business organizations - nca exam guru

TRANSCRIPT

Business Organizations

2

INTRODUCTION ...................................................................................................................... 9

Main Features of the 3 major Corporate Forms: ................................................................................... 9

1. Sole Proprietorship 9 2. Partnerships 9 3. Corporations 9

SOLE PROPRIETORSHIP ..................................................................................................... 10

Registration: 10 PARTNERSHIPS ..................................................................................................................... 11

The legal nature of Partnerships 11 Scheme of Partnership Act 11

Formation / Definition of the Partnerships (S. 2-5) .............................................................................. 12

Definition of Partnership ...................................................................................................................................... 12 Test to identify Partnerships 12 1. “Carrying on a Business” 12 2. “In Common” 12

Green v Harnum ..................................................................................................................................... 12 Cressman et al v Furniss ......................................................................................................................... 12 Red Burito............................................................................................................................................... 13

3. “View to a profit” 13 Backman v R SCC ................................................................................................................................... 13 Spire Freezers SCC ................................................................................................................................. 13

Sharing of Profits Critical but not essential and not always sufficient for partnership 13 Cox v Hickman – Mutual Agency test for Partnerships ............................................................................. 13 Pooley v Driver – rights and behaviour of an alleged partner will determine if they are a partner ............ 13

Factors indicating NO partnership: Co-ownership 14 LePage v. Kamex – No partnership where there was co-ownership .......................................................... 14

Factors Indicating Partnership: Co- Ownership 14 Volzke Construction v. Westlock Foods .................................................................................................... 14

Agreeing to be a Partner ...................................................................................................................................... 15

W v. MNR ............................................................................................................................................... 15 Surerus Construction............................................................................................................................... 15

Factors Suggesting a Partnership Relationship 15

The Relationship of Partners to Each other ......................................................................................... 15

Some of the important default rules 15 Fiduciary Duty 16

Rochwerg v Truster ................................................................................................................................. 16 Mohammadamin v Zameni ...................................................................................................................... 16 Olson v Gullo .......................................................................................................................................... 17

Partnership Property 17

Liability of the Partnership to Third Parties ........................................................................................ 17

Test for Triggering Partnership Liability ............................................................................................................ 17

Ernst & Young v Falconi ......................................................................................................................... 17 Dubai Aluminium v Salaam ..................................................................................................................... 17 3464920 Canada Inc. v Strother SCC 2007 .............................................................................................. 18

3

Holding out and Related Liabilities ..................................................................................................................... 18

Holding out of Retired Partners: 18

Dissolution of a partnership .................................................................................................................. 19

When mandatory dissolution under the Act occurs 19

Partnership Agreements........................................................................................................................ 19

Considerations that should go into drafting partnership agreements ................................................................. 19 a. Name 19 b. Description of Business 20 c. Membership of Partnership 20 d. Capitalization 20 e. Arrangements regarding Profits and their distribution 20 f. Management 20 g. Dissolution 21

Joint Ventures ....................................................................................................................................... 21 Central Mortgage v Graham ................................................................................................................... 21

Wonsch Construction v Danzig Enterprises ............................................................................................. 21

Limited partnerships ............................................................................................................................. 22

Definition and Liability 22 Limited Partners Rights 22 When Limited Liability disappears 23

Limited Liability Partnerships – s.10, 44.1-44.4 ................................................................................... 23

New provisions on limited liability partnerships: 23

Partnership Summary .......................................................................................................................................... 24

CORPORATIONS ................................................................................................................... 24

Jurisdiction to Incorporate / regulate .................................................................................................................. 24

Incorporation and Organization of Corporations ................................................................................ 25

To incorporate you MUST ................................................................................................................................... 25 1. File Articles of Incorporation 25 2. Hole a Directors’ Meeting 25 3. Hold a Shareholders’ Meeting 25

Function of Corporate Law ................................................................................................................... 25

1. Corporate Law increases returns by decreasing costs 26 2. Corporate Law decreases shareholder risk 26 3. Corporate Law balances mandatory rules protecting non shareholder Stakeholders 27 Relationship Between Corporate and Securities Law 27

The Nature of the Corporation / Separate legal Existence ................................................................... 28

Salomon v Salomon & Co. corporation is a separate legal entity ......................................................... 28 Kosmopoulos v. Constitution Insurance (1987) SCC ................................................................................ 28 Lee v Lee’s Air Farming One can be an employee of their own Corporation ......................................... 28

4

disregard of the Separate Legal Identity of Corporations ................................................................... 29

Grounds for Piercing the Corporate Veil............................................................................................................. 29 1. Unfairness 29

Wildman v Wildman flagrantly opposed to justice therefore disregard the corporate entity .................. 29

2. Variety of Objectionable purposes for which the court will pierce the corporate veil 29 Big Bend Hotel Fraud therefore disregard corporate entity ................................................................. 29 Preeco I v Bon Street Holdings ................................................................................................................ 29 Gilford Motor Co. v Horne avoiding contractual obligation therefore disregard corporate entity ........ 30 Rogers Cantel v Elbanna Sales avoiding contractual obligation therefore disregard corporate entity ... 30 De Salaberry Improper tax purpose therefore disregard the corporate entity ....................................... 30 Stubart Opposite to De Salaberry........................................................................................................ 30 Smith -TEST for Agency leading the court to lift the corporate veil ........................................................... 30 Alberta Gas Ethylene v MNR ................................................................................................................... 31 Gregorio v Intrans- Corp ........................................................................................................................ 31

Professional Corporations 31 THE PROCESS OF INCORPORATION ............................................................................... 32 Items included in the articles: .............................................................................................................................. 32

Number of Directors 32 Registered Office (s. 14) 32 Class and Number of Shares 32 Restrictions on issuing, transferring or owning shares 32 Restrictions on the Business the corporation may carry on 33 Other Provisions 33

Incorporation: other details ................................................................................................................................. 33

Pre Incorporation Contract .................................................................................................................. 33

Common Law Position ......................................................................................................................................... 33 Kelner v Baxter ....................................................................................................................................... 33 Black v smallwood .................................................................................................................................. 34

Statutory Reform.................................................................................................................................................. 34 When Does Contract Adoption Occur? 34

Sherwood Design Services Inc. v 872935 Ltd. .......................................................................................... 34 s.21 OBCA – Pre-incorporation Statutory reform (what happens if the corporation is not incorporated yet) 35

THE CORPORATION IN ACTION....................................................................................... 35

Liability of Corporations for crimes ..................................................................................................... 35

1. Common law Absolute Liability Offences 35 2. Common law Strict liability offences: 36 3. Common law Mens Rea Offence 36

R v Waterloo Mercury Sales Ltd. ............................................................................................................. 36 R v Safety-Kleen Canada ......................................................................................................................... 36 Canadian Dredge and Dock STILL GOOD LAW ................................................................................. 36 Oger v Cheifscope ................................................................................................................................... 37

Criminal Liability Under The Criminal Code ...................................................................................... 37

Bill c-45 An act to amend the criminal Code (Criminal Liability of Organizations) 37 Criminal negligence crimes s. 22.2 37 Criminal Offences requiring intent or recklessness 37

5

Liability of Corporations in Tort .......................................................................................................... 38

1. Vicarious Liability 38 Bazley v Curry ........................................................................................................................................ 38

2. Direct Liability 38

Liability of Corporations in Contract ................................................................................................... 38

Common law rules for corporate liability in Contract ........................................................................................ 39 Actual Authority 39

SMC Electronics v Akhter Computers Ltd. implied authority is actual Authority ................................... 39 Apparent Authority 39

CDN lab supplies Ltd. v Engelhard Industries of Canada Behaviour sufficient for Apparent Authority . 40

Statutory reform on Corporate Liability in Contracts ........................................................................................ 40

MANAGEMENT AND CONTROL OF THE CORPORATION .......................................... 40

OBCA provides enhanced roles for shareholders / how they exercise power ...................................... 41

How Shareholders Exercise their power .............................................................................................................. 41 Shareholder meetings and resolutions 41 Remedies available to shareholders for management misbehavior 44

Directors and how they Exercise their Power....................................................................................... 44

Director Qualifications 44 Election and appointment of Directors 45 Filing Vacancies on the board s. 124 45 Number of Directors s. 125 45 Directors Meetings 45

Officers .................................................................................................................................................. 45

Delegation 46 Delegation outside the Corporation – Cannot lose all control 46

Kennerson v Burbank Amusement – case of delegation limits being exceeded ........................................... 46 Remuneration and Indemnification of Directors and Officers 47 Director Remuneration 47

