bkaa 3023 - topic 4 - completing the audit

TRANSCRIPT

COMPLETING

THE AUDITCHAPTER 4

LEARNING OBJECTIVES To understand audit issue related to contingent liabilities and commitments

To know the types and procedures for subsequent events

To conduct a review on related parties disclosure

To reassess going concern considerations To reassess accounting estimates To integrate audit evidence and evaluate audit result

To communicate audit matter with those charged with corporate governance

INTRODUCTIONAs previously discussed, in conducting detailed audit work, the auditor divides (conceptually) the client’s accounting system into sub-systems or audit segments.

Once the detailed audit work is complete, the auditor approaches the audit holistically, and the completion and review stage is conducted on an entity-wide basis, which include: Review for contingent liabilities and commitments; Review for subsequent events and re-asses going concern assumption;

Review financial statements and audit working papers;

Evaluate evidence and form audit opinion.

1. REVIEW FOR CONTINGENT LIABILITIES AND COMMITMENTS

Contingent Liabilities (CL) – potential future obligation to outside party for an unknown amount resulting from activities already taken place. Three conditions to exist are:Possible future payment to outside party or impairment of asset due to existing condition

The amount of future payment or impairment is uncertain

The outcome will be resolved by some future events or event

E.g.: taxation in dispute and pending litigation for infringement (environmental, product safety, etc)

Management is responsible for identifying and deciding the appropriate accounting treatment for CL. Auditor’s objectives are to evaluate the accounting treatment of known CL and to identify, to the extent practical, any CL not already identified by the mgmt.

FRS 137: CL – (1) Possible obligation arises from past events, whose existence will be confirmed by uncertain future events not wholly within control; or (2) A present obligation but not recognized because: a) outflow of resources is not probable, or b) the amount of the obligation can’t be measured reliably.

Financial Statement Treatment

Likelihood of Occurrence

Financial Statement Treatment

Remote (slight chance)

Possible (likely to occur)

Reasonably possible

No disclosure

amount can be reasonably estimated – adjust FS

amount can’t be reasonably estimated – note disclosure

Footnote disclosure

Contingent liabilities of considerable concern to the auditor includes:

pending litigation for patent infringement, product liabilities, etc

income tax dispute product warranties note receivable discounted guarantees of obligations of others

Commitments – are contractual undertakings -e.g. commitment to purchase raw materials or lease facilities at certain price, agreement to sell at a fixed price, bonus plans, royalty agreement etc.

Audit Procedures for Finding Contingencies & Commitments

Inquire of mgmt (not useful to uncover intentional failure to disclose CL & C)

Review current and previous years internal revenue agent reports for income tax settlement/dispute.

Review the minutes of directors and shareholders meetings for indications of lawsuits and other CL & C.

Analyze legal expense for payment related to CL Obtain a letter from major solicitor as to the status of pending litigation or other CL & C

Review audit docs for info that may indicate CL

2. REVIEW FOR SUBSEQUENT EVENTS

The auditor is responsible express opinion on the fairness of auditee’s financial statement at balance sheet date.

Therefore, the auditor has to consider events between the balance sheet date and the audit report’s date, which might affect a financial statement user’s assessment.

The auditor must review transactions and events occurring after the balance sheet (BS) date to determine whether anything occurred that might affect the fair presentation or disclosure of the FS.

