administrative report - wbcomtax.gov

TRANSCRIPT

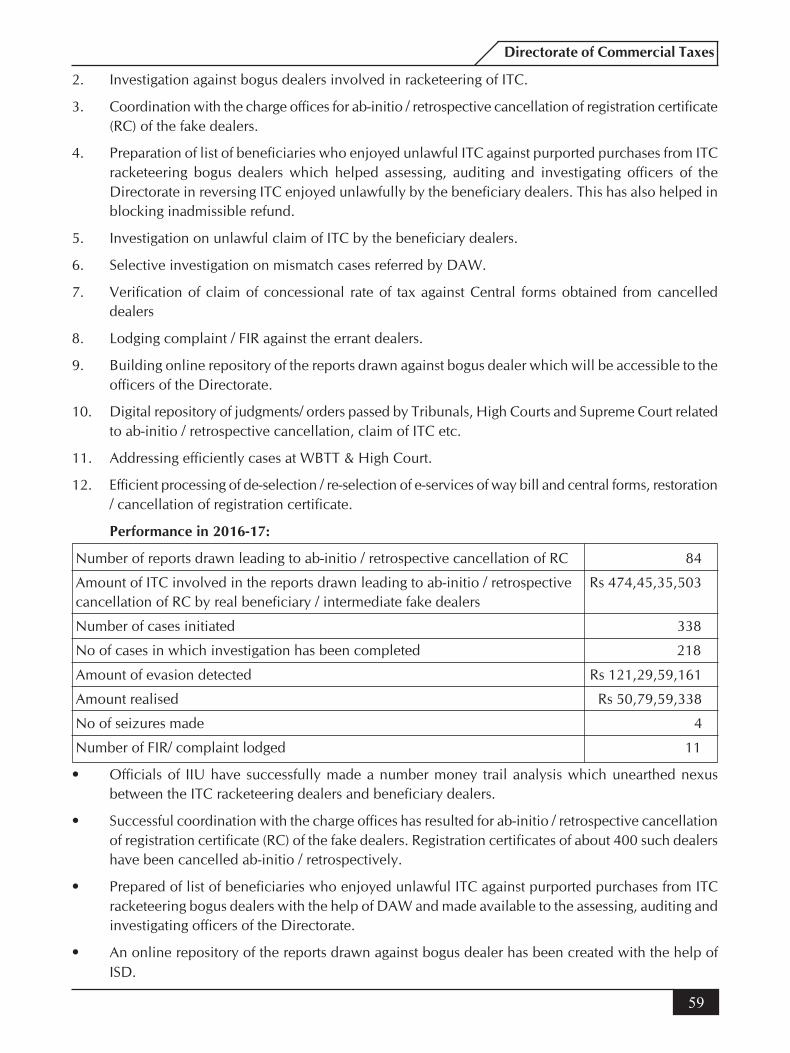

ADMINISTRATIVEREPORT2016 – 2017

DIRECTORATE OF COMMERCIAL TAXESGOVERNMENT OF WEST BENGAL

www.wbcomtax.gov.in

PREFACE

I have the pleasure to present the Annual Administrative Report for the year 2016-17 of theDirectorate of Commercial Taxes, West Bengal.

This has been a very significant year for the directorate as major emphasis has been on thepreparedness for entering into the new unified Tax Regime of GST departing from the federal taxstructure. Team of officers worked hard in drafting of new legal provisions so far they relate to WestBengal. As renewed legal situations will demand suitably equipping our Human Resources, ateam of master trainers has accordingly been developed. Employee database has been updatedfor mapping of duties for each individual in GST regime.

In order to promote e-governance in the exisiting tax law, compulsory use of Digital Signature forfiling online application for Registration has been introduced. Digital Signature for submission ofreturns by registered dealers having turnover of sales in excess of rupees fifty lakhs in the previousyear, or having registration under the Companies Act, is now mandatory. I would like to congratulateall the officers and staff for their ceaseless efforts and also the dealers for their co-operation inmaking the initiatives successful.

When this publication reaches you, the new tax era has already taken its own course puttingbefore us new situations and challanges which I believe all of us would be able to face with duecare and diligence. Though unique to our experiences, I hope that our concerted effort andendeavour in the new tax regime will usher in fiscal prosperity of the State.

Any suggestions for improving the future publications are welcome.

(Smaraki Mahapatra, IAS)Commissioner,

Commercial Taxes, West Bengal

Sl. No. Subject Page No.1. Directorate of Commercial Taxes: 1

(i) Prelude, Pioneering e-governance initiatives and New era Taxation regime 1(ii) Responsibilities Outlined 2(iii) GST and Future of Tax Administration 2-3(iv) Collection of Sales Tax since 1941 3-4(v) Role of Different Branches 6-11

2. Innovative Procedures introduced in 2016-17 113. Major Achievements of Commercial Tax Directorate From 2011-12 to 2016-17 124. Graphical Presentation of Some Achievements 14-185. Awards and Accolades in Credit 19-216. The Organisation 227. Collection and Expenditure 23-248. Circle, Charge and District wise Comparative Collection Figures 24-289. Registration 28

10. Assessment, Appeal Cases 2911. VAT Audit, Revision & Review 3012. Profession Tax Assessment 3013. Compliance to Budget Proposals of 2016-17 3114. Bureau of Investigation 3115. Central Registration Unit 3516. Central Audit Unit 3617. Interstate Verification Cell (H.Q.) 3718. Special Cell 3919. Industrial Promotion Assistance Cell 3920. Internal Audit Wing 4221. Certificate Organisation 4322. Collection Cell 4323. Human Resource Development Cell 4424. Sales Tax Deducted at Source (S.T.D.S.) Cell 4725. Law Section 5126. Fast Track Revisional Authority 5327. The West Bengal Commercial Taxes Appellate and Revisional Board 5428. Public Relation Section 5629. ITC Investigation Unit (IIU) 5830. Online Grievance Redressal System 6031. Central Section 6132. Central Refund Unit 6233. Information Systems Division 6434. Profession Tax Wing 7935. Infrastructure Development 8036. Commodity wise Rate of Tax under Vat Act (Web Link) 8137. Commodity Name with Codes (Web Link) 8138. Profession Tax Schedule (Web Link) 8139. Contact numbers of the offices of this Directorate 8240. Important e-mail Addresses 8541. Email addresses (by name) (Web link) 87

CONTENTS

1

Directorate of Commercial Taxes

DIRECTORATE OF COMMERCIAL TAXES, Government of West Bengal

PRELUDE

A single-point sales tax system was introduced by the then Bengal Government in July 1941 in pre-independent India by the enactment of the Bengal Finance (Sales Tax) Act, 1941.The British Governmentwas obliged to levy tax on sale or consumption primarily to support additional expenditure of the WorldWar-II. But it continued beyond the warring days, and over the years, it has undergone evolutionaryphases till the present day. Today, this form of indirect tax levied on the distributive trade part of commodityvalue chain is the mainstay for the State revenue under the federal setup. Directorate of CommercialTaxes, Government of West Bengal has been administering the tax which accounts for nearly 60% of theState tax-revenue receipts almost across the board.

Substantial research has taken place in the realm of indirect taxation, primarily to deal with itsdynamic nature. Incidence of tax, points of levy, reasonable restriction on movement of goods, easingout cascading effect on the final price, incentives and exemptions and to ensure uniformity of tax infederal setup are a few of the important challenges facing the administrator. Managing evasion is also acritical area. After a lot of deliberations over a considerable period of time, the concept of value-addedtax system, in keeping with the global trend, dawned on our country and was enacted in our state as WestBengal Value Added Tax Act, 2003 w.e.f 01.04.2005. Despite the success of Value Added Tax Act fromrevenue point of view the deliberation is going on at national level for introduction of a more improvedtax structure in the form of the Goods and Service Tax Act (in short GST Act) w.e.f. 01.07.2017 –beingstated as the biggest indirect taxation reform in India.

PIONEERING e-GOVERNANCE INITIATIVES

With the dawning of an era of Information and Communication Technology, citizen-centric onlineservices, to bring in efficiency, accountability and transparency have hogged the limelight. Under theInformation Technology (IT) driven new era of tax administration, extensive Government Process Re-engineering (GPR) took place under the Mission Mode Project for Commercial Taxes (MMP-CT) as a partof the National e-Governance Plan (NeGP). In the dedicated Mission Mode Project for Commercial Taxes(MMP-CT), the Directorate pioneered in introducing Government Process Re-engineering for ensuringcitizen-centric measures to bring in pace, ease of compliance and transparency in the system. It is needlessto mention that for the above purposes, apart from the fund available under MMPCT scheme the state isalso utilizing its own resources on equal sharing.

NEW ERA TAXATION REGIME

Before introduction of VAT, in the sales tax regime, apart from the problem of multiple taxation andburden of adverse cascading effect of taxes there was also no harmony in the rate of sales tax on differentcommodities among the States and there was often an unhealthy competition among States in the formof ‘rate war’.

West Bengal Value Added Tax Act 2003 entails multi-point levy of tax at each stage of transactionin a value chain, till it reaches the consumer. At each stage, credit of the tax paid on purchase is given inthe form of set off on the tax payable on the corresponding sale.

Incidentally, the concept of VAT has revolutionized the entire indirect taxation system in India.Though it was practiced variously in production part and thereafter introduced in the distributive part ofthe commodity tax, the need for integrating both the parts has also been envisaged in the forthcomingGoods and Service Tax (GST) Act, billed as mother of all indirect taxation reforms in India.

2

Administrative Report 2016-17

RESPONSIBILITIES OUTLINED

The Directorate has to maintain a very close interface for the Government of the day with the tradeand industry by way of tax administration. Starting from monitoring closely the trade and commerce ofthe State to regulating the movement of goods, besides catering to the primary obligation of revenuemobilization, form few of its critical tasks.

In doing so, the Directorate administers hosts of commodity taxation related Acts, like

i. The West Bengal Value Added Tax Act, 2003

ii. The West Bengal Sales Tax Act, 1994

iii. The Central Sales Tax Act, 1956

iv. The West Bengal State Tax on Profession, Trades, Callings and Employments Act, 1979

v. The West Bengal Primary Education Act, 1973. (for the limited purpose of Education Cess)

vi. The West Bengal Rural Employment and Production Act, 1976 (for the limited purpose ofRural Employment Cess)

vii. The West Bengal Transport Infrastructure Development Fund Act, 2002

viii. The West Bengal Sales Tax (Settlement of Dispute) Act, 1999

ix. The West Bengal Tax on Entry of Goods in Local Areas Act , 2012

This apart, anti-evasion activity that forms a vital part of tax administration requires close observanceof the provisions of Indian Penal Code 1860 and The Code of Criminal Procedure 1973.

Besides, the day-to-day tax administration entails a good part of general administration and officeprocedures, by closely observing West Bengal Treasury Rules, 2008, West Bengal Financial Rules, 1979& West Bengal Service Rules, 2009.

GST AND FUTURE OF TAX ADMINISTRATION

The proposed Goods and Service Tax is being identified by experts as the most important leaptowards future of tax administration in which public policy changes are to come about in a big way. Acomprehensive Goods and Services Tax (GST) based on VAT principle is targeted to be a simple, transparentand efficient system of indirect taxation as has been adopted by over 150 countries around the world.This involves taxation of goods and services in an integrated manner as the blurring of line of demarcationbetween goods and services has made separate taxation of goods and services untenable.

GST has also been identified as a singularly complex project where mission-critical IT systems needto be applied to introduce Government Process Re-engineering (GPR). The government is working on aspecial IT platform for smooth implementation of GST christened as GSTN (Goods and Services TaxNetwork).

Thus we have a twin task at hand. GST is going to be dual tax levied both by Central and StateGovt, when it subsumes State VAT, Central Excise, Service Tax and few other indirect taxes. It will belevied at every stage of production-distribution chain of goods and services in a broad-based, single,comprehensive tax regime. So far as administering State GST (SGST), the Directorate is going to assumea dominant role, while Central GST (CGST) is to be governed by Central Government and IGST shallhave dual jurisdiction. And equally important role awaits us when under the proposed command thenew concept of destination-based tax system takes place, as we would move up from the sub-nationaldomain to integrate in a pan Indian scenario.

3

Directorate of Commercial Taxes

On the technology front, the spotlight is going to be on this part of the world as significant changesare underway in terms of reforms of the system and application of Information and CommunicationTechnology (ICT) to bring about the desired change. For IT driven governance initiatives the administrationof indirect tax can well be the home page for Government of the State.

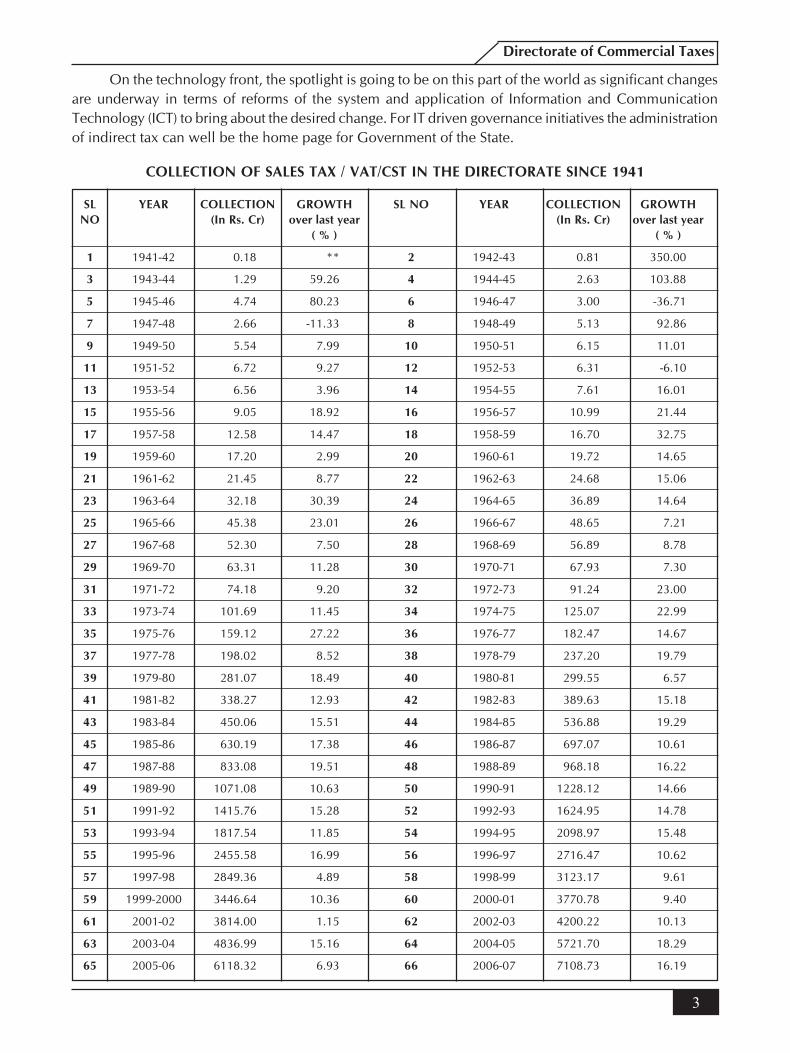

COLLECTION OF SALES TAX / VAT/CST IN THE DIRECTORATE SINCE 1941

SL YEAR COLLECTION GROWTH SL NO YEAR COLLECTION GROWTHNO (In Rs. Cr) over last year (In Rs. Cr) over last year

( % ) ( % )

1 1941-42 0.18 ** 2 1942-43 0.81 350.00

3 1943-44 1.29 59.26 4 1944-45 2.63 103.88

5 1945-46 4.74 80.23 6 1946-47 3.00 -36.71

7 1947-48 2.66 -11.33 8 1948-49 5.13 92.86

9 1949-50 5.54 7.99 10 1950-51 6.15 11.01

11 1951-52 6.72 9.27 12 1952-53 6.31 -6.10

13 1953-54 6.56 3.96 14 1954-55 7.61 16.01

15 1955-56 9.05 18.92 16 1956-57 10.99 21.44

17 1957-58 12.58 14.47 18 1958-59 16.70 32.75

19 1959-60 17.20 2.99 20 1960-61 19.72 14.65

21 1961-62 21.45 8.77 22 1962-63 24.68 15.06

23 1963-64 32.18 30.39 24 1964-65 36.89 14.64

25 1965-66 45.38 23.01 26 1966-67 48.65 7.21

27 1967-68 52.30 7.50 28 1968-69 56.89 8.78

29 1969-70 63.31 11.28 30 1970-71 67.93 7.30

31 1971-72 74.18 9.20 32 1972-73 91.24 23.00

33 1973-74 101.69 11.45 34 1974-75 125.07 22.99

35 1975-76 159.12 27.22 36 1976-77 182.47 14.67

37 1977-78 198.02 8.52 38 1978-79 237.20 19.79

39 1979-80 281.07 18.49 40 1980-81 299.55 6.57

41 1981-82 338.27 12.93 42 1982-83 389.63 15.18

43 1983-84 450.06 15.51 44 1984-85 536.88 19.29

45 1985-86 630.19 17.38 46 1986-87 697.07 10.61

47 1987-88 833.08 19.51 48 1988-89 968.18 16.22

49 1989-90 1071.08 10.63 50 1990-91 1228.12 14.66

51 1991-92 1415.76 15.28 52 1992-93 1624.95 14.78

53 1993-94 1817.54 11.85 54 1994-95 2098.97 15.48

55 1995-96 2455.58 16.99 56 1996-97 2716.47 10.62

57 1997-98 2849.36 4.89 58 1998-99 3123.17 9.61

59 1999-2000 3446.64 10.36 60 2000-01 3770.78 9.40

61 2001-02 3814.00 1.15 62 2002-03 4200.22 10.13

63 2003-04 4836.99 15.16 64 2004-05 5721.70 18.29

65 2005-06 6118.32 6.93 66 2006-07 7108.73 16.19

4

Administrative Report 2016-17

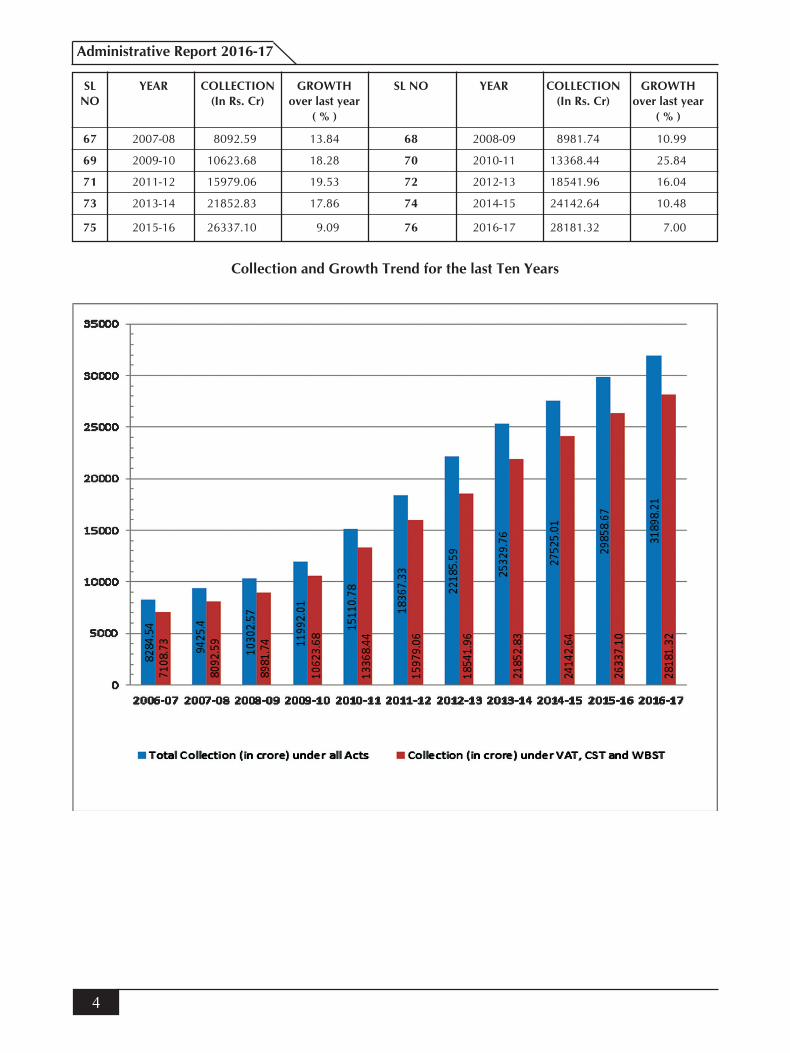

67 2007-08 8092.59 13.84 68 2008-09 8981.74 10.99

69 2009-10 10623.68 18.28 70 2010-11 13368.44 25.84

71 2011-12 15979.06 19.53 72 2012-13 18541.96 16.04

73 2013-14 21852.83 17.86 74 2014-15 24142.64 10.48

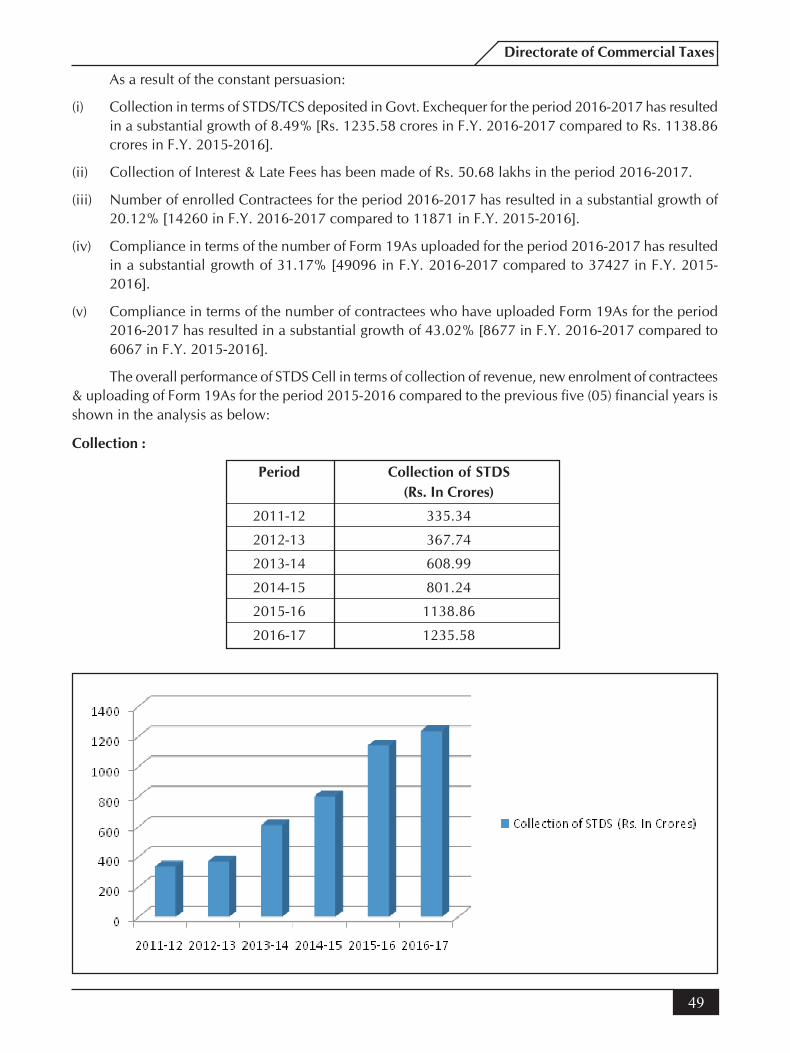

75 2015-16 26337.10 9.09 76 2016-17 28181.32 7.00

Collection and Growth Trend for the last Ten Years

SL YEAR COLLECTION GROWTH SL NO YEAR COLLECTION GROWTHNO (In Rs. Cr) over last year (In Rs. Cr) over last year

