apt-cpa review-std costing

TRANSCRIPT

Apt Financial Consultants CPA Review

FLEXIBLE BUDGETS AND STANDARD COSTINGMaster budget (or static budget), which was prepared basing on the expected volume of operation. Normally actual volume attained differs with the expected volume in the master budget; therefore comparing the two will lead to a misleading view. In order to make a better comparison between actual results and the budget, we must revise the budget so that it reflects the actual results. This revised budget is known as a flexible budget.

How Standards are established.Standards may be established by using any of the following ways or their combination: Negotiation between workers and management Basing on historical data Product engineering

In most cases the product engineering is used to establish standards. When standards are established basing on product engineering, engineers will specify akind(s) of raw material, quantity of raw material, quality of raw material, quantity of labour and quality of labour. They will also establish the colour, shape, weight, height and other attributes of the product.Purchasing department, on the other hand, will locate the supplier(s) of raw materials and price for each unit of raw material. In this way therefore, standards will be established of the quantity of raw materials and cost per each unit of raw material.

Standards for labour base on operations to be performed in order to have a finished product. Each operation may be performed by one person or a group of persons. When a group of persons perform one operation the average rate will be used to determine the number of hours and the rate per hour.

IllustrationPapias Company Ltd produces a product P using three types of labour known as unskilled labour, semi-skilled labour and skilled labour. The cutting operation involves 3 persons namely Mr.Gedau, Mr.Ngapo and Mr.Nache. The following data arerelevant for one unit of product P Rate applicable Name Hours to each Shs .Mr.Gedau (unskilled) 2 ½ hours 100/= 250/=Mr.Ngapo (semi-skilled) 1 ½ hours 200/= 300/=Mr.Nache (skilled) 1 hour 400/= 400/= 5 hours 950/=

1

Apt Financial Consultants CPA Review

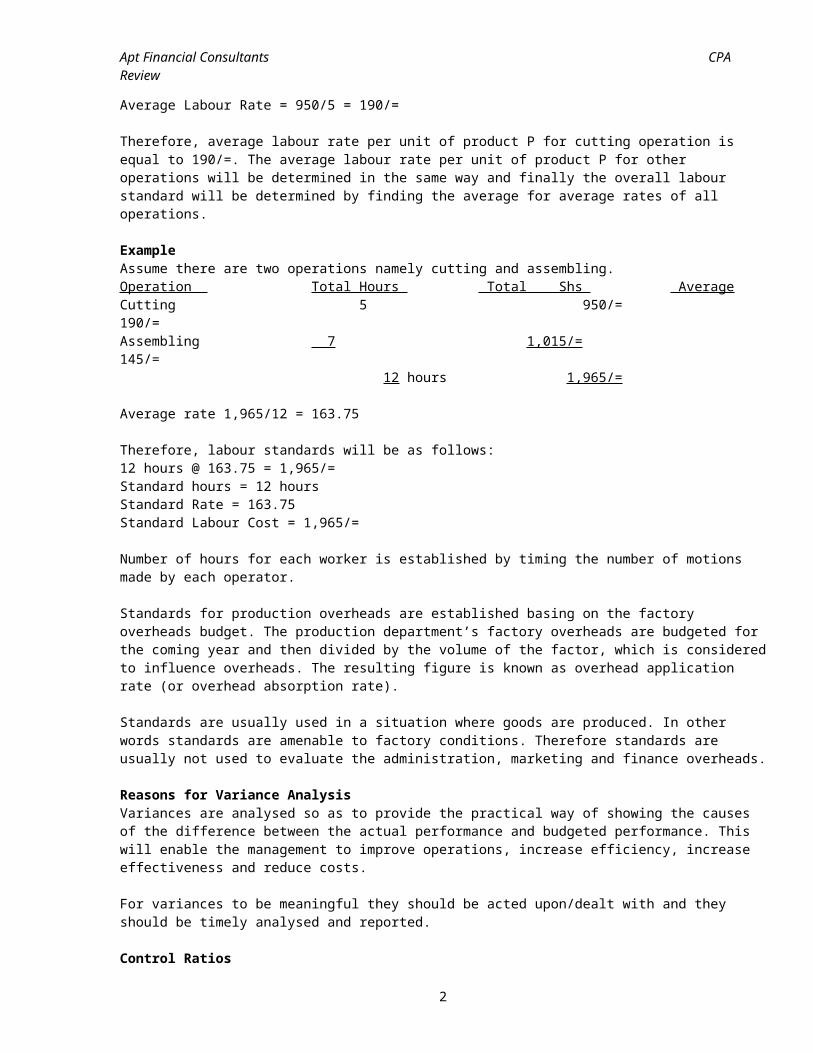

Average Labour Rate = 950/5 = 190/=

Therefore, average labour rate per unit of product P for cutting operation is equal to 190/=. The average labour rate per unit of product P for other operations will be determined in the same way and finally the overall labour standard will be determined by finding the average for average rates of all operations.

ExampleAssume there are two operations namely cutting and assembling.Operation Total Hours Total Shs AverageCutting 5 950/= 190/=Assembling 7 1,015/= 145/= 12 hours 1,965/=

Average rate 1,965/12 = 163.75

Therefore, labour standards will be as follows: 12 hours @ 163.75 = 1,965/=Standard hours = 12 hoursStandard Rate = 163.75Standard Labour Cost = 1,965/=

Number of hours for each worker is established by timing the number of motions made by each operator.

Standards for production overheads are established basing on the factory overheads budget. The production department’s factory overheads are budgeted for the coming year and then divided by the volume of the factor, which is consideredto influence overheads. The resulting figure is known as overhead application rate (or overhead absorption rate).

Standards are usually used in a situation where goods are produced. In other words standards are amenable to factory conditions. Therefore standards are usually not used to evaluate the administration, marketing and finance overheads.

Reasons for Variance AnalysisVariances are analysed so as to provide the practical way of showing the causes of the difference between the actual performance and budgeted performance. This will enable the management to improve operations, increase efficiency, increase effectiveness and reduce costs.

For variances to be meaningful they should be acted upon/dealt with and they should be timely analysed and reported.

Control Ratios

2

Apt Financial Consultants CPA Review

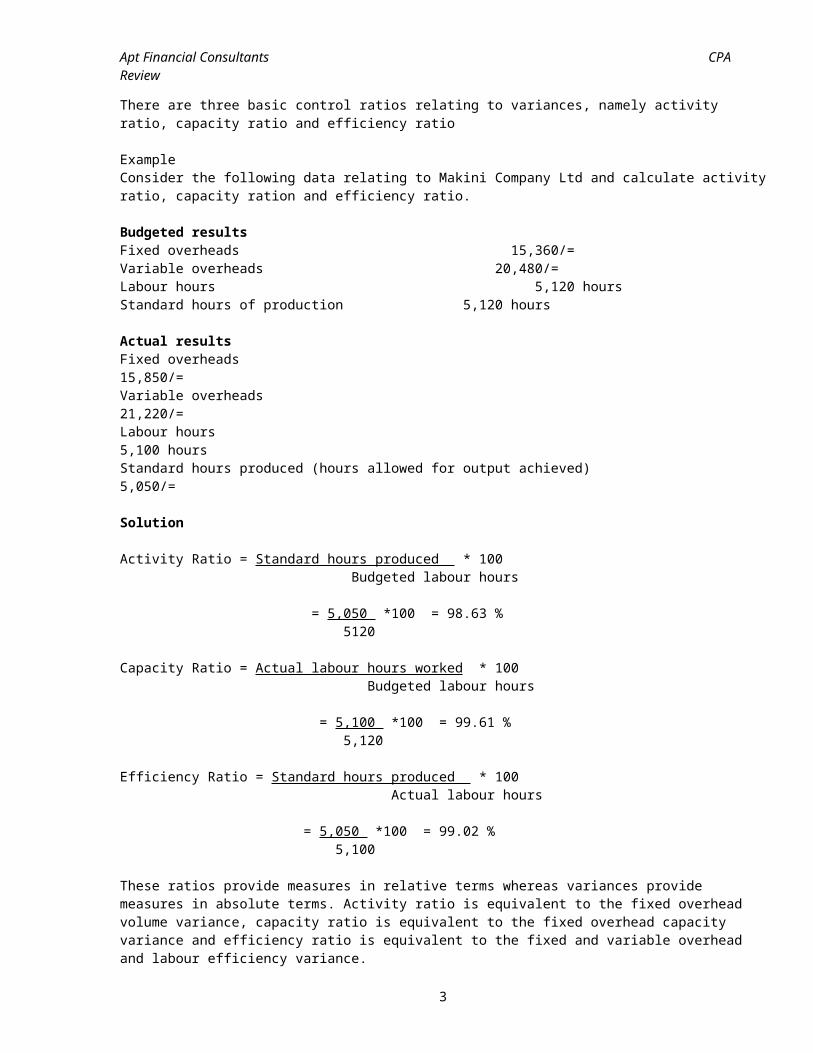

There are three basic control ratios relating to variances, namely activity ratio, capacity ratio and efficiency ratio

Example Consider the following data relating to Makini Company Ltd and calculate activityratio, capacity ration and efficiency ratio.

Budgeted resultsFixed overheads 15,360/=Variable overheads 20,480/=Labour hours 5,120 hoursStandard hours of production 5,120 hours

Actual resultsFixed overheads 15,850/=Variable overheads 21,220/=Labour hours 5,100 hoursStandard hours produced (hours allowed for output achieved) 5,050/=

Solution

Activity Ratio = Standard hours produced * 100 Budgeted labour hours

= 5,050 *100 = 98.63 % 5120

Capacity Ratio = Actual labour hours worked * 100 Budgeted labour hours

= 5,100 *100 = 99.61 % 5,120 Efficiency Ratio = Standard hours produced * 100 Actual labour hours

= 5,050 *100 = 99.02 % 5,100

These ratios provide measures in relative terms whereas variances provide measures in absolute terms. Activity ratio is equivalent to the fixed overhead volume variance, capacity ratio is equivalent to the fixed overhead capacity variance and efficiency ratio is equivalent to the fixed and variable overhead and labour efficiency variance.

3

Apt Financial Consultants CPA Review

Flexible Budgets A flexible budget is the budget prepared for any level of activity attained by using standards. A master budget is prepared taking into consideration the expected volume of activity. When this master budget is compared to actual results, that comparison gives a misleading view because they represent differentvolumes. The actual results must be “flexed” so that the comparison between actual results and the budget become meaningful. The comparison between actual results figures and master budget figures gives us a misleading view. However, when performance evaluation is based on flexible budget, the variance (or deviation) is analyzed into two groups, namely deviation attributable to changes in the price of inputs and variance attributable to efficiency in the usage of inputs.

