auditing, governance and scandals group assignment

TRANSCRIPT

N13505 Auditing, Governance and ScandalsGroup Assignment

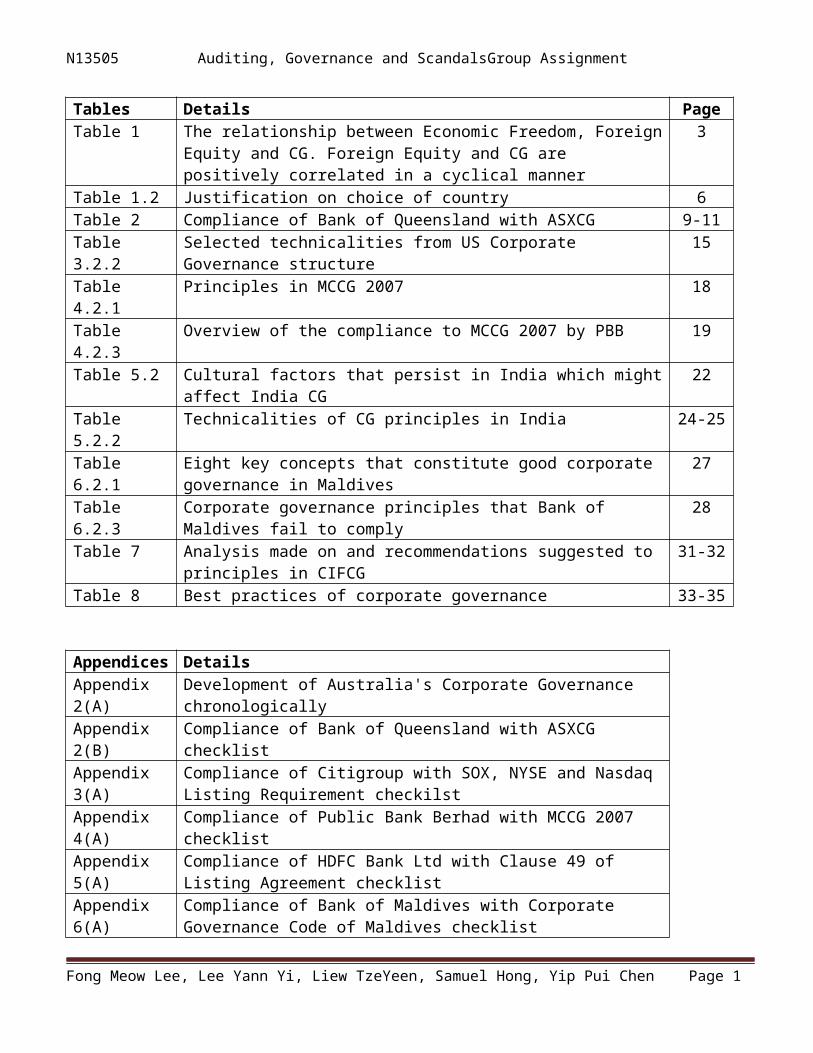

Tables Details PageTable 1 The relationship between Economic Freedom, Foreign

Equity and CG. Foreign Equity and CG are positively correlated in a cyclical manner

3

Table 1.2 Justification on choice of country 6Table 2 Compliance of Bank of Queensland with ASXCG 9-11Table 3.2.2

Selected technicalities from US Corporate Governance structure

15

Table 4.2.1

Principles in MCCG 2007 18

Table 4.2.3

Overview of the compliance to MCCG 2007 by PBB 19

Table 5.2 Cultural factors that persist in India which mightaffect India CG

22

Table 5.2.2

Technicalities of CG principles in India 24-25

Table 6.2.1

Eight key concepts that constitute good corporate governance in Maldives

27

Table 6.2.3

Corporate governance principles that Bank of Maldives fail to comply

28

Table 7 Analysis made on and recommendations suggested to principles in CIFCG

31-32

Table 8 Best practices of corporate governance 33-35

Appendices DetailsAppendix 2(A)

Development of Australia's Corporate Governance chronologically

Appendix 2(B)

Compliance of Bank of Queensland with ASXCG checklist

Appendix 3(A)

Compliance of Citigroup with SOX, NYSE and Nasdaq Listing Requirement checkilst

Appendix 4(A)

Compliance of Public Bank Berhad with MCCG 2007 checklist

Appendix 5(A)

Compliance of HDFC Bank Ltd with Clause 49 of Listing Agreement checklist

Appendix 6(A)

Compliance of Bank of Maldives with Corporate Governance Code of Maldives checklist

Fong Meow Lee, Lee Yann Yi, Liew TzeYeen, Samuel Hong, Yip Pui Chen Page 1

N13505 Auditing, Governance and ScandalsGroup Assignment

Appendix 7(A)

Compliance of respective country’s corporate governance structure to CIFCG checklist

Appendix 7(B)

Observation on compliance of respective country’s corporate governance structure to CIFCG

Fong Meow Lee, Lee Yann Yi, Liew TzeYeen, Samuel Hong, Yip Pui Chen Page 2

N13505 Auditing, Governance and ScandalsGroup AssignmentTable of Content

1.0 Introduction1.1 Objective1.2 Justification on choice of industry, country and listed company

2.0 Australia 2.1 Introduction to Bank of Queensland2.2 Australian Stock Exchange Corporate Governance

2.2.1 Principles 2.2.2 Technicalities 2.2.3 Compliance of bank with ASXCG2.2.4 Criticisms and critical evaluation of ASXCG

2.3 Whistle Blowing Policy

3.0 United States3.1 Introduction to Citigroup 3.2 Sarbanes-Oxley Act 2002, NYSE, Nasdaq Listing Requirement

3.2.1 Principles 3.2.2 Technicalities

3.2.3 Compliance of bank with SOX, NYSE and Nasdaq Listing Requirement

3.2.4 Criticisms and critical evaluation of SOX, NYSE and Nasdaq Listing Requirement3.3 Whistle Blowing Policy

4.0 Malaysia 4.1 Introduction to Public Bank Berhad4.2 Malaysian Code on Corporate Governance (MCCG)

4.2.1 Principles 4.2.2 Technicalities

4.2.3 Compliance of bank with MCCG4.2.4 Criticisms and critical evaluation of MCCG

4.3 Whistle Blowing Policy

5.0 India5.1 Introduction to HDFC Bank Ltd5.2 Clause 49 of Listing Agreement

5.2.1 Principles 5.2.2 Technicalities

Fong Meow Lee, Lee Yann Yi, Liew TzeYeen, Samuel Hong, Yip Pui Chen Page 3

N13505 Auditing, Governance and ScandalsGroup Assignment 5.2.3 Compliance of bank with Clause 49 of Listing Agreement

5.2.4 Criticisms and critical evaluation of Clause 49 of Listing Agreement5.3 Whistle Blowing Policy

6.0 Maldives6.1 Introduction to Bank of Maldives6.2 Corporate Governance Code of Maldives

6.2.1 Principles 6.2.2 Technicalities

6.2.3 Compliance of bank with Corporate Governance Code of Maldives

6.2.4 Criticisms and critical evaluation of Bank of Maldives6.3 Whistle Blowing Policy

7.0 Composite International Framework of Corporate Governance (CIFCG)7.1 Observation on compliance of respective country’s corporate governance structure to CIFCG7.2 Analysis on cross country differences 7.3 Recommendation

8.0 Best Practices of Corporate Governance

9.0 Conclusion

10.0 Appendices

11.0 References

Fong Meow Lee, Lee Yann Yi, Liew TzeYeen, Samuel Hong, Yip Pui Chen Page 4

N13505 Auditing, Governance and ScandalsGroup Assignment1.0 Introduction

Mentions of CG (CG) first appeared in 16th century England when thetrading monarchy erected its first central bank alongside joint stock companies that mushroomed into existence.

Contradictory to the meticulous nature of accounting, CG still remains an enigma to many who attempt to describe it. To this date, there is no set definition of CG (CIIA, 2012) due to constantly developing ideas of what CG should be. The Cadbury Report attempts to formalize the ambiguous concept by describing CG as ‘the system by which companies are directed and controlled’ (Cadbury Committee, 1992) which is solely the responsibility of the board of directors.

As CG developed, it began to allude to different concepts in a wider context and shows its recommendations emerging naturally in the course of a company’s evolution such as accountability and sound ethicsin managing a company (Financial Times, 2012) and further expansion of ‘responsibility’ to include the executive management and employees (IFAC, 2009; OECD, 2004).

However, all definitions point towards the same theme; structure and procedures that enable a company to achieve its goals without compromising on subjective areas of ethics that are not regulated by law. CG is a catchall phrase that covers grey areas of righteousness that constantly varies in the virtue of context (Broshko and Li, 2006).

The practice of good CG is an element of scrutiny of all listed companies as the scope of the company’s accountability now extends to the public masses that invest in them. Following the explosion of international trade at the end of the industrial revolution, formal intervention by countries’ respective Securities Exchange Commissions was necessary to encourage and maintain the inflow of foreign equity.

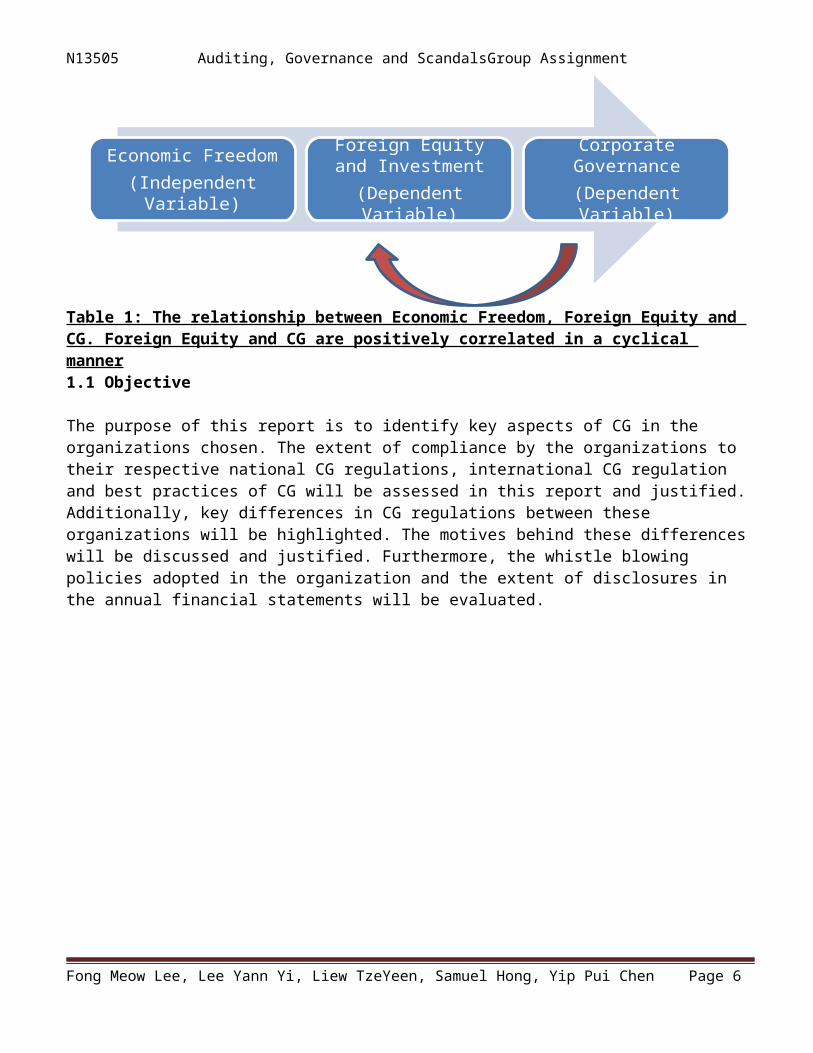

On the other hand, foreign trade and equity flow is positively correlated to a country’s economic freedom, as illustrated in the diagram below:

Fong Meow Lee, Lee Yann Yi, Liew TzeYeen, Samuel Hong, Yip Pui Chen Page 5

N13505 Auditing, Governance and ScandalsGroup Assignment

Table 1: The relationship between Economic Freedom, Foreign Equity and CG. Foreign Equity and CG are positively correlated in a cyclical manner1.1 Objective

The purpose of this report is to identify key aspects of CG in the organizations chosen. The extent of compliance by the organizations to their respective national CG regulations, international CG regulation and best practices of CG will be assessed in this report and justified.Additionally, key differences in CG regulations between these organizations will be highlighted. The motives behind these differenceswill be discussed and justified. Furthermore, the whistle blowing policies adopted in the organization and the extent of disclosures in the annual financial statements will be evaluated.

Fong Meow Lee, Lee Yann Yi, Liew TzeYeen, Samuel Hong, Yip Pui Chen Page 6

Economic Freedom(Independent Variable)

Foreign Equity and Investment(Dependent Variable)

Corporate Governance(Dependent Variable)

N13505 Auditing, Governance and ScandalsGroup Assignment1.2 Justification on choice of industry, country and listed company

The banking industry is our scope of analysis in this study of CG. Thisindustry has high exposure to wide range of risks in their daily operations and therefore, any misconduct could adversely affect its stakeholders including depositors, customers, shareholders, employees, creditors and society. The ripple effect can extend to causing turbulence in national economy. Deregulation opened way for increased global competition to this industry. Therefore, the banking industry issaid to be the backbone of the financial system in a nation.

Banks chosen in respective countries are based on availability of information relating to CG in order to assist us in this study and their qualification as listed company in stock exchanges. All these banks are believed to represent a diverse picture of the nations’ banking industries that they represent.