( % ) ( % )

5

Directorate of Commercial Taxes

6

Administrative Report 2016-17

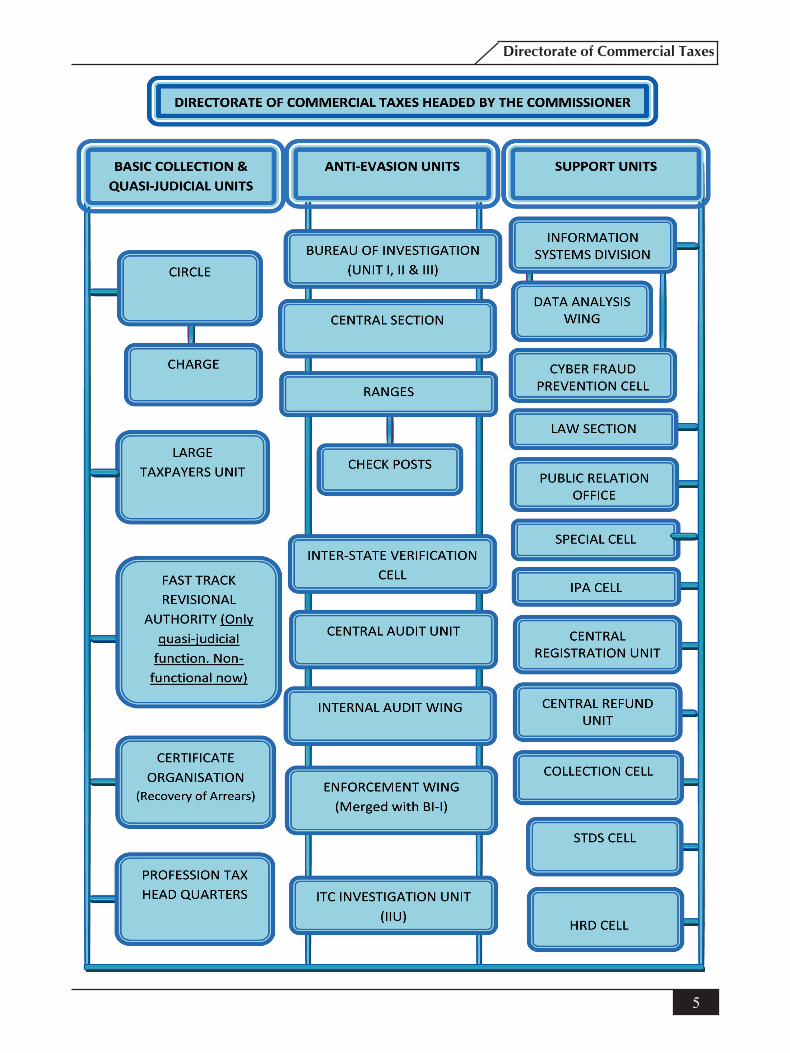

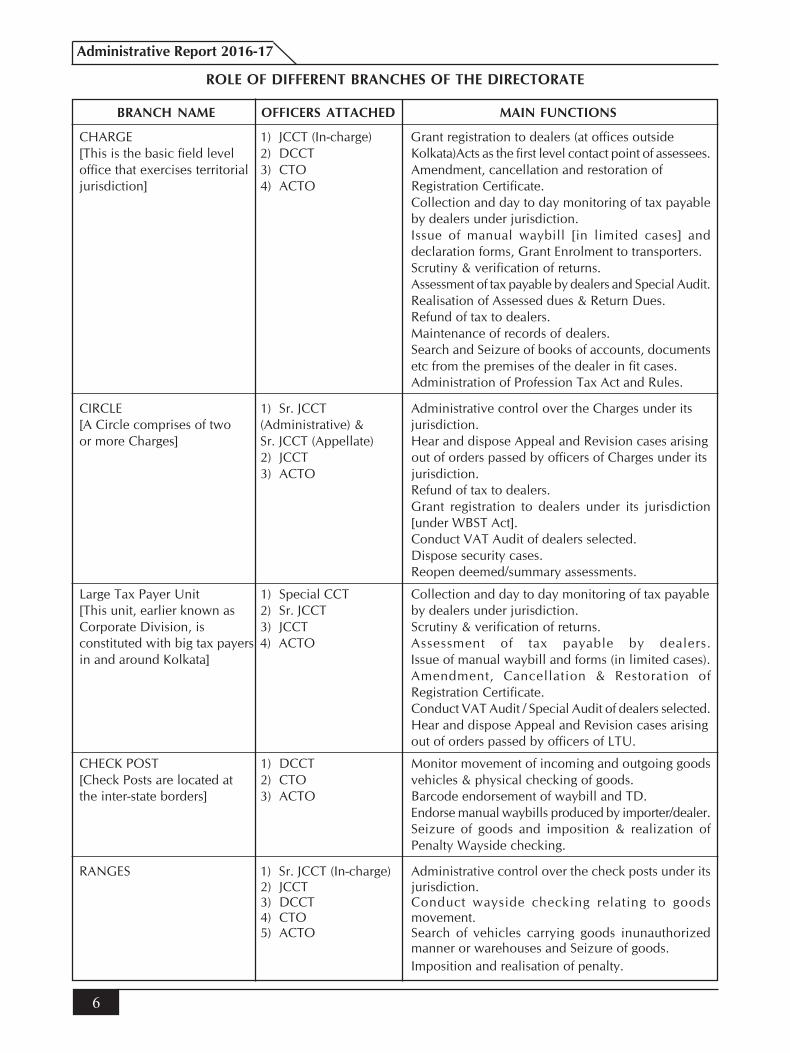

ROLE OF DIFFERENT BRANCHES OF THE DIRECTORATE

BRANCH NAME OFFICERS ATTACHED MAIN FUNCTIONS

CHARGE 1) JCCT (In-charge) Grant registration to dealers (at offices outside[This is the basic field level 2) DCCT Kolkata)Acts as the first level contact point of assessees.office that exercises territorial 3) CTO Amendment, cancellation and restoration ofjurisdiction] 4) ACTO Registration Certificate.

Collection and day to day monitoring of tax payableby dealers under jurisdiction.Issue of manual waybill [in limited cases] anddeclaration forms, Grant Enrolment to transporters.Scrutiny & verification of returns.Assessment of tax payable by dealers and Special Audit.Realisation of Assessed dues & Return Dues.Refund of tax to dealers.Maintenance of records of dealers.Search and Seizure of books of accounts, documentsetc from the premises of the dealer in fit cases.Administration of Profession Tax Act and Rules.

CIRCLE 1) Sr. JCCT Administrative control over the Charges under its[A Circle comprises of two (Administrative) & jurisdiction.or more Charges] Sr. JCCT (Appellate) Hear and dispose Appeal and Revision cases arising

2) JCCT out of orders passed by officers of Charges under its3) ACTO jurisdiction.

Refund of tax to dealers.Grant registration to dealers under its jurisdiction[under WBST Act].Conduct VAT Audit of dealers selected.Dispose security cases.Reopen deemed/summary assessments.

Large Tax Payer Unit 1) Special CCT Collection and day to day monitoring of tax payable[This unit, earlier known as 2) Sr. JCCT by dealers under jurisdiction.Corporate Division, is 3) JCCT Scrutiny & verification of returns.constituted with big tax payers 4) ACTO Assessment of tax payable by dealers.in and around Kolkata] Issue of manual waybill and forms (in limited cases).

Amendment, Cancellation & Restoration ofRegistration Certificate.Conduct VAT Audit / Special Audit of dealers selected.Hear and dispose Appeal and Revision cases arisingout of orders passed by officers of LTU.

CHECK POST 1) DCCT Monitor movement of incoming and outgoing goods[Check Posts are located at 2) CTO vehicles & physical checking of goods.the inter-state borders] 3) ACTO Barcode endorsement of waybill and TD.

Endorse manual waybills produced by importer/dealer.Seizure of goods and imposition & realization ofPenalty Wayside checking.

RANGES 1) Sr. JCCT (In-charge) Administrative control over the check posts under its2) JCCT jurisdiction.3) DCCT Conduct wayside checking relating to goods4) CTO movement.5) ACTO Search of vehicles carrying goods inunauthorized

manner or warehouses and Seizure of goods.Imposition and realisation of penalty.

7

Directorate of Commercial Taxes

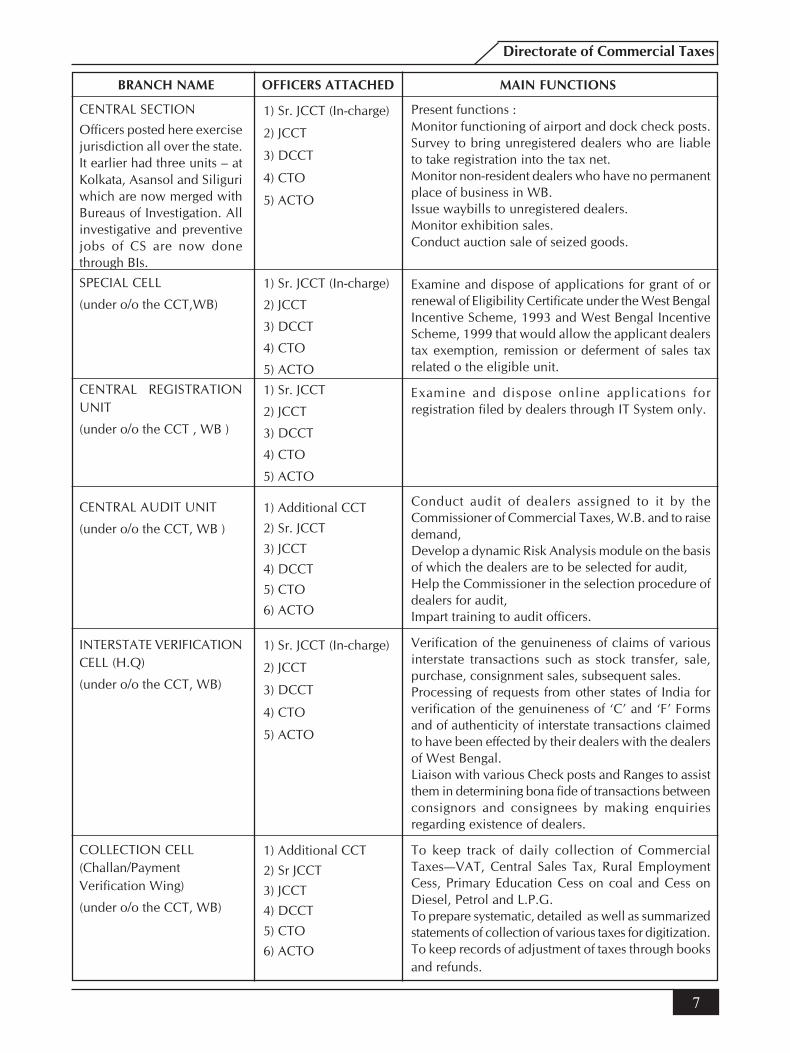

Present functions :Monitor functioning of airport and dock check posts.Survey to bring unregistered dealers who are liableto take registration into the tax net.Monitor non-resident dealers who have no permanentplace of business in WB.Issue waybills to unregistered dealers.Monitor exhibition sales.Conduct auction sale of seized goods.

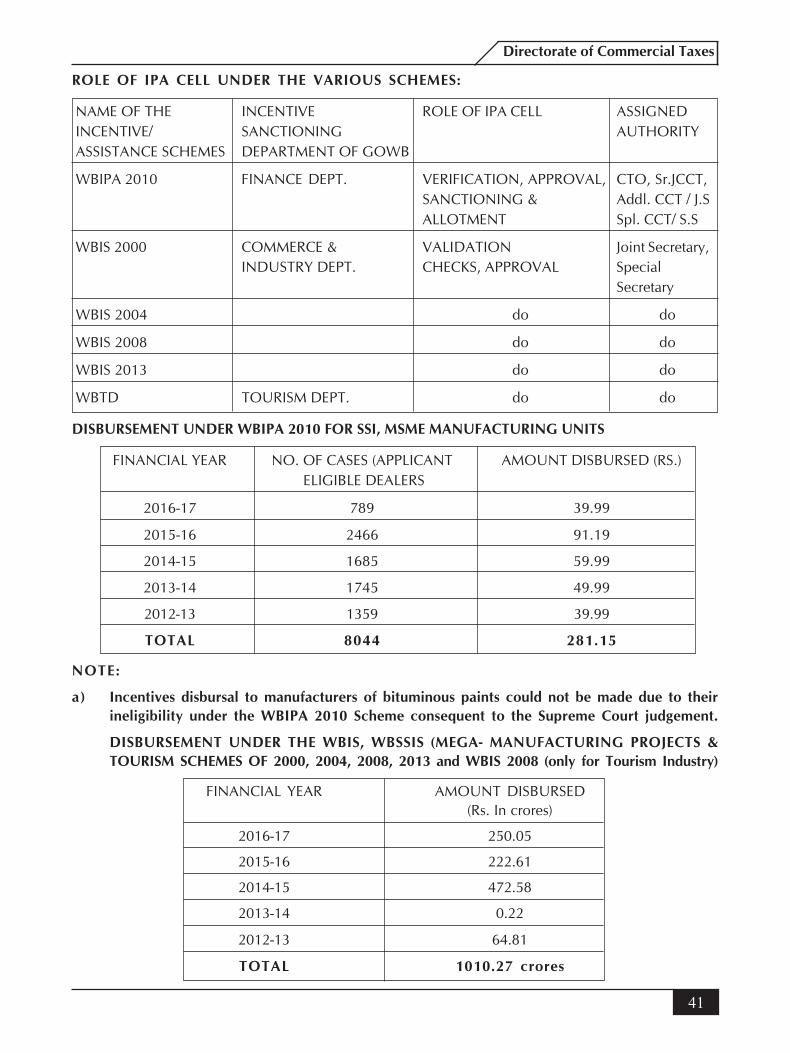

Examine and dispose of applications for grant of orrenewal of Eligibility Certificate under the West BengalIncentive Scheme, 1993 and West Bengal IncentiveScheme, 1999 that would allow the applicant dealerstax exemption, remission or deferment of sales taxrelated o the eligible unit.

Examine and dispose online applications forregistration filed by dealers through IT System only.

Conduct audit of dealers assigned to it by theCommissioner of Commercial Taxes, W.B. and to raisedemand,Develop a dynamic Risk Analysis module on the basisof which the dealers are to be selected for audit,Help the Commissioner in the selection procedure ofdealers for audit,Impart training to audit officers.

Verification of the genuineness of claims of variousinterstate transactions such as stock transfer, sale,purchase, consignment sales, subsequent sales.Processing of requests from other states of India forverification of the genuineness of ‘C’ and ‘F’ Formsand of authenticity of interstate transactions claimedto have been effected by their dealers with the dealersof West Bengal.Liaison with various Check posts and Ranges to assistthem in determining bona fide of transactions betweenconsignors and consignees by making enquiriesregarding existence of dealers.

To keep track of daily collection of CommercialTaxes—VAT, Central Sales Tax, Rural EmploymentCess, Primary Education Cess on coal and Cess onDiesel, Petrol and L.P.G.To prepare systematic, detailed as well as summarizedstatements of collection of various taxes for digitization.To keep records of adjustment of taxes through booksand refunds.

BRANCH NAME OFFICERS ATTACHED MAIN FUNCTIONS

CENTRAL SECTION

Officers posted here exercisejurisdiction all over the state.It earlier had three units – atKolkata, Asansol and Siliguriwhich are now merged withBureaus of Investigation. Allinvestigative and preventivejobs of CS are now donethrough BIs.

1) Sr. JCCT (In-charge)

2) JCCT

3) DCCT

4) CTO

5) ACTO

SPECIAL CELL

(under o/o the CCT,WB)

1) Sr. JCCT (In-charge)

2) JCCT

3) DCCT

4) CTO

5) ACTOCENTRAL REGISTRATIONUNIT

(under o/o the CCT , WB )

1) Sr. JCCT

2) JCCT

3) DCCT

4) CTO

5) ACTO

CENTRAL AUDIT UNIT

(under o/o the CCT, WB )

1) Additional CCT

2) Sr. JCCT

3) JCCT

4) DCCT

5) CTO

6) ACTO

INTERSTATE VERIFICATIONCELL (H.Q)

(under o/o the CCT, WB)

1) Sr. JCCT (In-charge)

2) JCCT

3) DCCT

4) CTO

5) ACTO

COLLECTION CELL(Challan/PaymentVerification Wing)

(under o/o the CCT, WB)

1) Additional CCT2) Sr JCCT3) JCCT4) DCCT

5) CTO6) ACTO

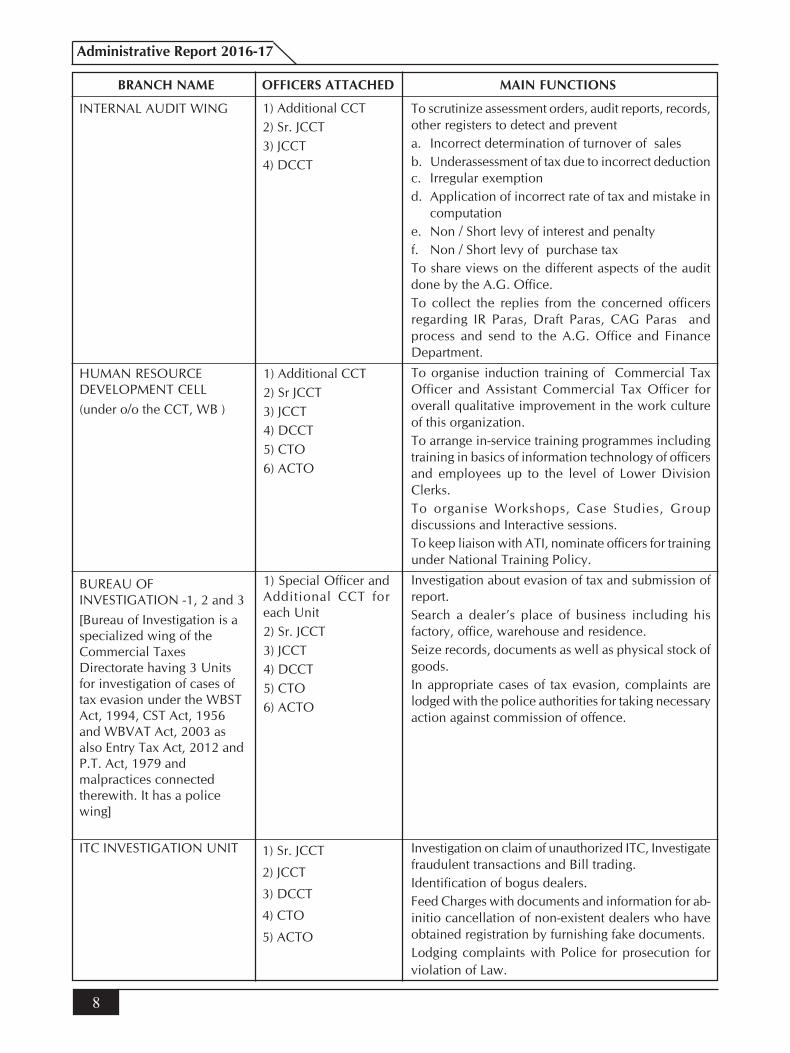

8

Administrative Report 2016-17

INTERNAL AUDIT WING To scrutinize assessment orders, audit reports, records,other registers to detect and preventa. Incorrect determination of turnover of salesb. Underassessment of tax due to incorrect deductionc. Irregular exemptiond. Application of incorrect rate of tax and mistake in

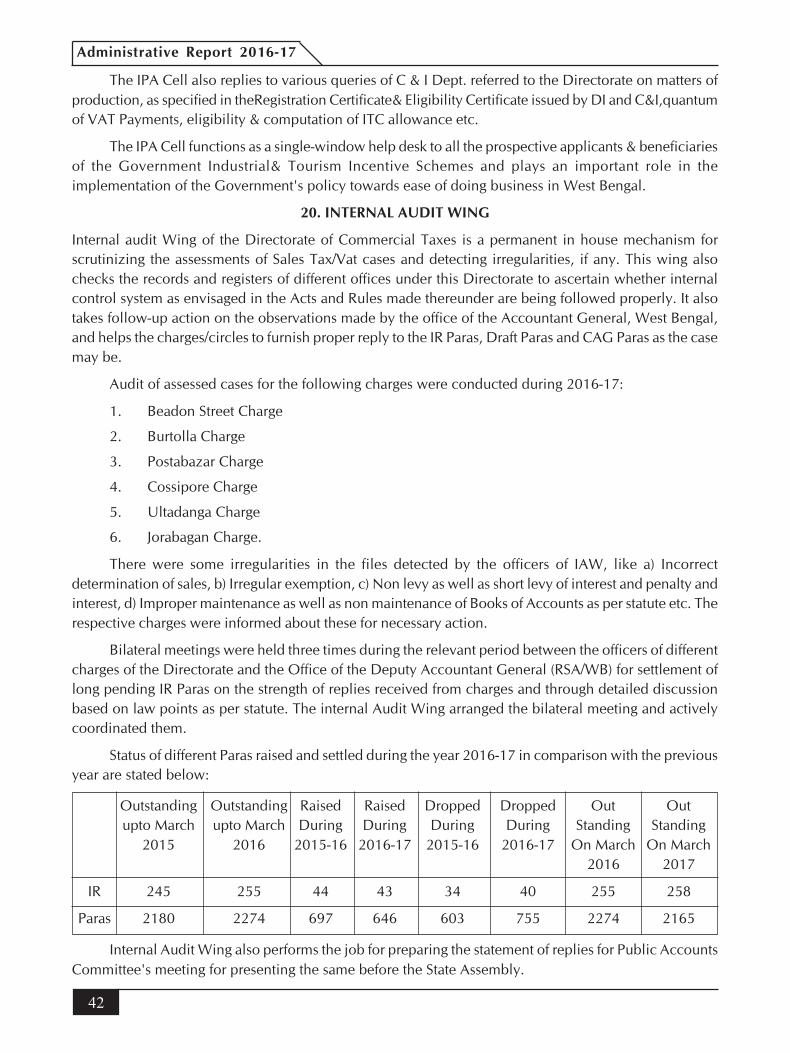

computatione. Non / Short levy of interest and penaltyf. Non / Short levy of purchase taxTo share views on the different aspects of the auditdone by the A.G. Office.To collect the replies from the concerned officersregarding IR Paras, Draft Paras, CAG Paras andprocess and send to the A.G. Office and FinanceDepartment.

