asignment#3, task 3

TRANSCRIPT

Assignment Three

Course:

Submitted To:

Submitted By:

Submission Date:

1 | P a g e

2 | P a g e

Table of ContentsTask 3...............................................................2Investment Appraisal Techniques......................................2Net Present Value (NPV):............................................2Internal Rate of Return:............................................4Accounting Rate of Return:..........................................5Payback Period:.....................................................5Discounted payback period:..........................................5Modified internal rate of return....................................6

Investment Appraisal for ABC Ltd.....................................6USA:................................................................7Table: 1............................................................7Conversion of Dollars to Pounds.....................................7Table: 2............................................................7Cash flow and Present Value of plant in USA:........................7France:.............................................................8Table: 3............................................................8Conversion of Euros to Pounds.......................................8Table: 4............................................................8Cash flow and Present Value of Plant in France......................8Switzerland:........................................................9Table: 5............................................................9Conversion of Swiss Franc to Pounds.................................9Table: 6............................................................9Cash flow and Present Value of Plant in Switzerland.................9

Judging the Soundness of the Financial Projections:.................10Scenario Analysis:.................................................10Sensitivity Analysis:..............................................11

International Risks Associated With ABC Ltd:........................11Exchange Rate Risk:................................................11

3 | P a g e

Country Risk:......................................................12Political Risk:....................................................12Economic Risk:.....................................................12Cultural Risk:.....................................................13

Financial Risk Management...........................................13Exchange Rate Risk:................................................13Futures:.........................................................14Forwards:........................................................14Options:.........................................................14

Country Risk:......................................................15Cultural Risk:.....................................................15

4 | P a g e

Task 3

Investment Appraisal Techniques

Following are the investment appraisal techniques used to measure

investment appraisal of a project of business.

Net Present Value (NPV):

NPV is an investment appraisal technique used to examine the

investment decision and make the management able to imagine a

clear picture regarding the investment, that weather it will add

value or not to the company. Normally whenever a project have a

positive net present value, it is a value adding option for the

company, and is going to benefit the shareholders.

Net present value can b calculated for the sake of assessment of

either a current acquisition, or for a future capital project. It

is the most widely used tool for investment appraisal.

