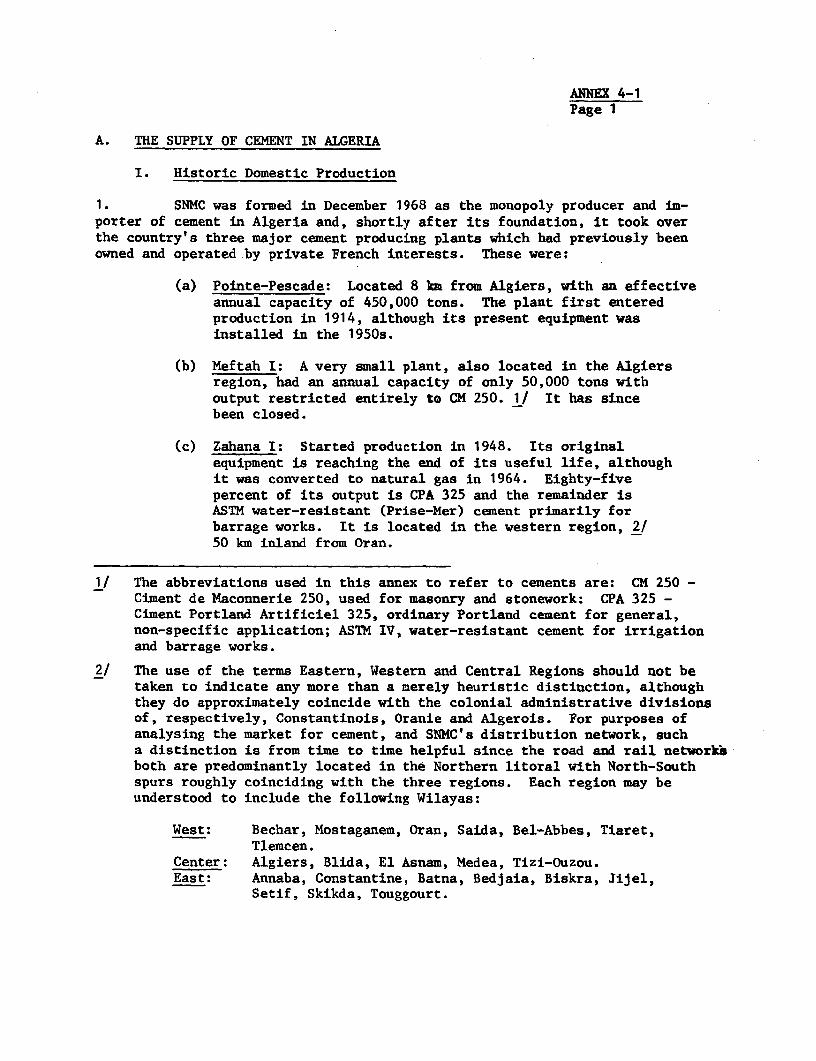

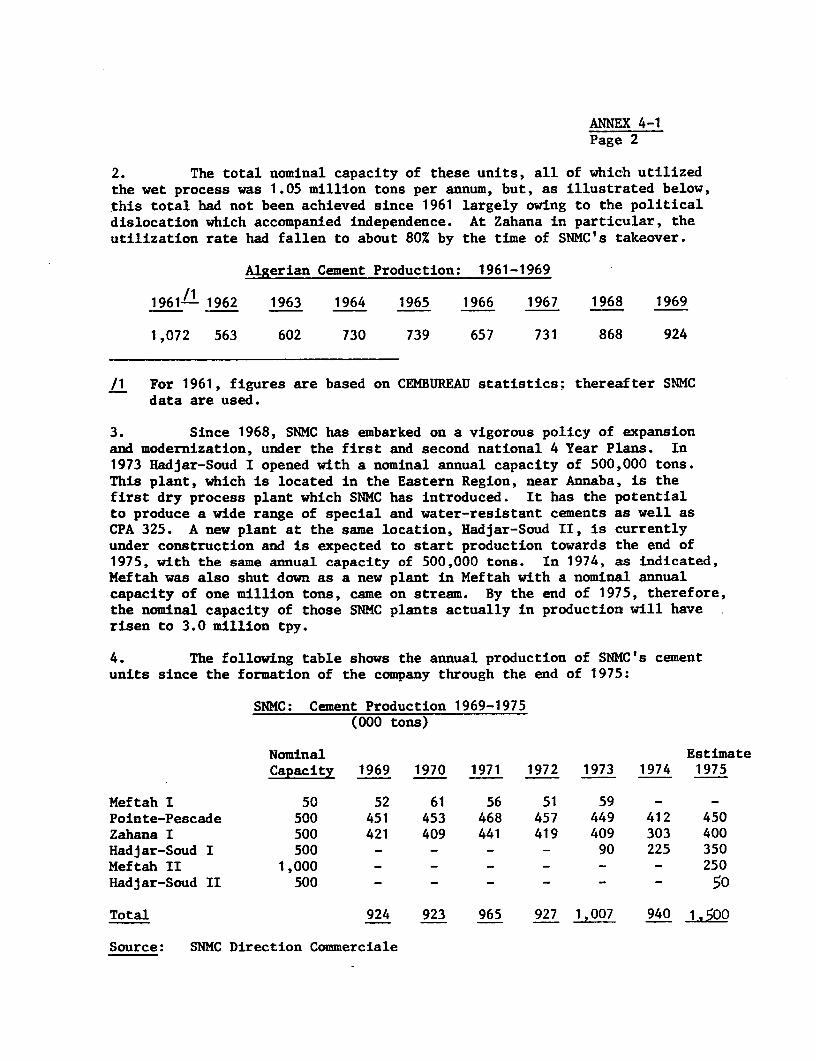

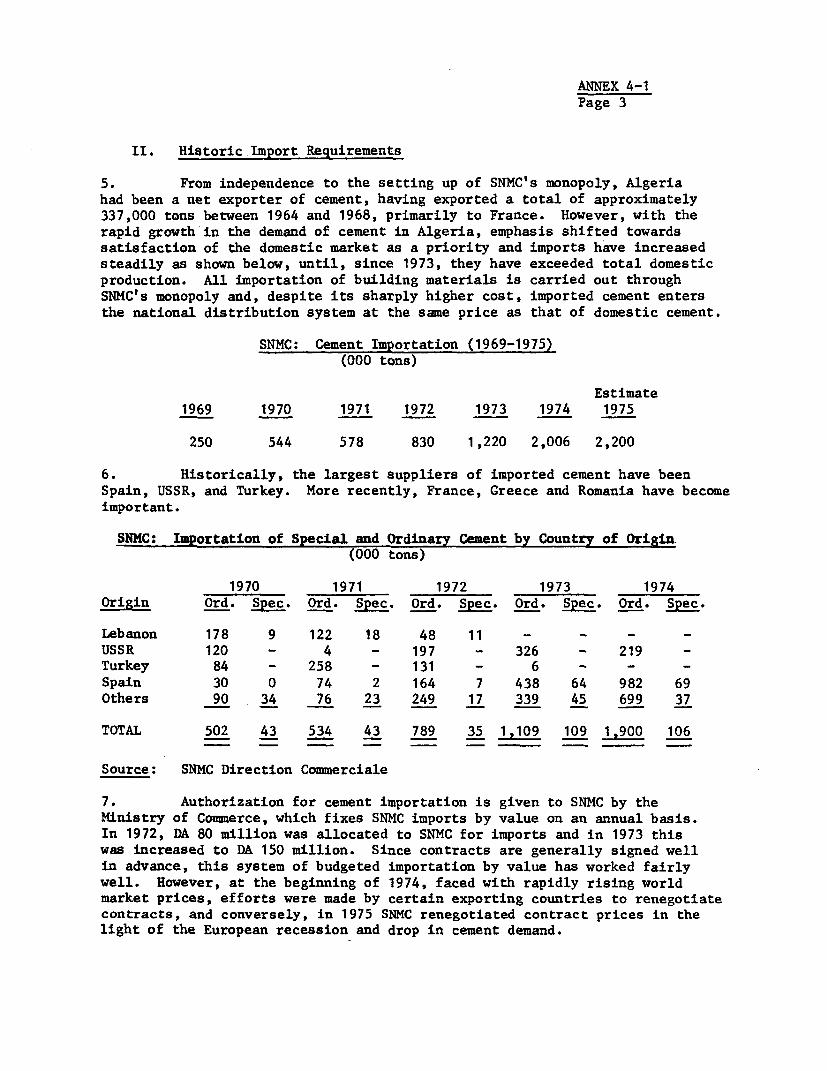

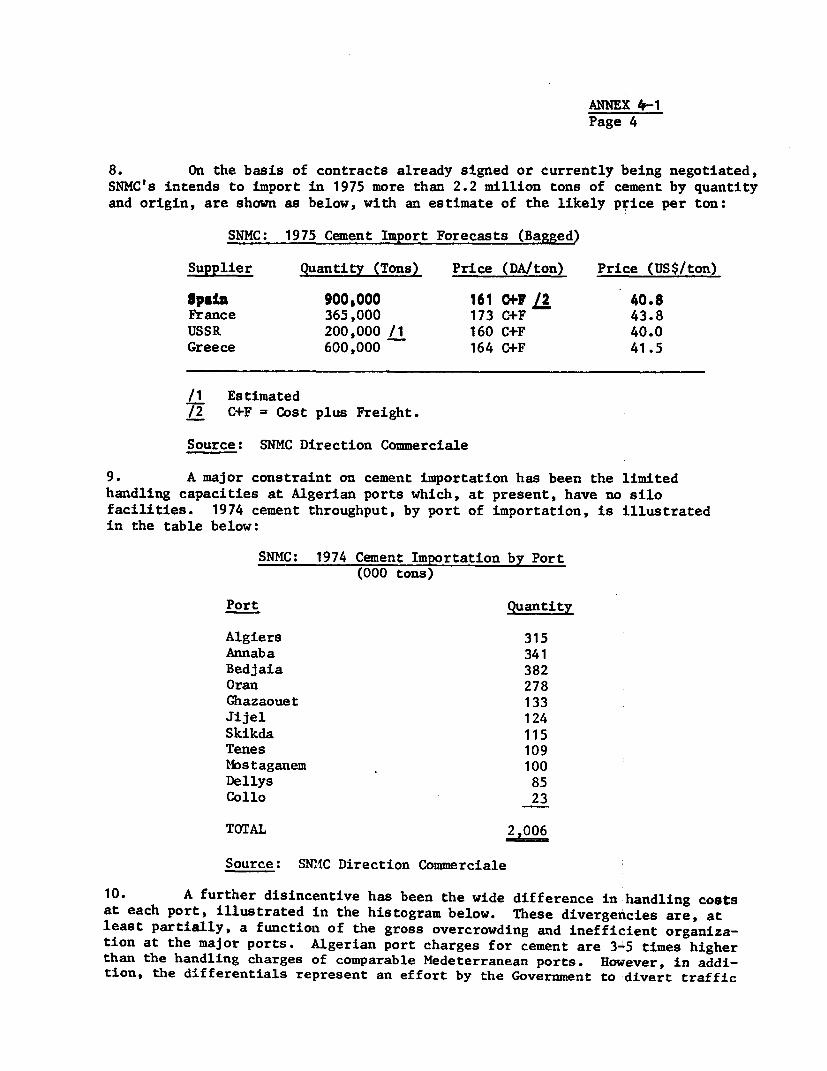

appraisal of the snmc expansion project algeria - world

TRANSCRIPT

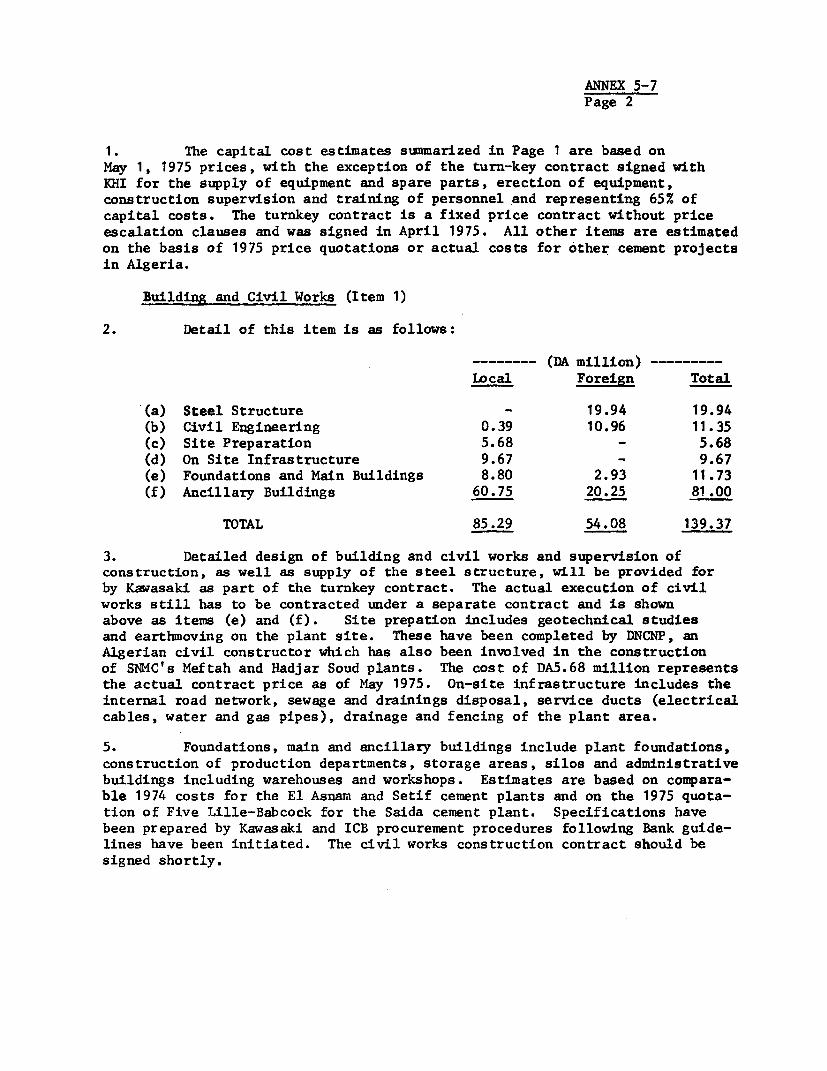

Report No. 874-AL COPYAppraisal of theSNMC Expansion ProjectAlgeriaNovember 25, 1975

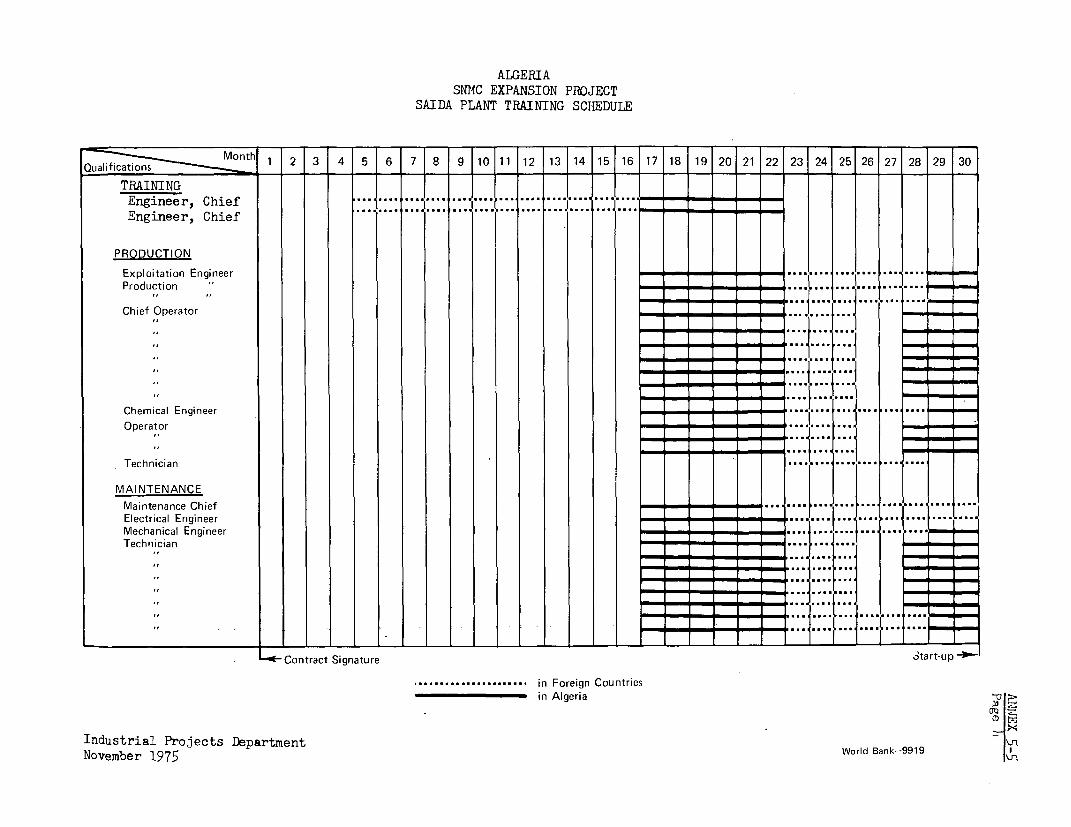

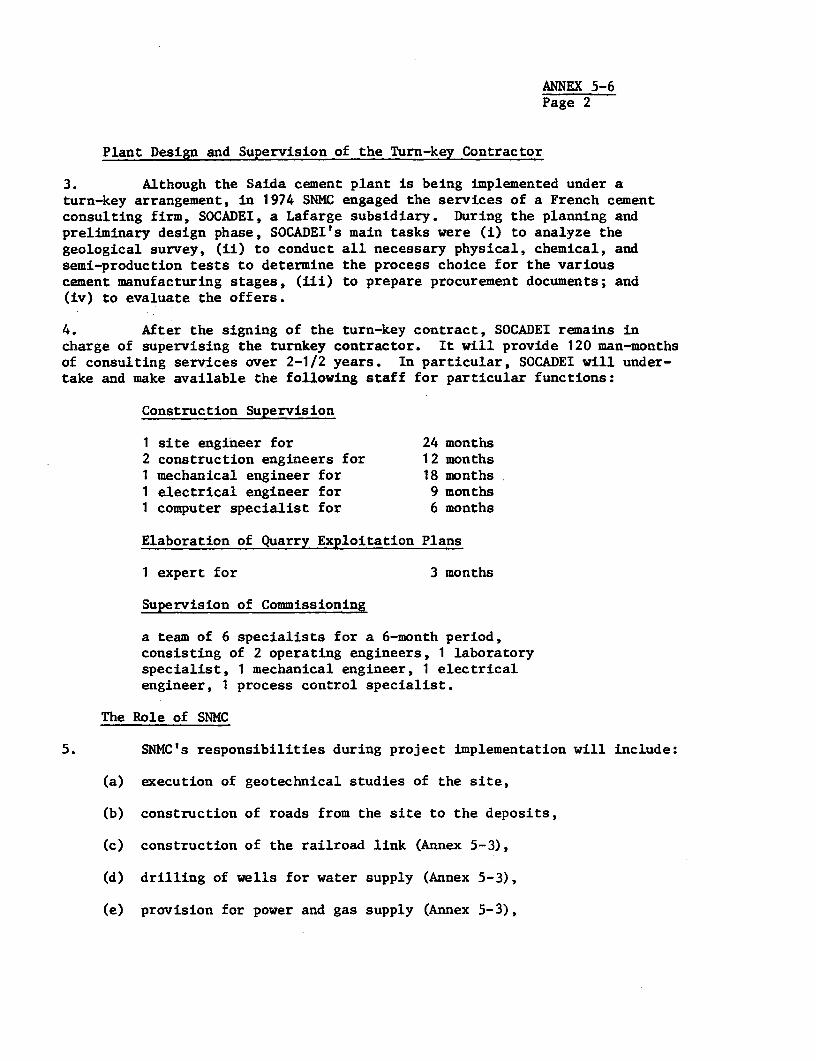

Industrial Projects Department

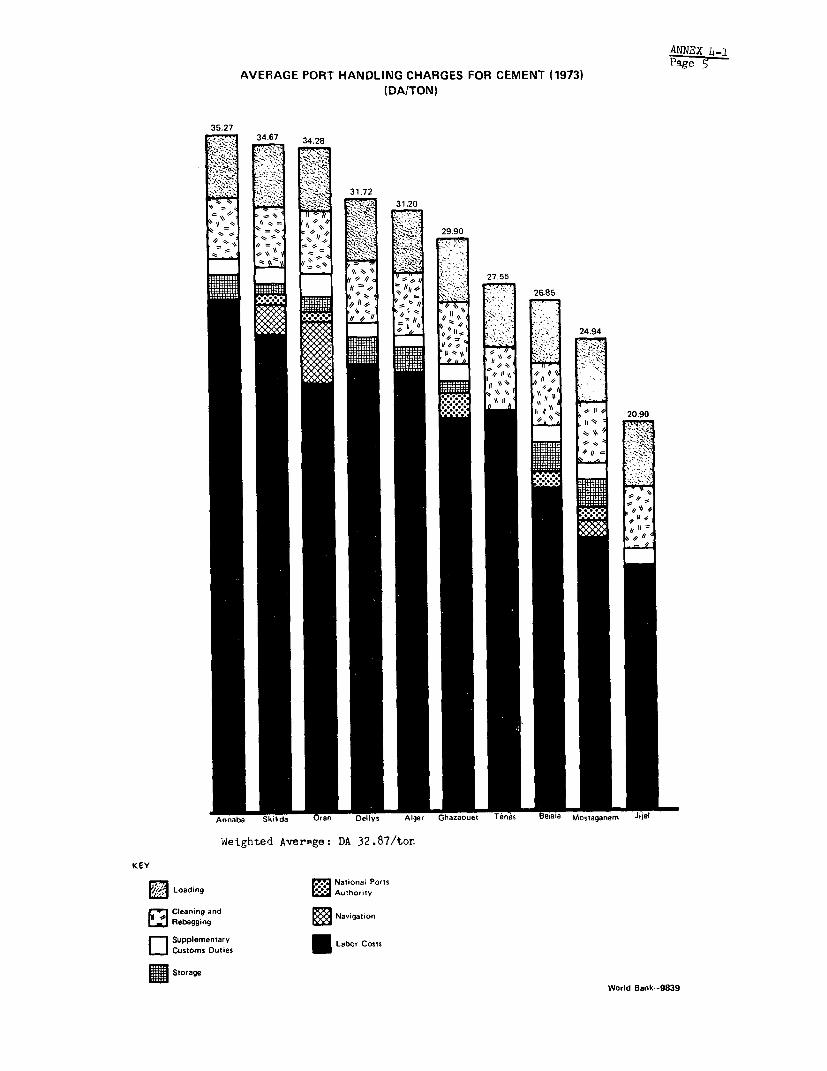

Not for Public Use

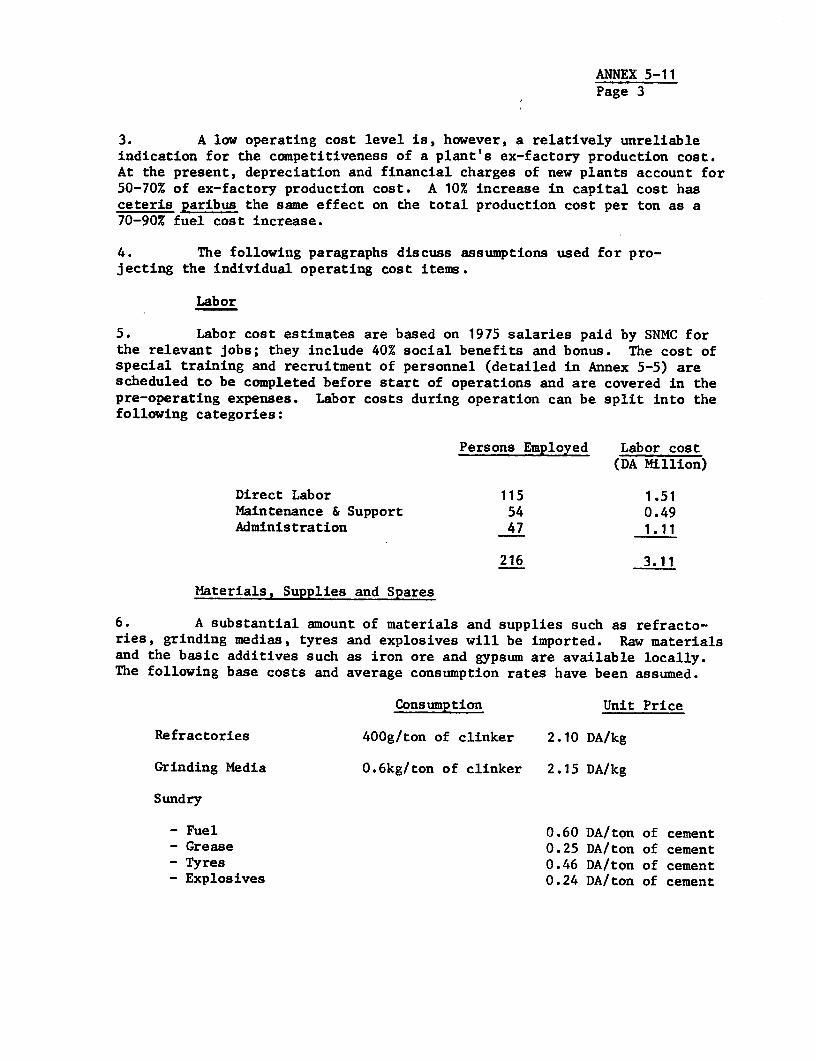

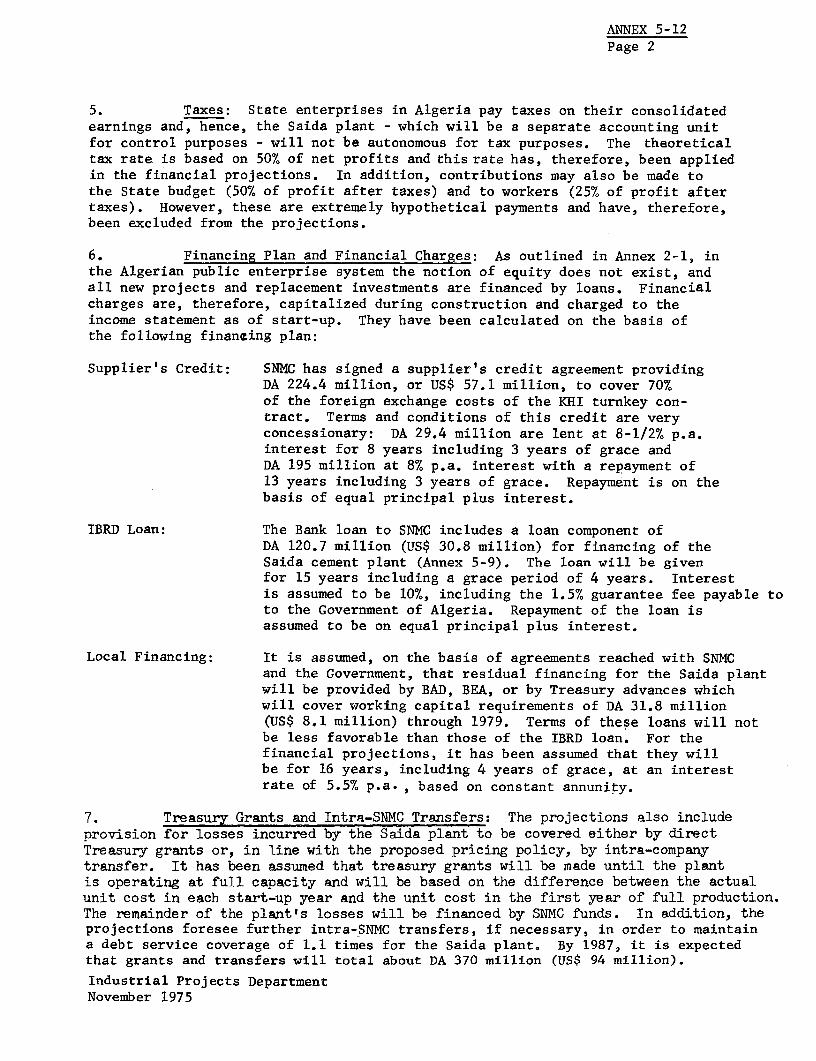

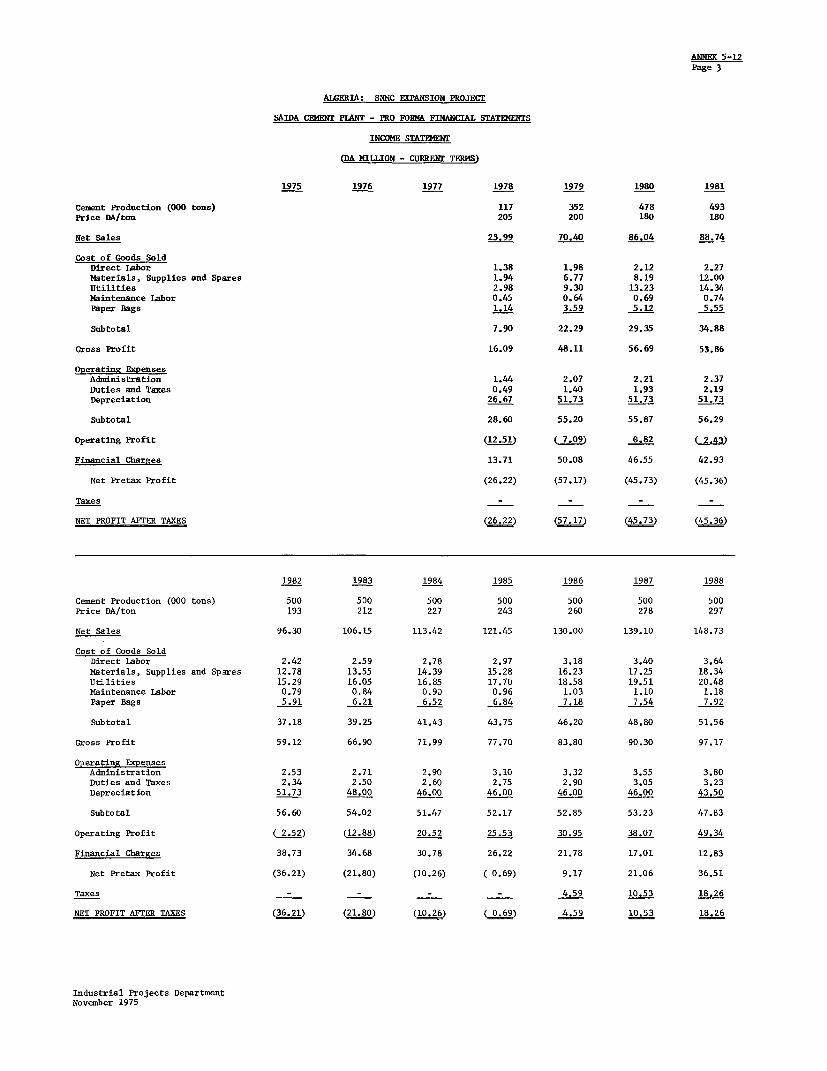

Document of the Worid Bank

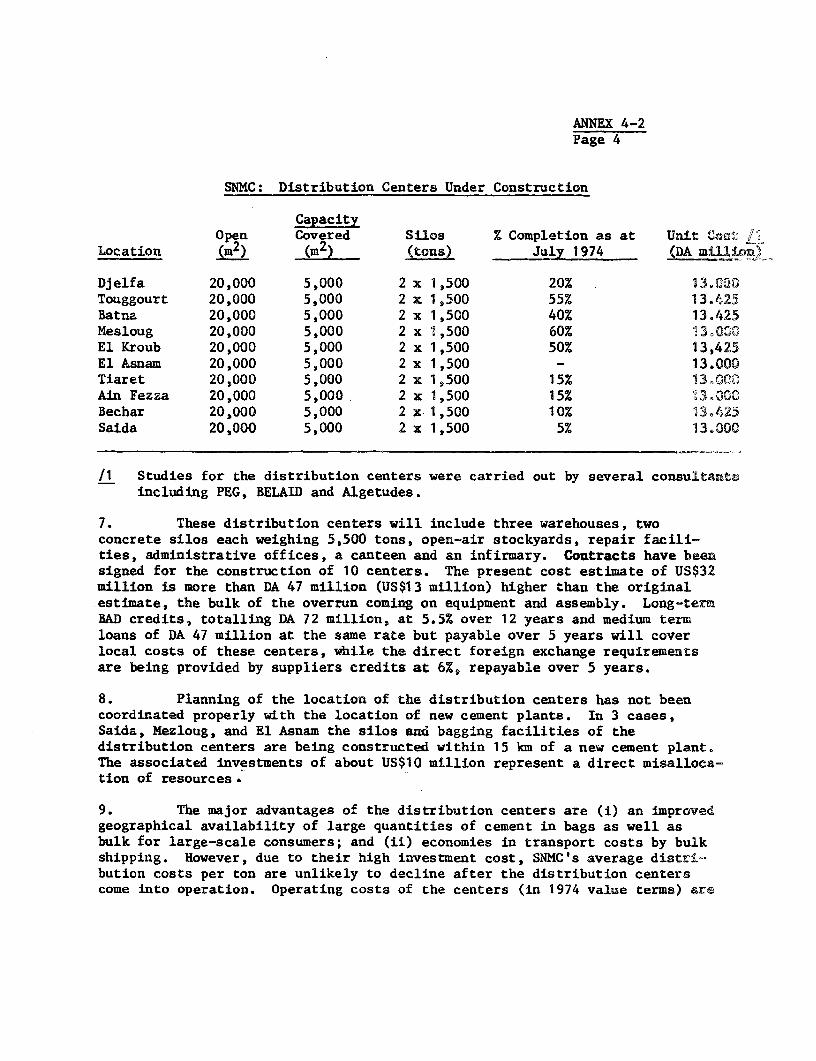

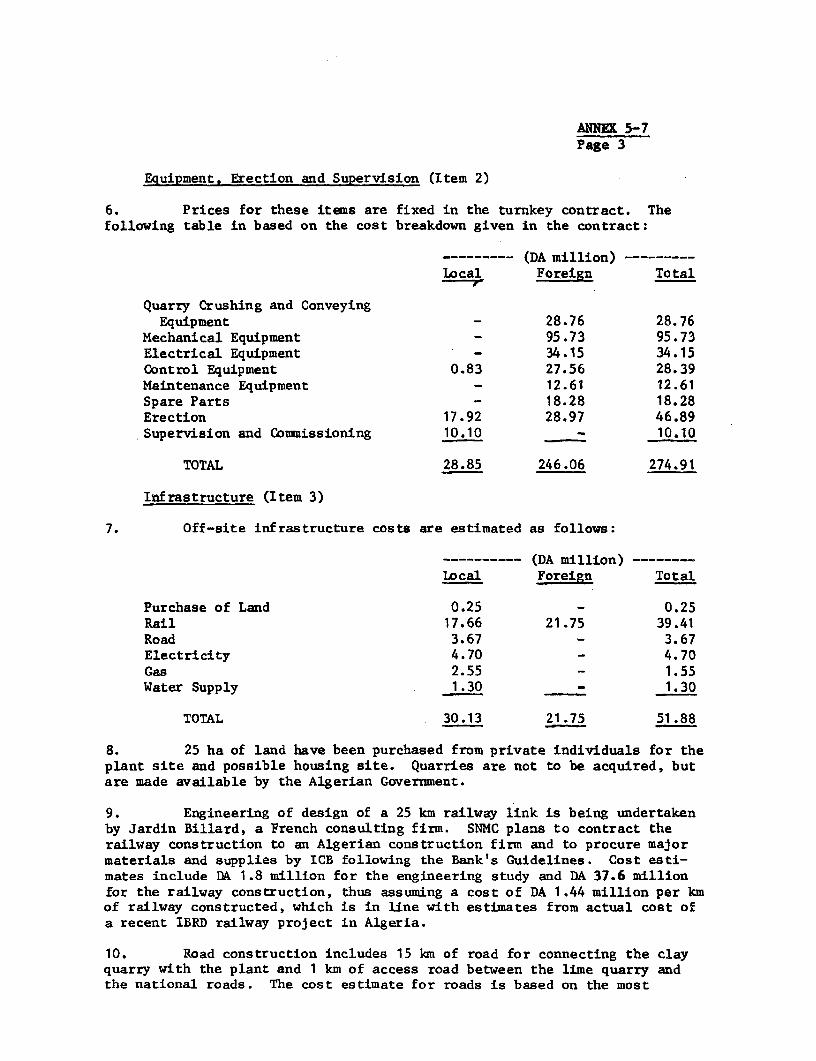

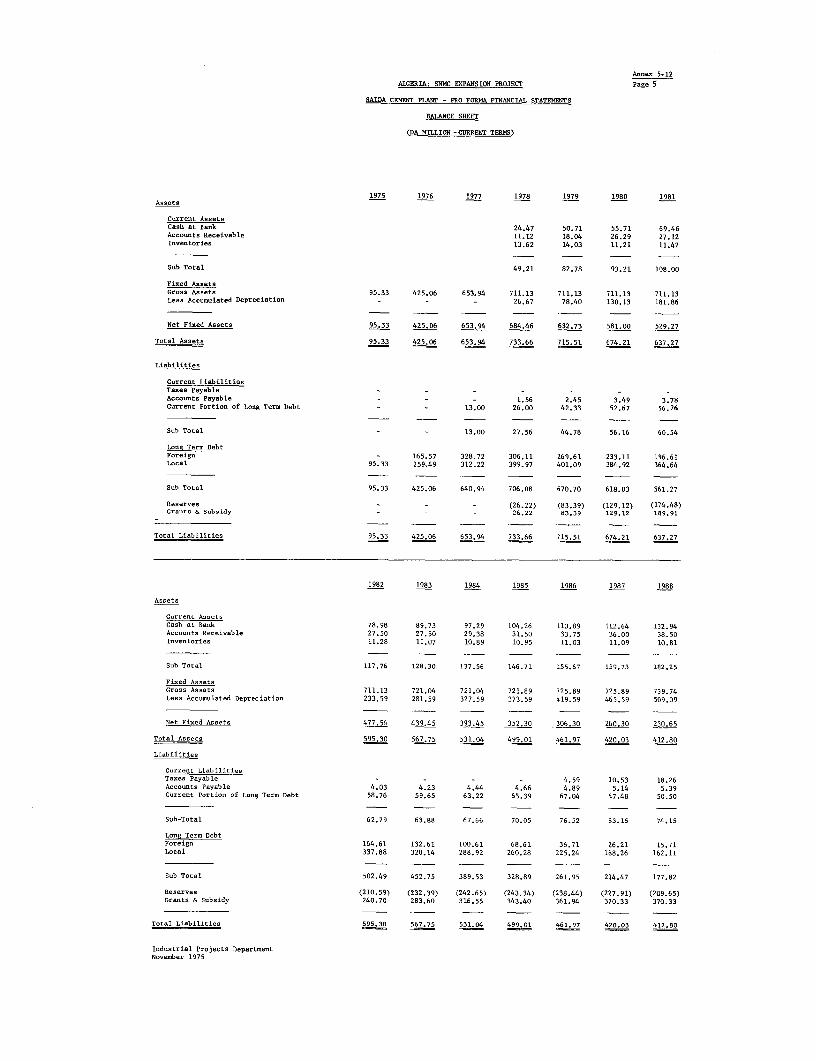

This document has a restricted distribution and may be used by recipientsonly in the performance of their official duties. Its contents may nototherwise be disclosed without Wor[d Bank authorization.

