board remuneration, company performance, and ownership concentration: evidence from publicly listed...

TRANSCRIPT

MONASH UNIVERSITY

AUSTRALIA

Department of Economics Discussion Papers ISSN 1441-5429

Board Remuneration, Company Performance, and Corporate Governance:

Evidence from Publicly Listed Malaysian Companies

Ergun Dogan and Russell Smyth

No. 10101

Monash University Victoria 3800

Australia

O 200 1 Ergun Dogan and Russell Smyth All rights reserved. No part of this paper may be reproduced in any form, or stored in a retrieval system, without the prior written permission of the author.

BOARD REMUNERATION, COMPANY PERFORMANCE, AND CORPORATE GOVERNANCE: EVIDENCE FROM PUBLICLY

-

LISTED MALAYSIAN COMPANIES

Ergun Dogan '

and

Russell smythtf

School of Business and Information Technology, Monash University, Malaysia Department of Economics, Monash University, Australia Earlier versions of this paper were presented at "Whose Milleniurn?" the 13'

Biennial Conference of the Asian Studies Association of Australia (ASAA), University of Melbourne, July 2000 and the National Workshop on Capacity Building Towards Excellence in Economic Research and Policy Formulation, Universiti Utara, Malaysia, April 2001. We thank participants at these conferences, Mita Bhattacharya and Dietrich Fausten for helpful comments that have improved the final version. Funding for this project was supplied by a grant from Monash University, Malaysia.

Abstract

Corporate governance is hotly debated in Malaysia and elsewhere in the

Asian-Pacific region. The reason for this is that several of the problems

that Asian-Pacific countries faced during the crisis of 1997-1 999 are

blamed on weak corporate governance structures. In this study we

examine the determinants of Board compensation in Malaysian

companies listed on the Kuala Lumpur Stock Exchange over the period

1989 to 2000. Our objective is to examine whether corporate governance

affects the relationship between performance and remuneration. We find

evidence of a statistically significant positive relationship between Board

remuneration and sales turnover and a statistically significant negative

relationship between Board remuneration and ownership concentration.

However, the relationship between Board remuneration and firm

performance is ambiguous, while there is no evidence of a significant.

relationship between Board remuneration and sector performance.

JEL: L1

Keywords: Malaysia, Board Remuneration, Corporate Governance

1. INTRODUCTION

This study investigates the relationship between total board remuneration

and corporate performance in a sample of firms listed on the Kuala

Lumpur Stock Exchange (KLSE). Our objective is to examine whether

corporate governance affects the relationship between performance and

executive salaries. This has been a widely debated issue in Malaysia and

elsewhere in Asia, particularly following the Asian financial crisis. This

,paper makes two main contributions to the existing literature on executive

compensation and corporate performance. First, there are several studies

that investigate the relationship between executive compensation and

corporate performance in Europe and the United States (USA) (see eg

Murphy 1985, Main et a1 1996, Brunello et a1 1997, Conyon 1997, Crespi

and Gispert 1998). There has, however, been little investigation of the

relationship between corporate performance, performance criteria and

executive compensation in firms in Asian countries.

This is an important gap in the literature. As Schleifer and Vishny (1997)

point out, there is a pressing need for studies of corporate governance

arrangements in countries other than the United Kingdom (UK) and USA.

This reflects the fact that corporate governance arrangements in other

parts of the world, including Asia, are often different from those in the

UK or USA. Berle and Means' (1932) classic description suggests that

ownership in the USA is dispersed among small shareholders with control

concentrated in the hands of managers. This description has been

questioned in more recent research. La Porta et a1 (1999) found that

ownership in countries other than the USA is more concentrated than

depicted in Berle and Means (1932). There is some evidence to suggest

that even in the USA ownership is more concentrated than when Berle

and Means (1932) wrote. Studies such as Morck et a1 (1988) and Shleifer

and Vishny (1986) have found at least a moderate degree of ownership

concentration in the USA. Nevertheless, it is clear that concentration of

ownership is greater in most Asian countries than in either the UK or the

USA (see eg Claessens et a1 1999, OECD 1999). In governance structures

where ownership is more dispersed there is greater potential for takeovers

to act as a disciplining mechanism relative to the contractual relationship

between management and shareholders.

A second contribution of this paper is to use total board remuneration as a

proxy for executive compensation. There are only a couple of studies

that look at the relationship between total board remuneration and

corporate performance (Main et a1 1996, Brunello et a1 1997). Most

studies, instead, use compensation of the highest paid director or chief

executive officer (CEO). Main et a1 (1996 p. 1634) suggest that in most

cases this has been because data has not been available for the board as a

whole. Where data is available, total board remuneration is a better proxy

for executive compensation. This is because, in terms of agency it is the

board collectively, rather than the CEO or individual directors that act on

behalf of the principals or shareholders (Main et a1 1996 p. 1634, Crespi

and Gispert 1998, p. 2).

The paper is set out as follows. The next section sets out several

hypotheses based on previous research on firms in the UK and USA and

considers the implications of these hypotheses for Asian corporate

governance arrangements. Section three discusses the data set and

empirical specification used in the study. The results are examined in

section four. The last section contains some concluding comments.

2. CONCEPTUAL FRAMEWORK

Hypotheses Based on Studies in Anglo-American Economies

The design of compensation contracts for managers has been an

important topic of investigation in the principal-agent literature. The

objective is to formulate an optimal compensation scheme that motivates

managers to maximise firm performance, taking into account governance

arrangements. The specific governance conditions depend on the

institutional rules and markets in which the firm operates, which are

related, among other things, to factors such as industry or sector

performance, firm size and the structure and composition of ownership.

These factors are able to influence the board-shareholder relationship,

impacting on problems of information asymmetries. This, in turn,

influences the manner in which control and supervision of managers is

exerted (Crespi and Gispert, 1998, p. 8). The existing theoretical and

empirical literature, based primarily on corporate governance

arrangements in Anglo-American economies, suggests several hypotheses

about the relationship between executive compensation and each of

corporate performance, firm size, industry or sector performance and the

degree of ownership concentration.

The first hypothesis is that there is a positive relationship between firm

performance and board remuneration. Principal-agent models of the firm

explain firm performance in terms of manager's effort and a set of

randomly distributed variables that are outside the manager's control and

not observable (see eg Tirole 1988 and Rosen 1992). These models.

suggest that in order to increase manager's effort, compensation should

be sensitive to performance. This assumes that effort and firm

performance move in the same direction, otherwise the observability of

performance would be irrelevant in motivating managers to increase

effort (Crespi and Gispert 1998). While the existing literature is far from

definitive on the point, several empirical studies support the existence of

a positive relationship between executive compensation and performance

(see eg Murphy 1985, Main et a1 1996, Gibbons and Murphy 1990).

