annual report 2012

TRANSCRIPT

ANNUAL REPORT 2012

1 40th

AnnuAl report 2012

1 40th

Our Bank’s 140-year history reminds us that BSI’s uniqueness lies in its ability to forge trusted relationships by combining our expertise and security with a strong personal touch for the benefit of our clients. This is our DNA, a solid base upon which we have obtained excellent results, allowing us to look towards the future with optimism.

Stefano CoduriGroup CEO

«

»

__ 3

5 __ HIGHLIGHTS 2012

7 __ FOREWORD

10 __ CORPORATE GOVERNANCE 18 __ OUR ORGANISATIONAL STRUCTURE

20 __ HUMAN RESOURCES

22 __ OUR IDENTITY

31 __ MANAGEMENT REPORT 2012

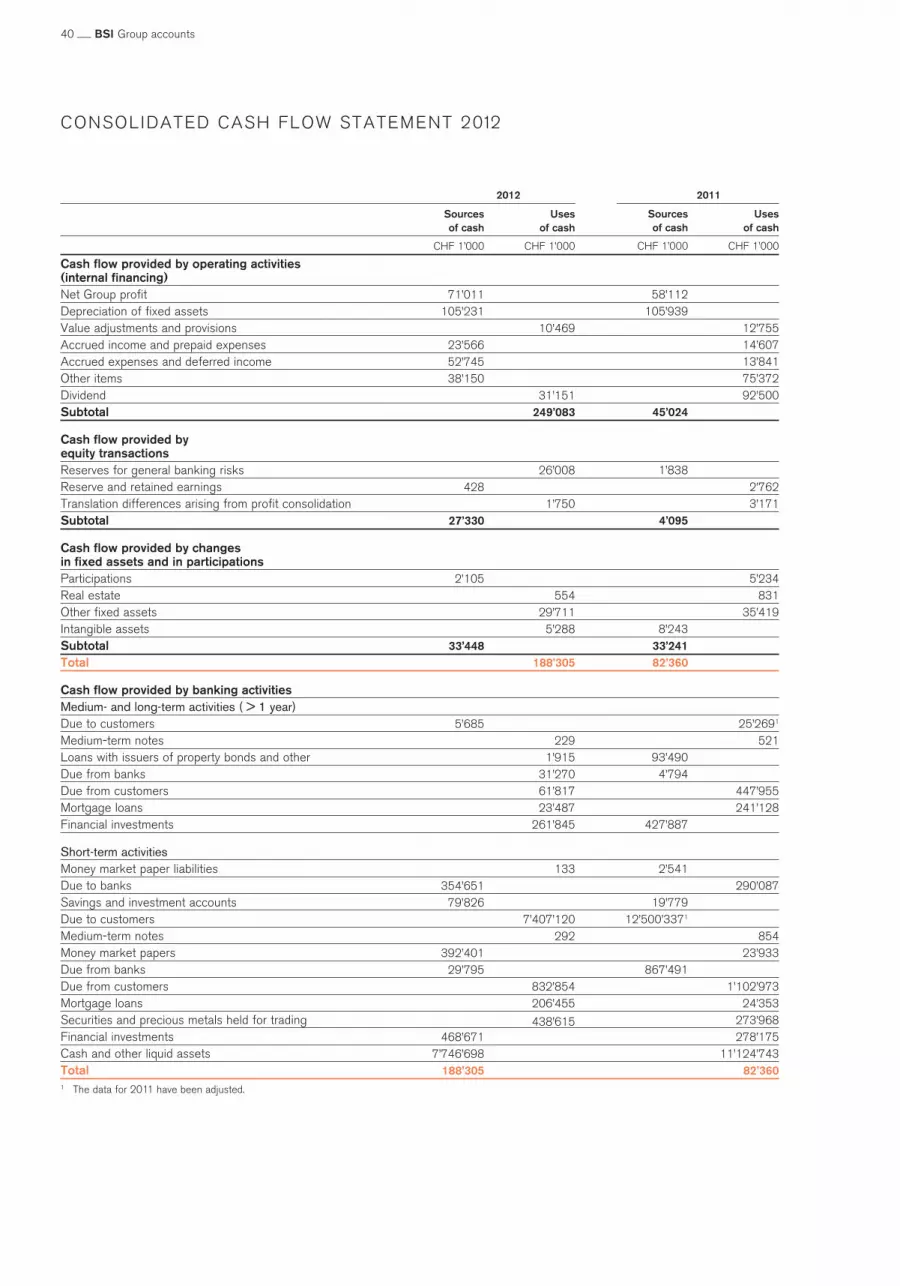

37 __ GROUP ACCOUNTS Consolidated balance sheet as of 31 December 2012 Consolidated profit and loss statement 2012 Consolidated cash flow statement 2012 Notes to the 2012 Group accounts Report of the statutory auditor on the consolidated financial statements

75 __ BSI AG ACCOUNTS Parent Bank balance sheet as of 31 December 2012 Parent Bank profit and loss statement 2012 Notes to the 2012 Parent Bank accounts Report of the statutory auditor on the financial statements

84 __ GLOSSARY OF SELECTED TERMS AND ABBREVIATIONS

88 __ CONTACTS

Annual Report as submitted to the ordinaryGeneral Meeting of 18 April 2013

A company of the Generali Group

Contents

This is a translation into English of the Annual Report issued in the Italian language and is intended solely for the con-venience of English speaking readers. This report includes information specifically required by Swiss law. In the event of contradictions or inconsistencies between the Italian and the English version of the Annual Report, the Italian version shall prevail.

“For BSI, investing in culture has always had a precise significance: helping to broaden the consciousness that science and art play a fundamental part in the every- day life and the sustainable development of society.BSI Architectural Foundation was constituted for the purpose of fostering knowledge, training and studies in this fascinating discipline, which is capable of com-bining technology and aesthetics in the service of a changing society. For BSI, a commitment to the field of architecture is a patrimony of the whole Group. Communicating research and innovation in its various forms is a challenge to us and a continuous stimulus which we seek purposefully.We are proud to work with the Academy of Archi-tecture and the Archivio del Moderno of Mendrisio (Università della Svizzera italiana) and, through its pa-tronage, with the Federal Office of Culture of Berne. This cooperation not only strengthens our relation-ship with the world of architecture in Switzerland and with the architect Mario Botta in particular, in his role as President of the Jury of the Award, but also ena-bles us to help bring important issues to the attention of the international public, which are not purely con-centrated on aesthetics but extend to the search for sustainability in works in the context in which they are embedded”.Alfredo GysiChairman of the Board of Directors of BSI

BSI Swiss Architectural Award

“In the wake of what, rightly, we can describe as a success story that began in 2007, the BSI Swiss Architectural Award is garnering increasing plaudits and emerging as a landmark in the cultural debate and among awards dedicated to contemporary architec-ture. The prestige of the Jury and Advisors, the grow-ing interest expressed by experts and international public opinion and above all the quality of the works presented have given this award a considerable di-mension. Its international dimension took us first to Latin America, with Solano Benitez (Paraguay, winner in 2008), then to Africa, with Diébédo Francis Kéré (Burkina Faso/Germany, winner in 2010), and then to India with Studio Mumbai, a team of architects and craftsmen, the winners of the third edition. But the credit for this success is also attributable to the far-sightedness of the objective of the Award: to sustain architecture that is attentive to the context in which it is set and sensitive to environmental issues, without neglecting the aesthetic factor on which the discipline of architecture rests. An ambitious goal achieved by the BSI Architectural Foundation togeth-er with the Academy of Architecture and the Archivio del Moderno of Mendrisio (Università della Svizzera italiana) and sponsored by the Federal Office of Cul-ture in Bern.For all these reasons, BSI decided to promote and support this award. And today more than ever, faced with the difficulties of the historical period we are traversing, we are convinced of the validity of this choice, which represents BSI’s commitment to the cultural sphere. A commitment that seeks to contrib-ute positively to the sustainable development of the communities where we operate. An award with which this institution is increasingly identified”.Stefano CoduriGroup CEO BSI

Mar

io B

otta

“The BSI Swiss Architectural Award is to be assigned biennially for a period of 10 years, subject to further extension. This appears to be a long time as evi-denced by the important changes which we are wit-nessing. Economic shifts of enormous proportions, the ever increasing political, social and economic importance of countries and regions outside Europe and the United States, and the seemingly unstoppa-ble ascent of new technologies are just a few premo-nitions of what are likely to be far-reaching paradigm shifts over a relatively short period of time. In these turbulent times, architecture has its specific place and function. Its continued relevance demonstrates that human beings will always continue to give form, shape and content to space, to express these values, creating culturally meaningful traces of their existence. It is of particular significance that the 2008, 2010 and 2012 awards recognised the achievements of archi-tects from South America, Africa and India”.Felix R. EhratPresident of BSI Architectural Foundation

