business opportunities in water sector in india

TRANSCRIPT

Water Sector in India Tapping the Opportunities

By

G.MD.ATIQUE

Development Consultant

M: +919703726628

E-Mail: [email protected]

Contents 1. Sector Background ............................................................................................................................... 2

2. Snapshot on “Sources-Supply-Consumption” ..................................................................................... 3

3. Creating Infrastructure -An Opportunity ............................................................................................. 4

4. Market Leaders ..................................................................................................................................... 8

5. Policy and Legislation ......................................................................................................................... 10

6. Water in 12th Five year Plan; Few initiatives ..................................................................................... 10

7. Indicative Opportunity Spaces ........................................................................................................... 11

8. Public Private Partnerships ................................................................................................................ 12

9. Fiscal Incentives .................................................................................................................................. 13

2 | P a g e

With the growing population, which is urbanizing at a brisk pace, the mechanisms to store, clean and deliver water are increasingly becoming important and presenting business opportunities. We estimate that the total potential business in the water sector in India can amount to US$30 bn annually.

Kotak Institutional Equities Estimate, US

1. Sector Background: India, home to 16% of the world’s population, has only 2.5% of the world’s land area and 4 % of the

world’s water resources at its disposal. Precipitation in the form of rain and snowfall provide over

4,000 trillion liters of fresh water to India. Most of this freshwater returns to the seas and ocean via

the many large rivers flowing across the subcontinent. A portion of this water is absorbed by the soil

and is stored in underground aquifers. A much smaller percentage is stored in inland water bodies

both natural (lakes and ponds) and man-made (tanks and reservoirs). Of the 1,869 trillion liters of

water reserves, only an estimated 1,122 trillion liters can be exploited due to topographic

constraints and distribution effects. The demand for water has been increasing at a high pace in the

past few decades. The current consumption in the country is approximately 581 trillion liters with

irrigation requirements accounting for a staggering 85 percent followed by domestic use at 7

percent and industrial use at 8%.

Growing Demand and Mismatching Supply:

Demand in the country is projected to very soon overtake the availability of water. In some regions

of the country, it has already happened. The rapid

increase in population, urbanization and

industrialization has led to a significant increase in

water requirement. In the next decade the demand

in water is expected to grow by 20 percent, fueled

primarily by the industrial requirements which are

projected to double from 23.2 trillion liters at

present to 47 trillion liters. Domestic demand is

expected to grow by 40 percent from 41 to 55

trillion liters while irrigation will require only 14

percent more ten years hence, 592 trillion liters up

from 517 trillion liters currently.

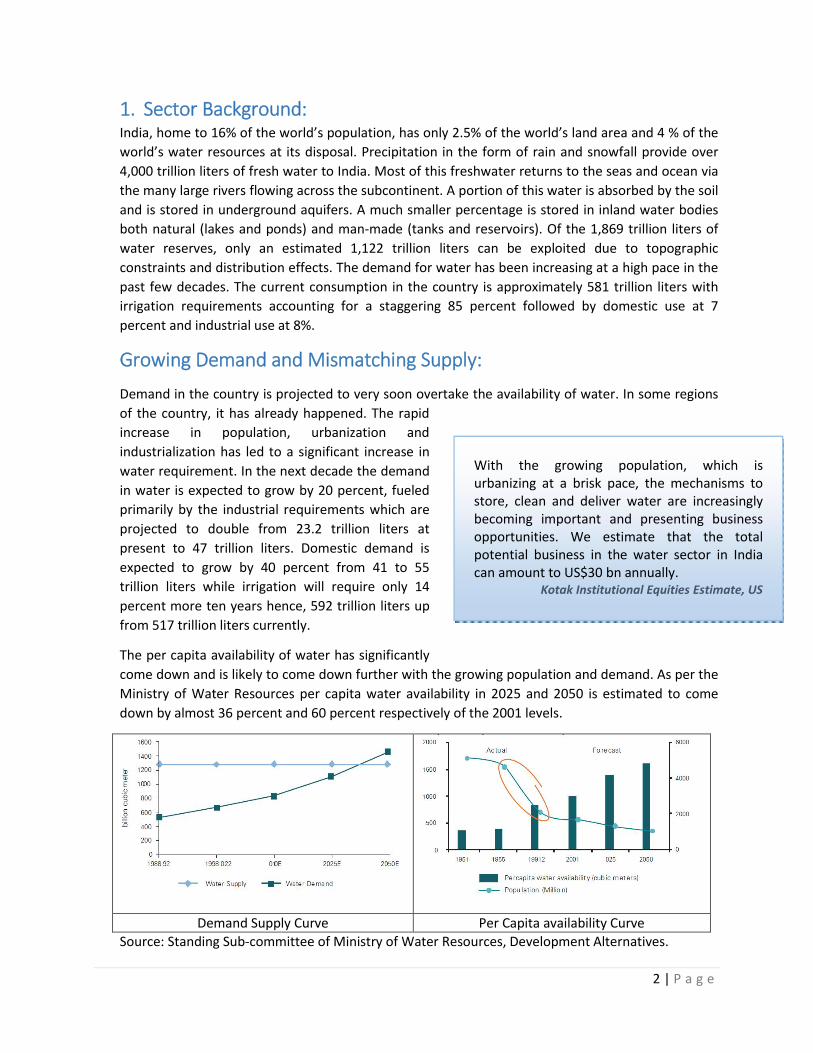

The per capita availability of water has significantly

come down and is likely to come down further with the growing population and demand. As per the

Ministry of Water Resources per capita water availability in 2025 and 2050 is estimated to come

down by almost 36 percent and 60 percent respectively of the 2001 levels.