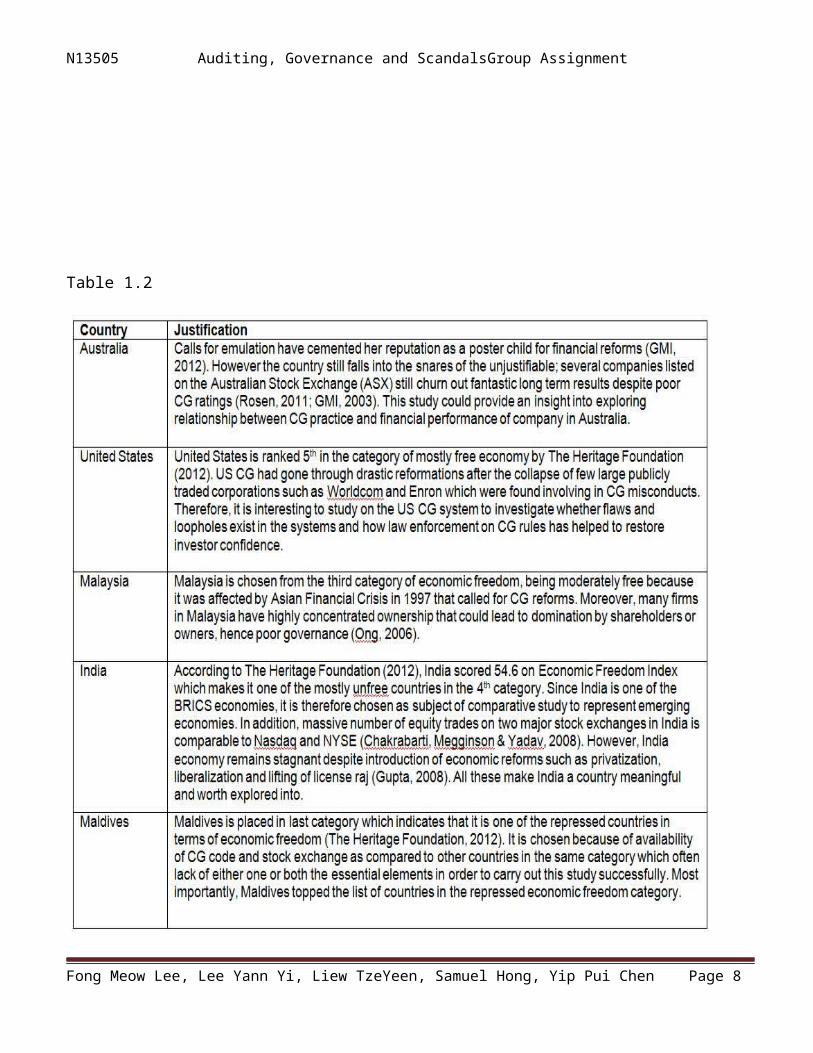

One country is selected from each category of differing economic levelsof economic freedom due the same reasons stated above. Table 1.2 below is a summary of justification on choice of country:

Fong Meow Lee, Lee Yann Yi, Liew TzeYeen, Samuel Hong, Yip Pui Chen Page 7

N13505 Auditing, Governance and ScandalsGroup Assignment

Table 1.2

Fong Meow Lee, Lee Yann Yi, Liew TzeYeen, Samuel Hong, Yip Pui Chen Page 8

N13505 Auditing, Governance and ScandalsGroup Assignment

2.0 Australia

2.1 Introduction to Bank of Queensland

Bank of Queensland is the one of the oldest banks in Australia. Initially established as a building society, it was converted into a bank in 1887, subsequently a trading bank in 1942 and then a public listed financial institution in 1971. Apart from providing the usual banking services, it is actively involved in high profile merger and acquisition activities. On top of the current notable issues explored in Table 1.2, its implicit involvement in the collapsed Storm Financial, also known as ‘Australia’s Champion Wealth Destroyer’ (Barry, 2011), has thrust the bank into negative spotlight.

2.2 Australian Stock Exchange CG

The history of CG in Australia traces back to the early 1960s, where the economic boom led to companies that mushroomed both in number and size. Subsequent foreign investment channeled equity to Australia’s rapidly growing industries and the ASX soon began to necessitate disclosures in financial reports of companies. This marked the beginning of the institutionalization of CG in Australia.

However, loopholes and lax enforcement of regulation soon manifested resulting in the eventual crash of ASX in the late 1980s, with investors exiting the country in search for other places of economic prosperity. The limitations of ASX’s regulation soon mitigated attention of investors to CG as an integral element of self-regulation which was more effective in combating agency problems (Smith, 1776).

Fong Meow Lee, Lee Yann Yi, Liew TzeYeen, Samuel Hong, Yip Pui Chen Page 9

N13505 Auditing, Governance and ScandalsGroup AssignmentThe enactment of the United Kingdom Companies Act in 1948 made certain disclosures mandatory, which then contextually evolved into its currentCompanies Act Code (Farrar, 1999).

The role of the legal system in CG continued to diminish and was eventually superseded in 2002 by the formation of the ASX CG Council, which comprises of 20 independent industrial boards (ASX, 2012) and codifies the highly flexible ‘Principles of Good Governance and Best Practice Recommendations’, which is voluntary in nature. Current developments in Australia’s CG currently mirror that of USA (Robins, 2006). The development of Australia’s Corporate Governance is shown chronologically in Appendix 2(A).

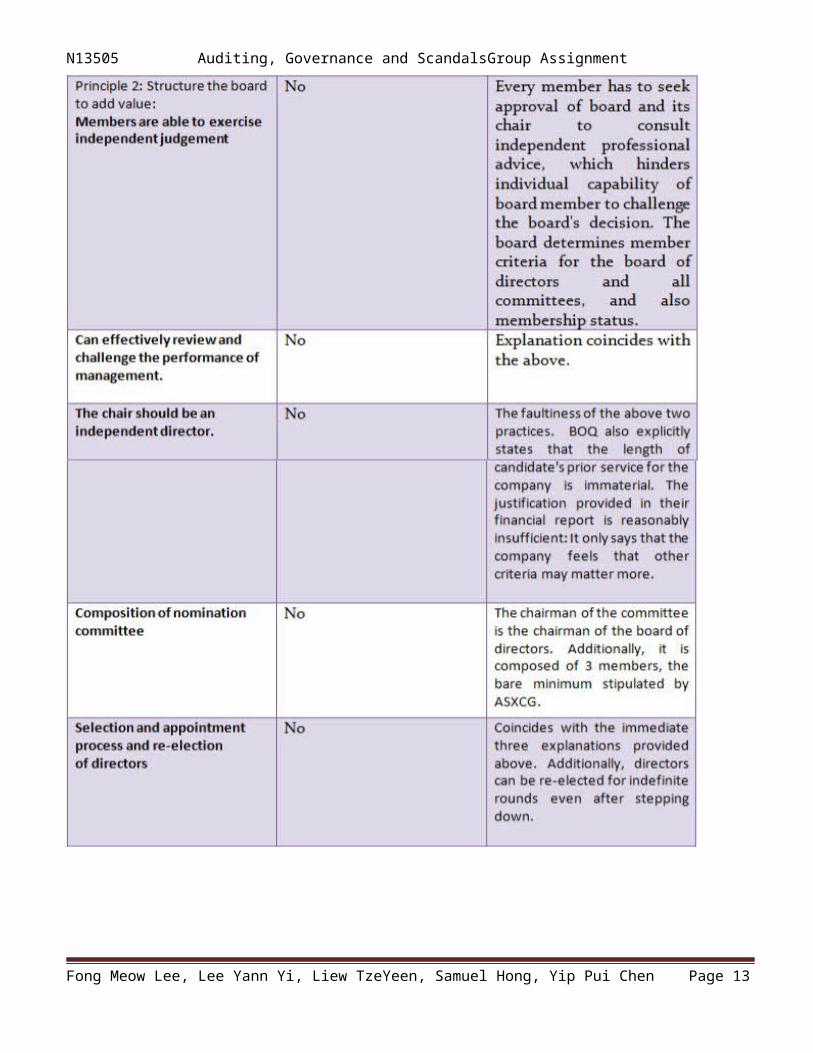

2.2.1 Principles

The “If not, Why not’ approach is suggestive of the country’s attempt of going over and above the OECD framework (as with their gender diversity recommendations) as the ASXCG has 8 principles, in contrast to the OECD set of 5, although the former is simply a rewording of the latter (refer to Appendix A for a table on OECD and ASXCG’s matching ofcorporate governance principles).

2.2.2 Technicalities

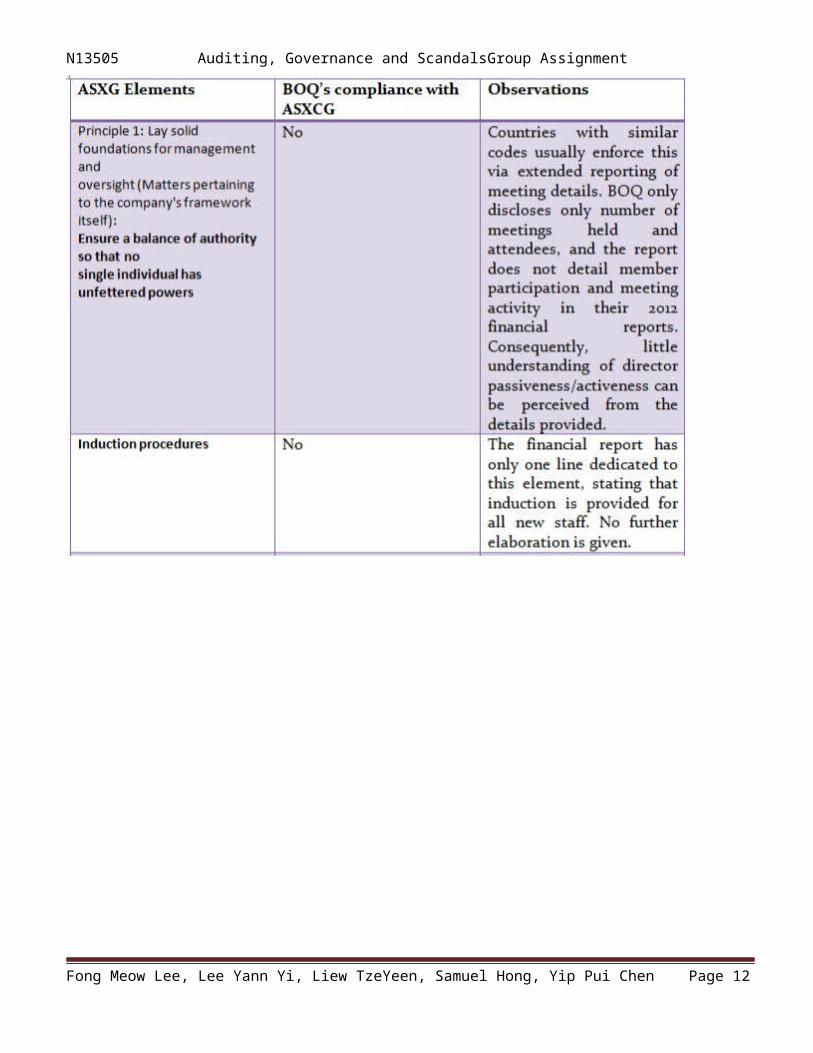

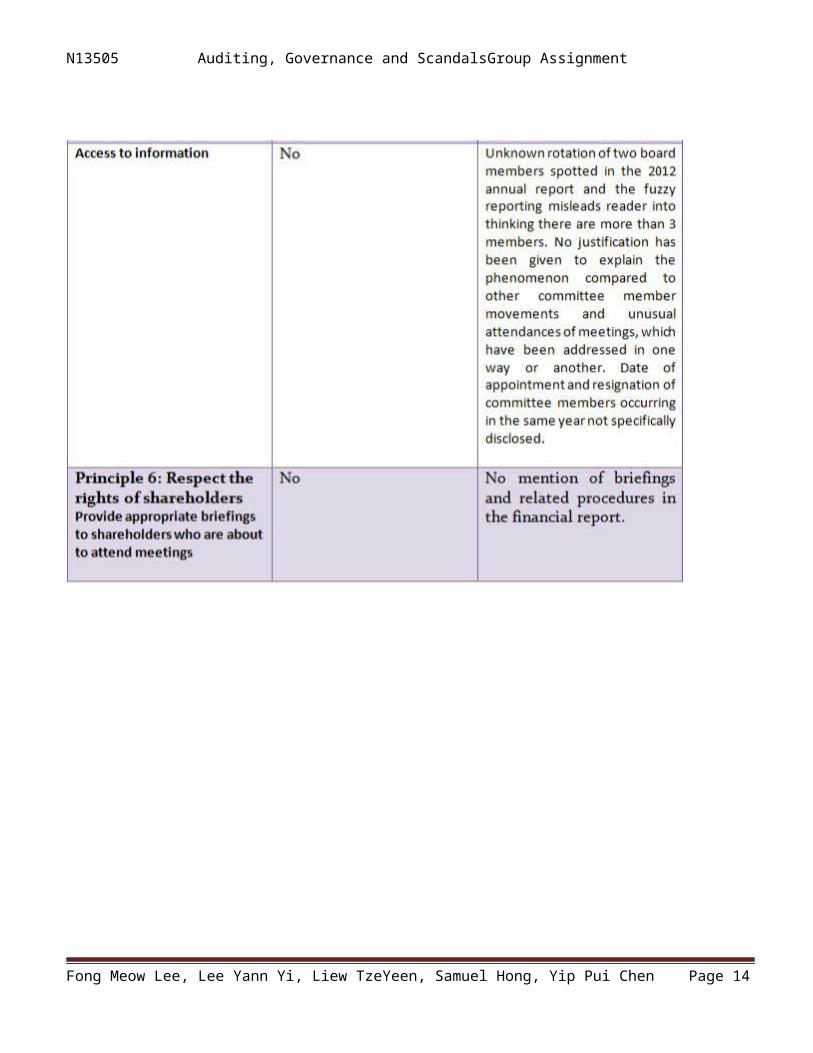

There are 43 core elements in ASXCG. BOQ has complied with 34, equalling to 79% compliance rate. It is observed that non compliances usually stem from the same vagueness that plagues the ASXCG has explained above; the grey areas that are trodden upon lead to illogical

Fong Meow Lee, Lee Yann Yi, Liew TzeYeen, Samuel Hong, Yip Pui Chen Page 10

N13505 Auditing, Governance and ScandalsGroup Assignmentoutcomes as illustrated in the table below. Additionally, minor errors in reporting have also been spotted:

2.2.3 Compliance of Bank with ASXCG

BOQ complies with every principle stated in the ASXCG and has structured their report in such a way that all elements and sub-elements of compliance follow the exact order of the ASXCG. This is possibly due to general awareness that as a large financial institutiontheir compliance to CG codes are constantly under high public scrutiny(evident due to repetitive and prominent placement of their CG statements on its website) and doing such will facilitate reading.

Table 2:

Fong Meow Lee, Lee Yann Yi, Liew TzeYeen, Samuel Hong, Yip Pui Chen Page 11

N13505 Auditing, Governance and ScandalsGroup Assignment

Fong Meow Lee, Lee Yann Yi, Liew TzeYeen, Samuel Hong, Yip Pui Chen Page 12

N13505 Auditing, Governance and ScandalsGroup Assignment

Fong Meow Lee, Lee Yann Yi, Liew TzeYeen, Samuel Hong, Yip Pui Chen Page 13

N13505 Auditing, Governance and ScandalsGroup Assignment

Fong Meow Lee, Lee Yann Yi, Liew TzeYeen, Samuel Hong, Yip Pui Chen Page 14

N13505 Auditing, Governance and ScandalsGroup Assignment

2.2.4 Criticisms and critical evaluation of ASXCG

Many critics have spoken out against the lack of (any) specific technicalities and criteria, which makes in depth comparison difficult even with a composite framework as shown in Appendix 7(A).

The approach seems to cause low quality disclosures (Sheehan, 2009; Seidl et al, 2009) and poses four major setbacks:

a) Companies can easily convey merely outward compliance by ‘speaking’in the same code, hence misleading shareholders (Sheehan, 2009) b) Companies often provide scattered, irrelevant information c) Difficulty in judging extent of compliance as there is no set criteria 4) Negates inter firm and interstate comparison due to lack of standardization (Woodward, 2004).

