a comparison between corporate and public sector business ethics in sweden

TRANSCRIPT

A comparison betweencorporate and public sectorbusiness ethics in Sweden

G˛ran Svensson,GregWoodandMichael Callaghann

Introduction

The establishment of a code of ethics has been

seen by many as an indicator that an organization

is beginning to show an interest in its ethical

performance. The notion that a code of ethics

should exist as a means of enhancing the ethical

environment of an organization has been pro-

posed by a plethora of writers (Gellerman 1989,

Stoner 1989, Laczniak & Murphy 1991, Sims

1991, Harrington 1991, Fraedrich 1992, Adams

et al. 2001, Somers 2001, Wood 2002, Carasco &

Singh 2003). Codes of ethics are not only a signal

to the general public, but they also bring into

sharp focus for all staff the need to examine the

ethical precepts upon which the business is

predicated (Wood 2002).

In the USA, codes of ethics have been in

evidence in many organizations (Baumhart 1961,

De George 1987, Benson 1989, Weaver et al.

1999) since the early 1960s. In Britain, the

development of codes of ethics seems to have

occurred mainly as a direct response to the stock

market crashes of the late 1980s (Schlegelmilch

1989, Donaldson & Davis 1990, Mahoney 1990,

Maclagan 1992). In Sweden, however, the use of

codes of ethics in either the corporate or the

public sectors has not been investigated prior to

this study. One study has been published in the

wider area of business ethics (Brytting 1997), but

it appears that there has been nothing specifically

done on codes of ethics in the largest organiza-

tions in Sweden.

The suggestion has been made that organi-

zations consider the implementation of a code

of ethics because they value the document and

perceive that such a document is important to the

organization (Adams et al. 2001, Somers 2001,

Wotruba et al. 2001). If organizations do have this

view of their codes, then surely they should be

committed to them. For if they are not committed

to their code of ethics, one could view it ostensibly

as a public relations exercise that is a cynical

attempt to capitalize on a real desire by the

marketplace to deal with ethical organizations

(Wood & Rimmer 2003).

A code can be seen as the first indicator of

commitment, but the existence of a code is not of

and in itself enough to ensure ethical behaviour by

staff, nor does a code guarantee an ethical

corporate culture. In and of itself, a code is only

one of a range of measures that corporations

should have in place to inculcate an ethical ethos

into the heart and soul of the organization.

Corporations must go beyond this initial level of

commitment and enact procedures that will

ensure that the ethical ethos of the organization

permeates all levels of the corporation (McDo-

nald & Zepp 1989, Sims 1991, Fraedrich 1992,

Sims 1992, Weaver et al. 1999, Somers 2001,

Wood 2002, Wood & Callaghan 2003). The

nRespectively: Associate Professor, Halmstad University, Sweden;

Senior Lecturer, Bowater School of Management and Marketing,

Deakin University, Australia; and Lecturer, Bowater School of

Management and Marketing, Deakin University, Australia.

r Blackwell Publishing Ltd. 2004. 9600 Garsington Road, Oxford OX4 2DQ, UKand 350 Main St, Malden, MA 02148, USA.166

Volume 13 Numbers 2/3 April/July 2004

establishment of a code of ethics is the first

tangible step on the road to a commitment to

business ethics (Townley 1992).

The concept of ‘commitment’ to business ethics

is integral to this research. Commitment is not a

simple idea that can be quantified easily. It is a

complex concept that embraces a number of

elements. Six areas of questioning were asked.

The intent of these questions was as follows. First,

how common are codes of ethics? Second, who

was involved in the development of these codes

and why? Third, how are they implemented?

Fourth, do organizations inform internal and

external publics of the codes? Fifth, what are the

reasons for the codes? Sixth, what are the

prescribed benefits of codes?

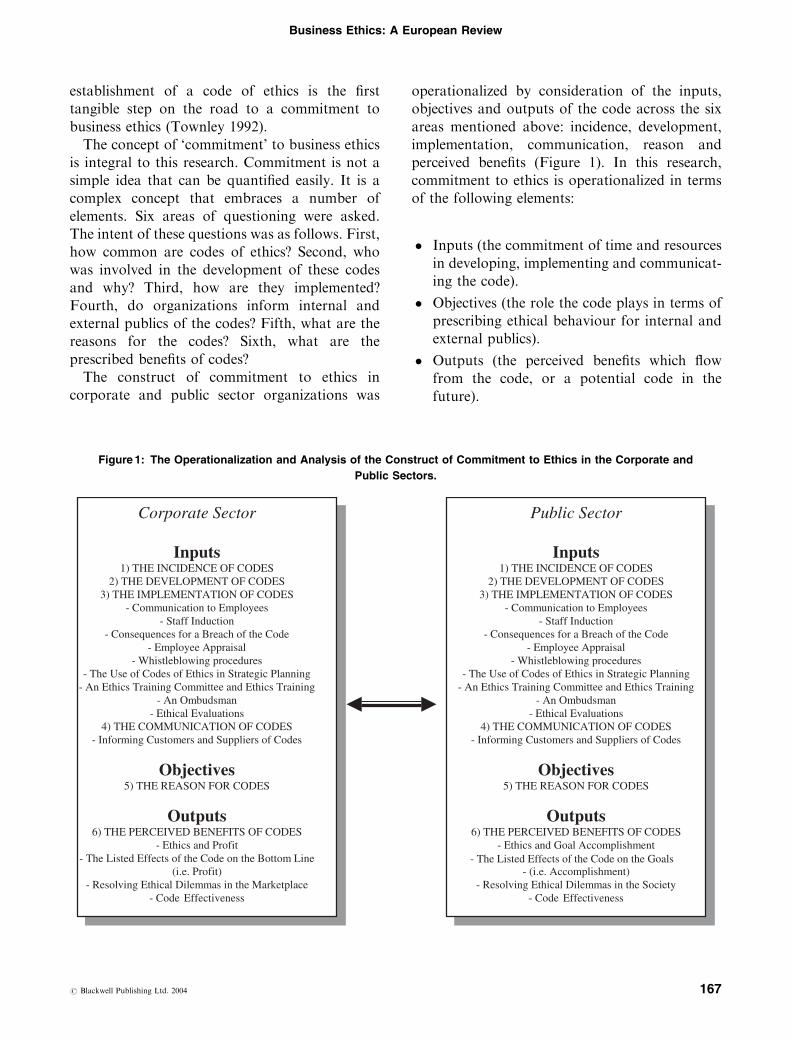

The construct of commitment to ethics in

corporate and public sector organizations was

operationalized by consideration of the inputs,

objectives and outputs of the code across the six

areas mentioned above: incidence, development,

implementation, communication, reason and

perceived benefits (Figure 1). In this research,

commitment to ethics is operationalized in terms

of the following elements:

� Inputs (the commitment of time and resources

in developing, implementing and communicat-

ing the code).

� Objectives (the role the code plays in terms of

prescribing ethical behaviour for internal and

external publics).

� Outputs (the perceived benefits which flow

from the code, or a potential code in the

future).

´´

Public Sector

Inputs 1) THE INCIDENCE OF CODES

2) THE DEVELOPMENT OF CODES 3) THE IMPLEMENTATION OF CODES

- Communication to Employees - Staff Induction

- Consequences for a Breach of the Code - Employee Appraisal

- Whistleblowing procedures - The Use of Codes of Ethics in Strategic Planning

- An Ethics Training Committee and Ethics Training- An Ombudsman

- Ethical Evaluations 4) THE COMMUNICATION OF CODES

- Informing Customers and Suppliers of Codes

Objectives 5) THE REASON FOR CODES

Outputs 6) THE PERCEIVED BENEFITS OF CODES

- Ethics and Goal Accomplishment - The Listed Effects of the Code on the Goals

- (i.e. Accomplishment)- Resolving Ethical Dilemmas in the Society

- Code Effectiveness

Corporate Sector

Inputs 1) THE INCIDENCE OF CODES

2) THE DEVELOPMENT OF CODES 3) THE IMPLEMENTATION OF CODES

- Communication to Employees - Staff Induction

- Consequences for a Breach of the Code - Employee Appraisal

- Whistleblowing procedures - The Use of Codes of Ethics in Strategic Planning

- An Ethics Training Committee and Ethics Training- An Ombudsman

- Ethical Evaluations 4) THE COMMUNICATION OF CODES

- Informing Customers and Suppliers of Codes

Objectives 5) THE REASON FOR CODES

Outputs 6) THE PERCEIVED BENEFITS OF CODES

- Ethics and Profit - The Listed Effects of the Code on the Bottom Line

(i.e. Profit) - Resolving Ethical Dilemmas in the Marketplace

- Code Effectiveness

Figure 1: The Operationalization and Analysis of the Construct of Commitment to Ethics in the Corporate and

Public Sectors.

Business Ethics: A European Review

r Blackwell Publishing Ltd. 2004 167

Methodology

In order to evaluate the use of codes of ethics by

corporate and public sector organizations operat-

ing in Sweden, a three-stage research procedure

was used and conducted in 2002. First, a

questionnaire was sent to the public relations

managers of the top 100 Swedish organizations

(based on revenue) operating in the corporate

sector (SCB 2002): firms that, for several reasons

such as size of turnover, employee numbers and

business profile, are more likely to have developed

a formal code of ethics (Brytting 1997). A

questionnaire was also sent to the human resource

managers of 100 top Swedish public sector

organizations. The public sector in Sweden is

divided into three categories of organizations,

namely entities of government, county councils,

and municipalities. The questionnaires were sent

to the top 40 entities of government, 40 munici-

palities, and 20 county councils. The selection of

these organizations was based upon staff numbers

in the public sector (SCB 2002). These organiza-

tions were asked to answer up to 29 questions and

to supply a copy of their code of ethics. The

second stage involved content analysis of the

codes of ethics supplied by survey respondents.

The third stage involved a more detailed follow-

up of a smaller group of organizations that

appeared to be close to best practice. Findings

from the first stage of the research are reported in

this article.

The package sent to each of the organizations in

the corporate and public sectors contained a

covering letter and a questionnaire. The package

was sent to the public relations managers in the

corporate sector and human resource managers in

the public sector organizations rather than the top

management or leadership of these organizations.

This was done in the hope that these professionals

would be more focused on staff concerns and that

they were more knowledgeable and committed to

the task at hand than other organizational func-

tionaries. Each respondent was assured of complete

anonymity as the results were to be aggregated.