Demand Supply Curve Per Capita availability Curve

Source: Standing Sub-committee of Ministry of Water Resources, Development Alternatives.

3 | P a g e

2. Snapshot on “Sources-Supply-Consumption”: India’s skew towards agriculture is more pronounced on account of low yield per drop of water and also free or (low) fixed cost electricity offered to farmers, promoting unchecked usage. With urbanization, demand from energy and industry will significantly outgrow agricultural and residential demand. Brahmaputra and Ganga provide 60% of India’s annual water availability. Water availability in India by river basin: Source of Water

Source Water in BCM

Brahmaputra, Barak and Others 586 Ganga 525 West flowing rivers from Tadri to Kanyakumari

114

Godavari 111 West flowing rivers from Tapit to Tadri

87

Krishna 78 Indus 73 Mahanadi 67 Narmada 46 Others 183 Total 1869

Source Water in BCM

Annual Precipitation

4000

Average Annual Availability

1869

Estimated Water Resources

1123

Source: Ministry of Water Resources India has enough supply-side and demand management options to meet its water needs. India’s water supply is plentiful. The monsoons supply 4,000 bcm of rain to India every year. It is sometimes fashionable to show declining water availability per capita in India since the population is growing while the average usable water has not and cannot change materially. We note that India’s per capita availability works out to 1,600 cubic meters per person, which is just at the threshold of water scarcity. However, it is more pertinent to note that this average hides large inter-regional imbalances. The Water majorly consumed in following forms;

Usage in Billion Cubic meters Breakdown (in %)

Indian Water Consumption

4 | P a g e

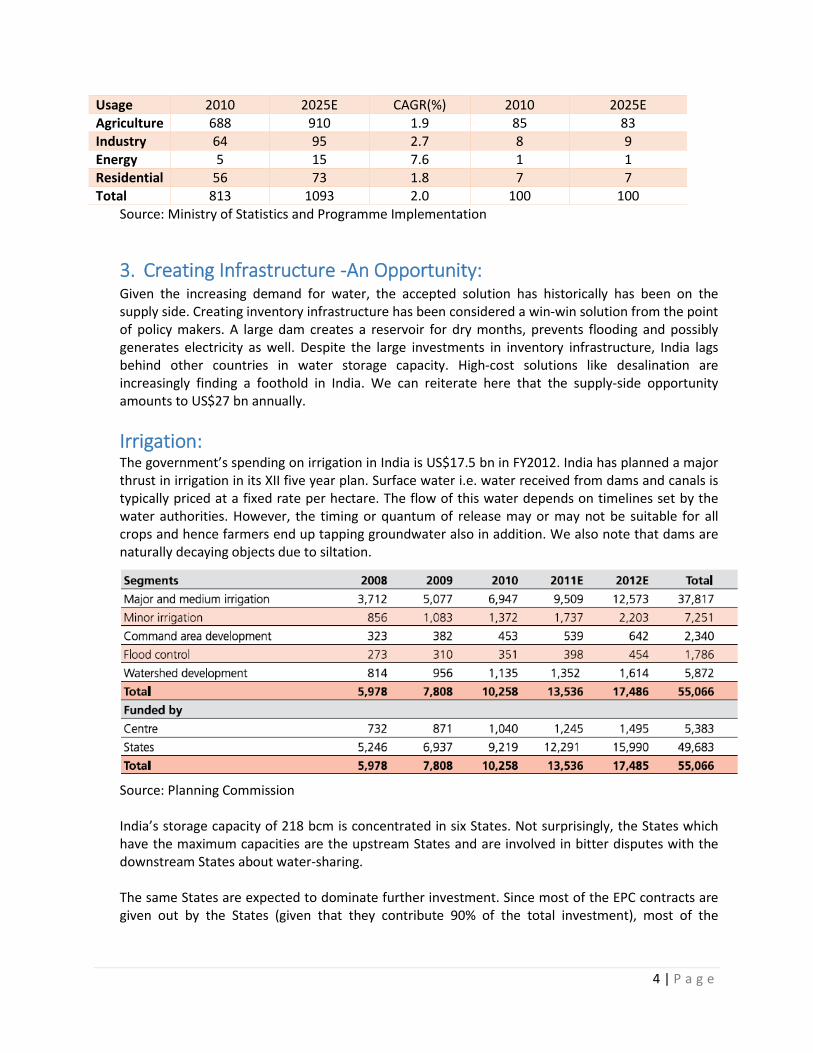

Usage 2010 2025E CAGR(%) 2010 2025E Agriculture 688 910 1.9 85 83 Industry 64 95 2.7 8 9 Energy 5 15 7.6 1 1 Residential 56 73 1.8 7 7 Total 813 1093 2.0 100 100

Source: Ministry of Statistics and Programme Implementation

3. Creating Infrastructure -An Opportunity: Given the increasing demand for water, the accepted solution has historically has been on the supply side. Creating inventory infrastructure has been considered a win-win solution from the point of policy makers. A large dam creates a reservoir for dry months, prevents flooding and possibly generates electricity as well. Despite the large investments in inventory infrastructure, India lags behind other countries in water storage capacity. High-cost solutions like desalination are increasingly finding a foothold in India. We can reiterate here that the supply-side opportunity amounts to US$27 bn annually.

