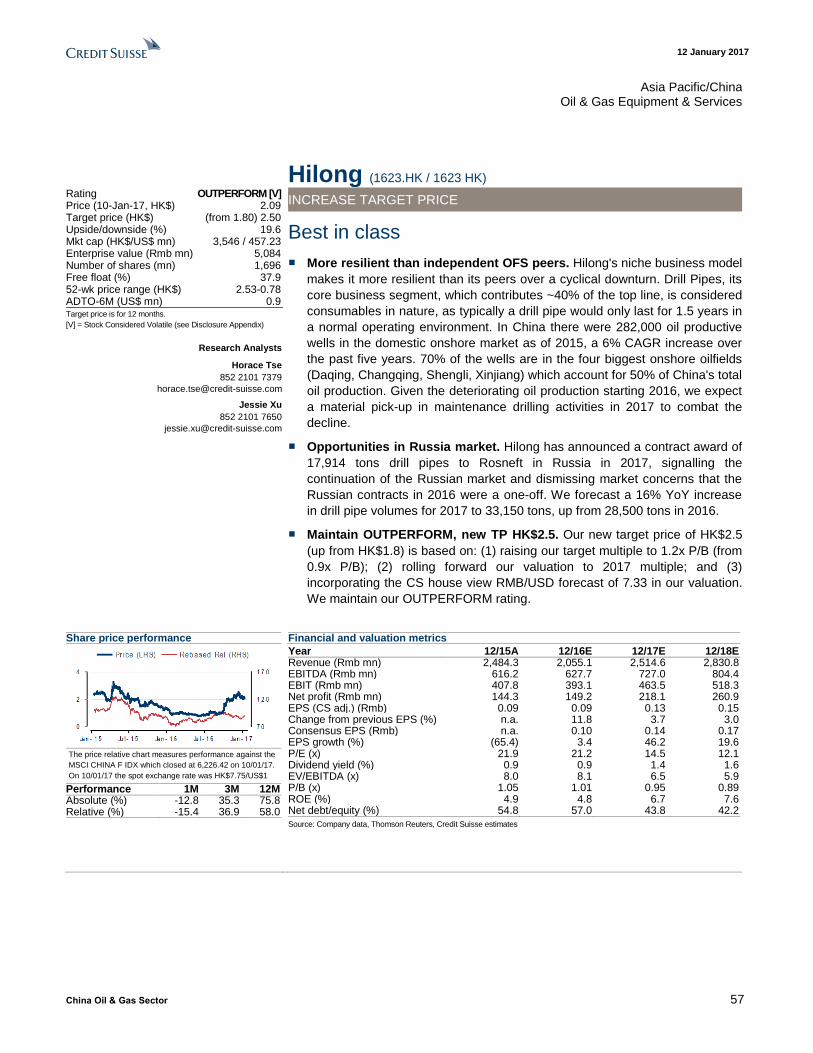

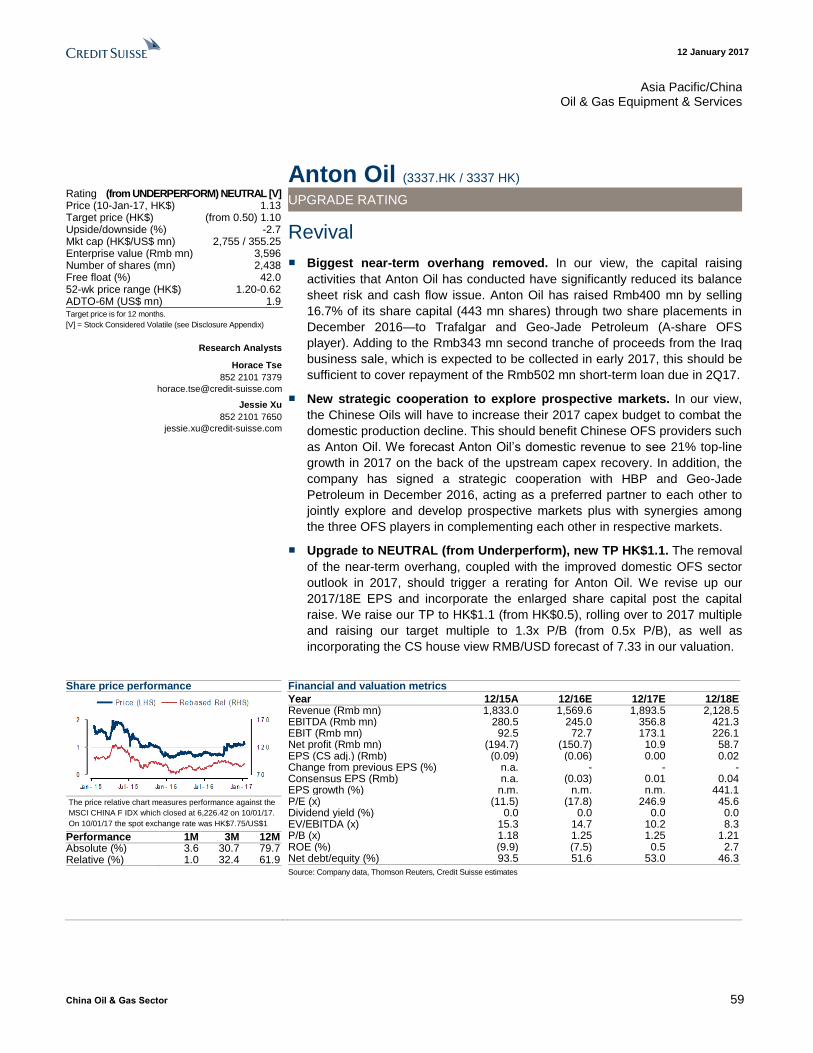

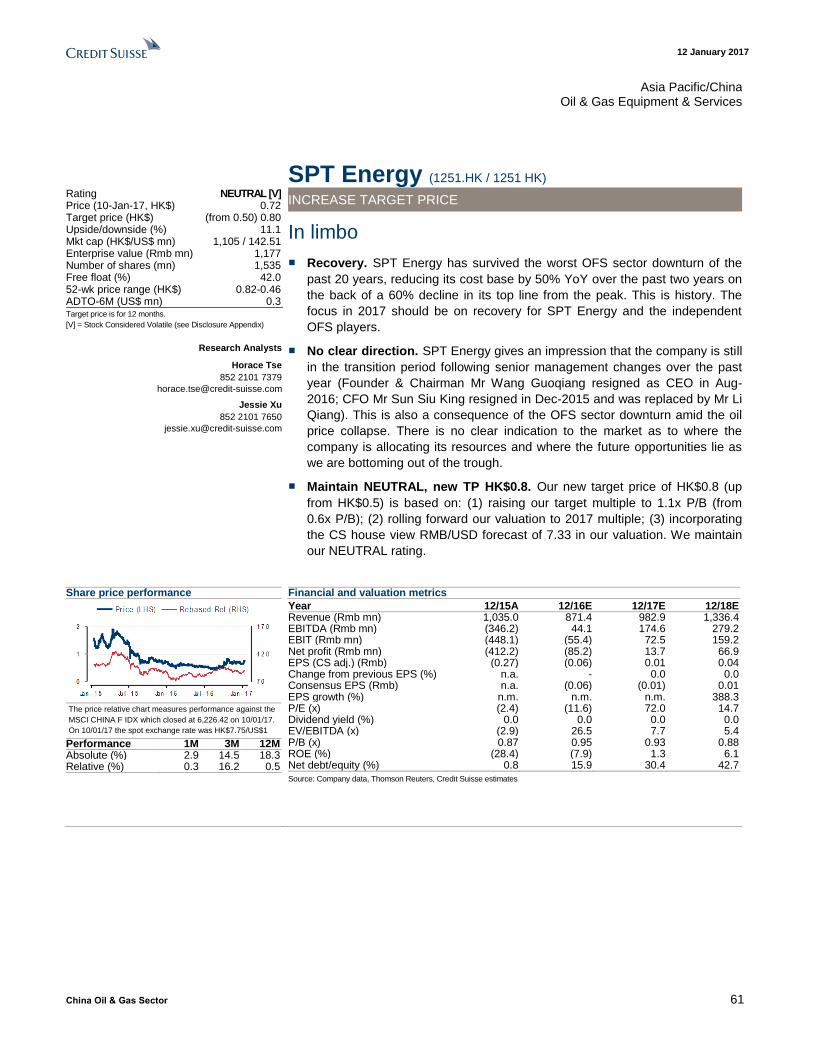

china oil & gas sector - credit suisse | plus

TRANSCRIPT

DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS, LEGAL ENTITY DISCLOSURE AND THE STATUS OF NON-US ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

12 January 2017 Asia Pacific/Hong Kong

Equity Research Energy

China Oil & Gas Sector Research Analysts

Horace Tse

852 2101 7379

Jessie Xu

852 2101 7650

SECTOR FORECAST

2017: A year of second-phase recovery

Figure 1: Chinese Oils typically see expansion of multiples during upcycle

Source: the BLOOMBERG PROFESSIONAL™ service, company data, Credit Suisse estimates

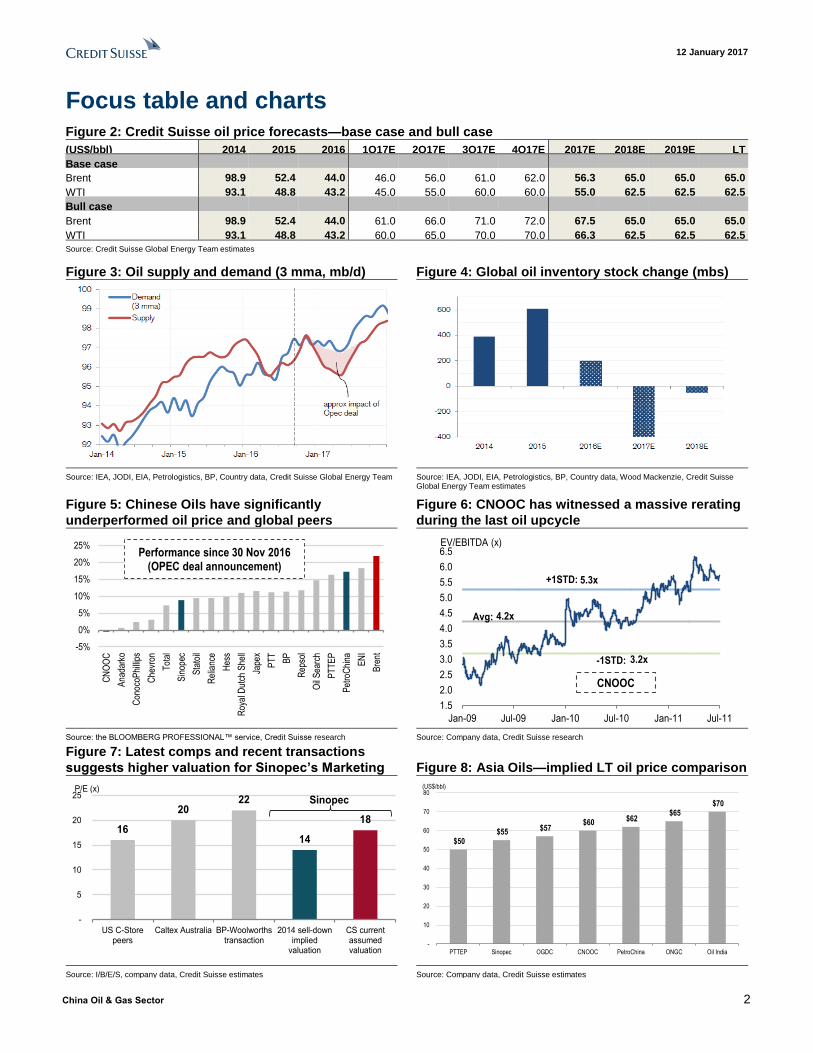

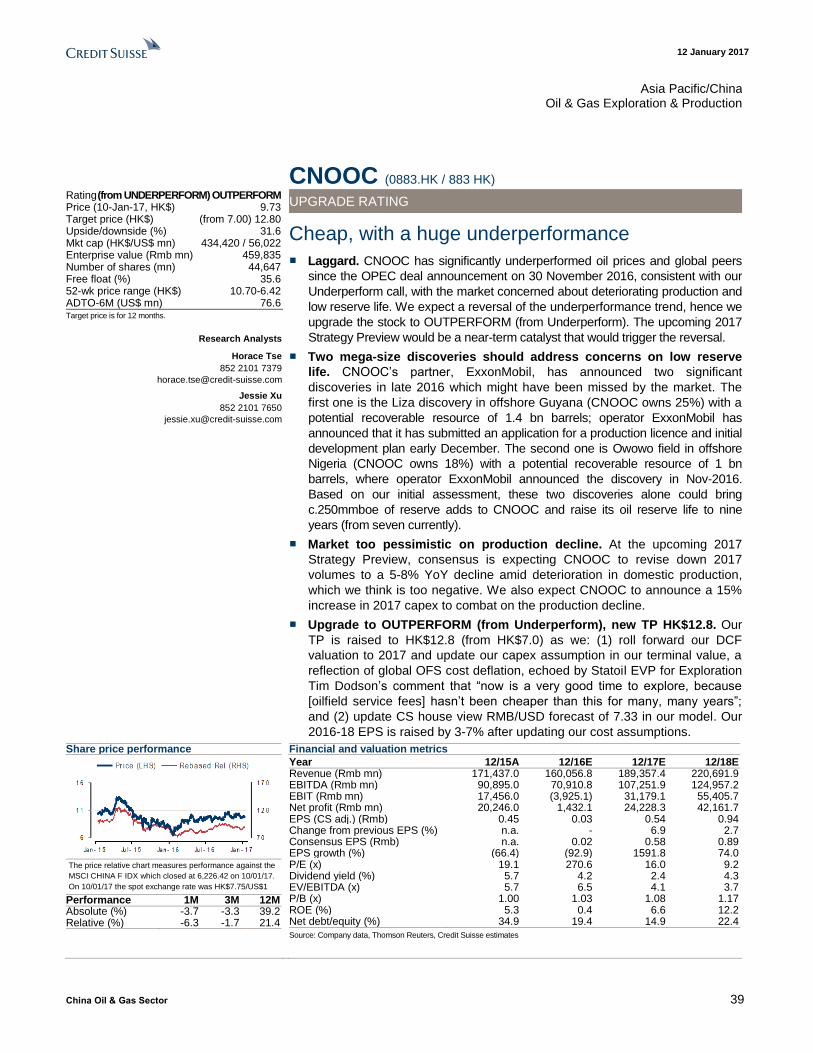

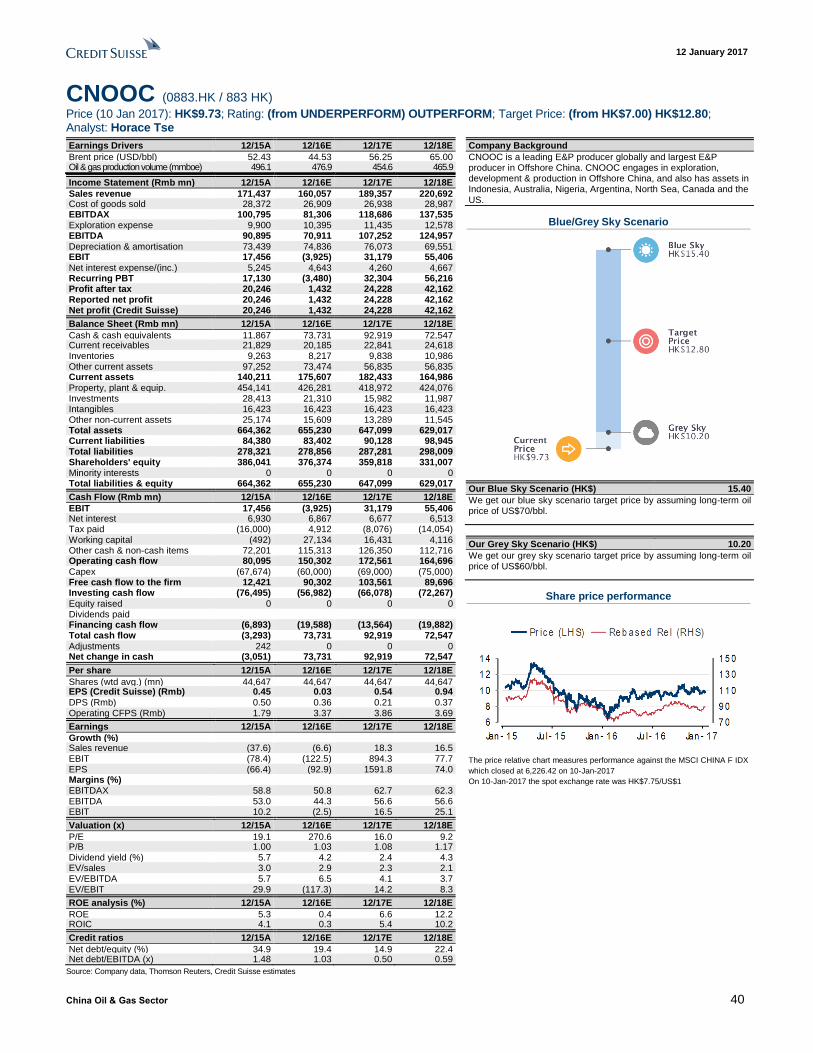

■ Accelerated oil market rebalancing post OPEC deal. We believe the OPEC cut effective from January, coupled with robust 1.5mb/d global oil demand growth, should induce 400mbs of inventory drawdown in 2017 and accelerate the global oil market rebalance. CS forecasts US$56/bbl Brent in 2017, with upside risk if OPEC adheres to the 32.5mb/d low-end output cut. Since the announcement of the OPEC deal, oil prices were up 22% and global peers have rallied 12%, but Chinese Oils, particularly CNOOC, have lagged. We expect a reversal of the underperformance trend.

■ Multiple catalysts ahead. (1) We think the market is too bearish on

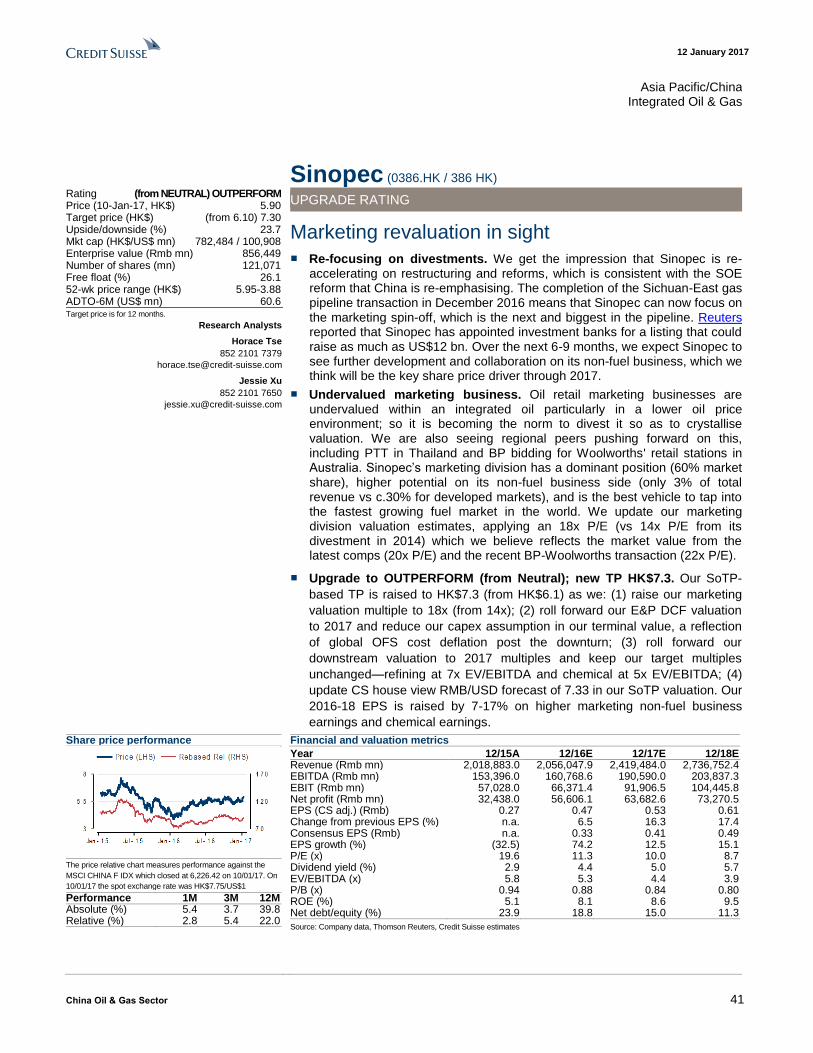

CNOOC’s production/reserves and its upcoming 2017 Strategy Preview could surprise on the upside. (2) Sinopec’s marketing business divestment could be the biggest catalyst this year; latest comps and recent transactions suggest 20x P/E valuation for the marketing business. We raise the marketing business valuation to 18x P/E (from 14x) in our Sinopec model.

■ Valuation rerating during an oil price upcycle. The Big 3 Oils are pricing

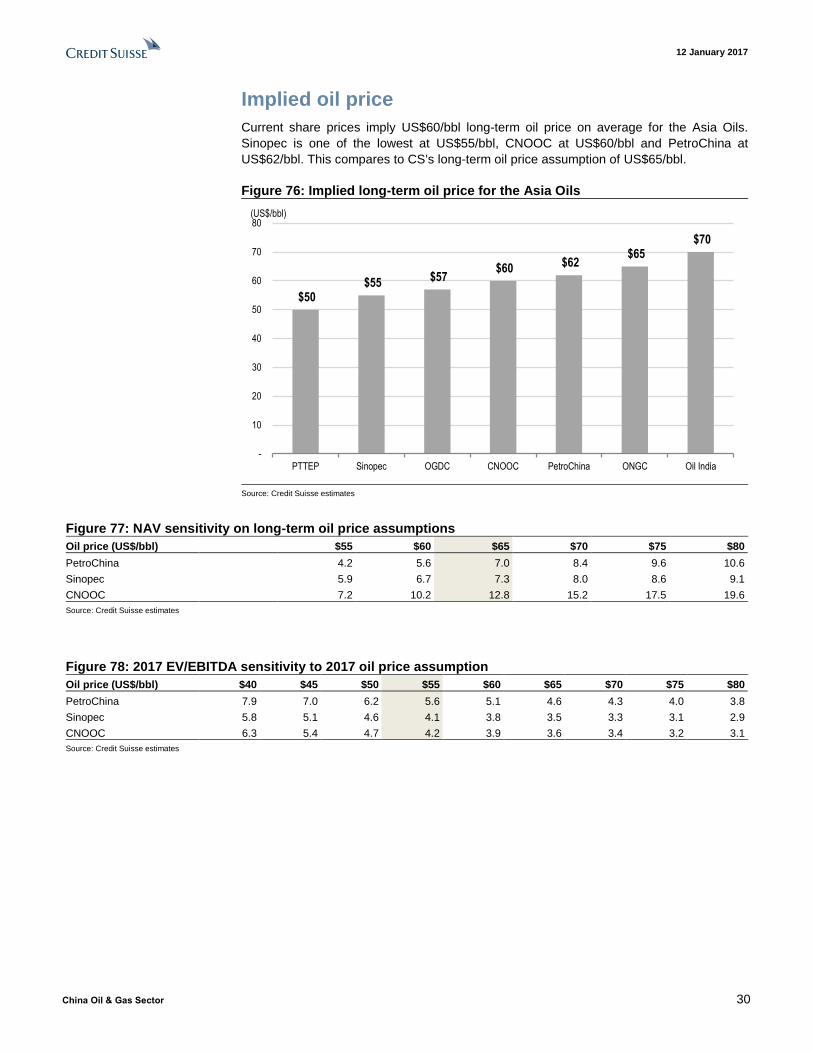

in 4.5x 2017E EV/EBITDA at our US$56/bbl assumption, >1 SD below the historical average. During the 2009-11 upcycle, the Big 3 Oils’ EV/EBITDA multiples rerated from 3x to 6x on average. In terms of implied oil prices, Sinopec is one of the lowest within the region at US$55/bbl long-term oil price, vs Asia Oils’ average of US$60 and CS’s long-term oil price assumption of US$65.

