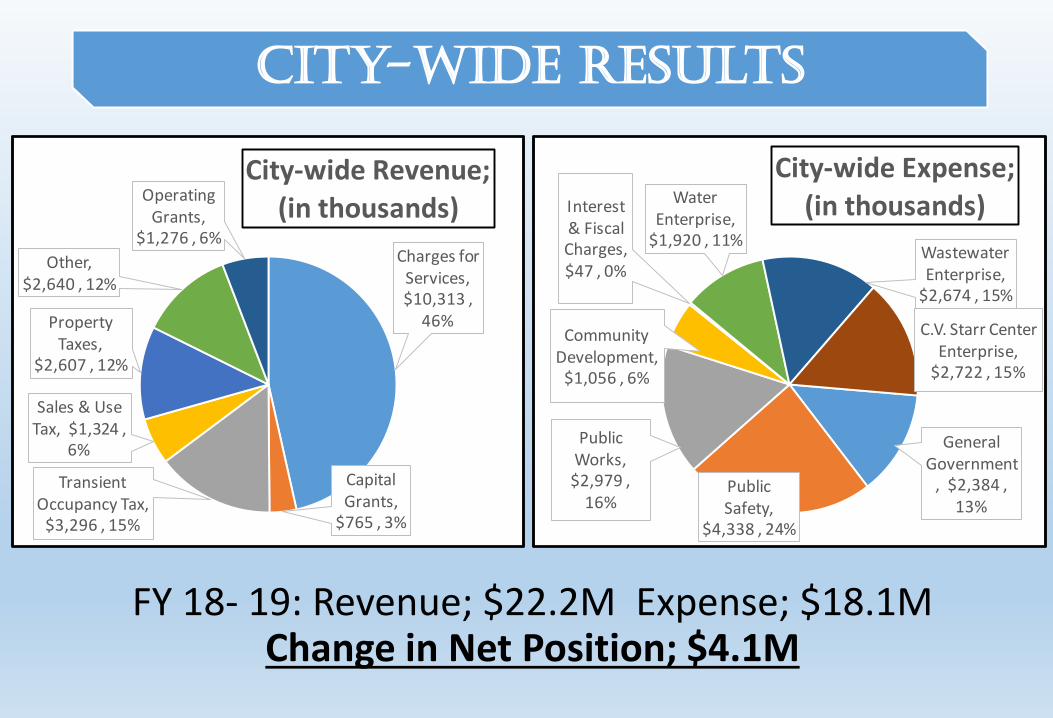

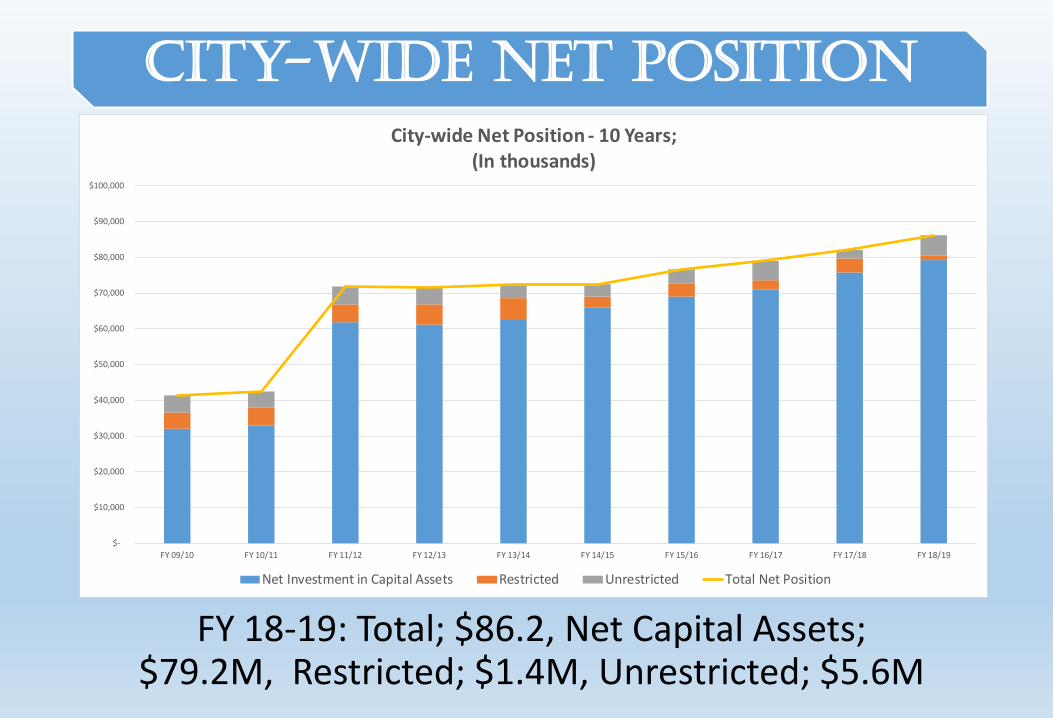

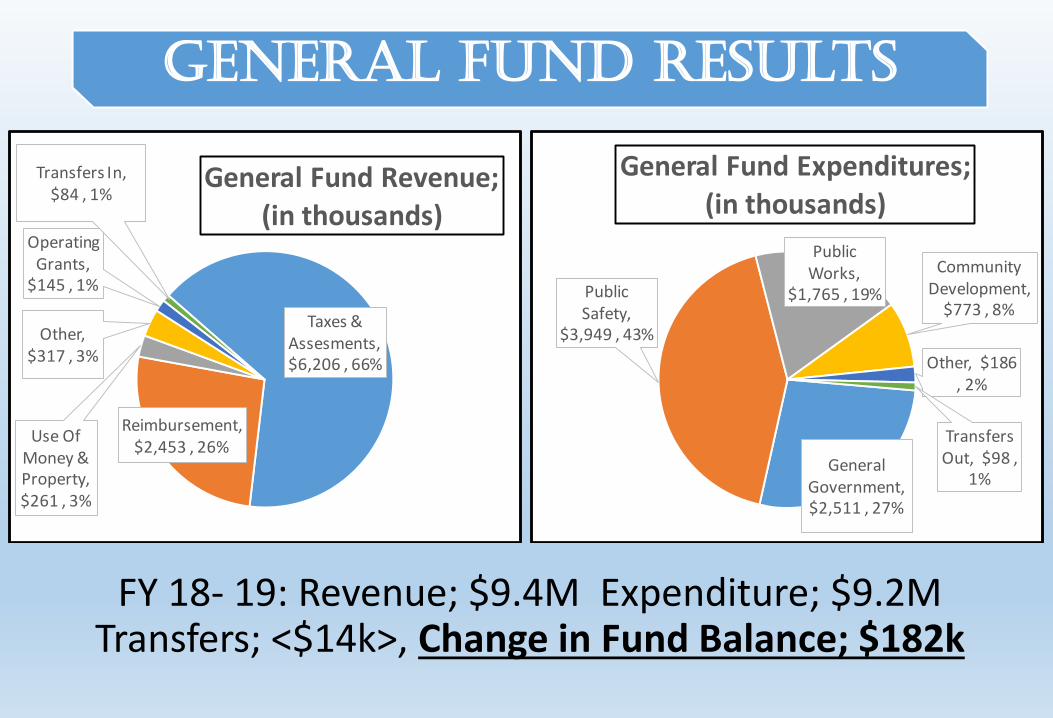

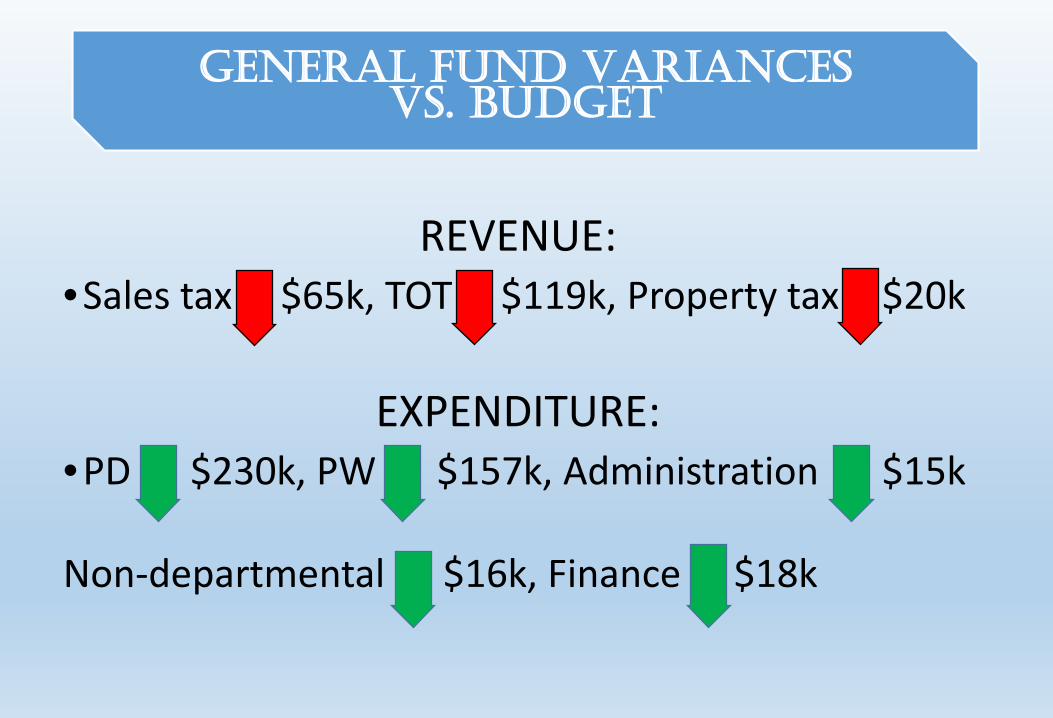

2019-12-09 CAFR Staff Report

Att 1 - CAFR, Including Auditor's Report

Att 2 - FY18-19 CAFR PowerPoint Presentation

Att 3 - Communications Letter 2019

Att 4 - Representation Letter

Att 5 - Fort Bragg Single Audit Report 2019

Attachments:

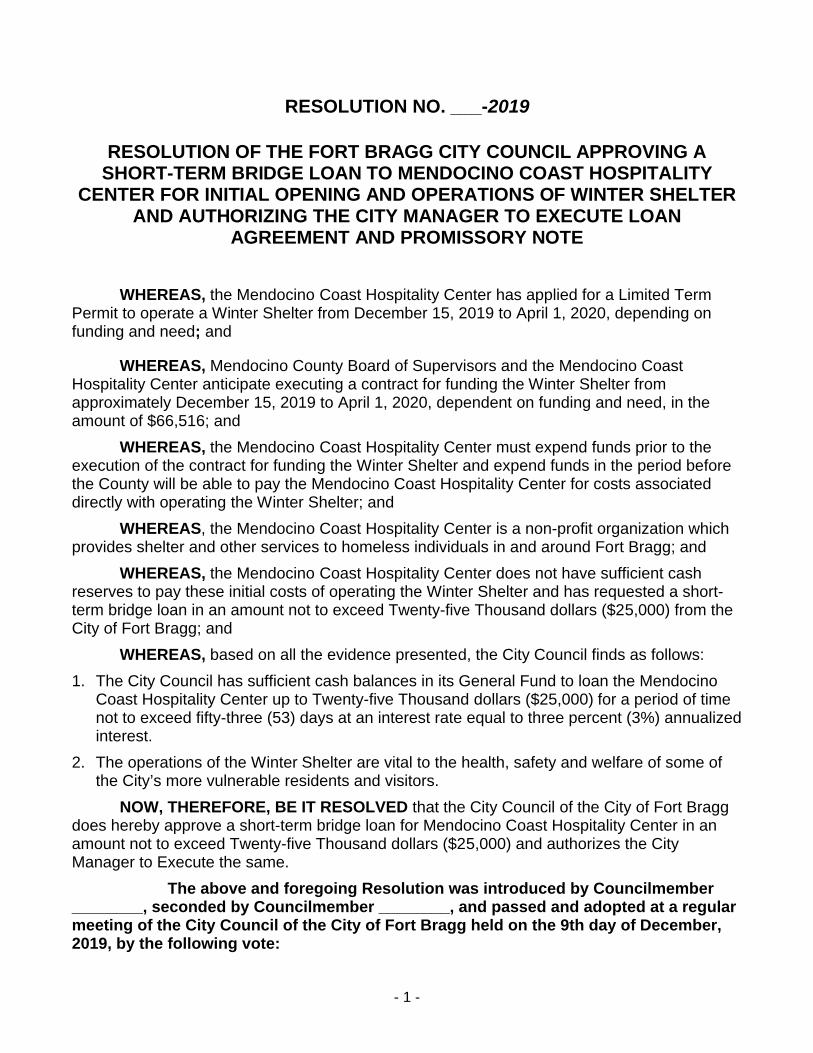

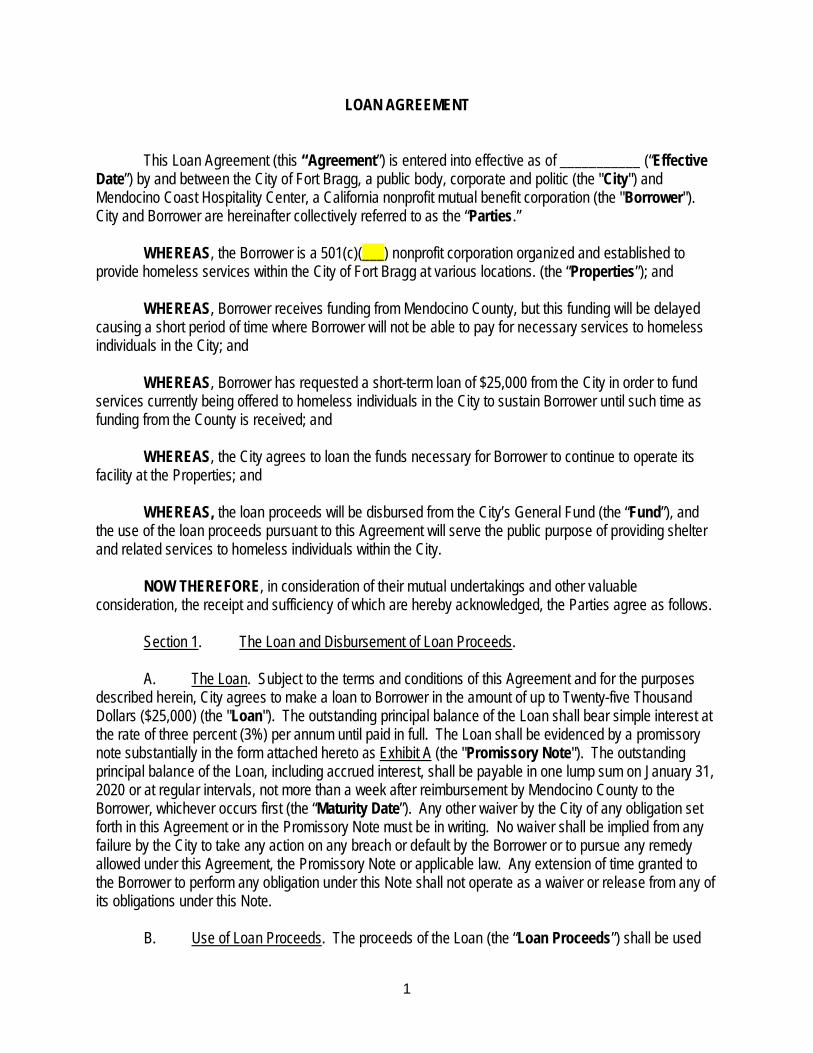

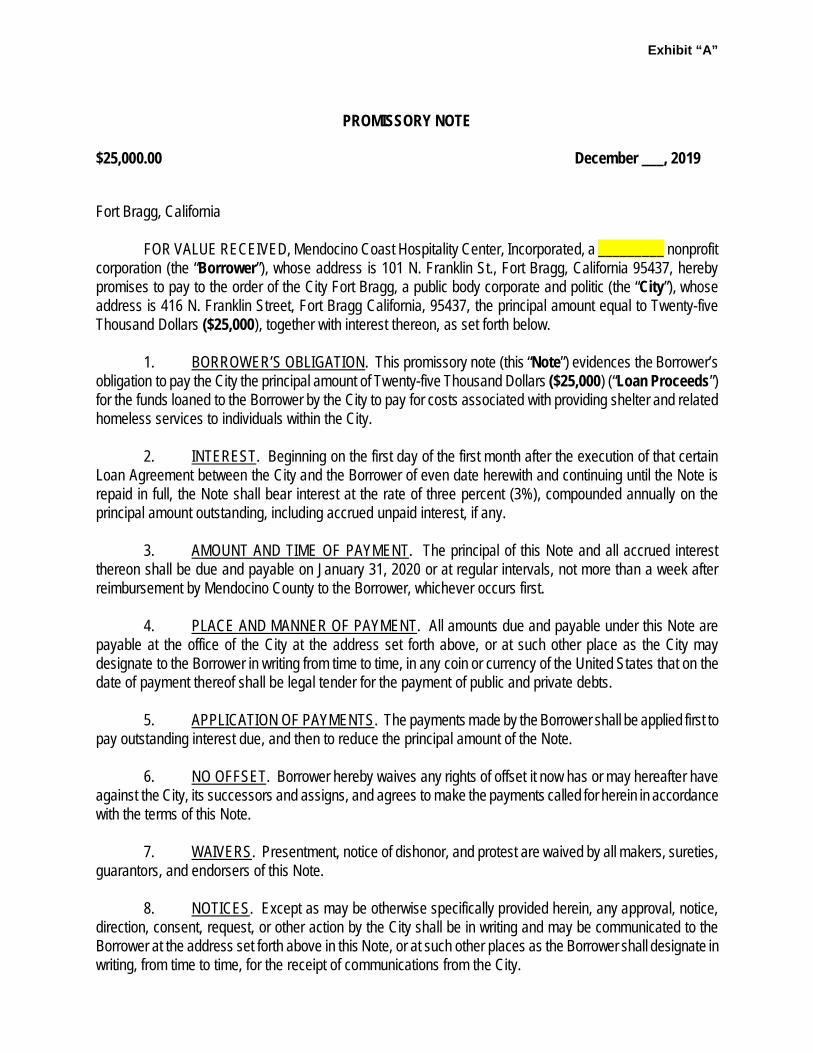

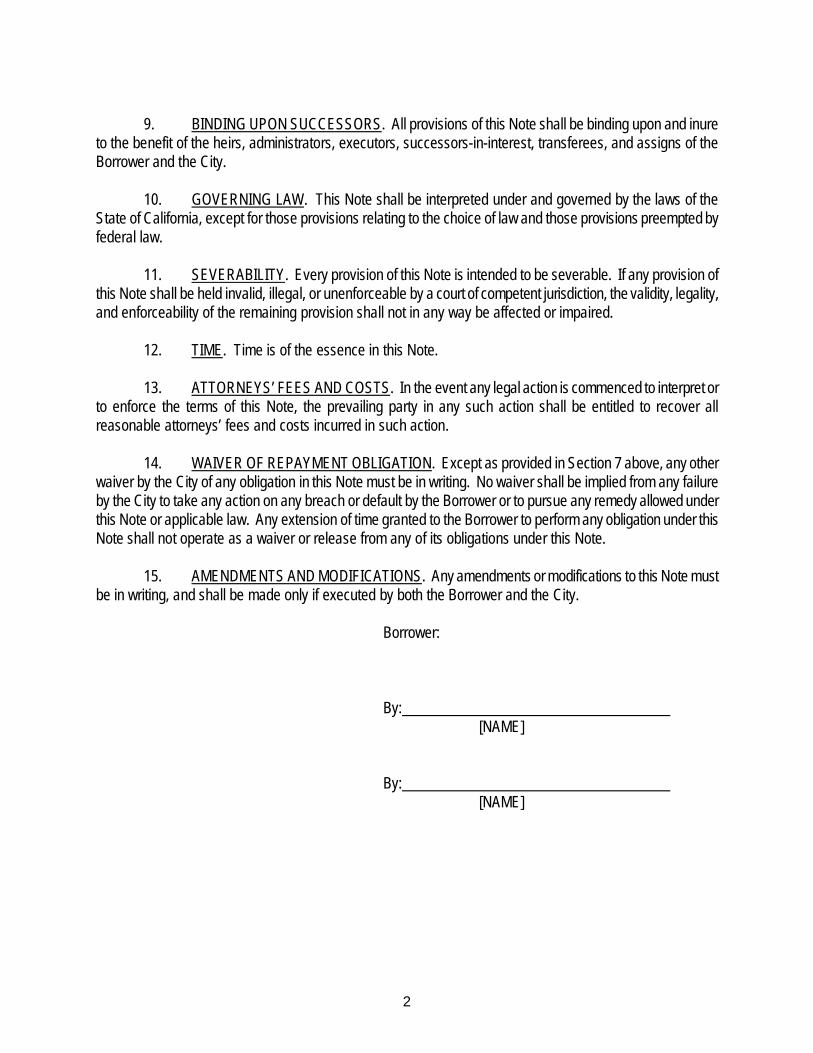

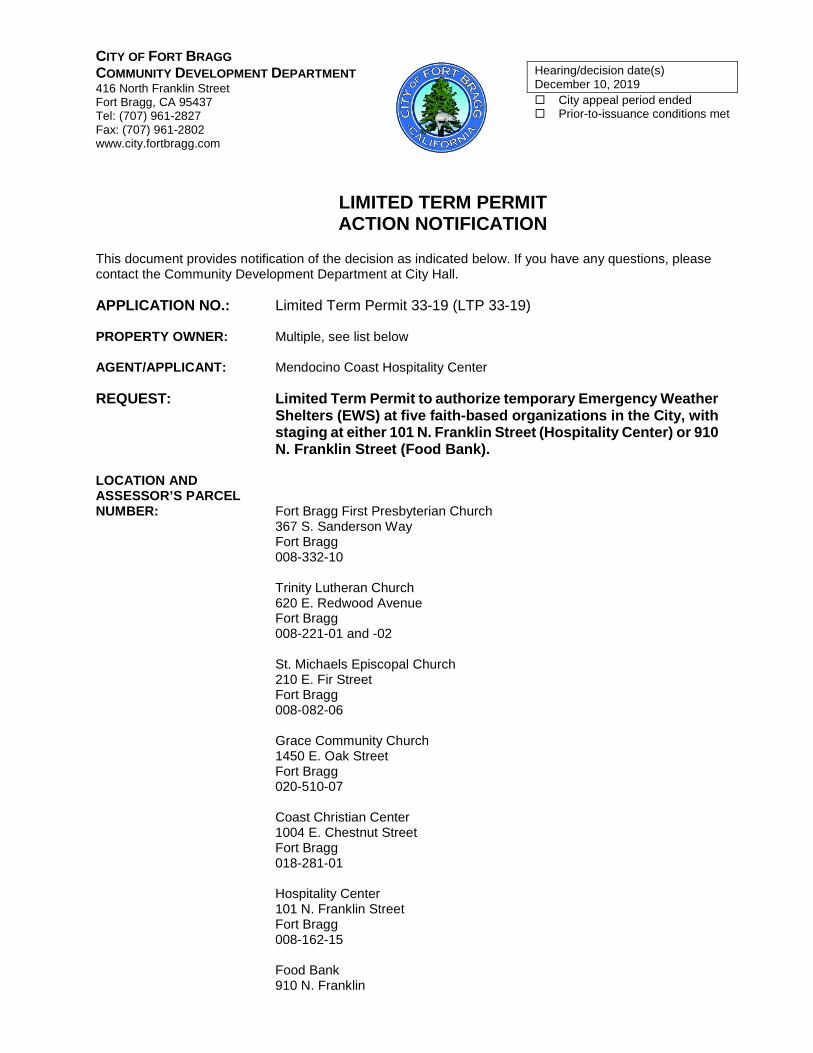

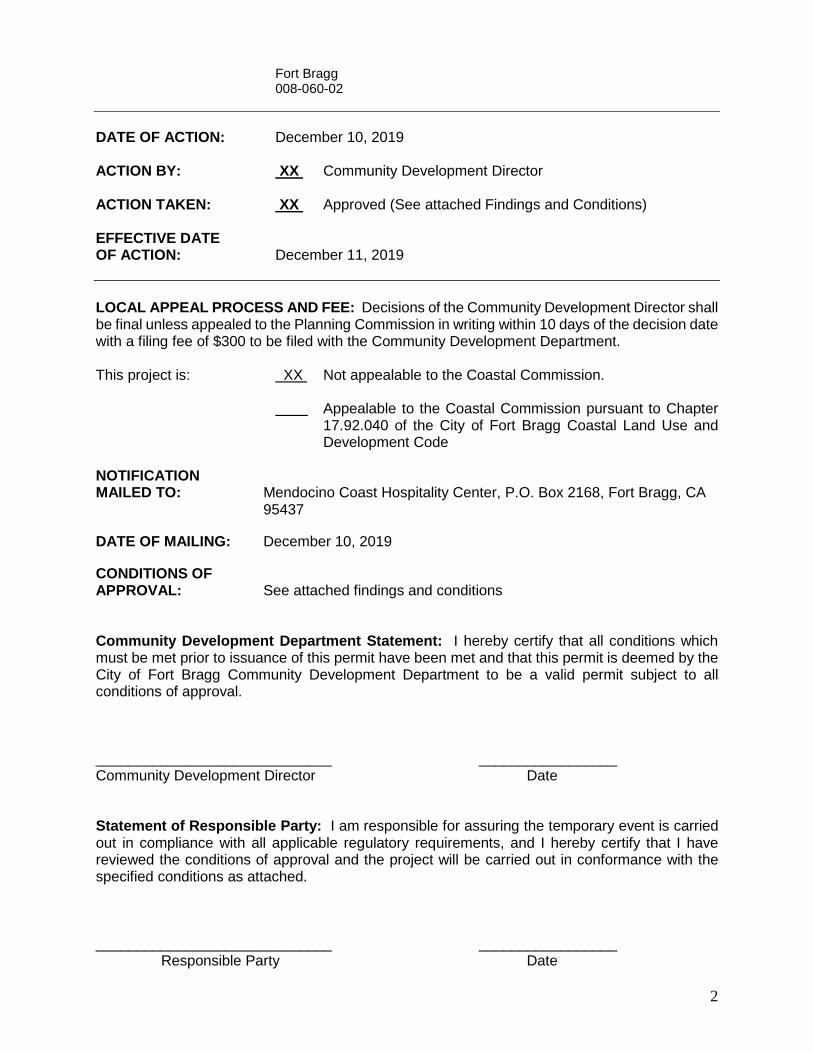

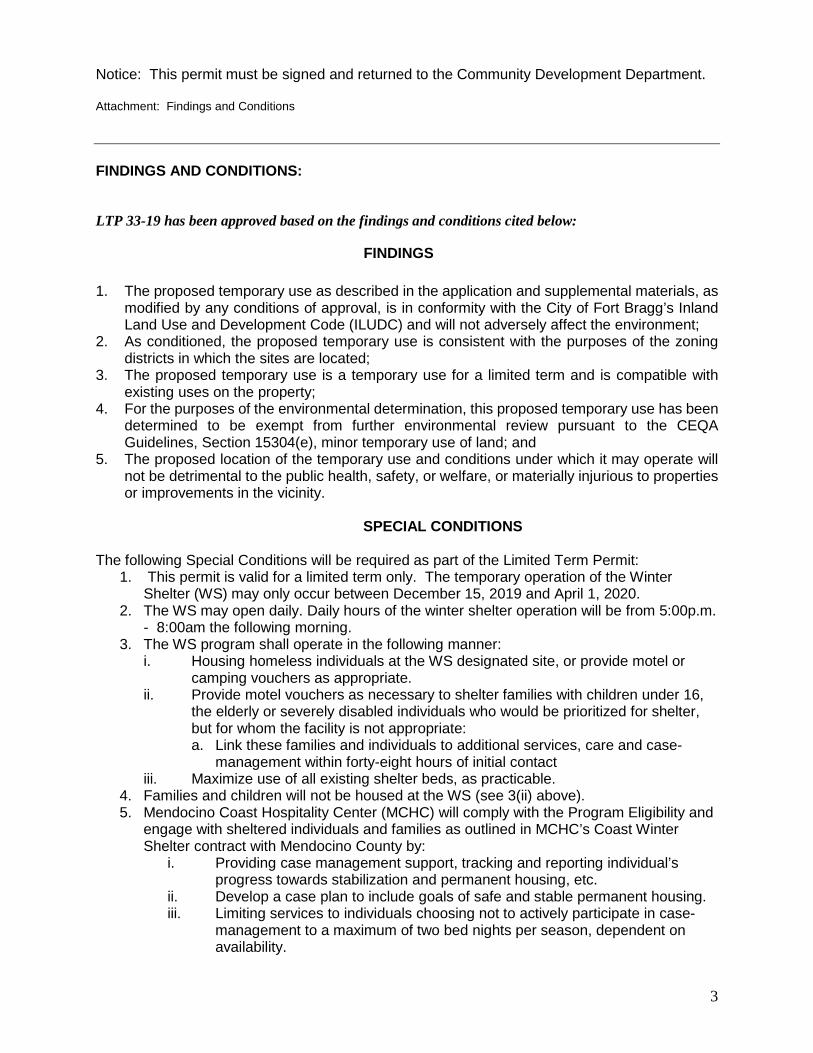

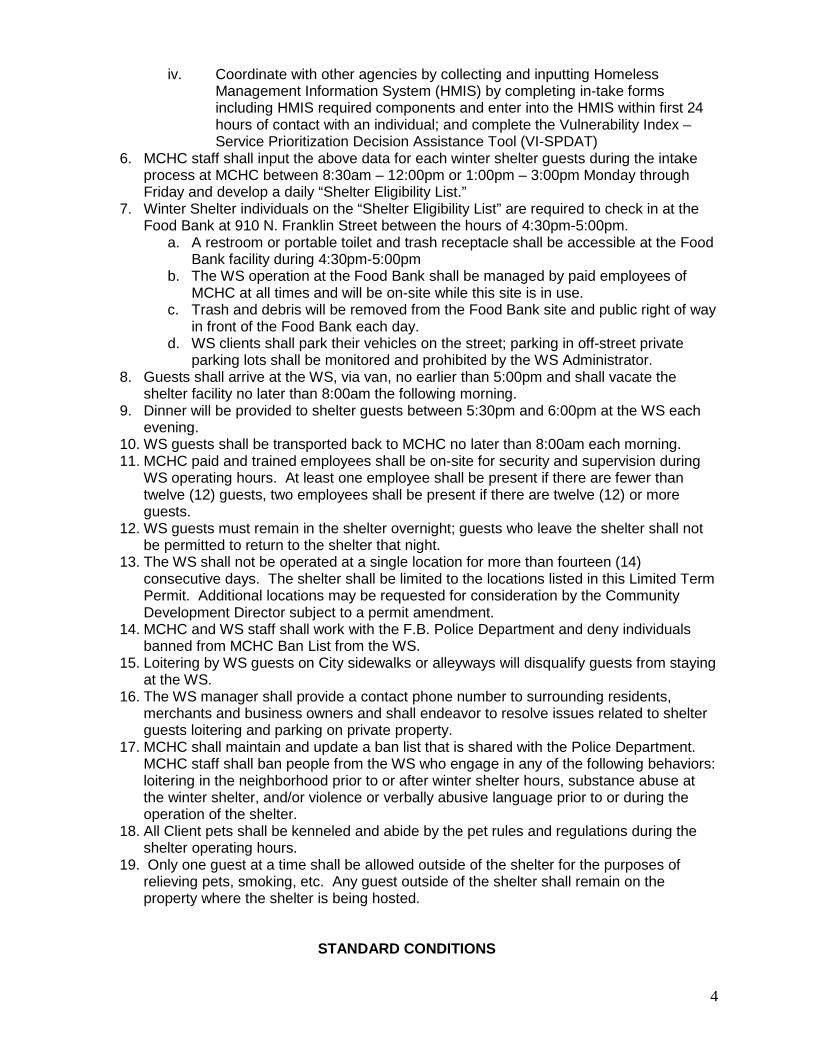

8D. 19-527 Receive Report on Limited Term Permit and Consider Adoption of City

Council Resolution Approving a Short-term Bridge Loan to Mendocino

Coast Hospitality Center for Initial Opening and Operations of Winter

Shelter and Authorizing City Manager to Execute Loan Agreement and

Promissory Note

Page 3 City of Fort Bragg Printed on 12/4/2019

December 9, 2019City Council Meeting Agenda

12092019 Winter Shelter

Att. 1 - Resolution

Att. 2 - Shelter Loan Agreement

Att. 3 - Promissory Note

Att. 4 - Draft Limited Term Permit for Winter Shelter

Att. 5 - Services for Mendocino County & MCHC Funding Agreement

Attachments:

8E. 19-537 Receive Report and Consider Introducing by Title Only and Waiving the

First Reading of Ordinance No. 956-2019 Repealing and Replacing

Chapter 15.04 (Construction Codes - Adopted by Reference) and Chapter

15.05 (California Fire Code) of Title 15 (Buildings and Construction) of the

Fort Bragg Municipal Code

12092019 Construction Ordinance

Att. 1 - ORD #956 Update to 2019 CA Building Codes

Attachments:

8F. 19-539 Receive Report and Consider Adoption of City Council Resolution

Adopting Legislative Findings Supporting Amendments and Changes to

the California State Building Standards Code as Contained in the Fort

Bragg International Fire Code and California Fire Code, Chapter 15.05 of

the Fort Bragg Municipal Code; and Consider Introducing by Title Only and

Waiving the First Reading of Ordinance No. 957-2019 Repealing and

Replacing Chapter 15.06 (Automatic Fire Sprinkler and Alarm Systems) of

Title 15 (Buildings and Construction) of the Fort Bragg Municipal Code

12092019 Fire Sprinkler Ordinance and Resolution

Att. 1 - RESO Findings 2019 Sprinkler

Att. 2 - Ex. A to RESO

Att. 3 - ORD #957 Sprinkler Update to 2019 CA Code

Attachments:

9. CLOSED SESSION

ADJOURNMENT

The adjournment time for all Council meetings is no later than 10:00 p.m. If the Council is still in session at

10:00 p.m., the Council may continue the meeting upon majority vote.