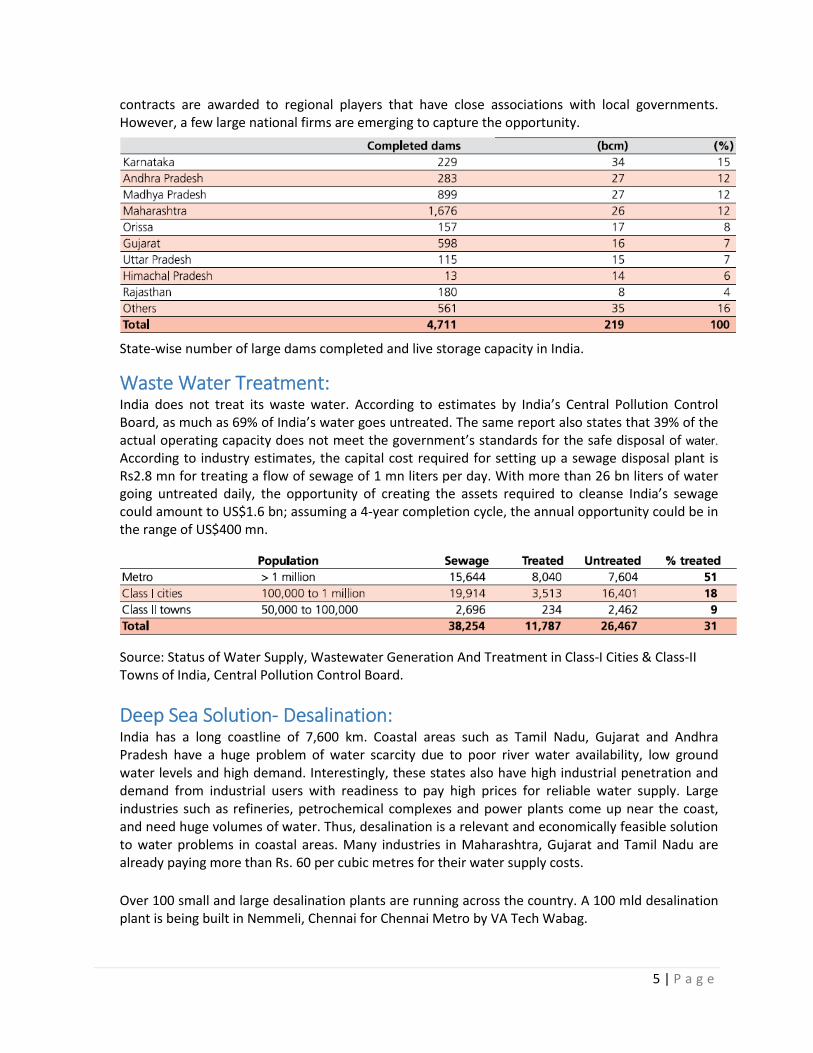

Irrigation: The government’s spending on irrigation in India is US$17.5 bn in FY2012. India has planned a major thrust in irrigation in its XII five year plan. Surface water i.e. water received from dams and canals is typically priced at a fixed rate per hectare. The flow of this water depends on timelines set by the water authorities. However, the timing or quantum of release may or may not be suitable for all crops and hence farmers end up tapping groundwater also in addition. We also note that dams are naturally decaying objects due to siltation.