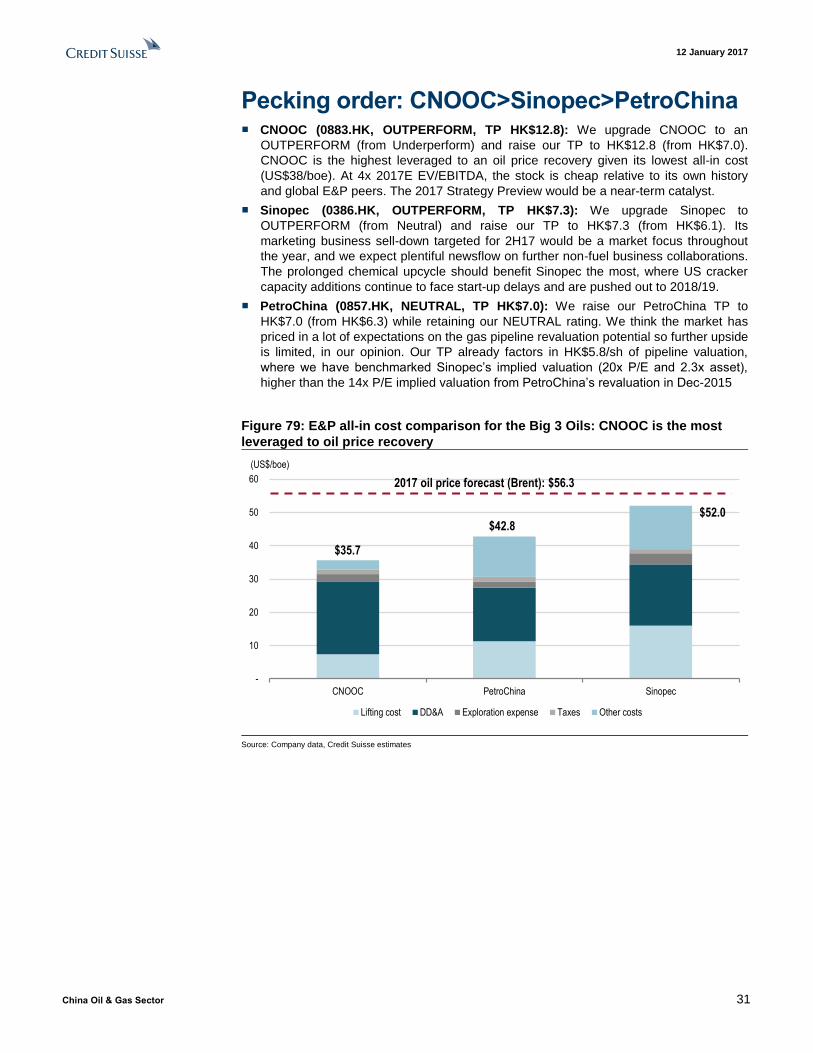

■ Pecking order: CNOOC > Sinopec > PetroChina. CNOOC (upgrade to

Outperform, TP HK$12.8) is the most leveraged to oil price recovery, cheap and has significantly underperformed global peers, with the 2017 Strategy Preview as a near-term catalyst. Sinopec (upgrade to Outperform, TP HK$7.3) should see valuation/earnings upside from its marketing business, plus tailwinds from a prolonged chemical upcycle. PetroChina (Neutral, TP HK$7.0) has priced in a lot of expectations on the gas pipeline revaluation potential so upside is limited. Please see the company pages at the back for the other ratings, TP and EPS changes made.

50

100

150

200

250

300

Jan-09 Jul-09 Jan-10 Jul-10 Jan-11 Jul-11Jan-16 Jul-16 Jan-17 Jul-17

(Rebased to 100)

Oil price trend - 2016-17 vs 2009-11

4.2x

5.3x

3.2x

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

6.0

6.5

Jan-09 Jul-09 Jan-10 Jul-10 Jan-11 Jul-11

Avg:

+1STD:

-1STD:

EV/EBITDA (x)

CNOOC

12 January 2017

China Oil & Gas Sector 2

Focus table and charts

Figure 2: Credit Suisse oil price forecasts—base case and bull case

(US$/bbl) 2014 2015 2016 1Q17E 2Q17E 3Q17E 4Q17E 2017E 2018E 2019E LT

Base case

Brent 98.9 52.4 44.0 46.0 56.0 61.0 62.0 56.3 65.0 65.0 65.0

WTI 93.1 48.8 43.2 45.0 55.0 60.0 60.0 55.0 62.5 62.5 62.5

Bull case

Brent 98.9 52.4 44.0 61.0 66.0 71.0 72.0 67.5 65.0 65.0 65.0

WTI 93.1 48.8 43.2 60.0 65.0 70.0 70.0 66.3 62.5 62.5 62.5

Source: Credit Suisse Global Energy Team estimates

Figure 3: Oil supply and demand (3 mma, mb/d) Figure 4: Global oil inventory stock change (mbs)

Source: IEA, JODI, EIA, Petrologistics, BP, Country data, Credit Suisse Global Energy Team Source: IEA, JODI, EIA, Petrologistics, BP, Country data, Wood Mackenzie, Credit Suisse Global Energy Team estimates

Figure 5: Chinese Oils have significantly

underperformed oil price and global peers

Figure 6: CNOOC has witnessed a massive rerating

during the last oil upcycle

Source: the BLOOMBERG PROFESSIONAL™ service, Credit Suisse research Source: Company data, Credit Suisse research

Figure 7: Latest comps and recent transactions

suggests higher valuation for Sinopec’s Marketing Figure 8: Asia Oils—implied LT oil price comparison

Source: I/B/E/S, company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

-5%

0%

5%

10%

15%

20%

25%

CN

OO

C

Ana

dark

o

Con

ocoP

hilli

ps

Che

vron

Tot

al

Sin

opec

Sta

toil

Rel

ianc

e

Hes

s

Roy

al D

utch

She

ll

Jape

x

PT

T

BP

Rep

sol

Oil

Sea

rch

PT

TE

P

Pet

roC

hina EN

I

Bre

nt

Performance since 30 Nov 2016(OPEC deal announcement)

4.2x

5.3x

3.2x

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

6.0

6.5

Jan-09 Jul-09 Jan-10 Jul-10 Jan-11 Jul-11

Avg:

+1STD:

-1STD:

EV/EBITDA (x)

CNOOC

16

2022

14

18

-

5

10

15

20

25

US C-Storepeers

Caltex Australia BP-Woolworthstransaction

2014 sell-downimplied

valuation

CS currentassumedvaluation

P/E (x)

Sinopec

$50 $55 $57

$60 $62 $65

$70

-

10

20

30

40

50

60

70

80

PTTEP Sinopec OGDC CNOOC PetroChina ONGC Oil India

(US$/bbl)

12 January 2017

China Oil & Gas Sector 3

2017: A year of second-phase recovery

Accelerated oil market rebalancing post OPEC deal

In our view, the OPEC cut effective from 1 January 2017, coupled with robust 1.5mb/d

global oil demand growth, should induce 400mbs of inventory drawdown in 2017 and

accelerate the rebalance of the global oil market. CS' Global Energy Team forecasts

US$56/bbl Brent for 2017, but acknowledges that there could be upside risk to oil prices

should OPEC adhere to the 32.5mb/d low-end of the agreed cut. Despite oil prices going

up 22% since OPEC struck the deal in November 2016, the Big 3 Oils’ underperformance

is significant, particularly CNOOC. CNOOC is down 1% since then, having hugely

underperformed global peers and consistent with our Underperform stance; Sinopec and

PetroChina are up 9% and 17%, respectively. We expect a reversal of the

underperformance trend, with multiple catalysts in sight.

Multiple catalysts ahead

We expect company-specific catalysts to drive share prices, on top of an oil price

recovery: (1) The market is concerned about CNOOC’s deteriorating production and low

reserve life, and expectations are low heading into the 2017 Strategy Preview, but we

believe it should bring positive surprises. Its 2017 production decline should be limited to

low single digits vs market expectations of a 5-8% decline. Two mega-size discoveries

recently announced by its partner, ExxonMobil, suggests successful exploration effort

under a low capex environment and will address concerns on its low reserve life. (2)

Sinopec's marketing business divestment, which is coherent with the SOE reform that

China is re-emphasising, would be a big catalyst for this year. Latest comps and recent

transactions suggest 20x P/E valuation for the marketing business; hence, we raise the

marketing business valuation to 18x P/E (from 14x) in our Sinopec model. Over the next 6-

9 months, we expect Sinopec to see further development and collaboration on its non-fuel

business.

Valuation rerating during an oil price upcycle

Under our US$56/bbl base-case oil price assumption, the Big 3 Oils are currently pricing in

4.5x 2017E EV/EBITDA, which is more than 1 SD below the historical average. Our

analysis of the past oil cycles suggests that during the 2009-11 recovery, the Big 3 Oils’

EV/EBITDA multiples have rerated from 3x to 6x on average. In terms of implied oil prices,

Sinopec is one of the lowest within the region at US$55/bbl long-term oil price, vs Asia

Oils’ average of US$60/bbl and CS’s long-term oil price assumption of US$65/bbl.

Pecking order: CNOOC > Sinopec > PetroChina

■ CNOOC (0883.HK, OUTPERFORM, TP HK$12.8): We upgrade CNOOC to an

OUTPERFORM (from Underperform) and raise our TP to HK$12.8 (from HK$7.0).

CNOOC is the highest leveraged to an oil price recovery given its lowest all-in cost

(US$38/boe). At 4x 2017E EV/EBITDA, the stock is cheap relative to its own history

and global E&P peers. The 2017 Strategy Preview would be a near-term catalyst.

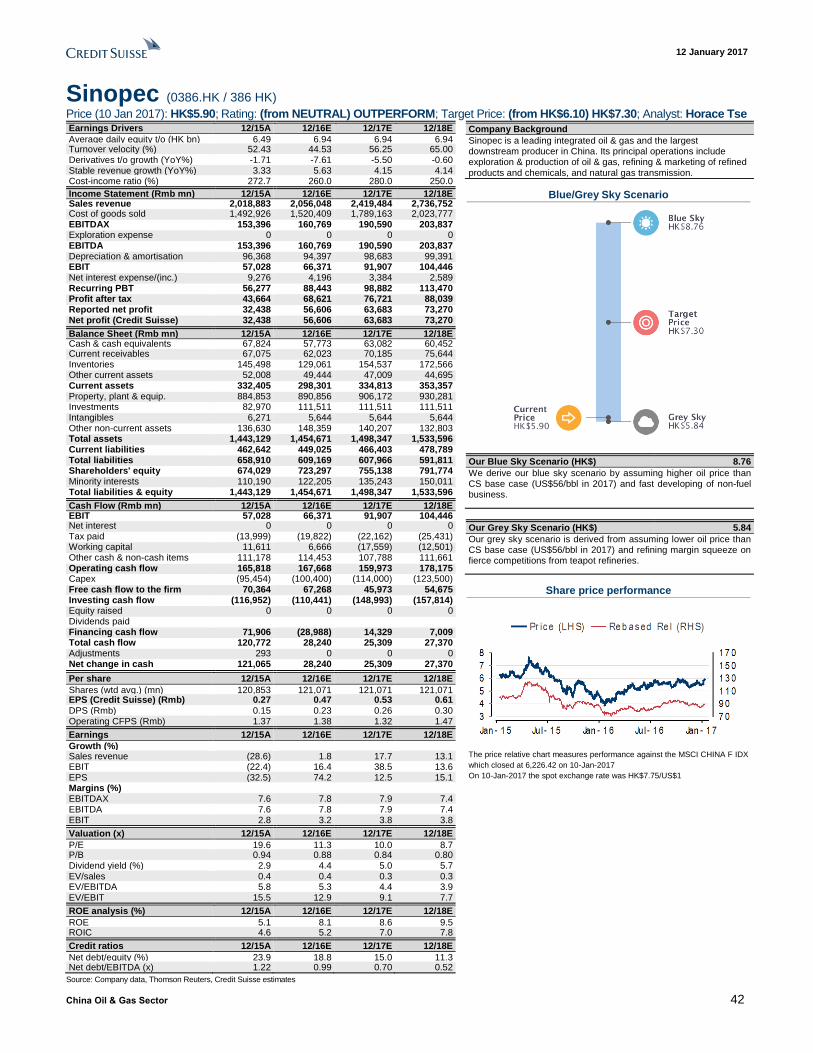

■ Sinopec (0386.HK, OUTPERFORM, TP HK$7.3): We upgrade Sinopec to

OUTPERFORM (from Neutral) and raise our TP to HK$7.3 (from HK$6.1). Its

marketing business sell-down targeted for 2H17 would be a market focus throughout

the year, and we expect plentiful newsflow on further non-fuel business collaborations.

The prolonged chemical upcycle should benefit Sinopec the most, where US cracker

capacity additions continue to face start-up delays and are pushed out to 2018/19.

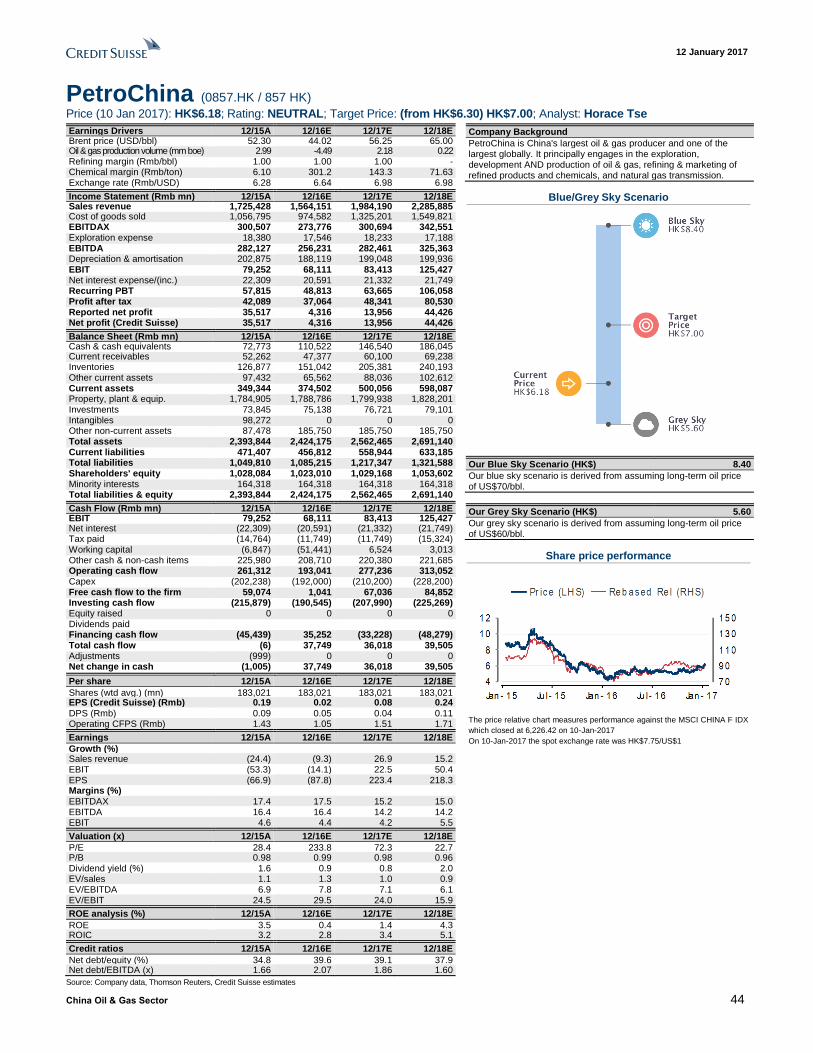

■ PetroChina (0857.HK, NEUTRAL, TP HK$7.0): We raise our PetroChina TP to

HK$7.0 (from HK$6.3) while retaining our NEUTRAL rating. We think the market has

priced in a lot of expectations on the gas pipeline revaluation potential so further upside

is limited, in our opinion. Our TP already factors in HK$5.8/sh of pipeline valuation,

where we have benchmarked Sinopec’s implied valuation (20x P/E and 2.3x asset),

higher than the 14x P/E implied valuation from PetroChina’s revaluation in Dec-2015.

$56/bbl CS base case 2017 forecast (Brent)

We expect fundamental share price drivers over

the course of 2017 on top of an oil price

uptick

EV/EBITDA multiples expanded from 3x to 6x

during the 2009-11 upcycle

China Oil & Gas Sector 4

12 J

an

uary

201

7

Ch

ina O

il & G

as S

ecto

r 4

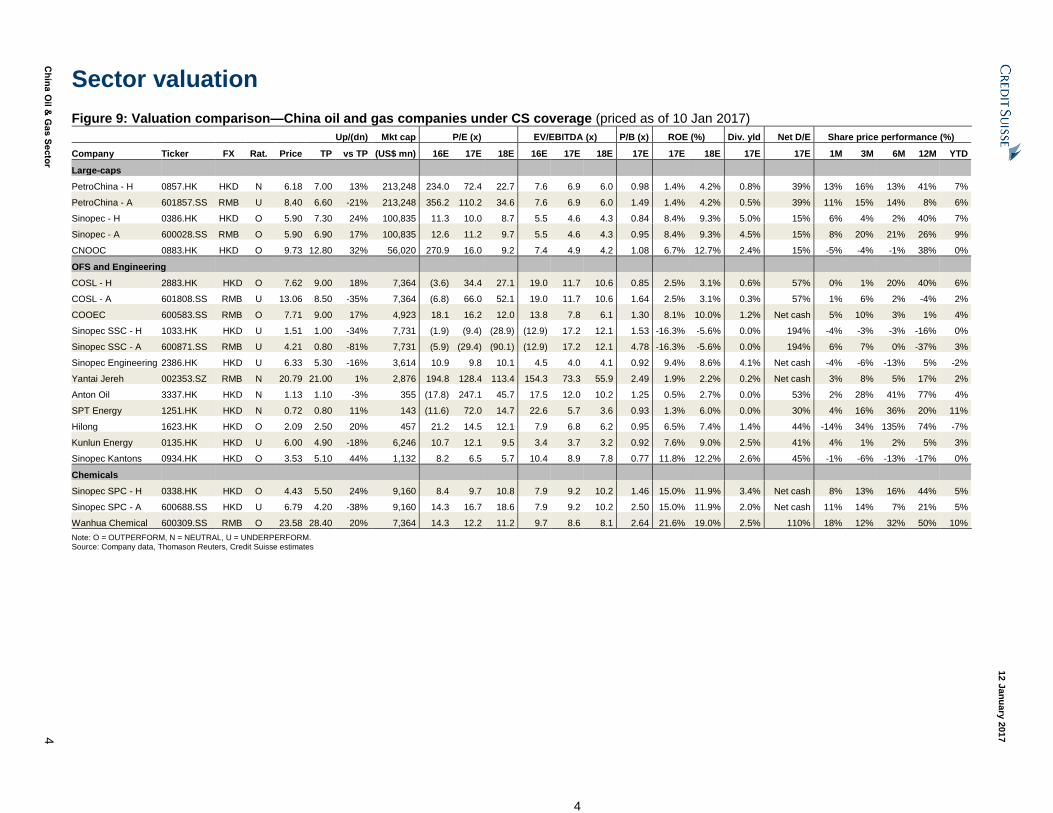

Sector valuation

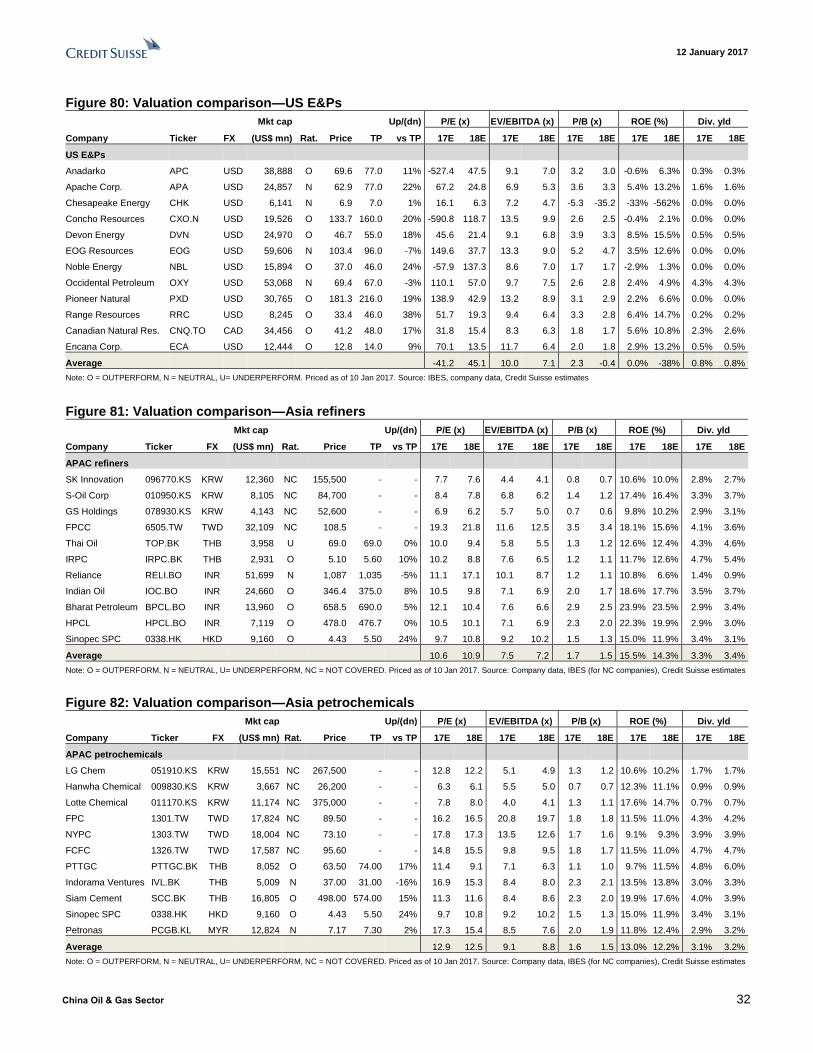

Figure 9: Valuation comparison—China oil and gas companies under CS coverage (priced as of 10 Jan 2017)

Up/(dn) Mkt cap P/E (x) EV/EBITDA (x) P/B (x) ROE (%) Div. yld Net D/E Share price performance (%)

Company Ticker FX Rat. Price TP vs TP (US$ mn) 16E 17E 18E 16E 17E 18E 17E 17E 18E 17E 17E 1M 3M 6M 12M YTD

Large-caps

PetroChina - H 0857.HK HKD N 6.18 7.00 13% 213,248 234.0 72.4 22.7 7.6 6.9 6.0 0.98 1.4% 4.2% 0.8% 39% 13% 16% 13% 41% 7%

PetroChina - A 601857.SS RMB U 8.40 6.60 -21% 213,248 356.2 110.2 34.6 7.6 6.9 6.0 1.49 1.4% 4.2% 0.5% 39% 11% 15% 14% 8% 6%

Sinopec - H 0386.HK HKD O 5.90 7.30 24% 100,835 11.3 10.0 8.7 5.5 4.6 4.3 0.84 8.4% 9.3% 5.0% 15% 6% 4% 2% 40% 7%

Sinopec - A 600028.SS RMB O 5.90 6.90 17% 100,835 12.6 11.2 9.7 5.5 4.6 4.3 0.95 8.4% 9.3% 4.5% 15% 8% 20% 21% 26% 9%

CNOOC 0883.HK HKD O 9.73 12.80 32% 56,020 270.9 16.0 9.2 7.4 4.9 4.2 1.08 6.7% 12.7% 2.4% 15% -5% -4% -1% 38% 0%

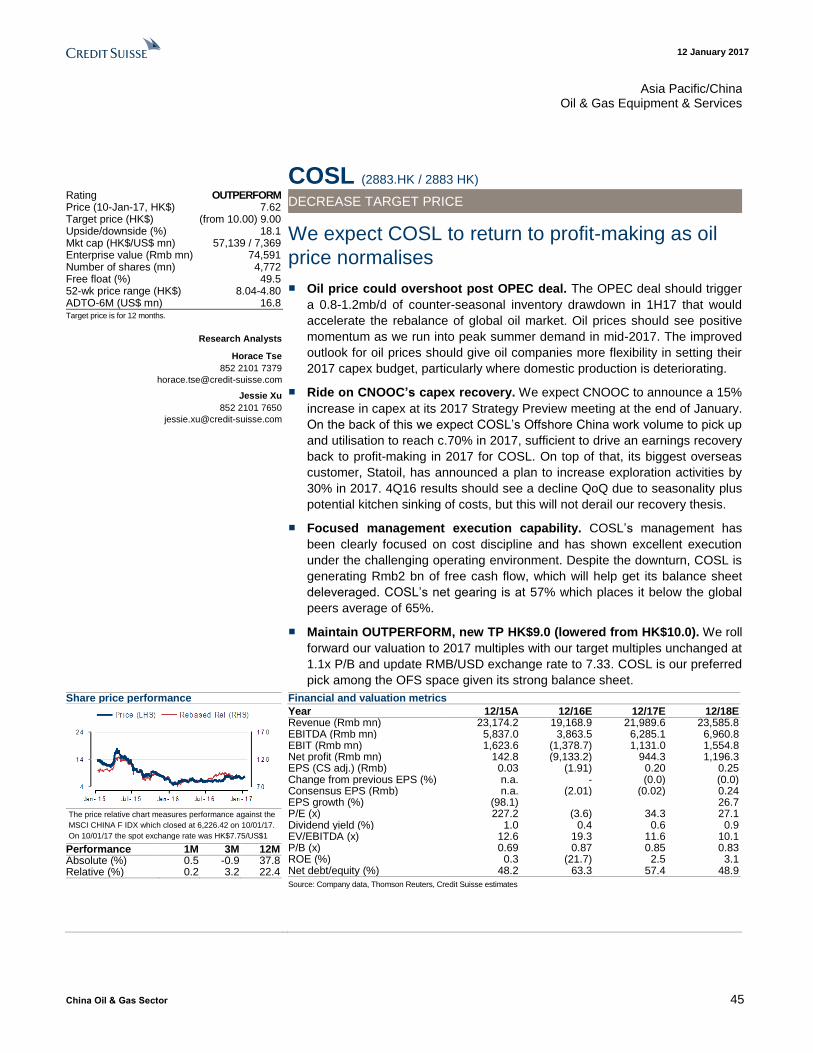

OFS and Engineering

COSL - H 2883.HK HKD O 7.62 9.00 18% 7,364 (3.6) 34.4 27.1 19.0 11.7 10.6 0.85 2.5% 3.1% 0.6% 57% 0% 1% 20% 40% 6%

COSL - A 601808.SS RMB U 13.06 8.50 -35% 7,364 (6.8) 66.0 52.1 19.0 11.7 10.6 1.64 2.5% 3.1% 0.3% 57% 1% 6% 2% -4% 2%

COOEC 600583.SS RMB O 7.71 9.00 17% 4,923 18.1 16.2 12.0 13.8 7.8 6.1 1.30 8.1% 10.0% 1.2% Net cash 5% 10% 3% 1% 4%