A substantial amount of work was performed in

the preparation, implementation, control and

conclusion of the mail survey. Each respondent

at each organization was initially contacted by

phone in order to confirm their appropriateness to

respond to the questionnaire, and eventually to

promote the importance of the survey. Each

respondent was also briefly introduced to the

research project to stimulate his or her interest

and willingness to participate in the survey. Those

executives who initially did not answer the

questionnaire were contacted again by telephone

in order to stimulate their interest to fill in the

required answers. The close attention to this part

of the research led to the achievement of a high

response rate. The response rate for the corporate

sector organizations was 74% with 72 organiza-

tions returning the completed questionnaire. For

the public sector there was a response rate of 83%.

The comparisons between the corporate and

public sectors are in part tested by the aid of

different statistical bivariate tests (Norusis 1993,

1994). One parametric test is applied, namely the

Independent Samples T-test. In addition, four non-

parametric tests are applied as a complement,

namely the Pearson Chi-Square, the Continuity

Correction, the Likelihood Ratio and the Linear-

by-Linear Association. The selection forms two-

way tables and provides a variety of measures of

association for two-way tables.

In all forthcoming reporting of results the

corporate sector univariate responses will be in

normal font and the public sector responses will

be in italics.

The incidence of codes

The respondents upon whom this research focuses

comprise those 40 organizations in the corporate

sector and the 27 organizations in the public

sector with a code of ethics.

It would appear that the majority of codes

(57.5%:81.5%) have been constructed in the last

six years. This phenomenon may well be indica-

tive of an awakening in Sweden of the need for a

code of ethics. It is of interest that 32.5% of

corporate sector organizations with codes cannot

say when the code was developed. This may

indicate earlier code development than the overall

figures may appear to suggest. If organizations

Volume 13 Numbers 2/3 April/July 2004

168 r Blackwell Publishing Ltd. 2004

cannot give a definite response it may well

indicate that the codes were established prior to

recent institutional memory. In the public sector

the interest in codes of ethics is very recent.

The development of codes

The development of a code is a task to which an

organization must devote time and energy as the

code will showcase the organization’s value

system to the world. It should not be a document

that is rushed or one that is not representative of

the views of all staff members and even other

stakeholders. The code must be of relevance and

significance to all staff and as such they should be

involved in its construction (Raiborn & Payne

1990, Stead et al. 1990).

The individuals involved in establishing a code

are: Senior Managers (70%:51.9%), Chief Execu-

tive Officers (67.5%:63.0%), Board of Directors

(50%:63.0%), and Other Staff (26.4%:14.8%). It

is of interest that in corporate sector organiza-

tions the Boards, which have responsibility for

overseeing the policies of the organizations, are

involved less than the senior managers of organi-

zations who surprisingly are involved more than

the CEO; yet in the public sector organizations

the Board are as involved as often as the CEO

and more than senior managers. The initiatives

and responsibility appear to rest with CEOs and

Boards more in the public sector in Sweden than

in the corporate sector. If good corporate

governance is to be practised then CEOs and

Boards should be at the forefront of code

development. They should not abrogate their

responsibility to senior managers.

Both sectors seem to have missed an opportu-

nity to involve all staff in a manner that makes the

code more real for these staff. Staff members who

are not in senior management (26.4%:14.8%)

appear not to play a large role within the

establishment of the code in either sector. This is

disappointing as not involving other employees is

a lost opportunity to establish universal owner-

ship of the ethos of the code throughout the

organization. To impose a code on them can run

the risk of being seen as an act of imposition

rather than one of engagement. If the staff do not

own the code, then organizations run the very real

risk that they will bear less allegiance to it (Wood

2002).

Organizations were asked for their reasons for

developing a code of ethics. The major reasons

given tend to centre upon ‘instill organization

values, culture, and philosophy’ (45.0%:66.7%),

‘adherence to policy, procedures, and objectives’

(52.5%:29.6%) and ‘staff integrity and behaviour

standards’ (12.5%:40.7%). Organizations appear

to be wanting to instil values of the organizational

philosophy into their staff and in many cases at the

same time wanting to formalize in the code of ethics

organizational policies and procedures. These

ideas, one could suggest, can be seen to link, as

one would hope, policy, procedures, and objectives

are aligned in organizations with values, philoso-

phy and culture. The Swedish approach appears to

strive towards creating an understanding of ethical

considerations among the employees in the organi-

zation. It is done voluntarily, since there are no

explicit legal requirements asking for it. The ethical

values in society are integrated within the opera-

tions of the organizations.

Organizations were asked about the time lines to

develop their codes. The researchers were inter-

ested in whether there were any apparent patterns.

When the respondent knew when their code was

developed, it was usually in less than a year

(32.5%:40.7%). In both sectors of Sweden, these

documents appear to be ones over which organiza-

tions do not linger. Once the decision has been

made to establish a code, then organizations get on

and do it. A point of interest in the public sector is

that 25.9% of organizations take between 1 and 2

years to develop a code. This longer length of time

could well be a feature of being a public sector

organization that needs to report to outside

political or regulatory bodies for the ratification

of the code and, therefore, delays may well be a

feature of process rather than intent.

Implementing codes

The methods that organizations institute to

implement their codes tend to reveal their level

Business Ethics: A European Review

r Blackwell Publishing Ltd. 2004 169

of commitment to the process. If they adapt

existing processes, then that is an indicator of a

level of commitment, but if they create new

processes to assist in code implementation, then

one could say that this is evidence of a higher level

of commitment. The adaptation of existing

processes can relate to communication with

employees, induction, discipline, staff appraisal,

and strategic planning. If the organization intro-

duces new initiatives such as an ombudsman,

whistleblowing protection for employees, ethics

committees, ethics education committees, and

ethics education, then one could say that a higher

level of commitment has been achieved (Wood &

Rimmer 2003).

Communication to employees

Electronic Communication (55%:37.0%), a

Booklet (40%:48.1%), Induction (32.5%:55.6%)

and Internal Publications (32.5%:37.0%) are

the major methods of code communication to

employees in both sectors. The fact that electro-

nic communication is the most used means in

the corporate sector is to be expected, because the

growth in intranets within organizations in the

last few years has meant that we have become

more reliant on technology in all of our business

activities. The most used means of communica-

tion in the public sector is induction of employees.

Inducting employees is important, as not to do so

devalues the code for all employees. If the code

is not of significant enough importance to be on

the corporate radar at induction time, then the

message to staff about its importance is surely

devalued. The Swedish public sector seems to be

more in tune here with best practice than its

counterpart corporate sector organizations.

Staff induction

The use of training and discussion (65%:51.9%)

at the time of staff induction is a preferred option

to just distributing a booklet (30%:44.4%) con-

taining the code. The impact that the organization

wants the code to make upon the employee may

be lost if the attention required is not given at the

time of induction. How is the employee meant to

know that the code is important if it is not

discussed or education given in its nuances?

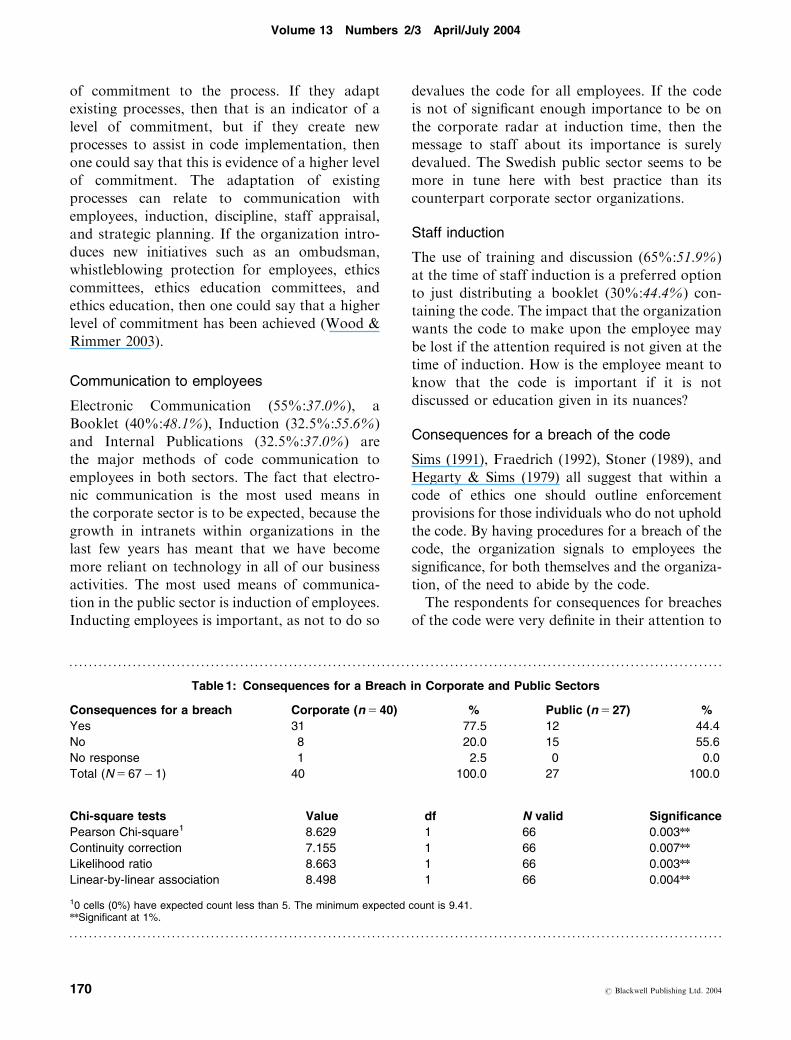

Consequences for a breach of the code

Sims (1991), Fraedrich (1992), Stoner (1989), and

Hegarty & Sims (1979) all suggest that within a

code of ethics one should outline enforcement

provisions for those individuals who do not uphold

the code. By having procedures for a breach of the

code, the organization signals to employees the

significance, for both themselves and the organiza-

tion, of the need to abide by the code.

The respondents for consequences for breaches

of the code were very definite in their attention to

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Table 1: Consequences for a Breach in Corporate and Public Sectors

Consequences for a breach Corporate (n5 40) % Public (n5 27) %

Yes 31 77.5 12 44.4

No 8 20.0 15 55.6

No response 1 2.5 0 0.0

Total (N567�1) 40 100.0 27 100.0

Chi-square tests Value df N valid Significance

Pearson Chi-square1 8.629 1 66 0.003nn

Continuity correction 7.155 1 66 0.007nn

Likelihood ratio 8.663 1 66 0.003nn

Linear-by-linear association 8.498 1 66 0.004nn

10 cells (0%) have expected count less than 5. The minimum expected count is 9.41.nnSignificant at 1%.