The second hypothesis is that there is a positive relationship between

board remuneration and firm size. The theoretical underpinning of this

hypothesis is the notion that there are complementarities between

individual talent and the productivity of control. Hence, it is efficient to

assign greater control to more talented individuals (Brunello et a1 1997 p.

2). Most studies have used firm size as a control variable because larger

firms pay higher salaries (see eg Murphy 1985, Crespi and Gispert 1998).

Firm size could also be considered as another measure by which

companies judge the performance of their managers. Since firm size is

typically measured by sales or turnover, managers who have increased

company sales are viewed as more successful. There are a number of

empirical studies which support the contention that there is a positive

relationship between firm size and executive compensation (see eg

Murphy 1985, Baker et a1 1988, Gregg et a1 1993, Main et a1 1996). In a

relatively recent study Murphy (1998) also found a positive relationship

between compensation paid to CEOs and firm size, but suggests that the

relationship has weakened over time.

The third hypothesis is that there is an inverse relationship between board

remuneration and sector performance. The performance of other

managers in the same sector provides additional information that can be

used to decide appropriate compensation. Principal-agent models suggest

that a more accurate picture of manager's effort decreases the variance of

observable outcomes. This reduces the risk differential that needs to be

built into the contract (see eg Holmstrom 1979, Zwiebel 1995). Empirical

studies that have found a statistically significant inverse relationship

between executive compensation and either industry or sector

performance include Conyon and Leech (1994) and Gibbons and Murphy

(1990).'

The fourth hypothesis is that there is an inverse relationship between

board remuneration and ownership concentration. In companies where

ownership is dispersed, the discretionary power of managers will be

higher. Thus higher levels of compensation will be needed to increase

manager effort. However, when ownership is concentrated shareholders

have better information and are better placed to monitor manager effort.

In these cases compensation can be tied more closely to actual effort.

Using data on Spanish listed companies, Crespi and Gispert (1998) found

that ownership concentration had a negative and significant effect on

remuneration.

Malaysian Corporate Governance and Implications for Board Remuneration

Ownership is generally more concentrated in Asia than the UK or USA.

Ownership concentration in Malaysia is indicative of most Asian

countries (Lim 1981). In Malaysia, the three largest shareholders own 54

per cent of the shares in the ten largest non-financial private firms and 46

per cent of the ten largest firms (OECD 1999 p. 7). One reason for this is

that family control of listed companies is more prevalent in Asia than

. Anglo-American economies. Claessens et a1 (1 999) examined ownership

concentration in 2,980 publicly listed companies in nine East Asian

countries (Hong Kong, Indonesia, Japan, Malaysia, the Philippines,

Singapore, South Korea, Taiwan and Thailand). Their conclusion was

that there was significant family control in more than half of East Asia's

corporations. This is certainly true for Malaysia. According to Claessens

et a1 (1999), in 1998 in Malaysia, the top five families controlled 17.3 per

cent of market capitalization; the top ten families controlled 24.8 per cent

of market capitalization and the fifteen families with the largest

shareholding controlled 28.3 per cent of market capitalization on the

KLSE.

Another reason for ownership concentration in countries such as

Indonesia Korea, Malaysia, Singapore and Thailand is significant

amounts of state control of listed firms. In Malaysia both of the main

political parties - United Malay National Organization and the Malaysian

Indian Congress - have substantial business holdings. Claessens et a1

(1 999) report that using the percentage of shares owned by the largest ten

shareholders as a benchmark the State controls 17.8 per cent of publicly

listed companies in Malaysia. If we focus on the 20 largest publicly

listed companies this figure increases to 36.3 per cent. This is the second

highest figure in the Claessens et a1 (1999) study after Singapore, where

the comparable figure is 45.8 per cent.

An important implication of ownership concentration in Malaysia, and

Asia more generally, is that the agency problems arising from the

separation of ownership and control are not as pronounced as in Anglo-

American economies. his suggests that the relationship between board

remuneration and firm performance should be weaker than in the UK or

USA. Whether this is in fact the case is an empirical question. Studies of

firms in continental Europe, where ownership is also more concentrated

than the UK or the USA have still found a positive relationship between

compensation and firm performance. Crespi & Gispert (1998) found a

strong relationship between board remuneration and firm performance in

a sample of 113 Spanish listed companies. Brunello et a1 (1997) also

found a positive relationship between board remuneration and firm

performance in a sample of Italian listed companies, where there was a

large proportion of State-controlled firms in the sample.

3. DATA, METHODOLOGY AND SPECIFICATION

We used total Board remuneration as our measure of pay (denoted as

REM).* This includes salaries and fees paid to all directors. We regressed

this variable on measures of firm performance, sector performance and

firm size. We used two alternative measures of firm and sector

performance. In the first set of regressions we defined firm and sector

performance in terms of stockholder wealth (SHW) and sector

stockholder wealth (SSHW) respectively. Stockholder wealth is defined

as [(P, + dt)/Pt-l)]*MVt-I, where P, is the current period stock market

price, d, is the dividend per share, is the previous period stock market

price, and MV,, is the market value of the firm. This definition is

consistent with that used in Conyon and Leech (1994) for their study

using data on UK listed companies and is similar to that used by Murphy

(1985) and Jensen and Murphy (1990) for US listed companies. The

sector performance measure is stockholder wealth averaged over firms in

each sector.

The advantage of using shareholder wealth rather than accounting profits

to measure firm performance is that in principal-agent theories,

shareholders are generally considered to be the principals (Murphy 1985,

p. 21). This, of course, assumes that share price movements always

dominate fm performance. Thus, for comparative purposes, in the

second set of regressions we used return on assets and sector return on

assets as alternative measures of firm and sector performance

respectively. These variables were entered into the regressions as

(l+ROA) and (l+SROA), which is the standard practice in the literature

(see eg Crespi and Gispert, 1998). Following the definition used by the

KLSE, return on assets was calculated by dividing either the firm's profit

or loss before extraordinary items by total assets. The sector performance

measure in the second set of regressions was return on assets averaged

over firms in each sector. We used the sector classification guidelines in

KLSE publications to determine which firms are in each sector. In both

sets of regressions, firm size was measured using sales turnover (TRN).