Sinopec SSC - H 1033.HK HKD U 1.51 1.00 -34% 7,731 (1.9) (9.4) (28.9) (12.9) 17.2 12.1 1.53 -16.3% -5.6% 0.0% 194% -4% -3% -3% -16% 0%

Sinopec SSC - A 600871.SS RMB U 4.21 0.80 -81% 7,731 (5.9) (29.4) (90.1) (12.9) 17.2 12.1 4.78 -16.3% -5.6% 0.0% 194% 6% 7% 0% -37% 3%

Sinopec Engineering 2386.HK HKD U 6.33 5.30 -16% 3,614 10.9 9.8 10.1 4.5 4.0 4.1 0.92 9.4% 8.6% 4.1% Net cash -4% -6% -13% 5% -2%

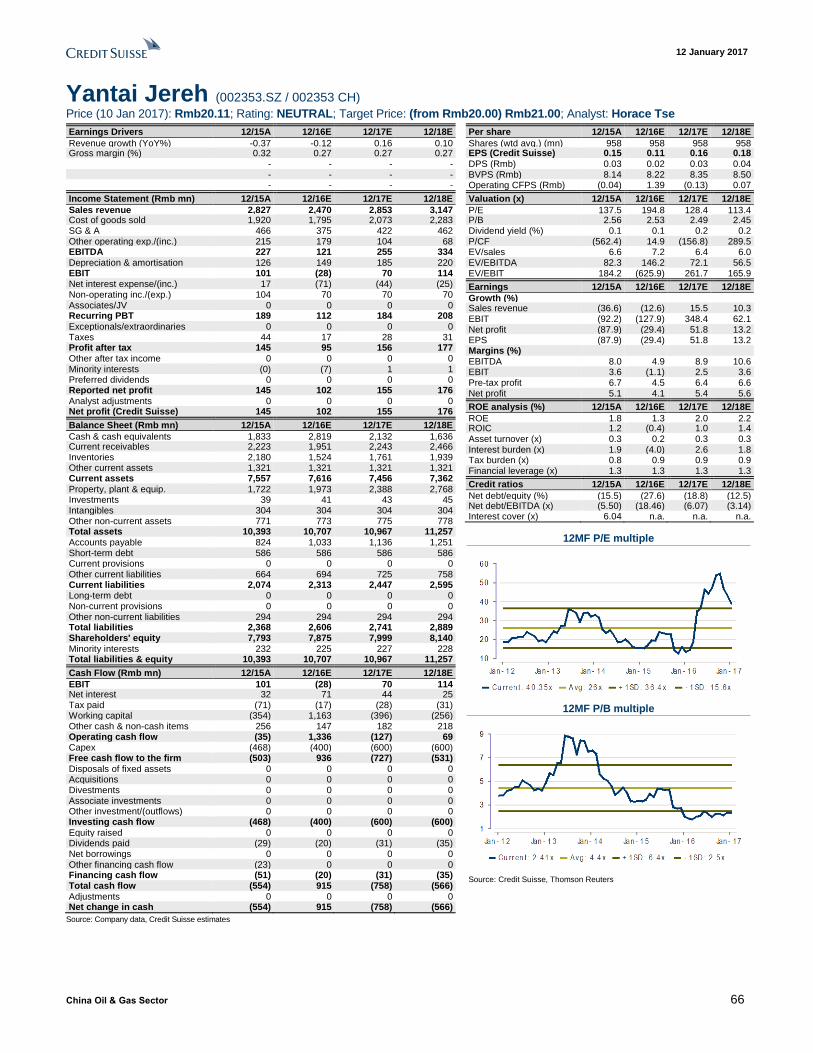

Yantai Jereh 002353.SZ RMB N 20.79 21.00 1% 2,876 194.8 128.4 113.4 154.3 73.3 55.9 2.49 1.9% 2.2% 0.2% Net cash 3% 8% 5% 17% 2%

Anton Oil 3337.HK HKD N 1.13 1.10 -3% 355 (17.8) 247.1 45.7 17.5 12.0 10.2 1.25 0.5% 2.7% 0.0% 53% 2% 28% 41% 77% 4%

SPT Energy 1251.HK HKD N 0.72 0.80 11% 143 (11.6) 72.0 14.7 22.6 5.7 3.6 0.93 1.3% 6.0% 0.0% 30% 4% 16% 36% 20% 11%

Hilong 1623.HK HKD O 2.09 2.50 20% 457 21.2 14.5 12.1 7.9 6.8 6.2 0.95 6.5% 7.4% 1.4% 44% -14% 34% 135% 74% -7%

Kunlun Energy 0135.HK HKD U 6.00 4.90 -18% 6,246 10.7 12.1 9.5 3.4 3.7 3.2 0.92 7.6% 9.0% 2.5% 41% 4% 1% 2% 5% 3%

Sinopec Kantons 0934.HK HKD O 3.53 5.10 44% 1,132 8.2 6.5 5.7 10.4 8.9 7.8 0.77 11.8% 12.2% 2.6% 45% -1% -6% -13% -17% 0%

Chemicals

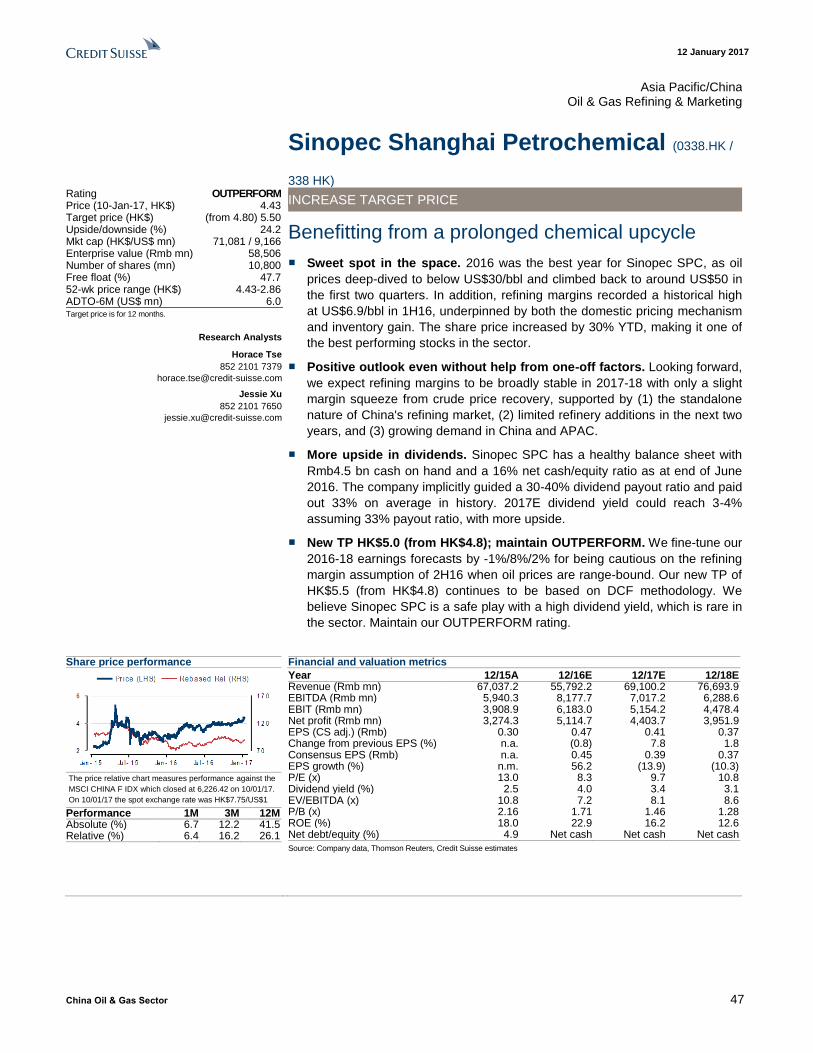

Sinopec SPC - H 0338.HK HKD O 4.43 5.50 24% 9,160 8.4 9.7 10.8 7.9 9.2 10.2 1.46 15.0% 11.9% 3.4% Net cash 8% 13% 16% 44% 5%

Sinopec SPC - A 600688.SS HKD U 6.79 4.20 -38% 9,160 14.3 16.7 18.6 7.9 9.2 10.2 2.50 15.0% 11.9% 2.0% Net cash 11% 14% 7% 21% 5%

Wanhua Chemical 600309.SS RMB O 23.58 28.40 20% 7,364 14.3 12.2 11.2 9.7 8.6 8.1 2.64 21.6% 19.0% 2.5% 110% 18% 12% 32% 50% 10%

Note: O = OUTPERFORM, N = NEUTRAL, U = UNDERPERFORM. Source: Company data, Thomason Reuters, Credit Suisse estimates

China Oil & Gas Sector 5

12 J

an

uary

201

7

Ch

ina O

il & G

as S

ecto

r 5

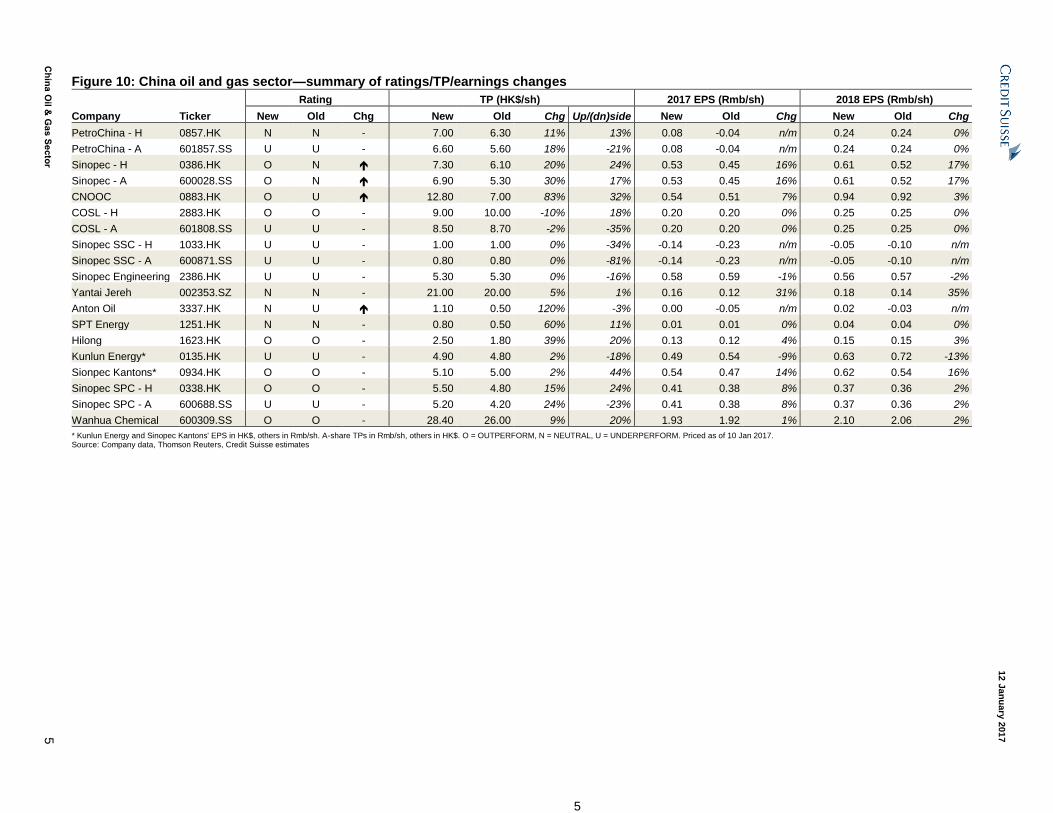

Figure 10: China oil and gas sector—summary of ratings/TP/earnings changes

Rating TP (HK$/sh) 2017 EPS (Rmb/sh) 2018 EPS (Rmb/sh)

Company Ticker New Old Chg New Old Chg Up/(dn)side New Old Chg New Old Chg

PetroChina - H 0857.HK N N - 7.00 6.30 11% 13% 0.08 -0.04 n/m 0.24 0.24 0%

PetroChina - A 601857.SS U U - 6.60 5.60 18% -21% 0.08 -0.04 n/m 0.24 0.24 0%

Sinopec - H 0386.HK O N 7.30 6.10 20% 24% 0.53 0.45 16% 0.61 0.52 17%

Sinopec - A 600028.SS O N 6.90 5.30 30% 17% 0.53 0.45 16% 0.61 0.52 17%

CNOOC 0883.HK O U 12.80 7.00 83% 32% 0.54 0.51 7% 0.94 0.92 3%

COSL - H 2883.HK O O - 9.00 10.00 -10% 18% 0.20 0.20 0% 0.25 0.25 0%

COSL - A 601808.SS U U - 8.50 8.70 -2% -35% 0.20 0.20 0% 0.25 0.25 0%

Sinopec SSC - H 1033.HK U U - 1.00 1.00 0% -34% -0.14 -0.23 n/m -0.05 -0.10 n/m

Sinopec SSC - A 600871.SS U U - 0.80 0.80 0% -81% -0.14 -0.23 n/m -0.05 -0.10 n/m

Sinopec Engineering 2386.HK U U - 5.30 5.30 0% -16% 0.58 0.59 -1% 0.56 0.57 -2%

Yantai Jereh 002353.SZ N N - 21.00 20.00 5% 1% 0.16 0.12 31% 0.18 0.14 35%

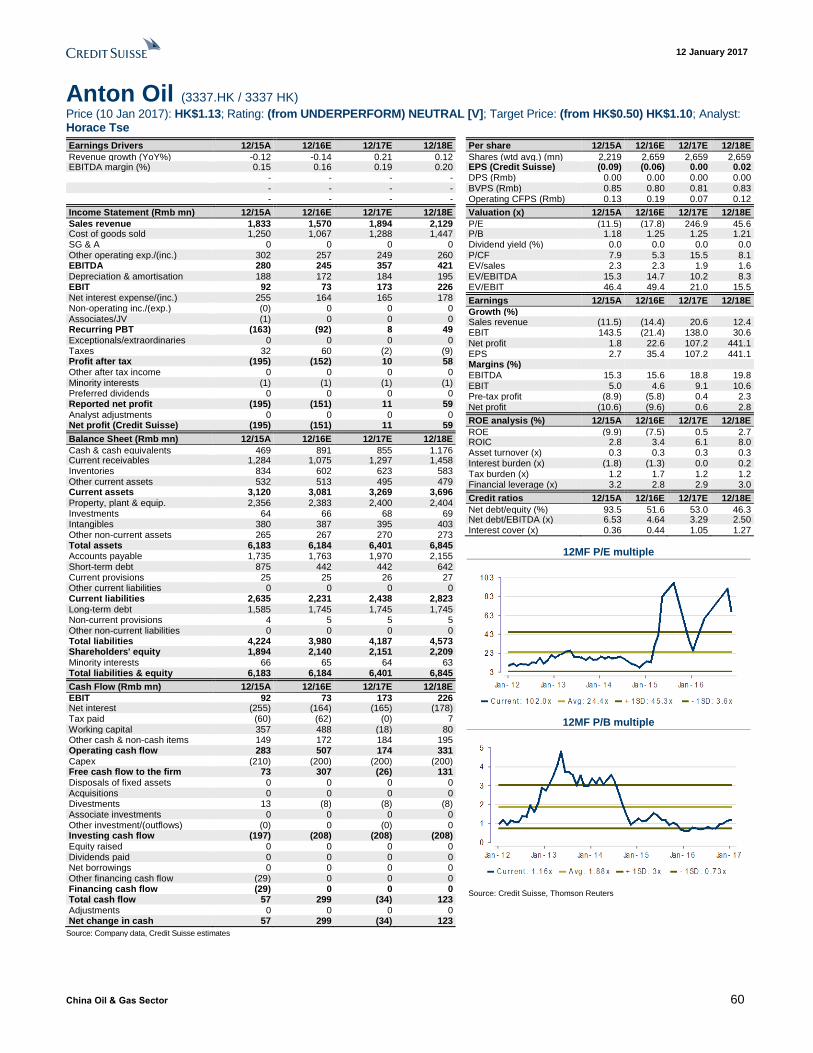

Anton Oil 3337.HK N U 1.10 0.50 120% -3% 0.00 -0.05 n/m 0.02 -0.03 n/m

SPT Energy 1251.HK N N - 0.80 0.50 60% 11% 0.01 0.01 0% 0.04 0.04 0%

Hilong 1623.HK O O - 2.50 1.80 39% 20% 0.13 0.12 4% 0.15 0.15 3%

Kunlun Energy* 0135.HK U U - 4.90 4.80 2% -18% 0.49 0.54 -9% 0.63 0.72 -13%

Sionpec Kantons* 0934.HK O O - 5.10 5.00 2% 44% 0.54 0.47 14% 0.62 0.54 16%

Sinopec SPC - H 0338.HK O O - 5.50 4.80 15% 24% 0.41 0.38 8% 0.37 0.36 2%

Sinopec SPC - A 600688.SS U U - 5.20 4.20 24% -23% 0.41 0.38 8% 0.37 0.36 2%

Wanhua Chemical 600309.SS O O - 28.40 26.00 9% 20% 1.93 1.92 1% 2.10 2.06 2%

* Kunlun Energy and Sinopec Kantons' EPS in HK$, others in Rmb/sh. A-share TPs in Rmb/sh, others in HK$. O = OUTPERFORM, N = NEUTRAL, U = UNDERPERFORM. Priced as of 10 Jan 2017. Source: Company data, Thomson Reuters, Credit Suisse estimates