To organise induction training of Commercial TaxOfficer and Assistant Commercial Tax Officer foroverall qualitative improvement in the work cultureof this organization.To arrange in-service training programmes includingtraining in basics of information technology of officersand employees up to the level of Lower DivisionClerks.To organise Workshops, Case Studies, Groupdiscussions and Interactive sessions.To keep liaison with ATI, nominate officers for trainingunder National Training Policy.

Investigation about evasion of tax and submission ofreport.Search a dealer’s place of business including hisfactory, office, warehouse and residence.Seize records, documents as well as physical stock ofgoods.In appropriate cases of tax evasion, complaints arelodged with the police authorities for taking necessaryaction against commission of offence.

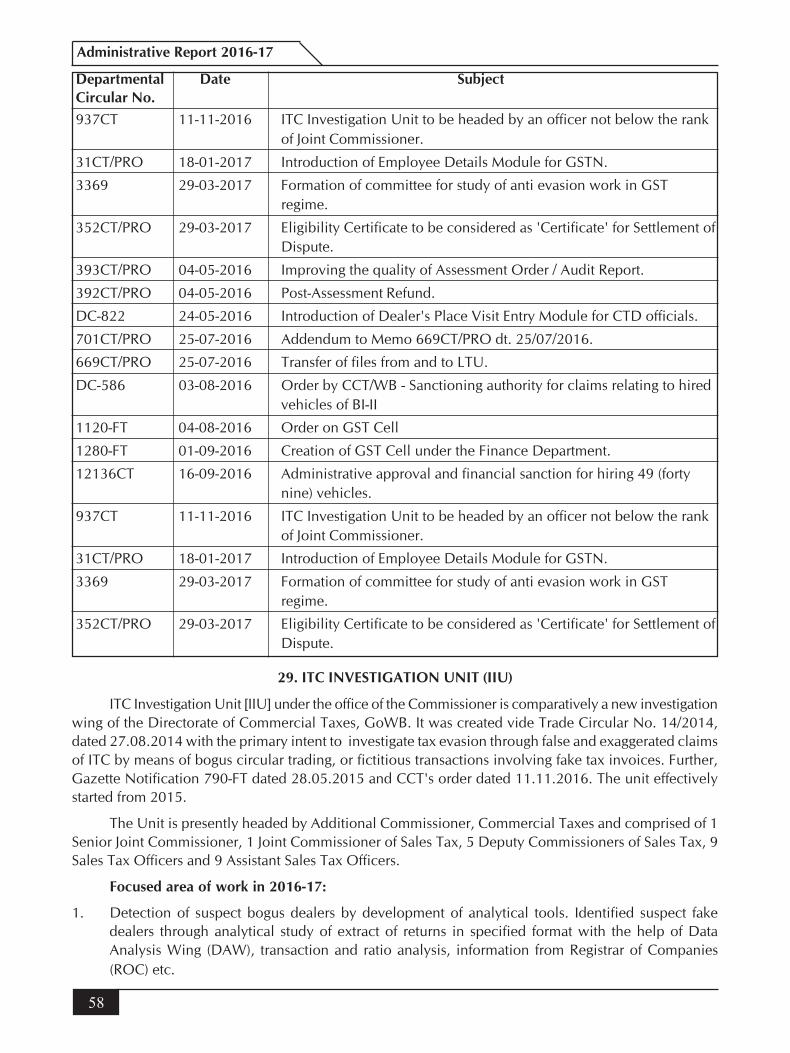

ITC INVESTIGATION UNIT Investigation on claim of unauthorized ITC, Investigatefraudulent transactions and Bill trading.Identification of bogus dealers.Feed Charges with documents and information for ab-initio cancellation of non-existent dealers who haveobtained registration by furnishing fake documents.Lodging complaints with Police for prosecution forviolation of Law.

BRANCH NAME OFFICERS ATTACHED MAIN FUNCTIONS

1) Additional CCT2) Sr. JCCT3) JCCT4) DCCT

HUMAN RESOURCEDEVELOPMENT CELL(under o/o the CCT, WB )

1) Additional CCT2) Sr JCCT3) JCCT4) DCCT5) CTO6) ACTO

BUREAU OFINVESTIGATION -1, 2 and 3[Bureau of Investigation is aspecialized wing of theCommercial TaxesDirectorate having 3 Unitsfor investigation of cases oftax evasion under the WBSTAct, 1994, CST Act, 1956and WBVAT Act, 2003 asalso Entry Tax Act, 2012 andP.T. Act, 1979 andmalpractices connectedtherewith. It has a policewing]

1) Special Officer andAdditional CCT foreach Unit2) Sr. JCCT3) JCCT4) DCCT5) CTO6) ACTO

1) Sr. JCCT

2) JCCT

3) DCCT

4) CTO

5) ACTO

9

Directorate of Commercial Taxes

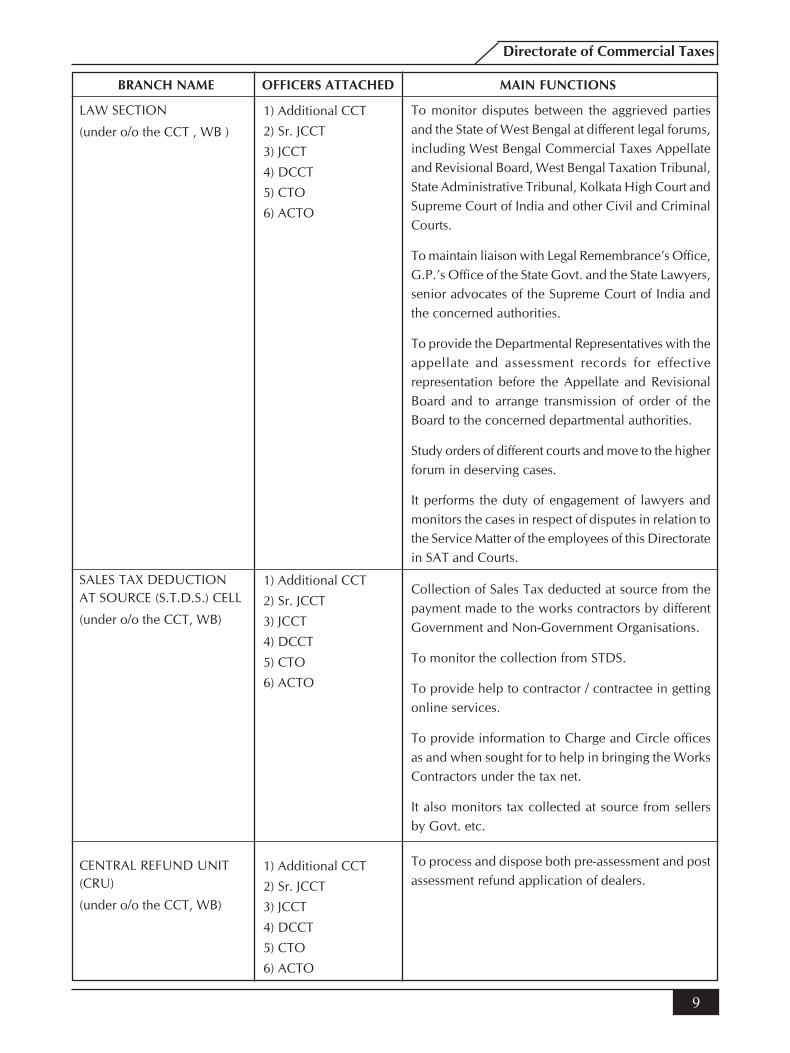

To monitor disputes between the aggrieved partiesand the State of West Bengal at different legal forums,including West Bengal Commercial Taxes Appellateand Revisional Board, West Bengal Taxation Tribunal,State Administrative Tribunal, Kolkata High Court andSupreme Court of India and other Civil and CriminalCourts.

To maintain liaison with Legal Remembrance’s Office,G.P.’s Office of the State Govt. and the State Lawyers,senior advocates of the Supreme Court of India andthe concerned authorities.

To provide the Departmental Representatives with theappellate and assessment records for effectiverepresentation before the Appellate and RevisionalBoard and to arrange transmission of order of theBoard to the concerned departmental authorities.

Study orders of different courts and move to the higherforum in deserving cases.

It performs the duty of engagement of lawyers andmonitors the cases in respect of disputes in relation tothe Service Matter of the employees of this Directoratein SAT and Courts.

Collection of Sales Tax deducted at source from thepayment made to the works contractors by differentGovernment and Non-Government Organisations.

To monitor the collection from STDS.

To provide help to contractor / contractee in gettingonline services.

To provide information to Charge and Circle officesas and when sought for to help in bringing the WorksContractors under the tax net.

It also monitors tax collected at source from sellersby Govt. etc.

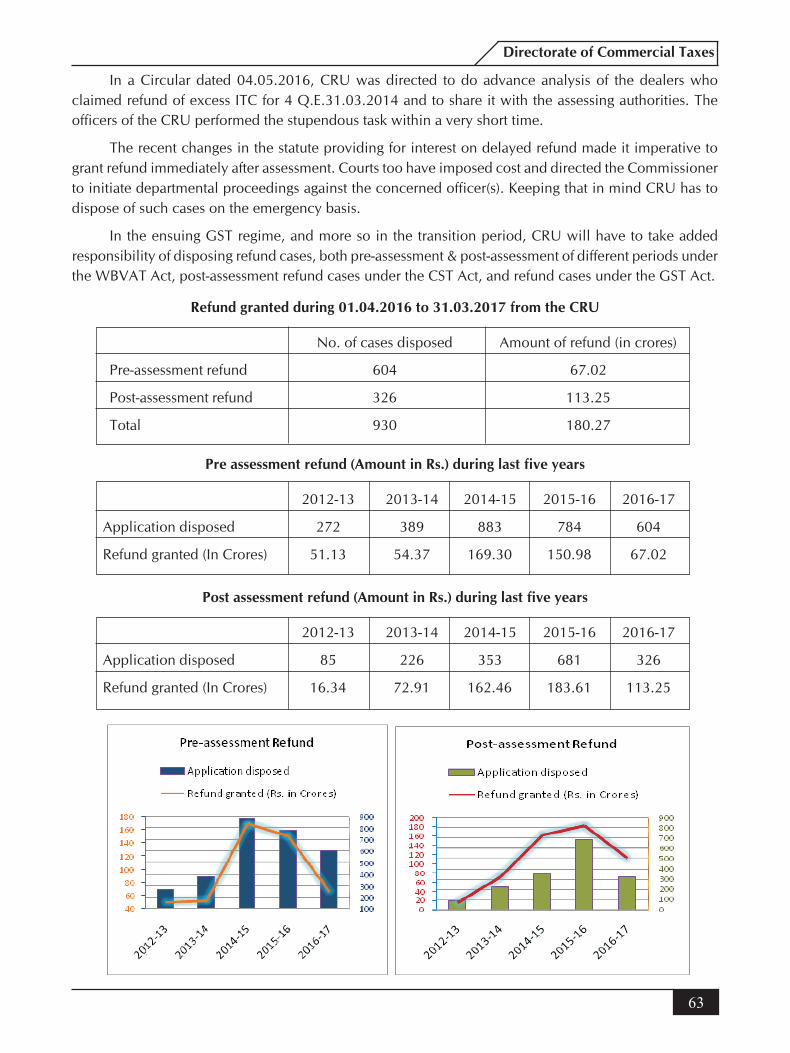

To process and dispose both pre-assessment and postassessment refund application of dealers.

BRANCH NAME OFFICERS ATTACHED MAIN FUNCTIONS

LAW SECTION

(under o/o the CCT , WB )

1) Additional CCT

2) Sr. JCCT

3) JCCT

4) DCCT

5) CTO

6) ACTO

SALES TAX DEDUCTIONAT SOURCE (S.T.D.S.) CELL

(under o/o the CCT, WB)

1) Additional CCT

2) Sr. JCCT

3) JCCT

4) DCCT

5) CTO

6) ACTO

CENTRAL REFUND UNIT(CRU)

(under o/o the CCT, WB)

1) Additional CCT

2) Sr. JCCT

3) JCCT

4) DCCT

5) CTO

6) ACTO

10

Administrative Report 2016-17

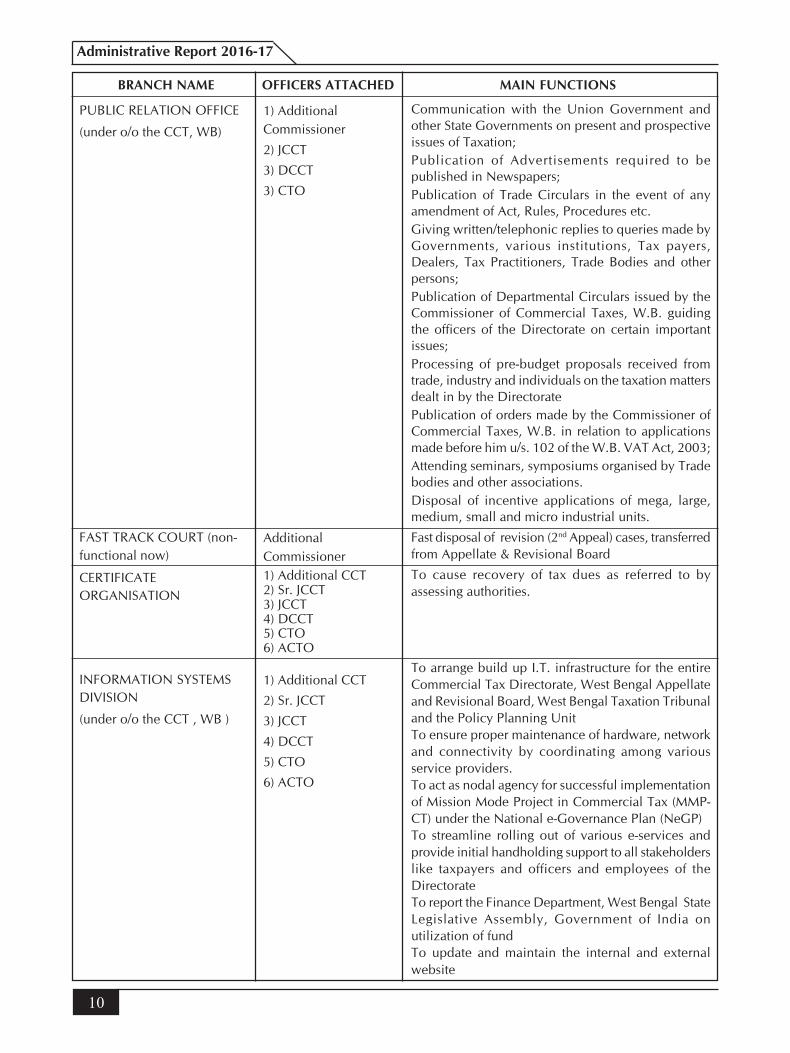

Communication with the Union Government andother State Governments on present and prospectiveissues of Taxation;Publication of Advertisements required to bepublished in Newspapers;Publication of Trade Circulars in the event of anyamendment of Act, Rules, Procedures etc.Giving written/telephonic replies to queries made byGovernments, various institutions, Tax payers,Dealers, Tax Practitioners, Trade Bodies and otherpersons;Publication of Departmental Circulars issued by theCommissioner of Commercial Taxes, W.B. guidingthe officers of the Directorate on certain importantissues;Processing of pre-budget proposals received fromtrade, industry and individuals on the taxation mattersdealt in by the DirectoratePublication of orders made by the Commissioner ofCommercial Taxes, W.B. in relation to applicationsmade before him u/s. 102 of the W.B. VAT Act, 2003;Attending seminars, symposiums organised by Tradebodies and other associations.Disposal of incentive applications of mega, large,medium, small and micro industrial units.

Fast disposal of revision (2nd Appeal) cases, transferredfrom Appellate & Revisional Board

To cause recovery of tax dues as referred to byassessing authorities.

To arrange build up I.T. infrastructure for the entireCommercial Tax Directorate, West Bengal Appellateand Revisional Board, West Bengal Taxation Tribunaland the Policy Planning UnitTo ensure proper maintenance of hardware, networkand connectivity by coordinating among variousservice providers.To act as nodal agency for successful implementationof Mission Mode Project in Commercial Tax (MMP-CT) under the National e-Governance Plan (NeGP)To streamline rolling out of various e-services andprovide initial handholding support to all stakeholderslike taxpayers and officers and employees of theDirectorateTo report the Finance Department, West Bengal StateLegislative Assembly, Government of India onutilization of fundTo update and maintain the internal and externalwebsite

BRANCH NAME OFFICERS ATTACHED MAIN FUNCTIONS

PUBLIC RELATION OFFICE

(under o/o the CCT, WB)

1) AdditionalCommissioner

2) JCCT

3) DCCT

3) CTO

FAST TRACK COURT (non-functional now)

AdditionalCommissioner

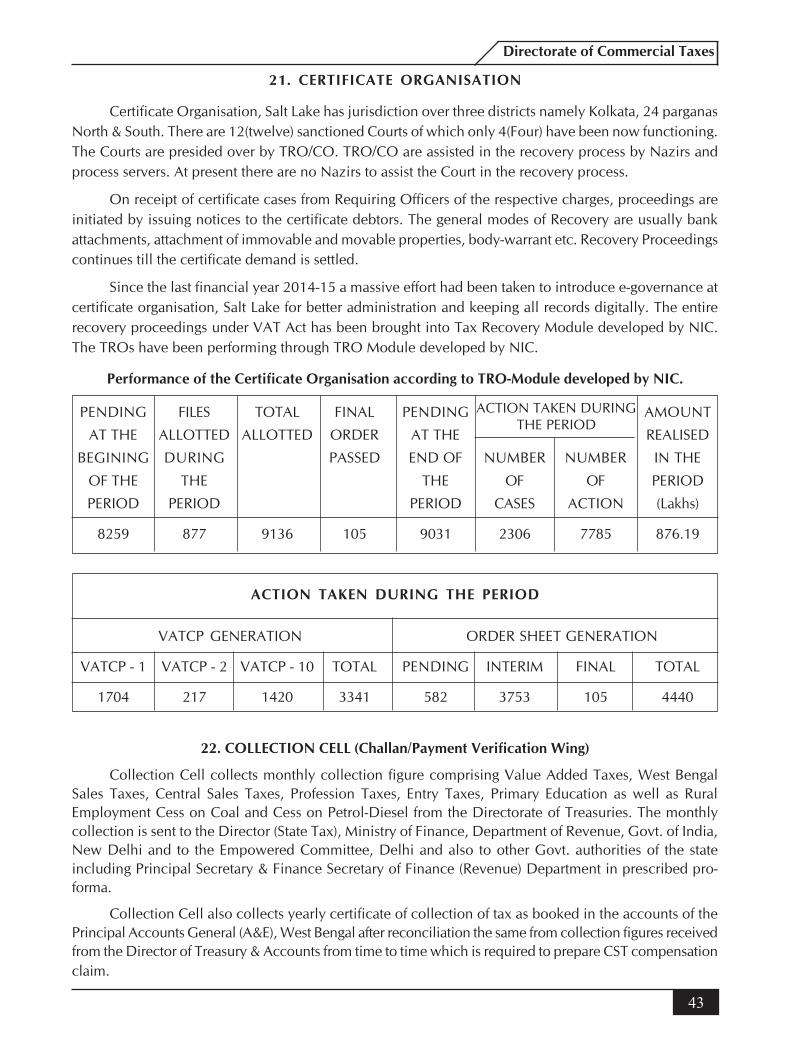

CERTIFICATEORGANISATION

1) Additional CCT2) Sr. JCCT3) JCCT4) DCCT5) CTO6) ACTO

INFORMATION SYSTEMSDIVISION

(under o/o the CCT , WB )