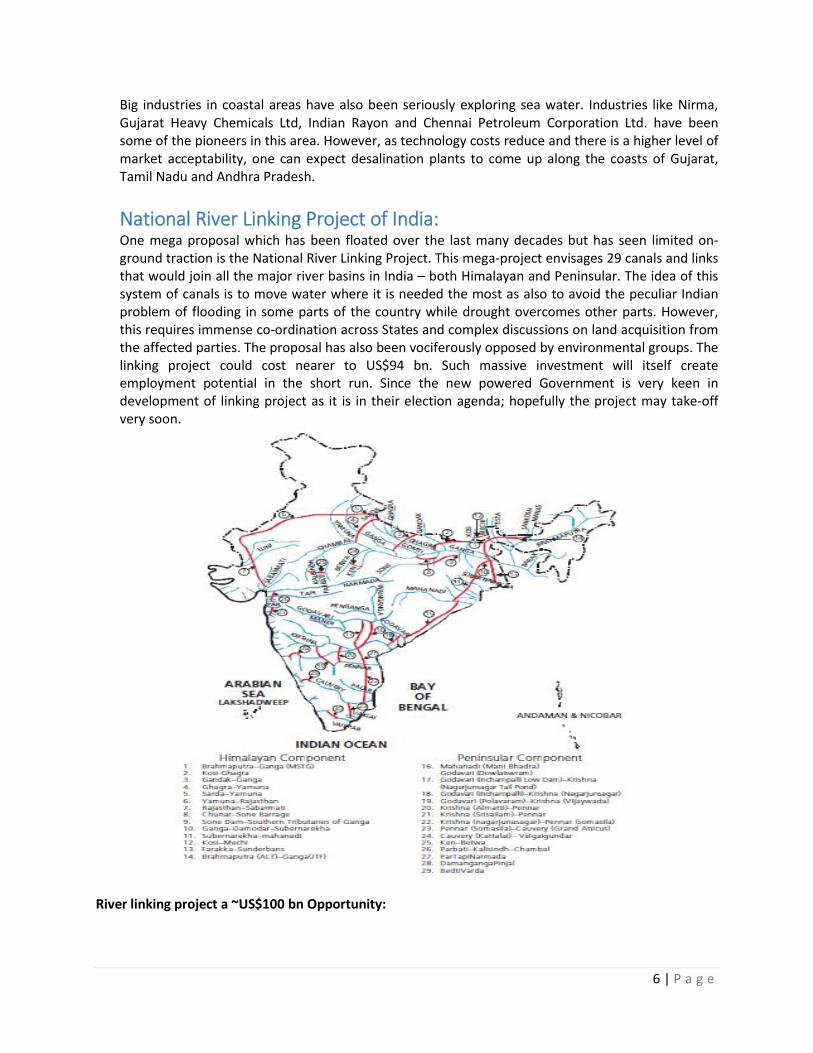

Source: Planning Commission India’s storage capacity of 218 bcm is concentrated in six States. Not surprisingly, the States which have the maximum capacities are the upstream States and are involved in bitter disputes with the downstream States about water-sharing. The same States are expected to dominate further investment. Since most of the EPC contracts are given out by the States (given that they contribute 90% of the total investment), most of the

5 | P a g e

contracts are awarded to regional players that have close associations with local governments. However, a few large national firms are emerging to capture the opportunity.

State-wise number of large dams completed and live storage capacity in India.

Waste Water Treatment: India does not treat its waste water. According to estimates by India’s Central Pollution Control Board, as much as 69% of India’s water goes untreated. The same report also states that 39% of the actual operating capacity does not meet the government’s standards for the safe disposal of water. According to industry estimates, the capital cost required for setting up a sewage disposal plant is Rs2.8 mn for treating a flow of sewage of 1 mn liters per day. With more than 26 bn liters of water going untreated daily, the opportunity of creating the assets required to cleanse India’s sewage could amount to US$1.6 bn; assuming a 4-year completion cycle, the annual opportunity could be in the range of US$400 mn.

Source: Status of Water Supply, Wastewater Generation And Treatment in Class-I Cities & Class-II Towns of India, Central Pollution Control Board.

Deep Sea Solution- Desalination: India has a long coastline of 7,600 km. Coastal areas such as Tamil Nadu, Gujarat and Andhra Pradesh have a huge problem of water scarcity due to poor river water availability, low ground water levels and high demand. Interestingly, these states also have high industrial penetration and demand from industrial users with readiness to pay high prices for reliable water supply. Large industries such as refineries, petrochemical complexes and power plants come up near the coast, and need huge volumes of water. Thus, desalination is a relevant and economically feasible solution to water problems in coastal areas. Many industries in Maharashtra, Gujarat and Tamil Nadu are already paying more than Rs. 60 per cubic metres for their water supply costs.

Over 100 small and large desalination plants are running across the country. A 100 mld desalination plant is being built in Nemmeli, Chennai for Chennai Metro by VA Tech Wabag.

6 | P a g e

Big industries in coastal areas have also been seriously exploring sea water. Industries like Nirma, Gujarat Heavy Chemicals Ltd, Indian Rayon and Chennai Petroleum Corporation Ltd. have been some of the pioneers in this area. However, as technology costs reduce and there is a higher level of market acceptability, one can expect desalination plants to come up along the coasts of Gujarat, Tamil Nadu and Andhra Pradesh.