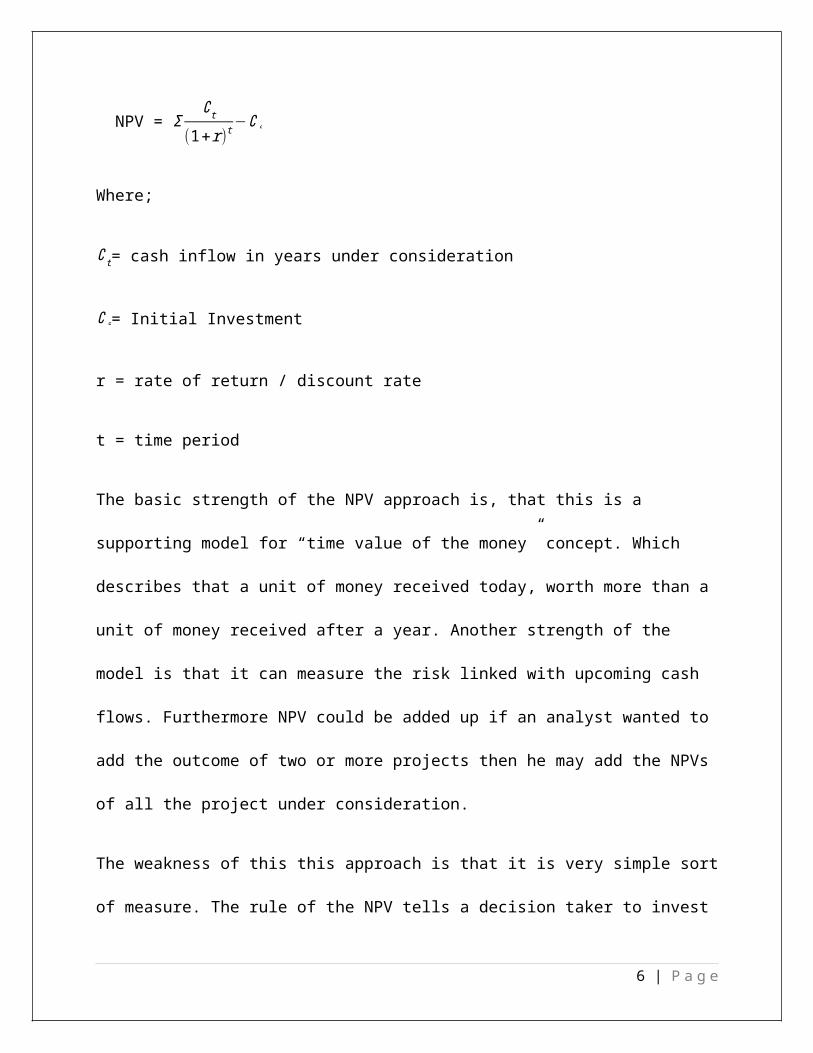

Formula of the net present value is;

5 | P a g e

NPV = Σ∁t

(1+r)t−∁°

Where;

∁t= cash inflow in years under consideration

∁°= Initial Investment

r = rate of return / discount rate

t = time period

The basic strength of the NPV approach is, that this is a

supporting model for “time value of the money” concept. Which

describes that a unit of money received today, worth more than a

unit of money received after a year. Another strength of the

model is that it can measure the risk linked with upcoming cash

flows. Furthermore NPV could be added up if an analyst wanted to

add the outcome of two or more projects then he may add the NPVs

of all the project under consideration.

The weakness of this this approach is that it is very simple sort

of measure. The rule of the NPV tells a decision taker to invest

6 | P a g e

the money in the project which is having an NPV greater than

zero. But the tool does not tell that when the positive NPV will

be realized.

The other restraint of the NPV approach that this model takes an

assumption that the capital is plentiful, and no capital

rationing exists. If there are limited and rare resources, the

analyst have to watch not only NPV of each individual project,

also to the size of the each individual investment. Luckily,

there is another tool that can control this weakness which is

IRR.

Internal Rate of Return:

IRR can be defined and explained as the discount rate at which the NPV

of the cash flows of the project become equivalent to the zero. If the

IRR of the projects comes greater than the projects benchmark rate or

WACC of the project then the proposed project gets accepted and vice

versa.

Most of the times IRR and NPV generates similar results but

whenever there are different or irregular cash flows a project

may have multiple IRR. In such a case NPV is t better option to

7 | P a g e

use. As the IRR help the analyst to accept the project which is

having the IRR greater than WACC, but what if the IRR is changing

each year, in that case it not valid tool to use.

As mentioned above the NPV of the multiple projects

could be added in one another but unfortunately IRR of

the multiple projects could not be added in one

another.

The IRR have options to calculate one is through trial and error

method that the analyst slowly change the number discount rate

until NPV don’t comes to the zero. Other than trial error long

process there is another method too from which the IRR can be

calculated quickly and immediately within seconds that is through

financial calculator that can perform this calculation

automatically. There are one more tool to calculate the IRR is

that spreadsheet application built-I function of the Microsoft

excel.

Formula:

The formula of IRR is as follows:

8 | P a g e

0 = PO + P1 / (1+ IRR) 1 +P2 / (1+ IRR) 2 …. PN / (1 +

IRR) N

Accounting Rate of Return:

Accounting rate of return is an investment appraisal tool in

which we divide total profit with the total investment. The rule

of decision in ARR is same as of IRR, if the ARR of a project is

greater than the benchmark rate of the project then it would be

accepted and vice versa. ARR is also known as ROCE which is

Return on Capital Employed.

Payback Period:

Pay back allows an analyst to examine that how soon will be the

cost of the project would be recovered , simply payback model is

an outdated and invalid tool to use because of time value of the

money concept, which is not being considered in the payback at

all.

Formula of the payback period;

Payback Period = Initial Investment .

9 | P a g e

Cash Inflow per Period

Discounted payback period:

The flaws noticed by the experts in payback period have been

rectified in discounted payback period as the time value of the

money concept have been considered in it. Now instead of putting

straight the value of the cash inflows periods, they are firstly

discounted backed to the time zero and then they putted in the

formula makes it a valid tool to measure the time span to recover

the initial cost of project.

Discounted Payback Period =Initial Investment .