The vagueness is negatively evident in many notable elements of the ASXCG, as summarized in the table below and will be further elaborated in sections 7.0 and 8.0 in Appendix

2.3 Whistle Blowing Policy

The code of ethics provision in the ASXCG doubles as an inferior whistle blowing policy; instead of falling into the ambit of securitiesexchange regulation, ASXCG delegates the power to individual companies,recommending them to create an environment at the workplace that ‘encourages’ whistle blowing behavior. The whistle blowing legislation was first recommended by an Australian Senate back in 1994 but never materialized. A.J Brown offers a few explanations for this (Brown, 2012):

1. Whistle blowing policies are not needed in federal government agencies

Fong Meow Lee, Lee Yann Yi, Liew TzeYeen, Samuel Hong, Yip Pui Chen Page 15

N13505 Auditing, Governance and ScandalsGroup Assignment2. Uncertain that whistle blowing issues were popular amongst or even

needed by the Australian Public3. Ambiguity of whistle blowing policies worldwide make it difficult

to distinguish what works and what does not4. Lack of Political Support

The absence of corporate whistle blowing policies is reflected uniformly across all banks, including the Bank of Queensland, where anysuggestion of whistle blowing activity lies in its code of ethics. Ironically, Queensland has a state-centric Whistleblower’s Protection Act 1994 that only protects government employees.

3.0 United States

3.1 Introduction to Citigroup

Citigroup is a multinational financial services entity listed on the NYSE. It was established in 1812 and has been operating in the industryfor 200 years. It caters to around 200 million customer accounts globally and has a broad business network over 160 countries (Citigroup.com, 2012), providing a wide category of financial products and services to the consumers, corporations, governments and institutions. Currently, it is the third largest bank in the U.S. (National Information Center, 2012). Despite having bagged prominent awards synonymous for excellence in integrity, the bank was fined $2.56billion USD for their involvement in the Worldcom fiasco.

3.2 Sarbanes-Oxley Act 2002, NYSE, Nasdaq Listing Requirement

Management practices for large public corporations in United States before the 1980s paid little attention on the shareholders’ interests (Kaplan and Holmstrom, 2003). Most corporations emphasize on generatinggrowth instead of maximizing shareholders’ interests and only some

Fong Meow Lee, Lee Yann Yi, Liew TzeYeen, Samuel Hong, Yip Pui Chen Page 16

N13505 Auditing, Governance and ScandalsGroup Assignmentsignificant stakeholders’ interests get attention from the management (Kaplan and Holmstrom, 2003), leading to poor governance mechanisms.

To adapt to the changing business environment in US, Kaplan and Holmstrom (2003) comment that few aspects of US CG has undergone gradual transformations to ensure relevancy. However, US CG system was bombarded with criticisms after collapses of few large publicly traded corporations such as Enron and Worldcom that were found committing frauds in its financial reporting (Jackson, 2010). Jackson suggests that market-based system is an insufficient approach for CG and furtherquips that the causes that drove the wrongdoings were the increasing importance of performance-based judgment in corporations and the equity-based compensation scheme to the managers.

Eventually, US introduced SOX legislation in 2002 and the Securities Commissions (SEC) amended listing requirements of New York Stock Exchange (NYSE) and National Association of Securities Dealers Automated Quotations (NASDAQ) as the remedies for the issues. Sewe (2012) contends that “SOX is a federal law that sets new or enhanced standards for all U.S. public company boards, management and public accounting firms”. While Kaplan and Holmstrom suggest that the governance guidelines by NYSE and NASDAQ is a form of regulatory control for CG.

3.2.1 Principles

ICAEW (2006) suggests that the CG in US “can be characterized as a regulator-led system predominantly enforced through SEC regulation, stock exchange listing rules and state law”. Owing to the federal nature of the US constitution, ICAEW (2006) and Hansen (n.d.) conclude that CG code is not present in US.

Fong Meow Lee, Lee Yann Yi, Liew TzeYeen, Samuel Hong, Yip Pui Chen Page 17

N13505 Auditing, Governance and ScandalsGroup Assignment

There are two existing CG reports from the Cadbury and OECD discussing about general CG principles that should follow by corporations (Insolvency Guardian Australia, 2012). Insolvency Guardian Australia (2012) suggests that SOX is actually derived from several principles recommended in the Cadbury and OECD reports. Combination of SOX and stock exchange requirements forms the rules-based CG in US (Broshko & Kai Li, 2006).

3.2.2 Technicalities

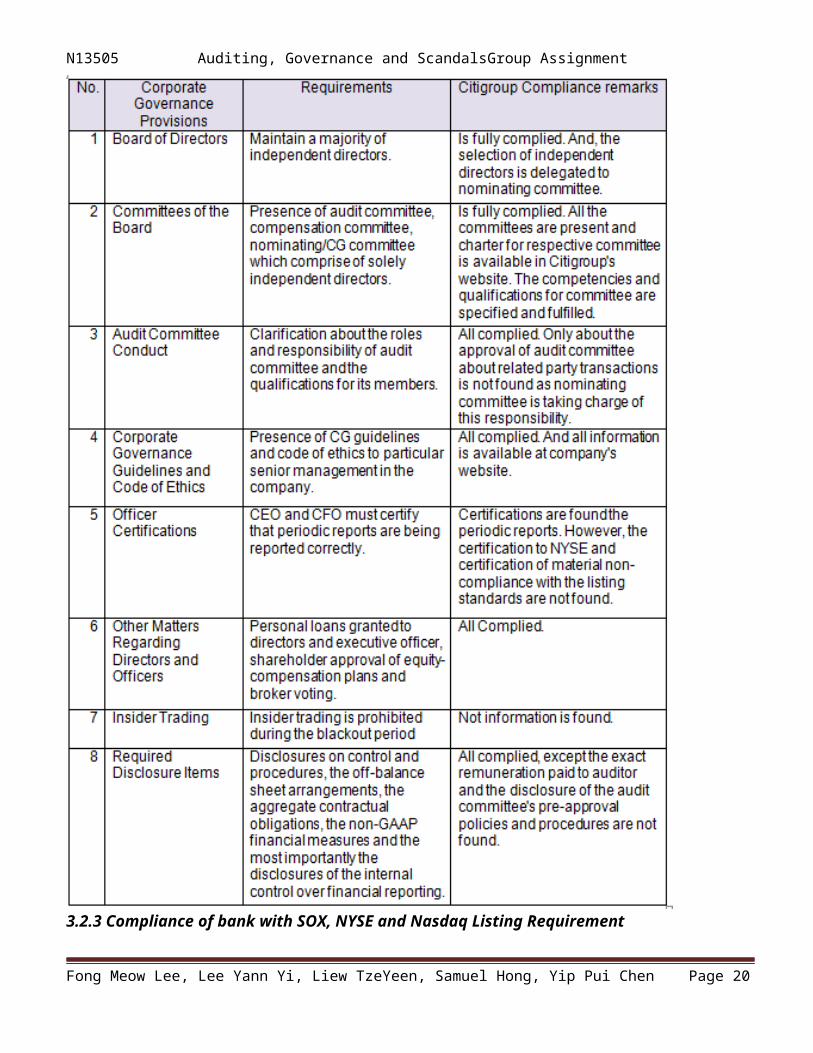

Selected technicalities are shown in Table 3.2.2.

Fong Meow Lee, Lee Yann Yi, Liew TzeYeen, Samuel Hong, Yip Pui Chen Page 18

N13505 Auditing, Governance and ScandalsGroup Assignment

Table 3.2.2:

Fong Meow Lee, Lee Yann Yi, Liew TzeYeen, Samuel Hong, Yip Pui Chen Page 19

N13505 Auditing, Governance and ScandalsGroup Assignment

3.2.3 Compliance of bank with SOX, NYSE and Nasdaq Listing Requirement

Fong Meow Lee, Lee Yann Yi, Liew TzeYeen, Samuel Hong, Yip Pui Chen Page 20

N13505 Auditing, Governance and ScandalsGroup AssignmentSince US CG is regulatory-led and on a mandatory basis, Citigroup has declared that it does its best to comply with all CG rules in US. Despite a 85% compliance rate, cross checks between Citigroup’s compliance to US CG shown in Table 3.2.2 reflected missing gaps which Citigroup failed to fulfill. Evaluation is based on current available information from Citigroup and therefore concluding that Citigroup failed to comply is premature. It is suggested that Citigroup should enhance its transparency in disclosing information necessary to educatestakeholders about their compliance to US CG.

3.2.4 Criticisms and critical evaluation of SOX, NYSE and Nasdaq Listing Requirements

Criticisms of US regulatory-led CG arose since it was implemented. Costs associated with compliance to the SOX and compulsory stock exchange requirements are perceived as burdensome by the corporations listed on US stock exchange (Jackson, 2010). As a result of the need torestructure internal control systems and audit procedures, audit firms demand a higher audit fee from corporations. The regulations pose additional cost when firms are required to hire only competent directors and independent directors.

Wade (2008) also suggests that it is difficult to justify what constitutes good CG. There is no promise that law can ensure effective CG when they claim they actually do. For example, the law can fail to justify why maintaining an independent audit committee can enhance company’s performance and restore stakeholders’ confidence.

3.3 Whistle Blowing Policy

It is notable that whistle-blowing procedures have been provisioned by the US legal system. However, Citigroup scores poorly in acting upon complaints brought by whistle-blower. No formal procedures and actions have been executed audit committee of Citigroup in tackling this issue.However, there are no observable drawbacks in whistle blower protectionas SOX prohibits retaliation against whistle blower.

Fong Meow Lee, Lee Yann Yi, Liew TzeYeen, Samuel Hong, Yip Pui Chen Page 21

N13505 Auditing, Governance and ScandalsGroup Assignment

4.0 Malaysia

4.1 Introduction to Public Bank Berhad

PBB is a bank under Public Bank Group, the third largest banking group by asset size in Malaysia. It had been listed on Bursa Malaysia since 1967 and is a growing regional player in finance industry with high commitment towards CG. The bank believes strong CG will deliver higher value to its stakeholders, especially investors (PBB, 2011).

4.2 Malaysian Code on CG (MCCG)

Following the 1997 Asian financial crisis, Malaysian government established a High Level Finance Committee on CG (FCCG) in 1998 to dealwith CG issues that surfaced (Mallin, 2010). Malaysian Code on CG (MCCG) 2010 that formalizes CG standard was published and the Minority Shareholder Watchdog Group (MSWG) consequently established to assist inimplementation and improvement of Malaysia’s CG. Compliance is voluntary. However, since 2001, MCCG has been incorporated into KLSE Listing Requirement (now Bursa Malaysia). PLCs are required to comply or explain for non-compliance (Wahab, 2010). Revisions were made to MCCG in 2007 and are superseded by MCCG 2012 (Securities Commission Malaysia, 2011b).

Malaysia draws the Code mainly from UK’s Cadbury Report (1992) and Hampel Report (1998) and adopts a hybrid approach similar to Combined Code 2003 in UK. It focuses more on commitment to the principles and practices instead of just ‘box-ticking’ (Securities Commission Malaysia, 2007).However, a study by Dora et al. (2012) shown that many companies, including top 250 PLCs in Malaysia are merely ‘outwardly-

Fong Meow Lee, Lee Yann Yi, Liew TzeYeen, Samuel Hong, Yip Pui Chen Page 22

N13505 Auditing, Governance and ScandalsGroup Assignmentcomplying’ with the Code , which allows directors to execute their oversight responsibility effectively and efficiently instead of enhancing firms’ value and performance.

MCCG 2007 consists of three parts that provide guidelines on Principlesand Best Practices. The revised MCCG 2012 is arranged in a way to provide principles together with recommendations and commentaries. Bursa Malaysia requires PLCs to provide a Statement of CG that includesa narrative statement on application of the Principles and a statement on compliance with the Best Practices or Recommendations to be displayed prominently in the annual reports. Commentaries on each itemsof compliance are not required but non-compliance and alternatives mustbe disclosed (Bursa Malaysia, 2012).

Government intervention in economy through National Economic Policy andprivatization aims to eliminate economic trademark by race. It targets to achieve 30% of ‘Bumiputra’s ownership in the corporate sector and this allows more political intervention of companies in Malaysia. Such cronyism and political ties ease firms in obtaining resources owned by government. Hence, fraud and corruption seem prevalent in these companies (Abidin and Ahmad, 2007). These characteristics are deemed closely tied with reformation of MCCG.

4.2.1 Principles

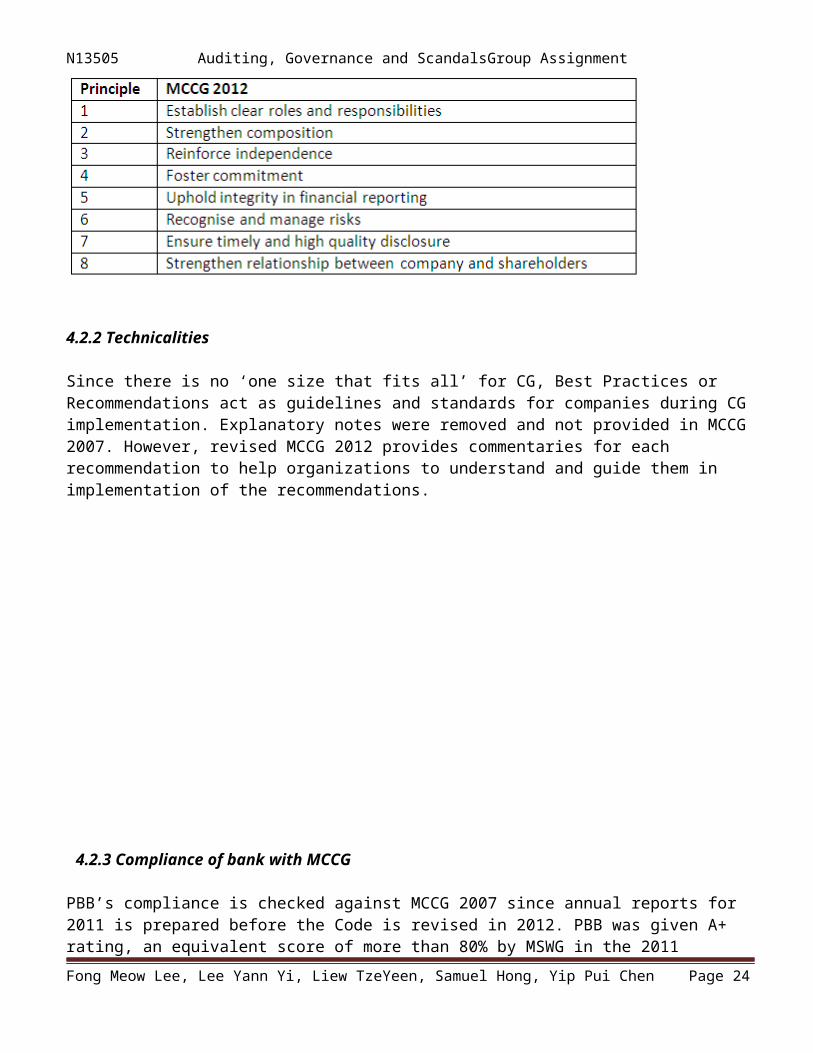

Principles of the Code cover broad concepts of good CG to allow for flexible implementation suited to individual companies. In MCCG 2007, the Principles covered are on directors, directors’ remuneration, shareholders and accountability and audit. Latest revision to MCCG extends the number of Principles covered from 4 to 8 as shown below in Table 4.2.1.