NEXT REGULAR CITY COUNCIL MEETING:

6:00 P.M., MONDAY, JANUARY 13, 2020

Page 4 City of Fort Bragg Printed on 12/4/2019

December 9, 2019City Council Meeting Agenda

STATE OF CALIFORNIA )

)ss.

COUNTY OF MENDOCINO )

I declare, under penalty of perjury, that I am employed by the City of Fort Bragg and that I caused

this agenda to be posted in the City Hall notice case on December 4, 2019.

_______________________________________________

June Lemos, CMC

City Clerk

NOTICE TO THE PUBLIC:

DISTRIBUTION OF ADDITIONAL INFORMATION FOLLOWING AGENDA PACKET

DISTRIBUTION:

• Materials related to an item on this Agenda submitted to the Council/District/Agency after distribution of

the agenda packet are available for public inspection in the lobby of City Hall at 416 N. Franklin Street during

normal business hours.

• Such documents are also available on the City of Fort Bragg’s website at http://city.fortbragg.com subject

to staff’s ability to post the documents before the meeting.

ADA NOTICE AND HEARING IMPAIRED PROVISIONS:

It is the policy of the City of Fort Bragg to offer its public programs, services and meetings in a manner that is

readily accessible to everyone, including those with disabilities. Upon request, this agenda will be made

available in appropriate alternative formats to persons with disabilities.

If you need assistance to ensure your full participation, please contact the City Clerk at (707) 961-2823.

Notification 48 hours in advance of any need for assistance will enable the City to make reasonable

arrangements to ensure accessibility.

The Council Chamber is equipped with a Wireless Stereo Headphone unit for use by the hearing impaired. The

unit operates in conjunction with the Chamber’s sound system. You may request the Wireless Stereo

Headphone unit from the City Clerk for personal use during the Council meetings.

This notice is in compliance with the Americans with Disabilities Act (28 CFR, 35.102-35.104 ADA Title II).

Page 5 City of Fort Bragg Printed on 12/4/2019

*** THIS PAGE INTENTIONALLY LEFT BLANK ***

Text File

City of Fort Bragg 416 N Franklin Street

Fort Bragg, CA 95437

Phone: (707) 961-2823

Fax: (707) 961-2802

File Number: 19-533

Agenda Date: 12/9/2019 Status: Mayor's OfficeVersion: 1

File Type: ProclamationIn Control: City Council

Agenda Number: 1A.

Presentation of Proclamation to Ricardo Garcia for Providing Life-Saving Actions

Page 1 City of Fort Bragg Printed on 12/4/2019

P R O C L A M A T I O N

COMMENDING RICARDO GARCIA FOR

PROVIDING LIFE-SAVING ACTIONS

WHEREAS, late in the evening of November 23, 2019, local citizen Ricardo Garcia made a startling discovery that a home on Redwood Avenue was on fire; and

WHEREAS, thinking quickly, Mr. Garcia immediately called 911 to report the fire; and

WHEREAS, seeing no movement coming from inside, Mr. Garcia proceeded to run into the smoky house to help those inside; and

WHEREAS, Mr. Garcia saw a little girl just 10 feet away from the flames and rescued her while assisting her siblings out of the burning building; and

WHEREAS, this family was able to escape due to the quick thinking of Mr. Garcia, a fellow parent and Fort Bragg resident; and

WHEREAS, thanks to the efforts of Ricardo Garcia, the police department, and fire department personnel, the family was safe and no one was badly hurt or injured; and

WHEREAS, if it were not for Ricardo Garcia’s quick action and bravery this family could have been lost to this tragedy.

NOW, THEREFORE, I, William V. Lee, Mayor of the City of Fort Bragg, on behalf of the entire City Council, do hereby commend Ricardo Garcia for providing immediate assistance and rescuing this family from the flames.

SIGNED this 9th day of December, 2019

WILLIAM V. LEE, Mayor

ATTEST:

June Lemos, CMC, City Clerk

No. 18-2019

P R O C L A M A C I Ó N

ENCOMENDANDO RICARDO GARCIA POR

SUMINISTRAR ACCIONES QUE SALVARON VIDAS

CONSIDERANDO que, por la tarde, el día 23 de noviembre de 2019 el ciudadano local Ricardo García hizo un descubrimiento sorprendente de que una casa en Redwood Avenue estaba en llamas; y

CONSIDERANDO, pensando rápidamente, el Sr. García llamó de inmediato al 911 para reportar el incendio; y

CONSIDERANDO, al no ver movimiento desde adentro, el Sr. García procedió a correr hacia la casa llena de humo para ayudar a los que estaban adentro; y

CONSIDERANDO, el Sr. García vio a una niña a solo 10 pies de distancia de las llamas y la rescató mientras ayudaba a sus hermanos a salir del edificio en llamas; y

CONSIDERANDO, esta familia pudo escapar debido al rápido pensamiento del Sr. García, un padreel mismo y residente de Fort Bragg; y

CONSIDERANDO, gracias a los esfuerzos de Ricardo García, el departamento de policía y el personal del departamento de bomberos, la familia estuvo a salvo y nadie resultó gravemente herido; y

CONSIDERANDO, si no fuera por la acción rápida y la valentía de Ricardo García, esta familia podría haberse perdido en esta tragedia.

AHORA, POR LO TANTO, yo, William V. Lee, alcalde de la ciudad de Fort Bragg, en nombre de todo el Concejo Municipal, felicito a Ricardo García por brindar asistencia inmediata y rescatar a esta familia de las llamas.

FIRMADO el 9 de diciembre de 2019

WILLIAM V. LEE, Mayor

DAR FE:

June Lemos, CMC, City Clerk

No. 18-2019

*** THIS PAGE INTENTIONALLY LEFT BLANK ***

Text File

City of Fort Bragg 416 N Franklin Street

Fort Bragg, CA 95437

Phone: (707) 961-2823

Fax: (707) 961-2802

File Number: 19-532

Agenda Date: 12/9/2019 Status: Mayor's OfficeVersion: 1

File Type:

Recognition/Announcements

In Control: City Council

Agenda Number: 1B.

Receive Presentation from Mendocino Coast Humane Society Executive Director Chuck

Tourtillott

Page 1 City of Fort Bragg Printed on 12/4/2019

Presentation Synopsis – December 9, 2019

The MCHS currently maintains a contract to provide animal care and sheltering services to the citizens of Fort Bragg. These services include

• Accepting and providing shelter and care for all cats and dogs impounded by FBPD.

• Accepting and providing shelter and care for stray cats and dogs found within city limits.

• Accepting and providing shelter and care for cats and dogs that are surrendered by Fort Bragg residents.

• Accepting and providing shelter and care for cats and dogs that are surrendered or found stray by Coastal County residents.

• We administer city dog licenses.

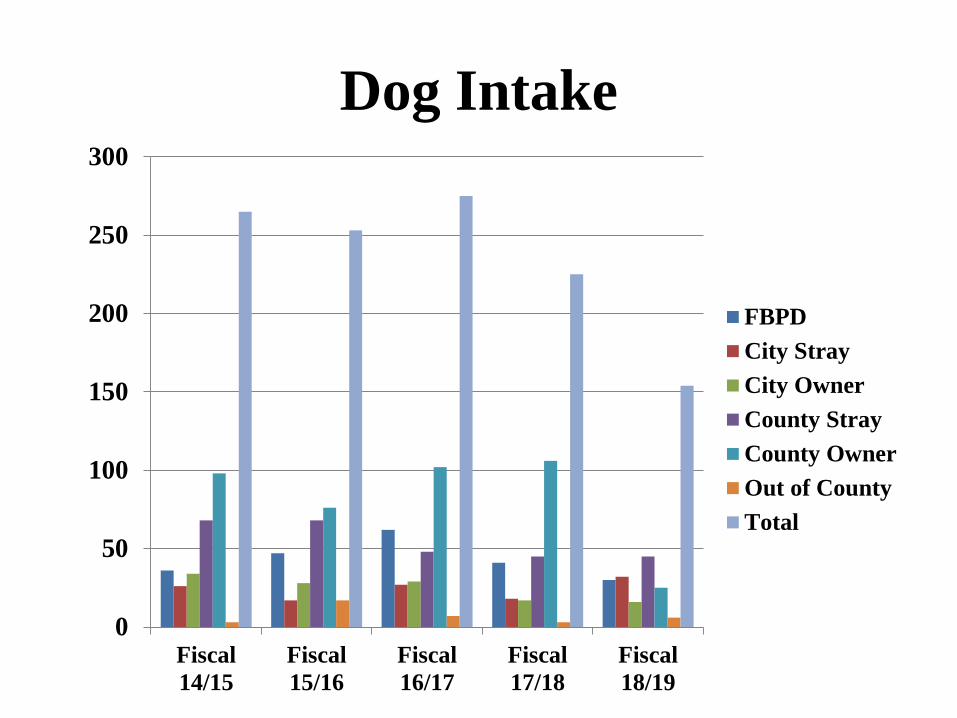

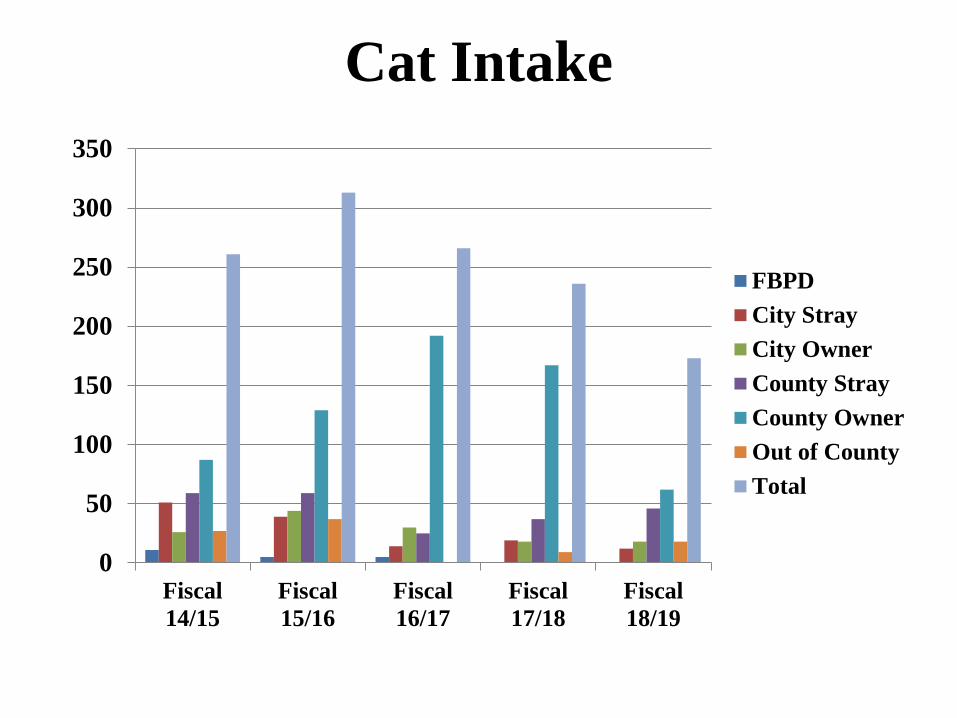

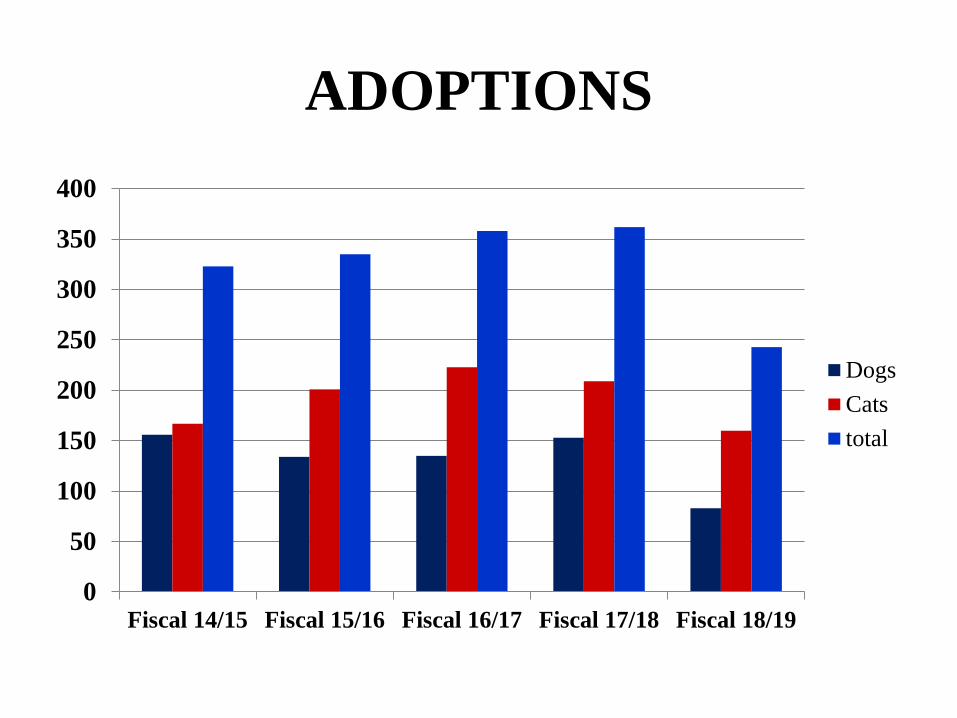

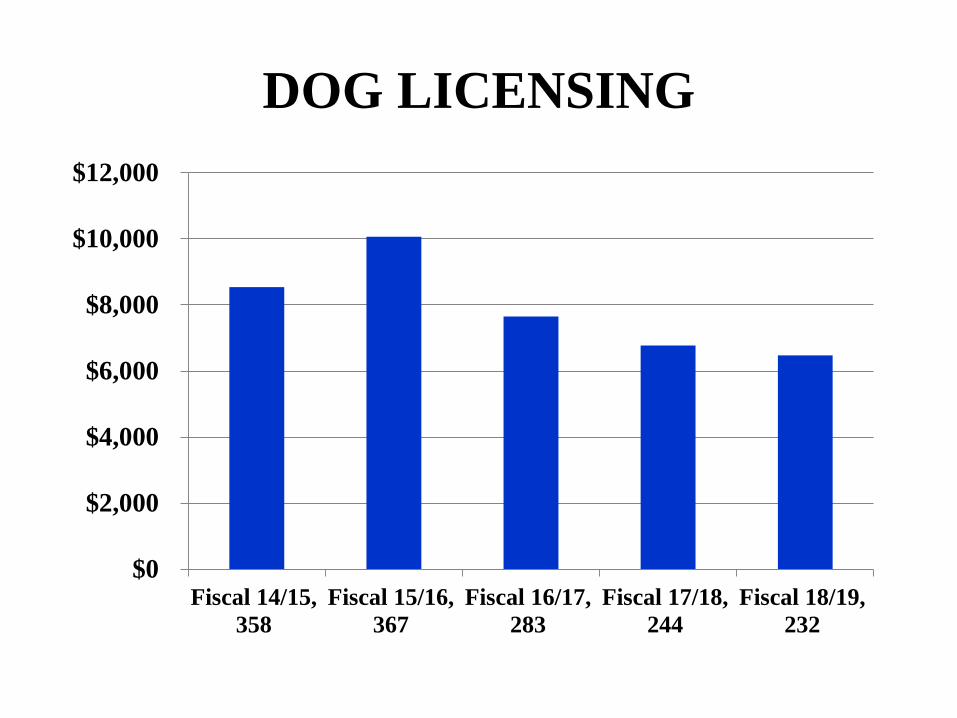

Presentation of shelter statistics for Fiscal 2018/2019

• Dog and Cat Intake• Animal Adoptions• Return to Owner Rates• Dog License Revenue• Spay/Neuter Surgeries

o New veterinarian hired November 2019

Questions and Discussion

Presentation to the Fort Bragg City Council

December 9, 2018

Chuck Tourtillott, Executive Director

We are a nonprofit 501c3 organization

OUR MISSIONis to contribute to a better life for

animals and to inspire public awareness of animal’s needs.