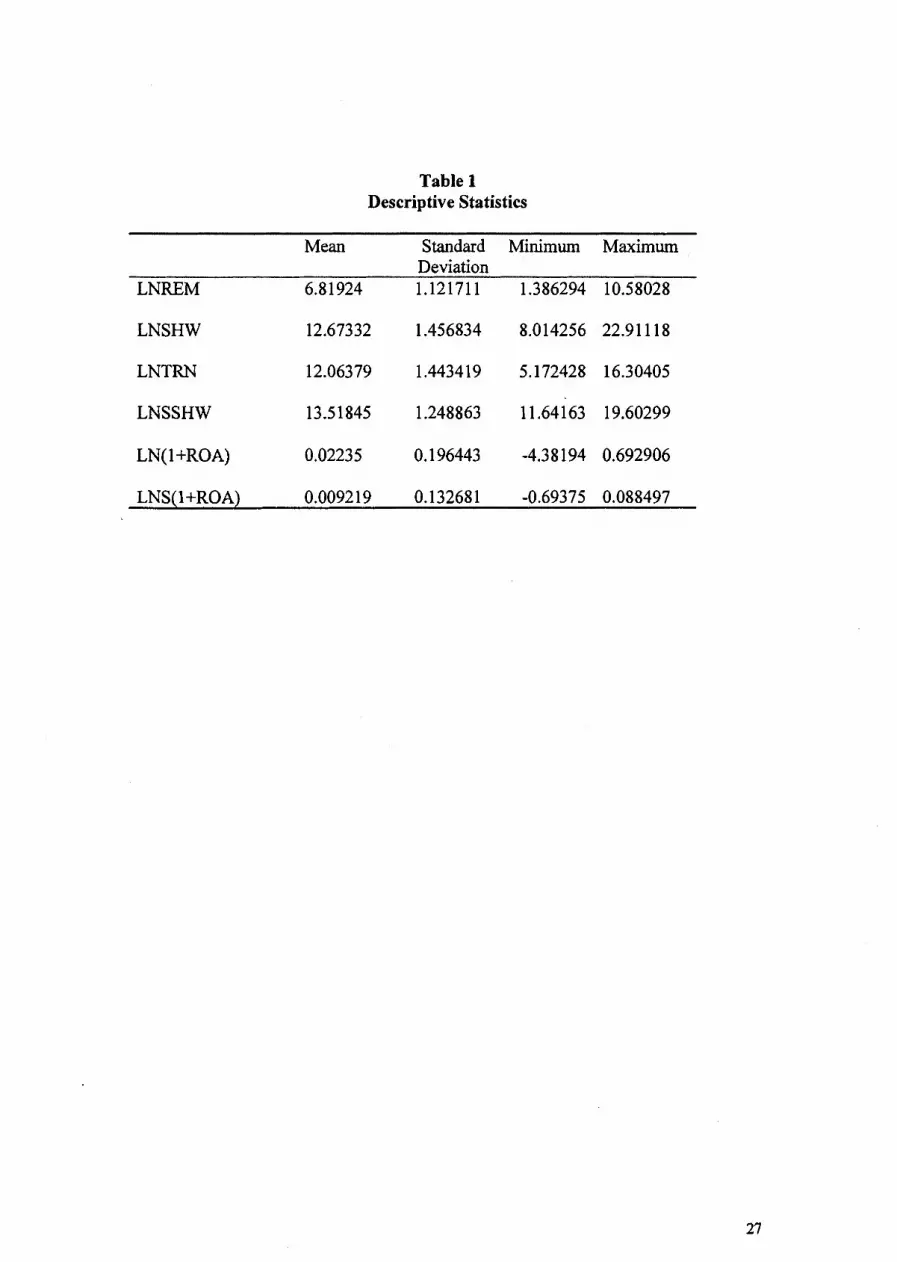

LNREM, LNSHW, LNSSHW, LN(1 +ROA), LN(1 +SROA) and LNTRN

are the natural logs of REM, SHW, SSHW, (l+ROA), (l+SROA) and

TRN. Table l provides some basic descriptive statistics for LNREM,

LNSHW, LNTRN and LNSSHW, LN(l+ROA), and LN(l+SROA).

Ownership concentration is employed to measure the effect of corporate

governance on board remuneration. Following Crespi and Gispert (1998)

we use the percentage of shares owned by the largest stockholder (CRl)

to measure concentration." Consistent with Crespi and Gispert (1998), a

dummy variable (denoted by DCR1) is used, which takes the value of one

if the concentration measure is above the median level and is otherwise

zero. This dummy variable is entered as time invariant. We used the latest

ownership data available to construct this dummy variable. Time

dummies were included in all initial regressions (reported in table 2) to

control for the effects of economy wide shocks. However, in later

specifications (reported in table 3) we examine the impact of the financial

crisis on remuneration. In these specifications, instead of using time

dummies, we substituted a crisis dummy variable (denoted as DCRISIS),

set equal to one for the period 1997 to 2000 and was zero otherwise.

To test the hypotheses in section two we used the first-differences model,

which is standard in the literature (see eg Conyon and Leech, 1994,

Crespi and Gispert, 1998). Specifically, in the first set of regressions we

regressed DLNREMi, on different combinations of DLNSHW,

DLNSSHW and DLNTRN in period t and period t-l and DCRl. In the

second set of regressions we used DLN(l+ROA) and DLN(l+SROA)

instead of DLNSHW and DLNSSHW as proxies for firm and sector

performance, where for a variable X, DLNX, is LNXt- L W I and

DLNX(t- 1) is LNX,-,- LN&.

We used pooled cross sectional and time series data for companies listed

on the KLSE over the period 1989-2000. The number of companies and

observation vary according to which specification is used with the

maximum number of companies and observations being 223 and 1092

respectively. Our sample only includes those companies for which we

have data on remuneration, performance variables and sales turnover for

at least three consecutive years over the sample period. There were 307

companies listed on the KLSE in 1989 and this number increased to 795

by 2000.

Financial data are available for most of these firms, but it was not

possible to collect ownership data on all of these companies for pooled

consecutive time series over the sample period. We also excluded fiom

the sample firms that operate in the finance, plantation and mining

sectors. These sectors use different accounting procedures than the ones

in other sectors. In addition, firms in the infrastructure (6), technology

(1 l), hotels (6) and closed end funds (1) sectors as well as trusts (4) have

also been excluded since there are only a handfd of companies listed on

the KLSE board for these sectors. Thus our sample includes those

companies operating in the consumer products, industrial products,

construction, trading/services, and property sectors.

Financial data such as sales turnover, last transacted price4 and market

value are measured at financial year-ends. Ownership data are measured

as of any month during the financial year (there is no fixed date at which

to report these data). Financial year-ends are not the same for all firms.

