australian first edition - credit suisse | plus

TRANSCRIPT

Note: If the rating of a company shown on the cover of First Edition is in bold type, a rating change has taken place

CREDIT SUISSE SECURITIES RESEARCH & ANALYTICS BEYOND INFORMATIONTM

Client-Driven Solutions, Insights, and Access

EQUITY RESEARCH CREDIT SUISSE EQUITIES (AUSTRALIA) LIMITED ABN 35 068 232 708 ACN 068 232 708 | Participating Organisation of the Australian Stock Exchange

Australia & NZ Daily Research Friday, 14 February 2014

COMPANIES & SECTORS

AWK Airwork Holdings NEUTRAL 13 .NZ Engineering a competitive advantage

ASX ASX UNDERPERFORM 26 Revenue growth across the board

DJS David Jones NEUTRAL 39 2Q14 sales

GMG Goodman Group NEUTRAL 43 Earnings achieved in a transition period

GPT GPT Group OUTPERFORM 48 Grinding away

IRE IRESS NEUTRAL 54 Glass half empty or glass half full?

MYX Mayne Pharma NEUTRAL 58 US portfolio expanded with another acquisition

SGP Stockland NEUTRAL 60 Entering the upgrade cycle

SGN STW Communications Group NEUTRAL 73 Soft underlying result, acquisitions yet to

generate solid returns

TLS Telstra Corporation OUTPERFORM 80 Mobile performance remains strong

WEB Webjet NEUTRAL 90 Risks to the core, but becoming full service

RESULT PREVIEW

AWC Alumina Limited OUTPERFORM 95 2013 results preview; reports on 20 Feb

Australian Transport Sector 98 1H14 preview: Cost-outs will be rewarded

against volume headwinds

BEN Bendigo and Adelaide Bank NEUTRAL 115 1H14 results preview; reports on 17 Feb

FMG Fortescue Metals Group OUTPERFORM 123 1H14 results preview; reports on 19 Feb

ILU Iluka Resources NEUTRAL 125 2013 results preview and operation analysis;

reports on 21 Feb

MGX Mount Gibson Iron UNDERPERFORM 136 1H14 results preview and exploration success;

reports on 19 Feb

UGL UGL NEUTRAL 142 HY14 results preview; reports on 17 Feb

STRATEGY & ECONOMICS

Australian Investment Strategy 146 Strategy Portfolio Changes - SUN out ASX in

DISCLOSURE APPENDIX CONTAINS ANALYST CERTIFICATIONS AND THE STATUS OF NON-US ANALYSTS. FOR OTHER IMPORTANT DISCLOSURES, visit www.credit-suisse.com/ researchdisclosures or call +1 (877) 291-2683. U.S. Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

MARKET EVENTS

Results, Automotive Hldgs Group 14 Feb

Results, Charter Hall Retail REIT 14 Feb

Results, Newcrest Mining 14 Feb

Results, Sims Metal Mgmt 14 Feb

UPCOMING CONFERENCES

2014 HOLT Conference 2014 – London

25 Feb

2014 5th Annual DC Defense Conference – Washington

25 Feb

For more scheduled conferences refer to page 2

TABLES

Credit Suisse Ratings – Australia 148

Top 100 Earnings & Dividends 151

Small Caps Earnings & Dividends 154

Sector Aggregates 157

Reporting Season Calendar 158

March 24-28, Hong Kong

Australia and NZ First Edition 2

Australia & NZ Market Reports

Australia Index +/- %Day %Wk %Mth %YrRol

All Ordinaries 5318.7 -1.1 0.0% 3.3% 1.9% 5.9% S&P/ASX 50 5478.0 -2.2 0.0% 3.3% 1.8% 7.4% S&P/ASX 200 5308.1 -2.0 0.0% 3.4% 1.8% 6.1% Financials 5790.7 -12.5 -0.2% 3.9% 1.0% 10.9% REITs 1009.6 0.6 0.1% 2.1% 1.8% -1.0% Industrials 3904.2 9.2 0.2% 3.0% 1.6% 0.8% Materials 10356.0 -0.1 0.0% 4.9% 5.7% -6.0% Cons. Discreet 1786.7 6.2 0.3% 3.4% 0.9% 18.2% NEW ZEALAND

NZX 50 4873.5 3.556 0.1% 1.4% 0.2% 15.4%

Currencies, Interest Rates & Gold

Index +/- %Day %Wk %Mth %YrRol

AUD/USD 0.893 -0.009 -1.0% -0.2% -0.4% -13.8% AUD/GBP 0.544 0.000 0.0% -0.9% -0.3% -18.3% EURAUD 1.505 0.000 0.0% -0.7% -1.3% 15.9% NZD/USD 0.830 -0.002 -0.3% 0.6% -1.0% -1.9% AUD/NZD 1.084 0.000 0.0% -0.1% 1.4% -11.5% TWI 0.697 0.003 0.4% 1.6% 0.4% -10.3% Aust 90Day 2.450 0.000 0.0% 0.0% 0.0% Aust 10Y 4.244 0.024 0.6% 2.8% 1.0% 20.7% NZ 90Day 3.220 NZ 10Y 4.630 0.005 0.1% 1.1% -1.6% 19.0% Gold Spot 1,291 -0.820 -0.1% 2.7% 3.7% -21.4%

Best Performers Worst Performers

Close % ‘000 Close % ‘000

Webjet 3.16 26.4% 1571 Sundance Rsc 0.10 27146 Nexus Energy 0.07 15.3% 11476 Goodman Fielder 0.59 -7.1% 34886 Mayne Pharma 0.87 9.5% 5662 Primary Health Care 4.55 -5.4% 8365 Qantas Airways 1.19 6.3% 31188 OM Holdings 0.56 -4.3% 4 Silver Chef 5.55 5.3% 46 Whitehaven Coal 1.61 -3.9% 8287 GMEL 0.21 5.0% 780 Skilled Group 2.97 -3.9% 2393 Teranga Gold 1.08 4.9% 180 MacMahon Hldgs 0.13 -3.8% 1559 McMillan Shakespeare 11.57 4.7% 601 Dulux Group 5.49 -3.7% 1499 Western Areas 3.14 4.7% 1654 Elemental 0.28 -3.5% 368 NewSat Limited 0.46 4.5% 1589 Intrepid Mines 0.29 -3.4% 566 Imdex 0.57 3.7% 77 Crowe Horwath 0.28 -3.4% 529 PanAust 1.85 3.7% 8403 Boart Longyear Grp 0.44 -3.3% 1675

Source: ASX, Bloomberg, Reuters

Commodity Prices Spot* Forward Curve Credit Suisse Forecasts 3mth 15mth 1Q14 2014 2015

Bulks Iron Ore $/t 121.0 125.0 111.3 95.0 Coking Coal $/t 143.0 153.3 167.5 Thermal Coal $/t 76.8 85.0 85.0 90.0 Base Metals Aluminium USc/lb 76.8 78.2 83.1 77.1 82.2 90.7 Copper USc/lb 326.5 324.5 321.5 317.5 300.5 306.2 Nickel USc/lb 651.3 653.0 656.1 635.0 629.4 646.4 Zinc USc/lb 91.6 91.7 92.6 90.7 95.3 107.7 Lead USc/lb 95.3 96.2 96.8 99.8 103.2 108.9 Tin USc/lb 1020.4 1019.5 1043.3 1071.6 1128.3

Precious Metals Gold US$/oz 1290.6 1160.0 1082.5 990.0 Silver US$/oz 20.2 18.7 18.2 18.5 Platinum US$/oz 1402.0 1380.0 1430.0 1562.5

Energy Oil (Brent) US$/bbl 108.5 108.0 102.9 107.0 101.8 97.5 Oil (WTI) US$/bbl 100.4 99.2 90.1 94.0 91.8 87.5

*Fiscal year averages used, Steel prices are contract prices. Spot as of 10PM AEST.

VIX (S&P 500 Options Implied Volatility)

0.00

10.00

20.00

30.00

40.00

50.00

60.00

70.00

80.00

90.00

Jan

-96

Au

g-9

6

Ap

r-97

Dec-9

7

Au

g-9

8

Ap

r-99

Dec-9

9

Au

g-0

0

Ap

r-01

Dec-0

1

Au

g-0

2

Ap

r-03

Dec-0

3

Au

g-0

4

Ap

r-05

Dec-0

5

Au

g-0

6

Ap

r-07

Dec-0

7

Au

g-0

8

Ap

r-09

Dec-0

9

Au

g-1

0

Ap

r-11

Nov-1

1

Jul-1

2

Dec-1

2

Jun

-13

Dec-1

3

Daily VIX (S&P 500 Options Implied Volatility)

VIX Index Average -1 StDev +1 StDev

VIX – Current 1mth rol(avg) 3mth rol(avg) 6mth rol(avg) 14.30 15.78 14.28 14.51 Freight Spot 1 wk (avg) 1 mth (avg) 3 mth (avg) 6 mth (avg) 1 yr (avg)

Baltic Dry 1091.0 1093 1219 1644 1653 1278

Source: Bloomberg

Upcoming Credit Suisse Global Conferences New additions this week in bold.

February 2014 to November 2014

Feb-Mar 2014 Q1 Media Seminar – London

25 Feb 2014 HOLT Conference 2014 – London

25 Feb 2014 5th Annual DC Defense Conference – Washington

4-5 Mar 2014 Global Healthcare Conference – London

5 Mar 2014 Geneva Autos Show 2014 – Geneva

10-12 Mar 2014 Global Services Conference – Scottsdale, Arizona

11-12 Mar 2014 European Banks Conference 2014 – London

13 Mar 2014 Global Flagship event – London

13 Mar 2014 9th Annual European Cable and Telecoms Conf – London

13-16 Mar 2014 DCM Winter Conference 2014 – Silvaplana-Surlej

19-21 Mar 2014 Prime Services 2014 Hedge Fund Leadership Conf. – Florida

24 - 28 Mar 2014 Asian Investment Conference – Hong Kong

25 Mar 2014 Asian Hedge Fund Forum 2014 – Hong Kong

26-28 Mar 2014 Global Trading Forum 2014 – Miami

8 May 2014 Stockholm Consumer IR Day – Stockholm

14-15 May 2014 Chemicals & Ag Conference – London

May-Jun 2014 Q2 Media Seminar – London

3-4 Jun 2014 Energy Conference – London

5 Jun 2014 European Gaming Companies Conference – London

11 Jun 2014 Global Small & Midcap Conference – London

12 Jun 2014 European Buildings Conference – London

Jun 2014 Swiss Midcap Healthcare Conference – Zurich

Aug-Sep 2014 Q3 Media Seminar – London

10-12 Sep 2014 Asian Technology Conference – Taiwan

15-16 Sep European Telecoms 1:1 Conference – London

17-18 Sep Pan European Capital Goods Conference – London

24-25 Sep Global Steel & Mining Conference – London

3-4 Oct Paris Auto Conference – Paris

Oct-Nov Q4 Media Seminar – London

1 Nov Global Consumer IR Day – London

Nov Swiss Midcap Conference – Zurich

If you would like to attend any of the above conferences, please contact the Australian Corporate Access team: Cathy Kermond [email protected] or your Credit Suisse sales representative

Research Production

Adam Indikt – Supervisory Analyst 61 3 9280 1659 Patricia Rocis – Supervisory Analyst 61 3 9280 1678

Web Access Research Distribution [email protected] Email: [email protected]

Database Jason Swinbourne 612 8205 4591

Bottom Liners

14 February 2014

Australia and NZ First Edition 3

At a Glance Australia/NZ equities executive summary

COMPANIES & SECTORS

Engineering a competitive advantage Airwork Holdings (AWK.NZ)

We initiate coverage on AWK with a DCF-based 12-month target price of $3.00 and a NEUTRAL rating. AWK is a specialist aviation business operating in fixed wing and helicopter leasing and maintenance. AWK owns, operates and maintains a fleet of aircraft that are supported by a world-class maintenance, repair and overhaul (MRO) capability backed by extensive local and international certification. In June 2013 AWK received European Aviation Safety Authority (EASA) certification. This has the potential to step change revenue and earnings of its Helicopter Engineering division and represents an area of upside risk to forecasts. Early benefits of EASA certification have been encouraging, with a key contract signing in Germany. Canada and South Africa are other markets that have been assessed as offering strong potential. Helicopter demand remains strong, particularly in the oil and gas sectors, and AWK’s upgrade capability positions the company for pursuing offshore leasing contracts. Potential exists to deploy further helicopters in markets such as Africa over and above what our current forecasts assume, particularly if mining related exploration and development activity expand. AWK has embarked on a programme of productivity measures within the Fixed Wing division to improve cost efficiency and fleet utilisation. Benefits from this programme are expected to commence from FY14. AWK will report its interim result on Wednesday 19 February.