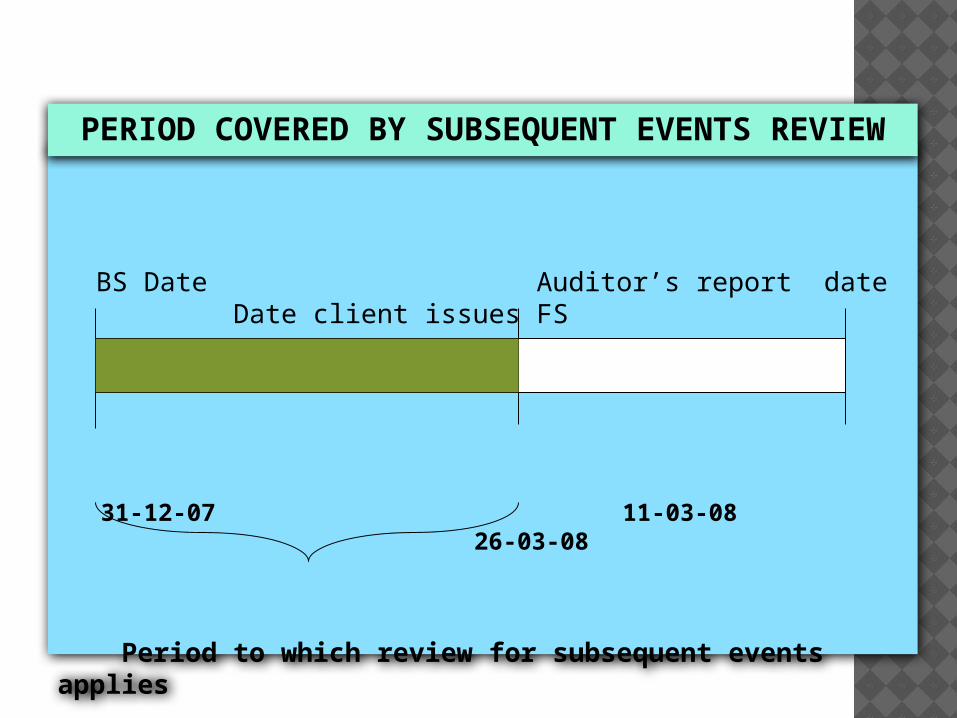

The auditor responsibility to review subsequent events is normally limited to the period beginning with the BS date and ending with the date of the auditor’s report.

BS Date Auditor’s report date Date client issues FS

31-12-07 11-03-08 26-03-08

Period to which review for subsequent events applies

PERIOD COVERED BY SUBSEQUENT EVENTS REVIEW

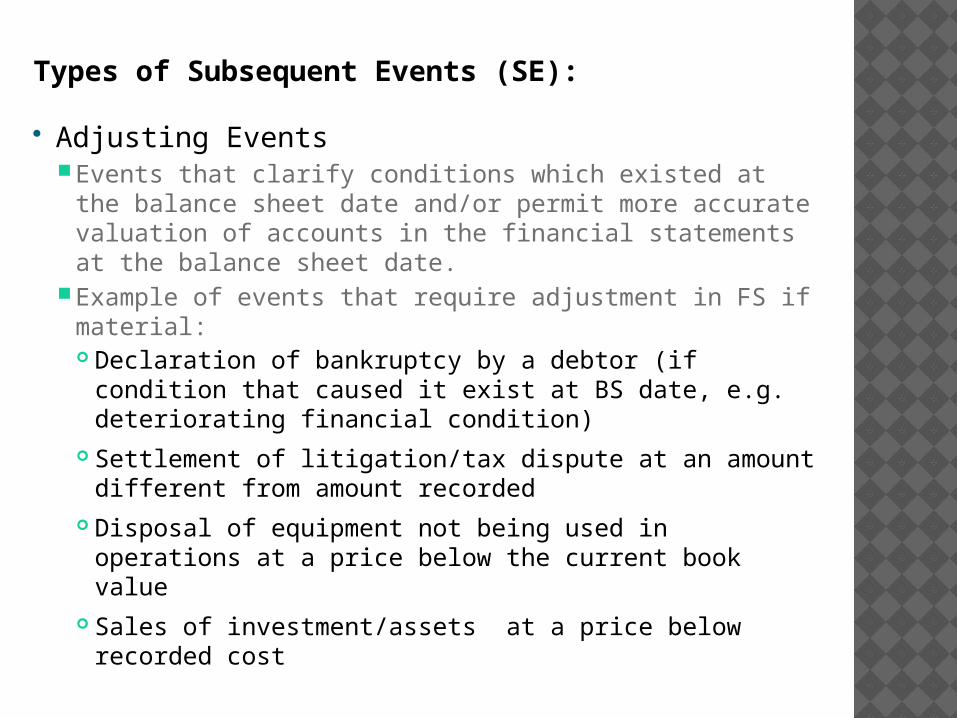

Types of Subsequent Events (SE):

Adjusting EventsEvents that clarify conditions which existed at the balance sheet date and/or permit more accurate valuation of accounts in the financial statements at the balance sheet date.