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Volume 13 Numbers 2/3 April/July 2004

170 r Blackwell Publishing Ltd. 2004

staff behaviour in this situation (Table 1). The

overwhelming majority of organizations in the

corporate sector (77.5%) do have consequences

for a breach of the code, yet in the public sector

only 44.4% of organizations do so. This is an

interesting disparity. The public sector organiza-

tions support the employees more than in the

corporate sector where business considerations

are taken more into account. The public servant

should focus on ways to serve the citizen and as a

consequence should behave appropriately in his

or her dealings.

The second part of this question asked the

organizations to clarify the nature of the con-

sequences of the breach. One gets a ‘verbal

warning’ (58.1%:100.0%) as the preferred choice

of disapproval at the employee’s actions in both

sectors. A ‘formal reprimand’ is also a method of

action taken (35.5%:66.7%). The difference may

be explained by the actual consequences that a

verbal warning and a formal reprimand may have

on the employee. The impact that these actions

have on the employee may be more severe in the

corporate sector due to the fact that a public

servant, through government legislation, has

stronger legal support in the workplace. The

ultimate weapon against the employee is ‘cessa-

tion of employment’ and it would appear that this

course of action is one that is not as acceptable in

Swedish corporate organizations or public sector

organizations as it may be in other management

cultures (35.5%:33.3%). The Swedish manage-

ment style is one of more participatory manage-

ment, where employees are coached and coaxed

into doing the ‘right thing’. The manager is not

seen as a disciplinarian there to ensure employee

compliance as may be the case in other cultures,

but the Swedish manager perceives their role

more as a mentor to lead and guide the staff

members to their own enlightenment and self-

correction in the areas where their performance

may be lacking.

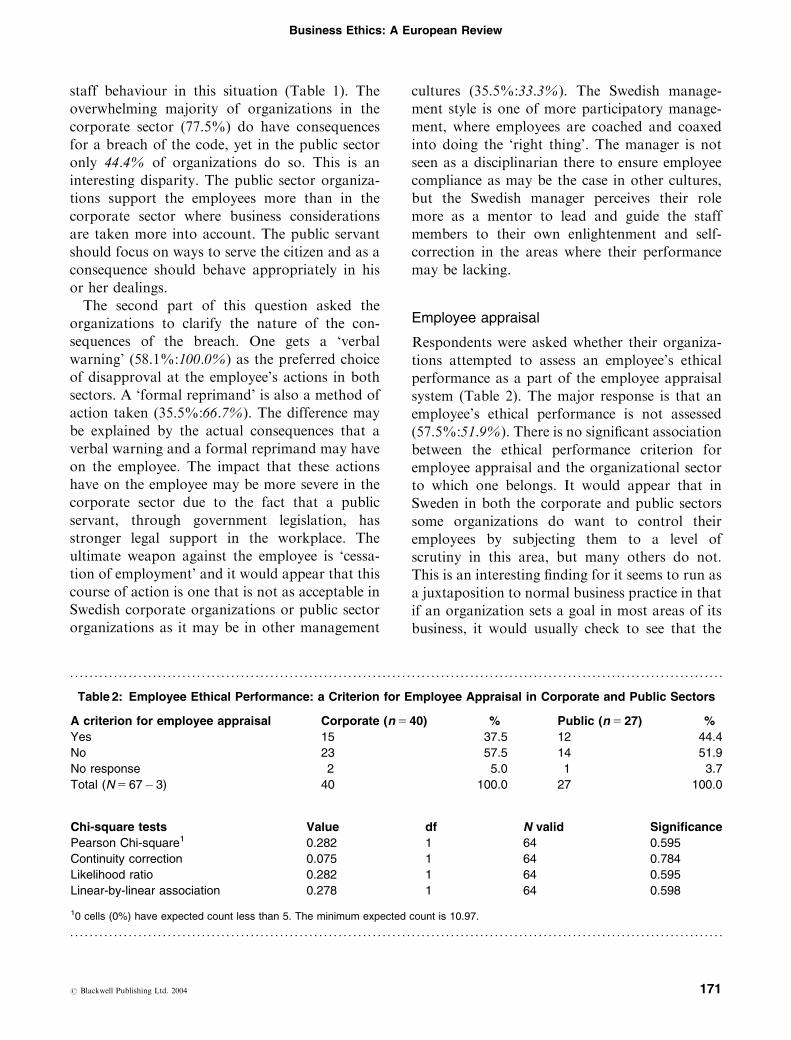

Employee appraisal

Respondents were asked whether their organiza-

tions attempted to assess an employee’s ethical

performance as a part of the employee appraisal

system (Table 2). The major response is that an

employee’s ethical performance is not assessed

(57.5%:51.9%). There is no significant association

between the ethical performance criterion for

employee appraisal and the organizational sector

to which one belongs. It would appear that in

Sweden in both the corporate and public sectors

some organizations do want to control their

employees by subjecting them to a level of

scrutiny in this area, but many others do not.

This is an interesting finding for it seems to run as

a juxtaposition to normal business practice in that

if an organization sets a goal in most areas of its

business, it would usually check to see that the

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Table 2: Employee Ethical Performance: a Criterion for Employee Appraisal in Corporate and Public Sectors

A criterion for employee appraisal Corporate (n540) % Public (n5 27) %

Yes 15 37.5 12 44.4

No 23 57.5 14 51.9

No response 2 5.0 1 3.7

Total (N567�3) 40 100.0 27 100.0

Chi-square tests Value df N valid Significance

Pearson Chi-square1 0.282 1 64 0.595

Continuity correction 0.075 1 64 0.784

Likelihood ratio 0.282 1 64 0.595

Linear-by-linear association 0.278 1 64 0.598

10 cells (0%) have expected count less than 5. The minimum expected count is 10.97.

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Business Ethics: A European Review

r Blackwell Publishing Ltd. 2004 171

employee is adhering to the espoused organiza-

tional standards. The reason for this finding

cannot be answered from this study but could

usefully be addressed in future research.

If an employee appraisal regarding ethics is

practised then a review by superiors is practised

(53.3%:58.3%). However, it must be acknowledged

that the relevant sample size is only 15 organ-

izations in the corporate sector and only 12

organizations in the public sector. This in itself

reveals that this type of practice may not be

widespread in either sector of Sweden. Even so,

there are some concerns raised with these figures. If

only two organizations (13.3%, of the sample in the

corporate sector) and only one organization (8.3%

of the respondents in the public sector) evaluate

ethical performance against formal organizational

standards then there is reason for concern. If there

are no formal standards in the other 86% of

corporate sector organizations and no standards in

the other 91% of public sector organizations in

Sweden, then against what criteria would the

assessment of staff performance be judged?

Employee appraisal is an area in which one

must try to be as objective as possible. However,

not having formal guidelines for appraisal places

both the supervisor and the subordinate in an

extremely precarious position. Each one could

suffer through the assessment which may ad-

versely affect them, but which neither party can

compare against formal guidelines to either

substantiate or refute the assessment.

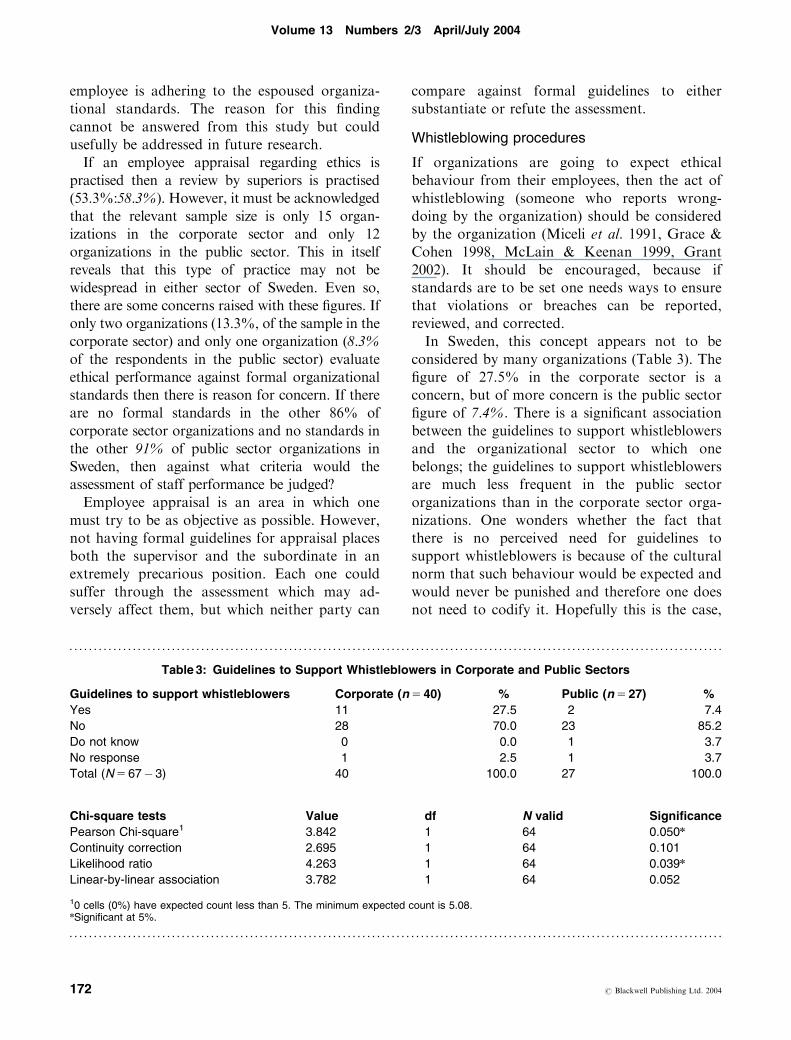

Whistleblowing procedures

If organizations are going to expect ethical

behaviour from their employees, then the act of

whistleblowing (someone who reports wrong-

doing by the organization) should be considered

by the organization (Miceli et al. 1991, Grace &

Cohen 1998, McLain & Keenan 1999, Grant

2002). It should be encouraged, because if

standards are to be set one needs ways to ensure

that violations or breaches can be reported,

reviewed, and corrected.