• For all dogs and cats impounded by FBPD.

•For dogs and cats that are surrendered or found stray by Fort Bragg residents.

• For dogs and cats that are surrendered or found stray by Coastal County residents.

•Issue dog licenses for Fort Bragg dog owners

•Operate an on-site veterinary clinic offering low cost spay/neuter services

Dog Intake

0

50

100

150

200

250

300

Fiscal14/15

Fiscal15/16

Fiscal16/17

Fiscal17/18

Fiscal18/19

FBPD

City Stray

City Owner

County Stray

County Owner

Out of County

Total

Cat Intake

0

50

100

150

200

250

300

350

Fiscal14/15

Fiscal15/16

Fiscal16/17

Fiscal17/18

Fiscal18/19

FBPD

City Stray

City Owner

County Stray

County Owner

Out of County

Total

ADOPTIONS

0

50

100

150

200

250

300

350

400

Fiscal 14/15 Fiscal 15/16 Fiscal 16/17 Fiscal 17/18 Fiscal 18/19

Dogs

Cats

total

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

Fiscal 14/15,358

Fiscal 15/16,367

Fiscal 16/17,283

Fiscal 17/18,244

Fiscal 18/19,232

DOG LICENSING

0102030405060708090

100

Fiscal 14/15 Fiscal 15/16 Fiscal 16/17 Fiscal 17/18

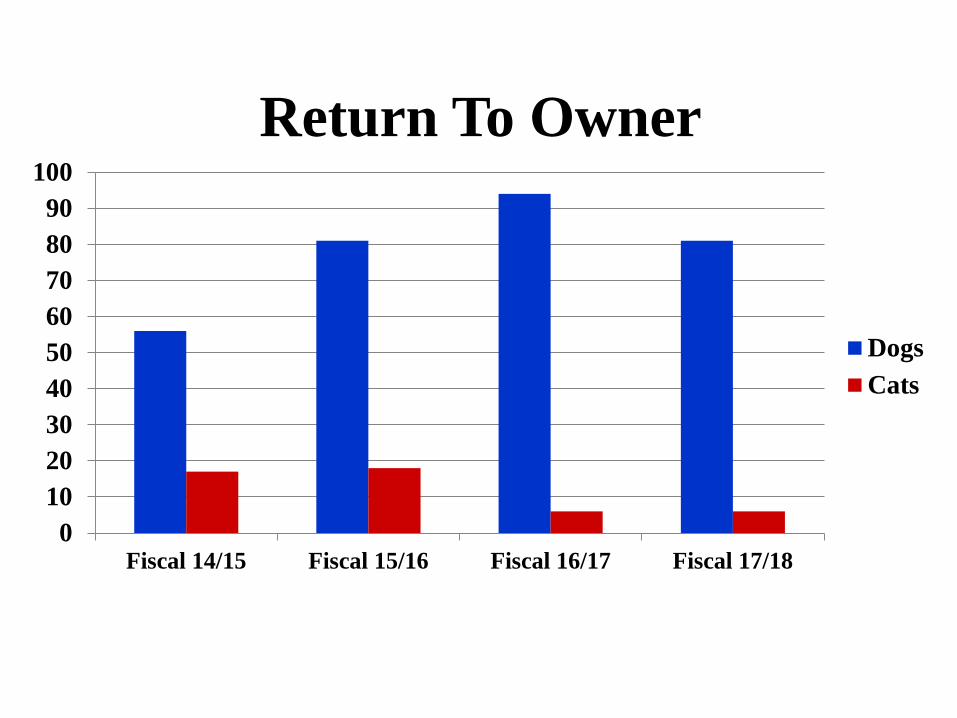

Return To Owner

Dogs

Cats

0

100

200

300

400

500

600

700

800

900

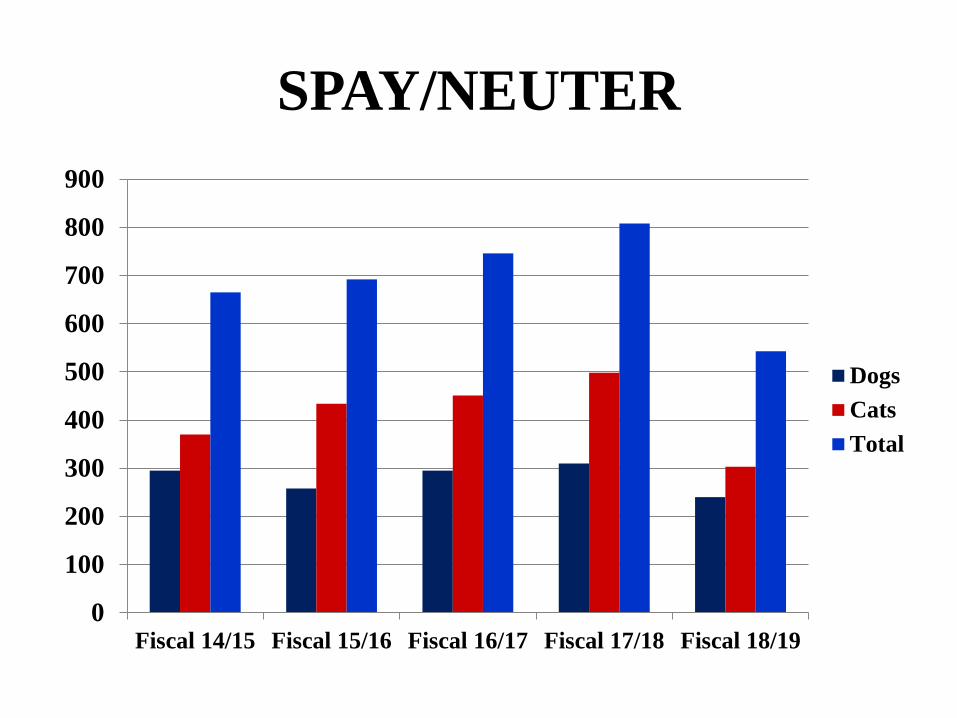

Fiscal 14/15 Fiscal 15/16 Fiscal 16/17 Fiscal 17/18 Fiscal 18/19

Dogs

Cats

Total

SPAY/NEUTER

QUESTIONSand

DISCUSSION

The picture can't be displayed.

THANK YOU!Mendocino Coast Humane Society

*** THIS PAGE INTENTIONALLY LEFT BLANK ***

Text File

City of Fort Bragg 416 N Franklin Street

Fort Bragg, CA 95437

Phone: (707) 961-2823

Fax: (707) 961-2802

File Number: 19-528

Agenda Date: 12/9/2019 Status: Mayor's OfficeVersion: 1

File Type:

Recognition/Announcements

In Control: City Council

Agenda Number: 1C.

Presentation by Mendocino County Fifth District Supervisor Ted Williams on the County's

Proposed Transient Occupancy Tax (TOT) on Campground and Recreational Vehicle Parks

Page 1 City of Fort Bragg Printed on 12/4/2019

*** THIS PAGE INTENTIONALLY LEFT BLANK ***

Text File

City of Fort Bragg 416 N Franklin Street

Fort Bragg, CA 95437

Phone: (707) 961-2823

Fax: (707) 961-2802

File Number: 19-525

Agenda Date: 12/9/2019 Status: Consent AgendaVersion: 1

File Type: ResolutionIn Control: City Council

Agenda Number: 5A.

Adopt Resolution of the Fort Bragg City Council Amending the FY 2019-20 Budget (Amendment

No. 2020-06) Approving the Use of $91,000.00 of General Fund Fund Balance to Make a

Prepayment to CalPERS Against the City’s Unfunded Pension Liability ( Account

110-0000-0220)

Per Fiscal Policy 9G, the City proposes making a prepayment against our pension unfunded

liability in the amount of $91,000. A budget amendment is required to do so.

Page 1 City of Fort Bragg Printed on 12/4/2019

- 1 -

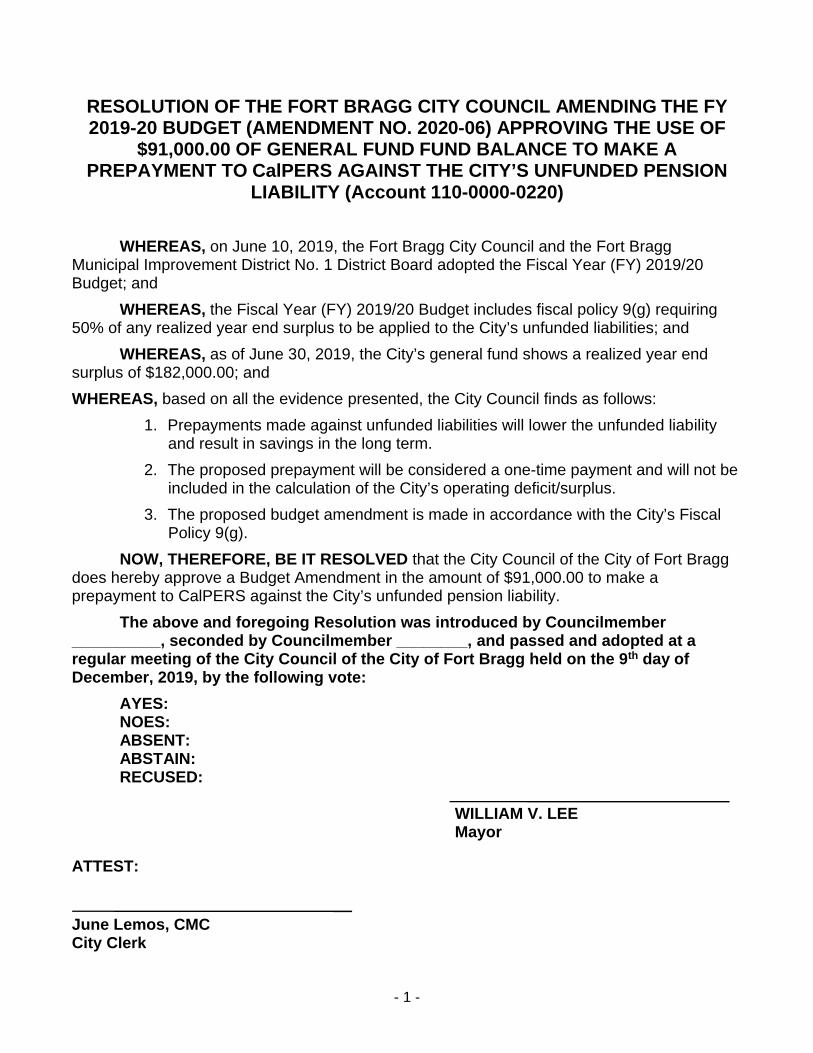

RESOLUTION OF THE FORT BRAGG CITY COUNCIL AMENDING THE FY 2019-20 BUDGET (AMENDMENT NO. 2020-06) APPROVING THE USE OF

$91,000.00 OF GENERAL FUND FUND BALANCE TO MAKE A PREPAYMENT TO CalPERS AGAINST THE CITY’S UNFUNDED PENSION

LIABILITY (Account 110-0000-0220)

WHEREAS, on June 10, 2019, the Fort Bragg City Council and the Fort Bragg Municipal Improvement District No. 1 District Board adopted the Fiscal Year (FY) 2019/20 Budget; and

WHEREAS, the Fiscal Year (FY) 2019/20 Budget includes fiscal policy 9(g) requiring 50% of any realized year end surplus to be applied to the City’s unfunded liabilities; and

WHEREAS, as of June 30, 2019, the City’s general fund shows a realized year end surplus of $182,000.00; and

WHEREAS, based on all the evidence presented, the City Council finds as follows:

1. Prepayments made against unfunded liabilities will lower the unfunded liability and result in savings in the long term.

2. The proposed prepayment will be considered a one-time payment and will not be included in the calculation of the City’s operating deficit/surplus.

3. The proposed budget amendment is made in accordance with the City’s Fiscal Policy 9(g).

NOW, THEREFORE, BE IT RESOLVED that the City Council of the City of Fort Bragg does hereby approve a Budget Amendment in the amount of $91,000.00 to make a prepayment to CalPERS against the City’s unfunded pension liability.

The above and foregoing Resolution was introduced by Councilmember __________, seconded by Councilmember ________, and passed and adopted at a regular meeting of the City Council of the City of Fort Bragg held on the 9th day ofDecember, 2019, by the following vote:

AYES:NOES:ABSENT:ABSTAIN:RECUSED:

WILLIAM V. LEEMayor

ATTEST:

June Lemos, CMCCity Clerk

Text File

City of Fort Bragg 416 N Franklin Street

Fort Bragg, CA 95437

Phone: (707) 961-2823

Fax: (707) 961-2802

File Number: 19-529

Agenda Date: 12/9/2019 Status: Consent AgendaVersion: 1

File Type: OrdinanceIn Control: City Council

Agenda Number: 5B.

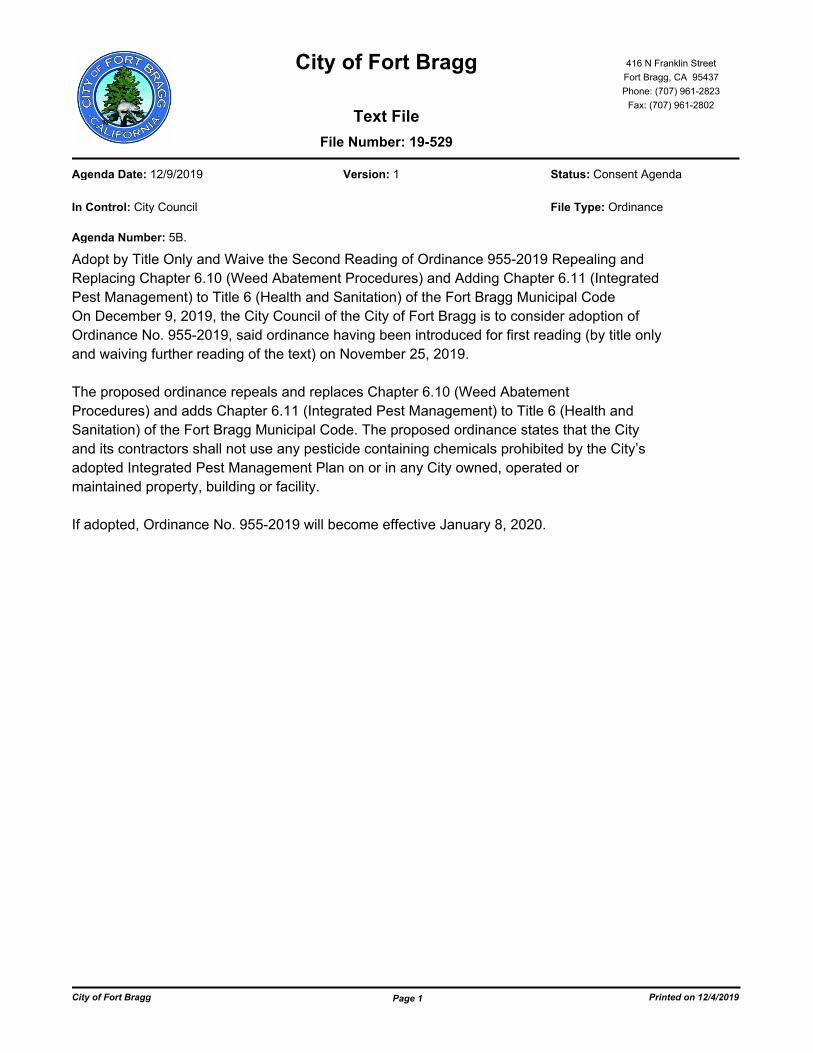

Adopt by Title Only and Waive the Second Reading of Ordinance 955-2019 Repealing and

Replacing Chapter 6.10 (Weed Abatement Procedures) and Adding Chapter 6.11 (Integrated

Pest Management) to Title 6 (Health and Sanitation) of the Fort Bragg Municipal Code

On December 9, 2019, the City Council of the City of Fort Bragg is to consider adoption of

Ordinance No. 955-2019, said ordinance having been introduced for first reading (by title only

and waiving further reading of the text) on November 25, 2019.