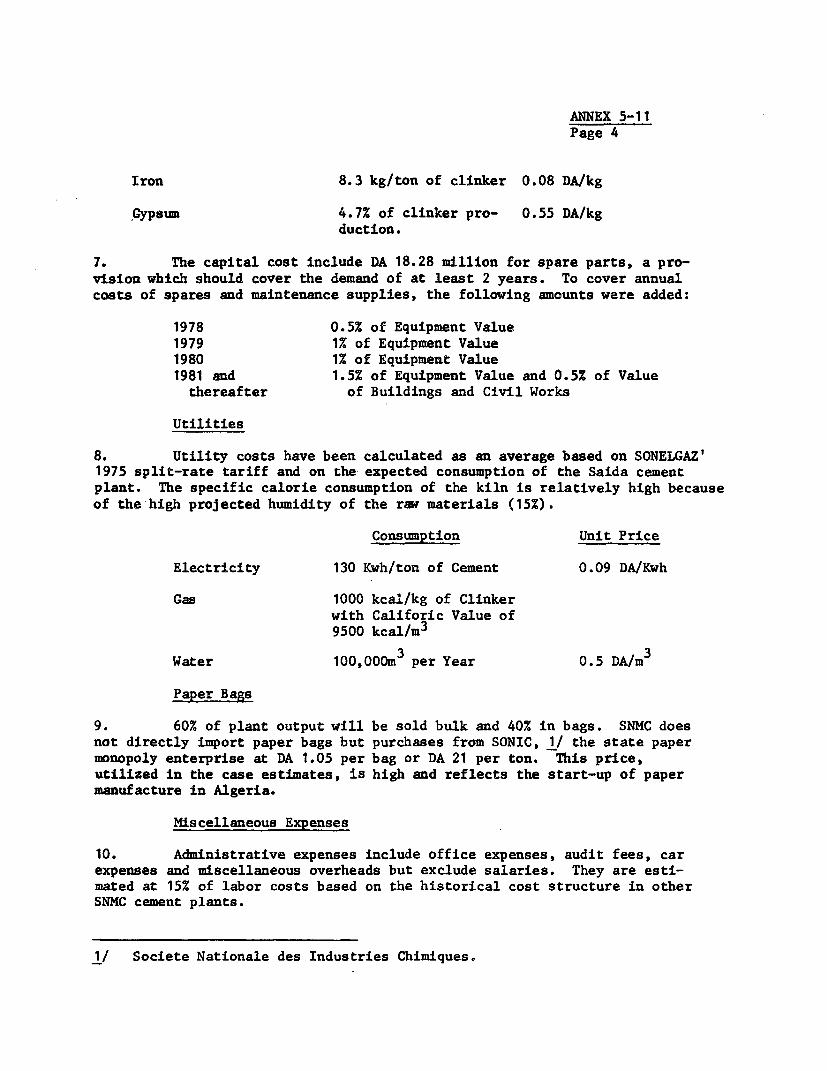

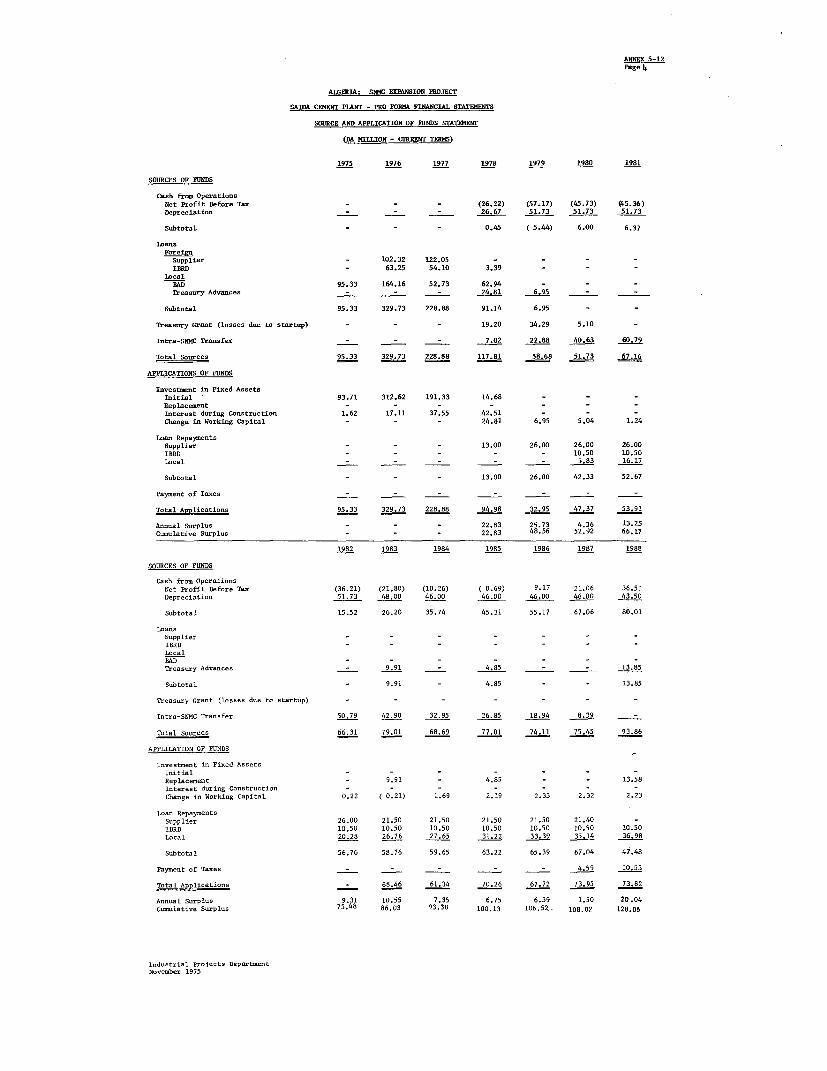

Pub

lic D

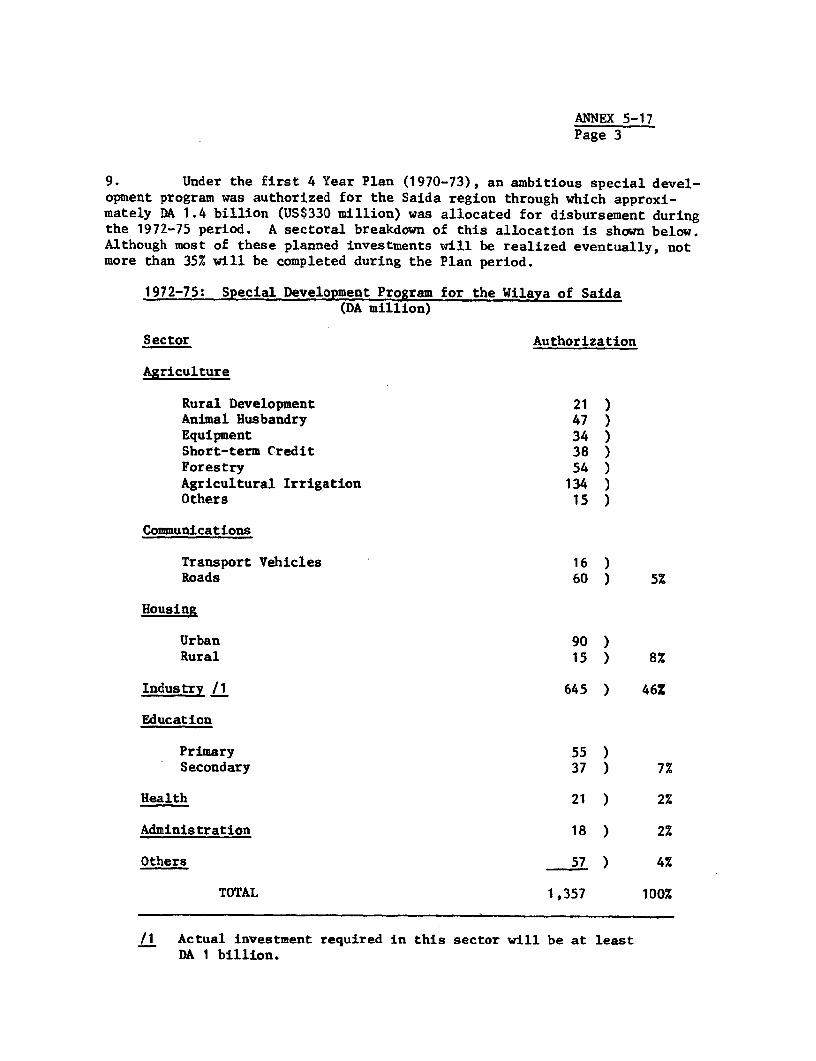

iscl

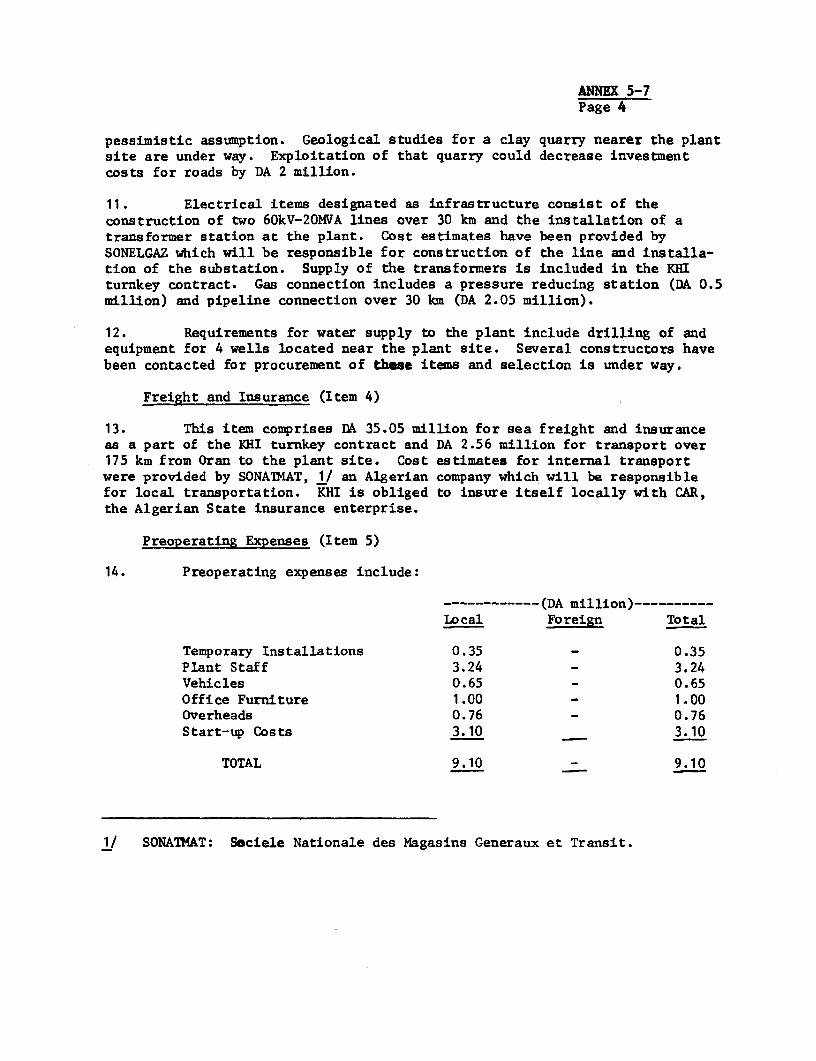

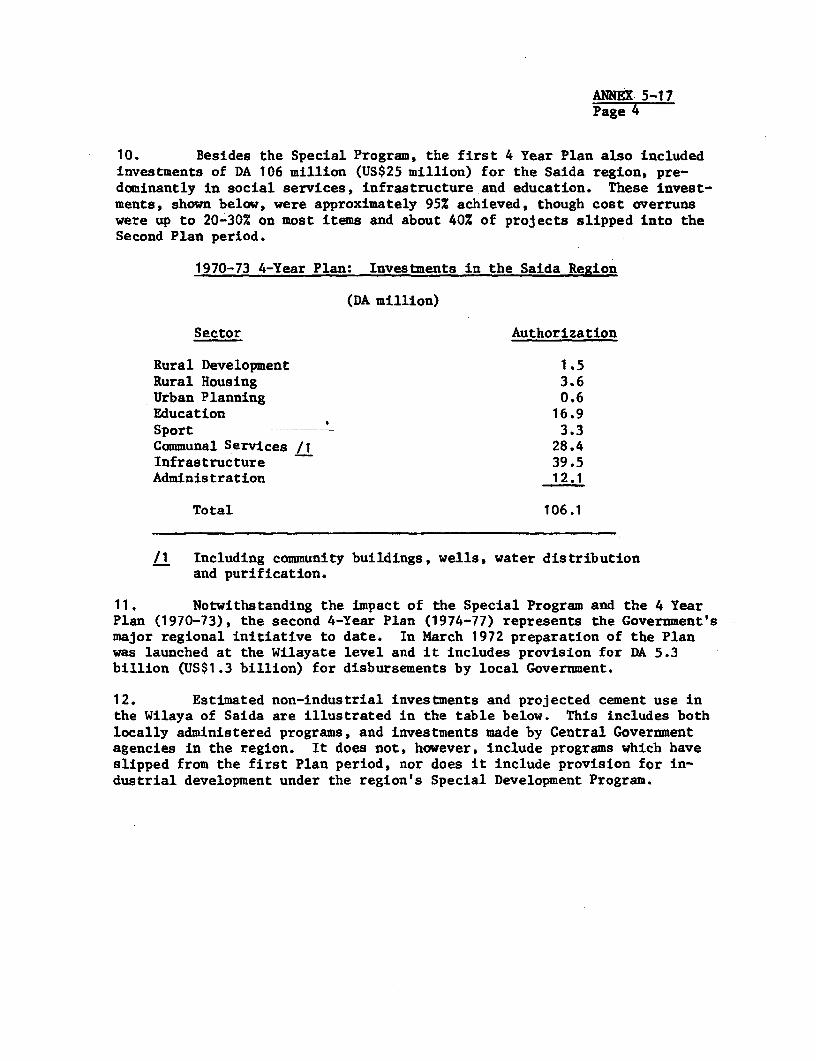

osur

e A

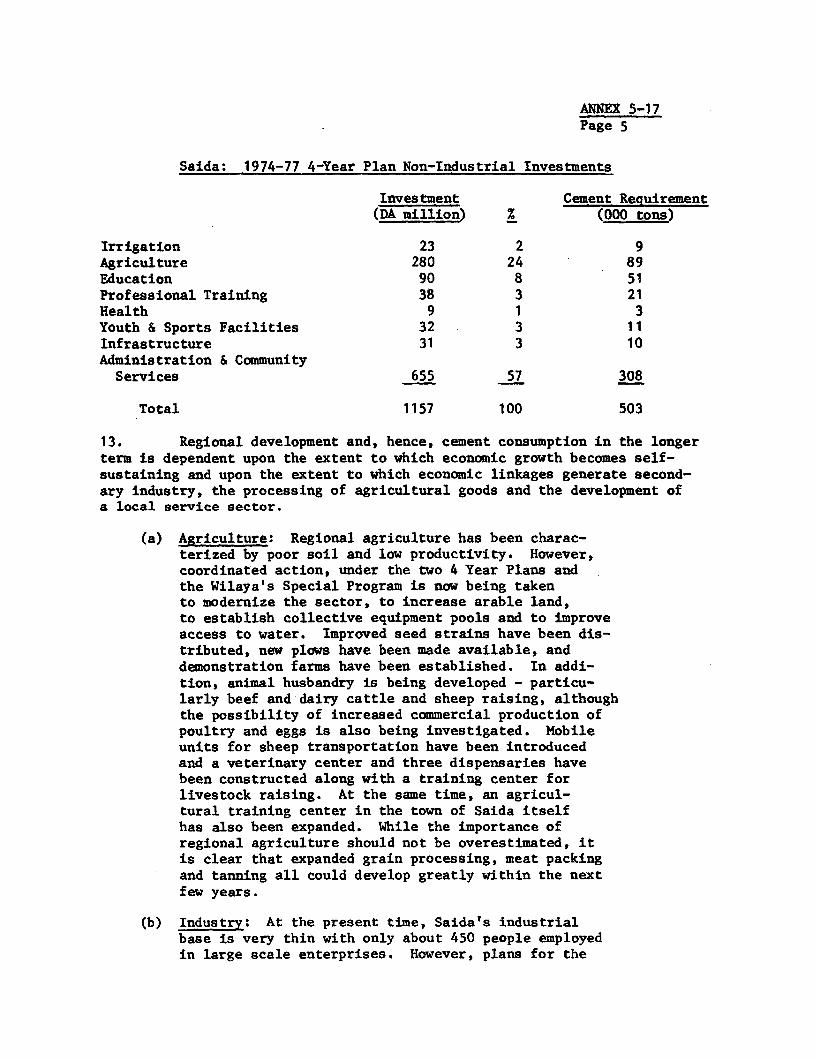

utho

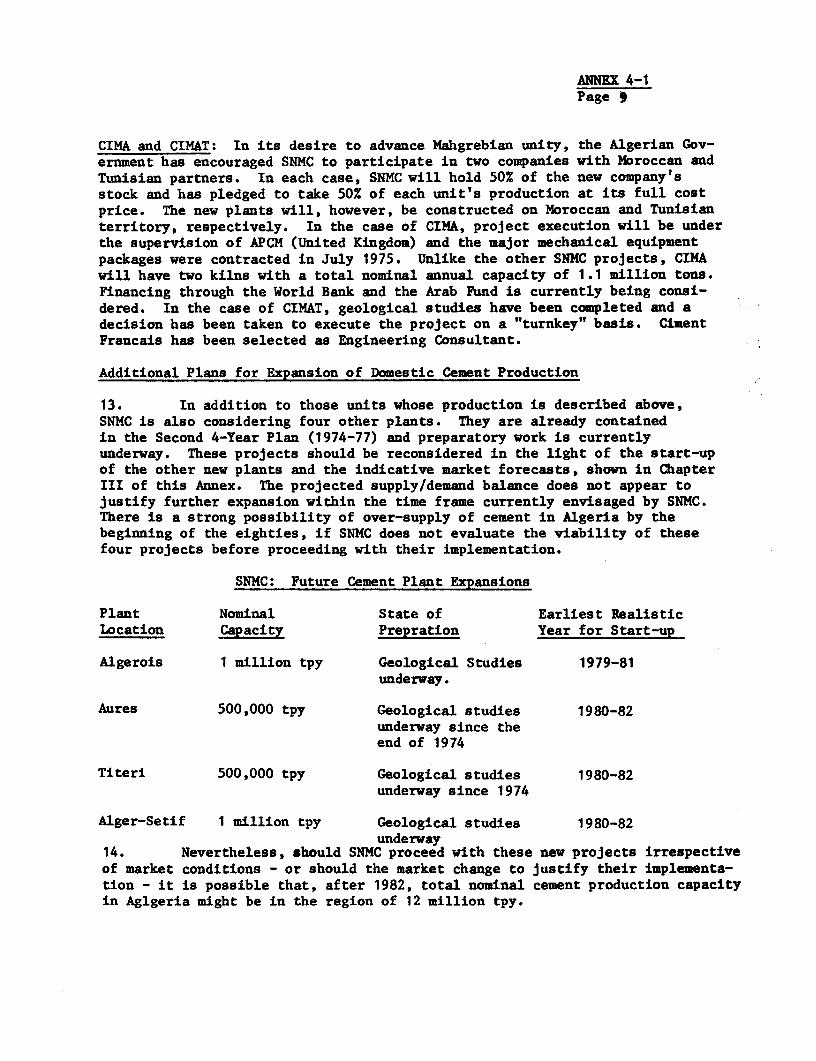

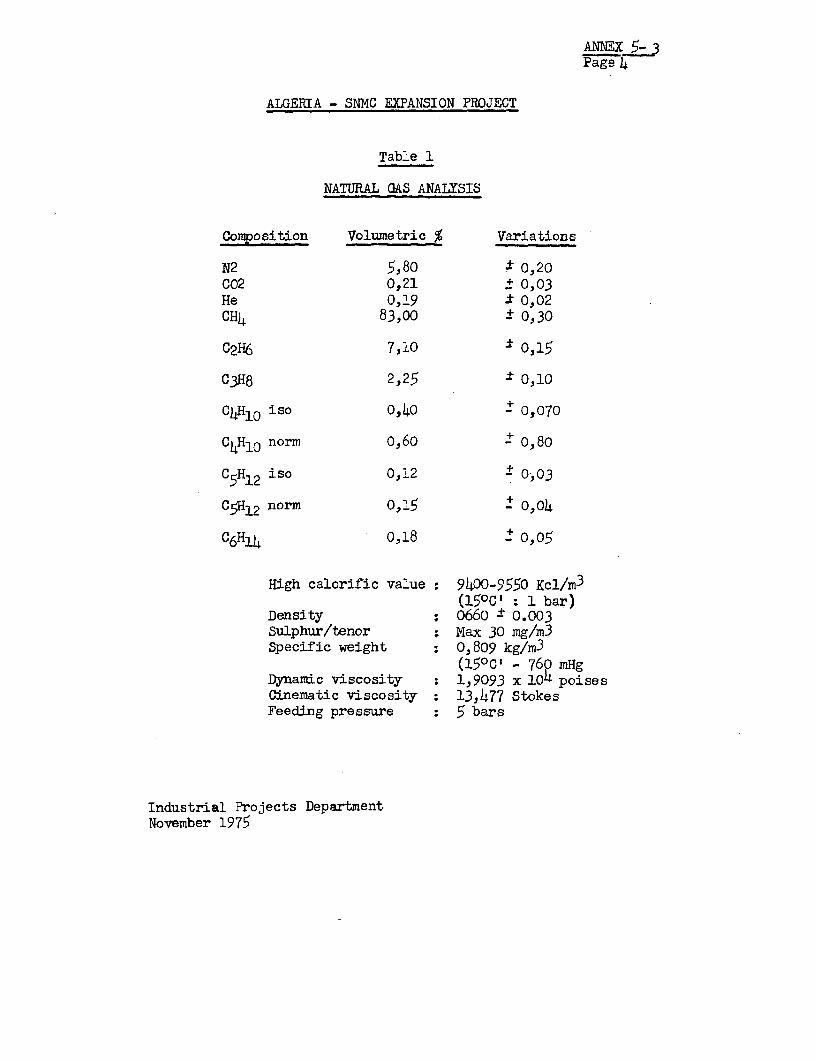

rized

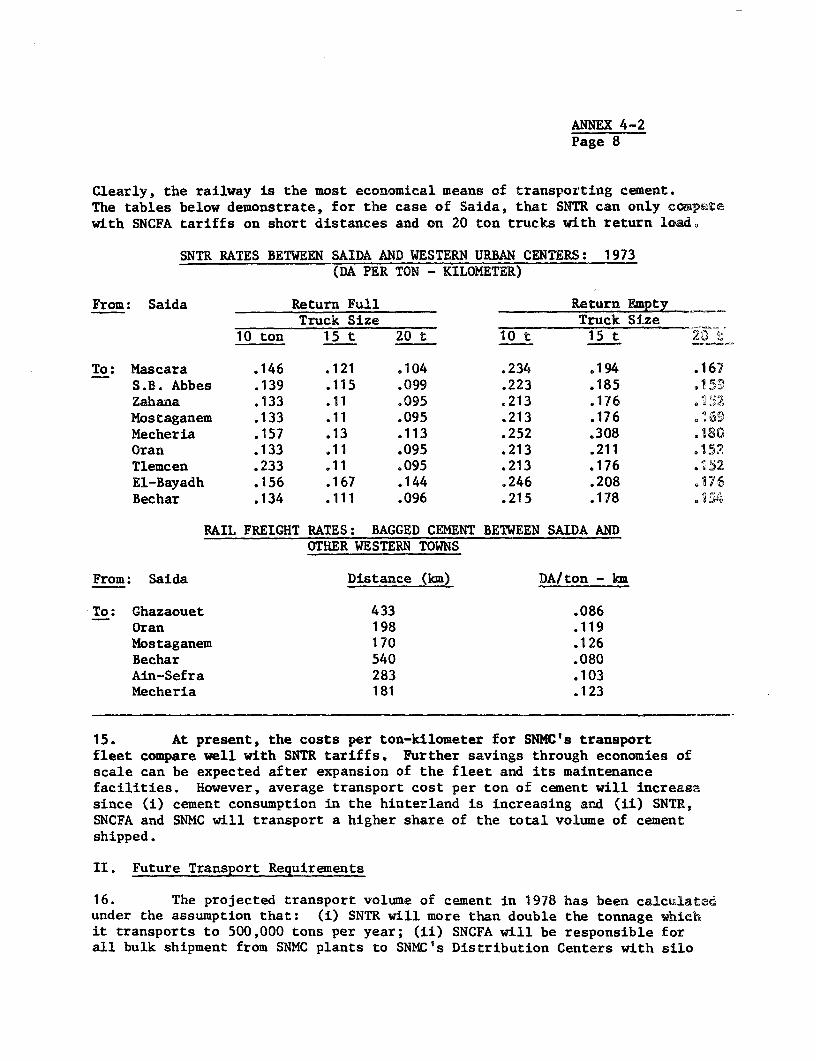

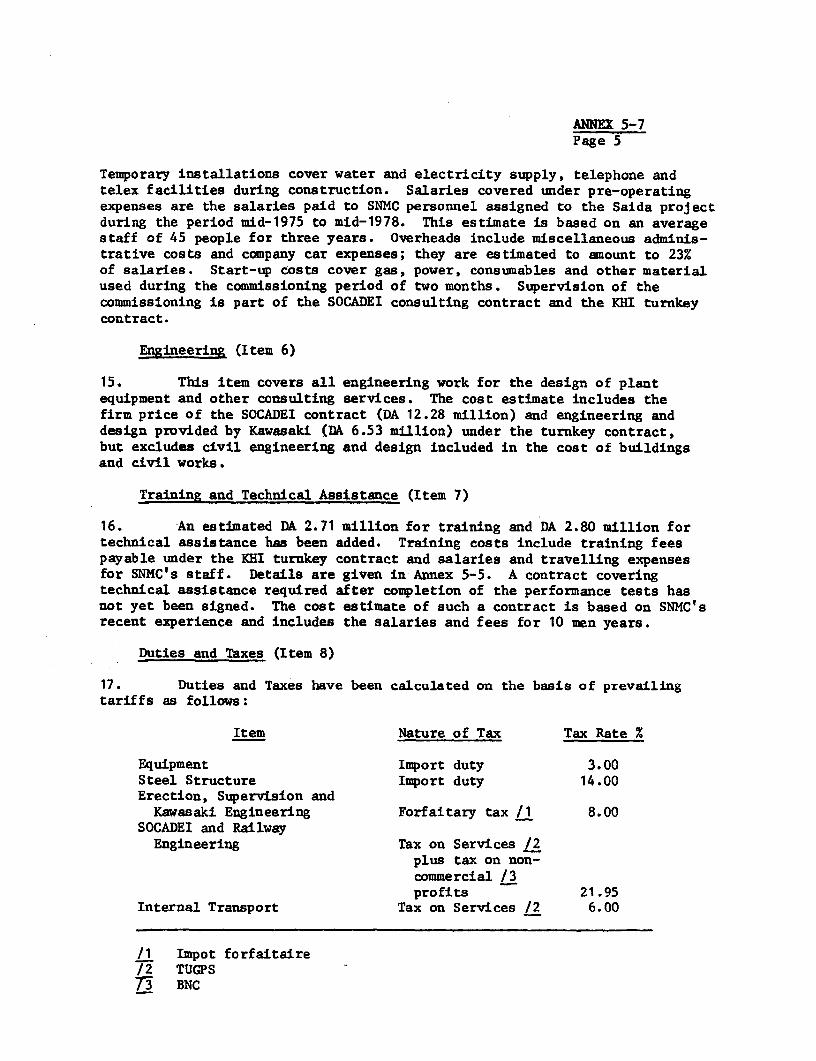

Pub

lic D

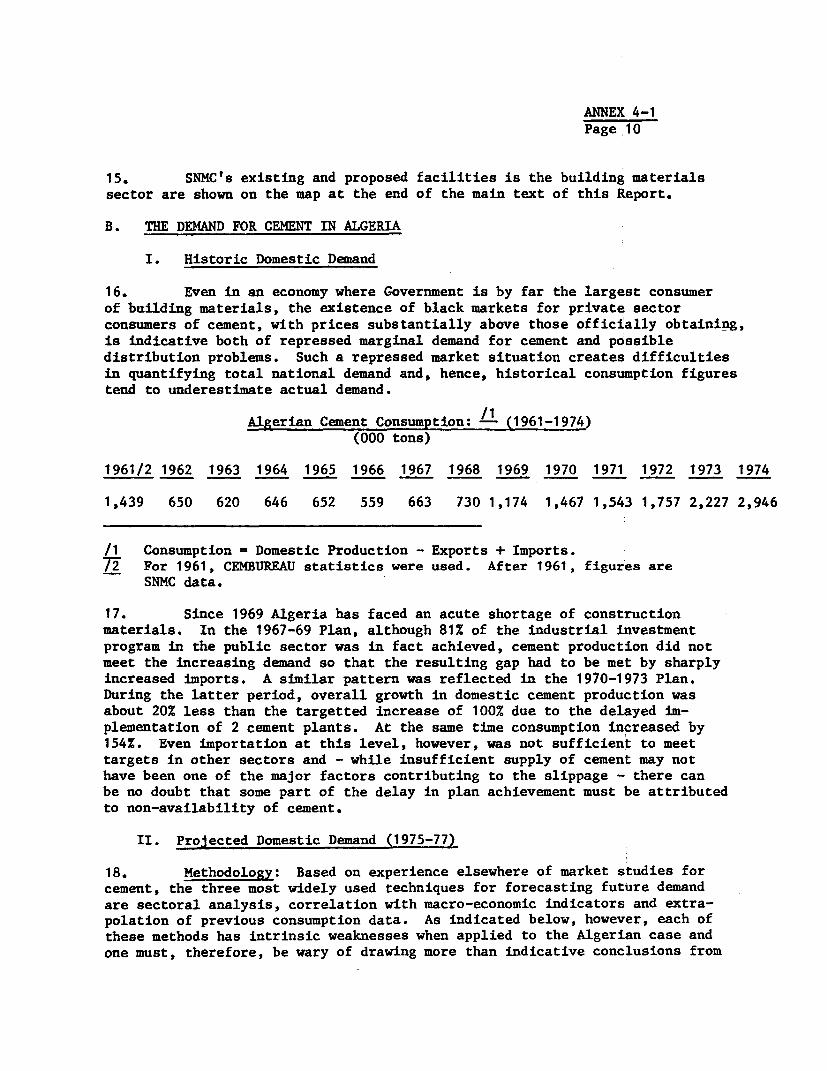

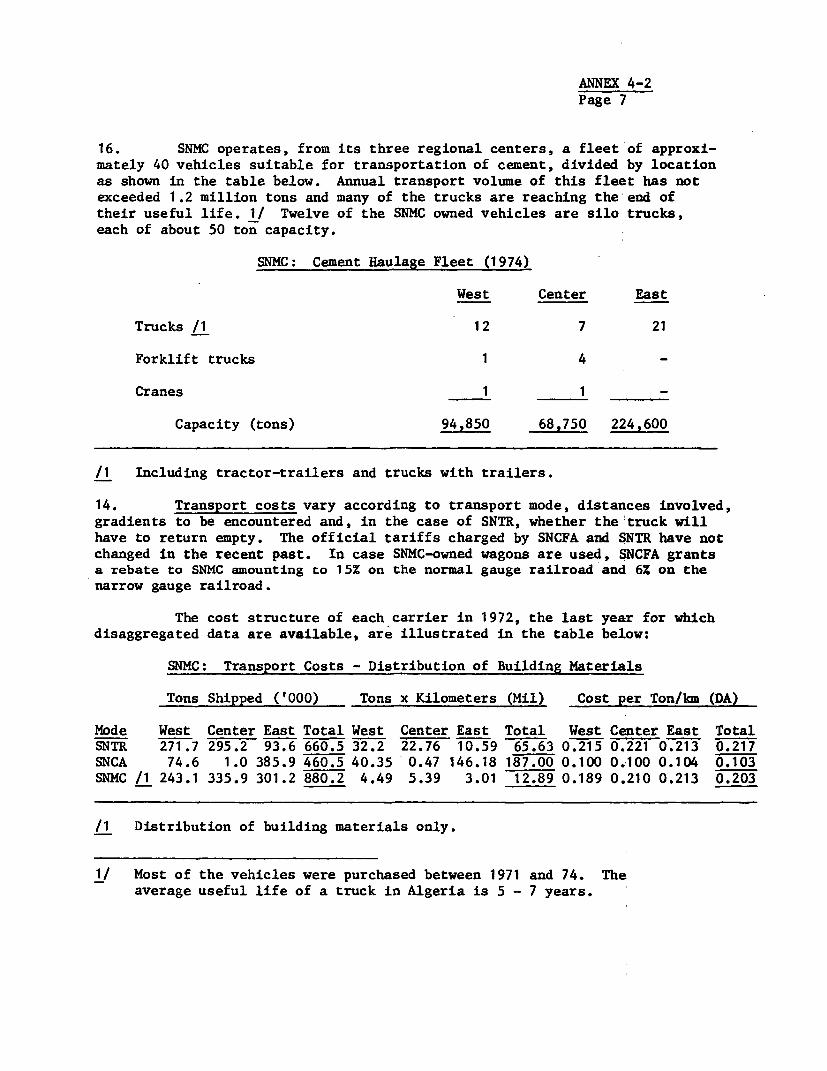

iscl

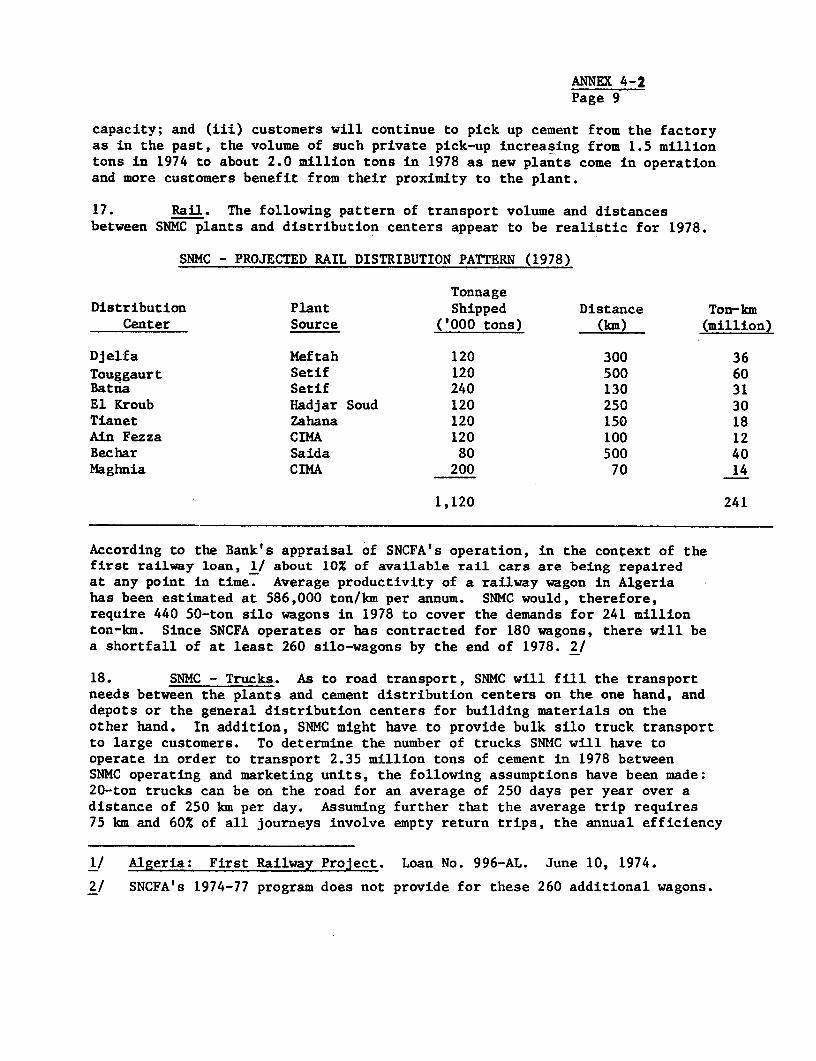

osur

e A

utho

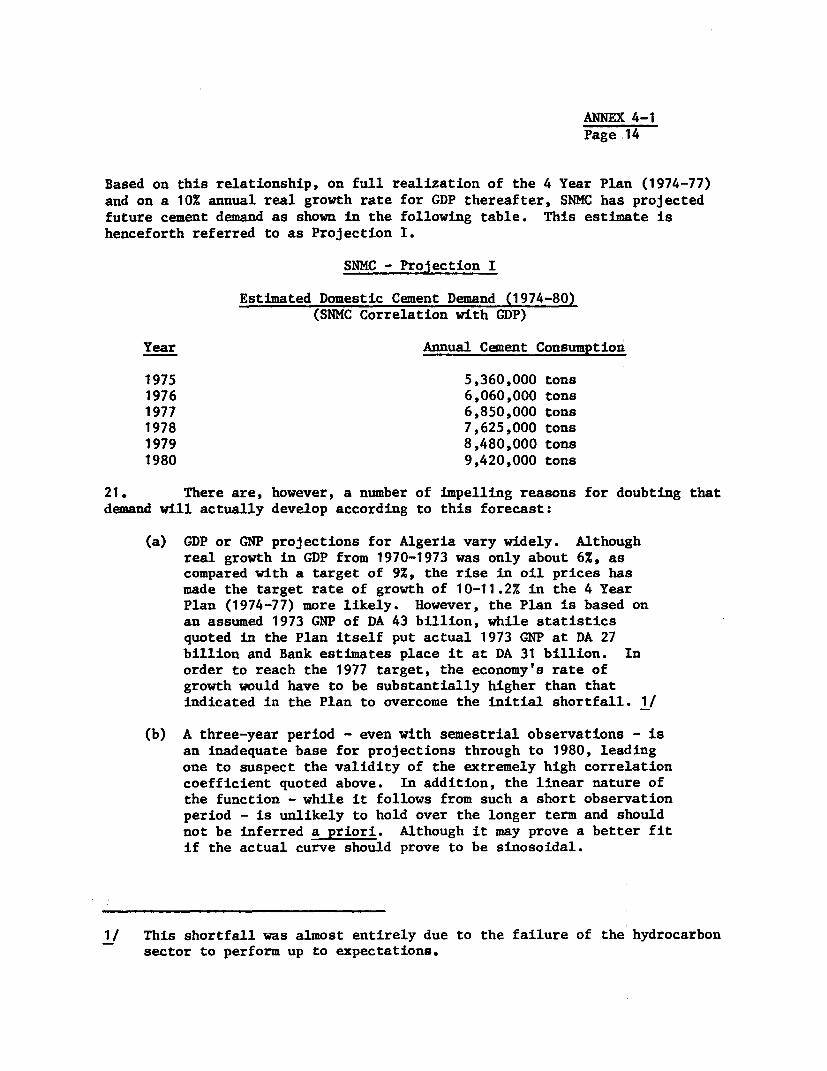

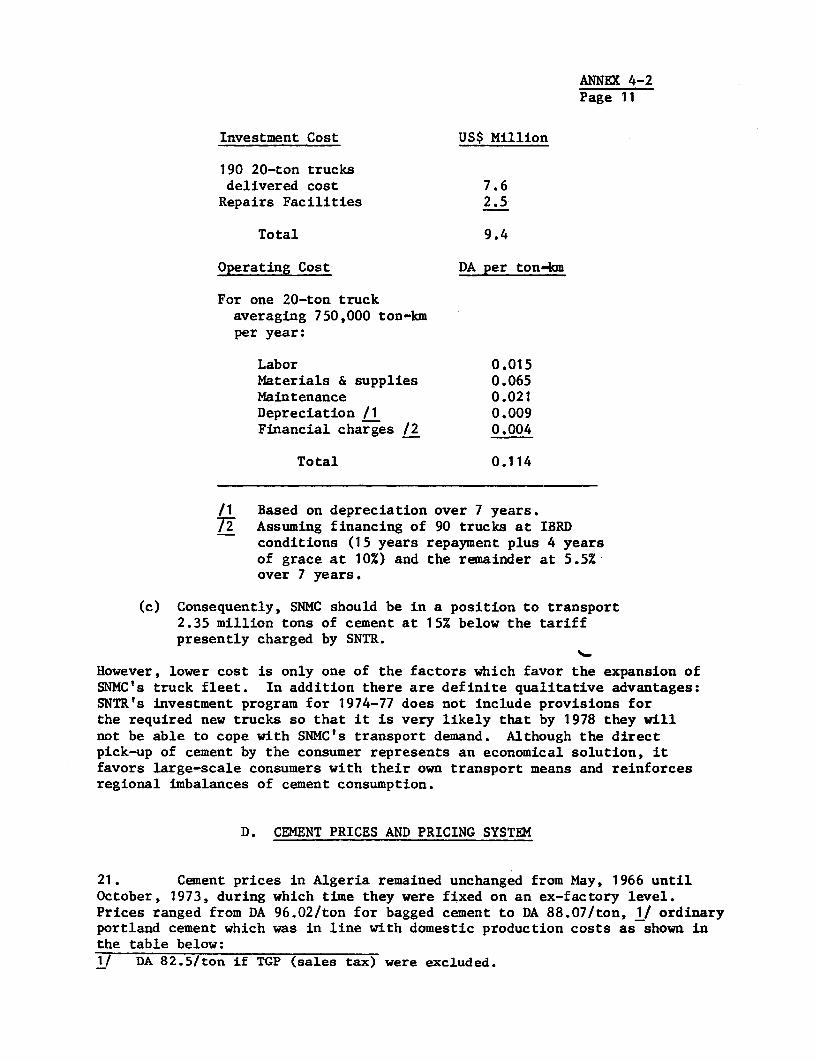

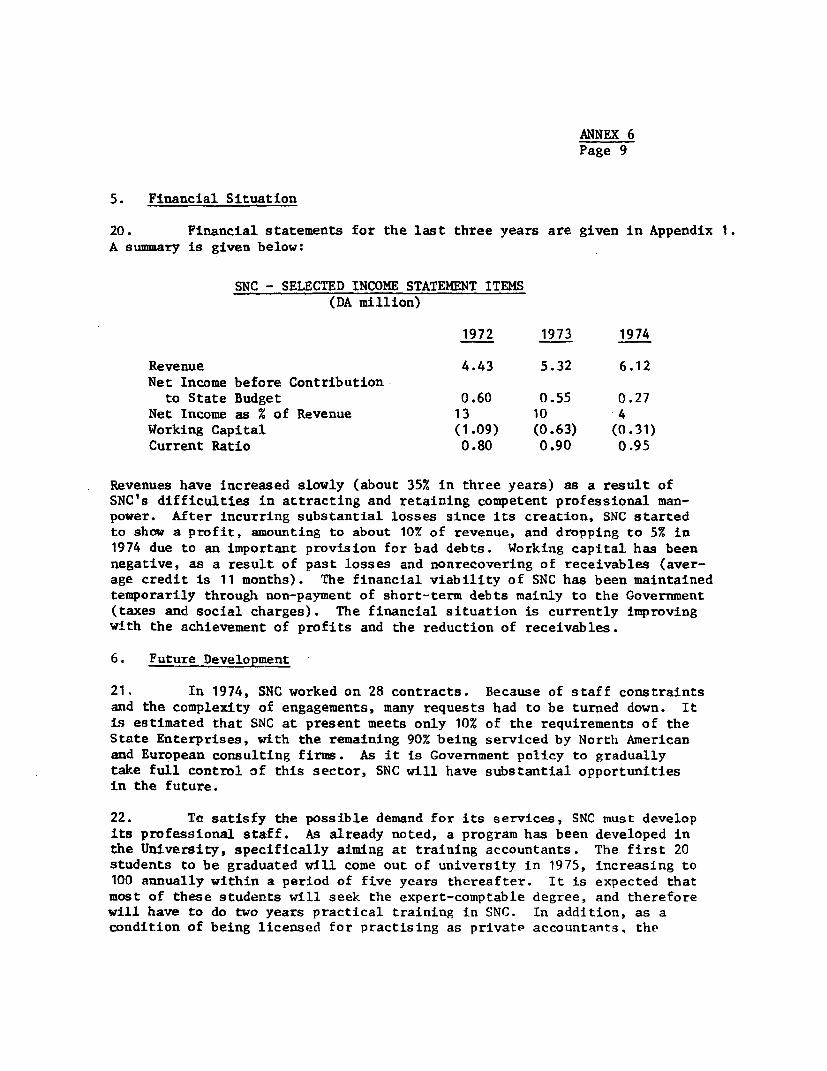

rized

Pub

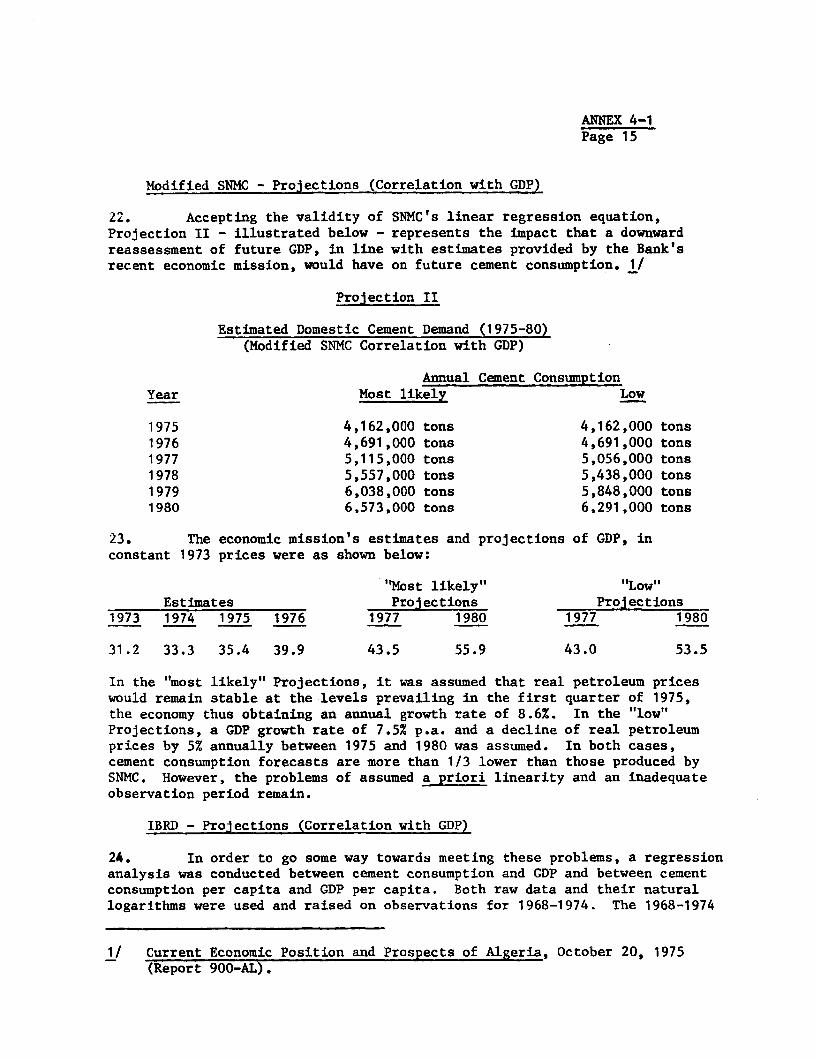

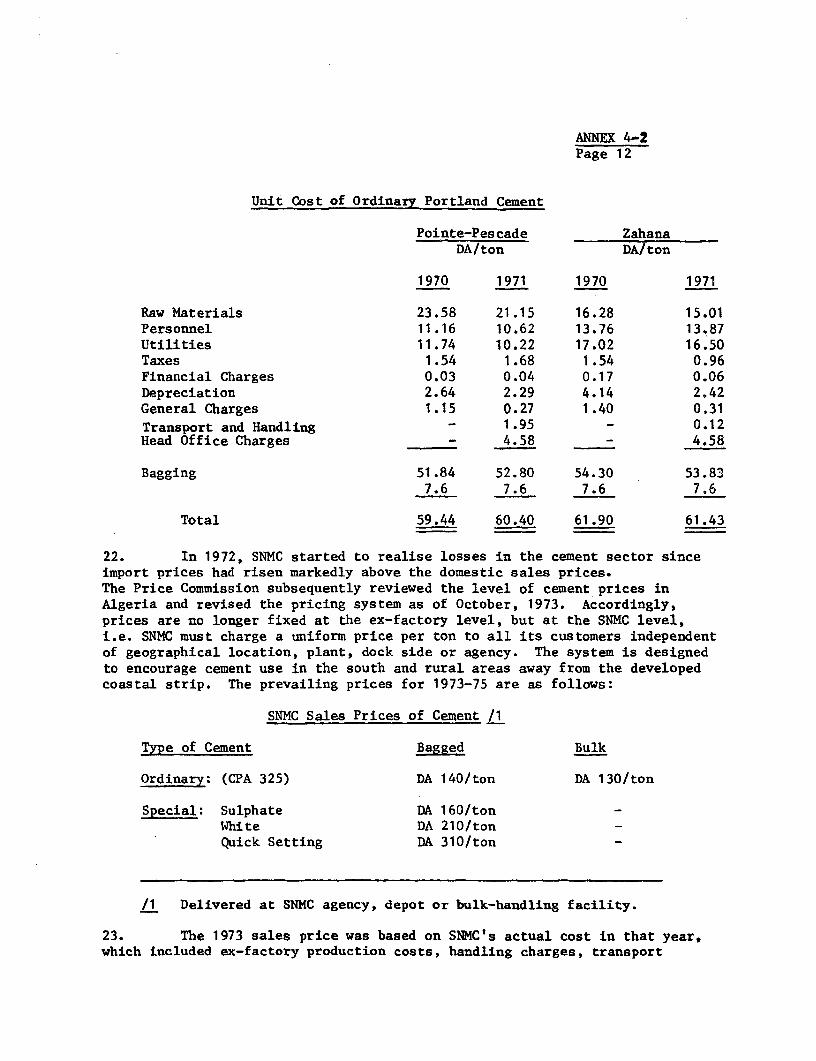

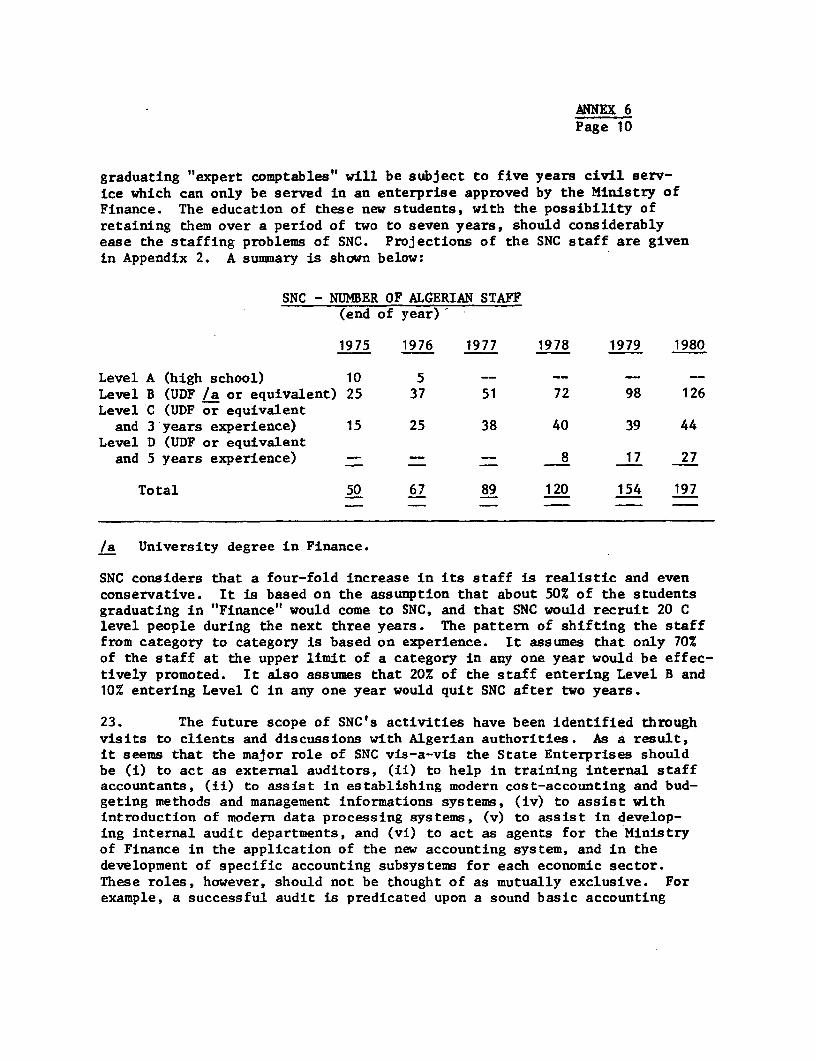

lic D

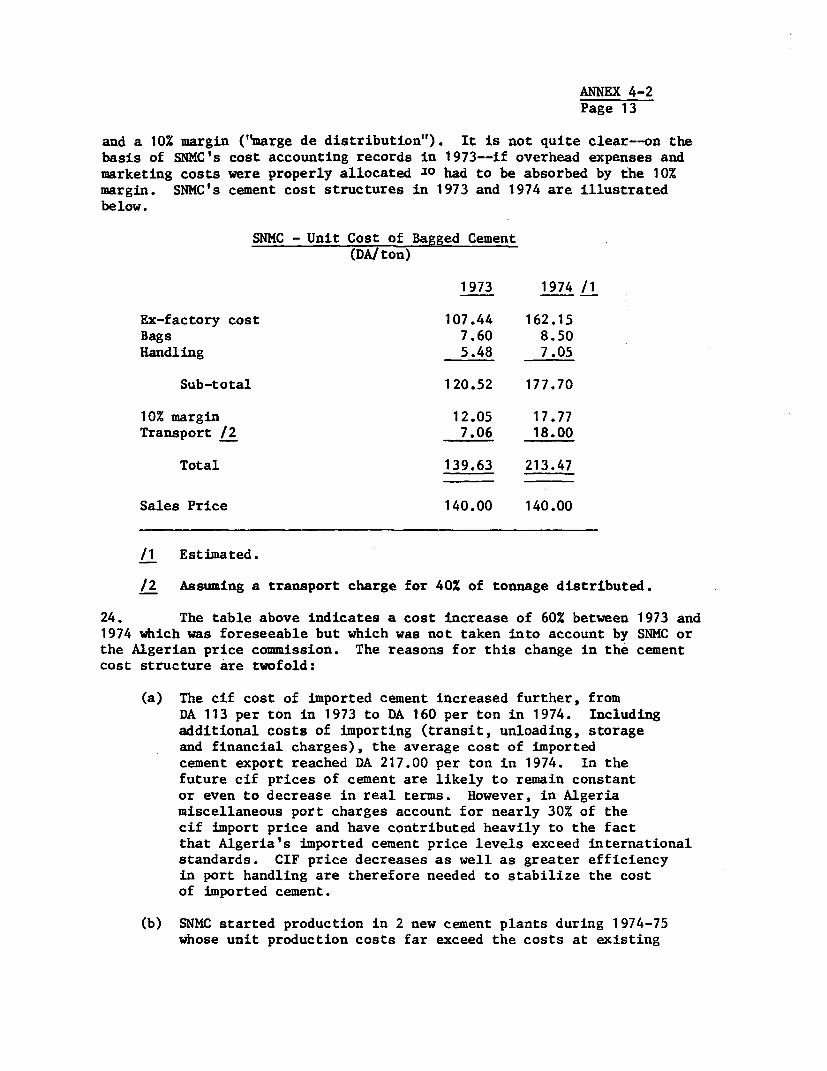

iscl

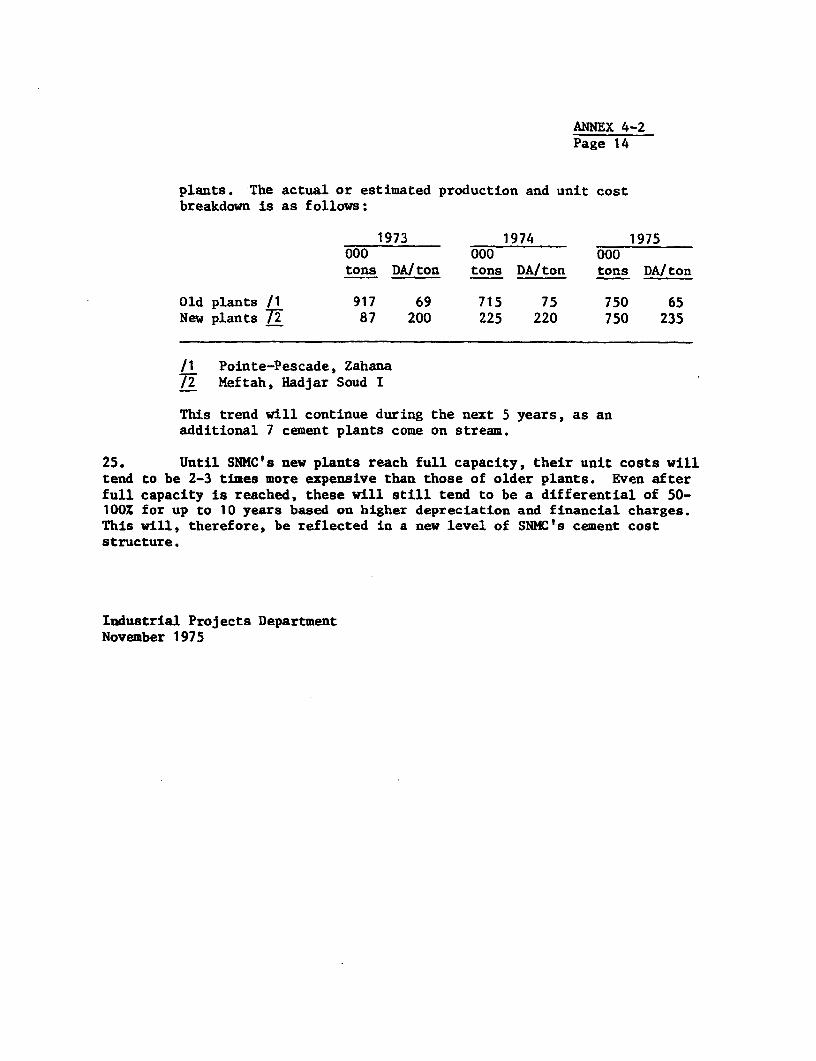

osur

e A

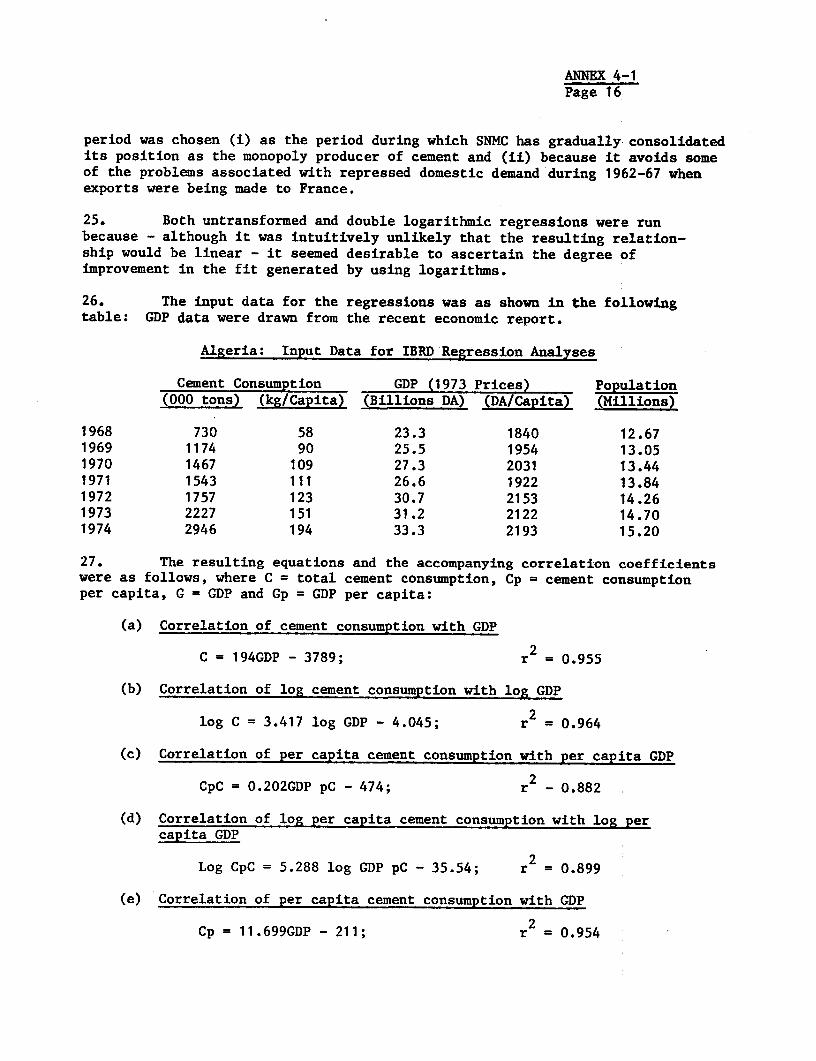

utho

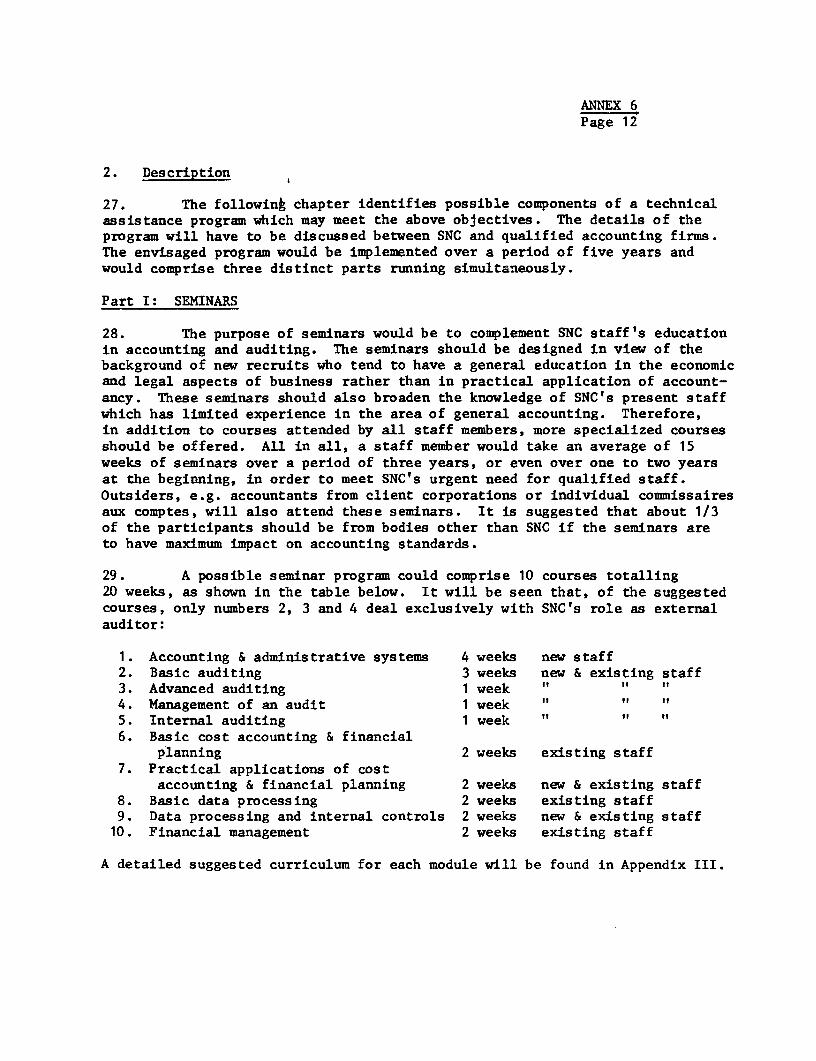

rized

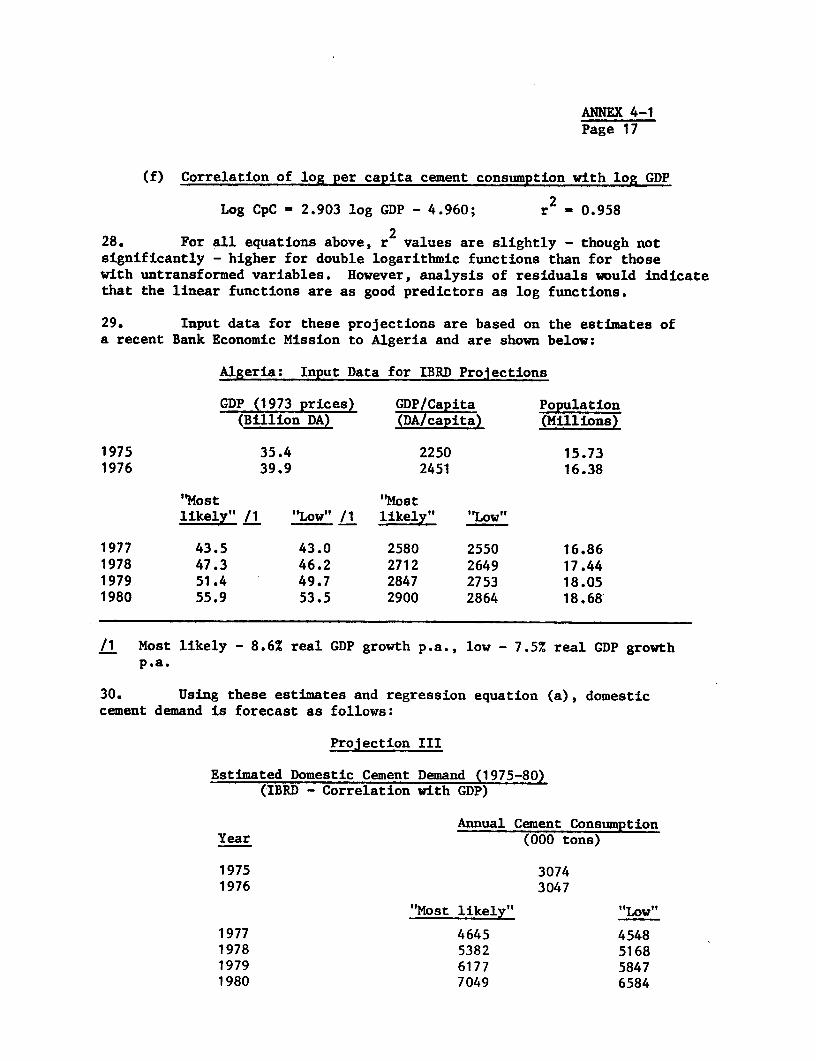

Pub

lic D

iscl

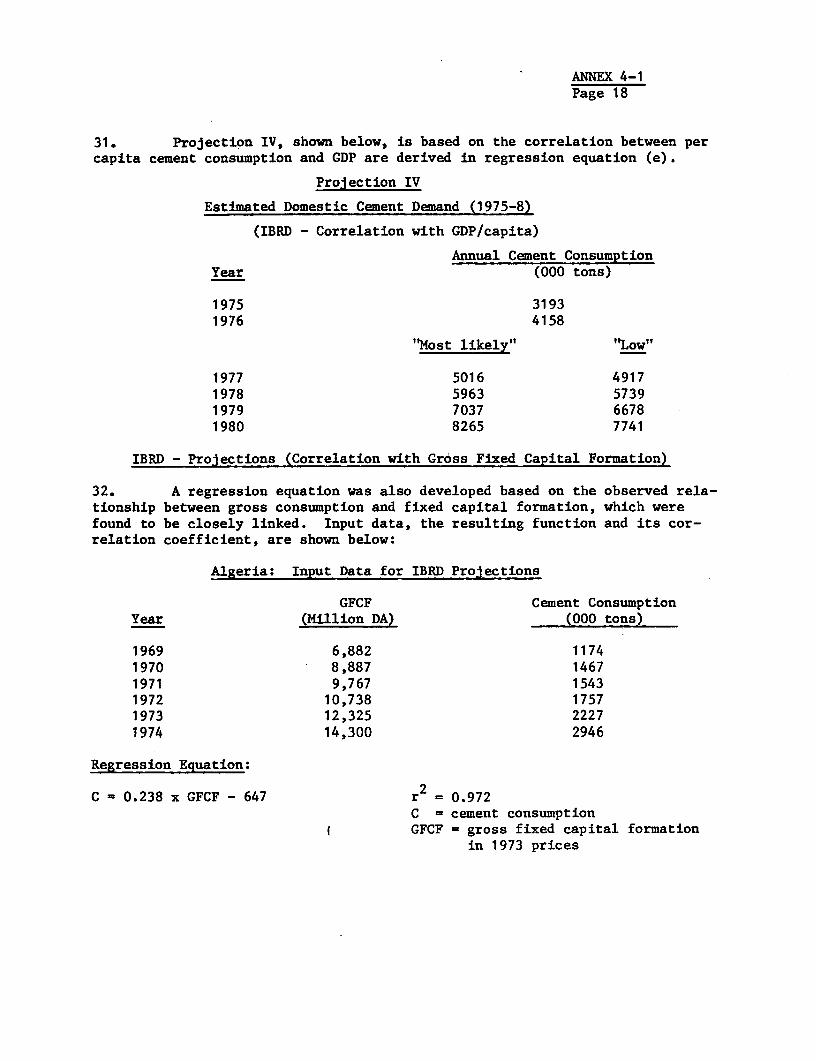

osur

e A

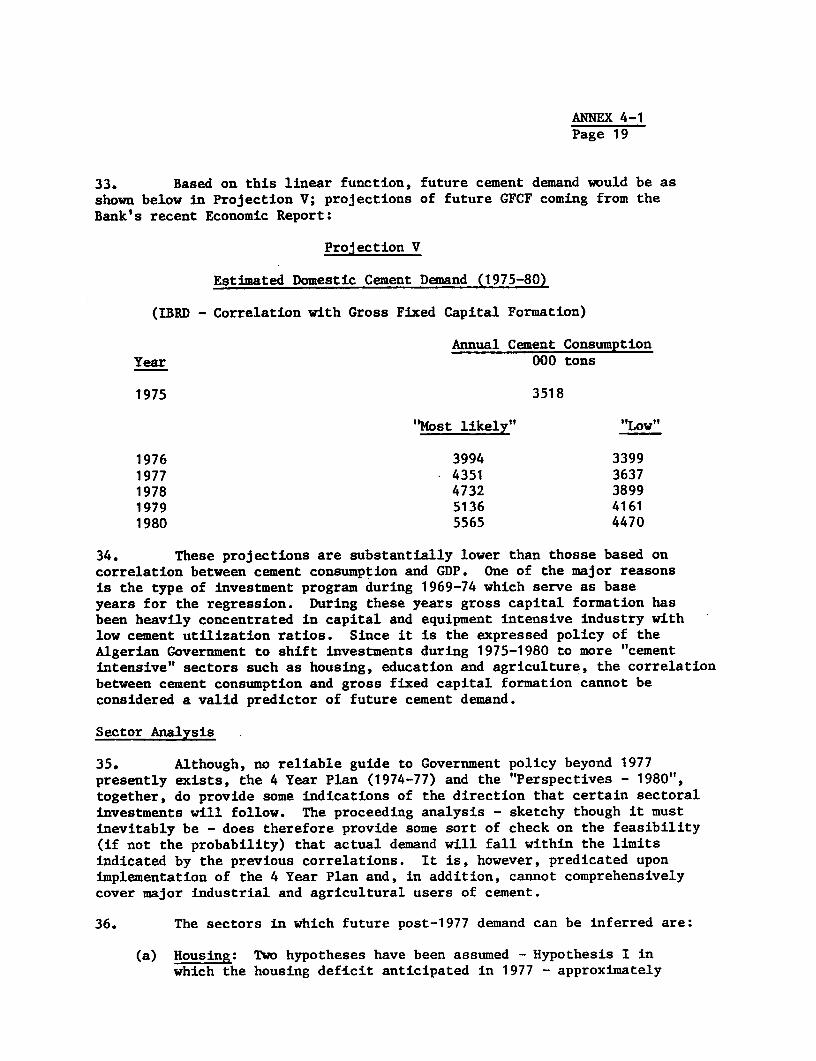

utho

rized