In Sweden, this concept appears not to be

considered by many organizations (Table 3). The

figure of 27.5% in the corporate sector is a

concern, but of more concern is the public sector

figure of 7.4%. There is a significant association

between the guidelines to support whistleblowers

and the organizational sector to which one

belongs; the guidelines to support whistleblowers

are much less frequent in the public sector

organizations than in the corporate sector orga-

nizations. One wonders whether the fact that

there is no perceived need for guidelines to

support whistleblowers is because of the cultural

norm that such behaviour would be expected and

would never be punished and therefore one does

not need to codify it. Hopefully this is the case,

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Table 3: Guidelines to Support Whistleblowers in Corporate and Public Sectors

Guidelines to support whistleblowers Corporate (n5 40) % Public (n5 27) %

Yes 11 27.5 2 7.4

No 28 70.0 23 85.2

Do not know 0 0.0 1 3.7

No response 1 2.5 1 3.7

Total (N567�3) 40 100.0 27 100.0

Chi-square tests Value df N valid Significance

Pearson Chi-square1 3.842 1 64 0.050n

Continuity correction 2.695 1 64 0.101

Likelihood ratio 4.263 1 64 0.039n

Linear-by-linear association 3.782 1 64 0.052

10 cells (0%) have expected count less than 5. The minimum expected count is 5.08.nSignificant at 5%.

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Volume 13 Numbers 2/3 April/July 2004

172 r Blackwell Publishing Ltd. 2004

because the downside to employees often is not

pleasant and in most cases may be hostile. Also

this concept may be one that has not previously

warranted consideration in Sweden. Employees

should be able to report infractions they witness,

and feel secure that they will be free of potential

retribution for their actions. Not to have such

safeguards in place for staff leaves genuine

individuals exposed and does not promote a

confidence in them to report their concerns.

Of the organizations that do have whistleblow-

ing procedures, many of them have tried to put in

place measures to support the individual. The

concern is that only 27.3% of these organizations

in the corporate sector and only 50% of public

sector organizations (only two respondents) have

a ‘formal resolution process’. This ambiguity is

not acceptable for all parties, as all parties need

protection in this area. Not to have a ‘formal

resolution process’ can often provide an environ-

ment that is prone to inconsistencies of policy and

in turn can lead to vagaries of interpretation.

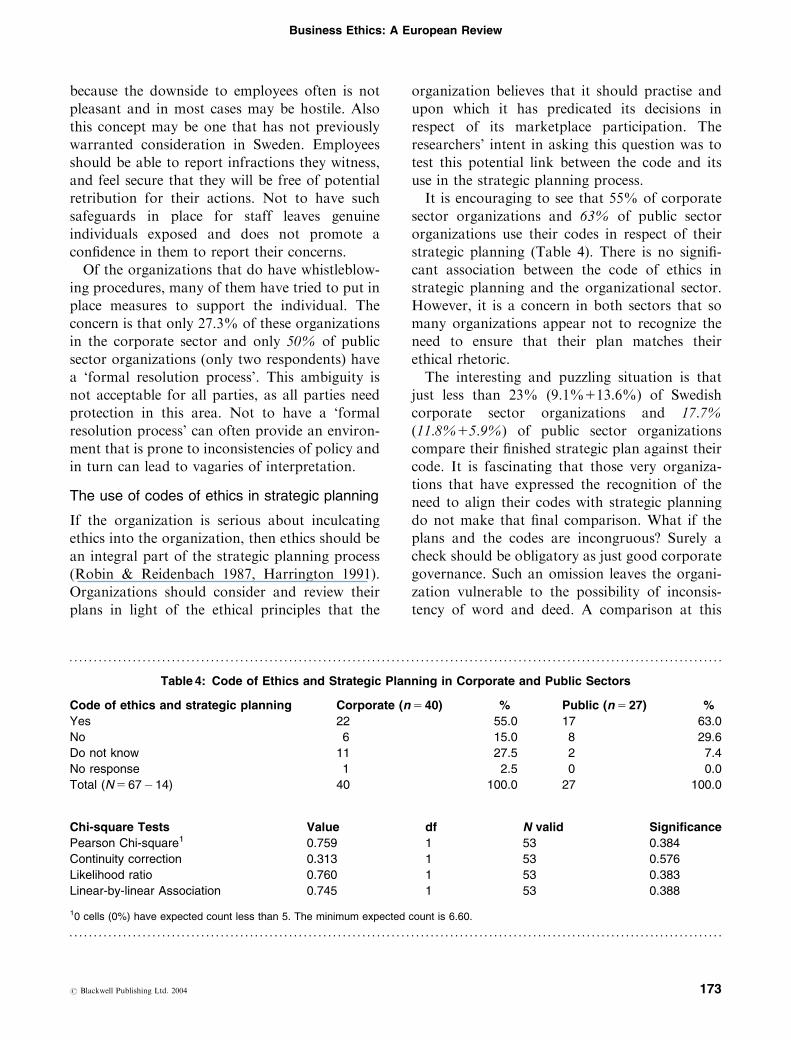

The use of codes of ethics in strategic planning

If the organization is serious about inculcating

ethics into the organization, then ethics should be

an integral part of the strategic planning process

(Robin & Reidenbach 1987, Harrington 1991).

Organizations should consider and review their

plans in light of the ethical principles that the

organization believes that it should practise and

upon which it has predicated its decisions in

respect of its marketplace participation. The

researchers’ intent in asking this question was to

test this potential link between the code and its

use in the strategic planning process.

It is encouraging to see that 55% of corporate

sector organizations and 63% of public sector

organizations use their codes in respect of their

strategic planning (Table 4). There is no signifi-

cant association between the code of ethics in

strategic planning and the organizational sector.

However, it is a concern in both sectors that so

many organizations appear not to recognize the

need to ensure that their plan matches their

ethical rhetoric.

The interesting and puzzling situation is that

just less than 23% (9.1%113.6%) of Swedish

corporate sector organizations and 17.7%

(11.8%15.9%) of public sector organizations

compare their finished strategic plan against their

code. It is fascinating that those very organiza-

tions that have expressed the recognition of the

need to align their codes with strategic planning

do not make that final comparison. What if the

plans and the codes are incongruous? Surely a

check should be obligatory as just good corporate

governance. Such an omission leaves the organi-

zation vulnerable to the possibility of inconsis-

tency of word and deed. A comparison at this

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Table 4: Code of Ethics and Strategic Planning in Corporate and Public Sectors

Code of ethics and strategic planning Corporate (n540) % Public (n5 27) %

Yes 22 55.0 17 63.0

No 6 15.0 8 29.6

Do not know 11 27.5 2 7.4

No response 1 2.5 0 0.0

Total (N567�14) 40 100.0 27 100.0

Chi-square Tests Value df N valid Significance

Pearson Chi-square1 0.759 1 53 0.384

Continuity correction 0.313 1 53 0.576

Likelihood ratio 0.760 1 53 0.383

Linear-by-linear Association 0.745 1 53 0.388

10 cells (0%) have expected count less than 5. The minimum expected count is 6.60.

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Business Ethics: A European Review

r Blackwell Publishing Ltd. 2004 173

time is a chance to prevent future heartache and

dissonance in the marketplace.

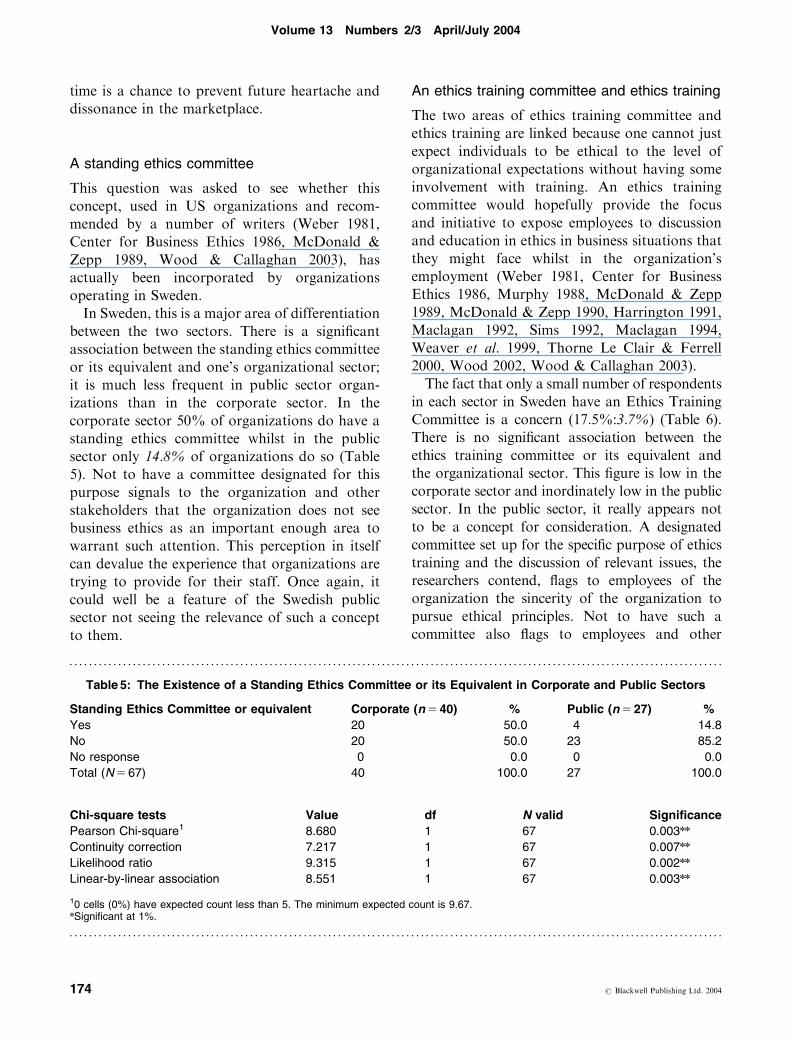

A standing ethics committee

This question was asked to see whether this

concept, used in US organizations and recom-

mended by a number of writers (Weber 1981,

Center for Business Ethics 1986, McDonald &

Zepp 1989, Wood & Callaghan 2003), has

actually been incorporated by organizations

operating in Sweden.

In Sweden, this is a major area of differentiation

between the two sectors. There is a significant

association between the standing ethics committee

or its equivalent and one’s organizational sector;

it is much less frequent in public sector organ-

izations than in the corporate sector. In the

corporate sector 50% of organizations do have a

standing ethics committee whilst in the public

sector only 14.8% of organizations do so (Table

5). Not to have a committee designated for this

purpose signals to the organization and other

stakeholders that the organization does not see

business ethics as an important enough area to

warrant such attention. This perception in itself

can devalue the experience that organizations are

trying to provide for their staff. Once again, it

could well be a feature of the Swedish public

sector not seeing the relevance of such a concept

to them.

