bmcg ecb welcome remarks isabel schnabel

TRANSCRIPT

The monetary policy non-puzzle in bond markets

Isabel Schnabel, Member of the ECB’s Executive BoardBond Market Contact Group, Frankfurt am Main, 15 September 2021

Rubric

www.ecb.europa.eu ©

Exceptionally low yield environment proves persistent despite recovery

10-year US Treasury and euro area GDP-weighted yield

(percentage)

Source: ECB calculations and Bloomberg.Latest observation: 10 September 2021.

Source: ECB calculations.Latest observation: 10 September 2021.

10-year sovereign bond spreads over German Bunds

(basis points)

2

-1

0

1

2

3

4

Jan-18 Jan-19 Jan-20 Jan-21

Euro area US

0

50

100

150

200

250

300

350

400

450

Jan-18 Jan-19 Jan-20 Jan-21

Italy Greece Portugal Spain

Rubric

www.ecb.europa.eu ©

Inflation expectations are rising, putting upward pressure on nominal rates…

Sources: ECB calculations.Latest observation: 10 September 2021.

Decomposition of nominal 10-year euro area OIS rate

(cumulative change since January 2021; percentage points)

Euro area 5y5y inflation swap forward rate

(percent)

3

Source: Bloomberg.Latest observation: 10 September 2021.

-0.6

-0.4

-0.2

0.0

0.2

0.4

0.6

0.8

Jan-21 Apr-21 Jul-21

10Y real OIS rate10Y inflation swap rate10Y nominal OIS rate

Could you start the chart in Jan-17?

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

Jan-17 Nov-17 Sep-18 Jul-19 May-20 Mar-21

Pre-pandemic level

Rubric

www.ecb.europa.eu ©

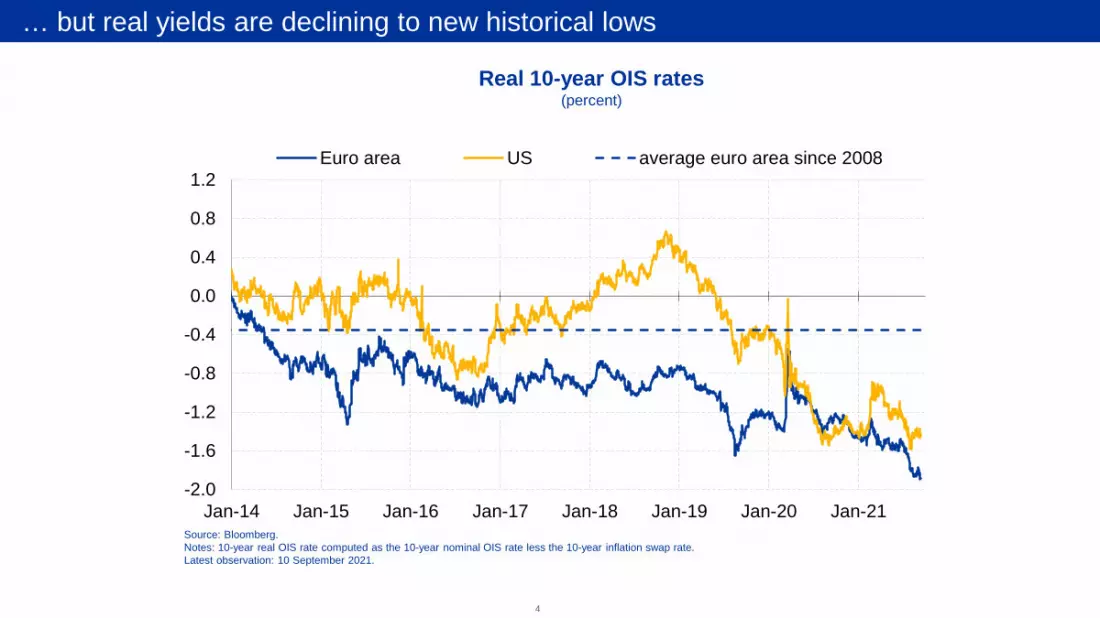

… but real yields are declining to new historical lows

Source: Bloomberg.Notes: 10-year real OIS rate computed as the 10-year nominal OIS rate less the 10-year inflation swap rate.Latest observation: 10 September 2021.

