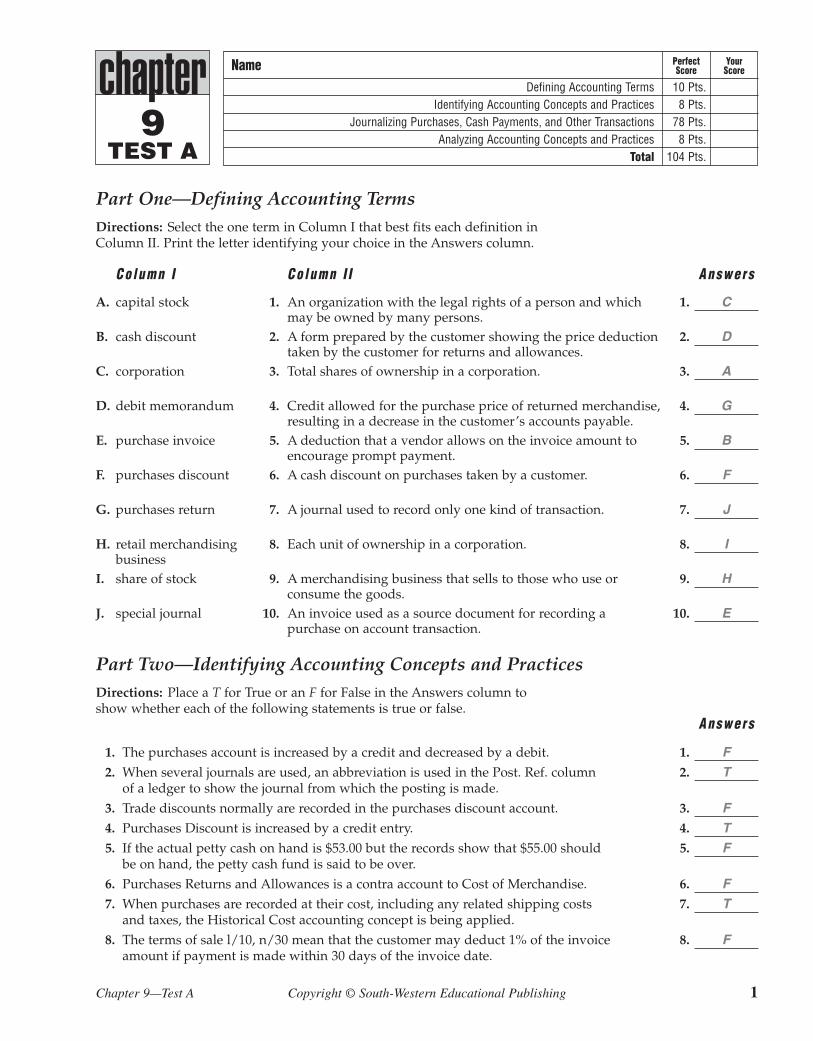

century 21 accounting 8e multicolumn journal chapter and

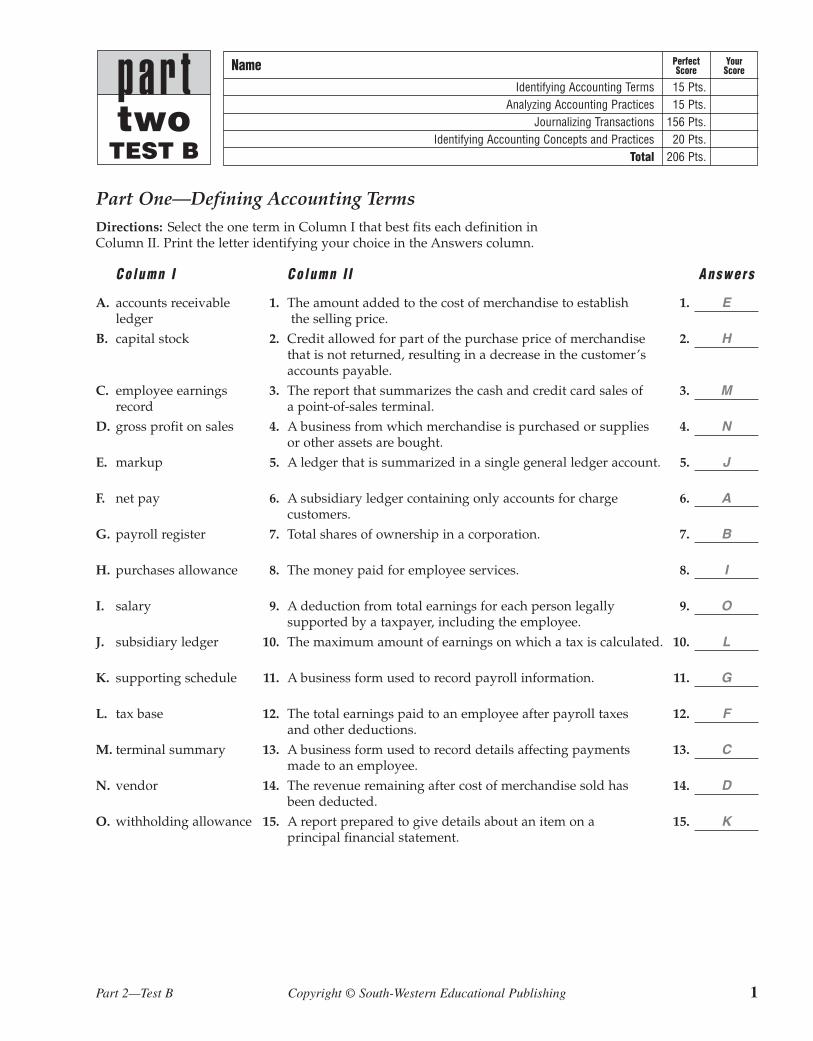

TRANSCRIPT

L U M N J O U R N A L • M U L T I C O L U M N J O U R N A L • M U L T I C O L U M N J O U R N A L • M U L T I C O L U M N J O U R N A L

AccountingS O U T H - W E S T E R NCentury 21

8E

C L A U D I A B I E N I A S G I L B E R T S O N , C PATeaching ProfessorNorth Hennepin Community CollegeBrooklyn Park, Minnesota

M A R K W . L E H M A N , C P AAssistant ProfessorSchool of AccountancyMississippi State UniversityStarkville, Mississippi

K E N T O N E . R O S S , C P AProfessor Emeritus of AccountingTexas A&M University—CommerceCommerce, Texas

Chapter and Part Tests · Teacher’s Edition

A u s t r a l i a · B r a z i l · C a n a d a · M e x i c o · S i n g a p o r e · S p a i n · U n i t e d K i n g d o m · U n i t e d S t a t e s

VP/Editorial DirectorJack W. Calhoun

VP/Editor-in-ChiefKaren Schmohe

Acquisitions EditorMarilyn Hornsby

Project ManagerCarol Sturzenberger

VP/Director of EducationalMarketingCarol Volz

Marketing ManagerCourtney Schulz

Marketing CoordinatorAngela Russo

Production ManagerPatricia Matthews Boies

Ancillary CoordinatorKelly Resch

Manufacturing CoordinatorKevin Kluck

Production HouseA.W. Kingston Publishing Services

Art DirectorTippy McIntosh

Cover/Internal DesignAnn Small, a small design studio

Cover IllustrationPhilip Brooker

PrinterGlobusMinster, OH

COPYRIGHT © 2006 Thomson South-Western, a partof The Thomson Corporation.Thomson, the Star logo, andSouth-Western are trademarksused herein under license.

Printed in the United Statesof America1 2 3 4 5 08 07 06 05

ISBN 0-538-44139-9

ALL RIGHTS RESERVED.No part of this work covered by thecopyright hereon may be repro-duced or used in any form or byany means—graphic, electronic,or mechanical, including photo-copying, recording, taping, Webdistribution or information storageand retrieval systems, or in anyother manner—without the writtenpermission of the publisher.

For permission to use materialfrom this text or product, submit arequest online athttp://www.thomsonrights.com.

For more information about ourproducts, contact us at:

Thomson Higher Education5191 Natorp BoulevardMason, Ohio 45040USA

Century 21 Accounting, Multicolumn Journal, Chapter and Part Tests, Eighth EditionTeacher’s Edition

Claudia Bienias Gilbertson, CPA; Mark W. Lehman, CPA; Kenton E. Ross, CPA

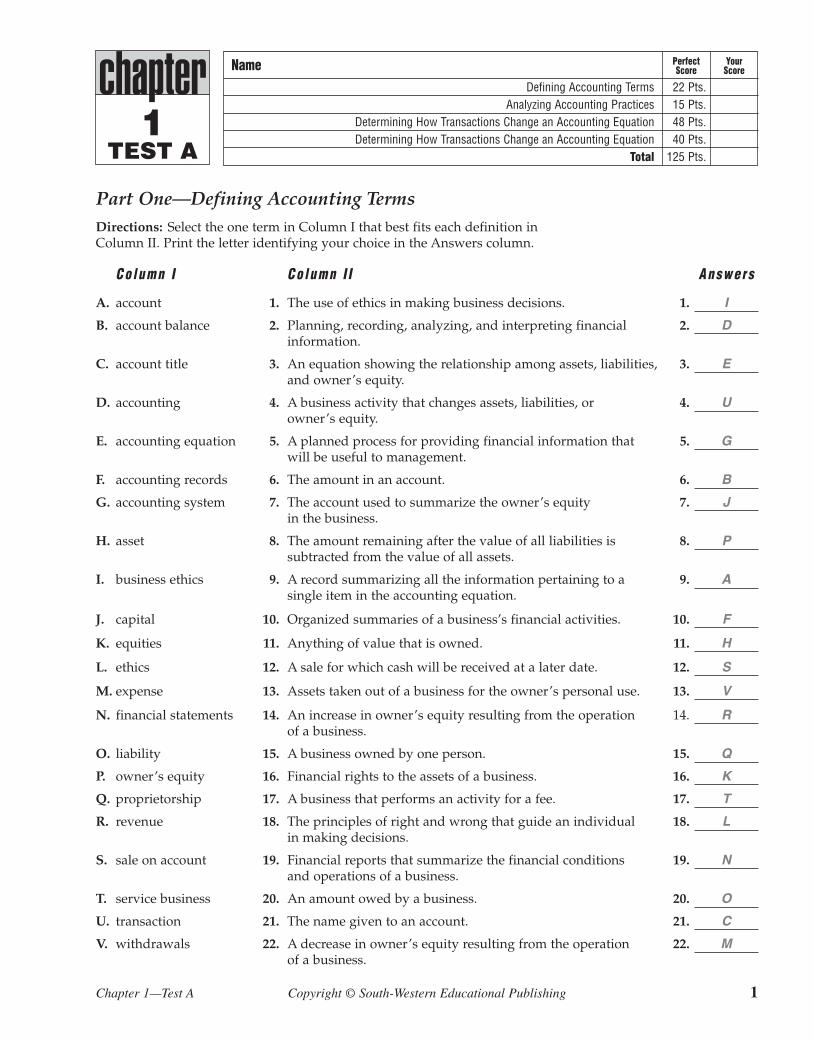

chapterTEST A

PerfectScore

YourScoreName

Defining Accounting Terms 22 Pts.Analyzing Accounting Practices 15 Pts.

Determining How Transactions Change an Accounting Equation 48 Pts.Determining How Transactions Change an Accounting Equation 40 Pts.

Total 125 Pts.

Chapter 1—Test A Copyright © South-Western Educational Publishing 1

1

Part One—Defining Accounting TermsDirections: Select the one term in Column I that best fits each definition inColumn II. Print the letter identifying your choice in the Answers column.

Co lumn I Co lumn I I Answers

A. account 1. The use of ethics in making business decisions. 1. I

B. account balance 2. Planning, recording, analyzing, and interpreting financial 2. Dinformation.

C. account title 3. An equation showing the relationship among assets, liabilities, 3. Eand owner’s equity.

D. accounting 4. A business activity that changes assets, liabilities, or 4. Uowner’s equity.

E. accounting equation 5. A planned process for providing financial information that 5. Gwill be useful to management.

F. accounting records 6. The amount in an account. 6. B

G. accounting system 7. The account used to summarize the owner’s equity 7. Jin the business.

H. asset 8. The amount remaining after the value of all liabilities is 8. Psubtracted from the value of all assets.

I. business ethics 9. A record summarizing all the information pertaining to a 9. Asingle item in the accounting equation.

J. capital 10. Organized summaries of a business’s financial activities. 10. F

K. equities 11. Anything of value that is owned. 11. H

L. ethics 12. A sale for which cash will be received at a later date. 12. S

M. expense 13. Assets taken out of a business for the owner’s personal use. 13. V

N. financial statements 14. An increase in owner’s equity resulting from the operation 14. Rof a business.

O. liability 15. A business owned by one person. 15. Q

P. owner’s equity 16. Financial rights to the assets of a business. 16. K

Q. proprietorship 17. A business that performs an activity for a fee. 17. T

R. revenue 18. The principles of right and wrong that guide an individual 18. Lin making decisions.

S. sale on account 19. Financial reports that summarize the financial conditions 19. Nand operations of a business.

T. service business 20. An amount owed by a business. 20. O

U. transaction 21. The name given to an account. 21. C

V. withdrawals 22. A decrease in owner’s equity resulting from the operation 22. Mof a business.

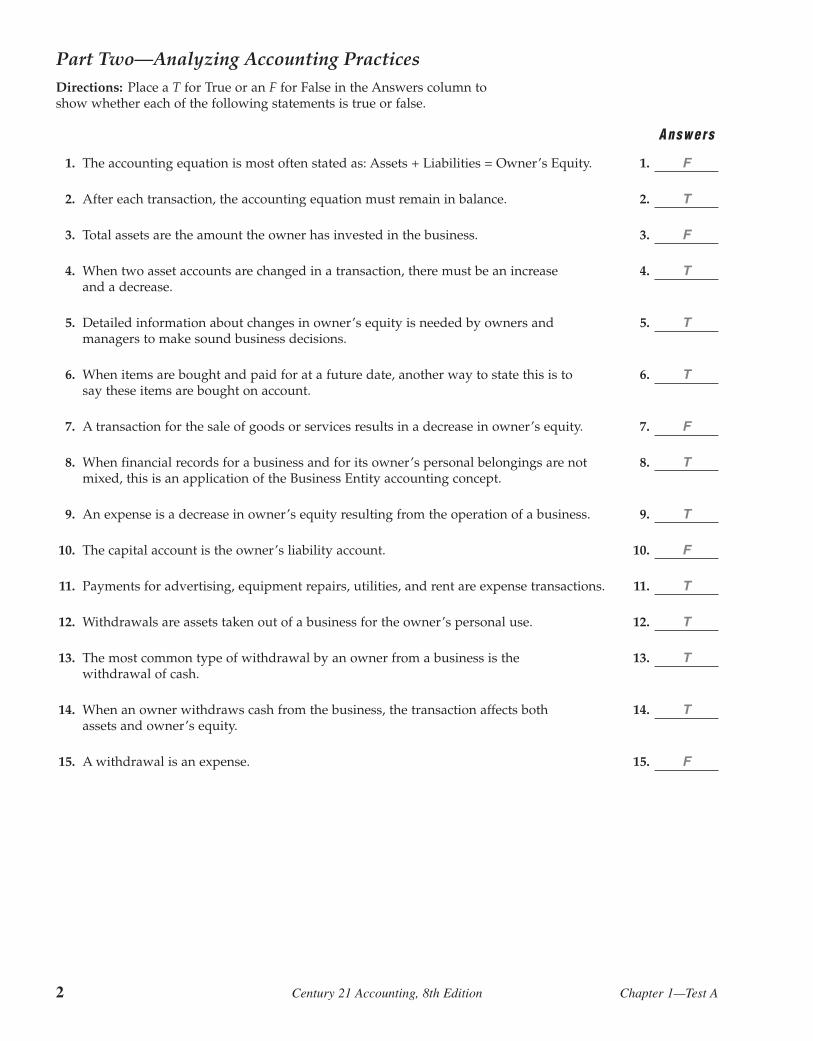

2 Century 21 Accounting, 8th Edition Chapter 1—Test A

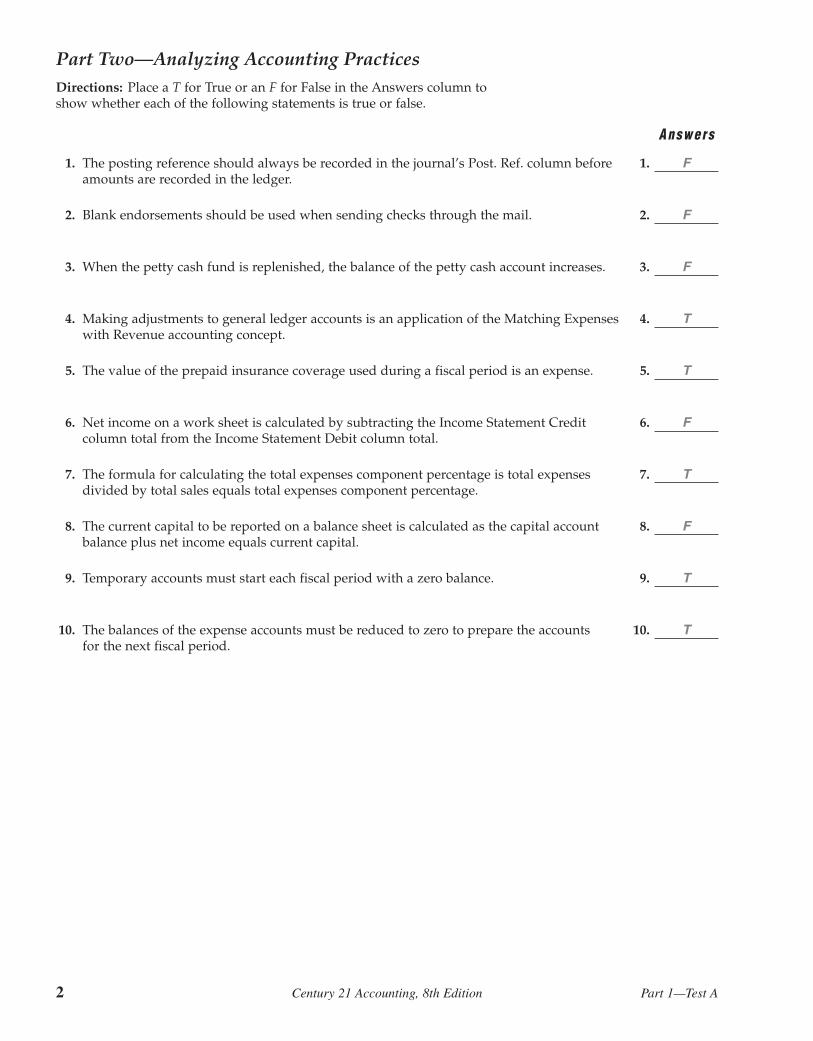

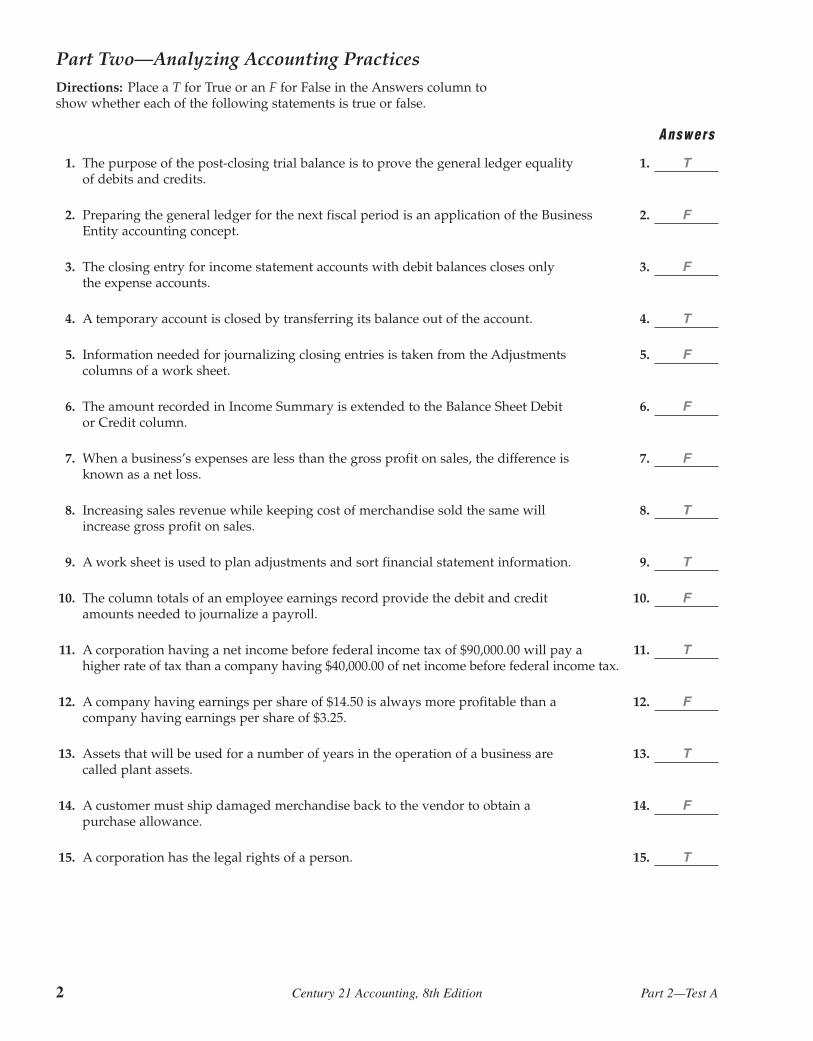

Part Two—Analyzing Accounting PracticesDirections: Place a T for True or an F for False in the Answers column toshow whether each of the following statements is true or false.

Answers

1. The accounting equation is most often stated as: Assets + Liabilities = Owner’s Equity. 1. F

2. After each transaction, the accounting equation must remain in balance. 2. T

3. Total assets are the amount the owner has invested in the business. 3. F

4. When two asset accounts are changed in a transaction, there must be an increase 4. Tand a decrease.

5. Detailed information about changes in owner’s equity is needed by owners and 5. Tmanagers to make sound business decisions.

6. When items are bought and paid for at a future date, another way to state this is to 6. Tsay these items are bought on account.

7. A transaction for the sale of goods or services results in a decrease in owner’s equity. 7. F

8. When financial records for a business and for its owner’s personal belongings are not 8. Tmixed, this is an application of the Business Entity accounting concept.

9. An expense is a decrease in owner’s equity resulting from the operation of a business. 9. T

10. The capital account is the owner’s liability account. 10. F

11. Payments for advertising, equipment repairs, utilities, and rent are expense transactions. 11. T

12. Withdrawals are assets taken out of a business for the owner’s personal use. 12. T

13. The most common type of withdrawal by an owner from a business is the 13. Twithdrawal of cash.

14. When an owner withdraws cash from the business, the transaction affects both 14. Tassets and owner’s equity.

15. A withdrawal is an expense. 15. F

Name

Chapter 1—Test A Copyright © South-Western Educational Publishing 3

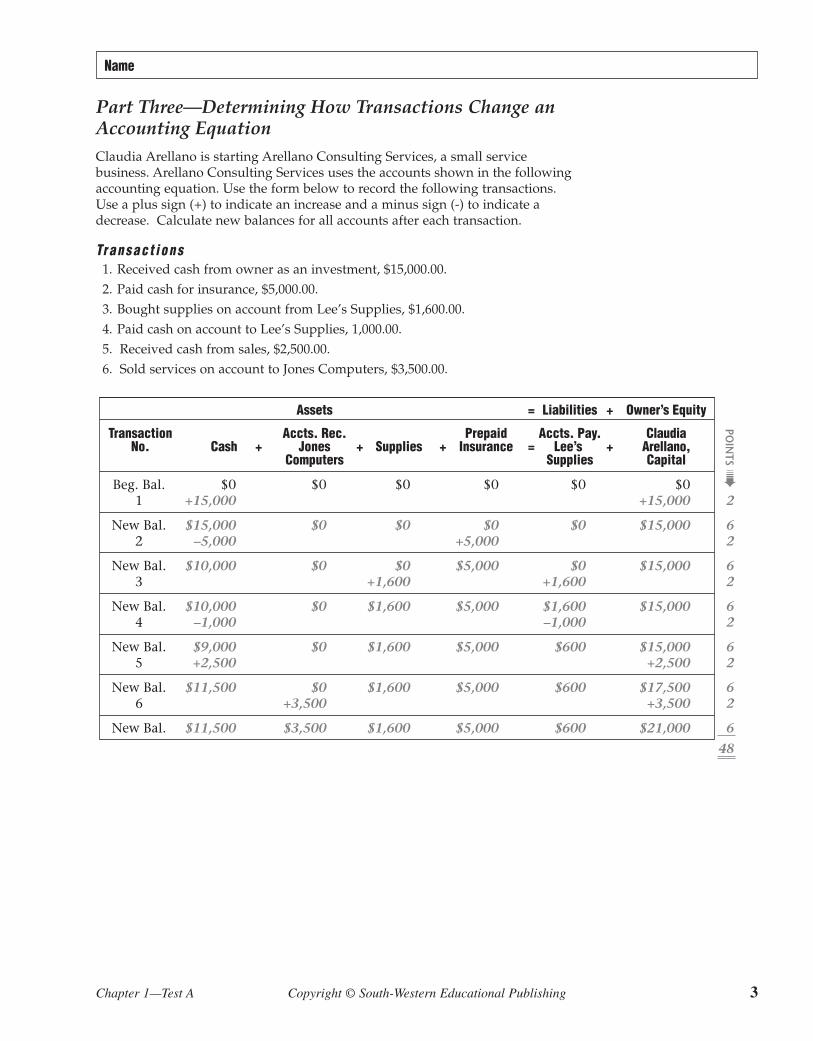

Part Three—Determining How Transactions Change anAccounting EquationClaudia Arellano is starting Arellano Consulting Services, a small servicebusiness. Arellano Consulting Services uses the accounts shown in the followingaccounting equation. Use the form below to record the following transactions.Use a plus sign (+) to indicate an increase and a minus sign (-) to indicate adecrease. Calculate new balances for all accounts after each transaction.

Transac t ions

Assets = Liabilities + Owner’s Equity

Transaction Accts. Rec. Prepaid Accts. Pay. ClaudiaNo. Cash + Jones + Supplies + Insurance = Lee’s + Arellano,

Computers Supplies Capital

Beg. Bal. $0 $0 $0 $0 $0 $01 +15,000 +15,000

New Bal. $15,000 $0 $0 $0 $0 $15,0002 –5,000 +5,000

New Bal. $10,000 $0 $0 $5,000 $0 $15,0003 +1,600 +1,600

New Bal. $10,000 $0 $1,600 $5,000 $1,600 $15,0004 –1,000 –1,000

New Bal. $9,000 $0 $1,600 $5,000 $600 $15,0005 +2,500 +2,500

New Bal. $11,500 $0 $1,600 $5,000 $600 $17,5006 +3,500 +3,500

New Bal. $11,500 $3,500 $1,600 $5,000 $600 $21,000

POIN

TS �

2

62

62

62

62

62

6

48

1. Received cash from owner as an investment, $15,000.00.2. Paid cash for insurance, $5,000.00.3. Bought supplies on account from Lee’s Supplies, $1,600.00.4. Paid cash on account to Lee’s Supplies, 1,000.00.5. Received cash from sales, $2,500.00.6. Sold services on account to Jones Computers, $3,500.00.