An ethics training committee and ethics training

The two areas of ethics training committee and

ethics training are linked because one cannot just

expect individuals to be ethical to the level of

organizational expectations without having some

involvement with training. An ethics training

committee would hopefully provide the focus

and initiative to expose employees to discussion

and education in ethics in business situations that

they might face whilst in the organization’s

employment (Weber 1981, Center for Business

Ethics 1986, Murphy 1988, McDonald & Zepp

1989, McDonald & Zepp 1990, Harrington 1991,

Maclagan 1992, Sims 1992, Maclagan 1994,

Weaver et al. 1999, Thorne Le Clair & Ferrell

2000, Wood 2002, Wood & Callaghan 2003).

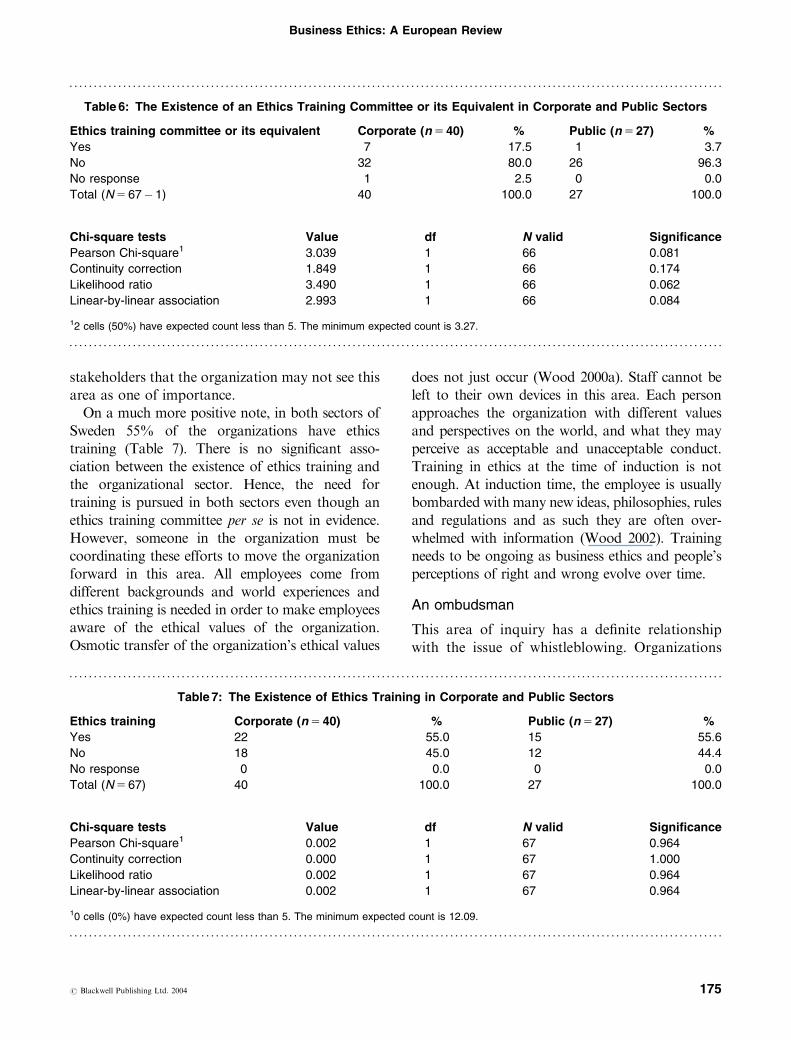

The fact that only a small number of respondents

in each sector in Sweden have an Ethics Training

Committee is a concern (17.5%:3.7%) (Table 6).

There is no significant association between the

ethics training committee or its equivalent and

the organizational sector. This figure is low in the

corporate sector and inordinately low in the public

sector. In the public sector, it really appears not

to be a concept for consideration. A designated

committee set up for the specific purpose of ethics

training and the discussion of relevant issues, the

researchers contend, flags to employees of the

organization the sincerity of the organization to

pursue ethical principles. Not to have such a

committee also flags to employees and other

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Table 5: The Existence of a Standing Ethics Committee or its Equivalent in Corporate and Public Sectors

Standing Ethics Committee or equivalent Corporate (n5 40) % Public (n5 27) %

Yes 20 50.0 4 14.8

No 20 50.0 23 85.2

No response 0 0.0 0 0.0

Total (N567) 40 100.0 27 100.0

Chi-square tests Value df N valid Significance

Pearson Chi-square1 8.680 1 67 0.003nn

Continuity correction 7.217 1 67 0.007nn

Likelihood ratio 9.315 1 67 0.002nn

Linear-by-linear association 8.551 1 67 0.003nn

10 cells (0%) have expected count less than 5. The minimum expected count is 9.67.nSignificant at 1%.

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Volume 13 Numbers 2/3 April/July 2004

174 r Blackwell Publishing Ltd. 2004

stakeholders that the organization may not see this

area as one of importance.

On a much more positive note, in both sectors of

Sweden 55% of the organizations have ethics

training (Table 7). There is no significant asso-

ciation between the existence of ethics training and

the organizational sector. Hence, the need for

training is pursued in both sectors even though an

ethics training committee per se is not in evidence.

However, someone in the organization must be

coordinating these efforts to move the organization

forward in this area. All employees come from

different backgrounds and world experiences and

ethics training is needed in order to make employees

aware of the ethical values of the organization.

Osmotic transfer of the organization’s ethical values

does not just occur (Wood 2000a). Staff cannot be

left to their own devices in this area. Each person

approaches the organization with different values

and perspectives on the world, and what they may

perceive as acceptable and unacceptable conduct.

Training in ethics at the time of induction is not

enough. At induction time, the employee is usually

bombarded with many new ideas, philosophies, rules

and regulations and as such they are often over-

whelmed with information (Wood 2002). Training

needs to be ongoing as business ethics and people’s

perceptions of right and wrong evolve over time.

An ombudsman

This area of inquiry has a definite relationship

with the issue of whistleblowing. Organizations

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Table 6: The Existence of an Ethics Training Committee or its Equivalent in Corporate and Public Sectors

Ethics training committee or its equivalent Corporate (n540) % Public (n527) %

Yes 7 17.5 1 3.7

No 32 80.0 26 96.3

No response 1 2.5 0 0.0

Total (N567�1) 40 100.0 27 100.0

Chi-square tests Value df N valid Significance

Pearson Chi-square1 3.039 1 66 0.081

Continuity correction 1.849 1 66 0.174

Likelihood ratio 3.490 1 66 0.062

Linear-by-linear association 2.993 1 66 0.084

12 cells (50%) have expected count less than 5. The minimum expected count is 3.27.

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Table 7: The Existence of Ethics Training in Corporate and Public Sectors

Ethics training Corporate (n5 40) % Public (n527) %

Yes 22 55.0 15 55.6

No 18 45.0 12 44.4

No response 0 0.0 0 0.0

Total (N567) 40 100.0 27 100.0

Chi-square tests Value df N valid Significance

Pearson Chi-square1 0.002 1 67 0.964

Continuity correction 0.000 1 67 1.000

Likelihood ratio 0.002 1 67 0.964

Linear-by-linear association 0.002 1 67 0.964

10 cells (0%) have expected count less than 5. The minimum expected count is 12.09.

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Business Ethics: A European Review

r Blackwell Publishing Ltd. 2004 175

need individuals who are designated in this

position, in order that individuals within the

organization who have genuine concerns can feel

free to voice them to an independent arbiter. Such

a position can only but enhance the ethical health

of the organization.

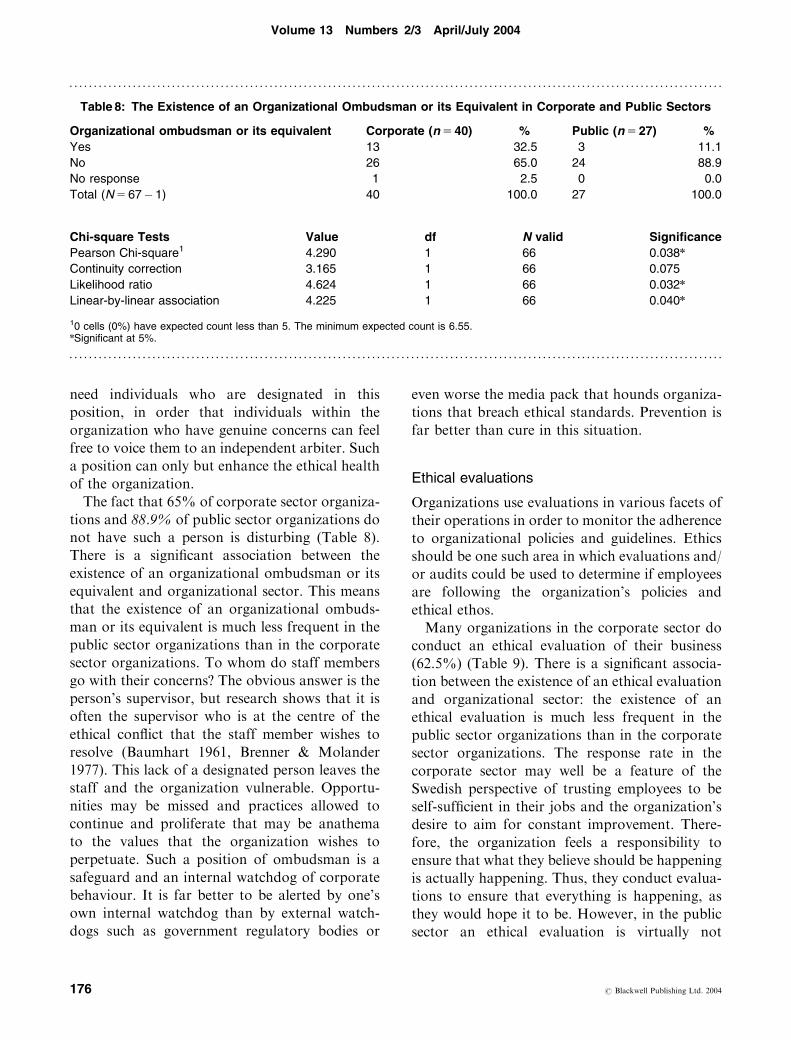

The fact that 65% of corporate sector organiza-

tions and 88.9% of public sector organizations do

not have such a person is disturbing (Table 8).

