analisis-kasus-coca-cola-company 2

TRANSCRIPT

MANAJEMEN STRATEGIK

ANALISIS KASUS

COCA-COLA COMPANY Dosen Pengampu: Lilik Wahyudi, S.E., M.Si.

Kelompok H

1. Fatania Latifa F0307049

2. Hermin Arifianti F0307055

3. Jarmiatun F0307059

4. Ratih Indah F0307075

JURUSAN AKUNTANSI FAKULTAS EKONOMI

UNIVERSITAS SEBELAS MARET SURAKARTA

2009

1

Kelompok H

PENDAHULUAN

Industri Minuman Ringan

Sekarang ini perkembangan dunia industri semakin maju, hal itu terbukti dengan banyaknya

industri-industri baru yang mengelola berbagai macam produk. Dengan demikian, kebutuhan akan

faktor-faktor produksi menjadi bertambah banyak.

Di Indonesia, minuman ringan mudah sekali diperoleh di berbagai tempat, mulai dari

warung sampai toko-toko kecil. Minuman ringan dikonsumsi oleh semua lapisan masyarakat dari

berbagai latar belakang pendidikan dan pekerjaan. Dengan konsumsi minuman ringan yang

sedemikian luasnya, produk minuman ringan bukanlah barang mewah melainkan barang biasa.

Saat ini, Indonesia mencatat tingkat konsumsi produk-produk Coca-Cola terendah (hanya 13

porsi saji seukuran 236 ml per orang per tahun), dibandingkan dengan Malaysia (33), Filipina (122)

dan Singapura (141). Karena minuman ringan merupakan barang yang permintaannya elastis

terhadap harga, berbagai upaya dilakukan agar harga produk-produk minuman ringan tetap

terjangkau. Elastisitas harga minuman ringan terhadap permintaan adalah -1.19 yang berarti bahwa

saat terjadi kenaikan harga, volume penjualan akan berkurang dengan prosentase yang lebih besar

daripada prosentase kenaikan harga tersebut.

Ditinjau dari segi penciptaan kesempatan kerja, industri minuman ringan memiliki efek

multiplier yang besar pada tenaga kerja. Dengan rasio sebesar 4,025, industri minuman ringan

menduduki pringkat ke - 14 dari 66 sektor industri lainya di seluruh Indonesia. Ini berarti bahwa

untuk setiap peluang pekerjaan yang tercipta, atau hilang, di industri minuman ringan, empat

kesempatan kerja akan tercipta, atau hilang, di tingkat nasional.

Delapan puluh persen penjualan minuman ringan dilakukan oleh

pengecer dan pedagang grosir dimana 90% diantaranya termasuk

dalam kategori pengusaha kecil. Bagi para pengusaha kecil tersebut,

produk minuman ringan merupakan barang dagangan terpenting

mereka dengan kontribusi sebesar 35% dari total penjualan dan nilai keuntungan sebesar 34%.

Industri-industri penunjang lainnya yang terkena dampak kegiatan industri minuman ringan

meliputi gelas, tutup botol, transportasi dan media.

2

Kelompok H

Coca-Cola Bottling Indonesia merupakan salah satu produsen

dan distributor minuman ringan terkemuka di Indonesia. Perusahaan

ini memproduksi dan mendistribusikan produk-produk berlisensi dari

The Coca-Cola Company.

Coca-Cola Bottling Indonesia merupakan nama dagang yang

terdiri dari perusahaan-perusahaan patungan antara perusahaan-

perusahaan lokal yang dimiliki oleh pengusaha-pengusaha

independen dan Coca-Cola Amatil Limited, yang merupakan salah

satu produsen dan distributor terbesar produk-produk Coca-Cola di

dunia.

asi yang tinggi dalam memproduksi dan mengelola

berbagai aspek teknis dan pengawasan mutu.

tur melaksanakan

audit di bidang pengawasan mutu, lingkungan, kesehatan dan keselamatan kerja.

melampaui standar yang ditetapkan untuk

pabrik-pabrik sejenis di berbagai lokasi lain di dunia.

PEMBUATAN COCA-COLA

sumen berawal dari bahan baku pilihan

berkualitas tinggi yang diproses melalui beberapa tahapan:

Semua produk yang dijual dan didistribusikan oleh Coca-Cola

Bottling Indonesia diproduksi di Indonesia. Saat ini terdapat 10 pabrik

pembotolan yang tersebar di seluruh Indonesia. Walaupun kebijakan

dan pengembangan produksi diarahkan oleh National Office yang

berkedudukan di Cibitung, Bekasi, setiap pabrik memiliki manajemen

yang memiliki pengalaman luas dan kualifik

Semua pabrik diwajibkan mematuhi dan bahkan kerap kali melampaui berbagai ketentuan

internasional dan peraturan perundang-undangan yang berlaku, dan secara tera

Selama ini pabrik-pabrik kami di Indonesia telah menerima berbagai penghargaan dari The

Coca-Cola Company atas pencapaian standar yang

Minuman Coca-Cola sebelum sampai ke tangan kon

3

Kelompok H

1. Tahap pertama untuk menhasilkan Coca-Cola sangat

sederhana, yaitu membuat sirup yang terdiri dari gula

dan air. Airnya disaring dengan seksama karena bagi

"Coca-Cola" bahan baku berkualitas tinggi sangat

mutlak diperlukan.

2. Untuk memastikan bahwa air yang digunakan untuk

produk botol dan kaleng benar-benar bersih dan murni,

air tersebut disaring. Para teknisi pengawasan mutu

menguji air tersebut berkali-kali sebelum digunakan

untuk membuat produk akhir.

3. Pemeriksaan dan pengujian berlanjut. Perangkat

canggih membantu para teknisi memeriksa segala segi

proses, mulai dari kondisi tiap kemasan hingga kadar

karbondioksida, rasa dan kandungan sirup. Pada tahap

ini, campuran sirup diperiksa.

4

Kelompok H

4. Sirup kemudian ditambahkan dengan konsentrat

"Coca-Cola". Sari rasa untuk "Coca-Cola ini dibuat di

pabrik-pabrik The Coca-Cola Company dan hingga

kini tetap merupakan rahasia dagang terbesar di dunia.

Teknisi kemudian mencicipi, memeriksa dan mencatat

campuran setiap batch sirup dengan seksama. Setelah

pencampuran, cairan siap untuk diberi tambahan

karbondioksida. Pengawasan mutu yang amat ketat

adalah alas an mengapa "Coca-Cola" dikenal sebagai

minuman yang memiliki kadar soda yang paling

sempurna.

5. Rangkaian botol dari gelas atau plastik PET

(Polyethelyne terephthalate) maupun kaleng sekarang

dalam jumlah sangat besar siap untuk diisi dengan

produk akhir. Botol-botol harus melalui pemeriksaan

yang amat teliti. Pertama-tama dicuci dan dibasuh

kemudian diperiksa secara elektronik dan manual.

Barulah boto-botol tersebut siap untuk diisi dengan

minuman ringan paling popular di dunia saat ini.

6. Botol demi botol diletakkan di atas ban berjalan agar

dapat terisi secara otomatis. Cara tersebut menjamin

jumlah dalam tiap botol akurat, dan penutupan botol

secara otomatis menjamin kadar higienis yang

sempurna pula.

7. Akhirnya, botol-botol diberi label, kode produksi dan

dikemas dalam karton-karton atau dimasukkan ke

dalam krat. Selanjutnya, pusat penjualan siap untuk

mengirimkan produk-produk "Coca-Cola menuju lebih

dari 420.000 gerai (outlet) yang menjual produk-

produk "Coca-Cola" di Indonesia.

5

Kelompok H

ISI

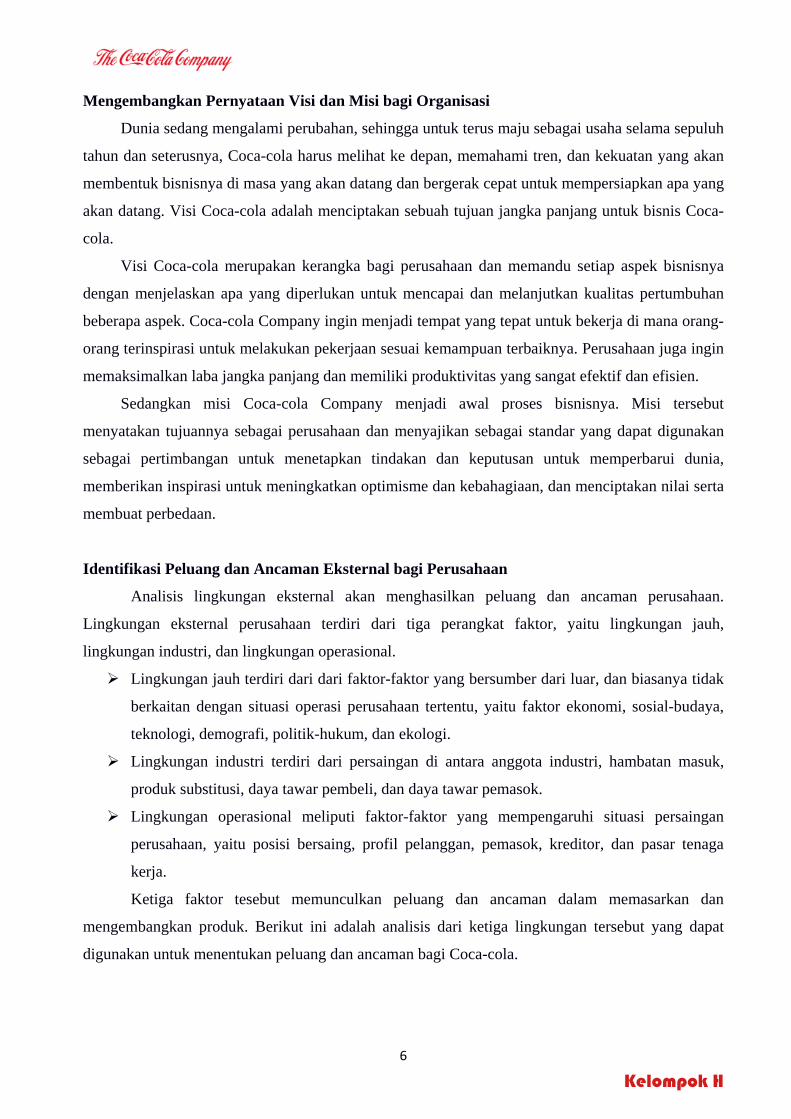

Identifikasi Visi, Misi, dan Nilai Perusahaan yang Ada

Visi, misi, maupun nilai-nilai yang ada merupakan cerminan dari apa yang dicari oleh

perusahaan untuk dicapai serta bagaimana mencapai hal tersebut. Semuanya memberikan arahan

atau petunjuk yang jelas pada perusahaan dan membantu perusahaan untuk memastikan bahwa

mereka yang ada di dalam perusahaan itu bekerja untuk tujuan yang sama. Berikut adalah

penjabaran dari visi, misi, dan nilai Coca-cola Company:

Our Vision Our vision serves as the framework for our Roadmap and guides every aspect of our business by describing what we need to accomplish in order to continue achieving sustainable, quality growth.