VariancesA variance is the difference between the budget and actual results. A variance may indicate that performance was better than what was expected or worse than what was expected. A variance, which looks better than what was expected, is termed as favourable variance (F) whereas a variance, which looks worse, than expected, is termed as adverse variance (A) or unfavourable variance (U).

Formulae

Material Price Variance = (AP-SP) * AQ

Where, AP = Actual Price, SP = Standard Price, AQ = Actual Quantity

Material Efficiency Variance = (AQ – SQ) * SP

Where, AQ = Actual Quantity, SQ = Standard Quantity, SP = Standard Price

Labour Rate Variance = (AR-SR) * AQ

Where, AR = Actual Rate, SR = Standard Rate, AQ = Actual Quantity

Labour Efficiency Variance = (AH-SH) * SR

Where, AH = Actual Hours, SH = Standard Hour, SR = Standard Rate

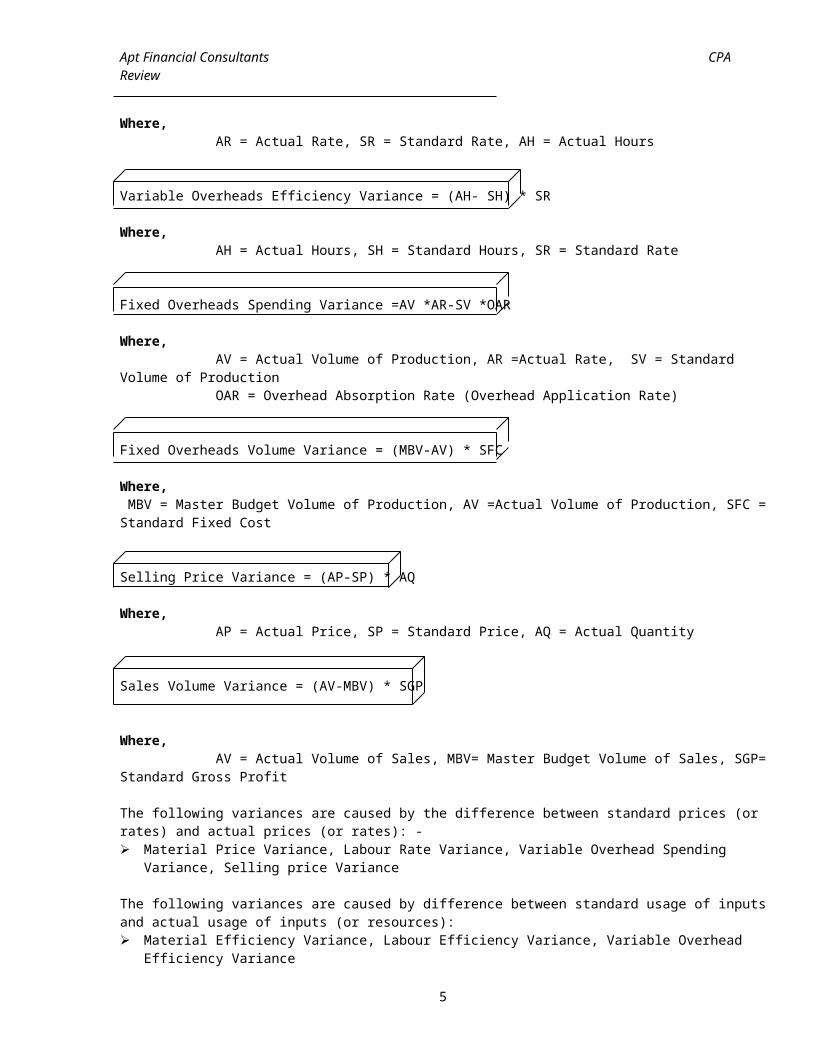

Variable Overheads Spending Variance = (AR-SR) * AH4

Apt Financial Consultants CPA Review

Where, AR = Actual Rate, SR = Standard Rate, AH = Actual Hours

Variable Overheads Efficiency Variance = (AH- SH) * SR

Where, AH = Actual Hours, SH = Standard Hours, SR = Standard Rate

Fixed Overheads Spending Variance =AV *AR-SV *OAR

Where, AV = Actual Volume of Production, AR =Actual Rate, SV = Standard Volume of Production OAR = Overhead Absorption Rate (Overhead Application Rate)

Fixed Overheads Volume Variance = (MBV-AV) * SFC

Where, MBV = Master Budget Volume of Production, AV =Actual Volume of Production, SFC =Standard Fixed Cost

Selling Price Variance = (AP-SP) * AQ

Where, AP = Actual Price, SP = Standard Price, AQ = Actual Quantity

Sales Volume Variance = (AV-MBV) * SGP

Where, AV = Actual Volume of Sales, MBV= Master Budget Volume of Sales, SGP=Standard Gross Profit

The following variances are caused by the difference between standard prices (or rates) and actual prices (or rates): - Material Price Variance, Labour Rate Variance, Variable Overhead Spending

Variance, Selling price Variance

The following variances are caused by difference between standard usage of inputsand actual usage of inputs (or resources): Material Efficiency Variance, Labour Efficiency Variance, Variable Overhead

Efficiency Variance

5

Apt Financial Consultants CPA Review

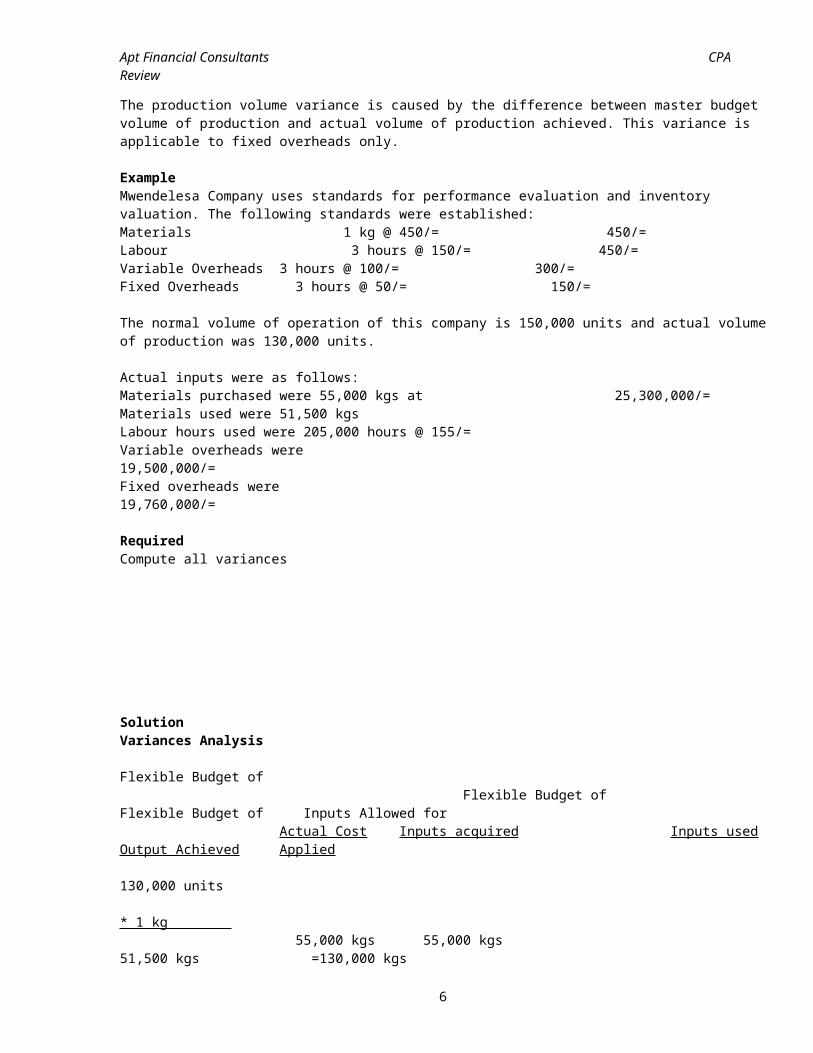

The production volume variance is caused by the difference between master budget volume of production and actual volume of production achieved. This variance is applicable to fixed overheads only.

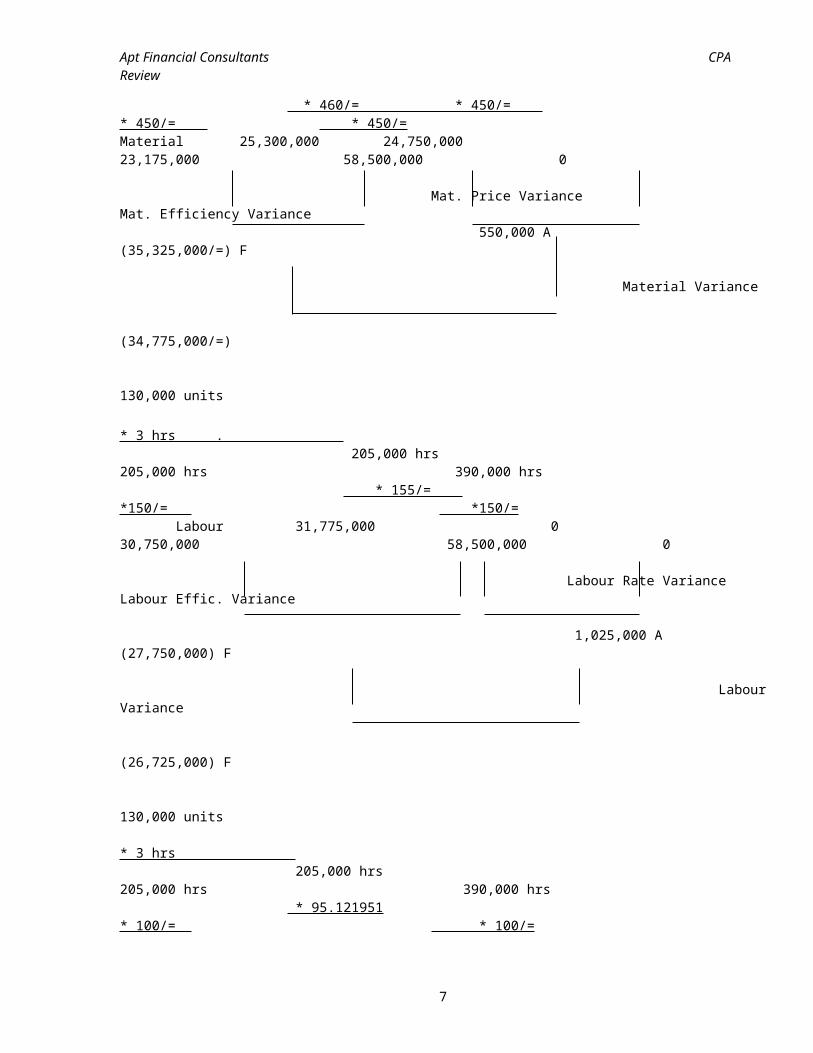

ExampleMwendelesa Company uses standards for performance evaluation and inventory valuation. The following standards were established: Materials 1 kg @ 450/= 450/=Labour 3 hours @ 150/= 450/=Variable Overheads 3 hours @ 100/= 300/=Fixed Overheads 3 hours @ 50/= 150/=

The normal volume of operation of this company is 150,000 units and actual volumeof production was 130,000 units.