There is a significant association between the

existence of an organizational ombudsman or its

equivalent and organizational sector. This means

that the existence of an organizational ombuds-

man or its equivalent is much less frequent in the

public sector organizations than in the corporate

sector organizations. To whom do staff members

go with their concerns? The obvious answer is the

person’s supervisor, but research shows that it is

often the supervisor who is at the centre of the

ethical conflict that the staff member wishes to

resolve (Baumhart 1961, Brenner & Molander

1977). This lack of a designated person leaves the

staff and the organization vulnerable. Opportu-

nities may be missed and practices allowed to

continue and proliferate that may be anathema

to the values that the organization wishes to

perpetuate. Such a position of ombudsman is a

safeguard and an internal watchdog of corporate

behaviour. It is far better to be alerted by one’s

own internal watchdog than by external watch-

dogs such as government regulatory bodies or

even worse the media pack that hounds organiza-

tions that breach ethical standards. Prevention is

far better than cure in this situation.

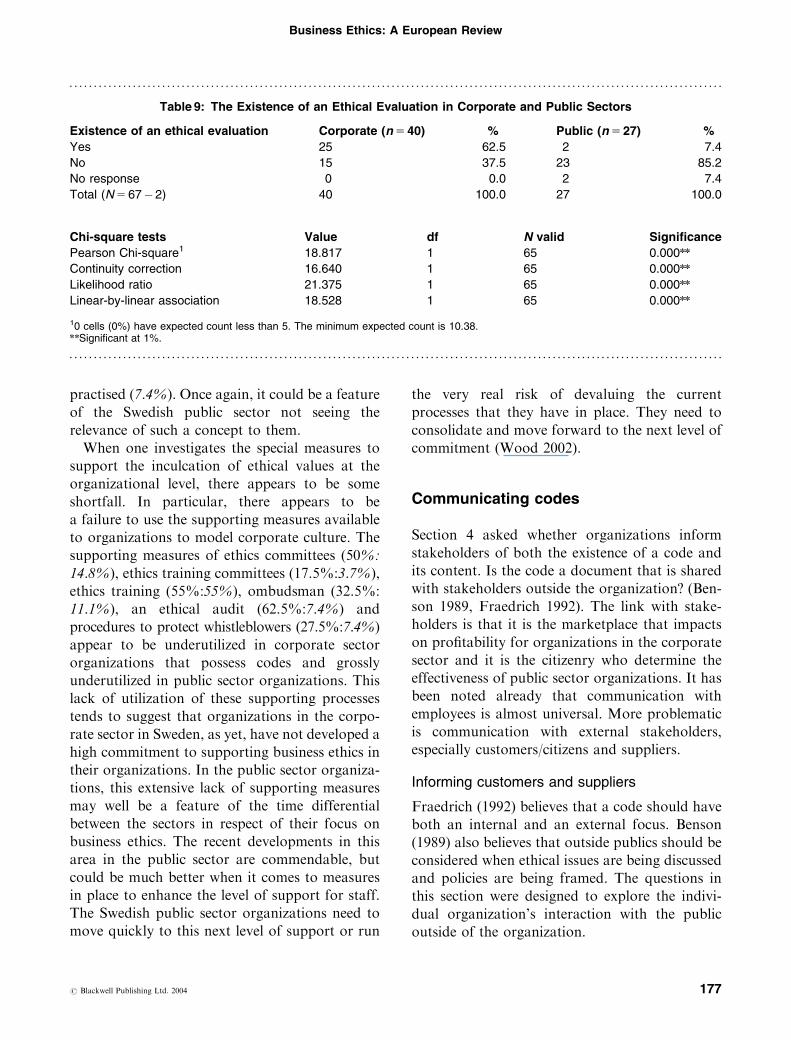

Ethical evaluations

Organizations use evaluations in various facets of

their operations in order to monitor the adherence

to organizational policies and guidelines. Ethics

should be one such area in which evaluations and/

or audits could be used to determine if employees

are following the organization’s policies and

ethical ethos.

Many organizations in the corporate sector do

conduct an ethical evaluation of their business

(62.5%) (Table 9). There is a significant associa-

tion between the existence of an ethical evaluation

and organizational sector: the existence of an

ethical evaluation is much less frequent in the

public sector organizations than in the corporate

sector organizations. The response rate in the

corporate sector may well be a feature of the

Swedish perspective of trusting employees to be

self-sufficient in their jobs and the organization’s

desire to aim for constant improvement. There-

fore, the organization feels a responsibility to

ensure that what they believe should be happening

is actually happening. Thus, they conduct evalua-

tions to ensure that everything is happening, as

they would hope it to be. However, in the public

sector an ethical evaluation is virtually not

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Table 8: The Existence of an Organizational Ombudsman or its Equivalent in Corporate and Public Sectors

Organizational ombudsman or its equivalent Corporate (n5 40) % Public (n5 27) %

Yes 13 32.5 3 11.1

No 26 65.0 24 88.9

No response 1 2.5 0 0.0

Total (N567�1) 40 100.0 27 100.0

Chi-square Tests Value df N valid Significance

Pearson Chi-square1 4.290 1 66 0.038n

Continuity correction 3.165 1 66 0.075

Likelihood ratio 4.624 1 66 0.032n

Linear-by-linear association 4.225 1 66 0.040n

10 cells (0%) have expected count less than 5. The minimum expected count is 6.55.nSignificant at 5%.

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Volume 13 Numbers 2/3 April/July 2004

176 r Blackwell Publishing Ltd. 2004

practised (7.4%). Once again, it could be a feature

of the Swedish public sector not seeing the

relevance of such a concept to them.

When one investigates the special measures to

support the inculcation of ethical values at the

organizational level, there appears to be some

shortfall. In particular, there appears to be

a failure to use the supporting measures available

to organizations to model corporate culture. The

supporting measures of ethics committees (50%:

14.8%), ethics training committees (17.5%:3.7%),

ethics training (55%:55%), ombudsman (32.5%:

11.1%), an ethical audit (62.5%:7.4%) and

procedures to protect whistleblowers (27.5%:7.4%)

appear to be underutilized in corporate sector

organizations that possess codes and grossly

underutilized in public sector organizations. This

lack of utilization of these supporting processes

tends to suggest that organizations in the corpo-

rate sector in Sweden, as yet, have not developed a

high commitment to supporting business ethics in

their organizations. In the public sector organiza-

tions, this extensive lack of supporting measures

may well be a feature of the time differential

between the sectors in respect of their focus on

business ethics. The recent developments in this

area in the public sector are commendable, but

could be much better when it comes to measures

in place to enhance the level of support for staff.

The Swedish public sector organizations need to

move quickly to this next level of support or run

the very real risk of devaluing the current

processes that they have in place. They need to

consolidate and move forward to the next level of

commitment (Wood 2002).

Communicating codes

Section 4 asked whether organizations inform

stakeholders of both the existence of a code and

its content. Is the code a document that is shared

with stakeholders outside the organization? (Ben-

son 1989, Fraedrich 1992). The link with stake-

holders is that it is the marketplace that impacts

on profitability for organizations in the corporate

sector and it is the citizenry who determine the

effectiveness of public sector organizations. It has

been noted already that communication with

employees is almost universal. More problematic

is communication with external stakeholders,

especially customers/citizens and suppliers.

Informing customers and suppliers

Fraedrich (1992) believes that a code should have

both an internal and an external focus. Benson

(1989) also believes that outside publics should be

considered when ethical issues are being discussed

and policies are being framed. The questions in

this section were designed to explore the indivi-

dual organization’s interaction with the public

outside of the organization.

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Table 9: The Existence of an Ethical Evaluation in Corporate and Public Sectors

Existence of an ethical evaluation Corporate (n540) % Public (n527) %

Yes 25 62.5 2 7.4

No 15 37.5 23 85.2

No response 0 0.0 2 7.4

Total (N567�2) 40 100.0 27 100.0

Chi-square tests Value df N valid Significance

Pearson Chi-square1 18.817 1 65 0.000nn

Continuity correction 16.640 1 65 0.000nn

Likelihood ratio 21.375 1 65 0.000nn

Linear-by-linear association 18.528 1 65 0.000nn

10 cells (0%) have expected count less than 5. The minimum expected count is 10.38.nnSignificant at 1%.

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Business Ethics: A European Review

r Blackwell Publishing Ltd. 2004 177

Nearly 63% of organizations in the corporate

sector report that their customers are aware of the

existence of their codes (Table 10). This is a high

figure and a commendable one. There is a

significant association between the customer

knowledge of the existence of the code and the

organizational sector; customer knowledge of

the existence of the code is much less frequent in

the public sector than in the corporate sector.

When communicating the code to customers,

the use of informal methods (60%) was by far the

highest individual category (Table 11). There is no

significant association between the communica-

tion of the code to customers and the organiza-

tional sector. The reliance on informal methods

raises the issue of an ad hoc approach, in that

organizations cannot be sure that the organiza-

tion’s ethics policy is being communicated to cus-

tomers. If it is done in an informal manner, then

the depth of understanding by the customers may

at best be superficial and at worst non-existent.

In the public sector, only 29.6% of organiza-

tions communicate their code to their customers

and of this small group, 62.5% do it informally.

The Swedish public sector appears to have missed

an opportunity to engage with its external

stakeholders for the improvement of their busi-

ness practices.

In respect of supplier knowledge of the codes,

just over two-thirds of organizations (67.5%) in

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Table 10: Customer Knowledge of the Existence of the Code in Corporate and Public Sectors

Customer knowledge of the existence of the code Corporate (n5 40) % Public (n5 27) %

Yes 25 62.5 8 29.6

No 9 22.5 13 48.1

Do not Know 5 12.5 6 22.2

No response 1 2.5 0 0.0

Total (N567�1) 40 100.0 27 100.0

Chi-square Tests Value df N valid Significance

Pearson Chi-square1 7.647 2 66 0.022n

Likelihood ratio 7.821 2 66 0.020n

Linear-by-linear association 5.444 1 66 0.020n

11 cells (16.7%) have expected count less than 5. The minimum expected count 4.50.nSignificant at 5%.

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Table 11: Communicating the Code to Customers in Corporate and Public Sectors

Communicating the code to customers Corporate (n525) % Public (n58) %

Formal 9 36.0 1 12.5

Informal 15 60.0 5 62.5

Other 1 4.0 2 25.0

No response 0 0.0 0 0.0

Total (N533) 25 100.0 8 100.0

Chi-square tests Value df N valid Significance

Pearson Chi-square1 4.051 2 33 0.132

Likelihood ratio 3.740 2 33 0.154

Linear-by-linear association 3.335 1 33 0.068

14 cells (66.7%) have expected count less than 5. The minimum expected count is 0.73.