• People: Be a great place to work where people are inspired to be the best they can be.

• Portfolio: Bring to the world a portfolio of quality beverage brands that anticipate and satisfy people's desires and needs.

• Partners: Nurture a winning network of customers and suppliers, together we create mutual, enduring value.

• Planet: Be a responsible citizen that makes a difference by helping build and support sustainable communities.

• Profit: Maximize long‐term return to shareowners while being mindful of our overall responsibilities.

• Productivity: Be a highly effective, lean and fast‐moving organization.

Our Mission

Our Roadmap starts with our mission, which is enduring. It declares our purpose as a company and serves as the standard against which we weigh our actions and decisions.

• To refresh the world... • To inspire moments of optimism and happiness... • To create value and make a difference.

Live Our Values Our values serve as a compass for our actions and describe how we behave in the world.

• Leadership: The courage to shape a better future • Collaboration: Leverage collective genius • Integrity: Be real • Accountability: If it is to be, it's up to me • Passion: Committed in heart and mind • Diversity: As inclusive as our brands • Quality: What we do, we do well

6

Kelompok H

Mengembangkan Pernyataan Visi dan Misi bagi Organisasi

Dunia sedang mengalami perubahan, sehingga untuk terus maju sebagai usaha selama sepuluh

tahun dan seterusnya, Coca-cola harus melihat ke depan, memahami tren, dan kekuatan yang akan

membentuk bisnisnya di masa yang akan datang dan bergerak cepat untuk mempersiapkan apa yang

akan datang. Visi Coca-cola adalah menciptakan sebuah tujuan jangka panjang untuk bisnis Coca-

cola.

Visi Coca-cola merupakan kerangka bagi perusahaan dan memandu setiap aspek bisnisnya

dengan menjelaskan apa yang diperlukan untuk mencapai dan melanjutkan kualitas pertumbuhan

beberapa aspek. Coca-cola Company ingin menjadi tempat yang tepat untuk bekerja di mana orang-

orang terinspirasi untuk melakukan pekerjaan sesuai kemampuan terbaiknya. Perusahaan juga ingin

memaksimalkan laba jangka panjang dan memiliki produktivitas yang sangat efektif dan efisien.

Sedangkan misi Coca-cola Company menjadi awal proses bisnisnya. Misi tersebut

menyatakan tujuannya sebagai perusahaan dan menyajikan sebagai standar yang dapat digunakan

sebagai pertimbangan untuk menetapkan tindakan dan keputusan untuk memperbarui dunia,

memberikan inspirasi untuk meningkatkan optimisme dan kebahagiaan, dan menciptakan nilai serta

membuat perbedaan.

Identifikasi Peluang dan Ancaman Eksternal bagi Perusahaan

Analisis lingkungan eksternal akan menghasilkan peluang dan ancaman perusahaan.

Lingkungan eksternal perusahaan terdiri dari tiga perangkat faktor, yaitu lingkungan jauh,

lingkungan industri, dan lingkungan operasional.

Lingkungan jauh terdiri dari dari faktor-faktor yang bersumber dari luar, dan biasanya tidak

berkaitan dengan situasi operasi perusahaan tertentu, yaitu faktor ekonomi, sosial-budaya,

teknologi, demografi, politik-hukum, dan ekologi.

Lingkungan industri terdiri dari persaingan di antara anggota industri, hambatan masuk,

produk substitusi, daya tawar pembeli, dan daya tawar pemasok.

Lingkungan operasional meliputi faktor-faktor yang mempengaruhi situasi persaingan

perusahaan, yaitu posisi bersaing, profil pelanggan, pemasok, kreditor, dan pasar tenaga

kerja.

Ketiga faktor tesebut memunculkan peluang dan ancaman dalam memasarkan dan

mengembangkan produk. Berikut ini adalah analisis dari ketiga lingkungan tersebut yang dapat

digunakan untuk menentukan peluang dan ancaman bagi Coca-cola.

7

Kelompok H

A. Analisis Lingkungan Jauh

Berdasarkan analisis lingkungan jauh, diperoleh hasil sebagai berikut:

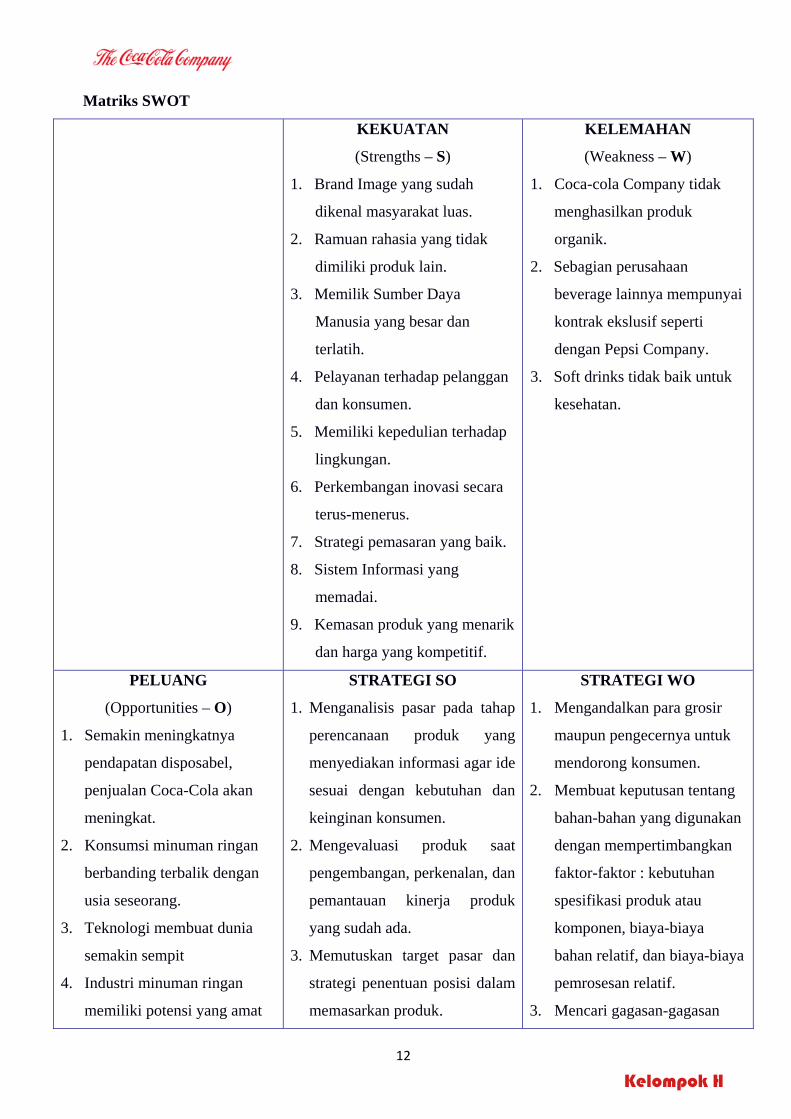

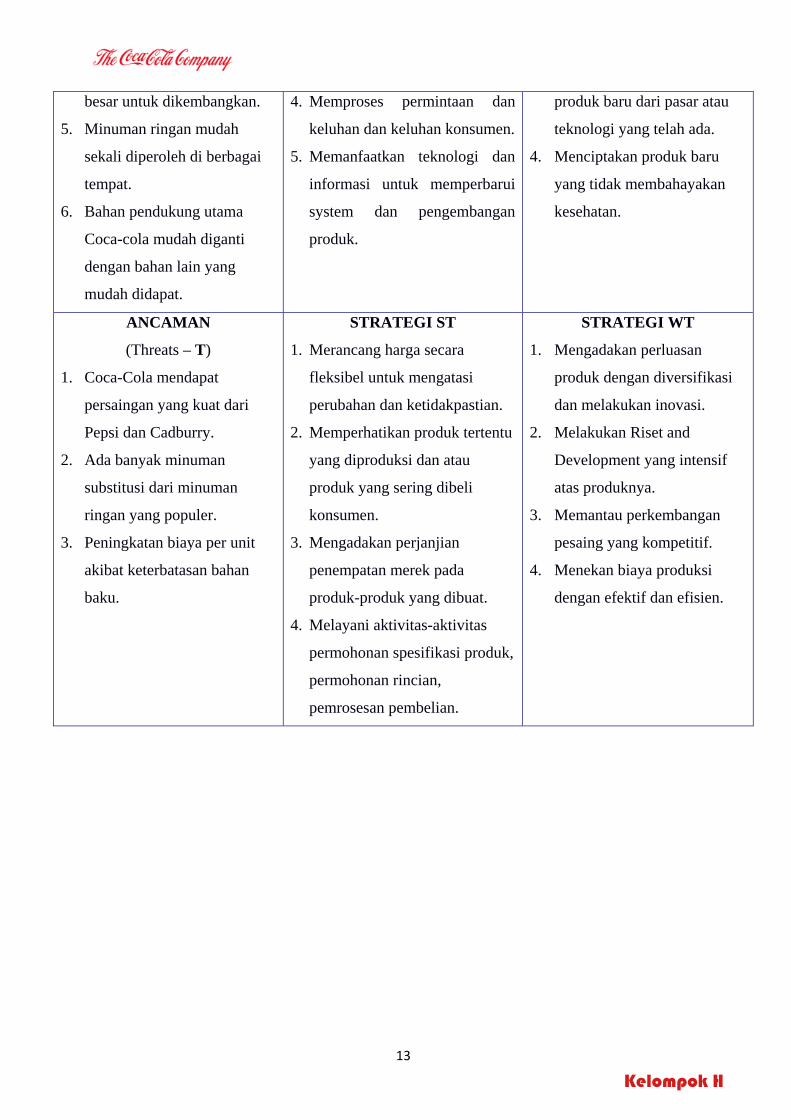

1. Semakin meningkatnya pendapatan disposabel, penjualan Coca-Cola akan meningkat.

Pendapatan disposable adalah sisa pendapatan perseorangan yang meliputi

pembayaran transfer setelah pembayaran semua pajak langsung dan sumbangan asuransi

nasional. Pendapatan disposable merupakan faktor penentu tingkat pengeluaran untuk

konsumsi dan tabungan dalam suatu perekonomian. Pada hakikatnya pendapatan disposable

digunakan oleh para penerimanya yaitu semua rumah tangga yang ada dalam perekonomian,

untuk membeli barang-barang dan jasa-jasa yang mereka ingini. Hal ini menjadi peluang

bagi perusahaan Coca-cola.