1) Additional CCT

2) Sr. JCCT

3) JCCT

4) DCCT

5) CTO

6) ACTO

11

Directorate of Commercial Taxes

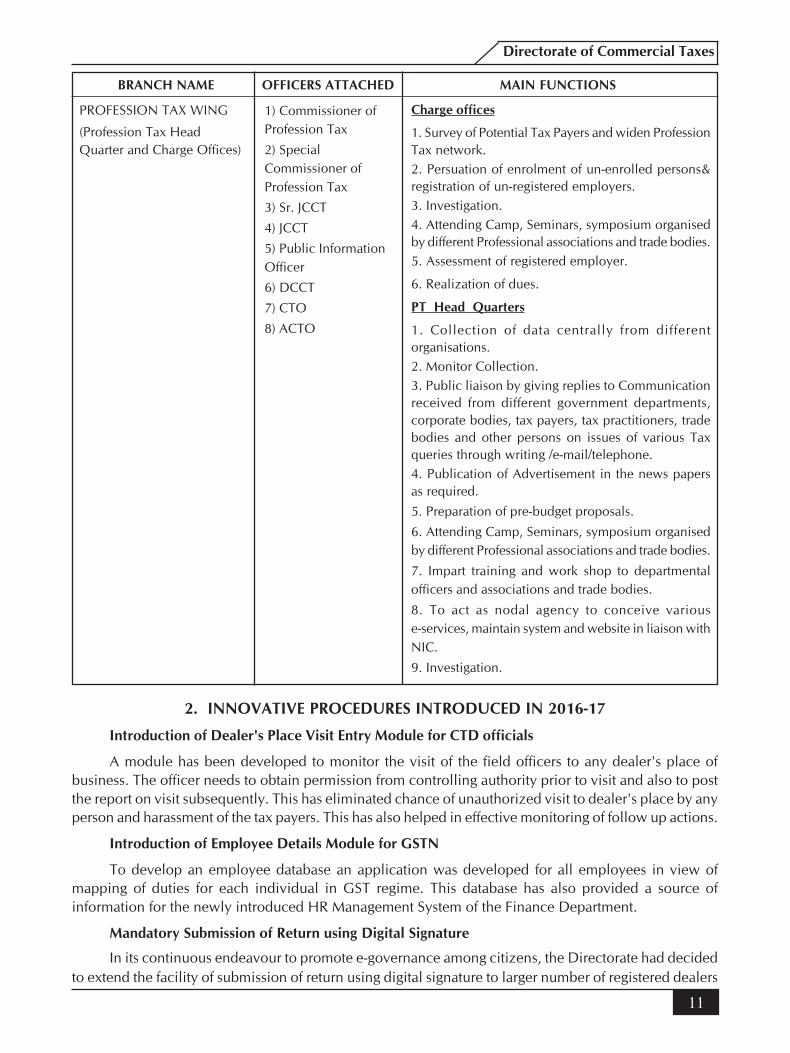

Charge offices

1. Survey of Potential Tax Payers and widen ProfessionTax network.2. Persuation of enrolment of un-enrolled persons®istration of un-registered employers.3. Investigation.4. Attending Camp, Seminars, symposium organisedby different Professional associations and trade bodies.5. Assessment of registered employer.

6. Realization of dues.

PT Head Quarters

1. Collection of data centrally from differentorganisations.2. Monitor Collection.3. Public liaison by giving replies to Communicationreceived from different government departments,corporate bodies, tax payers, tax practitioners, tradebodies and other persons on issues of various Taxqueries through writing /e-mail/telephone.4. Publication of Advertisement in the news papersas required.5. Preparation of pre-budget proposals.

6. Attending Camp, Seminars, symposium organisedby different Professional associations and trade bodies.

7. Impart training and work shop to departmentalofficers and associations and trade bodies.

8. To act as nodal agency to conceive variouse-services, maintain system and website in liaison withNIC.

9. Investigation.

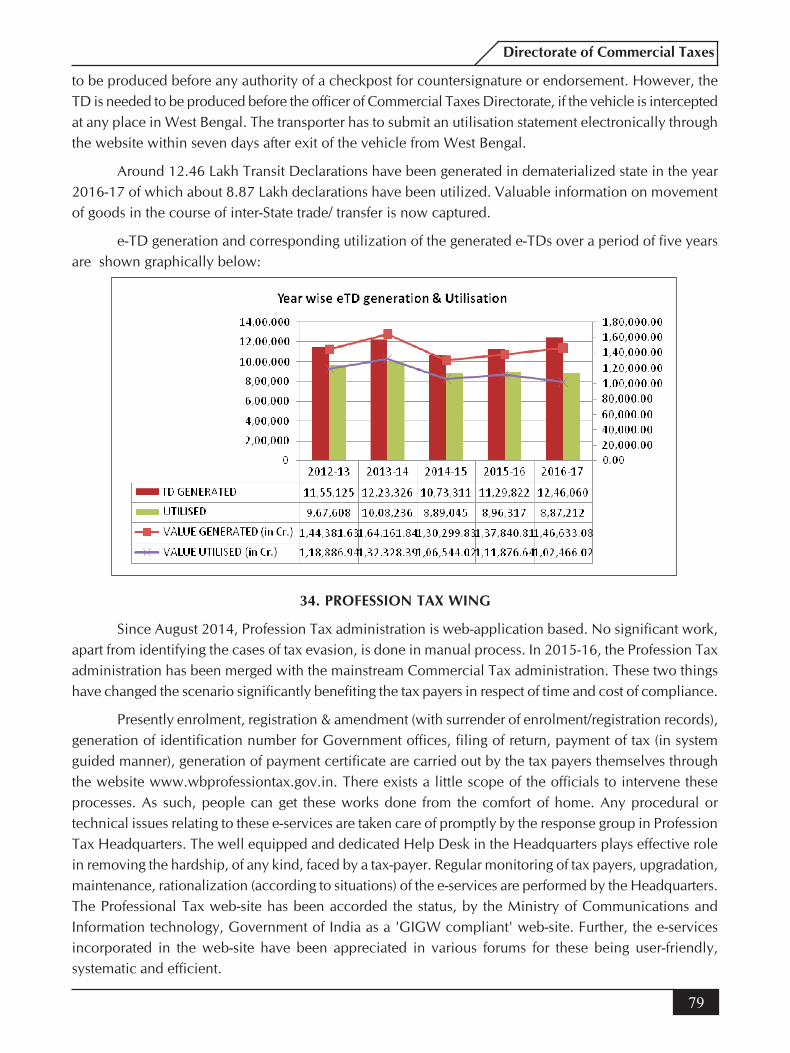

2. INNOVATIVE PROCEDURES INTRODUCED IN 2016-17

Introduction of Dealer's Place Visit Entry Module for CTD officials

A module has been developed to monitor the visit of the field officers to any dealer's place ofbusiness. The officer needs to obtain permission from controlling authority prior to visit and also to postthe report on visit subsequently. This has eliminated chance of unauthorized visit to dealer's place by anyperson and harassment of the tax payers. This has also helped in effective monitoring of follow up actions.

Introduction of Employee Details Module for GSTN

To develop an employee database an application was developed for all employees in view ofmapping of duties for each individual in GST regime. This database has also provided a source ofinformation for the newly introduced HR Management System of the Finance Department.

Mandatory Submission of Return using Digital Signature

In its continuous endeavour to promote e-governance among citizens, the Directorate had decidedto extend the facility of submission of return using digital signature to larger number of registered dealers

BRANCH NAME OFFICERS ATTACHED MAIN FUNCTIONS

PROFESSION TAX WING

(Profession Tax HeadQuarter and Charge Offices)

1) Commissioner ofProfession Tax

2) SpecialCommissioner ofProfession Tax

3) Sr. JCCT

4) JCCT

5) Public InformationOfficer

6) DCCT

7) CTO

8) ACTO

12

Administrative Report 2016-17

with effect from quarter ending 30 th June, 2016. Accordingly the West Bengal Value Added Tax Rules2005, has been amended. According to the amendment, all registered dealers filing return in Form 14/14D/15/15R having turnover of sales or contractual transfer price or both in the immediate previous year,i.e., 2015-16, in excess of rupees fifty lakhs or having registration under the Companies Act, 1956, or theCompanies Act, 2013, shall have to furnish return using digital signature mandatorily from quarter ending30th June, 2016, in terms of amended rule 34A(3) of WBVAT Rules, 2005. These dealers need not submitany signed hard copy of the said return furnished on line or the acknowledgement thereof.

Discontinuation of submission of printed copy of returns

Compulsory use of Digital Signature for filing online application for Registration

To make registration process under the West Bengal Value Added Tax Act, 2003 simpler and toensure quick disposal of the applications for new registration the West Bengal Finance Act, 2017 (WB ActIII), has introduced some changes in the registration process. Sending of printed copies of supportingdocuments has been done away with. This has reduced the time required for disposal of new registrationapplications as the delay in postal communication will be fully eliminated.

Settlement of Dispute

A new Settlement of Dispute Scheme had been introduced on 30th December, 2016 to dispose anumber of assessment and audit cases under all Acts completed on or before 31st March, 2014. Morethan Rs. 300 Crore was collected from this scheme.

3. MAJOR ACHIEVEMENTS OF COMMERCIAL TAX DIRECTORATE FROM 2011-12 TO 2016-17

Universal computerisation of all processes of Commercial Taxes with state of the art data and webservers at State Data Centre. All erstwhile manual processes have been replaced by computerisedprocesses reducing service delivery time and physical interface.

The e-governance initiative in Commercial Tax Directorate has got several national level awards:

(a) CSI Nihilent e-governance award for back end processes through IMPACT in 2013-14

(b) Won Trophy at 13th National Conference on e-Governance in 2014-15

(c) Skoch Award for e-Grievances and GRIPS in 2014-15

(d) Skoch Order of Merit for GRIPS and e-Grievances in 2014-15

(e) Skoch Order of Merit for Promoting, Simplification, Transparency and Ease in the CommercialTax Processes in 2014-15

(f) Skoch Award for e-Governance in Profession Tax, 2014-15

(g) National Silver Award for e-Governance, 2014-15 for e-Initiatives in Commercial Taxes forExcellence in Government Process Re-engineering

(h) Golden Peacock Innovative Product / Service Award, 2016

(i) CII Appreciation for Contribution of Commercial Tax Directorate towards success of synergyGourBanga, 2014.

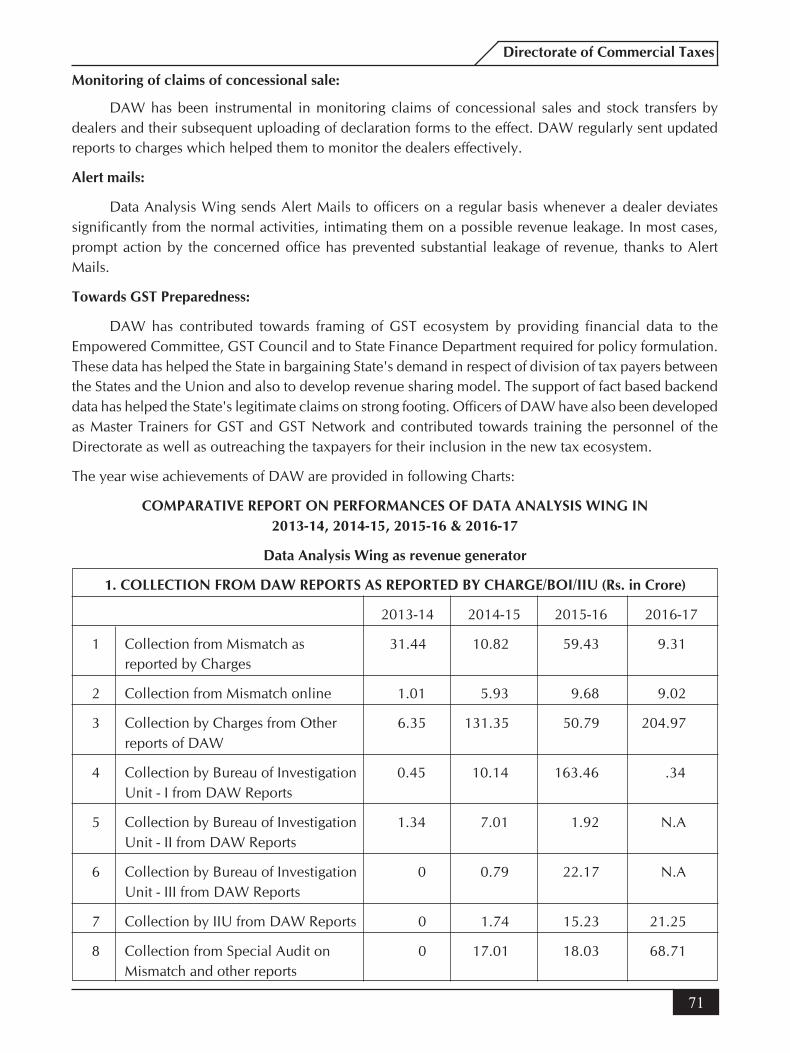

These e-initiatives have helped in collection of transaction data. Analysis of collected data resultedin identification of evasion and fraud. The contribution of Data Analysis towards revenue collectionhas grown up from Rs. 174.61 Crore in 2013-14, the starting year, to Rs. 1648.57 Crore in 2016-17.

For the period from 2011-12 to 2016-17 total revenue collection has grown by 74% fromRs. 18367.33 Crore to Rs. 31898.21 Crore.

13

Directorate of Commercial Taxes

Online payments and refund of tax has been made mandatory. In 2012-13, 71.45% payment wasmade online which achieved 100% from 2015-16. All services including submission of return,generation of waybill and statutory forms, filing of appeals have been covered by e-services duringthis period.

Statutory processes for service delivery have been simplified. Granting of Registration within 24hours is compulsory as per statutory provision with removal of pre-registration verification. Thesystem of sending of physical documents for registration has been done away with introduction offiling of application for registration using digital signature and uploading of relevant documents.Procedure for amendment of registration has been made simpler with introduction of onlineamendment facility.

Further to provide relief to small traders the statutory threshold for registration has been increasedfrom five lakh to 10 lakh in 2014-15 and to 20 lakh from 01/04/2017.

Refund processes have been made simpler by reducing procedural steps. The average time ofrefund has been reduced to 258 days in 2011-12 to 44 days (including holidays) in 2015-16. Forapplications made after 01/04/2015, the number of days for refund has been further reduced to twoweeks.

Previously, pre-assessment refund was given against exports and zero-rated sales. The facility hasbeen extended from 2015-16 to dealers having inter-state sale more than 50% of turnover to preventblocking of working capital for them. Post assessment refund has been made compulsory withinone month of disposal of assessment through statute.

To make service of statutory notices and orders and storage of electronic documents DataManagement System has been introduced. This has made all services instant with necessary audittrail of service delivery.

To save taxpayers from unnecessary harassment, the discretionary power for selection of assessmentcases has been replaced by risk-based selection on approval of the Commissioner.

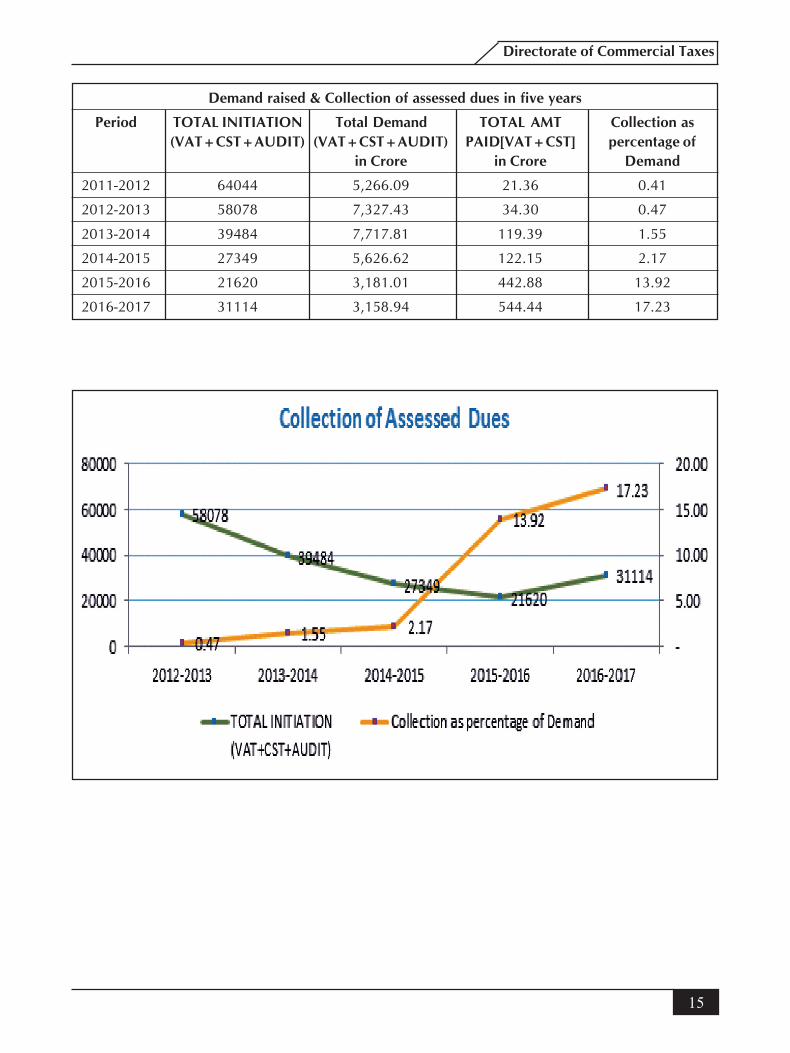

For the sake of transparency and natural justice, issue of draft order of assessment or audit has beenmade mandatory which has reduced the scope of litigation. This coupled with provision of depositof 15% of disputed tax for filing appeal has enabled quick recovery of dues. In 2011-12, collectionof assessed dues in was 21.36 Crore which has grown to 544.44 Crore in 2016-17 registering anaverage annual growth rate of 381%. Regular updated information of assessed dues provided throughdata analysis also has helped in better recovery.

For quick disposal of appeal cases, the statutory time limitation for disposal of appeal has beenreduced to 6 months from earlier one year period. Monitoring of appeal and pre-deposit of 15% ofdisputed tax have been introduced through data analysis. To clear backlog revision cases at theAppellate Board, Fast Track Courts have been set up for their early disposal.

Settlement of Dispute Schemes have been introduced twice one in 2015-16 and another in 2016-17 to clear off old cases pending before appellate and revisional authorities. This has resulted inone time disposal of many long pending cases and realisation of locked dues to the tune of Rs. 112Crore in 2015-16 and 290.80 Crore in 2016-17.

For small and medium business enterprises simplified annual return has been introduced. From2013-14, a new scheme has been introduced for small entrepreneurs for registration with provisionfor payment of lump sum tax without maintenance of statutory formalities including filing of returnswith guarantee of non-interference of the administration in their business affairs. This has increasedtax compliance among small entrepreneurs and helped them do their business without fear.