ALGERIA

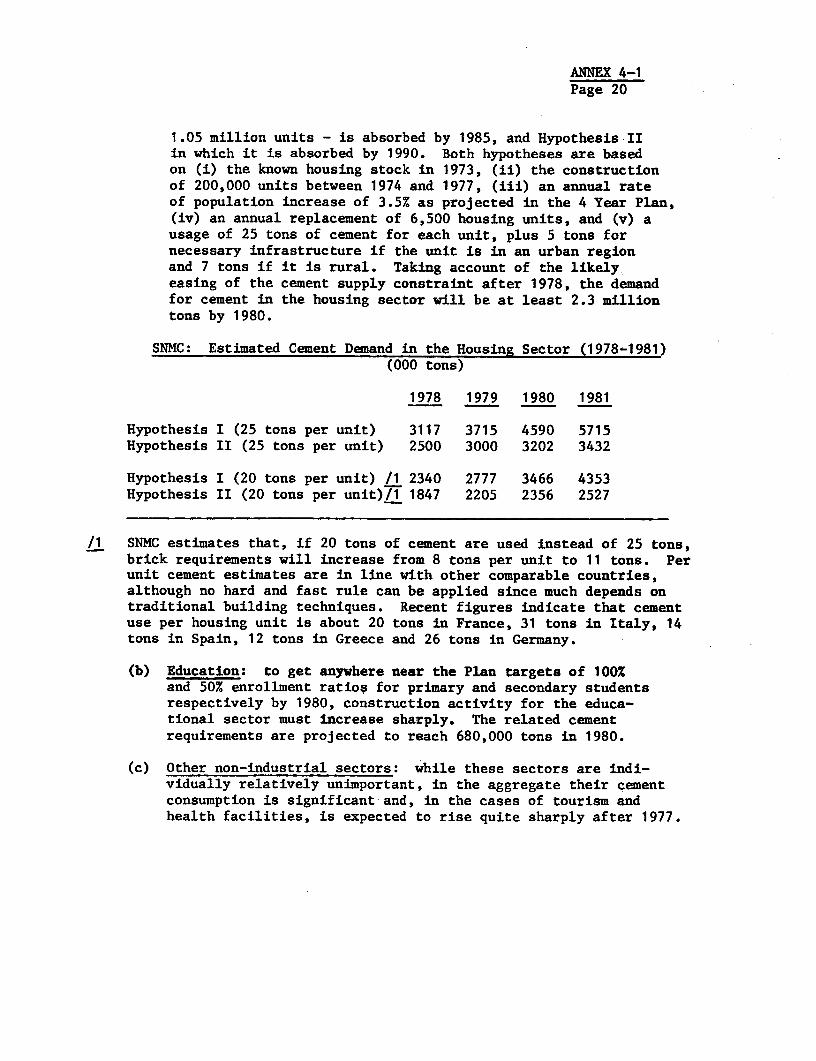

SNMC EXPANSION PROJECT

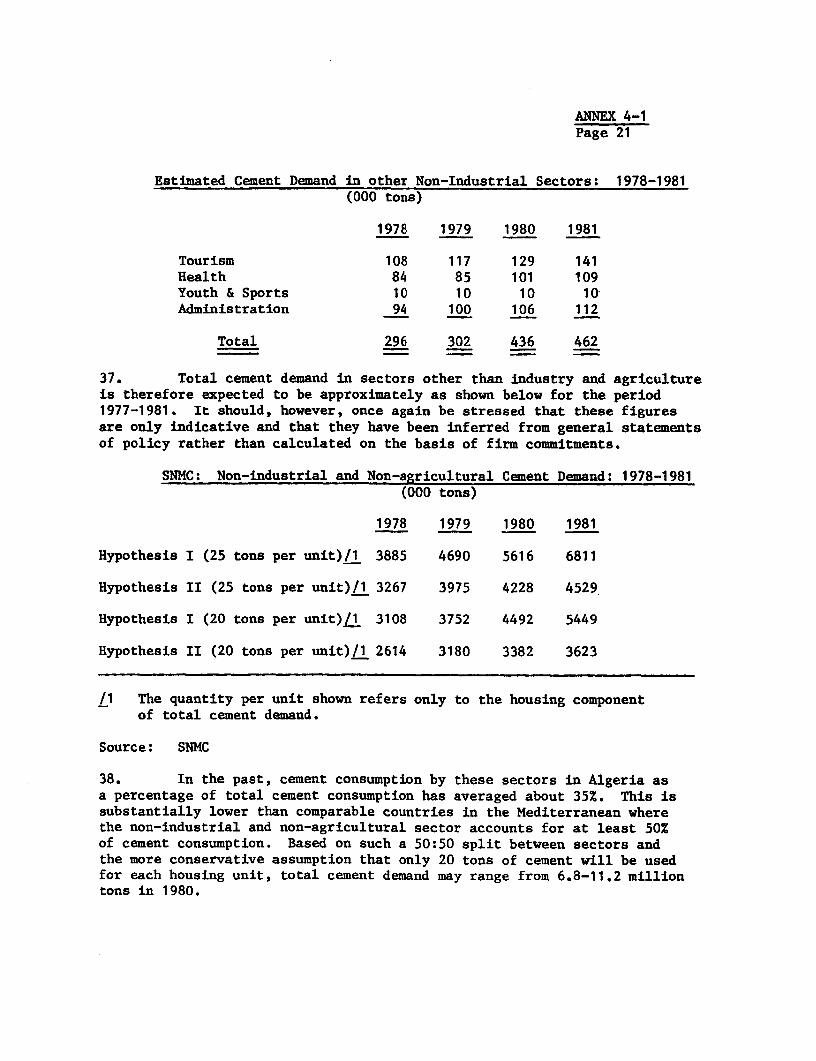

CURRENCY EQUIVALENTS

Except where otherwise notedall figures are quoted inAlgerian Dinars (DA)

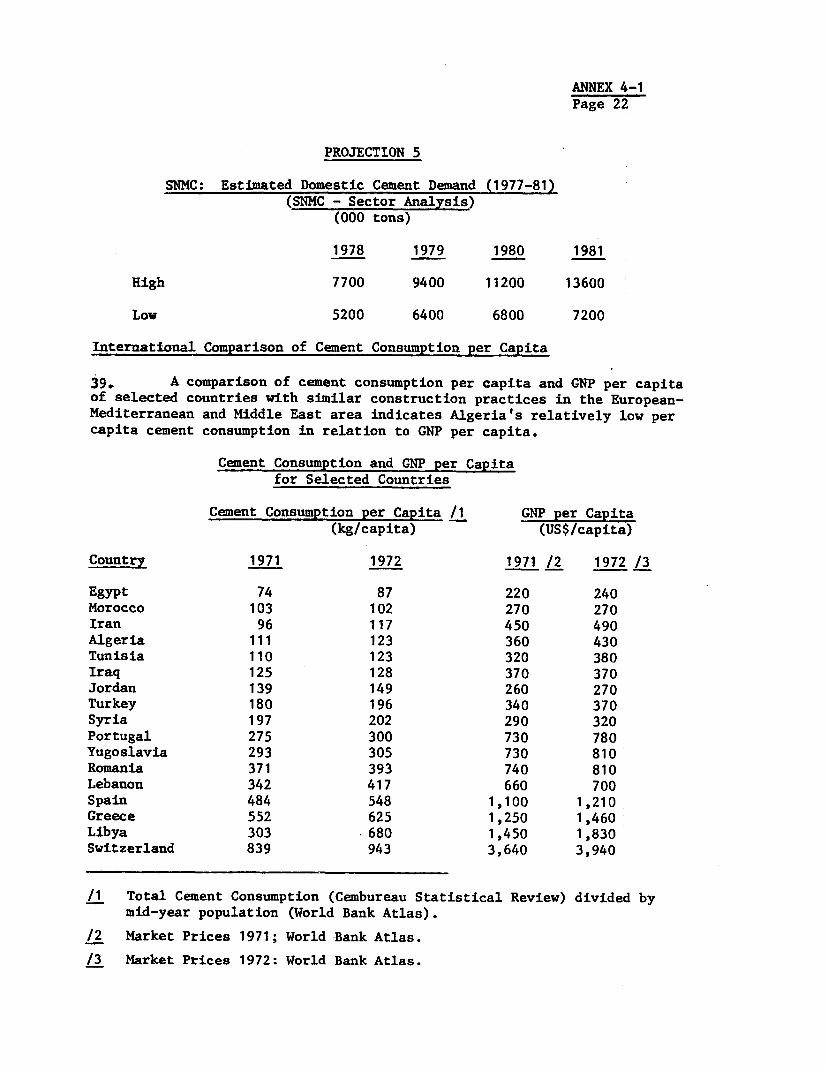

US$ 1 DA 3.92DA 1 US$ 0.26

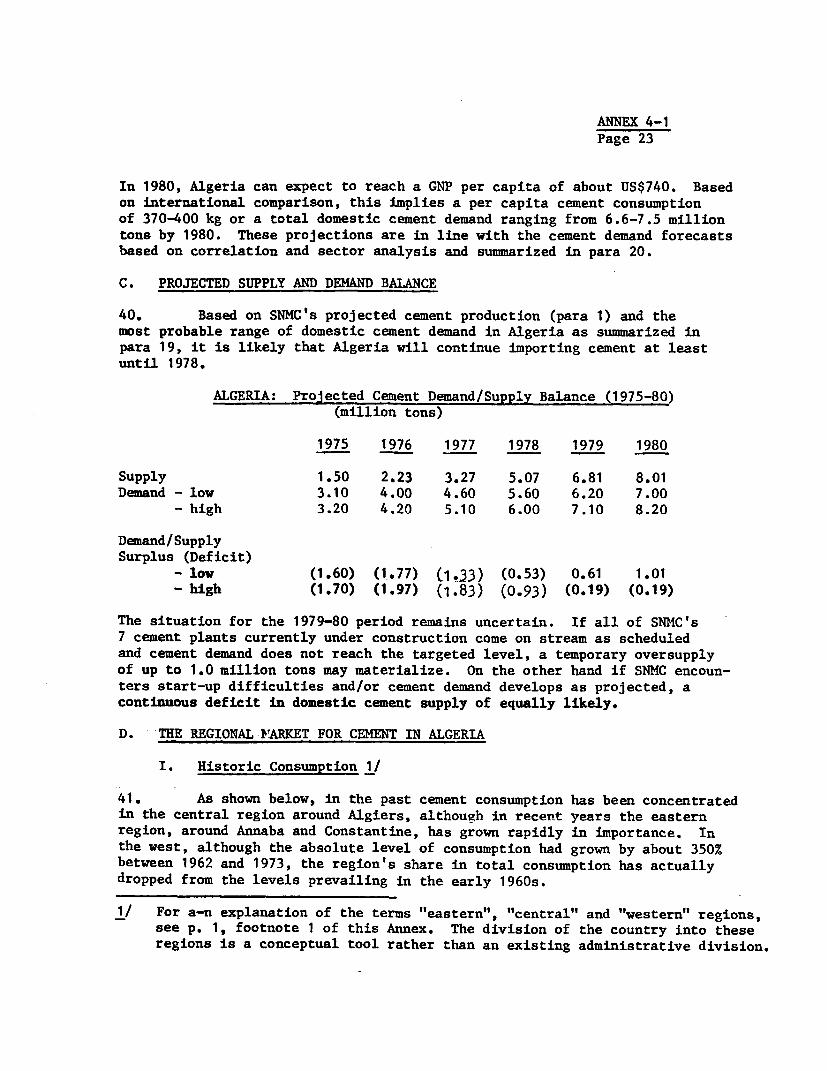

WEIGHTS AND MEASURES

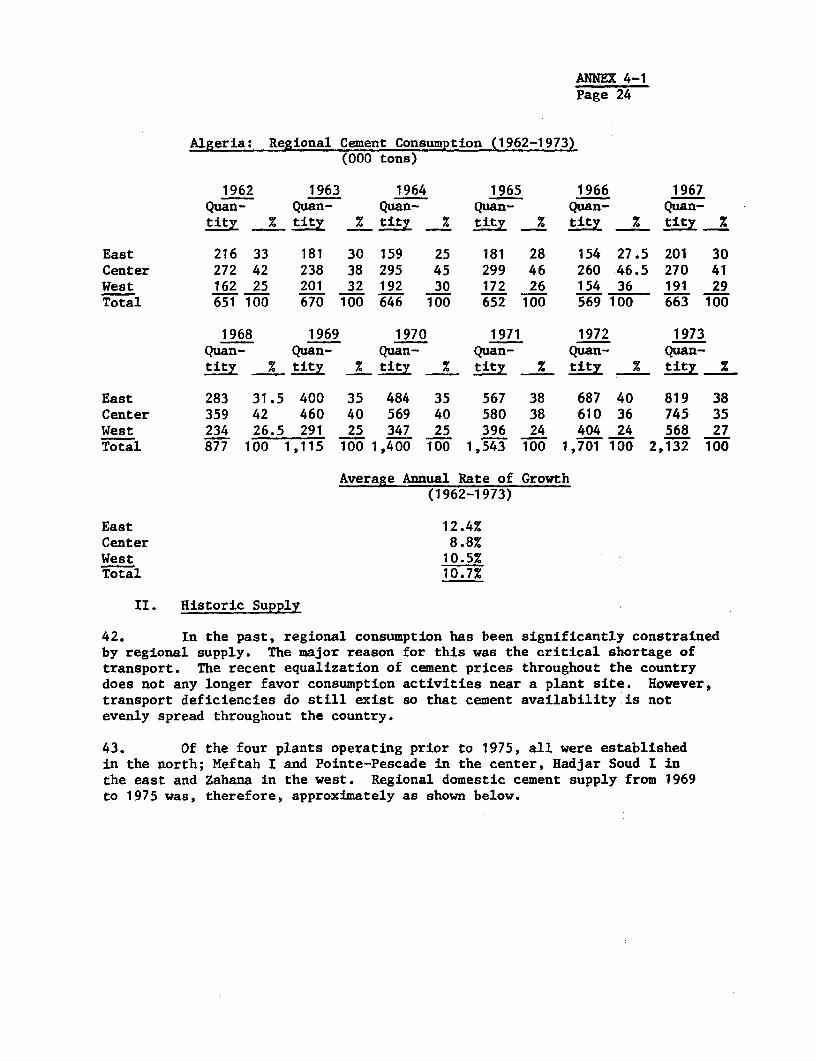

All weights and measures arein metric units

1 metric ton (ton) = 1,000 kilograms (kg)1 metric ton (ton) = 2,205 pounds1 kilometer (km) = 0.62 miles1 meter (m) = 39.3 inches1 hectare (ha) = 2.47 acres1 cubic meter (m3) 35.31 cubic feet1 kilo calorie (kcal) = 3.9685 BTU

ABBREVIATIONS AND ACRONYMS

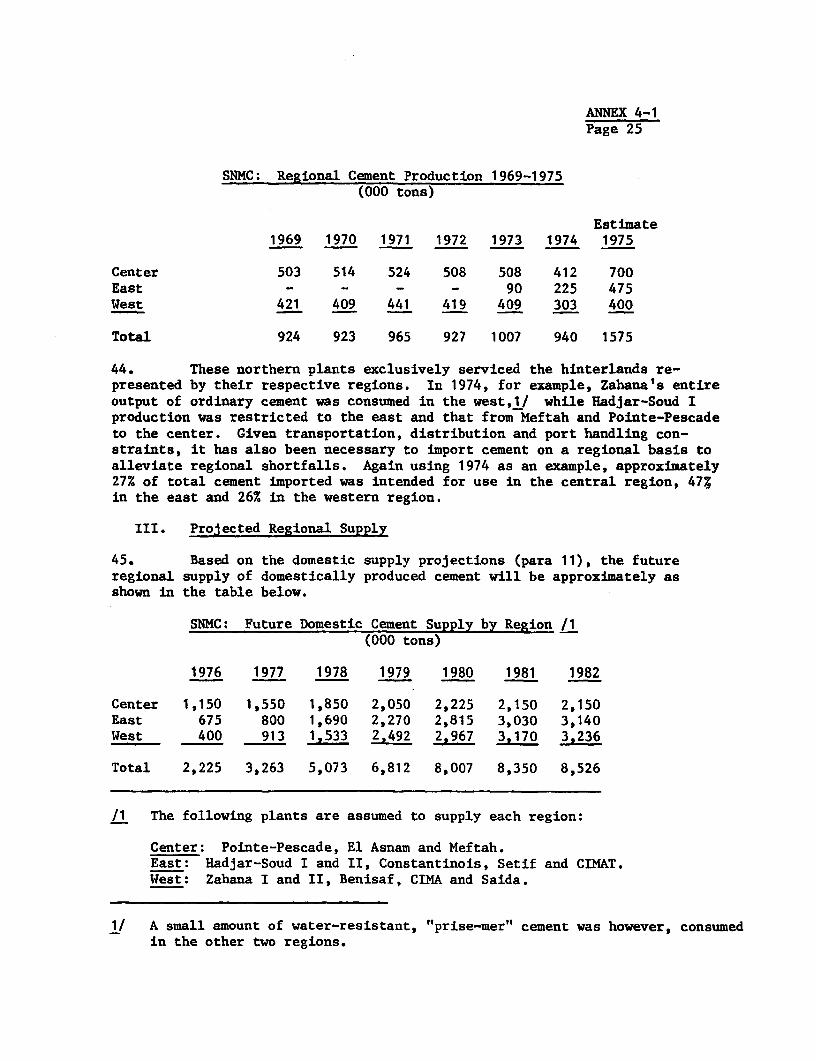

BAD Banque Algerienne de DeveloppementBEA Banque D'Exterieur AlgerienneSNC Societe Nationale de ComptabiliteSNMC Societe Nationale des Materiaux de ConstructionSONELGAZ Societe Nationale d"Electricite et de GazSNCFA Societe Nationale de Chemins de Fer AlgeriensSNTR Societe Nationale de Transport Routiertpy metric ton per year

Fiscal Year

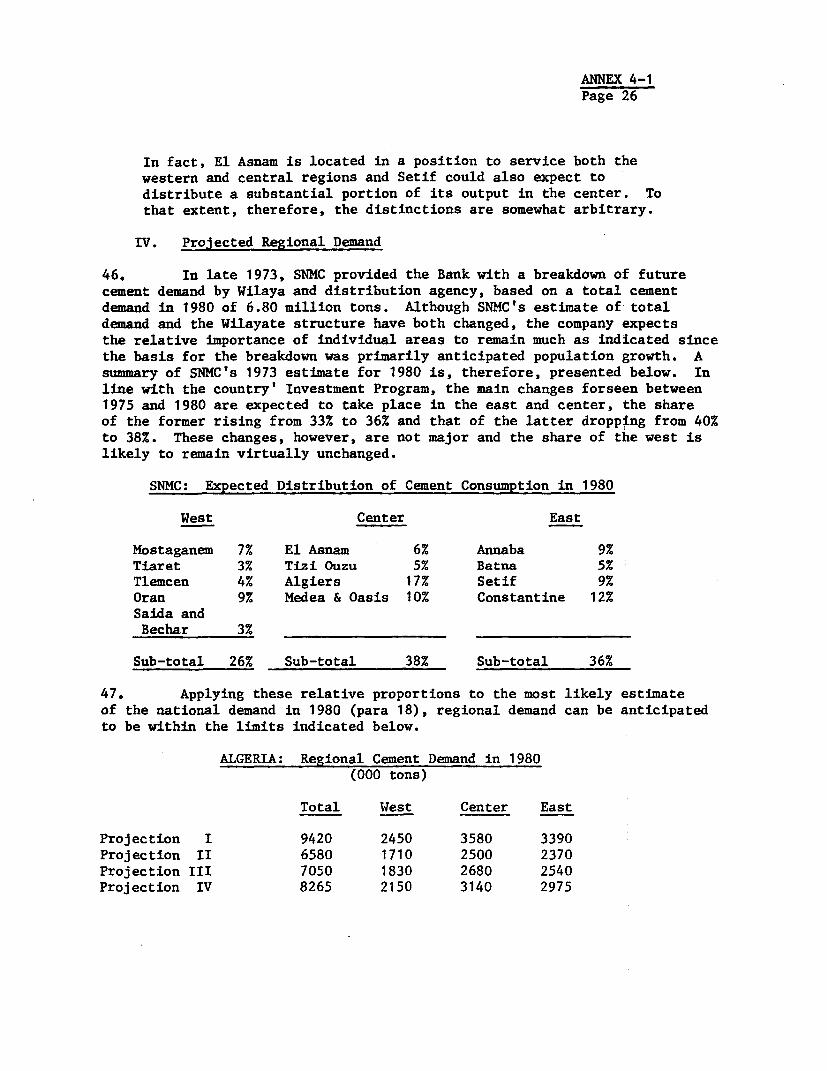

January 1 - December 31

ALGERIA

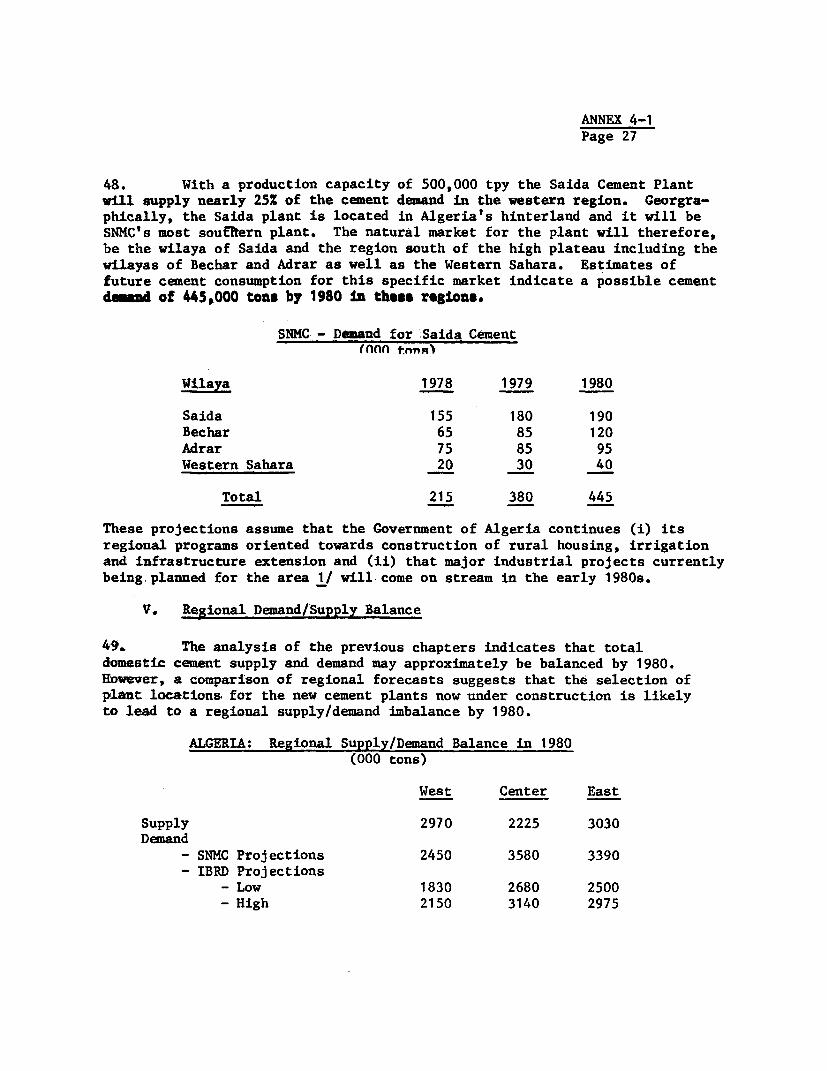

APPRAISAL OF THE SNMC EXPANSION PROJECT

TABLE OF CONTENTS

Page No.