The proposed ordinance repeals and replaces Chapter 6.10 (Weed Abatement

Procedures) and adds Chapter 6.11 (Integrated Pest Management) to Title 6 (Health and

Sanitation) of the Fort Bragg Municipal Code. The proposed ordinance states that the City

and its contractors shall not use any pesticide containing chemicals prohibited by the City’s

adopted Integrated Pest Management Plan on or in any City owned, operated or

maintained property, building or facility.

If adopted, Ordinance No. 955-2019 will become effective January 8, 2020.

Page 1 City of Fort Bragg Printed on 12/4/2019

1

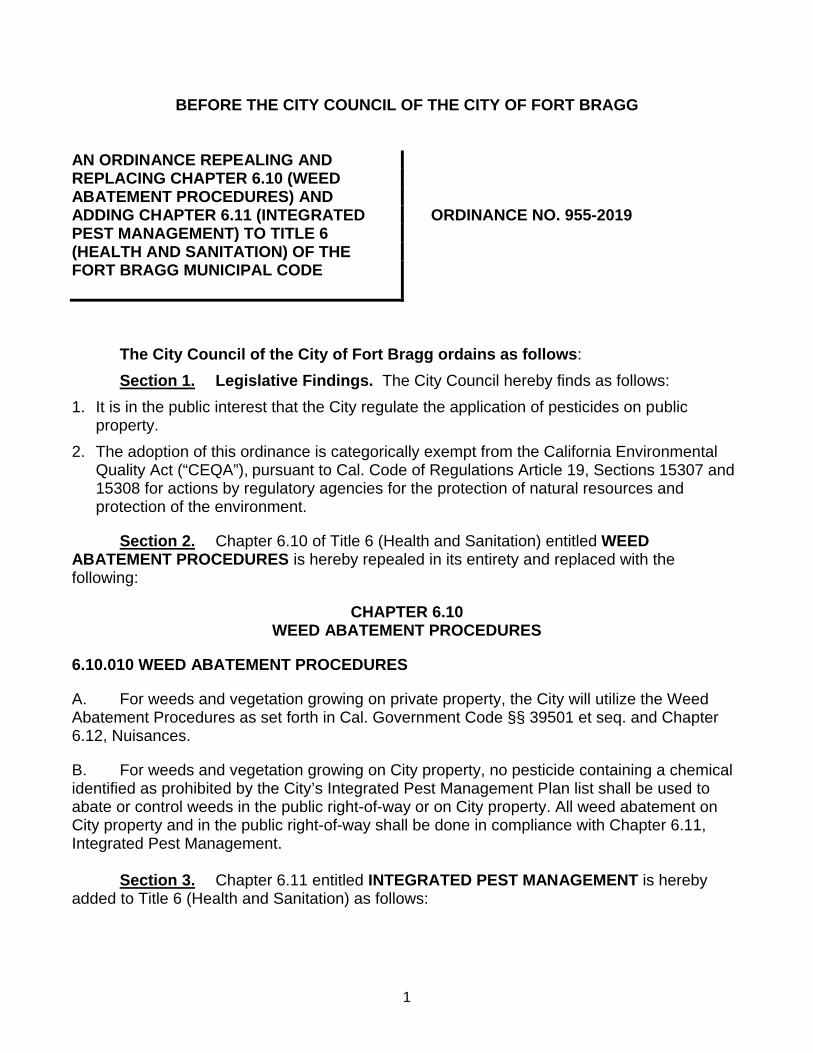

BEFORE THE CITY COUNCIL OF THE CITY OF FORT BRAGG

AN ORDINANCE REPEALING AND REPLACING CHAPTER 6.10 (WEED ABATEMENT PROCEDURES) AND ADDING CHAPTER 6.11 (INTEGRATED PEST MANAGEMENT) TO TITLE 6 (HEALTH AND SANITATION) OF THE FORT BRAGG MUNICIPAL CODE

ORDINANCE NO. 955-2019

The City Council of the City of Fort Bragg ordains as follows:

Section 1. Legislative Findings. The City Council hereby finds as follows:

1. It is in the public interest that the City regulate the application of pesticides on public property.

2. The adoption of this ordinance is categorically exempt from the California Environmental Quality Act (“CEQA”), pursuant to Cal. Code of Regulations Article 19, Sections 15307 and 15308 for actions by regulatory agencies for the protection of natural resources and protection of the environment.

Section 2. Chapter 6.10 of Title 6 (Health and Sanitation) entitled WEED ABATEMENT PROCEDURES is hereby repealed in its entirety and replaced with the following:

CHAPTER 6.10WEED ABATEMENT PROCEDURES

6.10.010 WEED ABATEMENT PROCEDURES

A. For weeds and vegetation growing on private property, the City will utilize the Weed Abatement Procedures as set forth in Cal. Government Code §§ 39501 et seq. and Chapter 6.12, Nuisances.

B. For weeds and vegetation growing on City property, no pesticide containing a chemical identified as prohibited by the City’s Integrated Pest Management Plan list shall be used to abate or control weeds in the public right-of-way or on City property. All weed abatement on City property and in the public right-of-way shall be done in compliance with Chapter 6.11, Integrated Pest Management.

Section 3. Chapter 6.11 entitled INTEGRATED PEST MANAGEMENT is hereby added to Title 6 (Health and Sanitation) as follows:

2

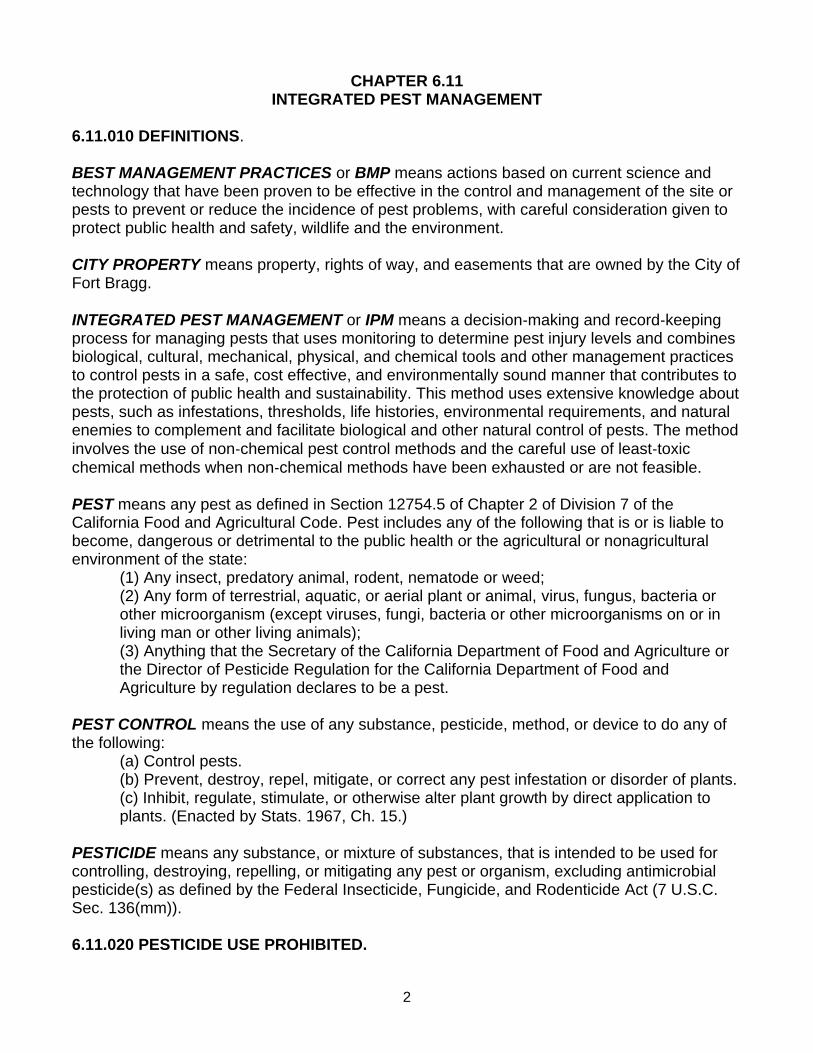

CHAPTER 6.11INTEGRATED PEST MANAGEMENT

6.11.010 DEFINITIONS.

BEST MANAGEMENT PRACTICES or BMP means actions based on current science and technology that have been proven to be effective in the control and management of the site or pests to prevent or reduce the incidence of pest problems, with careful consideration given to protect public health and safety, wildlife and the environment.

CITY PROPERTY means property, rights of way, and easements that are owned by the City of Fort Bragg.

INTEGRATED PEST MANAGEMENT or IPM means a decision‐making and record‐keeping process for managing pests that uses monitoring to determine pest injury levels and combines biological, cultural, mechanical, physical, and chemical tools and other management practices to control pests in a safe, cost effective, and environmentally sound manner that contributes to the protection of public health and sustainability. This method uses extensive knowledge about pests, such as infestations, thresholds, life histories, environmental requirements, and natural enemies to complement and facilitate biological and other natural control of pests. The method involves the use of non‐chemical pest control methods and the careful use of least‐toxic chemical methods when non‐chemical methods have been exhausted or are not feasible.

PEST means any pest as defined in Section 12754.5 of Chapter 2 of Division 7 of the California Food and Agricultural Code. Pest includes any of the following that is or is liable to become, dangerous or detrimental to the public health or the agricultural or nonagricultural environment of the state:

(1) Any insect, predatory animal, rodent, nematode or weed;(2) Any form of terrestrial, aquatic, or aerial plant or animal, virus, fungus, bacteria or other microorganism (except viruses, fungi, bacteria or other microorganisms on or in living man or other living animals);(3) Anything that the Secretary of the California Department of Food and Agriculture or the Director of Pesticide Regulation for the California Department of Food and Agriculture by regulation declares to be a pest.

PEST CONTROL means the use of any substance, pesticide, method, or device to do any of the following:

(a) Control pests.(b) Prevent, destroy, repel, mitigate, or correct any pest infestation or disorder of plants.(c) Inhibit, regulate, stimulate, or otherwise alter plant growth by direct application to plants. (Enacted by Stats. 1967, Ch. 15.)

PESTICIDE means any substance, or mixture of substances, that is intended to be used for controlling, destroying, repelling, or mitigating any pest or organism, excluding antimicrobial pesticide(s) as defined by the Federal Insecticide, Fungicide, and Rodenticide Act (7 U.S.C. Sec. 136(mm)).

6.11.020 PESTICIDE USE PROHIBITED.

3

A. The City Council shall adopt by Resolution an Integrated Pest Management Plan for use of pesticides on City property.

B. The City shall not use any pesticide containing a chemical prohibited by the City’s adopted Integrated Pest Management Plan on or in any City owned, operated or maintained property, building or facility except in accordance with the City's Pest Management Plan.

C. Exemption. A City department may apply for an exemption to the pesticide prohibition in the event that a pest outbreak poses an immediate threat to public health, will result in detriment to the environment or an environmentally sensitive habitat area or significant economic damage will result from failure to use a pesticide prohibited pursuant to Section 6.11.020, provided that all other options contained in the Integrated Pest Management Plan have been investigated and a compelling need to use the pesticide exists. The application for an exemption shall be filed with the Public Works Director.

This exemption shall not apply to the use of any pesticide for the purpose of improving or maintaining water quality for drinking water treatment, waste water treatment, and related water collection, distribution and treatment facilities.

6.11.030 BEST MANAGEMENT PRACTICES FOR PESTICIDES APPLICATION.

In approaching a pest management issue, the following steps shall be taken to ensure that any pesticide use as authorized by this Chapter is reduced to the maximum extent practicable.

A. Any employee or contractor hired to apply pesticides on City Property must have pesticide safety training prior to the use of any pesticide, regardless of toxicity. A record must be made of each employee applying pesticides, and evidence of training certified by the trainer/supervisor.

B. No pesticides or fertilizers shall be applied during irrigation or within 48 hours of predicted rainfall with greater than 50% probability as predicted by the National Oceanic and Atmospheric Administration (NOAA).

C. Pesticide Storage, Transportation and Disposal.1. Storage – Pesticides used by the City shall be stored in a manner consistent with

the label requirements of the products being used.2. Transportation – Pesticides shall be transported in a manner consistent with the

label requirements of the products being used. Containers shall be secured during transport in a manner that will prevent spillage into or out of the vehicle.

3. Empty Containers – Empty pesticide containers, other than bags, must be rinsed and drained into the spraying equipment on site by the applicator, at the time of use, using the triple rinse method. Rinse solution should be applied to the treated areas or otherwise safely disposed of.

4. Required Labels – All pesticide containers must be labeled with the following information:a) Name of pesticideb) Category of pesticide

4

c) EPA registration numberd) Active ingredient

5. Spills - Small spills of pesticides shall be cleaned up immediately with absorbent material. For major toxic pesticide spills, the Police Department must be contacted to request Emergency Response Personnel for spill clean-up. The location of the spill, what pesticide was spilt, the pesticide’s category, and its proximity to storm drains.

Section 4. Severability. If any section, subsection, sentence, clause or phrase of this Ordinance is for any reason held by a court of competent jurisdiction to be invalid or unconstitutional, such decision shall not affect the validity of the remaining portions of the Ordinance. The City Council of the City of Fort Bragg hereby declares that it would have passed this Ordinance and each section, subsection, sentence, clause and phrase thereof irrespective of the fact that one or more sections, subsections, sentences, clauses or phrases may be held invalid or unconstitutional.

Section 5. Effective Date and Publication. This ordinance shall be and the same is hereby declared to be in full force and effect from and after thirty (30) days after the date of its passage. Within fifteen (15) days after the passage of this Ordinance, the City Clerk shall cause a summary of said Ordinance to be published as provided in Government Code §36933, in a newspaper of general circulation published and circulated in the City of Fort Bragg, along with the names of the City Council voting for and against its passage.

The foregoing Ordinance was introduced by Councilmember Peters at a regular meeting of the City Council of the City of Fort Bragg held on November 25, 2019 and adopted at a regular meeting of the City of Fort Bragg held on December 9, 2019 by the following vote:

AYES:NOES:ABSENT:ABSTAIN:RECUSED:

____________________________________William V. LeeMayor

ATTEST:

______________________________________June Lemos, CMCCity Clerk

PUBLISH: November 27, 2019 and December 19, 2019 (by summary).EFFECTIVE DATE: January 8, 2020.

*** THIS PAGE INTENTIONALLY LEFT BLANK ***

Text File

City of Fort Bragg 416 N Franklin Street

Fort Bragg, CA 95437

Phone: (707) 961-2823

Fax: (707) 961-2802

File Number: 19-487

Agenda Date: 12/9/2019 Status: Consent AgendaVersion: 1

File Type: Consent CalendarIn Control: City Council

Agenda Number: 5C.

Approve Maddy Act Notice Providing List of Appointed Terms Expiring in 2020

The City is required by Government Code Section 54972 to post a list of Commission,

Committee and Board openings for the upcoming year. The legislative body (City Council) needs

to approve the list and direct the City Clerk to post and publish it. Attached is the list showing the

vacancies for 2020.