Radtke..................................................................................................................................................... 47 Director Indemnification 47

Consolidated Enfield Corp v Blair ........................................................................................................... 48 Catalyst Fund General Partner v Hollinger ............................................................................................. 48 Bennett v Bennett Environmental Inc ....................................................................................................... 48 Cytrnbaum v Look Communications ........................................................................................................ 48 R. v. Bata Industries case ........................................................................................................................ 49

Shareholder Agreements- Management and control of Corporations ................................................. 49

Share Transfer 49 Unanimous shareholder agreement 49 Final issues on Corporate Governance 49

SHARES ................................................................................................................................... 50

Terminology 50 Priority structure on dissolution: 51

6

Creation or Authorization ..................................................................................................................... 51

Class – Incorporator or Shareholders 51 The basic rights associated with shares s. 24(3) 51 Distinction between Classes and Series of Shares: 52 Issuance of Shares 52 Dividends 52

Solvency Tests – HARD TEST S. 42 ................................................................................................ 52

Redemption/Retraction/Purchase 53 DUTIES AND LIABILITIES OF DIRECTORS AND OFFICERS ...................................... 53

Fiduciary Duty ....................................................................................................................................... 53

“Best interest” of the Corporation 54 BCE Inc. v 1976 Debenture Holders ........................................................................................................ 54

Fiduciary Duty / Breach of Best interests may arises in 3 Scenarios ................................................................... 54

1. Transacting with the Corporation at common law 54

OBCA S. 132 - Statutory Test - when director / officer CAN transact with their own corporation .................. 55

Alternative transaction Saving Provision - s. 132(8) 55 Zysko v. Thorarin .................................................................................................................................... 55 Exide Canada v. Hilts .............................................................................................................................. 55 Rooney v. Cree Lake................................................................................................................................ 56 Repap Case ............................................................................................................................................. 56

2. Taking corporate opportunities 56 Cook v. Deeks ......................................................................................................................................... 57 Regal v Gulliver ...................................................................................................................................... 57 Peso Silver Mines v Cropper ................................................................................................................... 57 Canaero – land mark case ....................................................................................................................... 57

Test for whether Appropriation of an Opportunity is a Breach of Fiduciary Duty Canaero 57 3. Fiduciary duty not to compete with a company 58 4. Fiduciary Duties and Take Over Bid Transactions 58 Things Directors can do to defend against a Bid 58

Views on whether defensive measures against takeover bids should be allowed: ............................................... 58

Free Market View 58 View in favour of defensive measures by directors against takeover bids 59 Other Breaches of Fiduciary Duty 59 DEFENSE: Being Able to Use Reliance as a defence 59 Shareholder Ratification of Breach 59

DUTY OF CARE ................................................................................................................................... 60

RE City Equitable Fire Insurance Co. Ltd (1925) ..................................................................................... 60

Standard of Care ................................................................................................................................... 60

Francis v United Jersey Bank .................................................................................................................. 60 Fraser v MNR ......................................................................................................................................... 61 Peoples v Wise ........................................................................................................................................ 61

7

Other Duties imposed on Directors and Officers ................................................................................. 61

Liabilities of Directors and Officers for Torts ...................................................................................... 61

Negligence 62 Inducing a breach of contract 62

SHAREHOLDER REMEDIES ............................................................................................... 62

1. Personal Action............................................................................................................................... 63

2. Derivative Action ............................................................................................................................ 63

Test for when the Court will allow Derivative Action 63 Procedural Matters .............................................................................................................................................. 63

3. Oppression Remedy........................................................................................................................ 64

The Statutory Scheme .......................................................................................................................................... 64

Oppression Remedy Provision 241 64 WHO may claim Relief from Oppression: The Complainant 64 Section 245 - The Complainant 64 What can the complainant complain about? 65 What relief is available? 248(3) 65 Interim Costs 65 The Complainants Continued: 65

Cask v Aumon –whether applicants claiming a right to become security holders are complainants ........... 65 Affiliates can also be Complainants under the Oppression remedy 65 Oppression is also available to Creditors and others… 66 The Complainant can also be the majority shareholders, 66 245(b) – director or officer or former director or officer 66 The corporation itself as complainant 66 The SCC in BCE developed a new analytical framework for finding oppression (VD, pg. 432- 33): 67 BCE Explaining the terms of the Oppression Remedy 67

Arthur v. Signum Communications – some examples to show the remedy can be invoked .......................... 68 Other Procedural Issues 68

Remedies Available to the court for successful Oppression Applications ........................................... 69

a. Share purchase 69 b. Liquidation and Dissolution 69 c. Remedies against other oppressing shareholders 69 d. Compliance 69 Other possible oppression remedies 69 Oppression Remedy Framework: 69

Shareholder remedies ............................................................................................................................ 70