14

Administrative Report 2016-17

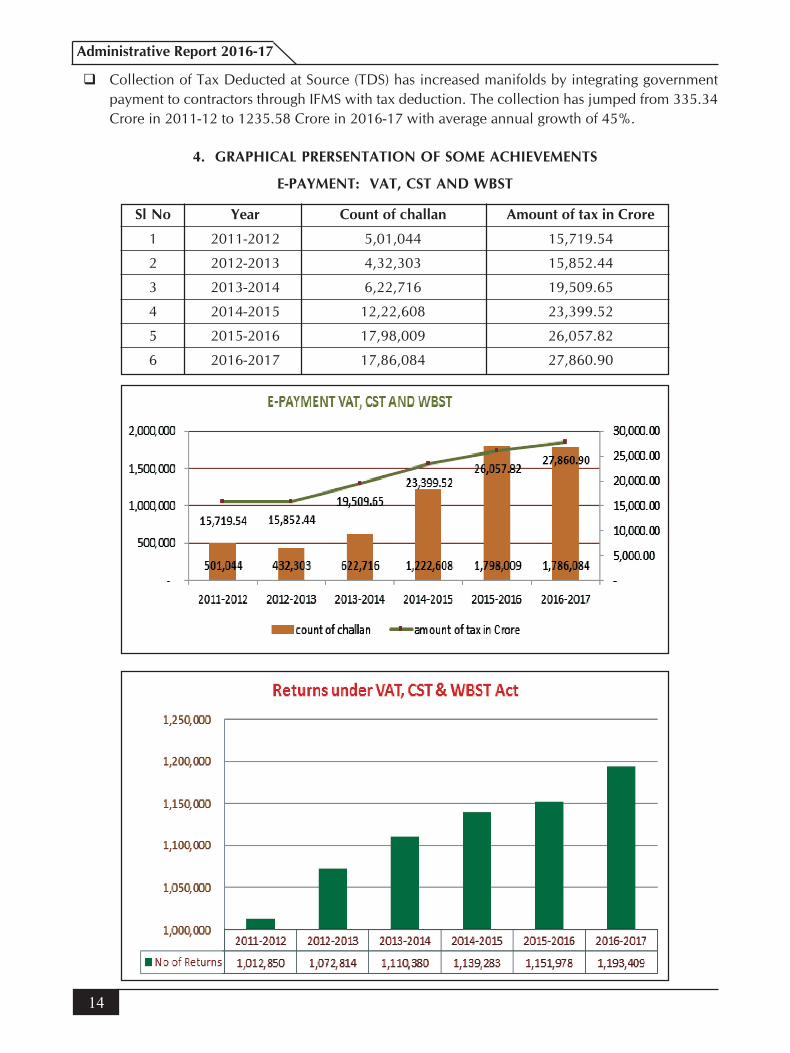

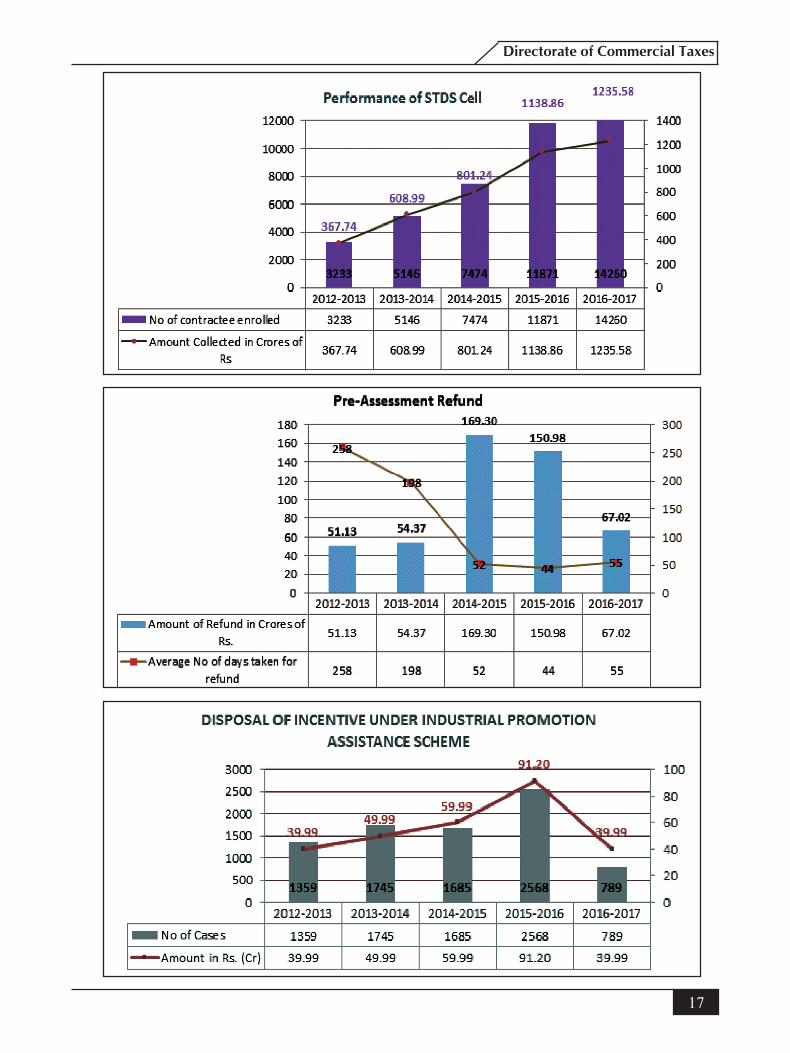

Collection of Tax Deducted at Source (TDS) has increased manifolds by integrating governmentpayment to contractors through IFMS with tax deduction. The collection has jumped from 335.34Crore in 2011-12 to 1235.58 Crore in 2016-17 with average annual growth of 45%.

4. GRAPHICAL PRERSENTATION OF SOME ACHIEVEMENTS

E-PAYMENT: VAT, CST AND WBST

Sl No Year Count of challan Amount of tax in Crore

1 2011-2012 5,01,044 15,719.54

2 2012-2013 4,32,303 15,852.44

3 2013-2014 6,22,716 19,509.65

4 2014-2015 12,22,608 23,399.52

5 2015-2016 17,98,009 26,057.82

6 2016-2017 17,86,084 27,860.90

15

Directorate of Commercial Taxes

Demand raised & Collection of assessed dues in five years

Period TOTAL INITIATION Total Demand TOTAL AMT Collection as(VAT+CST+AUDIT) (VAT+CST+AUDIT) PAID[VAT+CST] percentage of

in Crore in Crore Demand

2011-2012 64044 5,266.09 21.36 0.41

2012-2013 58078 7,327.43 34.30 0.47

2013-2014 39484 7,717.81 119.39 1.55

2014-2015 27349 5,626.62 122.15 2.17

2015-2016 21620 3,181.01 442.88 13.92

2016-2017 31114 3,158.94 544.44 17.23

16

Administrative Report 2016-17

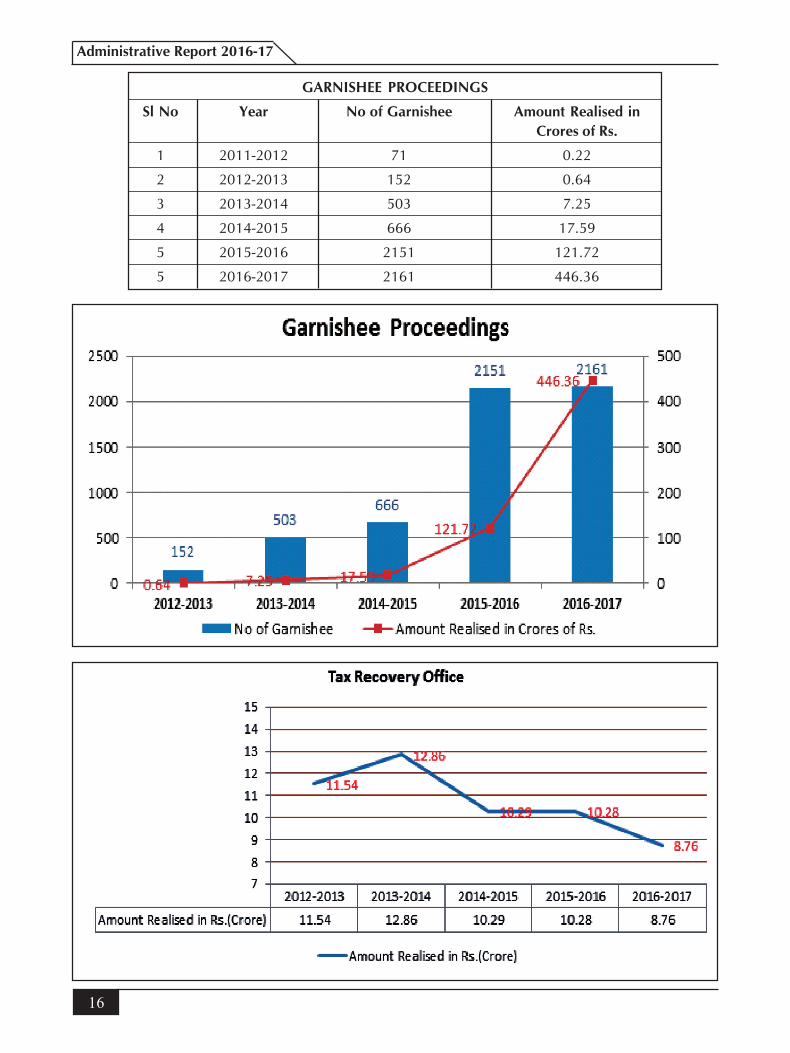

GARNISHEE PROCEEDINGS

Sl No Year No of Garnishee Amount Realised inCrores of Rs.

1 2011-2012 71 0.22

2 2012-2013 152 0.64

3 2013-2014 503 7.25

4 2014-2015 666 17.59

5 2015-2016 2151 121.72

5 2016-2017 2161 446.36

17

Directorate of Commercial Taxes

18

Administrative Report 2016-17

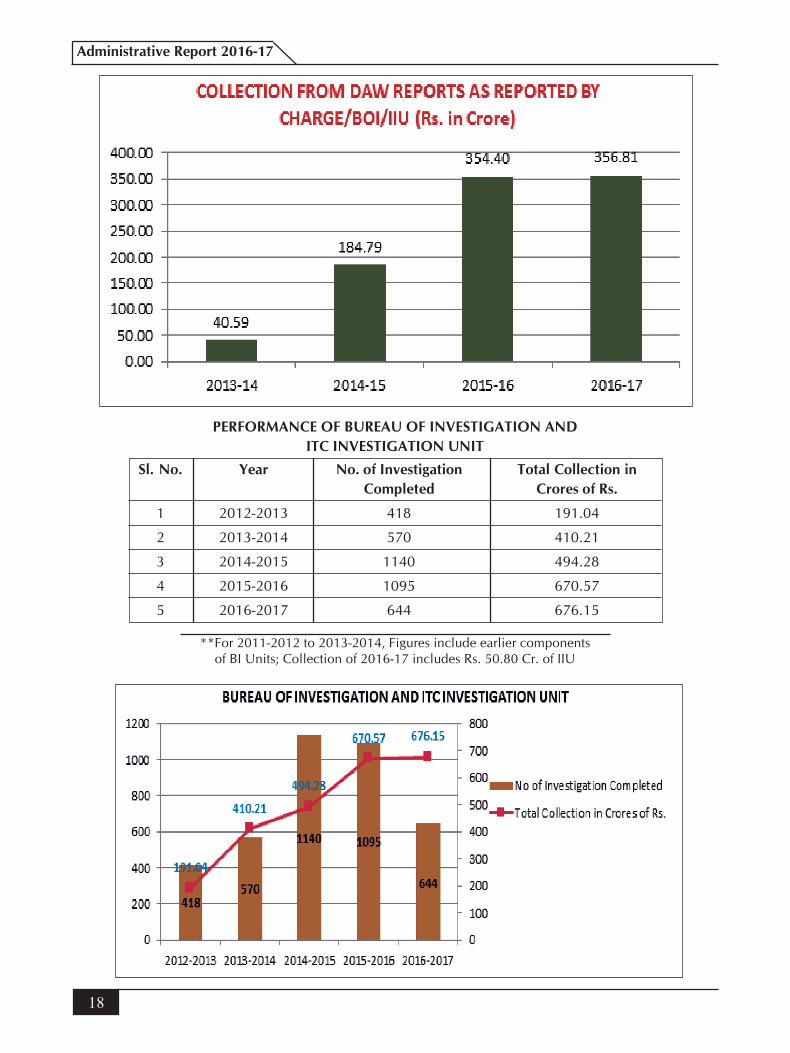

PERFORMANCE OF BUREAU OF INVESTIGATION ANDITC INVESTIGATION UNIT

Sl. No. Year No. of Investigation Total Collection inCompleted Crores of Rs.

1 2012-2013 418 191.04

2 2013-2014 570 410.21

3 2014-2015 1140 494.28

4 2015-2016 1095 670.57

5 2016-2017 644 676.15

**For 2011-2012 to 2013-2014, Figures include earlier componentsof BI Units; Collection of 2016-17 includes Rs. 50.80 Cr. of IIU

19

Directorate of Commercial Taxes

5. Awards and Accolades in credit5. Awards and Accolades in credit5. Awards and Accolades in credit5. Awards and Accolades in credit5. Awards and Accolades in credit

CSI-NIHILENTE-GOVERNANCE

AWARDSFOR IMPACT

2013-14

TROPHY WONAT 13TH NATIONALCONFERENCE ONE-GOVERNANCE

2014-15

SKOCH AWARDFOR

E GRIEVANCES ANDGRIPS

2014-15

20

Administrative Report 2016-17

SKOCH ORDER OF MERITFOR

GRIPS2014-15

SKOCH ORDER OF MERITFOR

E GRIEVANCES2014-15

SKOCH ORDER OF MERITFOR

PROMOTING SIMPLIFICATION,TRANSPARENCY AND EASE IN

THE COMMERCIAL TAXESPROCESSES

2014-15

SKOCH AWARDFOR

E GOVERNANCE INPROFESSION TAX

2014-15

21

Directorate of Commercial Taxes

NATIONAL SILVERAWARD FOR

E GOVERNANCE, 2014-15FOR

E INITIATIVES INCOMMERCIAL TAXESFOR EXCELLANCE IN

GOVERNMENT PROCESSRE-ENGINEERING

WINNEROF

GOLDEN PEACOCK INNOVATIVE PRODUCT/SERVICEAWARD

2016

CII APPRECIATION FORCONTRIBUTION OF

CT DTE TOWARDS SUCCESSOF

SYNERGY GOUR BANGA, 2014

22

Administrative Report 2016-17

6. THE ORGANISATION

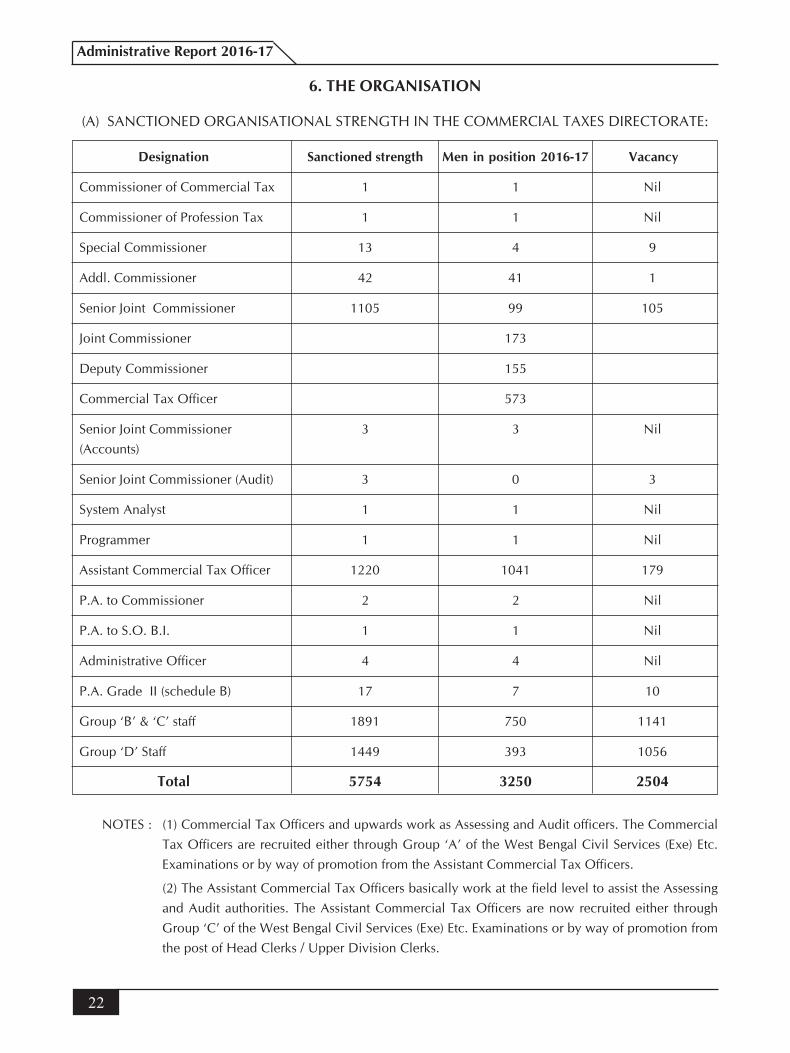

(A) SANCTIONED ORGANISATIONAL STRENGTH IN THE COMMERCIAL TAXES DIRECTORATE:

Designation Sanctioned strength Men in position 2016-17 Vacancy

Commissioner of Commercial Tax 1 1 Nil

Commissioner of Profession Tax 1 1 Nil

Special Commissioner 13 4 9

Addl. Commissioner 42 41 1

Senior Joint Commissioner 1105 99 105

Joint Commissioner 173

Deputy Commissioner 155

Commercial Tax Officer 573

Senior Joint Commissioner 3 3 Nil(Accounts)

Senior Joint Commissioner (Audit) 3 0 3

System Analyst 1 1 Nil

Programmer 1 1 Nil

Assistant Commercial Tax Officer 1220 1041 179

P.A. to Commissioner 2 2 Nil

P.A. to S.O. B.I. 1 1 Nil

Administrative Officer 4 4 Nil

P.A. Grade II (schedule B) 17 7 10

Group ‘B’ & ‘C’ staff 1891 750 1141

Group ‘D’ Staff 1449 393 1056

Total 5754 3250 2504

NOTES : (1) Commercial Tax Officers and upwards work as Assessing and Audit officers. The CommercialTax Officers are recruited either through Group ‘A’ of the West Bengal Civil Services (Exe) Etc.Examinations or by way of promotion from the Assistant Commercial Tax Officers.

(2) The Assistant Commercial Tax Officers basically work at the field level to assist the Assessingand Audit authorities. The Assistant Commercial Tax Officers are now recruited either throughGroup ‘C’ of the West Bengal Civil Services (Exe) Etc. Examinations or by way of promotion fromthe post of Head Clerks / Upper Division Clerks.

23

Directorate of Commercial Taxes

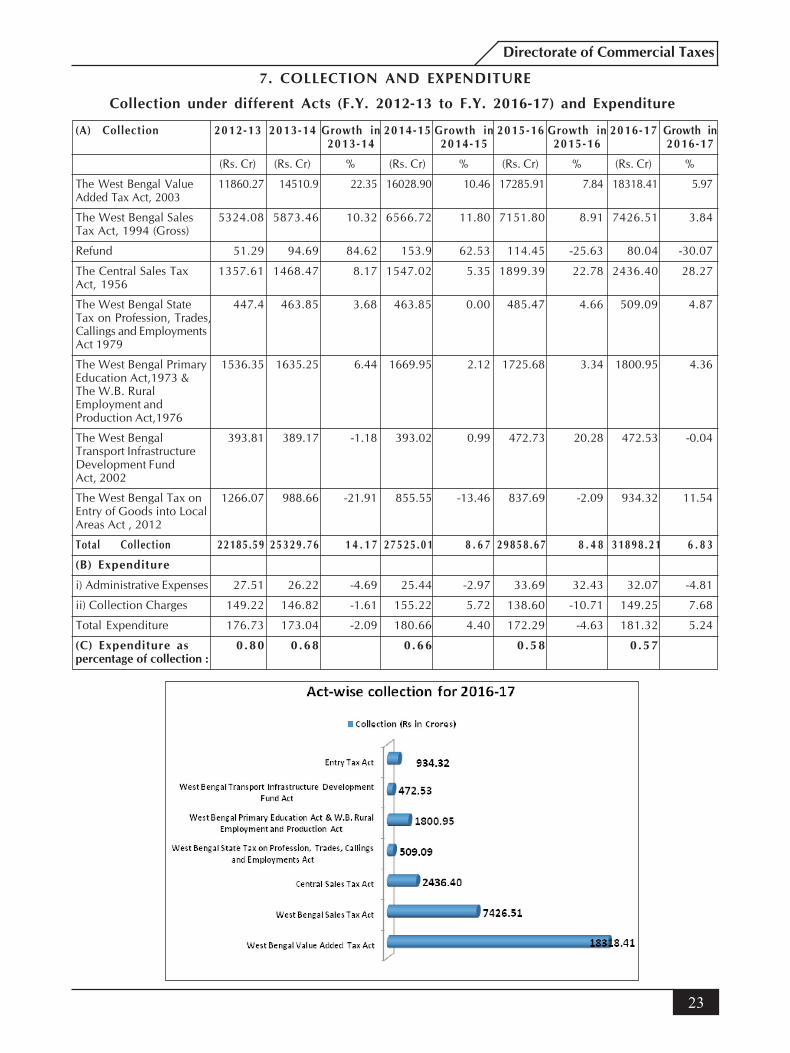

7. COLLECTION AND EXPENDITURE

Collection under different Acts (F.Y. 2012-13 to F.Y. 2016-17) and Expenditure

(A) Collection 2012 -13 2013 -14 Growth in 2014 -15 Growth in 2015 -16 Growth in 2016 -17 Growth in2013 -14 2014 -15 2015 -16 2016 -17

(Rs. Cr) (Rs. Cr) % (Rs. Cr) % (Rs. Cr) % (Rs. Cr) %

The West Bengal Value 11860.27 14510.9 22.35 16028.90 10.46 17285.91 7.84 18318.41 5.97Added Tax Act, 2003

The West Bengal Sales 5324.08 5873.46 10.32 6566.72 11.80 7151.80 8.91 7426.51 3.84Tax Act, 1994 (Gross)

Refund 51.29 94.69 84.62 153.9 62.53 114.45 -25.63 80.04 -30.07

The Central Sales Tax 1357.61 1468.47 8.17 1547.02 5.35 1899.39 22.78 2436.40 28.27Act, 1956

The West Bengal State 447.4 463.85 3.68 463.85 0.00 485.47 4.66 509.09 4.87Tax on Profession, Trades,Callings and EmploymentsAct 1979

The West Bengal Primary 1536.35 1635.25 6.44 1669.95 2.12 1725.68 3.34 1800.95 4.36Education Act,1973 &The W.B. RuralEmployment andProduction Act,1976

The West Bengal 393.81 389.17 -1.18 393.02 0.99 472.73 20.28 472.53 -0.04Transport InfrastructureDevelopment FundAct, 2002

The West Bengal Tax on 1266.07 988.66 -21.91 855.55 -13.46 837.69 -2.09 934.32 11.54Entry of Goods into LocalAreas Act , 2012

Total Collection 22185.59 25329 .76 1 4 . 1 7 27525 .01 8 . 6 7 29858 .67 8 . 4 8 31898 .21 6 . 8 3

(B) Expenditure

i) Administrative Expenses 27.51 26.22 -4.69 25.44 -2.97 33.69 32.43 32.07 -4.81

ii) Collection Charges 149.22 146.82 -1.61 155.22 5.72 138.60 -10.71 149.25 7.68

Total Expenditure 176.73 173.04 -2.09 180.66 4.40 172.29 -4.63 181.32 5.24

(C) Expenditure as 0 .80 0 .68 0 .66 0 .58 0 .57percentage of collection :