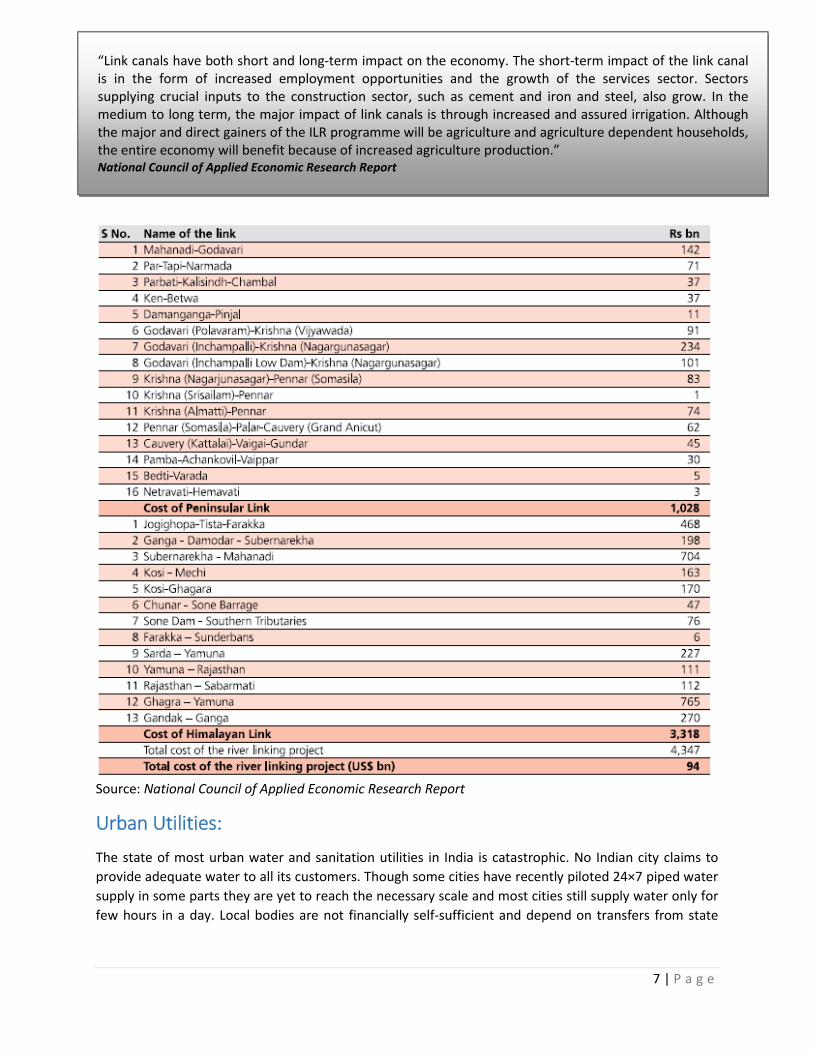

National River Linking Project of India: One mega proposal which has been floated over the last many decades but has seen limited on-ground traction is the National River Linking Project. This mega-project envisages 29 canals and links that would join all the major river basins in India – both Himalayan and Peninsular. The idea of this system of canals is to move water where it is needed the most as also to avoid the peculiar Indian problem of flooding in some parts of the country while drought overcomes other parts. However, this requires immense co-ordination across States and complex discussions on land acquisition from the affected parties. The proposal has also been vociferously opposed by environmental groups. The linking project could cost nearer to US$94 bn. Such massive investment will itself create employment potential in the short run. Since the new powered Government is very keen in development of linking project as it is in their election agenda; hopefully the project may take-off very soon.

River linking project a ~US$100 bn Opportunity:

7 | P a g e

“Link canals have both short and long-term impact on the economy. The short-term impact of the link canal is in the form of increased employment opportunities and the growth of the services sector. Sectors supplying crucial inputs to the construction sector, such as cement and iron and steel, also grow. In the medium to long term, the major impact of link canals is through increased and assured irrigation. Although the major and direct gainers of the ILR programme will be agriculture and agriculture dependent households, the entire economy will benefit because of increased agriculture production.” National Council of Applied Economic Research Report

Source: National Council of Applied Economic Research Report

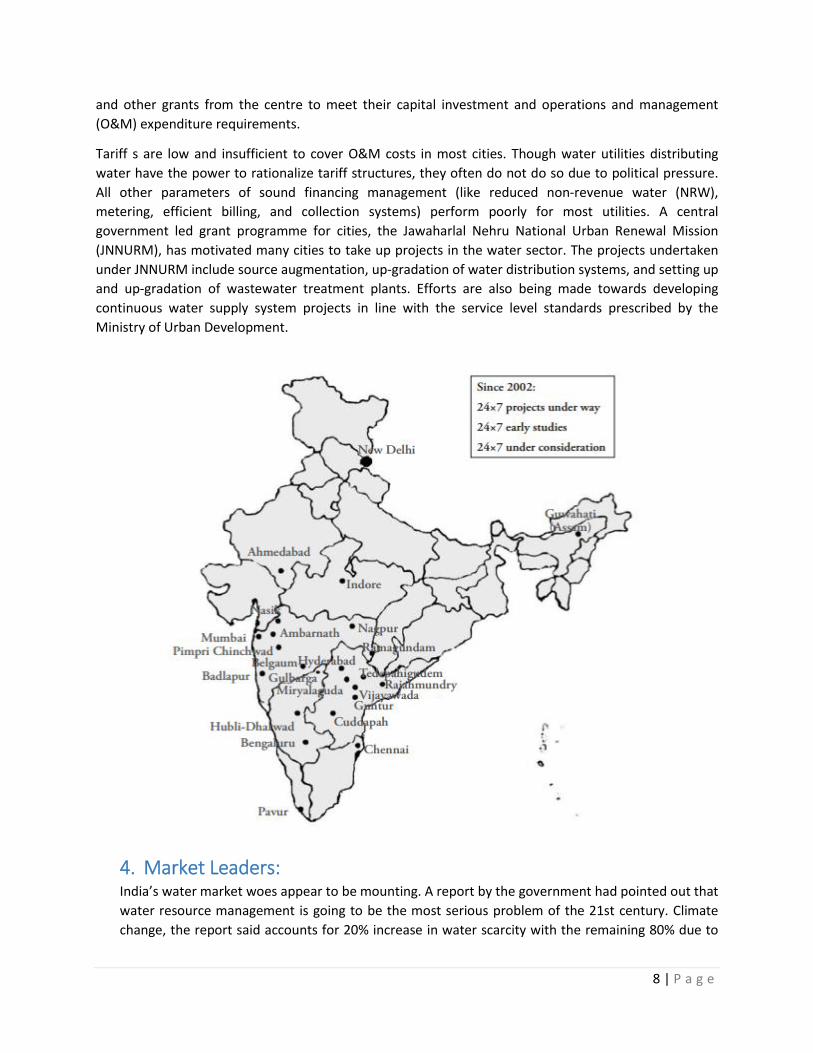

Urban Utilities:

The state of most urban water and sanitation utilities in India is catastrophic. No Indian city claims to

provide adequate water to all its customers. Though some cities have recently piloted 24×7 piped water

supply in some parts they are yet to reach the necessary scale and most cities still supply water only for

few hours in a day. Local bodies are not financially self-sufficient and depend on transfers from state

8 | P a g e

and other grants from the centre to meet their capital investment and operations and management

(O&M) expenditure requirements.