Discounted Cash Inflow per Period

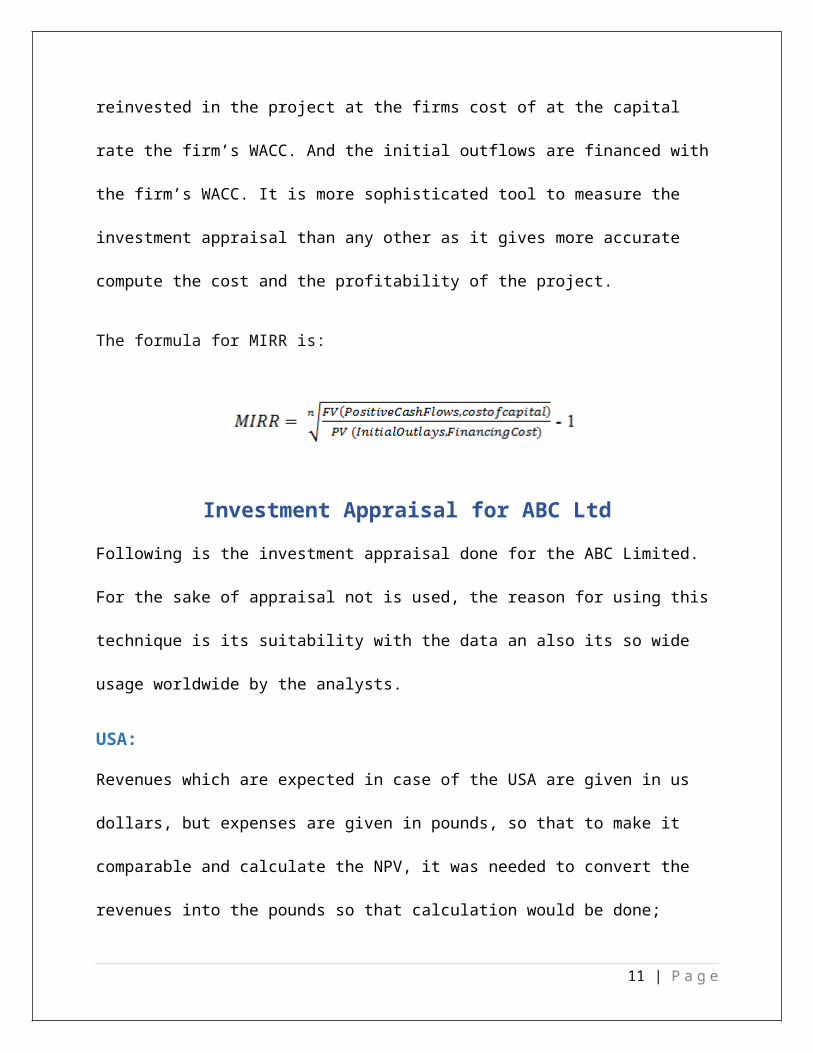

Modified internal rate of return

As the internal rate of return (IRR), calculated by discounting

the cash flows of the project with the different random numbers

until its NPV comes equal to zero. In modified rate of return

(MIRR), it’s assumed that all the positive cash flows would be

10 | P a g e

reinvested in the project at the firms cost of at the capital

rate the firm’s WACC. And the initial outflows are financed with

the firm’s WACC. It is more sophisticated tool to measure the

investment appraisal than any other as it gives more accurate

compute the cost and the profitability of the project.

The formula for MIRR is:

Investment Appraisal for ABC LtdFollowing is the investment appraisal done for the ABC Limited.

For the sake of appraisal not is used, the reason for using this

technique is its suitability with the data an also its so wide

usage worldwide by the analysts.