Example of events that require adjustment in FS if material: Declaration of bankruptcy by a debtor (if condition that caused it exist at BS date, e.g. deteriorating financial condition)

Settlement of litigation/tax dispute at an amount different from amount recorded

Disposal of equipment not being used in operations at a price below the current book value

Sales of investment/assets at a price below recorded cost

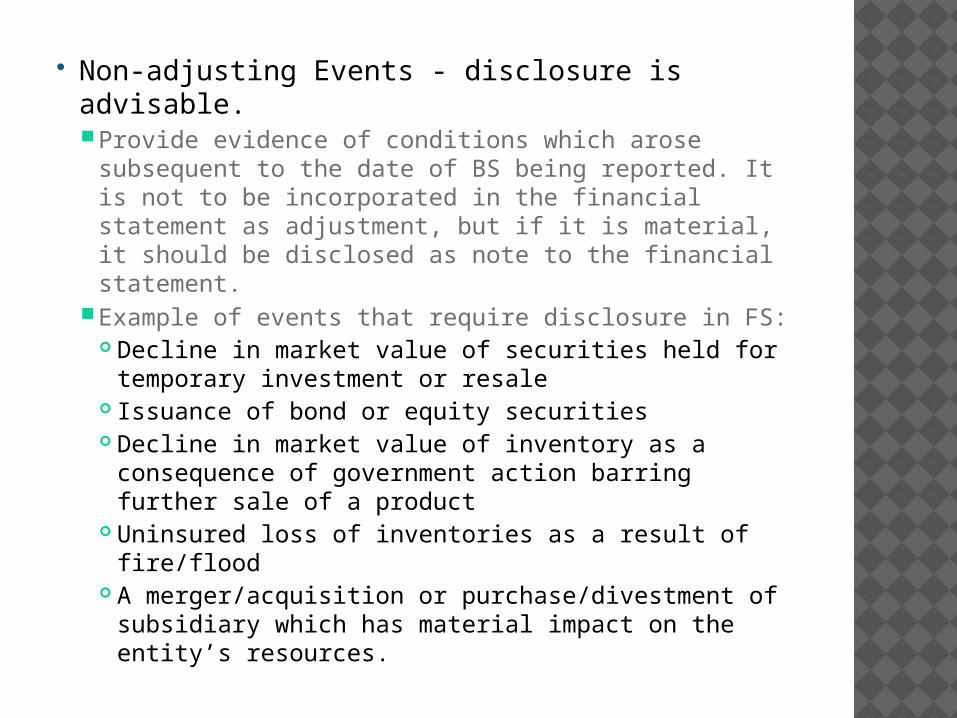

Non-adjusting Events - disclosure is advisable.Provide evidence of conditions which arose subsequent to the date of BS being reported. It is not to be incorporated in the financial statement as adjustment, but if it is material, it should be disclosed as note to the financial statement.

Example of events that require disclosure in FS: Decline in market value of securities held for temporary investment or resale

Issuance of bond or equity securities Decline in market value of inventory as a consequence of government action barring further sale of a product

Uninsured loss of inventories as a result of fire/flood

A merger/acquisition or purchase/divestment of subsidiary which has material impact on the entity’s resources.

Audit Test for SE Proc normally integrated as part of verification of year end acct balanceE.g. it is common to test the collectability of acct receivable by reviewing subsequent period cash receipts and to compare subsequent period purchase price of inventory with the recorded cost as a test of lower of cost or market valuation.

