budgeting systems of kyrgyzstan, germany, and the united states compared

TRANSCRIPT

1

Nodir Ataev

Professor Balázs Romhányi

ECON 5229 - Fiscal Policy in Practice

October 10, 2012

Budgeting Systems of Kyrgyzstan, Germany, and the United States Compared

INTRODUCTION

In this paper, I compare the budgeting systems of three diverse countries, namely

Kyrgyzstan, Germany, and the United States of America. It will be quite interesting to contrast the

public budgeting systems of these countries that are so different from one another from an

institutional, cultural, political, economic, and geographical point of view. The U.S. has by far the

largest economy the world has ever known in terms of consumption, production, and spending.

Kyrgyzstan, on the other hand, is a small, mountainous country that just recently went through a

dampened and crippled process of transition into a market-based economy from a centrally planned

economy. Finally, Germany has an economy that is characterized by a highly skilled labor force, a

large capital stock, and a high level of innovation. Despite these stark differences, each of these

countries faces the same problem of outlining and implementing a national fiscal plan for taxing,

spending and borrowing.

U.S. Economy at a Glance

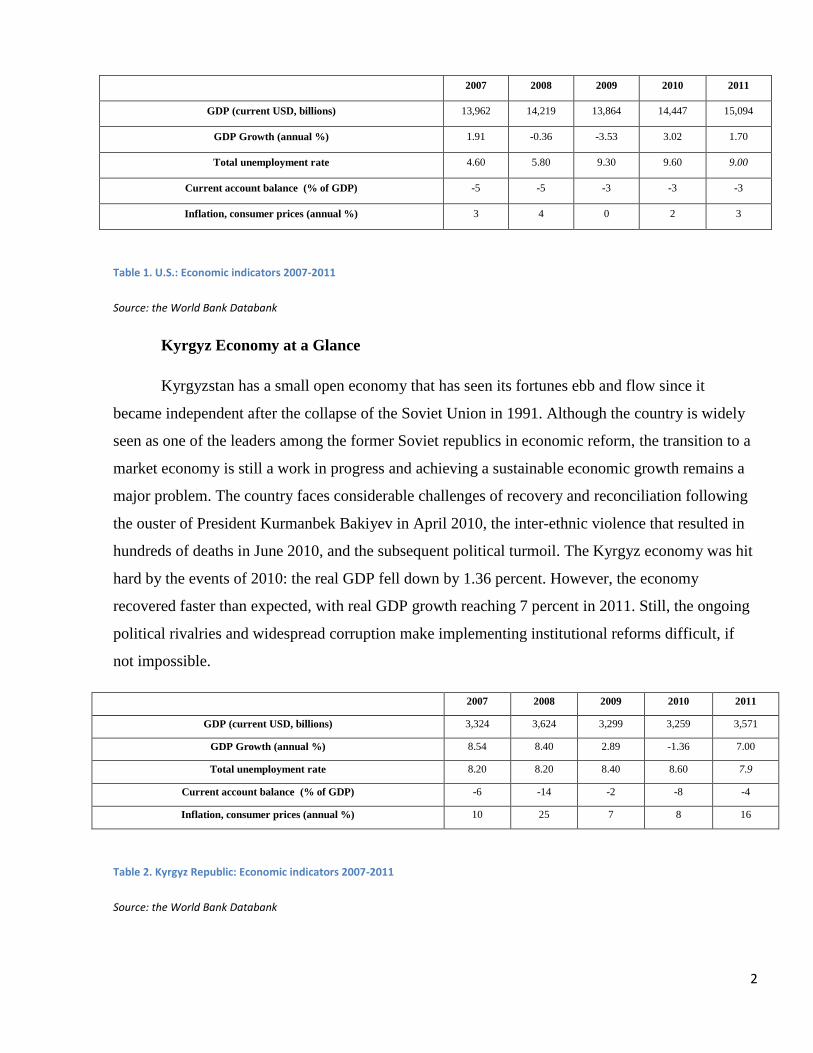

The U.S. ranks first in the world in the total value of its economic production. The nation's

GDP was more than $15 trillion in 2011. This is two times as large as the GDP of China, which

ranked second. The U.S. economy is also the most technologically powerful economy in the world

and American citizens enjoy very high standards of living.