24

Administrative Report 2016-17

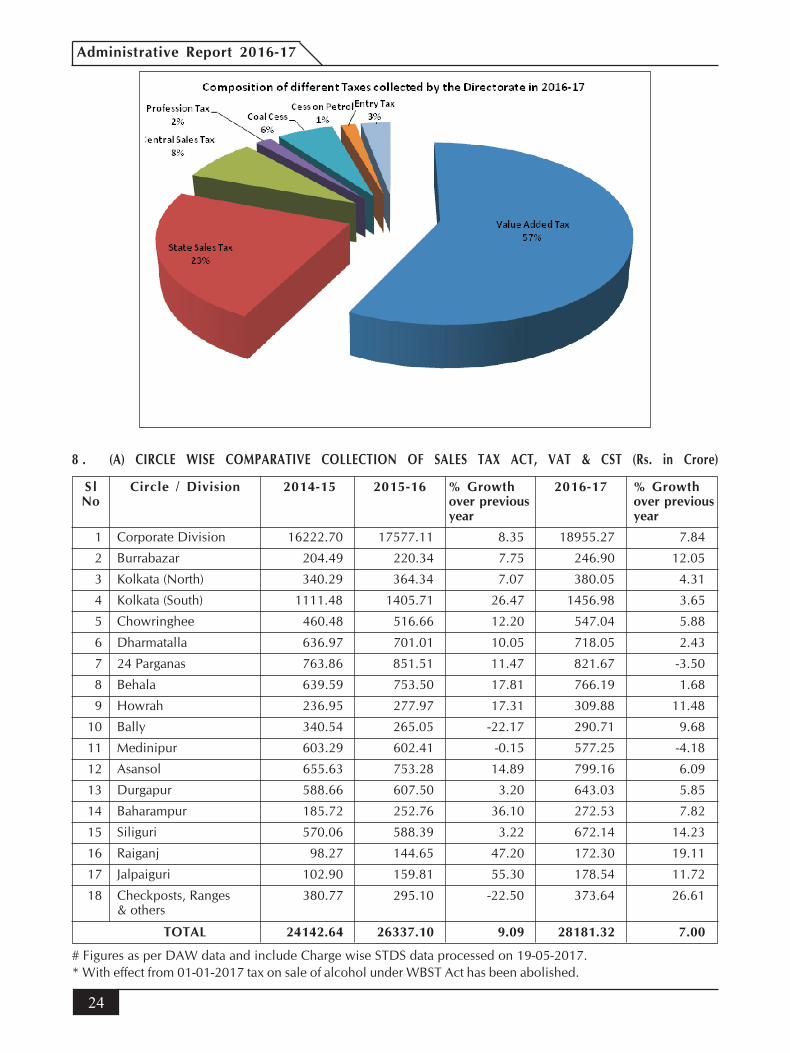

8 . (A) CIRCLE WISE COMPARATIVE COLLECTION OF SALES TAX ACT, VAT & CST (Rs. in Crore)

S l Circle / Division 2014-15 2015-16 % Growth 2016-17 % GrowthNo over previous over previous

year year

1 Corporate Division 16222.70 17577.11 8.35 18955.27 7.84

2 Burrabazar 204.49 220.34 7.75 246.90 12.05

3 Kolkata (North) 340.29 364.34 7.07 380.05 4.31

4 Kolkata (South) 1111.48 1405.71 26.47 1456.98 3.65

5 Chowringhee 460.48 516.66 12.20 547.04 5.88

6 Dharmatalla 636.97 701.01 10.05 718.05 2.43

7 24 Parganas 763.86 851.51 11.47 821.67 -3.50

8 Behala 639.59 753.50 17.81 766.19 1.68

9 Howrah 236.95 277.97 17.31 309.88 11.48

10 Bally 340.54 265.05 -22.17 290.71 9.68

11 Medinipur 603.29 602.41 -0.15 577.25 -4.18

12 Asansol 655.63 753.28 14.89 799.16 6.09

13 Durgapur 588.66 607.50 3.20 643.03 5.85

14 Baharampur 185.72 252.76 36.10 272.53 7.82

15 Siliguri 570.06 588.39 3.22 672.14 14.23

16 Raiganj 98.27 144.65 47.20 172.30 19.11

17 Jalpaiguri 102.90 159.81 55.30 178.54 11.72

18 Checkposts, Ranges 380.77 295.10 -22.50 373.64 26.61& others

TOTAL 24142.64 26337.10 9.09 28181.32 7.00

# Figures as per DAW data and include Charge wise STDS data processed on 19-05-2017.* With effect from 01-01-2017 tax on sale of alcohol under WBST Act has been abolished.

25

Directorate of Commercial Taxes

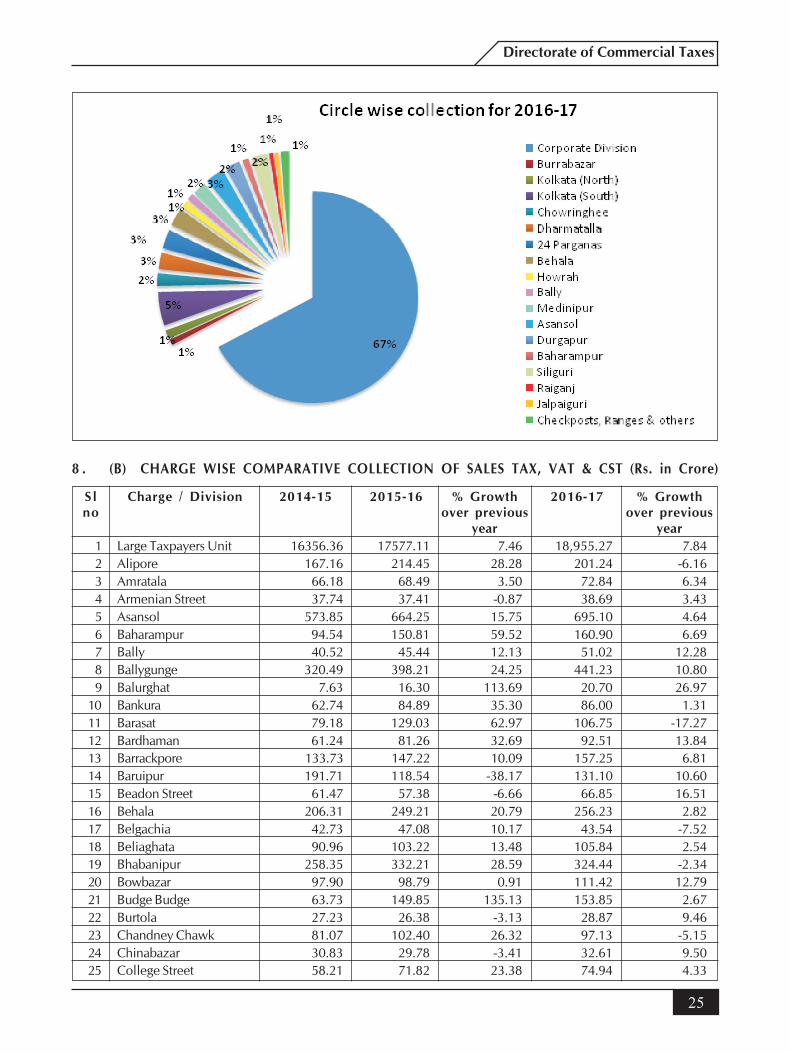

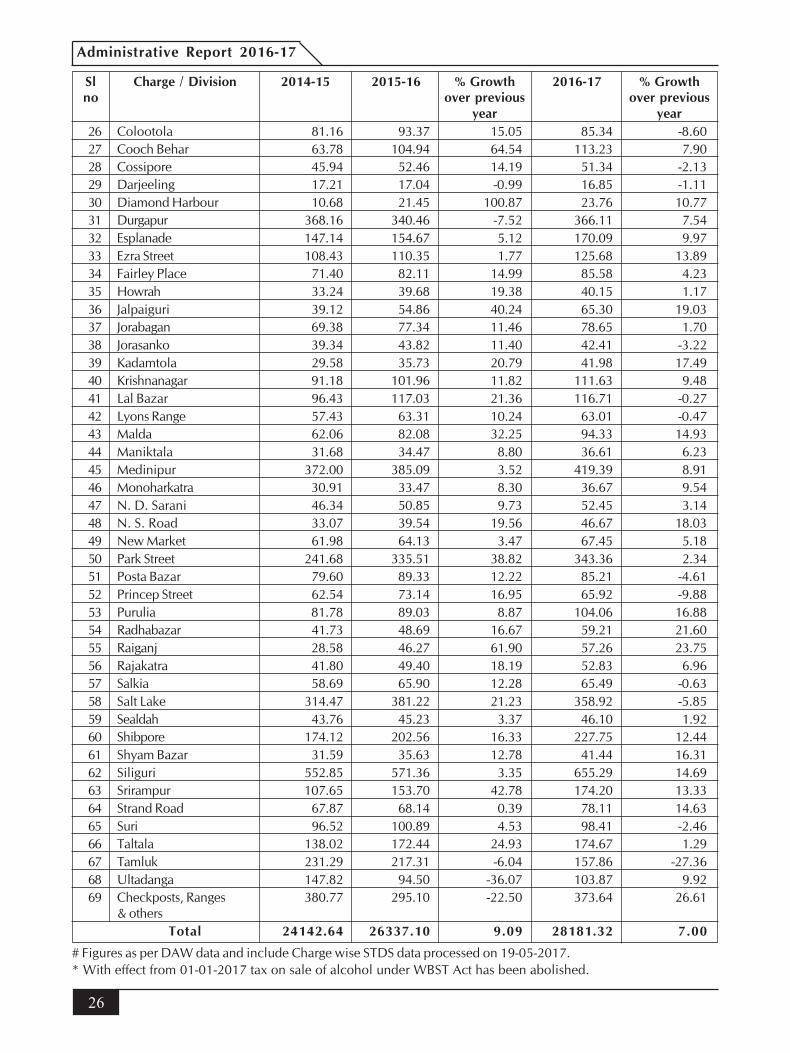

8 . (B) CHARGE WISE COMPARATIVE COLLECTION OF SALES TAX, VAT & CST (Rs. in Crore)

S l Charge / Division 2014-15 2015-16 % Growth 2016-17 % Growthno over previous over previous

year year1 Large Taxpayers Unit 16356.36 17577.11 7.46 18,955.27 7.842 Alipore 167.16 214.45 28.28 201.24 -6.163 Amratala 66.18 68.49 3.50 72.84 6.344 Armenian Street 37.74 37.41 -0.87 38.69 3.435 Asansol 573.85 664.25 15.75 695.10 4.646 Baharampur 94.54 150.81 59.52 160.90 6.697 Bally 40.52 45.44 12.13 51.02 12.288 Ballygunge 320.49 398.21 24.25 441.23 10.809 Balurghat 7.63 16.30 113.69 20.70 26.97

10 Bankura 62.74 84.89 35.30 86.00 1.3111 Barasat 79.18 129.03 62.97 106.75 -17.2712 Bardhaman 61.24 81.26 32.69 92.51 13.8413 Barrackpore 133.73 147.22 10.09 157.25 6.8114 Baruipur 191.71 118.54 -38.17 131.10 10.6015 Beadon Street 61.47 57.38 -6.66 66.85 16.5116 Behala 206.31 249.21 20.79 256.23 2.8217 Belgachia 42.73 47.08 10.17 43.54 -7.5218 Beliaghata 90.96 103.22 13.48 105.84 2.5419 Bhabanipur 258.35 332.21 28.59 324.44 -2.3420 Bowbazar 97.90 98.79 0.91 111.42 12.7921 Budge Budge 63.73 149.85 135.13 153.85 2.6722 Burtola 27.23 26.38 -3.13 28.87 9.4623 Chandney Chawk 81.07 102.40 26.32 97.13 -5.1524 Chinabazar 30.83 29.78 -3.41 32.61 9.5025 College Street 58.21 71.82 23.38 74.94 4.33

26

Administrative Report 2016-17

26 Colootola 81.16 93.37 15.05 85.34 -8.6027 Cooch Behar 63.78 104.94 64.54 113.23 7.9028 Cossipore 45.94 52.46 14.19 51.34 -2.1329 Darjeeling 17.21 17.04 -0.99 16.85 -1.1130 Diamond Harbour 10.68 21.45 100.87 23.76 10.7731 Durgapur 368.16 340.46 -7.52 366.11 7.5432 Esplanade 147.14 154.67 5.12 170.09 9.9733 Ezra Street 108.43 110.35 1.77 125.68 13.8934 Fairley Place 71.40 82.11 14.99 85.58 4.2335 Howrah 33.24 39.68 19.38 40.15 1.1736 Jalpaiguri 39.12 54.86 40.24 65.30 19.0337 Jorabagan 69.38 77.34 11.46 78.65 1.7038 Jorasanko 39.34 43.82 11.40 42.41 -3.2239 Kadamtola 29.58 35.73 20.79 41.98 17.4940 Krishnanagar 91.18 101.96 11.82 111.63 9.4841 Lal Bazar 96.43 117.03 21.36 116.71 -0.2742 Lyons Range 57.43 63.31 10.24 63.01 -0.4743 Malda 62.06 82.08 32.25 94.33 14.9344 Maniktala 31.68 34.47 8.80 36.61 6.2345 Medinipur 372.00 385.09 3.52 419.39 8.9146 Monoharkatra 30.91 33.47 8.30 36.67 9.5447 N. D. Sarani 46.34 50.85 9.73 52.45 3.1448 N. S. Road 33.07 39.54 19.56 46.67 18.0349 New Market 61.98 64.13 3.47 67.45 5.1850 Park Street 241.68 335.51 38.82 343.36 2.3451 Posta Bazar 79.60 89.33 12.22 85.21 -4.6152 Princep Street 62.54 73.14 16.95 65.92 -9.8853 Purulia 81.78 89.03 8.87 104.06 16.8854 Radhabazar 41.73 48.69 16.67 59.21 21.6055 Raiganj 28.58 46.27 61.90 57.26 23.7556 Rajakatra 41.80 49.40 18.19 52.83 6.9657 Salkia 58.69 65.90 12.28 65.49 -0.6358 Salt Lake 314.47 381.22 21.23 358.92 -5.8559 Sealdah 43.76 45.23 3.37 46.10 1.9260 Shibpore 174.12 202.56 16.33 227.75 12.4461 Shyam Bazar 31.59 35.63 12.78 41.44 16.3162 Siliguri 552.85 571.36 3.35 655.29 14.6963 Srirampur 107.65 153.70 42.78 174.20 13.3364 Strand Road 67.87 68.14 0.39 78.11 14.6365 Suri 96.52 100.89 4.53 98.41 -2.4666 Taltala 138.02 172.44 24.93 174.67 1.2967 Tamluk 231.29 217.31 -6.04 157.86 -27.3668 Ultadanga 147.82 94.50 -36.07 103.87 9.9269 Checkposts, Ranges 380.77 295.10 -22.50 373.64 26.61

& othersTotal 24142.64 26337.10 9.09 28181.32 7.00

# Figures as per DAW data and include Charge wise STDS data processed on 19-05-2017.* With effect from 01-01-2017 tax on sale of alcohol under WBST Act has been abolished.

Sl Charge / Division 2014-15 2015-16 % Growth 2016-17 % Growthno over previous over previous

year year

27

Directorate of Commercial Taxes

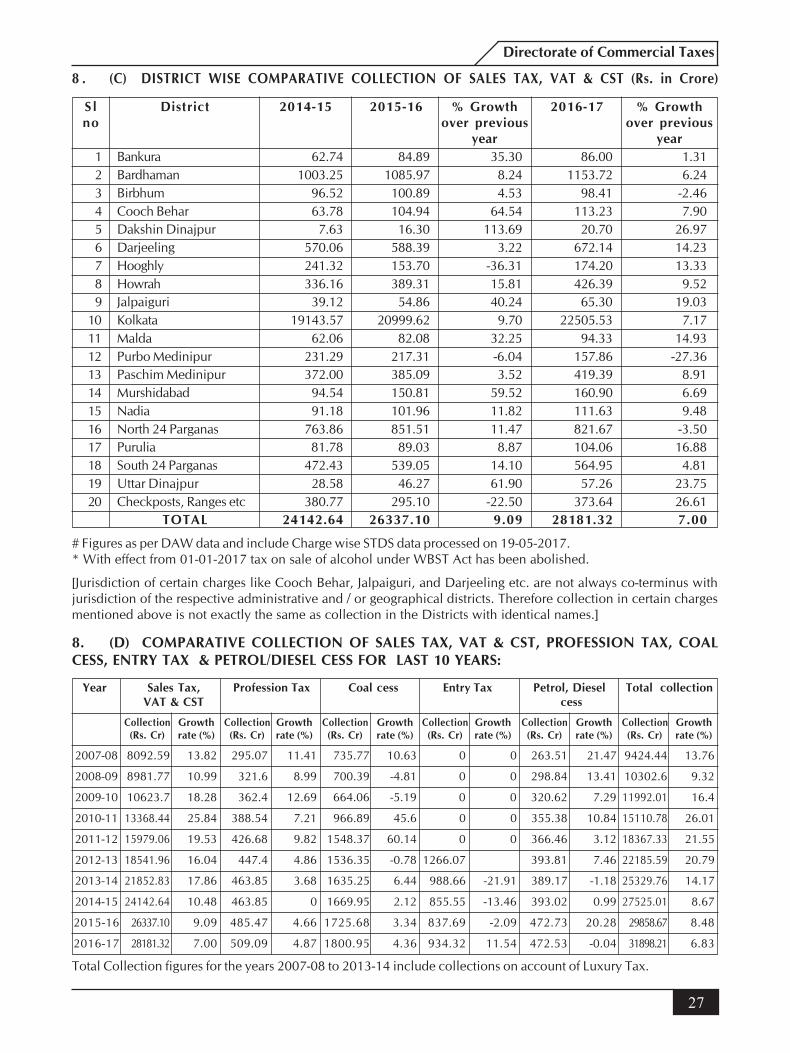

8 . (C) DISTRICT WISE COMPARATIVE COLLECTION OF SALES TAX, VAT & CST (Rs. in Crore)

S l District 2014-15 2015-16 % Growth 2016-17 % Growthno over previous over previous

year year1 Bankura 62.74 84.89 35.30 86.00 1.312 Bardhaman 1003.25 1085.97 8.24 1153.72 6.243 Birbhum 96.52 100.89 4.53 98.41 -2.464 Cooch Behar 63.78 104.94 64.54 113.23 7.905 Dakshin Dinajpur 7.63 16.30 113.69 20.70 26.976 Darjeeling 570.06 588.39 3.22 672.14 14.237 Hooghly 241.32 153.70 -36.31 174.20 13.338 Howrah 336.16 389.31 15.81 426.39 9.529 Jalpaiguri 39.12 54.86 40.24 65.30 19.03

10 Kolkata 19143.57 20999.62 9.70 22505.53 7.1711 Malda 62.06 82.08 32.25 94.33 14.9312 Purbo Medinipur 231.29 217.31 -6.04 157.86 -27.3613 Paschim Medinipur 372.00 385.09 3.52 419.39 8.9114 Murshidabad 94.54 150.81 59.52 160.90 6.6915 Nadia 91.18 101.96 11.82 111.63 9.4816 North 24 Parganas 763.86 851.51 11.47 821.67 -3.5017 Purulia 81.78 89.03 8.87 104.06 16.8818 South 24 Parganas 472.43 539.05 14.10 564.95 4.8119 Uttar Dinajpur 28.58 46.27 61.90 57.26 23.7520 Checkposts, Ranges etc 380.77 295.10 -22.50 373.64 26.61

TOTAL 24142.64 26337.10 9.09 28181.32 7.00

# Figures as per DAW data and include Charge wise STDS data processed on 19-05-2017.* With effect from 01-01-2017 tax on sale of alcohol under WBST Act has been abolished.

[Jurisdiction of certain charges like Cooch Behar, Jalpaiguri, and Darjeeling etc. are not always co-terminus withjurisdiction of the respective administrative and / or geographical districts. Therefore collection in certain chargesmentioned above is not exactly the same as collection in the Districts with identical names.]

8. (D) COMPARATIVE COLLECTION OF SALES TAX, VAT & CST, PROFESSION TAX, COALCESS, ENTRY TAX & PETROL/DIESEL CESS FOR LAST 10 YEARS:

Year Sales Tax, Profession Tax Coal cess Entry Tax Petrol, Diesel Total collectionVAT & CST cess

Collection Growth Collection Growth Collection Growth Collection Growth Collection Growth Collection Growth(Rs. Cr) rate (%) (Rs. Cr) rate (%) (Rs. Cr) rate (%) (Rs. Cr) rate (%) (Rs. Cr) rate (%) (Rs. Cr) rate (%)

2007-08 8092.59 13.82 295.07 11.41 735.77 10.63 0 0 263.51 21.47 9424.44 13.76

2008-09 8981.77 10.99 321.6 8.99 700.39 -4.81 0 0 298.84 13.41 10302.6 9.32

2009-10 10623.7 18.28 362.4 12.69 664.06 -5.19 0 0 320.62 7.29 11992.01 16.4

2010-11 13368.44 25.84 388.54 7.21 966.89 45.6 0 0 355.38 10.84 15110.78 26.01

2011-12 15979.06 19.53 426.68 9.82 1548.37 60.14 0 0 366.46 3.12 18367.33 21.55

2012-13 18541.96 16.04 447.4 4.86 1536.35 -0.78 1266.07 393.81 7.46 22185.59 20.79

2013-14 21852.83 17.86 463.85 3.68 1635.25 6.44 988.66 -21.91 389.17 -1.18 25329.76 14.17

2014-15 24142.64 10.48 463.85 0 1669.95 2.12 855.55 -13.46 393.02 0.99 27525.01 8.67

2015-16 26337.10 9.09 485.47 4.66 1725.68 3.34 837.69 -2.09 472.73 20.28 29858.67 8.48

2016-17 28181.32 7.00 509.09 4.87 1800.95 4.36 934.32 11.54 472.53 -0.04 31898.21 6.83

Total Collection figures for the years 2007-08 to 2013-14 include collections on account of Luxury Tax.