Tariff s are low and insufficient to cover O&M costs in most cities. Though water utilities distributing

water have the power to rationalize tariff structures, they often do not do so due to political pressure.

All other parameters of sound financing management (like reduced non-revenue water (NRW),

metering, efficient billing, and collection systems) perform poorly for most utilities. A central

government led grant programme for cities, the Jawaharlal Nehru National Urban Renewal Mission

(JNNURM), has motivated many cities to take up projects in the water sector. The projects undertaken

under JNNURM include source augmentation, up-gradation of water distribution systems, and setting up

and up-gradation of wastewater treatment plants. Efforts are also being made towards developing

continuous water supply system projects in line with the service level standards prescribed by the

Ministry of Urban Development.

4. Market Leaders: India’s water market woes appear to be mounting. A report by the government had pointed out that

water resource management is going to be the most serious problem of the 21st century. Climate

change, the report said accounts for 20% increase in water scarcity with the remaining 80% due to

9 | P a g e

population increase and economic development resulting in water pollution and contamination of

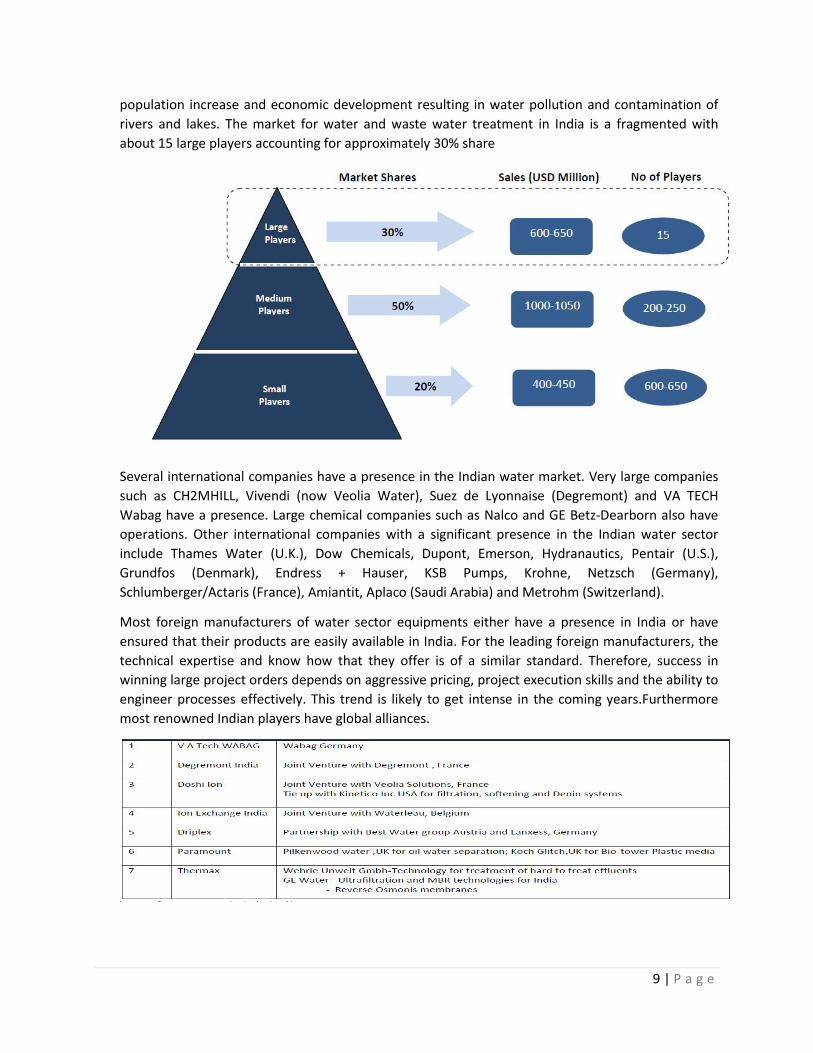

rivers and lakes. The market for water and waste water treatment in India is a fragmented with

about 15 large players accounting for approximately 30% share

Several international companies have a presence in the Indian water market. Very large companies

such as CH2MHILL, Vivendi (now Veolia Water), Suez de Lyonnaise (Degremont) and VA TECH

Wabag have a presence. Large chemical companies such as Nalco and GE Betz-Dearborn also have

operations. Other international companies with a significant presence in the Indian water sector

include Thames Water (U.K.), Dow Chemicals, Dupont, Emerson, Hydranautics, Pentair (U.S.),

Grundfos (Denmark), Endress + Hauser, KSB Pumps, Krohne, Netzsch (Germany),

Schlumberger/Actaris (France), Amiantit, Aplaco (Saudi Arabia) and Metrohm (Switzerland).

Most foreign manufacturers of water sector equipments either have a presence in India or have

ensured that their products are easily available in India. For the leading foreign manufacturers, the

technical expertise and know how that they offer is of a similar standard. Therefore, success in

winning large project orders depends on aggressive pricing, project execution skills and the ability to

engineer processes effectively. This trend is likely to get intense in the coming years.Furthermore

most renowned Indian players have global alliances.