2. Konsumsi minuman ringan berbanding terbalik dengan usia seseorang. Artinya semakin tua,

semakin berkurang minum minuman ringan, sebaliknya kelompok muda yang paling banyak

minum minuman ringan.

3. Teknologi membuat dunia semakin sempit, sehingga dapat menciptakan segmen pasar baru

kemudian munculnya pasar “kaum muda” baru yang lebih mudah dijangkau.

B. Analisis Lingkungan Industri

Berdasarkan analisis lingkungan industri, diperoleh hasil sebagai berikut:

1. Industri minuman ringan memiliki potensi yang amat besar untuk dikembangkan.

Hal ini didukung dengan jumlah konsumsi per kapita yang masih rendah dan

penduduk berusia muda yang sangat besar. Dengan konsumsi minuman ringan yang

sedemikian luasnya, produk minuman ringan bukanlah barang mewah melainkan barang

biasa.

2. Minuman ringan mudah sekali diperoleh di berbagai tempat.

Coca-cala merupakan salah satu minuman ringan yang mudah diperoleh mulai dari

warung sampai toko-toko kecil. Minuman ringan dikonsumsi oleh semua lapisan masyarakat

dari berbagai latar belakang pendidikan dan pekerjaan.

3. Coca-Cola mendapat persaingan yang kuat dari Pepsi dan Cadburry.

Coca-Cola Company mempunyai dua pesaing utama yaitu: PepsiCo dan Cadbury

Schweppes PLC. PepsiCo mempunyai jumlah karyawan dua kali lebih banyak dari Coca-

Cola Company. Sedangkan Cadbury Schweppes PLC mempunyai diversifikasi produk yang

mana tidak dimiliki oleh dua pesaingnya. Diversifikasi itu meliputi: industry minuman,

coklat dan permen karet.

8

Kelompok H

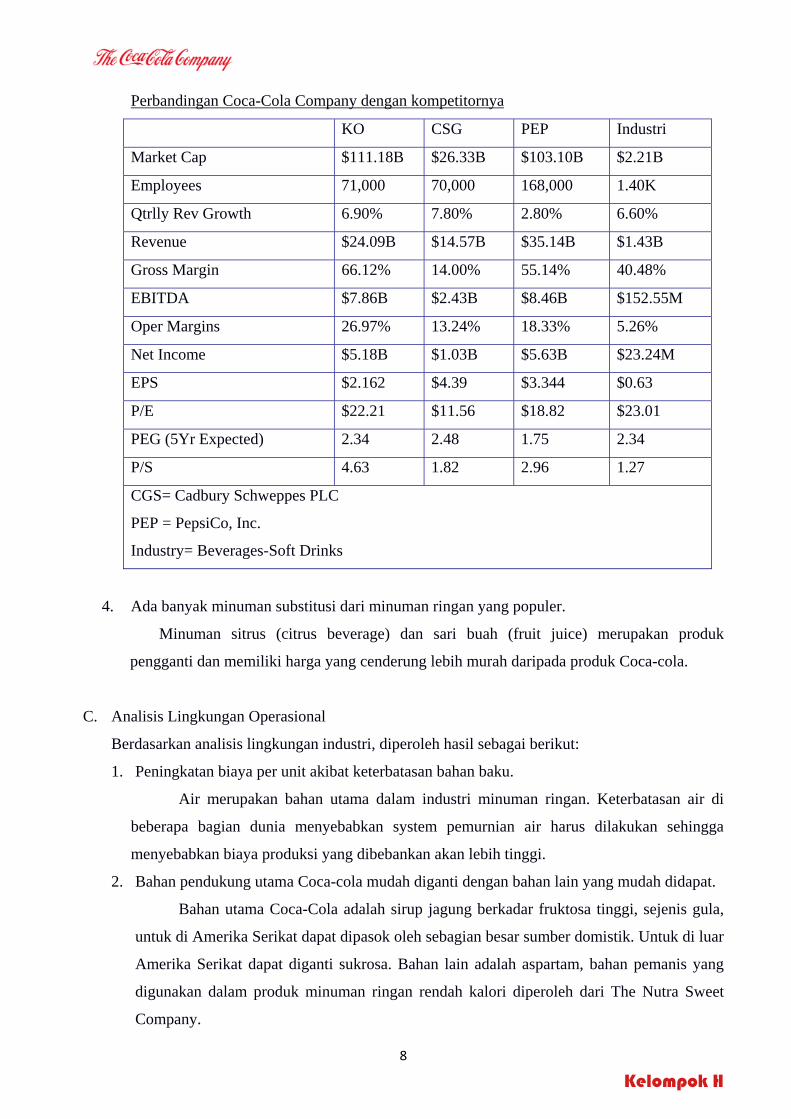

Perbandingan Coca-Cola Company dengan kompetitornya

KO CSG PEP Industri

Market Cap $111.18B $26.33B $103.10B $2.21B

Employees 71,000 70,000 168,000 1.40K

Qtrlly Rev Growth 6.90% 7.80% 2.80% 6.60%

Revenue $24.09B $14.57B $35.14B $1.43B

Gross Margin 66.12% 14.00% 55.14% 40.48%

EBITDA $7.86B $2.43B $8.46B $152.55M

Oper Margins 26.97% 13.24% 18.33% 5.26%

Net Income $5.18B $1.03B $5.63B $23.24M

EPS $2.162 $4.39 $3.344 $0.63

P/E $22.21 $11.56 $18.82 $23.01

PEG (5Yr Expected) 2.34 2.48 1.75 2.34

P/S 4.63 1.82 2.96 1.27

CGS= Cadbury Schweppes PLC

PEP = PepsiCo, Inc.

Industry= Beverages-Soft Drinks

4. Ada banyak minuman substitusi dari minuman ringan yang populer.

Minuman sitrus (citrus beverage) dan sari buah (fruit juice) merupakan produk

pengganti dan memiliki harga yang cenderung lebih murah daripada produk Coca-cola.

C. Analisis Lingkungan Operasional

Berdasarkan analisis lingkungan industri, diperoleh hasil sebagai berikut:

1. Peningkatan biaya per unit akibat keterbatasan bahan baku.

Air merupakan bahan utama dalam industri minuman ringan. Keterbatasan air di

beberapa bagian dunia menyebabkan system pemurnian air harus dilakukan sehingga

menyebabkan biaya produksi yang dibebankan akan lebih tinggi.

2. Bahan pendukung utama Coca-cola mudah diganti dengan bahan lain yang mudah didapat.

Bahan utama Coca-Cola adalah sirup jagung berkadar fruktosa tinggi, sejenis gula,

untuk di Amerika Serikat dapat dipasok oleh sebagian besar sumber domistik. Untuk di luar

Amerika Serikat dapat diganti sukrosa. Bahan lain adalah aspartam, bahan pemanis yang

digunakan dalam produk minuman ringan rendah kalori diperoleh dari The Nutra Sweet

Company.

9

Kelompok H

Identifikasi Kekuatan dan Kelemahan Internal bagi Perusahaan

Analisis lingkuangan internal akan menghasilkan kekuatan dan kelemahan perusahaan.

Analisis Internal Perusahaan dikenal juga dengan nama Analisis Profil Perusahaan. Analisis ini

menggambarkan kekuatan perusahaan, baik kuantitas maupun kualitas pemasaran, sumberdaya

manusia, sumberdaya fisik, operasi, keuangan, manajemen dan organisasi.

Kekuatan dan kelemahan pemasaran dapat dilihat dari reputasi perusahaan, pangsa pasar,

kualitas produk, kualitas pelayanan, efektifitas penetapan harga, efektifitas distribusi, efektifitas

promosi, kekuatan penjualan, efektifitas inovasi dan cakupan geografis.

Kekuatan dan kelemahan sumberdaya manusia dapat ditunjukkan dari manajemen

sumberdaya manusia, ketrampilan dan moral karyawan, kemampuan dan perhatian manajemen

puncak, produktivitas karyawan, kualitas kehidupan karyawan, fleksibilitas karyawan, ketaatan

hokum karyawan, efektivitas imbalan dalam memotivasi karyawan, dan pengalaman karyawan.

Keuangan terdiri dari ketersediaan modal, arus kas, stabilitas keuangan, hubungan dengan

pemilik dan investor, kemampuan berhubungan dengan bank, besarnya modal yang ditanam,

keuntungan yang diperoleh (nilai saham), efektivitas dan efisiensi system akuntansi untuk

perencanaan biaya-anggaran dan keuntungan dan sumber tingkat perusahaan.

Operasi meliputi fasilitas perusahaan, skala ekonomi, kapasitas produksi, kemampuan

berproduksi tepat waktu, keahlian dalam berproduksi, biaya bahan baku dan ketersediaan pemasok,

lokasi, layout, optimalisasi fasilitas, persediaan, penelitian dan pengembangan, hak paten, merk

dagang, proteksi hokum, pengendalian operasi dan efisiensi serta biaya-manfaat peralatan.

Kekuatan dan kelemahan organisasi dan manajemen dapat diperoleh dari struktur organisasi,

citra dan prestasi perusahaan, catatan perusahaan dalam mencapai sasaran, komunikasi dalam

organisasi, system pengendalian organisasi keseluruhan, budaya dan iklim organisasi, penggunaan

system yang efektif dalam pengambilan keputusan, system perencanaan strategik, sinergi dalam

organisasi, sistem informasi yang baik dan manajemen kualitas yang baik.