Table 4.2.1:

Fong Meow Lee, Lee Yann Yi, Liew TzeYeen, Samuel Hong, Yip Pui Chen Page 23

N13505 Auditing, Governance and ScandalsGroup Assignment

4.2.2 Technicalities

Since there is no ‘one size that fits all’ for CG, Best Practices or Recommendations act as guidelines and standards for companies during CGimplementation. Explanatory notes were removed and not provided in MCCG2007. However, revised MCCG 2012 provides commentaries for each recommendation to help organizations to understand and guide them in implementation of the recommendations.

4.2.3 Compliance of bank with MCCG

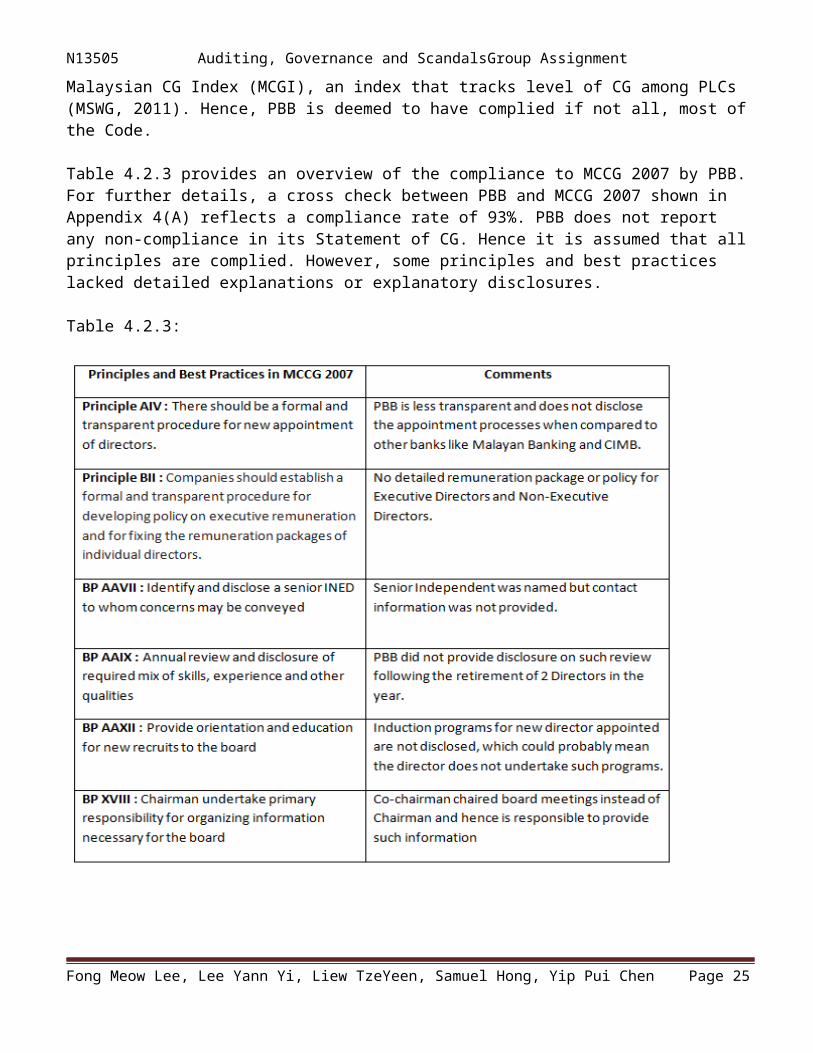

PBB’s compliance is checked against MCCG 2007 since annual reports for 2011 is prepared before the Code is revised in 2012. PBB was given A+ rating, an equivalent score of more than 80% by MSWG in the 2011 Fong Meow Lee, Lee Yann Yi, Liew TzeYeen, Samuel Hong, Yip Pui Chen Page 24

N13505 Auditing, Governance and ScandalsGroup AssignmentMalaysian CG Index (MCGI), an index that tracks level of CG among PLCs (MSWG, 2011). Hence, PBB is deemed to have complied if not all, most ofthe Code.

Table 4.2.3 provides an overview of the compliance to MCCG 2007 by PBB.For further details, a cross check between PBB and MCCG 2007 shown in Appendix 4(A) reflects a compliance rate of 93%. PBB does not report any non-compliance in its Statement of CG. Hence it is assumed that allprinciples are complied. However, some principles and best practices lacked detailed explanations or explanatory disclosures.

Table 4.2.3:

Fong Meow Lee, Lee Yann Yi, Liew TzeYeen, Samuel Hong, Yip Pui Chen Page 25

N13505 Auditing, Governance and ScandalsGroup AssignmentNevertheless, unlike many Malaysian organizations, PBB did disclose remunerations on each director. The bank outperforms the others in using AGMs as a mean of communication with investors, proven by high participation rate and awards by MSWG for Best Conduct of AGM for 3 consecutive years.

4.2.4 Criticisms and critical evaluation of MCCG

MCCG’s compliance is voluntary “to allow for a more constructive and flexible approach response” to enhance the standard of CG (Securities Commission Malaysia, 2007, p.2). In the absence of strict enforcement, Directors take CG issues and compliance lightly. However, it is also noted that compliance in substance is better than compliance in form (Securities Commission Malaysia, 2007).

Additional risk exposure and poor risk management is seen as factors that caused the 1997 crisis (Ong, 2006). Despite the increasing importance of risk management, MCCG does not require companies to set up risk management committees and risk policies. MCCG also neglects theimportance of auditors in ensuring good CG.

4.3 Whistle Blowing Policy

PBB has an Anti-Fraud Policy that specifies the responsibilities of employees in prevention, detection and reporting of fraudulent activities within the organization, including measures that will be taken against employees that are involved in frauds. Neither channels of whistle blowing or protection for whistleblowers are provided.

Fong Meow Lee, Lee Yann Yi, Liew TzeYeen, Samuel Hong, Yip Pui Chen Page 26

N13505 Auditing, Governance and ScandalsGroup Assignment

5.0 India

5.1 Introduction to HDFC Bank Ltd

HDFC Bank Ltd is a subsidiary of Housing Development Finance Corporation Limited (HDFC) Group incorporated in 1994 (Hdfcbank.com, 2012). It provides a wide range of business services, categorised into three main segments: wholesale banking, retail banking and treasury. The Bank highly values the importance of good CG to ensure fairness forall stakeholders and create shareholder value. Fundamental principles such as independence, accountability, responsibility, transparency, fair and timely disclosures and credibility are deemed as good CG practices by the bank.

5.2 Clause 49 of Listing Agreement

NFCG (2004) proposes that CG framework in India consists of Companies Act, 1956, Securities (Contracts) Regulation Act, 1956, Securities and Exchange Board of India (SEBI) Act, 1992, Depositories Act, 1996 and Clause 49 of the Listing Agreement.

Confederation of Indian Industry (CII) was the first to develop and promote “Desirable CG: A Code” in 1998 on voluntary adoption basis (Pande, 2011). Subsequently, SEBI enacted Clause 49 of the Listing Agreement applicable to listed companies for regulation of CG practicesin 2000 (Business.gov.in, 2012). Over the years, many special committees are set up to revise Clause 49. Provisions in Clause 49 resemble Anglo-American CG standards such as the Cadbury Report, the OECD Principles and SOX (Pande, 2011). However, differences that arise from contextualization are apparent and will be discussed later in 7.0.

Fong Meow Lee, Lee Yann Yi, Liew TzeYeen, Samuel Hong, Yip Pui Chen Page 27

N13505 Auditing, Governance and ScandalsGroup Assignment

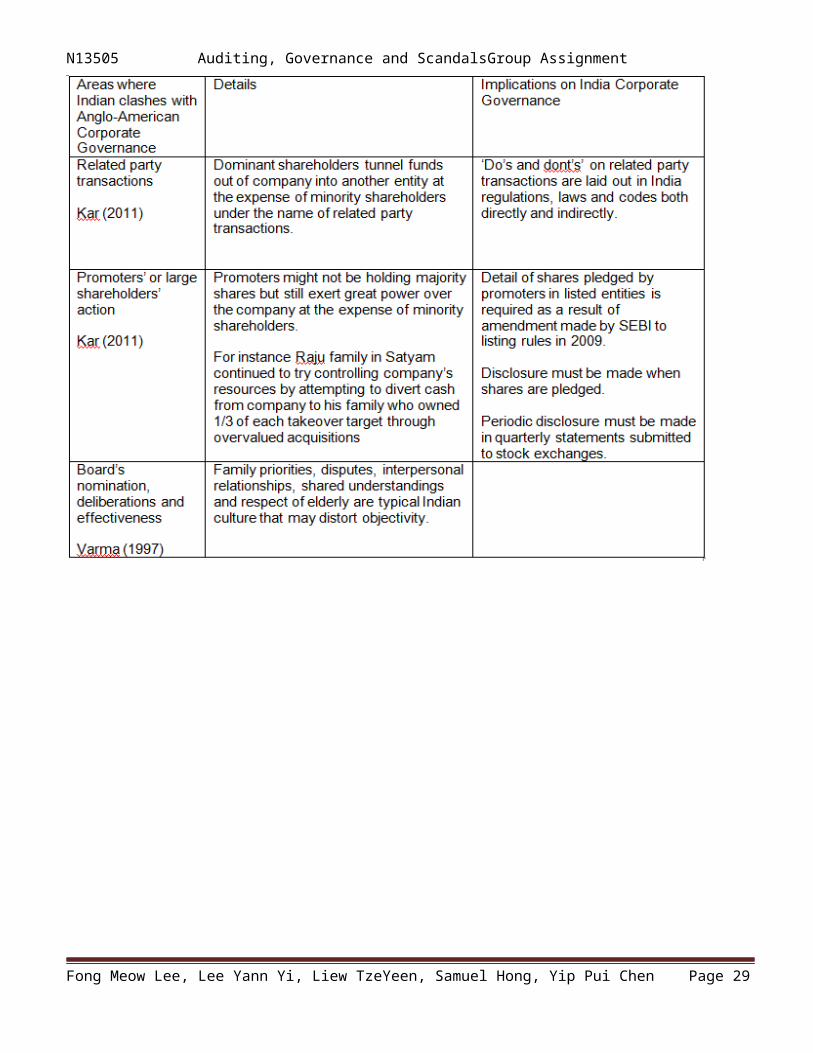

Table 5.2 below shows cultural factors that persist in India which might affect India’s CG:

Table 5.2:

Fong Meow Lee, Lee Yann Yi, Liew TzeYeen, Samuel Hong, Yip Pui Chen Page 28

N13505 Auditing, Governance and ScandalsGroup Assignment

Fong Meow Lee, Lee Yann Yi, Liew TzeYeen, Samuel Hong, Yip Pui Chen Page 29

N13505 Auditing, Governance and ScandalsGroup Assignment5.2.1 Principles

According to Gupta (2008), absence of principles on bank governance in India is due to multiplicity and sophistication of up to five legislations, which are RBI Act, SBI Act, Bank Nationalization Act, Banking Regulation Act and Companies Act. Clause 49 of Listing Agreement centered around six aspects: Board of directors, audit committee, subsidiary companies, disclosures, CEO/CFO certification, report on CG and compliance.

5.2.2 Technicalities

Selective significant technicalities of CG principles in India are appeared as sub-section in Table 5.2.2 below.