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Volume 13 Numbers 2/3 April/July 2004

178 r Blackwell Publishing Ltd. 2004

the corporate sector report that their suppliers are

aware of the existence of their codes. In the public

sector, the code is communicated to suppliers in

33.3% of cases (Table 12). There is a significant

association between the supplier knowledge of the

existence of the code and the organizational

sector. This means that supplier knowledge of

the existence of the code is much less frequent in

the public sector than in the corporate sector.

It is of interest that in both sectors, organiza-

tions communicate their codes formally to sup-

pliers (63.0%:66.6%) (Table 13). There is no

significant association between the communica-

tion of the code to suppliers and the organiza-

tional sector. It is of interest that organizations

communicate the code much more formally to

suppliers (63.0%:66.6%) than they do to their

customers (36%:12.5%). This disparity could well

be indicative of the perceived difference in the

power relationship that the organizations have

with suppliers as compared to their customers.

With suppliers, organizations can be more in

control and can take charge of the relationship,

whereas with customers they are open more to the

whims of the customers. Organizations have

power over suppliers from whom they may

withdraw business if they consider that the

supplier’s performance is not of a sufficient

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Table 12: Supplier Knowledge of the Existence of the Code in Corporate and Public Sectors

Supplier knowledge of the existence of the code Corporate (n540) % Public (n5 27) %

Yes 27 67.5 9 33.3

No 5 12.5 8 29.6

Do not know 8 20.0 10 37.0

No response 0 0.0 0 0.0

Total (N567) 40 100.0 27 100.0

Chi-square tests Value df N valid Significance

Pearson Chi-square1 7.681 2 67 0.021n

Likelihood ratio 7.801 2 67 0.020n

Linear-by-linear association 5.673 1 67 0.017n

10 cells (0%) have expected count less than 5. The minimum expected count is 5.24.nSignificant at 5%.

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Table 13: Communicating the Code to Suppliers in Corporate and Public Sectors

Communicating the code to suppliers Corporate (n5 27) % Public (n5 9) %

Formal 17 63.0 6 66.6

Informal 6 22.2 3 33.3

Other 2 7.4 0 0.0

No response 2 7.4 0 0.0

Total (N534) 27 100.0 9 100.0

Chi-square tests Value df N valid Significance

Pearson Chi-square1 0.940 2 34 0.625

Likelihood ratio 1.439 2 34 0.487

Linear-by-linear association 0.081 1 34 0.776

13 cells (50.0%) have expected count less than 5. The minimum expected count is 0.53.

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Business Ethics: A European Review

r Blackwell Publishing Ltd. 2004 179

standard. However, in their relationship with

customers, power usually lies with the customer.

Hence, organizations may have been reticent to

reveal a code because of the fear that customers/

citizens may have used a perceived disparity

between the code and actual practice to criticize

the organization. This situation may not be a

conscious decision, but one that has been made in

a ‘subconscious’ manner by the organization in

response to its perceptions of its interactions with

its marketplace. This disparity, however, does

open up the debate about whether organizations

in both sectors of business in Sweden have missed

the salient point of being ethical in their business

dealings. One needs to ensure that one’s employ-

ees always engage in open and honest interaction

with all parties with whom they come into

contact.

Perceived benefits

In the previous sections of this paper, commit-

ment has been viewed in terms of inputs: the areas

of managerial time, implementation, resources,

and communications that may signify whether a

code is considered of marginal significance or of

importance to an organization’s operation. An-

other perspective is to consider outputs. What

benefits do firms expect to derive? If these benefits

are significant, commitment is more beneficial

than if they believe that they do not derive any or

at best limited benefit.

Ethics, profit and outcomes

There was an interest in discovering whether

organizations perceive that having an ethical

commitment has assisted organizational out-

comes. In the corporate sector this is usually

judged by the impact on profitability, whilst in the

public sector the measure is usually with respect to

how these processes have assisted goal accom-

plishment. In the corporate sector, the link

between profit and being ethical has perplexed

researchers for many years. It is a debate about

which it is difficult to be definitive, because there

are so many variables and uncertainties. Yet, it is

a question that needs to be asked, in order to view

the concept from the perspective of the organiza-

tions surveyed. An effect of a code of ethics on the

bottom line was acknowledged by 60% of

organizations in the corporate sector whilst

74.1% of organizations in the public sector saw

the code as having an effect on their organization.

The listed effects of the code

Organizations were asked to list the effects on

them of having a code of ethics. The responses

could be classified into a number of types. The

responses centred around altruistic ideals such as

being good corporate citizens; mercenary ideals

that focused on improving the position of the

organization; and regulatory ideals that were fixed

on ensuring that the employees of the organiza-

tions were controlled and prevented from doing

damage to the organization.

Organizations pursue ethical practices and

behaviours for a wide range of reasons. Not all

of these, it would appear, are based upon the

highest ethical considerations. The corporate

sector seems to have a stronger focus on those

ideals that may be indicative of a more mercenary

perspective (72% of listed effects), while the

public sector organizations seem to focus more

upon altruistic ideals (50% of listed effects). This

difference in focus could well be just as a result of

their different roles and goals within society.

More investigation is needed here before more

definite opinions can be expressed and as such

further speculation is outside the current scope of

this study.

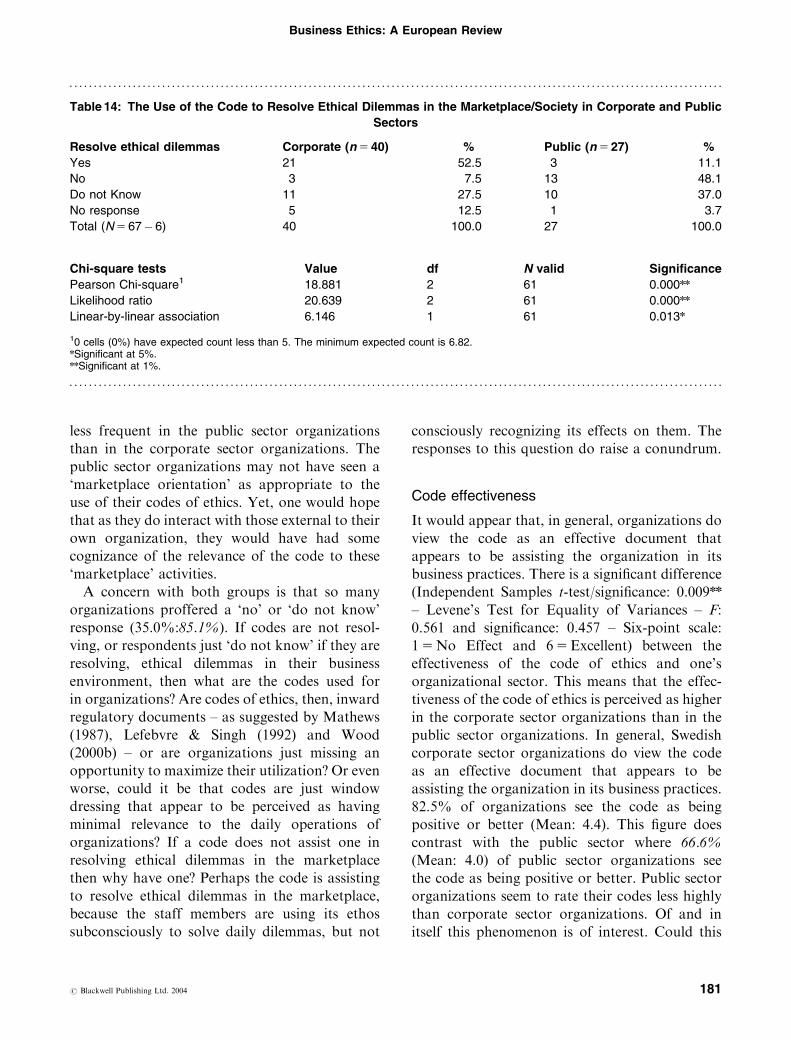

Resolving ethical dilemmas in the marketplace

This question was designed to determine practical

examples of the code being of use in the market-

place with other organizations and/or individuals

with whom the organization has dealt.

Just over 50% of corporate sector organizations

use their code to resolve ethical dilemmas in the

marketplace, whereas the concept was not one

that appeared relevant to the public sector

organizations (11.1%) (Table 14). There is sig-

nificant association between the use of the code to

resolve ethical dilemmas in the marketplace/

society and the organizational sector; it is much

Volume 13 Numbers 2/3 April/July 2004

180 r Blackwell Publishing Ltd. 2004

less frequent in the public sector organizations

than in the corporate sector organizations. The

public sector organizations may not have seen a

‘marketplace orientation’ as appropriate to the

use of their codes of ethics. Yet, one would hope

that as they do interact with those external to their

own organization, they would have had some

cognizance of the relevance of the code to these

‘marketplace’ activities.

A concern with both groups is that so many

organizations proffered a ‘no’ or ‘do not know’

response (35.0%:85.1%). If codes are not resol-

ving, or respondents just ‘do not know’ if they are

resolving, ethical dilemmas in their business

environment, then what are the codes used for

in organizations? Are codes of ethics, then, inward

regulatory documents – as suggested by Mathews

(1987), Lefebvre & Singh (1992) and Wood

(2000b) – or are organizations just missing an

opportunity to maximize their utilization? Or even

worse, could it be that codes are just window

dressing that appear to be perceived as having

minimal relevance to the daily operations of

organizations? If a code does not assist one in

resolving ethical dilemmas in the marketplace

then why have one? Perhaps the code is assisting

to resolve ethical dilemmas in the marketplace,

because the staff members are using its ethos

subconsciously to solve daily dilemmas, but not

consciously recognizing its effects on them. The

responses to this question do raise a conundrum.

Code effectiveness

It would appear that, in general, organizations do

view the code as an effective document that

appears to be assisting the organization in its

business practices. There is a significant difference

(Independent Samples t-test/significance: 0.009nn

– Levene’s Test for Equality of Variances – F:

0.561 and significance: 0.457 – Six-point scale:

15No Effect and 65Excellent) between the

effectiveness of the code of ethics and one’s

organizational sector. This means that the effec-

tiveness of the code of ethics is perceived as higher

in the corporate sector organizations than in the

public sector organizations. In general, Swedish

corporate sector organizations do view the code

as an effective document that appears to be

assisting the organization in its business practices.