SUMMARY AND CONCLUSIONS .......................... i - iv

I. INTRODUCTION ........ .............................. 1

II. THE INDUSTRIAL SYSTEM AND TUE COMPANY .... ........ 1

A. Industrial Policy and the Public Enterprise

System in Algeria ......................... 1

B. SNMC: Company Background and ExistingFacilities .... ............................... 2

C. SNMC: M4anagement and Organization .... ....... 3

D. SNMC: Past Performance and Financial Results. 3

E. SNMC: Accounts and Audits ..... .............. 5

F. SNMC: Future Investment Program .... ......... 6

G. SNMC: Future Financial Viability .... ........ 7

III. THE PROJECT ...................................... 9

A. Project Objective ............................ 9

B. Project Description .......................... 9

C. Allocation of Bank Loan and DisbursementSchedule .................................. il

IV. THE MARKET FOR CEMENT ............................ il

A. Supply and Demand Balance ..... ............... il

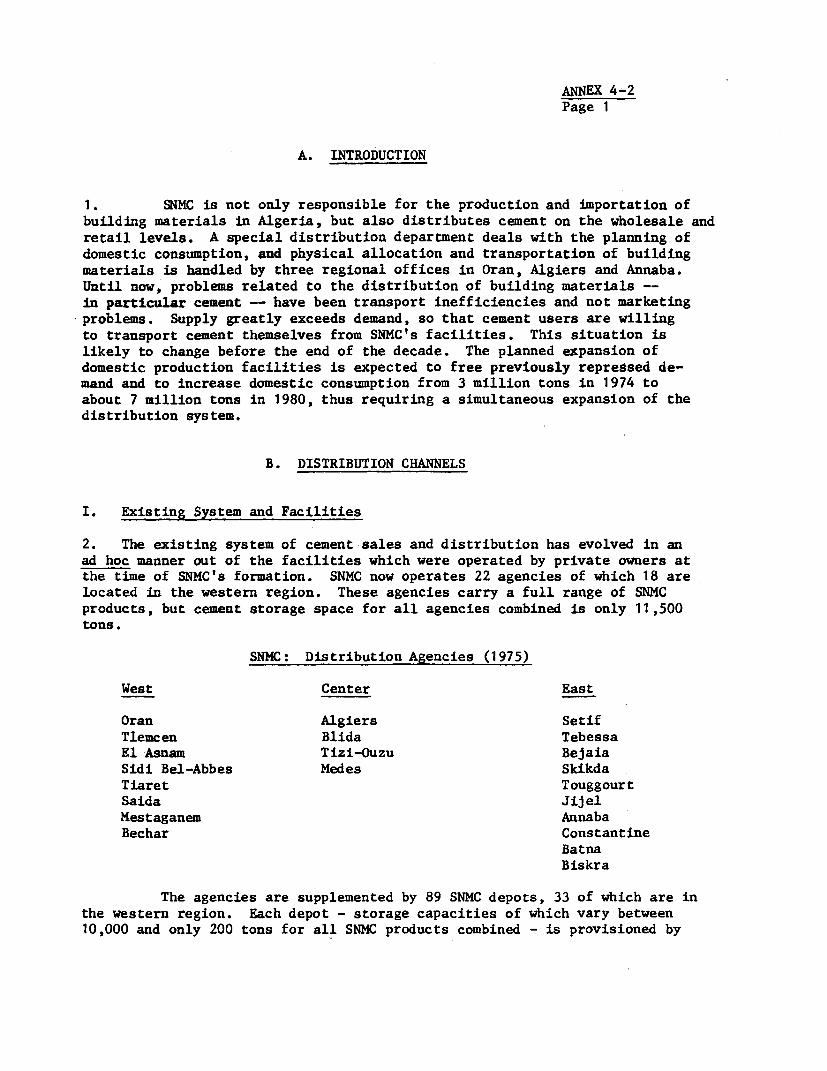

B. SNMC Distribution Network ..... ............... 15

C. Pricing of Cement ............................ 17

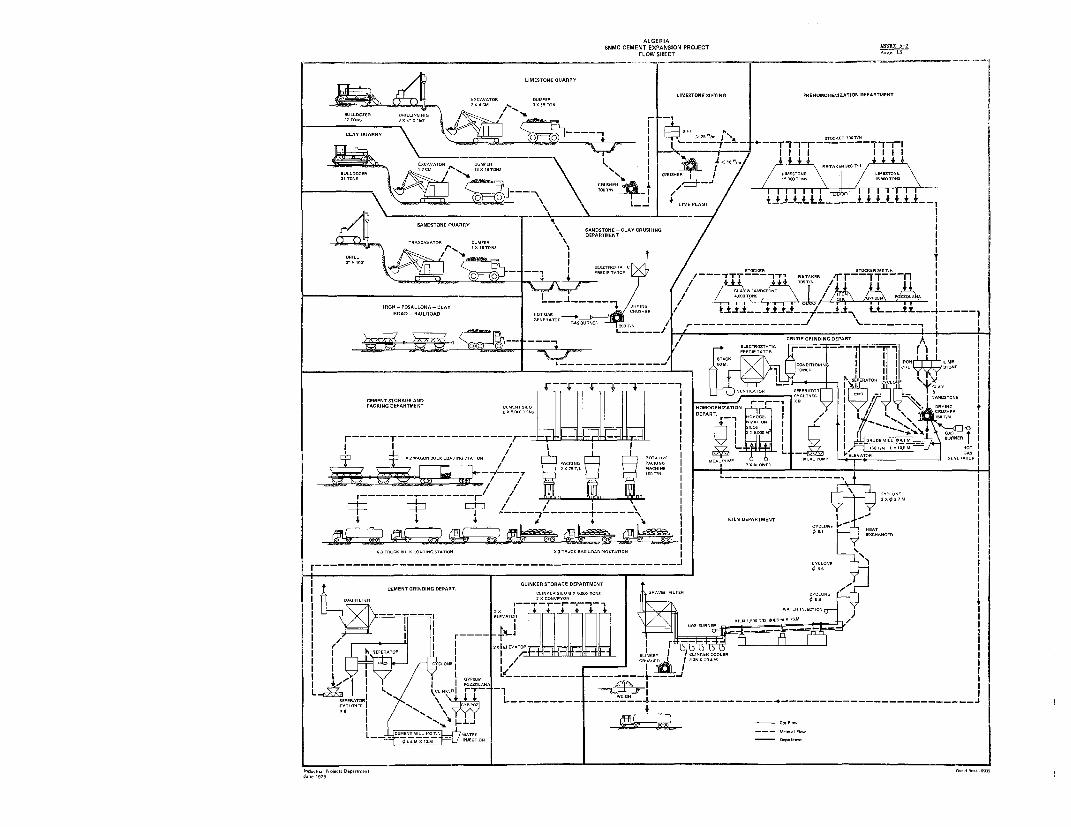

V. THE SAIDA CEMENT PLANT ............................ 18

A. Technical Aspects ............................ 18

B. Capital Cost and Financing Plan for the

Saida Plant . ............................... 22

C. Financial Analysis . ........................... 25

D. Major Risks .................................. 26

E. Economic Justification ....................... 27

VI. SNC TECHNICAL ASSISTANCE ......................... 28

A. SNC - Background ............................. 28

B. Program Objective and Description .... ........ 29

VII. AGREEMENTS ..................... .................. 30

This report was prepared by Miss Haug and Messrs. Hilton and Cognet, of theIndustrial Projects Department, and Mr. Basman, Consultant.

TABLE OF CONTENTS (Cont'd)

MAPS

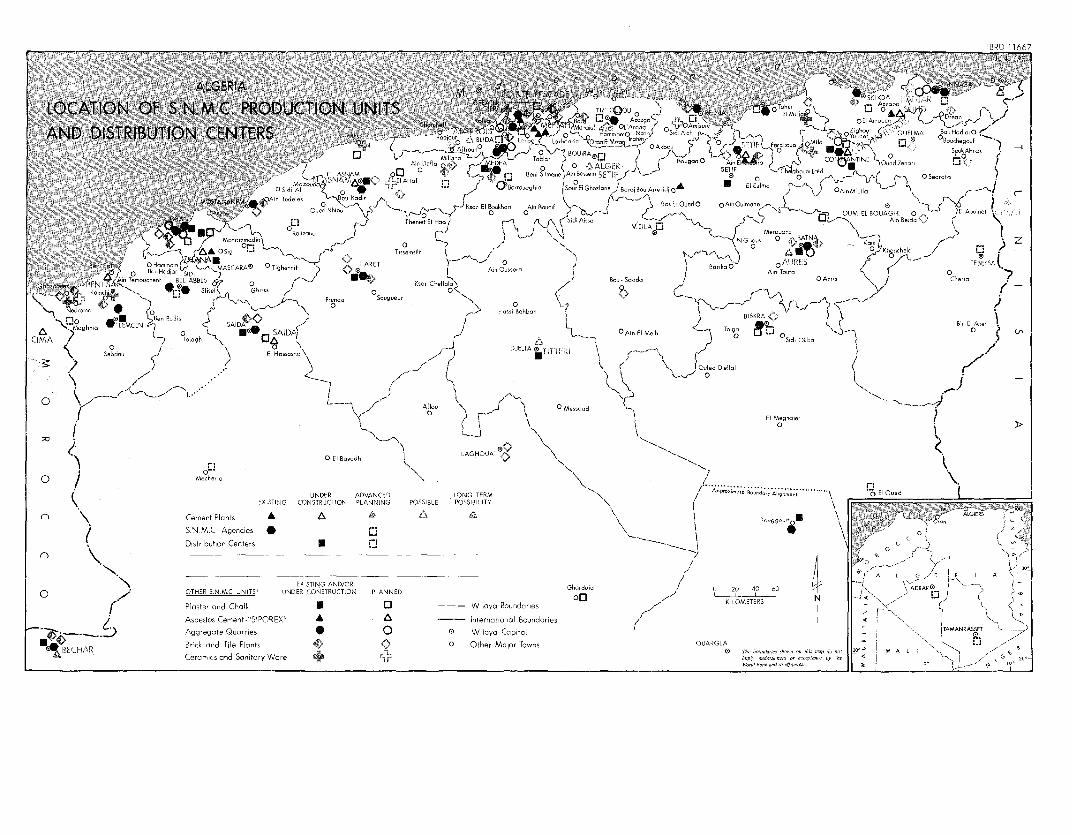

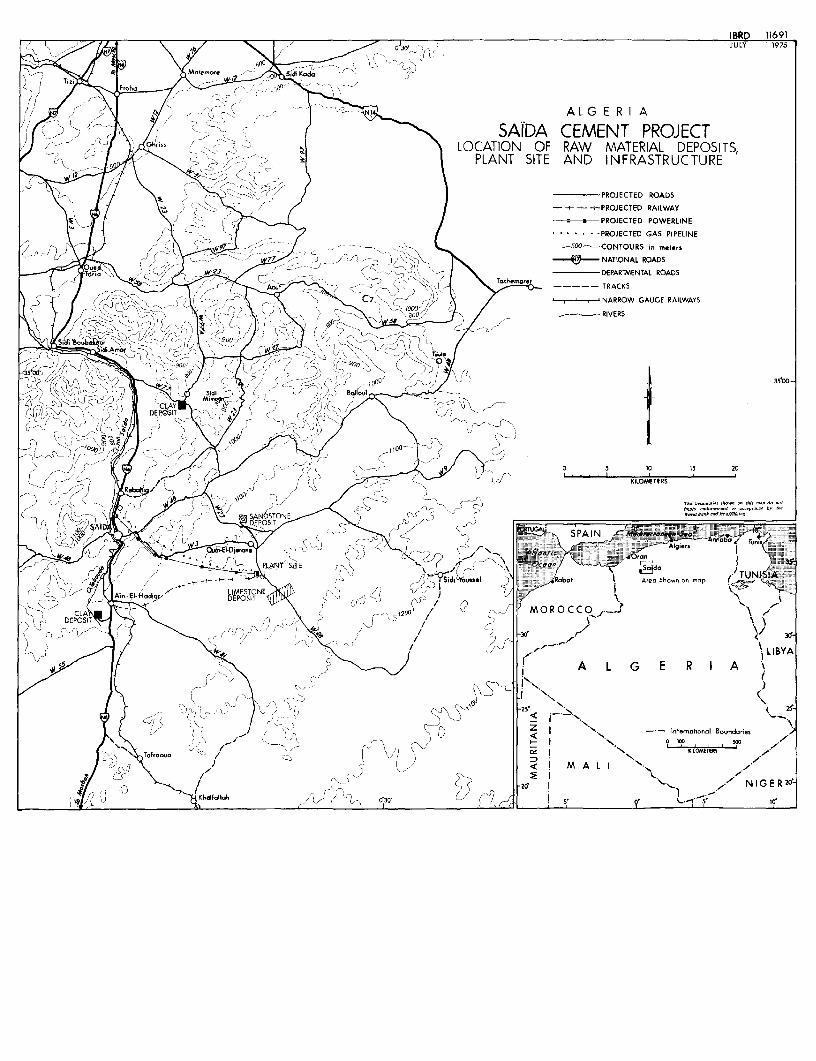

1. Location of Existing and Planned SNMC Facilities (IBRD 11667).2. Location of Saida Plant and Quarries (IBRD 11669).

ANNEXES

1 Technical Terms and Process Description

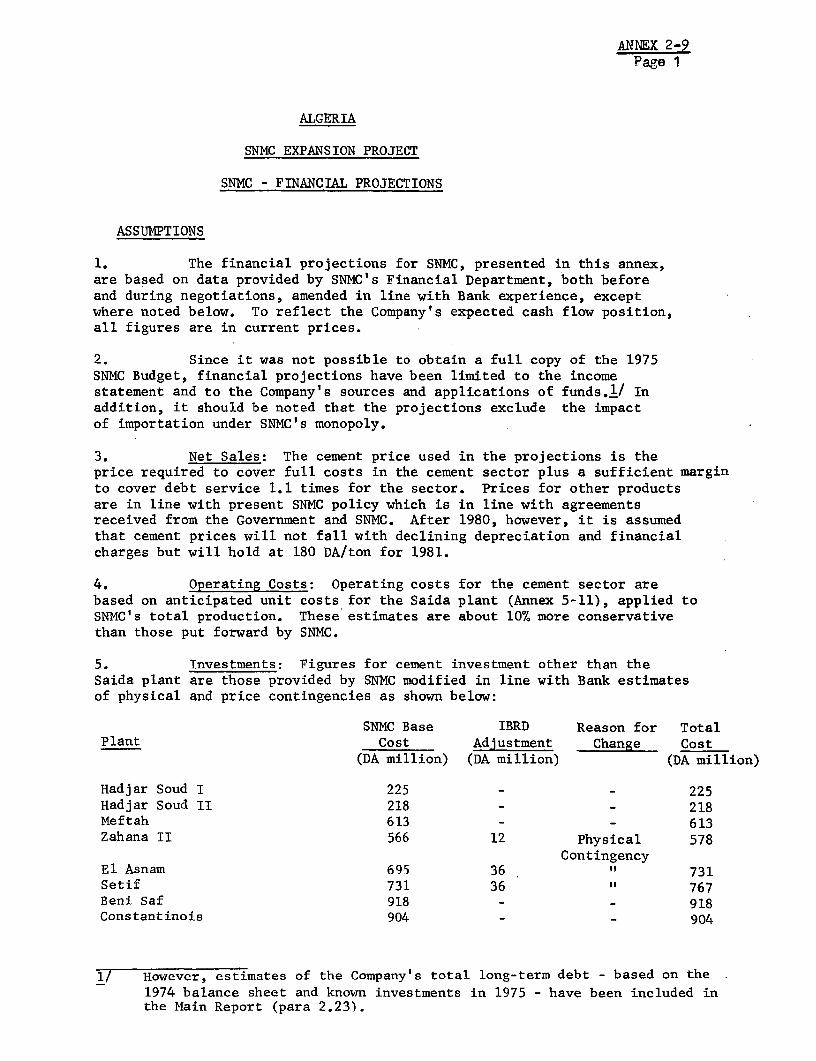

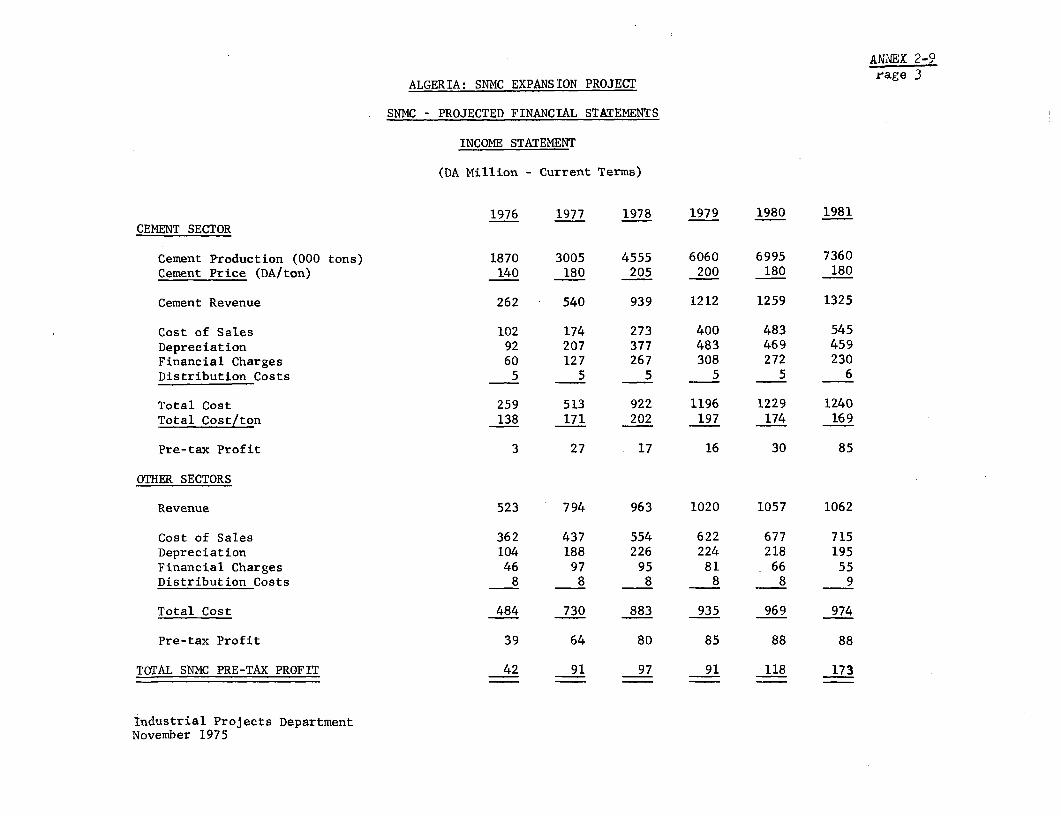

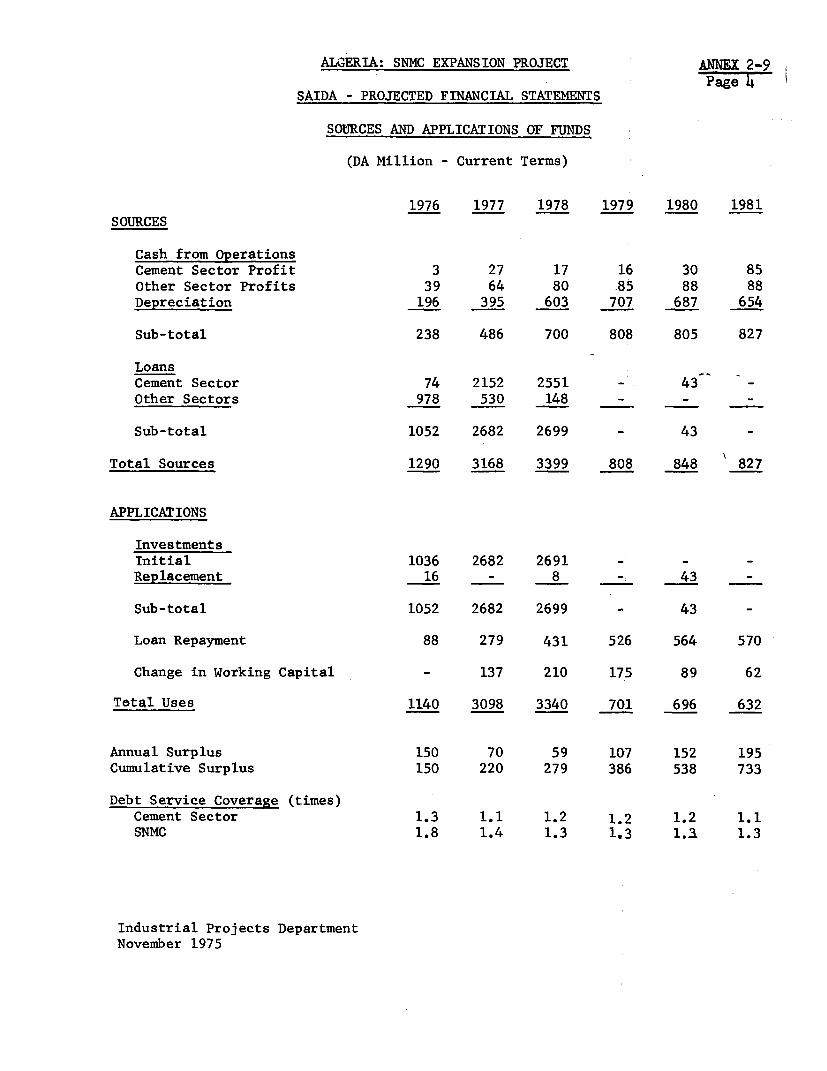

2-1 The Algerian Economy and the Industrial Sector2-2 The Public Enterprise System in Algeria2-3 SNMC - Existing Facilities2-4 SNMC - Organizational and Managerial Structure2-5 SNMC - Organization Chart2-6 SNMC - Historical Income Statement (1970-74)2-7 SNMC - Historical Balance Sheet (1970-74)2-8 SNMC - Plants Under Construction and New Investment Projects2-9 SNMC - Financial Projections

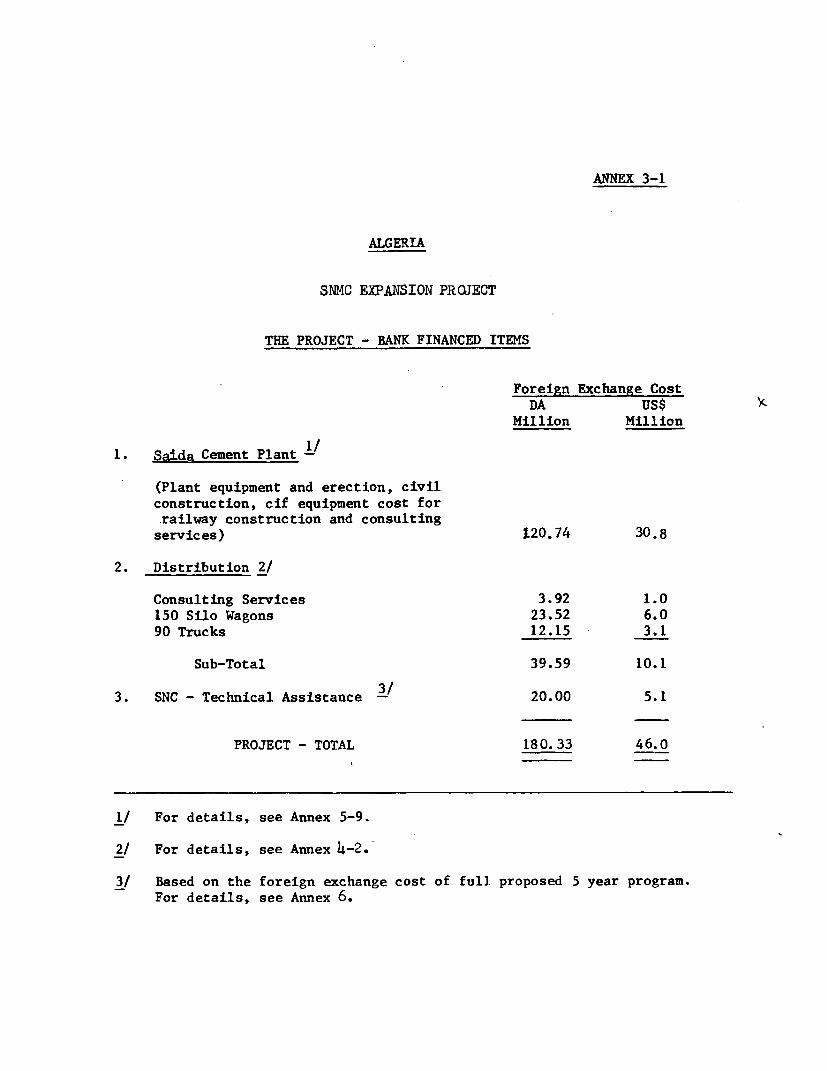

3-1 The Project - Bank Financed Items3-2 The Project - Implementation Schedule3-3 The Project - Estimated Disbursement Schedule

4-1 The Market for Cement in Algeria4-2 Distribution and Pricing of Cement in Algeria

5-1 Saida Cement Plant - Raw Material Availability and Analysis5-2 - Detailed Description5-3 - Infrastructure and Utilities5-4 - Ecology5-5 - Manpower Requirements, Training and Technical

Assistance5-6 - Plant Implementation5-7 Saida Cement Plant - Capital Cost Estimates5-8 " - Projected Working Capital Requirements5_9 si - Bank-Financed Items5-10 - Disbursement Schedule5-11 - Operating Cost Projection

and Production Build-up5-12 Saida Cement Plant - Financial Projections5-13 - Break-even Point Analysis5-14 - Financial Rate of Return and Sensitivity

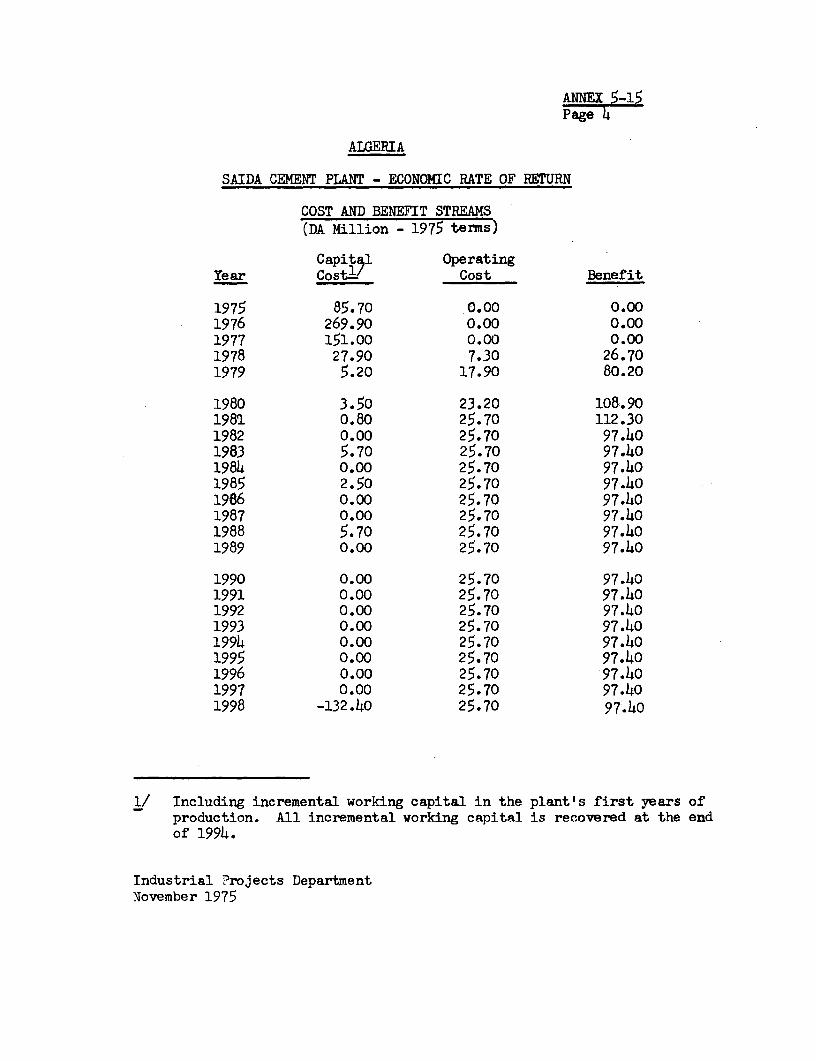

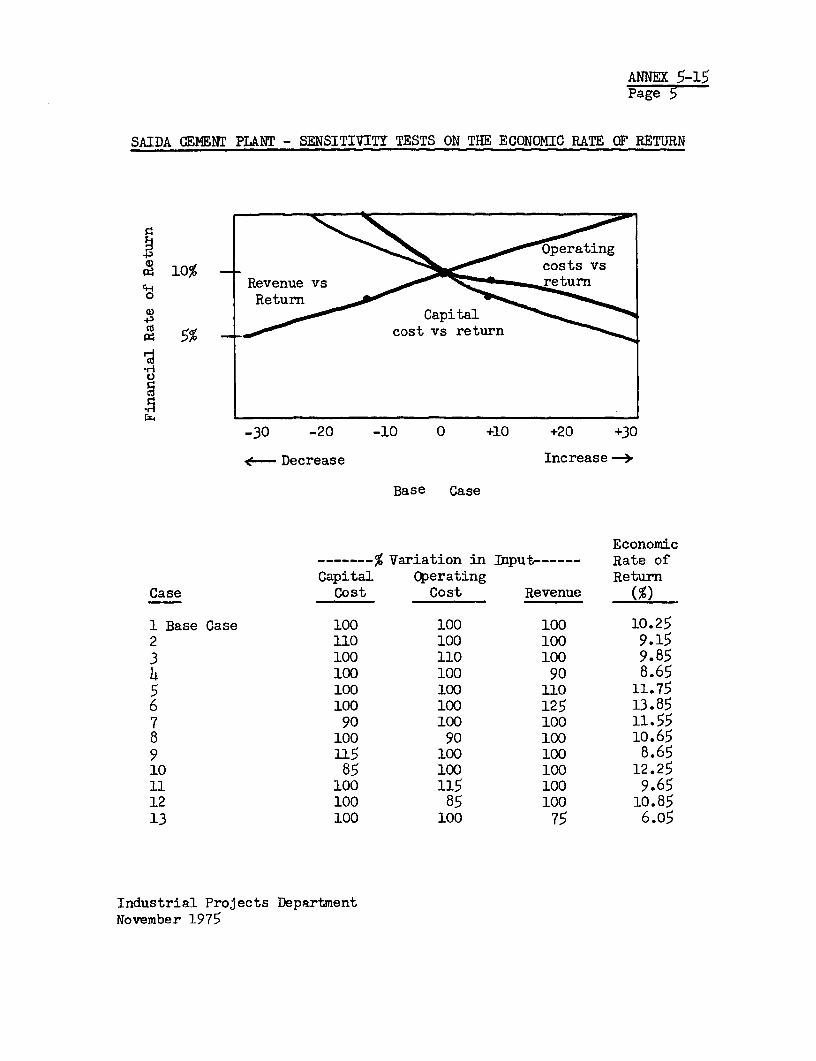

Analysis5-15 - Economic Rate of Return and Sensitivity

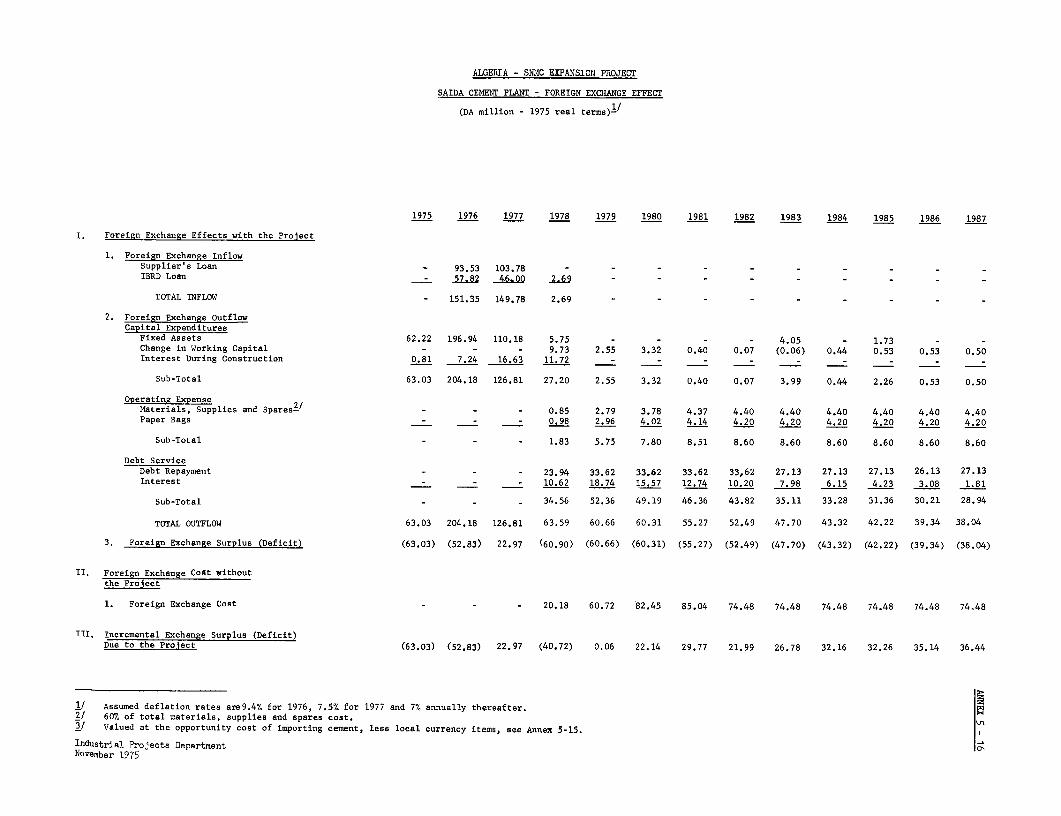

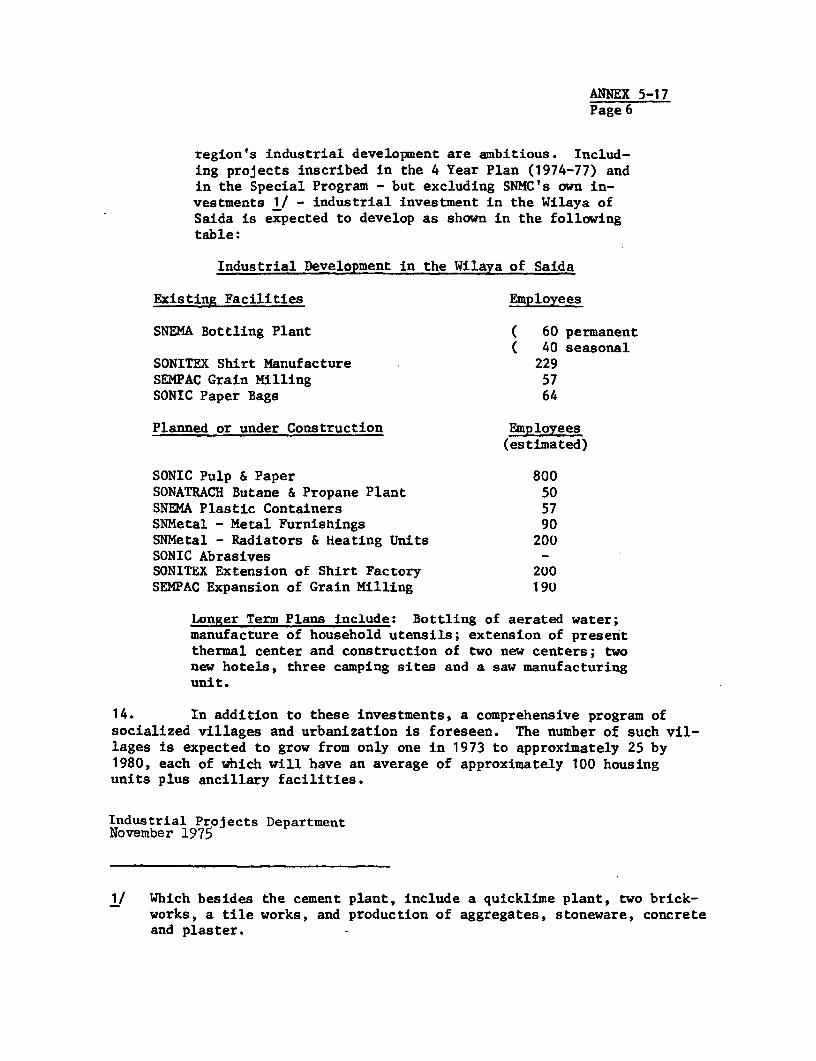

Analysis5-16 - Foreign Exchange Effect5-17 - Regional Development Impact

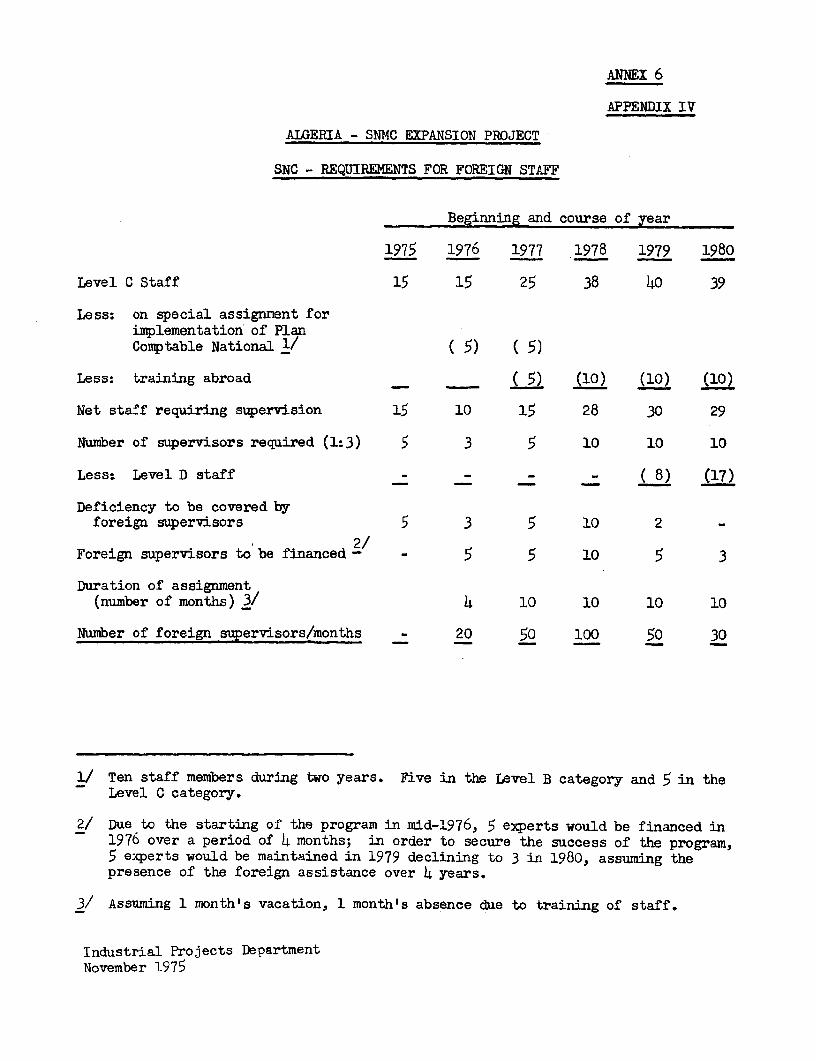

6 SNC - Technical Assistance Program

ALGERIA

APPRAISAL OF THE SNMC EXPANSION PROJECT

SUMMARY AND CONCLUSIONS

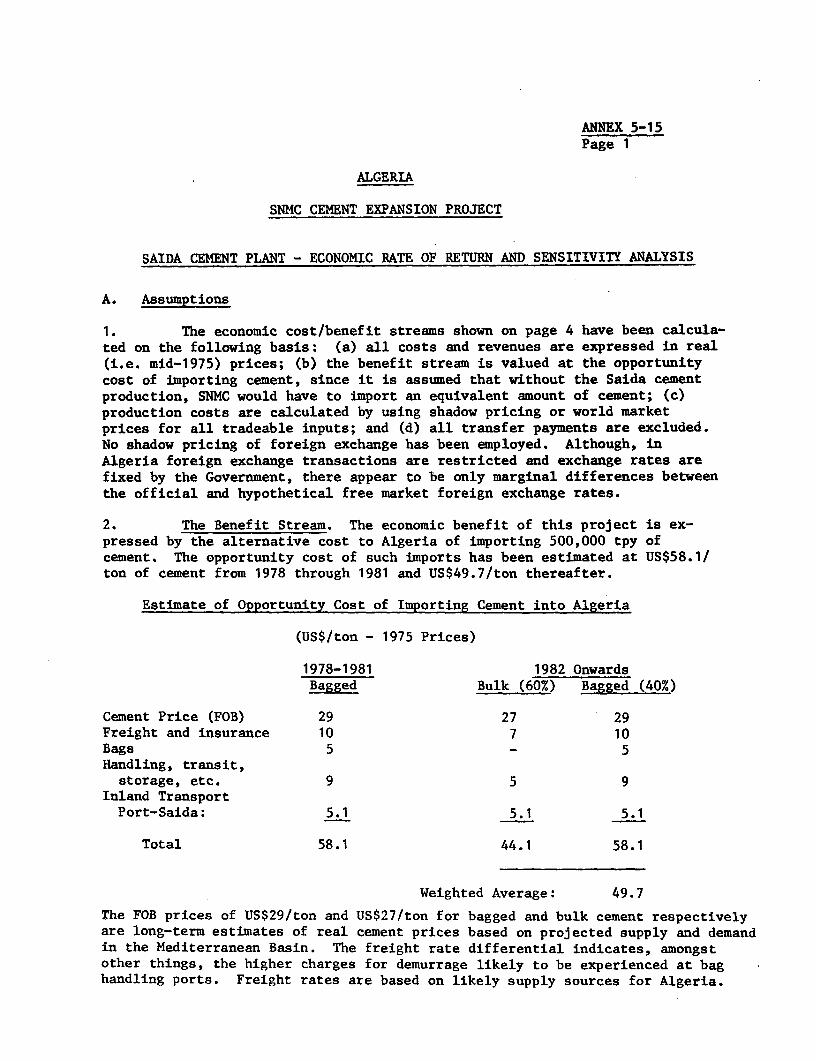

i. This report appraises a proposed Bank loan of US$46,0 million tohelp finance: (a) part of the ongoing expansion of the Societe Nationale desMateriaux de Construction (SNMC), the Algerian state enterprise for construc-tion materials, through erection of a new 500,000 ton per year cement plantnear Saida away trom the coast in the rural south; (b) the expansion of theCompany's distribution network; and (c) a technical assistance program to theSociete Nationale de Comptabilite (SNC), the state accounting and auditingcompany. If approved, the loan would be the Bank's first direct industrialoperation since lending was resumed in FY1973.

ii. The prime purpose of the proposed Bank loan lies not so much inïts tinancial contribution of somewhat more than 20% of estimated projectcosts as in its effort at institution building in Algeria's building materialsector. The project attempts to help SNMC cope with present and future or-ganizational and financial problens created by an ambitious investment pro-gram which, between 1974 and 1980, is expected to require fixed asset expendi-tures in excess of US$2.0 billion and which aims at making Algeria indepen-dent in cement and some other building materials by the end of this decade._76thls end, cerent production is expected to increase from about 1.5 xi31iontons in 1975 to about 8.0 mdllion tons by 1980.

iii. SNMC was established in 1968 as a state enterprise to promote thedevelopment of the Algerian construction materials industry and to manufac-ture, import and distribute a wide range of building materials. The basisfor SNMC's operations were 51, formerly privately-owned, production unitsand their distribution network which were nationalized between 1968 and1972. Since then the Company has expanded substantially and now includesabout 70 enterprises accounting for more than 65% of production in theconstruction materials sector (with a monopoly in cement), the renainderbeing produced by other state enterprises or by small factories owned byregional authorities or private operators.

iv. Industrial state enterprises, such as SNMC, operate under the closesupervision and guidance of the Government which, through the Ministry ofIndustry and Energy, defines individual companies' corporate strategy, appointssenior personnel, formulates investment programs in line with overall economicobjectives, determines the location and capacities of production units, setsprices for industrial products and controls the financing of such enterprisesboth through the allocation of funds from Government-owned banks and by thecollection of surplus funds for reinvestment in the economy. The firm centralcontrol and the absence of a free market price mechanism for primary productsand staples has undoubtedly led to some misallocation of resources and certainimbalances in industrial development in Algeria.