12 January 2017

China Oil & Gas Sector 6

Table of contents

2017: A year of second-phase recovery 3

Sector valuation 4

Accelerated oil market rebalancing post OPEC deal 7

Multiple catalysts ahead 20

Valuation rerating during an oil price upcycle 28

Pecking order: CNOOC>Sinopec>PetroChina 31

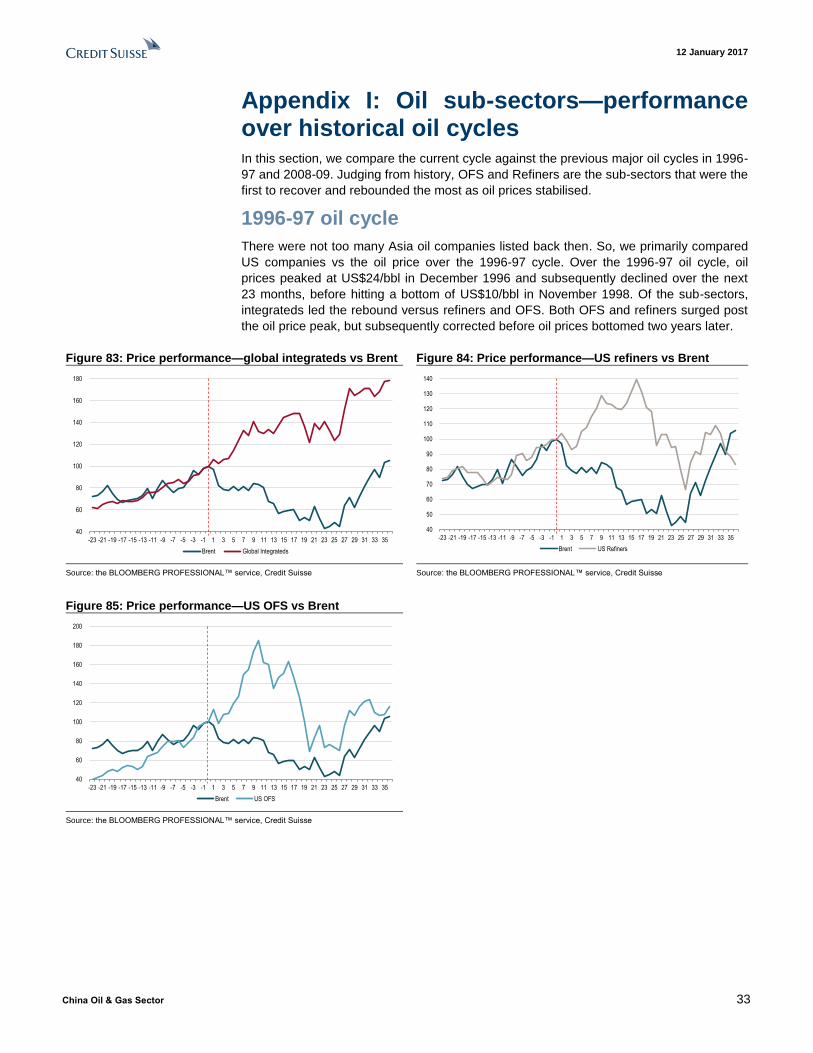

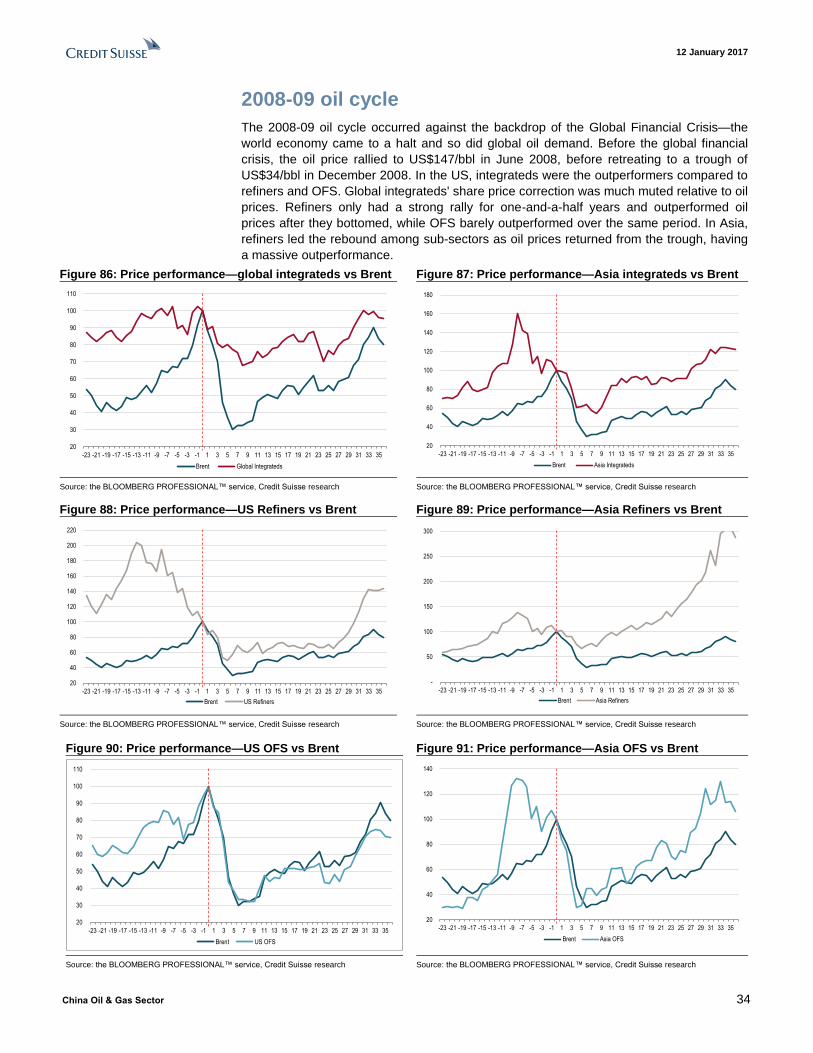

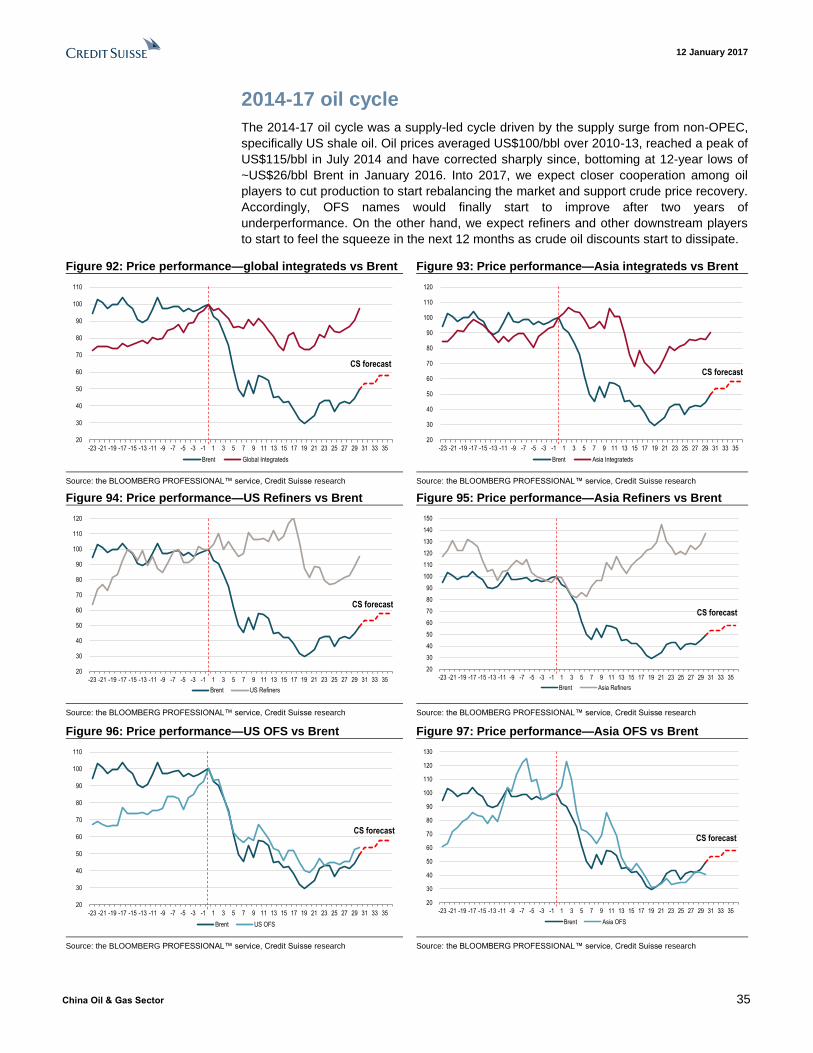

Appendix I: Oil sub-sectors—performance over historical oil cycles 33

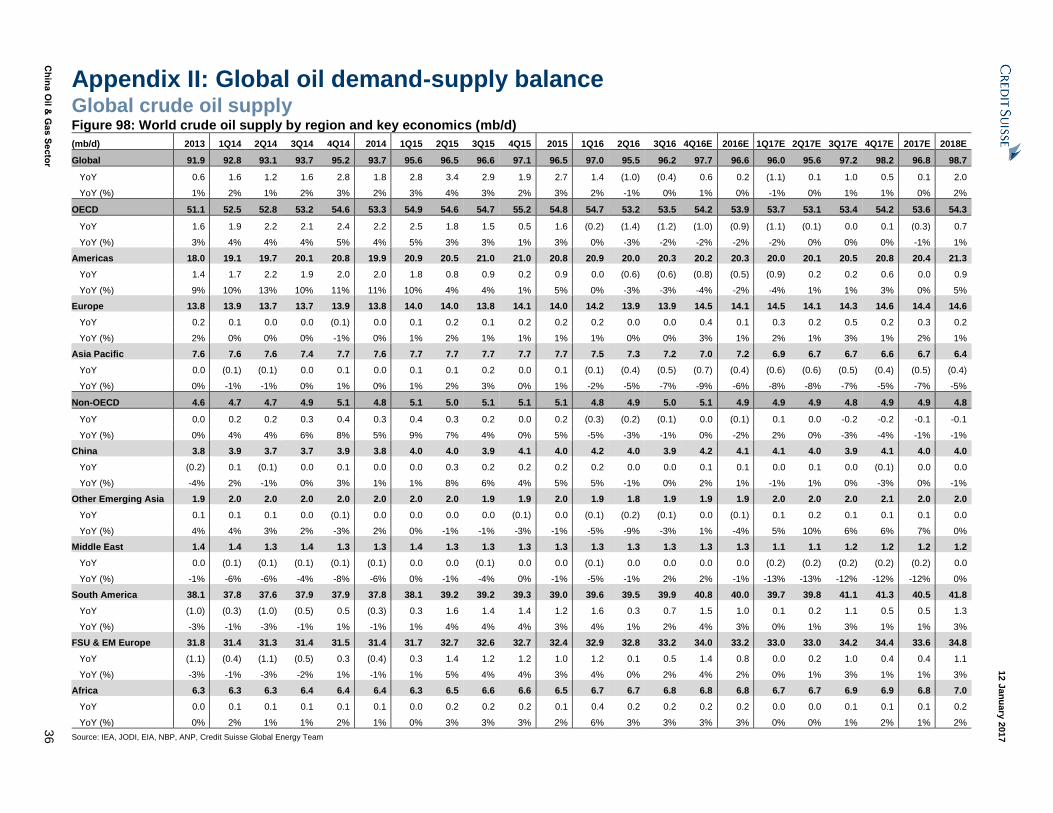

Appendix II: Global oil demand-supply balance 36

CNOOC (0883.HK / 883 HK) 39

Sinopec 41

PetroChina 43

COSL (2883.HK / 2883 HK) 45

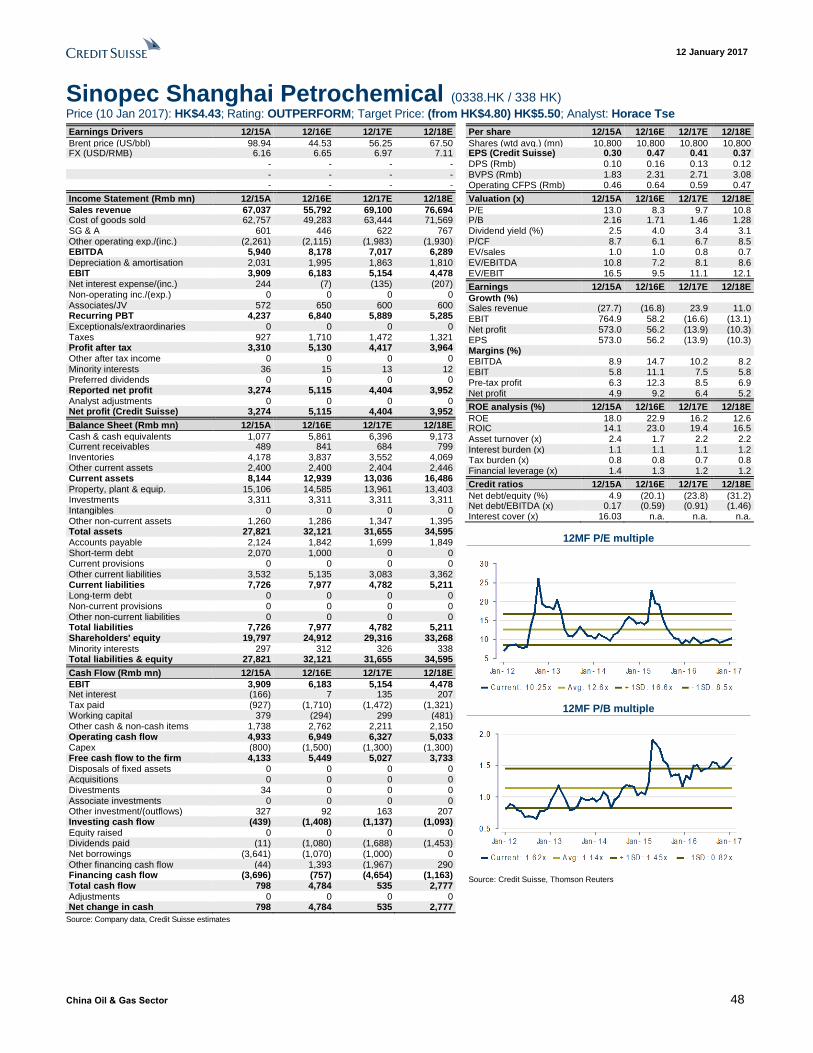

Sinopec Shanghai Petrochemical (0338.HK / 338 HK) 47

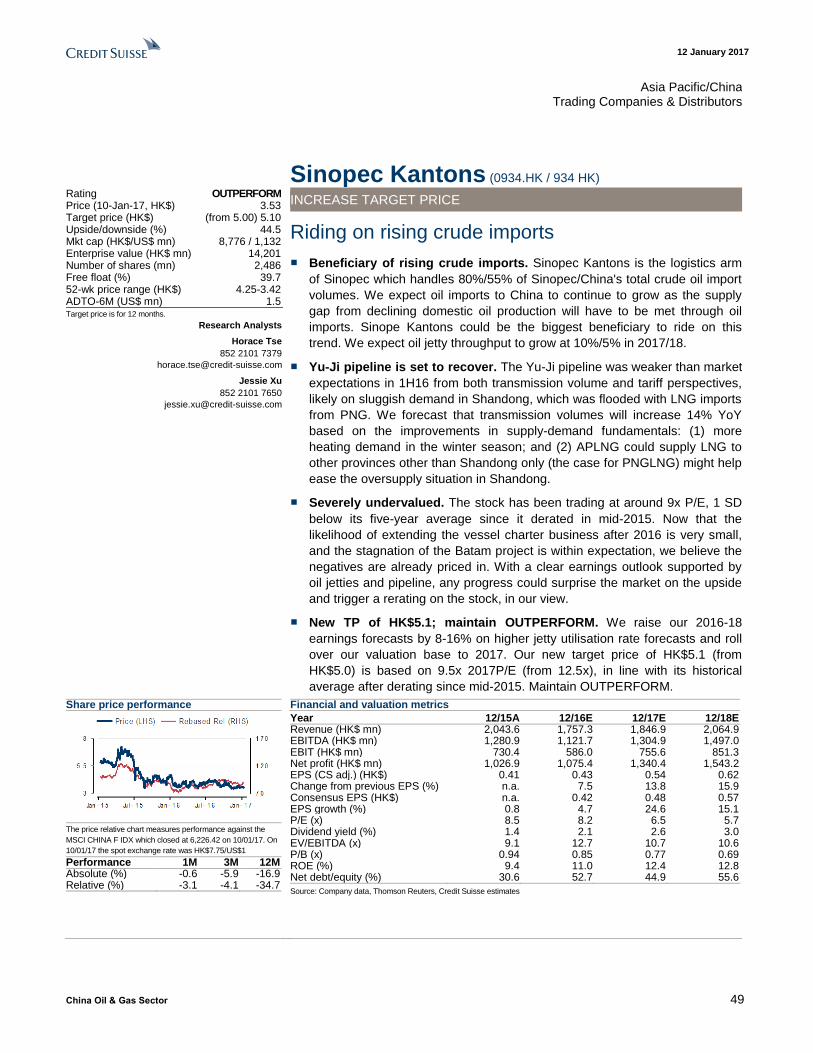

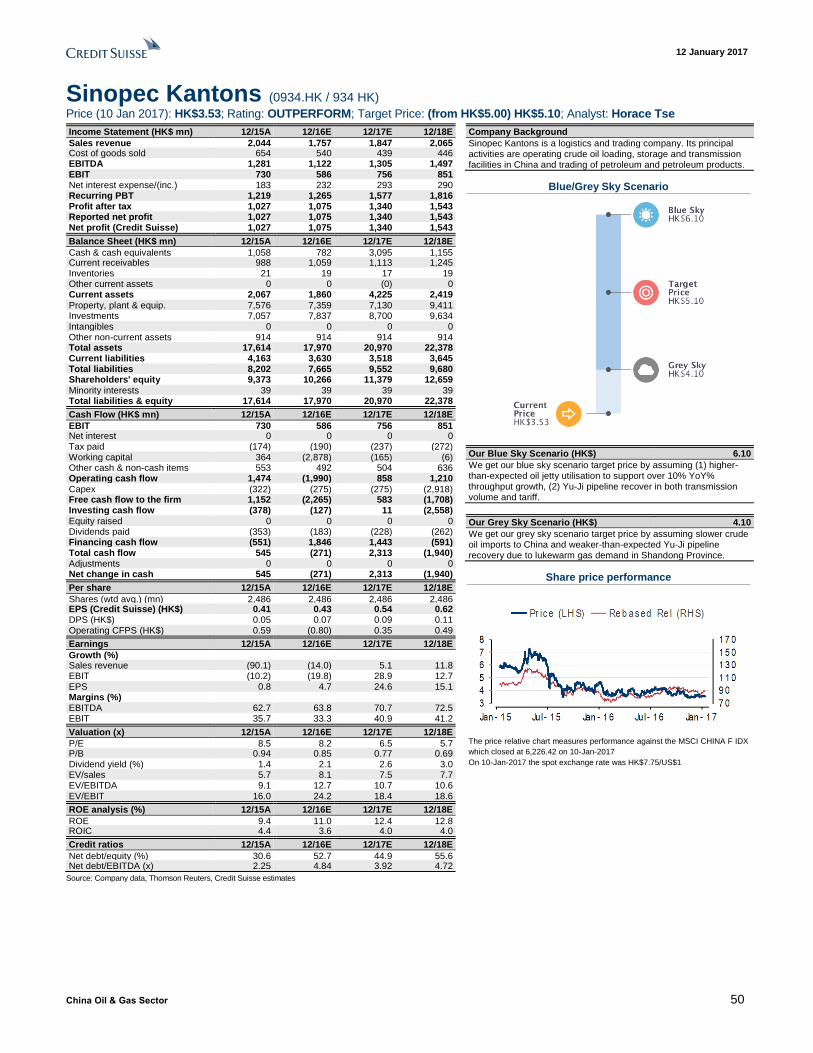

Sinopec Kantons 49

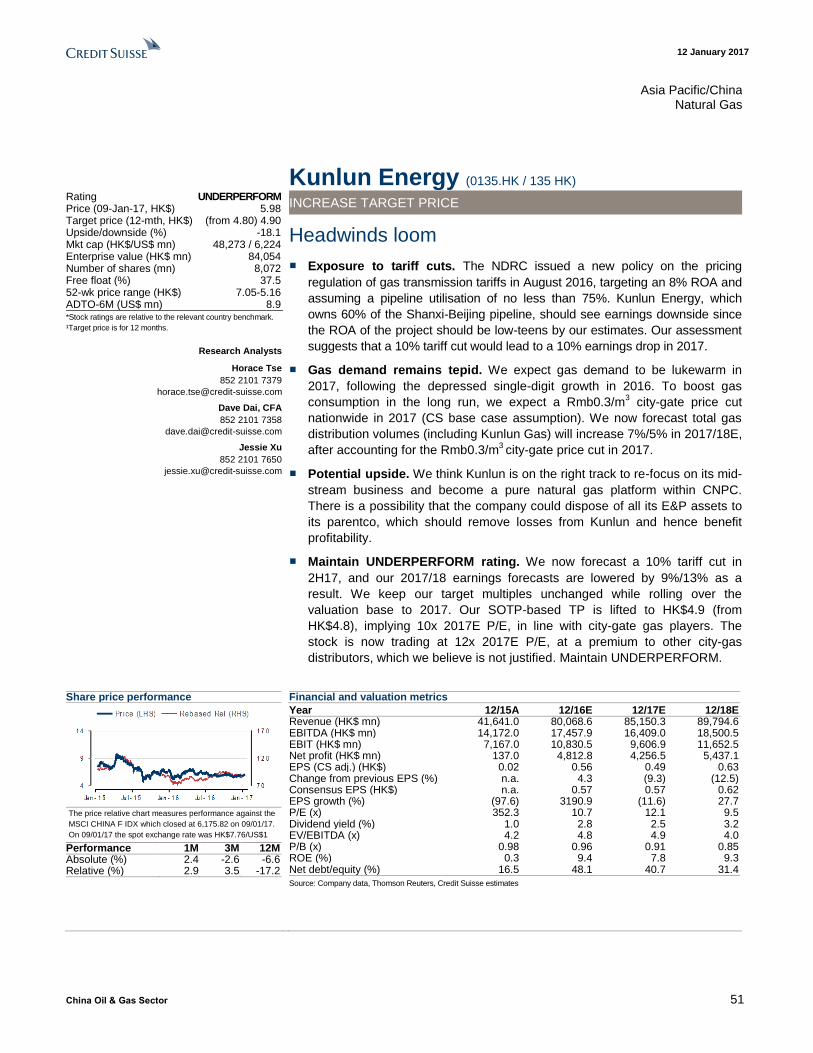

Kunlun Energy (0135.HK / 135 HK) 51

Sinopec Engineering (2386.HK / 2386 HK) 53

Sinopec SSC (1033.HK / 1033 HK) 55

Hilong (1623.HK / 1623 HK) 57

Anton Oil (3337.HK / 3337 HK) 59

SPT Energy (1251.HK / 1251 HK) 61

Wanhua Chemical (600309.SS / 600309 CH) 63

Yantai Jereh (002353.SZ / 002353 CH) 65

12 January 2017

China Oil & Gas Sector 7

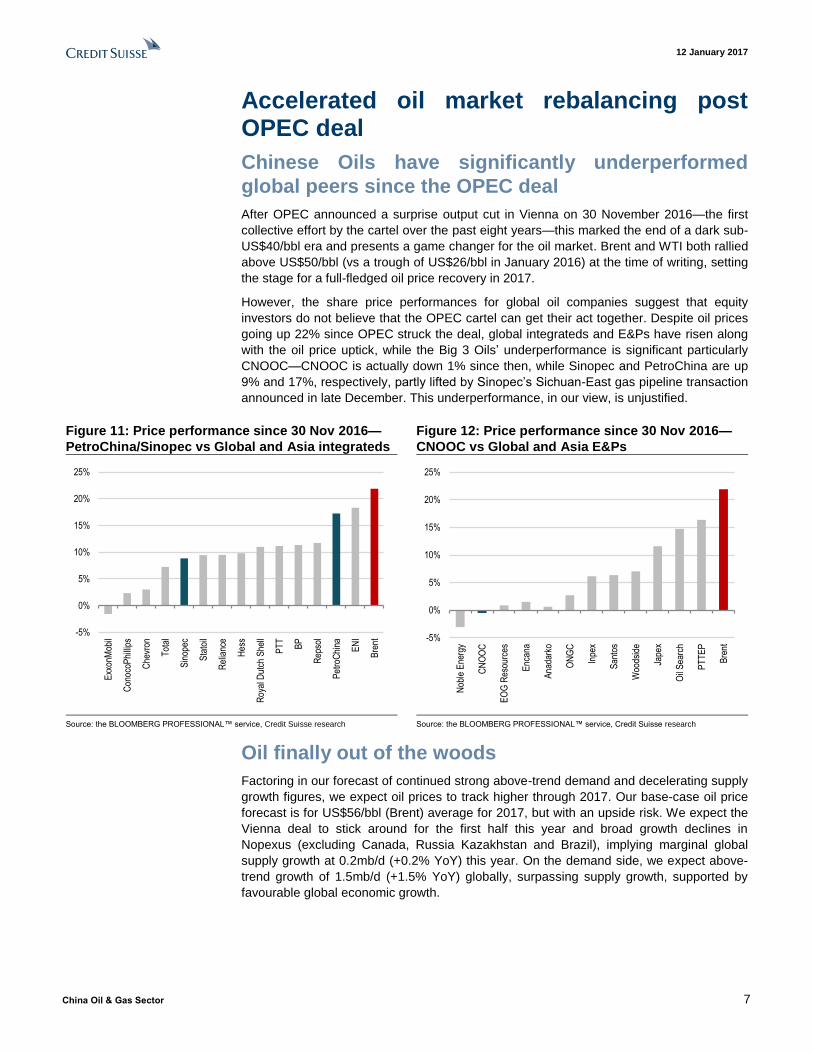

Accelerated oil market rebalancing post OPEC deal

Chinese Oils have significantly underperformed

global peers since the OPEC deal

After OPEC announced a surprise output cut in Vienna on 30 November 2016—the first

collective effort by the cartel over the past eight years—this marked the end of a dark sub-

US$40/bbl era and presents a game changer for the oil market. Brent and WTI both rallied

above US$50/bbl (vs a trough of US$26/bbl in January 2016) at the time of writing, setting

the stage for a full-fledged oil price recovery in 2017.

However, the share price performances for global oil companies suggest that equity

investors do not believe that the OPEC cartel can get their act together. Despite oil prices

going up 22% since OPEC struck the deal, global integrateds and E&Ps have risen along

with the oil price uptick, while the Big 3 Oils’ underperformance is significant particularly

CNOOC—CNOOC is actually down 1% since then, while Sinopec and PetroChina are up

9% and 17%, respectively, partly lifted by Sinopec’s Sichuan-East gas pipeline transaction

announced in late December. This underperformance, in our view, is unjustified.

Figure 11: Price performance since 30 Nov 2016—

PetroChina/Sinopec vs Global and Asia integrateds

Figure 12: Price performance since 30 Nov 2016—

CNOOC vs Global and Asia E&Ps

Source: the BLOOMBERG PROFESSIONAL™ service, Credit Suisse research Source: the BLOOMBERG PROFESSIONAL™ service, Credit Suisse research

Oil finally out of the woods

Factoring in our forecast of continued strong above-trend demand and decelerating supply

growth figures, we expect oil prices to track higher through 2017. Our base-case oil price

forecast is for US$56/bbl (Brent) average for 2017, but with an upside risk. We expect the

Vienna deal to stick around for the first half this year and broad growth declines in

Nopexus (excluding Canada, Russia Kazakhstan and Brazil), implying marginal global

supply growth at 0.2mb/d (+0.2% YoY) this year. On the demand side, we expect above-

trend growth of 1.5mb/d (+1.5% YoY) globally, surpassing supply growth, supported by

favourable global economic growth.

-5%

0%

5%

10%

15%

20%

25%

Exx

onM

obil

Con

ocoP

hilli

ps

Che

vron

Tot

al

Sin

opec

Sta

toil

Rel

ianc

e

Hes

s

Roy

al D

utch

She

ll

PT

T

BP

Rep

sol

Pet

roC

hina EN

I

Bre

nt -5%

0%

5%

10%

15%

20%

25%

Nob

le E

nerg

y

CN

OO

C

EO

G R

esou

rces

Enc

ana

Ana

dark

o

ON

GC

Inpe

x

San

tos

Woo

dsid

e

Jape

x

Oil

Sea

rch

PT

TE

P

Bre

nt

12 January 2017

China Oil & Gas Sector 8

Figure 13: Abbreviated CS base case oil balance CS Model 3Q16 4Q16E 2016E 1Q17E 2Q17E 3Q17E 4Q17E 2017E

Supply (mb/d) 96.2 97.7 96.6 96 95.6 97.2 98.2 96.7

YoY -0.4 0.6 0.1 -1.1 0.1 1 0.5 0.1

OPEC 14 39.9 40.8 40 39.7 39.8 41 41.3 40.5

YoY 0.7 1.5 1 0 0.2 1.1 0.5 0.5

Non-OPEC (includes processing gains) 56.2 56.9 56.6 56.3 55.8 56.1 56.9 56.3

YoY -1.1 -0.9 -0.9 -1.1 -0.2 -0.1 0.1 -0.3

Demand (mb/d) 96.9 97.6 96.4 97.1 96.8 98.4 99 97.8

YoY 1.1 1.8 1.6 1.4 1.2 1.5 1.4 1.4

OECD 47.2 47.2 46.8 47 46.3 47.6 47.6 47.1

YoY 0.3 0.8 0.4 0.3 0.3 0.4 0.4 0.3

Non-OECD 49.6 50.4 49.6 50 50.5 50.8 51.4 50.7

YoY 0.8 1 1.2 1.1 0.9 1.2 1 1.1

Implied inventory change (mb/d) -0.6 0.1 0.2 -1.0 -1.2 -1.1 -0.8 -1.1

Call on OPEC crude 33.9 33.9 33 34.1 34.2 35.4 35.2 34.7

YoY 2.1 2.5 2.2 2.5 1.4 1.5 1.3 1.7

OPEC crude 33.2 34 33.2 33 33 34.2 34.4 33.6

YoY 0.5 1.3 0.8 0 0.2 1 0.4 0.4 Source: Credit Suisse Global Energy Team estimates

Figure 14: CS oil price forecast and scenarios Figure 15: OPEC taking share (trended SA, mb/d)

Source: the BLOOMBERG PROFESSIONAL™ service, Credit Suisse Global Energy Team estimates

Source: IEA, JODI, EIA, Petrologistics, BP, country data, Credit Suisse Global Energy Team

Upside risk to CS’s 2017 oil price forecast, should

OPEC stick to its act

In November 2016, OPEC agreed to the outline of a deal that would cut production to

32.5mb/d from a record-high output in excess of 34mb/d in October. In addition, an

unprecedented 11 non-OPEC countries also pledged a collective 558kb/d cut in their

production. In effect, CS' Global Energy Team thinks this involves a cut of 1mb/d to

33.0mb/d, which we project as the average OPEC production in 1H17. We have also fine-

tuned our global forecasts to reflect lower oil production from Russia and Oman.