4 Century 21 Accounting, 8th Edition Chapter 1—Test A

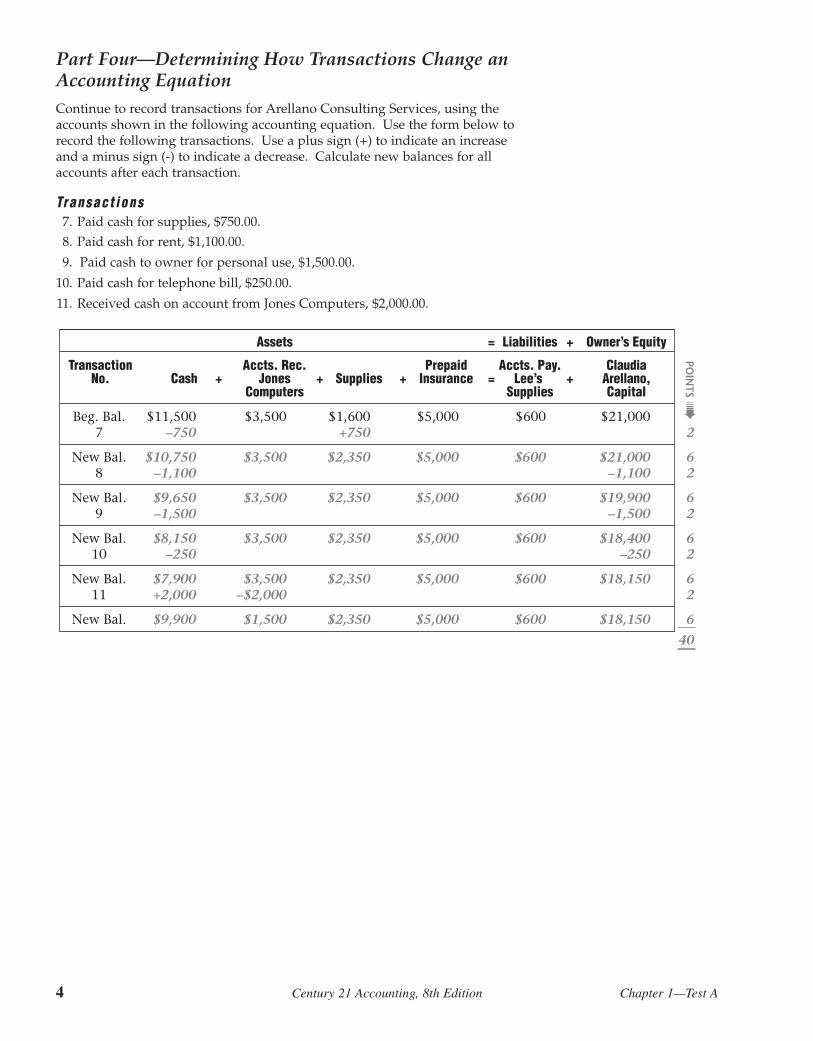

Part Four—Determining How Transactions Change anAccounting EquationContinue to record transactions for Arellano Consulting Services, using theaccounts shown in the following accounting equation. Use the form below torecord the following transactions. Use a plus sign (+) to indicate an increaseand a minus sign (-) to indicate a decrease. Calculate new balances for allaccounts after each transaction.

Transac t ions7. Paid cash for supplies, $750.00.8. Paid cash for rent, $1,100.00.

9. Paid cash to owner for personal use, $1,500.00.

10. Paid cash for telephone bill, $250.00.

11. Received cash on account from Jones Computers, $2,000.00.

Assets = Liabilities + Owner’s Equity

Transaction Accts. Rec. Prepaid Accts. Pay. ClaudiaNo. Cash + Jones + Supplies + Insurance = Lee’s + Arellano,

Computers Supplies Capital

Beg. Bal. $11,500 $3,500 $1,600 $5,000 $600 $21,0007 –750 +750

New Bal. $10,750 $3,500 $2,350 $5,000 $600 $21,0008 –1,100 –1,100

New Bal. $9,650 $3,500 $2,350 $5,000 $600 $19,9009 –1,500 –1,500

New Bal. $8,150 $3,500 $2,350 $5,000 $600 $18,40010 –250 –250

New Bal. $7,900 $3,500 $2,350 $5,000 $600 $18,15011 +2,000 –$2,000

New Bal. $9,900 $1,500 $2,350 $5,000 $600 $18,150

POIN

TS �

2

62

62

62

62

6

40

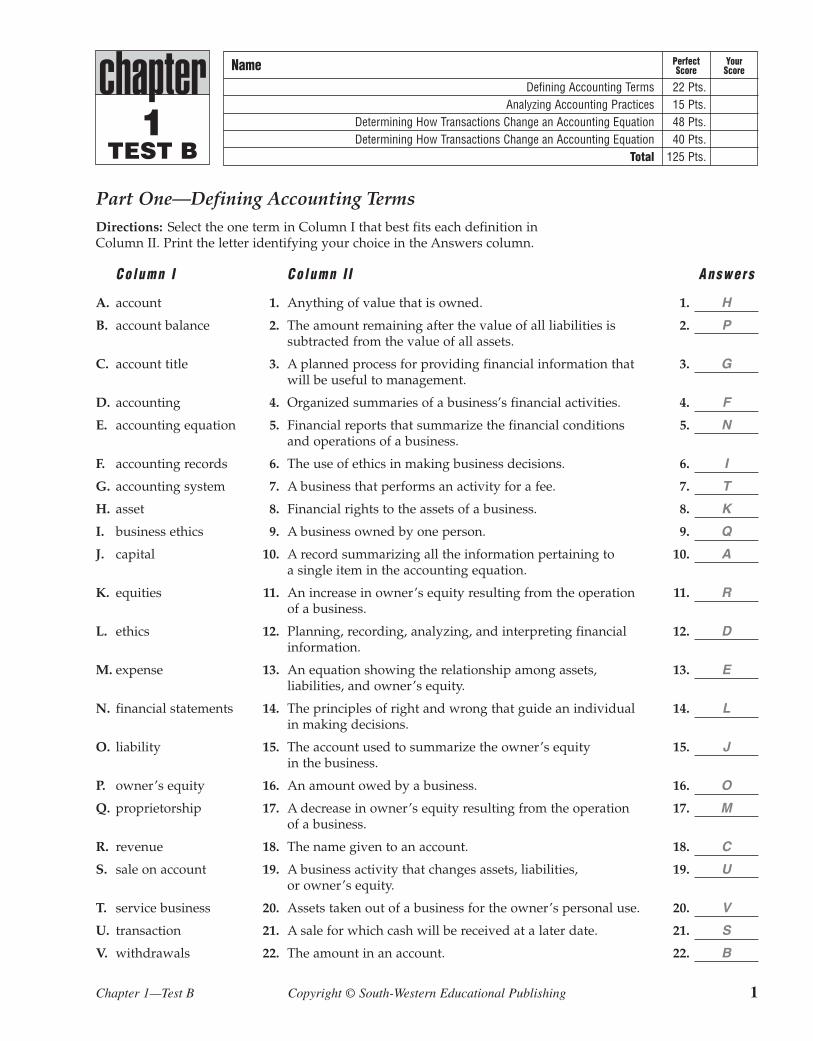

chapterTEST B

PerfectScore

YourScoreName

Defining Accounting Terms 22 Pts.Analyzing Accounting Practices 15 Pts.

Determining How Transactions Change an Accounting Equation 48 Pts.Determining How Transactions Change an Accounting Equation 40 Pts.

Total 125 Pts.

Chapter 1—Test B Copyright © South-Western Educational Publishing 1

1

Part One—Defining Accounting TermsDirections: Select the one term in Column I that best fits each definition inColumn II. Print the letter identifying your choice in the Answers column.

Co lumn I Co lumn I I Answers

A. account 1. Anything of value that is owned. 1. H

B. account balance 2. The amount remaining after the value of all liabilities is 2. Psubtracted from the value of all assets.

C. account title 3. A planned process for providing financial information that 3. Gwill be useful to management.

D. accounting 4. Organized summaries of a business’s financial activities. 4. F

E. accounting equation 5. Financial reports that summarize the financial conditions 5. Nand operations of a business.

F. accounting records 6. The use of ethics in making business decisions. 6. I

G. accounting system 7. A business that performs an activity for a fee. 7. T

H. asset 8. Financial rights to the assets of a business. 8. K

I. business ethics 9. A business owned by one person. 9. Q

J. capital 10. A record summarizing all the information pertaining to 10. Aa single item in the accounting equation.

K. equities 11. An increase in owner’s equity resulting from the operation 11. Rof a business.

L. ethics 12. Planning, recording, analyzing, and interpreting financial 12. Dinformation.

M. expense 13. An equation showing the relationship among assets, 13. Eliabilities, and owner’s equity.

N. financial statements 14. The principles of right and wrong that guide an individual 14. Lin making decisions.

O. liability 15. The account used to summarize the owner’s equity 15. Jin the business.

P. owner’s equity 16. An amount owed by a business. 16. O

Q. proprietorship 17. A decrease in owner’s equity resulting from the operation 17. Mof a business.

R. revenue 18. The name given to an account. 18. C

S. sale on account 19. A business activity that changes assets, liabilities, 19. Uor owner’s equity.

T. service business 20. Assets taken out of a business for the owner’s personal use. 20. V

U. transaction 21. A sale for which cash will be received at a later date. 21. S

V. withdrawals 22. The amount in an account. 22. B

2 Century 21 Accounting, 8th Edition Chapter 1—Test B

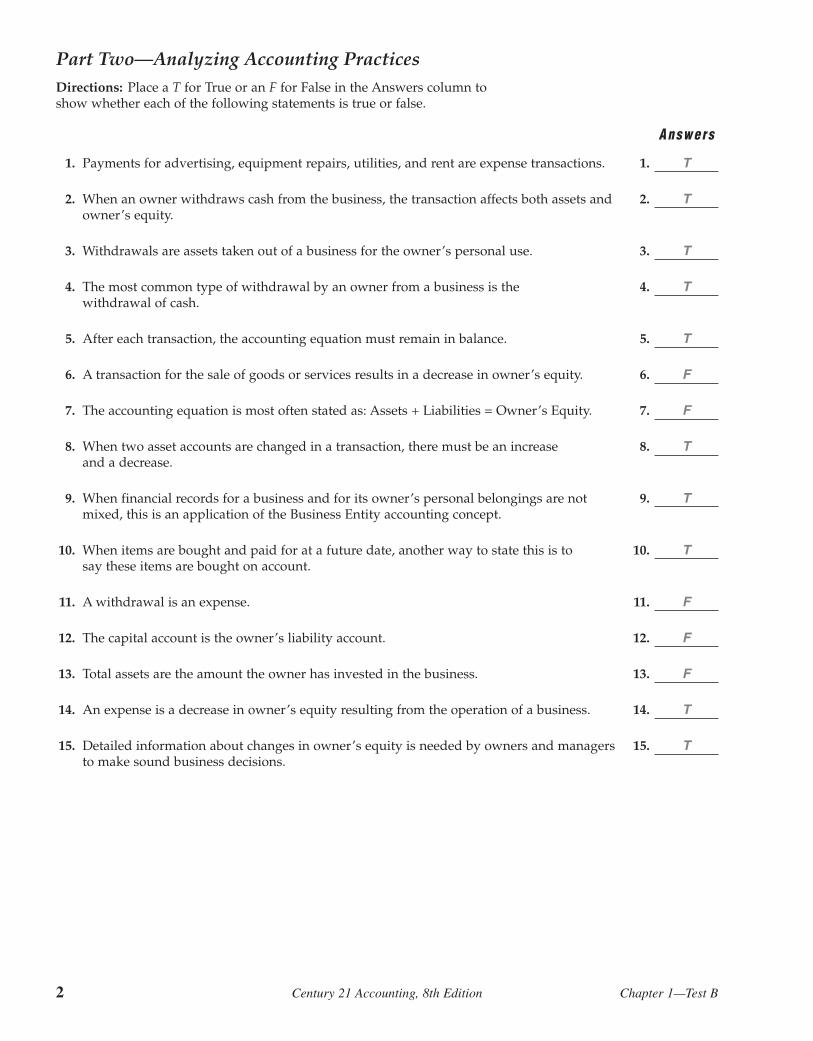

Part Two—Analyzing Accounting PracticesDirections: Place a T for True or an F for False in the Answers column toshow whether each of the following statements is true or false.

Answers

1. Payments for advertising, equipment repairs, utilities, and rent are expense transactions. 1. T

2. When an owner withdraws cash from the business, the transaction affects both assets and 2. Towner’s equity.

3. Withdrawals are assets taken out of a business for the owner’s personal use. 3. T

4. The most common type of withdrawal by an owner from a business is the 4. Twithdrawal of cash.

5. After each transaction, the accounting equation must remain in balance. 5. T

6. A transaction for the sale of goods or services results in a decrease in owner’s equity. 6. F

7. The accounting equation is most often stated as: Assets + Liabilities = Owner’s Equity. 7. F

8. When two asset accounts are changed in a transaction, there must be an increase 8. Tand a decrease.

9. When financial records for a business and for its owner’s personal belongings are not 9. Tmixed, this is an application of the Business Entity accounting concept.

10. When items are bought and paid for at a future date, another way to state this is to 10. Tsay these items are bought on account.

11. A withdrawal is an expense. 11. F

12. The capital account is the owner’s liability account. 12. F

13. Total assets are the amount the owner has invested in the business. 13. F

14. An expense is a decrease in owner’s equity resulting from the operation of a business. 14. T

15. Detailed information about changes in owner’s equity is needed by owners and managers 15. Tto make sound business decisions.

Name

Chapter 1—Test B Copyright © South-Western Educational Publishing 3

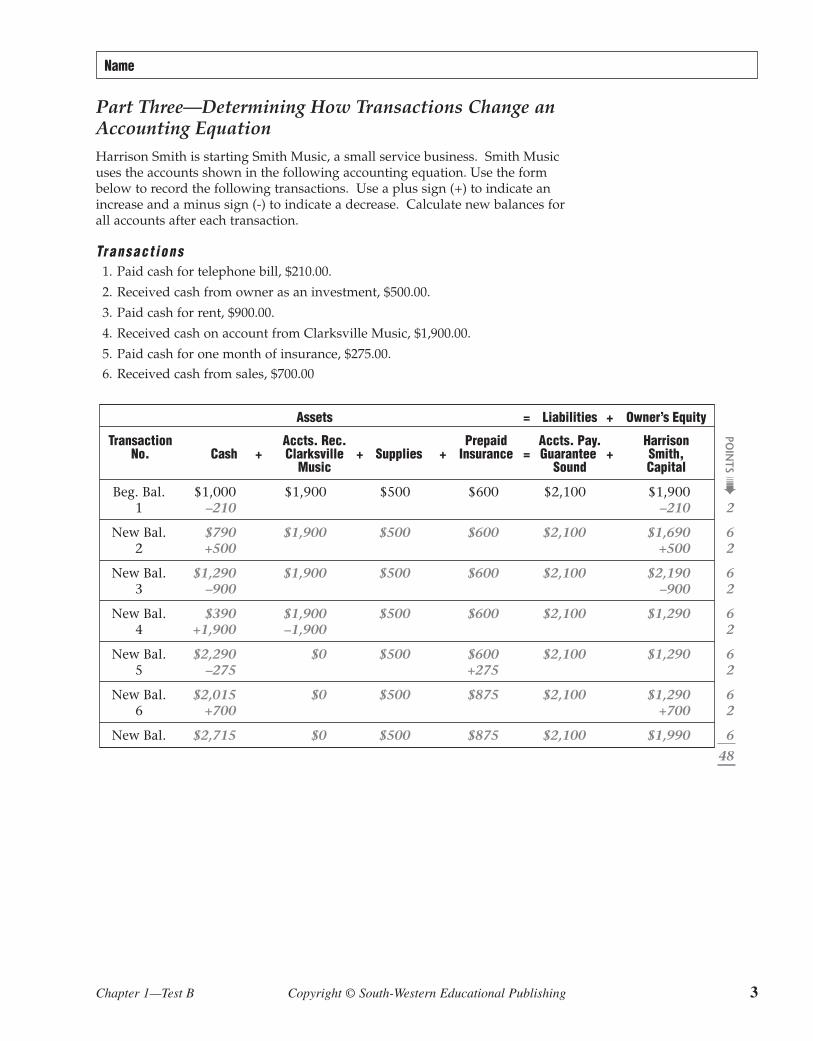

Part Three—Determining How Transactions Change anAccounting EquationHarrison Smith is starting Smith Music, a small service business. Smith Musicuses the accounts shown in the following accounting equation. Use the formbelow to record the following transactions. Use a plus sign (+) to indicate anincrease and a minus sign (-) to indicate a decrease. Calculate new balances forall accounts after each transaction.

Transac t ions1. Paid cash for telephone bill, $210.00.

2. Received cash from owner as an investment, $500.00.

3. Paid cash for rent, $900.00.

4. Received cash on account from Clarksville Music, $1,900.00.

5. Paid cash for one month of insurance, $275.00.6. Received cash from sales, $700.00

Assets = Liabilities + Owner’s Equity

Transaction Accts. Rec. Prepaid Accts. Pay. HarrisonNo. Cash + Clarksville + Supplies + Insurance = Guarantee + Smith,

Music Sound Capital

Beg. Bal. $1,000 $1,900 $500 $600 $2,100 $1,9001 –210 –210

New Bal. $790 $1,900 $500 $600 $2,100 $1,6902 +500 +500

New Bal. $1,290 $1,900 $500 $600 $2,100 $2,1903 –900 –900

New Bal. $390 $1,900 $500 $600 $2,100 $1,2904 +1,900 –1,900

New Bal. $2,290 $0 $500 $600 $2,100 $1,2905 –275 +275

New Bal. $2,015 $0 $500 $875 $2,100 $1,2906 +700 +700

New Bal. $2,715 $0 $500 $875 $2,100 $1,990

POIN

TS �

2

62

62

62

62

62

6

48

4 Century 21 Accounting, 8th Edition Chapter 1—Test B

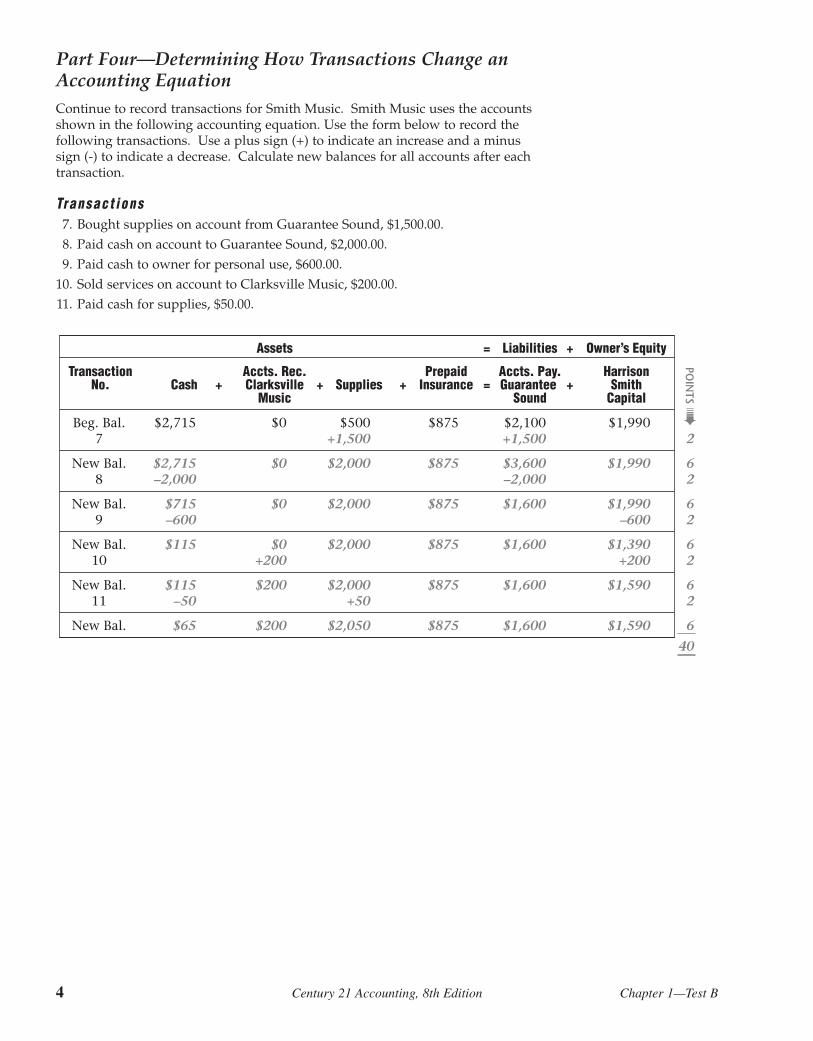

Part Four—Determining How Transactions Change anAccounting EquationContinue to record transactions for Smith Music. Smith Music uses the accountsshown in the following accounting equation. Use the form below to record thefollowing transactions. Use a plus sign (+) to indicate an increase and a minussign (-) to indicate a decrease. Calculate new balances for all accounts after eachtransaction.

Transac t ions7. Bought supplies on account from Guarantee Sound, $1,500.00.8. Paid cash on account to Guarantee Sound, $2,000.00.9. Paid cash to owner for personal use, $600.00.

10. Sold services on account to Clarksville Music, $200.00.11. Paid cash for supplies, $50.00.

Assets = Liabilities + Owner’s Equity

Transaction Accts. Rec. Prepaid Accts. Pay. HarrisonNo. Cash + Clarksville + Supplies + Insurance = Guarantee + Smith

Music Sound Capital

Beg. Bal. $2,715 $0 $500 $875 $2,100 $1,9907 +1,500 +1,500

New Bal. $2,715 $0 $2,000 $875 $3,600 $1,9908 –2,000 –2,000

New Bal. $715 $0 $2,000 $875 $1,600 $1,9909 –600 –600

New Bal. $115 $0 $2,000 $875 $1,600 $1,39010 +200 +200

New Bal. $115 $200 $2,000 $875 $1,600 $1,59011 –50 +50

New Bal. $65 $200 $2,050 $875 $1,600 $1,590

POIN

TS �

2

62

62

62

62

6

40

chapterTEST A

PerfectScore

YourScoreName

Analyzing Accounting Concepts and Practices 20 Pts.Analyzing the Effect of Transactions 9 Pts.

Determining the Normal Balance, Increase, and Decrease Sides for Accounts 36 Pts.Analyzing Transactions into Debit and Credit Parts 20 Pts.

Total 85 Pts.

Chapter 2—Test A Copyright © South-Western Educational Publishing 1

2

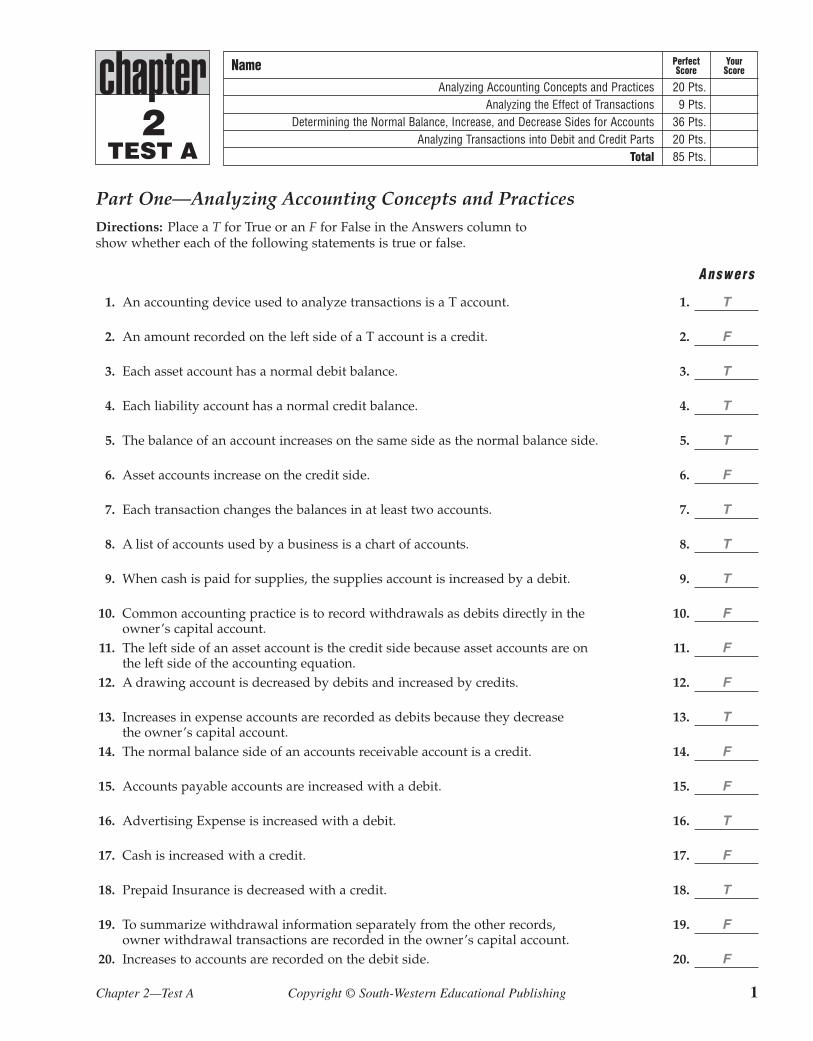

Part One—Analyzing Accounting Concepts and Practices Directions: Place a T for True or an F for False in the Answers column toshow whether each of the following statements is true or false.

Answers

1. An accounting device used to analyze transactions is a T account. 1. T

2. An amount recorded on the left side of a T account is a credit. 2. F

3. Each asset account has a normal debit balance. 3. T

4. Each liability account has a normal credit balance. 4. T

5. The balance of an account increases on the same side as the normal balance side. 5. T

6. Asset accounts increase on the credit side. 6. F

7. Each transaction changes the balances in at least two accounts. 7. T

8. A list of accounts used by a business is a chart of accounts. 8. T

9. When cash is paid for supplies, the supplies account is increased by a debit. 9. T

10. Common accounting practice is to record withdrawals as debits directly in the 10. Fowner’s capital account.

11. The left side of an asset account is the credit side because asset accounts are on 11. Fthe left side of the accounting equation.

12. A drawing account is decreased by debits and increased by credits. 12. F

13. Increases in expense accounts are recorded as debits because they decrease 13. Tthe owner’s capital account.

14. The normal balance side of an accounts receivable account is a credit. 14. F

15. Accounts payable accounts are increased with a debit. 15. F

16. Advertising Expense is increased with a debit. 16. T

17. Cash is increased with a credit. 17. F

18. Prepaid Insurance is decreased with a credit. 18. T

19. To summarize withdrawal information separately from the other records, 19. Fowner withdrawal transactions are recorded in the owner’s capital account.

20. Increases to accounts are recorded on the debit side. 20. F

2 Century 21 Accounting, 8th Edition Chapter 2—Test A

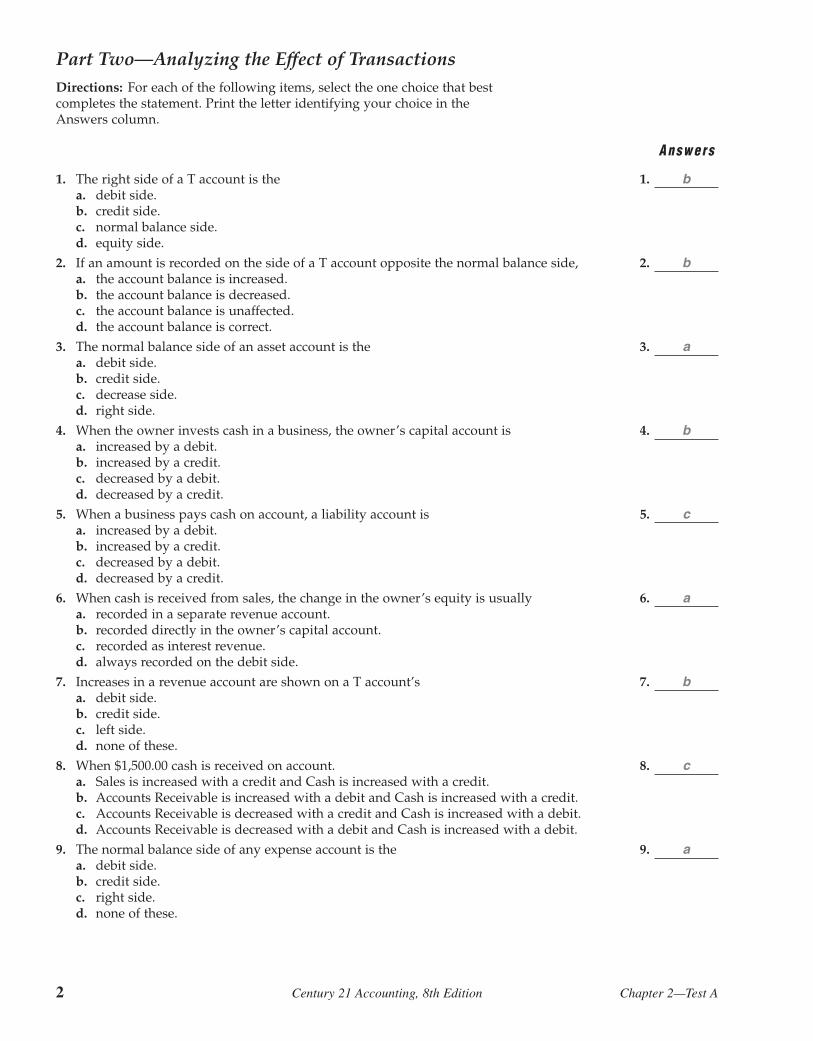

Part Two—Analyzing the Effect of TransactionsDirections: For each of the following items, select the one choice that bestcompletes the statement. Print the letter identifying your choice in theAnswers column.