Page 1 City of Fort Bragg Printed on 12/4/2019

CITY OF FORT BRAGG Incorporated August 5, 1889

416 N. Franklin Street Fort Bragg, CA 95437 Phone: (707) 961-2823

Fax: (707) 961-2802

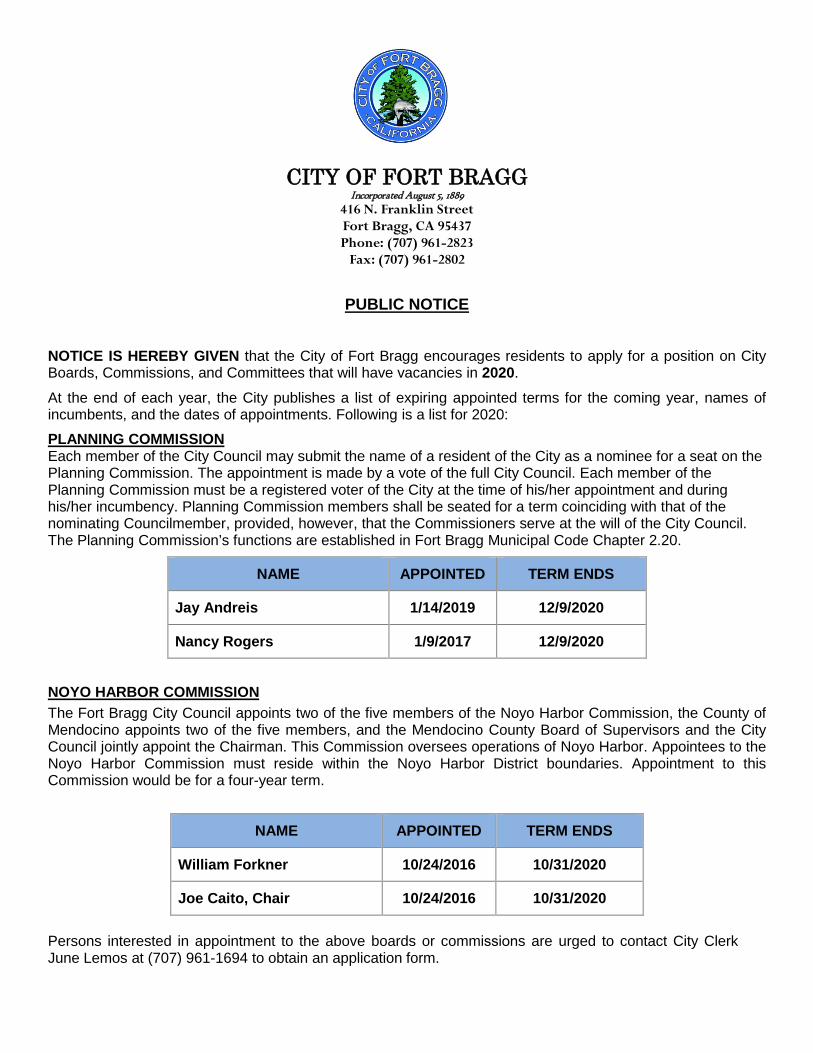

PUBLIC NOTICE

NOTICE IS HEREBY GIVEN that the City of Fort Bragg encourages residents to apply for a position on City Boards, Commissions, and Committees that will have vacancies in 2020.

At the end of each year, the City publishes a list of expiring appointed terms for the coming year, names of incumbents, and the dates of appointments. Following is a list for 2020:

PLANNING COMMISSION Each member of the City Council may submit the name of a resident of the City as a nominee for a seat on the Planning Commission. The appointment is made by a vote of the full City Council. Each member of the Planning Commission must be a registered voter of the City at the time of his/her appointment and during his/her incumbency. Planning Commission members shall be seated for a term coinciding with that of the nominating Councilmember, provided, however, that the Commissioners serve at the will of the City Council. The Planning Commission’s functions are established in Fort Bragg Municipal Code Chapter 2.20.

NAME APPOINTED TERM ENDS

Jay Andreis 1/14/2019 12/9/2020

Nancy Rogers 1/9/2017 12/9/2020

NOYO HARBOR COMMISSION

The Fort Bragg City Council appoints two of the five members of the Noyo Harbor Commission, the County of Mendocino appoints two of the five members, and the Mendocino County Board of Supervisors and the City Council jointly appoint the Chairman. This Commission oversees operations of Noyo Harbor. Appointees to the Noyo Harbor Commission must reside within the Noyo Harbor District boundaries. Appointment to this Commission would be for a four-year term.

NAME APPOINTED TERM ENDS

William Forkner 10/24/2016 10/31/2020

Joe Caito, Chair 10/24/2016 10/31/2020

Persons interested in appointment to the above boards or commissions are urged to contact City Clerk June Lemos at (707) 961-1694 to obtain an application form.

Residents of the City of Fort Bragg and persons owning a business or commercial property in the City shall be given preference for appointment to advisory committees. The City Council will review applications and interview applicants for appointment to the Noyo Harbor Commission in October of 2020. The two incoming Councilmembers will put forth their nominees for Planning Commissioner at the first meeting in January 2021.

ADDITIONAL BOARDS AND COMMISSIONS In addition to those listed above, the following is a list of all boards, commissions, and committees whose members serve at the pleasure of the legislative body, and the necessary qualifications for each position:

Library Advisory Board – The City Council will consider appointees to the Library Advisory Board in October 2021. Applicants must show an interest in development of quality improvements in the local library branches by exposing the membership to changes and innovations in the library world. Residents of Fort Bragg are given preference.

Fort Bragg Fire Protection Authority – The Joint Powers Authority Agreement that created the Fort Bragg Fire Protection Authority in 1990 provides, in part, that one member of the five member board shall be appointed jointly by the Board of Directors for the Fort Bragg Rural Fire District and the City Council of the City of Fort Bragg. In March of 2021, the District Board and City Council shall consult with the Fort Bragg Volunteer Fire Department prior to selecting the jointly-appointed member. At its option, the Fort Bragg Volunteer Fire Department may submit one or more candidates for this position. The appointee must be a resident of the Fire Protection area. Appointment to this Board would be for a two-year term.

Dated: December 13, 2019 __________________________________________ June Lemos, CMC, City Clerk

Published: December 19, 2019 and December 26, 2019 STATE OF CALIFORNIA ) ) ss. COUNTY OF MENDOCINO ) I declare, under penalty of perjury, that I am employed by the City of Fort Bragg and that I caused this notice to be posted in the City Hall notice case on December 13, 2019 and delivered to the Mendocino County Public Library, 499 East Laurel Street, Fort Bragg, California. __________________________________________ June Lemos, CMC, City Clerk

*** THIS PAGE INTENTIONALLY LEFT BLANK ***

Text File

City of Fort Bragg 416 N Franklin Street

Fort Bragg, CA 95437

Phone: (707) 961-2823

Fax: (707) 961-2802

File Number: 19-512

Agenda Date: 12/9/2019 Status: Consent AgendaVersion: 1

File Type: Committee MinutesIn Control: City Council

Agenda Number: 5D.

Receive and File Minutes of October 2, 2019 Finance and Administration Committee Meeting

Page 1 City of Fort Bragg Printed on 12/4/2019

416 N Franklin Street

Fort Bragg, CA 95437

Phone: (707) 961-2823

Fax: (707) 961-2802

City of Fort Bragg

Meeting Minutes

Finance and Administration Committee

11:00 AM Town Hall, 363 N. Main StreetWednesday, October 2, 2019

MEETING CALLED TO ORDER

Chair Peters called the meeting to order at 11:04 AM

ROLL CALL

Staff Present: Finance Director Victor Damiani, Senior Government Accountant II Isaac

Whippy, Administrative Assistant Brenda Jourdain and Administrative Assistant Cristal

Muñoz.

Lindy Peters and Tess Albin-SmithPresent: 2 -

1. APPROVAL OF MINUTES

1A. 19-449 Approve Minutes of August 7, 2019

The minutes where approved by the Committee as presented and will be

forwarded for Council review.

2. PUBLIC COMMENTS ON NON-AGENDA ITEMS

3. CONDUCT OF BUSINESS

3A. 19-446 Review Draft Water Shut-Off Policy in Preparation for SB 998

Implementation

The Committee reviewed the report prepared for this item. The committee report presented

by Finance Director Damiani who further explained the draft Water Shut-Off Policy in

preparation of SB 998 implementation. New implementations are discussed and a new

timeline is described. SB998 is well intended but may have the opposite effect might create a

hardship for residents in the long run.

Public Comment:

*None.

Discussion:

Finance Director Damiani expressed concern with regarding the implementation of SB 998

and offered assisting measures for customers.

Recommendation:

* There was consensus from committee to move forward to City Council on draft water shut-off

policy with water conservation efforts added.

* Spelling error on second graph on page 4, “April 4th monthly”

Page 1City of Fort Bragg Printed on 10/23/2019

October 2, 2019Finance and Administration

Committee

Meeting Minutes

3B. 19-378 Receive Oral Update from Staff on Departmental Activities

Department Update:

Government Accountant II Whippy reported on the following:

*Community Development Block Grant (CDBG) monitoring team on site auditing the grant

award of 2014. No discrepancies found.

*Auditors for City wide FY 2018, Comprehensive Annual Finance Report (CAFR) will be

brought to Council by December.

*US Bank awarded new City contract as of February 2020.

*JJACPA Audit for auditing of Citywide books for FY 2018/19 concluded on Friday.

*Transient Occupancy Tax (TOT) audit was concluded last Friday. Findings will be done by the

end of October.

*Wells Fargo to eliminate printing of their bills. New utility billing to begin in-house.

*Interactive Voice Response (IVR): The Pay-Over-the-Phone process has been implemented.

4. MATTERS FROM COMMITTEE / STAFF

* Committee Member inquired if the MuniServices TOT Audit findings payed for the consultant

services.

ADJOURNMENT

Chair Peters adjourned the meeting at 11:46 AM.

Page 2City of Fort Bragg Printed on 10/23/2019

*** THIS PAGE INTENTIONALLY LEFT BLANK ***

Text File

City of Fort Bragg 416 N Franklin Street

Fort Bragg, CA 95437

Phone: (707) 961-2823

Fax: (707) 961-2802

File Number: 19-514

Agenda Date: 12/9/2019 Status: Consent AgendaVersion: 1

File Type: Committee MinutesIn Control: City Council

Agenda Number: 5E.

Receive and File Minutes of August 21, 2019 Public Safety Committee Meeting

Page 1 City of Fort Bragg Printed on 12/4/2019

416 N Franklin Street

Fort Bragg, CA 95437

Phone: (707) 961-2823

Fax: (707) 961-2802

City of Fort Bragg

Meeting Minutes

Public Safety Committee

10:00 AM Town Hall, 363 N. Main StreetWednesday, August 21, 2019

MEETING CALLED TO ORDER

Committee Chair Peters opened the Meeting at 10:13a.m.

ROLL CALL

Bernie Norvell, Lindy Peters, Tabatha Miller, Fabian Lizarraga and Lesley BryantPresent: 5 -

Tom Varga and Steve OrsiAbsent: 2 -

1. APPROVAL OF MINUTES

19-394 Approve Minutes of July 17, 2019 Public Safety Committee Meeting

A motion was made by Committee Member Norvell, seconded by Chair Peters

that the Minutes of July 17, 2019 Meeting be approved. The motion was carried

by unanimous vote.

2. PUBLIC COMMENTS ON NON-AGENDA ITEMS

None

3. CONDUCT OF BUSINESS

3A. 19-392 Receive Oral Update from Staff on Safeway and Alcohol Shoplifting Issues

Chief Lizarraga explained Executives from Safeway are visiting Fort Bragg during the week

commencing 16th September. Any future discussion would have imput from ABC, Probation,

DA's Office, and School District. Hopefully by pointing out the monetary loss to the store may

help with security.

3B. 19-393 Receive Oral Update from Staff on Gang Prevention Efforts

Chief Lizarraga pointed out there have been no major incidents lately. The Department is

continuing it's suppression efforts as well as efforts to reach out to the Hispanic community.

FBUSD is applying for a grant for a School Resource Officer.

Committee Chair Peters talked about the increase in vehicle vs pedestrian accidents.

Committee Member Norvell mentioned the crowd of transients at the mid way point of the trail,

and City Manager Miller mentioned transients sleeping there overnight.

Committee Chair Peters talked about the lights in the parking lot at the CV Starr Center are

Page 1City of Fort Bragg Printed on 9/16/2019

August 21, 2019Public Safety Committee Meeting Minutes

not on in the early morning hours, which could prove a security issue. City Manager Miller

stated she will contact the CV Starr Center.

4. MATTERS FROM COMMITTEE / STAFF

Chief Lizarraga announced there would two officers graduating the Police Academy on 22nd,

which would make the sworn officers fully staffed with the two on injury. The Community

Service Officer candidate is continuing through background which will fill all slots. An offer has

been made to a replacement Police Services Technician. With new staff comes new ideas

and new energy.

ADJOURNMENT

Chair Peters closed the Meeting at 10:37a.m.

Page 2City of Fort Bragg Printed on 9/16/2019

*** THIS PAGE INTENTIONALLY LEFT BLANK ***

Text File

City of Fort Bragg 416 N Franklin Street

Fort Bragg, CA 95437

Phone: (707) 961-2823

Fax: (707) 961-2802

File Number: 19-531

Agenda Date: 12/9/2019 Status: Consent AgendaVersion: 1

File Type: Committee MinutesIn Control: City Council

Agenda Number: 5F.

Receive and File Minutes of October 9, 2019 Public Works and Facilities Committee Meeting

Page 1 City of Fort Bragg Printed on 12/4/2019

416 N Franklin Street

Fort Bragg, CA 95437

Phone: (707) 961-2823

Fax: (707) 961-2802

City of Fort Bragg

Meeting Minutes

Public Works and Facilities Committee

3:00 PM Town Hall, 363 N. Main StreetWednesday, October 9, 2019

MEETING CALLED TO ORDER

Chair Lee called the meeting to order at 3:00 PM.

ROLL CALL

Will Lee and Jessica Morsell-HayePresent: 2 -

1. APPROVAL OF MINUTES

1A. 19-441 Approve Minutes of September 11, 2019

A motion was made by Chair Lee, seconded by Committee Member

Morsell-Haye, that these Committee Minutes be approved for Council review. The

motion carried by a unanimous vote.

2. PUBLIC COMMENTS ON NON-AGENDA ITEMS

Public comment was received from Paul Clark.

3. CONDUCT OF BUSINESS

3A. 19-454 Review the Potential Expansion of the Municipal Improvement District

Wastewater Facilities and City of Fort Bragg Water Facilities on the East

Side of the Fort Bragg City Limits and Improvement District Boundary

Public Works Director Varga presented the staff report on this agenda item.

Public Comment was received from:

· Casey Phillips spoke in opposition to annexation.

· Paul Clark was in support of annexation with affordable housing.

· Jacob Patterson supported looking into annexation.

Discussion: The Committee Members agreed that further exploration and research needed to

be developed regarding annexation and recommended that this matter return to Committee in

the next month or two prior to being discussed by the full Council.

This Staff Report was referred to staff.

3B. 19-099 Receive Oral Update from Staff on Departmental Activities

Public Works Director Varga gave updates on the 2019 Street Rehabilitation Project, storm

drain pumps, Guest House Clock, CalTrans permit for Welcome to Fort Bragg sign at

Page 1City of Fort Bragg Printed on 10/18/2019

October 9, 2019Public Works and Facilities

Committee

Meeting Minutes

Simpson Lane roundabout, and PG&E power shutoff impacts.

4. MATTERS FROM COMMITTEE / STAFF

ADJOURNMENT

Chair Lee adjourned the meeting at 4:28 PM.

Page 2City of Fort Bragg Printed on 10/18/2019

*** THIS PAGE INTENTIONALLY LEFT BLANK ***

Text File

City of Fort Bragg 416 N Franklin Street

Fort Bragg, CA 95437

Phone: (707) 961-2823

Fax: (707) 961-2802

File Number: 19-536

Agenda Date: 12/9/2019 Status: Consent AgendaVersion: 1

File Type: MinutesIn Control: City Council

Agenda Number: 5G.

Approve Minutes of November 25, 2019

Page 1 City of Fort Bragg Printed on 12/4/2019

416 N Franklin Street

Fort Bragg, CA 95437

Phone: (707) 961-2823

Fax: (707) 961-2802

City of Fort Bragg

Meeting Minutes

City Council

THE FORT BRAGG CITY COUNCIL MEETS CONCURRENTLY AS

THE FORT BRAGG MUNICIPAL IMPROVEMENT DISTRICT NO. 1

AND THE FORT BRAGG REDEVELOPMENT SUCCESSOR

AGENCY

6:00 PM Town Hall, 363 N. Main StreetMonday, November 25, 2019

CALL TO ORDER

Mayor Lee called the meeting to order at 6:00 PM.

PLEDGE OF ALLEGIANCE

ROLL CALL

Mayor Will Lee, Vice Mayor Bernie Norvell, Councilmember Tess Albin-Smith and

Councilmember Lindy Peters

Present: 4 -

Councilmember Jessica Morsell-HayeAbsent: 1 -

AGENDA REVIEW

Mayor Lee noted that Item 1B, the Mendocino Coast Humane Society presentation, would be

moved to the next meeting of City Council on December 9, 2019. The Mayor announced that

Paula Cohen would give a short presentation to the Council on the 2020 Census under Item 1.