“Architecture means much more than just building ed-ifices. It shapes our living space and therefore has a role in how we feel in a given environment. Architects do not design and build for the purposes of material ob-jects, but always for people. In this way they contrib-ute to the identity of a society and the development of a country by endowing it with a face. The award offers the candidates, members of the ju-ry and the general public opportunities to meet, ex-change ideas and engage in fruitful discussions. For these reasons the BSI Swiss Architectural Award has become a special event for our national architecture as well as internationally, offering local architecture the opportunity to become known worldwide and so become part of the current debate”.Jean-Frédéric JauslinDirector of the Swiss Federal Office of Culture

“In seismology (a discipline with which we have es-tablished a tragic familiarity in recent years), at least three detector stations are necessary to determine the epicentre of an earthquake. If we apply this prin-ciple to a much less ominous field, this rule justifies us in seeing the BSI Swiss Architectural Award, as a kind of reliable “seismograph” which gives us a reading of the state of contemporary architecture. And if we approach it in this way, the reading we receive is two-fold: on the one hand it is heartening to our discipline to observe the quality of the works submitted to the attention of the jury: a level of quality that is guaran-teed, thanks to the selection procedure adopted, by the panel of advisors who identify the candidates. On the other hand this also leads one to reflect the fact that the winners actually come from countries outside “old” Europe, or with only partial links to it (as was the case of Diébédo Francis Kéré). And this, of course, is not due to any bias on the part of the different juries that have selected the short lists (immune, I believe, from the influence of any form of Orientalism), but the objective value of the winners. They, however, display different conceptual approaches and work with differ-ent formal languages: in short they have very different “poetics” which cannot be reduced to a common de-nominator, except, perhaps, for a particular concern with the craft component of the construction process and its consequent enhancement”.Mario BottaPresident of the Swiss Architectural Award Jury

THE PRIZE“This award represents an opportunity to recognise and raise the international profile of architects who can make an outstanding contribution to contempo-rary architectural culture. It is also a good occasion to reflect critically on ideas that favour first an ethical and then an aesthetic approach. The names selected can be considered as some of the most important ar-chitects working internationally today. Their sensitiv-ity and professional commitment in their countries of origin highlight their diverse hopes (both fanciful and realistic), in contrast to the contradictions and confu-sion that are rife today in the debates within the field”. Mario BottaPresident of the Swiss Architectural Award Jury

“For an artist to work with an architect is a moment of pure exchange. It is where the tensions and pos-sibilities of modernity come together. For an artist to design an architectural award is a strange role and it is also a moment to play. This award is precise and compact. It is designed to show a reflection of growth. A growth of ideas, a growth of new structures and a growth of new relationships. It is also designed to last, to be polished and to be thought of as a gift and a thank you from artist to architect”. Liam GillickConceptual Artist

PARTnERS

BSI Established in Lugano in 1873, BSI AG is one of the oldest banks in Switzerland and specialises in private wealth management. The bank places great emphasis on establishing and maintaining ongoing personal re-lationships with clients, while at the same time offering global asset management services with world-class products. Aware of the impact that its operations can have on the local areas in which it operates, BSI is at the forefront of promoting, through its foundations, partnerships and sponsorships, events and projects that contribute to the cultural, economic, and scien-tific development of our society. It is present in the major financial markets worldwide, in Europe, Latin America, the Middle East and Asia.

BSI ARCHITECTURAL FOUnDATIOnBSI Architectural Foundation was created by BSI for the promotion of knowledge, education and research in the field of architecture. It presents a biennial archi-tecture award (BSI Swiss Architectural Award) and sponsors activities and projects as part of that event, including exhibitions and publications.

ACADEMy OF ARCHITECTURE OF MEnDRISIO,UnIvERSITà DELLA SvIZZERA ITALIAnAThe Academy of Mendrisio aims to create a “new” architect able to make sense of the territory, critically transform it without erasing its identity, respond to the demands of living space creatively and effectively. The study curriculum is built on the integration of de-sign with historical-humanistic and technical-scientif-ic disciplines. The Academy of Architecture maintains relations and cooperates with numerous national and international institutions and schools, and is active in research, especially into the areas of history and urban studies.

ARCHIvIO DEL MODERnO, MEnDRISIO The Archivio del Moderno is an independent research institute that supports the Academy of Architecture of Mendrisio. Instituted in 1996, it was constituted as a Foundation on 20 February 2004 by the Uni-versità della Svizzera italiana. The objectives of the institute are: on the one hand the acquisition, protec-tion, preservation and valorisation of archives of archi-tecture, urban planning, engineering, design, art and photography; on the other the promotion of scientific research in fields such as the history of modern and contemporary architecture, art, design, the territory and civil engineering.

Limited edition by Liam Gillick 10 copies for BSI, Chromed steel Produced by Flury Modellbau GmbH, Egliswil

Any architect aged under 50 in the year in which the Award is launched, of any nationality, may enter, provided that they have designed at least three significant works that meet the aims of the competition.

FIRST EDITIOn2007-2008

JURyPresident

Mario BottaMendrisio (Switzerland)

Members

Emilio Ambasznew york (USA)

Valentin BearthChur (Switzerland)

Davide Croffvenice (Italy)

Wenjun ZhiShanghai (China)

Secretary

Nicola NavoneMendrisio (Switzerland)

ADvISORSLaurent Beaudouinnancy (France)

Gonçalo ByrneLisbon (Portugal)

Alberto Campo BaezaMadrid (Spain)

Massimo CarmassiFlorence (Italy)

Roberto CollovàPalermo (Italy)

Kenneth Framptonnew york (USA)

Dan S. HanganuMontreal (Canada)

Kengo KumaTokyo (Japan)

Paulo Mendes da RochaSão Paulo (Brasil)

Boris Podreccavienna (Austria)

Anant RajeAhmedabad (India)

Bruno ReichlinMendrisio (Switzerland)

Chang Yung HoBeijing (China)

WInnERSolano BenitezAsunción (Paraguay)

CAnDIDATES 3LHD(Saša Begovic , Marko Dabrovic , Tanja Grozdanic , Silvije novak)Zagreb (Croatia)

Manuel e FranciscoAires MateusLisbon (Portugal)

David AdjayeLondon (Great Britain)

Jesús AparicioMadrid (Spain)

Gion A. Caminadavrin (Switzerland)

Alfonso Cendronvenice (Italy)

Dominique CoulonStrasburg (France)

Richard Francis-JonesSidney (Australia)

Sean GodsellMelbourne (Australia)

Thomas HeatherwickLondon (Great Britain)

Rick JoyTucson (USA)

Alberto KalachMexico City (Mexico)

Francisco MangadoPamplona (Spain)

Luis L. Mansilla,Emilio Tuñón AlvarezMadrid (Spain)

Rahul MehrotraMumbai (India)

Quintus Miller, Paola MarantaBasel (Switzerland)

Marco Navarra(NOWA)Caltagirone (Italy)

Office dA(Monica Ponce de Leon,Nader Tehrani)Boston (USA)

Valerio OlgiatiChur (Switzerland)

Promontorio Architects(João Perloiro, João Luís Ferreira, Paulo Perloiro,Paulo Martins Barata,Pedro Appleton)Lisbon (Portugal)

Saša Randic , Idis TuratoRijeka (Croatia)

João Alvaro RochaMaia (Portugal)

Enric Ruiz Geli(Cloud 9)Barcelona (Spain)

S-M.A.O.(Juan Carlos Sancho,Sol Madridejos)Madrid (Spain)

Beniamino ServinoCaserta (Italy)

Shuhei EndoOsaka (Japan)

The next ENTERprise(Marie-Therese Harnoncourt,Ernst J. Fuchs)vienna (Austria)

Antonio Jimenez TorrecillasGranada (Spain)

Shu WangHang Zhou (China)

SECOnD EDITIOn 2009-2010

JURyPresident

Mario BottaMendrisio (Switzerland)

Members

Valentin BearthChur (Switzerland)

Solano BenitezAsunción (Paraguay)

Barry Bergdollnew york (USA)

Luis Fernandez GalianoMadrid (Spain)

Secretary

Nicola NavoneMendrisio (Switzerland)

ADvISORSEmilio Ambasznew york (USA)

Laurent Beaudouinnancy (France)

Gonçalo ByrneLisboa (Portugal)

Alberto Campo BaezaMadrid (Spain)

Massimo CarmassiFlorence (Italy)

Kenneth Framptonnew york (USA)

Dan S. HanganuMontreal (Canada)

Kengo KumaTokyo (Japan)

Boris Podreccavienna (Austria)

Bruno ReichlinMendrisio (Switzerland)

Wenjun ZhiShanghai (China)

WInnERDiébédo Francis KéréGando (Burkina Faso)Berlin (Germany)

CAnDIDATES Iñaqui Carnicero, Ignacio Vila,Alejandro VírsedaMadrid (Spain)

Adam Caruso, Peter St JohnLondon (Great Britain)

Davide Cristofani, Gabriele LelliFaenza (Italy)

João Pedro Falcão de CamposLisbon (Portugal)

Dietmar FeichtingerParis (France)vienna (Austria)

Arturo Franco DíazMadrid (Spain)

Sou FujimotoTokyo (Japan)

José Fernando GonçalvesPorto (Portugal)

Erich Hubmann, Andreas Vassvienna (Austria)

Bjarke IngelsCopenhagen (Denmark)

Junya IshigamiTokyo (Japan)