Answers

1. The right side of a T account is the 1. ba. debit side.b. credit side.c. normal balance side.d. equity side.

2. If an amount is recorded on the side of a T account opposite the normal balance side, 2. ba. the account balance is increased.b. the account balance is decreased.c. the account balance is unaffected.d. the account balance is correct.

3. The normal balance side of an asset account is the 3. aa. debit side.b. credit side.c. decrease side.d. right side.

4. When the owner invests cash in a business, the owner’s capital account is 4. ba. increased by a debit.b. increased by a credit.c. decreased by a debit.d. decreased by a credit.

5. When a business pays cash on account, a liability account is 5. ca. increased by a debit.b. increased by a credit.c. decreased by a debit.d. decreased by a credit.

6. When cash is received from sales, the change in the owner’s equity is usually 6. aa. recorded in a separate revenue account.b. recorded directly in the owner’s capital account.c. recorded as interest revenue.d. always recorded on the debit side.

7. Increases in a revenue account are shown on a T account’s 7. ba. debit side.b. credit side.c. left side.d. none of these.

8. When $1,500.00 cash is received on account. 8. ca. Sales is increased with a credit and Cash is increased with a credit.b. Accounts Receivable is increased with a debit and Cash is increased with a credit.c. Accounts Receivable is decreased with a credit and Cash is increased with a debit.d. Accounts Receivable is decreased with a debit and Cash is increased with a debit.

9. The normal balance side of any expense account is the 9. aa. debit side.b. credit side.c. right side.d. none of these.

Name

Chapter 2—Test A Copyright © South-Western Educational Publishing 3

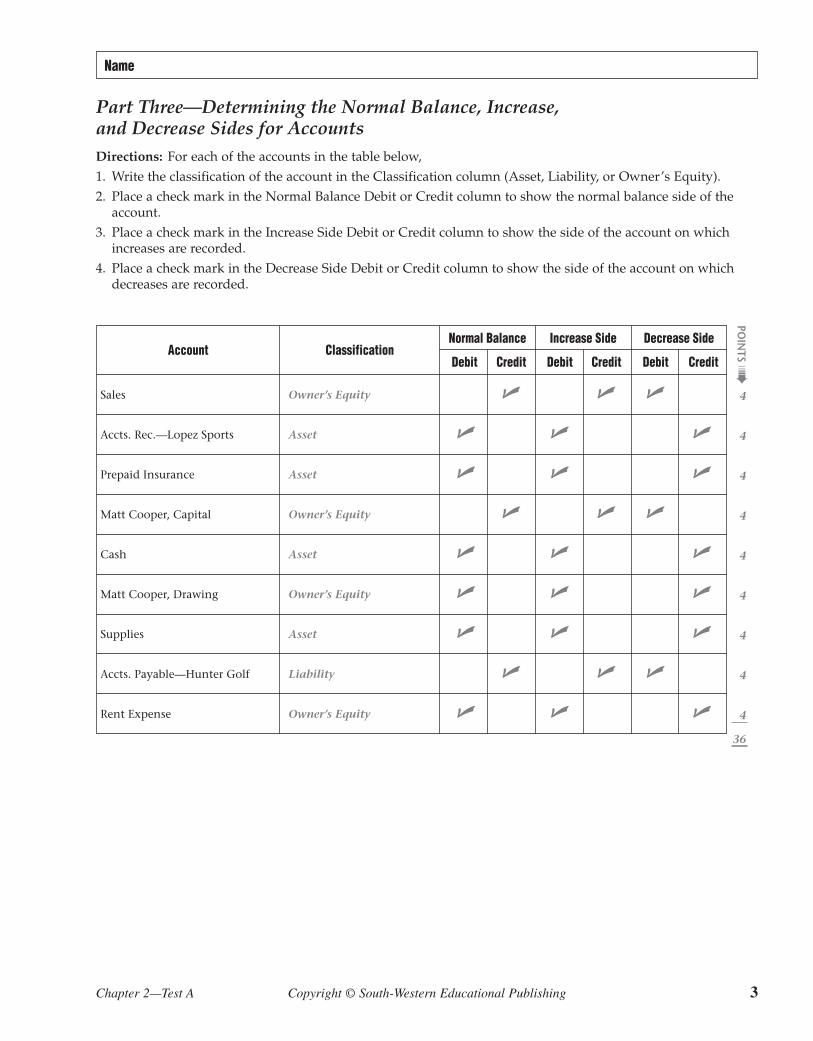

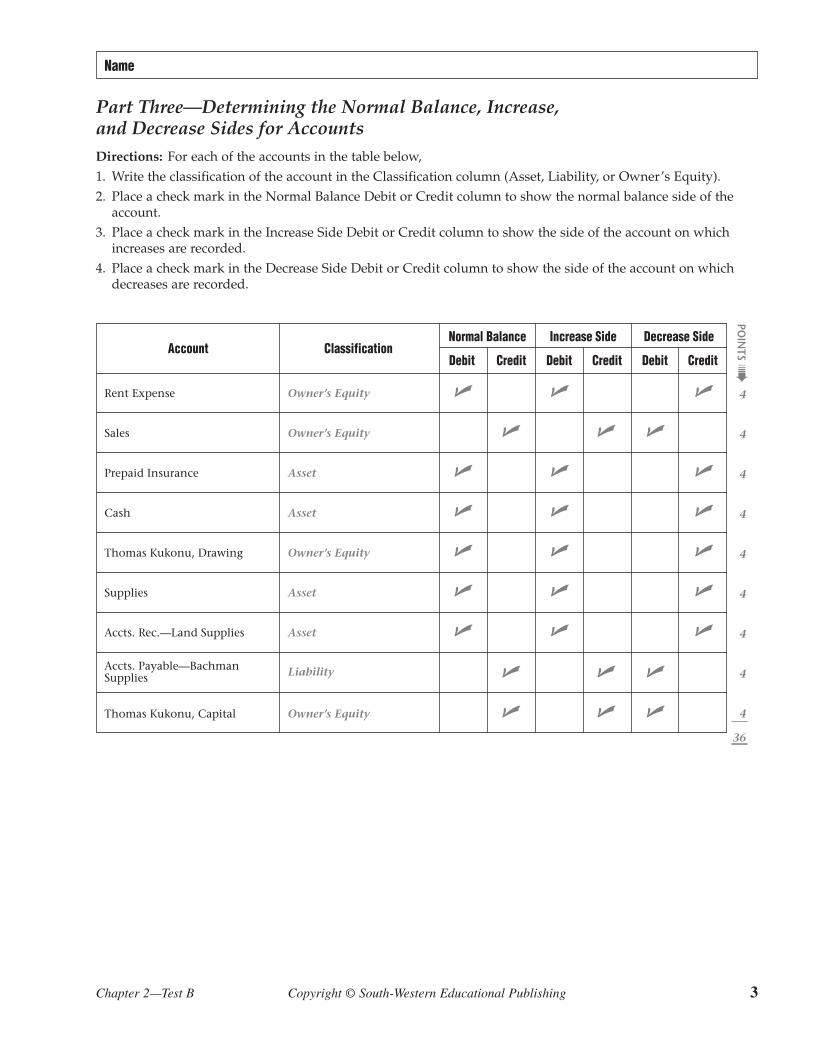

Part Three—Determining the Normal Balance, Increase,and Decrease Sides for AccountsDirections: For each of the accounts in the table below,1. Write the classification of the account in the Classification column (Asset, Liability, or Owner’s Equity).2. Place a check mark in the Normal Balance Debit or Credit column to show the normal balance side of the

account.3. Place a check mark in the Increase Side Debit or Credit column to show the side of the account on which

increases are recorded.4. Place a check mark in the Decrease Side Debit or Credit column to show the side of the account on which

decreases are recorded.

Account ClassificationNormal Balance Increase Side Decrease Side

Debit Credit Debit Credit Debit Credit

Sales Owner’s Equity � � �

Accts. Rec.—Lopez Sports Asset � � �

Prepaid Insurance Asset � � �

Matt Cooper, Capital Owner’s Equity � � �

Cash Asset � � �

Matt Cooper, Drawing Owner’s Equity � � �

Supplies Asset � � �

Accts. Payable—Hunter Golf Liability � � �

Rent Expense Owner’s Equity � � �

POIN

TS �

4

4

4

4

4

4

4

4

4

36

4 Century 21 Accounting, 8th Edition Chapter 2—Test A

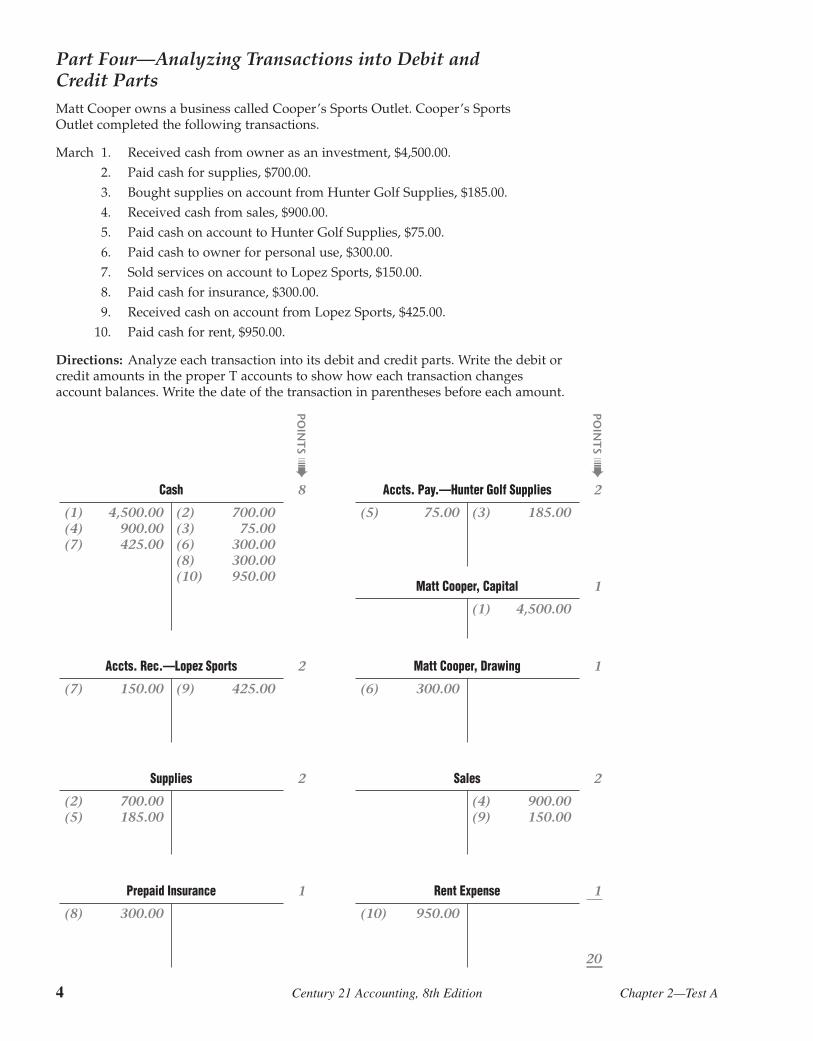

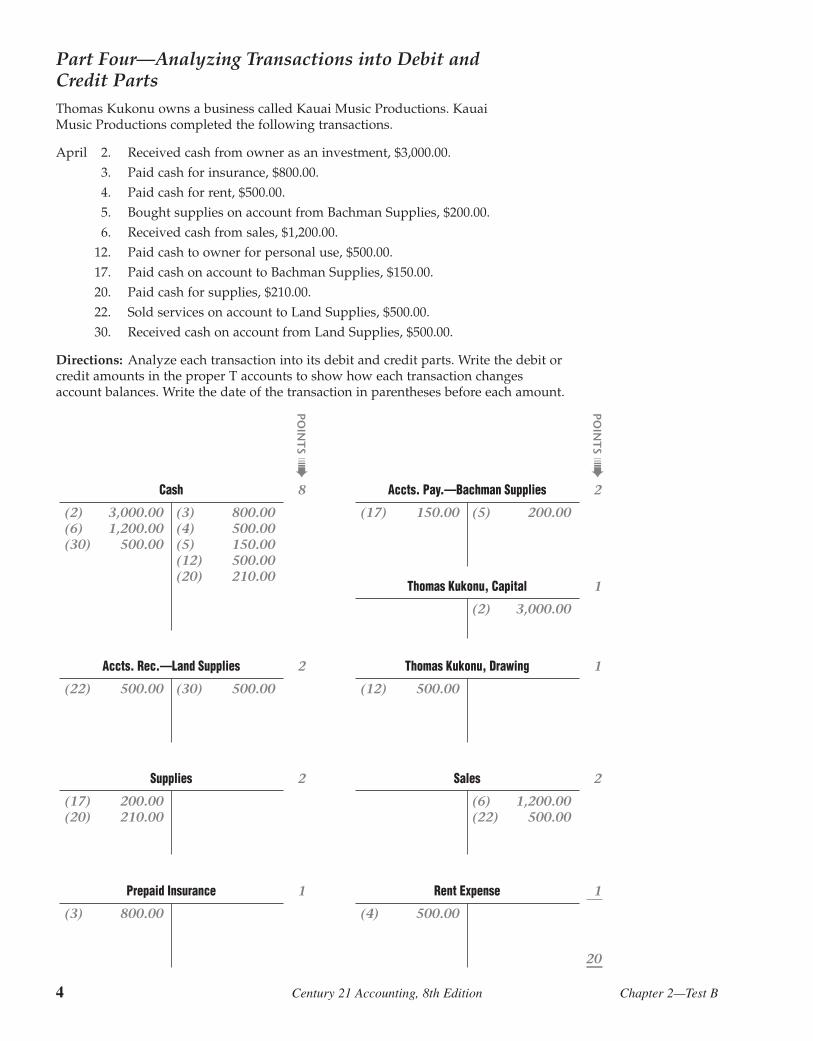

Part Four—Analyzing Transactions into Debit andCredit Parts Matt Cooper owns a business called Cooper’s Sports Outlet. Cooper’s SportsOutlet completed the following transactions.

March 1. Received cash from owner as an investment, $4,500.00.2. Paid cash for supplies, $700.00.3. Bought supplies on account from Hunter Golf Supplies, $185.00.4. Received cash from sales, $900.00.5. Paid cash on account to Hunter Golf Supplies, $75.00.6. Paid cash to owner for personal use, $300.00.7. Sold services on account to Lopez Sports, $150.00.8. Paid cash for insurance, $300.00.9. Received cash on account from Lopez Sports, $425.00.

10. Paid cash for rent, $950.00.

Directions: Analyze each transaction into its debit and credit parts. Write the debit orcredit amounts in the proper T accounts to show how each transaction changesaccount balances. Write the date of the transaction in parentheses before each amount.

Cash

(1) 4,500.00(4) 900.00(7) 425.00

(2) 700.00(3) 75.00(6) 300.00(8) 300.00(10) 950.00

Accts. Pay.—Hunter Golf Supplies

(5) 75.00 (3) 185.00

Matt Cooper, Capital

(1) 4,500.00

Accts. Rec.—Lopez Sports

(7) 150.00 (9) 425.00

Matt Cooper, Drawing

(6) 300.00

Supplies

(2) 700.00(5) 185.00

Sales

(4) 900.00(9) 150.00

Prepaid Insurance

(8) 300.00

Rent Expense

(10) 950.00

8

2

2

1

POIN

TS �

2

1

1

2

1

20

POIN

TS �

chapterTEST B

PerfectScore

YourScoreName

Analyzing Accounting Concepts and Practices 20 Pts.Analyzing the Effect of Transactions 9 Pts.

Determining the Normal Balance, Increase, and Decrease Sides for Accounts 36 Pts.Analyzing Transactions into Debit and Credit Parts 20 Pts.

Total 85 Pts.

Chapter 2—Test B Copyright © South-Western Educational Publishing 1

2

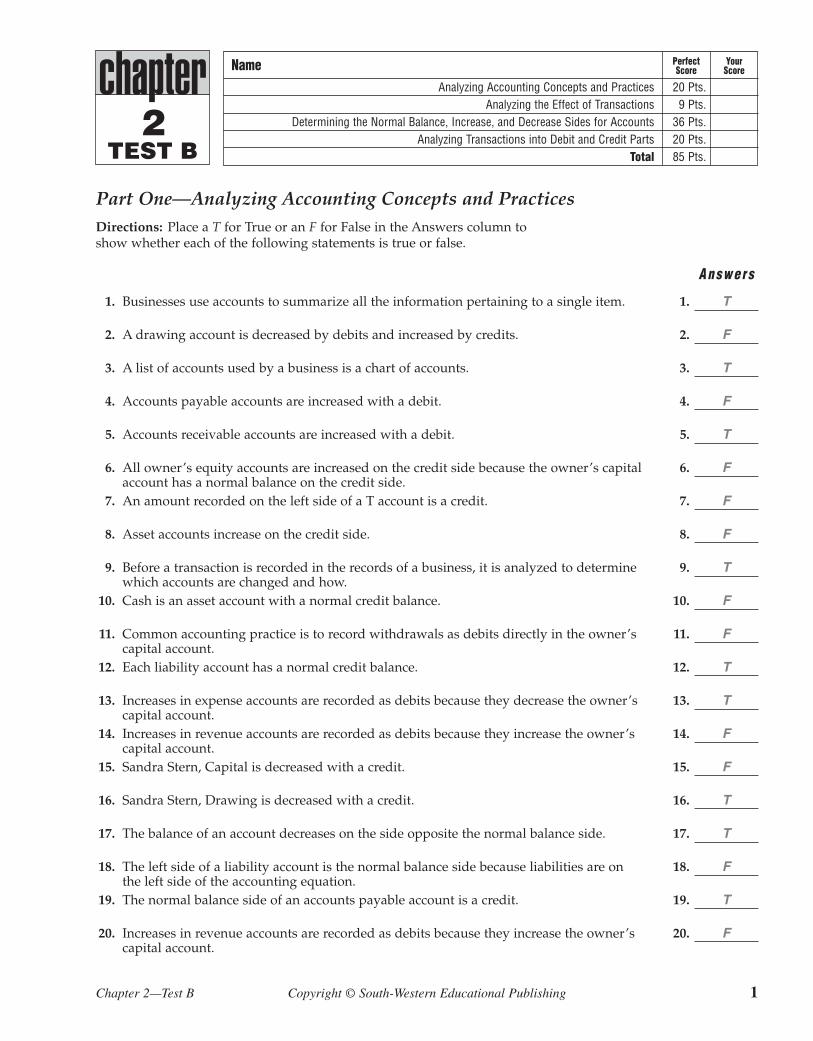

Part One—Analyzing Accounting Concepts and Practices Directions: Place a T for True or an F for False in the Answers column toshow whether each of the following statements is true or false.

Answers

1. Businesses use accounts to summarize all the information pertaining to a single item. 1. T

2. A drawing account is decreased by debits and increased by credits. 2. F

3. A list of accounts used by a business is a chart of accounts. 3. T

4. Accounts payable accounts are increased with a debit. 4. F

5. Accounts receivable accounts are increased with a debit. 5. T

6. All owner’s equity accounts are increased on the credit side because the owner’s capital 6. Faccount has a normal balance on the credit side.

7. An amount recorded on the left side of a T account is a credit. 7. F

8. Asset accounts increase on the credit side. 8. F

9. Before a transaction is recorded in the records of a business, it is analyzed to determine 9. Twhich accounts are changed and how.

10. Cash is an asset account with a normal credit balance. 10. F

11. Common accounting practice is to record withdrawals as debits directly in the owner’s 11. Fcapital account.

12. Each liability account has a normal credit balance. 12. T

13. Increases in expense accounts are recorded as debits because they decrease the owner’s 13. Tcapital account.

14. Increases in revenue accounts are recorded as debits because they increase the owner’s 14. Fcapital account.

15. Sandra Stern, Capital is decreased with a credit. 15. F

16. Sandra Stern, Drawing is decreased with a credit. 16. T

17. The balance of an account decreases on the side opposite the normal balance side. 17. T

18. The left side of a liability account is the normal balance side because liabilities are on 18. Fthe left side of the accounting equation.

19. The normal balance side of an accounts payable account is a credit. 19. T

20. Increases in revenue accounts are recorded as debits because they increase the owner’s 20. Fcapital account.

2 Century 21 Accounting, 8th Edition Chapter 2—Test B

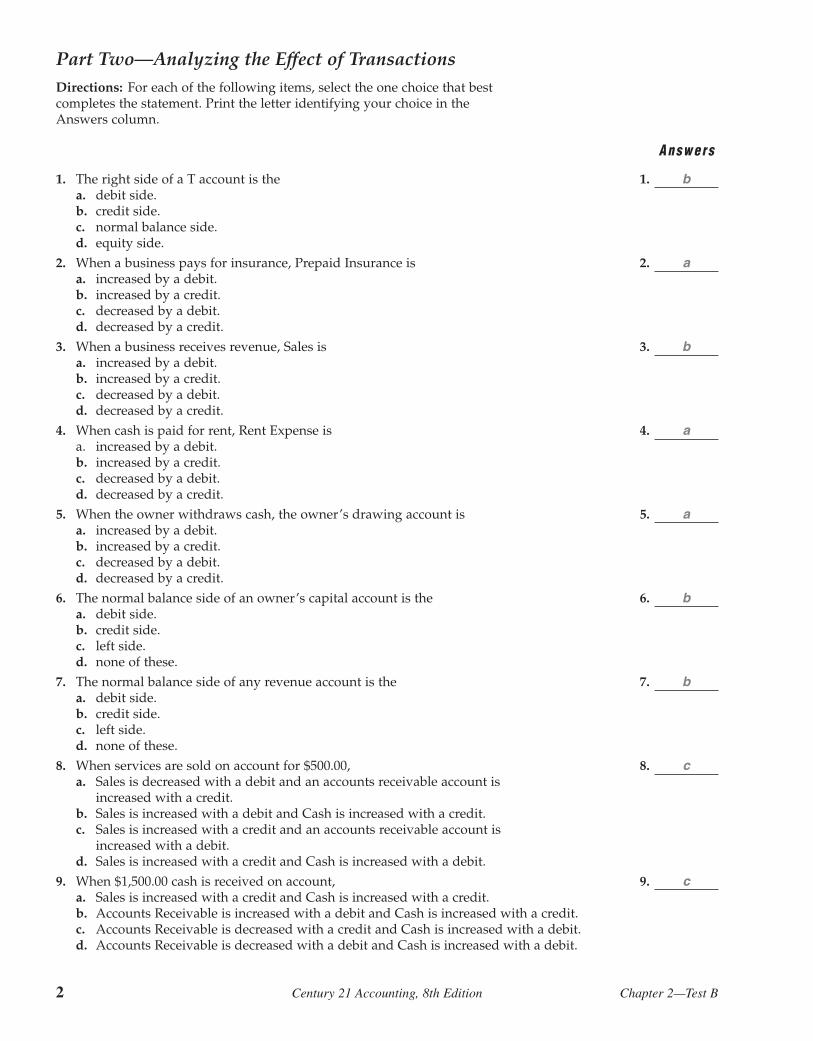

Part Two—Analyzing the Effect of TransactionsDirections: For each of the following items, select the one choice that bestcompletes the statement. Print the letter identifying your choice in theAnswers column.

Answers

1. The right side of a T account is the 1. ba. debit side.b. credit side.c. normal balance side.d. equity side.

2. When a business pays for insurance, Prepaid Insurance is 2. aa. increased by a debit.b. increased by a credit.c. decreased by a debit.d. decreased by a credit.

3. When a business receives revenue, Sales is 3. ba. increased by a debit.b. increased by a credit.c. decreased by a debit.d. decreased by a credit.

4. When cash is paid for rent, Rent Expense is 4. aa. increased by a debit.b. increased by a credit.c. decreased by a debit.d. decreased by a credit.

5. When the owner withdraws cash, the owner’s drawing account is 5. aa. increased by a debit.b. increased by a credit.c. decreased by a debit.d. decreased by a credit.

6. The normal balance side of an owner’s capital account is the 6. ba. debit side.b. credit side.c. left side.d. none of these.

7. The normal balance side of any revenue account is the 7. ba. debit side.b. credit side.c. left side.d. none of these.

8. When services are sold on account for $500.00, 8. ca. Sales is decreased with a debit and an accounts receivable account is

increased with a credit.b. Sales is increased with a debit and Cash is increased with a credit.c. Sales is increased with a credit and an accounts receivable account is

increased with a debit.d. Sales is increased with a credit and Cash is increased with a debit.

9. When $1,500.00 cash is received on account, 9. ca. Sales is increased with a credit and Cash is increased with a credit.b. Accounts Receivable is increased with a debit and Cash is increased with a credit.c. Accounts Receivable is decreased with a credit and Cash is increased with a debit.d. Accounts Receivable is decreased with a debit and Cash is increased with a debit.

Name

Chapter 2—Test B Copyright © South-Western Educational Publishing 3

Part Three—Determining the Normal Balance, Increase,and Decrease Sides for AccountsDirections: For each of the accounts in the table below,1. Write the classification of the account in the Classification column (Asset, Liability, or Owner’s Equity).2. Place a check mark in the Normal Balance Debit or Credit column to show the normal balance side of the

account.3. Place a check mark in the Increase Side Debit or Credit column to show the side of the account on which

increases are recorded.4. Place a check mark in the Decrease Side Debit or Credit column to show the side of the account on which

decreases are recorded.

Account ClassificationNormal Balance Increase Side Decrease Side

Debit Credit Debit Credit Debit Credit

Rent Expense Owner’s Equity � � �

Sales Owner’s Equity � � �

Prepaid Insurance Asset � � �

Cash Asset � � �

Thomas Kukonu, Drawing Owner’s Equity � � �

Supplies Asset � � �

Accts. Rec.—Land Supplies Asset � � �

Accts. Payable—BachmanSupplies Liability � � �

Thomas Kukonu, Capital Owner’s Equity � � �

POIN

TS �

4

4

4

4

4

4

4

4

4

36

4 Century 21 Accounting, 8th Edition Chapter 2—Test B

Part Four—Analyzing Transactions into Debit andCredit Parts Thomas Kukonu owns a business called Kauai Music Productions. KauaiMusic Productions completed the following transactions.

April 2. Received cash from owner as an investment, $3,000.00.3. Paid cash for insurance, $800.00.4. Paid cash for rent, $500.00.5. Bought supplies on account from Bachman Supplies, $200.00.6. Received cash from sales, $1,200.00.

12. Paid cash to owner for personal use, $500.00.17. Paid cash on account to Bachman Supplies, $150.00.20. Paid cash for supplies, $210.00.22. Sold services on account to Land Supplies, $500.00.30. Received cash on account from Land Supplies, $500.00.

Directions: Analyze each transaction into its debit and credit parts. Write the debit orcredit amounts in the proper T accounts to show how each transaction changesaccount balances. Write the date of the transaction in parentheses before each amount.

Cash

(2) 3,000.00(6) 1,200.00(30) 500.00

(3) 800.00(4) 500.00(5) 150.00(12) 500.00(20) 210.00

Accts. Pay.—Bachman Supplies

(17) 150.00 (5) 200.00

Thomas Kukonu, Capital

(2) 3,000.00

Accts. Rec.—Land Supplies

(22) 500.00 (30) 500.00

Thomas Kukonu, Drawing

(12) 500.00

Supplies

(17) 200.00(20) 210.00

Sales

(6) 1,200.00(22) 500.00

Prepaid Insurance

(3) 800.00

Rent Expense

(4) 500.00

8

2

2

1

POIN

TS �

2

1

1

2

1

20

POIN

TS �

chapterTEST A

PerfectScore

YourScoreName

Defining Accounting Terms 13 Pts.Analyzing Accounting Concepts and Practices 12 Pts.

Journalizing Transactions 100 Pts.Analyzing Journalizing Transactions 10 Pts.

Total 135 Pts.