1. MAYOR’S RECOGNITIONS AND ANNOUNCEMENTS

1A. 19-452 Introduction of New Employees: Sandy Arellano, Public Works

Administrative Analyst; Rory Beak, Community Services Officer; Laura

Godinez, Police Services Technician; Jacqueline Jimenez, Community

Services Officer; Colin McHugh, Community Services Officer; Cristal

Munoz, Administrative Assistant; and Tanner Smith, Police Officer

Chief Lizarraga, Public Works Director Varga, and City Manager Miller introduced their new

employees to the City Council. Mayor Lee extended a warm welcome to all the new City of

Fort Bragg employees.

1B. 19-510 Receive Presentation from Mendocino Coast Humane Society Executive

Director Chuck Tourtillott

Mayor Lee continued this presentation to December 9, 2019.

1C. 19-521 Presentation from Paula Cohen Regarding Census 2020

Paula Cohen gave a status update on the 2020 Census and the various ways in which people

can be counted - by mail, by phone and online.

Page 1City of Fort Bragg Printed on 12/3/2019

November 25, 2019City Council Meeting Minutes

2. PUBLIC COMMENTS ON: (1) NON-AGENDA, (2) CONSENT CALENDAR & (3)

CLOSED SESSION ITEMS

(1) Non-Agenda Items:

· Annemarie Weibel commented on wireless telecommunications issues.

(2) Consent Calendar Items:

· None.

(3) Closed Session Items:

· Leslie Kashiwada urged the Council to talk to other cities who had purchased property with

toxic cleanup issues.

· Annemarie Weibel recommended that the Council work closely with Department of Toxic

Substances Control regarding the Mill Site property.

3. STAFF COMMENTS

City Manager Miller provided updates on PG&E activities related to storm weather.

Councilmember Peters received a pledge from Comcast for the purchase of a generator for

use by the City during power outages that would keep the internet running for first responders.

Miller noted that City Hall will be closed Thursday and Friday for the Thanksgiving holiday. She

reported on Public Safety Power Shutdown preparedness and a meeting with the County

regarding sales tax matters. Public Works Director Varga reported on a meeting regarding

wireless/telecom mapping and pending lawsuits.

4. MATTERS FROM COUNCILMEMBERS

Councilmember Peters spoke about the Visit Fort Bragg Committee and the Fire Protection

Authority meetings. Councilmember Albin-Smith reported on Climate Action Advisory

Committee and Economic Development Finance Corporation meetings. Mayor Lee thanked

school staff and the Police Department personnel for quick work ensuring that the scene was

safe after a threat at the high school campus. He mentioned a home fire that occurred

Saturday night on Redwood Avenue and that Mendocino Coast Children's Fund is setting up a

fund to donate monies to help the family get back on their feet. A local citizen who alerted first

responders and saved the residents from the burning house will be honored by the City

Council at the next meeting.

5. CONSENT CALENDAR

Approval of the Consent Calendar

A motion was made by Vice Mayor Norvell, seconded by Councilmember Peters,

to approve the Consent Calendar. The motion carried by the following vote:

Aye: Mayor Lee, Vice Mayor Norvell, Councilmember Albin-Smith and Councilmember

Peters

4 -

Absent: Councilmember Morsell-Haye1 -

5A. 19-509 Adopt by Title Only and Waive the Second Reading of Ordinance

954-2019 Establishing a Capacity Fee Deferral Program

Page 2City of Fort Bragg Printed on 12/3/2019

November 25, 2019City Council Meeting Minutes

This Ordinance was adopted on the Consent Calendar.

Enactment No: ORD 954-2019

5B. 19-451 Adopt City Council Resolution Accepting the Public Drainage Easement

from Dennis Miller and Barbara DeOca, as Required by Lot Line

Adjustment LLA 1-19, and Authorize City Manager to Execute Certificate of

Acceptance

This Resolution was adopted on the Consent Calendar.

Enactment No: RES 4211-2019

5C. 19-486 Authorize Cancellation of the December 23, 2019 Meeting

Cancellation of the December 23, 2019 Meeting was approved on the Consent

Calendar.

5D. 19-499 Receive and File Minutes of October 9, 2019 Public Works and Facilities

Committee Meeting

These Committee Minutes were received and filed on the Consent Calendar.

5E. 19-505 Approve Minutes of November 12, 2019

These Minutes were approved on the Consent Calendar.

6. DISCLOSURE OF EX PARTE COMMUNICATIONS ON AGENDA ITEMS

None.

7. PUBLIC HEARING

7A. 19-463 Open Public Hearing and Immediately Continue Public Hearing to Date,

Time and Place Certain - January 13, 2020 at 6:00 PM in Town Hall, 363

N. Main Street - to Consider Appeal of Planning Commission Decision by

Mitch Bramlitt Regarding Denial of Coastal Development Permit (CDP

9-18), Design Review Permit (DR 3-18) and Minor Subdivision (DIV 1-18)

for the Proposed AutoZone Retail Store at 1151 South Main Street (APN

008-440-58)

Mayor Lee opened the public hearing at 6:44 PM and immediately continued the

hearing to January 13, 2020 at 6:00 PM or as soon thereafter as the matter may be

heard.

This Public Hearing was continued to January 13, 2020 at 6PM or as soon

thereafter as the matter may be heard.

7B. 19-507 Receive Report, Conduct Public Hearing, and Consider Adopting a City

Council Resolution Authorizing the Execution of a Joint Exercise Powers

Agreement Relating to the California Municipal Finance Authority and

Page 3City of Fort Bragg Printed on 12/3/2019

November 25, 2019City Council Meeting Minutes

Approving the Issuance of Revenue Bonds by the Authority for the Purpose

of Financing or Refinancing the Acquisition, Construction and Improvement

of Certain Facilities for the Benefit of Fort Bragg South Street LP

Mayor Lee opened the public hearing at 6:44 PM.

City Manager Miller presented the staff report on this agenda item. Chris Dart of Danco spoke

about the progress of the applications for this project, noting that he hoped the project will start

in July of 2020.

Public Comment: None.

Mayor Lee closed the public hearing at 6:54 PM.

A motion was made by Councilmember Albin-Smith, seconded by

Councilmember Peters, that this Resolution be adopted. The motion carried by

the following vote:

Aye: Mayor Lee, Vice Mayor Norvell, Councilmember Albin-Smith and Councilmember

Peters

4 -

Absent: Councilmember Morsell-Haye1 -

Enactment No: RES 4212-2019

8. CONDUCT OF BUSINESS

8A. 19-518 Receive Report and Consider Adoption of City Council Resolution

Approving Professional Services Agreement with Creative Thinking, Inc.,

DBA The Idea Cooperative for Marketing Strategy Development and

Execution and Authorizing the City Manager to Execute Contract (Amount

Not to Exceed $99,000: Account No. 110.4321.0319)

City Manager Miller gave the staff report on this agenda item. Tom Kavanaugh, President of

The Idea Cooperative, presented a slide show on the company and the proposed scope of

work for the project.

Public Comment was received from:

· Mary Rose Koczorowski commented on the need for brochures about Fort Bragg being

available at San Francisco hotels. She stated that marketing firms need to understand

algorithms and tags.

· Robert Maki Ellis said that Idea Cooperative clients are all on the Highway 101 corridor and

he doesn't see how they can bring business up to Fort Bragg.

· Gabriel Quinn Maroney spoke about the Big Idea and city identity.

Discussion: After a brief discussion, the Council agreed to accept the recommendation of

Visit Fort Bragg Committee to contract with this company.

A motion was made by Councilmember Peters, seconded by Vice Mayor Norvell,

that this Resolution be adopted. The motion carried by the following vote:

Aye: Mayor Lee, Vice Mayor Norvell, Councilmember Albin-Smith and Councilmember

Peters

4 -

Absent: Councilmember Morsell-Haye1 -

Enactment No: RES 4213-2019

Page 4City of Fort Bragg Printed on 12/3/2019

November 25, 2019City Council Meeting Minutes

8B. 19-479 Receive Report and Recommendation from Public Works and Facilities

Committee and Consider: (1) Adoption of City Council Resolution

Approving an Integrated Pest Management Plan; and (2) Introducing by

Title Only and Waiving the First Reading of Ordinance 955-2019 Repealing

and Replacing Chapter 6.10 (Weed Abatement Procedures) and Adding

Chapter 6.11 (Integrated Pest Management) to Title 6 (Health and

Sanitation) of the Fort Bragg Municipal Code

Engineering Technician O'Neal presented the staff report on this agenda item.

Public Comment was received from:

· Jenny Shattuck urged the Council to ban pesticides of any kind on the Guest House lawn and

gardens.

·Mary Rose Koczorowski asked Council to look at various ecosystems and prepare an

analysis for all properties affected by pesticides. She recommended engaging youth to work

on integrated pest management.

·Gabriel Quinn Maroney recommended hiring homeless people to mechanically remove

weeds and that the City be more creative in pest management methods.

Discussion: After deliberation, the Council agreed that the resolution should be amended to

contain language designating the Guest House property as a pesticide-free zone. Staff was

directed to research the herbicide Garlon and if not already included in the restricted

pesticides in Exhibit A, to add it to the list.

A motion was made by Councilmember Peters, seconded by Vice Mayor Norvell,

that this Resolution be adopted as amended. The motion carried by the following

vote:

Aye: Mayor Lee, Vice Mayor Norvell and Councilmember Peters3 -

No: Councilmember Albin-Smith1 -

Absent: Councilmember Morsell-Haye1 -

Enactment No: RES 4214-2019

A motion was made by Councilmember Peters, seconded by Vice Mayor Norvell,

that this Ordinance be introduced. The motion carried by the following vote:

Aye: Mayor Lee, Vice Mayor Norvell and Councilmember Peters3 -

No: Councilmember Albin-Smith1 -

Absent: Councilmember Morsell-Haye1 -

8C. 19-450 Receive Report and Consider Adoption of City Council Resolution

Amending the FY 2019-20 Budget (Amendment No. 2020-03), Approving

the Use of $17,213.15 of Forfeited Construction and Demolition Incentive

Deposits (from Account No. 190-0000-0309) to Fund the Purchase of Nine

(9) New Dual-Purpose Trash Receptacles to Replace Existing Garbage Bins in the Central Business District, in Accordance with Municipal Code Chapter 15.34.130 (Use of Construction and Demolition Recycling Incentive)

Page 5City of Fort Bragg Printed on 12/3/2019

November 25, 2019City Council Meeting Minutes

Mayor Lee recessed the meeting at 8:23 PM; the meeting reconvened at 8:28 PM. Public Works Director Varga gave the staff report on this agenda item.

Public Comment: None.

A motion was made by Vice Mayor Norvell, seconded by Councilmember

Albin-Smith, that this Resolution be adopted. The motion carried by the following

vote:

Aye: Mayor Lee, Vice Mayor Norvell, Councilmember Albin-Smith and Councilmember

Peters

4 -

Absent: Councilmember Morsell-Haye1 -

Enactment No: RES 4215-2019

8D. 19-508 Receive Report and Consider Adoption of City Council Resolution

Updating the City's Compensation Plan and Confirming the Pay

Rates/Ranges for all City of Fort Bragg Established Classifications

City Manager Miller presented the staff report on this agenda item. She noted that the

resolution and compensation schedule have been changed to remove items 1, 3 and 4; items

2, 5 and 6 will remain.

Public Comment: None.

Discussion: It was agreed that the resolution be amended to remove the 5th, 7th, 8th, 11th and

12th recital paragraphs.

A motion was made by Councilmember Peters, seconded by Vice Mayor Norvell,

that this Resolution be adopted as amended. The motion carried by the following

vote:

Aye: Mayor Lee, Vice Mayor Norvell, Councilmember Albin-Smith and Councilmember

Peters

4 -

Absent: Councilmember Morsell-Haye1 -

Enactment No: RES 4216-2019

9. CLOSED SESSION

Mayor Lee recessed the meeting at 8:45 PM; the meeting reconvened to Closed

Session at 8:51 PM.

9A. 19-519 CONFERENCE WITH REAL PROPERTY NEGOTIATORS FOR

POSSIBLE ACQUISITION OF REAL PROPERTY, Pursuant to Government

Code Section §54956.8: Real Property: APN 018-430-22-00, 90 W

Redwood Ave., Fort Bragg, CA 95437; City Negotiator: Tabatha Miller,

City Manager; Negotiating Party: Dave Massengill, Environmental Affairs,

Georgia Pacific Corporation; Under Negotiation: Terms of Acquisition,

Price

Mayor Lee reconvened the meeting to Open Session at 9:04 PM and reported that

no reportable action was taken on the Closed Session item.

Page 6City of Fort Bragg Printed on 12/3/2019

November 25, 2019City Council Meeting Minutes

ADJOURNMENT

Mayor Lee adjourned the meeting at 9:04 PM.

________________________________

WILLIAM V. LEE, MAYOR

_______________________________

June Lemos, CMC, City Clerk

IMAGED (___________)

Page 7City of Fort Bragg Printed on 12/3/2019

Text File

City of Fort Bragg 416 N Franklin Street

Fort Bragg, CA 95437

Phone: (707) 961-2823

Fax: (707) 961-2802

File Number: 19-530

Agenda Date: 12/9/2019 Status: BusinessVersion: 1

File Type: Staff ReportIn Control: City Council

Agenda Number: 8A.

Receive Report and Consider Adoption of City Council Resolution Approving Professional

Services Agreement with R.E.Y. Engineers, Inc. to Provide Design and Engineering Services for

the 2020 Maple Street Storm Drain and Alleys Rehab Project, City Project No. PWP-00116, and

Authorizing City Manager to Execute Contract (Amount Not to Exceed $144,342.00; Account

No.405-4870-0731)

Page 1 City of Fort Bragg Printed on 12/4/2019

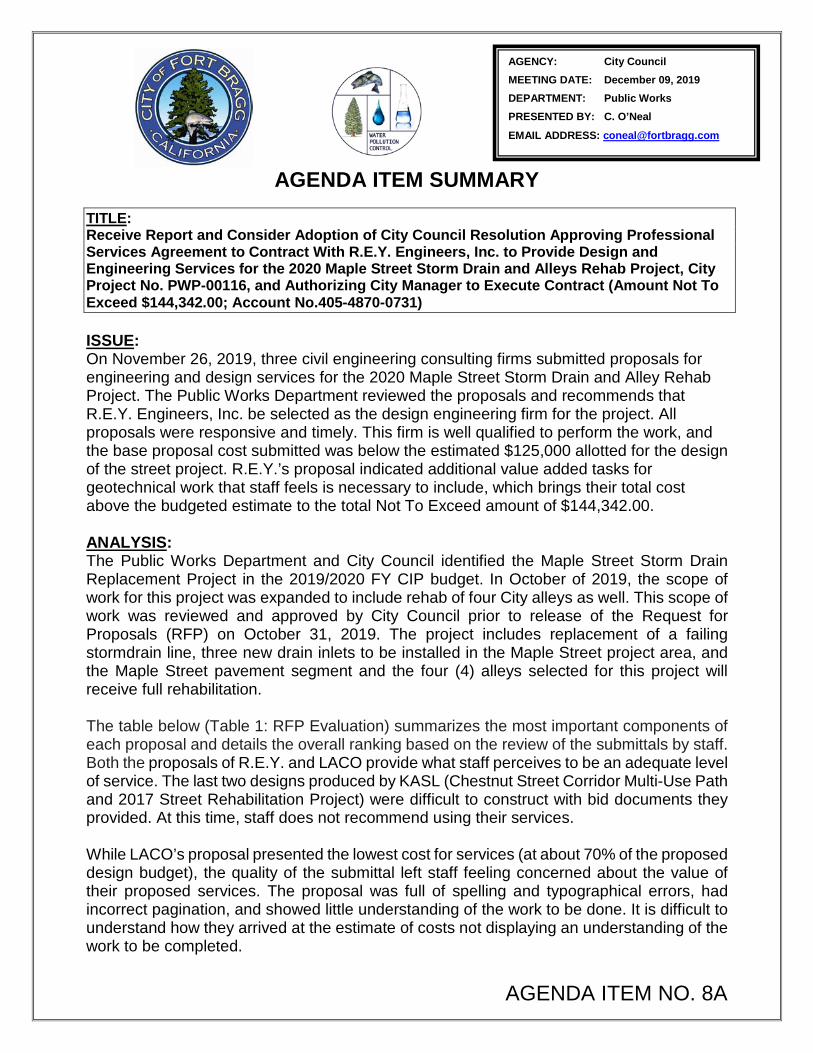

AGENDA ITEM SUMMARY

AGENDA ITEM NO. 8A

AGENCY: City Council

MEETING DATE: December 09, 2019

DEPARTMENT: Public Works

PRESENTED BY: C. O’Neal

EMAIL ADDRESS: [email protected]