Share Price 2.96 (NZD)

NEUTRAL

Target Price 3.00 (NZD)

Paul Turnbull Research Analyst 64 9 302 5559 This report is distributed in Australia by Credit Suisse Equities (Australia) Limited. Please see legal disclaimer and disclosure annex for further terms and information. Provided by First NZ Capital

Revenue growth across the board ASX (ASX.AX)

ASX reported 1H14 NPAT of $189.6mn, slightly below our $191mn (consensus $187mn) and an interim dividend of 88.2cps (consensus 89.8cps). Revenue was slightly above our expectations, however this was offset by an 8.3% increase in operating expenses. We maintain our UNDERPERFORM rating with a $35.20 target price. Key points: (1) all major ASX business lines increased revenue year-on-year in 1H14, for the first time since the end of 2008; (2) operating expenses increases 8.3% due to an increase in staff numbers; (3) capital expenditure guidance has increased from $40mn to $40-$45mn; (4) the largest business line, Derivatives, had the lowest growth and we note that the daily contract average for ASX 24 was down 11% on 2H13. Earnings changes: We have lowered our FY14 NPAT by 0.6% and increased FY15 by 1.1%. The increase in outer year revenue forecasts is driven by a base increase to information services revenue. While 1H14 expenses were higher than expected we have maintained our FY14 estimate and lowered outer years on the assumption of further cost savings in occupancy and equipment expenses. Investment view: ASX is currently trading at a ~20% PE premium to the market, the middle of the 10-30% range it has traded at over the past five years. While the 1H14 operating revenue growth was 8.0% on pcp, the growth on 2H13 was only 5.4% with the decline in activity late in 1H14 flowing through to the start of 2H14. With downside risk to earnings we consider the current share price as full and maintain our UNDERPERFORM rating.

Share Price 36.25 (AUD)

UNDERPERFORM

Target Price (from 33.20) 35.20 (AUD)

Andrew Adams Research Analyst 61 2 8205 4106

14 February 2014

Australia and NZ First Edition 4

2Q14 sales David Jones (DJS.AX)

DJS returned to positive LFL sales growth in 2Q14. Second-quarter sales of $618mn and LFL sales growth 2.1% were in line with forecast (CS $622mn, 2.0%). Online was above expectations and stands to boost total sales by 100–150bp through 2014. We have upgraded our second-half LFL sales forecasts 50bps to 3.0%. The upgrade reflects the improved run rate in on line sales and an assumption of steady growth in the market. Gross margin has been downgraded 50bp for 1H14 and 30bp for 2H14 due to higher levels of promotional activity. EPS has been downgraded 3% due to gross margin effect (-4%) and LFL sales upgrade (+1%). Online sales improved through the period: Online sales increased 150% in 2Q14 and accounted for 2.0% of group sales in the quarter. That outcome suggests online growth contributed ~60% of the total growth in comparable store sales. Commentary that online was 1.4% of first-half sales implies acceleration is ongoing and it is therefore likely to make an increasing contribution to 2H14 LFLs. There is likely to be a positive margin impact over time due to the growth of online. Promotional activity was higher than expected. Inventory issues in Target appeared to lead a period of higher-than-expected promotional expenditure. That effect is likely to be temporary due to Target's restructuring efforts. We expect some heightened promotional activity to continue through 3Q14. Earnings and valuation: We have downgraded EPS due to a reduction in gross margin. In our view, the sales lift is of greater materiality than the temporary increase in promotional activity thought 2Q14. DJS appears on the verge of successive quarters of sales and consequent profit growth.

Share Price 3.14 (AUD)

NEUTRAL

Target Price 3.14 (AUD)

Grant Saligari Research Analyst 61 3 9280 1720

Earnings achieved in a transition period Goodman Group (GMG.AX)

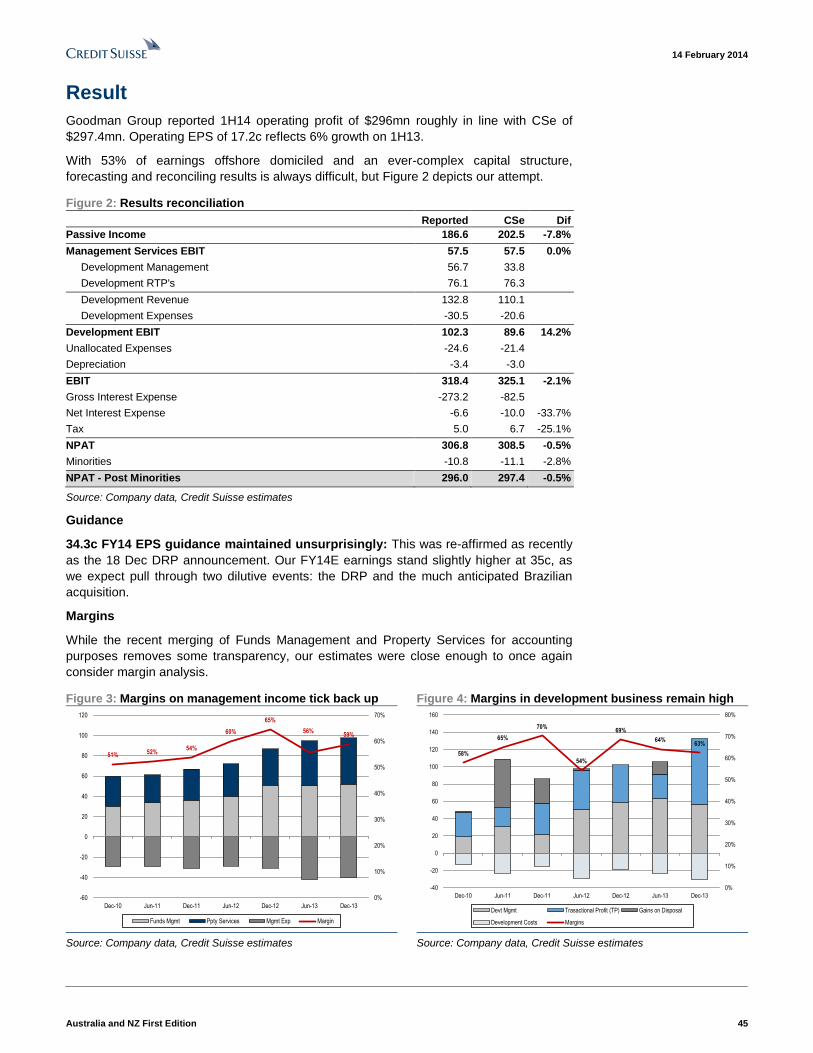

Not disappointed by guidance: Goodman Group reported 1H14 operating profit of $296mn roughly in line with CSe of $297.4mn. Operating EPS of 17.2c reflects 6% growth on 1H13. While some may be disappointed to note GMG merely re-iterated 6% EPS growth guidance for FY14 (34.3c) we remain slightly higher (35c) to be diluted back to guidance on inclusion of the DRP and our expectation that the Brazil deal will close towards the end of 3Q FY14. Investment case: Goodman Group trades on a 13.2x P/E representing a 0.92x P/E Rel, only slightly below the historical average of 0.96x. Growth expectations into Year Two stand at 7.3% relative to an average expectation of 7.8% over the past 12 months. For GMG to meaningfully outperform, the market will need to value the quality (sustainability) of GMG's growth, for which a market correction may be a catalyst. We also note, speculation about the "overhang" associated with the CIC block continues to weigh on pricing. Catalysts: This half saw the first meaningful Japanese development impact on the P&L. We expect the Japanese contribution will ramp up quickly from here with Osaka (~March), Nagoya (Dec Qtr) and Tokyo Bay (Dec Qtr) representing ~$550mn of completions this year. We expect WIP to remain at ~$2.5bn with these completions offset by Ichikawa commencement in 4Q and a US ramp-up to ~$250mn of WIP by year-end. Valuation: Our target price of $4.95 is struck at our June 2014 Net Asset Valuation applying: a 7.65% WACR to balance sheet NOI, 11.4x multiple to management EBIT and 12x to development EBIT. We apply an 8x multiple to unallocated expenses.

Share Price 4.76 (AUD)

NEUTRAL

Target Price 4.95 (AUD)

Stephen Rich Research Analyst 61 2 8205 4617

14 February 2014

Australia and NZ First Edition 5

Grinding away GPT Group (GPT.AX)

No magic bullets. GPT reported FY13 earnings of $471.8m as pre-released on 28 January. EPS of 25.7c represents a 6.1% increase on 2012. Having ridden a cost of debt reduction from 7.4% in 2010 to 5.1% today, we should now expect real estate type returns. To that end, 3% EPS growth is a reasonable outcome. Two concerns arise from GPT's strategy: (1) Management is incentivised to lever up to drive DPS growth and (2) the focus on tangible asset growth appears at odds with the desire to grow active earnings. OUTPERFORM rating retained due to value in real estate portfolio. Investment case. GPT owns and manages a high-quality portfolio of Australian Real Estate. At $3.66, GPT is trading on: a forward NOI yield of 7.2%, a dividend yield of 5.6% and a 13.6x FY14 FFO. While we see better value in Dexus, WRT and MGR, GPT combines inherent value with an active buyback, which we expect would be effective in a market correction. Catalysts. We note the buyback activity was not included in GPT's 3% EPS growth guidance but also note that GPT has significant capacity to buy back stocks on an earnings yield of ~7.2% versus a cost of debt of 5.1%. Operationally, we look forward to leasing success at Governor Macquarie Tower and/or MLC Centre or a recovery in retail lead indicators such as retention to refocus the market on the quality of the real estate. Valuation. We strike our target price in line with our December 2014 Net Asset Valuation at $4.00. Key inputs include: 5.8% cap rate on malls, 8.0% on industrial and a 6.56% implied cap rate on office as well as 10.0x on active earnings and 9.25x on costs. If GPT was to trade to our $4.00 NAV in 12 months, it would offer a 5.3% forward dividend yield at that time.