Proc performed specifically for the purpose of discovering SEInquire of management Correspond with solicitors Review internal statements subsequent to BS dateReview accounting records and latest available financial info subsequent to BS date

Examine minutes of BOD, audit and executives committees meeting issued subsequent to BS date

Obtain a letter of representation

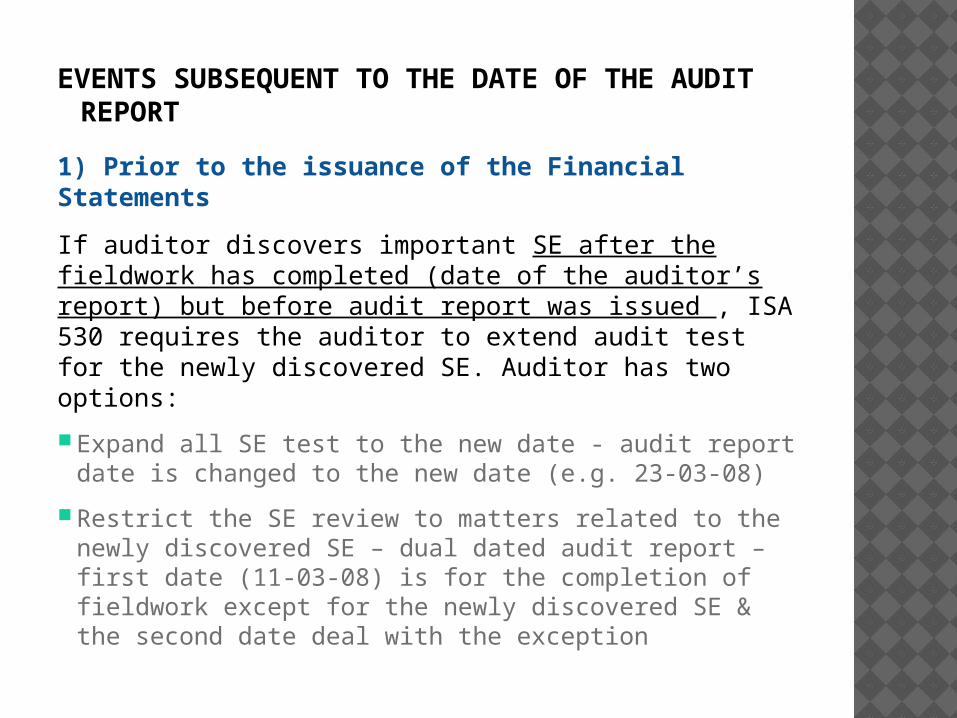

EVENTS SUBSEQUENT TO THE DATE OF THE AUDIT REPORT

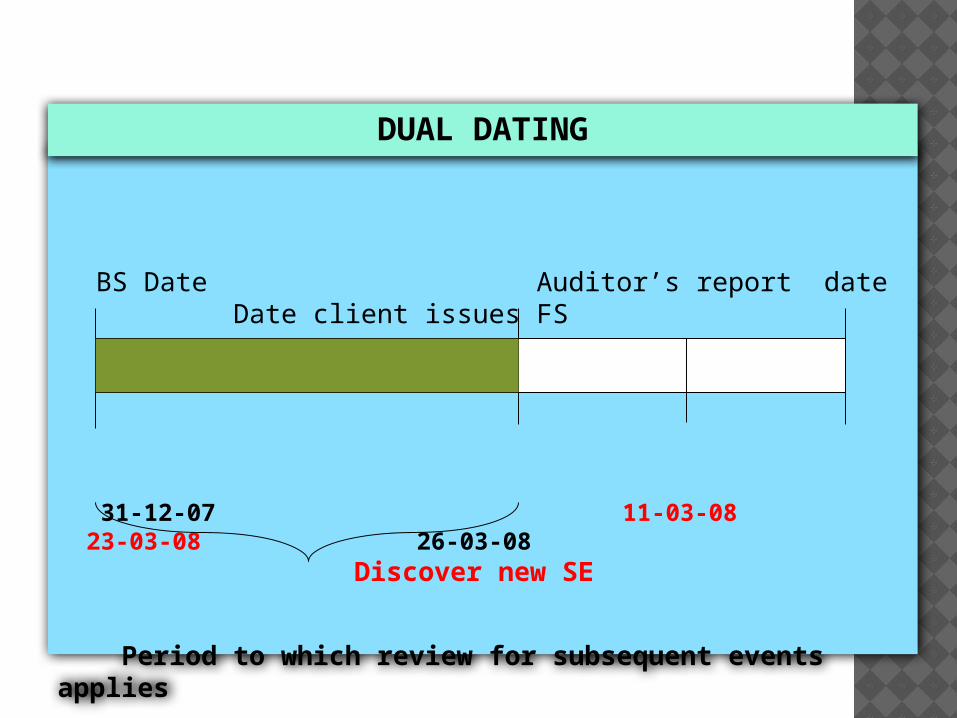

1) Prior to the issuance of the Financial StatementsIf auditor discovers important SE after the fieldwork has completed (date of the auditor’s report) but before audit report was issued , ISA 530 requires the auditor to extend audit test for the newly discovered SE. Auditor has two options:Expand all SE test to the new date - audit report date is changed to the new date (e.g. 23-03-08)

Restrict the SE review to matters related to the newly discovered SE – dual dated audit report –first date (11-03-08) is for the completion of fieldwork except for the newly discovered SE & the second date deal with the exception

BS Date Auditor’s report date Date client issues FS

31-12-07 11-03-08 23-03-08 26-03-08 Discover new SE

Period to which review for subsequent events applies

DUAL DATING

2) Subsequent to the issuance of the financial statement to the entity’s shareholders

If the auditor become aware after the audited FS has been issued that some is materially misleading, the auditor need to discuss with the client’s director and need to inform the users of the FS.

Desirable approach – issue revision containing explanation of the revision.

The FS must be recalled or reissued only when info that indicate the statement were not fairly presented already existed at the audit report date.

If client refuses to cooperate in disclosing it:Inform the BODNotify regulatory agenciesIf practical, to users who relies on the FS