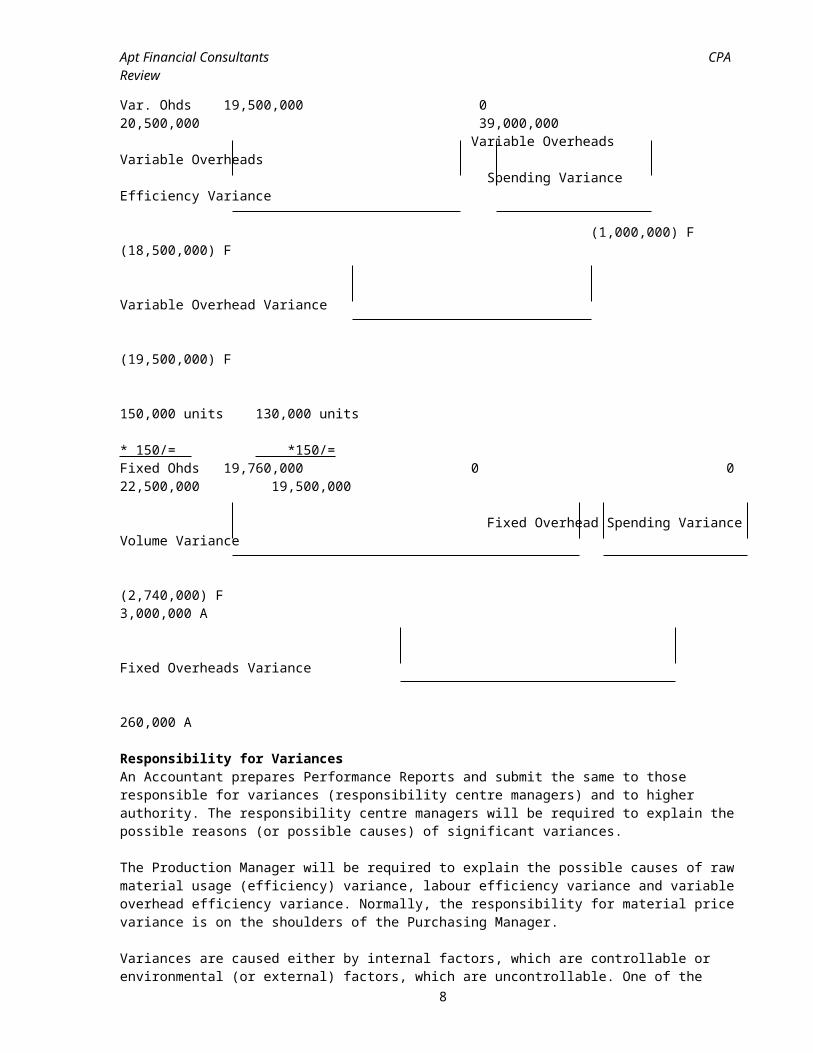

Actual inputs were as follows: Materials purchased were 55,000 kgs at 25,300,000/=Materials used were 51,500 kgs Labour hours used were 205,000 hours @ 155/=Variable overheads were 19,500,000/= Fixed overheads were 19,760,000/=

RequiredCompute all variances

SolutionVariances Analysis Flexible Budget of Flexible Budget of Flexible Budget of Inputs Allowed for Actual Cost Inputs acquired Inputs used Output Achieved Applied 130,000 units * 1 kg 55,000 kgs 55,000 kgs 51,500 kgs =130,000 kgs

6

Apt Financial Consultants CPA Review

* 460/= * 450/= * 450/= * 450/=Material 25,300,000 24,750,000 23,175,000 58,500,000 0 Mat. Price Variance Mat. Efficiency Variance 550,000 A (35,325,000/=) F

Material Variance (34,775,000/=)

130,000 units * 3 hrs . 205,000 hrs 205,000 hrs 390,000 hrs * 155/= *150/= *150/= Labour 31,775,000 0 30,750,000 58,500,000 0

Labour Rate Variance Labour Effic. Variance

1,025,000 A (27,750,000) F

LabourVariance

(26,725,000) F

130,000 units * 3 hrs 205,000 hrs 205,000 hrs 390,000 hrs * 95.121951 * 100/= * 100/=

7

Apt Financial Consultants CPA Review

Var. Ohds 19,500,000 0 20,500,000 39,000,000 Variable Overheads Variable Overheads Spending Variance Efficiency Variance

(1,000,000) F (18,500,000) F

Variable Overhead Variance (19,500,000) F

150,000 units 130,000 units * 150/= *150/=Fixed Ohds 19,760,000 0 0 22,500,000 19,500,000 Fixed Overhead Spending Variance Volume Variance

(2,740,000) F 3,000,000 A

Fixed Overheads Variance 260,000 A

Responsibility for VariancesAn Accountant prepares Performance Reports and submit the same to those responsible for variances (responsibility centre managers) and to higher authority. The responsibility centre managers will be required to explain the possible reasons (or possible causes) of significant variances.

The Production Manager will be required to explain the possible causes of raw material usage (efficiency) variance, labour efficiency variance and variable overhead efficiency variance. Normally, the responsibility for material price variance is on the shoulders of the Purchasing Manager.

Variances are caused either by internal factors, which are controllable or environmental (or external) factors, which are uncontrollable. One of the

8

Apt Financial Consultants CPA Review

internal factors, which may cause variances, is the operational factor. Operational decisions may cause favourable or unfavourable variances. For example, Purchasing Manager’s decision to purchase materials of inferior (or marginal) quality may cause favourable material price variance and may probably result into unfavourable material efficiency variance. Operational decisions of this kind may be for fraudulent purposes or negligence.

Operational decisions relating to labour may cause a labour rate variance. Standards may be established using rate of high-grade labour while actual operations use low-grade labour. This may cause the favourable labour rate variance and probably unfavourable labour efficiency variance.

It follows that price variances or rate variances may have an effect on efficiency variances. A favourable price variance (or rate variance) may mean that inferior inputs (or inputs of marginal quality) are acquired and used and this may affect the quantity used, and therefore unfavourable efficiency variancewill be a result.

Internal factors, which may affect efficiency in the use of material and labour, are: (i) The condition of the plant used in the production(ii) Pilferage of material(iii) Motivation Highly motivated personnel will use resources efficiently(iv) Supervision Good supervision will minimize blunders and misuse of materials(v) Coordination methods

Other reasons that we observed include: Recording errorsSometimes part of variance may be attributable to errors in recording the actual results but not the usage of material and labour. Planning errorsSometimes part of variance may be attributable to errors in planning the specifications of materials and labour. For example an organization may plan to use material of high quality whose production by its suppliers is not sufficient to cover its needs.

Overhead efficiency variance is attributable to the change in quantities of the factor used to absorb (or apply) overheads. For example if overhead is absorbed (or applied) using machine hours then a change in the volume of machine hours from the budget of hours allowed for output achieved will cause overhead efficiency variance.

All variances, which are significant, should be investigated in order to establish their causes. However, investigation should take into account a trade off between the cost of investigation and cost of failure to investigate.

9

Apt Financial Consultants CPA Review

Reporting of VariancesWe have seen that variances should be reported in summary form to higher authority and in detail to responsibility centre managers. There are various waysof reporting variances. The following are some of them: By appending variances to the Production Report If this approach is used, actual costs of operation will be compared to the budgeted costs and the difference will be reconciled by the total variance.

By appending variances to the Operating Report (that is Income Statement) If this approach is used, actual profit will be compared to the budgeted profit and the difference will be reconciled by sales variances and production variances.

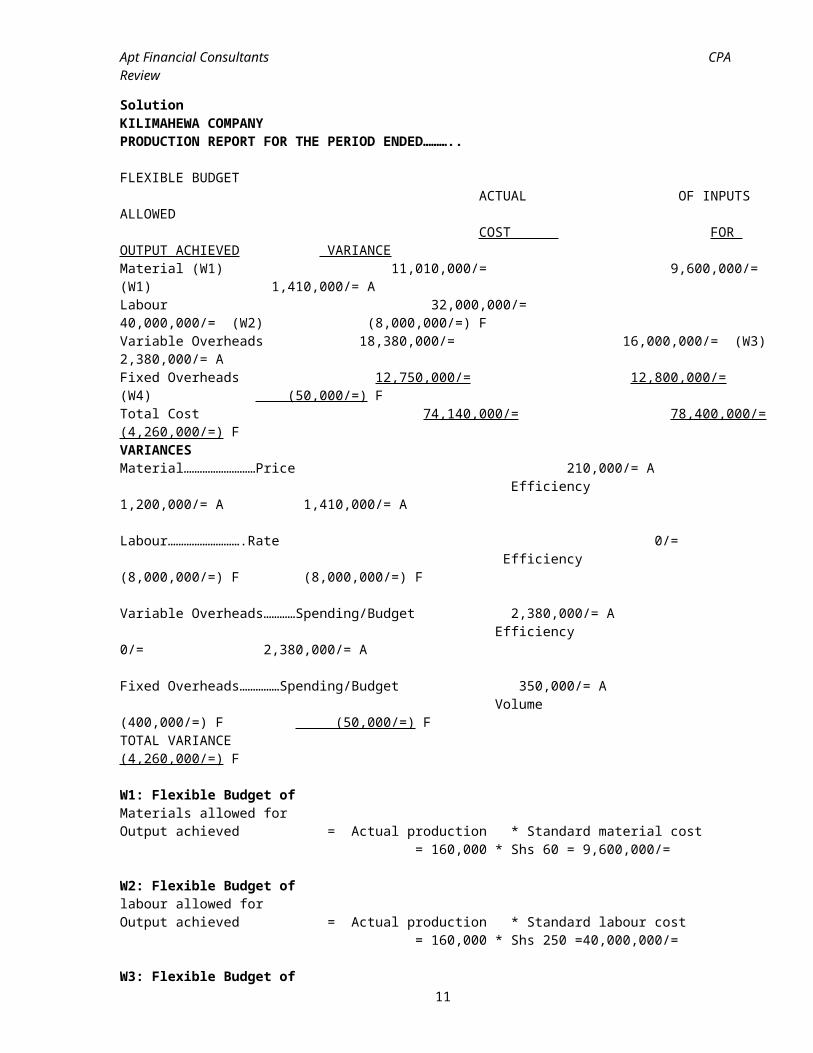

ExampleKilimahewa Company uses standards for performance evaluation and inventory valuation. During the previous quarter the company budgeted production and sales equal to 155,000 units (which is its normal operating capacity) but actual production turned out to be 160,000 units. Actual sales was equal to 170,000 units and each unit was sold at 650/=.