Share Price 3.66 (AUD)

OUTPERFORM

Target Price 4.00 (AUD)

Stephen Rich Research Analyst 61 2 8205 4617

Glass half empty or glass half full? IRESS (IRE.AX)

Pros and cons: A criticism of IRE is that for a stock with a fairly demanding multiple, it hasn't delivered much growth over the last few years. The counter to this is that for a company that has as much financial market exposure as IRE has, it has done remarkably well. As always, the forward-looking view is most important and in that regard we are starting to become more optimistic on the growth profile. This is not without its share of risks however, and for the time being we find that the pros and cons equal out at current valuation levels. We retain our Neutral rating. Paul Buys assumes coverage of IRE following a change in analyst responsibility. UK is the key driver: We have reviewed our key assumptions for IRE, but while our updated forecasts result in some revisions at a divisional level, the net impact on group EPS is fairly minor. We assume A&NZ Financial Markets remain flat into FY14 and some further growth for A&NZ Wealth Management, although at moderated levels. That leaves the UK business as the key growth driver. Key opportunities are the market size, regulatory change and IRE's competitive technology – basically, the potential to replicate IRE's XPLAN/VisiPlan experience. Key risks include integrating Avelo (the CEO has relocated to the UK to oversee this), managing legacy product and the different UK structure (greater dealer group independence). Valuation: Our target price increases from $8.75 to $9.60, due mainly to modest positive EPS revisions and a higher market multiple. On a PE basis, IRE trades in line with its long-term average premium of ~45% relative to the ASX Small Industrials (XSI). However, the stock looks more demanding on an EV/EBIT basis (~1 standard deviation expensive) given the introduction of debt to the balance sheet post the Avelo acquisition.

Share Price 9.25 (AUD)

NEUTRAL

Target Price (from 8.75) 9.60 (AUD)

Paul Buys Research Analyst 61 2 8205 4538

14 February 2014

Australia and NZ First Edition 6

US portfolio expanded with another acquisition Mayne Pharma (MYX.AX)

Brand franchises acquired: MYX has completed an A$18mn equity placement (~22.6mn shares) to fund the acquisition of the LORCET and ESGIC brands from Forest Pharmaceuticals for ~A$13.4mn (US$12mn). LORCET contains hydrocodone + paracetamol and is used to treat moderate to moderately severe pain, while ESGIC contains butalbital (a barbituate), paracetamol and caffeine and is indicated for tension headaches. Gross sales of both products were ~US$5mn in FY13 (implying a sales acquisition multiple of 2.4x). Manufacturing of both products is currently outsourced but MYX could look to bring this in-house in the medium term when contracts expire. Further, MYX will directly distribute both brands through its US Midlothian business and hence realise a high margin on sales. Management noted that investment in both products had been somewhat limited by Forest and that there was opportunity for MYX to grow share. Sound strategy: This brand acquisition is another example of MYX executing its core strategy of acquiring "unloved", complementary products to properly market and distribute with the intention of growing the brands. We suspect similar opportunities will continue to present themselves and that further acquisitions will follow. The strategy is in our view sound, prices paid are relatively undemanding and acquired assets are leveraged by MYX's existing infrastructure and business capabilities. As with all pharmaceutical companies we see some inherent regulatory risk with new products but see the company as a fundamentally attractive investment proposition. Catalysts: MYX 1H14 result (26 February) Valuation: While the acquisition is expected to be mid-single digit EPS accretive (pre-synergies) in its first full financial year (FY15), we will incorporate the transaction in our forecasts following MYX's formal 1H14 result. Our target price is based on DCF valuation.

Share Price 0.86 (AUD)

NEUTRAL

Target Price 0.86 (AUD)

Saul Hadassin Research Analyst 61 2 8205 4679

14 February 2014

Australia and NZ First Edition 7

Entering the upgrade cycle Stockland (SGP.AX)

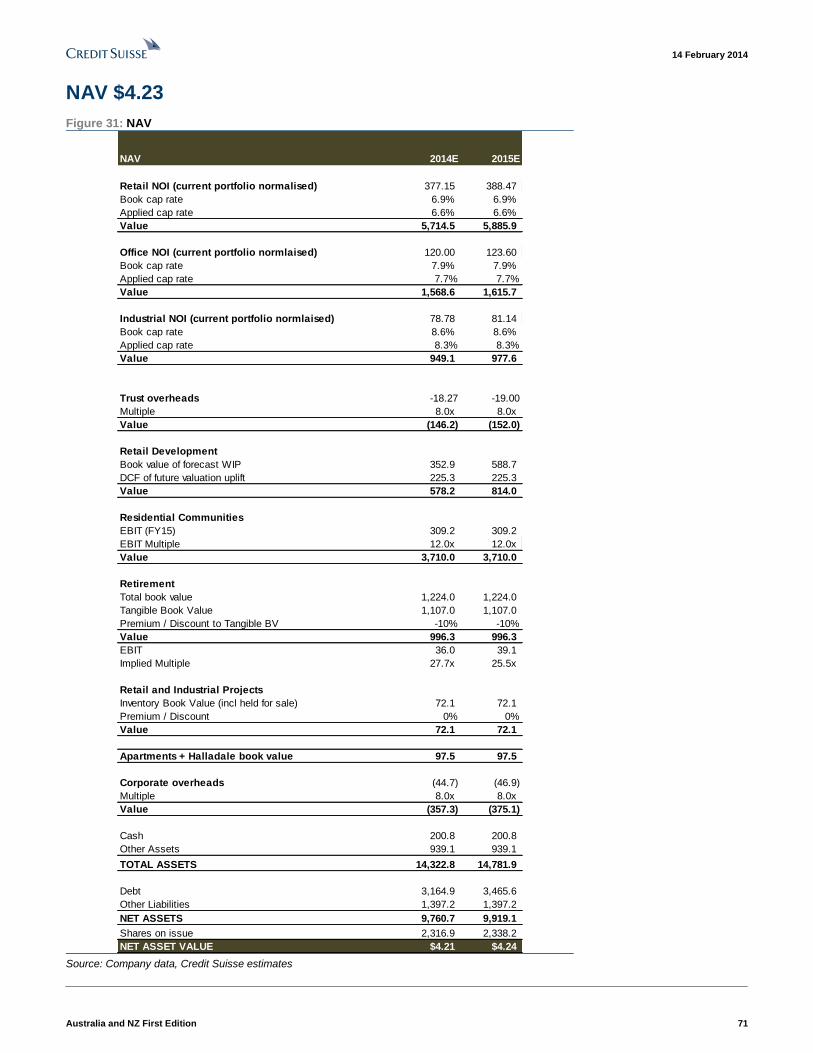

Entering the upgrade cycle. After two years of negative consensus earnings revisions, SGP has now entered the upgrade cycle, with management lifting its previous FY14 EPS growth guidance from 4-6% to 5-6% largely on the back of stronger residential earnings. We have lifted our earnings by 0.5%, and our FY14-16E EPS CAGR of 7.6% is the highest in our universe after LLC, and sits above SGP's upper EPS growth hurdle for LTI awards of 6.5% p.a. Higher quality earnings. SGP's 1H14 EPS of 11.6¢ was flat on 1H13 and was in line with our forecast (of 11.6¢). Quality improved on several fronts: (1) Operating cash increased 60% representing 113% of NPAT; (2) Net capitalised interest moved from $20m to -$29m representing -11% of NPAT, and (3) the tax benefit reduced from 10% of pre-tax profit to 7%. On the negative side, SGP's 12¢ DPS remains above both EPS (11.6¢) and AFFO (10.6¢). Residential delivers. Residential profit grew 49% due to 8% growth in settlements (2,253) and a lift in operating margins from 7.0% to 8.9%. Net deposits of 3,197 are running well ahead of settlements driving a 67% increase in pre-sales, which support our FY13-16 EBIT CAGR of 34% for the business. Commercial still tough. While developments on 11-13% IRR's supported 10% growth in retail NOI, operations are still tough. Retail comp NOI growth declined for the fifth consecutive period to 2.6% and comp spec MAT growth was -0.8% versus +2.7% in June. Office and industrial occupancy sit at <92%. Upside priced in. Despite positive EPS growth, improving market conditions and improved earnings quality, SGP offers a TSR of 14.6% in line with the AREIT sector at 13.6%, warranting a NEUTRAL rating. SGP currently trades on a 14.7x P/E and at a 6% P/E premium to ASX versus its historic 2% discount. Our $4.23 NAV applies a 7.0% WACR (versus 7.3% book), a 12x FY15E EBIT multiple for Communities and values Retirement at a 10% discount to tangible book.

Share Price 3.90 (AUD)

NEUTRAL

Target Price (from 4.00) 4.23 (AUD)

John Richmond Research Analyst 61 2 8205 4580

Soft underlying result, acquisitions yet to generate solid returns

STW Communications Group (SGN.AX)

Event: STW Communications reported a weaker-than-expected FY13 result. NPAT increased 12.5% vs consensus and guidance for 15% growth. EPS increased 2.5% vs consensus and guidance for mid-single-digit growth. The result was impacted by a number of acquisitions as well as changing business mix to lower margin research and field marketing businesses and office relocation and consolidation. STW Communications provided FY14 guidance for mid-single-digit NPAT growth which was below market expectations for high-single-digit growth. We have reduced our forecasts following a weaker-than-expected result and outlook. Our TP moves to $1.55 (from $1.63) per share and we maintain a NEUTRAL rating. Investment case: Underlying business fairly static, acquisitions yet to generate solid returns. Most of the profit growth in FY13 came from acquisitions within Australia, and to a lesser extent acquisitions in Asia. Whilst the acquisitions make strategic sense and are likely to increase STW Communications' market share, they do not appear to be driving synergies within the group or contributing meaningful profits at this point. With a mix shift to lower margin businesses such as research and field marketing, it will become increasingly important for STW Communications to leverage its core business capabilities to drive additional revenues. We need to see a reversal in the current declining return on invested capital trend. Fair value with upside: STW Communications is trading on 11x FY14 and 10x FY15 EPS, broadly in line with its historical ratios. We forecast mid-single-digit growth p.a. for the next several years. There is upside from successful expansion in Asia and further abroad (although some upside from recent acquisitions will be offset by additional earnout payments if certain earnings targets are met).