Since we define turnover and shareholder wealth consistently by financial

year, this should not be a problem for these variables. However, for sector

performance we use calendar years, that is, when we calculate the sector

performance measure for a given firm we include not just the firms with

the same financial year as the given firm, but all firms on which we have

data in our ca1cu1ations.' All data in ringgits are expressed in 1994

ringgits. The Consumer Price Index (CPI) has been used to convert the

nominal values to real values using 1994 as the base year. In the cases

where a firm is owned by a holding company, we have included only the

holding company to prevent double counting as holding company'

accounts consolidate the accounts of subsidiaries. In cases where we have

data on several subsidiaries and data on the holding company itself, we

have excluded the holding company from the sample to increase the

number of observations.

All data come from various KLSE publications. The main sources are the

KLSE Annual Companies Handbook and KLSE on Disc (which is the

electronic version of the Handbook). For Directors' Remuneration we

used the data provided on the web site of the KLSE Research Institute of

Investment Analysts Information ~ ~ s t e m s ! Data on this web site as well

as that in the KLSE handbook and KLSE on Disc are derived from the

annual reports of companies listed on the KLSE.

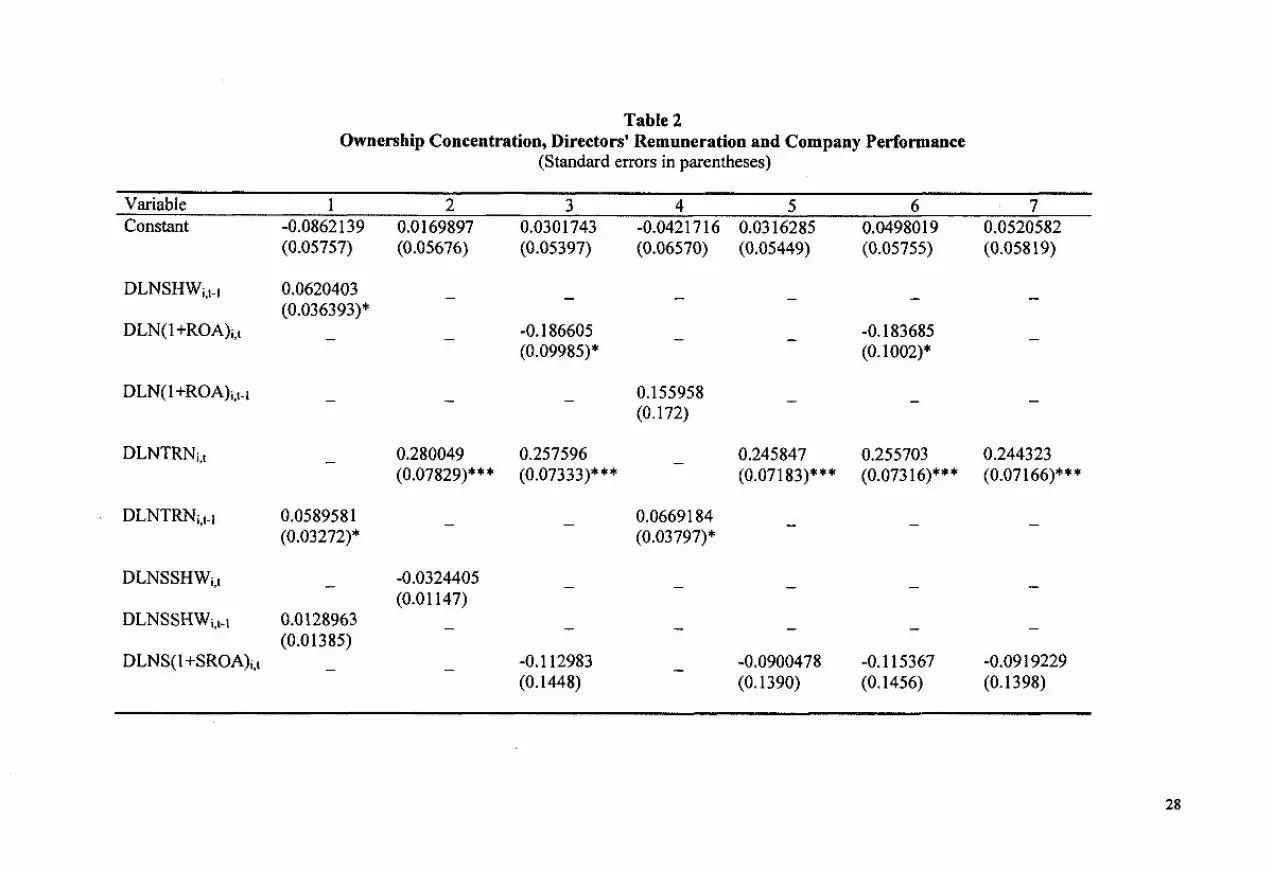

4. RESULTS

The results of various specifications using either stakeholder wealth or

return on assets as a proxy for performance, with time dummies to control

for shocks are reported in table 2. With the exception of the fourth

regression reported in table 2, both the Wald (time) and Wald (joint)

statistics are significant in each specification,which rejects the null

hypothesis that the tested coefficients are simultaneously zero. All

estimates were obtained using the Dynamic Panel Data (DPD) package of

Doornik et a1 (1999). These are one-step estimates obtained by using the

robust variance covariance matrix. In table 2 tests for the absence of first-

order and second-order serial correlation in the first-differenced residuals

are reported as AR(1) and AR(2) respectively. In the second, third, fifth

and seventh specification AR(1) is negative and significant and AR(2) is

insignificant, meaning that we can accept the null hypothesis that the

disturbance terms are not serially correlated in these ~~ecifications.~ For

this reason, we concentrate on the results in these specifications when

interpreting our findings in the following discus~ion.~

The first hypothesis, based on studies in the UK and USA, is that there is

a positive relationship between firm performance and board

remuneration. However, we noted above that the relationship between

board remuneration and firm performance might be weaker in Malaysia

than in the UK or USA because ownership is more concentrated. Our

results suggest that the relationship between board remuneration and firm

performance is ambiguous in Malaysia. In table 2 DLNSHWi,t-I is positive

and significant at 10 per cent in the first specification, but here we cannot

accept the null hypothesis that the disturbance terms are not serially

correlated. Turning to measures of accounting performance, in the third

specification in table 2, which does satisfy the null hypothesis that the

disturbance terms are not serially correlated DLN(l+ROA)i,t is significant

at the 10 per cent level with a perverse negative sign.