3. RELATED PARTIES DISCLOSURES ISA 550 – auditor should obtain sufficient appropriate evidence regarding the identification and disclosure by mgmt of related parties and the effect of related party transactions that are material to FS.

Related parties – refer to FRS 124. Related parties transaction – a transfer of resources, services or obligation between RP, regardless of price charged

If exist, auditor should perform modified, extended or additional audit procedures.

Mgmt is responsible for the identification and disclosure of related parties and transactions with such parties. However, auditor need to be aware of transactions or events that may result in a risk of material misstatement regarding related parties

Auditor should review info provided by management on names of related parties and conduct audit procedures to ensure the completeness of this info.

If availability of appropriate audit evidence of related parties transaction is limited, the auditor may perform audit procedures such as following: Confirm with the RP, the terms and amount of transaction.

Discuss with mgmt the purpose and nature of transaction

Inspect the documentary evidence in the possession of RP

In addition, ISA requires auditor to obtain mgmt representation letter concerning the completeness of info provided and adequacy of disclosure of RP in FS

4. REASSESSMENT OF GOING CONCERN ASSUMPTION ISA 570 requires auditor to evaluate whether there is substantial doubt about a client’s ability to continue as a going concern for at least 1 year beyond the BS date.

Going concern means the entity is to continue in operational existence for the foreseeable future

Example that could indicate going concern problem includes defaulted loan, lost of primary customer or plan to dispose substantial assets to pay off loans.

Analytical procedures could be used to assess going concern problem.

Auditor should also evaluate the management’s plan to avoid bankruptcy and the feasibility of achieving these plans.

If the auditor still had doubts about the ability of the company to continue going concern, the auditor was required to report these doubts in the audit report.