The stock levels were as follows: Raw materials Finished GoodsOpening Stock 50,000 kgs 20,000 unitsClosing Stock 40,000 kgs 10,000 units

The company purchased 350,000 kgs at 10,710,000/=Labour hours used were 320,000 at 32,000,000/=Variable overheads were 18,380,000/=Fixed overheads were 12,750,000/=

The following operating standards are used by the company: Materials 2 kgs @ 30/= 60Labour 2 ½ hours @ 100/= 250/=Variable overheads 2 hours @ 50/= 100/=Fixed overheads 2 hours @ 40/= 80/=Standard cost of a unit 490/=Standard selling price 612.50Standard gross profit 122.50

RequiredPrepare a Production Report reconciling actual costs and the budget

10

Apt Financial Consultants CPA Review

SolutionKILIMAHEWA COMPANYPRODUCTION REPORT FOR THE PERIOD ENDED……….. FLEXIBLE BUDGET ACTUAL OF INPUTS ALLOWED COST FOR OUTPUT ACHIEVED VARIANCEMaterial (W1) 11,010,000/= 9,600,000/= (W1) 1,410,000/= ALabour 32,000,000/= 40,000,000/= (W2) (8,000,000/=) FVariable Overheads 18,380,000/= 16,000,000/= (W3)2,380,000/= AFixed Overheads 12,750,000/= 12,800,000/= (W4) (50,000/=) FTotal Cost 74,140,000/= 78,400,000/=(4,260,000/=) FVARIANCESMaterial………………………Price 210,000/= A Efficiency 1,200,000/= A 1,410,000/= A

Labour……………………….Rate 0/= Efficiency (8,000,000/=) F (8,000,000/=) F

Variable Overheads…………Spending/Budget 2,380,000/= A Efficiency 0/= 2,380,000/= A

Fixed Overheads……………Spending/Budget 350,000/= A Volume (400,000/=) F (50,000/=) FTOTAL VARIANCE (4,260,000/=) F

W1: Flexible Budget ofMaterials allowed for Output achieved = Actual production * Standard material cost = 160,000 * Shs 60 = 9,600,000/=

W2: Flexible Budget oflabour allowed for Output achieved = Actual production * Standard labour cost = 160,000 * Shs 250 =40,000,000/=

W3: Flexible Budget of11

Apt Financial Consultants CPA Review

Variable overheads allowed for Output achieved = Actual production * Standard variable overhead cost = 160,000 * Shs 100 =16,000,000/=

W4: Overheads applied = Actual production * Overhead application (or absorption) rate = 160,000 * Shs 80 =12,800,000/=

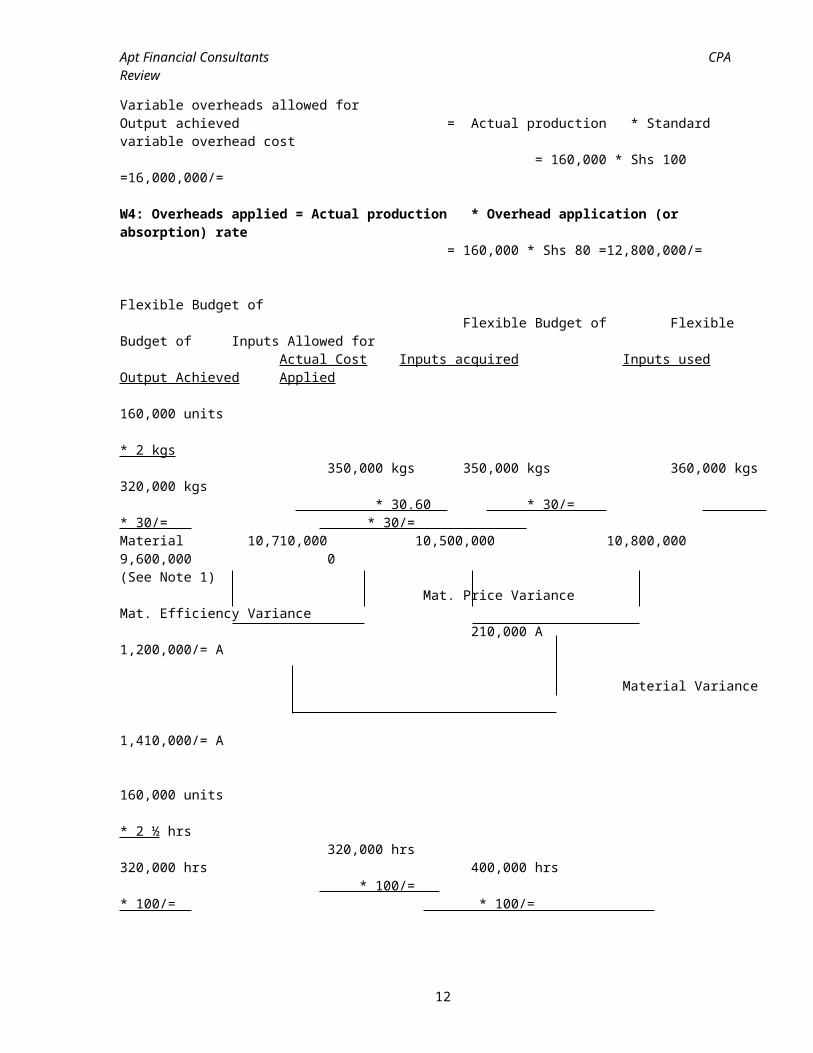

Flexible Budget of Flexible Budget of Flexible Budget of Inputs Allowed for Actual Cost Inputs acquired Inputs used Output Achieved Applied 160,000 units * 2 kgs 350,000 kgs 350,000 kgs 360,000 kgs 320,000 kgs * 30.60 * 30/= * 30/= * 30/= Material 10,710,000 10,500,000 10,800,000 9,600,000 0(See Note 1) Mat. Price Variance Mat. Efficiency Variance 210,000 A 1,200,000/= A

Material Variance 1,410,000/= A

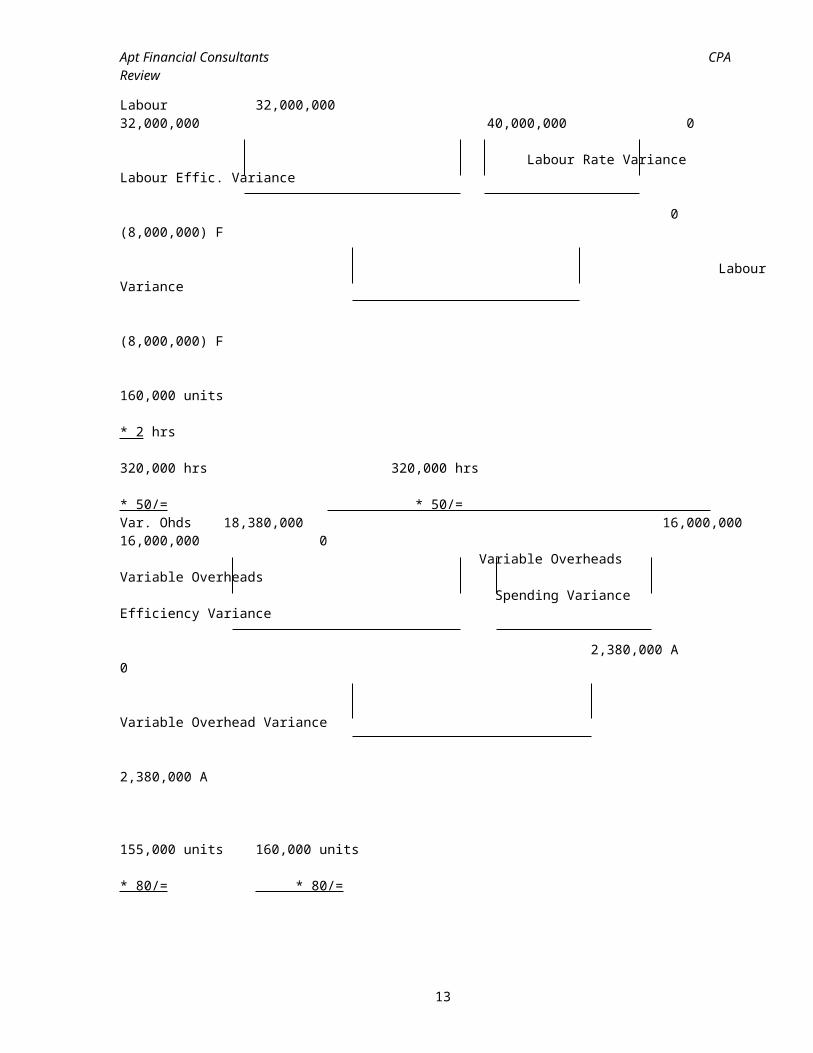

160,000 units * 2 ½ hrs 320,000 hrs 320,000 hrs 400,000 hrs * 100/= * 100/= * 100/=

12

Apt Financial Consultants CPA Review

Labour 32,000,000 32,000,000 40,000,000 0 Labour Rate Variance Labour Effic. Variance

0 (8,000,000) F

LabourVariance

(8,000,000) F

160,000 units * 2 hrs 320,000 hrs 320,000 hrs * 50/= * 50/= Var. Ohds 18,380,000 16,000,000 16,000,000 0 Variable Overheads Variable Overheads Spending Variance Efficiency Variance