Christian KerezZurich (Switzerland)

Andrea Liverani, Enrico MolteniMilan (Italy)

Fabio MarianiRimini (Italy)

João Mendes RibeiroCoimbra (Portugal)

MGM - Morales Giles MariscalJosé Morales Sanchez,Sara de Giles Dubois,Juan Gonzalez MariscalSeville (Spain)

Hiroshi NakamuraTokyo (Japan)

nARCHITECTSEric Bunge, Mimi Hoangnew york (USA)

Willem Jan Neutelings,Michiel RiedijkRotterdam (The netherlands)

Mauricio Pezo, Sofia vonEllrichshausenConception (Chile)

Joshua Prince-Ramusnew york (USA)

Bernard QuirotPesmes (France)

Jurij Sadar, Boštjan VugaLjubljana (Slovenia)

Markus SchererMerano (Italy)

José Selgas, Lucia CanoMadrid (Spain)

URBANUSXiaodu Liu, Yan Meng, Hui WangShenzhen (China)

Tiantian XuBeijing (China)

THIRD EDITIOn2011-2012

JURyPresident

Mario BottaMendrisio (Switzerland)

Members

Gonçalo ByrneLisbon (Portugal)

Marco Della TorreComo (Italy)

Diébédo Francis KéréGando (Burkina Faso)Berlin (Germany)

Mohsen MostafaviCambridge, Mass. (USA)

Secretary

Nicola NavoneMendrisio (Switzerland)

ADvISORSSolano BenitezAsunción (Paraguay)

Barry Bergdollnew york (Stati Uniti)

Ole BoumanRotterdam (The netherlands)

Luis Fernandez GalianoMadrid (Spain)

Kenneth Framptonnew york (USA)

Sean GodsellMelbourne (Australia)

Kengo KumaTokyo (JApan)

Shelley McNamaraDublin (Ireland)

Rahul MehrotraMumbai (India)Boston (USA)

Valerio OlgiatiFlims (Switzerland)

Eduardo Souto de MouraPorto (Portugal)

Shu WangHang Zhou (China)

WInnERStudio MumbaiMumbai (India)

CAnDIDATES Alejandro AravenaSantiago (Chile)

architecten de vylder vinck taillieu (Jan de Vylder, Inge Vinck, Jo Taillieu)Ghent (Belgium)

Atelier Bow-Wow(Yoshiharo Tsukamoto,Momoyo Kaijima)Tokyo (Japan)

Nuno Brandão CostaPorto (Portugal)

Angelo BucciSão Paulo (Brazil)

Marcus Donaghy, William DimondDublin (Ireland)

Ecosistema urbanoMadrid (Spain)

Antón García-Abril(Ensamble Studio)Madrid (Spain)

Anna HeringerSalzburg (Austria)

LTL Architects(Paul Lewis, Marc Tsurumaki,David Lewis)new york (USA)

Gurjit Singh MatharooAhmedabad (India)

Alberto MozóSantiago (Chile)

muf architecture/artLondon (Great Britain)

Hiroshi NakamuraTokyo (Japan)

Mauricio Pezo,Sofia von EllrichshausenConcepción (Chile)

Smiljan RadicSantiago (Chile)

Camilo RebeloPorto (Portugal)

Enric Ruiz-Geli (Cloud 9)Barcelona (Spain)

José María SaezQuito (Ecuador)

Joaõ Pedro Serôdio,Isabel FurtadoPorto (Portugal)

Dominic StevensCloone (Ireland)

Jonathan WoolfLondon (Great Britain)

Alejandro Zaera PoloLondon (Great Britain)Barcelona (Spain)

Ke Zhang (standardarchitecture)Beijing (China)

Lei Zhangnanjing (China)

-

The BSI Swiss Architectural Award is more than just a prize; it is the expression of the composite work of many people who, over and above their individual specialisations, identify with a common project for the greater social good.

«

Alfredo Gysi, Chairman of the Board of Directors of BSI

»

__ 5

BSI Group

Profit and loss statementNet operating result

Operating expenses

Gross profit

Depreciation of fixed assets

Value adjustments, provisions, and losses

Extraordinary income / expenses

Taxes

Net Group profit

Balance sheetTotal assets

Shareholders’ equity, including net Group profit

Client assetsTotal

Headcount (in FTEs)

Total

of which: in Switzerland

abroad

Capital ratios (Basel II)Total capital (Tier 1 and 2)

Tier 1 capital

BSI AG

Profit and loss statementNet operating result

Operating expenses

Gross profitNet profit Balance sheet Total assets

Shareholders’ equity after appropriation of profit

Dividend (proposal of the Board of Directors)

in CHF 1’000

in %

2011

CHF 1’000

834’151

-668’582

165’569

-105’939

-21’259

43’311

-23’570

58’112

32’164’674

2’463’585

CHF million

77’746

Unit

1’964

1’346

618

%

14.59

13.78

2011

CHF 1’000

643’765

-463’828

179’937

90’113

18’659’769

2’270’109

30’000

1.63

2012

CHF 1’000

865’038

-667’997

197’041

-105’231

-41’104

34’290

-13’985

71’011

24’286’931

2’476’115

CHF million

86’262

Unit

1’963

1’317

646

%

16.96

16.22

2012

CHF 1’000

656’677

-494’800

161’877

30’867

20’023’067

2’260’080

30’000

1.63

HIGHLIGHTS 2012

__ 7

The BSI Group ended 2012 on a positive note, giving renewed impetus to the implementation of its growth strategy. This was amidst a fragile world economy, volatile financial markets and major changes in the wealth ma- nagement sector.

In 2012 the world economy continued to grapple with the effects of the crisis that began in 2007. Global growth slowed due to economic weakness in the euro area es-pecially but also in the emerging economies, China in par-ticular, whose growth rates, while still high, decelerated. Conditions on financial markets improved partly due to the ECB’s actions in support of the euro. Nonetheless, investors remained wary primarily because of persistent uncertainty concerning the euro crisis, the slowdown in the Chinese economy and doubts about the sustainability and solidity of the recovery in the US economy.

Although slowing, the Swiss economy turned out to be one of the best performers among the developed coun-tries. On the monetary front, the Swiss National Bank continued to defend the minimum exchange rate of 1.20 francs to the euro with the goal of limiting the strong appreciation in the Swiss currency, which remained high throughout the year against both the euro and the dollar.

The Swiss banking sector overall continued to face politi-cal pressure centred predominantly on taxes. In 2012 the European Union established the regulatory compatibility of Switzerland’s proposal to introduce a final withholding tax for the assets of European clients held at Swiss banks. This proposal allows for the regularisation of assets not declared in the past as well as the introduction of a tax for the future that fully respects client privacy. Also in 2012, tax agreements to this effect were ratified by Austria and the United Kingdom, while the tax agreement signed with the German government became the centre of political debate in Germany, and despite being approved by the Bundestag was rejected by the Bundesrat. Other negoti-ating tables with important European partners, including Italy, are still open, and it is hoped that some positive conclusions will be reached.

Nationally, discussions continued in an effort to define a strategy for the Swiss financial centre in line with the most recent international developments such as recom- mendations from the Financial Action Task Force (FATF) for combating money laundering concerning the extension of bank diligence in conjunction with stepping up the fight against money laundering. In today’s times, marked by sweeping changes, we believe in maximum cooperation between the banking world, regulatory and government institutions to respond efficiently and lastingly to the chal-lenges that lie ahead for the financial centre.

In 2012, BSI succeeded in improving its performances signi- ficantly thanks to the effectiveness of our strategic choic-es, our attractiveness in the wealth management sec-tor and the professionalism of our staff, which has not only retained existing clients but acquired new ones as well. In terms of shareholder structure, the Generali Group has announced its plan to sell the Bank to focus on its core insurance business.

In 2012, net new money totalled CHF 7.5 billion (2011: CHF 6.7 billion), an all-time high for the BSI Group. Assets under management reached CHF 86.3 billion, up 11.0% from 2011’s CHF 77.7 billion, despite the continued strength of the Swiss franc against the euro and the dollar. Growth in volumes and cost containment helped improve margins significantly. Gross profit rose by 19.0% with respect to the previous financial year, settling at CHF 197 million (2011: CHF 165.6 million), while net profit grew by 22.0%, com-ing in at CHF 71 million compared to CHF 58.1 million in 2011. Also in 2012, BSI reinforced its position as a solid bank, with shareholders’ equity of CHF 2.5 billion and a total capital ratio of 17.0% (2011: 14.6%), further strength-ening the Group’s capital base.

Foreword

8 __ BSI Annual Report 2012

This positive trend reflects the effectiveness of BSI’s strategy, based on three main pillars: geographical di-versification, through which we have been able to take advantage of the development opportunities offered by more dynamic markets such as Asia, Latin America, Eastern and Central Europe and the Middle East and to consoli-date our position on the more traditional markets; the de-velopment of specialised service models for specific cli-ent segments; and increased operating efficiency along with strict risk control and capital management.