CS base case: 33.0mb/d of 2017 OPEC-14 crude production

With our modelling of an OPEC cut to 33.0mb/d in 1H17, we maintain our forecast for an

average US$56/bbl Brent oil price forecast for 2017, some 25% higher than the

~US$44/bbl of 2016 and 15% higher than the US$52/bbl of 2015. Our base case factors in

a partial implementation of the OPEC cut deal with 33.0mb/d of the 2017 OPEC-14 crude

production.

12 January 2017

China Oil & Gas Sector 9

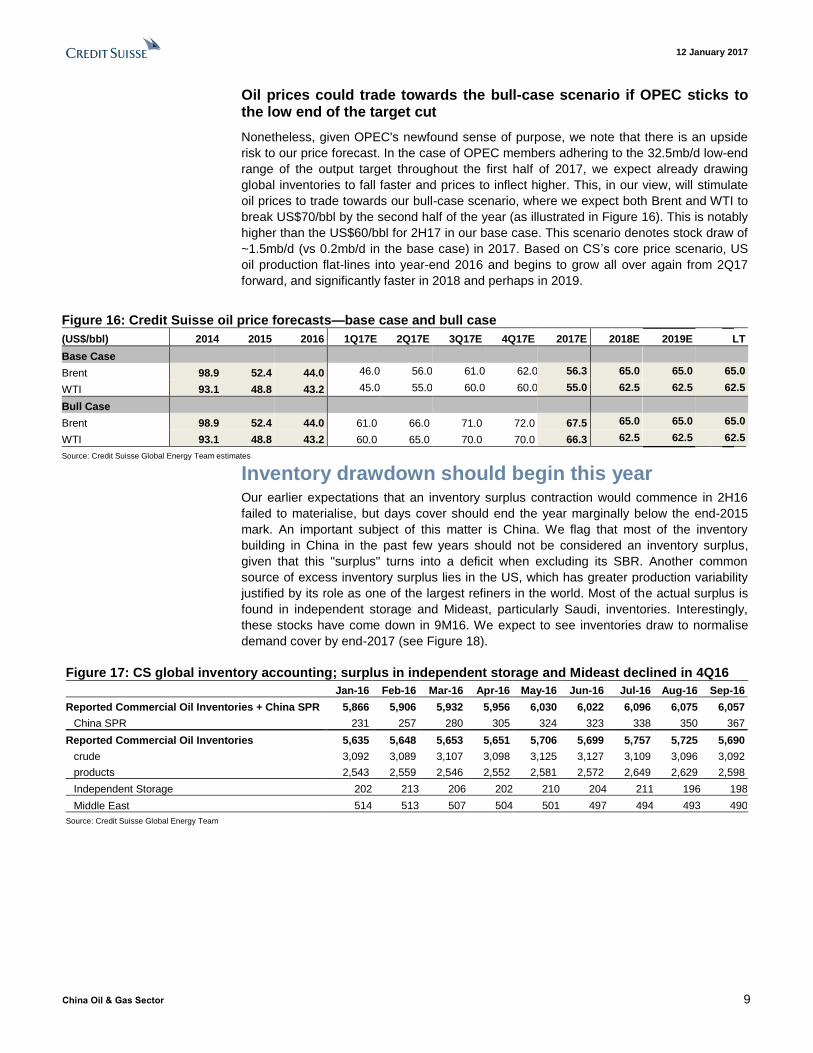

Oil prices could trade towards the bull-case scenario if OPEC sticks to the low end of the target cut

Nonetheless, given OPEC's newfound sense of purpose, we note that there is an upside

risk to our price forecast. In the case of OPEC members adhering to the 32.5mb/d low-end

range of the output target throughout the first half of 2017, we expect already drawing

global inventories to fall faster and prices to inflect higher. This, in our view, will stimulate

oil prices to trade towards our bull-case scenario, where we expect both Brent and WTI to

break US$70/bbl by the second half of the year (as illustrated in Figure 16). This is notably

higher than the US$60/bbl for 2H17 in our base case. This scenario denotes stock draw of

~1.5mb/d (vs 0.2mb/d in the base case) in 2017. Based on CS’s core price scenario, US

oil production flat-lines into year-end 2016 and begins to grow all over again from 2Q17

forward, and significantly faster in 2018 and perhaps in 2019.

Figure 16: Credit Suisse oil price forecasts—base case and bull case

(US$/bbl) 2014 2015 2016 1Q17E 2Q17E 3Q17E 4Q17E 2017E 2018E 2019E LT

Base Case

Brent 98.9 52.4 44.0 46.0 56.0 61.0 62.0 56.3 65.0 65.0 65.0

WTI 93.1 48.8 43.2 45.0 55.0 60.0 60.0 55.0 62.5 62.5 62.5

Bull Case

Brent 98.9 52.4 44.0 61.0 66.0 71.0 72.0 67.5 65.0 65.0 65.0

WTI 93.1 48.8 43.2 60.0 65.0 70.0 70.0 66.3 62.5 62.5 62.5

Source: Credit Suisse Global Energy Team estimates

Inventory drawdown should begin this year Our earlier expectations that an inventory surplus contraction would commence in 2H16

failed to materialise, but days cover should end the year marginally below the end-2015

mark. An important subject of this matter is China. We flag that most of the inventory

building in China in the past few years should not be considered an inventory surplus,

given that this "surplus" turns into a deficit when excluding its SBR. Another common

source of excess inventory surplus lies in the US, which has greater production variability

justified by its role as one of the largest refiners in the world. Most of the actual surplus is

found in independent storage and Mideast, particularly Saudi, inventories. Interestingly,

these stocks have come down in 9M16. We expect to see inventories draw to normalise

demand cover by end-2017 (see Figure 18).

Figure 17: CS global inventory accounting; surplus in independent storage and Mideast declined in 4Q16

Jan-16 Feb-16 Mar-16 Apr-16 May-16 Jun-16 Jul-16 Aug-16 Sep-16

Reported Commercial Oil Inventories + China SPR 5,866 5,906 5,932 5,956 6,030 6,022 6,096 6,075 6,057

China SPR 231 257 280 305 324 323 338 350 367

Reported Commercial Oil Inventories 5,635 5,648 5,653 5,651 5,706 5,699 5,757 5,725 5,690

crude 3,092 3,089 3,107 3,098 3,125 3,127 3,109 3,096 3,092

products 2,543 2,559 2,546 2,552 2,581 2,572 2,649 2,629 2,598

Independent Storage 202 213 206 202 210 204 211 196 198

Middle East 514 513 507 504 501 497 494 493 490

Source: Credit Suisse Global Energy Team

12 January 2017

China Oil & Gas Sector 10

Figure 18: Global inventory levels and forecasts Figure 19: China inventory surplus without SPR

Source: IEA, EIA, JODI, Country data, Credit Suisse Global Energy Team estimates Source: JODI, Country data, Credit Suisse Global Energy Team

Figure 20: Global oil inventory stock change (mbs) Figure 21: US weekly crude oil inventory (mbs)

Source IEA, JODI, EIA, Petrologistics, BP, Country data, Wood Mackenzie, Credit Suisse Global Energy Team estimates

Source: EIA, Credit Suisse Global Energy Team

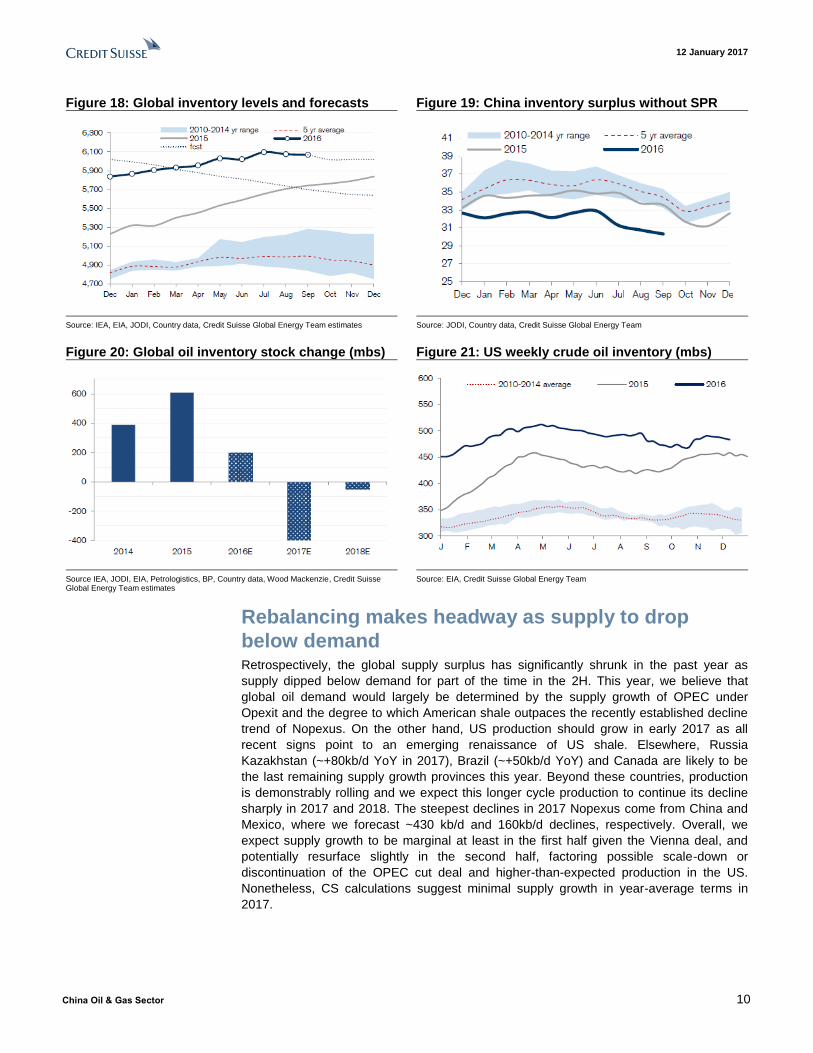

Rebalancing makes headway as supply to drop

below demand Retrospectively, the global supply surplus has significantly shrunk in the past year as

supply dipped below demand for part of the time in the 2H. This year, we believe that

global oil demand would largely be determined by the supply growth of OPEC under

Opexit and the degree to which American shale outpaces the recently established decline

trend of Nopexus. On the other hand, US production should grow in early 2017 as all

recent signs point to an emerging renaissance of US shale. Elsewhere, Russia

Kazakhstan (~+80kb/d YoY in 2017), Brazil (~+50kb/d YoY) and Canada are likely to be

the last remaining supply growth provinces this year. Beyond these countries, production

is demonstrably rolling and we expect this longer cycle production to continue its decline

sharply in 2017 and 2018. The steepest declines in 2017 Nopexus come from China and

Mexico, where we forecast ~430 kb/d and 160kb/d declines, respectively. Overall, we

expect supply growth to be marginal at least in the first half given the Vienna deal, and

potentially resurface slightly in the second half, factoring possible scale-down or

discontinuation of the OPEC cut deal and higher-than-expected production in the US.

Nonetheless, CS calculations suggest minimal supply growth in year-average terms in

2017.

12 January 2017

China Oil & Gas Sector 11

Figure 22: Oil supply and demand (3 mma, mb/d) Figure 23: US shale crude oil should now recover

Source: IEA, JODI, EIA, Petrologistics, BP, country data, Credit Suisse Global Energy Team estimates

Source: Credit Suisse Global Energy Team estimates

Figure 24: OPEC 14 crude production forecast Figure 25: China crude oil production (mb/d)

Source: IEA, JODI, EIA, Petrologistics, BP, country data, : Credit Suisse Global Energy Team estimates

Source: IEA, BP, NBS, Credit Suisse Global Energy Team research estimates

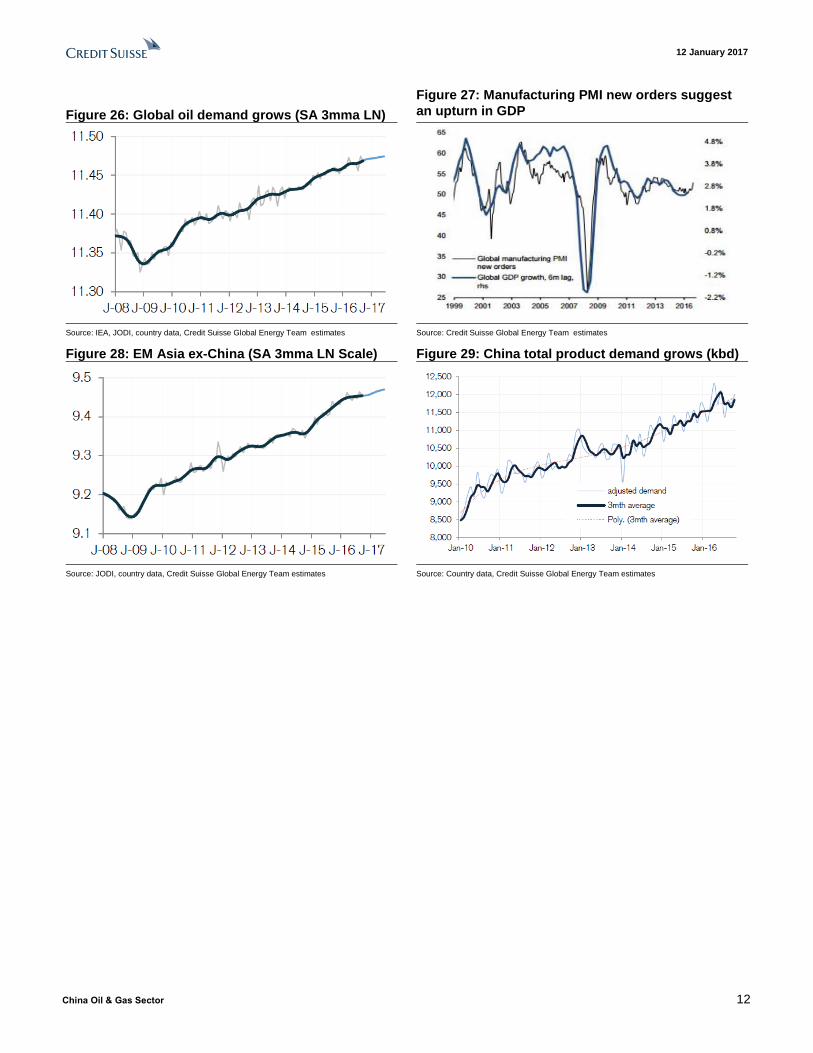

Solid demand extends into 2017; uncertainties

remain on macro volatility

With the OPEC deal locking down supply risks, demand becomes the most uncertain

component of the oil price equation. In the past three years, the market theory that an oil

price collapse would generate a fall in demand proved a fallacy as global demand soared

above the trend pace amid falling oil prices, increased EM consumers, the making of a

cyclical upturn in the US and a shallow recovery in Europe. In 2017, we expect global

growth of 1.5% YoY, which would outperform trend growth of around 1.3% YoY. We

estimate that the OECD will grow 0.9% YoY and EM demand growth will decelerate to

2.1% YoY. We flag three macro-environmental factors, crucial for shaping near-term oil

demand. (1) The latest strength of the greenback supported by rising interest rates and

inflationary promises would theoretically erode upstream costs and hence undermine the

upside to oil. (2) Accommodating easing and fiscal policies globally present upside to

oil. (3) China demands more. Notably, China's renewed increase in infrastructure

spending and an export boost due to Rmb weakness appear to be favourable to growth in

2017. We model around 3.5% YoY demand growth in the country in 2017.

In our model, we expect demand growth to decelerate slightly from ~1.6% in 2016 to

~1.5% in 2017. There are a few downside risks to our estimates, namely: (1) quicker-

than-expected demand growth deceleration owing to economic volatilities; (2) a short-

lived Trump "honeymoon"; (3) faltering consumer confidence; (4) European

elections and potentially ensuing disordered policy responses; and (5) further deflation

of global trade.

12 January 2017

China Oil & Gas Sector 12

Figure 26: Global oil demand grows (SA 3mma LN)

Figure 27: Manufacturing PMI new orders suggest

an upturn in GDP

Source: IEA, JODI, country data, Credit Suisse Global Energy Team estimates Source: Credit Suisse Global Energy Team estimates

Figure 28: EM Asia ex-China (SA 3mma LN Scale) Figure 29: China total product demand grows (kbd)

Source: JODI, country data, Credit Suisse Global Energy Team estimates Source: Country data, Credit Suisse Global Energy Team estimates

12 January 2017

China Oil & Gas Sector 13

Downstream: Positive outlook for 2016

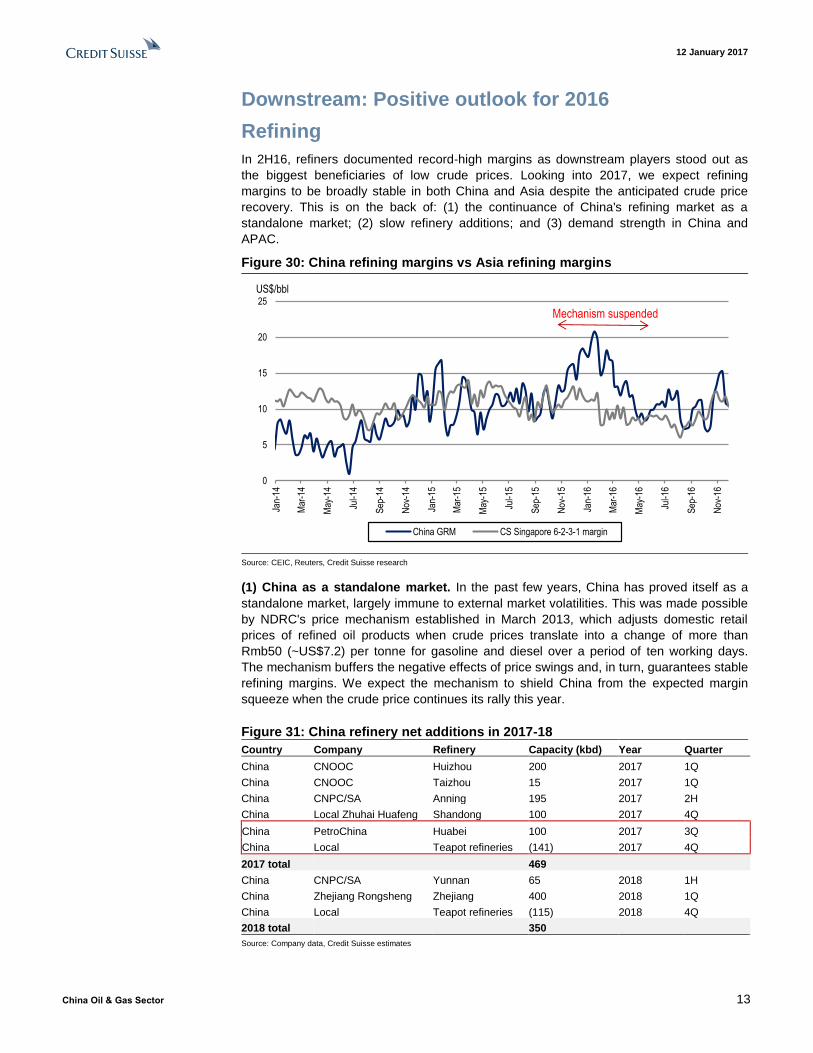

Refining

In 2H16, refiners documented record-high margins as downstream players stood out as

the biggest beneficiaries of low crude prices. Looking into 2017, we expect refining

margins to be broadly stable in both China and Asia despite the anticipated crude price

recovery. This is on the back of: (1) the continuance of China's refining market as a

standalone market; (2) slow refinery additions; and (3) demand strength in China and

APAC.

Figure 30: China refining margins vs Asia refining margins

Source: CEIC, Reuters, Credit Suisse research

(1) China as a standalone market. In the past few years, China has proved itself as a

standalone market, largely immune to external market volatilities. This was made possible

by NDRC's price mechanism established in March 2013, which adjusts domestic retail

prices of refined oil products when crude prices translate into a change of more than

Rmb50 (~US$7.2) per tonne for gasoline and diesel over a period of ten working days.

The mechanism buffers the negative effects of price swings and, in turn, guarantees stable

refining margins. We expect the mechanism to shield China from the expected margin

squeeze when the crude price continues its rally this year.

Figure 31: China refinery net additions in 2017-18

Country Company Refinery Capacity (kbd) Year Quarter

China CNOOC Huizhou 200 2017 1Q

China CNOOC Taizhou 15 2017 1Q

China CNPC/SA Anning 195 2017 2H

China Local Zhuhai Huafeng Shandong 100 2017 4Q

China PetroChina Huabei 100 2017 3Q

China Local Teapot refineries (141) 2017 4Q

2017 total 469

China CNPC/SA Yunnan 65 2018 1H

China Zhejiang Rongsheng Zhejiang 400 2018 1Q

China Local Teapot refineries (115) 2018 4Q

2018 total 350

Source: Company data, Credit Suisse estimates

0

5

10

15

20

25

Jan-

14

Mar

-14

May

-14

Jul-1

4

Sep

-14

Nov

-14

Jan-

15

Mar

-15

May

-15

Jul-1

5

Sep

-15

Nov

-15

Jan-

16

Mar

-16

May

-16

Jul-1

6

Sep

-16

Nov

-16

China GRM CS Singapore 6-2-3-1 margin

US$/bbl

Mechanism suspended

12 January 2017

China Oil & Gas Sector 14

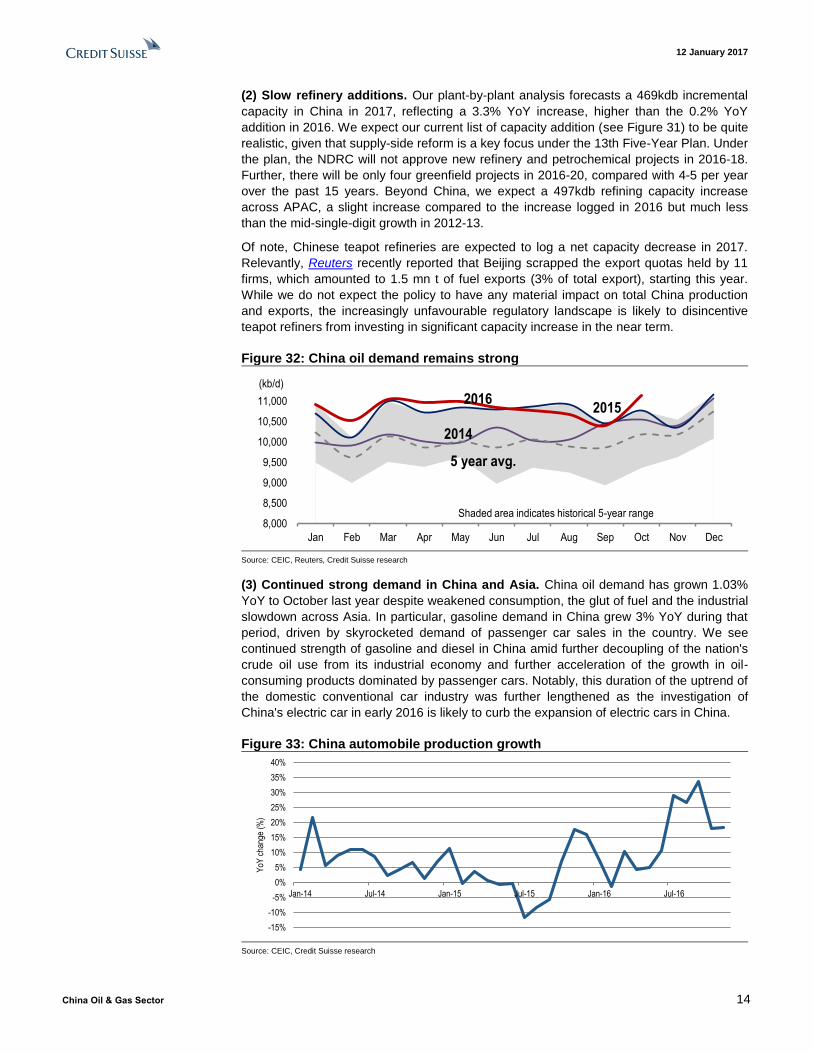

(2) Slow refinery additions. Our plant-by-plant analysis forecasts a 469kdb incremental

capacity in China in 2017, reflecting a 3.3% YoY increase, higher than the 0.2% YoY

addition in 2016. We expect our current list of capacity addition (see Figure 31) to be quite

realistic, given that supply-side reform is a key focus under the 13th Five-Year Plan. Under

the plan, the NDRC will not approve new refinery and petrochemical projects in 2016-18.

Further, there will be only four greenfield projects in 2016-20, compared with 4-5 per year

over the past 15 years. Beyond China, we expect a 497kdb refining capacity increase

across APAC, a slight increase compared to the increase logged in 2016 but much less

than the mid-single-digit growth in 2012-13.