10 | P a g e

5. Policy and Legislation: As per the Indian Constitution, water is in the domain of the states with the central government only advising the states by issuing a non-binding National Water Policy. Despite this asymmetry, various schemes devised by the central government have had a significant effect on addressing the gaps in the access to freshwater. Lately, the schemes have had a reformist agenda, which has been coupled with direct financial assistance for water sector projects at the state level and as well as channelling multilateral finance into the sector. The Ministry of Water Resources, River Development and Ganga Rejuvenation is the principal agency responsible for water in India and as such, oversees the planning and development of the resource from policy formulation to infrastructure support. Other central departments working in water are:

The Ministry of Agriculture: Watershed development and irrigation The Ministry of Power: Hydropower development The Ministry of Environment and Forests: Water quality The Ministry of Rural Development: Watershed development and drinking

water provision The Ministry of Industry: Industrial uses of water The Ministry of Urban Development: Urban drinking water provision and

sanitation The Central Pollution Control Board: Water quality monitoring The Indian Council of Agricultural Research: Development of water management

techniques. Within each state, the water sector is fragmented, with separate agencies responsible for irrigation, domestic and industrial water supply. Supply to domestic consumers, especially in the urban areas, is further fragmented. Even within a state there can be different service arrangements and service delivery models, such as state level departmental supply, state-level autonomous boards, city-level utilities and municipal departments. Crucially, in many instances, capital expenditure is the responsibility of a state-level entity, while the actual responsibility of service delivery rests with city municipal bodies, which makes even day-to-day management of the sector unnecessarily complex which makes any reform or improvement difficult as the entire departments/boards/utilities are constantly in firefighting modes to accomplish day-to-day activities. India’s National Water Policy 2012 prioritizes water use in the following order: drinking, irrigation, hydropower, ecology, agricultural and non-agricultural industries, navigation and other uses. The policy also encourages private participation in the planning and operation of water systems. The policy will specifically look into sustainable use of water, effects of climate change and rationalisation of water pricing. Apart from that the water sector is governed by the different environmental legislations, pollution control acts, and rules and notifications.

6. Water in 12th Five year Plan; Few initiatives: XII Plan envisages a move away approach from engineering construction centric approach to multidisciplinary participatory approach and to bridge the gap between potential creation and utilization with prioritize investment in command area development and management programme.

11 | P a g e

Focus Areas: i. Reform of major and minor irrigation (MMI) projects:

The 12th plan document outlines the different ways in which we can works towards better water use efficiency of irrigation projects. It calls for a move away from a narrowly engineering construction- centric approach to a more multidisciplinary, participatory management approach to our major and medium irrigation projects,with central emphasis on command area development.

ii. Ground Water:

Groundwater accounts for nearly two-thirds (66%) of India’s irrigation and 80% of domestic water needs, thus the plan documents calls for a participatory approach to sustainable management of groundwater based on a new programme of aquifer mapping, as a prerequisite and a precursor to the National Groundwater Management Programme.

Further, the plan calls for launching a massive programme for watershed restoration and groundwater recharge by transforming Mahatma Gandhi National Rural Employment Guarantee Act (MGNREGA) into our largest watershed programme.

iii. Urban Water & Waste Management:

As far as management and supply of water is concerned, currently, it is estimated that as much as 40-50 per cent of the water is ‘lost’ in the distribution system! Even this is a guesstimate, as most cities do not have real accounts for the water that is actually supplied to consumers. The 12th Plan proposes that the water supply programme for each city must provide for demand management and reduction of the cost of supply.

iv. Integrated Watershed Management Program: There are new guidelines to IWMP proposed by the Mihir Shah Committee. The guidelines are it has been decided to make the IWMP a five-year programme with a renewed focus on professionalism, capacity building, institutional building and a greater role for civil society. Further, based on the experience of a lot of states, a new framework is proposed for convergence of IWMP with allied programmes such as MGNREGA, National Rural Livelihood Mission.

v. National Water Framework Law: A national law on water is considered even more necessary. To this end, a Sub Group in the 12th Plan has drafted a National Water Framework Law. It is important that, the proposed national water law is not intended to either centralise water management, or to change Centre-State relations or to alter the Constitutional position on water in any way.

7. Indicative Opportunity Spaces:

Joint ventures with Indian firms to offer integrated solutions in water treatment, including performing feasibility studies, designing, technical consulting and providing operation and online maintenance services.

12 | P a g e

Water supply and efficient use and reuse of water particularly in industrial processes for high polluting sectors, such as cement, pulp, paper and equipment for water saving and water recycling.

Provision of better design, manufacture and installation of various types of rainwater

harvesting systems to cater to the inherent and growing needs of the population to conserve and reuse rain water.

Water use efficiency solutions (including efficient irrigation solutions, such as sprinkler

or drip irrigation and low-flow faucets and other water use systems).

Water governance (including innovative and novel government policy approaches).

Water analysis and instruments (such as water-saving, household devices and domestic usage monitoring, equipment).

Municipal and household water purification systems.

Water consulting (including services to develop water conservation policy plans).

Sewerage treatment, and efficient use and reuse of water particularly in industrial

processes for high polluting sectors, such as cement, pulp, paper and equipment for wastewater treatment (including treatment technologies, biogas regeneration through anaerobic treatment of municipal and industrial wastewater, and water saving equipment and water recycling).