Chapter 3—Test A Copyright © South-Western Educational Publishing 1

3

Part One—Defining Accounting TermsDirections: Select the one term in Column I that best fits each definition inColumn II. Print the letter identifying your choice in the Answers column.

Co lumn I Co lumn I I Answers

A. check 1. Information for each transaction recorded in a journal. 1. CB. double-entry accounting 2. A form for recording transactions in chronological order. 2. FC. entry 3. A journal amount column headed with an account title. 3. MD. general amount column 4. A business paper from which information is obtained for 4. L

a journal entry.E. invoice 5. A journal amount column that is not headed with an 5. D

account title. F. journal 6. The recording of debit and credit parts of a transaction. 6. BG. journalizing 7. A form describing the goods or services sold, the quantity, 7. E

and the price. H. memorandum 8. Recording transactions in a journal. 8. GI. proving cash 9. Determining that the amount of cash agrees with the 9. I

accounting records.J. receipt 10. A business form ordering a bank to pay cash from a 10. A

bank account.K. sales invoice 11. An invoice used as a source document for recording a 11. K

sale on account. L. source document 12. A business form giving written acknowledgment for cash 12. J

received.M. special amount column 13. A form on which a brief message is written describing a 13. H

transaction.

Part Two—Analyzing Accounting Concepts and PracticesDirections: Place a T for True or an F for False in the Answers column toshow whether each of the following statements is true or false.

Answers

1. The source document for all cash payments is a sales invoice. 1. F2. A receipt is the source document for cash received from transactions other than sales. 2. T3. A calculator tape is the source document for daily sales. 3. T4. The source document used when supplies are bought on account is a memorandum. 4. T5. The journal columns used to record receiving cash from sales are Cash Debit and Sales Credit. 5. T6. To correct an error in a journal, simply erase the incorrect item and write the correct item 6. F7. A transaction recorded in a journal is not considered a permanent record. 7. F8. Transactions are recorded in a journal in chronological order. 8. T9. A complete entry consists of the date, the debit amount, and the credit amount. 9. F

10. The day of the month is written on each journal page only for the first entry. 10. F11. Double lines are ruled across a journal’s amount columns to indicate that the totals have 11. T

been verified as correct.12. Cash is always proved at the end of a month. 12. T

2 Century 21 Accounting, 8th Edition Chapter 3—Test A

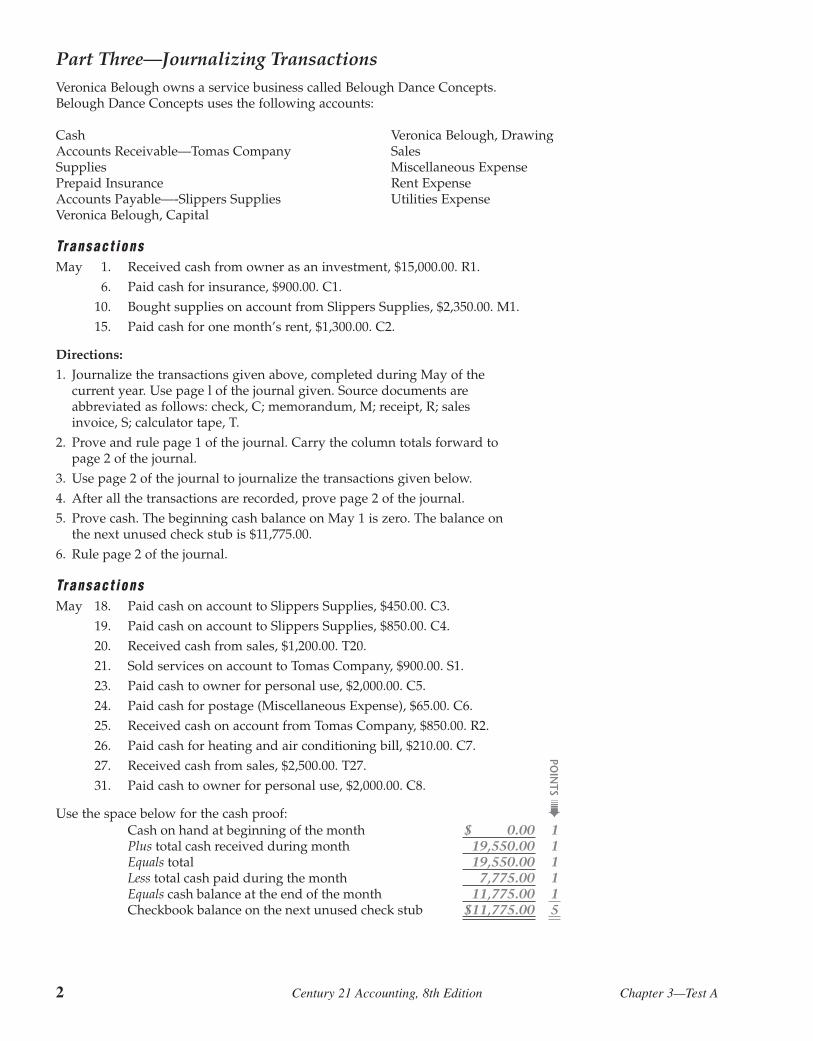

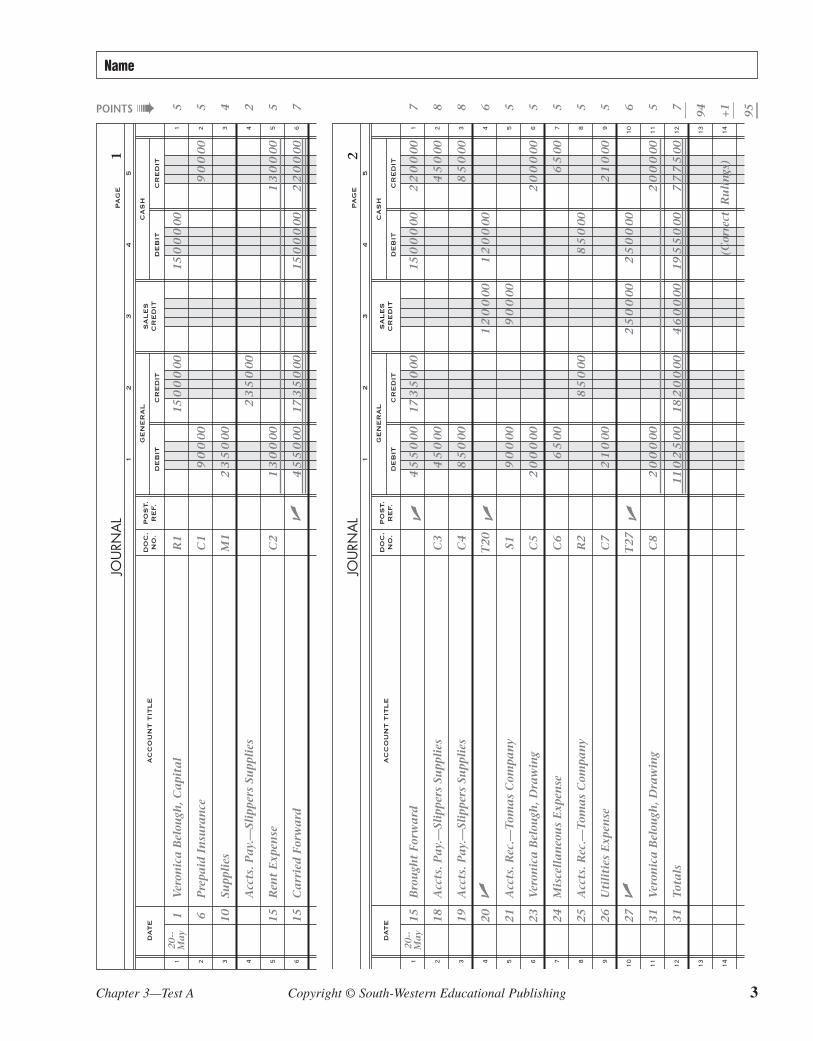

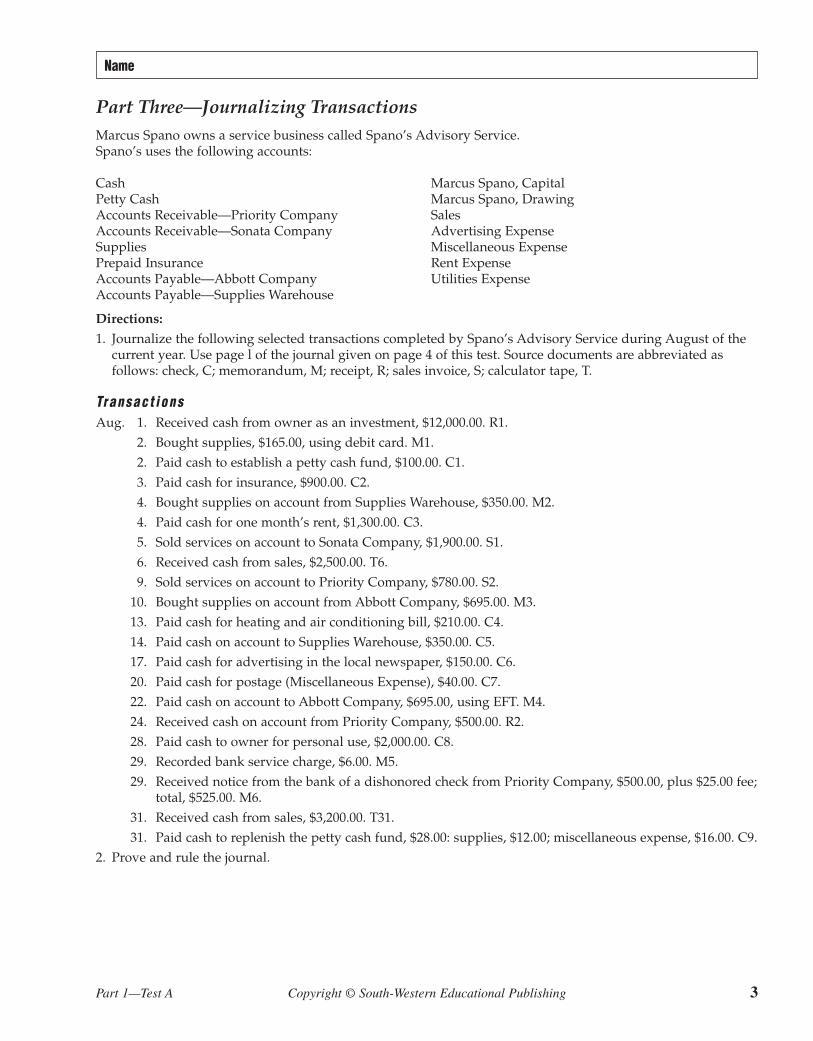

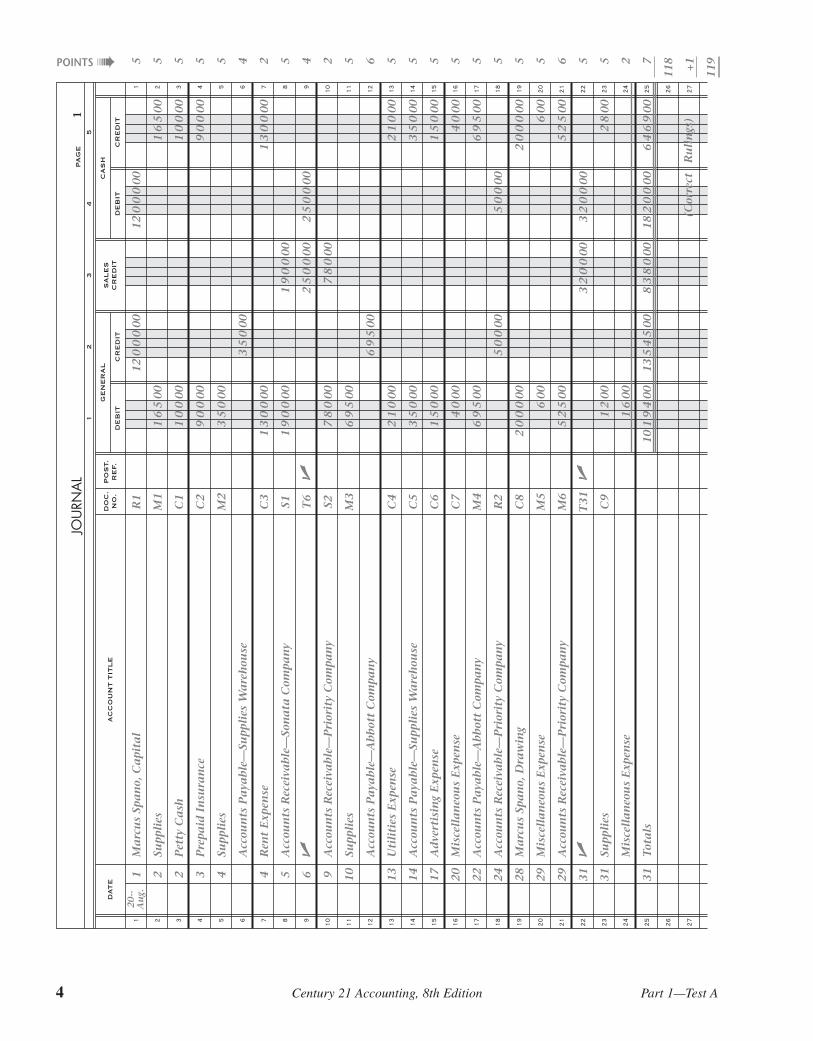

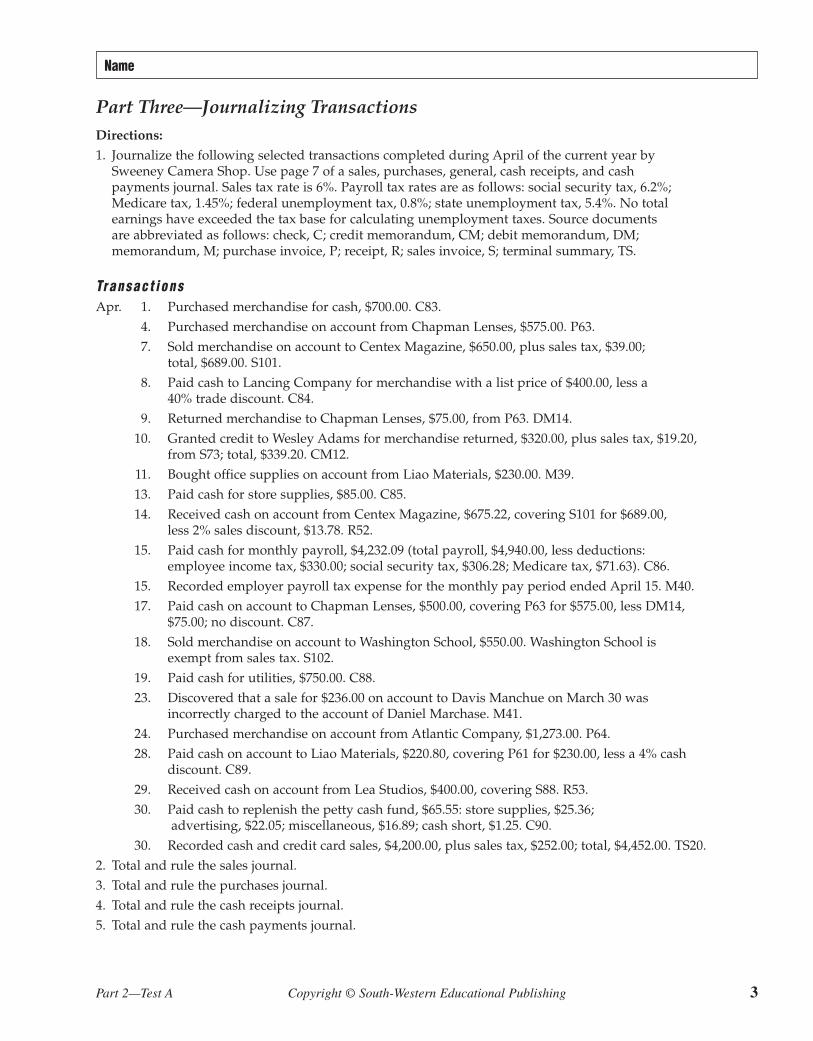

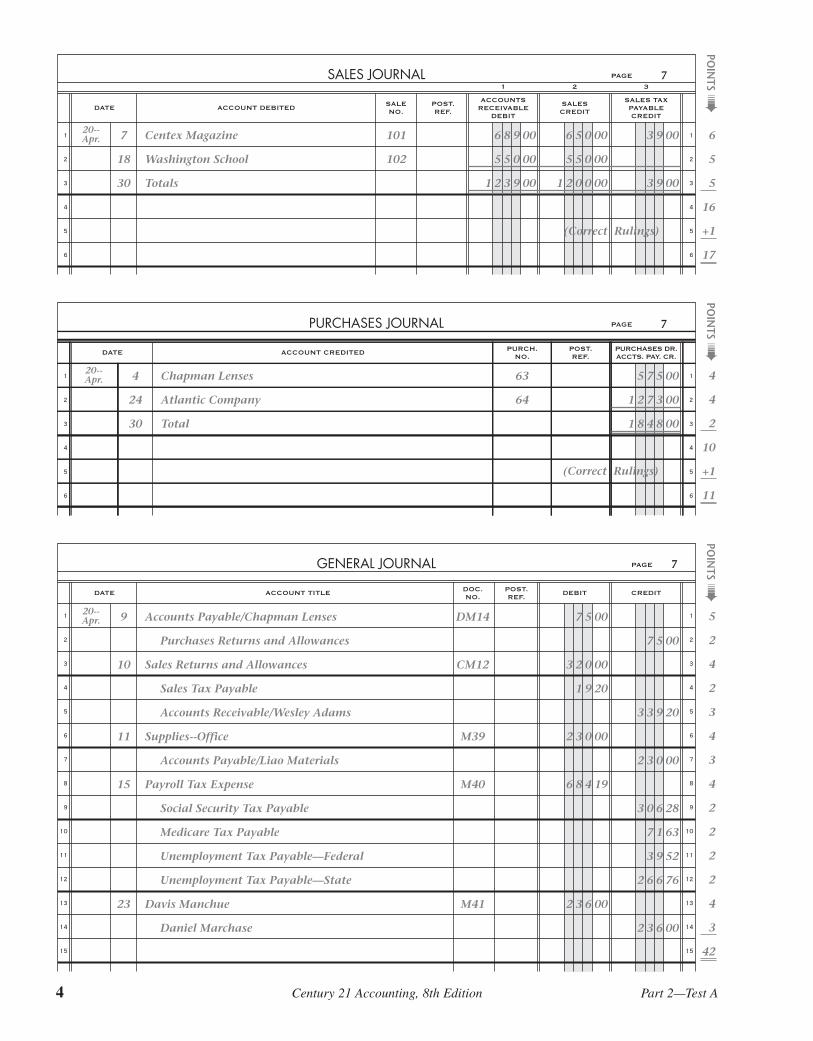

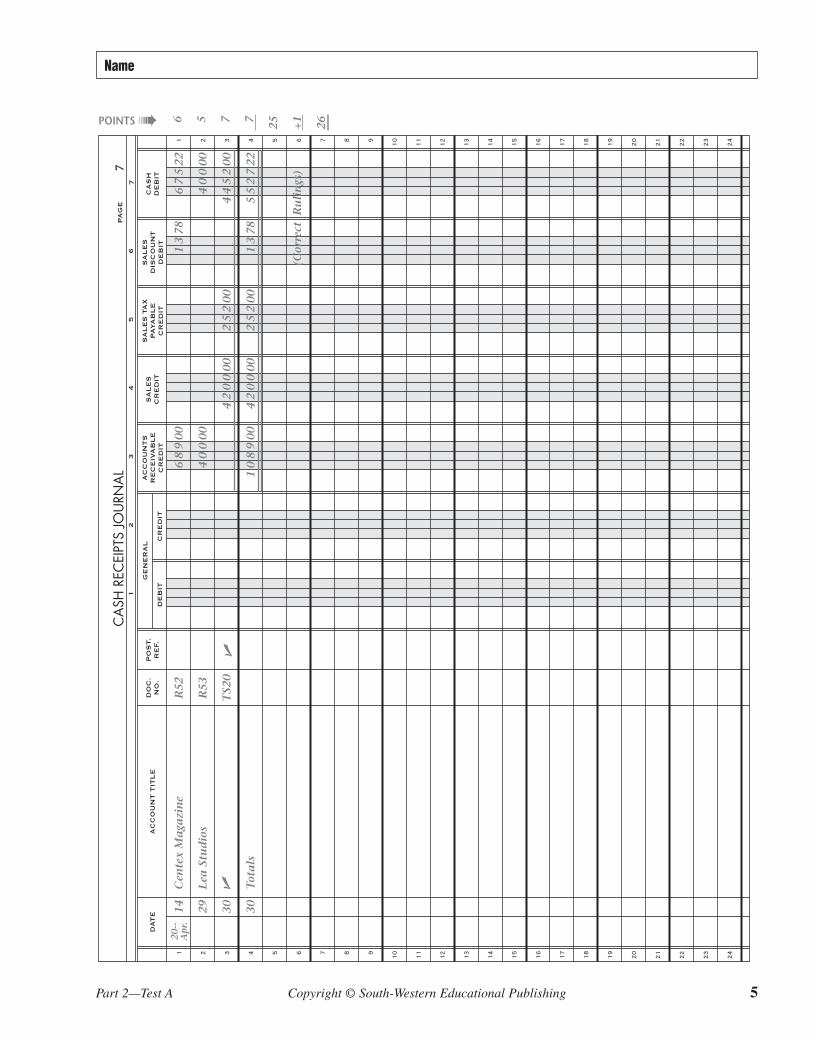

Part Three—Journalizing TransactionsVeronica Belough owns a service business called Belough Dance Concepts.Belough Dance Concepts uses the following accounts:

Cash Veronica Belough, DrawingAccounts Receivable—Tomas Company SalesSupplies Miscellaneous ExpensePrepaid Insurance Rent ExpenseAccounts Payable—-Slippers Supplies Utilities ExpenseVeronica Belough, Capital

Transac t ionsMay 1. Received cash from owner as an investment, $15,000.00. R1.

6. Paid cash for insurance, $900.00. C1.10. Bought supplies on account from Slippers Supplies, $2,350.00. M1.15. Paid cash for one month’s rent, $1,300.00. C2.

Directions:

1. Journalize the transactions given above, completed during May of thecurrent year. Use page l of the journal given. Source documents areabbreviated as follows: check, C; memorandum, M; receipt, R; salesinvoice, S; calculator tape, T.

2. Prove and rule page 1 of the journal. Carry the column totals forward topage 2 of the journal.

3. Use page 2 of the journal to journalize the transactions given below.4. After all the transactions are recorded, prove page 2 of the journal.5. Prove cash. The beginning cash balance on May 1 is zero. The balance on

the next unused check stub is $11,775.00.6. Rule page 2 of the journal.

Transac t ionsMay 18. Paid cash on account to Slippers Supplies, $450.00. C3.

19. Paid cash on account to Slippers Supplies, $850.00. C4.20. Received cash from sales, $1,200.00. T20.21. Sold services on account to Tomas Company, $900.00. S1.23. Paid cash to owner for personal use, $2,000.00. C5.24. Paid cash for postage (Miscellaneous Expense), $65.00. C6.25. Received cash on account from Tomas Company, $850.00. R2.26. Paid cash for heating and air conditioning bill, $210.00. C7.27. Received cash from sales, $2,500.00. T27.31. Paid cash to owner for personal use, $2,000.00. C8.

Use the space below for the cash proof:

POIN

TS �

Cash on hand at beginning of the month $11,770.00 1Plus total cash received during month 19,550.00 1Equals total 19,550.00 1Less total cash paid during the month 7,775.00 1Equals cash balance at the end of the month 11,775.00 1Checkbook balance on the next unused check stub $11,775.00 5

Name

Chapter 3—Test A Copyright © South-Western Educational Publishing 3

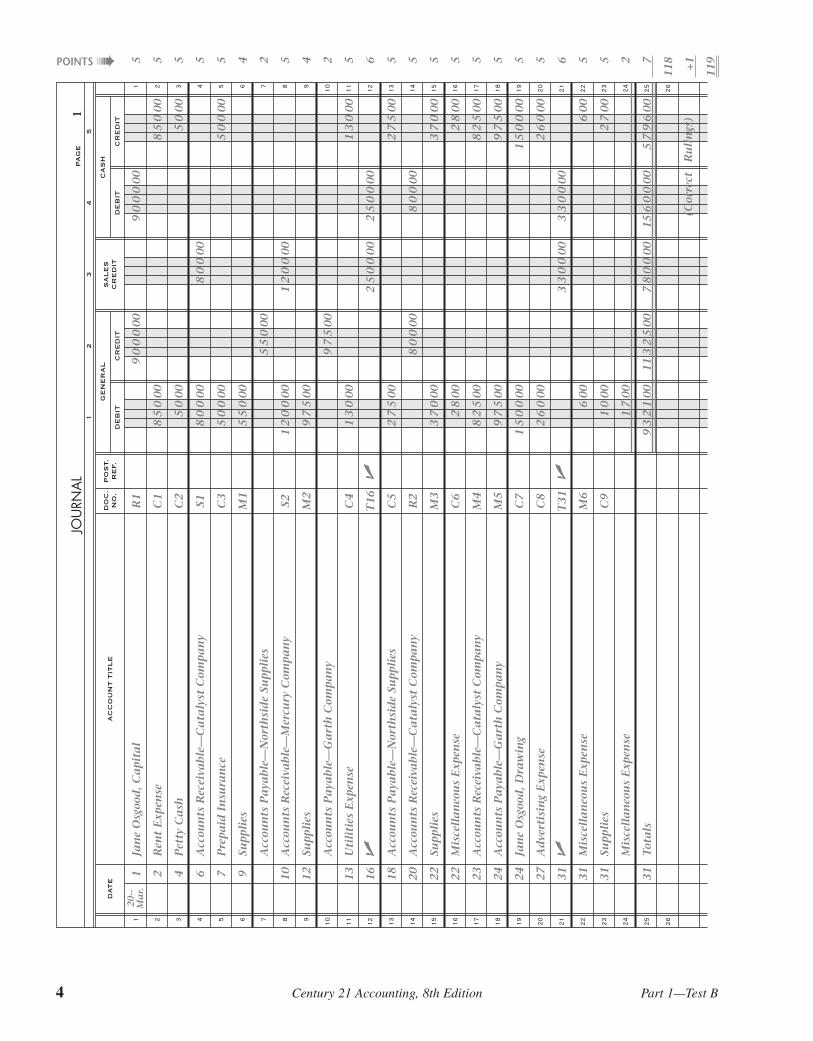

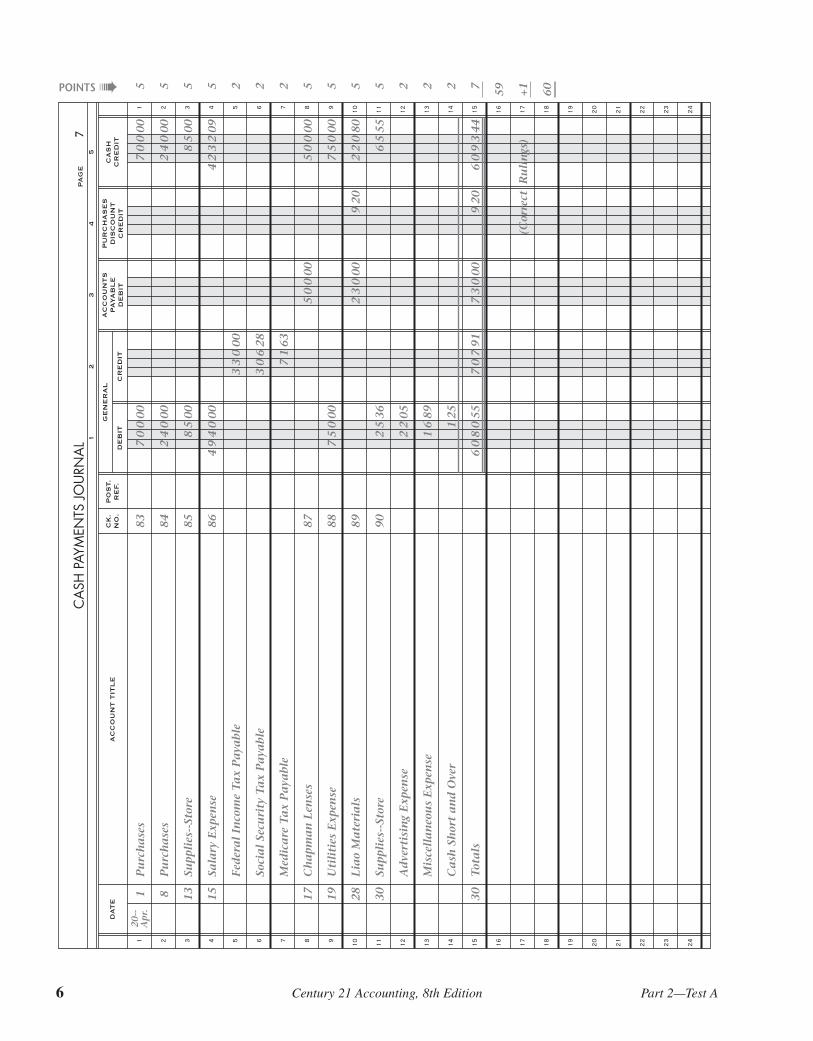

JOU

RNA

LP

AG

E

12

34

1 2 3 4 5 6

1 2 3 4 5 6

DAT

EA

CC

OU

NT

TIT

LE

DO

C.