Of note, Chinese teapot refineries are expected to log a net capacity decrease in 2017.

Relevantly, Reuters recently reported that Beijing scrapped the export quotas held by 11

firms, which amounted to 1.5 mn t of fuel exports (3% of total export), starting this year.

While we do not expect the policy to have any material impact on total China production

and exports, the increasingly unfavourable regulatory landscape is likely to disincentive

teapot refiners from investing in significant capacity increase in the near term.

Figure 32: China oil demand remains strong

Source: CEIC, Reuters, Credit Suisse research

(3) Continued strong demand in China and Asia. China oil demand has grown 1.03%

YoY to October last year despite weakened consumption, the glut of fuel and the industrial

slowdown across Asia. In particular, gasoline demand in China grew 3% YoY during that

period, driven by skyrocketed demand of passenger car sales in the country. We see

continued strength of gasoline and diesel in China amid further decoupling of the nation's

crude oil use from its industrial economy and further acceleration of the growth in oil-

consuming products dominated by passenger cars. Notably, this duration of the uptrend of

the domestic conventional car industry was further lengthened as the investigation of

China's electric car in early 2016 is likely to curb the expansion of electric cars in China.

Figure 33: China automobile production growth

Source: CEIC, Credit Suisse research

8,000

8,500

9,000

9,500

10,000

10,500

11,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

20152016

2014

5 year avg.

Shaded area indicates historical 5-year range

(kb/d)

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

40%

Jan-14 Jul-14 Jan-15 Jul-15 Jan-16 Jul-16

YoY

cha

nge

(%)

12 January 2017

China Oil & Gas Sector 15

Chemicals

Ethylene

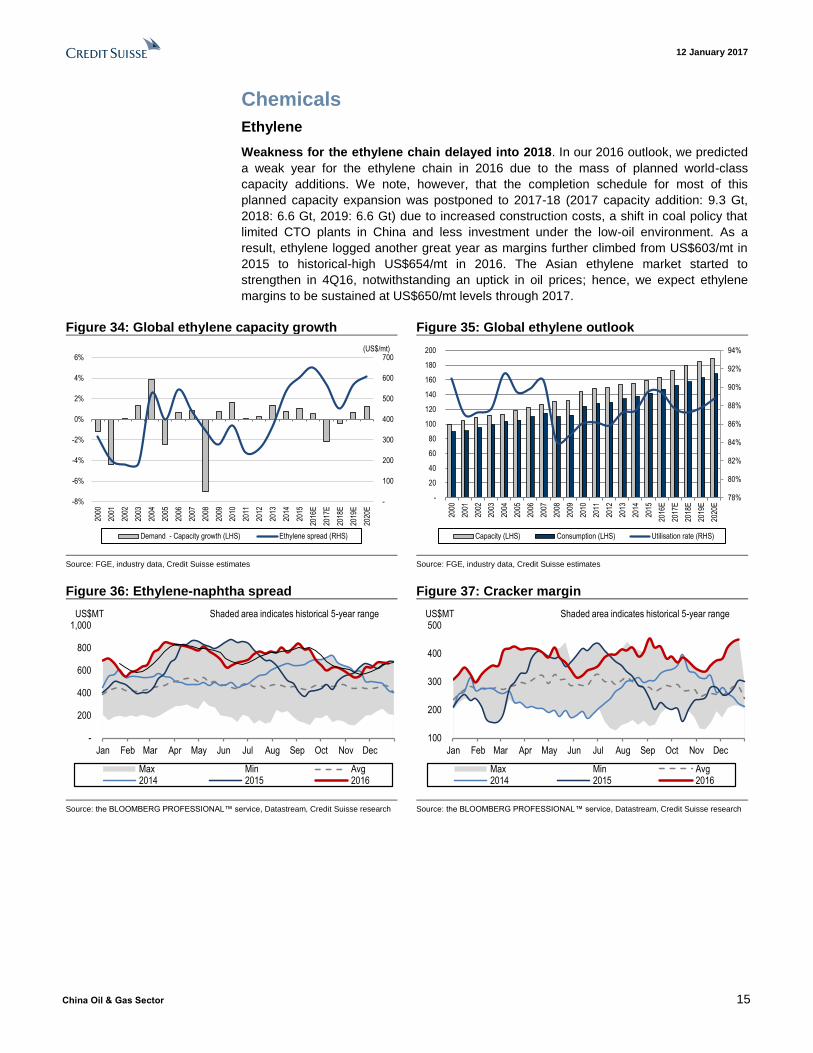

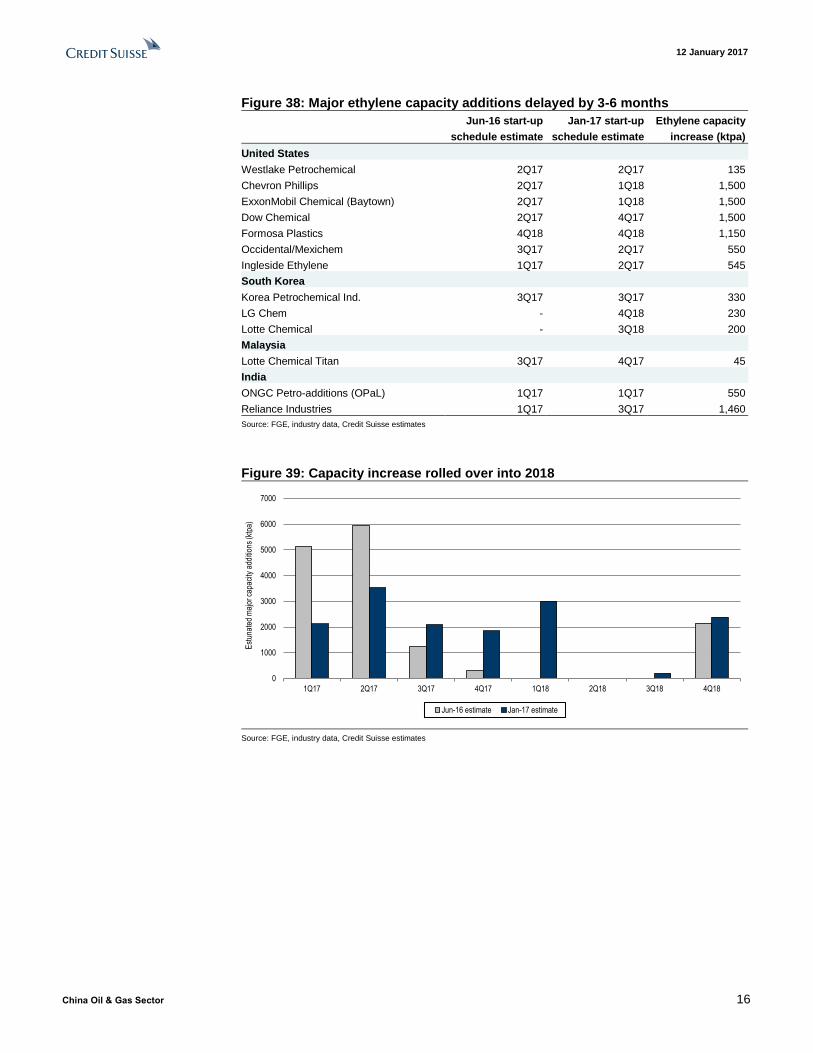

Weakness for the ethylene chain delayed into 2018. In our 2016 outlook, we predicted

a weak year for the ethylene chain in 2016 due to the mass of planned world-class

capacity additions. We note, however, that the completion schedule for most of this

planned capacity expansion was postponed to 2017-18 (2017 capacity addition: 9.3 Gt,

2018: 6.6 Gt, 2019: 6.6 Gt) due to increased construction costs, a shift in coal policy that

limited CTO plants in China and less investment under the low-oil environment. As a

result, ethylene logged another great year as margins further climbed from US$603/mt in

2015 to historical-high US$654/mt in 2016. The Asian ethylene market started to

strengthen in 4Q16, notwithstanding an uptick in oil prices; hence, we expect ethylene

margins to be sustained at US$650/mt levels through 2017.

Figure 34: Global ethylene capacity growth Figure 35: Global ethylene outlook

Source: FGE, industry data, Credit Suisse estimates Source: FGE, industry data, Credit Suisse estimates

Figure 36: Ethylene-naphtha spread Figure 37: Cracker margin

Source: the BLOOMBERG PROFESSIONAL™ service, Datastream, Credit Suisse research Source: the BLOOMBERG PROFESSIONAL™ service, Datastream, Credit Suisse research

-

100

200

300

400

500

600

700

-8%

-6%

-4%

-2%

0%

2%

4%

6%

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

E

2017

E

2018

E

2019

E

2020

E

Demand - Capacity growth (LHS) Ethylene spread (RHS)

(US$/mt)

78%

80%

82%

84%

86%

88%

90%

92%

94%

-

20

40

60

80

100

120

140

160

180

200

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

E

2017

E

2018

E

2019

E

2020

E

Capacity (LHS) Consumption (LHS) Utilisation rate (RHS)

-

200

400

600

800

1,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Max Min Avg2014 2015 2016

US$MT Shaded area indicates historical 5-year range

100

200

300

400

500

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Max Min Avg2014 2015 2016

US$MT Shaded area indicates historical 5-year range

12 January 2017

China Oil & Gas Sector 16

Figure 38: Major ethylene capacity additions delayed by 3-6 months

Jun-16 start-up

schedule estimate

Jan-17 start-up

schedule estimate

Ethylene capacity

increase (ktpa)

United States

Westlake Petrochemical 2Q17 2Q17 135

Chevron Phillips 2Q17 1Q18 1,500

ExxonMobil Chemical (Baytown) 2Q17 1Q18 1,500

Dow Chemical 2Q17 4Q17 1,500

Formosa Plastics 4Q18 4Q18 1,150

Occidental/Mexichem 3Q17 2Q17 550

Ingleside Ethylene 1Q17 2Q17 545

South Korea

Korea Petrochemical Ind. 3Q17 3Q17 330

LG Chem - 4Q18 230

Lotte Chemical - 3Q18 200

Malaysia

Lotte Chemical Titan 3Q17 4Q17 45

India

ONGC Petro-additions (OPaL) 1Q17 1Q17 550

Reliance Industries 1Q17 3Q17 1,460

Source: FGE, industry data, Credit Suisse estimates

Figure 39: Capacity increase rolled over into 2018

Source: FGE, industry data, Credit Suisse estimates

0

1000

2000

3000

4000

5000

6000

7000

1Q17 2Q17 3Q17 4Q17 1Q18 2Q18 3Q18 4Q18

Est

unat

ed m

ajor

cap

acity

add

ition

s (k

tpa)

Jun-16 estimate Jan-17 estimate

12 January 2017

China Oil & Gas Sector 17

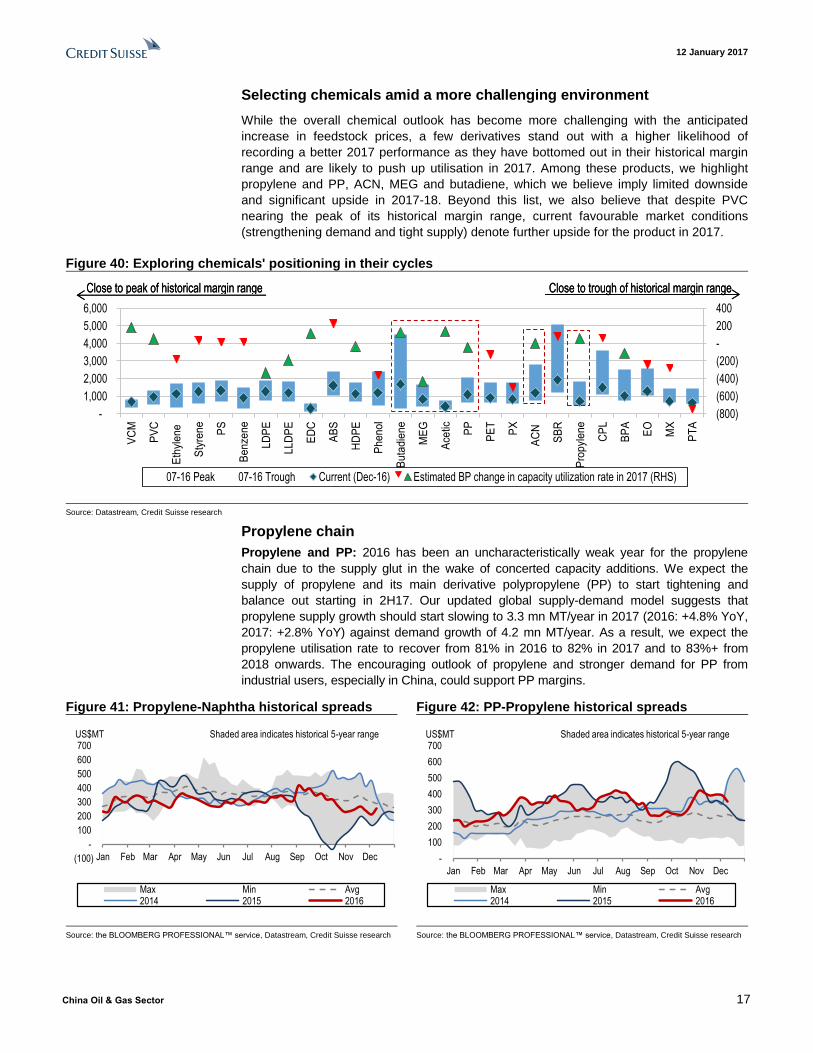

Selecting chemicals amid a more challenging environment

While the overall chemical outlook has become more challenging with the anticipated

increase in feedstock prices, a few derivatives stand out with a higher likelihood of

recording a better 2017 performance as they have bottomed out in their historical margin

range and are likely to push up utilisation in 2017. Among these products, we highlight

propylene and PP, ACN, MEG and butadiene, which we believe imply limited downside

and significant upside in 2017-18. Beyond this list, we also believe that despite PVC

nearing the peak of its historical margin range, current favourable market conditions

(strengthening demand and tight supply) denote further upside for the product in 2017.

Figure 40: Exploring chemicals' positioning in their cycles

Source: Datastream, Credit Suisse research

Propylene chain

Propylene and PP: 2016 has been an uncharacteristically weak year for the propylene

chain due to the supply glut in the wake of concerted capacity additions. We expect the

supply of propylene and its main derivative polypropylene (PP) to start tightening and

balance out starting in 2H17. Our updated global supply-demand model suggests that

propylene supply growth should start slowing to 3.3 mn MT/year in 2017 (2016: +4.8% YoY,

2017: +2.8% YoY) against demand growth of 4.2 mn MT/year. As a result, we expect the

propylene utilisation rate to recover from 81% in 2016 to 82% in 2017 and to 83%+ from

2018 onwards. The encouraging outlook of propylene and stronger demand for PP from

industrial users, especially in China, could support PP margins.

Figure 41: Propylene-Naphtha historical spreads Figure 42: PP-Propylene historical spreads

Source: the BLOOMBERG PROFESSIONAL™ service, Datastream, Credit Suisse research Source: the BLOOMBERG PROFESSIONAL™ service, Datastream, Credit Suisse research

(800)

(600)

(400)

(200)

-

200

400

-

1,000

2,000

3,000

4,000

5,000

6,000

VC

M

PV

C

Eth

yle

ne

Sty

ren

e

PS

Be

nze

ne

LD

PE

LL

DP

E

ED

C

AB

S

HD

PE

Ph

en

ol

Bu

tad

ien

e

ME

G

Ace

tic PP

PE

T

PX

AC

N

SB

R

Pro

pyl

en

e

CP

L

BP

A

EO

MX

PT

A

07-16 Peak 07-16 Trough Current (Dec-16) Estimated BP change in capacity utilization rate in 2017 (RHS)

Close to peak of historical margin range Close to trough of historical margin rangeClose to peak of historical margin range Close to trough of historical margin range

(100)

-

100

200

300

400

500

600

700

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Max Min Avg2014 2015 2016

US$MT Shaded area indicates historical 5-year range

-

100

200

300

400

500

600

700

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Max Min Avg2014 2015 2016

US$MT Shaded area indicates historical 5-year range

12 January 2017

China Oil & Gas Sector 18

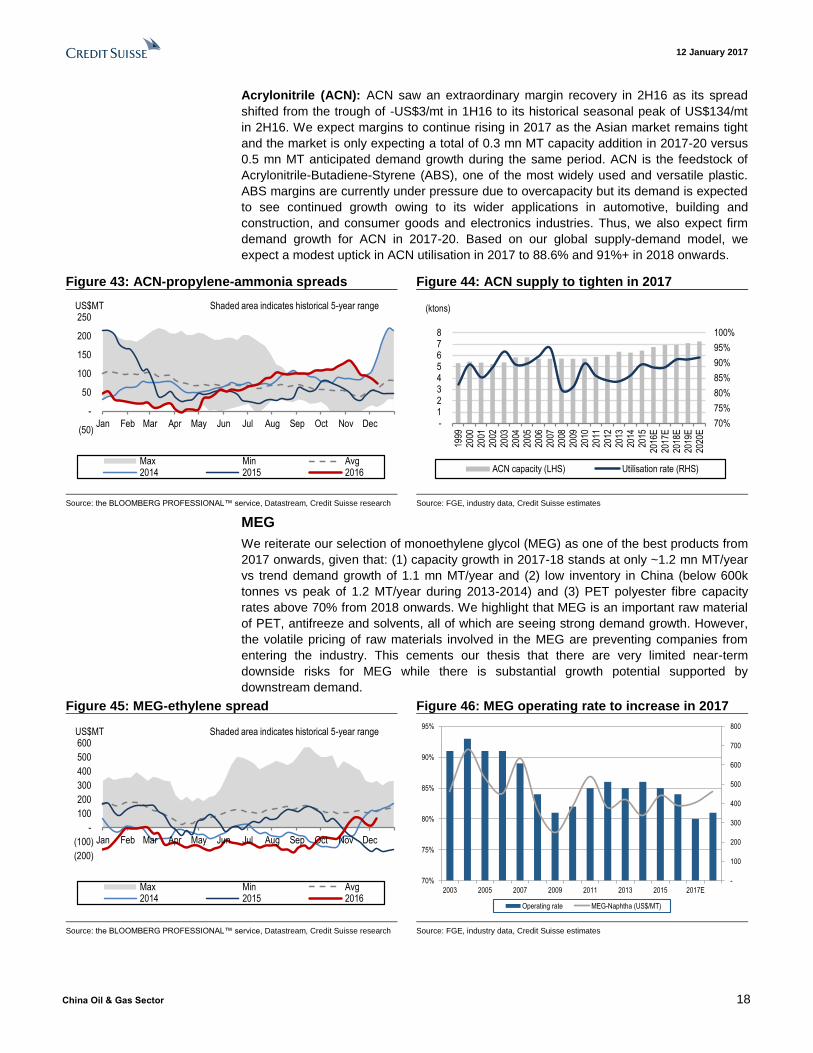

Acrylonitrile (ACN): ACN saw an extraordinary margin recovery in 2H16 as its spread

shifted from the trough of -US$3/mt in 1H16 to its historical seasonal peak of US$134/mt

in 2H16. We expect margins to continue rising in 2017 as the Asian market remains tight

and the market is only expecting a total of 0.3 mn MT capacity addition in 2017-20 versus

0.5 mn MT anticipated demand growth during the same period. ACN is the feedstock of

Acrylonitrile-Butadiene-Styrene (ABS), one of the most widely used and versatile plastic.

ABS margins are currently under pressure due to overcapacity but its demand is expected

to see continued growth owing to its wider applications in automotive, building and

construction, and consumer goods and electronics industries. Thus, we also expect firm

demand growth for ACN in 2017-20. Based on our global supply-demand model, we

expect a modest uptick in ACN utilisation in 2017 to 88.6% and 91%+ in 2018 onwards.

Figure 43: ACN-propylene-ammonia spreads Figure 44: ACN supply to tighten in 2017

Source: the BLOOMBERG PROFESSIONAL™ service, Datastream, Credit Suisse research Source: FGE, industry data, Credit Suisse estimates

MEG

We reiterate our selection of monoethylene glycol (MEG) as one of the best products from

2017 onwards, given that: (1) capacity growth in 2017-18 stands at only ~1.2 mn MT/year

vs trend demand growth of 1.1 mn MT/year and (2) low inventory in China (below 600k

tonnes vs peak of 1.2 MT/year during 2013-2014) and (3) PET polyester fibre capacity

rates above 70% from 2018 onwards. We highlight that MEG is an important raw material

of PET, antifreeze and solvents, all of which are seeing strong demand growth. However,

the volatile pricing of raw materials involved in the MEG are preventing companies from

entering the industry. This cements our thesis that there are very limited near-term

downside risks for MEG while there is substantial growth potential supported by

downstream demand.

Figure 45: MEG-ethylene spread Figure 46: MEG operating rate to increase in 2017

Source: the BLOOMBERG PROFESSIONAL™ service, Datastream, Credit Suisse research Source: FGE, industry data, Credit Suisse estimates

(50)

-

50

100

150

200

250

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Max Min Avg2014 2015 2016

US$MT Shaded area indicates historical 5-year range

70%

75%

80%

85%

90%

95%

100%

- 1 2 3 4 5 6 7 8

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

E20

17E

2018

E20

19E

2020

E

ACN capacity (LHS) Utilisation rate (RHS)

(ktons)

(200)

(100)

-

100

200

300

400

500

600

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Max Min Avg2014 2015 2016

US$MT Shaded area indicates historical 5-year range

-

100

200

300

400

500

600

700

800

70%

75%

80%

85%

90%

95%

2003 2005 2007 2009 2011 2013 2015 2017E

Operating rate MEG-Naphtha (US$/MT)

12 January 2017

China Oil & Gas Sector 19

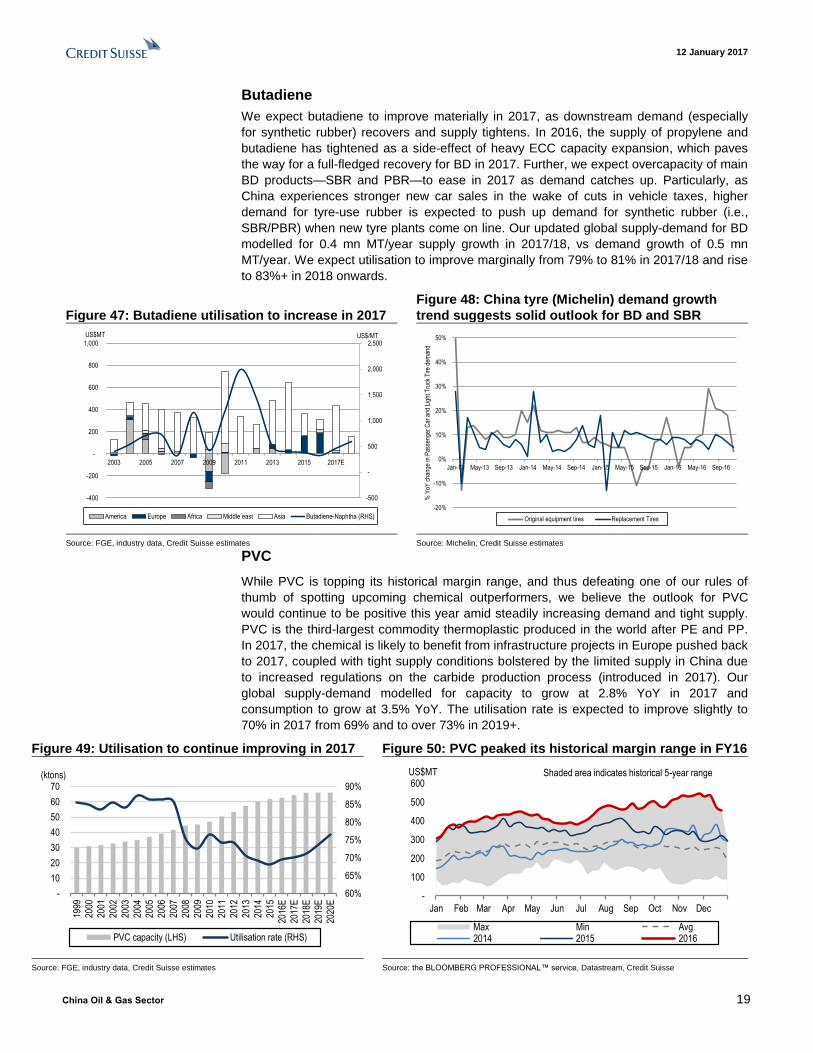

Butadiene

We expect butadiene to improve materially in 2017, as downstream demand (especially

for synthetic rubber) recovers and supply tightens. In 2016, the supply of propylene and

butadiene has tightened as a side-effect of heavy ECC capacity expansion, which paves

the way for a full-fledged recovery for BD in 2017. Further, we expect overcapacity of main

BD products—SBR and PBR—to ease in 2017 as demand catches up. Particularly, as

China experiences stronger new car sales in the wake of cuts in vehicle taxes, higher

demand for tyre-use rubber is expected to push up demand for synthetic rubber (i.e.,

SBR/PBR) when new tyre plants come on line. Our updated global supply-demand for BD

modelled for 0.4 mn MT/year supply growth in 2017/18, vs demand growth of 0.5 mn

MT/year. We expect utilisation to improve marginally from 79% to 81% in 2017/18 and rise

to 83%+ in 2018 onwards.