5.2.3 Compliance of bank with Clause 49 of Listing Agreement

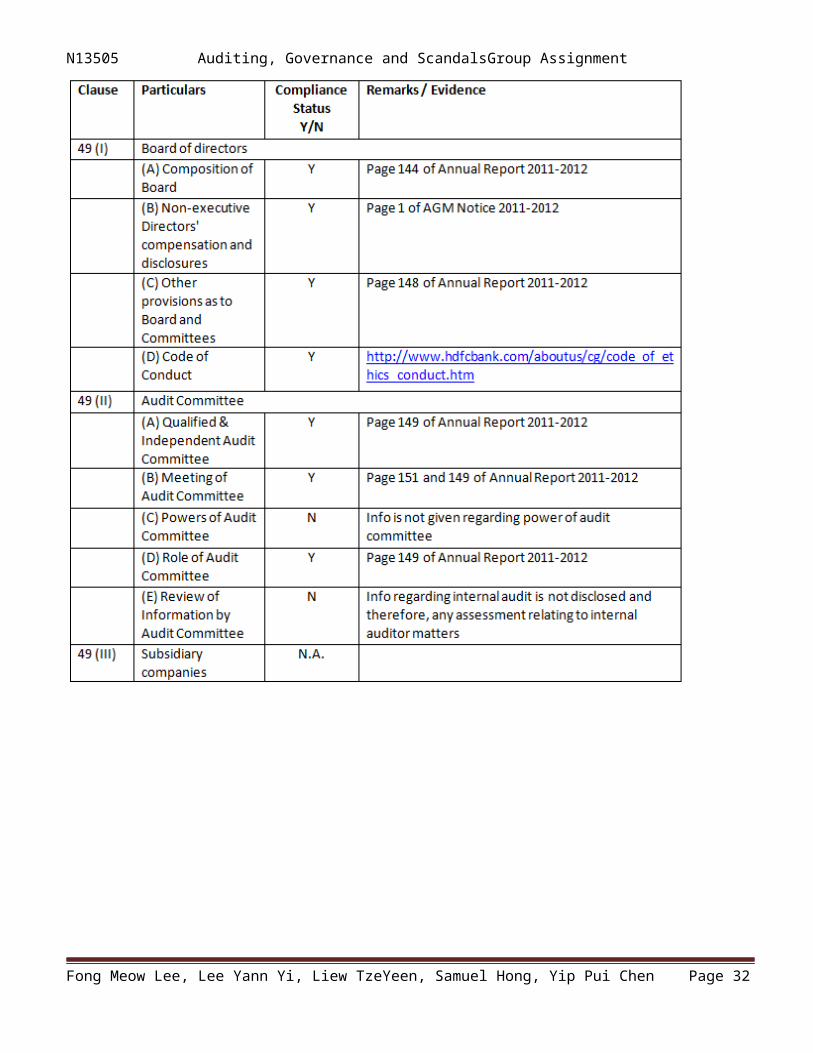

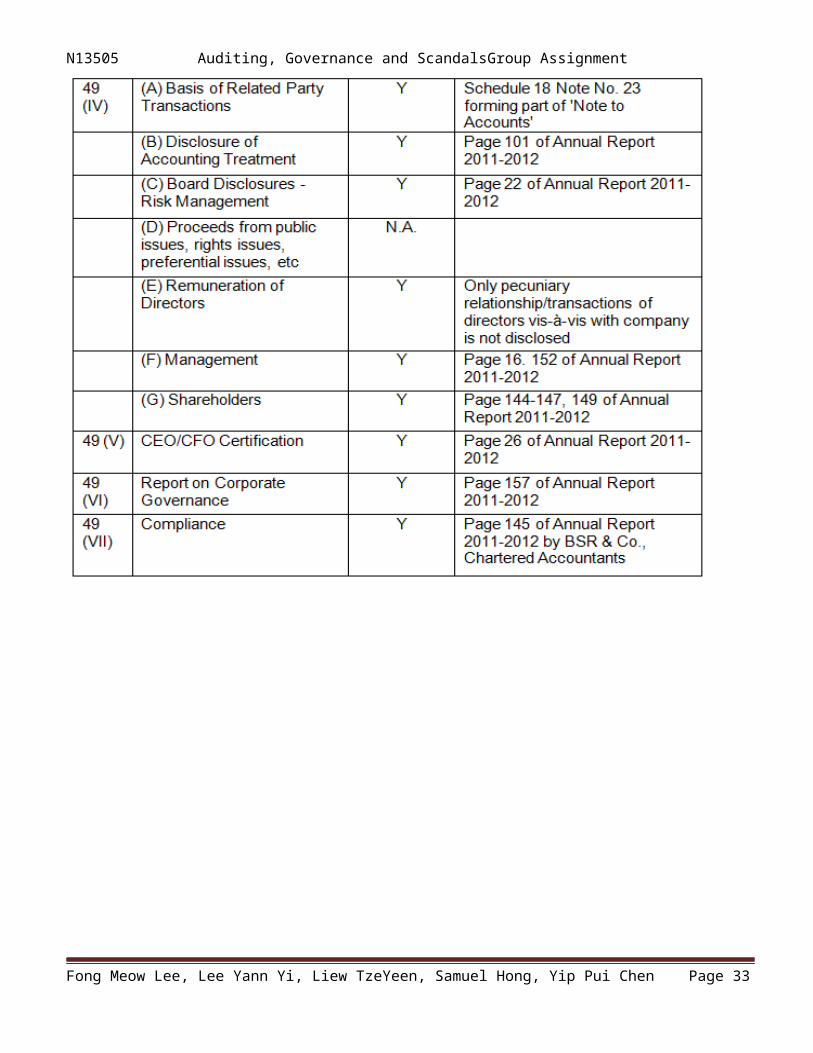

Due to resource constraints, compliance of HDFC Bank with section in Clause 49 cannot be assessed individually in detail. Despite BSR & Co.,Chartered Accountant’s validation of the bank’s compliance to CG as stipulated in Clause in its annual report 2011-2012, it is observed in Table 5.2.2 that there is insufficient evidence disclosed to support their compliance (for elaboration please refer to Appendix 5(A)). For instance, neither the authority nor actual activities carried out by the audit committee were disclosed. As much as transparency is needed particularly in internal control aspects, internal audit reports of HDFC Bank are not made available to the public, restricting outsiders from assessment of CG compliance in this aspect. Other unavailable information includes letter of internal control weaknesses and disclosure of pecuniary relationships between non-executive directors and the bank. Limited information on whistle blower mechanisms, audit qualifications and the procedures on evaluation on non-executive Board members further restrict our analysis. Nevertheless, HDFC Bank has adopted all voluntary CG practices.

Despite the bank being 83% in compliance with Clause 49, it is still predominantly controlled by foreign institutional investors with 30.68%shareholdings and followed by promoters with 23.15% shareholdings. This

Fong Meow Lee, Lee Yann Yi, Liew TzeYeen, Samuel Hong, Yip Pui Chen Page 30

N13505 Auditing, Governance and ScandalsGroup Assignmentraises red flags suggesting potential abuse of power by dominant shareholders. HDFC Bank scores less well in disclosure of post board meeting, disclosure and transparency and disclosure of stakeholders’ interests (Shah and Gupta, 2012). Conversely, the bank fulfills other aspects in Clause 49 which makes it ranked 4th out of 12 banks assessed in the country.

Table 5.2.2:

Fong Meow Lee, Lee Yann Yi, Liew TzeYeen, Samuel Hong, Yip Pui Chen Page 31

N13505 Auditing, Governance and ScandalsGroup Assignment

Fong Meow Lee, Lee Yann Yi, Liew TzeYeen, Samuel Hong, Yip Pui Chen Page 32

N13505 Auditing, Governance and ScandalsGroup Assignment

Fong Meow Lee, Lee Yann Yi, Liew TzeYeen, Samuel Hong, Yip Pui Chen Page 33

N13505 Auditing, Governance and ScandalsGroup Assignment

5.2.4 Criticisms and critical evaluation of Clause 49 of Listing Agreement

Reed (2002) argues that CG reform in India has been shifting towards the Anglo-Saxon model in which its efficacy in India is highly questionable, possibly because CG problems faced in India are very different from that of US and UK(Varma, 1997). Agency problems in US and UK prompted CG reforms to focus on increasing Board Independence byestablishing Audit Committees and Compensation Committees to exercise considerable restraint of CEO for best interests of shareholders Conflict between dominant and minority shareholders is a central problem in India. This can be overcome by either regulatory intervention or capital market forces. The former often entails micro-management of regular business operations while the latter is preferable for its ability to make business judgments and levying of sanctions in the form of denial of market access. Weak legal protection, poor disclosure prerequisites and overriding owners are other factors that thwart the development of efficient CG principles inIndia (Gupta, 2008).

Joint publication by ACGA and CLSA Asia-Pacific Markets suggests that India has particularly low score in enforcement and culture of CG (ACGALtd, 2012). Poor enforcement of CG mechanism is further accentuated by research showing that no sanctions have been imposed by SEBI despite recording an excess of a thousand companies that fail to file their CG compliance reports for the quarter ended September 30, 2008 (Khanna, 2009). Current CG mechanisms in India are alleged to be more on the “form” than “content”, epitomized by companies like Satyam and Reliancethat violated governance practices in the same period they were awardedto good CG (Pande, 2011).

5.3 Whistle Blowing Policy

HDFC Bank has adopted and disclosed Whistle Blowing Policy in its annual report. Extent of disclosure is limited to its objectives and

Fong Meow Lee, Lee Yann Yi, Liew TzeYeen, Samuel Hong, Yip Pui Chen Page 34

N13505 Auditing, Governance and ScandalsGroup Assignmentmodus operandi. It serves as a mechanism where employees can report anyissues relating to fraud, malpractice or any other activity or event which is against the interests of the bank and society as a whole, to the attention of Audit and Compliance Committee (HDFCBank.com, 2012). Complaints received are reviewed and acted upon if valid.

Strangely, there are no further records on actual whistle blower activities or complaints made by employees. Most importantly, no information regarding protection of whistle blowers and methods of safeand confidential reporting were provided. The bank’s whistle blowing mechanism generally lacks transparency as compared to that of other banks such as United Bank of India.

Fong Meow Lee, Lee Yann Yi, Liew TzeYeen, Samuel Hong, Yip Pui Chen Page 35

N13505 Auditing, Governance and ScandalsGroup Assignment6.0 Maldives

6.1 Introduction to Bank of Maldives

Bank of Maldives (BoM) is the only locally operated bank which has a broad banking network that can accommodate the whole nation. BoM was founded in 1982 and has 30 years of experience in providing modern banking products that to cater individuals, businesses and institutional investors’ needs.

6.2 CG Code of Maldives

Under the Maldives Securities Act 2/2006, the Capital Market Development Authority (CMDA) was formed in 2006 to bring up the CG issues amongst private and state-owned firms (Shareef and Sodique, n.d.). The CG code was formulated in 2006 and enforced on PLCs in 2008.Consequently, Capital Markets and CG Institute (CMCGI) were establishedto provide training for adopting good CG practices among the board of directors and company secretaries. Practicing good CG is important in Maldives as it adds values for corporations to raise capital funds in global competitive market (CMDA, 2012). Most importantly, compliance ismandatory for PLCs and voluntary for other non-listed entities.

6.2.1 Principles

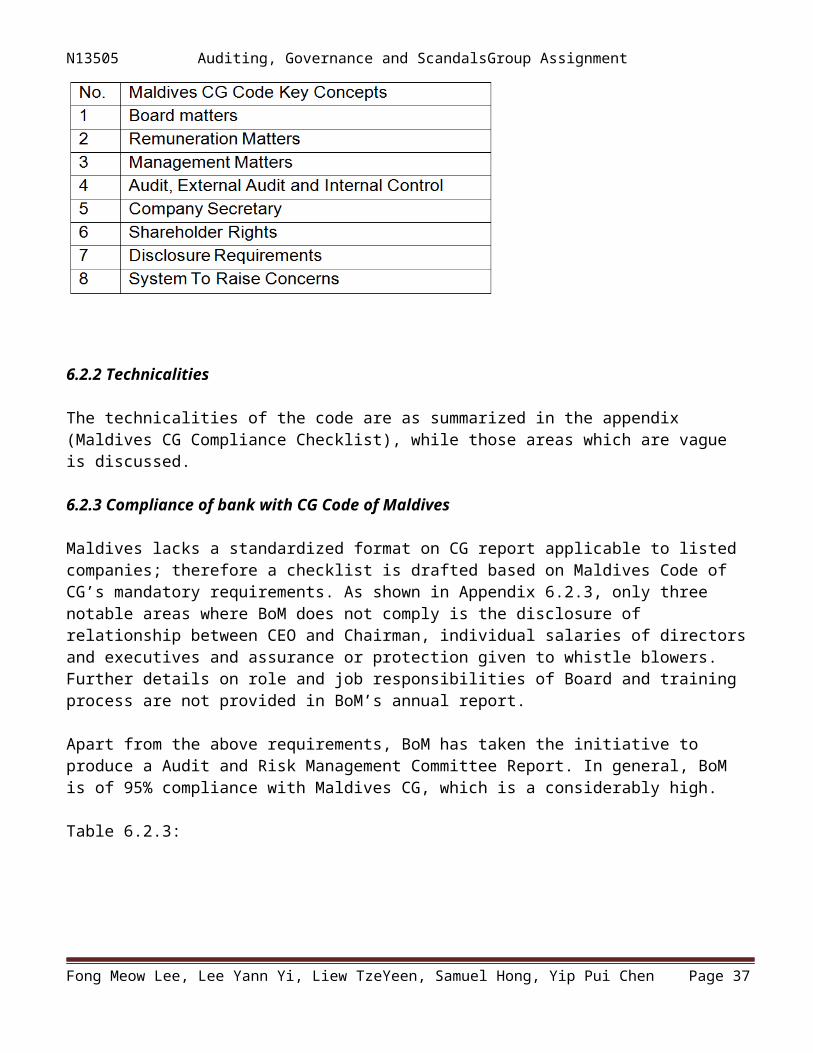

There is no certain measurement of what constitutes a good CG. Therefore, eight key concepts that constitute good CG are identified inthis code and respective recommendations for each element are discussedas shown in Table 6.2.1.

Table 6.2.1:

Fong Meow Lee, Lee Yann Yi, Liew TzeYeen, Samuel Hong, Yip Pui Chen Page 36

N13505 Auditing, Governance and ScandalsGroup Assignment

6.2.2 Technicalities

The technicalities of the code are as summarized in the appendix (Maldives CG Compliance Checklist), while those areas which are vague is discussed.

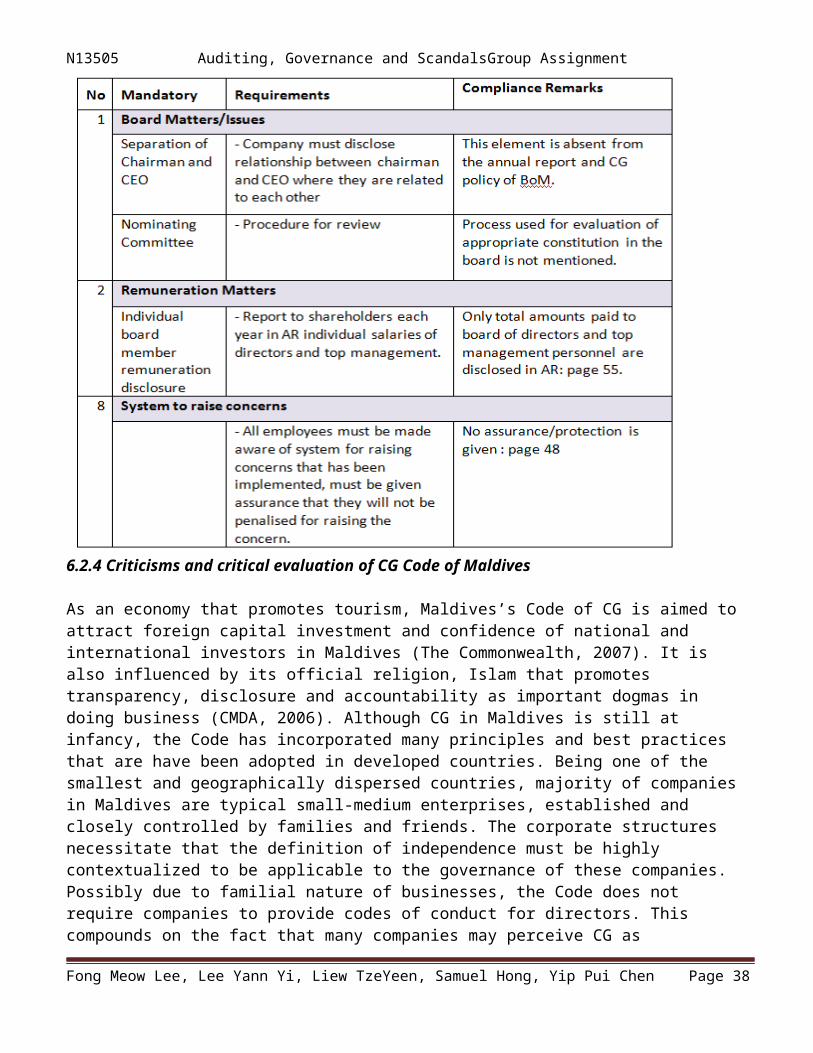

6.2.3 Compliance of bank with CG Code of Maldives

Maldives lacks a standardized format on CG report applicable to listed companies; therefore a checklist is drafted based on Maldives Code of CG’s mandatory requirements. As shown in Appendix 6.2.3, only three notable areas where BoM does not comply is the disclosure of relationship between CEO and Chairman, individual salaries of directorsand executives and assurance or protection given to whistle blowers. Further details on role and job responsibilities of Board and training process are not provided in BoM’s annual report.