Overall, the important goals reached in 2012 demonstrate that the BSI Group has laid down a solid foundation for sustainable long-term growth. In this 140th year of our Insti-tution, the BSI Board of Directors and Executive Board are determined to continue on the path of growth success-fully followed for so many years. We would like to thank our clients for the trust they place in our Institution, and we would like to take this opportunity to extend our apprecia- tion and thanks to our staff, who dedicate every day, with unwavering commitment and professionalism, to provid-ing the services that our clients demand and deserve. Thank you again.

Alfredo Gysi Stefano CoduriChairman of the Group Chief Executive Officer

Board of Directors

__ 9

10 __ BSI Annual Report 2012

Corporate governanCe

In light of the new structure that was implemented at BSI AG effective 1 January 2012, the corporate governance principles of the Bank, which were amended to meet the new organisational situation, have been included in the updated versions of the General Management Regulations as well as in the Articles of Incorporation.

orDInArY GenerAl MeetInGThe duties and responsibilities of the Ordinary General Meeting, which is held within four months of the end of the financial year, include the approval and amendment of the Articles of Incorporation; the appointment of mem-bers of the Board of Directors and the external auditor; and the approval of the annual report, and the Group and BSI AG financial statements including resolutions re-garding the appropriation of profit, the discharge of the Board members and other decisions attributed to it by national law (art. 6 and 9 of the Articles of Incorporation). The Ordinary General Meeting, for which minutes are ta-ken, is generally chaired by the Chairman of the Board of Directors (art. 7 of the Articles of Incorporation). The share capital of BSI is equal to CHF 1.84 billion and is divided into 18.4 million registered shares (nominal value of CHF 100). The capital is fully paid up and is held by a sole shareholder: Participatie Maatschappij Graafschap Holland N. V. of Diemen, which is in turn wholly owned directly and indirectly by Assicurazioni Generali SpA of Trieste. The employees of BSI AG do not hold any of the Bank’s share capital.

BoArD oF DIreCtorSAnD tHe BoArD CoMMItteeSThe duties, responsibilities, composition and function of the Board of Directors are regulated by federal law, and in particular by FINMA circular 2008/24 “Supervision and internal control in the banking sector”, and are defined in the Articles of Incorporation (art. 10-14) and in the new General Management Regulations of the Bank (art. 1-10).

The Board of Directors is responsible for the ultimate su-pervision, monitoring and control of the Bank’s manage-ment in accordance with the Swiss Federal Law on Banks and Savings Banks, as well as the applicable articles of the Swiss Code of Obligations.Thus, the Board of Directors is responsible for instituting, regulating, maintaining, supervising and checking on a re-gular basis that there is a suitable internal control system for BSI AG and the Group.

At least one-third of the Board of Directors must com-prise members who satisfy the requirements for inde-pendence stipulated in the FINMA provisions. The Board constitutes itself every year at the meeting following the Ordinary General Meeting. The members are elected for a period of three years and may be re-elected. Their term of office expires on the day of the third Ordinary General Meeting following their appointment. The Board of Di-rectors makes the appointments required in the Articles of Incorporation. In particular, it appoints the Chairman and Vice-Chairman. It has the authority to appoint up to two Vice-Chairmen. The Board of Directors also appoints a secretary, who may also not be a member of the Board.

The composition of the Board of Directors, which for 2012 has nine members, is in compliance with the independen-ce requirements fixed by the FINMA Circular 2008/24 (margin no. 20-24). Meetings of the Board of Directors are called by the Chairman or, if he is unavailable, by the Vice-Chairman. The Board must meet at least four times each year. For decisions to be valid, a majority of the Board members, including the Chairman or the Vice-Chairman, must be present. The Board of Director’s de-cisions are made based on an absolute majority among members present. In the case of a tied vote, the Chairman or the Vice-Chairman has the casting vote. The Board of Directors may also make decisions by correspondence, using the usual methods of telecommunication. The new General Management Regulations stipulate a new deci-sion-making procedure for extremely urgent cases: the Chairman, or if he is not available, the Vice-Chairman, with at least two other members of the Board, may make urgent decisions by unanimity under certain conditions. Minutes of decisions made under this procedure must be written down at the latest during the following meeting of the Board of Directors, with an indication of the members who took the decision.

__ 11

The Chairman or, if he is not available, the Vice-Chairman convenes the Board of Directors at least ten days before the meeting date with a communication indicating the agenda. The Chairman or, if he is not available, the Vice-Chairman chairs the meetings, to which members of the Group Executive Board may also be invited. Any member of the Board of Directors, the Group Executive Board, the Group CEO or, in his absence, the Group Deputy CEO may convene meetings of the Board, indicating their re-asons.

The Board of Directors must, as a committee, satisfy the requirements necessary to execute its tasks in terms of professional competences, experience and availability. For this purpose, the Board of Directors evaluates and documents in writing the achievement of objectives and its working methodology. This self-evaluation was done, as in the previous year, with the support of an external consultant.

The tasks and main powers of the Board of Directors include issuing and modifying the necessary regulations and general directives for organising, managing and su-pervising the activities of BSI AG and the Group, as well as setting the competencies for the Bank’s governing bodies, if these tasks have not been delegated to the Group Executive Board. Furthermore, the Board of Di-rectors decides the medium-term plan for the Bank’s corporate policy, management principles and global risk control as well as approving its risk management policy. It also approves the structure of the general organisational chart and designates the persons authorised to represent the Bank.The Board of Directors prepares the current annual re-port, the annual accounts and the Group accounts, which are presented to the Ordinary General Meeting for ap-

proval, together with a proposal for the appropriation of profit. As part of its monitoring and control duties, the Board of Directors, with the support of the Audit & Risk Committee, examines the reports of the external auditor and Internal Audit, the quarterly Global Risk Report, the trend in large exposures, the financial result, the financial positions, the Bank’s liquidity and the shareholders’ equity at Bank and Group level. Finally, the Board of Directors appoints the Chief Audit Executive, who is responsible for internal auditing at Group level.

The Board of Directors appoints an Audit & Risk Commit-tee, comprising at least three members. They supervise and assess the integrity of the annual financial state-ments, compliance with legal requirements and regula-tions, the effectiveness of the internal and external audits, and the adequacy and effectiveness of the control system of BSI AG and the Group. The duties and responsibilities of the Audit & Risk Committee are defined in specific re-gulations. The Committee meets at least four times each year. Together with the Group Executive Board, Internal Audit and the external auditor, the Audit & Risk Commit-tee examines the annual financial statement. The respon-sibility for the tasks assigned to the Committee remains with the Board of Directors.

The Appointments & Remuneration Committee, appoin-ted by the Board of Directors, comprises at least two members. It is responsible for approving the principles go-verning employees’ fixed and variable remuneration, and the global plan for promotions and development. In par-ticular, this Committee sets salaries for the members of the Board of Directors. It also approves the employment contracts and sets the remuneration of the Group Execu-tive Board and the Chief Audit Executive. The duties and responsibilities of the Committee are defined in specific regulations.

At the meetings of 19 January 2012, 19 April 2012 and 25 September 2012, the Ordinary General Meeting appointed the following new members to the Board of Directors: Mr Ilan Hayim, Mr Pierre E. Genecand and Mr Mario Greco.

12 __ BSI Annual Report 2012

the Year in 2004. In the same year he was also appoin-ted to the Board of Managing Directors of Allianz AG. In 2005 he became the CEO of EurizonVita of the Sanpaolo IMI Group, and thus CEO of Eurizon Financial Group. In 2007 he became the Vice CEO Global Life for Zurich Financial Services, and one year later was appointed CEO and member of the Executive Committee. In 2010 he was appointed CEO General Insurance for Zurich Insurance Group. He held this position until 4 June 2012. He is currently CEO of the Fondazione Assicurazioni Generali and of Generali PPF Holding B.V., and is also chairman of the Board of Directors of Generali (Schweiz) Holding AG. On 1 August 2012, he was appointed Group CEO of Assicurazioni Generali.

Ilan Hayim was born in Geneva, Switzerland, on 3 Novem-ber 1951. He obtained a degree in economics at the HEC business school of the University of Geneva in 1975 and worked there as an assistant for three years. He then held positions at various banking institutions in Switzerland: Paribas (Switzerland), Banca della Svizzera Italiana (as General Manager of the Geneva branch from 1988 to 1992), Banque Unigestion, Union Bancaire Privée, HSBC Guyerzeller initially as a Member of the Executive Board, then as Deputy CEO and finally as Chief Executive Of-ficer. In 2006, he was appointed Vice-Chairman of the Board of Directors of HSBC Private Bank (Suisse) SA, Geneva, and he retained this role until the end of 2011. He joined the Board of Directors of BSI AG, Lugano, on 20 January 2012.

Alfredo Gysi was born in Sorengo, Switzerland, on 3 Oc-tober 1948 and studied in Italy and Switzerland. After earning an undergraduate degree, he went on to obtain a doctorate in mathematics from Milan’s Università Statale in 1973. From 1994 to 2011 he was Chief Executive Of- ficer of BSI AG. He is Chairman of the Association of Fo-reign Banks in Switzerland and a Member of the Board of Directors and the Committee of the Board of Directors of the Swiss Bankers Association (SBA). Since March 2011, he has been a member of the Bank Council of the Swiss National Bank (SNB). He is Chairman of the Foundation Board for the faculties of Università della Sviz- zera Italiana in Lugano, a member of the Board of Direc-tors of that university, and a member of the Foundation Board of the Swiss Finance Institute. A great lover of art and music, Mr Gysi is Vice-Chairman of the Fondazione dell’Orchestra della Svizzera Italiana.