- ii -

v. While SNMC is a very active company and vas able to double the valueof its sales between 1970 and 1974, losses have rapidly increased and reached25% of net sales in 1974. This was largely due to prices not having beenadjusted adequately or frequently enough to reflect increasing operating costsand higher import prices for the products SNMC is selling in Algeria, the lackof an effective budgeting and cost control system, and the fact that all cashshortfalls were financed by additional short-term debt thereby aggravatingthe Company's financial strains even further. In addition, there vere anumber of non-recurring costs associated with the takeover of the previouslyprivate companies and a greatly increased wage bill as all workers were puton a permanent salaried basis. At present, therefore, SNMC is nôt a finan-cially viable enterprise.

vi. Discussions have been held with the Algerian Government to putSNMC on a sounder financial basis, independent of continuous subsidies,so that it is able to meet at least its cost and debt service obligations.It has been agreed that, to achieve such an objective, (i) SNMC will plan andimplement a financial planning, cost control and budgeting system, (ii) pricesof all of SNMC's products will be reviewed annually and new prices will beproposed at such levels as to cover at least average unit costs plus a margin tocover debt incurred for that product group, and (iii) if necessary funds willbe made available to SNMC in such a way that the Company can cover its debtservice obligations at least 1.1 times and be able to pay whatever currentliabilities fall due.

vii. Historicaliy, Algerian cement demand has not been met becauseoa lack of domestic production and insufficient cement imports. Morerecently, domestic production rose by 60% between 1969 and 1975 and atthe same time, imports increased almost ten-fold and, since 1973, havesurpassed actual domestic production. Based on the Government's ambitiouseconomic development programs, demand for cement is expected to continueits rapid growth in rural and urban areas where a concerted effort is beingmade to improve the housing situation, expand irrigation and increase theindustrial base. It is estimated that by 1981 cement demand will be between8.0 and 9.5 million tons per year, representing an annual growth rate ofbetween 13 and 16% as compared to 20% in the recent past. Saida is one ofat least seven new plants that are to come on stream between now and the endof the decade to help meet this demand.

viii. An increase in cement production and demand of the magnitude envi-saged requires a concurrent expansion of SNMC's marketing and distributioncapability and the Company is currently establishing a number of distribu-tion centers to handle bulk cement as well as formulating longer-term plansfor distributing a full range of building materials, including those producedby other state companies. This, however, is not yet enough and in order toservice these centers and to transport cement and other construction materialsmore effectively in the rural regions, substantial transport equipment--bothrail silo wagons and trucks--are required. SNMC will also undertake studiesdesigned to determine the location and method of operation of its futuregreatly expanded distribution network and to analyze its long-term transportneeds.

- iii -

ix. SNMC's present financial position is not untypical of Algerian

state enterprises and underlines the importance of the technical assistance

program to SNC. The proposed program aims to develop SNC's capabilities in

external auditing, implementing basic accounting systems and modern manage-

ment accounting techniques. The program would require collaboration betweenSNC and a qualified international accounting and auditing firm over five

years and is expected to include both practical training of Algerian staff

abroad and joint operations in Algeria. Given the impracticality of makingindividual loans to state enterprises for improvement of each accounting

department, SNC represents the best available vehicle for effecting a general

improvement in accounting standards.

x. Of the Bank loan (US$46.0 million) to be made to SNMC, US$30.8 mil-

lion will cover approximately 25% of the estimated foreign exchange cost of

the Saida plant; US$10.1 million will provide the foreign cost of the Most

urgent requirements of trucks and silo wagons plus the foreign exchange

expenditures of the related distribution studies; and US$5.1 million will

be onlent to SNC to cover the foreign exchange component of the technical

assistance program. Residual financing for the Saida plant will be provided

by a supplier's credit (US$57.1 million)Ynand by loans from Algerian financial

institutions, probably Banque Algerienne de Developpement (BAD), BanqueExterieure d'Algerie (BEA), and Treasury advances, together amounting to

approximately US$98 million. The Government will also provide the remaining

financing tor the distribution network and the technical assistance component

to SNC as well as any overrun financing that might become necessary to

complete all project elements.

xi. Procurement of equipment, erection and civil works for the Saida

plant is being carried out in accordance with the Bank's international com-

petitive bidding procedures. A turnkey contract, excluding the civil works,

has been signed with Kawasaki Reavy Industries of Japan. The portion of the

Bank loan allocated directly to the Saida plant will finance: 30% of the

outstanding foreign exchange cost of the turnkey contract (representing 15%

of the total cost); 25% of the civil construction cost, representing its

estimated direct and indirect foreign exchange component; the foreign exchange

cost of a railway spur connecting the plant with the existing network as well

as consultant services and technical assistance connected with the implementation

and initial operation of the cement plant. It is proposed that US$300,000 of

the Bank loan be used for retroactive financing of consultant services.

xii. The price the Saida plant will receive for its cement is expected

to be based on average industry costs plus a margin sufficient to cover

SNMC's debt service obligations in the cement sector. The Saida plant will,

however, not be able to maintain a positive cash flow until its third year of

operations. The main reasons for the fact that the Saida plant will be a

higher than average cost producer are the plant's high capital cost, due to

its relatively small size, expensive design features such as a high degree

of automation, ample built-in security margins, above average performance

guarantees, the decision to proceed with a turnkey contract and, in partic-

ular, the special environment in which SNMC has been contracting for cement

plants. Nevertheless, the êconomic rate of return of the Saida plant is

- iv -

still about 10%. Once the plant is operating at full capacity, the netforeign exchange savings vill be significant and are expected to recoverthe plant's total foreign exchange costs in 6 years.

xiii. A number of the beneficial effects of the project are diffiultto quantify. The benefit of the Saida plant lies also in the broader de-velopmental impact that it will have on a region which so far has lagged behindthe coastal strip in the north. In addition to the institution-building imi-pact of the project on SNMC and SNC, the strengthening of the accounting andauditing functions in public sector firms can be expected to result in betterfinancial management and economic planning in Algeria. Most importantly, theproject is expected to permit continuation of a constructive dialogue withSNMC and the Goverument on hov to improve the efficiency of industrial develop-ment in Algeria.

xiv. The technical and comuercial risks that the project faces are notmajor. Difficulties may, however, arl:se if SNMC and SNC cannot recruit andretain sufficient qualified staff to implement their expansion progrem.But it muet be recognized that the financial viability of SNMC, and theSaida plant as part of it, depends on the continued functioning ofAlgeria's public enterprise and finance system, and therefore on the readyavailability to SNMC of funds from the Government particularly during theperiod of its rapid expansion.

xv. Based on the assurances and agreements summarized at the end ofthis report, the project is suitable for a Bank loan of US$46,0 millionequivalent to SNMC, for 15 years including 4 years of grace, at an annualinterest rate of 8.5% plus a guarantee fee of 1.5% per annum payable bySNMC to the Government on that portion of the loan which is not onlent toSNC.

I. INTRODUCTION

1.01 This report appraises a proposed Bank loan of US$46.0 million tohelp finance: (i) part of the ongoing expansion of the Societe Nationale desMateriaux de Construction (SNMC), the Algerian state enterprise for construc-tion materials, through erection of a new 500,000 metric tons per year (tpy)cement plant near Saida, about 200 km south of Oran (Map IBRD 11667); (ii)the expansion of the Company's distribution network; and (iii) a technicalassistance program to the Societe Nationale de Comptabilite (SNC), the stateaccounting and auditing company.

1.02 The Saida plant is part of the Algerian Four-Year Plan (t974-77)which stipulates an increase in the country's cement production capacityfrom about 1.6 million tpy in 1975 to 7.5 million by 1978 and forms anintegral component of the Special Development Program (1972-75) for thePlateau Region; this program aims at fostering industry and agriculture ofAlgeria's less developed regions away from the coastal strip.

1.03 The various project components were appraised in May and July of1975. The Bank mission consisted of Miss Haug (Chief) and Messrs. Cognetand Hilton of the Industrial Project8 Department and Mr. Basman (Consult-ant). Technical terms used in the report are described in Annex 1.

II. THE INDUSTRIAL SYSTEM AND THE COMPANY

A. Industrial Policy and the Public Enterprise System in Algeria

2.01 SNMC's organizational structure, investment plans, decision-makingprocess and financial situation must be seen in the context of the Algerianeconomic and public enterprise system and the country's industrial policywhich are described in Annexes 2-1 and 2-2.

2.02 Algeria's economy is characterized by heavy concentration on in-dustrial development and by the absence of the balancing mechanism of anautonomous pricing system or of other free market forms of financial discipline.Production of goods and services is dominated by state enterprises with theprivate sector accounting for only a minor share. Since 1971, all stateenterprises have had to rely entirely on long or medium-term bank loans fortheir investments since financing through equity or retained earnings is nolonger permissible. They are considered instruments of Government policyand, as such, are not only financed by the state through Government-ownedbanks but, in turn, are expected to contribute to Government finances throughtax contributions and investment of internally generated funds with theTreasury in the form of Government bonds.

2.03 Industrial state enterprises, such as SNMC, operate under thesupervision and guidance of the Ministry of Industry and Energy whichdefines their strategy, appoints senior personnel, determines - in collabora-tion with the Ministry of Finance - the allocation of profits and proposes

-2-

investment program-s to the Plan Secretariat for final approval. Althoughstate enterprîses participate in formulating their investment programs, thePlaa Secretariat influences not only production targets in line with overalleconuric objectives, but also the location and capacities of important newproduction units. In the past, enterprises seldom questioned the economicfeasibility of investments inscribed in the Four-Year Plans and emphasisvas instead put on physical Plan fulfillment.

B. SNNC: Company Background and Existing Facilities

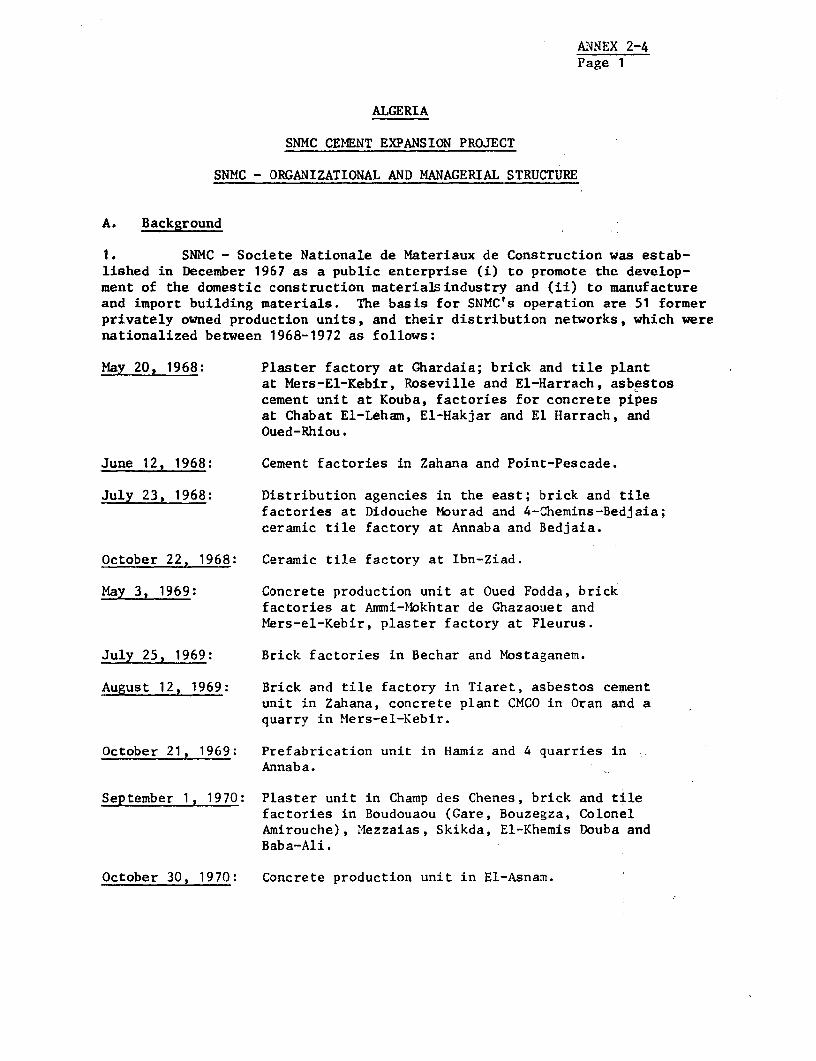

2.04 SNMC was established in December 1968 as a State enterprise to pro-mote the development of the domestic construction materials industry and tomanufacture, import and distribute a wide range of building materials. Thebasis for SNMC's operations were 51 formerly privately-owned production unitsand their distribution network which were nationalized between 1968 and 1972.Compensation for take-over of the private assets vas resolved to mutual satis-faction and, by the end of 1974, SNMC dominated the markets for cement (100%),ready mixed concrete (100%), bricks (80%), tiles (75%), and plaster (55%).The Company accounts for more than 65% of production in the Algerian construc-tion materials sector, the remainder being produced by other state monopolies(responsible for metal products, glass, wood, etc.) and by small factoriesowned by regional authorities or private operators.

2.05 The Company produces, imports and markets, in addition to the basicconstruction materials just mentioned, manufactured products of either con-crete (pipes, props, support structures, etc.) or asbestos cement, as wellas ceramicse, sanitary ware, aggregates, sand/cement mixtures and miscella-neous building materials. Recently, SNMC introduced two new product lines,SIPOREX, a sand/cement based brick developed in Sweden for housing con-struction, and some plastic building materials.

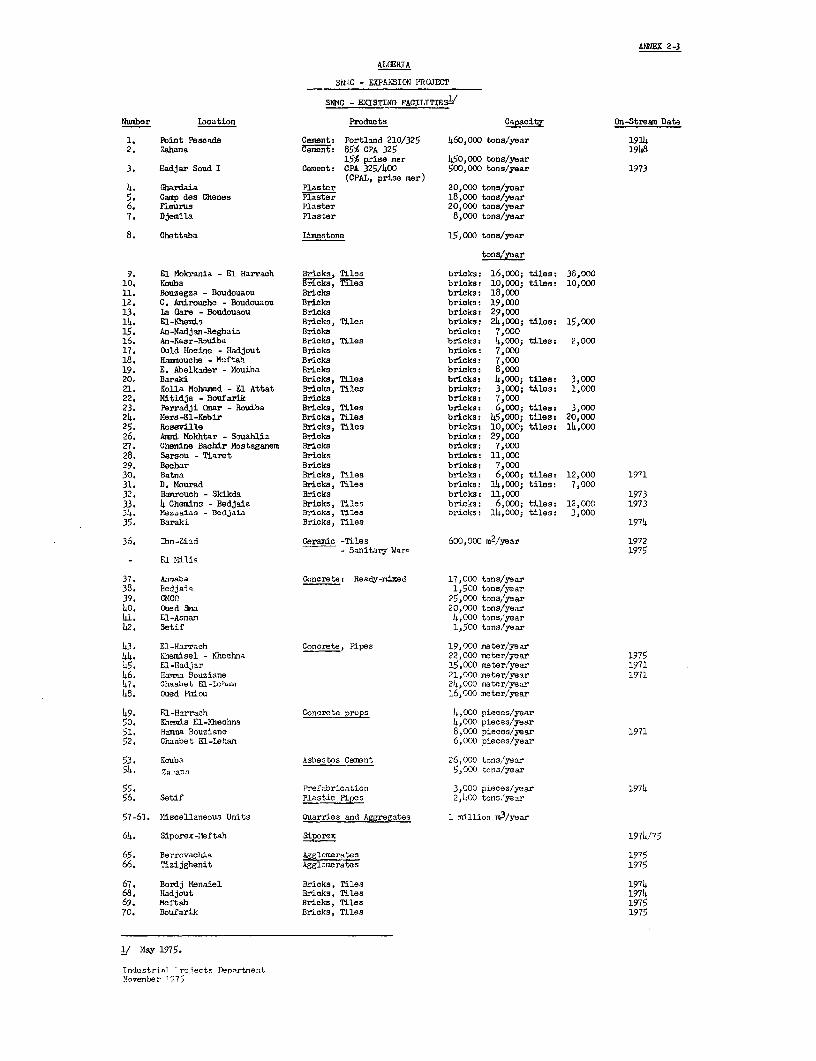

2.06 Since its creation, SNMC has invested more than US$400 million innew production facilities, including 8 quarries, 8 brick and tile plants, 5plants for manufacturing concrete products, 3 sanitary ware factories and2 cement plants. The Company currently operates 70 production units, a fleetof trucks, a construction company and a nationwide distribution system with22 agencies and 89 depots. As illustrated in Map 11667, the existing facil-ities, which, are given in some detail in Annex 2-3, are concentrated alongthe coastal strip with few plants or agencies serving the rural high plateauxand nomadic south.

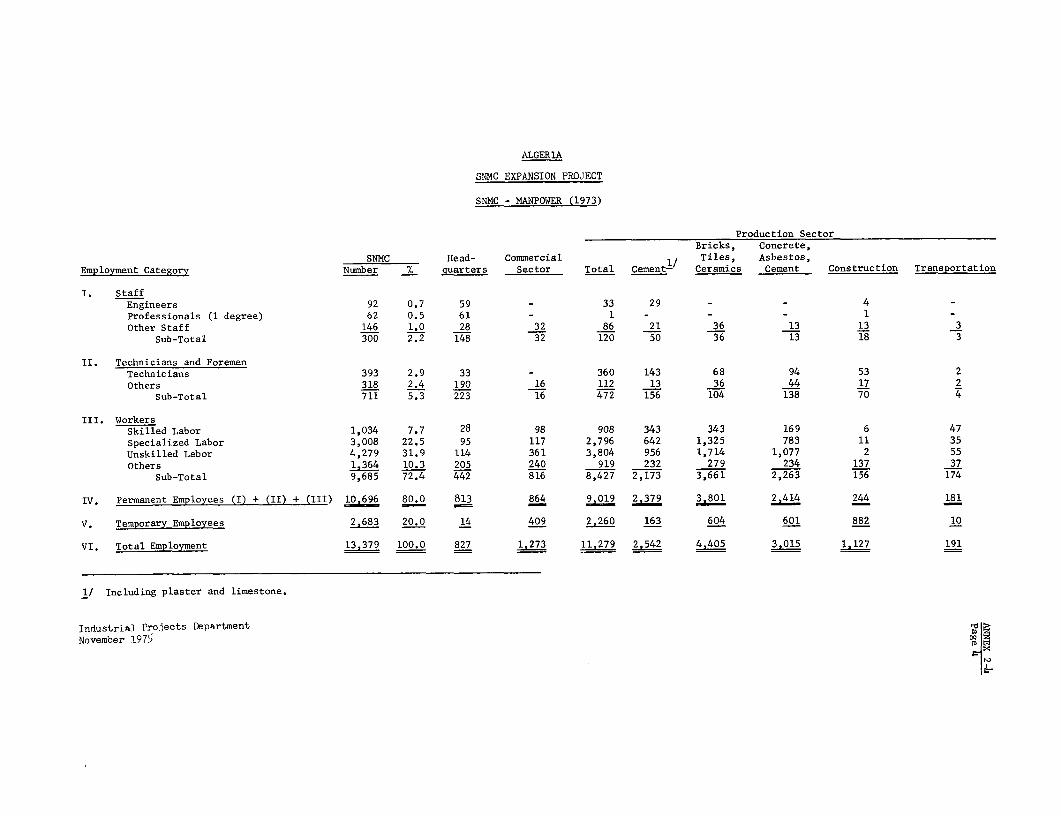

2.07 SNHC's manpower increased from about 6,000 people in 1970 to nearly15,000 people by mid-1975, of whom 92% are employed in production (Annex 2-4).During the past five years, SNMC has been able to maintain productivity levelsin thq formerly private companies and has been operating its plants consis-tently close to capacity.

2.08 The build-up of new capacity in the building materials sector is,however, far behind schedule. During the first Four-Year Plan (1970-73)only 55% of the planned increase was actually attained although investmentscame to 90Z of planned expenditures. The main causes of SNMC's failure to

-3-

implement investments according to targets were: (i) unrealistically tightconstruction schedules, imposed by the Plan and unchallenged by the Companybecause of inadequate project preparation and implementation capacity due tolack of experienced staff, the absence of proper feasibility studies, un-satisfactory experiences with consultants and continued time pressures; and(il) administrative difficulties within Algeria for approving contracts,clearing customs and arranging transport and the need for time-consumingspecial procedures for the financing of overruns which, due to severe ini-tial underestimation of costs, often occurred.

C. SNMC: Management and Organization

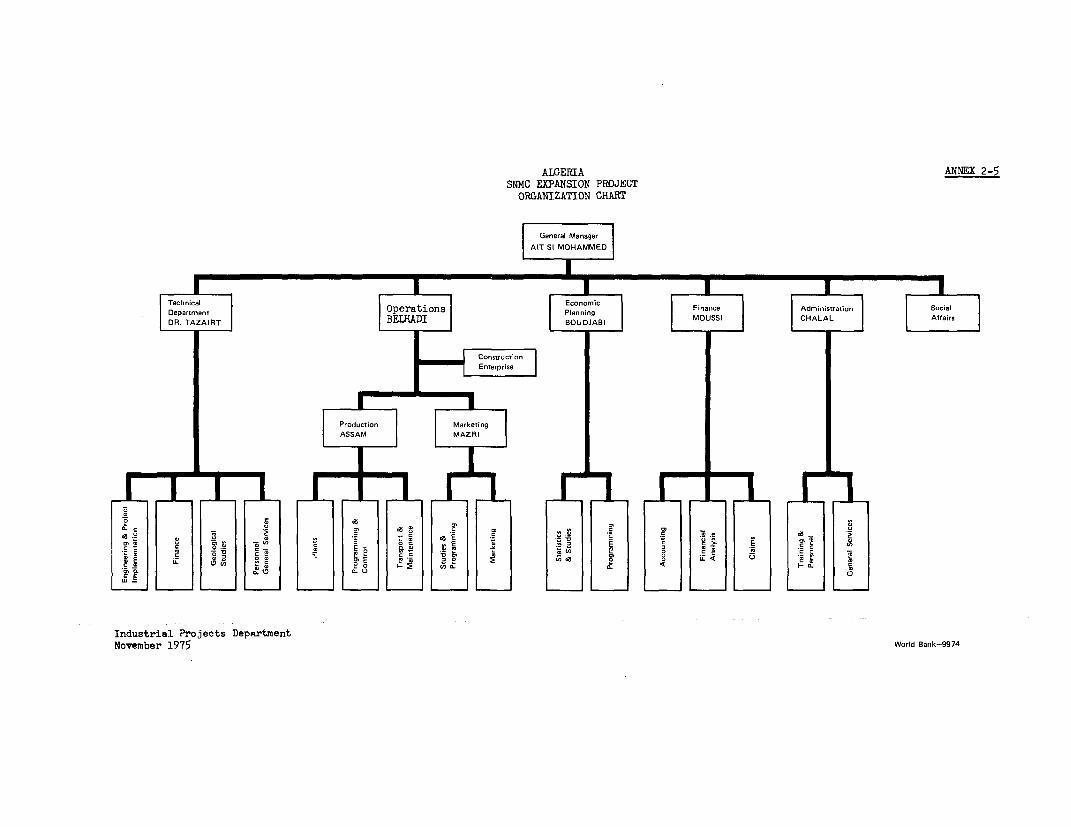

2.09 The Company, with headquarters in Algiers, is managed by a DirectorGeneral, Mr. Ait Si Mohamed, who is an engineer by training and who joinedSNMC in 1973. He is assisted by five directors, respectively responsiblefor Finance, Economic Planning, Technical Planning, Operations and Admin-istration. Annex 2-5 illustrates SNMC's organizational structure. TheCompany has been reorganized several times over the past five years. SNMC'spresent organizational structure is basically acceptable and inefficienciesstem more from (i) lack of coordination between the Technical, Financial andEconomic Planning Departments; (ii) inadequate numbers of qualified staff;and (iii) insufficient guidance and supervision of middle management, thanfrom flaws in the organizational set-up.

2.10 SNMC's management efforts are dominated by the need to meet timeachedules and fulfill production and investment targets. Therefore, at theSMMC level, economic planning and financial control of investments havebecome secondary. Lately, examples of resource misallocation have increasedincluding, in particular, overcapacities in certain sectors and regions.

2.11 To help realize, on schedule, its ambitious investment program witha limited number of qualified staff, SNMC has opted for the turnkey approachfor all its major projects and is making a continuous effort to train andrecruit personnel at all levels in Algeria and abroad. To operate its newplants at capacity, an additional safety margin is provided by a tendencyto overdesign new production units in order to safeguard against productionshortfalls in the future.

D. SNMC: Past Performance and Financial Results

2.12 The Algerian state-controlled economic system is characterizedby: (i) the fixing of domestic prices by a Governmental price commission;(ii) the centralization of financial decisions through the requirement thatinvestments be approved by the relevant Ministries and the Banque Algeriennede Developpement (BAD) which is the source of all local and some foreign ex-change credits for investments in the country; and (iii) as mentioned inpara 2.02, the financing of all investments and working capital by debt andthe immediate back-flow of any surplus funds to the Treasury.

- 4 -

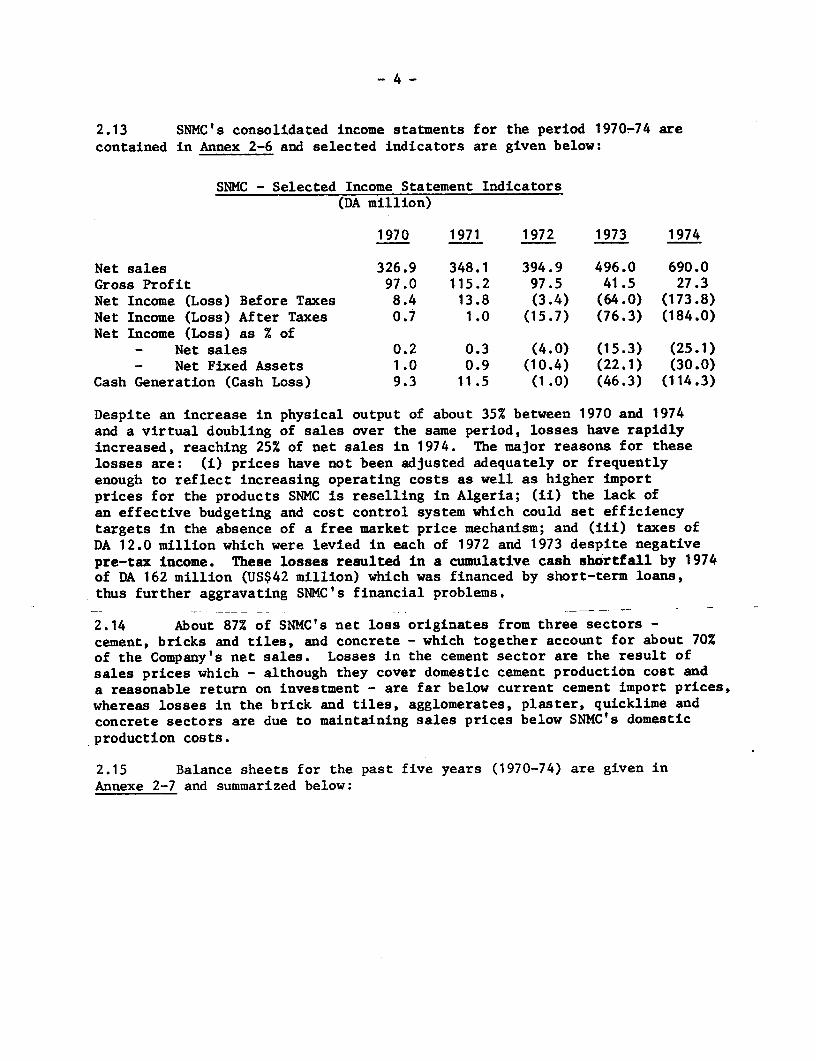

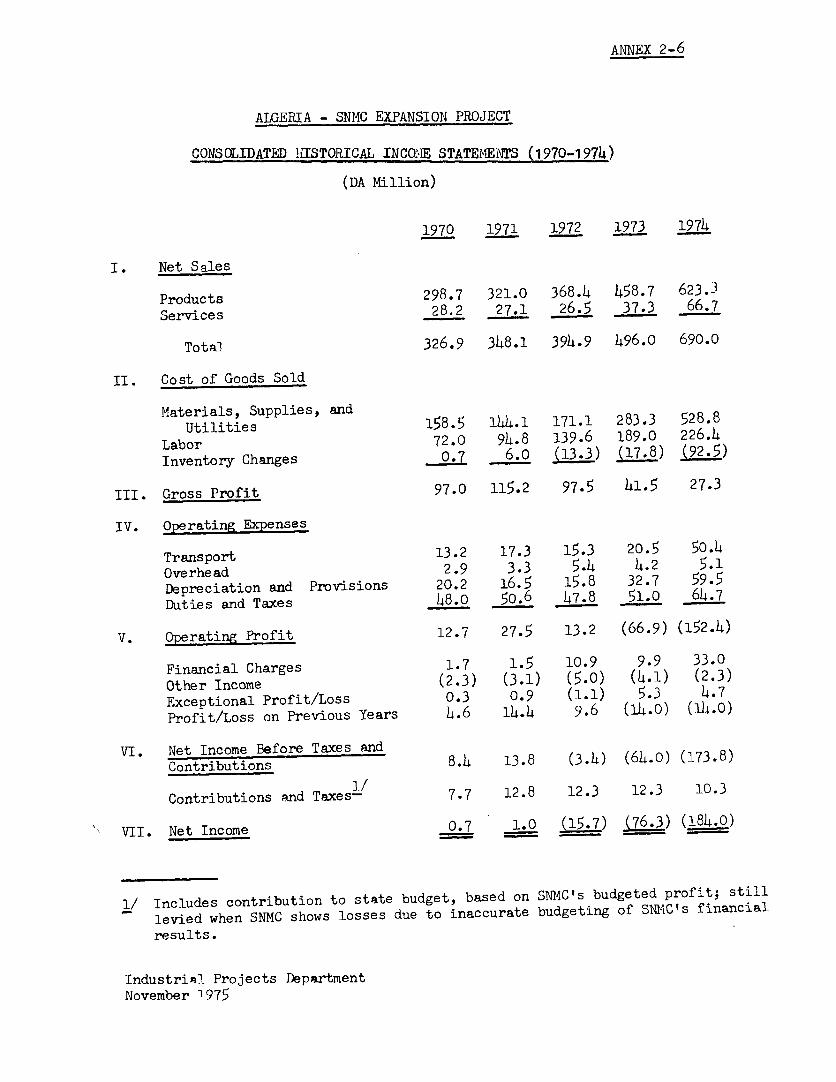

2.13 SNMC's consolidated income statments for the period 1970-74 arecontained in Annex 2-6 and selected indicators are given below:

SNMC - Selected Income Statement Indicators(DA million)

1970 1971 1972 1973 1974

Net sales 326.9 348.1 394.9 496.0 690.0Gross Profit 97.0 115.2 97.5 41.5 27.3Net Income (Loss) Before Taxes 8.4 13.8 (3.4) (64.0) (173.8)Net Income (Loss) After Taxes 0.7 1.0 (15.7) (76.3) (184.0)Net Income (Loss) as % of

- Net sales 0.2 0.3 (4.0) (15.3) (25.1)- Net Fixed Assets 1.0 0.9 (10.4) (22.1) (30.0)

Cash Generation (Cash Loss) 9.3 11.5 (1.0) (46.3) (114.3)

Despite an increase in physical output of about 35% between 1970 and 1974and a virtual doubling of sales over the same period, losses have rapidlyincreased, reaching 25% of net sales in 1974. The major reasons for theselosses are: (i) prices have not been adjusted adequately or frequentlyenough to reflect increasing operating costs as well as higher importprices for the products SNMC is reselling in Algeria; (ii) the lack ofan effective budgeting and cost control system which could set efficiencytargets in the absence of a free market price mechanism; and (iii) taxes ofDA 12.0 million which were levied in each of 1972 and 1973 despite negativepre-tax income. These losses resulted in a cumulative cash shortfall by 1974of DA 162 million (US$42 million) which was financed by short-term loans,thus further aggravating SNMC's financial problems.

2.14 About 87% of SNMC's net los originates from three sectors -cement, bricks and tiles, and concrete - which together account for about 70%of the Company's net sales. Losses in the cement sector are the result ofsales prices which - although they cover domestic cement production cost anda reasonable return on investment - are far below current cement import prices,whereas losses in the brick and tiles, agglomerates, plaster, quicklime andconcrete sectors are due to maintaining sales prices below SNMC's domesticproduction costs.

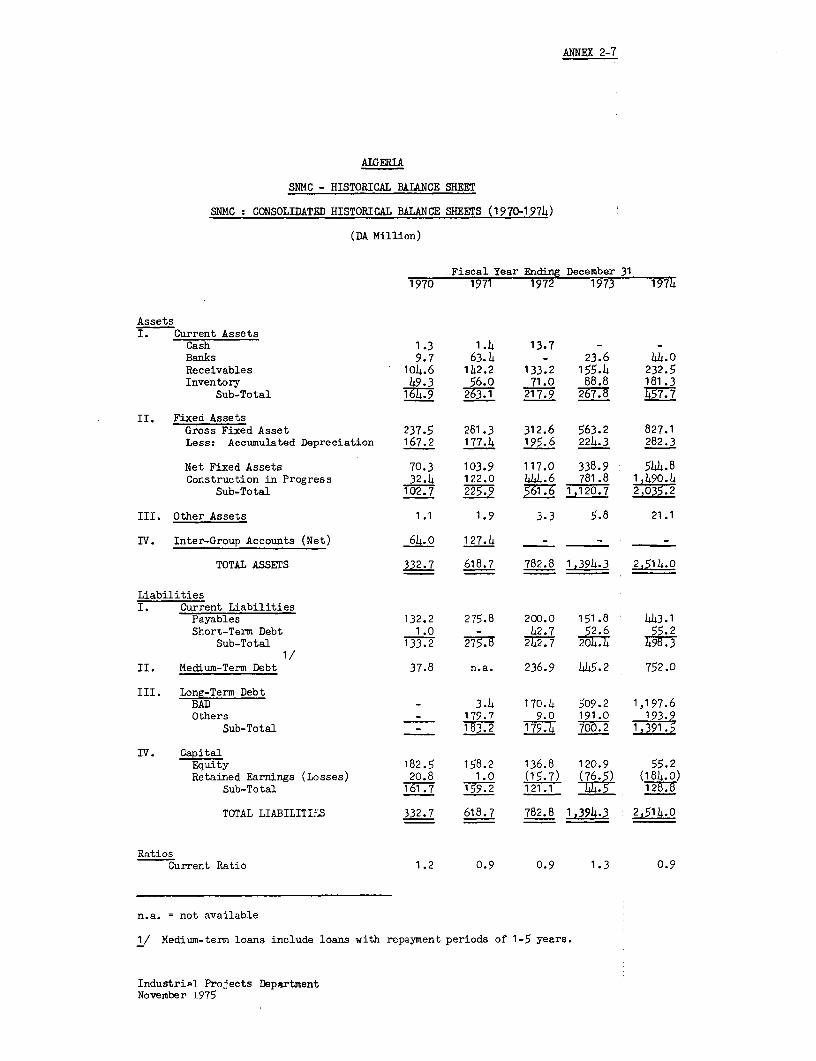

2.15 Balance sheets for the past five years (1970-74) are given inAnnexe 2-7 and summarized below:

-5-

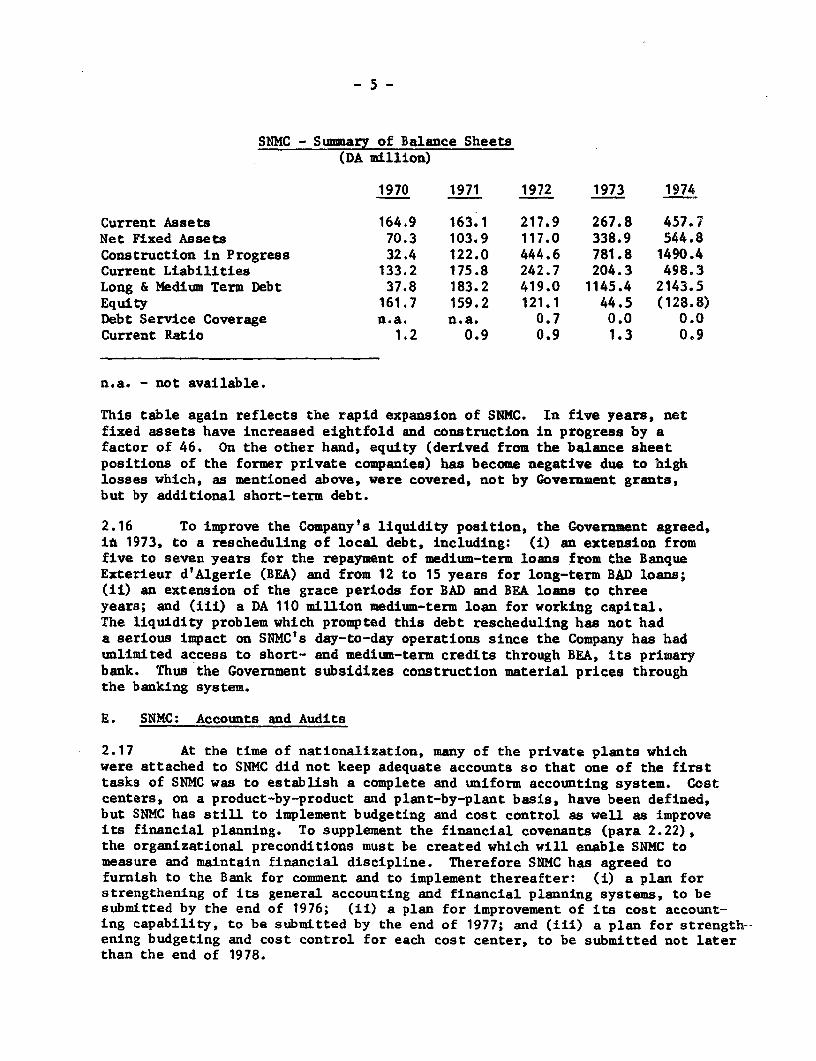

SNMC - Summary of Balance Sheets(DA million)

1970 1971 1972 1973 1974

Current Assets 164.9 163.1 217.9 267.8 457.7Net Fixed Assets 70.3 103.9 117.0 338.9 544.8Construction in Progress 32.4 122.0 444.6 781.8 1490.4Current Liabilities 133.2 175.8 242.7 204.3 498.3Long & Medium Term Debt 37.8 183.2 419.0 1145.4 2143.5Equity 161.7 159.2 121.1 44.5 (128.8)Debt Service Coverage n.a. n.a. 0.7 0.0 0.0Current Ratio 1.2 0.9 0.9 1.3 0.9

n.a. - not available.

This table again reflects the rapid expansion of SNMC. In five years, netfixed assets have increased eightfold and construction in progress by afactor of 46. On the other hand, equity (derived from the balance sheetpositions of the former private companies) has become negative due to highlosses which, as mentioned above, vere covered, not by Government grants,but by additional short-term debt.

2.16 To improve the Company's liquidity position, the Governwent agreed,iû 1973, to a rescheduling of local debt, including: (i) an extension fromfive to seven years for the repayment of medium-term loans from the BanqueExterieur d'Algerie (BEA) and from 12 to 15 years for long-term BAD loans;(ii) an extension of the grace perioda for BAD and BEA loans to threeyears; and (iii) a DA 110 million medium-term loan for working capital.The liquidity problem which prompted this debt rescheduling has not hada serious impact on SNMC's day-to-day operations since the Company has hadunlimited access to short- and medium-term credits through BEA, its primarybank. Thus the Goverament subsidizes construction material prices throughthe banking system.