In 2008, the U.S. economy sank into a recession as a result of the sub-prime mortgage crisis,

bank failures, falling home prices, tight credit, and the overall global economic downturn. The U.S.

GDP contracted by 0.36 percent in 2008 and by 3.53 percent in 2009. This recession is the deepest

and longest downturn since the Great Depression. Currently the U.S. economy faces enormous

challenges. Economic stagnation, sizable current account and budget deficits, rising external debt,

and rising unemployment – these are just a handful of many critical issues that need to be addressed.

2

2007 2008 2009 2010 2011

GDP (current USD, billions) 13,962 14,219 13,864 14,447 15,094

GDP Growth (annual %) 1.91 -0.36 -3.53 3.02 1.70

Total unemployment rate 4.60 5.80 9.30 9.60 9.00

Current account balance (% of GDP) -5 -5 -3 -3 -3

Inflation, consumer prices (annual %) 3 4 0 2 3

Table 1. U.S.: Economic indicators 2007-2011

Source: the World Bank Databank

Kyrgyz Economy at a Glance

Kyrgyzstan has a small open economy that has seen its fortunes ebb and flow since it

became independent after the collapse of the Soviet Union in 1991. Although the country is widely

seen as one of the leaders among the former Soviet republics in economic reform, the transition to a

market economy is still a work in progress and achieving a sustainable economic growth remains a

major problem. The country faces considerable challenges of recovery and reconciliation following

the ouster of President Kurmanbek Bakiyev in April 2010, the inter-ethnic violence that resulted in

hundreds of deaths in June 2010, and the subsequent political turmoil. The Kyrgyz economy was hit

hard by the events of 2010: the real GDP fell down by 1.36 percent. However, the economy

recovered faster than expected, with real GDP growth reaching 7 percent in 2011. Still, the ongoing

political rivalries and widespread corruption make implementing institutional reforms difficult, if

not impossible.