Mario Greco was born in Naples on 16 June 1959. He received a degree in economics in Rome in 1983 and went on to obtain a Master’s Degree in International Eco-nomics and Monetary Theory at the University of Roche-ster in New York in 1986. He started his professional career in 1986 at McKinsey & Company. He became a partner in 1992 and continued working there until 1994. He worked primarily as a financial consultant at banks and insurance companies. In 1995 he became the head of the Claims Division at RAS, in the following year he took on the position of General Manager, and in 1998 he became the Managing Director. In 2000 he was appointed the Chief Executive Officer of Ras, a position he held until 2005. He obtained some major results and awards for the company and for himself, including Insurance CEO of

Alfredo Gysi

Mario Greco

Ilan Hayim

Eugenio Brianti Luigi Butti

Pierre Genecand

Tiziano Moccetti

Nicola Mordasini

Renzo Respini

1 Vice-Chairman until 16 January 2013.

2 Independent member in accordance with FINMA Circular 2008/24.

Appointments & Remuneration

Committee

Vice-Chairman

Chairman

Audit & RiskCommittee

Vice-Chairman

Member

Member

Chairman

Mandateexpires

2014

2015

2014

2013

2013

2015

2013

2014

2014

1, 2

2

2

2

2

2

2

Boardof Directors

Chairman

Vice-Chairman

Vice-Chairman

Member

Member

Member

Member

Member

Member

As at 1 January 2013, the composition of the Board of Directors was as follows:

__ 13

Tiziano Moccetti was born in Caslano, Switzerland, on 4 December 1938. After earning a degree in medicine from the University of Zurich, he specialised in internal medicine and cardiology. He deepened his knowledge of various sectors at university and specialist hospitals in Zurich, returning to Ticino in 1972 to the Ospedale Civico in Lugano as chief cardiologist and medical director. As a Professor at the Faculty of Medicine of the University of Zurich since 1981, he has written more than 300 inter-national scientific publications in the field of cardiology. He is a member and Director of the Cardiocentro Ticino Foundation, Lugano, which he founded in 1995. In addi-tion, he is Chairman and member of various associations and committees for health, in particular cardiology, in Switzerland and abroad. He has held a seat on the Board of Directors of BSI AG since 1985.

Nicola Mordasini was born in Bellinzona, Switzerland, on 7 July 1950. After graduating from the University of Geneva with a degree in economics, he started his professional career in 1974 at Banca del Gottardo. He held numerous positions in various sectors of this bank. In October 1991, he was appointed Senior Executive Vice President with responsibility for the activities of Private & Commercial Banking. In 1998, he took on the position of Vice-Chair- man of the Executive Board, again with responsibilities related to clients and affiliates. He held this position until the beginning of 2008, when he was appointed to the Board of Directors of BSI AG. Lastly, he has held and still holds various mandates with boards of companies and foundations.

Renzo Respini was born in Sorengo, Switzerland, on 2 July 1944. After studying law, he qualified as a lawyer and notary. He has been the Public Prosecutor, and from 1983 to 1995 he was a State Councillor for the Canton of Ticino in charge of the Department of Law, Economics and the Military, and subsequently for the Department of Home Affairs. Until 1999, he was a member of the Council of States in Berne. He is currently joint principal of a law firm and notary’s office in Lugano and Locar-no. He holds positions on the Board of Directors of Alp Transit Gottardo SA, Lucerne, and on the boards of other small and medium-sized companies in Ticino. He is also active in various cultural and humanitarian associations that operate in Switzerland and internationally. He was a Member of Banca del Gottardo’s Board of Directors until early 2008, when he was appointed to the Board of Directors of BSI AG.

Eugenio Brianti was born in Trieste, Italy, on 4 June 1953 and is a Swiss citizen. After finishing high school in Lu-gano, he studied at the University of Parma, where he received a doctorate in economics and business in 1979. He worked briefly at UBS before starting at BSI in 1980. Over the years he has held various positions, including the coordination of the development and control office for the Swiss branches. In 1989, he became manager of the St. Moritz branch, and a year later he was appointed manager of the Chiasso branch.In 2003, he took on the position of head of Private Banking for Ticino and Graubünden. In 2005, he was na-med Executive Vice President, and in 2008 Senior Exe-cutive Vice President. Since 1 January 2011 he has been a member of the Board of Directors of BSI and a member of the Board of Directors of FINMA, the Swiss financial market supervisory authority, by appointment of the Swiss Federal Council. He is Chairman of Funicolare Lugano-Paradiso-Monte San Salvatore SA, Vice-Chairman of Società Autolinee Regionali Luganesi and a Member of Finnat Gestioni SA.

Luigi Butti was born in Vacallo, Switzerland, on 25 Novem-ber 1940. After graduating from the Business College of Maria-Hilf (canton of Schwyz), he honed his professional skills at various credit institutions and brokers, such as Credit Suisse in Zurich, Rued, Blass & Cie in Zurich, and Hirsch & Co. in New York. He began his career at BSI AG in 1969 as a relationship manager, and then took over responsibility for the financial division and private clients department. In 1990, he was appointed Senior Executive Vice-President, and in 1998 he became Deputy CEO of BSI AG, a position he held until 2004, when he became a member of the Board of Directors of BSI AG. He is also a member of the Cardiocentro Ticino Foundation, Lugano, and since 2011 he has been Chairman of the San Salva-tore Foundation, Lugano.

Pierre E. Genecand was born in Geneva, Switzerland, on 26 March 1950. He has many years of experience in the international banking and insurance sector, particularly in portfolio management for life insurance and pension funds. He spent most of his career working at Gesrep SA, a Geneva-based company that operates in insurance portfolio management for private and institutional clients. He managed the company from 1982 and was its Chair- man from 1992 until 2005. Among his other roles, he has been Chairman of the PatrimoniA Foundation, an entity that supports small and medium-sized companies in the area of pension funds. Until 2003 he was Vice-Chairman of the Swiss Insurance Brokers Association (SIBA). From 2003 until 2011 Pierre Genecand was also a member of the Board of Directors at HSBC Private Bank Suisse and at HSBC Guyerzeller Bank.

14 __ BSI Annual Report 2012

Group exeCutIve BoArDThe Group Executive Board (hereinafter: GEB) is responsi-ble for the operational management of the Bank. Its mem-bers are appointed by the Board of Directors. It manages the Bank, in particular, by carrying out the following tasks. It decides the short- and medium-term objectives within the general framework set by the Board of Directors, takes all measures needed to achieve these objectives, presents proposals in support of decisions taken by the Board of Directors, and proposes to the Board of Directors the general policies and strategies of the Bank. In carrying out its functions, the GEB represents the Bank, drafts the medium-term plan and the annual budget (both of which are submitted to the Board of Directors for appro-val), implements the risk management policy, monitors trends and prepares the quarterly report on liquidity and shareholders’ equity, appoints Assistant Vice Presidents and Assistant Treasurers, signs agreements with profes-sional associations, establishes the human resources po-licy, and issues provisions required for the execution of the General Management Regulations. The GEB is required to keep the Board of Directors informed of business trends and the Bank’s situation by presenting to the Board and commenting upon respective reports and documents. The GEB acts as a collective body in carrying out its functions. Its tasks, responsibilities and reporting duties are defined in the General Management Regulations (art. 11-16).

The GEB is supported in its activities by several perma-nent committees with decision-making powers: the Finan-cial Risk & Capital Allocation Committee, the Operational Risk & Compliance Committee, the Operational Efficiency Committee, the Business Policy & Development Commit-tee, the Credit Committee and the Counterparty & Broker Committee.

Lastly, the GEB proposes the composition of the Group Advisory Board, which is approved by the Board of Direc-tors. The Group Advisory Board is a committee with adviso-ry powers chiefly in relation to strategic issues surrounding business development at BSI AG and the Group.

As at 1 January 2013, the composition of the Group Exe-cutive Board was as follows:

Stefano Coduri, Group CEOGianni Aprile, Deputy Group CEO, Strategic Planning & Corporate FinanceNicola Battalora, Senior Executive Vice President, BSI EuropeHanspeter Brunner, Senior Executive Vice President, BSI AsiaRajiv Pradhan, Senior Executive Vice President, Corporate ServicesGérald Robert, Senior Executive Vice President, BSI Latin America & Middle EastRenato Santi, Senior Executive Vice President, BSI Switzerland

CoMpenSAtIon 2012 (CHF GroSS AMountS) oF tHe MeMBerS oF tHe Group exeCutIve BoArD

Annual base salary

Short term incentive

Long term plan (deferred payment)

Total

The disclosed amounts refer to seven members of the Group Executive Board. One member of the Board left (retirement) at the end of June 2012 and two ones (new appointments) joined in July 2012. All the amounts but the ones related to the long term plan, do not include the employer contributions to social securities as well as all other additional insurances and unemployment. The long term plan amounts are deferred and paid by instalments according to the rules of the Plan.