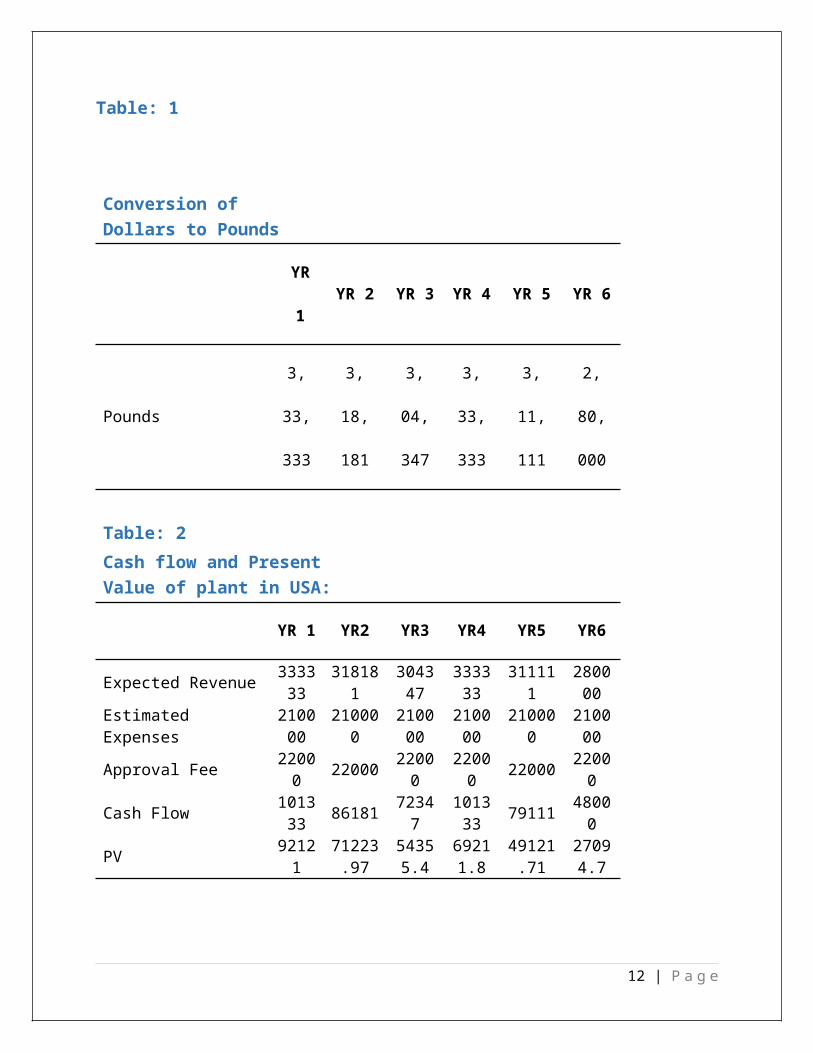

USA:

Revenues which are expected in case of the USA are given in us

dollars, but expenses are given in pounds, so that to make it

comparable and calculate the NPV, it was needed to convert the

revenues into the pounds so that calculation would be done;

11 | P a g e

Table: 1

Conversion of Dollars to Pounds

YR

1YR 2 YR 3 YR 4 YR 5 YR 6

Pounds

3,

33,

333

3,

18,

181

3,

04,

347

3,

33,

333

3,

11,

111

2,

80,

000

Table: 2Cash flow and Present Value of plant in USA:

YR 1 YR2 YR3 YR4 YR5 YR6

Expected Revenue 333333

318181

304347

333333

311111

280000

Estimated Expenses

210000

210000

210000

210000

210000

210000

Approval Fee 22000 22000 2200

022000 22000 2200

0

Cash Flow 101333 86181 7234

7101333 79111 4800

0

PV 92121

71223.97

54355.4

69211.8

49121.71

27094.7

12 | P a g e

NPV of the use is

given below;