The second hypothesis is that there is a positive relationship between

remuneration and firm size. Our results provide strong evidence for this

hypothesis. In the second, third, fifth and seventh specification in table 2,

DLNTRNi, has a positive sign and is statistically significant at the 1 per

cent level. The magnitude of the coefficient on DLNTRNi,t varies

between .24 and .28, which is consistent with the findings of US studies

that have repeatedly found the elasticity of pay with respect to sales to be

around .3 (see Rosen 1992). Baker et a1 (1998, p. 609) suggest that this is

"the best documented empirical regularity regarding levels of executive

compensation". The magnitude on DLNTRNi,t-l in the first and fourth

specification is in the range .05 to .07. This result is consistent with that

of Conyon and Leech (1994) who estimate that the elasticity of the

highest paid director with respect to lagged turnover is .07 for the UK.

However, it is lower than Main et a1 (1996) who estimate the elasticity of

total board remuneration with respect to lagged turnover to be .28 for the

UK.

The third hypothesis is that there is an inverse relationship between board

remuneration and sector performance. Our results reject this hypothesis.

In table 2, DLNSSHWi, has a negative sign but is insignificant in the

second specification, while DLNS(l+SROA)i, has a negative sign, but is

insignificant in the third, fifth and seventh specification. Our results

suggest that those who set Board remuneration in Malaysia do not take

account of contemporaneous sector performance. Conyon and Leech's

(1994) findings for the UK suggest that pay setters take account of lagged

industry performance. However, we note that in one of the few existing

studies to use sector performance rather than industry performance to

measure relative performance, Main et a1 (1996) also found that

contemporaneous sector performance had a statistically insignificant

effect on Board remuneration in UK listed companies.

The fourth hypothesis is that there is an inverse relationship between

board remuneration and ownership concentration. In the seventh

specification in table 3, DCRl is negative and significant at 10 per cent.9

This suggests that ownership concentration has a negative and at least a

weakly significant effect on remuneration. This result differs from that of

Conyon and Leech (1994) who found that ownership concentration has

no effect on executive compensation in the UK. Our results, though, are

not surprising, given the higher levels of ownership concentration in

Malaysia than the UK. Because ownership is more concentrated, one

would expect that shareholders would have better information and be

better placed to monitor manager effort in Malaysia than in the UK. Our

findings are consistent with those of Crespi and Gispert (1998) for

Spanish listed companies. In Spain, where ownership concentration is

also much higher than the UK, Crespi and Gispert (1998) found that

ownership concentration had a negative and significant effect on

remuneration.