Share Price 1.44 (AUD)

NEUTRAL

Target Price (from 1.63) 1.55 (AUD)

Samantha Carleton Research Analyst 61 2 8205 4148

14 February 2014

Australia and NZ First Edition 8

Mobile performance remains strong Telstra Corporation (TLS.AX)

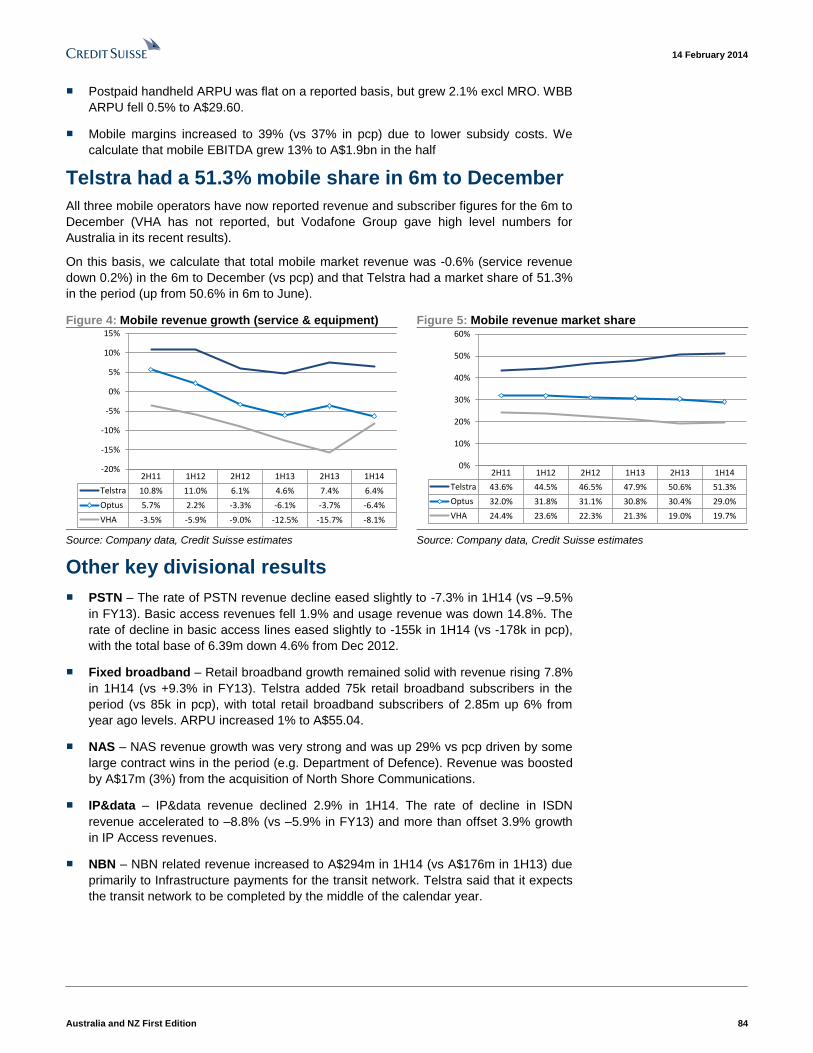

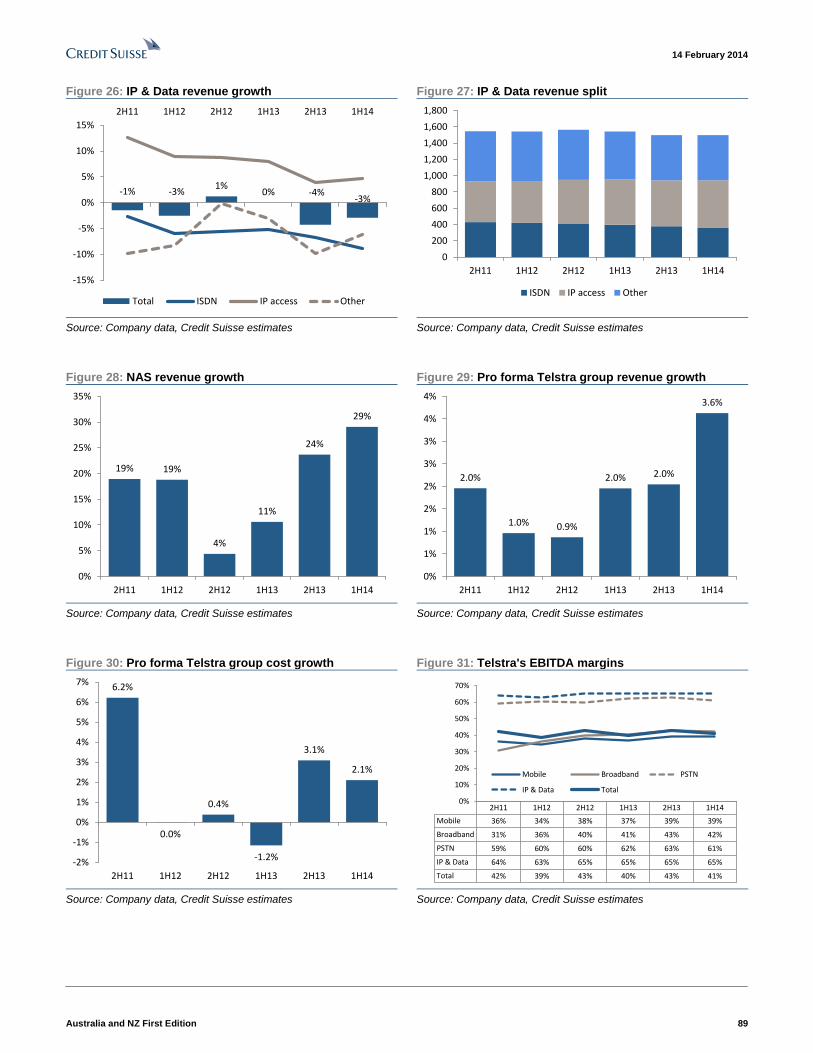

Solid 1H14 result: Telstra's 1H14 EBITDA of A$5.29bn (ex Sensis) was in line with our A$5.27bn forecast and up 7% vs pcp (+5% ex A$127m Telstra Clear impairment charge in pcp and ASB119). 1H14 NPAT of A$1.93bn was 2.6% ahead of our A$1.88bn forecast on lower depreciation. FY14 guidance for 'low-single digit EBITDA growth' (incl Sensis) was maintained. We raise our FY14F EBITDA by 0.8% to A$10.86bn (ex Sensis). FY14F NPAT is increased 2.6% to A$4.1bn due to lower depreciation. The interim dividend was raised to 14.5c (fully franked) and we forecast 29c for the full year. Mobile performance remained strong: Mobile growth remained strong, with mobile revenue rising 6.4% in 1H14 (vs +6.0% in FY13). Telstra added 739k mobile SIOs (vs 608k in pcp), although the majority were prepaid (postpaid handheld +103k). Postpaid handset ARPU (ex MRO) grew 2%. Mobile margins expanded to 39% (from 37% in pcp) and mobile EBITDA was up 13%. We calculate that the total mobile market declined 0.6% in the 6m to Dec and Telstra's market share rose to 51.3% (vs 50.6% in 6m to June). Costs slightly higher than expected: Costs grew 2.1% in the half, due to investment in NAS growth and lower efficiency savings (A$230m). The company said that efficiency savings will increase in 2H14 and it continues to target A$1bn in savings per annum for the next few years. OUTPERFORM rating and A$5.70 target price unchanged: We remain positive on the Telstra investment story with strong cashflows being supported by continued mobile growth, cost savings and NBN payments. We see upside from the emerging Asian growth strategy. Finalisation of NBN negotiations should be a key catalyst.

Share Price 5.15 (AUD)

OUTPERFORM

Target Price 5.70 (AUD)

Fraser McLeish Research Analyst 61 2 8205 4069

Risks to the core, but becoming full service Webjet (WEB.AX)

Zuji and LoH positive, but core still under pressure: Zuji appears on track and the TTV result for Lots of Hotels was ahead of expectations with the run rate now $65mn (up from $40mn at FY13). Backing out of the result the $2.1mn other gains and losses and adding back the $1mn in duplicated IT costs we believe the underlying EBITDA for 1H14 was ~$11.2mn and that it is supportive of FY14 guidance. However, we remain cautious given that we believe volumes in the core flights business remain negative, that in the 2H there will be the $2mn of incremental marketing spend for Zuji and that WEB is focused on scale in LoH and not on the short-term profitability ($0.4mn 1H14 loss may be carried into 2H). NEUTRAL rating retained. Key takeaways: (1) WEB's revenue margin increased ~23% to 10.3% (revenue / TTV) due to mix shift (higher proportion of accommodation TTV), 1H14 includes the full annualisation of the September 2012 increase in booking fees and improved commercial agreements with the airlines; (2) management gave no guidance into the air booking volumes in 1H14, and we believe that the negative run rate in 2H13 has likely continued, implying that WEB's booking volumes have continued to decline in its core flights business; (3) the weakness in WEB's booking volumes is not due to a single factor, it is a combination of many (cycling strong comps, slowing shift online, increased competition from airlines and other OTAs, growth in lower conversion mobile traffic); (4) the outlook for WEB's core flights business is softer, with Zuji and other initiatives required to drive earnings growth in FY14 and beyond; and (5) Lots of

Hotels is growing ahead of expectations, but management has changed its focus from profitability to scale ($0.4mn EBITDA loss in 1H14, previous guidance was for it to be profitable). Target price: $3.25 (from $2.90) moving back to an equally blended PER and DCF-based valuation methodology. Modest EPS revisions.

Share Price 3.16 (AUD)

NEUTRAL

Target Price (from 2.90) 3.25 (AUD)

Chris Smith Research Analyst 61 2 8205 4210

14 February 2014

Australia and NZ First Edition 9

RESULT PREVIEW

2013 results preview; reports on 20 Feb Alumina Limited (AWC.AX)

Expecting a messy result. The read-through from Alcoa results to AWC is poor when profits are weak because accounting translations from GAAP to AIFRS, plus black box retirement benefits and embedded derivative valuations overwhelm low values, swinging the results. On top of these problems, this year we have the true-up of the Alba settlements between Alcoa and AWC, another swing factor. AWC's share of Alcoa's profit was $41mn, but after finance, corporate costs, and accounting translations, we believe that the underlying NPAT will be US$17mn. Consensus is $12mn. We estimate FCF was US$60mn. AWC previously announced that new debt was down to $135mn at December. Cash inflows were the agreed AWAC dividends of US$105mn over the year. We forecast no dividend, but recognise risk. AWC has not paid a dividend since 2011, but having made positive FCF and with low net debt, it may decide a modest final dividend is warranted. But with commodity prices remaining weak and capital injections into AWAC of over $30mn being likely in 2014, we believe a wiser course would be to apply cash to reducing debt and set the company up for a better future. Our DCF valuation remains A$1.60/sh, and our target price is A$1.30/sh.

Share Price 1.25 (AUD)

OUTPERFORM

Target Price 1.30 (AUD)

Matthew Hope Research Analyst 61 2 8205 4669

1H14 preview: Cost-outs will be rewarded against volume headwinds

Australian Transport Sector

1H14 cost-out and self-help candidates should be rewarded against a weak volume backdrop and top-line outlook: With weak volumes and demand impacting the bulk of the Australian transport sector, we expect that evidence of cost-outs and solid execution at 1H14 results will be rewarded with relative outperformance. All stocks (excluding Qube) have publicly announced cost-out programmes, though the biggest upside in cost-out execution remains with AIO, AZJ and QAN. Asciano and Aurizon: cost-out upside baked in for AZJ, but what about AIO? While the cost-out opportunity is well understood for Aurizon, with the market already baking in 75% operating margins from FY15 (and then some), the opportunity for AIO is perhaps less well understood, but equally still available in Ports and PN Rail. We are optimistic that management can, in time, exceed the $150mn in cost-outs initially targeted under the BIP programme. For AZJ, the upside remains bringing forward the time frame for reaching 25% EBIT margins, currently expected in FY15. "One Toll" margin improvement? In the absence of a volume-led recovery, we believe evidence of productivity improvements elsewhere in the business in the form of margin expansion will be well received. While hard to quantify "One Toll" benefits, we believe they could progressively materialise from 1H14, as we start to see the first results of management turning its focus on consolidation instead of acquisitive growth. BXB back to more appropriate multiples: With BXB now trading back in line with its historical market multiple, and with management likely to reaffirm FY14 guidance, we see the result more about the timeline for growth in emerging markets as well as RPC penetration in North America. Following this note, we have removed Recall, resulting in 12% changes to earnings over the forecast period. We lower our target price from $9.83 to $9.29 leaving a NEUTRAL rating. Airlines: With guidance already given for both stocks and a looming "transformational" strategy day for Qantas, we see 1H14 results as perhaps less meaningful than in previous years. For VAH, we have lowered earnings over the forecast period and our target price to $0.38 (from $0.42). Qube – forecasts and target price upgraded into 1H14, based on volume expectations in Ports and Bulk as Qube progressively tender for contracts on the North West Shelf. Target price raised to $2.20, previously ($1.90), NEUTRAL rating maintained.