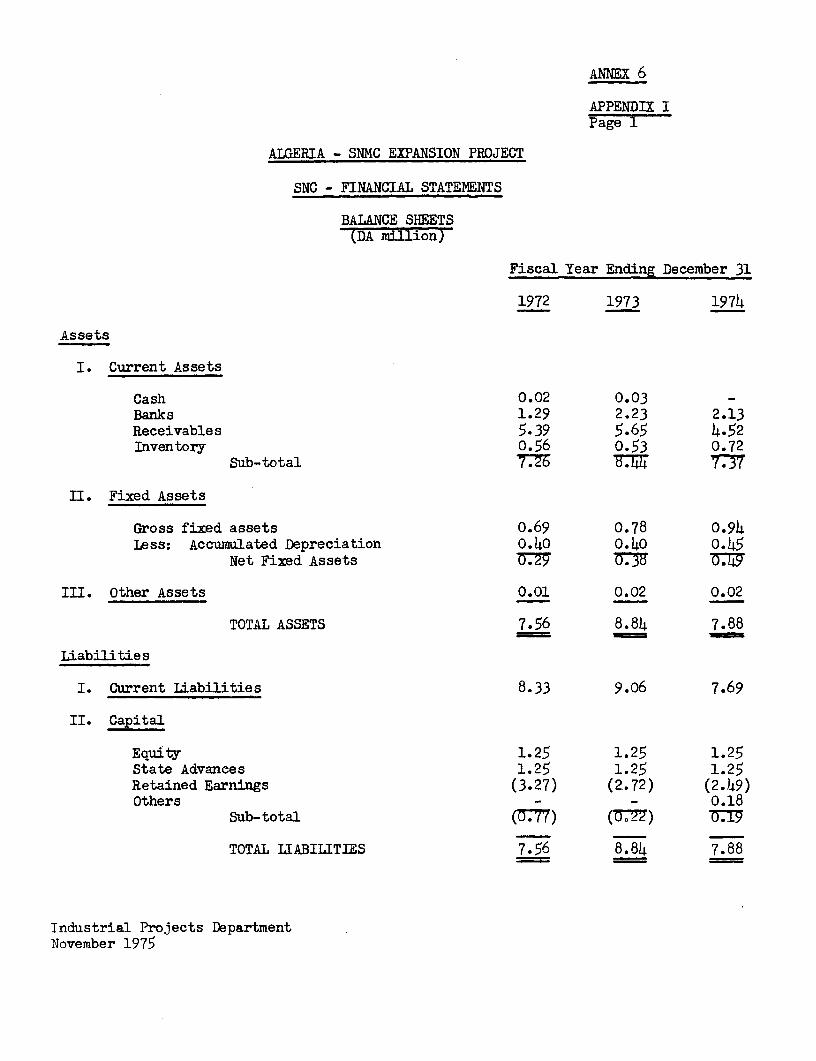

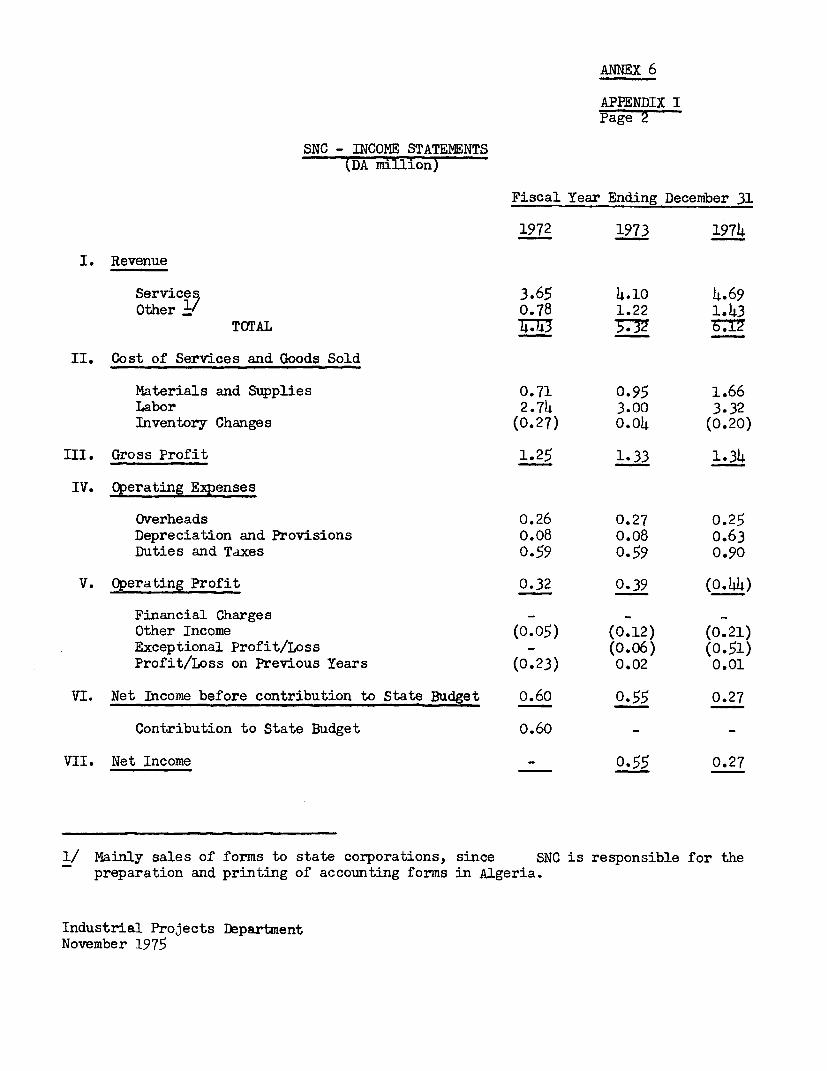

E. SNMC: Accounts and Audits

2.17 At the time of nationalization, many of the private plants whichwere attached to SNMC did not keep adequate accounts so that one of the firsttasks of SNMC was to establish a complete and uniform accounting system. Costcenters, on a product-by-product and plant-by-plant basis, have been defined,but SNMC has still to implement budgeting and cost control as well as improveits financial planning. To supplement the financial covenants (para 2.22),the organizational preconditions must be created which will enable SNMC tomeasure and maintain financial discipline. Therefore SNMC has agreed tofurnish to the Bank for comment and to implement thereafter: (i) a plan forstrengthening of its general accounting and financial planning systems, to besubmitted by the end of 1976; (ii) a plan for improvement of its cost account-ing capability, to be submitted by the end of 1977; and (iii) a plan for strength-ening budgeting and cost control for each cost center, to be submitted not laterthan the end of 1978.

-6-

2.18 SNMC's accounts are reviewed by the Commissaires aux Comptes, theofficial State auditors. Staff constraints do not allow them to conductaudits according to the Bank's standards. As part of the project, a trainingprogram for the Societe Nationale de Comptabilite (SNC), the state auditing andaccounting firm, will be executed under which SNC staff will inter alia betrained to perform audits consistent with Bank requirements (paras 6.05-6.09).Agreement was reached that SNMC's accounts will be audited by an independentauditing firm acceptable to the Bank. The Government and SNMC have agreedto appoint SNC to this task. Should SNC prove unable to meet the requirementsof an independent audit, the Bank will so inform SNMC and the Goverament andwill review with them ways and means of ensuring a satisfactory audit.

F. SNMC: Future Investment Program

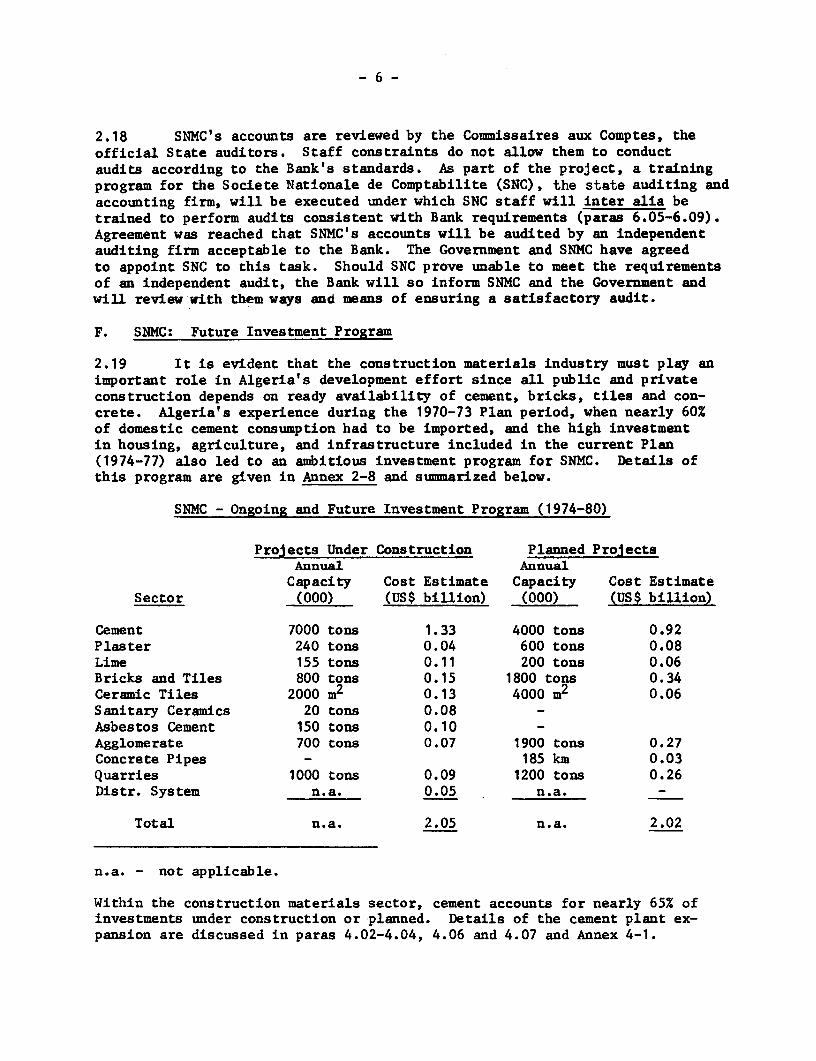

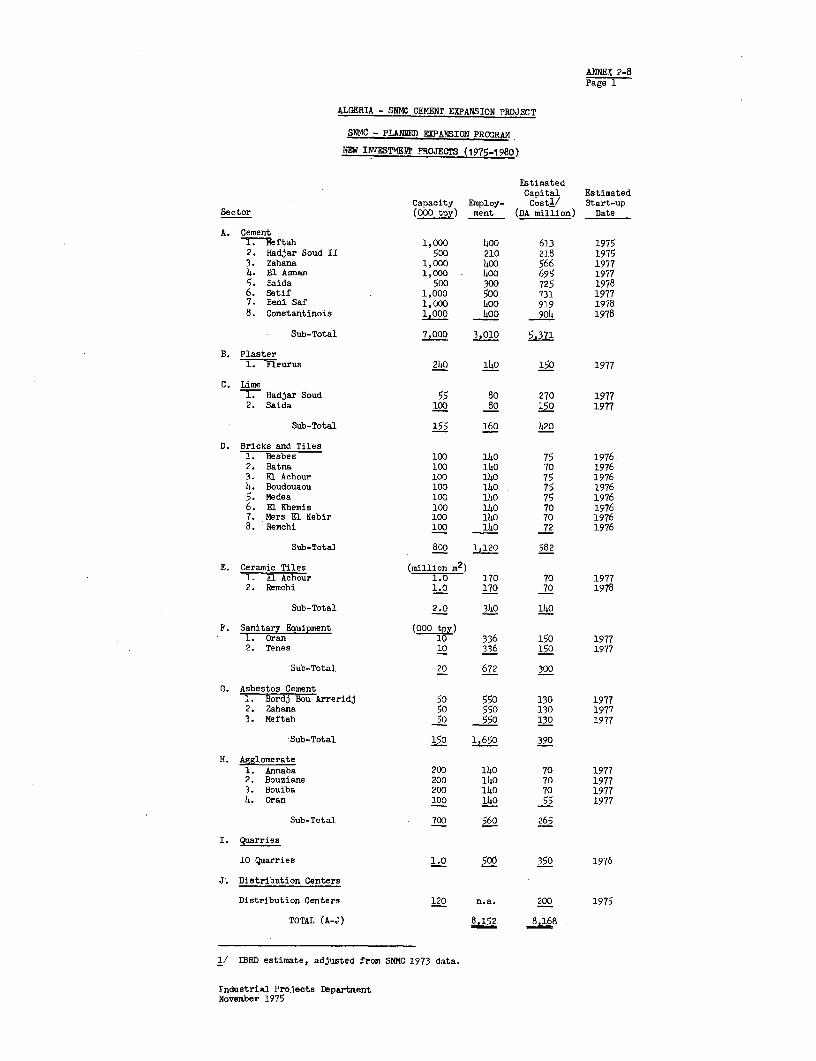

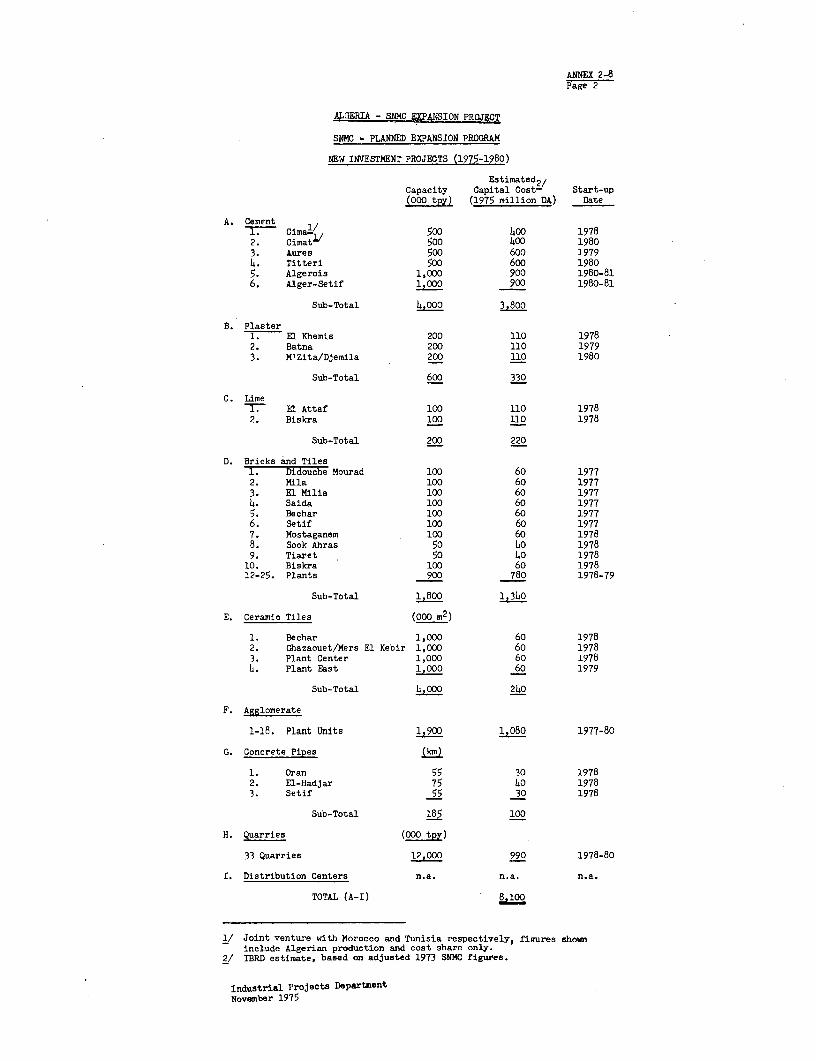

2.19 It is evident that the construction materials industry must play animportant role in Algeria's development effort since all public and privateconstruction depends on ready availability of cement, bricks, tiles and con-crete. Algeria's experience during the 1970-73 Plan period, when nearly 60%of domestic cement consumption had to be imported, and the high investmentin housing, agriculture, and infrastructure included in the current Plan(1974-77) also led to an ambitious investment program for SNMC. Details ofthis program are given in Annex 2-8 and sumrarized below.

SNMC - Ongoing and Future Investment Program (1974-80)

Projects Under Construction Planned ProjectsAnnual Annual

Capacity Cost Estimate Capacity Cost EstimateSector (000) (US$ billion) (000) (US$ billion)

Cement 7000 tons 1.33 4000 tons 0.92Plaster 240 tons 0.04 600 tons 0.08Lime 155 tons 0.11 200 tons 0.06Bricks and Tiles 800 tons 0.15 1800 tons 0.34Ceramic Tiles 2000 m2 0.13 4000 m2 0.06Sanitary Ceramics 20 tons 0.08 -Asbestos Cement 150 tons 0.10 -Agglomerate 700 tons 0.07 1900 tons 0.27Concrete Pipes - 185 km 0.03Quarries 1000 tons 0.09 1200 tons 0.26Distr. System n.a. 0.05 n.a. -

Total n.a. 2.05 n.a. 2.02

n.a. - not applicable.

Within the construction materials sector, cement accounts for nearly 65% ofinvestments under construction or planned. Details of the cement plant ex-pansion are discussed in paras-4.02-4.04, 4.06 and 4.07 and Annex 4-1.

2.20 As mentioned previously (para. 2.03), in practice, the responsibilityfor financing SNMC's investment program does not lie with the Company but withthe Ministry of Finance and funds are provided through bilateral development orsuppliers' credits and by BAD and BEA loans. Availability of such financingdepends not so much on SNMC's present and future financial position as onAlgeria's ability to generate sufficient funds internally and to attractforeign credits for meeting the economy's overall investment needs. In thepast, this system has not encouraged SNMC to adequately control capitalcosts or to make optimal technical and economic investment choices. The Bankrecently made a loan of US$40 million equivalent to the Banque Algerienne deDeveloppement (BAD) for smaller projects (other than cement production) inthe construction and building materials sector. 1/ The BAD project is expectedto improve investment decisions and financial control in the public sectorand provides for the establishment of a Project Evaluation Unit at BAD. BADwill also be invited to participate in the Bank's supervision of the proposedSNMC expansion project.

G. SNMC: Future Financial Viability

2.21 Although SNMC is at present not a financially viable independententerprise, it can be argued that, in a centrally-planned economy, the sub-sidization of the building material sector through transfer payments fromanother sector or unlimited credit from the Treasury is a legitimate meansof implementing a country's priorities. In theory, such a system may leadto optimal resource allocation if minimum cost and efficiency objectives arefollowed and there is rigorous control of transfers among sectors on themacro-economic level. Both conditions have not yet been fulfilled with regardto SNMC. In 1975, for example, the company budget indicates a net loss ofDA 397 million (US$101 million) of which DA 310 million (US$79 million) isattributable to imports. As a percentage of sales, the loss is expected tobe about 42%. Making allowance for depreciation, the cash loss is expectedto be around DA 303 million (US$77 million). It is, therefore, desirable toreestablish SNMC as a self-contained enterprise independent of subsidies inthe long run, i.e. at least to enable it to meet its cost and debt serviceobligations.

2.22 During appraisal and negotiations, ways and means of establishingSNMC on a sounder long-term financial basis were, therefore, discussed withthe Government and the Company. A number of measures were agreed upon withthe Government and SNMC which should meet this objective. In particular:

1/ Report No. 782-AL-Appraisal of an Industrial Project to Banque Algeriennede Developpement, dated June 10, 1975.

(a) SNMC agreed to review prices of all its products annually onthe basis of audited financial statements and to propose pricesequal to the average unit cost of each product plus a margin tocover debt service associated with that product or product group;the Government undertook to take all steps necessary with a viewto setting SNMC's prices at a level consistent with theseprovisions; 1/

(b) SNMC agreed to maintain a debt service coverage of 1.1 times ineach year and to meet its current liabilities as and when theyfall due; the Government specifically undertook to ensure thatSNMC will have adequate funds (other than short-term loans)sufficient to meet these financial covenants; and

(c) the Government agreed that SNMC's accumulated losses through toDecember 31, 1975 should be refinanced on adequate terms andconditions and confirmed that all losses through to the end of1974 had already been covered by long-term loans.

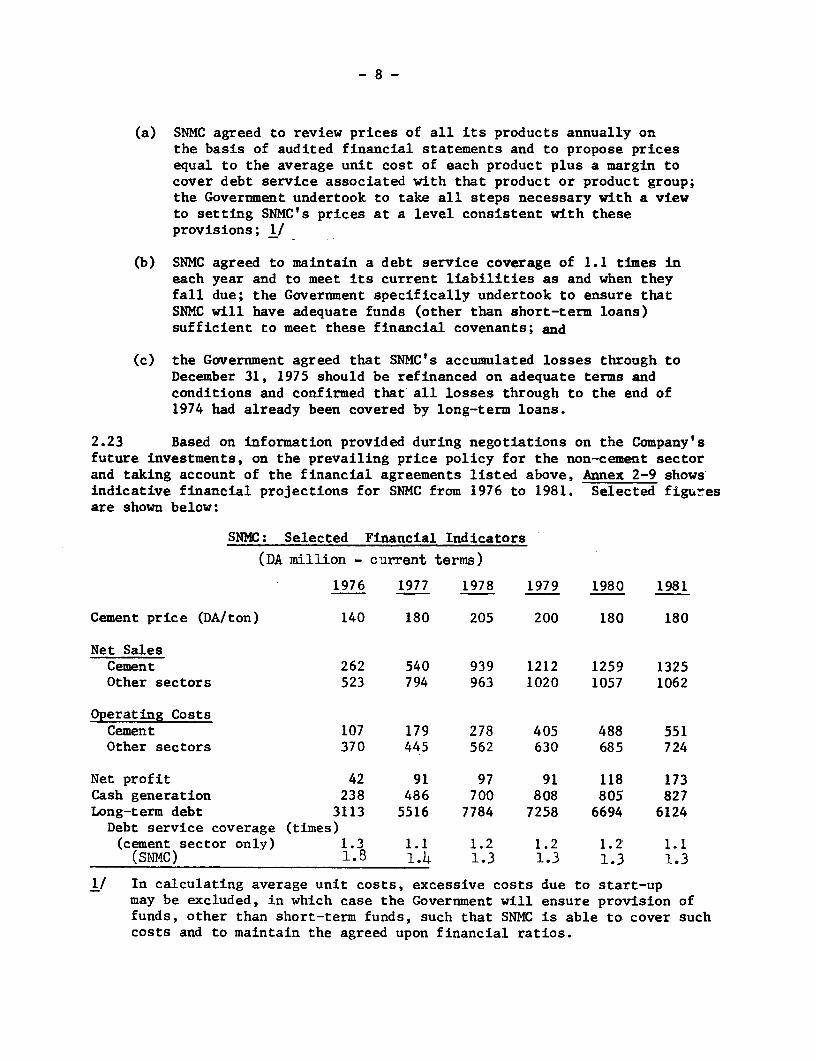

2.23 Based on information provided during negotiations on the Company'sfuture investments, on the prevailing price policy for the non-cement sectorand taking account of the financial agreements listed above, Annex 2-9 showsindicative financial projections for SNMC from 1976 to 1981. Selected figuresare shown below:

SNMC: Selected Financial Indicators

(DA million - current terms)

1976 1977 1978 1979 1980 1981

Cement price (DA/ton) 140 180 205 200 180 180

Net SalesCement 262 540 939 1212 1259 1325Other sectors 523 794 963 1020 1057 1062

Operating CostsCement 107 179 278 405 488 551Other sectors 370 445 562 630 685 724

Net profit 42 91 97 91 118 173Cash generation 238 486 700 808 805 827Long-term debt 3113 5516 7784 7258 6694 6124Debt service coverage (times)(cement sector only) 1.3 1.1 1.2 1.2 1.2 1.1(SNMC) 1.8 1.4 1.3 1.3 1.3 1.3

1/ In calculating average unit costs, excessive costs due to start-upmay be excluded, in which case the Governnent will ensure provision offunds, other than short-term funds, such that SNMC is able to cover suchcosts and to maintain the agreed upon financial ratios.

- 9 -

2.24 It can be seen that, until about 1978, other sectors will remainmore important for the Company than cement, in terms of revenue, but thatcement will increase rapidly as new plants come on stream. In 1976 cementis expected to account for approximately 33% of sales and for about 55% by1981.

III. THE PROJECT

A. Project Objective

3.01 The emphasis of the project lies on its institution building effecton the building materials sector. The project attempts to help SNMC cope viththe present and future organizational and financial problems created by anambitious investment program. SNMC has to develop from a financially weakenterprise which is struggling to meet its production targets under the Plan,to one which can meet production and distribution targets as well as maintainfinancial discipline and strict cost control. The proposed loan attempts tocontribute to this development by dealing with 3 critical aspects: (i)cement production, (ii) distribution means and planning, and (iii) accounting,financial planning and auditing.

B. Prolect Description

3.02 The project has three inter-related components:

(a) The Saida Plant: the largest single element in the projectis the construction of a new 500,000 tpy dry-process cementplant at Saida in the underdeveloped high plateau region.Including interest during construction and incremental workingcapital the plant is expected to cost DA 728 million (US$186million). It is part of a plan to increase domestic cementproduction by about 300% between 1975 and 1978.

(b) The Distribution System: SNMC is presently preoccupied withimplementing new projects and has not yet focused adequatelyon its distribution requirements resulting from the immenseexpansion of capacity. The distribution component of theproject includes, therefore, (i) a program of studies definingSNMC's future distribution facilities, and transport require-ments; and (ii) acquisition of an estimated 260 silo wagonsand 190 20-ton trucks with related repair facilities plus anyadditional transport or maintenance equipment as indicatedon the basis of the above studies. Total cost of this programis expected to be about DA 82 million (US$21 million).

(c) SNC: The Government intends to develop SNC, the state enter-prise for accounting and auditing (i) to perform regularindependent external audits and (ii) to provide consultingservices in accounting, cost control and budgeting to state

- 10 -

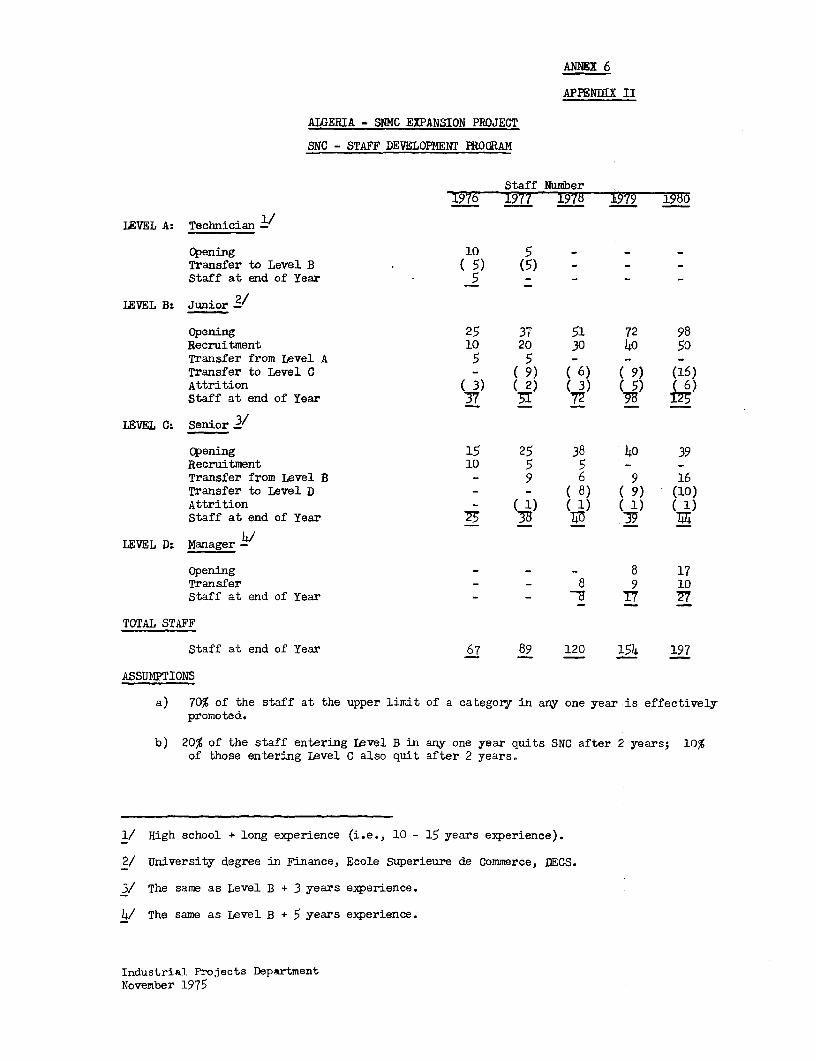

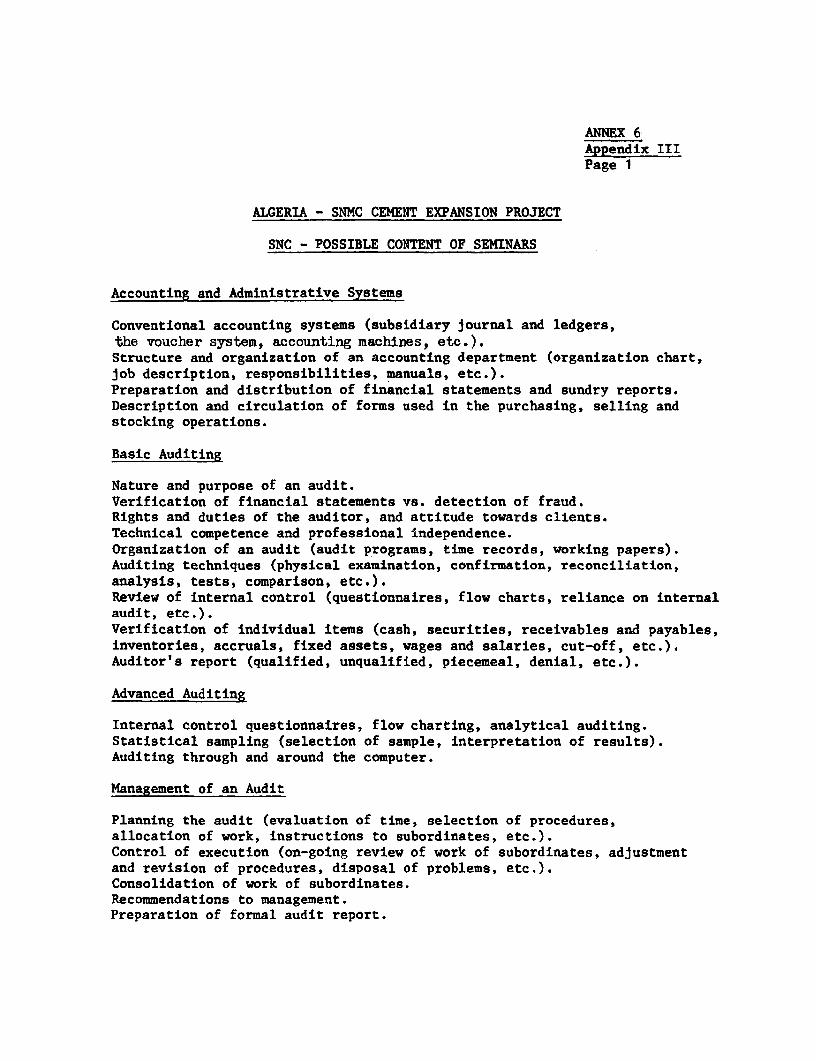

enterprises, including SNMC. The project includes a 5-yeartechnical assistance and training program for SNC to developits inhouse accounting, cost control and auditing capabilities.The program is estimated to cost DA 29 million (US$7.4 million).Aside from the immediate objective of ensuring for SNMC anindependent audit satisfactory to the Bank and the possibilityof providing expert assistance when establishing the requiredfinancial planning, cost control and budgeting system (para 2.17),the strengthening of SNC will help improve accounting standardsmore generally throughout Algeria.

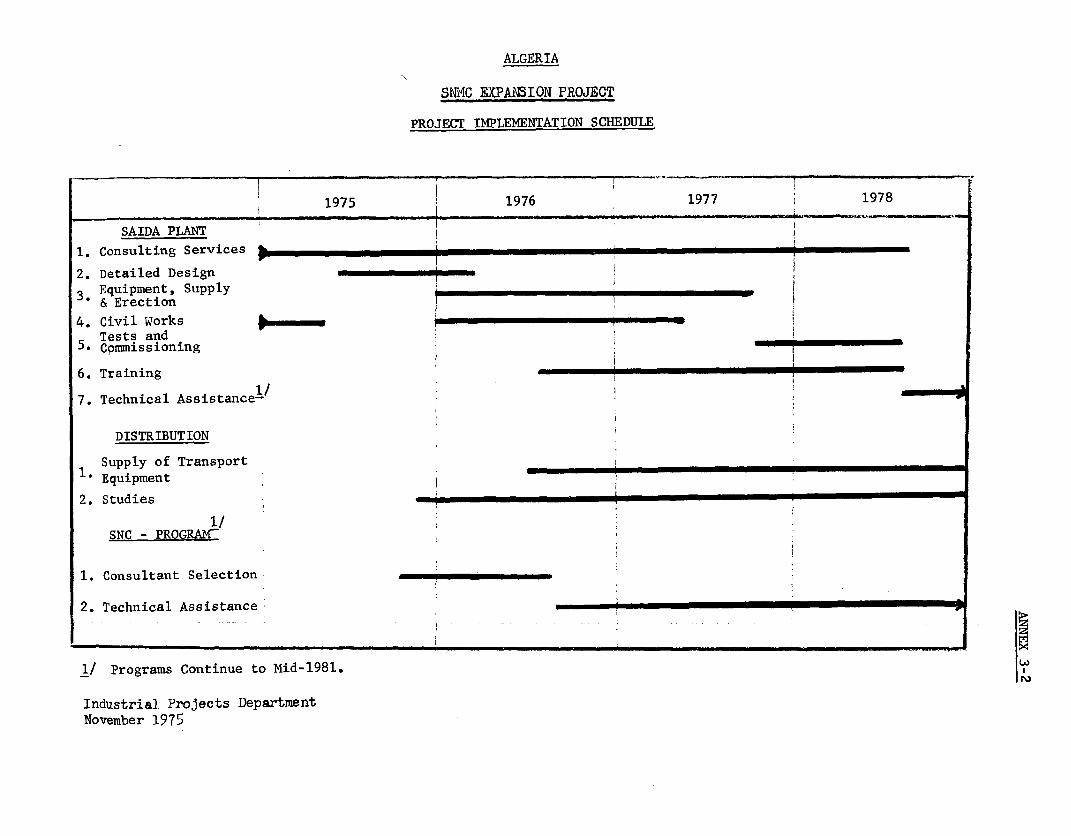

3.03 A list of Bank-financed items under the project is contained inAnnex 3-1 and a summary capital cost table for the project as a whole isshown below. Each component is discussed separately in Chapters IV, V andVI and more detailed information is available in Annexes 4-2, 5-7, 5-9 and6-1. A project implementation schedule is contained in Annex 3-2.

Summary of Capital Cost Estimates

Local Foreign Total Local Foreign Total %-- DA million ----- ---- US$ million ----

1. Saida PlantFixed Assets 199.2 413.1 612.3 50.8 105.4 156.2 72.8Working CapitalRequirement 15.3 16.4 31.6 3.9 4.2 8.1 3.9

Interest DuringConstruction 41.9 42.3 84.3 10.7 10.8 21.5 10.0Sub-total 256.4 471.8 728.2 65.4 120.4 185.8 86.7

2. DistributionVehicles - 67.0 67.0 - 17.1 17.1 7.9Studies 2.4 3.9 6.3 0.6 1.0 1.6 0.8Repair Facilities 7.8 1.0 8.8 2.0 0.5 2.5 1.2Sub-total 10.2 71.9 82.1 2.6 18.6 21.2 9.9

3. SNC5-year Program 9.0 20.0 29.0 2.3 5.1 7.4 3.4

FinancingRequirement 275.6 563.7 839.3 70.3 144.1 214.4 100.0

3.04 The total estimated financing requirement of US$214.4 million forthe project is to be covered by a supplier's credit of US$57.1 million, theBank loan of US$46 million and local financing as shown in the table below:

- il1 -

Financing Plan(US$ Million)

Saida SNC (5-yearPlant Distribution Program) Total %

IBRD Loan 30.8 10.1 5.1 46.0 21.5Supplier's Credit 57.1 57.1 26.6Local Debt

(BAD, BEA orTreasury Advances) 97.9 11.1 2.3 111.3 51.9

185.8 21.2 7.4 214.4 100.0

To ensure project completion under any eventuality, the Goverament has agreedto provide a cost overrun guarantee, i.e. to make available any additionallocal or foreign funds as may be needed to complete the project on terms con-sistent with maintenance of the financial covenants referred to in paras. 2.22and 5.25.

C. Allocation of Bank Loan and Disbursement Schedule

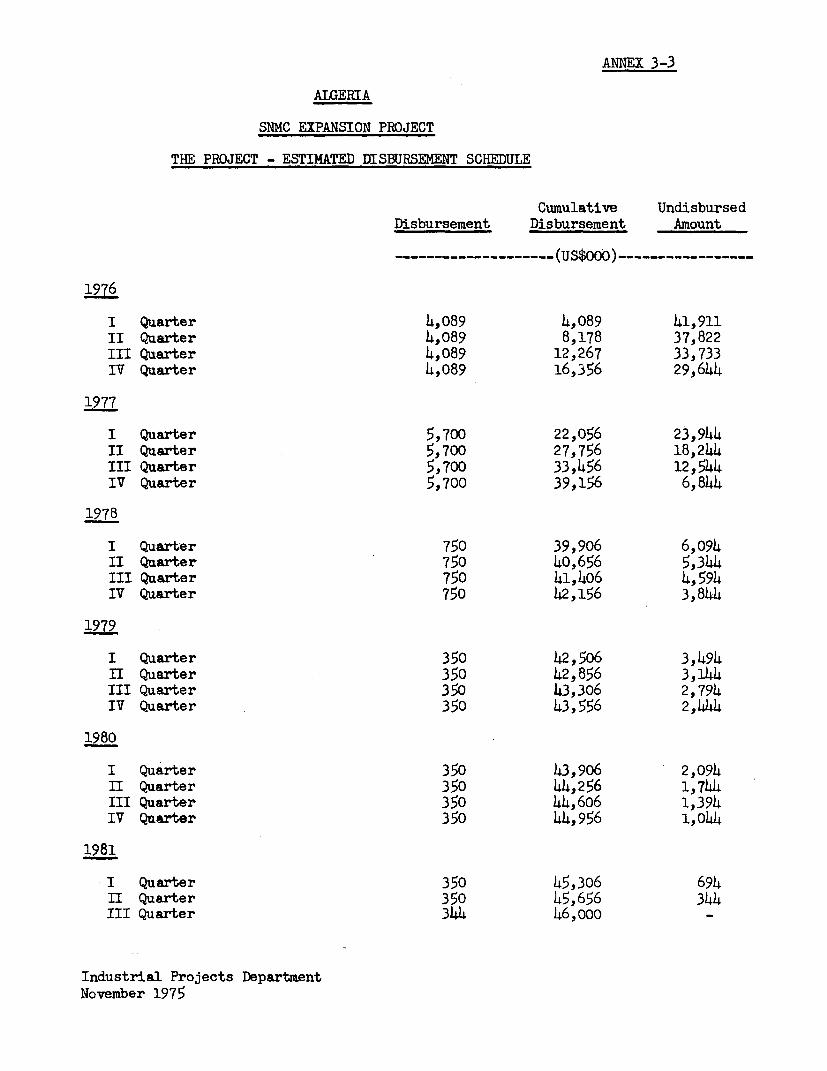

i.0O5 The Bank loan will be used to finance part or all of the estimatedforeign exchange costs of equipment, construction and consultant fees asdetailed in Annexes 3-1, 4-2, 5-9 and 6. The disbursement schedule for allproject components combined is contained in Annex 3-3. Any loan funds re-maining uncommitted for items on the Bank list would be used to finance otherproject components, if found justified, or othervise be cancelled.

IV. THE MARKET FOR CEMENT

4.01 A detailed description of the market for cement in Algeria, includ-ing a discussion of export prospects, transportation requirements and pricingpolicy, is presented in Annexes 4-1 and 4-2.

A. Supply and Demand Balance

4.02 Historic Demand/Supply: While cement has been produced in Algeriaat least since the early years of the century, SNMC did not begin manufactureuntil 1969 when it took over three cement plants (Pointe-Pescade, Meftah Iand Zahana I) of a combined annual capacity of 1.05 million tons. Since then,SNMC has concentrated on the satisfaction of domestic demand by installingnew production capacity and by importation. The results of this expansionare just beginning to be felt, as shown in the following table:

- 12 -

Algeria: Cement Supply (1969-75)('000 tons)

(est.)1969 1970 1971 1972 1973 1974 1975

Domestic Production

Meftah I 52 61 56 51 59 - -Pointe-Pescade 451 453 468 457 449 412 450Zahana I 421 409 441 419 409 303 400Hadjar-Soud I - - - - 90 225 350Meftah II - - - - - - 250Hadjar-Soud II - - - 5°

Total DomesticProduction 924 923 965 927 1007 940 1500

Imports 250 544 578 830 1220 2006 2200

Total Supply 1174 1467 1543 1757 2227 2946 3700

4.03 The major achievements in SNMC's program so far include: (i) start-up of a new 500,000 tpy plant, Hadjar-Soud I, (1973); (ii) the closure of thesmall Meftah I plant (1974); (iii) start-up of a new 1 million tpy plant,Meftah II, (1974); and (iv) construction of an extension to the Hadjar-Soudplant, Hadjar-Soud II, with an incremental annual capacity of 500,000 tons,which is due to come on stream in late 1975.

4.04 Despite the relatively high level of imports, accounting for about60% of consumption, and an average annual consumption increase of about 20%during 1969-1974, actual cement demand continues to exceed supply as illus-trated by black market prices 50-100% above official levels. The scarcityof cement in Algeria is not only due to inadequate imports and domesticproduction, but also due to inefficiencies in the distribution system, inparticular port handling of imports.

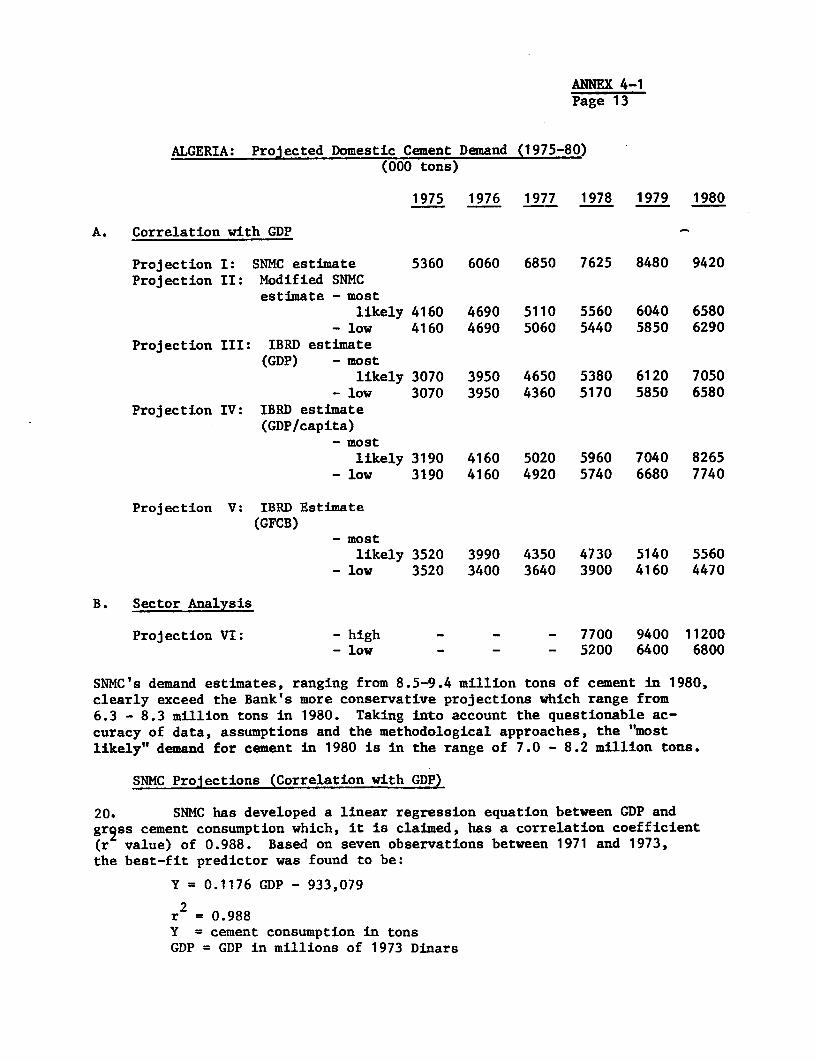

4.05 Projected Demand: Algeria's second Four-Year Plan (1974-77)stipulates an average annual cement demand of almost 7 million tons by 1977.However, past experience indicates that it is unlikely that the Plan will becarried out on schedule and this figure must be seen as an optimistic upperlimit for cement demand. In the period after 1977, when the Saida plant willcome on stream, demand projections can only be based on notional data since noreliable post-1977 planning document exists and secondary effects of economicgrowth are limited in centrally planned economies. The following tableindicates a range within which future cement demand might fall based on variousprojection methods. It should be noted that SNMC's estimates, which are basedon full implementation of the 1974-77 Plan, are consistently higher than thoseof the Bank (Annex 4-1).