28

Administrative Report 2016-17

9. REGISTRATION

(A) Sales Tax Act:

* Number of Registered Dealers

2014-15 2015-16 2016-17

(a) Opening Balance 259045 254384 267920

(b) New Registration Granted 16882 20297 21956

(c) Dealers Cancelled 22262 7596 15332

(d) Dealers Restored 719 835 1945

(e) Closing Balance 254384 267920 276489

(B) New Registration (Online):

2016-17

VAT CST Total

(a) No of NR applications filed 25034 13166 38200

(b) No of Registration Granted 21944 11016 32960

(c) No of Applications Rejected 2937 1908 4845

(C) Profession Tax Act:

Number of registered employers and enrolled persons under the Profession Tax Act, 1979

2014-15 2015-16 2016-17

i) Number of Registered Employers 105593 106002 111074

ii) Number of Enrolled Persons 1707955 1712897 1859713

29

Directorate of Commercial Taxes

10. ASSESSMENT, APPEAL CASES

(A) ASSESSMENT CASES (ASSESSMENT YEAR WISE) – (VAT+CST)

Initiated during (year) 2012-13 2013-14 2014-15 2015-16 2016-17

For Financial Year 2010-11 2011-12 2012-13 2013-14 2014-15

(a) Total cases initiated during the year 86140 29113 22565 20419 31759

(b) Net Initiation 49148 25111 18519 18109 28768

(c) Demand Initiated 48284 25024 18484 18096 6756

(d) Demand amount (in Rs. Crore) 4598.76 2358.40 2003.44 1321.69 859.76

The figures have been compiled and submitted by NIC & DAW from central database. Figures include both VAT andCST assessment cases but exclude Audit Cases. Some initiation cases were dropped after initiation.* As a part of reducing cost of compliance, routine assessment has been replaced with risk based assessment only.

10 (B) APPEAL CASES:

Sales Tax Acts (VAT+CST):

2014-15 2015-16 2016-17

(a) Opening Balance 12902 7502 4852

(b) Cases initiated during the year 9286 6673 6290

(c) Cases disposed of during the year 14686 9323 7319

(d) Cases pending at the end of the year 7502 4852 3823

30

Administrative Report 2016-17

11 (A) DISPOSAL OF VAT AUDIT CASES (ASSESSMENT YEAR WISE)

Assessment/Audit Year Cases initiated Demand Notice Generated Demand Amount(in Rs. crore)

2010-2011 N.A. 4606 2875.56

2011-2012 7556 7118 3308.68

2012-2013 5943 5783 1060.26

2013-2014 4527 2802 534.90

2014-2015 4703 1383 274.67

The figures have been compiled and submitted by NIC and DAW from central database. Figures include both VAT andCST audit cases. During the FY 2010-2011, there was manual system of generation of initiation notice and onlinegeneration of demand notice. For the period 2014-15, disposal of cases is still under process.

11 (B) REVISION & REVIEW CASES

Sales Tax Acts (Financial Year-wise) (VAT+CST):

2014-15 2015-16 2016-17

(a) Opening Balance 196 542 482

(b) Cases initiated during the year 903 560 885

(c) Cases disposed of during the year 557 620 724

(d) Cases pending at the end of the year 542 482 643

12. PROFESSION TAX ASSESSMENT CASES

Profession Tax Act (Financial Year-wise):

2013-14 2014-15 2015-16 2016-17

(a) Opening Balance 6572 2346 2378 2447

(b) Cases initiated during the year 14847 12571 5325 44663

(c) Cases disposed of during the year 19073 12539 5256 44984

(d) Cases pending at the end of the year 2346 2378 2447 2126

31

Directorate of Commercial Taxes

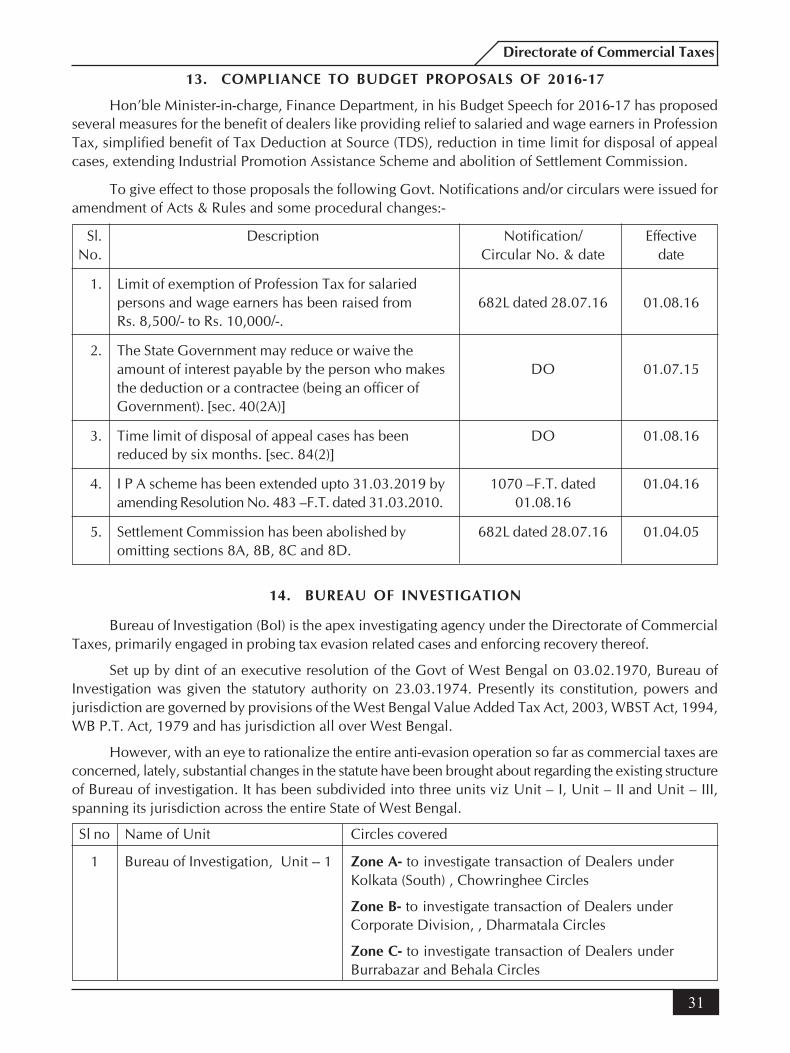

13. COMPLIANCE TO BUDGET PROPOSALS OF 2016-17

Hon’ble Minister-in-charge, Finance Department, in his Budget Speech for 2016-17 has proposedseveral measures for the benefit of dealers like providing relief to salaried and wage earners in ProfessionTax, simplified benefit of Tax Deduction at Source (TDS), reduction in time limit for disposal of appealcases, extending Industrial Promotion Assistance Scheme and abolition of Settlement Commission.

To give effect to those proposals the following Govt. Notifications and/or circulars were issued foramendment of Acts & Rules and some procedural changes:-

Sl. Description Notification/ EffectiveNo. Circular No. & date date

1. Limit of exemption of Profession Tax for salariedpersons and wage earners has been raised from 682L dated 28.07.16 01.08.16Rs. 8,500/- to Rs. 10,000/-.

2. The State Government may reduce or waive theamount of interest payable by the person who makes DO 01.07.15the deduction or a contractee (being an officer ofGovernment). [sec. 40(2A)]

3. Time limit of disposal of appeal cases has been DO 01.08.16reduced by six months. [sec. 84(2)]

4. I P A scheme has been extended upto 31.03.2019 by 1070 –F.T. dated 01.04.16amending Resolution No. 483 –F.T. dated 31.03.2010. 01.08.16

5. Settlement Commission has been abolished by 682L dated 28.07.16 01.04.05omitting sections 8A, 8B, 8C and 8D.

14. BUREAU OF INVESTIGATION

Bureau of Investigation (BoI) is the apex investigating agency under the Directorate of CommercialTaxes, primarily engaged in probing tax evasion related cases and enforcing recovery thereof.

Set up by dint of an executive resolution of the Govt of West Bengal on 03.02.1970, Bureau ofInvestigation was given the statutory authority on 23.03.1974. Presently its constitution, powers andjurisdiction are governed by provisions of the West Bengal Value Added Tax Act, 2003, WBST Act, 1994,WB P.T. Act, 1979 and has jurisdiction all over West Bengal.

However, with an eye to rationalize the entire anti-evasion operation so far as commercial taxes areconcerned, lately, substantial changes in the statute have been brought about regarding the existing structureof Bureau of investigation. It has been subdivided into three units viz Unit – I, Unit – II and Unit – III,spanning its jurisdiction across the entire State of West Bengal.

Sl no Name of Unit Circles covered

1 Bureau of Investigation, Unit -- 1 Zone A- to investigate transaction of Dealers underKolkata (South) , Chowringhee Circles

Zone B- to investigate transaction of Dealers underCorporate Division, , Dharmatala Circles

Zone C- to investigate transaction of Dealers underBurrabazar and Behala Circles

32

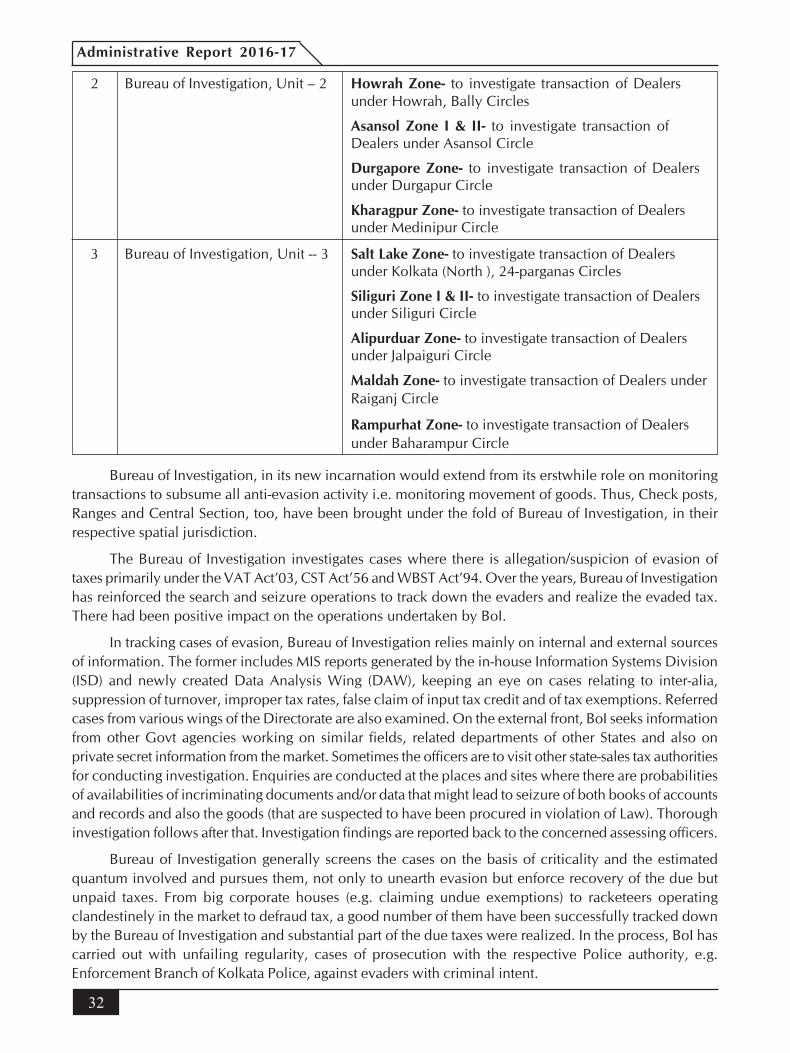

Administrative Report 2016-17

2 Bureau of Investigation, Unit – 2 Howrah Zone- to investigate transaction of Dealersunder Howrah, Bally Circles

Asansol Zone I & II- to investigate transaction ofDealers under Asansol Circle

Durgapore Zone- to investigate transaction of Dealersunder Durgapur Circle

Kharagpur Zone- to investigate transaction of Dealersunder Medinipur Circle

3 Bureau of Investigation, Unit -- 3 Salt Lake Zone- to investigate transaction of Dealersunder Kolkata (North ), 24-parganas Circles

Siliguri Zone I & II- to investigate transaction of Dealersunder Siliguri Circle

Alipurduar Zone- to investigate transaction of Dealersunder Jalpaiguri Circle

Maldah Zone- to investigate transaction of Dealers underRaiganj Circle

Rampurhat Zone- to investigate transaction of Dealersunder Baharampur Circle

Bureau of Investigation, in its new incarnation would extend from its erstwhile role on monitoringtransactions to subsume all anti-evasion activity i.e. monitoring movement of goods. Thus, Check posts,Ranges and Central Section, too, have been brought under the fold of Bureau of Investigation, in theirrespective spatial jurisdiction.

The Bureau of Investigation investigates cases where there is allegation/suspicion of evasion oftaxes primarily under the VAT Act’03, CST Act’56 and WBST Act’94. Over the years, Bureau of Investigationhas reinforced the search and seizure operations to track down the evaders and realize the evaded tax.There had been positive impact on the operations undertaken by BoI.

In tracking cases of evasion, Bureau of Investigation relies mainly on internal and external sourcesof information. The former includes MIS reports generated by the in-house Information Systems Division(ISD) and newly created Data Analysis Wing (DAW), keeping an eye on cases relating to inter-alia,suppression of turnover, improper tax rates, false claim of input tax credit and of tax exemptions. Referredcases from various wings of the Directorate are also examined. On the external front, BoI seeks informationfrom other Govt agencies working on similar fields, related departments of other States and also onprivate secret information from the market. Sometimes the officers are to visit other state-sales tax authoritiesfor conducting investigation. Enquiries are conducted at the places and sites where there are probabilitiesof availabilities of incriminating documents and/or data that might lead to seizure of both books of accountsand records and also the goods (that are suspected to have been procured in violation of Law). Thoroughinvestigation follows after that. Investigation findings are reported back to the concerned assessing officers.

Bureau of Investigation generally screens the cases on the basis of criticality and the estimatedquantum involved and pursues them, not only to unearth evasion but enforce recovery of the due butunpaid taxes. From big corporate houses (e.g. claiming undue exemptions) to racketeers operatingclandestinely in the market to defraud tax, a good number of them have been successfully tracked downby the Bureau of Investigation and substantial part of the due taxes were realized. In the process, BoI hascarried out with unfailing regularity, cases of prosecution with the respective Police authority, e.g.Enforcement Branch of Kolkata Police, against evaders with criminal intent.

33

Directorate of Commercial Taxes

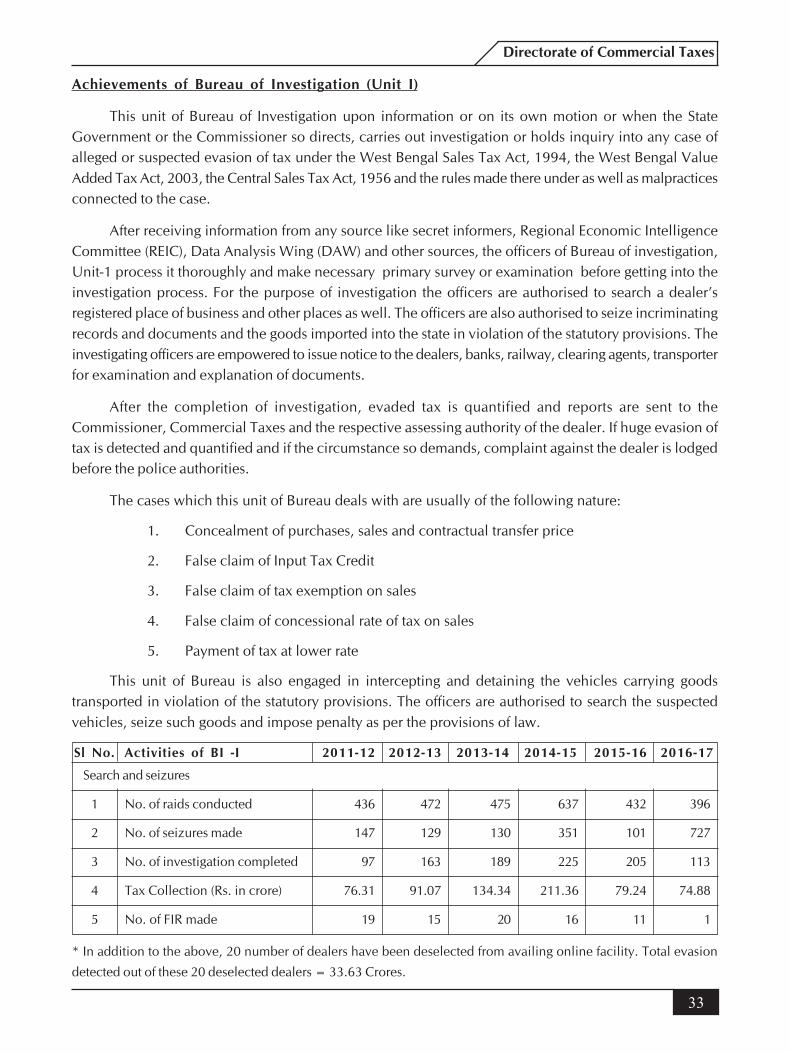

Achievements of Bureau of Investigation (Unit I)

This unit of Bureau of Investigation upon information or on its own motion or when the StateGovernment or the Commissioner so directs, carries out investigation or holds inquiry into any case ofalleged or suspected evasion of tax under the West Bengal Sales Tax Act, 1994, the West Bengal ValueAdded Tax Act, 2003, the Central Sales Tax Act, 1956 and the rules made there under as well as malpracticesconnected to the case.

After receiving information from any source like secret informers, Regional Economic IntelligenceCommittee (REIC), Data Analysis Wing (DAW) and other sources, the officers of Bureau of investigation,Unit-1 process it thoroughly and make necessary primary survey or examination before getting into theinvestigation process. For the purpose of investigation the officers are authorised to search a dealer’sregistered place of business and other places as well. The officers are also authorised to seize incriminatingrecords and documents and the goods imported into the state in violation of the statutory provisions. Theinvestigating officers are empowered to issue notice to the dealers, banks, railway, clearing agents, transporterfor examination and explanation of documents.

After the completion of investigation, evaded tax is quantified and reports are sent to theCommissioner, Commercial Taxes and the respective assessing authority of the dealer. If huge evasion oftax is detected and quantified and if the circumstance so demands, complaint against the dealer is lodgedbefore the police authorities.

The cases which this unit of Bureau deals with are usually of the following nature:

1. Concealment of purchases, sales and contractual transfer price

2. False claim of Input Tax Credit

3. False claim of tax exemption on sales

4. False claim of concessional rate of tax on sales

5. Payment of tax at lower rate

This unit of Bureau is also engaged in intercepting and detaining the vehicles carrying goodstransported in violation of the statutory provisions. The officers are authorised to search the suspectedvehicles, seize such goods and impose penalty as per the provisions of law.

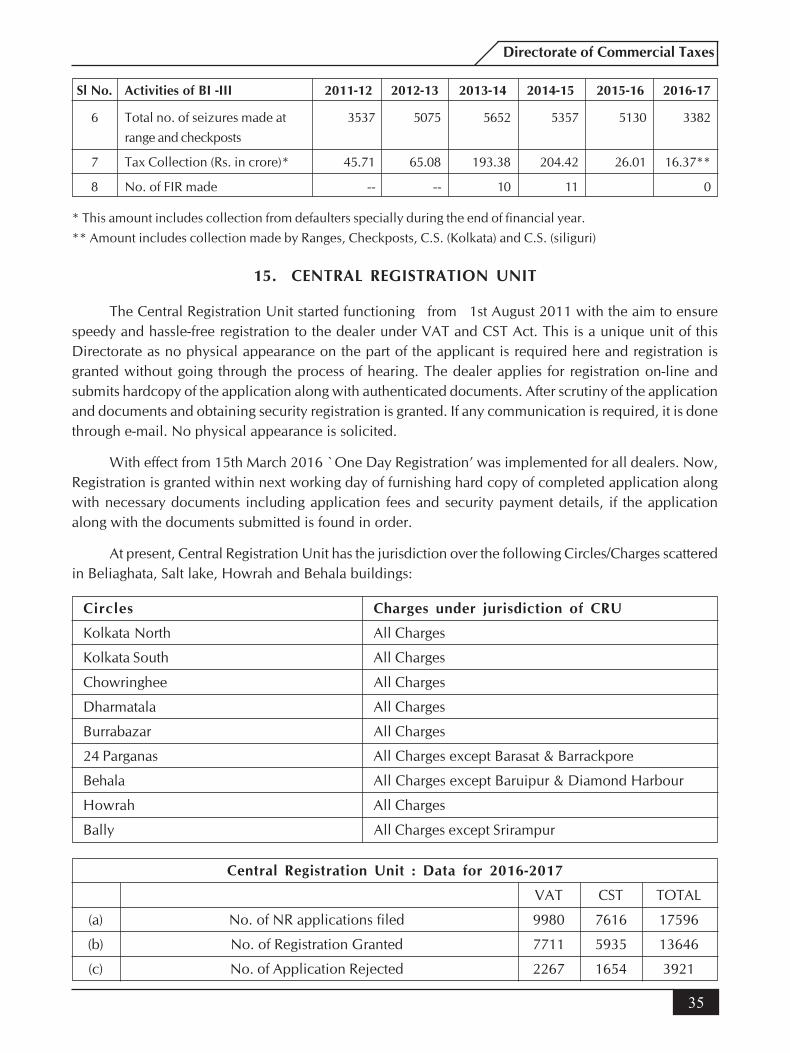

Sl No. Activities of BI -I 2011-12 2012-13 2013-14 2014-15 2015-16 2016-17

Search and seizures

1 No. of raids conducted 436 472 475 637 432 396

2 No. of seizures made 147 129 130 351 101 727

3 No. of investigation completed 97 163 189 225 205 113

4 Tax Collection (Rs. in crore) 76.31 91.07 134.34 211.36 79.24 74.88

5 No. of FIR made 19 15 20 16 11 1

* In addition to the above, 20 number of dealers have been deselected from availing online facility. Total evasion

detected out of these 20 deselected dealers = 33.63 Crores.