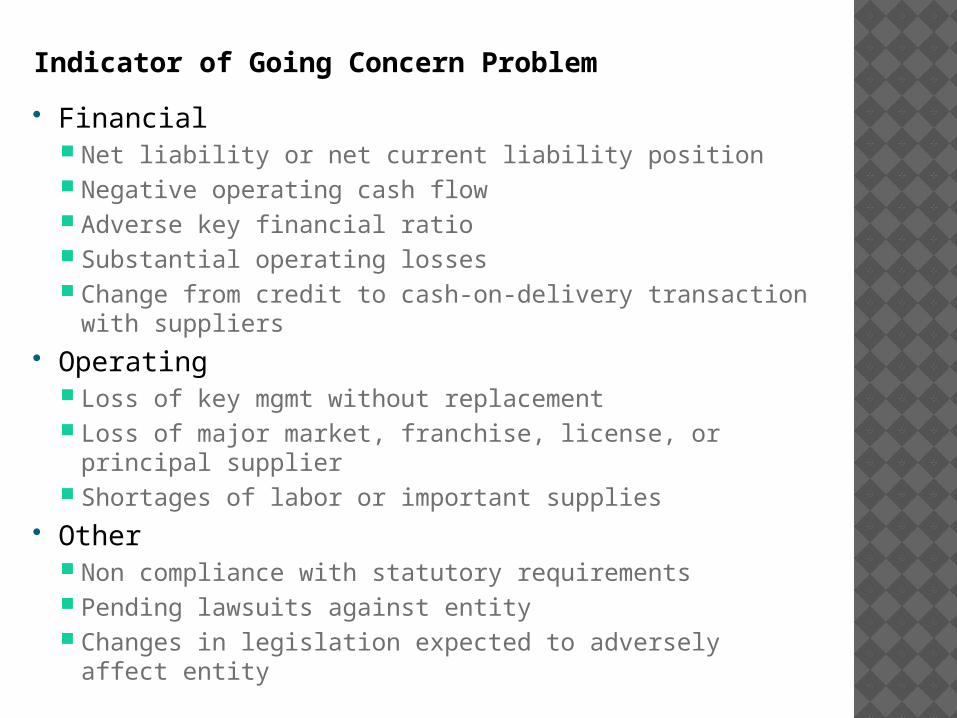

Indicator of Going Concern Problem Financial

Net liability or net current liability position Negative operating cash flow Adverse key financial ratio Substantial operating losses Change from credit to cash-on-delivery transaction with suppliers

Operating Loss of key mgmt without replacement Loss of major market, franchise, license, or principal supplier

Shortages of labor or important supplies Other

Non compliance with statutory requirements Pending lawsuits against entity Changes in legislation expected to adversely affect entity

5. EVALUATION OF ACCOUNTING ESTIMATES ISA 540 - Accounting estimates means an approximation of the amount of an item in the absence of precise means of measurement, e.g.: Allowance to reduce inventory and AR to their estimated realizable value

Provision to allocate cost of fixed assets over useful lives

Provision for a loss from lawsuit Provision to meet warranty claims

The auditor should: Review and test process used to develop the estimate

Use independent estimate for comparison Review subsequent events which provides audit evidence of the reasonableness of the estimate made