2007 2008 2009 2010 2011

GDP (current USD, billions) 3,324 3,624 3,299 3,259 3,571

GDP Growth (annual %) 8.54 8.40 2.89 -1.36 7.00

Total unemployment rate 8.20 8.20 8.40 8.60 7.9

Current account balance (% of GDP) -6 -14 -2 -8 -4

Inflation, consumer prices (annual %) 10 25 7 8 16

Table 2. Kyrgyz Republic: Economic indicators 2007-2011

Source: the World Bank Databank

3

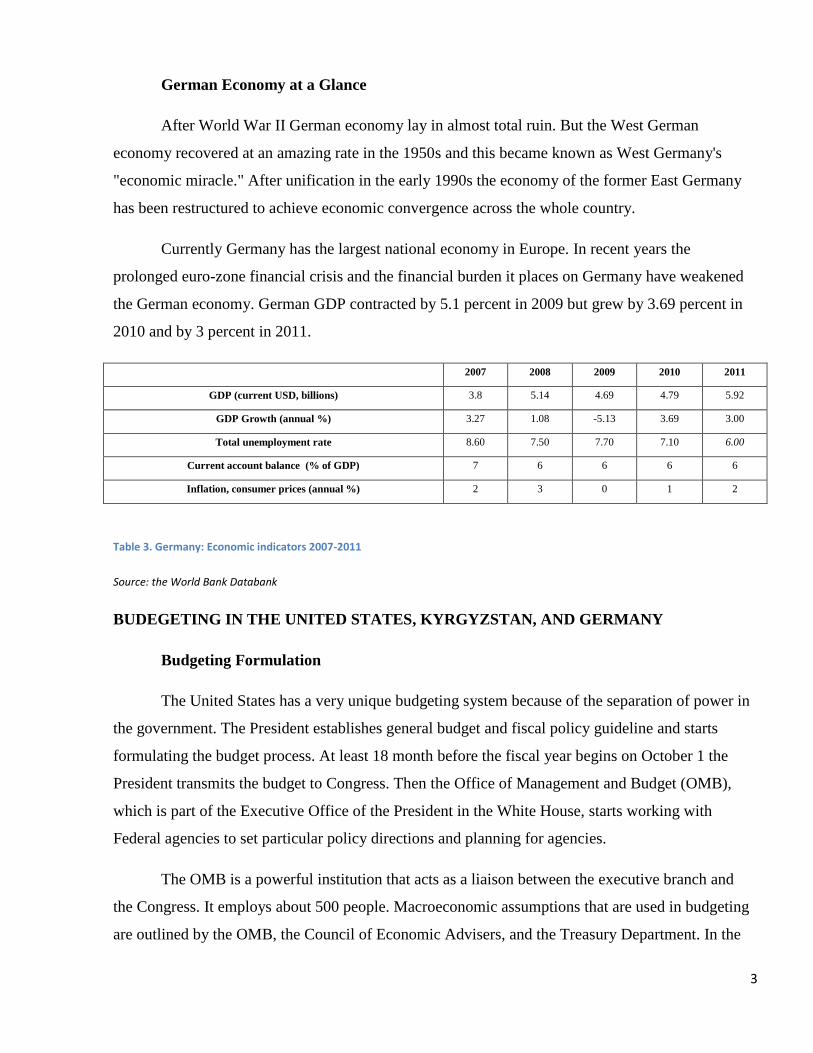

German Economy at a Glance

After World War II German economy lay in almost total ruin. But the West German

economy recovered at an amazing rate in the 1950s and this became known as West Germany's

"economic miracle." After unification in the early 1990s the economy of the former East Germany

has been restructured to achieve economic convergence across the whole country.

Currently Germany has the largest national economy in Europe. In recent years the

prolonged euro-zone financial crisis and the financial burden it places on Germany have weakened

the German economy. German GDP contracted by 5.1 percent in 2009 but grew by 3.69 percent in

2010 and by 3 percent in 2011.

2007 2008 2009 2010 2011

GDP (current USD, billions) 3.8 5.14 4.69 4.79 5.92

GDP Growth (annual %) 3.27 1.08 -5.13 3.69 3.00

Total unemployment rate 8.60 7.50 7.70 7.10 6.00

Current account balance (% of GDP) 7 6 6 6 6

Inflation, consumer prices (annual %) 2 3 0 1 2

Table 3. Germany: Economic indicators 2007-2011

Source: the World Bank Databank

BUDEGETING IN THE UNITED STATES, KYRGYZSTAN, AND GERMANY

Budgeting Formulation

The United States has a very unique budgeting system because of the separation of power in

the government. The President establishes general budget and fiscal policy guideline and starts

formulating the budget process. At least 18 month before the fiscal year begins on October 1 the

President transmits the budget to Congress. Then the Office of Management and Budget (OMB),

which is part of the Executive Office of the President in the White House, starts working with

Federal agencies to set particular policy directions and planning for agencies.

The OMB is a powerful institution that acts as a liaison between the executive branch and

the Congress. It employs about 500 people. Macroeconomic assumptions that are used in budgeting

are outlined by the OMB, the Council of Economic Advisers, and the Treasury Department. In the

4

U.S., econometric modeling and informed judgment are both used in specifying macroeconomic

assumptions.

Public expenditure is determined by two types of legislation: substantive and appropriations

legislation. Substantive legislation specifies what programs the American government has to

implement and controls direct spending. Appropriations legislation, on the other hand, gives public

authorities the right to spend on certain obligations and controls discretionary spending. As one

would expect, substantive legislation is superior to appropriations legislation in the U.S.

The Budget Enforcement Act (BEA) is used to control the American budgeting process. The

BEA is based on the Pay-As-You-Go (PAYGO) principle. This means that any rise in mandatory

spending or any fall in tax revenue that results from changes in legislation must be offset in order to

keep the deficit from rising. To achieve this goal, the effects of changes in legislation are recorded

on a scoreboard that covers a five-year period.