2,380,000 A 0

Variable Overhead Variance 2,380,000 A

155,000 units 160,000 units * 80/= * 80/=

13

Apt Financial Consultants CPA Review

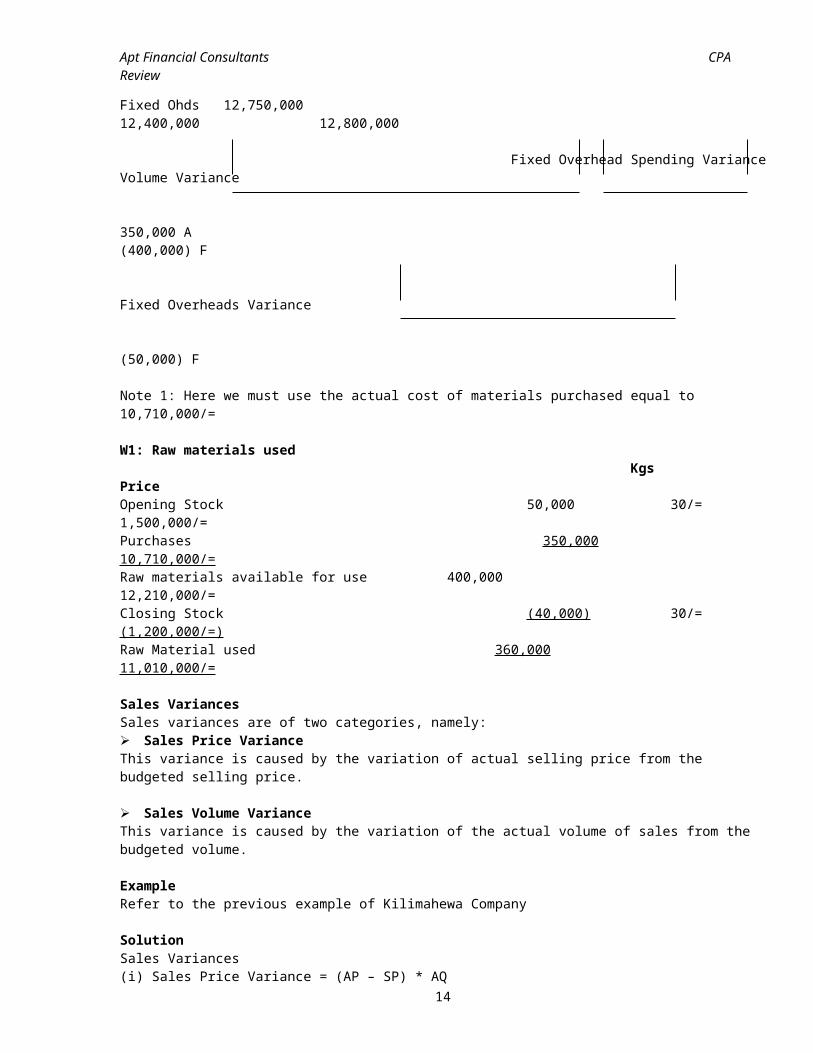

Fixed Ohds 12,750,000 12,400,000 12,800,000 Fixed Overhead Spending VarianceVolume Variance

350,000 A (400,000) F

Fixed Overheads Variance (50,000) F

Note 1: Here we must use the actual cost of materials purchased equal to 10,710,000/=

W1: Raw materials used Kgs PriceOpening Stock 50,000 30/= 1,500,000/=Purchases 350,000 10,710,000/=Raw materials available for use 400,000 12,210,000/=Closing Stock (40,000) 30/= (1,200,000/=)Raw Material used 360,000 11,010,000/=

Sales VariancesSales variances are of two categories, namely: Sales Price VarianceThis variance is caused by the variation of actual selling price from the budgeted selling price.

Sales Volume VarianceThis variance is caused by the variation of the actual volume of sales from the budgeted volume. ExampleRefer to the previous example of Kilimahewa Company

SolutionSales Variances(i) Sales Price Variance = (AP – SP) * AQ

14

Apt Financial Consultants CPA Review

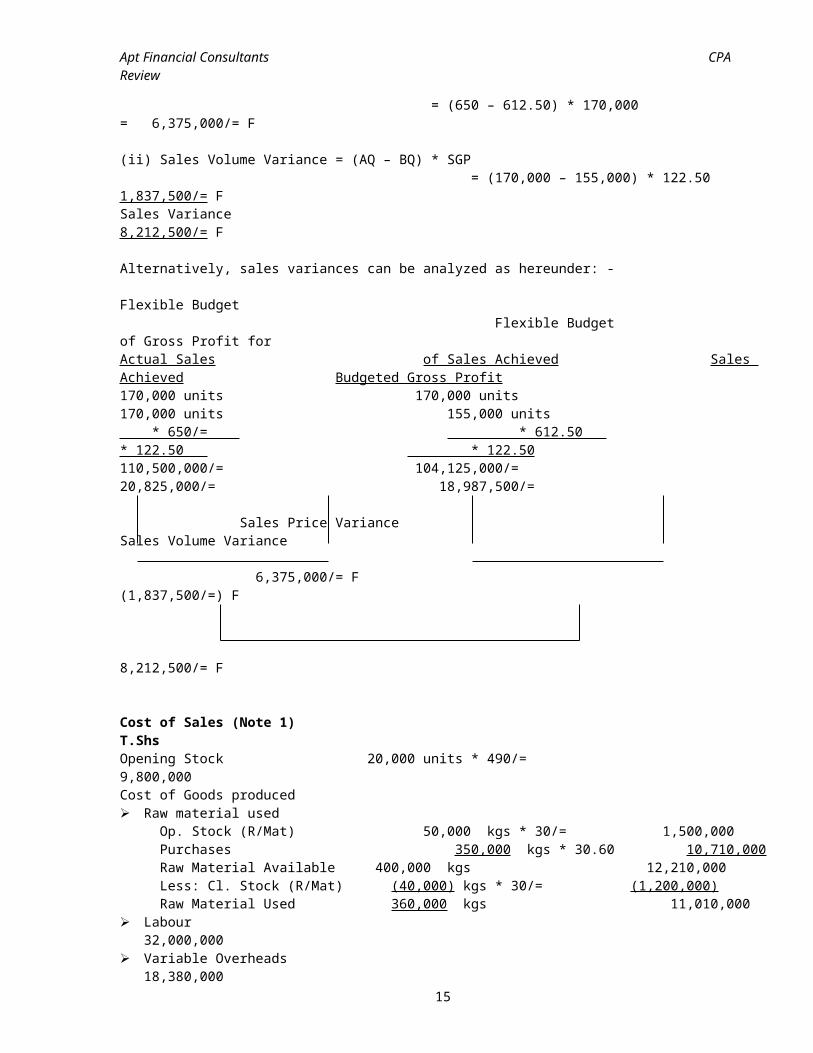

= (650 – 612.50) * 170,000 = 6,375,000/= F

(ii) Sales Volume Variance = (AQ – BQ) * SGP = (170,000 – 155,000) * 122.50 1,837,500/= FSales Variance 8,212,500/= F

Alternatively, sales variances can be analyzed as hereunder: - Flexible Budget Flexible Budget of Gross Profit for Actual Sales of Sales Achieved Sales Achieved Budgeted Gross Profit170,000 units 170,000 units 170,000 units 155,000 units * 650/= * 612.50 * 122.50 * 122.50110,500,000/= 104,125,000/= 20,825,000/= 18,987,500/= Sales Price Variance Sales Volume Variance

6,375,000/= F (1,837,500/=) F

8,212,500/= F

Cost of Sales (Note 1) T.ShsOpening Stock 20,000 units * 490/= 9,800,000Cost of Goods produced Raw material used Op. Stock (R/Mat) 50,000 kgs * 30/= 1,500,000 Purchases 350,000 kgs * 30.60 10,710,000 Raw Material Available 400,000 kgs 12,210,000 Less: Cl. Stock (R/Mat) (40,000) kgs * 30/= (1,200,000) Raw Material Used 360,000 kgs 11,010,000 Labour

32,000,000 Variable Overheads

18,380,00015

Apt Financial Consultants CPA Review

Fixed Overheads 12,750,000

Cost of goods produced 74,140,000Goods Available for Sale 83,940,000Less: Closing Stock (4,900,000)Cost of Sale 79,040,000

NB: This report is less detailed because it is intended for higher authority. Normally reports to higher authority highlights exceptional items only and detailed information is appended to the report.

Reconciliation of Actual Results and Budgeted ResultsOne of the ways of measuring the operating results of an organization is by way of profit attained. Therefore performance will be reported to the management in areport that shows the comparison of actual gross profit and budgeted gross profit. Any difference (or variance) between the two should be reflected by the total of sales variance and production variance.

ExampleRefer to the previous example of Kilimahewa Company

RequiredPrepare a report, which shows the performance attained in the previous quarter and show the variances within that report. NB: This question can be answered in the form of the Management Report. Within the management report a reconciliation is done between actual results and budgeted results.

SolutionReconciliation of Actual Results and Budgeted Results

KILIMAHEWA COMPANYMANAGEMENT REPORT FOR THE PERIOD ENDED…………..

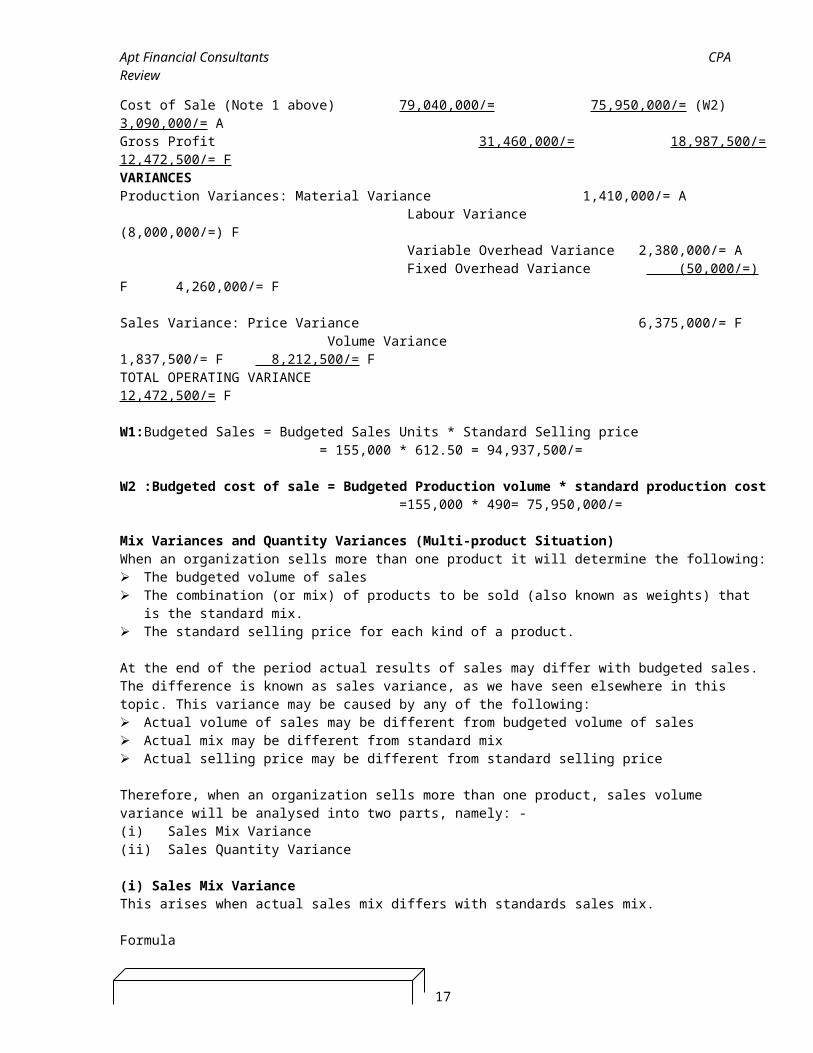

ACTUAL RESULTS BUDGET VARIANCESales Units 170,000 155,000 15,000 FProduction Units 160,000 155,000 5,000 FSales 110,500,000/= 94,937,500/= (W1) 15,562,500/= F

16

Apt Financial Consultants CPA Review

Cost of Sale (Note 1 above) 79,040,000/= 75,950,000/= (W2) 3,090,000/= AGross Profit 31,460,000/= 18,987,500/=12,472,500/= FVARIANCESProduction Variances: Material Variance 1,410,000/= A Labour Variance (8,000,000/=) F Variable Overhead Variance 2,380,000/= A Fixed Overhead Variance (50,000/=) F 4,260,000/= F

Sales Variance: Price Variance 6,375,000/= F Volume Variance 1,837,500/= F 8,212,500/= FTOTAL OPERATING VARIANCE 12,472,500/= F

W1:Budgeted Sales = Budgeted Sales Units * Standard Selling price = 155,000 * 612.50 = 94,937,500/=

W2 :Budgeted cost of sale = Budgeted Production volume * standard production cost =155,000 * 490= 75,950,000/=

Mix Variances and Quantity Variances (Multi-product Situation)When an organization sells more than one product it will determine the following: The budgeted volume of sales The combination (or mix) of products to be sold (also known as weights) that

is the standard mix. The standard selling price for each kind of a product.