- 13 -

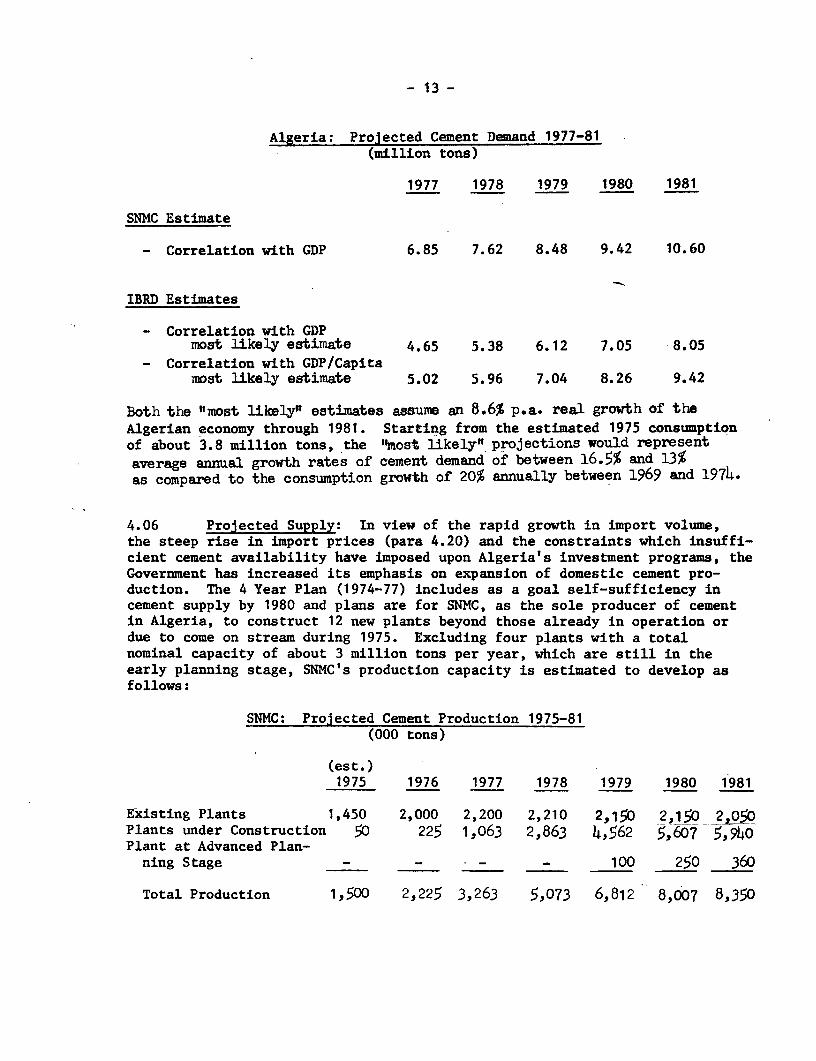

Algeria: Projected Cement Demand 1977-81(million tons)

1977 1978 1979 1980 1981

SNMC Estimate

- Correlation with GDP 6.85 7.62 8.48 9.42 10.60

IBRD Estimates

- Correlation with GDPmost likely estimate 4.65 5.38 6.12 7.05 8.05

- Correlation with GDP/Capitamost likely estimate 5.02 5.96 7.04 8.26 9.42

Both the "most likely" estimates assume an 8.6% p.a. real growth of theAlgerian economy through 1981. Starting from the estimated 1975 consumptionof about 3.8 million tons, the "most likely" projections would representaverage annual growth rates of cement demand of between 16.5% and 13%as compared to the consumption growth of 20% annually between 1969 and 1974.

4.06 Projected Supply: In view of the rapid growth in import volume,the steep rise in import prices (para 4.20) and the constraints which insuffi-cient cement availability have imposed upon Algeria's investment programs, theGovernment has increased its emphasis on expansion of domestic cement pro-duction. The 4 Year Plan (1974-77) includes as a goal self-sufficiency inceement supply by 1980 and plans are for SNMC, as the sole producer of cementin Algeria, to construct 12 new plants beyond those already in operation ordue to come on stream during 1975. Excluding four plants with a totalnominal capacity of about 3 million tons per year, which are still in theearly planning stage, SNMC's production capacity is estimated to develop asfollows:

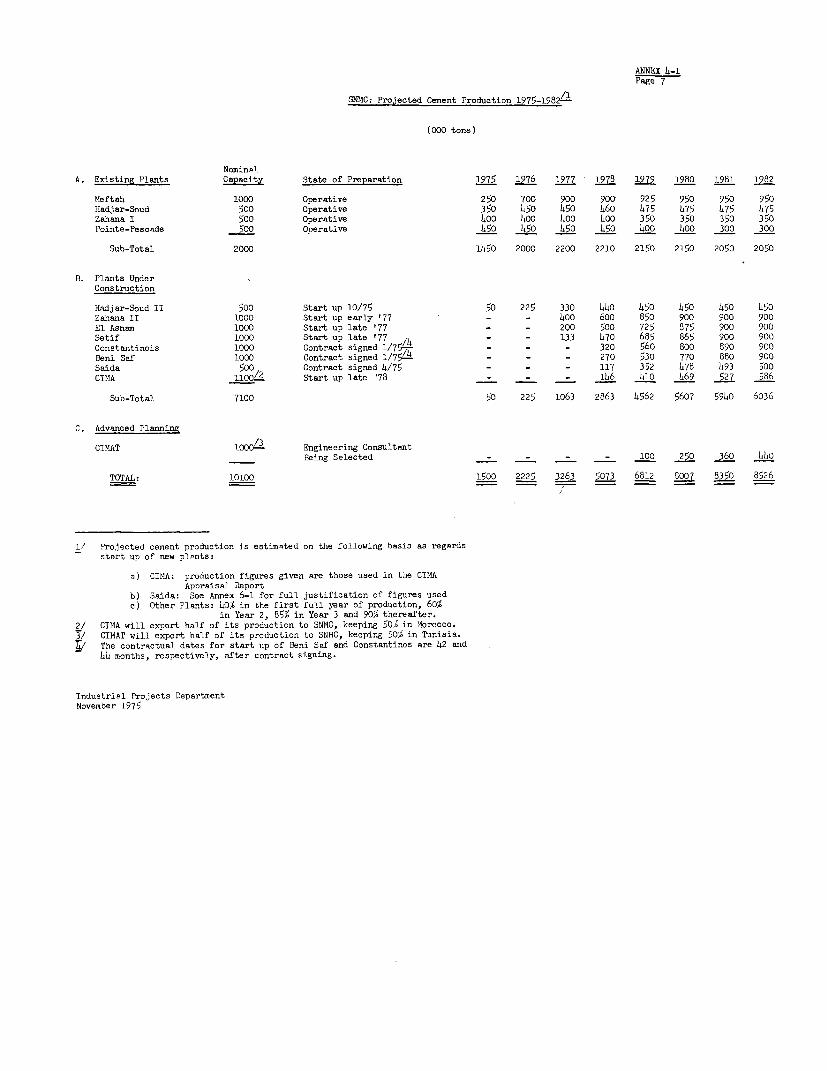

SNMC: Projected Cement Production 1975-81(000 tons)

(est.)1975 1976 1977 1978 1979 1980 1981

Existing Plants 1,450 2,000 2,200 2,210 2,150 2,150 2,050Plants under Construction 50 225 1,063 2,863 4,562 5,607 5,940Plant at Advanced Plan-ning Stage - - - - 100 250 360

Total Production 1,500 2,225 3,263 5,073 6,812 8,007 8,350

- 14 -

4.07 The above build-up in cement production is based on capacity utiliza-tion rates of 40% during the first year of production, 60% in year 2, 85% inyear 3, and 90% thereafter. Individual capacities, present status andexpected start-up dates for each new plant and assumed production rates forall plants are given in Annex 4-1. With the exception of CIMA, a joint ven-ture between SNMC and Morocco, all these plants are being contracted on a"turnkey" basis, which is expected to help SNMC assure timely implementationof the expansion program. Substantial foreign exchange financing is beingsecured on concessional terms through bilateral credits for all plants.

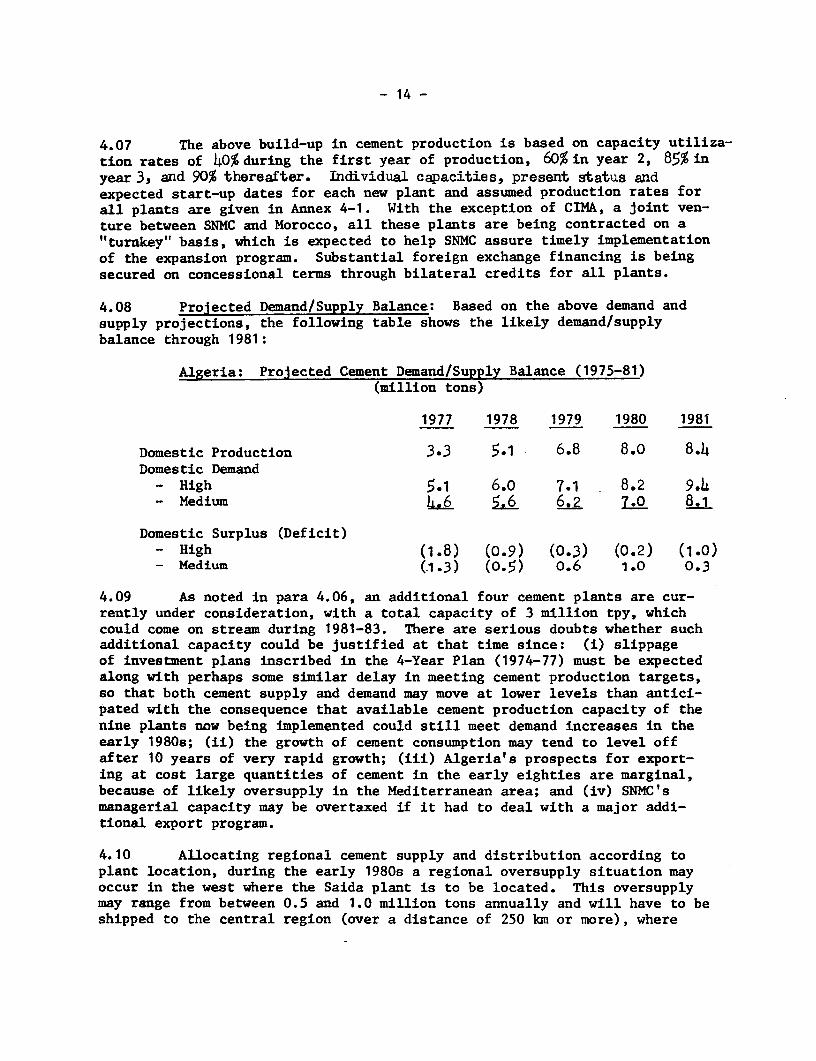

4.08 Projected Demand/Supply Balance: Based on the above demand andsupply projections, the following table shows the likely demand/supplybalance through 1981:

Algeria: Projected Cement Demand/Supply Balance (1975-81)(million tons)

1977 1978 1979 1980 1981

Domestic Production 3.3 5.1 6.8 8.0 8.4Domestic Demand

- High 5.1 6.0 7.1 8.2 9.4- Medium 4u6 5t 6.2 7.0 8.1

Domestic Surplus (Deficit)- High (1.8) (0.9) (0.3) (0.2) (1.0)- Medium (1.3) (0-5) 0.6 1.0 0.3

4.09 As noted in para 4.06, an additional four cement plants are cur-rently under consideration, with a total capacity of 3 million tpy, whichcould come on stream during 1981-83. There are serious doubts whether suchadditional capacity could be justified at that time since: (i) slippageof investment plans inscribed in the 4-Year Plan (1974-77) must be expectedalong with perhaps some similar delay in meeting cement production targets,s0 that both cement supply and demand may move at lower levels than antici-pated with the consequence that available cement production capacity of thenine plants now being implemented could still meet demand increases in theearly 1980s; (ii) the growth of cement consumption may tend to level offafter 10 years of very rapid growth; (iii) Algeria's prospects for export-ing at cost large quantities of cement in the early eighties are marginal,because of likely oversupply in the Mediterranean area; and (iv) SNMC'smanagerial capacity may be overtaxed if it had to deal with a major addi-tional export program.

4.10 Allocating regional cement supply and distribution according toplant location, during the early 1980s a regional oversupply situation mayoccur in the west where the Saida plant is to be located. This oversupplymay range from between 0.5 and 1.0 million tons annually and will have to beshipped to the central region (over a distance of 250 km or more), where

- 15 -

excess demand is expected to prevail. Such shipments will put an additionalstrain on the existing transportation and distribution system, and might havebeen avoided by more careful planning of plant locations. However, theregional supply/demand imbalance only indirectly affects the market for theSaida plant since from a transportation point of view it is optimally locatedto meet the projected cement demand on the high plateau around Saida and inthe southern desert where it does not compete with any other cement plant.

4.11 In view of SNMC's additional expansion plans and because of theexpected regional cement supply/demand imbalance in the early 1980s, SNMChas agreed to provide the Bank, during 1978, with a detailed cement marketstudy whose proposed content shall have been discussed with the Bank. ShouldSNMC decide to invest in further cement capacity prior to completion of thisstudy, the Company agreed to carry out all necessary preparatory studies,the scope and content of which will be the subject of an exchange of informa-tion and views with the Bank, and to furnish them to the Bank upon theircompletion for a further exchange of views.

B. SNMC Distribution Network

4.12 A description of SNMC's present and planned distribution systemis contained in Annex 4-2 and summrarized below.

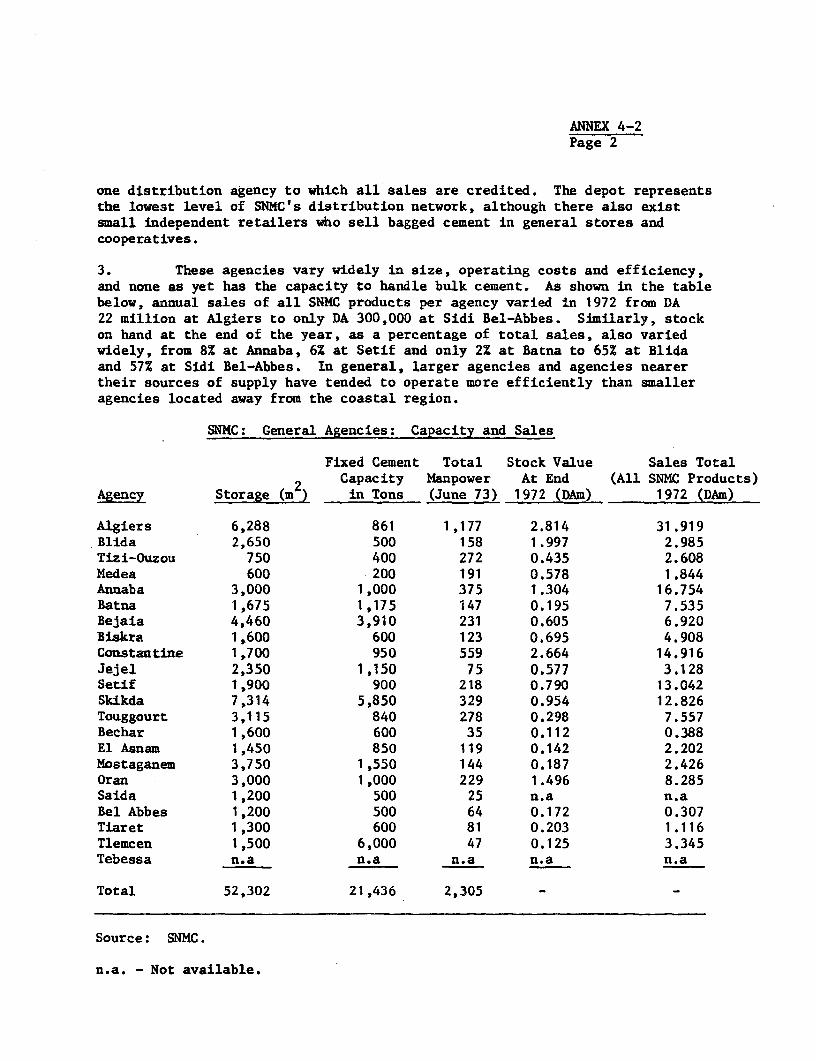

4.13 Distribution Channels: SNHC's current distribution system hasevolved in an ad hoc manner out of the facilities which the Company inheritedin 1968. It consists of 89 depots and 22 agencies operated by SNMC. Whilethe agencies handle the entire range of the Company's products, their cementstorage space totals only about 22,000 tons and individual agencies varygreatly in size, turnover and level of efficiency.

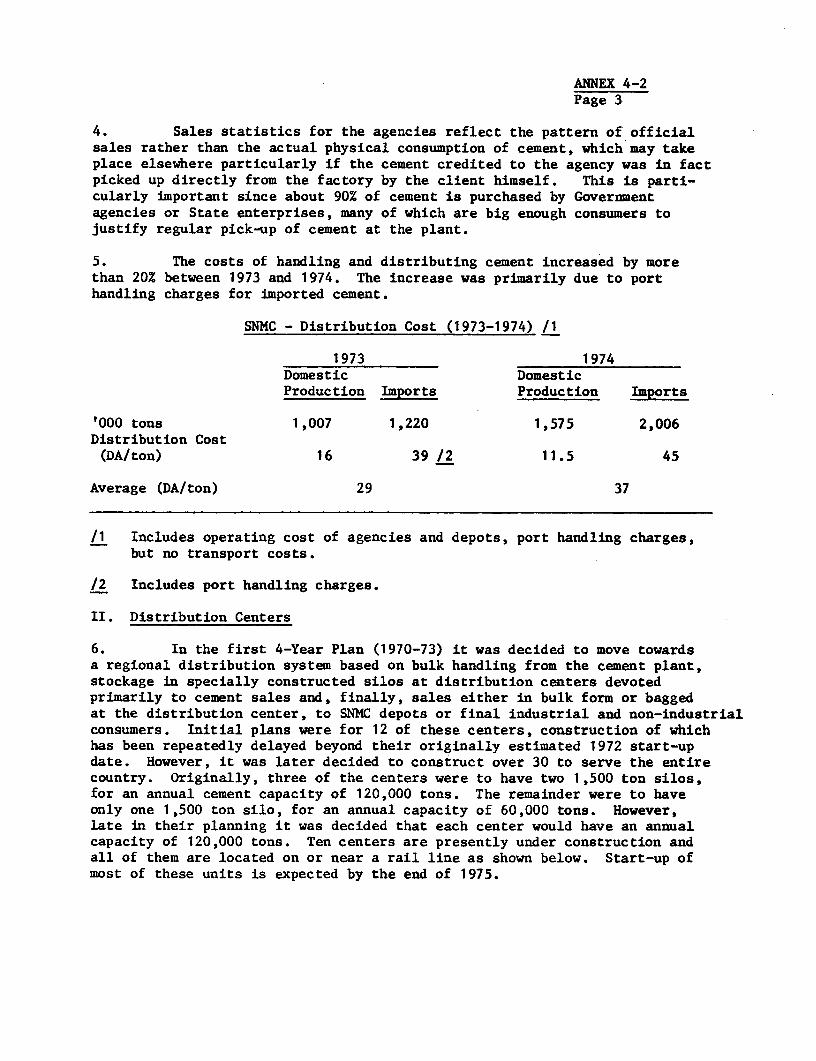

4.14 On account of the limitations of the existing network, the 4-YearPlan (1974-77) stipulated a shift to a regional cement distribution systembased on bulk-handling from the plants and storage in bulk-silos at 37 newdistribution centers. These centers, to be operated by SNMC, were to sellcement, either bagged or in bulk, to SNMC agencies and depots or final con-sumers and were to result in greater accessibility of bulk cement to largeconsumers and lower transportation and overall distribution costs. Ten ofthese centers were to be completed in 1975 at a total cost of DA 132 million(US$33 million) and each of them will have approximately 30,000 mr of openstorage, 5,000 m2 of covered storage and two cement silos of 1,500 ton capa-city each. However, three problems have arisen which have caused the conceptof the centers to be re-evaluated: (i) owing to the high initial investmentcost, it is unlikely that SNMC's average per ton distribution costs - whichrose from DA 20/ton (US$5.1/ton) to DA 37/ton (US$9.4/ton) between 1973 and1974 - will decline when the centers come into operation since their operatingcosts alone, in 1974 terms, are now estimated at about DA 10/ton; (ii) theoriginal concept of the centers limited them to cement sales while a largepart of total demand in the rural areas is for a wide range of buildingmaterials; and (iii) the number of customers able to receive bulk cement issmall and their needs can be adequately handled by the plants and the 10distribution centers soon starting operation.

- 16 -

4.15 In addition, the location of some of the centers appears question-able since three of those under construction are located within 15 km of anew cement plant with similar bagging'and storage facilities. It has, there-fore, been decided that: (i) only a few centers (in addition to those underconstruction) will be built; and (ii) the existing agencies and depots aswell as the new centers will be absorbed into a national network of distri-bution centers for construction materials which are to sell building materialsmanufactured by SNMC as well as by other state enterprises. The planningand timing of this new network are discussed in para 4.19.

4.16 Transport: Cement shipments fall under the monopolies of eitherSociete Nationale de Transport Routier (SNTR) or Societe Nationale des Cheminsde Fer d'Algerie (SNFCA) but neither has the capacity to handle all SNMC'soutput. SNMC is therefore allowed to own its own trucks and silo wagons,the latter being operated, through a leasing arrangement under which SNMCpays a preferential tariff, by SNCFA. The present transport capacity isinadequate and 50% of cement sales are picked up by consumers at theplant or dockside. Of the remainder, approximately 35% (on a ton km basis)is at present transported by SNCFA (rail); 10% by SNTR (road); and only 5%by SNMC (road). Road transport is about twice as expensive as rail haulage(DA 0.21 vs. 0.10/ton km) and the weight of this disadvantage will furtherincrease as demand in the hinterland grows and average truck journeys becomelonger.

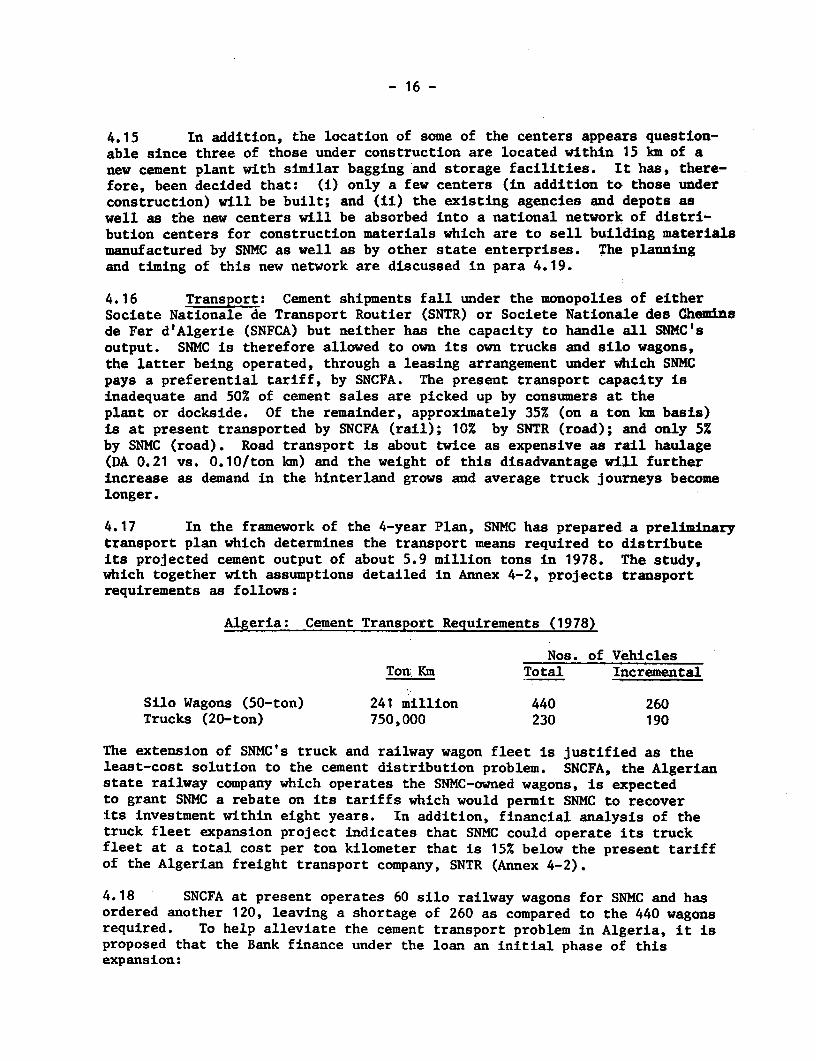

4.17 In the framework of the 4-year Plan, SNMC has prepared a preliminarytransport plan which determines the transport means required to distributeits projected cement output of about 5.9 million tons in 1978. The study,which together with assumptions detailed in Annex 4-2, projects transportrequirements as follows:

Algeria: Cement Transport Requirements (1978)

Nos. of VehiclesTon Km Total Incremental

Silo Wagons (50-ton) 241 million 440 260Trucks (20-ton) 750,000 230 190

The extension of SNMC's truck and railway wagon fleet is justified as theleast-cost solution to the cement distribution problem. SNCFA, the Algerianstate railway company which operates the SNMC-owned wagons, is expectedto grant SNMC a rebate on its tariffs which would permit SNMC to recoverits investment within eight years. In addition, financial analysis of thetruck fleet expansion project indicates that SNMC could operate its truckfleet at a total cost per ton kilometer that is 15% below the present tariffof the Algerian freight transport company, SNTR (Annex 4-2).

4.18 SNCFA at present operates 60 silo railway wagons for SNMC and hasordered another 120, leaving a shortage of 260 as compared to the 440 wagonsrequired. To help alleviate the cement transport problem in Algeria, it isproposed that the Bank finance under the loan an initial phase of thisexpansion:

- 17 -

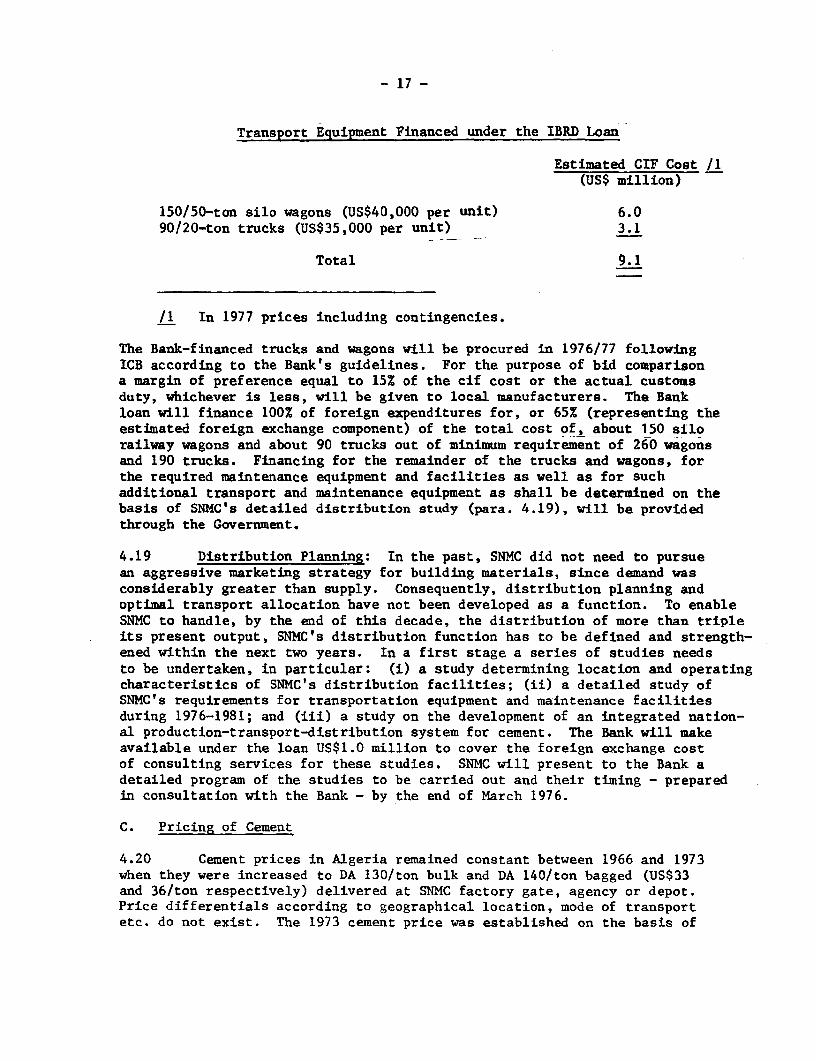

Transport Equipment Financed under the IBRD Loan

Estimated CIF Cost /1(US$ million)

150/50-ton silo wagons (US$40,000 per unit) 6.090/20-ton trucks (US$35,000 per unit) 3.1

Total 9.1

/1 In 1977 prices including contingencies.

The Bank-financed trucks and wagons will be procured in 1976/77 followingICB according to the Bank's guidelines. For the purpose of bid comparisona margin of preference equal to 15% of the cif cost or the actual customsduty, whichever is less, will be given to local manufacturers. The Bankloan will finance 100% of foreign expenditures for, or 65% (representing theestimated foreign exchange component) of the total cost of, about 150 silorailway wagons and about 90 trucks out of minimum requirement of 260 wagonsand 190 trucks. Financing for the remainder of the trucks and wagons, forthe required maintenance equipment and facilities as well as for suchadditional transport and maintenance equipment as shall be determined on thebasis of SNMC's detailed distribution study (para. 4.19), will be providedthrough the Governnent.

4.19 Distribution Planning: In the past, SNMC did not need to pursuean aggressive marketing strategy for building materials, since demand wasconsiderably greater than supply. Consequently, distribution planning andoptimal transport allocation have not been developed as a function. To enableSNMC to handle, by the end of this decade, the distribution of more than tripleits present output, SNMC's distribution function has to be defined and strength-ened within the next two years. In a first stage a series of studies needsto be undertaken, in particular: (i) a study determining location and operatingcharacteristics of SNMC's distribution facilities; (ii) a detailed study ofSNMC's requirements for transportation equipment and maintenance facilitiesduring 1976-1981; and (iii) a study on the development of an integrated nation-al production-transport-distribution system for cement. The Bank will makeavailable under the loan US$1.0 million to cover the foreign exchange costof consulting services for these studies. SNMC will present to the Bank adetailed program of the studies to be carried out and their timing - preparedin consultation with the Bank - by the end of March 1976.

C. Pricing of Cement

4.20 Cement prices in Algeria remained constant between 1966 and 1973when they were increased to DA 130/ton bulk and DA 140/ton bagged (US$33and 36/ton respectively) delivered at SNMC factory gate, agency or depot.Price differentials according to geographical location, mode of transportetc. do not exist. The 1973 cement price was established on the basis of

- 18 -

SNMC's average unit cost of producing, importing, transporting and dis-tributing cement in 1972, plus a fixed margin. However, while cement pricesin Algeria have been kept constant since then, costs have risen sharply:(i) the average dockside price of imported cement increased from DA 120/tonin 1973 to DA 200/ton in 1975, and (ii) at present, the average productioncost of Algeria's new plants which have not yet reached full capacity isestimated at up to three times that in older plants. Therefore, in orderto cover its present cost of cement production and distribution, SNMC wouldrequire a delivered price of about DA 230/ton versus the 1975 price of DA 130/ton for bulk cement and DA 140/ton for bagged cement. This cost structurewill improve as new plants reach full production at which time costs shouldbe about DA160/ton - below comparable import prices.

4.21 In July 1975, SNMC requested a price increase for all its products.Subsequently a new pricing policy for all building materials but cement wasdecided upon, which determines SNMC's sales prices at cost plus a 10% profitmargin. Cement pricing is still under review and a decision is expectedbefore end 1975. However, it is understood that cement prices will also beadjusted periodically to reflect production costs plus a margin sufficientto cover debt service obligations (para. 2.22).

4.22 Average cost-plus pricing as used in Algeria is widely applied incapital-intensive industries, such as cement. New plants have high unitcosts as they are gradually brought up to capacity operation and pre-oper-ating expenses are written off. Thereafter, costs decrease by some 20-30%and experience an even larger reduction when, after about 10 years of oper-ations, depreciation and financial charges become negligible. Average costpricing systems in countries with a relatively even mix of old and newplants or, as is the case of industrialized countries, a marginal capac-ity increase relative to existing capacity, tend therefore to result in afair amount of intra-industry or intra-company subsidization at graduallyincreasing prices, whereas in countries, such as Algeria, with primarilynew plants such pricing systemns imply high initial and then decreasingcemènt prices over time. This situation is, of course, aggravated bythe fact that, in Algeria, all investrents are financed by debt.

V. THE SAIDA CEMENT PLANT

A. Technical Aspects

5.01 Scope and ObJectives: The plant is part of a lime and cement complex,to be constructed and operated by SNMC near Saida. The cement plant, witha rated capacity of 500,000 tpy will use dry process technology and produceOrdinary Portland cement and possibly some special cement types. The cementplant is being constructed under a turnkey contract, except for civil works,with the Japanese firm, Kawasaki Heavy Industries (KHI), having been selectedas contractor following international competitive bidding.