The annual budget process starts more than a year before the beginning of the fiscal year.

The American budget formulation timetable can be roughly summarized as follows (Blöndal, Kraan

and Ruffner 2003):

April - the OMB issues a letter called planning guidance to departments

specifying general funding levels;

June/July - the OMB issues detailed guidance on the information that agencies

should include in their budget submissions;

July/September - departments submit budget requests to OMB;

October/November - OMB gives its decisions to departments on budget totals;

November/December - final decisions are made by the president;

December/January - OMB and departments finalize budget documentation.

Before First Tuesday of February - president’s budget is sent to Congress.

The budgeting system of Kyrgyzstan is more similar to the budgeting system of Russia. The

Ministry of Finance of the Kyrgyz Republic carries out the country’s budgeting operations. The

Ministry operates according to established laws. The law of the Kyrgyz Republic “On Fundamental

Principles of the Budgetary Law in the Kyrgyz Republic” regulates short- and medium-term

budgetary planning.

5

Medium-term plans are developed annually in Kyrgyzstan. They provide the whole picture

of revenues and expenditures of the state budget. They consist of a macro-fiscal memorandum, a

medium-term revenue forecast, a description of medium-term expenditures, the public debt

management strategy, the scope of external financing, and detailed budget and expenditure

strategies of the different sectors of the economy. (Ministry of Finance of the Kyrgyz Republic

2011)

The timetable of the budgetary process in Kyrgyzstan has changed several times in the past.

The timetable that the Ministry of Finance is currently using can be summarized as follows: (The

Ministry of Finance of the Kyrgyzs Republic 2012)

Before May 15 – Coordination Council on Macroeconomic Issues and Investment

Policies issues a statement on projected budget;

Before May 31 – The Ministry of Finance issues its budgetary circular to the

ministries;

Before June 15 – Each ministry agrees on its budgetary program;

Before July 1 – Ministries submit their budget proposals to the Ministry of Finance;

July 1 – July 30 – Discussion of the budget proposals of the ministries;

Before August 31 – Government budget is submitted to the Supreme Council;

September- November – The Supreme Council considers the state budget.

The third country under discussion, namely Germany, has a very comprehensive legal

framework for budget processes at different levels of government. Basic Law for the Federal

Republic of Germany defines the roles of the key actors in budget processes. It gives detailed

descriptions of the responsibilities of both the Federal German Government and the sixteen states

that make up the Federal Republic of Germany.

Germany has a cabinet-level Ministry of Finance that governs revenue administration of the

country. Germany is unquestionably one of the most important countries of the European Union.

Therefore it is no surprise that in addition to being responsible for all aspects of tax and revenue

policy in Germany, the German Finance Ministry plays a significant role in European Union policy.

The finance minister of Germany is the only cabinet minister who can veto a decision of the

government if it would lead to additional expenditure.

In Germany, the fiscal year for all levels of government is the calendar year. The budget

processes in the German Parliament can be summarized as follows: (Germany 2004)

6

● Simultaneous introduction of draft budget to both chambers;

● First stage in the Bundesrat; It must state its position within six weeks;

● First reading in the Bundestag – usually in September, when the Federal

Minister of Finance gives his/her budget speech and outlines the

government’s fiscal policy strategy;

● Budget Committee of the Bundestag examines budget proposals, prepares a

report, and proposes amendments if necessary;

● Second reading in the Bundestag; Budget Committee’s findings presented,

plenary session debate on departmental budgets, with separate decisions

on each;

● Third reading in the Bundestag; Vote on the budget as a whole;

● Bundestag resolution transmitted to Bundesrat;

● If necessary, vote on any amendments proposed by the Mediation Committee;

● Second stage in the Bundesrat; Bundesrat may enter objection. This can be rejected by the

Bundestag with the required majority;

● Budget statute signed into law by the Federal President (countersigned by

the Federal Chancellor and the Federal Minister of Finance);

● Publication in the Federal Law Gazette.