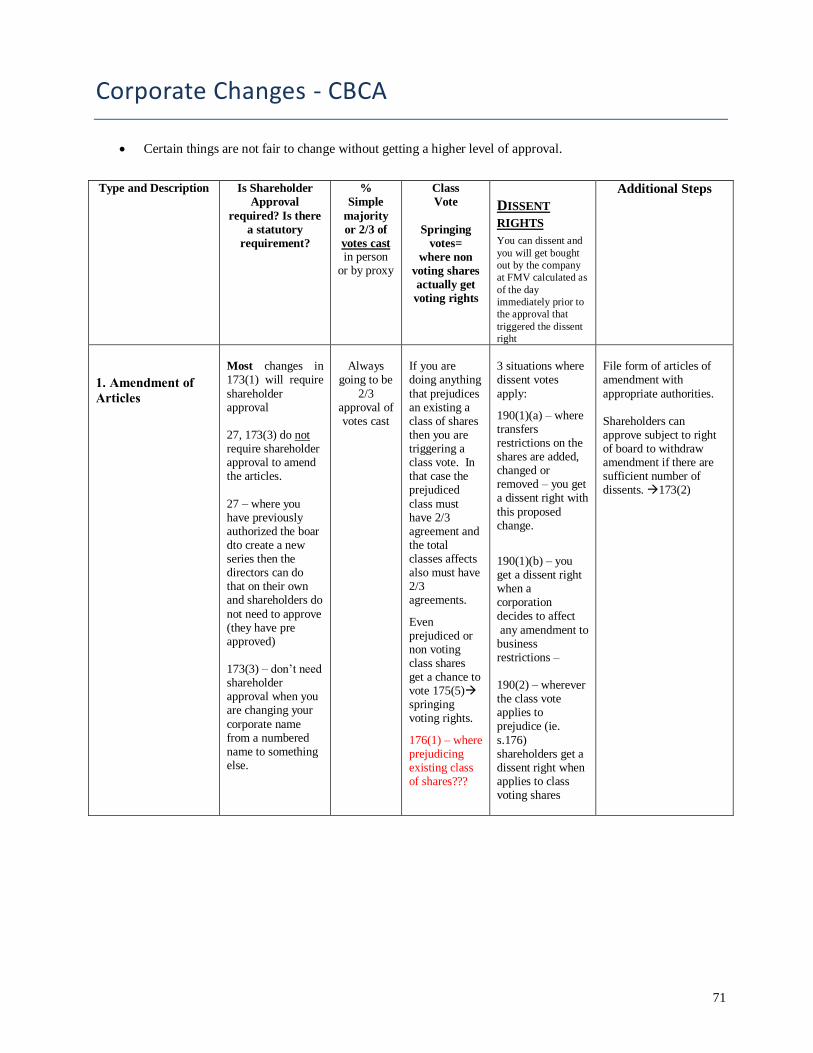

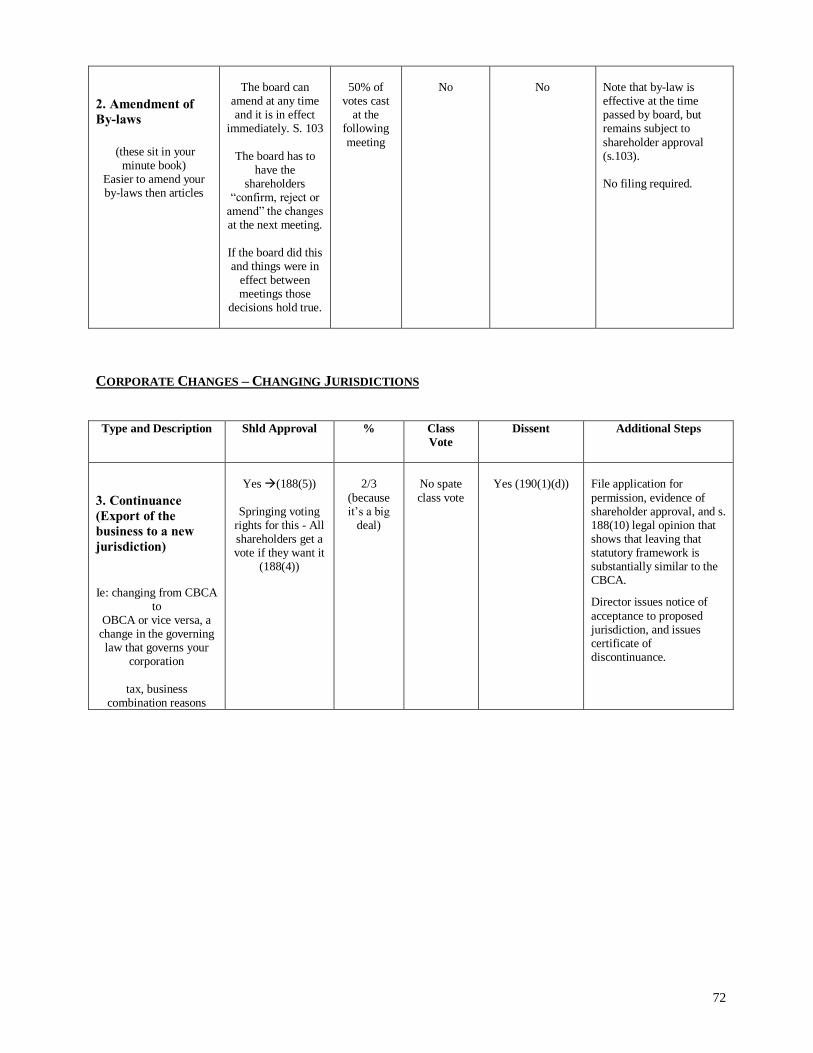

CORPORATE CHANGES - CBCA ........................................................................................ 71

Dissent rights ......................................................................................................................................... 71

1. Amendment of Articles 71 2. Amendment of By-laws 72

Corporate Changes – Changing Jurisdictions ...................................................................................... 72

3. Continuance (Export of the business to a new jurisdiction) 72

8

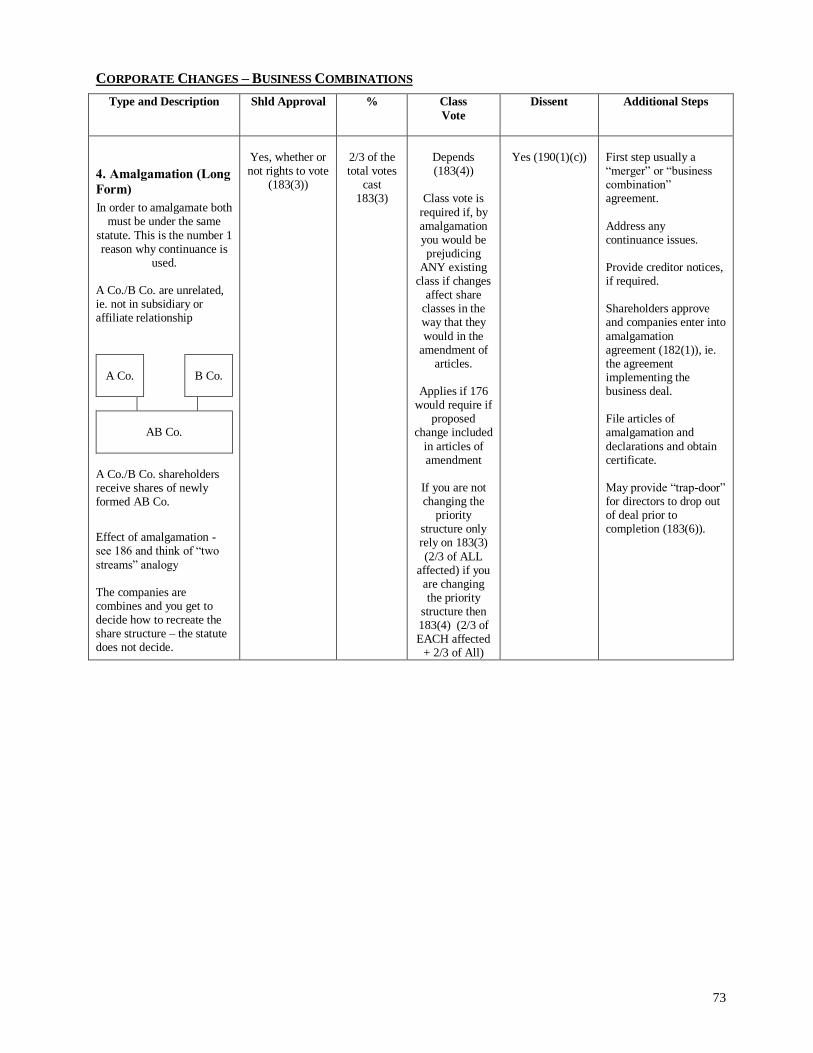

Corporate Changes – Business Combinations ...................................................................................... 73