- 19 -

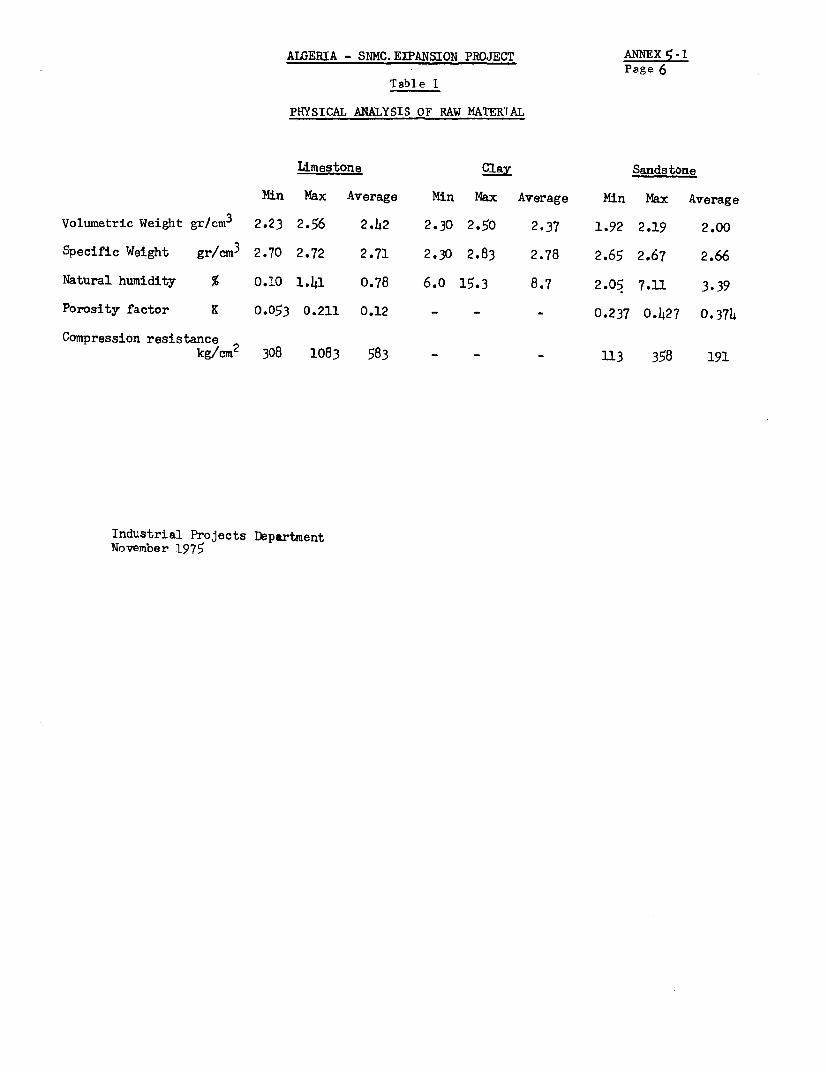

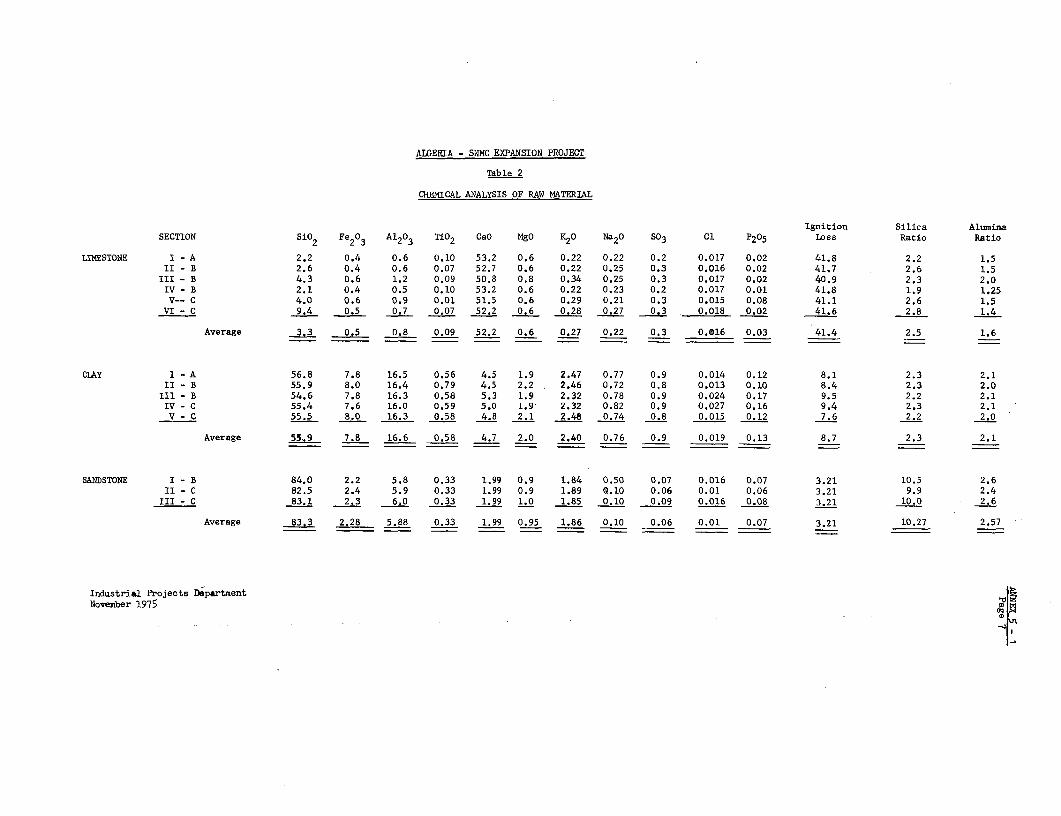

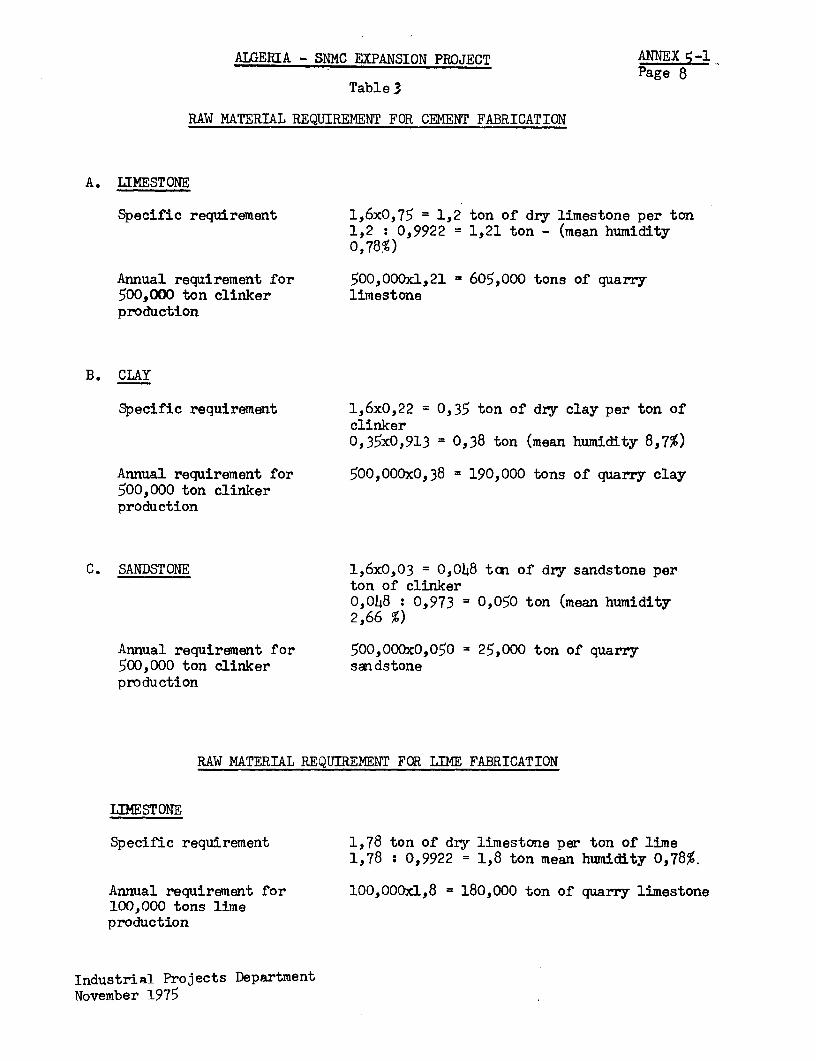

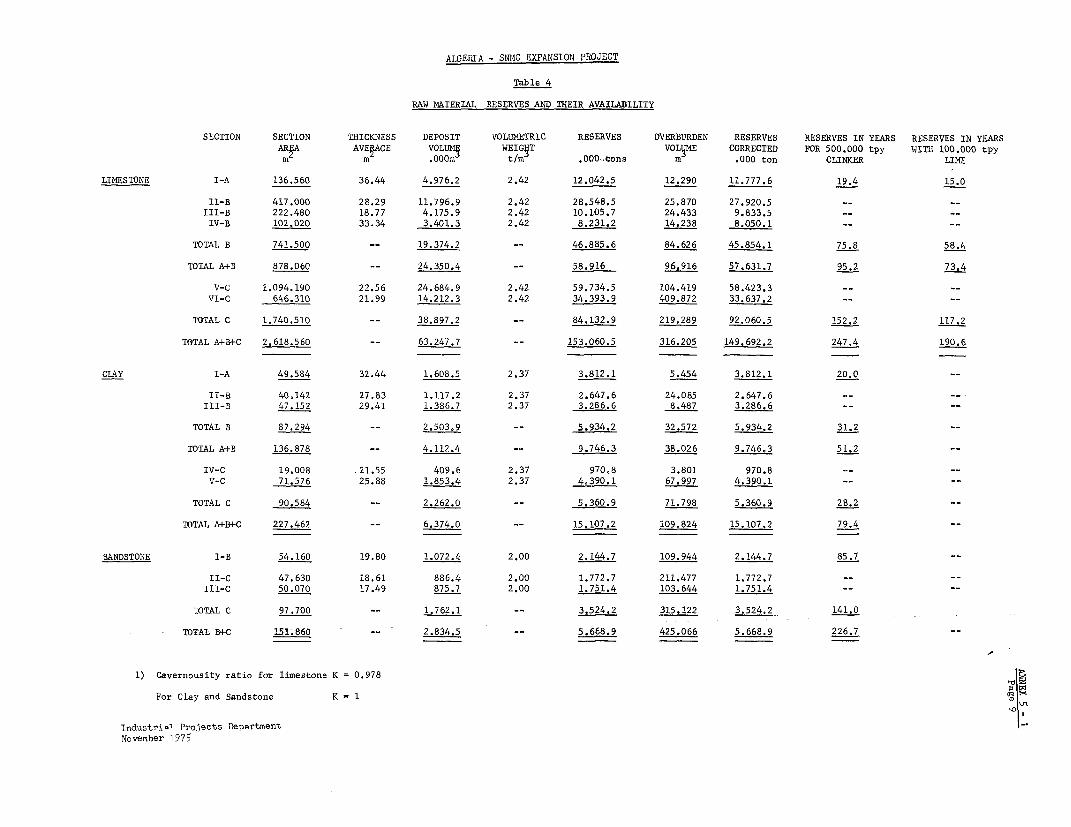

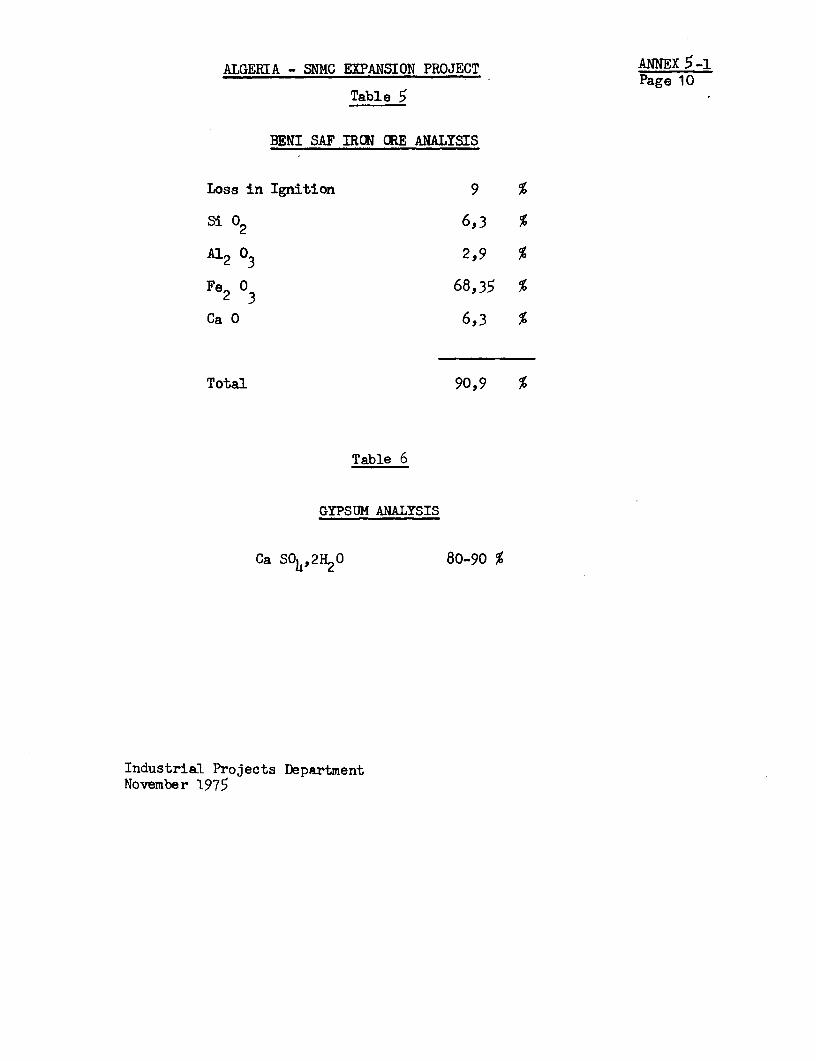

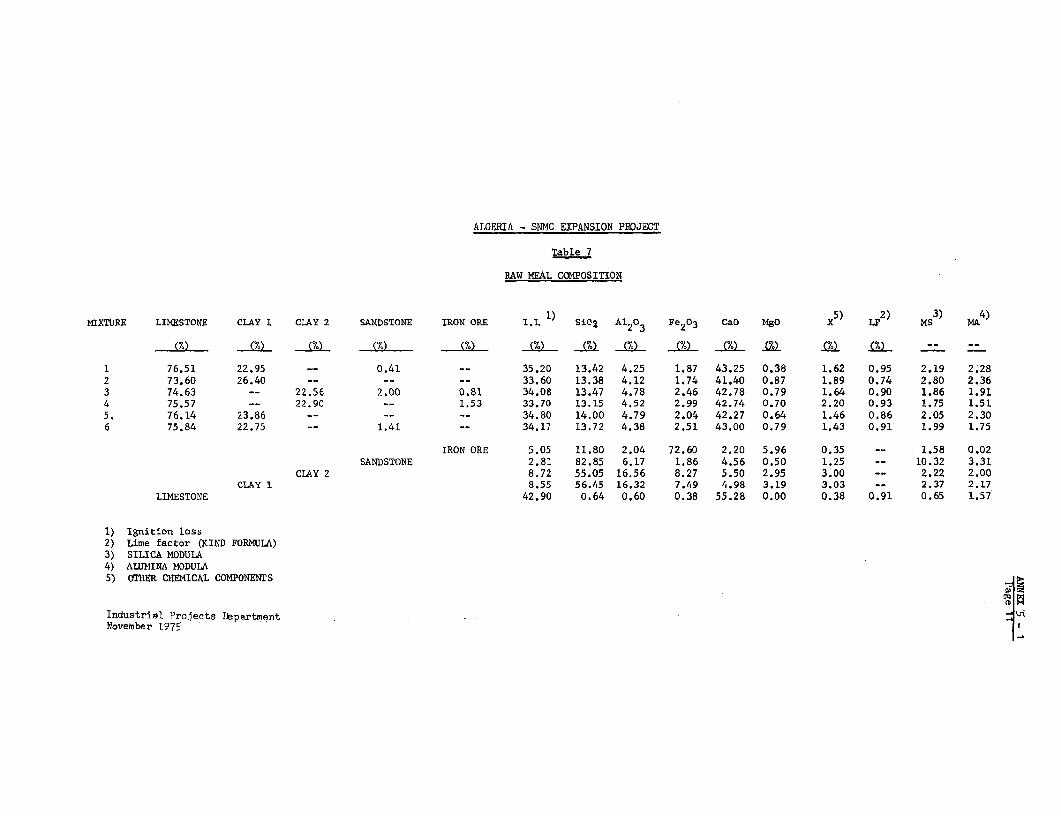

5.02 Raw Material Availability and Analysis: Geological investigationswere undertaken by a Bulgarian company during 1972/73, confirming the avail-ability of sufficient reserves of limestone, clay and sandstone to operatethe cement - lime complex at full capacity for more than 50 years. Abundantlimestone reserves exist about 1.5 km from the plant site but the clay depositis located more than 35 km distant. The clay samples show low silica andhigh alumina components which necessitate sandstone and iron ore additionsas corrective components for dry process production. Sufficient sandstoneis available at a deposit 30 km from the site and other additives (e.g. gypsum)are quarried by SNMC, purchased locally (iron ore), or imported (pozzolana).Details on raw material deposits and sources of supply are given in Annex 5-1.

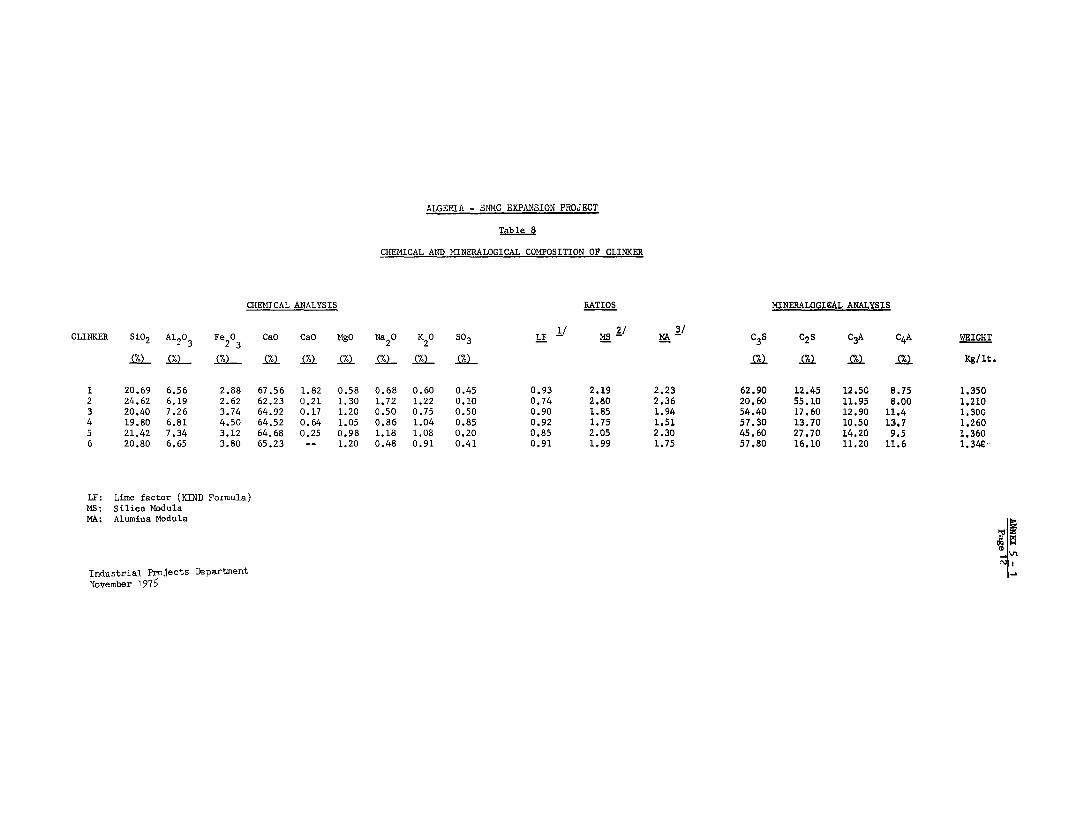

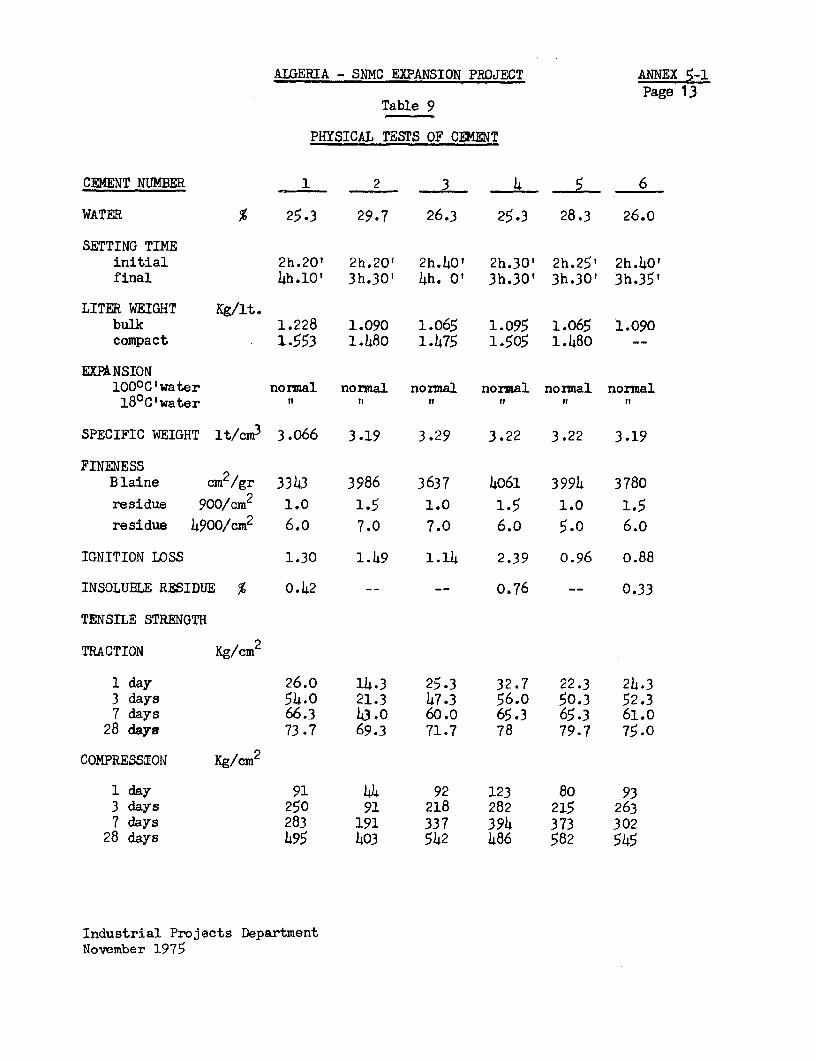

5.03 Plant Description: A detailed technical description of the plant,as proposed by KHI, is contained in Annex 5-2. Dry process technologywas chosen because of the acceptable humidity of the raw materials, thesubstantial fuel savings associated with this process and the objective ofstandardizing cement-making technology in Algeria. The plant will be fullyautomated in line with SNMC's desire to incorporate the latest technology; itincludes a complete line of mechanical and electrical cement machinery witha kiln of a rated capacity of 1,500 tons per day of clinker and all othernecessary auxiliary installations as well as extensive workshops, a laboratoryand administrative and social buildings.

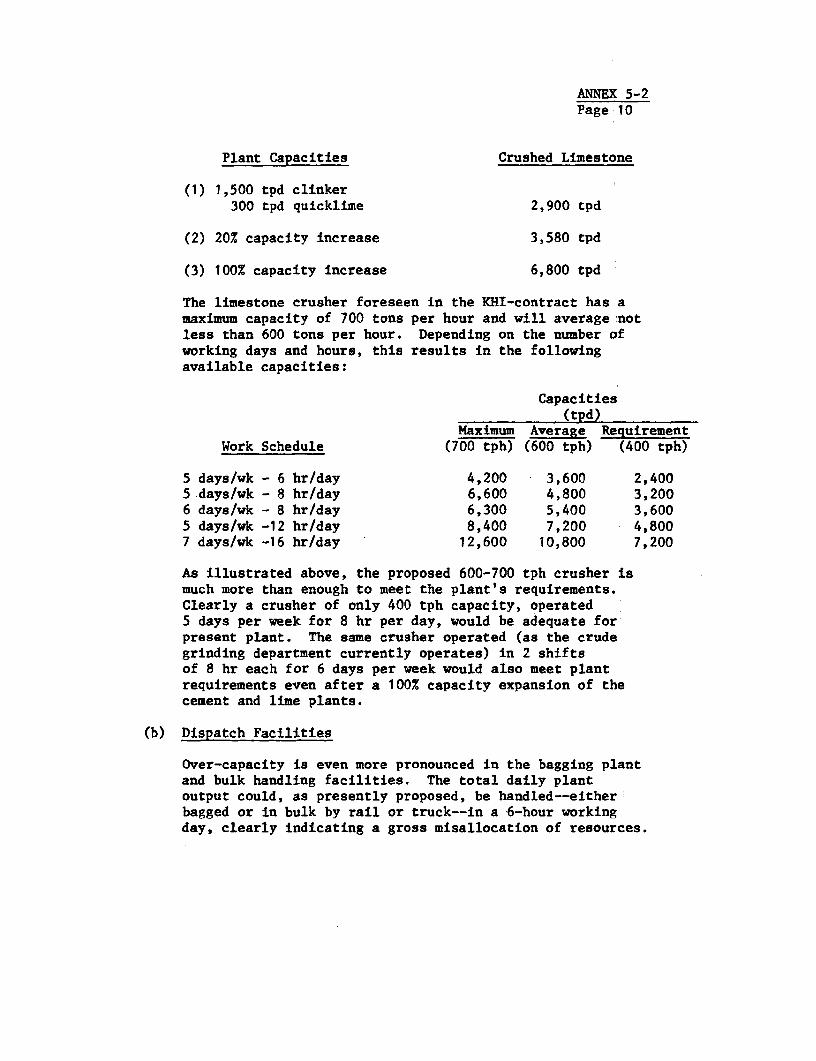

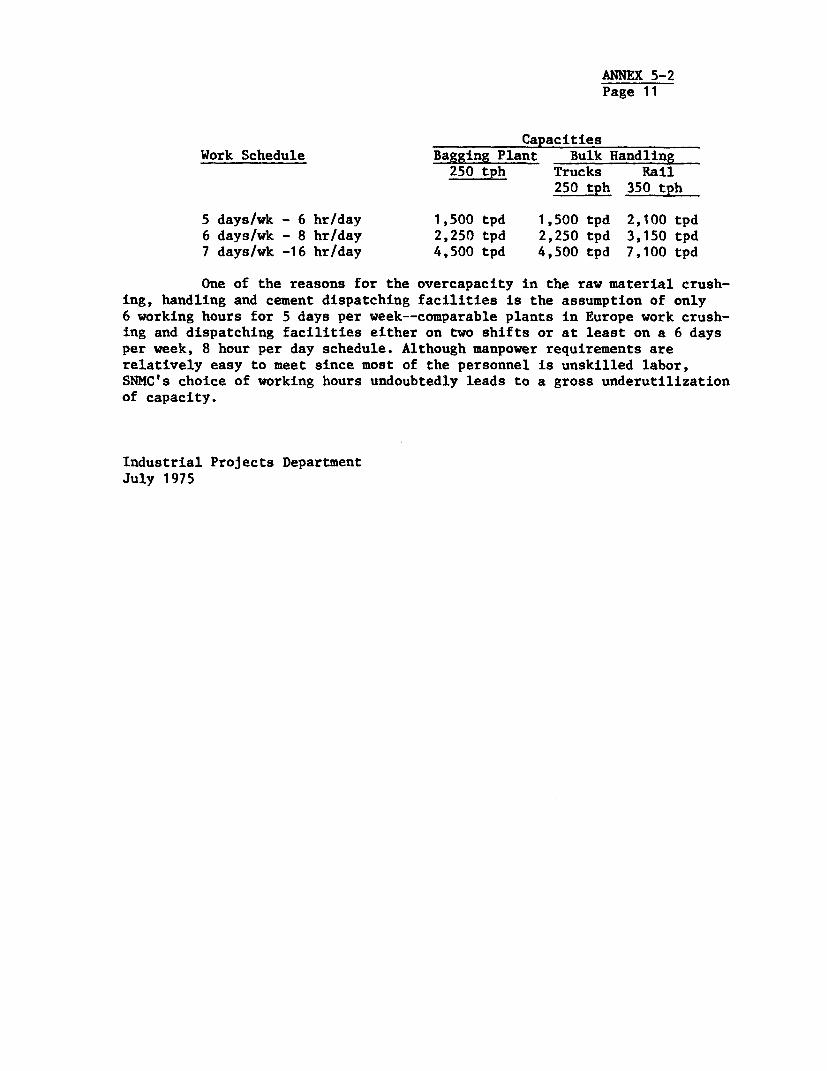

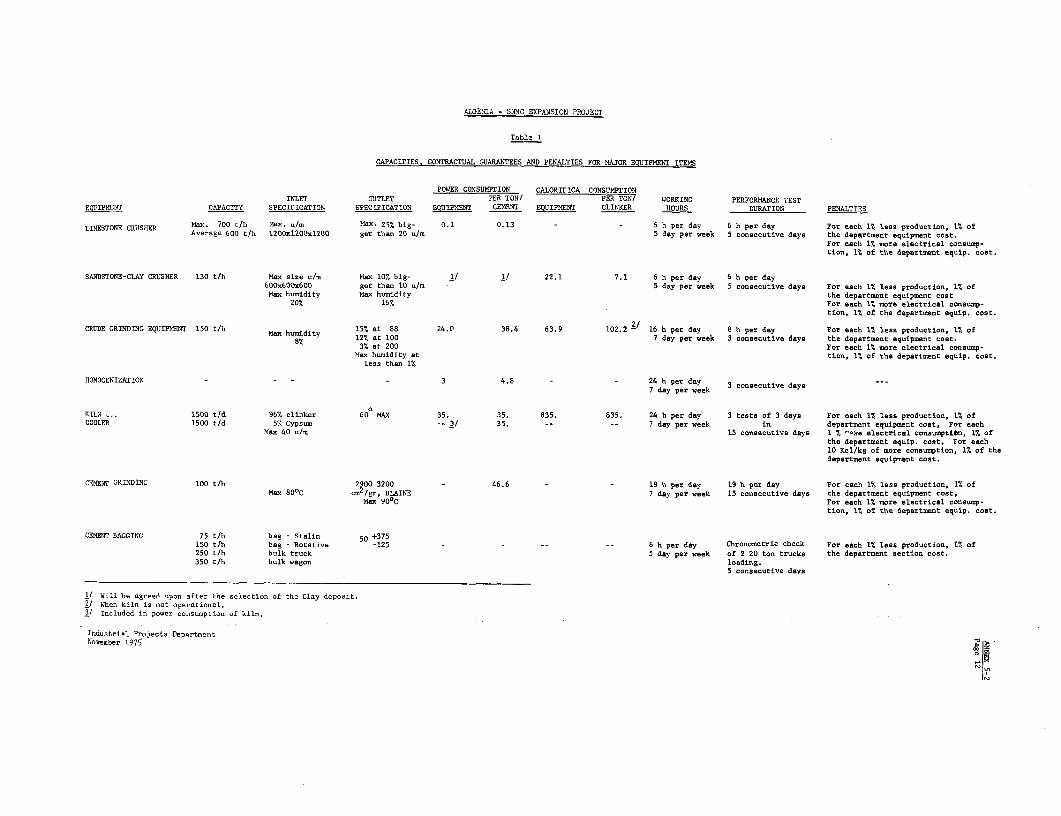

5.04 The design of the plant provides for a doubling of capacity with aminimum of new equipment and no infrastructure additions and includes amplesecurity margins in all but the kiln and cement grinding departments. Asdetailed in Annex 5-2, the raw material quarrying and handling equipment,the limestone crusher and the dispatching facilities are substantially over-designed, with their capacities exceeding by 3-10 times the required normfor handling 1,800 ton per day of clinker during a 30 working hour week.During negotiations, SNMC was asked to review with KHI the possibility ofeliminating these overcapacities. The possible investment saving could beup to US$5.0 million. This issue is further discussed in para 5.13.

5.05 Infrastructure and Utilities: Infrastructure and utilities aredescribed in Annex 5-3. The plant requires the construction of roads connectingthe quarries and the plant site and of a 25 km railway link to the SNCFA mainrail network. SNMC is responsible for undertaking and financing, as part of theproject, all necessary infrastructure work except for the provision of housing.

5.06 Power for the cement - lime complex will be supplied by SONELGAZ 1/through its distribution center north of Saida and a pressure reducing stationat the site. SONELGAZ will be responsible for the construction of the con-necting lines whereas the related investment costs will be covered by SNMCand are provided for in the plant's capital cost. Assurances were obtainedthat SNMC will take all necessary steps to ensure timely availability of gasand electricity for the project.

1/ Societe Nationale d'Electricite et de Gaz

- 20 -

5.07 Ecology: The plant is designed to meet anti-pollution standardsrequired by Western European c untries (Annex 5-4): (i) to prevent a dustdischarge of mare than 50 mg/m , electrical precipitators and filters will beinstalled which amount to nearly 7% of equipment cost; (ii) the sulphate-alkalimixture of the raw meal and the stack height is to be such as to maintainan annual mean of below 100 micrograms/m ; (iii) noise pollution will be keptto a minimum because of the fully automatic operation of the plant; and (iv)sewerage discharge will be treated by the normal bio-chemical process.SNMC agreed to construct and operate the Saida plant according to soundecological and environmental considerations and to establish and maintaina monitoring system for dust, gas and noise pollution at the plant.

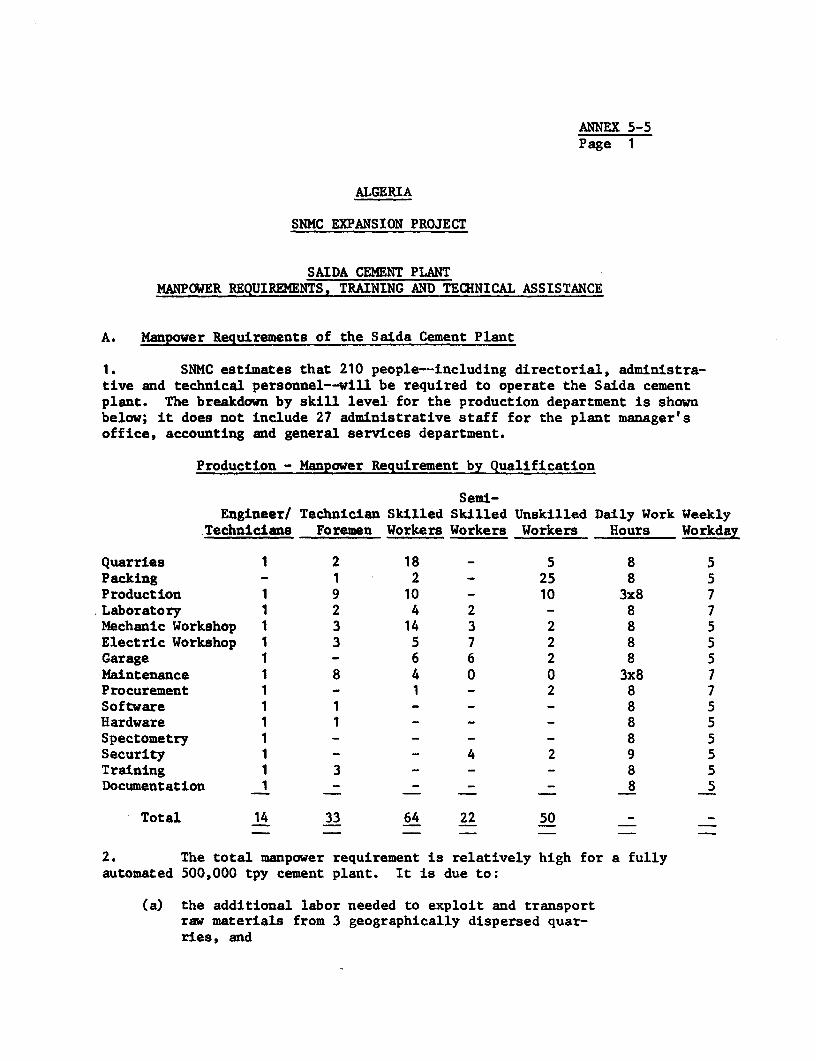

5.08 Manpower and Training: Details of labor force projections andtraining are contained in Annex 5-5. Cement factories have high capital/laborratios; thus the plant will provide direct employment for only about 220persons, including 50 unskilled workers. Training of all personnel will beprovided by KHI as part of the turnkey contract and take place at KHI'sworkshops, similar dry-process plants in Europe and at Saida. In addition,by 1976, SNMC intends to create its own Permanent Technical Training Center,with UNDP/UNIDO assistance, which will supplement the supplier's training.The training plans are satisfactory provided the Company will be able torecruit the required personnel. Assurances were obtained from SNMC that itwill make adequate and tinmly arrangements for recruiting and training ofpersonnel for the Saida plant.

5.09 Procurement: As mentioned above, the Saida plant will be builtunder a turnkey contact. While this approach entails normally higher capitalcosts, it offers in the Algerian context certain clear advantages. First,the number of SNMC's qualified technical staff is very small and clearlyinsufficient to plan and supervise the ambitious ongoing investment program.Second, this concept allows a single contractor to be held responsible forcompletion dates, performance guarantees and costs.

5.10 Procurement procedures for the Saida cement plant were initiated inNovember 1973. Following pre-qualification and ICB according to theBank's guidelines and including two-stage bidding, KHI was chosen aslowest evaluated bidder and a contract signed in April 1975. The turnkeycontract includes detailed engineering, supervision of civil works, supplyand erection of equipment, commissioning and training. It excludes theexecution of the actual construction work for the plant. In May 1975, sitepreparation was completed by a local firm and SNMC has started ICB proceduresfor the plant's civil construction contract. SNMC will also bid internationallythe materials and supplies for the construction of the railroad, followingBank procedures. Details on procurement are given in Annexes 5-6 and 5-7.

- 21 -

5.11 Plant Implementation and Technical Assistance: SNMC has engagedSOCADEI (France), a Lafarge subsidiary, to provide consulting services.The selection of this company followed Bank procedures. SOCADEI wasinstrumental in preparing procurement documents and evaluating offers andwill be supervising construction and commissioning, and vill elaborate thequarry exploitation plan. The plant implementation schedule is given inAnnex 5-6. The plant is forecast to start operating in mid-1978 andperformance tests are expected to be concluded by end 1978.

5.12 Both SOCADEI's and KHI's responsibilities end with the completionof the performance tests about six months after start-up. SNMC has signedagreements with Lafarge, Asland and COMSIP International for the provisionof technical assistance if SNMC so requires. The companies may not be able,however, to meet SNMC's needs during 1977-80, when five new cement plants willcome on stream. Although SNMC's training program is commendable, SNMC'sexperience with new cement plants during the next two years may prove thatconsiderable technical assistance will be required. Therefore, SNMC hasagreed to make, by December 1977, adequate arrangements for technical services,satisfactory to the Bank, for operation of the Saida cement plant.

- 22 -

B. Capital Cost and Financing Plan for the Saida Plant

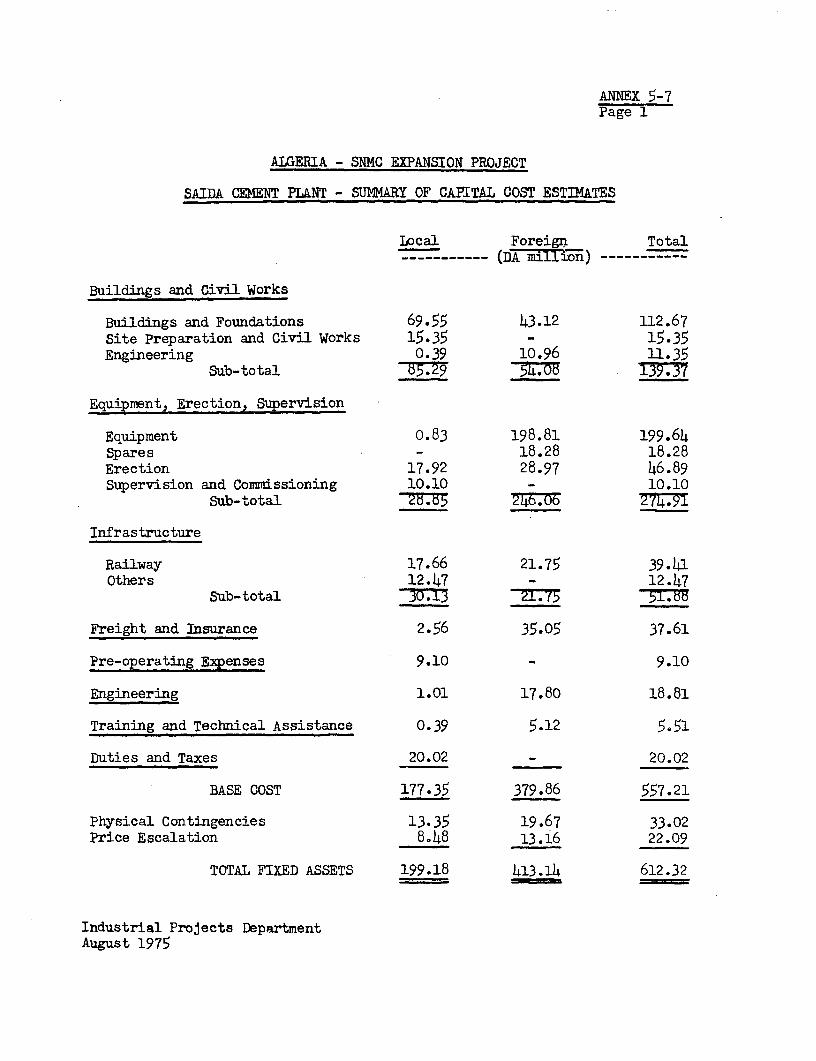

5.13 Capital Cost: Capital cost estimates are detailed in Annex 5-7 andsummarized below:

Saida Plant - Summary of Capital Cost Estimates

DA Million US$ MillionLocal Foreign Total Local Foreign Total %

Building § Civil Works 85.3 54.2 139.5 21.8 13.8 35.6 21.8Equipment Supply, Erec-tion & Supervision 28.8 246.1 274.9 7.4 62.8 70.2 42.9

Infrastructure 30.1 21.8 51.9 7.6 5.6 13.2 8.1Freight & Insurance 2.6 35.0 37.6 0.7 8.9 9.6 5.9Preoperating &

Engineering 10.2 17.8 28.0 2.5 4.5 7.0 4.4Training & Tech. Assist. 0.4 5.1 5.5 0.1 1.3 1.4 0.8Duties & Taxes 20.0 - 20.0 5.1 - 5.1 3.2

Base Cost 177.4 380.0 557.4 45.2 96.9 142.1 87.1

Physical Contingencies 13.4 23.5 36.9 3.4 6.0 9.4 5.1Price Contingencies 8.5 9.7 18.2 2.2 2.5 4.7 2.8

Fixed Assets 199.3 413.2 612.5 50.8 105.4 156.2 95.0Working Capital 15.3 16.4 31.6 3.9 4.2 8.1 5.0

Total Plant Cost 214.6 429.6 644.1 54.7 109.6 164.3 100.0

Interest duringConstruction 41.9 42.3 84.3 10.7 10.8 21.5

Total FinancingRequired 256.5 471.9 728.4 65.4 120.4 185.8

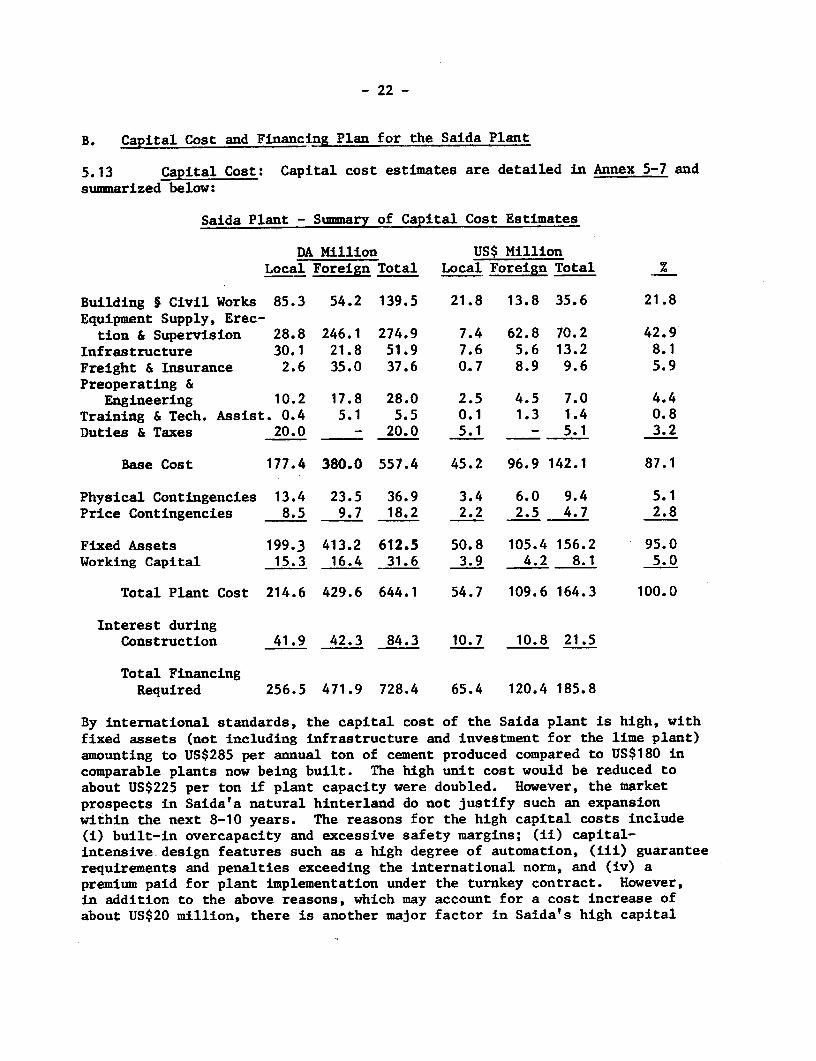

By international standards, the capital cost of the Saida plant is high, withfixed assets (not including infrastructure and investment for the lime plant)amounting to US$285 per annual ton of cement produced compared to US$180 incomparable plants now being built. The high unit cost would be reduced toabout US$225 per ton if plant capacity were doubled. However, the marketprospects in Saida'a natural hinterland do not justify such an expansionwithin the next 8-10 years. The reasons for the high capital costs include(i) built-in overcapacity and excessive safety margins; (ii) capital-intensive design features such as a high degree of automation, (iii) guaranteerequirements and penalties exceeding the international norm, and (iv) apremium paid for plant implementation under the turnkey contract. However,in addition to the above reasons, which may account for a cost increase ofabout US$20 million, there is another major factor in Saida's high capital

- 23 -

cost: During the past 2 years, SNMC has signed other turnkey contracts for5 cement plants with leading cement contractors. These suppliers are wellaware of: (i) the prevailing working conditions in Algeria; and (ii) SN4C'semphasis on time achedules, technical quality and output guarantees ratherthan on the level of capital costs. SNMC$a approach and. the Algerian systemhave, therefore, created a procurement climate which induces high priced offers.Under such circumstances the normal cost-reducing effect of internationalcompetitive bidding has not materialized.

5.14 The above capital cost estimates can be considered accurate: Theturnkey, consulting and site preparation contracts are firm so that costs ofequipment, erection, engineering and supervision representing 75% of the base

cost estimate, are not subject to price escalation. The estimate for buildingsand civil works reflects a May 1975 quote of a European contractor andSNMC's current experience with other cement plants. Infrastructure costs

are based on quotes from SONELGAZ, SNCFA and local contractors. Importduties and taxes of about 7% have been added to equipment and erectionand 22% to consulting services. An estimated DA 2.7 million for trainingand DA 2.8 million for technical assistance have also been included. Pre-

operating start-up expenses and engineering fees include SOCADEI's and KHI'sfees, the cost of the SNMC project team, and material and supplies duringcommissioning of the plant. To cover possible omissions and changes inproject design, physical contingencies of 5% and 10% have been added respec-tively to the base cost of items for which contracte have or have not beensigned. The allowance for price escalation amounts to 14% of that 25% ofthe base cost plus physical contingencies that remains subject to priceescalation. The annual escalation rates used during the constructionperiod are 15% for foreign equipment and construction, 10% for foreign

services, 5% for local equipment and supplies and 7% for local services.

5.15 As mentioned previously, the Saida cement plant is part of a cement-

lime production complex. The above capital cost includes DA 17.9 million(US$4.6 million) for land, infrastructure, civil works and equipment whichcan be allocated to the lime plant.

5.16 Working Capital Requirements: Working capital requirements through1979, i.e. the first full year of operations of the plant are estimated at

DA 31.8 million (US$8.1 million). The detailed build-up is given in Annex 5-8.

The amount is high due to the fact that the majority of SNMC's customers arestate enterprises or Government agencies which pay only three months afterdelivery.

5.17 Financing Plan: In accordance with financing practices in Algeria(para 2.02) the total financing required for the Saida plant of DA 728.4 million(US$185.8 million) will be covered by loans as follows:

- 24 -

Saida Plant - Financing Plan

Source DA million US$ million %

Supplier's credit 224.0 57.1 30.7IBRD 120.7 30.8 16.6BAD, BEA or TreasuryAdvances 383.7 97.9 52.7

Total 728.4 185.8 100.0

5.18 In May 1975, SNMC signed a supplier's credit agreement, as part ofthe KHI turnkey contract, totalling DA 224 million, of which DA 194.5 million(87%) is for 13 years including 3 years of grace, bearing an annual interestof 8.0%, and DA 29.5 million, covering KHI's services, is for 8 years, includ-ing 3 years of grace at 8.5% interest. In line with similar Japanese creditsto Algeria, the credit covers 70% of the turnkey contract's foreign exchangecost, equivalent to 48% of the Saida plant's total foreign exchange cost.The Saida plant component of the proposed Bank loan to SNMC is US$30.8 mil-lion equivalent. The Bank loan will cover about 25% of the plant's totalforeign exchange requirements. Both the supplier's credit and the IBRD loanwill be guaranteed by the Government of Algeria; the foreign exchange riskrests with SNMC.

5.19 Financing of incremental working capital requirements (estimated atUS$8.1 million) will be provided by Treasury advances on terms at least asfavourable as those of the IBRD loan. The remaining financing gap (estimatedat US$89.8 million) will be covered by long-term loans from BAD or otherappropriate domestic lending institutions. The latter generally carryinterest at 5.5% per annum and repayment periods in line with a project'sfinancial prospects. The financial projections are based on a repaymentperiod of 16 years, including four years of grace, calculated from the yearin which the disbursement is made. The Government indicated that the BADloan would be on terms at least as favourable at those of the IBRD loan.

5.20 Allocation of Bank Loan and Disbursement: The Bank loan will financepart of the foreign exchange cost of goods and services for the Saida plant,in accordance with a list of items shown in Annex 5-9, consisting of (i) 30%of the outstanding foreign exchange cost of the KHI turnkey contract for supplyand erection of the Saida plant, representing about 15% of the contract's totalforeign exchange cost; (ii) 25% of the cost of the plant's civil constructioncontracti representing the estimated direct and indirect foreign exchangecomponent; (iii) the cif cost of materials and supplies for the constructionof the railway link; (iv) the foreign exchange cost of the SOCADEI engineeringcontract; and (v) the technical assistance contract after commissioning. Sincethe services of SOCADEI were important during project preparation and werecontracted upon the Bank's request, it is recommended that the Bank financethe SOCADEI contract retroactively from May 1, 1975 up to a maximum ofUS$300,000.

- 25 -

5.22 The disbursement schedule for Bank financed items connected withthe cement plant is given in Annex 5-10. It is based on detailed estimatesof order placement and payment conditions in line with the expected deliveryand construction schedule.

C. Financial Analysis

5.22 Operating Costs: Production cost and revenue estimates are basedon the proposed product mix of 60:40 bulk and bagged Ordinary Portland cementand a production start-up in mid-1978 gradually leading to full capacity ope-ration by 1982. Projections in 1975 constant terms are given in Annex 5-11and those in current terms in Annex 5-12. To reflect inflationary cost changes,it has been assumed that local labor rates will increase by 7% p.a., otherlocal coste by 5% p.a. and foreign inputs by 15% p.a. in 1975-77, 10% in 1978,8% in 1979 and 7% thereafter. In 1982, at full production of 500,000 tpy, theSaida plant is projected to reach a direct operating cost of 55 DA/ton inconstant terms and 86 DA/ton in current terms.