At the end of the period actual results of sales may differ with budgeted sales. The difference is known as sales variance, as we have seen elsewhere in this topic. This variance may be caused by any of the following: Actual volume of sales may be different from budgeted volume of sales Actual mix may be different from standard mix Actual selling price may be different from standard selling price

Therefore, when an organization sells more than one product, sales volume variance will be analysed into two parts, namely: -(i) Sales Mix Variance(ii) Sales Quantity Variance

(i) Sales Mix VarianceThis arises when actual sales mix differs with standards sales mix.

Formula

17

Apt Financial Consultants CPA Review

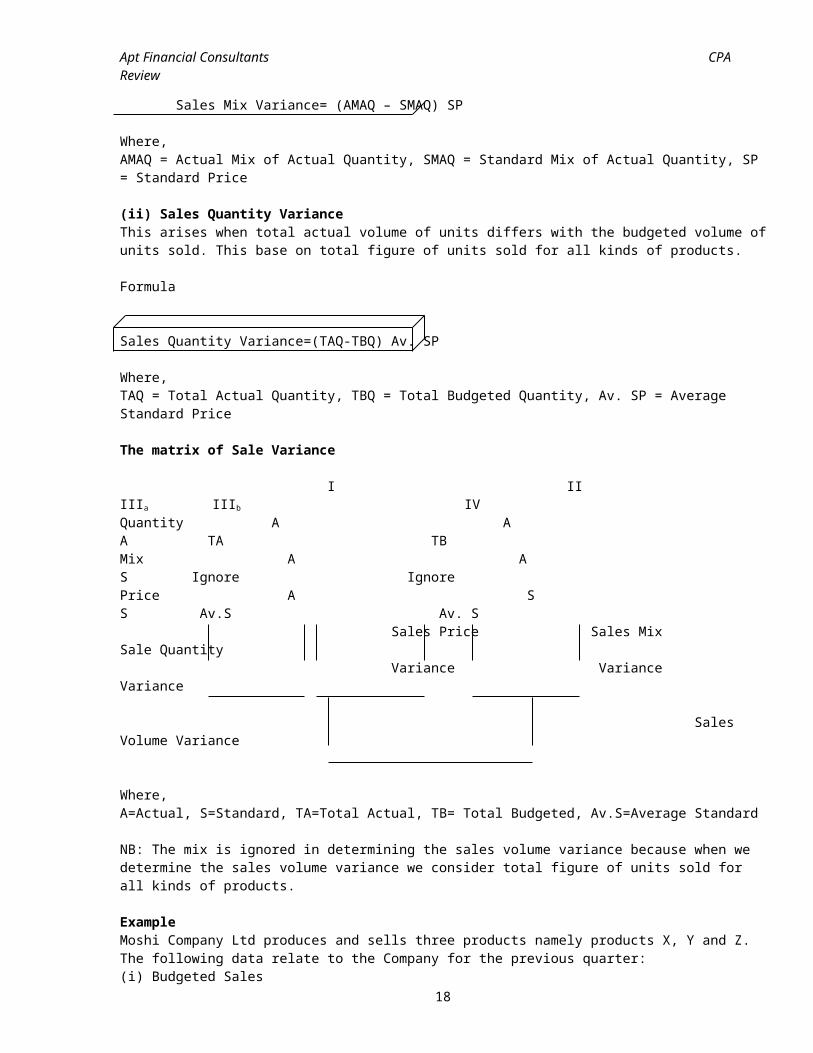

Sales Mix Variance= (AMAQ – SMAQ) SP

Where,AMAQ = Actual Mix of Actual Quantity, SMAQ = Standard Mix of Actual Quantity, SP = Standard Price

(ii) Sales Quantity VarianceThis arises when total actual volume of units differs with the budgeted volume ofunits sold. This base on total figure of units sold for all kinds of products.

Formula

Sales Quantity Variance=(TAQ-TBQ) Av. SP

Where,TAQ = Total Actual Quantity, TBQ = Total Budgeted Quantity, Av. SP = Average Standard Price

The matrix of Sale Variance

I II IIIa IIIb IVQuantity A A A TA TBMix A A S Ignore IgnorePrice A S S Av.S Av. S Sales Price Sales Mix Sale Quantity Variance Variance Variance

Sales Volume Variance

Where,A=Actual, S=Standard, TA=Total Actual, TB= Total Budgeted, Av.S=Average Standard

NB: The mix is ignored in determining the sales volume variance because when we determine the sales volume variance we consider total figure of units sold for all kinds of products.

ExampleMoshi Company Ltd produces and sells three products namely products X, Y and Z. The following data relate to the Company for the previous quarter: (i) Budgeted Sales

18

Apt Financial Consultants CPA Review

Units Selling Price (TShs) Product X 10,000 130/= Y 8,000 150/= Z 2,000 185/= 20,000

(ii) Actual Sales Units Selling Price (TShs) Product X 8,000 140/= Y 8,500 120/= Z 2,500 145/= 19,000

Required (i) Determine the following:

(a) Sales Price Variance (b) Sales Mix Variance, (c) Sales Quantity Variance, (d) Sales Volume Variance

Solution Actual MixProduct X: 80/190 Y: 85/190 Z: 25/190

Budgeted MixProduct X: 100/200 Y: 80/200 Z: 20/200

Average Standard Price=[130+150+185]/3= 155

Column I: Actual Quantity, Actual Mix and Actual PriceProduct X: 19,000 * [80/190] : 8,000 * 140 = 1,120,000 Y: 19,000 * [85/190] : 8,500 * 120 = 1,020,000 Z: 19,000 * [25/190] : 2,500 * 145 = 362,500 19,000 2,502,500

Column II: Actual Quantity, Actual Mix and Standard PriceProduct X: 19,000 * [80/190] : 8,000 * 130 = 1,040,000 Y: 19,000 * [85/190] : 8,500 * 150 = 1,275,000 Z: 19,000 * [25/190] : 2,500 * 185 = 462,500 19,000 2,777,500

19

Apt Financial Consultants CPA Review

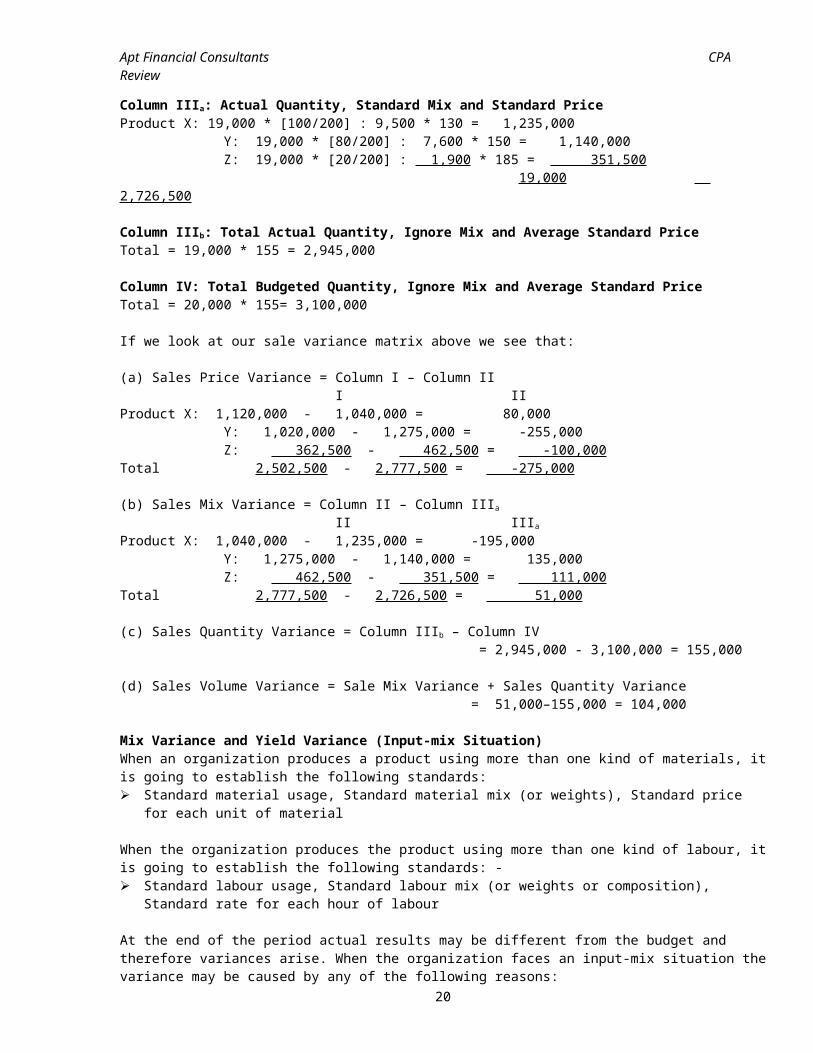

Column IIIa: Actual Quantity, Standard Mix and Standard Price Product X: 19,000 * [100/200] : 9,500 * 130 = 1,235,000 Y: 19,000 * [80/200] : 7,600 * 150 = 1,140,000 Z: 19,000 * [20/200] : 1,900 * 185 = 351,500 19,000 2,726,500

Column IIIb: Total Actual Quantity, Ignore Mix and Average Standard Price Total = 19,000 * 155 = 2,945,000

Column IV: Total Budgeted Quantity, Ignore Mix and Average Standard Price Total = 20,000 * 155= 3,100,000

If we look at our sale variance matrix above we see that:

(a) Sales Price Variance = Column I – Column II I IIProduct X: 1,120,000 - 1,040,000 = 80,000 Y: 1,020,000 - 1,275,000 = -255,000 Z: 362,500 - 462,500 = -100,000Total 2,502,500 - 2,777,500 = -275,000