NO

.P

OS

T.

RE

F.

GE

NE

RA

L

DE

BIT

CR

ED

IT

SA

LE

SC

RE

DIT

CA

SH

DE

BIT

CR

ED

IT

5

1 6 10 15 15

20--

Ma

yV

eron

ica

Bel

ough

, Ca

pita

l

Pre

paid

In

sura

nce

Supp

lies

Acc

ts. P

ay.

—Sl

ippe

rs S

upp

lies

Ren

t E

xpen

se

Ca

rrie

d F

orw

ard

R1

C1

M1

C2

�

90

000

23

50

00

13

00

00

45

50

00

150

00

00

23

50

00

173

50

00

150

00

00

150

00

00

90

000

13

00

00

22

00

001

5 5 4 2 5 7

JOU

RNA

LP

AG

E

12

34

1 2 3 4 5 6 7 8 9

10 11 12 13 14

1 2 3 4 5 6 7 8 9

10 11 12 13 14

DAT

EA

CC

OU

NT

TIT

LE

DO

C.

NO

.P

OS

T.

RE

F.

GE

NE

RA

L

DE

BIT

CR

ED

IT

SA

LE

SC

RE

DIT

CA

SH

DE

BIT

CR

ED

IT

5

15 18 19 20 21 23 24 25 26 27 31 31

20--

Ma

yB

rou

ght

For

wa

rd

Acc

ts. P

ay.

—Sl

ippe

rs S

upp

lies

Acc

ts. P

ay.

—Sl

ippe

rs S

upp

lies

� Acc

ts. R

ec.—

Tom

as

Com

pan

y

Ver

onic

a B

elou

gh, D

raw

ing

Mis

cell

an

eou

s E

xpen

se

Acc

ts. R

ec.—

Tom

as

Com

pan

y

Uti

liti

es E

xpen

se

� Ver

onic

a B

elou

gh, D

raw

ing

Tot

als

C3

C4

T20 S1 C5

C6

R2

C7

T27 C8

� � �

45

50

00

45

000

85

000

90

000

20

00

00

65

00

21

000

20

00

00

110

25

00

173

50

00

85

000

182

00

00

150

00

00

12

00

00

85

000

25

00

00

195

50

00

22

00

00

45

000

85

000

20

00

00

65

00

21

000

20

00

00

77

75

002

7 8 8 6 5 5 5 5 5 6 5 7 94 +1 95

12

00

00

90

000

25

00

00

46

00

00

(Cor

rect

Ru

lin

gs)

POINTS �

4 Century 21 Accounting, 8th Edition Chapter 3—Test A

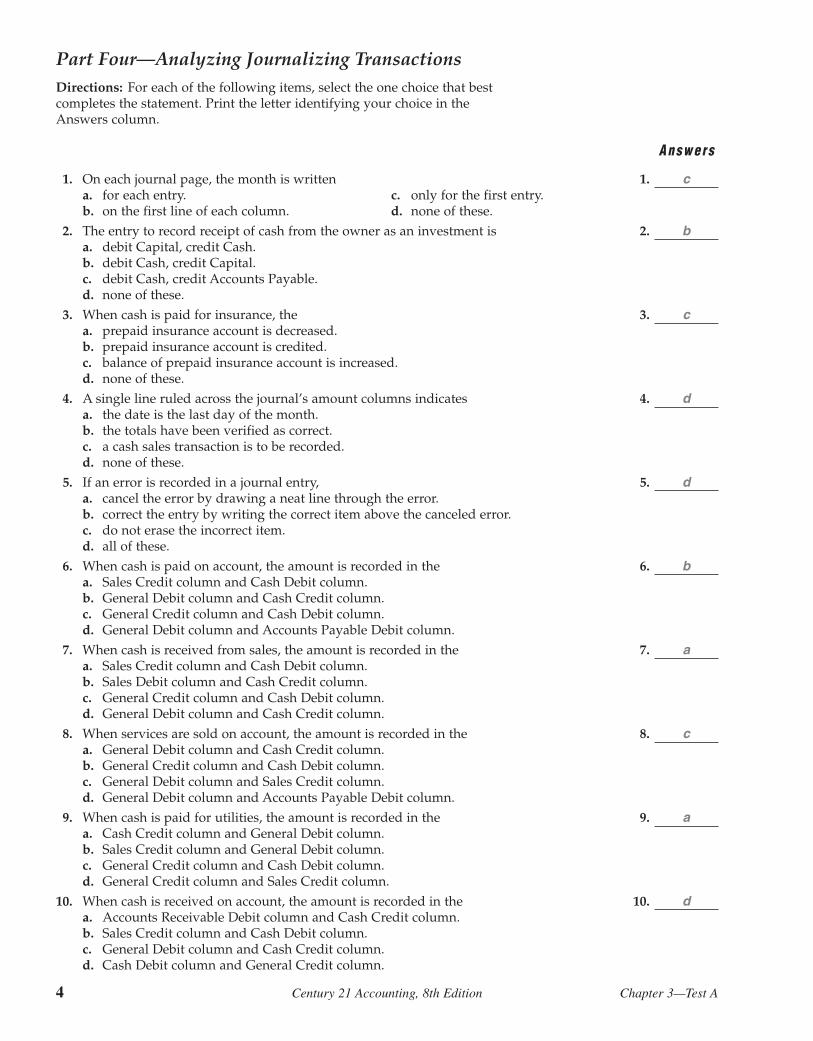

Part Four—Analyzing Journalizing TransactionsDirections: For each of the following items, select the one choice that bestcompletes the statement. Print the letter identifying your choice in theAnswers column.

Answers

1. On each journal page, the month is written 1. ca. for each entry. c. only for the first entry.b. on the first line of each column. d. none of these.

2. The entry to record receipt of cash from the owner as an investment is 2. ba. debit Capital, credit Cash.b. debit Cash, credit Capital.c. debit Cash, credit Accounts Payable.d. none of these.

3. When cash is paid for insurance, the 3. ca. prepaid insurance account is decreased.b. prepaid insurance account is credited.c. balance of prepaid insurance account is increased.d. none of these.

4. A single line ruled across the journal’s amount columns indicates 4. da. the date is the last day of the month.b. the totals have been verified as correct.c. a cash sales transaction is to be recorded.d. none of these.

5. If an error is recorded in a journal entry, 5. da. cancel the error by drawing a neat line through the error.b. correct the entry by writing the correct item above the canceled error.c. do not erase the incorrect item.d. all of these.

6. When cash is paid on account, the amount is recorded in the 6. ba. Sales Credit column and Cash Debit column.b. General Debit column and Cash Credit column.c. General Credit column and Cash Debit column.d. General Debit column and Accounts Payable Debit column.

7. When cash is received from sales, the amount is recorded in the 7. aa. Sales Credit column and Cash Debit column.b. Sales Debit column and Cash Credit column.c. General Credit column and Cash Debit column.d. General Debit column and Cash Credit column.

8. When services are sold on account, the amount is recorded in the 8. ca. General Debit column and Cash Credit column.b. General Credit column and Cash Debit column.c. General Debit column and Sales Credit column.d. General Debit column and Accounts Payable Debit column.

9. When cash is paid for utilities, the amount is recorded in the 9. aa. Cash Credit column and General Debit column.b. Sales Credit column and General Debit column.c. General Credit column and Cash Debit column.d. General Credit column and Sales Credit column.

10. When cash is received on account, the amount is recorded in the 10. da. Accounts Receivable Debit column and Cash Credit column.b. Sales Credit column and Cash Debit column.c. General Debit column and Cash Credit column.d. Cash Debit column and General Credit column.

chapterTEST B

PerfectScore

YourScoreName

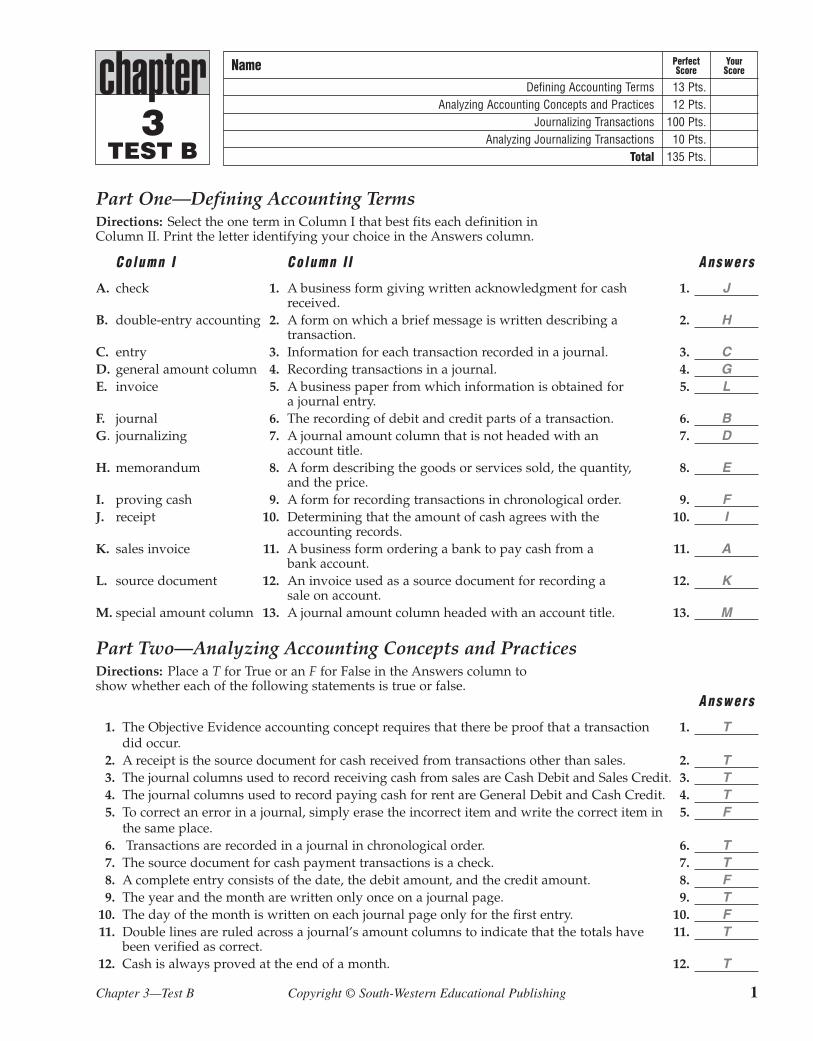

Defining Accounting Terms 13 Pts.Analyzing Accounting Concepts and Practices 12 Pts.

Journalizing Transactions 100 Pts.Analyzing Journalizing Transactions 10 Pts.

Total 135 Pts.

Chapter 3—Test B Copyright © South-Western Educational Publishing 1

3

Part One—Defining Accounting TermsDirections: Select the one term in Column I that best fits each definition inColumn II. Print the letter identifying your choice in the Answers column.

Co lumn I Co lumn I I Answers

A. check 1. A business form giving written acknowledgment for cash 1. Jreceived.

B. double-entry accounting 2. A form on which a brief message is written describing a 2. Htransaction.

C. entry 3. Information for each transaction recorded in a journal. 3. CD. general amount column 4. Recording transactions in a journal. 4. GE. invoice 5. A business paper from which information is obtained for 5. L

a journal entry.F. journal 6. The recording of debit and credit parts of a transaction. 6. BG. journalizing 7. A journal amount column that is not headed with an 7. D

account title.H. memorandum 8. A form describing the goods or services sold, the quantity, 8. E

and the price. I. proving cash 9. A form for recording transactions in chronological order. 9. FJ. receipt 10. Determining that the amount of cash agrees with the 10. I

accounting records. K. sales invoice 11. A business form ordering a bank to pay cash from a 11. A

bank account. L. source document 12. An invoice used as a source document for recording a 12. K

sale on account. M. special amount column 13. A journal amount column headed with an account title. 13. M

Part Two—Analyzing Accounting Concepts and PracticesDirections: Place a T for True or an F for False in the Answers column toshow whether each of the following statements is true or false.

Answers

1. The Objective Evidence accounting concept requires that there be proof that a transaction 1. Tdid occur.

2. A receipt is the source document for cash received from transactions other than sales. 2. T3. The journal columns used to record receiving cash from sales are Cash Debit and Sales Credit. 3. T4. The journal columns used to record paying cash for rent are General Debit and Cash Credit. 4. T5. To correct an error in a journal, simply erase the incorrect item and write the correct item in 5. F

the same place.6. Transactions are recorded in a journal in chronological order. 6. T7. The source document for cash payment transactions is a check. 7. T8. A complete entry consists of the date, the debit amount, and the credit amount. 8. F9. The year and the month are written only once on a journal page. 9. T

10. The day of the month is written on each journal page only for the first entry. 10. F11. Double lines are ruled across a journal’s amount columns to indicate that the totals have 11. T

been verified as correct.12. Cash is always proved at the end of a month. 12. T

2 Century 21 Accounting, 8th Edition Chapter 3—Test B

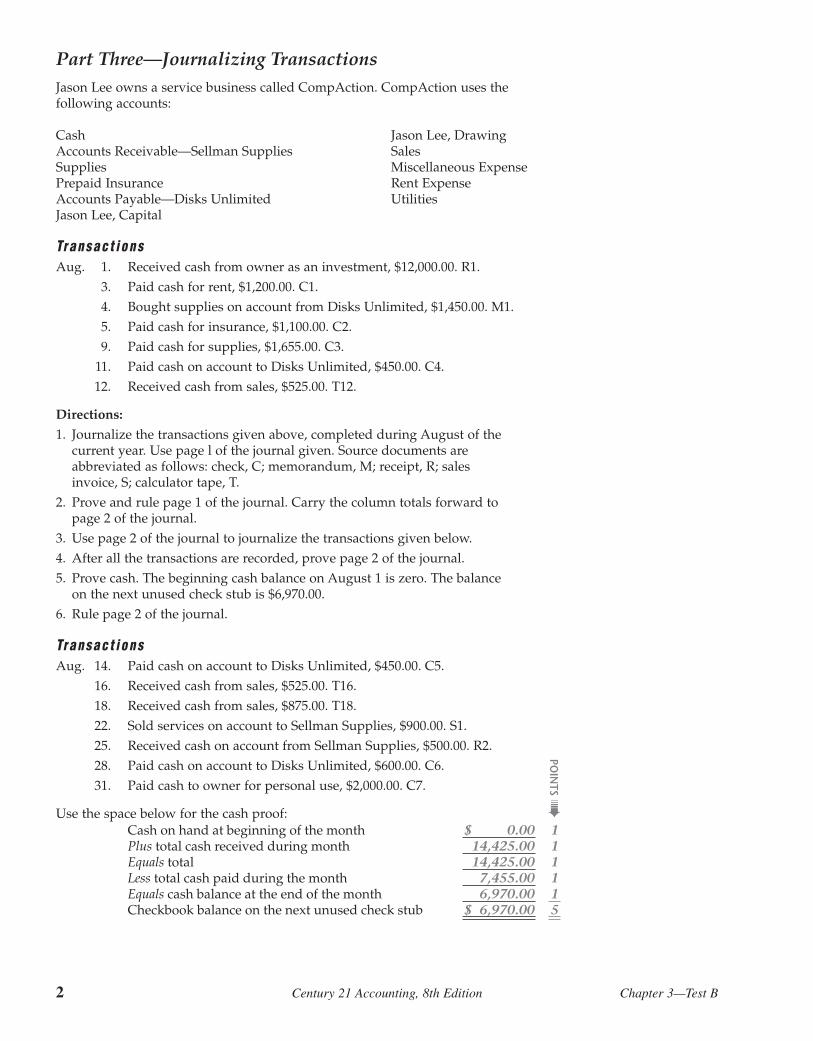

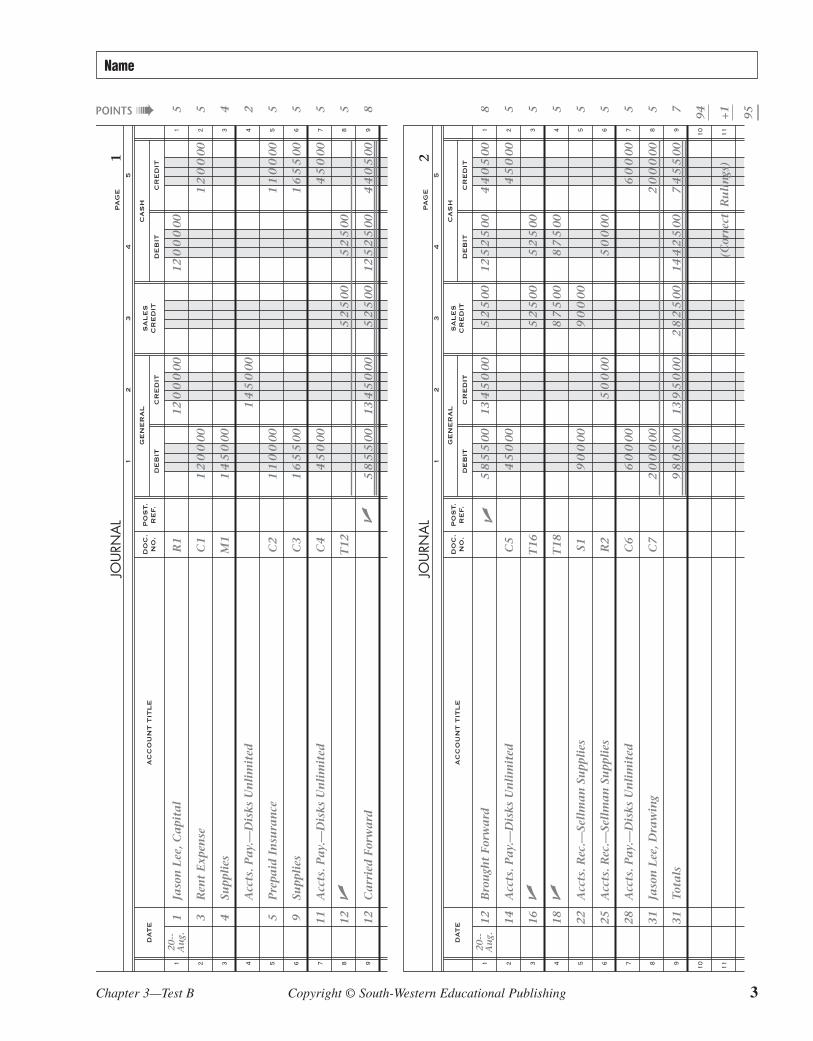

Part Three—Journalizing TransactionsJason Lee owns a service business called CompAction. CompAction uses thefollowing accounts:

Cash Jason Lee, DrawingAccounts Receivable—Sellman Supplies SalesSupplies Miscellaneous ExpensePrepaid Insurance Rent ExpenseAccounts Payable—Disks Unlimited UtilitiesJason Lee, Capital

Transac t ionsAug. 1. Received cash from owner as an investment, $12,000.00. R1.

3. Paid cash for rent, $1,200.00. C1.4. Bought supplies on account from Disks Unlimited, $1,450.00. M1.5. Paid cash for insurance, $1,100.00. C2.9. Paid cash for supplies, $1,655.00. C3.

11. Paid cash on account to Disks Unlimited, $450.00. C4.12. Received cash from sales, $525.00. T12.

Directions:

1. Journalize the transactions given above, completed during August of thecurrent year. Use page l of the journal given. Source documents areabbreviated as follows: check, C; memorandum, M; receipt, R; salesinvoice, S; calculator tape, T.

2. Prove and rule page 1 of the journal. Carry the column totals forward topage 2 of the journal.

3. Use page 2 of the journal to journalize the transactions given below.4. After all the transactions are recorded, prove page 2 of the journal.5. Prove cash. The beginning cash balance on August 1 is zero. The balance

on the next unused check stub is $6,970.00.6. Rule page 2 of the journal.

Transac t ionsAug. 14. Paid cash on account to Disks Unlimited, $450.00. C5.

16. Received cash from sales, $525.00. T16.18. Received cash from sales, $875.00. T18.22. Sold services on account to Sellman Supplies, $900.00. S1.25. Received cash on account from Sellman Supplies, $500.00. R2.28. Paid cash on account to Disks Unlimited, $600.00. C6.31. Paid cash to owner for personal use, $2,000.00. C7.

Use the space below for the cash proof:

POIN

TS �

Cash on hand at beginning of the month $0,0000.00 1Plus total cash received during month 14,425.00 1Equals total 14,425.00 1Less total cash paid during the month 7,455.00 1Equals cash balance at the end of the month 6,970.00 1Checkbook balance on the next unused check stub $06,970.00 5

Name

Chapter 3—Test B Copyright © South-Western Educational Publishing 3

JOU

RNA

LP

AG

E

12

34

1 2 3 4 5 6 7 8 9

1 2 3 4 5 6 7 8 9

DAT

EA

CC

OU

NT

TIT

LE

DO

C.

NO

.P

OS

T.

RE

F.

GE

NE

RA

L

DE

BIT

CR

ED

IT

SA

LE

SC

RE

DIT

CA

SH

DE

BIT

CR

ED

IT

5

1 3 4 5 9 11 12 12

20--

Au

g.Ja

son

Lee

, Ca

pita

l

Ren

t E

xpen

se

Supp

lies

Acc

ts. P

ay.

—D

isks

Un

lim

ited

Pre

paid

In

sura

nce

Supp

lies

Acc

ts. P

ay.

—D

isks

Un

lim

ited

� Ca

rrie

d F

orw

ard

R1

C1

M1

C2

C3

C4

T12

�

12

00

00

14

50

00

11

00

00

16

55

00

45

000

58

55

00

120

00

00

14

50

00

134

50

00

120

00

00

52

500

125

25

00

12

00

00

11

00

00

16

55

00

45

000

44

05

001

5 5 4 2 5 5 5 5 8

52

500

52

500

JOU

RNA

LP

AG

E

12

34

1 2 3 4 5 6 7 8 9

10 11

1 2 3 4 5 6 7 8 9

10 11

DAT

EA

CC

OU

NT

TIT

LE

DO

C.

NO

.P

OS

T.

RE

F.

GE

NE

RA

L

DE

BIT

CR

ED

IT

SA

LE

SC

RE

DIT

CA

SH

DE

BIT

CR

ED

IT

5

12 14 16 18 22 25 28 31 31

20--

Au

g.B

rou

ght

For

wa

rd

Acc

ts. P

ay.

—D

isks

Un

lim

ited

� � Acc

ts. R

ec.—

Sell

ma

n S

upp

lies

Acc

ts. R

ec.—

Sell

ma

n S

upp

lies

Acc

ts. P

ay.

—D

isks

Un

lim

ited

Jaso

n L

ee, D

raw

ing

Tot

als

C5

T16

T18 S1 R2

C6

C7

�5

85

500

45

000

90

000

60

000

20

00

00

98

05

00

134

50

00

50

000

139

50

00

125

25

00

52

500

87

500

50

000

144

25

00

44

05

00

45

000

60

000

20

00

00

74

55

002

8 5 5 5 5 5 5 5 7 94 +1 95

52

500

52

500

87

500

90

000

28

25

00

(Cor

rect

Ru

lin

gs)

POINTS �

4 Century 21 Accounting, 8th Edition Chapter 3—Test B

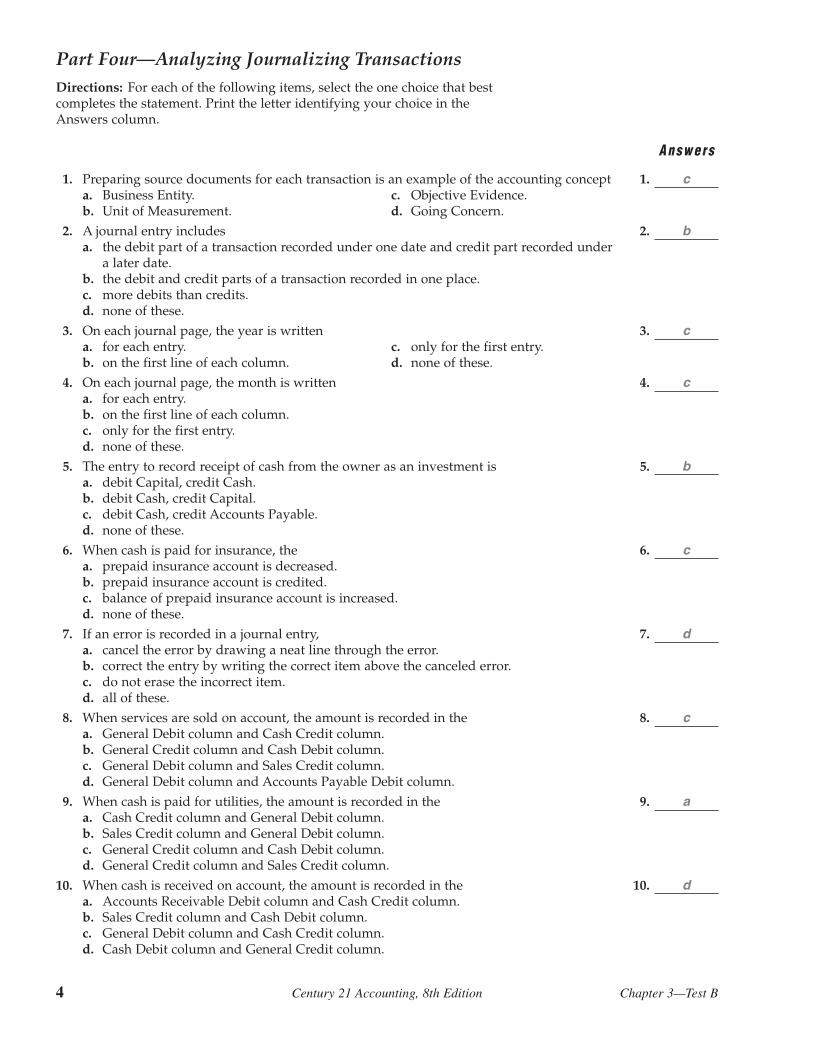

Part Four—Analyzing Journalizing TransactionsDirections: For each of the following items, select the one choice that bestcompletes the statement. Print the letter identifying your choice in theAnswers column.

Answers

1. Preparing source documents for each transaction is an example of the accounting concept 1. ca. Business Entity. c. Objective Evidence.b. Unit of Measurement. d. Going Concern.

2. A journal entry includes 2. ba. the debit part of a transaction recorded under one date and credit part recorded under

a later date.b. the debit and credit parts of a transaction recorded in one place.c. more debits than credits.d. none of these.

3. On each journal page, the year is written 3. ca. for each entry. c. only for the first entry.b. on the first line of each column. d. none of these.

4. On each journal page, the month is written 4. ca. for each entry.b. on the first line of each column.c. only for the first entry.d. none of these.

5. The entry to record receipt of cash from the owner as an investment is 5. ba. debit Capital, credit Cash.b. debit Cash, credit Capital.c. debit Cash, credit Accounts Payable.d. none of these.

6. When cash is paid for insurance, the 6. ca. prepaid insurance account is decreased.b. prepaid insurance account is credited.c. balance of prepaid insurance account is increased.d. none of these.

7. If an error is recorded in a journal entry, 7. da. cancel the error by drawing a neat line through the error.b. correct the entry by writing the correct item above the canceled error.c. do not erase the incorrect item.d. all of these.