Real 10-year OIS rates(percent)

4

-2.0

-1.6

-1.2

-0.8

-0.4

0.0

0.4

0.8

1.2

Jan-14 Jan-15 Jan-16 Jan-17 Jan-18 Jan-19 Jan-20 Jan-21

Euro area US average euro area since 2008

Rubric

www.ecb.europa.eu ©

Delta variant affects bond yields and prolongs supply bottlenecks

5

Euro area PMI manufacturing: suppliers’ delivery times

(50 indicates no change over previous month)

Source: MarkitLatest observation: August 2021

0

10

20

30

40

50

60

70

1999 2003 2007 2011 2015 20190

10

20

30

40

50

60

70

2019 2020 2021-1.0

-0.8

-0.6

-0.4

-0.2

0.0

0.2

0.4

0.6

May-21 Jun-21 Jul-21 Aug-21 Sep-21

10-year Treasurydomestic macrodomestic policy

foreign macroforeign policyglobal risk

Sources: Sources: Refinitiv Datastream and ECB.Note: Shock contributions are estimated using a daily BVAR model for the US using a combinationof sign, magnitude and narrative restrictions.Latest observation: 10/09/2021.

Drivers of 10-year US Treasury yield(contribution in basis points)

Rubric

www.ecb.europa.eu ©

0

1

2

3

4

Jan-17 Jan-19 Jan-21

US

0

1

2

3

4

Jan-17 Jan-19 Jan-21

Europe

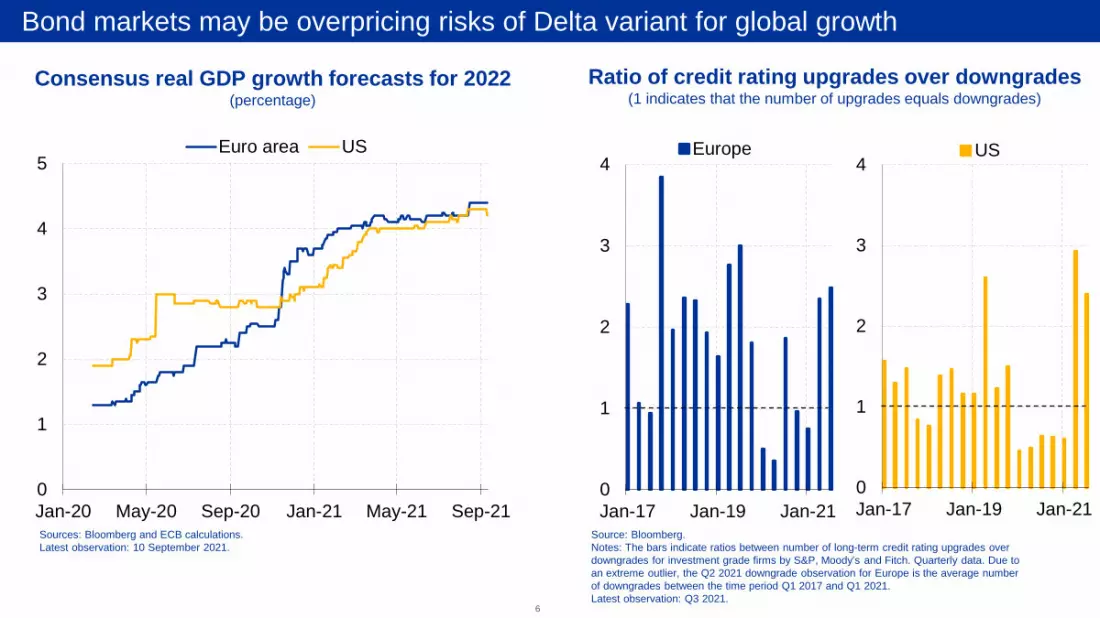

Bond markets may be overpricing risks of Delta variant for global growth

Consensus real GDP growth forecasts for 2022(percentage)

Sources: Bloomberg and ECB calculations.Latest observation: 10 September 2021.