(b) Sales Mix Variance = Column II – Column IIIa

II IIIa

Product X: 1,040,000 - 1,235,000 = -195,000 Y: 1,275,000 - 1,140,000 = 135,000 Z: 462,500 - 351,500 = 111,000Total 2,777,500 - 2,726,500 = 51,000

(c) Sales Quantity Variance = Column IIIb – Column IV = 2,945,000 - 3,100,000 = 155,000

(d) Sales Volume Variance = Sale Mix Variance + Sales Quantity Variance = 51,000–155,000 = 104,000

Mix Variance and Yield Variance (Input-mix Situation)When an organization produces a product using more than one kind of materials, itis going to establish the following standards: Standard material usage, Standard material mix (or weights), Standard price

for each unit of material

When the organization produces the product using more than one kind of labour, itis going to establish the following standards: - Standard labour usage, Standard labour mix (or weights or composition),

Standard rate for each hour of labour

At the end of the period actual results may be different from the budget and therefore variances arise. When the organization faces an input-mix situation thevariance may be caused by any of the following reasons:

20

Apt Financial Consultants CPA Review

Actual material price (or labour rate) may be different from the standard material price (or labour rate)

Actual material mix (or labour composition) may be different from the standardmaterial mix (or labour composition)

Actual material usage (or labour usage) may be different from the budgeted material usage (or labour usage)

When the organization faces an input-mix situation the following variances may arise: Price varianceThis is that part of the variance attributable to the usage of inputs whose prices (or rates) are different from standard prices (or rates) Mix varianceThis is that part of the variance attributable to applying inputs whose mix (or composition) is different from standard mix (or composition)

Yield varianceThis is that part of the variance attributable to the usage of inputs quantities different from standard material usage.

The matrix of input variances in the input-mix situation is as follows:

I II III IV Quantity A A ASMix A A S SPrice A S S S

Price Variance Mix Variance Yield Variance

Efficiency Variance A - Stands for ActualS - Stands for Standard

Efficiency variance can be segregated into two variances namely mix variance and yield variance. Therefore,

Efficiency Variance = Mix Variance + Yield Variance

21

Apt Financial Consultants CPA Review

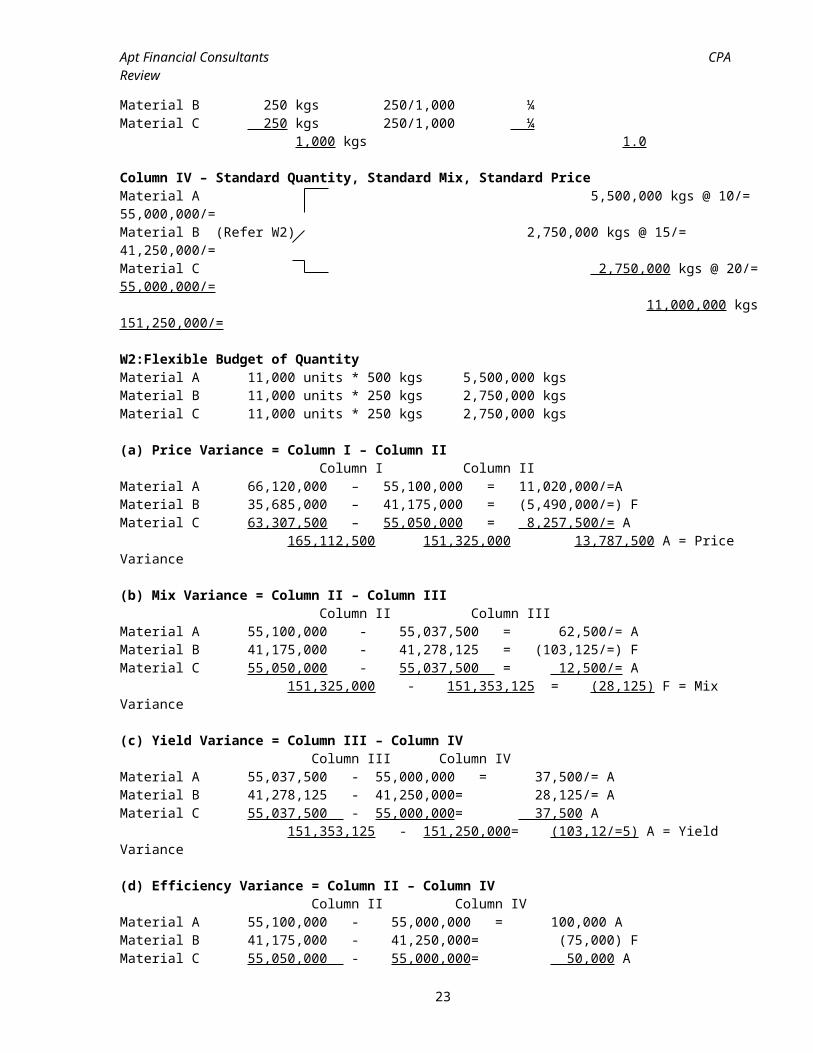

ExampleMongwe Company produces a product known as N using materials A, B and C. ChemicalEngineers of the Company has established the following standards for producing one unit of product N: Material A 500 kgs @ 10/=Material B 250 kgs @ 15/=Material C 250 kgs @ 20/=

Its production budget for the previous week was 10,000 units.

The following were the actual results for the previous week: Actual production was 11,000 units.Actual Material usage Material A 5,510,000 kgs @ 12/= Material B 2,745,000 kgs @ 13/= Material C 2,752,500 kgs @ 23/=

Required: -Calculate the following material variances: (a) Price Variance, (b) Mix Variance, (c) Yield Variance, (d) Efficiency Variance

Solution: -Column I – Actual Quantity, Actual Mix, Actual PriceMaterial A 5,510,000 kgs @ 12/= 66,120,000/=Material B 2,745,000 kgs @ 13/= 35,685,000/=Material C 2,752,500 kgs @ 23/= 63,307,500/= 11,007,500 kgs 165,112,500/=

Column II – Actual Quantity, Actual Mix, Standard PriceMaterial A 5,510,000 kgs @ 10/= 55,100,000/=Material B 2,745,000 kgs @ 15/= 41,175,000/=Material C 2,752,500 kgs @ 20/= 55,050,000/= 11,007,500 kgs 151,325,000/=

Column III – Actual Quantity, Standard Mix, Standard PriceMaterial A 11,007,500 kgs * ½ 5,503,750 kgs @ 10/= 55,037,500/=Material B 11,007,500 kgs * ¼ 2,751,875 kgs @ 15/= 41,278,125/=Material C 11,007,500 kgs * ¼ 2,751,875 kgs @ 20/= 55,037,500/= 11,007,500 kgs 151,353,125/=

W1: For standard mix calculationMaterial A 500 kgs 500/1,000 ½

22

Apt Financial Consultants CPA Review

Material B 250 kgs 250/1,000 ¼ Material C 250 kgs 250/1,000 ¼ 1,000 kgs 1.0

Column IV – Standard Quantity, Standard Mix, Standard PriceMaterial A 5,500,000 kgs @ 10/= 55,000,000/=Material B (Refer W2) 2,750,000 kgs @ 15/= 41,250,000/=Material C 2,750,000 kgs @ 20/= 55,000,000/= 11,000,000 kgs 151,250,000/=

W2:Flexible Budget of QuantityMaterial A 11,000 units * 500 kgs 5,500,000 kgs Material B 11,000 units * 250 kgs 2,750,000 kgs Material C 11,000 units * 250 kgs 2,750,000 kgs

(a) Price Variance = Column I – Column II Column I Column II Material A 66,120,000 – 55,100,000 = 11,020,000/=AMaterial B 35,685,000 – 41,175,000 = (5,490,000/=) F Material C 63,307,500 – 55,050,000 = 8,257,500/= A 165,112,500 151,325,000 13,787,500 A = Price Variance

(b) Mix Variance = Column II – Column III Column II Column IIIMaterial A 55,100,000 - 55,037,500 = 62,500/= AMaterial B 41,175,000 - 41,278,125 = (103,125/=) F Material C 55,050,000 - 55,037,500 = 12,500/= A 151,325,000 - 151,353,125 = (28,125) F = Mix Variance

(c) Yield Variance = Column III – Column IV Column III Column IV Material A 55,037,500 - 55,000,000 = 37,500/= AMaterial B 41,278,125 - 41,250,000= 28,125/= AMaterial C 55,037,500 - 55,000,000= 37,500 A 151,353,125 - 151,250,000= (103,12/=5) A = Yield Variance

(d) Efficiency Variance = Column II – Column IV Column II Column IVMaterial A 55,100,000 - 55,000,000 = 100,000 AMaterial B 41,175,000 - 41,250,000= (75,000) FMaterial C 55,050,000 - 55,000,000= 50,000 A

23

Apt Financial Consultants CPA Review

151,325,000 - 151,250,000= (75,000) A = Efficiency Variance

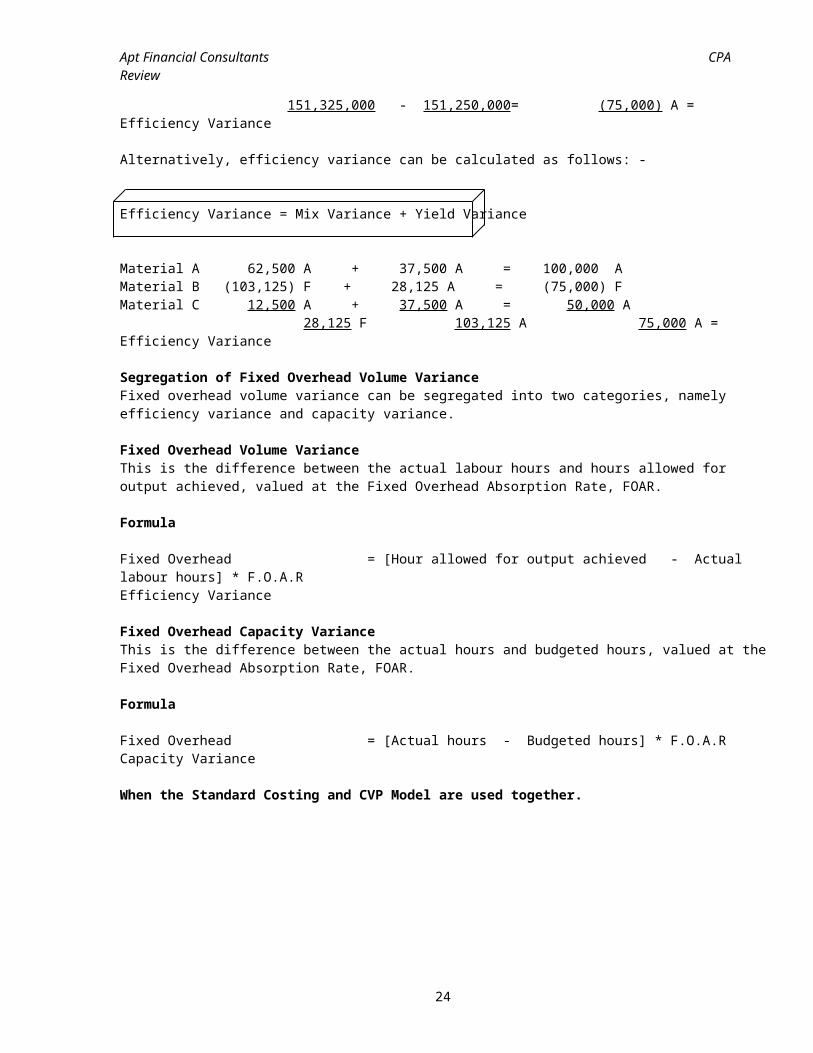

Alternatively, efficiency variance can be calculated as follows: -

Efficiency Variance = Mix Variance + Yield Variance

Material A 62,500 A + 37,500 A = 100,000 AMaterial B (103,125) F + 28,125 A = (75,000) FMaterial C 12,500 A + 37,500 A = 50,000 A 28,125 F 103,125 A 75,000 A = Efficiency Variance

Segregation of Fixed Overhead Volume VarianceFixed overhead volume variance can be segregated into two categories, namely efficiency variance and capacity variance.