NPV =

36312

8

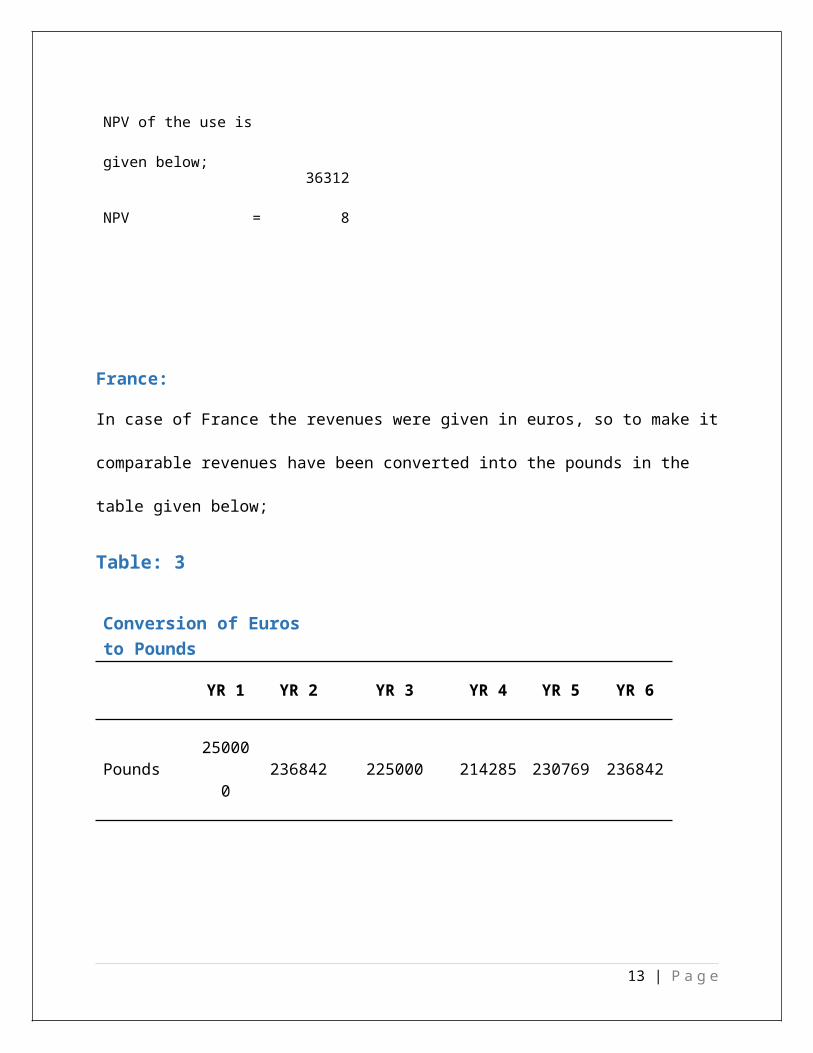

France:

In case of France the revenues were given in euros, so to make it

comparable revenues have been converted into the pounds in the

table given below;