34

Administrative Report 2016-17

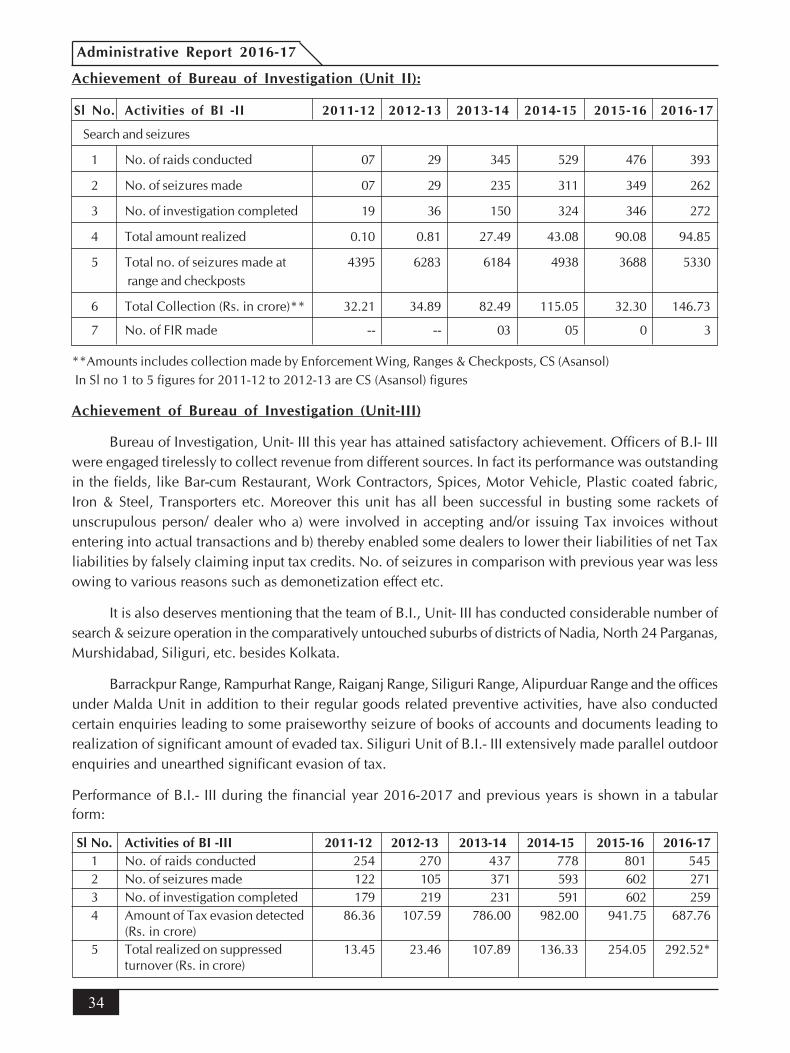

Achievement of Bureau of Investigation (Unit II):

Sl No. Activities of BI -II 2011-12 2012-13 2013-14 2014-15 2015-16 2016-17

Search and seizures

1 No. of raids conducted 07 29 345 529 476 393

2 No. of seizures made 07 29 235 311 349 262

3 No. of investigation completed 19 36 150 324 346 272

4 Total amount realized 0.10 0.81 27.49 43.08 90.08 94.85

5 Total no. of seizures made at 4395 6283 6184 4938 3688 5330 range and checkposts

6 Total Collection (Rs. in crore)** 32.21 34.89 82.49 115.05 32.30 146.73

7 No. of FIR made -- -- 03 05 0 3

**Amounts includes collection made by Enforcement Wing, Ranges & Checkposts, CS (Asansol) In Sl no 1 to 5 figures for 2011-12 to 2012-13 are CS (Asansol) figures

Achievement of Bureau of Investigation (Unit-III)

Bureau of Investigation, Unit- III this year has attained satisfactory achievement. Officers of B.I- IIIwere engaged tirelessly to collect revenue from different sources. In fact its performance was outstandingin the fields, like Bar-cum Restaurant, Work Contractors, Spices, Motor Vehicle, Plastic coated fabric,Iron & Steel, Transporters etc. Moreover this unit has all been successful in busting some rackets ofunscrupulous person/ dealer who a) were involved in accepting and/or issuing Tax invoices withoutentering into actual transactions and b) thereby enabled some dealers to lower their liabilities of net Taxliabilities by falsely claiming input tax credits. No. of seizures in comparison with previous year was lessowing to various reasons such as demonetization effect etc.

It is also deserves mentioning that the team of B.I., Unit- III has conducted considerable number ofsearch & seizure operation in the comparatively untouched suburbs of districts of Nadia, North 24 Parganas,Murshidabad, Siliguri, etc. besides Kolkata.

Barrackpur Range, Rampurhat Range, Raiganj Range, Siliguri Range, Alipurduar Range and the officesunder Malda Unit in addition to their regular goods related preventive activities, have also conductedcertain enquiries leading to some praiseworthy seizure of books of accounts and documents leading torealization of significant amount of evaded tax. Siliguri Unit of B.I.- III extensively made parallel outdoorenquiries and unearthed significant evasion of tax.

Performance of B.I.- III during the financial year 2016-2017 and previous years is shown in a tabularform:

Sl No. Activities of BI -III 2011-12 2012-13 2013-14 2014-15 2015-16 2016-171 No. of raids conducted 254 270 437 778 801 5452 No. of seizures made 122 105 371 593 602 2713 No. of investigation completed 179 219 231 591 602 2594 Amount of Tax evasion detected 86.36 107.59 786.00 982.00 941.75 687.76

(Rs. in crore)5 Total realized on suppressed 13.45 23.46 107.89 136.33 254.05 292.52*

turnover (Rs. in crore)

35

Directorate of Commercial Taxes

6 Total no. of seizures made at 3537 5075 5652 5357 5130 3382range and checkposts

7 Tax Collection (Rs. in crore)* 45.71 65.08 193.38 204.42 26.01 16.37**

8 No. of FIR made -- -- 10 11 0

* This amount includes collection from defaulters specially during the end of financial year.** Amount includes collection made by Ranges, Checkposts, C.S. (Kolkata) and C.S. (siliguri)

15. CENTRAL REGISTRATION UNIT

The Central Registration Unit started functioning from 1st August 2011 with the aim to ensurespeedy and hassle-free registration to the dealer under VAT and CST Act. This is a unique unit of thisDirectorate as no physical appearance on the part of the applicant is required here and registration isgranted without going through the process of hearing. The dealer applies for registration on-line andsubmits hardcopy of the application along with authenticated documents. After scrutiny of the applicationand documents and obtaining security registration is granted. If any communication is required, it is donethrough e-mail. No physical appearance is solicited.

With effect from 15th March 2016 `One Day Registration’ was implemented for all dealers. Now,Registration is granted within next working day of furnishing hard copy of completed application alongwith necessary documents including application fees and security payment details, if the applicationalong with the documents submitted is found in order.

At present, Central Registration Unit has the jurisdiction over the following Circles/Charges scatteredin Beliaghata, Salt lake, Howrah and Behala buildings:

Circles Charges under jurisdiction of CRU

Kolkata North All Charges

Kolkata South All Charges

Chowringhee All Charges

Dharmatala All Charges

Burrabazar All Charges

24 Parganas All Charges except Barasat & Barrackpore

Behala All Charges except Baruipur & Diamond Harbour

Howrah All Charges

Bally All Charges except Srirampur

Central Registration Unit : Data for 2016-2017

VAT CST TOTAL

(a) No. of NR applications filed 9980 7616 17596

(b) No. of Registration Granted 7711 5935 13646

(c) No. of Application Rejected 2267 1654 3921

Sl No. Activities of BI -III 2011-12 2012-13 2013-14 2014-15 2015-16 2016-17

36

Administrative Report 2016-17

16. CENTRAL AUDIT UNIT

In order to strengthen the audit of accounts referred to section 43 of the WBVAT Act, 2003, CentralAudit Unit (CAU) was formed with effect from 01.06.2010. The CAU has started functioning from01.07.2010 with its two wings; one at Sales Tax Building, Beliaghata and the other at Salt Lake Building.

Audit in the context of section 43 of the VAT Act relates not only to the examination of the accounts,registers and documents maintained or kept by the dealer to verify whether the books of accountsmaintained give true state of affairs of business but also to the examination of the correctness of returnsfurnished and the admissibility of various claims for the relevant period and most significantly it alsospecifically involves quantification of tax, interest or late fee payable by the dealer.

It is to be noted here that necessary amendments in the statutory provisions were made - to enablethe audit report to be treated as deemed assessment order after expiry of stipulated period - just to stop therepetition of work as envisaged and stressed upon by the Hon'ble Finance Minister, Govt. of West Bengal,while delivering his budget speech for the financial year 2012-13. In chapter 3.11 of the heading of'Fundamental Reforms of the Tax Administration as enumerated in 'Annual Financial Statement for theFinancial Year 2012-13', he commented : "I now propose to take the reform further to the effect thatwhere the audit report is not accepted by the dealer, no further assessment will be initiated. The auditreport, on expiry of the prescribed time, shall automatically become a notice of demand. The proposedamendment will reduce the time for dealers by at least 12 months."

The Central Audit Unit will have the following responsibilities:

I. Develop a dynamic Risk Analysis module on the basis of which the dealers are to be selectedfor audit,

II. Help the Commissioner in the selection procedure of the dealers for audit,

III. Improve the existing Audit Manual wherever it is felt necessary,

IV. Impart training to audit officers of Central Audit Unit and audit officers of different Charge andCircle,

V. Conduct audit of dealers assign to it by the Commissioner of Commercial Taxes, W.B.,

VI. Planning and monitoring of audit work,

VII. E-governance in audit system,

VIII. Developing an MIS for audit reporting,

IX. To facilitate the production of books of accounts as well as the examination of records, theaudit proceedings of the dealer under Corporate Divisions are being conducted now at dealer's“place of business” in terms of provisions under section 66 of the said Act read with rule94(2)(b) of WBVAT Rules, 2005 for the purpose of audit u/s 43 of the said Act,

X. Any other work connected with audit under the WBVAT Act, 2003 as may be assigned by theCommissioner of Commercial taxes, West Bengal.

Officers posted in the Central Audit Unit shall have jurisdiction over the whole of the State of WestBengal exercising the power of that of officers posted in Central Section in terms of notification issued forthis purpose.

37

Directorate of Commercial Taxes

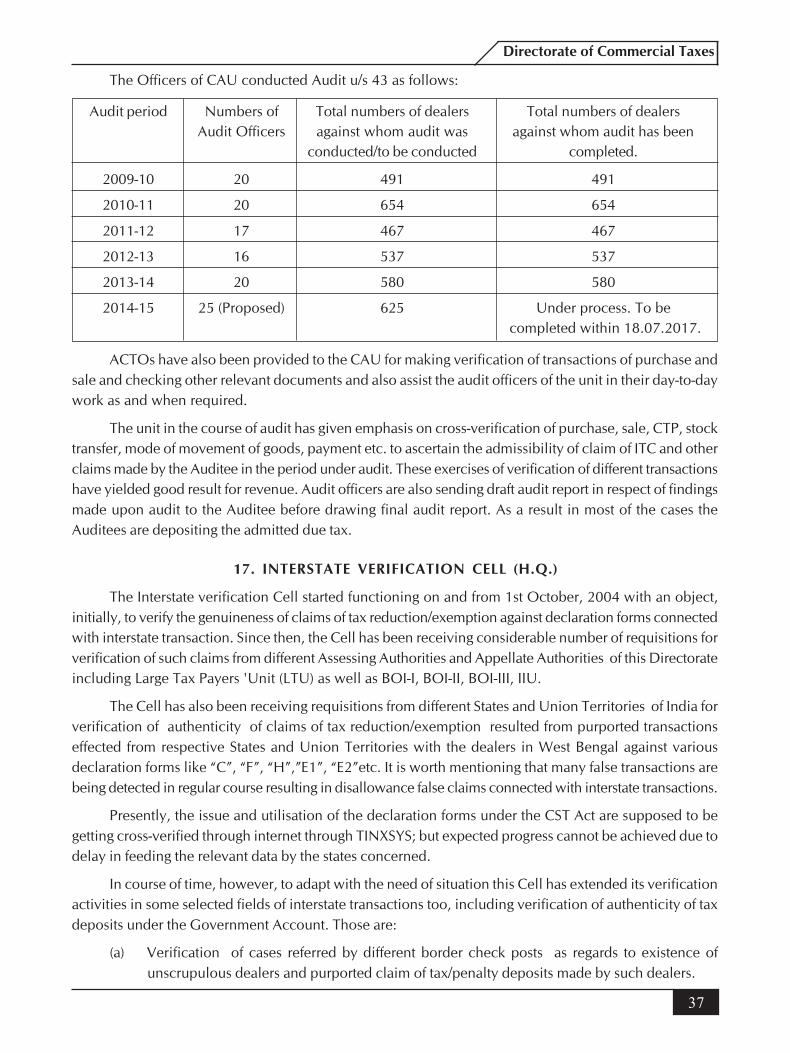

The Officers of CAU conducted Audit u/s 43 as follows:

Audit period Numbers of Total numbers of dealers Total numbers of dealersAudit Officers against whom audit was against whom audit has been

conducted/to be conducted completed.

2009-10 20 491 491

2010-11 20 654 654

2011-12 17 467 467

2012-13 16 537 537

2013-14 20 580 580

2014-15 25 (Proposed) 625 Under process. To be completed within 18.07.2017.

ACTOs have also been provided to the CAU for making verification of transactions of purchase andsale and checking other relevant documents and also assist the audit officers of the unit in their day-to-daywork as and when required.

The unit in the course of audit has given emphasis on cross-verification of purchase, sale, CTP, stocktransfer, mode of movement of goods, payment etc. to ascertain the admissibility of claim of ITC and otherclaims made by the Auditee in the period under audit. These exercises of verification of different transactionshave yielded good result for revenue. Audit officers are also sending draft audit report in respect of findingsmade upon audit to the Auditee before drawing final audit report. As a result in most of the cases theAuditees are depositing the admitted due tax.

17. INTERSTATE VERIFICATION CELL (H.Q.)

The Interstate verification Cell started functioning on and from 1st October, 2004 with an object,initially, to verify the genuineness of claims of tax reduction/exemption against declaration forms connectedwith interstate transaction. Since then, the Cell has been receiving considerable number of requisitions forverification of such claims from different Assessing Authorities and Appellate Authorities of this Directorateincluding Large Tax Payers 'Unit (LTU) as well as BOI-I, BOI-II, BOI-III, IIU.

The Cell has also been receiving requisitions from different States and Union Territories of India forverification of authenticity of claims of tax reduction/exemption resulted from purported transactionseffected from respective States and Union Territories with the dealers in West Bengal against variousdeclaration forms like “C”, “F”, “H”,”E1”, “E2”etc. It is worth mentioning that many false transactions arebeing detected in regular course resulting in disallowance false claims connected with interstate transactions.

Presently, the issue and utilisation of the declaration forms under the CST Act are supposed to begetting cross-verified through internet through TINXSYS; but expected progress cannot be achieved due todelay in feeding the relevant data by the states concerned.

In course of time, however, to adapt with the need of situation this Cell has extended its verificationactivities in some selected fields of interstate transactions too, including verification of authenticity of taxdeposits under the Government Account. Those are:

(a) Verification of cases referred by different border check posts as regards to existence ofunscrupulous dealers and purported claim of tax/penalty deposits made by such dealers.

38

Administrative Report 2016-17

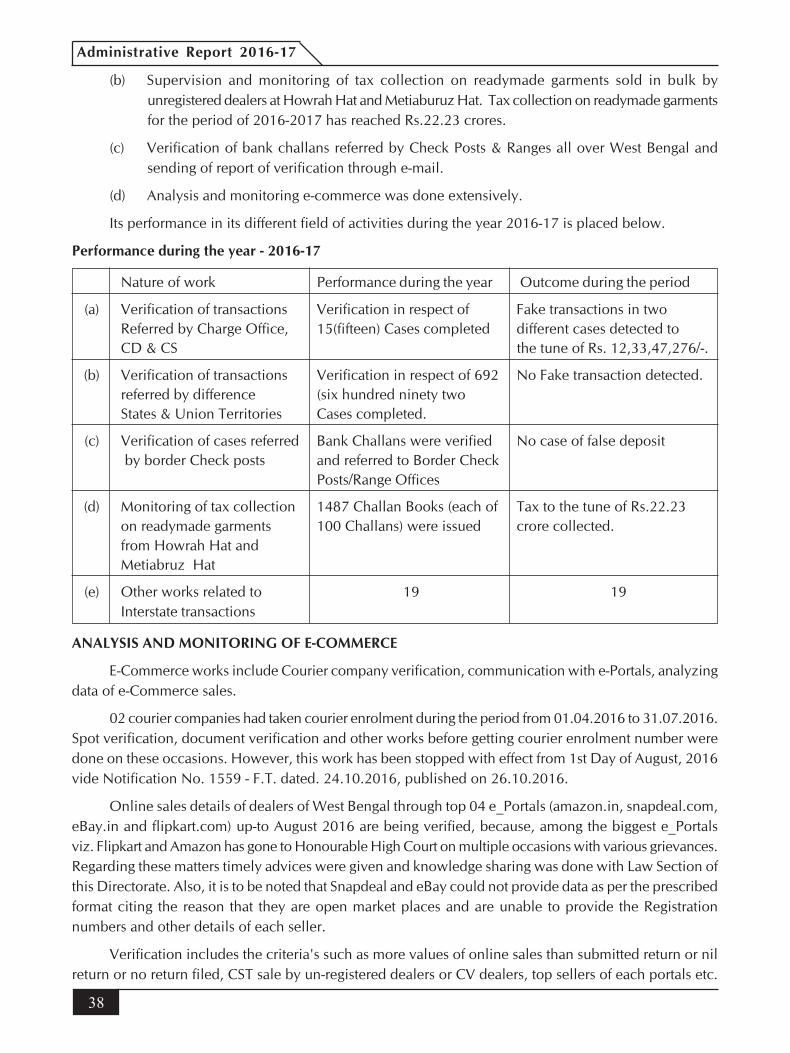

(b) Supervision and monitoring of tax collection on readymade garments sold in bulk byunregistered dealers at Howrah Hat and Metiaburuz Hat. Tax collection on readymade garmentsfor the period of 2016-2017 has reached Rs.22.23 crores.

(c) Verification of bank challans referred by Check Posts & Ranges all over West Bengal andsending of report of verification through e-mail.

(d) Analysis and monitoring e-commerce was done extensively.

Its performance in its different field of activities during the year 2016-17 is placed below.

Performance during the year - 2016-17

Nature of work Performance during the year Outcome during the period

(a) Verification of transactions Verification in respect of Fake transactions in twoReferred by Charge Office, 15(fifteen) Cases completed different cases detected toCD & CS the tune of Rs. 12,33,47,276/-.

(b) Verification of transactions Verification in respect of 692 No Fake transaction detected.referred by difference (six hundred ninety twoStates & Union Territories Cases completed.

(c) Verification of cases referred Bank Challans were verified No case of false deposit by border Check posts and referred to Border Check

Posts/Range Offices

(d) Monitoring of tax collection 1487 Challan Books (each of Tax to the tune of Rs.22.23on readymade garments 100 Challans) were issued crore collected.from Howrah Hat andMetiabruz Hat

(e) Other works related to 19 19Interstate transactions

ANALYSIS AND MONITORING OF E-COMMERCE

E-Commerce works include Courier company verification, communication with e-Portals, analyzingdata of e-Commerce sales.

02 courier companies had taken courier enrolment during the period from 01.04.2016 to 31.07.2016.Spot verification, document verification and other works before getting courier enrolment number weredone on these occasions. However, this work has been stopped with effect from 1st Day of August, 2016vide Notification No. 1559 - F.T. dated. 24.10.2016, published on 26.10.2016.

Online sales details of dealers of West Bengal through top 04 e_Portals (amazon.in, snapdeal.com,eBay.in and flipkart.com) up-to August 2016 are being verified, because, among the biggest e_Portalsviz. Flipkart and Amazon has gone to Honourable High Court on multiple occasions with various grievances.Regarding these matters timely advices were given and knowledge sharing was done with Law Section ofthis Directorate. Also, it is to be noted that Snapdeal and eBay could not provide data as per the prescribedformat citing the reason that they are open market places and are unable to provide the Registrationnumbers and other details of each seller.

Verification includes the criteria's such as more values of online sales than submitted return or nilreturn or no return filed, CST sale by un-registered dealers or CV dealers, top sellers of each portals etc.

39

Directorate of Commercial Taxes

This verification work is done after collecting sales details from different e_Portals, mismatches werescrutinized with CDT data. Dealers' online sales details were then informed to respective Charges fortaking necessary action whose mismatches were found.

During verification, sales data of 10 dealers ware verified, out of which 03 registered dealers paidtotal Rs. 6,45,000/- which were collected by imposing tax and penalty in connection with tax evasion.

Future prospect of online sales is very wide as it is getting popularity in a geometric shape. So focuson future e-commerce is need of the hour, hence proposal for an E-Commerce Cell was placed beforeSpecial Commissioner of Commercial Taxes-1/West Bengal.

18. SPECIAL CELL