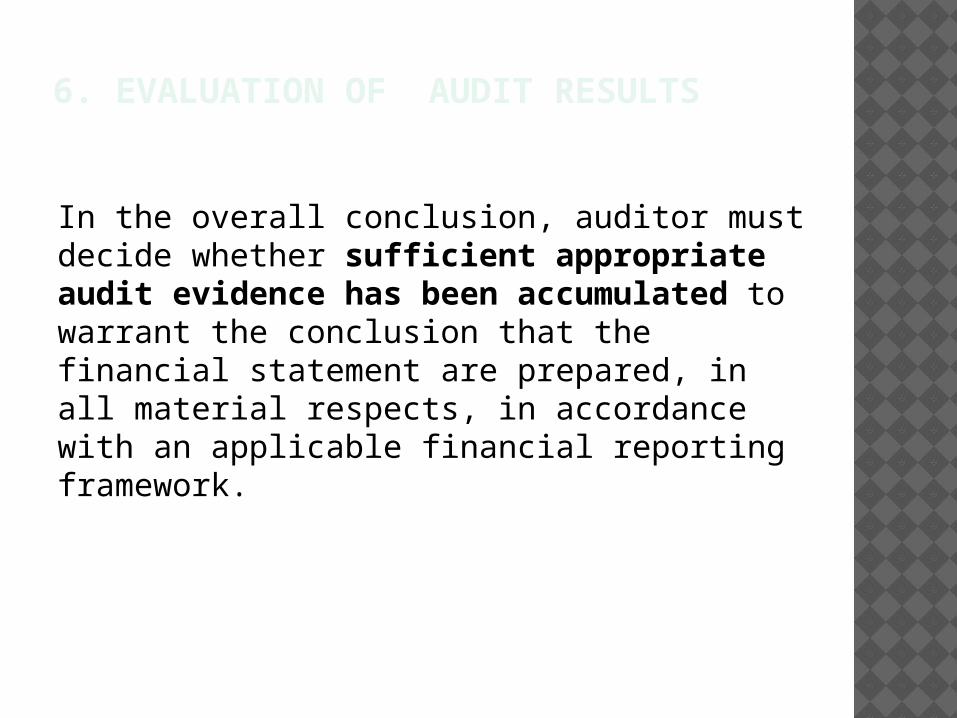

6. EVALUATION OF AUDIT RESULTS

In the overall conclusion, auditor must decide whether sufficient appropriate audit evidence has been accumulated to warrant the conclusion that the financial statement are prepared, in all material respects, in accordance with an applicable financial reporting framework.

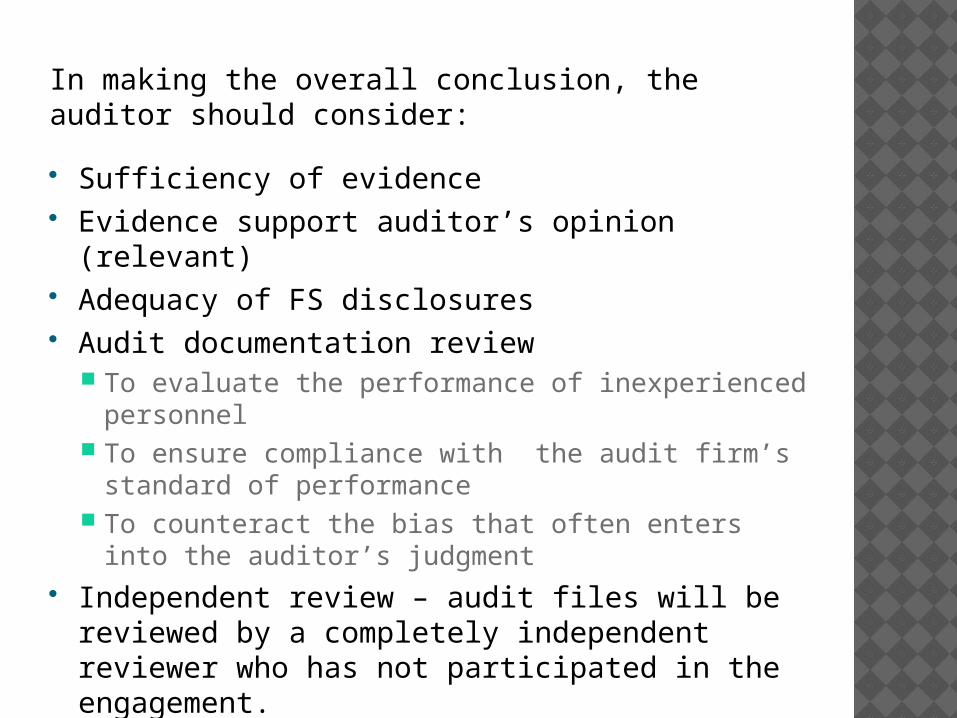

In making the overall conclusion, the auditor should consider: Sufficiency of evidence Evidence support auditor’s opinion (relevant)