Kekuatan Internal Coca-Cola Company

1. Brand Image yang sudah dikenal masyarakat luas.

Brand Image menyebabkan kesetiaan pelanggan terhadap produk (brand loyalty).

2. Ramuan rahasia yang tidak dimiliki produk lain.

Sari rasa untuk "Coca-Cola” dibuat di pabrik-pabrik The Coca-Cola Company dan

hingga kini tetap merupakan rahasia dagang terbesar di dunia.

3. Memilik Sumber Daya Manusia yang besar dan terlatih.

Coca-cola Company memiliki tim khusus yang bertugas meningkatkan keterampilan

fungsi teknis, bidang manajemen, dan kepemimpinan karyawan.

10

Kelompok H

4. Pelayanan terhadap pelanggan dan konsumen.

Misalnya, Coca-Cola Bottling Indonesia (CCBI) menyediakan National Contact

Centre (NCC), yaitu pusat layanan bagi pelanggan dan konsumen di seluruh Indonesia.

NCC berfungsi sebagai media bagi para pelanggan dan konsumen yang membutuhkan

informasi atau layanan apapun terkait dengan Perusahaan dan produk-produk Coca-Cola.

Layanan dari NCC meliputi:

• Layanan Pelanggan yang mencakup permohonan menjadi pelanggan, alat pendingin,

pemesanan produk baik dari outlet tradisional maupun modern, serta hal lain yang

terkait dengan distribusi atau penjualan;

• Layanan Konsumen yang mencakup informasi produk, kualitas produk dan kemasan,

kegiatan promosi produk;

• Pertanyaan Umum yang mencakup penelitian, praktek kerja/magang dan lowongan

pekerjaan di CCBI, permohonan kunjungan ke pabrik CCBI, penawaran jasa dan

produk untuk CCBI.

5. Memiliki kepedulian terhadap lingkungan.

PT Coca-Cola Bottling Indonesia memiliki komitmen untuk senantiasa memahami,

mencegah dan memperkecil setiap dampak buruk terhadap lingkungan sehubungan dengan

kegiatan produksi minuman ringan, serta terus berupaya memberikan pelayanan dan produk

berkualitas yang diharapkan konsumen maupun pelanggan, dan menciptakan lingkungan

kerja yang aman bagi seluruh karyawan.

6. Perkembangan inovasi secara terus-menerus.

Selain berinovasi pada produk-produk baru, Coca-Cola selalu meningkatkan

kualitasnya.

7. Strategi pemasaran yang baik.

Strategi pemasaran Coca-Cola mempunyai ciri khas tersendiri, yang unik dan kreatif.

Berbagai program promosi diadakan sesuai dengan event yang sedang berlangsung, baik

melalui konser musik, pameran, promo penukaran tutup botol, hadiah kejutan, maupun iklan

TV.

8. Sistem Informasi yang memadai.

Pengembangan pendekatan manajemen Sistem Informasi (Information System / IS)

yang terarah pada organisasi merupakan bentuk pengaruh evolusi teknologi terhadap dunia

usaha dewasa ini.

9. Kemasan produk yang menarik dan harga yang kompetitif.

Coca-Cola juga mencoba mengembangkan desain kemasan minuman, serta

meningkatkan kualitasnya. Setelah meluncurkan Frestea dalam kemasan botol, pada akhir

11

Kelompok H

tahun 2002, Coca-Cola Indonesia meluncurkan Frestea dalam kemasan Tetra Wedge yang

lebih mudah dan praktis untuk dibawa. Pada akhir 2003, Coca-Cola, Sprite, dan Fanta hadir

dalam kemasan kaleng ramping baru yang unik. Pada tahun 2004 ini, Coca-Cola hadir

dengan inovasi terbaru yaitu botol gelas berbobot lebih ringan 30 % dengan desain mungil,

imut, tapi kuat. Inovasi kemasan produk akan terus dikembangkan sesuai dengan

perkembangan teknologi terbaru.

Kelemahan Internal Coca-cola Company

1. Coca-cola Company tidak menghasilkan produk organik

Di Amerika sedang mengembangkan produk organik, dan perkembangannya telah

mencapai 70%. Dan sampai saat ini pun produk organik semakin popular. Sedangkan Coca-cola

Company tidak mengadakan inovasi dalam hal produk organik, padahal hal ini dapat dijadikan

peluang bisnis yang potensial.

2. Sebagian pengecer mempunyai kontrak ekslusif dengan PepsiCo.

Sebagian perusahaan beverage seperti Pepsi Co. telah melakukan kontrak ekslusif dengan

restoran-restoran misalnya saja KFC, Mac D, dan lainnya. Sehingga Coca Cola tidak bisa masuk

ke area tersebut.

3. Soft drinks tidak baik untuk kesehatan

Soft drinks tidak punya nilai gizi (dalam hal vitamin dan mineral). Mereka punya

kandungan gula lebih tinggi, lebih asam, dan banyak zat aditif seperti pengawet dan pewarna.

Sementara orang suka meminum soft drink dingin setelah makan, Akibatnya, Tubuh kita

mempunyai suhu optimum 37 supaya enzim pencernaan berfungsi. Suhu dari soft drink dingin

jauh di bawah 37, terkadang mendekati 0. Hal ini mengurangi keefektivan dari enzim dan

memberi tekanan pada sistem pencernaan kita, mencerna lebih sedikit makanan. Bahkan

makanan tersebut difermentasi. Makanan yang difermentasi menghasilkan bau, gas, sisa busuk

dan racun, yang diserap oleh usus, di edarkan oleh darah ke seluruh tubuh. Penyebaran racun ini

mengakibatkan pembentukan macam-macam penyakit.

12

Kelompok H

Matriks SWOT

KEKUATAN

(Strengths – S)

1. Brand Image yang sudah

dikenal masyarakat luas.

2. Ramuan rahasia yang tidak

dimiliki produk lain.

3. Memilik Sumber Daya

Manusia yang besar dan

terlatih.

4. Pelayanan terhadap pelanggan

dan konsumen.

5. Memiliki kepedulian terhadap

lingkungan.

6. Perkembangan inovasi secara

terus-menerus.

7. Strategi pemasaran yang baik.

8. Sistem Informasi yang

memadai.

9. Kemasan produk yang menarik

dan harga yang kompetitif.

KELEMAHAN

(Weakness – W)

1. Coca-cola Company tidak

menghasilkan produk

organik.

2. Sebagian perusahaan

beverage lainnya mempunyai

kontrak ekslusif seperti

dengan Pepsi Company.

3. Soft drinks tidak baik untuk

kesehatan.

PELUANG

(Opportunities – O)

1. Semakin meningkatnya

pendapatan disposabel,

penjualan Coca-Cola akan

meningkat.

2. Konsumsi minuman ringan

berbanding terbalik dengan

usia seseorang.

3. Teknologi membuat dunia

semakin sempit

4. Industri minuman ringan

memiliki potensi yang amat

STRATEGI SO

1. Menganalisis pasar pada tahap

perencanaan produk yang

menyediakan informasi agar ide

sesuai dengan kebutuhan dan

keinginan konsumen.

2. Mengevaluasi produk saat

pengembangan, perkenalan, dan

pemantauan kinerja produk

yang sudah ada.

3. Memutuskan target pasar dan

strategi penentuan posisi dalam

memasarkan produk.

STRATEGI WO

1. Mengandalkan para grosir

maupun pengecernya untuk

mendorong konsumen.

2. Membuat keputusan tentang

bahan-bahan yang digunakan

dengan mempertimbangkan

faktor-faktor : kebutuhan

spesifikasi produk atau

komponen, biaya-biaya

bahan relatif, dan biaya-biaya

pemrosesan relatif.

3. Mencari gagasan-gagasan

13

Kelompok H

besar untuk dikembangkan.

5. Minuman ringan mudah

sekali diperoleh di berbagai

tempat.

6. Bahan pendukung utama

Coca-cola mudah diganti

dengan bahan lain yang

mudah didapat.

4. Memproses permintaan dan

keluhan dan keluhan konsumen.

5. Memanfaatkan teknologi dan

informasi untuk memperbarui

system dan pengembangan

produk.

produk baru dari pasar atau

teknologi yang telah ada.

4. Menciptakan produk baru

yang tidak membahayakan

kesehatan.

ANCAMAN

(Threats – T)

1. Coca-Cola mendapat

persaingan yang kuat dari

Pepsi dan Cadburry.

2. Ada banyak minuman

substitusi dari minuman

ringan yang populer.

3. Peningkatan biaya per unit

akibat keterbatasan bahan

baku.

STRATEGI ST

1. Merancang harga secara

fleksibel untuk mengatasi

perubahan dan ketidakpastian.

2. Memperhatikan produk tertentu

yang diproduksi dan atau

produk yang sering dibeli

konsumen.

3. Mengadakan perjanjian

penempatan merek pada

produk-produk yang dibuat.

4. Melayani aktivitas-aktivitas

permohonan spesifikasi produk,

permohonan rincian,

pemrosesan pembelian.

STRATEGI WT

1. Mengadakan perluasan

produk dengan diversifikasi

dan melakukan inovasi.

2. Melakukan Riset and

Development yang intensif

atas produknya.

3. Memantau perkembangan

pesaing yang kompetitif.

4. Menekan biaya produksi

dengan efektif dan efisien.

14

Kelompok H

PENUTUP

KESIMPULAN

1. Persaingan Industri dan Globalisasi era sekarang ini menuntut organisasi / perusahaan untuk

lebih mengembangkan kreativitas dan inovasi demi kemajuan organisasi / perusahaan

khususnya dalam menghasilkan produk demi kemajuan perusahaan dan tidak kalah dalam

persaingan.

2. Produk adalah sesuatu atau kebutuhan yang dapat memberikan kepuasan, bagi

konsumen ataupun pemakai produk.

3. Posisi PT. Coca-Cola Bottling Indonesia berada pada kuadran I dengan wilayah kekuatan lebih

besar dari pada peluang sehingga perusahaan harus bisa menggunakan kekuatan dengan

memanfaatkan peluang.