Medium-term financial planning is very developed in Germany. (Lubke 2008) When budget

preparation stars, about 6,000 revenue and expenditure titles are re-evaluated. Medium-term plans

usually involve four- or five-year periods. While preparing mid-range budgetary plans the Federal

Ministry of Finance of Germany evaluates the overall economic situation on the basis of available

macroeconomic data.

Role of the Legislature

Unlike the legislative bodies of Kyrgyzstan and Germany, the U.S. legislative body, that is,

the United States Congress, plays an extensive role in the budgeting process. The United States

Congress is a bicameral legislature that is made of the House of Representatives and the Senate. The

7

legislature, the executive, and the judiciary are all equal parts of the U.S. government. The

Constitution of the United States holds that “No Money shall be drawn from the Treasury, but in

Consequence of Appropriations made by Law.” This gives the U.S. Congress the “power of the

purse.” The Congressional Budget Office (CBO) acts as a nonpartisan agency to provide objective

analyses of budgetary and economic issues to support the U.S. Congress.

Unlike in other OECD countries, the American president’s budget is only a recommendation

that the Congress takes into consideration while making budget decisions. The assumptions made by

the MBO and CBO may and do differ and the Congress pays much attention to “Congressional

Justifications” (or CJs) submitted by departments when analyzing the president’s submission.

The Congressional Budget Act points of order are used when a member of the Congress

wants to object a piece of legislation. Most of the points of order can only be waived by a three-

fifths majority approval.

The Congressional budget timeline can be summarized as follows:

Early February - president submits the executive budget recommendation;

March and April - Budget Committees develop the Congressional Budget

Resolution;

15 April - Congress passes Concurrent Budget Resolution;

Summer - Congress passes 13 appropriations bills;

30 September - fiscal year ends; all appropriations bills should be passed.

1 October - fiscal year begins.

In Kyrgyzstan, the Jogorku Kenesh (literally Supreme Council) is the legislative branch of

the government. It is a unicameral parliament. Members of the Supreme Council meet periodically

during the year to consider budget, tax, and appointment issues. The Supreme Council receives the

budget proposals of the ministries by the end of August. In the period from September to November

the Council considers and approves the state budget.

Germany has a two-chamber Parliament for the federal government, composed of a

Bundestag with 603 members and a Bundesrat, which represents the interests of the 16 states. The

Bundestag makes and changes the Constitution, federal laws, and the annual budged. It passes the

8

budget as an addendum to the annual or bi-annual budget act. Revenues and expenses are divided

into groups by ministries and other administrative entities.

The German Federal Budget Code requires that “the draft budget law be submitted to the

Bundestag and Bundesrat, together with the draft budget, before the beginning of the fiscal year. As

a rule, this should be not later than the first week of the Bundestag’s session following September

1.” (Germany 2004) The budget preparation process actually starts three months earlier when the

Ministry of Finance sends the annual budget circular to different departments.

Budget Execution

In the U.S., the Office of Management and Budget sends budgetary resources to departments

and agencies in a process known as “apportionment”. Apportionment is made in a way that makes

sure that appropriations will be enough for the whole fiscal year. Usually apportionment is done in

quarterly installments. The U.S. Department of the Treasury is responsible for the daily management

of cash. Most money is paid directly from the Treasury.

An appropriations bill is treated as an ordinary legislative bill. It gets sent to the President

who has to approve or veto the bill. If the U.S. Congress disagrees with the president, it can override

the president’s veto with a two-thirds vote of each chamber. This rarely takes place.

According to the OECD, managerial flexibility in the budgeting process is low in the United

States compared to most other member countries. (Blöndal, Kraan and Ruffner 2003) This is due to

the strong role that the Congress plays in the budget process. Congress has enacted about 80 very

detailed general management laws which are a big impediment to achieving greater flexibility in the

American budgeting system.