Adequacy of FS disclosures Audit documentation review

To evaluate the performance of inexperienced personnel

To ensure compliance with the audit firm’s standard of performance

To counteract the bias that often enters into the auditor’s judgment

Independent review – audit files will be reviewed by a completely independent reviewer who has not participated in the engagement.

7. COMMUNICATIONS OF AUDIT MATTERS WITH THOSE CHARGED WITH CORPORATE GOVERNANCE

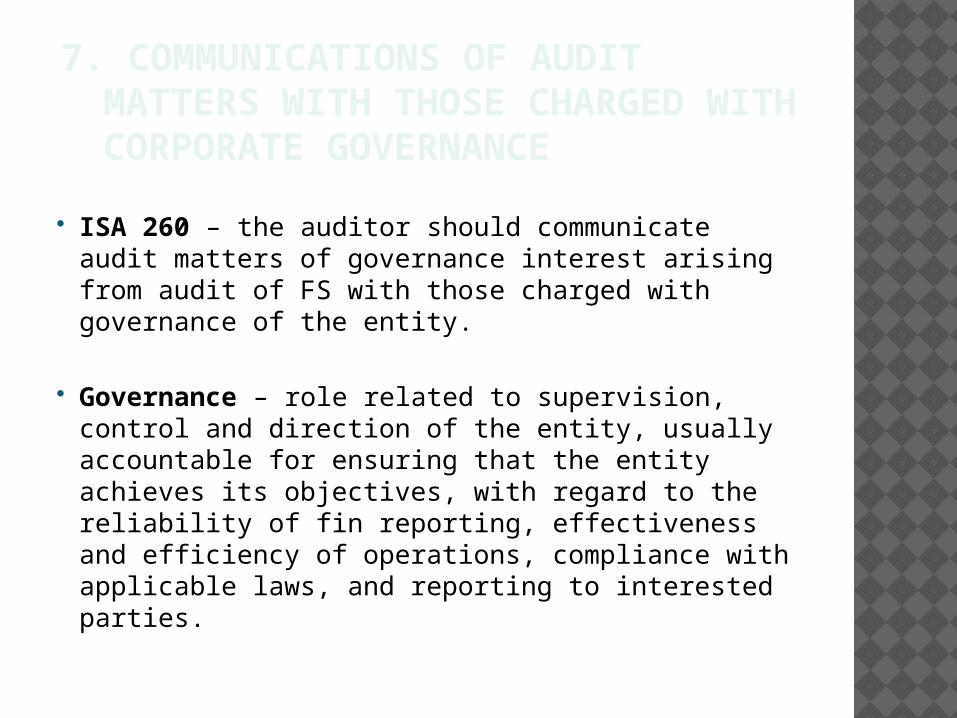

ISA 260 – the auditor should communicate audit matters of governance interest arising from audit of FS with those charged with governance of the entity.

Governance – role related to supervision, control and direction of the entity, usually accountable for ensuring that the entity achieves its objectives, with regard to the reliability of fin reporting, effectiveness and efficiency of operations, compliance with applicable laws, and reporting to interested parties.

Para 11, ISA 260 - The auditor should consider audit matters of governance interest and communicate them with those charged with governance, i.e.:General approach and overall scope of the auditSelection of accounting policies that might have material effect on FS

Potential effect on FS of any material risk and exposures, such as pending litigation, that require disclosures

Audit adjustmentMaterial uncertainties on entity’s ability to continue as a going concern

Disagreements with management about matters that could be significant to FS or the auditor’s report.

Auditor should also inform on uncorrected misstatement aggregated by the auditor during the audit that were determined by mgmt to be immaterial.