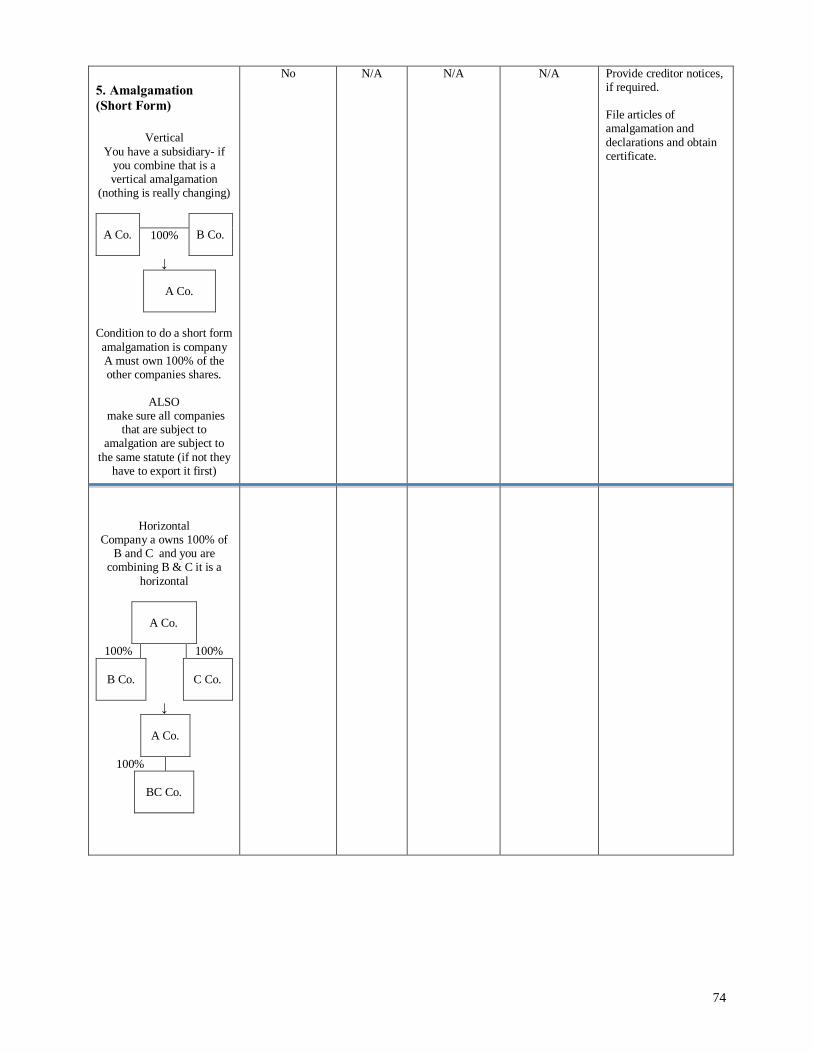

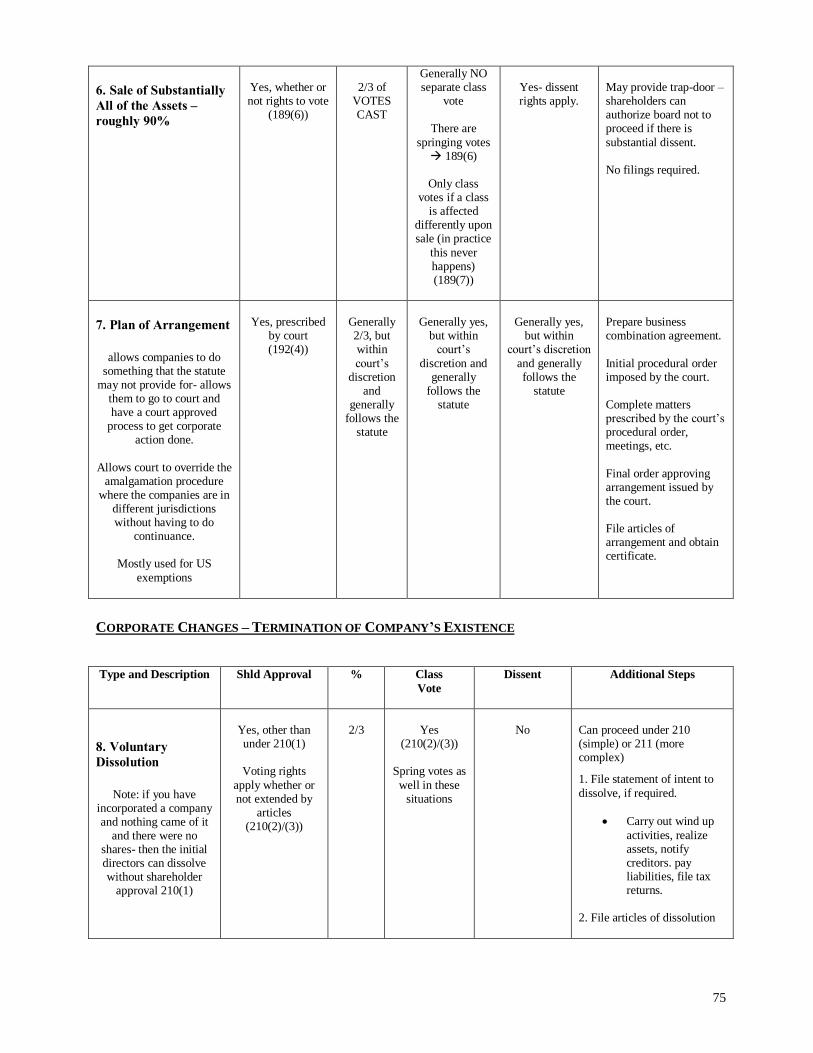

4. Amalgamation (Long Form) 73 5. Amalgamation (Short Form) 74 6. Sale of Substantially All of the Assets – roughly 90% 75 7. Plan of Arrangement 75

Corporate Changes – Termination of Company’s Existence ............................................................... 75

8. Voluntary Dissolution 75

9

Introduction

MAIN FEATURES OF THE 3 MAJOR CORPORATE FORMS:

1. Sole Proprietorship

Both own and manage their business

Formation occurs when an individual carries on business with his or her own account

SP is the sole owner

SP cannot employ self

All benefits accrue to SP

You are responsible for all contracts, any torts you commit yourself, or committed b employees, and income

is taxed to you and you have unlimited personal liability.

2. Partnerships

Partners are owners and managers (similar to sole proprietorship in legal form)

This is 2 or more persons carrying on business in common with a view to a profit Partnerships Act (PA)

S. 2

The characteristics of partnerships include internal relationships with other partners. This is governed by

default rules in the PA ss. 20- 31.

Partners cannot be employees?

All Benefits of partnership accrue to partners

All obligations of partnerships are personally attached to the partners regardless of which partner actually

commits the partnership to doing it

Each partner is responsible for tortious acts of self or employees subject to the Partnerships Law Amendment

act for some professional partnerships (often seen in law)

Income tax – income is calculated at the partnership level

Each partner has unlimited personal liability

Liability of partnerships to third parties is governed by the PA ss. 6-19 e

Each partner is an agent of the partnership which means that each partner can bind the partnership when

acting the normal course of business

How to manage risk of unauthorized obligations?

- Legal protections

Partnership agreements

Law of partnership

Limited liability partnerships under the partnership Statute Law Amendment Act

- Practical protections

Relationships of trust and confidence

Opportunities for informal monitoring

3. Corporations

Corporations are incorporated under a statute either the Canada business Corporations Act or a provincial

act.

Like with partnerships, corporations can customize their relationship and structure by augmenting the

statutory scheme with agreements and within the corporate constitution

No registration of the corporation is required

Run by directors and officers

Ask yourself… are the shareholders really owners? (NO)

Formation: Filing incorporation documents with appropriate government authority

10

Characteristics:

Separate legal entity- separate from shareholders

It is a juridical person (NOTE: core difference between partnerships, sole Prop. And corporations)

The corporation carries on business, owns the property of the business

Is solely responsible for obligations of business, contracts, torts and taxes

Only entity that is entitled to income from the business (unlike the other two)

A person can be a shareholder and an employee

The corporation has perpetual existence

There is a separation of ownership and management -managed by paid agents who are directors and officers

Shareholders DO vote in the directors however it is the directors that appoint the officers.

Key Issues:

How do shareholders ensure that management (directors and officers) act in their interest?

How do they ensure that there is no negligence?

How do they ensure that management interests are placed ahead of personal interests?

In response to these concerns the following items are in place:

1. Controls in the corporate constitution (articles, by laws, and shareholder agreements)

2. Duty of care, fiduciary duty and obligation not to oppress

3. Access to information rights (Bundle of shareholder rights)

4. Shareholder voting (Bundle of shareholder rights)

5. Shareholder remedies (Bundle of shareholder rights)

Sole Proprietorship

Simplest form of business organization

Comes into being whenever an individual starts to carry on business on own account without taking steps

necessary to use some other form of organization

Sole proprietor is the sole business owner and the only person entitled to manage the business. Cannot

contract with herself

The sole proprietor is exclusively responsible for preforming all contracts entered into in the course of

business and is exclusively responsible for all torts committed by her personally in connection with the

business and is vicariously liable for all torts committed by employees in the course of employment.

All of the sole proprietors personal assets, as well as those contributed to the business may be seized to fulfill

the obligations of the business

For income tax purposes the income or less from the business is included with the income or loss from other

sources in calculating the sole proprietors personal tax liability.

Obligations applying to all new businesses apply to all SP’s upon commencement of business- E.g. licenses

under Municipal Act; Securities Act; Registered Real Estate Brokers Act

advantage = ease to open a business;

disadvantages = risk of unlimited personal liability, difficulty of raising money, it is not possible to divide

up ownership of the sole proprietorship so the only method of financing is to borrow money directly.

Registration:

s. 2(2) of the Business Names Act (ONBA) Governance of Ontario registration of a sole proprietorship

Registration is required if a sole proprietor is using a name other than her own.

S. 4 says that a sole proprietor may also register voluntarily.

S. 7 If you do not register when you have to you cannot sue to ensure a business obligation in Ontario (and

you may be liable for a fine of up to $2000 s.10

These are the sticks to get you to register. It ensures that there is public record which can be relied on by

those dealing with SP to identify the individual who is liable for SP’s obligations

11

Partnerships

Common law partnership law codified in 1890. In Canada most provinces base their partnership related

statutes on 1890 statute from Great Britain. This means that the statute does not reflect how businesses

function today.

Note that QC’s partnership law is based on the civil code. There are 2 major categories of partnerships in

QC- declared partnerships where the individuals register or there are undeclared partnerships, which are

similar to that in the common law.

3 types of partnerships

1. General partnerships (simple)

Each partner has unlimited liability (Partnerships act s.6, 10-13)

2. Limited Liability Partnership

Same as general except that each partner is only liable for his or her own negligence or that of

persons under direct supervision or control

3. Limited Partnerships

At least one general partner and one limited partner contribute to partnership. All you are liable for

is the amount you invest and the general partners will take the rest of the liability risk amounting to

the same amount of risk that would be taken in a general partnership. Used in risky partnerships.

History of limited liability partnerships:

Until August 1, 2007, LLP was a general partnership except An individual partner not liable for negligence

of other partners or Employees - unless directly supervised by the partner affecting ss. 10 (2-4), 13, 24 and

44 OPA.

After Aug. 1, 2007, LLPs will have “full shield” limited liability protection for debts or obligations but

liability is enlarged if criminal or fraud involved or knew or ought to have known of negligent or wrongful

act. See sec. 10(2), 10(3).