In Kyrgyzstan, members of the Supreme Council meet to prepare the country’s budget. The

president can issue orders on budgetary matters. The Supreme Council has the power to impeach the

president if it opposes the president’s decision. Since Kyrgyzstan has become a parliamentary

republic, the budgeting process has become inflexible like in the U.S.

In Germany, a bill that is approved by members of the Bundestag is sent to the Minister of

Finance. The minister has to sign the annual budget. Neither the Federal President nor the Federal

Chancellor has the right to veto the budget approved by the Bundestag and the Bundesrat, the two

chambers of Parliament. Budgetary Principles Act and budget codes govern budget execution.

9

German law incorporates articles on efficient cash management strategies. It requires that money be

spent as and when necessary and the Bundesbank have a liquid reserve at all times. German

budgeting process is probably the most flexible of the three countries being discussed.

Accounting

In the U.S., the Government Accountability Office (GAO) is the audit, evaluation, and

investigative arm of the U.S. Congress. In addition to carrying out accounting functions, the GAO

also publishes much important information about the U.S. budget. A unique feature of the GAO is

that even though it is an accounting institution, its most important function is as an analyst of the

effectiveness of different programs. The GAO presents the U.S. deficit on a cash rather than

accruals basis.

Accounting procedures used in formulating the budget of Kyrgyzstan are regulated by law.

The official website of the Ministry of Finances lists several laws on accounting procedures.

However, it is not easy to get data about the use of accrual information in the country’s budgeting

processes.

In federal countries like the United States, state laws are different from federal laws. In

contrast, in Germany a federal law requires nation-wide consistency of budget and accounting

systems. The budget and accounting principles included in a federal law are also adopted by states.

This has resulted in a coherent set of budgeting and accounting practices across the whole country.

The German Constitution requires annual accounts to cover revenues, expenditures, assets, and debt

liabilities. (Germany 2004) German states have experimented with accrual accounting but it has not

become the standard in the country.

Transparency

The U.S. budgeting system is frequently cited as one of the most transparent systems in the

world. Detailed and comprehensive information about Federal and State budgets are readily

available for public and U.S. citizens can participate in the budgeting process in one way or another.

According to the International Open Budget Survey, the United States has the 7th

most transparent

budgeting system in the world. (International Budget Partnership 2010) The Government

Accountability Office publishes almost all of its reports on its website, www.gao.gov.

10

In contrast, the situation is very different in Kyrgyzstan. Corruption is rife in the country.

According to Transparency International, an independent nonprofit organization dedicated to

exposing and fighting corruption, Kyrgyzstan was the 164th

least corrupt country in the world out of

the 182 surveyed in 2010. The budget process is far from transparent in the country. According to

the International Budget Partnership, the transparency of the budget of Kyrgyzstan was only 15

percent in 2010 and that the country’s budgeting processes are not transparent. (Ministry of Finance

on Transparency 2010) In fact, the average Kyrgyzstani citizen thinks that the country’s budgeting

system is not transparent at all and that the Ministry of Finance is a corrupt institution. Even though

the website of the Ministry of Finance has a page listing documents about the benefits of having a

transparent budgeting system and the role of internal auditing as the basis of effective budgeting,

these documents largely remain paper tigers.

Finally, the German national budgeting process ranks high in terms of transparency and

accountability. According to the International Open Budget Survey, Germany has lower levels of

transparency than the United States, but it is more transparent than in most other countries.

(International Budget Partnership 2010)

In Germany, internal auditing is decentralized. All the departments carry out internal

auditing on their own. The Federal Court of Audit (Bundesrechnungshof) carries out external audit

functions. The Federal Court of Audit is not part of the legislative, judicial or, executive branches of

government. It is an independent institution and is regulated by law only. The Federal Court of

Audit is required by law to submit an annual report directly to the federal government as well as to

the two houses. (Germany 2004)

The German Constitution requires the Minister of Finance to submit annual accounts to the

Bundestag and the Bundesrat. The reports must have information about revenues, expenditures,

property, and debt. Such reports are readily available for the general public, which is an indication

of the transparency of the German budgeting processes.