82.5% of organizations see the code as being

positive or better (Mean: 4.4). This figure does

contrast with the public sector where 66.6%

(Mean: 4.0) of public sector organizations see

the code as being positive or better. Public sector

organizations seem to rate their codes less highly

than corporate sector organizations. Of and in

itself this phenomenon is of interest. Could this

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Table 14: The Use of the Code to Resolve Ethical Dilemmas in the Marketplace/Society in Corporate and Public

Sectors

Resolve ethical dilemmas Corporate (n5 40) % Public (n527) %

Yes 21 52.5 3 11.1

No 3 7.5 13 48.1

Do not Know 11 27.5 10 37.0

No response 5 12.5 1 3.7

Total (N567�6) 40 100.0 27 100.0

Chi-square tests Value df N valid Significance

Pearson Chi-square1 18.881 2 61 0.000nn

Likelihood ratio 20.639 2 61 0.000nn

Linear-by-linear association 6.146 1 61 0.013n

10 cells (0%) have expected count less than 5. The minimum expected count is 6.82.nSignificant at 5%.nnSignificant at 1%.

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Business Ethics: A European Review

r Blackwell Publishing Ltd. 2004 181

impression be the result of the fact that public

sector organizations may well have implemented

codes of ethics as a direct result of outside

political and regulatory pressure to do so and,

therefore, whilst the artefact has appeared, the

ethos behind the artefact may well not have been

embraced as was expected or even for which the

creators had hoped?

A code within the next 2 years

The organizations that did not have a code were

asked of their intentions to establish a code within

the next two years (Table 15). There is a

significant association between the intention to

establish a code within the next 2 years and the

organizational sector; it is lower in public sector

organizations than in corporate sector organiza-

tions. The positive response rate in the corporate

sector was 68.8%. Based on these figures, it would

appear that the movement towards having a code

of ethics in the corporate sector will continue to

grow within Sweden. However, in the public

sector, the growth of the movement in respect of

codes is much less assured. Only 25.0% of

organizations reported that a code is on their

agenda within the next two years. If these figures

are indicative of the interest that will be shown in

the next 2 years, then the divergence between code

numbers in the corporate and public sectors will

grow dramatically.

Codes will be increasingly more prevalent in the

corporate sector as compared to the public sector.

The current figures show 40/72 (55.6%) codes in

the corporate sector and 27/83 (32.5%) in the

public sector. In two years, if one adds the figures

for the current code usage and the figures for the

proposed code usage, the situation in Sweden may

well look like 62/72 (86.1%) codes in the corporate

sector as compared to 41/83 (49.4%) codes in the

public sector. Sweden effectively may have its two

sectors of business becoming highly divergent in

their acceptance of business ethics practices as a

norm. Moving in parallel would surely be a more

desirable outcome than such a marked disparity

that may lead to intersector concerns and machi-

nations about the precepts upon which business

interaction in Sweden is predicated.

Conclusion

Within both the corporate and the public sectors

of Sweden, the processes involved in business

ethics have begun to be recognized and acted

upon at an organizational level. Evidence is now

available to show that codes of ethics are well

developed in many of Sweden’s largest corporate

organizations and a lesser number of public sector

organizations: organizations that from their

responses see a diverse range of benefits in

developing the area of business ethics. These

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Table 15: Intention to Establish a Code within the Next 2 Years in Corporate and Public Sectors

Code within the next 2 years Corporate (n5 32) % Public (n5 56) %

Yes 22 68.8 14 25.0

No 4 12.5 24 42.9

Do not Know 4 12.5 18 32.1

No response 2 6.3 0 0.0

Total (N588�2) 32 100.0 56 100.0

Chi-square tests Value df N valid Significance

Pearson Chi-square1 18.834 2 86 0.000nn

Likelihood ratio 19.294 2 86 0.000nn

Linear-by-linear association 13.434 1 86 0.000nn

10 cells (0%) have expected count less than 5. The minimum expected count is 7.67.nnSignificant at 1%.

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Volume 13 Numbers 2/3 April/July 2004

182 r Blackwell Publishing Ltd. 2004

organizations are beginning to implement not

only a code of ethics, but also other complemen-

tary initiatives that reinforce the need for the

culture of the organization to focus more on

business ethics than has been done until recently.

The movement towards business ethics varies

between the corporate and the public sectors.

This may well be just a feature of the current

spotlight being upon corporate excesses and the

need for business to be seen to be doing the ‘right

thing’. The relevance to the public sector of this

need and perhaps even a requirement to be ethical

may not yet have become as apparent as it has

become within the corporate world in Sweden.

The researchers have concerns in both sectors

with the lack of use of the range of support

measures that one could invoke to inculcate the

ethos of the code into the organization and that

individually and collectively are indicative of a

high commitment to being ethical. There is an

obvious lack of staff training, ethics committees,

whistleblowing procedures, and ombudsmen in

both sectors. It is not enough to have the artefacts

of an ethical culture, such as codes, without

ensuring that all employees are assisted to under-

stand what is required of them.

These observations are not meant to be seen to

admonish the corporate and public sectors in

Sweden, but to highlight that the Swedish business

ethics experience is one that is in its early forms of

evolution and if organizations wish to move to the

next level of ethical development they need to

seriously consider these higher-order indicators of

organizational commitment. Such initiatives are

designed to ensure better outcomes for all.

References

Adams, J.S., Tashchian, A. and Stone, T.H. 2001.

‘Codes of ethics as signals for ethical behavior’.

Journal of Business Ethics, 29:3, 199–211.

Baumhart, R.C. 1961. ‘How ethical are businessmen?’

Harvard Business Review, July–August 6–12, 16, 19,

156–166.

Benson, G.C.S. 1989. ‘Codes of ethics’. Journal of

Business Ethics, 8:5, 305–319.

Brenner, S.N. and Molander, E.A. 1977. ‘Is the ethics of

business changing?’. Harvard Business Review, 55:1,

57–71.

Brytting, T. 1997. ‘Moral support structures in private

industry – the Swedish case’. Journal of Business

Ethics, 16:7, 663–697.

Carasco, E.F. and Singh, J.B. 2003. ‘The content and

focus of the codes of ethics of the world’s largest

transnational corporations’. Business and Society

Review, 108:1, 71–94.

Center for Business Ethics. 1986. ‘Are corporations

institutionalizing ethics?’ Journal of Business Ethics,

5:2, 85–91.

De George, R.T. 1987. ‘The status of business ethics: past

and future’. Journal of Business Ethics, 6:3, 201–211.

Donaldson, J. and Davis, P. 1990. ‘Business ethics?

Yes, but what can it do for the bottom line?’ Man-

agement Decision (UK), 28:6, 29–33.

Fraedrich, J.P. 1992. ‘Signs and signals of unethical

behavior’. Business Forum, 17:2, 13–17.

Gellerman, S.W. 1989. ‘Managing ethics from the top

down’. Sloan Management Review, 30:2, 73–79.

Grace, D. and Cohen, S. 1998. Business Ethics:

Australian Problems and Cases, 2nd edition. Mel-

bourne: Oxford University Press.

Grant, C. 2002. ‘Whistle blowers: saints of secular

culture’. Journal of Business Ethics, 39:4, 391–399.

Harrington, S.J. 1991. ‘What corporate America is

teaching about ethics’. Academy of Management

Executive, 5:1, 21–30.

Hegarty, W.H. and Sims, H.P. 1979. ‘Organizational

philosophy, policies, and objectives related to

unethical decision behavior: a laboratory experi-

ment’. Journal of Applied Psychology, 64:3, 331–338.

Laczniak, G.R. and Murphy, P.E. 1991. ‘Fostering

ethical marketing decisions’. Journal of Business

Ethics, 10:10, 259–271.

Lefebvre, M. and Singh, J.B. 1992. ‘The content and

focus of Canadian corporate codes of ethics’.

Journal of Business Ethics, 11:2, 799–808.

Maclagan, P. 1992. ‘Management development and

business ethics: a view from the UK.’ Journal of

Business Ethics, 11:4, 321–328.

Maclagan, P. 1994. ‘Education and development for

corporate ethics’. Industrial and Commercial Train-

ing, 26:4, 3–7.

Mahoney, J. 1990. ‘An international look at business ethi-

cs: Britain’. Journal of Business Ethics, 9:7, 545–550.

Mathews, M.C. 1987. ‘Codes of ethics: organizational

behavior and misbehavior’. Research in Corporate

Social Performance and Policy, 9, 107–130.

McDonald, G.M. and Zepp, R.A. 1989. ‘Business

ethics: practical proposals’. Journal of Management

Development, 8:1, 55–66.

Business Ethics: A European Review

r Blackwell Publishing Ltd. 2004 183

McDonald, G.M. and Zepp, R.A. 1990. ‘What should

be done? A practical approach to business ethics’.

Management Decision (UK), 28:1, 9–14.

McLain, D.L. and Keenan, J.P. 1999. ‘Risk, informa-

tion, and the decision about response to wrongdoing

in an organization’. Journal of Business Ethics, 19:3,

255–271.

Miceli, M.P., Near, J.P. and Schwenk, C.R. 1991.

‘Who blows the whistle and why?’. Industrial and

Labor Relations Review, 45:1, 113–130.

Murphy, P.E. 1988. ‘Implementing business ethics’.

Journal of Business Ethics, 7, 907–915.

Norusis, M.J. 1993. SPSS for Windows: Base System

User’s Guide Release 6.0. Chicago, IL: SPSS Inc.

Norusis, M.J. 1994. SPSS Professional Statistics 6.1.

Chicago, IL: SPSS Inc.

Raiborn, C.A. and Payne, D. 1990. ‘Corporate codes

of conduct: a collective conscience and continuum’.

Journal of Business Ethics, 9:11, 879–889.

Robin, D.P. and Reidenbach, R.E. 1987. ‘Social

responsibility, ethics, and marketing strategy: clos-

ing the gap between concept and application’.

Journal of Marketing, 51:1, 44–58.

SCB 2002. Foretagsregister. Stockholm: Statistiska

Centralbyran.

Schlegelmilch, B. 1989. ‘The ethics bap between Britain

and the United States: a comparison of the state of

business ethics in both countries’. European Man-

agement Journal, 7:1, 57–64.

Sims, R.R. 1991. ‘The institutionalization of organi-

zational ethics’. Journal of Business Ethics, 10,

493–506.

Sims, R.R. 1992. ‘The challenge of ethical behavior

in organizations’. Journal of Business Ethics, 11:7,

505–513.

Somers, M.J. 2001. ‘Ethical codes of conduct and

organizational context: a study of the relationship