Limited liability partnerships are formed by signing agreement designating as Limited Liability Partnership,

and registering its name, inc. LLP or s.r.l. under the Business Names Act. There are also requirements set out

in ss. 44.1 to 44.4 OPA

The legal nature of Partnerships

General and limited liability partnerships must register under the Ontario Business Names Act s. 2(3)

The act triggers default rules unless you contract out of them as you structure your partnership. Partnerships

should learn how to contract out and make alternate agreements because the act is outdated

Partnerships are like a sole proprietorship in that partners themselves carry on business directly

Unlike corporations, the partnership is not a legal entity separate from the partners

Each partner is liable to the full extent of his personal assets for debts and other liabilities of the partnership

business

Existence of any partnership depends on the continuing participating of the partners. If a partner leaves the

partnership it is terminated.

For income tax purposes, the income from the partnership business is calculated at the firm / partnership

level, adding up all of the revenues of the partnership and deducting all related expenses.

A partnerships assets and liabilities are not separate from each of the partners personal assets and liabilities.

Scheme of Partnership Act

– Nature of partnership ss. 2-5 - formation

– Relationship of partners to persons dealing with them ss. 6-19 – mandatory

– Relationships of partners to each other ss. 20-31 –default rules

– Dissolution of Partnership ss. 32-44

12

FORMATION / DEFINITION OF THE PARTNERSHIPS (S. 2-5)

Definition of Partnership

S. 2 “relation between persons carrying on business in common with a view to a profit”

Test to identify Partnerships

To determine if there is in fact a partnership assess whether:

1. A business is being carried on

2. In common

3. With a view to profit

1. “Carrying on a Business”

Business is defined as including every trade, occupation and profession OPA s. 1

“Any ongoing activity or even a single transaction” Thrush v Read

The idea of carrying on a business together usually suggests the need for an enduring relationship, but even

that factor may be inconclusive of identifying a partnership.

Preparation for a restaurant that never opens could be understood as carrying on a business identifying a

partnership Kahn v Miah

partnership may arise in relation to carrying on a business for a one time limited activity Spire Freezers

SCC

Principle indicia of carrying on a business together was sharing profits but now that is a rebuttable

presumption

OPA s.5 a partnership is called a firm, e.g. law firms. Actions against a partnership may be commenced

and defended using the firm name, but any judgment can be enforced against the partnership assets and those

of the individual partners.

A business is less likely to be found a partnership if the people involved are merely passive investors for

example, if several people jointly own an apartment building and collect rent their relationship may not be

found to be a partnership

2. “In Common”

Carrying on bus together, based on some kind of agreement. Agreement may be – written, oral, or implied

Whether agreement exists determined objectively- meaning persons may be characterized as Ps w/out their

knowledge, even contrary to their express intention.

Provisions stating the intention of parties may help clarify the agreement where clauses are not clear

Agreement must demonstrate intention to participate in a relationship that fits w/in definition of partnership.

Whether Ps describe themselves as such or not in an agreement is not conclusive of a partnership. Nor is

express provision denying intention to be Ps (but may help clarify other clauses of the agreement where such

clauses not clear)

S. 15 OPA states that if you hold yourself out to be a partner you are a partner

Several cases have addressed what is needed to establish the existence of an agreement:

Green v Harnum

2 men buy a fishing boat together, shared profits and borrowed equal amounts to fund the business but there

were no formal agreements. The court still held that this was a partnership because of a clear intention.

Cressman et al v Furniss

Where a partnership agreement was drafted but not signed there was insufficient evidence of a

partnership business based on the terms of the agreement, which contemplated each partner having an

ownership interest in an optometry business (here the court seems to be wrong- this is inconsistent case law).

13

Red Burito

If it is clear from their actions that the partners were planning to carry on business together the court

may find a partnership. The two parties had entered into a letter of understanding which provided that they

would incorporate. This never happened though the court still held that it was clear that they were going to

carry on business together and did so.

3. “View to a profit”

Need not actually make profit—but must have making money as a goal—ie: not for the purpose of carrying

out charitable, social, or cultural purposes

Backman v R SCC

if only purpose is to take advantage of loss then there is no view to profit in the business

Spire Freezers SCC

“Ancillary purpose to make profit suffices for a partnership”. Making profits need not be main or sole

intention in order for there to be a view to a profit there just needs to be some intention. Even if you have

losses for a long time you might still have an intention to make profit.

Sharing of Profits Critical but not essential and not always sufficient for partnership

Under legislation, sharing profits alone NOT sufficient to create a partnership OPA s. 3

The focus is on whether there is an interest in how the business is managed to produce profits.

If a person is compensated out of revenues she only has a stake in how much the business sells – may not be

sufficient to indicate a partnership. If a person is sharing profits, that person must also be concerned with

how the business is managed. Agreements to share losses and profits are strongly indicative of partnerships.

Cox v Hickman – Mutual Agency test for Partnerships

Facts: C & W were creditors of an ironworks business, appointed trustees; while the business was being operated by

the trustees, it became indebted to Hickman; Hickman sued them, alleging that they were partners

Rule: Where there is profit sharing but no mutual agency = no partnership The fundamental characteristic of

the relationship of partnership is mutual agency. A partnership exists where each person alleged to be in

a partnership carries on the business on behalf of the other alleged partners. The case also illustrates the

difficulty with drawing a clear line between partnership relationships and creditor relationships.

Analy: To find a partnership between cox and wheatcroft the business had to be carried on for the benefit of cox and

wheat croft . Here they were simply trustees acting for the benefit of the creditor and the actual principles,

which was the iron company.

Held: not partners, true relationship found to be debtor & creditor (business not carried on for benefit of C & W as

principals). Sharing profits not sufficient to find partnership relationship

NOTE: Vanduzer states that the case shows how the same facts may give rise to different interpretations of whether a

partnership exists and illustrates difficulty of determining whether a partnership exists even where an

individual or creditor is involved in the management of the business.

Pooley v Driver – rights and behaviour of an alleged partner will determine if they are a partner

Facts: Partners in manure business agreed to split profits with “Lenders” in accordance with their capital interests.

Complex relationship that was expressly designed to ensure that the Lenders were not found to be partners

(tried to fit into the equivalent of BCPA s.4(c)(iv))

Rule: in every case, court must decide if, based on all the circumstances, the most accurate characterization of the

relationship is one of a partnership, or some other relationship (eg. Debtor and creditor)

Held: In looking at the whole relationship between the Lenders and the partnership as described in the partnership &

loan agreements, court concluded the Lenders were partners (had interest in capital, had a degree of

14

participation & control unusual for Lenders, etc.) The return to alleged partner depended on profits; simply

meant that the sharing of profits in these circumstances does not by itself give rise to presumption of

partnership

Profit sharing does NOT always create inference of partnership -Ex.’s s. 3.3

- Repayment of debt out of profits to a lender

- Compensation to lender in the form of share of profits or interest rate varying with profits

- Employee profit sharing

- Annuity to spouse or child of deceased partner

- Payment of purchase price for sale of business out of profits

- DO NOT CONFUSE THESE WITH REAL PARTNERSHIPS

Note on Creditors

May be ongoing payments out of profits each month (s.4 says ok)…

Look at initial reason for investment – investing for sake of carrying on the business?

Look at how relationship will end – when some fixed amount repaid? Or, if only repaid in full when business

ends – may be interpreted as equity investment & so partnership

Factors indicating NO partnership: Co-ownership

Co-ownership is a form of tenancy in property law, managed by a trustee, and they get the profits (but not

carrying on a business together, as in partnership)

Co-Ownership does not in and of itself create partnership even if profits are shared s. 3.1 OPA

To create a partnership, something more than simply co-owning property & sharing profits – some active

involvement in management or other business activity must exist to find a partnership among co-owners

If co owners do cross the line and go into management and did not intend to you may still end up in a

partnership agreement

To avoid partnership hire a management company instead of trying to do it yourself!

LePage v. Kamex – No partnership where there was co-ownership

Facts: Apt. Building, co-owners have invested; individual co-owner signed K with real estate agent, who is now

trying to sue “partnership” not just individual

Rule: To determine if there is a partnership of co-owners ask: whether the intention of the co-owner was to “carry on

business” or simply to provide by an agreement for the regulation of their rights and obligations as co-owners

of a property?

Rule: Where co-owners want to deal with their individual interests separately, like by exercising a first right of refusal

over their own portion of a property, that desire is incompatible with the intention that a piece of property

become part of a partnership.

Held: Not partners, each co-owner had a “right of first refusal” on their own share.

Factors Indicating Partnership: Co- Ownership

Where, in addition to co-ownership and sharing of profits, there is substantial participation in the activities

associated with the management of the co-owned property, a partnership will likely be found.