Use of Performance Information

Performance information is used to some extent in the U.S. budgeting process. The

Government Performance and Results Act (GPRA) is a law designed to improve government project

management. GPRA outlines the basic approach to performance-based management for the

executive branch. In simple terms GPRA requires the different departments of the U.S. government

11

to set departmental and annual goals and report to the Congress about any progress made. A

procedure called the Program Assessment Rating Tool (PART) is used to evaluate government

programs. The method involves making a decision by analyzing four sections of the budgeting

process, namely program purpose, strategic planning, management, and results.

However, it should be noted that the U.S. has only a basic performance management system.

According to the OECD, “… it is incorrect to say that the United States has a performance

budgeting system despite the current administration’s attempt to inform its budget choices with

performance information.” (Blöndal, Kraan and Ruffner 2003) This problem still remains

unaddressed in the U.S.

In Kyrgyzstan, since the budgeting process is so opaque, performance information is not

used explicitly in the budget process. The Ministry of Finance does not use any fixed technique to

measure performance. However, the Finance Ministry publishes news releases every now and then

about whether the state budget is higher or lower than projected. Usually the latter is the case.

Finally, in Germany the system is very different. Department budgets are written up using

comprehensive classification. Since appropriations are not openly based on an activity basis, the

German Law does not require program performance indicators to be submitted along with budget

submissions. (Germany 2004)

CONCLUDING REMARKS

In this paper, I compared the budgeting systems of three different nations. Each of them has

different systems that have been shaped by their own history. The United States has a very

sophisticated and transparent system that could be a role model for many countries. However, the

American system also has its weaknesses. Because the system is so complex and the goals of the

president and the Congress often diverge, it is inherently inflexible and suffers from inefficiencies in

many areas.

As a newly established country, Kyrgyzstan has a very inefficient and opaque budgeting

system. Political rivalry and corruption keep the country from establishing a well-functioning

system. There are so many issues that need to be addressed that it is almost mind-boggling. Still, it

should be noted that with the help of Western countries and international organizations the country

has made some progress in improving its budgeting system.

12

Finally, Germany has a very comprehensive system of budget processes that is seen as a role

model for many European countries. The country has established a very detailed legal framework

for budget processes at both federal and state levels of government. Still, the sixteen German states

have not all achieved efficient and balanced budgeting systems and there is a lot more room for

improvement. The current euro-zone financial crisis and the financial burden it places on Germany

have been seriously straining the country’s budget.

13

WORKS CITED

Blöndal, Jón R., Dirk-Jan Kraan, and Michael Ruffner. "Budgeting in the United States." OECD

Jouranl on Budgeting, 2003: 8-53.

"Germany." OECD Journal on Budgeting, 2004: 219-254.

International Budget Partnership. "OBI 2010 Scores." 2010. http://internationalbudget.org/wp-

content/uploads/2011/06/2010_Rankings.pdf (accessed October 17, 2012).

Lubke, Astrid. "Medium-term Financial Planning in the Federal ." 2008.

http://www.ief.es/documentos/recursos/publicaciones/revistas/presu_gasto_publico/51_Astri

dL%C3%BCbke.pdf (accessed October 17, 2012).

Ministry of Finance of the Kyrgyz Republic. "Medium Term Budget Framework for 2012-2014."

Global Agriculture and Food Safety Program. 2011.

http://www.gafspfund.org/gafsp/sites/gafspfund.org/files/Documents/$MTBF%20for%2020

12-2014.pdf (accessed October 17, 2012).

"Ministry of Finance: Statements on Kyrgyzstan’s budget transparency - incorrect and biased."

24.kg. October 27, 2010. http://eng.24.kg/business/2010/10/27/14472.html (accessed

October 17, 2012).

The Ministry of Finance of the Kyrgyzs Republic. "Budgetary Circular." May 5, 2012.

http://www.minfin.kg/index.php?option=com_content&view=article&id=1316:-2013-2014-

2015-&catid=49:2010-10-05-10-26-01&Itemid=119 (accessed October 18, 2012).