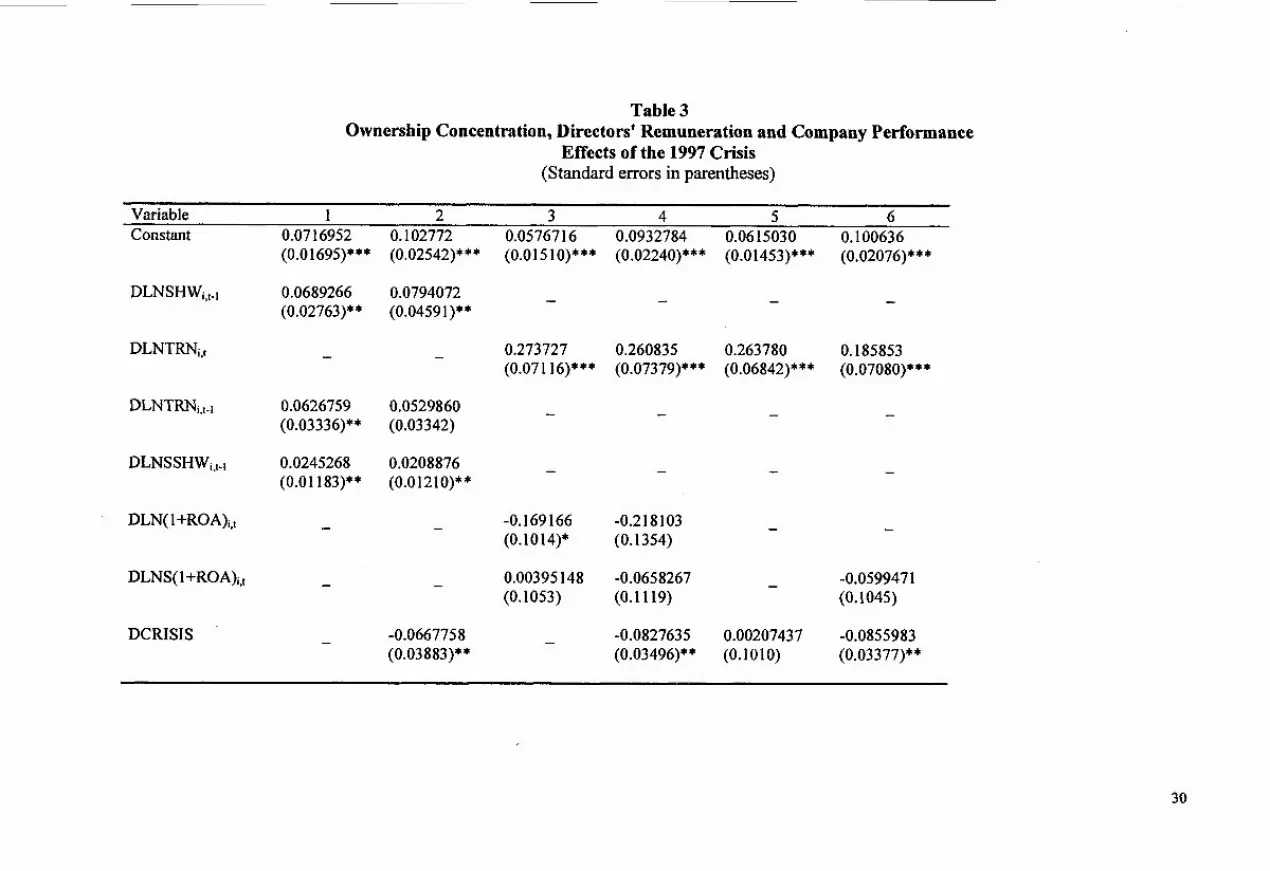

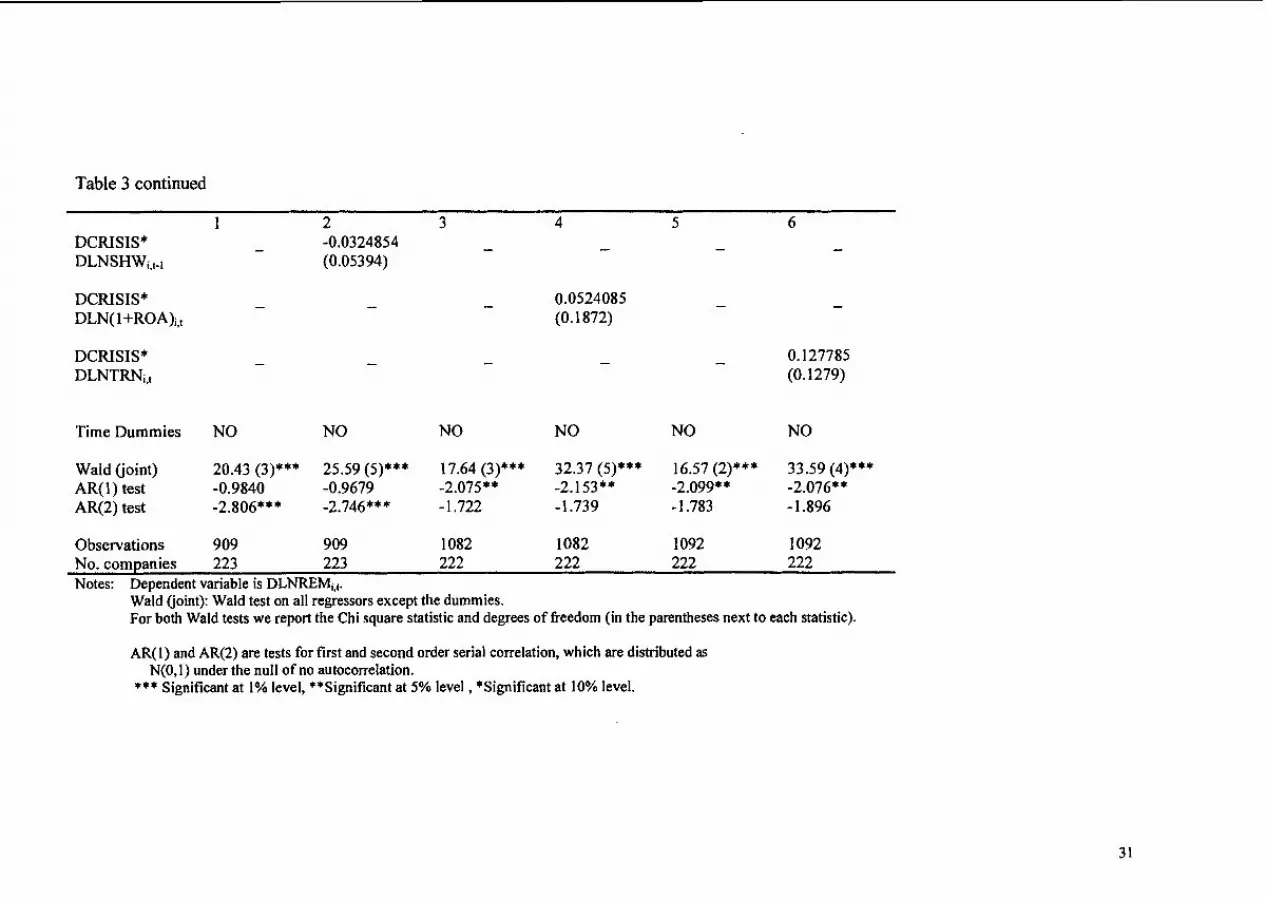

Table 3 examines the impact of the 1997 Asian financial crisis on Board

remuneration. It substitutes a crisis dummy variable (DCRISIS), which is

set equal to 1 for the period 1997 to 2000, for the time dummies in table

2. Table 3 also considers the effect of interactive variables - DCRISIS*DLNSHWi,t-I, DCRISIS*DLN( 1 +ROA)i,t and

DCRISIS*DLNTRNit - on Board remuneration. The Wald (joint) test is

significant at 1 per cent in each specification in table 3, while AR(1) is

negative and significant and AR(2) is insignificant in specifications three

through to six, which means that we can accept the null hypothesis that

the disturbance terms are not serially correlated in four of the six

specifications.

Focusing on these four specifications, the results in table 3 are generally

consistent with the findings with respect to the four hypotheses based on

table 2. The coefficient on the crisis dummy variable is negative and

significant at 5 per cent in specifications four and six, but insignificant in

specification five. In table 3, none of the crisis interactive variables are

significant. This suggests that as one would expect the Asian crisis had a

statistically significant negative effect on Board remuneration, but the

Asian financial crisis did not affect the role of either stockholder wealth,

return on assets or sales turnover as potential factors determining Board

remuneration.

5. CONCLUSIONS AND FUTURE RESEARCH

Most existing studies examine executive compensation in the UK or

USA. This study contributes to the literature through examining the

determinants of executive compensation in Malaysia, where ownership is

usually much more concentrated than in either of these countries. In

, addition, while most studies use the remuneration of the CEO or highest

paid director, we use Board remuneration which is more justifiable in

terms of principal-agent theory because it is the Board as a whole rather

than the highest paid director which can be best regarded as the

shareholders' agent. In section four, we tested four hypotheses based on

the existing literature. Our results provide support for two of the four

hypotheses. We found evidence of a statistically significant positive

relationship between Board remuneration and sales turnover and a

statistically significant negative relationship between Board remuneration

and ownership concentration. Our results suggest that the relationship

between Board remuneration and firm performance is ambiguous, while

there is no evidence of a significant relationship between Board

remuneration and sector performance.

Future research could extend this study in several ways. First, the

reference period for the concentration dummies could be changed fiom

later years to earlier years. If ownership has become more dispersed after

the crisis the pay performance relationship should have strengthened.

Second, by using data on share distribution it should be possible to

determine, for example, whether or not the pay performance relationship

differs between firms where ownership is concentrated in the hands of

Malaysian owners and the firms where there is a high proportion of

foreign ownership. Third, it might be desirable to use a dynamic model,

in the sense this term is used in panel data estimation, employed in Main

et a1 (1996) instead of the static one we use in order to account for the

delay in the administration of pay. To do this it would necessary to

include a lagged dependent variable on the right hand side.

References

Baker, G., M. Jensen and K. Murphy, 1988, Compensation and

Incentives: Practice vs Theory, Journal of Finance 43, 593-61 6.

Berle, A and G. Means, 1932, The Modern Corporation and Private

Property (Harcourt, New York)

Brunello,G., C. Graziano and B. Parigi, 1997, Executive Compensation

and Firm Performance in Italy, Unpublished manuscript, Department of

Economics, University of Udine, Udine, Italy.