Stefano Coduri, born in Mendrisio, Switzerland, on 25 May 1964, has been CEO of BSI since 1 January 2012. After obtaining a degree in finance and accounting from the University of St. Gallen, he joined BSI in 1989 and has spent his entire career at the bank. He was appointed to the Executive Board in 2004. He successfully led the most important projects involving the Bank in recent years, inclu-ding the integration of Banca Unione di Credito (BUC), ac-quired in 2006, and Banca del Gottardo, acquired in 2007, and the implementation of a new IT platform for the entire BSI Group. Before taking over his present position, Stefano Coduri was Head of Banking Platform (group operations), a position that enabled him to acquire a wealth of expe-rience in various segments of the Bank, including private banking, product management and organisation.

2012

CHF

3’583’265

3’924’336

2’507’224

10’014’824

__ 15

Gianni Aprile, born in Zurich, Switzerland, on 18 October 1951, has been CEO of BSI Strategic Planning & Corpo-rate Finance since January 2013 and deputy CEO of the BSI Group since 2007. After obtaining degrees in eco-nomics and sociology from the University of Geneva, in 1978 he received a Master’s Degree in econometrics and he began his career as scientific researcher at the Federal Polytechnic of Zurich and the University of Geneva, where he earned a PhD in economics and social sciences in 1983. After three years at Paribas Suisse as Head of In-ternal Control and Risk Treasury Management, he joined BSI in 1987, where he successfully filled important roles of responsibility inside the BSI Group. In 1999 he was appointed General Director. Before taking over his pre-sent position, Gianni Aprile was Head of Private Banking Switzerland of the BSI Group, Head of Corporate Center, Head of Financial Services, thus acquiring a wealth of experience in various segments of the Bank, including asset management, products and services, logistics and operations. Gianni Aprile also fills other important institu- tional positions: he is Chairman of the Board of Directors of Patrimony 1873, member of the Board of Directors of B-Source and member of the Scientific Board of Univer-sity of Applied Sciences and Arts of Southern Switzerland (SUPSI).

Nicola Battalora, born in Lugano (Switzerland) on 10 January 1962, has been CEO of BSI Europe since July 2012 and Head of BSI Luxembourg since 2010. After graduating in Business & Administration at the St. Gallen University, in 1987, he began his professional career as General Manager Assistant at the Ente per il Turismo Ticinese. Nicola Battalora joined the BSI Group in 1989 and started work in the Offshore Banking Operations unit at the Lugano head office. He subsequently worked in the Control of Overseas Subsidiaries unit until 1992, gaining considerable experience in international banking. Subse-quently Mr Battalora obtained Securities & Financial De-rivates Representative Certification in London and had various roles in the offices of Guernsey and Nassau, where he spent a long period as Senior Vice President. Before taking over his present position, Mr Battalora filled the role of CEO BSI Bank Ltd. Singapore from 2005 to 2010.

Hanspeter Brunner, born in Steckborn (Switzerland) on 12 April 1952, has been CEO of BSI Asia since 2010, over-seeing Singapore operations and heading up the strategic development of BSI in the Asian markets. He has thirty years’ experience and an in-depth knowledge of the private banking sector. After the degree, Mr Brunner worked di-rectly in the Asian markets for over 20 years, first with Cre-dit Suisse and then with RBS Coutts, including positions such as CEO of RBS Coutts International and Executive Chairman of RBS Coutts Asia. He thus acquired a deep knowledge and understanding of the Asian private banking landscape. During his career, Mr Brunner was classified “Outstanding Private Banker Asia Pacific” in 2008 by Pri-vate Banker International, and “Asian Private Banker of the Year 2010” by the Asian Private Banker publication in 2011. A Swiss National, Hanspeter Brunner became a Singapore Permanent Resident in 2007 and has held numerous extra-professional positions in both Singapore and Hong Kong as a Board member of the Association of Foreign Banks in Switzerland, Council member for the British Swiss Chamber of Commerce, and the President of the Swiss Business Council.

Rajiv Pradhan, born in New Delhi (India) on 11 June 1955, has been CEO of BSI Corporate Services since 2010, with responsibility for the departments of Finance, Risk Management, Group Credit Officer, Legal & Compliance, Group Investment Services, Capital Markets and Banking Platform. After obtaining a degree in Economics from the London School of Economics, a professional qualification as a Chartered Accountant at Peat Marwick in London, and an MBA from INSEAD of Fontainebleau, he began his professional career as an internal auditor of Olivetti Group subsidiaries worldwide. He then continued his professional development at Hermes Precisa International (Yverdon/Lausanne), a company then acquired by Olivetti. He has been at BSI since 1987, holding many important roles in the Group Accounting, Budgeting, Planning, Operations and Logistics. In 2001 Rajiv Pradhan was appointed as a mem-ber of BSI Executive Board and Head of Operations & Logistics, a position that he kept until 2004. In 2005 he became CEO of B-Source, a company providing Informa-tion Technology Outsourcing (ITO) & Business Process Outsourcing (BPO) services, which during those years was wholly owned by the BSI Group. In 2008 he was appointed Chief Financial & Risk Officer of BSI Group and has assu-med his current position from 2010.

16 __ BSI Annual Report 2012

Gérald Robert, born in Rome (Italy) on 14 November 1957, has been CEO of BSI Latin America & Middle East since July 2012 and since 2001 he has been Director at BSI and Branch Manager in Geneva, as well as Area Manager of Latin America. In this role, he is responsible for mana-ging both domestic and international banking for Gene-va branch in addition to Latin America worldwide. After graduating in International politics and economics from George Washington University, he studied for a Master of Arts at the John Hopkings University of Washington D.C., specialising in Economics and Finance, and worked as Research Associate for the Department of state arms and control and disarmament agency. From 1983 to 1985 he worked for the Banker Trust Company of New York as a private banking relationship manager for Europe and Latin America. In 1985 he joined the New York branch of BSI as Account Manager and was responsible for maintai-ning and developing private banking clients in Latin America and Europe. In 1987 he moved to Venezuela, where he has managed the bank since 1989 and in 1990 he became Senior Representative of BSI in Argentina. From 1993 to 2001 he was Director of BSI Monte Carlo.

Renato Santi, born in San Vittore, Switzerland, on 27 Oc-tober 1969, has been CEO of BSI Switzerland since 1 January 2013. Santi started working for BSI in 1994 and has spent his entire career with the bank. In 2011 he joined the bank’s Executive Board as the head of the Personal Banking division. Renato Santi is a graduate in economics from the University of St. Gallen. In the course of his career at BSI he has successfully taken charge of va-rious strategic development projects. Since entering the management of BSI AG’s Private Banking division in 1996 and subsequently becoming head of the division in 2002, Santi has been responsible for Product Manage-ment (Lugano), Corporate Services at BSI Ifabanque (Pa-ris) and Strategic Marketing & Support Services (Lugano).

InternAl AuDItInternal Audit is the department that, at group level, per-forms independent evaluations and reviews of the inter-nal control system, thereby contributing to the ongoing adjustment of the control system as needed. It coordina-tes its activities with those of the external auditor. Internal Audit reports directly to the Board of Directors and thus to the Audit & Risk Committee. Internal Audit reports pe-riodically to the Committee on the actions it has carried out, and it also reports to the Board of Directors once a year. Written reports on the results of audits conducted by Internal Audit are produced and sent to the Chairman of the Board of Directors and the Audit & Risk Committee. A copy is also sent to the members of the Group Executive Board and to the external auditor. The scope, authorities and responsibilities of Internal Audit are defined in the General Management Regulations and in the Group In-ternal Audit Regulations. The Chief Audit Executive, who is appointed by the Board of Directors, is Mr Nicola Gu-scetti. He has held this position since 1 January 2012.

externAl AuDItorThe external auditor checks the Group accounts and the annual reports of the Bank in accordance with legal provi-sions and regulations in force in Switzerland. The exter-nal auditors’ mandate as defined in the Swiss Code of Obligations was granted for the last financial year to the Geneva branch of Ernst & Young in Lancy, Switzerland. It was renewed by the Ordinary General Meeting of BSI AG on 31 March 2011 for the period 2011-2013. The head auditor is Mr Didier Müller.