Nicholas Markiewicz Research Analyst 61 2 8205 4107

14 February 2014

Australia and NZ First Edition 10

1H14 results preview; reports on 17 Feb Bendigo and Adelaide Bank (BEN.AX)

Credit Suisse assumptions/variance to market Our FY14E $378mn cash earnings estimate sits 1% above the IBES $376mn consensus, while our corresponding DPS estimate of $0.64 is in line with the consensus. What to look for We would look for: 1) Some relief emerging for net interest margins, with term deposit spread pressures easing and the re-pricing of parts of the Community Bank originated portfolio; 2) Accelerating operating costs, reflecting new premises costs and acceleration of the Basel advanced accreditation programme; 3) Rural Bank asset quality (given on-going deterioration within half a dozen North Queensland cattle exposures, reflecting live export bans, drought and lower stock prices); and 4) Update on medium-term issues such as the progress of the Great Southern litigation and the Basel advanced accreditation programme. Share price implications BEN currently trades on 12.4x 12-month prospective earnings (equating to a 4% discount to the major banks vs an 8% four-year average discount and compared with Bank of Queensland on 12.3x) and a corresponding book multiple of 1.1x (major banks 2.1x, Bank of Queensland 1.3x).

Share Price 11.65 (AUD)

NEUTRAL

Target Price 12.20 (AUD)

James Ellis Research Analyst 61 2 8205 4531

1H14 results preview; reports on 19 Feb Fortescue Metals Group (FMG.AX)

We already have a good estimate of the key P&L items following the DecQ results. We can estimate revenue and expenses from received prices and C1 costs, and we know net debt and gearing as FMG has kept the market informed while calling in debt for repayment. Having the exact figures will be interesting, but there is unlikely to be anything in the results to change the view. We expect EPS of 53¢ps (consensus 55¢ps). Management provided an investor call less than three weeks ago, so we doubt much has changed. We will be looking for updates on the ramp-up of the Kings OPF and status of the Cloud Break wet front-end fix due for completion this month. We expect an interim dividend of 5¢/sh, ahead of zero last year, given the strong DecH result. This would represent a payout ratio of only 9% versus the policy of 30%-40%, but we understand the first priority is debt repayment. We doubt the market would welcome a dividend above consensus while gearing remains high. We expect the dividend payout will rise towards the payout policy once gearing reaches the targeted 40% level. Our DCF valuation remains A$9.60/sh and our target price A$7.50.

Share Price 5.62 (AUD)

OUTPERFORM

Target Price 7.50 (AUD)

Matthew Hope Research Analyst 61 2 8205 4669 All material presented in this report, unless specifically indicated otherwise, is under copyright to CS. None of the material, nor its content, nor any copy of it, may be altered in any way, transmitted to, copied or distributed to any other party, without the prior express written permission of CS.

14 February 2014

Australia and NZ First Edition 11

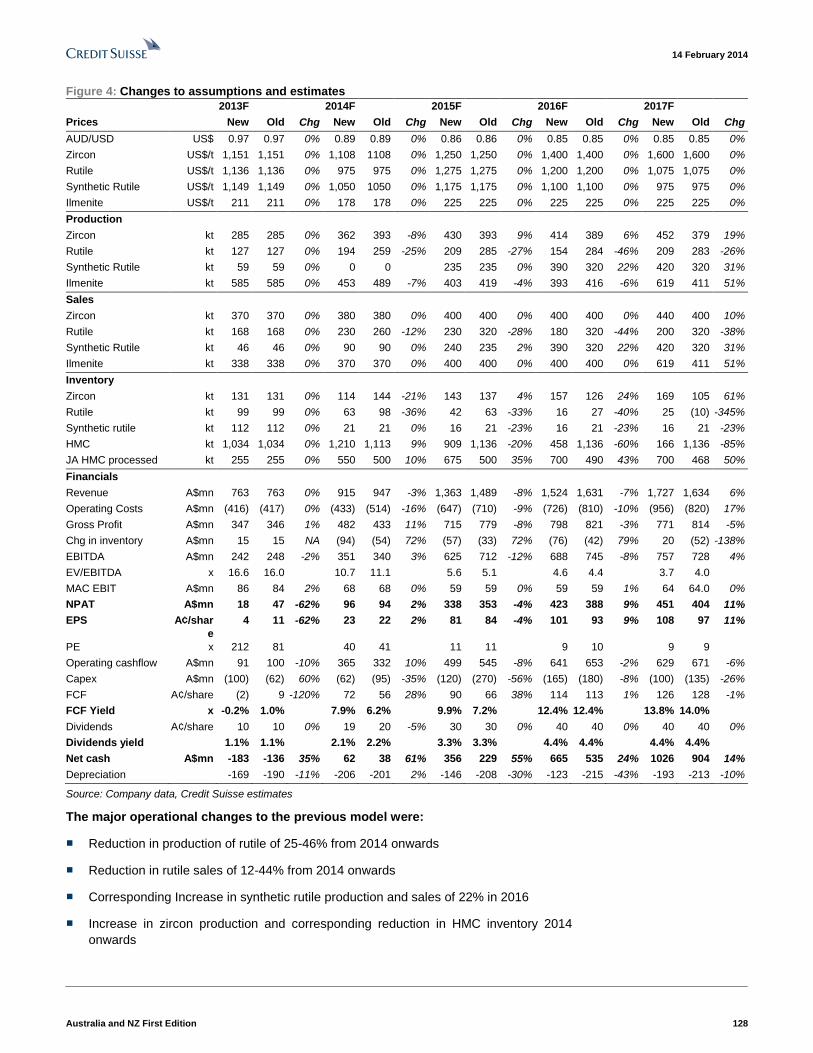

2013 results preview and operation analysis; reports on 21 Feb

Iluka Resources (ILU.AX)

Following the quarterly results and the 11 Feb report that NPAT is $18mn after impairments, we now have the main items of the P&L. Dividend – we expect policy-breaking 5¢/sh final dividend, matching interim. Payout policy is +40% of FCF measured after all capital. Capex for DecH is uncertain, but guidance was $100mn for the year. On that basis, we estimate 2013 FCF to be -$3mn. Interim dividend of 5¢/sh (A$21mn) looked beyond a hefty tax payment towards a stronger DecH, which did not eventuate. Policy would indicate no final dividend, given it would be funded with debt, but with a comfortable balance sheet, it may match interim at 5¢. Management call and cost guidance for the current year should be key catalysts for the outlook. We believe ILU is heading for a loss in the first half of 2014 with pricing now lower than the average for 2013. We will be interested in management response, although we doubt ILU has any further useful cuts available. We look closer at this issue in this note. MAC changes – ILU has given responsibility for the MAC royalty to a development manager and may begin moves to develop and spin off the royalty business. Our DCF valuation remains A$9.10/sh and our target price is $10.

Share Price 9.22 (AUD)

NEUTRAL

Target Price 10.00 (AUD)

Matthew Hope Research Analyst 61 2 8205 4669

1H14 results preview and exploration success; reports on 19 Feb

Mount Gibson Iron (MGX.AX)

Sales revenue can be estimated from the received prices (CS: $589mn, consensus $525mn), but we have no lead on cash costs. For EBITDA, CS: $230mn, consensus $224mn. A large swing factor in reaching NPAT is D&A, particularly amortisation of stripping, which is driven by earth moving at Koolan Island. We estimate NPAT of $142mn, consensus mean is $109mn, but with a $65mn range. MGX provided its cash balance in the DecQ report (A$484mn) which implies net cash of $465mn. Interim dividend nil: MGX has a policy of providing only final dividends. MGX today announced exploration success at Iron Hill prospect, 3km from Extension Hill mine. Successful Dec drilling and historical work (drilling and adits) has provided MGX with an exploration target of 5-7Mt at a grade of 58-61% Fe, which could extend the mine life by two years. Iron Hill is one of three prospects known at Extension Hill South lease from historical work. Extension Hill mine is due to end in 2017 on most recent reserves. A two-year life extension might increase our DCF valuation by 5¢ps if there is no capex, and costs are similar to the current mine. Nevertheless, earnings will improve if the mine life could be extended to 2021 like Koolan Island. Our DCF valuation and target price remain A$1.05/sh.

Share Price 1.12 (AUD)

UNDERPERFORM

Target Price 1.05 (AUD)

Matthew Hope Research Analyst 61 2 8205 4669

14 February 2014

Australia and NZ First Edition 12

HY14 results preview; reports on 17 Feb UGL (UGL.AX)

Credit Suisse assumptions/variance to market: We forecast HY14 underlying NPAT of $52.9mn, up 4% vs. pcp. Our forecasts imply 1H earnings seasonality of 41%, below the historical average (45%). What to look for: Reiterate FY14 guidance of $120-130mn underlying NPAT. Credit Suisse FY14 forecasts ($128mn) are 4% above consensus ($123mn). Solid property result to offset engineering: We forecast 24% growth in DTZ EBIT vs pcp driven by revenue growth (+8%) & margin uplift (to 5.7%). In contrast, we forecast an 11% decline in engineering EBIT in 1H14 with stronger projects EBIT offset by a weaker rail result. Demerger on track for FY15: We expect UGL to confirm it remains on track to have its property and engineering businesses structurally separated in FY14 and the demerger completed in FY15 subject to market conditions. UGL to focus on solid outlook for property supported by the US cyclical recovery and integration of DTZ. We are still cautious on engineering outlook: UGL is likely to identify the Dec-13 LNG maintenance contract win as evidence that resources maintenance activity is picking up. However, we need to see further contract wins to turn more positive on the outlook. UGL appears fair value: Trading at 10x 12-month fwd PE, valuation upside from the demerger is likely to be offset by the weak outlook for engineering.

Share Price 7.11 (AUD)

NEUTRAL

Target Price 7.75 (AUD)

Emma Alcock Research Analyst 61 2 8205 4403

STRATEGY & ECONOMICS

Strategy Portfolio Changes - SUN out ASX in Australian Investment Strategy

Strategy Short Ideas, Suncorp Out – We are taking profits from our short Suncorp position. The stock has been in our Short Ideas list since inception. Andrew Adams has been cautious on Suncorp given the stocks lofty valuations, aggressive insurance assumptions and likelihood of cutting revenue growth targets. Andrew notes that the upcoming results

announcement could be an additional negative for the share price.

Strategy Short Ideas, ASX In – In place of Suncorp, we are adding ASX to our Short Ideas. We believe the general pressures on the equity industry will continue to weigh on ASXs share price. Meanwhile, the company currently pays out 90% of free cash-flow in the form of dividends. FCF growth is expected to remain anaemic. Andrew Adams has recently assumed coverage on the stock with an Underperform rating.