Claessens, S., S. Djankov and L. Lang, 1'999, Who Controls East Asian

Corporations?, Unpublished manuscript, World Bank and the University

of Chicago.

Conyon, M.J., 1997, Corporate Governance and Executive

Compensation, International Journal of Industrial Organization 15, 493-

509.

Conyon, M.J., and D. Leech, 1994, Top Pay, Company Performance and

Corporate Governance, Oxford Bulletin of Economics and Statistics 56,

Crespi, R and C. Gispert, 1998, Board Remuneration, Performance and

Corporate Governance in Large Spanish Companies, Unpublished

manuscript, Department d'Economia de I'Empresa, Universitat

Autonoma de Barcelona.

Doornik, J.A., M. Arellano and S. Bond, 1999, Panel Data Estimation

using DPD for Ox, Unpublished.

Gibbons, R and K. Murphy, 1990, Relative Performance Evaluation for

Chief Executive Officers, Industrial and Labor Relations Review 43, 30-

49

Gregg, P., S. Machin and S. Szymanski, 1993, The Disappearing

Relationship Between Directors' Pay and Corporate Performance, British

Journal of Industrial Relations 30, 1 - 1 0.

Holmstrom, B. 1979, Moral Hazard and Observability, Bell Journal of

Economics 10,74-9 1.

Jensen, M. and K. Murphy, 1990, Performance Pay and Top Management

Incentives, Journal of Political Economy 98,225-264

La Porta, R., F. Lopez-De-Silanes and A Shleifer, 1999, Corporate

Ownership Around the World, Journal of Finance 54,47 1-5 13

Lim, M.H., 1981, Ownership and Control of the One Hundred Largest

Corporations in Malaysia (Oxford University Press, Oxford).

Main, B., A. Bruce and T. Buck, 1996, Total Board Remuneration and

Company Performance, Economic Journal 106, 1 627- 1 644.

Morck, R., A. Shleifer and R. Vishny, 1988, Management, Ownership

and Market Valuation: An Empirical Analysis, Journal of Financial

Economics 20,293-3 15.

Murphy, K, 1985, Corporate Performance Pay and Managerial

Remuneration: An Empirical Analysis, Journal of Accounting and

Economics 7,ll-42.

Murphy, K., 1998, Executive Compensation, in: 0. Ashenfelter and D.

Card, eds, Handbook of Labor Economics, Vol. 3 (North Holland,

Amsterdam).

Organisation of Economic Cooperation and Development (OECD), 1999,

Corporate Governance in Asia: A Comparative Perspective (OECD and

World Bank, Seoul)

Rosen, S., 1992, Contracts and the Market for Executives, in: L. Werin

and H. Wijkander, eds, Contract Economics (Basil Blackwell, Oxford)

181-217.

Shleifer, A and R. Vishny, 1986, Large Shareholders and Corporate

Control, Journal of Political Economy 94,46 1-488.

Schleifer, A and R. Vishny, 1997, A Survey of Corporate Governance,

Journal of Finance 94,461 -488.

Tirole, J., 1988, The Theory of Industrial Organization (MIT Press,

Cambridge Mass.)

Zwiebel, J., 1995, Corporate Conservatism and Relative Compensation,

Journal of Political Economy 103, 1-25.

Table 1 Descriptive Statistics

Mean Standard Minimum Maximum Deviation

LNREM 6.8 1924 1.121711 1 .386294 10.58028

LNSHW 12.67332 1.456834 8.014256 22.91 1 18

LNTRN 12.06379 1 .443419 5.172428 16.30405

LNSSHW 13.51845 1 .248863 1 1.641 63 19.60299

LN(1 +ROA) 0.02235 0.196443 -4.38 194 0.692906

LNS(1 +ROA) 0.0092 19 0.13268 1 -0.69375 0.088497

Table 2 Ownership Concentration, Directors' Remuneration and Company Performance

(Standard errors in parentheses)

Constant

DLNSHWi,t-l

DLN(1 +ROA)i,t

DLN(1 +ROA)i,t-I

DLNTRNi,t

DLNTRNi,t-l

DLNSSH WiVt

DLNSSHWi,t-l

DLNS(1 +SROA)i,t

Variable 1 2 3 4 5 6 7 -0.0862 139 0.0 169897 0.0301 743 -0.0421 7 16 0.03 16285 0,04980 19 0.0520582

Table 2 continued

DCRl

Time Dummies YES YES YES YES YES YES YES

Wald (time) 19.6 1 18.91 20.79 (7)*** 28.00 19.91 (7)*** 20.65 (7)*** 19.80 (7)*** (7)* * * (7)* * * (7)* * *

Wald (joint) 7.930 19.2 1 15.49 (3) *** 5.761 (3) 11.84 (2) *** 16.45 (4)*** 12.94 (3) *** (3)** (2)* * *

AR(1) test -1.014 -2.055 ** -2.156 ** -2.062** -2.172** -2.188** -2.213** AR(2) test -2.679*** -1.893 -1.724 -2.672*** -1.783 -1.768** -1.822

Observations 909 966 1082 1152 1092 1082 1092 No. companies 223 223 222 223 222 222 222 Notes: Dependent variable is DLNREI4i.p

wild (time): Wald test on time dummies only. Wald (joint): Wald test on all regressors except the dummies. For both Wald tests we report the Chi square statistic and degrees of freedom (in the parentheses next to each statistic). AR(1) and AR(2) are tests for first and second order serial correlation, which are distributed as

N(0,I) under the null of no autocorrelation. *** Significant at 1% level, **Significant at 5% level , *Significant at 10% level.

Table 3 Ownership Concentration, Directors' Remuneration and Company Performance

Effects of the 1997 Crisis (Standard errors in parentheses)

Variable 1 2 3 4 5 6 Constant 0.07 16952 0.102772 0.057671 6 0.0932784

DLNSHWi,,.,

DLNTRNi,t

DLNTRNi,,.,

DLNSSHWi,t.l

DLN( l +ROA)i,t

DLNS(1 +ROA)i,t

DCRISIS

Table 3 continued

1 2 3 4 5 6 DCRISIS* - -0.0324854 - - - - DLNSHWis+l (0.05394)

DCRISIS* - - - 0.0524085 - - DLN( l +ROA)i,l (0.1872)

Time Dummies NO NO NO NO NO NO

Wald (joint) 20.43 (3)*** 25.59 (5)*** 17.64 (3)*** 32.37 (5)*** 16.57 (2)*** 33.59 (4)*** AR(1) test -0.9840 -0.9679 -2.075** -2.153** -2.099** -2.076** AR(2) test -2.806*** -2.746*** - 1.722 -1.739 - 1.783 - 1 .S96

Observations 909 909 1082 1082 1092 1092 No. companies 223 223 222 222 222 222 Notes: Dependent variable is DLNREMi,,.