Apart from the above requirements, BoM has taken the initiative to produce a Audit and Risk Management Committee Report. In general, BoM is of 95% compliance with Maldives CG, which is a considerably high.

Table 6.2.3:

Fong Meow Lee, Lee Yann Yi, Liew TzeYeen, Samuel Hong, Yip Pui Chen Page 37

N13505 Auditing, Governance and ScandalsGroup Assignment

6.2.4 Criticisms and critical evaluation of CG Code of Maldives

As an economy that promotes tourism, Maldives’s Code of CG is aimed to attract foreign capital investment and confidence of national and international investors in Maldives (The Commonwealth, 2007). It is also influenced by its official religion, Islam that promotes transparency, disclosure and accountability as important dogmas in doing business (CMDA, 2006). Although CG in Maldives is still at infancy, the Code has incorporated many principles and best practices that are have been adopted in developed countries. Being one of the smallest and geographically dispersed countries, majority of companies in Maldives are typical small-medium enterprises, established and closely controlled by families and friends. The corporate structures necessitate that the definition of independence must be highly contextualized to be applicable to the governance of these companies. Possibly due to familial nature of businesses, the Code does not require companies to provide codes of conduct for directors. This compounds on the fact that many companies may perceive CG as

Fong Meow Lee, Lee Yann Yi, Liew TzeYeen, Samuel Hong, Yip Pui Chen Page 38

N13505 Auditing, Governance and ScandalsGroup Assignmentunimportant rendering the degree of compliance questionable (CMDA, 2006).

6.3 Whistle Blowing Policy

A “Whistle Blowing System” was established in 2009 in BoM aiming to provide its employees a channel to raise concerns and grievances of anyillegal or unethical practices within the bank to the Audit and Risk Management Committee. Issues raised will then be handled by Audit and Risk Management Committee. However, no information regarding the definition of whistle blowing or protection to whistle blowers and its implementation are given. This could be partly attributable to vague provisions in the CG Code of Maldives.

7.0 Composite International Framework of CG (CIFCG)

7.1 Observation on compliance of respective country’s CG structure to CIFCG

Fong Meow Lee, Lee Yann Yi, Liew TzeYeen, Samuel Hong, Yip Pui Chen Page 39

N13505 Auditing, Governance and ScandalsGroup AssignmentCompliance of national CG in Australia, US, Malaysia, India and Maldives are compared against CIFCG as shown in Appendix 7(A) and 7(B).

7.2 Analysis on cross country differences

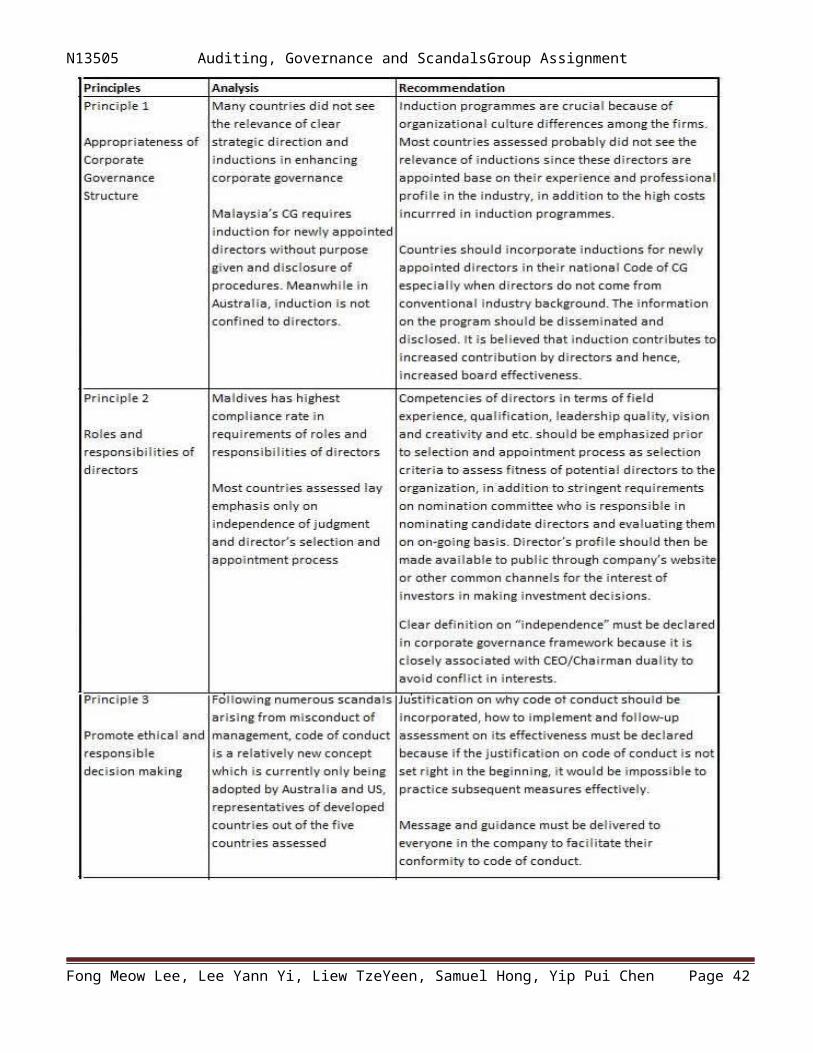

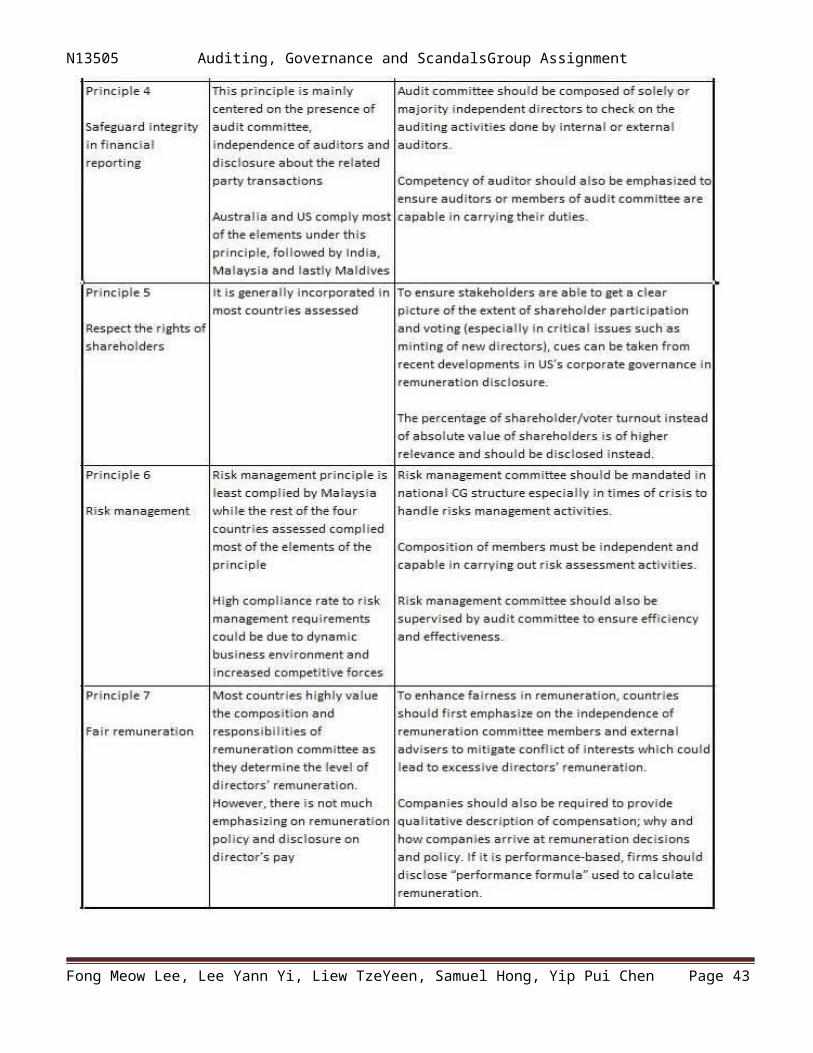

Analysis on the differences in terms of country compliance to CIFCG is shown in Table 7.

7.3 Recommendation

Recommendations made to principles in CIFCG that still requires attention and further room for improvement is shown in Table 7.

Fong Meow Lee, Lee Yann Yi, Liew TzeYeen, Samuel Hong, Yip Pui Chen Page 40

N13505 Auditing, Governance and ScandalsGroup Assignment

Table 7:

Fong Meow Lee, Lee Yann Yi, Liew TzeYeen, Samuel Hong, Yip Pui Chen Page 41

N13505 Auditing, Governance and ScandalsGroup Assignment

Fong Meow Lee, Lee Yann Yi, Liew TzeYeen, Samuel Hong, Yip Pui Chen Page 42

N13505 Auditing, Governance and ScandalsGroup Assignment

Fong Meow Lee, Lee Yann Yi, Liew TzeYeen, Samuel Hong, Yip Pui Chen Page 43

N13505 Auditing, Governance and ScandalsGroup Assignment

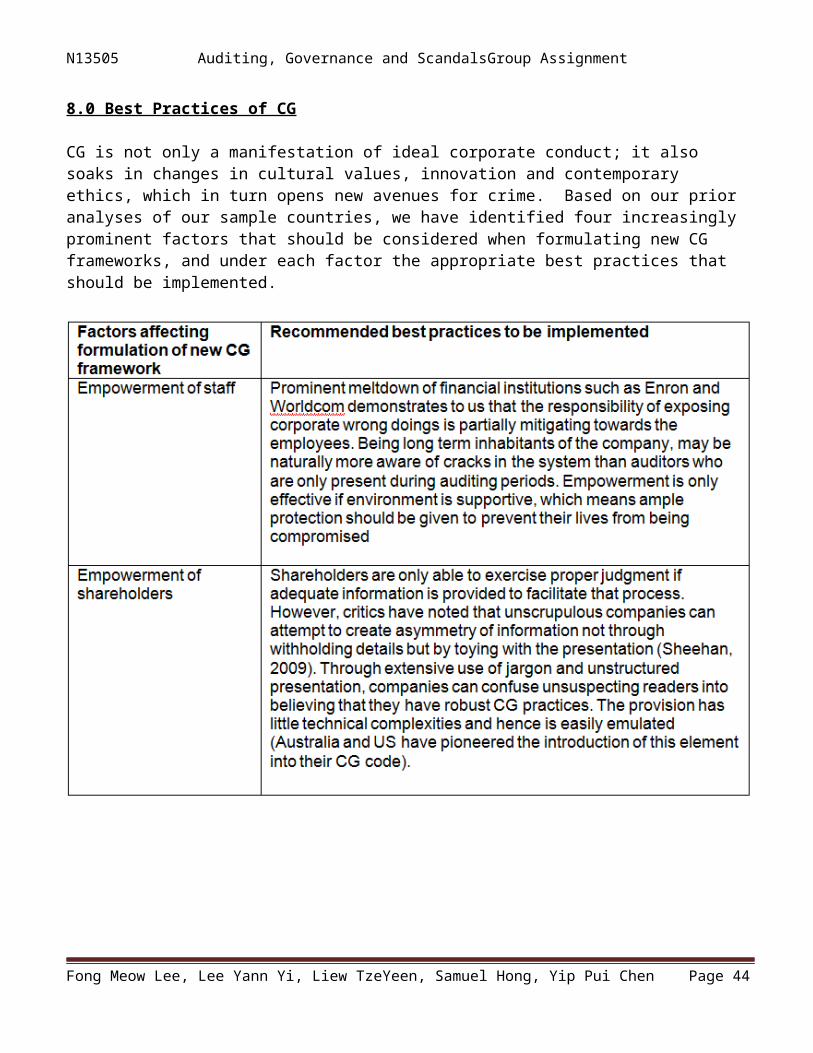

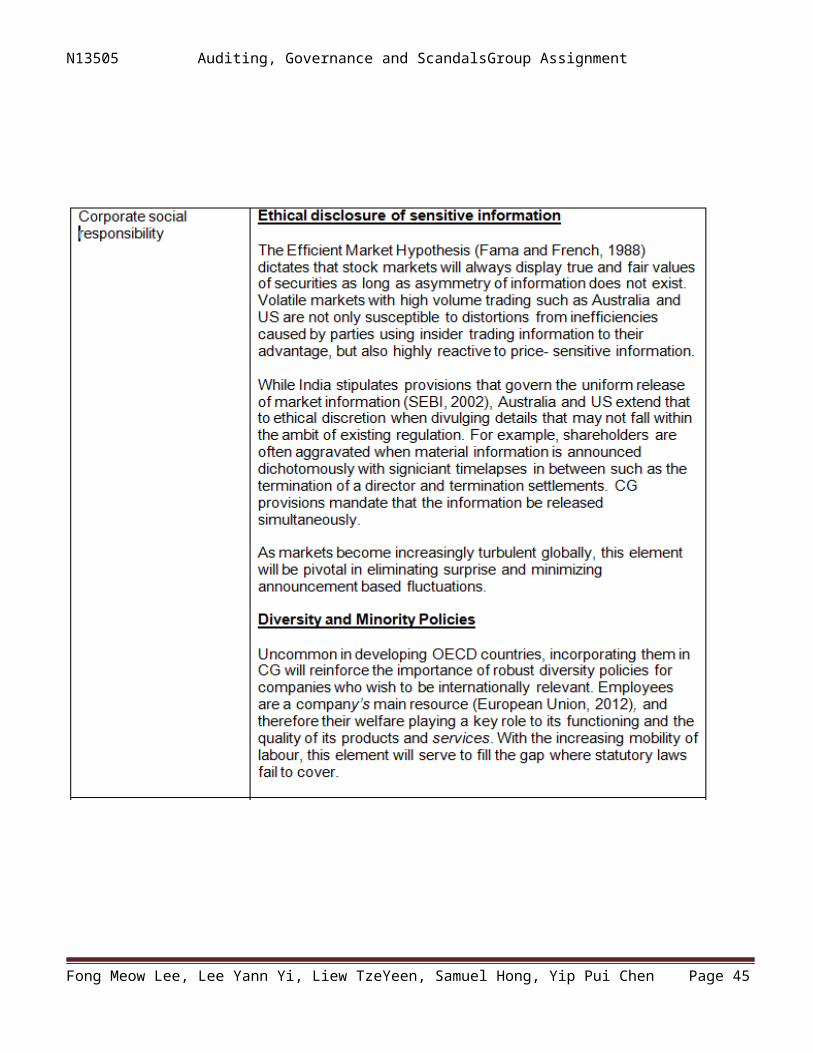

8.0 Best Practices of CG

CG is not only a manifestation of ideal corporate conduct; it also soaks in changes in cultural values, innovation and contemporary ethics, which in turn opens new avenues for crime. Based on our prior analyses of our sample countries, we have identified four increasingly prominent factors that should be considered when formulating new CG frameworks, and under each factor the appropriate best practices that should be implemented.