8. When services are sold on account, the amount is recorded in the 8. ca. General Debit column and Cash Credit column.b. General Credit column and Cash Debit column.c. General Debit column and Sales Credit column.d. General Debit column and Accounts Payable Debit column.

9. When cash is paid for utilities, the amount is recorded in the 9. aa. Cash Credit column and General Debit column.b. Sales Credit column and General Debit column.c. General Credit column and Cash Debit column.d. General Credit column and Sales Credit column.

10. When cash is received on account, the amount is recorded in the 10. da. Accounts Receivable Debit column and Cash Credit column.b. Sales Credit column and Cash Debit column.c. General Debit column and Cash Credit column.d. Cash Debit column and General Credit column.

chapterTEST A

PerfectScore

YourScoreName

Analyzing Accounting Concepts and Procedures 20 Pts.Preparing a Chart of Accounts 37 Pts.

Posting to a General Ledger 47 Pts.Analyzing Posting Procedures 10 Pts.

Total 114 Pts.

Chapter 4—Test A Copyright © South-Western Educational Publishing 1

4

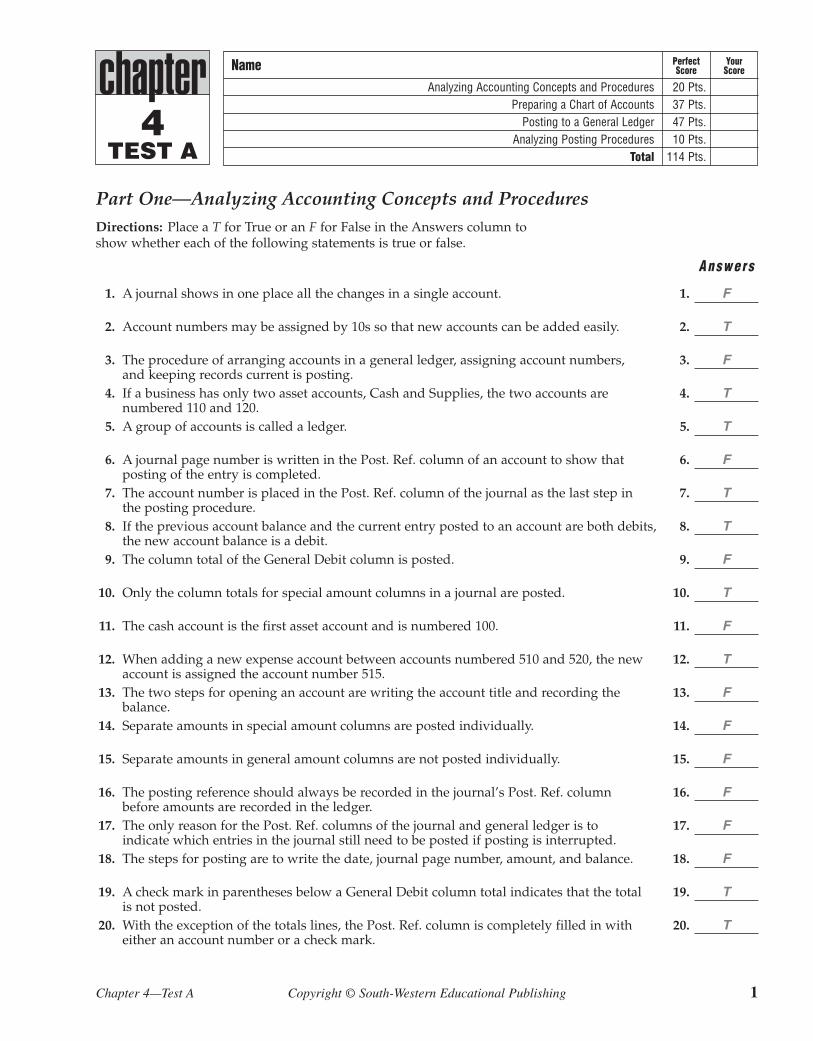

Part One—Analyzing Accounting Concepts and ProceduresDirections: Place a T for True or an F for False in the Answers column toshow whether each of the following statements is true or false.

Answers

1. A journal shows in one place all the changes in a single account. 1. F

2. Account numbers may be assigned by 10s so that new accounts can be added easily. 2. T

3. The procedure of arranging accounts in a general ledger, assigning account numbers, 3. Fand keeping records current is posting.

4. If a business has only two asset accounts, Cash and Supplies, the two accounts are 4. Tnumbered 110 and 120.

5. A group of accounts is called a ledger. 5. T

6. A journal page number is written in the Post. Ref. column of an account to show that 6. Fposting of the entry is completed.

7. The account number is placed in the Post. Ref. column of the journal as the last step in 7. Tthe posting procedure.

8. If the previous account balance and the current entry posted to an account are both debits, 8. Tthe new account balance is a debit.

9. The column total of the General Debit column is posted. 9. F

10. Only the column totals for special amount columns in a journal are posted. 10. T

11. The cash account is the first asset account and is numbered 100. 11. F

12. When adding a new expense account between accounts numbered 510 and 520, the new 12. Taccount is assigned the account number 515.

13. The two steps for opening an account are writing the account title and recording the 13. Fbalance.

14. Separate amounts in special amount columns are posted individually. 14. F

15. Separate amounts in general amount columns are not posted individually. 15. F

16. The posting reference should always be recorded in the journal’s Post. Ref. column 16. Fbefore amounts are recorded in the ledger.

17. The only reason for the Post. Ref. columns of the journal and general ledger is to 17. Findicate which entries in the journal still need to be posted if posting is interrupted.

18. The steps for posting are to write the date, journal page number, amount, and balance. 18. F

19. A check mark in parentheses below a General Debit column total indicates that the total 19. Tis not posted.

20. With the exception of the totals lines, the Post. Ref. column is completely filled in with 20. Teither an account number or a check mark.

2 Century 21 Accounting, 8th Edition Chapter 4—Test A

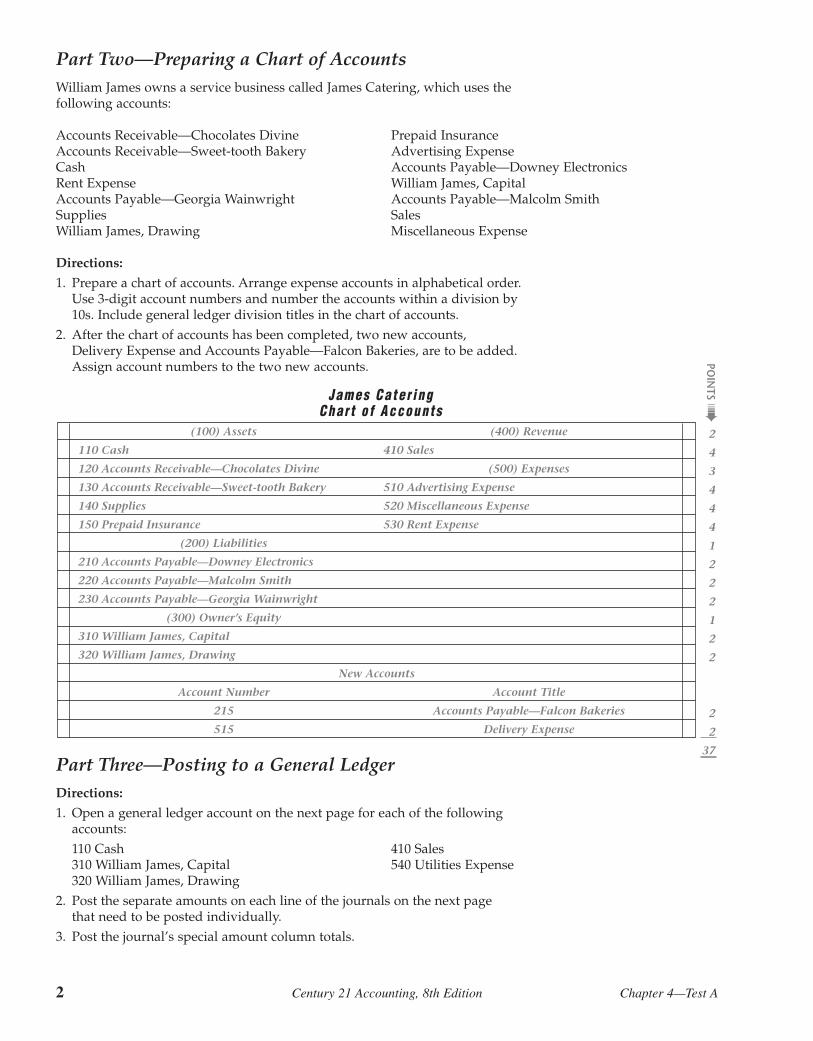

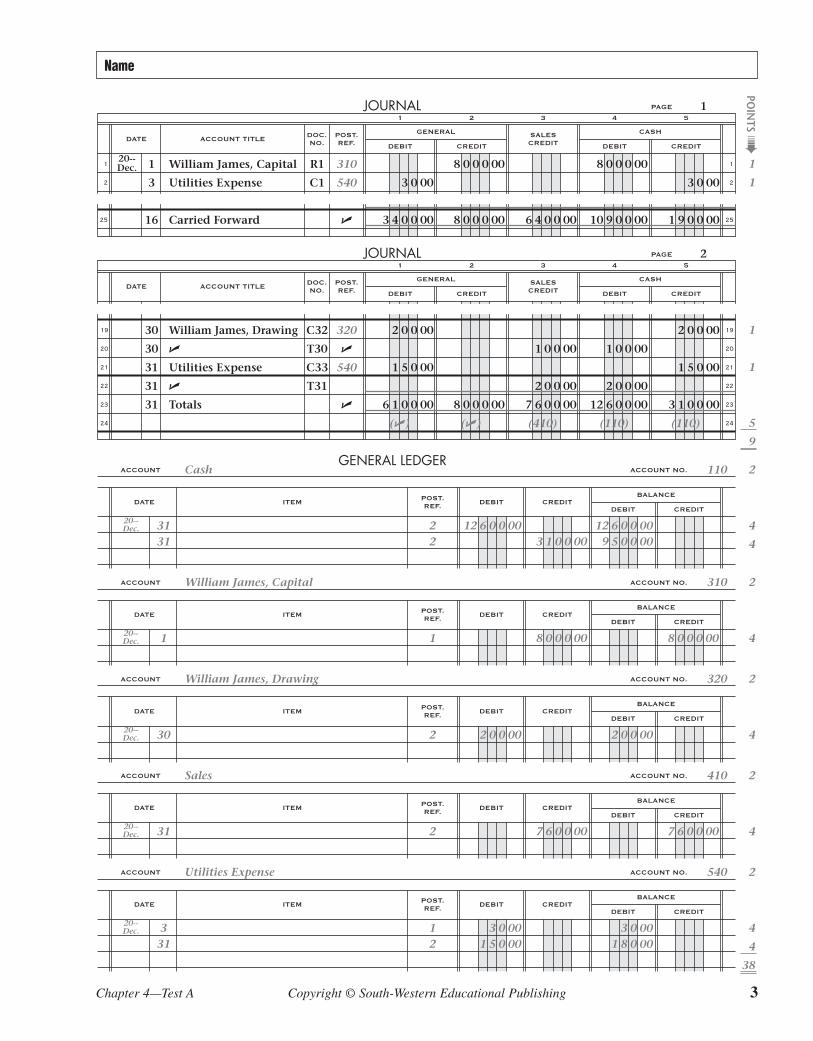

Part Two—Preparing a Chart of AccountsWilliam James owns a service business called James Catering, which uses thefollowing accounts:

Accounts Receivable—Chocolates Divine Prepaid InsuranceAccounts Receivable—Sweet-tooth Bakery Advertising ExpenseCash Accounts Payable—Downey ElectronicsRent Expense William James, CapitalAccounts Payable—Georgia Wainwright Accounts Payable—Malcolm SmithSupplies SalesWilliam James, Drawing Miscellaneous Expense

Directions:

1. Prepare a chart of accounts. Arrange expense accounts in alphabetical order.Use 3-digit account numbers and number the accounts within a division by10s. Include general ledger division titles in the chart of accounts.

2. After the chart of accounts has been completed, two new accounts,Delivery Expense and Accounts Payable—Falcon Bakeries, are to be added.Assign account numbers to the two new accounts.

Part Three—Posting to a General LedgerDirections:

1. Open a general ledger account on the next page for each of the followingaccounts:110 Cash 410 Sales310 William James, Capital 540 Utilities Expense320 William James, Drawing

2. Post the separate amounts on each line of the journals on the next pagethat need to be posted individually.

3. Post the journal’s special amount column totals.

(100) Assets (400) Revenue

110 Cash 410 Sales

120 Accounts Receivable—Chocolates Divine (500) Expenses

130 Accounts Receivable—Sweet-tooth Bakery 510 Advertising Expense

140 Supplies 520 Miscellaneous Expense

150 Prepaid Insurance 530 Rent Expense

(200) Liabilities

210 Accounts Payable—Downey Electronics

220 Accounts Payable—Malcolm Smith

230 Accounts Payable—Georgia Wainwright

(300) Owner’s Equity

310 William James, Capital

320 William James, Drawing

New Accounts

Account Number Account Title

215 Accounts Payable—Falcon Bakeries

515 Delivery Expense

James Cate r ingChar t o f Accounts

POIN

TS �

2

4

3

4

4

4

1

2

2

2

1

2

2

2

2

37

Name

Chapter 4—Test A Copyright © South-Western Educational Publishing 3

JOURNAL PAGE

1 2 3 4

1

2

25

1

2

25

DATE ACCOUNT TITLE DOC.NO.

POST.REF.

GENERAL

DEBIT CREDIT

SALESCREDIT

CASH

DEBIT CREDIT

5

1

3

16

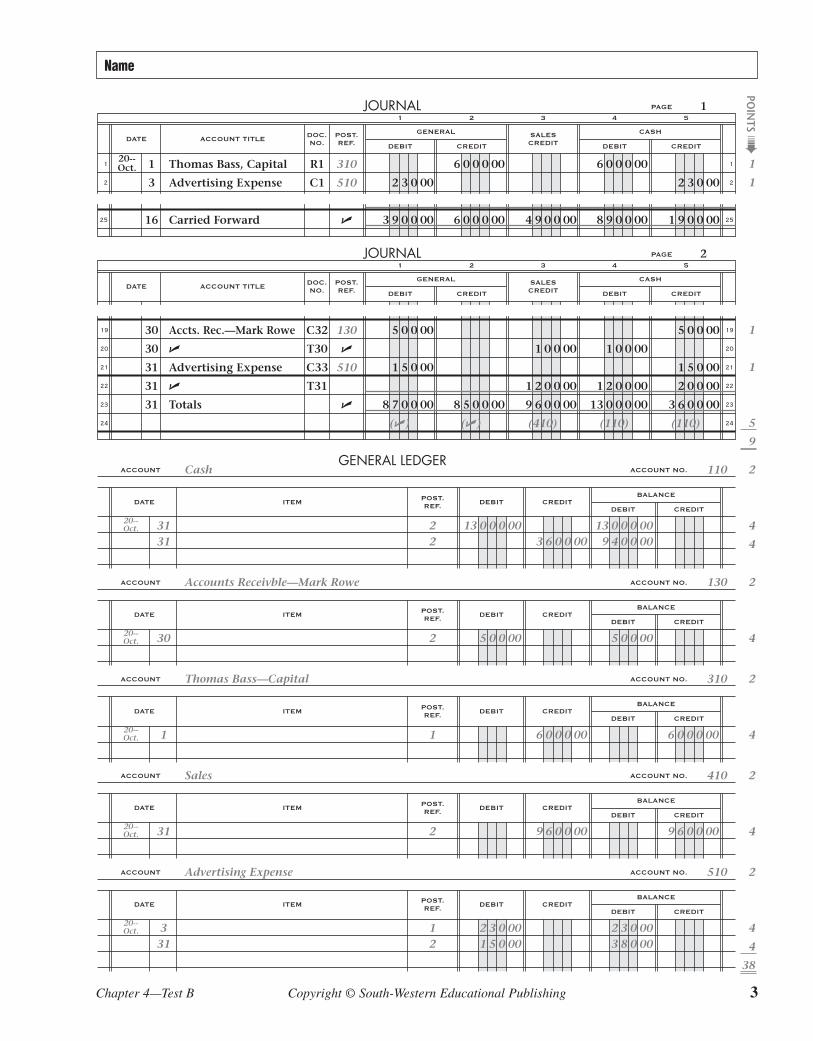

20--Dec. William James, Capital

Utilities Expense

Carried Forward

R1

C1

310

540

�

3 0 00

3 4 0 0 00

8 0 0 0 00

8 0 0 0 00 6 4 0 0 00

8 0 0 0 00

10 9 0 0 00

3 0 00

1 9 0 0 00

1

1

1

POIN

TS �

JOURNAL PAGE

1 2 3 4

19

20

21

22

23

24

19

20

21

22

23

24

DATE ACCOUNT TITLE DOC.NO.

POST.REF.

GENERAL

DEBIT CREDIT

SALESCREDIT

CASH

DEBIT CREDIT

5

30

30

31

31

31

2

1

1

5

9

William James, Drawing

�

Utilities Expense

�

Totals

C32

T30

C33

T31

320

�

540

�

2 0 0 00

1 5 0 00

6 1 0 0 00

(�)

8 0 0 0 00

(�)

1 0 0 00

2 0 0 00

7 6 0 0 00

(410)

1 0 0 00

2 0 0 00

12 6 0 0 00

(110)

2 0 0 00

1 5 0 00

3 1 0 0 00

(110)

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

3131

20--Dec. 2

2

110

12 6 0 0 00

Cash

3 1 0 0 0012 6 0 0 00

9 5 0 0 004

4

2

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

120--Dec. 1

310William James, Capital

8 0 0 0 00 4

2

8 0 0 0 00

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

3020--Dec. 2

320William James, Drawing

2 0 0 00 4

2

2 0 0 00

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

3120--Dec. 2

410Sales

7 6 0 0 00 4

2

7 6 0 0 00

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

331

20--Dec. 1

2

540

3 0 001 5 0 00

Utilities Expense

3 0 001 8 0 00

4

4

38

2

GENERAL LEDGER

4 Century 21 Accounting, 8th Edition Chapter 4—Test A

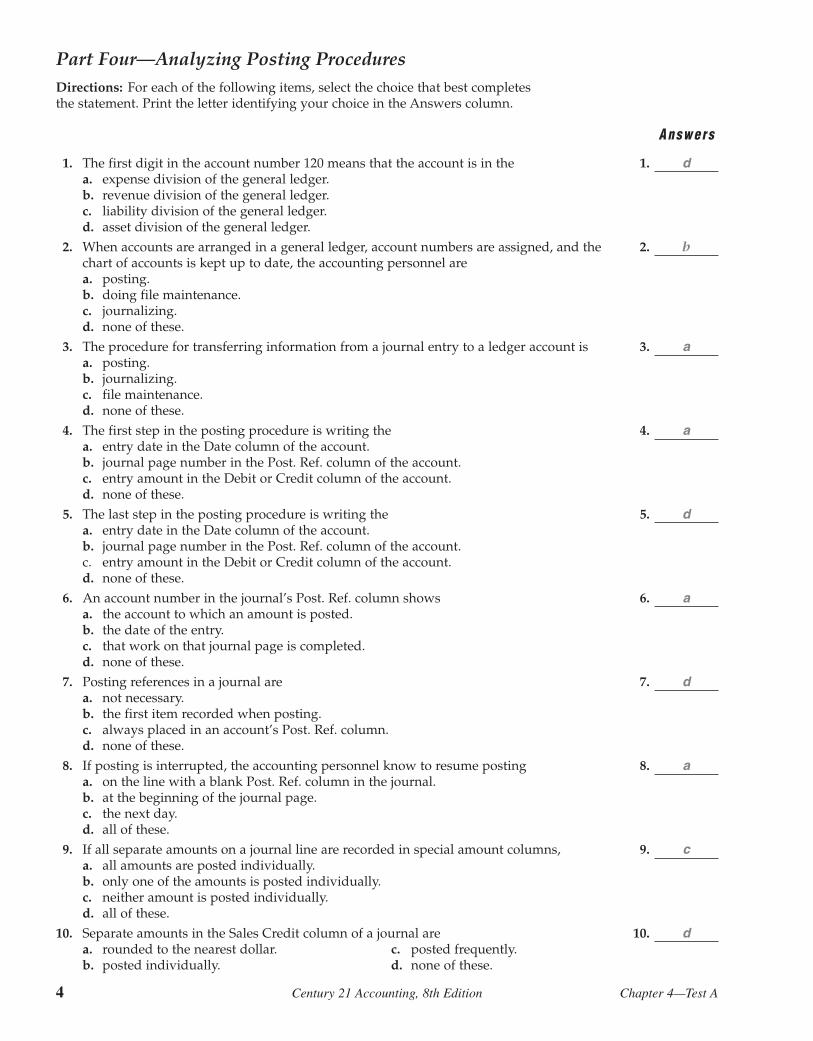

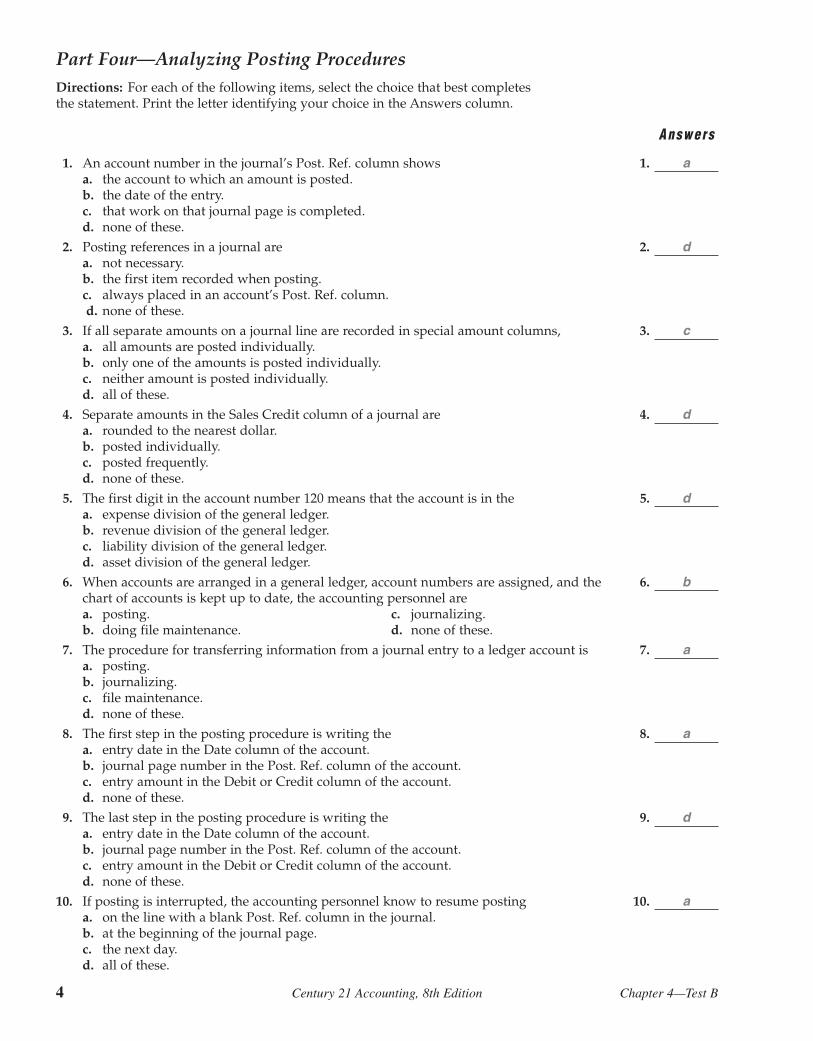

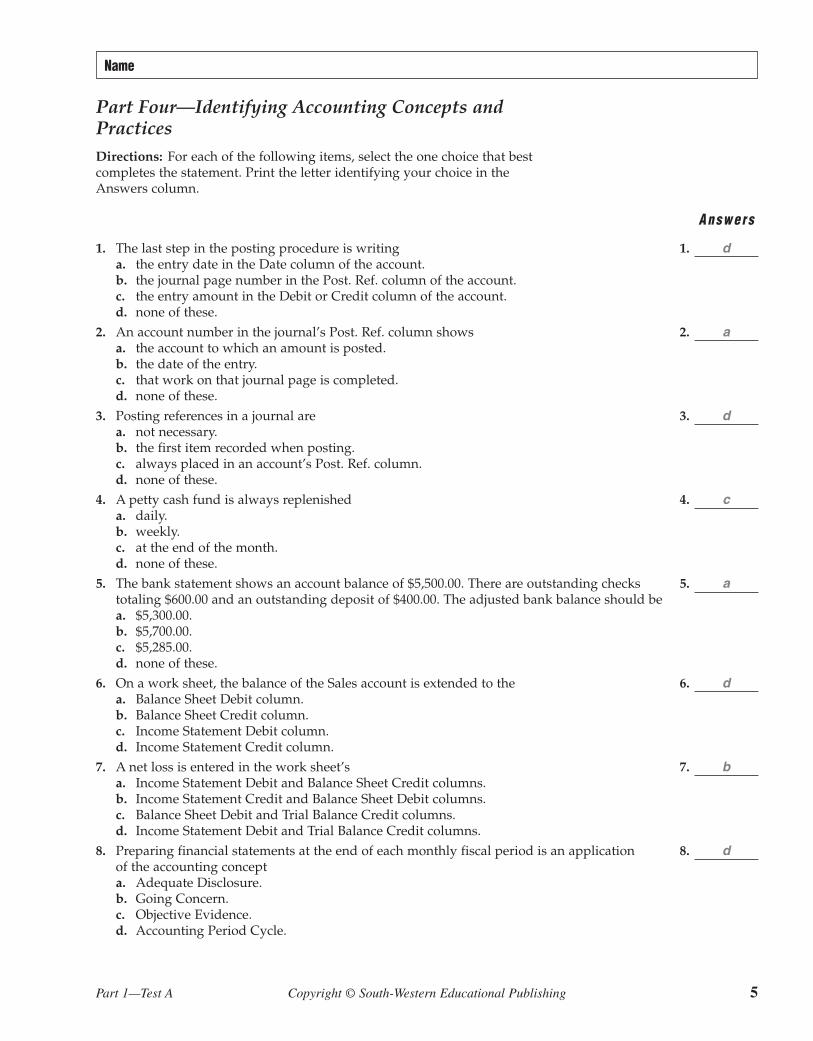

Part Four—Analyzing Posting ProceduresDirections: For each of the following items, select the choice that best completesthe statement. Print the letter identifying your choice in the Answers column.

Answers

1. The first digit in the account number 120 means that the account is in the 1. da. expense division of the general ledger.b. revenue division of the general ledger.c. liability division of the general ledger.d. asset division of the general ledger.

2. When accounts are arranged in a general ledger, account numbers are assigned, and the 2. bchart of accounts is kept up to date, the accounting personnel area. posting.b. doing file maintenance.c. journalizing.d. none of these.

3. The procedure for transferring information from a journal entry to a ledger account is 3. aa. posting.b. journalizing.c. file maintenance.d. none of these.

4. The first step in the posting procedure is writing the 4. aa. entry date in the Date column of the account.b. journal page number in the Post. Ref. column of the account.c. entry amount in the Debit or Credit column of the account.d. none of these.

5. The last step in the posting procedure is writing the 5. da. entry date in the Date column of the account.b. journal page number in the Post. Ref. column of the account.c. entry amount in the Debit or Credit column of the account.d. none of these.

6. An account number in the journal’s Post. Ref. column shows 6. aa. the account to which an amount is posted.b. the date of the entry.c. that work on that journal page is completed.d. none of these.

7. Posting references in a journal are 7. da. not necessary.b. the first item recorded when posting.c. always placed in an account’s Post. Ref. column.d. none of these.

8. If posting is interrupted, the accounting personnel know to resume posting 8. aa. on the line with a blank Post. Ref. column in the journal.b. at the beginning of the journal page.c. the next day.d. all of these.

9. If all separate amounts on a journal line are recorded in special amount columns, 9. ca. all amounts are posted individually.b. only one of the amounts is posted individually.c. neither amount is posted individually.d. all of these.