Figure 47: Butadiene utilisation to increase in 2017

Figure 48: China tyre (Michelin) demand growth

trend suggests solid outlook for BD and SBR

Source: FGE, industry data, Credit Suisse estimates Source: Michelin, Credit Suisse estimates

PVC

While PVC is topping its historical margin range, and thus defeating one of our rules of

thumb of spotting upcoming chemical outperformers, we believe the outlook for PVC

would continue to be positive this year amid steadily increasing demand and tight supply.

PVC is the third-largest commodity thermoplastic produced in the world after PE and PP.

In 2017, the chemical is likely to benefit from infrastructure projects in Europe pushed back

to 2017, coupled with tight supply conditions bolstered by the limited supply in China due

to increased regulations on the carbide production process (introduced in 2017). Our

global supply-demand modelled for capacity to grow at 2.8% YoY in 2017 and

consumption to grow at 3.5% YoY. The utilisation rate is expected to improve slightly to

70% in 2017 from 69% and to over 73% in 2019+.

Figure 49: Utilisation to continue improving in 2017 Figure 50: PVC peaked its historical margin range in FY16

Source: FGE, industry data, Credit Suisse estimates Source: the BLOOMBERG PROFESSIONAL™ service, Datastream, Credit Suisse

-500

-

500

1,000

1,500

2,000

2,500

-400

-200

-

200

400

600

800

1,000

2003 2005 2007 2009 2011 2013 2015 2017E

US$/MTUS$MT

America Europe Africa Middle east Asia Butadiene-Naphtha (RHS)

-20%

-10%

0%

10%

20%

30%

40%

50%

Jan-13 May-13 Sep-13 Jan-14 May-14 Sep-14 Jan-15 May-15 Sep-15 Jan-16 May-16 Sep-16

% Y

oY c

hang

e in

Pas

seng

er C

ar a

nd L

ight

Tru

ck T

ire d

eman

d

Original equipment tires Replacement Tires

60%

65%

70%

75%

80%

85%

90%

-

10

20

30

40

50

60

70

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

E

2017

E

2018

E

2019

E

2020

E

PVC capacity (LHS) Utilisation rate (RHS)

(ktons)

-

100

200

300

400

500

600

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Max Min Avg2014 2015 2016

US$MT Shaded area indicates historical 5-year range

12 January 2017

China Oil & Gas Sector 20

Multiple catalysts ahead

(1) CNOOC’s Strategy Preview CNOOC will be hosting its annual Strategy Preview on 19 January 2017. Over the past

year, the market has been concerned about CNOOC’s deteriorating production and low

reserve life, and expectations are low heading into the Preview, but we believe it should

surprise the market on the upside.

First, on production, we believe that CNOOC should announce a 3-5% YoY decline in

2017 volume target which is more resilient than previous projections. The market is

predicting a 5-8% YoY decline in 2017 volumes, so the guidance should be a positive

surprise to the market, in our opinion.

Second, two recent mega-size discoveries should address concerns on low reserve life.

ExxonMobil has announced/confirmed two significant discoveries in late 2016, but given

CNOOC is not the operator, the company has not made a public announcement and might

have missed by the market. Based on our initial assessment, these two discoveries alone

could bring c.250mmboe of reserve adds to CNOOC and raise its oil reserve life to nine

years (from seven currently).

■ Liza discovery: The Liza discovery is located in offshore Guyana with a potential

recoverable resource of 1.4 bn barrels. ExxonMobil is the operator with a 45% interest

in the block and CNOOC owns 25% interest. On 20 December 2016, ExxonMobil has

announced that it has submitted an application for a production licence and initial

development plan early December and will look to fast-track the development.

ExxonMobil confirmed the discovery through the Liza-2 exploration well, which has

encountered more than 58 meters of oil-bearing sandstone reservoirs in Upper

Cretaceous formations. The well was drilled to 5,475m in 1,692m of water. The second

well has confirmed the presence of high-quality oil from the high-porosity sandstone

reservoirs seen in the Liza-1 well.

■ Owowo discovery: The Owowo discovery is located in offshore Nigeria with a

potential recoverable resource of 1bn barrels. ExxonMobil announced the discovery on

27 October 2016. ExxonMobil is the operator with a 27% interest in the block and

CNOOC owns an 18% interest. The Owowo-3 exploration well encountered about 140

meters of oil-bearing sandstone reservoir. Owowo-3 extends the resource discovered

by the Owowo-2 well, which encountered about 157m of oil-bearing sandstone

reservoir.

(2) Sinopec’s marketing divestment: Paving the way

for non-fuel business expansion Reuters reported on 4 January that Sinopec has appointed investment banks for a

potential listing that could raise as much as US$12 bn. Back in 2014, Sinopec had sold

down a 30% stake in its marketing division, raising Rmb107 bn (US$17.5 bn) through a

capital injection agreement with 25 investors, with plans to make further divestment. In this

section we reiterate the potential upside of Sinopec’s non-fuel retail business, both in

terms of earnings and valuation upside.

Sinopec's marketing unit encompasses several businesses, including its 25,000 Easy Joy

convenience stores out of its 30,560 service station network, its B2C online shopping mall

(www.ejoy365.com; launched in 2011) and restaurant collaborations with McDonald's and

KFC (launched in 2009). A further divestment of the marketing unit would raise funds that

Sinopec could invest in more non-fuel businesses, such as vehicle maintenance and

advertising, which would allow Sinopec to better utilise the business potential of its existing

distribution network in China.

12 January 2017

China Oil & Gas Sector 21

Figure 51: Sinopec's major non-fuel strategic cooperation in recent years

Date Partner Terms

Jun-2006 McDonald's Agreement to set up its Drive-Thru restaurants at selected Sinopec service station sites across China

Nov-2011 Yum! Brands Agreement to open drive-through outlets at Sinopec's gas stations and expressway service stations

May-2014 China Taiping Insurance Group Sinopec Sales will leverage its network and carry out car insurance and life insurance business of China

Taiping in selected stations under Sinopec's traditional service network such as convenience stores and car

service. Meanwhile, both parties will share customer resources and cross market.

Jul-2014 Ruentex Group (Taiwan retailer) Agreement to develop non-oil businesses, including convenience stores, e-commerce and financial services

Aug-2014 Tibet Highland Natural Water Ltd Agreement to establish a glacier water brand and use Sinopec's retailing network to sell it nationwide

Aug-2014 S.F. Express Sinopec EasyJoy will connect its nationwide retail stores with S.F. Express’ logistics network to achieve

greater synergy.

Aug-2014 yhd.com The parties will start and explore the prospects of cooperation in areas such as joint procurement, O2O

(online-to-offline) business, cooperation in e-commerce platforms, oil product sales, etc.

Aug-2014 Tencent, Inc EasyJoy will cooperate with Tencent to explore business development, mobile payment, brand promotion,

online to offline, map navigation, customer loyalty management, big data application and cross marketing

opportunities.

Sep-2014 Haier Electronics Group, Sinopec would cooperate with Haier in interactive marketing and logistics. In return, Sinopec would provide

Haier with fuel for transportation and delivery operations.

Dec-2014 Beijing Aiyihang Auto Services Ltd Jointly operate automotive services business at the gas stations within the Sinopec Hubei network.

Jul-2015 Beiqi Foton Motor Co. Partnership on information and market interaction and jointly develop electric vehicle charging stations

May-2016 Zhongbai Holdings Group Co Ltd The supermarket will set up outlets in Sinopec’s charging stations

Source: Company data, Credit Suisse research

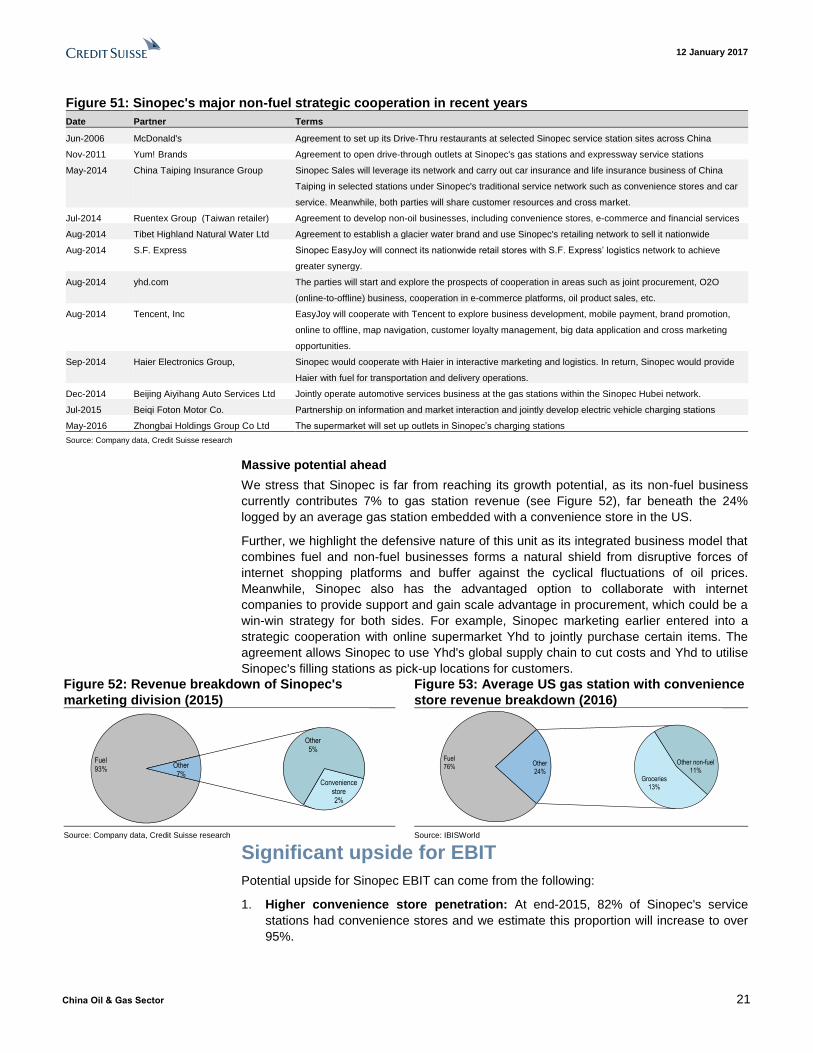

Massive potential ahead

We stress that Sinopec is far from reaching its growth potential, as its non-fuel business

currently contributes 7% to gas station revenue (see Figure 52), far beneath the 24%

logged by an average gas station embedded with a convenience store in the US.

Further, we highlight the defensive nature of this unit as its integrated business model that

combines fuel and non-fuel businesses forms a natural shield from disruptive forces of

internet shopping platforms and buffer against the cyclical fluctuations of oil prices.

Meanwhile, Sinopec also has the advantaged option to collaborate with internet

companies to provide support and gain scale advantage in procurement, which could be a

win-win strategy for both sides. For example, Sinopec marketing earlier entered into a

strategic cooperation with online supermarket Yhd to jointly purchase certain items. The

agreement allows Sinopec to use Yhd's global supply chain to cut costs and Yhd to utilise

Sinopec's filling stations as pick-up locations for customers.

Figure 52: Revenue breakdown of Sinopec's

marketing division (2015)

Figure 53: Average US gas station with convenience

store revenue breakdown (2016)

Source: Company data, Credit Suisse research Source: IBISWorld

Significant upside for EBIT

Potential upside for Sinopec EBIT can come from the following:

1. Higher convenience store penetration: At end-2015, 82% of Sinopec's service

stations had convenience stores and we estimate this proportion will increase to over

95%.

Fuel93%

Convenience store2%

Other5%

Other 7%

Fuel76%

Groceries13%

Other non-fuel11%

Other24%

12 January 2017

China Oil & Gas Sector 22

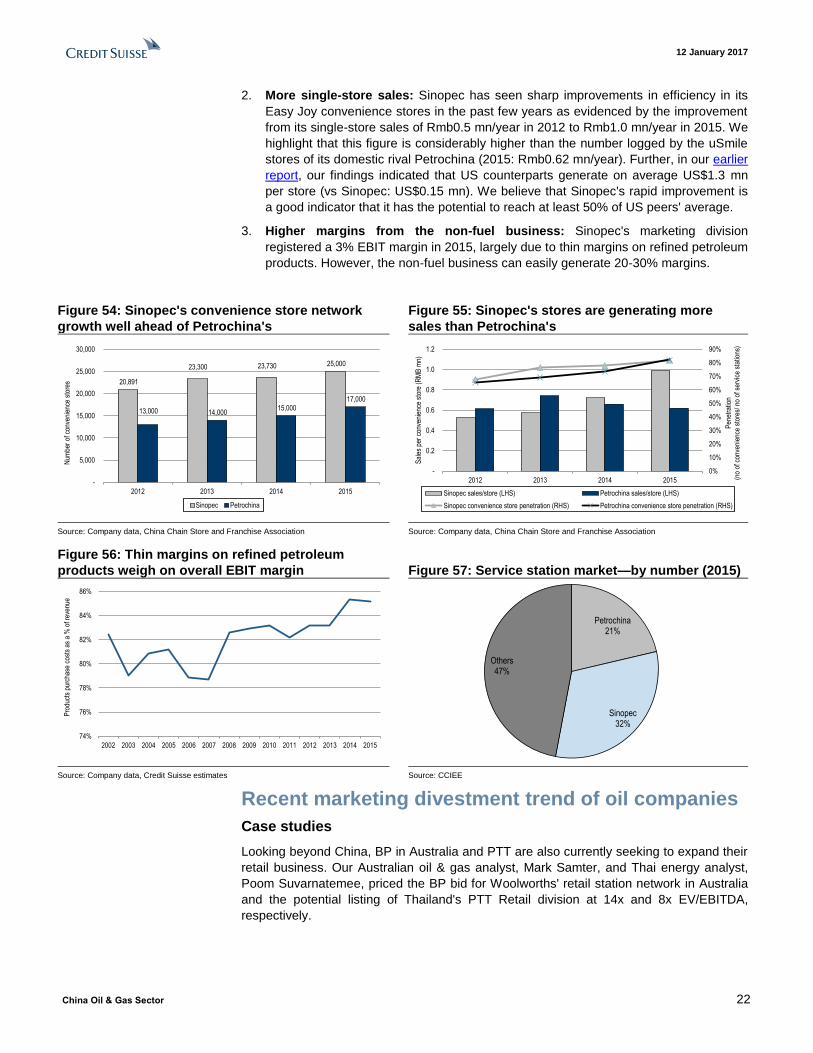

2. More single-store sales: Sinopec has seen sharp improvements in efficiency in its

Easy Joy convenience stores in the past few years as evidenced by the improvement

from its single-store sales of Rmb0.5 mn/year in 2012 to Rmb1.0 mn/year in 2015. We

highlight that this figure is considerably higher than the number logged by the uSmile

stores of its domestic rival Petrochina (2015: Rmb0.62 mn/year). Further, in our earlier

report, our findings indicated that US counterparts generate on average US$1.3 mn

per store (vs Sinopec: US$0.15 mn). We believe that Sinopec's rapid improvement is

a good indicator that it has the potential to reach at least 50% of US peers' average.

3. Higher margins from the non-fuel business: Sinopec's marketing division

registered a 3% EBIT margin in 2015, largely due to thin margins on refined petroleum

products. However, the non-fuel business can easily generate 20-30% margins.

Figure 54: Sinopec's convenience store network

growth well ahead of Petrochina's

Figure 55: Sinopec's stores are generating more

sales than Petrochina's

Source: Company data, China Chain Store and Franchise Association Source: Company data, China Chain Store and Franchise Association

Figure 56: Thin margins on refined petroleum

products weigh on overall EBIT margin Figure 57: Service station market—by number (2015)

Source: Company data, Credit Suisse estimates Source: CCIEE

Recent marketing divestment trend of oil companies

Case studies

Looking beyond China, BP in Australia and PTT are also currently seeking to expand their

retail business. Our Australian oil & gas analyst, Mark Samter, and Thai energy analyst,

Poom Suvarnatemee, priced the BP bid for Woolworths' retail station network in Australia

and the potential listing of Thailand's PTT Retail division at 14x and 8x EV/EBITDA,

respectively.

20,891

23,300 23,730 25,000

13,000 14,000 15,000

17,000

-

5,000

10,000

15,000

20,000

25,000

30,000

2012 2013 2014 2015

Num

ber

of c

onve

nien

ce s

tore

s

Sinopec Petrochina

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

-

0.2

0.4

0.6

0.8

1.0

1.2

2012 2013 2014 2015

Pen

etra

tion

(no

of c

onve

nien

ce s

tore

s/ n

o of

ser

vice

sta

tions

)

Sal

es p

er c

onve

nien

ce s

tore

(R

MB

mn)

Sinopec sales/store (LHS) Petrochina sales/store (LHS)

Sinopec convenience store penetration (RHS) Petrochina convenience store penetration (RHS)

74%

76%

78%

80%

82%

84%

86%

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Pro

duct

s pu

rcha

se c

osts

as

a %

of r

even

ue

Petrochina21%

Sinopec32%

Others47%

12 January 2017

China Oil & Gas Sector 23

Woolworths

In Australia, BP recently acquired embattled supermarket chain Woolworths. Unlike

Sinopec, Woolworths's specialty lies in grocery retailing as the retail giant only forayed into

the petrol business in 1996. In 2016, Woolworths operated 527 petrol stations with

convenience stores, accounting for 21% share of the Australian fuel market. Prior to 2014,

Woolworths jointly operated 131 additional sites with Caltex. However, in 2015, under

changes to the Woolworths-Caltex alliance, 131 Caltex-operated sites were no longer

recognised.

In an effort to entice customers to spend money at their non-fuel stores, Woolworths

stations offer a per-litre discount off pump prices for customers who spend a qualifying

amount at its own-branded convenience stores or supermarkets, hence generating

synergy between Woolworths’s businesses. Woolworths also provides a loyalty

programme that extends across all of its chain businesses, including supermarkets and

hotels.

In a recent note, our Australian analyst, Mark Samter, noted that Woolworths is the winner

in the acquisition. BP paid A$1.785 bn upfront and would fund 2cpl of the redemption

going forward. Pre-synergies, but post Woolworths funding 2cpl of the redemption (but not

the 2cpl redemption BP will now have to fund at some of its sites), this is for A$153 mn of

EBIT. Adjusting for A$300-400 mn of lease liabilities and they are paying >14x EV/EBIT.

Mark thinks that while BP would definitely claw some back with the supply agreement,

even at 2cpl (and remember they will use a lot of third-party infrastructure) it is ~10x

EV/EBIT. We estimate that the deal is valued at approximately 22x P/E.

Figure 58: Woolworths' petrol revenue breakdown Figure 59: Stable per-store sales throughout the years

Source: Company data, Credit Suisse research Source: Company data, Credit Suisse research

Figure 60: Transaction valuation estimates

Revenue (Australia Food and Petrol segment) (A$ mn) 39,410

- Fuel 4,612

- Non-fuel 34,798

EBITDA–Fuel (A$ mn) 225

EBIT–Fuel (A$ mn) 151

Net profit–Fuel (A$ mn) 84

Implied P/E (x) 22x

Implied EV/EBITDA (x) 8x

Source: Company data, Credit Suisse estimates

PTT Retail Marketing Plc

In Thailand, PTT Public Company Limited plans to spin off its marketing arm, PTTOR

(PTT Oil and Retail Business Company Ltd in 4Q17 or 2018. PTT plans to own only 45-

50% of PTTOR after the sell-down from 100% currently. PTTOR will be PTT's flagship

company in the oil and retail business.

14% 14% 15% 15% 15% 14% 12%

86% 86% 85% 85% 85% 86% 88%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2010 2011 2012 2013 2014 2015 2016

Fuel Non-fuel 60

70

80

90

2010 2011 2012 2013 2014 2015 2016

Per

-sto

re s

ales

(A

$ m

n)

12 January 2017

China Oil & Gas Sector 24

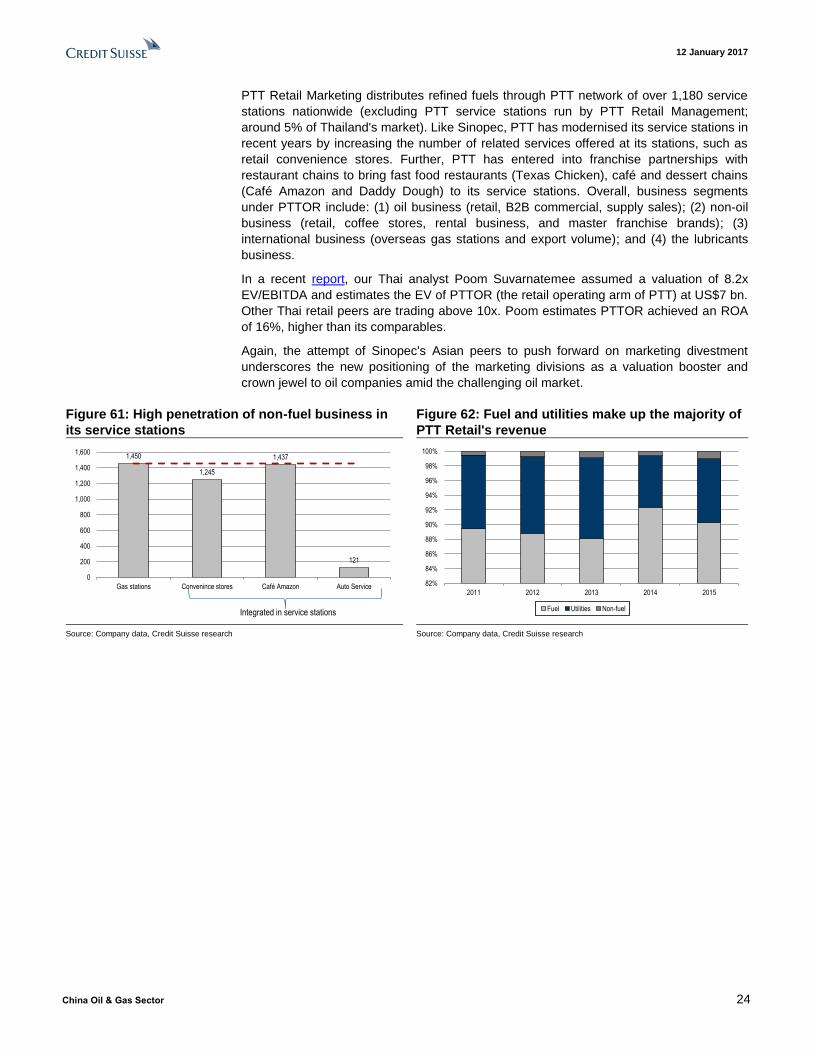

PTT Retail Marketing distributes refined fuels through PTT network of over 1,180 service

stations nationwide (excluding PTT service stations run by PTT Retail Management;

around 5% of Thailand's market). Like Sinopec, PTT has modernised its service stations in

recent years by increasing the number of related services offered at its stations, such as

retail convenience stores. Further, PTT has entered into franchise partnerships with

restaurant chains to bring fast food restaurants (Texas Chicken), café and dessert chains

(Café Amazon and Daddy Dough) to its service stations. Overall, business segments

under PTTOR include: (1) oil business (retail, B2B commercial, supply sales); (2) non-oil

business (retail, coffee stores, rental business, and master franchise brands); (3)

international business (overseas gas stations and export volume); and (4) the lubricants

business.

In a recent report, our Thai analyst Poom Suvarnatemee assumed a valuation of 8.2x

EV/EBITDA and estimates the EV of PTTOR (the retail operating arm of PTT) at US$7 bn.

Other Thai retail peers are trading above 10x. Poom estimates PTTOR achieved an ROA

of 16%, higher than its comparables.

Again, the attempt of Sinopec's Asian peers to push forward on marketing divestment

underscores the new positioning of the marketing divisions as a valuation booster and

crown jewel to oil companies amid the challenging oil market.