SARAN

Perusahaan harus menerapkan strategi pemasaran yang cukup agresif agar dapat tetap

mempertahankan persaingan pada industri minuman ringan. Dengan perubahan dan penyesuaian

sistem perekonomian di Indonesia maupun dunia saat ini, di mana sistem perekonomian saat ini

mengacu pada persaiangan dalam penciptaan produk/jasa pada sistem pembelajaran berbasis Mutu

dan Kualitas serta formasi produk / jasa di mata konsumen yang ke depan dihadapkan pada sistem

perekonomian global.

Sumber:

David, Fred R. 2006. Strategic Management: Concepts and Cases, 10th edition. Jakarta: Salemba

Empat

Handoko, Hani T. 1984. Dasar-dasar Manajemen Produksi dan Operasi. Yogyakarta: BPFE

Pratama, Yudha, SE, dkk. 2006. Kamus Ekonomi Lengkap. Jakarta: Wipress

Sukirno, Sadono. 2003. Pengantar Teori Makroekonomi. Jakarta: PT Raja Grafindo Persada

http://www.coca-cola.com

http://finance.yahoo.com

http://www.indosripsi.com

http://www.medanonline.net

http://www.google.com

1998

1988

2008

Per Capita Consumption of Company Beverage Products*

© 2009 The Coca-Cola Company, all rights reserved

* Based on U.S. 8 fluid ounces of a finished beverage

United States

Australia

Argentina

Spain

South Africa

Panama

Canada

Romania

Brazil

Great Britain

Greece

Germany

Japan

Italy

Turkey

France

Philippines

Poland

Colombia

Worldwide

Morocco

Thailand

Russia

Egypt

Kenya

China

Nigeria

Indonesia

India

Mexico

Chile

0

0

3

7

8

13

22

29

27

0.4

8

28

45

31

36

22

31

49

1.3

21

69

31

60

81

24

65

81

39

65

85

102

104

94

3

50

108

87

142

130

31

96

130

12

74

140

78

99

141

94

148

176

127

200

179

132

203

187

72

122

196

84

132

199

4

72

223

168

232

237

61

132

249

123

154

252

118

219

303

119

218

312

205

282

324

275

406

412

110

325

427

229

408

635

20FEB200406462039

UNITED STATESSECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K� ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES

EXCHANGE ACT OF 1934For the fiscal year ended December 31, 2005

OR

� TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THESECURITIES EXCHANGE ACT OF 1934

For the transition period from to

Commission File No. 1-2217

(Exact name of Registrant as specified in its charter)

DELAWARE 58-0628465(State or other jurisdiction of (IRS Employerincorporation or organization) Identification No.)

One Coca-Cola PlazaAtlanta, Georgia 30313

(Address of principal executive offices) (Zip Code)Registrant’s telephone number, including area code: (404) 676-2121

Securities registered pursuant to Section 12(b) of the Act:

Title of each class Name of each exchange on which registered

COMMON STOCK, $0.25 PAR VALUE NEW YORK STOCK EXCHANGESecurities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.Yes � No �

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or Section 15(d) of theExchange Act. Yes � No �

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) ofthe Securities Exchange Act of 1934 during the preceding 12 months and (2) has been subject to such filing requirementsfor the past 90 days. Yes � No �

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not containedherein, and will not be contained, to the best of Registrant’s knowledge, in definitive proxy or information statementsincorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. �

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer or a non-acceleratedfiler. See definition of ‘‘accelerated filer’’ or ‘‘large accelerated filer’’ in Rule 12b-2 of the Exchange Act.

Large accelerated filer � Accelerated filer � Non-accelerated filer �Indicate by check mark if the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes � No �The aggregate market value of the common equity held by non-affiliates of the Registrant (assuming for these

purposes, but without conceding, that all executive officers and Directors are ‘‘affiliates’’ of the Registrant) as of July 1,2005, the last business day of the Registrant’s most recently completed second fiscal quarter, was $87,349,477,246 (basedon the closing sale price of the Registrant’s Common Stock on that date as reported on the New York Stock Exchange).

The number of shares outstanding of the Registrant’s Common Stock as of February 21, 2006 was 2,367,883,247.DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Company’s Proxy Statement for the Annual Meeting of Shareowners to be held on April 19, 2006, areincorporated by reference in Part III.

Table of Contents

Page

Forward-Looking Statements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

Part I

Item 1. Business . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1Item 1A. Risk Factors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12Item 1B. Unresolved Staff Comments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18Item 2. Properties . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18Item 3. Legal Proceedings . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19Item 4. Submission of Matters to a Vote of Security Holders . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23Item X. Executive Officers of the Company . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24

Part II

Item 5. Market for the Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases ofEquity Securities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27

Item 6. Selected Financial Data . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations . . . . . . . . . 30Item 7A. Quantitative and Qualitative Disclosures About Market Risk . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 62Item 8. Financial Statements and Supplementary Data . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 63Item 9. Changes in and Disagreements with Accountants on Accounting and Financial Disclosure . . . . . . . . . 124Item 9A. Controls and Procedures . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 124Item 9B. Other Information . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 124

Part III

Item 10. Directors and Executive Officers of the Registrant . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 125Item 11. Executive Compensation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 125Item 12. Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters 125Item 13. Certain Relationships and Related Transactions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 125Item 14. Principal Accountant Fees and Services . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 125

Part IV

Item 15. Exhibits and Financial Statement Schedules . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 126Signatures . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 132

FORWARD-LOOKING STATEMENTS

This report contains information that may constitute ‘‘forward-looking statements.’’ Generally, the words‘‘believe,’’ ‘‘expect,’’ ‘‘intend,’’ ‘‘estimate,’’ ‘‘anticipate,’’ ‘‘project,’’ ‘‘will’’ and similar expressions identify forward-looking statements, which generally are not historical in nature. All statements that address operating performance,events or developments that we expect or anticipate will occur in the future—including statements relating to volumegrowth, share of sales and earnings per share growth, and statements expressing general optimism about futureoperating results—are forward-looking statements. As and when made, management believes that these forward-looking statements are reasonable. However, caution should be taken not to place undue reliance on any suchforward-looking statements because such statements speak only as of the date when made. Our Company undertakesno obligation to publicly update or revise any forward-looking statements, whether as a result of new information,future events or otherwise. In addition, forward-looking statements are subject to certain risks and uncertainties thatcould cause actual results to differ materially from our Company’s historical experience and our present expectationsor projections. These risks and uncertainties include, but are not limited to, those described in Part I, ‘‘Item 1A. RiskFactors’’ and elsewhere in this report and those described from time to time in our future reports filed with theSecurities and Exchange Commission.

PART I

ITEM 1. BUSINESS

General

The Coca-Cola Company is the largest manufacturer, distributor and marketer of nonalcoholic beverageconcentrates and syrups in the world. Finished beverage products bearing our trademarks, sold in the UnitedStates since 1886, are now sold in more than 200 countries and include the leading soft drink products in most ofthese countries. In this report, the terms ‘‘Company,’’ ‘‘we,’’ ‘‘us’’ or ‘‘our’’ mean The Coca-Cola Company andall subsidiaries included in our consolidated financial statements.

Our business is nonalcoholic beverages—principally carbonated soft drinks, but also a variety ofnoncarbonated beverages. We manufacture beverage concentrates and syrups, which we sell to bottling andcanning operations, fountain wholesalers and some fountain retailers, as well as some finished beverages, whichwe sell primarily to distributors. We also produce, market and distribute certain juice and juice drinks andcertain water products. In addition, we have ownership interests in numerous bottling and canning operations,although most of these operations are independently owned and managed.

We were incorporated in September 1919 under the laws of the State of Delaware and succeeded to thebusiness of a Georgia corporation with the same name that had been organized in 1892.

Our Company is one of numerous competitors in the commercial beverages market. Of the approximately50 billion beverage servings of all types consumed worldwide every day, beverages bearing trademarks owned byor licensed to us account for more than 1.3 billion.

We believe that our success depends on our ability to connect with consumers by providing them with awide variety of choices to meet their desires, needs and lifestyle choices. Our success further depends on theability of our people to execute effectively, every day.

Our goal is to use our Company’s assets—our brands, financial strength, unrivaled distribution system, andthe strong commitment of management and employees—to become more competitive and to accelerate growthin a manner that creates value for our shareowners.

1

Operating Segments

The Company’s operating structure is the basis for our Company’s internal financial reporting. As ofDecember 31, 2005, our operating structure included the following operating segments, the first six of which aresometimes referred to as ‘‘operating groups’’ or ‘‘groups.’’

• North America

• Africa

• East, South Asia and Pacific Rim

• European Union

• Latin America

• North Asia, Eurasia and Middle East

• Corporate

Our operating structure as of December 31, 2005, reflected the changes we made during the second quarterof 2005, when we replaced our then existing Europe, Eurasia and Middle East operating segment and Asiaoperating segment with three new operating segments: European Union; East, South Asia and Pacific Rim; andNorth Asia, Eurasia and Middle East. The North America operating segment included the United States,Canada and Puerto Rico. The European Union operating segment included our operations in all currentmember states of the European Union as well as the European Free Trade Association countries, Switzerland,Israel and the Palestinian Territories, and Greenland. The North Asia, Eurasia and Middle East operatingsegment included our operations in China, Japan, Eurasia, the Middle East (other than Israel and thePalestinian Territories), Russia, Ukraine and Belarus, and those in other European countries not included in theEuropean Union operating segment. The East, South Asia and Pacific Rim operating segment included ouroperations in India, the Philippines, Southeast and West Asia, and South Pacific and Korea.

In the first quarter of 2006, the Company made certain changes to its operating structure primarily toestablish a new, separate internal organization for its consolidated bottling operations and its unconsolidatedbottling investments. This new structure will result in the reporting of a separate operating segment, along withthe six existing geographic operating segments and Corporate, beginning with the first quarter of 2006.

Except to the extent that differences between operating segments are material to an understanding of ourbusiness taken as a whole, the description of our business in this report is presented on a consolidated basis.

For financial information about our operating segments and geographic areas, refer to Note 5 and Note 20of Notes to Consolidated Financial Statements set forth in Part II, ‘‘Item 8. Financial Statements andSupplementary Data’’ of this report, incorporated herein by reference. For certain risks attendant to ournon-U.S. operations, refer to ‘‘Item 1A. Risk Factors’’ below.