Design, manufacture and installation of various types of wastewater systems, sewage

system rehabilitation and septic system rehabilitation and alternatives, packaged and transportable sewerage and wastewater treatments, waterless composting toilets, water treatment controllers, design, manufacture and/or maintain equipment for disinfecting water by electrolysis.

Wastewater consulting (including services to develop water conservation policy

plans).

8. Public Private Partnerships:

Private sector’s participation in publicly owned setups: There has been a thrust at the policy level to encourage private sector participation as a means to improve performance delivered by publicly owned utilities. The National Water Policy of

2002, the National Water Policy 2012, as well the Planning Commission’s Five Year Plans explicitly encourage private sector participation in the water sector. Furthermore, the flagship urban development programs of the Government, such as the Jawaharlal Nehru National Urban Renewal Mission (JNNURM), and the Urban Infrastructure Development Scheme for Small & Medium Towns (UIDSSMT), encourage institutional reform in a publicly owned sector through private sector capital and capabilities. There have been several attempts to mobilize private

13 | P a g e

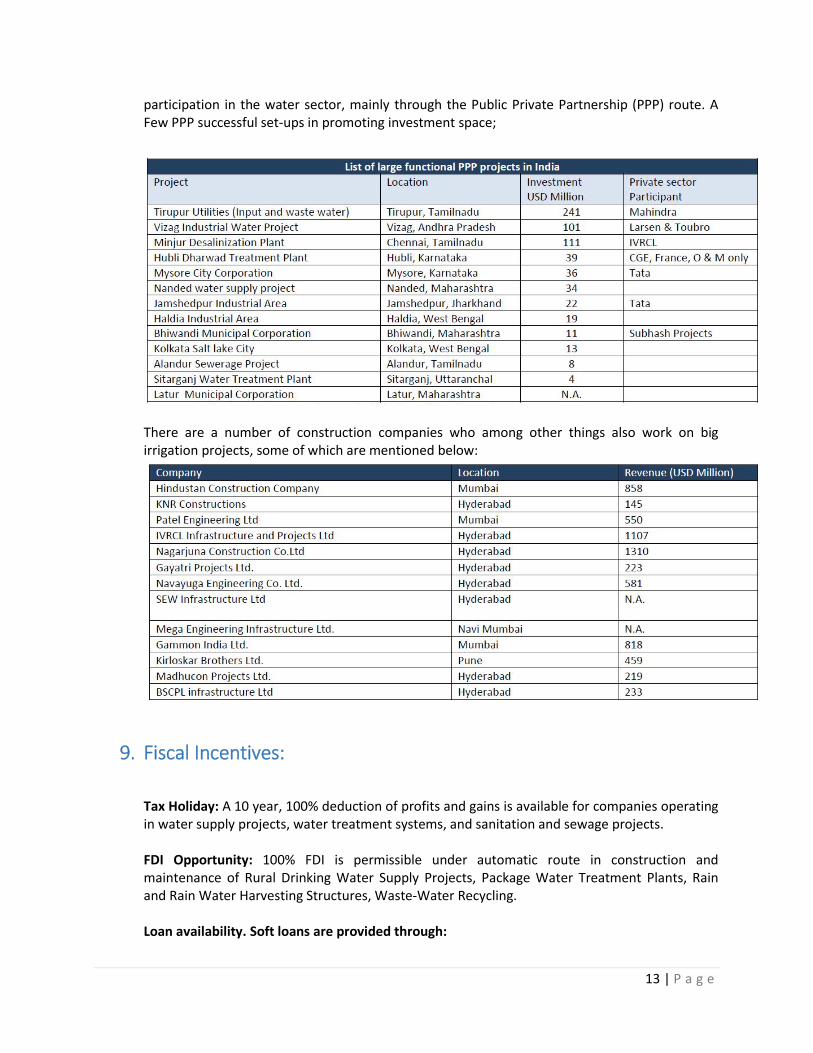

participation in the water sector, mainly through the Public Private Partnership (PPP) route. A Few PPP successful set-ups in promoting investment space;

There are a number of construction companies who among other things also work on big irrigation projects, some of which are mentioned below:

9. Fiscal Incentives:

Tax Holiday: A 10 year, 100% deduction of profits and gains is available for companies operating in water supply projects, water treatment systems, and sanitation and sewage projects. FDI Opportunity: 100% FDI is permissible under automatic route in construction and maintenance of Rural Drinking Water Supply Projects, Package Water Treatment Plants, Rain and Rain Water Harvesting Structures, Waste-Water Recycling. Loan availability. Soft loans are provided through:

14 | P a g e

IREDA, a public sector company of the Ministry. Nationalised banks and other financial institutions for identified technologies / systems. Tax / Duties Relief:

Direct taxes: 100% depreciation within 1st year of project installation. Exemption / reduction in excise duty. Exemption from Central Sales Tax, and customs duty concessions on the import of

material, components and equipment used in “Renewable Energy” RE projects. Duty-free import of renewable energy equipment. Exemptions from electricity taxes.

Subsidies:

CETPs, TSDF, and conveyance pipelines for treated wastewater disposal into deep sea are eligible for a 25% state subsidy.

Capital subsidies and concessionary financing from the Indian Renewable Energy

Development Agency are available.