Fixed Overhead Volume VarianceThis is the difference between the actual labour hours and hours allowed for output achieved, valued at the Fixed Overhead Absorption Rate, FOAR.

Formula

Fixed Overhead = [Hour allowed for output achieved - Actual labour hours] * F.O.A.R Efficiency Variance

Fixed Overhead Capacity VarianceThis is the difference between the actual hours and budgeted hours, valued at theFixed Overhead Absorption Rate, FOAR.

Formula

Fixed Overhead = [Actual hours - Budgeted hours] * F.O.A.R Capacity Variance

When the Standard Costing and CVP Model are used together.

24

Apt Financial Consultants CPA Review

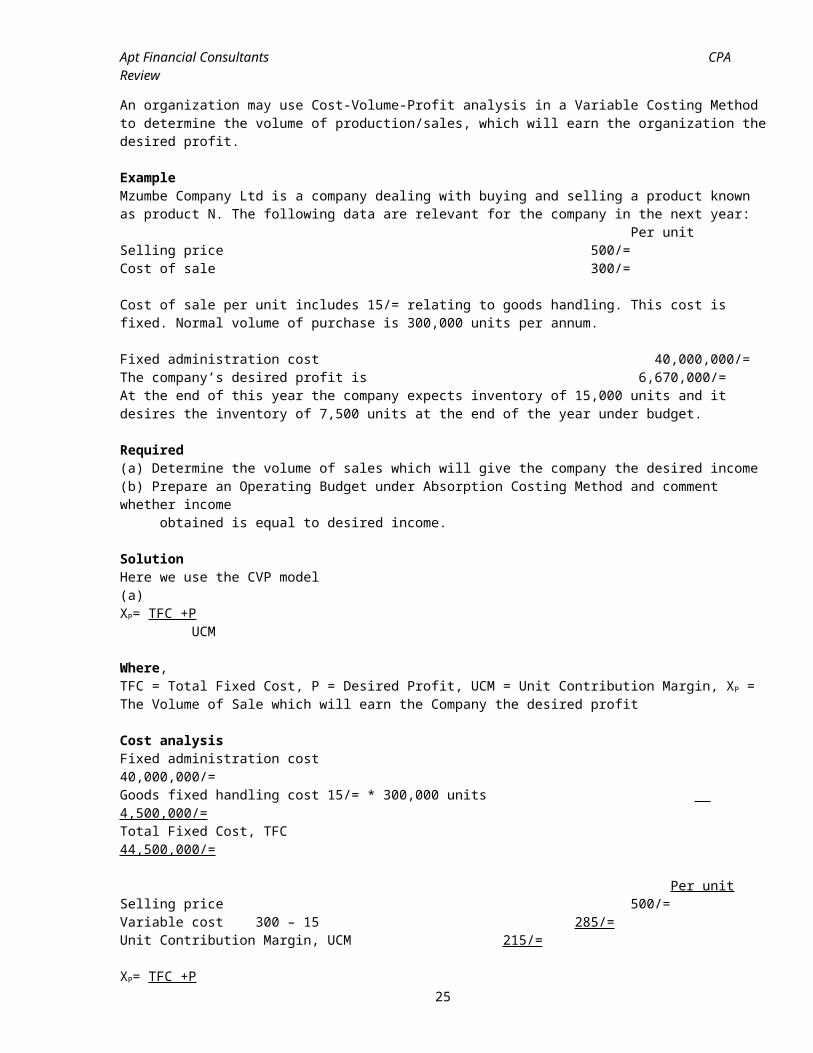

An organization may use Cost-Volume-Profit analysis in a Variable Costing Method to determine the volume of production/sales, which will earn the organization thedesired profit.

Example Mzumbe Company Ltd is a company dealing with buying and selling a product known as product N. The following data are relevant for the company in the next year: Per unitSelling price 500/=Cost of sale 300/=

Cost of sale per unit includes 15/= relating to goods handling. This cost is fixed. Normal volume of purchase is 300,000 units per annum.

Fixed administration cost 40,000,000/=The company’s desired profit is 6,670,000/=At the end of this year the company expects inventory of 15,000 units and it desires the inventory of 7,500 units at the end of the year under budget.

Required(a) Determine the volume of sales which will give the company the desired income(b) Prepare an Operating Budget under Absorption Costing Method and comment whether income obtained is equal to desired income.

SolutionHere we use the CVP model(a)XP= TFC +P UCM

Where, TFC = Total Fixed Cost, P = Desired Profit, UCM = Unit Contribution Margin, XP = The Volume of Sale which will earn the Company the desired profit

Cost analysisFixed administration cost 40,000,000/=Goods fixed handling cost 15/= * 300,000 units 4,500,000/=Total Fixed Cost, TFC 44,500,000/=

Per unitSelling price 500/=Variable cost 300 – 15 285/=Unit Contribution Margin, UCM 215/=

XP= TFC +P25

Apt Financial Consultants CPA Review

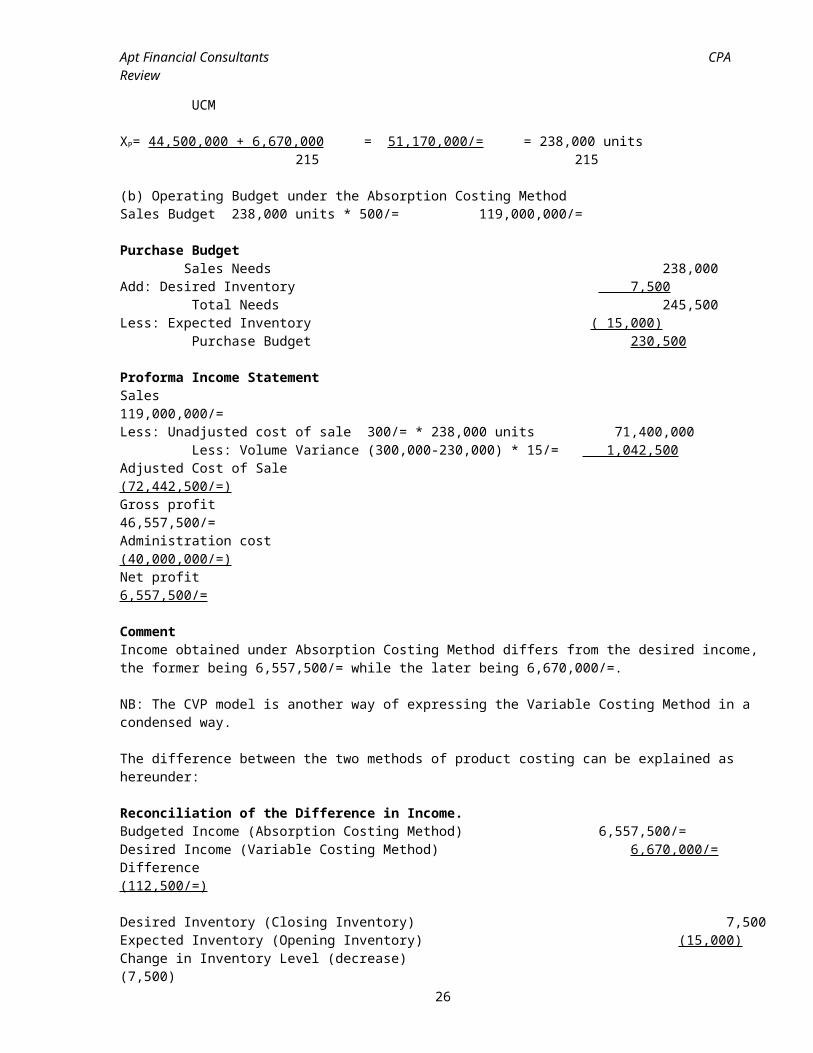

UCM

XP= 44,500,000 + 6,670,000 = 51,170,000/= = 238,000 units 215 215

(b) Operating Budget under the Absorption Costing MethodSales Budget 238,000 units * 500/= 119,000,000/=

Purchase Budget Sales Needs 238,000Add: Desired Inventory 7,500 Total Needs 245,500Less: Expected Inventory ( 15,000) Purchase Budget 230,500

Proforma Income StatementSales 119,000,000/=Less: Unadjusted cost of sale 300/= * 238,000 units 71,400,000 Less: Volume Variance (300,000-230,000) * 15/= 1,042,500Adjusted Cost of Sale (72,442,500/=)Gross profit 46,557,500/=Administration cost (40,000,000/=)Net profit 6,557,500/=

CommentIncome obtained under Absorption Costing Method differs from the desired income, the former being 6,557,500/= while the later being 6,670,000/=.

NB: The CVP model is another way of expressing the Variable Costing Method in a condensed way.

The difference between the two methods of product costing can be explained as hereunder:

Reconciliation of the Difference in Income.Budgeted Income (Absorption Costing Method) 6,557,500/=Desired Income (Variable Costing Method) 6,670,000/=Difference (112,500/=)

Desired Inventory (Closing Inventory) 7,500Expected Inventory (Opening Inventory) (15,000) Change in Inventory Level (decrease) (7,500)

26

Apt Financial Consultants CPA Review

Goods fixed handling cost per unit *15/= Difference (as above) (112,500/=)

OR

Purchases 230,500Sales (238,000)Change in Inventory (decrease) (7,500)Goods fixed handling cost per unit *15/=Difference (as above) (112,500/=)

27