Table: 3

Conversion of Euros to Pounds

YR 1 YR 2 YR 3 YR 4 YR 5 YR 6

Pounds25000

0236842 225000 214285 230769 236842

13 | P a g e

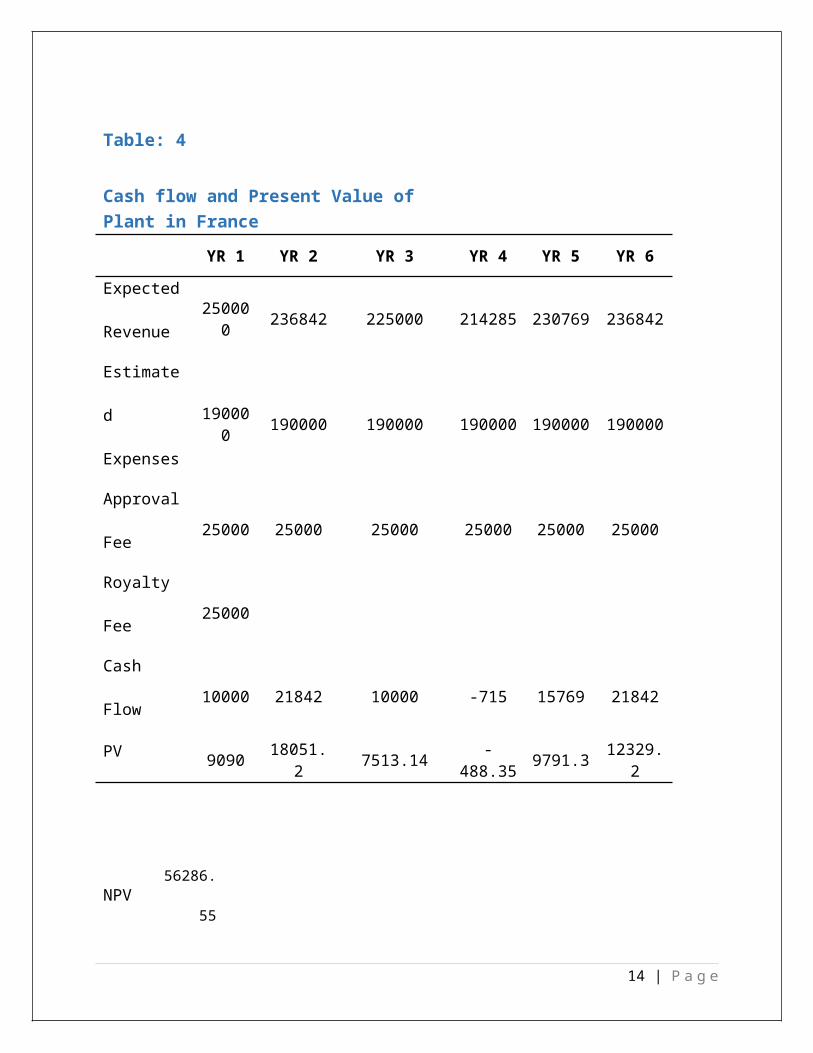

Table: 4

Cash flow and Present Value of Plant in France

YR 1 YR 2 YR 3 YR 4 YR 5 YR 6

Expected

Revenue 25000

0 236842 225000 214285 230769 236842

Estimate

d

Expenses

190000 190000 190000 190000 190000 190000

Approval

Fee 25000 25000 25000 25000 25000 25000

Royalty

Fee 25000

Cash

Flow 10000 21842 10000 -715 15769 21842

PV 9090 18051.2 7513.14 -

488.35 9791.3 12329.2

NPV56286.

55

14 | P a g e

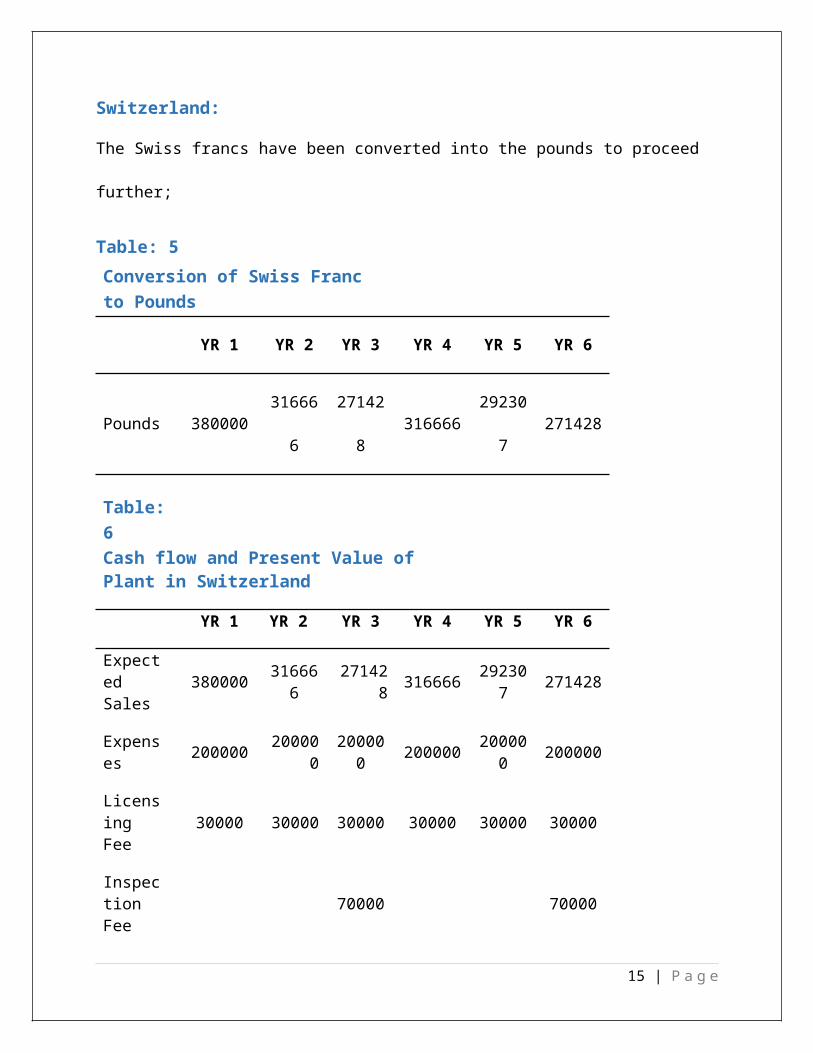

Switzerland:

The Swiss francs have been converted into the pounds to proceed

further;