Volzke Construction v. Westlock Foods

Ratio: co-owners Involvement in management need not amount to control for courts to find a partnership exists.

Use of common bank account (even if only signing authority, agreement to share the costs and profits,

common participating in financing the business & dealing with tenants concerns, and talking to eachother as

partners were all held to be indicative of a partnership here

Held: control of management had an effect on whether partnership a partnership arose.

15

Agreeing to be a Partner

Q: Is the case law becoming too vague in identifying what constitutes a partnership?

W v. MNR

Rule: Agreeing to be a partner can be enough to find a partnership.

Held: Courts have also held that Participation in management or other contribution not necessary to find a

partnership. In this case the Court also focused on the fact that the widows had left their deceased husbands

capital with the partnership and had not withdrawn it, so indicated an INTENTION to continue the partnership,

even though they were “silent or sleeping” partners.

Q: Does the focus on intention give sufficient guidance to lawyers to determine when a partnership exists?

Surerus Construction

Even stated intention to be partners were not found to be sufficient to find a partnership agreement, as parties

had not agreed to when the partnership would commence or their respective contributions.

Factors Suggesting a Partnership Relationship

1. Sharing profits

2. Sharing responsibilities for losses including guaranteeing partner debts

3. Jointly owning property

4. Controlling the partnership business

5. Participating in management

6. Stating an intention to form a partnership in a contract

7. Making government filings showing partnership

8. Access to information request regarding that business

9. Singing authority for contracts and bank accounts

10. Contributing money, services, or property as capital

11. Full time involvement in the business

12. Use of a firm name, perhaps in advertising

13. The firm having its own personnel and address

THE RELATIONSHIP OF PARTNERS TO EACH OTHER

Nature of partnership relationship will be specified in the partnership agreement

OPA ss. 20-31 default rules to govern parties relation which can be altered by specific agreements

The default rules may be displaced by conduct, but conduct must show a clear intention to displace the rules

Default rules are archaic and based on an archetypal conception of partnership. Most partnerships use their

partnership agreements to contract out of the default rules

Some of the important default rules

1. Each partner shares equally, both in the capital of the partnership and in any profits and must contribute

equally to any losses incurred s. 24.1

This seems out of date. Modern partnerships would maybe consider apportioning capital and

profits based on how much each partner contributes.

2. Each partner is entitled to be indemnified (if one partner incurs liability, if the other partner is responsible the

first can get the money back from the other partner) in respect of payments made or liabilities incurred in the

ordinary course of the partnership business or to preserve the business property of the firm s.24.2

This does not seem too out of date because it is a safety valve against he mistake and idiocy of

the other partner’s actions.

3. A partner making, for the purpose of the partnership, any actual payment or advance beyond the amount of

capital that he or she has agreed to subscribe is entitled to interest at the rate of 5 per cent per annum from

the date of the payment or advance. 24.3 NOTE: this is still the case today

16

4. A partner is not entitled, before the ascertainment of profits, to interest on the capital subscribed by the

partner s.24.4

5. Every partner may take part in the management of the partnership business s. 24.5

6. No partner is entitled to remuneration for acting in the partnership business s.24.6

7. No person may be introduced as a partner without the consent of all existing partners s.24.7

8. Any difference arising as to ordinary matters connected with the partnership business may be decided by a

majority of the partners, but no change may be made in the nature of the partnership business without the

consent of all existing partners s.24.8

9. The partnership books are to be kept at the place of business of the partnership, or the principal place, if there

is more than one, and every partner may, when he or she thinks fit, have access to and inspect and copy any

of them. (s.24.9)

10. No majority of the partners can expel any partner unless a power to do so has been conferred by express

agreement between the partners. (s.25)

11. Any person who takes an assignment of a partners interest, whether as a purported transfer or for the

purposes of taking security for the performance of some obligation of the partner, has no rights as a partner,

except to receive the share of the partnership profits to which the assigning partner would otherwise be

entitled (s.31)

12. Any partner may terminate the partnership by giving notice to the others (s. 26 & 32)

13. Any variation of the default rules requires unanimous consent (s. 20)

Fiduciary Duty

In addition to the default rules, common law says that partners owe each other a fiduciary duty: they must

deal with the partnership and partners with the utmost good faith and loyalty and integrity

Partners must never put their personal interests ahead of the interests of the partnership

Each partner is required to render to each other partner “true account and full information regarding matters

affecting the partnership s. 28

Have to account for any and all use of partnership property

Each partner has a right to access documents prepared by and for the partnership Dockrill v Coopers

Each partner must make full and accurate discloser of activities such that the partnership is fully aware of the

nature and significance of the activities but by agreement may exclude things McKnight v Hutchinson

Rochwerg v Truster

Facts: a partner in a firm of accountants became a director of one of the firm’s clients. He also purchased 8000

common shares in the client for what was fair price at the time and acquired options to purchase an additional

set of shares. The partner disclosed the directorship to his partners and paid the directors fees he received to

the partnership. He did not disclose the investment of the shares because he believed it was a private

investment.

Rule : The precise content of the fiduciary duty is dependent on the facts.

Held: The court held that he had to disclose in accordance with the fiduciary duty. He was required to account for the

profits

NOTE: that you can contract out of having to give up profits of shares and options as long as you disclose that you

will be getting them! Negotiate at the outset of the partnership.

Mohammadamin v Zameni

Facts: Zameni sold his interest in the partnerships auto parts business and set up a competing business nearby

Rule: Partner’s non competition obligation should extend beyond the termination as a part of fiduciary duties

Held: He breached his fiduciary duty by not complying with non-competition obligations

17

Olson v Gullo

A partner who sold part of the real property owns by the partnership had to pay the profits of the sale over to

the partnership based on s. 29(1) as well as the common law principles of fiduciary duties – a partner in

breach of his duty and receiving a benefit from the breach must share over the profits from that breach.

Partnership Property

Partnership property consists of all property contributed to the partnership and all property acquired on

behalf of the partnership.

Once property becomes partnership property, it must be held and used exclusively for the purposes of the

partnership and in accordance with the terms of the partnership agreement. Ex if someone decides to give

their truck for the partnership, even if that individual has legal title to the property, because it is regarded as

property of the partnership it cannot be sold because he agreed that it is part of the partnership.

An individual partner looses his individual beneficial interest in property contributed to a partnership

LIABILITY OF THE PARTNERSHIP TO THIRD PARTIES

Ss. 6-19 govern when partnerships are liable to third parties. These rules are mandatory and cannot be

contracted out of like other parts of the act. (READ THESE CAREFULLY!)

Test for Triggering Partnership Liability

Any business conducted by any partner in the usual way of business will trigger responsibility for the partnership as a

whole UNLESS the partner had no authority AND the third party dealing with the partners knows of the lack of

authority or does not know but believed him to be a partner s.6

Everything turns on “in the usual way of business”

Partnerships become liable to third parties when someone who is an agent of the firm enters into a contract

on its behalf. Each partner is considered an agent of the firm and of all other partners.

There is no partnership liability for acts outside the usual scope of partnership business

Partnerships are liable for the obligations torts and wrongful acts or omissions of its agents or employees

A partner is not responsible for the liabilities of the firm that arose prior to him becoming a partner

Some cases show that even if a partner is acting in a tortious way that might be considered to be in the “usual

or ordinary course of business”. This is where things get tricky.

Ernst & Young v Falconi

Facts: the estate partner in a law firm was held liable for the acts of another partner who assisted bankrupt clients with

fraudulently disposing of their property contrary to the bankruptcy act. The activity was held to be in the

ordinary course of the law firms business. The firm gave him authority to do this kind of fraud. The partner

here knew he was acting fraudulently as did the firm.

Rule: partners may be held liable for Wrongs, including torts and fraud, authorized in the ordinary course of business

of the partnership or with authority of all partners s. 11. The court in that case said that the test for whether

the activity could be held to be in the ordinary court of business was whther the unlawful acts are the sort that

would be within the scope of the partnership if done for legitimate (rather then illegitimate) purposes as seen

from the perspective of the overall business partnership.

Dubai Aluminium v Salaam

Rule: So long as the dishonest conduct was sufficiently closely connected to acts that the partners were authorized to

engage in the conduct may ne regarded as done in the course of business.

Held: House of lords held that a law firm partnership was liable for the dishonest acts of one of the partners. Their

actions were found to be in the usual course of business.