__ 17

BSI AG – ORGANISATION CHART

(situation as of 1 January 2013)BOARD OFDIRECTORS

INTERNAL AUDIT

Nicola Guscetti

CORPORATE SERVICES

Rajiv Pradhan 1

GROUP HR, ORGANISATION & INTERNAL COMMUNICATION

Vincenzo Martino

STRATEGIC PLANNING & CORPORATE FINANCE

Gianni Aprile 1

GROUP ExECUTIVE OFFICE

David Matter

MERCHANT &INVESTMENTBANKING

Vincenzo Piantedosi

BSI EUROPE

Nicola Battalora 1

BSI SWITZERLAND

Renato Santi 1

BSI ASIA

Hanspeter Brunner 1

BSI LATIN AMERICA& MIDDLE EAST

Gérald Robert 1

GROUP CHIEF ExECUTIVE OFFICER

Stefano Coduri 1

1 Members of the Group Executive Board.

18 __ BSI Annual Report 2012

oUr organIsatIonaL strUCtUre

After the consolidation of the new organisation structure in three regions based on Private Banking activities was completed and the structure of Corporate Services and the staff units were strengthened in 2011, the year 2012 saw an additional organisational optimisation. This in-volved separating the activities focused on the markets of Latin America and the Middle East from BSI Switzerland and defining a new dedicated region to them. Additionally, the Institutional & Family Office division was transformed into an independent legal entity, wholly owned by BSI AG, called Patrimony 1873. This represents an additional fine-tuning of the service excellence offered in integrated asset management for wealthy clients, through the use of dedicated tools entirely organised to guarantee wide-ranging protection and management of risks, as well as continual monitoring of investments. This new structure is compatible with both the original objective – to guarantee greater client focus depending on the specific market area, both with respect to individual needs and to devel-oping specific opportunities for private and institutional clients – and the ongoing improvement of internal pro-cesses and services.

BSI SwItzerlAnDThe BSI Switzerland region continued its strategic devel-opment activities in the Private Banking segment in the following key geographical areas. A branch will be opened in the Italian market, which has always been of central importance to BSI. This strategic choice will strengthen the banking services offered in Italy. Consequently, the EOS Servizi Fiduciari SpA and BSI Wealth & Family SIM SpA units were assigned to BSI Switzerland. In the Swiss domestic market, measures were also taken to accelerate the pace of growth in the regions of Zurich and French-speaking Switzerland by enhancing the current advisory and wealth management process. Activities also con-tinued to strengthen the offering and service model for the growth segment of External Asset Managers in the three main Swiss cities. Additionally, the Personal Bank-ing service model was further developed towards an efficient, innovative, multi-channel model dedicated to clients in this segment. Moreover, it was clear that BSI’s international outlook and the attractiveness of the Swiss financial centre are appreciated by foreign clients. In par-ticular, entrepreneurs and professionals from the rapidly developing markets in Central and Eastern Europe value the opportunity to diversify their assets and investments geographically, and they appreciate the excellent service provided. Against this backdrop, the central role of the staff units was confirmed, especially of the CEO CH Of-fice, Investment Solutions and Wealth Planning, which act as specialist competency centres for the entire Swiss structure.

In particular, the CEO CH Office provided structured sup-port in terms of reporting and controlling, coordinated management for all the project activities that impact the front office structures, and the basis for integrated use of the different marketing resources. The Investment Solutions unit, which is responsible for managing and administering mandates as well as providing specialist support in the area of investment advice, contributed to the development of the range of products and services dedicated to various client segments and made it possi-ble to better personalise advisory activities at the invest-ment level. Finally, thanks to the Wealth Planning unit, which is specialised in tax, company, succession, pension and insurance planning, it is possible to offer clients first-class advice in a highly complex, constantly changing re- gulatory environment.

BSI europeThe region BSI Europe retains responsibility for the Eu-ropean affiliates BSI Monaco SAM, BSI Luxembourg SA and Oudart SA, as well for Spain and Germany, which are assigned to the Geneva and Zurich branches respectively. The structure includes the CEO Europe Office, whose mission is to provide targeted, coordinated support that is focused on business development and related manage-ment tools, the optimisation of processes, and controlling and reporting activities.

BSI ASIA The Bank continued to develop its operations in Asia in 2012. BSI Bank Ltd (Singapore) is the main affiliate out-side Lugano, with over 250 employees. BSI obtained a banking license from the Hong Kong Monetary Authority (HKMA), allowing the Bank to best take advantage of growth opportunities in North Asia. BSI Asia is moving ahead with its development in a key region for the success of the Bank’s growth and business diversification stra- tegy.

BSI lAtIn AMerICA & MIDDle eAStIn view of the need to increase geographical focus on international markets, the new Latin America & Middle East region was set up in 2012. It has taken on activities in these areas that were previously covered by BSI Switzer-land. The Latin America & Middle East region is responsi-ble for client management activities in Latin America (via its local presence in Argentina, Uruguay and Panama),

__ 19

the Middle East, Turkey and the Eastern Mediterranean. The BSI Group’s presence was developed further in the Middle East with the transformation of the representative office in Bahrain into a branch. In addition, the Bank has applied to obtain authorisation to open a representati-ve office in Istanbul. Approval is expected to be granted in early 2013. This is another major step in the Group’s international expansion strategy, and it reflects the im-portance that BSI attaches to the Turkish market, which offers significant growth potential in wealth management.

CorporAte ServICeSThe Corporate Services division includes the departments of Finance, Risk Management, Group Credit Office, Le-gal & Compliance, Banking Platform, Group Investment Services, and Capital Markets. The division provides sup-port services for the BSI Group. This includes the risk framework and risk policies, as well as financial manage-ment, including the consolidated financial statements. In addition, the division provides logistics and IT services, and also defines banking processes. It is responsible for investment policy, provides analyses and strategies, de-velops products and services for clients, and manages all activities on the financial markets. Additionally it provides support to the committees of the Group Executive Board.In addition to its ordinary activities in 2012, the Finance unit improved the analytical accounting instruments that support management. Risk Management prepared the Bank for the implementation of the Basel III requirements, and also focused on improving the management of capi-tal. A new organisational structure was defined for the Group Credit Office, which also consolidated its operat-ing processes. The Legal & Compliance unit monitored and integrated the recent developments in the regula- tory environment, including the implications of the tax agreements. Following the major IT migration that was completed during the previous year, the Banking Platform consolidated and stabilised the new IT platform. Group Investment Services obtained positive results in its in- vestment fund management and provision of services to the various units of the Group. The Capital Markets unit contributed positively to the Group’s results, whilst ex- panding its foreign exchange services by offering a 24-hour service.

MerCHAnt & InveStMent BAnkInGThe main objective of the Merchant & Investment Banking division is to provide highly specialised services and iden-tify investment opportunities for institutional and private clients at international level. The division supports Private Banking by analysing and implementing corporate finan-ce and extraordinary financing solutions, as well as acting as a point of reference for private equity operations and

estate planning. In addition, the division is responsible for monitoring the affiliate BSI Overseas (Bahamas), and it recently strengthened its service offering with the ope-ning of BSI Merchant in Milan.

StrAteGIC plAnnInG & CorporAte FInAnCeThe objective of the new Strategic Planning & Corporate Finance division is to provide corporate financial advisory services to individual, corporate and institutional clients, in particular as regards mergers and acquisitions, IPOs, feasibility studies and business plans. It also acts as a centre of competence for the various business areas with regard to corporate development. In addition, the division has responsibility at Group level for strategic planning. Specifically, the division undertakes ongoing analyses of the business model and different strategic options, coor-dinates business plans and monitors the implementation and the returns from its various activities.

Group HuMAn reSourCeS, orGAnISAtIon & InternAl CoMMunICAtIonThe Human Resources, Organisation and Internal Com-munication division has been entrusted with the funda-mental mission of developing and managing the Group’s human resources. This involves: selection, recruitment and internal mobility measures to ensure the Bank has the right staff; remuneration policies; and all administra-tive services relating to compliance with legal provisions. Moreover, in addition to the traditional but also, at times, advanced activities of training, developing and managing new staff, the division also manages the internal organi-sation and its compliance with business objectives, and ensures that the Mission, Vision, Values and Competen-cies are in line with the corporate culture by defining and managing internal communication policies.

Group exeCutIve oFFICeThe Group Executive Office supports the CEO in the ex-ercise of his duties, and in particular, in the drafting and coordinating of strategic decisions; the Group’s internal control activities; relations with the shareholder, the au-thorities and other entities and institutions; and exter-nal communication activities. For all these activities, the department acts as a comprehensive service centre at Group level. The Group Executive Office thus consists of the following services: General Secretariat, Strategic Planning & Marketing, Media Relations, and Group Inter-nal Controls.

20 __ BSI Annual Report 2012

HeADCountIn 2012 the number of full-time equivalent (FTEs) em-ployees at the BSI Group remained largely unchanged, at 1,962.55 on 31 December 2012 compared with 1,964.40 at the end of 2011. The number of FTE employees in Switzerland reduced slightly, from 1,345.95 to 1,317.15, while the Bank’s presence in Asia continued to grow, with 316.50 employees as at 31 December 2012 compared with 310 at the end of 2011. The total number of employees outside Switzerland as at 31 December 2012 was 645.40. reMunerAtIon polICYBSI has a careful remuneration policy that aims to uphold the Bank’s competitiveness in the market and maintain fairness within the Bank, as well as a balance between short- and long-term incentivisation in order to create value for the company over time.

orGAnISAtIonThe activities associated with corporate organisation in 2012 focused on constantly fine-tuning the processes for the new Corporate Governance and the publication of Human Resources Policies in support of it.

trAInInG & DevelopMentTraining & Development activities in 2012 were primarily focused on the management of organisational develop-ment projects linked to the Group’s first climate survey conducted in the autumn of 2011. The participation rate in the survey was very high (87%). The careful analysis of the results produced action in individual sectors, under the coordination of Human Resources. In addition, the survey resulted in some cross-divisional initiatives, such as the Young People Program and a course on Gender Diversity (WhatWomenWant@BSI). In addition to the usual team-building and outdoor activities based on spe-cific requests and the management of numerous indi-vidual development plans launched in the previous year, the year 2012 also saw the start of the BSI Leadership Academy. All internal management training programmes will now fall under the BSI Leadership Academy with the completion of the courses that had been launched previ- ously under the Leadership Programme. In addition, 2012 saw the start of a course focused on BSI Asia, as well as the first International Leadership Programme, which was held in Lugano. Managers from all BSI loca-tions attended this event. In the area of technical and professional training, the BSI Private Banking Business Academy offered educational activities aimed at adapting regulatory and fiscal com- petencies to the changing environment, in addition to its usual catalogue of internal training courses on banking behaviour and managing ad hoc training programmes.