6

Ratio of credit rating upgrades over downgrades(1 indicates that the number of upgrades equals downgrades)

Source: Bloomberg.Notes: The bars indicate ratios between number of long-term credit rating upgrades over downgrades for investment grade firms by S&P, Moody’s and Fitch. Quarterly data. Due to an extreme outlier, the Q2 2021 downgrade observation for Europe is the average number of downgrades between the time period Q1 2017 and Q1 2021.Latest observation: Q3 2021.

0

1

2

3

4

5

Jan-20 May-20 Sep-20 Jan-21 May-21 Sep-21

Euro area US

Rubric

www.ecb.europa.eu ©

60

70

80

90

100

110

120

130

140

150

Jan-20 May-20 Sep-20 Jan-21 May-21 Sep-21

EURO STOXX S&P 500

Continued rally in stock markets is mainly driven by better earnings outlook

7

Source: Bloomberg.Latest observation: 10 September 2021.

Equity market developments(index: Jan-20 = 100)

Drivers of equity prices in the euro area(cumulative change since January 2020, percentages)

Sources: Refinitiv, IBES, Consensus Economics, Bloomberg and ECB calculations.Notes: The decomposition is based on a dividend discount model. The model includes share-buybacks, discounts future cash-flows with interest rates of appropriate maturity, and includes fiveexpected dividend growth horizons. See ECB Economic Bulletin, Issue 4/2018 for more details.Latest observation: 3 September 2021 (weekly data).

Please remove vertical line and change bar on the right side

-80

-60

-40

-20

0

20

40

60

80

Jan-20 Jul-20 Jan-21 Jul-21

Equity risk premiumRisk-free discount ratesLonger-term earnings expectationsShort-term earnings expectationsDividends and share buybacksEA Total Economy Index

38%

16%

Rubric

www.ecb.europa.eu ©

Stock of acquired assets is putting persistent downward pressure on bond yields

30

35

40

45

50

55

2009 2011 2013 2015 2017 2019

Free-floating EA-4 bond supply(percent)

Sources: ECB.Notes: The free-float measure for the four largest euro area economies (Germany, France, Italy and Spain) isdefined as holdings of general government bonds by price-sensitive private-sector investors as a share of totaloutstanding bond supply, both expressed in ten-year maturity equivalents. Price sensitive investors are defined asall sectors other than the foreign official sector, insurance companies and pension funds, and the Eurosystem.Latest observation: March 2021 (quarterly data).

8

Sources: ECB calculations.Notes: Impacts derived from the model of Eser et al. (2019) and a recalibrated version of the model so that the model-implied yield reactions to the March PEPP announcement match the two-day yield changes observed after 18 March(average estimates). Results refer to GDP-weighted averages of the zero-coupon yields of the big-four sovereign issuers(DE, FR, IT, ES). Future assumptions are based on results from the ECB’s survey of monetary analysts, i.e. APP (PEPP)end of net purchases: June 2024 (March 2022); APP (PEPP) end of reinvestments: June 2026 (December 2024).Latest observation: March 2021 for past estimates.

Estimates of APP and PEPP holdings on EA-4 sovereign term premia

(basis points)

-200-180-160-140-120-100-80-60-40-20

0

2015 2017 2019 2021 2023 2025

2y 5y 10y

Rubric

www.ecb.europa.eu ©

-1

0

1

2

3

4

0 1 2 3 4

2010-Feb 2020March 2020-todayLast obs (10-Sep-21)

-1

0

1

2

3

4

0 1 2 3 4

2010-Feb 2020 (ex. 2012-13)March 2020-todayLast obs (10-Sep-21)