10. Separate amounts in the Sales Credit column of a journal are 10. da. rounded to the nearest dollar. c. posted frequently.b. posted individually. d. none of these.

chapterTEST B

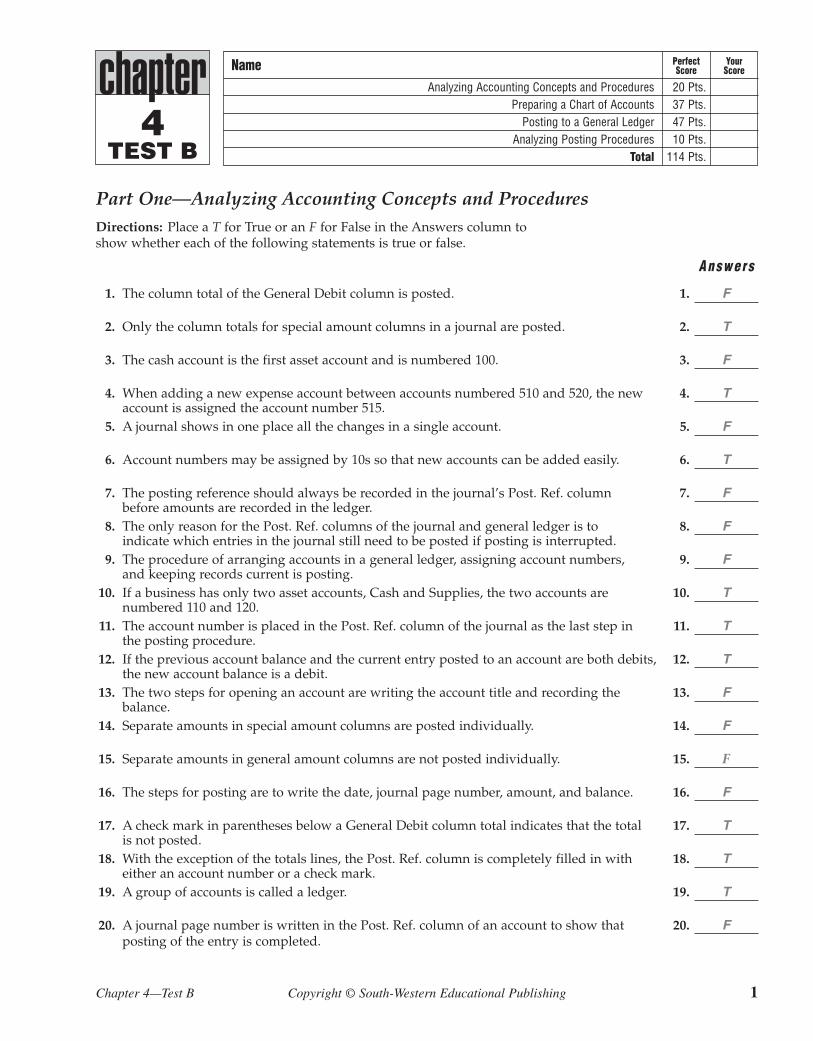

PerfectScore

YourScoreName

Analyzing Accounting Concepts and Procedures 20 Pts.Preparing a Chart of Accounts 37 Pts.

Posting to a General Ledger 47 Pts.Analyzing Posting Procedures 10 Pts.

Total 114 Pts.

Chapter 4—Test B Copyright © South-Western Educational Publishing 1

4

Part One—Analyzing Accounting Concepts and ProceduresDirections: Place a T for True or an F for False in the Answers column toshow whether each of the following statements is true or false.

Answers

1. The column total of the General Debit column is posted. 1. F

2. Only the column totals for special amount columns in a journal are posted. 2. T

3. The cash account is the first asset account and is numbered 100. 3. F

4. When adding a new expense account between accounts numbered 510 and 520, the new 4. Taccount is assigned the account number 515.

5. A journal shows in one place all the changes in a single account. 5. F

6. Account numbers may be assigned by 10s so that new accounts can be added easily. 6. T

7. The posting reference should always be recorded in the journal’s Post. Ref. column 7. Fbefore amounts are recorded in the ledger.

8. The only reason for the Post. Ref. columns of the journal and general ledger is to 8. Findicate which entries in the journal still need to be posted if posting is interrupted.

9. The procedure of arranging accounts in a general ledger, assigning account numbers, 9. Fand keeping records current is posting.

10. If a business has only two asset accounts, Cash and Supplies, the two accounts are 10. Tnumbered 110 and 120.

11. The account number is placed in the Post. Ref. column of the journal as the last step in 11. Tthe posting procedure.

12. If the previous account balance and the current entry posted to an account are both debits, 12. Tthe new account balance is a debit.

13. The two steps for opening an account are writing the account title and recording the 13. Fbalance.

14. Separate amounts in special amount columns are posted individually. 14. F

15. Separate amounts in general amount columns are not posted individually. 15. F

16. The steps for posting are to write the date, journal page number, amount, and balance. 16. F

17. A check mark in parentheses below a General Debit column total indicates that the total 17. Tis not posted.

18. With the exception of the totals lines, the Post. Ref. column is completely filled in with 18. Teither an account number or a check mark.

19. A group of accounts is called a ledger. 19. T

20. A journal page number is written in the Post. Ref. column of an account to show that 20. Fposting of the entry is completed.

2 Century 21 Accounting, 8th Edition Chapter 4—Test B

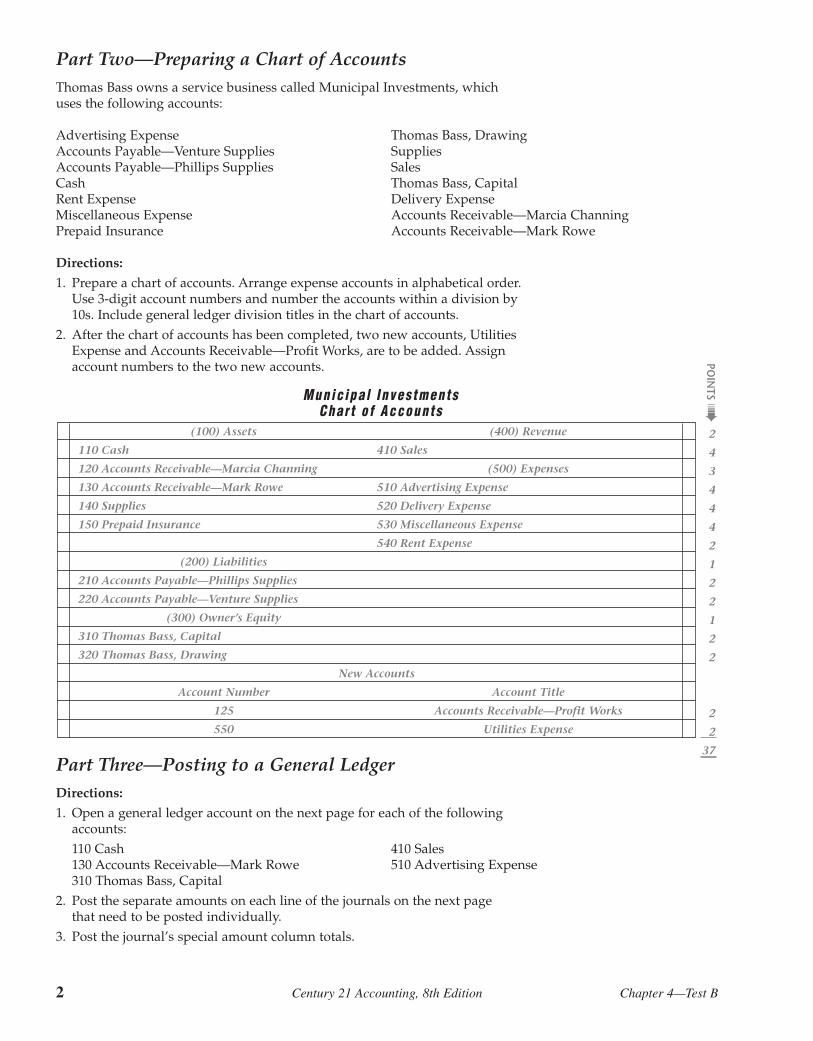

Part Two—Preparing a Chart of AccountsThomas Bass owns a service business called Municipal Investments, whichuses the following accounts:

Advertising Expense Thomas Bass, DrawingAccounts Payable—Venture Supplies SuppliesAccounts Payable—Phillips Supplies SalesCash Thomas Bass, CapitalRent Expense Delivery ExpenseMiscellaneous Expense Accounts Receivable—Marcia ChanningPrepaid Insurance Accounts Receivable—Mark Rowe

Directions:

1. Prepare a chart of accounts. Arrange expense accounts in alphabetical order.Use 3-digit account numbers and number the accounts within a division by10s. Include general ledger division titles in the chart of accounts.

2. After the chart of accounts has been completed, two new accounts, UtilitiesExpense and Accounts Receivable—Profit Works, are to be added. Assignaccount numbers to the two new accounts.

Part Three—Posting to a General LedgerDirections:

1. Open a general ledger account on the next page for each of the followingaccounts:110 Cash 410 Sales130 Accounts Receivable—Mark Rowe 510 Advertising Expense310 Thomas Bass, Capital

2. Post the separate amounts on each line of the journals on the next pagethat need to be posted individually.

3. Post the journal’s special amount column totals.

(100) Assets (400) Revenue

110 Cash 410 Sales

120 Accounts Receivable—Marcia Channing (500) Expenses

130 Accounts Receivable—Mark Rowe 510 Advertising Expense

140 Supplies 520 Delivery Expense

150 Prepaid Insurance 530 Miscellaneous Expense

540 Rent Expense

(200) Liabilities

210 Accounts Payable—Phillips Supplies

220 Accounts Payable—Venture Supplies

(300) Owner’s Equity

310 Thomas Bass, Capital

320 Thomas Bass, Drawing

New Accounts

Account Number Account Title

125 Accounts Receivable—Profit Works

550 Utilities Expense

Munic ipa l I nves tmentsChar t o f Accounts

POIN

TS �

2

4

3

4

4

4

2

1

2

2

1

2

2

2

2

37

Name

Chapter 4—Test B Copyright © South-Western Educational Publishing 3

GENERAL LEDGER

JOURNAL PAGE

1 2 3 4

1

2

25

1

2

25

DATE ACCOUNT TITLE DOC.NO.

POST.REF.

GENERAL

DEBIT CREDIT

SALESCREDIT

CASH

DEBIT CREDIT

5

1

3

16

20--Oct. Thomas Bass, Capital

Advertising Expense

Carried Forward

R1

C1

310

510

�

2 3 0 00

3 9 0 0 00

6 0 0 0 00

6 0 0 0 00 4 9 0 0 00

6 0 0 0 00

8 9 0 0 00

2 3 0 00

1 9 0 0 00

1

1

1

POIN

TS �

JOURNAL PAGE

1 2 3 4

19

20

21

22

23

24

19

20

21

22

23

24

DATE ACCOUNT TITLE DOC.NO.

POST.REF.

GENERAL

DEBIT CREDIT

SALESCREDIT

CASH

DEBIT CREDIT

5

30

30

31

31

31

2

1

1

5

9

Accts. Rec.—Mark Rowe

�

Advertising Expense

�

Totals

C32

T30

C33

T31

130

�

510

�

5 0 0 00

1 5 0 00

8 7 0 0 00

(�)

8 5 0 0 00

(�)

1 0 0 00

1 2 0 0 00

9 6 0 0 00

(410)

1 0 0 00

1 2 0 0 00

13 0 0 0 00

(110)

5 0 0 00

1 5 0 00

2 0 0 00

3 6 0 0 00

(110)

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

3131

20--Oct. 2

2

110

13 0 0 0 00

Cash

3 6 0 0 0013 0 0 0 00

9 4 0 0 004

4

2

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

3020--Oct. 2

130Accounts Receivble—Mark Rowe

5 0 0 00 4

2

5 0 0 00

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

120--Oct. 1

310Thomas Bass—Capital

6 0 0 0 00 4

2

6 0 0 0 00

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

3120--Oct. 2

410Sales

9 6 0 0 00 4

2

9 6 0 0 00

ACCOUNT NO.

DATE ITEMBALANCE

DEBIT CREDIT

POST.REF.

ACCOUNT

DEBIT CREDIT

331

20--Oct. 1

2

510

2 3 0 001 5 0 00

Advertising Expense

2 3 0 003 8 0 00

4

4

38

2

4 Century 21 Accounting, 8th Edition Chapter 4—Test B

Part Four—Analyzing Posting ProceduresDirections: For each of the following items, select the choice that best completesthe statement. Print the letter identifying your choice in the Answers column.

Answers

1. An account number in the journal’s Post. Ref. column shows 1. aa. the account to which an amount is posted.b. the date of the entry.c. that work on that journal page is completed.d. none of these.

2. Posting references in a journal are 2. da. not necessary.b. the first item recorded when posting.c. always placed in an account’s Post. Ref. column.d. none of these.

3. If all separate amounts on a journal line are recorded in special amount columns, 3. ca. all amounts are posted individually.b. only one of the amounts is posted individually.c. neither amount is posted individually.d. all of these.

4. Separate amounts in the Sales Credit column of a journal are 4. da. rounded to the nearest dollar.b. posted individually.c. posted frequently.d. none of these.

5. The first digit in the account number 120 means that the account is in the 5. da. expense division of the general ledger.b. revenue division of the general ledger.c. liability division of the general ledger.d. asset division of the general ledger.

6. When accounts are arranged in a general ledger, account numbers are assigned, and the 6. bchart of accounts is kept up to date, the accounting personnel area. posting. c. journalizing.b. doing file maintenance. d. none of these.

7. The procedure for transferring information from a journal entry to a ledger account is 7. aa. posting.b. journalizing.c. file maintenance.d. none of these.

8. The first step in the posting procedure is writing the 8. aa. entry date in the Date column of the account.b. journal page number in the Post. Ref. column of the account.c. entry amount in the Debit or Credit column of the account.d. none of these.

9. The last step in the posting procedure is writing the 9. da. entry date in the Date column of the account.b. journal page number in the Post. Ref. column of the account.c. entry amount in the Debit or Credit column of the account.d. none of these.

10. If posting is interrupted, the accounting personnel know to resume posting 10. aa. on the line with a blank Post. Ref. column in the journal.b. at the beginning of the journal page.c. the next day.d. all of these.

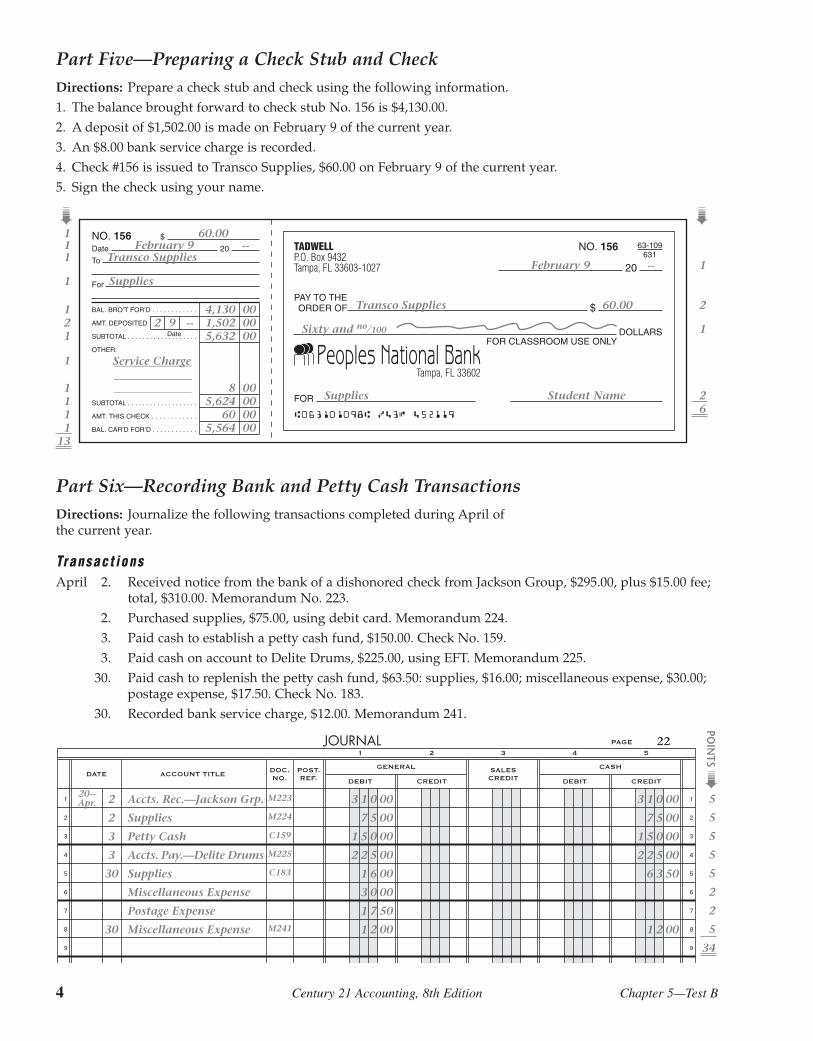

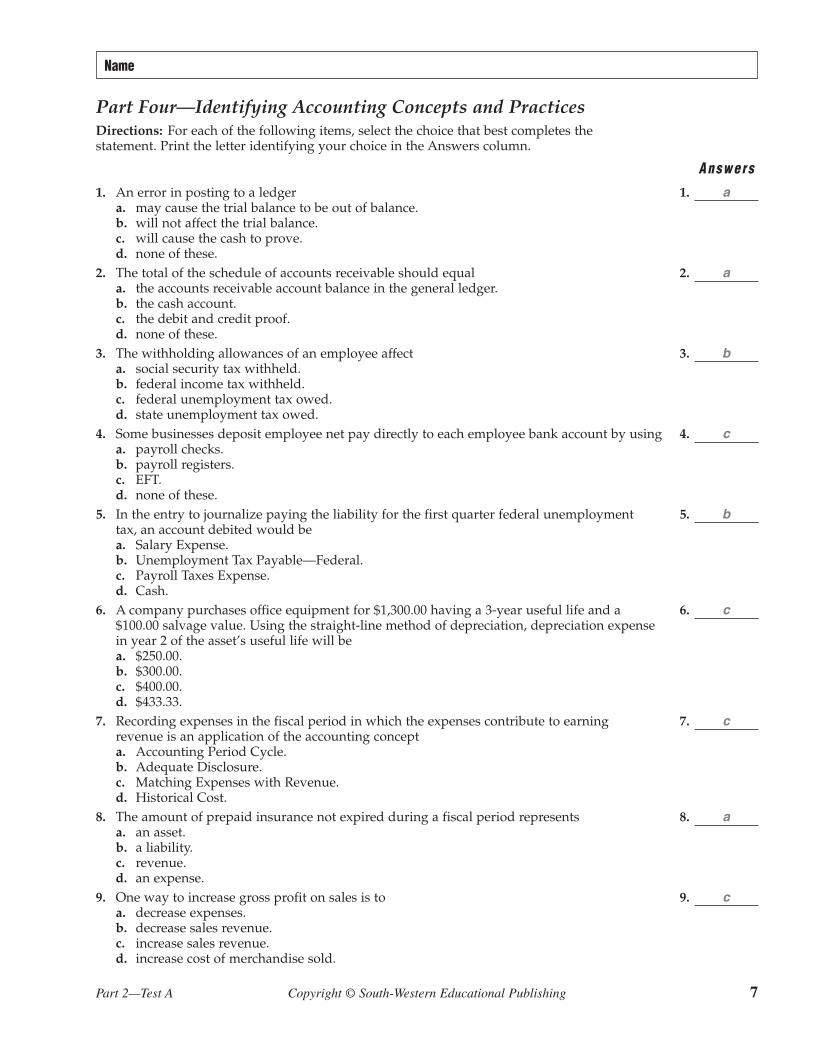

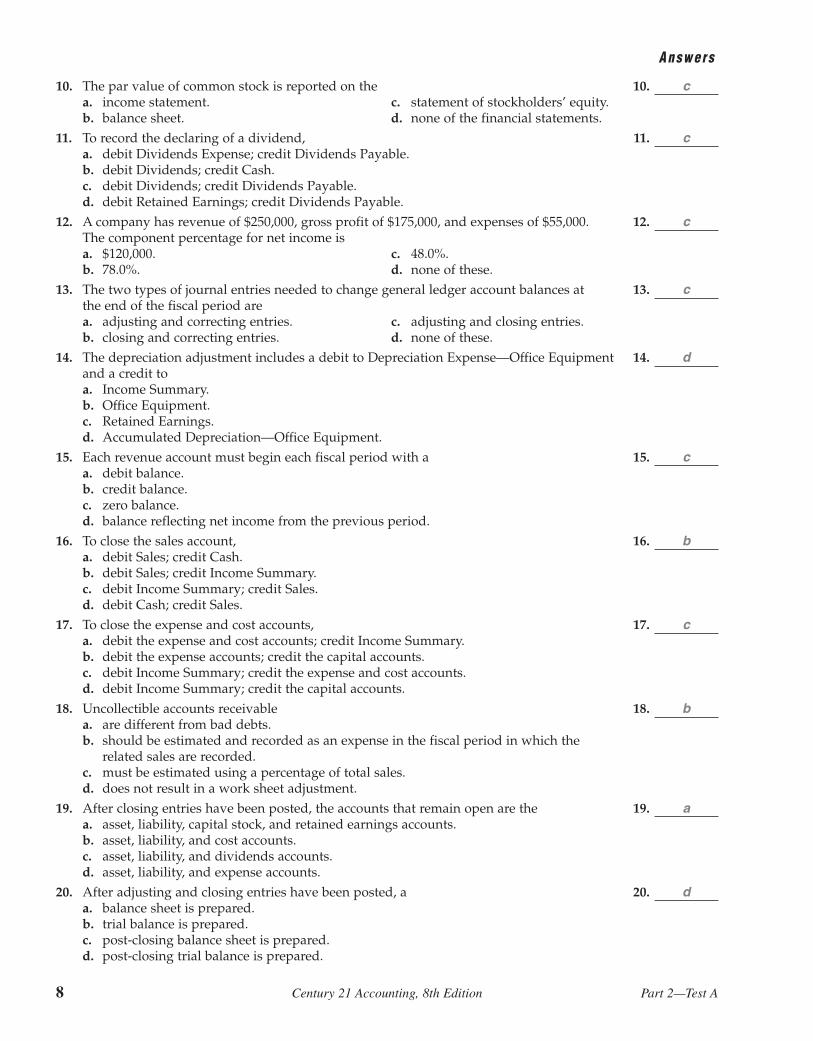

chapterTEST A

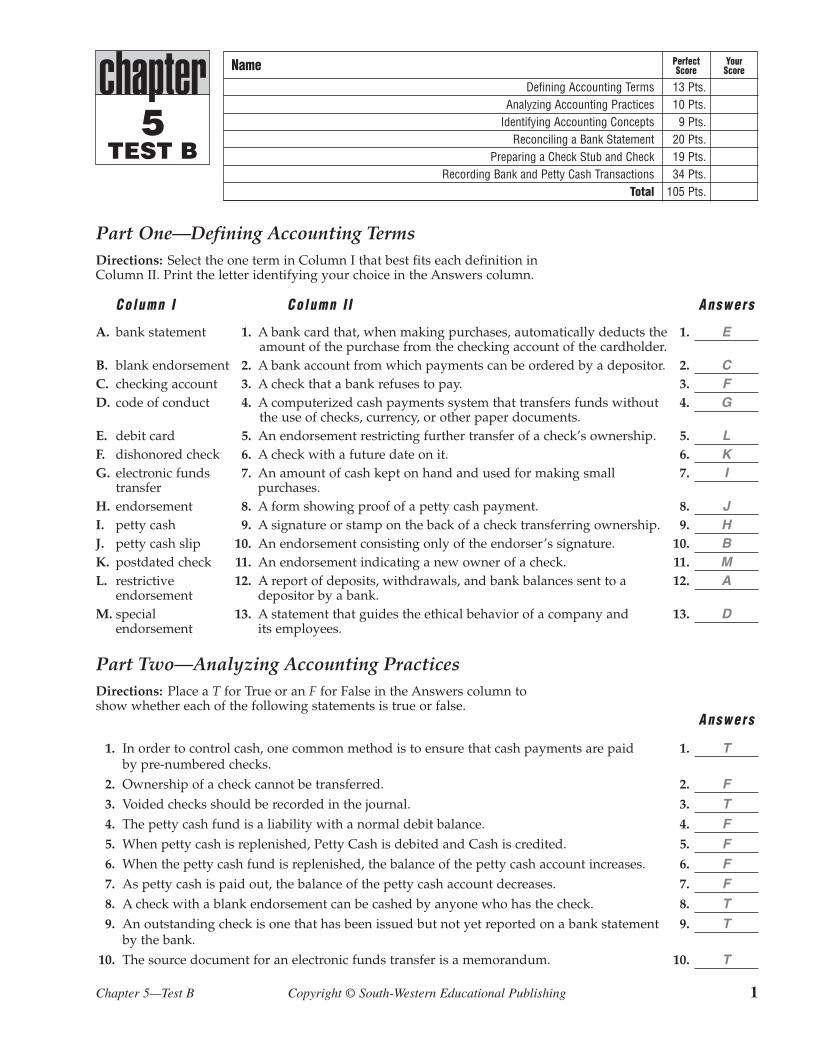

PerfectScore

YourScoreName

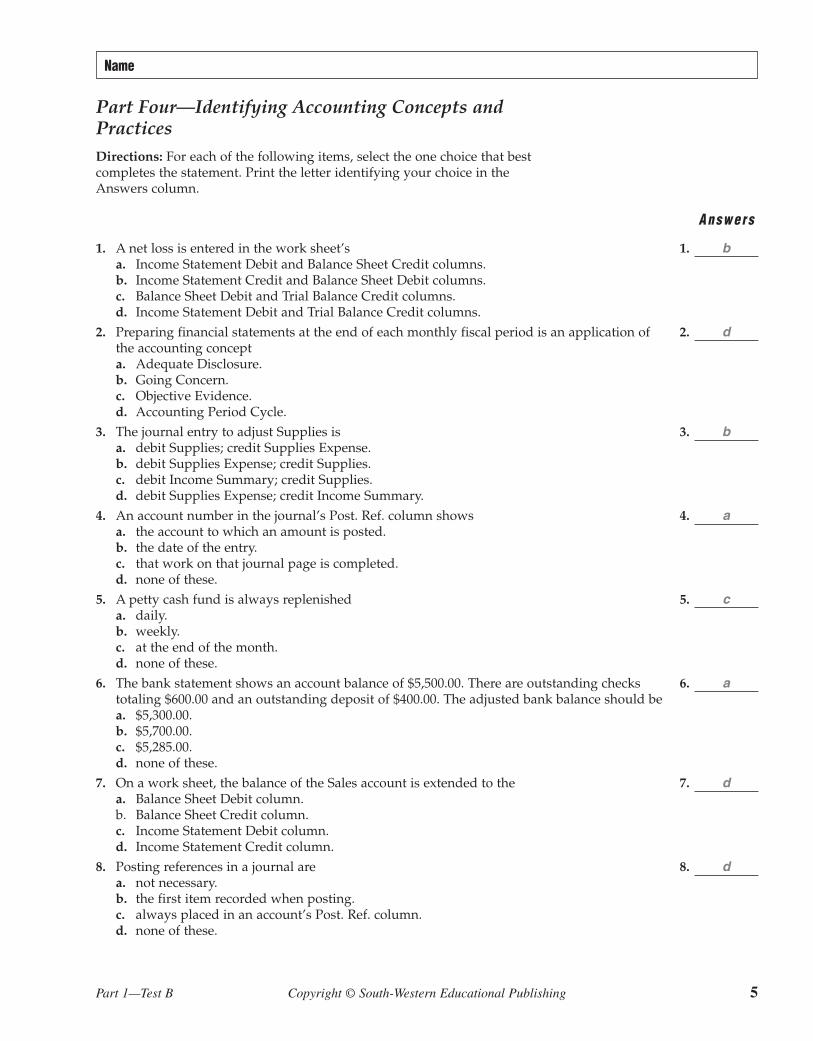

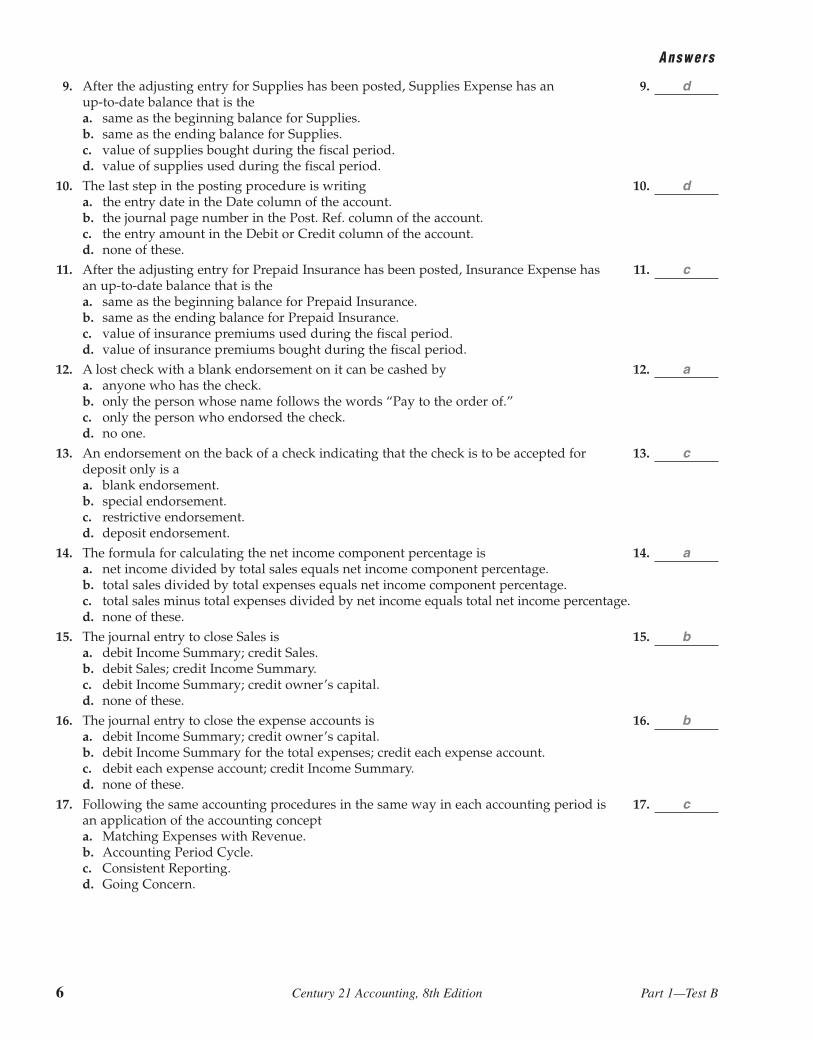

Defining Accounting Terms 13 Pts.Analyzing Accounting Practices 10 Pts.