HUman resoUrCes

__ 21

InternAl CoMMunICAtIonInternal Communication made a major change to its traditional approach by placing increasing emphasis on multimedia channels and launching a monthly newsletter from the Group Executive Board for all employees. In ad-dition, Internal Communication acts as an interface for all the initiatives set up to disseminate the Bank’s Mission, Vision, Values and Competencies throughout the organi-sation in order to maintain a strong corporate culture and identity. In particular, several informal gatherings between top management and employees were organised. These events were met with widespread satisfaction.

BSI StAFF CoMMItteeIn 2012 the staff committee continued its important work representing staff’s information and participation rights. To meet the needs of employees and to give due at- tention to environmental and traffic issues, the Bank decided to promote the corporate Arcobaleno programme once again as part of the internal project “Environmental sustainability in cooperation with the Staff Committee”. The corporate Arcobaleno programme allows employees to use all public transport within the zones indicated on their travel pass, or to obtain an annual pass at a discount.

Companies with a strong identity have the ability to pros-per across various economic cycles, during various tech-nological phases and in various parts of the world, while also helping to develop the societies in which they oper-ate. These are companies, such as BSI, that have been able to reinvent themselves over time while maintaining a distinct identity.

our HIStorY The Banca della Svizzera Italiana, with its head office in Lugano, was founded in 1873 thanks to the financial support of Kreditanstalt in Zurich, the Basler Bankverein and the Banca Generale di Roma, and with the participa-tion of local backers in Ticino (Carlo Battaglini, Annibale Bollati, Luigi Enderlin, Rodolfo Landerer, Pasquale Luc-chini, Giuseppe Soldini, Pasquale Veladini, Giovan Battista Ferrazzini and Clemente Maraini sen.). A few years after its founding, the Bank moved to the 18th century home of the Marquis of Riva, which it still owns and uses as its head office. In the final decades of the 19th century, the institution was active on the domestic market. In particu-lar, it supported initiatives to develop regional transport and the hotel and catering sector. Nonetheless, the Bank was also active in Italy thanks to the personal relation-ships of its directors. The Bank survived the banking cri-sis of 1914, although two cantonal institutions – Banca Cantonale Ticinese di Bellinzona and Credito Ticinese di Locarno – did not. The Banca Popolare Ticinese di Bellinzona was also forced into liquidation. Following this crisis, the Banca della Svizzera Italiana continued to grow its presence in the Swiss market, and later, starting in the 1960s, it also expanded internationally. Total assets rose from CHF 102 million in 1950 to more than CHF 1 bil-lion in 1970 and to CHF 9.2 billion in 1990. This growth was also accompanied by an increase in the number of employees, from 357 in 1970 to 1,761 in 1990, of whom 1,638 were working in Switzerland. In the early 1990s the Bank restructured its business and organisation, spe- cialising in wealth management for private Swiss and international clients. The Bank, which has meanwhile changed its name to BSI, has expanded again in recent years through client acquisition and also thanks to the recovery of banks in general operating in the Ticino finan-cial centre. At the same time, the Bank has undergone a major international expansion, especially in Asia, in order to diversify its market presence.

keY DAteS 1873 Founding of the bank with the name Banca della Svizzera Italiana. 1874 Opening of agency in Locarno, transformed into a branch in 1914. 1879 Opening of agency in Bellinzona, later sold to the new company Banca Popolare Ticinese in 1884.1881 The Bank begins issuing banknotes, a function it maintains until the Swiss National Bank is founded in 1907. Opening of agency in Mendrisio, transformed into a branch in 1955 (closed midway through the 1990s). 1905 Opening of agency in Chiasso, transformed into a branch in 1924. 1908 Acts as an agency for the Swiss National Bank in the Sottoceneri region of Ticino.1914 Opening of branch in Bellinzona. 1935 Opening of branch in Zurich. 1969 Swiss Italian Banking Corporation Ltd, Nassau, is founded, marking the start of the Bank’s international expansion.1971 Acquisition of Adler Bank Basel AG, Basel. 1973 Opening of branch in St. Moritz. On the occasion of the bank’s centenary, the Fondazione del Centenario della Banca della Svizzera Italiana is founded. 1975 Acquisition of a majority stake in Banque Romande in the French-speaking part of Switzerland. 1976 Acquisition of a significant stake in Compagnie Monegasque de Banque, Monaco. Opening of a representative office in Caracas. 1980 Acquisition of a participation in Domus Bank, Zurich. 1990 Opening of BSI Finanziaria SpA, Milan, which in 2002 becomes Banca BSI Italia SpA, Milan, and which is later sold to Banca Generali, Milan.

22 __ BSI Annual Report 2012

oUr IdentIty

__ 23

CHAIrMen oF tHe BoArD oF DIreCtorS• Pasquale Veladini, 1873-1874• Pasquale Lucchini, 1874-1892• Clemente Maraini, 1893-1905• Giacomo Blankart, 1905-1920• Adolfo Soldini, 1920-1927• Otto Maraini, 1927-1944• Marco Antonini, 1944-1955• Antonio Lory, 1955-1966• Carlo Pernsch jr., 1966-1974• Ettore Tenchio, 1975-1983• Gianfranco Antognini, 1983-1991• Franco Masoni, 1991-1993• Alberto Togni, 1993-1998• Hugo von der Crone, 1998-2004• Giorgio Ghiringhelli, 2004-2011• Alfredo Gysi, since 1 January 2012

exeCutIve DIreCtorS• Giacomo Blankart, Director 1873-1888• Innocente Gianinazzi, Director 1888-1918• Carlo Pernsch sen., Director 1918-1926• Guido Petrolini, Director 1926-1927 • Adolfo Hediger, 1928• Antonio Lory, Director 1928-1942 and Managing Director 1943-1955• Carlo Pernsch jr., Director 1943-1955 and Managing Director 1956-1966• Gianfranco Antognini, Senior Executive Vice President 1966-1968 and Managing Director 1969-1983• Giorgio Ghiringhelli, Chief Executive Officer 1983-1994• Alfredo Gysi, Senior Executive Vice President and Chief Executive Officer 1994-2011• Stefano Coduri, Group CEO, since 1 January 2012

1993 Separation of assets and liabilities related to commercial activity, founding of the company SBSI Holding SA, Lugano. 1994 The asset management company in Monaco is transformed into a bank (the current BSI SAM Monaco).1995 Founding of Boss Lab SA, an IT services company for financial institutions and which later becomes B-Source. 1998 On the occasion of the 125th anniversary of BSI, the BSI Gamma Foundation is created, a foundation that supports academic research in the financial field. 2000 The company’s name is changed to BSI AG. Opening of office in Lausanne, which is later transformed into a branch.2005 Opening of BSI Bank Ltd, Singapore. 2006 Acquisition of Banca Unione di Credito, Lugano. 2008 Acquisition of Banca del Gottardo, Lugano. Licence obtained for operating in the Kingdom of Bahrain. 2010 Opening of an agency in Crans-Montana.2011 Sale of 51% of B-Source and IT migration from the BOSS system to Avaloq.2012 BSI expands its Asian business and opens a branch in Hong Kong. Incorporation of Patrimony 1873, a wholly controlled wealth management company. Middle East business continues to grow with the representative office in the Kingdom of Bahrain being upgraded to a branch.

SHAreHolDerS1910 Acquisition of a majority share package by Banca Commerciale Italiana, Milan.1983 Irving Trust Co., New York, takes over the share package from Banca Commerciale Italiana. 1988 Unigestion SA, Geneva, obtains the share package from Irving Trust Co. and later sells a minority stake to Tayio Kobe Bank. 1991 Swiss Bank Corporation, Basel, becomes the majority shareholder. 1998 Assicurazioni Generali, Trieste, becomes the sole shareholder.

24 __ BSI Annual Report 2012

our vAlueSOur values represent who we are, our DNA. They make us a unique Bank, different from the competition.Our values are a beacon that guides us in the midst of the great changes that are transforming our company on a constant basis. They always remind us of who we are, inspiring our actions as we pursue our objectives.

CoMpetenCe

Our craft is private wealth management. We carry out our business earnestly, reliably and discreetly, to offer our clients – year after year, generation after generation – a high-quality service based on a variety of special com-petencies and characterised by a balanced risk/return profile.