18

3464920 Canada Inc. v Strother SCC 2007

Facts: A partner in a firm breached his fiduciary duty and the terms of his retainer with a client when he took a direct

financial interest in a direct competitor to that client. The court saw this as a conflict of interest that would lead

the lawyer not to act as a zealous advocate in accordance with the rules of professional conduct.

Rule: Liability of the firm under the partnerships statutes is not limited to common-law torts, the language of the

statute include liability for omissions and breach of fiduciary duty. Where a partner goes out on a frolic on his

own it does not matter, if the liability happens in the ordinary course of business, all of the partners are liable.

(The partner’s act could not be separated from the firms ordinary course of business).

Held: Despite the fact that the firm did not know this was going on the court held that the firm was still responsible

because the partners act was so closely connected with the business of the firm as to be within the ordinary

course of business.

Holding out and Related Liabilities

“Every person, who by words spoken or written or by conduct represents himself or herself or who knowingly suffers

himself or herself to be represented as a partner in a particular firm, is liable as a partner to any person who has on the

faith of any such representation given credit to the firm, whether the representation has or has not been made or

communicated to the persons so giving credit by or with the knowledge of the apparent partner making the

representation or suffering it to be made.” S. 15 OPA

If a person is held out, OR is knowingly holding out to be a partner of a firm then that person may be held

liable for the obligations of a partnership even though he was never a partner or was not a partner at the time

the partnership incurred the obligation s. 15 OPA

s. 15, s. 18 & 36(2) May be liable under these provisions even if never were or no longer a partner.

This might include use of a persons name in the firm name, on a sign or on the firms invoices or letterhead

Holding out of Retired Partners:

RULE: A retired partner is liable to every person who dealt with the firm prior to his retirement for obligations of the

firm incurred after retirement

UNLESS actual notice of the retirement is given to the person (OPA s.36 (1),

UNLESS the person never knew that the retiring partner was a partner (OPA s. 36(3), or

UNLESS the partner left the firm because he became insolvent or died (s. 36(3).

Holding out must be with the knowledge of the partner held out Tower v. Ingram must be some type of

action by the person to hold themselves out. If they did nothing it is sort of like a limitation on the liability.

In this case Ingram, the retired partner had not knowingly suffered himself to be represented as a partner.

To ensure that there is no liability

after retirement it is best to put a

notice in the gazette

19

DISSOLUTION OF A PARTNERSHIP

Under the Act, partnerships are dissolved if:

Formed for a fixed period on expiry of the term s. 32 OPA.

If not for fixed term, on notice by one partner to all others s. 26. 33(c).

If formed for a single adventure or undertaking, on termination of that business s. 32 (b).

If there is a death or insolvency of any partner s.33 (a).

But partnership agreement can make durability more stable or unstable, e.g. inability of one of the partners to

continue partners’ work.

NOTE: This is a default rule you want to stay away from: Partnership agreements should deal directly with these

dissolution rules and not rely on the default.

When mandatory dissolution under the Act occurs

When business of partnership becomes illegal or illegal to be carried on by partners s. 34

Court may order dissolution on a variety of grounds, e.g. mental incapacity of a partner, persistent breaches

of the partnership agreement, and residuary power where it is just and equitable to do so (e.g. where majority

of partners refuse to allow a partner to exercise her rights to participate in the management of the partnership

as she has a right to do (s. 24.5) or irreconcilable differences between partners. These types of events amount

to breach of fiduciary duties between partners.

Sec. 44 OPA deals with settlement of claims against partnership on dissolution and what occurs with the

assets. As with shareholders in a company, debts to creditors paid first, then debts to partners, then return of

capital (original contribution that the partners had made). Statutory scheme re partners share can be tailored

in a partnership agreement.

PARTNERSHIP AGREEMENTS

We have talked about the default rules, the mandatory rules and the liabilities, but much of the time in these

types of law will be spent drafting partnership agreements for clients to ensure that their partnership is

tailored and takes into account the default rules which will be replaced as decided upon by clients.

It is commonplace for partners to enter into partnership agreements, which allow for tailoring of specifics.

Through the agreement the partners can provide a structure for operating the partnership where the

legislation is silent or where the partners want something different from what it provides

Agreements can also be used to respond to mandatory provisions in the OPA, especially those providing for

liability to third parties by structuring the relations among partners to address liability (S. 6-19).

Considerations that should go into drafting partnership agreements

a. Name

A partnership may carry on business using any name it likes Name should be registered

Name constitutes part of goodwill of the business and belongs to the partners. Thus any partner could

use the name on dissolution and thus an agreement might consider identifying who the name would

“belong to”.

The agreement might outwardly allow for the continued use of the name of a dead or retired partner in

order to help limit liability for the retired partner

The use of a persons name as a part of the firm name with his knowledge constitutes holding out that

person as a partner within the meaning of the OPA. Any person held out after they leave the partnership

retains liability. Accordingly, if a persons name is going to be used after she leaved the remaining

parties of the firm should agree to indemnify her against liability. Such an agreement will not protect her

from third parties but it gives her the right to recover any amount she has to pay from her former

partners

There is no need for such indemnity where there is a deceased partner’s name used in the firm name

20

b. Description of Business

Each partner is an agent of the partnership capable of binding the firm to obligations and thus each

partners authority as an agent is limited by the nature of the business undertaken

The scope of a partners authority to bind the partnership to a third party will be determined by what the

partnership actually does rather then by any limit in the partnership agreement. Nevertheless make it

clear what activities are considered to be carried on for the benefit of the partnership

Directors fees and options should be dealt with here as well and a discussion of how much capital each

partner will contribute

Ex: In a law firm partnership partners may want to describe that the business includes teaching a law

school course or writing papers so any fees received are income for the partnership

Ex: a partnership agreement may explicitly list that all partners must put their full attention into the

business or have permission of other partners to carry on another business.

Permitting activities in the description of business that would otherwise be a breach of fiduciary duty

allows the partner to engage in activities without fear of being required to account of all profits

A non compete clause may also be included

Describing the scope provides the basis for the firm to claim against a partner for liabilities imposed for

carrying on activities that that are outside the scope

c. Membership of Partnership

Default rules talk about all partners consenting to admission and expulsion and retirement leaves to

dissolution. OPA says that in the absence of agreement to the contrary all partners have to agree to the

admission of a new partner.

This requirement is often adapted in partnership agreements and often include criteria for admission of a

new partner

Amount of capital a new partner has to contribute should be addressed in agreements

The expulsion of a partner is prohibited under the default rules of the OPA so many agreements find a

way to change this

Retirement should not dissolve a partnership so this default rule should be changed as well.

d. Capitalization

The amount contributed by the partners to the firm is called the firms capital.

Default rules say that in absence of a specific agreement to how partners should share capital all partners

share equally.

Capital contributions and partners’ entitlement to capital should be dealt with in the partnership

agreement.

e. Arrangements regarding Profits and their distribution

Pursuant to OPA, all profits are to be divided equally among the partners. This provision is almost

always changed to allocate to each partner a share commensurate with her contribution to the firm.

Each partnership must decide what kinds of contributions to take into account and what weight to give

to each for the purpose of allocating profits. These contributions might include capital contributions

(how much you put in), billable hours worked, hours worked on matters that were not billable but

contribute to the firm, or not, fees billed and collected, totally billings to new clients brought in by that

partner, total billings and business development

Each partners entitlement will change each time the factors are evaluated

It is also necessary o decide how the profits would be distributed

f. Management

The default rules in the OPA provide that all partners are entitled to participate in management and that

decisions on ordinary matters are to be made by a majority of partners but decisions relating to the

nature of the partnership requires consent of all partners

Agreements usually alter the requirements for consent by numerical majority to something that better

reflects the power structure of the partnership

Reality is that most medium and large firms delegate the management to one or a few people sometimes

not even a partner.

21

g. Dissolution

Provincial law allows for dissolution of partnerships in a variety of ways

Partners often agree to change the many ways that the OPA identifies automatically dissolve a

partnership

In some agreements dissolution may be precluded altogether and replaced by a provision dealing with

withdrawal

S. 44 of the OPA can be fleshed out in an agreement

JOINT VENTURES

Joint ventures are neither a distinct form of business organization nor a relationship that has legal meaning

Joint Venture is a term used to describe a relationship among persons who agree by contract to combine their

money, property, knowledge, skills, experience, time and other resources for some common purpose

The distinguishing feature of a joint venture is that it is set up for a limited amount of time for a

limited purpose or both

You can have a joint venture by partnership and by corporation or by contract alone.