Products and Distribution

Our Company manufactures and sells beverage concentrates, sometimes referred to as ‘‘beverage bases,’’and syrups, including fountain syrups. We also manufacture and sell some finished beverages, both carbonatedand noncarbonated, including certain juice and juice-drink products; sports drinks; ready-to-drink coffees andteas; and water products.

As used in this report:

• ‘‘concentrates’’ means flavoring ingredients and, depending on the product, sweeteners used to preparebeverage syrups or finished beverages;

2

• ‘‘syrups’’ means the beverage ingredients produced by combining concentrates and, depending on theproduct, sweeteners and added water;

• ‘‘fountain syrups’’ means syrups that are sold to fountain retailers, such as restaurants, that use dispensingequipment to mix the syrups with carbonated or noncarbonated water at the time of purchase to producefinished beverages that are served in cups or glasses for immediate consumption;

• ‘‘soft drinks’’ means nonalcoholic carbonated beverages containing flavorings and sweeteners, excluding,among others, waters and flavored waters, juice and juice drinks, sports drinks, teas and coffees;

• ‘‘noncarbonated beverages’’ means nonalcoholic beverages without carbonation including, but not limitedto, waters and flavored waters, juice and juice drinks, sports drinks, teas and coffees;

• ‘‘Company Trademark Beverages’’ means beverages bearing our trademarks and certain other beverageproducts licensed to us for which we provide marketing support and from the sale of which we derive netrevenues; and

• additional terms used in this report are defined in the Glossary beginning on page 122.

We sell the concentrates and syrups for bottled and canned beverages to authorized bottling and canningoperations. In addition to concentrates and syrups for soft-drink products and flavored noncarbonatedbeverages, we also sell concentrates for purified water products such as Dasani to authorized bottlingoperations.

Authorized bottlers or canners either combine our syrups with carbonated water or combine ourconcentrates with sweeteners (depending on the product), water and carbonated water to produce finished softdrinks. The finished soft drinks are packaged in authorized containers bearing our trademarks—such as cans andrefillable and nonrefillable glass and plastic bottles (‘‘bottle/can products’’)—and are then sold to retailers(‘‘bottle/can retailers’’) or, in some cases, wholesalers.

For our fountain products in the United States, we manufacture fountain syrups and sell them to authorizedfountain wholesalers and some fountain retailers. The wholesalers are authorized to sell the Company’s fountainsyrups by a nonexclusive appointment from us that neither restricts us in setting the prices at which we sellfountain syrups to the wholesalers, nor restricts the territory in which the wholesalers may resell in the UnitedStates. Outside the United States, fountain syrups typically are manufactured by authorized bottlers fromconcentrates sold to them by the Company. The bottlers then typically sell the fountain syrups to wholesalers ordirectly to fountain retailers.

Finished beverages manufactured by us include a variety of carbonated and noncarbonated beverages. Wesell most of these finished beverages and certain water products to authorized bottlers or distributors, who inturn sell these products to retailers or, in some cases, wholesalers. We manufacture and sell juice and juice-drinkproducts and certain water products to retailers and wholesalers in the United States and numerous othercountries both directly and through a network of business partners, including certain Coca-Cola bottlers.

Our beverage products include Coca-Cola, Coca-Cola Classic, caffeine free Coca-Cola, caffeine freeCoca-Cola Classic, Diet Coke (sold under the trademark Coca-Cola Light in many countries other than theUnited States), caffeine free Diet Coke, Diet Coke Sweetened with Splenda, Coca-Cola with Lime, Diet Cokewith Lime, Cherry Coke, Diet Cherry Coke, Coca-Cola C2, Coca-Cola Zero, Fanta brand soft drinks, Sprite,Diet Sprite Zero/Sprite Zero (sold under the trademark Sprite Light in many countries other than the UnitedStates), Sprite Remix, Pibb Xtra, Mello Yello, Tab, Fresca brand soft drinks, Barq’s, Powerade, Minute Maidbrand soft drinks, Aquarius, Sokenbicha, Ciel, Bonaqa/Bonaqua, Dasani, Dasani brand flavored waters, Lift,Thums Up, Kinley, Pop Cola, Eight O’Clock, Qoo, Full Throttle, DOBRIY, Rich, Nico and other productsdeveloped for specific countries (including Georgia brand ready-to-drink coffees). In many countries (excludingthe United States, among others), our Company’s beverage products also include Schweppes, Canada Dry, DrPepper and Crush. Our Company produces, distributes and markets juice and juice-drink products including

3

Minute Maid juice and juice drinks, Simply Orange orange juice, Odwalla nutritional juices, Five Aliverefreshment beverages, Bacardi tropical fruit mixers concentrate (manufactured and marketed under a licensefrom Bacardi & Company Limited) and Hi-C ready-to-serve fruit drinks. We have a license to manufacture andsell concentrates for Seagram’s mixers, a line of carbonated drinks, in the United States and certain othercountries. Our Company is the exclusive master distributor of Evian bottled water in the United States andCanada and of Rockstar, an energy drink, in most of the United States and in Canada. Beverage PartnersWorldwide (‘‘BPW’’), the Company’s 50 percent-owned joint venture with Nestlé S.A. (‘‘Nestlé’’), marketsready-to-drink teas and coffees in certain countries.

Consumer demand determines the optimal menu of Company product offerings. Consumer demand canvary from one locale to another and can change over time within a single locale. Employing our businessstrategy, and with special focus on core brands, our Company seeks to build its existing brands and, at the sametime, to broaden its historical family of brands, products and services in order to create and satisfy consumerdemand locale by locale.

Our Company introduced a variety of new brands, brand extensions and new beverage products in 2005.Among numerous examples, we introduced Nanairo-Acha in Japan; Bonaqua BonActive in Hong Kong; andnew Fanta flavors including strawberry, pineapple and apple in Angola, Ghana and Nigeria, respectively. InNorth America, we launched Coca-Cola Zero, a new calorie-free cola, Diet Coke Sweetened with Splenda brandsweetener, Sugar Free Full Throttle; and Powerade Option, a new low-calorie, low-carbohydrate sports drinks.We also rebranded our Fresca line and added two new calorie-free extensions—Sparkling Peach Citrus Frescaand Sparkling Black Cherry Citrus Fresca. In Thailand and Vietnam we launched Minute Maid juice and juicedrinks under the Splash brand name. We extended the rebranding of Diet Sprite to Diet Sprite Zero/SpriteZero, which began in Greece in 2002, to now include a total of 77 countries, including the United States. In2006, we launched Black Cherry Vanilla Coca-Cola, Diet Black Cherry Vanilla Coca-Cola, Full Throttle Fury,Tab Energy and Coca-Cola Blak, a new Coca-Cola and coffee fusion beverage designed to appeal to adultconsumers, in France, and we plan to introduce this beverage in the United States later in 2006.

Our Company measures the volume of products sold in two ways: (1) unit cases of finished products and(2) gallons. As used in this report, ‘‘unit case’’ means a unit of measurement equal to 192 U.S. fluid ounces offinished beverage (24 eight-ounce servings); and ‘‘unit case volume’’ means the number of unit cases (or unitcase equivalents) of Company beverage products directly or indirectly sold by the Coca-Cola bottling system tocustomers. Unit case volume primarily consists of beverage products bearing Company trademarks. Alsoincluded in unit case volume are certain products licensed to, or distributed by, our Company, and brands ownedby Coca-Cola system bottlers for which our Company provides marketing support and from the sale of which itderives income. Such products licensed to, or distributed by, our Company or owned by Coca-Cola systembottlers account for a minimal portion of total unit case volume. In addition, unit case volume includes sales byjoint ventures in which the Company is a partner. Although most of our Company’s revenues are not baseddirectly on unit case volume, we believe unit case volume is one of the measures of the underlying strength of theCoca-Cola system because it measures trends at the consumer level. The unit case volume numbers used in thisreport are based on estimates received by the Company from its bottling partners and distributors. As used inthis report, ‘‘gallon’’ means a unit of measurement for concentrates (sometimes referred to as ‘‘beveragebases’’), syrups, finished beverages and powders (in all cases, expressed in equivalent gallons of syrup) sold byour Company to its bottling partners or other customers. Most of our revenues are based on gallon sales, aprimarily ‘‘wholesale’’ activity. Unit case volume and gallon sales growth rates are not necessarily equal duringany given period. Items such as seasonality, bottlers’ inventory practices, supply point changes, timing of priceincreases, new product introductions and changes in product mix can impact unit case volume and gallon salesand can create differences between unit case volume and gallon sales growth rates.

4

In 2005, concentrates and syrups for beverages bearing the trademark ‘‘Coca-Cola’’ or including thetrademark ‘‘Coke’’ (‘‘Coca-Cola Trademark Beverages’’) accounted for approximately 55 percent of theCompany’s total gallon sales.

In 2005, gallon sales in the United States (‘‘U.S. gallon sales’’) represented approximately 27 percent of theCompany’s worldwide gallon sales. Approximately 58 percent of U.S. gallon sales for 2005 was attributable tosales of beverage concentrates and syrups to 78 authorized bottler ownership groups in 393 licensed territories.Those bottlers prepare and sell finished beverages bearing our trademarks for the food store and vendingmachine distribution channels and for other distribution channels supplying products for home and immediateconsumption. Approximately 33 percent of 2005 U.S. gallon sales was attributable to fountain syrups sold tofountain retailers and to 522 authorized fountain wholesalers, some of which are authorized bottlers. Theremaining approximately 9 percent of 2005 U.S. gallon sales was attributable to sales by the Company of finishedbeverages, including juice and juice-drink products and certain water products. Coca-Cola Enterprises Inc.,including its bottling subsidiaries and divisions (‘‘CCE’’), accounted for approximately 50 percent of theCompany’s U.S. gallon sales in 2005. At December 31, 2005, our Company held an ownership interest ofapproximately 36 percent in CCE, which is the world’s largest bottler of Company Trademark Beverages.

In 2005, gallon sales outside the United States represented approximately 73 percent of the Company’sworldwide gallon sales. The countries outside the United States in which our gallon sales were the largest in2005 were Mexico, Brazil, China and Japan, which together accounted for approximately 27 percent of ourworldwide gallon sales. Approximately 91 percent of non-U.S. unit case volume for 2005 was attributable to salesof beverage concentrates and syrups to authorized bottlers together with sales by the Company of finishedbeverages other than juice and juice-drink products, in 511 licensed territories. Approximately 5 percent of 2005non-U.S. unit case volume was attributable to fountain syrups. The remaining approximately 4 percent of 2005non-U.S. unit case volume was attributable to juice and juice-drink products.