Wald (joint): Wald test on all regressors except the dummies. For both Wald tests we report the Chi square statistic and degrees of freedom (in the parentheses next to each statistic).

AR(I) and AR(2) are tests for first and second order serial correlation, which are distributed as N(0,l) under the null of no autocorrelation.

*** Significant at 1% level, **Significant at 5% level , *Significant at 10% level.

Notes

' In the regressions reported later in the paper we use sectors rather than industries.

Companies listed on the KLSE board are grouped into 12 sectors: construction,

consumer products, finance, industrial products, trading and services, hotel,

infrastructure, mining, plantation, properties, trusts and closed end h d s . Each sector

is divided into a number of industries. Some previous studies use industries and

others use sectors to get a comparative performance measure. Typically, the choice of

measure depends on the availability of data; industry data is not always available. In

this study it was not possible to use industries because we needed data for at least

three firms in one sector or industry to be able to calculate a comparative performance

measure and in many cases we did not have that many at the industry level. By

including a sector performance measure instead of an industry one we assume that

when directors' salaries are set, the former is used.

The median level of directors' remuneration in real terms was Rh4 679 536 in 1991,

Rh4 1 099 000 in 1995, and RM 1 127 508 in1 999 for the companies in the sample.

We also experimented with alternative concentration measures such as the

percentage of shares owned by the largest five and largest 10 shareholders. The

results were similar to those reported below using the largest shareholder.

For some companies the stock market data for earlier years provided in the latest

issue of KLSE on Disc (Volume 1 : No.4) are inconsistent with the ones provided in

previous issues. (For example for certain companies 1993 data on latest transacted

price in volume 4 do not match the 1993 data in earlier discs). We used the latest data

in these cases.

In our data set data from, say, 1999-2000 financial year appears as year 2000

information. To calculate sector returns for a year we use all data available for that

year, no matter when the financial year ends.

http://www.klse-ris.com.mv/

According to the DPD manual: "If the disturbances v,, are not serially correlated,

there should be evidence of significant negative first order serial correlation in

.. .. differenced residuals, (Le v ,,- v and no evidence of second order serial

correlation in the differenced residuals. These tests are based on the standardized

average residual autocovariances which are asymptotically N(0; l) variables under the

null of no autocorrelation" (Doornik et. al., 1999, p.8).

We experimented with a number of different lag structures to remove serial

correlation in the first fourth and six specifications without success. We report the

results even though they are impaired by serial correlation to allow the reader to

compare our results with those in the previous literature.

We have not reported the results with DCRl from the first and second specification

in table 2 because they are impaired by serial correlation.

Titles in the Department of Economics Discussion Papers (New Series commenced October 1999)

01-99 Should China be Promoting Large-scale Enterprises and Enterprise Groups? Russell Smyth

02-99 Division of Labor, Coordination, and Underemployment Heling Shi

03-99 Attitude Choice, Economic Change, and Welfare Yew-Kwang Ng and Jianguo Wang

04-99 Economic Reform, Overlapping Property Rights, and Polarisation in the Real Estate Market J. Ram Pillarisetti

05-99 Economic Reform, Growth and Inequality in Human Development in Transitional Economies J. Ram Pillarisetti and Mark Mcgillivray

, 06-99 Efficiency and Liquidity in the Electricity Market: A Preliminary Analysis Barry A. Goss and S. Gulay Avsar

01-00 Effects of Externality-Corrective Taxation on the Extent of the Market and Network Size of Division of Labor Yew-Kwang Ng and Xiaokai Yang

02-00 Incomplete Contingent Labor Contract, Asymmetric Residual Rights and Authority, and the Theory of the Firm Xiaokai Yang

03-00 The Effects of Education on the Timing of Marriage and First Conception in Pakistan Lata Gangadharan and Ptrshkar Maitra

04-00 A Production Theory Approach to the Imports and Wage Inequality Nexus Christis G. Tombazos

05-00 Simultaneity, Rationality and Price Determination in US Live Cattle Barry A. Goss, S. Gulay Avsar and Brett A. Inder

06-00 Free Riding and the Welfare Effects of Parallel Imports Jong-Say Yong

07-00 The Determinants of Judicial Prestige and Influence: Some Empirical Evidence from the High Court of Australia Mita Bhattacharya and Russell Smyth

08-00 Causality in International Capital Movements: The Income Mobility of Australian Investment Abroad Robert D Brooks, Dietrich K Fausten and Param Silvapulle

01-01 Outside Options and the Competitiveness of Vertical Alliances: A Core Theoretic Approach Jong-Say Yong

02-01 Resource Inflows and Household Composition: Evidence From South African Panel Data Pushkar Maitra and Ranjan Ray

03-0 1 School Dropouts and Economic Growth: A Cross-Country Analysis Kausik Chaudhuri and Pushkar Maitra

04-0 1 HOGLEX demand systems and welfare policy in major ASEAN developing countries: A Bayesian analysis using expenditure unit records Hikaru Hasegawa, Tran Van Hoa, Ma. Rebecca Valenzuela

05-01 Unprotective Tariffs, Ineffective Liberalization and Other Mysteries: An Investigation of the Endogenous Dimensions of Trade Policy Formation in Australia Christis G. Tombazos

06-0 1 Strategic FDI and Industrial Ownership Structure Christopher J. Ellis and Dietrich Fausten

07-0 1 Forecast Errors and Efficiency in the US Electricity Futures Market S. Gulay Avsar and Barry A. Goss

08-0 1 Good Capitalism Versus Bad Capitalism: Effects of Political Monopoly of the Ruling Elite on the Extent of the Market, Income Distribution, and Development Wai-Man Liu and Xiaokai Yang

09-0 1 Birth-spacing and Child Survival: Comparative Evidence fiom India and Pakistan Pushkar Maitra and Sarmistha Pal

10-01 Board remuneration, Company Performance and Corporate Governance: Evidence fiom Publicly Listed Malaysian Companies Ergun Dogan and Russell Smyth

11-01 Externality, Pigou and Coase: A Case for Bilateral Taxation and Amenity Rights Yew-Kwang Ng

12-0 1 Division of Labour, Specialisation and the Enforcement of a System of Property Rights: A General Equilibrium Analysis Li Ke and Russell Smyth

1 3-0 1 Optimal Environmental ChargeslTaxes: Easy to Estimate and Surplus Yielding Yew-Kwang Ng