He highlights falling value per trade and lower turnover velocity.

While we expect the Australian equity market to rally from here, we still anticipate ASX to underperform. Its historical beta has been less than one. Stock Themes – A number of themes run through our stock selection

process. First, Selfies continue to dominate the Australian investor base

and we know they have an acute focus on dividends. We do not want to stand in the way of these flows. Most of our long ideas are in a position to increase dividends. While our shorts generally operate on lower FCF yields and have less capacity to return capital to share-holders. Second,

we believe Australian companies will be operating in a low growth environment. Those companies in a position to generate returns,

irrespective of the macro backdrop, should be valued more highly. For this

reason, we have many restructuring candidates amongst our Long

Ideas. Third, while we believe bottom-up factors will continue to become more important in driving stock prices, there will continue to be macro

influences. One of the most important will be the RBA to cutting rates as mining investment unwinds. This supports our long position in a

number of consumer and residential housing exposed stocks.

Hasan Tevfik ,CFA Research Analyst 61 2 8205 4284

Australia and NZ First Edition 13

14 February 2014

Asia Pacific/New Zealand

Equity Research

Transportation Infrastructure (Industrials)

■

■

Airwork Holdings

(AWK.NZ) INITIATION

Engineering a competitive advantage

■ We initiate coverage on AWK with a DCF-based 12-month target price

of $3.00 and a NEUTRAL rating. AWK is a specialist aviation business

operating in fixed wing and helicopter leasing and maintenance. AWK owns,

operates and maintains a fleet of aircraft that are supported by a world-class

maintenance, repair and overhaul (MRO) capability backed by extensive

local and international certification.

■ In June 2013 AWK received European Aviation Safety Authority (EASA)

certification. This has the potential to step change revenue and earnings of

its Helicopter Engineering division and represents an area of upside risk to

forecasts. Early benefits of EASA certification have been encouraging, with a

key contract signing in Germany. Canada and South Africa are other

markets that have been assessed as offering strong potential.

■ Helicopter demand remains strong, particularly in the oil and gas sectors,

and AWK’s upgrade capability positions the company for pursuing offshore

leasing contracts. Potential exists to deploy further helicopters in markets

such as Africa over and above what our current forecasts assume,

particularly if mining related exploration and development activity expand.

■ AWK has embarked on a programme of productivity measures within

the Fixed Wing division to improve cost efficiency and fleet utilisation.

Benefits from this programme are expected to commence from FY14.

■ AWK will report its interim result on Wednesday 19 February.

Share price performance

90.0

95.0

100.0

105.0

110.0

2.00

2.50

3.00

3.50

4.00

Dec-13 Jan-14

Airwork Holdings Limited LHS Relative to NZX50 (RHS)

The price relative chart measures performance against the

NZX50 index which closed at 4870.0 on 12 Feb 14

The spot exchange rate was NZ$1.202/US$1 on 13 Feb 14

Performance over 1M 3M 12M

Absolute (%) 8.4 N/A N/A

Rel-NZX50(%) 9.0 N/A N/A

Year to 30 Jun 2012A 2013A 2014F 2015F 2016F

Adjusted Earnings NZ$m 8.0 10.1 12.0 13.2 13.9

EPS Adjusted NZc. 18.8 23.7 23.9 26.2 27.6

EPS Grow th % -32.6 25.8 0.8 9.8 5.5

P/E x 15.7 12.5 12.4 11.3 10.7

CPS NZc. 56.5 68.7 66.3 70.6 72.5

P/CF x 5.2 4.3 4.5 4.2 4.1

EV/EBITDA x 7.6 6.2 5.6 4.8 4.4

Net DPS NZc. 7.5 7.5 13.4 14.0 15.3

Imputation % 50.0 50.0 50.0 50.0 50.0

Net Yield % 2.5 2.5 4.5 4.7 5.2

Gross Yield % 3.0 3.0 5.4 5.6 6.2

Financial and valuation metrics

Source: Company data, NZX, First NZ Capital estimates

Rating NEUTRAL* Price (13 Feb 2014, NZ$) 2.96 Target price (NZ$) 3.00¹ Market cap. (NZ$mn) 148.71 Projected return: 0 Capital gain (%) 1.4 Dividend yield (net %) 4.6 Total return (%) 6.0 52-week price range (NZ$) 2.70-3.05

* Stock ratings are relative to the relevant country

benchmark.

¹Target price is for 12 months.

Research Analysts

Paul Turnbull

+64 9 302 5559

This report is distributed in Australia by Credit Suisse

Equities (Australia) Limited. Please see legal disclaimer and

disclosure annex for further terms and information

Provided by First NZ Capital

14 February 2014

Australia and NZ First Edition 14

Figure 1: Airwork Holdings financial summary

Sector: Transportation NZX Code: AWK

PROFIT & LOSS ($m) BALANCE SHEET ($m)Year to 30 Jun 2012A 2013A 2014F 2015F 2016F Year to 30 Jun 2012A 2013A 2014F 2015F 2016F

Operating Rev enue 103 118 126 134 143 Cash & Equiv alents 2.6 4.7 4.8 7.6 15.4

Operating Ex penses -72.3 -81.3 -86.5 -90.4 -96.8 Debtors & Inv entories 14.5 18.4 15.4 16.4 17.5

Operating EBITDA 30.4 37.1 39.2 43.2 45.9 Other Current Assets 39.6 31.7 24.5 26.5 28.3

Depreciation -16.0 -19.1 -21.3 -22.3 -22.6 Current Assets 56.8 54.8 44.7 50.5 61.1

Amortisation -0.2 -0.3 -0.2 -0.6 -0.6 Fix ed Assets 122 126 135 134 130

Operating EBIT 14.2 17.7 17.8 20.4 22.7 Inv estments 0.0 0.0 0.0 0.0 0.0

Other Income 0.0 0.0 0.0 0.0 0.0 Intangibles 1.0 1.7 3.7 3.8 3.9

Abnormals -10.6 -3.7 -0.9 0.1 0.0 Other Non-Current Ass. 4.4 1.8 2.1 2.0 2.0

Reported EBIT 3.7 14.0 16.9 20.5 22.7 Total Assets 185 185 189 194 201

Net Interest -5.2 -5.3 -4.4 -3.2 -3.5

Pretax Profit -1.5 8.7 12.5 17.2 19.3 Interest Bearing Debt 87.4 84.9 67.4 65.7 65.7

Tax 0.5 -2.2 -4.0 -5.1 -5.3 Other Liabilities 31.6 30.9 31.4 31.4 32.1

Minority Interests 0.0 0.0 0.0 0.0 0.0 Total Liabilities 119 116 98.7 97.1 97.8

Equity Accounted Profit 0.0 0.0 0.0 0.0 0.0 Minorities 0.0 0.0 0.0 0.0 0.0

Reported NPAT -1.1 6.5 8.6 12.2 13.9 Conv ertible Capital 0.0 0.0 0.0 0.0 0.0

Abnormals (net of tax ) -9.1 -3.6 -3.4 -1.0 0.1 Ordinary Equity 65.6 68.8 90.2 95.5 102

Adjusted Earnings 8.0 10.1 12.0 13.2 13.9 Total Funds Emp. 185 185 189 193 200

RATIOS AND CAPITAL STRUCTURE CASH FLOW ($m)Year to 30 Jun 2012A 2013A 2014F 2015F 2016F Year to 30 Jun 2012A 2013A 2014F 2015F 2016F

Profitability & Growth

EBITDA/Op Rev % 29.6 31.3 31.2 32.4 32.2 Operating EBITDA 30.4 37.1 39.2 43.2 45.9

EBIT/Op Rev % 13.9 14.9 14.2 15.2 15.9 Other Cash Income 1.7 -2.3 -1.8 0.1 0.0

Effectiv e Tax Rate % 30.5 25.5 31.6 29.4 27.7 Interest Paid -5.2 -5.3 -4.4 -3.2 -3.5

Return On Equity % 11.8 15.0 15.1 14.2 14.1 Tax Paid 0.5 -2.2 -4.0 -5.1 -5.3

ROCE % 9.5 11.8 11.8 13.3 14.9 Working Capital / Other -3.1 -4.8 5.2 -1.9 -2.2

EPS Adjusted c. 18.8 23.7 23.9 26.2 27.6 Operating Cash Flow 24.3 22.5 34.4 33.2 34.9

EPS Grow th % -32.6 25.8 0.8 9.8 5.5

Net DPS c. 7.5 7.5 13.4 14.0 15.3 Total Capex -31.0 -16.3 -31.2 -21.1 -18.8

Div idend Cov er x 2.5 3.2 1.8 1.9 1.8 Acquisitions -0.6 -0.9 -4.9 -0.7 -0.7

Asset Backing & Capital Structure Div estments 4.9 0.7 5.2 0.0 0.0

Net Cash (Debt) $m -84.8 -80.2 -62.5 -58.1 -50.3 Div idends -3.2 -3.2 -6.7 -7.0 -7.7

NTA / Share $ 1.5 1.6 1.9 1.8 1.9 Equity Raised 0.0 0.0 20.0 0.0 0.0

Equity / Tot Assets % 35.5 37.3 47.8 49.4 50.8 Other 0.0 0.0 -0.5 0.1 0.0

Net Debt / EBITDA x 2.8 2.2 1.6 1.3 1.1 Change in Net Debt -5.6 2.7 16.2 4.5 7.7

Interest Cov er x 2.7 3.3 4.1 6.3 6.6

Shares on Issue Capex /Depn % 194 85.3 147 94.7 83.2

Ordinary m 42.6 42.6 50.2 50.2 50.2 Capex /Rev % 30.2 13.8 24.8 15.8 13.2

Fully Diluted m 42.6 42.6 46.4 50.2 50.2

EBITDA BREAKDOWNYear to 30 Jun 2012A 2013A 2014F 2015F 2016F

Fix ed Wing 22 24.22 26.58 26.36 27.1

Helicopters 11.93 17.06 18.96 22.21 24.24

Other -3.5 -4.21 -6.31 -5.33 -5.49

Group 30.43 37.07 39.23 43.24 45.85

Fix ed Wing Margin % 37.52 37.09 41.48 41.24 41.24

Helicopters Margin % 27.07 32.17 30.77 31.87 31.53

Group Margin % 29.63 31.32 31.21 32.37 32.16

Fixed Wing51%

Helicopter Leasing

17%

Helicopter Engineering

32%

SEGMENT REVENUE

Source: Company data, NZX, First NZ Capital estimates

14 February 2014

Australia and NZ First Edition 15

Introduction

Airwork Holdings Limited (AWK) is a specialist aviation business operating in two well-

defined niches of fixed wing and helicopter leasing and maintenance. AWK owns,

operates and maintains a fleet of aircraft that are supported by a world-class maintenance,

repair and overhaul (MRO) capability backed by extensive local and international

certification.

AWK’s Fixed Wing business derives most of leasing income from the provision of B737

aircraft, maintenance and crew for carriage of express freight in Australia and New

Zealand for major courier companies. Helicopter operations encompass leasing, crewing

and chartering of helicopters for emergency medical services (EMS), search and rescue

(SAR), police, military, mining, oil and gas and tourism sectors. A full helicopter MRO

service supports the helicopter leasing business and provides third-party MRO services in

New Zealand and internationally.