Table: 5Conversion of Swiss Franc to Pounds

YR 1 YR 2 YR 3 YR 4 YR 5 YR 6

Pounds 38000031666

6

27142

8316666

29230

7271428

Table:6Cash flow and Present Value of Plant in Switzerland

YR 1 YR 2 YR 3 YR 4 YR 5 YR 6

Expected Sales

380000 316666

271428 316666 29230

7 271428

Expenses 200000 20000

020000

0 200000 200000 200000

Licensing Fee

30000 30000 30000 30000 30000 30000

Inspection Fee

70000 70000

15 | P a g e

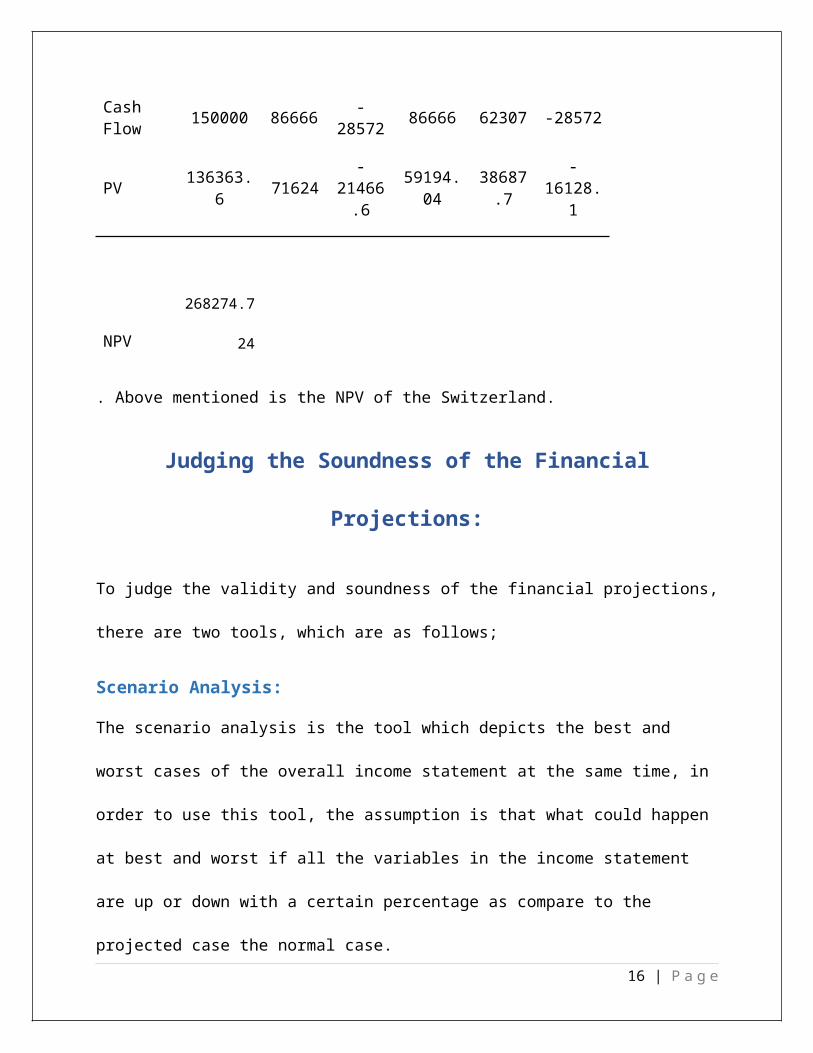

Cash Flow 150000 86666 -

28572 86666 62307 -28572

PV 136363.6 71624

-21466.6

59194.04

38687.7

-16128.

1

NPV

268274.7

24

. Above mentioned is the NPV of the Switzerland.

Judging the Soundness of the Financial

Projections:

To judge the validity and soundness of the financial projections,

there are two tools, which are as follows;

Scenario Analysis:

The scenario analysis is the tool which depicts the best and

worst cases of the overall income statement at the same time, in

order to use this tool, the assumption is that what could happen

at best and worst if all the variables in the income statement

are up or down with a certain percentage as compare to the

projected case the normal case.16 | P a g e

Sensitivity Analysis:

Sensitivity analysis is a tool which is used to evaluate

occurrence of changes in the amounts of the other variable if one

of them got changed in a projection. In this way the impact of

the changes occurred n a specific variable could be clearly in

the cash flows of the project. And it can be determined that if

any of the factor in the income statement do not seems suitable

for the project or business, then in such a case what and how

much worst a business would be suffered in result. It gives an

analyst the idea that how much sensitive is the each factor for

the business if up or down any thing would happen with it.

International Risks Associated With ABC Ltd:All the firms going to expansion globally have to face certain

types and level of the international risks which threaten the

firms to operate globally, but it is also other side of the coin

that operating globally gives a firm more opportunities and more

growth profit potentials, risks which are expected to face by the

ABC Ltd are mention below;

o Exchange Rate Risk

17 | P a g e

o Country Risk

o Cultural Risk

Exchange Rate Risk:

Exchange rate risks are those which are risks which a firm face

due to difference in the exchange rates of the two countries.