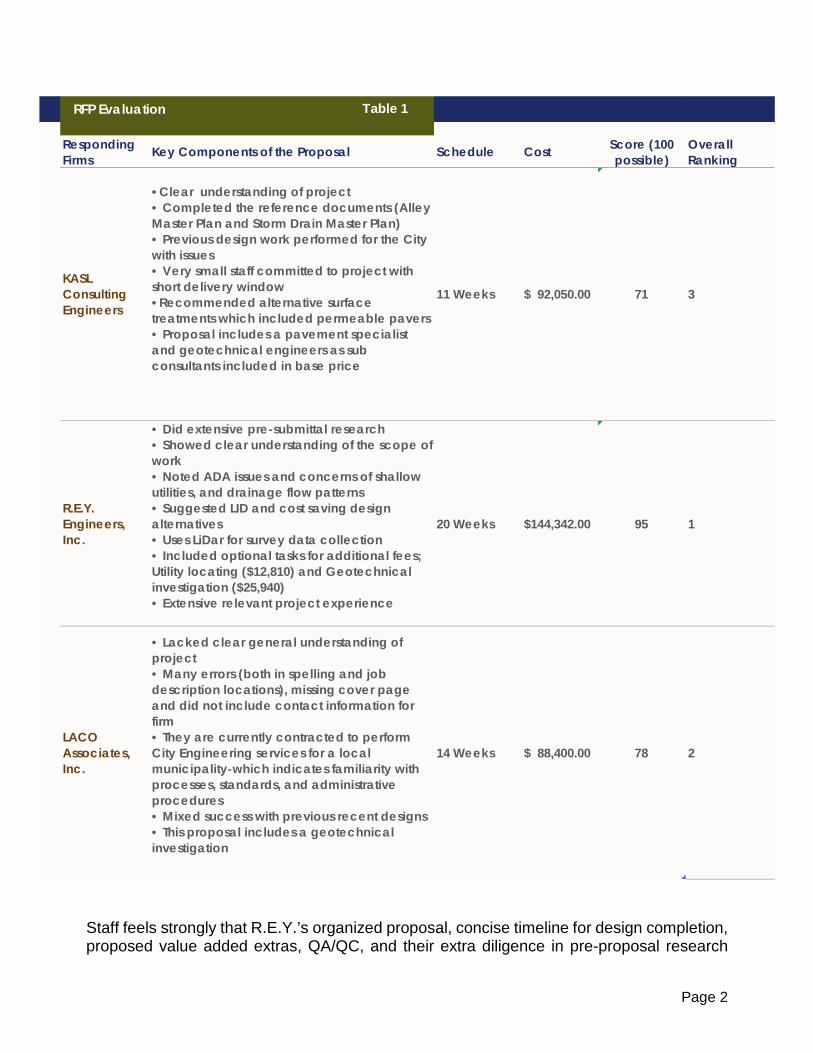

TITLE: Receive Report and Consider Adoption of City Council Resolution Approving Professional Services Agreement to Contract With R.E.Y. Engineers, Inc. to Provide Design and Engineering Services for the 2020 Maple Street Storm Drain and Alleys Rehab Project, City Project No. PWP-00116, and Authorizing City Manager to Execute Contract (Amount Not To Exceed $144,342.00; Account No.405-4870-0731) ISSUE: On November 26, 2019, three civil engineering consulting firms submitted proposals for engineering and design services for the 2020 Maple Street Storm Drain and Alley Rehab Project. The Public Works Department reviewed the proposals and recommends that R.E.Y. Engineers, Inc. be selected as the design engineering firm for the project. All proposals were responsive and timely. This firm is well qualified to perform the work, and the base proposal cost submitted was below the estimated $125,000 allotted for the design of the street project. R.E.Y.’s proposal indicated additional value added tasks for geotechnical work that staff feels is necessary to include, which brings their total cost above the budgeted estimate to the total Not To Exceed amount of $144,342.00. ANALYSIS: The Public Works Department and City Council identified the Maple Street Storm Drain Replacement Project in the 2019/2020 FY CIP budget. In October of 2019, the scope of work for this project was expanded to include rehab of four City alleys as well. This scope of work was reviewed and approved by City Council prior to release of the Request for Proposals (RFP) on October 31, 2019. The project includes replacement of a failing stormdrain line, three new drain inlets to be installed in the Maple Street project area, and the Maple Street pavement segment and the four (4) alleys selected for this project will receive full rehabilitation. The table below (Table 1: RFP Evaluation) summarizes the most important components of each proposal and details the overall ranking based on the review of the submittals by staff. Both the proposals of R.E.Y. and LACO provide what staff perceives to be an adequate level of service. The last two designs produced by KASL (Chestnut Street Corridor Multi-Use Path and 2017 Street Rehabilitation Project) were difficult to construct with bid documents they provided. At this time, staff does not recommend using their services. While LACO’s proposal presented the lowest cost for services (at about 70% of the proposed design budget), the quality of the submittal left staff feeling concerned about the value of their proposed services. The proposal was full of spelling and typographical errors, had incorrect pagination, and showed little understanding of the work to be done. It is difficult to understand how they arrived at the estimate of costs not displaying an understanding of the work to be completed.

Page 2

Staff feels strongly that R.E.Y.’s organized proposal, concise timeline for design completion, proposed value added extras, QA/QC, and their extra diligence in pre-proposal research

Responding Firms Key Components of the Proposal Schedule Cost Score (100

possible)Overall Ranking

KASL Consulting Engineers

•Clear understanding of project• Completed the reference documents (Alley Master Plan and Storm Drain Master Plan)• Previous design work performed for the City with issues• Very small staff committed to project with short delivery window•Recommended alternative surface treatments which included permeable pavers• Proposal includes a pavement specialist and geotechnical engineers as sub consultants included in base price

11 Weeks $ 92,050.00 71 3

R.E.Y. Engineers, Inc.

• Did extensive pre-submittal research• Showed clear understanding of the scope of work• Noted ADA issues and concerns of shallow utilities, and drainage flow patterns• Suggested LID and cost saving design alternatives • Uses LiDar for survey data collection• Included optional tasks for additional fees; Utility locating ($12,810) and Geotechnical investigation ($25,940)• Extensive relevant project experience

20 Weeks $144,342.00 95 1

LACO Associates, Inc.

• Lacked clear general understanding of project• Many errors (both in spelling and job description locations), missing cover page and did not include contact information for firm• They are currently contracted to perform City Engineering services for a local municipality-which indicates familiarity with processes, standards, and administrative procedures• Mixed success with previous recent designs• This proposal includes a geotechnical investigation

14 Weeks $ 88,400.00 78 2

RFP Evaluation Table 1

Page 3

about this project shows their commitment to delivering the City a successful project. One of the most important components of a good design is attention to detail and quality control of the submittal, something that was best represented by the submittal from R.E.Y. An example of this from their proposal is their assertion that up to $50,000 in construction costs can be saved by utilizing the in-depth geotechnical information from their geotechnical investigation option to optimize the street thickness design and minimize materials used. If selected, City staff would continue to work with R.E.Y. to find other substantial construction cost savings reflecting their higher level care and detail during design. Engineering staff also believes that optimized or inventive designs can be used in other future projects. The City is always looking at bringing new and innovative designers to perform work on the coast and staff feels that R.E.Y. will make us a regular client. Nevertheless, the R.E.Y. proposal (with the geotechnical and utility location options) is $144,342 which is $55,942 (or about 63%) greater than LACO’s. While high quality design and construction bid documents are always desirable, staff is looking for direction from Council as to whether they agree that the extra cost is merited. RECOMMENDED ACTION: Adopt Resolution approving Professional Services Agreement with R.E.Y. Engineers Inc. to Provide Design and Engineering Services for the 2020 Maple Street Storm Drain and Alley Rehab Project, City Project No. PWP-00116, and Authorizing City Manager to Execute Contract (Amount Not To Exceed $144,342.00). ALTERNATIVE ACTION(S): 1. Adopt Resolution approving Professional Services Agreement with LACO Associates,

Inc. to Provide Design and Engineering Services for the 2020 Maple Street Storm Drain and Alley Rehab Project, City Project No. PWP-00116, and Authorizing City Manager to Execute Contract (Amount Not To Exceed $88,400.00); or

2. Reject all proposals and solicit a new Request for Proposals (RFPs). FISCAL IMPACT: The Design and Engineering portion of this project was estimated at $125,000, and a total project budget of $1,800,000. The 2020 Maple Street Storm Drain and Alley Rehab Project is funded in part through SB-1 Local Partnership Program (LPP) funds in the amount of $100,000 and the remaining amount of $1,700,000 is verified as being available for funding with City’s Special Sales Tax money. City Special Street Sales tax monies are received from a half-cent sales tax which is restricted to City Street and alley repairs/rehabilitation. Staff will bring forward a budget amendment in the spring of 2020 once the engineers estimate is substantially complete and prior to the project going out to bid. GREENHOUSE GAS EMISSIONS IMPACT: There is little to no increase in Greenhouse gas emissions associated with the Design Engineering portion of this project. There is a slightly higher emissions impact associated with the selection of either R.E.Y. Engineers, Inc. or KASL Consulting Engineers versus LACO Associates, Inc. due to the increased driving distance required to travel to Fort Bragg.

Page 4

CONSISTENCY: The Maple Street portion of this project is consistent with the City’s Capital Improvement Plan (CIP) budget for street repair. The primary funding source for this project is Special Street Sales Tax, Measure H. This special purpose transaction and use tax was passed by the voters in 2004 and extended again in 2014. The special sales tax is currently scheduled to sunset in 2024. This City’s Special Street Sales Tax, makes us a “Self-Help” City under RMRA, which entitles us to the additional $100,000 in state funds described above as available for this project. The proposed use of both the Special Street Sales tax and RMRA funds is consistent with their intended use for repairing, maintaining and reconstructing City streets and underlying infrastructure. IMPLEMENTATION/TIMEFRAMES: Project design engineering is scheduled for this winter and spring. Once designed, the project will be released for bid in late spring/early summer of 2020 with the intent of catching the most competitive bidding environment. The construction contract will likely be sixty (60) to ninety (90) working days and construction should be complete for final billing by November 2020. ATTACHMENTS: 1. Resolution to Approve Professional Services Agreement with R.E.Y. Engineers Inc. NOTIFICATION: 1. KASL Consulting Engineers; John C. Scroggs, PE Principal-in-Charge 2. LACO Associates, Inc.; Holly Cinkutis, PE Senior Engineer 3. R.E.Y. Engineers, Inc.; Aaron Brusatori, PE Project Manager

- 1 -

RESOLUTION NO. ___-2019

RESOLUTION OF THE FORT BRAGG CITY COUNCILAPPROVING PROFESSIONAL SERVICES AGREEMENT WITH R.E.Y.

ENGINEERS, INC. TO PROVIDE DESIGN AND ENGINEERING SERVICES FOR THE 2020 MAPLE STREET STORM DRAIN AND ALLEYS REHAB PROJECT, CITY PROJECT NO. PWP-00116, AND AUTHORIZING CITY

MANAGER TO EXECUTE CONTRACT (AMOUNT NOT TO EXCEED $144,342.00; ACCOUNT NO.405-4870-0731)

WHEREAS, on October 24, 2019 City Council directed the Public Works Department to move forward with releasing a request for proposals to design improvements for the 2020 Maple Street Storm Drain and Alleys Rehabilitation Project; and

WHEREAS, on November 26, 2019, the City received three proposals for engineering design services for the street rehabilitation project. Proposing firms included KASL Consulting Engineers, LACO Associates, and R.E.Y. Engineers; and

WHEREAS, those proposals were reviewed and evaluated on the basis of capabilities, qualifications, and responsiveness; and

WHEREAS, the Project is exempt pursuant to the California Environmental Quality Act (“CEQA”) and Title 14, the California Code of Regulations (“CEQA Guidelines”), Section 15301 (c) &21080 b. (1); and

WHEREAS, funds in the amount of $650,000 were appropriated in the FY 2019/2020 budget for this activity and sufficient funds are available for this contract; and

WHEREAS, based on all the evidence presented, the City Council finds as follows:

1. R.E.Y. Engineers, Inc. is qualified to provide necessary professional services to complete plans and specifications for the 2020 Maple Street Storm Drain and Alleys Rehabilitation Project.

NOW, THEREFORE, BE IT RESOLVED that the City Council of the City of Fort Bragg does hereby approve a Professional Services Agreement with R.E.Y. Engineers, Inc. for the 2020 Maple Street Storm Drain and Alleys Rehabilitation Project design and authorizes the City Manager to execute the same upon execution by Contractor (Amount Not to Exceed $144,342.00 Account 405-4870-0731).

The above and foregoing Resolution was introduced by Councilmember ________, seconded by Councilmember ________, and passed and adopted at a regular meeting of the City Council of the City of Fort Bragg held on the 9th day of December, 2019, by the following vote:

AYES:NOES:ABSENT:ABSTAIN:RECUSED:

- 2 -

WILLIAM V. LEEMayor

ATTEST:

June Lemos, CMCCity Clerk

*** THIS PAGE INTENTIONALLY LEFT BLANK ***

Text File

City of Fort Bragg 416 N Franklin Street

Fort Bragg, CA 95437

Phone: (707) 961-2823

Fax: (707) 961-2802

File Number: 19-520

Agenda Date: 12/9/2019 Status: BusinessVersion: 1

File Type: ReportIn Control: City Council

Agenda Number: 8B.

Receive Report and Recommendation from the Election Systems Review Ad Hoc Committee

Page 1 City of Fort Bragg Printed on 12/4/2019

AGENDA ITEM SUMMARY

AGENDA ITEM NO. 8B

AGENCY: City Council

MEETING DATE: December 9, 2019

DEPARTMENT: City Council

PRESENTED BY: Tess Albin-Smith

EMAIL ADDRESS: [email protected]

TITLE:Receive Report and Recommendation from the Election Systems Review Ad Hoc Committee

THIS WILL BE AN ORAL PRESENTATION BYCOUNCILMEMBER TESS ALBIN-SMITH

P a g e | 1

FINAL REPORT

ELECTIONS REVIEW AD HOC COMMITTEE (ERC)

DECEMBER 9, 2019

BACKGROUND

In April 2018, the “Coast Committee for Responsive Representation” (CCRR), sent a

letter alleging that the City of Fort Bragg violated the California Voting Rights Act of 2001

(CVRA, California Elections Code §§ 14025-14032). The CVRA protects the voting rights

of minorities from dilution and can require communities to form districts when there is

“racially-polarized1” voting.

That allegation was based on a theory that a lack of Latinos running or winning a seat on

the Fort Bragg City Council happens because voting at large causes racially polarized

voting in favor of the non-Hispanic majority.

The ERC would like to point out that the statement is incorrect. Historically Latinos have

indeed run for Fort Bragg City Council seats during elections in 2002, 2004, 2006, and

2018. Brian Baltierra served from 2002 to 2006.

To enforce the CVRA, the plaintiff must demonstrate that Fort Bragg DOES indeed have

racially-polarized voting with respect to City Council elections. In essence there is one

test in California:

Do the voters who are not in the protected class vote in a bloc to defeat the

preferred candidates of the protected class?

This test is significantly broader than the test at the federal level under the Voting Rights

Act of 1965.

1 Racially polarized voting exists when voters of different racial or ethnic groups exhibit very different candidate preferences in an election. It means simply that voters of different groups are voting in opposite directions, rather than in a coalition.

P a g e | 2

The City of Fort Bragg hired a professional demographer consultant through the National

Demographics Corporation (Douglas Johnson, president) to provide demographic and

election history profiles, and to examine the claim of “racially-polarized voting” in Fort

Bragg City Council elections.

The demographer’s findings provided the following conclusions:

• There is no evidence of racially polarized voting in past elections.

• Dividing the city into five separate districts could not produce a majority bloc of

Latinos or any one ethnic group.

• Using surnames is not a reliable way to identify minorities within district lines.

• For example, Mayor Lee may be grouped with Asians, Portuguese may be

grouped with Latinos, and one of the spouses in a mixed Latino/Caucasian

marriage will be misidentified.

A Settlement Agreement was drawn up whereby the CCRR agreed to rescind their

letter if the City, which had already contracted for a demographic analysis, further

agreed to:

1. Cover candidate statement fees, making it less expensive for candidates to

run for election.

2. Promote civic engagement by doing more public outreach to include