Figure 2: Revenue by division FY13 Figure 3: EBITDA by division FY13

Fixed Wing54%

Helicopters46%

Fixed Wing24.2m

Helicopters17.0m

Source: Company data

Source: Company data

Helicopter operations

AWK’s Helicopter business principally operates in the small- to medium-sized (5-9 pax),

twin engine, turbine powered helicopter market. These helicopters are typically used for

support services in the mining/oil and gas sector, emergency medical services (EMS),

search and rescue (SAR), police, military and tourism/charter market.

An active secondary market exists for helicopters, with around 80% of all turbine

helicopters produced since commercial production commenced in 1955 estimated to

remain in active service. Helicopters depreciate relatively modestly over a useful life that

can span several decades with appropriate service. Individual components are frequently

replaced to meet regulatory requirements or safety standards. The global fleet of twin-

engine BK117 helicopters in operation is around 295.

In FY13 helicopter leasing contributed 39% of divisional revenue compared with 61% from

maintenance, repair and overhaul (MRO). AWK’s external MRO business has roughly

doubled over the past five years.

Helicopter MRO

A healthy secondary market for helicopters together with AWK’s MRO capability provides

opportunity for AWK to source helicopters to overhaul and upgrade them and either lease

or on-sell. Upgraded helicopters are a highly cost-competitive alternative to new

helicopters. The high value of helicopter components and maintenance and low cost of

transporting components relative to their value has created a global MRO market. This

feature of the helicopter business allows AWK’s NZ-based MRO facility to support the

offshore growth aspirations of AWK’s helicopter leasing business and compete effectively

with high valued new helicopters.

14 February 2014

Australia and NZ First Edition 16

AWK’s MRO capability is supported by an increasing range of certifications which offer a

barrier to entry and international growth opportunity. Key certifications underpinning

helicopter MRO growth:

■ Only accredited service centre for Honeywell LTS-101 turbine engine in the Asia

Pacific excluding Japan (and only one of six worldwide);

■ One of two facilities in Asia Pacific approved to repair and overhaul BK117 dynamic

components (and only one of three worldwide);

■ One of three accredited service centres in Asia Pacific to repair and overhaul

Eurocopter AS350/355 dynamic components (and one of six facilities globally

excluding OEM providers);

■ The only helicopter engineering facility in the Asia Pacific with test cell capability for

Honeywell LTS-101 engines and Eurocopter AS350/355 and BK117 dynamic

components.

In addition AWK holds the only certification for BK117-850 engine upgrade, a modification

developed with Honeywell which replaces the engine on the BK117 helicopter with a more

powerful version. This upgrade has been approved by the New Zealand, European and

Canadian authorities. This significantly improves the Category A performance of the

BK117 helicopter, especially in hot and high altitude conditions to enable upgraded

helicopters to match alternative models in this area, but at a significantly lower cost.

Helicopter leasing

AWK manages a fleet of 29 helicopters which are leased or chartered on a range of terms

tailored to customer requirements. Of these helicopters 25 are owned and four are

operated on behalf of third parties. Helicopters are currently leased in New Zealand,

Australia, Papua New Guinea and Africa. The fleet in service has grown by two helicopters

over the past five years.

Figure 4: Helicopter fleet in service

Eurocopter AS 355F1

Kawasaki BK-117

Augusta Westland A109

Eurocopter AS 350BA

McDonnell Douglas 500

Robinson R44 Bell 427

Number Owned 10 12 - 2 1 - -

Number Operated - 1 1 - - 1 1

Capacity 5 passengers 9 passengers 5 passengers 6 passengers 4 passengers 3 passengers 7

passengers

Max Range 703km 500km 990km 660km 605km 560km 685km

Source: Company data

There are two types of leases:

■ “dry lease” where the helicopter is supplied (with full or partial engineering support) – in

this case the customer is responsible for crew, fuel, insurance and operation; and

■ “wet lease” where AWK provides all services (aircraft, crew, maintenance and

insurance) and the customer is only responsible for variable charges (eg. fuel).

AWK’s helicopter fleet operates in the following sectors: mining/oil and gas exploration,

tourism/charter, emergency medical services (EMS), police and search and rescue (SAR).

In addition to its long-term leasing operations AWK offers helicopter charter services on an

ad hoc basis in NZ and offshore. Around two thirds of forecast FY14 revenue is covered

by existing contracts.

14 February 2014

Australia and NZ First Edition 17

Figure 5: Helicopter leasing revenue by industry FY13

Oil & Gas48%

Mining17%

Tourism / Charter14%

Emergency / Govt Services

20%

Other1%

Source: Company data

Major customers currently include:

■ New Zealand Police.

■ Heli Niugini – a helicopter provider to the oil and gas industry in PNG.

■ Rio Tinto.

■ Bristow Group – for contracting to the offshore oil and gas industry in Australia.

■ The Helicopter Line.

AWK is in a commercial dispute with The Helicopter Line (a subsidiary of Skyline

Enterprises Ltd) with respect to the dry lease of eight Squirrel AS355 helicopters. The

Helicopter Line is not flying the helicopters and has been threatening to terminate the

lease for some months alleging that AWK has breached the contract. AWK has filed

proceedings in the High Court seeking payment of outstanding invoices amounting to

$2.5mn. The contract extends for a further nine years and provides for minimum revenue

of approximately $17mn ($1.9mn pa). While the company is confident of success in the

summary judgment, no income from this contract is allowed for in FY14 or FY15 forecasts.

Fixed Wing Operations

AWK’s Fixed Wing flight operations business is based around the provision of aircraft on a

wet lease basis (providing aircraft, crew. maintenance and insurance) in the specialist

airfreight sector in New Zealand and Australia. Over 70% of revenue is derived from

leasing and operating aircraft and related services to the airfreight industry with the

balance of revenue mainly derived from passenger charters, dry leasing of aircraft and

third party maintenance. Over 80% of revenue is secured by long-term contracts. AWK

has little direct fuel price risk or operating risk. FY13 accounts disclose that AWK’s two

largest customers were both in Fixed Wing and contributed approximately 72% of Fixed

Wing revenue.

14 February 2014

Australia and NZ First Edition 18

Figure 6: Revenue by sector FY13

Air Freight70%

Passenger Charters

18%

Dry Leasing5%

Other7%

Source: Company data

Express Freight Services

This business comprises two contracts:

■ In New Zealand, AWK Flight Operations lease a B737 to Express Couriers (NZ Post

subsidiary) on an ACMI lease and operates five turboprop aircraft on their behalf under

AWK’s New Zealand Air Operators certificate. The relationship with NZ Post extends

back to 1989.

■ In Australia, AWK Flight Operations leases five B737-300 freighters to Toll Priority for

its Australian express freight business under an ACMI lease. When the contract was

first awarded in 2007, three B737-300 aircraft were leased. Two B737-300 aircraft have

since been added as routes have grown. The contract was renegotiated in FY11 and

extended from 2014 to 2018 in conjunction with the addition of capacity. Multiple

services are operated between Brisbane, Sydney, Melbourne and Perth and additional

services are operated as required.

In both NZ and Australia the express freight market are duopolies. AWK lease and operate

the aircraft fleet for one of the two major players in each market. In NZ, AWK’s customer

NZ Express (NZ Post subsidiary) competes against Freightways. In Australia, AWK’s

customer Toll Priority competes against Qantas Freight.

Passenger services

AWK leases or operates the following passenger aircraft:

■ A B737-400 passenger aircraft was leased to Alliance Airways up until December

2013. Since then the aircraft has been redeployed for charters and short term lease. A

B737-300 passenger aircraft is based in Brisbane which is leased on short-term

contracts often in support of small airlines operating in the Pacific.

■ A Fairchild Metroliner is leased to Life Flight Trust Auckland as an air ambulance

service under an ACMI lease. AWK also uses 2 uncommitted aircraft (Metroliner and

Piper Chieftain) for commercial charters.

■ AWK also owns 50% of Infinite Charters Ltd, a corporate charter joint venture that

operates two Jetstream 32 aircraft which are crewed and operated by AWK.

14 February 2014

Australia and NZ First Edition 19

Dry leasing

AWK leases two B737-400 passenger aircraft to Romanian low-cost carrier Blue Air, which

operates services out of Bucharest. AWK receives a monthly lease fee and an hourly rate

per flight hour. Blue Air operates, insures and maintains the aircraft.

Figure 7: Fixed Wing fleet in service

Boeing 737 300

Boeing

737-400

IAI Westwind

II Jet Stream 32

Fokker

F27-500

Fairchild

SA227

Metroliner

Piper PA31

Cheiftain

Number Owned 5 freight

1 passenger

1 freight

3 passenger - - - 2 1

Number Operated - - 1 2 2 3 -

Capacity 17,000kg

136 passengers

19,500kg

162 passengers

1,155kg

7 passengers

1,908kg

19 passengers 5,500kg

2,200kg

18 passengers

800kg

8 passengers

Max Range 6,000km 6,000km 4,167km 1,875km 2,000km 2,750km 2,750km

Source: Company data

Maintenance

AWK is certified to perform the full range of engineering services on all aircraft within its

fleet including heavy maintenance C checks for B737-300 and B737-400, C and D checks

on Fokker 27 aircraft and Phase and SSV checks of Metroliner aircraft. AWK also provides

MRO services to some external customers.

The key competitive advantage of AWK’s Fixed Wing business is its cost competiveness

supported by its in-house engineering capability and certifications held to operate fixed

wing aircraft in the jurisdictions it operates. Also, through mutual recognition of Australia

and New Zealand aviation regulations, AWK can operate in Australia on a partial New

Zealand cost base.

Key opportunities

Helicopter MRO certification leverage. In June 2013 AWK received European Aviation

Safety Authority (EASA) certification of its Ardmore facility. This followed initial submission

back in October 2010 and expanded the acceptance of maintenance and engine upgrade

sales to most of jurisdictions worldwide (other than USA). This is expected to be a key

driver of further MRO growth in the years ahead. Early signs of the benefits of EASA

accreditation are encouraging. AWK recently contracted with ADAC, the largest

automotive club in Germany to progressively purchase its fleet of 14 BK117 helicopters

over the next five years while also supplying parts, engines and components during that

period. Canada and South Africa are other markets that have been assessed as offering

strong potential for BK117 upgrades. In anticipation of further sustained growth AWK is

upgrading capacity at its Ardmore facility.

EASA certification has the potential to step change BK 117 engine sales and we would

highlight this as a key area of upside risk to medium-term forecasts. We forecast

Helicopter Engineering revenue will grow to $40.5mn in FY14 up 26% on pcp. This slightly

exceeds PFI forecasts but we would highlight helicopter trading revenue as presenting

further upside risk. Between FY14 and FY18 we forecast Helicopter Engineering revenue

will grow at an average 11% p.a.

Helicopter lease fleet growth. Helicopter demand remains strong, particularly in the oil

and gas sectors, and AWK’s upgrade capability (and cost-effective products) positions the

company strongly for pursuing offshore leasing contracts. Potential exists to deploy further

helicopters in Africa, particularly if mining related exploration and development activity

expands. Our base case valuation assumes AWK grows its helicopter fleet by one BK117

p.a. through the explicit forecast period.