In addition to conducting our own independent advertising and marketing activities, we may providepromotional and marketing services or funds to our bottlers. In most cases, we do this on a discretionary basisunder the terms of commitment letters or agreements, even though we are not obligated to do so under theterms of the bottling or distribution agreements between our Company and the bottlers. Also, on a discretionarybasis in most cases, our Company may develop and introduce new products, packages and equipment to assist itsbottlers. Likewise, in many instances, we provide promotional and marketing services and/or funds and/ordispensing equipment and repair services to fountain and bottle/can retailers, typically pursuant to marketingagreements. The aggregate amount of funds provided by our Company to bottlers, resellers or other customersof our Company’s products, principally for participation in promotional and marketing programs wasapproximately $3.7 billion in 2005.

Bottler’s Agreements and Distribution Agreements

Most of our products are manufactured and sold by our bottling partners. We typically sell concentrates andsyrups to our bottling partners who convert them into finished packaged products which they sell to distributorsand other customers. Separate contracts (‘‘Bottler’s Agreements’’) exist between our Company and each of ourbottling partners regarding the manufacture and sale of Company products. Subject to specified terms andconditions and certain variations, the Bottler’s Agreements generally authorize the bottlers to prepare specifiedCompany Trademark Beverages, to package the same in authorized containers, and to distribute and sell thesame in (but, subject to applicable local law, generally only in) an identified territory. The bottler is obligated topurchase its entire requirement of concentrates or syrups for the designated Company Trademark Beveragesfrom the Company or Company-authorized suppliers. We typically agree to refrain from selling or distributing,or from authorizing third parties to sell or distribute, the designated Company Trademark Beverages throughoutthe identified territory in the particular authorized containers; however, we typically reserve for ourselves or ourdesignee the right (1) to prepare and package such beverages in such containers in the territory for sale outside

5

the territory, and (2) to prepare, package, distribute and sell such beverages in the territory, in any other manneror form. Territorial restrictions on bottlers vary in some cases in accordance with local law.

The Bottler’s Agreements between us and our authorized bottlers in the United States differ in certainrespects from those in the other countries in which Company Trademark Beverages are sold. As furtherdiscussed below, the principal differences involve the duration of the agreements; the inclusion or exclusion ofcanned beverage production rights; the inclusion or exclusion of authorizations to manufacture and distributefountain syrups; in some cases, the degree of flexibility on the part of the Company to determine the pricing ofsyrups and concentrates; and the extent, if any, of the Company’s obligation to provide marketing support.

Outside the United States

The Bottler’s Agreements between us and our authorized bottlers outside the United States generally are ofstated duration, subject in some cases to possible extensions or renewals of the term of the contract. Generally,these contracts are subject to termination by the Company following the occurrence of certain designated events.These events include defined events of default and certain changes in ownership or control of the bottler.

In certain parts of the world outside the United States, we have not granted comprehensive beverageproduction rights to the bottlers. In such instances, we or our authorized suppliers sell Company TrademarkBeverages to the bottlers for sale and distribution throughout the designated territory, often on a nonexclusivebasis. A majority of the Bottler’s Agreements in force between us and bottlers outside the United Statesauthorize the bottlers to manufacture and distribute fountain syrups, usually on a nonexclusive basis.

Our Company generally has complete flexibility to determine the price and other terms of sale of theconcentrates and syrups we sell to bottlers outside the United States. In some instances, however, we haveagreed or may in the future agree with the bottler with respect to concentrate pricing on a prospective basis forspecified time periods. Outside the United States, in most cases, we have no obligation to provide marketingsupport to the bottlers. Nevertheless, we may, at our discretion, contribute toward bottler expenditures foradvertising and marketing. We may also elect to undertake independent or cooperative advertising andmarketing activities.

Within the United States

In the United States, with certain very limited exceptions, the Bottler’s Agreements for Coca-ColaTrademark Beverages and other cola-flavored beverages have no stated expiration date. Our standard contractsfor other soft-drink flavors and for noncarbonated beverages are of stated duration, subject to bottler renewalrights. The Bottler’s Agreements in the United States are subject to termination by the Company fornonperformance or upon the occurrence of certain defined events of default that may vary from contract tocontract. The ‘‘1987 Contract,’’ described below, is terminable by the Company upon the occurrence of certainevents, including:

• the bottler’s insolvency, dissolution, receivership or the like;

• any disposition by the bottler or any of its subsidiaries of any voting securities of any bottler subsidiarywithout the consent of the Company;

• any material breach of any obligation of the bottler under the 1987 Contract; or

• except in the case of certain bottlers, if a person or affiliated group acquires or obtains any right toacquire beneficial ownership of more than 10 percent of any class or series of voting securities of thebottler without authorization by the Company.

Under the terms of the Bottler’s Agreements, bottlers in the United States are authorized to manufactureand distribute Company Trademark Beverages in bottles and cans. However, these bottlers generally are notauthorized to manufacture fountain syrups. Rather, as described above, our Company manufactures and sells

6

fountain syrups to authorized fountain wholesalers (including certain authorized bottlers) and some fountainretailers. These wholesalers in turn sell the syrups or deliver them on our behalf to restaurants and otherretailers.

In the United States, the form of Bottler’s Agreement for cola-flavored soft drinks that covers the largestamount of U.S. gallon sales (the ‘‘1987 Contract’’) gives us complete flexibility to determine the price and otherterms of sale of concentrates and syrups for Company Trademark Beverages. In some instances, we have agreedor may in the future agree with the bottler with respect to concentrate pricing on a prospective basis for specifiedtime periods. Bottlers operating under the 1987 Contract accounted for approximately 89 percent of ourCompany’s total U.S. gallon sales for bottled and canned beverages in 2005, excluding direct sales by theCompany of juice and juice-drink products and other finished beverages (‘‘U.S. bottle/can gallon sales’’). Certainother forms of U.S. Bottler’s Agreements, entered into prior to 1987, provide for concentrates or syrups forcertain Coca-Cola Trademark Beverages and other cola-flavored Company Trademark Beverages to be pricedpursuant to a stated formula. Bottlers accounting for approximately 10 percent of U.S. bottle/can gallon sales in2005 have contracts for certain Coca-Cola Trademark Beverages and other cola-flavored Company TrademarkBeverages with pricing formulas that generally provide for a baseline price. This baseline price may be adjustedperiodically by the Company, up to a maximum indexed ceiling price, and is adjusted quarterly based uponchanges in certain sugar or sweetener prices, as applicable. Bottlers accounting for the remaining (less than1 percent) U.S. bottle/can gallon sales in 2005 operate under our oldest form of contract, which provides for afixed price for Coca-Cola syrup used in bottles and cans. This price is subject to quarterly adjustments to reflectchanges in the quoted price of sugar.

We have standard contracts with bottlers in the United States for the sale of concentrates and syrups fornon-cola-flavored soft drinks and certain noncarbonated beverages in bottles and cans; and, in certain cases, forthe sale of finished noncarbonated beverages in bottles and cans. All of these standard contracts give theCompany complete flexibility to determine the price and other terms of sale.

Under the 1987 Contract and most of our other standard soft-drink and noncarbonated beverage contractswith bottlers in the United States, our Company has no obligation to participate with bottlers in expenditures foradvertising and marketing. Nevertheless, at our discretion, we may contribute toward such expenditures andundertake independent or cooperative advertising and marketing activities. Some U.S. Bottler’s Agreementsthat predate the 1987 Contract impose certain marketing obligations on us with respect to certain CompanyTrademark Beverages.

As a practical matter, our Company’s ability to exercise its contractual flexibility to determine the price andother terms of sale of its syrups, concentrates and finished beverages under various agreements described aboveis subject, both outside and within the United States, to competitive market conditions.

Significant Equity Method Investments and Company Bottling Operations

Our Company maintains business relationships with three types of bottlers:

• bottlers in which the Company has no ownership interest;

• bottlers in which the Company has invested and has a noncontrolling ownership interest; and

• bottlers in which the Company has invested and has a controlling ownership interest.

In 2005, bottling operations in which we had no ownership interest produced and distributed approximately25 percent of our worldwide unit case volume. We have equity positions in 51 unconsolidated bottling, canningand distribution operations for our products worldwide. These cost or equity method investees produced anddistributed approximately 58 percent of our worldwide unit case volume in 2005. Controlled and consolidatedbottling operations produced and distributed approximately 7 percent of our worldwide unit case volume in2005. The remaining approximately 10 percent of our worldwide unit case volume in 2005 was produced and

7

distributed by our fountain operations plus our juice and juice drink, sports drink and other finished beverageoperations.

We make equity investments in selected bottling operations with the intention of maximizing the strengthand efficiency of the Coca-Cola system’s production, distribution and marketing systems around the world.These investments are intended to result in increases in unit case volume, net revenues and profits at the bottlerlevel, which in turn generate increased gallon sales for our Company’s concentrate and syrup business. Whenthis occurs, both we and our bottling partners benefit from long-term growth in volume, improved cash flows andincreased shareowner value.

The level of our investment generally depends on the bottler’s capital structure and its available resourcesat the time of the investment. Historically, in certain situations, we have viewed it as advantageous to acquire acontrolling interest in a bottling operation, often on a temporary basis. Owning such a controlling interest hasallowed us to compensate for limited local resources and has enabled us to help focus the bottler’s sales andmarketing programs and assist in the development of the bottler’s business and information systems and theestablishment of appropriate capital structures.

In line with our long-term bottling strategy, we may periodically consider options for reducing ourownership interest in a bottler. One such option is to combine our bottling interests with the bottling interests ofothers to form strategic business alliances. Another option is to sell our interest in a bottling operation to one ofour equity method investee bottlers. In both of these situations, our Company continues to participate in thebottler’s results of operations through our share of the strategic business alliances’ or equity method investees’earnings or losses.

In cases where our investments in bottlers represent noncontrolling interests, our intention is to provideexpertise and resources to strengthen those businesses.