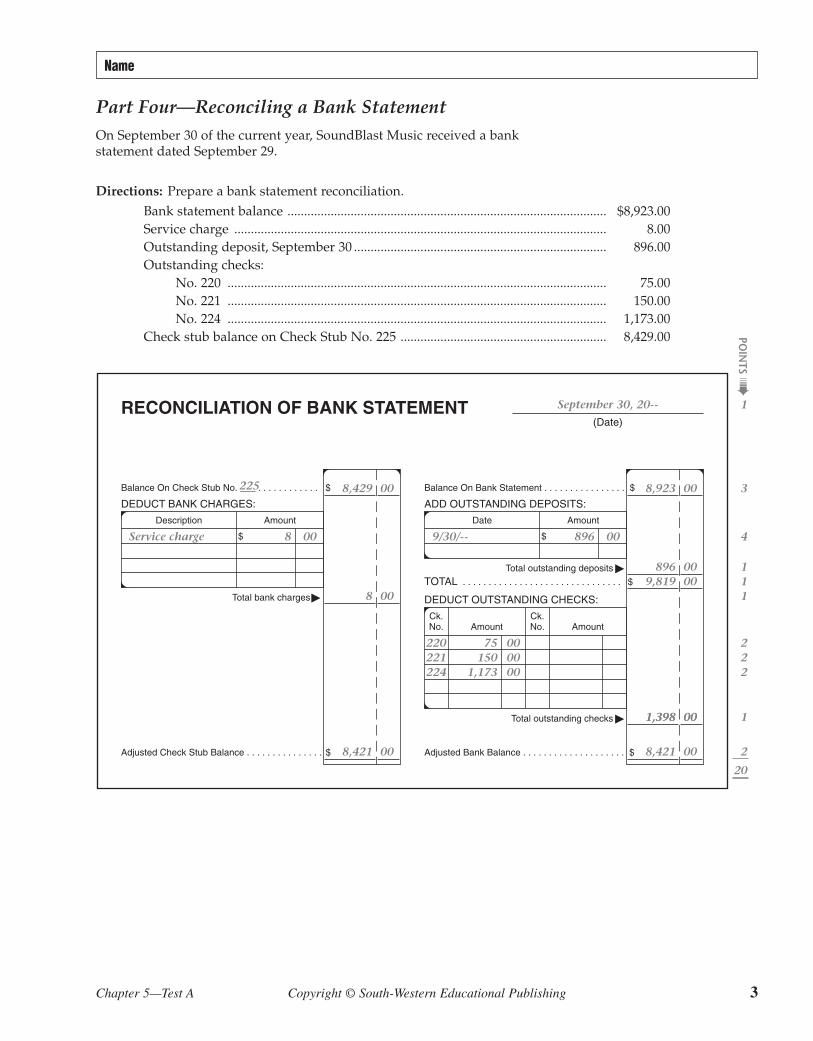

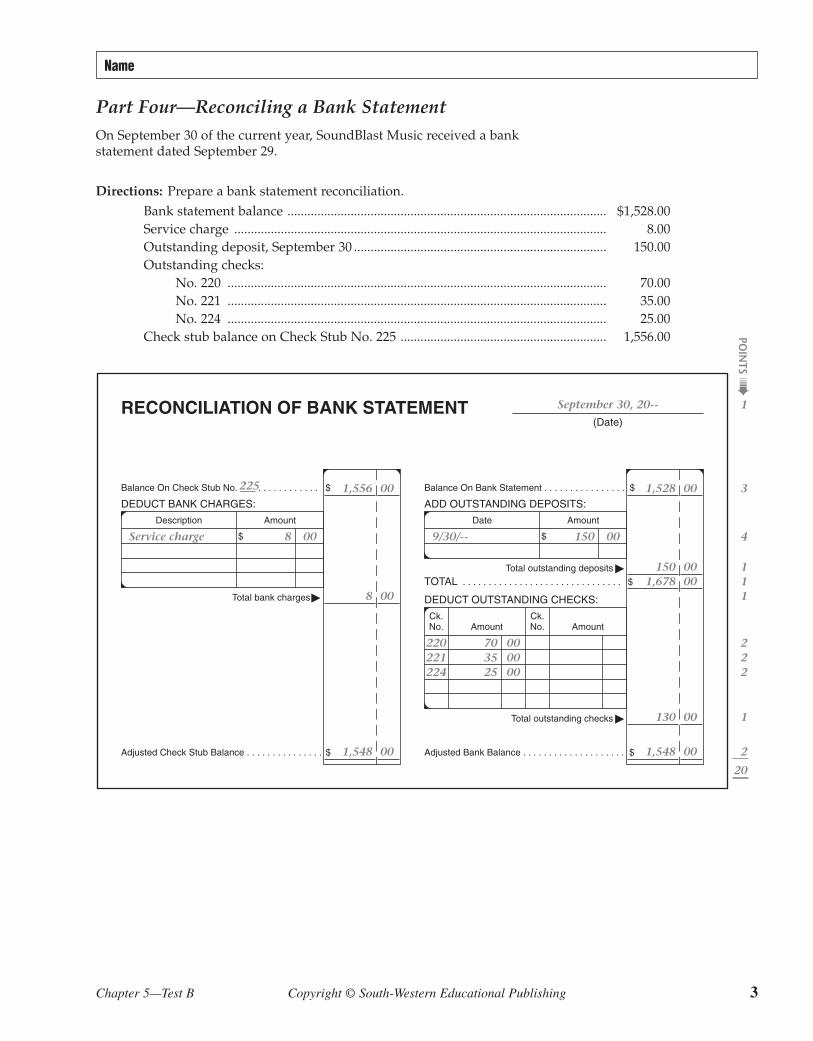

Identifying Accounting Concepts 9 Pts.Reconciling a Bank Statement 20 Pts.

Preparing a Check Stub and Check 19 Pts.Recording Bank and Petty Cash Transactions 34 Pts.

Total 105 Pts.

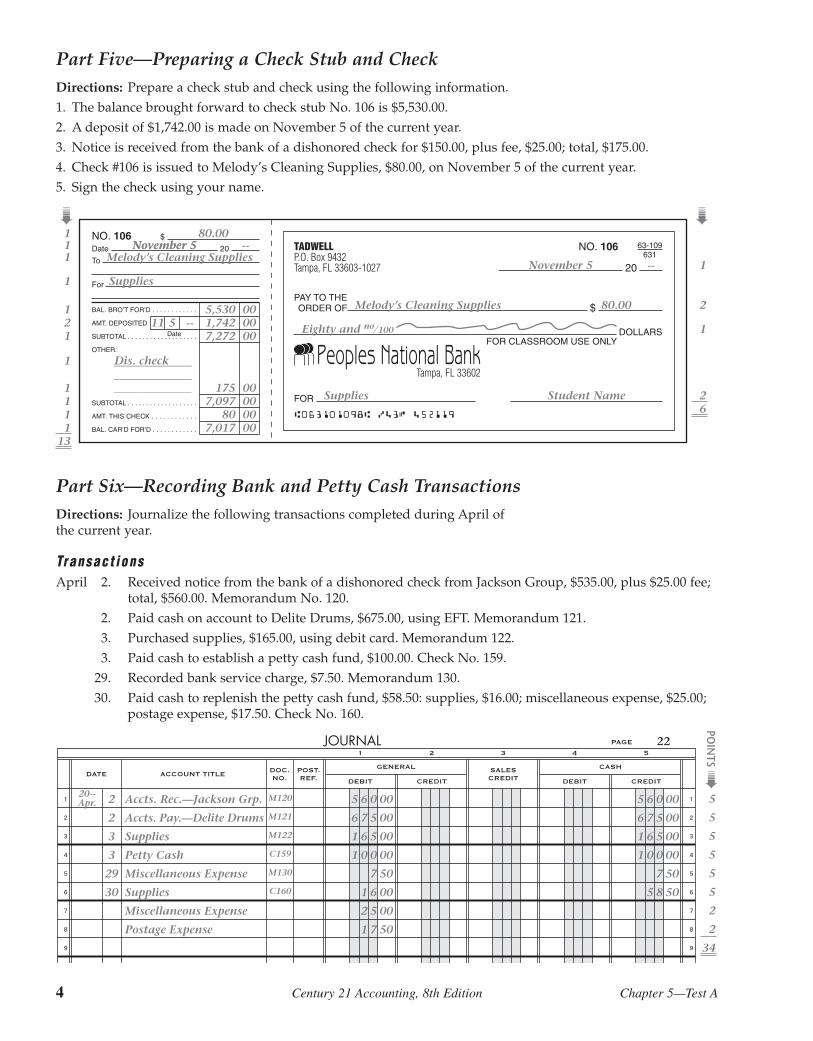

Chapter 5—Test A Copyright © South-Western Educational Publishing 1

5

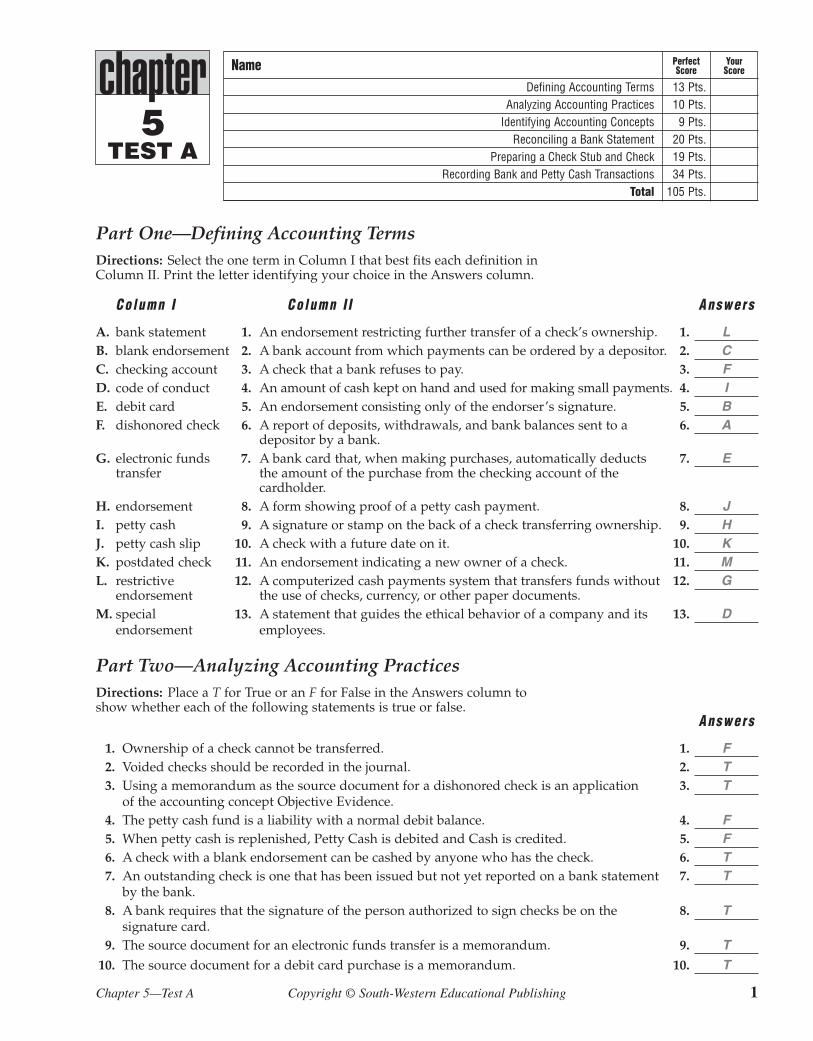

Part One—Defining Accounting TermsDirections: Select the one term in Column I that best fits each definition inColumn II. Print the letter identifying your choice in the Answers column.

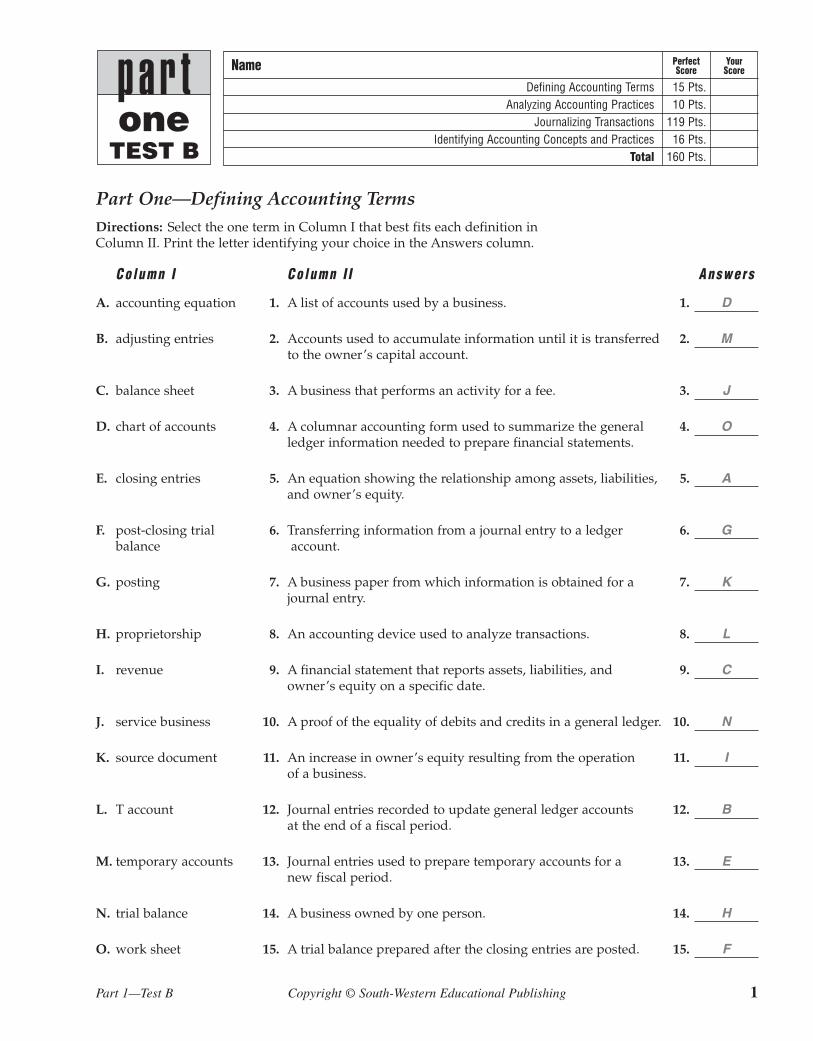

Co lumn I Co lumn I I Answers

A. bank statement 1. An endorsement restricting further transfer of a check’s ownership. 1. LB. blank endorsement 2. A bank account from which payments can be ordered by a depositor. 2. CC. checking account 3. A check that a bank refuses to pay. 3. FD. code of conduct 4. An amount of cash kept on hand and used for making small payments. 4. IE. debit card 5. An endorsement consisting only of the endorser’s signature. 5. BF. dishonored check 6. A report of deposits, withdrawals, and bank balances sent to a 6. A

depositor by a bank.G. electronic funds 7. A bank card that, when making purchases, automatically deducts 7. E

transfer the amount of the purchase from the checking account of the cardholder.

H. endorsement 8. A form showing proof of a petty cash payment. 8. JI. petty cash 9. A signature or stamp on the back of a check transferring ownership. 9. HJ. petty cash slip 10. A check with a future date on it. 10. KK. postdated check 11. An endorsement indicating a new owner of a check. 11. ML. restrictive 12. A computerized cash payments system that transfers funds without 12. G

endorsement the use of checks, currency, or other paper documents.M. special 13. A statement that guides the ethical behavior of a company and its 13. D

endorsement employees.

Part Two—Analyzing Accounting PracticesDirections: Place a T for True or an F for False in the Answers column toshow whether each of the following statements is true or false.

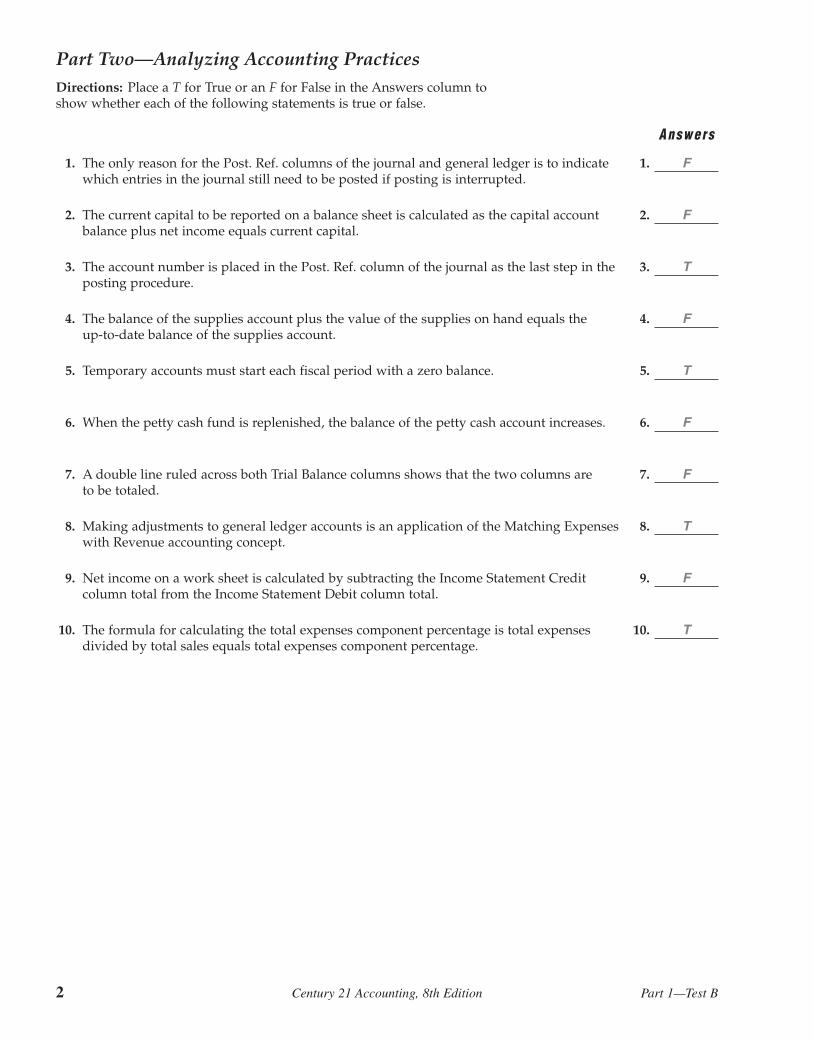

Answers

1. Ownership of a check cannot be transferred. 1. F2. Voided checks should be recorded in the journal. 2. T3. Using a memorandum as the source document for a dishonored check is an application 3. T

of the accounting concept Objective Evidence.4. The petty cash fund is a liability with a normal debit balance. 4. F5. When petty cash is replenished, Petty Cash is debited and Cash is credited. 5. F6. A check with a blank endorsement can be cashed by anyone who has the check. 6. T7. An outstanding check is one that has been issued but not yet reported on a bank statement 7. T

by the bank.8. A bank requires that the signature of the person authorized to sign checks be on the 8. T

signature card.9. The source document for an electronic funds transfer is a memorandum. 9. T

10. The source document for a debit card purchase is a memorandum. 10. T

2 Century 21 Accounting, 8th Edition Chapter 5—Test A

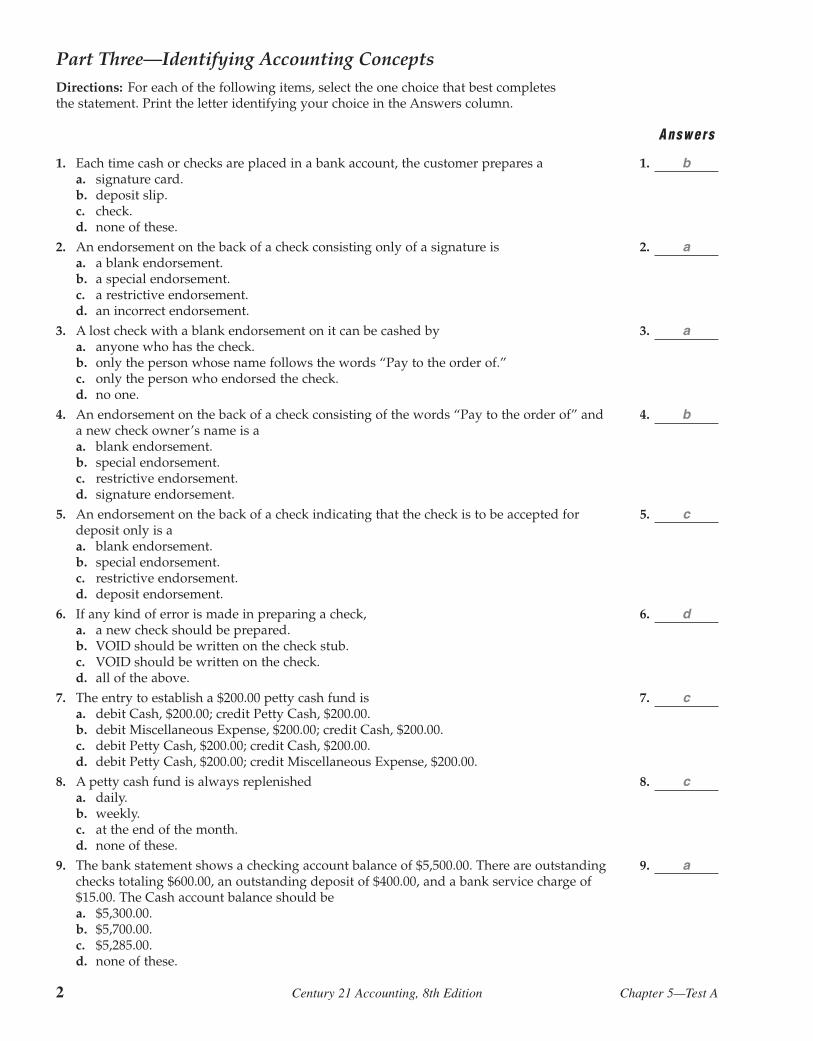

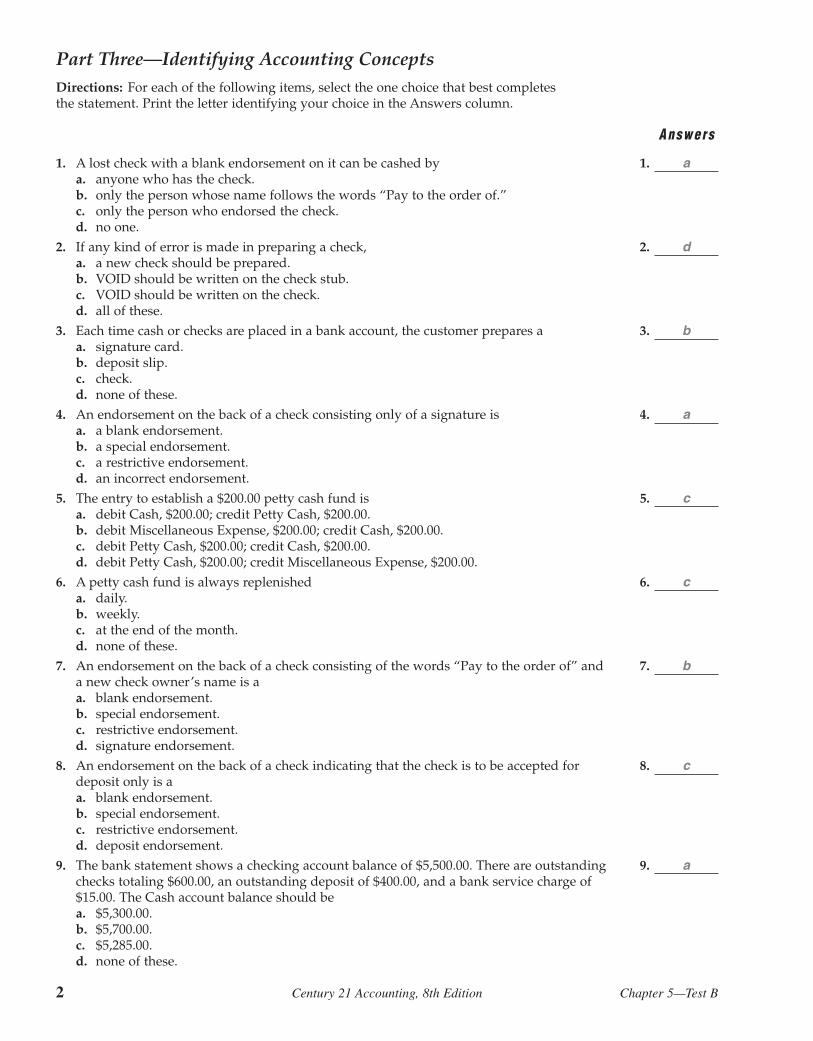

Part Three—Identifying Accounting ConceptsDirections: For each of the following items, select the one choice that best completesthe statement. Print the letter identifying your choice in the Answers column.

Answers

1. Each time cash or checks are placed in a bank account, the customer prepares a 1. ba. signature card.b. deposit slip.c. check.d. none of these.

2. An endorsement on the back of a check consisting only of a signature is 2. aa. a blank endorsement.b. a special endorsement.c. a restrictive endorsement.d. an incorrect endorsement.

3. A lost check with a blank endorsement on it can be cashed by 3. aa. anyone who has the check.b. only the person whose name follows the words “Pay to the order of.”c. only the person who endorsed the check.d. no one.

4. An endorsement on the back of a check consisting of the words “Pay to the order of” and 4. ba new check owner’s name is aa. blank endorsement.b. special endorsement.c. restrictive endorsement.d. signature endorsement.

5. An endorsement on the back of a check indicating that the check is to be accepted for 5. cdeposit only is aa. blank endorsement.b. special endorsement.c. restrictive endorsement.d. deposit endorsement.

6. If any kind of error is made in preparing a check, 6. da. a new check should be prepared.b. VOID should be written on the check stub.c. VOID should be written on the check.d. all of the above.