14 February 2014

Australia and NZ First Edition 20

Fixed Wing efficiency improvement. Expansion of the business footprint in Fixed Wing

in Australia in recent years has been accompanied by a significant lift in the capital and

cost base. Management is now focusing on consolidating the Fixed Wing business (to

extract improved ROIC) and has embarked on a programme of productivity measures to

improve cost efficiency in its Australian operation. Management is targeting annual cost

reduction of A$3mn from a variety of initiatives including more robust planning, logistics,

crewing and internalisation of staff maintenance functions. These cost-reduction benefits

will commence in FY14.

In addition to targeting greater efficiency, focus is on increasing capacity utilisation in

Fixed Wing charter. FY14 PFI forecasts assume that the expiry of a Boeing 737-400 fixed

price contract in Australia in December 2013 will only be partly offset by charter hours.

However, with current charter activity strength in Australia we believe there is upside risk

to this assumption as well as our Fixed Wing revenue forecast in FY14 of $64.1mn.

AWK has also signalled that organic growth may be supplemented with strategic

acquisitions of businesses and assets that complement its existing operations.

Key issues / risks

Key contract risk. AWK derives a significant portion of revenue from key customers. The

FY13 financial statements note that the two largest customers (both in Fixed Wing)

accounted for 72% of Fixed Wing revenue and 40% of FY13 group revenue. AWK’s

largest customer, Toll Holdings Ltd, accounted for 28% of group revenue in FY13 and

although this contract does not expire until 2018 we would nominate this renegotiation as

a key medium-term risk. To reflect this risk in our valuation we assume a 5% nominal

decline in Fixed Wing lease revenue per flying hour in FY19. We also note that a four-year

extension of the Toll contract in FY11 coincided with declining yield trends in the Fixed

Wing division. Another key Fixed Wing lease contract with NZ Post is up for renewal in

FY16.

Fixed Wing accelerated depreciation. AWK has accelerated the depreciation of its Fixed

Wing fleet such that the implied economic life of this asset base has fallen from around 15

years in FY11 to nine years currently. Fixed Wing depreciation as a percentage of revenue

increased from 13.6% in FY11 to 19.4% in FY13. This led to a significant decline in Fixed

Wing EBIT margin during the period. Rather than a change in useful life, we believe that

the key driver of the higher depreciation charge has been a significant decline in the

market value of B737 aircraft. We estimate that the present over-depreciation of Fixed

Wing assets equates to around $4mn relative to maintenance capex indicated by

management. In addition to the accelerated depreciation, an impairment of $11.8mn was

recognised in FY12. This related to adjustments in the carrying value of AWK’s Fixed Wing

engines, specifically the Boeing 737 fleet.

Supplier and accreditation risk. In conducting its MRO activities AWK relies on

accreditations and parts supply agreements with OEMS, including Eurocopter and

Honeywell. Given that OEMs can compete with AWK’s MRO business potential

commercial tension exists between AWK and MROs. While AWK proactively manages

such relationships any impairment of these relationships could negatively impact on AWK.

Cyclical industry exposure. Many of AWK’s customers are exposed to cyclical sectors

including oil and gas, mining, logistics and tourism. AWK’s helicopter leasing division has

enjoyed growth in recent years as a recovery in the oil and gas and mining sectors drove

improved fleet utilisation. Three BK-117 helicopters were added to the fleet during FY12

with two of those deployed in a full service contract to Guinea, Africa, to support Rio

Tinto’s Simandou iron ore project. While charter activity in Australia has shown recent

strength, tourism related helicopter activity in NZ has remained weak.

Foreign exchange risk. AWK transacts much of its revenue and expenses in foreign

currencies such that AWK calculates that a 1 cent appreciation of the USD against the

14 February 2014

Australia and NZ First Edition 21

NZD will increase EBITDA by around $0.343mn, while a 1 cent appreciation of the AUD

against the NZD will increase EBITDA by $0.136mn.

Accident/incident risk. An accident or incident involving any aircraft or equipment

operated, designed or maintained by AWK could incur reputational damage or financial

loss. In January 2014 the right side main landing gear of a B737 aircraft owned by AWK

and servicing Toll Holdings Ltd collapsed, causing the plane to come to a sudden halt on

the runway shortly after landing. A full investigation is in progress to determine the cause

of the incident. The aircraft was fully insured and AWK had spare capacity to continue to

fully service the Toll contract.

Historical financial information and FNZC forecasts

Figure 8: AWK revenue and earnings breakdown

Year end 30 June (NZ$mn) FY11A FY12A FY13A FY14F FY15F FY16F

Revenue

Fixed Wing 53.7 58.6 65.3 64.1 63.9 65.7

Helicopter - leasing 17.2 18.8 21.0 21.1 23.7 26.6

Helicopter - engineering 26.1 25.2 32.0 40.5 46.0 50.3

Total Revenue 97.0 102.7 118.3 125.7 133.6 142.6

Operating Expenses

Parts & material purchases -23.9 -30.4 -31.6 -33.0 -37.9 -42.3

Employee & related expenses -17.1 -28.9 -35.3 -33.9 -33.5 -34.3

Aircraft operating expenses 0.0 -4.0 -4.1 -6.2 -6.8 -7.2

Other expenses -22.1 -9.1 -10.3 -13.4 -12.1 -13.0

Total Operating Expenses -63.1 -72.3 -81.3 -86.5 -90.4 -96.7

EBITDA

Fixed Wing 24.1 22.0 24.2 26.6 26.4 27.1

Helicopters 12.2 11.9 17.1 19.0 22.2 24.2

Other -1.8 -3.5 -4.2 -6.3 -5.3 -5.5

EBITDA 34.6 30.4 37.1 39.2 43.2 45.9

Depreciation & amortisation -12.8 -16.2 -19.4 -21.4 -22.9 -23.1

EBIT

Fixed Wing 16.9 12.2 11.6 12.0 11.7 12.5

Helicopters 7.9 6.9 11.9 13.8 16.8 18.7

Other -3.0 -4.9 -5.8 -8.1 -8.2 -8.4

EBIT 21.8 14.2 17.7 17.8 20.4 22.7

Impairment expenses -1.3 -12.0 -2.0 0.0 0.0 0.0

Other gains/(losses) 11.5 1.5 -1.7 -0.9 0.1 0.0

Net Financing Expense -5.1 -5.2 -5.3 -4.4 -3.2 -3.5

Profit before tax 26.9 -1.5 8.7 12.5 17.2 19.3

Tax Expense -7.9 0.5 -2.2 -4.0 -5.1 -5.3

NPAT 19.0 -1.1 6.5 8.6 12.2 13.9

NPAT - Normalised 11.9 8.0 10.1 12.0 13.2 13.9

EBIT margin

Fixed Wing 31.4% 20.8% 17.7% 18.8% 18.3% 19.0%

Helicopters 18.2% 15.6% 22.5% 22.4% 24.1% 24.3%

Group 22.4% 13.9% 14.9% 14.2% 15.2% 16.0%

Operating Fleet

Fixed Wing 17 20 20 21 21 21

Helicopter 22 25 26 27 28 29

Source: Company data, FNZC estimates

■ Earnings in FY11 were boosted relative to other years by excellent returns achieved

from the purchase, parting and sale of two MD90 aircraft engines in the Fixed Wing

division.

■ Margin expansion was achieved in the Helicopter division between FY11 and FY13 as

scale benefits more than offset the increasing skew from higher margin leasing

revenue towards lower margin engineering revenue.

14 February 2014

Australia and NZ First Edition 22

■ FY14 and FY15 do not recognise any revenue for the eight helicopters contracted to

The Helicopter Line Limited. FY16 does assume that these helicopters are re-leased

albeit at less than the current terms of the disputed contract.

Return on Invested Capital (ROIC)

Investment in additional Boeing 737 fleet in the Fixed Wing division and higher working

capital requirements to support the growth in Helicopter engineering revenue has led to

invested capital growth of 35% between FY09 and FY13. Earnings growth was unable to

keep pace with the increasing capital base, with Group after tax ROIC declining from

11.2% in FY09 to 9.1% in FY13. Key drivers of the lower return were the accelerated

depreciation and declining yields in the Fixed Wing division. Encouragingly we estimate

that the faster growing Helicopter division saw ROIC improve from around 11.0% in FY11

to 11.7% in FY13.

After adjusting for the accelerated depreciation and elevated fleet book value in Fixed

Wing, we calculate a normalised ROIC of 12.7% in FY13. Over the explicit forecast period

we assume a gradual decline in ROIC to 12.0% in our terminal year as a declining profile

in Fixed Wing is offset by scale benefits in the Helicopter division. With a calculated

WACC of 10.0% in the terminal year, and therefore an excess return of 2.1%, we are

implicitly ascribing a value of $40mn to intangible assets within AWK that are not carried

on balance sheet. Specifically we believe this intangible value is supported by AWK’s long-

standing relationships with a number of key customers and more importantly the extensive

local and international Helicopter Engineering certification that AWK holds.

Capex

Capex of $31.2mn is forecast in FY14 with maintenance capex of $13.8mn and growth

capex of $17.4mn. Implicit within this forecast is the assumption that Fixed Wing

maintenance capex will again be lower than Fixed Wing depreciation due to the

accelerated depreciation profile of the Boeing 737 asset base. Growth capex in FY14 and

FY15 includes investment in helicopter engineering plant capacity at AWK’s Ardmore

facility as well as the initial purchase of fleet from ADAC under the terms of the new parts

supply contract.

AWK estimated in the PFI that, based on the current fleet size, the addition of one

helicopter to the leasing fleet each year and provision of plant, inventories and spare parts

to support fleet and engineering growth, net annual capex would approximate $15mn to

$17mn. This includes average maintenance capex estimated at $13.5mn ($9.5mn Fixed

Wing, $4.0mn Helicopter). Our capex forecasts exceed management guidance, with

maintenance capex averaging around $17mn p.a. over the next five years. So as to take

into consideration a fleet replacement cycle we then forecast maintenance capex lifting to

$20mn p.a. from FY19 which equates to 1.13x depreciation.

Valuation

Our 12-month target price of $3.00 is established using a DCF valuation methodology. We

also compare AWK against the metrics of a basket of listed peer stocks. We consider an

adjusted EV/EBIT methodology the most relevant comparative multiple.

DCF valuation

DCF is our preferred valuation methodology due to a lack of directly comparable peer

companies for multiple-based analysis and due to the capital intensity of the business.

AWK is also suited to DCF analysis due to the contractual nature of its revenue stream, its

inconsistent capex profile and the accelerated depreciation of its Fixed Wing assets in the

medium term.

Our spot DCF valuation of $2.70 and 12-month forward valuation of $3.00 per share

assume that one BK-117 helicopter is added each year between FY16 and FY24.

14 February 2014

Australia and NZ First Edition 23

We provide a summary below of the sensitivity of our AWK 12-month forward DCF

valuation to a change in WACC and terminal growth rate inputs under two alternative

growth scenarios.

The low scenario assumes that the operating environment for helicopter leasing is not

supportive for BK-117 fleet growth. In this instance we do not grow the BK-117 fleet and

revert to a lower long-term ROIC for the Group.

The high scenario assumes that the operating environment remains buoyant for helicopter

leasing and is supportive for BK-117 fleet growth. In this scenario we grow the BK-117

fleet by two aircraft each year between FY16 and FY24 and long-term ROIC for the Group

improves and is sustained at an elevated level.