Significant investees in which we have noncontrolling ownership interests include the following:

Coca-Cola Enterprises Inc. Our ownership interest in CCE was approximately 36 percent atDecember 31, 2005. CCE is the world’s largest bottler of the Company’s beverage products. In 2005, sales ofconcentrates, syrups and finished products by the Company to CCE were approximately $5.1 billion. CCEestimates that the territories in which it markets beverage products to retailers (which include portions of 46states and the District of Columbia in the United States, the United States Virgin Islands, Canada, GreatBritain, continental France, the Netherlands, Luxembourg, Belgium and Monaco) contain approximately78 percent of the United States population, 98 percent of the population of Canada, and 100 percent of thepopulations of Great Britain, continental France, the Netherlands, Luxembourg, Belgium and Monaco. In 2005,CCE’s net operating revenues were approximately $18.7 billion. Excluding fountain products, in 2005,approximately 62 percent of the unit case volume of CCE consisted of Coca-Cola Trademark Beverages, 31percent of its unit case volume consisted of other Company Trademark Beverages and 7 percent of its unit casevolume consisted of beverage products of other companies.

Coca-Cola Hellenic Bottling Company S.A. (‘‘Coca-Cola HBC’’). At December 31, 2005, our ownershipinterest in Coca-Cola HBC was approximately 24 percent. Coca-Cola HBC has bottling and distribution rights,through direct ownership or joint ventures, in Armenia, Austria, Belarus, Bosnia-Herzegovina, Bulgaria,Croatia, the Czech Republic, Estonia, Former Yugoslavian Republic of Macedonia, Greece, Hungary, Italy,Latvia, Lithuania, Moldova, Nigeria, Northern Ireland, Poland, Republic of Ireland, Romania, Russia, Serbiaand Montenegro, Slovakia, Slovenia, Switzerland and Ukraine. Coca-Cola HBC estimates that the territories inwhich it markets beverage products contain approximately 67 percent of the population of Italy and 100 percentof the populations of the other countries named above in which Coca-Cola HBC has bottling and distributionrights. In 2005, Coca-Cola HBC’s net sales of beverage products were approximately $5.8 billion. In 2005,approximately 46 percent of the unit case volume of Coca-Cola HBC consisted of Coca-Cola TrademarkBeverages, approximately 47 percent of its unit case volume consisted of other Company Trademark Beverages

8

and approximately 7 percent of its unit case volume consisted of beverage products of Coca-Cola HBC or othercompanies.

Coca-Cola FEMSA, S.A. de C.V. (‘‘Coca-Cola FEMSA’’). Our ownership interest in Coca-Cola FEMSAwas approximately 40 percent at December 31, 2005. Coca-Cola FEMSA is a Mexican holding company withbottling subsidiaries in a substantial part of central Mexico, including Mexico City and southeastern Mexico;greater São Paulo, Campinas, Santos, the state of Matto Grosso do Sul and part of the state of Goias in Brazil;central Guatemala; most of Colombia; all of Costa Rica, Nicaragua, Panama and Venezuela; and greater BuenosAires, Argentina. Coca-Cola FEMSA estimates that the territories in which it markets beverage productscontain approximately 48 percent of the population of Mexico, 16 percent of the population of Brazil, 98 percentof the population of Colombia, 47 percent of the population of Guatemala, 100 percent of the populations ofCosta Rica, Nicaragua, Panama and Venezuela and 30 percent of the population of Argentina. In 2005,Coca-Cola FEMSA’s net sales of beverage products were approximately $4.5 billion. In 2005, approximately62 percent of the unit case volume of Coca-Cola FEMSA consisted of Coca-Cola Trademark Beverages,34 percent of its unit case volume consisted of other Company Trademark Beverages and 4 percent of its unitcase volume consisted of beverage products of Coca-Cola FEMSA or other companies.

Coca-Cola Amatil Limited (‘‘Coca-Cola Amatil’’). At December 31, 2005, our Company’s ownershipinterest in Coca-Cola Amatil was approximately 32 percent. Coca-Cola Amatil has bottling and distributionrights, through direct ownership or joint ventures, in Australia, New Zealand, Fiji, Papua New Guinea,Indonesia and South Korea. Coca-Cola Amatil estimates that the territories in which it markets beverageproducts contain 100 percent of the populations of Australia, New Zealand, Fiji, South Korea and Papua NewGuinea, and 98 percent of the population of Indonesia. In 2005, Coca-Cola Amatil’s net sales of beverageproducts were approximately $3.0 billion. In 2005, approximately 51 percent of the unit case volume ofCoca-Cola Amatil consisted of Coca-Cola Trademark Beverages, approximately 40 percent of its unit casevolume consisted of other Company Trademark Beverages, approximately 8 percent of its unit case volumeconsisted of beverage products of Coca-Cola Amatil and less than 1 percent of its unit case volume consisted ofbeverage products of other companies.

Other Interests. We own a 50 percent interest in BPW, a joint venture with Nestlé and certain of itssubsidiaries that is focused upon the ready-to-drink tea and coffee businesses. BPW had sales in the UnitedStates and 65 other countries during the year ended December 31, 2005. BPW serves as the exclusive vehiclethrough which our Company and Nestlé participate in the ready-to-drink tea and coffee businesses, except inJapan. BPW markets ready-to-drink tea products primarily under the Nestea, Belté, Yang Guang, Nagomi,Heaven and Earth, Funchum, Frestea, Ten Ren, Modern Tea Workshop, Café Zu, Shizen and Tian Teytrademarks, and ready-to-drink coffee products primarily under the Nescafé, Taster’s Choice and Georgia Clubtrademarks. We also own a 50 percent interest in Multon, a Russian juice business (‘‘Multon’’), which weacquired in April 2005 jointly with Coca-Cola HBC. Multon produces and distributes juice products under theDOBRIY, Rich, Nico and other trademarks in Russia, Ukraine and Belarus.

Seasonality

Sales of our ready-to-drink nonalcoholic beverages are somewhat seasonal, with the second and thirdcalendar quarters accounting for the highest sales volumes. The volume of sales in the beverages business maybe affected by weather conditions.

Competition

Our Company competes in the nonalcoholic beverages segment of the commercial beverages industry.Based on internally available data and a variety of industry sources, we believe that, in 2005, worldwide sales ofCompany products accounted for approximately 10 percent of total worldwide sales of nonalcoholic beverageproducts. The nonalcoholic beverages segment of the commercial beverages industry is highly competitive,

9

consisting of numerous firms. These include firms that, like our Company, compete in multiple geographic areasas well as firms that are primarily local in operation. Competitive products include carbonated soft drinks;packaged water; juices and nectars; fruit drinks and dilutables (including syrups and powdered drinks); sportsand energy drinks; coffee and tea; still drinks and other beverages. Nonalcoholic beverages are sold toconsumers in both ready-to-drink and not-ready-to-drink form. In many of the countries in which we dobusiness, including the United States, PepsiCo, Inc. is one of our primary competitors. Other significantcompetitors include Nestlé, Cadbury Schweppes plc, Groupe Danone and Kraft Foods Inc.

Most of our beverages business currently is in soft drinks, as that term is defined in this report. The softdrink business, which is part of the nonalcoholic beverages segment, is itself highly competitive, and soft drinksface significant competition from other nonalcoholic beverages. Our Company is the leading seller of soft drinkconcentrates and syrups in the world. Numerous firms, however, compete in that business. These consist of arange of firms, from local to international, that compete against our Company in numerous geographic areas.

Competitive factors impacting our business include pricing, advertising, sales promotion programs, productinnovation, increased efficiency in production techniques, the introduction of new packaging, new vending anddispensing equipment, and brand and trademark development and protection.

Our competitive strengths include powerful brands with a high level of consumer acceptance; a worldwidenetwork of bottlers and distributors of Company products; sophisticated marketing capabilities; and a talentedgroup of dedicated employees. Our competitive challenges include strong competition in all geographicalregions and, in many countries, a concentrated retail sector with powerful buyers able to freely choose amongCompany products, products of competitive beverage suppliers and individual retailers’ own store-brandbeverages.

Raw Materials

The principal raw materials used by our business are nutritive and non-nutritive sweeteners. In the UnitedStates, the principal nutritive sweetener is high fructose corn syrup, a form of sugar, which is available fromnumerous domestic sources and is historically subject to fluctuations in its market price. The principal nutritivesweetener used by our business outside the United States is sucrose, another form of sugar, which is alsoavailable from numerous sources and is historically subject to fluctuations in its market price. Our Companygenerally has not experienced any difficulties in obtaining its requirements for nutritive sweeteners. In theUnited States, we purchase high fructose corn syrup to meet our and our bottlers’ requirements with theassistance of Coca-Cola Bottlers’ Sales & Services Company LLC (‘‘CCBSS’’). CCBSS is a limited liabilitycompany that is owned by authorized Coca-Cola bottlers doing business in the United States. Among otherthings, CCBSS provides procurement services to our Company for the purchase of various goods and services inthe United States, including high fructose corn syrup.

The principal non-nutritive sweeteners we use in our business are aspartame, saccharin, sucralose,acesulfame potassium and cyclamate. Generally, these raw materials are readily available from numeroussources. However, our Company purchases aspartame, an important non-nutritive sweetener that is used aloneor in combination with other important non-nutritive sweeteners such as saccharin or acesulfame potassium inour low-calorie soft drink products, primarily from The NutraSweet Company, Holland Sweetener Companyand Ajinomoto Co., Inc., which we consider to be our only viable sources for the supply of this product. Wecurrently purchase acesulfame potassium from Nutrinova Nutrition Specialties & Food Ingredients GmbH,which we consider to be our only viable source for the supply of this product. Our Company generally has notexperienced any difficulties in obtaining its requirements for non-nutritive sweeteners.

Our Company sells a number of products sweetened with sucralose, a non-nutritive sweetener. We workclosely with Tate & Lyle, our sucralose supplier, to maintain continuity of supply. Although Tate & Lyle is oursingle source for sucralose, we do not anticipate difficulties in obtaining our requirements for sucralose.

10

With regard to juice and juice-drink products, citrus fruit, particularly orange juice concentrate, is ourprincipal raw material. The citrus industry is subject to the variability of weather conditions. In particular,freezing weather or hurricanes in central Florida may result in shortages and higher prices for orange juiceconcentrate throughout the industry. Due to our ability to source orange juice concentrate from the SouthernHemisphere (particularly from Brazil), the supply of orange juice concentrate available that meets ourCompany’s standards is normally adequate to meet demand.

Patents, Copyrights, Trade Secrets and Trademarks