This is the risk which is attached with expectations of

fluctuation in the future spot rate. If in case the currency’s

value got appreciated against currency of any other currency,

then consequently the higher amount would be needed to pay to get

the similar amount of the currency required. There are two

methods to follow for dealing in exchange rates when preparing

financial statement of the subsidiary and reporting to the

parent;

1) All Current Method

2) Temporal Method.

Country Risk:

Country is further categorized in to two kinds;

1) Political Risk

2) Economic Risk

18 | P a g e

Political Risk:

The political risk is risk which is related with the political

instability and consequently the change in rules and regulations

of a country. If in case the alteration in the political setup

are very major and frequent, then there are huge chances and

risk that ABC Ltd would not receive any constant set of policies

which enable them to operate with sound-mind in an effective and

efficient manner. So ABC Ltd would be needed to ensure before

entering into an international market. Whether the political

environment of the country is stable or not.

Economic Risk:

The economic risks linked with the deprived performance of a

country’s economy. As a double-digit inflation, a greater

unemployment and a declining GDP are the economic indicators of

the underperforming country which indicates that making investing

in such a country will give back the required profits which may

also lead to the losses. So economic risk is one of the risks

which must be prevented and measured before entering in to the

international market.

19 | P a g e

Cultural Risk:

Same as economic risks and political risks there are cultural

risks prevailing while going globally, because there are

difference among the cultures of the country with other, and when

thinking to expand globally these risk must be analyzed by the

firm, because adaption of the culture is the key to do successful

business global, a company should not behave at every corner of

the world in the same way, people living in different countries

have different norms and etiquettes, as the meanings of the

similar objects and symbols get change when the environment is

different. ABC Ltd needs to adapt the culture of the each country

in an appropriate manner to be successful.

Financial Risk ManagementRisks is somehow manageable up to a range by utilizing different

hedging tools. Risks which are mentioned above are manageable by

following the ways stated below;

Exchange Rate Risk:

Risks associated with the fluctuation in the exchange rate of the

currency is manageable by using following hedging tools;

20 | P a g e

1) Currency Futures

2) Currency Forwards

3) Options

Futures:

Futures are the one of the hedging tool used for managing

exchange rate risk, it is basically an agreement to buy or sell a

particular amount of the currency at a predetermined rate in the

future time. It is a standardized form of contract, that are

normally transected in stock markets, and it is tool which can

help the firms to lock the rate at which the currency could be

purchased or sold at a future date. These are the legally

enforceable if once agreed to form a contract of such nature.

Forwards:

Forwards are just like futures but the difference between these

two is that the forwards are traded outside the stock exchange as

privately, e.g. in commercial banks and etc. forwards are not

standardized sort of tool, it has flexibility of negation and

customization in terms of time, amount, and rate etc. the purpose

21 | P a g e

behind both of these is same, to hedge the exchange rate and

avoid uncertainty and potential losses.

Options:

Options are right to purchase or sale a particular currency at a

predefined rate just to avoid minimize the potential risk. In

order to get this right a premium is needed to pay, so that you

may exercise the option if needed. And it works as shield to

protect yourself from the possible changes in the currency rates.

So options are right of the person who pays the premium to

exercise if needed, but not his obligation to perform. It can

give a company with a better shield to protect their self against

the risk than the forwards and futures, because of the reason

that forwards and futures require cost as penalty in order to

cancel them. But option does not have such compulsion. Buyer can

exercise the options I he feels favorable to exercise them.

Country Risk:

The country risk is a risk which could be avoided by observing

the country under consideration before entering in to that wit

business. The performance and consistency trends of a country

22 | P a g e

could be analyzed from the past that how consistently they have

implemented the policies and regulation in the past time, in

terms of global investments and business people. For the sake of

protection of economic risk through a keen eye one must observe

the employment rate, GDP of the country, and purchasing power of

the natives of the country and also the inflation rates too.

Through a proper analysis decision should be made.

Cultural Risk:

Cultural risks are avoidable in a way that one should hire the

local workforce and local management who could behave in the same

way as of the natives of that country. And take those decisions

which are appropriate in order to operate successfully in that

region, and also to avoid blunders which could be committed

unconsciously by the management hired from the outside of that

country. Humor resource is the most carefully hired if expansion

is intended.

23 | P a g e

24 | P a g e