Figure 61: High penetration of non-fuel business in

its service stations

Figure 62: Fuel and utilities make up the majority of

PTT Retail's revenue

Source: Company data, Credit Suisse research Source: Company data, Credit Suisse research

1,450

1,245

1,437

121

0

200

400

600

800

1,000

1,200

1,400

1,600

Gas stations Convenince stores Café Amazon Auto Service

Integrated in service stations

82%

84%

86%

88%

90%

92%

94%

96%

98%

100%

2011 2012 2013 2014 2015

Fuel Utilities Non-fuel

12 January 2017

China Oil & Gas Sector 25

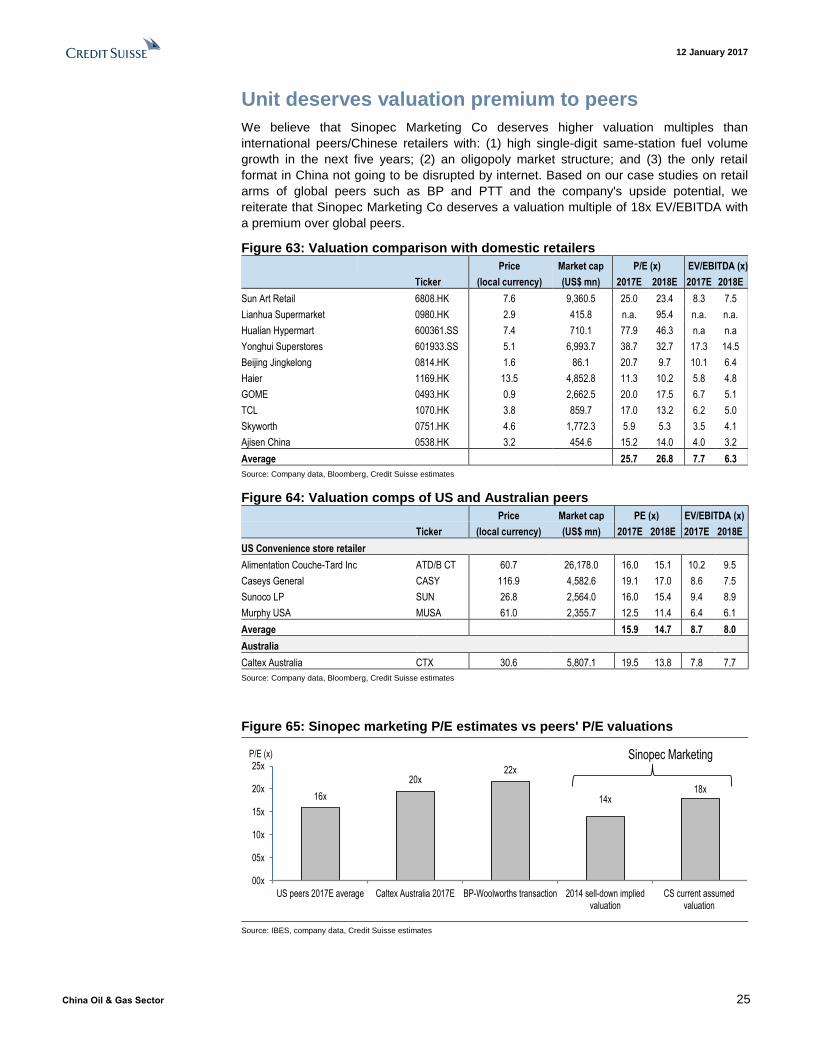

Unit deserves valuation premium to peers

We believe that Sinopec Marketing Co deserves higher valuation multiples than

international peers/Chinese retailers with: (1) high single-digit same-station fuel volume

growth in the next five years; (2) an oligopoly market structure; and (3) the only retail

format in China not going to be disrupted by internet. Based on our case studies on retail

arms of global peers such as BP and PTT and the company's upside potential, we

reiterate that Sinopec Marketing Co deserves a valuation multiple of 18x EV/EBITDA with

a premium over global peers.

Figure 63: Valuation comparison with domestic retailers

Price Market cap P/E (x) EV/EBITDA (x)

Ticker (local currency) (US$ mn) 2017E 2018E 2017E 2018E

Sun Art Retail 6808.HK 7.6 9,360.5 25.0 23.4 8.3 7.5

Lianhua Supermarket 0980.HK 2.9 415.8 n.a. 95.4 n.a. n.a.

Hualian Hypermart 600361.SS 7.4 710.1 77.9 46.3 n.a n.a

Yonghui Superstores 601933.SS 5.1 6,993.7 38.7 32.7 17.3 14.5

Beijing Jingkelong 0814.HK 1.6 86.1 20.7 9.7 10.1 6.4

Haier 1169.HK 13.5 4,852.8 11.3 10.2 5.8 4.8

GOME 0493.HK 0.9 2,662.5 20.0 17.5 6.7 5.1

TCL 1070.HK 3.8 859.7 17.0 13.2 6.2 5.0

Skyworth 0751.HK 4.6 1,772.3 5.9 5.3 3.5 4.1

Ajisen China 0538.HK 3.2 454.6 15.2 14.0 4.0 3.2

Average 25.7 26.8 7.7 6.3

Source: Company data, Bloomberg, Credit Suisse estimates

Figure 64: Valuation comps of US and Australian peers

Price Market cap PE (x) EV/EBITDA (x)

Ticker (local currency) (US$ mn) 2017E 2018E 2017E 2018E

US Convenience store retailer

Alimentation Couche-Tard Inc ATD/B CT 60.7 26,178.0 16.0 15.1 10.2 9.5

Caseys General CASY 116.9 4,582.6 19.1 17.0 8.6 7.5

Sunoco LP SUN 26.8 2,564.0 16.0 15.4 9.4 8.9

Murphy USA MUSA 61.0 2,355.7 12.5 11.4 6.4 6.1

Average 15.9 14.7 8.7 8.0

Australia

Caltex Australia CTX 30.6 5,807.1 19.5 13.8 7.8 7.7

Source: Company data, Bloomberg, Credit Suisse estimates

Figure 65: Sinopec marketing P/E estimates vs peers' P/E valuations

Source: IBES, company data, Credit Suisse estimates

16x

20x22x

14x18x

00x

05x

10x

15x

20x

25x

US peers 2017E average Caltex Australia 2017E BP-Woolworths transaction 2014 sell-down impliedvaluation

CS current assumedvaluation

P/E (x) Sinopec Marketing

12 January 2017

China Oil & Gas Sector 26

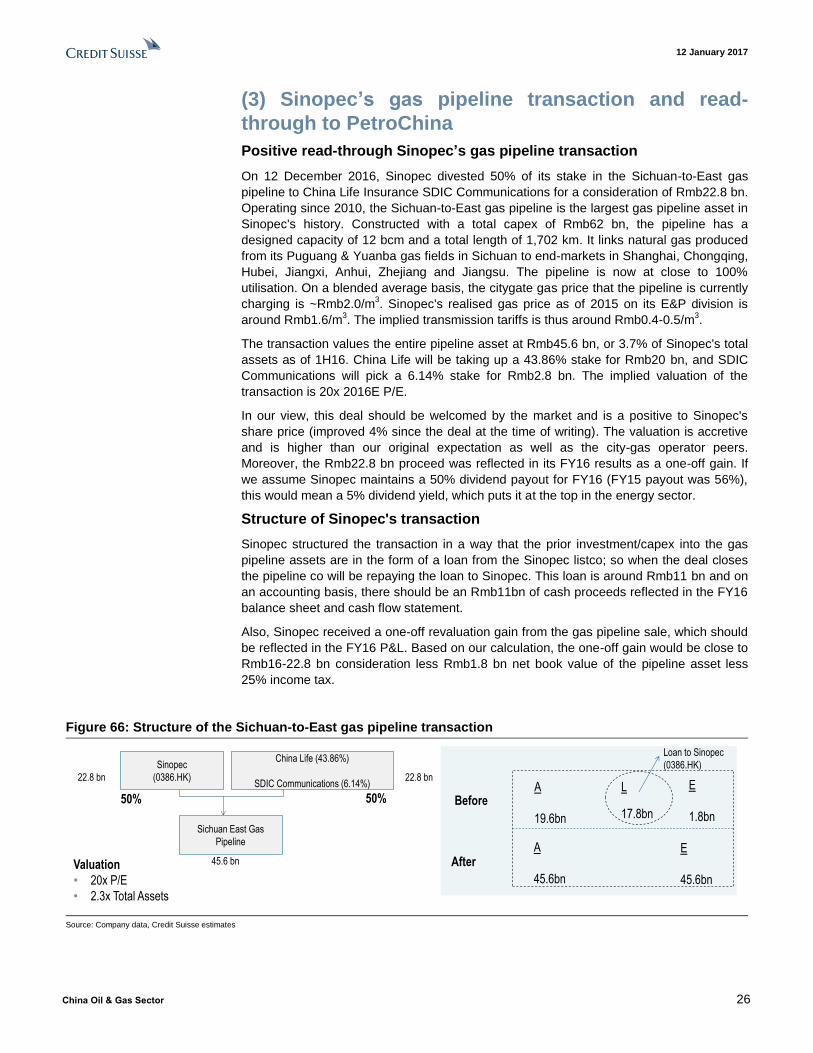

(3) Sinopec’s gas pipeline transaction and read-

through to PetroChina

Positive read-through Sinopec’s gas pipeline transaction

On 12 December 2016, Sinopec divested 50% of its stake in the Sichuan-to-East gas

pipeline to China Life Insurance SDIC Communications for a consideration of Rmb22.8 bn.

Operating since 2010, the Sichuan-to-East gas pipeline is the largest gas pipeline asset in

Sinopec's history. Constructed with a total capex of Rmb62 bn, the pipeline has a

designed capacity of 12 bcm and a total length of 1,702 km. It links natural gas produced

from its Puguang & Yuanba gas fields in Sichuan to end-markets in Shanghai, Chongqing,

Hubei, Jiangxi, Anhui, Zhejiang and Jiangsu. The pipeline is now at close to 100%

utilisation. On a blended average basis, the citygate gas price that the pipeline is currently

charging is ~Rmb2.0/m3. Sinopec's realised gas price as of 2015 on its E&P division is

around Rmb1.6/m3. The implied transmission tariffs is thus around Rmb0.4-0.5/m

3.

The transaction values the entire pipeline asset at Rmb45.6 bn, or 3.7% of Sinopec's total

assets as of 1H16. China Life will be taking up a 43.86% stake for Rmb20 bn, and SDIC

Communications will pick a 6.14% stake for Rmb2.8 bn. The implied valuation of the

transaction is 20x 2016E P/E.

In our view, this deal should be welcomed by the market and is a positive to Sinopec's

share price (improved 4% since the deal at the time of writing). The valuation is accretive

and is higher than our original expectation as well as the city-gas operator peers.

Moreover, the Rmb22.8 bn proceed was reflected in its FY16 results as a one-off gain. If

we assume Sinopec maintains a 50% dividend payout for FY16 (FY15 payout was 56%),

this would mean a 5% dividend yield, which puts it at the top in the energy sector.

Structure of Sinopec's transaction

Sinopec structured the transaction in a way that the prior investment/capex into the gas

pipeline assets are in the form of a loan from the Sinopec listco; so when the deal closes

the pipeline co will be repaying the loan to Sinopec. This loan is around Rmb11 bn and on

an accounting basis, there should be an Rmb11bn of cash proceeds reflected in the FY16

balance sheet and cash flow statement.

Also, Sinopec received a one-off revaluation gain from the gas pipeline sale, which should

be reflected in the FY16 P&L. Based on our calculation, the one-off gain would be close to

Rmb16-22.8 bn consideration less Rmb1.8 bn net book value of the pipeline asset less

25% income tax.

Figure 66: Structure of the Sichuan-to-East gas pipeline transaction

Source: Company data, Credit Suisse estimates

A

45.6bn

Sinopec

(0386.HK)

China Life (43.86%)

SDIC Communications (6.14%)

Sichuan East Gas

Pipeline

50% 50%

22.8 bn 22.8 bn

45.6 bnValuation

• 20x P/E

• 2.3x Total Assets

Before

After

A

19.6bn

L

17.8bn

E

1.8bn

Loan to Sinopec

(0386.HK)

E

45.6bn

12 January 2017

China Oil & Gas Sector 27

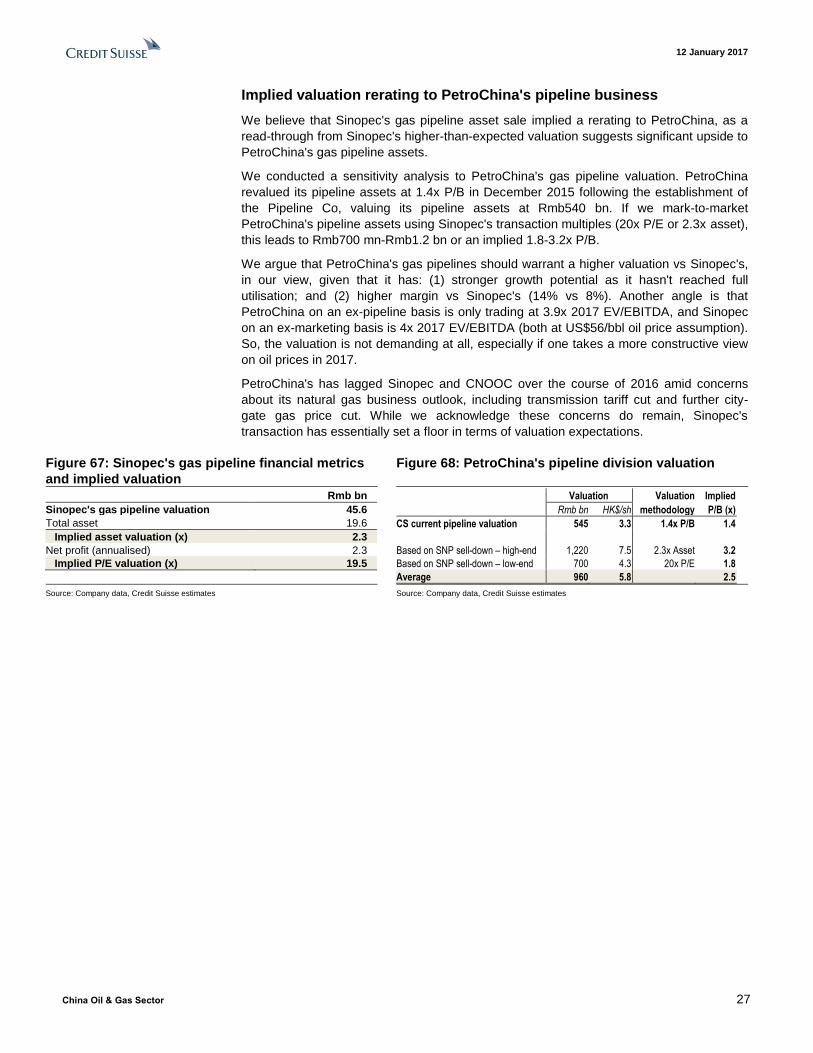

Implied valuation rerating to PetroChina's pipeline business

We believe that Sinopec's gas pipeline asset sale implied a rerating to PetroChina, as a

read-through from Sinopec's higher-than-expected valuation suggests significant upside to

PetroChina's gas pipeline assets.

We conducted a sensitivity analysis to PetroChina's gas pipeline valuation. PetroChina

revalued its pipeline assets at 1.4x P/B in December 2015 following the establishment of

the Pipeline Co, valuing its pipeline assets at Rmb540 bn. If we mark-to-market

PetroChina's pipeline assets using Sinopec's transaction multiples (20x P/E or 2.3x asset),

this leads to Rmb700 mn-Rmb1.2 bn or an implied 1.8-3.2x P/B.

We argue that PetroChina's gas pipelines should warrant a higher valuation vs Sinopec's,

in our view, given that it has: (1) stronger growth potential as it hasn't reached full

utilisation; and (2) higher margin vs Sinopec's (14% vs 8%). Another angle is that

PetroChina on an ex-pipeline basis is only trading at 3.9x 2017 EV/EBITDA, and Sinopec

on an ex-marketing basis is 4x 2017 EV/EBITDA (both at US$56/bbl oil price assumption).

So, the valuation is not demanding at all, especially if one takes a more constructive view

on oil prices in 2017.

PetroChina's has lagged Sinopec and CNOOC over the course of 2016 amid concerns

about its natural gas business outlook, including transmission tariff cut and further city-

gate gas price cut. While we acknowledge these concerns do remain, Sinopec's

transaction has essentially set a floor in terms of valuation expectations.

Figure 67: Sinopec's gas pipeline financial metrics

and implied valuation

Figure 68: PetroChina's pipeline division valuation

Rmb bn

Sinopec's gas pipeline valuation 45.6

Total asset 19.6

Implied asset valuation (x) 2.3

Net profit (annualised) 2.3

Implied P/E valuation (x) 19.5

Valuation Valuation Implied

Rmb bn HK$/sh methodology P/B (x)

CS current pipeline valuation 545 3.3 1.4x P/B 1.4

Based on SNP sell-down – high-end 1,220 7.5 2.3x Asset 3.2

Based on SNP sell-down – low-end 700 4.3 20x P/E 1.8

Average 960 5.8 2.5

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

12 January 2017

China Oil & Gas Sector 28

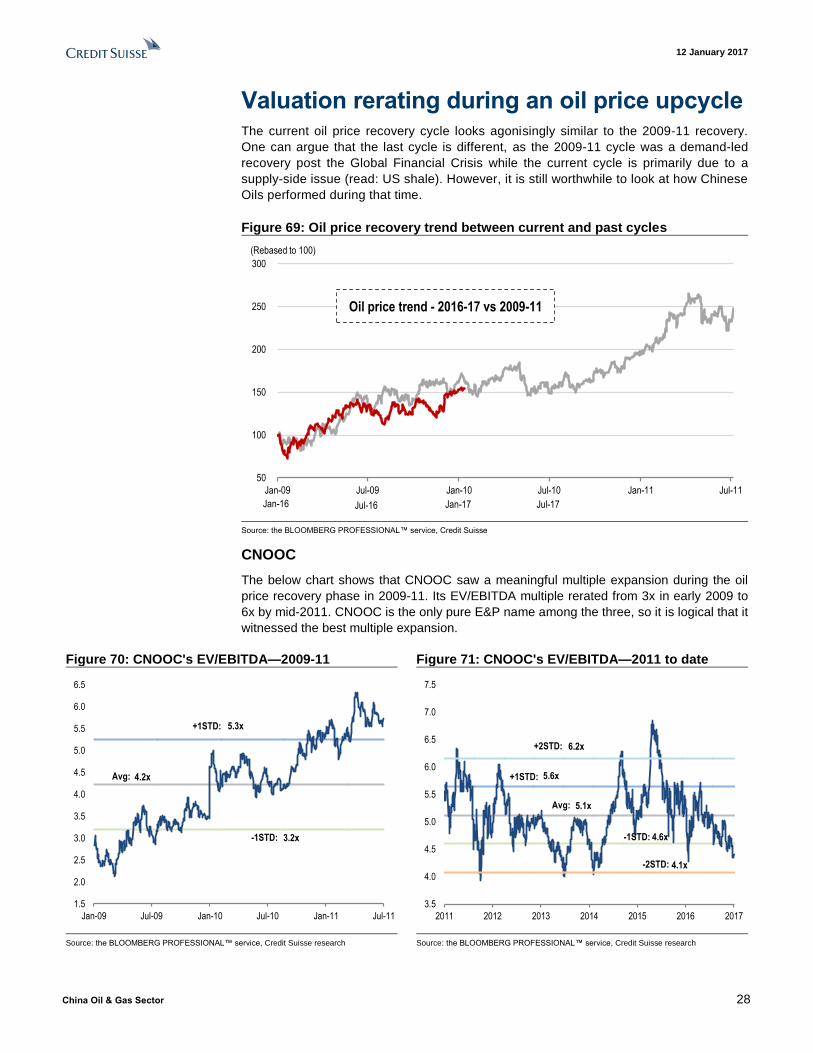

Valuation rerating during an oil price upcycle The current oil price recovery cycle looks agonisingly similar to the 2009-11 recovery.

One can argue that the last cycle is different, as the 2009-11 cycle was a demand-led

recovery post the Global Financial Crisis while the current cycle is primarily due to a

supply-side issue (read: US shale). However, it is still worthwhile to look at how Chinese

Oils performed during that time.

Figure 69: Oil price recovery trend between current and past cycles

Source: the BLOOMBERG PROFESSIONAL™ service, Credit Suisse

CNOOC

The below chart shows that CNOOC saw a meaningful multiple expansion during the oil

price recovery phase in 2009-11. Its EV/EBITDA multiple rerated from 3x in early 2009 to

6x by mid-2011. CNOOC is the only pure E&P name among the three, so it is logical that it

witnessed the best multiple expansion.

Figure 70: CNOOC's EV/EBITDA—2009-11 Figure 71: CNOOC's EV/EBITDA—2011 to date

Source: the BLOOMBERG PROFESSIONAL™ service, Credit Suisse research Source: the BLOOMBERG PROFESSIONAL™ service, Credit Suisse research

50

100

150

200

250

300

Jan-09 Jul-09 Jan-10 Jul-10 Jan-11 Jul-11

Jan-16 Jul-16 Jan-17 Jul-17

(Rebased to 100)

Oil price trend - 2016-17 vs 2009-11

4.2x

5.3x

3.2x

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

6.0

6.5

Jan-09 Jul-09 Jan-10 Jul-10 Jan-11 Jul-11

Avg:

+1STD:

-1STD:

5.1x

5.6x

4.6x

6.2x

4.1x

3.5

4.0

4.5

5.0

5.5

6.0

6.5

7.0

7.5

2011 2012 2013 2014 2015 2016 2017

Avg:

+1STD:

-1STD:

-2STD:

+2STD:

12 January 2017

China Oil & Gas Sector 29

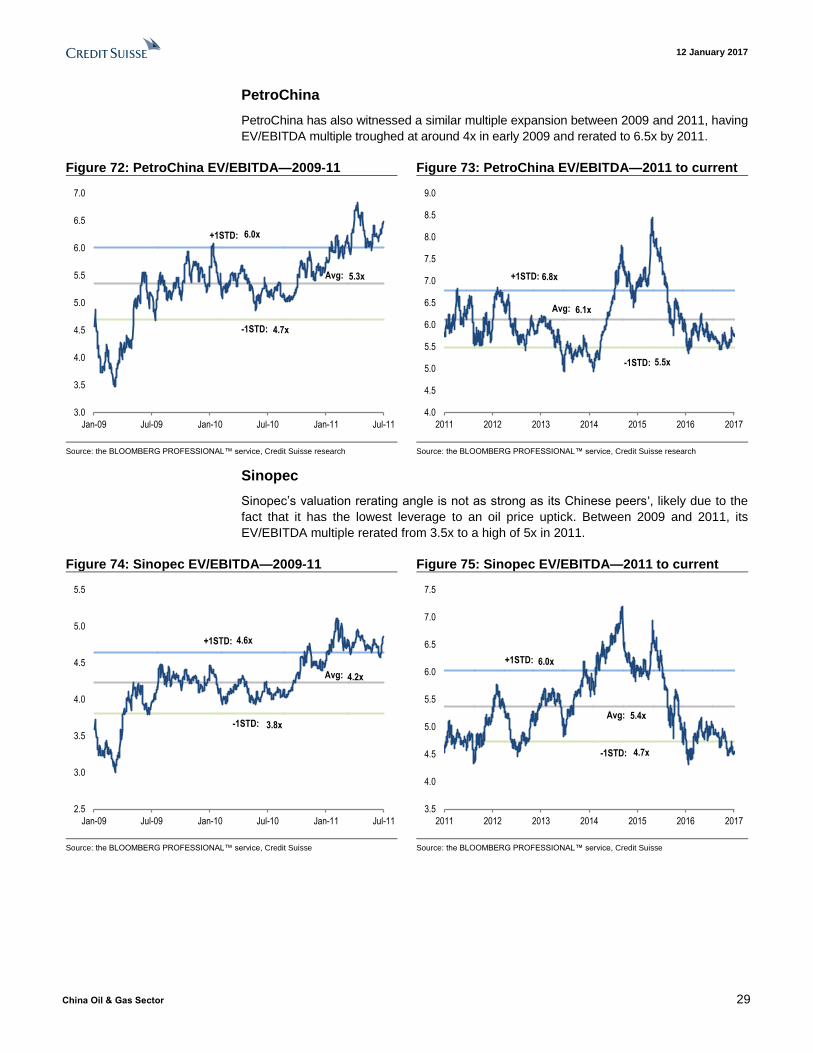

PetroChina

PetroChina has also witnessed a similar multiple expansion between 2009 and 2011, having

EV/EBITDA multiple troughed at around 4x in early 2009 and rerated to 6.5x by 2011.

Figure 72: PetroChina EV/EBITDA—2009-11 Figure 73: PetroChina EV/EBITDA—2011 to current

Source: the BLOOMBERG PROFESSIONAL™ service, Credit Suisse research Source: the BLOOMBERG PROFESSIONAL™ service, Credit Suisse research

Sinopec

Sinopec’s valuation rerating angle is not as strong as its Chinese peers', likely due to the

fact that it has the lowest leverage to an oil price uptick. Between 2009 and 2011, its

EV/EBITDA multiple rerated from 3.5x to a high of 5x in 2011.

Figure 74: Sinopec EV/EBITDA—2009-11 Figure 75: Sinopec EV/EBITDA—2011 to current

Source: the BLOOMBERG PROFESSIONAL™ service, Credit Suisse Source: the BLOOMBERG PROFESSIONAL™ service, Credit Suisse