The legal consequences of joint venture that is NOT a partnership or corporation are NOT clear

Main issues of joint ventures = consequences of the relationship outside of the agreement to the relationship

EX: a small mineral exploration business may go in on a joint venture by combining resources with a

business with financial strength

Central Mortgage v Graham

Facts: Central Mortgage initiated a relationship with a builder under which it provided the financing for that company

to build some houses to specifications provided by Central Mortgage. The financing was secured by a

mortgage on the property in favour of central mortgage. Central Mortgage was consulted during construction

and had the right to approve purchases. Graham bought one of the houses from the second company which

assumed that he would take on the mortgage payments. He stopped paying the mortgage

Rule: In a joint venture with the following characteristics, each party in the joint venture is responsible for all

obligations of the joint venture (just as each partner is responsible for all obligations of a partnership). This is a

partnership – like liability

Contributions by both parties of money, property, skill or knowledge to a common undertaking

Joint interest in the subject matter of the joint venture

Mutual control and management

Arrangement limited to one project

Expectation of profit AND

Mutual profit sharing

Held: Based on the indicia listed, such a relationship can trigger partnership liabilities. This was a joint venture and

therefore Central mortgage was liable for the obligations of its fellow venturing company

NOTE: this is the only case to ever find that a joint venture has partnership like characteristics but it is VALID LAW

The label of joint venture seems not to actually have any effect other than to create a partnership like relationship.

Some courts have held that joint ventures may have more limited legal consequences.

Some courts have held that parties to a joint venture owe each other a fiduciary duty. An aspect of the

fiduciary duty is the obligation not to disclose confidential information provided by one joint venturer to the

other for the purposes of the joint venture.

Wonsch Construction v Danzig Enterprises

Facts: These two parties entered into a joint venture to build and operate an apartment building. Wonsch was

responsible for construction and incurred debt to the Bank. Danzig negotiated an assignment of the debt

owed, paying the bank significantly less than the full amount owed.

Held: The court decided Danzig owed a fiduciary duty to Wonsch, which precluded it from trying to make a profit

from dealing in Wonsch’s debt incurred for the purposes of the joint venture.

22

LIMITED PARTNERSHIPS

For investors who want to be able to share in partnerships profits but limit their liability for losses.

Limited partners are not usually interested in participating in management- they are usually passive investors

In Ontario these partnerships are governed by the Ontario Limited Partnership Act (OLPA)

Limited partners are only responsible for their limited risk that they put in and the general partners have

unlimited liability. There is always one general partner and often several limited partners.

Tax motivation bus likely to have losses in early stages of its life. LPs able to deduct these losses against

other income. One of the ways the tax law is trying to promote these partnerships, if companies buy

expensive equipment, they can write off capital cost depreciation (a percentage of the value of that

equipment). This will bring down the tax bracket of the companies.

Definition and Liability

RULE: Every limited partnership must consist of at least one general partner with unlimited liability and at least one

limited partner with limited liability OLPA s. 2(2)

RULE: A declaration must be filed with the registrar appointed under the Business names Act to identify the limited

partners OLPA s.3

RULE: The declaration of the limited liability partnership expires after years unless it is renewed. Expiry does not

terminate the limited partnership, but an additional fee must be paid for renewal OLPA s.3(3).

RULE: The general partner in a limited partnership has all the rights and powers and is subject to the same

restrictions and unlimited personal liability as a partner in a general partnership subject to certain additional

constraints designed to protect the limited partners OLPA s.8

RULE: Limited partners have certain narrowly defined rights and their liability is limited to the extent of their

contribution OLPA s. 9

Limited Partners Rights

RULE: Limited partners have a right to share in profits and to have their investment returned OLPA ss. 11

RULE: right to demand and receive return of investment when: OLPA s.15(1)

a. Dissolution of the LP’ship

b. At the time specified in the p’ship agreement

c. On 6 mos notice, if no time specified in PA

d. On unanimous consent of all Ps

RULE: No return of a limited partner’s investment may occur if there are not enough assets to pay the claims of all

creditors OLPA 15(1)

RULE: In addition, Section 10 of the Ontario Act provides that a limited partner has the same rights as a general

partner to: 1) inspect the books and make copies, 2) get full and true information regarding the limited

partnership and to be given a complete and formal account of the affairs and 3) to obtain dissolution by court

order. OLPA s. 10

RULE: A limited partner may transact business with the limited partnership including lending it money but cannot

hold a security interest in its assets and cannot receive anything from the limited partnership if its insolvent

RULE: Unlike a general partner, a limited partner may be an employee of the partnership OLPA s. 12

RULE: A limited partners interest is transferable, but the transferee has the full rights of the transferor OLPA s. 18

RULE: A person can be both a limited and general partner OLPA s. 5(1) Governments allow this because it

allows for involvement in high risk activities especially people who do not have money or people with mney

but no special skills

23

When Limited Liability disappears

Limited Liability disappears if partner:

(a) "takes part in the control of the business" [LPA s. 13(1)]; or

(b) allows their name to be used in firm name [LPA s. 6(2)]

The limited partner can advise (not control) the firm management [12(2)(a)]

Hard to distinguish between giving advice and when in control. In this case the limited partner lost his status

when he acted as the manager Houghton Graphics

A limited partner actng only in their capacities as directors and officers of a corporate general partner, they are

not liable as general partners Nordile Holdings,

o BUT will lose his limited liability if he is also the controlling shareholder because as such, he is in

control of the general partner (corporation) (Houghton Graphics).

Limited Partners have similar rights to those in the default rules under general partnerships

Dissolution occurs if

(a) no more general partner

(b) no more limited partners

(c) the limited partner’s contribution not repaid when required (d) assets are not enough to pay liabilities.

LIMITED LIABILITY PARTNERSHIPS – S.10, 44.1-44.4

After Aug. 1, 2007, LLPs will have “full shield” limited liability protection for debts or obligations but that

liability can be enlarged if criminal or fraud involved and the partners knew or ought to have known of the

criminal or fraudulent act or omission. See sec. 10(2), 10 (3).

This is done by all partners signing an agreement called LLP under the Business Names Act and must be all

requirement set out in ss. 44.1 – 44.4 of the OPA

The government statute of the profession – LSUC – has to allow this type of coverage to allow the

professional associations to operate under LLP’s

LLP’s must carry a mandatory minimum amount of insurance.

Minimizes risk for partners, but increases risk for clients/creditors. FIRM REMAINS LIABLE- scheme

protects Ps from claims against personal assets. Assets of the firm are still available.

New provisions on limited liability partnerships:

10(2)(a) An individual partner not liable for debts or obligations of partnership or another partner arising out of

negligence, or wrongful acts or omissions of Other partners or Employees, agent, or representative of the

partnership

10(2)(b) Not liable for any other debts or obligations of p’ship incurred while p’ship is LLP

UNLESS:

• Act or omission of other partner or employee (not directly supervised) constitutes a crime or fraud

(criminal or civil) [10(3)(c)(i)] OR

• Partner knew or ought to have known of act or omission and did not take actions to prevent it that a

reasonable person would have taken [10(3(c)(ii)]

REMAINS LIABLE for:

own negligence or wrongful act or omission [10(3)(a)]

that of person directly supervised or controlled by the Partner [10(3)(b)]

24

Partnership Summary

1. Partnership has no existence separate from the partners who comprise it. Therefore partners have unlimited

personal liability for the obligations of the partnership business

2. In absence of any agreement to the contrary, partnerships may be dissolved by any of the partners in

accordance with the default rules

3. Partnerships come into existence without any formality – it is sufficient if two or more persons begin to carry

on business together with a view to profit.

4. The test for this intention = whether the business is being carried on for the benefit of the alleged partners

5. The most significant indicia of such an intention is sharing of profits from the business activity

6. Other important indicia of partnership include management, control of the partnership, and common

ownership of property.

7. The relationship of partners to each other is governed by default rules in the OPA unless the parties agree on

some other arrangement.

8. The relationship between partners and third parties are governed by a set of mandatory rules

9. In general, all partners are liable for all obligations incurred in the course of the partnership

10. After a person dies or becomes bankrupt he is no longer liable for the obligations incurred afterwards

11. If a partner leaved for other reason he may continue to be liable

12. Persons who are not partner will nevertheless be liable as partners if they are knowingly being held out as

partners

13. Partnership agreements alter the default laws of partnerships

14. Joint ventures are not partnerships but may have some lesser partnership like legal consequences

15. Joint Venterurs have fiduciary duty not to put their personal interests ahead of the interests of the venture.

16. Limited partnerships are like general partnerships except that the liability of at least one partner is limited to