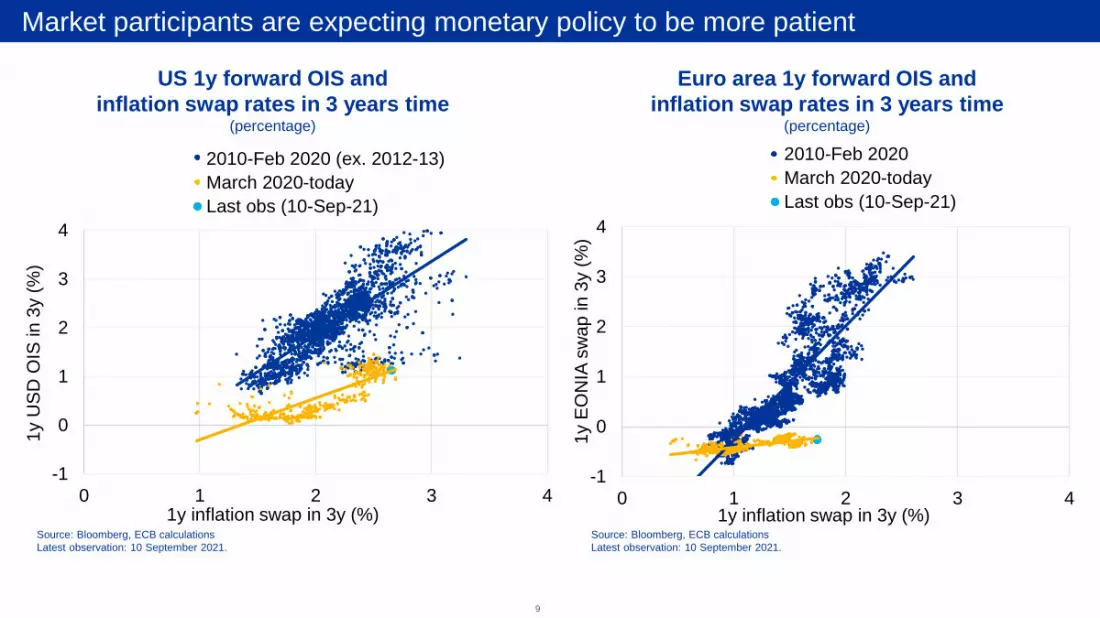

Market participants are expecting monetary policy to be more patient

US 1y forward OIS and inflation swap rates in 3 years time

(percentage)

Euro area 1y forward OIS and inflation swap rates in 3 years time

(percentage)

Source: Bloomberg, ECB calculationsLatest observation: 10 September 2021.

Source: Bloomberg, ECB calculationsLatest observation: 10 September 2021.

9

1y E

ON

IA s

wap

in 3

y (%

)

1y inflation swap in 3y (%)1y inflation swap in 3y (%)

1y U

SD O

IS in

3y

(%)

Rubric

www.ecb.europa.eu ©

New strategy and revised forward guidance truncate risk distribution from the top

10

Source: ECB calculations.

Probabilities of future evolution of 3-month Euribor(percentage)

Source: ECB calculations.

7 July 2021 (pre-strategy announcement) 23 July 2021 (post-July GovC)

Rubric

www.ecb.europa.eu ©

Markets increasingly price risks of higher inflation

11

Probability of inflation exceeding 2% over the next five years

(percentage)

Sources: Bloomberg and ECB calculations.Notes: Probabilities implied by five-year zero-coupon inflation options, smoothed over five businessdays. Risk-neutral probabilities may differ significantly from physical, or true, probabilities.Latest observation: 10 September 2021.

0

10

20

30

40

50

60

70

80

90

100

Jan-14 Jan-16 Jan-18 Jan-20

Euro area US

10-year inflation risk premium(percentage)

Source: Refinitiv, Haver and ECB calculations.Notes: The euro area inflation risk premium represents average estimates based on two affine term structure models applied to ILS rates adjusted for the indexation lag as in Camba-Mendez and Werner (2017). This estimation method follows Joslin, Singleton and Zhu (2011). The US inflation risk premium is estimated by the Federal Reserve Board DKW Model.Latest observation: August 2021.

-1.0

-0.5

0.0

0.5

1.0

Jan-06 Jan-09 Jan-12 Jan-15 Jan-18 Jan-21

Euro area US

Rubric

www.ecb.europa.eu ©

Thank you for your attention!