Fong Meow Lee, Lee Yann Yi, Liew TzeYeen, Samuel Hong, Yip Pui Chen Page 44

N13505 Auditing, Governance and ScandalsGroup Assignment

Fong Meow Lee, Lee Yann Yi, Liew TzeYeen, Samuel Hong, Yip Pui Chen Page 45

N13505 Auditing, Governance and ScandalsGroup Assignment

Fong Meow Lee, Lee Yann Yi, Liew TzeYeen, Samuel Hong, Yip Pui Chen Page 46

N13505 Auditing, Governance and ScandalsGroup Assignment

9.0 Conclusion

Our analyses of the above corporate governance frameworks have successfully met the objectives of this study. We have discovered that the extent of international convergence and domestic compliance resemble a funnel comprising of two dichotomies: Individual national codes of corporate governance never are completely identical to existing elements and principles of international frameworks and corporate codes of governance rarely entirely comply with their national codes.

To justify the adequacy of this situation, we reiterate our early discussions on the nature of corporate governance in 1.0. What separates corporate governance from the rigid frameworks of accounting is the high level of contextualization necessary to ensure that it achieves its objectives. The structure of an entity’s corporate governance covers an exhaustive list of factors such as cultural valuesand integrity (Australia), historical incidences (USA), government intervention in the market (Malaysia), prevailing structures of corporate ownership (India) and current economic goals (Maldives), epitomized by our countries in our study.

Our analyses also show that all companies disappointingly subscribe to ‘outward-compliant’ behavior, manifested in superficial box ticking activity, minimalistic disclosures and meeting only the bare requirements. This implies that any attempt to rely on definite, codified procedures of CG will only perpetuate this behavior as regulation can only cover a limited amount of aspects, allowing companies to get by what possibly could be contextually critical items.

Fong Meow Lee, Lee Yann Yi, Liew TzeYeen, Samuel Hong, Yip Pui Chen Page 47

N13505 Auditing, Governance and ScandalsGroup AssignmentWe conclude our study by emphasizing that further improvements of

CG frameworks, both national and international, should factor this while continually exploring what practices work and what should be discarded while considering the implications of other systematic factors such as inherent economic structure and cultural values.

Fong Meow Lee, Lee Yann Yi, Liew TzeYeen, Samuel Hong, Yip Pui Chen Page 48

N13505 Auditing, Governance and ScandalsGroup Assignment11.0 References

Abd. Hamid, A., Abdul Aziz, R., Dora, D. and Said, J. (2012) Corporate Governance Reporting Of Top 250 Companies: Recent Evidence from Emerging Economy. British Journal of Economics, Finance and Management Sciences, 4 (2), p.95-112.

Abdul Samad, F. (2004) Corporate Governance and Ownership Structure in the Malaysian Corporate Sector. Advances in Financial Economics. 9: pp.355-385 [online]. Available at: http://dx.doi.org/10.1016/S1569-3732(04)09014-0 [Accessed: 27 November 2012].

Abdul Wahab, E. A. (2010) Corporate governance in Malaysia: Corporate Governance Reform in Malaysia. Saarbrücken: LAP Lambert Academic Publishing.

Aguilera, R.V., Williams, C.A., Conley, J.M. and Rupp, D.E. (2006) Corporate Governance and Social Responsibility: A Comparative Analysis of the UK and the US [online]. Available at: http://business.illinois.edu/aguilera/pdf/CGIR%202006.pdf[Accessed: 20th November 2012].

Asian Corporate Governance Association and CSLA Asia-Pacific Markets (2012) CG Watch 2012: Market Rankings [online]. Available at: http://www.acga-asia.org/public/files/CG_Watch_2012_ACGA_Market_Rankings.pdf [Accessed: 3 December 2012].

ASX Corporate Governance (2009) Analysis of Corporate Governance Disclosures in Annual Reports for year ended 31 December 2009 August. [online] Available at: http://www.asx.com.au/documents/about/corporate_governance_disclosures_31_dec_2009_analysis.pdf [Accessed: 4 Dec 2012].

ASX Corporate Governance Council (2004) Analysis of Corporate Governance Practices reported in 2004 Annual Reports. [online] Available at: http://www.asx.com.au/documents/about/analysis_of_cg_practice_disclosure_may_16_2005.pdf [Accessed: 4 Dec 2012].

Fong Meow Lee, Lee Yann Yi, Liew TzeYeen, Samuel Hong, Yip Pui Chen Page 49

N13505 Auditing, Governance and ScandalsGroup AssignmentASX Corporate Governance Council (2007) Marked-Up Amendments dated 30 June 2010 to the Second Edition August 2007 of the Corporate GovernancePrinciples and Recommendations. [online] Available at: http://www.asx.com.au/documents/about/cg_marked_up_amendments_30_june_10.pdf [Accessed: 4 Dec 2012].

ASX Corporate Governance Council (2008) 2005 Analysis of corporate governance practice disclosure Listed trusts. [online] Available at: http://www.asx.com.au/documents/about/analysis_2005_corporate_governance_disclosures_listedtrusts.pdf [Accessed: 4 Dec 2012].

ASX Corporate Governance Council (2009) Analysis of Corporate Governance Disclosures in Annual Reports for year ended 30 June 2009. [online] Available at: http://www.asx.com.au/documents/about/analysis_corporate_governance_disclosures_in_annual_reports_.pdf [Accessed: 4 Dec 2012].

ASX Corporate Governance Council (2010) Changes annotated from 2nd Edition of the principles published 2007 to the amendments to 2nd edition published June 2010. [online] Available at: http://www.asx.com.au/documents/about/cg_comparative_table_june_2010.pdf [Accessed: 4 Dec 2012].

ASX Corporate Governance Council (2010) Corporate Governance Principlesand Recommendations with 2010 Amendments. [report] Sydney: ASX Corporate Governance Council.

ASX Corporate Governance Group (2012) Corporate Governance Council. [online] Available at: http://www.asxgroup.com.au/corporate-governance-council.htm [Accessed: 4 Dec 2012].

Bank of Maldives (2012) Annual Report 2011 [online]. Available at: http://www.bankofmaldives.com.mv/SiteCollectionDocuments/BML%20Annual%20Report%202011%20-%20English.pdf [Accessed: 12 November 2012].

Bank of Queensland (2009) Statement From Bank Of Queensland Regarding Storm Financial [online]. Available at: http://www.boq.com.au/aboutus_media_250609.htm [Accessed: 17th November2012].

Fong Meow Lee, Lee Yann Yi, Liew TzeYeen, Samuel Hong, Yip Pui Chen Page 50

N13505 Auditing, Governance and ScandalsGroup Assignment

Bank of Queensland (2011) BOQ Appoints Stuart Grimshaw as CEO [online].Available at: http://afr.com/rw/2009-2014/AFR/2011/08/22/Photos/6b195752-cd0e-11e0-a648-3567d5de62fd_BOQ_01209543.pdf [Accessed: 17th November 2012].

Bank of Queensland (2012) Corporate Governance [online]. Available at: http://www.boq.com.au/aboutus_corporate_governance.htm [Accessed: 17th November 2012].

Barnes, L. (2006) Nordic Governance in the Context of International Best Practice [online]. Available at: http://132.234.243.22/school/gbs/afe/symposium/2008/Barnes.pdf [Accessed: 3 December 2012].

Barry, P. (2011) In the Eye of the Storm: The Collapse of Storm Financial [online]. Available at: http://www.themonthly.com.au/collapse-storm-financial-eye-storm-paul-barry-2980 [Accessed: 20th November 2012].

Beltratti, A. and Stulz, R. (2009) Why Did Some Banks Perform Better during the Credit Crisis? A Cross-Country Study of the Impact of Governance and Regulation. p.1-38. Available at: http://papers.ssrn.com/sol3/papers.cfm?abstract_id=1433502 [Accessed: 4th December 2012].

Bode, M. (2009) Investors Furious At Storm Inquiry [online]. Available at: http://www.sunshinecoastdaily.com.au/news/banks-let-off-lightly-furious-investors-say/413883/ [Accessed: 20th November 2012].

Boq.com.au (2012) Corporate governance - BOQ. [online] Available at: http://www.boq.com.au/aboutus_corporate_governance.htm [Accessed: 4 Dec2012].

Broshko, E.B. and Kai Li (2006) Corporate Governance Requirements in Canada and the United States: A Legal and Empirical Comparison of the Principles-based and Rules-Based Approaches [online]. Available at: http://finance.sauder.ubc.ca/~kaili/BroshkoLi.pdf [Accessed: 3 December2012].

Fong Meow Lee, Lee Yann Yi, Liew TzeYeen, Samuel Hong, Yip Pui Chen Page 51

N13505 Auditing, Governance and ScandalsGroup AssignmentBrown, A.J. (2012) Everyone backs whistleblowing laws. So why are we still waiting for them? [online]. Available at: http://www.canberratimes.com.au/national/public-service/everyone-backs-whistleblowing-laws-so-why-are-we-still-waiting-for-them-20120929-26ryr.html [Accessed: 20th November 2012].

Bursa Malaysia Securities Berhad (2012) Listing Requirements | Bursa Malaysia Market. [online]. Available at: http://www.bursamalaysia.com/market/regulation/rules/listing-requirements/main-market/listing-requirements [Accessed: 17 November 2012].

Business.gov.in (2012.) Business Portal of India : Government of India,Indian Economy, Investment, Incentives, Trade, Infrastructure, Legal Aspects. [online] Available at: http://business.gov.in [Accessed: 20 November 2012].

Capital Market Development Authority (2006) Corporate Governance in Maldives. In: Developments, Structures, Capacity & Roadmap for Enhancing Corporate Standards in Commonwealth Countries, 17-18 June 2006, Bandos Island Resort. Capital Market Development Authority, p.1-11.

Capital Market Development Authority (2008) Corporate Governance [online]. Available at: http://cmda.gov.mv/corporate-governance/ [Accessed: 3 December 2012].

Capital Market Development Authority (2012) Corporate Governance Code [online]. Available at: http://cmda.gov.mv/docs/Revised%20CG%20Code_12.02.12.pdf [Accessed 1 December 2012].

Chakrabarti, R. (2005) Corporate Governance in India - Evolution and Challenges. Social Science Research Network, Available at: http://unpan1.un.org/intradoc/groups/public/documents/APCITY/UNPAN023826.pdf [Accessed: 3 December 2012].

Fong Meow Lee, Lee Yann Yi, Liew TzeYeen, Samuel Hong, Yip Pui Chen Page 52

N13505 Auditing, Governance and ScandalsGroup AssignmentChakrabarti, R. Megginson, W. and Yadav, P. (2008) Corporate Governancein India. Journal of Applied Corporate Finance, 20 (1), p.59-72. Available at: http://onlinelibrary.wiley.com/doi/10.1111/j.1745-6622.2008.00169.x/abstract [Accessed: 16 November 2012].

Cheah, F. S., and Lee, L. S. (2009) Corporate governance in Malaysia: principles and practice. Petaling Jaya, Selangor, Malaysia, August Pub.

Christiansen, H. and Koldertsova, A. (2009) The Role of Stock Exchange in Corporate Governance. Available at: http://www.oecd.org/finance/financialmarkets/43169104.pdf [Accessed: 20th November 2012].

Citigroup (2012). Governance Documents [online]. Available at: http://www.citigroup.com/citi/investor/corporate_governance.html [Accessed: 3 December 2012].

Coghill, K., Mohamed Ariff, On, K.T. and Wilkins, L. (n.d) Rating Governance in Australia [online]. Available at: http://govrank.in/Misc/coghill-prato.pdf [Accessed: 17th November 2012].

Considine, M. and Lewis, J.M. (2003) Bureaucracy, Network, or Enterprise? Comparing Models of Governance in Australia, Britain, the Netherlands, and New Zealand [online]. Available at: http://web.ebscohost.com/ehost/detail?sid=a0b81d10-681e-4c05-8a2c-368f20f9306c%40sessionmgr14&vid=1&hid=21&bdata=JnNpdGU9ZWhvc3QtbGl2ZQ%3d%3d#db=buh&AN=9199208 [Accessed: 17th November 2012].

CRISIL (2012) Credit Rating List – CRISIL [online]. Available at: http://crisil.com/ratings/credit-ratings-list.jsp [Accessed: 3 December2012].

Deloitte Touche Tohmatsu India (2010) Welcome to the Center for Corporate Governance [online]. Available at: http://www.corpgov.deloitte.com/site/in [Accessed: 3 December 2012].

Fama, E. and French, K. (1988) Permanent and Temporary Components of Stock Prices. The Journal of Political Economy, 96 (2), p.246-273.

Fong Meow Lee, Lee Yann Yi, Liew TzeYeen, Samuel Hong, Yip Pui Chen Page 53

N13505 Auditing, Governance and ScandalsGroup AssignmentFanning, E. (2010) BOQ Docs Show Problems with Storm Loans [online]. Available at: http://sixtyminutes.ninemsn.com/stories/1064746/boq-docs-show-problems-with-storm-loans [Accessed: 17th November 2012].Governance Metrics International (2003) GMI Launches Ratings on Australia’s ASX50 Governance Generally Good But Concern Over Related-Party Transactions Have Cross Shareholdings [online]. Available at: http://www.gmiratings.com/Release20030609.html [Accessed: 17th November2012].

Grant Thornton (2012) Corporate Governance in India and the UK: A Comparative Analysis [online]. Available at: http://thinking.grant-thornton.co.uk/emergingmarkets/index.php/article/corporate_governance_in_india_and_the_uk_a_comparative_analysis [Accessed: 3 December 2012].

Gupta, P. (2008) Corporate Governance In Indian Banking Sector. Undergraduate. University of Nottingham.

Hansen, B. R. (n.d.) Effective Corporate Governance? Sarbanes-Oxley in the Courts. [online]. Available at: http://people.carleton.edu/~amontero/Bridget%20Hansen.pdf [Accessed: 29November 2012].

HDFCBank.com (2012) HDFC Bank - Leading Bank in India, Banking Services, Private Banking, Personal Loan, Car Loan. [online] Available at: http://www.hdfcbank.com/aboutus/cg/Corporate_Governance.htm [Accessed: 3 December 2012].

Holmstrom, B. and Kaplan, S. (2003) The State of U.S. Corporate Governance: What’s right and what’s wrong? [online]. Available at: http://www.nber.org/papers/w9613.pdf?new_window=1 [Accessed: 19 November 2012].

Hossain, M. and Reaz, M. (2007) The determinants and characteristics ofvoluntary disclosure by Indian banking companies. Corporate Social Responsibility and Environmental Management, 14 (5), p.274-288. Available at: http://onlinelibrary.wiley.com/doi/10.1002/csr.154/pdf [Accessed: 16 November 2012].

Fong Meow Lee, Lee Yann Yi, Liew TzeYeen, Samuel Hong, Yip Pui Chen Page 54

N13505 Auditing, Governance and ScandalsGroup Assignmenthttp://www.asx.com.au/documents/about/media_release_cg_reporting_18_june_08.pdf (2008) Continued Improvement in Corporate Governance Reporting. [press release] 18 June 2008.

ICAEW (2006) Effective Corporate Governance Frameworks [online]. Available at: http://www.icaew.com/~/media/Files/Technical/Corporate-governance/dialogue-in-corporate-governance/effective-corporate-governance-frameworks.pdf [Accessed: 24 November 2012].

Ifac.org (2009) Evaluating and Improving Governance in Organizations | IFAC. [online] Available at: https://www.ifac.org/publications-resources/evaluating-and-improving-governance-organizations [Accessed: 4 Dec 2012].

Insolvency Guardian Australia (2012) Corporate Governance [online]. Available at: https://insolvencyguardian.com.au/corporategovernance [Accessed: 3 December 2012].

Iu, J. and Batten, J. (2001) The Implementation of OECD Corporate Governance Principles in Post-Crisis Asia [online]. Available at: http://www.greenleaf-publishing.com/content/pdfs/jcc04iuba.pdf [Accessed: 20th November 2012].

Jackson, G. (2010) Understanding Corporate Governance in United States.[online]. Available at: http://www.boeckler.de/pdf/p_arbp_223.pdf [Accessed: 19 November 2012].

Kar, P. (2011). Culture and Corporate Governance Principles in India: Reconcilable Clashes?. [pdf] Washington DC: World Bank. Available through: International Finance Corporation http://www1.ifc.org/wps/wcm/connect/1fe292804a4785e6824d9faa52ef3b86/PSO_23_Pratip.pdf?MOD=AJPERES [Accessed 1 December 2012].

Khanna, V. (2009). Law Enforcement and Stock Market Development: Evidence from India. [pdf] e.g. Chester: CDDRL. Available at: University of Michigan Law School, http://iis-db.stanford.edu/pubs/22401/No_97_Khanna_Law_enforcement_stock_market.pdf [Accessed 3 December 2012].

Fong Meow Lee, Lee Yann Yi, Liew TzeYeen, Samuel Hong, Yip Pui Chen Page 55

N13505 Auditing, Governance and ScandalsGroup AssignmentLocke Liddell & Sapp LLP (2006) U.S. Corporate Governance Standards: A Checklist Covering Sarbanes-Oxley, SEC Rulemaking and the New NYSE and NASDAQ Listing Requirements [online]. Available at: http://www.lockelord.com/files/Publication/24390dea-a4ab-498f-a9e0-5ba6db4e2f0b/Presentation/PublicationAttachment/9f40f340-e9c1-4cda-859d-5cefc0b030f5/Corp%20Gov%20Checklist.pdf [Accessed: 20 November 2012].

Maldives Stock Exchange (2012) Listed Companies [online]. Available at:http://www.mse.com.mv/#mse_listed-companies [Accessed 1 December 2012].

Mallin, C.A. (2010) Corporate Governance. 3rd ed. New York: Oxford University Press Inc.Marx, A. (2012) Banks put profit ahead of Storm clients, court hears. Available: http://www.couriermail.com.au/realestate/news/banks-put-profit-ahead-of-storm-clients/story-fnczc3if-1226480777255 [Accessed: 17th November 2012].

May, J. (2008) ANZ Ranked World's Most Sustainable Bank [online]. Available at: http://www.investordaily.com.au/cps/rde/xchg/id/style/4951.htm?rdeCOQ=SID-3F579BCE-FAF630CF&rdeCOQ=SID-0A3D9632-B53A41D1 [Accessed: 17th November 2012].

McMurray, J. (2003) The Facts About Corporate Governance [online]. Available at: http://www.gmiratings.com/%28y1f3egn2mj0jjqbsiyj5cm55%29/news/crikey_6_11_03.htm [Accessed: 17th November 2012].

Melis, A. (2004) Corporate Governance Failures. To What Extent is Parmalat a Particularly Italian Case?. p.1-29. Available at: http://papers.ssrn.com/sol3/papers.cfm?abstract_id=563223 [Accessed: 4th December 2012].

Minority Shareholder Watchdog Group (2011) MSWG | MCG Index. [online]. Available at: http://www.mswg.org.my/web/page.php?pid=47&menu=sub [Accessed: 17 December 2012].

Mohamad Mokhtar, S., Muhamad Sori, Z., Abdul Hamid, M.A., et. al. (2009) Corporate Governance Practices and Firms' Performance: The

Fong Meow Lee, Lee Yann Yi, Liew TzeYeen, Samuel Hong, Yip Pui Chen Page 56

N13505 Auditing, Governance and ScandalsGroup AssignmentMalaysian Case. Journal of Money, Investment and Banking, 11 p.45-59. [online]. Available at: http://www.eurojournals.com/jmib_11_04.pdf [Accessed: 20 November\ 2012].

National Foundation for Corporate Governance (2004) Reports on the Observance of Standards and Codes - Corporate Governance Country Assessment INDIA [online]. Available at: http://www.nfcgindia.org/rosc.htm [Accessed: 3 December 2012].

National Foundation for Corporate Governance (2004) Corporate Governance: India [online]. Available at: http://www.nfcgindia.org/library.htm [Accessed: 3 December 2012].

National Information Center (2012) Top 50 Holding Companies [online]. Available at: http://www.ffiec.gov/nicpubweb/nicweb/Top50Form.aspx [Accessed: 18 November 2012].

Nfcgindia.org (2011) National Foundation for Corporate Governance : Library. [online] Available at: http://www.nfcgindia.org/library.htm [Accessed: 25 November 2012].

O'Brien, J. (2012) Attack on ASIC Chief Draws Corporate Governance IntoPolitical Mire [online]. Available at: http://theconversation.edu.au/attack-on-asic-chief-draws-corporate-governance-into-political-mire-8251 [Accessed: 20th November 2012].

OECD Steering Group on Corporate Governance (2007) Methodology for Assessing The Implementation Of The OECD Principles Of Corporate Governance [online]. Available: http://www.oecd.org/daf/corporateaffairs/corporategovernanceprinciples/37776417.pdf [Accessed: 20th November 2012].

Ong, W.J. (2006) Corporate Governance Disclosure in Malaysia. MA in Risk Management Dissertation. University of Nottingham.

PAIB (2009) Evaluating and Improving Governance in Organizations, International Good Practice Guidance. [e-book] New York: Professional Accountants in Business (PAIB) Commitee. Available through: https://www.ifac.org/sites/default/files/publications/files/IGPG-Evaluating-and-Improving-Governance.pdf [Accessed: 30th November 2012].

Fong Meow Lee, Lee Yann Yi, Liew TzeYeen, Samuel Hong, Yip Pui Chen Page 57

N13505 Auditing, Governance and ScandalsGroup Assignment

Pande, S. (2011) An Overview of Corporate Governance Reforms in India. [pdf] New Delhi: Available through: Google Scholar SSRN: http://ssrn.com/abstract=1958031 [Accessed: 16 November 2012].

Papers.ssrn.com (2009) Why Did Some Banks Perform Better during the Credit Crisis? A Cross-Country Study of the Impact of Governance and Regulation by Andrea Beltratti , Rene Stulz :: SSRN. [online] Availableat: http://papers.ssrn.com/sol3/papers.cfm?abstract_id=1433502 [Accessed: 4 Dec 2012].

Public Bank Berhad (2012a) 2011 Annual Report [online]. Available at: http://www.pbebank.com/corporate/PBB_AR2011_CorporateBook.pdf [Accessed: 12 November 2012].

Public Bank Berhad (2012b) 2011 Annual Report: Financial Statements [online]. Available at: http://www.pbebank.com/corporate/PBB_AR2011_Financial%20Book.pdf [Accessed: 12 November 2012].

Reed, A. (2002) Corporate Governance Reforms in India. Journal of Business Ethics, 37 p.249-268. Available at: http://download.springer.com/static/pdf/45/art%253A10.1023%252FA%253A1015260208546.pdf?auth66=1354025687_c23e65e99fd14122855f522bf2146a5b&ext=.pdf [Accessed: 27 November 2012].

Robins, R. (2006) Corporate Governance after Sarbanes-Oxley: an Australian Perspective [online]. Available at: http://www.emeraldinsight.com/journals.htm?issn=1472-0701&volume=6&issue=1&articleid=1545691&show=html&PHPSESSID=0a7q8jkptqs7ac9qhng9lddp30 [Accessed: 17th November 2012].

Rosen, J. (2011) News Corp is Bad News [online]. Available at: http://www.abc.net.au/unleashed/3683736.html [Accessed: 20th November 2012].

Fong Meow Lee, Lee Yann Yi, Liew TzeYeen, Samuel Hong, Yip Pui Chen Page 58

N13505 Auditing, Governance and ScandalsGroup AssignmentRussian Economic Freedom(2010) Kremlin Gets Blingy. [online] Available at: http://russianeconomicfreedom.org/tag/corporate-governance/ [Accessed: 4 Dec 2012].

Sakar, J. and Sakar, S. (2000) Large Shareholder Activism in Corporate Governance in Developing Countries: Evidence from India. [e-book] Mumbai: Indira Gandhi Institute of Development Research. Available through: Google Scholar Indira Gandhi Institute of Development Research[Accessed: 16 November 2012].

Securities Commission Malaysia (2007) Malaysian Code on Corporate Governance (Revised 2007). [report] Kuala Lumpur: p.1-19.

Securities Commission Malaysia (2011a) Corporate Governance Blueprint 2011. [report] Kuala Lumpur: p.1-81.

Securities Commission Malaysia (2011b) Corporate Governance: Malaysian Code on Corporate Governance 2012. [online]. Available at: http://www.sc.com.my/main.asp?pageid=1088&menuid=332&newsid=&linkid=&type=S [Accessed: 17 November 2012].

Securities Commission Malaysia (2012a) Malaysian Code on Corporate Governance 2012. [report] Kuala Lumpur: p.1-28.

Securities Commission Malaysia (2012b) MCCG 2012: Other Frequently-Asked Questions [online]. Available at: http://www.sc.com.my/main.asp?pageid=1154&menuid=1035&newsid=&linkid=&type= [Accessed: 17 November 2012].

Security Exchange Commisions (SEC) of USA (2002) Sarbanes-Oxley Act of 2002 Corporate responsibility 15 USC 7201 note.. [report] Public Law 107–204: p.745-801.

Sewe, F. O. (2012) The Sarbanes Oxley Act and Its Impacts on Corporate Finance and Corporate Governance Behavior [online]. Available at: http://papers.ssrn.com/sol3/papers.cfm?abstract_id=2111505 [Accessed: 16 November 2012].

Fong Meow Lee, Lee Yann Yi, Liew TzeYeen, Samuel Hong, Yip Pui Chen Page 59

N13505 Auditing, Governance and ScandalsGroup AssignmentSexton, E. (2012) Pair Pin Storm's Fall on Bank and ASIC Failures [online]. Available at: http://www.smh.com.au/business/pair-pin-storms-fall-on-bank-and-asic-failures-20120207-1r587.html#ixzz2E4bRgvb5 [Accessed: 17th November 2012].

Shah, C. and Gupta, A. (2012) Corporate Governance in Banking Sector. Indian Journal of Applied Research, 2 (1), p.115-117. Available at: http://www.ijar.in/oct2012$/41.pdf [Accessed: 25 November 2012].

Shareef, F. and Sodique, H. (n.d.) Baseline Study on Corporate Social Responsibility Practices in Maldives [online]. Available at: http://www.trade.gov.mv/downloads/4cd26412809fb_CSR%20Baseline%20Study%20Report%20Maldives.pdf [Accessed: 3 December 2012].

The Commonwealth (2007) Corporate governance in Maldives [online]. Available at: http://www.thecommonwealth.org/news/34580/34581/168621/2900807maldives.htm [Accessed: 1 December 2012].

The Heritage Foundation (2012) 2012 Index of Economic Freedom [online].Available at: http://www.heritage.org/index/country/australia [Accessed: 20th November 2012].

The Star Online (2009) Corporate Governance Index, to be launched Tuesday. [online]. Available at: http://biz.thestar.com.my/news/story.asp?file=/2009/6/9/business/4076690&sec=business [Accessed: 29 November 2012].

Thinking.grant-thornton.co.uk (2010) Corporate governance in India and the UK: A comparative analysis. [online]. Available at: http://thinking.grant-thornton.co.uk/emergingmarkets/index.php/article/corporate_governance_in_india_and_the_uk_a_comparative_analysis [Accessed: 24 November 2012].

UKEssays.com. (2012) Corporate Governance in India: Past, Present and Future [online]. Available at: http://www.ukessays.com/essays/accounting/corporate-governance-in-india-past-present-and-future-accounting-essay.php [Accessed: 3 December 2012].

Fong Meow Lee, Lee Yann Yi, Liew TzeYeen, Samuel Hong, Yip Pui Chen Page 60

N13505 Auditing, Governance and ScandalsGroup AssignmentVarma, J. (1997) Corporate Governance in India: disciplining the dominant shareholder. IIMB Management Review, 9 (4), p.5-18. [online]. Available at: http://www.iimahd.ernet.in/~jrvarma/papers/iimbr9-4.pdf [Accessed: 16 November 2012].

Wade, C. L. (2008) Sarbanes-Oxley Five Years Later: Will Criticism of SOX Undermine Its Benefits? [online]. Available at: http://www.leadershape.luc.edu/law/activities/publications/lljdocs/vol39_no3/wade.pdf [Accessed: 23 November 2012].

Wall Street Journal (2010) Russia's Khordokovsky Discount. [online] Available at: http://online.wsj.com/article/SB10001424052748704138604576029683014614212.html [Accessed: 4 Dec 2012].White, A.L. (2012) Redefining Value: The Future of Corporate Sustainability Ratings [online]. Available at: http://www1.ifc.org/wps/wcm/connect/7d9c6f804d9bd08baeb7bf48b49f4568/IFC+PSO+29.pdf?MOD=AJPERES [Accessed: 3 December 2012].

Williams, R. and Johnston, E. (2009) BOQ to Review Its Practices [online]. Available at: http://www.businessday.com.au/business/boq-to-review-its-practices-20090911-fkra.html [Accessed: 17th November 2012].

Worldbank.org (2009) World Bank Group - ROSC. [online]. Available at: http://www.worldbank.org/ifa/rosc_cg.html [Accessed: 25 November 2012].

Zainal Abidin, N.A. and Ahmad, H. (2012) Corporate Governance in Malaysia: The Effect of Corporate Reforms and State Business Relation in Malaysia. Asian Academy of Management Journal, 12 (1), p.23-34.

Fong Meow Lee, Lee Yann Yi, Liew TzeYeen, Samuel Hong, Yip Pui Chen Page 61